Embed Size (px)

Citation preview

Asia’s MobileAdvertising

Marketplace Has Gone Full Circle

WHITE PAPER

Prepared by Nick Lane Chief Analyst, mobileSQUARED

June 2012

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 2

Rising smartphone uptake and lowering cost of data plans for consumers have caused an influx of mobilenetworks and resellers into the SEA ecosystem over the past 18-months, offering more compellingsolutions at scale to advertisers. More recently, the rising adoption of screen-neutral channel planning and thinking by agencies has seen the inclusion ofmobile into top-level discussions for maturemarkets like Singapore, with the rest of theregion following closely. But more significantly,as we live in an increasingly socially-enabledenvironment, advertisers are experiencing first-handas consumers themselves, that mobile providesreal-time access to the world. They have realisedthat to be social is to be mobile, and accepted that the time to embrace the space is now... if they haven’t already done so.

Ian LoonDirector Starcom MediaVest

The latest developments in mobile advertising will see brandscreating richer, more immersive mobile ad campaigns, while the next generation of smaller brands, businesses and apps willbolster spend on standard mobile ad banners.

The mobile advertising ecosystem is expanding and will start to command a greater percentage of digital ad spend across Asia.

For the purposes of this report, mobileSQUARED has looked at 10 markets (Australia, China, India, Indonesia, Japan, Malaysia,Singapore, South Korea, Thailand and Vietnam) representing 2.7 billion mobile subscriptions.

The research reveals that the mobile advertising industry has gone full circle and now not only incorporates brands of all sizes, but is embracing the developer community also.

The model is becoming self-perpetuating and generatingsignificant growth and opportunities for all brands andbusinesses alike.

Consequently, mobileSQUARED forecasts mobile advertisingrevenues across the Asia10 region of US$3.13 billion, increasing to US$3.96 billion in 2013, and US$6.21 billion by 2015.

Of this, mobile display market will be worth US$2.02 billion in 2012 and US$2.98 billion in 2015. In 2012, mobile display will ac-count for 64% of total mobile spend.

Smartphones are driving this change.

Summary

2.7 BillionMobile subscriptions

across the Asia10 in 2012

$3.13 BillionMobile advertising revenues

across the Asia10 in 2012

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 3

Across much of Asia, the mobile advertising marketplace isreaching new levels of maturity, and with it, comes a number of developments that are reshaping and defining the industry for the long term.

Consequently, the Asian mobile advertising marketplace is nowundergoing a two-pronged growth spurt driven by the big brands looking to diversify their mobile strategy into a broader marketingmix, while the rise of smartphones and apps, has spawned theresurrection of the mobile content companies investing inmobile advertising.

It can be said, that the mobile content industry was, in effect, the ‘Founding Father’ of the mobile advertising industry. Before thearrival of the “Big Brands” into the mobile advertising scene, the marketplace was dominated by the mobile content providerspromoting their games, “Crazy Frog” ringtones, and wallpapers. In 2005 mobile content companies represented approximately 80%of total global mobile advertising spend which stood atapproximately US$500 million.

Then the Big Brands arrived, massively upped the ante anddominated the mobile advertising spend landscape. Today,mobile advertising spend across the Asia10 region will be worth US$3.13 billion in 2012, rising to US$6.21 billion in 2015.

Mobile advertising spend across the Asia10 markets is dominated by mobile banner campaigns which account for 64% of campaign spend in 2012. While the mobile banner market in the Asia10 isprojected to increase from US$2.02 billion in 2012 to US$2.98billion in 2015, it will be competing with alternative mobileadvertising formats (especially permission-based messagingadvertising and search), and that will see mobile banner spendaccount for 48% of total spend by the end of the forecast period.

