Embed Size (px)

Citation preview

ACG 201

AUDITING - I

SPECIAL GROUP : A - ACCOUNTING GROUP

M. Com (M 17) – Part I

Semester - II

YYYYYASHWASHWASHWASHWASHWANTRAANTRAANTRAANTRAANTRAO CHAO CHAO CHAO CHAO CHAVVVVVAN MAHARASHTRA OPEN UNIVERSITYAN MAHARASHTRA OPEN UNIVERSITYAN MAHARASHTRA OPEN UNIVERSITYAN MAHARASHTRA OPEN UNIVERSITYAN MAHARASHTRA OPEN UNIVERSITYDnyangangotri, Near Gangapur Dam, Nashik 422 222, Maharashtra

Copyright © Yashwantrao Chavan Maharashtra

Open University, Nashik.

All rights reserved. No part of this publication which is materialprotected by this copyright notice may be reproduced or transmittedor utilized or stored in any form or by any means now known orhereinafter invented, electronic, digital or mechanical, includingphotocopying, scanning, recording or by any information storageor retrieval system, without prior written permission from thePublisher.

The information contained in this book has been obtained byauthors from sources believed to be reliable and are correct to thebest of their knowledge. However, the publisher and its authorsshall in no event be liable for any errors, omissions or damagearising out of use of this information and specially disclaim anyimplied warranties or merchantability or fitness for anyparticular use.

YASHWANTRAO CHAVAN MAHARASHTRA OPEN UNIVERSITY

Vice-Chancellor : Dr. M. M. Salunkhe

Director (I/C), School of Commerce & Management : Dr. Prakash Deshmukh

State Level Advisory Committee

Dr. Pandit Palande Dr. Suhas Mahajan Dr. V. V. Morajkar

Hon. Vice Chancellor Ex-Professor Ex-Professor

Dr. B. R. Ambedkar University Ness Wadia College of Commerce B.Y.K. College, Nashik

Muaaffarpur, Bihar Pune

Dr. Mahesh Kulkarni Dr. J. F. Patil Dr. Ashutosh Raravikar

Ex-Professor Economist Kolhapur Director, EDMU,

B.Y.K. College, Nashik Ministry of Finance, New Delhi

Dr. A. G. Gosavi Dr. Madhuri Sunil Deshpande Dr. Prakash Deshmukh

Professor Professor Director (I/C)

Modern College, Swami Ramanand Teerth Marathwada School of Commerce & Management

Shivaji Nagar, Pune University, Nanded Y.C.M.O.U., Nashik

Dr. Parag Prakash Saraf Dr. S. V. Kuvalekar Dr. Surendra Patole

Director, Institute of Management Associate Professor and Assistant Professor

Science, Pimpri, Pune Associate Dean (Training)(Finance ) School of Commerce & Management

National Institute of Bank Management, Y.C.M.O.U., Nashik

Pune

Dr. Latika Ajitkumar Ajbani

Assistant Professor

School of Commerce & Management

Y.C.M.O.U., Nashik

Authors & Editors

Dr. Parag Prakash Saraf

Director, Institute of Management Science, Pimpri, Pune

Dr. Latika Ajitkumar Ajbani

Assistant Professor, School of Commerce & Management, Y.C.M.O.U., Nashik

Instructional Technology Editing & Programme Co-ordinator

Dr. Latika Ajitkumar Ajbani

Assistant Professor, School of Commerce & Management, Y.C.M.O.U., Nashik

Production

Shri. Anand Yadav

Manager, Print Production Centre

Y.C.M. Open University, Nashik - 422 222.

Copyright © Yashwantrao Chavan Maharashtra Open University, Nashik.

(First edition developed under DEC development grant)

q First Publication : September 2015

q Type Setting : Avinash R. Varpe (Sangamner, Mob.9960252514)

q Cover Print :

q Printed by :

q Publisher : Dr. Prakash Atkare, Registrar, Y.C.M.Open University, Nashik - 422 222.

INTRODUCTION

I am very please to placing the first and enlarge edition of this study material

on 'Auditing' to the students and practitioners of this subject. This book is design as

per the revise syllabus prescribed by the YCMOU Nashik from August 2015. It

gives equal importance to the theoretical aspects as well as to the practical case

studies. Hence this edition will be an ideal companion not only to the scholars but

also to the average students. I am sure that this present work a result of my sincere

and dedicated efforts would subserve the genuine interest of all the students concerned

in enriching their knowledge of this ever-growing Auditing discipline.

I have made a sincere attempt to make the subject easy to understand. For

this purpose the theory on each topic is written in a simple and lucid language to

enable the students to grasp the essence of subject. This book is also useful to the

students of CA, CWA and CS course.

It gives me great pleasure to introduce you to the world of Auditing and

Assurance. This book has got knowledge oriented and exam oriented approach. I

am tried to cover all Audit Assurance Standards (AAS) and provisions of amended

Company Act 2013. So let's start this lovely journey of learning in a positive way.

Any suggestions will be appreciated.

I am confident, that students will welcome new edition of this book.

With knowledge, hard work, marvelous success is just around the corner.

All The Best!

- Dr.Parag Prakash Saraf

Index

Unit No. Unit Name Page No.

