Embed Size (px)

Citation preview

07

Arbor Memorial Services Inc.

Annual Report 2007

Global Reports LLC

corporate profile Arbor Memorial Services Inc. (“Arbor” or the “Company”) is a

Canadian market leader in providing interment rights, cremations, funerals and associated

merchandise and services to customers across Canada. At October 3 1 , 2007, Arbor owned 4 1

cemeteries, 27 crematoria, 3 reception centres and 9 1 funeral homes in communities in eight

provinces of Canada. The Company’s cemeteries and funeral homes have been successful in

developing and providing customized products and services to many ethnic and religious groups

in Canada.

Cover: Funerary model of boat with 1 2 rowers and coxswain, 2055-2004 BC, Middle Kingdom, 1 1th Dynasty; Mentuhotepll, Deir el-Bahri, Egypt

This wooden model of a boat was excavated from the tomb of King Mentuhotep II at Deir el-Bahri, near modern Luxor. This model was

The model depicts a galley with twelve rowers and a coxswain, who steers the boat and has charge of the crew. Such a galley might have been

used to haul barges of produce or manufactured items. Models were placed in tombs to ensure the deceased everlasting prosperity, for it was

thought that both would magically come to life and work for the tomb owner in the afterlife.

reconstructed using the material from several other models strewn across the tomb floor and using other Middle Kingdom boat models as a guide.

.

Mark Agate,

Regional Director, South Eastern Ontario

Leonard Marceau,

Regional Director, South Western Ontario

Peter Bancroft,

Regional Director, Atlantic Canada

CEMETERY OPERATIONS

REGIONAL MANAGEMENT

James Risbey,

Regional Property Manager,

Alberta and British Columbia

Terry Bokshowan,

Regional Property Manager,

Manitoba and Saskatchewan

Rodger W. Halden,

Regional Property Manager,

Western Ontario

Donn Bailey,

Regional Property Manager,

Central/Western Ontario

Kenneth Gurney,

Regional Property Manager,

Niagara and Thunder Bay

P. Bradley Hunter,

Regional Property Manager,

Eastern Ontario

William E. Grady,

Regional Property Manager,

Eastern Canada

CEMETERY ADMINISTRATION

REGIONAL MANAGEMENT

Diane E. Vinje,

Regional Manager, Calgary, British

Columbia and Saskatchewan

Teresa M. Bastin,

Regional Manager, Edmonton, Manitoba

and Thunder Bay

Mary A. Brandoline,

Regional Manager, Western Ontario

and Toronto

Liane Coviensky,

Regional Manager, Toronto West and

South Western Ontario

Barbara E. Weatherdon,

Regional Manager, Quebec, Eastern

Ontario and Atlantic

FUNERAL OPERATIONS

REGIONAL MANAGEMENT

James M. Fletcher,

Regional Director, Western Canada

Alenka Manners,

Regional Director, South Western Ontario

Terry A. Eccles,

Regional Director, Central Ontario

Denis Marcoux,

Regional Director, Quebec and

Northern New Brunswick

David McEachnie,

Regional Director, Atlantic Canada

Valerie Scott,

Manager, Funeral Planning Services,

Ontario and New Brunswick

HEAD OFFICE

2 Jane Street, Toronto, Ontario

M6S 4W8

Telephone: (416) 763-4531

WEB SITE

www.arbormemorial.com

AUDITORS

Deloitte & Touche LLP

PRINCIPAL BANKERS

TD Bank Financial Group

Bank of Montreal

TRANSFER AGENT AND

REGISTRAR

Computershare Investor Services Inc.

Phone: 514-982-7555 or 1-800-564-6253

Fax: 416-263-9524 or 1-866-249-7775

PRINCIPAL TRUSTEES OF FUNDS

TD Canada Trust Company

The Bank of Nova Scotia Trust Company

ANNUAL MEETING

The annual meeting of Arbor

Memorial Services Inc. will be held

in the Brulé Room,

The Old Mill, 21 Old Mill Road,

Toronto, Ontario,

on Thursday, February 28th, 2008

at 10:00 a.m. (Toronto time).

Global Reports LLC

1A r b o r M e m o r i a l S e r v i c e s I n c .

2007highlights

Company Highlights 2

Report to Shareholders 3

Management’s Discussion and Analysis 8

Management’s Report 38

Auditors’ Report 39

Consolidated Financial Statements 40

Notes to Consolidated Financial Statements 44

Company Information 66

0

50

100

150

200

250

0706050403

Fiscal Year

REVENUE($Millions)

0

200

400

600

800

1000

1200

0706050403

Fiscal Year

TOTAL ASSETS($Millions)

2007 ARBOR 14-01-08 1/14/08 2:52 PM Page 1

Global Reports LLC

2A r b o r M e m o r i a l S e r v i c e s I n c .

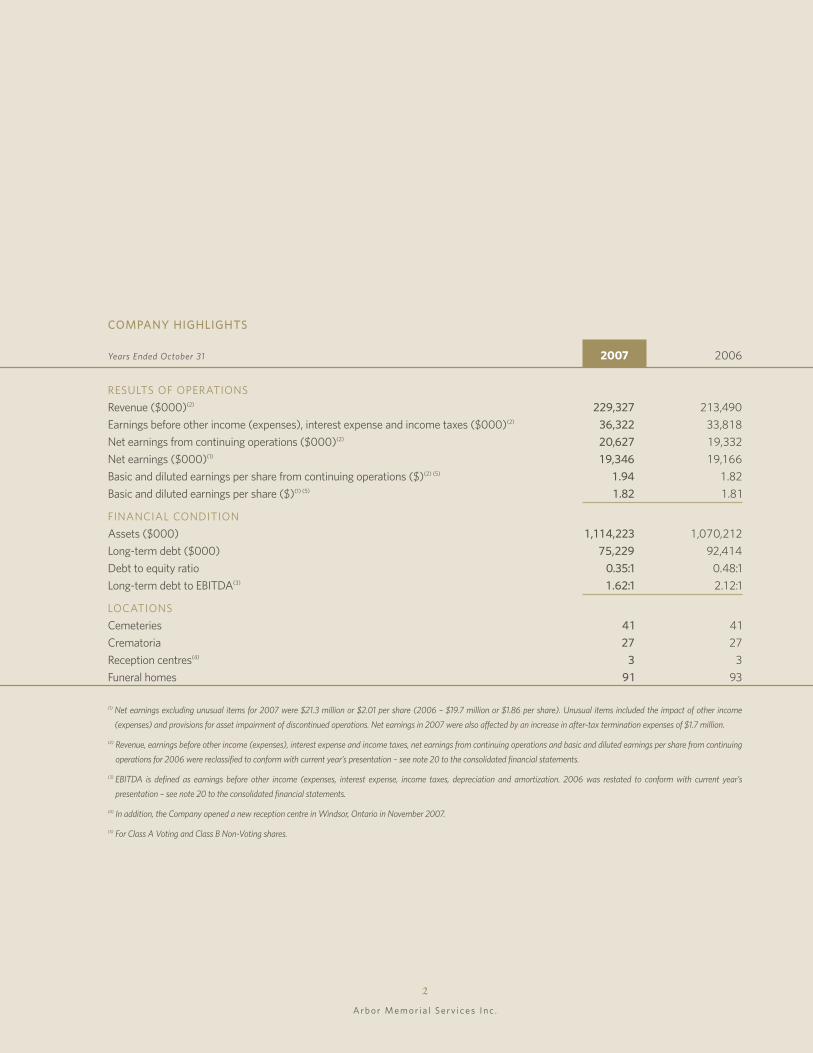

COMPANY HIGHLIGHTS

Years Ended October 31 2007 2006

RESULTS OF OPERATIONS

Revenue ($000)(2) 229,327 213,490

Earnings before other income (expenses), interest expense and income taxes ($000)(2) 36,322 33,818

Net earnings from continuing operations ($000)(2) 20,627 19,332

Net earnings ($000)(1) 19,346 19,166

Basic and diluted earnings per share from continuing operations ($)(2) (5) 1 .94 1 .82

Basic and diluted earnings per share ($)(1) (5) 1 .82 1 .81

FINANCIAL CONDITION

Assets ($000) 1 ,1 14,223 1 ,070,212

Long-term debt ($000) 75,229 92,414

Debt to equity ratio 0.35:1 0.48:1

Long-term debt to EBITDA(3) 1 .62:1 2.12:1

LOCATIONS

Cemeteries 41 41

Crematoria 27 27

Reception centres(4) 3 3

Funeral homes 91 93

(1) Net earnings excluding unusual items for 2007 were $21.3 million or $2.01 per share (2006 – $19.7 million or $1.86 per share). Unusual items included the impact of other income

(expenses) and provisions for asset impairment of discontinued operations. Net earnings in 2007 were also affected by an increase in after-tax termination expenses of $1.7 million.

(2) Revenue, earnings before other income (expenses), interest expense and income taxes, net earnings from continuing operations and basic and diluted earnings per share from continuing

operations for 2006 were reclassified to conform with current year’s presentation – see note 20 to the consolidated financial statements.

(3) EBITDA is defined as earnings before other income (expenses, interest expense, income taxes, depreciation and amortization. 2006 was restated to conform with current year’s

presentation – see note 20 to the consolidated financial statements.

(4) In addition, the Company opened a new reception centre in Windsor, Ontario in November 2007.

(5) For Class A Voting and Class B Non-Voting shares.

2007 ARBOR 14-01-08 1/14/08 3:01 PM Page 2

Global Reports LLC

3A r b o r M e m o r i a l S e r v i c e s I n c .

2007report to shareholders

2007 PERFORMANCE

By any measure, 2007 was a very successful year. The Company’s revenue was $229.3 million and net earnings were $19.3 million or

$1 .82 per share. Revenue grew 7.4% during 2007 as our dedicated employees continued to meet the needs of our customers in record

numbers. The Company performed 21 ,777 funeral services in 2007, which represented an increase of 5.9% over 2006. Arbor’s revenue

growth was also driven by a 4.1% increase in interments and a 1 .1% increase in cremations performed over 2006. In addition to growth

in the base business, the Company benefited from the opening of a new reception centre at our Mount Lawn cemetery in Whitby, Ontario.

