Embed Size (px)

Citation preview

This document was prepared by Axon Consulting for the use of the client to whom it is addressed. No part of it may be copied or reused in any way without our prior written consent.

Assessment of the cost of providing wholesale roaming services and mobile voice termination in the EU/EEA countries – SMART 2017/0091

Presentation of the model’s results

28 May 2019

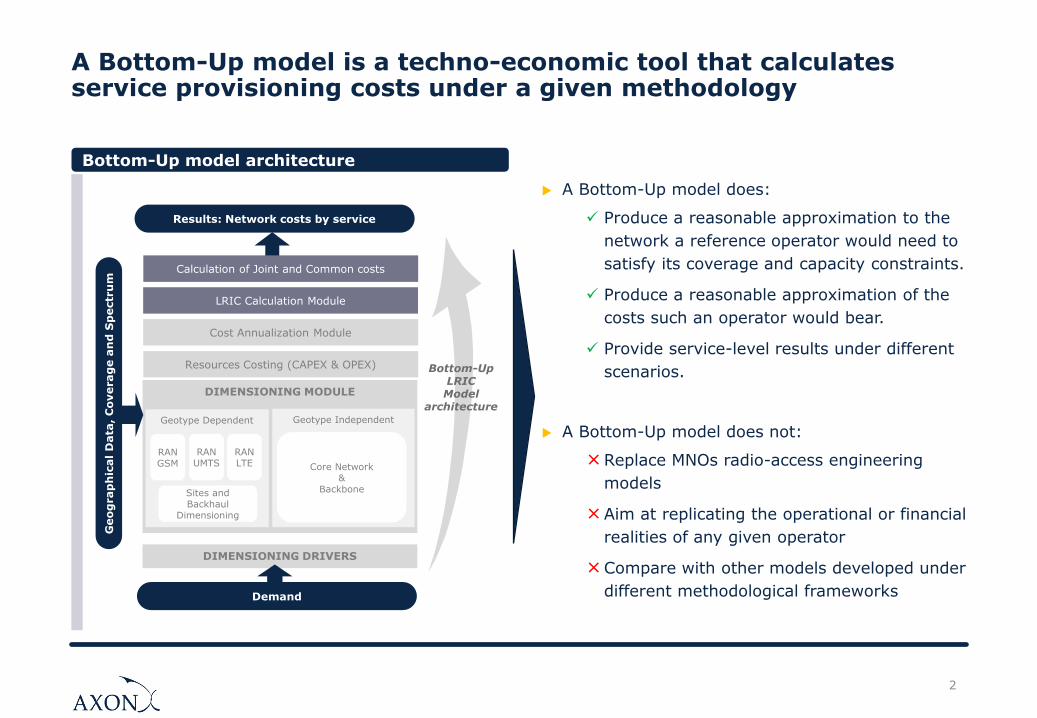

A Bottom-Up model is a techno-economic tool that calculates service provisioning costs under a given methodology

2

Bottom-Up model architecture

LRIC Calculation Module

Cost Annualization Module

Resources Costing (CAPEX & OPEX)

DIMENSIONING MODULE

Geotype Dependent Geotype Independent

RAN GSM

RAN UMTS

RAN LTE

Sites and Backhaul

Dimensioning

Core Network&

Backbone

DIMENSIONING DRIVERS

Results: Network costs by service

Bottom-Up LRICModel

architecture

Geo

grap

hic

al

Data

, C

overag

e a

nd

Sp

ectr

um

Demand

Calculation of Joint and Common costs

A Bottom-Up model does:

✓ Produce a reasonable approximation to the

network a reference operator would need to

satisfy its coverage and capacity constraints.

✓ Produce a reasonable approximation of the

costs such an operator would bear.

✓ Provide service-level results under different

scenarios.

A Bottom-Up model does not:

×Replace MNOs radio-access engineering

models

×Aim at replicating the operational or financial

realities of any given operator

×Compare with other models developed under

different methodological frameworks

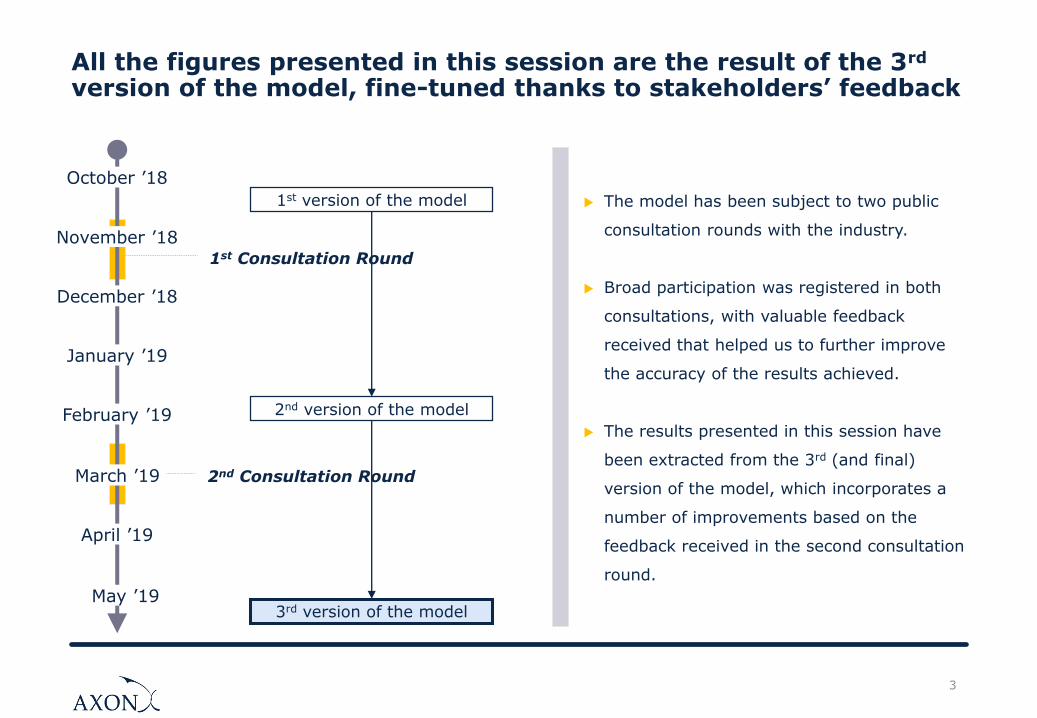

2nd Consultation Round

All the figures presented in this session are the result of the 3rd

version of the model, fine-tuned thanks to stakeholders’ feedback

3

October ’18

December ’18

November ’18

January ’19

February ’19

March ’19

1st Consultation Round

April ’19

May ’19

1st version of the model

2nd version of the model

3rd version of the model

The model has been subject to two public

consultation rounds with the industry.

Broad participation was registered in both

consultations, with valuable feedback

received that helped us to further improve

the accuracy of the results achieved.

The results presented in this session have

been extracted from the 3rd (and final)

version of the model, which incorporates a

number of improvements based on the

feedback received in the second consultation

round.

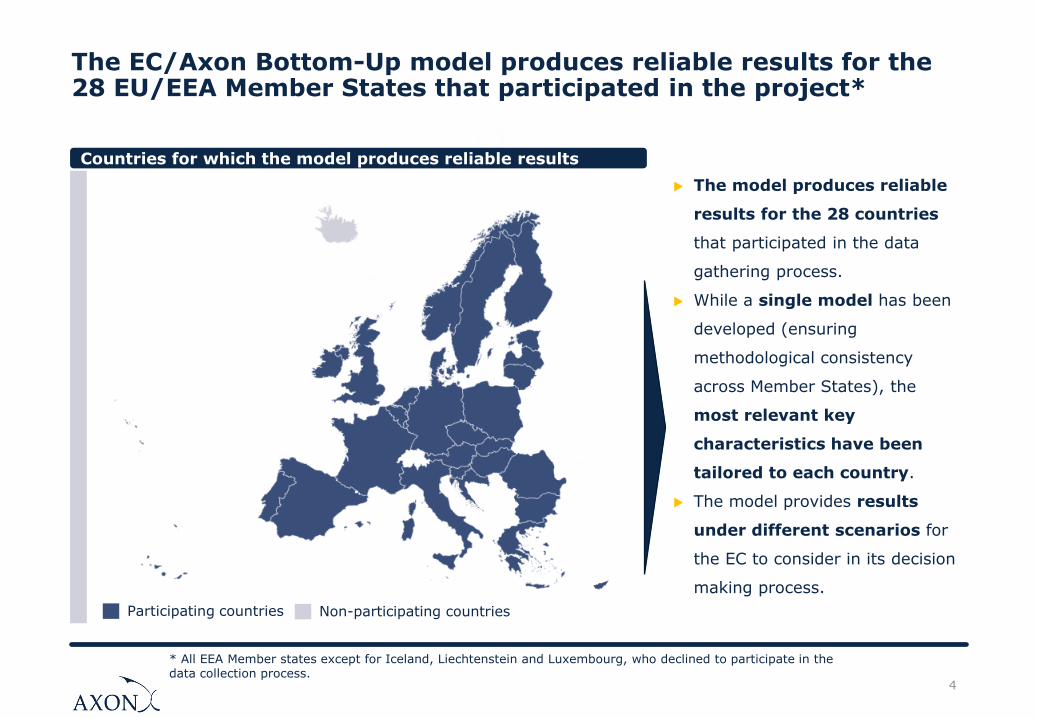

The EC/Axon Bottom-Up model produces reliable results for the28 EU/EEA Member States that participated in the project*

4

* All EEA Member states except for Iceland, Liechtenstein and Luxembourg, who declined to participate in the data collection process.

Countries for which the model produces reliable results

The model produces reliable

results for the 28 countries

that participated in the data

gathering process.

While a single model has been

developed (ensuring

methodological consistency

across Member States), the

most relevant key

characteristics have been

tailored to each country.

The model provides results

under different scenarios for

the EC to consider in its decision

making process.

