Embed Size (px)

Citation preview

1

Association of Investment Bankers of India raising the credibility standard

Contents Page

Notice 2

Directors' Report 3

Auditors' Report 19

Balance Sheet 21

Income & Expenditure 22Account

Notes to the Financial 23Statements

List of Members 28

Board of Directors

Mr. Sanjay Sharma Chairman

Mr. B. Madhuprasad Vice Chairman

Mr. Anay Khare Director

Mr. T.R.Prashanth Kumar Director

Mr. Ranganath Char Director

Mr. Abhay Bongirwar Director

Ms. Gesu Kaushal Director

Mr. Ajay Pancholi Director

Mr. K. Srinivas Director

Mr. Avinash Kulkarni Director( w.e.f. 3RD December 2012)

Honorary Advisor

Mr. Prithvi Haldea

Chief Executive Officer

Mr. V.S. Narayanan

Auditors

M/S. Chandabhoy & Jassoobhoy

Chartered Accountants

208, “A” Wing, 2ND Floor

Phoenix House

462, Senapati Bapat Marg

Mumbai – 400 013.

Bankers

Central Bank Of India

Axis Bank Ltd.

Registered Office

505/506, Dalamal Chambers

29, New Marine Lines

Mumbai – 400 020.

2

20th Annual Report 2012-13 raising the credibility standard

Notice is hereby given that the Twentieth Annual General Meeting of the Association of Investment

Bankers of India will be held on Monday the 30th September 2013 at 3.00 pm at Hotel West End,

45, New Marine Lines, Mumbai- 400 020 to transact the following business:

1. To consider, approve and adopt the Directors’ Report, the Audited Income & ExpenditureAccount for the year ended 31st March 2013, the Audited Balance Sheet as at that date andthe Auditor’s report thereon.

2. To elect a Director in place of Mr. T. R. Prashanth Kumar, who retires by rotation and is eligiblefor re-appointment.

3. To elect a Director in place of Mr. Ajay Pancholi, who retires by rotation and is eligible for re-appointment.

4. To elect a Director in place of Mr. Avinash Kulkarni, who retires by rotation and is eligible forre-appointment.

5. To appoint Auditors to hold office from the conclusion of the Twentieth Annual General

Meeting until the conclusion of the Twenty First Annual General Meeting and to authorise theBoard to fix their remuneration.

NOTICE

Registered Office : 505-506, Dalamal Chambers,

5th Floor, 29, New Marine Lines, Mumbai - 400 020.

By the order of the Board

SANJAY SHARMA

Chairman

Place : Mumbai

Date : 28th August 2013

NOTES :

A) As per Article 45 of the Articles of Association of the Association of Investment Bankers of India

(AIBI) the total number of Directors on the Board of Directors shall not be more than fifteen out of

which ten will be elected by members, two will be elected by Associates and three will be nominee

Directors (not subject to retirement by rotation) of the Securities & Exchange Board of India (SEBI).

Accordingly, the Board of Directors was constituted. The authorised representatives of Members are

entitled to be appointed on the Board of Directors, if elected. At the AGM the ballot papers with

necessary instructions will be handed over to the Members for electing the Directors.

As Investment Bankers belonging to Categories II, III and IV are no longer registered with SEBI,

there will be no Director from the category of Associates. SEBI has decided not to nominate any

Director on the Board. The reservation for public sector Directors and Non-public sector Directors

does not exist any more.

B) A Member entitled to attend and vote is entitled to appoint a proxy to attend and vote instead of

himself provided that the proxy is a Member or an officer of any other Member and registered with

AIBI as per provisions of Article 15 of the Articles of Association.

The Proxy Form should be deposited at the Registered Office of the Association of Investment

Bankers of India, not less than 48 hours before the meeting.

3

Association of Investment Bankers of India raising the credibility standard

DIRECTORS’ REPORT

Your Directors have great pleasure in presenting the Twentieth Annual Report of the Association of

Investment Bankers of India together with the Income and Expenditure Account for the year ended

31st March 2013 and the Balance Sheet as at that date.

FINANCIAL RESULTS

Membership Fees 2,787 2,675

Summit Income 2,030 0

Other Income 5,179 4,713

Total Income 9,996 7,388

Employees benefits expenses 2,875 2,253

Other Expenses 1,582 1,317

Summit Expenses 1,491 0

Depreciation and amortization expense 425 465

Total Expenses 6,373 4,035

Excess of Income over Expenditure for the Year befor tax 3,623 3,353

Less: Tax expense

(1) Current tax 1,140 1,100

(2) Deferred tax (27) (17)

Excess of Income over Expenditure after tax 2,510 2,270

Less: Short /(Excess) provision for income tax of earlier years (38) (57)

Excess of Income over Expenditure carried to Balance Sheet 2,548 2,213

CHAIRMAN AND VICE CHAIRMAN

At the Board Meeting held on the 27th September 2012, Mr. Sanjay Sharma, Managing Director,

Deutsche Equities India Pvt. Ltd and Mr. B. Madhuprasad, Vice Chairman, Keynote Corporate

Services Ltd. were unanimously re-elected Chairman and Vice Chairman respectively of the Association

till the conclusion of the next Annual General Meeting.

(`. ‘000s)

ParticularsYear ended Year ended31-3-2013 31-3-2012

4

20th Annual Report 2012-13 raising the credibility standard

DIRECTORS

The following Directors are due to retire by rotation at the end of the 20th Annual General Meeting

and are eligible for re-appointment by election.

1) Mr. Avinash Kulkarni

2) Mr. Ajay Pancholi

3) Mr. T.R.Prashanth Kumar

HONORARY ADVISOR

Mr. Prithvi Haldea, Chairman & Managing Director of PRIME Database, continued as the Honorary

Advisor to AIBI .The Board would like to express its special appreciation for his continued support

and guidance, especially in successfully conducting our Summit 2012.

MEMBERSHIP

Between the last AGM and the ensuing AGM two new Investment Banking entities viz. IL&FS

Capital Advisors Ltd. and Chartered Finance Management Ltd. were admitted as Members. We

warmly welcome the new Members and look forward to their contribution to making our Association

and industry stronger.

The total number of members as on the date of this report is 57.

MARKET SCENARIO

EQUITY CAPITAL MARKETS - SECONDARY

SUMMARY

The secondary market was quite volatile during the year. A number of factors contributed to this

volatility such as political uncertainty, rising oil prices, weak macroeconomic indicators and

volatile exchange rates. After being range bound during April 2012, the indices lost more than

6% in May 2012 (Sensex and Nifty were down by 1100 points and 324 points respectively as

compared to April 2012 closing). The Sensex was one of the worst performing global indices in

the last week of July 2012 on account of concerns regarding RBI monetary policy rates remaining

unchanged and weak FII inflows. By September, the markets gathered some momentum, with

Sensex and Nifty moving up by 1330 (7.35%) and 444 points (8.46%) respectively, as compared

to the previous month’s closing. This was mainly on account of positive FII inflows during the

month, announcement of FDI reforms in insurance and pension sectors and brief strengthening

5

Association of Investment Bankers of India raising the credibility standard

of the rupee. November 2012 saw positive investor interest on account of discussions on FDI in

multi brand retail in the upper house of Parliament. In January 2013, the indices (Sensex at

20203.66 and Nifty at 6111.8) touched the high of the financial year though the closing levels

for the month were not much higher than the previous month. However, in February 2012, the

indices lost nearly two thirds of the gains made in the last four months with the Sensex and Nifty

falling by more than 1000 points and 300 points respectively. The Sensex and Nifty at the end of

the Financial Year were at 18835 and 5682.55 (representing a gain of 8.23% and 7.31%)

respectively over the previous year’s closing (Sensex 17404 and Nifty 5295.22). The performance

of the indices in the last quarter of FY 13 was influenced by events such as the Union Budget

falling short of market expectations, weak global cues and lower GDP numbers among other

factors.

