Embed Size (px)

Citation preview

ASSET FINANCE INTERNATIONAL

IN ASSOCIATION WITHWHITE CLARKE GROUP

AUTO & EQUIPMENT FINANCE SURVEY 2017

United States

United States Auto & Equipment Finance Survey 2017

2

United States Auto & Equipment Finance Survey 2017

White Clarke GroupWhite Clarke Group is the market leader in software solutions and business consultancy to the automotive and equipment finance sector for retail, fleet and wholesale. White Clarke Group solutions enable end-to-end credit processing and administration to streamline business practice, cut operational cost and deliver outstanding customer service. White Clarke Group has a 25-year track record of leadership and innovation in finance technology, consultancy and new market entry. Clients value White Clarke Group’s industry knowledge, market intelligence and innovation. The company employs some 600 finance and technology professionals, with offices in the USA, UK, Canada, Australia, Austria, Germany, India and China.

whiteclarkegroup.com

www.assetfinanceinternational.com

Publisher: Edward Peck

Editors: John Maslen and Brian Rogerson

Author: Jonathan Manning

Asset Finance International Ltd.39 Manor WayLondon SE3 9XGUNITED KINGDOMTelephone: +44 (0) 207 617 7830

© Asset Finance International, 2017, All rights reserved. No part of this publication may be reproduced or used in any form or by any means–graphic; electronic; or mechanical, including photocopying, recording, taping or information storage and retrieval systems–without the written permission from the publishers.

United States Auto & Equipment Finance Survey 2017

3

United States Auto & Equipment Finance Survey 2017

Acknowledgements

This year’s United States Auto & Equipment Finance Survey 2017 features the views of more than 20 industry leaders, based on interviews, submissions and desk research. We would like to thank them all for their support and express our thanks to:

Gary Amos, CEO, commercial finance - Americas, Siemens Financial Services

Bill Bosco, principal, Leasing 101

Nicolas Brush, CEO, BlaBlaCar

Jamie Dimon, chairman and CEO, JPMorgan Chase & Co

Mark Fields, former president and chief executive officer of Ford

Jason Grohotolski, vice president - senior credit officer, Moody’s

Thomas Jaschik, president, BB&T Equipment Finance

Jason Laky, senior vice president and automotive business leader, TransUnion

Lou Loquasto, VP auto lender and dealer vertical leader, Equifax

Dave Mirsky, CEO, Pacific Rim Capital

Matthias Müller, chief executive officer, Volkswagen Group

Tom Partridge, president, Fifth Third Equipment Finance

Ralph Petta, president and CEO, Equipment Leasing and Finance Association

Mark Scarpelli, chairman, NADA

Alan Sikora, chief executive officer, First American Equipment Finance

Bill Stephenson, CEO, De Lage Landen

Steven Szakaly, chief economist, NADA

Mark Vitner, managing director and senior economist, Wells Fargo

Adam Warner, president, Key Equipment Finance

Stephen Whelan, partner, Blank Rome LLP

Melinda Zabritski, Experian’s senior director of automotive finance

Tracey Zhen, president, Zipcar

United States Auto & Equipment Finance Survey 2017

4

United States Auto & Equipment Finance Survey 2017

Contents

Acknowledgements 3

Executive summary 6

The US economy 8

Politics: focus on delivering promises 10

US Auto Finance 12

Finance maintains strong demand in auto market 13

Floorplan finance shows growth 15

Used car oversupply threatens residual values 16

Shift to SUVs presents RV challenge for 18 finance companies

Industry responds to sub-prime auto credit fears 19

Negative equity threat to new business 21

Start-up mobility companies challenge car 22 ownership models

US Equipment Finance 25

Performance and prospects for equipment finance 26

US equipment finance industry 27

United States Auto & Equipment Finance Survey 2017

5

United States Auto & Equipment Finance Survey 2017

Equipment finance enjoys steady growth 28

Where next for interest rates? 30

The smart data revolution 32

Mixed fortunes ahead for 2018 34

A year of mixed fortunes 36

Government urged to drive growth in 2018 37

The Legal and Regulatory Environment 38

TRAC auto leases 38

Amended and restated: oops 38

Hell or high water: bundled contracts 39

Waiver of defenses: maybe, maybe not 39

Electronic chattel paper 39

Lease accounting - transitioning to Topic 842 41

Where are we now? 41

The positives 41

The negatives 41

Lessee preparedness 42

Other lessee concerns 42

Lessor concerns 43

Other lessor concerns 43

Conclusions 44

United States Auto & Equipment Finance Survey 2017

6

Executive summary

ƴ The arrival in the White House of arguably the most business-friendly administration in history sent business and consumer confidence soaring. The vital next step is delivery on pre-election promises in terms of regulatory reform, fiscal changes and federal spending.

ƴ The US economy expanded by 2.6% in the second quarter of 2017, and analysts forecast growth of up to 3% for 2017.

ƴ Although new car sales are down 2.2% year-on-year, they are still heading for one of the highest annual totals in history. Half year registrations were just over 8.4 million and the National Automobile Dealers Association is forecasting full year sales of 17.1 million new cars and light trucks. This is slightly down on last year’s record-breaking 17.55 million new registrations, but still makes it only the third year on record with sales of more than 17 million.

ƴ The average loan amount for a new vehicle reached a record high last year of $30,621, up 3.6% compared to the end of 2015.

ƴ Trucks accounted for more than 60% of new vehicle sales in 2016, up from 45% in 2009. Sales of sedans are falling.

ƴ The average loan for a used vehicle has reached a record high of $19,329 in Q4 2016, compared to $18,850 in Q4 2015.

United States Auto & Equipment Finance Survey 2017

7

ƴ An oversupply of used vehicles is undermining residual values. The annual depreciation rate on two to six-year-old vehicles rose to 17.3% in 2016, compared to 13% or lower from 2011 to 2016.

ƴ Auto lenders are being more cautious with their lending criteria, credit-checking customers more carefully amid underlying concerns over sub-prime lending.

ƴ A growing market for mobility services is challenging car ownership models, but the need for lease and asset finance continues to be strong.

ƴ New business volumes in the equipment leasing and finance market were up 6% year-on-year to $54.5 billion for the first seven months of 2017. Last year the market grew by 2.5% to $114.7 billion in 2016, a more modest increase than the 12.4% rise recorded in 2015, but marking the eighth consecutive year of growth.

ƴ New technology is cutting out the middleman from equipment finance and leasing, and making the lending process swifter and more efficient.

ƴ Big data will enable lessors and their clients to manage leased assets far more effectively.

ƴ A steadily growing economy, the promise of a more business-friendly approach by the Trump Administration, and gradual increases in interest rates by the Fed are paving the way for future growth in the equipment finance sector.

ƴ Legal developments in the equipment and auto finance market include bundled contracts, waiver of defenses and electronic chattel paper.

ƴ A wave of lease, revenue and credit loss accounting rule changes is sweeping through finance departments and this means significant work and financial changes for the industry.

ƴ The Consumer Financial Protection Bureau, which oversees financial institutions such as banks, credit card companies and lenders, faces a reduced role from 2018 as executive orders and proposed budget cuts limit its activity.

The United States Auto and Equipment Finance Survey paints a positive picture for the future, with ongoing growth and signs of accelerating economic activity. To maximise this growth, the industry will need to adapt to approaching challenges and ensure that innovation is at the heart of future product development

David Slider group executive vice-president White Clarke Group

United States Auto & Equipment Finance Survey 2017

8

Martin Nixon

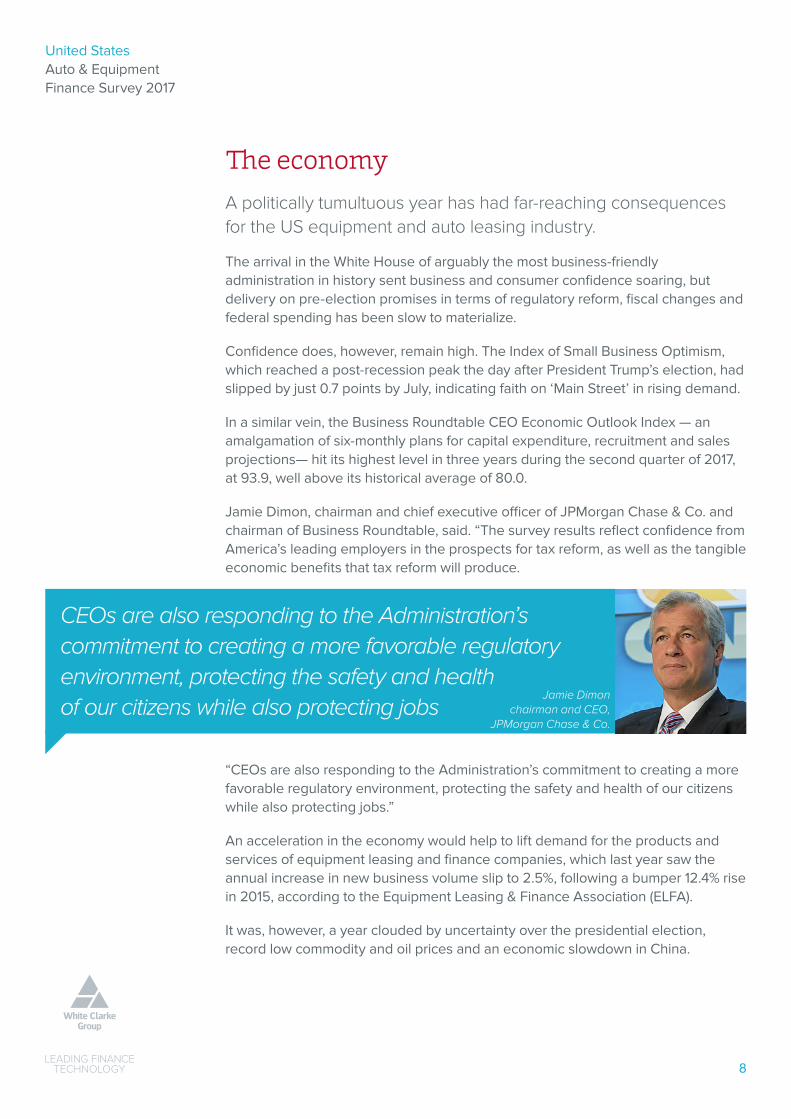

The economy A politically tumultuous year has had far-reaching consequences for the US equipment and auto leasing industry.