Participating countries Non-participating countries

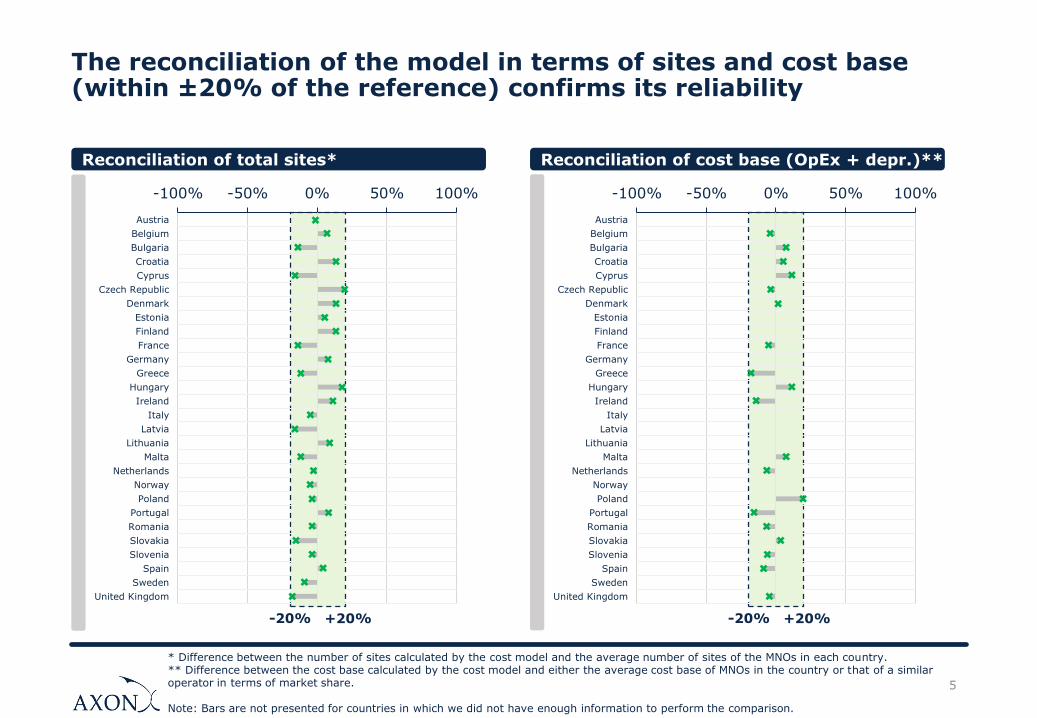

The reconciliation of the model in terms of sites and cost base (within ±20% of the reference) confirms its reliability

5

-100% -50% 0% 50% 100%

Austria

Belgium

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Latvia

Lithuania

Malta

Netherlands

Norway

Poland

Portugal

Romania

Slovakia

Slovenia

Spain

Sweden

United Kingdom

Reconciliation of total sites*

+20%-20%

-100% -50% 0% 50% 100%

Austria

Belgium

Bulgaria

Croatia

Cyprus

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Latvia

Lithuania

Malta

Netherlands

Norway

Poland

Portugal

Romania

Slovakia

Slovenia

Spain

Sweden

United Kingdom

Reconciliation of cost base (OpEx + depr.)**

+20%-20%

* Difference between the number of sites calculated by the cost model and the average number of sites of the MNOs in each country.** Difference between the cost base calculated by the cost model and either the average cost base of MNOs in the country or that of a similar operator in terms of market share.

Note: Bars are not presented for countries in which we did not have enough information to perform the comparison.

Relevant notes on the assessment of the model’s reconciliation

6

The model is not aimed at replicating the operational or financial realities of any given operator,

but to produce a reasonable approximation of the assets and costs of a reference operator. The

reconciliation exercise needs to be performed at a high level (i.e. the reconciliation of the

number of MGWs or the transmission costs is not that meaningful).

The model represents a reference or average operator in each country (calculated based on the

information provided by NRAs for each MNO in their country). Therefore, comparisons between

specific real MNOs and the model’s KPIs may not be fully representative.

The reconciliation of the cost base needs to be assessed with care. The comparison of the cost

base needs to be made on the basis of MNOs’ OpEx and depreciation + amortization

related to the assets included in the model.

Given the techno-economic nature of the model, it can’t be expected to produce the exact

same number of sites or cost base as the average in a country. A reasonable confidence

range of ±20% needs to be accepted given its nature and applicability to 28 countries.

7

2. Results for Data Roaming services

3. Results for Voice Roaming services

4. Results for Voice Call Termination services

1. Definition of scenarios

5. Results for SMS roaming services

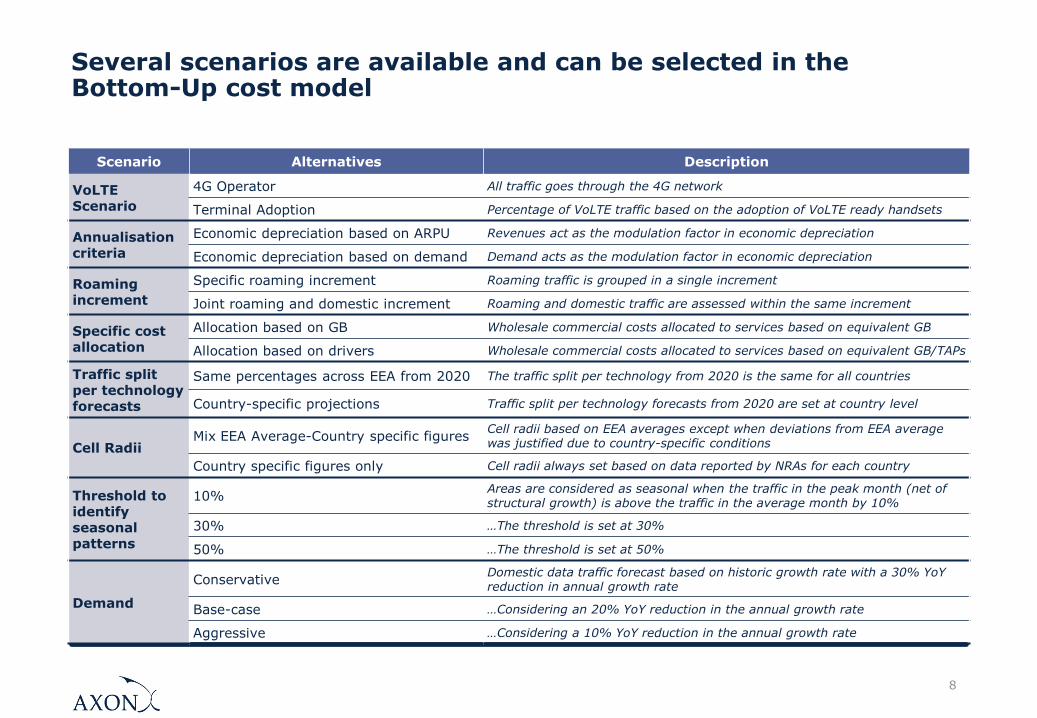

Several scenarios are available and can be selected in the Bottom-Up cost model

8

Scenario Alternatives Description

VoLTE Scenario

4G Operator All traffic goes through the 4G network

Terminal Adoption Percentage of VoLTE traffic based on the adoption of VoLTE ready handsets

Annualisationcriteria

Economic depreciation based on ARPU Revenues act as the modulation factor in economic depreciation

Economic depreciation based on demand Demand acts as the modulation factor in economic depreciation

Roaming increment

Specific roaming increment Roaming traffic is grouped in a single increment

Joint roaming and domestic increment Roaming and domestic traffic are assessed within the same increment

Specific cost allocation

Allocation based on GB Wholesale commercial costs allocated to services based on equivalent GB

Allocation based on drivers Wholesale commercial costs allocated to services based on equivalent GB/TAPs

Traffic split per technology forecasts

Same percentages across EEA from 2020 The traffic split per technology from 2020 is the same for all countries

Country-specific projections Traffic split per technology forecasts from 2020 are set at country level

Cell RadiiMix EEA Average-Country specific figures

Cell radii based on EEA averages except when deviations from EEA average was justified due to country-specific conditions

Country specific figures only Cell radii always set based on data reported by NRAs for each country

Threshold to identify seasonal patterns

10%Areas are considered as seasonal when the traffic in the peak month (net of structural growth) is above the traffic in the average month by 10%

30% …The threshold is set at 30%

50% …The threshold is set at 50%

Demand

ConservativeDomestic data traffic forecast based on historic growth rate with a 30% YoY reduction in annual growth rate

Base-case …Considering an 20% YoY reduction in the annual growth rate

Aggressive …Considering a 10% YoY reduction in the annual growth rate

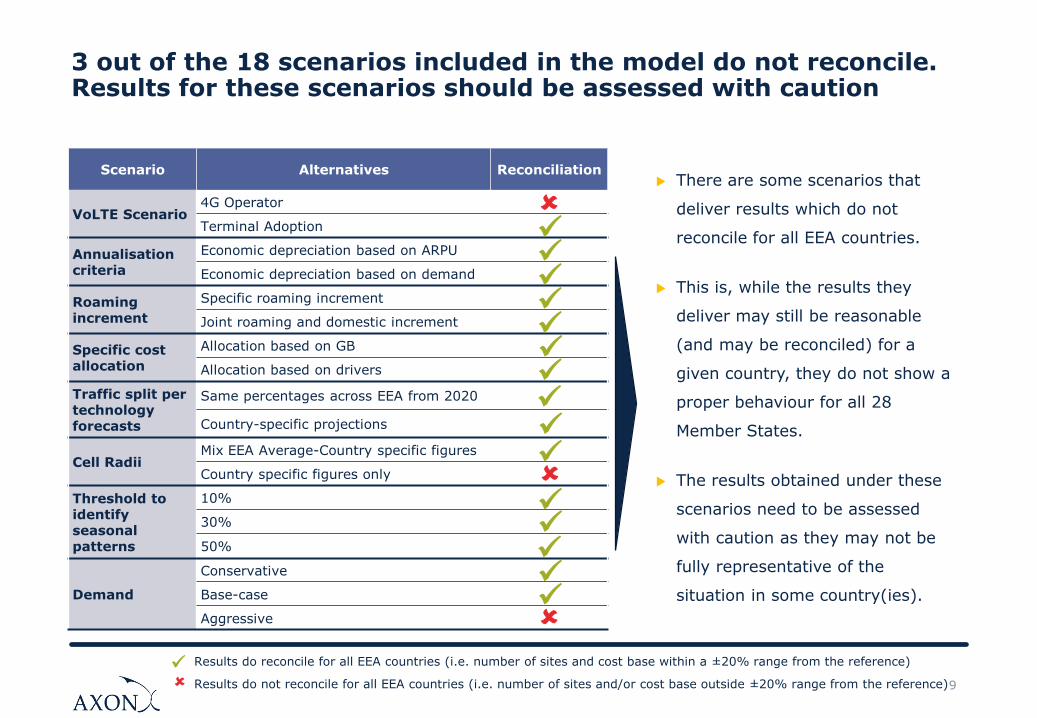

3 out of the 18 scenarios included in the model do not reconcile. Results for these scenarios should be assessed with caution

