Embed Size (px)

Citation preview

Assessing Supply Chain Risk

Costs, Availability, and Logistics Pressure

Manufacturing Supply Chains

Presented by:

Katherine Lewis

Senior Manager, IHS Global Insight

Andrea Borruso

Director of Middle East Operations, SRIC Consulting

Eric Pratt

Vice President, iSuppli

Chris Pålsson

Director, IHS Fairplay

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 2

Agenda

• Introductions

• Themes

• Key Inputs to Production

• Labor Markets

• Chemicals & Plastics

• Electronic Components

• Shipping

• Conclusions

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 3

Where have all the suppliers gone?

Demand is returning, but to new supplier conditions

• Many suppliers have gone out of business, and consolidation means pricing power

The Strong (or Big) Survive

• Vertical integration is the new reality in many markets

Economies of Scale

• Constantly changing technology means some suppliers that were hot when demand flagged haven’t weathered the storm

Staying Relevant

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 4

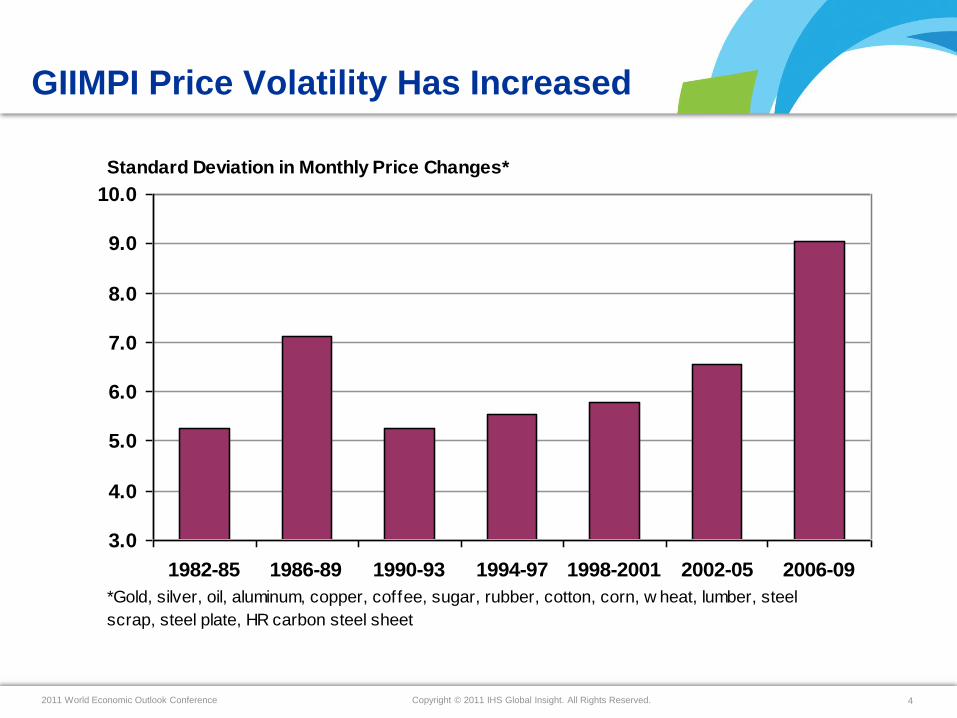

GIIMPI Price Volatility Has Increased

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1982-85 1986-89 1990-93 1994-97 1998-2001 2002-05 2006-09

Standard Deviation in Monthly Price Changes*

*Gold, silver, oil, aluminum, copper, coffee, sugar, rubber, cotton, corn, w heat, lumber, steel

scrap, steel plate, HR carbon steel sheet

Assessing Supply Chain Risk

Labor Markets

Presented by:

Katherine Lewis

Senior Manager, IHS Global Insight

Pricing and Purchasing

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 6

Emerging Market Wage Rates Rising

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

Labour Rates, Manufacturing(U.S. dollars per hour)

China India Indonesia Thailand Vietnam

Assessing Supply Chain Risk

Petrochemical Industry

Presented by:

A. Borruso

Director Middle East Operations

IHS – SRI Consulting

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 8

Agenda

• Overcapacity or time to invest

• Price volatility

• Has the industry model changed

• Elasticity to crude price

Assessing Supply Chain Risk: Electronics

Impact of Japanese Disaster

Presented by:

Eric Pratt

Vice President, iSuppli

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 101010

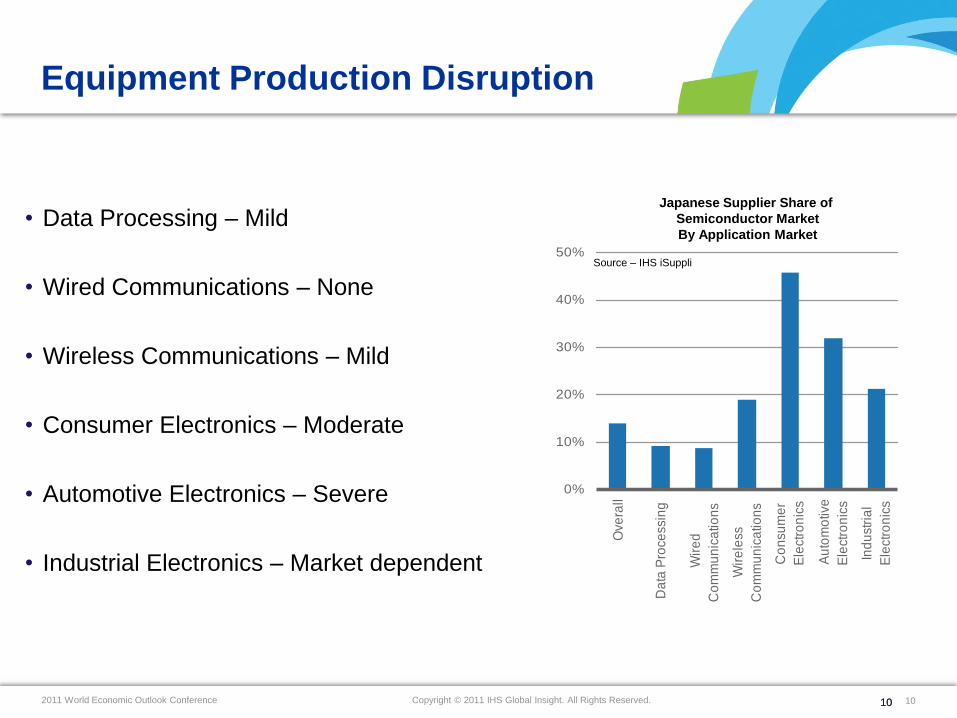

Equipment Production Disruption

• Data Processing – Mild

• Wired Communications – None

• Wireless Communications – Mild

• Consumer Electronics – Moderate

• Automotive Electronics – Severe

• Industrial Electronics – Market dependent

0%

10%

20%

30%

40%

50%

Ove

rall

Da

ta P

roce

ssin

g

Wir

ed

Co

mm

un

ica

tion

s

Wir

ele

ss

Co

mm

un

ica

tion

s

Co

nsu

me

r

Ele

ctro

nic

s

Au

tom

otiv

e

Ele

ctro

nic

s

Ind

ust

ria

l

Ele

ctro

nic

s

Japanese Supplier Share of

Semiconductor Market

By Application Market

Source – IHS iSuppli

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 11

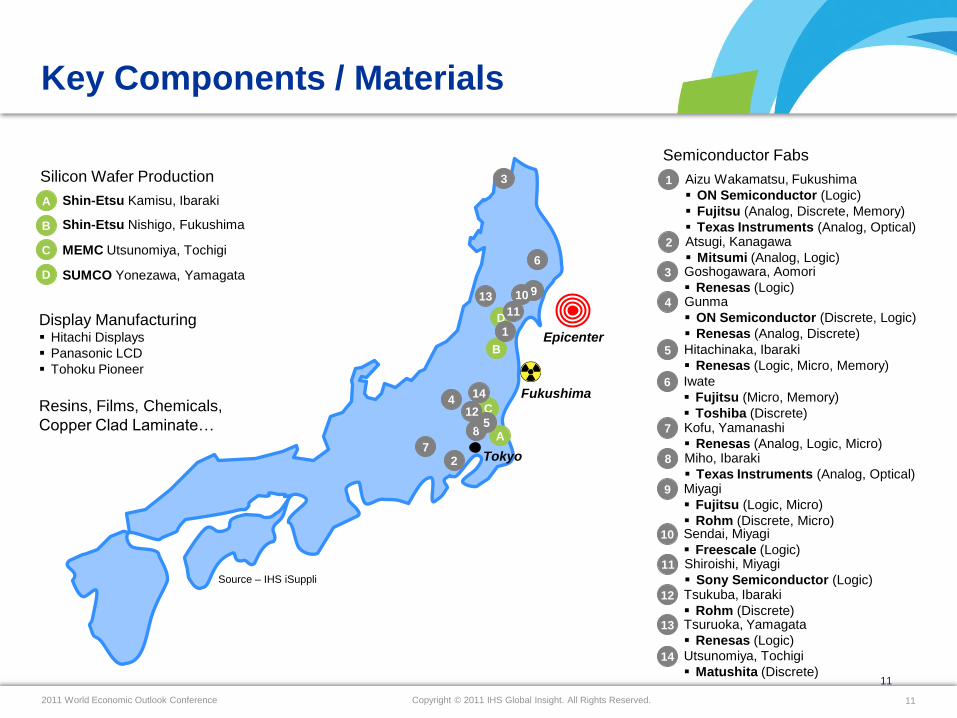

Semiconductor Fabs

1 Aizu Wakamatsu, Fukushima

ON Semiconductor (Logic)

Fujitsu (Analog, Discrete, Memory)

Texas Instruments (Analog, Optical)2 Atsugi, Kanagawa

Mitsumi (Analog, Logic)3 Goshogawara, Aomori

Renesas (Logic)4 Gunma

ON Semiconductor (Discrete, Logic)

Renesas (Analog, Discrete)

5 Hitachinaka, Ibaraki

Renesas (Logic, Micro, Memory)

6 Iwate

Fujitsu (Micro, Memory)

Toshiba (Discrete)7 Kofu, Yamanashi

Renesas (Analog, Logic, Micro)8 Miho, Ibaraki

Texas Instruments (Analog, Optical)9 Miyagi

Fujitsu (Logic, Micro)

Rohm (Discrete, Micro)10 Sendai, Miyagi

Freescale (Logic)11 Shiroishi, Miyagi

Sony Semiconductor (Logic)12 Tsukuba, Ibaraki

Rohm (Discrete)13 Tsuruoka, Yamagata

Renesas (Logic)

