Embed Size (px)

Citation preview

Asymmetric Information

Snyder and Nicholson, Copyright ©2008 by Thomson South-Western. All rights reserved.

Asymmetric Information• Transactions can involve a considerable

amount of uncertainty– can lead to inefficiency when one side has

better information

• The side with better information is said to have private information or asymmetric information

The Value of Contracts• Contractual provisions can be added in

order to circumvent some of the inefficiencies associated with asymmetric information– rarely do they eliminate them

Principal-Agent Model• The party who proposes the contract is

called the principal

• The party who decides whether or not to accept the contract and then performs under the terms of the contract is the agent– typically the party with asymmetric

information

Leading Models• Two models of asymmetric information

– the agent’s actions affect the principal, but the principal does not observe the actions directly

• called a hidden-action model or a moral hazard model

– the agent has private information before signing the contract (his type)

• called a hidden-type model or an adverse selection model

First, Second, and Third Best• In a full-information environment, the

principal could propose a contract that maximizes joint surplus– could capture all of the surplus for himself,

leaving the agent just enough to make him indifferent between agreeing to the contract or not

• This is called a first-best contract

First, Second, and Third Best• The contract that maximizes the

principal’s surplus subject to the constraint that he is less well informed than the agent is called a second-best contract

• Adding further constraints leads to the third best, fourth best, etc.

Hidden Actions• The principal would like the agent to take

an action that maximizes their joint surplus

• But, the agent’s actions may be unobservable to the principal– the agent will prefer to shirk

• Contracts can mitigate shirking by tying compensation to observable outcomes

Hidden Actions• Often, the principal is more concerned

with outcomes than actions anyway– may as well condition the contract on

outcomes

Hidden Actions• The problem is that the outcome may

depend in part on random factors outside of the agent’s control– tying the agent’s compensation to

outcomes exposes the agent to risk– if the agent is risk averse, he may require

the payment of a risk premium before he will accept the contract

Owner-Manager Relationship• Suppose a firm has one representative

owner and one manager– the owner offers a contract to the manager– the manager decides whether to accept the

contract and what action e 0 to take• an increase in e increases the firm’s gross

profit but is personally costly to the manager

Owner-Manager Relationship• The firm’s gross profit is

g = e + – where represents demand, cost, and

other economic factors outside of the agent’s control

• assume ~ (0,2)

– c(e) is the manager’s personal disutility from effort

• assume c’(e) > 0 and c’’(e) < 0

Owner-Manager Relationship• If s is the manager’s salary, the firm’s

net profit isn = n – s

• The risk-neutral owner wishes to maximize the expected value of profit

E(n) = E(e + – s) = e – E(s)

Owner-Manager Relationship• We will assume the manager is risk

averse with a constant risk aversion parameter of A > 0

• The manager’s expected utility will be

ecsA

sEuE Var2

First-Best• With full information, it is relatively easy

to design an optimal salary contract– the owner can pay the manager a salary if

he exerts a first-best level of effort and nothing otherwise

– for the manager to accept the contract

E(u) = s* - c(e*) 0

First-Best• The owner will pay the lowest salary

possible [s* = c(e*)]

• The owner’s net profit will be

E(n) = e* - E(s*) = e* - c(e*)

– at the optimum, the marginal cost of effort equals the marginal benefit

Second Best• If the owner cannot observe effort, the

contract cannot be conditioned on e– the owner may still induce effort if some of

the manager’s salary depends on gross profit

– suppose the owner offers a salary such as

s(g) = a + bg

– a is the fixed salary and b is the power of the incentive scheme

Second Best• This relationship can be viewed as a

three-stage game– owner sets the salary (choosing a and b)– the manager decides whether or not to

accept the contract– the manager decides how much effort to

put forth (conditional on accepting the contract)

Second Best• Because the owner cannot observe e

directly and the manager is risk-averse, the second-best effort will be less than the first-best effort– the risk premium adds to the owner’s cost

of inducing effort

First- versus Second-Best Effort

ee**

MB1

e*

MC in first bestc’(e)

The owner’s MC is higher in the second best, leading to lower effort by the manager

