Embed Size (px)

Citation preview

ASSESSMENT OF THE RELATIONSHIP BETWEEN WORKING

CAPITAL MANAGEMENT AND PROFITABILITY OF LISTED

COMPANIES IN DAR ES SALAAM STOCK EXCHANGE

ASSESSMENT OF THE RELATIONSHIP BETWEEN WORKING

CAPITAL MANAGEMENT AND PROFITABILITY OF LISTED

COMPANIES IN DAR ES SALAAM STOCK EXCHANGE

By

Ngianael Paul Minja

A Dissertation Submitted to MUDCC in Partial Fulfillment of the Requirements for

the Award of the Degree of Master of Business Administration in Corporate

Management (MBA-CM) of Mzumbe University.

2014

ii

CERTIFICATION

We, the undersigned, certify that we have read and hereby recommend for

acceptance by the Mzumbe University, a thesis entitled Assessment of the

Relationship Between Working Capital Management and Profitability of Listed

Companies in Dar es Salaam Stock Exchange, in partial fulfillment of the

requirements for award of the degree of Master of Business Administration in

Corporate Management (MBA-CM) of Mzumbe University

___________________________

Major Supervisor

___________________________

Internal Examiner

Accepted for the Board of …………………….

_______________________________________________________

CHAIRPERSON, FACULTY/DIRECTORATE BOARD

iii

DECLARATION

AND

COPYRIGHT

I, Ngianael Paul Minja, I do hereby declare that this dissertation t is my own

original work and it has not been presented and will not be presented to any other

University for a similar any other degree award.

Signature: _____________________________

Date: _________________________________

© 2014

This dissertation is a copyright material protected under the Berne Convention, the

Copyright Act 1999 and other international and national enactments, in that behalf,

on intellectual property. It may not be reproduced by any means in full or in part,

except for short extracts in fair dealings, for research or private study, critical

scholarly review or discourse with an acknowledgement, without the written

permission of Mzumbe University, on behalf of the author.

iv

ACKWOLEDGEMENT

To God are the glory, honor and praise for his abundant love, inspiration and good

health throughout my study period at Mzumbe University Dar es Salaam Campus

College.

I thank the lecturing staff of Mzumbe University especially Business Administration

Department, whose support over fourteen months provided me with the necessary

background skills to undertake and complete this study. A special thanks to my

supervisor, Ms. Sarah R. Mngoya of Mzumbe University for her guidance, insight

and encouragement in the writing and compilation of this thesis. Your invaluable

support and patience throughout this journey has been unreal and is appreciated from

the bottom of my heart.

This work would not have been complete without the support and effort from my

employer ELCT – ECD and employees of Keko Lutheran Parish I am grateful to

them. I am also grateful to Chairperson and Treasurer of Financial committee of

Keko Parish for their cooperation and support.

It is practically impossible to mention all those who took me and made efforts to help

me. As such collective thanks go to all those who have not been acknowledged by

name I also give the same weight as those whose name appears.

Lastly but not least, I would like to express my heartfelt gratitude to my close fellow

Masters students at Mzumbe University.

MAY OUR GOD BLESS YOU ALL!

v

DEDICATION

This dissertation work is dedicated to my lovely family of Paul C. Minja, for their

patience, contribution and support throughout the study period. I am appreciative of

their prayers, moral, financial and material support. I am wishing them a lot of

success and happiness throughout, the blessings of the Lord be with them always.

vi

LIST OF ABBREVIATIONS AND ACRONYMS

CACLR - Current ratio

CCC - Cash Conversion Cycle

DSE - Dar es Salaam Stock Exchange

ECD - Eastern and costal Diocese

ECD - Eastern and Costal Diocese

ELCT - Evangelism Lutheran church of Tanzania

ELCT - Evangelism Lutheran church of Tanzania

FPD - Focus Panel Discussion

ROA - Return on assets

ROIC/ROE - Return on equity

SPSS - Statistical Package for Social Sciences

URT - United Republic of Tanzania

WCM - Working capital management

vii

ABSTRACT

The aim of this study was to investigate the relationship between working capital

management and profitability of listed companies in Dar es Salaam Stock Exchange.

The objectives of the study were; to determine relationship between working capital

management and return on assets, to determine relationship between working capital

management (WCM) and return on equity (ROE) and to determine relation between

WCM and cash conversion cycle (CCC).

Data was gathered from selected sample of seven (7) listed companies from 2008 up

to 2013. Most of the data collected was secondary data obtained from the companies

audited financial statements, internet surfing, DSE, CMSA, companies achieves and

National Board of Accountants and Auditors Library. Literature from both published

and unpublished documents were employed in this study.

The study findings shows a negative significant relationship exists between cash

conversion cycle (CCC) and return on assets and there is also a negative significant

relationship between cash conversion cycle (CCC) and return on equity. However,

the relationship between current ratio and return on equity is insignificant. The study

findings also show that there exist negative relationship between number of day’s

accounts receivable, number of day’s inventories, member of days accounts payable,

cash conversion cycle and profitability.

Based on the study findings the study recommends that listed companies must adopt

suitable policy for financing and assets turnover in order to increase in return on

assets rates and profitability. The study also recommends that listed Companies must

adopt policies and plans to reduce number of day accounts receivable this will

improve their operation and increase in shareholder’s wealth.

viii

TABLE OF CONTENTS

Pages

CERTIFICATION ................................................................................................. ii DECLARATION AND COPYRIGHT ................................................................ iii

ACKWOLEDGEMENT ....................................................................................... iv DEDICATION ........................................................................................................v

LIST OF ABBREVIATIONS AND ACRONYMS .............................................. vi ABSTRACT ......................................................................................................... vii

TABLE OF CONTENTS .................................................................................... viii LIST OF TABLES ................................................................................................ xi

LIST OF FIGURES ............................................................................................. xii

CHAPTER ONE .....................................................................................................1 INTRODUCTION AND PROBLEM SETTING ...................................................1

1.0 Introduction ............................................................................................1 1.1 Background Information to the Study .....................................................1

1.2 Problem Statement ..................................................................................2 1.3 Objectives of the Study ...........................................................................3

1.3.1 General Objective ...................................................................................3 1.3.2 Specific objectives ..................................................................................3

1.4 Research Questions .................................................................................4 1.4.1 Broad Research Question ........................................................................4

1.4.2 Specific Research Questions ...................................................................4 1.5 Scope of the Study ..................................................................................4

1.6 Significance and Necessity of the Study ..................................................4 1.7 Limitation of the Study ...........................................................................5

1.8 Organization of the Dissertation ..............................................................6

CHAPTER TWO ....................................................................................................7 LITERATURE REVIEW .......................................................................................7

2.0 Introduction ............................................................................................7 2.1 Definitions of Key Terms and Meaning of Concepts ...............................7

2.1.1 Working Capital .....................................................................................7 2.1.2 Working Capital Management ................................................................8

2.1.3 Profitability Returns on Assets ................................................................8 2.1.4 Return on Equity .....................................................................................9

2.1.5 Meaning of Cash Conversion Cycle ........................................................9 2.1.6 Effects of Working Capital Management on a Firm’s Profitability ..........9

2.1.7 Determinants of Trade Credit ................................................................ 12 2.1.7.1 Financial Motives ................................................................................. 12

2.1.7.2 Operational Motives ............................................................................. 13 2.1.7.3 Commercial Motives............................................................................. 13

2.1.7.4 Other Motives of Extending Trade Credit ............................................. 14 2.1.7.5 Studies on Determinants of Trade Credit ............................................... 15

2.1.8 Determinants of Inventories .................................................................. 16 2.1.8.1 Just-In-Time Inventory System ............................................................. 17

ix

2.1.8.2 Higher Inventory Levels and Production Costs ..................................... 17

2.1.8.3 Other Determinants of Inventory Management...................................... 18 2.2 Theoretical Framework ......................................................................... 18

2.2.1 The Cash Conversion Cycle (CCC) ....................................................... 18 2.2.2 Working Capital and Its Management ................................................... 20

2.2.3 Enough Liquidity .................................................................................. 23 2.2.4 Minimizing Risk ................................................................................... 23

2.2.5 Maximizing Firm’s Value ..................................................................... 23 2.2.6 Measures of Profitability ....................................................................... 23

2.2.7 Measures of firms working capital ........................................................ 24 2.3 Empirical Literature Review ................................................................. 24

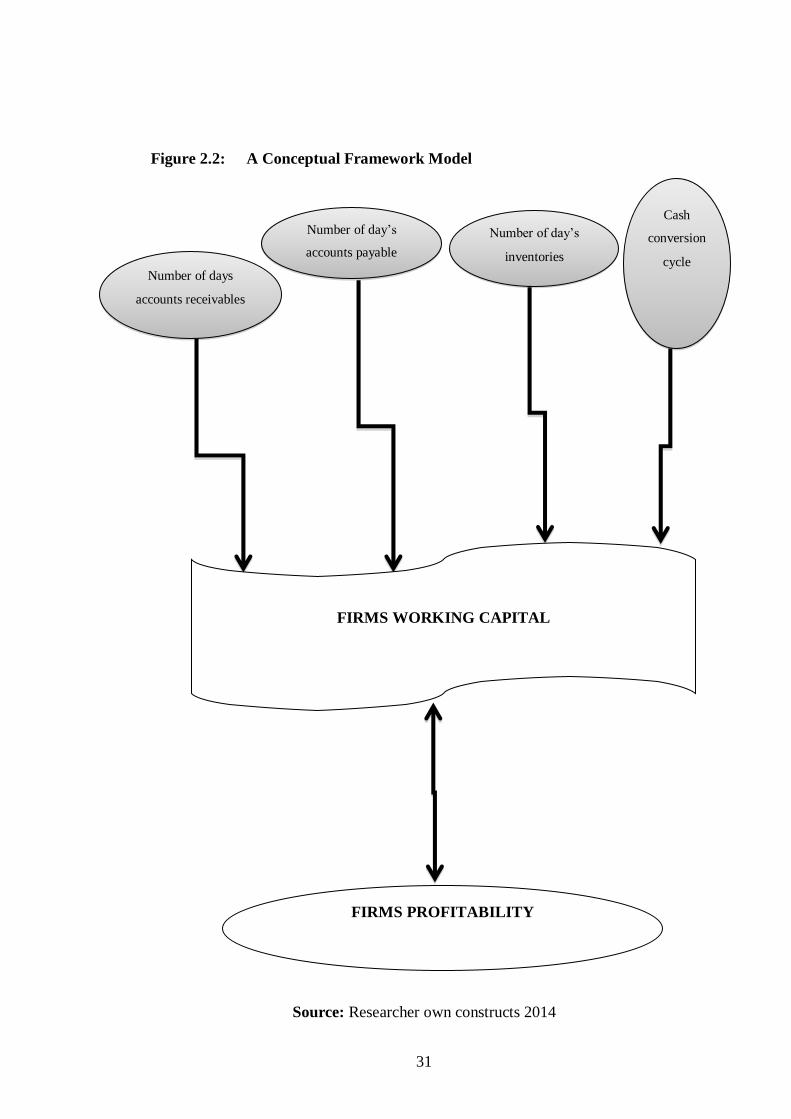

2.4 Research Gap ........................................................................................ 29 2.5 Conceptual Framework ......................................................................... 29

2.5.1 Number of days accounts receivables .................................................... 32 2.5.2 Number of days accounts payable ......................................................... 32

2.5.3 Number of days inventories .................................................................. 32 2.5.4 Cash conversion cycle .......................................................................... 32

2.5.5 Firms working capital ........................................................................... 33 2.5.6 Firms Profitability................................................................................. 33

2.6 Research Model .................................................................................... 33

CHAPTER THREE .............................................................................................. 35 RESEARCH METHODOLOGY ......................................................................... 35

3.0 Introduction .......................................................................................... 35 3.1 Research Design ................................................................................... 35

3.2 Study Area ............................................................................................ 35 3.3 Population of the Study ......................................................................... 35

3.4 Sample Size .......................................................................................... 36 3.5 Sampling Procedure .............................................................................. 37

3.6 Types and Sources of Data .................................................................... 37 3.7 Data Collection Technique .................................................................... 37

3.7.1 Documentation ..................................................................................... 37 3.7.2 Focused Panel Dialogue ........................................................................ 37

3.8 Data Presentation and Analysis ............................................................. 37 3.9 Chapter Summary ................................................................................. 38

CHAPTER FOUR................................................................................................. 39

PRESENTATION AND DISCUSSION OF FINDINGS ..................................... 39 4.0 Introduction .......................................................................................... 39

4.1 Companies Information ........................................................................ 39 4.1.1 Productions Firms ................................................................................. 39

4.1.2 Insurance Firms .................................................................................... 41 4.1.3 Manufacturing Firms ............................................................................ 42

4.1.4 Agricultural Sector Firms...................................................................... 42 4.1.5 Transportation Services Firms............................................................... 42

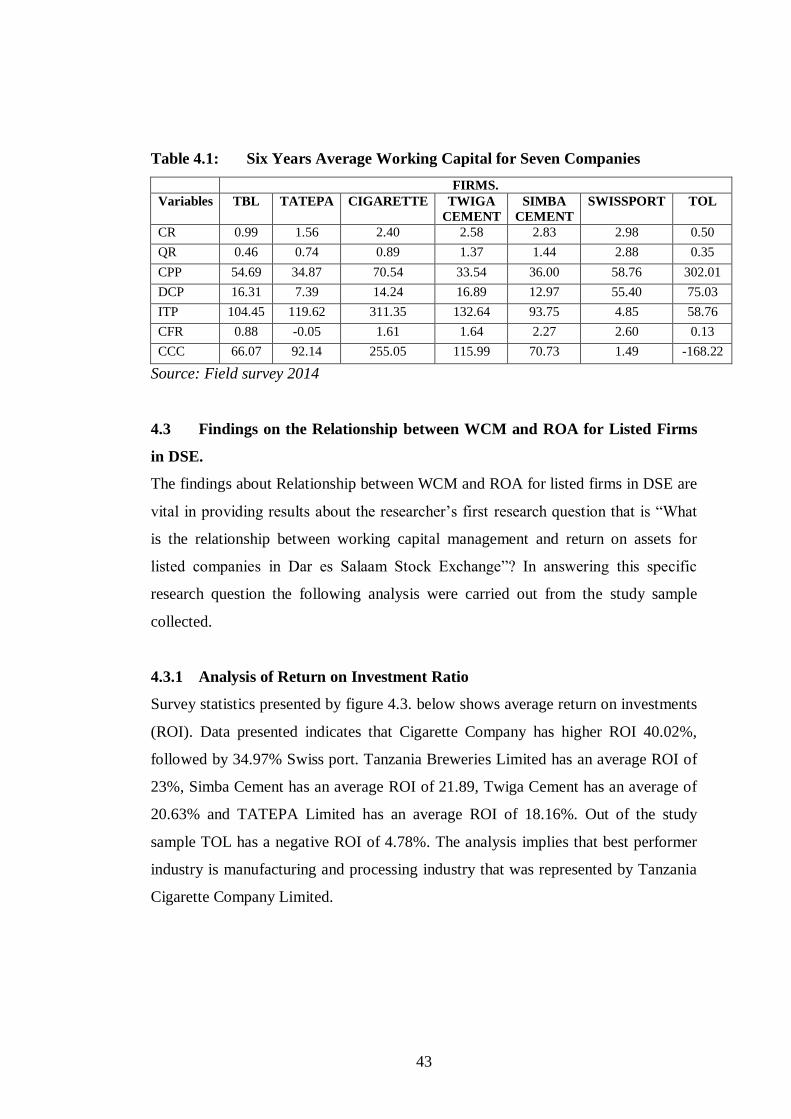

4.2 Findings on the Working Capital Analysis ............................................ 42

x

4.3 Findings on the Relationship between WCM and ROA for Listed Firms

in DSE. ................................................................................................. 43 4.3.1 Analysis of Return on Investment Ratio ................................................ 43