Mobile advertising is going back to basics

Chart 1: Mobile ad spend, Asia10 (Billions US$)7

64%Mobile banner campaigns of total mobile advertising spend in 2012

$2 BillionMobile banner market worth

across the Asia in 2012

2010

6

5

4

3

2

1

0

Messaging

Search

Rich Media (incl. video)

Banner

Source: mobileSQUARED

2011 2012 2013 2014 2015

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 4

A breakdown of the rich media campaign spend as a percentage of total banner campaign spend will increase from 12% in 2012 to almost 50% in 2015. Regardless, spend in mobile banners across Asia10 will be driven by two factors.

Firstly, the content and service providers as previously outlinedthose smaller brands, businesses and app developers lookingto promote their apps by typically spending on averageUS$500-3,000 per campaign.

While this level of campaign is unlikely to have a major impact on the developed mobile advertising markets of Australia, Japan,Singapore and South Korea, and to a certain extent China, thisactivity will have a phenomenal impact on emerging anddeveloping mobile advertising markets of India, Indonesia,Malaysia, Thailand and Vietnam.

It is estimated that the smaller brands, businesses and appdevelopers now account for 60% of mobile banner campaigns indeveloping and emerging markets.

Then there are the bigger brands that are looking to engageconsumers with a more compelling experience by developingcreative, rich-media mobile ad campaigns.

mobileSQUARED research reveals that on average across the Asia10, approximately 16% of campaigns are rich media-based, with markets such as Australia and Japan experiencing around40-45% of all campaigns based on rich media. While there is an increased creative cost attached to rich mediamobile advertising campaigns, the click-through rate of 0.8% is at least double that of standard mobile banner ad campaigns.

Chart 2: Banner spend breakdown, Asia10 (Millions)

2010

Banner

Rich Media (incl. video)

Source: mobileSQUARED

2011 2012 2013 2014 2015

50%Increase of mobile rich mediaads across the Asia10 by 2015

1200

1000

800

600

400

200

0

2000

1600

1400

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 5

Although rich media campaigns are not the norm across the Asia10 markets, the research revealed that there is a significantpent-up demand to migrate existing campaigns into asignificantly richer and immersive experience.

From a brands’ perspective, they are now looking to develop a 1-2-1 communication with consumers, and have identifiedmobile as the primary media to achieve that goal.

In a region dominated by prepaid, user profiling is very limitedwhich makes the delivery of targeted and relevant ads to mobile users all-the-more challenging.

The obvious way to overcome this is to develop an opt-in userdatabase.

That means brands in the more advanced Asia10 markets are now starting to migrate towards a CRM-based model to deliverpromotions, vouchers and discounts to a brand’s opt-incustomer base directly.

While this strategy will ensure mobile becomes more immersed in the broader marketing mix, it will require the support ofawareness campaigns – and most likely, rich media campaigns –provided by mobile banner advertising to continually boost and refresh each brands’ database.

The emergence of smartphones and prevalence of theaccompanying “apps” has spurred on the content – and nowservices – sectors across Asia over the last 12 months.

Where the market has evolved significantly, is that in the firstmobile content era of 2004-2007 (i.e. pre smartphones), access was limited via the mobile internet and most likely an operator portal.

What’s more, the content portfolio was largely restricted to games, music and entertainment.

While these categories still feature prominently, in this ‘2.0mobile world’ dominated by app stores, the breadth of howcontent and services extends to business, reading, education,finance, health & fitness, medical, navigation, photography,productivity, reference, travel and utilities.

There is an app for everything, and more importantly, behindevery app is an app developer or a brand or business funding its creation and its promotion.

But the one over-riding factor that is the glue behind all of thedevelopments outlined in this white paper thus far is the rapidadoption of the smartphone.

