Embed Size (px)

Citation preview

Tom Steffens

Office of the Assistant

Secretary of the Army

(Financial Management

and Comptroller)

Alaleh Jenkins

Office of the Under

Secretary of Defense

(Comptroller)

Steve Quentmeyer

Office of the Assistant

Secretary of the Navy

(Financial Management

and Comptroller)

Steve Herrera

Office of the Assistant

Secretary of the Air Force

(Financial Management

and Comptroller)

Audit & Audit Readiness

What Is Next For DoD?

v1

American Society of Military Comptrollers (ASMC) – PDI

May 28, 2015

Simone Reba

Defense Logistics

Agency, Finance & Audit

Readiness

• DoD’s Approach To Audit‒ Statutory Direction

‒ Path to Full Financial Statement Audit

‒ DoD’s Consolidated Audit Strategy

‒ History of Audit Efforts to Date

• Current Status Demonstrates Significant Progress‒ Overview

‒ Army

‒ Navy

‒ Air Force

‒ Defense Logistics Agency

• Final Thoughts

Agenda

2

3

Statutory Direction

The Chief Financial Officers (CFO) Act of 1990 requires federal agencies to

prepare annual financial statements, and the Government Management Reform

Act (GMRA) of 1994 requires the financial statements to be audited. In addition

to the CFO Act and GMRA, Congress legislated the following:

• Sec. 1003 of the National Defense Authorization Act (NDAA) for FY 2012

requires the plan to include the interim objectives and a schedule of milestones for

each Military Department and Defense Agency to support the goal established by

the Secretary of Defense that the SBR be validated for audit by not later than

September 30, 2014

• Sec. 1003 of the NDAA for FY 2010 requires the Department to develop and

maintain a plan that ensures DoD financial statements are validated as ready for

audit by not later than September 30, 2017

The Financial Audit Requirement and DoD Approach

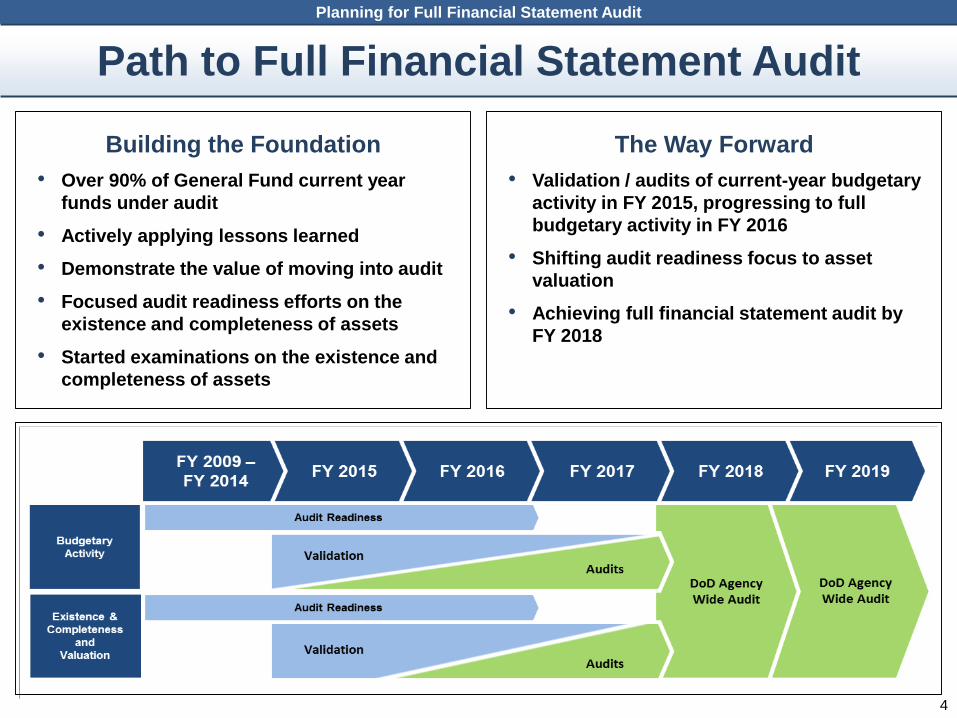

The Way Forward

• Validation / audits of current-year budgetary

activity in FY 2015, progressing to full

budgetary activity in FY 2016

• Shifting audit readiness focus to asset

valuation

• Achieving full financial statement audit by

FY 2018

Path to Full Financial Statement Audit

Building the Foundation

• Over 90% of General Fund current year

funds under audit

• Actively applying lessons learned

• Demonstrate the value of moving into audit

• Focused audit readiness efforts on the

existence and completeness of assets

• Started examinations on the existence and

completeness of assets

4

Planning for Full Financial Statement Audit

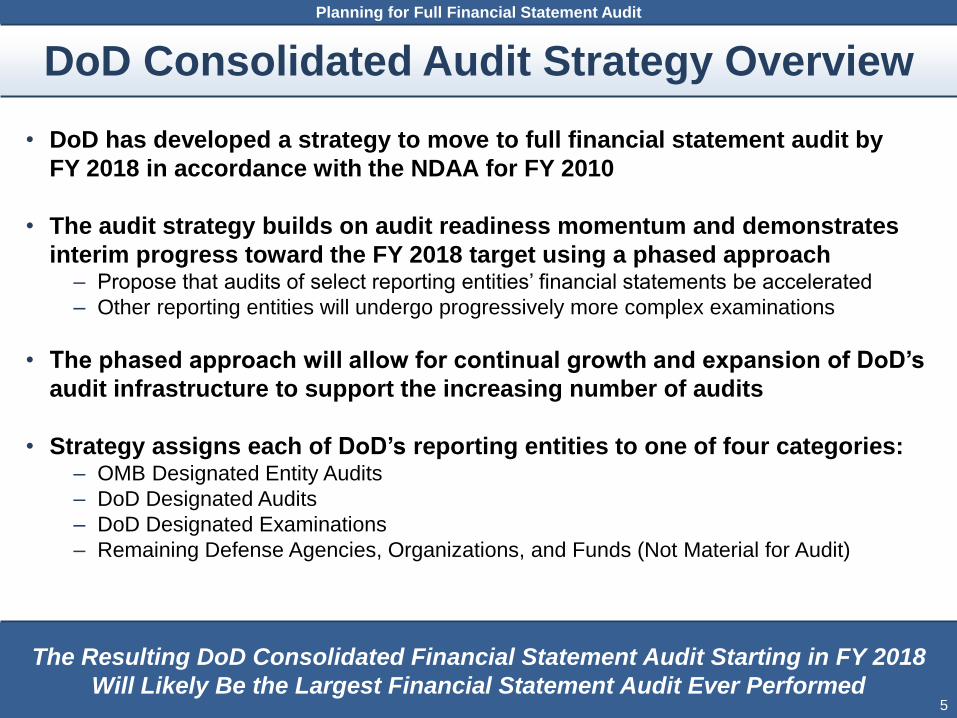

DoD Consolidated Audit Strategy Overview

• DoD has developed a strategy to move to full financial statement audit by

FY 2018 in accordance with the NDAA for FY 2010

• The audit strategy builds on audit readiness momentum and demonstrates

interim progress toward the FY 2018 target using a phased approach– Propose that audits of select reporting entities’ financial statements be accelerated

