Embed Size (px)

Citation preview

ASB Update

Analyst Briefing

8th September 2006

Disclaimer

The material that follows is general background information about ASB’s activities

current at the date of the presentation, 8 September 2006. It is information given in

summary form and does not purport to be complete. It is not intended to be relied

upon as advice.

Note all financial numbers are reported in NZD.

Agenda

• Team Introductions

• Introduction Hugh Burrett

• Financial Performance Stewart McRobie

• Retail Banking Ross McEwan

• Business & Rural Banking James Mitchell

• Q & A

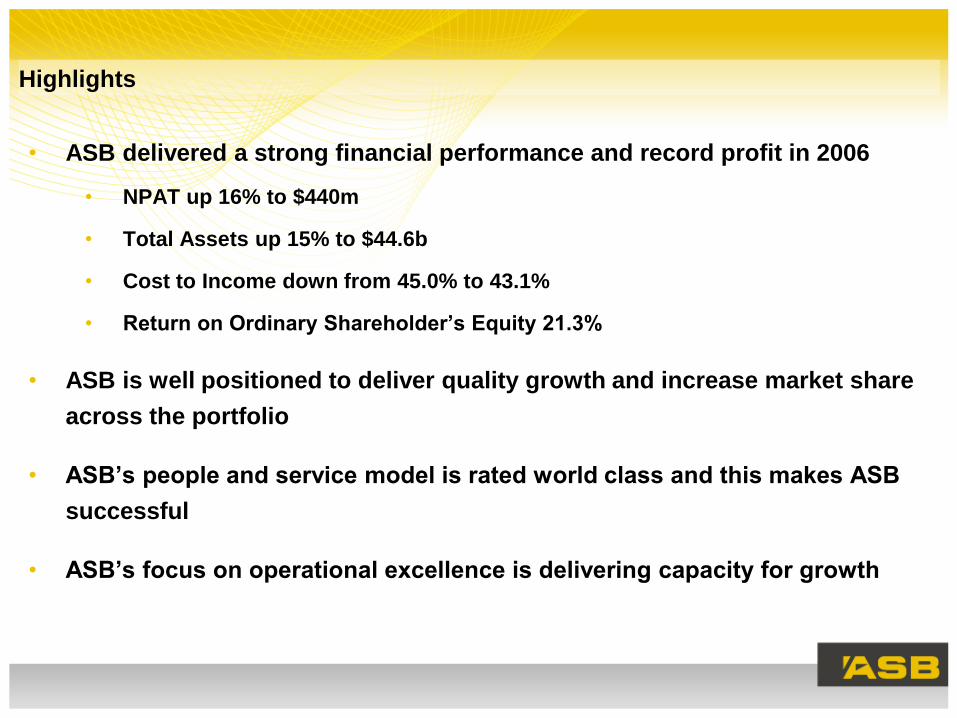

Highlights

• ASB delivered a strong financial performance and record profit in 2006

• NPAT up 16% to $440m

• Total Assets up 15% to $44.6b

• Cost to Income down from 45.0% to 43.1%

• Return on Ordinary Shareholder’s Equity 21.3%

• ASB is well positioned to deliver quality growth and increase market share

across the portfolio

• ASB’s people and service model is rated world class and this makes ASB

successful

• ASB’s focus on operational excellence is delivering capacity for growth

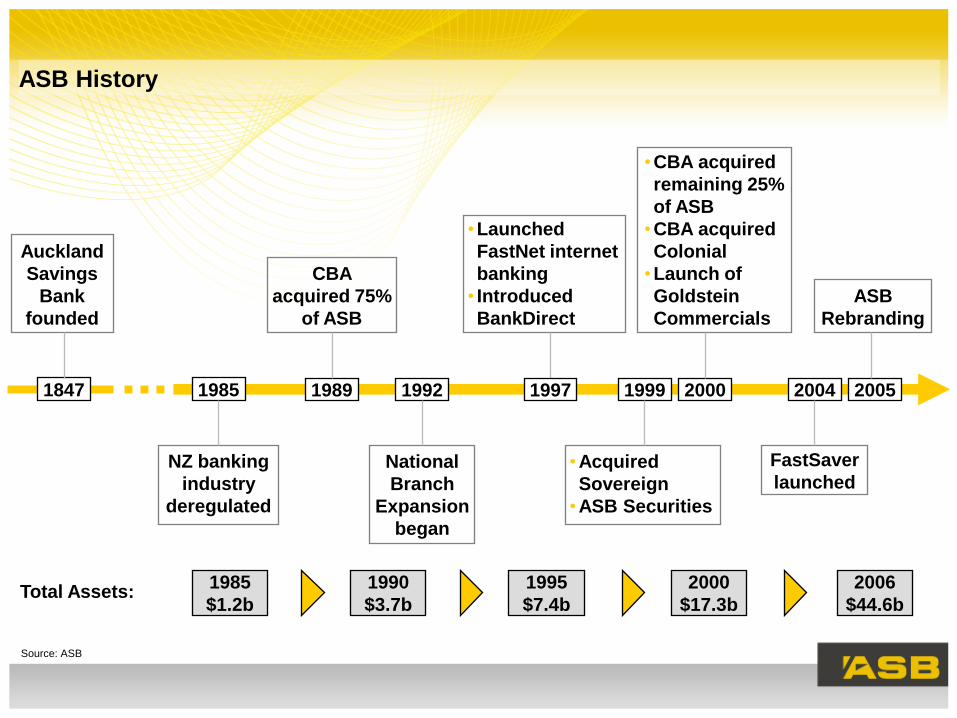

ASB History

Auckland

Savings

Bank

founded

National

Branch

Expansion

began

•Launched

FastNet internet

banking

• Introduced

BankDirect

•Acquired

Sovereign

•ASB Securities

•CBA acquired

remaining 25%

of ASB

•CBA acquired

Colonial

•Launch of

Goldstein

Commercials

ASB

Rebranding

1847 1985 1989 1992 1999 2000 20051997

CBA

acquired 75%

of ASB

FastSaver

launched

2004

1985

$1.2bTotal Assets:

2006

$44.6b

1990

$3.7b

1995

$7.4b

2000

$17.3b

NZ banking

industry

deregulated

Source: ASB

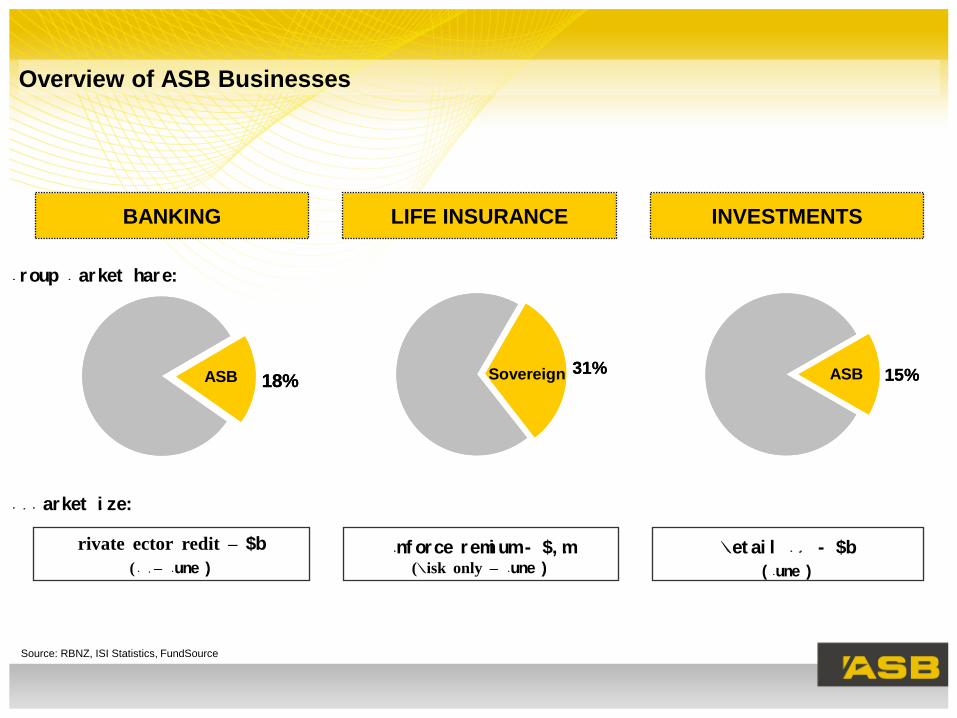

Overview of ASB Businesses

Private Sector Credit – $215b

(M3 – June 2006)

Inf orce Premi um - $1, 033m(Risk only – June 2006)

Ret ai l FUM - $22b

( June 2006)

BANKING LIFE INSURANCE INVESTMENTS

NZ Market Si ze:

Group Market Share:

Source: RBNZ, ISI Statistics, FundSource

18%ASB31%Sovereign 15%ASB18%ASB31%Sovereign 15%ASB

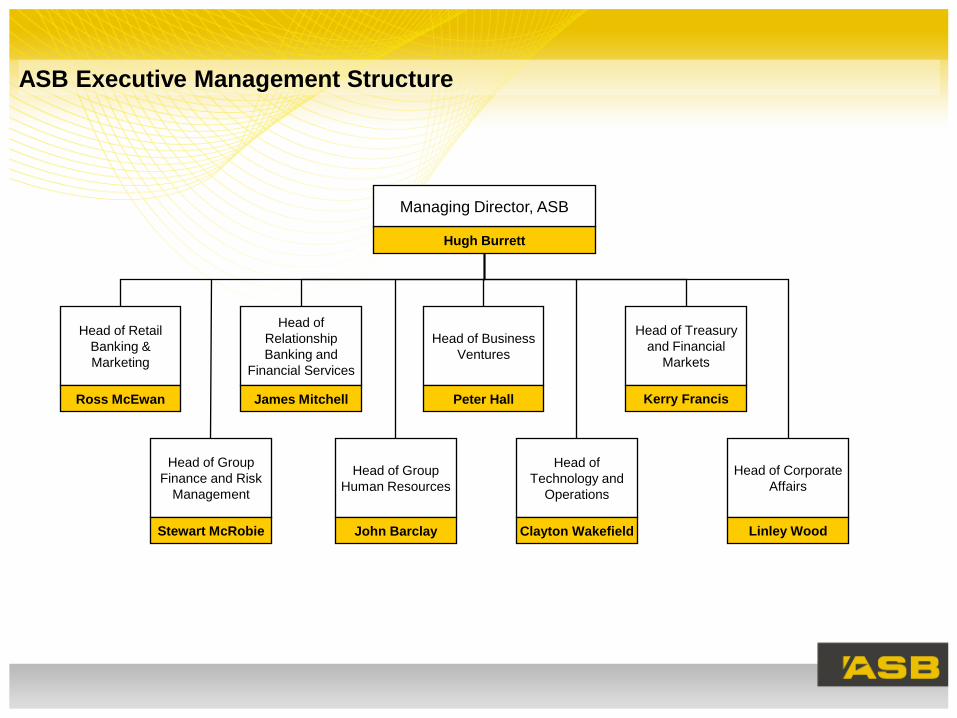

Head of Retail

Banking &

Marketing

Head of

Relationship

Banking and

Financial Services

Head of Treasury

and Financial

Markets

Head of Business

Ventures

Head of Group

Human Resources

Head of

Technology and

Operations

Head of Corporate

Affairs

Head of Group

Finance and Risk

Management

Ross McEwan James Mitchell Peter Hall

Stewart McRobie

Kerry Francis

Clayton WakefieldJohn Barclay Linley Wood

Hugh Burrett

Managing Director, ASB

ASB Executive Management Structure

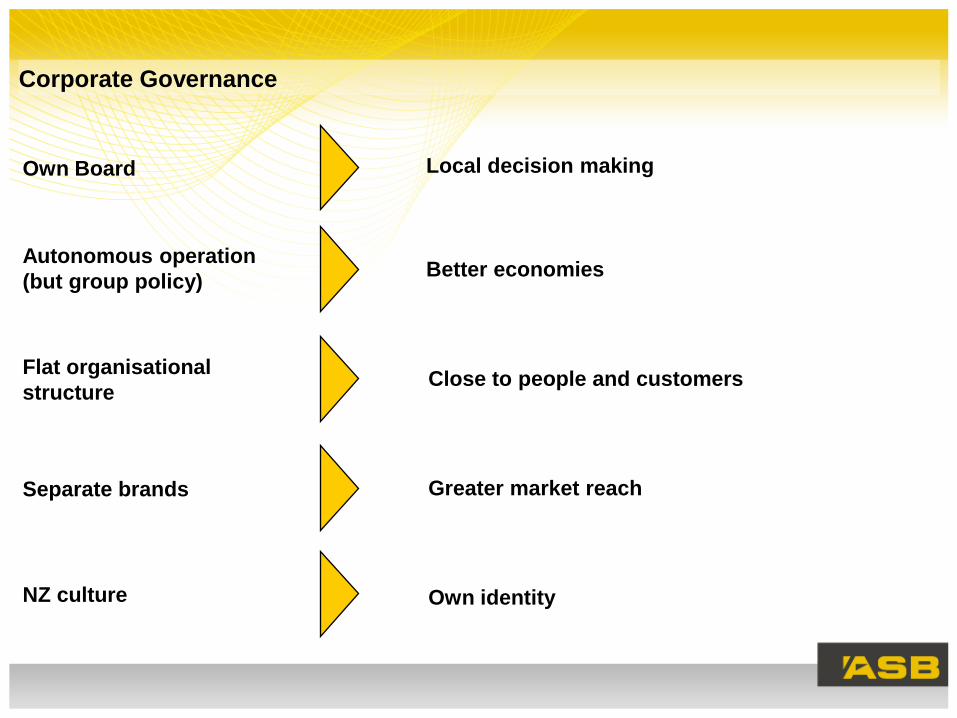

Corporate Governance

Own Board Local decision making

Autonomous operation

(but group policy)Better economies

Flat organisational

structureClose to people and customers

Separate brands Greater market reach

NZ culture Own identity

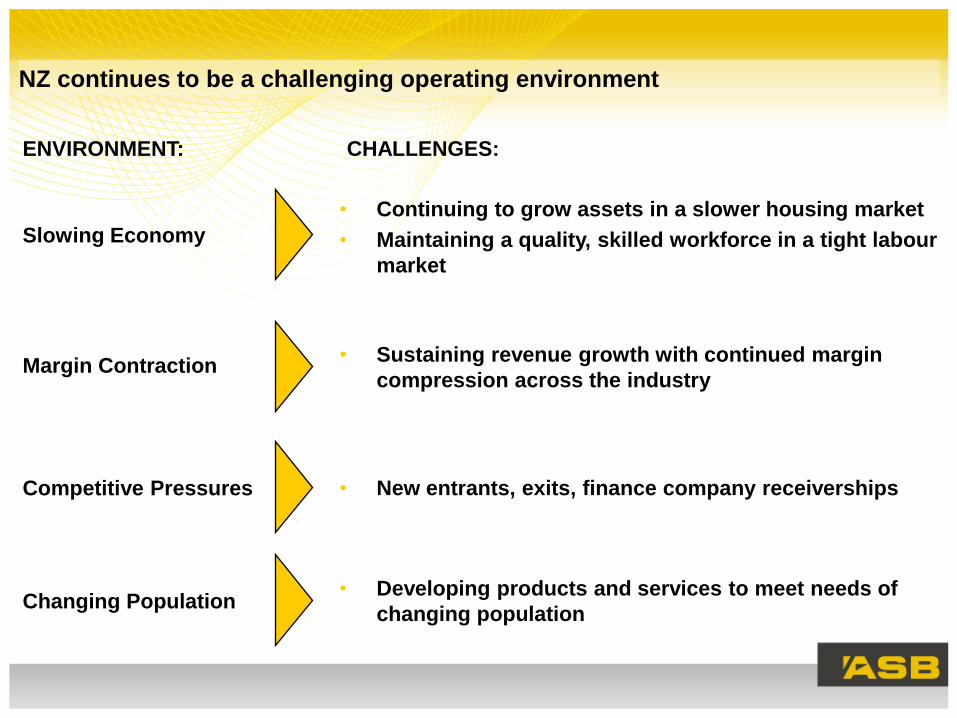

NZ continues to be a challenging operating environment

Slowing Economy

• Continuing to grow assets in a slower housing market

• Maintaining a quality, skilled workforce in a tight labour

market

Margin Contraction• Sustaining revenue growth with continued margin

compression across the industry

Competitive Pressures • New entrants, exits, finance company receiverships

Changing Population• Developing products and services to meet needs of

changing population

ENVIRONMENT: CHALLENGES:

To be New Zealand’s best bank and financial services provider

excelling in customer service

BEST SERVICE

BEST PROCESSES

BEST TEAM, Passionate People

BEST DISTRIBUTION

DELIVER

CONTINUOUS

QUALITY GROWTH

and

ABOVE MARKET

SHAREHOLDER

RETURNS

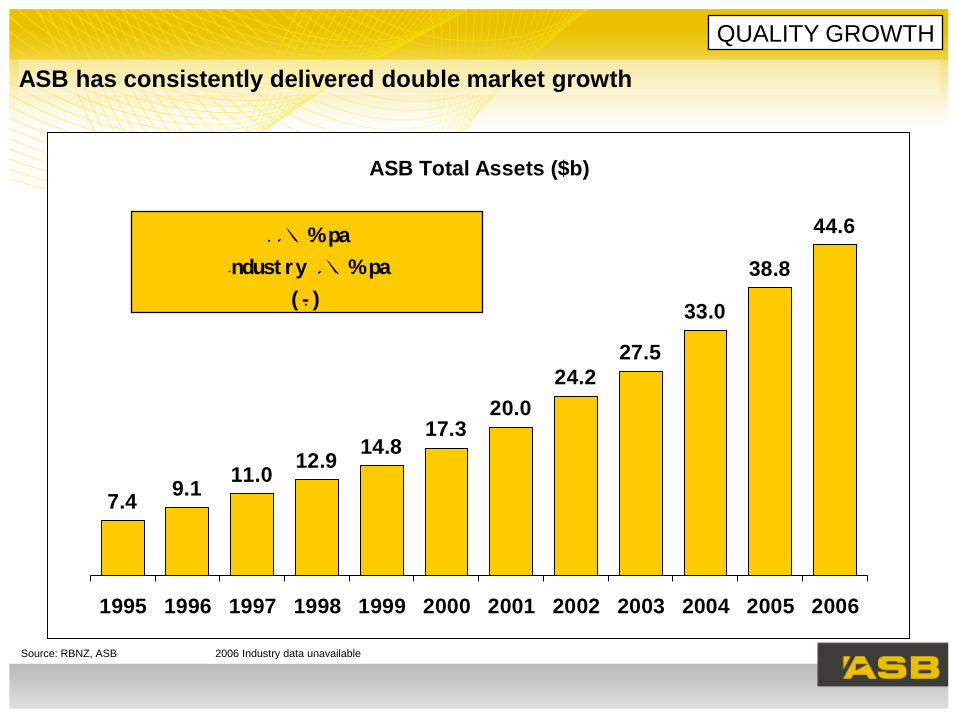

QUALITY GROWTH

However ASB is well positioned for growth

ASB Total Assets ($b)

7.49.1

11.012.9

14.817.3

20.0

24.2

27.5

33.0

38.8

44.6

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

ASB has consistently delivered double market growth

QUALITY GROWTH

Source: RBNZ, ASB 2006 Industry data unavailable

ASB CAGR 18% pa

Indust ry CAGR 9% pa

( 1995- 2005)

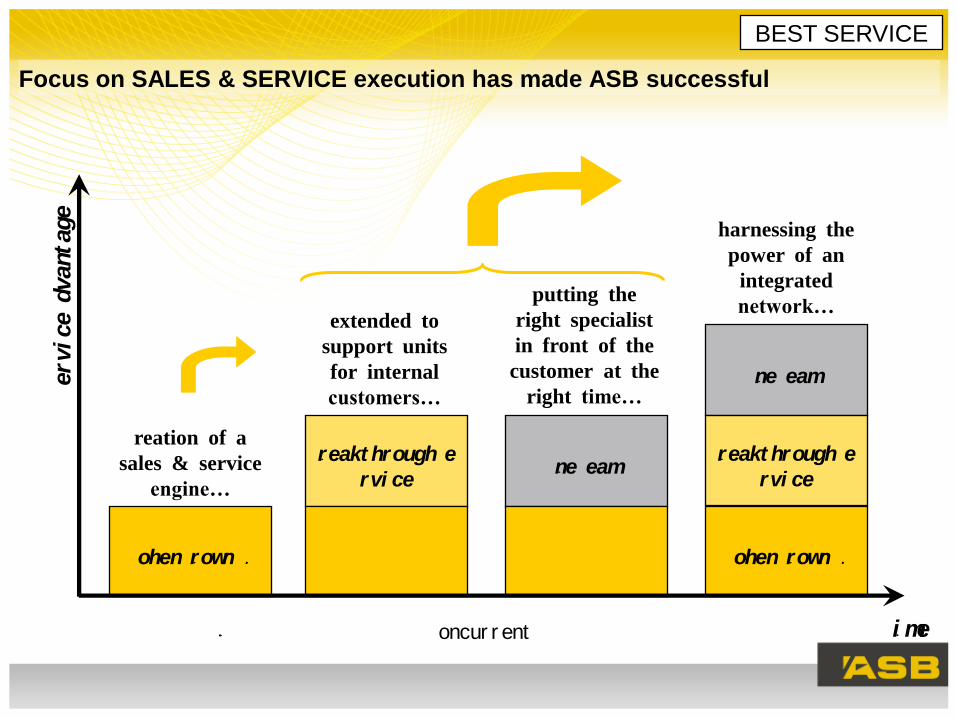

Focus on SALES & SERVICE execution has made ASB successful

BEST SERVICE

Cohen Brown SUCCESS

Service Ad

vantage

Ti me

Creation of a

sales & service

engine…

extended to

support units

for internal

customers…

putting the

right specialist

in front of the

customer at the

right time…

harnessing the

power of an

integrated

network…

Concur r ent1994

Breakt hrough Se

rvi ceOne Team

One Team

Breakt hrough Se

rvi ce

Cohen Brown SUCCESS

Increasingly diversified throughout New Zealand

BEST DISTRIBUTION

1990 Today New branch f i t - out and

brandi ng

84 Auckl and

17 Sout h Isl and

10 Nort hl and

71 Auckl and

14 Lower Nort h

Isl and

12 Cent ral Nort h

Isl and

14 Nort hl and

7 Sout h Isl and

Ret ai l Branches 105

Korean & Mi grant 0

Busi ness Cent res 0

Rural Cent res 0

FTE 1, 950

Ret ai l Branches 124

Korean & Mi grant 2

Busi ness Cent res 18

Rural Cent res 24

FTE 3, 868

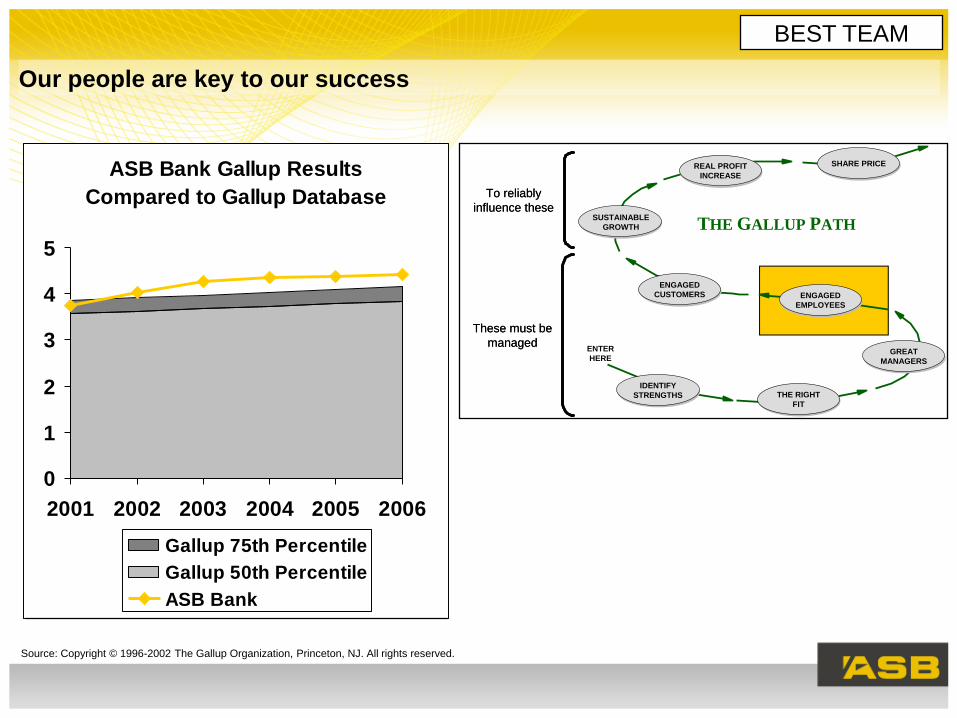

Our people are key to our success

THE GALLUP PATH

ENTER

HERE

IDENTIFY

STRENGTHS THE RIGHT

FIT

GREAT

MANAGERS

ENGAGED

EMPLOYEES

ENGAGED

CUSTOMERS

SUSTAINABLE

GROWTH

REAL PROFIT

INCREASE

SHARE PRICE

To reliably

influence these

To reliably

influence these

These must be

managed

These must be

managed

Source: Copyright © 1996-2002 The Gallup Organization, Princeton, NJ. All rights reserved.

