Embed Size (px)

Citation preview

ed-CK / sa- YM, PY

Flying a little lower

Airline earnings in 2017 to see margin pressure

from higher fuel cost

Aircraft deliveries reaccelerating after two-year

slowdown, yields to see downwards pressure

Structural regional growth in fleet and passengers

bodes well for aeronautical support and airport

players

ASEAN airline picks: AIRA MK, AAV TB, CEB PM;

other aviation picks: AOT TB, CAO SP, STE SP

Carrier earnings moving out of sweet spot as fuel prices

depart from bottom. ASEAN airlines are (for the most part) on track for record CY16 performances on the back of the trough in jet fuel prices. However, the CY17 outlook is less benign as fuel has tracked crude oil prices’ upward trend. We think margins will be squeezed from the bottom, as average cost/available-seat-kilometre (ASKs) will be pushed up – our current CY2017 forecast for jet fuel is US$60/bbl, c.13% higher than 2016’s US$52.9/bbl average.

More planes to fill the skies. Capacity growth is on the cards for most airlines after a general lull in 2015-16, as strong CY16 earnings bolstered balance sheets and expansion plans. Even those adding fewer aircraft aim to improve volume. We think competition is set to rise which will pull down average fares as airlines attempt to drive up or maintain load factors.

Preference for airlines with market share strongholds.

Overall, we are unperturbed by the likely step-down in airline profits as it comes from a high base. In this environment, we prefer airlines with stronger market shares and thus more flexibility in tweaking the levers (price / volume) to strengthen their position or achieve their desired bottomlines. Top BUY recommendations along this theme are: AirAsia (AIRA MK), Asia Aviation (AAV TB), and Cebu Air (CEB PM).

AoT remains a favoured pick while we also like CAO and

ST Engineering. We prefer AoT to MAHB given the former’s strong earnings growth prospects, which is driven by Thailand’s dynamic tourism sector. We also like China Aviation Oil (CAO) as a proxy for China’s firm civil air travel demand growth and finally, we prefer ST Engineering to SIA Engineering as it has a strong order pipeline to underpin earnings and dividend visibility.

KLCI : 1,688.50 STI : 3,071.64 SET : 1,589.29

Analyst Marvin KHOR +60 32604 3911 Paul YONG CFA +65 6682 3712 [email protected] [email protected]

Suvro SARKAR +65 6682 3720 Namida ARTISPONG +66 2657 7833 [email protected] [email protected]

Singapore Research Team [email protected]

Source: AllianceDBS, DBS Bank, Bloomberg Finance L.P. Closing price as of 9 Feb 2017

AirAsia : Low cost carrier based in Malaysia with similar-branded associates across Asia AirAsia X : Long-haul low cost carrier based in Malaysia Airports of Thailand : The national airport operator managing six international airports throughout Thailand, including Suvarnabhumi Airport in Bangkok. Asia Aviation : Majority owner of Thai AirAsia, low cost carrier based in Thailand Bangkok Airways : Full service regional carrier with hubs in Bangkok and Samui, and is also a major and controlling shareholder of Samui Airport Property Fund Cebu Air : Low cost carrier based in the Philippines China Aviation Oil : CAO is the largest physical jet fuel trader in the Asia Pacific region and the key importer of jet fuel into the PRC. Garuda Indonesia : Garuda Indonesia (GIAA) is the national flag carrier of Indonesia focusing in passenger and cargo service. Malaysia Airports : Malaysia's primary airport operator, also operating the Istanbul Sabiha Gokcen airport SIA Engineering : Provision of aviation maintenance, repair and overhaul services Singapore Airlines : Singapore Airlines owns and operates SIA, SIA Cargo and Silk Air, Scoot. They also own majority stakes in SGX-listed SIA Engineering and Tigerair. ST Engineering : An integrated engineering group providing solutions and services in aerospace, electronics, land systems and marine sectors. Thai Airways : National Carrier of Kingdom of Thailand

DBS Group Research . Equity 10 Feb 2017

ASEAN Industry Focus

ASEAN Aviation

Refer to important disclosures at the end of this report

STOCKS

12-mth

Price Mkt Cap Target Price Performance (%)

RM US$m RM 3 mth 12 mth Rating

AirAsia 2.70 2,032 3.25 (4.3) 92.9 BUY AirAsia X 0.41 383 0.38 (4.7) 70.8 HOLD Airports of Thailand 42.00 1,713 45.50 12.6 12.3 BUY Asia Aviation 6.10 845 7.60 (14.1) 9.9 BUY Bangkok Airways 21.30 1,277 26.30 (13.8) (11.3) BUY Cebu Air 96.40 1,171 125 (9.5) 24.4 BUY China Aviation Oil 1.48 900 1.70 6.1 126.9 BUY Garuda Indonesia 338 658 475 (4.5) (17.2) BUY Malaysia Airports 6.70 2,504 6.80 4.2 9.1 HOLD SIA Engineering 3.61 2,856 3.58 2.9 3.7 HOLD Singapore Airlines 9.80 8,175 10.10 (0.2) (12.8) HOLD ST Engineering 3.33 7,309 3.68 8.5 20.7 BUY Thai Airways 21.90 1,365 23.25 (19.6) 163.9 HOLD

Industry Focus

ASEAN Aviation

Page 2

Executive summary – airline earnings coming off peak

Aviation players in the ASEAN region are (mostly) largely on track to achieve stellar earnings in 2016, on the back of earlier anticipated factors of 1) bottoming of effective jet fuel prices, and 2) favourable supply-demand conditions from slower aircraft deliveries.

Moving into 2017, we think margins are set to come under some pressure as those factors unwind, with a number of airlines under our coverage expected to see dips in core earnings – except those charting low 2016 bases from underperformance due to respective specific reasons.

Regional airlines’ 9M16 core earnings (local currency)

9MCY16 9MCY15 % variance

AAV (THB m) 1,674 1,047 +60%AAX (RM m) 151 (217) turnaround AIRA (RM m) 923 165 +>100% BA (THB m) 2,535 1,740 +46% CEB (PHP m) 7,574 4,449 +70% GIAA (US$ m) (22) 16 n.m. SIA (S$ m)* 546 356 53% THAI (THB m) 3,349 (4,621) turnaround

Source: Companies, DBS Bank, AllianceDBS * FYE Mar

However, we are not overly concerned with a prospective decline – as it would not be outside the norm for global airline peers. The International Air Transport Association (IATA) has forecasted 2017 global airline industry net profit of US$29.8bn, 16% down from US$35.6bn it projected for 2016. For Asia-Pacific carriers in particular, IATA forecasted an aggregated 14% decline in 2017 net profit to US$6.3bn, from US$7.3bn expected for 2016. We observe two key reasons for the broad decline for ASEAN airline earnings: 1) the gradual uptick in fuel prices, and 2) easing of average fares due to competition. Industry traffic growth is expected to record a decent pace, though unable to overcome margin erosion implied by the two headwind factors. Airlines we favour under such circumstances are those with higher control over volume – i.e. with strong demand positioning or captive markets.

Regional airlines’ FY16/17F core earnings forecasts (local

currency)

FY17F FY16F % variance

AAV (THB m) 2,215 2,322 (5%)AAX (RM m) 189 206 (8%)AIRA (RM m) 975 1,334 (27%)BA (THB m) 3,011 3,286 (8%)CEB (PHP m) 9,480 9,892 (4%)GIAA (US$ m) 49 10 >100%SIA (S$ m)* 684 629 9%THAI (THB m) 4,882 4,590 6%

Source: Companies, DBS Bank, AllianceDBS * FYE Mar, figures are FY18F/FY17F respectively

Given this outlook, we also find other aviation plays like airports and aerospace maintenance, report & operations (MRO) firms provide a good avenue for exposure to ASEAN aviation. Passenger traffic demand is picking up in both Malaysia and Singapore, while Thailand is expected to rebound to being a key ASEAN tourist draw after a short blip given the crackdown on ‘zero-dollar’ tours that hurt China visitations. MRO players are a natural beneficiary of higher aircraft volumes in the region, for which Asia is also a good longer-term prospect as the propensity to travel grows.

Airlines regaining growth ambitions

ASEAN airlines are looking at larger fleet growth in 2017. We think this is in part incentivised by strong financial performances in 2016 – which had for many airlines grew or rejuvenated cash piles and book values. Across our coverage, we expect a net fleet growth of 35 (from 27 expected in 2016), which adds on the expected growth from competitors as well. This is led by Malaysia and Thai AirAsia with planned increases of seven and six, respectively, which we view as the group’s strategy to entrench its domestic market share dominance. Notably, demand appears to be skewed towards short-haul and/or low-cost aircraft; and with less demand for new long-haul capacity. No new planes are expected for Malaysia AirAsia X, and players like Bangkok Air and Garuda are only adding to their short-haul aircraft (the latter via low-cost unit Citilink).

Page 2

Industry Focus

ASEAN Aviation

Page 3

Expected year-end active fleet counts (non-exhaustive)

2017F Net chg 2016E

Net chg 2015

Thailand

Thai AirAsia 57 +6 51 +6 45

Bangkok Air 39 +4 35 +4 31

Thai Airways 97 +2 95 - 95

Nok Airways 34 +1 33 +5 28

Thai AirAsia X 6 - 6 +1 5

Thai Lion 24 +6 18

Thai VietJet 3 +2 1

NokScoot 5 +2 3 - 3

Malaysia

Malaysia AirAsia 84 +7 77 -3 80

Malaysia AirAsia X 22 - 22 +2 20

Malaysia Airlines 87 +9 78

Malindo / Batik M’sia 52 +10 42 +15 27

Singapore

Singapore Airlines (main) 110 1 109 7 102

Silk Air 35 4 31 2 29

Tiger + Scoot 38 3 35 - 35

Philippines

Cebu Air 59 +2 57 +2 55

PAL 66 +4 62 +4 58

Philippines AirAsia 18 +4 14 - 14

Indonesia

Garuda (mainline) 144 - 144 +1 143

Citilink 56 +4 52 +8 44

Indonesia AirAsia 24 +2 22 -2 25

Indonesia AirAsia X 2 - 2 - 2

Lion Air (+Wings + Batik) 233 +22 204 +16 188

Source: CAPA, companies, DBS Bank, AllianceDBS Major unlisted player Lion Group continues to be a major contender in terms of capacity through its network comprising Indonesian LCCs (Lion Air, Wings Air) and FSC (Batik Air), Malaysian FSC (Malindo – soon Batik Malaysia), and Thai LCC (Thai Lion Air). The group’s burgeoning orderbook of 442 aircraft at the start of 2017 implies that growth must continue, despite a slowdown in deliveries in 2016, which had contributed to the sector’s stronger margin performance. CAPA estimates that the group is set to receive 32 (non-turboprop) aircraft in 2017 – which after removing the 10 slated for Malindo, leaves 22 to be split among Thai Lion Air and its Indonesian units.

