Embed Size (px)

Citation preview

AUDIT REPORT

ON

THE ACCOUNTS OF

TELECOMMUNICATION SECTOR

AUDIT YEAR 2007-08

AUDITOR-GENERAL OF PAKISTAN

CONTENTS Page

Abbreviations & Acronyms i

Preface

ii

Executive Summary

iii

Section-I Audit Report

Cabinet Division

1. Pakistan Telecommunication Authority

1

2. Frequency Allocation Board Ministry of Defence Production

3. National Radio Telecommunication Corporation

17

20

Ministry of Information Technology (IT& Telecom Division)

4. National Telecommunication Corporation

27

5. Special Communications Organization

43

Section-II Evaluation of Internal Controls

47

ABBREVIATIONS & ACRONYMS

1. APC : Access Promotion Contribution

2. CCRB : Cabinet Committee on Regulatory Bodies

3. DAC : Departmental Accounts Committee

4. ECC : Economic Coordination Committee

5. FAB : Frequency Allocation Board

6. LDI : Long Distance and International 7. MoIT : Ministry of Information Technology 8. IT&T : Information Technology & Telecom

9. MoF : Ministry of Finance

10. MoDP : Ministry of Defence Production

11. NTC : National Telecommunication Corporation

12. NRTC : National Radio Telecommunication Corporation

13. PTA : Pakistan Telecommunication Authority

14. PAO : Principal Accounting Officer

15. PTCL : Pakistan Telecommunication Company Limited

16. R&D : Research & Development

17. SCO : Special Communications Organization

18. USF : Universal Service Fund

19. WLL : Wireless Local Loop

PREFACE

The Auditor-General of Pakistan is authorized to conduct the audit of expenditure and

receipts of the Federal Consolidated Fund and Public Account under Article 169 of the Constitution of the Islamic Republic of Pakistan read with Sections 8 and 12 of the Auditor-General’s (Functions, Powers and Terms and Conditions of Service) Ordinance, 2001. Section 15 of the aforesaid Ordinance also authorizes the Auditor-General to conduct audit of Government commercial undertakings.

This report is based on audit of the accounts for the year 2006-07 of five Public Sector Telecommunication entities. It includes comments on the accounts of audited entities and findings of compliance audit. The audit was conducted on a test check basis during 2007-08, by the Directorate General of Audit, Posts, Telegraphs and Telephones, Lahore, with a view to report significant findings to the stakeholders.

The findings indicate the need for adherence to regulatory framework, prudent decision

making, professional financial management, instituting and strengthening of internal controls to avoid recurrence of similar type of irregularities.

Audit observations included in the report were discussed with the concerned Principal Accounting Officers in the meetings of the Departmental Accounts Committee and have been finalized in the light of written response and discussion.

The report is submitted to the President of Pakistan in pursuance of Article 171 of the Constitution of the Islamic Republic of Pakistan.

Islamabad Dated:

TANWIR ALI AGHA Auditor-General of Pakistan

EXECUTIVE SUMMARY

The report presents comments on the accounts and results of audit for the year 2006-07 of the Telecommunication Sector, which comprises Pakistan Telecommunication Authority (PTA), Frequency Allocation Board (FAB), National Radio Telecommunication Corporation (NRTC), National Telecommunication Corporation (NTC), and Special Communications Organization (SCO). PTA, FAB and NTC were established under Pakistan Telecommunication (Re-organization) Act 1996. PTA and FAB are under the administrative control of Cabinet Division. SCO and NTC are under Ministry of Information & Technology. SCO was established under the directives of Prime Minister in 1976. NRTC is a private limited company incorporated under the Companies Ordinance 1984 and is administered by the Ministry of Defence Production. PTA regulates telecommunication industry in Pakistan and FAB allocates frequency spectrum to the Government and other operators. NRTC manufactures all kinds of radio/wireless sets for Defence Services and PTCL. NTC provides telecommunication services to the designated customers of the public sector. SCO provides telecommunication services in AJ&K and Northern Areas. The accounts of PTA, NTC and NRTC are commercial accounts and are audited by the Chartered Accountants. Certain issues were identified while conducting the audit of above organizations on test check basis. The report includes observations involving Rs 9,644 million. These were discussed and accepted in almost all cases by the Principal Accounting Officers in Departmental Accounts Committee meetings. A brief narration of these issues is given below whereas the evaluation of the internal controls has been given in Section-II of this report. 1. PTA incurred irregular expenditure on purchase of vehicles and foreign TA/DA worth Rs 38.565 million (Paras 1.2 & 1.3). Its receivables management remained a weak area, which resulted in non-recovery of huge amount of dues of Rs 2,412.882 million from various telecom/mobile operators (Paras1.4 & 1.5). The Authority made irregular/unjustified payments of Rs 19.699 million on account of pay & allowances, Proficiency incentive/honorarium and appointment of consultants (Paras 1.6 to 1.10). PTA irregularly allowed to WLL, LL and LDI operators to transfer Radio Spectrum Licenses/business to other parties which cause loss of Rs 3,207.800 million (Para 1.11). 2. FAB is preparing only ‘Receipt & Expenditure Account which do not reflect the status of its liabilities & assets. It should maintain the accounts on double entry system (Para 2.1). The Board made excess payment of Rs 4.107 million on account of HRA (Para 2.2). FAB allowed the frequencies to certain telecom operators through open tenders but the frequencies were actually utilized by some other companies/operators. FAB failed to block the use of frequencies by operators who had neither been allocated the radio spectrum nor paid auction price of radio spectrum. This resulted into a loss of Rs 3,544.600 million (Para 2.3).

3. NRTC sustained loss of Rs 15.255 million on account of exchange rate fluctuations, negligence of management and deduction of liquidated damages due to non-supply of goods within the stipulated period (Paras 3.2, 3.3 & 3.5). It was not adhering to the Public Procurement Rules, which resulted into irregular procurements of stores worth Rs 73.143 million (Para 3.4). NRTC management continued the practice of granting unjustified advances and also hurt the public exchequer by Rs 1.434 millions on account of Income Tax and Sales Tax (Para 3.6). 4. NTC incurred irregular expenditure of Rs 77.635 million on purchase of vehicles, stores and construction of new exchange building (Paras 4.2, 4.3, 4.5 & 4.6). It could not recover liquidated damages of Rs 10.292 million from different agencies (Paras 4.8 to 4.11) and made payments on account of pay & fringe benefits worth Rs 82.204 million without obtaining approval of Finance Division (Para 4.13). 5. SCO was not adhering to the Public Procurement Rules, which resulted into irregular procurements worth Rs 14.731 million (Para 5.2). It blocked public money due to un-necessary purchase of stores worth Rs 29.551 million (Para 5.3). AUDIT OUTCOMES The PAC while discussing this report on 01-08-2011, 26-10-2015, 07-05-2015 and 10-08-2015 issued direction out of which none of the directives was fully complied. However, in compliance of PAC directives recovery of an amount Rs.234.821 million has been made up till now. An amount of Rs 1,199 was recovered on initiation of Audit. The management of these organizations was sensitized with the importance of effective internal control system to achieve the efficiency gains in deregulated environment. RECOMMENDATIONS Audit recommends that Principal Accounting Officers / Management of above organizations should take effective measures to strengthen the internal controls systems, receivables management, and ensure adherence to rules and regulations.

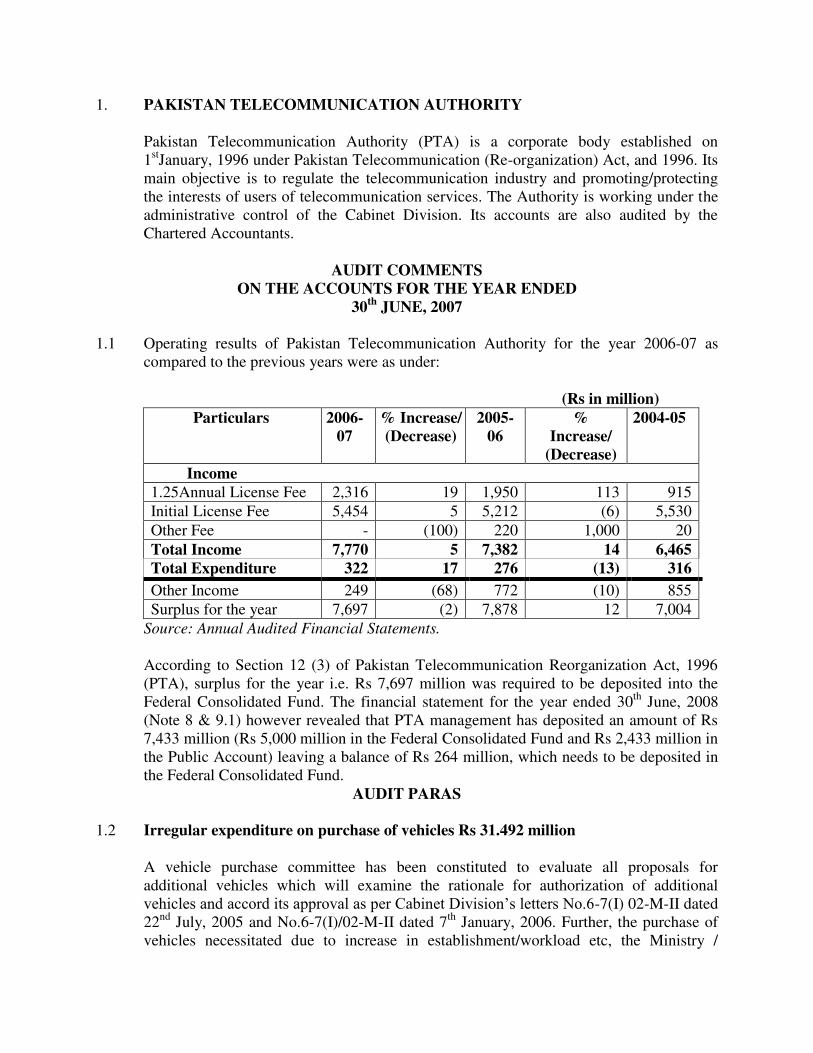

1. PAKISTAN TELECOMMUNICATION AUTHORITY

Pakistan Telecommunication Authority (PTA) is a corporate body established on 1stJanuary, 1996 under Pakistan Telecommunication (Re-organization) Act, and 1996. Its main objective is to regulate the telecommunication industry and promoting/protecting the interests of users of telecommunication services. The Authority is working under the administrative control of the Cabinet Division. Its accounts are also audited by the Chartered Accountants.

AUDIT COMMENTS

ON THE ACCOUNTS FOR THE YEAR ENDED 30th JUNE, 2007

1.1 Operating results of Pakistan Telecommunication Authority for the year 2006-07 as

compared to the previous years were as under:

(Rs in million) Particulars 2006-

07 % Increase/ (Decrease)

2005-06

% Increase/

(Decrease)

2004-05

Income 1.25Annual License Fee 2,316 19 1,950 113 915

Initial License Fee 5,454 5 5,212 (6) 5,530

Other Fee - (100) 220 1,000 20

Total Income 7,770 5 7,382 14 6,465 Total Expenditure 322 17 276 (13) 316

Other Income 249 (68) 772 (10) 855

Surplus for the year 7,697 (2) 7,878 12 7,004

Source: Annual Audited Financial Statements.

According to Section 12 (3) of Pakistan Telecommunication Reorganization Act, 1996 (PTA), surplus for the year i.e. Rs 7,697 million was required to be deposited into the Federal Consolidated Fund. The financial statement for the year ended 30th June, 2008 (Note 8 & 9.1) however revealed that PTA management has deposited an amount of Rs 7,433 million (Rs 5,000 million in the Federal Consolidated Fund and Rs 2,433 million in the Public Account) leaving a balance of Rs 264 million, which needs to be deposited in the Federal Consolidated Fund.

AUDIT PARAS

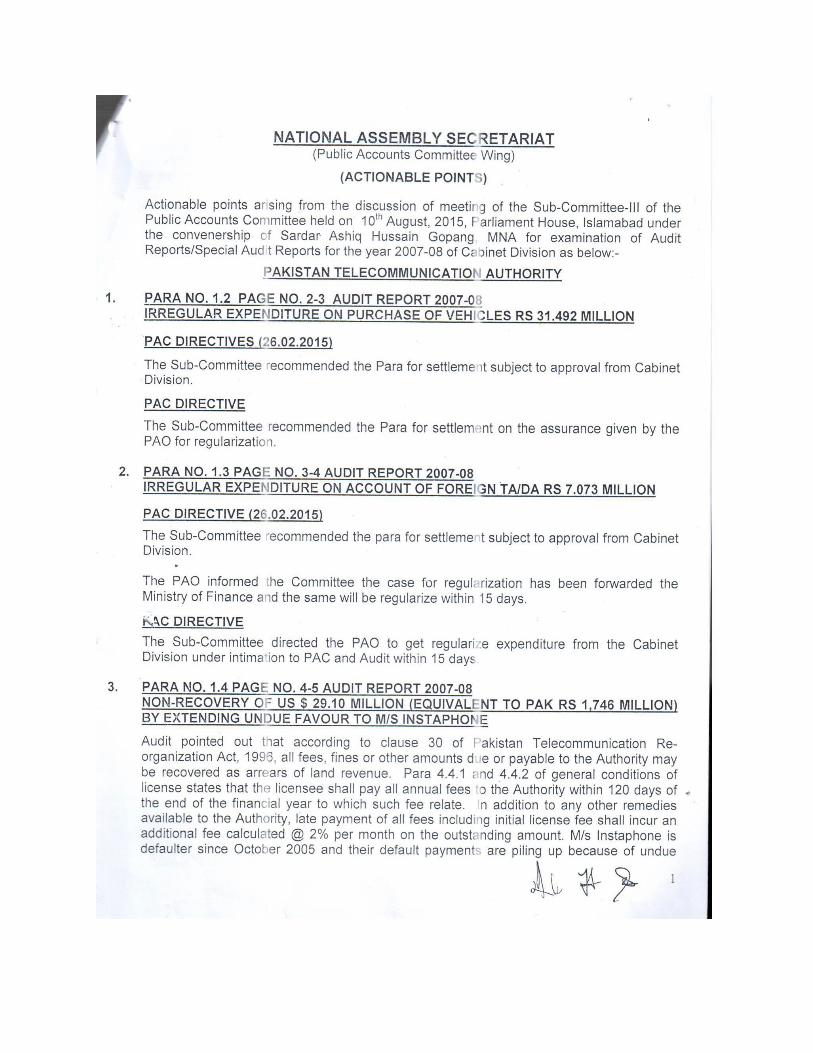

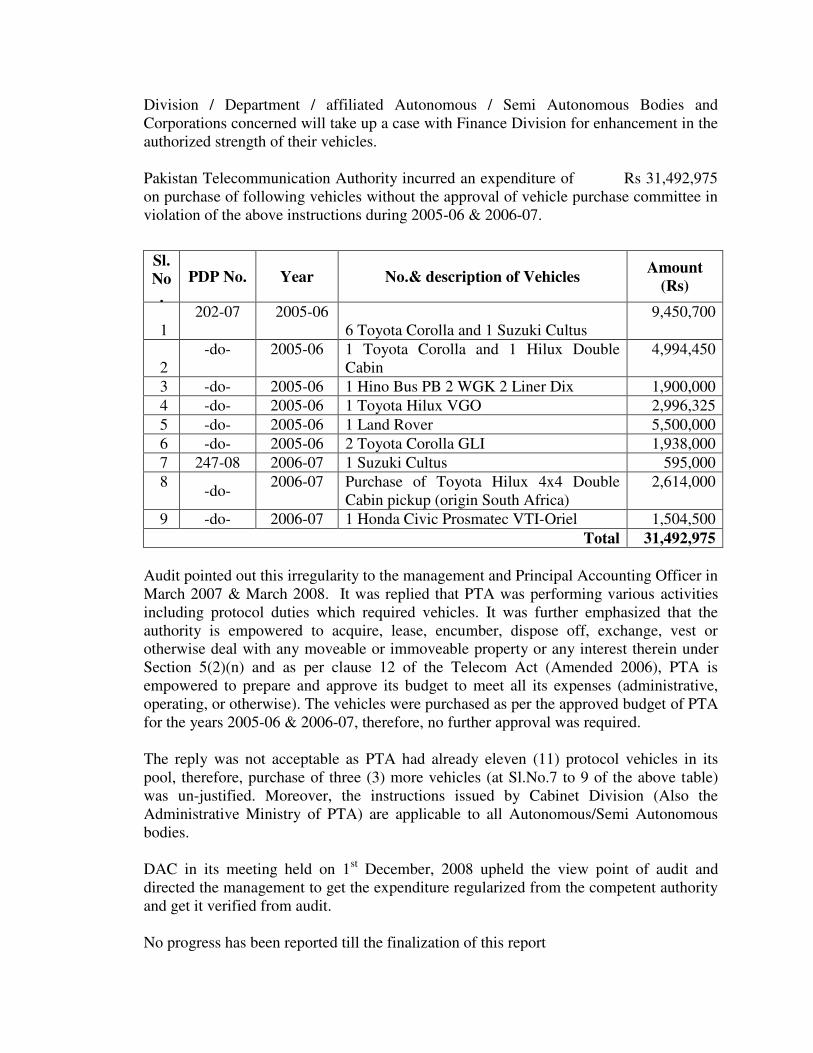

1.2 Irregular expenditure on purchase of vehicles Rs 31.492 million

A vehicle purchase committee has been constituted to evaluate all proposals for additional vehicles which will examine the rationale for authorization of additional vehicles and accord its approval as per Cabinet Division’s letters No.6-7(I) 02-M-II dated 22nd July, 2005 and No.6-7(I)/02-M-II dated 7th January, 2006. Further, the purchase of vehicles necessitated due to increase in establishment/workload etc, the Ministry /

Division / Department / affiliated Autonomous / Semi Autonomous Bodies and Corporations concerned will take up a case with Finance Division for enhancement in the authorized strength of their vehicles.

Pakistan Telecommunication Authority incurred an expenditure of Rs 31,492,975 on purchase of following vehicles without the approval of vehicle purchase committee in violation of the above instructions during 2005-06 & 2006-07.

Sl. No.