The driving force behind this nextwave of mobile advertising activity

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 6

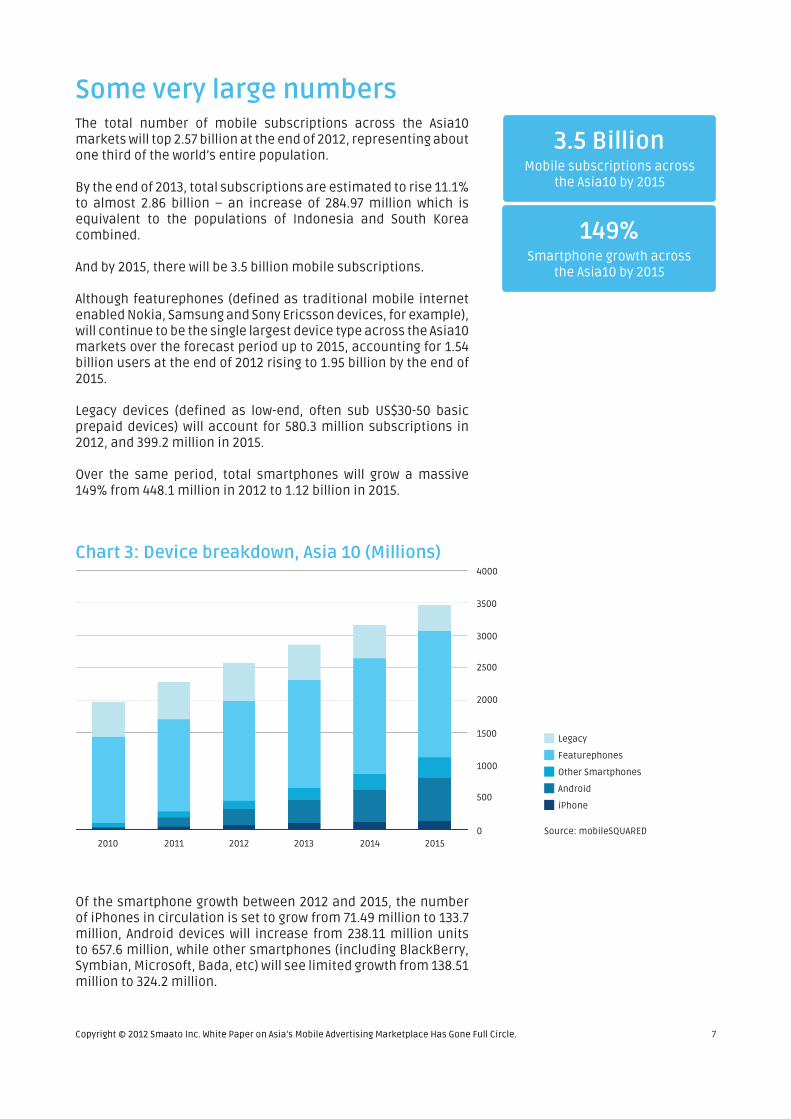

Some very large numbersThe total number of mobile subscriptions across the Asia10markets will top 2.57 billion at the end of 2012, representing about one third of the world’s entire population.

By the end of 2013, total subscriptions are estimated to rise 11.1% to almost 2.86 billion – an increase of 284.97 million which isequivalent to the populations of Indonesia and South Koreacombined.

And by 2015, there will be 3.5 billion mobile subscriptions.

Although featurephones (defined as traditional mobile internetenabled Nokia, Samsung and Sony Ericsson devices, for example), will continue to be the single largest device type across the Asia10 markets over the forecast period up to 2015, accounting for 1.54billion users at the end of 2012 rising to 1.95 billion by the end of 2015.

Legacy devices (defined as low-end, often sub US$30-50 basicprepaid devices) will account for 580.3 million subscriptions in 2012, and 399.2 million in 2015.

Over the same period, total smartphones will grow a massive 149% from 448.1 million in 2012 to 1.12 billion in 2015.

Chart 3: Device breakdown, Asia 10 (Millions)

3500

2010

3000

2500

2000

1500

1000

500

0

Featurephones

Other Smartphones

Android

iPhone

Source: mobileSQUARED

2011 2012 2013 2014 2015

4000

Legacy

Of the smartphone growth between 2012 and 2015, the number of iPhones in circulation is set to grow from 71.49 million to 133.7million, Android devices will increase from 238.11 million units to 657.6 million, while other smartphones (including BlackBerry, Symbian, Microsoft, Bada, etc) will see limited growth from 138.51 million to 324.2 million.