BEST TEAM

ASB Bank Gallup Results

Compared to Gallup Database

0

1

2

3

4

5

2001 2002 2003 2004 2005 2006

Gallup 75th Percentile

Gallup 50th Percentile

ASB Bank

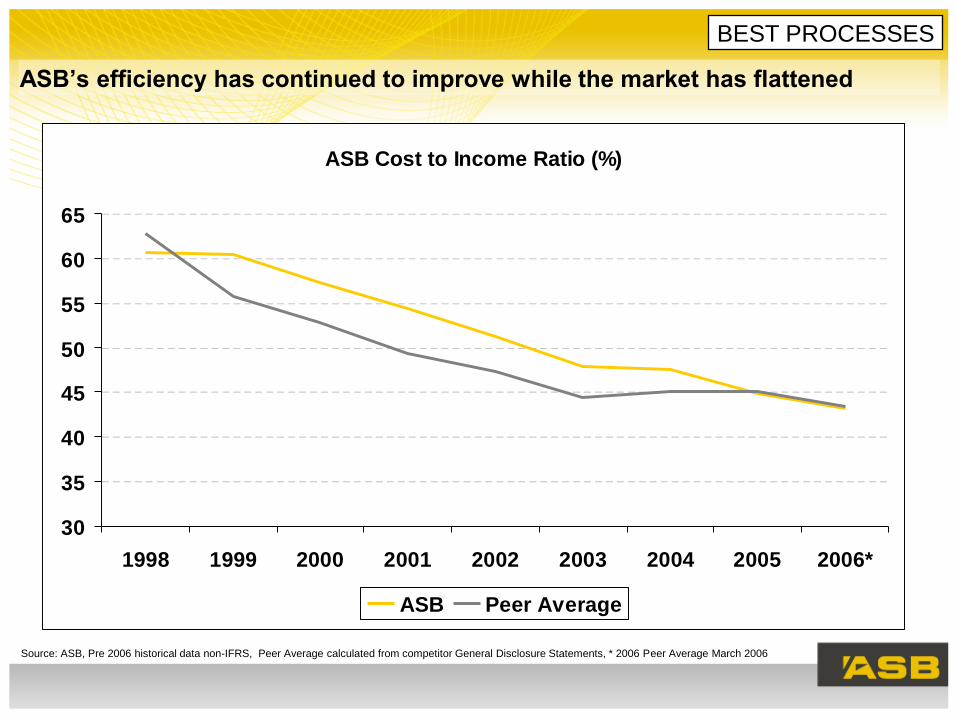

ASB’s efficiency has continued to improve while the market has flattened

Source: ASB, Pre 2006 historical data non-IFRS, Peer Average calculated from competitor General Disclosure Statements, * 2006 Peer Average March 2006

BEST PROCESSES

ASB Cost to Income Ratio (%)

30

35

40

45

50

55

60

65

1998 1999 2000 2001 2002 2003 2004 2005 2006*

ASB Peer Average

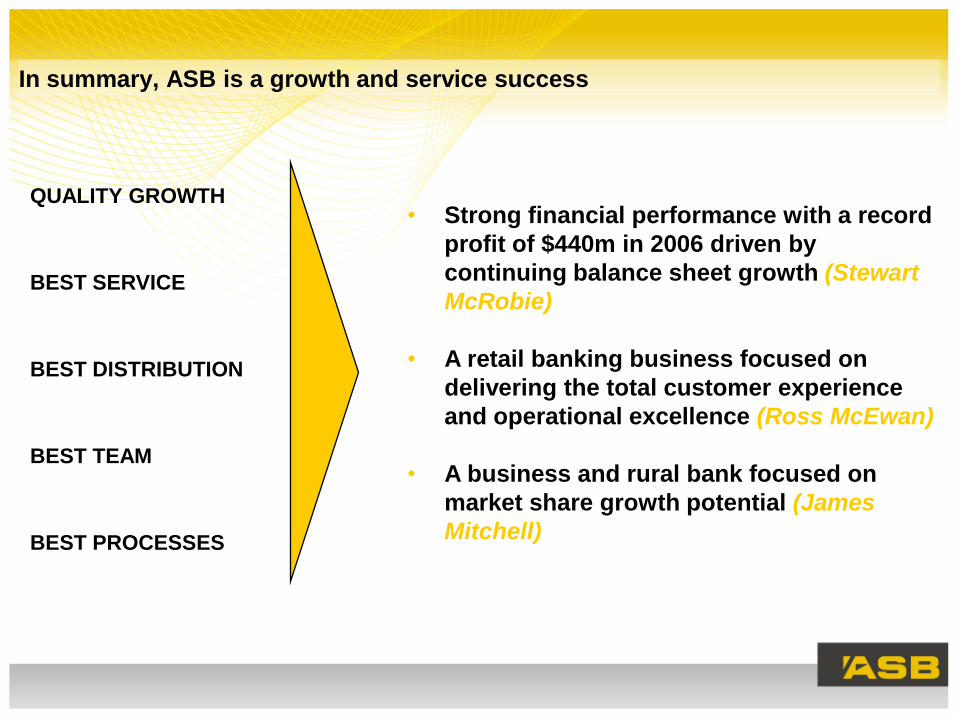

• Strong financial performance with a record

profit of $440m in 2006 driven by

continuing balance sheet growth (Stewart

McRobie)

• A retail banking business focused on

delivering the total customer experience

and operational excellence (Ross McEwan)

• A business and rural bank focused on

market share growth potential (James

Mitchell)

In summary, ASB is a growth and service success

BEST SERVICE

BEST PROCESSES

BEST TEAM

BEST DISTRIBUTION

QUALITY GROWTH

Agenda

• Team Introductions

• Introduction Hugh Burrett

• Financial Performance Stewart McRobie

• Retail Banking Ross McEwan

• Business & Rural Banking James Mitchell

• Q & A

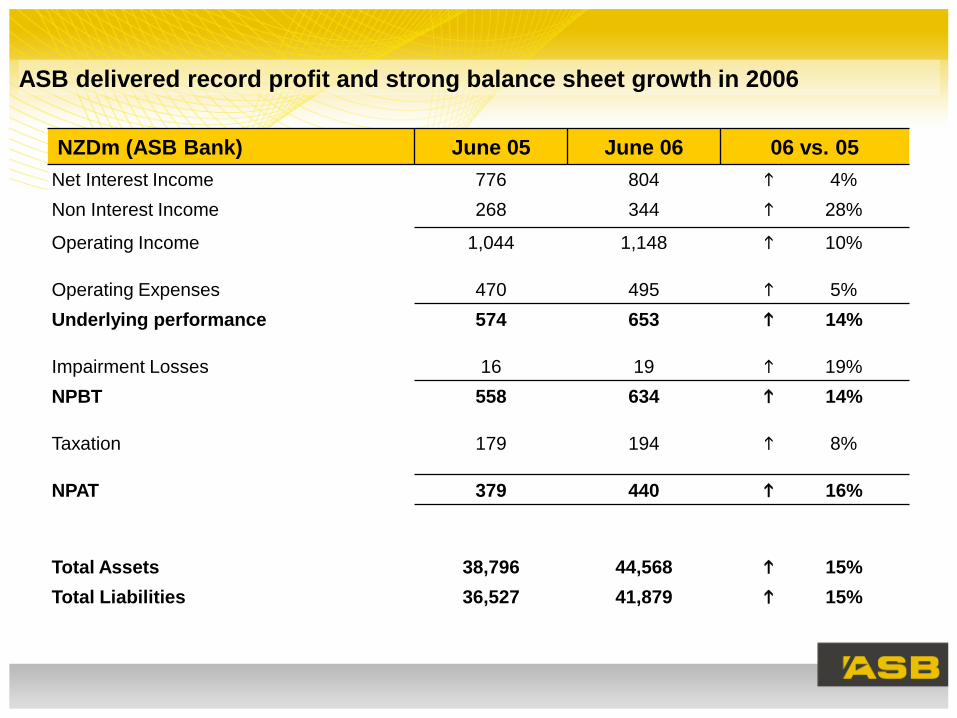

ASB delivered record profit and strong balance sheet growth in 2006

NZDm (ASB Bank) June 05 June 06 06 vs. 05

Net Interest Income 776 804 4%

Non Interest Income 268 344 28%

Operating Income 1,044 1,148 10%

Operating Expenses 470 495 5%

Underlying performance 574 653 14%

Impairment Losses 16 19 19%

NPBT 558 634 14%

Taxation 179 194 8%

NPAT 379 440 16%

Total Assets 38,796 44,568 15%

Total Liabilities 36,527 41,879 15%

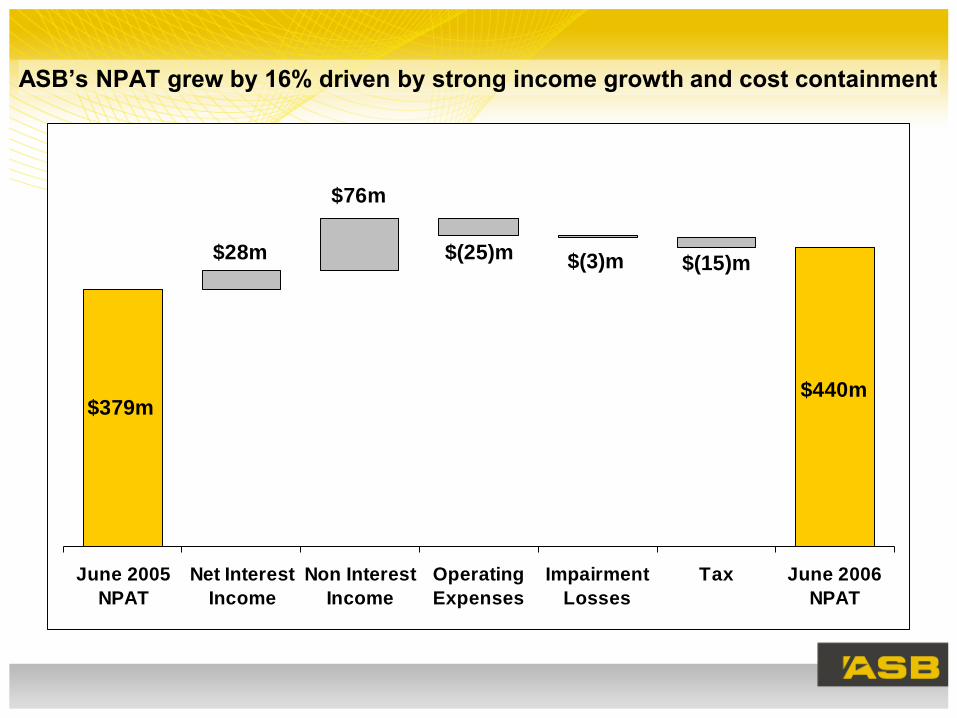

ASB’s NPAT grew by 16% driven by strong income growth and cost containment

June 2005

NPAT

Net Interest

Income

Non Interest

Income

Operating

Expenses

Impairment

Losses

Tax June 2006

NPAT

$379m

$28m

$76m

$(25)m $(3)m

)m

$(15)m

$440m

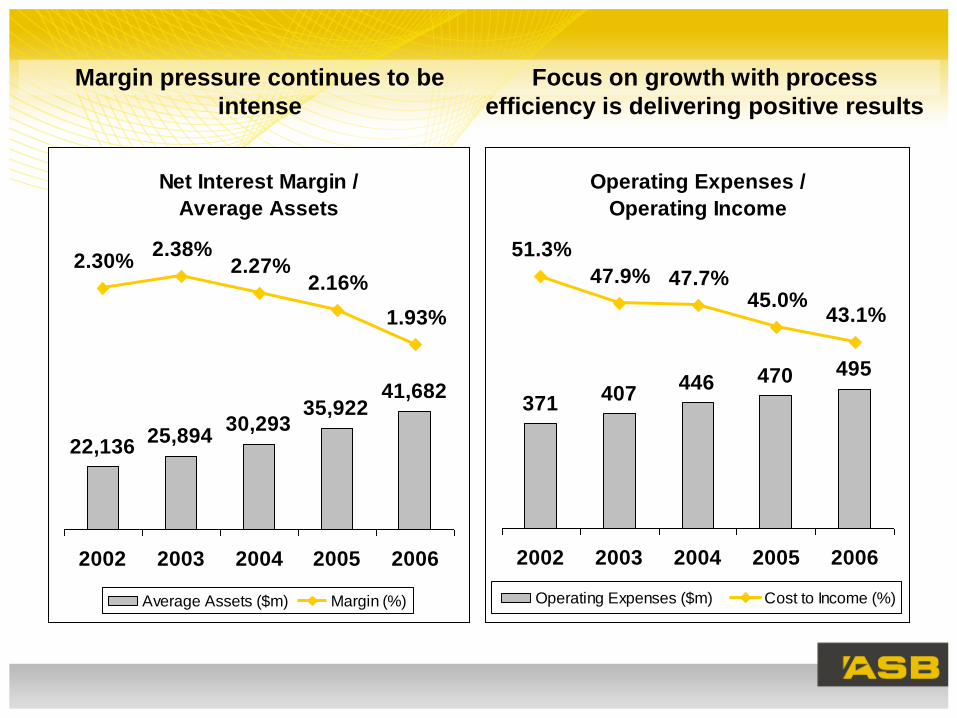

Margin pressure continues to be

intense

Focus on growth with process

efficiency is delivering positive results

Net Interest Margin /

Average Assets

22,13625,894

30,29335,922

41,682

2.30%2.38%

2.27%2.16%

1.93%

2002 2003 2004 2005 2006

Average Assets ($m) Margin (%)