4.3.2 Analysis of Firms Gross Profit Margin .................................................. 44 4.3.3 Analysis of Firms Return on Assets (ROA) ........................................... 45

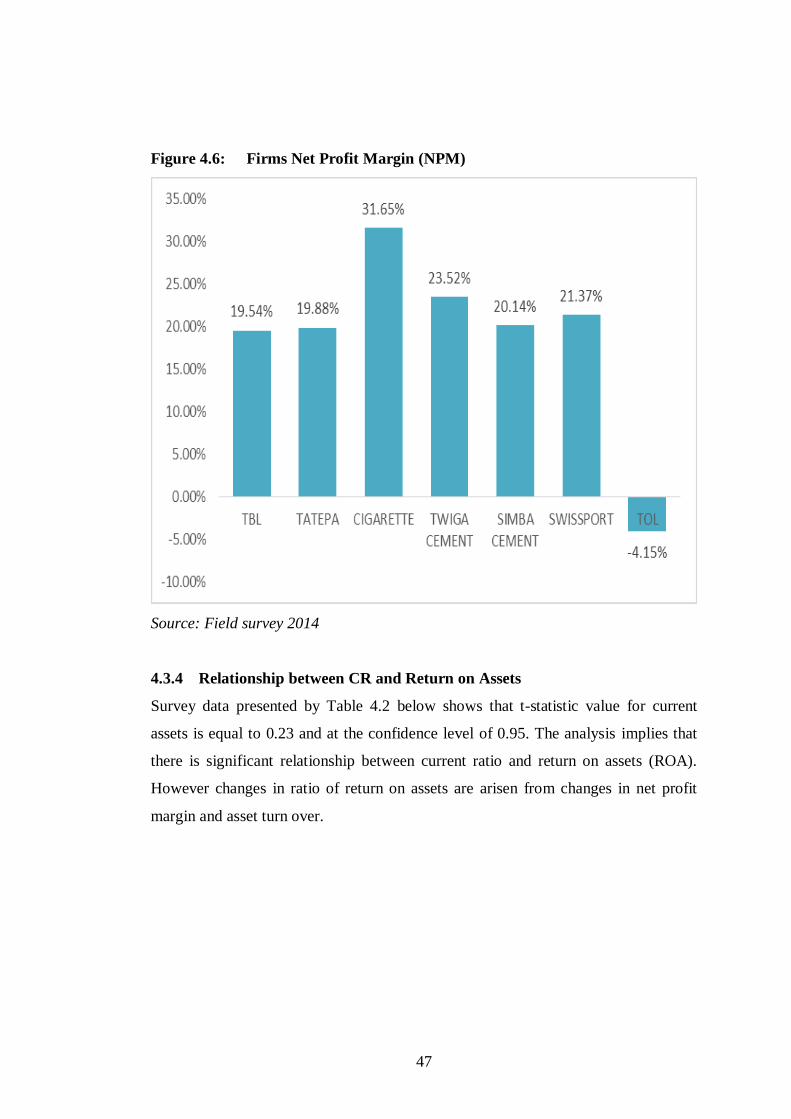

4.3.4 Firms Net Profit Margin (NPM) ............................................................ 46 4.3.4 Relationship between CR and Return on Assets .................................... 47

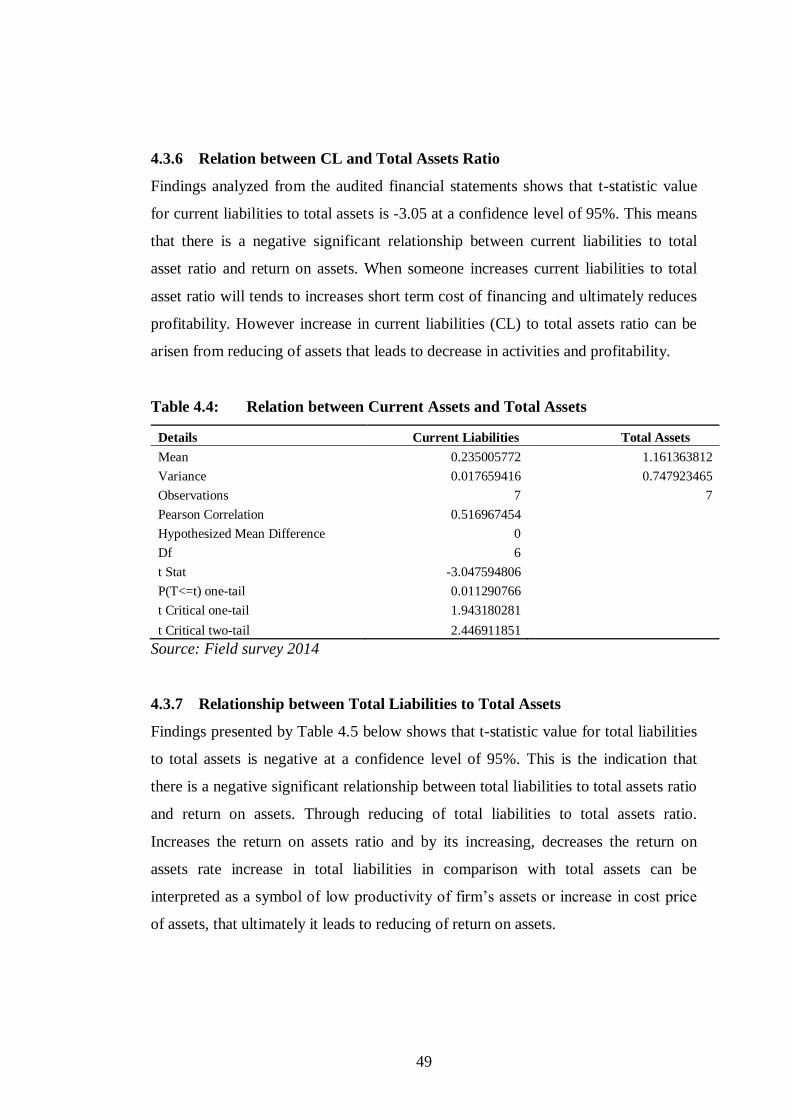

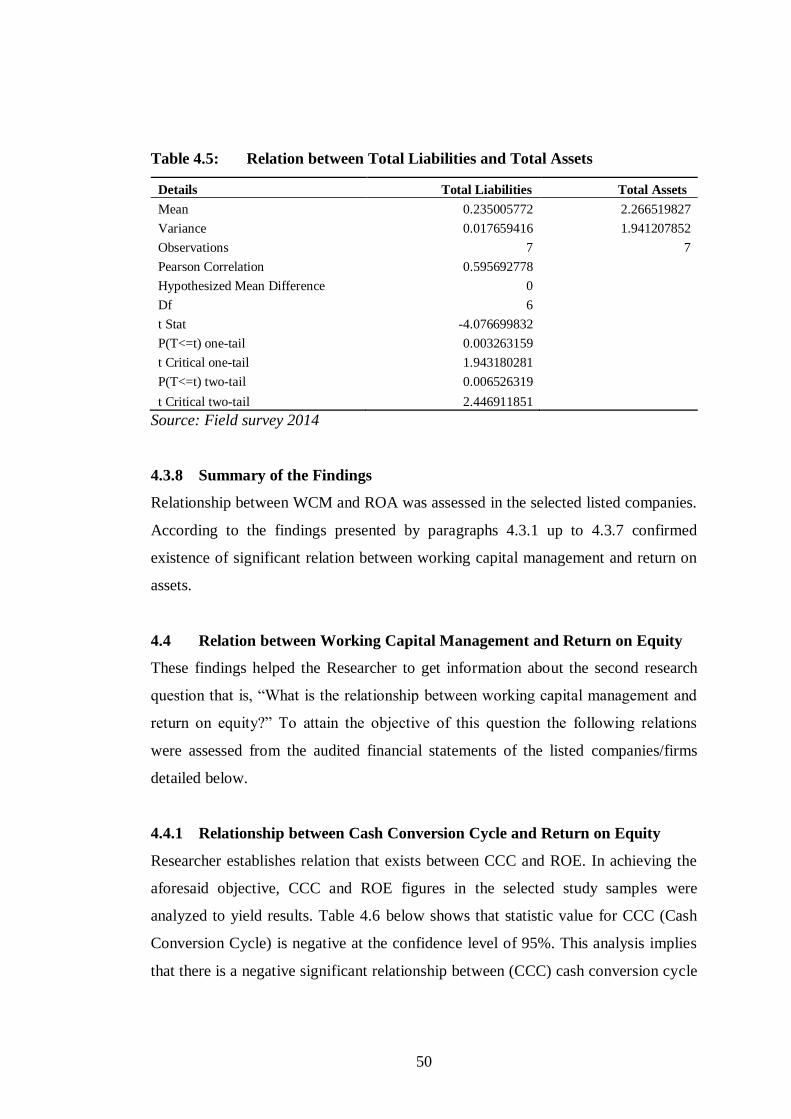

4.3.5 Relation between ROA and Current Assets to Total Assets Ratio .......... 48 4.3.6 Relation between CL and Total Assets Ratio......................................... 49

4.3.7 Relationship between Total Liabilities to Total Assets .......................... 49 4.3.8 Summary of the Findings ...................................................................... 50

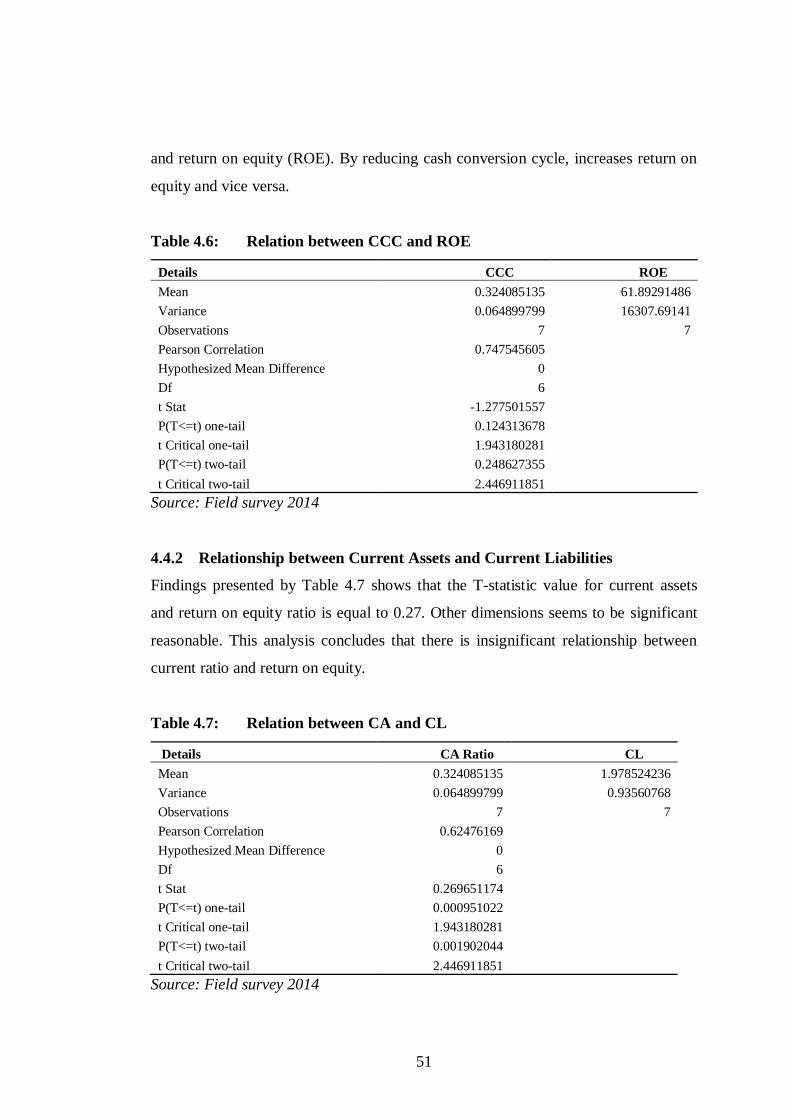

4.4 Relation between Working Capital Management and Return on Equity. 50 4.4.1 Relationship between Cash Conversion Cycle and Return on Equity ..... 50