PDP No. Year No.& description of Vehicles Amount

(Rs)

1 202-07 2005-06

6 Toyota Corolla and 1 Suzuki Cultus 9,450,700

2 -do- 2005-06 1 Toyota Corolla and 1 Hilux Double

Cabin 4,994,450

3 -do- 2005-06 1 Hino Bus PB 2 WGK 2 Liner Dix 1,900,000

4 -do- 2005-06 1 Toyota Hilux VGO 2,996,325

5 -do- 2005-06 1 Land Rover 5,500,000

6 -do- 2005-06 2 Toyota Corolla GLI 1,938,000

7 247-08 2006-07 1 Suzuki Cultus 595,000

8

-do- 2006-07

Purchase of Toyota Hilux 4x4 Double Cabin pickup (origin South Africa)

2,614,000

9 -do- 2006-07 1 Honda Civic Prosmatec VTI-Oriel 1,504,500

Total 31,492,975

Audit pointed out this irregularity to the management and Principal Accounting Officer in March 2007 & March 2008. It was replied that PTA was performing various activities including protocol duties which required vehicles. It was further emphasized that the authority is empowered to acquire, lease, encumber, dispose off, exchange, vest or otherwise deal with any moveable or immoveable property or any interest therein under Section 5(2)(n) and as per clause 12 of the Telecom Act (Amended 2006), PTA is empowered to prepare and approve its budget to meet all its expenses (administrative, operating, or otherwise). The vehicles were purchased as per the approved budget of PTA for the years 2005-06 & 2006-07, therefore, no further approval was required.

The reply was not acceptable as PTA had already eleven (11) protocol vehicles in its pool, therefore, purchase of three (3) more vehicles (at Sl.No.7 to 9 of the above table) was un-justified. Moreover, the instructions issued by Cabinet Division (Also the Administrative Ministry of PTA) are applicable to all Autonomous/Semi Autonomous bodies.

DAC in its meeting held on 1st December, 2008 upheld the view point of audit and directed the management to get the expenditure regularized from the competent authority and get it verified from audit. No progress has been reported till the finalization of this report

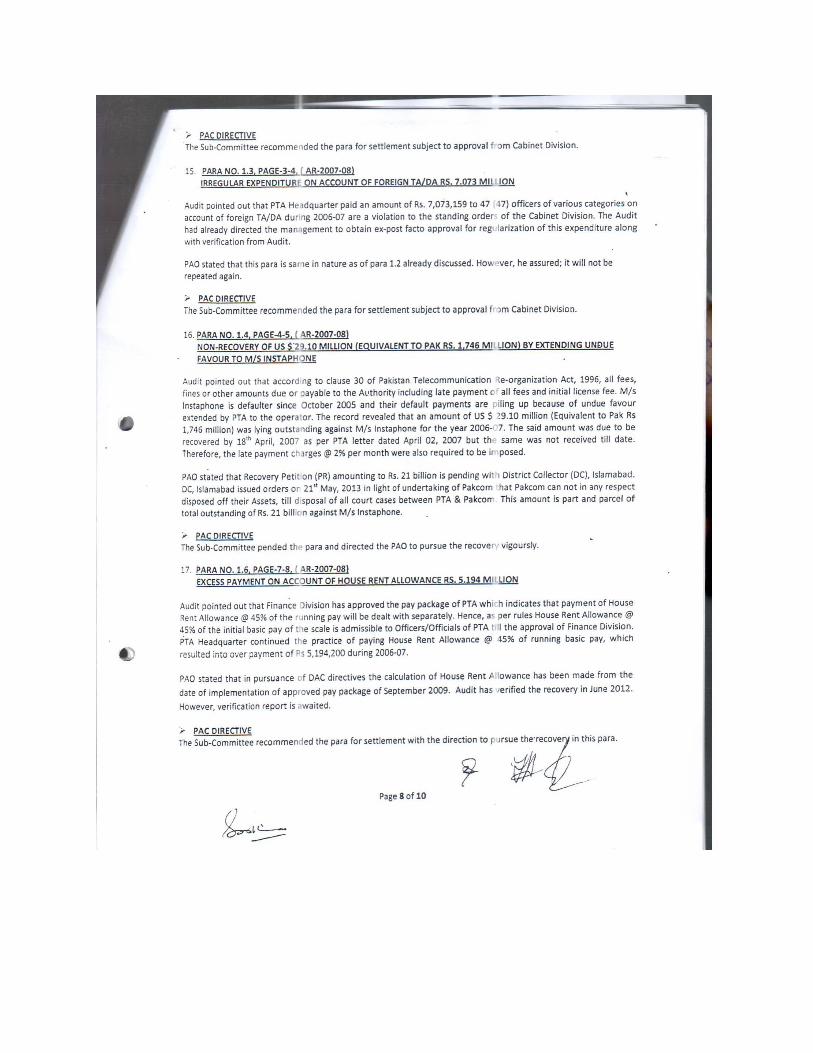

1.3 Irregular expenditure on account of foreign TA/DA Rs 7.073 million

The visits abroad by officers/officials upto and including BPS-20 and their equivalent working in Autonomous/Semi Autonomous bodies and where no Government funding is involved, Secretary/Additional Secretary incharge of Ministry/Division concerned will be competent to accord permission according to Cabinet Division circular No.F-9-148/2002-Min dated 19th February, 2003 and letter No.7-25/2006-RA-I/PTA dated 18th January, 2007.

PTA Headquarter paid an amount of Rs 7,073,159 to forty seven (47) officers of various categories on account of foreign TA/DA during 2006-07 in violation to the standing orders of the Cabinet Division.

Audit pointed out this irregularity to the management during March 2008. It was replied that PTA is specifically empowered under its Act, to prepare its budget, submitted to Cabinet Division for information. The approval is not required for any expenditure from any Ministry including the administrative Ministry of PTA i.e Cabinet Division. In the light of above mentioned clarification the administrative as well as the financial approval of Chairman PTA was sought in all foreign TA/DA cases of PTA officers. However, in accordance with the directives of DAC dated 10th January, 2007 held to discuss the report for year 2005-06, a case has been referred to Cabinet Division for ex-post facto approval of the Prime Minister.

The reply was not acceptable as the instructions issued by the Cabinet Division were applicable to all Autonomous/Semi Autonomous bodies and the same irregularity was pointed out in 2005-06 but the management did not take care for the audit objection and DAC directives prior to processing the cases of foreign tours in the year 2006-07.

DAC in its meeting held on 1st December, 2008 directed the management to obtain ex-post facto approval for regularization of expenditure and get it verified from audit.

No progress has been reported so far.

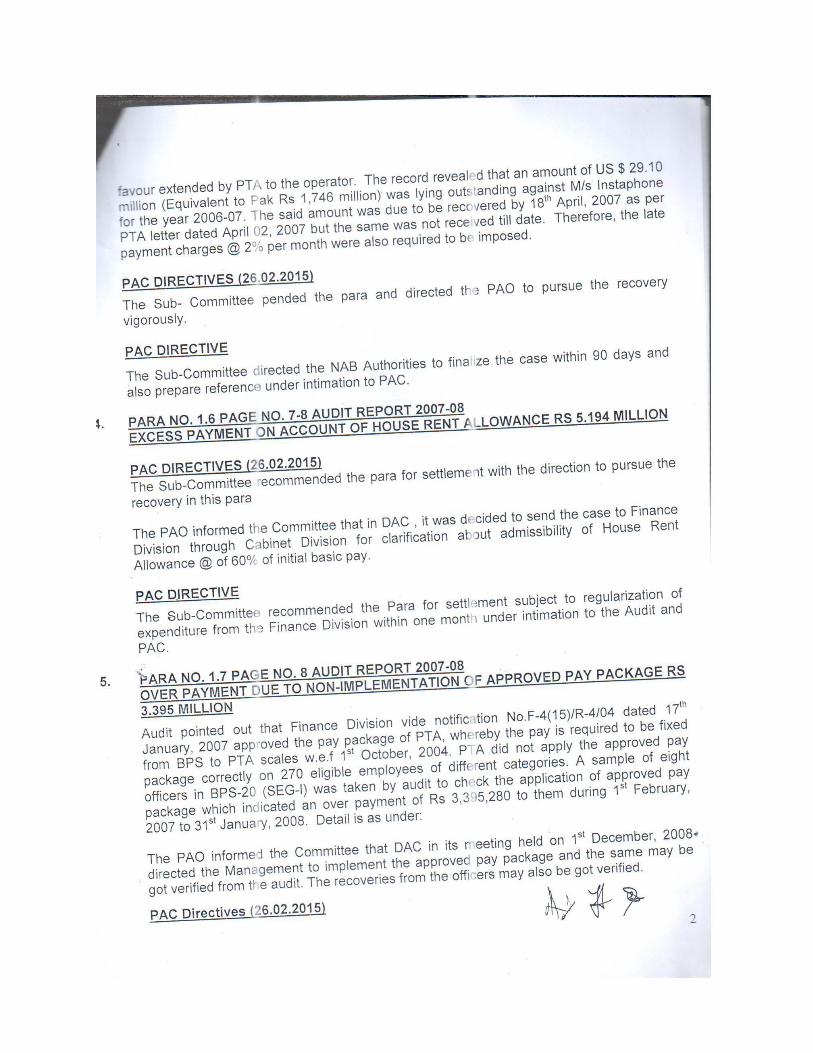

1.4 Non-recovery of US $ 29.10 million (Equivalent to Pak Rs 1,746 million) by extending undue favour to M/s Instaphone

According to clause 30 of Pakistan Telecommunication Re-organization Act, 1996, all fees, fines or other amounts due or payable to the Authority may be recovered as arrears of land revenue. Para 4.4.1 and 4.4.2 of general conditions of license states that the licensee shall pay all annual fees to the Authority within 120 days of the end of the financial year to which such fee relate. In addition to any other remedies available to the Authority, late payment of all fees including initial license fee shall incur an additional fee calculated @ 2% per month on the outstanding amount.

M/s Instaphone is defaulter since October 2005 and their default payments are piling up because of undue favour extended by PTA to the operator. The record revealed that an amount of US $ 29.10 million (Equivalent to Pak Rs 1,746 million) was lying outstanding against M/s Instaphone for the year 2006-07. The said amount was due to be recovered by 18th April, 2007 as per PTA letter dated April 02, 2007 but the same was not received till date. Therefore, the late payment charges @ 2% per month were also required to be imposed.

Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied that a number of show cause notices had been issued and hearing was conducted. The Authority tried its best to recover the amount and even allowed extension in period of payment keeping in view the interest of the subscribers and state. An enforcement order was issued to the company on 4th March, 2008 with the decision of the Authority that in case the company fails to clear its dues on or before 21st

May, 2008, its license shall stand terminated under section 23 of the Act. The case is still pending in the Islamabad High Court Islamabad and the last date of hearing was 5th December, 2008.

The reply was not acceptable as the Authority issued show-cause notices w.e.f February, 2006 but neither the license was terminated nor any amount was received from the company. The reply proves that undue favour was extended by the Authority which provided an opportunity to the company for accumulation of amount.

DAC in its meeting held on 1st December, 2008 directed the management to pursue the case in Court of Law vigorously and give updated status to the PAO as well as to audit.

No further progress has been reported so far.

1.5 Non-recovery of Rs 666.882 million from mobile/telecom operators

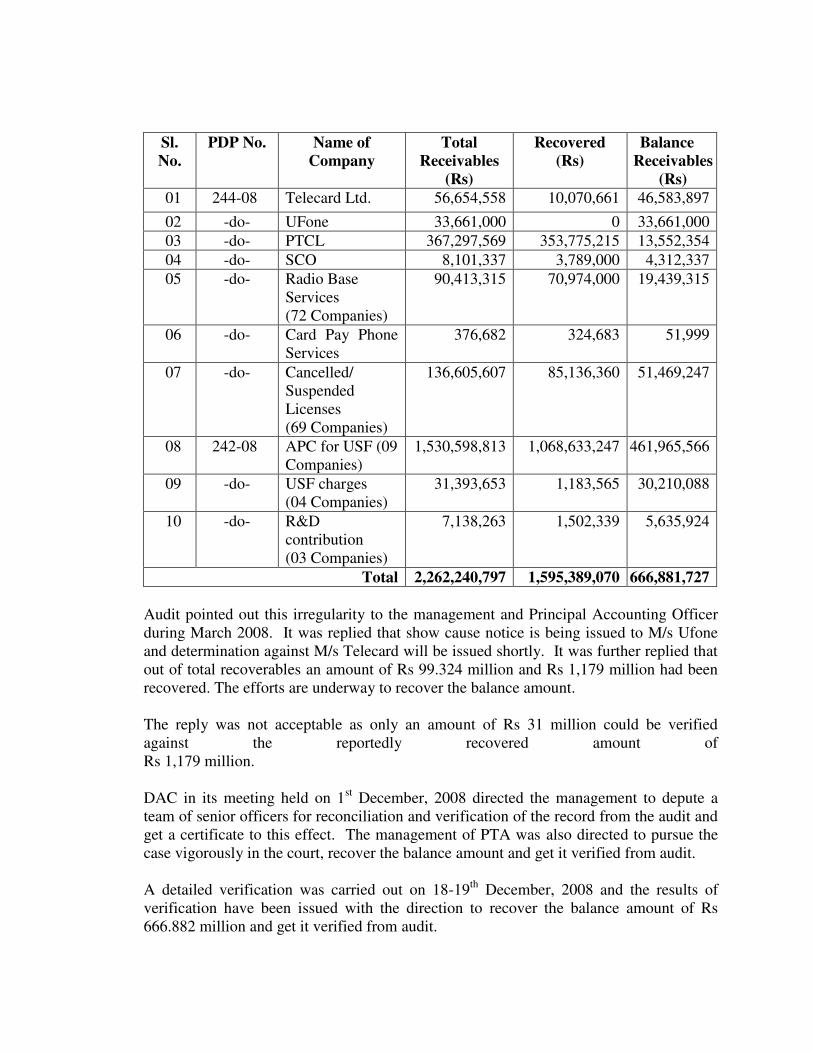

According to section 30 of Pakistan Telecommunication (Re-organization) Act, 1996, all fees, fines or other amounts due or payable to the Authority may be recovered as arrears of land revenue. Para 4.4.1 of General conditions of license revealed, that the licensee shall pay all annual fees to the Authority within 120 days of the end of the financial year to which such fees relate. Further, para-7(2) of Card Pay Phone Service (CPPS) Regulations, 2004 provides that the licensee shall make payment of the annual license fee to the Authority but not later than 120 days of the close of financial year of the licensee. As per Sub Section (2) of Section 10 of Access Promotion Regulations 2005, “An LDI licensee shall make payment into the designated bank account within a time period not exceeding ninety (90) days from the close of the month to which such payment relates”. PTA did not recover an amount of Rs 666,881,727 from various mobile/telecom operators upto 30th June, 2007. The detail is given below:

Sl. No.

PDP No. Name of Company

Total Receivables

(Rs)

Recovered (Rs)

Balance Receivables

(Rs) 01 244-08 Telecard Ltd. 56,654,558 10,070,661 46,583,897

02 -do- UFone 33,661,000 0 33,661,000

03 -do- PTCL 367,297,569 353,775,215 13,552,354

04 -do- SCO 8,101,337 3,789,000 4,312,337

05 -do- Radio Base Services (72 Companies)

90,413,315 70,974,000 19,439,315

06 -do- Card Pay Phone Services

376,682 324,683 51,999

07 -do- Cancelled/ Suspended Licenses (69 Companies)

136,605,607 85,136,360 51,469,247

08 242-08 APC for USF (09 Companies)

1,530,598,813 1,068,633,247 461,965,566

09 -do- USF charges (04 Companies)

31,393,653 1,183,565 30,210,088

10 -do- R&D contribution (03 Companies)

7,138,263 1,502,339 5,635,924

Total 2,262,240,797 1,595,389,070 666,881,727 Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied that show cause notice is being issued to M/s Ufone and determination against M/s Telecard will be issued shortly. It was further replied that out of total recoverables an amount of Rs 99.324 million and Rs 1,179 million had been recovered. The efforts are underway to recover the balance amount. The reply was not acceptable as only an amount of Rs 31 million could be verified against the reportedly recovered amount of Rs 1,179 million. DAC in its meeting held on 1st December, 2008 directed the management to depute a team of senior officers for reconciliation and verification of the record from the audit and get a certificate to this effect. The management of PTA was also directed to pursue the case vigorously in the court, recover the balance amount and get it verified from audit.

A detailed verification was carried out on 18-19th December, 2008 and the results of verification have been issued with the direction to recover the balance amount of Rs 666.882 million and get it verified from audit.

No further progress has been reported so far.

1.6 Excess payment on account of House Rent Allowance Rs 5.194 million

Finance Division has approved the pay package of PTA vide O.M No.F.4(15)R-4/04 dated 17th January, 2007 which indicates that payment of House Rent Allowance @ 45% of the running pay will be dealt with separately. Hence, as per rules House Rent Allowance @ 45% of the initial basic pay of the scale is admissible to Officers/Officials of PTA till the approval of Finance Division.

PTA Headquarter continued the practice of paying House Rent Allowance @ 45% of running basic pay, which resulted into over payment of Rs 5,194,200 during 2006-07.

Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied that the decision regarding House Rent Allowance was pended with the Finance Division and payment of HRA @ 45% of running basic pay was paid to the employees as approved by the Authority. The reply was not acceptable as the House Rent Allowance @ 45% on running basic pay was not approved by the Finance Division and the same could have been discontinued till the approval of Finance Division.

DAC in its meeting held on 1st December, 2008 directed the Management that approval of Finance Division be obtained within 15 days and submit report to the PAO. No progress has been reported till the finalization of this report.