1 INTRODUCTION OF AUDIT 9

2 TYPES OF AUDIT 18

3 VOUCHER & VOUCHING 26

4 INTERNAL CHECK & ROLE OF INTERNAL

AUDITOR 36

5 DOCUMENTATION 45

6 FRAUDS - THEIR DETECTION & PREVENTION 52

7 VALUATION & VERIFICATION OF ASSETS 63

8 VALUATION & VERIFICATION OF LIABILITIES 73

9 COMPANY AUDIT IN BROAD LINE,

PROFIT AVAILABLE FOR DIVIDEND,

AUDITOR'S DUTIES REGARDING RESERVES 79

10 QUALIFICATION & APPOINTMENT OF

A COMPANY AUDITOR 89

11 RIGHTS, DUTIES AND RESPONSIBILITIES OF

A COMPANY AUDITOR 96

12 MISCELLANOUS MATTERS IN

COMPANY AUDIT 103

SYLLABUS - AUDIT -I

1) INTRODUCTION OF AUDIT

Definition, Objectives of an Audit, Scope of an Audit,

Restriction of scope, Advantages of an Audit, Limitations of an

audit, Audit Programme, Contents of Audit Programme,

Advantages of an Audit Programme, Disadvantages of an Audit

Programme, Audit Working Papers, Commencement of New Audit

2) TYPES OF AUDIT

Kinds of Audit, Statutory / Mandatory Audit, Voluntary /

Independent Audit, Interim Audit, Concurrent Audit, Continuous

Audit, Balance Sheet Audit, Financial Audit, Cost Audit,

Management Audit, Audit Techniques

3) VOUCHER & VOUCHING

Vouching, Purpose of vouching, Objectives of vouching,

Voucher, General Consideration in Audit of Ledger, Audit of

Different Ledgers, Bought Ledger, Sales Ledger, General Ledger,

Kinds of Frauds in relation to Ledgers

4) INTERNAL CHECK & ROLE OF INTERNAL

AUDITOR

Internal Control, Objectives of Internal Control, Essentials

of Good Internal Control System, Inherent Limitations of Internal

Control, Methods for the Proper Review & Evaluation of the

Adequacy of the Internal Control, Internal Check, Objects of

Internal Check, Internal Audit, Basic Principles of Establishing

Internal Auditing, Objectives of Internal Audit, Role of Internal

Auditor, Possible areas of co-operation & co-ordination

5) DOCUMENTATION

Documentation, Importance of Working Papers, Form &

Content of Working Papers, Lien on Working Papers, Classification

of Working Papers, Audit Note Book

6) FRAUDS - THEIR DETECTION & PREVENTION

Frauds, Errors, Reasons & Circumstances of Frauds &

Errors, Auditor's responsibility for non detection of frauds & errors,

Events which increases the risk of fraud or error, Inherent limitation

of an audit in relation to frauds & errors, Types of fraud, Internal

Audit, Internal Control, Elements of internal control, Investigation

for suspected frauds

7) VALUATION & VERIFICATION OF ASSETS

Verification of Assets, General Consideration for Valuation

& Verification of Assets, Valuation of Assets, Valuation of Fixed

Assets, Valuation of Current / Floating Assets, Inventories (Stock

in Trade), Long term Work in Progress, Trade Debtors, Investments,

Loans, Advances, Bank Balance, Cash balance on Hand

8) VALUATION & VERIFICATION OF LIABILITIES

General principles to be followed in verification of liabilities,

Verification of Liabilities, Valuation of Liabilities, Trade Creditors,

Bills Payables, Outstanding Liabilities for expenses, Provision for

Taxation, Contingent Liabilities, Debentures

9) COMPANY AUDIT IN BROAD LINE, PROFIT

AVAILABLE FOR DIVIDEND, AUDITOR'S DUTIES

REGARDING RESERVES

Company Audit, Share Capital Audit, Auditor's duties

regarding to audit of share capital, Shares underwritten placed for

commission, Shares issued at premium, Shares issued at a discount,

Audit of debentures, Preliminary Expenses, Statutory Meeting &

Statutory Report, Dividend, Interim dividend, Auditor's duty with

regard to payment of dividend, Transfer to reserve, Capita profits,

Revaluation reserve

10) QUALIFICATION & APPOINTMENT OF A

COMPANY AUDITOR

Qualification of Auditors, Disqualification of Auditors,

Appointment of Company Auditor, Removal of the auditor, Auditor's

Remuneration

11) RIGHTS, DUTIES AND RESPONSIBILITIES OFA

COMPANY AUDITOR

Rights & Powers of an Auditor, Duties & responsibilities

of the auditor, Scope of duties of an auditor

12) MISCELLANOUS MATTERS IN COMPANY

AUDIT

Statutory report, Audit of branch Accounts, Powers of

accompany auditor in relation to branch, Exemption to Branch

Audit, Special audit on direction of Central Government, Cost audit

Intoduction of AuditUNIT - 1

INTRODUCTION OF AUDIT

Structure

1.0 Introduction

1.1 Objectives

1.2 Definition

1.3 Objectives of an Audit

1.4 Scope of an Audit

1.4.1 Restriction of scope

1.5 Advantages of an Audit

1.6 Limitations of an audit

1.7 Audit Programme

1.7.1 Contents of Audit Programme

1.7.2 Advantages of an Audit Programme

1.7.3 Disadvantages of an Audit Programme

1.8 Audit Working Papers

1.9 Commencement of New Audit

1.10 Key concepts

1.11 Summary

1.12 Exercise & Questions

1.13 Further Reading and References

1.0 Introduction

The industrial revolution and the consequent explosion of technology have

resulted in an enormous increase in the size of all organizations, business

undertakings. So control on various aspects is required. This growth has had far

reaching effects on accounting and auditing. Auditing has now become an analytical

exercise which involves evaluating the effectiveness of internal control procedures

by examining selected samples of transactions and applying analytical procedure.

1.1 Objectives

After this unit you should be able :

1. To understand the concept of audit.

2. To find out scope and limitations of audit.

3. To know in detail the audit program.

4. To understand the importance of audit working papers.

1.2 Definition of an Audit

"An audit is independent examination of financial information of

any entity, whether profit oriented or not, and irrespective of its size or

legal form, when such an examination is conducted with a view to expressing

an opinion thereon."

CHECK YOUR

PROGRESS

Define objectives of

Audit?

AUDITING - I (9)

NOTES

AUDITING - I

(10) AUDITING - I

NOTES

According to general guidelines on internal Auditing issued by ICAI, auditing

is defined as a

"Systematic and independent examination of data, statements,

records, operations and performances (financial or otherwise) of an enterprise

for a stated purpose. In any auditing situation, the auditor receives and

recognizes the propositions before him for examination, collects evidence,

evaluates the same and on this basis, formulates his judgement which is

communicated through his Audit Report".

The above definitions of auditing have certain important elements. They

are:

1. Independence - The auditor has to express an opinion on the financial

statements examined by him. Therefore, auditor should be free from any

interest which might detract his objectivity.

2. Auditor's opinion - The auditor has to express an opinion on the financial

statements examined in the form of an audit report. The audit report is an

expression of opinion rather than a statement of verified facts.

3. Financial statements -. The financial statements comprise of Balance Sheet,

Profit and Loss Account, notes and other statements, which collectively are

intended to give a proper understanding of the financial position. The auditor

has to express an opinion on the financial statements.

These three elements are contained in any kind of audit, whether profit oriented

or not and irrespective of its size or legal form.

1.3 Objectives of an Audit

1. Reporting: The primary objective of auditing is reporting - whether

the Financial Statements present a "true and fair view" of the financial position

(Balance Sheet) and the financial performance (Profit and Loss Account)

during the period.

2. Expression of Opinion: The objective of an audit of Financial Statements,

prepared within a framework of recognized accounting policies and relevant

statutory requirements, is to enable an auditor to express an opinion on such

Financial Statements.

3. True and Fair View: The Auditor's duty is to express an opinion on financial

statements.

(a) Auditor's opinion helps to determine the true and fair view of the operating

results & financial position of an enterprise.

(b) The user, however, should not assume that the Auditor's opinion is an

assurance as to the future viability of the enterprise of the efficiency or

effectiveness.

4. Management Responsibility:

(a) The Management of an enterprise is primarily responsible for the preparation

of Financial Statements

(b) Management's responsibilities include maintenance of adequate accounting

records and internal controls, selection and application of accounting policies

CHECK YOUR

PROGRESS

Define Concept of

Audit?

AUDITING - I (11)

NOTES

Intoduction of Auditand safeguarding the assets of the enterprise.

(c) Hence, the audit of the Financial Statements does not relieve Management

of its responsibilities.

1.4 Scope of an Audit

lllll Scope:

Auditor will be determined the scope of an audit of financial statements with

regards to -

a) The terms of the engagements

b) The pronouncements of ICAI

c) The requirements of relevant legislation

lllll Coverage of work:

The auditor should be organized to cover all operational aspects relevant to

the financial statements. He has to make study & evaluate the accounting

system & internal controls on which auditor wishes to rely.

lllll Disclosure:

Auditor should ensure whether all relevant information is properly disclosed

in financial statements & as per statutory requirement. The disclosure

requirement can be verified by performing-

- Financial statement analysis &

- Evaluation of accounting policies.

lllll Judgment:

Absolute certainty is not attainable in auditing because of the need to exercise

judgment. Auditor is also required to examine the reasonableness of judgment.

lllll Materiality:

Material items are those, which might influence the decision of the users of

financial statements. Auditor should exercise his professional experience &

judgment with material items.

lllll Technical aspects:

Auditor is not expected to perform duties, which fall outside the scope of his

competence. Auditor is not an expert in all fields. So, auditor can take the

advice of an expert for technical work.

1.4.1 Restriction of scopea) The terms of engagement cannot restrict the scope of an audit in relation

to matters,which are prescribed by legislation or by the pronouncement of

the Institute.

b) Where the scope of work impairs the auditors ability to express an

unqualified opinion on such financial statements & he should state the

restriction.

1.5 Advantages of an AuditThe principle advantage of an audit is to get an informed, objectives &

forthright opinion on financial statements of the enterprises. This can be used in

making significant decisions by interested parties like shareholders, creditors, banks

CHECK YOUR

PROGRESS

Give Scope of Audit?

AUDITING - I

(12) AUDITING - I

NOTES

etc. With the help of audit the shareholders of the company are assured that the

funds invested by them are safe & are used for the purpose for which they were

raised.

1) A proprietary concern accounts may be audited to get funds from banks.

2) In case of partnership firm accounts may be audited for the decision making

like valuation of goodwill of firms or settlement of accounts at the time of

admission, retirement or death of partner.

3) There is a separation of ownership & management in case of company.

Shareholders have no direct control on the administration on the company. So

audited accounts may help to shareholders to get complete understanding

about company's affairs.

4) Audit helps in locating the weaknesses, inadequacies in the financial statements.

5) An audit also helps in detection of wastages & losses and suggests ways by

which they might be checked.

6) Sometimes government may require audited & certified statements for giving

assistance or issue a license.

7) An audit helps in setting liability of taxes, negotiating loans, determining purchase

consideration of business, setting trade disputes for higher wages & bonus.

8) An audit also helps to control over inefficiency.

These are some advantages of an audit.

1.6 Limitations of an Audit

Though auditing has its advantages, it has certain limitations too.

1. An auditor has to depend on the books of accounts & other records presented

before him. If these accounts are prepared with malafide intentions, the auditor

may not fully detect them.

2. Auditor is not expected to be an expert in all the fields. He has to depend upon

the opinion of the expert.

3. Auditor has to depend upon the explanations & information given by the client.

But it is possible that such information & explanations may not be correct.

4. Audit evidence persuasive rather than conclusive in nature. Eg. Confirmation

of a debt by a customer is not conclusive that the debt is good & recoverable.

5. The auditor's independence is necessary to serve the purpose of audit. Though

under law shareholders appoint the auditor. In reality, directors appoint the

auditors.

6. Auditor has to make an assessment of internal control system & rely on them

if they are effective. However, there will always some risk of internal control;

it may be ineffective against fraud involving collusion among employees.

1.7 Audit Programme

An audit programme is a predetermined plan of the auditing work to be

performed, specifying the procedure to be followed in verification of each item in

the financial statement, allocation of the audit staff and the time framed to be

followed in conducting audit. Audit programme is the written plan of audit work

CHECK YOUR

PROGRESS

Give advantages of

Audit?

AUDITING - I (13)

NOTES

Intoduction of Auditwhich contains the audit objectives It also specifying what work to be done, when

to be done, & by whom to be done.

1) An Audit programme is detailed plan of work, prepared by the auditor

for carrying out an audit.

2) It constitutes the plan of the work which provides a basis for supervision

& control of work. It is a set techniques & procedures which auditor applies for

forming an opinion on financial statements.