Statistics Canada annually provides information regarding the number of deaths for the 12-month period ended June 30. During the

period ended June 30, 2007, the number of deaths increased by 3.1% nationally. The Company benefited both from the increase in the

number of deaths as well as growth in market share.

Earnings per share increased to $1 .82 from $1 .81 in 2006. This was achieved despite termination costs of $3.0 million in the year, with

an after-tax impact on earnings of $2.0 million. The personnel changes that gave rise to these costs will help position Arbor to achieve its

full potential. Unusual items in 2007 included $2.3 million in after-tax provisions for asset impairment, of which $1 .5 million was included

in discontinued operations, which were offset by a $0.3 million after-tax net gain on disposal of assets. This resulted in a loss from unusual

items of $0.19 per share. Unusual items in 2006 included $0.6 million in after-tax provisions for asset impairment, offset by a $0.1 million

after-tax net gain on disposal of assets. This resulted in a loss from unusual items of $0.05 per share. Unusual items in 2002 through

2005 included similar items.

Excluding unusual items, earnings per share increased 8.1% to $2.01 from $1 .86 in 2006. Over the last 5 years earnings per share

excluding unusual items has increased by 66.1%.

Years Ended October 31 2007 2006 2005 2004 2003 2002

Earnings per share

excluding unusual items $2.01 $1.86 $1.71 $1 .65 $1 .31 $1 .21

During the year, the Company reduced its long-term debt by $17.2 million due to surplus cash on hand. The surplus cash was the result

of strong financial performance and a $6.8 million payment received against a mortgage receivable. The Company’s debt to equity ratio

at the end of the year was 0.35:1 .

As at October 31 2007 2006 2005 2004 2003 2002

Long-term debt ($000) 75,229 92,414 76,163 77,471 83,164 96,767

2007 ARBOR 14-01-08 1/14/08 3:01 PM Page 3

Global Reports LLC

4A r b o r M e m o r i a l S e r v i c e s I n c .

Shareholders’ equity increased 10.9% over 2006 to $212.3 million in 2007. Over the past 5 years, shareholders’ equity has increased

by 87.9%. Return on average shareholders’ equity was 9.6% versus 10.5% last year. The termination costs and provisions for asset

impairment had a significant downward impact on 2007’s profitability.

As at October 31 2007 2006 2005 2004 2003 2002

Shareholders’ equity ($000) 212,296 191 ,385 172,961 156,178 137,636 1 13,010

Share prices continued to increase in 2007. Over the latest 5-year period, the price of Class A shares has increased by 162.5% while

Class B shares have advanced by 147.9%. Total return (share price appreciation plus dividends reinvested) in 2007 on Class B shares

was 26.5% and the 5-year compounded annual return on investment was 20.4%.

As at October 31 2007 2006 2005 2004 2003 2002

Market price

Class A Voting $32.8 1 $24.10 $20.1 1 $17.95 $14.50 $12.50

Class B Non-Voting $30.99 $24.50 $20.20 $16.50 $13.50 $12.50

We continued to add to our base of pre-need customers by entering into pre-need cemetery and funeral contracts during the year. While

pre-need merchandise and services sales, including funerals, and certain interment right sales that do not meet minimum deposit

requirements, are not included immediately in the Company’s reported sales until delivery, installation or performance, they do contribute

to building future market share and future reported sales.

Pre-need cemetery contracts written during the year achieved a new record of $73.1 million, up 5.7% from 2006. The total undelivered

pre-need cemetery contracts and associated investment income accumulated at the end of 2007 was $332 million, the equivalent of

3.3 years of 2007 cemetery sales.

Pre-need funeral contracts written during the year achieved a new record of $55.2 million, up 6.6% from 2006. The total undelivered pre-

need funeral contracts and associated investment income accumulated at the end of 2007, including the off-balance sheet annuity funds,

was $377 million, the equivalent of 3.3 years of 2007 funeral sales.

INVESTING FOR THE FUTURE

While we are very proud of our strong and consistent financial performance, our primary focus is on strengthening our competitive

position and investing in projects for which the return exceeds our cost of capital. This should allow us to capitalize on the projected

market growth for our services and enhance long-term shareholder value.

In 2007, the Company continued to make capital investments to ensure that our business will continue to grow and prosper in the future.

• In November 2007, the Company completed construction of the Victoria Greenlawn Memorial Chapel and Reception Centre in

Windsor, Ontario and officially opened its doors to the public. This facility is expected to give Arbor a high-profile presence in the

Windsor market and increase our market share.

• The Company continued with its strategic initiative of building chapels and reception centres on its cemetery properties in Ontario. We

are currently working on plans and building permits for seven such buildings with construction expected to start in fiscal 2008 at four

cemeteries. The budgeted capital spending in 2008 on these buildings is $24.0 million.

• The Company prepared for construction to commence on mausolea at Glendale Memorial Gardens in Toronto, Ontario and Glen Oaks

Memorial Gardens in Oakville, Ontario. The estimated cost of construction for these two buildings is $22.7 million and they will add

approximately 6,200 crypts to our burial space inventory.

2007 ARBOR 14-01-08 1/14/08 3:02 PM Page 4

Global Reports LLC

5A r b o r M e m o r i a l S e r v i c e s I n c .

• Construction of a new sales office at Rideau Memorial Gardens in Dollard des Ormeaux, Quebec, renovation of the Chapel Lawn

Memorial Gardens sales office in Winnipeg, Manitoba and major renovations and expansions were completed at the Kelly Funeral

Home in Kanata, Ontario, Jenkens Funeral Home in Thunder Bay, Ontario and McDougall & Brown Funeral Home (Eglinton Chapel) in

Toronto, Ontario.

In addition to the above, the Company committed capital to the development of computerized sales presentation programs for at-need

and pre-need cemetery sales and pre-need funeral sales. The programs are expected to improve the “look and feel” of our sales

presentations and assist our sales counsellors through a combination of improved customer service, reduced administration and

improved productivity. Several years ago, the Company introduced a similar sales support tool for at-need funeral sales, which was well

received by the public and provided financial and other benefits as expected. The sales programs are expected to be completed and

implemented in phases over the next three years.

In an effort to reduce energy consumption and costs, the Company teamed up with an energy consulting firm during 2007. A three-

pronged strategy was adopted:

1 . reduce the cost of energy by purchasing electricity and natural gas at wholesale rates where energy markets had deregulated;

2. improve energy efficiency of buildings and mechanical systems for new construction and retrofits where there is an adequate

return; and

3. improve energy awareness in an effort to reduce consumption.

The benefits of the program have yet to be realized as the energy procurement agreements were effective for fiscal 2008 and the

Company will be launching an employee-awareness campaign, the Green Arbor Project, effective January 1 , 2008.

PERSONNEL

The 2007 year was marked by a number of management changes as noted below.

Effective October 31 , 2007, Richard Innes retired from the Company as its President and Chief Executive Officer, and resigned from the

Board of Directors. We are thankful to Mr. Innes for his 1 1 years of service and would like to recognize the financial success of the company

under his leadership.

Brian Snowdon was appointed President and Chief Executive Officer, and a member of the Board of Directors, effective November 1 ,

2007. Previously Mr. Snowdon was Vice-President and Chief Financial Officer.

In May 2007, David Scanlan was appointed Vice-President, Sales. Previously he was Assistant Senior Vice-President, Sales and Regional

Director, Ontario. Effective November 1 , 2007, Mr. Scanlan was promoted to Senior Vice-President, Sales.

Effective November 1 , 2007, Michael Scanlan was appointed Senior-Vice President, Marketing, Property and Construction and

Development. Previously, Mr. Scanlan was Vice-President, Marketing.

Also effective November 1 , 2007, Jeff Scott was appointed Senior Vice-President, Funeral Service. Previously Mr. Scott was Vice-

President, Funeral Service.

Effective November 1 , 2007, Laurel Ancheta was promoted to Vice-President and Chief Financial Officer. Previously Ms. Ancheta was

Senior Director of Finance.

We recognize that employee training is important and as a result created and developed an in-house management training program in

2007. The program is geared towards selected funeral directors who have shown management potential. The training includes rotational

work periods at several different funeral homes across the country, cross-training within certain areas of the company, experience with

pre-need funeral sales, and information sessions in areas such as finance, human resources, and leadership.

2007 ARBOR 14-01-08 1/14/08 3:03 PM Page 5

Global Reports LLC

6A r b o r M e m o r i a l S e r v i c e s I n c .

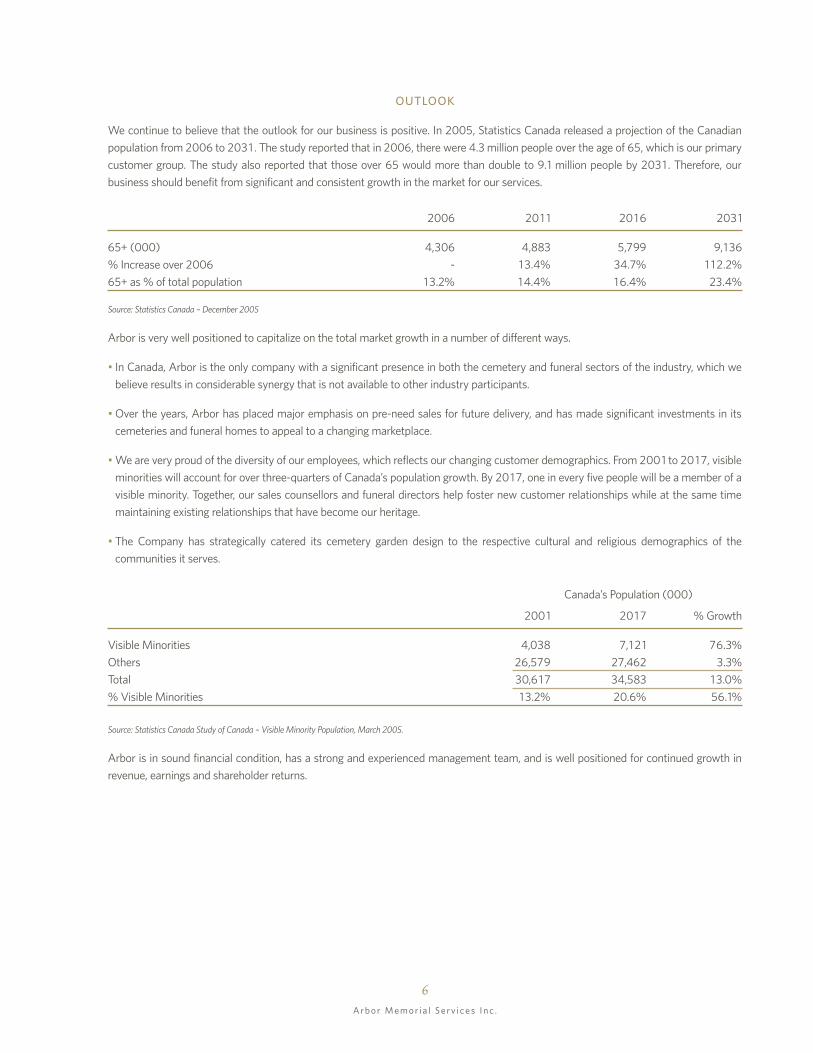

OUTLOOK

We continue to believe that the outlook for our business is positive. In 2005, Statistics Canada released a projection of the Canadian

