Embed Size (px)

Citation preview

Asia and Pacific Regional Economic Outlook

Sustaining the Momentum: Vigilance and Reforms

1

Romain DuvalAsia and Pacific Department, IMF

Tokyo, May 8, 2014

2

Key Messages

•Asia will remain the most dynamic region

•Risks from outside Asia have receded

•Actions taken to address vulnerabilities bearing fruit

•But need for vigilance and reforms

Roadmap

Outlook and broad policy challenges

1: Leverage— a fault line?

2: Responding to financial risks— what role for Macro-prudential policies?

3: China’s reforms— What impact?

4: Abenomics— temporary stimulus or break with the past?

5: ASEAN— what is happening to growth?

Key Regional Themes

3

6: Regional integration — Growing source of spillovers?

4

5

6

7

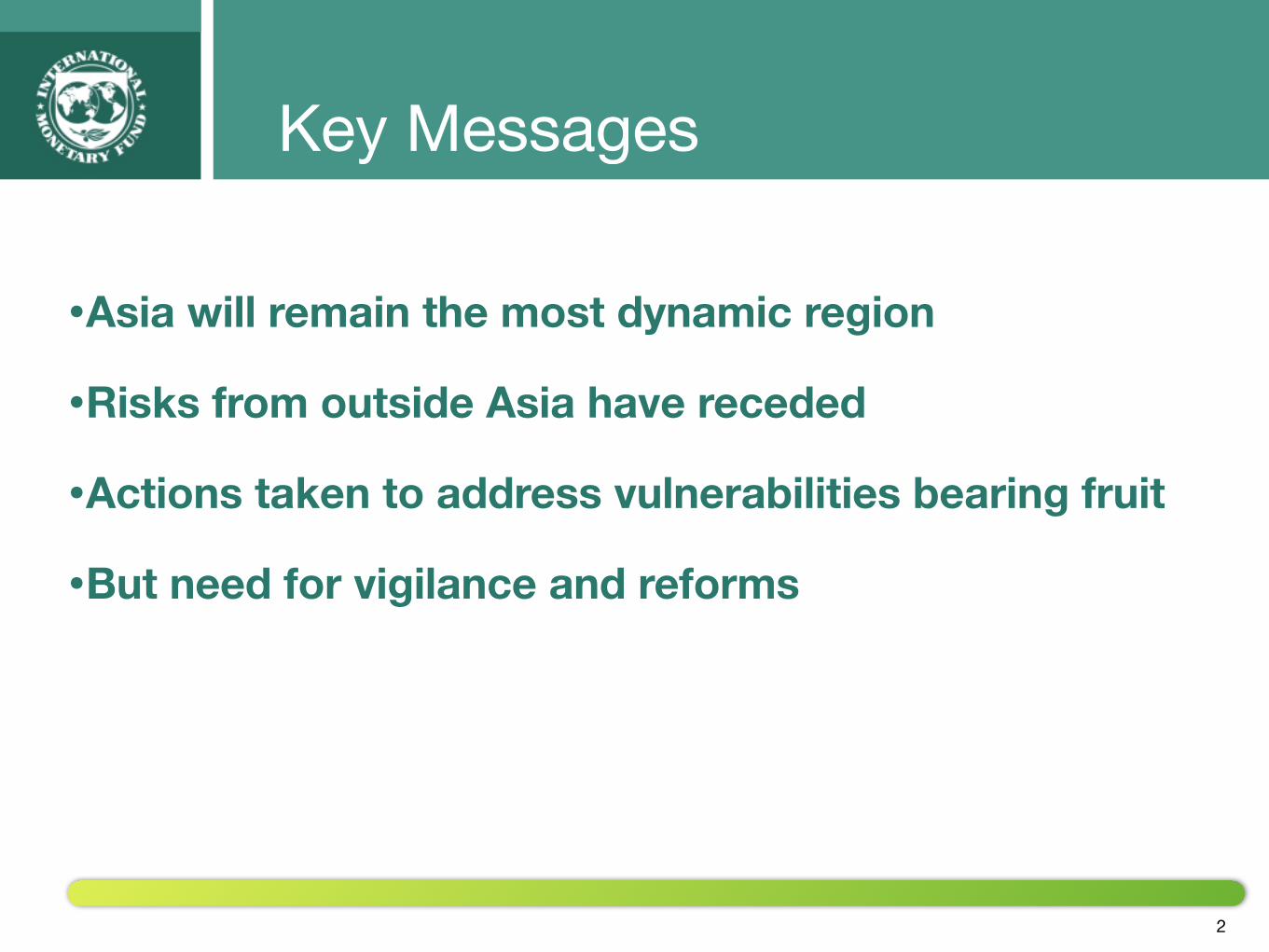

Asia Emerging Asia ASEAN-5 Frontier and Developing Asia

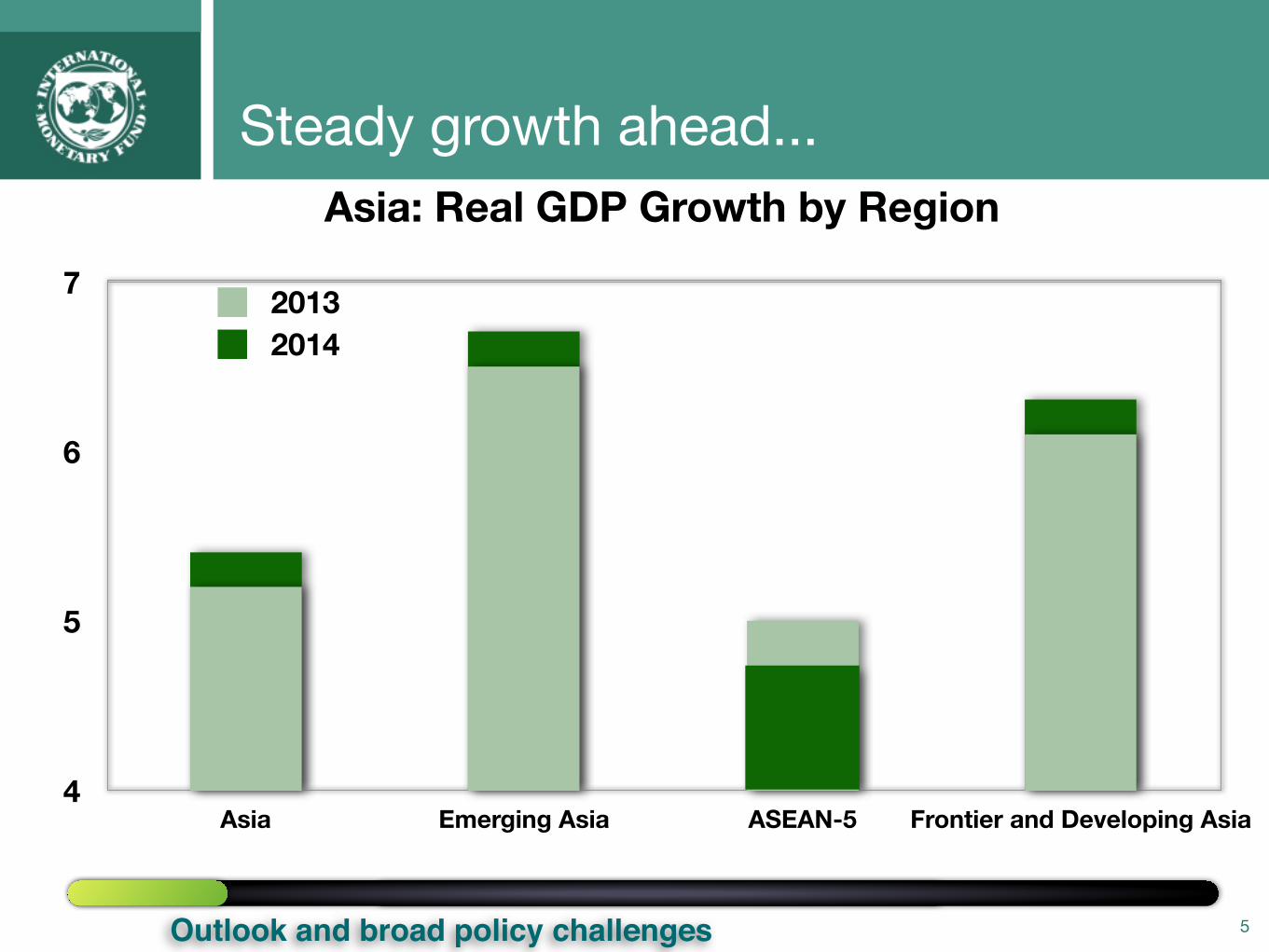

Steady growth ahead...

4

Asia: Real GDP Growth by Region

2013

Outlook and broad policy challenges

4

5

6

7

Asia Emerging Asia ASEAN-5 Frontier and Developing Asia

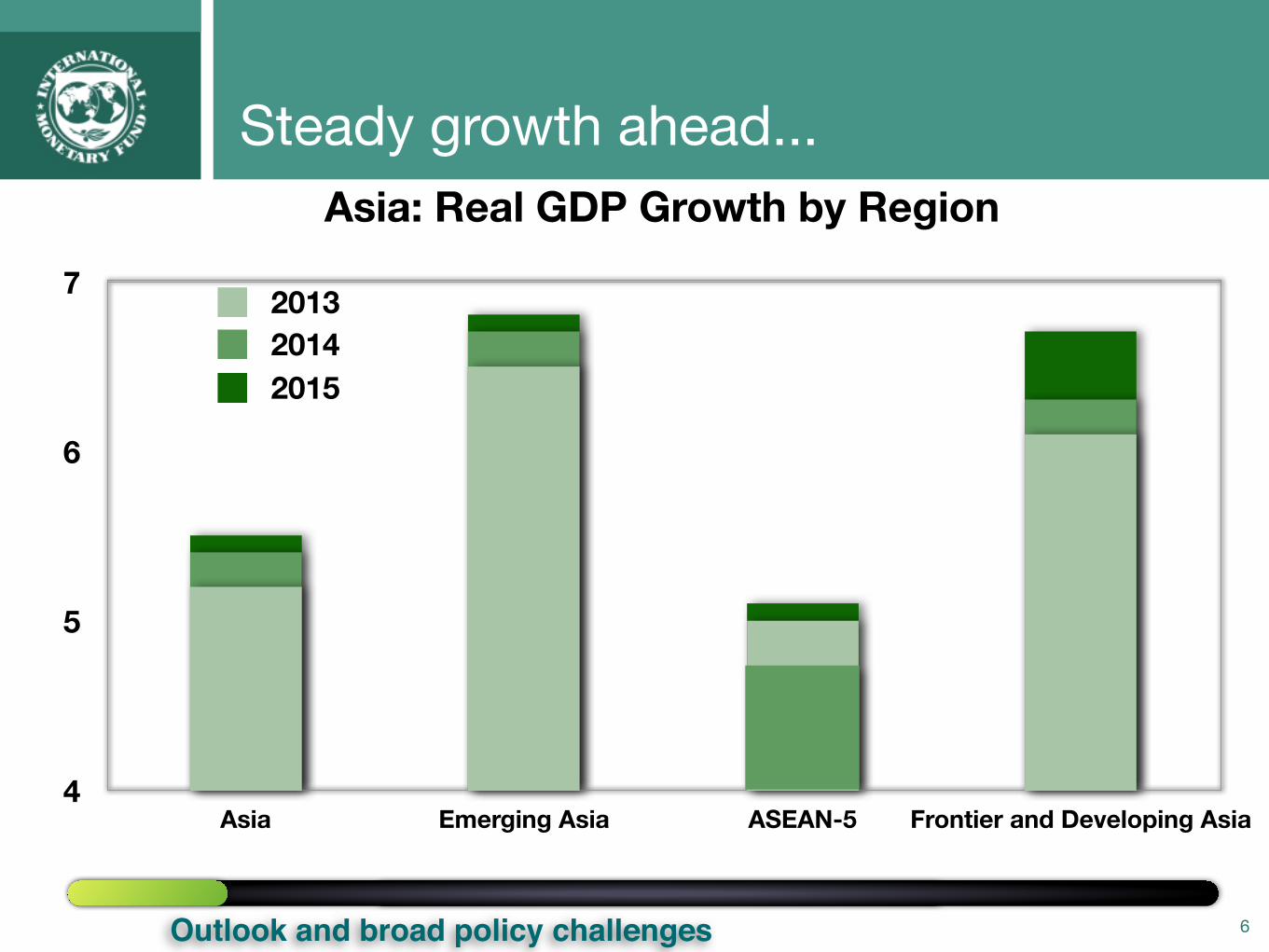

Steady growth ahead...

5

Asia: Real GDP Growth by Region

20132014

Outlook and broad policy challenges

Steady growth ahead...

6

Asia: Real GDP Growth by Region

20132014

4

5

6

7

Asia Emerging Asia ASEAN-5 Frontier and Developing Asia

2015

Outlook and broad policy challenges

-0.5

0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015

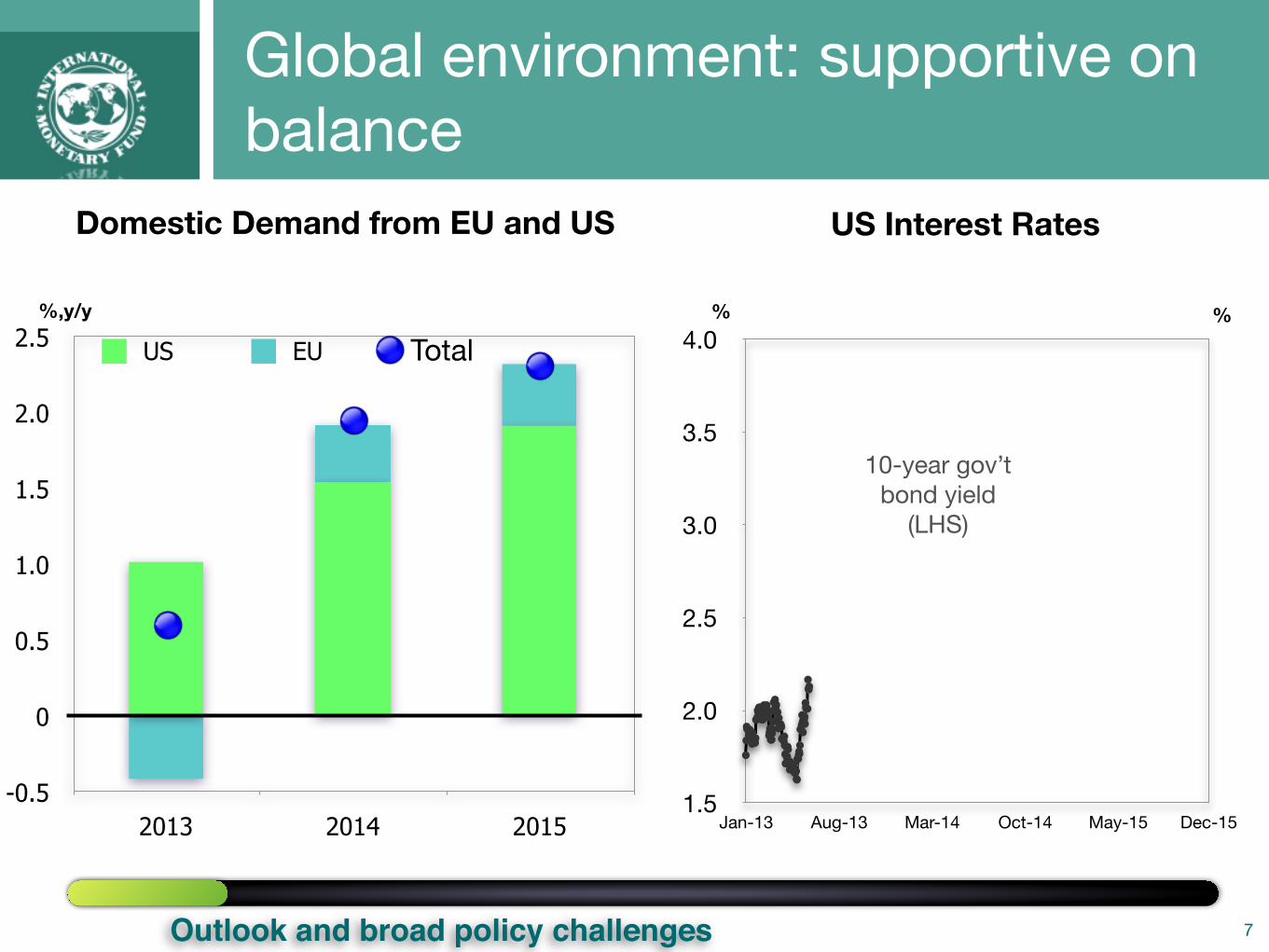

7

Domestic Demand from EU and US

US EU Total

US Interest Rates

%,y/y

1.5

2.0

2.5

3.0

3.5

4.0

Jan-13 Aug-13 Mar-14 Oct-14 May-15 Dec-15

% %

10-year gov’t bond yield

(LHS)