MC in second bestc’(e) + risk term

Moral Hazard in Insurance• If a person is fully insured, he will have

a reduced incentive to undertake precautions– may increase the likelihood of a loss

occurring

Moral Hazard in Insurance• The effect of insurance coverage on an

individual’s precautions, which may change the likelihood or size of losses, is known as moral hazard

Mathematical Model• Suppose a risk-averse individual faces

the possibility of a loss (l) that will reduce his initial wealth (W0)

– the probability of loss is – an individual can reduce this probability by

spending more on preventive measures (e)

Mathematical Model• An insurance company offers a contract

involving a payment of x to the individual if a loss occurs– the premium is p

• If the individual takes the coverage, his expected utility is

E[u(W)] = (1-)u(W0-e-p) + ()u(W0-e-p-l+x)

First-Best Insurance Contract

• In the first-best case, the insurance company can perfectly monitor e– should set the terms to maximize its expected

profit subject to the participation constraint• the expected utility with insurance must be at least

as large as the utility without the insurance

– will result in full insurance with x = l– the individual will choose the socially efficient

level of precaution

Second-Best Insurance Contract

• Assume the insurance company cannot monitor e at all– an incentive compatibility constraint must be

added

• The second-best contract will typically not involve full insurance– exposing the individual to some risk induces

him to take some precaution

Hidden Types• In the hidden-type model, the individual

has private information about an innate characteristic he cannot choose– the agent’s private information at the time

of signing the contract puts him in a better position

Hidden Types• The principal will try to extract as much

surplus as possible from agents through clever contract design– include options targeted to every agent

type

Nonlinear Pricing• Consider a monopolist who sells to a

consumer with private information about his own valuation for the good

• The monopolist offers a nonlinear price schedule– menu of different-sized bundles at different

prices– larger bundles sell for lower per-unit price

Mathematical Model• Suppose a single consumer obtains surplus

from consuming a bundle of q units for which he pays a total tariff of T

u = v(q) – T– assume that v’(q) > 0 and v’’(q) < 0– the consumer’s type is

H is the “high” type (with probability of )

L is the “low” type (with probability of 1-)

• 0 < L < H

Mathematical Model• Suppose the monopolist has a constant

average and marginal cost of c

• The monopolist’s profit from selling q units is

= T – cq

First-Best Nonlinear Pricing• In the first-best case, the monopolist

observes • At the optimum

v’(q) = c– the marginal social benefit of increased

quantity is equal to the marginal social cost

First-Best Nonlinear Pricing

q

T

U0L

This graph shows the consumers’ indifference curves (by type) and the firm’s isoprofit curves

U0H

First-Best Nonlinear Pricing

q

T

A

U0L

A is the first-best contract offered to the “high” type and B is the first-best offer to the “low” type

U0H

B

Second-Best Nonlinear Pricing• Suppose the monopolist cannot observe

– knows the distribution

• Choosing A is no longer incentive compatible for the high type– the monopolist must reduce the high-type’s

tariff

Second-Best Nonlinear Pricing

q

T

A

U0L

The “high” type can reach a higher indifference curve by choosing B

U0H

B

U2H

To keep him from choosing B, the monopolist must reduce the “high” type’s tariff by offering a point like C

C

Second-Best Nonlinear Pricing

q

T

A

U0L

The monopolist can also alter the “low” type’s bundle to make it less attractive to the high type

U0H

B

U2H

C

D

E

q**Hq**L

Monopoly Coffee Shop• The college has a single coffee shop

– faces a marginal cost of 5 cents per ounce

• The representative customer faces an equal probability of being one of two types– a coffee hound (H = 20)

– a regular Joe (L = 15)

• Assume v(q) = 2q0.5

First Best• Substituting such that marginal cost =

marginal benefit, we get

q = (/c)2

q*L = 9 q*H = 16

T*L = 90 T*H = 160

E() = 62.5

Incentive Compatibility when Types Are Hidden

• The first-best pricing scheme is not incentive compatible if the monopolist cannot observe type– keeping the cup sizes the same, the price

for the large cup would have to be reduced by 30 cents

– the shop’s expected profit falls to 47.5

Second Best

• The shop can do better by reducing the size of the small cup

• The size that is second best would be

LqL-0.5 = c + (H - L)qL

-0.5

q**L = 4

T**L = 60

E() = 50

Adverse Selection in Insurance• Adverse selection is a problem facing

insurers where the risky types are more likely to accept an insurance policy and are more expensive to serve– assume policy holders may be one of two