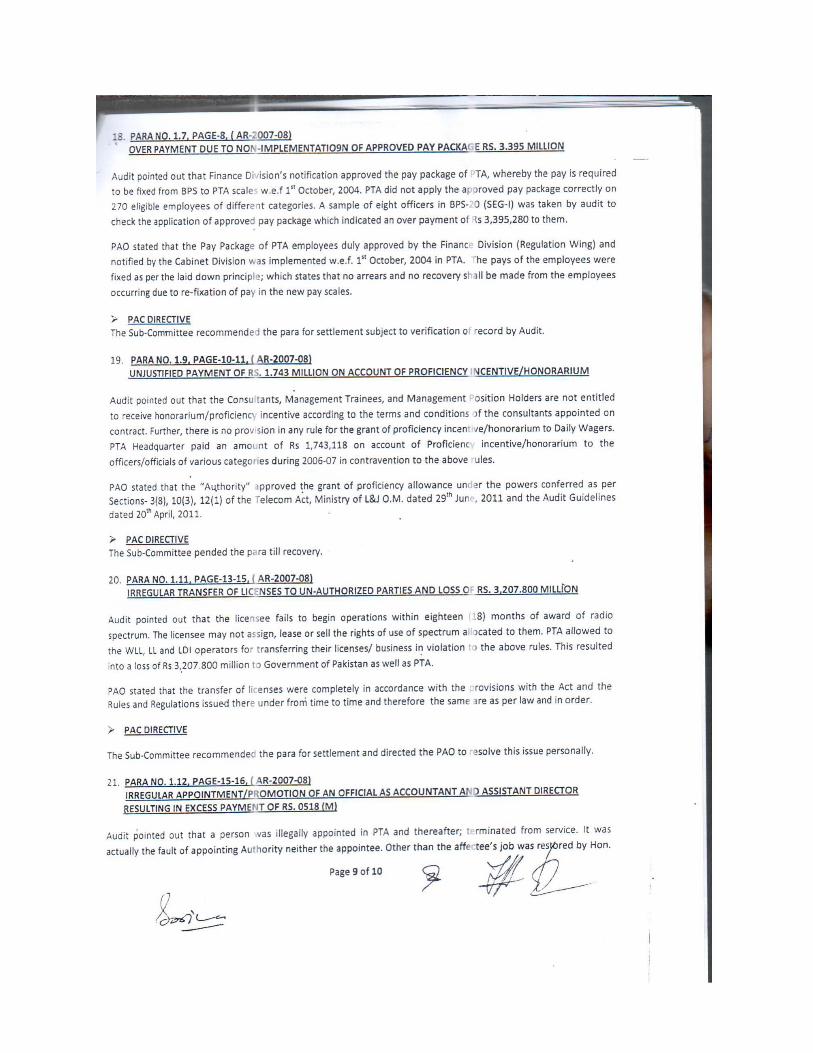

1.7 Over payment due to non-implementation of approved pay package Rs 3.395

million

Finance Division vide notification No.F-4(15)/R-4/04 dated 17th January, 2007 approved the pay package of PTA, whereby the pay is required to be fixed from BPS to PTA scales w.e.f 1st October, 2004.

PTA did not apply the approved pay package correctly on 270 eligible employees of different categories. A sample of eight officers in BPS-20 (SEG-I) was taken by audit to check the application of approved pay package which indicated an over payment of Rs 3,395,280 to them during 1st February, 2007 to 31st January, 2008 as detailed below:

Sl. No.

Head of Account

No. of Officers

Amount due (Rs)

Amount drawn (Rs)

Difference per month

(Rs)

Amount overpaid

(Rs)

01 Pay 07 501,600 572,900 71,300 855,600

02 Medical Allowance

06 73,440 99,260 25,820 309,840

03 Utility Allowance

06 73,440 99,260 25,820 309,840

04 Subsidy on HRA

08 -- 12,500 -- 1,200,000

05 CLA 08 -- 7500 -- 720,000

Total 3,395,280

Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied that the implementation of pay package as approved by Finance Division is under consideration. It was further replied in November 2008 that recoveries had been made from the officers. The reply was not acceptable as the pay package was approved on 17th January, 2007 by Finance Division but the fixation has not been made so far to implement the pay package. Furthermore, the recoveries made from the officers were not got verified from audit.

DAC in its meeting held on 1st December, 2008 directed the management to implement the approved pay package and the same may be got verified from the audit. The recoveries made from the officers may also be got verified. No progress has been made so far.

1.8 Irregular grant of House Building Advances of Rs 5.930 million

As per terms and conditions of the employees the officers were appointed for three years on deputation or on contract basis. The sanctions of the House Building Advances reveal that the advances will be recovered in 120 monthly installments.

PTA management granted heavy amount of Rs 5,930,000 on account of house building advance to the retired Army Officers appointed on contract basis. The detail is given below:

Sl. No.

Vr. No. & date

Name of officers Amount (Rs)

01 279/30-06-05 Col.(R) Ghulam Haidar 850,000

02 276/30-06-05 Col.(R) Muhammad Younis 1,050,000

03 273/30-06-05 Maj.(R) Sardar Mehmood Gul 850,000

04 149/14-06-06 Col.(R) Rizwan Ahmad Hyderi 1,000,000

05 197/19-06-06 Brig.(R) Muhammad Mazhar Qayyum Butt 2,180,000

Total 5,930,000 Audit pointed out this irregularity to the management in March 2008. It was replied that the officers mentioned in the paras are not on a 2 or 3 years contract. Their contract is upto superannuation age. Once an officer is employed, he is an employee of PTA and is

entitled to all benefits that were for other employees of PTA. Recovery of HBA given to these officers is being made regularly.

The reply was not acceptable as the orders of the officers clearly indicate that they were appointed for three years deputation or on contract. Therefore, the HBA was not admissible to them. Hence, recovery of the balance be made from the officers whether serving in PTA or had left the job. DAC in its meeting held on 1st December, 2008 directed the management to fix responsibility for violation of rules besides affecting the recovery of balance amount involved.

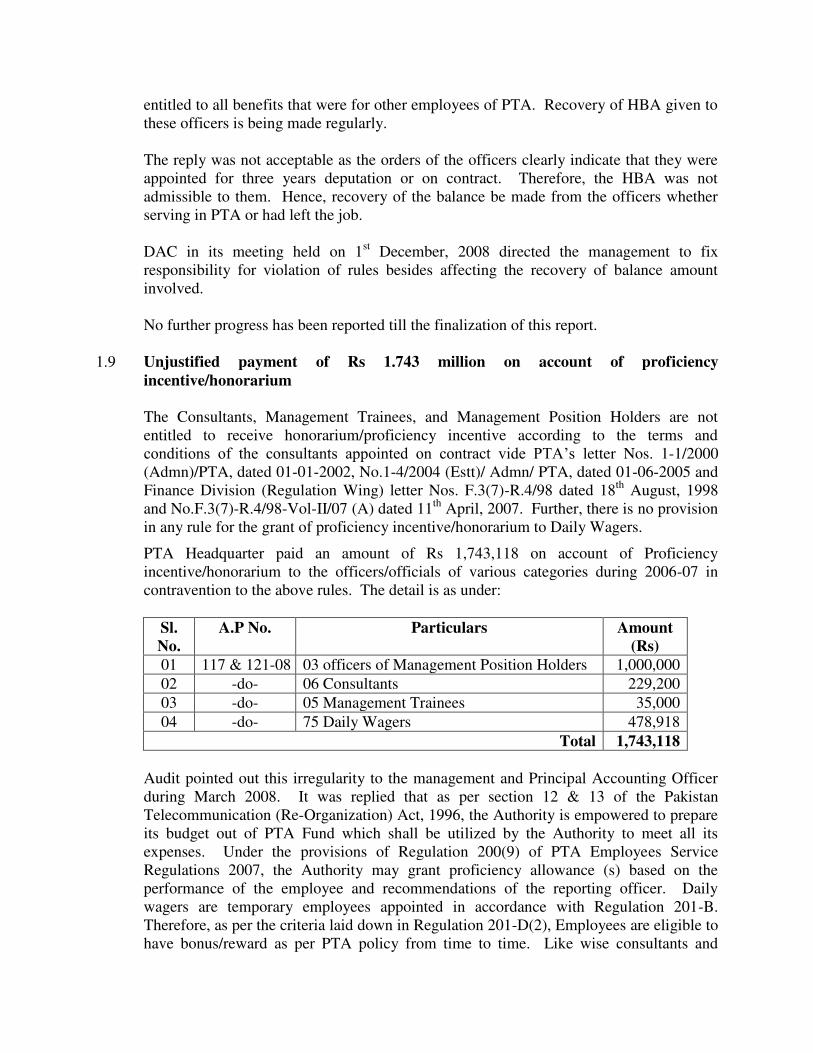

No further progress has been reported till the finalization of this report. 1.9 Unjustified payment of Rs 1.743 million on account of proficiency

incentive/honorarium

The Consultants, Management Trainees, and Management Position Holders are not entitled to receive honorarium/proficiency incentive according to the terms and conditions of the consultants appointed on contract vide PTA’s letter Nos. 1-1/2000 (Admn)/PTA, dated 01-01-2002, No.1-4/2004 (Estt)/ Admn/ PTA, dated 01-06-2005 and Finance Division (Regulation Wing) letter Nos. F.3(7)-R.4/98 dated 18th August, 1998 and No.F.3(7)-R.4/98-Vol-II/07 (A) dated 11th April, 2007. Further, there is no provision in any rule for the grant of proficiency incentive/honorarium to Daily Wagers.

PTA Headquarter paid an amount of Rs 1,743,118 on account of Proficiency incentive/honorarium to the officers/officials of various categories during 2006-07 in contravention to the above rules. The detail is as under:

Sl. No.

A.P No. Particulars Amount (Rs)

01 117 & 121-08 03 officers of Management Position Holders 1,000,000

02 -do- 06 Consultants 229,200

03 -do- 05 Management Trainees 35,000

04 -do- 75 Daily Wagers 478,918

Total 1,743,118

Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied that as per section 12 & 13 of the Pakistan Telecommunication (Re-Organization) Act, 1996, the Authority is empowered to prepare its budget out of PTA Fund which shall be utilized by the Authority to meet all its expenses. Under the provisions of Regulation 200(9) of PTA Employees Service Regulations 2007, the Authority may grant proficiency allowance (s) based on the performance of the employee and recommendations of the reporting officer. Daily wagers are temporary employees appointed in accordance with Regulation 201-B. Therefore, as per the criteria laid down in Regulation 201-D(2), Employees are eligible to have bonus/reward as per PTA policy from time to time. Like wise consultants and

management trainees have been appointed on contract basis. Proficiency incentive or bonus is a norm in all companies world over. If these incentives are not given, it can result in reduced employee morale and high turn over.

The reply was not acceptable as the payment was not covered under the terms and conditions of the contract appointment of the consultants and management trainees. Further, the regulation 201-D(2) is for bonus/cash reward and not for proficiency incentive. Besides, no documentary evidence was provided in support of drawing pay in SEG-II instead of MP Scales. DAC held on 1st December 2008 considered the para for discussion in Internal Meeting. An Internal Meeting was held on 19th December, 2008 wherein it was replied that the Chairman and Members were not drawing Pay in MP Scales when they were granted honorarium, therefore, the amount paid on account of Honorarium is justified. However, the amount paid to Consultants, Management Trainees and Daily Wagers will be recovered in due course of time. It was decided that the documentary evidence regarding non-drawing of pay by Chairman & Members in MP Scales (i.e Pay Slips of the officers of that period) be provided to audit. As regards payments to the Consultants, Management Trainees and Daily Wagers the recovery particulars be provided to audit for verification. No progress was reported so far.

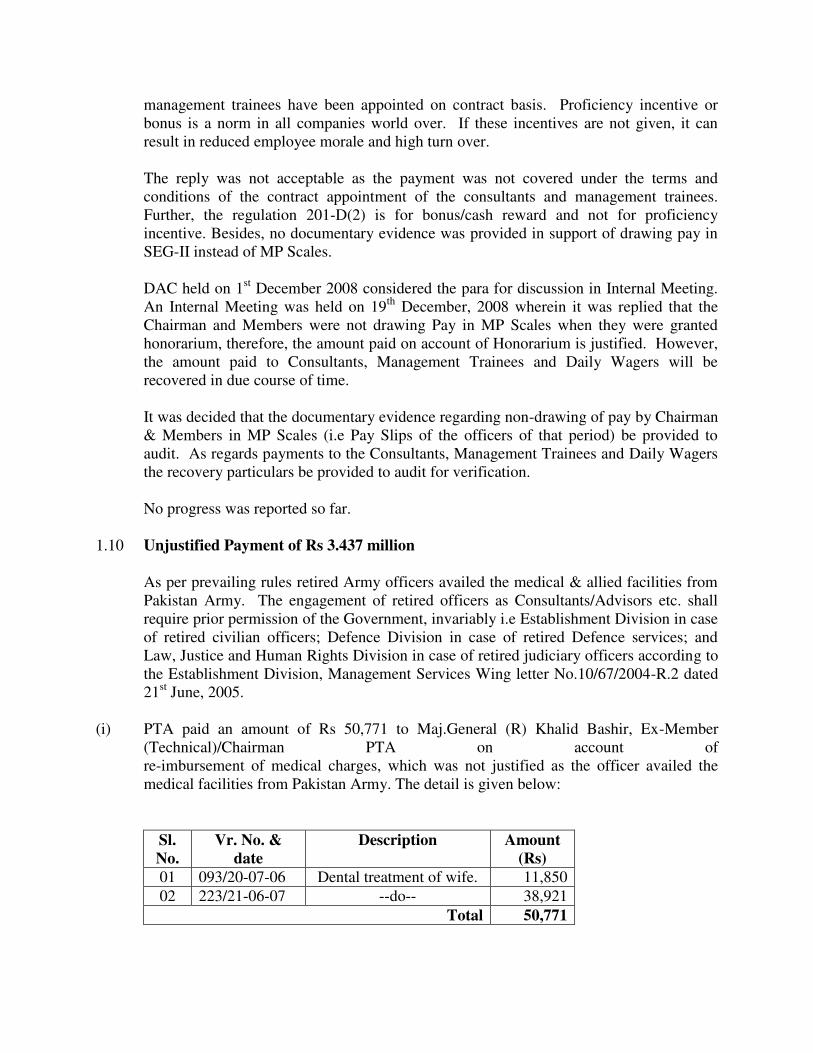

1.10 Unjustified Payment of Rs 3.437 million

As per prevailing rules retired Army officers availed the medical & allied facilities from Pakistan Army. The engagement of retired officers as Consultants/Advisors etc. shall require prior permission of the Government, invariably i.e Establishment Division in case of retired civilian officers; Defence Division in case of retired Defence services; and Law, Justice and Human Rights Division in case of retired judiciary officers according to the Establishment Division, Management Services Wing letter No.10/67/2004-R.2 dated 21st June, 2005.

(i) PTA paid an amount of Rs 50,771 to Maj.General (R) Khalid Bashir, Ex-Member

(Technical)/Chairman PTA on account of re-imbursement of medical charges, which was not justified as the officer availed the medical facilities from Pakistan Army. The detail is given below:

Sl. No.

Vr. No. & date

Description Amount (Rs)

01 093/20-07-06 Dental treatment of wife. 11,850

02 223/21-06-07 --do-- 38,921

Total 50,771

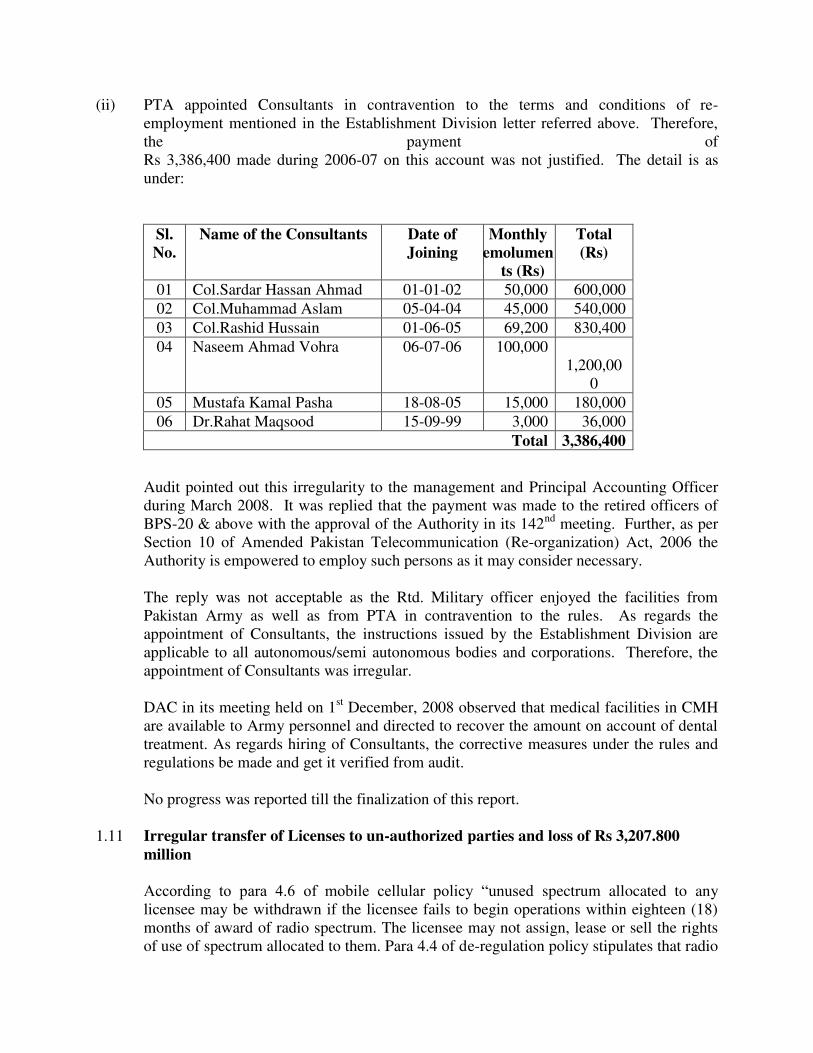

(ii) PTA appointed Consultants in contravention to the terms and conditions of re-employment mentioned in the Establishment Division letter referred above. Therefore, the payment of Rs 3,386,400 made during 2006-07 on this account was not justified. The detail is as under:

Sl. No.

Name of the Consultants Date of Joining

Monthly emolumen

ts (Rs)

Total (Rs)

01 Col.Sardar Hassan Ahmad 01-01-02 50,000 600,000

02 Col.Muhammad Aslam 05-04-04 45,000 540,000

03 Col.Rashid Hussain 01-06-05 69,200 830,400

04 Naseem Ahmad Vohra 06-07-06 100,000 1,200,00

0

05 Mustafa Kamal Pasha 18-08-05 15,000 180,000

06 Dr.Rahat Maqsood 15-09-99 3,000 36,000

Total 3,386,400

Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied that the payment was made to the retired officers of BPS-20 & above with the approval of the Authority in its 142nd meeting. Further, as per Section 10 of Amended Pakistan Telecommunication (Re-organization) Act, 2006 the Authority is empowered to employ such persons as it may consider necessary.