– Other reporting entities will undergo progressively more complex examinations

• The phased approach will allow for continual growth and expansion of DoD’s

audit infrastructure to support the increasing number of audits

• Strategy assigns each of DoD’s reporting entities to one of four categories:– OMB Designated Entity Audits

– DoD Designated Audits

– DoD Designated Examinations

– Remaining Defense Agencies, Organizations, and Funds (Not Material for Audit)

5

The Resulting DoD Consolidated Financial Statement Audit Starting in FY 2018

Will Likely Be the Largest Financial Statement Audit Ever Performed5

Planning for Full Financial Statement Audit

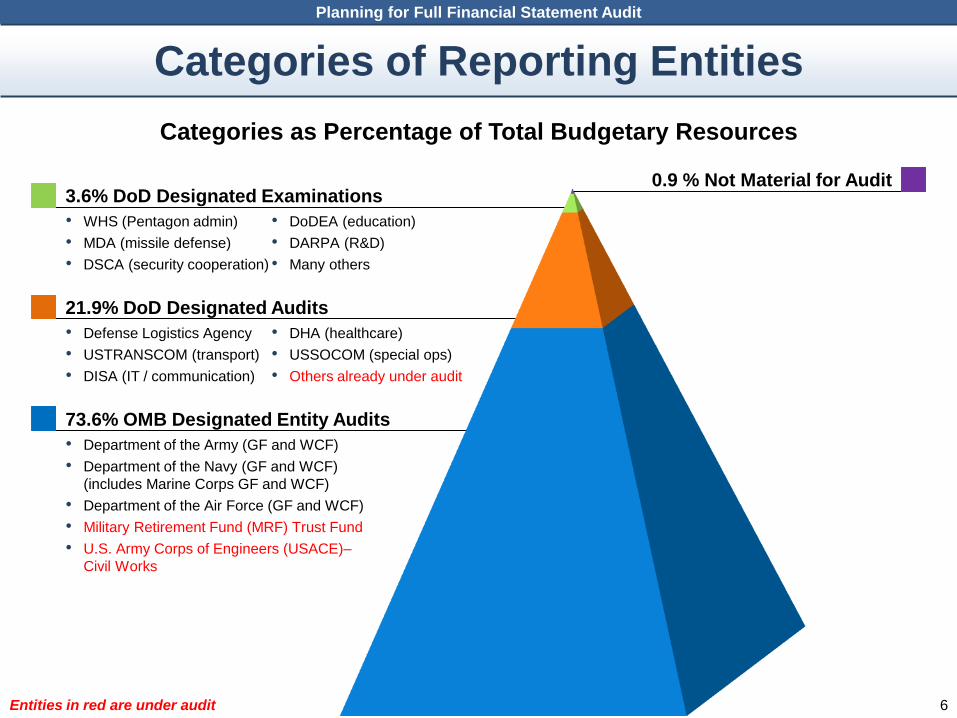

0.9 % Not Material for Audit3.6% DoD Designated Examinations

21.9% DoD Designated Audits

73.6% OMB Designated Entity Audits

Categories as Percentage of Total Budgetary Resources

6

• Department of the Army (GF and WCF)

• Department of the Navy (GF and WCF)

(includes Marine Corps GF and WCF)

• Department of the Air Force (GF and WCF)

• Military Retirement Fund (MRF) Trust Fund

• U.S. Army Corps of Engineers (USACE)–

Civil Works

• WHS (Pentagon admin)

• MDA (missile defense)

• DSCA (security cooperation)

• DoDEA (education)

• DARPA (R&D)

• Many others

• Defense Logistics Agency

• USTRANSCOM (transport)

• DISA (IT / communication)

• DHA (healthcare)

• USSOCOM (special ops)

• Others already under audit

Entities in red are under audit

Categories of Reporting Entities

Planning for Full Financial Statement Audit

Current Status

7

Over 90 percent of the Department’s FY 2015 General Funds are under audit.

Funds under audit represent most of the financial information reported in the SBR.

• Although the Department did not achieve the September 30, 2014, Statement

of Budgetary Resources deadline, significant progress was made

• Military Departments asserted audit readiness on their services’ General

Fund Schedules of Budgetary Activit– Audit contracts awarded December 2-4, 2014

– Audits began in January 2015

– Audits include financial transactions related to appropriation received in FY 2015 and do

not include financial transactions related to appropriations received in prior fiscal years

– DoD OIG oversees the IPA-conducted SBA audits

• Other Defense Organizations (ODOs)– By June 30, 2014, each of the other Defense organizations asserted audit readiness of