Fares and yields to pare down as airlines opt for volume

Given the competitive environment above, we expect yields (fares/RPK) to broadly pare down for the ASEAN airlines. We contrast the yield movement below relative to industry capacity growth for each of the major markets, where it had demonstratively fallen in higher competitive scenarios. The main exception will be the Thai airlines, in particular those serving domestic routes – which be imposing an additional Bt150-200 per flight to pass on newly hiked jet fuel excise taxes. See further elaboration in “Thailand’s domestic jet fuel excise quandary” section below. Additionally, yield, capacity and load factor also generally show a trade-off pattern, where higher capacity growth impact yield or load factor or both adversely, and vice versa. For example, ambitious capacity growth from Malaysia AirAsia X from 2Q13 to 1Q14 resulted in a concurrent severe decline in yield; it is apparent that during this time, AirAsia X sacrificed yield amid capacity growth to maintain a reasonable level of load factor. In contrast, after the capacity tapering, which started in 1Q14, Singapore Tigerair is now enjoying higher load factors. Another important factor in yields is the fuel surcharge which now has been abolished. Reaching as high as one-fifth of total yields at its peak, fuel surcharges have largely been removed by airlines following the collapse of jet fuel prices since late-2014, driving down yields external to supply-demand conditions. Malaysia Fare/RPK (in local currency) y-o-y changes - Malaysia

Source: Companies, DBS Bank, AllianceDBS

‐30%

‐20%

‐10%

0%

10%

20%

30%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Malaysia AirAsia Malaysia AirAsia X

Page 3

Industry Focus

ASEAN Aviation

Page 4

Capacity (y-o-y changes) - Malaysia

Source: Companies, DBS Bank, AllianceDBS Load factors - Malaysia

Source: Companies, DBS Bank, AllianceDBS Thailand Fare/RPK (local currency) y-o-y changes - Thailand

Source: Companies, DBS Bank, AllianceDBS

Capacity y-o-y changes - Thailand

Source: Companies, DBS Bank, AllianceDBS Load factors - Thailand

Source: Companies, DBS Bank, AllianceDBS Singapore Fare/RPK (local currency) y-o-y changes - Singapore

Source: Companies, DBS Bank, AllianceDBS

‐25%

‐20%

‐15%

‐10%

‐5%

0%

5%

10%

15%

20%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Thai AirAsia Bangkok Air Thai Airways Nok Air

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Malaysia AirAsia Malaysia AirAsia X

55%

60%

65%

70%

75%

80%

85%

90%

Malaysia AirAsia Malaysia AirAsia X

-10%

0%

10%

20%

30%

40%

50%

Thai AirAsia Bangkok Air Thai Airways Nok Air

55%

60%

65%

70%

75%

80%

85%

90%

Thai AirAsia Bangkok Air Thai Airways Nok Air

-15%

-10%

-5%

0%

5%

10%

SIA mainline Silkair Tigerair Scoot

Page 4

Industry Focus

ASEAN Aviation

Page 5

Capacity y-o-y changes - Singapore

Source: Companies, DBS Bank, AllianceDBS Load factors - Singapore

Source: Companies, DBS Bank, AllianceDBS Indonesia Fare/RPK (local currency) y-o-y changes - Indonesia

Source: Companies, DBS Bank, AllianceDBS

Capacity (y-o-y changes) - Indonesia

Source: Companies, DBS Bank, AllianceDBS Load factors - Indonesia

Source: Companies, DBS Bank, AllianceDBS Philippines Fare/RPK (local currency) y-o-y changes - Philippines

Source: Companies, DBS Bank, AllianceDBS

‐25%

‐20%

‐15%

‐10%

‐5%

0%

5%

10%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Cebu Air

‐20%

‐15%

‐10%

‐5%

0%

5%

10%

15%

20%

25%

1Q13

2Q13

3Q13

4Q13

1Q14

2Q14

3Q14

4Q14

1Q15

2Q15

3Q15

4Q15

1Q16

2Q16

3Q16

Garuda (group) Indonesia AirAsia

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

SIA mainline Silkair Tigerair Scoot

65%

70%

75%

80%

85%

90%

SIA mainline Silkair Tigerair Scoot

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Garuda (group) Indonesia AirAsia

65%

70%

75%

80%

85%

90%

Garuda (group) Indonesia AirAsia

Page 5

Industry Focus

ASEAN Aviation

Page 6

Capacity (y-o-y changes) and load factors - Philippines

Source: Companies, DBS Bank, AllianceDBS The LCC factor on yields

A factor frequently associated with easing average industry yield growth is the prevalence of low cost carriers or LCCs, which had been a key factor boosting air travel over the 00s. LCC market penetration for ASEAN air travel had stagnated for two years since 2014, implying it may be near to a mature level for ASEAN. LCC market share: intra- & to/from ASEAN

Source: CAPA, AllianceDBS, DBS Bank After peaking at 57% in 2014, the proportion of LCC seats over total seats available for intra-ASEAN flights had pared down to 56% in 2015 and further to 54% in 9M16. This trend was slightly less noticeable for flights to/from ASEAN, which has lower LCC share justified by mostly longer average flight times. Breaking it down, LCC seat growth for intra-ASEAN air travel had, for the first time since 2015, grown at a slower (9%) pace than that of total seat growth (10%). On one hand, this may be due to the simple maturing exposure of ASEAN to the LCC concept. However, the removal of fuel surcharges has

brought down the relative price difference between FSC and LCC average fares – which we think made FSCs more competitive and viable as a growth model. Going forward, we see LCC market penetration to be steady – evidenced by the two largest groups AirAsia and Lion Air choosing different tactics in service expansion (continued LCC for the former, and more FSC products for the latter). LCC vs total seat growth – intra-ASEAN segment

Source: CAPA, AllianceDBS, DBS Bank Jet fuel tracking crude oils tentative uphill climb

The severe collapse in oil and jet fuel prices were instrumental in the record profitability logged in 2016, but the bottom appears to have come to pass in 1Q16. Right now, jet fuel has reached levels of above US$60/bbl (our average forecast for 2017), contrasting with the average of US$52/bbl in 2016. This is expected to contribute to cost/ASK rising up to 7% among our coverage. Jet fuel price FOB Singapore (US$/barrel)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS

30

40

50

60

70

80

90

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

Spot jet fuel (US$/bbl) Calendar quarter average

70%

72%

74%

76%

78%

80%

82%

84%

86%

0%

5%

10%

15%

20%

25%

30%

35%

Cebu Air Load Factor (RHS) Cebu Air Capacity Growth (LHS)

32%37%

41%43%

45% 47%

54%57.0% 56.4%

54.2%

17% 19% 20% 21% 22% 22% 24% 24.2% 23.7% 23.7%

0%

10%

20%

30%

40%

50%

60%

2007 2008 2009 2010 2011 2012 2013 2014 2015 Jan-Sep2016

LCC market share - intra-ASEANLCC market share - to/from ASEAN

10.2%

9.0%

0%

5%

10%

15%

20%

25%

30%

35%

0

50

100

150

200

250

300

350

2007 2008 2009 2010 2011 2012 2013 2014 2015 Jan-Sep2016

Total seats - intra-ASEAN (m) LCC seats - intra-ASEAN (m)