14 Utsunomiya, Tochigi

Matushita (Discrete)11

Key Components / Materials

Silicon Wafer Production

A

B

C

D

Shin-Etsu Kamisu, Ibaraki

Shin-Etsu Nishigo, Fukushima

MEMC Utsunomiya, Tochigi

SUMCO Yonezawa, Yamagata

Display Manufacturing Hitachi Displays

Panasonic LCD

Tohoku Pioneer

Resins, Films, Chemicals,

Copper Clad Laminate…

Fukushima

Epicenter

A

B

D

C

1

3

2

4

Tokyo7

6

85

910

11

12

14

13

Source – IHS iSuppli

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 12

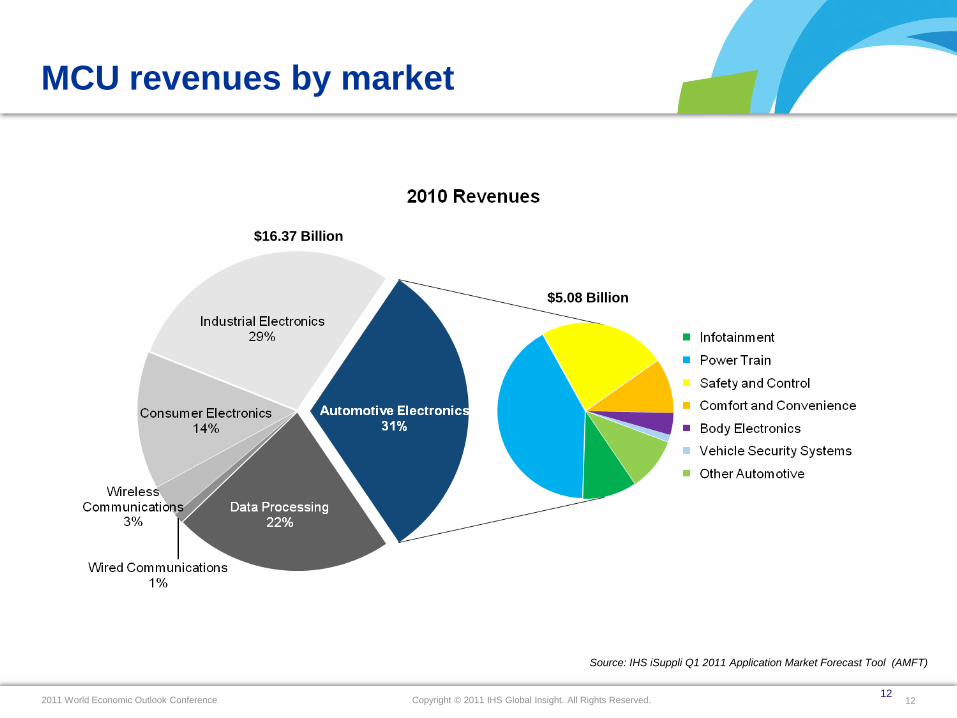

MCU revenues by market

12

Source: IHS iSuppli Q1 2011 Application Market Forecast Tool (AMFT)

$16.37 Billion

$5.08 Billion

Assessing Supply Chain Risk:

Shipping and Logistics

Presented by:

Chris Pålsson

Director, IHS Fairplay

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 14

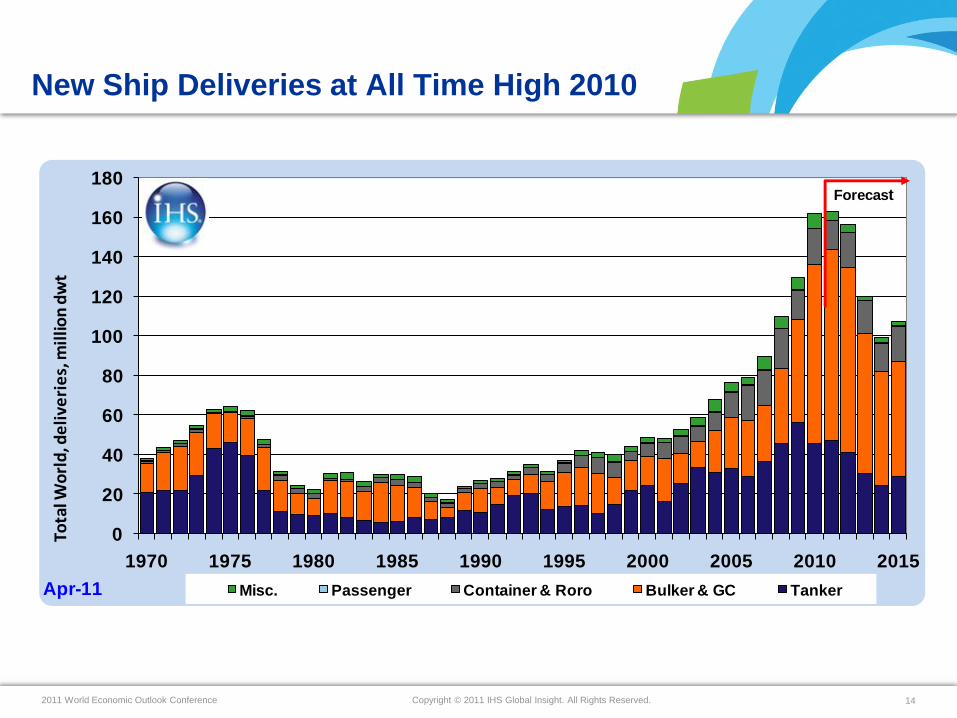

New Ship Deliveries at All Time High 2010

0

20

40

60

80

100

120

140

160

180

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Misc. Passenger Container & Roro Bulker & GC Tanker

Forecast

Tota

l Wo

rld

, de

live

rie

s, m

illio

n d

wt

Apr-11

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 15

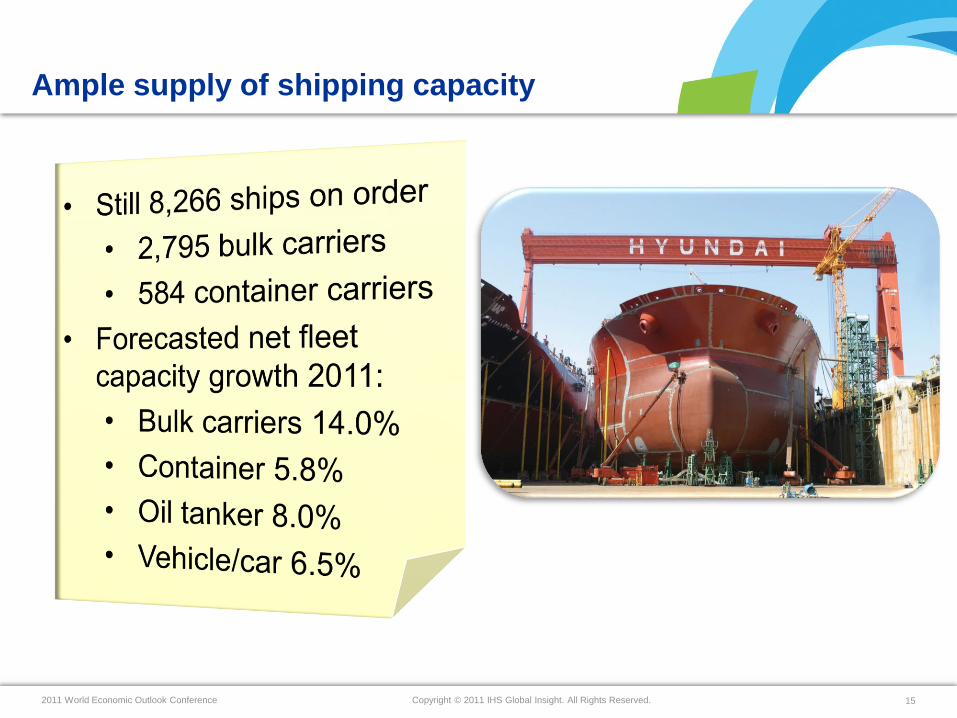

Ample supply of shipping capacity

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 16

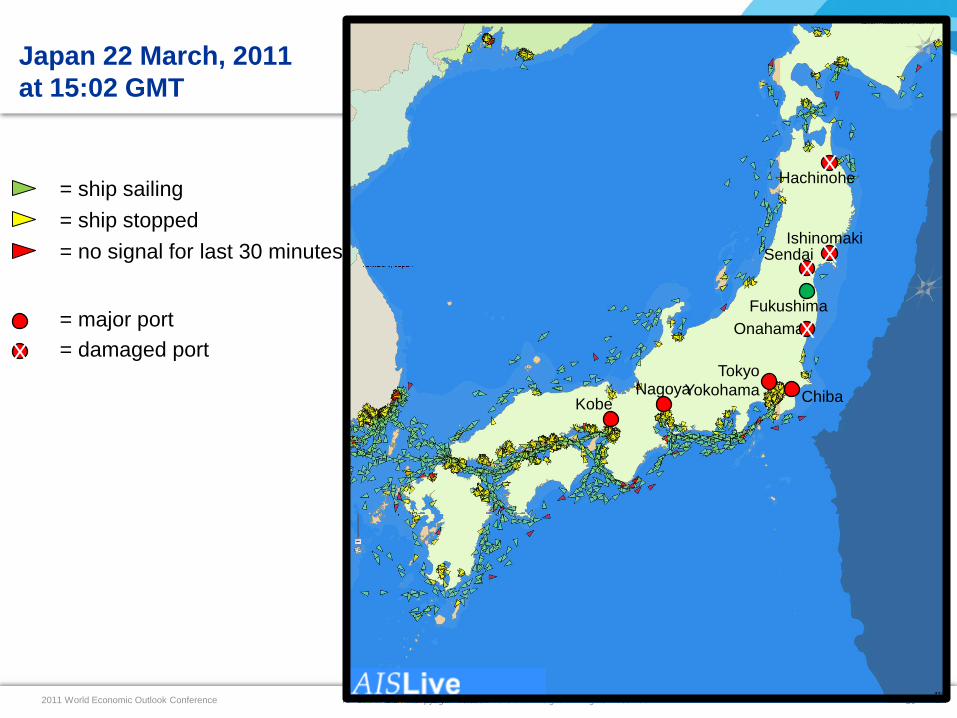

Japan 22 March, 2011

at 15:02 GMT

= ship sailing

= ship stopped

= no signal for last 30 minutes

NagoyaTokyo

Yokohama

Fukushima

ChibaKobe

XSendai

XHachinohe

XIshinomaki

OnahamaXX

= major port

= damaged port

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 17

Conclusions

• Price Volatility is increasing

• Sophisticated trading mechanisms

• Emerging market players

• Supplier conditions have changed

• Fewer players in several markets

• Vertical Integration of production

• Global flows of goods impacted by Emerging Market trends

• Demographic changes

• Income rise

• Rising demand for consumer goods will pressure prices & availability

Thank You for Your Participation!

