Embed Size (px)

Citation preview

Armenian Development

Agency

Russian, Georgian, Uzbek and Kazakhstani Market Research for Pharmaceutical Industry

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

TABLE OF CONTENTS

LIST OF TABLES AND FIGURES ................................................................................................................. 4

Harmonized System Codes (HS Code) for Pharmaceutical Products ...................................................... 6

Fast Facts about Pharmaceutical Products ............................................................................................. 6

GLOBAL PHARMACEUTICAL INDUSTRY OVERVIEW ................................................................................ 7

INTRODUCTION ................................................................................................................................... 7

EXECUTIVE SUMMARY ........................................................................................................................ 7

MARKET OVERVIEW ............................................................................................................................ 8

GROWTH DRIVERS ............................................................................................................................ 11

PHARMACEUTICAL INDUSTRY LEADERS ........................................................................................... 12

EXTERNAL TRADE .............................................................................................................................. 14

R&D PRODUCTIVITY .......................................................................................................................... 15

REGULATORY REQUIREMENTS.......................................................................................................... 16

PRICING ............................................................................................................................................. 17

PATENT EXPIRIES AND GENERICISATION .......................................................................................... 19

BUILDING TRUST ............................................................................................................................... 20

FORECAST .......................................................................................................................................... 20

CONCLUSION ..................................................................................................................................... 21

REFERENCES ...................................................................................................................................... 22

PHARMACEUTICAL INDUSTRY IN RUSSIA .............................................................................................. 23

EXECUTIVE SUMMARY ...................................................................................................................... 23

MARKET OVERVIEW .......................................................................................................................... 24

FOREIGN TRADE ................................................................................................................................ 30

INVESTMENT ..................................................................................................................................... 31

PRICES ............................................................................................................................................... 31

CITY KEY TRENDS ............................................................................................................................... 32

OTC REGISTRATION AND CLASSIFICATION ....................................................................................... 38

VITAMINS AND DIETARY SUPPLEMENTS REGISTRATION AND CLASSIFICATION .............................. 44

SELF-MEDICATION/SELF-CARE AND PREVENTATIVE MEDICINE ....................................................... 48

FORECAST .......................................................................................................................................... 48

REFERENCES ...................................................................................................................................... 52

PHARMACEUTICAL INDUSTRY IN GEORGIA .......................................................................................... 53

EXECUTIVE SUMMARY ...................................................................................................................... 53

MARKET OVERVIEW .......................................................................................................................... 54

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

FOREIGN TRADE ................................................................................................................................ 63

PRICES ............................................................................................................................................... 66

OTC REGISTRATION AND CLASSIFICATION ....................................................................................... 66

VITAMINS AND DIETARY SUPPLEMENTS REGISTRATION AND CLASSIFICATION .............................. 70

SELF-MEDICATION/SELF-CARE AND PREVENTATIVE MEDICINE ....................................................... 71

FORECAST .......................................................................................................................................... 72

REFERENCES ...................................................................................................................................... 73

PHARMACEUTICAL INDUSTRY IN UZBEKISTAN ..................................................................................... 74

EXECUTIVE SUMMARY ...................................................................................................................... 74

MARKET OVERVIEW .......................................................................................................................... 75

FOREIGN TRADE ................................................................................................................................ 80

INVESTMENT ..................................................................................................................................... 82

OTC REGISTRATION AND CLASSIFICATION ....................................................................................... 83

VITAMINS AND DIETARY SUPPLEMENTS REGISTRATION AND CLASSIFICATION .............................. 85

SELF-MEDICATION/SELF-CARE AND PREVENTATIVE MEDICINE ....................................................... 86

FORECAST .......................................................................................................................................... 86

REFERENCES ...................................................................................................................................... 87

PHARMACEUTICAL INDUSTRY IN KAZAKHSTAN.................................................................................... 88

EXECUTIVE SUMMARY ...................................................................................................................... 88

MARKET OVERVIEW .......................................................................................................................... 88

FOREIGN TRADE ................................................................................................................................ 94

INVESTMENT ..................................................................................................................................... 94

OTC REGISTRATION AND CLASSIFICATION ....................................................................................... 95

VITAMINS AND DIETARY SUPPLEMENTS REGISTRATION AND CLASSIFICATION .............................. 99

SELF-MEDICATION/SELF-CARE AND PREVENTATIVE MEDICINE ..................................................... 101

FORECAST ........................................................................................................................................ 102

REFERENCES .................................................................................................................................... 102

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

LIST OF TABLES AND FIGURES

1. GLOBAL PHARMACEUTICAL INDUSTRY OVERVIEW

Pie Chart 1. Share of Global Pharmaceutical Market for 2010 Bar Chart 1. Top Pharmaceutical Expenditure in GDP by Country in 2009, % Table 1. Consumer Expenditure on Pharmaceutical Products, Medical Appliances and Equipment Table 2. Production of Pharmaceuticals and Medicinal Chemicals by Countries Table 3. Top 25 Global Pharmaceutical Companies by 2011 Sales Table 4. Exports of Medicinal and Pharmaceutical Products Table 5. Imports of Medicinal and Pharmaceutical Products

2. PHARMACEUTICAL INDUSTRY IN RUSSIA

Table 6. Pharmaceutical Market Sizes in Russia Table 7. Production of Pharmaceuticals and Medicinal Chemicals in Russia Table 8. Sales of Consumer Health by Category in Russia Table 9. Sales of Consumer Health by City of Russia Table 10. Sales of Consumer Health by Distribution Format in Russia Table 11. Consumer Expenditure on Health Goods and Medical Services in Russia Table 12. Consumer Health Company Shares of Russia Table 13. Consumer Heath Brand Shares in Russia Table 14. Russia's Foreign Trade of Medicinal Agents Table 15. Investment in Health Care in Russia Table 16. Forecast Sales of Consumer Health by Category in Russia Table 17. Forecast Sales of Consumer Health by City of Russia

3. PHARMACEUTICAL INDUSTRY IN GEORGIA

Table 18. Production of Pharmaceuticals and Medicinal Chemicals in Georgia Table 19. Sales of Consumer Health by Category in Georgia Table 20. Sales of Consumer Health by Distribution Format in Georgia Table 21. Consumer Expenditure on Health Goods and Medical Services in Georgia Table 22. Consumer Health Company Shares of Georgia Table 23. Consumer Heath Brand Shares in Georgia Table 24. Georgia's Exports of Medicinal and Pharmaceutical Products Table 25. Georgia's Imports of Medicinal and Pharmaceutical Products Graph 1. FDI in Health and Social Work in Georgia Table 26. Forecast Sales of Consumer Health by Category in Georgia

4. PHARMACEUTICAL INDUSTRY IN UZBEKISTAN

Bar Chart 2. Manufacturing Output of Pharmaceutical Industry in Uzbekistan Pie Chart 2. Composition of Output of Main Medical Drugs in Uzbekistan for 2009 Table 27. Sales of Consumer Health by Category in Uzbekistan Table 28. Sales of Consumer Health by Distribution Format in Uzbekistan Table 29. Consumer Expenditure on Health Goods and Medical Services in Uzbekistan Table 30. Consumer Health Company Shares of Uzbekistan Table 31. Consumer Heath Brand Shares in Uzbekistan

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Table 32. Imports of Pharmaceutical Products of Uzbekistan Table 33. Forecast Sales of Consumer Health by Category in Uzbekistan

5. PHARMACEUTICAL INDUSTRY IN KAZAKHSTAN

Table 34. Production of Pharmaceuticals and Medicinal Chemicals in Kazakhstan Table 35. Sales of Consumer Health by Category in Kazakhstan Table 36. Sales of Consumer Health by Distribution Format in Kazakhstan Table 37. Consumer Expenditure on Health Goods and Medical Services in Kazakhstan Table 38. Consumer Health Company Shares of Kazakhstan Table 39. Consumer Heath Brand Shares in Kazakhstan Table 40. Exports of Medicinal and Pharmaceutical Products in Kazakhstan Table 41. Imports of Medicinal and Pharmaceutical Products in Kazakhstan Table 42. Forecast Sales of Consumer Health by Category in Kazakhstan

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Harmonized System Codes (HS Code) for Pharmaceutical Products

30 PHARMACEUTICAL PRODUCTS

3001 glands etc dry and ext, heparin, hum etc. subst nesoi

3002 human blood, animal blood, antisera, vaccines etc.

