Embed Size (px)

Citation preview

Weekly International Pricing and Analysis

Argus Asphalt Report

Copyright © 2013 Argus Media LtdPage 1 of 21

Asphalt prices at key locations 13-17 May

US (rack prices, fob) $/st Low High Change

Northern New Jersey/New York City Metro 500 540

Coastal Texas 550 560

Northern Illinois/eastern Iowa 530 550 3

Southern California 530 540

Western Washington/Oregon 525 530 -5

US (waterborne, fob) $/st

East Gulf coast (barge fob) 460 470 -3

West Gulf coast (barge fob) 455 460

Midwest (barge fob) 410 420

Canada (rack prices, fob)

Quebec 611 617 -9

Ontario 602 615 -9

Europe (rack prices, fob)

Rotterdam 578 591 -10

Southwest Spain 597 623 -11

Other international (rack prices, fob)

South Africa 670 690 -20

Singapore 625 630

Other international (waterborne, fob) $/t

Iran (cargo fob) 490 500 -5

Singapore (cargo fob) 605 612 -3

Taiwan (cargo fob) 600 608 -2

South China (ex-Singapore cfr) 617 658 -4

Note: st - short ton, t - metric tonne.

5M-20 17 May 2013

Summary

• WholesaleactivityinUSasphaltmarketswaslimitedduringmid-month.Retailmarketsremainslowtoopenup,backingupwhole-saledemand.Withthelatestarttotheseason,manyareexpectingUSvolumestobeofffromthe2012demandfigureof22.2mnshorttons.

• IntheUSMidwest,withalatestartandashortfinishexpectedthispavingseason,anunpredictablesummersupplysituationcouldemerge.Newcokingunitsexpectedtocomeonlinethisyearcouldshiftsupply-demanddynamicscausingtemporaryshort-fallsinsup-ply.

• USRockiesmarketsinchedupforwholesaledeals.Somerefin-ershaveachieveddealsat$400/stfobrailforthemonthofMayandarepushinghigherforJune.IntheGulfcoast,valuesfell,pressuredbydiminishedexportdemandandweakeningalternativemarkets.

• NorthwestEuropeanbitumendemandslowedafterabusymid-ApriltoearlyMayperiodofconstructionandproductfill-uprequire-ments.ShippingsourcesindicatedthatcargoflowshadslowedinthemiddleweekofMay,althoughtankersarestillfullyemployedonalreadyagreedbusinessthroughtoearlyJune.

• Lebanon’sbitumenconsumptionisexpectedtofallto40,000-50,000tthisyear,thelowestlevelforseveralyearsanddownmas-sivelyfrom75,000tin2012.

• WhileSouthAfricanbitumendemandisstartingtotaperoffwiththeapproachofwinter,aprolongedandextensiveseasonofrefinery

ContentsSummary 1

Global bitumen wholesale prices 2

US and Canada 3-9

East coast commentary 3

Gulf coast commentary 4

Midwest commentary 5

Rocky Mountain and west coast commentary 6

Canada commentary 7

Europe and Africa bitumen commentary 10

Asia and Middle East bitumen commentary 15

Crude oil 20

Oil industry briefs 20

Argus Media contact information 21argusmedia.com/euro-bitumen

Argus Europe/Africa Bitumen 2013 12-13 June | Cannes, France

Muliti-booking discounts now available!

5M-20 17 May 2013

Page 2 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

maintenanceinSouthAfricahasreduceddomesticsupply.This,coupledwitharebateonimportdutieswhichcameintoeffectinMarch,hasseenariseinimportsofdrummedmaterial.

• NegotiationswerecontinuingregardingtheawardoftheTunisianimporttenderfor60,000tofPen30/50fordeliveryintotheportsofRadesandGabesfromMay2013throughtoApril2014.Aseparatetenderwasreportedtohavebeenissuedfortheimportof12,000tofbitumen–mostlikelyinthree4,000tcargoes–intotheTunisianportofSfax.

• Singapore’sbulkpricesinchedlowerby$3/tto$605-612/tfob,assellerscutpricestofindhomesfortheirJune-loadingcargoes.ButSingaporecargoeswerestilldeemedtobeuncompetitiveintoVietnamorsouthChinawithcheaper-pricedalternativesfromSouthKorea,China,ThailandandTaiwan.

• Singaporeex-tanktruckpricesweredownslightlyto$590-600/tthisweek.OneSingaporerefinermovedasignificantnumberoftanktrucksintoMalaysiathisweekataround$600/t.Theincreasein

tanktruckdeliveriespromptedMalaysiandealersandthecountry’sstate-controlledrefinertocutpricesaswell.

• WeakbuyinginterestfromsouthChina,VietnamandAustraliameantthatThairefinersstruggledtofindoutletsfortheirJunecargoes.TankswerealmostfullinNorthVietnambutimporterswereseekingsmallvolumesinJunefortheirterminalsinthesouth.

• SpotpricesinSouthKoreaeasedby$2/tto$578-583/tfobthisweek.VerylittlespotdemandwasheardalthoughAustralianbuyerswillcontinuetoreceivetheirtermcommitmentsfromThailandandSingapore.

• ImportpricesintoChinaarestableat$613-620/tcfrinnorthernChinabutdownby$6/tto$615-663/tcfrineasternChinaanddownby$4/ttoat$617-658/tcfrinsouthChina.

• Indiahasraisedthecountry’sbitumenrackpriceby180rupees/t($3.2/t),effective15May.

Argus Market Map: Global wholesale bitumen prices, fob basis $/t

New Jersey

$513/t

West Gulf coast

$504/t

Bahrain

$550/t

Note: Med and NWE HSFO prices on 16-May were used to calculate Europe and Africa wholesale bitumen prices.

East Gulf coast

$513/t

Greece

$535/t

Ivory Coast

$638/t

Iran

$495/t

Italy

$503/t

Japan

$566/t

Netherlands

$558/t

Singapore

$609/t

South Korea

$581/t

Spain

$520/t

Taiwan

$604/t

Thailand

$603/t

5M-20 17 May 2013

Page 3 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

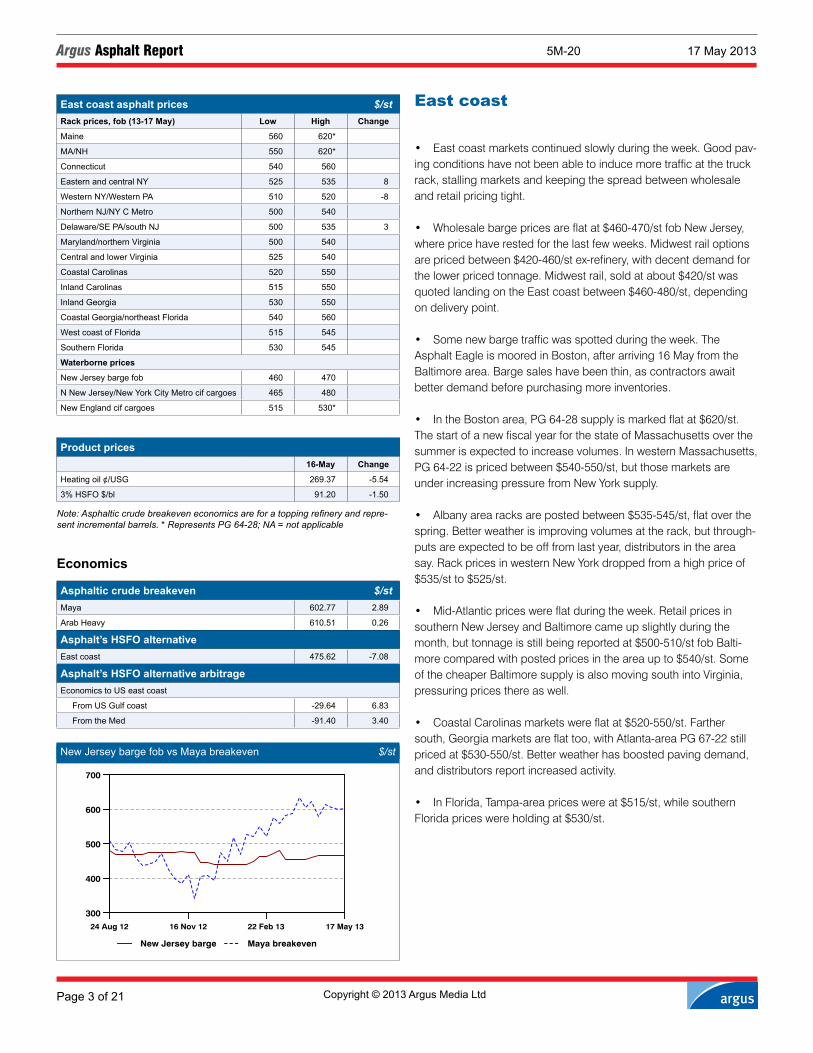

US and CanadaEast coast

• Eastcoastmarketscontinuedslowlyduringtheweek.Goodpav-ingconditionshavenotbeenabletoinducemoretrafficatthetruckrack,stallingmarketsandkeepingthespreadbetweenwholesaleandretailpricingtight.

• Wholesalebargepricesareflatat$460-470/stfobNewJersey,wherepricehaverestedforthelastfewweeks.Midwestrailoptionsarepricedbetween$420-460/stex-refinery,withdecentdemandforthelowerpricedtonnage.Midwestrail,soldatabout$420/stwasquotedlandingontheEastcoastbetween$460-480/st,dependingondeliverypoint.

• Somenewbargetrafficwasspottedduringtheweek.TheAsphaltEagleismooredinBoston,afterarriving16MayfromtheBaltimorearea.Bargesaleshavebeenthin,ascontractorsawaitbetterdemandbeforepurchasingmoreinventories.

• IntheBostonarea,PG64-28supplyismarkedflatat$620/st.ThestartofanewfiscalyearforthestateofMassachusettsoverthesummerisexpectedtoincreasevolumes.InwesternMassachusetts,PG64-22ispricedbetween$540-550/st,butthosemarketsareunderincreasingpressurefromNewYorksupply.

• Albanyarearacksarepostedbetween$535-545/st,flatoverthespring.Betterweatherisimprovingvolumesattherack,butthrough-putsareexpectedtobeofffromlastyear,distributorsintheareasay.RackpricesinwesternNewYorkdroppedfromahighpriceof$535/stto$525/st.

• Mid-Atlanticpriceswereflatduringtheweek.RetailpricesinsouthernNewJerseyandBaltimorecameupslightlyduringthemonth,buttonnageisstillbeingreportedat$500-510/stfobBalti-morecomparedwithpostedpricesintheareaupto$540/st.SomeofthecheaperBaltimoresupplyisalsomovingsouthintoVirginia,pressuringpricesthereaswell.

• CoastalCarolinasmarketswereflatat$520-550/st.Farthersouth,Georgiamarketsareflattoo,withAtlanta-areaPG67-22stillpricedat$530-550/st.Betterweatherhasboostedpavingdemand,anddistributorsreportincreasedactivity.

• InFlorida,Tampa-areapriceswereat$515/st,whilesouthernFloridapriceswereholdingat$530/st.

East coast asphalt prices $/stRack prices, fob (13-17 May) Low High Change

Maine 560 620*

MA/NH 550 620*

Connecticut 540 560

Eastern and central NY 525 535 8

Western NY/Western PA 510 520 -8

Northern NJ/NY C Metro 500 540

Delaware/SE PA/south NJ 500 535 3

Maryland/northern Virginia 500 540

Central and lower Virginia 525 540

Coastal Carolinas 520 550

Inland Carolinas 515 550

Inland Georgia 530 550

Coastal Georgia/northeast Florida 540 560

West coast of Florida 515 545

Southern Florida 530 545

Waterborne prices

New Jersey barge fob 460 470

N New Jersey/New York City Metro cif cargoes 465 480

New England cif cargoes 515 530*

Product prices16-May Change

Heating oil ¢/USG 269.37 -5.54

3% HSFO $/bl 91.20 -1.50

Note: Asphaltic crude breakeven economics are for a topping refinery and repre-sent incremental barrels. * Represents PG 64-28; NA = not applicable

Economics

Asphaltic crude breakeven $/stMaya 602.77 2.89

Arab Heavy 610.51 0.26

Asphalt’s HSFO alternativeEast coast 475.62 -7.08

Asphalt’s HSFO alternative arbitrageEconomics to US east coast

From US Gulf coast -29.64 6.83

From the Med -91.40 3.40

hhh

300

400

500

600

700

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

New Jersey barge Maya breakeven

New Jersey barge fob vs Maya breakeven $/st

5M-20 17 May 2013

Page 4 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Gulf coast

• Gulfcoastasphaltmarketsfellslightlyduringtheweekforwhole-salevalues.RetailmarketsineasternandwesternGulfcoastregionsstilllackmomentumandpricesareflat.

