Embed Size (px)

Citation preview

VALLOUREC

January 2018

INFORMATION

Quarterly financial statements are unaudited and are not subject to any review

Half year financial statements are subject to limited review by statutory auditors

Full year consolidated financial statements at 31 December are audited

Unless otherwise specified, indicated variations are expressed in comparison with the same period of the previous year

FORWARD-LOOKING STATEMENTS

This document contains forward-looking statements. These statements include financial forecasts and estimates

as well as assumptions on which they are based, statements related to projects, objectives and expectations

concerning future operations, products and services or future performance. Although Vallourec’s management believes

that these forward-looking statements are reasonable, Vallourec cannot guarantee their accuracy or completeness

and these forward-looking statements are subject to numerous risks and uncertainties that are difficult to foresee

and generally beyond Vallourec’s control, which may mean that actual results and developments may differ significantly

from those expressed, induced or forecasted in the forward-looking statements. These risks include those developed

or identified in the public documents filed by Vallourec with the AMF, including those listed in the “Risk Factors” section

of the Registration Document filed with the AMF on 21 March 2017 (N° D.17-0191).

2VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

VALLOUREC RE-POSITIONED TO FULLY BENEFIT FROM THE RECOVERY THANKS TO ITS TRANSFORMATION PLAN

3

1 Favourable long-term trends

Extensive technological expertise and brand trust-recognition2

A reshaped industrial set up with highly competitive low-cost

export routes3

Strong focus on cost reduction4

A solid liquidity position and long term maturity5

Start of recovery in activity and financial performance6

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

-2,5

-1,5

-0,5

0,5

1,5

2,5

3,5

4,5

90

92

94

96

98

100

102

Q113

Q213

Q313

Q413

Q114

Q214

Q314

Q414

Q115

Q215

Q315

Q415

Q116

Q216

Q316

Q416

Q117

Q217

Q317

Q417

Q118

Q218

Q318

Q418

mb/dmb/d

Stock Change (R) World Oil Supply World Oil Demand

347

441

536

433484

587

651679 702

493

352378

412 432480

527

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

Africa Asia-Pacific Europe Middle East

North America Russia & Caspian Latin America Global Capex

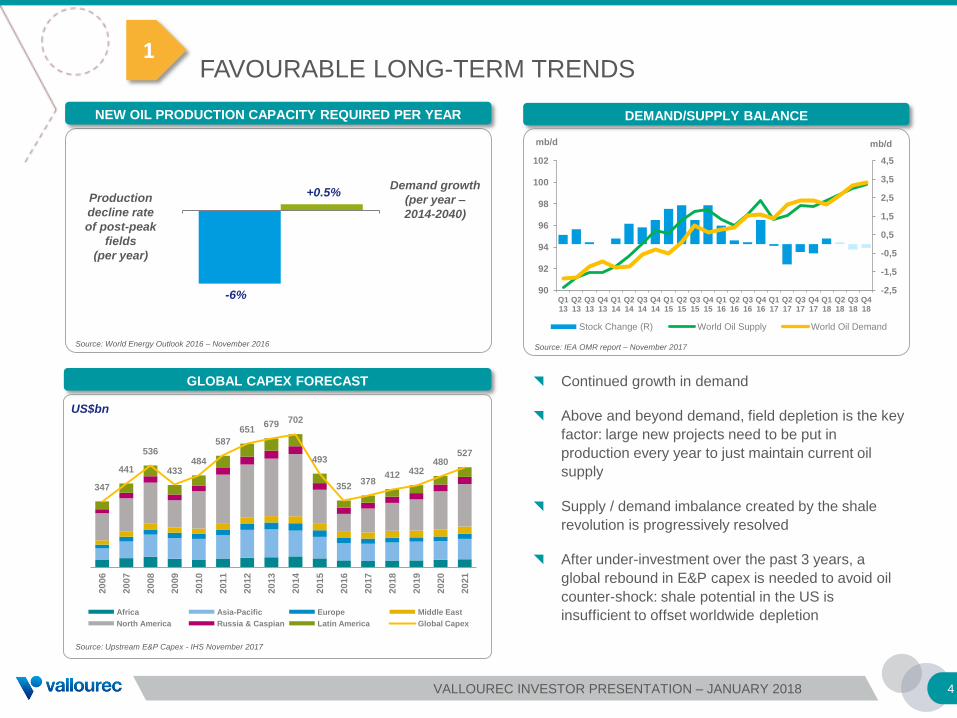

Continued growth in demand

Above and beyond demand, field depletion is the key

factor: large new projects need to be put in

production every year to just maintain current oil

supply

Supply / demand imbalance created by the shale

revolution is progressively resolved

After under-investment over the past 3 years, a

global rebound in E&P capex is needed to avoid oil

counter-shock: shale potential in the US is

insufficient to offset worldwide depletion

GLOBAL CAPEX FORECAST

US$bn

Source: Upstream E&P Capex - IHS November 2017

4

Demand growth

(per year –

2014-2040)

Production

decline rate

of post-peak

fields

(per year)

NEW OIL PRODUCTION CAPACITY REQUIRED PER YEAR

Source: World Energy Outlook 2016 – November 2016

+0.5%

-6%

Source: IEA OMR report – November 2017

DEMAND/SUPPLY BALANCE

1FAVOURABLE LONG-TERM TRENDS

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

EXTENSIVE TECHNOLOGICAL EXPERTISE AND BRAND TRUST-RECOGNITION

5

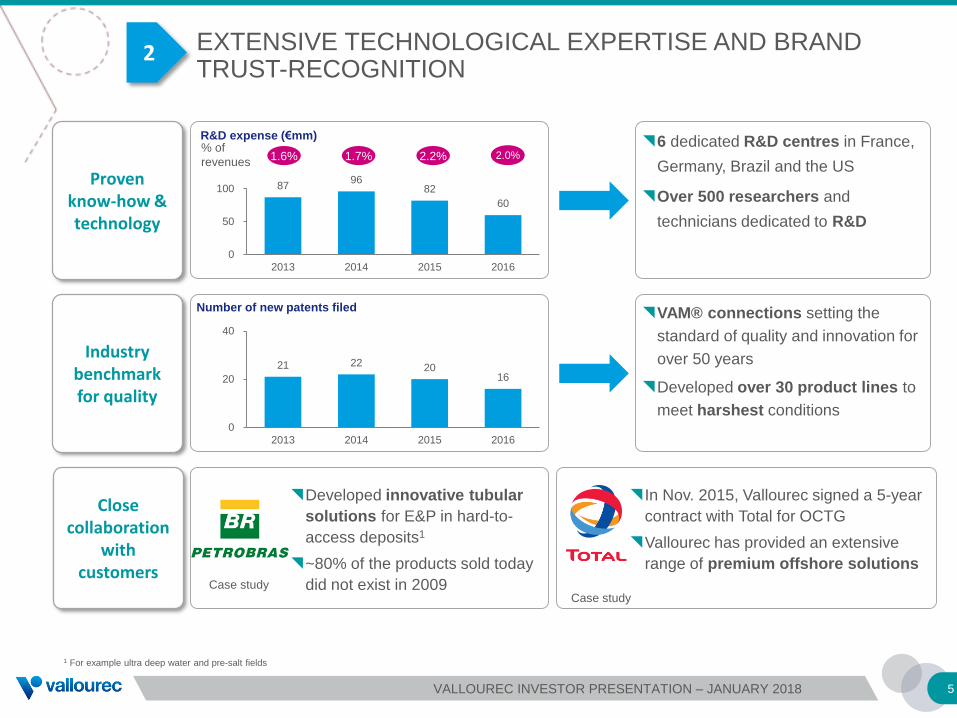

Proven know-how & technology

Industry benchmark for quality

Close collaboration

with customers

2

VAM® connections setting the

standard of quality and innovation for

over 50 years

Developed over 30 product lines to

meet harshest conditions

6 dedicated R&D centres in France,

Germany, Brazil and the US

Over 500 researchers and

technicians dedicated to R&D

21 22 20 16

0

20

40

2013 2014 2015 2016

Number of new patents filed

1 For example ultra deep water and pre-salt fields

In Nov. 2015, Vallourec signed a 5-year

contract with Total for OCTG

Vallourec has provided an extensive

range of premium offshore solutions

Developed innovative tubular

solutions for E&P in hard-to-

access deposits1

~80% of the products sold today

did not exist in 2009Case studyCase study

% of

revenues1.6% 1.7% 2.2% 2.2%

R&D expense (€mm)

87 96

82

60

0

50

100

2013 2014 2015 2016

2.0%

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

OPTIMIZED INDUSTRIAL FOOTPRINT

6

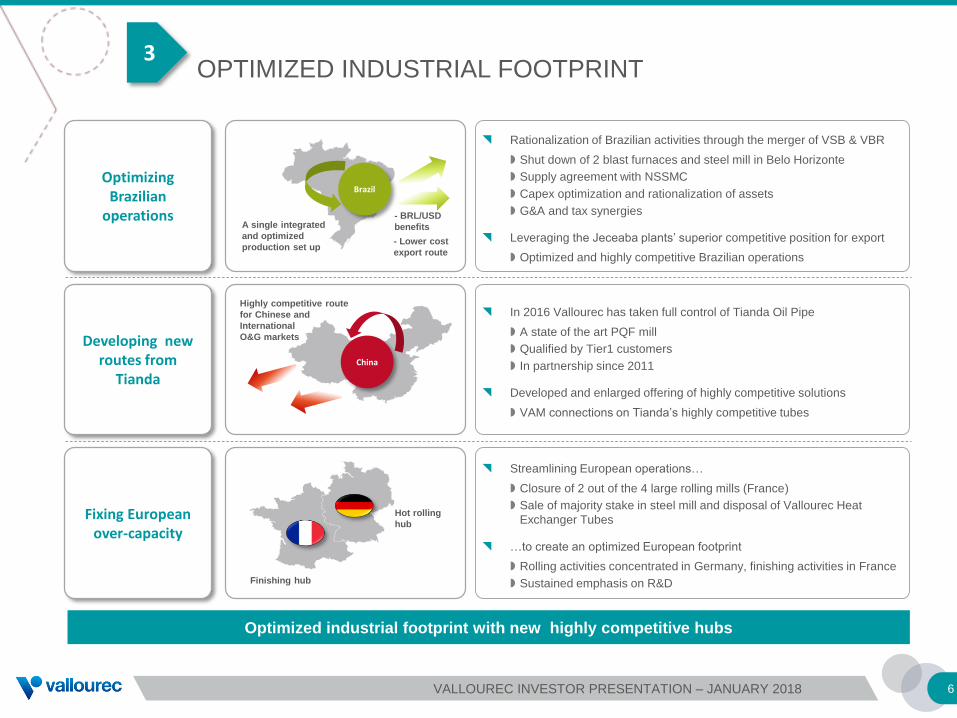

Optimizing Brazilian

operations

Developing new routes from

Tianda

Fixing European over-capacity

Optimized industrial footprint with new highly competitive hubs

Rationalization of Brazilian activities through the merger of VSB & VBR

Shut down of 2 blast furnaces and steel mill in Belo Horizonte

Supply agreement with NSSMC

Capex optimization and rationalization of assets

G&A and tax synergies

Leveraging the Jeceaba plants’ superior competitive position for export

Optimized and highly competitive Brazilian operations

In 2016 Vallourec has taken full control of Tianda Oil Pipe

A state of the art PQF mill

Qualified by Tier1 customers

In partnership since 2011

Developed and enlarged offering of highly competitive solutions

VAM connections on Tianda’s highly competitive tubes

Streamlining European operations…

Closure of 2 out of the 4 large rolling mills (France)