Operating Expenses /

Operating Income

371407

446 470 495

51.3%

47.9% 47.7%45.0%

43.1%

2002 2003 2004 2005 2006

Operating Expenses ($m) Cost to Income (%)

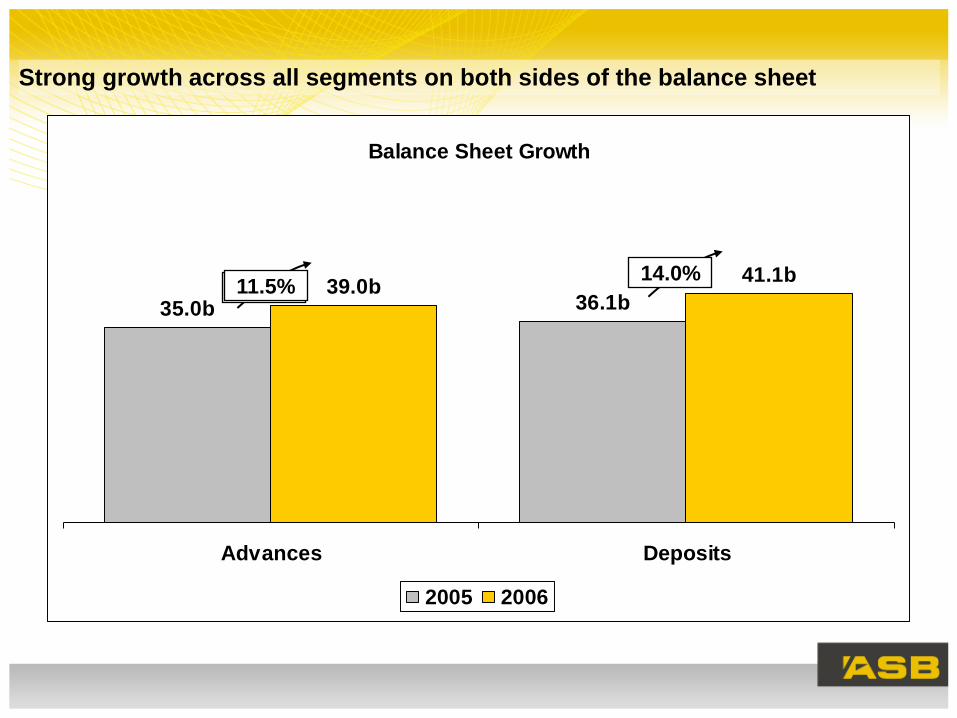

Balance Sheet Growth

36.1b35.0b

41.1b39.0b

Advances Deposits

2005 2006

Strong growth across all segments on both sides of the balance sheet

11.5%14.0%

11.5%

Underlying credit quality remains sound

• Provisions methodology has changed following the adoption of IFRS - $80m

of Collective and Specific Provisions are held as at 30 June 2006.

• Actual loan loss experience and specific provisioning levels continue to

represent only a small part of both P&L Net Impairment Loss expense and

Balance Sheet provisions for Bad Debts.

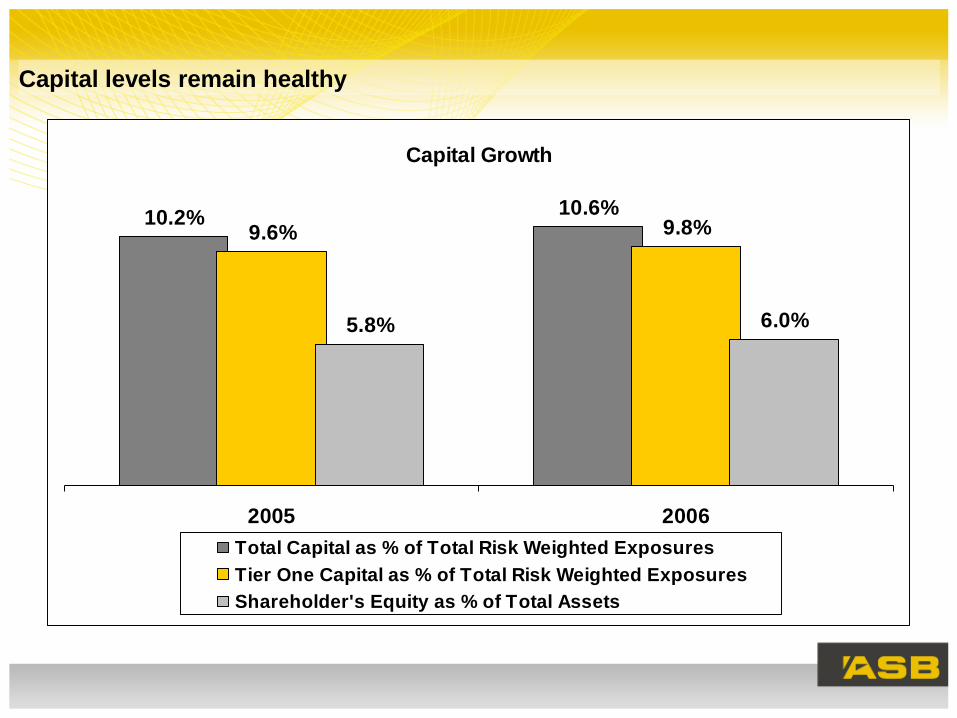

Capital levels remain healthy

Capital Growth

10.2%10.6%

9.6% 9.8%

5.8% 6.0%

2005 2006

Total Capital as % of Total Risk Weighted Exposures

Tier One Capital as % of Total Risk Weighted Exposures

Shareholder's Equity as % of Total Assets

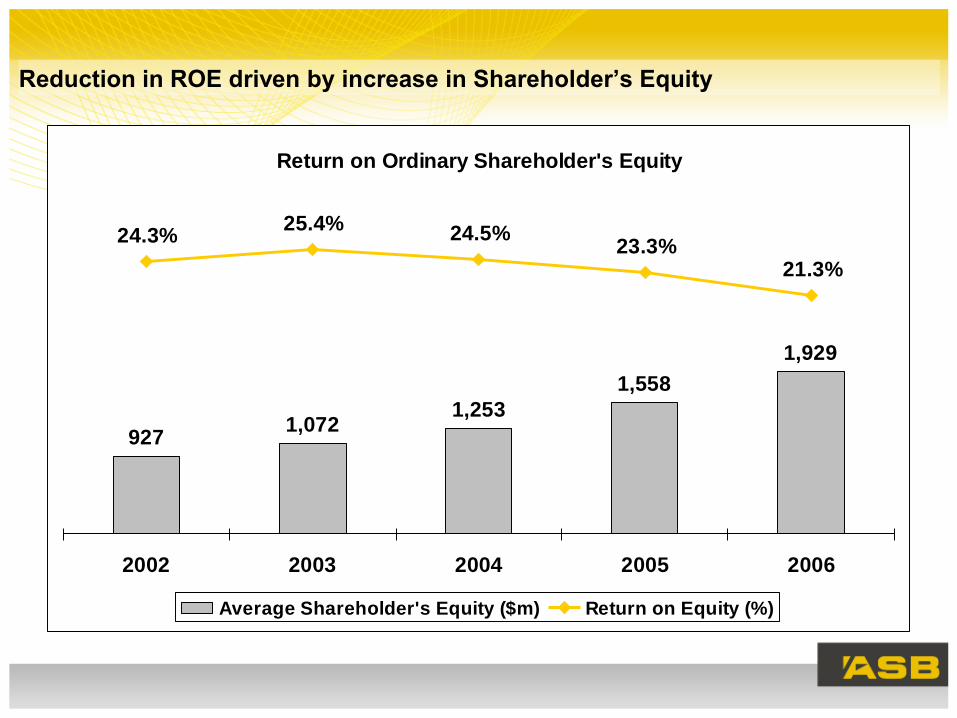

Reduction in ROE driven by increase in Shareholder’s Equity

Return on Ordinary Shareholder's Equity

9271,072

1,253

1,558

1,929

24.3%25.4% 24.5%

23.3%21.3%

2002 2003 2004 2005 2006

Average Shareholder's Equity ($m) Return on Equity (%)

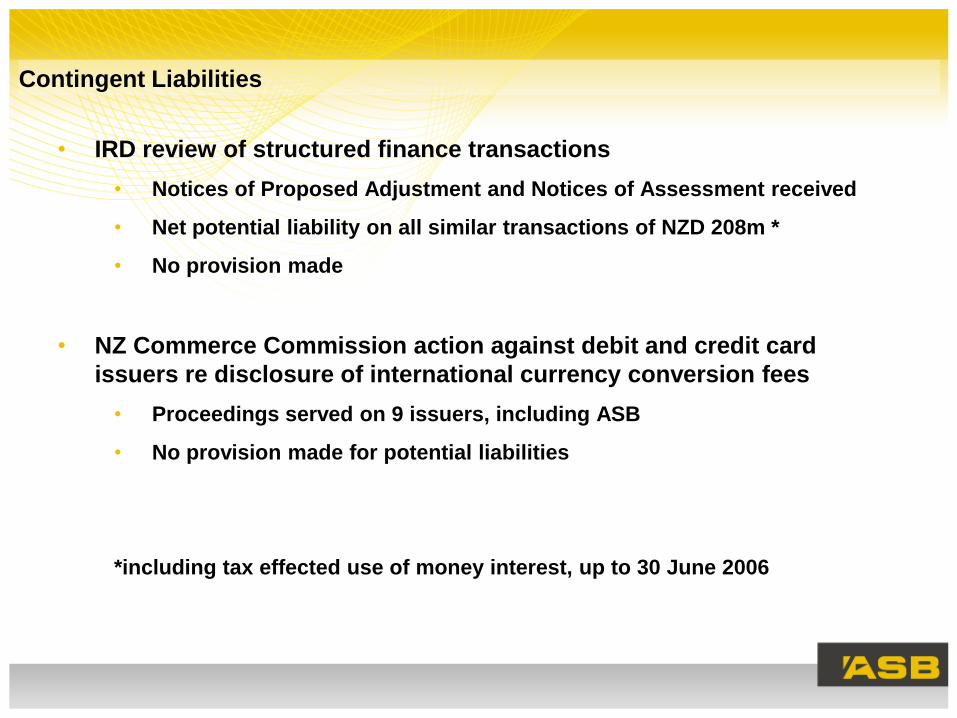

Contingent Liabilities

• IRD review of structured finance transactions

• Notices of Proposed Adjustment and Notices of Assessment received

• Net potential liability on all similar transactions of NZD 208m *

• No provision made

• NZ Commerce Commission action against debit and credit card

issuers re disclosure of international currency conversion fees

• Proceedings served on 9 issuers, including ASB

• No provision made for potential liabilities

*including tax effected use of money interest, up to 30 June 2006

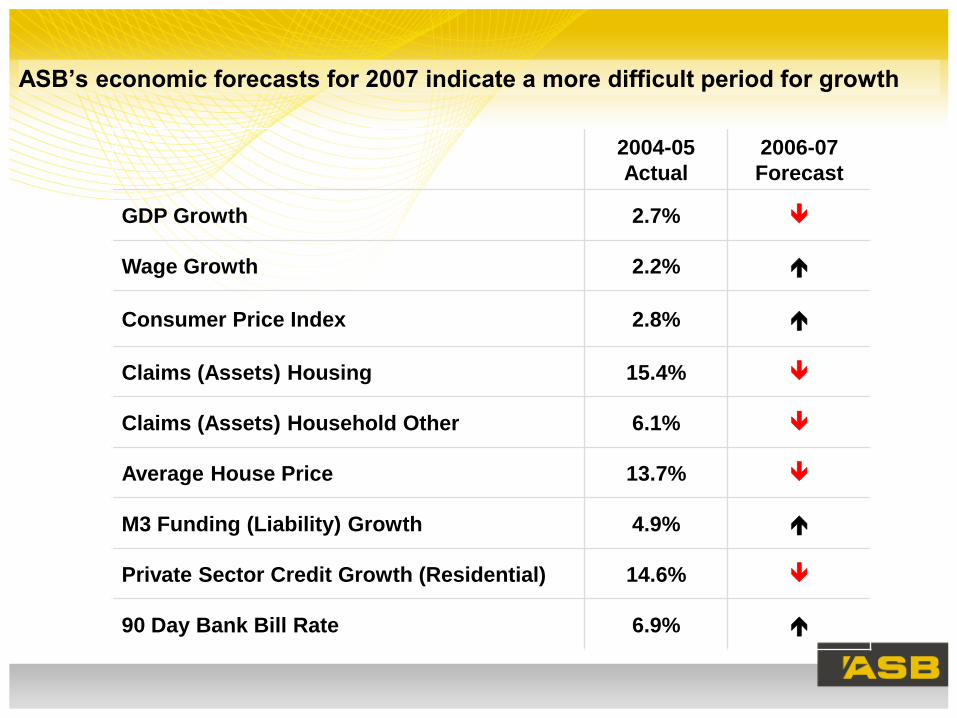

ASB’s economic forecasts for 2007 indicate a more difficult period for growth

2004-05

Actual

2006-07

Forecast

GDP Growth 2.7%

Wage Growth 2.2%

Consumer Price Index 2.8%

Claims (Assets) Housing 15.4%

Claims (Assets) Household Other 6.1%

Average House Price 13.7%

M3 Funding (Liability) Growth 4.9%

Private Sector Credit Growth (Residential) 14.6%

90 Day Bank Bill Rate 6.9%

Agenda

• Team Introductions

• Introduction Hugh Burrett

• Financial Performance Stewart McRobie

• Retail Banking Ross McEwan

• Business & Rural Banking James Mitchell

• Q & A

Source: RBNZ, ASB, June Year End

ASB continues to grow market share in retail lending

QUALITY GROWTH

ASB Household Lending ($b) and Market Share (%)