• Onenewcargoof30,000-34,000blofAC-20wasbookedforexportat$470/stfobbargeeasternGulfcoast,downfromlastweek’shigherpricesof$475/sttoadomesticcustomer,butthesalesuggestssomestrengthatlevelsabove$460/st–lastweek’slow.

• WesternGulfcoastmarketsareweaker,astalkscontinueforMaybarrelsat$455-460/stfobbarge.SomepricingdiscussionshavecommencedforJuneaswell,withinthesamerange.

• ExportdemandfromLatinAmericahasfallenoffsincetheendofApril,assomecountriesbreakforrainyseasons.ButtheappetiteforasphaltoverallisfallingoffforsomekeyexportoutletsforUSsupply.

• Somenewbargeactivitywasspottedintheweek.TheIverAs-phaltdeliveredtonnagePortMoin,CostaRicafromMobile,landing16May.CompetitionwithVenezuelacontinuesforseabornemarkets–theAsphaltTransporterisdeliveringacargotoHonolulufromVenezuela.

• Inretailmarkets,pricesstayedflat.FormuchoftheGulfcoastre-gion,springandearlysummerhaveyettodeliveranyincreasedactivity.

• InAlabama,inlandPG64-22supplyispostedat$555/st,flatontheweek,whiletothesouth,pricesareat$545/st.MississippipostedpricesforPG67-22are$560/stacrossthestate.ActivityinMississippihasbeenslowsinceheavyrainslastweek,andmomen-tumhasyettoreturn.

• TexasrackpriceshavebeenflatallyearforPG64-22at$550-560/stalongthecoastand$550/stinland.

• WesternGulfcoastasphalt’salternativevaluetocokehasfallenoff,withvaluesnearlyinlinewithwholesaleasphalt,accordingtolocalrefiners.

Gulf coast asphalt prices $/stRack prices, fob (13-17 May) Low High ChangeAlabama (southern) 545 565 -10

Alabama (inland) 555 565 -5

Louisiana/Mississippi (southern) 544 560 -8

Louisiana/Mississippi (inland) 560 560 -15

Arkansas/northeast Texas 580 600

Texas (coastal) 550 560

Texas (inland) 550 550

New Mexico 570 575

Waterborne fobEast Gulf coast 460 470 -3

West Gulf coast 455 460

Note: Asphaltic crude breakeven economics are for a topping refinery and repre-sent incremental barrels.

Product prices 16-May ChangeHeating oil ¢/USG 271.87 -5.92

3% HSFO $/bl 90.95 -1.50

EconomicsAsphaltic crude breakeven $/stMaya 576.97 3.86

Arab Heavy 611.52 0.43

Asphalt’s HSFO alternative $/stGulf coast 472.14 -6.83

General refining economicsFob US Gulf coast ($/bl)3-2-1 crackspread 23.34 1.32

2-1-1 crackspread 22.26 0.67

hhh

300

400

500

600

700

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

East Gulf coast barge Maya breakeven

East Gulf coast barge vs Maya breakeven $/st

hhh

550

560

570

580

590

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Inland Alabama Southern Alabama

Inland Alabama vs southern Alabama $/st

hhh

450

475

500

525

550

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

East Gulf coast barges HSFO alternative

East Gulf coast barge vs Asphalt's HSFO alternative $/st

5M-20 17 May 2013

Page 5 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Midwest asphalt prices $/stRack prices, fob (13-17 May) Low High Change

West Oklahoma/Texas Panhandle 540 550

NE Oklahoma/Kansas/southwest Missouri 530 555

North Illinois/eastern Iowa (Chicago) 530 550 3

South Illinois/eastern Missouri (St Louis) 500 550

Western Iowa/Nebraska 575 595

North Dakota/south Dakota 550 595 -13

Northern Minnesota/northern Wisconsin 535 550 -10

Southern Minnesota/southern Wisconsin 490 545 15

Northeast Indiana/north Ohio/Michigan 525 575

South Ohio/south Indiana/north Kentucky 540 545

South Kentucky/Tennessee 545 565

Waterborne fob

Midwest asphalt barge 410 420

Midwest roofing flux barge 510 540

Midwest

• Midwestmarketswereflat.Pricesonthewholesaleandretailsidearecaughtinmid-monthdoldrums,andweakdemandismatchedbylimitedsupplyfromrefineryturnarounds.

• Wholesalerailquoteswereflatontheweekat$420-440/st,withnosuppliersadjustingprices.Rivertrafficisscant,especiallywitharbitragewindowstoUSGulfcoastmarketsclosed,andpricesremainflatat$410-420/stfobbarge.SomeCanadiandemandcouldbeemergingforGreatLakesbargesatpricesinthesamerange.

• Withalatestartandashortfinishexpectedthispavingseason,marketsareexpectingavolatilesummer.Newcokingunitsexpectedtocomeonlineinthesummercouldshiftsupply-demanddynamicsandleavesomecontractorsshortofmaterial,oratleastshoppingforanewsupplier.

• Rackswereunchangedduringtheweekformostlocations.Manyareexpectingvolumestobeoffoflastyear’sthroughputs,asdemandremainsstubborn,andweatherstillhinderssomeregions.

• TheMichiganpricerangewidened.SupplyforPG64-22wasquotedbetween$520-545inthesouthernpartofthestateandupto$565/st(andsomelimitedamountsof$575/st)reportedinthenorthernpartofthestate.PG58-28retainsits$30/stpremiumoverPG64-22.

• NorthernOhioPG64-22wasreportedat$535/st,downfrompostednumbersashighas$565/st.

• InChicagomarkets,pricesforPG64-22movedupslightlyto$545-550/stfrom$530-545/stnitheweekprior.NorthernIndianapricesstayedflatat$545/st.

• MinnesotaandWisconsinretailmarketsremainquiet.Pavingconditionsarestilldifficultandlimitedproductismoving.Retailton-nagewasquotedinthemid-$500/stacrossnorthernWisconsinandMinnesota.SouthernWisconsinpriceswereslightlycheaper,withtonnagebeingmarkedat$545/st.

• TheDakota’spricesalsofell.Activityissimilarlythin,andpricesforretailwerequotedatmid-$500/st.

hhh

500

525

550

575

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Chicago St LouisOhio/Michigan

Chicago - St Louis - Ohio/Michigan $/st

hhh

540

550

560

570

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

N Ohio/S Indiana/N Kentucky S Kentucky/Tennesse

North OH - South IN - North KY vs South KY - TN $/st

hhh

350

400

450

500

550

600

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Midwest roofing flux barge Midwest asphalt barge

Midwest roofing flux barge vs Midwest asphalt barge $/st

5M-20 17 May 2013

Page 6 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Rocky Mountain and west coast

• Rockieswholesalemarketsweremixed.SomehigherwholesalenumberswerereportedforMaydeliveriesasrefinerspushsummerpriceshigher,butretailactivityremainsmiredinalull.LowerrackpricescontinueforRockiesandWestcoastmarkets.

• Wholesalerailpurchaseswerereportedat$400/tex-refinery,up$5/tfromapreviousrangeof$385-395/tsincetheendofApril.SomenascentconversationsforJunearebeginning.Purchasingremainscontainedtosmalllotstotopupliftedinventories,andnegotiationsoverpriceunderlielingeringresistancetothe$400/tmark.

• RackmarketswereflatordownintheRockiesandWestCoast.Demandremainsmutedandcompetitionhighinmanymarkets.

• LettingswerequietinthestateofMontana,duringtheweek.Pricesstayedflatat$515-525/stforPG64-22.Decentweatherhasboostedvolumesatsometruckracks,movingsupplyouttohighwayprojectsalreadyunderway.

• InDenver,cheapsupplyofPG64-22remainsprevalent.Somewholesaleofferingsarestillinthemarketat$450/st,withtherackspostedat$515/stforMay.Effortstoincreasethewholesalepricecouldbringsomeconvergencewiththeracknumbers.

• Arizonapriceswerestableat$510-515/stforPG64-22.Someweaknesspervades,asquotesonsupplyatsub-$500’s/starestillreported.MarketoutlookforthePhoenixregionisforpricestoremainflat,orslightlydownforMayandJune.

• SouthernCaliforniamarketsremainweak.MarketpricesforPG64-10and64-16stayedbetween$530-540/st.TheendofthefiscalyearfortheCaliforniaDepartmentofTransportationhasslowedworkoverthemonthofJune.Holidaysattheendofthemonthareexpectedslowbusinessevenmore,butJulycouldbringheaviervolumes.

• InthePacificNorthwest,marketpriceswereflat,havingsof-tenedoverthespring.SupplyofPG64-22issellingfor$530/stinOregon.Thestate’sbidseasonhasmostlyclosedfortheyear,thoughmoreworkwillcontinuetobereleased.Washingtonmar-ketsaresofterthanOregon,at$525/st,weakenedbycompetitionandlimiteddemand.

Rocky Mountain asphalt prices $/stRack prices, fob (13-17 May) Low High Change

Montana 515 525

Wyoming 515 525

Colorado 500 515 -3

Utah 500 550

Idaho/east Washington 570 600

Wholesale prices

Rocky Mountain (rail) fob 385 400 3

Product prices (Los Angeles) 16-May Change

EPA diesel oil ¢/USG 284.87 -6.04

HSFO 380cst $/bl 99.21

Asphalt’s HSFO alternative $/stWest coast 522.85 518.79

West coast asphalt prices $/stRack prices, fob (13-17 May) Low High Change

Western Washington/Oregon 525 530 -5

Northern California 580 600

Central California 550 560

Southern California 530 540

Arizona 510 515

Nevada 520 530

Roofing flux rack prices

Southern California 610 630

hhh

505

510

515

520

525

530

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Montana Colorado

Rocky mountain rack prices $/st

hhh

500

550

600

650

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Arizona South Californiawest Washington/Oregon

Arizona - southern California - west Washington/Oregon $/st

5M-20 17 May 2013

Page 7 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Canada

• Canadianasphaltmarketswereflatduringtheweek.Easternprovincesarestartingtoseevolumeimprovements,thoughoverall2013marketsarestillexpectedtobedowncomparedwithlastyear.Pricesareexpectedtobestablethroughmid-May.

• TheMontrealdepartmentoftransportationissuedtendersthisweekforPG58-34and64-34overtheweek.ForPG58-34,thelowofferfromsupplierswasC$782.50/t,andthehighofferwasC$835/t.ForPG64-34thelowestofferwasC$862.50/tandthehighestofferwasC$895/t.

• PostedpricesforPG58-28inQuebecwereflatintheweek,pricedbetweenC$685-695/t.Lastweek,springweightrestrictionsontruckswereliftedandgoodweatherboostedvolumes,butthe

marketoutlookisstillcallingforaslowyear.Volumescouldbeoffbyasmuchas20pccomparedwith2012,accordingtosomedistribu-tors.

• OntariopriceswereflatduringtheweekforPG58-28.PriceshavebeenflatoverthespringonlimitedactivityatC$675-690/t.

• InwesternCanada,wholesalerailpriceshavebeenflatsincethebeginningofMayatUS$380-390/stfobrefinery.

• Manitobamarketsarestillquiet.Thepavingbudgetfortheprov-inceremainsuncertainuntilfloodrepaireffortsarecompleted.

