Embed Size (px)

Citation preview

MAYER BROWN JSM | 1

Asia Tax BulletinAutumn 2016

Americas | Asia | Europe | Middle East www.mayerbrownjsm.com

2 | Asia Tax Bulletin MAYER BROWN JSM | 3

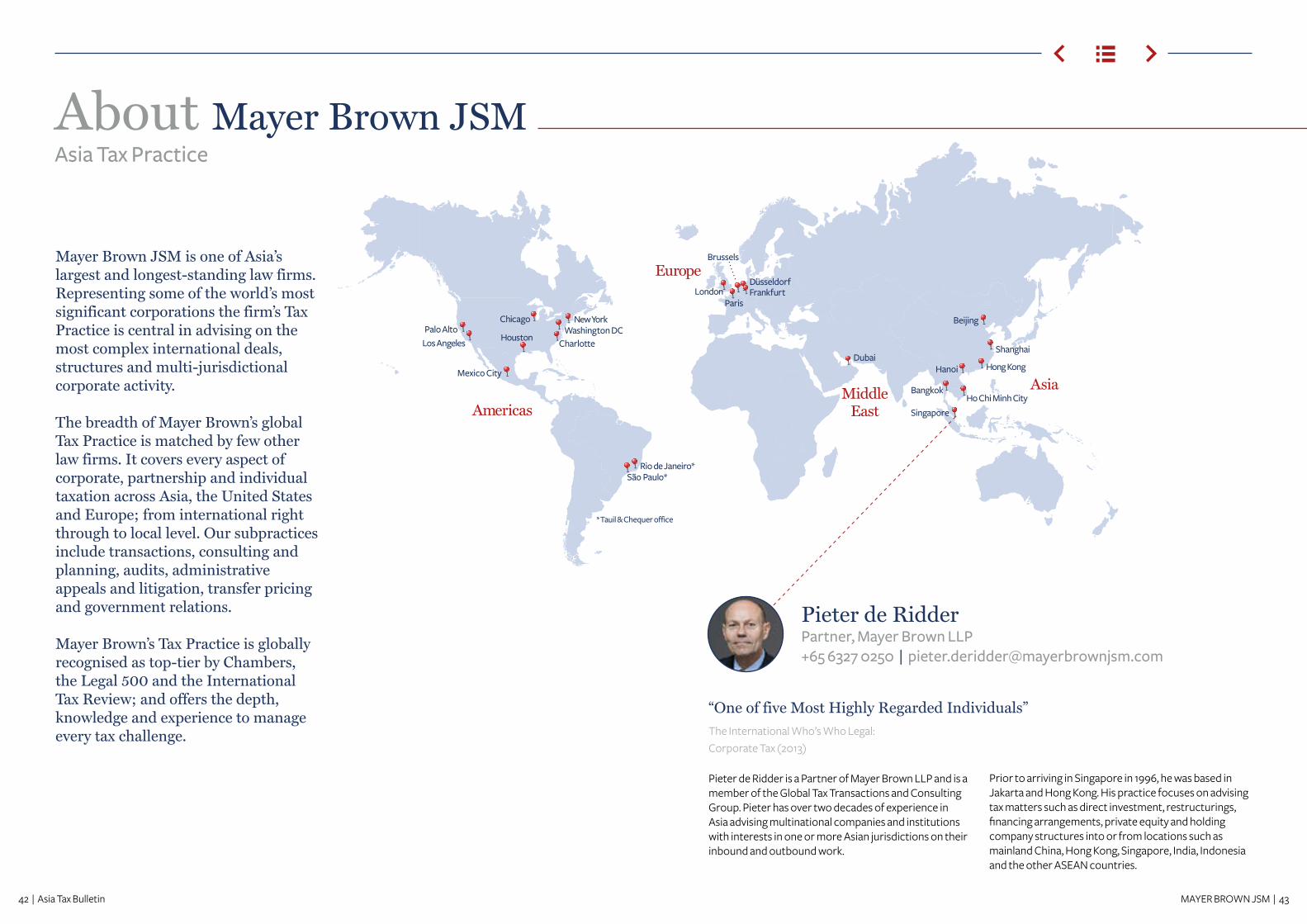

Asia

Europe

MiddleEastAmericas

Charlotte

Rio de Janeiro*São Paulo*

Palo Alto Los Angeles

Houston

Chicago

Brussels

Bangkok

New YorkWashington DC

ParisLondon Frankfurt

DubaiShanghai

Hong Kong

Ho Chi Minh City

Hanoi

Beijing

Singapore

Düsseldorf

*Tauil & Chequer office

Mexico City

Pieter de RidderPartner, Mayer Brown LLP+65 6327 0250 | [email protected]

This EditionWe would like to thank you for your continued interest in the Asia Tax Bulletin.Here is the Autumn edition which features important developments in Southeast Asia, China, Taiwan, Japan, Korea and India.

Let me highlight here just a few of the items contained in this issue. In China, there has never been a better, or more critical, time than now for enterprises to review their operations and activities that are subject to scrutiny and regulation by China Customs. In Hong Kong, there is guidance on taxation of corporate treasury activity, and in India, a new rule is relaxing the statutory requirement of withholding tax at a higher rate on payments to non-residents. In India, we bring news about the new Goods and Services Tax and about the new tax treaty with Mauritius.

In Indonesia, we bring you further news on the regulations of the recent tax amnesty and the proposed tax law amendments for 2017 in Korea, while in Malaysia, there could be sweeping changes on the horizon for digital platforms which are being targeted with a proposed new tax. In Singapore, the IRAS issued guidance on the application of the M&A tax deductions and a circular was issued on the application of the General Anti Avoidance Rule. Taiwan’s Ministry of Finance has issued clarifying notes on the application of the new anti avoidance rules concerning Controlled Foreign Companies and the place of effective management.

We hope you will find this bulletin useful. As always we look forward to receiving your feedback if there are things we can improve – and do not hesitate to contact us if we can be of assistance with any tax or legal matters in Asia.

With kind regards,

Pieter

4 | Asia Tax Bulletin MAYER BROWN JSM | 5

ContentsTAIWAN

34 Rules on exchange of information published

35 Visa waiver pilot programme for certain Asian countries announced

35 Anti avoidance rules in respect of individuals

35 VAT Act on cross-border sale of digital services

35 Deductibility of management fees

36 Anti-avoidance measures

36 Income tax policy for talented foreign employees

THAILAND

37 Personal income tax rates for 2016

37 VAT

38 Foreign Business Licenses are no longer required for certain banking and finance services

VIETNAM

39 Indirect transfers of Vietnamese companies

39 Circular on tax incentives issued

40 International tax developments

KOREA

23 2017 Tax Proposals

27 International tax developments

MALAYSIA

28 Tax on digital business platforms proposed

28 Group relief for companies

29 International tax developments

PHILIPPINES

30 Treaty benefits for dividends, interest and royalty income

30 Paying taxes via credit, debit and prepaid cards

31 National Budget 2017 proposed

31 Employment permit exemption for corporate officers

SINGAPORE

32 Mergers and acquisitions

32 General anti avoidance rule

33 Minimum qualifying salary for employment passes to increase

CHINA

6 New rules on transfer pricing documentation

7 Certificate of residence

7 China amends inbound investment laws

8 Customs duties

8 Financial reporting standards regarding financial instruments

8 VAT incentive for generating electricity through solar energy

9 Tax exemptions for animation industry

9 VAT

9 Reduction of tariffs for 201 IT products

10 New income tax policy on stock options and capital contributions

10 Cost contribution arrangement on intra-group services

11 International Tax Developments

HONG KONG

12 Advance ruling on amalgamation

13 Guidance on taxation of corporate treasury activity

14 Automatic exchange of financial account information

14 Open-ended fund company

15 International tax developments

INDIA

16 Relaxation of higher withholding tax rate in case no PAN

16 New tax treaty with Mauritius

17 Grant of call option is treated as capital gain

18 The new Goods and Services Tax

INDONESIA

19 Tax amnesty law

JAPAN

21 Guidance on new transfer pricing documentation rules

22 International tax developments

Key: Jurisdiction (Click to navigate)

6 | Asia Tax Bulletin MAYER BROWN JSM | 7

China (PRC)New rules on transfer pricing documentation

The State Administration of Taxation (SAT) issued an announcement on 29 June 2016 concerning the reporting on related transactions and contemporaneous documentation of transfer pricing (SAT Gong Gao [2016] No. 42). The Shanghai State Tax Bureau published the announcement on its website on 12 July 2016. The new rules apply to the tax year 2016 and subsequent years.