Sale of majority stake in steel mill and disposal of Vallourec Heat

Exchanger Tubes

…to create an optimized European footprint

Rolling activities concentrated in Germany, finishing activities in France

Sustained emphasis on R&DFinishing hub

Hot rolling

hub

Brazil

A single integrated

and optimized

production set up

- BRL/USD

benefits

China

Highly competitive route

for Chinese and

International

O&G markets

- Lower cost

export route

3

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

Steel mills

Tube mills

R&D

Finishing unit

Sales & Services office

Plantation and mine

NorthAmerica

Brazil

Europe

China

A RESHAPED INDUSTRIAL SET-UP WITH HIGHLY COMPETITIVE LOW-COST EXPORT ROUTES

7

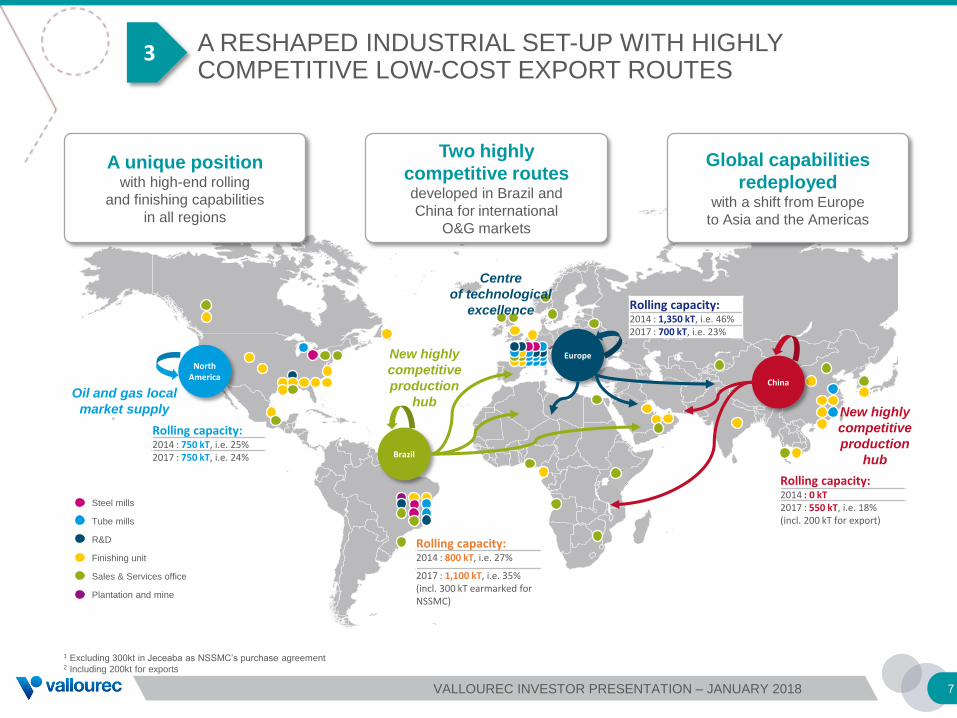

3

A unique positionwith high-end rolling

and finishing capabilities

in all regions

Global capabilities

redeployedwith a shift from Europe

to Asia and the Americas

Two highly

competitive routesdeveloped in Brazil and

China for international

O&G markets

Oil and gas local

market supply

New highly

competitive

production

hubNew highly

competitive

production

hub

Centre

of technological

excellence

1 Excluding 300kt in Jeceaba as NSSMC’s purchase agreement2 Including 200kt for exports

Rolling capacity:2014 : 750 kT, i.e. 25%2017 : 750 kT, i.e. 24%

Rolling capacity:2014 : 800 kT, i.e. 27%

2017 : 1,100 kT, i.e. 35%(incl. 300 kT earmarked for NSSMC)

Rolling capacity:2014 : 1,350 kT, i.e. 46%2017 : 700 kT, i.e. 23%

Rolling capacity:2014 : 0 kT2017 : 550 kT, i.e. 18%(incl. 200 kT for export)

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

268

175

86

2015 2016 9M 2017

116109 106

117113

10810217%

14%15%

14% 14%

12%11%

8%

18%

Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017

SG&A m€ % Sales

130 150

78

2015 2016 H1 2017

8

CAPEX,

in €m

SG&A,

in €m

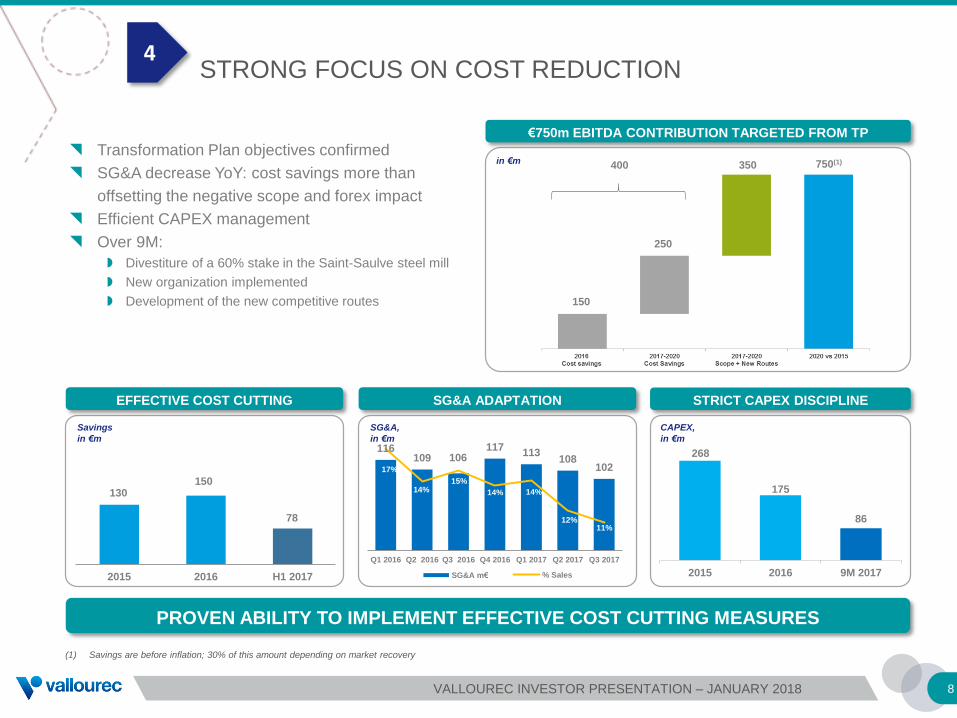

(1) Savings are before inflation; 30% of this amount depending on market recovery

Savings

in €m

150

250

350 750(1)400

€750m EBITDA CONTRIBUTION TARGETED FROM TP

EFFECTIVE COST CUTTING SG&A ADAPTATION STRICT CAPEX DISCIPLINE

PROVEN ABILITY TO IMPLEMENT EFFECTIVE COST CUTTING MEASURES

in €m Transformation Plan objectives confirmed

SG&A decrease YoY: cost savings more than

offsetting the negative scope and forex impact

Efficient CAPEX management

Over 9M:

Divestiture of a 60% stake in the Saint-Saulve steel mill

New organization implemented

Development of the new competitive routes

4STRONG FOCUS ON COST REDUCTION

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

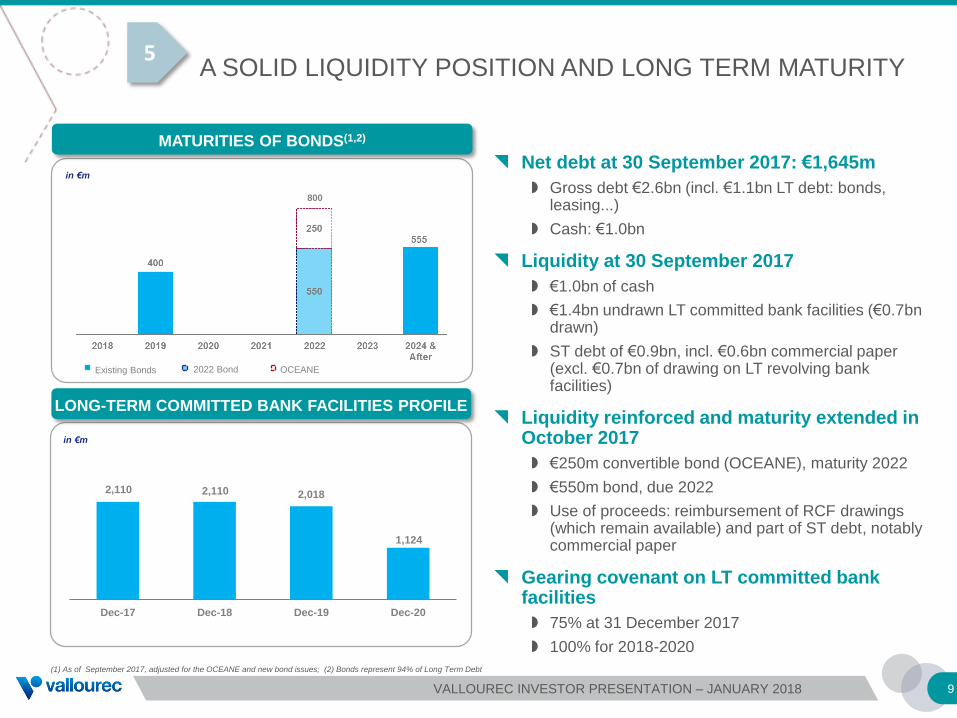

2,110 2,110 2,018

1,124

Dec-17 Dec-18 Dec-19 Dec-20

9

in €m

(1) As of September 2017, adjusted for the OCEANE and new bond issues; (2) Bonds represent 94% of Long Term Debt

LONG-TERM COMMITTED BANK FACILITIES PROFILE

Net debt at 30 September 2017: €1,645m

Gross debt €2.6bn (incl. €1.1bn LT debt: bonds, leasing...)