3003 medicaments nesoi of mixtures, not dosage etc. form

3004 medicaments nesoi, mixed or not, in dosage etc. fm

3005 bandages etc. coated etc. or in retail medic etc. fm

3006 pharmaceutical goods (specified sterile prod etc.)

Fast Facts about Pharmaceutical Products

It takes 10-15 years to develop a medicine or vaccine.

The research-based pharmaceutical industry currently spends over USD 100

billion (EUR 75 billion) on R&D.

It costs in average of USD 1.38 billion to develop a single medicine.

Nearly 20% of the world's top medicines were discovered and developed in

Britain.

In world terms, the UK industry has 9% of pharmaceutical R&D expenditure:

only the USA (49%) and Japan (15%) are ahead.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

GLOBAL PHARMACEUTICAL INDUSTRY OVERVIEW

INTRODUCTION

PHARMACEUTICAL INDUSTRY The pharmaceutical industry deals with the study,

development, mass production and distribution of the medicinal agent designed for

prophylaxis, pain relief and disease treatment.

TYPES OF MEDICINAL AGENTS The medicaments are included in the following two

categories: (1) prescription and (2) over-the-counter drugs. Usually no advertising campaign

is implemented for the prescription drugs. As a rule, these medicaments are introduced

with the patients by their doctors. And the patients can get them only when possessing the

doctor’s prescription. The over-the-counter drugs can be bought without any prescription.

Aspirin, cough medicine and others can be set as an example for over-the-counter drugs.

These medicaments relieve temporal pains and cure minor ailments.

PRODUCTION OF A NEW MEDICAMENT There is no a standing rule for a successful

development of a new product. Usually the developers of medicaments start to operate as

soon as there is a well-devised program and precisely defined aim. The production of a new

pharmaceutical includes the following three procedures: (1) study, (2) development and

production, (3) sale.

NAME OF A NEW MEDICAMENT The name of a new pharmaceutical is as much

important as to produce it. As a rule, a medicament has three names: (1) chemical name,

which defines its chemical composition (the chemical name of aspirin is “2-actoxybenzoic

acid”), (2) general name, which is the non-proprietary name of a medicament (the generic

name of aspirin is “Acetylsalicylic acid”), and (3) trade name, which enables a patient to

recognize the medicament (“Aspirin”).

EXECUTIVE SUMMARY Today pharmaceuticals have become an indispensable part of health care system around

the globe. Historically pharmaceuticals have played a vital role in the human development

by improving the quality of life and reducing the time spent in the hospitals. Thanks to

innovative pharmaceutical industry that almost all epidemics and chronic diseases are

curable today. Due to its direct link with the welfare and wellbeing of human beings,

pharmaceutical industry is of strategic importance for the development of a healthy and

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

productive nation. Nowadays, pharmaceutical industry is considered to be one of the largest

and rapidly growing global industries. It is a major source of employment generation and

foreign exchange earnings for many countries around the globe. However, despite all these

extraordinary achievements it’s a harsh reality that every year millions of people die across

the world, mostly in low income developing countries, due to unavailability and

inaccessibility of necessary medicines. According to the World Health Organization (WHO),

on average, 30% of the world population lacks access to life-saving medicines; whereas, in

some countries in Asia and Africa, the number may be as high as 50%.

Many developing countries have insufficient or no manufacturing capacities in the

pharmaceutical industry. Consequently, medicines are neither available nor accessible to a

large fraction of population and hundreds and thousands of people die of preventable and

treatable diseases.

MARKET OVERVIEW MARKET DATA The world pharmaceutical market grew by 4.5% in 2011. Average revenue

growth in established markets was 2.8% while that in emerging markets was over 4 times

higher at 12%. The top five pharmaceutical markets in the world remained the USA, Japan,

Germany, France and China, with the US representing 38.1% of global prescription

pharmaceutical sales (2010: 38.5%). While demand for medicines and world pharmaceutical

markets continued to grow in 2011, research-based pharmaceutical companies faced a

challenging marketplace. Industry returns are under pressure from declining R&D

productivity and intensifying pricing pressures, particularly in Established Markets facing

rising healthcare costs. We also face increased competition from generic medicines as some

of the world’s most successful drugs come off patent. In addition, greater regulatory

constraints are being placed on the pharmaceutical industry by governments and those who

pay for our medicines.

The industry remains highly competitive. Our competitors are other large research-based

pharmaceutical companies that develop and sell innovative, patent-protected prescription

medicines and vaccines, as well as smaller biotechnology and vaccine companies, and

companies that produce generic medicines. While many of our peers are confronting similar

challenges, strategically these challenges are being met in different ways. For example,

some companies have chosen to diversify by acquiring or building branded generics

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

businesses or consumer portfolios, arguing that this enables them to better meet changing

customer needs and smooth risk for shareholders.

Most companies continued to pursue their existing strategies in 2011, with some continuing

to diversify and others pursuing a focused strategy. There were, however, exceptions with

examples of companies shedding diversified assets. Key trends included efforts to improve

R&D productivity, expansion of geographic scope, especially in Emerging Markets and Japan,

and the pursuit of operational efficiency. Industry consolidation continued with both merger

activity and acquisitions of specific assets and capabilities.

The global pharmaceutical industry, after experiencing a shrink during the past 2-3 years, is

now in its recovery period, which will be followed by its growth. Decline in global

pharmaceutical market was largely due to the economic recession. Meanwhile,

pharmaceutical markets in some developing regions, like Asia and Latin America have been

continuously witnessing huge growth rate for the last few years on account of increasing

prevalence of diseases, rising healthcare spending, and increasing affordability. United

States is still the largest pharmaceutical market in the world with a market size of around

USD 300 billion and it is expected to reach USD 370 to USD 390 billion by 2015 (see the pie

chart below).

Source: www.businessvibes.com

33%

30%

18%

7%6%

2% 2% 1% 1%

Pie Chart 1. Share of Global Pharmaceutical Market for 2010

USA Europe Japan

Latin America China Middle East

Australia Canada Africa

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Today’s major pharmaceutical markets, consisting of 17 countries, are slated to grow in the

range of 15-17% in 2012, representing sales of USD 170-180 billion. China, which is now the

third largest market in the world, is expected to grow 25-27% to more than USD 50 billion in

2012. As far as developed markets are concerned, Japan is slated to grow 5-7% in 2012.

Major European markets like the UK, Germany, France, Italy and Spain are expected to

deliver combined growth of 13%.

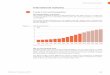

In 2009, the USA was a global leader in pharmaceutical expenditure in GDP with 2.14%. The

bar chart below represents the top leader countries in pharmaceutical expenditure in GDP

for 2009.

Source: www.businessvibes.com

The data of consumer expenditure on pharmaceutical products, medical appliances and

equipment are displayed in the table below.

Table 1. Consumer Expenditure on Pharmaceutical Products, Medical Appliances and Equipment

mln USD

Country 2006 2007 2008 2009 2010 2011 WORLD 677492.5 753760.0 831961.9 865376.1 954592.7 1061056.8

USA 320890.2 340695.1 352307.1 366235.8 384350.3 410189.0 China 36916.6 43621.9 53718.5 74949.6 90537.0 112497.7 Japan 38107.9 36509.9 44897.0 53269.5 65428.9 72703.4

Germany 25981.7 29207.5 33649.2 31667.8 31709.5 34497.8 France 20042.2 22745.1 25946.5 25159.9 24522.3 26474.9 Canada 14766.4 17009.8 17926.8 17527.8 20341.7 22431.4 Russia 8748.8 11908.7 15883.2 14591.8 17766.0 22227.1 Italy 15832.3 17540.4 19163.6 17646.0 17007.2 18375.6

Switzerland 7680.2 7973.8 10245.2 10396.2 12334.1 15127.7 UK 13439.3 15367.5 14265.7 12635.9 12407.8 13316.8

2.14

1.58

1.54

1.53

1.28

USA

Japan

Spain

France

Belgium

Bar Chart 1. Top Pharmaceutical Expenditure in GDP by Country in 2009, %

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Spain 8099.4 9599.9 10939.5 10346.7 10099.7 10701.8

Source: www.portal.euromonitor.com

The figures in the table above prove that the world consumer expenditure on

pharmaceutical products, medical appliances and equipment is growing steadily: an 11.2%

growth in 2011 over the 2010 record. The figures prove the growing trend in consumer

expenditures of this category as the world population has a growing trend. USA, China and

Japan are in the first, second and third place respectively.