The arrival in the White House of arguably the most business-friendly administration in history sent business and consumer confidence soaring, but delivery on pre-election promises in terms of regulatory reform, fiscal changes and federal spending has been slow to materialize.

Confidence does, however, remain high. The Index of Small Business Optimism, which reached a post-recession peak the day after President Trump’s election, had slipped by just 0.7 points by July, indicating faith on ‘Main Street’ in rising demand.

In a similar vein, the Business Roundtable CEO Economic Outlook Index — an amalgamation of six-monthly plans for capital expenditure, recruitment and sales projections— hit its highest level in three years during the second quarter of 2017, at 93.9, well above its historical average of 80.0.

Jamie Dimon, chairman and chief executive officer of JPMorgan Chase & Co. and chairman of Business Roundtable, said. “The survey results reflect confidence from America’s leading employers in the prospects for tax reform, as well as the tangible economic benefits that tax reform will produce.

“CEOs are also responding to the Administration’s commitment to creating a more favorable regulatory environment, protecting the safety and health of our citizens while also protecting jobs.”

An acceleration in the economy would help to lift demand for the products and services of equipment leasing and finance companies, which last year saw the annual increase in new business volume slip to 2.5%, following a bumper 12.4% rise in 2015, according to the Equipment Leasing & Finance Association (ELFA).

It was, however, a year clouded by uncertainty over the presidential election, record low commodity and oil prices and an economic slowdown in China.

CEOs are also responding to the Administration’s commitment to creating a more favorable regulatory environment, protecting the safety and health of our citizens while also protecting jobs

Jamie Dimonchairman and CEO,

JPMorgan Chase & Co.

United States Auto & Equipment Finance Survey 2017

9

Domestically, official figures reveal the economy grew at an annualised rate of 2.6% in the second quarter of 2017, more than twice as fast as in Q1, while Goldman Sachs is not alone in identifying other activity indicators that estimate the ‘real’ figure to be in excess of 3% for most of 2017.

Internationally, a buoyant global economy is forecast to expand by 3.5% this year, according to both the International Monetary Fund and Organization for Economic Cooperation and Development, holding out the prospect of rising exports.

Domestically, official figures reveal the economy grew at an annualised rate of 2.6% in the second quarter of 2017, more than twice as fast as in Q1

United States Auto & Equipment Finance Survey 2017

10

Politics: focus on delivering promisesFollowing the impasse in Washington during the final few years of President Obama’s administration, business and consumer confidence soared in the wake of the 2017 election results.

This signalled a belief that a Republican White House and a Republican Congress together would improve the Affordable Care Act, rationalize regulation and pass comprehensive tax reform, according to Adam Warner, president of Key Equipment Finance.

However, the challenge of achieving political momentum to deliver on ambitions for major economic change is proving difficult.

Warner said: “It is becoming clearer now that there is dysfunction in the White House and the Republican Party is fractured, so all early attempts to pass meaningful economic legislation have failed. Business confidence has eroded and will likely continue to be challenged in 2018.”

The challenge for the relatively new administration is to bridge the gap between rhetoric and reality.

Bill Stephenson, chief executive officer De Lage Landen Leasing, said: “The Trump administration continues to promise the right things for business... infrastructure spending, tax cuts and deregulation, all of which should spur economic growth.

“That said, translating all of those promises into concrete actions has appeared to be more difficult, at least if judged by the initial six months of this new administration.

If there is continued division, gridlock and uncertainty coming from Washington DC, at some point those factors will have an adverse impact on business spending and our industry Bill Stephenson

CEO, De Lage Landen Leasing

United States Auto & Equipment Finance Survey 2017

11

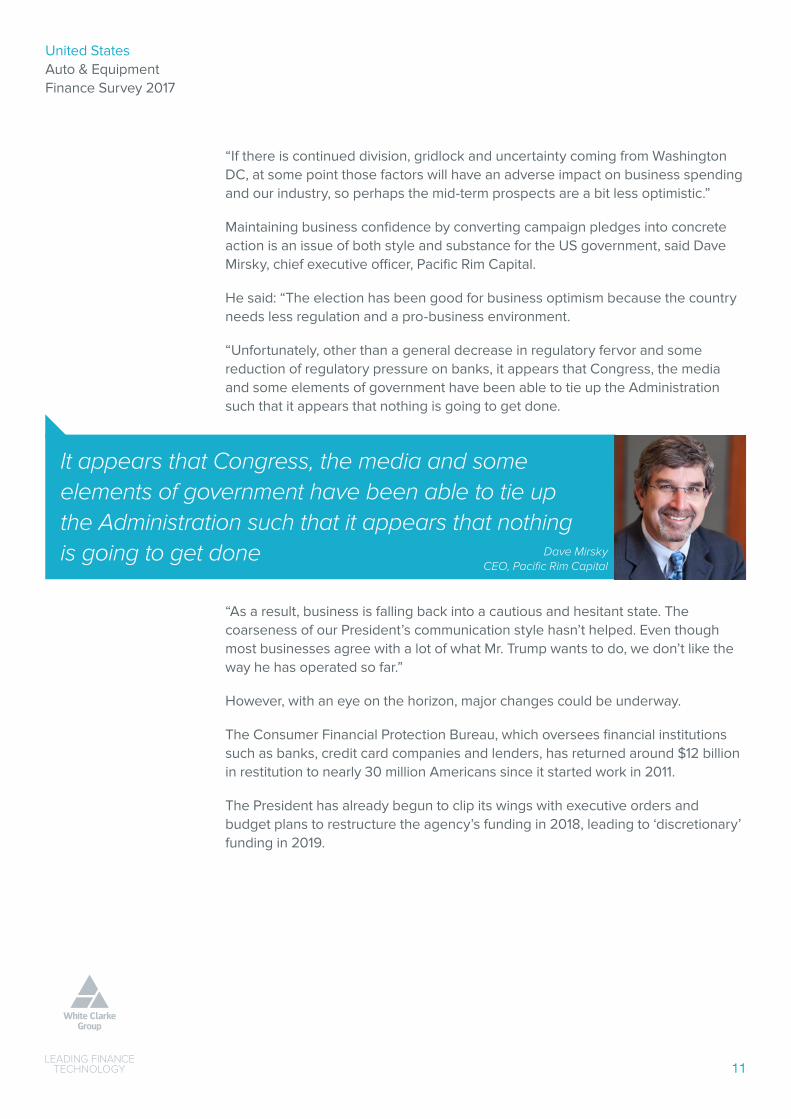

“If there is continued division, gridlock and uncertainty coming from Washington DC, at some point those factors will have an adverse impact on business spending and our industry, so perhaps the mid-term prospects are a bit less optimistic.”

Maintaining business confidence by converting campaign pledges into concrete action is an issue of both style and substance for the US government, said Dave Mirsky, chief executive officer, Pacific Rim Capital.

He said: “The election has been good for business optimism because the country needs less regulation and a pro-business environment.

“Unfortunately, other than a general decrease in regulatory fervor and some reduction of regulatory pressure on banks, it appears that Congress, the media and some elements of government have been able to tie up the Administration such that it appears that nothing is going to get done.

“As a result, business is falling back into a cautious and hesitant state. The coarseness of our President’s communication style hasn’t helped. Even though most businesses agree with a lot of what Mr. Trump wants to do, we don’t like the way he has operated so far.”

However, with an eye on the horizon, major changes could be underway.

The Consumer Financial Protection Bureau, which oversees financial institutions such as banks, credit card companies and lenders, has returned around $12 billion in restitution to nearly 30 million Americans since it started work in 2011.

The President has already begun to clip its wings with executive orders and budget plans to restructure the agency’s funding in 2018, leading to ‘discretionary’ funding in 2019.

It appears that Congress, the media and some elements of government have been able to tie up the Administration such that it appears that nothing is going to get done Dave Mirsky

CEO, Pacific Rim Capital

United States Auto & Equipment Finance Survey 2017

12

United States Auto & Equipment Finance Survey 2017

Auto Finance

United States Auto & Equipment Finance Survey 2017

13

Finance maintains strong demand in auto marketNew vehicle sales remain among the highest on record as consumers show an insatiable appetite for new cars and light trucks, funded through cheap finance.

The National Automobile Dealers Association (NADA) is forecasting total sales of 17.1 million new cars and light trucks in 2017, after they reached 8.4 million during the first six months of 2017.

This was 2.2% down on the same period of 2016, continuing a trend that has seen sales slip year-on-year for the first seven months of 2017 until August stopped the slide.

Despite the falls, this year is still shaping up to be one of the highest performances on record, and NADA insists the overall trends fuelling consumer demand remain positive, with strong employment growth and low unemployment levels, and says there is little to indicate a broader weakness in the market that some analysts have suggested.

Steven Szakaly, NADA chief economist, said: “[The] typical stresses and strains from rising interest rates, excessive lending and overall weak consumer spending are not visible in the broader economy. There is little indication that the Fed’s rate raising actions have as yet had any impact on overall growth.”

Indeed, since the financial crash and recession of 2008-09, US light-vehicle sales have delivered seven consecutive annual gains, the longest upwards streak in decades, peaking at 17.55 million new registrations in 2016.

The combination of pent up consumer demand, attractive lease deals and easy credit availability have pushed sales ever higher since the downturn.

Demand is being funded through finance, with credit agency Experian calculating that the average loan amount for a new vehicle reached a record high last year, at $30,621. Used vehicle finance also achieved new peaks at $19,329 per car.

However, to lower the cost of monthly repayments, consumers are turning to longer term loans, with a 29% Q4 2016 year-on-year rise in loans of 73 to 84 months for new vehicles.

Melinda Zabritski, Experian’s senior director of automotive finance, said: “With the average loan amount for new and used vehicles hitting all-time highs, we are seeing the need for affordability drive consumer purchasing behaviour. Our latest research shows an $11,000 gap between the average loan amount on a new and used vehicle — the widest we have ever seen.

United States Auto & Equipment Finance Survey 2017

1414

“This upward trend is causing many consumers to find alternative methods like extending loan terms, getting a short-term lease or opting for a used vehicle to get what they want while staying within their monthly budget.”