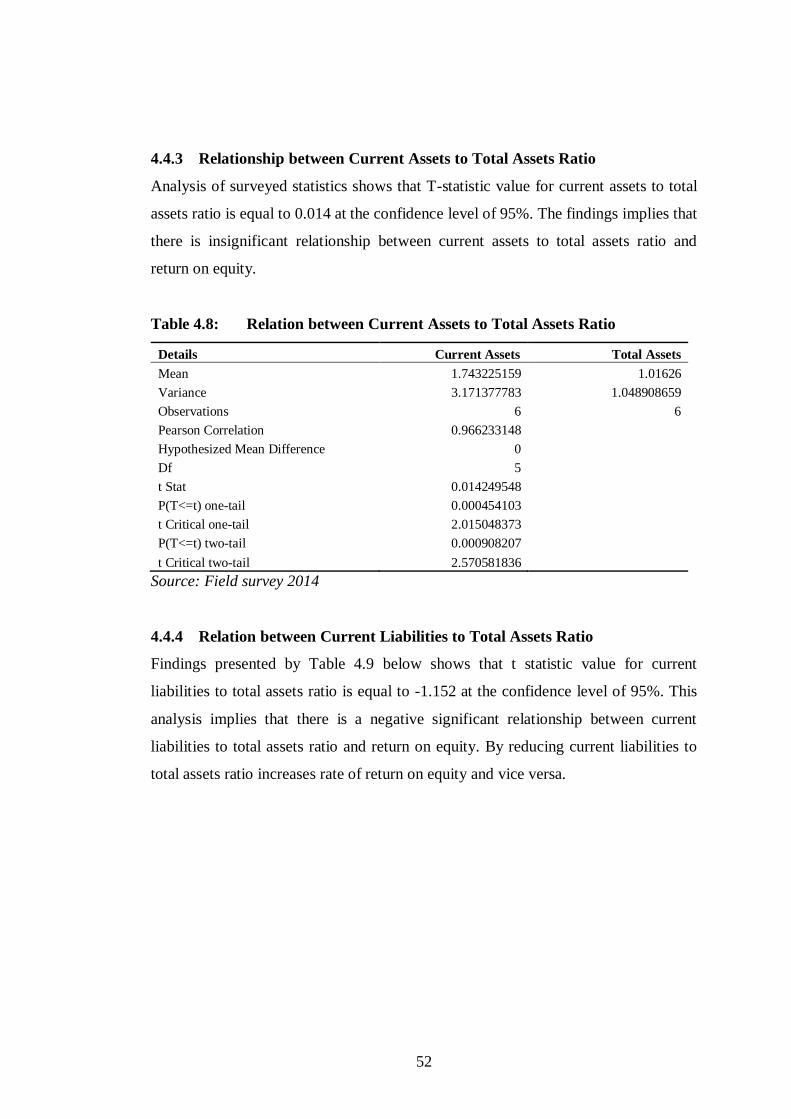

4.4.2 Relationship between Current Assets and Current Liabilities ................ 51 4.4.3 Relationship between Current Assets to Total Assets Ratio ................... 52

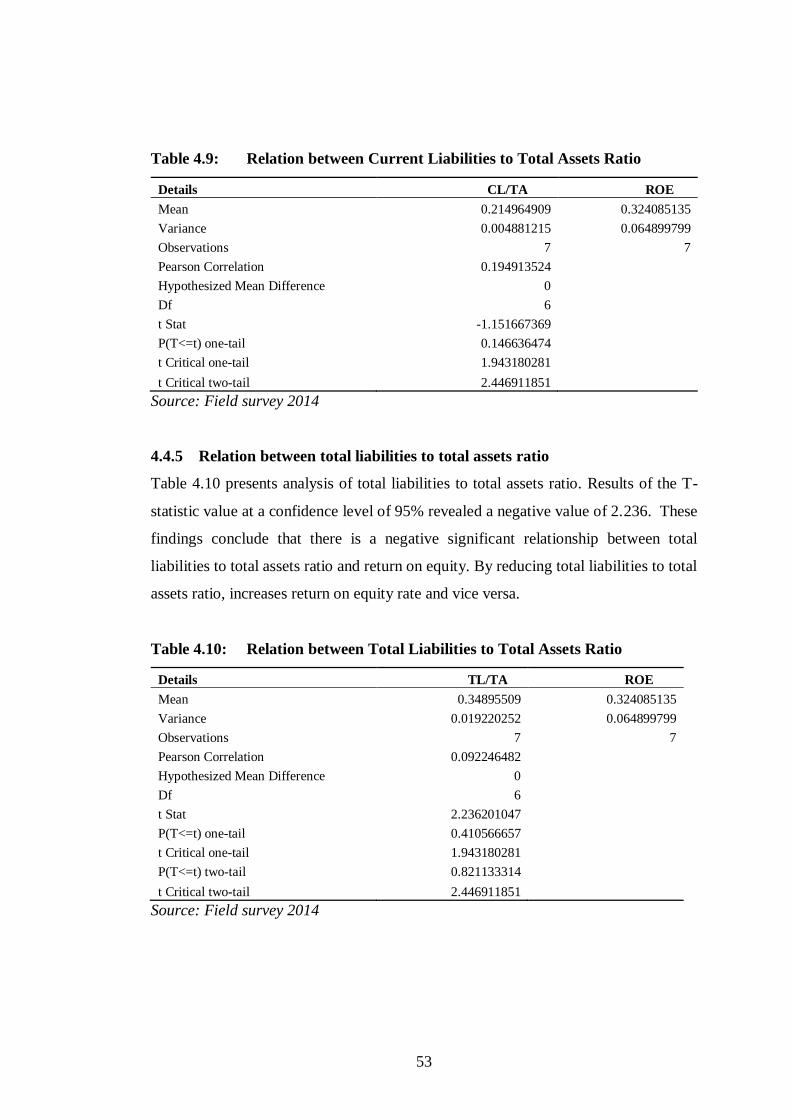

4.4.4 Relation between Current Liabilities to Total Assets Ratio .................... 52 4.4.5 Relation between total liabilities to total assets ratio.............................. 53

4.4.6 Summary of the Findings ...................................................................... 54 4.5 Relation between Working Capital Management and Cash Conversion

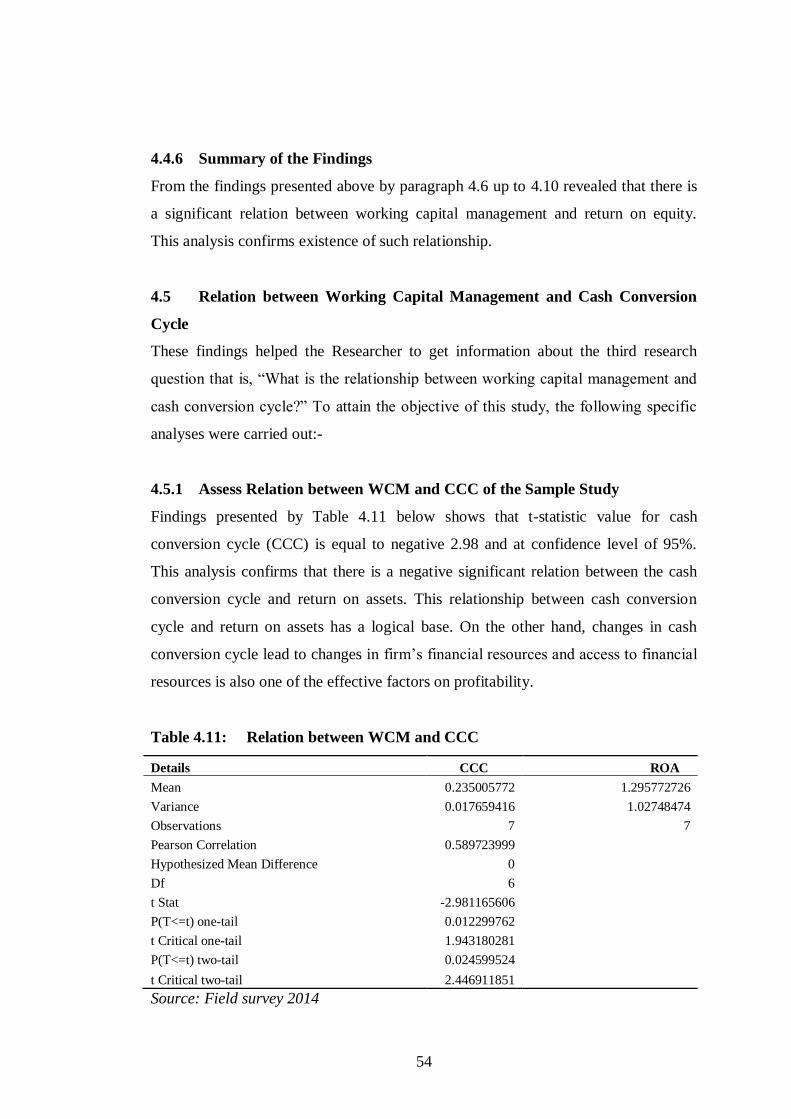

Cycle .................................................................................................... 54 4.5.1 Assess Relation between WCM and CCC of the Sample Study ............. 54

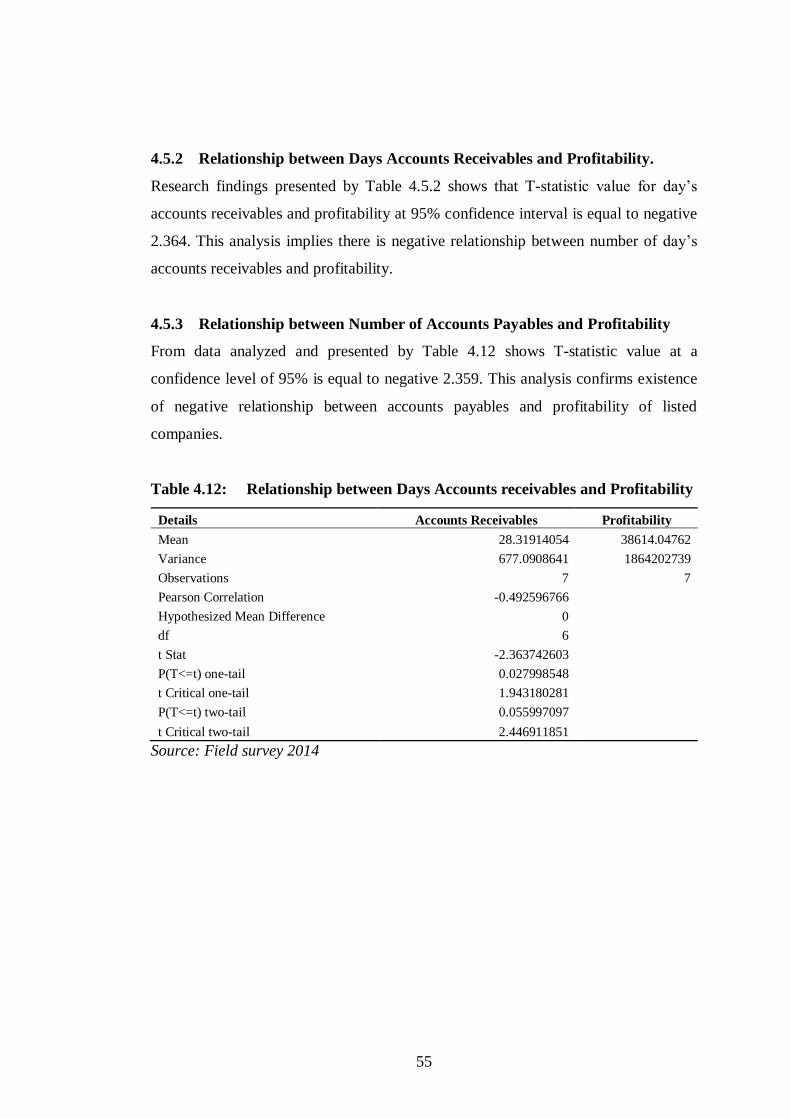

4.5.2 Relationship between Days Accounts Receivables and Profitability. ..... 55 4.5.3 Relationship between Number of Accounts Payables and Profitability .. 55

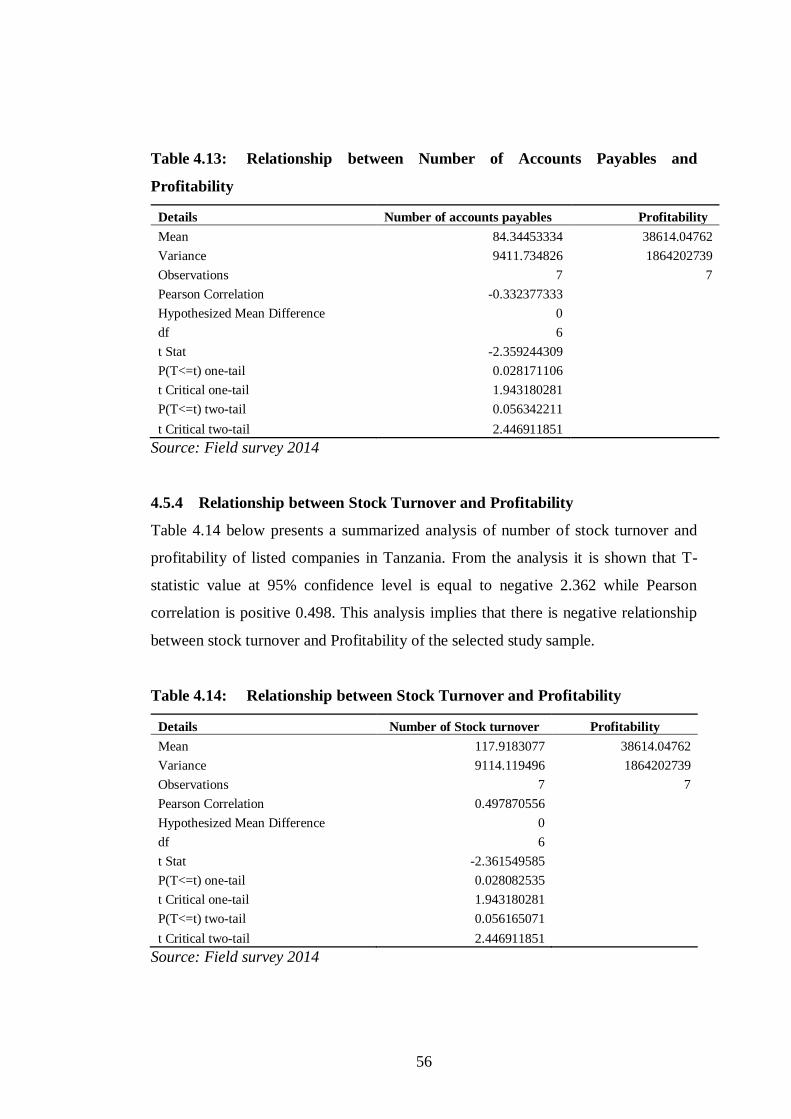

4.5.4 Relationship between Stock Turnover and Profitability ......................... 56 4.5.5 Summary of the Findings ...................................................................... 57

CHAPTER FIVE .................................................................................................. 58

SUMMARY, RECOMMENDATIONS AND CONCLUSION ........................... 58 5.0 Introduction .......................................................................................... 58

5.1 Summary of the Main Findings ............................................................. 58 5.1.1 Relationship between WCM and ROA. ................................................. 58

5.1.2 Relationship between WCM and ROE. ................................................. 58 5.1.3 Relationship between WCM and CCC. ................................................. 59

5.2 Conclusion............................................................................................ 59 5.2.1 Research objective 1: Relationship between WCM and ROA for listed

firms. .................................................................................................... 59 5.2.2 Research objective 2: Relationship between WCM and ROE. ............... 59

5.2.3 Research objective 3: Relationship between WCM and CCC. ............... 59 5.3 Recommendations ................................................................................ 60

5.3.1 Research objective 1: Relationship between WCM and ROA for listed

firms. .................................................................................................... 60