1.7.1 Contents of Audit ProgrammeContents of an audit programme maybe divided as under:

1) A review of the system of internal check.

2) Audit of Balance Sheet accounts.

3) Audit of Profit and Loss account items.

4) Preparation of the audit report and co-ordination of all the

above-mentioned items.

1.7.2 Advantages of an Audit Programme:

1) Instructions: The audit programme specifies the extent & manner of checking

& verification of different aspects of the accounting records.

2) Checklist: It serves as a ready checklist of procedures and techniques to be

applied and minimizes the possibility of overlooking any of the important audit

steps.

3) Phasing work: The work can be planned and phased properly.

4) Selection of Team Members: The audit programme helps in selection of

assistants for jobs on the basis of their capability.

5) Supervision: The work can be supervised and controlled better by periodic

reference to the programme.

6) Work Review: The progress of the work at any point of time can be readily

known by reference to the entries on the audit programme.

7) Future Planning: It serves as a guide for carrying out the current audit and

as a basis for drawing the future audit programmer-

8) Responsibility: Responsibility for an audit examination is fixed on the team

member who has signed after completing a particular procedure under the

programme.

9) Basis for opinion: It serves as evidence of the work performed and provides

a sound basis for the expression of the Auditor's opinion.

10) Record of Work: All work performed by auditor should be recorded. It is

the sufficient proof that the work was carried out with reasonable skill & care

that is of expected a professional.

1.7.3 Disadvantages of Audit Programme.

Following are the disadvantages of Audit Programme -

1) Mechanical work: The audit may be performed mechanically without

reference to the special circumstances of the client or to the development of

any new or unusual features in the client's business.

CHECK YOUR

PROGRESS

Give limitations of

Audit?

AUDITING - I

(14) AUDITING - I

NOTES

2) Rigidity: Additional procedures or techniques may be called for by the special

circumstances.

3) False sense of security: Audit members may feel that everything is taken

care by the audit programme. They may fail to apply their mind in

circumstances that arise during the course of work.

4) Lack of Initiative: Independent judgment and initiative of the staff may be

restricted. It may frustrate talented and efficient audit staff.

5) Lack of Suitability: Procedures may be undertaken which may be

inappropriate to the circumstances of the client's business.

How will you overcome from disadvantages of Audit Programme?

1. Suitability: Audit programme should be suitable to the nature of entity, scale

of operations & volume of transactions & the efficacy of internal controls.

2. Review of the internal controls: Internal controls should be reviewed and

evaluated to obtain knowledge of changes in the controls and systems and

procedures.

3. Changed business operations: The Auditor should obtain information about

new systems to carry on the old business. The audit programme should be

recast or modified to suit the changed business operations and practices.

4. Participative approach: The Auditor should encourage his audit assistants

to keep an open mind and make suggestions for amending the programmes.

5. Flexibility: The audit programme should not become stereotyped. There

should be revision from time to time according to circumstances even though

no material change has taken place in the client's business operations and the

business practice. It means audit programme should be flexible according to

situation.

6. Minimum Requirement: It should be impressed upon the audit assistants

that the programme provides for the minimum tests that should be carried out

and they should undertake tests and surprise checks, considered appropriate,

even though not provided in the programme

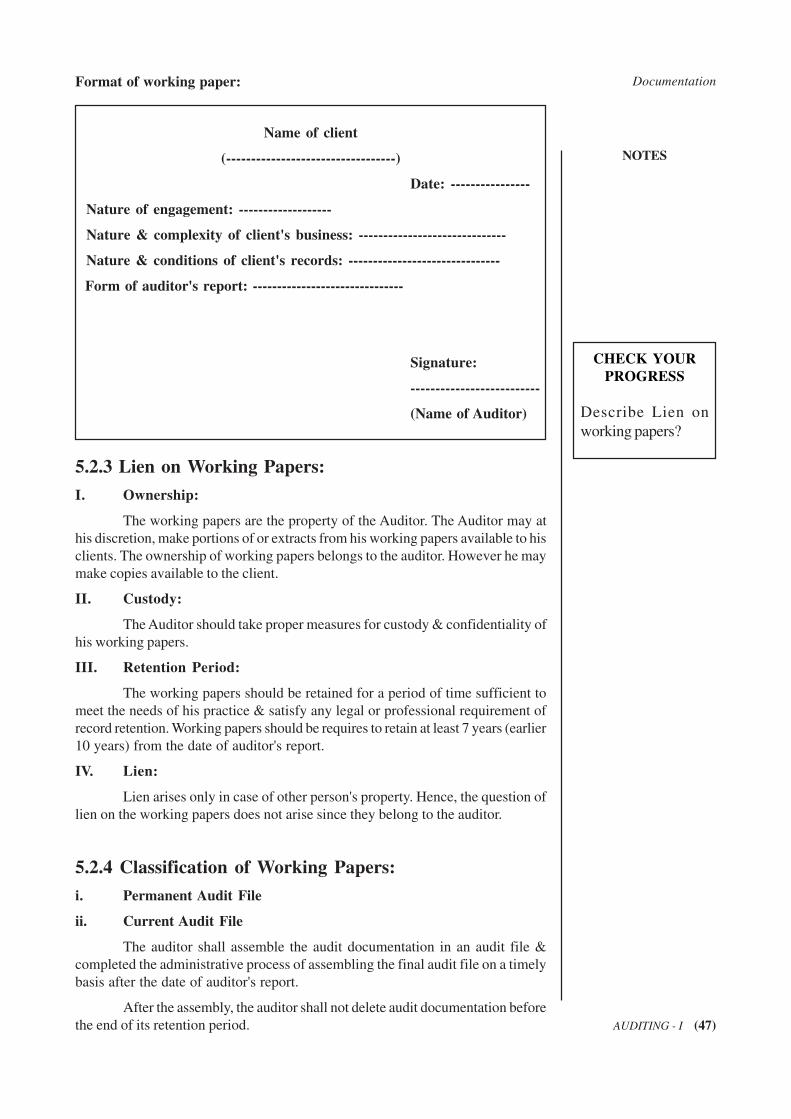

1.8 Audit working papers

The audit working paper constitutes the link between the auditor's report

and the client's records.SA 230 on "Documentation" refers to working papers

prepared or obtained by the auditor and retained by him in connection with the

performance of his audit. Working papers should record audit plans. The working

papers should provide for-

a. Means of controlling current audit work.

b. Supervision and review of the audit work.

c. Evidence of audit work performed to support the auditor's opinion.

Working papers should also prove the evidence of work performed in case

of charge of negligence brought against the auditors.

CHECK YOUR

PROGRESS

Define Audit

program, its

advantages and

limitations?

AUDITING - I (15)

NOTES

Intoduction of Audit1.9 Commencement of New Audit

Auditor should prepare himself before the commencement of a new audit;

following points should consider:

lllll Initial Engagement: Initial engagement means appointment of an auditor for

first time by the client. First of all auditor should confirm his appointment

letter that fulfilling all its legal requirements.

lllll Internal Control System: Auditor should evaluate the internal control system

of client's enterprise. The review of internal control system will helps the

auditor to know the weaknesses in system. Accordingly auditor develops the

audit plan.

lllll Books of Accounts: The auditor should obtain the list of all the books of

account and should see that all books have been kept in accordance with

required policies & procedures. Auditor should see that required standards

were followed.

lllll Documentation: The auditor should obtain the copy of the legal documents

and should study carefully before the commencement of audit. Eg.

Memorandum of association, Articles of association, Prospectus and Contract

with vendors etc.

lllll Complexity of Audit: Auditor should know the nature of audit so that he may

prepare himself accordingly. The scope of work & responsibility should be

taken into account in determining the complexity of audit.

lllll Internal Audit: Auditor should also study the internal audit system in the

business concern. He should make detailed inquiries, inspect books of

accounts and observe the actual procedure in operation.

lllll Accounting System: Auditor must know the accounting system adopted by

client concern, before the commencement of new audit. He should thoroughly

investigate the whole system of book keeping and accounting.

lllll Environment in which entity operates: Auditor should understand various

operational aspects of audit. Eg. Extent of computerization, general attitude

of personnel's, etc.

l l l l l Audit Programme: Audit program is predetermined plan of audit. Keeping in

view the nature of audit, nature of business and extent of work, auditor

should work out an audit programme for the commencement of new audit.

lllll List of important persons: Auditor should obtain the list of important persons

along with their powers & responsibilities.

lllll Previous Experience with the client: Auditor should observe the last balance

sheet for the purpose of checking the opening entries for the period under

audit. The previous auditor report should also be inspected. Auditor should

pay particular attention to matters that required special consideration.

These are some points which are necessary to understand before the

commencement of audit. This will help the auditor to determine the nature,

timing & extent of audit.

CHECK YOUR

PROGRESS

Give brief about new

Audit concept?

AUDITING - I

(16) AUDITING - I

NOTES

1.10 Key Concepts

Audit - "An audit is independent examination of financial information of

any entity, whether profit oriented or not, and irrespective of its size or legal form,

when such an examination is conducted with a view to expressing an opinion

thereon."