Cash: €1.0bn

Liquidity at 30 September 2017

€1.0bn of cash

€1.4bn undrawn LT committed bank facilities (€0.7bn drawn)

ST debt of €0.9bn, incl. €0.6bn commercial paper (excl. €0.7bn of drawing on LT revolving bank facilities)

Liquidity reinforced and maturity extended in October 2017

€250m convertible bond (OCEANE), maturity 2022

€550m bond, due 2022

Use of proceeds: reimbursement of RCF drawings (which remain available) and part of ST debt, notably commercial paper

Gearing covenant on LT committed bank facilities

75% at 31 December 2017

100% for 2018-2020

800

in €m

MATURITIES OF BONDS(1,2)

Existing Bonds OCEANE2022 Bond

5A SOLID LIQUIDITY POSITION AND LONG TERM MATURITY

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

10

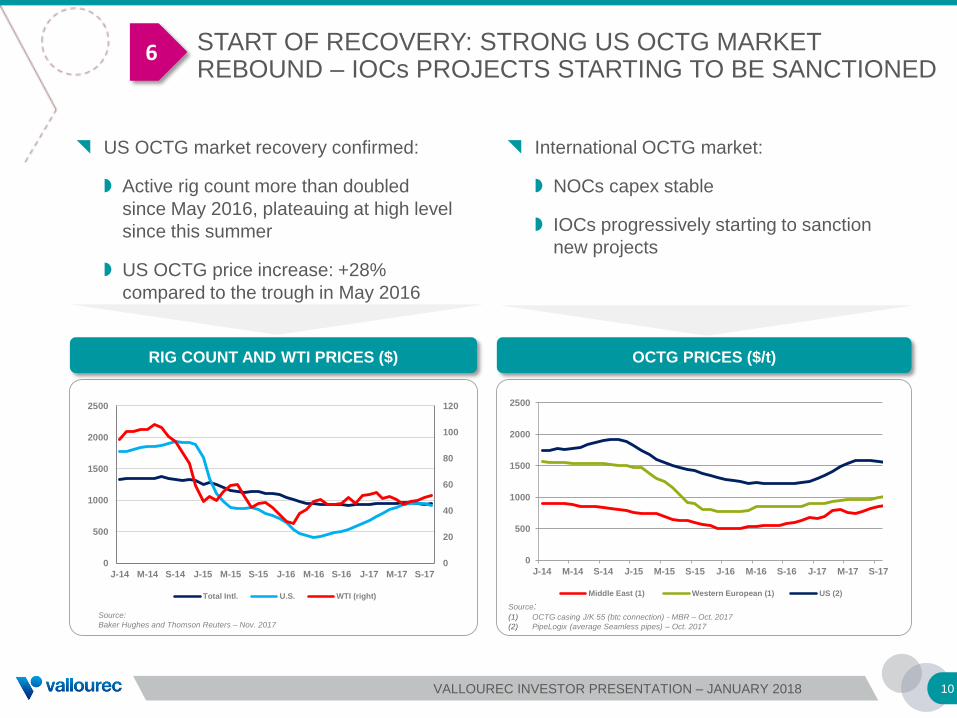

START OF RECOVERY: STRONG US OCTG MARKET REBOUND – IOCs PROJECTS STARTING TO BE SANCTIONED

6

OCTG PRICES ($/t)

Source: (1) OCTG casing J/K 55 (btc connection) - MBR – Oct. 2017

(2) PipeLogix (average Seamless pipes) – Oct. 2017

US OCTG market recovery confirmed:

Active rig count more than doubled

since May 2016, plateauing at high level

since this summer

US OCTG price increase: +28%

compared to the trough in May 2016

International OCTG market:

NOCs capex stable

IOCs progressively starting to sanction

new projects

Source:

Baker Hughes and Thomson Reuters – Nov. 2017

RIG COUNT AND WTI PRICES ($)

0

500

1000

1500

2000

2500

J-14 M-14 S-14 J-15 M-15 S-15 J-16 M-16 S-16 J-17 M-17 S-17

Middle East (1) Western European (1) US (2)

0

20

40

60

80

100

120

0

500

1000

1500

2000

2500

J-14 M-14 S-14 J-15 M-15 S-15 J-16 M-16 S-16 J-17 M-17 S-17

Total Intl. U.S. WTI (right)

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

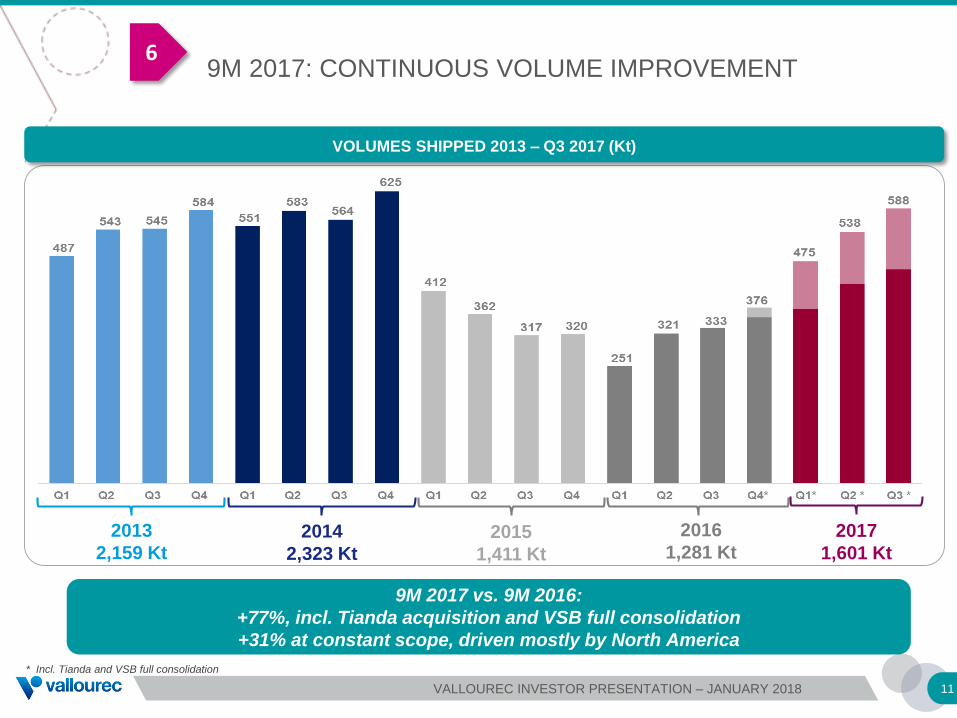

2013

2,159 Kt2014

2,323 Kt

2015

1,411 Kt

2016

1,281 Kt

* Incl. Tianda and VSB full consolidation

2017

1,601 Kt

11

VOLUMES SHIPPED 2013 – Q3 2017 (Kt)

9M 2017 vs. 9M 2016:

+77%, incl. Tianda acquisition and VSB full consolidation

+31% at constant scope, driven mostly by North America

69M 2017: CONTINUOUS VOLUME IMPROVEMENT

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

1,287

1,613 1,645

31 Dec 2016 30 June 2017 30 Sept. 2017

- 156

- 9

9M 2016 9M 2017

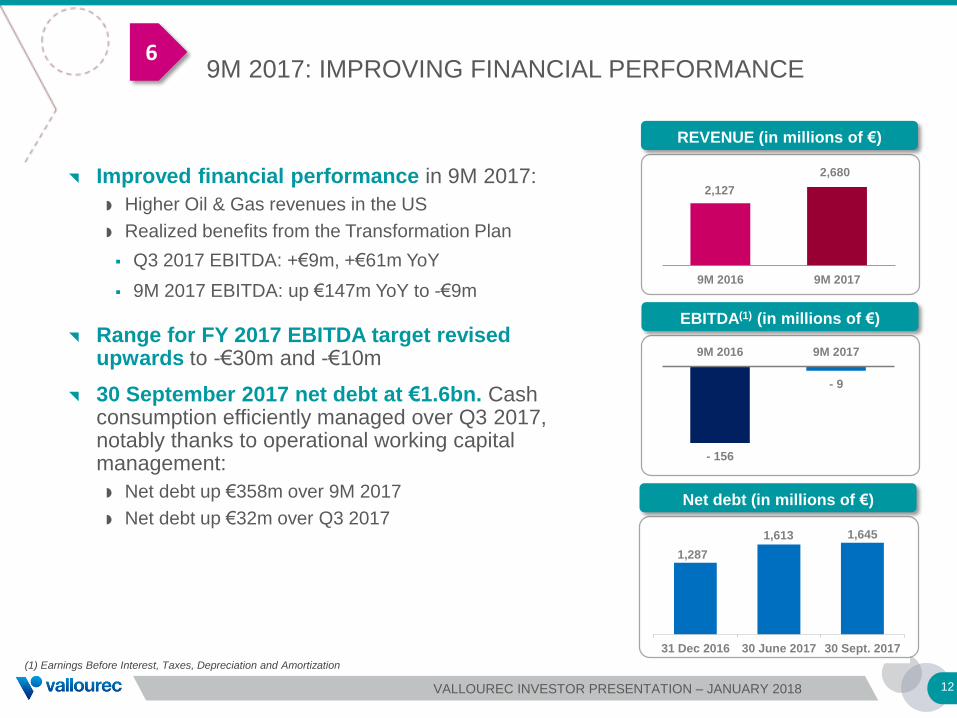

9M 2017: IMPROVING FINANCIAL PERFORMANCE

(1) Earnings Before Interest, Taxes, Depreciation and Amortization

Improved financial performance in 9M 2017:

Higher Oil & Gas revenues in the US

Realized benefits from the Transformation Plan

Q3 2017 EBITDA: +€9m, +€61m YoY

9M 2017 EBITDA: up €147m YoY to -€9m

Range for FY 2017 EBITDA target revised upwards to -€30m and -€10m

30 September 2017 net debt at €1.6bn. Cash consumption efficiently managed over Q3 2017, notably thanks to operational working capital management:

Net debt up €358m over 9M 2017

Net debt up €32m over Q3 2017

REVENUE (in millions of €)

6

2,127

2,680

9M 2016 9M 2017

EBITDA(1) (in millions of €)

Net debt (in millions of €)

12VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

OUTLOOK FOR THE MONTHS TO COME

13

Q4 2017 EBITDA to be slightly negative or nearing breakeven

FY 2017 EBITDA target revised upwards: to range between -€30m and -€10m

BRAZIL

O&G: Petrobras’ drilling activity expected to

remain stable

Industry: better momentum in a competitive

environment

Q4 2017: impacted by a less favorable mix

NORTH AMERICA

Rig count expected to plateau, assuming no

significant change in WTI price

High load of Vallourec domestic facilities

EAMEA O&G

IOCs: Progressively starting to sanction new projects

NOCs: Expected to remain sustained

Q4 2017: impacted by a less favorable mix

Industry: better momentum in a competitive

environment

Power Generation: to be progressively impacted

by a reduced number of conventional power plant

projects

Group results dependant notably on the evolution

of raw material costs and forex

Focused on sustained implementation of its

Transformation Plan which will continue to

generate significant savings

EAMEA

6

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

Q&A

EXANE CEO CONFERENCE - JUNE 2017

APPENDIX

16

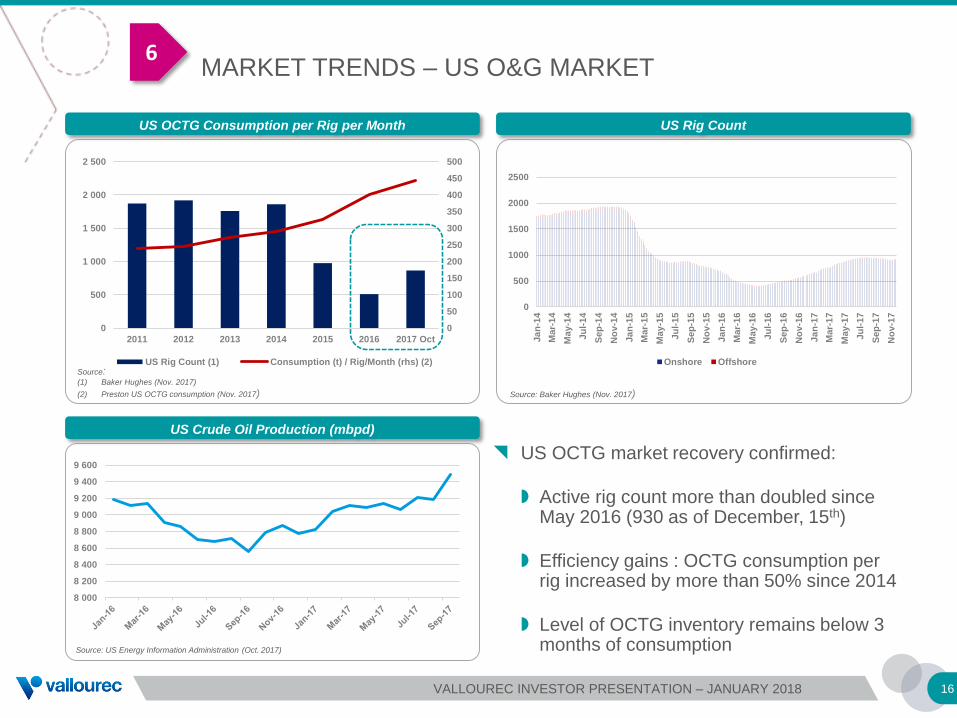

6MARKET TRENDS – US O&G MARKET

8 000

8 200

8 400

8 600

8 800

9 000

9 200

9 400

9 600

0

50

100

150

200

250

300

350

400

450

500

0

500

1 000

1 500

2 000

2 500

2011 2012 2013 2014 2015 2016 2017 Oct

US Rig Count (1) Consumption (t) / Rig/Month (rhs) (2)

Source: Baker Hughes (Nov. 2017)

US OCTG market recovery confirmed:

Active rig count more than doubled since May 2016 (930 as of December, 15th)

Efficiency gains : OCTG consumption per rig increased by more than 50% since 2014

Level of OCTG inventory remains below 3 months of consumption

US Rig CountUS OCTG Consumption per Rig per Month

Source: (1) Baker Hughes (Nov. 2017)

(2) Preston US OCTG consumption (Nov. 2017)

Source: US Energy Information Administration (Oct. 2017)

US Crude Oil Production (mbpd)

0

500

1000

1500

2000

2500

Ja

n-1

4

Mar-

14

May

-14

Ju

l-14

Sep

-14

No

v-1

4

Ja

n-1

5

Mar-

15

May

-15

Ju

l-15

Sep

-15

No

v-1

5

Ja

n-1

6

Mar-

16

May

-16

Ju

l-16

Sep

-16

No

v-1

6

Ja

n-1

7

Mar-

17

May

-17

Ju

l-17

Sep

-17

No

v-1

7

Onshore Offshore

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

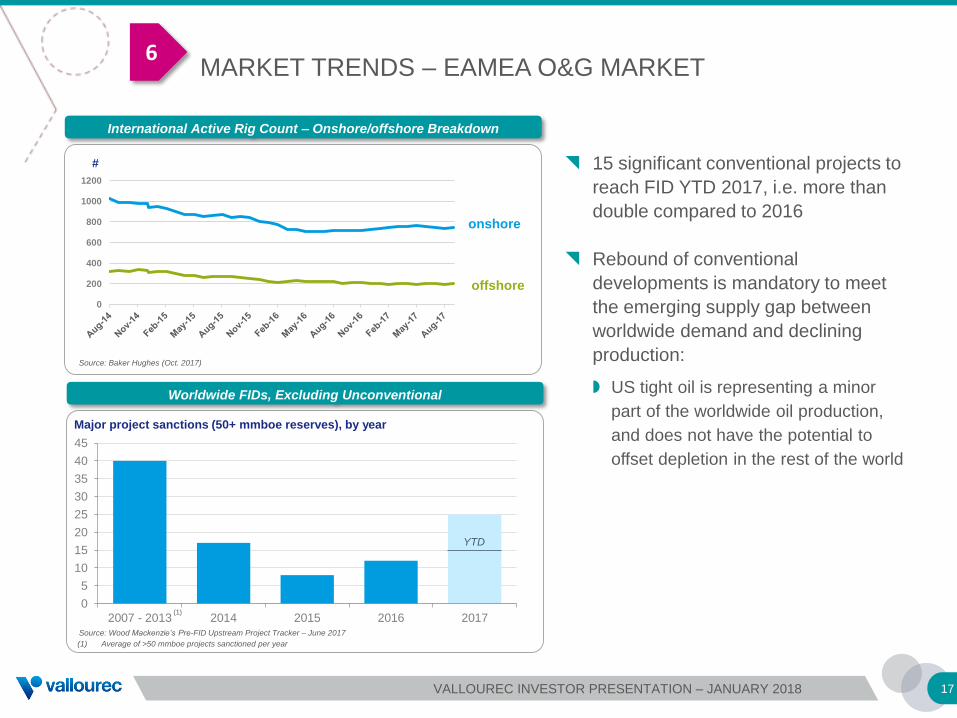

17

15 significant conventional projects to

reach FID YTD 2017, i.e. more than

double compared to 2016

Rebound of conventional

developments is mandatory to meet

the emerging supply gap between

worldwide demand and declining

production:

US tight oil is representing a minor

part of the worldwide oil production,

and does not have the potential to

offset depletion in the rest of the world

6MARKET TRENDS – EAMEA O&G MARKET

offshore

Worldwide FIDs, Excluding Unconventional

International Active Rig Count – Onshore/offshore Breakdown

Source: Baker Hughes (Oct. 2017)

Source: Wood Mackenzie’s Pre-FID Upstream Project Tracker – June 2017

onshore

#

0

5

10

15

20

25

30

35

40

45

2007 - 2013 2014 2015 2016 2017

Major project sanctions (50+ mmboe reserves), by year

(1) Average of >50 mmboe projects sanctioned per year

(1)

YTD

0

200

400

600

800

1000

1200

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

0,0

1,0

2,0

3,0

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Mar-17 Jun-17 Sep-17

2016–17 for 2017 2017 for 2018

18

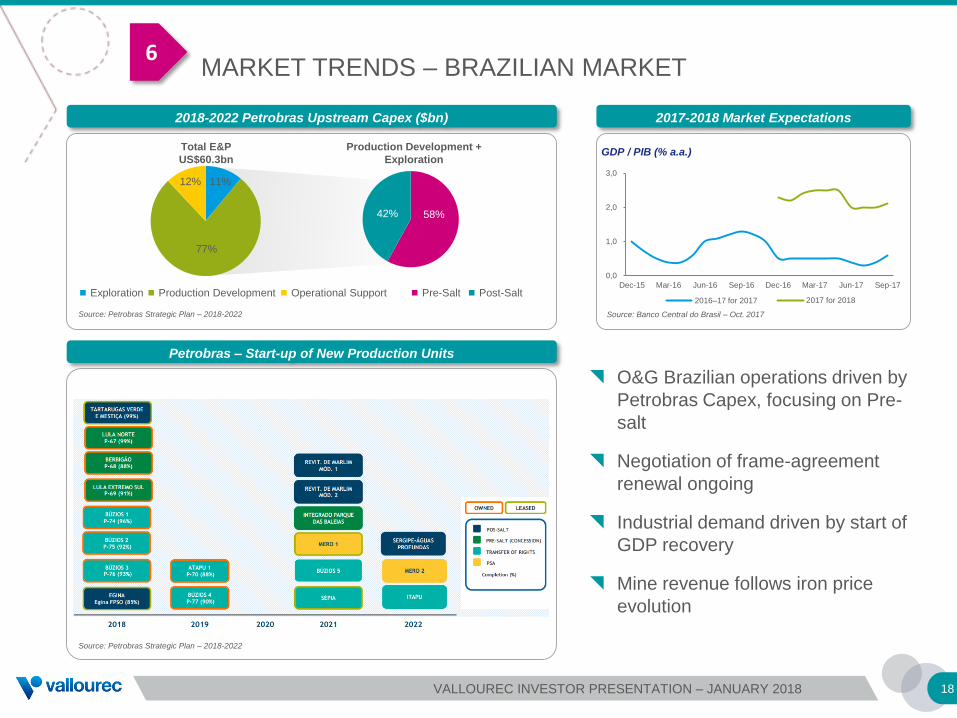

2018-2022 Petrobras Upstream Capex ($bn)

Petrobras – Start-up of New Production Units

2017-2018 Market Expectations

O&G Brazilian operations driven by

Petrobras Capex, focusing on Pre-

salt

Negotiation of frame-agreement

renewal ongoing

Industrial demand driven by start of

GDP recovery

Mine revenue follows iron price

evolution

Source: Petrobras Strategic Plan – 2018-2022

Source: Banco Central do Brasil – Oct. 2017

GDP / PIB (% a.a.)

Exploration Production Development Operational Support Post-SaltPre-Salt

Total E&P

US$60.3bn

Production Development +

Exploration

Concession

Transfer of Rights

Production Sharing

(Libra)

Source: Petrobras Strategic Plan – 2018-2022

11%

77%

12%

58%42%

6MARKET TRENDS – BRAZILIAN MARKET

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

19

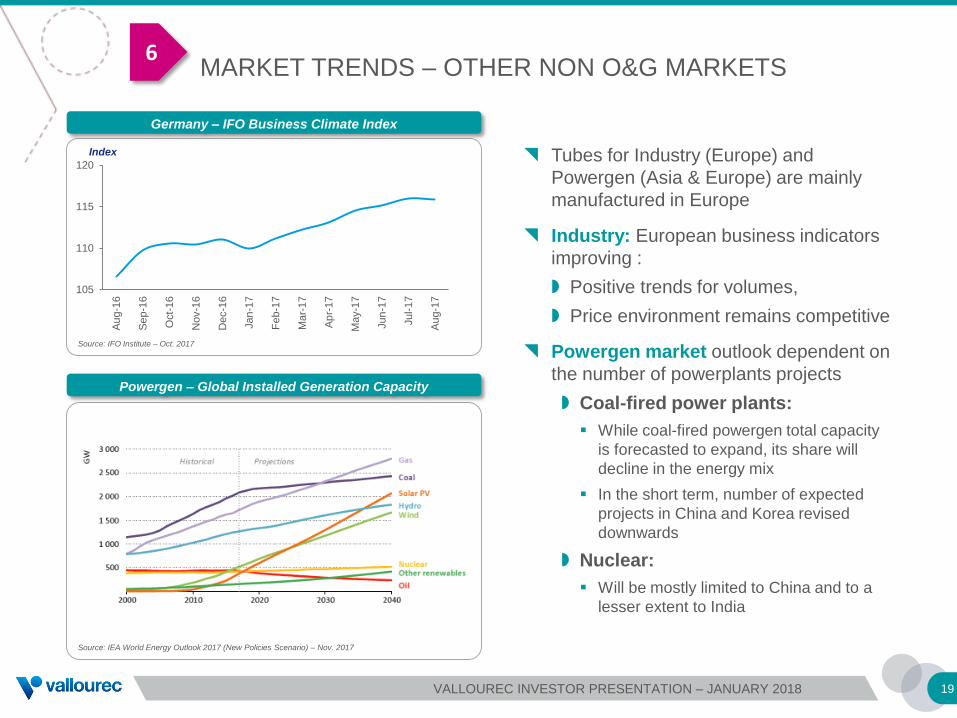

Tubes for Industry (Europe) and

Powergen (Asia & Europe) are mainly

manufactured in Europe

Industry: European business indicators

improving :