population from 2006 to 2031 . The study reported that in 2006, there were 4.3 million people over the age of 65, which is our primary

customer group. The study also reported that those over 65 would more than double to 9.1 million people by 2031 . Therefore, our

business should benefit from significant and consistent growth in the market for our services.

2006 201 1 2016 2031

65+ (000) 4,306 4,883 5,799 9,136

% Increase over 2006 - 13.4% 34.7% 1 12.2%

65+ as % of total population 13.2% 14.4% 16.4% 23.4%

Source: Statistics Canada – December 2005

Arbor is very well positioned to capitalize on the total market growth in a number of different ways.

• In Canada, Arbor is the only company with a significant presence in both the cemetery and funeral sectors of the industry, which we

believe results in considerable synergy that is not available to other industry participants.

• Over the years, Arbor has placed major emphasis on pre-need sales for future delivery, and has made significant investments in its

cemeteries and funeral homes to appeal to a changing marketplace.

• We are very proud of the diversity of our employees, which reflects our changing customer demographics. From 2001 to 2017, visible

minorities will account for over three-quarters of Canada’s population growth. By 2017, one in every five people will be a member of a

visible minority. Together, our sales counsellors and funeral directors help foster new customer relationships while at the same time

maintaining existing relationships that have become our heritage.

• The Company has strategically catered its cemetery garden design to the respective cultural and religious demographics of the

communities it serves.

Canada’s Population (000)

2001 2017 % Growth

Visible Minorities 4,038 7,121 76.3%

Others 26,579 27,462 3.3%

Total 30,617 34,583 13.0%

% Visible Minorities 13.2% 20.6% 56.1%

Source: Statistics Canada Study of Canada – Visible Minority Population, March 2005.

Arbor is in sound financial condition, has a strong and experienced management team, and is well positioned for continued growth in

revenue, earnings and shareholder returns.

2007 ARBOR 14-01-08 1/14/08 3:04 PM Page 6

Global Reports LLC

7A r b o r M e m o r i a l S e r v i c e s I n c .

ACKNOWLEDGEMENTS

For the third consecutive year, Arbor’s marketing department won two Ginny Awards at the 89th annual convention of the Cremation

Association of North America. Arbor won first place in the Public Relations category for the creation of the “Veterans’ Wall of

Remembrance”. This award-winning project involved the production of eleven granite walls with over 13,000 inscriptions at cemetery

locations across Canada. In addition, Arbor received an honourable mention in the Advertising category for its “Ching Ming” celebration

work. Ching Ming is known as “Remembrance of Ancestors Day” to the Chinese community.

The success achieved by the Company in 2007 was due to the skill and commitment of our employees. The Directors extend a sincere

thank you to all.

On behalf of the Board of Directors,

Brian D. SnowdonPresident and Chief Executive Officer

This Report to Shareholders contains forward-looking statements about Arbor Memorial Services Inc.’s outlook. Reference should be made to “Information

Regarding Forward-Looking Statements” on page 8 of this Annual Report. For a description of material factors and assumptions see page 8 of this Annual

Report and for a description of risks and uncertainties that could cause actual results to differ materially from the forward-looking statements in this

Report to Shareholders, please see the Company’s 2007 Management’s Discussion and Analysis, particularly under “Risks, Events and Uncertainties” on

page 35, and the Company’s 2007 Annual Information Form under “Description of the Business – Risk Factors”.

2007 ARBOR 14-01-08 1/14/08 3:05 PM Page 7

Global Reports LLC

8A r b o r M e m o r i a l S e r v i c e s I n c .

2007management’s discussion and analysis

Management’s Discussion and Analysis for Arbor Memorial

Services Inc. (“Arbor” or the “Company”) has been prepared for

the fiscal year ended October 31 , 2007 and includes material

information available up to December 7, 2007. The financial

data provided has been prepared in accordance with Canadian

generally accepted accounting principles (“GAAP”) and all

figures provided are in Canadian dollars. Management’s

Discussion and Analysis herewith provided is the responsibility

of the Company’s management. The Board of Directors is

responsible for reviewing and approving Management’s

Discussion and Analysis. Additional information relating to

Arbor, including the Company’s Annual Information Form, can

be found on SEDAR at www.sedar.com.

Information Regarding Forward-Looking Statements

Certain statements contained in this Management’s Discussion

and Analysis including, but not limited to, information regarding

the status and progress of the Company’s operating and capital

activities, the plans and objectives of the Company and

assumptions regarding the Company’s future performance are

forward-looking statements. Forward-looking statements may

include words such as “believes”, “may”, “should”, “estimates”,

“continues”, “indicates”, “suggests”, “anticipates”, “intends”,

“plans”, “expects” and similar expressions. These forward-looking

statements are based on current expectations and various factors

and assumptions. Accordingly, these forward-looking statements

are subject to certain risks and uncertainties. The material factors

and assumptions that were applied in making the forward-looking

statements in this Management’s Discussion and Analysis

include, but are not limited to: reliance on third-party reports from

government bodies and industry associations, the use of

economic forecasts prepared by various financial institutions,

historical experience, and financial reporting of competitors and

suppliers. Risks and uncertainties that could cause or contribute to

actual results differing from such statements include, but are not

limited to, those discussed elsewhere in this Management’s

Discussion and Analysis, particularly under “Events and

Uncertainties”, and in the Company’s 2007 Annual Information

Form under “Description of the Business – Risk Factors” and 2007

Annual Report under “Risks, Events and Uncertainties”. The

Company cannot provide any assurance that forward-looking

statements will materialize. The Company assumes no obligation

to publicly release any revisions to these forward-looking

statements to reflect events or circumstances after the date

hereof or to reflect the occurrence of unanticipated events.

Non-GAAP Financial Measures

In addition to the GAAP results provided in this Management’s

Discussion and Analysis, some of the discussion of operating

performance is based on earnings before other income

(expenses), interest expense and income taxes (“EBOIT”) and

earnings before interest expense and income taxes (“EBIT”). In

addition, management uses net earnings excluding unusual items

(“NEEUI”) to assess its total financial results. EBOIT, EBIT and

NEEUI are non-GAAP financial measures. EBOIT excludes the

impact of other income (expenses), interest expense and income

taxes as disclosed in the statement of earnings, EBIT excludes the

impact of interest expense and income taxes as disclosed in the

statements of earnings and NEEUI excludes the after-tax impact

of other income (expenses) and provisions for asset impairment

of discontinued operations. EBOIT, EBIT and NEEUI are non-

GAAP financial measures that do not have any standardized

meaning prescribed by GAAP and are therefore unlikely to be

comparable to similar measures presented by other companies.

These non-GAAP financial measures are provided as a

supplement, and should not be considered an alternative to

measurements required by GAAP. Management uses both EBOIT

and EBIT to assess its operating results, as it believes it is

important to assess the cemetery, funeral, and corporate activities

without these non-operating components. Management uses

NEEUI to analyze sustainable net earnings. Management believes

that these measures provides useful additional information to

management and investors regarding the Company’s

performance as it provides a basis for analyzing the ongoing

operating results, which may vary due to different market and

economic factors than those that affect interest expense and

income taxes.

2007 ARBOR 14-01-08 1/14/08 3:06 PM Page 8

Global Reports LLC

9A r b o r M e m o r i a l S e r v i c e s I n c .

COMPANY AND CORE BUSINESSES

Arbor Memorial Services Inc. is a Canadian company

incorporated in Ontario which, through wholly owned

subsidiaries, is a market leader in providing interment rights,

cremations, funerals and associated merchandise and services to

customers across Canada. At October 31 , 2007, the Company

owned 41 cemeteries, 27 crematoria, 3 reception centres and

91 funeral homes in communities in eight provinces of Canada. In

addition, the Company opened a new reception centre in Windsor,

Ontario in November 2007.

Arbor is the successor to a business formed in 1947 to establish a

national system of garden cemeteries in which memorials were

set flush with the ground. In the 1980’s, Arbor began to provide

funeral services. The Company’s cemeteries and funeral homes

have developed and provided customized products and services

for many ethnic and religious groups in Canada.

The Company sells all of its products and services on a “pre-need”

basis, or prior to death, in addition to selling on an “at-need” basis.

Pre-need sales allow customers to make their cemetery and/or

funeral arrangements in advance, thereby avoiding additional

emotional and financial stress during a time of bereavement. The

Company believes that it is one of the industry leaders in

marketing pre-need cemetery and funeral arrangements, which is

an integral part of Arbor’s long-term business strategy.

Cemetery Operations

Cemetery operations offer interment rights (traditional ground

burial, cremation ground burial, mausolea, columbaria and other

cremation products including benches and pedestals), bronze

memorials, upright monuments, vaults, urns, interment services,

cremation services and other related merchandise and services.