The announcement contains 27 provisions and defines the related enterprises and related transactions for the purpose of the announcement. Article 5 requires large multinational enterprises (MNEs with total consolidated revenue of more than CNY5.5 billion) to submit country-by-country reports, and the Chinese tax authority is authorisedd to exchange such country-by-country reports with other tax jurisdictions according to the tax treaties or other agreements concluded by China.

Moreover, detailed rules on contemporaneous documentation – which includes a master file, local file and special items file – are provided. These detailed rules are related to the kind of information and analysis that should be conveyed in each file. Enterprises dealing only with associated enterprises located in China or which have concluded an advance pricing agreement covering the relevant related transactions do not need to prepare the three aforementioned files. The documents must be written in Chinese and kept for 10 years. As to the administrative issues, the announcement provides:

• The master file must be finalisedd within 12 months after the accounting year of the ultimate holding company;

• The local file and special items file must be finalised within 6 months of the following year in which the relevant related transactions take place; and

• The contemporaneous documentation must be finalised within 30 days upon the request of the tax authority.

Certificate of residence

The State Administration of Taxation (SAT) published an announcement concerning the issuing of the certificate of residence on 28 June 2016 (SAT Gong Gao [2016] No. 40). The announcement applies from 1 October 2016, and on the same date Guo Shui Han [2008] No. 829, Guo Shui Han [2010] No. 218, and article 28 of SAT Gong Gao [2011] No. 45 will be abolished. The taxpayer must lodge the application for a certificate of residence with its competent state tax bureau or local tax bureau (in the case of an individual). For a domestic or foreign branch of a Chinese resident enterprise, the tax bureau where the head office is located is the competent tax bureau for this purpose and the head office has to lodge the application. In the case of a partnership, the Chinese partner has to lodge the application with the tax bureau where the Chinese partner is located. The documents must be submitted in Chinese, and need to include the following:

• The application form for the certificate of residence;• The documents related to the income being eligible

for treaty benefits – such as contracts, agreements or resolutions of the board of directors or a shareholder meeting – and evidence of payments;

• In the case of an individual who has a dwelling within China, evidence of an habitual abode by virtue of registration, family or economic interest, including personal information on the applicant and other information required;

• In the case of an individual who does not have a dwelling within China and has resided in China for less than one year, evidence of the actual duration of residence in China including the entrance and exit data of the passport and other information required;

• The application filed by the head office for its domestic or foreign branch must contain information on the registration of the head office; and

• The application filed by the Chinese partner of a partnership must contain information on the registration of the partnership.

The competent tax bureau must make a decision on the resident status within 10 days after the relevant documents have been submitted. If the competent tax bureau is not able to make a decision the case can be submitted to its superior, which has to make a decision within 20 days.

All of the issued certificates will be numbered. If the contracting state has special requirements for the format of the certificate, the applicant must provide an example.

China amends inbound investment laws

On 3 September 2016, the National People’s Congress (NPC) Standing Committee approved the amendments to the Laws on Wholly Foreign-Owned Enterprises (中华人民共和国外资企业法), the Laws on Sino-Foreign Equity Joint Ventures (中华人民共和国中外合资经营企业法), the Laws on Sino-Foreign Cooperative Joint Ventures (中华人民共和国中外合作经营企业法) and the Laws on the Protection of Investment of Taiwan Compatriots (中华人民共和国台湾同胞投资保护法) (“FIE Laws”), expanding the “negative list” regime currently applicable within the free trade zones (FTZs) of Shanghai, Guangdong, Tianjin and Fujian across the country starting from 1 October 2016 (“NPC Decision”).

The NPC Decision will mean significant change in relation to the establishment and structure of foreign invested enterprises (FIEs) in China – they will not require approval from the Ministry of Commerce (MOFCOM) or its local branches, as long as the business undertaken is not on a “negative list”. In particular the NPC Decision will impact:

• Incorporation of FIEs;• Changes to the structure of FIEs, including (among

other things) increase or decrease of registered capital, merger or division, termination, extension of business term, changes to capital contribution schedule; and

• Equity transfers relating to FIEs.

JURISDICTION:

There has never been a better, or more critical, time than now for enterprises to review their operations.

”“

8 | Asia Tax Bulletin MAYER BROWN JSM | 9

Tax exemptions for animation industry On 1 August 2016, the Ministry of Finance, the Customs General Administration and the State Administration of Taxation (SAT) jointly issued a notice (Cai Guang Shui [2016] No. 36) extending the existing tax incentives granted to the animation industry. The notice was published on the SAT’s website on 17 August 2016. According to the notice, enterprises engaged in the animation industry are exempt from import duties and value added tax (VAT) at the import stage on imports of equipment or other necessities, provided they qualify (as per the instructions of the relevant government department) for enjoying the incentives during the period from 1 January 2016 to 31 December 2020. The notice contains an attachment detailing the requirements for enterprises and animation products to be eligible for the incentives, as well as the administrative procedures for submitting the application.

VAT

On 18 August 2016, the State Administration of Taxation (SAT) issued an announcement (SAT Gong Gao [2016] No. 53) clarifying several issues concerning value added tax (VAT). The announcement, which applies from 1 September 2016, addresses the following issues:

• Services provided and intangibles used in full outside of China are not subject to VAT. These include postal parcels, exhibitions and construction services supplied abroad.

• Individuals letting immovable properties may apply the VAT exemption for small and low-profit enterprises. If the average monthly rental income does not exceed CNY30,000, it is exempt from VAT.

• The supply of (single-use or multiple-use) prepaid cards is exempt from VAT; the administrative costs charged are subject to VAT.

• The method of determining the acquisition price of restricted shares (funder’s shares).

• The timing of tax liability for lending services.• If a taxpayer is allowed to file a VAT return in respect of

the supply of certain goods or services on a quarterly

Customs duties

There has never been a better, or more critical, time than now for enterprises to review their operations and activities that are subject to scrutiny and regulation by China Customs. With the recent changes to the Regulations on Customs Audit as well as the boost in China Customs’ audit capabilities, enterprises can expect China Customs to heighten its efforts to complete audits of all importers, exporters and processing trade manufacturers.

On 7 July 2016, the State Council amended the Regulations on Customs Audit (State Council Order 670). The amended regulations will enter into force on 1 October 2016. The revised audit rules further clarify (among other things) the scope and period of a customs audit, the procedures and processes of an audit, the mechanisms for self-compliance and voluntary disclosure, and the involvement of third-party intermediaries in a customs audit.

The revised audit rules also formalise the sharing of enterprise information. This means that China Customs can collect information related to the import and export of certain commodities and industries from related industrial associations, government bodies and enterprises as required for a Customs audit.

China Customs has also increased the number of Customs-accredited third-party auditing firms which can be appointed to conduct post-clearance audits of enterprises. The assessments of these third-party auditing firms can form the basis of Customs audits.

Financial reporting standards regarding financial instruments

On 7 September 2016, the General Office of the Ministry of Finance published the draft of the amendments to Accounting Standards for Business Enterprises No. 37 – Presentation of Financial Instruments. The key changes are the following:

• The changes relate to the items presented in financial statements and to the disclosure contents resulting from the changes to the classification of financial instruments. The current financial assets are classified into four categories when they are initially recognised: the financial assets (the fair market value and the value fluctuations of which are recorded in the profit and loss account for the current period); investments held to maturity; loans and receivables; and financial assets available for sale. This classification has been removed from the proposed new standards.

• The disclosure of the devaluation of financial instruments: the draft indicates that the “incurred loss” model will be replaced by an “expected credit loss” model.

• The disclosure of hedge accounting: specifically, the draft specifies the financial statements’ requirements in respect of information on the devaluation of financial instruments, such as risk management activities, calculation and measurement of expected credit losses, and preparation of losses caused by devaluation.

VAT incentive for generating electricity through solar energy

The Ministry of Finance (MoF) and the State Administration of Taxation (SAT) jointly issued a notice on 25 July 2016 (Cai Shui [2016] No. 81, which was published on 25 August 2016) concerning an extension of the preferential value added tax (VAT) policy on the generation of solar energy.

The notice states that electricity generated by an individual taxpayer through solar energy continues to be subject to the “50% VAT refund” policy, which means that 50% of the collected VAT will be repaid to the taxpayer through a financial subsidy from 1 January 2016 to 31 December 2018. The refund to which the taxpayer is entitled but is not repaid before the publication of this notice can be offset against the VAT payable in the following months, or simply be repaid to the taxpayer.