5.3.2 Research objective 2: Relationship between WCM and ROE. ............... 60 5.3.3 Research objective 3: Relationship between WCM and CCC. ............... 60

5.4 Recommendations Further Research ..................................................... 60

REFERENCES ..................................................................................................... 61

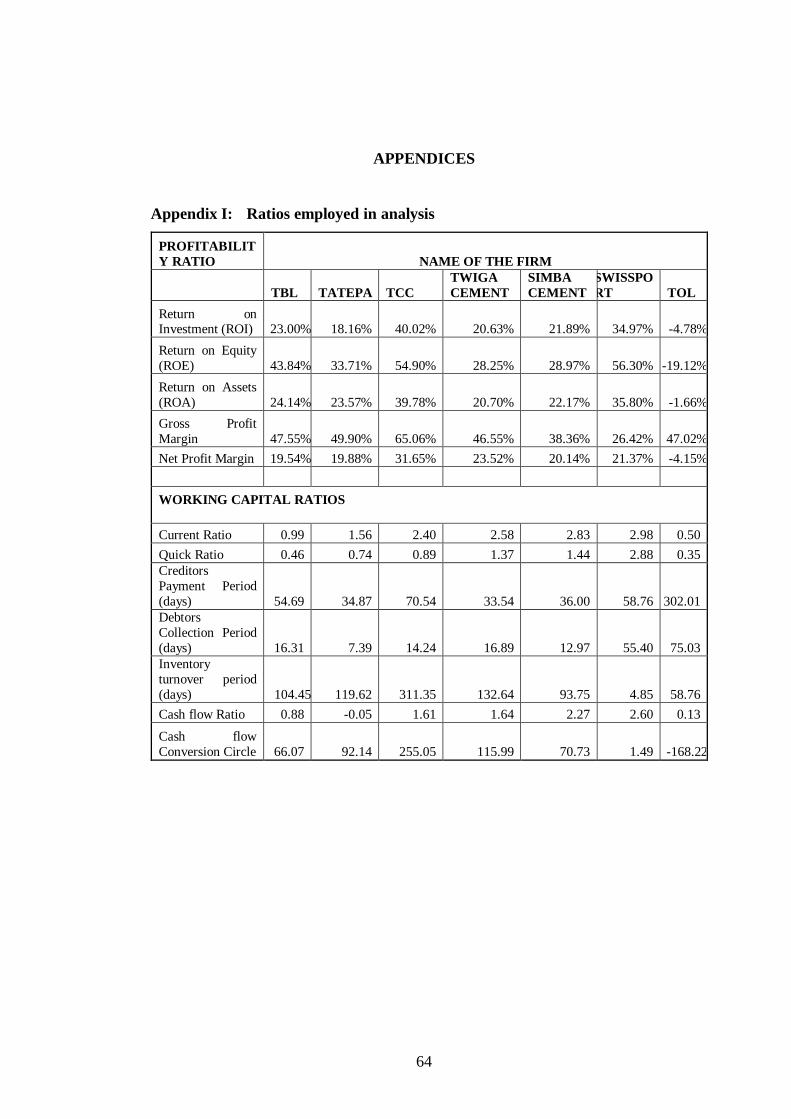

APPENDICES ....................................................................................................... 64 Appendix I: Ratios employed in analysis ........................................................ 64

xi

LIST OF TABLES

Pages

Table 2.1: Showing Components of Working Capital ..........................................7

Table 2.2: Showing Nature of Working Capital...................................................8

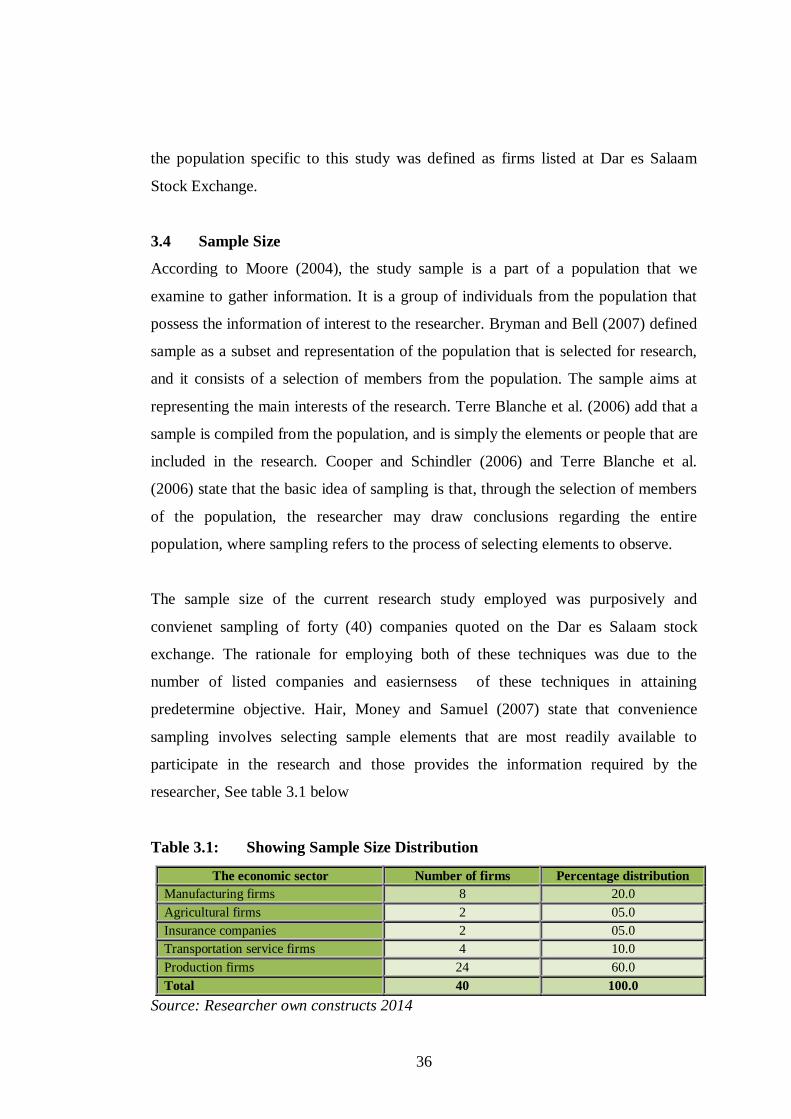

Table 3.1: Showing Sample Size Distribution ................................................... 36

Table 4.1: Six Years Average Working Capital for Seven Companies ............... 43

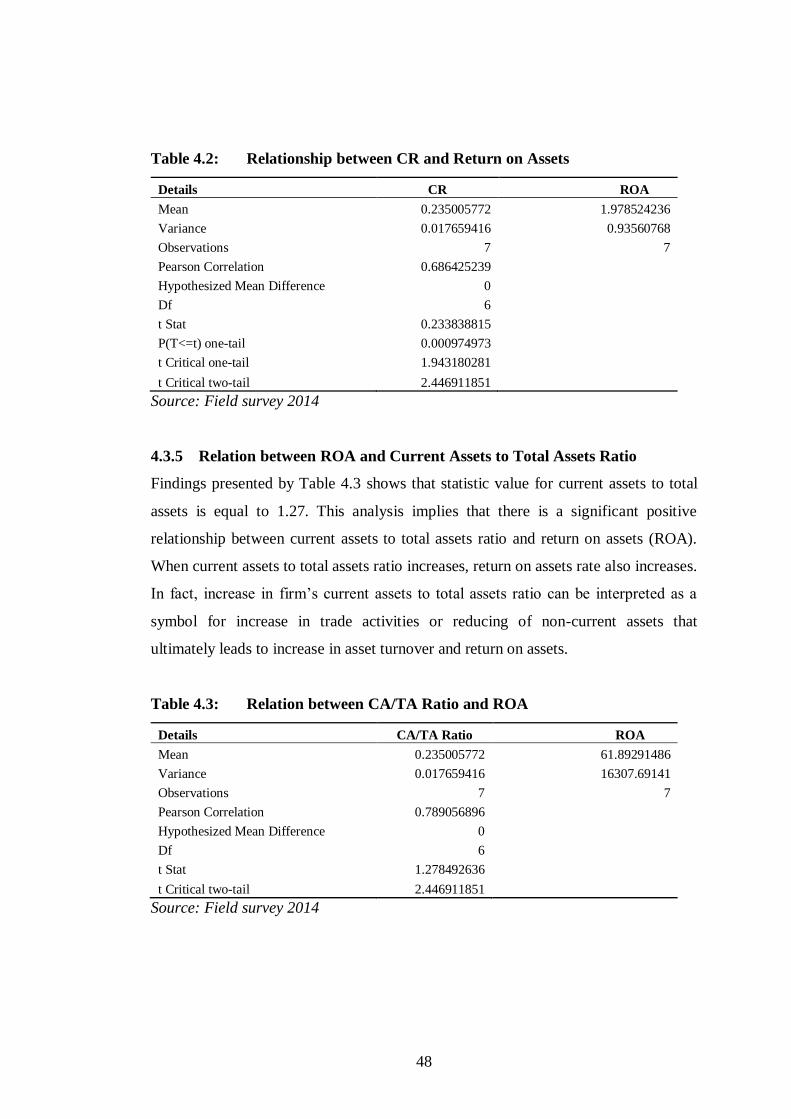

Table 4.2: Relationship between CR and Return on Assets ............................... 48

Table 4.3: Relation between CA/TA Ratio and ROA ........................................ 48

Table 4.4: Relation between Current Assets and Total Assets ........................... 49

Table 4.5: Relation between Total Liabilities and Total Assets.......................... 50

Table 4.6: Relation between CCC and ROE ...................................................... 51

Table 4.7: Relation between CA and CL ........................................................... 51

Table 4.8: Relation between Current Assets to Total Assets Ratio ..................... 52

Table 4.9: Relation between Current Liabilities to Total Assets Ratio ............... 53

Table 4.10: Relation between Total Liabilities to Total Assets Ratio ................... 53

Table 4.11: Relation between WCM and CCC .................................................... 54

Table 4.12: Relationship between Days Accounts receivables and Profitability ... 55

Table 4.13: Relationship between Number of Accounts Payables and

Profitability ...................................................................................... 56

Table 4.14: Relationship between Stock Turnover and Profitability .................... 56

xii

LIST OF FIGURES

Pages

Figure 2.1: The Cash Conversion Cycle (CCC).............................................. 19

Figure 2.2: A Conceptual Framework Model ................................................. 31

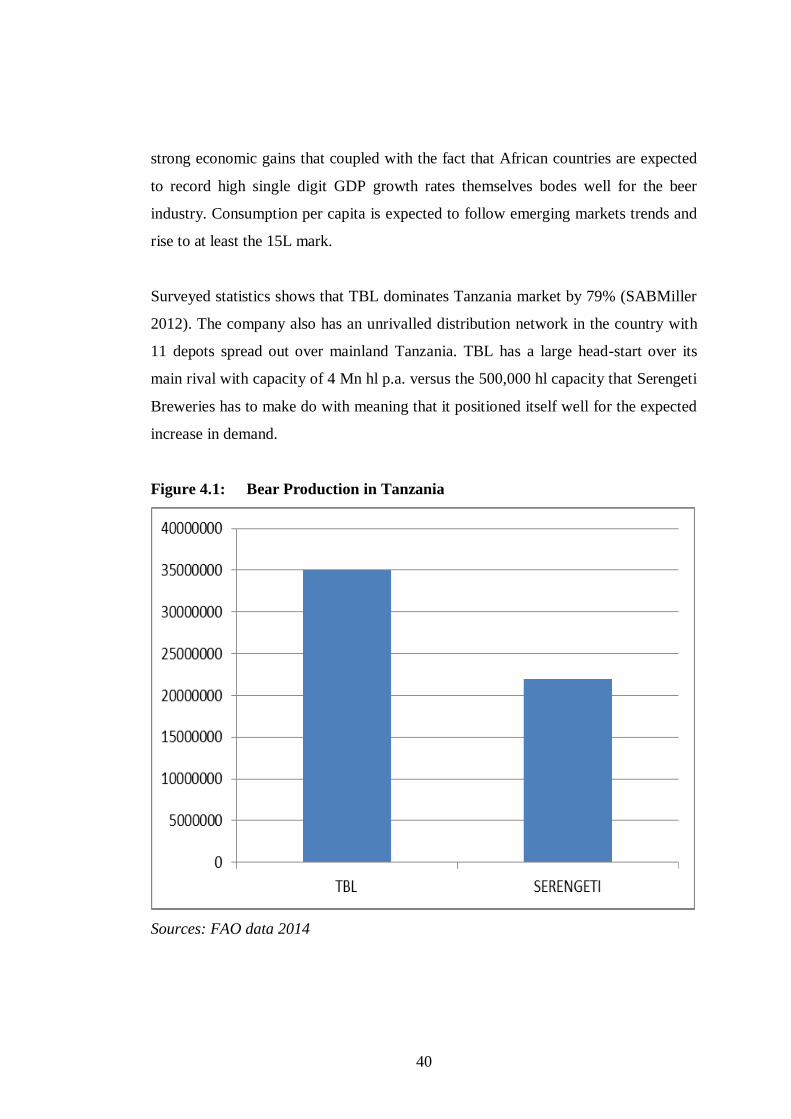

Figure 4.1: Bear Production in Tanzania ........................................................ 40