Volatility in the indices during the year was more than 28% with Sensex and Nifty touching a

high of 20203.66 points and 6111.8 points and a low of 15437 points and 4770.35 points

respectively.

In terms of other stock market indices, FMCG, Healthcare, IT, Bankex, Consumer Durables,

TECk, Oil & Gas and Realty closed in the positive while Auto, Midcap, Capital Goods, PSU,

Small Cap had negative closing.

• FMCG continued to show maximum growth with 31.7% followed by Healthcare and IT at

20.9% and 13.2% respectively. Consumer durables at 10.8% also registered a higher growth

as compared to the previous year (2.6% growth).

• Oil & Gas and Realty indices showed considerable gain while closing positive at 2.9% (-21%

in previous year) and 0.2% (-23.9% in the previous year) respectively.

• Auto sector and Midcap indices slipped to negative closing at -1.4% (9.1% previous year)

and -3.2%(7.7% previous year) respectively.

• Capital Goods, PSU, Small cap and Metal indices continued to have negative closing at

-10.1, -11.4%, – 12.4% and -22.8% respectively despite gains as compared to previous year.

• Power sector index remained negative at -21.3% without much change from the previous

year.

6

20th Annual Report 2012-13 raising the credibility standard

INDICES REPRESENTED IN BAR CHART

Indices 31/3/2012 31/3/2013 Growth Indices 31/3/2012 31/3/2013 Growth

% %

Sensex 17404.20 18835.77 8.23

BSE Sectorial Indices

FMCG 4493.10 5,919.19 31.74 Auto 10134.88 9,994.23 -1.39

Healthcare 6625.74 8,008.09 20.86 Midcap 6,346.38 6,142.06 -3.22

IT 6081.87 6,885.46 13.21 Capital 10027.92 9,017.59 -10.08

Goods

Bankex 11751.18 13,033.35 10.91 PSU 7311.47 6,481.16 -11.36

Consumer 6402.49 7,094.55 10.81 Small 6,629.38 5,804.65 -12.44

Durables Cap

TECK 3,562.41 3,900.94 9.50 Power 2090.97 1,646.50 -21.26

Oil & Gas 8087.50 8,326.60 2.96 Metal 11346.31 8,758.32 -22.81

Realty 1776.96 1,780.09 0.18

Source: www.bseindia.com

20000 18000 16000 14000 12000 10000 8000 6000 4000 2000

0

7

Association of Investment Bankers of India raising the credibility standard

SEBI REGULATIONS

The following new Regulations/ guidelines were issued by SEBI by way of Amendments/Circulars:

between August 22, 2012 and August 28, 2013 (date of this Directors’Report)

Sr. Date of Regulation / Gist of Regulations/Circular/

# Regulation / Circular/ Notification/ Notification/Circular / General Order General Order

Notification/General Order

SEBI (ICDR) REGULATIONS 2009

1. August 24, 2012 SEBI (ICDR) Third 1) New Proviso added to Regulation 14 (1) to align

Amendment the miniumum subscription received in an IPO

with Regulation, 2011 the minimum allotment

prescribed under 19(2)(b) of Securities

Contracts (Regulations) Rules 1957.

2) Regulation 91G(1) substituted by new

Regulation 91G(1) putting restriction of the sale

by Promoter/Promoter Group through IPP or

Stock Exchange Mechanism.

2. Oct. 12, 2012 SEBI (ICDR) 1) Definition General Corporate Purposes (GCP)

Fourth Amendment included and the total amount of GCP restricted

Regulation, 2012 to 25 of Objects of Issue.

2) Average Market Capitalisation of public

shareholding reduced to Rs. 3000 crs for Fast

track issues.

3) Fast track issues not to open before 3 days of

filing of RHP with RoC.

4) Non-underwritable portion increased from 50%

to 75% in case of Issues not complying with

eligibility criteria.

5) Track record for eligibility criteria under

Regulation 26 (1) (b) changed to minimum

average pre-tax operating profit of Rs. 15 crs

during the most profitable 3 years of the

preceding 5 years.

6) Change in Regulation 26 (2) - Net offer to

Public increased to 75% for companies not

meeting eligibility criteria stipulated under

Regulation 26(1).

7) Change in Regulation 30 (1) – Period for

announcing Price band increased to at least

before 5 days of opening of bid.

8) Regulation 33(1)(b) and 36 (a) – Investment by

alternate investment fund to be a part of

Promoters’ contribution.

8

20th Annual Report 2012-13 raising the credibility standard

9) New Sub Regulation 43 (2A) to align with new

Regulation 26 (2).

10) Regulation 49(1) - Minimum application value –

range increased to Rs. 10,000 and Rs. 15,000.

11) New Regulation 50 (1A) – compulsory

allotment to each retail individual investor (RII),

subject to availability of shares in the RII

category.

12) New Regulation 51A – Annual updation of

Offer document .

13) New proviso to sub regulation 57(b) introduced

in case of follow on and rights offer.

14) New proviso to sub regulation 85(1) – discount

on QIP.

15) New “Point # 17” added to DD Certificate from

Lead Managers in Form A under Schedule VI.

16) Schedule VII – Updation and Refiling of Offer

documents – restricted to only increase in Issue

size and the limit increased from 10% to 20%.

17) Marketing lead manager’s name to appear on

the Cover page.

18) Sub clause (i) in Schedule XI – Part A – RIIs

allowed to withdraw or revise the bid until

finalization of allotment.

19) Sub clause (j) in Schedule XI – Part A – QIBs

cannot lower their bids.

20) Manner of allocation/allotment modified - para

15 of Schedule XI Part A .

21) Schedule XIV substituted by new Schedule XIV.

22) Schedule XV substituted by new Schedule XV.

3. February 27, SEBI (ICDR) Regulation 100 – existing regulation substituted by

2013 Amendment new Regulation.

Regulation, 2013

4. August 26, 2013 SEBI (ICDR) Changes in Preferential Allotment Regulations-

Second Amendment 1) sub clause (e ) in Regulation 73 (1) modified to

Regulation, 2013 included beneficial owners.

2) New sub Regulation 74 (4) introduced allotment

only in dematerialized form.

3) New sub Regulations (5) and (6) included in

Regulation 74 – in respect of cash receipt for

allotment of shares.

9

Association of Investment Bankers of India raising the credibility standard

4) Sub Regulations (1), (2), (4) and (6) to

Regulation 78 – “date of allotment” substituted

by “date of trading approval”.

5) New sub Regulation (79) (2) introduced – inter

se transfer of locked-in shares not permitted till

the date of trading approval.