• Lastweek,onerefinerincreasedrack(postedspot)pricesin

Eastern Canada posted prices for asphaltCompany (location) Asphalt grade Posted prices (C$/t) Differentials Effective dateKildair (Sorel-Tracy, Quebec) PG 58-28 712 19 Apr

PG 64-28 762 50 19 Apr

PG 58-34 polymer 802 90 19 Apr

PG 64-34 polymer 852 140 19 Apr

PG 70-28 polymer 852 140 19 Apr

Suncor Energy Inc. (Montreal, Quebec) PG 58-28 695 09 May

PG 64-28 - - 09 May

PG 58-34 polymer - - 09 May

PG 64-34 polymer - - -

Note: st - short ton, t - metric. *BUR = Built-up roofing.

Eastern Canada asphalt pricesRack prices, fob (13-17 May) C$/t $/st

Low High Change Low High Change

Quebec 685 692 611 617 -9

Ontario 675 690 602 615 -9

Roofing BUR* liquid prices

Ontario 800 820 714 731 -11

Western Canada asphalt pricesRetail prices, fob (13-17 May) Base Asphalt grade C$/t $/st

Low High Change Low High Change

British Columbia 150/200A or PG 64-25(80/100A) 570 590 508 526 -8

Alberta 150/200A 570 585 508 522 -8

Saskatchewan 150/200A 580 600 517 535 -8

Manitoba 150/200A 560 600 500 535 -8

Western Canada Posted Spot Prices for AsphaltCurrent Posted Spot Price Effective Date

Company (Location) Asphalt Grade (C$/t) ($/st)

Husky (Edmonton, AB) 150/200A 675 602 10 May

Husky ( Vancouver, BC) PG 64-25 (80/100A) 715 638 10 May

Husky (Prince George, BC) 150/200A 735 656 10 May

Husky (Kamloops, BC) 150/200A 725 647 10 May

Husky (Winnipeg, Manitoba) 150/200A 715 638 10 May

5M-20 17 May 2013

Page 8 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Canada – Methodology

Eastern Canada posted prices for asphalt: These are posted prices announced by suppliers and refiners in the Quebec market for asphalt grades they supply (conventional and polymer). The prices are listed by company, location and grades supplied, along with differentials for premium grades. The posted prices are reported in C$/t with effective dates.Eastern Canada asphalt prices for Quebec: This is actual selling prices in the Quebec market for grade PG 58-28.Eastern Canada asphalt prices for Ontario: This is actual selling prices in the Ontario market for grade PG 58-28. Roofing BUR liquid prices: This is built-up roofing pricing in the Ontario market.Western Canada posted spot prices for asphalt: These prices are also known as “rack postings” in western Canada. They represent pricing to stationary asphalt plants at various locations. Grades represented are Pen 150/200A for Edmonton, Price George, Kamloops and Winnipeg. The grade for Vancouver is PG 64-25 (Pen 80/100A).Western Canada asphalt prices for British Columbia, Alberta, Saskatchewan and Manitoba: These prices represent the “current market” and include winning quotes at highway tenders. Winning quotes are “fob the closest” supplier. Grade represented is Pen 150/200A.

hhh

600

625

650

675

700

725

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Quebec Ontario

Quebec/Ontario C$/t

hhh

570

580

590

600

610

620

630

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Alberta C$/t

westernCanadabyC$50/t,mostlyforPen150/200specifications.Thepriceincreaseswhichtookeffecton10Mayremainedun-changedthisweek.

• InManitoba,WinnipegPen150/200rack(postedspot)pricesincreasedtoC$715/tfromC$665/tpreviously.InAlberta,Edmon-

tonrack(postedspot)pricesforPen150/200increasedtoC$675/tfromC$625/t.InBritishColumbia,Vancouverrack(postedspot)pricesforPG64-25(Pen80/100A)increasedtoC$715/tfromC$665/t.InKamloops,Pen150/200wasraisedtoC$725/tfromC$675/t.InPrinceGeorge,Pen150/200wasraisedtoC$735/tfromC$685/t.

5M-20 17 May 2013

Page 9 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

European bitumen pricesRack prices, fob* 13-17 May €/t**** 13-17 May $/t

Low High Change Low High Change

Netherlands-Rotterdam 445 455 578 591 -10

Belgium - Antwerp 445 455 578 591 -10

Brussels** 450 460 584 597 -10

Germany north 455 470 591 610 -10

northeast 455 470 591 610 -10

south 460 475 597 617 -10

southwest 455 470 591 610 -10

west 460 475 597 617 -10

France north** 465 485 604 630 -11

central** 470 490 610 636 -11

south** 480 500 623 649 -11

UK south (UKP) 480 500 733 763 -12

Italy*** 450 470 584 610 -10

Spain northeast 480 500 623 649 -11

southwest 460 480 597 623 -11

fob Mediterranean cif northwest Europe 16-May Change 16-May Change

Straight-run fuel oil 3.5% sul. $/t 581.00 -3.75 Straight-run fuel oil 3.5% sul. $/t 598.25 -4.25

Vacuum gasoil 0.5 % sul. $/t 749.00 22.88 Vacuum gasoil 0.5 % sul. $/t 751.75 25.63

* truck prices, fob refinery or terminal. **Delivered price. *** Price includes €31/t tax. ****UK prices in Pounds.

Bitumen’s HSFO alternative $/t 16-May Change

Mediterranean 537.85 -10.13

hhh

575

600

625

650

675

700

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Italy Spain

Italy vs Spain rack $/t

hhh

500

550

600

650

700

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Rotterdam rack HSFO

Rotterdam rack vs NW Europe HSFO barges $/t

hhh

480

490

500

510

520

530

540

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

UK south UKP/t

hhh

600

650

700

750

800

850

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

South Africa West Africa

South Africa rack vs West Africa cargo cfr $/t

5M-20 17 May 2013

Page 10 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Europe and Africa bitumen Northwest Europe

• Pricesheldsteadyinmid-Mayaftertypical€10-15/tdeclinesthattookeffectfromthestartofthemonth.

• Costpressuresweredownwardovertheweekbutstillwellupmonth-on-month.Prompthigh-sulphurfueloilbargepricesslippedto$586.75/tfobRotterdamon16Mayfrom$591/taweekearlier,butthepricelevelwasstill$18/thigherthanon16Aprilwhenitstoodat$568.5/t.Thedailyaveragepricefor1-16Maywasat$583/t,downamodest$4.5/tfrom$587.5/tinthe1-16Aprilperiod.

• DatedNorthSeaphysicalcrudeoilstoodat$104.37/bl,up89¢/blfromaweekearlierandup$5.05/blfrom16April.

• Bitumendemandslowedafterabusymid-ApriltoearlyMayperiodofconstructionandproductfill-uprequirements.ShippingsourcesindicatedthatcargoflowshadslowedinthemiddleweekofMay,althoughtankersarestillfullyemployedonalreadyagreedbusinessthroughtoearlyJune.

• CargoflowsintoFranceremainwelldownonlastyear,reflectingthestillweakstateofthateconomyandofconstructionsectoractiv-itythere,withScandinavia,UKandIrelandcurrentlythemainexportoutletsforcargoesemanatingfromnorthwestEuropeanexportterminals,principallyRotterdam.

• NofreshSouthAfricaboundrequirementswerereportedasthe6,300DWTtankerBitRedomadeitswaytowardsthecountrywithitslatest5,000tcargofromtheColasspecialityproductsrefineryinDunkirkonthenorth-easterncoastofFrance.Thecargoissched-uledtoarriveinDurbanon28May.

• WhiletheFrencheconomyenteredatriple-diprecession,andtheoveralleconomicpictureacrossEUeconomiesremainedpoor,thereweresignsofverymodestGDPgrowthinGermanyandtheUK.

• EUdatashowedthattherecessionacrossthe17-nationeuro-zonehascontinuedintoasixthquarter.Arecessionisdefinedastwoconsecutivequartersofnegativegrowth.

• Theeconomyofthe17-nationblocshrankby0.2%intheJanu-arytoMarchperiod,accordingtotheEU’sstatisticsofficeEurostat,withnineofitsmembersnowinrecession.

• Germany’seconomy,generallyconsideredtobetheeurozone’sstrongest,grewbyjust0.1%inthequarter,farweakerthanexpect-ed.Economistshavingexpectedarateof0.3%.Annualfiguresfromthecountry’sStatisticsOfficealsoshowtheGermaneconomyhasshrunkby1.4%whencomparedwithayearago.

• Butinastatementitsaidthiswaspartlyduetoseverewinterweather:“TheGermaneconomyisonlyslowlypickingupsteam.Theextremewinterweatherplayedaroleinthisweakgrowth.”

• TheoutgoingGovernoroftheBankofEngland,MervynKing,issuedaseparateforecastthatUKGDPgrowthwouldbemorethan1pcin2013,upfromtheBanks’spreviousforecastof0.9pc.

France

• Ageneralriseinpost-winterconstructionactivityacrossEuropesinceearlytomid-Aprilhasmaskedanespeciallypooryear-on-yearperformancebyFrance,wherebitumendemandisexpectedtobewelldownonlastyearwhenitdroppedbyaround20pctoanestimated2.32mnt.

• Indicationsofthatslowdownwerebeingseenontheshippingmarket,wheretankerbrokerspointedtomuchlowercargomove-mentsintoFrenchdestinationslikeNantesandBayonnethanaroundthesametimelastyear.

• TheweakstateoftheFrencheconomywasunderlinedbyofficialfiguresthatshowedthecountryhadslippedintorecessioninthefirstquarterof2013,makingitthethirdtimeithasdonesoinfouryears.TheFrencheconomyshrankby0.2pcinthefirstquarterafter0.2pcfallinthefourthquarterof2012.FrenchPresidentFrancoisHollandesaidheexpectszerogrowthin2013,comparedwiththegovern-ment’spreviousforecastof0.1pcgrowth.EurostatsingledoutFranceinitsEU-widesurveyasacountrywithrecordunemploymentandlowbusinessandconsumerconfidence.

Europe/Africa wholesale bitumen differentials to HSFO $/tMarket Bitumen’s differential to HSFO

The Netherlands (Rotterdam) -15 to -5

Spain -55 to -40

Italy -70 to -60

Greece -40 to -25

Ivory Coast +65 to +75

Grade represented Pen 60/70 or equivalent grade

hhh

-100

0

100

01 Jun 12 24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Netherlands (Rotterdam) SpainItaly GreeceIvory Coast

Europe/Africa wholesale bitumen differentials to HSFO $/t

5M-20 17 May 2013

Page 11 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

• ThebitumentankerSanMatteowasscheduledtodischargea5,000tcargointotheLBCstorageterminalatLaveraon17May.

Benelux

• Theshutdownofapropanede-asphaltingunitatShell’sPernisrefineryonRotterdambecauseofa2MayfirewashavingnoimpactondomesticsuppliesintheBeneluxorneighbouringmarkets.Buttheshutdown,whichisthoughttohavehitbitumenproductionattherefinerythatmainlyproduceshardgradesoftheproduct,didhaveatemporaryimpactontheinternationalcargomarket.ShippingsourcespointedtodelaystocargoloadingsfromfromRotterdamaround8-11MayasaresultofthePernissituation,butsaidthesituationhadreturnedtonormalbythemiddleofMay.

• ShellhasconsistentlydeclinedtocommentontheimpactofthefireandshutdownonitsbitumenproductionatPernis,andithasalsorefusedtocommentonthegeneraloperationalstatusoftherefinerysinceitsfirststatementsjustafterthefire.TheoilmajorwasbelievedtohavemovedstoredcargoesontobitumentankersorintoRotterdamstoragetankswhileproductionwasbeinghitattherefinery.

Hungary

• Trans-borderprojectsbetweenHungaryandSlovakiawillbeontheagendawhentheprimeministersofthetwocountriesmeetinJulythisyear.AccordingtotheHungaryprimeminister’soffice,Hungaryproposedlaunching60border-crossingroadconstructionprojectsduringthe2014-2020EUfinancialframeworkperiod.Thereareonly28crossingpointscurrently.Theprogrammewouldincludeconstructionof43roads,reconstructionof14roadsandthreeprior-ityprojects:constructionoftheM15andM2dualcarriagewaysandanewroadbridgeovertheDanubeatKomarom.Thetotalcostoftheprojectswouldamountto€170mn.Atmorethan700kmlong,theSlovak-HungarianbordersectionislongerthanthatofGermanyandFrance.