The Company offers a complete range of options for personalized

memorialization and provides the highest quality products and

services to its customers. In fiscal 2007, cemetery sales

accounted for 43% of the Company’s total revenues and

cemetery investment and other income accounted for an

additional 4% of total revenues.

The cemetery properties range in size from 19 to over 200 acres

and are staffed by permanent maintenance, administrative and

sales personnel. At October 31 , 2007, the Company’s developed

and undeveloped cemetery land totalled approximately

2,862 acres, of which 43% was available for future development.

Of the Company’s 41 cemeteries at October 31 , 2007, 24

had a crematorium on site, 13 had a funeral home on site and

3 had a reception centre on site. The Company’s growth in

the cemetery segment is focused on development of new

cemeteries and reception centres, and expansion of existing

locations where warranted.

Funeral Operations

Funeral homes provide a range of services that includes

embalming, registration of death, the use of funeral home facilities

for visitation, memorial services and funeral receptions,

transportation services, cremation and the sale of caskets, urns,

flowers, custom books and cards and other related merchandise

and services. Many Arbor funeral homes have reception lounges

with fully equipped kitchens and extensive seating. In fiscal 2007,

funeral operations sales accounted for 49% of the Company’s

total revenues and funeral investment and other income

accounted for an additional 2% of total revenues.

The Company’s growth in the funeral segment is focused on

construction of new funeral homes and expansion or replacement

of existing facilities where warranted. The Company owns 96% of

its funeral facilities and leases 4%.

Pre-Need Trust Funds, Cemetery Care Funds and

Referral and Annuity Fees

The Company is required by provincial regulation to deposit

specific amounts, received in respect of pre-need merchandise

and services contracts, into trust or with third-party insurers

under group annuity programs, pending the delivery of the

products and services. Upon delivery of the products and services,

the Company is entitled to receive related amounts placed into

trust and accumulated investment income earned thereon. The

Company also recognizes revenue from these products and

services upon delivery.

In respect of interment rights, the Company is required to deposit

into cemetery care funds amounts specified by provincial

regulation. The investment income from the cemetery care funds

is available to the Company to defray the costs of ongoing care

and maintenance of cemeteries, mausolea and columbaria.

The Company receives fees on the balance of pre-need cemetery

and funeral funds under the trust program (“referral fees”) and

receives fees on the deposit of funeral funds under the group

annuity program (“annuity fees”). These fees are recognized as

received, net of an allowance for those fees subject to refund.

2007 ARBOR 14-01-08 1/14/08 3:06 PM Page 9

Global Reports LLC

10A r b o r M e m o r i a l S e r v i c e s I n c .

DEATH CARE INDUSTRY AND COMPETITION

The following contains forward-looking statements regarding the

Company’s and its industry’s outlook. Reference should be made to

“Information Regarding Forward-Looking Statements” on page 8.

For a description of material factors and assumptions see page 8

and for a description of risks and uncertainties that could cause

actual results to differ materially from forward-looking statements

see “Risks, Events and Uncertainties” on page 35, and the

Company’s 2007 Annual Information Form under “Description of

the Business – Risk Factors”.

Cemetery Operations

In Canada, cemetery operations are owned by a large number of

religious, municipal governments and other “not-for-profit”

organizations in addition to commercial owners. One large multi-

national firm owns a small number of cemeteries in Canada;

however, its presence in the cemetery business is significantly less

than in the funeral business. In addition, the Company competes

with monument dealers and other providers of cemetery products

and services in certain of its markets. Based on the number of deaths

in Canada as reported by Statistics Canada, the Company has

calculated that it performed interment services for 7.5% of all

deaths in Canada for the period from July 1 , 2006 to June 30, 2007.

Only a small number of organizations have developed large

modern cemeteries and even fewer provide a full range of services

due to the significant barriers to entry. Specifically, entry into the

cemetery industry can be difficult due to:

• complex cemetery regulations and zoning restrictions;

• the significant capital investment required and high land values,

particularly in metropolitan areas;

• land for new cemetery development being difficult to locate; and

• the desire for families to return to the same cemetery for

generations.

Arbor competes in the cemetery segment by presenting well-

maintained premises and a wide variety of burial space selection.

In addition, the Company provides products and services that

appeal to the different cultural backgrounds of its customers.

There is active competition in every major community in which

Arbor’s cemeteries are located.

Funeral Operations

Although Arbor competes with one large multi-national firm that

operates funeral homes in Canada, small independently owned

firms, controlling one or two funeral homes, account for the

largest number of funeral home operators in Canada. The

Company also competes with casket retailers, discount funeral

providers and other providers of funerary products and services in

certain of its markets. Based on the number of deaths in Canada

as reported by Statistics Canada, the Company has calculated

that it performed services for 9.1% of all deaths in Canada for the

period from July 1 , 2006 to June 30, 2007. Barriers to entry are

high due to the significant capital investment required, increasing

regulatory complexity and the importance of an established

reputation in competing for market share.

Operations by Province

The following table provides the number of funeral homes, cemeteries, reception centres and crematoria by province at October 31 , 2007:

Funeral ReceptionHomes Cemeteries Centres(1) Crematoria

British Columbia 8 3 - 3

Alberta 8 5 - 4

Saskatchewan 4 3 - 3

Manitoba 4 3 - 1

Ontario 45 21 3 12

Quebec 7 2 - 2

New Brunswick 8 1 - 1

Nova Scotia 7 3 - 1

91 41 3 27

(1) In addition, the Company opened a new reception centre in Windsor, Ontario in November 2007.

2007 ARBOR 14-01-08 1/14/08 3:07 PM Page 10

Global Reports LLC

11A r b o r M e m o r i a l S e r v i c e s I n c .

Throughout most of the 1980’s and 1990’s, the Company and its

competitors engaged in the acquisition of independently owned

funeral homes. However, this trend slowed in early 1999 when the

Company and its competitors generally applied lower valuation

criteria and many potential sellers withdrew their businesses from

the market rather than pursuing transactions at lower prices.

Arbor competes in the funeral segment by providing unique,

personalized funeral services and by offering well-maintained,

attractive facilities that cater to its customers’ requirements.

Industry Trends

Establishment of new cemeteries is declining: The establishment of

individual cemeteries by religious, municipal governments and

other “not-for-profit” organizations has declined. Many existing

religious cemeteries are nearing full capacity and few religious

organizations have the funds to acquire new cemetery facilities.

Additionally, the interest of municipal governments in fulfilling the

requirement for cemetery facilities has been declining.

Cremation is increasing: There has been a growing acceptance of

cremation as an alternative to traditional burial in Canada and

internationally. In 2006, the Cremation Association of North

America (“CANA”) reported that the number of cremations in 1996

represented 40% of total Canadian deaths and that this percentage

grew to 56% in 2004. The CANA projections that were provided for

five of the provinces also indicated that the percentages for three of

these five provinces would grow further by 2010.

While cremation was originally seen as a less costly alternative to

traditional burial, it is increasingly accompanied by traditional

funeral services and memorialization. Cremation also provides the

Company with an opportunity to better serve its families by

offering unique products and services. Arbor has been developing

cremation gardens in a number of its cemeteries. These gardens

are landscaped with flowers, trees, shrubs, walkways, waterfalls

and ponds and provide the Company’s customers with

alternatives for burial or scattering, which can be accompanied by

various other memorial products such as benches, pedestals,

rocks, trees and memorial walls.

Need for products and services is increasing: There is an inevitable

need for the products and services the industry offers. In addition,

the number of deaths in Canada is expected to increase at a

steady, moderate pace. Annual population estimates by Statistics

Canada in December 2005 indicated that Canada’s population

would grow by 0.8% annually from 2005 to 2031 . In addition, the

estimates from Statistics Canada indicated that the Company’s

primary customer group, those aged 65 and older, is expected to

grow by 4.5% annually over the same period.

ARBOR’S STRATEGY

Key Objectives

Arbor has four key objectives:

• to generate a return to shareholders that exceeds the Company’s

cost of capital;

• to maintain Arbor’s Canadian market position in combined

cemetery/funeral revenue;

• to generate consistent growth in earnings per share with a

limited risk profile; and

• to achieve operational excellence.

Competitive Strengths

Industry leader: Arbor is one of the leading providers of combined

funeral and cemetery products and services in Canada and has

been in business for close to 60 years.

Experienced senior management team: Arbor’s senior management

team has been with the Company for an average of 20 years

and has a wealth of knowledge and history with the Company and

the industry.

Focus on high quality customer service and facilities: Arbor has been

providing its customers with high quality service for many years.

The Company believes that it operates one of the premier death

care facilities in most of its principal markets and that it generally

provides superior funeral and cemetery services that meet or

exceed customer expectations.

Funeral homes and reception centres located on cemetery properties:

Locating funeral homes and reception centres on cemetery

properties allows the Company to provide superior customer

service. On-site funeral and reception operations provide families

with the convenience of complete death care services at a single

location and provide the Company with the ability to share

certain costs and resources. At October 31 , 2007, the Company

had 13 funeral homes and 3 reception centres located on

cemetery properties.

National presence in both the cemetery and funeral sectors of the

death care industry: The Company’s national presence in both the

cemetery and funeral sectors allows for sharing of certain costs and

resources and referral opportunities between sectors.

2007 ARBOR 14-01-08 1/14/08 3:07 PM Page 11

Global Reports LLC

12A r b o r M e m o r i a l S e r v i c e s I n c .

Established base of pre-arranged services: Arbor has a significant

history in pre-arrangement of products and services. Pre-need

planning enables families to specify their preferred cemetery and

funeral products and services in advance and to pre-pay for these

products and services. Arbor’s focus on pre-need business is also

important to the Company’s results since these sales generate

future revenues.

Competitive Challenges

Ontario cemetery and funeral regulations: Existing cemetery and

funeral regulations in Ontario do not allow the Company to

operate funeral homes on cemetery properties. While legislation

has been passed that will ultimately allow this to occur, based on

the Company’s experience, it is uncertain when the regulations

will be finalized so that the legislation can be proclaimed.