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 19

Key Themes for Supply Chain Operations

• Supplier Continuity

• Supplier or Material Substitution

• Managing input costs & availability

• Uneven Demand

• Inventory management

• Strategic Planning

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 20

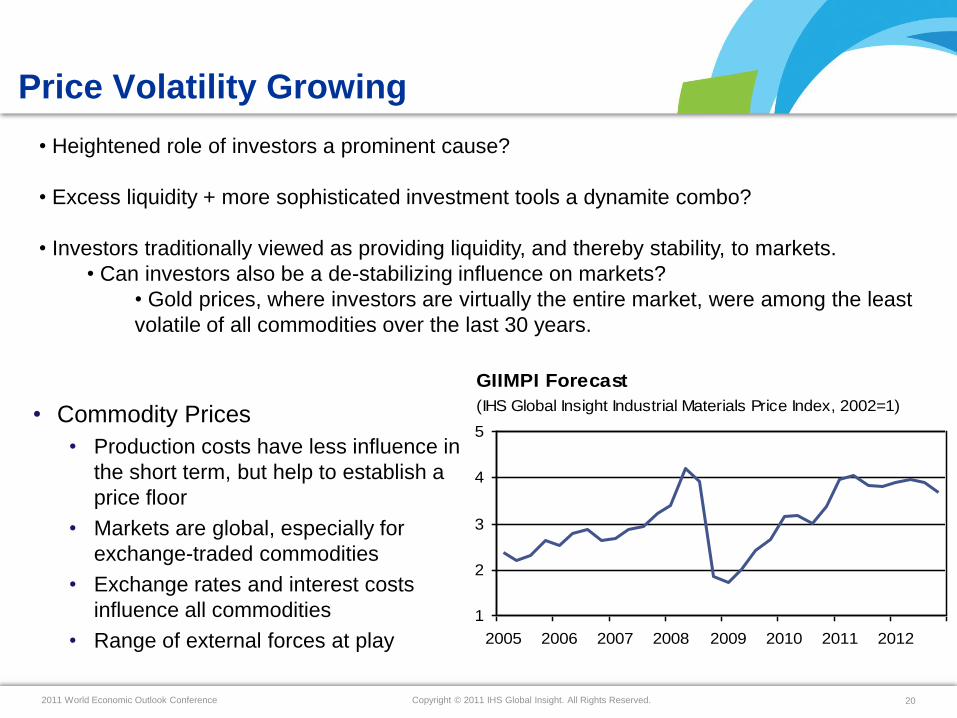

Price Volatility Growing

1

2

3

4

5

2005 2006 2007 2008 2009 2010 2011 2012

GIIMPI Forecast

(IHS Global Insight Industrial Materials Price Index, 2002=1)• Commodity Prices

• Production costs have less influence in

the short term, but help to establish a

price floor

• Markets are global, especially for

exchange-traded commodities

• Exchange rates and interest costs

influence all commodities

• Range of external forces at play

• Heightened role of investors a prominent cause?

• Excess liquidity + more sophisticated investment tools a dynamite combo?

• Investors traditionally viewed as providing liquidity, and thereby stability, to markets.

• Can investors also be a de-stabilizing influence on markets?

• Gold prices, where investors are virtually the entire market, were among the least

volatile of all commodities over the last 30 years.

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 21

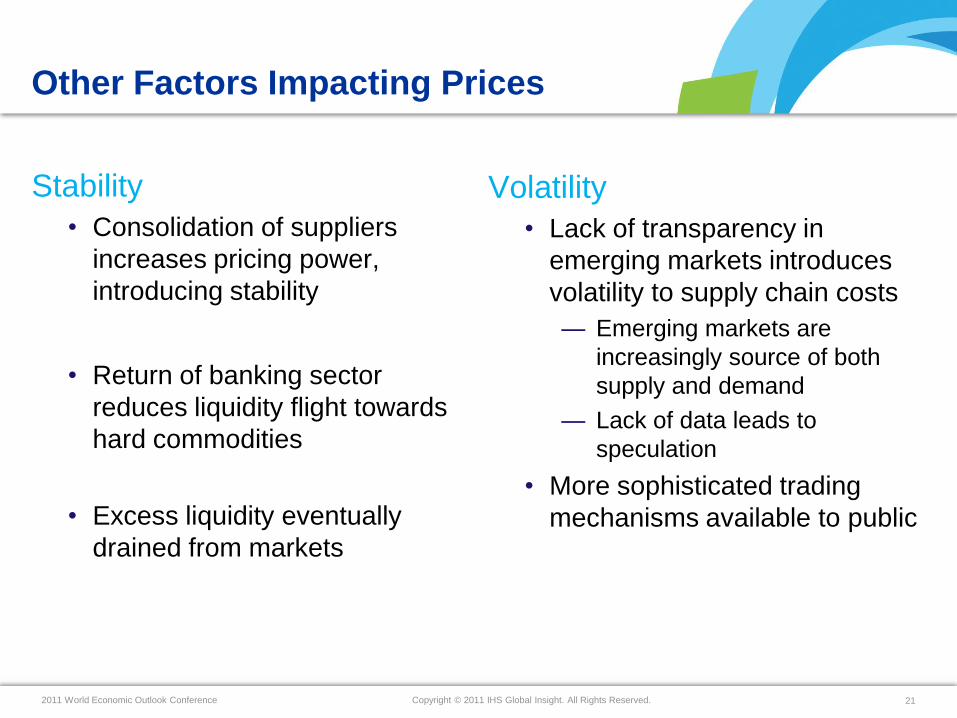

Other Factors Impacting Prices

Stability

• Consolidation of suppliers

increases pricing power,

introducing stability

• Return of banking sector

reduces liquidity flight towards

hard commodities

• Excess liquidity eventually

drained from markets

Volatility

• Lack of transparency in

emerging markets introduces

volatility to supply chain costs

— Emerging markets are

increasingly source of both

supply and demand

— Lack of data leads to

speculation

• More sophisticated trading

mechanisms available to public

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 22

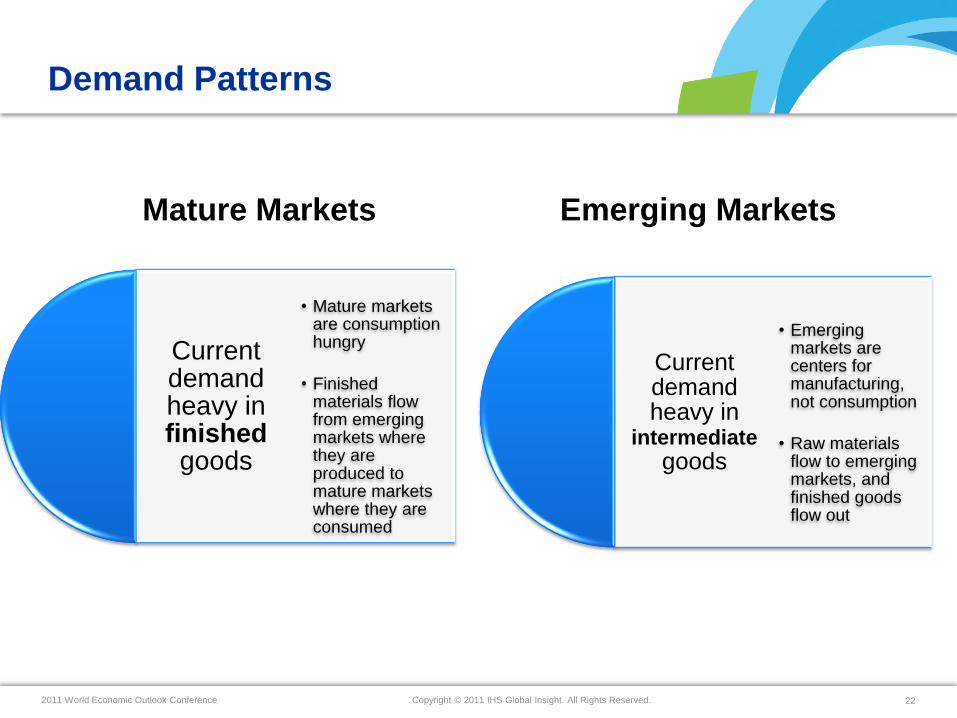

Demand Patterns

Mature Markets Emerging Markets

Current demand heavy in

intermediategoods

• Emerging markets are centers for manufacturing, not consumption

• Raw materials flow to emerging markets, and finished goods flow out

Current demand heavy in finishedgoods

• Mature markets are consumption hungry

• Finished materials flow from emerging markets where they are produced to mature markets where they are consumed

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 23

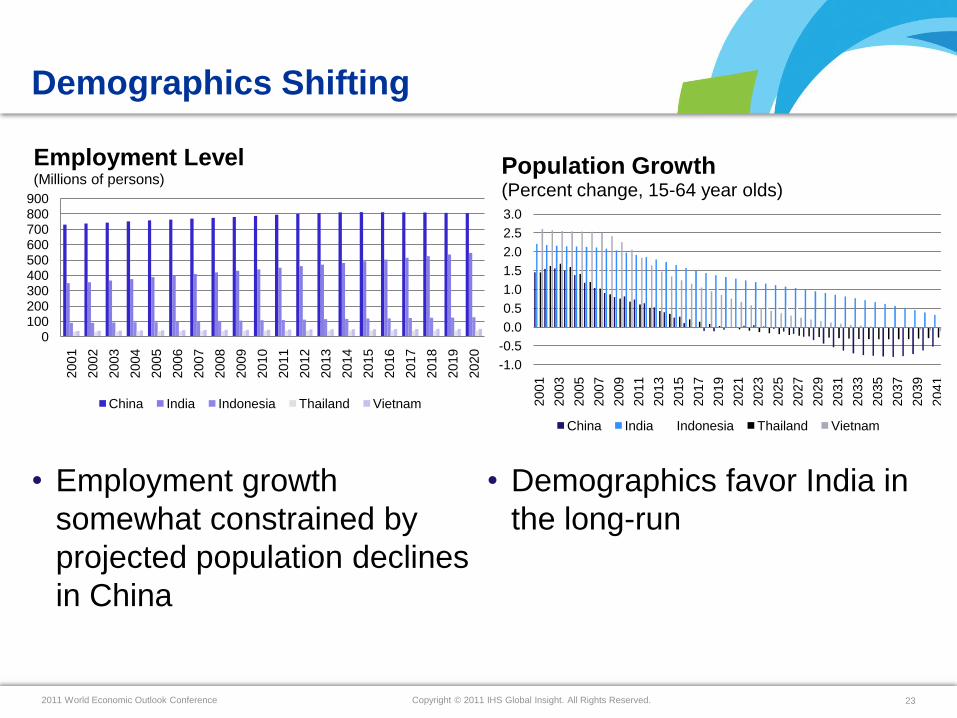

Demographics Shifting

• Demographics favor India in

the long-run

• Employment growth

somewhat constrained by

projected population declines

in China

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

Population Growth(Percent change, 15-64 year olds)

China India Indonesia Thailand Vietnam

0100200300400500600700800900

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Employment Level(Millions of persons)