Audit programme is the written plan of audit work which contains the

audit objectives It also specifying what work to be done, when to be done, & by

whom to be done.

Audit Working Paper constitutes the link between the auditor's report and the

client's records.

1.11 Summary

Systematic and independent examination of data, statements, records,

operations and performances (financial or otherwise) of an enterprise for a stated

purpose is known as audit.

Reporting, expression of auditor's opinion in a fair manner are some of the

objectives of an audit. It is beneficial for getting loan from bank valuation of goodwill.

Audit helps in locating the weaknesses, inadequacies in the financial statements. It

also helps in detection of wastages etc.

There are certain weaknesses of audit such as Auditor has to depend

upon the explanations & information given by the client which may not be correct.

An Audit programme is detailed plan of work, prepared by the auditor for

carrying out an audit. Auditor should prepare himself before the commencement

of a new audit.

1.12 Exercise & Questions

1. Define the term Audit & state the advantages of audit?

2. What is mean by Audit Programme? State the disadvantages of Audit

Programme & how will you overcome from disadvantages of Audit

Programme?

3. State the importance of Audit working papers?

4. Which points should considered while commencement of new audit?

lllll Fill in the blanks:

1) The primary objective of auditing is ________________.

(Expression of opinion, Reporting, Vouching, Verification)

2) The Auditor's duty is ___________________on financial statements.

(Reporting, to express an opinion, Vouching,

3) The principle advantage of an audit is to get an informed, _____________

& forthright opinion on financial statements of the enterprises.

(Scope, Objectives, Disadvantages, Audit procedure)

AUDITING - I (17)

NOTES

Intoduction of Audit4) Audit evidence _________________ rather than conclusive in nature.

(True, Persuasive, Fair, Correct)

5) ____________________ is detailed plan of work, prepared by the auditor

for carrying out an audit.

(Audit Programme, Audit Plan, Audit Technique, Audit Working papers)

6) --------------- should also prove the evidence of work performed in case of

charge of negligence brought against the auditors.

(Audit Programme, Internal Control, Working Papers, Internal Audit)

7) Auditor should also study the ________________ in the business concern.

(Environment, Internal audit system, Business policies, Internal control)

8) The -------------- constitutes the link between the auditor's report and the

client's records.

(Audit Working Papers, Audit Programme, Audit Plan, Internal Audit)

9) Audit programme should be ______________ according to situation.

(Fixed, Flexible, Semi Flexible, Classified)

10) All work performed by ____________ should be recorded.

(Director, Auditor, Management, Secretary)

11) There is a separation of ____________ & management in case of company.

(Directorship, Responsibilities, Ownership, Control)

12) Auditor can take the advice of an _______________for technical work.

(Internal auditor, cost auditor, Management, Expert)

13) ________________items are those, which might influence the decision of

the users of financial statements.

(Material, Capital, Revenue, Technical)

14) Auditor should be free from any _____________which might detract his

objectivity.

(Item, Interest, Challenge, None)

15) Reporting is beneficial for getting loan from bank valuation of

________________.

(Goodwill, Fixed assets, Current assets, Share capital)

(Answers: 1) Reporting, 2) to express an opinion, 3) objectives, 4) Persuasive,

5) Audit programme, 6) Working papers, 7) Internal audit system, 8) Audit

working papers, 9) Flexible, 10) Auditor, 11) Ownership, 12) Expert, 13)

Material, 14) Interest, 15) Goodwill)

1.13 Further Reading and References

1. Audit Assurance Standards ( AAS) issued by ICAI

2. N.D.Kapoor's Audit Procedure

3. Dr. Mahesh Kulkarni's Audit practices

AUDITING - I

(18) AUDITING - I

NOTES

UNIT - 2

TYPES OF AUDIT

Structure

2.0 Introduction

2.1 Objectives

2.2 Kinds of Audit

2.2.1 Statutory / Mandatory Audit

2.2.2 Voluntary / Independent Audit

2.2.3 Interim Audit

2.2.4 Concurrent Audit

2.2.5 Continuous Audit

2.2.6 Balance Sheet Audit

2.2.7 Financial Audit

2.2.8 Cost Audit

2.2.9 Management Audit

2.3 Audit Techniques

2.4 Key concepts

2.5 Summary

2.6 Exercise & Questions

2.7 Further Reading and References

2.0 Introduction

There are various types of audit. Auditor may choose any audit procedure

for conducting audit of financial statements. Audit procedure may vary from

enterprise to enterprise according to the nature of business, audit period, etc.

2.1 Objectives

After this unit you should be able:

1. To be familiar with various types of audit.

2. To understand new audit techniques.

lllll AUDIT:

"An audit is independent examination of financial information of

any entity, whether profit oriented or not, and irrespective of its size or

legal form, when such an examination is conducted with a view to expressing

an opinion thereon."

AUDITING - I (19)

NOTES

2.2 Kinds of Audit

2.2.1 Statutory / Mandatory Audit:The audit which is prescribed by law i.e. governing by statute or by

regulations is called statutory audit. Where scope is defined by law, it can't be

restricted by the appointing authority. Only a person possessing the prescribed

qualification shall conduct the audit. The matters to be covered in the auditor's

report are generally defined by law.

Examples of Statutory Audit

Enterprise Governing Statute

Companies Companies Act, 1956

Co-operative Multi-state Co-operative Societies Act and

Societies also State enactments

Banking Companies Banking Regulation Act, 1949

Insurance Companies Insurance Act and Companies Act, 1956

Electricity Companies Indian Electricity Act, 1910 and Companies Act, 1956

Corporations Statute by which the Corporation is created

e.g. IDBI Act, LIC, etc.

2.2.2Voluntary / Independent Audit:This audit is purely optional and at discretion of the governing body. The

scope of audit is defined by the letter of engagement between the auditor and the

client. The format of report is prescribed by the scope of work.

Examples: Individuals, Private trusts, Partnership firms etc. which are

not governed by any audit provisions of act.

2.2.3 Interim Audit:An audit which is conducted between two annual audits is called an interim

audit. Such type of audit conducted at a specific date as per client's requirement.

Eg. 30th September, 31st December. Financial statements are prepared for interim

audit period. Assets and liabilities are verified for interim balance sheet purposes.

Advantages of Interim audit

lllll Immediate detection of errors & frauds: Errors & Frauds, if any, easily

detected.

lllll Upto date accounts: The accounting staff of the client is motivated to keep

the books of accounts upto date.

lllll Early final audit: The final audit can be completed in a short span of time.

lllll Interim dividend: It helps the company to publish interim financial statements

for declaration of interim dividend.

lllll Act as deterrent: Frequent attendance by audit staff deters persons from

committing a fraud.

lllll Staff planning: Staff can be sent regularly by proper planning. Work scheduling

can be done effectively.

Types of Audit

CHECK YOUR

PROGRESS

Explain different types

of Audit?

AUDITING - I

(20) AUDITING - I

NOTES

lllll Interim reporting: Interim financial statement can be prepared easily & in

timely manner.

lllll Detailed coverage: All verifications are carried out in detailed than in final

audit.

Disadvantages of Interim audit

lllll Failure to keep track: Since work is carried out in several installments, the

audit staff may fail to keep track of things. As a result some of the transactions

may escape.

lllll Tampering: The staff of the client may alter entries in the books of accounts

after checking thereof.

lllll Uneconomic: The audit is uneconomic for small size concern as a great deal

of time & efforts would be wasted.

lllll Missing links: Continuity in work may be lost when work is executed

lllll Time consuming: Since all transactions are verified. Continuous audit will be

time consuming.

lllll No guarantee for fraud detection: Complete verification of all transactions in

detail, does not guarantee detection of all errors & frauds. Some material

misstatements may still exist.

2.2.4 Concurrent Audit:It implies verification of transactions of a year on a continuous basis. The

period of verification is primarily determined by the auditor. Financial statements

are not prepared. Assets & liabilities are verified only at the time of finalization at

the year end.

2.2.5 Continuous Audit:When the Auditor's staff is engaged continuously in checking the accounts

of the client during the whole year round or when the staff attends audit work at

some intervals, it is called a Continuous Audit.

Advantages of continuous audit

lllll Immediate errors and frauds detection: Management can exercise a stricter

control over the accounts in as much as it is able to check sooner the causes

of any errors or frauds uncovered by such an audit.

lllll Acts as Deterrent: The frequent attendance of the audit staff deters persons

from committing fraud.

lllll Upto date accounts: The accounting staff of the client is motivated to keep

the books of account upto date.

lllll Early Final Audit: The final audit can be completed in short span of time..

lllll Knowledge of clients' affairs: The Auditor can obtain a more detailed

knowledge of the client's affairs, which helps the auditor to discharge his

duties more efficiently.

lllll Detailed Coverage: All aspects of verification are carried out in detail than in

final audit.

CHECK YOUR

PROGRESS

Define interim Audit,

its advantages and

disadvantages?