Global environment: supportive on balance

Outlook and broad policy challenges

-0.5

0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015

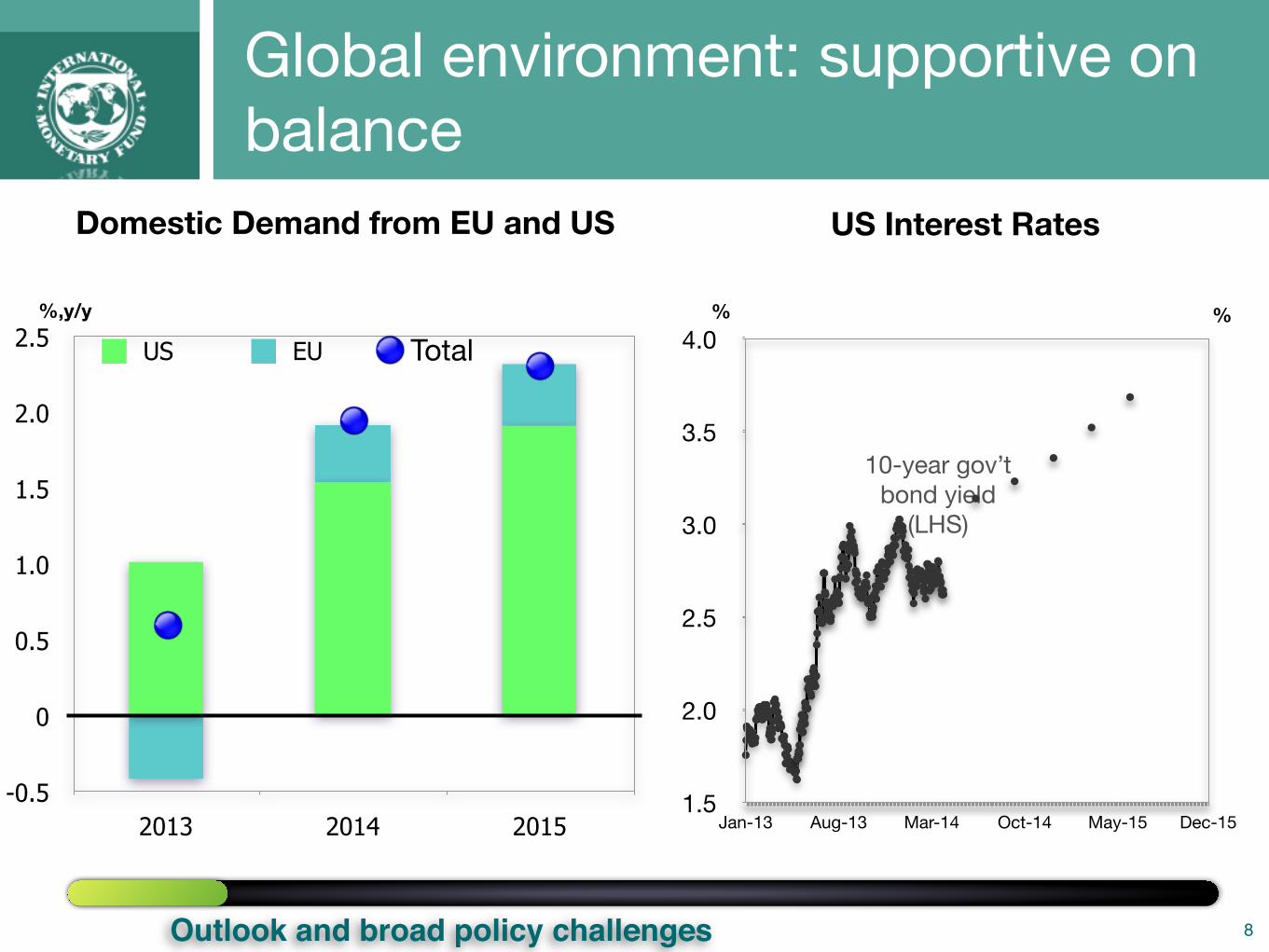

8

Domestic Demand from EU and US

US EU Total

US Interest Rates

%%,y/y %

10-year gov’t bond yield

(LHS)

Global environment: supportive on balance

1.5

2.0

2.5

3.0

3.5

4.0

Jan-13 Aug-13 Mar-14 Oct-14 May-15 Dec-15

Outlook and broad policy challenges

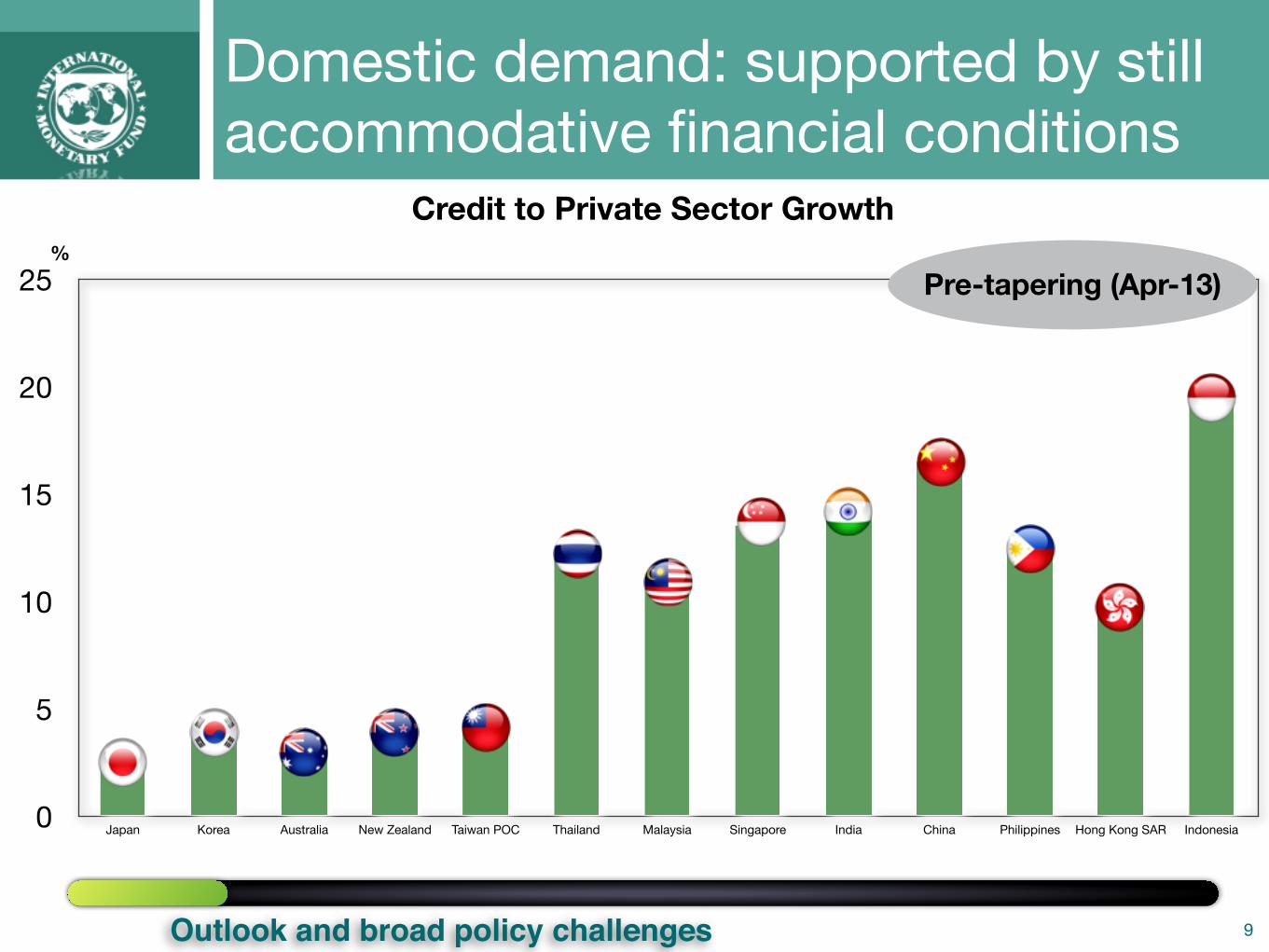

9

0

5

10

15

20

25

Japan Korea Australia New Zealand Taiwan POC Thailand Malaysia Singapore India China Philippines Hong Kong SAR Indonesia

Pre-tapering (Apr-13)

Credit to Private Sector Growth%

Domestic demand: supported by still accommodative financial conditions

Outlook and broad policy challenges

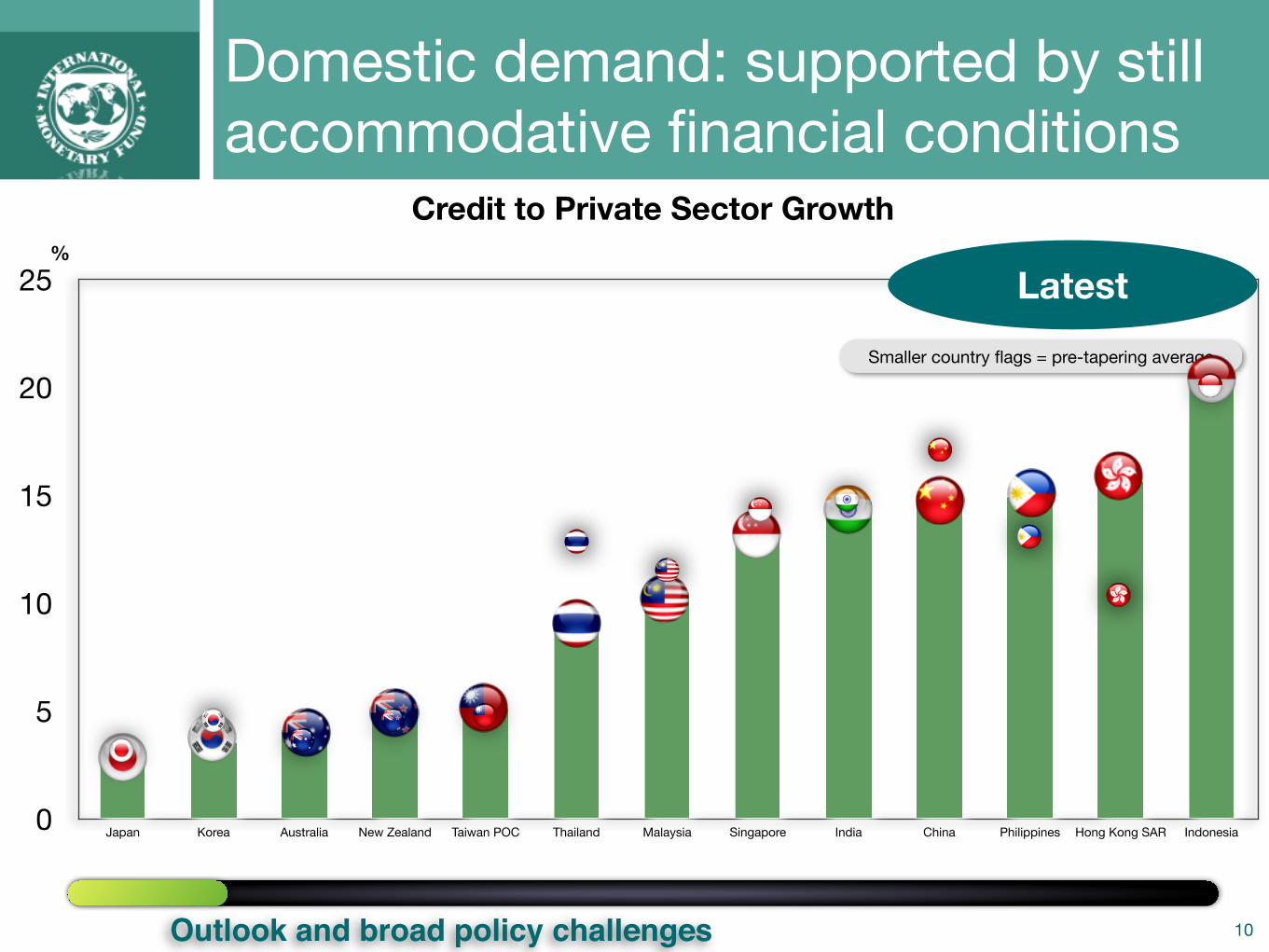

10

0

5

10

15

20

25

Japan Korea Australia New Zealand Taiwan POC Thailand Malaysia Singapore India China Philippines Hong Kong SAR Indonesia

Latest

Credit to Private Sector Growth%

Smaller country flags = pre-tapering average

Domestic demand: supported by still accommodative financial conditions

Outlook and broad policy challenges

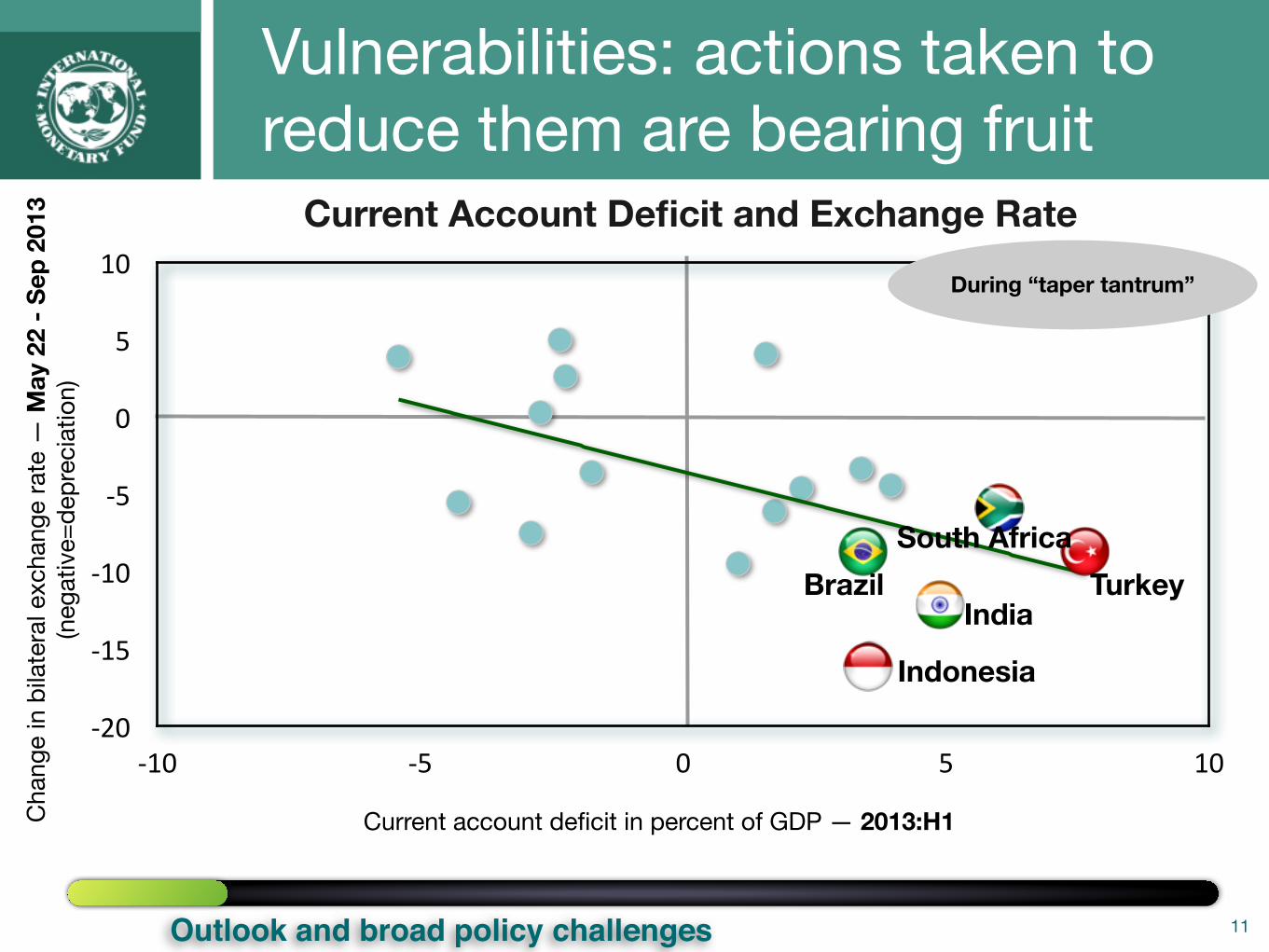

-‐20

-‐15

-‐10

-‐5

0

5

10

-‐10 -‐5 0 5 10

Current Account Deficit and Exchange Rate

11

Indonesia

India

Cha

nge

in b

ilate

ral e

xcha

nge

rate

— M

ay 2

2 - S

ep 2

013

(neg

ativ

e=de

prec

iatio

n)

Current account deficit in percent of GDP — 2013:H1

During “taper tantrum”

BrazilSouth Africa

Turkey

Vulnerabilities: actions taken to reduce them are bearing fruit

Outlook and broad policy challenges

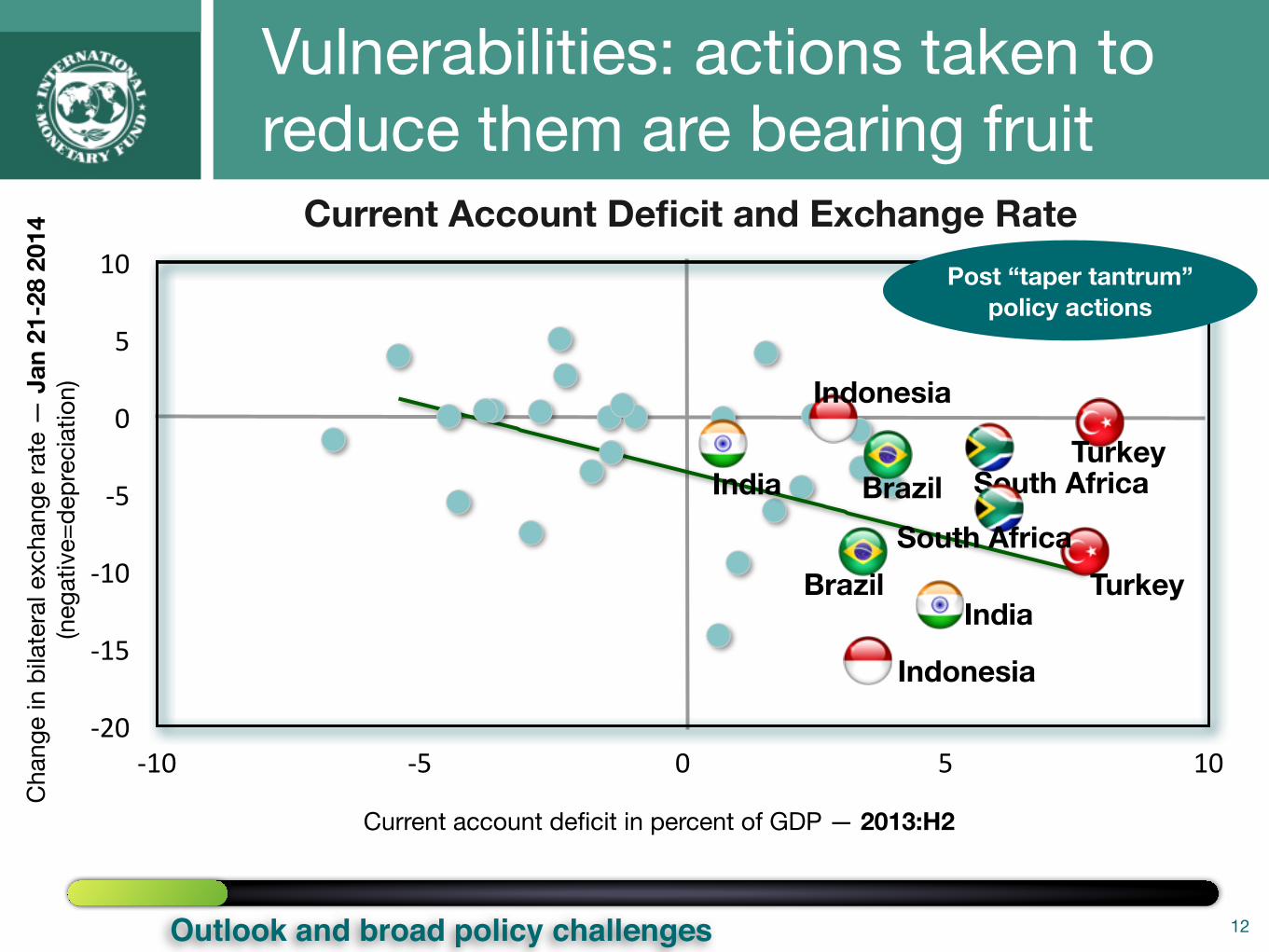

-‐20

-‐15

-‐10

-‐5

0

5

10

-‐10 -‐5 0 5 10

Current Account Deficit and Exchange Rate

12

Cha

nge

in b

ilate

ral e

xcha

nge

rate

— J

an 2

1-28

201

4(n

egat

ive=

depr

ecia

tion)

Current account deficit in percent of GDP — 2013:H2

Post “taper tantrum” policy actions

India

Indonesia

Indonesia

India

Brazil South AfricaTurkey

Brazil TurkeySouth Africa

Vulnerabilities: actions taken to reduce them are bearing fruit

Outlook and broad policy challenges

13

Policy settings and challenges- Monetary: progressive normalization as conditions warrant

- Fiscal: gradual consolidation

- Macroprudential: remains part of the toolkit

- Structural: key for both short-term financial stability and medium-term growth

- But no one size-fits-all: subregional specificities

Outlook and broad policy challenges

Theme 1. Leverage

Theme 1: Leverage: a fault line?