their applicable assessable units or of specific SBR line-items

– ODOs material to the DoD Consolidated Financial Statements are undergoing SBA

mock audits or IPA examinations

Overview: Significant Progress Made

8

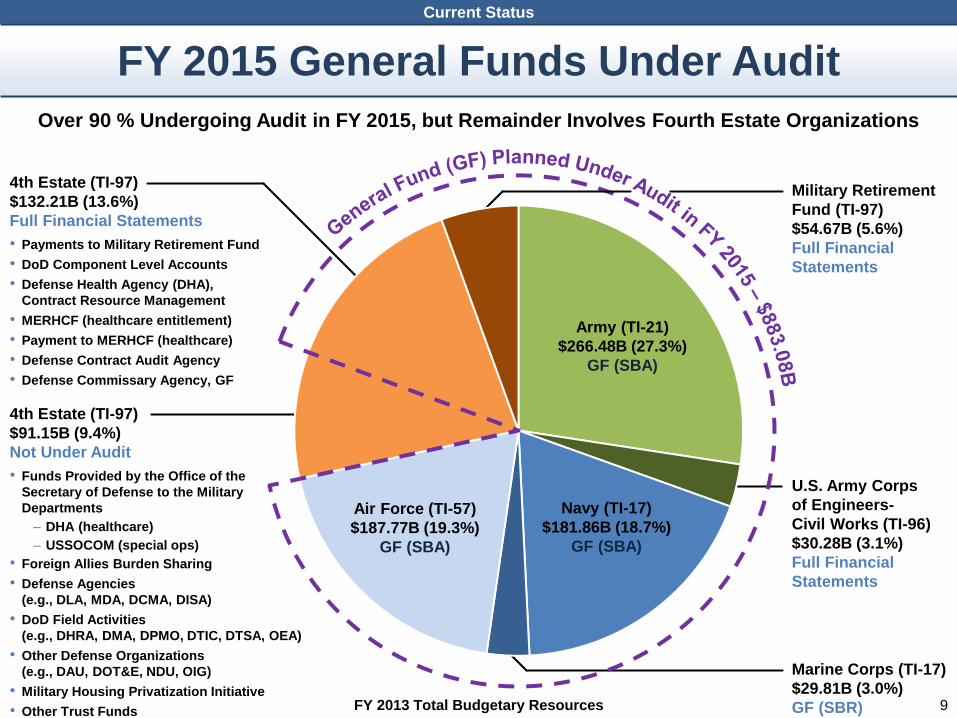

Current Status

Over 90 % Undergoing Audit in FY 2015, but Remainder Involves Fourth Estate Organizations

U.S. Army Corps

of Engineers-

Civil Works (TI-96)

$30.28B (3.1%)

Full Financial

Statements

Military Retirement

Fund (TI-97)

$54.67B (5.6%)

Full Financial

Statements

Marine Corps (TI-17)

$29.81B (3.0%)

GF (SBR)

Air Force (TI-57)

$187.77B (19.3%)

GF (SBA)

Navy (TI-17)

$181.86B (18.7%)

GF (SBA)

Army (TI-21)

$266.48B (27.3%)

GF (SBA)

4th Estate (TI-97)

$132.21B (13.6%)

Full Financial Statements

4th Estate (TI-97)

$91.15B (9.4%)

Not Under Audit

• Payments to Military Retirement Fund

• DoD Component Level Accounts

• Defense Health Agency (DHA),

Contract Resource Management

• MERHCF (healthcare entitlement)

• Payment to MERHCF (healthcare)

• Defense Contract Audit Agency

• Defense Commissary Agency, GF

• Funds Provided by the Office of the

Secretary of Defense to the Military

Departments

– DHA (healthcare)

– USSOCOM (special ops)

• Foreign Allies Burden Sharing

• Defense Agencies

(e.g., DLA, MDA, DCMA, DISA)

• DoD Field Activities

(e.g., DHRA, DMA, DPMO, DTIC, DTSA, OEA)

• Other Defense Organizations

(e.g., DAU, DOT&E, NDU, OIG)

• Military Housing Privatization Initiative

• Other Trust Funds FY 2013 Total Budgetary Resources 9

FY 2015 General Funds Under Audit

Current Status

SSBA Audit Status

10

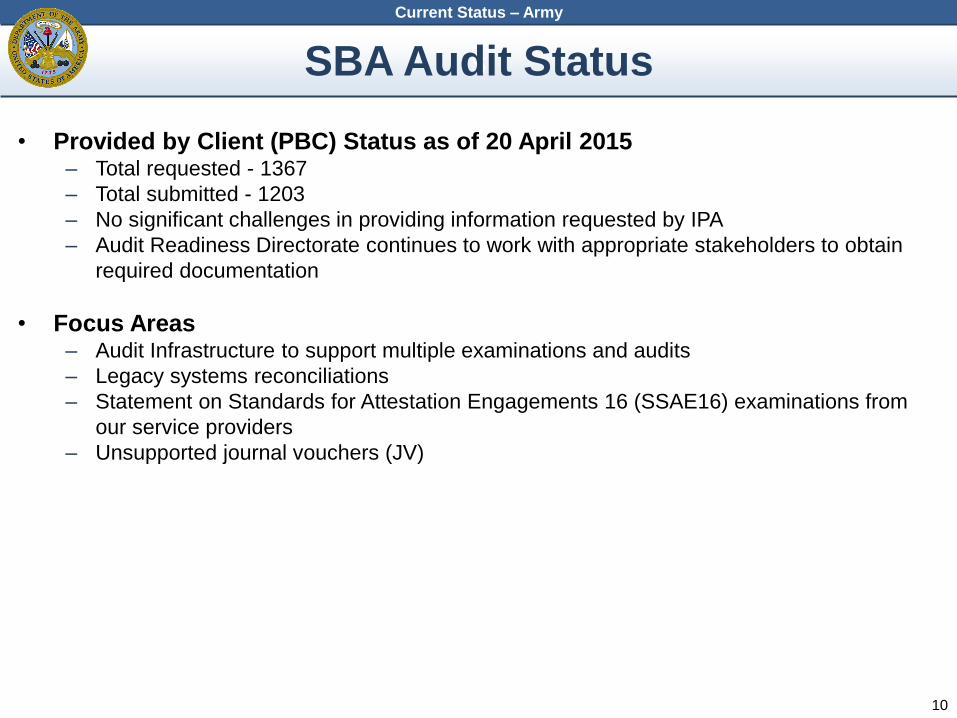

Current Status – Army

• Provided by Client (PBC) Status as of 20 April 2015– Total requested - 1367

– Total submitted - 1203

– No significant challenges in providing information requested by IPA

– Audit Readiness Directorate continues to work with appropriate stakeholders to obtain

required documentation

• Focus Areas– Audit Infrastructure to support multiple examinations and audits

– Legacy systems reconciliations

– Statement on Standards for Attestation Engagements 16 (SSAE16) examinations from

our service providers

– Unsupported journal vouchers (JV)