The reply was not acceptable as the Rtd. Military officer enjoyed the facilities from Pakistan Army as well as from PTA in contravention to the rules. As regards the appointment of Consultants, the instructions issued by the Establishment Division are applicable to all autonomous/semi autonomous bodies and corporations. Therefore, the appointment of Consultants was irregular.

DAC in its meeting held on 1st December, 2008 observed that medical facilities in CMH are available to Army personnel and directed to recover the amount on account of dental treatment. As regards hiring of Consultants, the corrective measures under the rules and regulations be made and get it verified from audit. No progress was reported till the finalization of this report.

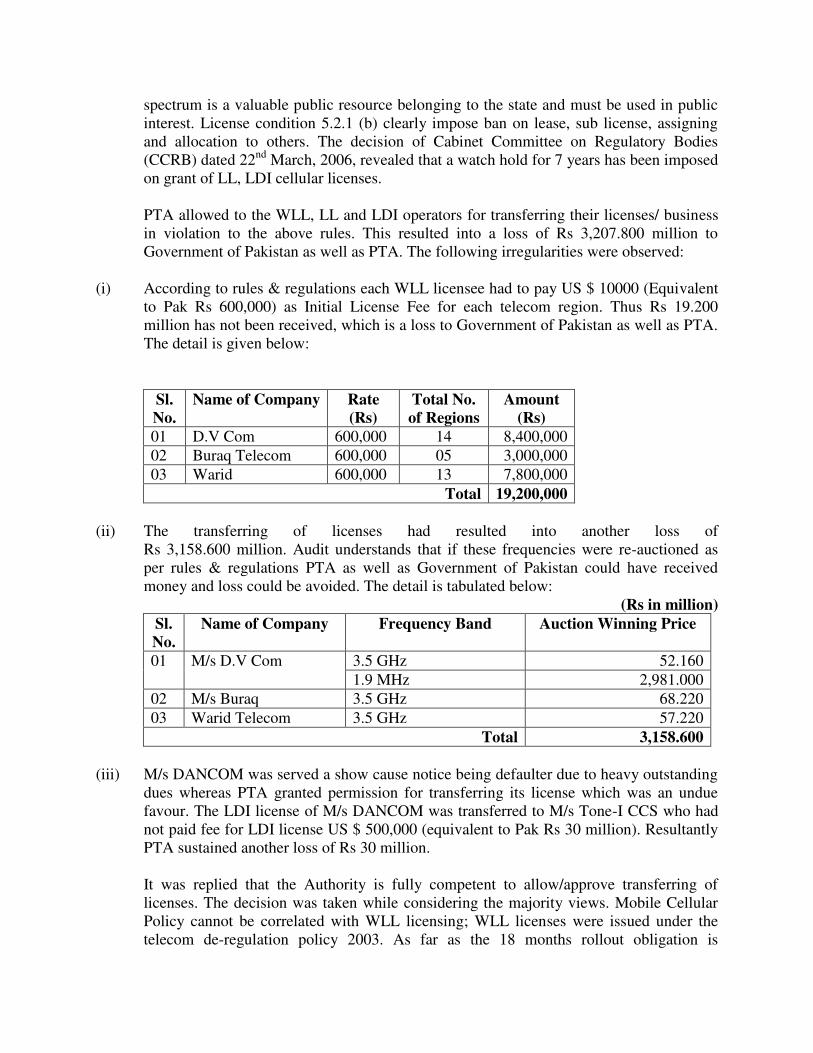

1.11 Irregular transfer of Licenses to un-authorized parties and loss of Rs 3,207.800 million According to para 4.6 of mobile cellular policy “unused spectrum allocated to any licensee may be withdrawn if the licensee fails to begin operations within eighteen (18) months of award of radio spectrum. The licensee may not assign, lease or sell the rights of use of spectrum allocated to them. Para 4.4 of de-regulation policy stipulates that radio

spectrum is a valuable public resource belonging to the state and must be used in public interest. License condition 5.2.1 (b) clearly impose ban on lease, sub license, assigning and allocation to others. The decision of Cabinet Committee on Regulatory Bodies (CCRB) dated 22nd March, 2006, revealed that a watch hold for 7 years has been imposed on grant of LL, LDI cellular licenses.

PTA allowed to the WLL, LL and LDI operators for transferring their licenses/ business in violation to the above rules. This resulted into a loss of Rs 3,207.800 million to Government of Pakistan as well as PTA. The following irregularities were observed:

(i) According to rules & regulations each WLL licensee had to pay US $ 10000 (Equivalent to Pak Rs 600,000) as Initial License Fee for each telecom region. Thus Rs 19.200 million has not been received, which is a loss to Government of Pakistan as well as PTA. The detail is given below:

Sl. No.

Name of Company Rate (Rs)

Total No. of Regions

Amount (Rs)

01 D.V Com 600,000 14 8,400,000

02 Buraq Telecom 600,000 05 3,000,000

03 Warid 600,000 13 7,800,000

Total 19,200,000

(ii) The transferring of licenses had resulted into another loss of Rs 3,158.600 million. Audit understands that if these frequencies were re-auctioned as per rules & regulations PTA as well as Government of Pakistan could have received money and loss could be avoided. The detail is tabulated below:

(Rs in million) Sl. No.

Name of Company Frequency Band Auction Winning Price

01 M/s D.V Com 3.5 GHz 52.160

1.9 MHz 2,981.000

02 M/s Buraq 3.5 GHz 68.220

03 Warid Telecom 3.5 GHz 57.220

Total 3,158.600

(iii) M/s DANCOM was served a show cause notice being defaulter due to heavy outstanding dues whereas PTA granted permission for transferring its license which was an undue favour. The LDI license of M/s DANCOM was transferred to M/s Tone-I CCS who had not paid fee for LDI license US $ 500,000 (equivalent to Pak Rs 30 million). Resultantly PTA sustained another loss of Rs 30 million. It was replied that the Authority is fully competent to allow/approve transferring of licenses. The decision was taken while considering the majority views. Mobile Cellular Policy cannot be correlated with WLL licensing; WLL licenses were issued under the telecom de-regulation policy 2003. As far as the 18 months rollout obligation is

concerned, the Authority had extended the period for operators to facilitate them in the rollout. As regard to the change of management of M/s DANCOM, the same has been made with the approval of the Authority. The license was transferred to the subsidiary of DANCOM which have no adverse effects on the capabilities for provision of telecom services. There were no outstanding dues against this license. Further, in case the spectrum had been withdrawn, it would have resulted in wastage of precious resources as under the Government decision we cannot award further WLL licenses for 7 years. The reply was not acceptable as the Authority have 3 Pillars, Chairman, Member (F), Member (T) and the remaining employees are not considered Authority. The transfer has been made without the unanimous decision. Member (Finance) who is the Financial Manager has not been considered and transfer approved through the recommendations of the committee who was not the Authority. Further, the CCRB has made a (hold on) for 7 years, which was accepted in the reply. Hence, another way in the shape of transferring was used for trading. Further, para 211 of note sheet clearly indicated that there were outstanding dues against M/s DANCOM. The matter may be investigated at appropriate level, responsibility may be fixed for a heavy loss to Government of Pakistan and non-observance of rules & regulations. The DAC in its meeting held on 1st December 2008 recommended to settle the para in the light of reply given by the PTA.

Audit had different view from DAC and decided to place it before PAC by including in the Audit Report.

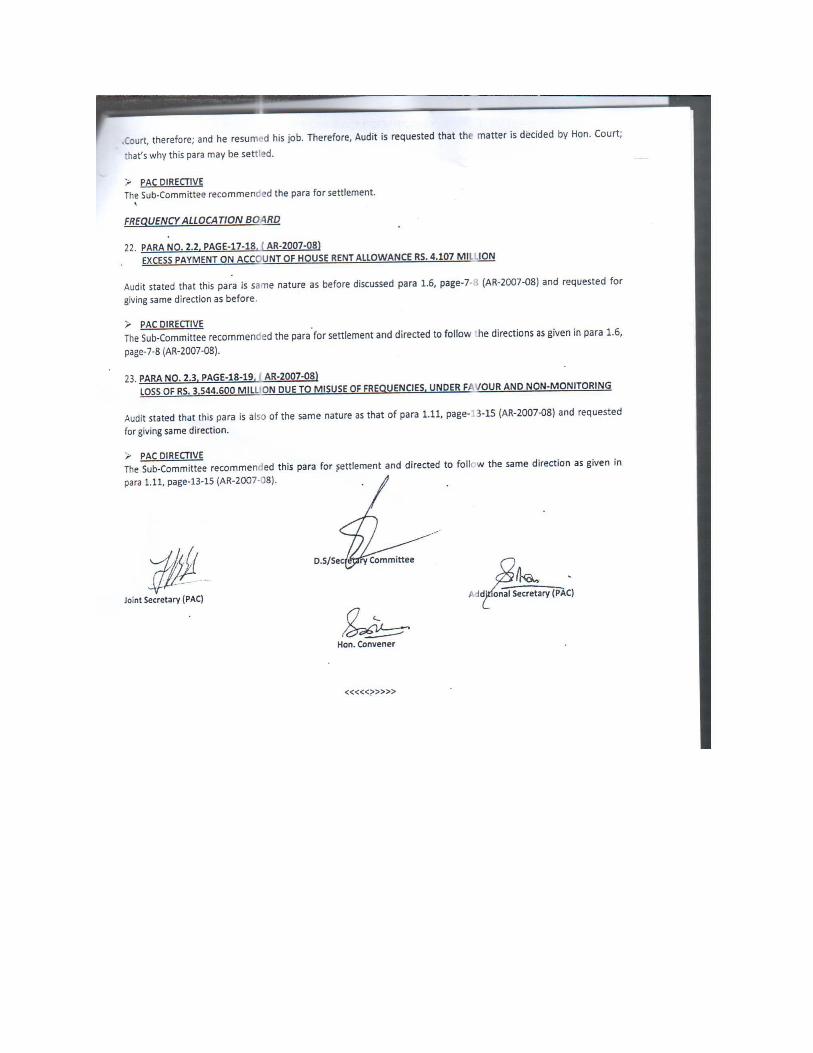

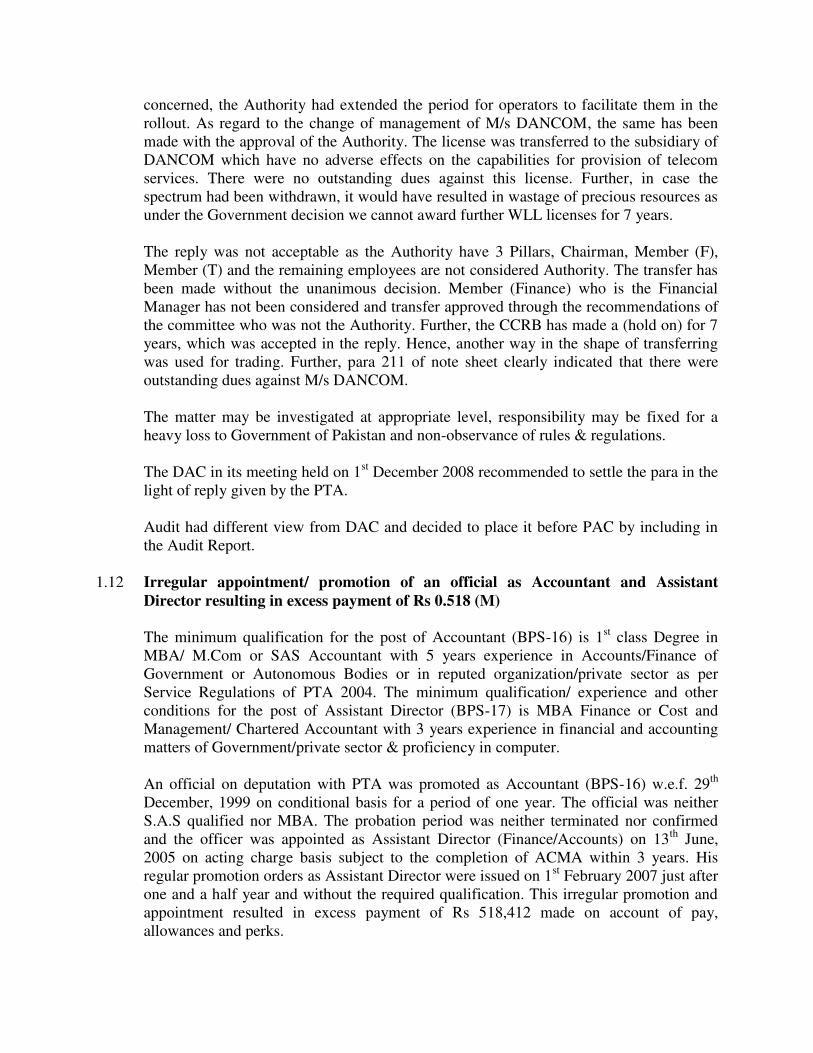

1.12 Irregular appointment/ promotion of an official as Accountant and Assistant Director resulting in excess payment of Rs 0.518 (M)

The minimum qualification for the post of Accountant (BPS-16) is 1st class Degree in MBA/ M.Com or SAS Accountant with 5 years experience in Accounts/Finance of Government or Autonomous Bodies or in reputed organization/private sector as per Service Regulations of PTA 2004. The minimum qualification/ experience and other conditions for the post of Assistant Director (BPS-17) is MBA Finance or Cost and Management/ Chartered Accountant with 3 years experience in financial and accounting matters of Government/private sector & proficiency in computer. An official on deputation with PTA was promoted as Accountant (BPS-16) w.e.f. 29th December, 1999 on conditional basis for a period of one year. The official was neither S.A.S qualified nor MBA. The probation period was neither terminated nor confirmed and the officer was appointed as Assistant Director (Finance/Accounts) on 13th June, 2005 on acting charge basis subject to the completion of ACMA within 3 years. His regular promotion orders as Assistant Director were issued on 1st February 2007 just after one and a half year and without the required qualification. This irregular promotion and appointment resulted in excess payment of Rs 518,412 made on account of pay, allowances and perks.

Audit pointed this out to the management in March 2007 and the Principal Accounting Officer in May 2007. It was replied in June & August 2007 that the official was promoted as Accountant in (BPS-16) in accordance with the Annexure-C of PTA Service Regulations. The officer was appointed as Assistant Director (Finance/Accounts) on Acting charge basis in accordance with the qualification/experience criteria defined and advertised in Daily Dawn Islamabad as per rule-55 (4) of the Service Regulations of PTA. Further, three years service was required as Accountant (B-16) for promotion as Assistant Director (B-17) as per Annexure-C of PTA Regulations. The reply was not acceptable as the promotion/appointment was against the Government as well as PTA Rules which required minimum education/level. The list of other candidates provided with the reply indicated that there were a number of qualified ACMA candidates who were ignored while appointing this officer. The DAC observed in the meeting held on 10th January, 2008 that PTA did not have cogent reasons to defend irregular promotion of the incumbent as Accountant and later on as Assistant Director. The DAC directed that the para may be placed before the PAC for order.

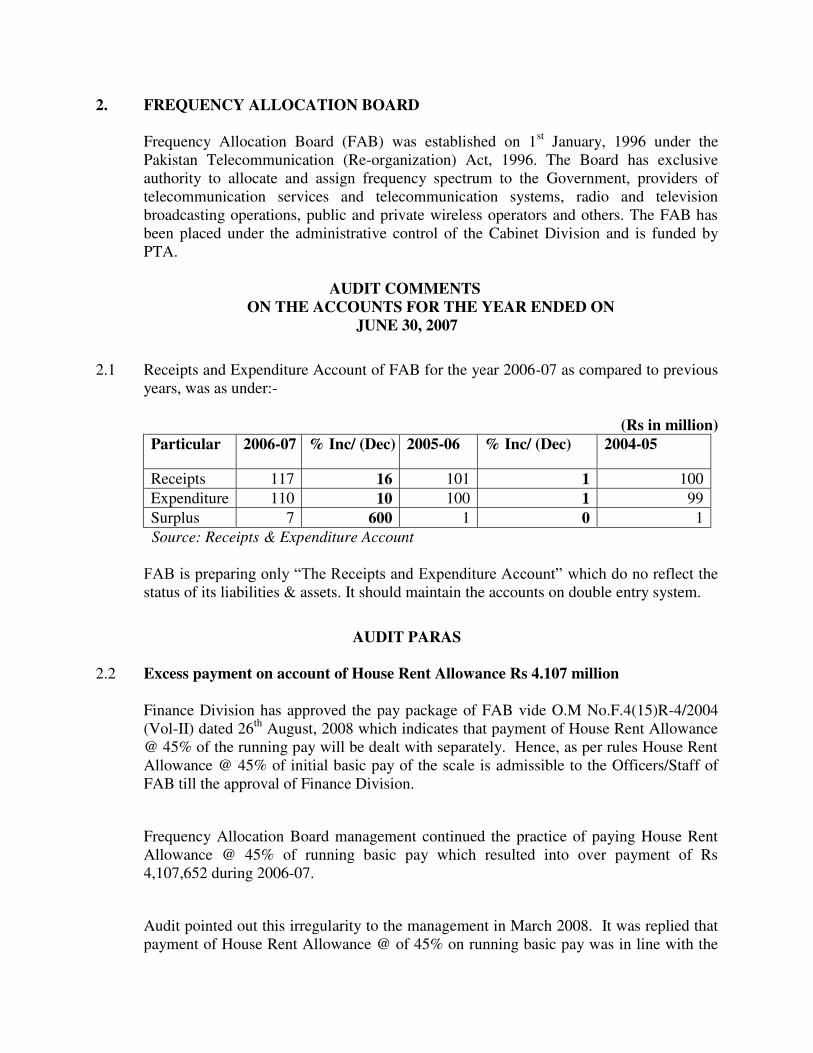

2. FREQUENCY ALLOCATION BOARD

Frequency Allocation Board (FAB) was established on 1st January, 1996 under the Pakistan Telecommunication (Re-organization) Act, 1996. The Board has exclusive authority to allocate and assign frequency spectrum to the Government, providers of telecommunication services and telecommunication systems, radio and television broadcasting operations, public and private wireless operators and others. The FAB has been placed under the administrative control of the Cabinet Division and is funded by PTA.