China (PRC) cont’d

JURISDICTION:

basis, it may file the quarterly return for all the goods and services.

• The documentation requirements for adjusting the VAT advance payment in respect of construction services have been changed. There is no need to present the original contract; a stamped copy of the contract will suffice.

• New VAT codes have been introduced to supplement the existing VAT codes for a number of goods and services.

Reduction of tariffs for 201 IT products On 3 September 2016, the National People’s Congress (NPC) Standing Committee approved the “Amendments to WTO Tariff Concessions Schedule of the People’s Republic of China”. According to the amendments, China will gradually reduce the tariffs of 201 information technology (IT) products imported from WTO members, with a view to a final abolition of these tariffs. The products eligible for tariff reduction include information and communication products, semi-conductor products plus their production facilities, audio and visual products, medical devices, instruments and apparatuses, etc. The phasing-out period for import tariffs on most products is three or five years, with seven years applicable to a small number of products. The State Council is authorised by the NPC to make further technical adjustments.

This amendment not only represents the first time the tariff schedule has been amended since China’s accession to the WTO, but also the first time the NPC has considered amending the tariff reduction.

The reduction and final abolition is one of the most impressive achievements in tariff reduction realised by the WTO in the past 20 years. The volume of annual global trade represented by these products amounts to USD1.3 trillion, with China being responsible for producing 25% of them. This achievement will effectively promote the development of global trade, investment and IT development.

10 | Asia Tax Bulletin MAYER BROWN JSM | 11

China (PRC) cont’d

JURISDICTION:

New income tax policy on stock options and capital contributions

The Ministry of Finance and the State Administration of Taxation (SAT) jointly issued a notice regarding the tax treatment of stock options and capital contributions in the form of technology on 20 September 2016 (Cai Shui [2016] No. 101).

Employees participating in stock incentive schemes such as stock options, equity options, restricted shares and bonuses in shares granted by unlisted companies are not subject to individual income tax at the time of granting, but are taxable at the time of disposal of the underlying stocks provided that the company granting such schemes has filed them with the tax authority and the following requirements are met:

• The scheme is initiated by a resident enterprise;• The scheme has been approved by the board of

directors;• The scheme concerns only the resident company’s

own shares;• The employees receiving the incentives are the

key technical staff and managers and account for a maximum of 30% of the average total personnel in the last six months;

• The holding period for stock and equity options is three years from the granting date and that for restricted shares is one year after the restriction is removed;

• The time span between the granting date of the schemes and the date of exercise of the rights is less than 10 years; and

• The company granting the schemes is not listed in the catalogue of the sectors in which stock incentive schemes are not permitted.

The income derived from the disposal is calculated as the difference between the sales proceeds of the shares and the purchase price of the options, plus fees and taxes associated with the disposal; and is taxed as income from transfer of property at a rate of 20%. The individual income tax on income from the disposal of listed stock can be paid within 12 months after the

date of the disposal if the schemes are filed with the tax authority. With the publication of this notice, Cai Shui [2009] No. 40 is abolished.

Enterprises and individuals participating in a resident company by using technology to subscribe the shares of the company may opt to apply the tax deferral treatment, which means no realization of the value of the technology if the consideration for the contribution of the technology is fully in shares. Income tax is deferred to the time at which the acquired shares are disposed and the income is calculated as the sale proceeds of the shares minus the original value of the technology, plus the taxes and fees associated with the transfer.

To enjoy the incentives mentioned above, the company has to file the schemes with the relevant tax authority.

Cost contribution arrangement on intra-group services

The state and local tax bureaus of Nanjing (the provincial capital of Jiangsu Province) have reportedly signed a cost contribution arrangement (CCA) on intra-group services with a multinational company after a negotiation of more than four months. This is the first CCA case in Nanjing and is reported as a significant achievement of transfer pricing management.

The taxpayer is a multinational company which has its headquarters located and listed in Hong Kong. The agreement involves eight enterprises in Nanjing with two of the eight enterprises falling under the jurisdiction of the local tax bureau. The agreement covers centralised services such as professional, technical and administrative services. After the conclusion of the agreement, the enterprise income tax for the year 2015 is adjusted to be increased by CNY1.5 million, and the CCA policy established by the company is accepted by the tax authority.

To conclude this CCA, the tax bureaus have prepared the case at an early stage and gave full consideration to the reasonable demands of the taxpayer, and provided the taxpayer with the advice in respect of the services, ratio of allocation and the use of the cost plus method.

International Tax Developments

Macao On 19 July 2016, China and Macau signed an amending protocol to their tax treaty, as amended by the 2009 and 2011 protocols.

NetherlandsOn 12 September 2016, China and the Netherlands signed a social security agreement in The Hague.

12 | Asia Tax Bulletin MAYER BROWN JSM | 13

Hong KongJURISDICTION:

A financial institution is not entitled to the profits tax concession even if it only performs corporate treasury activities for its associated corporations.

”

“assessable profits for the year of assessment 2016/17 and subsequent years of assessment, provided that such assessable profits are derived by Company A from the same trade or business carried on by Company B up to the day immediately before the Amalgamation.

Guidance on taxation of corporate treasury activity

The Inland Revenue Department (IRD) issued Departmental Interpretation and Practice Notes No. 52 (DIPN 52) on the taxation of corporate treasury activities on 9 September 2016. DIPN 52 sets out the IRD’s interpretation and practice in relation to the relevant provisions under the Inland Revenue (Amendment) (No. 2) Ordinance 2016, which enables the government to implement a new interest deduction rule for the intra-group financing business of corporations and the concessionary profits tax rate for qualifying corporate treasury centres (QCTCs). Key features of DIPN 52 are set out below.

A corporation carrying on an intra-group financing business borrows money from, and lends money to, associated corporations in the ordinary course of its business. To constitute an intra-group financing business, a sufficient number of intra-group borrowing and lending transactions with a number of associated corporations is required, involving a significant amount of funds, taking into account the nature and scale of the business operations of the multinational corporation. In general, in the opinion of the Commissioner, a corporation carries on an intra-group financing business if:

• The corporation conducts at least four borrowing or lending transactions per month;

• Each borrowing or lending transaction exceeds HKD250,000; and

• Borrowing or lending transactions involve at least four associated corporations in the relevant basis period.

A corporate borrower carrying on an intra-group financing business in Hong Kong is allowed to deduct the interest payable on money borrowed from a non-

Advance ruling on amalgamation

On 18 August 2016, the Inland Revenue Department (IRD) published an advance ruling (Advance Ruling Case No. 58) in respect of the application of sections 14, 19C(4), 51(1), 61A and 61B of the Inland Revenue Ordinance (IRO) which sets out the profits tax treatment of amalgamation. The ruling will apply as from the year of assessment 2016/17 and subsequent years of assessment. The ruling is consistent with the guidance note issued by the IRD in December 2015.

To give an example, Company A and Company B are incorporated in Hong Kong as part of the same international group. Company A, the group’s regional holding company, is principally engaged in investment holding. Company B, which is wholly owned by Company A, is principally engaged in the provision of services. To streamline the overall group structure, enhance management and reduce cost, the management of the group has planned to amalgamate Company B vertically into Company A (the Amalgamation). Company B incurs tax losses which will remain unutilised prior to the Amalgamation. Company A agrees that, following the Amalgamation, it will utilise such tax losses only to set them off against profits derived by it from the same trade or business succeeded from Company B.

Company B will be amalgamated into Company A in 2016.

The Amalgamation is governed by the amalgamation provisions included in the Companies Ordinance. The legal effects of the Amalgamation on and after the effective date of the Amalgamation are as follows:

• Company B ceases to exist as an entity separately from Company A; and

• Company A succeeds to all property, rights and privileges, and all liabilities and obligations, of Company B.

The ruling states that no profits or losses will arise or be deemed to arise for Company A or Company B as a result of the Amalgamation. Any unutilised tax losses incurred by Company B prior to the Amalgamation will be available for set-off against Company A’s

Hong Kong associated corporation subject to specific conditions:

• The deduction claimed is in respect of interest payable by a corporation (i.e. the borrower) on money borrowed from a non-Hong Kong associated corporation (i.e. the lender) in the ordinary course of an intra-group financing business;

• In respect of the interest, the lender is subject to a similar tax in a territory outside Hong Kong at a rate that is not lower than the reference rate; and

• The lender’s right to use and enjoy the interest is not restricted by a contractual or legal obligation to transfer such interest to another person, unless the obligation arises as a result of a transaction between the lender and a person other than the borrower dealing with each other at arm’s length.