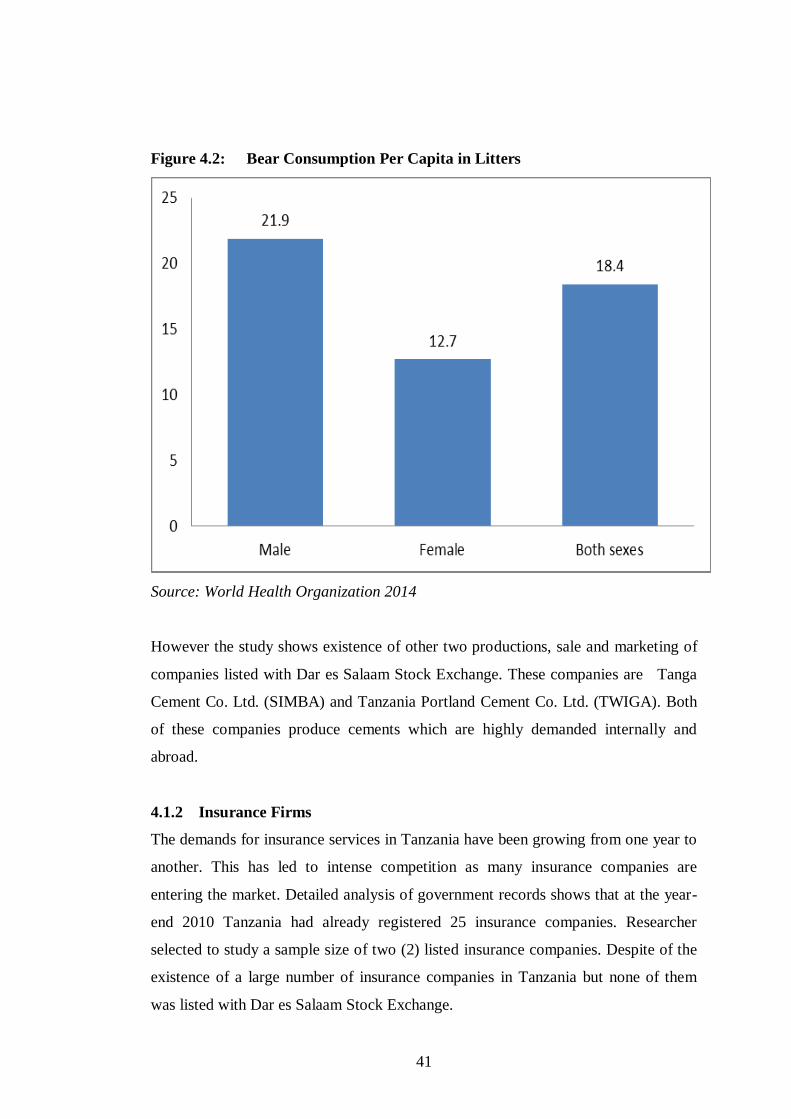

Figure 4.2: Bear Consumption Per Capita in Litters ....................................... 41

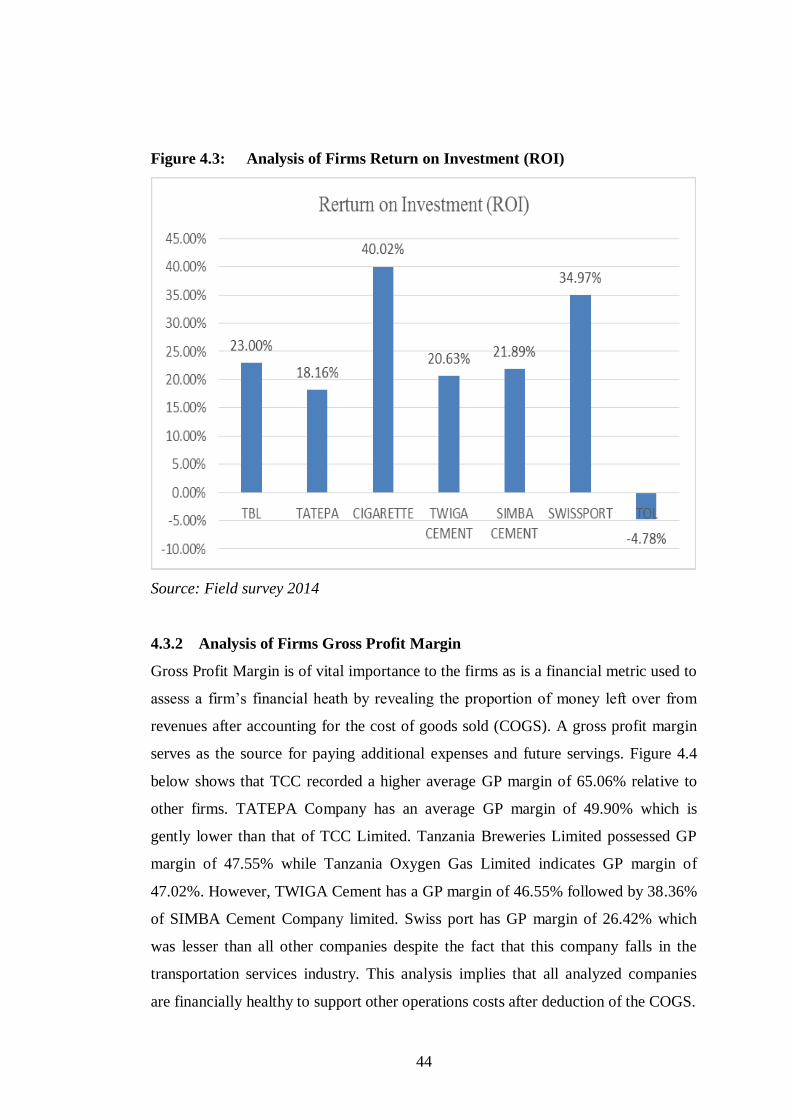

Figure 4.3: Analysis of Firms Return on Investment (ROI) ............................ 44

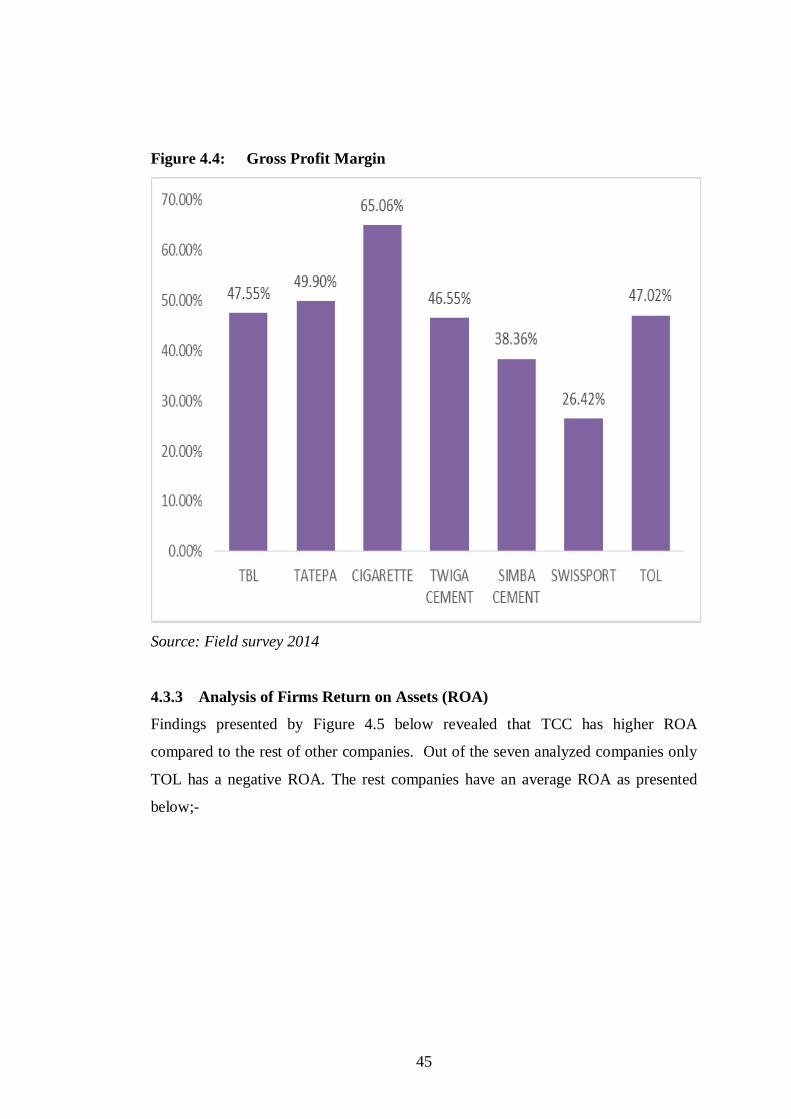

Figure 4.4: Gross Profit Margin ..................................................................... 45

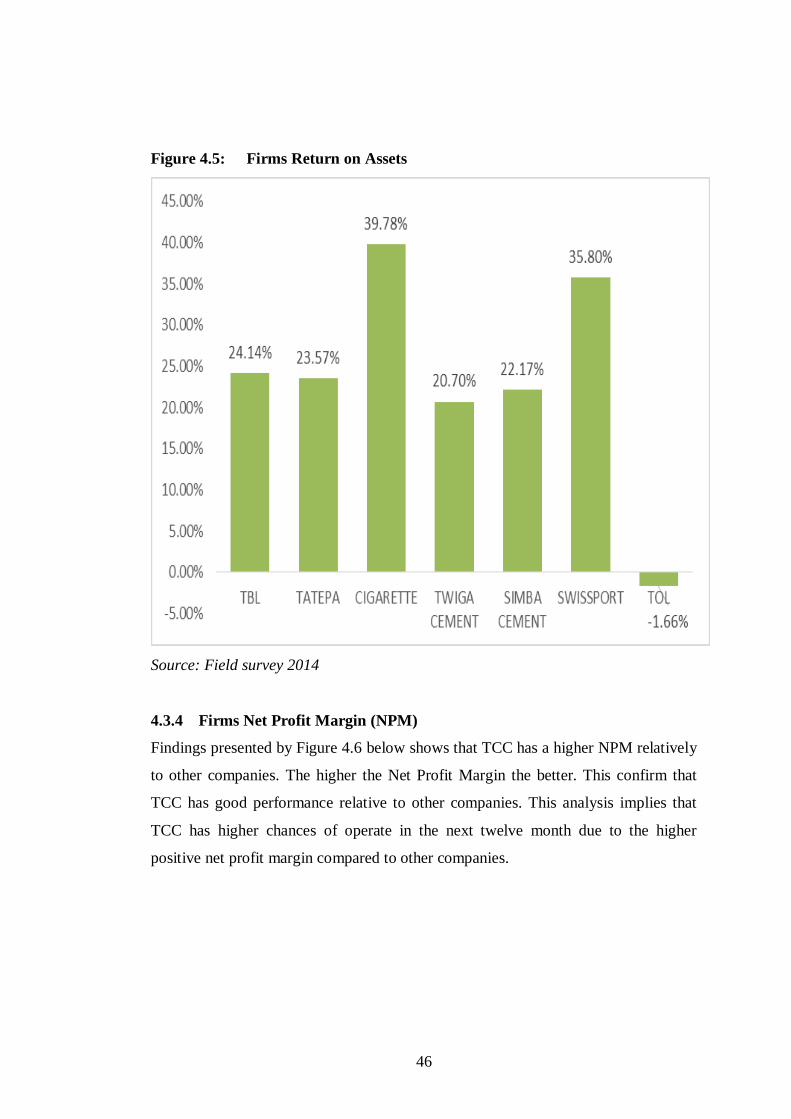

Figure 4.5: Firms Return on Assets ................................................................ 46

Figure 4.6: Firms Net Profit Margin (NPM) ................................................... 47

1

CHAPTER ONE

INTRODUCTION AND PROBLEM SETTING

1.0 Introduction

This chapter is classified into eight sections. The first section airs the background to

the study. The second section focuses the problem statement. The third section

focuses on the study objectives. The fourth section exposes research questions. The

fifth section exposes the scope. The sixth section focuses on the significance of the

study. The seventh section exposes limitations of the study and the final section

exposes organization of the rest of this thesis.

1.1 Background Information to the Study

Capital is one of the most important trade factor and largest instrument for attracting

the profit. Each firm should have capital in order to access profit from its trade.

Importance of trade unit can be understood by their capital. Subject of capital, also

forms the fundamental discussion in the financial management and can be claimed

that all trade activities need to have capital. Capital refers to all financial resources

that trade unit consumes it and in this connection, financial management determines

the framework of the relationship between capital and firm. Generally, in all

organizations particularly in small size, a great part of organization capital is working

capital. Working capital includes all assets which companies use it in daily activities.

Working capital is an indicator for measuring the liquidity, which is defined as

adequacy of cash for doing firm’s obligations.

Firm with proper situation of liquidity, has enough cash for the payment of bills. On

the contrary, companies with improper situation cannot pay their bills on the maturity

date (Pike and Bill, 2006). Thus, working capital management is very important and

should be done on the basis of supply chain management. Working capital

management refers to determination of volume and combination of resources and

consumptions of working capital so that leads to increase in shareholder's wealth

(Neveu, 2001). Working capital management indicates policies and is adopting about

2

working capital in order to change types of current assets and financial resources.

Correct controlling the working capital management can affect importantly on the

firm’s profitability.

1.2 Problem Statement

One of the main purposes of any firm is maximize the profit. But, maintaining

liquidity of the firm also is an important objective. The problem is that at the cost of

liquidity can bring serious problems to firm. Thus, strategy of firm must be a balance

between these two objectives of the firms. Because the importance of profit and

liquidity are the same so, one objective should not be at the cost of the other. If firm

ignores about profit, firm cannot survive for a longer period. Conversely, if firm does

not care about liquidity, firm may face the problem of insolvency and bankruptcy

(Rahman and Nasr, 2007). Therefore, when a trade unit operates, have to maintain an

optimal balance between liquidity and profitability and preserve always it. Liquidity

as a precondition warrants trade unit ability to trade obligations and in fact, indicates

that the firm operates continuously. Liquidity and profitability are two important

subjects for scientists and financial executives. In this connection, it is said that Non-

profitable firm, called as a patient case in the economy. However, firm with lack of

liquidity has less life expectancy.

One of the major determinant of firm’s market valuation is their profitability which

it’s changes affect the market valuation and ultimately has impact on shareholder’s

wealth. Firms’ working capital management affects directly the profitability of firms.

Thus, it can be said that firms’ working capital management is one of the

determinants of firms’ market valuation, shareholders’ wealth which its changes has

non-denial impacts on the changes of shareholders’ wealth. Therefore, working

capital management is important due to its impact on firm’s profitability and risk as

well as its value. In fact, working capital management, to maintain on optimal

balance between trade activities cycle and liquidity circulation of firm for the

purpose of profitability and increase in firm’s value.

3

Therefore, the lack of understanding about the impact of working capital

requirements on profitability, the lack of clarity about its determinants, and the lack

of management’s ability to plan and control its components may lead to insolvency

and bankruptcy, so that a large number of business failures may come from the

inability of financial manager to plan and control current assets and current liabilities

of their respective firms (Gill, 2011). If impact of working capital requirement on

profitability, clarity about its determinants and proper management plans and

controls of its components were well known by firm’s stakeholder’s insolvency and

bankruptcy will cease. Existence of mentioned matters is the major reason for

undertaking this study. The study was aimed at determining the relationship between

working capital management and profitability for listed companies at Dar es Salaam

Stock Exchange.

1.3 Objectives of the Study

1.3.1 General Objectives

The study main objective was: Determination of relationship between working

capital management and profitability for listed companies in Dar es Salaam Stock

Exchange.

1.3.2 Specific objective

The study was specifically addressing the following objectives;-

(i.) Determination of relationship between working capital management and

return on assets for listed companies in Dar es Salaam Stock Exchange.

(ii.) Determination of relationship between working capital management and

return on equity.

(iii.) Determination of relationship between working capital management and cash

conversion cycle.