9

Scenario Alternatives Reconciliation

VoLTE Scenario4G Operator

Terminal Adoption

Annualisationcriteria

Economic depreciation based on ARPU

Economic depreciation based on demand

Roaming increment

Specific roaming increment

Joint roaming and domestic increment

Specific cost allocation

Allocation based on GB

Allocation based on drivers

Traffic split per technology forecasts

Same percentages across EEA from 2020

Country-specific projections

Cell RadiiMix EEA Average-Country specific figures

Country specific figures only

Threshold to identify seasonal patterns

10%

30%

50%

Demand

Conservative

Base-case

Aggressive

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓✓

✓

✓

✓

✓ Results do reconcile for all EEA countries (i.e. number of sites and cost base within a ±20% range from the reference)

Results do not reconcile for all EEA countries (i.e. number of sites and/or cost base outside ±20% range from the reference)

There are some scenarios that

deliver results which do not

reconcile for all EEA countries.

This is, while the results they

deliver may still be reasonable

(and may be reconciled) for a

given country, they do not show a

proper behaviour for all 28

Member States.

The results obtained under these

scenarios need to be assessed

with caution as they may not be

fully representative of the

situation in some country(ies).

10

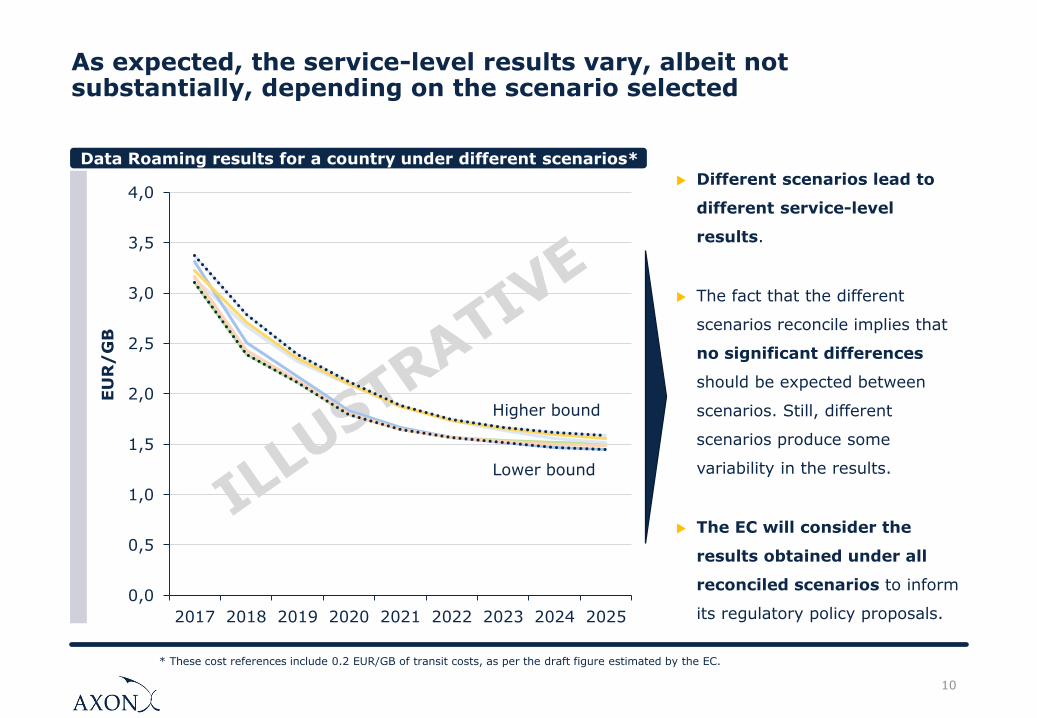

As expected, the service-level results vary, albeit not substantially, depending on the scenario selected

Data Roaming results for a country under different scenarios*

Different scenarios lead to

different service-level

results.

The fact that the different

scenarios reconcile implies that

no significant differences

should be expected between

scenarios. Still, different

scenarios produce some

variability in the results.

The EC will consider the

results obtained under all

reconciled scenarios to inform

its regulatory policy proposals.0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

2017 2018 2019 2020 2021 2022 2023 2024 2025

EU

R/

GB

Higher bound

Lower bound

* These cost references include 0.2 EUR/GB of transit costs, as per the draft figure estimated by the EC.

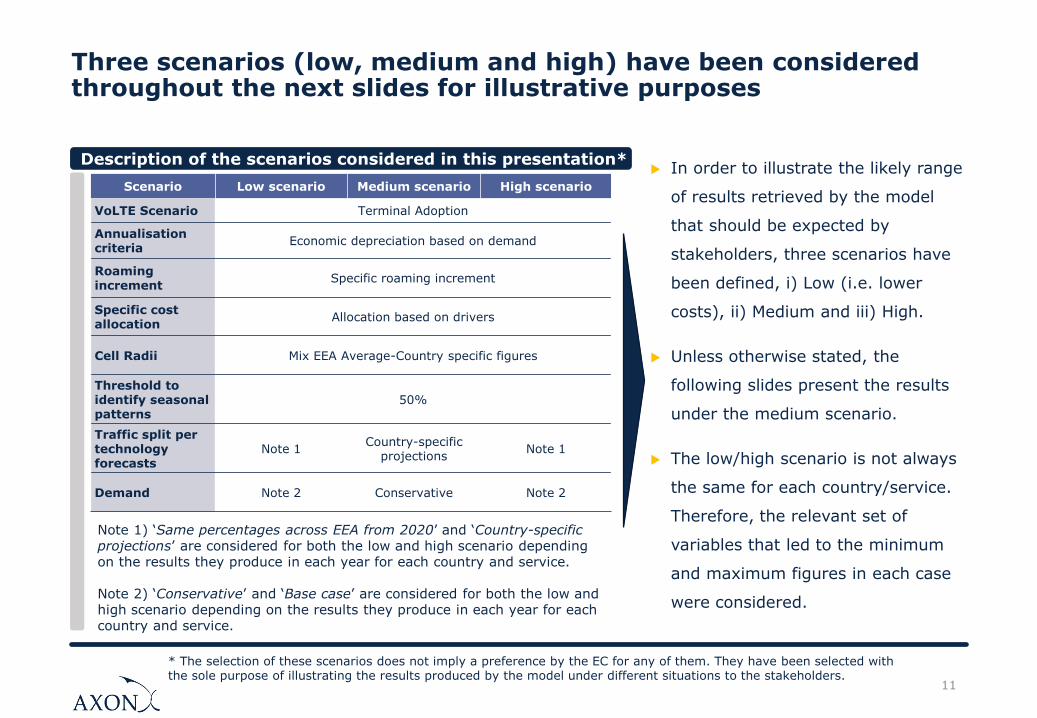

Three scenarios (low, medium and high) have been considered throughout the next slides for illustrative purposes

In order to illustrate the likely range

of results retrieved by the model

that should be expected by

stakeholders, three scenarios have

been defined, i) Low (i.e. lower

costs), ii) Medium and iii) High.

Unless otherwise stated, the

following slides present the results

under the medium scenario.

The low/high scenario is not always

the same for each country/service.

Therefore, the relevant set of

variables that led to the minimum

and maximum figures in each case

were considered.

Scenario Low scenario Medium scenario High scenario

VoLTE Scenario Terminal Adoption

Annualisationcriteria

Economic depreciation based on demand

Roaming increment

Specific roaming increment

Specific cost allocation

Allocation based on drivers

Cell Radii Mix EEA Average-Country specific figures

Threshold to identify seasonal patterns

50%

Traffic split per technology forecasts

Note 1Country-specific

projectionsNote 1

Demand Note 2 Conservative Note 2

Description of the scenarios considered in this presentation*

* The selection of these scenarios does not imply a preference by the EC for any of them. They have been selected with the sole purpose of illustrating the results produced by the model under different situations to the stakeholders.

11

Note 1) ‘Same percentages across EEA from 2020’ and ‘Country-specific projections’ are considered for both the low and high scenario depending on the results they produce in each year for each country and service.

Note 2) ‘Conservative’ and ‘Base case’ are considered for both the low and high scenario depending on the results they produce in each year for each country and service.