AUDIT COMMENTS

ON THE ACCOUNTS FOR THE YEAR ENDED ON JUNE 30, 2007

2.1 Receipts and Expenditure Account of FAB for the year 2006-07 as compared to previous years, was as under:-

(Rs in million)

Particular 2006-07 % Inc/ (Dec) 2005-06 % Inc/ (Dec) 2004-05

Receipts 117 16 101 1 100

Expenditure 110 10 100 1 99

Surplus 7 600 1 0 1

Source: Receipts & Expenditure Account

FAB is preparing only “The Receipts and Expenditure Account” which do no reflect the

status of its liabilities & assets. It should maintain the accounts on double entry system.

AUDIT PARAS

2.2 Excess payment on account of House Rent Allowance Rs 4.107 million

Finance Division has approved the pay package of FAB vide O.M No.F.4(15)R-4/2004 (Vol-II) dated 26th August, 2008 which indicates that payment of House Rent Allowance @ 45% of the running pay will be dealt with separately. Hence, as per rules House Rent Allowance @ 45% of initial basic pay of the scale is admissible to the Officers/Staff of FAB till the approval of Finance Division.

Frequency Allocation Board management continued the practice of paying House Rent Allowance @ 45% of running basic pay which resulted into over payment of Rs 4,107,652 during 2006-07.

Audit pointed out this irregularity to the management in March 2008. It was replied that payment of House Rent Allowance @ of 45% on running basic pay was in line with the

policies of PTA. The funds were provided / approved in the Budget Estimates 2006-07.

The reply was not acceptable as the House Rent Allowance @ 45% on running basic pay was not approved by the Finance Division in case of PTA and even now in case of FAB and the same could have been discontinued till the approval of Finance Division.

DAC in its meeting held on 1st December, 2008 directed the management that approval of Finance Division be obtained within 15 days and submit report to the PAO.

No progress has been reported till the finalization of this report.

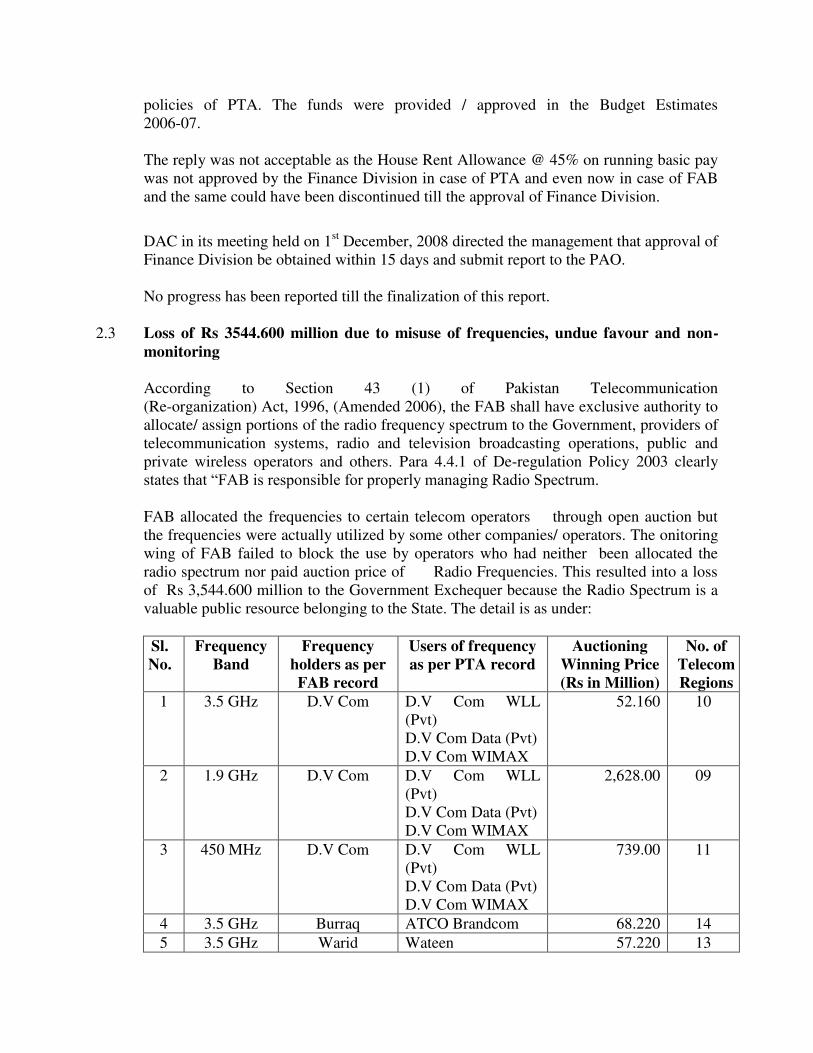

2.3 Loss of Rs 3544.600 million due to misuse of frequencies, undue favour and non-monitoring According to Section 43 (1) of Pakistan Telecommunication (Re-organization) Act, 1996, (Amended 2006), the FAB shall have exclusive authority to allocate/ assign portions of the radio frequency spectrum to the Government, providers of telecommunication systems, radio and television broadcasting operations, public and private wireless operators and others. Para 4.4.1 of De-regulation Policy 2003 clearly states that “FAB is responsible for properly managing Radio Spectrum. FAB allocated the frequencies to certain telecom operators through open auction but the frequencies were actually utilized by some other companies/ operators. The onitoring wing of FAB failed to block the use by operators who had neither been allocated the radio spectrum nor paid auction price of Radio Frequencies. This resulted into a loss of Rs 3,544.600 million to the Government Exchequer because the Radio Spectrum is a valuable public resource belonging to the State. The detail is as under:

Sl. No.

Frequency Band

Frequency holders as per FAB record

Users of frequency as per PTA record

Auctioning Winning Price (Rs in Million)

No. of Telecom Regions

1 3.5 GHz D.V Com D.V Com WLL (Pvt) D.V Com Data (Pvt) D.V Com WIMAX

52.160 10

2 1.9 GHz D.V Com D.V Com WLL (Pvt) D.V Com Data (Pvt) D.V Com WIMAX

2,628.00 09

3 450 MHz D.V Com D.V Com WLL (Pvt) D.V Com Data (Pvt) D.V Com WIMAX

739.00 11

4 3.5 GHz Burraq ATCO Brandcom 68.220 14

5 3.5 GHz Warid Wateen 57.220 13

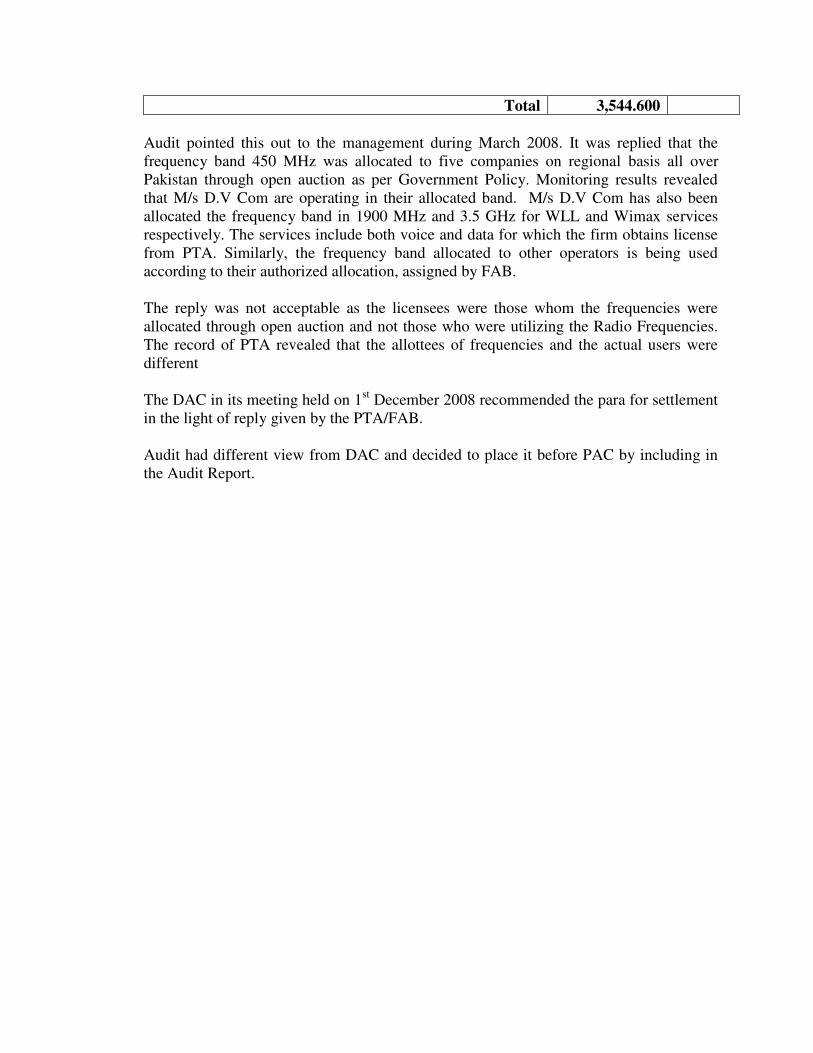

Total 3,544.600

Audit pointed this out to the management during March 2008. It was replied that the frequency band 450 MHz was allocated to five companies on regional basis all over Pakistan through open auction as per Government Policy. Monitoring results revealed that M/s D.V Com are operating in their allocated band. M/s D.V Com has also been allocated the frequency band in 1900 MHz and 3.5 GHz for WLL and Wimax services respectively. The services include both voice and data for which the firm obtains license from PTA. Similarly, the frequency band allocated to other operators is being used according to their authorized allocation, assigned by FAB. The reply was not acceptable as the licensees were those whom the frequencies were allocated through open auction and not those who were utilizing the Radio Frequencies. The record of PTA revealed that the allottees of frequencies and the actual users were different The DAC in its meeting held on 1st December 2008 recommended the para for settlement in the light of reply given by the PTA/FAB. Audit had different view from DAC and decided to place it before PAC by including in the Audit Report.

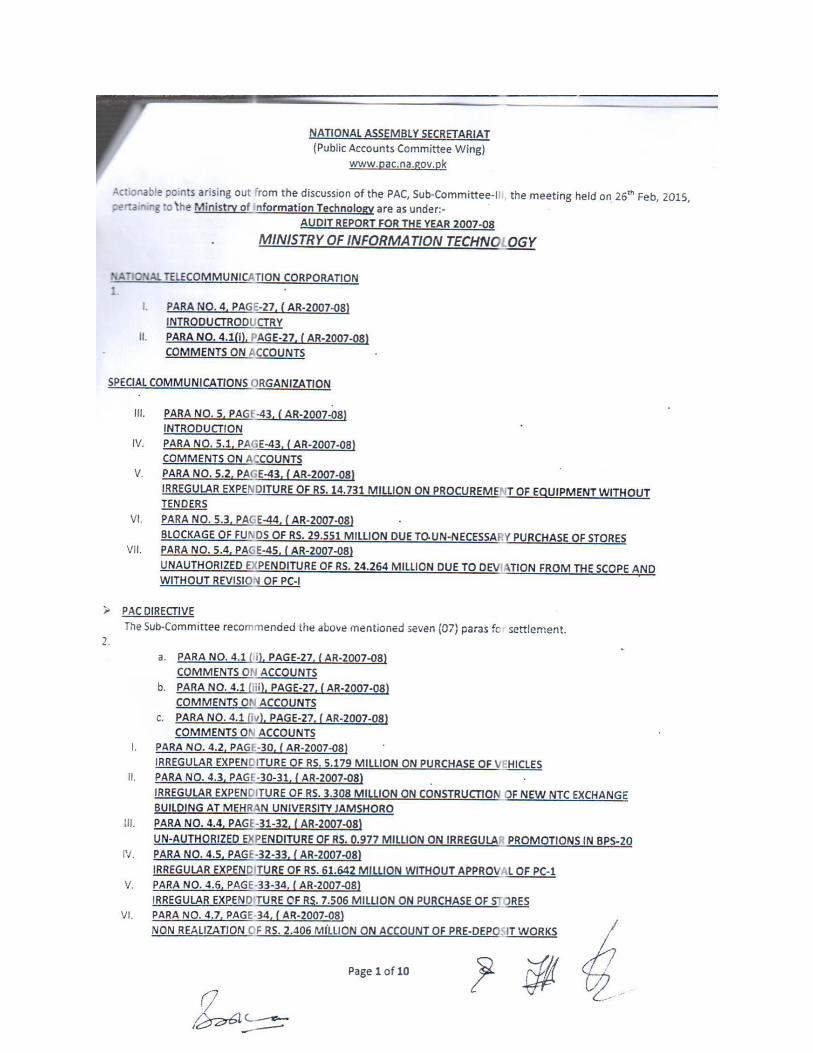

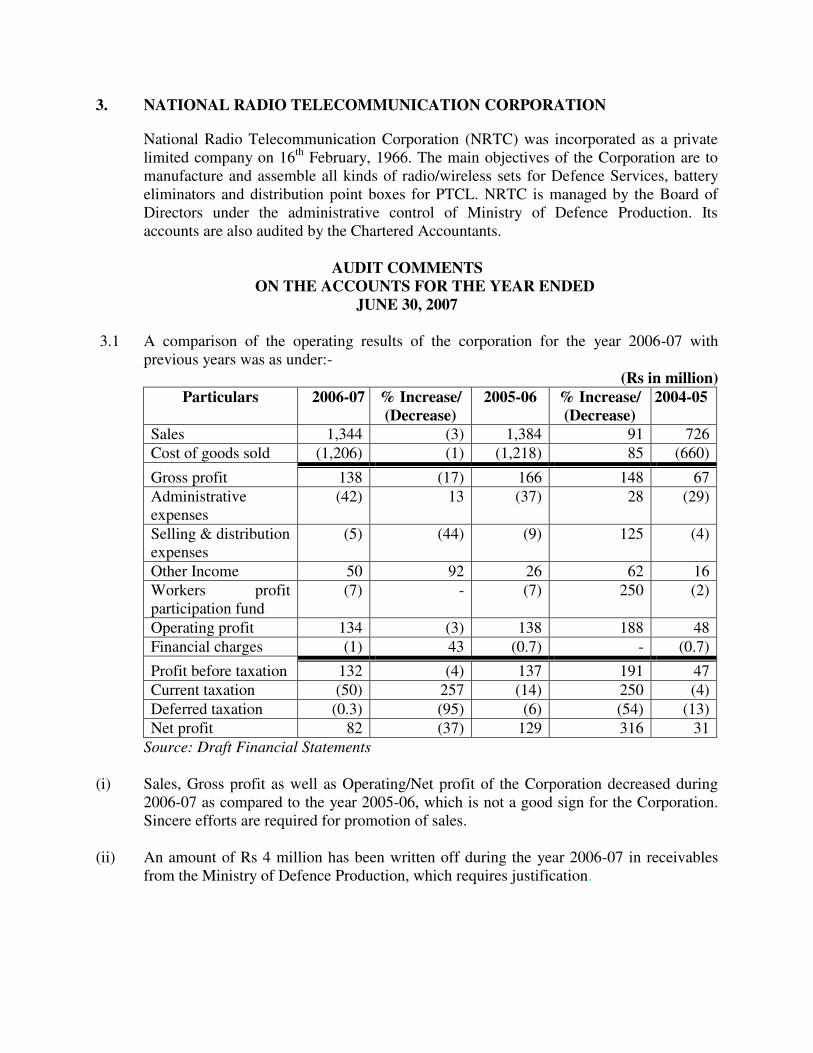

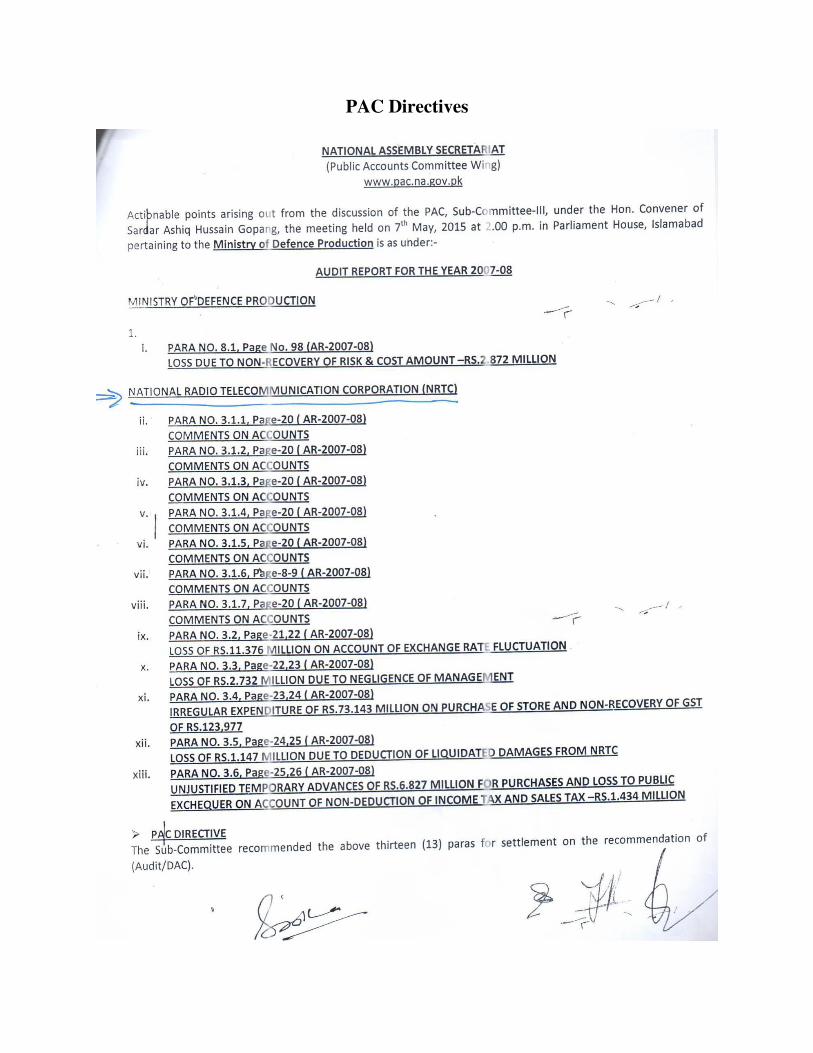

3. NATIONAL RADIO TELECOMMUNICATION CORPORATION

National Radio Telecommunication Corporation (NRTC) was incorporated as a private limited company on 16th February, 1966. The main objectives of the Corporation are to manufacture and assemble all kinds of radio/wireless sets for Defence Services, battery eliminators and distribution point boxes for PTCL. NRTC is managed by the Board of Directors under the administrative control of Ministry of Defence Production. Its accounts are also audited by the Chartered Accountants.