AUDITING - I (21)

NOTES

Disadvantages of continuous audit

lllll Failure to keep track: Since work is carried out in several installments, the

audit staff may fail to keep track of things. As a result some of the transactions

may escape.

lllll Tampering: The Client's staff may alter entries in the books of account, after

checking thereof.

lllll Uneconomic: The audit is uneconomic for small sized concerns as a great

deal of time and effort would be wasted each time in preparing for the audit.

lllll Interruption of work: The presence of audit staff at regular intervals may

affect the regular work-flow of the client.

lllll Boredom: Routine checking on a continuous basis may become mechanical.

lllll Time consuming: Since all transactions are verified, continuous audit will be

time-consuming.

lllll No guarantee for fraud detection: Complete verification of all transactions in

detail, does not guarantee detection of all errors and frauds. Some material

misstatements may still exist

How will you overcome the disadvantages of Continuous Audit?

Following are some precautions -

lllll Stage-wise completion: The work should be completed upto a definite stage

during the .course of each visit. This will eliminate the possibility of loose

ends.

lllll Documentation: Important balances should be noted down at the end of each

visit and the same should be compared at the time of the next visit. Proper

documentation should be maintained.

lllll Surprise visit: The visits should be conducted at irregular intervals. Client

staff would not know the exact dates of the proposed visit.

lllll Special auditing marks: The client's staff should be instructed not to alter or

correct audited figures. The Auditor should also device a special form of

ticks and places the same, against altered figures. The purpose or the

significance of such special marks should not be disclosed to the client's

staff.

2.2.6 Balance sheet audit:The Balance Sheet Audit means Auditor reviews the Balance Sheet and

works back to the books of original entry and other evidences. In balance sheet

audit it is assumed that there is a reliable system of internal check & internal audit.

Much of the vouching, casting and posting and other routine audit is eliminated

considering the soundness of internal control system. Where internal controls are

considered weak, the Auditor might prefer more elaborate testing procedures to

obtain audit assurance.

Auditor performs analytical review of the items in the Financial Statements and

investigates the followings-

l l l l l Material deviations from budgeted amounts;

l l l l l Items of unusual and non-recurring nature;

l l l l l Items requiring statutory disclosure.

Types of Audit

CHECK YOUR

PROGRESS

Explain continuous

Audit?

AUDITING - I

(22) AUDITING - I

NOTES

Need for Balance sheet audit: The need for Balance Sheet Audit by departing

away from routine "ticking" of vouchers and "post and vouch" audit arises due to -

l l l l l Development of Industries.

l l l l l Adoption of very formal control system by organization.

l l l l l Growth in size of business.

l l l l l Increase in number of transactions of homogeneous nature.

2.2.7 Financial Audit:Financial audit means examination of financial statements to express an

opinion thereon. This audit is mandatory for all enterprises. It covers all the items

which form part of the financial statements. This audit helps to determine the true

& fair view of financial statements. Here propriety aspect is not considered in

detailed.

2.2.8 Cost Audit:Cost audit means review of decisions & actions of management to analyse

performance. This is applicable to those companies specified under law. Cost audit

primarily covers the cost aspects of the enterprise.

2.2.9 Management Audit:Review of decisions & actions of management. Propriety & efficiency of

decisions & managerial actions are studied. It covers all aspects like organizational

objectives, policies, procedures, structure, control & system.

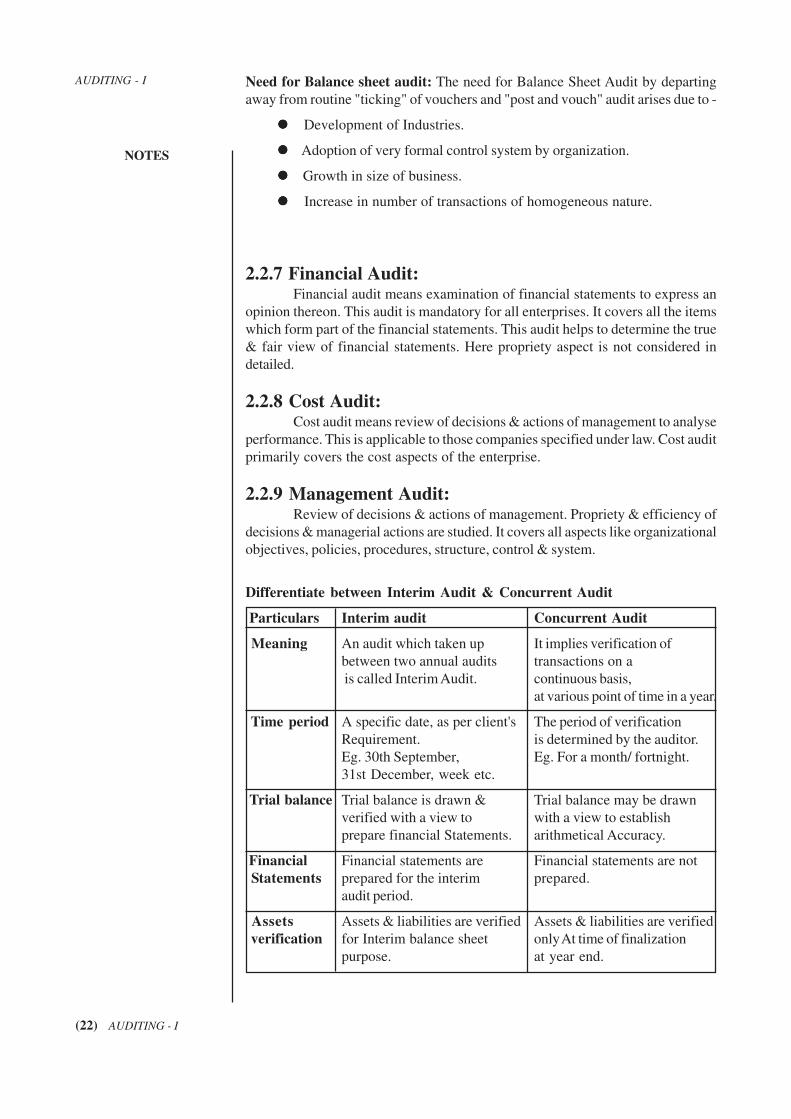

Differentiate between Interim Audit & Concurrent Audit

Particulars Interim audit Concurrent Audit

Meaning An audit which taken up It implies verification of

between two annual audits transactions on a

is called Interim Audit. continuous basis,

at various point of time in a year.

Time period A specific date, as per client's The period of verification

Requirement. is determined by the auditor.

Eg. 30th September, Eg. For a month/ fortnight.

31st December, week etc.

Trial balance Trial balance is drawn & Trial balance may be drawn

verified with a view to with a view to establish

prepare financial Statements. arithmetical Accuracy.

Financial Financial statements are Financial statements are not

Statements prepared for the interim prepared.

audit period.

Assets Assets & liabilities are verified Assets & liabilities are verified

verification for Interim balance sheet only At time of finalization

purpose. at year end.

AUDITING - I (23)

NOTES

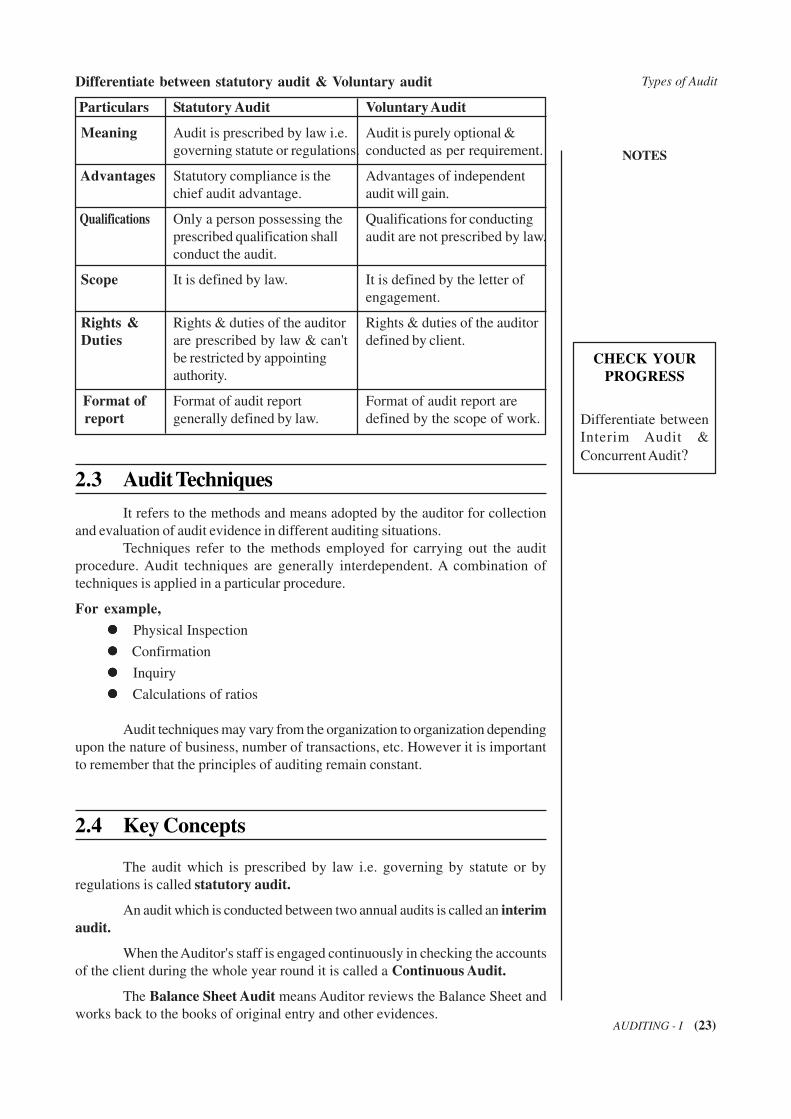

Differentiate between statutory audit & Voluntary audit

Particulars Statutory Audit Voluntary Audit

Meaning Audit is prescribed by law i.e. Audit is purely optional &

governing statute or regulations. conducted as per requirement.