SEBI (BUY BACK OF SECURITIES) REGULATION, 1998

5. August 8, 2013 SEBI Key amendments in the Buy back Regulations

(Buy back of included :

Securities) 1) Regulation 4 modified - Buy back through

Amendment Open Market route restricted to 15% of share

Regulation, 2013 capital and reserves.

2) New sub Regulation (14) (4 ) introduced – one

year gap between two Buy back offers.

3) New sub Regulation 14 (2) (3) introduced – for

successful Buy back minimum 50% of amount

reserved for Buy back has to be utilized.

4) Sub Regulation 15(i) changed – information on

Buy back to be put up Company’s website on a

daily basis.

5) New sub Regulation 15(k) – Buy back offer

period restricted to six months.

6) New sub Regulation 15A introduced – Buy back

of physical shares.

7) New sub Regulation 15B introduced –

providing for minimum 25% of Buy back

amount to be kept in escrow account and other

operational matters.

8) New sub regulation 16 (3) – extinguishment of

shares.

9) Sub Regulation 19 (e ) changed – restricting the

promoters’ right in dealing in the shares from

the date of Buy back resolution to closing of

offer.

10) New sub Regulation 19 (f) introduced –

restriction of one year for further raising of

capital.

10

20th Annual Report 2012-13 raising the credibility standard

SEBI (SUBSTANTIAL ACQUISITION OF SHARES AND TAKEOVER ) REGULATION 2011

6. March 26, 2013 SEBI (Substantial 1) At several places in the Regulation, the words

Acquisition of “on which the voting rights so increase” has

Shares and been substituted by “the date of closure of buy

Takeover) back offer”.

Amendment 2) The relevant date for Public announcement

Regulation 2013 under Regulation 13 (2) (g) amended.

3) New sub Regulation 13(2A) introduced to

provide of Public announcement.

4) New sub Regulation 22 (2) introduced – to

provide for shares to be kept in escrow account.

5) New Proviso introduced to Regulation 23 (1)

(c) – restricting the acquirers’ right to withdraw

the open offer.

6) Existing sub clause 29(2) substituted by new

clause.

SEBI (CERTIFICATION OF ASSOCIATE PERSONS IN THE SECURITIES

MARKET) REGULATION 2007

7. August 2, 2013 Notification Certification from NISM for at least two key

under personnel involved in Primary Capital market

Regulation 3 activities made compulsory by passing NISM-

Series IX (Merchant Banking Certification

Examination).

GENERAL ORDER UNDER SECTION 11 A OF SEBI ACT, 1992

8. October 9, 2012 SEBI 1) Criteria for rejection of Offer Documents.

(Framework for 2) Applicability of the General Order.

Rejection of Draft 3) One time withdrawal Opportunity.

Offer Documents) 4) Consequences of Rejection.

Order 2012.

NISM CERTIFICATION

Vide Notification dated August 2, 2013 SEBI has mandated that a Registered Merchant Banker

should have at least two of its key personnel involved in Primary Capital Market activities, should

pass the NISM Series IX examination conducted by National Institute of Securities Management.

We are glad to inform you that AIBI was involved in developing the course content for this

examination.

11

Association of Investment Bankers of India raising the credibility standard

SUMMARY OF OFFERINGS – EQUITY CAPITAL MARKET

During year the total amount raised through equity offerings were higher at Rs. 55,018 crores (from

100 issues) as compared Rs. 28,547 crores (from 65 issues) during the previous Financial Year.

And more than Rs. 28,024 crores (51%) were from OFS as compared Rs. 13,518 crores (55%).

a) IPOs:

During FY 2012-13, there were almost similar number of IPOs compared to the previous year

(33 as against 34) which mobilized a slightly higher amount of Rs. 6,497 crores against Rs.

5,893 crores during the previous FY, thus representing a marginal increase of about 10%.

b) FPOs:

There was no FPO during FY 2012-13 as against one FPO for Rs. 4,578 crores in the previous FY.

c) QIPs:

Similar to Rights Issues, QIPs also witnessed a substantial increase, up from Rs.1,713 crores (11

issues) in FY 2011-12 to Rs. 10,818 crores (14 issues) representing an increase of 532% . in the

amount raised during the year.

d) IPPs:

IPP was a new product introduced in January 2012 to enable companies to meet minimum

public shareholding requirements. During FY 2012-13, Rs. 734 crores was raised from 2

Institutional Placement Programmes (IPPs) thus witnessing an increase from Rs.471 crores of

funds raised through IPP issue when compared to 1 (one) IPP during FY 2011-12.

e) OFS:

Offers for Sale through the Stock Exchange mechanism witnessed a huge increase, up from 2

offers in the previous year for Rs. 13518 crores to 35 offers for Rs. 28024 crores in FY 2012-13.

This was also on account of the fact that most companies were required to meet the minimum

public shareholding requirements by June 2013.

f) Rights Issues:

During FY 2012-13, the number of Rights Issues remained the same at 16 as the last year.

However, the total amount mobilized increased significantly to Rs.8,945 crores as against Rs.

2,375 crores (FY 2011-12), thus up by 277%.

SUMMARY OF OFFERINGS - DEBT CAPITAL MARKET

During year the total amount raised through debt offerings were higher at Rs. 369108 crores (from

1854 issues) as compared Rs. 289819 crores (from 1386 issues) during the previous Financial

Year. Out of these Private Placement of Bonds/NCDs were much higher at 348875 crores (1890

issues) as compared Rs. 252181 crores (1360 issues). Public Issue of Tax free bonds were lower at

Rs. 14764 (14 issues) crores as compared to Rs. 27987 crores (5 issues) during the last Financial

Year.

12

20th Annual Report 2012-13 raising the credibility standard

Public Issues

a) NCDs/Bonds:

During FY 2012-13, the number of Public Issue NCDs reduced to 6 as compared to 15 in FY

2011-12. The amount raised also decreased from Rs. 7,624 crores in fiscal 2012 to Rs. 2,217

crores in fiscal 2013.

b) Tax-free Bonds:

During FY 2012-13, the number of Public Issues of Tax-free Bonds increased to 14 as compared

to 5 in FY 2011-12. However, the amount raised decreased significantly from Rs. 27,987 crores

in fiscal 2012 to Rs. 14,764 crores in fiscal 2013.

Private Placements

a) NCDs/Bonds:

The total amount raised through this mode increased by more Rs, 96,694 crores during FY

2012-13, up from Rs. 2,52,181 crores in previous year to Rs. 3,48,875 crores). The number of

issues also increased from 1360 to 1820.

b) Tax-free Bonds:

The Private Placements of Tax-free Bonds increased to 14 in FY 2012-13 from 6 during FY

2011-12, raising Rs. 3,252 crores raised as against Rs. 2,027 crores in FY 2011-12.

