Embed Size (px)

Citation preview

Accounting Standards for Private EnterprisesPrivate Enterprises

Transition – Middle of the Road

A DISCLAIMER BEFORE WE BEGIN...

Although the presentation and Although the presentation and related materials have been carefully prepared neither the carefully prepared, neither the presentation authors, firm, nor any persons involved in the preparation persons involved in the preparation and/or instruction of the materials accepts any legal responsibility for accepts any legal responsibility for its contents or for any consequences arising from its usearising from its use.

OBJECTIVESConcentrate on presentation and disclosure of ASPE transition F/S with specific reference to:ASPE transition F/S with specific reference to:

Fair value Prepaid vs Capital Asset Government payables Government payables Income taxes Preferred shares disclosure Subsidiaries Business combinations Callable debt Opening balance sheet Retained earnings and cash flow reconciliations for

application of new standards Insights and industry observations Audit or review engagement report example Audit or review engagement report - example

REVIEW OF ASPE Adoption – private enterprises must adopt either

ASPE IFRS f fi l b i i ft ASPE or IFRS for fiscal years beginning on or after January 1, 2011.

A private enterprise is a profit-oriented entity that is neither a publicly accountable enterprise nor an entity in the public sector.

Handbook – now located in Part II

Retrospective - is applying a new accounting policy to transactions, other events and conditions as if that policy had always been applied.

TIMELINE

ASPE AFFECTSASPE AFFECTS:• Fair value• Prepaids• Government payables• Asset retirement obligations (ARO)• Asset retirement obligations (ARO)• Election for Property, Plant & Equipment• Intangibles• Employee future benefits• Stock-based compensation• Business combinations and Joint Ventures• Business combinations and Joint Ventures• Goodwill• Income taxes• Opening balance sheet

CHANGES TO THE NUMBERS: OPENING BALANCE SHEET

Entities must show an opening balance sheet that is prepared in balance sheet that is prepared in accordance with ASPE

This includes a reconciliation of t i d i i l retained earnings, previously

reported income and cash flows

CASE STUDYOff the Ground Incorporated (OGI)( )

INTRO TO CASE STUDY:OFF THE GROUND INCORPORATED (OGI) Large, privately owned company located in Niagara Falls. It

owns a fleet of large cargo helicopters which it rents to businesses and charitable organizations.

The Company also owns a building which it rents.

The Company has three foreign subsidiaries located in New Zealand and Bolivia. There are some related party transactions.

The Company currently uses differential reporting for income taxes, investment in subsidiaries, financial instruments and preferred shares issued in a tax arrangement.

The Company has a January 31 year-end, it is now March 2012 and the controller is starting to prepare the financial statements and working papers for the year-end audit.

CHANGES TO THE NUMBERS:FAIR VALUE OF INVESTMENTS

Fair value – the consideration that would be Fair value the consideration that would be agreed upon in an arm’s length transaction between knowledgeable and willing parties.

Investments in equity instruments quoted in an active market are subsequently measured an active market are subsequently measured at fair value.

Investments not quoted in an active market are subsequently measured at cost less impairment.