3.5 BillionMobile subscriptions across

the Asia10 by 2015

149%Smartphone growth across

the Asia10 by 2015

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 7

Breakdown by deviceFeaturephone users will continue to dominate the Asia10marketplace, although their market share will decrease slightly over the period from 60% in 2012 to 56% in 2015.

This of course means that the market for smartphones isexploding with one-in-five users throughout the Asia10 owning asmartphone by the end of 2013.

The overall market share of smartphones is forecast to rise from 17.4% in 2012 to 32% in 2015 – primarily driven by the growingdominance of Android devices and other smartphones such as Blackberry and Symbian in specific marketplaces.

Chart 4: Smartphone vs Featurephone penetration, Asia10

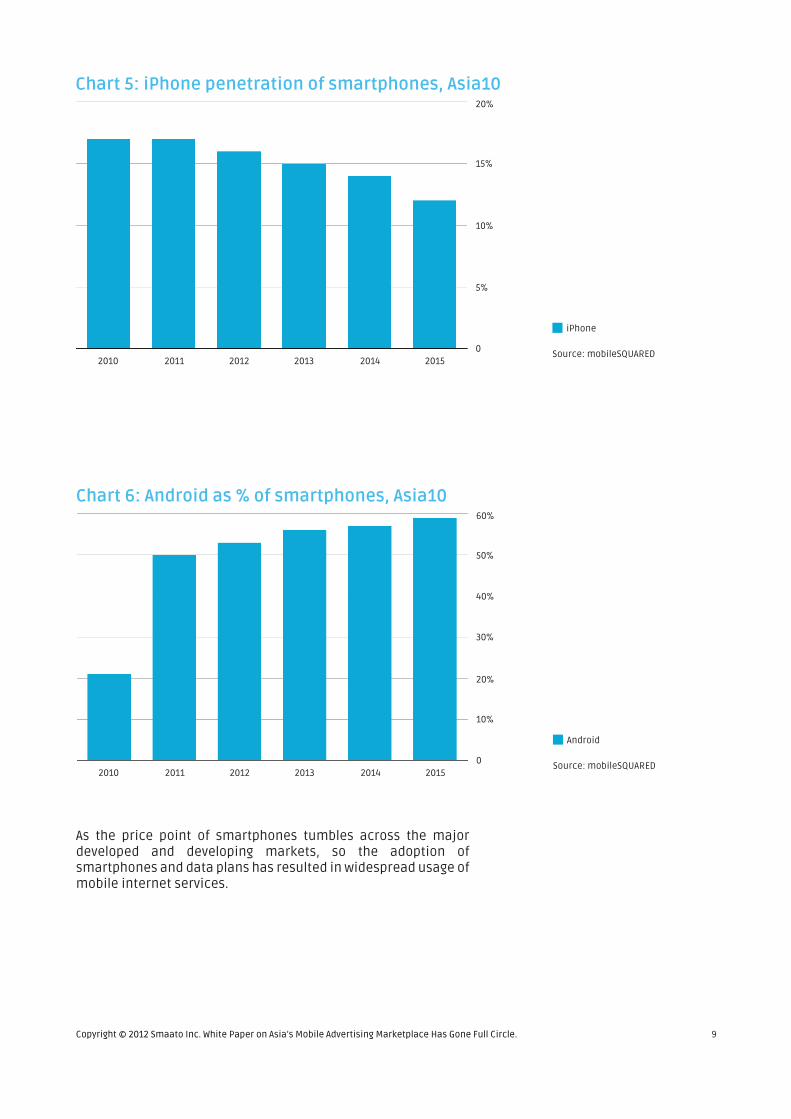

Despite growth in the overall number of iPhones across the Asia10, Apple’s share of the smartphone market will fall from 16% in 2012 to 12% in 2015 as growth in Android continues to outpace.