Amount of funds raised from capital markets during the year:

2011-12 2012-13

Particulars No. of Amount No. of Amount

Issues (Rs. Crores) Issues (Rs. Crores)

EQUITY

i) Public Issues

Public Issue out of which: 38 24460 70 35255

- IPOs 34 5893 33 6497

- FPOs 1 4578 0 0

- QIPs 11 1713 14 10818

- IPP 1 471 2 734

- OFS 2 13518 35 28024

ii) Rights Issues 16 2375 16 8945

Total (i +ii) 65 28547 100 55018

DEBT

i) Public Issues 20 35611 20 16981

- Bonds/NCDs 15 7624 6 2217

- Tax-free Bonds 5 27987 14 14764

ii) Private Placement of Debt 1366 254208 1834 352127

- Bonds/NCDs 1360 252181 1820 348875

- Tax-free Bonds 6 2027 14 3252

Total (i +ii) 1386 289819 1854 369108

Source: PRIME Database

13

Association of Investment Bankers of India raising the credibility standard

AIBI SUMMIT 2012

On December 19, 2012 AIBI held its “Summit 2012” at Grand Hyatt, Mumbai. The Summit was

well attended with nearly 300 participants. All the three Stock Exchanges viz. BSE, NSE and

MCX-SX were the Principal Sponsors while Mysys, CCL and Western Printers were the Associate

Sponsors for the Summit. Prime Database was the Summit Advisor and CARE Ratings was the

Knowledge Partner for the Summit.

The Summit commenced with formal inauguration of the Summit by lighting of the ceremonial

lamp by Mr. U.K. Sinha, Chairman SEBI. Mr. Sanjay Sharma, Chairman AIBI welcomed the Chief

Guest and other dignitaries and members. This was followed by Mr. U.K. Sinha releasing a

“Background Paper” prepared by our Knowledge Partner, CARE.

Dr. P. Harsh Vardhan, Partner Bain and Company made a presentation on “Global Investment

Banking Trends. This presentation focused on three issues – the aftermath of 2008 crisis and the

implications of the crisis in 2008 on the way the investment banking business evolved overseas. Dr.

Harsh Vardhan touched upon Cost Management, ROE, change in business model from “Originate

to Whole captive” principle to “Originate to manage’ principle. The concluding remarks of the

presentation stressed on the important role of Regulations in striking a balance between evolution

of financial system with the real system, Regulatory role, Corporate Governance and talent at

reasonable price.

In his Keynote Address, Mr. U.K. Sinha outlined the various measures taken by SEBI for protecting

the investors and urged the Investment Bankers to raise the standard of due diligence, be reasonable

in pricing the IPOs and strive to restore the credibility in the minds of the retail investors to revive

the Primary Capital Market.

This was followed by a speech by Mr. V.S. Sundaresan, CGM, SEBI who stressed that SEBI is

always willing to engage with the market participants to make the market a better place. He also

stressed that all efforts have to be made to bring the retail investors, the backbone of Indian

Primary Capital Market, to support the IPOs and subscribe to the IPOs.

There were four Technical Sessions which were moderated by eminent persons including Mr.Tamal

Bandhyopadhyay, Editor, Mint, Mr. Vivek Law, Editor, Bloomberg, Mr. Prithvi Haldea, Chairman

and Managing Director, Prime Database and Mr. Sanjay Sharma, Chairman AIBI and MD, Deutsche

Equities India Private Ltd.

The Panel Members for each session had representation from the Investment Banking community,

Corporates, Lawyers and Regulators and there was lively interaction between all panel members.

There was also an interesting talk by the eminent Leadership Consultant, Mythologist and Author,

Dr. Devdutta Pattanaik. The topic was “Rannbhoomi to Rangbhoomi” in which Dr. Pattanaik

compared the market and market participants to various characters from mythology wherein the

rights and wrongs are always a perception and depend on the point of view of the player.

14

20th Annual Report 2012-13 raising the credibility standard

Mr. Madhuprasad, Vice Chairman of AIBI and Vice Chairman, Keynote Capital succinctly summarized

the entire proceedings of the Summit 2012 in his Vote of Thanks speech.

Key takeaways from the Technical Sessions are -

1st Technical Session – “Are Regulations fostering or hampering growth of Primary

Capital Market” –

• Moderator - Mr. Tamal Bandyopadhyay, Deputy Managing Editor, Mint.

• Mr. Ashishkumar Chauhan, Managing Director & Chief Executive Officer, BSE - Period

between issue closing and listing has to be shortened. Safety Net is a good idea for the

protection of the small investors.

• Mr. K. Hari, Vice President, NSE - Equity is a risk capital and investors must be aware of the

risks. Subscription from Retail Individual Investors should be routed through Mutual Funds and

ETF.

• Mr. U. Venkataraman, Chief Executive Officer and Whole time Director, MCX – Capital

formation will be easier if we quicken the process of listing. This will generate more allocation of

investment for productive purposes and create more jobs.

• Dr. S. Subramanian, Managing Director, Investment Banking, Axis Capital – Instruments like

NCDs with warrants, IDRs and REITs can play an important role in mobilizing subscription from

Retail Individual Investors.

• Mr. V. K. Bansal, Chairman and Managing Director, Morgan Stanley India - Long term

capital gains must be extended to IDRs and Insurance Companies must be allowed to participate

in IDRs to bring in deep pocket investors. QIP route should be used for FCCB issues. The

investment limit of Insurance Companies, PF and Pension Funds needs to be increased.

• Mr. Somasekhar Sundaresan, Partner, J. Sagar Associates - Regulations have to do a

balancing role between being excessive and market development. Materiality should be very

clearly defined and should be only threshold for disclosures in Offer Documents. Regulators

should not be obsessed about pricing and Merchant Bankers found wanting in due diligence

must be punished. Action must be swift and not after 24-36 months.

2nd Technical Session - “Expectations from Investment Bankers by Regulators, Investors

and Issuers – A Reality Check”

• Moderator - Mr. Vivek Law, Editor, Bloomberg TV India.

• Mr. Prithvi Haldea, Chairman and Managing Director, PRIME Database - IPO structure and

process needs to be overhauled. The role of Investment Bankers needs to be defined more

clearly.

15

Association of Investment Bankers of India raising the credibility standard

• Ms. Neelam Bhardwaj, former General Manager, SEBI - Due diligence by Investment Bankers

needs a lot of improvement. The Due Diligence manual should help the Investment bankers in

due diligence.

• Mr. Girish Nadkarni, Executive Director, Avendus Capital - Allotment to QIBs should be

discretionary. In proportionate allotment everyone is a price taker and not a price giver. Defaulters

of Regulations have to be severely punished.

• Mr. Mahesh Chhabria, Partner, Actis PE – There is not enough appetite from Institutional

Investors forIPOs and hence PEs find it difficult to exit.

• Mr. V. Srinivasa Rangan, Executive Director, HDFC Ltd – In the debt market pricing and

quality of issuance is very transparent. But pricing an IPO is a tough because issuers want

maximum price and the issue of optimum price or maximum price is debatable. There is no

benchmark for IPOs from new or growing sectors.

• Mr. Sanjay Bajaj, Managing Director, HSBC Securities – Institutional participation is necessary

for getting retail participation. Indian Investors are obsessed with “listing gains”. Forward looking

statements with enough caveats must be allowed in Offer Documents. Greed and fear should be

replaced by rational expectations on returns.

• Mr. V.G.Kannan, President & Chief Operating Officer, SBI Capital – Retail investors are

followers and come to the IPO only when the market is euphoric and more regulations and

regulatory actions happen only when the market is down. QIP is the best way of fund raising

and will be order of the day in future.

3rd Technical Session – “Re-examining the role of small investors in an IPO Market”

• Moderator - Mr. Prithvi Haldea, Chairman and Managing Director, PRIME Database.