11.112.5

14.6

17.1

21.6

25.8

29.7

2000 2001 2002 2003 2004 2005 2006

23.1%23.0%22.4%20.8%19.8%18.3%17.3%

ASB Household Lending ($b) and Market Share (%)

11.112.5

14.6

17.1

21.6

25.8

29.7

2000 2001 2002 2003 2004 2005 2006

23.1%23.0%22.4%20.8%19.8%18.3%17.3%

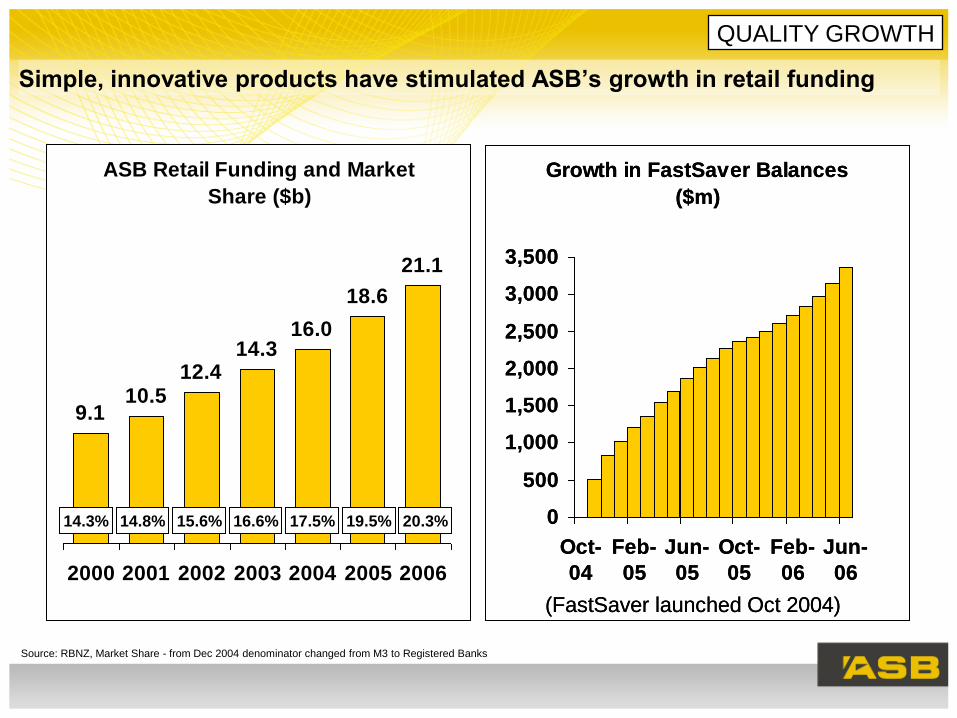

Simple, innovative products have stimulated ASB’s growth in retail funding

Source: RBNZ, Market Share - from Dec 2004 denominator changed from M3 to Registered Banks

QUALITY GROWTH

Growth in FastSaver Balances

($m)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Oct-

04

Feb-

05

Jun-

05

Oct-

05

Feb-

06

Jun-

06

(FastSaver launched Oct 2004)

ASB Retail Funding and Market

Share ($b)

9.110.5

12.414.3

16.0

18.6

21.1

2000 2001 2002 2003 2004 2005 2006

14.3% 14.8% 15.6% 16.6% 17.5% 19.5% 20.3%

Growth in FastSaver Balances

($m)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Oct-

04

Feb-

05

Jun-

05

Oct-

05

Feb-

06

Jun-

06

(FastSaver launched Oct 2004)

ASB Retail Funding and Market

Share ($b)

9.110.5

12.414.3

16.0

18.6

21.1

2000 2001 2002 2003 2004 2005 2006

14.3% 14.8% 15.6% 16.6% 17.5% 19.5% 20.3%

Focus on under 30’s market - YOUTH

Source: ASB

Sample Advertisement

QUALITY GROWTH

Growth in Headstart Account

Numbers and Balances

0

20

40

60

80

100

120

140

2002 2003 2004 2005 2006

Accounts ('000) Balances ($M)

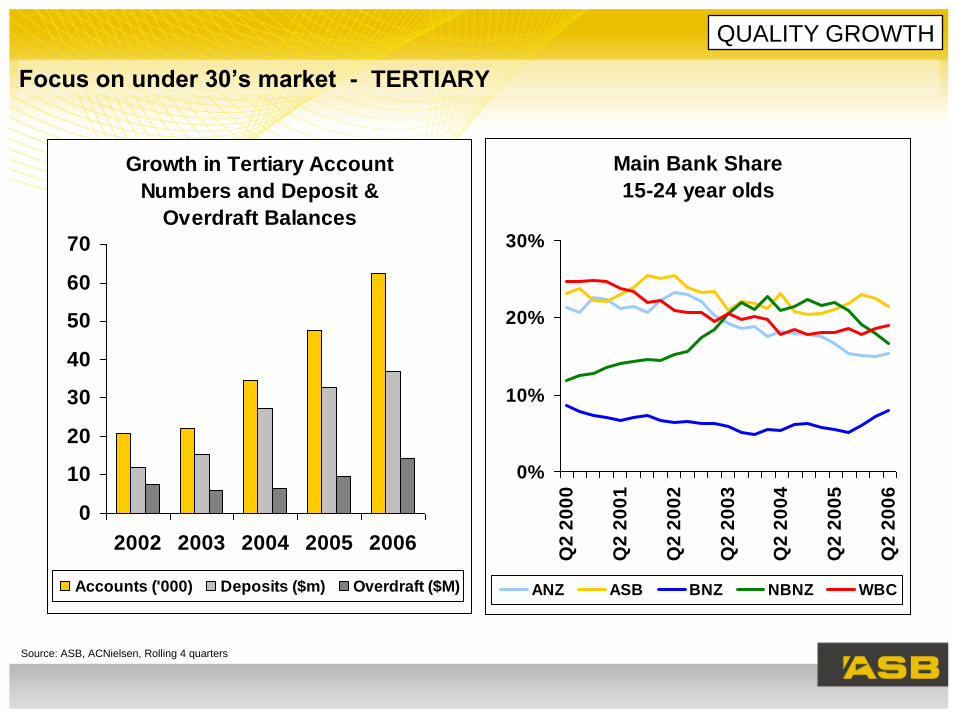

Focus on under 30’s market - TERTIARY

Source: ASB, ACNielsen, Rolling 4 quarters

QUALITY GROWTH

Growth in Tertiary Account

Numbers and Deposit &

Overdraft Balances

0

10

20

30

40

50

60

70

2002 2003 2004 2005 2006

Accounts ('000) Deposits ($m) Overdraft ($M)

Main Bank Share

15-24 year olds

0%

10%

20%

30%

Q2

20

00

Q2

20

01

Q2

20

02

Q2

20

03

Q2

20

04

Q2

20

05

Q2

20

06

ANZ ASB BNZ NBNZ WBC

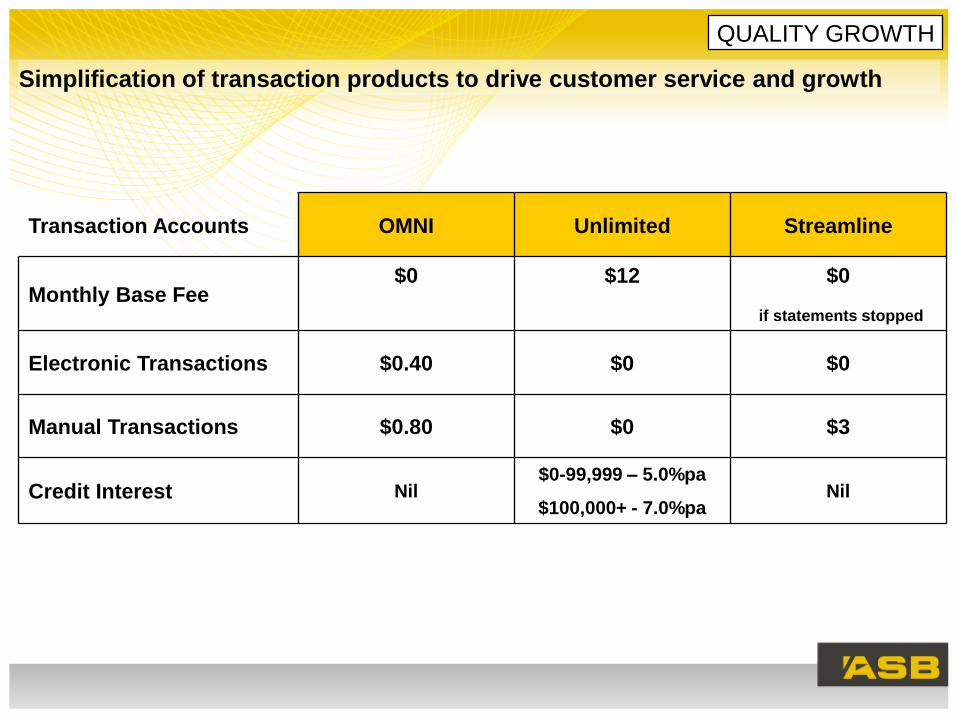

Simplification of transaction products to drive customer service and growth

Transaction Accounts OMNI Unlimited Streamline

Monthly Base Fee$0 $12 $0

if statements stopped

Electronic Transactions $0.40 $0 $0

Manual Transactions $0.80 $0 $3

Credit Interest Nil$0-99,999 – 5.0%pa

$100,000+ - 7.0%paNil

QUALITY GROWTH

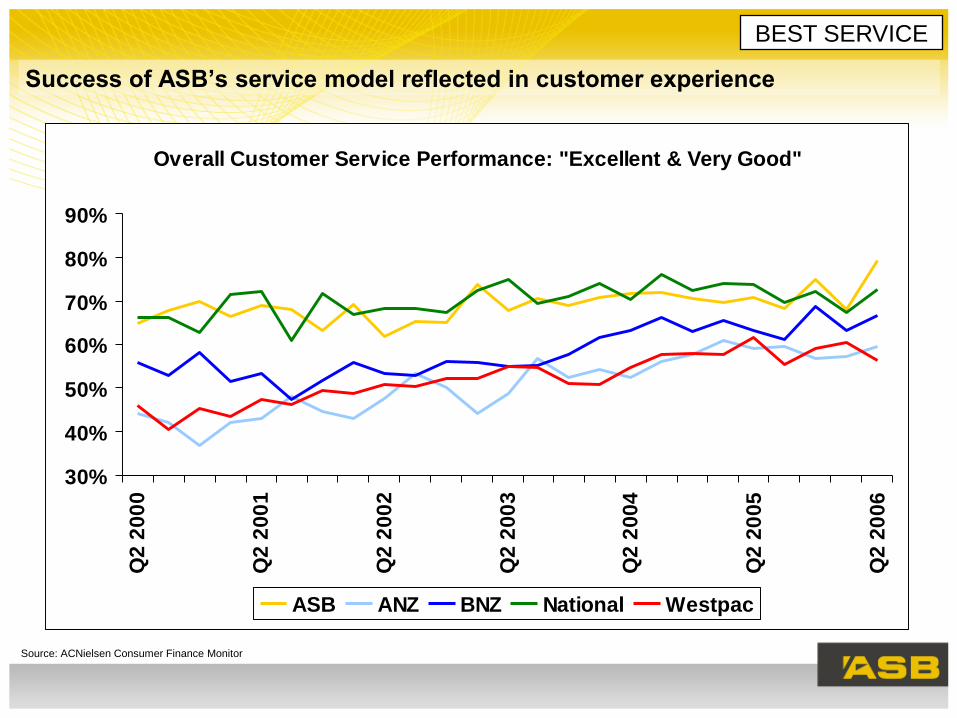

Success of ASB’s service model reflected in customer experience

BEST SERVICE

Source: ACNielsen Consumer Finance Monitor

Overall Customer Service Performance: "Excellent & Very Good"