typesH = high risk

L = low risk

First Best• The insurer can observe the individual’s

risk type

• First best involves full insurance– different premiums are charged to each

type to extract all surplus

First Best

certainty line

W1

W2

U0L

Without insurance each type finds himself at E

U0H

A

B

E

A and B represent full insurance

Second Best• If the insurer cannot observe type, first-

best contracts will not be incentive compatible– if the insurer offered A and B, the high-risk

type would choose B– the insurer must change the coverage

offered to low-risk individuals to make it unattractive to high-risk individuals

First Best

certainty line

W1

W2

U0L

U0H

A

B

E

U1H

The high-risk type is fully insured, but his premium is higher (than it would be at B)

C

The low-risk type is only partially insured

D

Market Signaling• If the informed player moves first, he

can “signal” his type to the other party– the low-risk individual would benefit from

providing his type to insurers• he should be willing to pay the difference

between his equilibrium and his first-best surplus to issue such a signal

Market for Lemons• Sellers of used cars have more

information on the condition of the car– but the act of offering the car for sale can

serve as a signal of car quality• it must be below some threshold that would

have induced the owner to keep it

Market for Lemons• Suppose there is a continuum of

qualities from low-quality lemons to high-quality gems– only the owner knows a car’s type

• Because buyers cannot determine the quality, all used cars sell for the same price– function of average car quality

Market for Lemons• A car’s owner will choose to keep a car

that is in the upper end of the spectrum– reduces the average quality– reduces the market price– leads sellers of the high end of the

remaining cars to keep their cars• reduces average quality and market price

Adverse Selection• Consider a used car market.

• Two types of cars; “lemons” and “peaches”.

• Each lemon seller will accept $1,000; a buyer will pay at most $1,200.

• Each peach seller will accept $2,000; a buyer will pay at most $2,400.

Adverse Selection• If every buyer can tell a peach from a

lemon, then lemons sell for between $1,000 and $1,200, and peaches sell for between $2,000 and $2,400.

• Gains-to-trade are generated when buyers are well informed.

Adverse Selection• Suppose no buyer can tell a peach from

a lemon before buying.

• What is the most a buyer will pay for any car?

Adverse Selection• Let q be the fraction of peaches.

• 1 - q is the fraction of lemons.

• Expected value to a buyer of any car is at mostEV q q $1200( ) $2400 .1

Adverse Selection• Suppose EV > $2000.

• Every seller can negotiate a price between $2000 and $EV (no matter if the car is a lemon or a peach).

• All sellers gain from being in the market.

Adverse Selection• Suppose EV < $2000.

• A peach seller cannot negotiate a price above $2000 and will exit the market.

• So all buyers know that remaining sellers own lemons only.

• Buyers will pay at most $1200 and only lemons are sold.

Adverse Selection• Hence “too many” lemons “crowd out”

the peaches from the market.

• Gains-to-trade are reduced since no peaches are traded.

• The presence of the lemons inflicts an external cost on buyers and peach owners.

Adverse Selection• How many lemons can be in the market

without crowding out the peaches?

• Buyers will pay $2000 for a car only if

2000$2400$)1(1200$ qqEV

Adverse Selection• How many lemons can be in the market

without crowding out the peaches?

• Buyers will pay $2000 for a car only if

• So if over one-third of all cars are lemons, then only lemons are traded.

.32

2000$2400$)1(1200$

q

qqEV

Adverse Selection• A market equilibrium in which both types of

cars are traded and cannot be distinguished by the buyers is a pooling equilibrium.

• A market equilibrium in which only one of the two types of cars is traded, or both are traded but can be distinguished by the buyers, is a separating equilibrium.

Adverse Selection• What if there is more than two types of

cars?

• Suppose that car quality is Uniformly distributed

between $1000 and $2000 any car that a seller values at $x is valued

by a buyer at $(x+300).

• Which cars will be traded?

Adverse SelectionThe expected value of anycar to a buyer is $1500 + $300 = $1800.