12

2. Results for Data Roaming services

3. Results for Voice Roaming services

4. Results for Voice Call Termination services

1. Definition of scenarios

5. Results for SMS roaming services

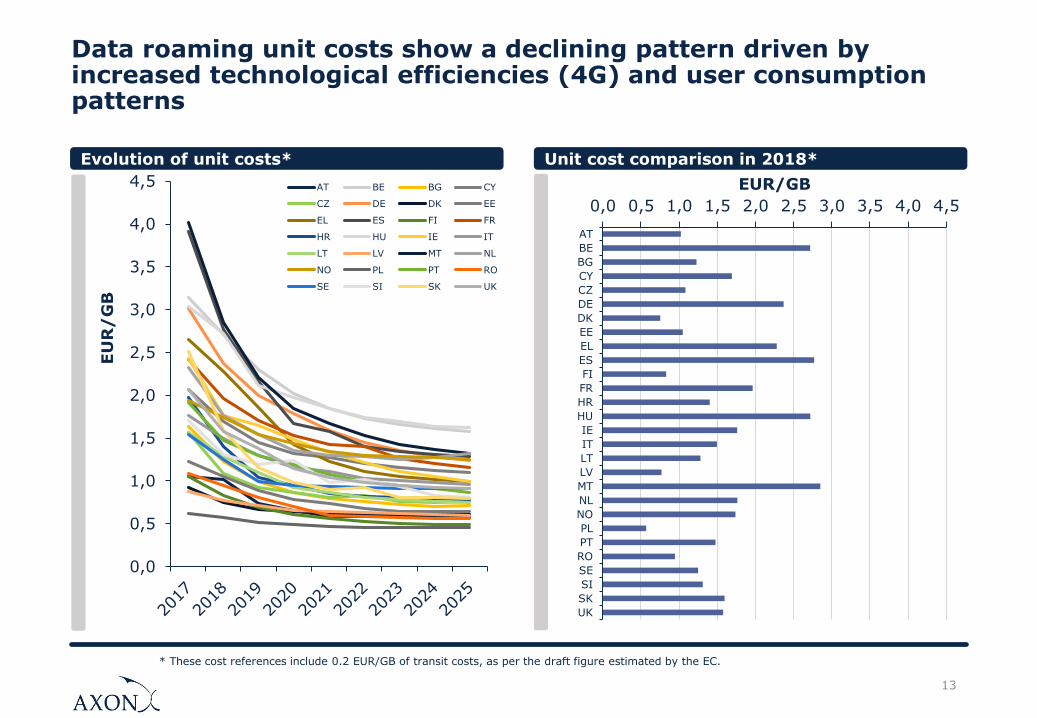

Data roaming unit costs show a declining pattern driven by increased technological efficiencies (4G) and user consumption patterns

13

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

EU

R/

GB

AT BE BG CY

CZ DE DK EE

EL ES FI FR

HR HU IE IT

LT LV MT NL

NO PL PT RO

SE SI SK UK

Evolution of unit costs* Unit cost comparison in 2018*

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5

AT

BE

BG

CY

CZ

DE

DK

EE

EL

ES

FI

FR

HR

HU

IE

IT

LT

LV

MT

NL

NO

PL

PT

RO

SE

SI

SK

UK

EUR/GB

* These cost references include 0.2 EUR/GB of transit costs, as per the draft figure estimated by the EC.

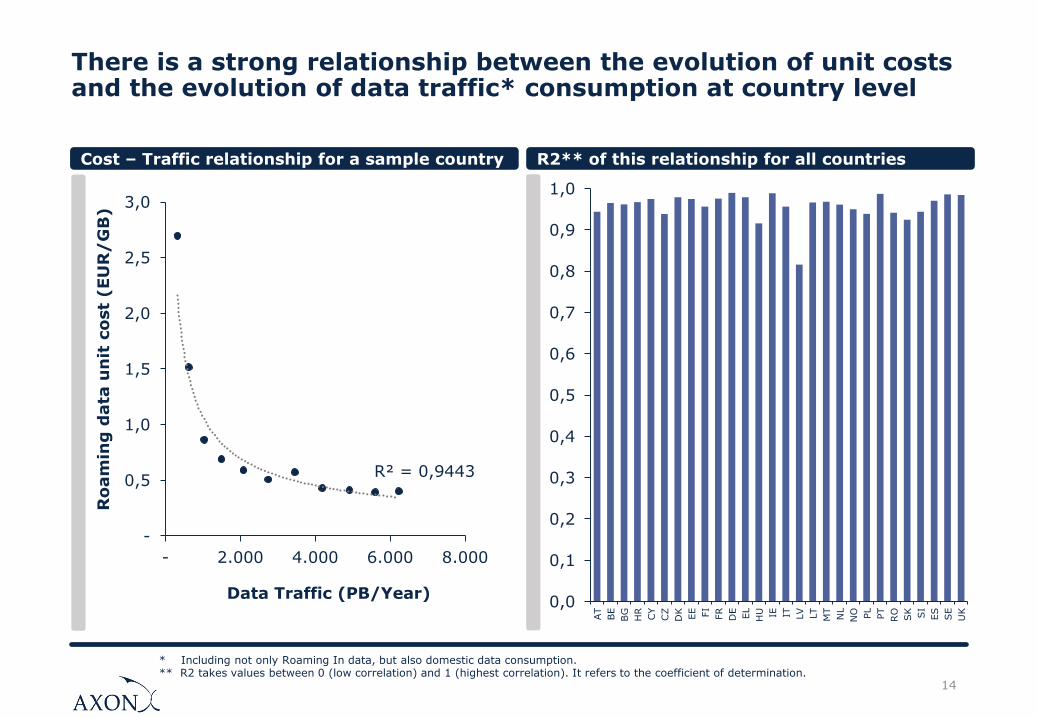

There is a strong relationship between the evolution of unit costs and the evolution of data traffic* consumption at country level

14

* Including not only Roaming In data, but also domestic data consumption.** R2 takes values between 0 (low correlation) and 1 (highest correlation). It refers to the coefficient of determination.

Cost – Traffic relationship for a sample country R2** of this relationship for all countries

R² = 0,9443

-

0,5

1,0

1,5

2,0

2,5

3,0

- 2.000 4.000 6.000 8.000

Ro

am

ing

data

un

it c

ost

(EU

R/

GB

)

Data Traffic (PB/Year)0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

1,0

AT

BE

BG

HR

CY

CZ

DK

EE FI

FR

DE

EL

HU IE IT LV

LT

MT

NL

NO PL

PT

RO

SK SI

ES

SE

UK

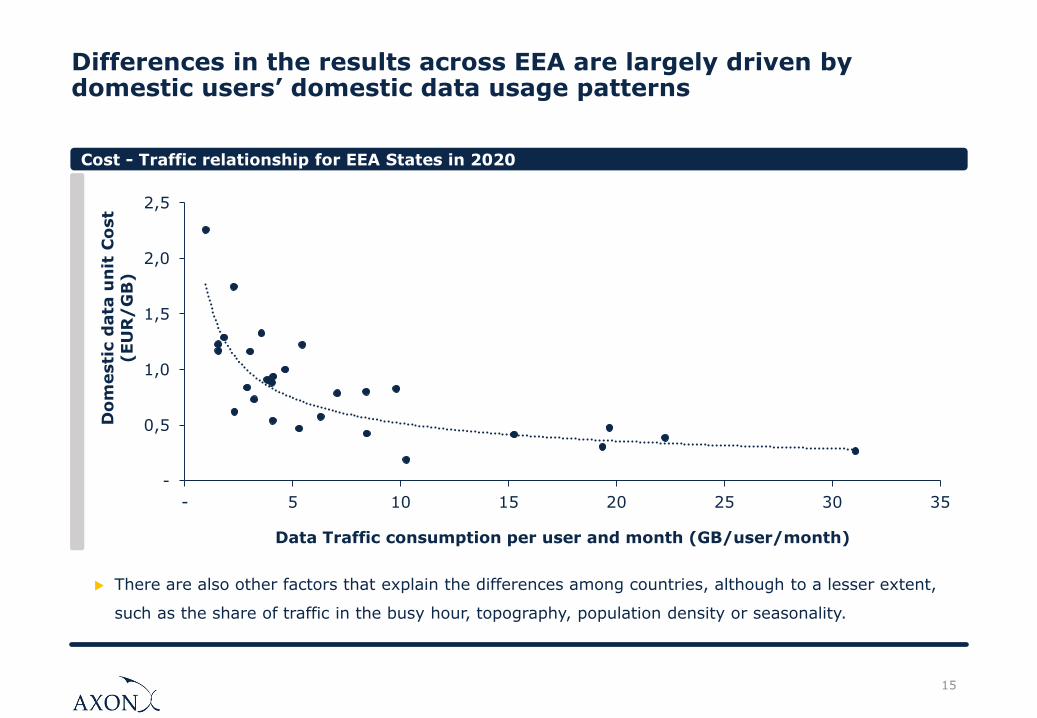

Differences in the results across EEA are largely driven by domestic users’ domestic data usage patterns

15

Cost - Traffic relationship for EEA States in 2020

There are also other factors that explain the differences among countries, although to a lesser extent,

such as the share of traffic in the busy hour, topography, population density or seasonality.

-

0,5

1,0

1,5

2,0

2,5

- 5 10 15 20 25 30 35

Do

mesti

c d

ata

un

it C

ost

(EU

R/

GB

)

Data Traffic consumption per user and month (GB/user/month)

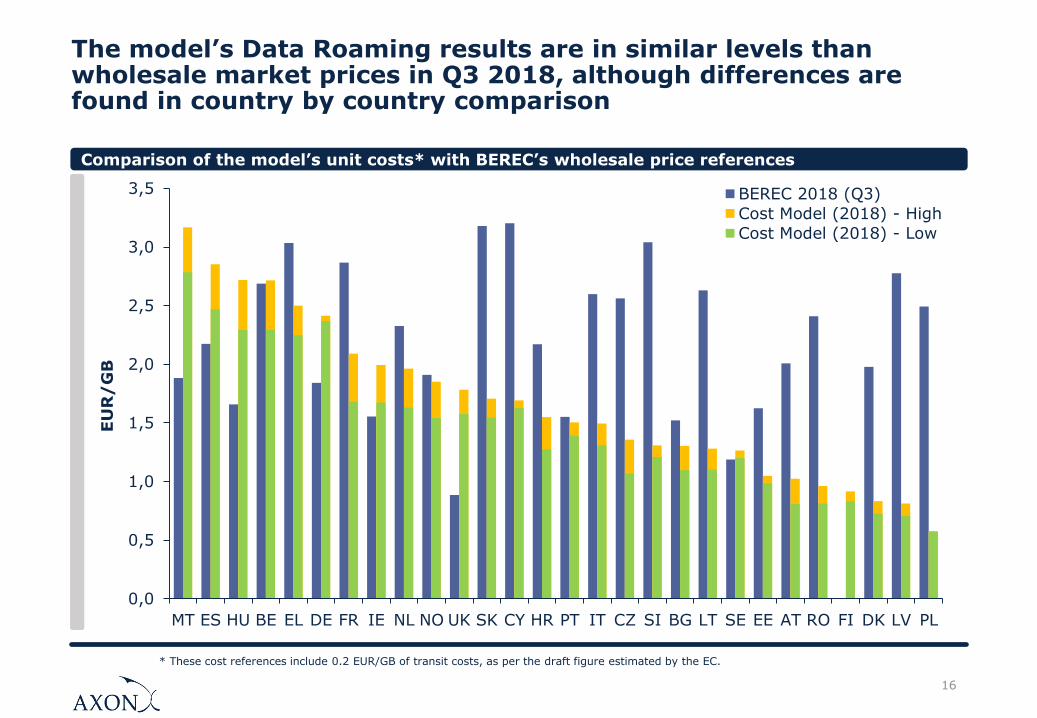

The model’s Data Roaming results are in similar levels than wholesale market prices in Q3 2018, although differences are found in country by country comparison

16

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

MT ES HU BE EL DE FR IE NL NO UK SK CY HR PT IT CZ SI BG LT SE EE AT RO FI DK LV PL

EU

R/

GB

BEREC 2018 (Q3)

Cost Model (2018) - High

Cost Model (2018) - Low

* These cost references include 0.2 EUR/GB of transit costs, as per the draft figure estimated by the EC.