30%

40%

50%

60%

70%

80%

90%

Q2

20

00

Q2

20

01

Q2

20

02

Q2

20

03

Q2

20

04

Q2

20

05

Q2

20

06

ASB ANZ BNZ National Westpac

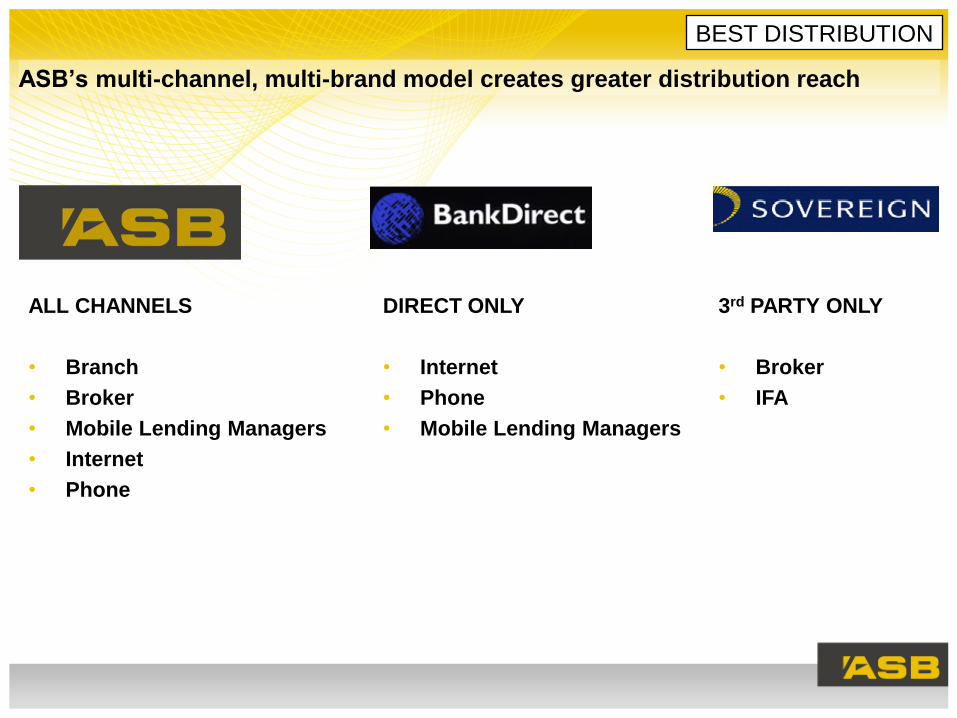

ASB’s multi-channel, multi-brand model creates greater distribution reach

BEST DISTRIBUTION

ALL CHANNELS

• Branch

• Broker

• Mobile Lending Managers

• Internet

• Phone

DIRECT ONLY

• Internet

• Phone

• Mobile Lending Managers

3rd PARTY ONLY

• Broker

• IFA

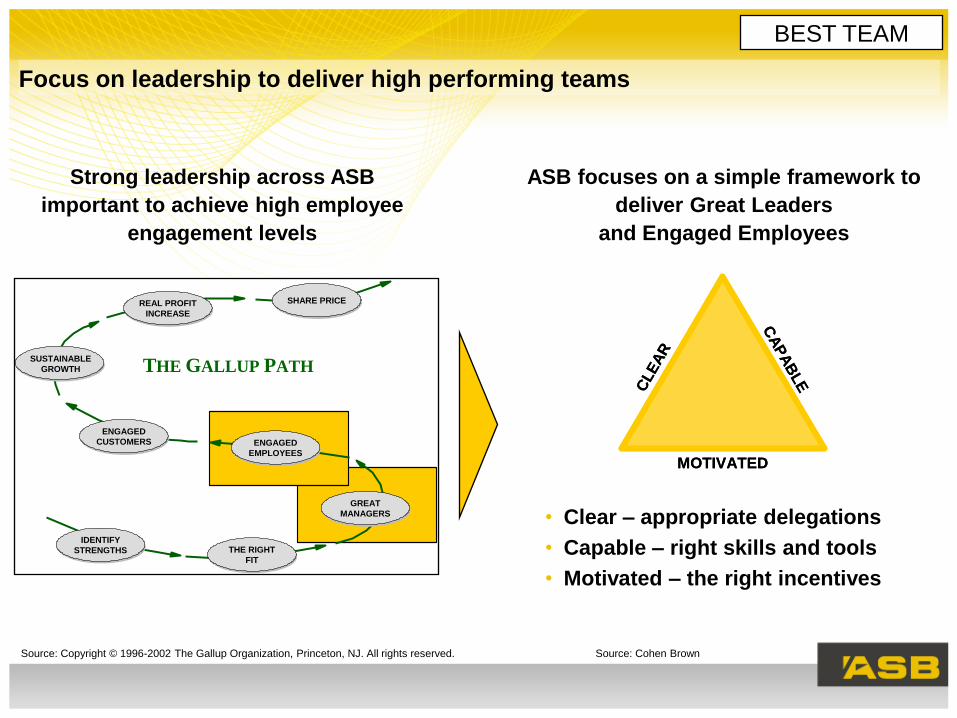

Focus on leadership to deliver high performing teams

THE GALLUP PATH

IDENTIFY

STRENGTHS THE RIGHT

FIT

GREAT

MANAGERS

ENGAGED

EMPLOYEES

ENGAGED

CUSTOMERS

SUSTAINABLE

GROWTH

REAL PROFIT

INCREASE

SHARE PRICE

BEST TEAM

Source: Copyright © 1996-2002 The Gallup Organization, Princeton, NJ. All rights reserved. Source: Cohen Brown

Strong leadership across ASB

important to achieve high employee

engagement levels

ASB focuses on a simple framework to

deliver Great Leaders

and Engaged Employees

• Clear – appropriate delegations

• Capable – right skills and tools

• Motivated – the right incentives

CLE

AR

CA

PA

BLE

MOTIVATED

CLE

AR

CA

PA

BLE

MOTIVATED

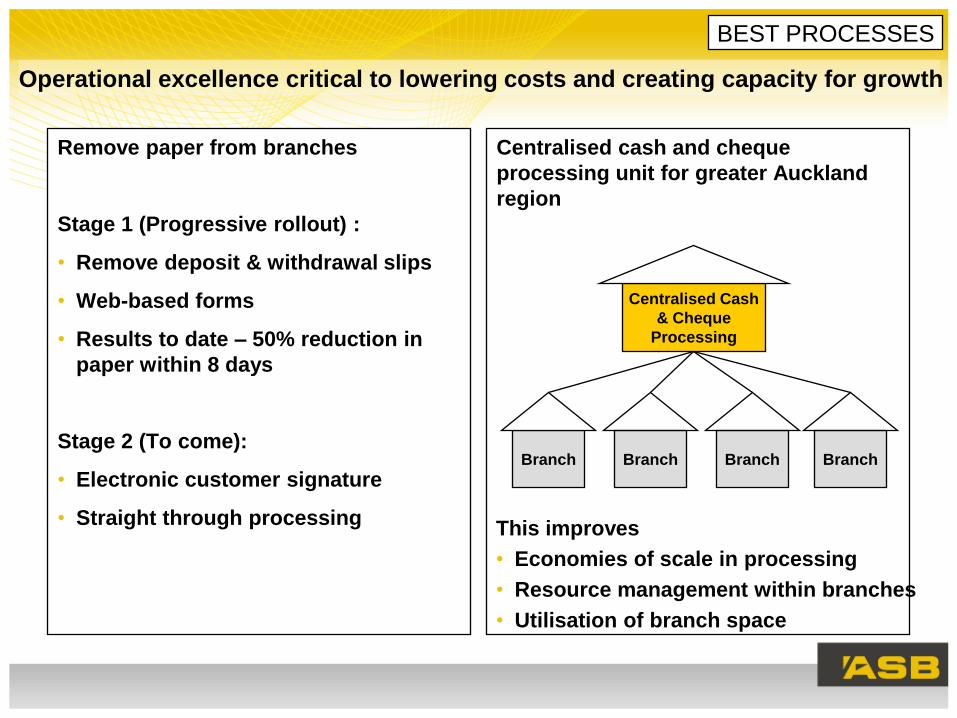

Operational excellence critical to lowering costs and creating capacity for growth

Remove paper from branches

Stage 1 (Progressive rollout) :

• Remove deposit & withdrawal slips

• Web-based forms

• Results to date – 50% reduction in

paper within 8 days

Stage 2 (To come):

• Electronic customer signature

• Straight through processing

BEST PROCESSES

Centralised Cash

& Cheque

Processing

Branch Branch Branch Branch

Centralised cash and cheque

processing unit for greater Auckland

region

This improves

• Economies of scale in processing

• Resource management within branches

• Utilisation of branch space

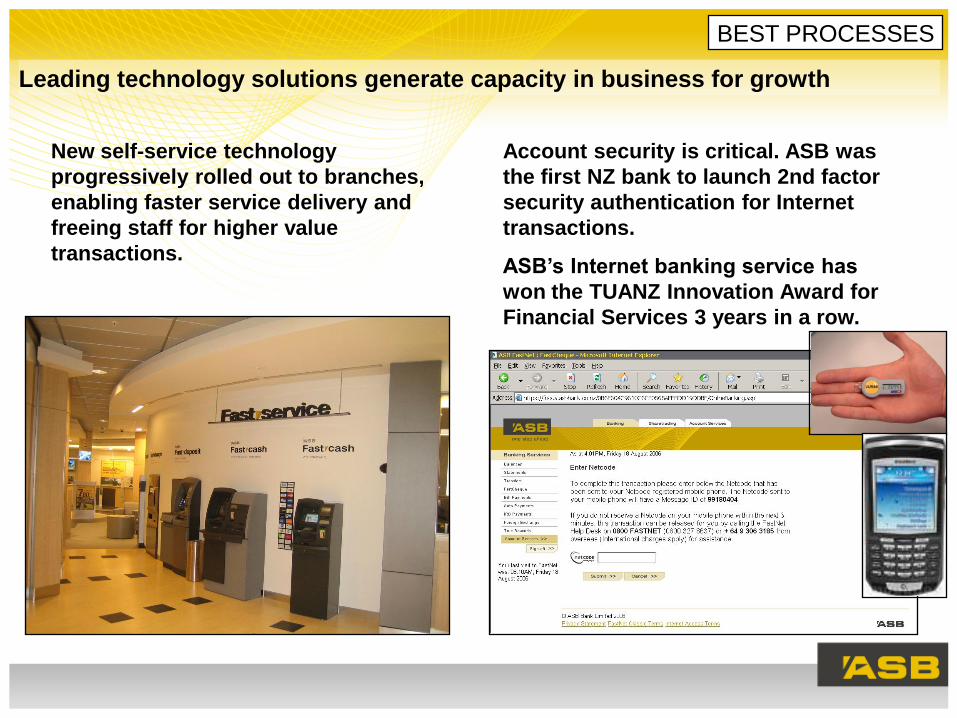

Leading technology solutions generate capacity in business for growth

New self-service technology

progressively rolled out to branches,

enabling faster service delivery and

freeing staff for higher value

transactions.

Account security is critical. ASB was

the first NZ bank to launch 2nd factor

security authentication for Internet

transactions.

ASB’s Internet banking service has

won the TUANZ Innovation Award for

Financial Services 3 years in a row.