• Theseprojects,ifitgoesahead,willbeamuchneededboosttotheHungarybitumenmarketwhichhasseenconsumptiondeclineoverthepastseveralyearsowingtothefinancialcrisis.

• ButaglimmerofhopesurfacedthisweekwithpreliminarydataoutthisweekshowingthatHungary0.7pchighercomparedtoQ4lastyear.However,theministryofnationaleconomyconcededthatslowergrowthisstillexpectedduringthefirst-halfofthisyearalthoughitwaslikelytoimproveoverthelatterhalf.

Mediterranean

• Regionalactivitywasthin,withlackoftankeravailabilityakeyfactorlimitingspotbusinessbyindependenttradingfirms.Nev-ertheless,therewerestillspotbitumentankerslyingidleawaiting

business,includingtheIverBrightanchoredoffCeutaoffnorthernMoroccoandthemarVictoriaoffCartagena,Spain.

• AnItalianoilrefinerwasreportedseekingatankertomovea3,000tbitumencargofromItalytotheCypriotportofLimassolforsecondhalfMayshipment.NearlyallimportsintoCyprusaremadeintoLarnaca,butimportflowshavefallenoffsharplythisyearinthemidstofthedeepeconomicandfinancialcrisisinthecountry.TraderssaidtherareLimassol-boundshipmentwasinlargepartdependentonfinancialtermsbeingagreed.Shippingremainsanobstacle,withnospottankeravailabilityreportedintheeasternMediterraneanwiththeexceptionoftheSanBenjaminowhichwaslaidoffataTurkishshipyarduntilearlyJune.

• AMediterraneantradermeanwhileindicatedthathewassepa-ratelylookingtomovetwocargoesintoCyprusbytheendofJune.Shippingremainamajorobstacletosuchspotshipments,withnospottankeravailabilityreportedintheeasternMediterraneanwiththeexceptionoftheSanBenjaminowhichwaslaidoffataTurkishshipyarduntilearlyJune.

• Thepictureonexportpricediscountswasmixed,withItalianshipmentsstillindicatedat$60-70/tbelowfobMediterraneanhigh-sulphurfueloilquotes,Spanishcargoesvaluesaroundthe$50/tmarkandGreekflowspeggedinthe$25-40/trangeunderthesamefueloilquotes.

Italy

• TheweakstateoftheItalianmarketwasunderlinedonceagainbyfreshindustrydatashowinganothersteepyear-on-yeardemanddecline.

• UnionePetroliferafiguresshoweddomesticbitumenconsump-tionstoodat106,000tinApril,1.9pcupfrom104,000tinthesamemonthof2012(1.9pcup).ButfortheJanuarytoAprilperiod,totalconsumptionstoodat303,000tin2013versus377,000tinthesameperiodoflastyear,a19.6pcfall.

Spain

• GovernmentdatashowingSpainrecordeditsfirstevertradesurplusunderlinedthepoorstateofthedomesticeconomythatisreflectedinthebitumensector.Domesticbitumendemandsofarthisyearisrunningwellbelow2012volumes,whichstoodatanestimated1.65mn–itselfaround400,000tdownfrom2011.

• Thecountry’srefiners,CepsaandRepsol,arefocusingonexportactivitytomakeupforsomeofthelostvolumes,althoughinstalla-tionofcokingunitatSpanishrefineriesoverrecentyearshasgiventhemtheoptionofwhetherornottoproducebitumen.

• AlgeriaremainsakeyexportoutletforSpanishexports,partlybe-causeoftheheavyshortfallinMoroccanvolumesthisyearbecause

5M-20 17 May 2013

Page 12 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

ofalengthybitumenunitshut-downthere.Cepsaissupplyingsize-ablebitumenvolumestoAlgeria,inadditiontomorethan200,000tofbitumenbeingsuppliedtothecountrybyRepsolunderthisyear’sAlgerianimporttender.

• TradersarefindingitincreasinglydifficulttopickupfobcargoesoutofSpain,withthecountry’srefinerspreferringtoexporttheirownvolumesintoNorthAfricanandWestAfricandestinations–aswellasnorthwestEurope–onadeliveredbasisusingeithertheirownshipsortankerstakenbythemundertermcharteroroccasionalspotarrangements.Thathasreducedthetransparencyofspotexportprices,althoughtherewereindicationsthatdiscountstofobMediterraneanhigh-sulphurfueloilquotesforSpanishexportship-mentshavenarrowedtoaround$50/t.

Lebanon

• Domesticbitumenconsumptionisexpectedtofallto40,000-50,000tthisyear,thelowestlevelforseveralyearsanddownmassive-lyfrom75,000tin2012.Lackoffunds,slowanddelayedpayments,aswellaspaymentdefaultsforconstructionworkareallkeyfactorsinslowingdownprojectactivityandbitumendemand.ThelackofaLebanesegovernment-afterresignationofPrimeMinisterNajibMiqatiinMarch-isanothermajorfactorhamperingprojectandfundingapprovals,whiletheunlikelihoodofanylocalorcentralgovernmentelectionsduring2013promisesnopre-electionboostforthecoun-try’sroadsector.NegotiationshavebeenunderwayforsometimeonformationofanewCabinet,withnoimmediateresolutioninsight.

• AmajorLebaneseimporterhassofartakendeliveryofthree3,000tcargoesthisyear,allintoBeirut,thelastoneonboardtheKaterinaLthatarrivedinApril.Another2,500-3,000tcargocouldbemovedattheendofMayfromEgyptintoBeirutdependingontankeravailability.RecentimportsfromGreecehavebeenpricedat$5-12/tpremiumstofobMediterraneanhigh-sulphurfueloilquotes,cifbasisBeirut.Withfreightcostspeggedataround$40/t,thatwouldindicate$28-35/tdiscountstothefueloilquotesonafobGreecebasis.

• TheLebaneseimportpicturecouldchangedramaticallyintheeventofaresolutionintheSyrianconflictthatshouldtriggerasurgeinreconstructionactivityinthecountry.Thatwouldneces-sitateamajorboostinbitumenrequirementsthatisunlikelytobemetintheshorttermatleastbySyrianrefineries,principallythebitumen-producingBaniasrefineryontheMediterraneancoast.MuchoftheshortfallindomesticsupplywouldbemetbyLeba-neseimportsintoitscoastalstoragetanksbeforetruckshipmenttoSyrianlocations.

• ThebiggestLebaneseroadprojectthatwouldgeneratesig-nificantbitumenrequirementswouldbetheproposedmotorwayfromBeiruttotheSyrianborder.Thefirstsectionofthatprojectthatcouldpotentiallybegiventhego-aheadasearlyaslate2013isfromChtaura–inlandfromBeirut–totheSyrianborder.

Turkey

• ItalianconstructioncompanyAstaldisaidinitsfirstquarterre-sultson14MaythatanintensificationofworkontheThirdBospho-rusBridgewasplannedforthisyear.Thecompanyalsoreferredtoworkcarriedoutduringthefirstquarterof2013onthefirstphasesofconstructionoftheGebze-Orhangazi-Izmirmotorway.

• Initsfirstquarter2013financialresultsreleasedonalsoon14May,TurkishrefinerTuprasreferredto“majorbatteryshutdownsandunplannedoutagesatitsrefineries”duringthequarterthathadhitoveralloutputofoilproducts.

• Tuprassaidfirstquarter2013refinerycapacityutilisationforcrudeoilwas62.4pcandoverallcapacityutilisation(includ-ingalternativefeedstockslikestraight-runfueloilandvacuumgasoil)was64.6pcversus69.7pcand71.5pcrespectivelyinthefirstquarterof2012.BitumenyieldatTupras’refinerieswas9pcversus6pc,whilefueloilyieldstoodat19pcversus22pcayearago,highlightingagrowingshare.Bitumenproductioninthefirstquarterof2013was199,000t,comparedwith137,000tinsamequarterof2012.

• TotalTuprasbitumenproductionin2012stoodat2.8mnt,withanestimated100,000tofadditionalconsumptionintothecountry.DomesticasphaltplayersexpecttoseeasignificantriseinTurk-ishbitumendemandin2013,withonesourceforecastinga10pcrise.

Tunisia

• NegotiationswerecontinuingregardingtheawardoftheTunisianimporttenderfor60,000tofPen30/50fordeliveryintotheportsofRadesandGabesfromMay2013throughtoApril2014.Regionaltraderssaidfundingdifficultiescouldstandinthewayofanearlyconclusionofthetender,whichwastohavebeenawardedbyaround15May.

• Aseparatetenderwasreportedtohavebeenissuedfortheim-portof12,000tofbitumen–mostlikelyinthree4,000tcargoes–intotheTunisianportofSfax.

Libya

• HopesthatLibyanbitumenconsumptionandimportrequire-mentswouldrisesharplyfrom2013onwardsweredentedbyItalianpressreportsthatamajorplannedmotorwayfromEgypttoTunisiaviaLibyahadbeencancelled.TheprojectwastohavebeenlargelyfundedbyItaly.

• Therewasnoconfirmationofthatnews,butoccasionalimportscargoescontinuetoflowintoLibya.ThelatestcargoshipmentwasexpectedtobeloadedatEni’sLeghornexportterminalattheoilcompany’sLivornorefineryon28-30may,destinedforMisrata.

5M-20 17 May 2013

Page 13 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Morocco

• ThemainBituroxtechnologybitumenproductionunitattheSamirrefineryinMohammediawasstilldowninmid-May,asithasbeenforthemuchoftheyearsofar.ButSamirbegantoraisebitu-menproductionbyrunningthede-asphaltingunitattherefinery.Whiletherefinerexpectstosteadilyraisebitumenproductionoverthenextfewmonths,itwasanticipatingaslighttemporarydropinproductioninthelastweekofMay.

• Thedesigncapacityofthenewandlargerbituroxunit–installedinthesummerof2011andaffectedbythecurrentlengthyshutdown-wasslatedat280,000t/yr,althoughitcanproduceupto330,000t/yr.ThesmallerandolderbitumenunitatMohammediahasadesigncapacityof140,000t/yr.

West Africa

• StrongNigerianconstructionsectorgrowthremainsanimportantfactorindrawingsizeableimportvolumestothecountry.Themostrecentshipmentwasdischargedinmid-MaybythetankerFuNingWanattheEcomarine(ECM)terminalinCalabar,southeastNigeria.Delaysofseveraldayswerereportedincompletingthedischargeoperationforthe4,000-5,000tcargothatwasreportedtohavebeenpurchasedbyNigerianimporterWabeco.TheFuNingWanisaves-selintheSargeantMarineglobalbitumenfleet.

• Anothermajorglobalshippingandtradingcompanywasreport-edseekingratesforspotcargoshipmentsfromarangeofMediter-raneanexportpointsintostoragetanksacrossWestAfrica,althoughnofreshbookingwasreportedtohavebeencompleted.

• PricesfordeliveredcargoesintoNigeriaandGhanawerebeingreportedinthe$695-715/tonadeliveredbasis,equivalenttofobAbidjanpricepremiumstofobMediterraneanhigh-sulphurfueloilaveragingaround$70/t.

• Nigerianconstructionsectorgrowthhelpedboostthecountry’snon-oilGDPgrowthto7.89pcinthefirstquarterof2013evenasaweakeroilsectorshoweda0.54pcdropinitsGDPcontribution.OverallNigeriangrowthslowedslightlyinthequarterto6.56pccom-paredwith6.99pcinthefourthquarterof2012,stillinlinewithtrendgrowthof5-8pcinNigeriasince2003.

Zambia

• TheZambianRoadDevelopmentAgencyisupgradingtheD153fromtheGreatEastRoadatMoonoPolicecheckpointviaPalabanatoD151atLukoshiBasicschool(54km)includingD566SilverestRoad(4.7km),D156StateLodgeRoad(8km)andD154Palana-LeopardsHill(7.5km)roadinLusakaprovinceusingfundsapprovedinthe2012AnnualWorkPlanfortheRDA.SealedbidsmustbesubmittedbyFriday,24May.