China India Indonesia Thailand Vietnam

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 24

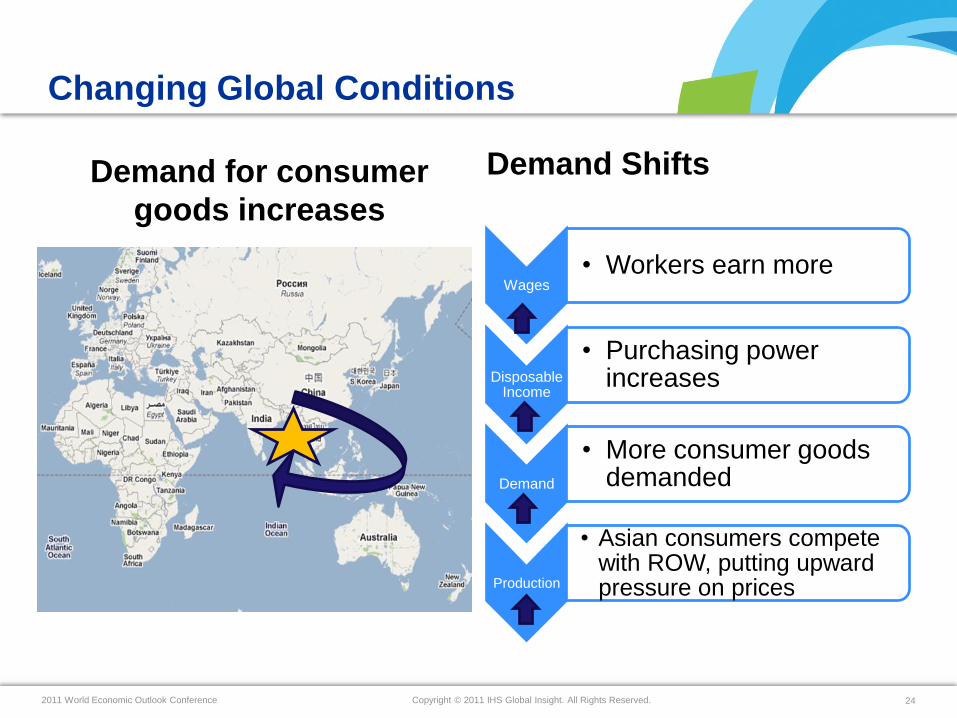

Changing Global Conditions

Demand for consumer

goods increases

Demand Shifts

Wages • Workers earn more

Disposable Income

• Purchasing power increases

Demand

• More consumer goods demanded

Production

• Asian consumers compete with ROW, putting upward pressure on prices

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 25

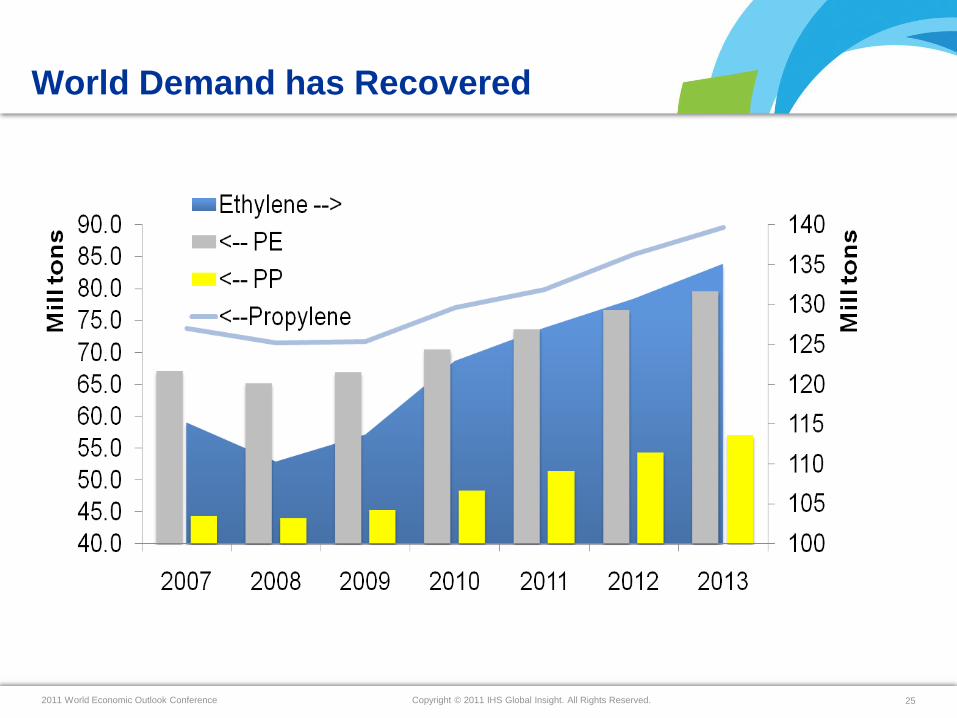

World Demand has Recovered

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 26

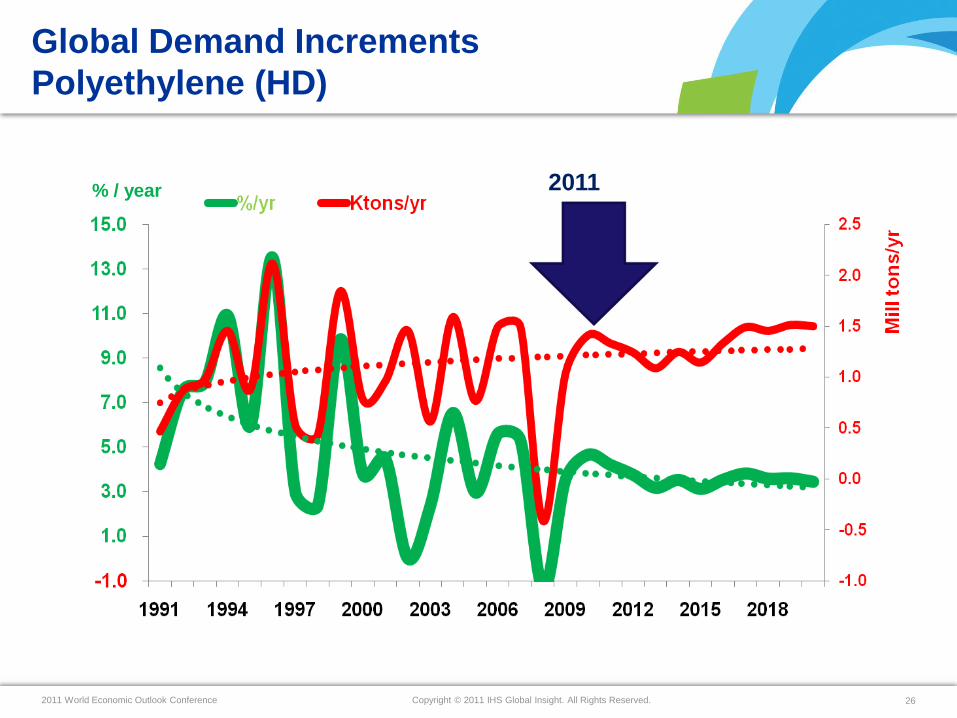

Global Demand Increments

Polyethylene (HD)

% / year 2011

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 27

0

20

40

60

80

100

120

140

160

180

0.0

2.0

4.0

6.0

8.0

10.0

12.0

1990199219941996199820002002200420062008201020122014201620182020

Mil

lio

n t

on

s

Announced Capacity

% Spare

avg 1990 -12

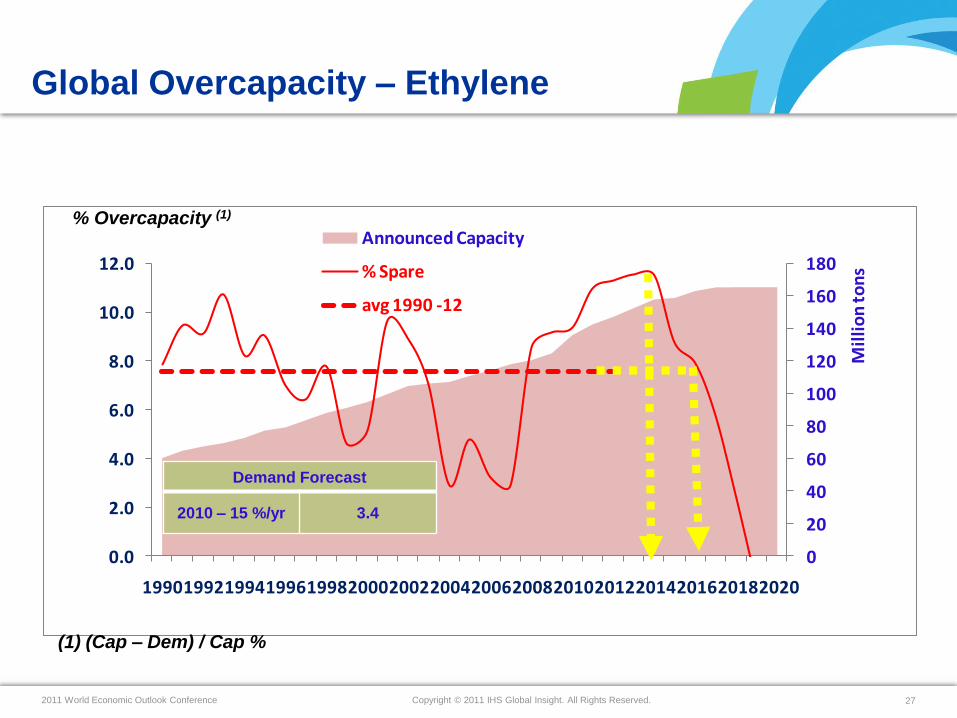

Global Overcapacity – Ethylene

% Overcapacity (1)

(1) (Cap – Dem) / Cap %

Demand Forecast

2010 – 15 %/yr 3.4

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 28

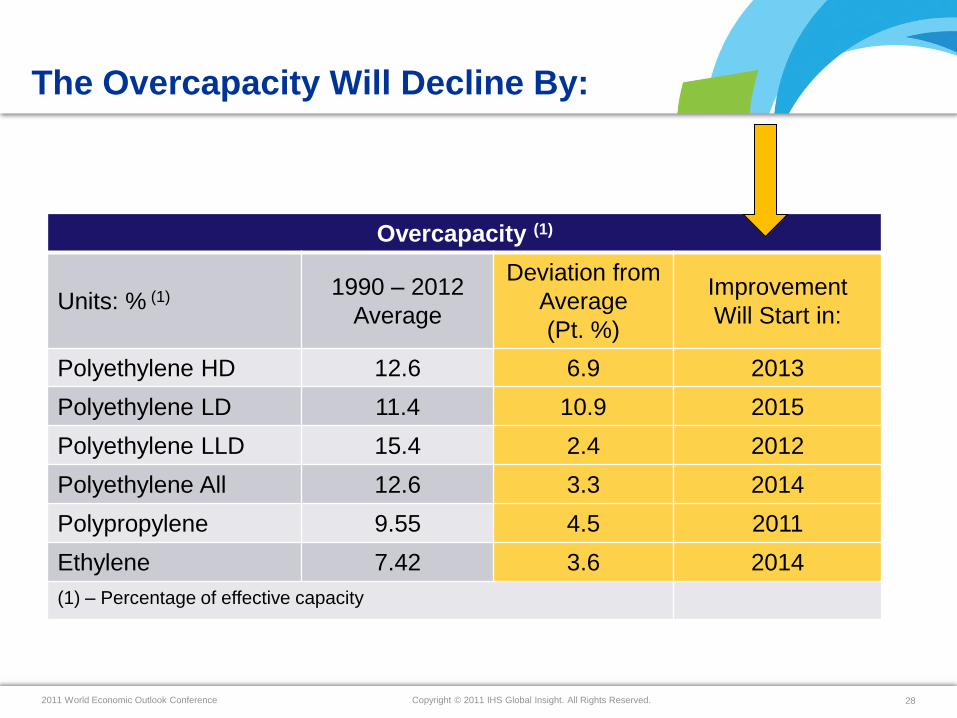

The Overcapacity Will Decline By:

Overcapacity (1)

Units: % (1) 1990 – 2012

Average

Deviation from

Average

(Pt. %)

Improvement

Will Start in:

Polyethylene HD 12.6 6.9 2013

Polyethylene LD 11.4 10.9 2015

Polyethylene LLD 15.4 2.4 2012

Polyethylene All 12.6 3.3 2014

Polypropylene 9.55 4.5 2011

Ethylene 7.42 3.6 2014

(1) – Percentage of effective capacity

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 29

0

5

10

15

20

25

30

350

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mil

lio

n t

on

s

Possible Delays

Announced

% Possible Delay

% of World Capacity that could be delayed

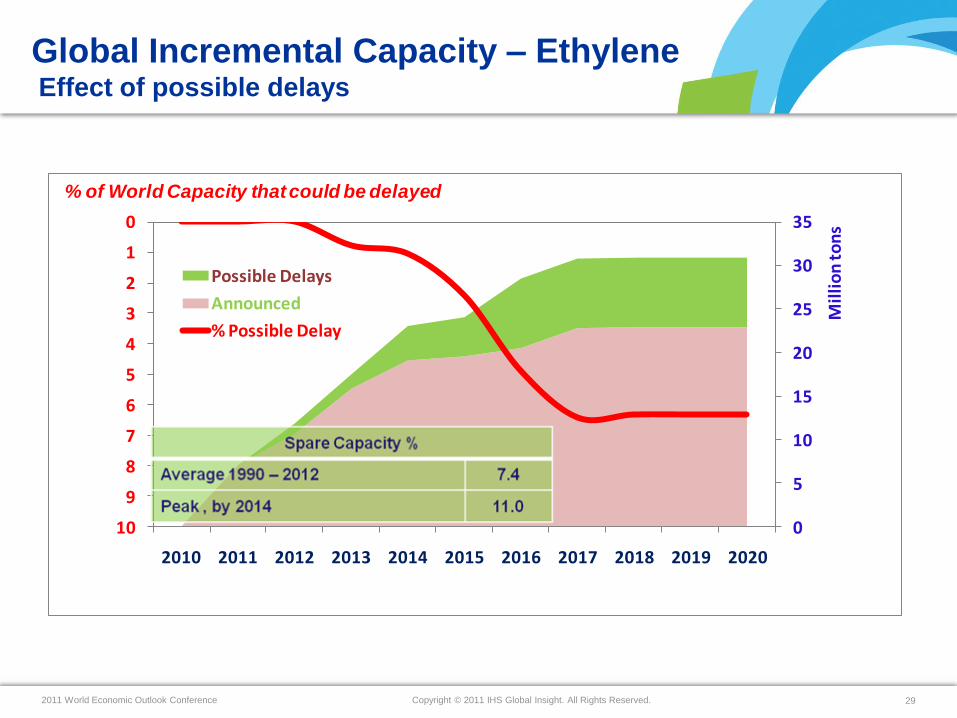

Global Incremental Capacity – EthyleneEffect of possible delays

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 30

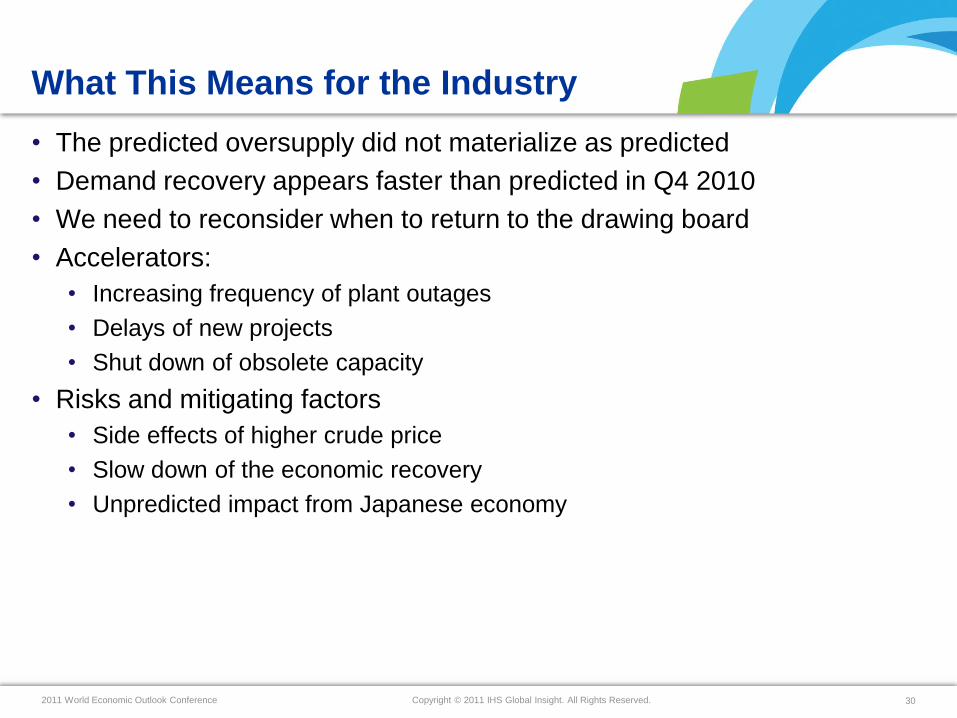

What This Means for the Industry

• The predicted oversupply did not materialize as predicted

• Demand recovery appears faster than predicted in Q4 2010

• We need to reconsider when to return to the drawing board

• Accelerators:

• Increasing frequency of plant outages

• Delays of new projects

• Shut down of obsolete capacity

• Risks and mitigating factors

• Side effects of higher crude price

• Slow down of the economic recovery

• Unpredicted impact from Japanese economy

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 31

PRICE VOLATILITY

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 32

Price Volatility Has Been Increasing

• Contributing Factors

• Crude price is now dependent on perception rather than actual S/D and

extraction costs

• Increased average plant scale and business Interruptions

• Information is now global –> ripple waves –> uncertainty –> price swings

• The commodity market has lost its traditional price reference

• More frequent plant outages

• On line deliveries across the chain

• Remedies?

• Commodity vs. Specialties

• Producers discipline

• Further Consolidation?

Implications for Buyers

•Difficult to predict

•Transactions terms even shorter

•Increasing difficulty to manage

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 33

HAS THE INDUSTRY MODEL

CHANGED?

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 34

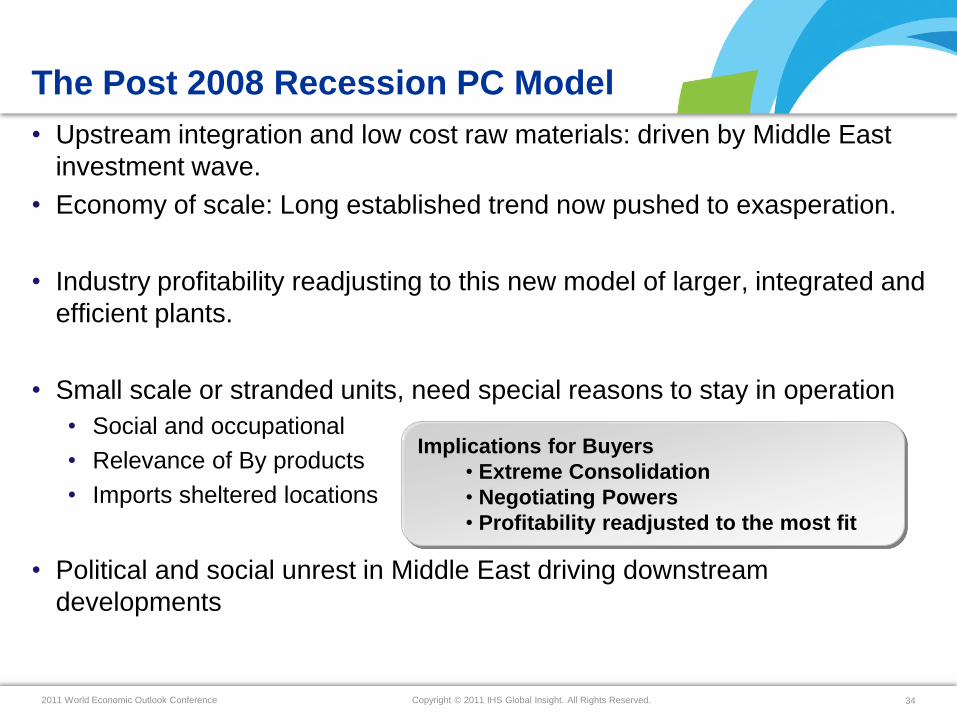

The Post 2008 Recession PC Model

• Upstream integration and low cost raw materials: driven by Middle East

investment wave.

• Economy of scale: Long established trend now pushed to exasperation.

• Industry profitability readjusting to this new model of larger, integrated and

efficient plants.

• Small scale or stranded units, need special reasons to stay in operation

• Social and occupational

• Relevance of By products

• Imports sheltered locations

• Political and social unrest in Middle East driving downstream

developments

Implications for Buyers

• Extreme Consolidation

• Negotiating Powers

• Profitability readjusted to the most fit

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 35

ELASTICITY TO CRUDE PRICE

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 36

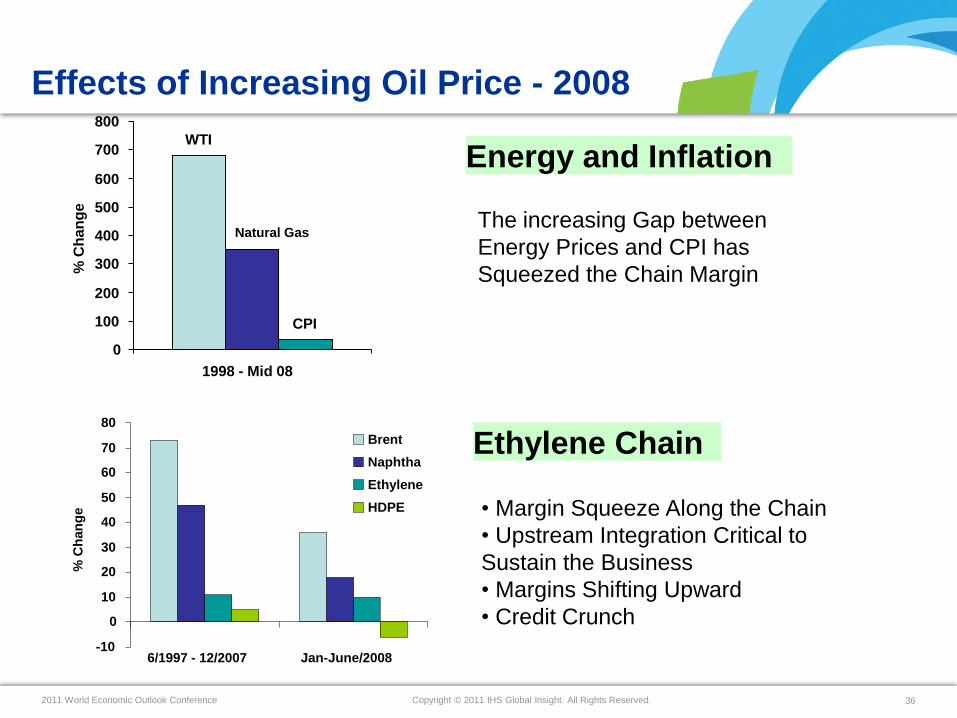

Increasing Oil Price Effects

Energy and Inflation

The increasing Gap between

Energy Prices and CPI has

Squeezed the Chain Margin

WTI

CPI

Natural Gas

0

100

200

300

400

500

600

700

800

1998 - Mid 08

% C

han

ge

Ethylene Chain

• Margin Squeeze Along the Chain

• Upstream Integration Critical to

Sustain the Business

• Margins Shifting Upward

• Credit Crunch

-10

0

10

20

30

40

50

60

70

80

6/1997 - 12/2007 Jan-June/2008

% C

han

ge

Brent

Naphtha

Ethylene

HDPE

Effects of Increasing Oil Price - 2008

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 37

Direct Effect of Crude Price

• Crude – Naphtha – Aromatics and Olefins – Derivatives

• Crude price and chain profitability : Profit squeeze?