Growth - Total Growth - LCC

Page 6

Industry Focus

ASEAN Aviation

Page 7

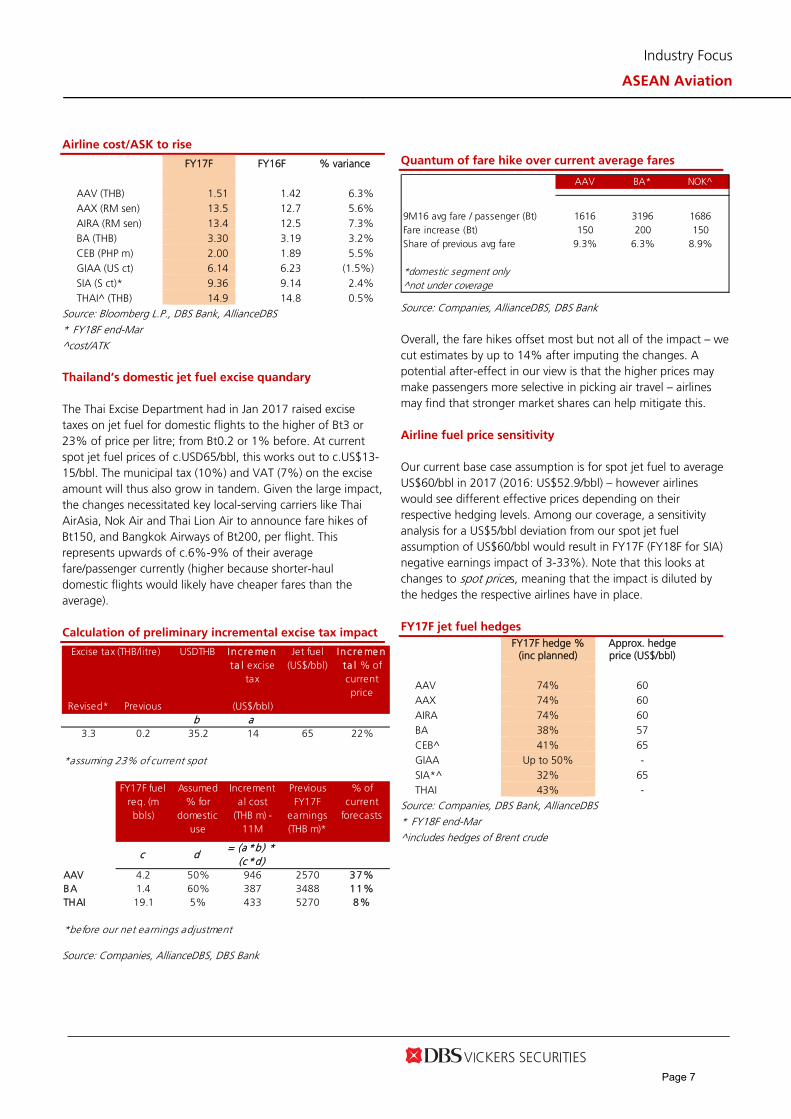

Airline cost/ASK to rise

FY17F FY16F % variance AAV (THB) 1.51 1.42 6.3% AAX (RM sen) 13.5 12.7 5.6% AIRA (RM sen) 13.4 12.5 7.3% BA (THB) 3.30 3.19 3.2% CEB (PHP m) 2.00 1.89 5.5% GIAA (US ct) 6.14 6.23 (1.5%) SIA (S ct)* 9.36 9.14 2.4% THAI^ (THB) 14.9 14.8 0.5%

Source: Bloomberg L.P., DBS Bank, AllianceDBS * FY18F end-Mar ^cost/ATK Thailand’s domestic jet fuel excise quandary

The Thai Excise Department had in Jan 2017 raised excise taxes on jet fuel for domestic flights to the higher of Bt3 or 23% of price per litre; from Bt0.2 or 1% before. At current spot jet fuel prices of c.USD65/bbl, this works out to c.US$13-15/bbl. The municipal tax (10%) and VAT (7%) on the excise amount will thus also grow in tandem. Given the large impact, the changes necessitated key local-serving carriers like Thai AirAsia, Nok Air and Thai Lion Air to announce fare hikes of Bt150, and Bangkok Airways of Bt200, per flight. This represents upwards of c.6%-9% of their average fare/passenger currently (higher because shorter-haul domestic flights would likely have cheaper fares than the average). Calculation of preliminary incremental excise tax impact

Source: Companies, AllianceDBS, DBS Bank

Quantum of fare hike over current average fares

Source: Companies, AllianceDBS, DBS Bank Overall, the fare hikes offset most but not all of the impact – we cut estimates by up to 14% after imputing the changes. A potential after-effect in our view is that the higher prices may make passengers more selective in picking air travel – airlines may find that stronger market shares can help mitigate this. Airline fuel price sensitivity

Our current base case assumption is for spot jet fuel to average US$60/bbl in 2017 (2016: US$52.9/bbl) – however airlines would see different effective prices depending on their respective hedging levels. Among our coverage, a sensitivity analysis for a US$5/bbl deviation from our spot jet fuel assumption of US$60/bbl would result in FY17F (FY18F for SIA) negative earnings impact of 3-33%). Note that this looks at changes to spot prices, meaning that the impact is diluted by the hedges the respective airlines have in place. FY17F jet fuel hedges

FY17F hedge %

(inc planned) Approx. hedge price (US$/bbl)

AAV 74% 60 AAX 74% 60 AIRA 74% 60 BA 38% 57 CEB^ 41% 65 GIAA Up to 50% - SIA*^ 32% 65 THAI 43% -

Source: Companies, DBS Bank, AllianceDBS * FY18F end-Mar ^includes hedges of Brent crude

AAV BA* NOK^

9M16 avg fare / passenger (Bt) 1616 3196 1686Fare increase (Bt) 150 200 150Share of previous avg fare 9.3% 6.3% 8.9%

*domestic segment only^not under coverage

USDTHB Inc re me nta l excise

tax

Jet fuel (US$/bbl)

Inc re me nta l % of current price

Revised* Previous (US$/bbl)b a

3.3 0.2 35.2 14 65 22%

*assuming 23% of current spot

FY17F fuel req. (m bbls)

Assumed % for

domestic use

Incremental cost

(THB m) - 11M

Previous FY17F

earnings (THB m)*

% of current

forecasts

c d= (a *b) *

(c *d)AAV 4.2 50% 946 2570 37%BA 1.4 60% 387 3488 11%THAI 19.1 5% 433 5270 8%

*before our net earnings adjustment

Excise tax (THB/litre)

Page 7

Industry Focus

ASEAN Aviation

Page 8

FY17F earnings forecasts changes per US$5/bbl

deviation from US$60/bbl base assumption for jet fuel

FY17F

adjusted FY17F % variance AAV (THB m) 2,113m 2,215m (5%) AAX (RM m) 143m 189m (24%) AIRA (RM m) 947m 975m (3%) BA (THB m) 2,898m 3,011m (4%) CEB (PHP m) 8,874m 9,480m (6%) GIAA (US$ m) 32.9m 49.3m (33%) SIA (S$ m)* 598m 682m (12%) THAI (THB m) 3,287m 4,882m (33%)

Source: Companies, DBS Bank, AllianceDBS * FY18F end-Mar This relatively mild increase (or indeed any further spikes) may not result in the immediate collapse of airline earnings, somewhat like the initial oil price collapse took time to raise airline profitability. This is simply because of the hedges airlines have employed are up to or even above half of their expected requirements in 2017. As such a sustained increase will only have more meaningful impact in 2018, wherein the operating landscape may yet shift again to accommodate the higher cost environment. Over the past five years, fuel costs as a % of overall cost/ASK has deteriorated from 23-50% to 20-40% AirAsia cost per ASK breakdown (RM sen)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS

Thai AirAsia cost per ASK breakdown (THB)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS SIA cost per ASK breakdown (S$ cents)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS Garuda cost per ASK breakdown (US cents)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS

42% 40%

0

2

4

6

8

10

12

14

2010 2011 2012 2013 2014 2015

Fuel Cost / ASK Cash Opex / ASK Asset Cost / ASK

38%28%

0

1

2

3

4

5

6

7

8

9

10

2011 2012 2013 2014 2015

Fuel Cost / ASK Cash Opex / ASK Asset Cost / ASK

37% 35%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2010 2011 2012 2013 2014 2015

Fuel Cost / ASK Cash Opex / ASK Asset Cost / ASK

35% 32%

0

2

4

6

8

10

12

2010 2011 2012 2013 2014 2015

Fuel Cost / ASK Cash Opex / ASK Asset Cost / ASK

Page 8

Industry Focus

ASEAN Aviation

Page 9

Cebu Air cost per ASK breakdown (PHP)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS Will fuel prices eventually raise fares for other countries? The developments from Thailand provide some reassurance that excessive fuel price-related escalations indeed will induce airlines to pass it on via higher fares or yields. In relation to spot jet price increases, however, the chance of reintroducing surcharges at present levels appear slim given that the last instances (before being removed) were in place when prices were above the US$100/bbl level (>50% higher than current) back in 2014 and prior. Air travel demand still looking robust Demand in ASEAN remains generally positive though still below peak conditions. Air travel demand has generally been tied to economic activity in a region (i.e. correlated with GDP growth), but with more underlying potential in region where propensity to travel has yet to mature. ASEAN GDP vs ASEAN passenger (RPK) y-o-y growth

Source: ASEAN, Boeing, DBS Bank, AllianceDBS *Includes, Africa, Asia Pacific, Europe, Middle East, North America As GDP expectations for ASEAN countries remain on the mild side for 2017, air travel is accordingly not expected to chart

excessive growth. Most countries are still expecting single-digit expansion. Still confident in Thailand tourism

For Thailand, the number of international tourist arrivals to the country has been strong in the first nine months of 2016, growing by 12.4%. However, tourist arrivals growth started to slow down in Oct as the impact from crackdown on low cost zero-dollar tours by the Thai and Chinese governments have kicked in, coupled with the passing of Thailand’s beloved late King Bhumibol Adulyadej in mid-Oct in which several forms of public entertainment were banned for one month until 13 November. As a result, the Ministry of Tourism reported only 0.5% growth in international tourist arrivals to Thailand in Oct and a 4.4% fall in arrivals in Nov. Note that Chinese tourist numbers fell for the first time in Oct by 16.2% and continued to decline by 29.7% in Nov. Nevertheless, the sentiment on tourism has improved after the Thai government announced in Nov that they will lift Bt1,000 visa fee for tourists who sought visas at Thai embassies and consulates for 19 countries (including China, Bhutan, India, Taiwan). Also, the visa on arrival fee will also be cut from Bt2,000 to Bt1,000. This has been implemented from 1 Dec 2016 to 28 Feb 2017. Thanks to the government’s effort to boost tourism, international tourist arrivals increased by 1.1% in Dec while the number of Chinese tourists fell by a smaller magnitude (-16% y-o-y). In line with Ministry of Tourism’s numbers, AOT's international passenger traffic growth started to slow down in Oct with growth of 3%, followed by a negative growth (in a low single digit) in Nov. Then international passenger growth rebounded to 4% in Dec. For the full year 2016, there were 32.6m international tourists visiting Thailand, representing an increase of 8.9%. AOT: International passenger traffic at its six airports

Source: AOT, DBS Vickers For year 2017, we maintain our positive view on Thailand tourism which has shown its resilience by rebounding rapidly in the wake of several unfavourable events in the past. We believe the impact from crackdown on zero-dollar tours should be temporary and that the zero-dollar tour ban will

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

2010 2011 2012 2013 2014 2015

ASEAN GDP growth Within ASEAN RPK growthASEAN to key regions* RPK growth

-5%0%5%10%15%20%25%30%35%40%45%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Dec