1000 20001500Seller values

So sellers who value their cars atmore than $1800 exit the market.

Adverse Selection

1000 1800

The distribution of valuesof cars remaining on offer

Seller values

Adverse Selection

1000 18001400

The expected value of anyremaining car to a buyer is $1400 + $300 = $1700.

So now sellers who value their carsbetween $1700 and $1800 exit the market.

Seller values

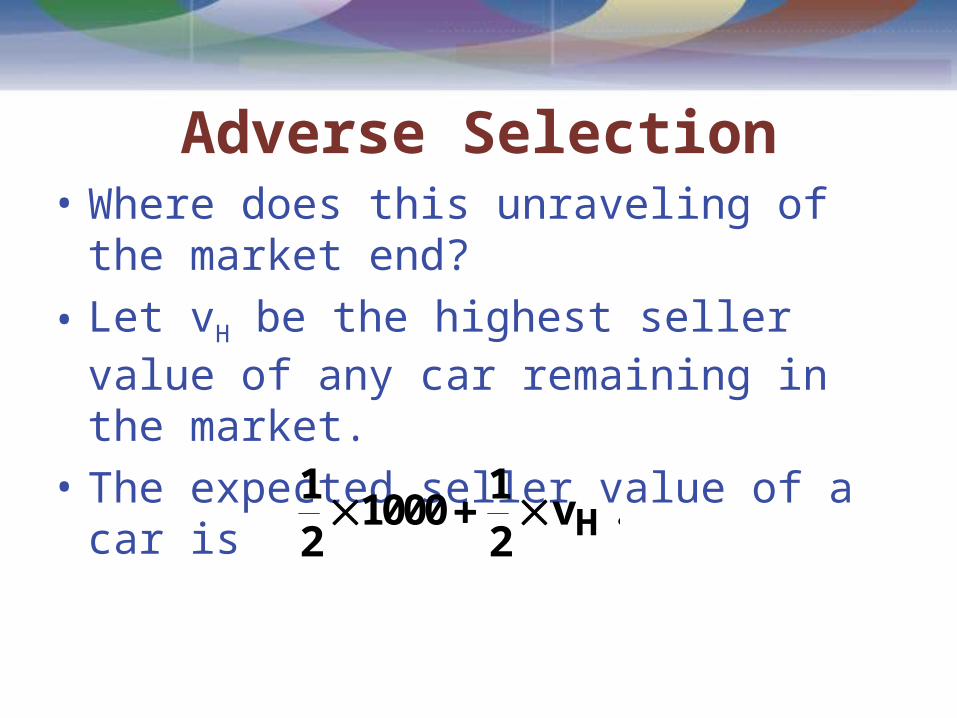

Adverse Selection• Where does this unraveling of the market

end?

• Let vH be the highest seller value of any car remaining in the market.

• The expected seller value of a car is121000

12

vH .

Adverse Selection

• So a buyer will pay at most

• This must be the price which the seller of the highest value car remaining in the market will just accept; i.e.

121000

12

300 vH .

121000

12

300 v vH H .

Adverse Selection

121000

12

300 v vH H

vH $1600.

Adverse selection drives out all carsvalued by sellers at more than $1600.

Signaling• Adverse selection is an outcome of an

informational deficiency.

• What if information can be improved by high-quality sellers signaling credibly that they are high-quality?

• E.g. warranties, professional credentials, references from previous clients etc.

Signaling• A labor market has two types of workers;

high-ability and low-ability.

• A high-ability worker’s marginal product is aH.

• A low-ability worker’s marginal product is aL.

• aL < aH.

• A fraction h of all workers are high-ability.

• 1 - h is the fraction of low-ability workers.

Signaling• Each worker is paid his expected

marginal product.

• If firms knew each worker’s type they would pay each high-ability worker wH = aH

pay each low-ability worker wL = aL.

Signaling• If firms cannot tell workers’ types then

every worker is paid the (pooling) wage rate; i.e. the expected marginal product wP = (1 - h)aL + haH.

Signaling• wP = (1 - h)aL + haH < aH, the wage rate

paid when the firm knows a worker really is high-ability.

• So high-ability workers have an incentive to find a credible signal.