PRODUCTION According to Euromonitor data, in 2011, China has exceeded its production

of pharmaceuticals and medicinal chemicals excelling even the USA production (by circa

9.2%). Japan has demonstrated a stable growth as the time series show: a 4.3% growth in

2010 over the 2009 record, and a 9.5% growth in 2011 over the 2010 record.

Table 2. Production of Pharmaceuticals and Medicinal Chemicals by Countries

mln USD

Country 2006 2007 2008 2009 2010 2011 China 71694.7 92582.2 119343.7 134128.5 159419.7 189005.7 USA 193194 184801.6 173401.6 163905.3 168072.1 173594.2

Japan 58181.6 59371.9 66883.8 67402.6 70322.5 77690.9 France 48936.8 54778.1 60290 59602.3 59513.2 65848.7

Germany 42597.4 49693.0 52563.9 46645.4 44316.8 49526.4 UK 32116.4 37105.4 35816.5 32424.7 34252.3 37489.8

Italy 30468.5 35411.7 36905.6 31984.1 31345.5 33786.7 Spain 15815.4 18589.5 23379.5 23063.6 21348.9 22949.6

Source: www.portal.euromonitor.com

GROWTH DRIVERS EXPANDING PATIENT POPULATIONS The world population has already passed 7 billion in

2011, increasing from 6 billion in 1998 and is expected to reach 9 billion by 2050. In

addition, the number of people who can access healthcare continues to increase,

particularly among the elderly. Globally, it is estimated that the number of people over 65

will be almost one billion by 2030, double what it was in 2005.

Faster-developing economies, such as China, India and Brazil, offer new opportunities for

the pharmaceutical industry to help an expanding number of patients who can benefit from

innovative medicines. Emerging markets now represent approximately 85% of the world

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

population. In addition, pharmaceutical revenues in those markets grew significantly faster

than those in established markets in 2011 and it is estimated that this trend will continue.

UNMET MEDICAL NEED In most established markets, ageing populations and certain

lifestyle choices such as smoking, poor diet and lack of exercise drive an increased incidence

of chronic diseases such as cancer, cardiovascular/metabolic and respiratory diseases which

require long-term management. The prevalence of chronic disease is increasing in middle

income countries and is also beginning to have an impact in low income countries. For

example, there are 36 million deaths every year from non-communicable diseases and, of

those, 80% are in lower and middle income countries. It is estimated that nearly 33% of the

world’s diabetes patients will come from India and China by 2030.

ADVANCES IN SCIENCE AND TECHNOLOGY Innovation leading to new drugs is critical to

meeting unmet medical need. Existing drugs will continue to be important in meeting the

growing demand for healthcare, particularly with the increasing use of generic medication.

At the same time, advances in disease understanding and the application of new

technologies will be required to ensure the delivery of new medicines. Such approaches

include personalized healthcare and predictive science as well as new types of therapy.

With advances in the technologies for the design and testing of novel compounds, new

opportunities exist for the use of innovative small molecules as new medicines. The use of

large molecules, or biologics, has also become an important source of innovation, with

biologics among the most commercially successful new products. Forecasts for 2016 predict

that of the world’s top 100 pharmaceutical products, 45% of sales will come from biologics.

This compares with only 33% in 2010 and 15% in 2002. Most pharmaceutical companies

now pursue both small molecules and biologics R&D.

PHARMACEUTICAL INDUSTRY LEADERS For 2011, the pharmaceutical industry analysts list the top industry leaders as Pfizer,

Novartis, Merck & Co, Sanofi-Aventis, Roche, GlaxoSmithKline, AstraZeneca, Johnson &

Johnson, Abbott, Eli Lilly and Bristol-Myers Squibb.

Headquartered in New York, Pfizer has over 110,000 employees and is the leading research-

based pharmaceutical company worldwide. Pfizer reported a 36% rise in revenue for 2010.

This is largely thanks to its acquisition of competitor Wyeth, which Pfizer purchased for USD

68 billion. Pfizer manufactures the 2010 number-one selling prescription drug in the US,

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Lipitor. Sales for Lipitor reached USD 7.2 billion in 2010 and represented 18% of the

company’s biopharmaceutical revenue. Lipitor is used to treat patients with raised levels of

cholesterol. Pfizer also acquired King Pharmaceuticals in 2010 at the cost of USD 3.6 billion.

King manufactures various medications for use in pain management, a market worth USD 22

billion. King products that will likely boost Pfizer sales include Embeda and Remoxy, which

are painkillers that pose less risk of addiction than other offerings on the market. Emeda

sales for the six-month period following its launch reached sales of almost USD 24 million.

Swiss-based Novartis was established in 1996 with the merger of Sandoz and Ciba-Geigy.

Among its well-known drugs are Gleevic, used in the treatment of chronic myeloid leukemia.

In one of its initiatives, Novartis supplied Gleevic to 27,000 patients spanning 80 countries.

In 2010, Novartis’s Gilenya was approved in the US by the FDA and also in Russia and

Switzerland. Gilenya is the first oral treatment used in the treatment of relapse-remitting

multiple sclerosis. In the second quarter of 2011, Novartis saw its net sales grow 27% to

almost USD 15 billion. Its core operating income increased 29% to USD 4.2 billion.

The following table represents the pharmaceutical company sales by country for 2011.

Table 3. Top 25 Global Pharmaceutical Companies by 2011 Sales

Country Ticker Company bln USD USA PFE Pfizer 57,70

Switzerland NVS Novartis 54,00 USA MRK Merck & Co 41,30

France SNY Sanofi-Aventis 37,00 Switzerland RHHBY Roche 34,90

UK GSK GlaxoSmithKline 34,40 UK AZN AstraZeneca 33,60

USA JNJ Johnson & Johnson 24,40 USA ABT Abbott 22,40 USA LLY Eli Lilly 21,90 USA BMY Brystol-Myers Squibb 21,20

Israel TEVA Teva 16,70 USA AMGN Amgen 15,30

Japan TKPYY Takeda 15,20 Germany N/A Boehringer Ingelheim 13,80 Germany BAYRY Bayer 12,80

Japan DSNKY Daiichi Sankyo 11,60 Denmark NVO Novo Nordisk 11,50

Japan ALPMY Astellas 11,40

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

USA GILD Gilead Sciences 8,10

Japan OTSKY Otsuka 7,40 Germany MKGAY Merck KGaA 7,20

USA BAX Baxter International 6,10 USA MYL Mylan 5,50

France N/A Servier 5,00 Source: Pharmaceutical Executive

The American Pfizer and Merck companies take the first and third places with the sales of

USD 57.7 and 41.3 billion respectively. The Swiss Novartis company is in the second place

with the sales of USD 54.0 billion.

EXTERNAL TRADE EXPORTS Top three leaders in exports of medicinal and pharmaceutical products are

Germany, Switzerland and Belgium. Despite the world leader in pharmaceutical and

medicinal chemical production is China, the leader in exports is Germany. The most famous

German pharmaceutical companies are Boehringer Ingelheim, Bayer and Merck KGaA.