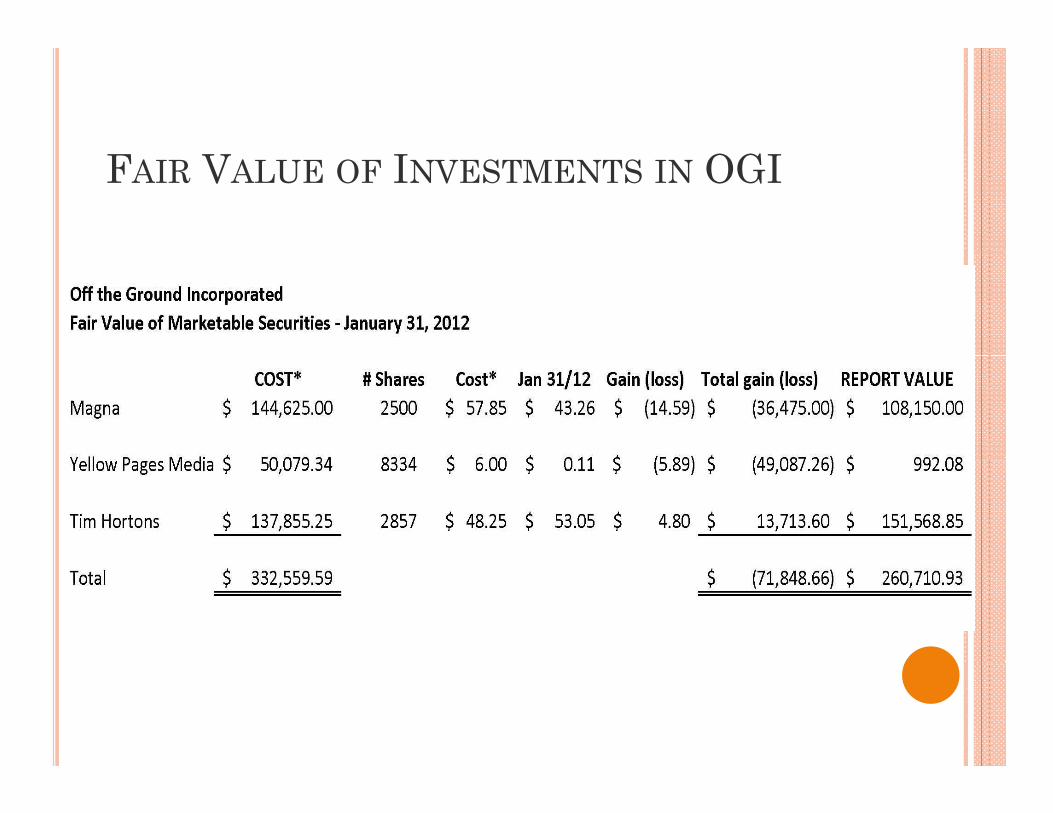

FAIR VALUE OF INVESTMENTS IN OGI

B k l i $250 000 hi h i th t f th Book value is $250,000, which is the cost of the original investments.

Marketable securities include common shares in: Marketable securities include common shares in:- Tim Horton’s- Yellow Media - Magna

At what dates do we need relevant market rates?

FAIR VALUE OF INVESTMENTS IN OGI

FAIR VALUE OF INVESTMENTS IN OGI

IS THIS A CURRENT ASSET - PREPAID? OGI purchases specialty spare parts needed to

maintain its fleet of helicopters. Currently at January 31, 2012 it has $140,000 in spare parts set-up as prepaid asset. When the spare parts are used, the p p p p ,Company DR repairs and maintenance expense and CR the prepaid account.

Is this correct?

PREPAID OR CAPITAL ASSET

1510.06 - Prepaid expenses that meet the p pdefinition of a current asset shall be classified as current assets1510 03 C t t h ll i l d th t 1510.03 - Current assets shall include those assets ordinarily realizable within one year from the date of the balance sheet or within the normal operating cycle Are spare parts “ordinarily realizable” within one

year? year? In some cases – yes if these are regularly replaced parts In some cases – no, as the repairs are sporadic or rare

PREPAID OR CAPITAL ASSET – CONT’D 3061.03 - Property, plant and equipment are p y, p q p

identifiable tangible assets that meet all of the following criteria:

(i) are held for use in the production or supply (i) are held for use in the production or supply of goods and services, for rental to others, for administrative purposes or for the development, construction maintenance or repair of other construction, maintenance or repair of other property, plant and equipment;

(ii) have been acquired, constructed or developed with the intention of being used on a developed with the intention of being used on a continuing basis; and

(iii) are not intended for sale in the ordinary f b icourse of business.

CHANGES TO THE NUMBERS: GOVERNMENT PAYABLES

ASPE now requires the separate disclosure of q pamounts payable for government remittances other than income taxes including federal and provincial sales taxes payroll taxes health taxes provincial sales taxes, payroll taxes, health taxes and worker safety insurance premiums.

Section 1510.15 specifically refers to “payables” and not “receivables”.

This disclosure can be a separate line on the BS or a note disclosureor a note disclosure.

INCOME TAXES

Differential reporting option to account for taxes p g punder the taxes payable method is now part of the handbook. Unanimous consent of shareholders is no longer requiredshareholders is no longer required.