Comparison of the model’s unit costs* with BEREC’s wholesale price references

17

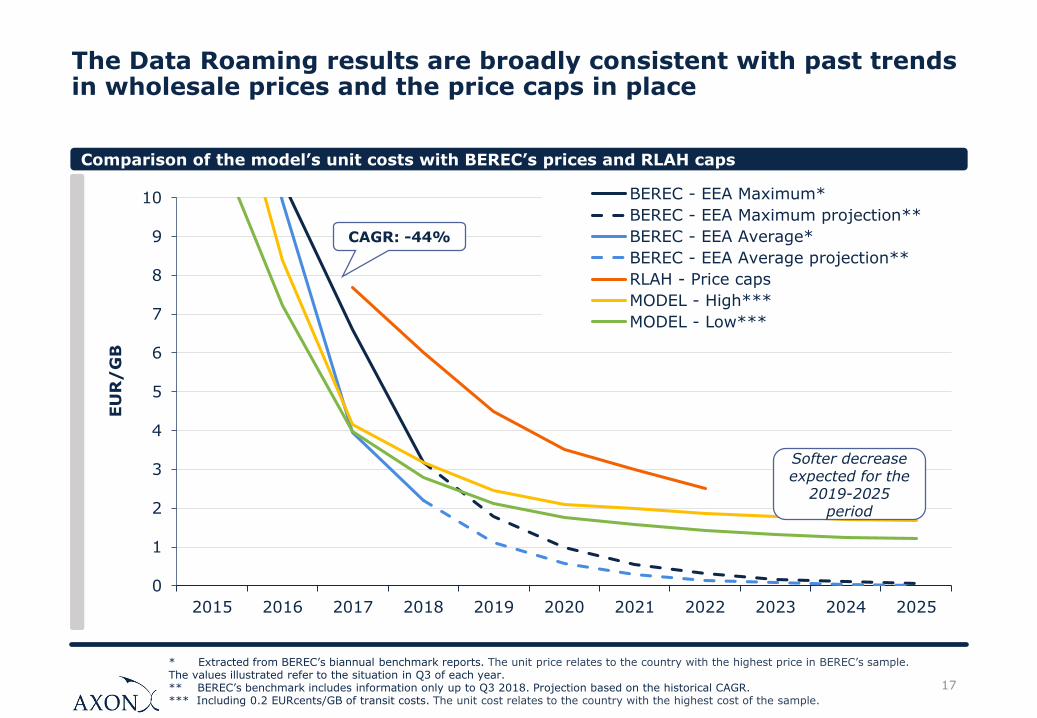

The Data Roaming results are broadly consistent with past trends in wholesale prices and the price caps in place

0

1

2

3

4

5

6

7

8

9

10

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EU

R/

GB

BEREC - EEA Maximum*

BEREC - EEA Maximum projection**

BEREC - EEA Average*

BEREC - EEA Average projection**

RLAH - Price caps

MODEL - High***

MODEL - Low***

CAGR: -44%

Softer decrease expected for the

2019-2025 period

* Extracted from BEREC’s biannual benchmark reports. The unit price relates to the country with the highest price in BEREC’s sample. The values illustrated refer to the situation in Q3 of each year.** BEREC’s benchmark includes information only up to Q3 2018. Projection based on the historical CAGR.*** Including 0.2 EURcents/GB of transit costs. The unit cost relates to the country with the highest cost of the sample.

Comparison of the model’s unit costs with BEREC’s prices and RLAH caps

18

2. Results for Data Roaming services

3. Results for Voice Roaming services

4. Results for Voice Call Termination services

1. Definition of scenarios

5. Results for SMS roaming services

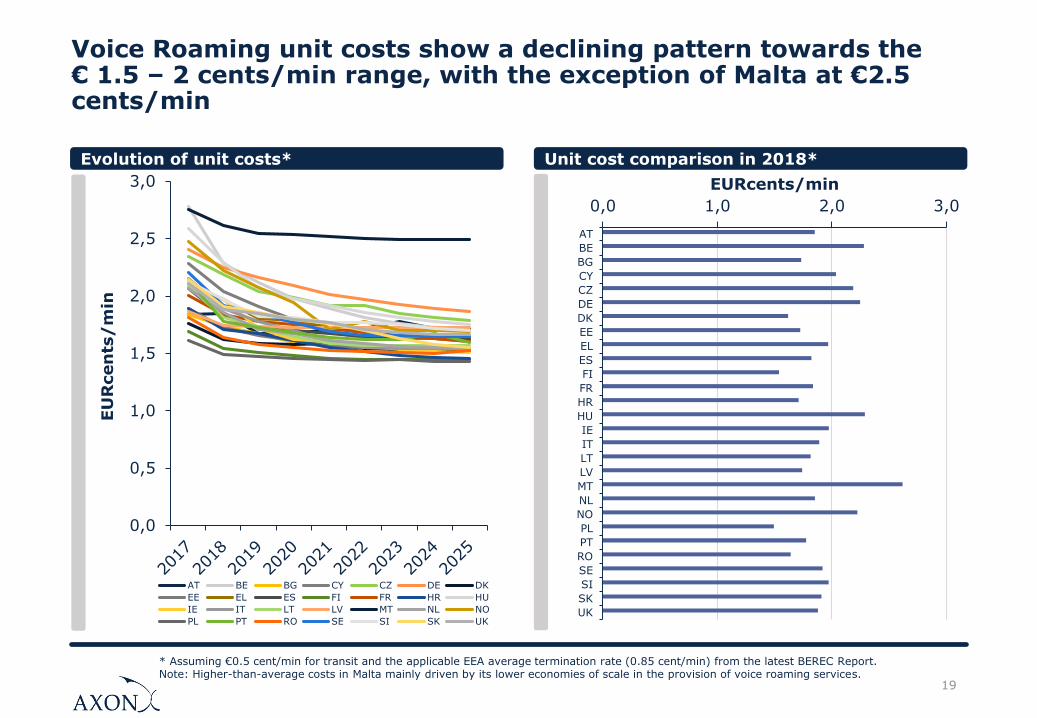

Voice Roaming unit costs show a declining pattern towards the € 1.5 – 2 cents/min range, with the exception of Malta at €2.5 cents/min

19

Evolution of unit costs* Unit cost comparison in 2018*

0,0 1,0 2,0 3,0

AT

BE

BG

CY

CZ

DE

DK

EE

EL

ES

FI

FR

HR

HU

IE

IT

LT

LV

MT

NL

NO

PL

PT

RO

SE

SI

SK

UK

EURcents/min

* Assuming €0.5 cent/min for transit and the applicable EEA average termination rate (0.85 cent/min) from the latest BEREC Report.Note: Higher-than-average costs in Malta mainly driven by its lower economies of scale in the provision of voice roaming services.

0,0

0,5

1,0

1,5

2,0

2,5

3,0

EU

Rcen

ts/

min

AT BE BG CY CZ DE DK

EE EL ES FI FR HR HU

IE IT LT LV MT NL NO

PL PT RO SE SI SK UK

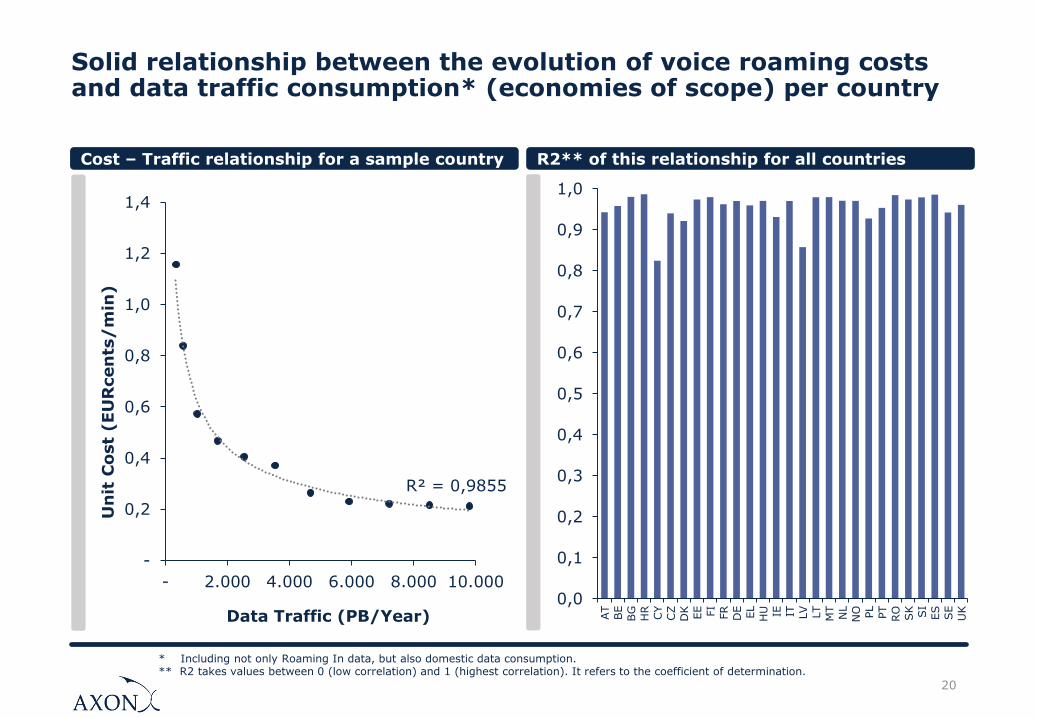

Solid relationship between the evolution of voice roaming costs and data traffic consumption* (economies of scope) per country

20

Cost – Traffic relationship for a sample country R2** of this relationship for all countries

R² = 0,9855

-

0,2

0,4

0,6

0,8

1,0

1,2

1,4

- 2.000 4.000 6.000 8.000 10.000

Un

it C

ost

(EU

Rcen

ts/

min

)

Data Traffic (PB/Year)0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

1,0

AT

BE

BG

HR

CY

CZ

DK

EE FI

FR

DE

EL

HU IE IT LV

LT

MT

NL

NO PL

PT

RO

SK SI

ES

SE

UK

* Including not only Roaming In data, but also domestic data consumption.** R2 takes values between 0 (low correlation) and 1 (highest correlation). It refers to the coefficient of determination.