• Economic Growth, GDP, Demand

• 1996 – 97 and 2008 – 09 experience

• Demand related to

— Construction and infrastructure

— Automotive and consumer goods

— Food and related packaging

Implications for the Industry

• Each Industry Model, defined by:

• the extent of the chain

• Crude Price Threshold

• Profitability readjusted to the most fit

• Readjustment of Feedstock dependency

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 38

Summary

• Demand has recovered and we should refocus on

opportunities

• Few factors may quickly turn around the supply demand

outlook

• Still few clouds in the short terms

• Political uncertainty

• Energy outlook

• Economic growth in the West

• Sustainability of Asian growth

• Price Volatility: becoming integral part of industry trends

• Crude and Economic growth appear countercyclical ??

• Crude price and profitability: will drive substantial changes in

the feedstock

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 393939

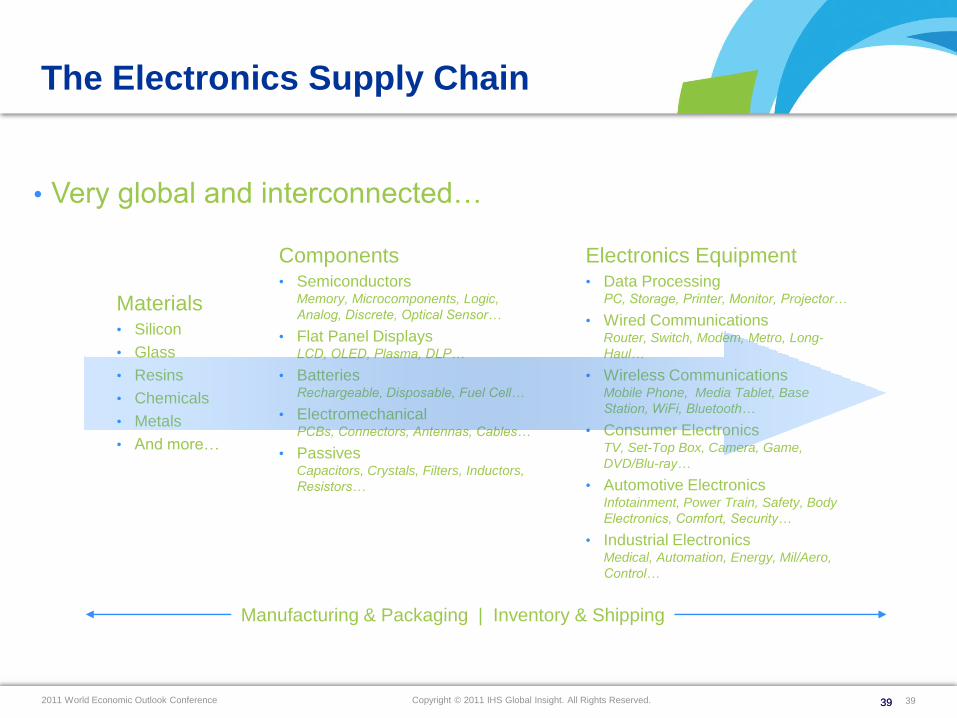

The Electronics Supply Chain

• Very global and interconnected…

Electronics Equipment• Data Processing

PC, Storage, Printer, Monitor, Projector…

• Wired CommunicationsRouter, Switch, Modem, Metro, Long-

Haul…

• Wireless CommunicationsMobile Phone, Media Tablet, Base

Station, WiFi, Bluetooth…

• Consumer ElectronicsTV, Set-Top Box, Camera, Game,

DVD/Blu-ray…

• Automotive ElectronicsInfotainment, Power Train, Safety, Body

Electronics, Comfort, Security…

• Industrial ElectronicsMedical, Automation, Energy, Mil/Aero,

Control…

Components• Semiconductors

Memory, Microcomponents, Logic,

Analog, Discrete, Optical Sensor…

• Flat Panel DisplaysLCD, OLED, Plasma, DLP…

• BatteriesRechargeable, Disposable, Fuel Cell…

• ElectromechanicalPCBs, Connectors, Antennas, Cables…

• PassivesCapacitors, Crystals, Filters, Inductors,

Resistors…

Materials• Silicon

• Glass

• Resins

• Chemicals

• Metals

• And more…

Manufacturing & Packaging | Inventory & Shipping

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 40

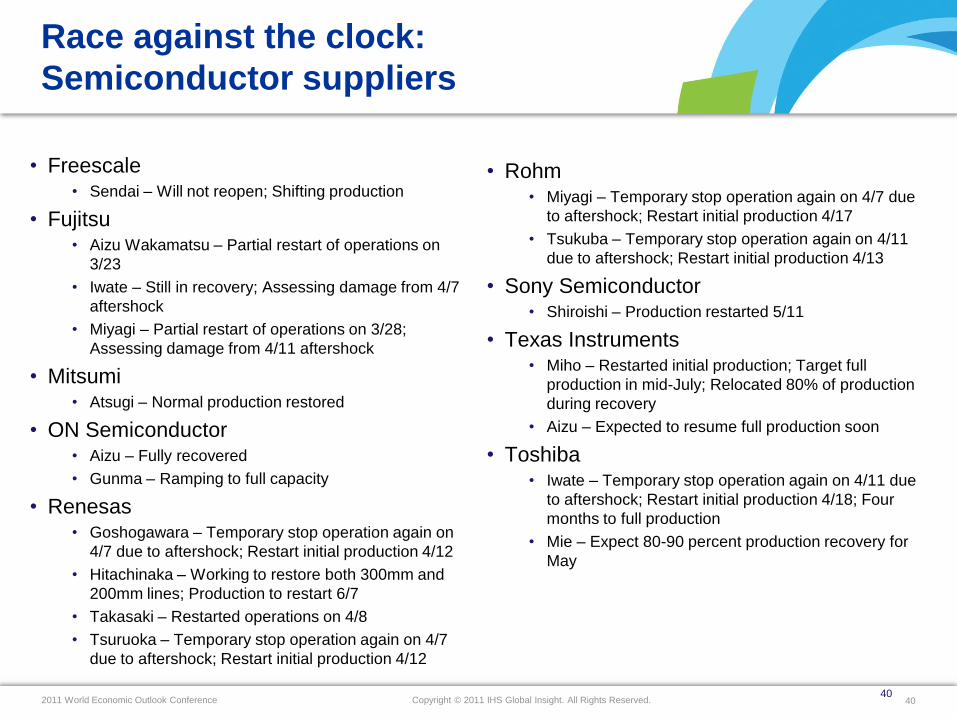

Race against the clock:

Semiconductor suppliers

• Freescale• Sendai – Will not reopen; Shifting production

• Fujitsu• Aizu Wakamatsu – Partial restart of operations on

3/23

• Iwate – Still in recovery; Assessing damage from 4/7

aftershock

• Miyagi – Partial restart of operations on 3/28;

Assessing damage from 4/11 aftershock

• Mitsumi• Atsugi – Normal production restored

• ON Semiconductor• Aizu – Fully recovered

• Gunma – Ramping to full capacity

• Renesas• Goshogawara – Temporary stop operation again on

4/7 due to aftershock; Restart initial production 4/12

• Hitachinaka – Working to restore both 300mm and

200mm lines; Production to restart 6/7

• Takasaki – Restarted operations on 4/8

• Tsuruoka – Temporary stop operation again on 4/7

due to aftershock; Restart initial production 4/12

• Rohm• Miyagi – Temporary stop operation again on 4/7 due

to aftershock; Restart initial production 4/17

• Tsukuba – Temporary stop operation again on 4/11

due to aftershock; Restart initial production 4/13

• Sony Semiconductor• Shiroishi – Production restarted 5/11

• Texas Instruments• Miho – Restarted initial production; Target full

production in mid-July; Relocated 80% of production

during recovery

• Aizu – Expected to resume full production soon

• Toshiba• Iwate – Temporary stop operation again on 4/11 due

to aftershock; Restart initial production 4/18; Four

months to full production

• Mie – Expect 80-90 percent production recovery for

May

40

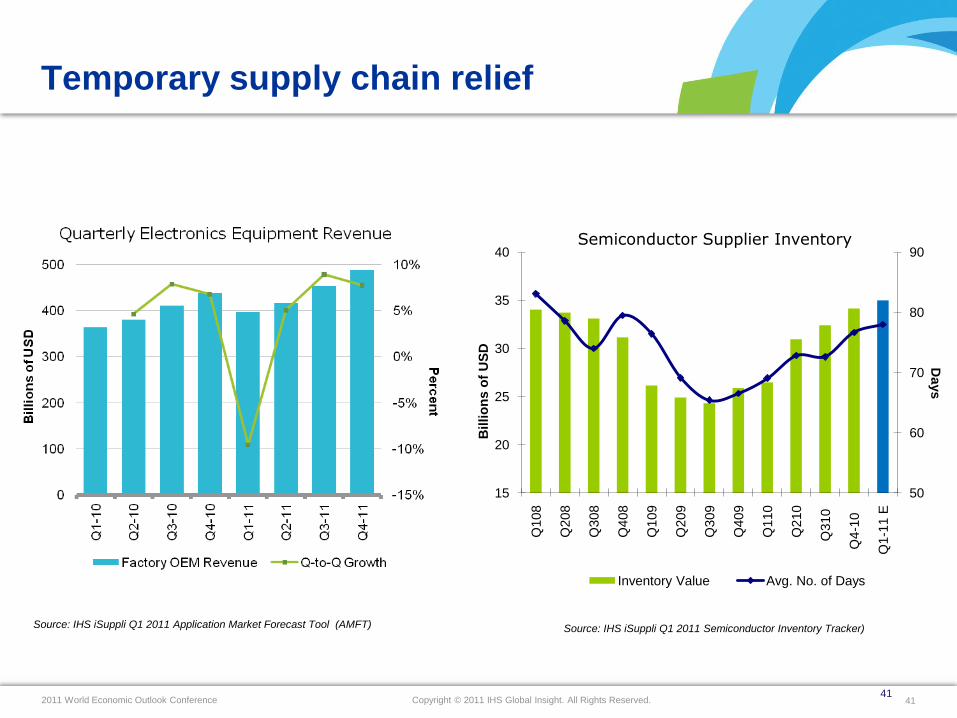

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 41

Temporary supply chain relief

50

60

70

80

90

15

20

25

30

35

40

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q4

-10

Q1-1

1 E

Days

Billio

ns o

f U

SD

Semiconductor Supplier Inventory

Inventory Value Avg. No. of Days

Source: IHS iSuppli Q1 2011 Application Market Forecast Tool (AMFT) Source: IHS iSuppli Q1 2011 Semiconductor Inventory Tracker)