As a result, Google will see its share of the smartphone spaceincrease from 53.1% to 59%.

32%Smartphone market shareacross the Asia10 by 2015

70%

2010

60%

50%

40%

30%

20%

10%

0

Featurephones

Smartphones

Source: mobileSQUARED

2011 2012 2013 2014 2015

59%Android smartphone market

share across the Asia10 by 2015

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 8

Chart 5: iPhone penetration of smartphones, Asia1020%

2010

15%

10%

5%

0

iPhone

Source: mobileSQUARED2011 2012 2013 2014 2015

As the price point of smartphones tumbles across the majordeveloped and developing markets, so the adoption ofsmartphones and data plans has resulted in widespread usage of mobile internet services.

Chart 6: Android as % of smartphones, Asia1060%

2010

50%

40%

10%

0

Android

Source: mobileSQUARED2011 2012 2013 2014 2015

30%

20%

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 9

Mobile internet numbersIn 2012, mobileSQUARED forecasts that 30% of the entiresubscription base across the Asia10 markets will access the mobile internet – equivalent to 772.9 million users. By the end of next year, this number is expected to reach 952.94 million – or 33.4% of theaddressable market. The landmark 1 billion mobile internetusers will be passed during 2014.

1 BillionMobile internet users across

the Asia10 by 2014

Chart 7: Mobile internet users, Asia 10 (Millions)

1350

2010

1050

900

750

600

300

150

0

Featurephones

Other Smartphones

Android

iPhone

Source: mobileSQUARED2011 2012 2013 2014 2015

1500

Legacy

Featurephones will account for over half of all mobile internetusers in 2012 – equivalent to 420.12 million users, or 54.4% of the entire mobile internet market, with 327.89 million smartphone users. By the end of 2013, the number of mobile browsers on a smartphone would have surpassed the number of featurephone users, while featurephones will hit 458.38 million in 2012, the number of smartphone users browsing will exceed 471.19 million.

1200

450

Chart 8: Smarphone’s impact on mobile internet usage, Asia10 (Millions)