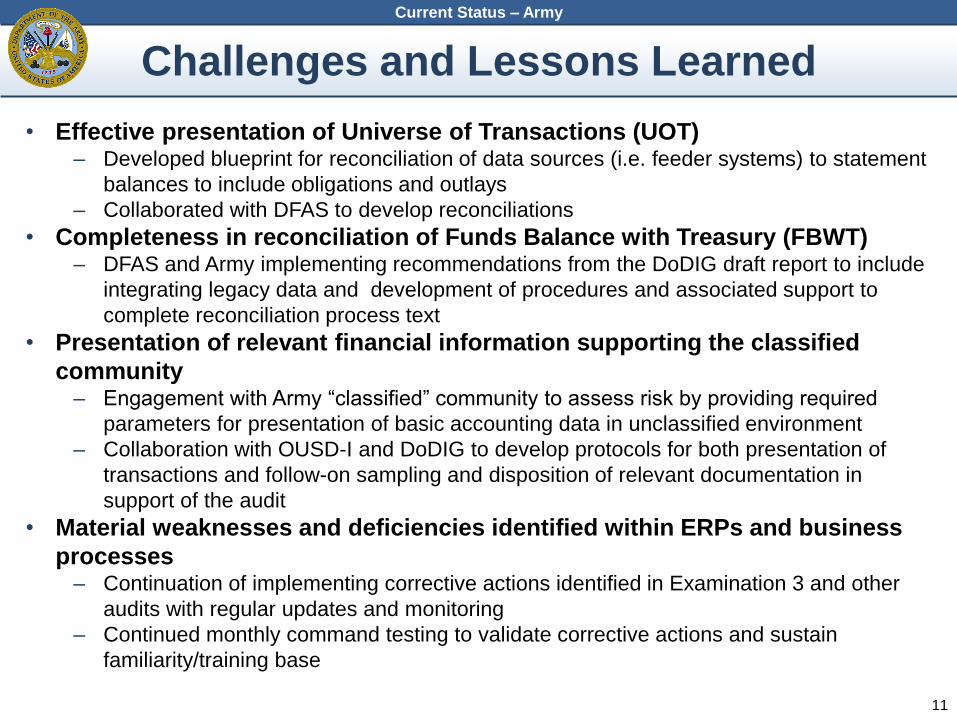

• Effective presentation of Universe of Transactions (UOT)– Developed blueprint for reconciliation of data sources (i.e. feeder systems) to statement

balances to include obligations and outlays

– Collaborated with DFAS to develop reconciliations

• Completeness in reconciliation of Funds Balance with Treasury (FBWT)– DFAS and Army implementing recommendations from the DoDIG draft report to include

integrating legacy data and development of procedures and associated support to

complete reconciliation process text

• Presentation of relevant financial information supporting the classified

community– Engagement with Army “classified” community to assess risk by providing required

parameters for presentation of basic accounting data in unclassified environment

– Collaboration with OUSD-I and DoDIG to develop protocols for both presentation of

transactions and follow-on sampling and disposition of relevant documentation in

support of the audit

• Material weaknesses and deficiencies identified within ERPs and business

processes– Continuation of implementing corrective actions identified in Examination 3 and other

audits with regular updates and monitoring

– Continued monthly command testing to validate corrective actions and sustain

familiarity/training base

Challenges and Lessons Learned

11

Current Status – Army

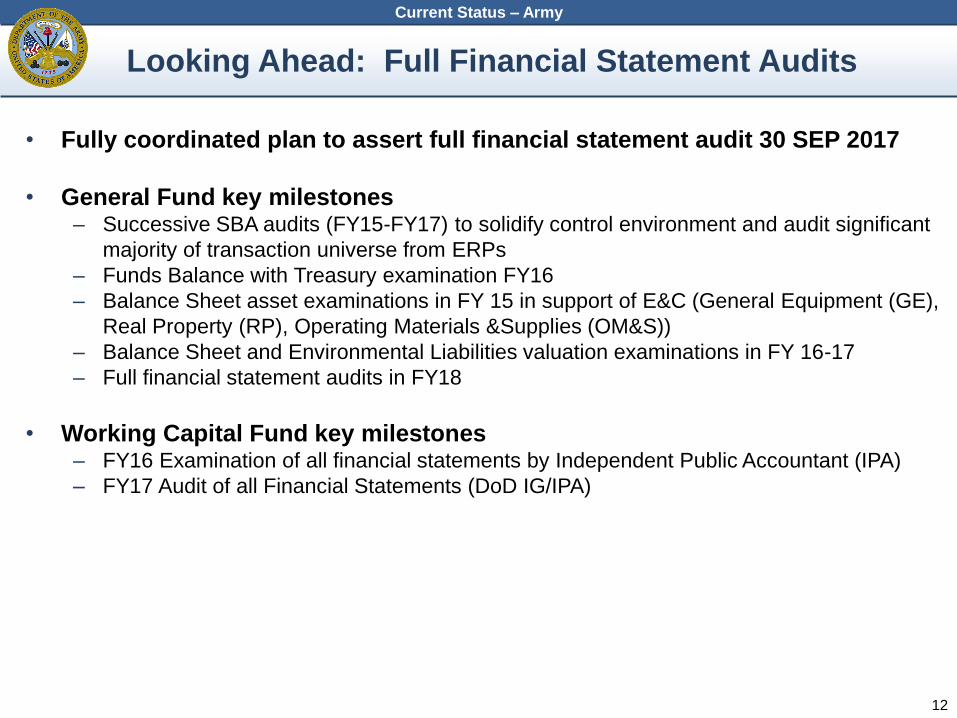

• Fully coordinated plan to assert full financial statement audit 30 SEP 2017

• General Fund key milestones– Successive SBA audits (FY15-FY17) to solidify control environment and audit significant

majority of transaction universe from ERPs

– Funds Balance with Treasury examination FY16

– Balance Sheet asset examinations in FY 15 in support of E&C (General Equipment (GE),

Real Property (RP), Operating Materials &Supplies (OM&S))

– Balance Sheet and Environmental Liabilities valuation examinations in FY 16-17

– Full financial statement audits in FY18

• Working Capital Fund key milestones– FY16 Examination of all financial statements by Independent Public Accountant (IPA)

– FY17 Audit of all Financial Statements (DoD IG/IPA)

