Embed Size (px)

Citation preview

ASSETS MATTER

Your Financial Road Trip

High School Financial Education Training

March 14-15, 2011

Washoe County School District

ASSETS MATTER

Assets Matter

Assets enable families to: Weather economic crisis

Make choices

Invest in their futures

Plan for retirement

Transfer wealth to future generations

Bottom Line: Income helps people get by, assets help people to get ahead.

ASSETS MATTER

Assets Build Better LivesFamilies without savings and assets are more likely to experience:

• Divorce• Increased health problems for themselves and

their children• Less stable housing• Greater job turnover• Higher drop-out rates for their children• Less connection to their community

ASSETS MATTER

What is Asset Poverty?

• A household is asset poor if it has insufficient net worth to support itself at the federal poverty level for three months in the absence of income.

• Federal poverty line for a family of four is $22,350 year (or, $430 per week)

• In Nevada, 34% of those earning $44,801-$68,800 are asset poor.

ASSETS MATTER

Asset Poverty by Race/Ethnicity

56.5

43.5

26.3

19.4

34

27

12

16

0

10

20

30

40

50

60

AfricanAmerican

Latino Caucasian Asian PacificIslander

Asset Poverty

Income Poverty

Source: http://scorecard.cfed.org/

ASSETS MATTER

Asset Poverty by Education

37.3

29.6

19.221.3

0

5

10

15

20

25

30

35

40

HighSchool

SomeCollege

BachelorDegree

AdvanceDegree

Asset Poverty 33%

Source: http://scorecard.cfed.org/

ASSETS MATTER

Financial Education Matters

• Nearly one-third of teens owe money to a person or company, with an average debt of $230.

• Average debt of young adults ages 22-29 is $16,120.

• People in the 18 to 24 age bracket spend nearly 30% of their monthly income just on debt repayment - double the percentage spent in 1992 (10% of net income is a recommended amount for debt obligation).

• The number of 18 to 24-year-olds declaring bankruptcy has increased 96% in 10 years.

ASSETS MATTER

Financial Education Matters

• While 71% agree that the best way for teens to learn about money is from guided, hands-on experience or their own example, only 20% involve their teen in the family’s budgeting and spending decisions.

• Americans shelled out more than $24 billion in credit card fees in 2004, an 18% increase over the previous year.

• In 2005, savings rates dipped to minus 0.5 percent, something that hasn't happened since the Great Depression in 1932 and 1933. A negative savings rate means that Americans spent all their disposable income and dipped into past savings or increased their borrowing.

Collected from Jumpstart Coalition as of April 2010

ASSETS MATTER

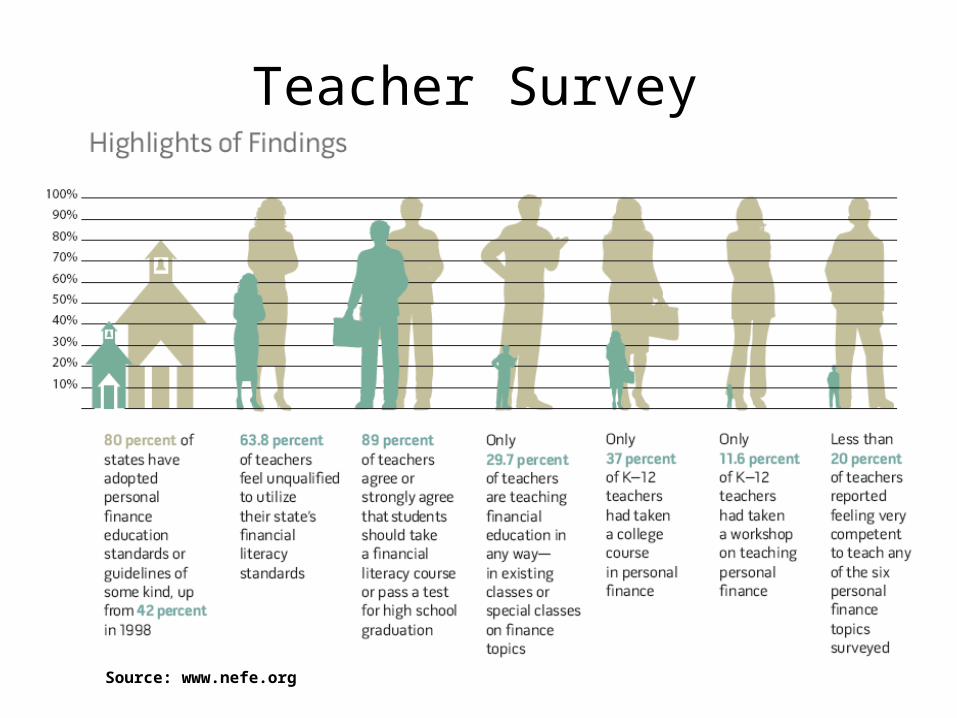

Teacher Survey

Source: www.nefe.org

ASSETS MATTER

Questions for Me?

ASSETS MATTER

Question for You

Do you think financial education is a stand-alone subject (like a physics course), or is it like reading – a skill to be learned and applied throughout life?

ASSETS MATTER

1. Review NEFE HSFPP material2. Review Recommended Curriculum Flow3. Walk through a lesson4. Review additional supplemental materials,

including tests5. Brainstorm – ideas, tips, deficits,

outstanding issues to be covered.

Roadmap of Today’s Trip

ASSETS MATTER

Recommended Resources

Building Wealth – Federal Reserve Bank of Dallashttp://www.dallasfed.org/ca/wealth/index.cfm

Practical Money Skills for Lifehttps://www.practicalmoneyskills.com/foreducators/lesson_plans/teens.php

Money Guide for Teenshttp://moneytalks4teens.ucdavis.edu/

Hands On Banking – Wells Fargohttp://www.handsonbanking.org