Advantages Statutory compliance is the Advantages of independent

chief audit advantage. audit will gain.

Qualifications Only a person possessing the Qualifications for conducting

prescribed qualification shall audit are not prescribed by law.

conduct the audit.

Scope It is defined by law. It is defined by the letter of

engagement.

Rights & Rights & duties of the auditor Rights & duties of the auditor

Duties are prescribed by law & can't defined by client.

be restricted by appointing

authority.

Format of Format of audit report Format of audit report are

report generally defined by law. defined by the scope of work.

2.3 Audit Techniques

It refers to the methods and means adopted by the auditor for collection

and evaluation of audit evidence in different auditing situations.

Techniques refer to the methods employed for carrying out the audit

procedure. Audit techniques are generally interdependent. A combination of

techniques is applied in a particular procedure.

For example,

l l l l l Physical Inspection

l l l l l Confirmation

l l l l l Inquiry

l l l l l Calculations of ratios

Audit techniques may vary from the organization to organization depending

upon the nature of business, number of transactions, etc. However it is important

to remember that the principles of auditing remain constant.

2.4 Key Concepts

The audit which is prescribed by law i.e. governing by statute or by

regulations is called statutory audit.

An audit which is conducted between two annual audits is called an interim

audit.

When the Auditor's staff is engaged continuously in checking the accounts

of the client during the whole year round it is called a Continuous Audit.

The Balance Sheet Audit means Auditor reviews the Balance Sheet and

works back to the books of original entry and other evidences.

Types of Audit

CHECK YOUR

PROGRESS

Differentiate between

Interim Audit &

Concurrent Audit?

AUDITING - I

(24) AUDITING - I

NOTES

Financial audit means examination of financial statements to express an

opinion thereon.

Management Audit - Review of decisions & actions of management.

Audit Techniques refer to the methods adopted by auditor for carrying

out audit procedure.

2.5 Summary

Types of audit includes Statutory / Mandatory Audit, Voluntary / Independent

Audit, Interim Audit, Concurrent Audit, Continuous Audit, Balance sheet audit,

Financial Audit, Cost Audit, Management Audit.

2.6 Exercise & Questions

1. How many types of Audit? Explain each one of them.

2. What are the disadvantages of Continuous Audit? How will you overcome

the disadvantages of Continuous audit?

3. Differentiate between statutory audit & Voluntary audit.

4. What is mean by Audit technique?

lllll Fill in the blanks:

1) Cost audit primarily covers the ___________aspects of the enterprise.

(Financial, Cost, Human, Behavioral)

2) When the Auditor's staff is engaged continuously in checking the accounts of

the client during the whole year round or when the staff attends audit work at

some intervals, it is called a _______________.

(Concurrent audit, Voluntary audit, Continuous audit, Balance sheet audit)

3) __________________means examination of financial statements to express

an opinion thereon.

(Financial Audit, Cost Audit, Balance Sheet Audit, Concurrent Audit)

4) Propriety & efficiency of decisions & managerial actions are studied in

_______________ Audit.

(Cost, Statutory, Management, Financial)

5) Audit technique refers to the methods and means adopted by the auditor for

collection and evaluation of ____________________.

(Financial Information, Audit Evidence, Cost Data, Audit Procedure)

6) The audit which is prescribed by law i.e. governing by statute or by regulations

is called _____________

(Concurrent Audit, Statutory Audit, Voluntary Audit, Financial Audit)

7) An audit which is conducted between two annual audits is called an

_________________.

(Interim Audit, Balance Sheet Audit, Concurrent Audit, Continuous audit)

8) ________________ implies verification of transactions of a year on a

AUDITING - I (25)

NOTES

continuous basis.

(Concurrent Audit, Continuous audit, Statutory Audit, Cost Audit)

9) The ___________________ means Auditor reviews the Balance Sheet

and works back to the books of original entry and other evidences.

(Balance sheet audit, Continuous audit, Concurrent Audit, Cost Audit)

10) ____________________ helps the company to publish interim financial

statements for declaration of interim dividend.

(Interim audit, Balance sheet audit, Continuous audit, Cost Audit)

11) The scope of Voluntary audit is defined by ________________________.

(Law, Letter of engagement, Pronouncement by ICAI, Prospectus)

12) Auditor performs ______________________ of the items in the Financial

Statements.

(analytical review, compliance procedure, testing, sampling)

13) _______________ refer to the methods employed for carrying out the audit

procedure.

(Sampling, Testing, Techniques, Materiality)

14) ____________________ is purely optional and at discretion of the governing

body.

(Concurrent Audit, Statutory Audit, Voluntary Audit, Financial Audit)

15) In _____________________Assets & liabilities are verified only at time

of finalization at year end.

(Concurrent Audit, Continuous audit, Statutory Audit, Cost Audit)

(Answers: 1) Cost, 2) Continuous audit, 3) Financial audit, 4) Management,

5) Audit evidence, 6) Statutory audit, 7) Interim audit, 8) Concurrent audit, 9)

Balance sheet audit, 10) Interim audit, 11) Letter of engagement, 12) Analytical

review, 13) Techniques, 14) Voluntary audit, 15) Concurrent audit)

2.7 Further Reading and References

1. Audit Assurance Standards (AAS) issued by ICAI

2. N.D.Kapoor's Audit Procedure

3. Dr. Mahesh Kulkarni's Audit practices

Types of Audit

AUDITING - I

(26) AUDITING - I

NOTES

UNIT - 3

VOUCHER & VOUCHING

Structure

3.0 Introduction

3.1 Objectives

3.2 Vouching

3.3 Purpose of vouching

3.4 Objectives of vouching

3.5 Voucher

3.6 General Consideration in Audit of Ledger

3.7 Audit of Different Ledgers

3.7.1 Bought Ledger

3.7.2 Sales Ledger

3.7.3 General Ledger

3.8 Kinds of Frauds in relation to Ledgers

3.9 Key Concepts

3.10 Summary

3.11 Exercise & Questions

3.12 Further Reading and References

3.0 Introduction

Auditing may be viewed as a practical application of the theory of evidence

or the science of proof to financial data. It is not just an inspection of evidence in

support and substantiation of accounting data but it involves and includes a critical

examination of the different business transactions themselves for an accounting

period. An auditor would like to assure himself of the validity, accuracy, adequacy,

authority and accountability.

3.1 Objectives

After this unit you should be able:

1. To understand the concept of Vouching.

2. To find out purpose and objectives of Vouching.

3. To be familiar with concept and various types of Voucher.

4. To know in detail about the audit of different ledgers.

5. To understand the nature of frauds in relation to ledgers.

AUDITING - I (27)

NOTES

3.2 Vouching

Vouching means inspection by an auditor of documentary evidence

supporting & substantiating transactions. Vouching is the process of

checking documentary evidence that the transactions are properly recorded

& accounted for.

The main aim of vouching is to inspect all receipts & payments are properly

accounted for & no fraudulent transactions are recorded. Vouching is a substantive

audit procedure to obtain evidence as to completeness, accuracy & validity. With

the help of vouching auditor come to know the genuineness of the transactions.

The duty of auditor is to see substantial accuracy of vouchers & then

make report thereon. Vouching is also the basis for assets & liabilities. Auditor

should be careful while vouching the transactions & entries in the books of accounts.

It is the backbone of auditing process. Thus, vouching may be considered as the

essence of auditing.

3.3 Purpose of Vouching

The purpose of vouching is to determine that-

lllll Classification: Transactions have been classified & disclose in accordance

with accounting policies.

lllll Accurate amount: Accurate amount has been recorded.

lllll Pertains to entity: Transactions are pertains to entity that took place during

the relevant period.

lllll Actual occurred: Transactions which have actually occurred have been

recorded.

lllll Proper Accounts: Transactions is recorded in proper account to proper

period.

3.4 Objectives of Vouching

Following are the objectives of vouching-

lllll To see that transactions & entries are properly recorded in the books of

accounts.

lllll To see that entries & transactions are properly authenticated by reasonable

person.

lllll To see that transactions have been properly classified & disclosed in

accordance with the accounting policies.

lllll To see that no fraudulent transactions are recorded in books of accounts.

lllll To see that all entries & transactions are supported by proper evidence.

