Embed Size (px)

Citation preview

Arvind: At An Inflection

Arvind’s Revenue is expected to grow at

CAGR of 17% to Rs. 10,000 cr by March 31, 2016

Arvind- A Changing Picture

About 36% of Arvind’s Revenue will come from its fast

growing B 2 C Business

5400

6600

8500

10000

3000

5000

7000

9000

11000

2013 2014 2015 2016

Revenue CAGR 17%

While Textile will continue to be significant part of Arvind’s Revenue, Arvind’s non denim business will

grow very rapidly

Textiles 68%

Brands &

Retail 29%

Others

3%

Revenue Mix 2013

Textiles 59%

Brands &

Retail 36%

Others

5%

Revenue Mix 2016

45% 33%

55% 67%

0%

20%

40%

60%

80%

100%

120%

2012 2016

Textile Revenue

Other Textiles

Denim

32% 20%

68% 80%

0%

20%

40%

60%

80%

100%

120%

2012 2016

Total Revenue

Revenue from others

Denim

Arvind- A Changing Picture

– Re-investment of Operating Cash Flows

– Cash flows from divestment of real-estate

• cash flows expected over next 5 years is Rs. 900 crores – Cash flows more or less equally spread every year.

– Scale Advantage

10.50%

13% 12%**

14%

16% 17%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

2011 2012 2013 2014 2015 2016

ROCE

**Earnings reduced due to strike in Q1-2013

1.30

1.05 1.00

0.80

0.90

1.00

1.10

1.20

1.30

1.40

2011 2012 2013

Debt: equity

Arvind- A Changing Picture

While Arvind’s revenue may double over 3 years, its ROCE and

leverage position is likely to significantly improve due to

Product Brands ( Licensed) Retail Brands

Product Brands (Owned)

JV Brand

Arvind has an Unmatched Portfolio of Owned & Licensed Brands and Retail Formats in the Fashion Industry

Aspirers (106)

Middle Class

Globals (3)

Affluent

Strivers &

Seekers (61)

Upper

Middle Class

Value Retail

Bridge to Luxury

Premium Brands

Income Pyramid in 2015 (households mn.)

India 1

India 2

Arvind Portfolio Caters to Addressable Market of 170 Mn Households

Arvind’s pursuit of Multi-Brand, Multi-Price Point and Multi-Channel Strategy over the last 5 years has grown the Business at a CAGR of 38%