41

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 424242

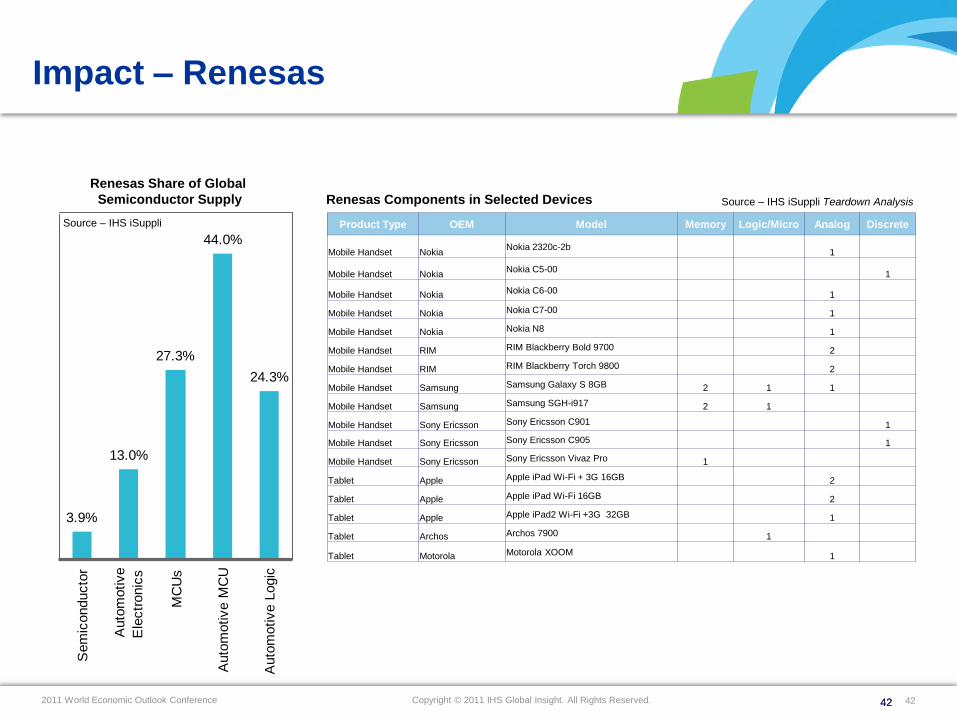

Impact – Renesas

Product Type OEM Model Memory Logic/Micro Analog Discrete

Mobile Handset NokiaNokia 2320c-2b

1

Mobile Handset NokiaNokia C5-00

1

Mobile Handset Nokia Nokia C6-00 1

Mobile Handset Nokia Nokia C7-00 1

Mobile Handset Nokia Nokia N8 1

Mobile Handset RIM RIM Blackberry Bold 9700 2

Mobile Handset RIM RIM Blackberry Torch 9800 2

Mobile Handset Samsung Samsung Galaxy S 8GB 2 1 1

Mobile Handset Samsung Samsung SGH-i917 2 1

Mobile Handset Sony Ericsson Sony Ericsson C901 1

Mobile Handset Sony Ericsson Sony Ericsson C905 1

Mobile Handset Sony Ericsson Sony Ericsson Vivaz Pro 1

Tablet Apple Apple iPad Wi-Fi + 3G 16GB 2

Tablet Apple Apple iPad Wi-Fi 16GB 2

Tablet Apple Apple iPad2 Wi-Fi +3G 32GB 1

Tablet Archos Archos 7900 1

Tablet Motorola Motorola XOOM 1

Renesas Components in Selected Devices Source – IHS iSuppli Teardown Analysis

3.9%

13.0%

27.3%

44.0%

24.3%

Sem

iconducto

r

Auto

motive

Ele

ctr

onic

s

MC

Us

Auto

motive M

CU

Auto

motive L

ogic

Renesas Share of Global

Semiconductor Supply

Source – IHS iSuppli

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 43

Japan and trade with goods

Container

• Some container ports

damaged

• Negative impact on exports

& imports

• Knock-on effects, e.g.

China’s electronic industry

Vehicles

• Japanese car exports falls

• Need for heavy vehicles

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 44

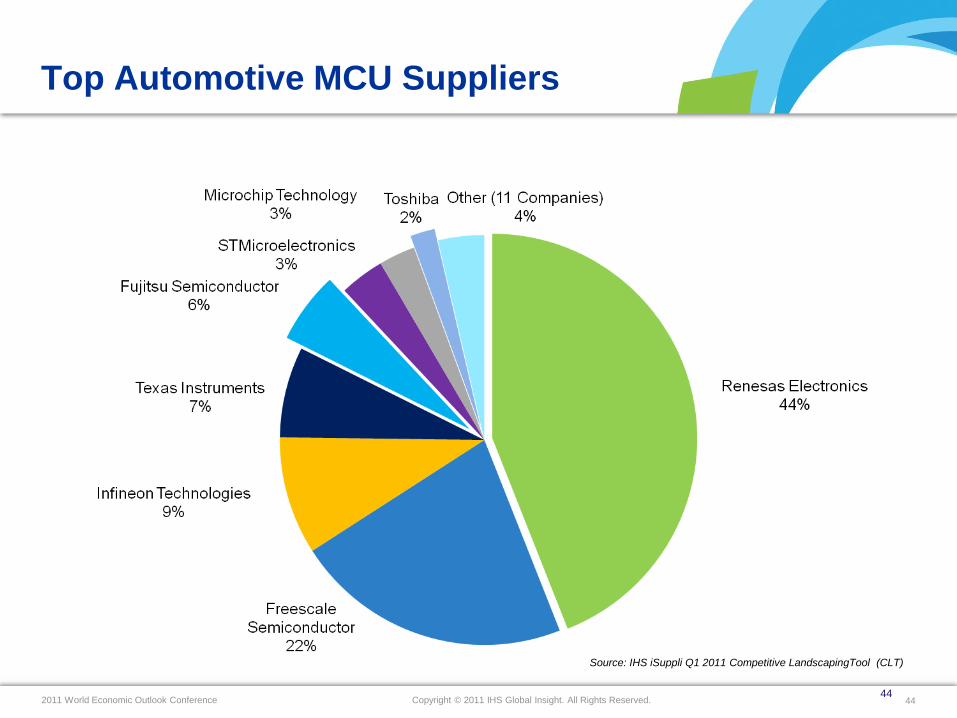

Top Automotive MCU Suppliers

44

Source: IHS iSuppli Q1 2011 Competitive LandscapingTool (CLT)

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 45

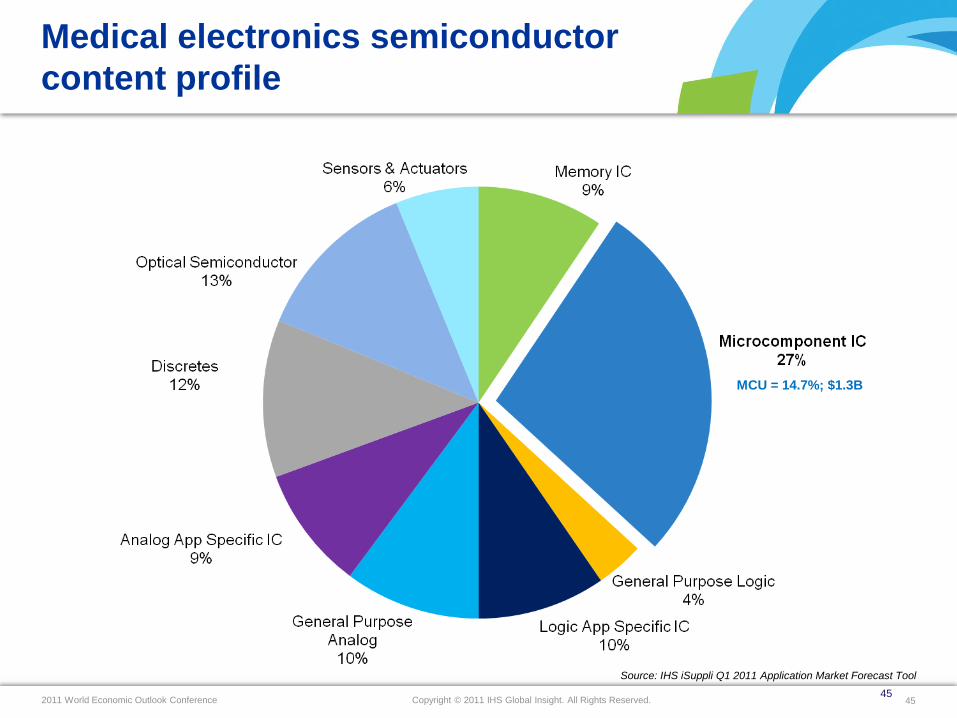

Medical electronics semiconductor

content profile

45

Source: IHS iSuppli Q1 2011 Application Market Forecast Tool

MCU = 14.7%; $1.3B

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 46

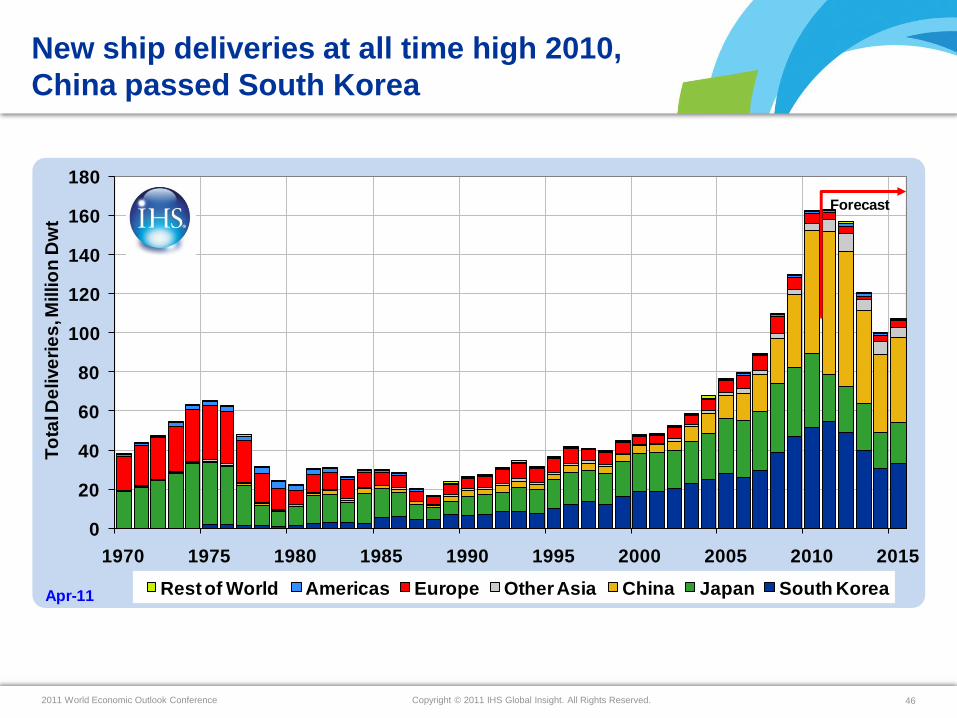

New ship deliveries at all time high 2010,

China passed South Korea

0

20

40

60

80

100

120

140

160

180

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

To

tal D

elive

rie

s, M

illio

n D

wt

Rest of World Americas Europe Other Asia China Japan South KoreaApr-11

Forecast

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 47

Demand for shipping capacity grows too…..