14Ja

n15

Feb1

5M

ar15

Apr

15M

ay15

Jun1

5Ju

l15

Aug

15Se

p15

Oct

15N

ov15

Dec

15Ja

n16

Feb1

6M

ar16

Apr

16M

ay16

Jun1

6Ju

l16

Aug

16Se

p16

Oct

16N

ov16

Dec

16

International movement growth yoy (RHS)

'000 passengers

43%38%

0.0

0.5

1.0

1.5

2.0

2.5

2010 2011 2012 2013 2014 2015

Fuel Cost / ASK Cash Opex / ASK Asset Cost / ASK

Page 9

Industry Focus

ASEAN Aviation

Page 10

benefit Thai tourism as a whole in a the long term from the qualitative improvement of Chinese tourists. Thailand will then be depending not only on the number of foreign tourist arrivals but also the quality of their spending per head. Nevertheless, we should see the return of Chinese tourist arrivals to Thailand given Thailand’s cost-competitive travelling and variety of destinations, as well as, the close proximity of these two countries and flight connectivity. The Tourism Authority of Thailand (TAT) expects international tourist arrivals to Thailand to grow by 7.7% to 35.1m in 2017 while Chinese arrivals are also expected to increase by 11.3% to 9.8m as tourists from zero-dollar tours were estimated to account for only 20% of arrivals last year. However, strong growth in other key feed markets such as Russia, India, the US, and the Middle East should compensate for Chinese arrivals if they were to continue to slow down. On a positive note, Russian tourists which account for 3.3% of total arrivals have showed positive signs of recovery, growing by 23.3% to 1.1m in 2016 after a long decline. Additionally, we believe the government will continue to support the tourism sector if any unfavourable event arises by lifting visa fee or offering tax rebates for domestic travel. Thailand: International tourist arrivals

Source: Ministry of Tourism and Sports (Thailand), DBS Vickers Passenger growth in Malaysia staved off two years of slowing progress, with Malaysia Airports (MAHB) reporting a 6% increase in 2016 (from 0.6% in 2015, 4.7% in 2014). Pax growth notched a long-unseen double-digit rate of c.10% in 2H16; appearing to shrug off a 24-month or 2-year slowdown (0.4% average growth) largely attributed to the airline incidences in 2014. Looking forward, MAHB’s MD Datuk Badlisham Ghazali stated its internal growth target of 5% for 2017 (and in a newer statement, 5-7%), likewise our forecast for the year. This represents a closer match with the pace of Malaysia’s nominal GDP growth from pre-2H14.

MAHB passenger growth by month, segment

Source: MAHB, DBS Bank, AllianceDBS Quarter pax growth vs Malaysia’s nominal GDP

Source: MAHB, Department of Statistics, DBS Bank, AllianceDBS In Singapore, Changi Airport pax growth charted a healthy +5.9% for 2016, showing a somewhat similar rebound trend to Malaysia. This continued improvements from 2015 (+2.5%), moving on from a relative slowdown in 2014 (+0.7%). Changi Airport’s y-o-y passenger growth

Source: Changi Airport, DBS Bank, AllianceDBS

(50%)

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%

50%

0

1

2

3

4

5

6

7

8

9

10

Jan-

13

Mar

-13

May

-…

Jul-1

3

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-…

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-…

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-…

Jul-1

6

Sep-

16

Nov

-16

% y-o-ym paxDomestic pax (lhs) International pax (lhs)Dom pax growth (rhs) Int pax growth (rhs)

Period of 2H14-1H16 averaged 0.4% growth

‐15%

‐10%

‐5%

0%

5%

10%

15%

20%

25%

30%1Q

FY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

2QFY11

3QFY11

4QFY11

1QFY12

2QFY12

3QFY12

4QFY12

1QFY13

2QFY13

3QFY13

4QFY13

1QFY14

2QFY14

3QFY14

4QFY14

1QFY15

2QFY15

3QFY15

4QFY15

1QFY16

2QFY16

3QFY16

4QFY16

Total passenger growth (y‐o‐y)

Malaysian GDP growth, current prices (y‐o‐y)

600

1,000

1,400

1,800

2,200

2,600

3,000

3,400

Jan

Feb

Mar

Apr

May Jun Jul

Aug Se

p

Oct

Nov

Dec

'000 People

2009 2010 2011 20122013 2014 2015 2016

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

36

40

44

48

52

56

60

2011 2012 2013 2014 2015 2016

Changi Airport passenger movements (m) y‐o‐y growth

Page 10

Industry Focus

ASEAN Aviation

Page 11

Aerospace MRO has steady growth potential but structural challenges persist Global air traffic outlook

Source: Boeing CMO 2016-2035 Increasing air traffic trend can be sustained in Asia. Facilitated by rapid economic growth, there has been increasing demand for air travel for the past 20 years. The air travel industry has weathered various major external shocks over the years to register a 5.4% CAGR over that period, almost double the average global GDP growth rate. Going forward, increasing per-capita income, increasing affordability and propensity to travel and the emergence of low cost carriers (LCCs) will continue to drive traffic growth, especially in emerging markets like Asia and spur the need for more aircraft and aircraft maintenance. Driven by China and India as the main engines of growth, passenger traffic in the region is forecast to grow by around 6.1% CAGR till 2035, outstripping the global growth rate of 4.8%. Liberalisation and policy initiatives like open skies and easing of visa regulations are also driving the traffic expansion in this region. Single aisle aircraft will dominate deliveries in future. Total jet aircraft fleet is expected to double over the next 20 years according to Boeing, and close to 71% of new deliveries will be single-aisle or narrowbody aircraft. Better fuel economics and lower maintenance requirements drive the replacement demand for the narrowbody fleet.

Expected global aircraft delivery demand

Source: Boeing CMO 2016-2035 Asia will dominate narrowbody aircraft demand. To accommodate the growing demand, Asia will need to add 15,130 aircraft over the next 20 years (5% CAGR), according to Boeing, nearly tripling the existing aircraft base. The growth will be driven by Low Cost Carriers (LCCs) and as a result, 40% of all new projected single aisle aircraft deliveries will be in Asia.

2380

28140

9100

0

5000

10000

15000

20000

25000

30000

Regional Jets Single Aisle Widebody

De livery demand (2016-2035)

Page 11

Industry Focus

ASEAN Aviation

Page 12

Regional variation in single aisle fleet demand

Source: Boeing CMO 2016-2035 Airline profitability trends holding up well. With oil prices falling up to 50% from the highs of 2014, airline profitability has improved significantly since 2015, as evident from the figure below. According to latest estimates from industry body IATA, airlines are expected to enjoy another good year in 2017, the third year in succession that airlines will record a return on invested capital (ROIC) that is better than the weighted average cost of capital (WACC). The strongest performance is from North America, which benefits from a strong local currency and consolidated industry structure. Airlines are likely to use the improved financial position to invest in interior upgrades, operational improvements and new planes, boosting prospects for aviation service companies like MRO providers. Airline profitability trends

Source: International Air Transport Association (IATA)

North American airlines leading profit projections

Source: International Air Transport Association (IATA) All this bodes well for MRO growth but heavy maintenance will lag. Industry consultant Oliver Wyman expects the global MRO market to grow at around 4.4% CAGR for the rest of the decade and at a slightly lower CAGR of 3.9% for the next five years to 2025. Engine MRO will remain the largest segment, with sustained engine MRO outsourcing trend. However, growth in heavy maintenance or airframe maintenance segment will be lower than average as new technology will lead to lower costs and longer schedules of heavy maintenance. Global MRO market size forecast

Source: Oliver Wyman In line with the fleet additions in the region, Asia is expected to drive the growth of the global MRO market at 6.6% CAGR over 2015-2025, with market share expanding from 27% to 35%. The North American MRO market is likely to stagnate though, as fleet additions will be offset to a large extent by retirements.

02000400060008000

100001200014000

Asia N.America

Europe MiddleEast

LatinAmerica

Africa Russiaand CIS

S ingle Aisle Fleet Development

2015 2035

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

Global airline industry profitability trends

Net profit/ loss (US$bn) (LHS) Net profit margin (%) (RHS)

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

NorthAmerica

Europe Asia-Pacific Middle East LatinAmerica

Africa

Industry Profitability by Region

2015 2016E 2017F

14.5 15.9 16.7

27.937.1

46.812.4

15.219.2

12.3

15.0

17.8

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2015 2020 2025

Airframe Engine Components Line

4.4% CAGR

3.8% CAGR

Page 12

Industry Focus

ASEAN Aviation

Page 13

Global MRO market size forecast by geography

Source: Oliver Wyman

Structural changes in industry here to stay. Despite the steady growth potential for the MRO industry in general, MRO operators will need to reinvent to stay relevant as Original Equipment Manufacturers (OEMs) are increasingly taking a bigger share of the aftermarket space, especially for new generation planes. MRO operators will also need to invest in big data analytics and predictive maintenance software to provide value-added services to customers, given the huge amount of operational data generated by new generation aircraft. Advances in data management may also result in lower downtimes for heavy checks and fewer repairs, resulting in lower manhour revenues in future. MROs will need to compensate for this by capturing more of the value chain in predicting maintenance cycle requirements for clients and providing fleet management services.

Key structural trends in MRO industry

OEMs will see increased aftermarket presence for newgeneration aircraft

Increased need for data analysis for new generationaircraft will necessitate MROs to design rigorous datamanagement software to value-add

Health monitoring and predictive maintenance willreduce overall time for individual checks with fewerrepairs

Mature markets are stagnating and nexus of MRO willcontinue to shift to Asia

Price and customer service are key levers to compete instagnant MRO markets

Source: Oliver Wyman

STE will continue to leverage its status as the largest 3rd party MRO provider. STE’s wholly owned subsidiary, ST Aerospace is the only major 3rd party MRO operator in the Asia Pacific region, and hence, is a natural choice for many low cost carriers operating in the region. Most LCCs tend to outsource MRO activities to a large extent, and ST Aerospace remains a partner of choice for operators like Air Asia, Jetstar Asia and Lion Air. SIA Engineering, on the other hand, has developed superior capabilities for modern wide body planes, as a direct beneficiary of the fact that parent SIA is a leader in adopting new generation aircraft. Thus, the two operators rarely compete in the same segments of the market and we believe the higher growth potential of LCCs in the region with their narrowbody fleet vis-à-vis the full service carriers, where new planes are mostly meant for fleet renewal, will likely benefit ST Engineering more than SIA Engineering.