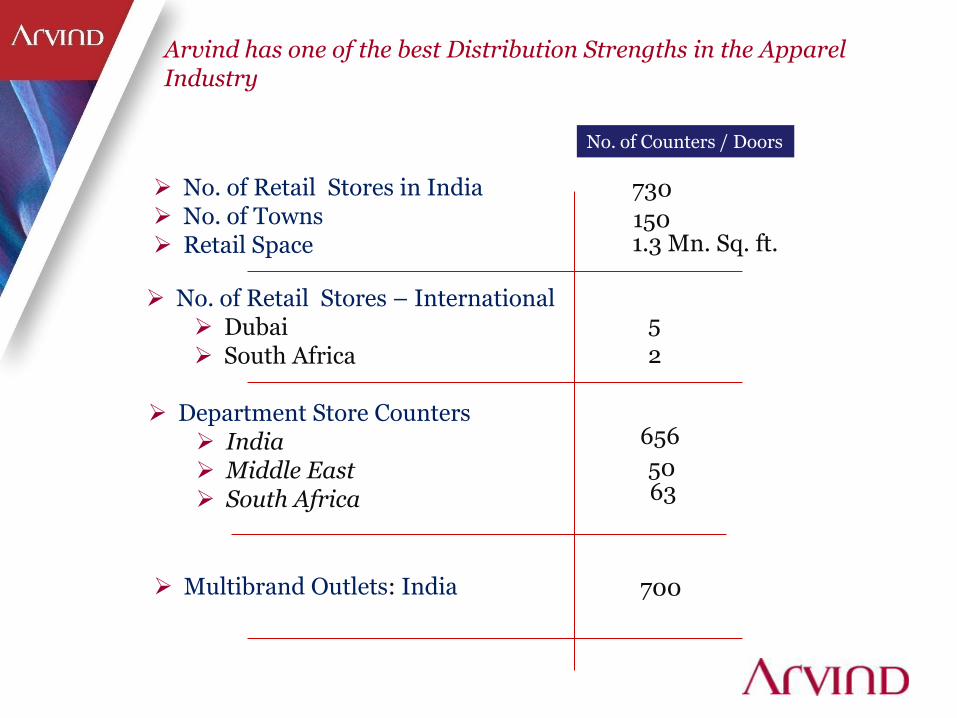

Arvind has one of the best Distribution Strengths in the Apparel Industry

No. of Counters / Doors

No. of Retail Stores in India No. of Towns Retail Space

Department Store Counters India Middle East South Africa

Multibrand Outlets: India

730

700

50 63

656

150 1.3 Mn. Sq. ft.

No. of Retail Stores – International Dubai South Africa

5

2

Competition

Now Future

Louis Philippe

Van Heusen

Allen Solly

Brooks Brothers

Pink

Kenneth Cole

Balanced Portfolio with Future Growth Drivers

Keep the Portfolio always

Future Ready

Premium Menswear No. 1

Apparel Specialty Retail

Arvind has already taken leadership position in Premium Menswear market

Best Portfolio in the Industry

Propose to add one large international brand in near future

Kids wear No. 1

Arvind has already taken leadership position in Premium Kids-wear market

International Brands Leverage Can Make Us No. 1

Competition

Now & Future

Denim & Youth

Arvind has some white spaces in youth and denim market

Bridge to Luxury Department Store

Premium Department Store

Fast Fashion Specialty Retail

Value

Discount

Kids

Youth

Arvind

Will be Among the Top 5 Players in the Apparel Retail Landscape

Family

India’s Retail play- Now & in future

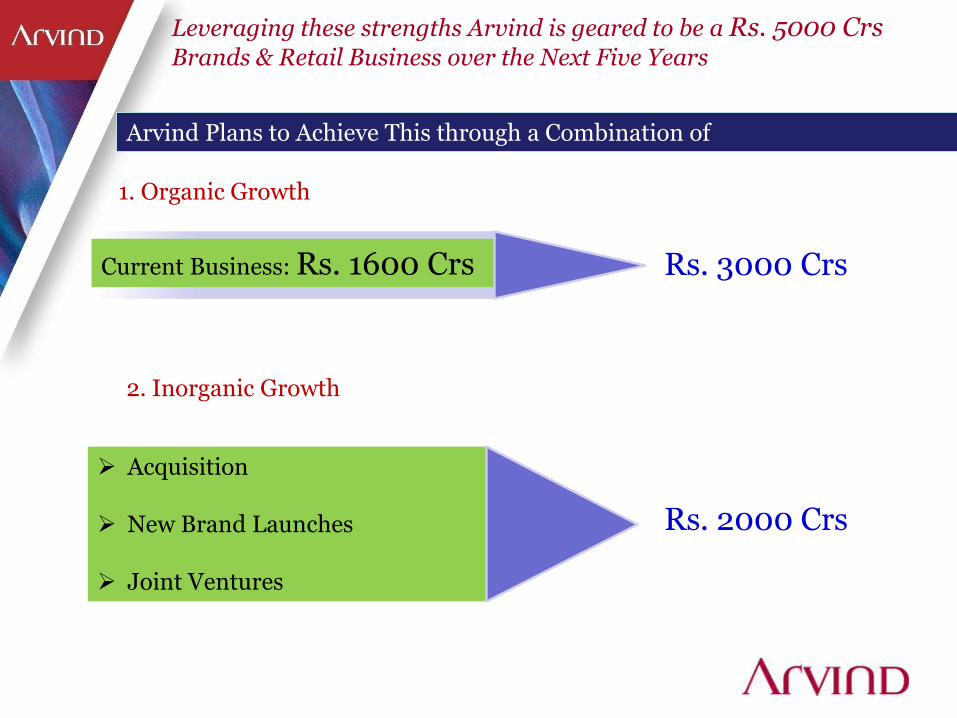

Leveraging these strengths Arvind is geared to be a Rs. 5000 Crs Brands & Retail Business over the Next Five Years