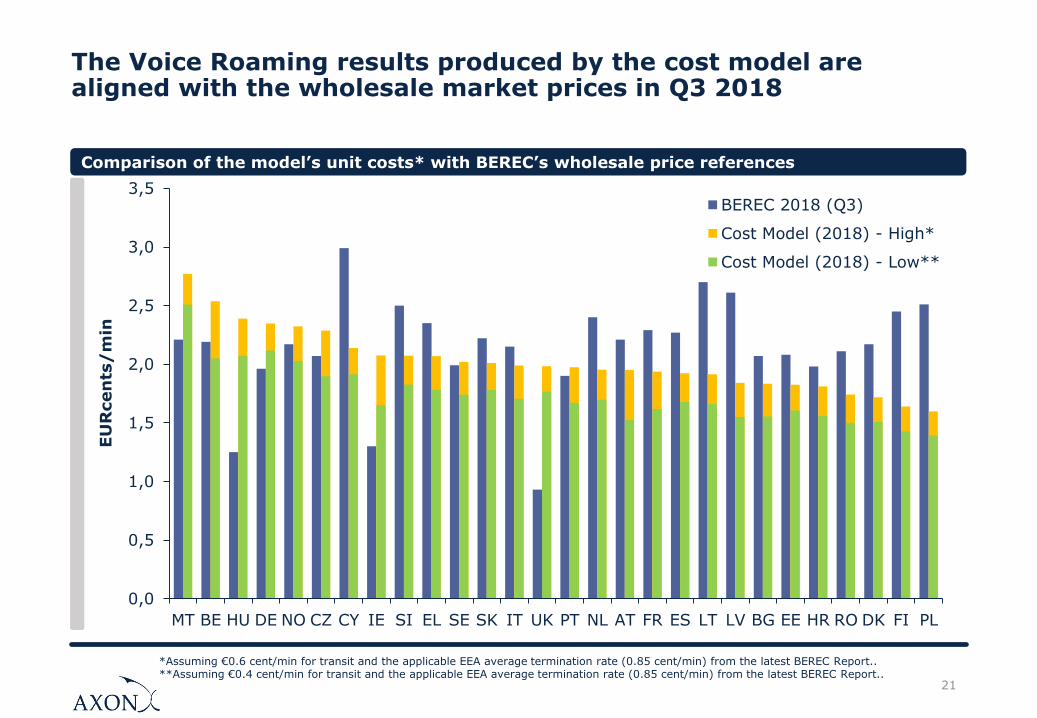

The Voice Roaming results produced by the cost model are aligned with the wholesale market prices in Q3 2018

21

Comparison of the model’s unit costs* with BEREC’s wholesale price references

*Assuming €0.6 cent/min for transit and the applicable EEA average termination rate (0.85 cent/min) from the latest BEREC Report.. **Assuming €0.4 cent/min for transit and the applicable EEA average termination rate (0.85 cent/min) from the latest BEREC Report..

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

MT BE HU DE NO CZ CY IE SI EL SE SK IT UK PT NL AT FR ES LT LV BG EE HR RO DK FI PL

EU

Rcen

ts/

min

BEREC 2018 (Q3)

Cost Model (2018) - High*

Cost Model (2018) - Low**

22

* Extracted from BEREC’s biannual benchmark reports. The unit price relates to the country with the highest price in BEREC’s sample. ** BEREC’s benchmark includes information only up to Q3 2018. Projection based on the historical CAGR. *** Considering 0.6-0.4 EURcents/min of transit costs for the high/low alternatives respectively, and 0.85 EURcents/min of mobile termination. The unit cost relates to the country with the highest cost of the sample.

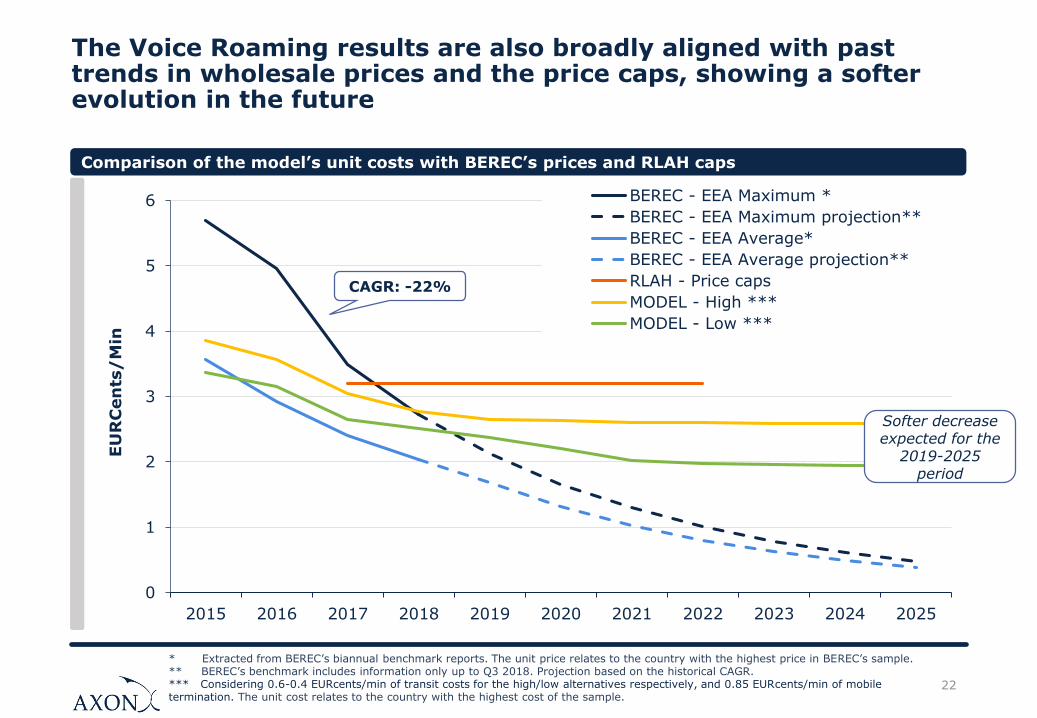

The Voice Roaming results are also broadly aligned with past trends in wholesale prices and the price caps, showing a softer evolution in the future

0

1

2

3

4

5

6

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EU

RC

en

ts/

Min

BEREC - EEA Maximum *

BEREC - EEA Maximum projection**

BEREC - EEA Average*

BEREC - EEA Average projection**

RLAH - Price caps

MODEL - High ***

MODEL - Low ***

CAGR: -22%

Softer decrease expected for the

2019-2025 period

Comparison of the model’s unit costs with BEREC’s prices and RLAH caps

23

2. Results for Data Roaming services

3. Results for Voice Roaming services

4. Results for Voice Call Termination services

1. Definition of scenarios

5. Results for SMS roaming services

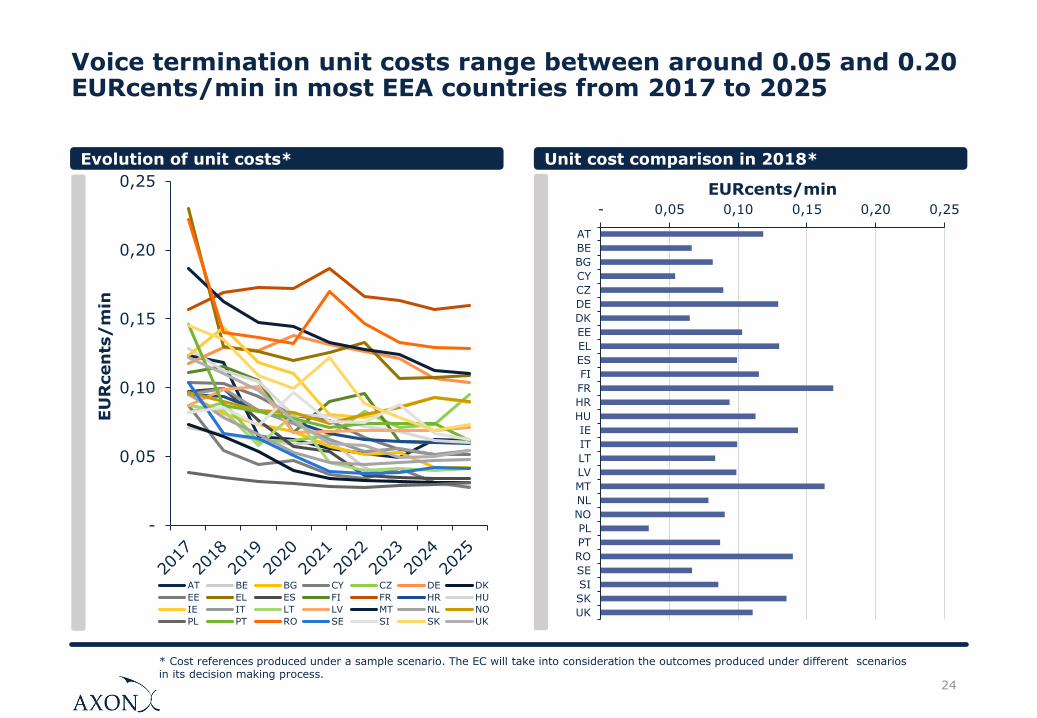

Voice termination unit costs range between around 0.05 and 0.20 EURcents/min in most EEA countries from 2017 to 2025

24

Evolution of unit costs* Unit cost comparison in 2018*

- 0,05 0,10 0,15 0,20 0,25

AT

BE

BG

CY

CZ

DE

DK

EE

EL

ES

FI

FR

HR

HU

IE

IT

LT

LV

MT

NL

NO

PL

PT

RO

SE

SI

SK

UK

EURcents/min

* Cost references produced under a sample scenario. The EC will take into consideration the outcomes produced under different scenarios in its decision making process.