Leasing remains the cheapest monthly solution to fund a vehicle, with Experian putting the average monthly rental for a new leased vehicle at $414, compared to $506 for a new vehicle purchase, a significant gap of $92.

Alongside the extension of loan terms, the size of down payments has increased, to the point where the percentage of car sales that are financed has declined for the first time in a decade, said Lou Loquasto, VP auto lender and dealer vertical leader, Equifax.

He said: “Currently it is 85% new and 55% used [in terms of the proportion of car sales that are financed], but a three-year-old car today is such good quality that customers may switch to used car finance instead.

“Annual car sales used to be two-thirds used and one-third new, but I could envisage that becoming 70% used and 30% new.”

US annual new light vehicle sales

20

18

16

14

12

10

8

6

4

2

0

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017(est)

Ann

ual s

ales

(mill

ion) 13.2

10.411.6

16.4414.5

12.7

15.5317.4 17.54 17.1

Source: NADA

United States Auto & Equipment Finance Survey 2017

15

Analysts are still assessing the impact of hurricane damage on the economy and the vehicle market, which could lead to a substantial increase in demand for new vehicles.

Hurricanes Harvey and Irma caused hundreds of billions of dollars worth of damage, with an estimate of more than one million vehicles destroyed.

Hurricane Harvey damaged 300,000 to 500,000 vehicles in Houston alone.

This will lead to substantial demand for new and used car replacements over the coming months.

Floorplan finance shows growth

The re-emergence of small and regional banks looking to expand services to existing manufacturers, dealers and retailers is continuing to spur growth in the floorplan finance market.

This is providing opportunities for many traditional lenders looking to diversify their businesses and expand into wholesale, with growth expected to continue throughout the year.

Lenders are fast realizing that the necessity for the right system partner to help them get to market quickly with low operating costs is imperative.

The key is finding a scalable solution that can provide an economical yet reliable, future-proof system to fit both the current size and growth of their businesses.

Kurt Ruhlin, chief operating officer at White Clarke Group, said: “We have seen a surge of expansion in the market and a need to increase operational efficiency.

“As a result, many new or expanding wholesale lenders have selected the CALMS Compass wholesale/floorplan platform to fulfil their needs.

“The need for a quick to market system has been required by all and the out-of-the-box functionality has allowed for many new implementations to go from decision to live in less than 90 days.”

New compliance and regulatory requirements are also playing a pivotal role in the emergence of start-ups, small companies and manufacturer captive lenders, which find it easier to raise capital due to their flexibility.

United States Auto & Equipment Finance Survey 2017

16

Used car oversupply threatens residual valuesOngoing high demand in the new car market is starting to ring alarm bells within the finance sector.

While the country’s general economic indicators remain strong, the danger of supply outstripping demand in the used market threatens residual values and exposes leasing companies to a greater risk of end-of-contract losses.

Black Book, the vehicle pricing expert, witnessed the annual depreciation rate on two- to six-year-old vehicles rise to 17.3% during 2016, compared to 13% or lower from 2011 to 2016, and forecasts a further marginal increase to 17.8% in 2017.

After the start of the recession in 2008, there was a sharp decline in new vehicle sales, which had led to a shortage of used vehicles stock in subsequent years that has kept prices high.

As new car demand has recovered along with the economy, the volume of cars being returned to the used vehicle market has risen steadily, leading to pressure on residual values.

The general economic outlook may continue to be rosy, but the risk of oversupply in the used market has led Black Book to forecast annual year-on-year declines in the value retained by vehicles as they return to the market at three years of age.

Taking an industry average, Black Book says that a 2014 model year vehicle would have retained 52% of its manufacturer’s suggested retail price (MSRP) in January 2017. However, an equivalent 2017 model will only be worth 48% of its MSRP when it returns to the used car market in 2020, a four percentage point decline.

This will challenge the profitability of lease contracts written in the last three years as a tide of ex-lease cars and light trucks returns to the market, according to analysts.

Lease volumes have risen sharply in recent years, helped by low interest rates and low monthly repayments, with leasing’s share of consumer vehicle finance exceeding 30% for the first time in 2016.

Industry estimates put the number of auto leases at 4.4 million for the year, an increase of 7% over 2015, and lease companies now have to brace themselves for oversupply in the used vehicle market, according to the Manheim Used Car Market Report 2017.

United States Auto & Equipment Finance Survey 2017

17

The report said: “The rise in new lease originations will produce a steady rise in off-lease volumes.

“It will be challenging for the industry to absorb these volumes without producing large residual losses.

“New lease originations generally peak at the top of the economic cycle when residual values are at their highest. That means off-lease volumes will rise as the economic down cycle begins. Given that the captive lessors have a residual exposure on some 10 million lease contracts outstanding, it is important that they balance future new vehicle volume objectives against the potential impact on used vehicle values.”

Lease return volumes grew by 27% in 2016, and in 2017 will continue to grow by an additional 15% over 2016 levels, according to the Vehicle Depreciation Report, jointly published by Black Book and Fitch Ratings.

Fitch predicts residual value performance to slow in 2017 as lease return volumes continue to climb, resulting in lower RVs in securitized auto lease asset-backed security pools.

However, as this report went to press, the wholesale market continued to buck the laws of economics, achieving its third consecutive record high in July, based on the Manheim Used Vehicle Value Index, 2.6% up on the previous year.

Manheim said: “Used vehicle sales are growing, driven by double-digit year-over-year growth in sales of vehicles less than four years old.

“Increased demand is absorbing the higher supply of newer vehicles.”

The other silver lining for leasing companies is the fact that most lease customers will return to the market for a new leased vehicle, as soon as their lease expires, whereas owners of loan-financed vehicles are more likely to delay replacing their car or truck until their confidence in the overall economic environment improves.

Finally, in areas affected by the recent hurricanes, used car prices have recently spiked as demand grows for replacement vehicles.

Used vehicle sales are growing, driven by double-digit year-over-year growth in sales of vehicles less than four years old

United States Auto & Equipment Finance Survey 2017

18

Shift to SUVs presents RV challenge for finance companies

Rapidly shifting demand among drivers is set to cause headaches for leasing companies. Accelerating enthusiasm for SUVs has been matched by a perilous decline in appetite for traditional sedans among both new and used vehicle buyers.

The result is a market where leasing companies are preparing to defleet hundreds of thousands of sedans into a market that may no longer want them.

As always with residual values, the devil is in the detail, and while headline figures suggest a used vehicle market in rude health, closer examination exposes widely diverging fortunes.

Mark Scarpelli, NADA chairman, said: “Sedans now account for 37% of sales, meaning that roughly two out of every three retail transactions are now a light truck, SUV or crossovers.

“Simply put, there is great demand for the utility that SUVs and light trucks provide.”

Trucks accounted for more than 60% of new vehicle sales in 2016, up from only 45% in 2009, and demand for this type of vehicle has carried over into the used market, at the expense of sedans.

The Manheim Used Car Market Report 2017 said: “Although overall wholesale prices have been very stable of late (a movement of only 1.2% over the past four years), the differences between market classes have been pronounced.”

“At the extremes, adjusted wholesale prices for pickups have risen 28% during this period, while compact car values fell 14%.”

The result is a market where leasing companies are preparing to defleet hundreds of thousands of sedans into a market that may no longer want them.

United States Auto & Equipment Finance Survey 2017

19

Industry responds to sub-prime auto credit fears Auto lenders face increased credit risks within the sub-prime sector, but many are taking action to minimize exposure to losses.

Sub-prime exposure is not substantial enough to destabilize the market, according to the American Financial Services Association, but the AFSA was sufficiently concerned to convene an expert panel earlier this year to investigate sub-prime lending in the auto market, before giving it a clean bill of health.

Experian data shows that auto lenders have become increasingly conservative, reducing their share of sub-prime loans and lending to customers with higher average credit scores.

Melinda Zabritski, senior director of automotive finance for Experian, said: “The sky is most definitely not falling on automotive lending. While we may have seen growth in sub-prime or deep sub-prime loans in recent years, it is important to keep it in perspective - the entire market has grown from a volume standpoint across all risk tiers.”

Nonetheless, lenders do appear to have adopted a slightly more cautious stance, with Experian figures indicating an increase in prime and super-prime risk tiers, and a decline in sub-prime and deep sub-prime market shares to 31.3% in the first quarter of 2017, compared to 34.3% in the same period a year earlier.

At TransUnion, Jason Laky, senior vice president and automotive business leader, said sub-prime auto finance today is very different from sub-prime mortgage lending 10 years ago.

TransUnion’s Industry Insights Report calculated that outstanding auto loan and lease balances for sub-prime consumers totaled $172 billion at the end of Q3 2016, representing 16% of the $1.1 trillion in total auto balances. In 2009, sub-prime auto lending accounted for in excess of 20% of the market.

While we may have seen growth in sub-prime or deep sub-prime loans in recent years, it is important to keep it in perspective - the entire market has grown from a volume standpoint across all risk tiers Melinda Zabritski

senior director, Experian Automotive

United States Auto & Equipment Finance Survey 2017

20

Laky said: “Sub-prime auto lending is much smaller than mortgage in terms of total outstanding loan balance and average loan size, so exposure from loss at a macro and micro level is likely to be less severe.

“Risk is also broadly distributed among lenders and investors, limiting the systemic risk stemming from one lender’s challenges.”

Trying to draw conclusions from the property mortgage market as a guide to what might happen in the auto lending market is a flawed approach, according to Lou Loquasto, VP auto lender and dealer vertical leader, Equifax, who rejected the idea of a car credit bubble.

He said: “Investors never lose money on auto securitisation and if it didn’t happen in 2008, it won’t happen now.”

He pointed to evidence of the more cautious approach of lenders, with Equifax recording a tripling of demand for its loan verification service in the past three years, as car dealers and lenders seek independent background information on customers prior to issuing a loan, rather than relying on self-certification.

Loquasto added: “Dealers are also being managed much more closely, to the extent that those who generate high levels of defaults can be cut off. In the same way, good dealers can receive better loan rates to reflect their reduced risk.”

Yet the trauma associated with sub-prime lending from the mortgage crisis of 2008-9 remains raw, and prompted two states to take firm action against Santander Consumer USA.