• Aggregate corporate leverage has remained stable in recent years

• But pockets of vulnerability: leveraged firms tend to be the weakest

• Leverage could amplify corporate stress created by higher global interest rates

• Leverage likely have adverse implications for investment

14

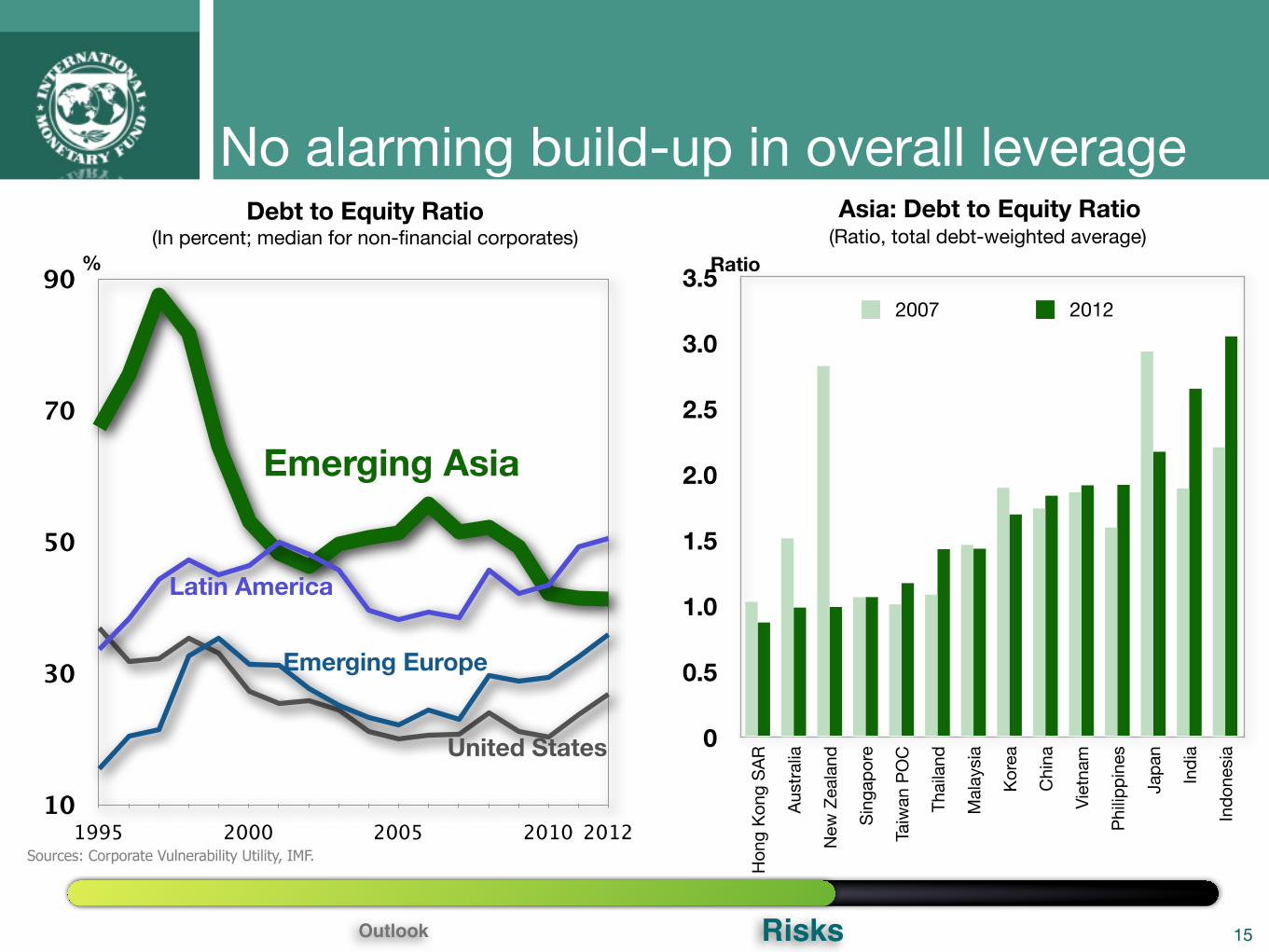

Debt to Equity Ratio (In percent; median for non-financial corporates)

Sources: Corporate Vulnerability Utility, IMF.

15

10

30

50

70

90

1995 2000 2005 2010 2012

Emerging Asia

Latin America

Emerging Europe

United States

RisksOutlook

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Hon

g Ko

ng S

AR

Aust

ralia

New

Zea

land

Sing

apor

e

Taiw

an P

OC

Thai

land

Mal

aysi

a

Kore

a

Chi

na

Viet

nam

Philip

pine

s

Japa

n

Indi

a

Indo

nesi

a

Asia: Debt to Equity Ratio (Ratio, total debt-weighted average)

2007 2012

% Ratio

No alarming build-up in overall leverage

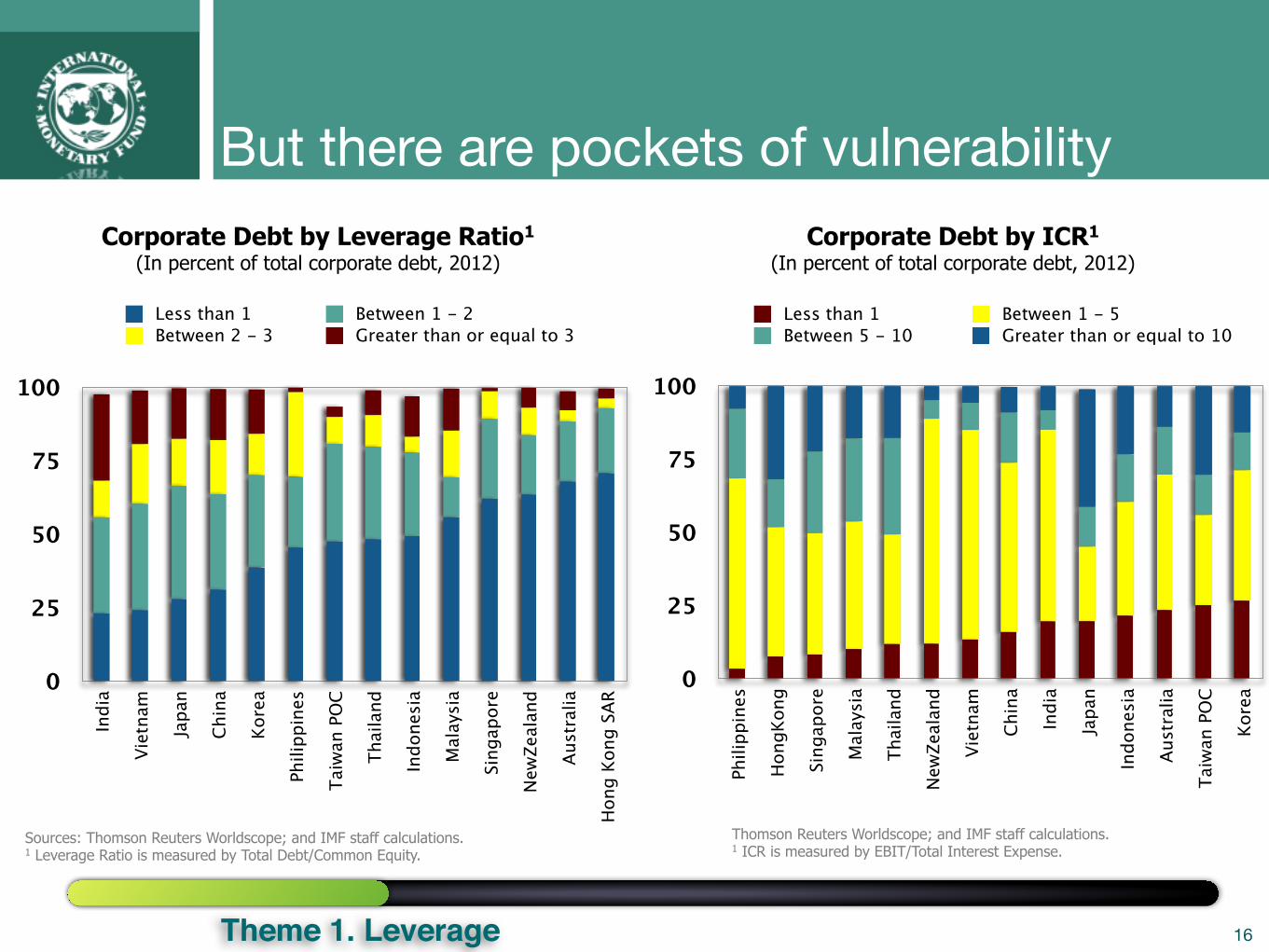

But there are pockets of vulnerability Corporate Debt by Leverage Ratio1

(In percent of total corporate debt, 2012) Corporate Debt by ICR1

(In percent of total corporate debt, 2012)

Sources: Thomson Reuters Worldscope; and IMF staff calculations.1 Leverage Ratio is measured by Total Debt/Common Equity.

Thomson Reuters Worldscope; and IMF staff calculations.1 ICR is measured by EBIT/Total Interest Expense.

16

0

25

50

75

100

Indi

a

Viet

nam

Japa

n

Chin

a

Kore

a

Phili

ppin

es

Taiw

an P

OC

Thai

land

Indo

nesi

a

Mal

aysi

a

Sing

apor

e

New

Zeal

and

Aust

ralia

Hon

g Ko

ng S

AR

Less than 1 Between 1 - 2Between 2 - 3 Greater than or equal to 3

0

25

50

75

100

Phili

ppin

es

Hon

gKon

g

Sing

apor

e

Mal

aysi

a

Thai

land

New

Zeal

and

Viet

nam

Chin

a

Indi

a

Japa

n

Indo

nesi

a

Aust

ralia

Taiw

an P

OC

Kore

a

Theme 1. Leverage

Less than 1 Between 1 - 5Between 5 - 10 Greater than or equal to 10

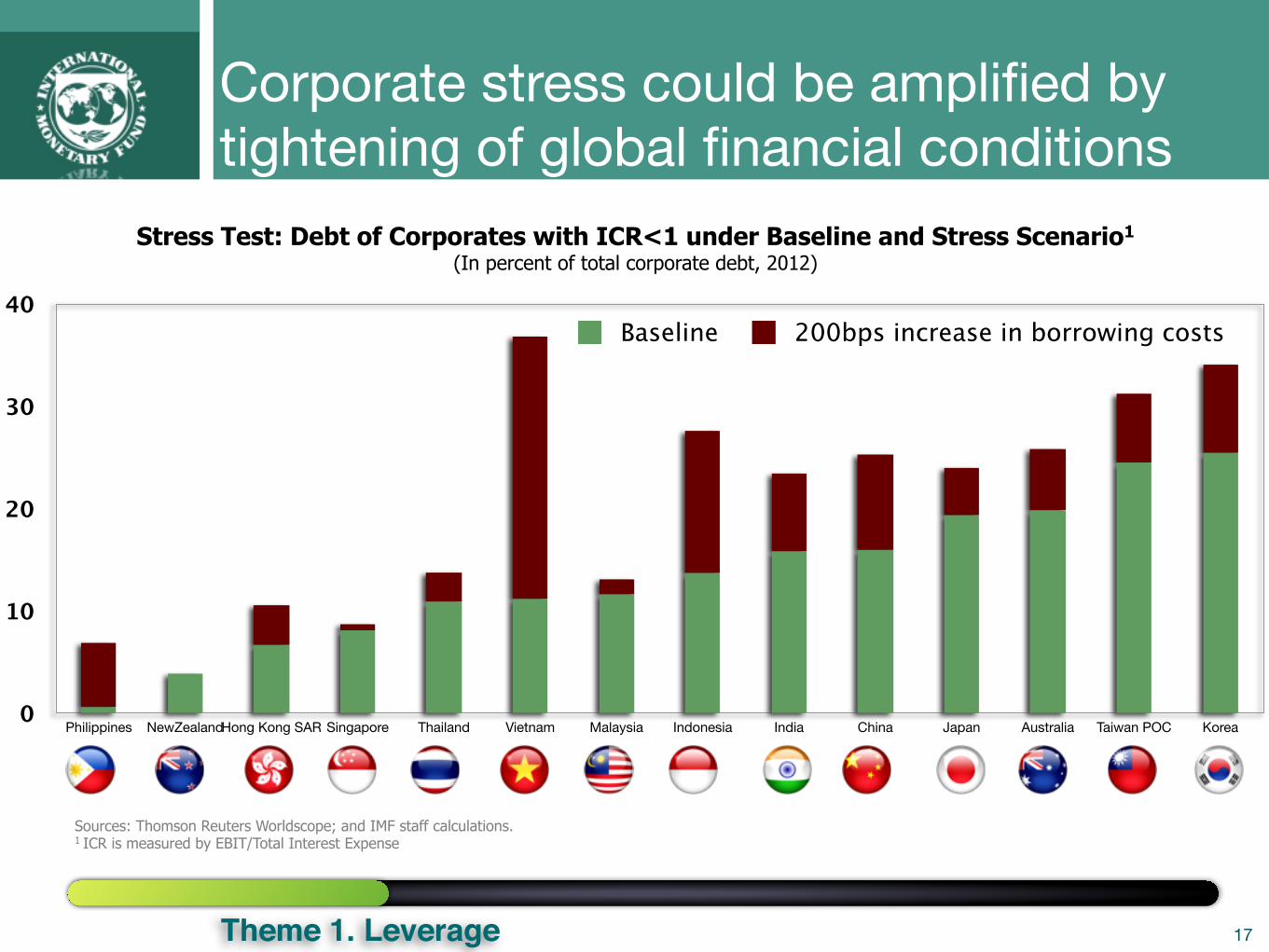

Corporate stress could be amplified by tightening of global financial conditions

Stress Test: Debt of Corporates with ICR<1 under Baseline and Stress Scenario1

(In percent of total corporate debt, 2012)

Sources: Thomson Reuters Worldscope; and IMF staff calculations.1 ICR is measured by EBIT/Total Interest Expense

17

0

10

20

30

40

Philippines NewZealandHong Kong SAR Singapore Thailand Vietnam Malaysia Indonesia India China Japan Australia Taiwan POC Korea

Baseline 200bps increase in borrowing costs

Theme 1. Leverage

Household debt: also a growing concern in some economies

Asia: Household Debt

Sources: CEIC Co. Ltd.; Haver Analytics; World Economic Outlook; OECD; National Authorities; and staff calculations.PHL=the Philippines, IND=India, IDN=Indonesia, CHN=China, TWN=Taiwan POC, HKG=Hong Kong SAR, MYS=Malaysia, SGP=Singapore, KOR=Korea, JPN=Japan, THA=Thailand, NZL=New Zealand, AUS=Australia.

18

0

25

50

75

100

2009

Late

st20

0020

08La

test

2010

Late

st20

0720

08La

test

2000

2008

Late

st20

0020

08La

test

2006

2008

Late

st20

0020

08La

test

2000

2008

Late

st20

0020

08La

test

2003

2008

Late

st20

0020

08La

test

2000

2008

Late

st

Housing Other

PHL IND IDN CHN TWN HKG MYS SGP KOR JPN THA NZL AUS

Theme 1. Leverage

% GDP

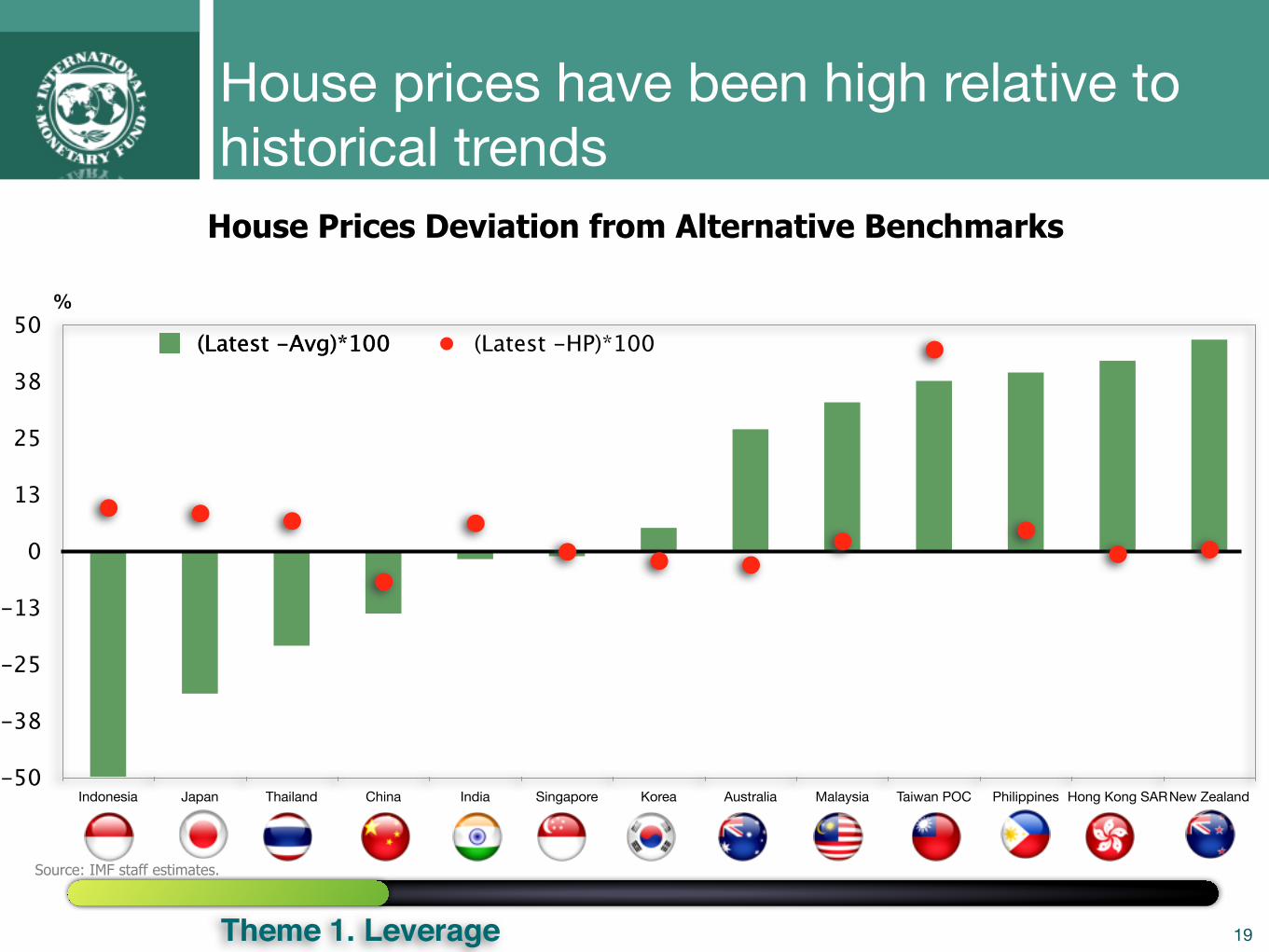

House prices have been high relative to historical trends

House Prices Deviation from Alternative Benchmarks(In percent)

Source: IMF staff estimates.