-

0,05

0,10

0,15

0,20

0,25

EU

Rcen

ts/

min

AT BE BG CY CZ DE DK

EE EL ES FI FR HR HU

IE IT LT LV MT NL NO

PL PT RO SE SI SK UK

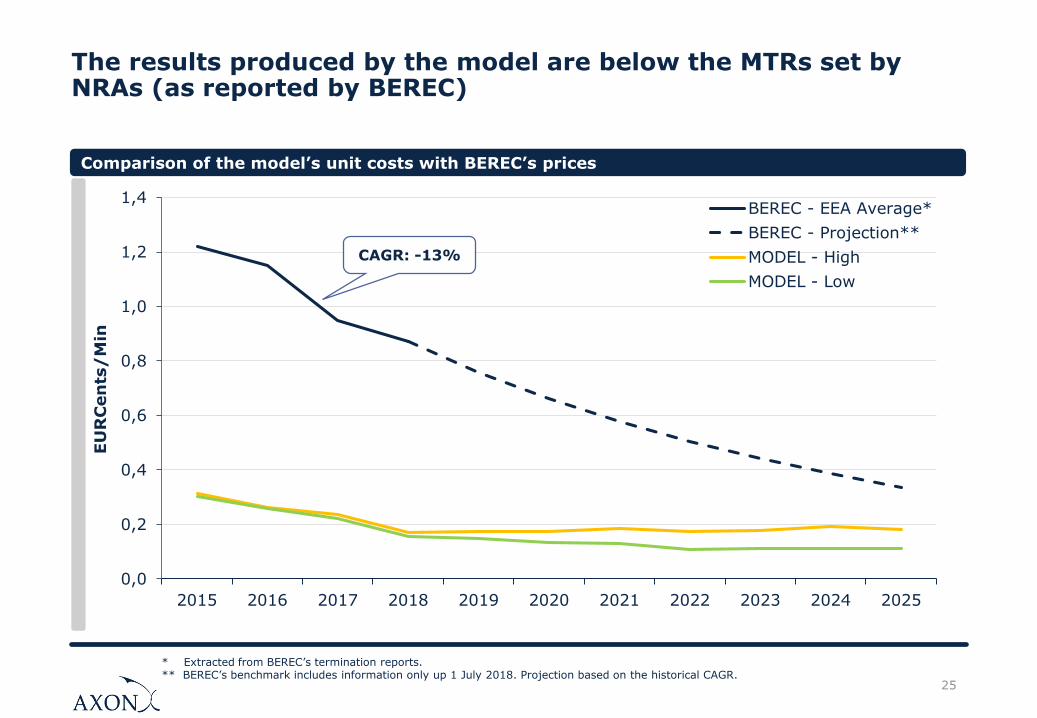

The results produced by the model are below the MTRs set by NRAs (as reported by BEREC)

25

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EU

RC

en

ts/

Min

BEREC - EEA Average*

BEREC - Projection**

MODEL - High

MODEL - Low

Comparison of the model’s unit costs with BEREC’s prices

* Extracted from BEREC’s termination reports. ** BEREC’s benchmark includes information only up 1 July 2018. Projection based on the historical CAGR.

CAGR: -13%

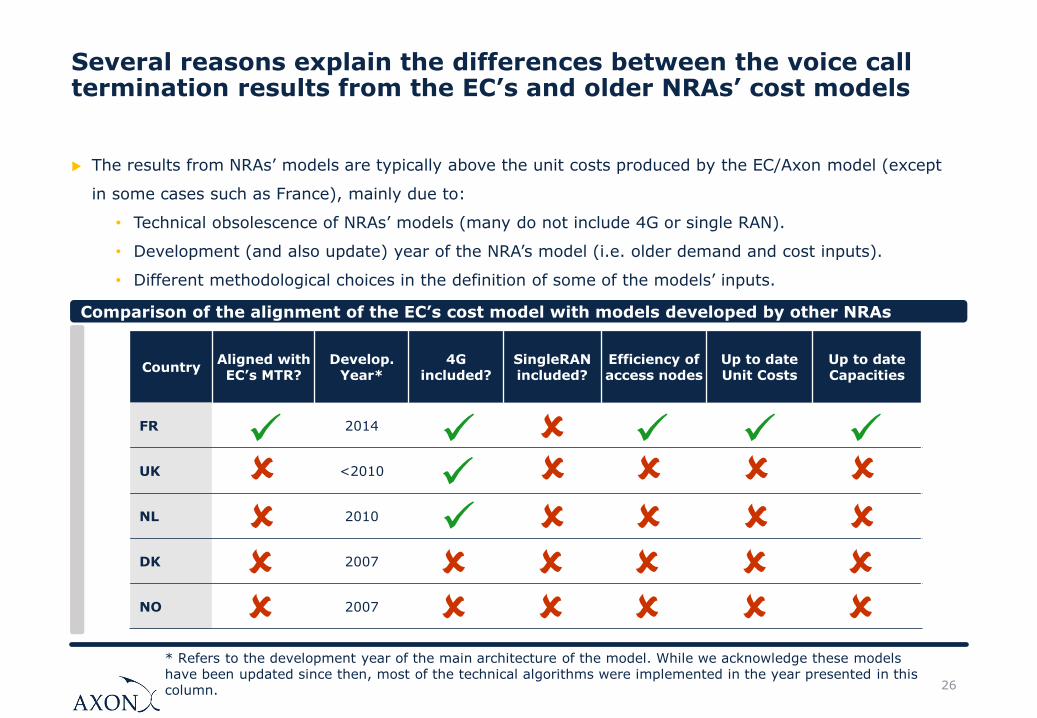

Several reasons explain the differences between the voice call termination results from the EC’s and older NRAs’ cost models

26

CountryAligned with EC’s MTR?

Develop. Year*

4G included?

SingleRAN included?

Efficiency of access nodes

Up to date Unit Costs

Up to date Capacities

FR 2014

UK <2010

NL 2010

DK 2007

NO 2007

Comparison of the alignment of the EC’s cost model with models developed by other NRAs

The results from NRAs’ models are typically above the unit costs produced by the EC/Axon model (except

in some cases such as France), mainly due to:

• Technical obsolescence of NRAs’ models (many do not include 4G or single RAN).

• Development (and also update) year of the NRA’s model (i.e. older demand and cost inputs).

• Different methodological choices in the definition of some of the models’ inputs.

* Refers to the development year of the main architecture of the model. While we acknowledge these models have been updated since then, most of the technical algorithms were implemented in the year presented in this column.

27

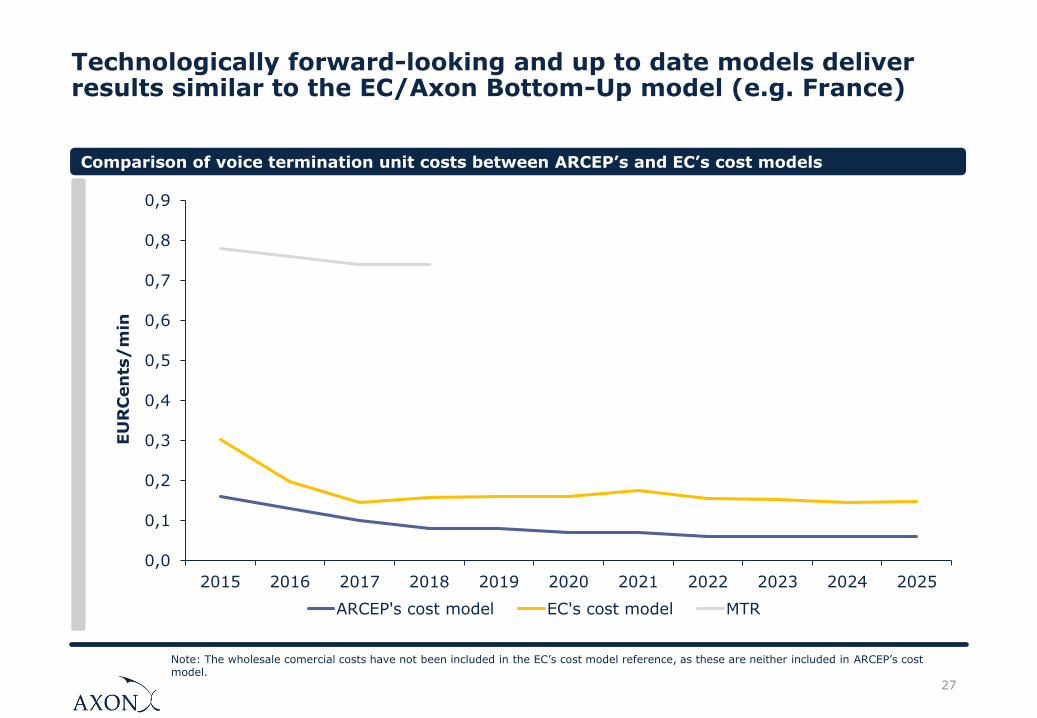

Technologically forward-looking and up to date models deliver results similar to the EC/Axon Bottom-Up model (e.g. France)

0,0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

0,8

0,9

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EU

RC

en

ts/

min

ARCEP's cost model EC's cost model MTR

Note: The wholesale comercial costs have not been included in the EC’s cost model reference, as these are neither included in ARCEP’s cost model.