However, interest paid to non-corporate associates outside Hong Kong (e.g. partnerships, trusts) is not eligible for deduction.

If a corporation (other than a financial institution) lends money to a non-Hong Kong associated corporation in the course of its intra-group financing business carried on in Hong Kong, the interest income and relevant gains or profits derived therefrom will be subject to profits tax.

A corporation is a QCTC if:

• It is a dedicated corporate treasury centre (CTC) which has not carried on any activity other than one or more corporate treasury activities in Hong Kong;

• It is a CTC which has satisfied relevant safe harbour rules, although it has carried on activities other than a corporate treasury activity in Hong Kong; or

• It is a CTC defined as such by the Commissioner.

A QCTC is subject to profits tax at a concessionary rate of 8.25% only if:

• In a year of assessment, the central management and control of the corporation is exercised in Hong Kong, and the activities that produce its qualifying profits in that year are carried on in Hong Kong by the

14 | Asia Tax Bulletin MAYER BROWN JSM | 15

Hong Kong cont’d

JURISDICTION:

corporation, or arranged by the corporation to be carried on in Hong Kong; and

• The corporation has elected in writing, which is irrevocable, that the half rate concession applies to it.

However, a financial institution is not eligible to be a QCTC. Therefore, a financial institution is not entitled to the profits tax concession even if it only performs corporate treasury activities for its associated corporations.

Automatic exchange of financial account information

Following the passage of the Inland Revenue (Amendment) (No.3) Ordinance 2016, the government will start implementing the new international standard for automatic exchange of financial account information in tax matters (AEOI). On 9 September 2016, the Inland Revenue Department (IRD) announced that the legislation for implementing the AEOI was in place. The relevant guidance will be provided to financial institutions wishing to comply with their obligations under the new legislation. The guidance is available on the official website of the IRD.

Open-ended fund company

The Hong Kong government gazetted the Securities and Futures (Amendment) Ordinance on 10 June 2016, which introduces the legal, regulatory and tax framework for an open-ended fund company (OFC) regime in Hong Kong. Thus far, an open-ended investment fund could only be established in Hong Kong in the form of a unit trust. With this ordinance, an alternative Hong Kong-domiciled investment vehicle is provided to the asset management sector.

We understand the market may be waiting for ‘operational rules and subsidiary legislation’ which is yet to come. Meanwhile, the following features of the OFC should be noted.

• OFCs are exempt from profits tax provided the relevant conditions under section 26A, section

20AC and section 20ACA of the IRO are satisfied. Publicly-offered OFCs will be exempt from profits tax regardless of whether the OFC’s central management and control is in or outside Hong Kong. However, for privately-offered OFCs, central management must be outside Hong Kong in order to enjoy the profits tax exemption, presenting a limitation in the usefulness of the OFCs for privately-offered OFCs.

• There is no stamp duty on the initial allotment and cancellation of OFC shares upon redemption. A transfer of OFC shares, however, is subject to stamp duty.

• With regard to an umbrella OFC, each sub-fund under an OFC is regarded as a separate OFC for stamp duty purposes. The conversion of interest from one sub-fund to another and the transfer of dutiable assets between different sub-funds are subject to stamp duty.

• Stock transactions involving in kind allotment and redemption of shares of public OFCs, which are open-ended collective investment schemes authorised by the Securities and Futures Commission, are not subject to stamp duty.

• OFCs are subject to the same profits tax filing requirements and obligations as corporations, partnerships, trustees, and any other entities under the IRO.

• An umbrella company will have the obligation to file a profits tax return to report the consolidated profits of the whole fund. Each sub-fund has to file separate profits tax returns.

• In order to ensure the success of the OFC framework, it should cater equally to privately-offered funds as well as retail funds; and be competitive and attractive compared to investment funds domiciled in other jurisdictions, such as the Cayman Islands and Luxembourg. Further work should be done on the tax aspects such as exploring ways to achieve profits tax exemption for onshore private OFCs.

International tax developments

RussiaOn 29 July 2016, the Hong Kong-Russia Income Tax Agreement (2016) entered into force. The new agreement generally applies from 1 January 2017 for Russia and from 1 April 2017 for Hong Kong. From this date, the new agreement generally replaces the avoidance of double taxation provision (article 12) of the Hong Kong-Russia Transport Tax Agreement (1999).

KoreaOn 27 September 2016, the Hong Kong-Korea (Rep.) Income Tax Agreement (2014) entered into force. The agreement generally applies for Hong Kong from 1 April 2017 and for Korea (Rep.) from 1 April 2017 for withholding taxes and from 1 January 2017 for other taxes.

16 | Asia Tax Bulletin MAYER BROWN JSM | 17

IndiaJURISDICTION:

Relaxation of higher withholding tax rate in case no PAN

The Central Board of Direct Taxes (CBDT) issued a new rule 35BC vide Notification No. 53/2016, dated 24 June 2016, that relaxes the statutory requirement of withholding tax at a higher rate on payments to non-residents (other than a company, or a foreign company) in the absence of tax registration (i.e. Permanent Account Number) under section 206AA of the Income Tax Act, 1961 (ITA).

The current provisions of section 206AA of the ITA require the payer to withhold taxes at the higher of the following:

• The rate prescribed in the relevant tax treaty;• The rate prescribed in the Income Tax Act, 1961; or• A rate of 20% on the gross amount.

The new rule 35BC is applicable to the non-resident, provided he/she furnishes the prescribed details and documents to the payer, in respect of payments in the nature of interest, royalty, fees for technical services and payments on transfer of any capital assets. Upon submission, the payer should mention “PAN not available” in Form 27Q (quarterly withholding tax statement in the case of non-residents).

New tax treaty with Mauritius

On 19 July 2016, the amending protocol, signed on 10 May 2016, to the India – Mauritius Income Tax Treaty (1982), entered into force. The protocol generally applies from:

• In India: 1 April 2017, for the provisions of article 1, article 2, article 3, article 4, article 5 and article 8;

• In Mauritius: 1 July 2017, for the provisions of article 1, article 2, article 3, article 4, article 5 and article 8;

• In India and Mauritius: 19 July 2016, for the provisions of article 6 (Exchange of information) and article 7 (Assistance in the collection of taxes).

The Bill paves the way for a uniform tax regime in the country and will replace most of the current central and state indirect tax levies.

”

“As a reminder, the key change brought about by the protocol is the amendment to Article 13 “Capital Gains,” whereby the taxing rights on capital gains (CG) will lie with India as from 1 April 2017.

In order to preserve the position of existing investors, a phase-wise approach has been proposed for the shift from residence-based taxation to source-based taxation, through the implementation of:

(i) A grandfathering provision for investments acquired prior to 1 April 2017; and

(ii) A two-year transition period from 1 April 2017 to 31 March 2019 when Mauritian companies will benefit from a reduced tax rate on CG subject to meeting the conditions of a newly-introduced “Limitation of Benefits” clause.

The other salient change was made to Article 11 of the treaty, with the introduction of withholding tax of 7.5% on the interest arising on debt claims/loans made by Mauritian resident banks to Indian companies after 31 March 2017.

Grant of call option is treated as capital gain

Courtesy of BMR Advisors in Mumbai, it was reported that a non-resident Indian (NRI) taxpayer had granted a call option which was treated as a capital gain under the tax treaty between Singapore and India. The taxpayer was an NRI individual who was a resident of Singapore. The NRI taxpayer held 99% of the shares in an Indian holding company (“Hold Co”), which in turn held 25% shares in an Indian operating company (“Op Co”). The remaining 75% shares in Op Co were held by a Mauritius company (“M Co”).

The taxpayer had entered into a call option agreement on November 19 2001 to sell his shareholding in Hold Co to M Co, and the consideration for the grant of this option was agreed at US$2.45 million. The call option was to be exercised within 150 years, and the call/strike price was agreed to be US$1.

Further, the taxpayer executed an irrevocable Power of Attorney (“POA”) in favour of an affiliate of M Co permitting the affiliate to participate in meetings of shareholders and all other powers qua the shares in Hold Co, and caused Hold Co to execute a similar irrevocable POA in favour of the affiliate in respect of shares held by Hold Co in Op Co. The taxpayer further undertook not to transfer the shares in Hold Co other than in exercise of the call option and not to have any further issue of shares in Hold Co.