AUDIT COMMENTS

ON THE ACCOUNTS FOR THE YEAR ENDED JUNE 30, 2007

3.1 A comparison of the operating results of the corporation for the year 2006-07 with

previous years was as under:- (Rs in million)

Particulars 2006-07 % Increase/ (Decrease)

2005-06 % Increase/ (Decrease)

2004-05

Sales 1,344 (3) 1,384 91 726

Cost of goods sold (1,206) (1) (1,218) 85 (660)

Gross profit 138 (17) 166 148 67

Administrative expenses

(42) 13 (37) 28 (29)

Selling & distribution expenses

(5) (44) (9) 125 (4)

Other Income 50 92 26 62 16

Workers profit participation fund

(7) - (7) 250 (2)

Operating profit 134 (3) 138 188 48

Financial charges (1) 43 (0.7) - (0.7)

Profit before taxation 132 (4) 137 191 47

Current taxation (50) 257 (14) 250 (4)

Deferred taxation (0.3) (95) (6) (54) (13)

Net profit 82 (37) 129 316 31

Source: Draft Financial Statements

(i) Sales, Gross profit as well as Operating/Net profit of the Corporation decreased during 2006-07 as compared to the year 2005-06, which is not a good sign for the Corporation. Sincere efforts are required for promotion of sales.

(ii) An amount of Rs 4 million has been written off during the year 2006-07 in receivables

from the Ministry of Defence Production, which requires justification.

(iii) A disclosure has not been made regarding payment of Rs 67 million on account of commission shown against export sales during 2006-07 whereas the same was not paid during 2005-06.

(iv) Provision for tax has been increased by Rs 54 million in 2006-07 against Rs 8 million in

2005-06 which is 575% more as compared to previous year. Further, current tax of the company also increased by 257 % from Rs 14 million in 2005-06 to Rs 50 million in 2006-07 whereas sales of the company decreased by 3% from the previous year which needs justification.

(v) Development advance has been increased by Rs 153 million in 2006-07 against Rs 26

million in 2005-06. This significant increase of 489% is not supported by any disclosure. (vi) Trade debts of the company increased by 28% from Rs 286 million in 2005-06 to Rs 367

million in 2006-07. Besides, receivables on account of importation and other charges of Rs 3 million exist for the last 03 years. All this shows weak receivables management.

(vii) There was significant decrease in saving bank balance of the Corporation from Rs 665

million to Rs 196 million during 2005-06 and 2006-07 respectively, which needs justification.

AUDIT PARAS

3.2 Loss of Rs 11.376 million on account of exchange rate fluctuation

The terms of contract must be precise and definite and there must be no room for ambiguity or misconstruction therein. Provision must be made in contracts for safeguarding Government property entrusted to a contractor according to Rule-18 (i) & (ix) of GFR Vol-I. A contract was made with Director General (Munitions Production) for supply of Frequency Hopping Radio Sets 9600 series. The total cost of the contract was US $ 21.451 million. The clause for fluctuation loss was not entered in the contract agreement. The exchange rate of US $ 1=Rs 58.50 was fixed. The actual exchange rate remained higher at the time of payment to NRTC. This resulted into a net loss of Rs 11,376,448.

Audit pointed out this irregularity to the management during March 2008. It was replied that due to non inclusion of the clause in the contract the fluctuation loss does not appear to be received even after hectic efforts by NRTC management at higher level.

The reply was not acceptable as no correspondence was on record showing the hectic efforts made for realization of loss. Furthermore, no responsibility was fixed to those at fault for non-inclusion of the fluctuation clause.

DAC in its meeting held on 13th December, 2008 directed the NRTC management to order an inquiry to fix responsibility besides affecting the recovery of amount involved. The recommendation/decision taken by the court of inquiry be submitted within 15 days to the PAO.

No progress has been reported till the finalization of this report.

3.3 Loss of Rs 2.732 million due to negligence of management

According to Para-11 of terms of payment, 100% Foreign Exchange will be released to NRTC under the provisions of Government letter No.07/81/DMP(E&T)/1844/D&B/70 dated 7th May, 1970; Amendment letter No.11/52/74/DP-4/ 1342/ 10/ DGDP/PC-3 dated 5th December, 1974; and No. 1557 / 40/ DGDP/PC-1/11/81/74/DP-4 dated 29th June, 2001.

A work order for up-gradation of sets AN/PRC-77 series was placed upon NRTC on 30th June, 2003 with a total cost of Rs 201,392,919 (FE US $ 3.443 million) by Director General, Munitions Production (DGMP). NRTC received an amount of Rs198,661,000 vide cheque No.E-683651 dated 12th March, 2004 leaving a balance of Rs 2,731,919 and presented a claim for less payment on 14th June, 2005 but the DGMP rejected the claim on the grounds that all payment had been released in March 2004 and re-appropriation of funds after fifteen months is not possible. This caused a loss of Rs 2,731,919 to NRTC due to its negligence. Audit pointed out this irregularity to the management during March 2008. It was replied that the case for re-appropriation of funds is under process with DG MP and further progress will be intimated in due course. It was further replied in December 2008 that despite continuous pursuance by NRTC management at all levels request for the release of short paid amount has not been acceded to by MoDP.

The reply was not acceptable as the payment was released in March 2004 whereas the claim for less payment was pursued after the delay of 15 months due to which the request was not acceded to by the MoDP. This indicates improper financial management by NRTC. DAC in its meeting held on 13th December, 2008 directed the NRTC management to order an inquiry to fix responsibility besides affecting the recovery of amount involved. The recommendation/decision taken by the court of inquiry be submitted within 15 days to the PAO.

No progress has been reported till the finalization of this report.

3.4 Irregular expenditure of Rs 73.143 million on purchase of store and non-recovery of GST of Rs 123,977

The procuring agencies shall announce in an appropriate manner all proposed procurements for each financial year and shall proceed accordingly without any splitting or re-grouping according to Rule-9 of Public Procurement Rules, 2004. Rule-21 further stipulates that if the cost of the object is more than one hundred thousand rupees, the procuring agency shall engage in open competitive bidding.

NRTC incurred an expenditure of Rs 73,142,786 on purchase of various store items in violation to the above rules during 2006-07. Further, the public exchequer sustained a loss of Rs 123,977 due to procurement from the firms not registered with the sales tax department.

Audit pointed out this irregularity to the management during March 2008. It was replied that all the purchases were made on the basis of open tenders and GST is not recoverable. The reply was not acceptable as only in two cases the tenders were floated and the remaining purchases were made on repeat order basis in violation to the PPRs, 2004.

DAC in its meeting held on 13th December, 2008 directed the management to take up the case with Secretary, (Defence Production Division) for regularization of expenditure and exemption from PPRA Rules, 2004. The amount of GST be recovered and get it verified from audit No further progress has been reported so far.

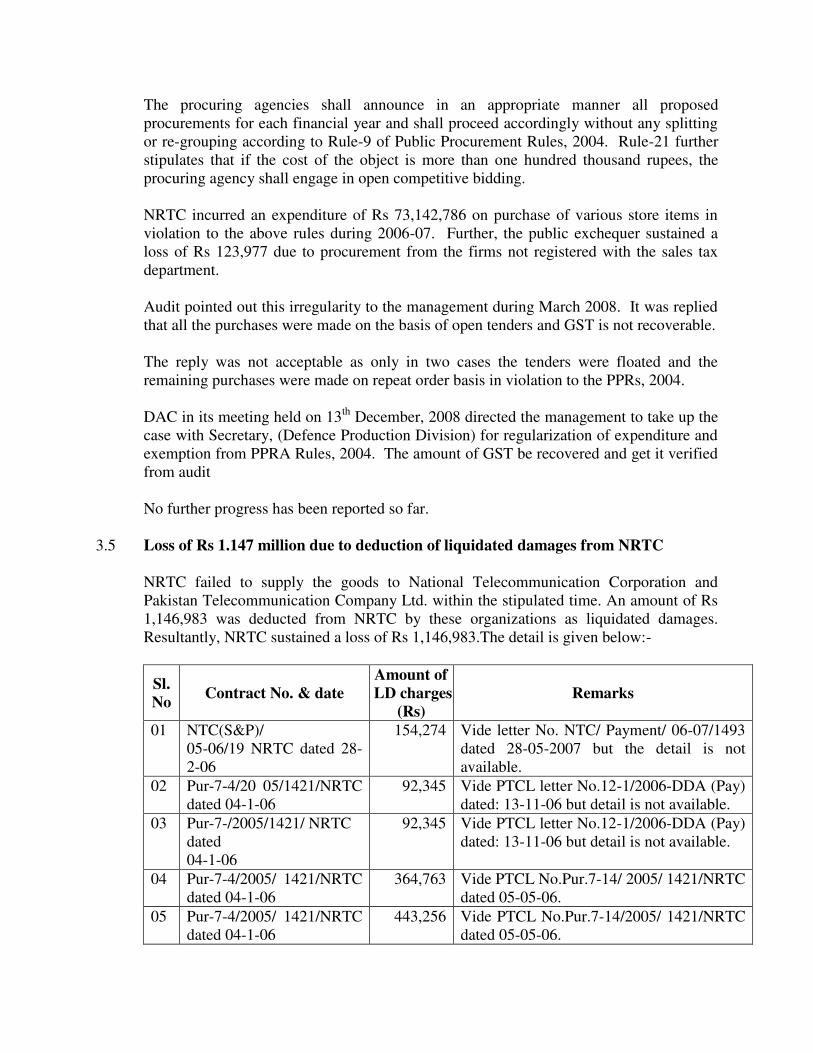

3.5 Loss of Rs 1.147 million due to deduction of liquidated damages from NRTC

NRTC failed to supply the goods to National Telecommunication Corporation and Pakistan Telecommunication Company Ltd. within the stipulated time. An amount of Rs 1,146,983 was deducted from NRTC by these organizations as liquidated damages. Resultantly, NRTC sustained a loss of Rs 1,146,983.The detail is given below:-

Sl. No

Contract No. & date Amount of LD charges

(Rs) Remarks

01 NTC(S&P)/ 05-06/19 NRTC dated 28-2-06

154,274 Vide letter No. NTC/ Payment/ 06-07/1493 dated 28-05-2007 but the detail is not available.

02 Pur-7-4/20 05/1421/NRTC dated 04-1-06

92,345 Vide PTCL letter No.12-1/2006-DDA (Pay) dated: 13-11-06 but detail is not available.

03 Pur-7-/2005/1421/ NRTC dated 04-1-06

92,345 Vide PTCL letter No.12-1/2006-DDA (Pay) dated: 13-11-06 but detail is not available.

04 Pur-7-4/2005/ 1421/NRTC dated 04-1-06

364,763 Vide PTCL No.Pur.7-14/ 2005/ 1421/NRTC dated 05-05-06.

05 Pur-7-4/2005/ 1421/NRTC dated 04-1-06

443,256 Vide PTCL No.Pur.7-14/2005/ 1421/NRTC dated 05-05-06.

Total 1,146,983

Audit pointed out this irregularity to the management in March 2008. It was replied that NRTC is pursuing the cases at personal level with top management of both the organizations. A series of meetings have been held for the settlement of NRTC claims. The case was not yet settled and NRTC is still making concerted efforts for refund of amount.

DAC in its meeting held on 13th December, 2008 directed the management to make all out efforts to recover the amount of liquidated damages from NTC & PTCL. Para stand till the recovery of amount involved. No progress was reported.

3.6 Unjustified temporary advances of Rs 6.827 million for purchases and loss to public exchequer on account of non-deduction of Income Tax and Sales Tax-Rs 1.434 million

The procuring agencies shall announce in an appropriate manner all proposed procurements for each financial year and shall proceed accordingly without any splitting or re-grouping according to Rule-9 of Public Procurement Rules, 2004. Rule-21 further stipulates that if the cost of the object is more than one hundred thousand, the procuring agency shall engage in open competitive bidding. Further, Rule-10 (i) of GFR Vol-I revealed that every public officer is expected to exercise the same vigilance in respect of expenditure incurred from public moneys as a person of ordinary prudence would exercise in respect of expenditure of his own money. NRTC continued the practice of granting heavy temporary advances for cash purchases. An amount of Rs 6,826,967 was paid on account of temporary advance for cash purchase during 2006-07. It was further added that an amount of Rs 6,046,762 was paid to only one officer during the year. As a result of heavy cash purchases the public exchequer sustained a loss of Rs 1,433,664 in the shape of non-deduction of Income Tax and procurement made from the firms not registered with the sales tax department.

Audit pointed out this irregularity to the management during March 2008. It was replied that Deputy Chief Engineer (Procurement) was authorized a permanent imprest of Rs 200,000 and purchases were made through this imprest. The Deputy Chief Engineer (Procurement) was authorized for cash purchases through temporary advances as per the procedure of the company. The payment of GST and deduction of Income Tax at source through cash purchases is not practicable as it tantamount to double taxation as the items procured were mostly of already manufactured nature, wherein the taxes are catered for by the manufacturers itself. The reply was not acceptable as the officer had a sufficient amount of imprest for cash purchase, therefore, heavy temporary advance to one officer was not justified. No approved cash purchase procedure was in vogue at present. Further, the practice was not

stopped despite pointing out in previous report and directions of the DAC. The amount of GST and Income Tax was required to be recovered as per rules. DAC in its meeting held on 13th December, 2008 directed the management to get the record verified from audit within 15 days and submit report to the PAO for further action. No progress was reported.

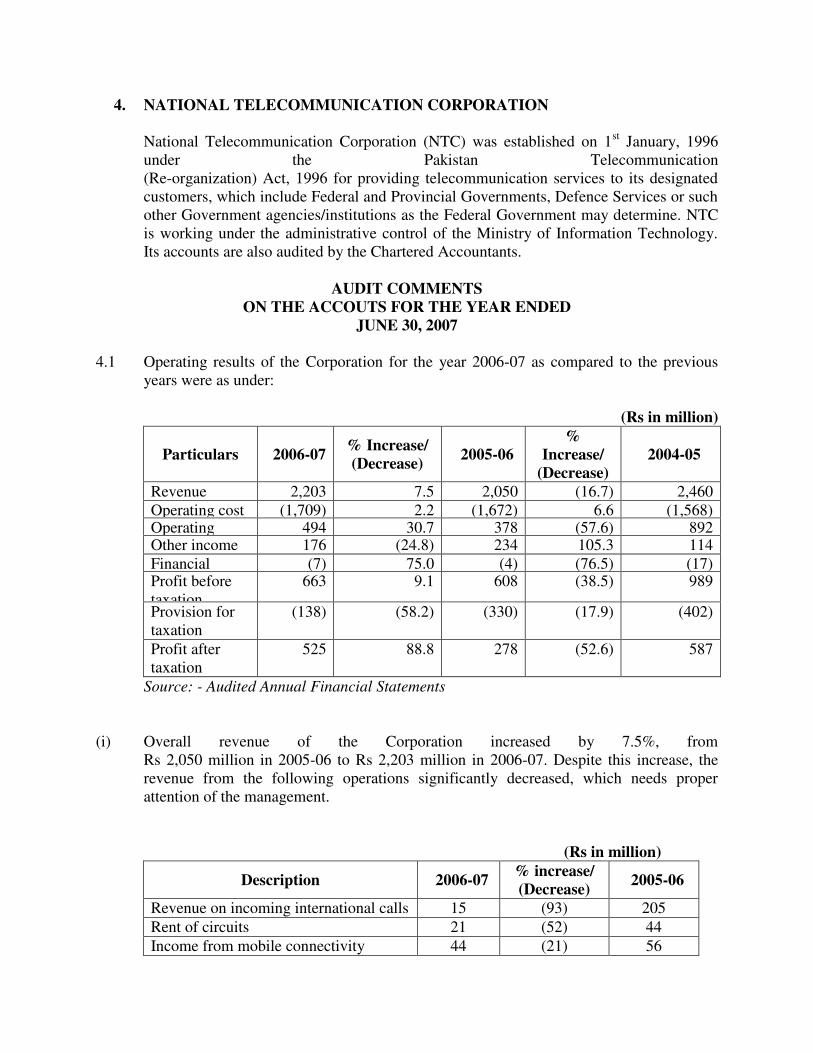

4. NATIONAL TELECOMMUNICATION CORPORATION

National Telecommunication Corporation (NTC) was established on 1st January, 1996 under the Pakistan Telecommunication (Re-organization) Act, 1996 for providing telecommunication services to its designated customers, which include Federal and Provincial Governments, Defence Services or such other Government agencies/institutions as the Federal Government may determine. NTC is working under the administrative control of the Ministry of Information Technology. Its accounts are also audited by the Chartered Accountants.

AUDIT COMMENTS

ON THE ACCOUTS FOR THE YEAR ENDED JUNE 30, 2007

4.1 Operating results of the Corporation for the year 2006-07 as compared to the previous

years were as under:

(Rs in million)

Particulars 2006-07 % Increase/ (Decrease)

2005-06 %

Increase/ (Decrease)

2004-05

Revenue 2,203 7.5 2,050 (16.7) 2,460 Operating cost (1,709) 2.2 (1,672) 6.6 (1,568) Operating profit

494 30.7 378 (57.6) 892 Other income 176 (24.8) 234 105.3 114 Financial charges

(7) 75.0 (4) (76.5) (17) Profit before taxation

663 9.1 608 (38.5) 989

Provision for taxation

(138) (58.2) (330) (17.9) (402)

Profit after taxation

525 88.8 278 (52.6) 587

Source: - Audited Annual Financial Statements

(i) Overall revenue of the Corporation increased by 7.5%, from

Rs 2,050 million in 2005-06 to Rs 2,203 million in 2006-07. Despite this increase, the revenue from the following operations significantly decreased, which needs proper attention of the management.