Comparison of voice termination unit costs between ARCEP’s and EC’s cost models

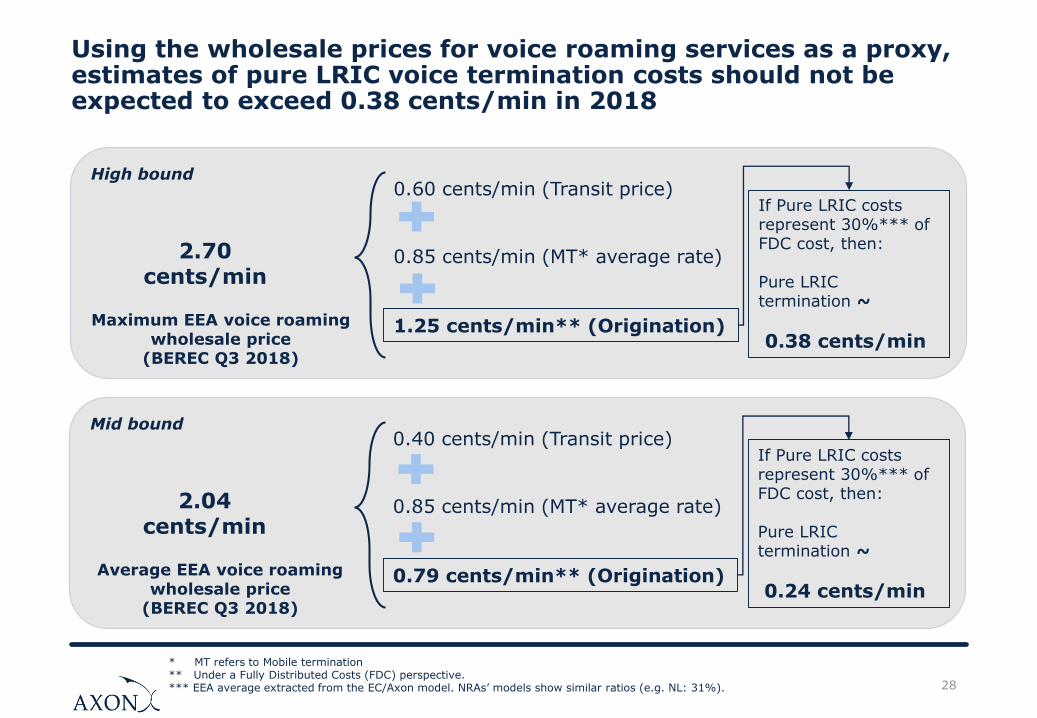

Using the wholesale prices for voice roaming services as a proxy, estimates of pure LRIC voice termination costs should not be expected to exceed 0.38 cents/min in 2018

28

* MT refers to Mobile termination** Under a Fully Distributed Costs (FDC) perspective.*** EEA average extracted from the EC/Axon model. NRAs’ models show similar ratios (e.g. NL: 31%).

High bound

Maximum EEA voice roaming wholesale price

(BEREC Q3 2018)

2.70 cents/min

0.60 cents/min (Transit price)

0.85 cents/min (MT* average rate)

1.25 cents/min** (Origination)

If Pure LRIC costs represent 30%*** of FDC cost, then:

Pure LRIC termination ~

0.38 cents/min

Mid bound

Average EEA voice roaming wholesale price

(BEREC Q3 2018)

2.04 cents/min

0.40 cents/min (Transit price)

0.85 cents/min (MT* average rate)

0.79 cents/min** (Origination)

If Pure LRIC costs represent 30%*** of FDC cost, then:

Pure LRIC termination ~

0.24 cents/min

29

2. Results for Data Roaming services

3. Results for Voice Roaming services

4. Results for Voice Call Termination services

1. Definition of scenarios

5. Results for SMS roaming services

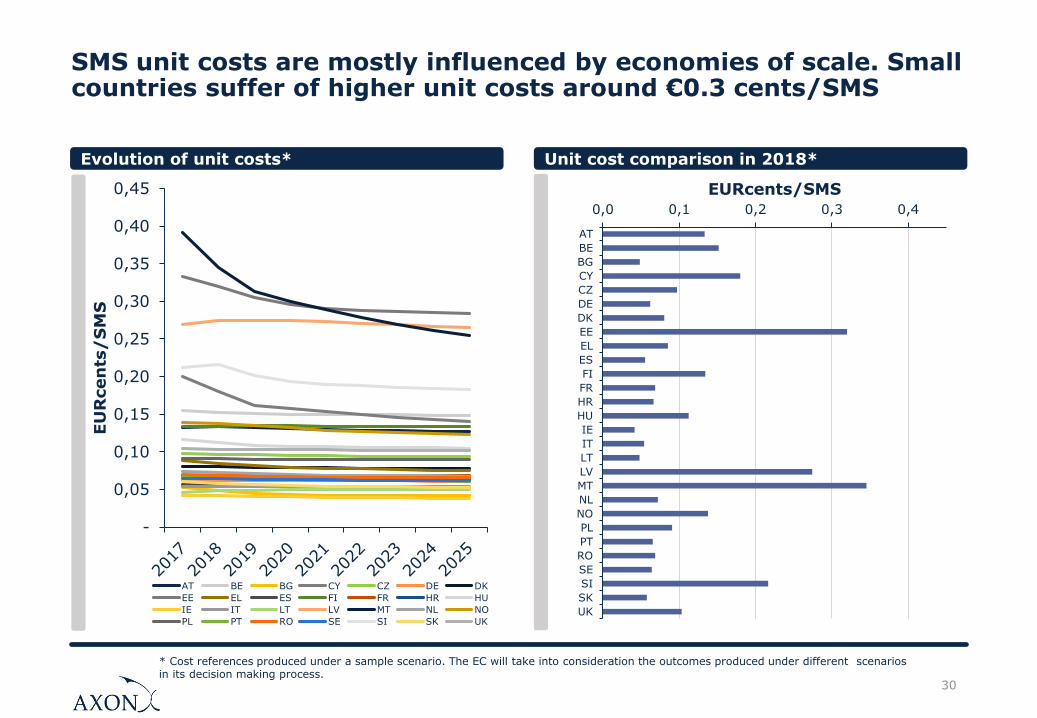

SMS unit costs are mostly influenced by economies of scale. Small countries suffer of higher unit costs around €0.3 cents/SMS

30

Evolution of unit costs* Unit cost comparison in 2018*

0,0 0,1 0,2 0,3 0,4

AT

BE

BG

CY

CZ

DE

DK

EE

EL

ES

FI

FR

HR

HU

IE

IT

LT

LV

MT

NL

NO

PL

PT

RO

SE

SI

SK

UK

EURcents/SMS

* Cost references produced under a sample scenario. The EC will take into consideration the outcomes produced under different scenarios in its decision making process.

-

0,05

0,10

0,15

0,20

0,25

0,30

0,35

0,40

0,45

EU

Rcen

ts/

SM

S

AT BE BG CY CZ DE DK

EE EL ES FI FR HR HU

IE IT LT LV MT NL NO

PL PT RO SE SI SK UK

31

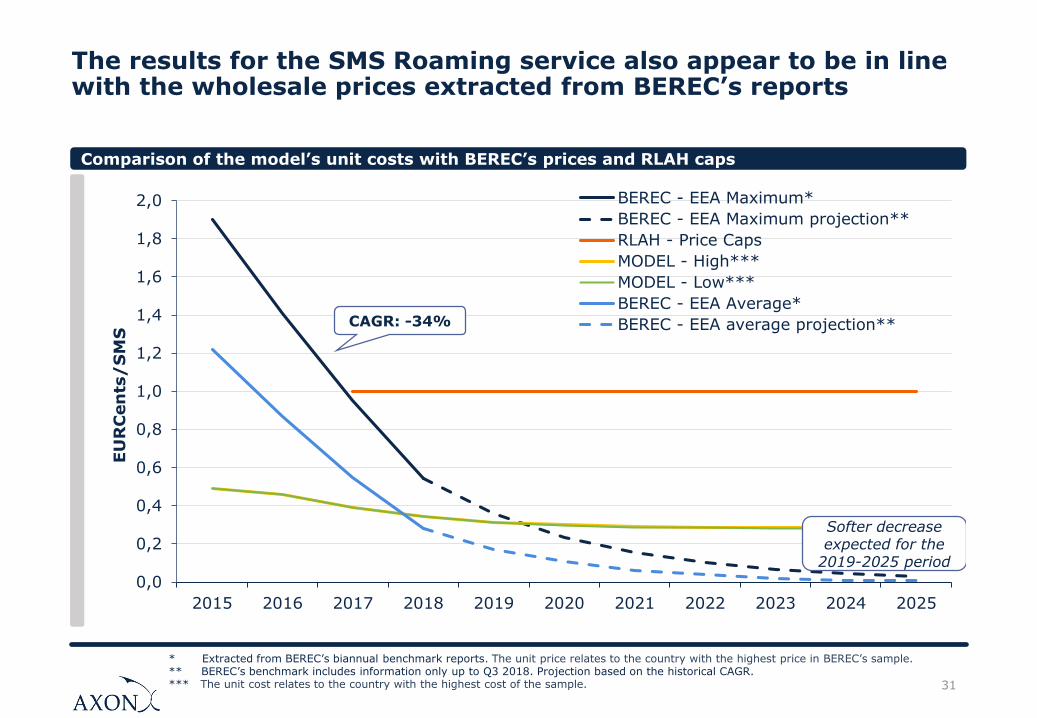

The results for the SMS Roaming service also appear to be in line with the wholesale prices extracted from BEREC’s reports

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

EU

RC

en

ts/

SM

S

BEREC - EEA Maximum*

BEREC - EEA Maximum projection**

RLAH - Price Caps

MODEL - High***

MODEL - Low***

BEREC - EEA Average*

BEREC - EEA average projection**

Softer decrease expected for the

2019-2025 period

CAGR: -34%

Comparison of the model’s unit costs with BEREC’s prices and RLAH caps

* Extracted from BEREC’s biannual benchmark reports. The unit price relates to the country with the highest price in BEREC’s sample. ** BEREC’s benchmark includes information only up to Q3 2018. Projection based on the historical CAGR.*** The unit cost relates to the country with the highest cost of the sample.

Any questions? Please, contact:

Principal

Jorge Martínez

Principal

Alfons Oliver

Axon Partners Group

Calle Sagasta 18, 3rd

28004 Madrid (Spain)

Tel: +34 91 310 28 94