Kenya

• Issuessurroundingdelayedandlackofpaymentforworkalreadydone,aswellasthelackofconcretegovernmentbudgetaryplansonnewspending,continuetosuppressKenya’sappetiteforimportedbitumen.

• SomeoftheexportsfromtheMideastGulfandIran,whichwouldnormallygotoKenya,arefindingalternativeoutletsinSouthAfricainstead.

South Africa

• WhileSouthAfricanbitumendemandisstartingtotaperoffwiththeapproachofwinter,aprolongedandextensiveseasonofrefinerymaintenanceinSouthAfricahasreduceddomesticsupply.This,coupledwitharebateonimportdutieswhichcameintoeffectinMarch,hasseenariseinimportsofdrummedmaterial.

5M-20 17 May 2013

Page 14 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Africa and Asia bitumen pricesLocal currency/t $/t

Rack prices, fob (13-17 May) Low High Change Low High Change

Africa

South Africa (rand) 6,240 6,426 41 670 690 -20

South Korea (won) 720,000 730,000 645 654 -14

Mumbai, India (rupees) 37,753 38,753 180 689 707 -3

Mumbai, India — drums (rupees) 40,833 41,833 180 745 763 -4

Thailand (baht) 18,287 18,436 173 615 620

Indonesia (rupiah) 6,357,000 6,357,000 11519 652 652

Singapore ($S) 782 788 14 625 630

Singapore ex-refinery (to Malaysia) 738 751 10 590 600 -2

Japan (¥) 68,000 74,000 665 724 -22

Export cargo/drum prices, fob

Iran - - - 490 500 -5

Iran — drums - - - 530 550

Bahrain (dinar) 207 207 550 550

Thailand (baht) 17,841 17,990 21 600 605 -5

Singapore ($S) 757 766 10 605 612 -3

Singapore — drums 888 901 16 710 720

Japan (¥) 57,554 58,065 1758 563 568

Taiwan ($) 18,012 18,252 299 600 608 -2

South Korea (won) 644,888 650,467 11706 578 583 -2

Cargo prices, cfr

West Africa Nfc* Nfc* - 695 715 38

China (yuan)

North coast 3,772 3,815 11 613 620

East central 3,784 4,079 -26 615 663 -6

South coast 3,796 4,049 -11 617 658 -4

North Vietnam — drums Nfc* Nfc* - 732 759

South Vietnam — drums Nfc* Nfc* - 732 751

*Not freely convertible. Note: All cargo prices are for heated tankers unless otherwise specified. Exchange rates used effective for Thursday of week reported.

Asia products Economics

fob Singapore Bitumen’s HSFO alternative $/t 16-May Change 16-May Change

HSFO 180cst $/t 606.00 -15.50 Singapore 562.89 -18.12

HSFO 380cst $/t 599.00 -13.25

Gasoil, high pour $/bl 113.70 -0.80

hhh

575

600

625

650

675

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Singapore rack Ex-refinery to Malaysia

Singapore rack vs ex-refinery prices to Malaysia $/t

hhh

600

650

700

750

800

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Singapore drum Singapore cargo

Singapore drums - Singapore fob $/t

5M-20 17 May 2013

Page 15 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

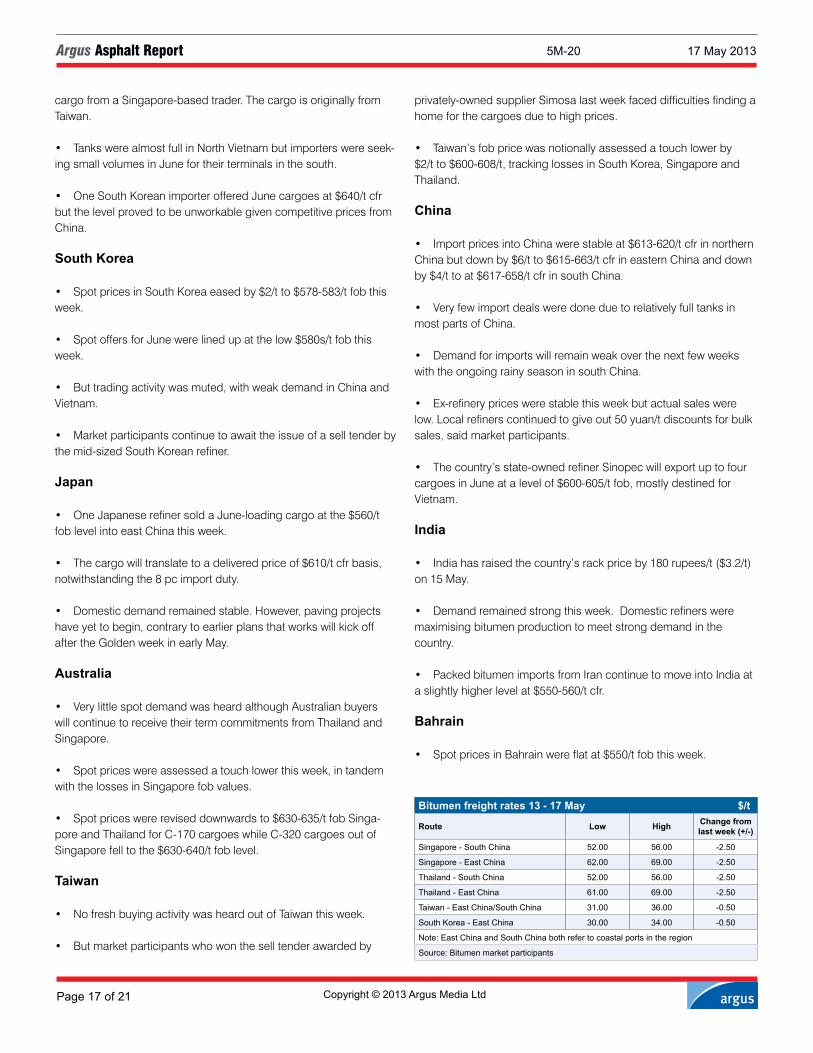

Asia and Middle East bitumen Singapore

• Singapore’sbulkpricesinchedlowerby$3/tto$605-612/tfob,assellerscutpricestofindhomesfortheirJune-loadingcargoes.

• Amplesuppliesintheregionalmarketpromptedseveralsellerstocuttheiroffersinthespotmarket.

• DealsforSingapore-bulkorigincargoesweredoneatawiderangeof$605-612/tfobthisweek,withthebulkoftheJunevolumesheadedforIndonesia.

• ButSingaporecargoeswerestilldeemedtobeuncompetitiveintoVietnamorsouthChinawithcheaper-pricedalternativesfromSouthKorea,China,ThailandandTaiwan.

• TheonlybrightspotinthephysicalmarketremainedinIndone-sia,withstate-ownedsupplierPertaminaseekingseveralsmall–sizedcargoesforend-May/JuneintoJava.BuyinginterestisalsosteadyinPhilippines,withthecountry’sthreesupplierslikelytotakeonecargoeachinJune.

• ButdemandremainedsoftinChina,VietnamandAustralia.

• Singapore’sbulkpricesforJunecargoeswereassessedatouchlowerby$3/tto$605-612/tfob,takingintoaccountofthephysicaldealsconcludedthisweek.

• Singaporedrumpriceswereunchangedat$710-720/tfobthisweek.Offersremainedat$720/tfobbutbuyinginterestfordrumswasweak.

• Singapore’srackpriceswereunchangedat$625-630/tthisweek.

• Singaporeex-tanktruckpricesweredownby$2/tto$590-600/tthisweek.OneSingaporerefinermovedasignificantnumberof

tanktrucksintoMalaysiathisweekataround$600/t.TheincreaseintanktruckdeliveriespromptedMalaysiandealersandthecountry’sstate-controlledrefinertocutpricesaswell.

• Singapore180cstfueloilpricesroseoncrudeandpapergains.OnshorestockpilesofresidualfuelsinSingaporerosetotheirhigh-estlevelsinceearlyDecember.ActivityduringtheafternoontradinginSingaporewasmuted.Offersfaroutnumberedbids13tofivewithinterestprimarilyin380cstoffers.Singapore’sonshorestocksofre-sidualfuelsroseby2.6mlnblasof15Mayto22.3mlnbl.Theboostrepresentsa13pcincreaseoverthepreviousweekandthehighestlevelsince5December2012.Importsoffueloilroseby11.7pcfromthepreviousweekto1.22mntfortheweekending15May.Exportsoffueloilalsorose,by36.9pcoverthesameperiodto316,690tfortheweek.

Malaysia

• Thecountry’sstate-controlledrefineranddealerscutpricesthisweekfollowingtheinfluxoftanktrucksfromSingaporethisweek.

• Thecountry’sstate-ownedrefinerwasproducingatclosetofullcapacity,leadingtoexpectationsofoversupply.

• Demandremainedlacklustrefollowingtheelectionsandlocaldealersexpectpricestocomeunderfurtherpressureinthenearterm.

Thailand

• BulkpricesinThailandfellby$5/tto$600-605/tfobthisweek.

• WeakbuyinginterestfromsouthChina,VietnamandAustraliameantthatThairefinersstruggledtofindoutletsfortheirJunecargoes.

• OneThairefinersoldacargointosouthChinaatthe$600-605/tfoblevelthisweek.

hhh

300

400

500

600

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Bahrain Iran

Bahrain cargo vs Iran cargo $/t

hhh

300

400

500

600

24 Aug 12 16 Nov 12 22 Feb 13 17 May 13

Drum Cargo

Iran drum vs cargo $/t

5M-20 17 May 2013

Page 16 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

• Domesticdemandstayedweak,astheThaigovernmenthasyettoissuefundingforpavingprojects.

Indonesia

• DemandinIndonesiaremainedsupportedbybuyingbythecountry’sstate-ownedsupplierPertamina.

• Pertaminaisseekingsmall-sizedcargoesforend-May/JuneloadingintoJava.Negotiationsremainedongoing.

• Demandisexpectedtopickupasthecountryentersintoitspeakpavingseason.

• SeveralotherimportersalsopickedupJune-loadingcargoesthisweekwhichweremostlydoneatadeliveredbasisofhigh-$630s/ttolow-$640s/t.

Prices of China main refineries 13 - 17 May Yuan/t

Place (Area, Province)

Refinery Grade Posted Price

Change from

previous week()

Contract Price

Change from

previous week()

Posted Price in

$/t

Contract Price in

$/t

Nothwest Xinjiang Petrochina Karamay AH-70, AH-90, AH-110, AH-130 4,800 4,720 780 767

AH-100, AH-140, AH-180 4,750 4,680 772 761

Sinopec Tahe 90-A 4,750 4,630 772 752

90-B 4,750 4,620 772 751

Gansu Petrochina Lanzhou AH-90 No sale - No sale - - -Shannxi Sinopec Xi’an AH-90 4,750 4,680 772 761

Northeast Liaoning Petrochina Liaohe AH-70, AH-90, AH-110, AH-100, AH-140 4,750 4,700 772 764

Panjin Northern AH-90, AH-110, AH-100, AH-140 4,750 4,710 772 765

North Hebei Petrochina Qinhuangdao AH-70, AH-90 4,870 4,800 791 780

Central Henan Sinopec Luoyang AH-90 4,750 4,700 772 764

East Shandong CNOOC asphalt AH-70, AH-90 4,900 4,850 796 788

Sinopec Qilu 70 -A 4,800 4,700 780 764

90 -A, 70-B 4,750 4,680 772 761

90-B 4,700 4,600 764 748

Sinopec Jinan AH-100 No sale - No sale - - -

Zhejiang Sinopec Zhenhai 70-A, 90-A 4,750 4,700 772 764

70-B, 90-B 4,850 4,800 788 780

CNOOC Daxie AH-70, AH-90 No sale - No sale - - -

Petrochina Wenzhou AH-70, AH-90 4,820 4,700 783 764

Shanghai Sinopec Shanghai AH-70 4,750 4,600 772 748

Jiangsu CNOOC Taizhou AH-70, AH-90 4,900 4,830 796 785

Sinopec Jinling 70-A, 90-A 4,830 4,750 785 772

South Guangdong Sinopec Maoming 70-A, 90-A 4,700 4,650 764 756

Sinopec Guangzhou 70-A, 90-A 4,700 4,650 764 756

Petrochina Gaofu AH-70, AH-90 4,800 4,700 780 764

Southwest Sichuan CNOOC Sichuan AH-70, AH-90 5,450 5,320 886 865

Source: China refiners and bitumen market participants

Australia import cargo prices $/tLow High Change

Thailand fob (Class 170) 630 635 -3Thailand fob (Class 320) 630 635 -3Singapore fob (Class 170) 630 640 -3Singapore fob (Class 320) 630 640 -3

Vietnam

• Thecountry’sstate-ownedsupplierwillbuyatleast2spotcar-goesforJunedeliveryfromChinesestate-ownedrefinerSinopec.