4

1.4 Research Questions

1.4.1 Broad Research Question

The general research question was: What is the relationship between working capital

management and profitability of listed companies in Dar es Salaam Stock Exchange?

1.4.2 Specific Research Questions

Specific research questions was the following;-

(i.) What is the relationship between working capital management and return on

assets for listed companies in Dar es Salaam Stock Exchange?

(ii.) What is the relationship between working capital management and return on

equity?

(iii.) What is the relationship between working capital management and cash

conversion cycle?

1.5 Scope of the Study

The study focus listed companies at Dar es Salaam Stock Exchange (DSE) in the

United Republic of Tanzania (URT). The main reason for this selection is the

accessibility to company’s annual reports. The data which was used for analysis

range from 2008 to 2013.

1.6 Significance and Necessity of the Study

Working capital management has been studied from 1995 to 2008 in other countries

by several researches including Soenen (2001), and Demirgunes (2008). General

results of these studies in different stock exchanges in America, Belgium, India,

Pakistan and Turkey are almost the same and indicate that there is significant

relationship between different variables of working capital management and

profitability. In respect of importance of working capital management and

inadequacy of researches on this subject in our century we will examine working

capital management in Dar es Salaam stock Exchange based on previous studies

which done in other countries, and also models or variables which were used in these

studies.

5

Working capital management is one of the parts which play vital role in structural

management of organization. So that, sometimes working capital management and

liquidity are resembled as a circulating blood in a trade unit. Management of working

capital is also known as a heart which pumps the blood to vessels of organization

(Kesseven, 2006). Examination of working capital management is particularly

important due to following reasons:

(i.) The study contributes to the existing body of literature on the relationship

between working capital management and company profitability based on

Tanzanian firms.

(ii.) The study is of useful to economists, financial analyst and firm’s

management to orient the efforts accordingly as the empirical evidence show

that deficiency of working capital is the main reason for their bankruptcy.

(iii.) Government has a need to study working capital management and company’s

profitability of an individual manufacturing companies or industry as a whole

for various reasons. Taxes, revenues, financial assistance, sanctioning,

subsidy, to a business organization or industry as well as price fixing policies,

frame outlines the key role of study for the Government lies in planning,

decision making and control process.

(iv.) The existence of inflationary situations and devaluation of money purchasing

power in Tanzania economy stimulated managers of trade units would rather

other types of properties than cash money. It caused managers face money

difficulties for the payment of their current debts.

1.7 Limitation of the Study

The research study was conducted based on secondary data of which some of them

was accessed from companies listed at Dar es Salaam Stock Exchange. The data

might be subjective due to unintended errors. But any typing and calculation errors

remain the weakness of the study or researcher should not be transmitted to the

management or owners of the analyzed companies.

Time and financial resources was a problem in whole process of conducting research

study since researcher is an employee. To overcome the funding challenge research

6

study was conducted in Dar es Salaam Tanzania so as to minimize cost and save

time.

1.8 Organization of the Dissertation

This dissertation is classified into five chapters. The first chapter discusses the

background information of the study, the statement of the problem, research

questions and objectives, scope of the study, significance and limitation of the study.

Chapter two focuses on the literature review and conceptual framework. The chapter

also includes definitions and meaning of variables and various concepts as used in

this study.

Chapter three presents the research methodology of the data and instruments for data

collections, ethical considerations and techniques employed in analyzing data in

order to attain objectives of the study.

Chapter four presents dissertation findings, analysis and discussion. Chapter five of

the dissertation presents summary of the main findings, recommendations and

conclusions. In this chapter recommendations for the prospects for further research

that may be of worth are put forward.

7

CHAPTER TWO

LITERATURE REVIEW

2.0 Introduction

This chapter brings out the literature review issues that have been explored and

studied on the two variables. The first variable is the working capital management

and the second variable is the profitability. The chapter also discusses the

relationship between the two variables.

2.1 Definitions of Key Terms and Meaning of Concepts

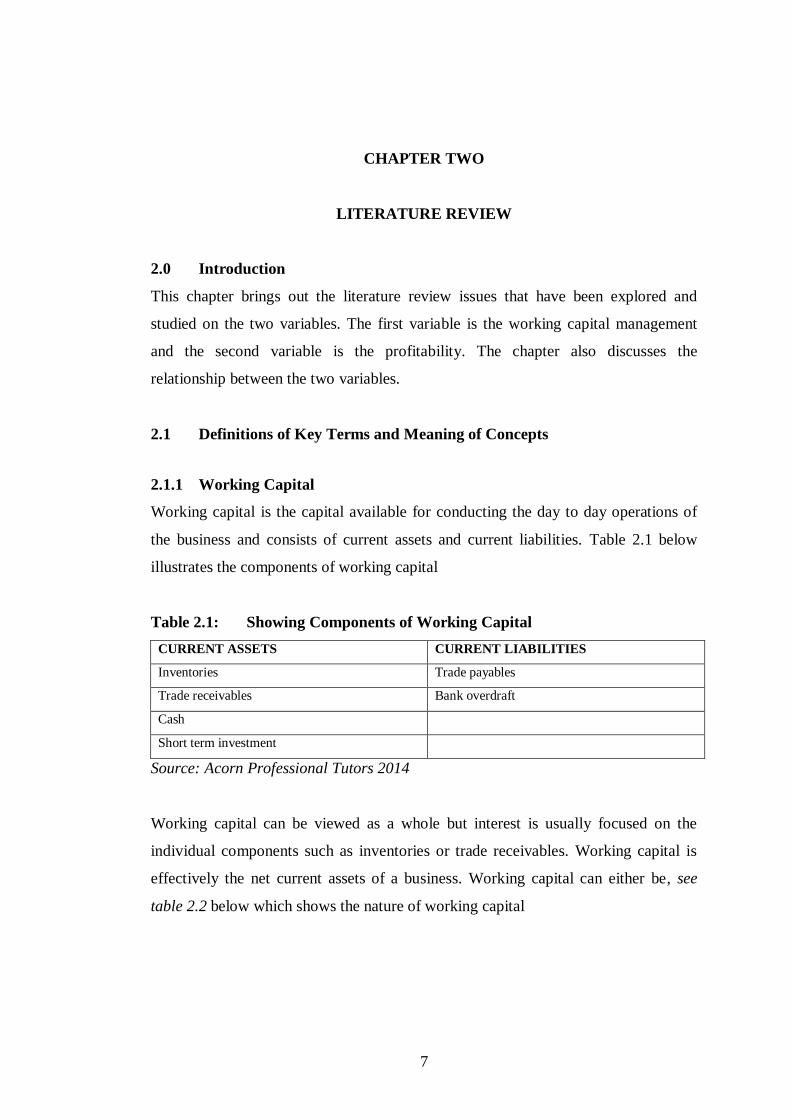

2.1.1 Working Capital

Working capital is the capital available for conducting the day to day operations of

the business and consists of current assets and current liabilities. Table 2.1 below

illustrates the components of working capital

Table 2.1: Showing Components of Working Capital

CURRENT ASSETS CURRENT LIABILITIES

Inventories Trade payables

Trade receivables Bank overdraft

Cash

Short term investment

Source: Acorn Professional Tutors 2014

Working capital can be viewed as a whole but interest is usually focused on the

individual components such as inventories or trade receivables. Working capital is

effectively the net current assets of a business. Working capital can either be, see

table 2.2 below which shows the nature of working capital

8

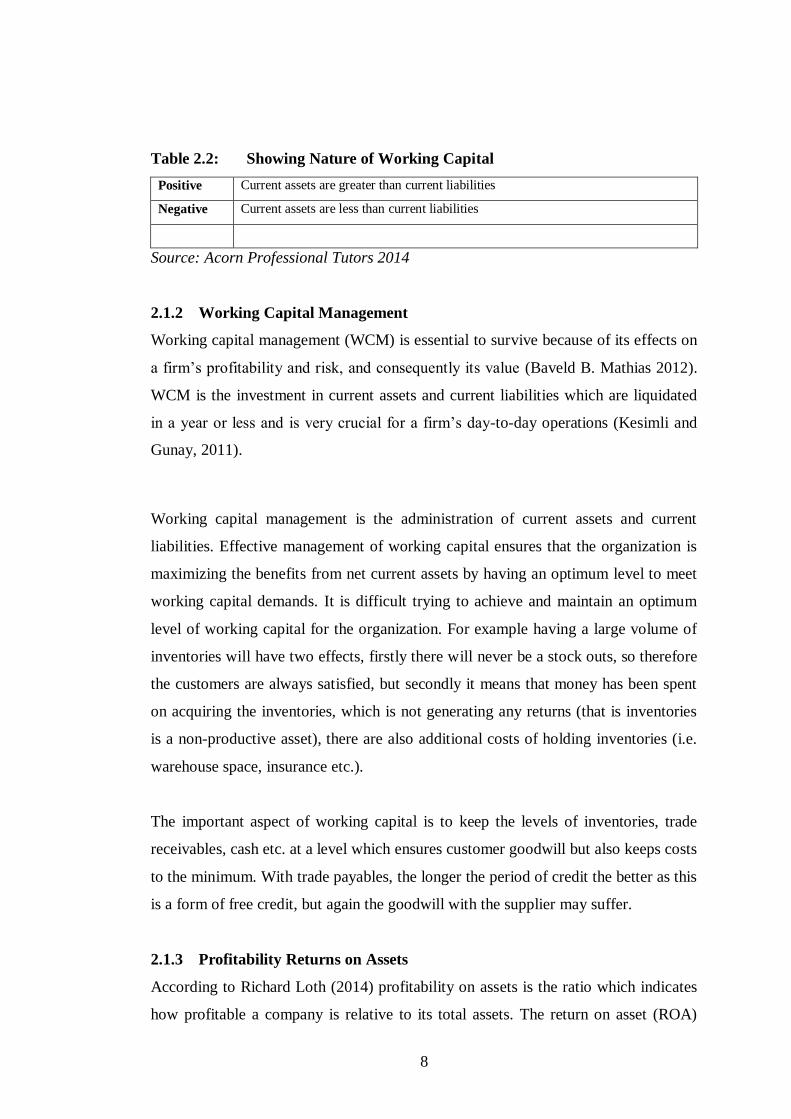

Table 2.2: Showing Nature of Working Capital

Positive Current assets are greater than current liabilities

Negative Current assets are less than current liabilities

Source: Acorn Professional Tutors 2014

2.1.2 Working Capital Management

Working capital management (WCM) is essential to survive because of its effects on

a firm’s profitability and risk, and consequently its value (Baveld B. Mathias 2012).

WCM is the investment in current assets and current liabilities which are liquidated

in a year or less and is very crucial for a firm’s day-to-day operations (Kesimli and

Gunay, 2011).

Working capital management is the administration of current assets and current

liabilities. Effective management of working capital ensures that the organization is

maximizing the benefits from net current assets by having an optimum level to meet

working capital demands. It is difficult trying to achieve and maintain an optimum

level of working capital for the organization. For example having a large volume of

inventories will have two effects, firstly there will never be a stock outs, so therefore

the customers are always satisfied, but secondly it means that money has been spent

on acquiring the inventories, which is not generating any returns (that is inventories

is a non-productive asset), there are also additional costs of holding inventories (i.e.

warehouse space, insurance etc.).

The important aspect of working capital is to keep the levels of inventories, trade

receivables, cash etc. at a level which ensures customer goodwill but also keeps costs

to the minimum. With trade payables, the longer the period of credit the better as this

is a form of free credit, but again the goodwill with the supplier may suffer.

2.1.3 Profitability Returns on Assets

According to Richard Loth (2014) profitability on assets is the ratio which indicates

how profitable a company is relative to its total assets. The return on asset (ROA)

9

ratio illustrates how well management is employing the company's total assets to

make a profit. The higher the return, the more efficient management is in utilizing its

asset base. The ROA ratio is calculated by comparing net income to average total

assets.

2.1.4 Return on Equity

Return on equity (ROE) is defined as the amount of net income returned as a

percentage of shareholders equity. It reveals how much profit a company earned in

comparison to the total amount of shareholder equity found on the balance sheet.

ROE is one of the most important financial ratios and profitability metrics. It is often

said to be the ultimate ratio or the ‘mother of all ratios’ that can be obtained from a

company’s financial statement. It measures how profitable a company is for the

owner of the investment, and how profitably a company employs its equity.

2.1.5 Meaning of Cash Conversion Cycle

Besley and Brigham (2005) describe cash conversion cycle as “the length of time

from the payment for the purchase of raw materials to manufacture a product until

the collection of account receivable associated with the sale of the product.” The

CCC length in days can be simply calculated as follows:

CCC days = inventory turnover days + debtor’s turnover days – payables

turnover days

2.1.6 Effects of Working Capital Management on a Firm’s Profitability

The main body of the literature of working capital focusses on studying the relation

between WCM and firm’s profitability. These studies evaluate WCM, by trying to

determine the effect of a firm’s working capital management on its profitability.

They argue that a WCM, which resulted in the highest profitability, must be the best

way of managing working capital that can be implemented. All these studies have

used regression analyses using different independent variables for profitability. The

main used independent variable operationalizing WCM is the Cash Conversion

Cycle (CCC). The CCC basically shows how long a firm takes to convert resource

10

inputs into cash flows (Quayyum, 2012). The CCC will be discussed in-depth in the

next subsection of this chapter. There are also several studies that have done research

on accounts receivables, accounts payables and inventories individually. Although

many studies have been carried out but all found a negative relation between WCM,

using the CCC, and firm profitability. This means that having a WCM policy which

results in a low as possible accounts receivables and inventories and the highest

amount of accounts payables leads to the highest profitability.

Contradicting evidence is found by Gill et al. (2010), whom did research in the USA

and found a positive relation between CCC and a firm’s profitability. But they did

find a highly significant negative relation between accounts receivables and a firm’s

profitability. They suggest that firm can enhance their profitability by keeping their

working capital to a minimum. This is because they argue that less profitable firms

will pursue a decrease of their accounts receivables in an attempt to reduce their cash

gap in the CCC (Gill et al., 2010).

Other studies have mainly focused on emerging market. These studies are Raheman

and Nasr (2007), Zariyawati et al. (2009), Falope and Ajilore (2009), Dong and Su

(2010), Mathuva (2010) and Quayyum (2012) whom did research in respectively

Pakistan, Malaysia, Nigeria, Vietnam, Kenya and Bangladesh. All these studies have

found a significant negative relation between the cash conversion cycle and a firm’s

profitability. This means that managers can create value for their firms, by keeping

their working capital to a reasonable minimum.