Massachusetts fined the finance company $22 million for its role in facilitating unfair, high-rate auto loans for thousands of car buyers.

Maura Healey, attorney general, said: “We found that Santander, a leading player in the business of packaging and reselling sub-prime auto loans, funded unfair and unaffordable auto loans for more than 2,000 Massachusetts residents.”

The fine followed a joint investigation with the state of Delaware, which claimed that Santander allegedly funded auto loans “without having a reasonable basis to believe that the borrowers could afford them”.

United States Auto & Equipment Finance Survey 2017

21

Negative equity threat to new business

Auto lenders could have to accept greater credit risk by rolling negative equity at trade-in into the next vehicle loan, according to credit ratings agency Moody’s.

The increase in negative equity is a risk that lenders have to face in order to secure deals to provide finance for the customer’s next new-car purchase. Longer loan terms and higher loan to value ratios keep the deals alive, while higher interest rates offer a degree of compensation for the higher risks involved.

Jason Grohotolski, a Moody’s vice president - senior credit officer, said: “Now that new vehicle-sales have plateaued, the competition for remaining loan supply will intensify, driving increased credit risk for auto lenders.”

In this fiercely fought market, car buyers have been able to purchase a new car while simultaneously rolling negative equity from a prior lending balance into their new loan.

This creates a ‘trade-in treadmill’ where car buyers are in a cycle of regularly renewing their loans at increased negative equity during trade-in, warns Moody’s. As a result, each successive loan is riskier.

Grohotolski said: “Consumers will have to get off the treadmill, and the industry’s response will help dictate how painful it is.”

United States Auto & Equipment Finance Survey 2017

22

Start-up mobility companies challenge car ownership modelsRead the headlines and hype and it would be easy to reach the conclusion that car ownership, whether fleet or private, is drinking in the last chance saloon.

The future, according to the hyperbole, lies in a brave new world of ride hailing, car sharing and multi-modal transport, where car ownership will be as rare as getting around by horse and carriage today.

Yet closer inspection of the triple digit growth figures by consultancy McKinsey has revealed that fewer than 1% of vehicle miles travelled (VMT) in the US last year came from ridesharing, while new car sales reached an all-time high.

True, ride hailing giants Uber and Lyft have delivered compound growth of more than 150% in the past three years, to generate over $10 billion in revenues last year, but this is a tiny fraction of the nation’s VMT.

McKinsey said: “Car ownership is still more economical and convenient for most car owners and users, and for all of the buzz and excitement, when we count VMT in absolute terms, ride sharing share is almost a rounding error,”

Yet there’s no doubt that companies with very different backgrounds, from automotive manufacturers to tech giants including Google and Apple, and start-ups like Uber and Zipcar, are all involved in a land grab to secure as much territory as possible in the new world of ‘mobility as a service’.

Mark Fields, the recently retired president and chief executive officer of Ford, said the blue oval was expanding its business, “to be both an auto and a mobility company,” and Volkswagen has declared its mobility solutions business unit to be the group’s 13th brand, anticipating sales revenues in the billions by 2025.

Matthias Müller, chief executive officer of the Volkswagen Group, said: “In future, many people will no longer own a car. But they can all be a Volkswagen customer in one way or another – because we will serve a much broader concept of mobility than is the case today.”

In future, many people will no longer own a car. But they can all be a Volkswagen customer in one way or another – because we will serve a much broader concept of mobility than is the case today Matthias Müller

CEO, Volkswagen Group

United States Auto & Equipment Finance Survey 2017

23

In the fleet sector, an increasing number of leasing companies have adopted the language of ‘mobility providers’, and the first references to total cost of mobility, rather than total cost of ownership are starting to appear.

So where does this leave the leasing and finance companies that fund fleet and private cars?

In the short-term the answer seems to be exactly where they are.

McKinsey calculates that the break-even point between owning a car and relying on mobility services is about 3,500 annual miles, a threshold exceeded by 90-95% of US car owners, so there’s unlikely to be a mad rush to hand in car keys.

In the longer term, however, the number of young people in the country with driving licences has fallen steadily in recent years, from 76% at the turn of the new millennium to 71% in 2013.

Navigant Research estimated that there were around 2 million car-sharing members in North America by the end of last year, and there’s growing consensus that private vehicle ownership no longer has a place in congested, environmentally-challenged cities.

Tracey Zhen, president of car club Zipcar, which operates in more than 50 cities across North America and Europe, said: “Urbanization is happening rapidly. In the past, we’ve been [building] cities around each person owning and parking a personal vehicle.

“There is no longer space for this one-to-one model. Instead of building more parking and more roads, we need to think about providing new mobility choices that are more sustainable and efficient.”

No surprise, then, to see manufacturers move into this space alongside rental firms and start-ups.

General Motors has launched Maven car club in the US; BMW, MINI and rental company Sixt are behind DriveNow; and Mercedes-Benz Vans is investing $50 million in a joint venture with US-based ride-hailing firm Via to offer on-demand shared shuttle services in European cities.

Instead of building more parking and more roads, we need to think about providing new mobility choices that are more sustainable and efficient Tracey Zhen

president, Zipcar

United States Auto & Equipment Finance Survey 2017

24

Leasing and finance companies are also eyeing this space, with Toyota Financial Services making strategic investments in Uber that will also see it offer leasing products to Uber drivers.

Across Europe, LeasePlan has also developed a full operational leasing solution for Uber drivers, with the leasing company saying that the rise in popularity of on-demand mobility is leading to significant growth opportunities.

In one of the most interesting developments, car leasing company ALD Automotive, owned by Société Générale, GM’s Opel, and long-distance carpooling start-up BlaBlaCar (which has 35 million members in 22 countries) have signed a three-way agreement to provide BlaBlaCar drivers with access to cars through zero-deposit finance, competitive monthly payments and fully-inclusive maintenance packages.

Drivers can also take advantage of a $24 (€20) discount on their lease for every month they share journeys on BlaBlaCar, increasing their opportunities to save on car costs through carpooling.

Nicolas Brush, chief executive officer of BlaBlaCar, said: “The BlaBlaCar community will purchase more than 1.3 million cars in 2017. The idea here is to leverage the strength of this community to unlock deals that would not otherwise be widely available to our members and pioneer a new approach to car ownership based on usage.”

While the development of such new mobility services may eventually result in lower sales of private-vehicle sales, McKinsey forecasts that this decline “is likely to be offset by increased sales in shared vehicles that need to be replaced more often due to higher utilization and related wear and tear”.

The customer may change, but the need for lease and asset finance continues.

United States Auto & Equipment Finance Survey 2017

25

United States Auto & Equipment Finance Survey 2017

Equipment Finance

United States Auto & Equipment Finance Survey 2017

26

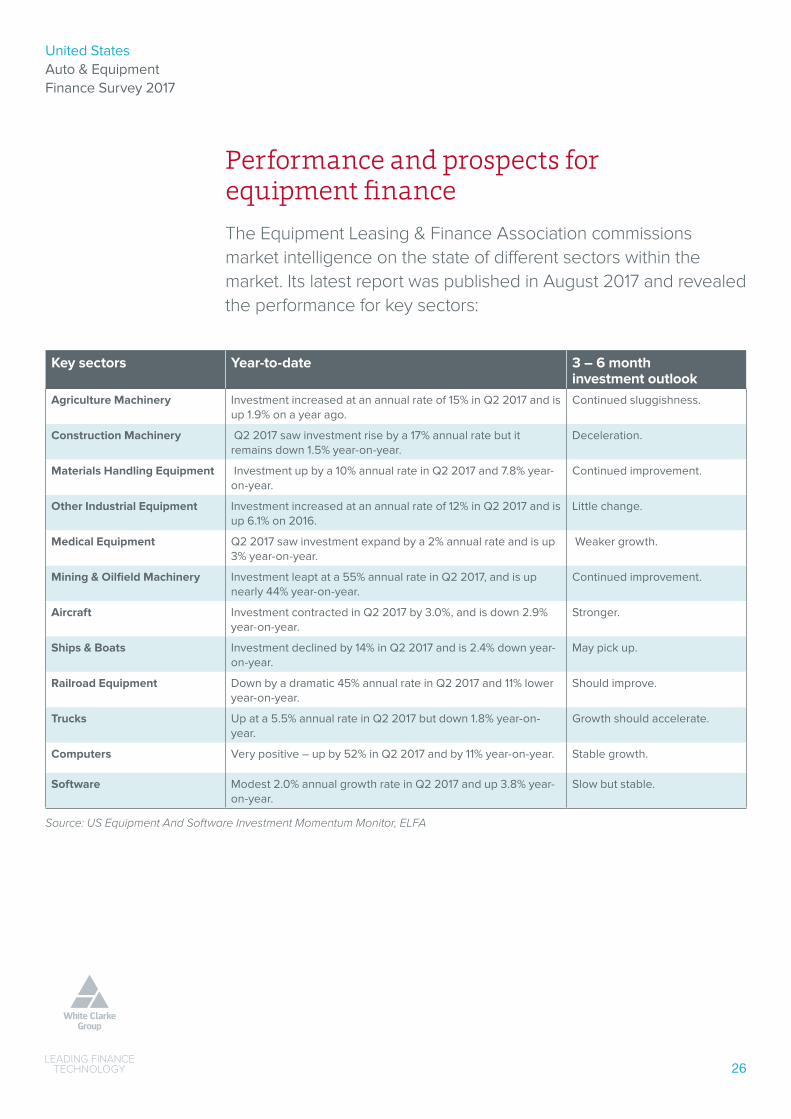

Performance and prospects for equipment financeThe Equipment Leasing & Finance Association commissions market intelligence on the state of different sectors within the market. Its latest report was published in August 2017 and revealed the performance for key sectors:

Key sectors Year-to-date 3 – 6 month investment outlook

Agriculture Machinery Investment increased at an annual rate of 15% in Q2 2017 and is up 1.9% on a year ago.

Continued sluggishness.

Construction Machinery Q2 2017 saw investment rise by a 17% annual rate but it remains down 1.5% year-on-year.

Deceleration.

Materials Handling Equipment Investment up by a 10% annual rate in Q2 2017 and 7.8% year-on-year.

Continued improvement.

Other Industrial Equipment Investment increased at an annual rate of 12% in Q2 2017 and is up 6.1% on 2016.