(Rs in million)

Description 2006-07 % increase/ (Decrease)

2005-06

Revenue on incoming international calls 15 (93) 205

Rent of circuits 21 (52) 44

Income from mobile connectivity 44 (21) 56

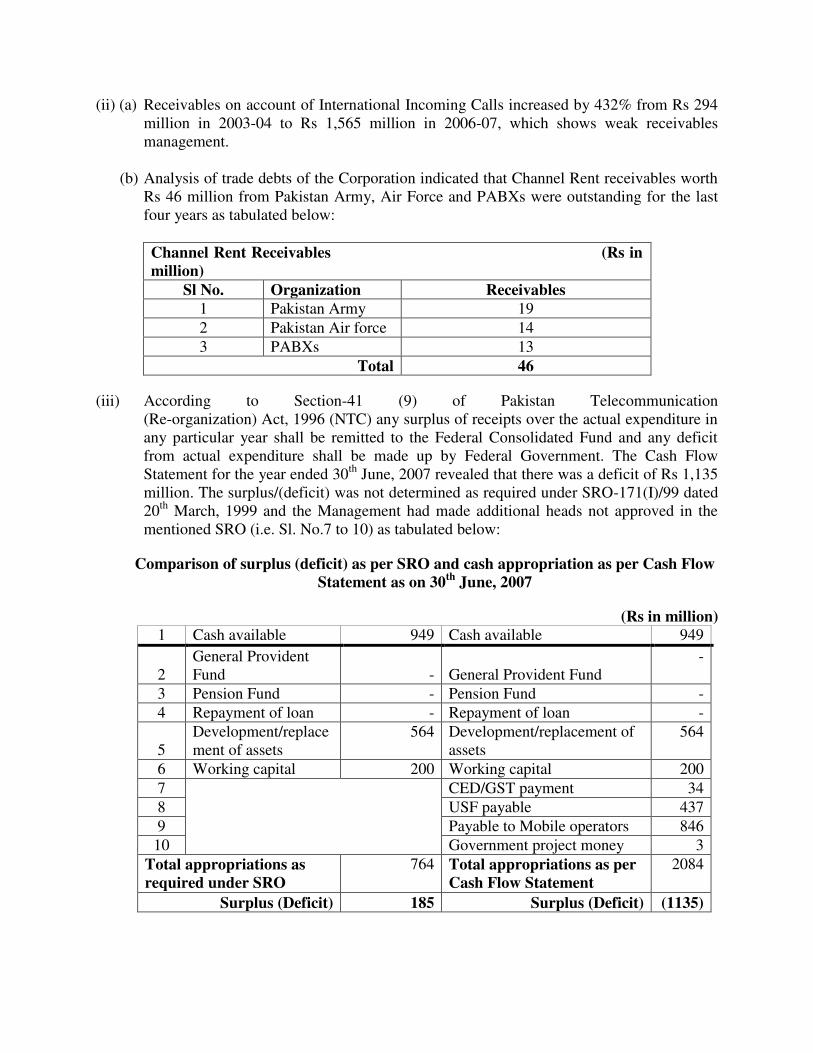

(ii) (a) Receivables on account of International Incoming Calls increased by 432% from Rs 294 million in 2003-04 to Rs 1,565 million in 2006-07, which shows weak receivables management.

(b) Analysis of trade debts of the Corporation indicated that Channel Rent receivables worth

Rs 46 million from Pakistan Army, Air Force and PABXs were outstanding for the last four years as tabulated below:

Channel Rent Receivables (Rs in million)

Sl No. Organization Receivables 1 Pakistan Army 19

2 Pakistan Air force 14

3 PABXs 13

Total 46

(iii) According to Section-41 (9) of Pakistan Telecommunication (Re-organization) Act, 1996 (NTC) any surplus of receipts over the actual expenditure in any particular year shall be remitted to the Federal Consolidated Fund and any deficit from actual expenditure shall be made up by Federal Government. The Cash Flow Statement for the year ended 30th June, 2007 revealed that there was a deficit of Rs 1,135 million. The surplus/(deficit) was not determined as required under SRO-171(I)/99 dated 20th March, 1999 and the Management had made additional heads not approved in the mentioned SRO (i.e. Sl. No.7 to 10) as tabulated below:

Comparison of surplus (deficit) as per SRO and cash appropriation as per Cash Flow Statement as on 30th June, 2007

(Rs in million) 1 Cash available 949 Cash available 949

2 General Provident Fund - General Provident Fund

-

3 Pension Fund - Pension Fund -

4 Repayment of loan - Repayment of loan -

5 Development/replacement of assets

564 Development/replacement of assets

564

6 Working capital 200 Working capital 200

7

CED/GST payment 34

8 USF payable 437

9 Payable to Mobile operators 846

10 Government project money 3

Total appropriations as required under SRO

764 Total appropriations as per Cash Flow Statement

2084

Surplus (Deficit) 185 Surplus (Deficit) (1135)

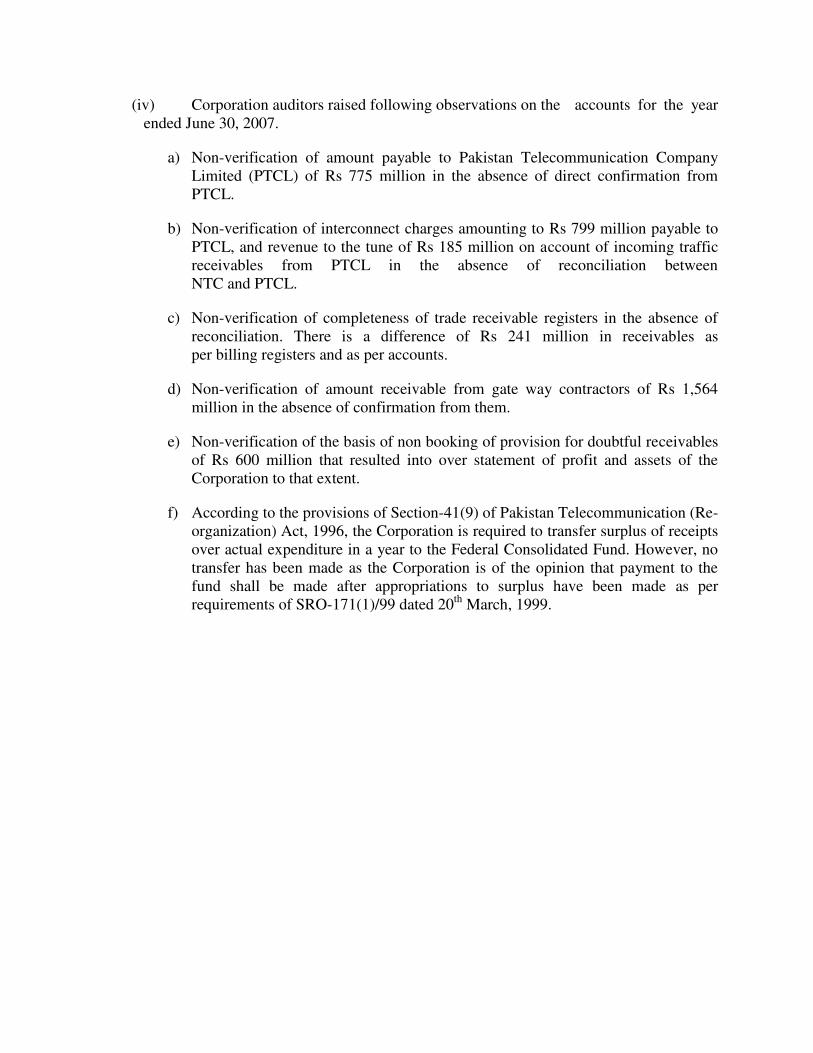

(iv) Corporation auditors raised following observations on the accounts for the year ended June 30, 2007.

a) Non-verification of amount payable to Pakistan Telecommunication Company Limited (PTCL) of Rs 775 million in the absence of direct confirmation from PTCL.

b) Non-verification of interconnect charges amounting to Rs 799 million payable to PTCL, and revenue to the tune of Rs 185 million on account of incoming traffic receivables from PTCL in the absence of reconciliation between NTC and PTCL.

c) Non-verification of completeness of trade receivable registers in the absence of reconciliation. There is a difference of Rs 241 million in receivables as per billing registers and as per accounts.

d) Non-verification of amount receivable from gate way contractors of Rs 1,564 million in the absence of confirmation from them.

e) Non-verification of the basis of non booking of provision for doubtful receivables of Rs 600 million that resulted into over statement of profit and assets of the Corporation to that extent.

f) According to the provisions of Section-41(9) of Pakistan Telecommunication (Re-organization) Act, 1996, the Corporation is required to transfer surplus of receipts over actual expenditure in a year to the Federal Consolidated Fund. However, no transfer has been made as the Corporation is of the opinion that payment to the fund shall be made after appropriations to surplus have been made as per requirements of SRO-171(1)/99 dated 20th March, 1999.

AUDIT PARAS

4.2 Irregular expenditure of Rs 5.179 million on purchase of vehicles

As per Cabinet Division’s D.O letters No.1/2/2000 Imp-II dated 28th February, 2000; No.6-35/2000 M-II dated 1st December, 2003; and No.6-7(1) 02 M-II dated 22nd July, 2005, the existing ban on purchase of new vehicles is applicable to all Ministries / Divisions/Autonomous/Semi-Autonomous Bodies, Corporations, Northern Areas and Fata and its relaxation can be granted by the Prime Minister only.

NTC Headquarter, Islamabad incurred an expenditure of Rs 5,178,624 on purchase of imported vehicles in violation of the above instructions during 2006-07.

Audit pointed out this irregularity to the management and Principal Accounting Officer in March 2008. It was replied in October 2008 that the foreign assembled vehicles were purchased after getting approval from the screening committee, Planning & Development Division. The reply was not acceptable as the screening committee was only empowered to grant NOC for purchase of vehicles against foreign aided projects. The approval of purchase committee set up by the Finance Division was not obtained.

DAC in its meeting held on 22nd October, 2008 directed the management to get the expenditure regularized from the committee set up by the Finance Division for purchase of vehicles. No progress has been reported till the finalization of this report.

4.3 Irregular expenditure of Rs 3.308 million on construction of new NTC exchange

building at Mehran University Jamshoro

According to the laid down procedure circulated by Ministry of I.T vide letter No. 3 (7) PSDP/04-AC-P, dated 31-01-2005, development schemes of NTC are required to be sanctioned by the Development Working Party (DWP) subject to endorsement of the NTC management. An expenditure of Rs 3,308,043 was incurred by Director, Development (South) NTC, Karachi on construction of new building at Mehran University, Jamshoro without the approval of NTC management board and DWP. Audit pointed this out to the head of the unit during February, 2008 and the management in April, 2008. It was replied in February & October 2008 that work was approved by the Chairman NTC Headquarters Islamabad. The reply was not acceptable as the approval of the NTC management board and DWP was not obtained.

DAC in its meeting held on 22nd October, 2008 directed the management to hold an inquiry within 15 days for fixing the responsibility and get it verified from audit. No progress has been reported till the finalization of this report.

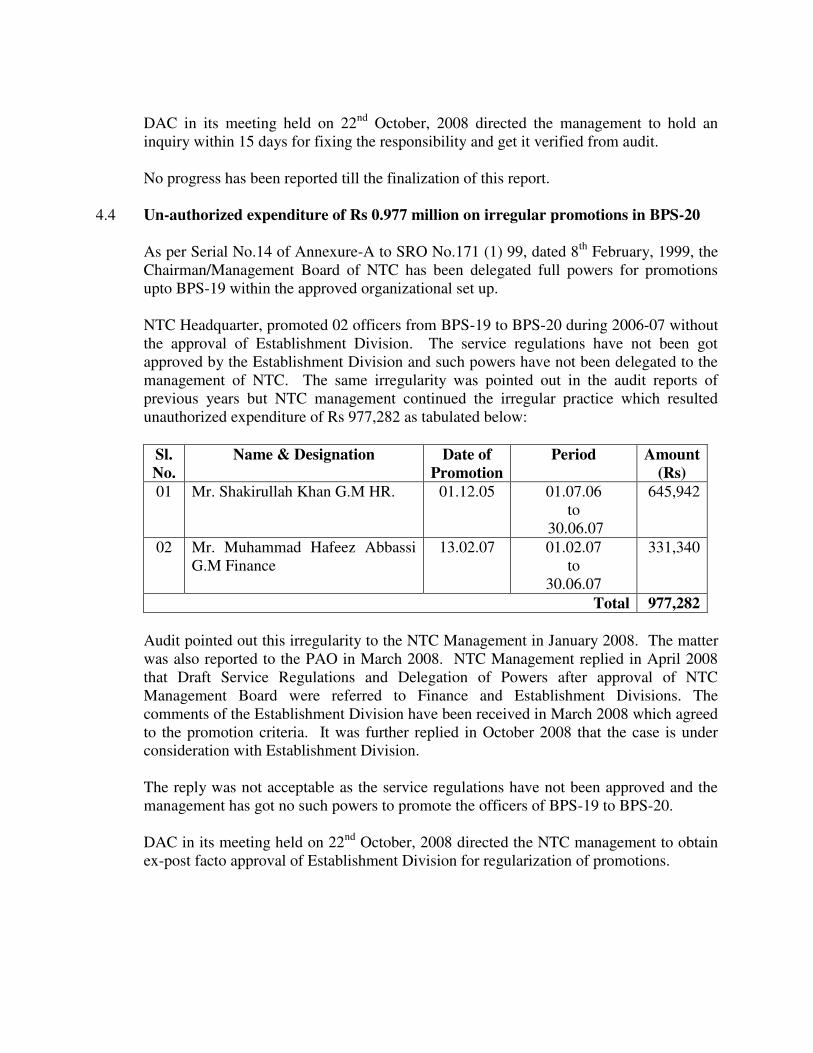

4.4 Un-authorized expenditure of Rs 0.977 million on irregular promotions in BPS-20

As per Serial No.14 of Annexure-A to SRO No.171 (1) 99, dated 8th February, 1999, the Chairman/Management Board of NTC has been delegated full powers for promotions upto BPS-19 within the approved organizational set up.

NTC Headquarter, promoted 02 officers from BPS-19 to BPS-20 during 2006-07 without the approval of Establishment Division. The service regulations have not been got approved by the Establishment Division and such powers have not been delegated to the management of NTC. The same irregularity was pointed out in the audit reports of previous years but NTC management continued the irregular practice which resulted unauthorized expenditure of Rs 977,282 as tabulated below:

Sl. No.

Name & Designation Date of Promotion

Period Amount (Rs)

01 Mr. Shakirullah Khan G.M HR. 01.12.05 01.07.06 to

30.06.07

645,942

02 Mr. Muhammad Hafeez Abbassi G.M Finance

13.02.07 01.02.07 to

30.06.07

331,340

Total 977,282 Audit pointed out this irregularity to the NTC Management in January 2008. The matter was also reported to the PAO in March 2008. NTC Management replied in April 2008 that Draft Service Regulations and Delegation of Powers after approval of NTC Management Board were referred to Finance and Establishment Divisions. The comments of the Establishment Division have been received in March 2008 which agreed to the promotion criteria. It was further replied in October 2008 that the case is under consideration with Establishment Division. The reply was not acceptable as the service regulations have not been approved and the management has got no such powers to promote the officers of BPS-19 to BPS-20.

DAC in its meeting held on 22nd October, 2008 directed the NTC management to obtain ex-post facto approval of Establishment Division for regularization of promotions.

4.5 Irregular expenditure of Rs 61.642 million without approval of PC-1

According to para 14 (4-iii) of Finance Division letter No.F-3(2) EXT.III/2006 dated 13th September, 2006 in case of disagreement of any number of Departmental Development Working Party to the project proposal, the case will be referred to the Central Development Working Party for consideration.

The PC-I for the provision of Optical Fiber Access Network costing Rs 39,366,920 was approved by the DDWP. Due to addition of supplementary works, the expenditure was enhanced to Rs 61,642,321. The revised PC-I was submitted to DDWP for sanction. The DDWP did not sanction the revised PC-I on the pretext that the same was beyond the competence of DDWP. The revised PC-I was not prepared for the approval of CDWP prior to implementation of the project. Audit pointed out this irregularity to the head of the formation during October 2007 and to the management in January 2008. It was replied in October 2008 that the revised PC-I including supplementary works was presented to DDWP for its approval. The DDWP did not consider the revision being beyond its competence. The case was then re-submitted to NTC Management Board which was approved in its 53rd meeting held 27th September, 2007.

The reply was not acceptable as the revised PC-I having cost more than 40 million was to be sanctioned by the Central Development Working Party.

DAC in its meeting held on 22nd October, 2008 directed the management to produce the approval of CDWP for verification by audit within 15 days and submit a report to Ministry. No further progress has been reported till the finalization of this report.

4.6 Irregular expenditure of Rs 7.506 million on purchase of stores

According to Rule-4 of Public Procurement Rules, 2004, the procuring agencies while engaging in procurements shall ensure that the procurements are conducted in a fair and transparent manner. The object of procurement brings value for money to the agency and the procurement process is efficient & economical. Rule-8 further stipulates that all procuring agencies shall devise a mechanism, for planning in detail for all proposed procurements with the object of realistically determining the requirements of the procuring agency.

NTC Headquarter, Islamabad incurred an expenditure of Rs 7,506,000 on procurement of CDMA WLL telephone sets, USB data cable, out door antenna and out door (wall mounted) antenna during 2006-07. The rates were called for only for two items whereas actually five items were purchased for which no competitive rates were obtained.