Table 4. Exports of Medicinal and Pharmaceutical Products

mln USD

Country 2006 2007 2008 2009 2010 2011 Germany 44963.7 55311.1 66722.1 63732.7 65335.2 69416.6

Switzerland 29872.7 34700.3 42118.5 43960.8 47612.2 54967.8 Belgium 38114.5 47394.2 50225.7 52278.9 51214.9 49772.0

USA 28794.1 32968.1 37711.8 44055.6 44437.0 42954.2 Ireland 17897.6 20205.0 24520.0 29981.8 32120.6 36723.5

UK 25425.6 29086.0 32073.1 32046.7 34367.4 36297.3 France 25186.3 28853.8 33973.0 35078.4 34672.8 33974.5

Italy 14053.4 15647.3 16696.2 16057.9 17591.1 20410.7 Netherlands 12620.7 15200.9 10448.5 11835.6 13873.6 15942.7

Spain 7570.6 9632.3 11288.7 10863.1 11754.2 14498.1 China 4488.2 5992.0 8079.3 8615.7 10685.1 11815.6

Source: www.portal.euromonitor.com

IMPORTS The list of medicinal and pharmaceutical product importers is represented below.

Table 5. Imports of Medicinal and Pharmaceutical Products

mln USD

Country 2006 2007 2008 2009 2010 2011 USA 44654.7 52344.9 58175.9 58569.1 63784.7 68220.0

Germany 34636.7 40806.1 45959.9 46049.5 46824.5 51370.9

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Belgium 35243.4 41445.5 43962.1 43722.6 42712.4 36807.7 France 19199.9 22793.5 25546.8 28188.5 28792.2 30083.6

UK 16860.1 20360.8 21020.6 21041.4 23902.4 26504.1 Italy 15702.6 18178.4 20273.4 21382.8 21698.2 25048.4

Japan 8517.5 9144.4 10997.2 14204.0 17352.0 21545.5 Switzerland 13804.9 15864.1 16789.3 16558.9 17893.0 21309.1

Spain 9514.4 11975.8 15203.2 17173.4 15161.7 17852.2 Netherlands 12831.6 16342.8 12730.7 12213.4 12340.9 14030.9

Canada 9533.0 10527.6 11227.8 12067.3 12320.7 13091.8 China 2716.3 3889.1 5528.1 6688.2 8018.4 11282.6

Source: www.portal.euromonitor.com

USA, Germany and Belgium are the top importers of pharmaceutical and medicinal products

despite the import volumes of Belgium have begun decreasing since 2009.

R&D PRODUCTIVITY Improving R&D productivity is a critical challenge for the pharmaceutical industry. Global

investment in pharmaceutical R&D by the top 500 pharmaceutical and biotech companies

reached an estimated USD 133 billion in 2011, a 93% increase from USD 69 billion in 2002.

Over the same period, the number of new drug launches per year in the US stayed broadly

the same. Increasing investment has not resulted in a sustained increase in output yet,

although the FDA approved 30 new drugs in 2011. At the same time, there appears to be a

shift away from regulatory submissions for broad primary care medicines to more specialist

drugs treating, for example, more complex diseases, together with orphan drugs for rare

medical conditions.

To ensure it delivers a sustainable return on its R&D investment, the industry is working to

increase its probability of success in developing commercially viable new drugs and moving

to a lower, more flexible cost base. It does so at a time when regulators and payers are

demanding more and better evidence of comparative effectiveness of compounds, which

lengthens development times and increases development costs.

Using the full range of innovative technologies, the industry is focused on two critical

milestones: proof of concept, which delivers candidate drugs with supporting data

demonstrating that the drug results in a clinical change with an acceptable endpoint or

surrogate in patients with the disease and, secondly, product approval.

Organizationally, companies are addressing productivity challenges in a variety of ways.

These include:

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

• focusing on a defined set of therapeutic areas and exiting those where success

has been poor;

• restructuring R&D organizations to create clearer accountabilities and smaller,

more entrepreneurial units;

• revamping decision making and governance, so that unsuccessful compounds

are identified early, before significant costs have been incurred;

• reducing costs and improving process efficiency, using lean business

improvement tools such as Six Sigma1 and outsourcing;

• a collaboration-centric business model that includes academic collaborations

and co-development agreements that provide for the sharing of development

risks and costs with third parties;

• looking externally for high quality science, technologies, targets, drug

candidates and/or entire drug pipelines.

REGULATORY REQUIREMENTS The pharmaceutical industry continues to be one of the most heavily regulated. This reflects

public interest in ensuring access to safe, effective and high quality medicines that are

responsibly promoted.

Efforts to harmonize regulations globally are ongoing, yet the number of regulations and

their impact continue to multiply. This is particularly evident in the conduct of clinical trials.

In order to support the registration of medical products in a given regulatory jurisdiction,

programs providing foreign clinical trial data must meet each individual health authority’s

requirements to ensure relevance to their population. Regulators also continue to redefine

their patient safety assessment processes. This includes the management of known and

emerging risks, both before and after product approval. In certain markets, additional safety

initiatives are developing locally which operate independently of already established

international standards, further increasing the complexity and disharmony of drug safety

monitoring and reporting. In addition, the growing complexity and globalization, of both

clinical studies and the manufacturing supply chain, has led to an increase in cross-regional

health authority collaborations and inspections in these areas.

1 Six Sigma seeks to improve the quality of process outputs by identifying and removing the causes of defects (errors) and minimizing variability in manufacturing and business processes.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Public demand for access to data, especially clinical data, to understand how health

authorities arrive at their regulatory decisions, has resulted in numerous transparency

proposals worldwide. In some instances, policies have been implemented without

guidelines that define personal, private and proprietary information. Thus there can be no

assurance that the data will be safeguarded against public disclosure.

There is mounting pressure from both health technology assessors and payers to assess not

only the safety of our products but also their relative effectiveness and value. Consequently

there is a heightened interest by health authorities in both the comparative clinical

effectiveness and the ongoing benefit/risk assessment of pharmaceuticals after approval.

The regulatory landscape is evolving with an increased focus on incorporating validated

health outcome quality measures into clinical trials and developing clinical comparative

evidence.

In spite of the challenges, regulators are approving drugs that address unmet medical needs

when supported by strong data and compelling benefit/risk propositions. In addition, health

authorities are increasing their collaboration with external stakeholders to drive innovation,

define and clarify approval requirements for personalized healthcare and drug-diagnostic

combinations and to accelerate the development of treatments that address public health

priorities.

PRICING The pricing of medicaments depends on numerous factors including development costs,

research costs and similarities to other medical agents in market, improvement upon other

pharmaceuticals and who are buying them. Hospitals and government organizations, such

as the military and Medicaid are able to negotiate the lowest prices because of their power

and volume that they buy the goods. Medicaid supports an immense amount of low wage

workers in the US and as a result pays for nearly 20% of all drugs sold in the US.

Most pharmaceutical sales continue to be generated in highly regulated markets where

governments and private payers, such as insurance companies, exert various levels of

control on pricing and reimbursement. Cost containment in healthcare, including

containment of pharmaceutical spending, continues to be a focus and the global economic

downturn has enhanced this trend. As a consequence, the pricing and reimbursement

environments in many markets continue to be highly dynamic. It is increasingly important

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

for companies to work with governments to promote innovation, while ensuring they

achieve adequate commercial returns.

Pricing pressures have arisen in the pharmaceutical industry in a number of ways in recent

years, particularly through the implementation of a variety of regulatory drug price control

mechanisms and other reforms. For example, in Europe, mandatory discounts have been

applied in Italy. In Germany, Europe’s largest pharmaceutical market, there have been

freezes on permitted pharmaceutical prices. In addition, recent German healthcare reforms

have transformed the way in which new patent protected drugs are assessed. There is no

longer a free market for the pricing and reimbursement for such drugs. Instead, the law in

Germany now requires manufacturers to prove the additional benefit of their drugs over

existing alternatives and demonstrate their value to regulators and payers. Only by showing

additional benefit can create opportunities for the drug to be transferred to the German

reference pricing system, where, for each drug group, a single reimbursement level or

reference price is set.

China has experienced 26 rounds of cuts to the maximum permitted retail drug prices in the

last seven years and in Japan and South Korea biennial cuts are expected to continue. We

are also seeing the introduction of fixed hospital tariffs, which can act as a method of

controlling drug costs by incentivizing hospitals to choose cheaper generic alternatives.