Little change.

Medical Equipment Q2 2017 saw investment expand by a 2% annual rate and is up 3% year-on-year.

Weaker growth.

Mining & Oilfield Machinery Investment leapt at a 55% annual rate in Q2 2017, and is up nearly 44% year-on-year.

Continued improvement.

Aircraft Investment contracted in Q2 2017 by 3.0%, and is down 2.9% year-on-year.

Stronger.

Ships & Boats Investment declined by 14% in Q2 2017 and is 2.4% down year-on-year.

May pick up.

Railroad Equipment Down by a dramatic 45% annual rate in Q2 2017 and 11% lower year-on-year.

Should improve.

Trucks Up at a 5.5% annual rate in Q2 2017 but down 1.8% year-on-year.

Growth should accelerate.

Computers Very positive – up by 52% in Q2 2017 and by 11% year-on-year. Stable growth.

Software Modest 2.0% annual growth rate in Q2 2017 and up 3.8% year-on-year.

Slow but stable.

Source: US Equipment And Software Investment Momentum Monitor, ELFA

United States Auto & Equipment Finance Survey 2017

27

Equipment acquisition continues to drive the supply chains across all US manufacturing and service sectors. Equipment leasing and financing provide the source of funding for a majority of US businesses to acquire the productive assets they need to operate and grow Ralph Petta

president and CEO, ELFA

$1.1 TRILLIONsize of the US

equipment finance industry

7 YEARS of consecutive

growth in the US equipment finance

industry

2.5%the increase in US equipment finance

new business volume in 2016

$1.5 TRILLION

expenditure this year by US businesses, non-profits and

government agencies on capital goods and fixed

business investment (including software)

US equipment finance industry

United States Auto & Equipment Finance Survey 2017

28

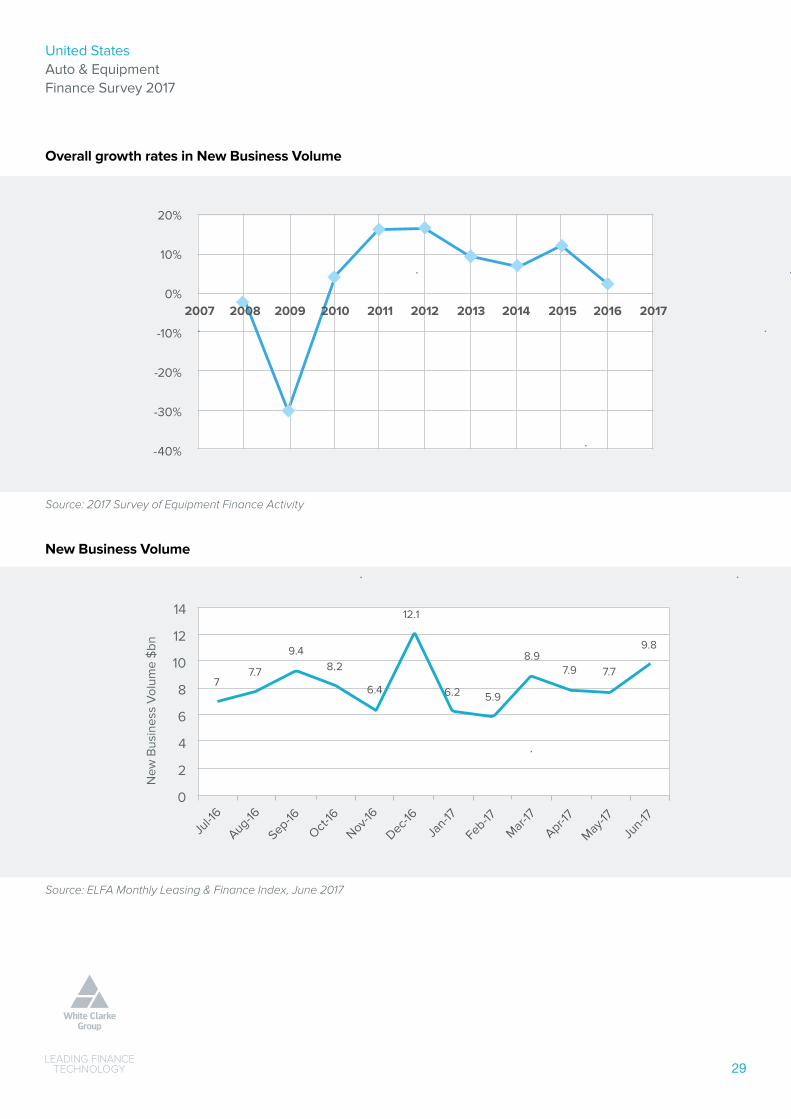

Equipment finance enjoys steady growthProspects are improving among leasing and finance companies after steady rather than stellar growth in the past 12 months.

Industry statistics compiled by the Equipment Leasing and Finance Association (ELFA) show an acceleration in new business volumes during the first half of 2017.

The ELFA’s Monthly Leasing and Finance Index (MLFI),, based on the economic activity of a cross-section of 25 companies, reported a 5% rise in overall new business volume (NBV) compared to the same period of 2016.

This snapshot of industry fortunes also revealed a spectacular 27% month-on-month increase from May to June 2017, when NBV totalled $9.8 billion.

Over the first six months of 2017, NBV totaled $54.5 billion, according to the MLFI.

Ralph Petta, ELFA president and CEO, said: “Business owners are taking advantage of low interest rates, favorable employment data, an equity market that continues to defy gravity, and other solid fundamentals to replace aging assets and, in some cases, expand operations, requiring installation of new equipment.”

The figures, which do not include data on auto leasing (including floorplan finance), real estate and ‘non-equipment finance operations’, are encouraging following modest growth in 2016.

The more representative 2017 Survey of Equipment Finance Activity by ELFA, consolidating figures from 115 members, revealed a 2.5% increase in NBV last year to $114.7 billion, compared to $111.9 billion in 2015.

While the figures were positive, they did mask a significant decline in the growth rate, which had slowed significantly from 2015’s spectacular 12.4% year-on-year rise.

In total, ELFA members’ assets under management rose by nearly 14% in 2016.

The biggest gains in new business were made in middle-ticket items, up 5.2% to $58.2 billion (2015: $55.3 billion), while small ticket items nudged ahead by 0.8% to $34.4 billion (2015: $34.1 billion), while large ticket items slipped back by 1.8%, down to $22.1 billion (2015: $22.5 billion) due to declines in demand for corporate aircraft, railroad and trucks and trailers.

United States Auto & Equipment Finance Survey 2017

29

20%

10%

0%

-10%

-20%

-30%

-40%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Overall growth rates in New Business Volume

New Business Volume

Jul-1

6

Oct-16

Sep-16

Feb-17

Apr-17

Jun-17

Aug-16

Dec-16

May-17

Nov-16

Jan-17

14

12

10

8

6

4

2

0

Mar-17

New

Bus

ines

s V

olum

e $

bn

77.7

9.48.2

6.4

12.1

6.2 5.9

8.97.77.9

9.8

Source: ELFA Monthly Leasing & Finance Index, June 2017

Source: 2017 Survey of Equipment Finance Activity

United States Auto & Equipment Finance Survey 2017

30

Where next for interest rates?Senior analysts forecast a further interest rate rise before the end of 2017, the fourth increase within 12 months.

In June, the US Federal Reserve put up its interest by 0.25% to 1.25%, the highest since the financial crisis of 2008, but still low by historic standards. Lower than anticipated inflation (below the Fed’s target 2%) limited the scale of the central bank’s intervention, but a tightening labor market suggests that the Fed will act again during this calendar year.

The latest increase followed rises of 0.25% in December 2016, and March 2017. Subsequent increases will be dependent on growth in the economy, and finance and leasing experts forecast no more than very small upward adjustments.

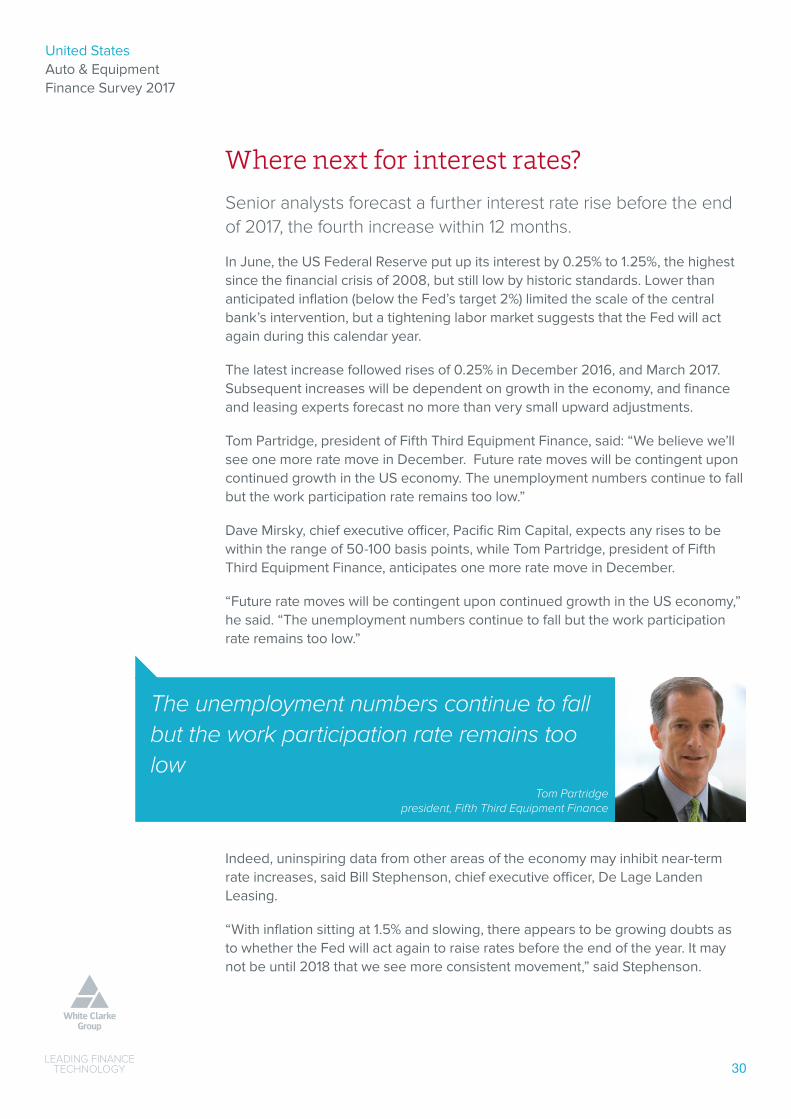

Tom Partridge, president of Fifth Third Equipment Finance, said: “We believe we’ll see one more rate move in December. Future rate moves will be contingent upon continued growth in the US economy. The unemployment numbers continue to fall but the work participation rate remains too low.”