Positive trends for volumes,

Price environment remains competitive

Powergen market outlook dependent on

the number of powerplants projects

Coal-fired power plants:

While coal-fired powergen total capacity

is forecasted to expand, its share will

decline in the energy mix

In the short term, number of expected

projects in China and Korea revised

downwards

Nuclear:

Will be mostly limited to China and to a

lesser extent to India

Germany – IFO Business Climate Index

105

110

115

120

Au

g-1

6

Se

p-1

6

Oct-

16

Nov-1

6

Dec-1

6

Jan

-17

Fe

b-1

7

Ma

r-17

Ap

r-17

Ma

y-1

7

Jun

-17

Ju

l-1

7

Au

g-1

7

Index

Source: IFO Institute – Oct. 2017

6MARKET TRENDS – OTHER NON O&G MARKETS

Powergen – Global Installed Generation Capacity

Source: IEA World Energy Outlook 2017 (New Policies Scenario) – Nov. 2017

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

VALLOUREC AT A GLANCE

20

Key clients

Key segments

Revenue share

(FY 2016)

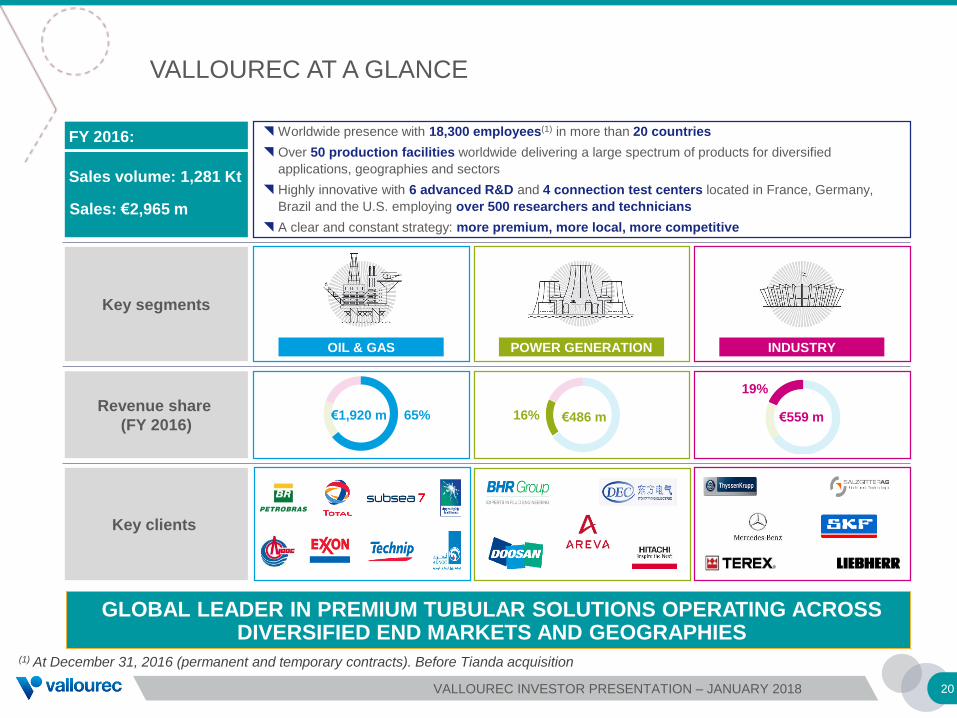

Worldwide presence with 18,300 employees(1) in more than 20 countries

Over 50 production facilities worldwide delivering a large spectrum of products for diversified

applications, geographies and sectors

Highly innovative with 6 advanced R&D and 4 connection test centers located in France, Germany,

Brazil and the U.S. employing over 500 researchers and technicians

A clear and constant strategy: more premium, more local, more competitive

FY 2016:

Sales volume: 1,281 Kt

Sales: €2,965 m

65% 16%

19%

€559 m€486 m€1,920 m

OIL & GAS POWER GENERATION INDUSTRY

(1) At December 31, 2016 (permanent and temporary contracts). Before Tianda acquisition

GLOBAL LEADER IN PREMIUM TUBULAR SOLUTIONS OPERATING ACROSS DIVERSIFIED END MARKETS AND GEOGRAPHIES

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

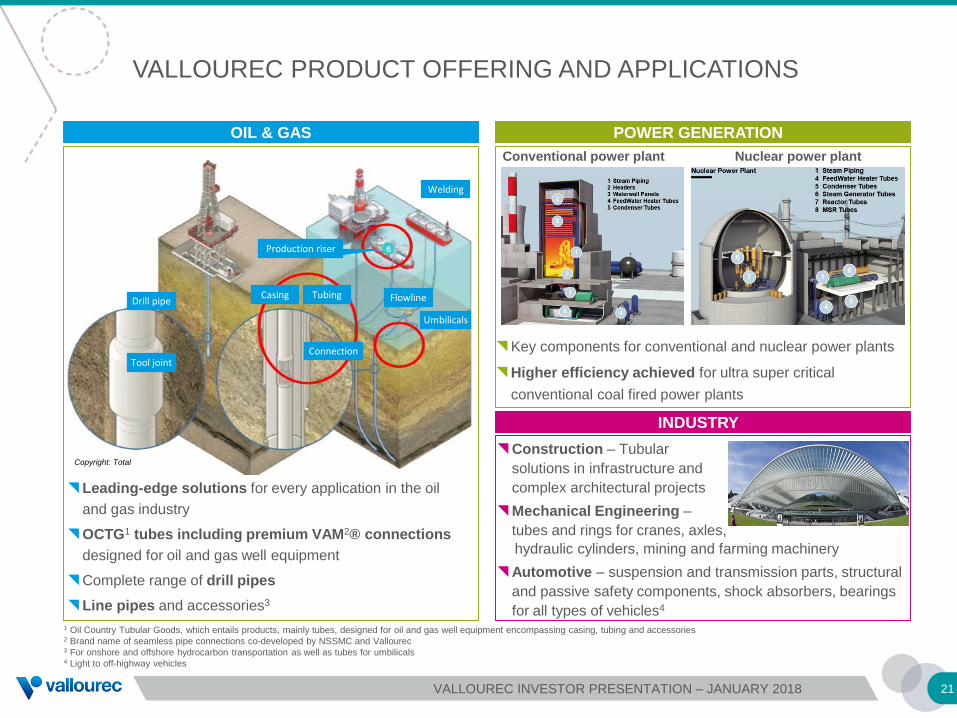

VALLOUREC PRODUCT OFFERING AND APPLICATIONS

21

OIL & GAS POWER GENERATION

Key components for conventional and nuclear power plants

Higher efficiency achieved for ultra super critical

conventional coal fired power plants

Drill pipe

Tool joint

Casing Tubing

Connection

Production riser

Flowline

Umbilicals

Welding

Conventional power plant Nuclear power plant

Leading-edge solutions for every application in the oil

and gas industry

OCTG1 tubes including premium VAM2® connections

designed for oil and gas well equipment

Complete range of drill pipes

Line pipes and accessories3

INDUSTRY

Construction – Tubular

solutions in infrastructure and

complex architectural projects

Mechanical Engineering –

tubes and rings for cranes, axles,

• hydraulic cylinders, mining and farming machinery

Automotive – suspension and transmission parts, structural

and passive safety components, shock absorbers, bearings

for all types of vehicles4

Copyright: Total

1 Oil Country Tubular Goods, which entails products, mainly tubes, designed for oil and gas well equipment encompassing casing, tubing and accessories2 Brand name of seamless pipe connections co-developed by NSSMC and Vallourec 3 For onshore and offshore hydrocarbon transportation as well as tubes for umbilicals4 Light to off-highway vehicles

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

WORLDWIDE LEADER IN PREMIUM TUBES

22

First seamless pipe actor to put new capacity

dedicated to shale in the US

Recognised technology leader globally for

complex well designs

Unmatched technical leadership and strong

R&D

Differentiation through global premium services

(network of over 200 VAM licensees, accessories

shop…)