Competition: In Canada, the funeral and cemetery industry is

characterized by a large number of locally owned, independent

operations. To compete successfully, our funeral service locations

and cemeteries must maintain good reputations and high

professional standards in the industry, as well as offer attractive

products and services at competitive prices. In addition, we must

market our Company in such a manner as to distinguish us from

our competitors. We have historically experienced price

competition from independent funeral home and cemetery

operators, monument dealers, casket retailers, low-cost funeral

providers and other non-traditional providers of services and

merchandise. If we are unable to successfully compete, the

Company’s financial condition, results of operations and cash

flows could be adversely affected.

Price competition, increased advertising, better marketing or

improvements in products and services offered by competitors in

any market in which Arbor competes could reduce the Company’s

market share or cause the Company to reduce prices or incur

increased costs in order to retain or recapture market share, either

of which would reduce revenues and/or margins. If the Company is

not able to respond effectively to changing consumer preferences,

its market share, sales and profitability could decrease.

Environmental legislation: Over the last several years, various

federal, provincial and municipal government agencies have

released environmental legislation that has caused the Company

to incur extra costs in order to comply with the legislation. The

Company believes that this trend will continue.

Business Strategies

Customer service: One of the Company’s most important strategies

is to meet or exceed customer expectations with respect to the

delivery of cemetery and funeral products and services, thereby

meeting or exceeding the standards set by the competition.

Products and services: The Company strives to provide the entire

spectrum of cemetery, funeral and related products and services

on a pre-need and an at-need basis and continues to develop new

products and services to meet the unique needs of the many

cultures the Company serves.

Pricing: The Company largely sets its prices in line with its

premium-priced, value-added competitors. However, it also

manages a few smaller operations that compete in lower-priced

market segments.

Pre-need sales: The Company intends to continue to emphasize pre-

need cemetery and funeral arrangements in order to better serve its

customers and to secure future revenues.

Cemetery/funeral synergy: The Company strives to maximize

the benefit of having a national presence in both the cemetery

and funeral sectors of the death care industry by encouraging

cross-referrals and combining cemetery and funeral operations

where possible.

Properties/facilities: Another of Arbor’s market strategies is to

meet or exceed the major competition in terms of the quality of

each cemetery and funeral home it owns and operates. One

exception to this basic strategy is where a facility has been

specifically designed to service the lower-priced market segment.

The Company currently operates a few facilities in the lower-

priced market segment.

Future investments: The Company’s present priorities for future

investment are:

• to establish funeral homes and reception centres within its

cemeteries or as stand-alone facilities in communities where

there is market justification and where the operation will achieve

the goal of complete service to customers;

• to acquire property to expand existing cemeteries or develop

new cemeteries;

• to continue to develop new products and services that meet the

unique needs of the many cultures the Company serves; and

• to establish or expand facilities to service the growing cremation

market.

2007 ARBOR 14-01-08 1/14/08 3:08 PM Page 12

Global Reports LLC

13A r b o r M e m o r i a l S e r v i c e s I n c .

Asset management: Arbor’s asset management strategy is to

achieve a return that exceeds the Company’s cost of capital both

on a consolidated basis and a location-by-location basis.

Individual branch operations that are achieving only marginal

returns are addressed either through return improvement

programs or divestiture.

NEW ACCOUNTING POLICIES

Financial Instruments

The Canadian Institute of Chartered Accountants (“CICA”) issued

the following new accounting standards, which were effective for

the Company’s first quarter of fiscal 2007: Financial Instruments –

Recognition and Measurement (“Section 3855”); Hedges

(“Section 3865”); Comprehensive Income (“Section 1530”),

Equity (“Section 3251”) and Disclosure and Presentation (“Section

3861”). Each of the standards requires prospective application.

Section 1530 introduces the concept of comprehensive income,

which consists of net income and other comprehensive income

(“OCI”), and represents changes in shareholders’ equity during a

period arising from transactions with non-owners. OCI includes

among its components, unrealized gains and losses on financial

assets classified as “available for sale” and changes in the fair value

of the effective portion of cash flow hedging instruments together

with income tax expenses or benefits associated with each

component. As a result of the implementation of this section, our

Consolidated Financial Statements include a Consolidated

Statement of Comprehensive Income and a Consolidated

Statement of Accumulated Other Comprehensive Income. In

addition, the cumulative amount of OCI, which is termed

“accumulated other comprehensive income” or “AOCI”, is

presented as a new category of shareholders’ equity in the

Consolidated Balance Sheets.

Section 3861 establishes standards for presentation of financial

instruments and identifies the information that should be

disclosed about them. This section deals with disclosure of

information about the nature and extent of an entity’s use of

financial instruments, the business purpose they serve, the risks

associated with them and management’s policies for controlling

those risks. The Company has expanded its discussion of financial

instruments and the related objectives, risks and risk

management policies throughout the notes to the consolidated

financial statements.

Section 3855 establishes standards for recognizing and measuring

financial instruments and non-financial derivatives. On application

of Section 3855, the Company classified the investments in the

pre-need cemetery and funeral trust funds and the investments in

the cemetery care funds as “available for sale” and changed the

basis of measurement for these assets from cost to fair value in the

Consolidated Balance Sheets. Unrealized gains and losses on these

“available for sale” financial assets are excluded from net earnings

and recorded, net of income taxes, as a component of OCI in the

Consolidated Statement of Comprehensive Income. Unrealized

gains and losses are then offset by the amounts attributable to non-

controlling interests in pre-need funds, non-controlling interests in

cemetery care funds or deferred revenue, as appropriate, as such

unrealized earnings have not been earned by the Company through

the performance of services or delivery of merchandise. The

Company continues to recognize as sales, amounts removed from

the pre-need funds upon the performance of services and delivery

of merchandise, including realized earnings accumulated in the

funds and the Company’s AOCI is ultimately not affected by the

revaluation of the pre-need cemetery and funeral trust funds and

the cemetery care funds.

The cemetery and funeral trust funds were measured at fair value

at November 1 , 2006, and the resulting unrealized net gain of

$9.5 million was recorded to OCI, net of income taxes of

$3.3 million. The subsequent changes in the fair value, totalling

$1 .8 million, were also recorded to OCI, net of income taxes of

$0.6 million. Both the initial unrealized net gain in the funds and

the subsequent changes therein have been offset by the amounts

attributable to “non-controlling interests in pre-need funds” or

“deferred revenue” as appropriate

In accordance with the Section, however, the prior period

comparative figures at October 31 , 2006, were not restated to fair

value and are therefore presented at cost.

Similarly, the cemetery care funds were measured at fair value at

November 1 , 2006, and the resulting unrealized net gain of

$6.1 million was recorded to OCI, net of income taxes of

$2.2 million. The subsequent changes in the fair value, totalling

$4.4 million, were also recorded to OCI, net of income taxes of

$1 .6 million. Both the initial unrealized net gain in the funds and

the subsequent changes therein have been offset by the amounts

attributable to “non-controlling interests in cemetery care funds”.

2007 ARBOR 14-01-08 1/14/08 3:09 PM Page 13

Global Reports LLC

14A r b o r M e m o r i a l S e r v i c e s I n c .

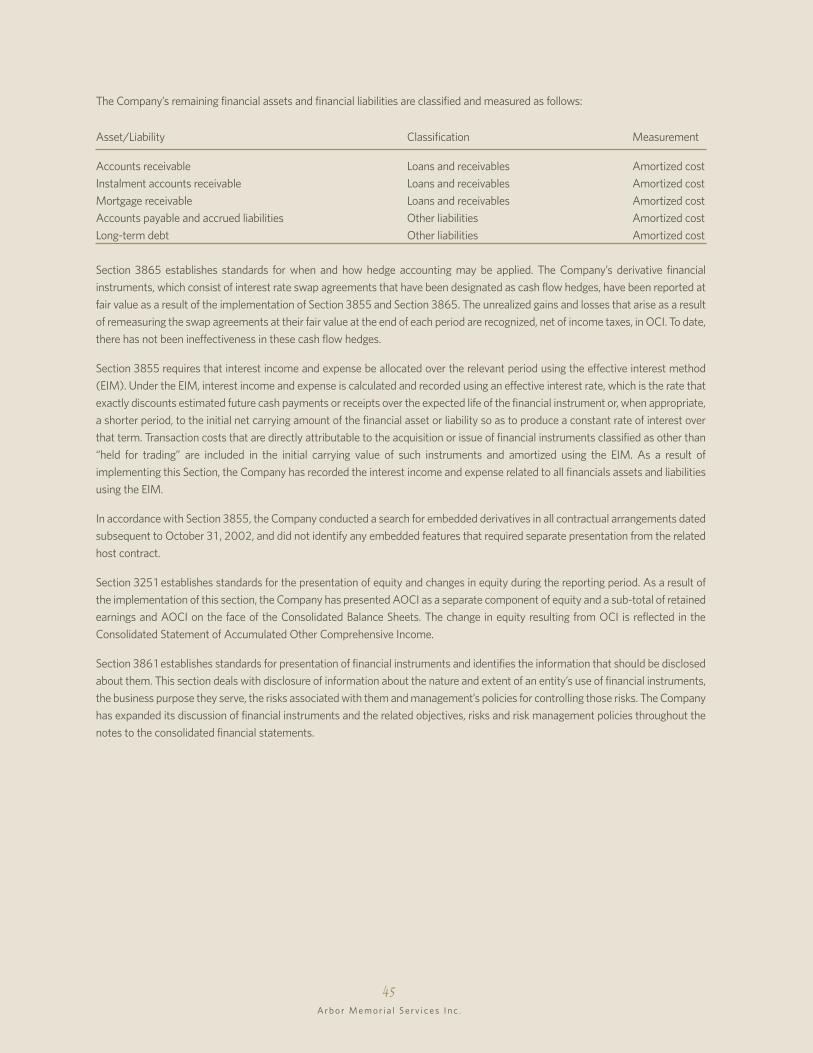

Section 3865 establishes standards for when and how hedge

accounting may be applied. The Company’s derivative financial

instruments, which consist of interest rate swap agreements that

have been designated as cash flow hedges, have also been

reported at fair value as a result of the implementation of Section

3855 and Section 3865. The unrealized gains and losses that

arise as a result of remeasuring the swap agreements at their fair

value at the end of each period are recognized, net of income

taxes, in OCI. To date there has not been any ineffectiveness in

these cash flow hedges. The accumulated loss at November 1 ,

2006, of $0.9 million was recorded, net of income taxes of

$0.3 million, as a transition adjustment to opening AOCI. The

estimated fair value of the interest rate swaps at October 31 ,

2007 was a gain of $0.1 million, which was recorded in “Other

liabilities”. The change in the loss in the period ended October 31 ,

2007 was recorded, net of income taxes, in OCI.