BEST PROCESSES

BEST SERVICE

BEST PROCESSES

BEST TEAM

BEST DISTRIBUTION

QUALITY GROWTH

In summary, ASB Retail is a growth and service success

• Outstanding service performance

• Technology and process redesign building capacity

for growth

• Focus on leadership excellence at all levels

• Broad distribution reach

• A strong business with focus on key segments to

maintain long term growth

Agenda

• Team Introductions

• Introduction Hugh Burrett

• Financial Performance Stewart McRobie

• Retail Banking Ross McEwan

• Business & Rural Banking James Mitchell

• Q & A

Source: ASB, June Year End

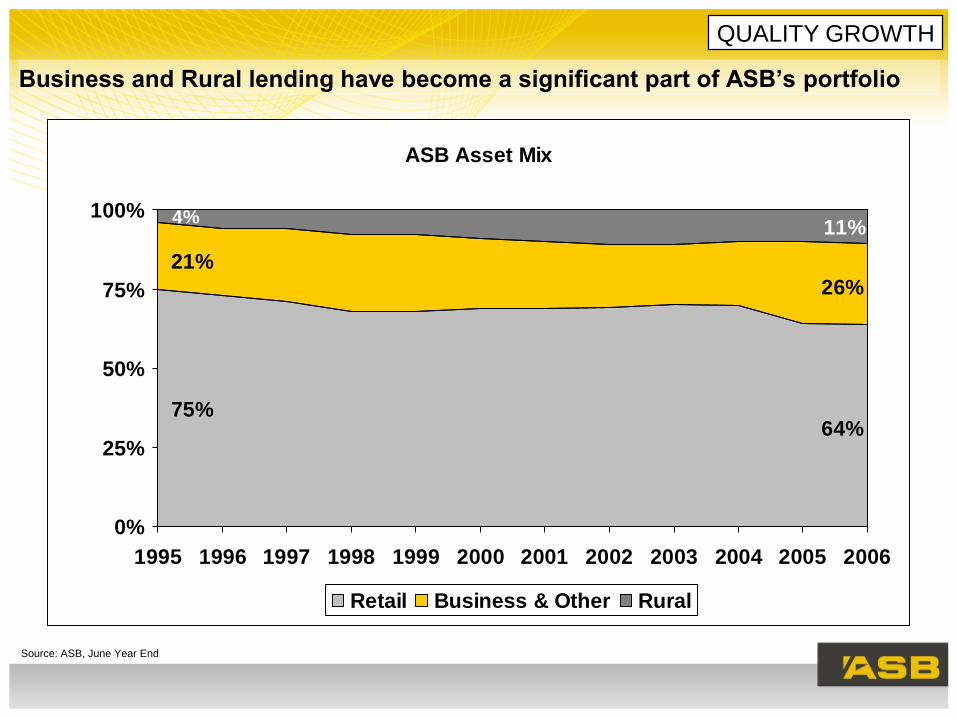

Business and Rural lending have become a significant part of ASB’s portfolio

QUALITY GROWTH

ASB Asset Mix

64%75%

26%

21%

11%4%

0%

25%

50%

75%

100%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Retail Business & Other Rural

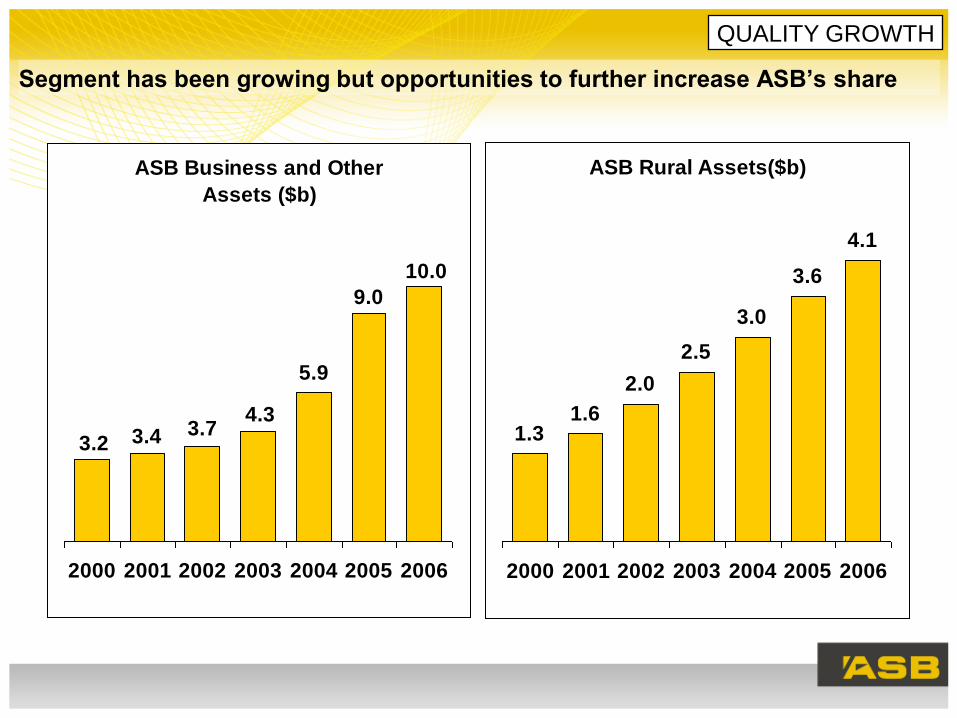

Segment has been growing but opportunities to further increase ASB’s share

QUALITY GROWTH

ASB Business and Other

Assets ($b)

10.0

9.0

5.9

4.33.73.43.2

2000 2001 2002 2003 2004 2005 2006

ASB Rural Assets($b)

1.31.6

2.0

2.5

3.0

3.6

4.1

2000 2001 2002 2003 2004 2005 2006

Source: TNS, 4 quarter roll Small Business <$5m turnover Middle business $5m to $100m turnover

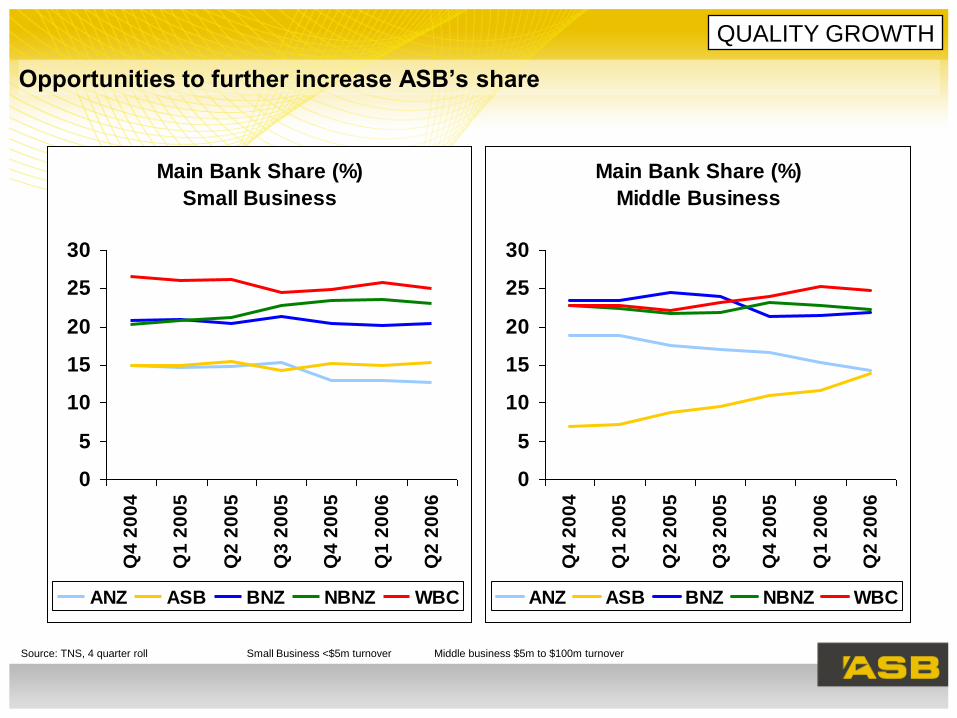

Opportunities to further increase ASB’s share

QUALITY GROWTH

Main Bank Share (%)

Small Business

0

5

10

15

20

25

30

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

Main Bank Share (%)

Middle Business

0

5

10

15

20

25

30

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

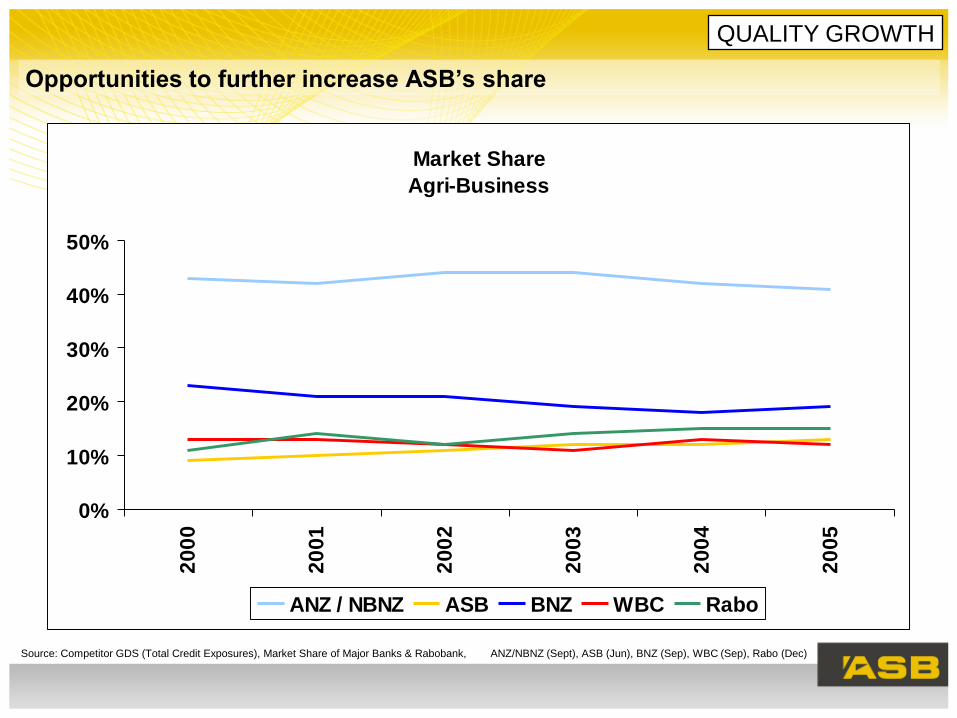

Opportunities to further increase ASB’s share

Source: Competitor GDS (Total Credit Exposures), Market Share of Major Banks & Rabobank, ANZ/NBNZ (Sept), ASB (Jun), BNZ (Sep), WBC (Sep), Rabo (Dec)

QUALITY GROWTH

Market Share

Agri-Business

0%

10%

20%

30%

40%

50%

20

00

20

01

20

02

20

03

20

04

20

05

ANZ / NBNZ ASB BNZ WBC Rabo

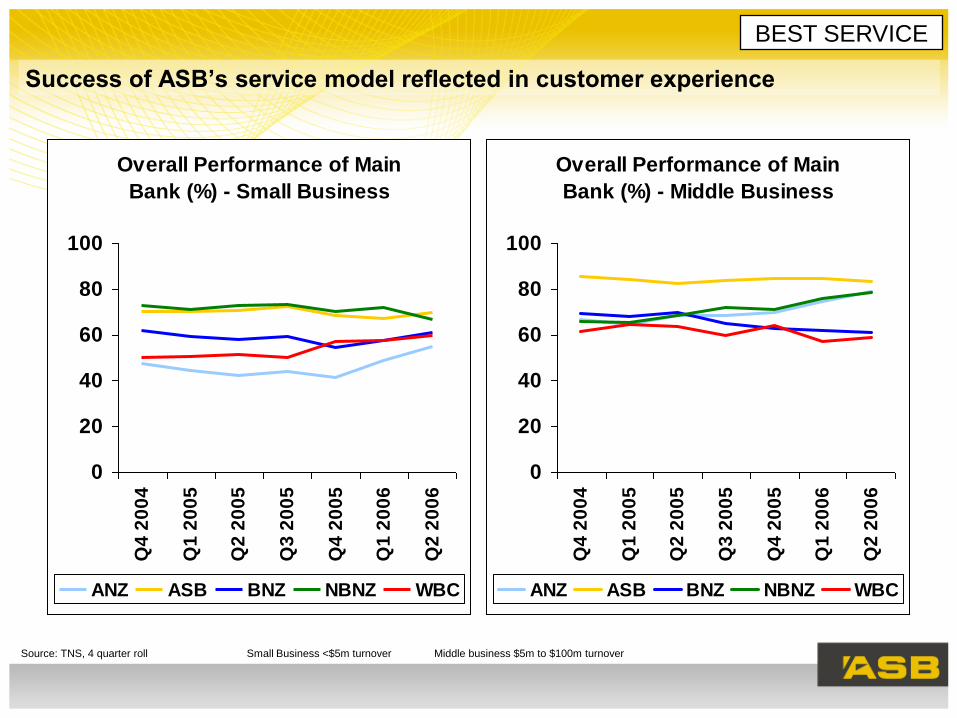

Success of ASB’s service model reflected in customer experience

BEST SERVICE

Source: TNS, 4 quarter roll Small Business <$5m turnover Middle business $5m to $100m turnover