Looking Ahead: Full Financial Statement Audits

12

Current Status – Army

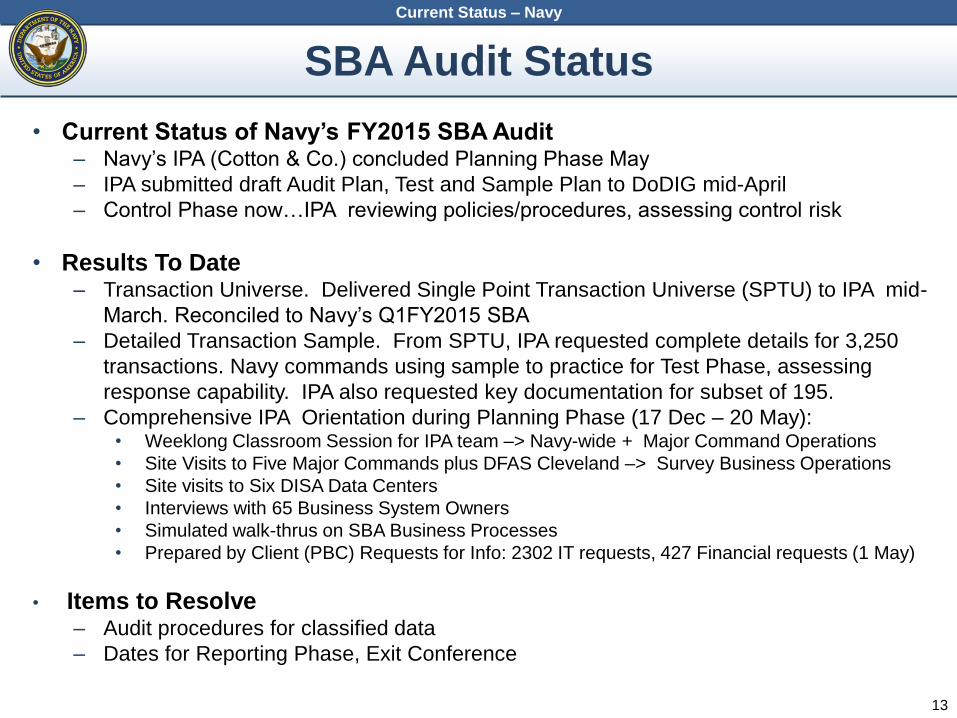

• Current Status of Navy’s FY2015 SBA Audit– Navy’s IPA (Cotton & Co.) concluded Planning Phase May

– IPA submitted draft Audit Plan, Test and Sample Plan to DoDIG mid-April

– Control Phase now…IPA reviewing policies/procedures, assessing control risk

• Results To Date– Transaction Universe. Delivered Single Point Transaction Universe (SPTU) to IPA mid-

March. Reconciled to Navy’s Q1FY2015 SBA

– Detailed Transaction Sample. From SPTU, IPA requested complete details for 3,250

transactions. Navy commands using sample to practice for Test Phase, assessing

response capability. IPA also requested key documentation for subset of 195.

– Comprehensive IPA Orientation during Planning Phase (17 Dec – 20 May):• Weeklong Classroom Session for IPA team –> Navy-wide + Major Command Operations

• Site Visits to Five Major Commands plus DFAS Cleveland –> Survey Business Operations

• Site visits to Six DISA Data Centers

• Interviews with 65 Business System Owners

• Simulated walk-thrus on SBA Business Processes

• Prepared by Client (PBC) Requests for Info: 2302 IT requests, 427 Financial requests (1 May)

• Items to Resolve – Audit procedures for classified data

– Dates for Reporting Phase, Exit Conference

SSBA Audit Status

13

Current Status – Navy

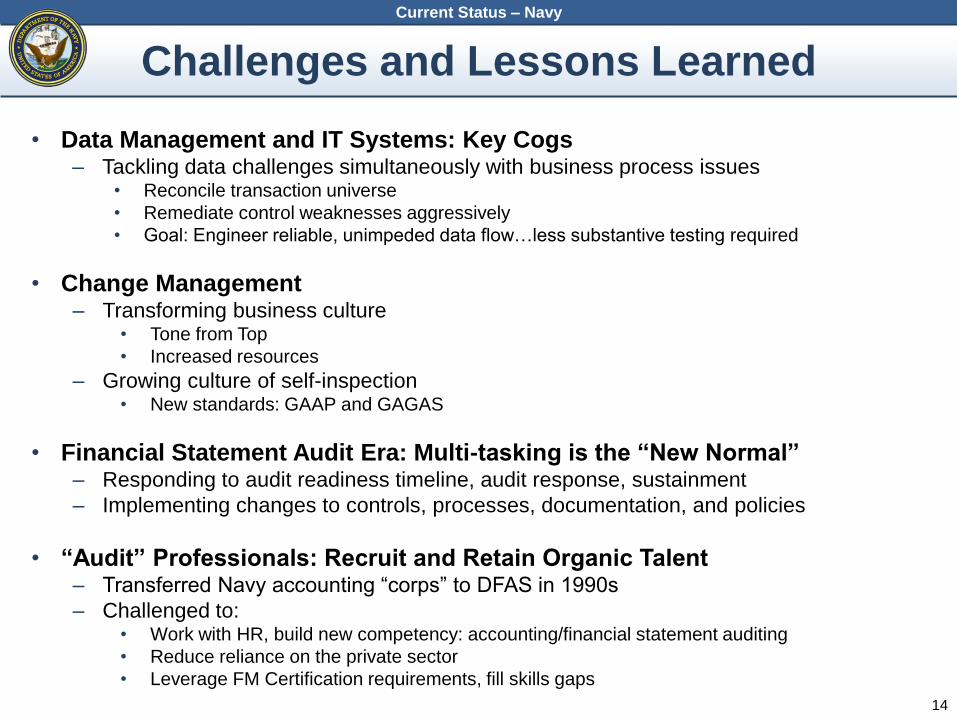

• Data Management and IT Systems: Key Cogs – Tackling data challenges simultaneously with business process issues

• Reconcile transaction universe

• Remediate control weaknesses aggressively

• Goal: Engineer reliable, unimpeded data flow…less substantive testing required

• Change Management ‒ Transforming business culture

• Tone from Top

• Increased resources

‒ Growing culture of self-inspection• New standards: GAAP and GAGAS

• Financial Statement Audit Era: Multi-tasking is the “New Normal” ‒ Responding to audit readiness timeline, audit response, sustainment

‒ Implementing changes to controls, processes, documentation, and policies

• “Audit” Professionals: Recruit and Retain Organic Talent ‒ Transferred Navy accounting “corps” to DFAS in 1990s

‒ Challenged to: • Work with HR, build new competency: accounting/financial statement auditing