Section 3855 requires that interest income and expense be

allocated over the relevant period using the effective interest

method (EIM). Under the EIM, interest income and expense is

calculated and recorded using an effective interest rate, which is

the rate that exactly discounts estimated future cash payments

or receipts through the expected life of the financial instrument

or, when appropriate, a shorter period, to the initial net carrying

amount of the financial asset or liability. Transaction costs that

are directly attributable to the acquisition or issue of financial

instruments classified as other than “held for trading” are

included in the initial carrying value of such instruments and

amortized using the EIM. As a result of implementing this

Section, the Company has recorded the interest income and

expense related to all financials assets and liabilities using the

EIM. The change to the EIM did not result in any significant

differences to the Company’s current calculation of interest

income and expense.

In accordance with Section 3855 the Company conducted a

search for embedded derivatives in all contractual arrangements

dated subsequent to October 31 , 2002 and did not identify any

imbedded features that required separate presentation from the

related host contract.

Section 3251 establishes standards for the presentation of equity

and changes in equity during the reporting period. As a result of

the implementation of this section, the Company has presented a

sub-total of retained earnings and AOCI on the face of the

Consolidated Balance Sheets.

FUTURE ACCOUNTING POLICY CHANGE

International Financial Reporting Standards

The Canadian Institute of Chartered Accountants has determined

that publicly accountable enterprises will transition from

Canadian generally accepted accounting principles (GAAP) to

international financial reporting standards (IFRS) and it is

expected that this transition will be effective for periods beginning

on or after January 1 , 201 1 . The Company will evaluate the

impact, if any, of the new standards on current financial reporting

practices and will implement these changes accordingly in order

to be compliant with IFRS.

RESULTS OF OPERATIONS

The data set forth herein should be read in conjunction with the

Company’s consolidated financial statements and accompanying

notes included in the Company’s 2007 Annual Report. Historical

information provided is not necessarily indicative of the results to be

expected in the future.

The Company operates on a weekly basis. The 2007, 2006 and

2005 fiscal years each comprised a 52-week period.

All other financial assets and financial liabilities are classified and measured as follows:

Asset/Liability Classification Measurement

Accounts receivable Loans and receivables Amortized cost

Instalment accounts receivable Loans and receivables Amortized cost

Mortgage receivable Loans and receivables Amortized cost

Accounts payable and accrued liabilities Other liabilities Amortized cost

Long-term debt Other liabilities Amortized cost

2007 ARBOR 14-01-08 1/14/08 3:09 PM Page 14

Global Reports LLC

15A r b o r M e m o r i a l S e r v i c e s I n c .

Revenue

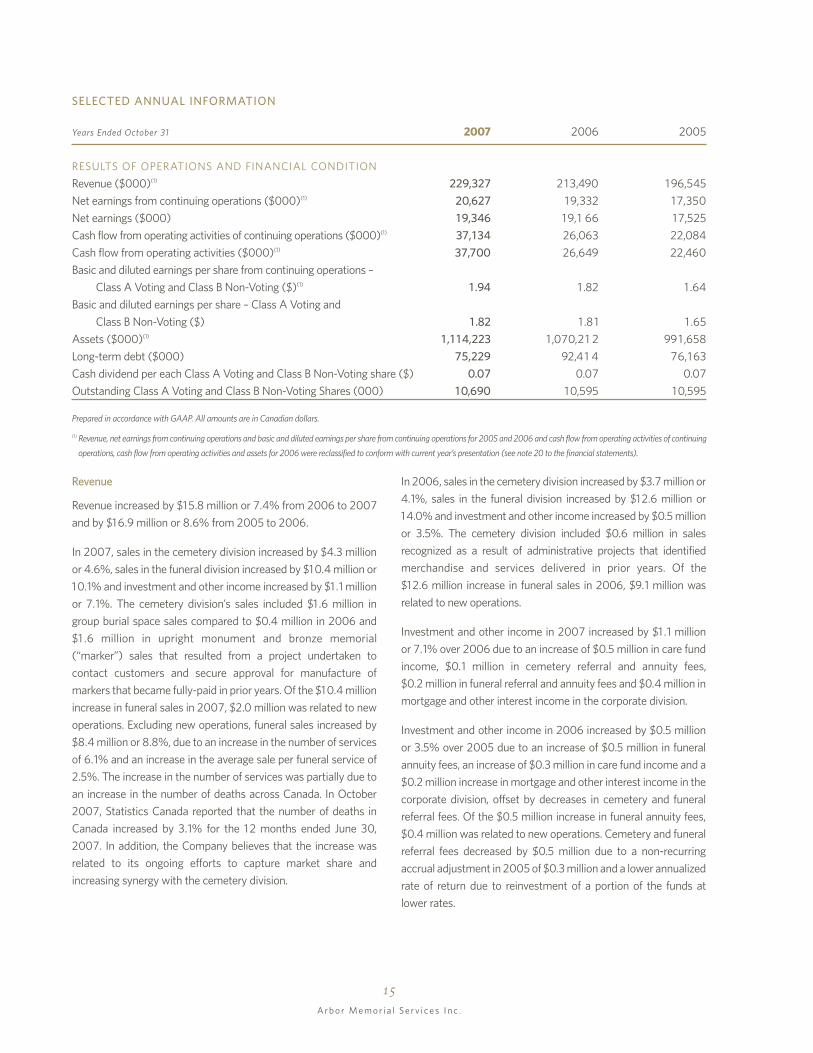

Revenue increased by $15.8 million or 7.4% from 2006 to 2007

and by $16.9 million or 8.6% from 2005 to 2006.

In 2007, sales in the cemetery division increased by $4.3 million

or 4.6%, sales in the funeral division increased by $10.4 million or

10.1% and investment and other income increased by $1 .1 million

or 7.1%. The cemetery division’s sales included $1 .6 million in

group burial space sales compared to $0.4 million in 2006 and

$1 .6 million in upright monument and bronze memorial

(“marker”) sales that resulted from a project undertaken to

contact customers and secure approval for manufacture of

markers that became fully-paid in prior years. Of the $10.4 million

increase in funeral sales in 2007, $2.0 million was related to new

operations. Excluding new operations, funeral sales increased by

$8.4 million or 8.8%, due to an increase in the number of services

of 6.1% and an increase in the average sale per funeral service of

2.5%. The increase in the number of services was partially due to

an increase in the number of deaths across Canada. In October

2007, Statistics Canada reported that the number of deaths in

Canada increased by 3.1% for the 12 months ended June 30,

2007. In addition, the Company believes that the increase was

related to its ongoing efforts to capture market share and

increasing synergy with the cemetery division.

SELECTED ANNUAL INFORMATION

Years Ended October 31 2007 2006 2005

RESULTS OF OPERATIONS AND FINANCIAL CONDITION

Revenue ($000)(1) 229,327 213,490 196,545

Net earnings from continuing operations ($000)(1) 20,627 19,332 17,350

Net earnings ($000) 19,346 19,1 66 17,525

Cash flow from operating activities of continuing operations ($000)(1) 37,134 26,063 22,084

Cash flow from operating activities ($000)(1) 37,700 26,649 22,460

Basic and diluted earnings per share from continuing operations –

Class A Voting and Class B Non-Voting ($)(1) 1 .94 1 .82 1 .64

Basic and diluted earnings per share – Class A Voting and

Class B Non-Voting ($) 1 .82 1 .81 1 .65

Assets ($000)(1) 1 ,1 14,223 1 ,070,21 2 991,658

Long-term debt ($000) 75,229 92,41 4 76,163

Cash dividend per each Class A Voting and Class B Non-Voting share ($) 0.07 0.07 0.07

Outstanding Class A Voting and Class B Non-Voting Shares (000) 10,690 10,595 10,595

Prepared in accordance with GAAP. All amounts are in Canadian dollars.

(1) Revenue, net earnings from continuing operations and basic and diluted earnings per share from continuing operations for 2005 and 2006 and cash flow from operating activities of continuing

operations, cash flow from operating activities and assets for 2006 were reclassified to conform with current year’s presentation (see note 20 to the financial statements).

In 2006, sales in the cemetery division increased by $3.7 million or

4.1%, sales in the funeral division increased by $12.6 million or

14.0% and investment and other income increased by $0.5 million

or 3.5%. The cemetery division included $0.6 million in sales

recognized as a result of administrative projects that identified

merchandise and services delivered in prior years. Of the

$12.6 million increase in funeral sales in 2006, $9.1 million was

related to new operations.

Investment and other income in 2007 increased by $1 .1 million

or 7.1% over 2006 due to an increase of $0.5 million in care fund

income, $0.1 million in cemetery referral and annuity fees,

$0.2 million in funeral referral and annuity fees and $0.4 million in

mortgage and other interest income in the corporate division.

Investment and other income in 2006 increased by $0.5 million

or 3.5% over 2005 due to an increase of $0.5 million in funeral

annuity fees, an increase of $0.3 million in care fund income and a

$0.2 million increase in mortgage and other interest income in the

corporate division, offset by decreases in cemetery and funeral

referral fees. Of the $0.5 million increase in funeral annuity fees,

$0.4 million was related to new operations. Cemetery and funeral

referral fees decreased by $0.5 million due to a non-recurring

accrual adjustment in 2005 of $0.3 million and a lower annualized

rate of return due to reinvestment of a portion of the funds at

lower rates.