• Mr. Anup Bagchi, Managing Director & Chief Executive Officer, ICICI Securities – Retail

Investors are price folIowers and not price setters and they should have the choice of subscribing

directly or through Mutual Funds in an IPO In an IPO with Offer for Sale, the pricing and gains

post listing are likely by muted. Fiscal incentive in RGESS is not a good idea to drive people to

the secondary market.

• Mr. D.R.Dogra, Managing Director & Chief Executive Officer, CARE Reatings – Discount of

15% to retail investors in PSU issues is a good idea. IPO grading has a great value and is seen

from high volatility in lower graded IPOs as compared to higher graded IPOs.

• Mr. Ankush Pitale, Managing Director, Religare Capital – Retail investors must be allowed in

OFS. Rs. 15 crores profitability criteria is a good move to distinguish companies with stable cash

flows and others.

16

20th Annual Report 2012-13 raising the credibility standard

• Mr. Sanjay Golecha, VP, MCX-SX – Equity investment gives more gains and hence retail

participation has to be promoted in every nook and corner of the country. Discount to retail in

FPOs by listed PSUs is a good idea but there should be lock-in for larger discounts.

• Mr. Ved Prakash Chaturvedi, Chief Executive Officer, L&T Finance – The over-arching

goal is that we should get larger and larger part of Indian retail savings in a structured, proper,

correct manner to risk assets like equity of individual companies preferably but not necessarily

through MF route.

• Ms. Vibha Padalkar, Executive Director & CFO, HDFC Standard Life – Retail Investors

should understand the risk in equity instrument but should not be banned from coming to the

primary market. But Safety Net is not the right protection measure. By giving discount in PSU

offers, the Government directly and the tax payers indirectly are the losers.

4th Technical Session – “Voluntary and Compulsory Delisting – What is the way

forward?”

• Moderator - Mr. Sanjay Sharma, Chairman, AIBI and MD Deutsche Equities India

• Mr. Sandip Bhagat, Partner, S&R Associates - Listing is a commercial decision, it is a

corporate decision. And hence delisting too should be a commercial decision keeping in mind

the interest of the minority. There is minority protection built in since delisting cannot be done

below the floor price. The concept of reverse book building is probably dated.

• Mr. Gautam Gupte, Director, Ambit Corporate Finance - Currently MNC pay a higher

premium for getting the shares delisted.In a reverse book building process currently being

followed for delisting, the book is not built like it is built in an IPO or follow offerings. Only the

person holding the maximum number of shares determines the price, others just participate but

do not determine the price, even though they are substantial majority in numbers.

• Mr. Yogesh Dhingra, Chief Operating Officer & Finance Director, Blue Dart - Delisting in

India is a very cumbersome, long drawn process with huge costs. You are not sure what price

will come in, secondly one has to wait for long period of time to get 100% though you may be

delisted after reaching 91%. Delisting process needs to be made simpler and has to be

commercially viable for both the parties.

• Mr. Rakesh Singh, Head-Investment Banking, HDFC Bank - Shareholders today may not be

well equipped to estimate the value of a company. Hence the board should guide the retail

shareholders by giving a direction to think. Some kind of a squeeze out provision has to be

brought in. Regulations should keep the company in mind and not the promoters in mind. The

listing fee could be linked to market cap.

• Mr. Nehal Vora, Chief Regulatory Officer, BSE - As in offer for sale on the exchange platform

today, have a T+2 rolling settlement for delisting. Have an “offer to buy” window which is

17

Association of Investment Bankers of India raising the credibility standard

available through the exchange window, Permit another group of promoter who is willing to

buy over the promoter shares. Intent is to maximize shareholder wealth. So use the merits of

the reverse book building by bringing some of the good points of the other systems which are

already in place and merge it with this process. The compliant community is burdened with

more regulation because of the 5% that continues to be non-compliant. There should be a

series of other actions against the group responsible for the non-compliance. So I think the

entire enforcement system needs to be revamped.

BOARD MEETINGS

It is stipulated that the Board of Directors should meet at least 4 times in an accounting year. The

Board of Directors met 10 times during the period the date of last AGM i.e. September 27, 2012 to

August 2013. The details of the attendance of the Directors are given below.

Name of Director Meetings Attended

Mr. Sanjay Sharma, Chairman 8

Mr. B. Madhuprasad, Vice Chairman 8

Mr. K. Srinivas 8

Ms. Gesu Kaushal 7

Mr. Anay Khare 7

Mr. Abhay Bongirwar 6

Mr. T.R. Prashanth Kumar 6

Mr. Ajay Pancholi 4

Mr. Avinash Kulkarni 3

Mr. Ranganath Char 2

AUDIT COMMITTEE

Given the nature of the Association’s functions, a separate Audit Committee is not considered

necessary.

REMUNERATION TO DIRECTORS

No remuneration is paid to any Director.

STATUTORY STATEMENT

No employee was covered under Section 217(2A) of the Companies Act, 1956 read with the

Companies (Particulars of Employees) Rules 1975.

18

20th Annual Report 2012-13 raising the credibility standard

AUDITORS

M/s. Chandabhoy & Jassoobhoy, Chartered Accountants, the statutory auditors of your company

hold office till the conclusion of the twentieth Annual General Meeting and are recommended for

re-appointment. The Association has received a certificate from them to the effect that their re-

appointment would be within the limits prescribed under Section 224(1) of the Companies Act

1956.

ACKNOWLEDGEMENTS

The Directors would like to thank Mr. U.K. Sinha for being the Chief Guest at our Summit 2012

and for delivering the Keynote Address. The Board would also like to thank Dr. P.Harsh Vardhan,

Mr. V.S.Sundaresan and Mr. Devdutta Pattanaik for their presentation and talks at our Summit

2012.

The Board would also like to put on record their special appreciation to all the Moderators and

Panel Members of the Technical Sessions at our Summit 2012.

The Board would like to profusely thank all the sponsors of our Summit especially BSE, NSE and

MCX. Special thanks are due to CARE for being the Knowledge Partner.

The Directors would like to thank all Members for their interest and co-operation in the Association’s

affairs. The Directors would also like to appreciate the services rendered by our Statutory Auditors

and all members of AIBI’s staff.

For and on behalf of the Board of Directors

SANJAY SHARMAChairman

Place : MumbaiDate : 28th August, 2013

19

Association of Investment Bankers of India raising the credibility standard

AUDITORS' REPORT

ToThe Members ofAssociation of Investment Bankers of India.

We have audited the accompanying financial statements of Association of Investment Bankers ofIndia, which comprise the Balance Sheet as at March 31, 2013, and the Income and ExpenditureAccount for the year then ended, and a summary of significant accounting policies and otherexplanatory information.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation of these financial statements that give a true and fairview of the financial position and financial performance of the Company in accordance with theAccounting Standards referred to in sub-section (3C) of section 211 of the Companies Act, 1956(“the Act”). This responsibility includes the design, implementation and maintenance of internalcontrol relevant to the preparation and presentation of the financial statements that give a true andfair view and are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with the Standards on Auditing issued by the Institute ofChartered Accountants of India. Those Standards require that we comply with ethical requirementsand plan and perform the audit to obtain reasonable assurance about whether the financial statementsare free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosuresin the financial statements. The procedures selected depend on the auditor’s judgment, includingthe assessment of the risks of material misstatement of the financial statements, whether due tofraud or error. In making those risk assessments, the auditor considers internal control relevant tothe Company’s preparation and fair presentation of the financial statements in order to designaudit procedures that are appropriate in the circumstances. An audit also includes evaluating theappropriateness of accounting policies used and the reasonableness of the accounting estimatesmade by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide abasis for our audit opinion.