Dave Mirsky, chief executive officer, Pacific Rim Capital, expects any rises to be within the range of 50-100 basis points, while Tom Partridge, president of Fifth Third Equipment Finance, anticipates one more rate move in December.

“Future rate moves will be contingent upon continued growth in the US economy,” he said. “The unemployment numbers continue to fall but the work participation rate remains too low.”

Indeed, uninspiring data from other areas of the economy may inhibit near-term rate increases, said Bill Stephenson, chief executive officer, De Lage Landen Leasing.

“With inflation sitting at 1.5% and slowing, there appears to be growing doubts as to whether the Fed will act again to raise rates before the end of the year. It may not be until 2018 that we see more consistent movement,” said Stephenson.

The unemployment numbers continue to fall but the work participation rate remains too low

Tom Partridge president, Fifth Third Equipment Finance

United States Auto & Equipment Finance Survey 2017

31

“We should also not lose sight of the $4.5 trillion in holdings the Fed accumulated during the financial crisis. A schedule for ‘balance sheet normalization’ is on the table and it appears likely the Fed will start acting to lower these balances later this year and into 2018. Those moves should put some upward pressure on long-term borrowing costs, and may start trickling down to our market(s) as well.”

Alan Sikora, chief executive officer, First American Equipment Finance, also foresees modest increases in interest rates throughout 2018, but with financing costs remaining low by historical standards, saying: “I don’t believe this will have much of an impact on the asset finance market.”

The impact of rate rises varies across the asset finance industry, depending on companies’ business models and routes to market, said Gary Amos, chief executive officer, Siemens Financial Services Commercial Finance North America.

“While banking systems have had increasing costs, independent financiers will continue to have a robust amount of access to liquidity in the debt markets,” said Amos. “Meanwhile, captive financiers will respond to their parent company strategies around equipment and software sales efforts, managing costs of the captive “lending arm” as needed.”

He added that as rates rise, financiers have to find and offer new ways to offset the effects of higher interest costs, particularly for the manufacturing sector.

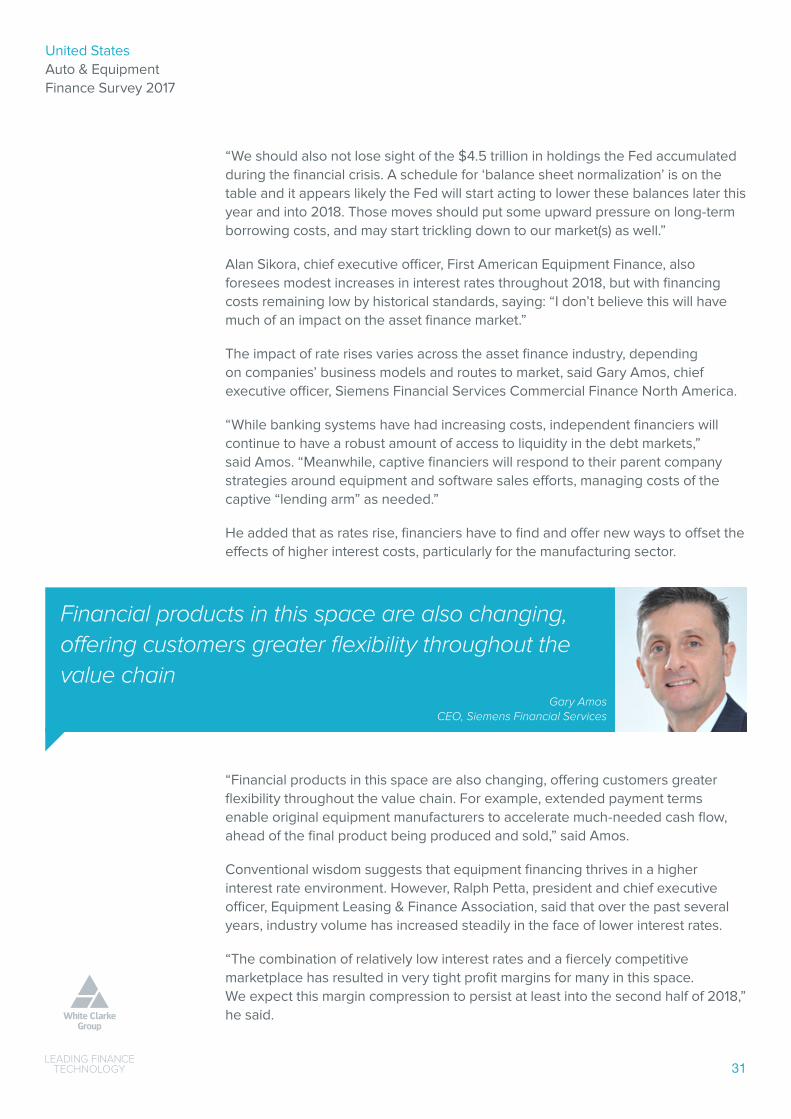

“Financial products in this space are also changing, offering customers greater flexibility throughout the value chain. For example, extended payment terms enable original equipment manufacturers to accelerate much-needed cash flow, ahead of the final product being produced and sold,” said Amos.

Conventional wisdom suggests that equipment financing thrives in a higher interest rate environment. However, Ralph Petta, president and chief executive officer, Equipment Leasing & Finance Association, said that over the past several years, industry volume has increased steadily in the face of lower interest rates.

“The combination of relatively low interest rates and a fiercely competitive marketplace has resulted in very tight profit margins for many in this space. We expect this margin compression to persist at least into the second half of 2018,” he said.

Financial products in this space are also changing, offering customers greater flexibility throughout the value chain

Gary AmosCEO, Siemens Financial Services

United States Auto & Equipment Finance Survey 2017

3232

The smart data revolution New technology and big data are transforming both the demand and delivery of equipment asset finance.

The increasing connectivity of assets has the power to generate data that will revolutionize their management by both their operators and financiers, while fintech companies increasingly demonstrate how technology can deliver financial services at lower costs and in innovative ways.

Alan Sikora, chief executive officer, First American Equipment Finance, said: “Commercial clients increasingly expect a convenient and frictionless client experience when obtaining financing.

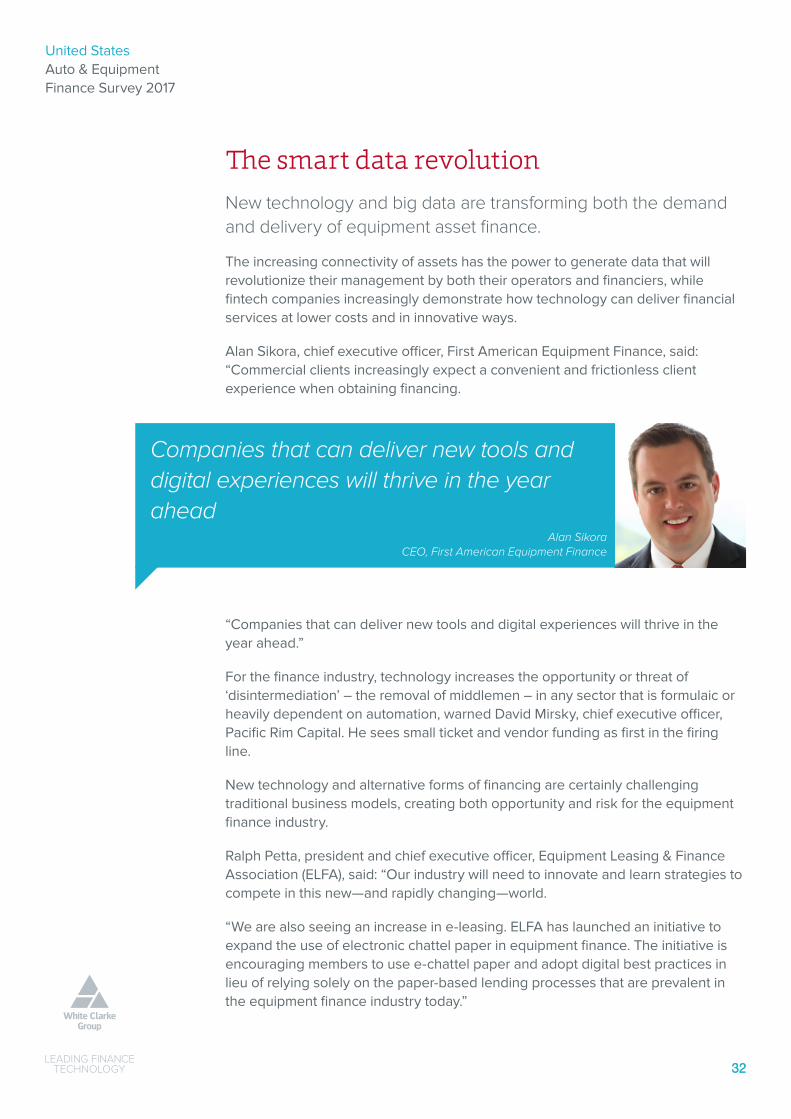

“Companies that can deliver new tools and digital experiences will thrive in the year ahead.”

For the finance industry, technology increases the opportunity or threat of ‘disintermediation’ – the removal of middlemen – in any sector that is formulaic or heavily dependent on automation, warned David Mirsky, chief executive officer, Pacific Rim Capital. He sees small ticket and vendor funding as first in the firing line.

New technology and alternative forms of financing are certainly challenging traditional business models, creating both opportunity and risk for the equipment finance industry.

Ralph Petta, president and chief executive officer, Equipment Leasing & Finance Association (ELFA), said: “Our industry will need to innovate and learn strategies to compete in this new—and rapidly changing—world.