Overall Performance of Main

Bank (%) - Small Business

0

20

40

60

80

100

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

Overall Performance of Main

Bank (%) - Middle Business

0

20

40

60

80

100

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

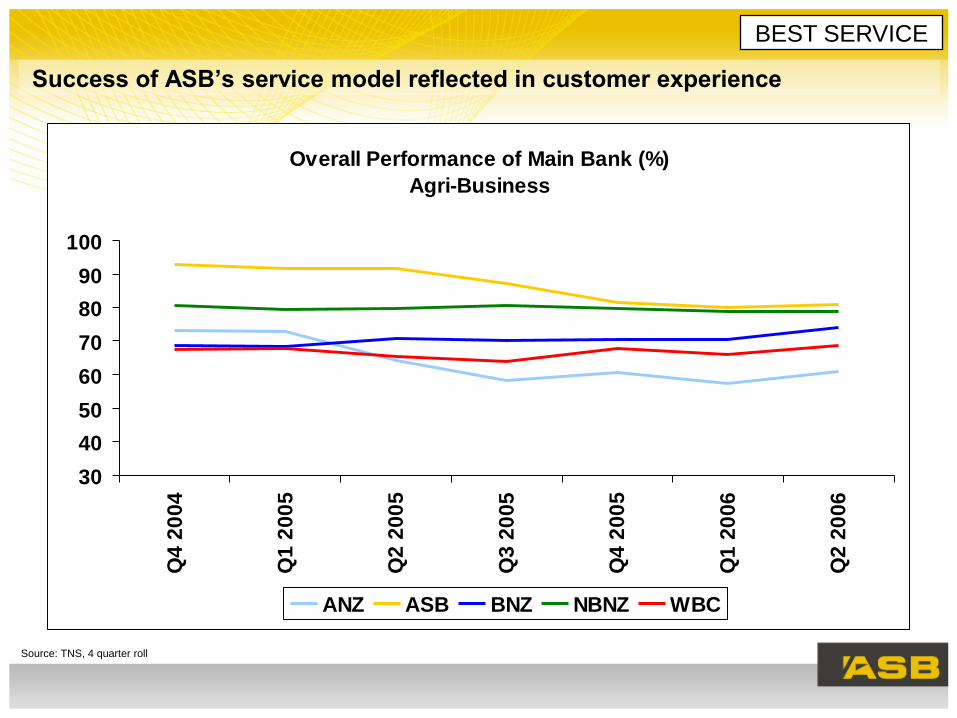

Success of ASB’s service model reflected in customer experience

BEST SERVICE

Source: TNS, 4 quarter roll

Overall Performance of Main Bank (%)

Agri-Business

30

40

50

60

70

80

90

100

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

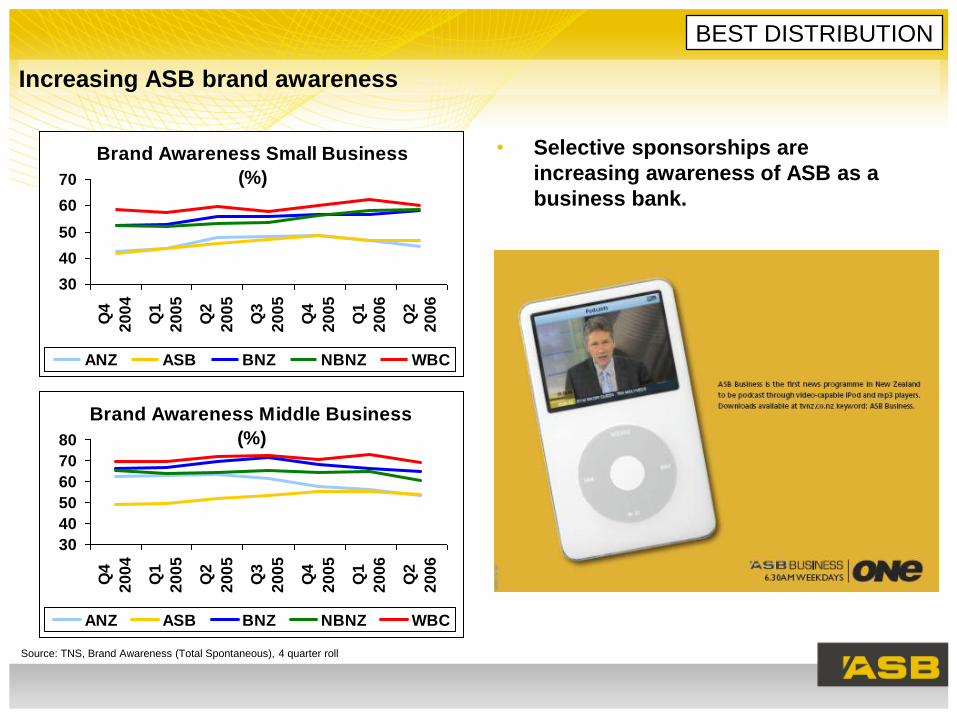

Increasing ASB brand awareness

• Selective sponsorships are

increasing awareness of ASB as a

business bank.

BEST DISTRIBUTION

Source: TNS, Brand Awareness (Total Spontaneous), 4 quarter roll

Brand Awareness Small Business

(%)

30

40

50

60

70

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

Brand Awareness Middle Business

(%)

30

40

50

60

70

80

Q4

20

04

Q1

20

05

Q2

20

05

Q3

20

05

Q4

20

05

Q1

20

06

Q2

20

06

ANZ ASB BNZ NBNZ WBC

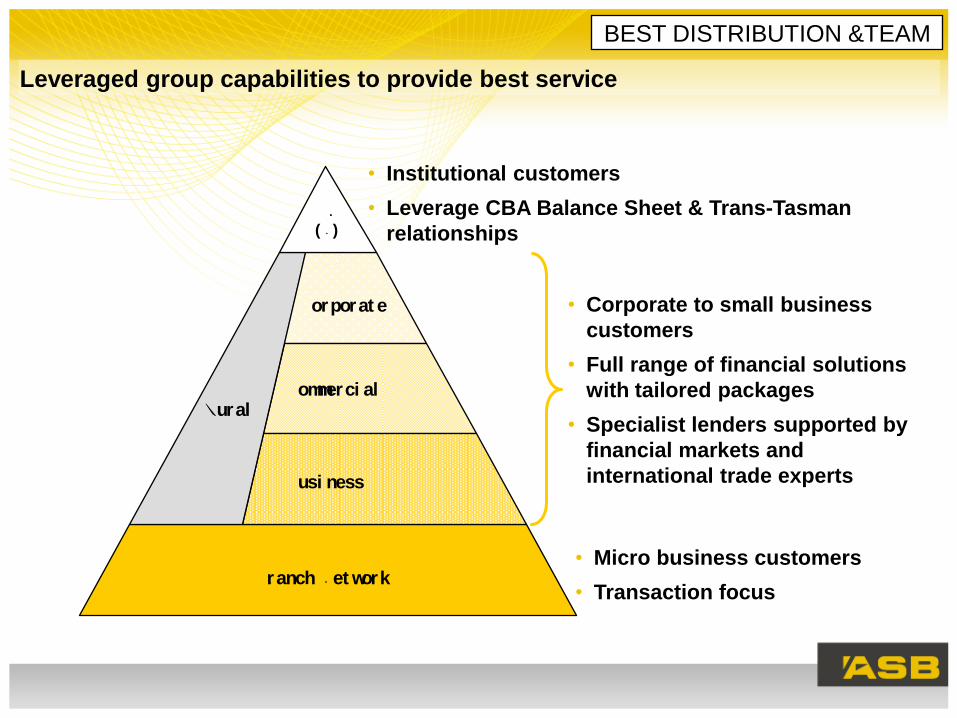

Leveraged group capabilities to provide best service

BEST DISTRIBUTION &TEAM

• Institutional customers

• Leverage CBA Balance Sheet & Trans-Tasman

relationships

• Micro business customers

• Transaction focus

• Corporate to small business

customers

• Full range of financial solutions

with tailored packages

• Specialist lenders supported by

financial markets and

international trade experts

CBA

(NZ)

Branch Net work

Corporat e

RuralCommerci al

Busi ness

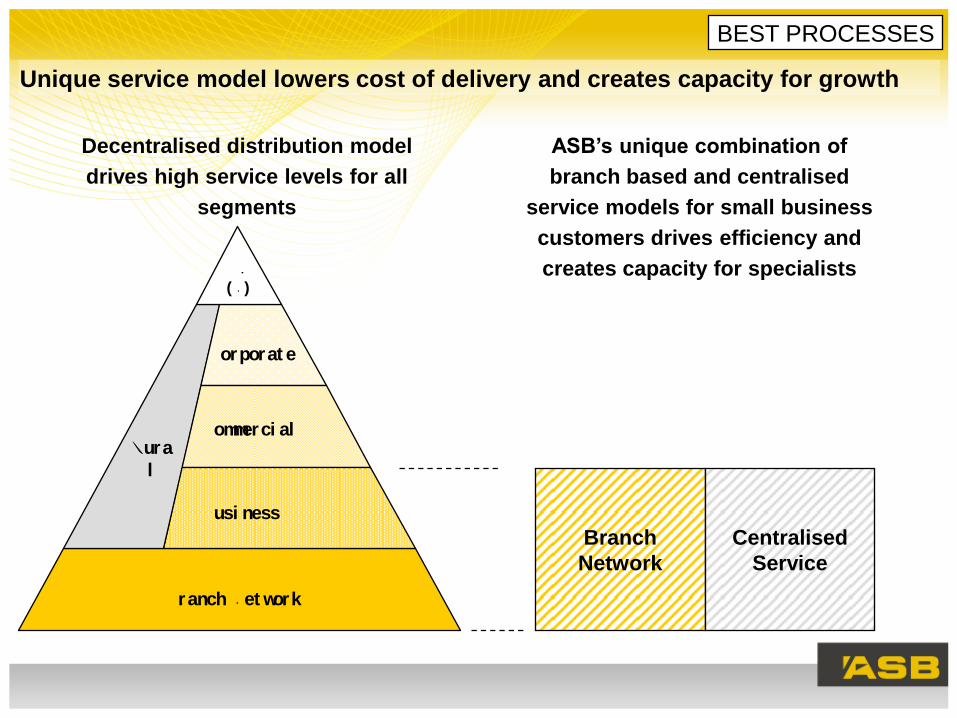

Unique service model lowers cost of delivery and creates capacity for growth

Decentralised distribution model

drives high service levels for all

segments

CBA

(NZ)

Branch Net work

Corporat e

Rura

l

Commerci al

Busi ness

ASB’s unique combination of

branch based and centralised

service models for small business

customers drives efficiency and

creates capacity for specialists

BEST PROCESSES

Branch

Network

Centralised

Service

BEST SERVICE

BEST PROCESSES

BEST TEAM

BEST DISTRIBUTION

QUALITY GROWTH

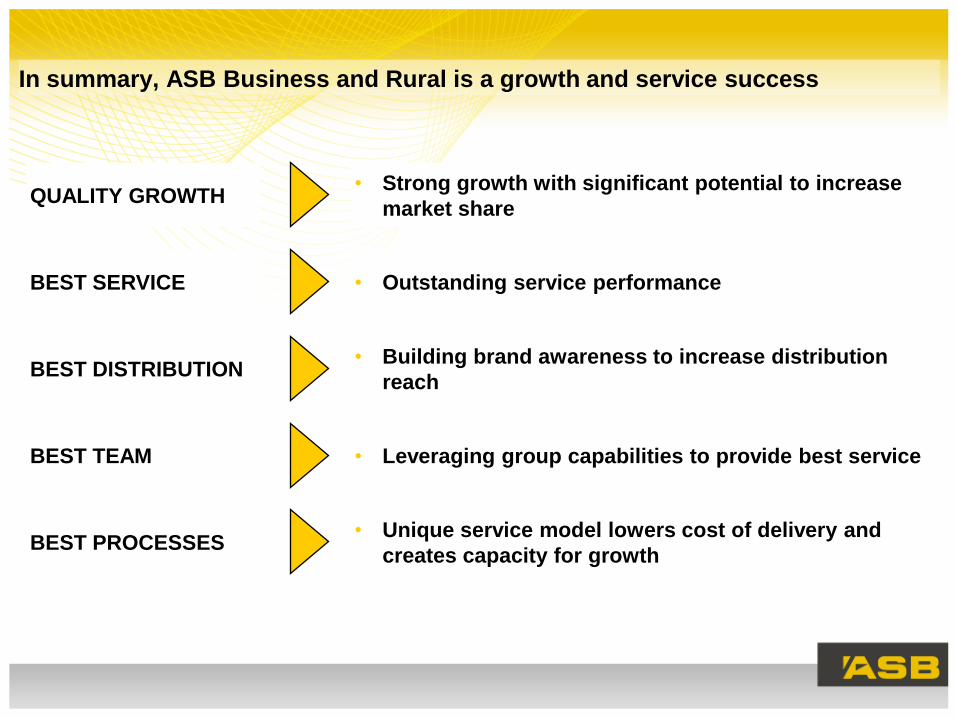

In summary, ASB Business and Rural is a growth and service success

• Outstanding service performance

• Unique service model lowers cost of delivery and

creates capacity for growth

• Leveraging group capabilities to provide best service

• Building brand awareness to increase distribution

reach

• Strong growth with significant potential to increase

market share

Agenda

• Team Introductions

• Introduction Hugh Burrett

• Financial Performance Stewart McRobie

• Retail Banking Ross McEwan

• Business & Rural Banking James Mitchell

• Q & A

ASB Update

Analyst Briefing

8th September 2006

![ASB The Changing Landscape - Chartered Institute of Housing Support/EM resources/ASB... · Recent ASB Case Law Wandsworth LBC v Maggott [2013] • ASB not found to be “in the locality”](https://img.pdfslide.us/doc/110x75/5c050c6d09d3f2133a8cde9d/asb-the-changing-landscape-chartered-institute-of-supportem-resourcesasb.jpg)