19

-50

-38

-25

-13

0

13

25

38

50

Indonesia Japan Thailand China India Singapore Korea Australia Malaysia Taiwan POC Philippines Hong Kong SARNew Zealand

(Latest -Avg)*100

Theme 1. Leverage

(Latest -Avg)*100 (Latest -HP)*100

%

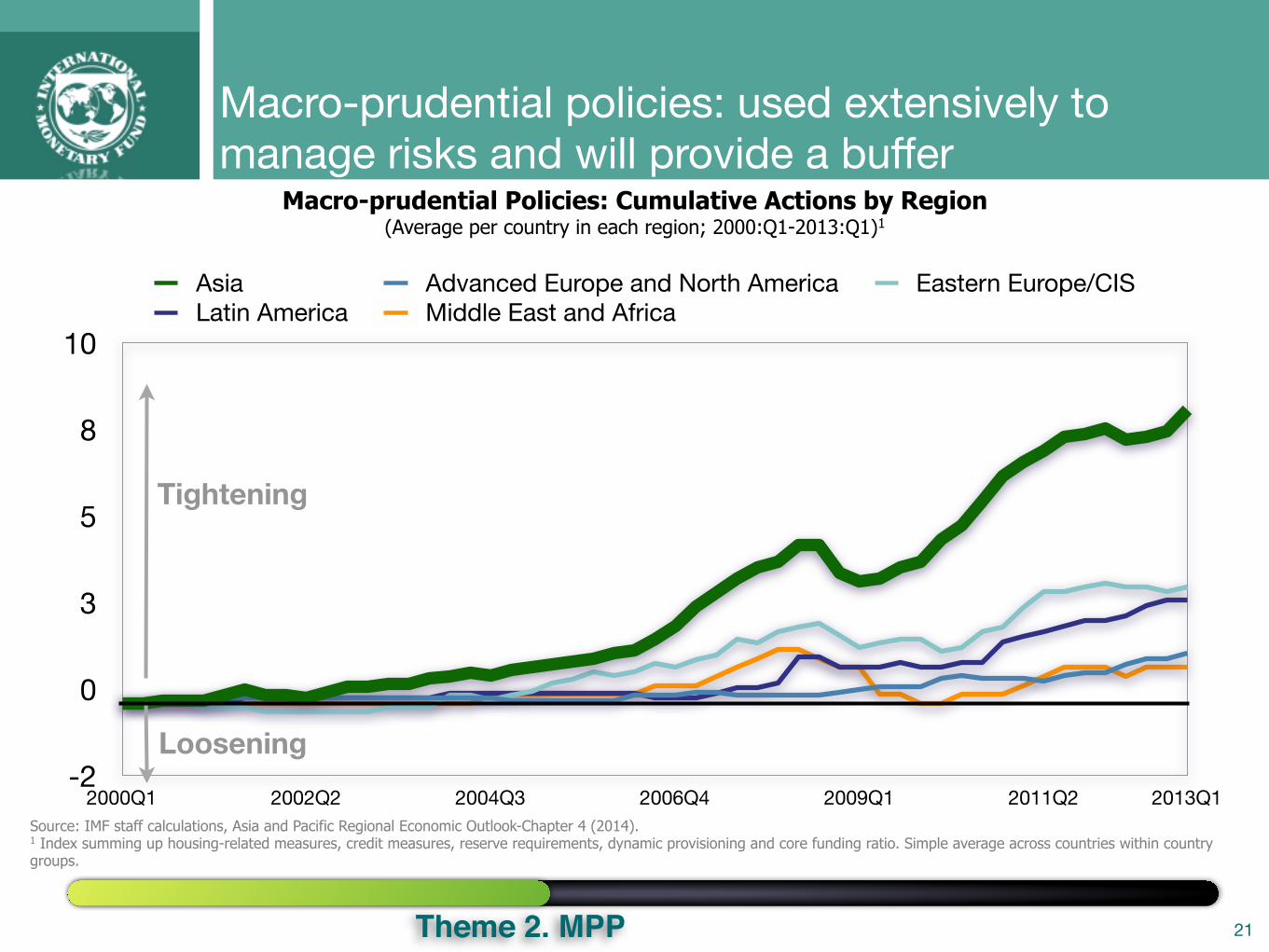

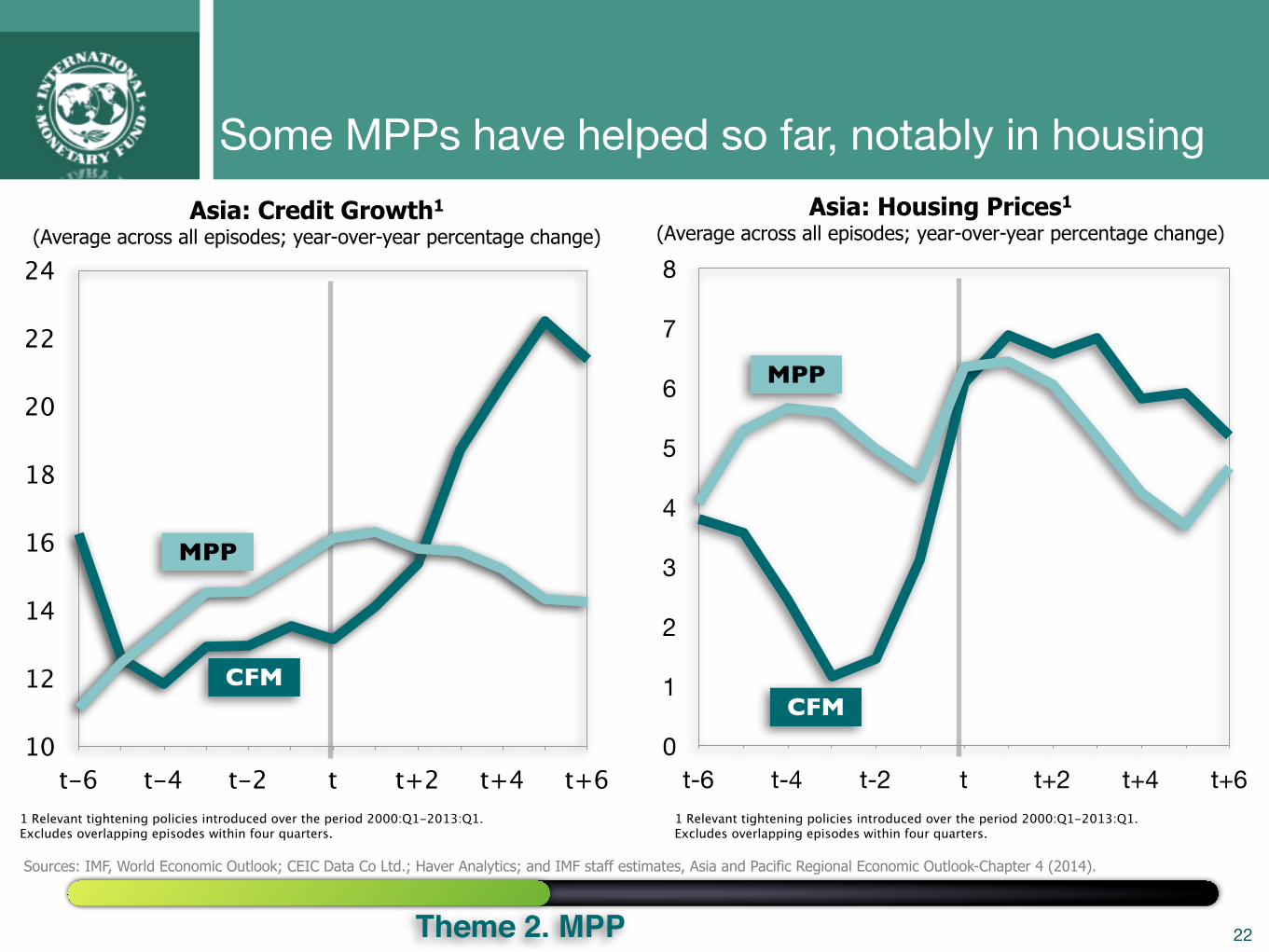

Theme 2: Responding to financial risks— what role for Macro-prudential policies?

• Asia has used MPPs more than other regions

• Some measures are effective, particularly in housing

• Should they be eased in case of downturn in financial cycle?

20Theme 2. MPP

-2

0

3

5

8

10

2000Q1 2002Q2 2004Q3 2006Q4 2009Q1 2011Q2 2013Q1

Asia Advanced Europe and North America Eastern Europe/CISLatin America Middle East and Africa

Tightening

Loosening

Macro-prudential policies: used extensively to manage risks and will provide a buffer

21

Macro-prudential Policies: Cumulative Actions by Region (Average per country in each region; 2000:Q1-2013:Q1)1

Source: IMF staff calculations, Asia and Pacific Regional Economic Outlook-Chapter 4 (2014). 1 Index summing up housing-related measures, credit measures, reserve requirements, dynamic provisioning and core funding ratio. Simple average across countries within country groups.

Theme 2. MPP

Some MPPs have helped so far, notably in housing

Sources: IMF, World Economic Outlook; CEIC Data Co Ltd.; Haver Analytics; and IMF staff estimates, Asia and Pacific Regional Economic Outlook-Chapter 4 (2014).

22Theme 2. MPP

Asia: Credit Growth1

(Average across all episodes; year-over-year percentage change)Asia: Housing Prices1

(Average across all episodes; year-over-year percentage change)

10

12

14

16

18

20

22

24

t-6 t-4 t-2 t t+2 t+4 t+61 Relevant tightening policies introduced over the period 2000:Q1-2013:Q1. Excludes overlapping episodes within four quarters.

0

1

2

3

4

5

6

7

8

t-6 t-4 t-2 t t+2 t+4 t+61 Relevant tightening policies introduced over the period 2000:Q1-2013:Q1. Excludes overlapping episodes within four quarters.

MPP

CFM

MPP

CFM

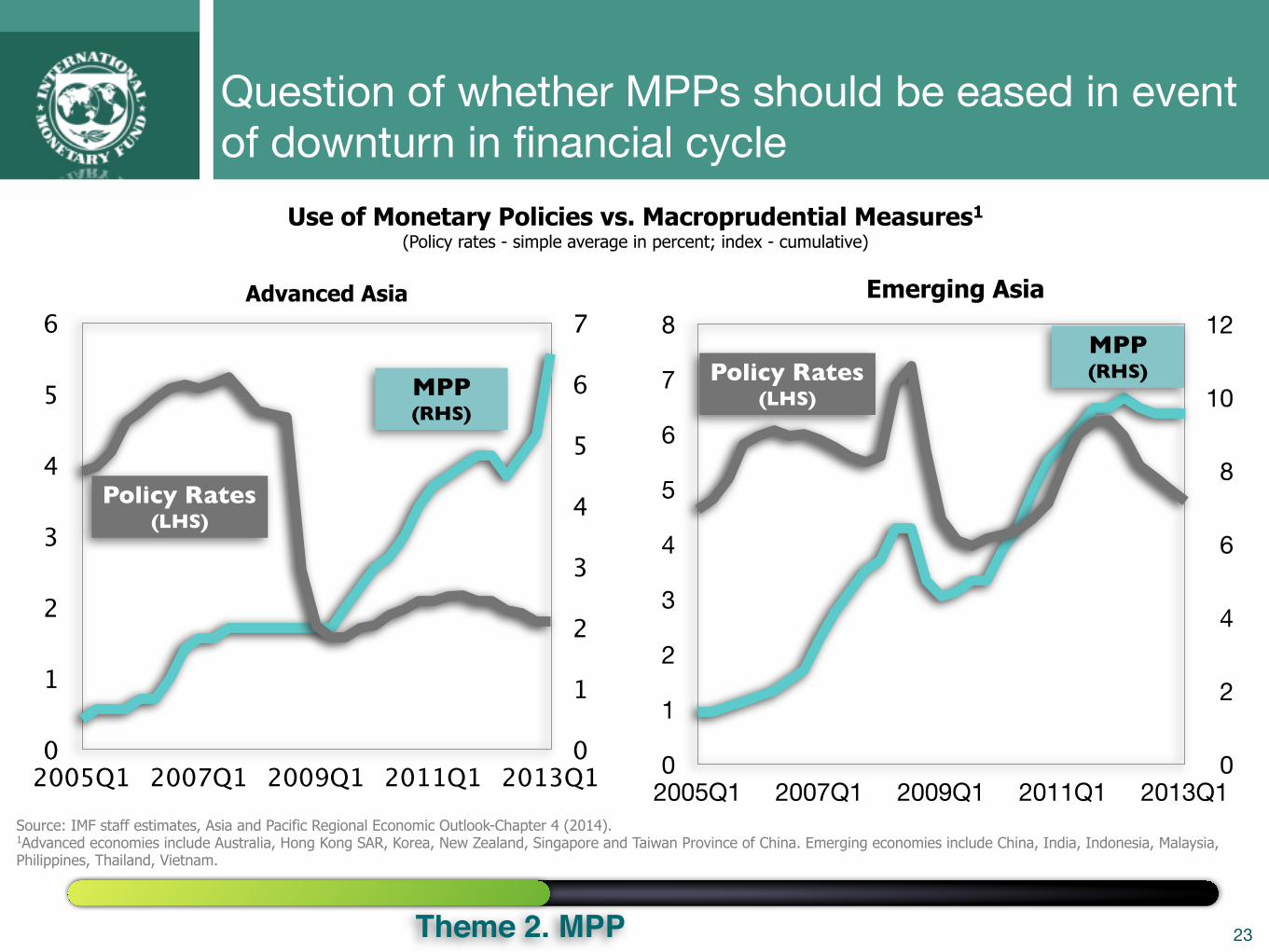

Question of whether MPPs should be eased in event of downturn in financial cycle

Use of Monetary Policies vs. Macroprudential Measures1

(Policy rates - simple average in percent; index - cumulative)

Source: IMF staff estimates, Asia and Pacific Regional Economic Outlook-Chapter 4 (2014).1Advanced economies include Australia, Hong Kong SAR, Korea, New Zealand, Singapore and Taiwan Province of China. Emerging economies include China, India, Indonesia, Malaysia, Philippines, Thailand, Vietnam.

23Theme 2. MPP

0

1

2

3

4

5

6

2005Q1 2007Q1 2009Q1 2011Q1 2013Q10

1

2

3

4

5

6

7Advanced Asia Emerging Asia

0

1

2

3

4

5

6

7

8

2005Q1 2007Q1 2009Q1 2011Q1 2013Q10

2

4

6

8

10

12

MPP (RHS)

Policy Rates (LHS)

MPP (RHS)Policy Rates

(LHS)

Theme 3. China

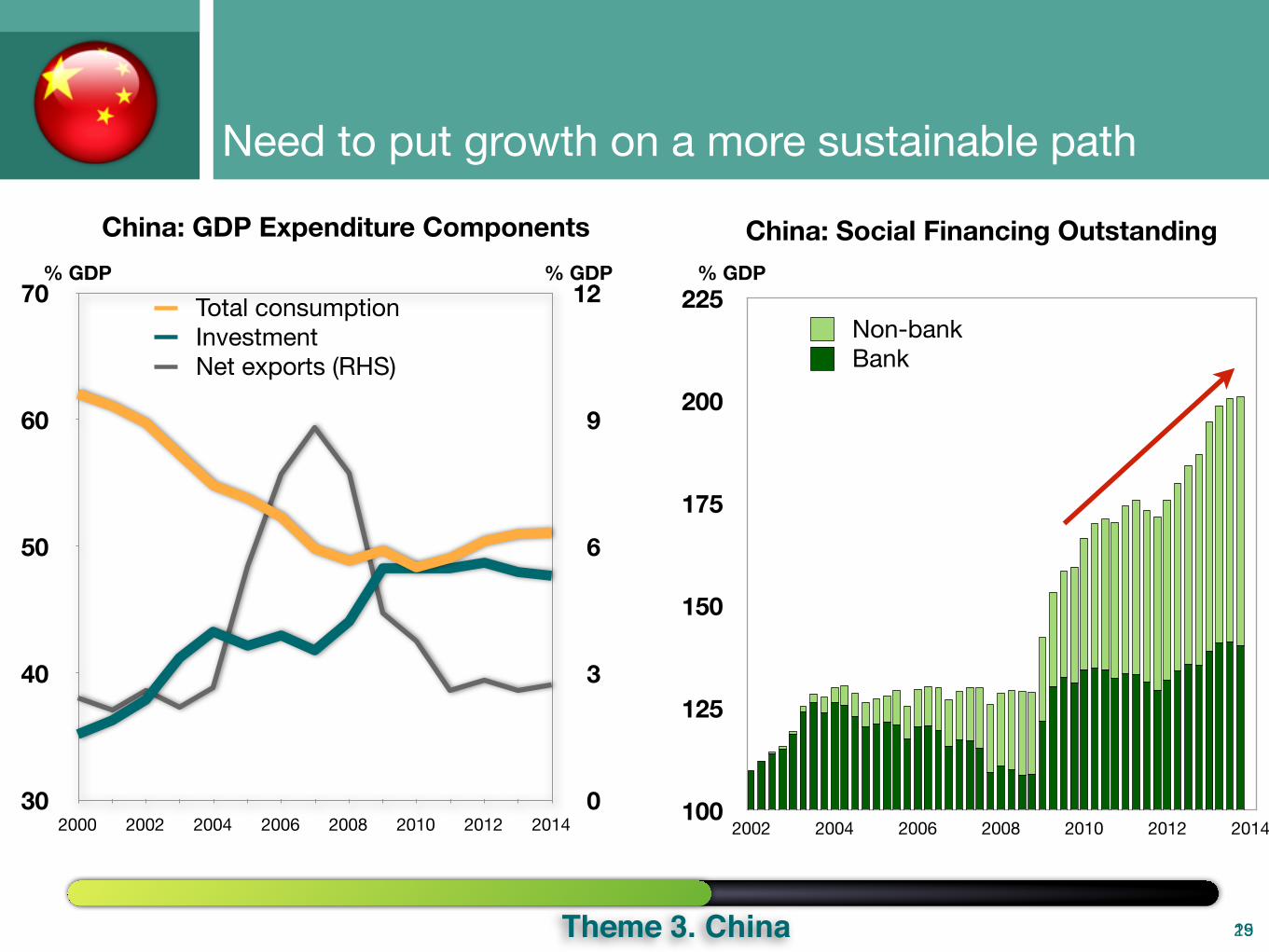

Theme 3: China’s reforms— what impact?