• Reduce reliance on the private sector

• Leverage FM Certification requirements, fill skills gaps

Challenges and Lessons Learned

14

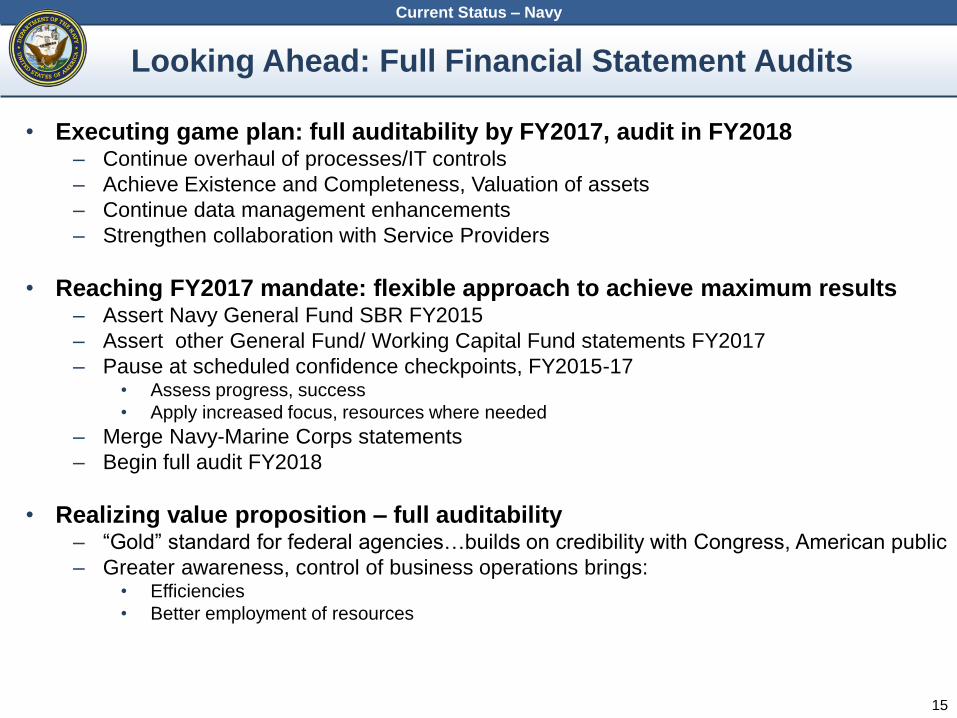

Current Status – Navy

• Executing game plan: full auditability by FY2017, audit in FY2018– Continue overhaul of processes/IT controls

– Achieve Existence and Completeness, Valuation of assets

– Continue data management enhancements

– Strengthen collaboration with Service Providers

• Reaching FY2017 mandate: flexible approach to achieve maximum results – Assert Navy General Fund SBR FY2015

– Assert other General Fund/ Working Capital Fund statements FY2017

– Pause at scheduled confidence checkpoints, FY2015-17 • Assess progress, success

• Apply increased focus, resources where needed

– Merge Navy-Marine Corps statements

– Begin full audit FY2018

• Realizing value proposition – full auditability– “Gold” standard for federal agencies…builds on credibility with Congress, American public

– Greater awareness, control of business operations brings: • Efficiencies

• Better employment of resources

Looking Ahead: Full Financial Statement Audits

15

Current Status – Navy

SSBA Audit Status

Current Status – Air Force

1616

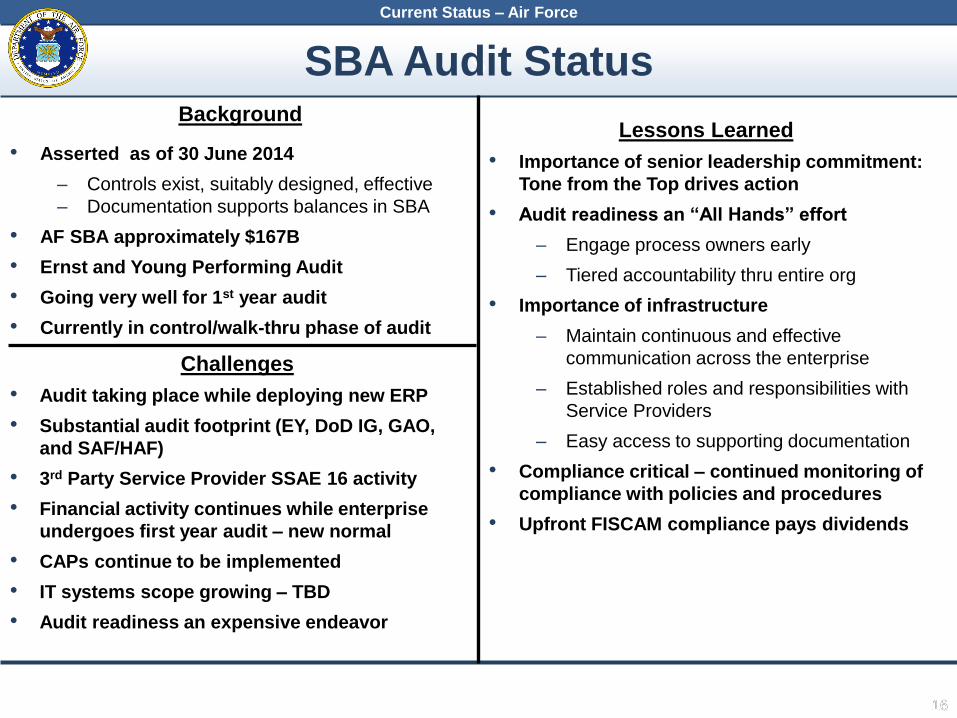

Background

• Asserted as of 30 June 2014

– Controls exist, suitably designed, effective

– Documentation supports balances in SBA

• AF SBA approximately $167B

• Ernst and Young Performing Audit

• Going very well for 1st year audit

• Currently in control/walk-thru phase of audit

Lessons Learned

• Importance of senior leadership commitment:

Tone from the Top drives action

• Audit readiness an “All Hands” effort

– Engage process owners early

– Tiered accountability thru entire org

• Importance of infrastructure

– Maintain continuous and effective

communication across the enterprise

– Established roles and responsibilities with

Service Providers

– Easy access to supporting documentation

• Compliance critical – continued monitoring of

compliance with policies and procedures

• Upfront FISCAM compliance pays dividends

Challenges

• Audit taking place while deploying new ERP

• Substantial audit footprint (EY, DoD IG, GAO,

and SAF/HAF)