3.5 Voucher

A voucher is documentary evidence in support of any transaction in books

of accounts. Voucher can originate within the organization or outside the organization

Voucher & Vouching

CHECK YOUR

PROGRESS

Define objectives of

vouching?

AUDITING - I

(28) AUDITING - I

NOTES

i.e. they can be internal or external. Eg. Internal voucher: invoices for purchase &

sale, receipts, counterfoils, slip of bank, etc. External voucher: consignment stock,

mortgage deed, etc.

Vouchers are of two types:

l l l l l Primary voucher: All written evidences in original are primary vouchers.

l l l l l Secondary voucher: Copies of original vouchers are called collateral vouchers.

Material Defects in Voucher:

Following are the material defect that disqualify the vouchers-

1. Voucher not addressed to the client.

2. Voucher not duly authorized for payment.

3. Voucher concerning purchases & expenses not related to business.

4. Voucher not pertaining to period under audit.

5. Payment not acknowledge against voucher.

6. Voucher in respect of which goods or services have not been received.

7. Date of voucher significantly different from the date on which entry was

made.

8. Amount of voucher not agreed with corresponding entry.

9. Amount altered, erased in voucher without proper authorization.

Care to be taken while Vouching:

1. Voucher must be dated & serially numbered.

2. Information on the voucher should fully explain the transactions.

3. Date of voucher should match with corresponding entry.

4. Auditor should satisfy that transactions are authentic i.e. genion

5. Voucher should be passed by responsible officer.

6. Distinction should be made between capital & revenue expenditure.

7. Amount on voucher should be checked.

8. The period for payment should be noted.

9. Proper care should be taken to see that transaction is not recorded twice.

10. Alteration in voucher must be authorized by proper person.

11. Prepare a list of missing & incomplete vouchers should be prepared.

12. Auditor should stamp the voucher seen.

3.6 General Considerations in Audit of Ledgers

Following steps involves in the audit of ledger-

1. Testing the strength & quality of internal check.

2. Tracing the opening balances from the previous year records.

3. Checking the posting from the subsidiary books.

AUDITING - I (29)

NOTES

4. Checking the closing balances of individual accounts.

5. Checking the totals of ledger accounts, trial balance, schedules.

6. Verifying the balances in personal accounts, either through statement of

accounts or external confirmation.

7. Scrutinizing the accounts generally & examining the composition of final

balances.

8. Ascertaining the clearness of balances brought forward from the previous

year.

9. Tallying the totals of balances in subsidiary ledgers which are kept on self

balancing system.

10. Verifying the balances in impersonal accounts viz. those of fixed assets,

bank balances, etc. with details of assets & liabilities.

Different ledgers:

l l l l l Bought ledger

l l l l l Sales ledger

l l l l l Nominal ledger

3.7 Audit of Different Ledgers

3.7.1 Bought Ledger:

Following are the steps for the audit of bought ledger-

a) Verification of opening balances: Opening balances of the bought ledger

would be verified from audited accounts & schedules. For that purpose auditor

has to know whether audit of that enterprise would actually conduct or not.

b) Internal Control System: Auditor has to check the internal control system.

He should verify the system & check whether proper allocation of functional

responsibilities within the organization.

c) Checking of posting: Next step of audit of bought ledger is the checking of

posting into ledger from cash book, purchase register, bills payable book,

journal, & other relevant books of accounts. While checking the posting auditor

should see that correct amounts are posted on the correct side of proper

account.

d) Checking of totals: Auditor should check the totals & casting of each

account. Carry forwards & brought forward should be properly checked.

e ) Checking of summary balances: Auditor should obtain the summary of

balances of the bought ledger. He should see the correct amount is shown

against every party.

f) General checking:

lllll Scanning Accounts: The client should be requested to write in the ledger

also the bill number for which credit is given. Similarly a reference bill while

making the payment should also be made when the party's account is debited.

This will enable both the accountant & the auditor to find out-

Voucher & Vouching

AUDITING - I

(30) AUDITING - I

NOTES

i. Whether there is any dispute in respect of any invoice.

ii. Whether any posting is left out or wrongly done.

iii. Whether goods have been received against advance made.

iv. The composition of the closing balances.

lllll Debit balances in the bought ledger: The auditor may come across

debit balances in some of the suppliers accounts in the bought ledger; this

requires a detailed scrutiny of such accounts. Sometimes, advance given

against the goods turn out to be more than the amount of bill. Here auditor

should find out whether the excess amount paid is received subsequently or

not. The auditor should verify in detailed & find out the reasons of such debit

balances & take all possible precautions.

lllll Confirmation of balances: The client may send the statement of account

to the party to confirm the same & then send it back. The client would be

requested to confirm the balance & write back. All replies should be

investigated independently of the person of in charge.

lllll Summary: Examination of the bought ledgers can be summarized as under-

- Review of the internal control system.

- Check up the opening balances.

- Check up postings, castings, etc.

- Check up the summary of bought ledger & compare with control

accounts.

- Review of confirmation received.

- At the year end examine the cut off procedure, review the transactions

after the balance sheet date,

& secure the certificates.

3.7.2 Sales Ledger:

Sales ledger contains the accounts of customer. So, client's capital blocked

up in debtors & receivables. There must be proper control on all the receivables.

In the absence of such control, the receivables would not be collected in time & as

a result they may become doubtful of recovery & time barred. Following are the

stages for audit of sales ledger-

a) Verification of Internal Control System: Auditor has to check the internal

control system. He should verify the system & check whether proper allocation

of functional responsibilities within the organization.

b) Verification of Opening balances: The auditor will check up the opening

balances of sales ledger. The control accounts should be verified in the general

ledger.

c) Checking of posting: The next stage of the audit of sales ledger is the

checking of posting into the ledger from cash book, Sales register, bills

receivable book, sales return register, & other relevant books of accounts.

While checking the posting, auditor should see that correct amounts are posted

on the correct side of the proper account.

lllll Credit balances in the sales ledger: If the party has sent money in

excess of the invoice value, then there may be a credit balances. If the credit

note is issued to the customer, the customer may send the amount after

deducting the amount of the credit note.

CHECK YOUR

PROGRESS

Define procedure of

sales ledger Audit?

AUDITING - I (31)

NOTES

lllll Confirmation of balances: Confirmation of balances received from

customer is one of the most important evidence in support of balances in

customer's ledgers.

d) Checking of totals & casting: After the checking of posting, auditor should

verify the totals, carry forwards & brought over in each accounts.

e ) Checking of summary of balances: Auditor should obtain the summary of

the balances of sales ledger. The balance in each account would be traced

into the summary. Proper care should be taken to see that correct amount is

shown against the appropriate party.

f) General checking:

lllll Scanning of accounts: The client should be requested to mention in the

sales ledger the reference of the sales invoice while debiting the account of

the customer & also while receiving the amount or while adjusting the credit

note. This will enable the auditor to find out-

i. Whether there is any dispute in respect of any sales invoice.

ii. Whether any posting has been left out or any wrong posting has been

made.

iii. Whether goods have been dispatched against advances received.

The internal auditor or any other responsible officer should periodically see

that all the debtors periodically, at least once in year confirm the balances.

lllll Credit Policy of the Client: Auditor should collect the data regarding all

the customers, credit terms granted to these customers. He should also study

the credit policy granted by competitors.

lllll Classification of Debtors: While obtaining the summary of balances,

auditor also obtains the classification of all such debtors. Credit balances of

customer's ledger should be classified separately. Following points should

considered while verifying the classification of debtors-

i. Debts considered secured.

ii. Debts considered unsecured but good.

iii. Debts considered unsecured but doubtful of recovery.

g) Yearly Examination:

Yearly examination should include-

i. Cut - off procedure.

ii. Review of post Balance sheet transactions.

iii. Comparisons & ratios.

iv. Review of adequacy of the reserve of doubtful debts & reserve for discount.

v. Securing the confirmation of balances.

vi. Securing various classifications of the debtors.

Voucher & Vouching

AUDITING - I

(32) AUDITING - I

NOTES

3.7.3 General Ledger:

General ledger is also called as 'Nominal Ledger' or 'Impersonal Ledger'.

It contains all the balances which are ultimately included in profit & loss account &

balance sheet, it contains:

i. Nominal Accounts

ii. Real or Property Accounts

iii. Capital & Loan Accounts

iv. Control Accounts, etc.

lllll Audit of General Ledger can be divided into following stages:

Following are the stages for the audit of general ledger-

a) Verification of Internal Control System: Auditor has to check the internal

control system. He should verify the system & check whether proper allocation

of functional responsibilities within the organization.

b) Checking of Opening balances: The opening balances of the general ledger

are checked from the audited accounts of the previous year.

c) Checking of posting: Sales Register, Purchase Register, Return Register,

& other appropriate accounts. Entries are posted in general ledger from almost

all the books of accounts. Corresponding control accounts are also posted

from these books. While checking the posting, auditor should see that correct

amounts are posted in correct account & on correct side. He should also see

the item has remained un-posted.

d) Checking of Totals & Casting: After the checking of posting auditor should

check up the totals & casting. He should check up whether figures are properly

& correctly carried over to the next page.

e ) Checking the balances in Trial Balance: The next stage of checking of

the balances of general ledger in trial balances. Because the books are

recorded on the principle of double entry system of book keeping. The total

of debit side must equal to the credit side of the trial balance.

f) Scrutiny & Scanning of ledger accounts: The auditor must scrutinize all

the ledgers one by one & find out whether necessary adjustments are already

recorded. While scrutinizing the partner's capital accounts, auditor should

see whether the conditions laid down by the partnership deed are complied

with. Interest should be allowed on the capital at a rate decided by the

partnership deed.