“We are also seeing an increase in e-leasing. ELFA has launched an initiative to expand the use of electronic chattel paper in equipment finance. The initiative is encouraging members to use e-chattel paper and adopt digital best practices in lieu of relying solely on the paper-based lending processes that are prevalent in the equipment finance industry today.”

Companies that can deliver new tools and digital experiences will thrive in the year ahead

Alan SikoraCEO, First American Equipment Finance

United States Auto & Equipment Finance Survey 2017

33

The development of big data and its analysis will give customers the tools to better assess their needs, “and make decisions with less input from their financial partners,” said Adam Warner, president, Key Equipment Finance.

Bill Stephenson, chief executive officer, De Lage Landen Leasing, said: “Our industry is just scratching the surface in terms of how big data and analytics can be used to enhance the customer experience, drive efficiencies and sharpen financial performance.”

As the collection of data improves and the Internet of Things connects related assets, both manufacturers and asset finance companies will have extraordinary new opportunities to enhance their product and service offerings.

“In the equipment markets we support, collected data can help customers manage their equipment more effectively and reduce overall utilization costs,” said Stephenson. “It can also help manufacturers and suppliers better understand when technology upgrades or new products should be introduced. With this type of visibility, they can better manage their supply chain, anticipating the return of assets and preparing for recycling or reuse.”

Pinpointing the real value in a sea of data will be a particular challenge for the asset finance industry and its clients.

Gary Amos, chief executive officer of Siemens Financial Services Commercial Finance Americas, said: “The era of ‘smart data’ sees the real and virtual worlds collide online, resulting in an overabundance of data requiring additional streamlining to determine the most valuable insights.

“In general, as the real and virtual worlds continue to merge through digitalization and the industrial Internet of Things – there will be constant demands for equipment and technology financing across verticals. Many smaller manufacturers and Original Equipment Manufacturers (OEMs) will require financing to stay competitive with larger manufacturers.”

United States Auto & Equipment Finance Survey 2017

34

Mixed fortunes ahead for 2018The asset finance industry faces mixed fortunes over the next 12 to 18 months, with tantalizing prospects of strong growth in danger of being undermined by political machinations and margin compression.

Base indicators all point in the right direction, with the labor market approaching full employment, wage growth, rising consumer confidence and increasing business investment, particularly in certain sectors of the economy.

A quarterly survey by Wells Fargo/Gallup in July 2017 found small business optimism to be at its highest level for more than a decade, driven by healthy finances, increasing revenues, and easy access to credit.

More than one-fifth (21%) had even increased their headcount in the past 12 months, with companies saying recruiting and retaining quality staff topped the list of challenges facing their businesses.

Mark Vitner, managing director and senior economist at Wells Fargo, said: “More businesses are planning to boost capital spending and hiring.”

Across the whole economy, investment in equipment and software is forecast to grow by 3.6% in 2017, according to the Equipment Leasing & Finance Foundation, with further grounds for optimism next year.

Ralph Petta, president and chief executive office, Equipment Leasing & Finance Association (ELFA), said: “Looking ahead to 2018, the outlook for a continued improving equipment finance sector is based on a variety of factors, including indications of a steadily growing economy, the promise of a more business-friendly approach by the Trump Administration, and the move by the Fed to gradually increase short-term interest rates.

“It is our hope that these factors will provide impetus for continued growth into 2018. It remains to be seen whether policy makers in Washington will succeed in making progress on important legislative matters that benefit the business community, including tax and regulatory reform.

“ELFA is currently engaging policy makers on Capitol Hill, in key regulatory agencies and in state capitals throughout the nation to be sure that public policy issues that are important to our industry are addressed.”

These political headwinds are buffeting the confidence of equipment finance companies, which are finding it a challenge to convert customers’ positive intentions into investment commitments.

Thomas Jaschik, president, BB&T Equipment Finance said: “US companies are poised to make significant investments in capital equipment.

United States Auto & Equipment Finance Survey 2017

35

“However, many continue to delay plans until tax and regulatory reform legislation gets on track. Until then it will be ‘wait and see.’ The equipment finance industry should see a significant increase in activity if and when this occurs.”

Elaborating on this theme, Dave Mirsky, chief executive officer, Pacific Rim Capital, said the business sector currently faces too much uncertainty to unleash its true growth potential.

He said: “Due to uncertainty about taxes, location of manufacturing centers, tariffs, banking, repatriation of money, etc. business will sit on its hands. I am seeing the same lessee behavior regarding equipment renewing rather than being replaced as I do during recessions.”

His comments were echoed by a number of commentators, frustrated by the Administration’s inability to put forth tangible plans for infrastructure spending, corporate tax cuts and reduced regulation.

At the same time, however, the availability of capital, combined with relatively low interest rates, is edging companies towards sorely needed efficiency upgrades.

Alan Sikora, chief executive officer, First American Equipment Finance, said: “Automation in manufacturing and other key industries provides an exciting business opportunity for equipment lessors as manufacturers invest in new technologies.”

Lessors are keeping a close eye on how the Trump Administration’s America First strategy reduces the globalization of manufacturing and returns it to the US, and whether this provokes any retaliatory reprisals from other countries in the form of trading tariffs.

And even if demand for asset finance does start to fulfil its potential, there’s no escaping the squeeze on margins.

Bill Stephenson, chief executive officer, De Lage Landen Leasing, said: “Our industry will continue to be challenged by increased competition, excess liquidity and downward pressure on margins.

“The ELFA Survey of Equipment Finance Activity noted a 10 basis points drop in weighted average spreads for 2016. More recently, if you look at the public filings of some of the industry’s major players, there has been further compression of seven to 10 basis points. Unfortunately, I don’t see this trend improving in 2018.”

Due to uncertainty about taxes, location of manufacturing centres, tariffs, banking, repatriation of money, etc. business will sit on its hands Dave Mirsky

CEO, Pacific Rim Capital

United States Auto & Equipment Finance Survey 2017

36

A year of mixed fortunes

Industry experts are predicting a year of mixed fortunes for different sectors in asset finance.

Among the growth markets will be construction.

Bill Stephenson, chief executive officer, De Lage Landen Leasing, said: “[Construction] should deliver solid single digit growth, unless we see some surprises coming out of Washington DC with regards to future infrastructure projects and investments.”

Technology infrastructure is also identified as a growth market by industry leaders.

However, Adam Warner, president of Key Equipment Finance, noted: “The buyers may be cloud and service providers (i.e. Amazon) rather than traditional corporate clients. Software and services financing should also continue to grow.”

Healthcare is seen as a static industry sector, with Gary Amos, chief executive officer, Siemens Financial Services Commercial Finance North America, saying: “Ongoing provider consolidation and a decrease in medical equipment production for the new year at 2.3%, according to Q3 ELFA US Economic Outlook, will delay customer buying decisions.

“This will also be affected by the backdrop of reform and policy discussion, all pointing to delayed buying decisions. However, that does not mean that equipment and technology cannot play an important role in supporting the development of the sector. The cost to replace diagnostic imaging equipment over 10 years old in the US is estimated to be almost €4 billion ($4.7 billion).”

Sectors that are reported to have declining demand include transport, with Tom Partridge, president, Fifth Third Equipment Finance saying: “The larger transportation assets, such as rail, marine, and corporate aircraft remain in a cyclical downturn.”

Agriculture is similarly downbeat, but there are signs of recovery.

Bill Stephenson, chief executive officer, De Lage Landen Leasing, said: “Another year of recovery for the agriculture sector, although we are starting the see the first green shoots of positive activity with our vendor partners.”

The buyers may be cloud and service providers (i.e. Amazon) rather than traditional corporate clients. Software and services financing should also continue to grow Adam Warner

presidentw, Key Equipment Finance

United States Auto & Equipment Finance Survey 2017

37

Government urged to drive growth in 2018A year that started with so much promise for the asset finance industry is in danger of stalling as modest GDP growth and political uncertainty delay commercial investment decisions.

For commentators with longer memories, any growth is good growth, but there’s an overwhelming sense within the sector that more could be done at a federal level to prime the pump.

Dave Mirsky, chief executive officer, Pacific Rim Capital, believes the economy has underperformed in 2017, growing too slowly, and he sees no signs for improvement in 2018 “unless Congress can actually pass laws to reduce the growth of government and reform taxes and Health Care.”

Of particular concern is the cautious approach of businesses towards investment, which despite GDP growth, has been undermined by federal policy uncertainty.

Although business spending rose by between 5% and 7% in the second quarter of 2017, according to Bill Stephenson, chief executive officer, De Lage Landen Leasing, this represented slower growth than the activity levels seen earlier in the year.

Stephenson said: “Is this the first signs that some of the uncertainties in Washington are starting to dampen confidence? Let’s wait and see.

“I look ahead with measured confidence, realizing that 2.5% economic growth has become the ‘new normal’. Let’s not forget this is the eighth consecutive year of economic expansion for the US market!”

And data from the Equipment Leasing & Finance Association reveals a steady improvement as this year has progressed.

Ralph Petta, president and chief executive officer, ELFA said: “Our latest data indicates that business is on the rise in the equipment finance industry in 2017. According to the July 2017 Monthly Leasing and Finance Index, new business volume was up 13% year-over-year in July 2017 compared to July 2016.

“Year to date, cumulative new business volume is up 6% in 2017 compared to 2016.”

United States Auto & Equipment Finance Survey 2017

38

The Legal and Regulatory EnvironmentStephen Whelan assesses recent developments in the US equipment and auto finance market.

There have been several interesting developments in equipment and auto finance from various courtrooms. This article will discuss some noteworthy decisions.

TRAC auto leases

Commercial vehicle lessors received a rude surprise in re: Lightning Bolt Leasing, a federal court decision in Florida ignoring the existence of the Florida statute which declares that the mere presence of a TRAC (terminal rent adjustment clause) provision in a lease does not destroy true lease treatment.

The court sided with the bankrupt lessee, which argued that the TRAC provision gave it the upside and downside potential at expiration of the lease term. This decision runs counter to the weight of authority in many states, following enactment of TRAC statutes, but nevertheless sounds a cautionary note for vehicle lessors in the State of Florida.

Amended and restated: oops

In re: Fair Finance Company, decided in August 2016 by the United States Court of Appeals for the Sixth Circuit, forced a lender to litigate whether it had lost its security interest in the collateral, when it entered into an amended and restated loan agreement which declared that it “supersedes all prior oral or written agreements related to the subject matter hereof.”