Looking at the ‘peculiar’ facts of the case, it was held that the taxpayer had irrevocably alienated substantive and valuable rights in the shares albeit without dejure alienating the shares themselves. Hence, the present case cannot be held as call option agreement simplicitor.

It was held that parting with valuable rights/interest in any asset or creating any substantive interest in the asset, directly or indirectly, would be reckoned as a ‘transfer’ of an asset under the provisions of section 2(47) of the Income-tax Act, 1961.

Having held that the consideration was taxable as capital gains under domestic tax law, the provisions of the DTAA were examined by the tribunal. It was held that in the absence of transfer of ‘shares’ in the present case, the residuary clause (6) of Article 13 of the DTAA was applicable – which thus gave exclusive taxing rights to the state of residence of the taxpayer (ie Singapore).

Taxpayer M. Co.

Op Co.

Affiliate

Hold Co.

Singapore Mauritius

99%25%

75%Call option agreement

Oversees

India

Irrevocable POA

& undertaking

Irrevocable POA

& undertaking

Call option agreement

18 | Asia Tax Bulletin MAYER BROWN JSM | 19

India cont’d

JURISDICTION:

The new Goods and Services Tax

Courtesy of BMR Advisors in Mumbai, it is reported that the much-awaited Goods and Services Tax (“GST”) is closer to becoming a reality as the Constitution (122nd Amendment) Bill, 2014 (“the Bill”) has received its unanimous approval from the Upper House of the Parliament. The Bill paves the way for a uniform tax regime in the country and will replace most of the current central and state indirect tax levies.

The process began its journey almost seven years ago in the year 2009 with the discussion paper on GST being issued by the Empowered Committee. The Constitution (115th Amendment) Bill, 2011 was initially tabled in the Lower House in 2011 but that bill lapsed. A revised bill was then tabled and passed by the Lower House in May 2015.

The Bill as passed by the Upper House will now have to be sent back to the Lower House for its approval of the amendments moved in the Upper House. Thereafter, the Bill would need to be ratified by more than half of the state legislatures. The ratified Bill will finally need to receive Presidential assent to be effective. After the Presidential assent, a GST Council would be set up for making recommendations on various aspects of the GST structure. GST legislation(s) would also need to be passed by the Parliament and respective state legislatures.

Passage of the Bill entailed an intense debate with primary focus on GST rates, threshold limits, administrative control, municipal taxes and other such matters. These aspects would be the subject matter of recommendations of the GST Council. One of the consistent demands by some of the parties in the Upper House was to introduce the Union GST bill(s) as a ‘Finance Bill’ instead of a ‘Money Bill’ to enable the GST bills to be put up for discussion and voting in both the houses of the Parliament.

With the critical parliamentary process of amending the Constitution nearing a closure, the industry is now closely watching developments around building a consensus between centre and states on various implementation issues including the GST

rate. The industry expects to be provided sufficient time for engaging with the law-makers to address various industry-specific issues. The timeline for implementation of GST, which as of now is expected to be 1 April 2017, would also be keenly watched.

International Tax Developments

CyprusAccording to a press release of 24 August 2016, published by the Indian government, the Union Cabinet of India authorised the signing of a new income tax treaty with Cyprus, initialled on 29 June 2016. Once signed, in force and effective, the new treaty will generally replace the old treaty of 1994.

SingaporeNegotiations have commenced on changes to the Singapore/India tax treaty as a result of the changes to the India/Mauritius tax treaty which removed capital gains tax protection. We will report news in due course.

IndonesiaJURISDICTION:

PMK-123 reaffirms that funds must be repatriated to special accounts with designated gateway banks.

”“

Tax amnesty law

The Ministry of Finance (MoF) recently issued further regulations in respect of the tax amnesty law. One of the new regulations is Regulation No. 123/PMK.08/2016 (PMK-123) which became effective on 8 August 2016. PMK-123 amends the MoF’s Regulation No. 119/PMK.08/2016 which details the procedure for repatriating funds back into the country and placing them in the financial market. PMK-123 reaffirms that funds must be repatriated to special accounts with designated gateway banks. Subsequently, the funds may be managed by other gateways such as investment management or related securities companies. Under PMK-123, repatriated funds may be invested in futures traded on the Indonesia Future Exchange and investment-linked products. PMK-123 also provides details of procedures for changing gateways within a three-year period. In total, 55 companies – comprising of banks, investment managers and brokers – have been designated as gateways by the MoF.

The MoF also issued Regulation No.122/PMK.08/2016 (PMK-122) of 8 August 2016 regarding details of and procedures for investing repatriated funds outside the financial market. The repatriation process is similar to that of investing them in the financial market. Initially, the funds must be transferred to special accounts with designated gateway banks. Under PMK-122, taxpayers are allowed to invest in other assets such as gold, infrastructure projects and properties.

Under Regulation No. PER-08/PJ/2016 of 1 August 2016, issued by the Directorate General of Taxes, for tax amnesty purposes registration and reactivation of taxpayers’ identification numbers may be done outside Indonesia; at the Consulate General of the Republic of Indonesia in Hong Kong, the Indonesian embassies in Singapore and London, and other places as determined by the Minister of Finance.

Special purpose companiesThe Indonesian Ministry of Finance (MoF) issued Regulation Number 127/PMK.010/2016 to clarify the situation where assets are indirectly held through a special purpose company (SPC).

20 | Asia Tax Bulletin MAYER BROWN JSM | 21

Indonesia cont’d

JURISDICTION:

Under the MoF Regulation No. 127/PMK.010/2016, the local Indonesian and international assets held indirectly through a passive SPC by the amnesty applicant must be transferred to the tax amnesty applicant’s direct name or assigned to an Indonesian limited company (Perseroan Terbatas, PT) owned by the tax amnesty applicant. As such, the ownership in such SPC must be released or such SPC must be liquidated. If the assets held through the SPC are local Indonesian assets, the amnesty applicant can still apply the 2%, 3% or 5% amnesty tax rates.

International assets held through an SPC will be subject to the 4%, 6% or 10% tax rates unless the international assets are repatriated to Indonesia and the applicant can apply for 2%, 3% or 5% amnesty tariffs. The transfer of assets will be entitled to an income tax waiver, but the transfer must be completed by 31 December 2017. Otherwise, the assets will be treated as taxable income at the prevailing income tax rate.

Another clarification provided in the MoF Regulation No. 127 indicates the value of assets and liabilities that can be declared for the assets held indirectly under an SPC. The liabilities in relation to the assets can still be used as a deduction to determine the net asset value (subject to specific requirements).

Following the issue of Regulation Number 127/PMK.010/2016 (“the Regulations”) for clarification on assets indirectly held through special purpose vehicles (“SPVs”), it is likely that some Indonesian amnesty applicants will need focused and timely advice on how to restructure and, in some instances, wind up their Bermuda, British Virgin Islands and Cayman Islands companies.

The Regulations provide that all international assets held indirectly through passive SPVs by an amnesty applicant must be transferred into the amnesty applicant’s direct name or be assigned to an Indonesian company owned by the tax amnesty applicant, in order for the applicant to utilise the 2%, 3% or 5% amnesty tariffs. For international assets held through an SPV, the applicable rates will be 4%, 6% or 10% unless the international assets are repatriated to Indonesia.

Amnesty applicants that hold assets indirectly through Bermuda, British Virgin Islands or Cayman Islands SPVs may therefore need to start considering how best to restructure those holdings or make the decision to wind up their SPVs in order to comply with the Regulations.

JapanJURISDICTION:

The new tax treaty between Japan and Germany came into force on 28 September 2016.

”

“Guidance on new transfer pricing documentation rules

Further to the 2016 tax reform outlined on 16 December 2015, the transfer pricing documentation rules have been amended in line with Action 13: transfer pricing documentation and country-by-country reporting of the OECD BEPS Project. In connection with this, on 30 June 2016, the National Tax Agency (NTA) released guidance on updated documentation requirements for the following:

• For specific multi-national groups (whose total consolidated revenue is JPY100 billion or more), a three-tiered approach consisting of country-by-country reports, master files and local files; and

• Local files.

The full guide is available (in English) on the NTA’s website. The website also contains reference material for the preparation of local files, but this is currently only available in Japanese.