2007 ARBOR 14-01-08 1/14/08 3:10 PM Page 15

Global Reports LLC

16A r b o r M e m o r i a l S e r v i c e s I n c .

Net Earnings From Continuing Operations and Earnings Per

Share From Continuing Operations

Net earnings from continuing operations and basic and diluted

earnings per share from continuing operations were $20.6 million

and $1 .94 in 2007 compared to $19.3 million and $1 .82 per share

in 2006. This represented an increase in net earnings from

continuing operations of $1 .3 million or 6.7% and an increase in

earnings per share from continuing operations of $0.1 2.

Comparatively, net earnings from continuing operations and basic

and diluted earnings per share from continuing operations

increased in 2006 from 2005 by $2.0 million or $0.18 per share.

This represented an increase in earnings from continuing

operations of 1 1 .4%.

Net earnings from continuing operations in 2007 were affected

by an increase in termination expenses and asset impairment

charges of $2.4 million. Excluding the affect of these items from

both years, net earnings from continuing operations increased by

$3.7 million or 19.0%.

Net earnings and earnings per share

Net earnings and basic and diluted earnings per share were

$19.3 million and $1 .82 in 2007 compared to $19.2 million and

$1 .81 per share in 2006. This represented an increase in net

earnings of $0.2 million or 0.9% and an increase in earnings

per share of $0.01 . Comparatively, net earnings and basic and

diluted earnings per share increased in 2006 from 2005 by

$1 .6 million or $0.16 per share. This represented an increase in

earnings of 9.7%.

Net earnings in 2007 were affected by an increase in termination

expenses and asset impairment charges of $3.4 million. Excluding

the affect of these items from both years, net earnings increased

by $3.6 million or 18.0%.

All years included a number of unusual items. The following

is a reconciliation of net earnings to net earnings excluding

unusual items.

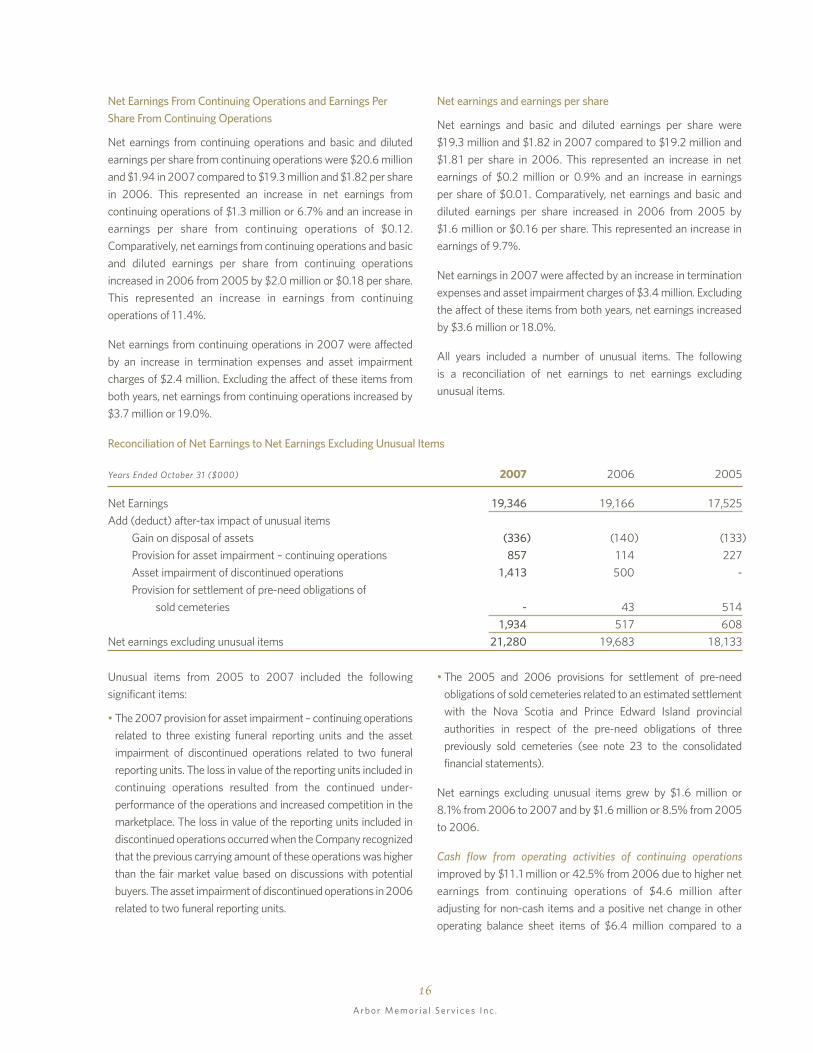

Unusual items from 2005 to 2007 included the following

significant items:

• The 2007 provision for asset impairment – continuing operations

related to three existing funeral reporting units and the asset

impairment of discontinued operations related to two funeral

reporting units. The loss in value of the reporting units included in

continuing operations resulted from the continued under-

performance of the operations and increased competition in the

marketplace. The loss in value of the reporting units included in

discontinued operations occurred when the Company recognized

that the previous carrying amount of these operations was higher

than the fair market value based on discussions with potential

buyers. The asset impairment of discontinued operations in 2006

related to two funeral reporting units.

• The 2005 and 2006 provisions for settlement of pre-need

obligations of sold cemeteries related to an estimated settlement

with the Nova Scotia and Prince Edward Island provincial

authorities in respect of the pre-need obligations of three

previously sold cemeteries (see note 23 to the consolidated

financial statements).

Net earnings excluding unusual items grew by $1 .6 million or

8.1% from 2006 to 2007 and by $1 .6 million or 8.5% from 2005

to 2006.

Cash flow from operating activities of continuing operations

improved by $1 1 .1 million or 42.5% from 2006 due to higher net

earnings from continuing operations of $4.6 million after

adjusting for non-cash items and a positive net change in other

operating balance sheet items of $6.4 million compared to a

Reconciliation of Net Earnings to Net Earnings Excluding Unusual Items

Years Ended October 31 ($000) 2007 2006 2005

Net Earnings 19,346 19,166 17,525

Add (deduct) after-tax impact of unusual items

Gain on disposal of assets (336) (140) (133)

Provision for asset impairment – continuing operations 857 1 14 227

Asset impairment of discontinued operations 1 ,413 500 -

Provision for settlement of pre-need obligations of

sold cemeteries - 43 514

1 ,934 517 608

Net earnings excluding unusual items 21,280 19,683 18,133

2007 ARBOR 14-01-08 1/14/08 3:10 PM Page 16

Global Reports LLC

17A r b o r M e m o r i a l S e r v i c e s I n c .

• Mortgage receivable decreased by $6.8 million due to a

payment received in 2007.

• Deferred obtaining costs and stored merchandise increased by

$4.0 million or 5.8% as a result of more pre-need contracts being

written than were delivered in the year.

Assets at the end of 2006 increased by $73.6 million or 7.4%

compared to 2005. Discussion of the main contributors to the

increase follows.

• Pre-need receivables and funds, including the current portion,

increased by $29.6 million or 6.6%, of which $18.0 million was

acquired from a group of 7 funeral homes that was purchased by

the Company in the first quarter of 2006. The remaining

increase of $1 1 .6 million was the result of growth in deposits to

the funds and realized earnings occurring at a higher rate than

deliveries of amounts out of trust.

• Fixed assets increased by $17.8 million or 10.9%, of which

$14.5 million was due to the acquisition of 7 funeral homes in

the year.

• Cemetery care funds increased by $1 1 .2 million or 7.7% due to

deposits made to the funds as a result of at-need and pre-need

cemetery interment right sales.

• Goodwill increased by $10.8 million, which was related to the

acquisition of 7 funeral homes in the year

• Cemetery land increased by $4.2 million due to the purchase of

two parcels of cemetery land for future development for

$4.9 million, which was partially offset by a reduction for lots

sold in the year.

Long-term debt decreased by $17.2 million from 2006 to 2007

due to principal repayments on the bank term loans. Long-term

debt increased by $16.3 million from 2005 to 2006 due to the

net impact of $19.9 million in new debt established on the

acquisition of 7 funeral homes in the year and $3.7 million in

principal repayments on the bank term loans.

negative net change in 2006 of $0.1 million. The adjustments

to net earnings for non-cash items included depreciation and

amortization, gain on disposal of assets, provision for asset

impairment, provision for settlement of pre-need obligations of

sold cemeteries and future income taxes.

Cash flow from operating activities of continuing operations

increased from 2005 to 2006 due to higher net cash collected in

2006 for at-need funerals and lower income taxes paid. Cash

attributed to at-need funerals was higher in 2006 due to new

operations. Income taxes paid in 2005 included $2.4 million paid

on behalf of a new subsidiary established in 2004 for which tax

instalments were not required during its first year. The positive

impact of these items was partially offset by higher additions to

developed land, crypts and niches of $2.0 million, due mainly to

$2.4 million spent on two mausoleum additions in 2006.

Cash flow from operating activities did not differ significantly from

cash flow from operating activities of continuing operations.

Assets at the end of 2007 increased by $44.0 million or 4.1%

compared to 2006. Discussion of the main contributors to the

increase follows.

• Cash increased by $12.6 million due to $37.7 million in cash

provided by operating activities and $7.2 million in cash

provided by financing activities, which were offset by

$32.3 million used for investing activities.

• Pre-need receivables and funds, including the current portion,

increased by $21 .4 million or 4.5%, of which $7.7 million was

due to a fair value adjustment recorded as a result of the

implementation of new accounting standards for financial

instruments in 2007. Excluding the fair value adjustment, pre-

need receivables and funds increased by $13.7 million or 2.9%

as a result of growth in deposits to the funds and realized

earnings occurring at a higher rate than deliveries of amounts

out of trust.

• Fixed assets increased by $6.6 million due to additions of

$16.6 million, which were offset by depreciation of $10.0 million.

Additions included $6.0 million for the development of new

reception centres.