In the US, the Affordable Care Act (Act) has already had a direct impact on healthcare

activities despite the fact that many of the healthcare coverage expansion provisions of the

Act do not take effect until 2014. For example, there has been an increase in drug rebates

and discounts. The pharmaceutical industry, including AstraZeneca, has continued to show

its commitment to expanding access to government healthcare programs through, for

example, helping to close the coverage gap in the Medicare Part D2 prescription drug

program and by paying an annual industry fee. The industry is working with policymakers

and regulators during the implementation of healthcare reform with a view to ensuring that

they strike a balance between containing costs, while also promoting an environment that

fosters medical innovation.

2 Medicare Part D, also called the Medicare prescription drug benefit, is a federal program to subsidize the costs of prescription drugs for Medicare beneficiaries in the US.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

PATENT EXPIRIES AND GENERICISATION Over the next few years some of the biggest selling drugs the industry has ever produced

face patent expiry. As a consequence, payers, physicians and patients in established markets

will have low price, generic alternatives in many important classes of primary care drugs. For

example, in the US, generics constitute 80% of the market by volume today and are

expected to be the single largest driver of value growth up to 2015.

Patents only protect pharmaceutical products for a finite period and the expiry or early loss

of patents may lead to the availability of generics. Generic versions of drugs are very

competitive with significantly lower pricing than the innovator equivalents. This is partly due

to lower investment by generic manufacturers in R&D and market development which

generic manufacturers do not need to recover. While generic competition has traditionally

occurred when patents expire, it can also occur where the validity of patents is disputed or

successfully challenged before expiry. Such early challenges by generics have increased with

generic companies increasingly willing to launch products “at risk”, for example, prior to

resolution of the relevant patent litigation. This trend is likely to continue, resulting in

significant market presence for the generic version during the period in which litigation

remains unresolved, even though the courts may subsequently rule that the innovative

product is properly protected by a valid patent. The unpredictable nature of patent litigation

has led innovators to seek to settle such challenges on terms acceptable to both innovator

and generic manufacturer. However, some competition authorities have sought to challenge

the scope or even availability of this type of settlement agreement.

Biologics have sustained longer life-cycles than traditional pharmaceuticals and have faced

less generic competition. This is due to a more complex manufacturing process for biologics

compared with small molecule medicines and the inherent difficulties in producing a copy of

a biologic, or biosimilar3, which is sufficiently similar to the innovator to meet regulatory

requirements. However, with regulatory authorities in Europe and the US continuing to

implement abbreviated approvals processes for biosimilar versions, biologics are becoming

subject to competition from biosimilars and other follow-on biologics.

3 Biosimilars are bio pharmaceuticals whose active drug substance are made by a living organism or derived from a living organism by means of recombinant DNA or controlled gene expression methods.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

BUILDING TRUST The pharmaceutical industry faces a challenge in building and maintaining trust, particularly

with governments and regulators. The last 10 years have seen a significant increase in the

number of settlements between innovator companies and governmental and regulatory

authorities for violations of a variety of laws. These include breaches of sales and marketing

practices, inducements of physicians to administer a company’s products and breaches of

anti-trust legislation. For some audiences, there is a perception that pharmaceutical

companies place their commercial goals above the interests of patients, physicians and

payers. Companies are taking steps to change this perception by embedding a culture of

ethics and integrity, adopting higher standards of governance and improving relationships

with employees, shareholders and other stakeholders.

FORECAST The global pharmaceutical industry is expected to be worth more than USD 1 trillion in

2014, marking a 5% compound annual growth rate according to research from Urch

Publishing.

The pharmaceutical market worldwide, after experiencing a slump during the past 2-3 years,

is now in its recovery period, which will be followed by its growth. Decline in global

pharmaceutical market was largely due to the economic slowdown and further aggravated

by patent expiry of key blockbusters together with saturation in key pharmaceutical

markets, such as the US and Western Europe. Meanwhile, pharmaceutical markets in some

developing regions, like Asia and Latin America have been continuously witnessing robust

growth rate for the last few years on account of increasing prevalence of diseases, rising

healthcare spending and increasing affordability. Overall, these markets will enjoy good

growth potential in coming few years.

According to the latest research “Global Pharmaceutical Market Forecast to 2012”, global

pharmaceutical industry is projected to grow at a CAGR of around 6.5% during 2011-2013.

The growth will be driven by low cost factor, increasing prevalence of diseases worldwide,

and rising per capita income of consumers. The sales of generic drugs will emerge as the

most prominent segment of the pharmaceutical market during the forecast period,

indicating large opportunities for generics manufacturers to tap.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Some regional level analysis found that the pharmaceutical industry is growing at a rapid

rate in emerging countries, such as India, China, Brazil, Russia, while a slowdown in the

growth has been encountered in the US and Western European countries.

CONCLUSION The market for pharmaceutical goods is increasing due to an aging global population,

advances in drug-based treatment research, increased investment in healthcare and

consumer-driven private health coverage and rising numbers of patients suffering from

cardiovascular disease, cancer and degenerative diseases. Market growth faces particular

challenges such as price pressures, strict regulation, lawsuits and expiring patents.

Expiring patents are paving the way for generic drugs to produce cheaper versions of

blockbuster drugs, cutting into pharmaceutical company profits. Many leading drugs on the

market are to see their patents expire over the next 5 years. According to many industry

reports, the patents for 10 top selling drugs will expire by 2013; namely, they are Lipitor,

Plavix, Seroquel, Actos, Enbrel, Singulair, Levaquin, Zyprexa, Concerta and Protonix.

Despite showing rapid growth over the years, global pharmaceutical industry remained

highly concentrated in the developed countries, which dominate the global pharmaceutical

production, consumption and trade. Although some developing countries emerged as major

contributor, the share of developing countries in global pharmaceutical industry remained

very low.

To this end, the following related concluding remarks can be made:

• Pharmaceutical production requires skilled human resources like scientists,

pharmacists, biologists and lab technicians. For this very reason, the future

professionals and experts in medicine should be provided with appropriate knowledge

and skills.

• Pharmaceutical industry relies heavily on research and development (R&D) activities.

Hence proper R&D facilities should be built and researchers and technicians should be

provided with necessary financial resources to develop an innovative pharmaceutical

industry.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

REFERENCES www.portal.euromonitor.com

http://www.imeche.org/knowledge/industries/process-industries/pharmaceuticals/facts-and-figures

http://www.businessvibes.com/blog/industry-insight-global-pharmaceutical-industry

http://topforeignstocks.com/2012/10/31/the-top-25-pharmaceutical-companies-by-2011-sales/

http://www.dsm.ru/content/file/1306924994.pdf

http://www.pharmexpert.ru/en/analytics/48/?y=2011

http://www.duke.edu/web/soc142/team2/political.html

http://www.researchandmarkets.com/reports/656457/global_pharmaceutical_market_forecast_to_2012

http://www.reportlinker.com/ci02257/Pharmaceutical.html

http://www.astrazeneca-annualreports.com/2011/our_strategy_and_performance/the_pharmaceutical_industry

http://www.foreign-trade.com/reference/hscode.cfm?cat=5

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

PHARMACEUTICAL INDUSTRY IN RUSSIA

EXECUTIVE SUMMARY The Russian pharmaceutical market comprises 2 basic segments: commercial segment and

state segment. The commercial segment of pharmaceutical industry includes the sales of

ready-to-use medicinal agents and parapharmaceuticals4 excluding the sales within the

framework of state reimbursement program. The state segment of pharmaceutical industry

implies the sales of ready-to-use medicinal agents, parapharmaceuticals and the sales

through medioprophilactic institutions within the framework of state reimbursement

program.

The main trend in 2011 for Russia was the formation of a “pharmaceutical clusters”. This

process takes place in the framework of the Strategy for the Development of

pharmaceutical industry that must have been implemented by 2020. Another significant

event in 2011, which will soon be reflected in the pharmaceutical market, was the signing of

documents on Russia's accession to the WTO. Russian pharmaceutical market is among the

10 largest pharmaceutical markets in the world. In 2011, Russia took the 8th place. The

volume of the pharmaceutical market in Russia in 2011 amounted to RUR 824 billion (or

USD 28 billion) in retail prices including VAT. The figure for 2010 was 12% less than the one

in 2011.