• 3rd Party Service Provider SSAE 16 activity

• Financial activity continues while enterprise

undergoes first year audit – new normal

• CAPs continue to be implemented

• IT systems scope growing – TBD

• Audit readiness an expensive endeavor

Looking Ahead: Full Financial Statement Audits

17

Current Status – Air Force

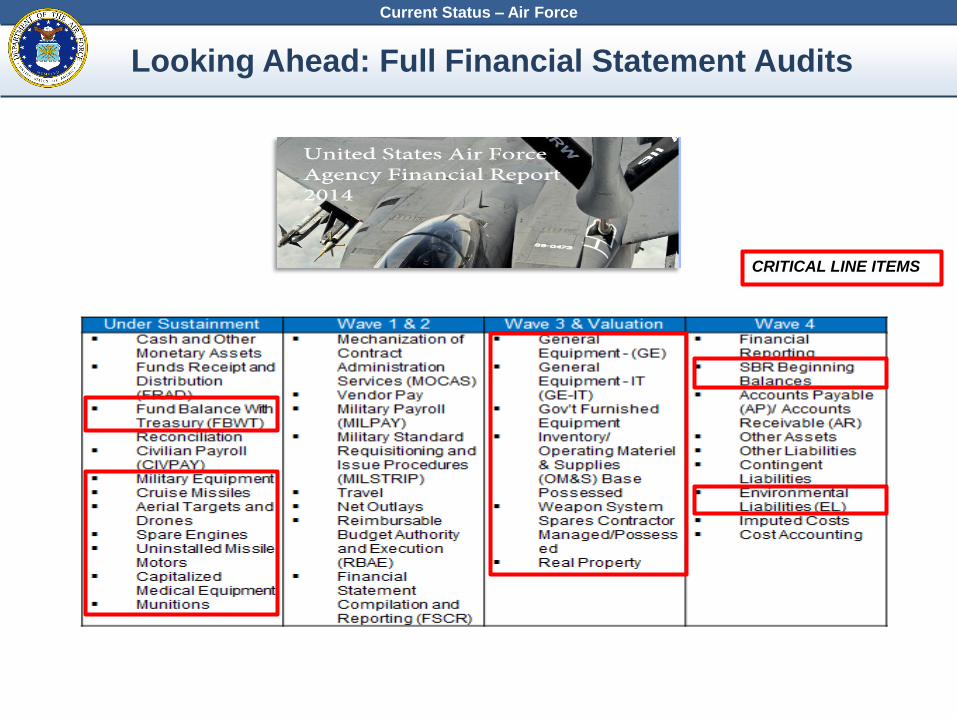

CRITICAL LINE ITEMS

Looking Ahead: Full Financial Statement Audits

18

Current Status – Air Force

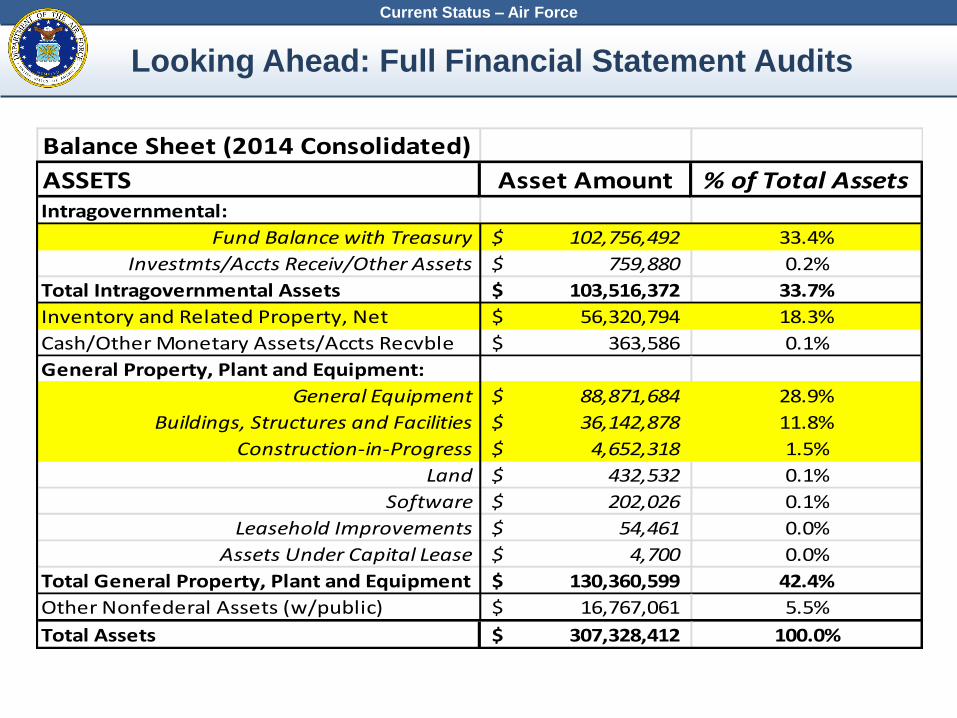

Balance Sheet (2014 Consolidated)

ASSETS Asset Amount % of Total AssetsIntragovernmental:

Fund Balance with Treasury 102,756,492$ 33.4%

Investmts/Accts Receiv/Other Assets 759,880$ 0.2%

Total Intragovernmental Assets 103,516,372$ 33.7%

Inventory and Related Property, Net 56,320,794$ 18.3%

Cash/Other Monetary Assets/Accts Recvble 363,586$ 0.1%

General Property, Plant and Equipment:

General Equipment 88,871,684$ 28.9%

Buildings, Structures and Facilities 36,142,878$ 11.8%

Construction-in-Progress 4,652,318$ 1.5%

Land 432,532$ 0.1%

Software 202,026$ 0.1%

Leasehold Improvements 54,461$ 0.0%

Assets Under Capital Lease 4,700$ 0.0%

Total General Property, Plant and Equipment 130,360,599$ 42.4%

Other Nonfederal Assets (w/public) 16,767,061$ 5.5%

Total Assets 307,328,412$ 100.0%

SSBA Audit Status

Current Status – DLA

1919

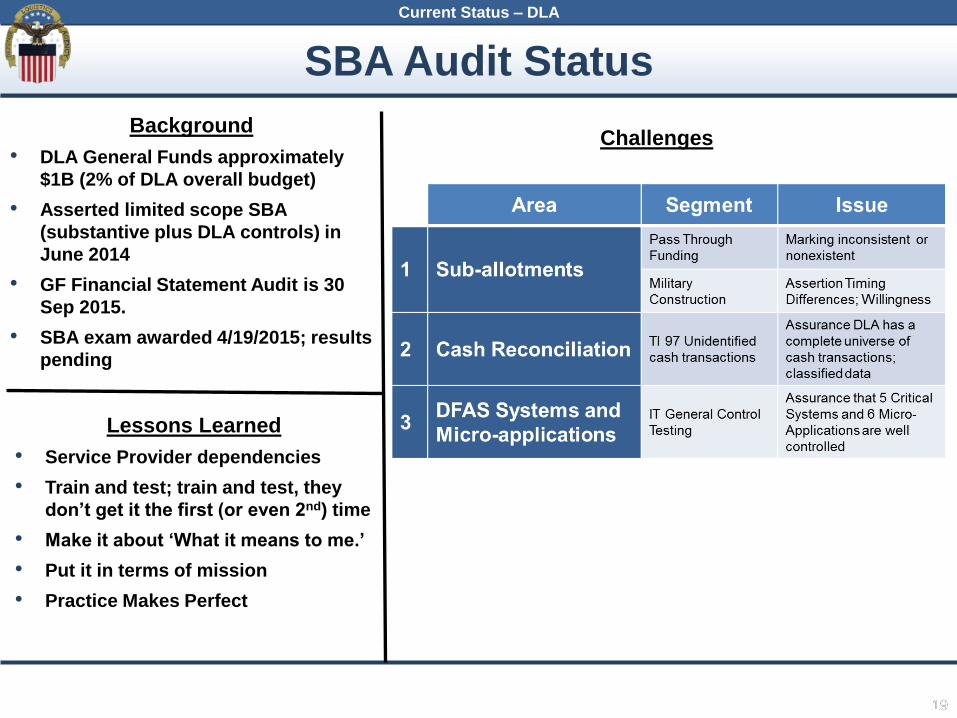

Background

• DLA General Funds approximately

$1B (2% of DLA overall budget)

• Asserted limited scope SBA

(substantive plus DLA controls) in

June 2014

• GF Financial Statement Audit is 30

Sep 2015.

• SBA exam awarded 4/19/2015; results

pending

Lessons Learned

• Service Provider dependencies

• Train and test; train and test, they

don’t get it the first (or even 2nd) time

• Make it about ‘What it means to me.’

• Put it in terms of mission

• Practice Makes Perfect

Challenges

Looking Ahead: Full Financial Statement Audit

20

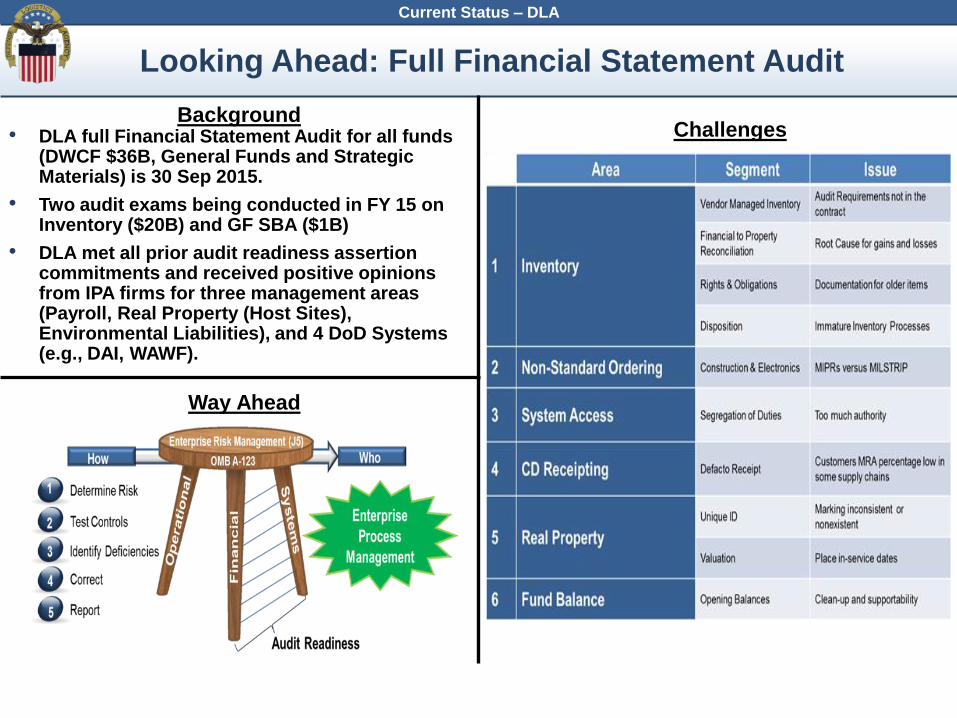

Current Status – DLA

Background• DLA full Financial Statement Audit for all funds

(DWCF $36B, General Funds and Strategic Materials) is 30 Sep 2015.

• Two audit exams being conducted in FY 15 on Inventory ($20B) and GF SBA ($1B)

• DLA met all prior audit readiness assertion commitments and received positive opinions from IPA firms for three management areas (Payroll, Real Property (Host Sites), Environmental Liabilities), and 4 DoD Systems (e.g., DAI, WAWF).

Challenges

Way Ahead

Final Thoughts

• This is a massive enterprise change management effort– The scale of DoD’s consolidated financial statement audit is unprecedented

– DoD is much more like a country than a corporation

• There is significant value in moving into an audit regimen

• Until audit opinions become routine, sustained emphasis will be needed from:– DoD senior leadership

– Congress

– Oversight organizations

• Budget stability is critical to our success

• This will be a multi-year effort– Federal Government experience indicates this is a 3-5 year process once audits begin

– We plan to do better, but need to manage expectations

21

The Department is Fully Committed to Improving the Quality of Our

Financial Information and Achieving Audit Readiness21

Stay Connected

• Visit the FIAR website – http://comptroller.defense.gov/FIAR.aspx

• Read the FIAR Plan Status Report– http://comptroller.defense.gov/FIAR/plan.aspx

• Subscribe to the DCFO’s ‘Defense Audit Readiness News’ – Join the distribution list by emailing

22