• Risks are building up...

• ...and any sharp slowdown would affect Asia twice as much as non-Asia

• Reform blueprint should make growth more balanced and sustainable...

• ...and benefit region despite short-term transitional costs

24

Need to put growth on a more sustainable path

25Theme 3. China 19

China: GDP Expenditure Components% GDP % GDP

100

125

150

175

200

225

2002 2004 2006 2008 2010 2012 2014

BankNon-bank

China: Social Financing Outstanding% GDP

30

40

50

60

70

2000 2002 2004 2006 2008 2010 2012 20140

3

6

9

12Total consumptionInvestmentNet exports (RHS)

-1.0

-0.8

-0.6

-0.3

-0.1

0.1

0.4

0.6

0.8

-1.5 -1.0 -0.5 0 0.5 1.0 1.5 2.0 2.5

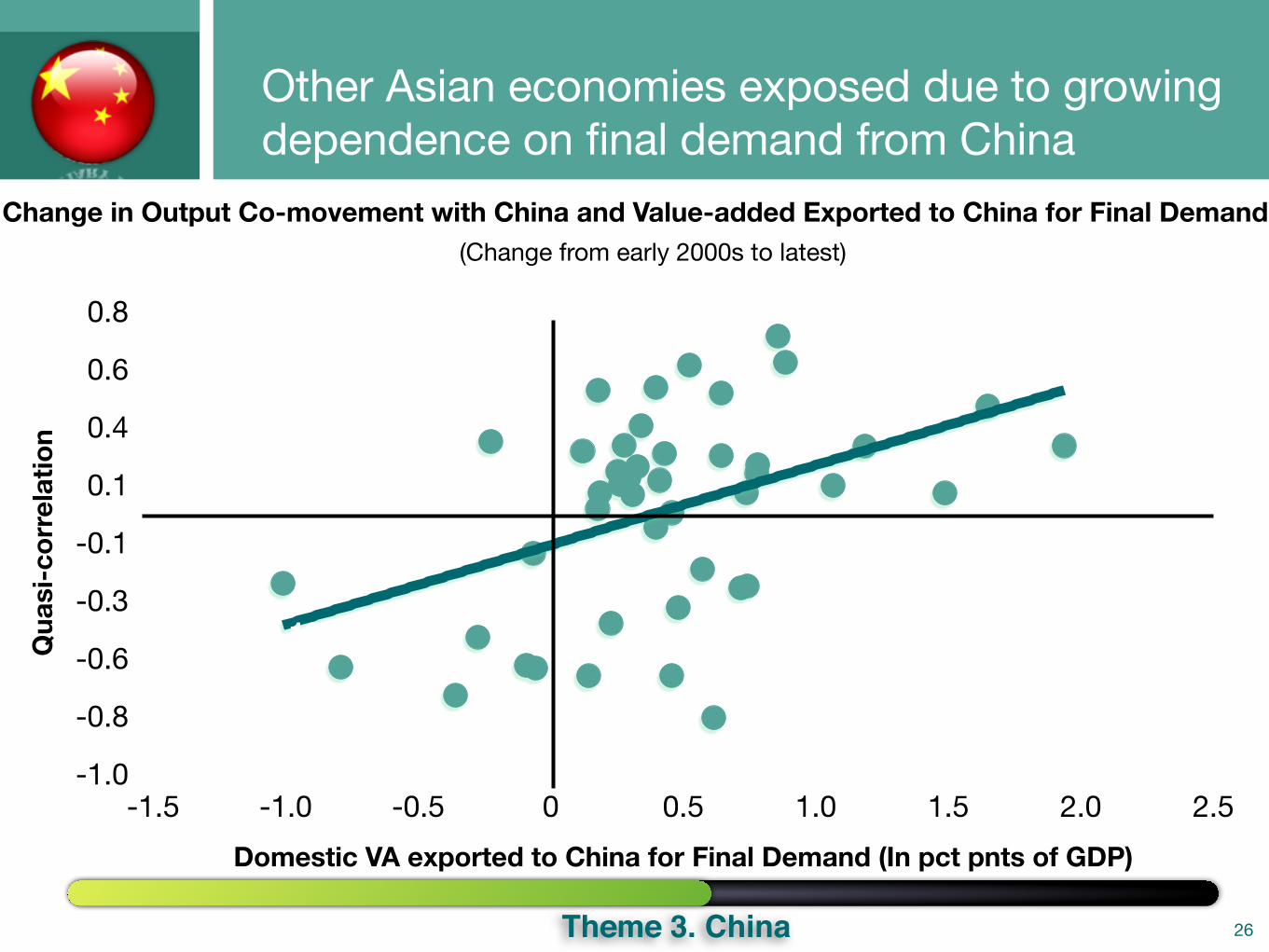

R² = 0.6395

R² = 0.1932Qua

si-c

orre

latio

n

Domestic VA exported to China for Final Demand (In pct pnts of GDP)

26

(Change from early 2000s to latest)Change in Output Co-movement with China and Value-added Exported to China for Final Demand

Other Asian economies exposed due to growing dependence on final demand from China

Theme 3. China

0

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

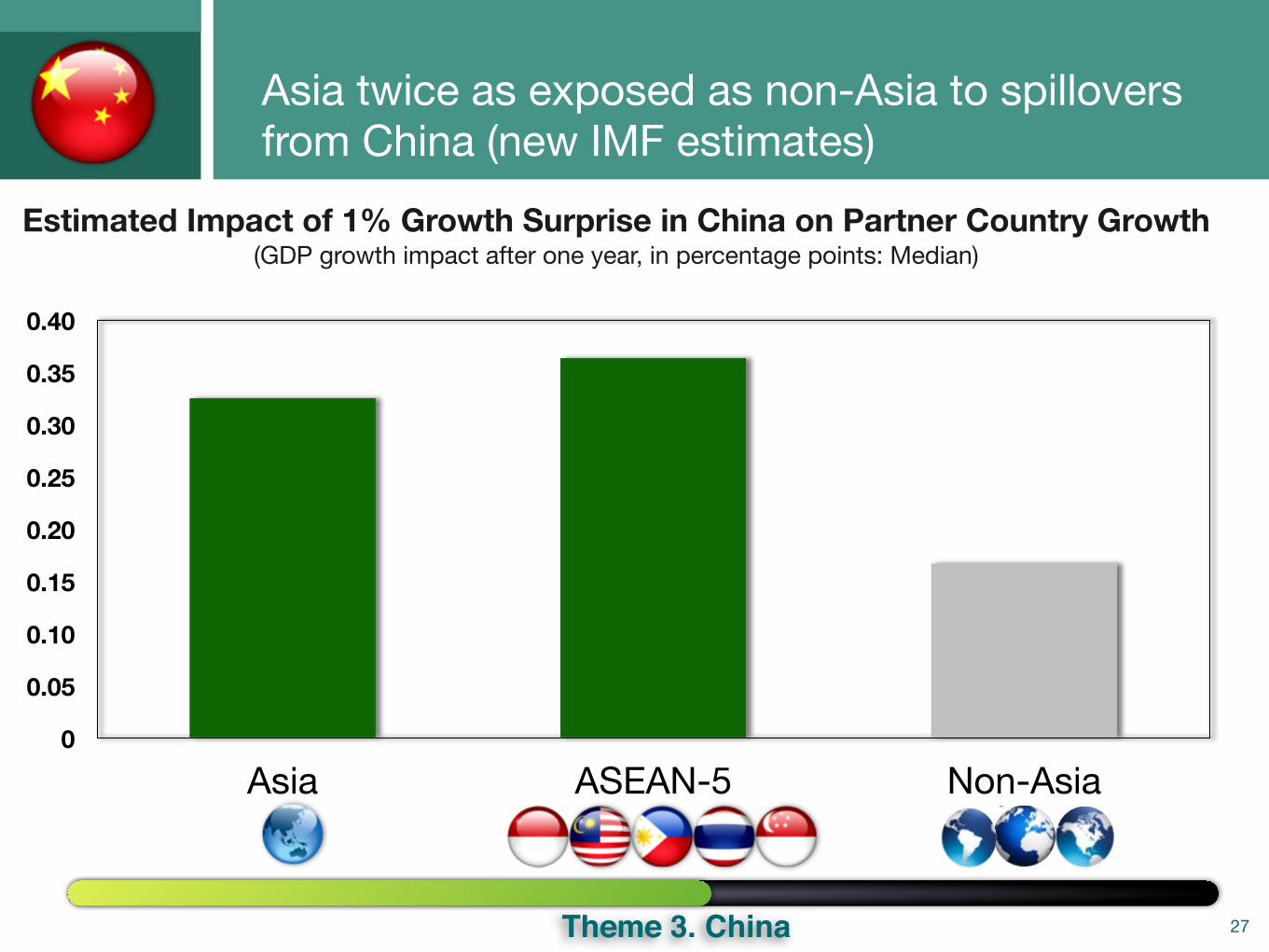

Asia ASEAN-5 Non-Asia

27

Asia twice as exposed as non-Asia to spillovers from China (new IMF estimates)

Estimated Impact of 1% Growth Surprise in China on Partner Country Growth(GDP growth impact after one year, in percentage points: Median)

Theme 3. China

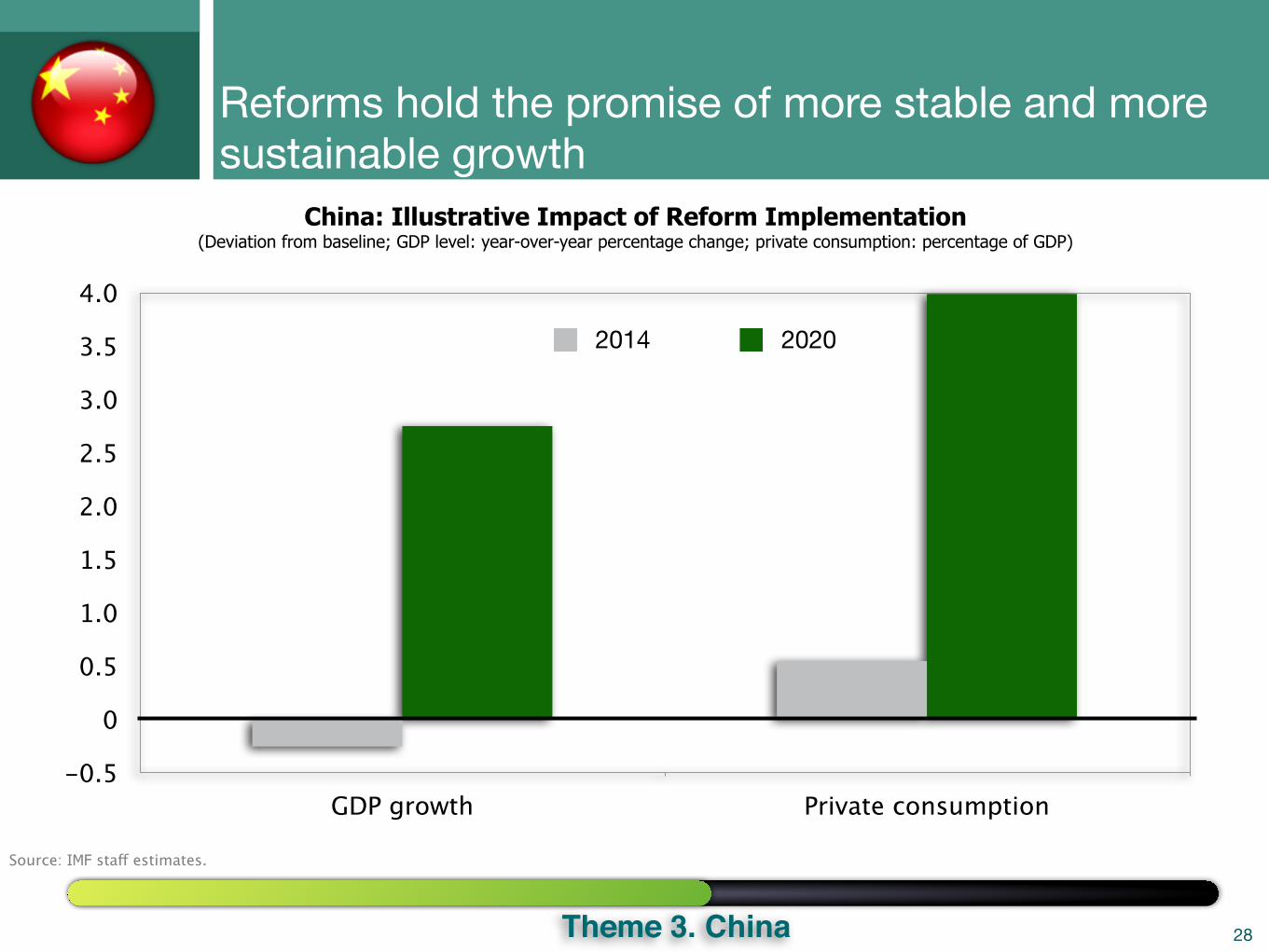

Reforms hold the promise of more stable and more sustainable growth

Source: IMF staff estimates.

China: Illustrative Impact of Reform Implementation(Deviation from baseline; GDP level: year-over-year percentage change; private consumption: percentage of GDP)

28Theme 3. China

-0.5

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

GDP growth Private consumption

2014 2020

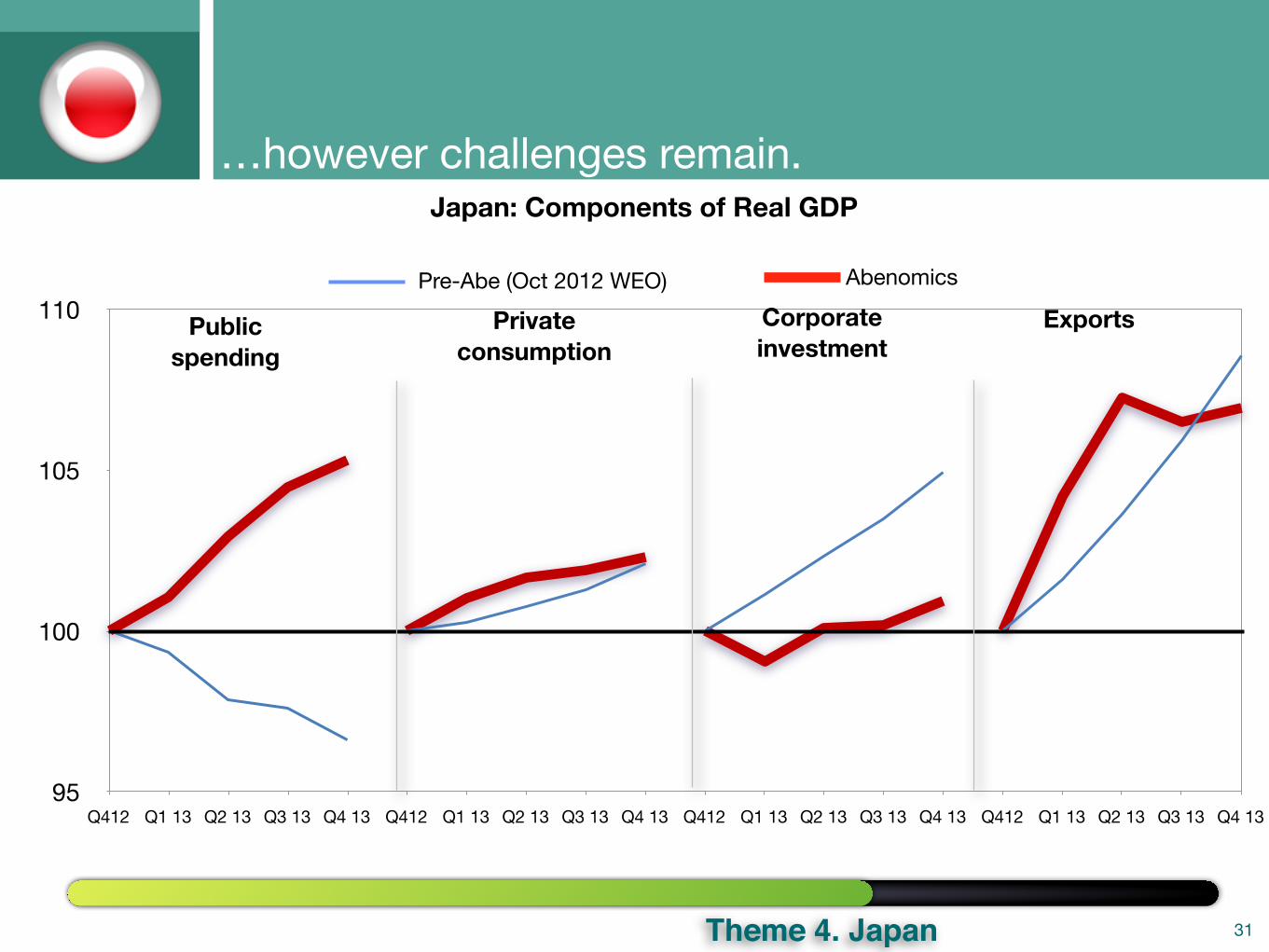

Theme 4: Abenomics— temporary stimulus or break with the past?