The Russian pharmaceutical market is import-oriented. The 76% of medicaments (in money

terms) in the Russian market is imported. The importance of the wholesaling remains very

high due to the geographical features of Russia. Big distributors support numerous branch

networks and representative offices. Smaller wholesalers are beginning to create an 4 Parapharmaceuticals - biologically active additives on the basis of extracts of medicinal plants - used for disease prevention, adjuvant therapy and maintenance of the functional activity of organs and systems. Their properties are determined belonging to the plant organic acids and other substances. Their role is to enhance the adaptive capacities of the organism in extreme circumstances.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

extensive network of warehouses (e.g., FC PULSE, Imperia Pharma). Leaders in the

distribution segment up to 2011 are “SIA International” and “Protek CV”. Their share in the

total market amounts to 33%. The distributors R-Pharm and Biotech are growing at high

growth rates.

2011 was marked as “business optimization” year for the pharmacies in the light of new

legislation and tax regulations. The largest deal of the year was the acquisition of the state

pharmacy network “Mosoblpharmacia”. The group of companies A5 and the investment

fund Hi Capital were the purchasers. As a result, the network of pharmacies was ranked 1st

by the number of drugstores (1,370 drugstores). The largest networks in turnover are

“36.6”, “Rigla”, “Impoziya” — their share amounts to 7.2%.

The drivers of market growth were inflation (+8.8%) and the transition to more expensive

drugs.

4.4 billion of packaged medicaments were sold in 2011. Almost the same amount was

consumed in 2010.

The parapharmaceutical segment has not recovered after the crisis yet. The capacity of this

segment in 2011 amounted to RUR 130 billion (or USD 4.4 billion). The figure for 2010 is

10% less than the 2011 one. Despite this phenomenon, the pharmacies continue to sell this

category of products under non-drug items.

In 2011, the public sector showed an increase of 7%. This is one of the most stable segments

of the pharmaceutical market because its development is based on state budget funds. At

the end of 2011 for the purchase of medicines for people entitled to benefits was spent 84.7

billion rubles. Increase compared to 2010 was about 4.7%.

MARKET OVERVIEW MARKET DATA The situation in the Russian pharmaceutical industry for 2011 can be

described as stable thanks to the stable economic situation and the lack of a strong

influence of external factors, such as abnormal weather conditions and the deterioration of

the epidemiological situation. Legislative initiatives as well have caused significant changes

in the organizational structure of the pharmaceutical market and its qualitative

development.

The growth of hospital medicaments’ share (14% or USD 4.57 billion over the previous year)

was also significant in 2011. Such dynamics is explained by the state funding in the

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

modernization program of healthcare. Financial means were assigned to purchase expensive

medicaments used in oncology, pulmonology, cardiology, etc. Taking into account that the

present program is planned to be executed within 2 years, its implementation progress in

hospital sector will be determined in 2012.

Macroeconomic stability is the basis for the development of all sectors of the

pharmaceutical market, and especially the ones that are dependent on public funding. The

increase in expenditure in hospital drugs improves not only the quality of medical care, but

also fosters the drug coverage and reimbursement and the development of the commercial

sector. This correlation is explained by the shift of funds from one segment to another. For

example, when there is insufficient funding for the purchase of medicines in hospital sector,

patients are forced to buy the necessary drugs on their own retail chain.

Regarding the drug coverage and reimbursement sector, it showed the lowest growth rate

— about 5% or USD 2.84 billion in 2011. This phenomenon took place due to the outflow of

the beneficiaries of the program. The substitution of domestic products with the imported

ones has also impacted on this process. The production of Russian origin oppressed the

imported ones in 2011 offering products for the treatment of hemophilia, multiple sclerosis,

pituitary dwarfism, etc.

Currently the Russian pharmaceutical market is developing steadily. According to

preliminary data, the following years will also end with growth in this sector.

The table below represents the volumes (in money terms).

Table 6. Pharmaceutical Market Sizes in Russia mln USD

SECTOR 2009 Growth (%) 2010 Growth (%) 2011

Commercial Sector 12054 11 13366 19 15964 Pharmacy Sector for Parapharmaceuticals 3649 7 3894 14 4438

Public Sector 6159 13 6944 11 7713 TOTAL 21862 11 24204 16 28116

Source: DSM Group. 9001:2008

The total pharmaceutical market sizes in Russia have the trend to grow. In 2011, the growth

amounted to 16% over the previous year.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

PRODUCTION The production of pharmaceutical agents and medicinal chemicals in Russia

is represented in the table below.

Table 7. Production of Pharmaceuticals and Medicinal Chemicals in Russia

mln USD

2006 2007 2008 2009 2010 2011 3197.2 4164.8 5096.4 4940.6 6149.4 7254.0

Source: www.portal.euromonitor.com

The drop by circa 3% in 2009 vis-à-vis 2008 was compensated with about 24.5% growth in

2010 over the 2009 record. In 2011, the growth in production amounted to 18% over the

previous year.

SALES In 2011, the total sales of consumer health amounted to 16%. Over the counter

(OTC) pharmaceutical sales dominate over the sales of sports nutrition, vitamins and dietary

supplements, weight management medicaments, herbal/traditional products, the

medicaments for allergy care and the medical agents for pediatric consumer health. The

table below represents the sales of consumer health by category for 2006-2011.

Table 8. Sales of Consumer Health by Category in Russia mln USD

Category 2006 2007 2008 2009 2010 2011 Over the Counter (OTC) 1680.4 2178.5 2812.0 2523.7 2863.2 3302.0 Sports Nutrition 21.3 29.4 39.6 36.3 43.1 50.1

Vitamins and Dietary Supplements 755.5 992.8 1244.6 1093.2 1219.2 1428.3

Weight Management 153.8 191.0 239.2 214.5 220.2 258.5

Herbal/Traditional Products 337.3 437.6 573.1 512.2 595.9 704.5

Allergy Care 82.9 114.0 154.0 140.3 165.8 177.1 Pediatric Consumer Health 62.6 88.4 116.2 109.7 134.7 162.3

Consumer Health 2637.8 3427.6 4384.2 3910.5 4396.8 5102.1

Note: all the figures were given in mln RUB in Euromonitor. The conversions from RUB to USD have been made according to the average annual exchange rates of the appropriate year.

Source: www.portal.euromonitor.com

Source: www.1prime.ru

The sales of consumer health by cities are represented below.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Table 9. Sales of Consumer Health by City of Russia

mln USD

Category 2006 2007 2008 2009 2010 2011 Moscow 529.5 694.4 915.2 780.7 886.5 1026.5 St Petersburg 162.6 218.3 286.0 257.8 292.6 336.6

Russia 2637.8 3427.6 4384.2 3910.5 4396.8 5102.1 Note: all the figures were given in mln RUB in Euromonitor. The conversions from RUB to USD have

been made according to the average annual exchange rates of the appropriate year.

Source: www.portal.euromonitor.com

Source: www.1prime.ru

The sales of consumer health by distribution format are represented below. As shown in the

table, store-based retailing has dominated over the non-store retailing.

Table 10. Sales of Consumer Health by Distribution Format in Russia % retail value rsp

Category 2006 2007 2008 2009 2010 2011 Store-Based Retailing 91.5 91.6 91.8 92.0 92.0 91.6 Grocery Retailers 2.1 1.9 1.9 1.8 1.9 1.9 Discounters 0.0 0.0 0.0 0.0 0.0 0.0 Health Food Shops 0.0 0.0 0.0 0.0 0.0 0.0 Hypermarkets 0.1 0.2 0.2 0.2 0.2 0.3 Small Grocery Retailers 0.4 0.4 0.4 0.4 0.4 0.4 Supermarkets 0.7 0.7 0.7 0.8 0.8 0.8 Other Grocery Retailers 0.9 0.7 0.5 0.4 0.4 0.4 Non-Grocery Retailers 89.4 89.7 89.9 90.2 90.1 89.7 Health and Beauty Retailers 87.6 87.6 88.1 88.2 88.5 88.0 Chemists/Pharmacies 87.1 87.2 87.7 87.7 87.9 87.4 Parapharmacies/Drugstores 0.0 0.0 0.0 0.0 0.0 0.1 Other Healthcare Specialist Retailers 0.5 0.5 0.5 0.5 0.5 0.5 Mixed Retailers 0.0 0.0 0.0 0.0 0.0 0.0 Department Stores 0.0 0.0 0.0 0.0 0.0 0.0 Mass Merchandisers 0.0 0.0 0.0 0.0 0.0 0.0 Variety Stores 0.0 0.0 0.0 0.0 0.0 0.0 Warehouse Clubs 0.0 0.0 0.0 0.0 0.0 0.0 Other Non-Grocery Retailers 1.9 2.1 1.8 2.0 1.6 1.7 Non-Store Retailing 8.5 8.4 8.2 8.0 8.0 8.4 Vending 0.0 0.0 0.0 0.0 0.0 0.0 Home Shopping 1.0 1.0 0.9 0.8 0.8 0.9 Internet Retailing 2.0 2.1 2.2 2.3 2.4 2.7 Direct Selling 5.5 5.3 5.1 4.9 4.8 4.9

TOTAL 100.0 100.0 100.0 100.0 100.0 100.0 Source: www.portal.euromonitor.com

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

The consumer expenditure on health goods and medical services in Russia is represented

below.