Opinion

In our opinion and to the best of our information and according to the explanations given to us,the financial statements give the information required by the Act in the manner so required andgive a true and fair view in conformity with the accounting principles generally accepted in India:

a) in the case of the Balance Sheet, of the state of affairs of the Company as at March 31, 2013;and

b) in the case of the Income and Expenditure Account, of the excess of income over expenditurefor the year ended on that date.

20

20th Annual Report 2012-13 raising the credibility standard

Report on Other Legal and Regulatory Requirements

1. The Association is licensed to operate under Section 25 of the Companies Act, 1956 and assuch the provisions of the Companies (Auditor’s Report) Order, 2003 are not applicable to theAssociation.

2. As required by section 227(3) of the Act, we report that:

a) we have obtained all the information and explanations, which to the best of our knowledge andbelief were necessary for the purpose of our audit;

b) in our opinion proper books of account as required by law have been kept by the Company sofar as appears from our examination of those books;

c) the Balance Sheet and Income and Expenditure Account dealt with by this Report are inagreement with the books of account;

d) in our opinion, the Balance Sheet and Income and Expenditure Account dealt with by thisreport comply with the Accounting Standards referred to in subsection (3C) of section 211 ofthe Companies Act, 1956; and

e) on the basis of written representations received from the directors as on March 31, 2013, andtaken on record by the Board of Directors, none of the directors is disqualified as on March 31,2013, from being appointed as a director in terms of clause (g) of sub-section (1) of section 274of the Companies Act, 1956.

For and on behalf ofCHANDABHOY & JASSOOBHOY

Chartered AccountantsFirm’s Registration No.- 101647W

BHUPENDRA T. NAGDAPartner

Membership No: F 102580

Place : MumbaiDate : 28th August, 2013

21

Association of Investment Bankers of India raising the credibility standard

BALANCE SHEET AS AT 31st MARCH, 2013

As at As atParticular Note 31.03.2013 31.03.2012

No. `̀̀̀̀ `

As per our report attached

For and on behalf ofCHANDABHOY & JASSOOBHOYChartered Accountants

Firm’s Registration No.- 101647W

BHUPENDRA T. NAGDA

Partner

Membership No: F 102580

Place : MumbaiDate : 28th August, 2013

For and on behalf of the Board of DirectorsASSOCIATION OF INVESTMENT BANKERS OF INDIA

SANJAY SHARMA

Chairman

B. MADHUPRASADVice Chairman

Place : MumbaiDate : 28th August, 2013

I.EQUITY AND LIABILITIES

1 Shareholders’ funds

(a) Reserves and surplus 1 5,95,26,403 5,64,78,450

2 Non-current liabilities

(a) Deffered tax liabilties (Net) 2 11,14,928 11,41,716

3 Current liabilities

(a) Other current liabilities 3 3,21,148 1,02,764

(b) Short-term provisions 4 1,29,107 1,85,777

TOTAL 6,10,91,586 5,79,08,707

II.ASSETS

1 Non-current assets

(a) Fixed assets

(i) Tangible assets 5 65,56,400 69,81,667

2 Non Current Investments 6 1,02,22,250 ––

3 Current assets

(a) Cash and cash equivalents 7 4,09,28,510 4,78,10,811

(b) Short-term loans and advances 8 2,13,206 69,259

(c) Other current assets 9 31,71,220 30,46,970

TOTAL 6,10,91,586 5,79,08,707

The accompanying notes 1 to 17 are an integral part of the financial statements.

22

20th Annual Report 2012-13 raising the credibility standard

INCOME AND EXPENDITURE ACCOUNT FORTHE YEAR ENDED MARCH 31, 2013

As per our report attached

For and on behalf ofCHANDABHOY & JASSOOBHOYChartered Accountants

Firm’s Registration No.- 101647W

BHUPENDRA T. NAGDA

Partner

Membership No: F 102580

Place : MumbaiDate : 28th August, 2013

For and on behalf of the Board of DirectorsASSOCIATION OF INVESTMENT BANKERS OF INDIA

SANJAY SHARMA

Chairman

B. MADHUPRASAD

Vice Chairman

Place : MumbaiDate : 28th August, 2013

Year ended Year ended

Note 31.03.2013 31.03.2012

No. `̀̀̀̀ `

I. Membership Fees 27,87,500 26,75,000

II. Summit Income 20,30,000 ––

III. Other Income 10 51,78,673 47,13,041

IV. Total Income 99,96,173 73,88,041

V. Expenses:

Employee benefits expense 11 28,74,909 22,52,855

Depreciation and amortization expense 4,25,267 4,64,970

Summit Expenses 14,91,152 ––

Other expenses 12 15,81,739 13,17,088

Total Expenses 63,73,067 40,34,913

VI. Excess of Income over Expenditure for

the year before tax (IV-V) 36,23,106 33,53,128

VII. Tax expense:

(1) Current tax 11,40,000 11,00,000

(2) Deferred tax (26,788) (17,350)

11,13,212 10,82,650

VIII. Excess of Income over Expenditure for

the year after tax (VI-VII) 25,09,894 22,70,478

IX. Less: Short /(Excess) provision for

income tax of earlier years (38,059) 57,446

X. Excess of Income over Expenditure (VIII-IX) 25,47,953 22,13,032.

The accompanying notes 1 to 17 are an integral part of the financial statements.

23

Association of Investment Bankers of India raising the credibility standard

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED MARCH 31, 2013

As at As at

31.03.2013 31.03.2012

`̀̀̀̀ `

NOTE : 1

RESERVES AND SURPLUS

General Reserve

As per Last Balance Sheet 5,64,78,450 5,27,65,418

Add: Entrance fees received during the year 5,00,000 15,00,000

Add: Excess of Income over expenditure during the year 25,47,953 22,13,032

5,95,26,403 5,64,78,450

NOTE : 2

DEFERRED TAX LIABILITIES (NET)

Deferred tax liabilties :

Differences between book and tax depreciation 11,54,822 11,77,511

Deferred tax assets :

Expense allowable on payment basis 39,894 35,795

Deferred tax liabilites (Net) 11,14,928 11,41,716

NOTE : 3

OTHER CURRENT LIABILITIES

Outstanding expenses 3,12,440 1,02,764

TDS Payable 8,708 ––

3,21,148 1,02,764

NOTE : 4

SHORT-TERM PROVISIONS

Provision for employee benefits 1,29,107 1,15,841

Provision for Income Tax (net of taxes paid) –– 61,995

Provision for Fringe Benefit tax (net of taxes paid) –– 7,941

1,29,107 1,85,777

24

20th Annual Report 2012-13 raising the credibility standard

NO

TE

: 5

FIX

ED

AS

SE

TS

Fix

ed

Ass

ets

Gro

ss B

lock

Acc

um

ula

ted

Dep

reci

atio

nN

et

Blo

ck

Bala

nce

as

at

1st

Ap

ril

20

12

Ad

ditio

ns

Dis

po

sals

Revalu

atio

ns/

(Im

pair

men

ts)