Contradicting evidence is found in India by Sharma and Kumar (2011). They found

evidence of a positive relation, which means that loosening the three parts of a firm

working capital management leads to higher profit. They argue that this is caused by

the fact that India is an emerging market and reputations of creditworthiness of firms

are not fully developed and therefore many companies loosen their working capital

management. Another reason they state is that only profitable firms can loosen their

working capital and therefore it’s because these firms are profitable, that they loosen

their working capital management and not the other way around.

11

Contradicting evidence is found on the effect of accounts payables on the

profitability of a firm. According to the cash conversion cycle, the number of days

accounts payables needs to be as large as possible. But researchers such as Deloof

(2003), Sharma and Kumar (2011), Lazaridis (2006), Banos-Caballero (2010) and

Karaduman (2011) have all found a negative relations between account payables and

profitability. The first reason for this could be that more profitable firms pay earlier

than less profitable firms, which in turn would affect the profitability and not the

other way round. An alternative reason is given by Deloof (2003); by arguing that if

a firm wait too long to pay their bills they have to pay without a discount. By

speeding up these payments a firm could receive this discount and which will

increase the profitability.

As mentioned before, authors have also studied the three parts of the CCC

individually. These parts are the number of day’s accounts receivables, inventories

and accounts payables. Almost all authors have found a negative effect of the three

parts on firm’s profitability. Sharma and Kumar (2011) argued that the positive

relation they found between accounts receivables and profitability is caused by the

fact that Indian firms have to grant more trade credit to sustain their competitiveness

with their foreign competitors, which have superior product and services.

Mathuva (2010) found contradicting evidence with the management of inventories in

Kenya. He argued that companies increase their inventory levels to reduce the cost of

possible production stoppages and the possibility of no access to raw materials and

other products. He further stated the findings of Blinder and Maccini (1991), which

indicate that higher inventory levels reduces the cost of supplying products and also

protects against price fluctuations caused by changing macroeconomic factors.

Also contradicting evidence is found by Mathuva (2010) with the management of

account payables. He found a positive effect of the number days accounts payables

on a firm’s profitability in Kenya. He explained this positive relation with two

reasons, first he argued that more profitable firms wait longer to pay their bills.

These firms use these accounts payables as a short-term source of funds. The second

12

argument why firms increase their accounts payables is that these firms are able to

increase their working capital levels and thus increasing their profitability. This is in

line with theory of a negative effect of the Cash Conversion Cycle (CCC) on the

profitability of a firm. This is caused by the fact that the number of days accounts

payables needs to be add in the measurement of the CCC. Thus a higher amount of a

number of day’s accounts payables leads to a higher profitability with a negative

relation between the CCC and a firm’s profitability.

2.1.7 Determinants of Trade Credit

The other main body of the literature of working capital focusses on trade credit.

Trade credit can either be given by a supplier in the form of accounts receivables, or

can be received by a customer in the form of accounts payables. The authors of this

body of literature on working capital are studying why firms decide to receive or to

grant trade credit. The literature offers various theories to explain this decision.

These are based on the advantages of either the supplier or customer, from the

operational, commercial and financial perspective (Garcia-Teruel and Martinez-

Solano, 2010). The motives for each perspective are elaborated in the next sub-

sections. Also some motives outside these perspectives are discussed.

The amount of trade credit extended by a supplier to the firm will appear as the

accounts payables. The amount of trade credit extended by the firm to its customer

will appear as the accounts receivables.

2.1.7.1 Financial Motives

Trade Credit extension to assess the Buyer’s Creditworthiness. The imperfect

information leads to the uncertainty about the buyer default risk. By extending a

trade credit to this buyer a seller can evaluate the creditworthiness by looking at the

buyer’s payment practices. These practices can identify which buyer may be in

financial difficulties. The common credit term given to these buyers is the two part

trade credit, where the buyer gets a discount if he pays within ten days. If this

discount is not taken, the buyer has to pay after the tenth day, with a very high

effective interest rate till the bill is paid. Failure to pay within the discount period

13

could signal financial distress and it would than merit to monitor the buyer more

closely.

The other motive which is in line with the above motive is the advantage a non

financial firm has when assessing creditworthiness compared to financial institutions.

This advantage enables certain non-financial firms with high creditworthiness to

financially aid their customers which have difficulties accessing capital market,

because of their low credit rating (Garcia-Teruel and Martínez-Solano, 2010). A

supplier has a greater ability for obtaining detailed information about its customers

creditworthiness, due to the continues contact with the customer. Also when a

customer is likely to default on a payment, the supplier can easily cut off the supply

of merchandise that is paid regularly (Garcia-Teruel and Martínez-Solano, 2010).

2.1.7.2 Operational Motives

Trade Credit and Variable Demand. An operational motive of using trade credit is

that it enables to operate in more efficient way. It also leads to cost improvements

through the separation of delivery of goods and the payment (Garcia-Teruel and

Martínez-Solano, 2010). This is because the separation reduces the uncertainty about

the level of cash that is needed to finish payment. Emery (1987) argued that this

provides more flexibility in the conduct of operations, because fluctuations can be

coped with the use of trade credit. He also argued that a firm can reward a customer

who acquires merchandise in a low demand period. According to Garcia-Teruel and

Martínez-Solano (2010) this relaxing of trade credit terms enables the supplier to

reduce the inventory costs of the excessive inventories that would elsewise

accumulate if they kept production constant. This is supported by the finding of Long

et al. (1993) where firms with variable demand extend more credit than firms with

stable demand.

2.1.7.3 Commercial Motives

Trade credit as price discrimination. Trade credit can be used as a form of price

discrimination by firms, according to weather delays and discount are given to its

customers (Brennan et al., 1998). There are two ways of implementing this price

14

discrimination to firms. The first is allowing a delay in payment and second is by

giving a discount in payment, which can be seen as a price reduction. This theory of

price discrimination is empirically tested by Petersen and Rajan (1997). They found

that firms with a high profit margin benefits when they raise their sales. Through

granting more trade credit, a firm is able to raise their sales. This is beneficial for

firms with high profit margins, because the profits of this raising of sales surpass the

costs of granting trade credit (Garcia-Teruel and Martínez-Solano, 2010).

Offering Delayed Payment to Guarantee Product Quality. Another commercial

motive of using trade credit is for the assessment of product quality. This is first

suggested by Smith in 1987, where he argued that suppliers can permit customers to

assess the quality of the products before payment, through granting trade credit

terms. When the quality of a product is difficult to assess, a supplier can extend the

agreed terms even longer. Lee and Stowe (1993) argued that trade credit is best way

to guarantee the quality of a product. Garcia-Teruel and Martínez-Solano (2010)

argued that therefore smaller and younger firms will give more trade credit, since

their customers don’t have any reasons to trust that the quality of their products is

sufficient. This argument is supported by the finding of Long et al. (1993). They

found that smaller firms, and firms who lack product quality reputation, extend more

trade credit relative to sales. More recently Pike et al. (2005) found that in the US,

UK and Australia trade credit can be used to reduce the information asymmetries

between a buyer and a seller, where product quality is a main part of.

2.1.7.4 Other Motives of Extending Trade Credit

Specific Investment in the Buyer-Seller Relationship. Smith (1987) argued that if a

supplier has a specialized and non-salvageable investment in a buyer, that this

investment could be an important determinant for extending trade credit to this

buyer. This credit term will give the seller the possibility to monitor the buyer more

closely and could determine the risk of this investment. This is based on the fact that

an investment can only be earned back if the buyer stays in business. In other words

the seller can protect the investment by using credit to learn about the financial

position of the buyer and act early if this buyer is in financial distress.

15

Scale Economies in Extending Credit. A firm’s size affects the extending of trade

credit to its customers. The larger the seller is, the larger its customer base will be.

This higher amount of customers increases the probability of a default on payment

among these customers. For this reason larger firms has to monitor its customers

more closely and an important tool for this monitoring is the extending of trade

credit.

2.1.7.5 Studies on Determinants of Trade Credit

Huyghebaert (2006) studied the trade credit use of Business start-ups. He found that

their high failure risk, financial constraints, and their lack of relation with banks and

suppliers significantly influence their trade credit use. These factors significantly

increase the use of trade credit by these start-up firms. He also found that suppliers

have an advantage in financing high-risk customers, but only in certain

circumstances. The first situation which brings an advantage is when raw materials

are often replaced and thus leads to a high frequency trade credit use. Second is when

these start-ups have high raw materials levels and third when these start-ups operate

in an industry with a low concentration ratio.

Garcia-Teruel and Martinez-Solano (2010) studied the trade credit use of Small and

Medium Enterprises (SMEs) in Europe. They found that the trade credit offered by

suppliers is especially important for SMEs, because they have more difficulties

obtaining finance through credit institutions. They also found that firms with greater

capacity of obtaining relatively cheap financial resources grant more trade credit to

their customers. These results support the theory that trade credit can be explained by

the advantages a supplying firm has over financial institutions. However, they didn’t

find evidence that support the quality assessment motive of using trade credit. They

did find support for the price discrimination motives, because the data indicate that

firms with higher profit margins grant more trade credit. Further support of this

argument is given by the fact that firms who faces a reduction in their sales; react by

increasing the trade credit to balance the decrease in sales. Evidence is also found

that when firms are able to access other cheaper financial resources, like bank loans,

they use less trade credit (substitution effect).

16

Petersen and Rajan (1997) did research on the theories and motives of the use or

granting of trade credit. They focused on smaller firms who have a limited access to

the capital market. They found that firms grant more trade credit to firms with higher

credit worthiness, but these firms use less trade credit when they have access to the

capital market. Also evidence is found which support the theory that supplying firms

have advantages over financial institutions concerning short-term financing. They

argue that this is mainly due to the fact that these suppliers have more current

information compared to the information of financial institutions. Also evidence is

found for the motives of these suppliers for extending trade credit when they have a

large interest in the survival of the customer and suppliers are able to liquidate the

goods without much loss. As mentioned before, they also found evidence supporting

the theory of price discrimination with firm with high profit margins.

2.1.8 Determinants of Inventories

As mentioned earlier in this study trade credit can either be accounts payables or

accounts receivables, but what of the other part of WCM, inventory management.

There are several motives for lower or higher levels of inventories and highly

depends on what business a company is in. The most widely and simple motive of

managing inventories is the cost motive, which is often based on the Transaction

Cost Economics (TCE) theory (Emery and Marques, 2011). To be competitive,

companies have to decrease their costs and this can be accomplished by keeping the

costs of stocking inventory to a reasonable minimum (Gaur et al., 2005). This

practice is also highly valued by stock market analysts (Sack, 2000). There are also

other motives of managing inventories which will be discussed in the following part

and empirical evidence will be given which supports these different motives.

Higher inventory levels and variable demand. The main motive of keeping high

levels of inventories, which are raw materials, work-in-progress, and finished goods,

is to keep them as a buffer against demand fluctuations, production stoppages and

other unexpected problems (Cuthbertson and Gasparro, 1993; Lieberman et al,

2009). This motive is supported by evidence found by Cachon and Olivares (2010),

who found that among automotive companies in the US, inventories are used as

17

safety stocks to better withstand demand fluctuations. Kahn (1987) also found

evidence that companies increase their amount of stocks to decrease the probability

of stock outs when demand is high and thus inventory levels are determined by the

fluctuations of sales of a company.

2.1.8.1 Just-In-Time Inventory System

Managerial decisions have a huge impact on the levels of inventories. During the

seventies and eighties of the 20th century Japanese manufacturing companies

increased their activities significantly in the U.S. markets. They also brought in new

ideas of managing companies and since they increased their market shares

substantially, it was apparent that some of these new ideas of managing were very

successful. One of these ideas affected the way of managing inventories, which was

called the Just-In-Time (JIT) inventory management system. The basic idea of this

system was that companies should deliver products to their customer just-in-time. By

doing this, companies won’t have to have large amounts of stocks to be able to

deliver goods. This saves a lot of costs concerning inventory stocking. The question

of whether companies in the U.S. did decrease their amount of stocks was studied by

Chen et al. (2005). They found that a large amount of companies did significantly

reduce their inventory levels. This reduction was mostly implemented on the levels

of work-in-progress inventory. This decrease in inventory levels is also found by

Rajagopalan and Malhorta (2001) who studied a number of industries in the

manufacturing sector in the U.S.

2.1.8.2 Higher Inventory Levels and Production Costs

Another reason for companies to increase their finished goods inventory levels is to

be able to produce in periods in which production costs are relatively low (Blinder

and Maccini, 1990; Eichenbaum, 1984; and Eichenbaum, 1989). A comparable

motive of increasing inventory levels is when companies can produce cheaper in

batches, which can result in relatively high inventory levels.

18

2.1.8.3 Other Determinants of Inventory Management

Lieberman et al. (2009) studied the determinants of inventory policies of automotive

companies in the United States. They found that both technological and managerial

factors have a significant influence on the determining of the levels of inventories.

Technological factors, like longer setup and processing times increases the level of

inventories. While the average price per piece of inventory decreases the inventory

levels. They also found that managerial factors, like more employee training and

problem solving training have a reducing effect on the inventory levels. Lieberman et

al. (2009) also found that when companies have a greater and more frequent

communications with their supplier, the inventory levels will be lower. This finding

is supported by Milgrom and Roberts (1988) that view inventory and communication

with a supplier as substitutes. Also macro-economic conditions have a profound

impact on the levels of the different types of inventories. Chen et al. (2005) found

that when interest rates are increasing, the levels of work-in-progress are decreased.

Also evidence is found that inflation has a positive effect on the acquiring of raw

materials. This is caused by the fact that companies wanted to buy these materials

before the prices of these materials rise even more. They also found that when

managers assume better economic conditions in the future, they increase the levels of

finished goods (Chen et al., 2005).

2.2 Theoretical Framework

2.2.1 The Cash Conversion Cycle (CCC)

Working capital are the funds which are used to operate in the short term. If

receivables are postponed there can be delays in payments and these could be

suspended causing a situation of illiquidity for the firm.