The A&R agreement also contained additional “boilerplate” language that it was “intended by the [parties] to be the final, complete, and exclusive expression of the agreement between them.”

The lender neglected to file a new financing statement when the A&R agreement was signed. Perhaps it assumed that its original financing

statement remained adequate, because two years later it (timely) filed a continuation statement. The lender was repaid three years after the A&R agreement, from proceeds of a new financing. That should have ended the story.

Regrettably, the borrower had changed its business model since the original loan agreement and two years after the lender was paid off, the FBI raided the borrower’s headquarters. The borrower’s top three officers were convicted and received substantial prison sentences.

Several creditors of the borrower filed an involuntary petition to place the borrower in bankruptcy proceedings and the trustee in bankruptcy sued the lender, under Ohio law, to recover moneys which it had received (at and prior to the refinancing) while the borrower was insolvent.

The Court of Appeals ruled (left undisturbed by the bankruptcy court’s March 2017 ruling) that the bankruptcy trustee had demonstrated a “plausible claim…that all payments made by the [borrower]…under the [A&R agreement] amount to fraudulent transfers” under the applicable Ohio statute. Consequently, the lender was inadvertently harmed by the use of conventional “boilerplate” language.

Although the decision can be criticized, because the original loan agreement declared that its grant of a security interest was to be collateral for “all present…and future obligations of Borrower to Lenders intended as replacements or substitutions for said Obligations,” the implications for auto and equipment lessors and lenders are that they must include language in an A&R loan agreement to disclaim that it constitutes a novation and to reconfirm the grant of a security interest in both the original and any new collateral.

United States Auto & Equipment Finance Survey 2017

39

Hell or high water: bundled contracts

CDK Global, LLC v. Tulley Automotive Group, Inc. involved a product increasingly in demand by equipment users: a so-called “bundled contract” under which the lessor provides not only the equipment, but also services and licensed software—the latter two elements often furnished by third parties to which the lessor has subcontracted these items.

The lessor had agreed, in a master agreement with the lessee, that (in addition to equipment “in good working order”) it would furnish software and services which would “conform to their respective functional and technical specifications”.

On that basis, the court denied the lessor’s motion to dismiss the lessee’s claims. Because of this kind of legal risk, many bundled contract lessors are including a hell or high water clause in their bundled contracts, thereby requiring customers to make the schedule contract payment in all events, and to pursue their claims for inadequate services or software against the third party providers thereof.

Waiver of defenses: maybe, maybe not

A corollary of a hell or high water clause is a waiver of defenses clause, under which the lessee or other account debtor waives—as against any third party receivables purchaser or financier--any defenses which it may against the originator of the contract.

This concept has been embodied in Uniform Commercial Code section 9-403, which generally provides that an agreement (such as a waiver of defenses clause) between an account debtor and an assignor (its counterparty) not to assert against an assignee any claims or defenses, which it may have against the assignor, is enforceable by a good faith assignee which takes for value and without notice of such claims or defenses.

Two decisions in the past twelve months produced divergent results. In a surprising result, the federal District Court sitting in Chicago, in React Presents, Inc. v. Sillerman, found that a guarantor had reserved

its right to assert defenses (to enforcement of the guaranty) based upon fraud.

Although the guaranty contained a waiver of defenses clause, it contained an exception for “(other than the defense of payment in full and fraud based defenses)”. The court ruled that, even where the contract contains a waiver of defenses clause, a “covenant of good faith and fair dealing is implied in every contract, absent express language to the contrary, even when a guaranty waives all defenses.”

The federal District Court sitting in Manhattan, NY reached a different result in Overseas Private Investment Corporation v. Moyer, where the waiver of defenses clause in the guaranty was “absolute, unconditional, irrevocable and continuing” and did not contain the “fraud based defenses” exception of the Sillerman case.

The decision notes that, under New York State law, “the only affirmative defenses that are not waived by an absolute and unconditional Guaranty are payment and lack of consideration.”

Electronic chattel paper

An increasing proportion of automobile installment sale contracts and loans are being documented electronically, using origination platforms such as DocuSign and electronic vaults such as those maintained by eOriginal, Inc.

Nevertheless, there has been a reluctance among many small ticket equipment lessors, and the lenders which provide financing, to accept the invitation of UCC section 9-105 and document those transactions exclusively using electronic records.

Although there have been no reported decisions, as of Summer 2017, involving enforcement of (or security interests in) electronic leases, two reported cases during the past twelve months have shed some light, in the context of electronic real estate mortgages.

In Riviera v. Wells Fargo Bank, N.A., the Florida state court ruled that Wells Fargo’s evidence “proved that Fannie Mae had control of the e-note by showing

United States Auto & Equipment Finance Survey 2017

40

that the bank, as Fannie Mae’s servicer, employed a system reliably establishing Fannie Mae as the entity to which the e-note was transferred” and that “the bank’s system stored the e-note in such a manner that a single authoritative copy of the e-note exists which is unique, identifiable, and unalterable.” This conclusion, based on the Florida version of the Uniform Electronic Transactions Act, tracks the language of an important element under UCC section 9-105.

In New York Community Bank v. McClendon, a New York State court construed a different statute, the Electronic Signatures in Global and National Commerce Act, to conclude that the lender (in a foreclosure situation) had control of the e-note because “the transfer history, together with the copy

of the e-Note itself, were sufficient…to establish the identity of the person [or entity] having control of” the e-Note.

Admittedly, these are fact-based decisions which do not supply definitive guidance for those who would provide financing for electronic auto loans or equipment leases, but they would be useful precedents in the event that a financier faced a challenge to its having perfected its security interest via control of electronic chattel paper.

Stephen T. Whelan is a partner in the New York City office of law firm Blank Rome LLP ([email protected]) and a member of the ELFA Board of Directors.

United States Auto & Equipment Finance Survey 2017

41

Lease accounting - transitioning to Topic 842 Bill Bosco, advisor to ELFA, provides an update on the latest developments in lease accounting

Where are we now?

There is relief in the US regarding the lease accounting rules change. The Equipment Leasing and Finance Association and the US leasing industry business were able to convince the Financial Accounting Standards Board (FASB) that their model should recognize that operating leases were economically different from finance leases for lessees and that lessor accounting need not be drastically changed. We still believe no major changes were necessary to lease accounting but the FASB believed they had to go down a recognition model path. We think users would have been served just as well with an improved disclosure model. Primary users of financial data, such as the rating agencies and large lenders in measuring compliance with covenants and for their analytical purposes, generally plan to unwind the new accounting for operating leases and revert to their former calculations.

The positives

We advocated that operating leases are executory contracts where the Right of Use (ROU) asset is unique – it disappears in a bankruptcy liquidation as the leased asset is returned to the lessor. We also argued that the liability is not debt in a bankruptcy as it disappears as well. Rating agencies recognized this as they call operating lease liabilities “debt-like.” We also argued that the expense pattern should be straight line as it best represents the level benefit monthly use of a rented asset. The FASB listened and preserved a two-lease model where operating lease accounting more faithfully reflects the economic nature of the contract. Despite the rules change, lessees should continue to lease as the reasons for leasing remain strong. Even though operating leases will not be off-balance-sheet, the economic fundamentals of leasing are not changed. The amount

capitalized is less than if the asset is purchased, resulting in partial off-balance-sheet treatment, the liability is not debt and the P&L cost is level versus front loaded in an asset purchase.

The negatives

On the negative side the new rules are complex for lessees, requiring a robust systems solution and extensive interdisciplinary internal controls. The transition could be costly for some due to the number of leases that most companies have; the decentralized authority to lease means the documents are in local offices, making it difficult to assemble the documents; and, finally, reading and extracting the many data points needed to capitalize leases is time consuming. Equipment sale leasebacks with fixed non-bargain purchase options will not be considered sales and operating leasebacks despite the fact they are sales under commercial and tax law. Financial institutions will have to raise capital as the regulators say they will risk weight operating lease ROU assets at 100%, thus requiring 10.5–13% regulatory capital despite the fact they never required it before as the leased asset is returned to the lessor in a liquidation. The FASB never intended for merely the change in financial presentation of leases to cause a change in capital requirements.

Some manufacturer lessors will lose the upfront income recognition in sales type leases. Leveraged lease accounting is eliminated going forward, thus increasing the cost of large-ticket leases. The definition of initial direct costs was changed so that it no longer matches that for loans. Lastly, there could be confusion in understanding the new financial presentation and ratios and measures with the first evidence that the bank regulators think operating lease assets need capital now that they are capitalized as assets.

United States Auto & Equipment Finance Survey 2017

42

Lessee preparedness

Lessee preparedness seems to be the biggest issue in transitioning to the new lease accounting rules. The major accounting firms have published polls that show many lessee preparers are behind in their transition plans. A recent Deloitte poll noted that 47% of lessees are concerned that they may not meet the transition date. The transition project is daunting and I think the FASB and preparers underestimated the task of transition particularly when they are also simultaneously dealing with the pervasive change in revenue recognition.

Any company with more than a handful of leases will need a lease accounting system to capitalize and account for the leases. A KPMG survey notes that 42% of respondents have more than 999 leases. As of this writing date, we have not heard that there is a commercially available system that is ready to use that has all the functionality the new standard requires. The reason is the calculations and requirements in the new rules are complex and it takes time to build and test systems. The complexities of operating lease accounting include calculating the ROU asset amortization to back into a straight line expense, switching ROU asset amortization in case of impairment, tracking CPI and floating lease payments if a lessee does not rebook the lease when the payments change (rebooking is only required if the lease is modified), and rebooking a lease when a payment under a residual guarantee becomes likely, as examples.

Companies then need to collect and assemble the lease documents for all leases in effect. Since operating leases are off-balance-sheet they are considered operating budget items while finance leases are capital items. This means that local managers have the authority to enter into operating leases where the rent is within their signing authority. These are generally equipment leases. The lease document is likely to be held in the local office. The only ways the CFO may know of the lease is if it was reported for footnote disclosures and by seeing rent expense in the general ledger coming from a local expense code.

A KPMG survey notes that 49% of respondents have lease documents in more than 9 locations. Real estate leases are generally managed centrally so it should be easy to locate those documents.