Bala

nce

as

at

31st

Marc

h2013

Bala

nce

as

at

1st

Apri

l 2012

Dep

reci

atio

nch

arg

e f

or

the

year

Ad

just

men

td

ue t

ore

valu

atio

ns

On

dis

po

sals

Bala

nce

as

at

31st

Marc

h2013

Bala

nce

as

at

31st

Marc

h2013

Bal

ance

as

at31

st M

arch

2012

NO

TES T

O T

HE F

INA

NC

IAL S

TATEM

ENTS

FOR

TH

E Y

EA

R E

ND

ED

MA

RC

H 3

1,

2013

Am

ou

nt

in `

Tan

gib

le A

sset

s

Off

ice

Pre

mis

es 1

,57

,96

,70

5––

––––

1,5

7,9

6,7

05

91

,88

,97

7 3

,30

,38

6––

–– 9

5,1

9,3

63

62

,77

,34

2 6

6,0

7,7

29

Off

ice

Eq

uip

men

ts 5

,44

,63

7––

––––

5,4

4,6

37

4,9

6,5

05

6,6

95

–– –

– 5

,03

,20

0 4

1,4

37

48

,13

2

Fu

rnitu

re &

Fix

ture

s 6

,73

,10

2––

––––

6,7

3,1

02

6,3

9,2

53

6,1

27

––––

6,4

5,3

80

27

,72

2 3

3,8

49

Ele

ctri

cal

Fitt

ings

1,4

3,8

83

––––

–– 1

,43

,88

3 1

,32

,60

7 1

,56

8––

–– 1

,34

,17

5 9

,70

8 1

1,2

76

Veh

icle

s 8

,70

,45

3––

––––

8,7

0,4

53

6,4

5,2

12

58

,31

5––

–– 7

,03

,52

7 1

,66

,92

6 2

,25

,24

1

Co

mp

ute

rs 2

,13

,54

9––

––––

2,1

3,5

49

1,5

8,1

08

22

,17

6––

–– 1

,80

,28

4 3

3,2

65

55

,44

0

Gra

nd T

ota

l 1

,82

,42

,32

9––

––

––1

,82

,42

,32

9 1

,12

,60

,66

2 4

,25

,26

7––

–– 1

,16

,85

,92

9 6

5,5

6,4

00

69

,81

,66

7

Pre

vio

us

Yea

r 1

,81

,72

,56

9 6

9,7

60

––––

1,8

2,4

2,3

29

1,0

7,9

5,6

92

4,6

4,9

70

––––

1,1

2,6

0,6

62

69

,81

,66

7

25

Association of Investment Bankers of India raising the credibility standard

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED MARCH 31, 2013

NOTE : 6

NON CURRENT INVESTMENTS

Other Investments :

Investments in Bonds :

(Unquoted, Non Traded, At cost)

50 (Previous year - Nil) 6.70 % Indian Railway Finance

Corporation Tax Free Bonds 2020 of Rs.100,000 each 48,95,000 ––

2,500 (Previous year - Nil) 8.20 % Power Finance

Corporation Tax Free Bonds 2022 of Rs.1,000 each 26,60,000 ––

25,00 (Previous year - Nil) 8.20% National Highway

authority of India Tax Free Bonds 2022 of Rs.1,000 each 26,67,250 ––

1,02,22,250 ––

NOTE : 7

CASH AND CASH EQUIVALENTS

a. Cash on hand 676 5,843

b. Balances with Banks:

In Savings Accounts 5,40,478 10,86,057

In Deposit Accounts 4,03,87,356 4,67,18,911

4,09,28,510 4,78,10,811

Balances with banks in deposits accounts includes bank

deposits with more than 12 months maturity - Rs.8,00,000

(Previous year - Rs. 12,055,019).

NOTE : 8

SHORT TERM LOANS AND ADVANCES

Unsecured, considered good :

Security Deposits 23,010 23,010

Staff Advances 25,520 12,630

Prepaid Expenses 33,235 33,619

Income Taxes paid (net of provisions) 1,31,441 ––

2,13,206 69,259

NOTE : 9

OTHER CURRENT ASSETS

Interest accrued on Fixed Deposits with banks 28,20,935 30,46,970

Interest accrued on Investments 3,50,285 ––

[Includes Rs.2,68,905 representing interest for the 31,71,220 30,46,970

broken period paid at the time of purchase of investments]

As at As at

31.03.2013 31.03.2012

`̀̀̀̀ `

26

20th Annual Report 2012-13 raising the credibility standard

NOTES TO THE FINANCIAL STATEMENTSFOR THE YEAR ENDED MARCH 31, 2013

For the For the

year ended year ended

31.03.2013 31.03.2012

`̀̀̀̀ `NOTE 10

OTHER INCOME

Interest :

On deposit with banks 50,87,115 47,06,157

On savings account with bank 9,933 5,874On Investments 81,380 ––

Miscellaneous Income 245 1,010

51,78,673 47,13,041

NOTE 11

EMPLOYEE BENEFIT EXPENSES

Salaries 25,75,016 19,49,458

Contribution to provident and other funds 1,99,495 2,44,753

Staff welfare expenses 1,00,398 58,644

28,74,909 22,52,855

NOTE 12

OTHER EXPENSES

Travelling & Conveyance 492,782 229,446

Website Expenses 333,900 330,900

Vehicle Expenses 119,882 100,494

Electrical Charges 106,832 74,652

Auditor’s Remuneration

- for Statutory Audit 35,000 35,000

- for taxation matters 30,000 36,500

- for company law matters 25,000 37,500

- for reimbursement of expenses 16,261 28,061

Printing and Stationery 91,860 78,757

Repairs and Maintenance - Others 77,899 48,120

Meeting Expenses 59,999 122,041

Telephone & Communication Charges 55,804 80,839

Office Expenses 40,552 48,909

Society Charges 35,541 35,360

Professional fees 33,000 16,000

Miscellaneous Expenses 11,715 5,908

Books & Periodicals 7,614 5,568

Rates & Taxes 5,000 ––

Insurance Charges 3,098 3,033

1,581,739 1,317,088

NOTES TO THE FINANCIAL STATEMENTS FORTHE YEAR ENDED 31ST MARCH, 2013

13. Significant Accounting Policies

13.1 The accounts of the Association are maintained on historical cost convention.

13.2 Income and expenses are accounted on accrual basis.

13.3 a) Membership fees is accounted as income except in cases where mem bership

ceases to be so in terms of Part E of Articles of Association.

b) Annual Subscription fees is accounted as income and Entrance fees is considered

as an addition to Reserves.

13.4 Fixed assets are stated at cost less accumulated depreciation.

13.5 Depreciation is provided on fixed assets on written down value basis at the rates

specified in Schedule XIV to the Companies Act, 1956.

13.6 Investments intended to be held for a period exceeding twelve months are classified as

long-term investments and are carried at cost. Provision for diminution, if any, in the

value of each long term investment is made to recognize a decline, other than of a

temporary nature.

13.7 a) Provident Fund is a defined benefit scheme and the contributions are charged to

profit and loss account of the year on accrual basis.

b) The liability for Gratuity and Superannuation is funded through Schemes

administered by the Life Insurance Corporation of India. Amounts payable under

the schemes are charged to revenue.

c) Liability for leave encashment of employees, in accordance with the rules of the

Company, is accrued for the un-availed encashable leave balance standing to the

credit of employees as at the balance sheet date.