22 | Asia Tax Bulletin MAYER BROWN JSM | 23

Japan cont’d

JURISDICTION:

International tax developments

GermanyThe new tax treaty between Japan and Germany came into force on 28 September 2016. The maximum rates of withholding tax are:

• 15% on dividends in general; 5% on dividends if the beneficial owner is a company (other than a partnership) that has owned directly, for a period of 6 months ending on the date on which entitlement to the dividends is determined, at least 10% of the voting shares of the company paying the dividends; and 0% if the beneficial owner of the dividends is a company (other than a partnership) that has owned directly, for a period of 18 months ending on the date on which entitlement to the dividends is determined, at least 25% of the voting shares of the company paying the dividends;

• 0% on interest; and• 0% on royalties.

IndiaOn 29 October 2016, the amending protocol, signed on 11 December 2015, to the India – Japan Income Tax Treaty (1989), as amended by the 2006 protocol, will enter into force. The protocol generally applies from 29 October 2016 for matters relating to the exchange of information and the assistance in the collection of taxes (articles 26 and 26A, as added by articles 2 and 3 of the amending protocol). For all other matters, it applies from 1 January 2017 for Japan and from 1 April 2017 for India.

2017 Tax Proposals

Corporate income taxOn 28 July 2016, the Ministry of Strategy and Finance (MOSF) announced its proposed tax law amendments for 2017 (the 2017 Tax Proposals). Unless otherwise stated, the following key 2017 Tax Proposals in respect of the taxation of corporations will be effective as of 1 January 2017.

Setting a deduction limit with respect to losses carried forward for foreign companies (article 91(1) of the Corporate Income Tax Law (CITL)):

This amendment will limit the amount of loss carried forward that a foreign company can deduct to 80% of the income earned in the relevant business year. The purport of the proposed amendment is to provide equal footing between foreign and domestic companies as domestic companies began to be subject to this rule from 1 January 2015. This rule will be effective from the beginning of the 2017 business year.

Expansion of the scope of personal service income among Korean-source income of non-residents/foreign companies (article 93(6) of the CITL and article 119(6) of the PITL):

Under the current CITL and PITL, income arising from services provided in Korea by entertainers, professional athletes and freelancers and services provided in Korea by persons with special scientific, technical or business management knowledge (technical services) is regarded as Korean-source personal service income and withheld at 22% (including local taxes).

According to the 2017 Tax Proposals, if prescribed by an applicable treaty, income occurring from provision of “technical services” will be subject to a 3% withholding tax where the consideration for such services is paid in Korea even though the services are provided outside of Korea. This amendment is particularly relevant to companies planning to conclude a technical services agreement with a Korean company in the future. The amendment will apply to applicable services provided after 1 January 2017.

KoreaJURISDICTION:

The amendment will extend the refund request period from three years to five years.

”“

24 | Asia Tax Bulletin MAYER BROWN JSM | 25

Korea cont’d

JURISDICTION:

Extension of the refund request period for non-resident taxpayers (articles 98-4(4), 98-5(2) and 98-6(4) of the CITL, articles 156-2(4), 156-4(2) and 156-6(4) of the PITL):

Under the current CITL and PITL, non-resident taxpayers that were subject to Korean withholding tax on income for which they were entitled to apply a treaty-reduced withholding tax rate, must file a request for refund within three years from the last day of the month in which the tax was withheld. The amendment will extend the refund request period from three years to five years. This rule will put foreign and domestic taxpayers on an equal footing because the same rule was introduced to domestic taxpayers from 1 January 2015. This amendment will be applicable to requests for refund made after 1 January 2017.

Individual income taxExtension of the reduced income tax benefit period for foreign workers and adjustment of the flat tax rate (article 18(2) of the Special Tax Treatment Control Law (STTCL)):

Under the current STTCL, foreign workers can choose to have their income taxed at a 17% flat rate for a period of five years from the date on which they first began providing services in Korea. This benefit was set to expire on 31 December 2016. The 2017 Tax Proposals extend the expiration of this benefit to 31 December 2019 for those who began to provide services in Korea from 1 January 2014. Those who started providing services prior to 1 January 2014 are eligible for this benefit only until 31 December 2018. The proposed amendment also increases the flat rate from the current 17% to 19%. The amended rate will be applicable to income earned after 1 January 2017.

Introduction of an “exit tax” (i.e. the imposition of tax on capital gains at the time of departure from

Korea) (newly added article 118(9) of the Personal Income Tax Law (PITL)):

According to the 2017 Tax Proposals, where a Korean resident departs from Korea for the purpose of emigration and (i) that person has lived in Korea for more than five years in the last 10 years before departure; and (ii) is a majority shareholder who is subject to capital gains tax (article 157(4) of the Enforcement Decree of the PITL), such person will be deemed to have transferred his Korean shares as of the departure date and will be taxed at 20% on the gains arising from such transfer (the tax rate applicable on the transfer of Korean shares by a majority shareholder).

A person who is subject to the exit tax will be required to report and pay the exit tax within three months from the last day of the month to which the departure date belongs. The penalty for non-compliance will be 20% of the tax amount payable. Tax credits will be allowed against foreign taxes paid on the same shares – and if the shares are subsequently transferred at a lower value than the value of the deemed transfer, a tax credit will be allowed reflecting this difference. Further, if a person who was subject to exit tax returns to Korea within five years from his departure, the exit tax paid will be refunded to that person. This amendment will be effective for departures from Korea that occur after 1 January 2018.

Other proposals include:

• Extension of the income tax deduction for credit card payments until the end of 2019; and

• Increase in the childbirth tax credit to KRW500,000 for the second child and KRW700,000 for the third child.

International tax aspectsExpansion of the scope of personal service income among Korean-source income of non-residents/

foreign companies (article 93(6) of the CITL and article 119(6) of the PITL):

As previously mentioned, under the current CITL and PITL, income arising from services provided in Korea by entertainers, professional athletes and freelancers and services provided in Korea by persons with special scientific, technical or business management knowledge (technical services, etc.) is regarded as Korean-source personal service income and tax should be withheld at 22% (including local taxes). According to the 2017 Tax Proposals, if prescribed by an applicable treaty, income occurring from provision of “technical services, etc.” will be subject to a 3% withholding tax where the consideration for such services is paid in Korea even though the services are provided outside of Korea. This amendment is particularly relevant to companies planning to conclude a technical services agreement with a Korean company in the future. The amendment is for applicable services provided after 1 January 2017.

Addition of a special case for which the statutory period for taxation relating to international transactions of multinational enterprises is applicable (article 23 of the LCITA):

Where a taxpayer files a request for commencing a mutual agreement procedure (MAP), the Korean tax authority suspends enforcement activities with respect to the taxable years subject to the MAP. However, under the current LCITA, if the taxpayer later withdraws the MAP, the tax authority does not have the power to assess tax against taxable years for which the statute of limitations has expired during the course of the MAP proceedings. The proposed amendment will grant the Korean tax authority an additional year from the date on which the taxpayer withdraws a MAP during which it can impose tax, even if the statute of limitations has expired during the MAP process. This amendment

will apply to MAP request withdrawals made after 1 January 2017.

Improvement of the MAP regime (article 22 of the LCITA, article 39 of the Enforcement Decree of the LCITA):

The amendment will expand the scope of MAP applicants so that even non-residents or foreign companies not having a place of business in Korea can request a MAP. In addition, if the Korean tax authority rejects the taxpayer’s MAP request, the amendment imposes on the Korean tax authority the duty to notify the taxpayer and the other contracting state of the rejection. The amendment reflects recent OECD recommendations relating to MAP. The amendment will be applicable to MAP requests and rejections of such requests made after 1 January 2017.

Regime relating to documentation requirements for multinational enterprisesImposition of duty to submit a country-by-country (CbC) report on multinational enterprises (article 11 of the LCITA and article 21(2) of the Enforcement Decree of the LCITA):

The 2017 Tax Proposals will require a Korean company which is the ultimate parent company of a multinational enterprise with a consolidated turnover of at least KRW1 trillion (approximately US$870 million) in the preceding year to submit a CbC report that includes information on the business activities (revenue, profits, number of employees, assets, etc.) and the taxes paid of the Korean company’s foreign subsidiaries. Under this amendment, a Korean ultimate parent company is required to submit a CbC report for the taxable year of 2016 by the end of 2017.

26 | Asia Tax Bulletin MAYER BROWN JSM | 27

Extension of the period for submitting Combined Report of International Transactions (CRIT) (article 11 of the LCITA):

This amendment extends the period for submitting the CRIT (i.e. the local file and master file) from the corporate tax return filing due date to within 12 months from the end of the relevant business year. The amendment will apply to the submissions made after 1 January 2017.