2010

Total Smarphones

Non-Smartphone

Source: mobileSQUARED

2011 2012 2013 2014 2015

630

540

450

360

270

180

0

900

810

720

90

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 10

471.19 MillionSmartphone users across

the Asia10 in 2012

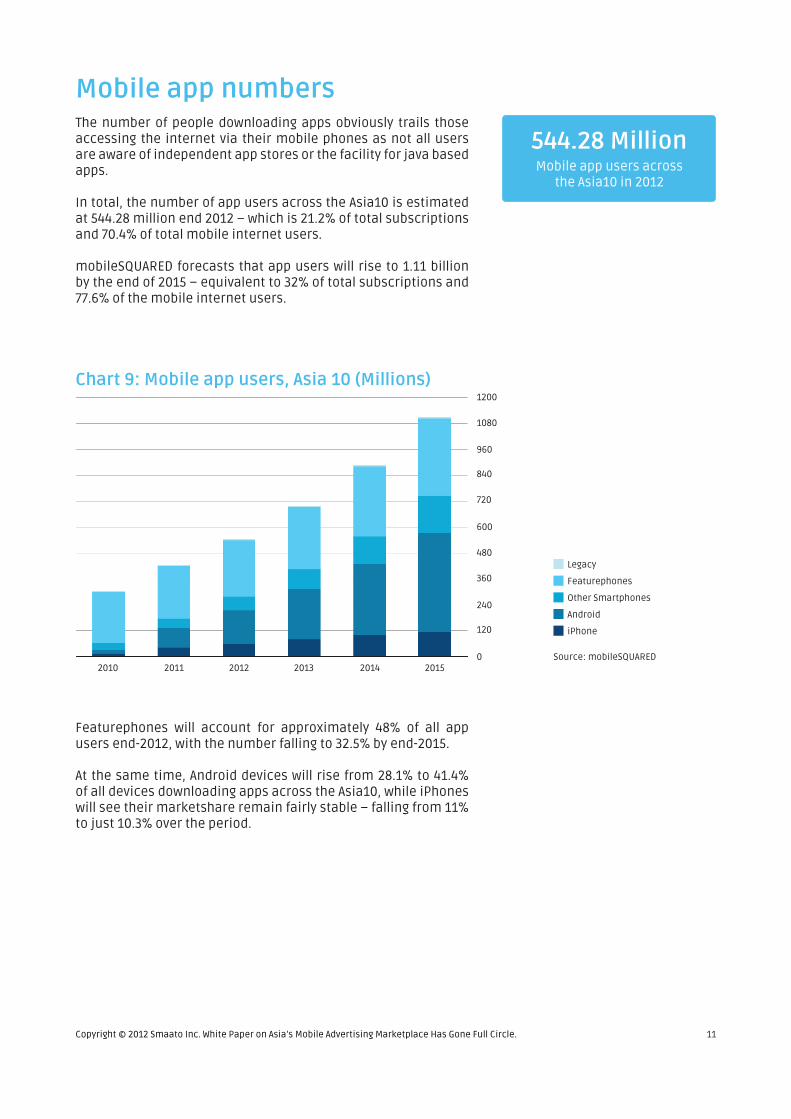

The number of people downloading apps obviously trails thoseaccessing the internet via their mobile phones as not all users are aware of independent app stores or the facility for java based apps.

In total, the number of app users across the Asia10 is estimated at 544.28 million end 2012 – which is 21.2% of total subscriptions and 70.4% of total mobile internet users.

mobileSQUARED forecasts that app users will rise to 1.11 billion by the end of 2015 – equivalent to 32% of total subscriptions and 77.6% of the mobile internet users.

Mobile app numbers

Chart 9: Mobile app users, Asia 10 (Millions)

1080

2010

840

720

600

480

240

120

0

Featurephones

Other Smartphones

Android

iPhone

Source: mobileSQUARED2011 2012 2013 2014 2015

1200

Legacy

960

360

Featurephones will account for approximately 48% of all appusers end-2012, with the number falling to 32.5% by end-2015.

At the same time, Android devices will rise from 28.1% to 41.4% of all devices downloading apps across the Asia10, while iPhones will see their marketshare remain fairly stable – falling from 11% to just 10.3% over the period.

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 11

544.28 MillionMobile app users across

the Asia10 in 2012

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 12

The Asia10 mobile advertising sector is on the cusp of a growth burst prompted by big brands looking to deliver a richer, more engaging experience, while smaller brands, business, and app developers are utilising mobile to promote their content andservices-based apps.

Ultimately, the mobile advertising ecosystem is expanding and will start to command a greater percentage of digital ad spend across Asia.

For the mobile advertising industry it has gone full circle:initiated by the mobile content companies, surpassed by the big brands, and now supplemented by the next generation of mobile advertising protagonists.

Consequently, mobileSQUARED forecasts mobile advertisingrevenues across the Asia10 region of US$3.13 billion in 2012,increasing to US$6.21 billion in 2015. Of this, mobile displaymarket will be worth US$2.02 billion in 2012 and US$2.98 billion in 2015.

In 2012, mobile display will account for 78% of total mobile spend, and 48% of total spend in 2015, as search and ad-basedmessaging campaigns rise in popularity.

Smartphones are inevitably providing the foundation for thisactivity, be it on web or app, but this is coupled with brands and businesses of all sizes, not forgetting app developers, to reach out to the broadest addressable audience available.

And that is mobile.

Conclusion

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 13

This report was researched and written by Nick Lane and GavinPatterson. Research was conducted between March and April 2012.

mobileSQUARED provides specialist research which enablesbrands, agencies and the mobile industry to increaseengagement with the mobile consumer.