80

90

100

110

120

130

140

150

2005 2006 2007 2008 2009 2010 2011

Seab

orn

e tr

ade

, In

de

x b

ase

d o

n to

nn

es,

teu

Crude & ref oil Dry bulk Containers Copyright © IHS, 2011All Rights reserved

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 48

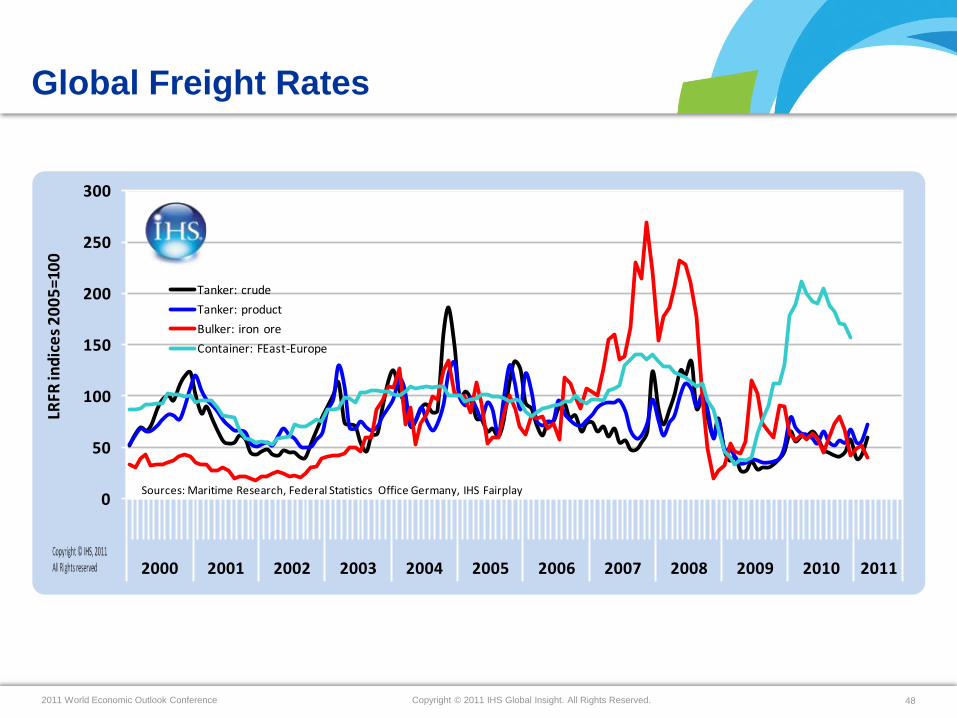

Global Freight Rates

0

50

100

150

200

250

300

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

LRFR

ind

ice

s 2

00

5=1

00

Tanker: crude

Tanker: product

Bulker: iron ore

Container: FEast-Europe

Sources: Maritime Research, Federal Statistics Office Germany, IHS Fairplay

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 49

Other factors ……

• Japan

• North Africa & Middle East

• Piracy

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 50

Japan and trade with commodities

Dry bulk cargo

• Reconstruction of:

• Construction industry

• Infrastructure

• Power plants

• Buildings

• Coal-fired generators at

capacity

• Some import terminals

damaged

Liquid bulk cargo

• 39 of 40 LNG terminals OK

• Substitution of nuclear &

coal shortfall by

• LNG

• Low sulphur fuels

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 51

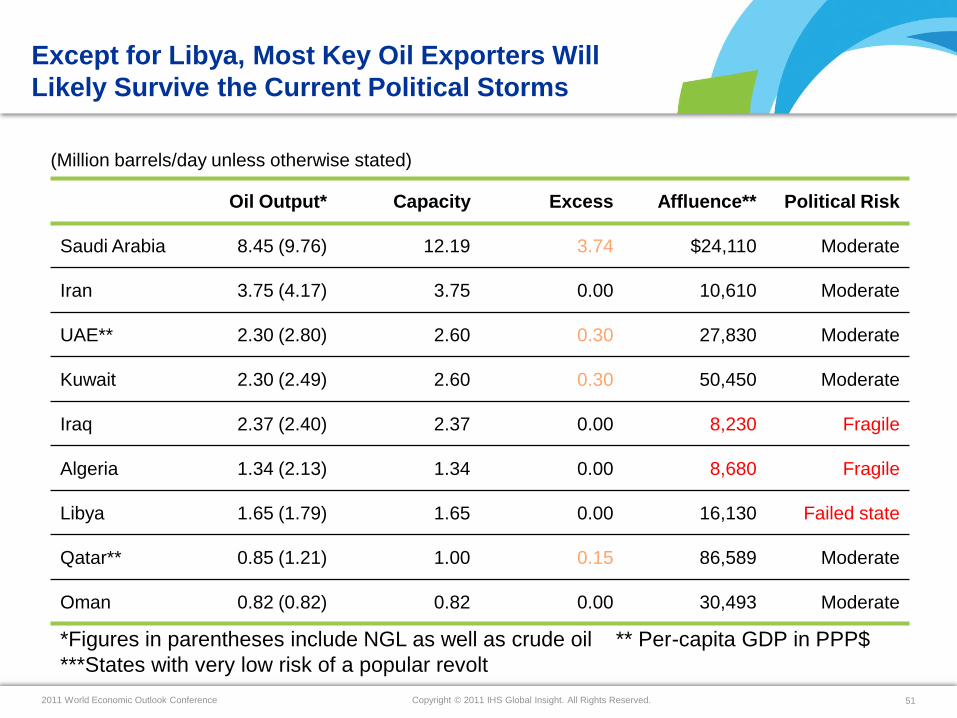

Oil Output* Capacity Excess Affluence** Political Risk

Saudi Arabia 8.45 (9.76) 12.19 3.74 $24,110 Moderate

Iran 3.75 (4.17) 3.75 0.00 10,610 Moderate

UAE** 2.30 (2.80) 2.60 0.30 27,830 Moderate

Kuwait 2.30 (2.49) 2.60 0.30 50,450 Moderate

Iraq 2.37 (2.40) 2.37 0.00 8,230 Fragile

Algeria 1.34 (2.13) 1.34 0.00 8,680 Fragile

Libya 1.65 (1.79) 1.65 0.00 16,130 Failed state

Qatar** 0.85 (1.21) 1.00 0.15 86,589 Moderate

Oman 0.82 (0.82) 0.82 0.00 30,493 Moderate

(Million barrels/day unless otherwise stated)

*Figures in parentheses include NGL as well as crude oil ** Per-capita GDP in PPP$

***States with very low risk of a popular revolt

Except for Libya, Most Key Oil Exporters Will

Likely Survive the Current Political Storms

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 52

N&WEUROPE

S EUROPE

EASTASIA

SOUTHASIA

SOUTHPACIFIC

EASTMIDDLE

EAST

EASTAFRICA

Clothes

Electronics

Manufactured goods

Cars

Energy commodities

Construction commodities

...etc

$686

Bn

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 53

N&WEUROPE

S EUROPE

EASTASIA

SOUTHASIA

SOUTHPACIFIC

EASTMIDDLE

EAST

EASTAFRICA

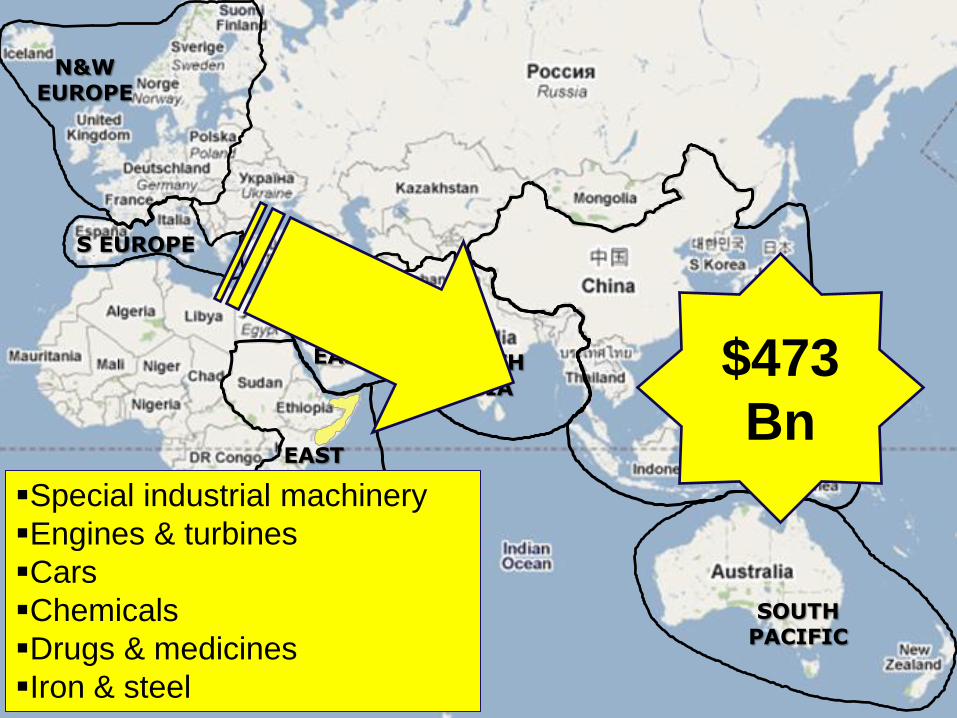

Special industrial machinery

Engines & turbines

Cars

Chemicals

Drugs & medicines

Iron & steel

$473

Bn

Copyright © 2011 IHS Global Insight. All Rights Reserved.2011 World Economic Outlook Conference 54

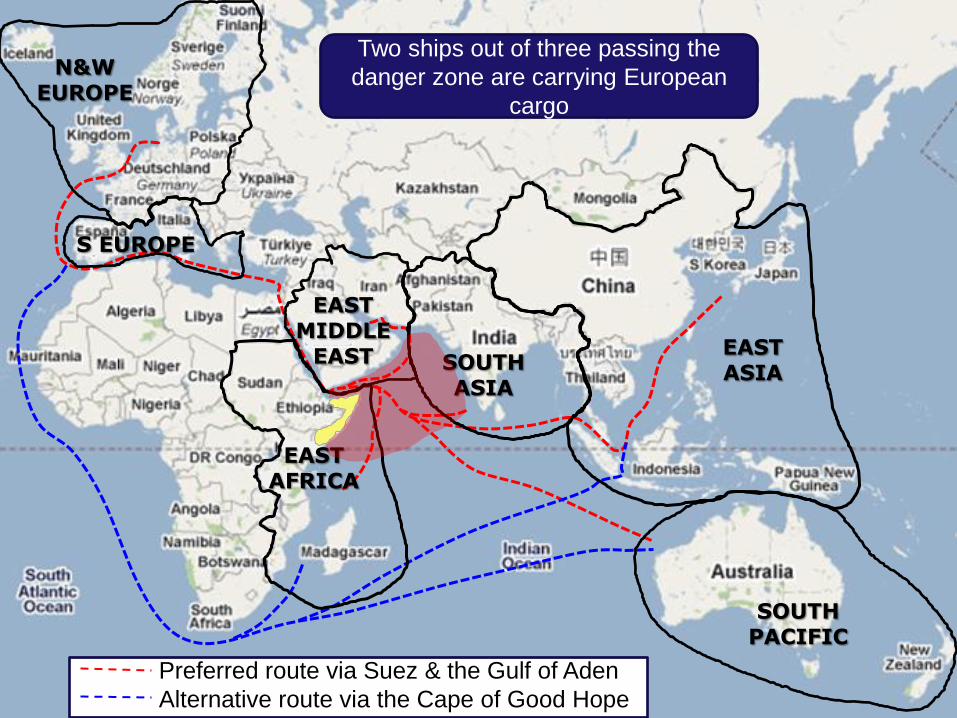

Preferred route via Suez & the Gulf of Aden

Alternative route via the Cape of Good Hope

N&WEUROPE

S EUROPE

EASTASIA

SOUTHASIA

SOUTHPACIFIC

EASTMIDDLE

EAST

EASTAFRICA

Two ships out of three passing the

danger zone are carrying European

cargo

![Assessing and Mapping the Supply Chain of Pineapple Production … · 2016-03-31 · to customers (Christopher, 1998 cited in Peck [11]). Again, Supply chain management seeks to enhance](https://img.pdfslide.us/doc/110x75/5e8fb61dcba4d84b225d6247/assessing-and-mapping-the-supply-chain-of-pineapple-production-2016-03-31-to-customers.jpg)