SIA Engineering has formed joint ventures with airframe OEMs. As a specialist widebody MRO provider servicing network airlines, SIE is facing a bigger challenge of OEMs bundling aftermarket services into new generation aircraft sales agreements. To overcome this, SIE has adopted a strategy of partnering with airframe OEMs to win back some of the lost revenues. In 2015, SIE incorporated a 49:51 JV with Boeing to provide fleet management services in the Asia Pacific region, having received regulatory approvals in the relevant geographies. This will help SIE to develop fleet management partnerships with airlines with Boeing fleet in the region and also open the doors for heavy maintenance business in the longer term. SIE has also established a heavy maintenance JV with Airbus (65:35) in 2016 to provide MRO services for A380, A350 and A330 aircraft in Asia Pacific and beyond. Airbus will develop the JV as its Centre of Excellence for Airbus A380 and A350 Heavy Maintenance in Asia. While near-term contribution from these JVs may not be significant, they will be crucial over the long term, in our view.

Narrowbody engine MRO is another driver for STE. As we saw earlier, global engine MRO is the largest MRO segment, and is expected to maintain the highest growth rate over the next 10 years. STE is well positioned for the growth in engine MRO with tie-ups with the top two engine manufacturers – GE and CFM. GE and CFM are expected to further increase their market share from around 57% in 2016 to 61% by 2025, according to industry consultant CAVOK/Oliver Wyman. To recall, STE has set up an engine MRO facility in Xiamen (China) for total support of CFM56 series of engines. STE also has an engine leasing joint venture with Marubeni Corp of Japan, which provides engine leasing services for CFM56-3, CFM56-5B, CFM56-7B engines that power narrow-body

20.0 21.3

17.9 24.93.2

6.57.5

12.818.3

34.8

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2015 2025

North America Europe Latin America Africa/ ME Asia

Page 13

Industry Focus

ASEAN Aviation

Page 14

aircraft such as the A320 and B737, and the opportunities in this segment in Asia Pacific region remains potentially huge. SIA Engineering, on the other hand, with its exposure to legacy widebody engines, has seen a structural decline in engine MRO demand and will hope for the Rolls Royce Trent series widebody engines to contribute to demand growth in future.

Cabin retrofitting and VIP reconfigurations will be a key business area for STE, going forward. In 2011, STE had launched AERIA Luxury Interiors in the US, a unit that focuses on refurbishing and outfitting of VIP aircraft. ST Aerospace is armed with endorsements from the world's leading aircraft OEMs – both an Airbus Corporate Jet service centre and an approved Boeing Business Jet completion centre. ST Aerospace has also extended its VIP aircraft interior business to Singapore, by unveiling a new facility at Seletar Aerospace Park to target demand for bespoke cabin interiors from Asian and Middle Eastern customers. In 2016, ST Aerospace’s VIP aircraft interiors business gained traction by securing five major maintenance and refurbishments contracts – for three Boeing Business Jet (BBJ), one Airbus Corporate Jet (ACJ) and a Boeing 757, from VIP customers in Asia Pacific and the US. ST Aerospace has also established an aircraft seats JV in Singapore to complement its cabin interiors business.

STE expanding into aircraft and engine leasing business to generate new maintenance streams. ST Aerospace has commenced its aircraft leasing business with acquisition of two aircraft in FY15, and added more aircraft in FY16. It has decided to collaborate with Sojitz Corporation of Japan in its aircraft leasing business, by divesting 50% stake the holding company for STE’s aircraft leasing investments.

STE has also further strengthened leadership position in PTF. ST Aerospace’s 55% owned European MRO centre in Dresden in collaboration with Airbus – EADS EFW – has successfully launched the A330 and the A320/321 Passenger to Freighter programmes. This will add to STE’s existing track record of PTF capabilities – MD11, B767-300, and B757-200 (14 &141/2

pallet). STE has also received the supplemental type certificate from US FAA for the 15-Pallet B757-200SF conversion.

Page 14

Industry Focus

ASEAN Aviation

Page 15

Valuations and stock picks

Airline valuations to cool off peak multiples

ASEAN airline share prices ended 2016 on a subdued note, as the cooling-off period started around Sep 16 – largely reacting to the rising jet fuel price and US dollar; despite a larger proportion of 2Q16 results being in line or beating consensus. This is not isolated to ASEAN as the Asia-Pacific Airlines Index has likewise deteriorated on similar factors.

Asia Pacific Airlines Index

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS

2H16 price movement, indexed (30 Jun 2016 = 100)

Source: Bloomberg Finance L.P., DBS Bank, AllianceDBS

Airlines under our coverage gave up gains from Sep 16 onwards, to close the year at slightly below end-1H16 levels. That said y-o-y performance at end-2016 remained mostly positive (6 out of 8).

Given a squeezed profit outlook, there may be some de-rating of valuations from a P/BV perspective – our chosen method of valuing airlines under coverage – easing from peak levels (see P/BV charts in Appendix below). That said, we think that there remains room for individual stocks to trade up to +1SD above mean as 1) performance may yet hold up until end 1HCY17, and 2) the performance gap may widen between performers and loss-makers. Further, given that fuel prices still remain far below peak of >US$100/bbl, we think that most players will have sufficient space for competitive, load-inducing yields without severely eating into equity values.

Look for market share winners among airlines

Despite expectations of thinner profitability, we still expect most airlines to be able to preserve book value – i.e. not fall into loss-making positions – barring a severe upswing in fuel price or the US dollar. In such conditions we expect valuations to edge down with the exception of airlines managing to expand their business position by growing market share without severely impacting profitability.

Top airline picks To that end, our BUY picks are AirAsia (BUY, TP: RM3.25), Asia Aviation (Buy, TP: Bt7.60), and Cebu Air (BUY, TP: P125). All three of AIRA, AAV and CEB are expected to handily maintain their domestic market share leads even despite growing competitor efforts in 2017. While earnings may indeed pare down, we think given their market positioning, price leadership and cost control; it’s more likely that their respective competition is squeezed out before the players units see overtly unfavourable financial impact.

Other calls For other stocks under our coverage, BA is also a pick as its focuses on relatively less contested markets of niche holiday routes, in particular to Samui (where it has the majority of flight slots to the key airport, which it also partly owns). GIAA remains a BUY on a valuation basis, as we think its discount to book value is unjustified as risks of severe prolonged loss-making has eased. AAX remains a HOLD given its heightened sensitivity to fuel or currency cost escalation. While THAI is expected to make progress on its Transformation Plan, risks still remain elevated in its unsold decommissioned fleet, and its high gearing of >4x.

0

50

100

150

200

250

300

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

Jul-1

6

Jan-

17

Mean

+2 SD

+1 SD

-1 SD

-2 SD

60

80

100

120

140

Jul‐16 Aug‐16 Sep‐16 Oct‐16 Nov‐16 Dec‐16

AsiaAviationAirAsia X

AirAsia

BangkokAirwaysCebu Air

GarudaIndonesiaSingaporeAirlinesThaiAirways

Page 15Page 15

Industry Focus

ASEAN Aviation

Page 16

Peer Comparison – Airlines

Sources: DBS Bank, Bloomberg Finance L.P. Prices as of 7 Feb 2017

Other Aviation Picks Airports of Thailand (BUY, TP Bt 455) For airport picks, AOT TB would be the best proxy for a Thailand tourism recovery in our view. We believe the decline in passenger traffic at its six airports should have already bottomed out in Nov last year as international passenger growth rebounded to 4% in Dec 2016 and 7% during 1-20 Jan 2017. AOT has maintained its FY17F total passenger movement target at its six airports at 8.7% (vs our assumptions of 6.5%). We expect the improving volume growth would support the share price. Another short-term catalyst for AOT will be the split of par value from Bt10 to Bt1 which will be subjected to shareholders' approval at AGM on 27 Feb. The par split should increase AOT's liquidity

China Aviation Oil (BUY, TP S$1.70). With the backing of its SOE parent, CNAF, and monopoly in the supply of bonded jet fuel in China, we like CAO as a proxy to the long-term growth of China's international air travel market, growing international presence, and for its exposure to Pudong International Airport's firm outlook through 33%-owned associate, SPIA. Currently trading at <10x FY17F PE, we believe that the group is poised to see a

structural re-rating to 12x on sustained earnings growth, especially if CAO can utilise its strong net cash balance of US$203m to further accelerate growth via M&A.

ST Engineering (BUY, TP S$3.50) STE is a relatively defensive stock with a healthy balance sheet, strong order book and secure dividend payouts. Its Aerospace segment has positioned itself well by investing in growth markets such as narrow-body aircraft Passenger-to-Freighter (PTF) conversions, the Chinese MRO market, and cabin interior solutions, to name a few. The Electronics segment should also benefit from the ‘Smart City’ trend, not only in Singapore but various overseas markets as well.

Other Calls MAHB remains a HOLD despite improving Malaysian pax growth and a recent extension of its operating agreement; as the group is still heavily dragged by its loss-making Turkish operations. SIA Engineering is seeing limited engines for growth, while core base maintenance and fleet management businesses are on declining trends given SIA’s fleet cycle. .