• Abenomics has provided a boost but major challenges remain

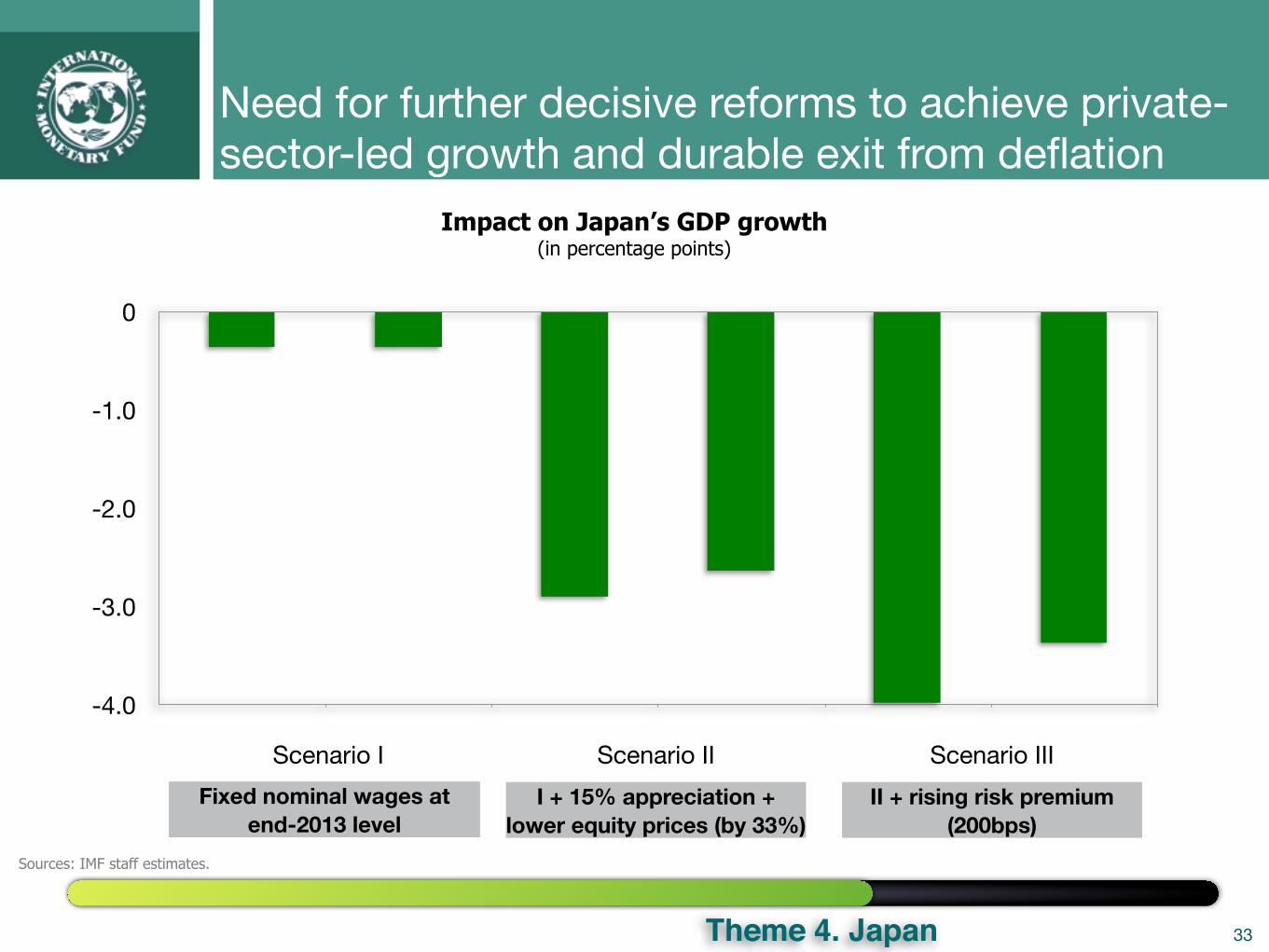

• Need for further decisive reforms to achieve private-sector-led growth and durable exit from deflation

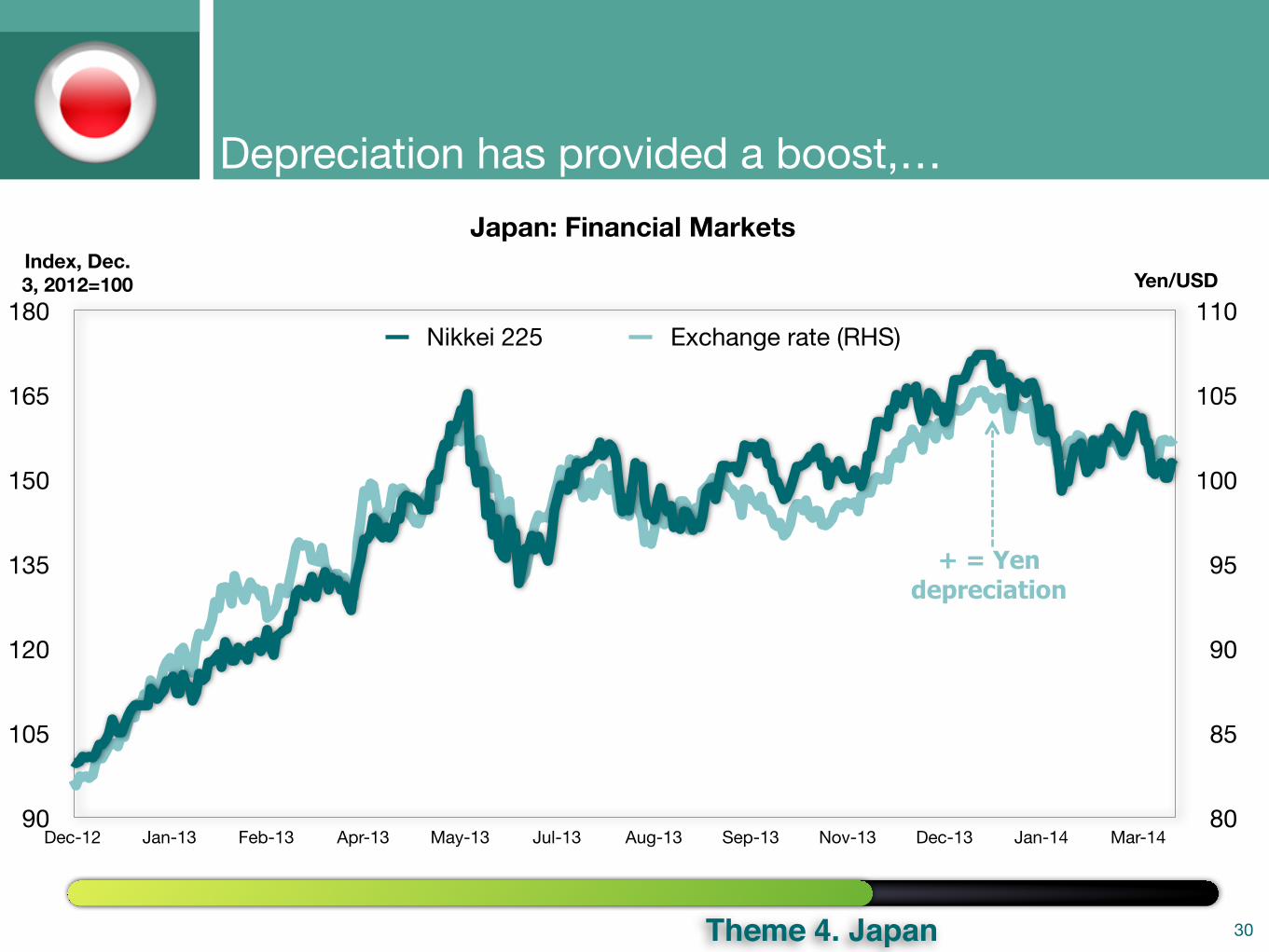

29Theme 4. Japan

Japan: Financial MarketsIndex, Dec. 3, 2012=100 Yen/USD

90

105

120

135

150

165

180

Dec-12 Jan-13 Feb-13 Apr-13 May-13 Jul-13 Aug-13 Sep-13 Nov-13 Dec-13 Jan-14 Mar-1480

85

90

95

100

105

110Nikkei 225 Exchange rate (RHS)

+ = Yen depreciation

Depreciation has provided a boost,…

30Theme 4. Japan

95

100

105

110

Q412 Q1 13 Q2 13 Q3 13 Q4 13 Q412 Q1 13 Q2 13 Q3 13 Q4 13 Q412 Q1 13 Q2 13 Q3 13 Q4 13 Q412 Q1 13 Q2 13 Q3 13 Q4 13

Privateconsumption

Corporate investment

ExportsPublicspending

Pre-Abe (Oct 2012 WEO) Abenomics

Japan: Components of Real GDP…however challenges remain.

31Theme 4. Japan

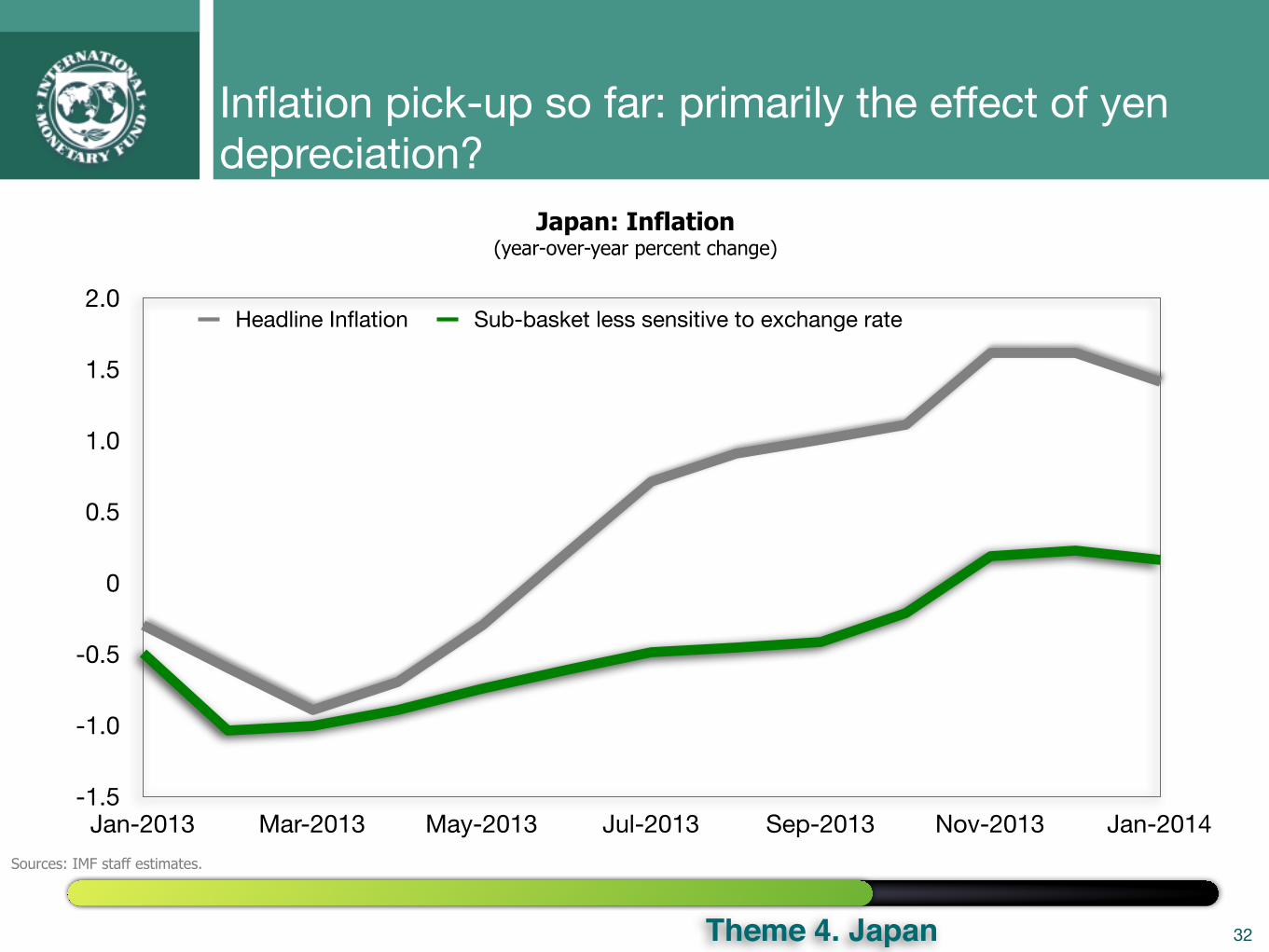

Inflation pick-up so far: primarily the effect of yen depreciation?

Sources: IMF staff estimates.

Japan: Inflation(year-over-year percent change)

32Theme 4. Japan

-1.5

-1.0

-0.5

0

0.5

1.0

1.5

2.0

Jan-2013 Mar-2013 May-2013 Jul-2013 Sep-2013 Nov-2013 Jan-2014

Headline Inflation Sub-basket less sensitive to exchange rate

Need for further decisive reforms to achieve private-sector-led growth and durable exit from deflation

Sources: IMF staff estimates.

Impact on Japan’s GDP growth(in percentage points)

33

Fixed nominal wages at end-2013 level

I + 15% appreciation + lower equity prices (by 33%)

II + rising risk premium (200bps)

Theme 4. Japan

-4.0

-3.0

-2.0

-1.0

0

Scenario I Scenario II Scenario III

Theme 5: ASEAN— what is happening to growth?