Exemption from duty to submit local file for Advance Pricing Agreement (APA) – approved transactions (article 21(2) of the Enforcement Decree of the LCITA):

In light of the similarity between APA documents and the local file, article 21(2) of the Enforcement Decree of the LCITA will be amended so that the duty to submit the local file will be exempted for APA-approved transactions. This amendment will be applicable to submissions made after 1 January 2017.

Indirect tax aspectsAllowing adjustments to the dutiable value of imported goods when the transaction price changes after the filing of an import declaration (article 16(1) of the Enforcement Decree of the Customs Law):

The amendment, which reflected the World Customs Organization’s guidelines, will change the existing position of the Korea Customs Service that prohibited a post-adjustment of the dutiable value of imported goods with respect to post-compensation adjustments made by multinational enterprises.

According to the amendment, where the transaction price of imported goods is adjusted after an import declaration is filed to reflect the

Korea cont’d

JURISDICTION:

normal value under the national tax methods for calculating such value, the dutiable value of the imported goods can be adjusted under certain conditions (e.g. submission of a post-adjustment plan before importing goods, and use of the method of calculating the normal value) by reporting the potential/determined price. This amendment will be applicable to import declarations made after the enforcement date of the Enforcement Decree of the Customs Law expected in early 2017.

Under this amendment, where a remittance is made through a post-compensation adjustment, the amount remitted will be included in the dutiable value of imported goods so that additional customs duties will be paid, and if the amount relating to post-compensation adjustment is received, the amount received will be excluded from the dutiable value of the imported goods so that customs duties already paid can be refunded.

Beneficial ownershipCourtesy of law firm Kim & Chang, it was reported that the Korean Supreme Court, on July 1, 2016, ruled on a case involving beneficial ownership, an issue which is the subject of many recent court cases. In its decision, the Supreme Court ruled that an intermediate UK holding company can be viewed as the beneficial owner of the Korean source dividends in light of various surrounding circumstances, and as such, the tax assessment – which treated the French parent company as the beneficial owner and denied the application of the Korea-UK Tax Treaty – is unlawful.

In 2014, Kim & Chang was successful in a similar Supreme Court case involving the beneficial ownership issue, where the Supreme Court ruled that the nominal investor should be viewed as the beneficial owner, and thus, a tax assessment that denied the nominal investor as the beneficial owner is unlawful.

Many foreign multinational companies and investors have acquired stocks of Korean companies, real estates, etc. and the incomes earned on the investments (i.e. dividends, capital gains, etc.) were subject to reduced withholding tax rates or exempt from tax under the relevant tax treaties. However, in recent years, the Korean tax authorities have assessed taxes in numerous cases alleging that the nominal investor that earned investment income is not the beneficial owner, but a mere conduit; and therefore the beneficial owner should be an upper-tier shareholder by application of the substance-over-form principle.

This new Supreme Court case was also a case where a French multinational company invested in a Korean company through an intermediate holding company in the UK and withheld tax on dividend by applying the reduced rate (5%) under the Korea-UK Tax Treaty. However, the Korean tax authority argued that since the intermediate holding company is a mere conduit established to take advantage of the lower withholding tax rate under the tax treaty, it cannot be recognised as the beneficial owner of the income under the Korea-UK Tax Treaty and assessed additional withholding tax on the taxpayer by alleging that the French parent company is the beneficial owner of the income and applying the reduced withholding tax rate available under the Korea-France Tax Treaty (15%).

As counsel for the taxpayer in the above Supreme Court case, Kim & Chang obtained a successful decision that the intermediate UK holding company should be respected as the beneficial owner of the dividend income and therefore the application of the reduced withholding tax rate under the Korea-UK Tax Treaty allowed when all of the following facts are taken into consideration:

(i) Incorporation background of the intermediate UK holding company (established 20 years prior to investment in Korea) and its business activities (invested in various other subsidiaries);

(ii) Decision-making on investment and assumption of investment-related costs (investment decisions were made by the board of directors of the intermediate UK holding company and the legal/accounting service costs were borne by the intermediate UK holding company); and

(iii) Source of the funds for investment (intermediate UK holding company used its own funds for investment).

This Supreme Court decision is meaningful in that taxpayers now have an opportunity to rescind similar tax assessments that denied the application of the tax treaty benefit through denial of the foreign nominal investor as the beneficial owner of the income by effectively advocating and substantiating key factual points such as the incorporation background.

International tax developments

USAFATCA. On 8 September 2016, the Korea-United States FATCA Model 1A Agreement (2015) entered into force.

28 | Asia Tax Bulletin MAYER BROWN JSM | 29

MalaysiaJURISDICTION:

Generally, every company within a group is treated as a separate entity and the tax liability of each company is determined separately.

”

“Tax on digital business platforms proposed

The Malaysian government on 10 August proposed to implement a tax on digital business platforms to ensure a fair level playing field between online and offline businesses.

The government already set up a team to study the development of taxation in the digital economy following the emergence of several digital platforms such as Uber, Netflix and Airbnb. The Inland Revenue Board (IRBM) also stated that it is currently monitoring those business activities in order to bring them under the tax net in the future. However, to realise the proposed plans, the government will need to ensure that all the necessary infrastructures (i.e. technology, organizational capability and the relevant legal frameworks) are in place.

Group relief for companies

On 22 August 2016, the Inland Revenue Board of Malaysia issued Public Ruling (PR) No. 6/2016, explaining the tax treatment of group relief for resident companies incorporated in Malaysia. Generally, every company within a group is treated as a separate entity and the tax liability of each company is determined separately. The PR also provides various examples of the computation of group relief.

Effective from year of assessment (YA) 2006, group relief is available to all locally incorporated resident companies subject to section 44A of the Income Tax Act, 1967 (ITA). The group relief allows a company to surrender (referred to as a “surrendering company”) not more than 70% of its adjusted loss to one or more related companies within the same group.

The PR also sets out the qualifying criteria for both the surrendering and claimant companies, as follows:

• Both companies must: - be resident and incorporated in Malaysia;- be related companies throughout the YA and 12

months immediately prior to that YA;- have more than MYR2.5 million ordinary paid-up

capital;- have a 12-month basis period ending on the same

date;- make an irrevocable election to surrender or claim

an amount of adjusted loss for that particular YA; and

- be subject to tax at the appropriate rate as specified in paragraph 2 of Part 1 of Schedule 1 of the ITA.

• The claimant company has an aggregate income for that YA.

Companies within the same group qualify for group relief if they fulfil two tests:

• First level test: the ordinary shareholding level of at least 70% is satisfied; and

• Second level test: the company concerned is beneficially entitled (directly or indirectly) to at least 70% of the residual profits and residual assets of the other company in proportion to their equity interest pursuant to subsection 44A(7) of the ITA.

International tax developments

InternationalOn 25 August 2016, Malaysia joined the multi-lateral Convention on Mutual Administrative Assistance in Tax Matters, signed on 25 January 1988 and the amending protocol, signed on 27 May 2010.

30 | Asia Tax Bulletin MAYER BROWN JSM | 31

PhilippinesJURISDICTION:

Treaty benefits for dividends, interest and royalty income

On 23 June 2016, the Bureau of Internal Revenue (BIR) issued Revenue Memorandum Order (RMO) No. 27-2016 on the new procedures for claiming preferential tax treaty benefits on dividend, interest and royalty payments to non-residents.

The effect of this Order is to allow Philippines taxpayers to directly apply the treaty rates on their dividend, interest and royalty payments to qualifying non-residents. As such, the filing of the tax treaty relief application (TPRA) for such payments is no longer required. Instead, taxpayers will be required to keep their records based on the guidelines outlined in the Order as supporting documentation for any future tax audit. In the case of other income, the procedures under RMO No. 72-2010 continue to apply and obtaining a ruling is still required.

Paying taxes via credit, debit and prepaid cards

On 23 March 2016, the Bureau of Internal Revenue (BIR) published Revenue Regulations No. 3-2016 of 12 January 2016, which prescribe the policies and guidelines on the adoption of credit, debit and prepaid card payments as additional voluntary or optional modes of paying taxes. Any convenience fee or other charges imposed by the banks or credit card companies for the use of such payment facilities are absorbed by taxpayers and not to be deducted from the tax amount due to the BIR. The full version of the Regulations is available on the BIR’s website.