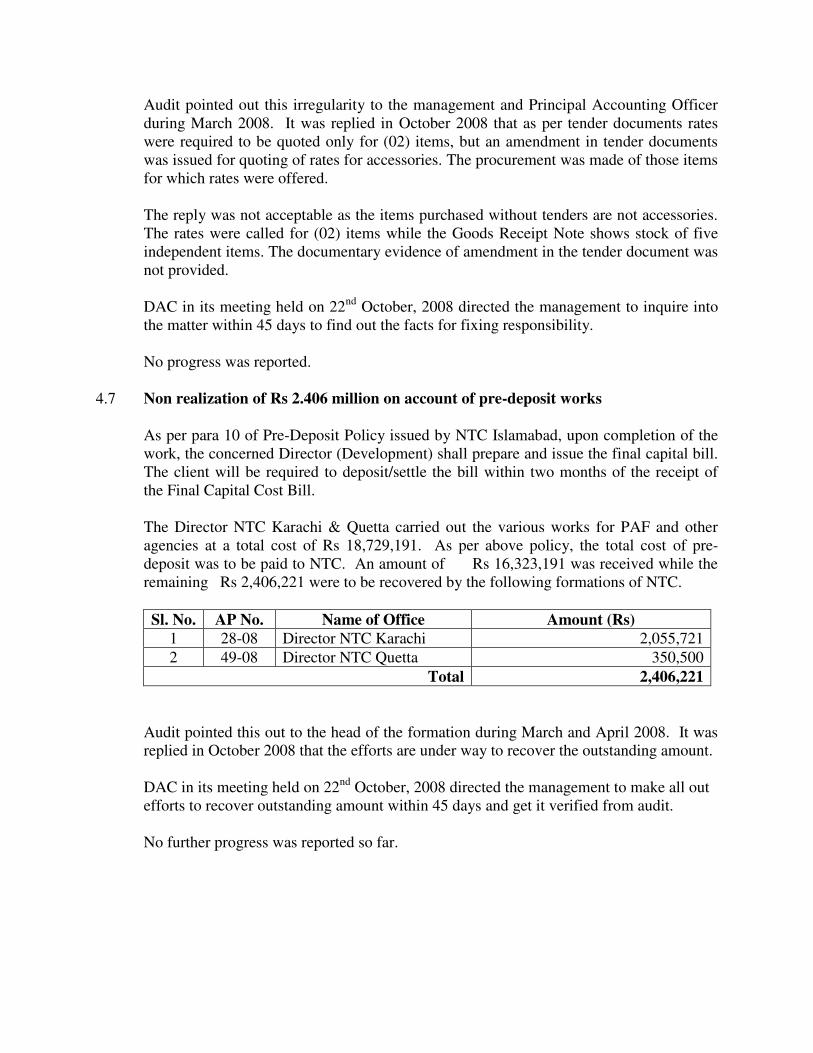

Audit pointed out this irregularity to the management and Principal Accounting Officer during March 2008. It was replied in October 2008 that as per tender documents rates were required to be quoted only for (02) items, but an amendment in tender documents was issued for quoting of rates for accessories. The procurement was made of those items for which rates were offered. The reply was not acceptable as the items purchased without tenders are not accessories. The rates were called for (02) items while the Goods Receipt Note shows stock of five independent items. The documentary evidence of amendment in the tender document was not provided. DAC in its meeting held on 22nd October, 2008 directed the management to inquire into the matter within 45 days to find out the facts for fixing responsibility. No progress was reported.

4.7 Non realization of Rs 2.406 million on account of pre-deposit works

As per para 10 of Pre-Deposit Policy issued by NTC Islamabad, upon completion of the work, the concerned Director (Development) shall prepare and issue the final capital bill. The client will be required to deposit/settle the bill within two months of the receipt of the Final Capital Cost Bill.

The Director NTC Karachi & Quetta carried out the various works for PAF and other agencies at a total cost of Rs 18,729,191. As per above policy, the total cost of pre-deposit was to be paid to NTC. An amount of Rs 16,323,191 was received while the remaining Rs 2,406,221 were to be recovered by the following formations of NTC.

Sl. No. AP No. Name of Office Amount (Rs) 1 28-08 Director NTC Karachi 2,055,721

2 49-08 Director NTC Quetta 350,500

Total 2,406,221

Audit pointed this out to the head of the formation during March and April 2008. It was replied in October 2008 that the efforts are under way to recover the outstanding amount. DAC in its meeting held on 22nd October, 2008 directed the management to make all out efforts to recover outstanding amount within 45 days and get it verified from audit. No further progress was reported so far.

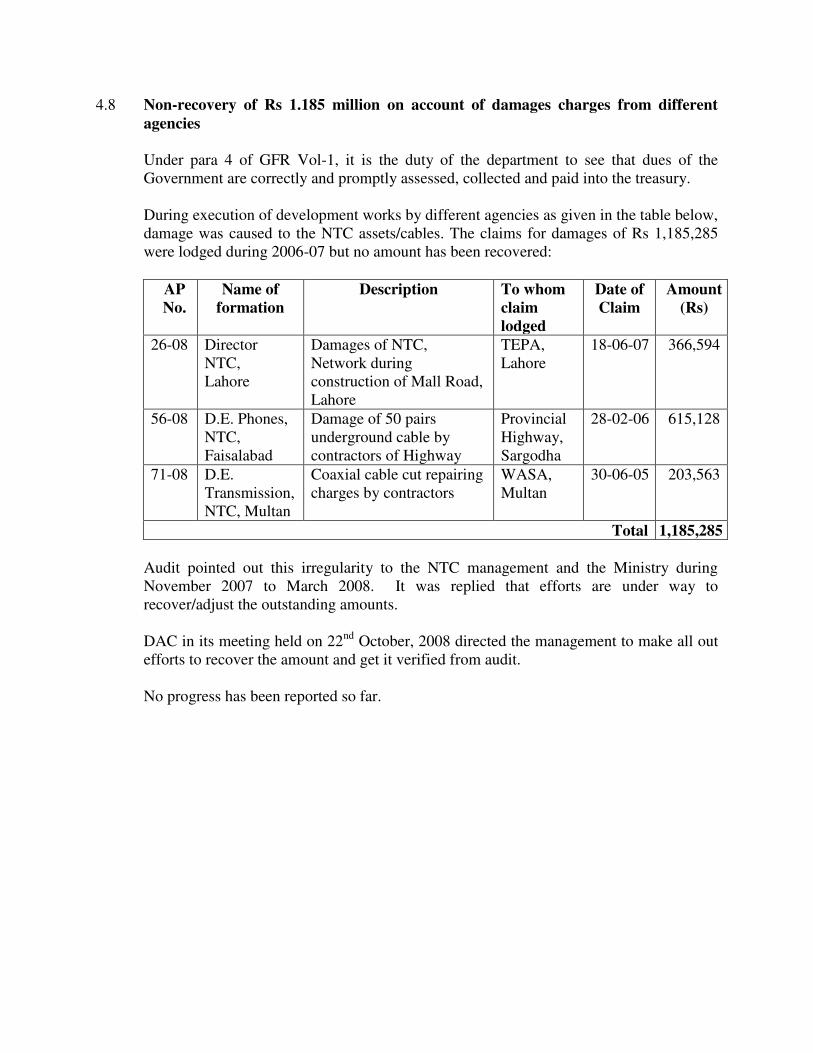

4.8 Non-recovery of Rs 1.185 million on account of damages charges from different agencies

Under para 4 of GFR Vol-1, it is the duty of the department to see that dues of the Government are correctly and promptly assessed, collected and paid into the treasury.

During execution of development works by different agencies as given in the table below, damage was caused to the NTC assets/cables. The claims for damages of Rs 1,185,285 were lodged during 2006-07 but no amount has been recovered:

AP No.

Name of formation

Description To whom claim lodged

Date of Claim

Amount (Rs)

26-08 Director NTC, Lahore

Damages of NTC, Network during construction of Mall Road, Lahore

TEPA, Lahore

18-06-07 366,594

56-08 D.E. Phones, NTC, Faisalabad

Damage of 50 pairs underground cable by contractors of Highway

Provincial Highway, Sargodha

28-02-06 615,128

71-08 D.E. Transmission,NTC, Multan

Coaxial cable cut repairing charges by contractors

WASA, Multan

30-06-05 203,563

Total 1,185,285 Audit pointed out this irregularity to the NTC management and the Ministry during November 2007 to March 2008. It was replied that efforts are under way to recover/adjust the outstanding amounts.

DAC in its meeting held on 22nd October, 2008 directed the management to make all out efforts to recover the amount and get it verified from audit. No progress has been reported so far.

4.9 Short-recovery of liquidated damages from contractors Rs 2.300 million

According to the clause 41 of the terms & conditions of the contract agreements, the contractor shall pay to NTC liquidated damages equivalent to 1% per week subject to a maximum of 10% of the contract value in case of non-completion of works within the stipulated period.

The contractors failed to complete the works within the stipulated periods as per agreements. The maximum liquidated damages of Rs 4,504,671 at the rate of 10% was required to be recovered from two contractors but Director Development NTC, Islamabad deducted liquidated damages of Rs 2,204,172 during 2006-07. This resulted into less recovery of Rs 2,300,499.

Audit pointed out this irregularity to the head of the formation during October 2007. The matter was brought to the notice of the NTC management and the Ministry during January 2008. It was replied in May & October 2008 that an amount of Rs 1.795 million has been recovered and the remaining will be recovered from the final payments and security withheld. The reply was not acceptable as no recovery has been made so far despite lapse of considerable time period. DAC in its meeting held on 22nd October, 2008 directed the management to recover the amount and get it verified from audit. No further progress has so far been reported.

4.10 Non-recovery of Rs 388,553 on account of liquidated damages by extending undue favour

As per contract clause-9 of the contract agreement, unless the delay in completion of work is caused by force majeure or the delay is not on the part of NTC, the contractor shall pay to NTC a sum equivalent to 0.5% of the total contract value for each week delay or part thereof subject to a maximum 10% of total contract value. A contract was executed on 26th July 2005 with M/s Huawei Technologies for Deployment of Next Generation Networks at the cost of Rs 5,977,738. As per clause-7, the contractual works were to be completed upto 15th November, 2005 but the firm completed the works on 13th February, 2006. NTC Headquarter asked the firm in May 2006 to intimate the solid reasons of delay otherwise liquidated damages of Rs 388,553 would be deducted. On the request of the contractor dated 5th May 2006, the completion period was enhanced upto 13th February, 2006 vide amendment dated 11th July, 2006 only to favour the contractor. The very purpose for inclusion of liquidated damages clause to ensure timely completion of work was therefore defeated.

Audit pointed this out to the head of the formation during January 2008. The matter was brought to the notice of the NTC management and the Ministry during March 2008. It was replied in October 2008 that the work was delayed due to non-availability of site for unloading equipment; Provisional Acceptance Test was offered in January 2006 but it took more than two months as the NTC staff was not trained; two extra weeks has also been taken by NTC.

The reply was not acceptable as the amendment for enhancement in completion period

was made after completion of work. The availability of site, trained NTC staff etc. should be foreseen before making contract to avoid delay in completion of works. Hence, responsibility needs to be fixed.

DAC in its meeting held on 22nd October, 2008 directed the management to inquire the matter for fixing responsibility. No further progress has been reported so far.

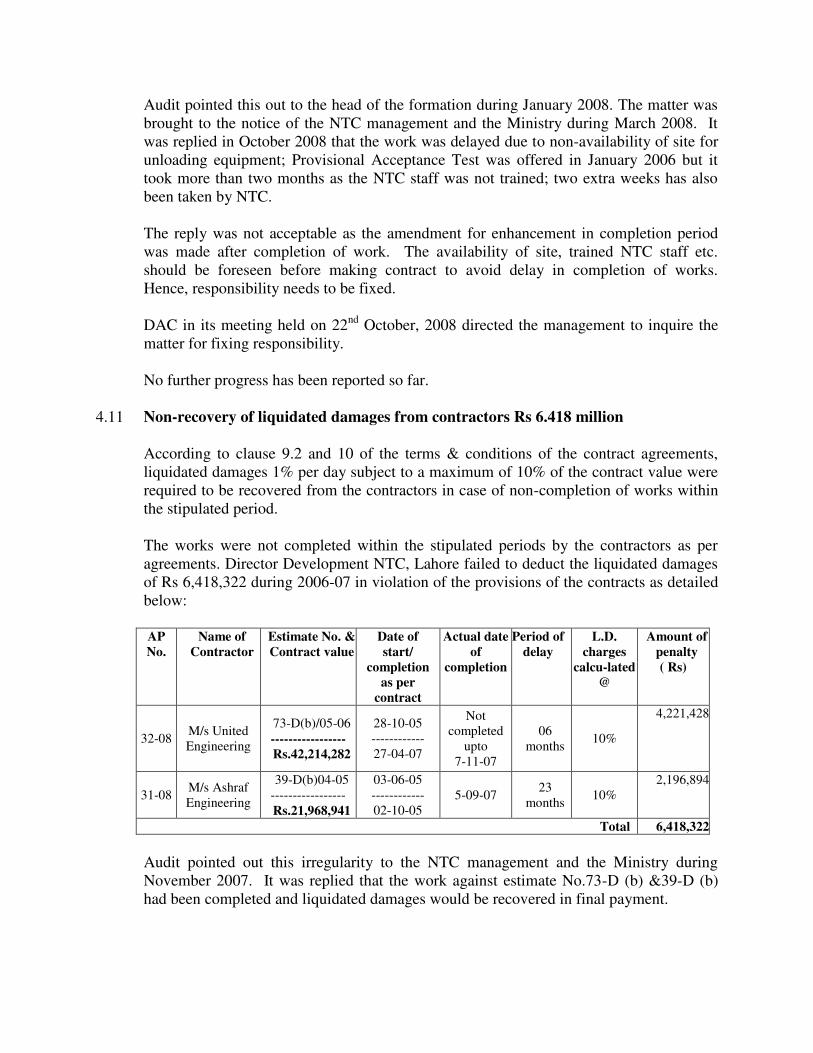

4.11 Non-recovery of liquidated damages from contractors Rs 6.418 million

According to clause 9.2 and 10 of the terms & conditions of the contract agreements, liquidated damages 1% per day subject to a maximum of 10% of the contract value were required to be recovered from the contractors in case of non-completion of works within the stipulated period.

The works were not completed within the stipulated periods by the contractors as per agreements. Director Development NTC, Lahore failed to deduct the liquidated damages of Rs 6,418,322 during 2006-07 in violation of the provisions of the contracts as detailed below: AP No.

Name of Contractor

Estimate No. & Contract value

Date of start/

completion as per

contract

Actual date of

completion

Period of delay

L.D. charges

calcu-lated @

Amount of penalty ( Rs)

32-08 M/s United Engineering

73-D(b)/05-06 ----------------- Rs.42,214,282

28-10-05 ------------ 27-04-07

Not completed

upto 7-11-07

06 months

10%

4,221,428

31-08 M/s Ashraf Engineering

39-D(b)04-05 ----------------- Rs.21,968,941

03-06-05 ------------ 02-10-05

5-09-07 23

months 10%

2,196,894

Total 6,418,322

Audit pointed out this irregularity to the NTC management and the Ministry during November 2007. It was replied that the work against estimate No.73-D (b) &39-D (b) had been completed and liquidated damages would be recovered in final payment.

The amount of liquidated damages be recovered and particulars of recovery be furnished for verification.

DAC in its meeting held on 22nd October, 2008 directed the management to recover amount of Rs 6,418,322 and get it verified from audit. No progress was made till finalization of this report.

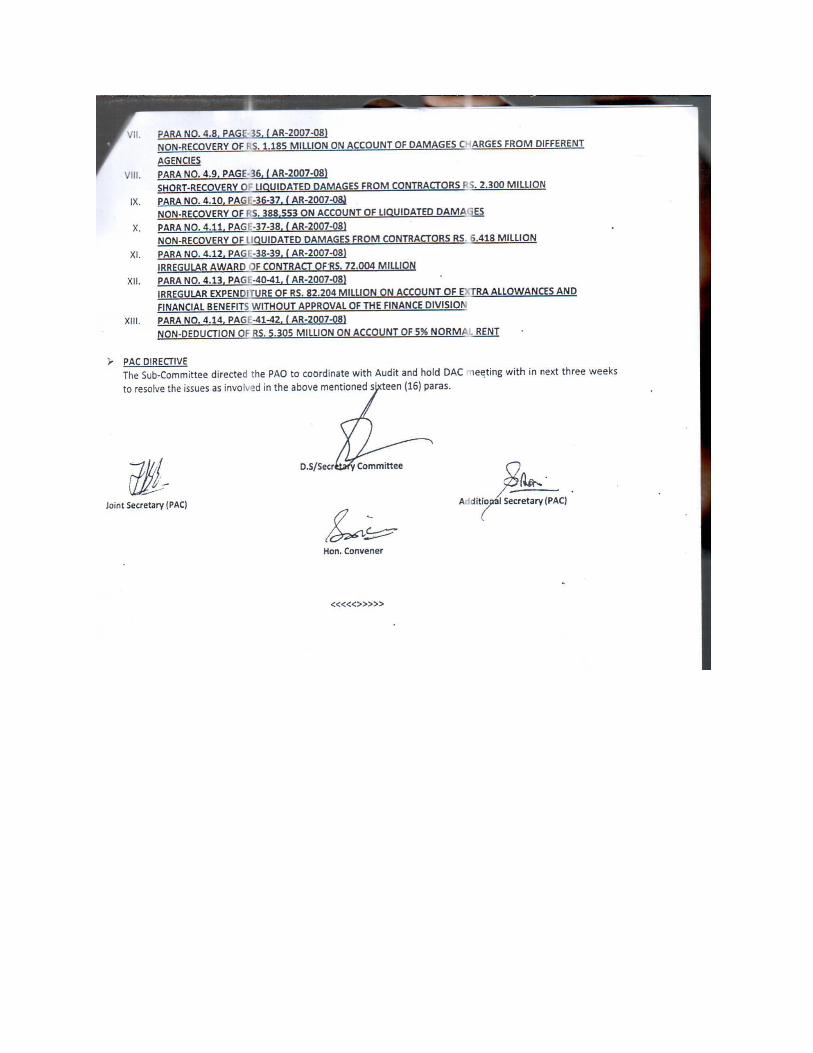

4.12 Irregular award of contract of Rs 72.004 million

According to the laid down procedure circulated vide Ministry of IT vide letter dated 31st January, 2005, development schemes of NTC are required to be sanctioned by the Development Working Party subject to endorsement of the NTC Management. Further, Rule 42 (c) (iv) of Public Procurement Rules 2004 provides that repeat order should not be placed exceeding 15% of the original contract.