• The recent growth slowdown in ASEAN-5 has been more cyclical than structural

• Domestic factors have played a bigger role

• But the pickup in global demand will help

34Theme 5. ASEAN

-1

0

1

2

3

4

5

6

7

8

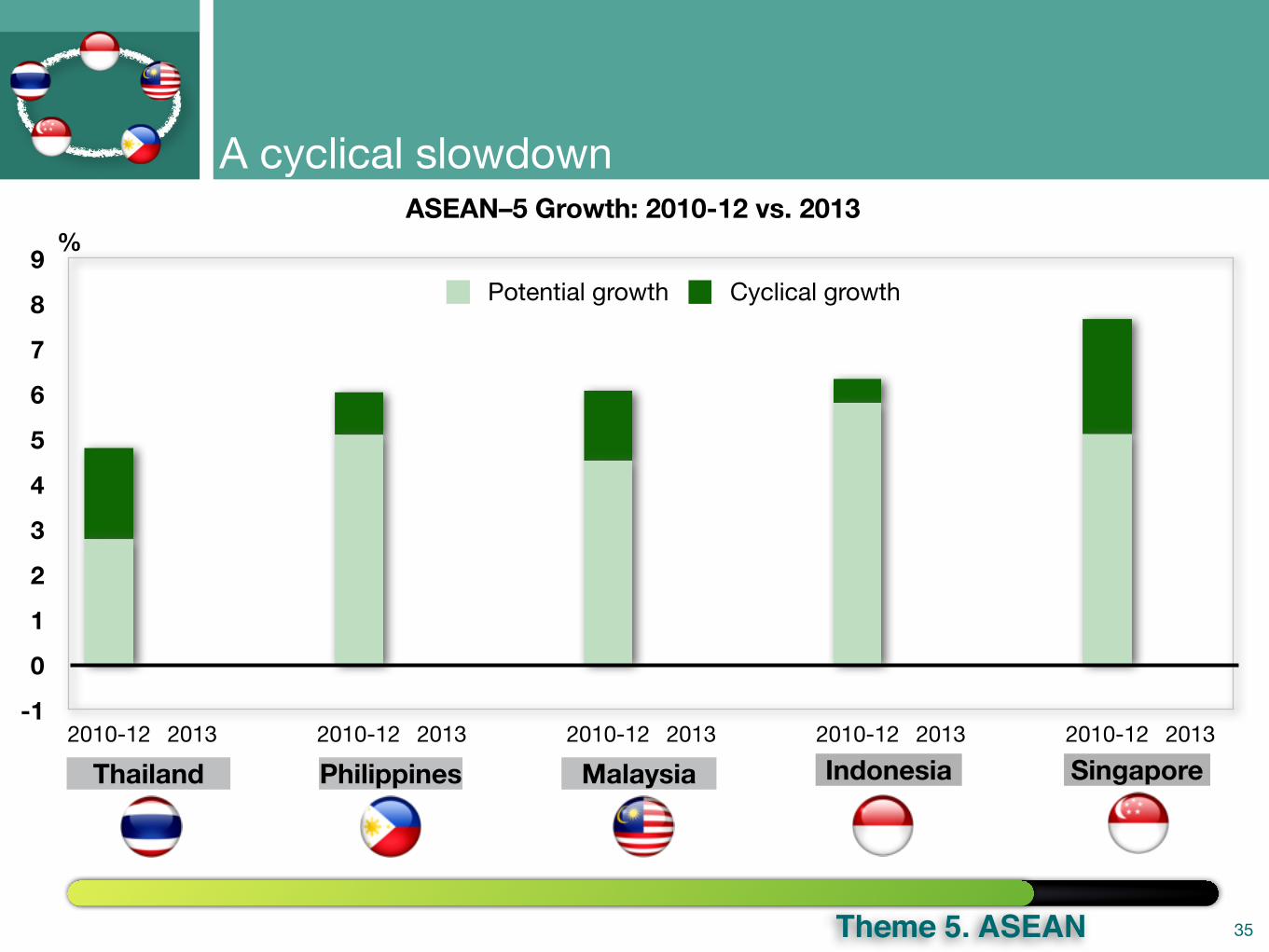

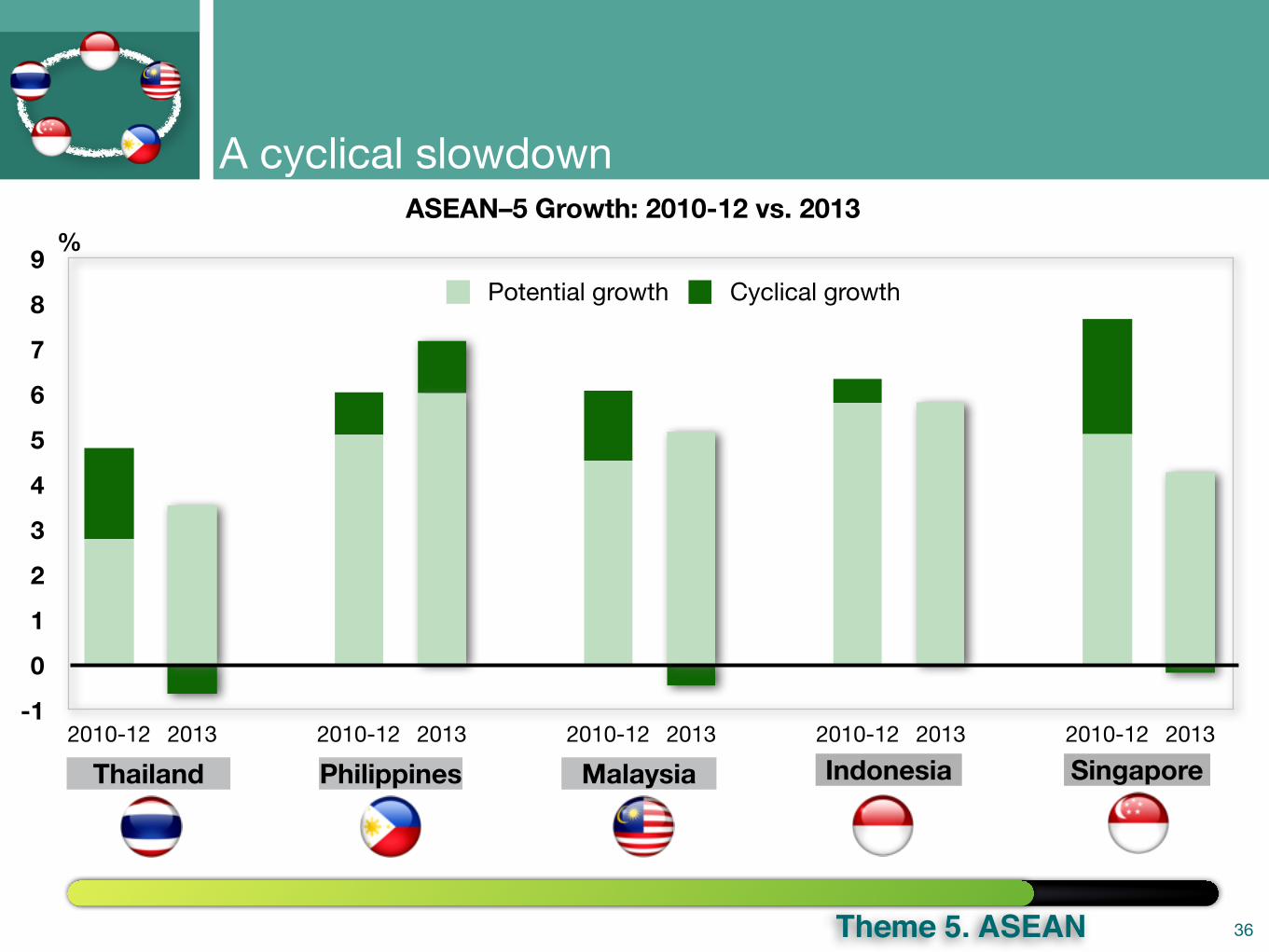

9

2010-12 2013 2010-12 2013 2010-12 2013 2010-12 2013 2010-12 2013

ASEAN–5 Growth: 2010-12 vs. 2013%

Potential growth Cyclical growth

Thailand Philippines Malaysia Indonesia Singapore

A cyclical slowdown

35Theme 5. ASEAN

-1

0

1

2

3

4

5

6

7

8

9

2010-12 2013 2010-12 2013 2010-12 2013 2010-12 2013 2010-12 2013

ASEAN–5 Growth: 2010-12 vs. 2013%

Potential growth Cyclical growth

Thailand Philippines Malaysia Indonesia Singapore

A cyclical slowdown

36Theme 5. ASEAN

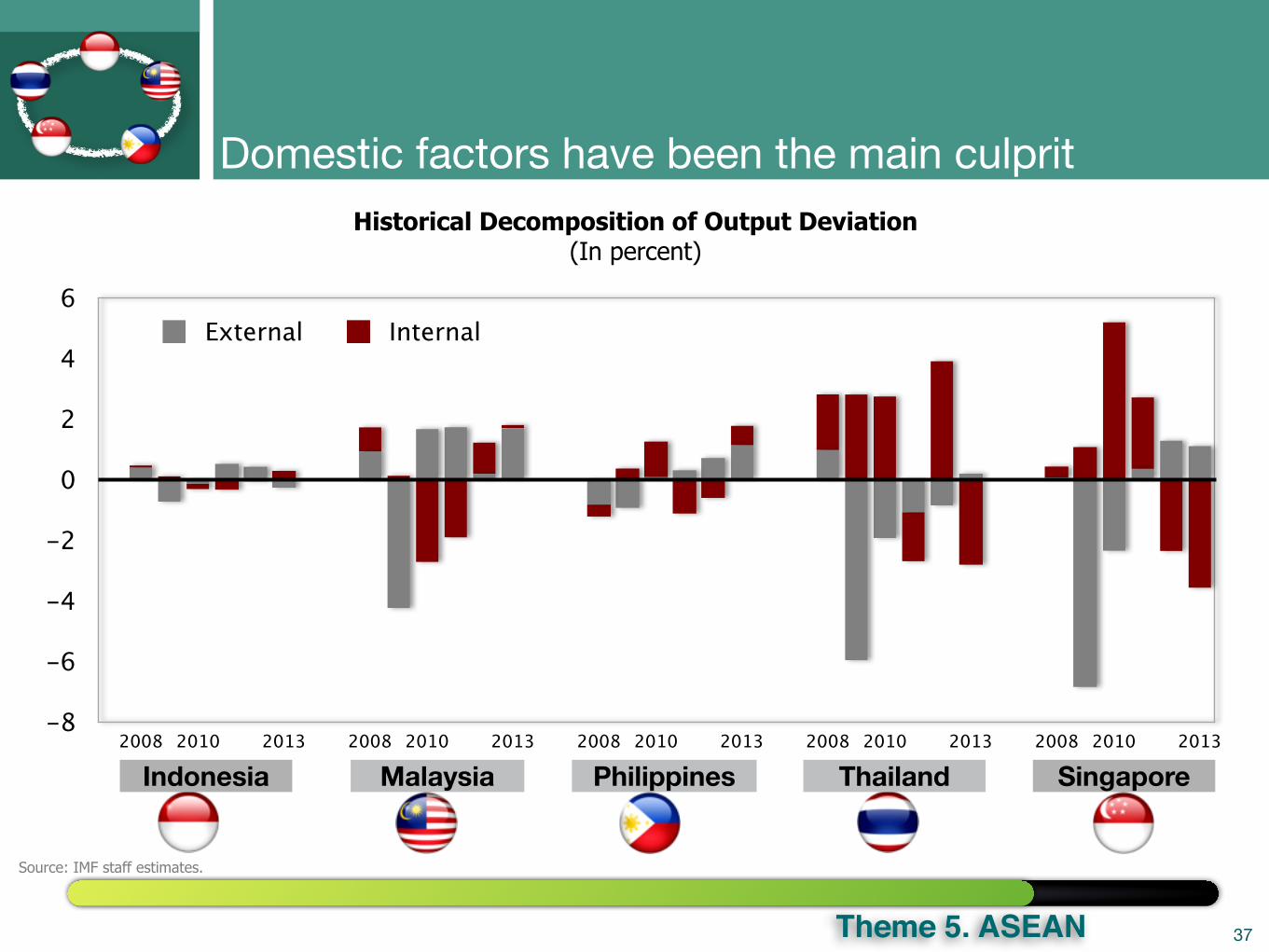

Domestic factors have been the main culprit

Source: IMF staff estimates.

Historical Decomposition of Output Deviation(In percent)

37Theme 5. ASEAN

-8

-6

-4

-2

0

2

4

6

2008 2010 2013 2008 2010 2013 2008 2010 2013 2008 2010 2013 2008 2010 2013

External Internal

ThailandPhilippinesMalaysiaIndonesia Singapore

Theme 6: Regional integration— growing source of spillovers?• Asian economies are moving increasingly in synch...

• ...partly due to growing trade integration (~ 1/4 of rise in comovement)

• ...which in turn reflects build-up of supply-chain linkages

• ...particularly around China, with Japan’s role declining

• The future: greater integration => greater growth comovement => role for regional and global financial safety nets

38Theme 5. ASEAN

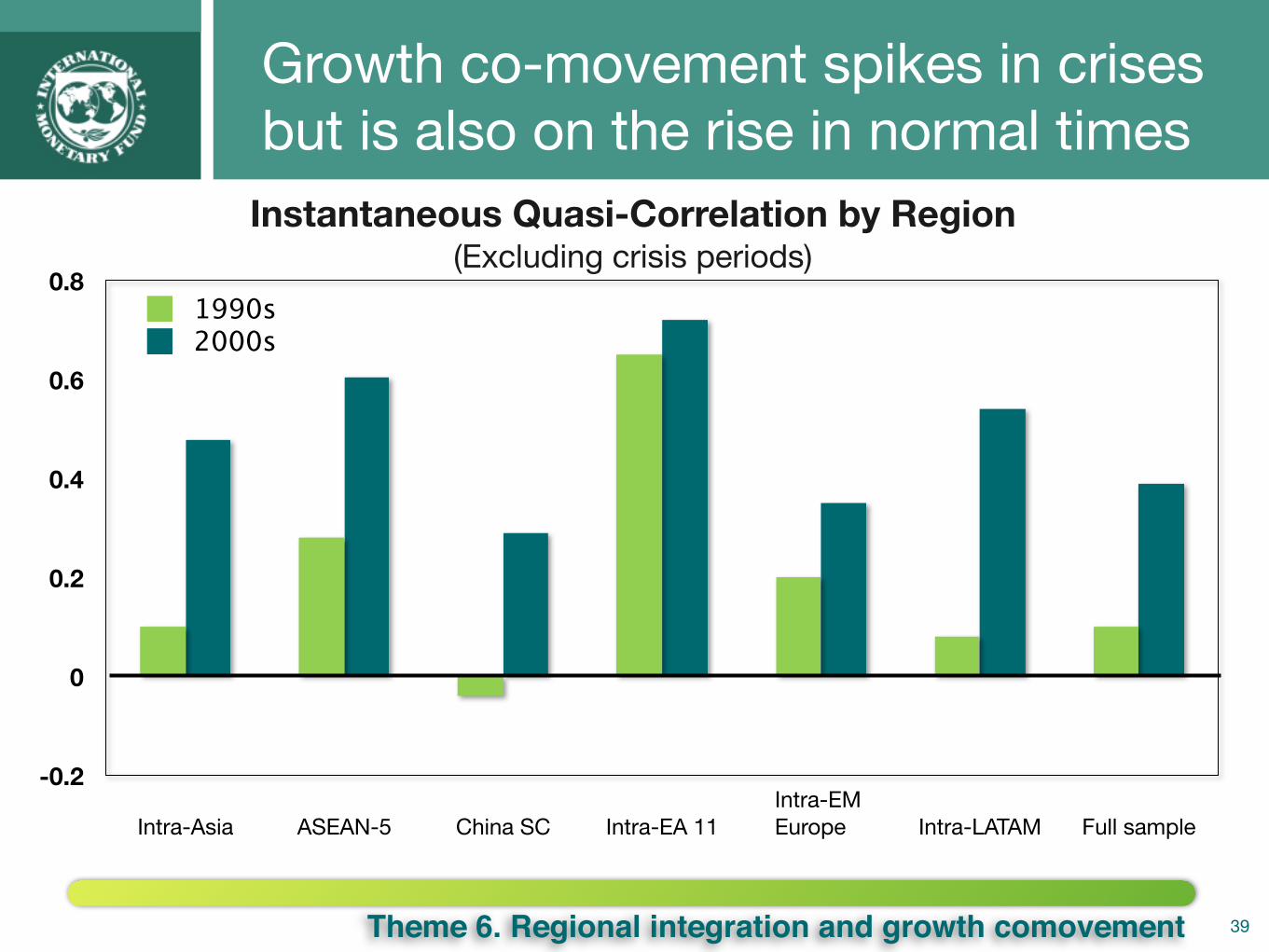

39

Instantaneous Quasi-Correlation by Region(Excluding crisis periods)

Growth co-movement spikes in crises but is also on the rise in normal times

-0.2

0

0.2

0.4

0.6

0.8

Intra-Asia ASEAN-5 China SC Intra-EA 11Intra-EM Europe Intra-LATAM Full sample

1990s2000s

Theme 6. Regional integration and growth comovement

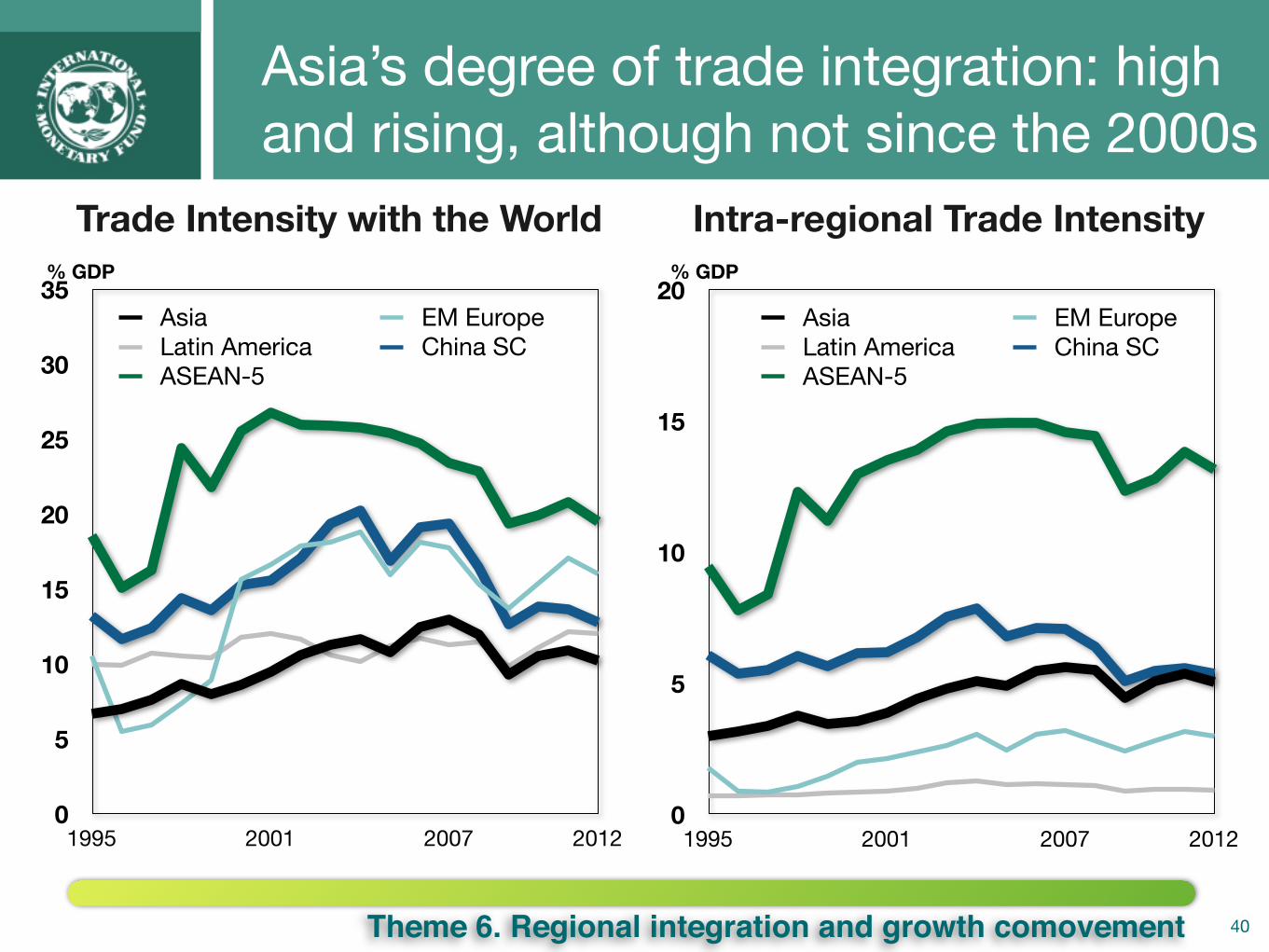

40

Trade Intensity with the World

Asia’s degree of trade integration: high and rising, although not since the 2000s

0

5

10

15

20

25

30

35

1995 2001 2007 2012

Asia EM EuropeLatin America China SCASEAN-5

% GDP

0

5

10

15

20

1995 2001 2007 2012

Asia EM EuropeLatin America China SCASEAN-5

Intra-regional Trade Intensity% GDP

Theme 6. Regional integration and growth comovement

0

5

10

15

20

25

30

35

AUS

KOR

HKG PH

L

TWN

JPN

MYS NZL

THA

IDN

SGP

IND

0

2

4

6

8

10

HKG PH

L

KOR

THA

TWN

SGP

MYS NZL IDN

IND

JPN

AUS

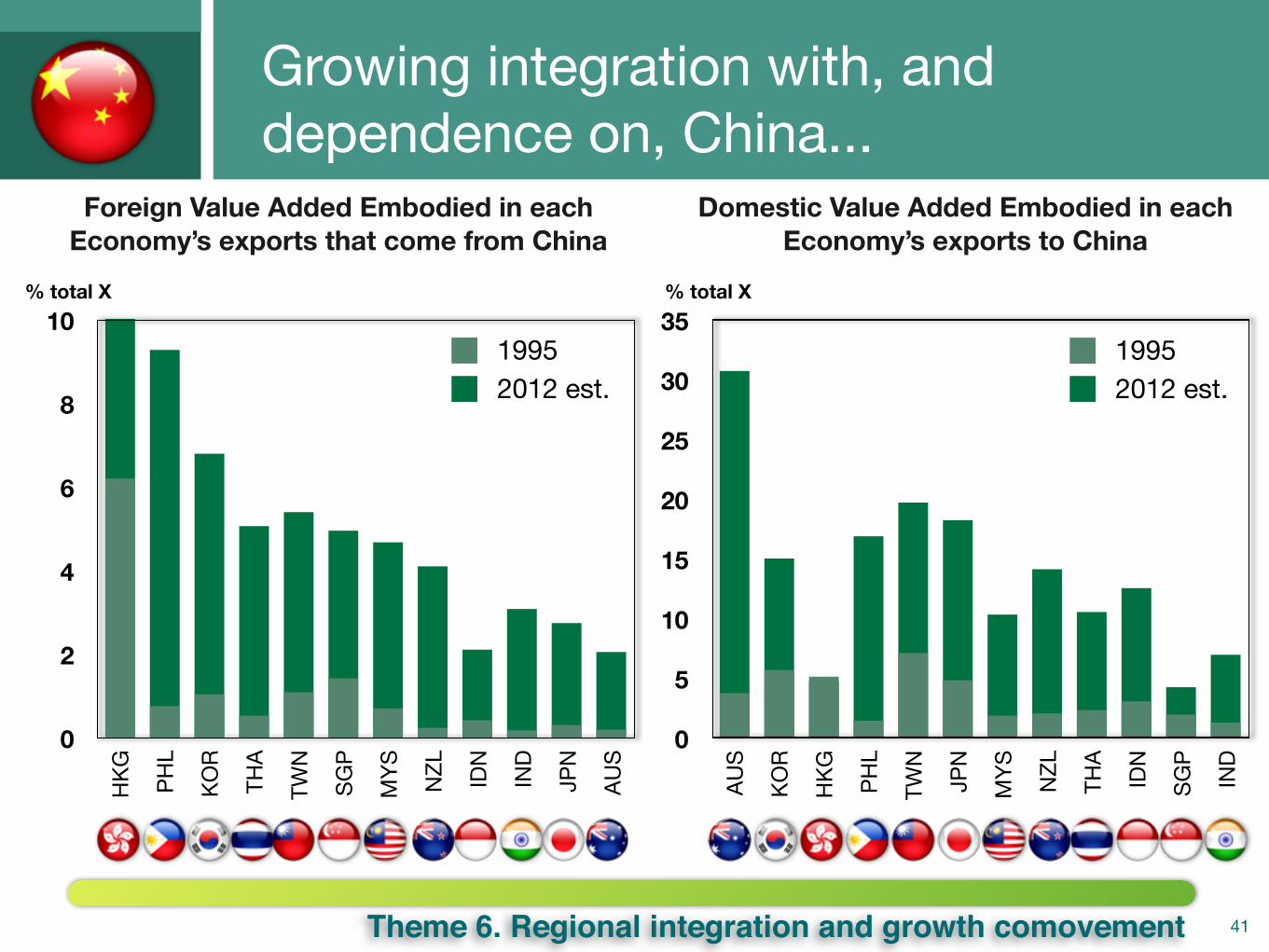

41

Growing integration with, and dependence on, China...