Disclosure changes are minimal and a consistent Disclosure changes are minimal and a consistent with current disclosures under existing GAAP.

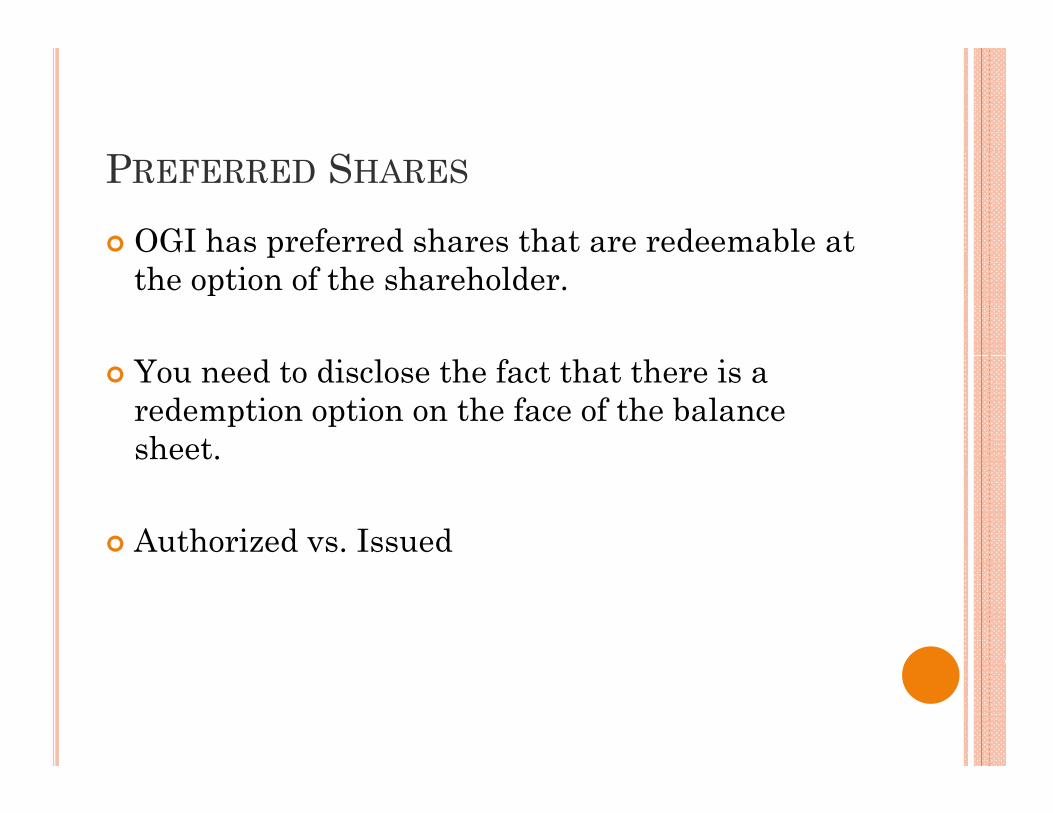

PREFERRED SHARES

OGI has preferred shares that are redeemable at pthe option of the shareholder.

You need to disclose the fact that there is a redemption option on the face of the balance sheet. sheet.

Authorized vs. Issued

SUBSIDIARIES

All the options that were available under pdifferential reporting exist under ASPE: Cost method

E it th d Equity method Consolidate However, all subsidiaries MUST be accounted for

using the same method. o There are changes to the note disclosure:

Significant accounting policy note % owned • Significant accounting policy note - % owned, “private”, name of subsidiary.

• Impairment disclosure has been expanded. • All other disclosures remain the same.

QUESTIONS?Q

COFFEE TIME!

AND WE’RE BACK!

BUSINESS COMBINATIONS

The acquisition method is the required method q q(used to be the purchase method).

The acquisition method – measures the fair value of what has been acquired (not what has been of what has been acquired (not what has been given up).

Any contingent consideration should be measured at fair value at the acquisition measured at fair value at the acquisition date (not just disclosed).

Identify the acquirer, acquisition date, and id if d h d li bili i identify and measure the assets and liabilities that were acquired.

Measurement period – once all facts known but pcannot exceed 1 year from date of acquisition.