Key partner in construction of modern

supercritical or ultra-supercritical thermal power

plants

European leader in seamless tubes for

mechanicals premium applications

Leading positions in various, niche markets across the globe

1 Ball-bearings manufactured from seamless tubes

Premium OCTG in the USA1

Premium OCTG in Brazil1

Ball-bearings1 tubes in Europe2

Premium tubes for power

generation applications

Drill pipes globally2

1

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

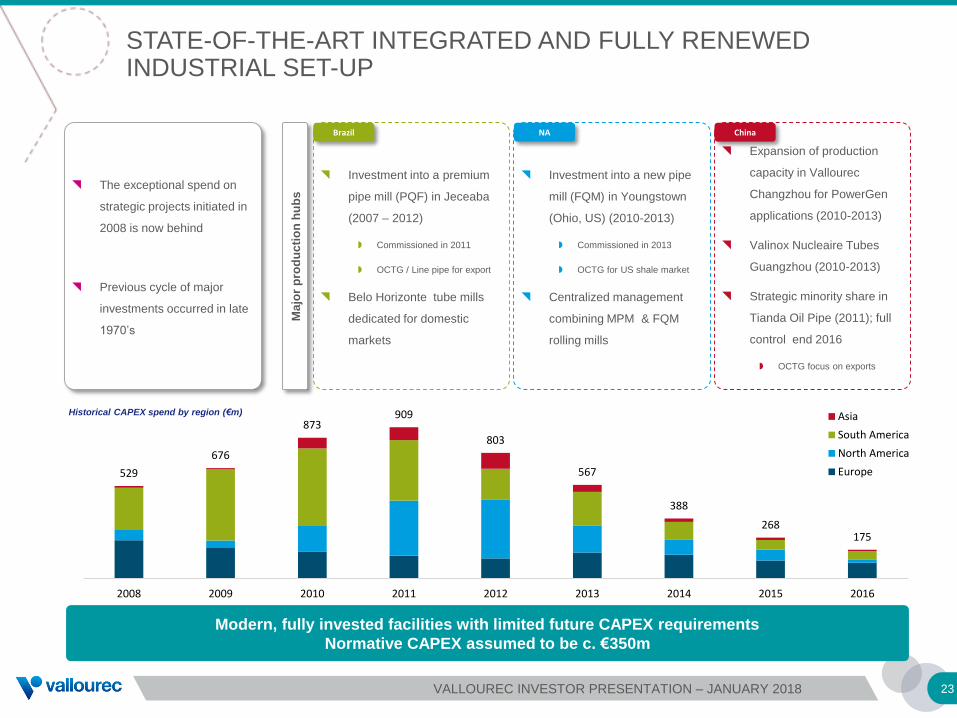

STATE-OF-THE-ART INTEGRATED AND FULLY RENEWED INDUSTRIAL SET-UP

23

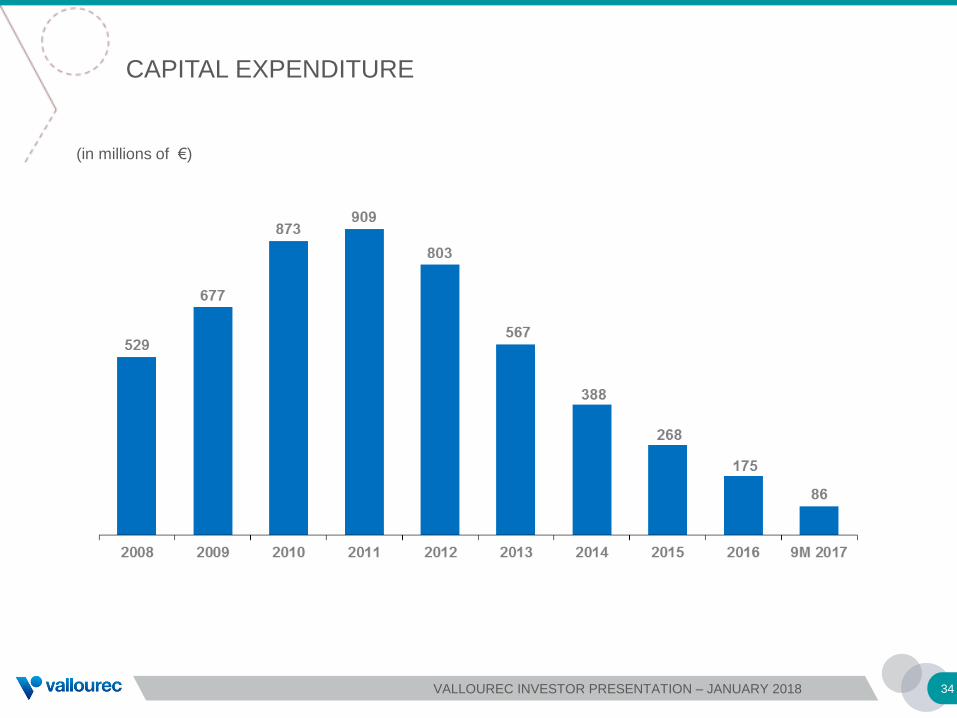

529

676

873909

803

567

388

268175

2008 2009 2010 2011 2012 2013 2014 2015 2016

Asia

South America

North America

Europe

Modern, fully invested facilities with limited future CAPEX requirements

Normative CAPEX assumed to be c. €350m

Investment into a premium

pipe mill (PQF) in Jeceaba

(2007 – 2012)

Commissioned in 2011

OCTG / Line pipe for export

Belo Horizonte tube mills

dedicated for domestic

markets

The exceptional spend on

strategic projects initiated in

2008 is now behind

Previous cycle of major

investments occurred in late

1970’s

Investment into a new pipe

mill (FQM) in Youngstown

(Ohio, US) (2010-2013)

Commissioned in 2013

OCTG for US shale market

Centralized management

combining MPM & FQM

rolling mills

Expansion of production

capacity in Vallourec

Changzhou for PowerGen

applications (2010-2013)

Valinox Nucleaire Tubes

Guangzhou (2010-2013)

Strategic minority share in

Tianda Oil Pipe (2011); full

control end 2016

OCTG focus on exports

Ma

jor

pro

du

cti

on

hu

bs

Historical CAPEX spend by region (€m)

Brazil NA China

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

24

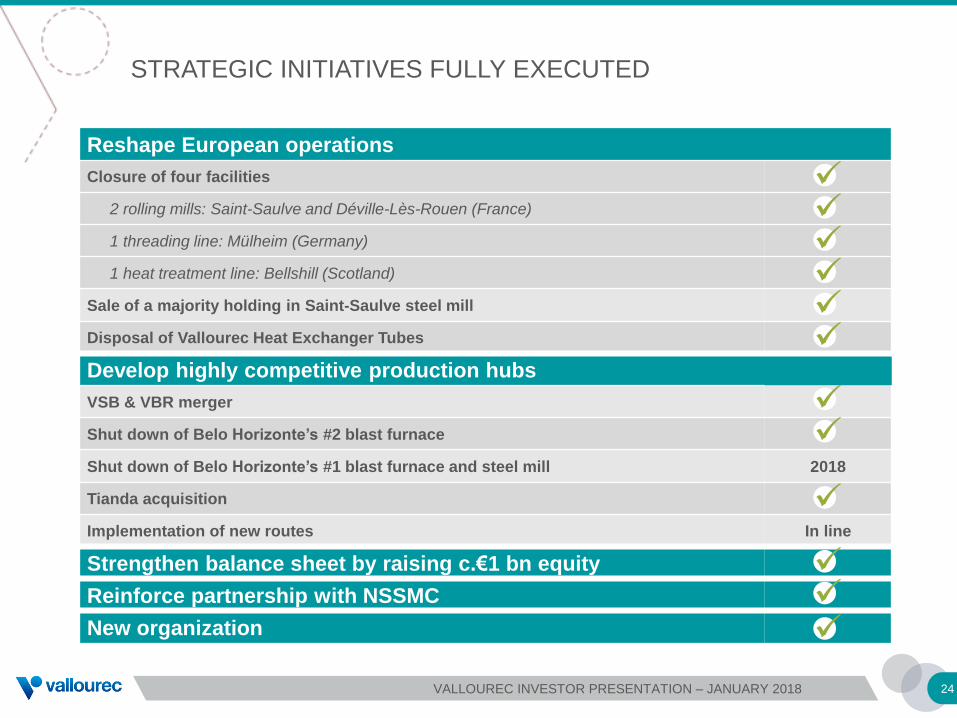

STRATEGIC INITIATIVES FULLY EXECUTED

Reshape European operations

Closure of four facilities

2 rolling mills: Saint-Saulve and Déville-Lès-Rouen (France)

1 threading line: Mülheim (Germany)

1 heat treatment line: Bellshill (Scotland)

Sale of a majority holding in Saint-Saulve steel mill

Disposal of Vallourec Heat Exchanger Tubes

Develop highly competitive production hubs

VSB & VBR merger

Shut down of Belo Horizonte’s #2 blast furnace

Shut down of Belo Horizonte’s #1 blast furnace and steel mill 2018

Tianda acquisition

Implementation of new routes In line

Strengthen balance sheet by raising c.€1 bn equity

Reinforce partnership with NSSMC

New organization

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

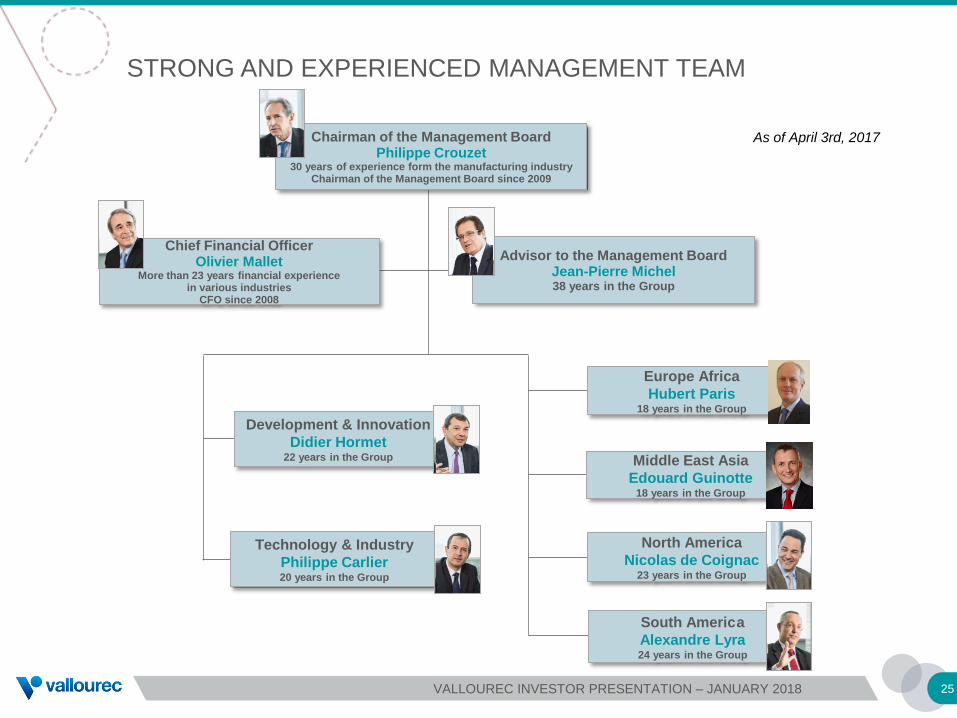

STRONG AND EXPERIENCED MANAGEMENT TEAM

Chairman of the Management BoardPhilippe Crouzet

30 years of experience form the manufacturing industryChairman of the Management Board since 2009

Chief Financial OfficerOlivier Mallet

More than 23 years financial experience in various industries

CFO since 2008

Advisor to the Management BoardJean-Pierre Michel38 years in the Group

Technology & Industry

Philippe Carlier20 years in the Group

Development & Innovation

Didier Hormet22 years in the Group

Europe Africa

Hubert Paris18 years in the Group

Middle East Asia

Edouard Guinotte18 years in the Group

South America

Alexandre Lyra24 years in the Group

North America

Nicolas de Coignac23 years in the Group

As of April 3rd, 2017

25VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

Q3 / 9M 2017 RESULTS

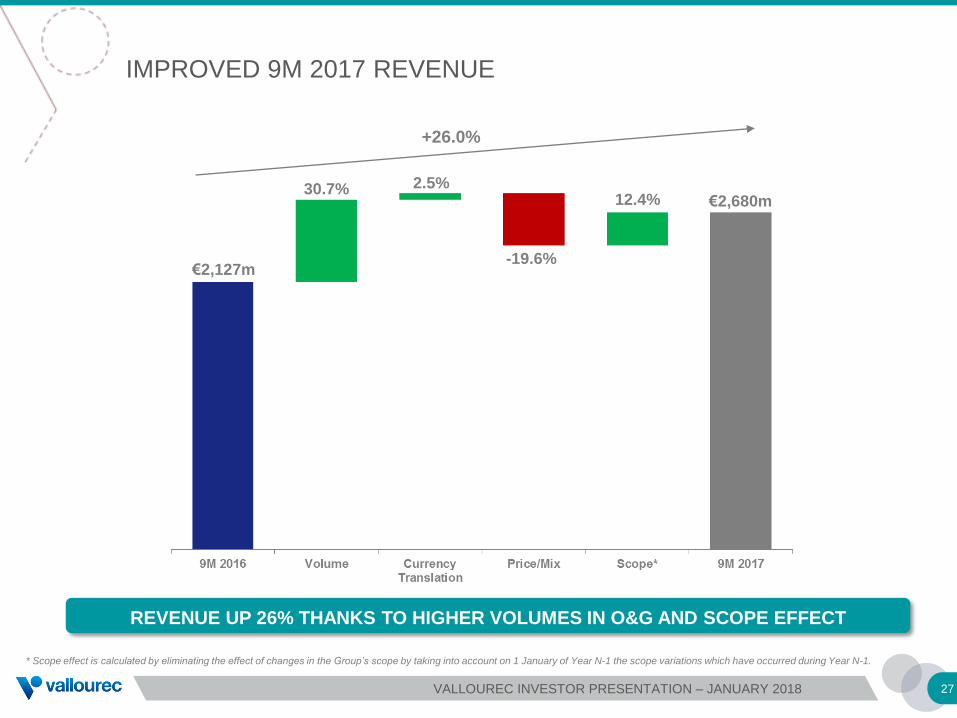

IMPROVED 9M 2017 REVENUE

€2,127m

30.7% 2.5%

-19.6%

12.4%

+26.0%

* Scope effect is calculated by eliminating the effect of changes in the Group’s scope by taking into account on 1 January of Year N-1 the scope variations which have occurred during Year N-1.