% total X

Foreign Value Added Embodied in each Economy’s exports that come from China

19952012 est.

1995

Domestic Value Added Embodied in each Economy’s exports to China

% total X

2012 est.

Theme 6. Regional integration and growth comovement

0

2

4

6

8

10

12

KOR

PHL

THA

MYS

HKG

TWN

SGP

CH

N

NZL IND

IDN

AUS

0

5

10

15

20

25

AUS

IDN

MYS TH

A

CH

N

NZL

KOR

PHL

TWN

IND

SGP

HKG

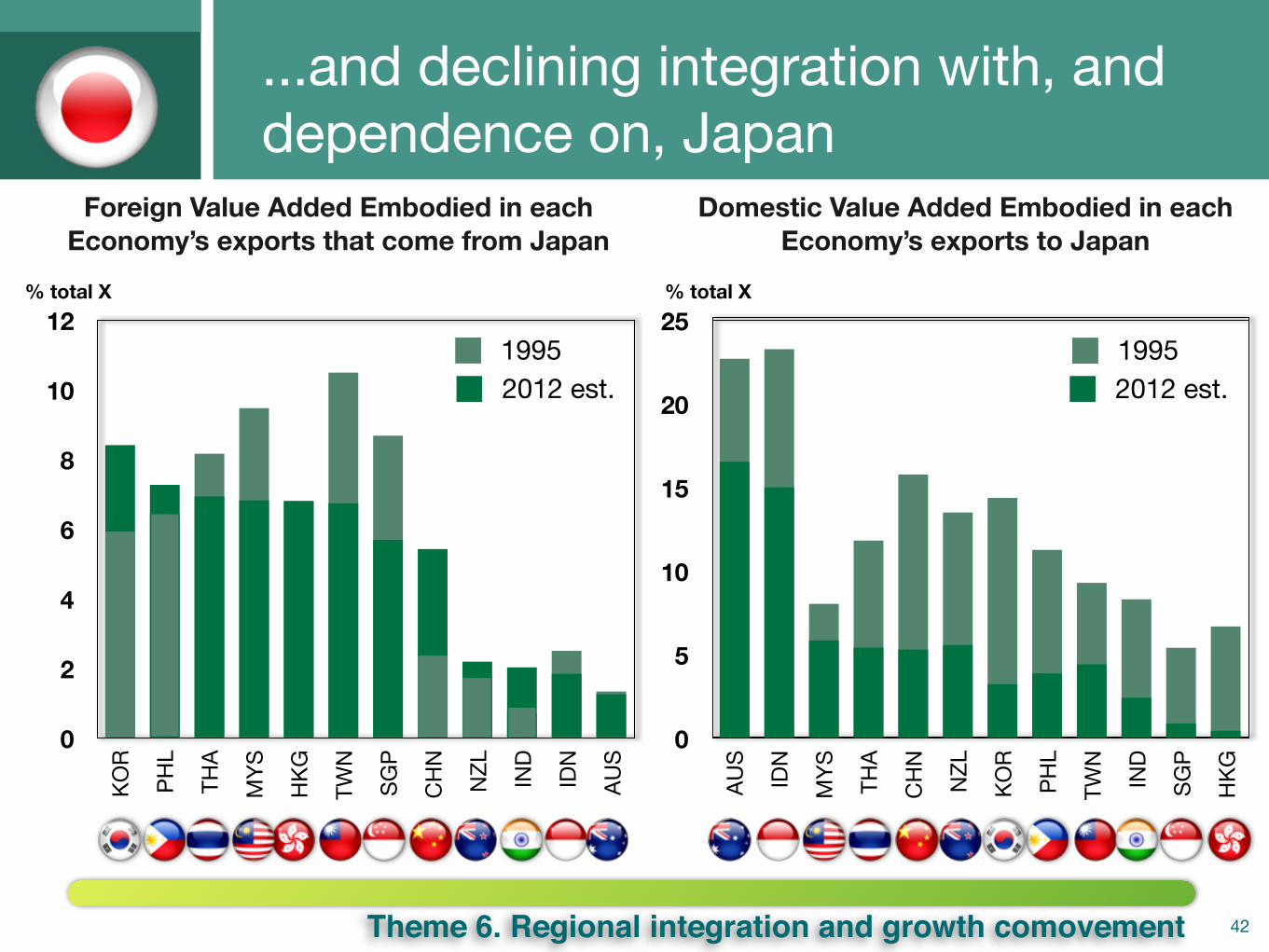

42

...and declining integration with, and dependence on, Japan

% total X

Foreign Value Added Embodied in each Economy’s exports that come from Japan

19952012 est.

1995

Domestic Value Added Embodied in each Economy’s exports to Japan

% total X

2012 est.

Theme 6. Regional integration and growth comovement

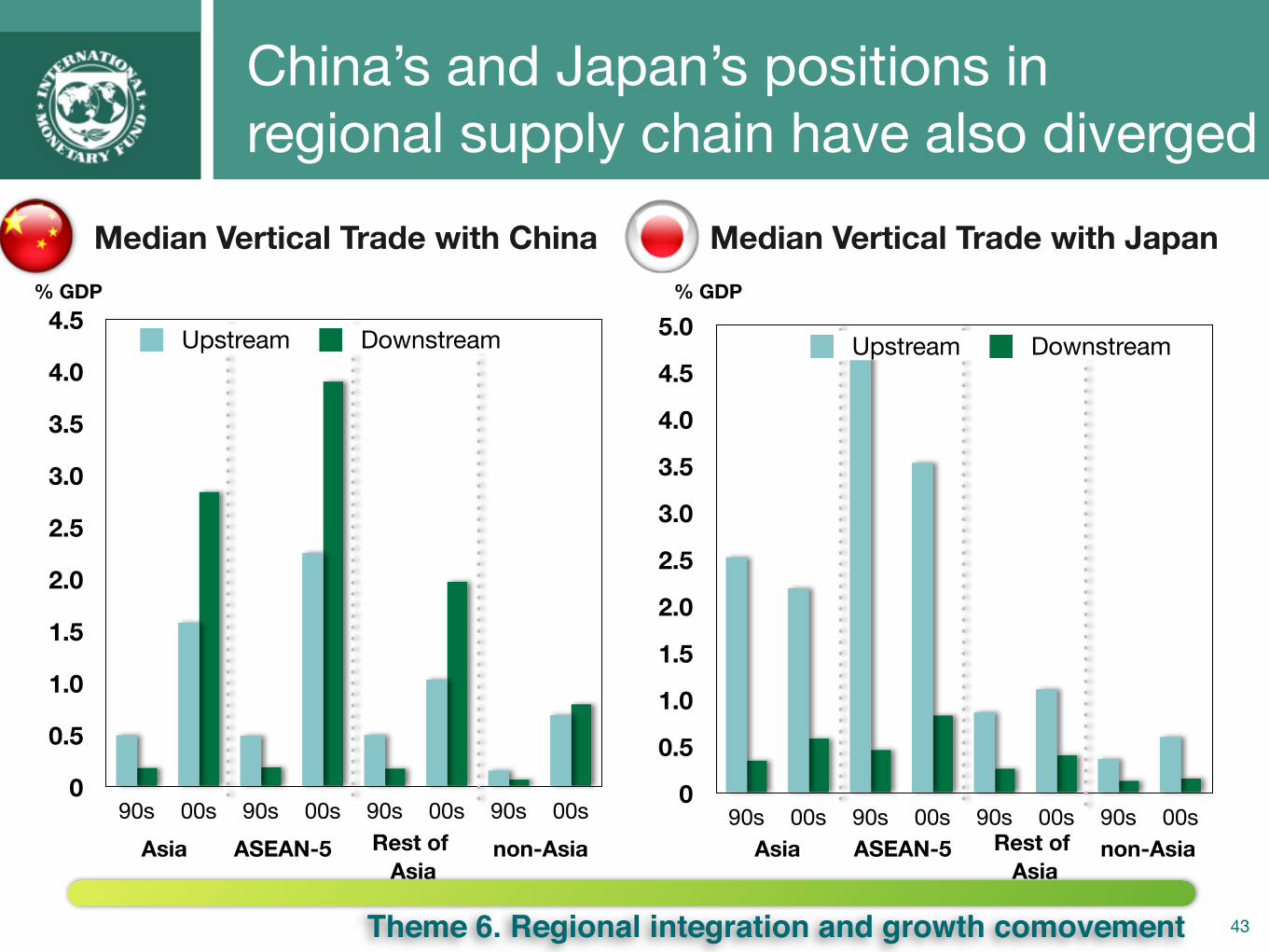

43

China’s and Japan’s positions in regional supply chain have also diverged

% GDP

Median Vertical Trade with China Median Vertical Trade with Japan% GDP

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

90s 00s 90s 00s 90s 00s 90s 00sAsia ASEAN-5 Rest of

Asianon-Asia

Upstream Downstream

0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

90s 00s 90s 00s 90s 00s 90s 00sAsia ASEAN-5 Rest of

Asianon-Asia

Upstream Downstream

Theme 6. Regional integration and growth comovement

0

1.0

2.0

3.0

4.0

5.0

Asia ASEAN-5 Non-Asia

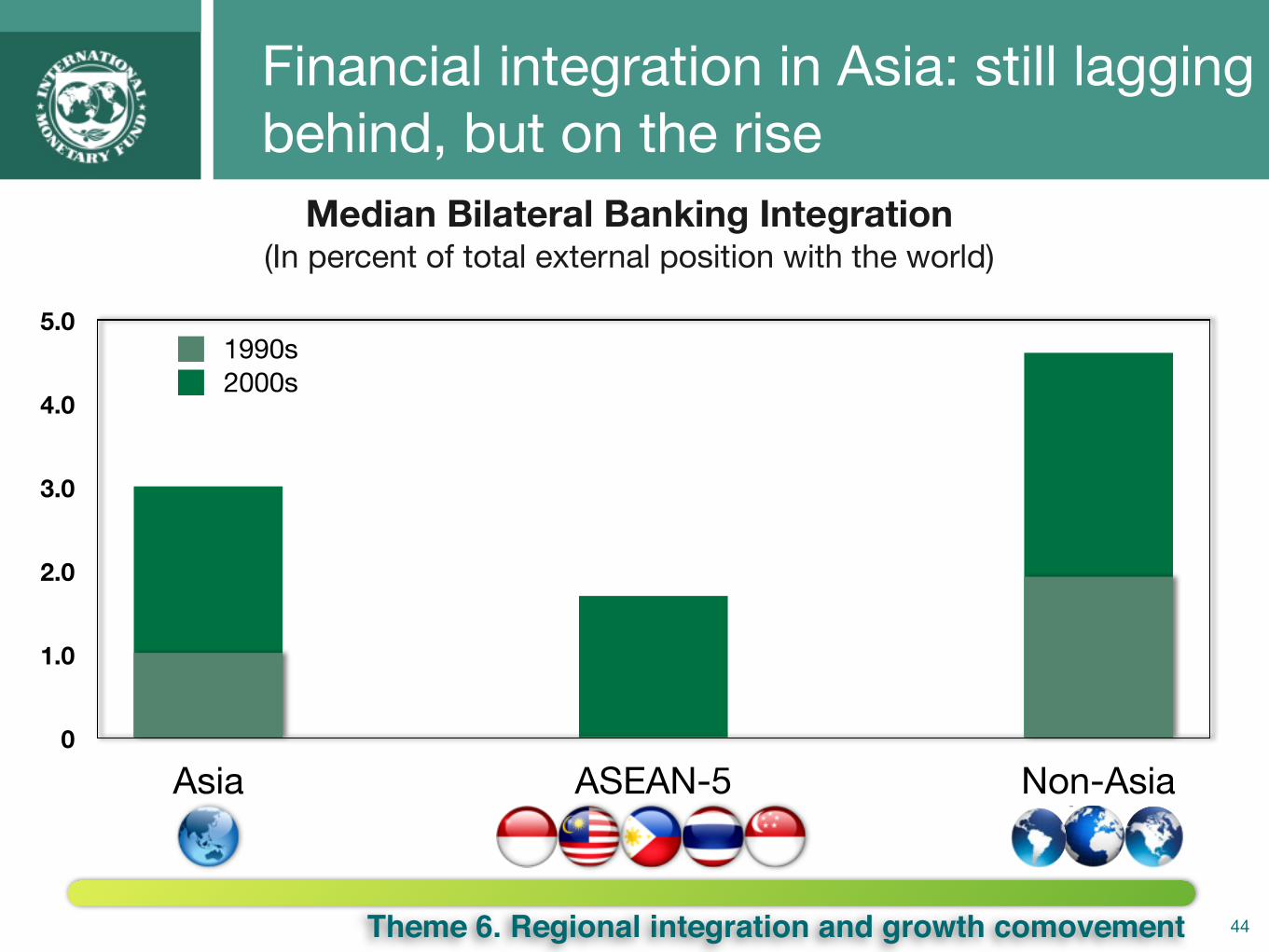

44

Financial integration in Asia: still lagging behind, but on the rise

Median Bilateral Banking Integration(In percent of total external position with the world)

1990s2000s

Theme 6. Regional integration and growth comovement

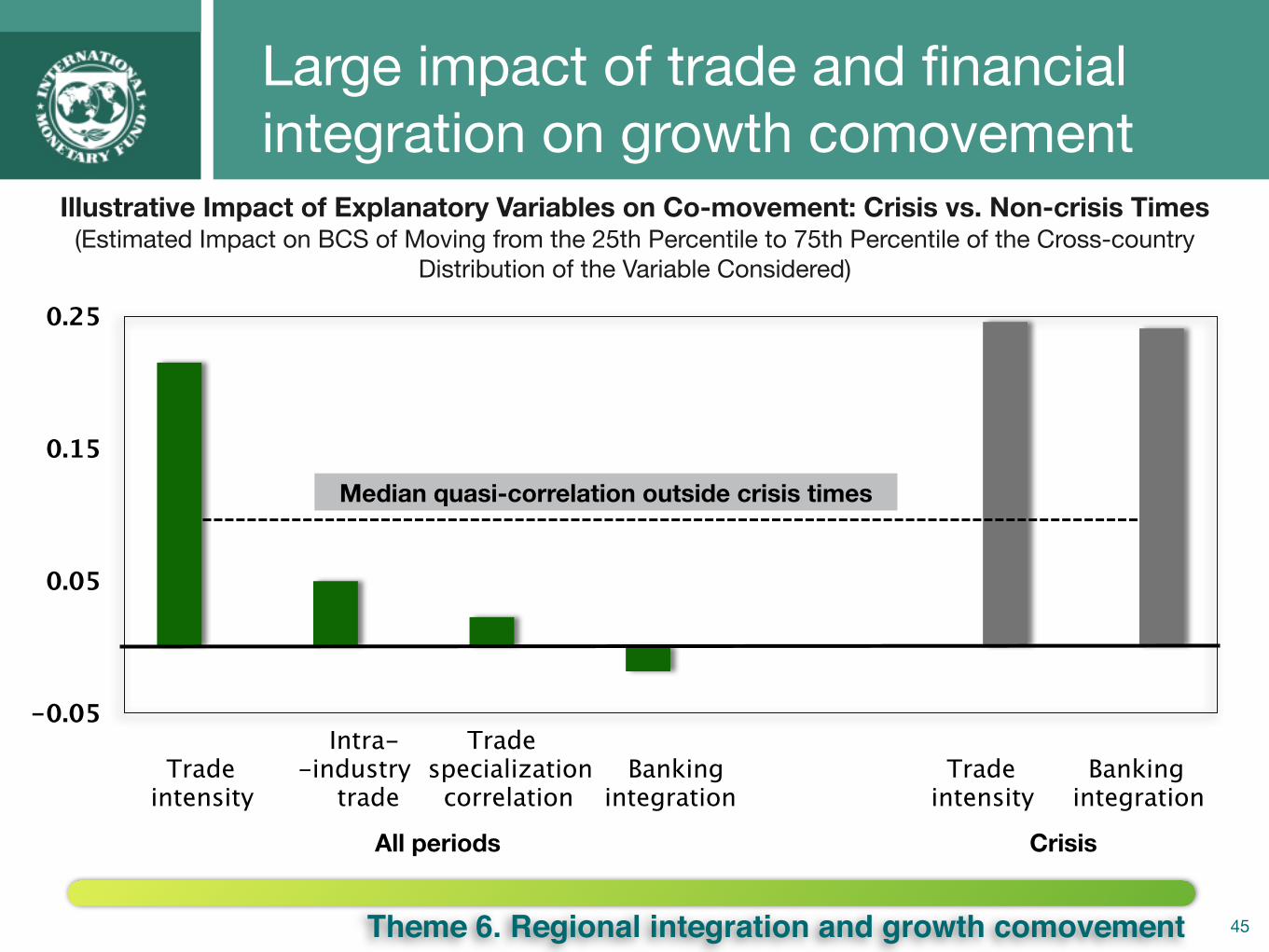

45

Large impact of trade and financial integration on growth comovement

Illustrative Impact of Explanatory Variables on Co-movement: Crisis vs. Non-crisis Times(Estimated Impact on BCS of Moving from the 25th Percentile to 75th Percentile of the Cross-country

Distribution of the Variable Considered)

-0.05

0.05

0.15

0.25

Trade intensity

Intra--industry trade

Trade specialization correlation

Banking integration

Trade intensity

Banking integration

Median quasi-correlation outside crisis times

All periods Crisis

Theme 6. Regional integration and growth comovement

46

Implications: The Future

• BCS to rise if economic integration increases further, especially in crisis times (financial integration)

• Role of China: increasing as a final demand source, declining as “assembly hub” ➡ greater spillovers from China shocks, but China less of a conduit for global shocks

• Higher BCS: bad for risk sharing ➡ need for individual policies to strengthen resilience and broad (regional and global) safety nets; global safety net especially useful in event of regional shocks/shocks originating from China

Theme 6. Regional integration and growth comovement

Thank You

Asia and Pacific Department, April 201447