In this context, CCC is an important tool of analysis that enables us to establish more

easily why and how the business needs more cash to operate and when and how it

will be in a position to refund the negotiated resources. The major ingredients of the

CCC turnover can be easily illustrated with the help of the following illustrated

figure 2.1:

19

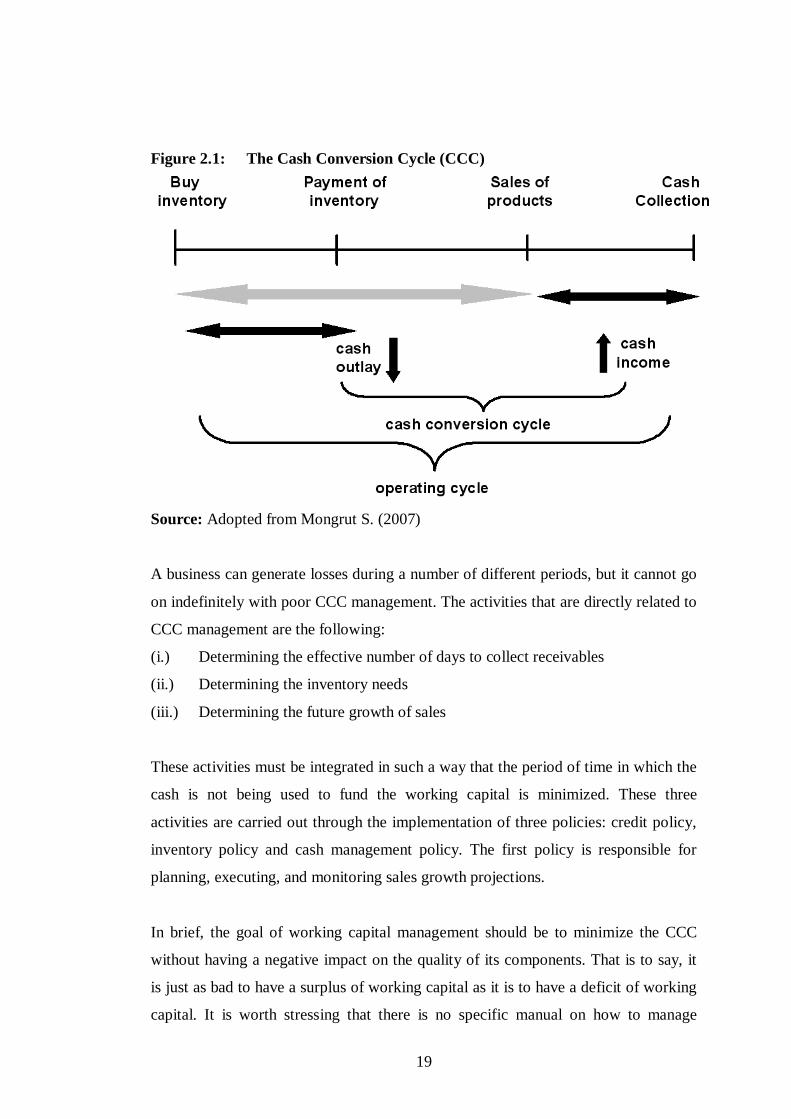

Figure 2.1: The Cash Conversion Cycle (CCC)

Source: Adopted from Mongrut S. (2007)

A business can generate losses during a number of different periods, but it cannot go

on indefinitely with poor CCC management. The activities that are directly related to

CCC management are the following:

(i.) Determining the effective number of days to collect receivables

(ii.) Determining the inventory needs

(iii.) Determining the future growth of sales

These activities must be integrated in such a way that the period of time in which the

cash is not being used to fund the working capital is minimized. These three

activities are carried out through the implementation of three policies: credit policy,

inventory policy and cash management policy. The first policy is responsible for

planning, executing, and monitoring sales growth projections.

In brief, the goal of working capital management should be to minimize the CCC

without having a negative impact on the quality of its components. That is to say, it

is just as bad to have a surplus of working capital as it is to have a deficit of working

capital. It is worth stressing that there is no specific manual on how to manage

20

working capital, since it depends to a very great extent on the specific circumstances

of each company.

2.2.2 Working Capital and Its Management

Working capital means the whole current assets owned by a firm. Net working

capital is the sum when short term liabilities are extracted from current assets. Return

of total assets of a firm as a result of an activity is closely related to level and

distribution of assets of the firm and efficiency in application of these assets. In lots

of firms current assets called working capital make up of a remarkable part of

community assets. But it is obvious that working capital is neglected in finance

literature compared to long term financing decisions. Studies on corporate finance

generally focus on main decisions like capital structure, dividend and capital

budgeting. However, the amount of assets group a significant part of total asset and

called working capital (money and quasi money, trade receivables, inventories and

short term liabilities) is a focus matter in all main books relating to corporate finance

where efficiency level of distribution and application of assets influence profitability

and risk level of the firm.

The main objective of a firm is to increase the market value. Working capital

management affects profitability of the firm, its risk, thus its value (Smith, 1980). In

other words, efficient management of working capital is an important component of

the general strategy aiming at increasing the market value (Howorth & Westhead,

2003; Deloof, 2003; Afza & Nazir, 2007). Since the flexibility of this group of assets

is very high in terms of adapting to changing conditions, and due to these

characteristics they can often be applied to realize the main objective of financial

management through policy changes. Success of a firm mainly depends on efficient

management capability of finance director to manage receivables, inventories and

liabilities (Filbeck & Krueger, 2005). Firms can strengthen their funding capabilities

or decrease the source cost reducing source amount they allocate to current assets.

The working capital meets the short-term financial requirements of a business

enterprise. It is a trading capital, not retained in the business in a particular form for

21

longer than a year. The money invested in it changes form and substance during the

normal course of business operations. The need for maintaining an adequate working

capital can hardly be questioned. Just as circulation of blood is very necessary in the

human body to maintain life, the flow of funds is very necessary to maintain

business. If it becomes weak, the business can hardly prosper and survive. Working

capital starvation is generally credited as a major cause if not the major cause of

small business failure in many developed and developing countries (Pike and bill,

2006). The success of a firm depends ultimately, on its ability to generate cash

receipts in excess of disbursements. Poor financial management exacerbates the cash

flow problems of many small business and in particular the lack of planning cash

requirements (Pike and bill, 2006).

Working capital is the total of the amounts invested in current assets of the company.

Generally, it is assumed that the current liabilities must be met by current assets.

Because, maturity date of current assets coincides with maturity date of current

liabilities (maximum maturity date is one year). Lack of coincidence between

maturity date of current assets and current liabilities lead to liquidity problems of the

firms. Of course, some of companies may try to secure a part of their current assets

through shareholders’ rights which is called fixed working capital. Current assets

including cash stock, short term investment, claims stock of raw materials and goods,

and also current liabilities means accounts and trade bills payable, pre receipts and

short term bank credits (Pike and bill, 2006). The working capital management from

financial managers’ point of view is a simple and clear concept ensuring the firm

ability to grasp differences between assets and short-term debts (Yaghob nejad,

2010).

While the performance levels of small businesses have traditionally been attributed

to general managerial factors such as manufacturing, marketing and operations,

working capital management may have a consequent impact on small business

survival and growth (Nikoomaram et al., 2004)). The management of working

capital is important to the financial health of businesses of all sizes. The amounts

invested in working capital are often high in proportion to the total assets employed

22

and so it is vital that these amounts are used in an efficient and effective way.

However, there is evidence that small businesses are not very good at managing their

working capital. Given that many small businesses suffer from undercapitalization,

the importance of exerting tight control over working capital investment is difficult

to overstate.

A firm can be very profitable, but if this is not translated into cash from operations

within the same operating cycle, the firm would need to borrow to support its

continued working capital needs. Thus, the twin objectives of profitability and

liquidity must be synchronized and one should not impinge on the other for long.

Investments in current assets are inevitable to ensure delivery of goods or services to

the ultimate customers and a proper management of same should give the desired

impact on either profitability or liquidity. If resources are blocked at the different

stage of the supply chain, this will prolong the cash operating cycle. Although this

might increase profitability (due to increase sales), it may also adversely affect the

profitability if the costs tied up in working capital exceed the benefits of holding

more inventory and/or granting more trade credit to customers.

Another component of working capital is accounts payable, but it is different in the

sense that it does not consume resources; instead it is often used as a short term

source of finance. Thus it helps firms to reduce its cash operating cycle, but it has an

implicit cost where discount is offered for early settlement of invoices.

Therefore, working capital management is one of the most important problems that

firms’ managers may face it. Working capital management plays an important role

for the firms’ maintenance and growth. Working capital management refers to

financing methods, investment and control of working capital. In other words,

working capital management is practical part of financing which includes all current

accounts of firm. Working capital management relates to adequacy of current assets

and risk resulting from current liabilities (Pike and Bill 2006). Working capital

management is of particular important due to its impact on risk, returns and

shareholders’ wealth. Companies by using various strategies related to working

23

capital management can affect the amount of firm’s liquidity. These strategies

determine their risk level and returns (Nikoomaram et al., 2004). In other words,

firms by using efficient working capital management can facilitate access to

following objectives:

2.2.3 Enough Liquidity

Firms face difficulties if they have not enough cash for the payment of their invoices

on maturity date. Thus one of the most important objectives of working capital

management is access to enough liquidity in order to undertake daily activities and

prevention of disturbances in trade cycle operations.

2.2.4 Minimizing Risk

Firms must ensure that their short term obligations do not exceed their current assets.

Comparison of assets and liabilities among the current accounts is a responsibility

which aims to minimize risk of inability to the payment of invoices and other

obligations.

2.2.5 Maximizing Firm’s Value

Firms maintain working capital for the same reason that maintain other assets, means

help to maximizing share’s value of the firms and consequently firms’ value.

Investment of idle moneys, minimizing the stocks, fast receipt of receivable and

elimination of costly short term financing, all lead to increase in firms’ value.

2.2.6 Measures of Profitability

In this research study, cash conversion cycle, current ratio, current assets to total

assets, current liabilities to total assets and total liabilities to total assets are used to

measure profitability. Also, profitability will includes return on assets rate and return

on equity rate.

(i.) Cash conversion cycle (CCC): is calculated by (number of days inventories +

number of days accounts receivable) – number of days accounts payable

(ii.) Return on assets (ROA): is calculated by = Operating Profit

Total assets

24

(iii.) Return on equity (ROIC/ROE): is calculated by = Net Profit

Total equities

(iv.) Current ratio (CACLR): is calculated by = Current Assets

Current Liabilities

2.2.7 Measures of firms working capital

In this research study, current ratio, quick ratio or acid test, trade payables (turnover),

trade receivables days (turnover), inventory days and inventory turnover are used to

measure working capital of the firms selected. These variables are calculated as

detailed below;-

(i.) Current ratio (CA): is calculated by = Current Assets (Times)

Current Liabilities

(ii.) Quick ratio (QR): is calculated by = Current Assets less Inventories (Times)

Current Liabilities

(iii.) Trade payables (turnover): is calculated = Year end trade payables X365 days

Credit Purchases or (Cost of Sales)

(iv.) Trade receivables days (turnover):Calculated =Yr end receivables X 365 days

Credit sales (Turnover)

(v.) Inventory days: is calculated by = Average inventory X 365 days

Cost of sales

(vi.) Inventory Turnover: is calculated by = Cost of sales (Times)

Average inventory

2.3 Empirical Literature Review

In 2010 Izadima and Taki examined the effects of working capital management on

capability of profitability for listed companies on Tehran Stock Exchange for the

25

period of 2001-2008. In this study return on total assets is considered as a measure

for capability of profitability. The results indicate that there is a negative significant

relationship between cash conversion cycle and return on assets and also a lot of

investment in inventories and accounts receivable leads to declining of profitability.

YaghoobNejad, et al. (2010) examined the relationship between working capital

management and profitability. For this purpose of this study sample size selected was

86 active companies on Tehran stock exchange for the period of 2002-2007.

Researchers employed regression and Pearson correlation while analyzing data

collected. The results show that there is a negative relationship between variables of

working capital management and profitability. Also, the results indicate that increase

in number of day’s accounts receivable, number of day’s accounts payable, number

of day’s inventories and cash conversion cycle leads to decrease in profitability of

companies. Managers can increase the shareholder’s wealth by reducing number of

day’s accounts receivable, number of day’s accounts payable, number of day’s

inventories and cash conversion cycle.

Mohmmadi (2009) examined the impact of working capital management on

profitability for listed companies on Tehran Stock Exchange. The study analyses a

sample of 92 companies for the period of 1996 up to 2005. Research findings show

that there exist negative relationship between number of day’s accounts receivable,

number of day’s inventories, member of days accounts payable, cash conversion

cycle and profitability.

Lazaridis and Tryfonidis (2006) conducted a statistical analysis of 131 firms in

Athens for the period 2001 to 2004 and arrived at the conclusion that managers may

create benefits for the companies if they manage an adequate level of CCC and

maintain each one of its components at an optimal level. They also detected a

negative relationship between the company’s working capital and its profitability.

A study conducted by Padachi in 2006 with an objective of examining the effect of

accounts receivables days, inventories days, accounts payable days and cash

26

conversion cycle on return on total assets. He also analyses the tendency in working

capital requirements of firms, for a sample of 58 small manufacturing firms in

Mauritius for the period 1998 to 2003. Using pooled OLS and fixed effect regression

model, he established that lower profitability was related with higher investment in

receivables and inventories. The findings also reveal a rising tendency in the short-

term component of financing working capital.

Mongrut et al. (2007) determine the factors that affect working capital management

in Latin American companies. Using an unbalanced panel data analysis for

companies quoted in five Latin American capital markets it is shown that companies

in Argentina, Brazil, Chile and Mexico are holding cash excesses, which could

destroy firm value. Findings of the study show that the industry cash conversion

cycle, the company market power, its future sales and country risk have an influence

on the way Latin American companies manage their working capital with significant

differences among countries in the region.

Soenen (2002) examined the relationship between net trade cycle as an indicator of

waking capital and investment return in American companies. Chai-Square Test

results showed a negative relationship between net trade cycle time and properties

return. Future, the negative relation is different for different industries. An important

significant relationship for almost half of considered companies indicated that

negative relation depends on type of industry.

Soenen and Shin (1998) investigated the relation between measure of the cash

conversion cycle and corporate profitability for a large sample of listed American

firms for the 1975 up to 1994 periods. They found a strong negative relation. This

result indicates that managers can create value for their shareholders by reducing the

cash conversion cycle to a reasonable minimum. In addition to this, Shin and Soenen

(1998) intended to come up with the determinants of working capital and found that

its management is correlated in a positive way to firm size. They also established that

industry concentration does not affect working capital management and that a greater

27

compensation paid to the CEO of the firm definitely improves the company’s

management of working capital. These results suggest that WCM has an important

impact on the profitability of the firms.

Deloof (2003) investigated the relationship between working capital management

and profitability for a sample of 1009 Belgian Companies for the period of 1960-

1992. In this study have been used cash conversion cycle inventories and number of

day’s accounts receivable as indicators of trade credit and cash conversion cycle as

comprehensive indicator of working capital management. The results show that

manager can increase profitability of trade by reducing the number of accounts

receivable, inventories and also by reducing cash conversion cycle.

Samiloglu and Demirgunes (2008) examined the effect of working capital

management on profitability for a sample of Turkish companies, for the period of

1998-2007. Empirical findings show that accounts receivables period, inventory

period and leverage affect firm profitability negatively; while growth (in sales)

affects firm profitability positively.