Signaling• Workers can acquire “education”.• Education costs a high-ability worker cH

per unit• and costs a low-ability worker cL per unit.• cL > cH.• Suppose that education has no effect on

workers’ productivities; i.e., the cost of education is a deadweight loss.

Signaling• High-ability workers will acquire eH

education units if(i) wH - wL = aH - aL > cHeH, and(ii) wH - wL = aH - aL < cLeH.

• (i) says acquiring eH units of education benefits high-ability workers.

• (ii) says acquiring eH education units hurts low-ability workers.

SignalingHHLH ecaa HLLH ecaa and

together require

.H

LHH

L

LH

caa

ecaa

Acquiring such an education level crediblysignals high-ability, allowing high-abilityworkers to separate themselves fromlow-ability workers.

Signaling• Q: Given that high-ability workers

acquire eH units of education, how much education should low-ability workers acquire?

• A: Zero. Low-ability workers will be paid wL = aL so long as they do not have eH units of education and they are still worse off if they do.

Signaling• Signaling can improve information in the

market.

• But, total output did not change and education was costly so signaling worsened the market’s efficiency.

• So improved information need not improve gains-to-trade.

Auctions• A seller can often do better if several

buyers compete against each other– high-value consumers are pushed to bid

high

• Different formats may lead to different outcomes– sellers should think carefully about how to

design the auction

First-Price Sealed Auction Bid• All bidders simultaneously submit secret

bids

• The auctioneer unseals the bids and awards the object to the highest bidder

• The highest bidder pays his own bid

First-Price Sealed Auction Bid• In equilibrium, it is a weakly dominated

strategy to submit a bid b greater than or equal to the buyer’s valuation v– a strategy is weakly dominated if there is

another strategy that does at least as well against all rivals’ strategies and strictly better against at least one

First-Price Sealed Auction Bid• A buyer receives no surplus if he bids

b=v no matter what his rivals bid– by bidding b < v, there is a chance for

some positive surplus

• Since players likely avoid weakly dominated strategies, we can expect bids to be lower then buyers’ valuations

Second-Price Sealed Auction Bid• The highest bidder pays the next

highest bid rather than his own

• All bidding strategies are weakly dominated by the strategy of bidding exactly one’s valuation– second-price auctions induce bidders to

reveal their valuations

Second-Price Sealed Auction Bid• The reason that bidding one’s valuation

is weakly dominant is that the winner’s bid does not affect the amount he has to pay– that depends on someone else’s bid

Common Values Auctions• In complicated economic environments,

different auction formats do not necessarily yield the same revenue

• Suppose the good has the same value to all bidders, but they do ot know exactly what that value is– common values auction

Common Values Auctions• The winning bidder realizes that every

other bidder probably though the object was worth less– means that he probably overestimated the

value when bidding

• This is often referred to as the winner’s curse

Important Points to Note:• Asymmetric information is often studied

using a principal-agent model in which a principal offers a contract to an agent who has private information– the two main variants of the model are the

models of hidden actions and hidden types

Important Points to Note:• In a hidden-action model (called a moral

hazard model), the principal tries to induce the agent to take appropriate actions by tying the agent’s payments to observable outcomes– doing so exposes the agent to random

fluctuations, which is costly for a risk-averse agent

Important Points to Note:• In a hidden-type model (called an

adverse selection model), the principal cannot extract all of the surplus from high types because they can always gain positive surplus by pretending to be a low type– the principal will offer a menu of contracts

from which different types of agents can select

Important Points to Note:• In a hidden-type model, the principal will

offer a menu of contracts from which different types of agents can select– the principal distorts the quantity offered to

low types in order to make the contract less attractive to high types

Important Points to Note:• Most of the insights gained from the

basic form of a principal-agent model, in which the principal is a monopolist, carry over to the case of competing principals– the main change is that agents obtain more

surplus

Important Points to Note:• The lemons problem arises when

sellers have private information about the quality of their goods– sellers whose goods are higher than

average quality may refrain from selling– the market may collapse, with goods of

only the lowest quality being offered for sale

Important Points to Note:

• The principal can extract more surplus from agents if several of them are pitted against one another in an auction setting– in a simple economic environment, a variety of

common auction formats generate the same revenue

– differences in auction format may generate different levels of revenue in more complicated settings