• Thedealiswidelyexpectedtobedoneat$600-605/tfoblevel.Thistranslatestoadeliveredbasisof$630s/tcfr.

• Thestate-ownedsupplierisalsoexpectedtobuyaJune-delivery

5M-20 17 May 2013

Page 17 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

cargofromaSingapore-basedtrader.ThecargoisoriginallyfromTaiwan.

• TankswerealmostfullinNorthVietnambutimporterswereseek-ingsmallvolumesinJunefortheirterminalsinthesouth.

• OneSouthKoreanimporterofferedJunecargoesat$640/tcfrbutthelevelprovedtobeunworkablegivencompetitivepricesfromChina.

South Korea

• SpotpricesinSouthKoreaeasedby$2/tto$578-583/tfobthisweek.

• SpotoffersforJunewerelinedupatthelow$580s/tfobthisweek.

• Buttradingactivitywasmuted,withweakdemandinChinaandVietnam.

• Marketparticipantscontinuetoawaittheissueofaselltenderbythemid-sizedSouthKoreanrefiner.

Japan

• OneJapaneserefinersoldaJune-loadingcargoatthe$560/tfoblevelintoeastChinathisweek.

• Thecargowilltranslatetoadeliveredpriceof$610/tcfrbasis,notwithstandingthe8pcimportduty.

• Domesticdemandremainedstable.However,pavingprojectshaveyettobegin,contrarytoearlierplansthatworkswillkickoffaftertheGoldenweekinearlyMay.

Australia

• VerylittlespotdemandwasheardalthoughAustralianbuyerswillcontinuetoreceivetheirtermcommitmentsfromThailandandSingapore.

• Spotpriceswereassessedatouchlowerthisweek,intandemwiththelossesinSingaporefobvalues.

• Spotpriceswerereviseddownwardsto$630-635/tfobSinga-poreandThailandforC-170cargoeswhileC-320cargoesoutofSingaporefelltothe$630-640/tfoblevel.

Taiwan

• NofreshbuyingactivitywasheardoutofTaiwanthisweek.

• Butmarketparticipantswhowontheselltenderawardedby

privately-ownedsupplierSimosalastweekfaceddifficultiesfindingahomeforthecargoesduetohighprices.

• Taiwan’sfobpricewasnotionallyassessedatouchlowerby$2/tto$600-608/t,trackinglossesinSouthKorea,SingaporeandThailand.

China

• ImportpricesintoChinawerestableat$613-620/tcfrinnorthernChinabutdownby$6/tto$615-663/tcfrineasternChinaanddownby$4/ttoat$617-658/tcfrinsouthChina.

• VeryfewimportdealsweredoneduetorelativelyfulltanksinmostpartsofChina.

• DemandforimportswillremainweakoverthenextfewweekswiththeongoingrainyseasoninsouthChina.

• Ex-refinerypriceswerestablethisweekbutactualsaleswerelow.Localrefinerscontinuedtogiveout50yuan/tdiscountsforbulksales,saidmarketparticipants.

• Thecountry’sstate-ownedrefinerSinopecwillexportuptofourcargoesinJuneatalevelof$600-605/tfob,mostlydestinedforVietnam.

India

• Indiahasraisedthecountry’srackpriceby180rupees/t($3.2/t)on15May.

• Demandremainedstrongthisweek.Domesticrefinersweremaximisingbitumenproductiontomeetstrongdemandinthecountry.

• PackedbitumenimportsfromIrancontinuetomoveintoIndiaataslightlyhigherlevelat$550-560/tcfr.

Bahrain

• SpotpricesinBahrainwereflatat$550/tfobthisweek.

Bitumen freight rates 13 - 17 May $/t

Route Low High Change from last week (+/-)

Singapore - South China 52.00 56.00 -2.50

Singapore - East China 62.00 69.00 -2.50

Thailand - South China 52.00 56.00 -2.50

Thailand - East China 61.00 69.00 -2.50

Taiwan - East China/South China 31.00 36.00 -0.50

South Korea - East China 30.00 34.00 -0.50

Note: East China and South China both refer to coastal ports in the region

Source: Bitumen market participants

5M-20 17 May 2013

Page 18 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

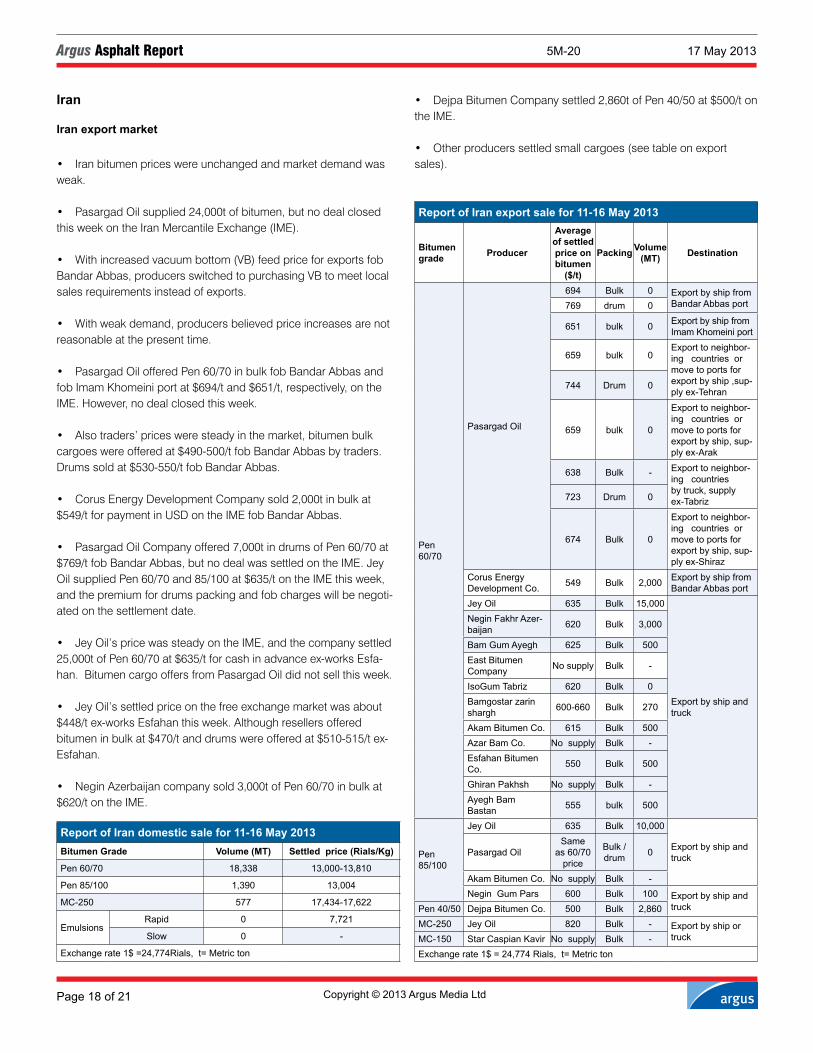

Iran

Iran export market

• Iranbitumenpriceswereunchangedandmarketdemandwasweak.

• PasargadOilsupplied24,000tofbitumen,butnodealclosedthisweekontheIranMercantileExchange(IME).

• Withincreasedvacuumbottom(VB)feedpriceforexportsfobBandarAbbas,producersswitchedtopurchasingVBtomeetlocalsalesrequirementsinsteadofexports.

• Withweakdemand,producersbelievedpriceincreasesarenotreasonableatthepresenttime.

• PasargadOilofferedPen60/70inbulkfobBandarAbbasandfobImamKhomeiniportat$694/tand$651/t,respectively,ontheIME.However,nodealclosedthisweek.

• Alsotraders’pricesweresteadyinthemarket,bitumenbulkcargoeswereofferedat$490-500/tfobBandarAbbasbytraders.Drumssoldat$530-550/tfobBandarAbbas.

• CorusEnergyDevelopmentCompanysold2,000tinbulkat$549/tforpaymentinUSDontheIMEfobBandarAbbas.

• PasargadOilCompanyoffered7,000tindrumsofPen60/70at$769/tfobBandarAbbas,butnodealwassettledontheIME.JeyOilsuppliedPen60/70and85/100at$635/tontheIMEthisweek,andthepremiumfordrumspackingandfobchargeswillbenegoti-atedonthesettlementdate.

• JeyOil’spricewassteadyontheIME,andthecompanysettled25,000tofPen60/70at$635/tforcashinadvanceex-worksEsfa-han.BitumencargooffersfromPasargadOildidnotsellthisweek.

• JeyOil’ssettledpriceonthefreeexchangemarketwasabout$448/tex-worksEsfahanthisweek.Althoughresellersofferedbitumeninbulkat$470/tanddrumswereofferedat$510-515/tex-Esfahan.

• NeginAzerbaijancompanysold3,000tofPen60/70inbulkat$620/tontheIME.

Report of Iran domestic sale for 11-16 May 2013Bitumen Grade Volume (MT) Settled price (Rials/Kg)

Pen 60/70 18,338 13,000-13,810

Pen 85/100 1,390 13,004

MC-250 577 17,434-17,622

Emulsions Rapid 0 7,721

Slow 0 -

Exchange rate 1$ =24,774Rials, t= Metric ton

Report of Iran export sale for 11-16 May 2013

Bitumen grade Producer

Average of settled price on bitumen

($/t)

Packing Volume (MT) Destination

Pen 60/70

Pasargad Oil

694 Bulk 0 Export by ship from Bandar Abbas port769 drum 0

651 bulk 0 Export by ship from Imam Khomeini port

659 bulk 0Export to neighbor-ing countries or move to ports for export by ship ,sup-ply ex-Tehran

744 Drum 0

659 bulk 0

Export to neighbor-ing countries or move to ports for export by ship, sup-ply ex-Arak

638 Bulk - Export to neighbor-ing countries by truck, supply ex-Tabriz723 Drum 0

674 Bulk 0

Export to neighbor-ing countries or move to ports for export by ship, sup-ply ex-Shiraz

Corus Energy Development Co. 549 Bulk 2,000 Export by ship from

Bandar Abbas portJey Oil 635 Bulk 15,000

Export by ship and truck

Negin Fakhr Azer-baijan 620 Bulk 3,000

Bam Gum Ayegh 625 Bulk 500East Bitumen Company No supply Bulk -

IsoGum Tabriz 620 Bulk 0Bamgostar zarin shargh 600-660 Bulk 270

Akam Bitumen Co. 615 Bulk 500Azar Bam Co. No supply Bulk -Esfahan Bitumen Co. 550 Bulk 500

Ghiran Pakhsh No supply Bulk -Ayegh Bam Bastan 555 bulk 500

Pen 85/100

Jey Oil 635 Bulk 10,000

Export by ship and truckPasargad Oil

Same as 60/70

price

Bulk /drum 0

Akam Bitumen Co. No supply Bulk -Negin Gum Pars 600 Bulk 100 Export by ship and

truckPen 40/50 Dejpa Bitumen Co. 500 Bulk 2,860MC-250 Jey Oil 820 Bulk - Export by ship or

truckMC-150 Star Caspian Kavir No supply Bulk -Exchange rate 1$ = 24,774 Rials, t= Metric ton

• DejpaBitumenCompanysettled2,860tofPen40/50at$500/tontheIME.