We conduct primary research on the mobile industry and mobile consumers, with a focus on delivering exclusive forward-looking data on mobile device usage, mobile web, app and commerce trends and usage, and mobile advertising responsiveness to help clients identify and respond to fast-changing mobile trends.

And for a wider view of the industry, we provide detailed mobileindustry user and revenue forecasts.

Our clients look to mobileSQUARED’s expertise to providecandid insight into the mobile market. We do this using our extensiveglobal network of senior contacts to research, collect and collate the latest data, developments, trends and insight on an ongoingbasis.

For more information www.mobilesquared.co.uk

About mobileSQUARED

The action is in mobile as a utility, first and foremost, for consumers to engage with brands’ services andproducts. And that’s where mobile is most interesting.The dilemma is that it’s an area of strategy anddevelopment, and business and marketing skills,which is not owned in a single place. It’s creatingchallenges for the growth. How can I let people know about how a client of mine can enhance people’slives. Notion of being able to use the addeddimension, based on physical location. The dream of having mobile ads at lunchtime and offer coupons for local restaurants. They are using time and proximity. That’s how you’re adding value to people’s lives. Main thrust, around the notion of delivering value andutility to people.

Jason KupermanVP, Omnicom Digital, APAC, India, Middle East & Africa

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. 14

Copyright © 2012 Smaato Inc. White Paper on Asia’s Mobile Advertising Marketplace Has Gone Full Circle. Designed by Hugo Candeias. 15

Smaato has rapidly expanded its APAC headquarters in Singapore to capitalize on the burgeoning mobileadvertising market in APAC - comprising developed markets like Singapore and Japan, and emergingones like Indonesia and Vietnam. As a long-terminvestor based in Asia, EDBI is well-placed to activelyconnect Smaato through our business andgovernment networks with potential partners in these countries to gain first-mover advantage andestablish itself as a preferred mobile advertisingpartner of choice. Smaato’s focus on “Ads for Apps” will be a competitive differentiator, as mobilecontent creation becomes democratized, leading tomobile becoming the preferred means to engage consumers.

Chua Boon PingSVP Investments, EDBI

More Smaato White Papers

www.smaato.com/whitepaper

Smaato provides Ads for Apps – operating the leading mobile advertising optimization platform called SOMA. More than 50,000 app developers and premium publishers have signed up with Smaato to monetize theircontent in 230+ countries with advanced realtime optimization features (RTB) and rich media ad formats.

SOMA’s unique feature is the aggregation of 80+ leading ad networks globally to maximize mobileadvertising revenues. Through an open API and the widest range of SDKs, SOMA can be easily integrated with ad networks, ad inventory owners (publishers, developers and operators) and 3rd party ad technology providers.

Smaato is an active member of the Mobile Marketing Association, Singapore Infocomm Industry (SITF),Singapore IT Federation and the German Digital Media Association BVDW. Smaato received a Top 100 Private Company Award by AlwaysOn Media (2012, 2011, 2009 & 2007), is one of the AlwaysOn Global 250 winners in the Mobile category (2011) and was recently named a “company to watch in 2010” by Financial Analyst company GP Bullhound, among other awards.

Smaato Inc. is based in San Francisco, California. The privately held company was founded in 2005 by anexperienced International management team. The European headquarters are in Hamburg, Germany and the Asia-Pacific presence of Smaato has been established in Singapore.

240 Stockton St, 10th FloorSan Francisco, CA 94108

T: +1 (650) 286-1198F: +1 (650) [email protected]

www.smaato.com

Gerhofstrasse 220354 Hamburg, Germany

T: +49 (0)40 3480 9490F: +49 (0)40 4921 [email protected]

twitter.com/smaato

333 North Bridge Rd, #05-00Singapore 188721

T: +65 3157 1444F: +65 6336 [email protected]

facebook.com/smaato

About Smaato

www.smaato.com [email protected]