Valuations – other ASEAN Aviation

Sources: DBS Bank, Bloomberg Finance L.P. Prices as of 7 Feb 2017

Cur Las t 12-mth Rtg Mkt Cap EPS Gth Fwd yld

Company Px Tgt Px US$m CY16 CY17 CY17 CY16 CY17 CY16 CY17 CY16 CY17 CY17

AirAsia MYR 2.65 3.25 BUY 1,999 6.6x 9.1x -27% 6.1x 7.6x 1.2x 1.1x 31.3% 13.0% 2.4%

AirAsia X MYR 0.42 0.38 HOLD 393 8.5x 9.2x -8% 5.6x 4.8x 2.1x 1.7x 28.4% 20.5% 0.0%

Asia Aviation THB 6.20 7.60 BUY 859 12.9x 13.6x -5% 6.7x 7.3x 1.4x 1.3x 10.6% 9.4% 2.8%

Bangkok Airways THB 21.20 26.30 BUY 1,271 13.5x 14.8x -8% 6.9x 7.2x 1.4x 1.3x 9.0% 9.1% 3.8%

Cebu Air PHP 95.0 125.0 BUY 1,162 5.8x 6.1x -4% 4.8x 4.5x 1.7x 1.4x 33.8% 25.8% 5.4%

Garuda Indonesia IDR 346.0 475.0 BUY 672 66.3x 13.6x >100% 4.4x 3.4x 0.7x 0.7x 1.1% 5.1% 0.0%

Singapore Airlines SGD 9.81 10.10 HOLD 8,228 14.2x 17.0x -17% 3.4x 3.9x 0.9x 0.9x 6.4% 5.4% 4.1%

Thai Airways THB 21.80 23.25 HOLD 1,359 10.4x 9.7x 6% 6.9x 7.2x 1.3x 1.1x 13.1% 12.2% 0.0%

ASEAN Airl ines Avg 17.3x 11.6x -9% 5.6x 5.7x 1.3x 1.2x 16.7% 12.6% 2.3%

-------- PER --------- EV/EBITDA P/BV ROAE

TP Las t 12-mth Rtg Mkt Cap EPS Gth Fwd yld

Company Crncy Px Tgt Px US$m CY16 CY17 CY17 CY16 CY17 CY16 CY17 CY16 CY17 CY17

Airports of Thailand THB 414.00 455.00 BUY 16,891 29.2x 25.6x 14% 17.8x 16.3x 4.7x 4.2x 17.1% 17.2% 0.0%

Malaysia Airports MYR 6.60 6.80 HOLD 2,472 238.2x 47.8x 398% 9.5x 8.1x 1.4x 1.4x 0.6% 2.9% 1.9%

China Aviation Oil SGD 1.53 1.70 BUY 935 11.8x 10.9x 9% 8.2x 6.8x 1.4x 1.3x 12.7% 12.6% 2.9%

SIA Engineering SGD 3.52 3.58 HOLD 2,800 23.1x 24.9x -7% 15.2x 16.0x 2.4x 2.4x 18.8% 12.0% 3.6%

ST Engineering SGD 3.34 3.68 BUY 7,371 21.3x 20.0x 7% 12.8x 12.1x 5.0x 4.8x 20.2% 24.5% 4.5%

Avg 64.7x 25.8x 84% 12.7x 11.9x 3.0x 2.8x 13.9% 13.9% 2.6%

-------- PER --------- EV/EBITDA P/BV ROAE

Page 16

Industry Focus

ASEAN Aviation

Page 17

Appendix

Valuation charts – P/BV

AirAsia PB Band (x)

AirAsia. AIRA MK (BUY, RM3.25 TP) had tracked back to its longer-term mean of near 1.3x P/BV as profitability began to recover as demonstrated by its earnings reports from 4Q15, as well as improvements in the standing of its receivables from loss-making associates. However concerns over a weakening ringgit dragged its share price from end-2016 onwards. As group performance steadies itself amid strong market shares in Malaysia and Thailand, we think the group should trade above mean valuations as its network and branding ensures longevity of the business.

AirAsia X PB Band (x)

AirAsia X. AAX MK (HOLD, RM0.38 TP) exceeded +1SD of its mean historical valuations after charting successive profit since 4Q15, and reaching high ROAEs given a severely beaten down net asset value from multiple FYs of losses. As its profitability outlook is more uncertain, we see it de-rating back towards historical mean levels.

Asia Aviation PB Band (x)

Asia Aviation. AAV TB (BUY, Bt7.60 TP) re-rated reaching +2SD of historical mean P/BV, but was dragged by growing concerns of Thai LCC competition plus the slowdown in tourist arrivals near end-2016 from the crackdown on zero-dollar tours. We think it has consolidated its position in 2016 and is poised to defend or grow its market share in 2017 even against competitors’ fleet expansion; while remaining financially.

Bangkok Airways PB Band (x)

Bangkok Airways. BA TB (BUY, Bt26.30 TP) has historically traded at a slight premium to airline peers averaging 1.6x P/BV, given its more secure profit stream with a stake in Samui Airport (where it also controls the majority of the slots). However a one-off taxation recognition dragged FY16 earnings and concerns on tourism growth dragged it to -1SD. We find this unjustified given its strong niche position servicing boutique routes in Thailand.

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Industry Focus

ASEAN Aviation

Page 18

Cebu Air PB Band (x)

Cebu Air. CEB PM (BUY, P125 TP) has typically traded far above regional peers at almost 2x P/BV, given its consistently strong ROAEs and solid profit track record even during peak oil prices. Valuations had come down in 2016 given a deceleration of its capacity growth due to infrastructure constraints in the Philippines, and caution on travel statistics with a new political regime. We remain confident on its maintenance of profit stability and expect a reversion to mean with good earnings reports.

Garuda Indonesia PB Band (x)

Garuda Indonesia. GIAA IJ (BUY, Rp475 TP) has typically traded below book value given a loss-making track record, in part due to a continuous weakening rupiah against the US dollar. We think it is nearer to profit stability after easing aircraft deliveries and restructuring efforts, and should trade nearer to mean of 0.9x P/BV with the production of profitable quarters.

Singapore Airlines PB Band (x)

Singapore Airlines. SIA SP (S$10.10 TP) is expected to trade to below or -1SD (0.9x) of its historical mean of 1x P/BV, as ROAEs decline to near 5% given a weak demand scenario while fuel cost savings are offset by softer yields and higher operating expenses.

Thai Airways PB Band (x)

Thai Airways. THAI TB (HOLD, Bt23.25 TP) re-rated very strongly to around +2SD from historical mean of below-book value as the beginning of its Transformation Plan coincided with low jet fuel to show sharply improved profitability. However low season still turned losses and we remain wary of a large unsold fleet and high gearing, which imply below-potential earnings until those items are resolved.

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Avg: 1.33x

+1sd: 1.62x

+2sd: 1.92x

‐1sd: 1.03x

‐2sd: 0.74x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Feb-13 Feb-14 Feb-15 Feb-16 Feb-17

(x)

Industry Focus

ASEAN Aviation

Page 19

COMPANY GUIDES

Page 19

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:BC, PY

BUYLast Traded Price ( 13 Dec 2016): RM2.51 (KLCI : 1,645.28) Price Target 12-mth : RM3.25 (29% upside) (Prev RM3.25)

Potential Catalyst: Value-accretive disposals, associate profit growth Where we differ: Lower yield forecasts than consensus

Analyst Marvin KHOR +60 32604 3911 [email protected]

Price Relative

Forecasts and Valuation FY Dec (RM m) 2015A 2016F 2017F 2018F Revenue 6,299 6,589 6,880 7,383 EBITDA 1,487 2,696 2,314 2,398 Pre-tax Profit 215 1,848 1,019 1,059 Net Profit 541 1,819 975 1,025 Net Pft (Pre Ex.) 412 1,334 975 1,025 Net Pft Gth (Pre-ex) (%) 56.0 224.2 (26.9) 5.1 EPS (sen) 19.4 54.4 29.2 30.7 EPS Pre Ex. (sen) 14.8 39.9 29.2 30.7 EPS Gth Pre Ex (%) 56 170 (27) 5 Diluted EPS (sen) 19.4 54.4 29.2 30.7 Net DPS (sen) 4.00 8.72 6.10 6.33 BV Per Share (sen) 160 214 235 259 PE (X) 12.9 4.6 8.6 8.2 PE Pre Ex. (X) 17.0 6.3 8.6 8.2 P/Cash Flow (X) 3.2 4.6 4.4 4.6 EV/EBITDA (X) 11.6 6.0 7.4 6.4 Net Div Yield (%) 1.6 3.5 2.4 2.5 P/Book Value (X) 1.6 1.2 1.1 1.0 Net Debt/Equity (X) 2.3 1.1 1.1 0.8 ROAE (%) 12.0 31.3 13.0 12.4 Earnings Rev (%): 0 0 0 Consensus EPS (sen): 45.8 39.0 39.3 Other Broker Recs: B: 16 S: 2 H: 4

Source of all data on this page: Company, AllianceDBS, Bloomberg Finance L.P.

Ambitions refuelled

Value emerging in market leader. AirAsia (AIRA) firmed up its leading position in the Malaysian air travel space with 15.6% revenue-passenger-kilometre (RPK) growth for 2016, on 86.5% load factor. This alongside lower average jet fuel prices secures strong FY16 profitability. We think the P/BV valuation at current prices appear unjustified given decent expected of ROAEs of 12-13% despite its aggressive growth plans. Potential catalysts may come from its plan to unlock value via divestments, or further improvements of associate performance.

Well equipped to defend market share. AirAsia (AIRA) has taken advantage of the restructuring of key competitor Malaysia Airlines (MAB) to expand its leading market share to c.32% from c.27% in 2014. Going into 2017, AIRA is prepared to expand capacity to absorb any pick-up in demand, with 7-8 new aircraft deliveries from 77 currently. We think that it is in a strong position to defend or grow its expanded market share given its active branding and digitalisation efforts.

Measures in place to manage margin pressure. AIRA has hedged c.74% of its jet fuel requirements at USD60/bbl, plus currencyor natural hedges for c.67% of USD-denominated borrowings. From the revenue perspective, yields (fares/RPK) are expected to pare down in light of steeper competition, which we account for by imputing 3% yield contraction in FY17. That said, we are reassured by the fact that MAB has a profitability priority going forward, implying fare competition should not reach the mutually damaging levels seen in pre-2014.