Table 11. Consumer Expenditure on Health Goods and Medical Services in Russia mln USD

Category 2006 2007 2008 2009 2010 2011

Pharmaceuticals, Medical Appliances and Equipment

8748.8 11908.7 15883.2 14591.8 17766.0 22227.1

Outpatient Services 6037.8 6982.6 9262.6 7508.3 8546.7 10232.0

Hospital Services 1646.7 2327.5 2526.2 2047.7 2330.9 2635.0

TOTAL 16433.3 21218.8 27672 24147.8 28643.6 35094.1 Source: www.portal.euromonitor.com

The consumer expenditure grew by 22.5% in 2011 vis-à-vis the previous year.

COMPETITION FIELD Pharmstandart, Novartis and Evalar are the top leaders in consumer

health company shares in Russia. Among these 3 companies, only Novartis is of Swiss origin.

The rest are Russian companies.

Table 12. Consumer Health Company Shares of Russia % retail value rsp

Company 2007 2008 2009 2010 2011 Pharmstandart OAO 5.6 5.6 5.1 5.2 5.8

Novartis Consumer Health OOO 4.3 5.2 5.5 4.7 4.8

Evalar ZAO 2.4 3.0 4.3 3.7 3.7 Sanofi-Aventis Russia 4.2 4.2 3.7 3.2 3.1

Sandoz ZAO 1.3 1.5 1.6 2.1 2.7 Berlin Chemie Russia 2.7 2.8 2.5 2.4 2.5

Johnson & Johnson OOO 1.2 1.3 1.5 1.7 2.3

Reckitt Benckiser Healthcare OOO 1.1 1.3 1.8 1.9 2.1

Nycomed Russia-CIS 1.6 1.7 1.8 1.7 1.8

Herbalife International RS OOO 1.1 1.2 1.1 1.4 1.8

Boehringer Ingelheim Pharma OOO 1.8 2.0 1.9 1.7 1.7

Unipharm Russia 1.5 1.6 1.6 1.6 1.7 Veropharm OAO 1.5 1.4 1.4 1.6 1.6

Amway OOO 1.1 1.3 1.7 1.6 1.5

GlaxoSmithKline Healthcare ZAO 3.0 2.5 1.8 1.6 1.5

Sagmel OOO 1.1 1.2 1.4 1.5 1.5

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Ferrosan Consumer Health OOO 1.0 1.1 1.1 1.2 1.3

Ratiopharm Russia 1.0 1.1 1.2 1.1 1.1 Akrikhin OAO 1.1 1.2 1.2 1.1 1.1

Solvay Pharma 0.8 0.9 1.0 0.9 1.0 Diod OAO 0.7 1.5 1.4 1.0 1.0

Akvion ZAO 0.6 0.8 0.8 0.8 1.0 Egis AO 1.0 1.0 1.1 1.1 1.0

Nizhpharm OAO 0.9 0.9 0.9 0.9 0.9 Lek Pharmaceuticals dd 0.9 0.9 0.8 0.8 0.8

AnviLab OOO — — 0.5 0.5 0.8 Ivax Pharmaceuticals sro 1.1 1.0 0.8 0.8 0.8

Schering-Plough Central East AG 0.6 0.7 0.7 0.9 0.8

Warner-Lambert Russia 1.0 0.9 0.8 0.8 0.8 Krka Pharm OOO 0.8 0.8 0.7 0.8 0.7

Others 52.9 49.7 48.3 49.8 46.9 TOTAL 100.0 100.0 100.0 100.0 100.0

Source: www.portal.euromonitor.com

The following table represents the brand shares in Russia.

Table 13. Consumer Heath Brand Shares in Russia % retail value rsp

Brand Company 2008 2009 2010 2011

Theraflu Novartis Consumer Health OOO 2.3 2.4 2.1 1.9

Nurofen Reckitt Benckiser Healthcare OOO 1.0 1.5 1.6 1.8

Linex Sandoz ZAO 1.3 1.3 1.6 1.5 Pentalgin Pharmstandart OAO 1.8 1.7 1.4 1.5 Nutrilite Amway OOO 1.2 1.6 1.5 1.5 Mezym Berlin Chemie Russia 1.3 1.2 1.2 1.3

Lasolvan Boehringer Ingelheim Pharma OOO 1.3 1.3 1.2 1.2

Vitrum Unipharm Russia 1.0 1.0 1.1 1.1 Complivit Pharmstandart OAO 0.9 0.8 0.9 1.1 Eczoderil Sandoz ZAO 0.2 0.2 0.4 1.1

Herbalife Thermojetics Herbalife International RS OOO 0.7 0.6 0.9 1.0

No-spa Sanofi-Aventis Russia 1.2 1.2 0.9 1.0

Bifiform Ferrosan Consumer Health OOO 0.8 0.8 0.8 0.8

Terpinkod Pharmstandart OAO 1.3 0.8 0.8 0.8 Turboslim Evalar ZAO 0.8 1.0 0.7 0.8

Relief Sagmel OOO 0.5 0.7 0.7 0.7

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Theraflu and Nurofen were the top leaders in 2011 despite the share of the first declined in

2011 vis-à-vis the 2010 figure. The brand share of Nurofen increases constantly. Linex,

Pentalgin and Nutrilite had the same share (1.5%) in 2011.

FOREIGN TRADE The table below shows the foreign trade of medicinal agents of Russia for 2000, 2005 and

2008-2010.

Table 14. Russia's Foreign Trade of Medicinal Agents mln USD

Category 2000 2005 2008 2009 2010

Total Exports of Medicinal Agents 103 162 258 260 289

Exports of Medicinal Agents to the CIS Countries 90.4 150 223 223 231

Exports of Medicinal Agents to Far Abroad 12.2 11.6 34.9 36.7 58.2

Total Imports of Medicinal Agents 1150 3865 7512 7136 9346

Imports of Medicinal Agents to the CIS Countries 59.2 47.9 65.3 75.0 106

Imports of Medicinal Agents to Far Abroad 1091 3817 7447 7061 9240

Afobazol Pharmstandart OAO 0.3 0.3 0.3 0.6 Halls Warner-Lambert Russia 0.7 0.6 0.6 0.6

Kodelak Pharmstandart OAO 0.6 0.7 0.7 0.6 Fastum Berlin Chemie Russia 0.9 0.8 0.6 0.6

Aqua Maris Jadran Galenski Laboratorij AO 0.4 0.5 0.6 0.6 Hylak Ratiopharm Russia 0.6 0.6 0.5 0.6

Antigrippin Anvi AnviLab OOO — 0.4 0.3 0.5 Hexoral Johnson & Johnson OOO 0.2 0.5 0.5 0.5

Herbalife Herbalife International RS OOO 0.4 0.3 0.4 0.5 Alphabet Akvion ZAO 0.3 0.3 0.4 0.5 Nasivin Nycomed Russia-CIS 0.5 0.6 0.5 0.5 Otrivin Novartis Consumer Health OOO 0.4 0.8 0.4 0.5

ACC Hexal AG 0.4 0.5 0.5 0.5 Ambrobene Ratiopharm Russia 0.4 0.5 0.5 0.5

Others — 76.3 74.3 75.4 73.1 TOTAL — 100.0 100.0 100.0 100.0

Source: www.portal.euromonitor.com

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Source: www.gks.ru

The table shows that the volumes of the imported medicinal agents dominate over the

exported ones. For 2008-2010, the growth rate of exported medicinal agents totaled 6% on

average. In 2009, the volume of imported medicaments decreased by 5% against the

previous year and increased by 31% in 2010. The volumes of exports in medicinal agents to

the CIS countries dominate over the volumes of imports.