13.8 a) The tax liability for the year is computed as per the provisions of the Income Tax

Act 1961, as amended.

b) Deferred tax is recognized on timing differences, being the differences between the

taxable income and accounting income that originate in one period and are

capable of reversal in one or more subsequent periods. The tax effect is calculated

on the accumulated timing difference at the year end based on the tax rates and

laws enacted or substantially enacted on the balance sheet date.

14. Association of Investment Bankers of India (Formerly Know as Association of Merchant bankers

of India) is a non-profit association registered under section 25 of the Companies Act, 1956.

15. There was no expenditure or income or remittance in foreign currency during the year.

16. Amounts due to Micro enterprises and Small enterprises is NIL (Previous Year – NIL).

17. Previous Year’s figures have been regrouped / rearranged wherever necessary.

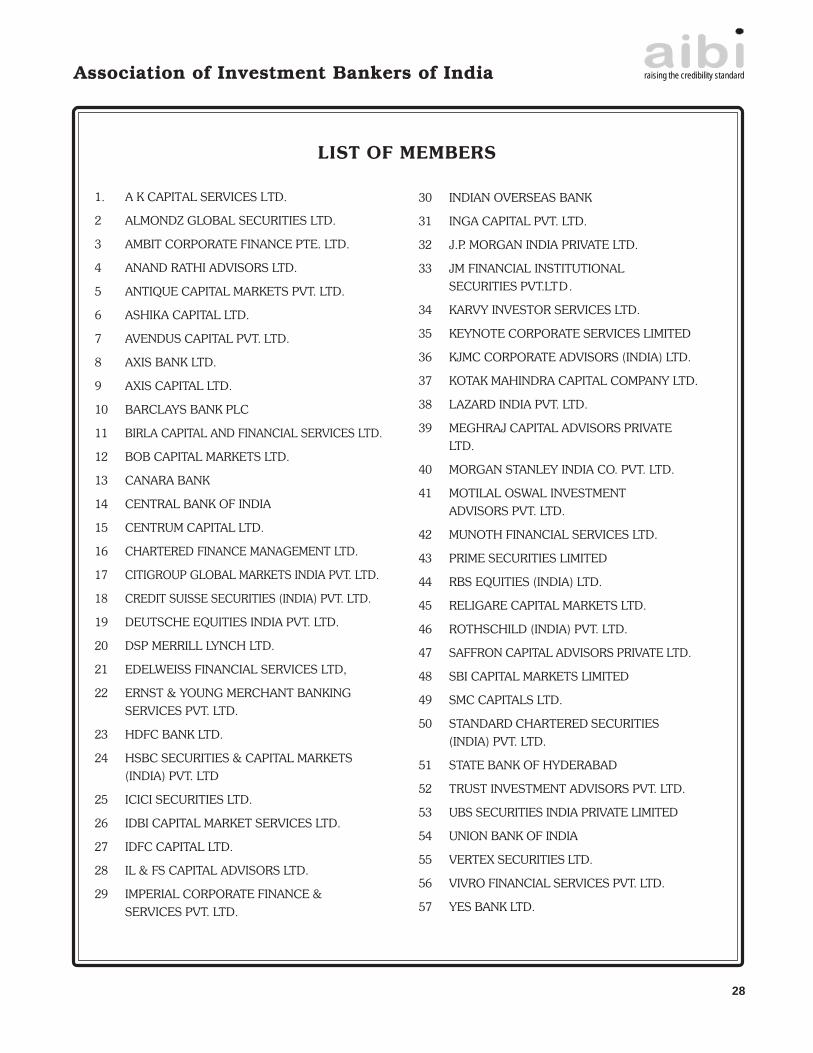

LIST OF MEMBERS

Association of Investment Bankers of India raising the credibility standard

28

1. A K CAPITAL SERVICES LTD.

2 ALMONDZ GLOBAL SECURITIES LTD.

3 AMBIT CORPORATE FINANCE PTE. LTD.

4 ANAND RATHI ADVISORS LTD.

5 ANTIQUE CAPITAL MARKETS PVT. LTD.

6 ASHIKA CAPITAL LTD.

7 AVENDUS CAPITAL PVT. LTD.

8 AXIS BANK LTD.

9 AXIS CAPITAL LTD.

10 BARCLAYS BANK PLC

11 BIRLA CAPITAL AND FINANCIAL SERVICES LTD.

12 BOB CAPITAL MARKETS LTD.

13 CANARA BANK

14 CENTRAL BANK OF INDIA

15 CENTRUM CAPITAL LTD.

16 CHARTERED FINANCE MANAGEMENT LTD.

17 CITIGROUP GLOBAL MARKETS INDIA PVT. LTD.

18 CREDIT SUISSE SECURITIES (INDIA) PVT. LTD.

19 DEUTSCHE EQUITIES INDIA PVT. LTD.

20 DSP MERRILL LYNCH LTD.

21 EDELWEISS FINANCIAL SERVICES LTD,

22 ERNST & YOUNG MERCHANT BANKING

SERVICES PVT. LTD.

23 HDFC BANK LTD.

24 HSBC SECURITIES & CAPITAL MARKETS

(INDIA) PVT. LTD

25 ICICI SECURITIES LTD.

26 IDBI CAPITAL MARKET SERVICES LTD.

27 IDFC CAPITAL LTD.

28 IL & FS CAPITAL ADVISORS LTD.

29 IMPERIAL CORPORATE FINANCE &

SERVICES PVT. LTD.

30 INDIAN OVERSEAS BANK

31 INGA CAPITAL PVT. LTD.

32 J.P. MORGAN INDIA PRIVATE LTD.

33 JM FINANCIAL INSTITUTIONAL

SECURITIES PVT.LTD.

34 KARVY INVESTOR SERVICES LTD.

35 KEYNOTE CORPORATE SERVICES LIMITED

36 KJMC CORPORATE ADVISORS (INDIA) LTD.

37 KOTAK MAHINDRA CAPITAL COMPANY LTD.

38 LAZARD INDIA PVT. LTD.

39 MEGHRAJ CAPITAL ADVISORS PRIVATE

LTD.

40 MORGAN STANLEY INDIA CO. PVT. LTD.

41 MOTILAL OSWAL INVESTMENT

ADVISORS PVT. LTD.

42 MUNOTH FINANCIAL SERVICES LTD.

43 PRIME SECURITIES LIMITED

44 RBS EQUITIES (INDIA) LTD.

45 RELIGARE CAPITAL MARKETS LTD.

46 ROTHSCHILD (INDIA) PVT. LTD.

47 SAFFRON CAPITAL ADVISORS PRIVATE LTD.

48 SBI CAPITAL MARKETS LIMITED

49 SMC CAPITALS LTD.

50 STANDARD CHARTERED SECURITIES

(INDIA) PVT. LTD.

51 STATE BANK OF HYDERABAD

52 TRUST INVESTMENT ADVISORS PVT. LTD.

53 UBS SECURITIES INDIA PRIVATE LIMITED

54 UNION BANK OF INDIA

55 VERTEX SECURITIES LTD.

56 VIVRO FINANCIAL SERVICES PVT. LTD.

57 YES BANK LTD.