Valuation: Reiterate BUY. Our TP of RM3.25 is based on 1.5x (historical mean) FY16/17F P/BV; on book value adjusted for cumulative unrecognised losses from associates.

Key Risks to Our View: Severe yield or ringgit depreciation. If yields or the ringgit sees severe sustained weakening, earnings and ROAE are at risk of erosion.

At A GlanceIssued Capital (m shrs) 2,783 Mkt. Cap (RMm/US$m) 6,985 / 1,577 Major Shareholders (%) Tune Air 16.7 Tune Live 15.5 Employees Provident Fund 4.5

Free Float (%) 75.4 3m Avg. Daily Val (US$m) 7.3 ICB Industry : Consumer Services / Travel & Leisure

DBS Group Research . Equity 14 Dec 2016

Malaysia Company Guide

AirAsia Version 7 | Bloomberg: AIRA MK | Reuters: AIRA.KL Refer to important disclosures at the end of this report

27

47

67

87

107

127

147

167

187

207

0.7

1.2

1.7

2.2

2.7

3.2

3.7

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Relative IndexRM

AirAsia (LHS) Relative KLCI (RHS)

Page 20

ASIAN INSIGHTS VICKERS SECURITIES Page 2

Company Guide

AirAsia

CRITICAL DATA POINTS TO WATCH

Earnings Drivers:

Returning to ASK growth. Airline capacity is measured via ASK (available seat kilometres), which is a function of the active fleet and flight distances of routes served. Malaysia AirAsia (MAA) is shrinking its fleet to 77 by end-2016 from 80 in 2015, but is looking at resuming growth by up to 7/8 new aircraft in FY17 as strong volumes had driven up load factors. However, we expect ASK to dive 8% in FY17. Nevertheless, efficiency improvements like reducing time of grounded aircraft may also help boost overall ASK. Load factors to ease after peaking in FY16. Load factors determine the ASK that is converted into RPKs (revenue passenger kilometres). AIRA’s passenger load factor averaged 80.2% in 2015 (+1.4ppts) as Malaysia Airlines’ (MAB) capacity cuts helped to rebalance supply and demand. We forecast an improved 86% load factor for FY16 (86.6% for 9M16) as supply-demand dynamics remain friendly, and easing to 84% from FY17F onwards as MAB replenishes some capacity. Expect yields to ease. Passenger yields (fare/RPK) were 5.1% lower in 2015 due to the spillover effect of the stiff competition, plus phasing out of the fuel surcharge in fares. Despite MAB carrying out rationalisation, we view that yields are not still due for an upcycle in 2016, having declined 1.1% in 9M16. Moving into FY17, resumption of MAB’s capacity growth may mean more fare competition, thus easing yields further. Forecast flattish ancillary income. AIRA has in the pipeline several initiatives to boost ancillary income (onboard WIFI, enhanced duty-free operation, new purchasing system, etc.). However, we conservatively assume flat growth in our forecast years to account for a slower pick-up in the more novel offerings, and the prevalence of value-sensitive passengers. Cheaper fuel leads cost savings. AIRA’s key expenses can be split into cash opex, asset costs and fuel costs. We expect cost/ASK to drop by 6% in FY16F (c.2% fall charted in 9M16), led by fuel cost/ASK falling 26%. Going into FY17F we expect a weaker ringgit to drive up costs/ASK by 7%, plus slightly higher fuel costs of USD60/bbl of which AIRA has hedged 74% of requirements. Our spot jet fuel assumptions are US$50/60/65/bbl in FY16/17/18F. Keeping a tab on regional associates. AIRA maintains a strong regional presence with its associates in Thailand, Indonesia, the Philippines, India and Japan. While the group gains from the extended network and brand image, challenging operating conditions have led to losses in a few associates. Of its associates, we are most positive on Thai AirAsia (TAA) (listed on the Stock Exchange of Thailand), and expect it to be the key contributor to associate income.

ASK growth (%)

Load Factor (%)

Fare / RPK (sen)

Ancillary income / pax (RM)

Cost / ASK (sen)

Source: Company, AllianceDBS

3.56

8.15

7

8

4.35

0.0

1.2

2.4

3.5

4.7

5.9

7.1

8.2

2014A 2015A 2016F 2017F 2018F

78.8 80.286 84 84

0.0

17.5

35.1

52.6

70.2

87.7

2014A 2015A 2016F 2017F 2018F

13.412.8 12.6 12.2 12.6

0.00

2.74

5.48

8.23

10.97

13.71

2014A 2015A 2016F 2017F 2018F

43.2 43.1 43.8 43.8 43.8

0.0

8.8

17.7

26.5

35.4

44.2

2014A 2015A 2016F 2017F 2018F

13.813.2

12.513.4 13.8

0.0

2.8

5.6

8.4

11.2

14.0

2014A 2015A 2016F 2017F 2018F

Page 21

ASIAN INSIGHTS VICKERS SECURITIES Page 3

Company Guide

AirAsia

Balance Sheet:

Expect gearing to improve. We expect AIRA’s net gearing to ease from 1.5x at end-Sep16 to 1.1x FY16/17F, given improved profits and aided by the c.RM1bn injection from major shareholders via a new share issuance. Any further divestments may serve to bring net gearing down further if proceeds are used to pare down debts. Share Price Drivers:

Continued profitability for the group. AIRA had notched losses in previous FYs due to forex translation items and losses from associates. As associate performance stabilises, and the group demonstrates profitability even against expected higher competition, we expect valuations to catch-up to mean. Value-accretive disposals and spin-offs. AIRA is mulling unlocking value by potentially 1) divesting its leasing arm, 2) conducting IPOs for IAA, PAA, and flight school AACE, and/or 3) entering JVs for its ground handling and cargo units. Favourable valuations by counterparties may prove accretive to the group, potentially in the form of cash proceeds to pare down borrowings or pay out in the form of dividends. Key Risks:

Further depreciation of the MYR against the USD. A stronger USD will pressure AIRA’s profitability as a significant portion of its operating and financing costs are in USD. Irrational competition. The emergence of irrational competition in the form of excessive capacity increases by AIRA’s competitors or new entrants pose threats to both yields and load factors. Besides the natural dilution of demand, the airline players would also drive down fares to recapture passengers. Company Background

AirAsia (AIRA) is a low-cost airline that operates short-haul, point-to point domestic and international route operating out of its hub in klia2, Malaysia. The group also has similarly-branded associates in Thailand, Indonesia, the Philippines, Japan and India, forming a network for its airlines to leverage on for passenger connectivity.

Leverage & Asset Turnover (x)

Capital Expenditure

ROE (%)

Forward PE Band (x)

PB Band (x)

Source: Company, AllianceDBS

0.2

0.2

0.2

0.3

0.3

0.3

0.3

0.3

0.4

0.4

0.4

0.00

0.50

1.00

1.50

2.00

2.50

2014A 2015A 2016F 2017F 2018F

Gross Debt to Equity (LHS) Asset Turnover (RHS)

0.0

500.0

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

2014A 2015A 2016F 2017F 2018F

Capital Expenditure (-)

RMm

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2014A 2015A 2016F 2017F 2018F

Avg: 14.4x

+1sd: 22.1x

+2sd: 29.8x

‐1sd: 6.8x

-0.8

4.2

9.2

14.2

19.2

24.2

29.2

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

(x)

Avg: 1.35x

+1sd: 1.64x

+2sd: 1.94x

‐1sd: 1.05x

‐2sd: 0.76x

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

(x)

Page 22

ASIAN INSIGHTS VICKERS SECURITIES Page 4

Company Guide

AirAsia

Key Assumptions

FY Dec 2014A 2015A 2016F 2017F 2018F ASK growth (%) 3.56 8.15 7.00 8.00 4.35 Load Factor (%) 78.9 80.2 86.0 84.0 84.0 Fare / RPK (sen) 13.4 12.8 12.6 12.2 12.6 Ancillary income / pax (RM) 43.2 43.1 43.8 43.8 43.8 Cost / ASK (sen) 13.8 13.2 12.5 13.4 13.8

Segmental Breakdown

FY Dec 2014A 2015A 2016F 2017F 2018F Revenues (RMm) MAA - Airline Operations 4,623 4,874 5,532 5,698 6,085 MAA - Aircraft leasing 793 1,425 1,057 1,182 1,299 Associates and JV 0.0 0.0 0.0 0.0 0.0 Total 5,416 6,299 6,589 6,880 7,383 Core PBT (RMm)

MAA - Airline Operations 262 386 1,077 640 559 MAA - Aircraft leasing 152 709 230 243 341 Associates and JV 27.6 (800) 149 136 158 Total 441 296 1,457 1,019 1,059 Core PBT Margins (%) MAA - Airline Operations 5.7 7.9 19.5 11.2 9.2 MAA - Aircraft leasing 19.2 49.8 21.8 20.6 26.3 Associates and JV N/A N/A N/A N/A N/A Total 8.2 4.7 22.1 14.8 14.3

Income Statement (RMm)

FY Dec 2014A 2015A 2016F 2017F 2018F Revenue 5,416 6,299 6,589 6,880 7,383 Other Opng (Exp)/Inc (4,590) (4,716) (4,799) (5,584) (6,028) Operating Profit 826 1,583 1,790 1,296 1,355 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc 27.6 (800) 149 136 158 Net Interest (Exp)/Inc (412) (488) (482) (413) (454) Exceptional Gain/(Loss) (419) (80.6) 391 0.0 0.0 Pre-tax Profit 22.7 215 1,848 1,019 1,059 Tax 60.1 326 (29.2) (43.8) (33.8) Minority Interest 0.0 0.09 0.0 0.0 0.0 Preference Dividend 0.0 0.0 0.0 0.0 0.0 Net Profit 82.8 541 1,819 975 1,025 Net Profit before Except. 264 412 1,334 975 1,025 EBITDA 1,573 1,487 2,696 2,314 2,398 Growth Revenue Gth (%) 5.9 16.3 4.6 4.4 7.3 EBITDA Gth (%) 3.8 (5.5) 81.3 (14.2) 3.6 Opg Profit Gth (%) (4.3) 91.7 13.0 (27.6) 4.6 Net Profit Gth (Pre-ex) (%) (41.6) 56.0 224.2 (26.9) 5.1 Margins & Ratio Opg Profit Margin (%) 15.3 25.1 27.2 18.8 18.4 Net Profit Margin (%) 1.5 8.6 27.6 14.2 13.9 ROAE (%) 1.7 12.0 31.3 13.0 12.4 ROA (%) 0.4 2.6 8.2 4.1 4.2 ROCE (%) 4.7 8.5 8.9 5.8 6.0 Div Payout Ratio (%) 100.8 20.6 16.0 20.9 20.7 Net Interest Cover (x) 2.0 3.2 3.7 3.1 3.0