INVESTMENT The investment volumes in heath care in Russia for 2005, 2009 and 2010 are given in the

table below.

Table 15. Investment in Health Care in Russia

Year mln USD % of Total Investments

2005 3550.8 2.6 2009 5700.9 2.3 2010 6938.8 2.3

Note: the figures in money terms are converted from RUR to USD according to the average annual exchange rates of the appropriate

year.

Source: www.gks.ru

Source: www.1prime.ru

The table shows a constant growth of investment funds for 2005-2010. Despite the

investment volumes in money terms grew in 2010, the share in total investments stayed

constant (2.3%). In 2010, the investment in health care grew by up to 21.7% over the

previous year.

PRICES The rise in prices of medicaments can be mentioned as a structural change. The

development of the market was due to the increase in retail sector. This situation is

explained by an increase in the tax burden on pharmacies, leading to lower profits. In

general, the growth rate of commercial retail market by the end of last year was about 16%

and amounted to USD 15.4 billion. As predicted, this trend will continue in the first half of

2012. For further development of the pharmaceutical market needs new stimulating factors.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

CITY KEY TRENDS MOSCOW Moscow accounts for a large share of sales in consumer health, accounting for

20% of overall value sales in the country in 2011. Its value share remained stable after the

economic situation in the city became better, with the labor market recovering and

disposable incomes growing after the depression seen in 2009-2010. It still has the highest

per capita consumption in the country for consumer health products, at RUR 2,584 (USD

87.9) in comparison with national per capita consumption of RUR 1,050 (USD 35.7).

Consumers in Moscow continue to be the most attractive target group, with the highest

incomes and a higher level of purchasing. At the same time consumers are more

sophisticated than in the country as a whole. Consequently, Moscow is a priority for

pharmacies and consumer health manufacturers. The city saw the strongest growth in new

pharmacies.

The pharmacies in the city try to offer higher value added products and a wider range of

products than in other regions. The Moscow labor market saw continuous recovery in 2011.

At the same time, uncertainty caused by global economic instability led to higher demands

from employers. Moscow is a business centre in Russia, and many of its citizens have to

work long hours. Manufacturers of vitamins and dietary supplements and consumer health

products promote them by targeting busy people with their marketing communications,

such as the advertisement for Afobazol, saying that the remedy helps consumers to deal

with constant stress, and helps to maintain high working efficiency. Working people do not

have enough time and use the opportunity to save valuable time by ordering healthcare

products online. Internet sales are growing in the whole of Russia and in the Moscow region

in particular. Besides convenience, internet pharmacies offer lower prices, which was an

additional stimulus for the development of the channel. The Moscow region saw strong

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

internet sales growth, benefiting from the high penetration of internet technology and

credit cards. Consumers became more sophisticated over the review period. Players in

pharmacies in Moscow realized that it was not enough to sell a customer a product; more

often people needed consultation and advice on the problem they had, not only the

presence of a particular product in stock. Along with the growing competition, the

atmosphere and service became increasingly important. Citizens in Moscow have higher

incomes than other Russians, and look for the most effective solutions to their problems.

This supports the sales of companies offering premium products. Companies such as

Amway, Herbalife, Nycomed and Novartis have a strong presence in the city.

Competition between pharmacies significantly increased in the Moscow market over the

review period. Many players started to consider new directions for business development,

differing from the traditional. Rebranding campaigns and new formats were announced. At

the end of the review period the Rigla pharmacy chain announced the launch of its new

format pharmacies “Bud’ Zdorov” (“Be Healthy”). The project was focused on the

development of pharmacy discounters and online sales. Over the review period in the

Moscow market there was a situation whereby wholesalers and pharmacies were motivated

to sell as expensive products as possible. This was due to tightening taxation, and control on

mark-ups for part of the pharmacy range. Domestic manufacturers with lower-priced

products were at a disadvantage, and were looking for ways to escape this trap. Many

domestic manufacturers developed motivation programs for pharmacies, reviewed their

portfolios of products and recruited company representatives to support sales. The largest

domestic manufacturer of dietary supplements, Evalar, started to develop its own pharmacy

retail chain in Moscow. Despite these moves, the share of domestic manufacturers in

Moscow did not increase in 2011.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

During the review period the Moscow market showed stable development, although this is

expected to slow down during the forecast period. Growth in the Moscow market over the

forecast period is expected to be lower than the growth in Russia as a whole. Whilst Russia

as a whole is expected to see a 4% constant value CAGR, Moscow is expected to see just a

3% constant value CAGR. The Moscow market accounted for 20% of the total value of the

Russian market in 2011. This largest regional market is characterized by the most developed

infrastructure, which is expected to see further development, with the largest pharmacies

trying new formats in Moscow. The city will continue to be a target market for companies

launching new products, with manufacturing facilities developed in the area surrounding

Moscow. The population has higher disposable incomes than in other regions, and

consumers are more open-minded, willing to buy the best and the most efficient products,

not paying much attention to price. The dynamic pace of life requires people to be always

moving, not allowing them the time to be ill. All kinds of preventive medicines and drugs

aiming to improve quality of life are expected to see continuous development in the city

over the forecast period.

The end of the review period saw an increasing birth rate in Russia, although in Moscow this

dynamic was less obvious. 2010 was the first year when the birth rate was higher than the

death rate in Moscow. The implementation of supportive government programs is expected

to maintain the relatively high birth rate in the forecast period. This will support the

development of pediatric consumer health and vitamins and dietary supplements in

Moscow.

The forecast period is expected to see continuous growth in demand for healthier nutrition

and remedies made from natural ingredients. The improving quality and decreasing number

of counterfeit products will positively affect the image of herbal/traditional products. The

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

number of people taking active actions to fight excess weight is expected to support

demand for weight management products. This is expected to support a current value CAGR

of 5% in both categories in Moscow during the forecast period. Sports nutrition and

vitamins and dietary supplements will also see significant growth of 5% and 4% respectively

in constant value terms.

ST PETERSBURG St Petersburg is the second largest city in Russia, and the second largest

market for consumer health. The population of the city is highly educated. Widespread

consumption habits close to those observed in Western countries are determined by the

high rate of travelers amongst the population. These people often go to the closest

neighboring countries, and tend to live a European-like lifestyle. People spend relatively

large amounts of money on consumer health, with per capita consumption being twice as

high as the average per capita consumption seen in Russia. Slower growth was seen in 2011,

because the market in St Petersburg was already well-developed. Growth was stronger in

the regions, which led to the underperformance of the city against the general background.

Sales of consumer health products in St Petersburg accounted for 7% of value sales in

consumer health in the whole of Russia. Sales saw 11% current value growth in 2011, which

was lower than the overall current value growth of 12% in Russia.

Although the second largest market for consumer health in Russia after Moscow, St

Petersburg was the market with the most developed pharmacy retail chain. At the end of

the review period there were about 1,000 pharmacies in the city, with a ratio of one

pharmacy per 4,500 people. This ratio is close to the level seen in Western European

countries such as Germany.

During the review period consumers in St Petersburg became increasingly health-conscious.

When diet is wrong, medicine is of no use. When diet is correct, medicine is of no need. Ancient Ayurvedic Proverb

Many categories showed a particularly strong performance, with health-enhancing products

and preventive medicines being amongst the leaders. Vitamins and dietary supplements

saw 12% growth and herbal/traditional products 11% current value growth in 2011 over the

previous year.

St Petersburg is the demographically oldest city in Russia, with almost every fourth citizen

being a pensioner. The high number of older people supported demand for eye care and