Arvind Plans to Achieve This through a Combination of

1. Organic Growth

Current Business: Rs. 1600 Crs

2. Inorganic Growth

Acquisition

New Brand Launches

Joint Ventures

Rs. 2000 Crs

Rs. 3000 Crs

Arvind’s Earnings :At Inflection Point

Arvind’s earnings likely to improve

substantially over next 3

years

• Textile Margins to improve as multiple product groups become large

• Apart from denim, woven fabrics, garments and technical textile to scale up rapidly

• Margin improvement • Consistency

• Brands business attaining maturity stage leading to

• Improved operating leverage resulting in margin improvement

• Mega Mart retail chain stabilising after the

derailment caused by imposing of excise duty

• Real-estate revenue and profits likely to kick in from next FY

Near term outlook is positive

Cost of increase in borrowing may significantly get off set by reduction in interest cost

Depreciation to increase at a lower pace than EBIDTA

PBT to sharply improve

Scale advantage

MegaMart margins steadily improving

Currency hedge almost getting over

Real-estate profits likely to kick in

EBIDTA margin may marginally

improve

Capacity expansion in woven fabrics completed

Garment plant in Bangladesh being set up

Established brands to continue growth momentum

Several new brands and retail formats acquired

Revenue growth @ 20% +

FY 2014

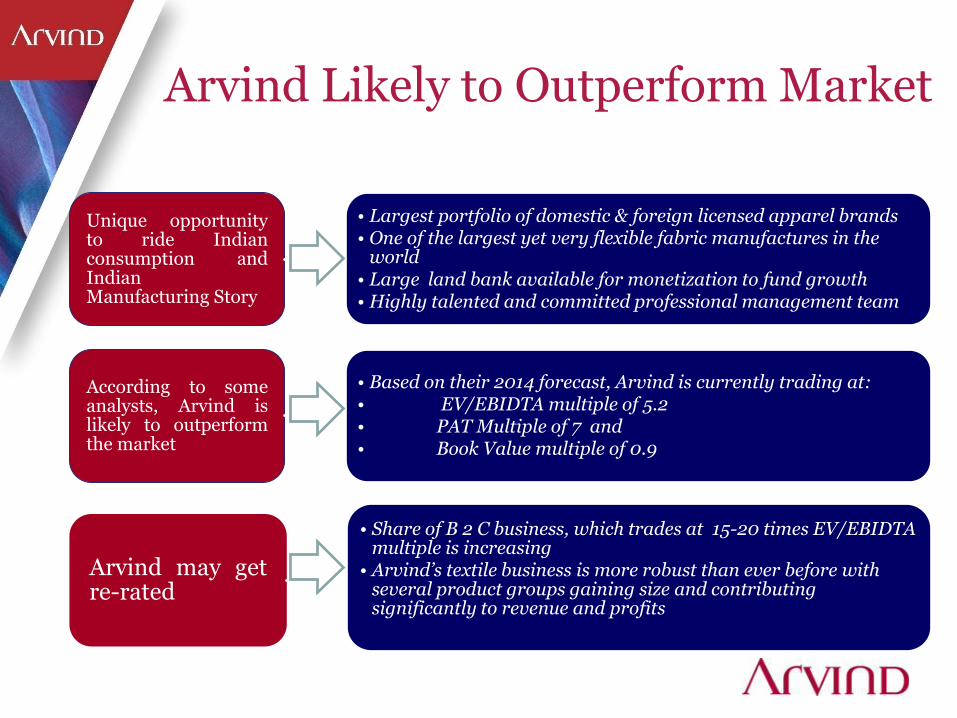

Arvind Likely to Outperform Market

Unique opportunity to ride Indian consumption and Indian Manufacturing Story

• Largest portfolio of domestic & foreign licensed apparel brands • One of the largest yet very flexible fabric manufactures in the

world • Large land bank available for monetization to fund growth • Highly talented and committed professional management team

According to some analysts, Arvind is likely to outperform the market

• Based on their 2014 forecast, Arvind is currently trading at: • EV/EBIDTA multiple of 5.2 • PAT Multiple of 7 and • Book Value multiple of 0.9

Arvind may get re-rated

• Share of B 2 C business, which trades at 15-20 times EV/EBIDTA

multiple is increasing • Arvind’s textile business is more robust than ever before with

several product groups gaining size and contributing significantly to revenue and profits

Thank You