An alien employment permit is typically required for a foreign national to engage in gainful employment in the Philippines.

”

“National Budget 2017 proposed

On 15 August 2016, the National Budget 2017 was presented to the House of Representatives.

Direct taxesIn order to increase the take-home pay for individual taxpayers and create a more favourable business climate in general, a decrease in income tax rates is proposed, as follows:

• For individuals: from the current ceiling of 32% to 25%; and

• For corporations: from the current ceiling of 30% to 25%.

Indirect taxes

• Broadening the value added tax base; and• Increasing excise tax rates on petroleum.

Other measuresTo curb tax leakages and tax evasion several measures are proposed, including:

• Relaxation of the Bank Secrecy Law; and• Amendment to the Anti-Money Laundering Act

to make tax evasion a predicate crime to money laundering.

Employment permit exemption for corporate officers

The Philippines Department of Labor and Employment (DOLE) has issued guidance identifying the supporting documents required for a Philippines company to obtain a certificate of exclusion (from alien employment permit requirements) for foreign officers.

An alien employment permit is typically required for a foreign national to engage in gainful employment in the Philippines. A September 2015 revision to these employment permit rules exempts certain categories of foreign nationals from employment permit requirements; these include foreign corporate officers such as president and CEO-level positions as well as board members of Philippine companies.

The DOLE guidance clarifies these revised rules and confirms that the exempted foreigners must not be involved in managing daily operations and must not receive a salary from a Philippine source.

32 | Asia Tax Bulletin MAYER BROWN JSM | 33

SingaporeJURISDICTION:

Mergers and acquisitions

The Inland Revenue Authority (IRAS) has issued a revised e-Tax Guide, to update the existing mergers and acquisition (M&A) scheme.

Pursuant to the announcement made during Budget 2016, the guide was updated to reflect that the cap on the value of qualifying acquisitions had been increased from SGD20 million to SG 40 million from 1 April 2016. Other terms and conditions of the M&A scheme remain unchanged.

General anti avoidance rule

Section 33 of the Income Tax Act contains the general anti avoidance rule. On 11 July the IRAS issued a practice note (‘E-Guide’) on how it will apply s.33 in practice. The practice note is largely based on the AQQ ruling by the Court of Appeals. The note explains that one should first look objectively at whether the manner in which an arrangement was implemented created a tax reduction. Secondly, one should look whether subjectively (from the perspective of the taxpayer) the taxpayer can refute a challenge based on s.33 because the arrangement was done for bona fide commercial reasons and had not as one of its main purposes the avoidance or reduction of income tax. Thirdly, if the taxpayer cannot sufficiently refute the challenge under s.33, one should examine whether the tax reduction obtained is consistent with the intention of a specific provision in the income tax law, based on which the income tax reduction is obtained.

The IRAS regards the following as having the purpose or effect of tax avoidance within the meaning of section 33:

• Circular flow or round-tripping of funds;• Setting-up of more than one entity for the sole

purpose of obtaining tax advantage;• Change in business form for the sole purpose of

obtaining tax advantage; and• Attribution of income that is not aligned with

economic reality.

EPs expiring between 1 January and 30 June 2017 may be renewed for a duration of one year at the current qualifying salary.

”

“Minimum qualifying salary for employment passes to increase

The Ministry of Manpower (MOM) announced on 26 July 2016 that it would be raising the qualifying salary for Employment Pass (EP) applications from S$3,300 per month to S$3,600 per month, effective 1 January 2017. By this date, all applications for new EPs must provide a monthly salary of at least S$3,600 per month.

EP applications set to expire before 1 January 2017 may be renewed for durations of up to three years at the current qualifying salary. EPs expiring between 1 January and 30 June 2017 may be renewed for a duration of one year at the current qualifying salary. Employers must renew EPs expiring after 30 June 2017 at the new qualifying salary.

Further information is available on the MOM website.

India According to a press release of 24 August 2016 published by the Indian government, negotiations for a revision to the India-Singapore Income Tax Treaty (1994), as amended by the 2005 and 2011 protocols, are underway.

South AfricaAn income tax treaty between Singapore and South Africa was signed on 23 November 2015 by South Africa and on 30 November 2015 by Singapore. Once in force and effective, the new treaty will generally replace the Singapore-South Africa Income Tax Treaty (1996).

AustraliaOn 6 September 2016, the Australia-Singapore Competent Authority Agreement on Automatic Exchange of Information (2016) was signed in Australia and in Singapore. The agreement specifies the details of which information will be exchanged and when, as set out in the OECD Automatic Exchange of Information Agreement (2014).

EthiopiaOn 24 August 2016, Singapore signed a tax treaty with Ethiopia on the sidelines of the 4th Africa Singapore Business Forum, held from 24 to 25 August 2016 in

Singapore. Further developments will be reported as they occur. MozambiqueOn 24 August 2016, Mozambique and Singapore signed an investment protection agreement (IPA).

UKOn 16 September 2016, the Inland Revenue Authority of Singapore (“IRAS”) and her counterpart in the UK signed a Competent Authority Agreement (“Agreement”) on the automatic exchange of financial account information (“AEOI”) based on the Common Reporting Standard (“CRS”). The CRS is an internationally agreed standard for AEOI, endorsed by OECD and Global Forum for Transparency and Exchange of Information for Tax Purposes (“GF”). More than 100 jurisdictions have endorsed the CRS and will commence AEOI in either 2017 or 2018.

As announced on 3 Nov 2014, Singapore will commence AEOI under the CRS in 2018. Such exchanges will be carried out on a bilateral basis with jurisdictions with whom Singapore has signed Agreements. This will be subject to the following conditions:

(i) There is a level playing field among all major financial centres to minimise regulatory arbitrage;

(ii) The IRAS will only engage in AEOI with jurisdictions that have a robust framework of law and can ensure the confidentiality of information exchanged and prevent its unauthorised use; and

(iii) There is full reciprocity with AEOI partners in terms of information exchanged. Singapore and the United Kingdom will commence AEOI under the CRS by September 2018. Under the Agreement, IRAS will automatically exchange with the UK financial account information of accounts in Singapore held by United Kingdom tax residents, while HMRC will automatically exchange with IRAS financial account information of accounts in the United Kingdom held by Singapore tax residents.

34 | Asia Tax Bulletin MAYER BROWN JSM | 35

TaiwanJURISDICTION:

On 22 September 2016, the Taiwanese Executive Yuan passed a draft bill to amend the VAT Act on the cross-border sale of digital services.

”

“Visa waiver pilot programme for certain Asian countries announced

Effective 1 August 2016, citizens of Thailand and Brunei may travel visa-free to Taiwan for up to 30 days. The pilot programme will be effective until 31 July 2017.

Anti avoidance rules in respect of individuals On 21 July 2016, the Cabinet of Taiwan passed the proposal for the Controlled Foreign Company (CFC) rules in respect of individuals. The legislative body of Taiwan had previously passed the amendment to basic income tax law in order to introduce the CFC rules for individuals on 12 July 2016.

According to the proposal, a CFC is any foreign company established in a low-tax jurisdiction in which more than 50% of the company’s capital directly or indirectly is owned by Taiwan individual shareholders, or on which the individuals have capacity to exercise significant influence. Companies with substantial business activities or whose revenue is below the prescribed threshold are excluded. Individuals who are resident in Taiwan or their up-to-second tier relatives who, separately or in the aggregate, hold more than 10% of equity interest in or capital of a CFC are required to include the income from CFCs in their taxable income of the current tax year in proportion to their holdings.

The losses of a CFC can be carried forward for 10 years. To avoid double taxation, the distributed dividends or profits will not be included in the taxable income and the foreign tax paid may be credited against Taiwanese basic income tax within 5 years after the date of the inclusion of the distributed income.

The CFC rules in respect of individuals will be enacted and implemented on the same date as the CFC rules in respect of companies and the date is yet to be determined by the Cabinet.

VAT Act on cross-border sale of digital services

On 22 September 2016, the Taiwanese Executive Yuan passed a draft bill to amend the VAT Act on the cross-border sale of digital services. The bill is drafted by the Ministry of Finance and refers to the proposals of the OECD and tax laws of the EU, Japan and Korea, and will be submitted to the Legislative Yuan. The bill addresses the following amendments:

• The concept of taxpayers who provide the cross-border sale of electronic services is redefined.

• The taxpayers must register or appoint tax agents for registration purposes.

• The taxpayers or the agents must file the VAT returns in the regulated period.