Source: Company, AllianceDBS

Page 23

ASIAN INSIGHTS VICKERS SECURITIES Page 5

Company Guide

AirAsia

Quarterly / Interim Income Statement (RMm)

FY Dec 3Q2015 4Q2015 1Q2016 2Q2016 3Q2016 Revenue 1,516 2,168 1,699 1,624 1,687 Other Oper. (Exp)/Inc (1,200) (1,367) (1,178) (1,209) (1,242) Operating Profit 316 801 521 415 445 Other Non Opg (Exp)/Inc 0.0 0.0 0.0 0.0 0.0 Associates & JV Inc (156) (225) 219 11.4 35.9 Net Interest (Exp)/Inc (150) (106) (111) (138) (88.9) Exceptional Gain/(Loss) (472) (34.5) 464 (33.9) 81.5 Pre-tax Profit (462) 435 1,093 254 474 Tax 56.0 120 (216) 88.1 (121) Minority Interest 0.0 (0.1) 0.85 0.24 1.43 Net Profit (406) 554 878 342 354 Net profit bef Except. 115 244 381 214 328 EBITDA 329 759 919 608 674 Growth Revenue Gth (%) 14.4 43.0 (21.6) (4.5) 3.9 EBITDA Gth (%) (19.6) 130.8 21.0 (33.9) 11.0 Opg Profit Gth (%) 37.1 153.4 (34.9) (20.4) 7.4 Net Profit Gth (Pre-ex) (%) nm 112.5 55.9 (43.9) 53.3 Margins Opg Profit Margins (%) 20.8 36.9 30.7 25.5 26.4 Net Profit Margins (%) (26.8) 25.6 51.7 21.1 21.0

Balance Sheet (RMm)

FY Dec 2014A 2015A 2016F 2017F 2018F Net Fixed Assets 13,034 11,593 11,102 12,859 11,912 Invts in Associates & JVs 422 1,185 1,334 1,470 1,628 Other LT Assets 4,675 4,690 4,690 4,690 4,690 Cash & ST Invts 1,338 2,431 4,562 3,524 5,205 Inventory 304 458 458 458 458 Debtors 891 923 1,083 1,131 1,214 Other Current Assets 0.0 0.0 0.0 0.0 0.0 Total Assets 20,664 21,279 23,228 24,132 25,106 ST Debt 2,275 2,432 2,432 2,432 2,432 Creditor 853 1,624 1,231 1,427 1,539 Other Current Liab 984 1,123 1,092 1,116 1,157 LT Debt 10,453 10,185 9,845 9,845 9,845 Other LT Liabilities 1,544 1,467 1,467 1,467 1,467 Shareholder’s Equity 4,555 4,447 7,161 7,845 8,666 Minority Interests 0.0 0.0 0.0 0.0 0.0 Total Cap. & Liab. 20,664 21,279 23,228 24,132 25,106 Non-Cash Wkg. Capital (642) (1,367) (782) (954) (1,024) Net Cash/(Debt) (11,390) (10,185) (7,715) (8,752) (7,072) Debtors Turn (avg days) 80.9 52.5 55.6 58.7 58.0 Creditors Turn (avg days) (409.3) (642.8) (688.5) (550.3) (611.8) Inventory Turn (avg days) (85.5) (197.9) (220.9) (189.6) (188.9) Asset Turnover (x) 0.3 0.3 0.3 0.3 0.3 Current Ratio (x) 0.6 0.7 1.3 1.0 1.3 Quick Ratio (x) 0.5 0.6 1.2 0.9 1.3 Net Debt/Equity (X) 2.5 2.3 1.1 1.1 0.8 Net Debt/Equity ex MI (X) 2.5 2.3 1.1 1.1 0.8 Capex to Debt (%) 14.3 (7.0) 2.2 21.5 (0.5) Z-Score (X) 0.8 0.8 1.2 1.2 1.3

Source: Company, AllianceDBS

Page 24

ASIAN INSIGHTS VICKERS SECURITIES Page 6

Company Guide

AirAsia

Cash Flow Statement (RMm)

FY Dec 2014A 2015A 2016F 2017F 2018F Pre-Tax Profit 22.7 215 1,848 1,019 1,059 Dep. & Amort. 720 703 757 882 885 Tax Paid (15.2) (31.0) (29.2) (43.8) (33.8) Assoc. & JV Inc/(loss) (27.6) 800 (149) (136) (158) Chg in Wkg.Cap. (871) (138) (585) 172 70.6 Other Operating CF 511 567 0.0 0.0 0.0 Net Operating CF 302 2,191 1,842 1,893 1,822 Capital Exp.(net) (1,823) 888 (266) (2,639) 61.9 Other Invts.(net) 49.3 (53.8) 0.0 0.0 0.0 Invts in Assoc. & JV (381) 258 0.0 0.0 0.0 Div from Assoc & JV 0.0 0.0 0.0 0.0 0.0 Other Investing CF 0.0 71.4 0.0 0.0 0.0 Net Investing CF (2,154) 1,164 (266) (2,639) 61.9 Div Paid (111) (83.5) (111) (291) (204) Chg in Gross Debt 1,888 (2,456) (340) 0.0 0.0 Capital Issues 2.06 0.0 1,006 0.0 0.0 Other Financing CF 0.0 (11.9) 0.0 0.0 0.0 Net Financing CF 1,779 (2,551) 555 (291) (204) Currency Adjustments 30.4 290 0.0 0.0 0.0 Chg in Cash (42.6) 1,093 2,131 (1,037) 1,680 Opg CFPS (sen) 42.2 83.7 72.6 51.5 52.4 Free CFPS (sen) (54.6) 111 47.1 (22.3) 56.4

Source: Company, AllianceDBS

Target Price & Ratings History

Source: AllianceDBS

Analyst: Marvin KHOR

S.No.Date of Report

Closing Price

12-mth Target Price

Rat ing

1: 29 Feb 16 1.47 1.90 BUY

2: 04 Apr 16 1.93 2.20 BUY

3: 06 Apr 16 1.90 2.20 BUY

4: 10 May 16 2.05 2.20 BUY

5: 27 May 16 2.40 2.70 BUY

6: 01 Aug 16 3.00 2.70 BUY

7: 30 Aug 16 3.00 3.20 HOLD

8: 01 Nov 16 2.84 3.20 HOLD

9: 25 Nov 16 2.71 3.25 BUY

Note : Share price and Target price are adjusted for corporate actions.

1

2

3

4 5

6 7

8

9

1.20

1.70

2.20

2.70

3.20

Dec-15 Apr-16 Aug-16 Dec-16

RM

Page 25

ASIAN INSIGHTS VICKERS SECURITIES ed: CK / sa:CS, PY

BUY Last Traded Price ( 6 Feb 2017): Bt6.20 (SET : 1,589.13) Price Target 12-mth: Bt7.60 (23% upside) (Prev Bt8.20)

Potential Catalyst: Positive yield or volume growth surprise Where we differ: More conservative margins than consensus Analyst Marvin KHOR +60 32604 3911 [email protected] Paul YONG CFA +65 6682 3712 [email protected]

What’s New FY16F earnings supported by 16% RPK growth

Expect cost escalation from hiked fuel excise, but

fare increases are set to help mitigate impact

Leading market share to drive FY17 volume

growth, but cut FY17/18F earnings by 14%/8% for

higher cost/ASK – offset by higher yields

Upside remains on reduced TP of Bt7.60 on more

conservative P/BV multiple, maintain BUY

Price Relative

Forecasts and Valuation FY Dec (Bt m) 2015A 2016F 2017F 2018F Revenue 29,507 33,374 38,491 43,067 EBITDA 3,898 6,092 6,093 6,660 Pre-tax Profit 2,109 4,325 4,116 4,400 Net Profit 1,078 2,212 2,105 2,250 Net Pft (Pre Ex.) 1,274 2,322 2,215 2,360 Net Pft Gth (Pre-ex) (%) 862.6 82.3 (4.6) 6.6 EPS (Bt) 0.22 0.46 0.43 0.46 EPS Pre Ex. (Bt) 0.26 0.48 0.46 0.49 EPS Gth Pre Ex (%) 863 82 (5) 7 Diluted EPS (Bt) 0.22 0.46 0.43 0.46 Net DPS (Bt) 0.10 0.15 0.15 0.17 BV Per Share (Bt) 4.15 4.46 4.74 5.03 PE (X) 27.9 13.6 14.3 13.4 PE Pre Ex. (X) 23.6 12.9 13.6 12.7 P/Cash Flow (X) 10.0 4.7 4.7 4.4 EV/EBITDA (X) 11.4 6.7 7.3 6.5 Net Div Yield (%) 1.6 2.4 2.4 2.8 P/Book Value (X) 1.5 1.4 1.3 1.2 Net Debt/Equity (X) 0.2 0.0 0.1 CASH ROAE (%) 6.4 11.1 9.9 10.0 Earnings Rev (%): 0 (14) (8) Consensus EPS (Bt): 0.46 0.50 0.52 Other Broker Recs: B: 12 S: 3 H: 7 Source of all data on this page: Company, AllianceDBS, Bloomberg Finance L.P