27

€2,680m

REVENUE UP 26% THANKS TO HIGHER VOLUMES IN O&G AND SCOPE EFFECT

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

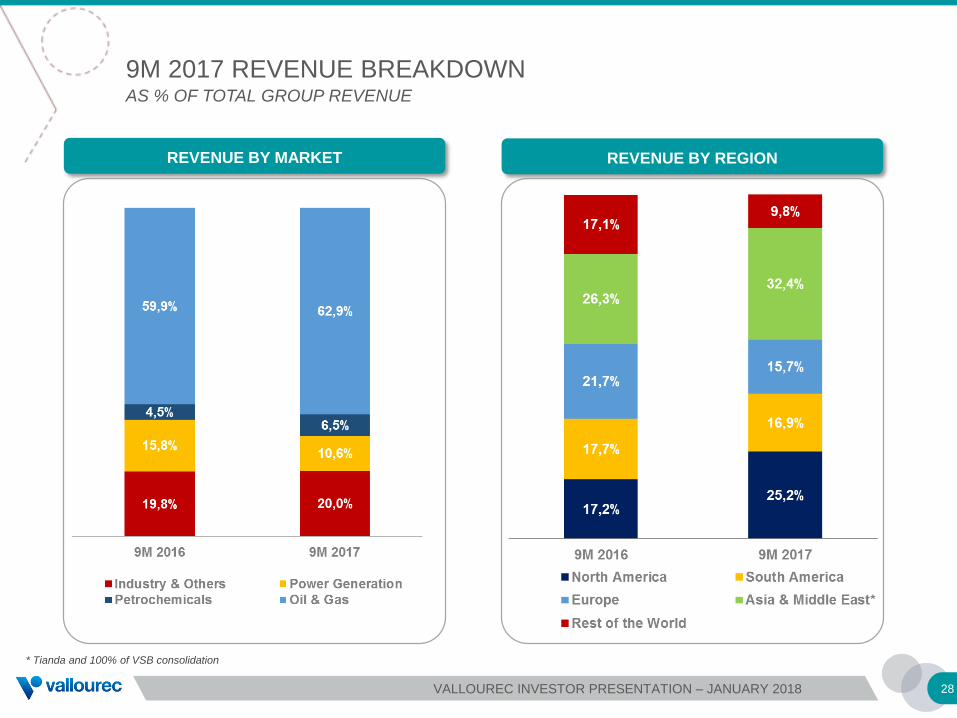

9M 2017 REVENUE BREAKDOWNAS % OF TOTAL GROUP REVENUE

* Tianda and 100% of VSB consolidation

28

REVENUE BY MARKET REVENUE BY REGION

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

* 9M 2017 versus 9M 2016

** at constant scope and exchange rates

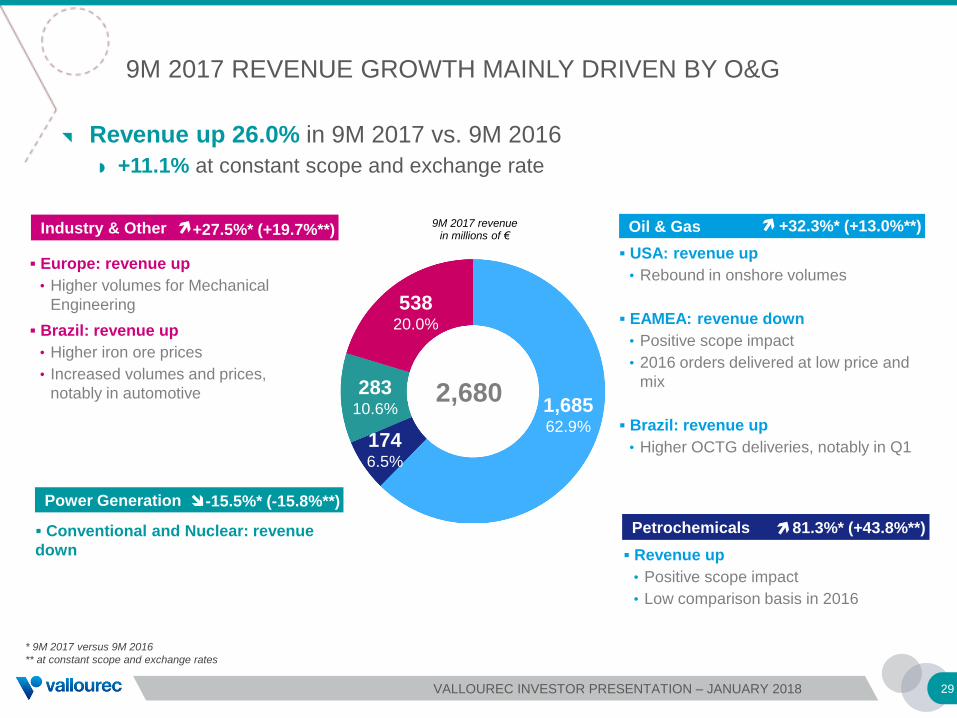

USA: revenue up

• Rebound in onshore volumes

EAMEA: revenue down

• Positive scope impact

• 2016 orders delivered at low price and

mix

Brazil: revenue up

• Higher OCTG deliveries, notably in Q1

Europe: revenue up

• Higher volumes for Mechanical

Engineering

Brazil: revenue up

• Higher iron ore prices

• Increased volumes and prices,

notably in automotive

Oil & GasIndustry & Other

Conventional and Nuclear: revenue

down

+27.5%* (+19.7%**)

Power Generation

Petrochemicals

+32.3%* (+13.0%**)

-15.5%* (-15.8%**)

81.3%* (+43.8%**)

53820.0%

28310.6%

1746.5%

1,68562.9%

2,680

9M 2017 REVENUE GROWTH MAINLY DRIVEN BY O&G

9M 2017 revenuein millions of €

Revenue up

• Positive scope impact

• Low comparison basis in 2016

Revenue up 26.0% in 9M 2017 vs. 9M 2016

+11.1% at constant scope and exchange rate

29VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

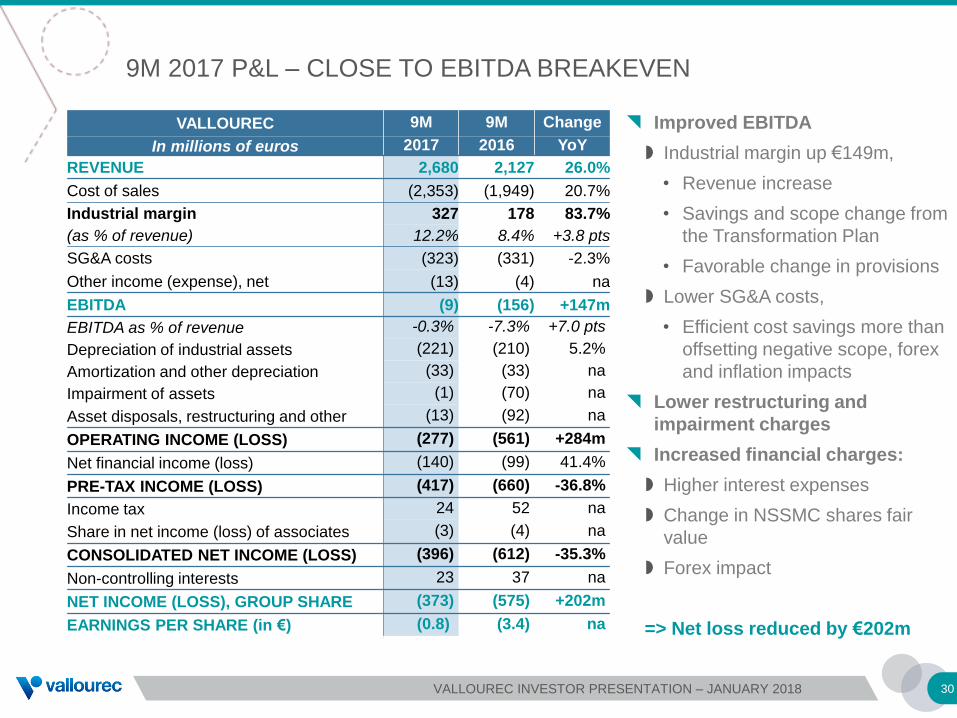

9M 2017 P&L – CLOSE TO EBITDA BREAKEVEN

VALLOUREC 9M 9M Change

In millions of euros 2017 2016 YoY

REVENUE 2,680 2,127 26.0%

Cost of sales (2,353) (1,949) 20.7%

Industrial margin 327 178 83.7%

(as % of revenue) 12.2% 8.4% +3.8 pts

SG&A costs (323) (331) -2.3%

Other income (expense), net (13) (4) na

EBITDA (9) (156) +147m

EBITDA as % of revenue -0.3% -7.3% +7.0 pts

Depreciation of industrial assets (221) (210) 5.2%

Amortization and other depreciation (33) (33) na

Impairment of assets (1) (70) na

Asset disposals, restructuring and other (13) (92) na

OPERATING INCOME (LOSS) (277) (561) +284m

Net financial income (loss) (140) (99) 41.4%

PRE-TAX INCOME (LOSS) (417) (660) -36.8%

Income tax 24 52 na

Share in net income (loss) of associates (3) (4) na

CONSOLIDATED NET INCOME (LOSS) (396) (612) -35.3%

Non-controlling interests 23 37 na

NET INCOME (LOSS), GROUP SHARE (373) (575) +202m

EARNINGS PER SHARE (in €) (0.8) (3.4) na

30

Improved EBITDA

Industrial margin up €149m,

• Revenue increase

• Savings and scope change from

the Transformation Plan

• Favorable change in provisions

Lower SG&A costs,

• Efficient cost savings more than

offsetting negative scope, forex

and inflation impacts

Lower restructuring and

impairment charges

Increased financial charges:

Higher interest expenses

Change in NSSMC shares fair

value

Forex impact

=> Net loss reduced by €202m

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

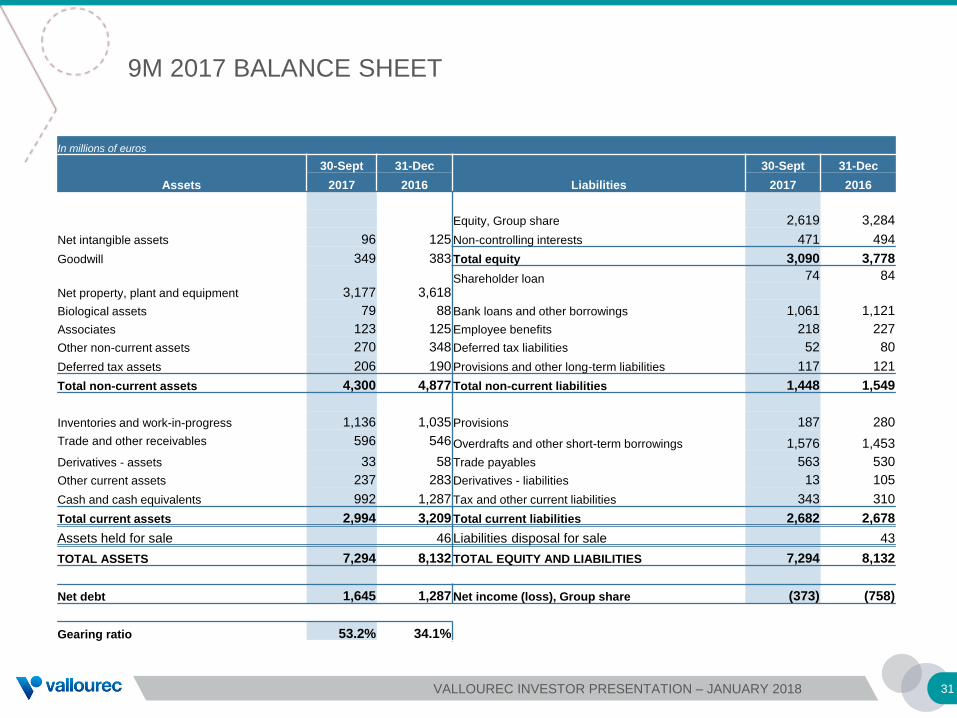

9M 2017 BALANCE SHEET

In millions of euros

Assets

30-Sept 31-Dec

Liabilities

30-Sept 31-Dec

2017 2016 2017 2016

Equity, Group share 2,619 3,284

Net intangible assets 96 125 Non-controlling interests 471 494

Goodwill 349 383 Total equity 3,090 3,778

Net property, plant and equipment 3,177 3,618Shareholder loan 74 84

Biological assets 79 88 Bank loans and other borrowings 1,061 1,121

Associates 123 125 Employee benefits 218 227

Other non-current assets 270 348 Deferred tax liabilities 52 80

Deferred tax assets 206 190 Provisions and other long-term liabilities 117 121

Total non-current assets 4,300 4,877 Total non-current liabilities 1,448 1,549

Inventories and work-in-progress 1,136 1,035 Provisions 187 280

Trade and other receivables 596 546 Overdrafts and other short-term borrowings 1,576 1,453

Derivatives - assets 33 58 Trade payables 563 530

Other current assets 237 283 Derivatives - liabilities 13 105

Cash and cash equivalents 992 1,287 Tax and other current liabilities 343 310

Total current assets 2,994 3,209 Total current liabilities 2,682 2,678

Assets held for sale 46 Liabilities disposal for sale 43

TOTAL ASSETS 7,294 8,132 TOTAL EQUITY AND LIABILITIES 7,294 8,132

Net debt 1,645 1,287 Net income (loss), Group share (373) (758)

Gearing ratio 53.2% 34.1%

31VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

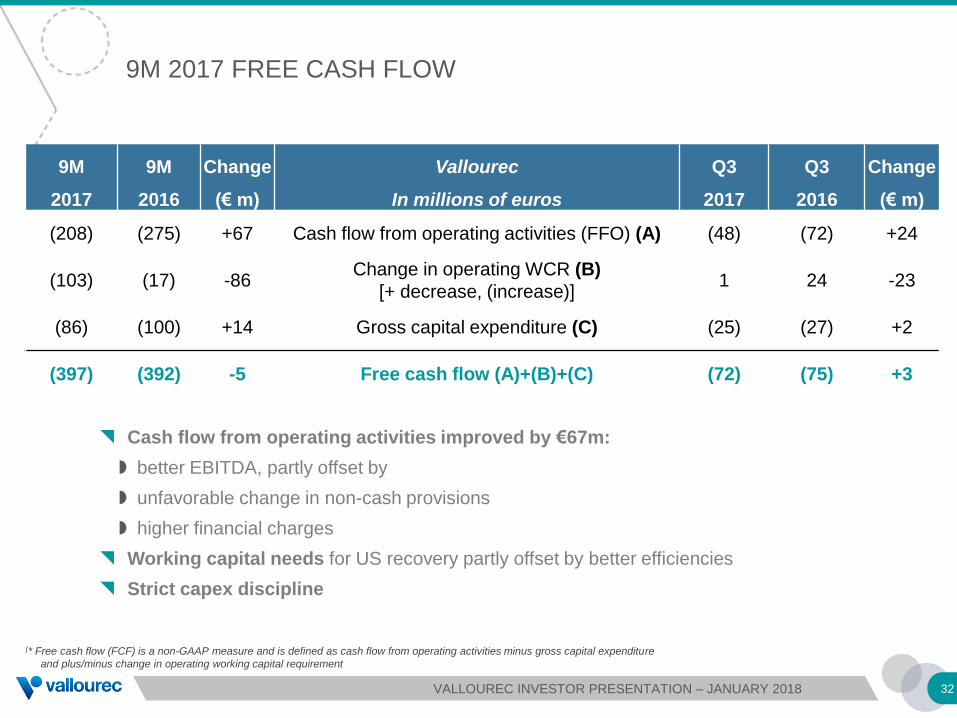

9M 2017 FREE CASH FLOW

(* Free cash flow (FCF) is a non-GAAP measure and is defined as cash flow from operating activities minus gross capital expenditure

and plus/minus change in operating working capital requirement

9M 9M Change Vallourec Q3 Q3 Change

2017 2016 (€ m) In millions of euros 2017 2016 (€ m)

(208) (275) +67 Cash flow from operating activities (FFO) (A) (48) (72) +24

(103) (17) -86Change in operating WCR (B)

[+ decrease, (increase)]1 24 -23

(86) (100) +14 Gross capital expenditure (C) (25) (27) +2

(397) (392) -5 Free cash flow (A)+(B)+(C) (72) (75) +3

32

Cash flow from operating activities improved by €67m:

better EBITDA, partly offset by

unfavorable change in non-cash provisions

higher financial charges

Working capital needs for US recovery partly offset by better efficiencies

Strict capex discipline

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

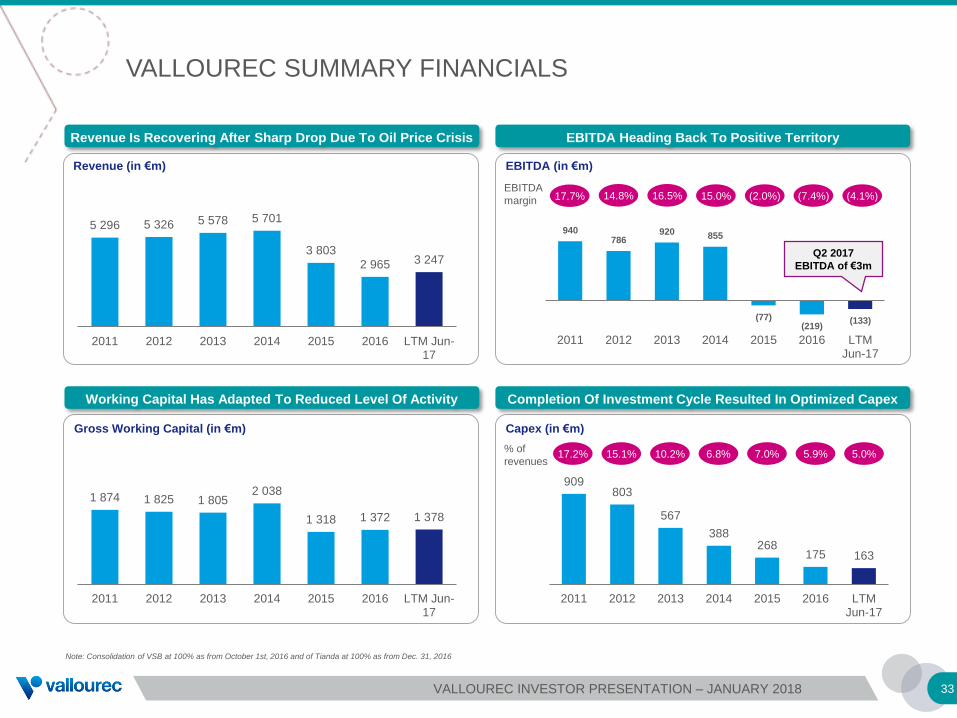

1 874 1 825 1 805 2 038

1 318 1 372 1 378

2011 2012 2013 2014 2015 2016 LTM Jun-17

VALLOUREC SUMMARY FINANCIALS

33

909 803

567

388 268

175 163

2011 2012 2013 2014 2015 2016 LTMJun-17

% of

revenues 17.2% 15.1% 10.2% 6.8% 7.0% 5.9%

5 296 5 326 5 578 5 701

3 803

2 965 3 247

2011 2012 2013 2014 2015 2016 LTM Jun-17

940 786

920 855

(77)(219)

(133)

2011 2012 2013 2014 2015 2016 LTMJun-17

EBITDA

margin 17.7% 14.8% 16.5% 15.0% (2.0%) (7.4%)

Revenue (in €m) EBITDA (in €m)

Gross Working Capital (in €m) Capex (in €m)

Note: Consolidation of VSB at 100% as from October 1st, 2016 and of Tianda at 100% as from Dec. 31, 2016

(4.1%)

5.0%

Q2 2017

EBITDA of €3m

Revenue Is Recovering After Sharp Drop Due To Oil Price Crisis EBITDA Heading Back To Positive Territory

Working Capital Has Adapted To Reduced Level Of Activity Completion Of Investment Cycle Resulted In Optimized Capex

VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

CAPITAL EXPENDITURE

(in millions of €)

34VALLOUREC INVESTOR PRESENTATION – JANUARY 2018

EURONEXT PARIS: ISIN CODE: FR0000120354, TICKER: VK

USA: AMERICAN DEPOSITARY RECEIPT (ADR) - ISIN CODE: US92023R2094, TICKER: VLOWY

Investor Relations Contact - Vallourec Group

Tel: +33 1 49 09 39 76

Email: [email protected]

www.vallourec.com