• Otherproducerssettledsmallcargoes(seetableonexportsales).

5M-20 17 May 2013

Page 19 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

• IMEcostsincludingbrokeragefeeandIMEcommissionwas$1.77/tforbuyersonthesettledpriceex-PasargadOilfobthisweek.

• Traders’priceswereheardat$490-500/tforbulkfobBandarAbbas.Also,traderssupplieddrumswereat$530-550/tfobBandarAbbas.

• MainproducersparticipatedinIMEthisweek,butmarketsentimentwasweakandexportsalesvolumedecreasedby7pcto35,230tofdifferentproducts.

Iran local market

• LocaldemandwasweakandIranlocalbitumenpricesweresteadyandproducerskeptpricesunchanged.

• Thehistoricaltrendshowedthatlocaldemandwillincreasesincenextmonthwithwarmerweatheranticipated,althoughupcomingpresidentialelectionsinIranwillimpactconstructionprojects.

• JeyOilhaskeptpricesunchangedandsettledPen60/70and85/100at13,004Rials/kgontheIME.

• PasargadOil’spricewasunchangedandthecompanysoldPen60/70and85/100at13,004Rials/kgex-Arakfactory.Also,theyset-tledon13,036Rials/kgex-Tehranfactory.

• PasargadOilsettledPen60/70at13,810Rials/kgex-BandarAb-basandShirazfactories.

• NeginFakhrAzerbaijansold410tofPen60/70at13,000Rials/kg.

• Shirazrefinery,AsphaltandBitumencompany,CorusEnergyandIsoGumTabrizsuppliedPen85/100and60/70,butnodealsclosedontheirofferedprices.

• JeyOilsettled17,622Rials/kgex-Esfahanthisweek.PasargadOilsettledMC-250at17,434Rials/kgex-AbadanandShirazfacto-riesthisweek.Otherproducersdidn’tparticipateontheIME.

• Producerssold20,305tofdifferentproductsontheIME.Salesvolumeshavenotchangedsignificantlychangedtothepreviousweek.

• Supplyofbitumenexceededdemandinthelocalmarket.Pro-ducerssupplied115,305tofdifferentproductsforlocalcustomersontheIME,butonly20,305tindemandwasregisteredthisweek.

• VBpricesdecreasedfromEsfahanandTehran,butwerefirmatotherrefineries.NationalIranianOilCompany(NIOC)sold15,000tex-Esfahanat10,807Rials/kg.Also,7,000twassoldat11,333Rials/kgex-Tabrizrefineryand15,000tex-Shirazrefineryat11,333Rials/kg.Theysettled20,000tofVBfeedex-Tehranrefineryat10,878Ri-als/kg.Nofeedsuppliedex-BandarAbbasrefinery.

5M-20 17 May 2013

Page 20 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

Oil industry briefs

• Crude benchmarks diverge:Crudepricesmovedindifferentdirections,asweakUSeconomicdatapulledvalueslower.AtlanticbasinbenchmarkNorthSeaDatedroseby89¢/blto

$104.37/blintheweekto16May,whileUSbenchmarkJuneWTIfellby$1.23/blto$95.16/bl.UpcomingmaintenanceattheNorthSea’sEkofiskfieldinJuneissupportingNorthSeaDated.WTI’sdiscounttoNorthSeaDatedwidenedto$9/blfrom$7/blaweekearlier.Butthespreadremainswellbelowthe$20/blseenearlierthisyear.Lastweek’snarrowerdiscountbrieflyopenedthearbitragefor

crudeshipmentstomovetotheUSGulfcoast.AtankerwasbookedtotakeacargofromHoundPointintheNorthSeainlateMaytotheUSGulfcoast.ThecargoissaidtobelightsweetForties,whichwouldbethefirstsuchfixturetomovetotheGulfcoastinamonth.WeakerrefiningmarginsinEuropeinMayaredampening

demandforlightsweetcrudes.PremiumsforlightsweetNigeriangradestoNorthSeaDatedhavefallen,andaround20NigeriancargoesremainunsoldforJuneaheadofthereleaseoftheJulyprogramme.WeaknortheastAsiandemandisweighingonlightsourMideast

Gulfcrude.Middledistillate-richAbuDhabiMurbanistradingatdiscountstotheAdnocofficialprice,despiteareductioninthelatestAdnocprice.HighgasoilexportsfromJapanhadbeendraggingdowngasoilmarginsintheregion,butmarginsarenowrecoveringaslowerChineseexportscountertheincreasedJapaneseavailabil-ity.TheEuropeanjetfuelmarketiswellsupplied,aslowerfreight

costsmakeitviableforAsia-Pacificcargoestomovetotheregion.ButacontangointheEuropeanjetfuelswapsmarket—whereforwardpricesarehigherthanpromptvalues—isincreasingtheincentivefortradingfirmsandairlinestostorecargoesaheadofthesummertravelseason.USsummerdrivingdemandisboostinggasolinevalues,but

othermarketslookvulnerable,andrelativelyweakcrudepriceshavedonelittletobolsterrefiningmargins.Globalmarketsarewellsuppliedwithotherproducts,asstutteringeconomicgrowthlimitsdemand,justasrefineriesreturningfrommaintenanceboostoutput.

Crude oil

Prices Americas $/bl 16-May ChangeWTI Cushing 95.16 -1.23

WTI Midland 95.57 -0.92

WTS Midland 95.50 -0.94

ANS USWC 105.24 -1.23

Mixed Sweet (MSW) 89.31 -0.05

Lloyd Blend (pipeline) 77.11 3.25

Western Canadian Select (WCS) 76.98 2.85

Maya del USGC 98.75 -0.86

Prices international $/bl Basis 16-May ChangeTapis 110.37 0.89

North Sea Dated 104.37 0.89

Dubai 100.10 -1.02

Arab Heavy, fob Ras Tanura

Differential to Asia Oman/Dubai -0.70

Differential to Europe Ice Bwave -4.40

Differential to US ASCI -3.30

Kuwait fob

Differential to Asia Oman/Dubai 0.50 0.45

Urals NWE 103.77 0.99

Urals Med 104.27 0.89

14

17

20

23

26

29

32

May-12 Aug-12 Nov-12 Feb-13 May-13

mn

bl

Source: EIA

Weekly US ending stocks of asphalt and road oil

hhh

10

15

20

25

30

26 Mar 13 12 Apr 13 30 Apr 13 16 May 13

WTI month 1 diff Lloyd Blend Hardisty month 1 $/bl

hhh

0

5

10

15

20

25

$/bl

22 Feb 14 Mar 05 Apr 25 Apr 16 May

Brent-WTI $/bl

5M-20 17 May 2013

Page 21 of 21 Copyright © 2013 Argus Media Ltd

Argus Asphalt Report

PublisherAdrian Binks Chief operating officerNeil BradfordCEO AmericasEuan CraikGlobal compliance officerJeffrey AmosCommercial managerKaren JohnsonEditor in chiefIan BourneManaging Editor, GlobalCindy GalvinManaging Editor, AmericasJim KennettEditor: Nasreen Tasker Tel: +1 203 261 [email protected]

Customer support and sales: email: [email protected]

Technical support: email: [email protected]

Houston, US Tel: +1 713 968 0000

New York, US Tel: +1 646 376 6130

Washington DC, US Tel: +1 202 775 0240 London, UK Tel: +44 20 7780 4200

Astana, Kazakhstan Tel: +7 7172 54 04 60

Beijing, China Tel: + 86 10 6515 6512

Dubai Tel: +971 4434 5112

Moscow, Russia Tel: +7 495 933 7571

Rio de Janeiro, Brazil Tel: +55 21 3514 1402

Singapore Tel: +65 6496 9966

Tokyo, Japan Tel: +81 3 3561 1805

Argus Asphalt Report is published by Argus Media Inc.

Registered office: Argus House,175 St John St, London, EC1V 4LW Tel: +44 20 7780 4200 Fax: +44 870 868 4338email: [email protected] 1462-8872Copyright noticeCopyright © 2013 Argus Media Ltd. All rights reserved.By reading this publication you agree that you will not copy or reproduce any part of its contents (including, but not limited to, single prices or any other individual items of data) in any form or for any purpose whatso-ever without the prior written consent of the publisher.

Trademark noticeARGUS, ARGUS MEDIA, the ARGUS logo, ARGUS ASPHALT REPORT, other ARGUS publication titles and ARGUS index names are trademarks of Argus Media Ltd.

Visit www.argusmedia.com/trademarks for more information.

DisclaimerThe data and other information published herein (the “Data”) are provided on an “as is” basis. Argus makes no warranties, express or implied, as to the accuracy, adequacy, timeliness, or completeness of the Data or fitness for any particular purpose. Argus shall not be liable for any loss or damage arising from any party’s reliance on the Data and disclaims any and all liability related to or arising out of use of the Data to the full extent permissible by law.

Slackrefiningmarginsarecurbingdemandforcrudeandthislookslikelytokeepalidonoilprices.

• Tensions leave investment plans in limbo:AmonthafterNicolasMadurowaselectedVenezuelanpresident,growingten-sionsinthecountryareleavingnervousforeignoilfirmsandevenclosealliesreluctanttomakebigenergyinvestmentsandloansthatCaracashopedtosecureoncethenewgovernmentwasinpower.Foreignoilcompanieswithsubstantialcapitalcommitmentsto

upstreamjointventureswithstate-ownedoilfirmPdVhavebeenunsettledbyMaduro’sinabilitytodispeloppositionchargesthatthe14Aprilelectionswerefraudulent.Madurothisweeksentthearmyontothestreetsinwhatthegovernmentsaysisacampaigntofightrecordviolentcrime.Maduro,whoreplacedthelateHugoChavez,isalsofacingasevereeconomiccrisismarkedbyshortfallsofbasicgoodsandgallopinginflation.PdVisstarvedforcashtofunditsambitiouscapitalexpenditure

(capex)planstodoublecrudecapacityto6mnb/dandgaspro-ductioncapacityto13bnft³/d(134bnm³/yr)by2019.ButCaracashassofarbeenunsuccessfulinsecuringfundsfromabroad,evenfromalliesChinaandRussia.State-runChinaDevelopmentBankconfirmeda$4bnloantoVenezueladuringavisittoVenezuelathisweekbyChinesevice-presidentLiYuanchao.ButLicalledformore“efficiency”inbilateralrelations,aremarkthathintsatfrustrationoverhowCaracashasusedChinesefundssofar.Andthevisitdidnotproduceanybreakthroughdealson$8bn-10bnofnewcash-for-oilloanssoughtbyMaduro.AplannedmeetingattheendofAprilbetweenRussianstate-

controlledoilfirmRosneft’spresident,IgorSechin,andVenezuelanenergyministerRafaelRamirezwascalledoffwithoutexplanation.RosneftandChina’sstate-ownedoilfirmCNPCarePdV’sbiggestupstreamjointventurepartners.Ramirez,whoisalsopresidentof

PdV,saidon4Maythatthecompanywillmakemorethan$208bnworthofcapexin2013-18toachieveitscrudeandgasproductiongrowthtargets.Thisfigureis$62bn,ornearly23pc,lowerthanPdV’srollingsix-year“SiembraPetrolera”spendingplan.PdVwillbedirectlyresponsibleforfunding80pcofthisinvest-

ment,including$25bnincorecapexthisyearalone,Ramirezsays.Ramirezhassince2011pressuredforeignoilcompanieswithminoritystakesinupstreamjointventureswithPdVtodevelopandexecuteaggressivecapexplanstoincreaseVenezuelancrudeproduction.ButevenVenezuela’sofficiallyreportedcrudeproductionfellby

3pcto2.90mnb/din2012.Argusandotherthirdpartiesestimatedproductionatabout2.35mnb/dlastyear.Ramirezwarnedthismonththatatleast10foreignoilfirmsinupstreamjointventureswithPdVcouldlosetheirlicencesiftheydonotstartsubstantialcapexrightaway.