3.8 Kinds of Frauds in Relation to Ledgers

Ledger keeper may commit some frauds by manipulating the entries in the

ledger. Some of the frauds which may be committed by ledger keeper are as

follows-

1. In the Bought Ledger/ Purchase Ledger/ Creditors Ledger:

Frauds may occurs like-

a. Crediting the supplier's account on the basis of a fictitious invoice.

CHECK YOUR

PROGRESS

Define different kinds

of frauds in relation to

ledger?

AUDITING - I (33)

NOTES

Subsequently misappropriating the payment made against the credit in

the suppliers account.

b. Suppressing a credit note issued by a supplier & misappropriating an

amount equivalent there to out of the payment made to him.

c. Crediting an amount due to a supplier not in his account but under a

fictitious name & misappropriating the amount paid against the credit

balance.

2. In the Sales Ledger / Debtors Ledger:

a. Fraud through Teeming & Lading method.

b. Adjusting a unauthorized credit on fictitious rebate, discount in the account

with a view to reduce the balance.

c. Writing off the amount receivable from a customer's bad debt account &

misappropriating an amount equivalent to credit.

3. In the Nominal Ledger:

a. Allocating an item of income or expenditure wrongly.

b. Understating or overstating the value of stocks, amount of prepaid expenses

or liabilities.

c. Capital expenditure charged as revenue expenditure or vice- versa.

3.9 Key Concepts

Vouching is the process of checking documentary evidence that the

transactions are properly recorded & accounted for.

A voucher is documentary evidence in support of any transaction in

books of accounts.

Primary voucher: All written evidences in original are primary vouchers.

Secondary voucher: Copies of original vouchers are called collateral

vouchers.

General ledger is also called as 'Nominal Ledger' or 'Impersonal

Ledger'. It contains all the balances which are ultimately included in profit

& loss account & balance sheet

3.10 Summary

Vouching means inspection by an auditor of documentary evidence

supporting & substantiating transactions. The main aim of vouching is to inspect all

receipts & payments are properly accounted for & no fraudulent transactions are

recorded. A voucher is documentary evidence in support of any transaction in

books of accounts. There are two types Vouchers i.e. Primary voucher and

Secondary voucher. Voucher must be dated & serially numbered. Voucher should

be passed by responsible officer. Auditor should checked opening and closing

balances, totals, trial balance, subsidiary books etc. while doing the audit of ledgers.

Specific consideration should be given while auditing Bought ledger, Sales ledger,

Nominal ledger.

Voucher & Vouching

AUDITING - I

(34) AUDITING - I

NOTES

3.11 Exercise & Questions

1. What is mean by Vouching? What are the objectives of vouching?

2. Which care should be taken while vouching?

3. What is Voucher? State the material defects that disqualify the voucher?

4. How will you conduct the audit of bought ledger?

5. Which stapes will you follow while checking the sales ledger?

6. Explain some kinds of frauds which may occur in bought ledger & nominal

ledger?

lllll Fill in the blanks:

1. ________________ is the process of checking documentary evidence that

the transactions are properly recorded & accounted for.

(Auditing, Vouching, Reporting, Verification)

2. _______________ is documentary evidence in support of any transaction

in books of accounts.

(Audit Program, Financial Statements, Voucher, Ledger)

3. Sales ledger contains the accounts of________________.

(Supplier, Customer, Lender, Banker)

4. _________________ is also called as 'Nominal Ledger' or 'Impersonal

Ledger'

(General ledger, Sales ledger, Bought ledger, None)

5. Ledger keeper may commit some ____________ by manipulating the entries

in the ledger.

(Error, Fraud, Plan, Program)

6. With the help of ____________auditor come to know the genuineness of

the transactions.

(Vouching, Reporting, Verification, Auditing)

7. The total of debit side must _______ to the credit side of the trial balance.

(more, lower, equal, more than or equal)

8. There are two types Vouchers i.e. Primary voucher and _____________

voucher.

(Duplicate, Secondary, Multiple, Triplicate)

9. Entries are posted in _____________from almost all the books of accounts.

(Journal, general ledger, trial balance, profit & loss a/c)

10. ____________ balances of customer's ledger should be classified separately.

(Credit, Debit, Both debit & credit, None)

11. ________________of balances received from customer is one of the most

important evidence in support of balances in customer's ledgers.

(Enquiry, Physical verification, Confirmation, Observation)

AUDITING - I (35)

NOTES

12. ______________ may be considered as the essence of auditing.

(Sampling, Vouching, Reporting, Verification)

(Answers: 1)Vouching, 2) Voucher, 3) customer, 4) General ledger, 5) Fraud,

6) Vouching, 7) equal, 8) secondary, 9) general ledger, 10) credit, 11)

Confirmation, 12) Vouching)

3.12 Further Reading and References

1. Audit Assurance Standards (AAS) issued by ICAI

2. N.D.Kapoor's Audit Procedure

3. Dr. Mahesh Kulkarni's Audit practices

Voucher & Vouching

AUDITING - I

(36) AUDITING - I

NOTES

UNIT 4

INTERNAL CHECK & ROLE OF

INTERNAL AUDITOR

Structure

4.0 Introduction

4.1 Objectives

4.2 Internal Control

4.3 Objectives of Internal Control

4.4 Essentials of Good Internal Control System

4.5 Inherent Limitations of Internal Control

4.6 Methods for the Proper Review & Evaluation of the Adequacy

of the Internal Control

4.7 Internal Check

4.7.1 Objects of Internal Check

4.8 Internal Audit

4.8.1 Basic Principles of Establishing Internal Auditing

4.8.2 Objectives of Internal Audit

4.9 Role of Internal Auditor

4.10 Possible areas of co-operation & co-ordination

4.11 Key Concepts

4.12 Summary

4.13 Exercise & Questions

4.14 Further Reading and References

4.0 Introduction

In big organization internal audit is a part and parcel of internal control

system. In order to have detailed audit, internal audit is usually conducted in addition

to internal check system. An internal auditing consist of a continuous critical review

of financial and operating activities by a staff of auditors functioning as full time

salaried employees.

4.1 Objectives

After this unit you should be able:

1. To understand the concept of internal control.

2. To understand the essentials of Good Internal Control System.

3. To find out objectives and limitations of internal control.

4. To be familiar with the concept of Internal Check and Internal Audit.

5. To understand the role of Internal Auditor.

6. To learn the documentation requirement for Internal Audit.

AUDITING - I (37)

NOTES

4.2 Internal Control

The system of internal control has been defined as-

"The plan of organization and all the methods & procedures adopted

by the management of an entity to assist in achieving management's

objective of ensuring, as far as practicable,

i. Orderly & efficient conduct of the business

ii. Adherence to management policies

iii. Safeguarding of assets

iv. Prevention & detection of frauds & errors

v. Ensuring accuracy & completeness of the accounting records

vi. Timely preparation of reliable finance information"

Usually the control is entirely centralized with the owner & there is no

significant delegation of duties. However as the business grows in size, it soon

reaches a stage where the owner can no longer keep himself intimately informed

about the detailed operations of his business in such a case internal control becomes

very important. The reliability of business operations can be judged by the

effectiveness of internal control.

4.3 Objectives of Internal Control

i. Transactions are executed in accordance with management authorization.

ii. All transactions are recorded with appropriate amount & in appropriate

account.

iii. To prevent & detect frauds & errors.

iv. To prevent the assets from unauthorized access, use.

4.4 Essentials of Good Internal Control System

i. Proper allocation of functional responsibilities within the organization.

ii. The quality of personnel is very important. They should be competent &

honest.

iii. Implementation of proper operating & accounting procedures to ensure

the accuracy & reliability.

iv. The review of the work of one individual by another whereby the possibility

of fraud or error in the absence of collusion is minimized.

4.5 Inherent Limitations of Internal Control

Due to some inherent limitations of internal control, objectives of internal

control cannot be absolutely achieved. These limitations are as follows-

1. Many times control does not tend to be directed at transactions of unusual

nature.

Internal Check & Role of

Internal Auditor

CHECK YOUR

PROGRESS

Define concept of

internal control

system?

AUDITING - I

(38) AUDITING - I

NOTES

2. Management's consideration that a control be cost effective.

3. The potential for human errors.

4. The possibility that the person having higher authority may override a

control.

5. The possibility of deception of control through collusion with outside parties

or with employees of the entity.