• Cemetery care funds increased by $14.0 million, of which

$1 .7 million was due to a fair value adjustment as a result of the

implementation of new accounting standards for financial

instruments. Excluding the fair value adjustment, cemetery care

funds increased by $12.3 million or 7.9% due to deposits made

to the funds as a result of at-need and pre-need cemetery

interment right sales.

2007 ARBOR 14-01-08 1/14/08 3:11 PM Page 17

Global Reports LLC

18A r b o r M e m o r i a l S e r v i c e s I n c .

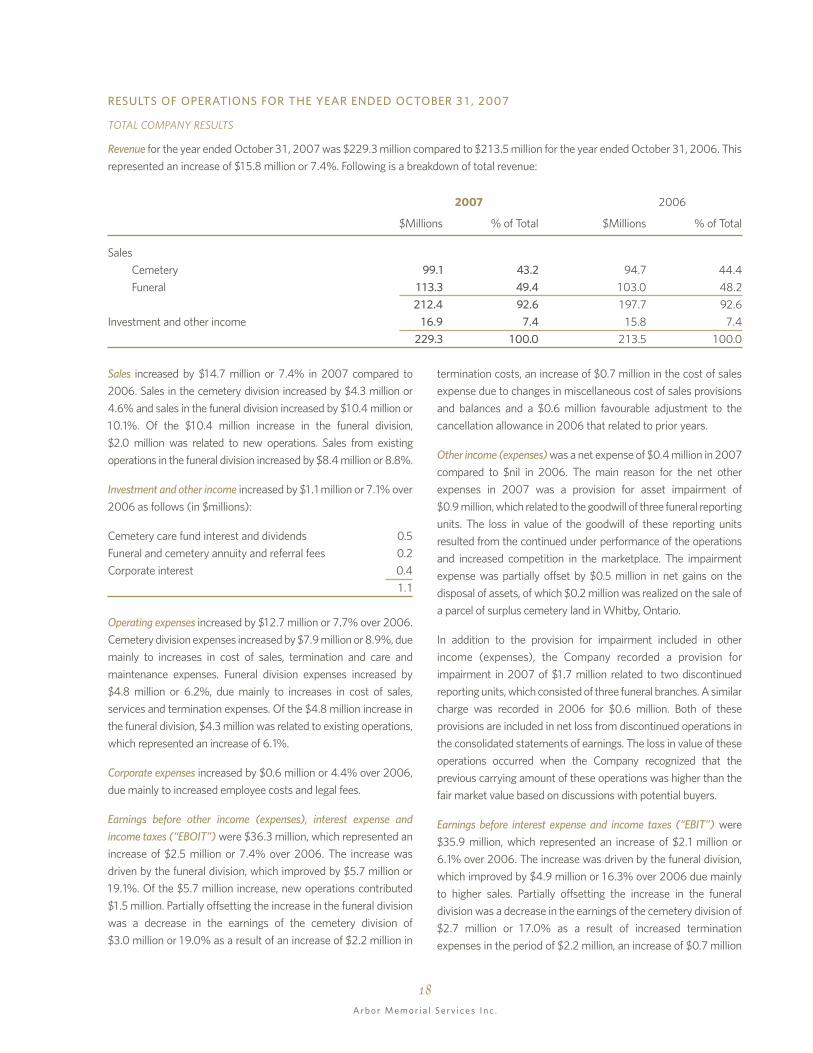

Sales increased by $14.7 million or 7.4% in 2007 compared to

2006. Sales in the cemetery division increased by $4.3 million or

4.6% and sales in the funeral division increased by $10.4 million or

10.1%. Of the $10.4 million increase in the funeral division,

$2.0 million was related to new operations. Sales from existing

operations in the funeral division increased by $8.4 million or 8.8%.

Investment and other income increased by $1 .1 million or 7.1% over

2006 as follows (in $millions):

Cemetery care fund interest and dividends 0.5

Funeral and cemetery annuity and referral fees 0.2

Corporate interest 0.4

1 .1

Operating expenses increased by $12.7 million or 7.7% over 2006.

Cemetery division expenses increased by $7.9 million or 8.9%, due

mainly to increases in cost of sales, termination and care and

maintenance expenses. Funeral division expenses increased by

$4.8 million or 6.2%, due mainly to increases in cost of sales,

services and termination expenses. Of the $4.8 million increase in

the funeral division, $4.3 million was related to existing operations,

which represented an increase of 6.1%.

Corporate expenses increased by $0.6 million or 4.4% over 2006,

due mainly to increased employee costs and legal fees.

Earnings before other income (expenses), interest expense and

income taxes (“EBOIT”) were $36.3 million, which represented an

increase of $2.5 million or 7.4% over 2006. The increase was

driven by the funeral division, which improved by $5.7 million or

19.1%. Of the $5.7 million increase, new operations contributed

$1 .5 million. Partially offsetting the increase in the funeral division

was a decrease in the earnings of the cemetery division of

$3.0 million or 19.0% as a result of an increase of $2.2 million in

termination costs, an increase of $0.7 million in the cost of sales

expense due to changes in miscellaneous cost of sales provisions

and balances and a $0.6 million favourable adjustment to the

cancellation allowance in 2006 that related to prior years.

Other income (expenses) was a net expense of $0.4 million in 2007

compared to $nil in 2006. The main reason for the net other

expenses in 2007 was a provision for asset impairment of

$0.9 million, which related to the goodwill of three funeral reporting

units. The loss in value of the goodwill of these reporting units

resulted from the continued under performance of the operations

and increased competition in the marketplace. The impairment

expense was partially offset by $0.5 million in net gains on the

disposal of assets, of which $0.2 million was realized on the sale of

a parcel of surplus cemetery land in Whitby, Ontario.

In addition to the provision for impairment included in other

income (expenses), the Company recorded a provision for

impairment in 2007 of $1 .7 million related to two discontinued

reporting units, which consisted of three funeral branches. A similar

charge was recorded in 2006 for $0.6 million. Both of these

provisions are included in net loss from discontinued operations in

the consolidated statements of earnings. The loss in value of these

operations occurred when the Company recognized that the

previous carrying amount of these operations was higher than the

fair market value based on discussions with potential buyers.

Earnings before interest expense and income taxes (“EBIT”) were

$35.9 million, which represented an increase of $2.1 million or

6.1% over 2006. The increase was driven by the funeral division,

which improved by $4.9 million or 16.3% over 2006 due mainly

to higher sales. Partially offsetting the increase in the funeral

division was a decrease in the earnings of the cemetery division of

$2.7 million or 17.0% as a result of increased termination

expenses in the period of $2.2 million, an increase of $0.7 million

RESULTS OF OPERATIONS FOR THE YEAR ENDED OCTOBER 3 1 , 2007

TOTAL COMPANY RESULTS

Revenue for the year ended October 31 , 2007 was $229.3 million compared to $213.5 million for the year ended October 31 , 2006. This

represented an increase of $15.8 million or 7.4%. Following is a breakdown of total revenue:

2007 2006

$Millions % of Total $Millions % of Total

Sales

Cemetery 99.1 43.2 94.7 44.4

Funeral 1 13.3 49.4 103.0 48.2

212.4 92.6 197.7 92.6

Investment and other income 16.9 7.4 15.8 7.4

229.3 100.0 213.5 100.0

2007 ARBOR 14-01-08 1/14/08 3:11 PM Page 18

Global Reports LLC

19A r b o r M e m o r i a l S e r v i c e s I n c .

in the cost of sales expense due to changes in miscellaneous cost

of sales provisions, and a $0.6 million favourable adjustment to

the cancellation allowance in 2006 that related to prior years.

Interest expense included interest on floating-rate bank term debt,

a capital lease and the cost of the Company’s interest rate swap

contracts. Interest expense decreased by $0.4 million or 8.2% to

$4.6 million in 2007 due to a lower weighted-average balance of

long-term debt outstanding of $9.4 million or 9.8% and lower

swap costs of $0.5 million. The decrease occurred despite a

higher average floating rate of interest of 5.2% compared to 4.6%

in 2006. The overall weighted-average rate of interest on long-

term debt for the period was 5.4% compared to 5.3% in 2006.

The weighted-average long-term debt balance decreased due to

repayments on the bank term loans in the fourth quarter of 2006

and the third and fourth quarters of 2007. The proportion of fixed-

rate debt at October 31 , 2007 was 47% compared to 49% at

October 31 , 2006.

Income taxes for 2007 resulted in an effective tax rate of 34.0%

compared to 32.8% in 2006. The increase in the effective rate of

1 .2 percentage points was mainly due to the non-deductible

portion of goodwill impairment charges, which increased the

effective rate by 0.9 of a percentage point.

Net earnings from continuing operations increased by $1.3 million or

6.7% to $20.6 million compared to 2006, despite an after-tax

increase in termination expenses of $1 .7 million and an after-tax

increase in asset impairment charges of $0.7 million. Excluding the

increase in termination expenses and asset impairment charges

from both years, net earning from continuing operations increased

by $3.7 million or 19.0%. The increase was mainly attributable to

improved earnings in the funeral division as a result of higher sales.

Net loss from discontinued operations increased by $1.1 million due

to an increase in after-tax impairment charges of $1.0 million.

The impairment provisions for both continuing and discontinued

operations resulted from continued under performance, despite

measures undertaken to improve the performance, increased

competition in the marketplace and in the case of two of the

discontinued reporting units, the recognition that the previous

carrying amount of these operations was higher than the fair

market value based on discussions with potential buyers.

Net earnings increased by 0.9% to $19.3 million. Net earnings

were affected by an increase in after-tax impairment provisions

of $1 .7 million and an increase in after-tax termination expenses

of $1 .7 million. Excluding the increase in termination expenses

and impairment charges from both years, net earnings increased

by $3.6 million or 18.0%.

Basic and diluted earnings per share from continuing operations

increased by $0.12 to $1 .94 per share in 2007, basic and diluted

loss per share from discontinued operations increased from $0.01

in 2006 to $0.12 in 2007 and basic and diluted earnings per

share increased by $0.01 to $1 .82 per share in 2007.

CEMETERY DIVISION

Cemetery sales in 2007 increased by $4.3 million or 4.6% over

2006 to $99.1 million. Sales in the year, including finance charges