BUSINESS COMBINATIONS CONT’D Any adjustments during the measurement period y j g p

will be apply retrospectively as if it was always known.A i iti t d Acquisition costs are expensed.

BUSINESS COMBINATIONS - EXAMPLE

Company ABC purchased 100% of the shares of p y pCompany XYZ on April 15, 2011.

Company XYZ net assets = $400,000 Company XYZ customer list was worth $150,000 Company XYZ had goodwill of $500,000

P h i $1 050 000 Purchase price – $1,050,000 Cash paid of - $650,000 and a note taken back of

$400,000 with payments in four equal (non-$ , p y q (interest bearing) instalments of $100,000 beginning Dec 31, 2011 if certain income targets are metare met.

WHAT ARE THE ENTRIES YOU WOULDRECORD: On acquisition?q

The date the 1st instalment is due if target is met?

Th d t th 1 t i t l t i d if th t t i The date the 1st instalment is due if the target in NOT met?

The date of 2nd instalment is due when the target is met in the 1st year but not subsequently?

BUSINESS COMBINATIONS - EXAMPLE

Initial entry on acquisitiony qDR Investment 1,030,000 CR Cash 650,000CR N t bl 380 000CR Note payable 380,000(entry considers time value of money – estimated for

example)

As the first payment of the note payable is within the measurement period there will be more data to measurement period there will be more data to assess the fair value at this point in time.

BUSINESS COMBINATIONS - EXAMPLE

First instalment date if target is met:gDR Note payable 95,000DR Interest expense 5,000CR C h 100 000CR Cash 100,000

First instalment date when target is NOT met: First instalment date when target is NOT met:DR Note payable 100,000CR Investment 100,000( i i i d )(on acquisition date)

This would indicate that goodwill is impaired and This would indicate that goodwill is impaired and should be tested.

BUSINESS COMBINATIONS - EXAMPLE

The date of 2nd instalment is due when the target gis met in the 1st year but not subsequently?DR Note payable 95,000DR I t t 5 000DR Interest expense 5,000CR Gain on purchase price adjustment 100,000

BUSINESS COMBINATIONS - DISCLOSURE

On April 15, 2011, Company ABC acquired 100% of th t t di h f XYZ C the outstanding shares of XYZ Company, a complimentary company providing services in the same industry as Company ABC. The payment was cash of $650,000 and a $400,000 note payable which $ , $ , p yis non-interest bearing and resulting in goodwill of $500,000.

Cash FVA t i bl FVAccounts receivable FVInvestments FVCapital assets FVLiabilities FVLiabilities FVL-T debt FV

Company ABC does not consolidate this subsidiary but accounts for it using the cost method.

CALLABLE DEBT There is now an option to show “callable loans”

(loans with regular payments and callable feature) as callable debt on the Balance Sheet.

The non-current portion is placed below current liabilities but before long-term liabilities liabilities but before long-term liabilities.

OPENING BALANCE SHEET

Common presentation is split between a Common presentation is split between a third column on the balance sheet or in a note to the F/S.

Remember, this opening balance sheet will include:

Fair value presentation of the investments (for our example)Other required and optional transition issues (ARO, goodwill, PPE etc)

RETAINED EARNINGS, NET INCOME ANDCASH FLOW RECONCILIATION

Retained earning reconciliation at transition date gis a note disclosure that outlines all the changes with respect to retrospective application of the new ASPE standardsnew ASPE standards.

INSIGHTS AND INDUSTRY OBSERVATIONS

Netting of government payables and receivablesg g p y Is it permitted? How to properly present on FS?

A R i Obli i Asset Retirement Obligations Watch for Leaseholds! Watch for Environmental Liabilities!Watch for Environmental Liabilities!

What have we heard from banks? What have we heard from clients?

EXAMPLE OF AUDIT REPORT UNDER ASPE

Comparative Information p “we are not engaged to report on the restated

comparative information, and as such, it is unaudited.”

Financial statements are not esthetically pleasing 3rd column can make Balance Sheet very busy 3 column can make Balance Sheet very busy Note formatting can also make columns look squished

(especially capital assets)

Financial statements can take additional time to set-up – especially if we have opening balance changeschanges

QUESTIONS?Q