Argus global asphalt/bitumen conferences:Europe/Africa Bitumen

Cannes, France — 12-13 June, 2013

Asia Bitumen Singapore — 25-27 September, 2013

Americas Asphalt SummitMarch, 2014

illuminating the markets

Argus Europe/ Africa Bitumen 2013

The fourth annual event will discuss market opportunities and challenges in Europe and Africa and how changing production and supply patterns are shaping the market.

Argus is the global leader in international asphalt pricing information — this event is part of a global series, with Argus bitumen/asphalt events also being held in Asia and the US.

Gold Sponsors

Petroleum

If you are interested in sponsorship and exhibition opportunities at the conference please contact Amber Ward on +44 20 7 780 4341 or [email protected]

12-13 June JW Marriott Cannes, France

Conference Topics:

The impact of crude prices on bitumen

prices

European re�nery economics

Growth of the Turkish market

Developments in north Africa and their

political impact on bitumen

consumption

French bitumen market overview

Update on emulsions and technology

Bitumen shipping and trade flows

Con�rmed Speakers:Ned Leary Risk Marketing, European, Team Leader, Shell International Trading and Shipping

Olaf Grodotzki General Manager, GKG Mineraloel Handel

Nasreen TaskerGlobal Editor - Argus Asphalt Report, Argus

Siamak EsfehanianExport Manager, Binas Baya Energy

Konstantinos PlousiosTrader, Asphaltos Trade

Jean Louis PettierGroup Procurement Manager, Icopal

Edman Nafrieh Managing Director, Gilda Tar

Media Partner

Exhibiting Sponsor

Kurt Wynendaele Business Area Director for Continental, Nynas Bitumen

Gülay Malkoc Technical Director, Turkish Asphalt Contractors Association (ASMUD)

Michael Zormelo Managing Director, Mustek Bitumen

Jean-Claude Ro é Senior International Advisor, COLAS

José Javier García Pardenilla Manager, Ditecpesa Asphalt Products (Ferrovial) Panelist: Keyvan Hedvat Deputy Editor, Europe Asphalt, Argus Panelist: Peter Ross General Manager Europe and South Africa, Shell

argusmedia.com/euro-bitumen Cannes, France

Agenda: Argus Europe/Africa Bitumen 201312 June

9.00 - 9.45 Registration and Co�ee 9.45 - 10.00Chairperson’s Opening RemarksNasreen Tasker, Global Editor - Argus Asphalt Report, Argus

Session One – Big Picture

10.00 - 10.25Keynote AddressRelationship between Crude and Bitumen

Impact of Light Tight Oil on crude marketsOutlook for the bottom of the barrelWhat could change in the next few years?

Ned Leary, Risk Marketing, European Team Leader, Shell International Trading and Shipping

Session Two – Europe and Growth Markets

10.25 - 10.40Overview of the French Bitumen Market

Impact of economic di�culties on European economyEuropean supply and demand zonesWhat re�nery closures mean to the bitumen market

Kurt Wynendaele, Business Area Director for Continental, Nynas Bitumen

10.40 - 11.00Questions and Answers Peter Ross, General Manager Europe and South Africa, Shell Kurt Wynendaele, Business Area Director for Continental, Nynas BitumenNed Leary, Risk Marketing, European Team Leader, Shell International Trading and Shipping

11.00 - 11.30 Morning Co�ee

11.30 - 11.55Turkish Bitumen Market and the opportunuties

Current market overviewProspects for the futureChallenges and the opportunities

Gülay Malkoc, Technical Director, Turkish Asphalt Contractors Association (ASMUD)

11.55 - 12.20Romania

12.20 - 12.50Black Sea Panel Discussion

Project �nance

12.50 - 14.10 Lunch 14.10 – 14.35Renewed Asphalt Products Market in Spain

Results from the crisis : technical solutionsSupply and demand changesTypes of projects : public administration

José Javier García Pardenilla, Manager, Ditecpesa Asphalt Products (Ferrovial)

Session Three – Roo�ng and Waterproo�ng

14.35 - 15.05Bitumen for Roo�ng and Waterproo�ng in the EUJean Louis Pettier, Group Procurement Manager, Icopal

15.05 - 15.40Speed Networking

15.40 - 16.10 A�ernoon Co�ee

Session Four – Middle East

16.10 - 16.40Middle East Bitumen

Overview of Middle East supply/demandCurrent Middle East trade with Europe and Africa Future prospects

Siamak Esfehanian, Export Manager, Binas Baya Energy

Session Five – Shipping

16.40 - 17.10 Bitumen Shipping and Trade Flows

New builds and market growth Arbitrage in bitumen tradeE�ects of piracy on trade flows

Konstantinos Plousios, Trader, Asphaltos Trade

17.10 - 17.15 Chairperson’s Closing Remarks End of Day One 17.15 - 19.30 Drinks Reception

argusmedia.com/euro-bitumen Cannes, France

Day 2: Argus Europe/Africa Bitumen 2013 13 June

9.00 - 10.00Registration and Co�ee

Session Six – Pricing

10.00 - 10.15Chairperson’s Opening Remarks Nasreen Tasker, Global Editor - Argus Asphalt Report, Argus 10.15 - 11.00Keynote AddressGlobal Bitumen Pricing TrendsNasreen Tasker, Global Editor - Argus Asphalt Report, Argus

Session Seven – Africa

11.00 - 11.25North Africa

11.25 - 11.50East and West AfricaEdman Nafrieh, Managing Director, Gilda Tar

11.50 - 12.20 Morning Co�ee 12.20 - 12.45Introducing New Products into Africa

Imports into East Africa Michael Zormelo, Managing Director, Mustek Bitumen

12.45 - 13.20

African Panel Discussion Edman Nafrieh, Managing Director, Gilda TarMichael Zormelo, Managing Director, Mustek Bitumen

13.20 - 14.30 Lunch

Session Eight – Emulsions and Technology 14.30 - 14.55Trends in Bitumen Modi�cation

Developmental trendsFuture growth

Olaf Grodotzki, General Manager, GKG Mineraloel Handel 14.55 - 15.20Bitumen for Roo�ng and Waterproo�ng in the EUJean Louis Pettier, Group Procurement Manager, Icopal

15.20 - 15.30Questions and Answers

15.30 - 15.40Chairperson’s Closing Remarks End of Conference

Argus Asphalt Report

An Argus market service, published weekly.

As the leading publication in asphalt assessments, the Argus Asphalt Report o�ers an international perspective on the markets. Historical prices are available dating back to 1998, facilitating charting and analysis of long-term trends.

For more information or to request a complimentary trial, please contact us on [email protected] or +44 (0) 20 7780 4200.

Event registration

DATES & VENUE 12-13 June 2013 JW Marriott Cannes, France STANDARD REGISTRATION RATE Two day conference rate: £1,245 €1,560 US $2,045*

MULTI-BOOKING DISCOUNTIf you wish to send 2 or more delegates contact us at: [email protected] receive a discounted rate.

*CONFERENCE FEE INCLUDES To see full details of what the conference fees include visit:www.argusmedia.com/euro-bitumen

PAYMENT METHOD Invoice my company Cheque enclosed (Make payable to “Argus Media Limited”) Credit card

Type of credit card (check one): Visa Amex Mastercard

Total fee to be deducted: Card number: Card holder’s name: Security code: Exp. date: / / Card billing address: Signature: (Credit card payments must be received before the expiration date)

EMAIL:Complete this form and email [email protected]

REGISTRATION FORM Return to: Gabriela Bonilla, Argus Media, Argus House, 175 St John Street, London, EC1V 4LW, UK Tel: +44 (0) 20 7780 4341 | Fax: +44 (0) 870 441 9873 [email protected] www. argusmedia.com/euro-bitumen COMPANY DETAILS: Company name: Address: City: Postal code: Country: VAT number: DELEGATE 1 DETAILSName: Dr/Mr/Ms: Job title: Telephone: Email: Special dietary/disability requirements (if any):

DELEGATE 2 DETAILSName: Dr/Mr/Ms: Job title: Telephone: Email: Special dietary/disability requirements (if any):

Argus Media VAT: GB229714941 - Company registration no. 1642534

Code: web

FAX:Complete this form and fax to +44 (0) 870 441 9873

MAIL:Complete this form in BLOCK letters and post to the address below

TERMS AND CONDITIONSIn these Terms and Conditions the expressions: “we”, “us” and “our” refer to Argus Media Limited a company incorporated in England with registered company number 01642534 and whose registered o¡ce is at Argus House, 175 St John Street, London, EC1V 4LW; and “you” and “your” refer to you. Subject to availability, we accept bookings for events through the online, electronic or postal submission of a registration form. Upon our communication to you (including by email) of our acceptance of your booking, there shall be a legally binding contract between you and us incorporating these Terms and Conditions. Payment 1. If payment is not received in full at the time of booking, your booking will be provisional until payment is received in full in accordance with paragraph 2 below. You acknowledge that we cannot guarantee bookings made on a provisional basis. 2. The event fee is payable within 30 days of the invoice date and in any event must be received in full 7 days before the event. 3. Fees are a §xed price and unless otherwise stated reductions and discounts cannot be o¨ered should you not wish to attend the entire event. 4. In order to qualify for any “early bird” discounts, booking and payment in full must be received prior to the date speci§ed above and on the invoice. 5. UK Excise Regulations, delegates from all countries are required to pay VAT on any event taking place in the UK.Cancellations & Substitutions 6. If you are unable to attend the event, you may send a substitute provided that you inform us in writing to [email protected] at least 48 hours before the commencement of the event. 7. Cancellations made in writing to [email protected] before 15 May 2013 will be refunded in full, less a 15% administration charge. No refunds will be given for cancellations received on or a«er 15 May 2013. 8. Failure to attend all or part of an event for any reason whatsoever will be treated as a late cancellation and no refunds will be given. 9. If the event is cancelled for any reason within our control, then the registration fee will be fully refunded. We shall not be liable for any other loss, damage, costs (including without limitation travel, visa or accommodation costs), expenses or other liabilities incurred by you in connection with such cancellation. Refunds may take up to 25 business days. Events 10. Our agendas are correct at the time of issue; however, it may be necessary to make some amendments to the content, speakers, location, and/or timing of the event. 11. Please advise us of any

special requirements (such as access or dietary requirements) at the time of booking. 12. We reserve the right to refuse admission to an event for any reason. 13. Views expressed by speakers at the event may not be the views of Argus. All event materials are provided to you on an “as is” basis and we make no warranty as to the completeness or accuracy of such materials. 14. You agree that, unless otherwise expressly stated, we own all intellectual property rights in all event materials and delegate lists. 15. You may not §lm, photograph or otherwise record all or any part of the event without our prior written consent. 16. You must comply with all applicable laws and any health and safety requirements (including no smoking signs) in respect of the event.Privacy & Marketing 17. Any personal data you disclose to us will be processed in accordance with the Data Protection Act 1998 and our privacy policy. 18. Your personal data may be used by us and carefully selected third parties to inform you about other products and services that may be of interest to you via telephone, post and/or email. If you do not wish to receive such marketing information, please contact us 19. You agree that we may use your company name in marketing promotions in connection with this event. 20. We may record (by audio and/or visual means) all or part of the event. You agree that we may use and distribute such recordings for the purposes of training, publicity and documentation.General 21. It is your responsibility to arrange appropriate insurance cover for your attendance at the event. 22. You are fully responsible and liable for any loss or damage caused by you to property or individuals at an event. 23. Except in respect of death or personal injury caused by our negligence or for fraud, our total aggregate liability in connection with the event shall be limited to the fee paid by you. 24. You are responsible for safeguarding your own property at the event. We accept no liability in respect of any damage to, or the« or loss of, your property. 25. These Terms and Conditions together with the registration form set out the entire agreement between you and us. 26. If any provision of these Terms and Conditions (in whole or in part) is found by any competent authority to be unenforceable or illegal, the remainder of provisions shall remain in force. 27. These Terms and Conditions shall be governed by the laws of England and you agree to submit to the exclusive jurisdiction of the English courts.