Embed Size (px)

Citation preview

Highlights from our April Fact Book

The SEC is scheduled to make a decision regarding its controversial “tick size pilot program” on May 6th. We provide a refresher on the details of the program and which securities could be affected.

Traditionally equity volumes in the U.S. and abroad surrounding Memorial Day have been abysmal… We shed some light on what to expect for the upcoming holiday using historical data.

Read all about these things, ETF volumes, U.S. equity market structure changes, major factor performance, upcoming index reviews and more in our Market Fact Book…

April Market Fact Book Weeden & Co.

Weeden Special Situations Group

April 2015

Disclosure: This publication is prepared by Weeden & Co.'s trading department, and not its research department. This publication is for

information purposes only and is based on information and data from sources considered to be reliable, but it is not guaranteed as to accuracy and

does not purport to be complete and are subject to change without notice. This publication is neither intended nor should be considered as an offer or the solicitation of an offer to sell or buy any security or other financial product. Nothing contained herein is intended to be, nor shall it be

construed as, investment advice. Information contained herein provides insufficient information upon which to base an investment decision. Any

comments or statements made herein do not necessarily reflect those of Weeden & Co. LP or its affiliates. 2015 Weeden & Co. LP. Sources: See Contact Page

2

Tick Size & Trade-At Pilot Program Refresher

After extending its preliminary ruling date in March the SEC is due to make a decision on its

controversial tick size pilot program this Wednesday, May 6th

. As of February, the SEC had received

over 70 letters commenting on the proposed new program. Below we provide a summary of the

previously announced rules outlined by the SEC, which could be implemented as soon as this summer.

Eligible Pilot Securities & Test Group Selection

Eligibility Criteria:

1) Market cap below $5Bln,

2) Consolidated Average Daily Volume of one million shares or less

3) Price of at least $2

Stratified Random Sampling Selection o Eligible securities will be broken into 27 groups based on liquidity, market cap, and price

(VWAP). Four hundred securities will then be randomly selected from each of these sub-

groups, and the remaining securities will constitute the control group.

Test Groups

In order to test the effectiveness of wider tick sizes and the “trade-at” rule the program will consist of

three test groups and one control group. Each group will be subject the following rules:

Test Group I: o Stocks will be quoted in $0.05 minimum increments

o May trade at any price increment that is currently permitted

o Orders entered into an exchange’s retail liquidity program may be accepted in increments

of less than $0.05

Test Group II: o Must be quoted and must trade in $0.05 minimum increments both on AND off

exchanges with a few exceptions: Midpoint, retail orders with price improvement of

$0.005 or better, and negotiated trades (tied to any pre-arranged benchmark)

Test Group III: o Same rules as Test Group II, plus the additional trade-at rule

Control Group

o Securities will continue to be quoted and traded in increments currently allowed

Trade-At Rule Exemptions

Orders of “block size”

Retail orders executed with at least $0.005 price improvement

The order is identified as an ISO

The order is executed by a venue that concurrently sent ISO orders to the venue with the best

displayed Bid or Offer against the full displayed size

The order is executed as part of a negotiated trade

Stopped orders for customers that are priced at the BBO when the stop is elected

3

-2.6%-1.2%

-5.4%

-25.2%

-7.1%-5.8% -5.3%

3.5%

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

%2

0D

AD

V

Total U.S. Volumes Drop Off Around After Memorial Day(2009-2014, excl. 2011)

-64% -61%

-54%

-26%-20%

-16%

-75%

-60%

-45%

-30%

-15%

0%

15%

T-1 Memorial Day T+1 T+2

%2

0D

AD

V

International Volumes Impacted on Memorial Day (2009-2014, excl. 2011)

Europe Mexico Canada Hong Kong Australia Japan

U.S. & Intl. Volumes Surrounding Memorial Day While most Americans are eager for the upcoming Memorial Day weekend, those relying on liquidity in

equity markets worldwide will have little to cheer about. In this study we review historical U.S. equity

volumes surrounding Memorial Day and also take a quick look at how international volumes have

traditionally been affected by the holiday.

Total U.S. Average Daily Volume

International Average Daily Volume

For those of you trading internationally on Memorial Day be prepared for a very slow day. This is

especially true in Europe (measured by Bloomberg’s BE500 Composite Index), Mexico, and Canada

where volumes have been down over the past five years 64%, 61%, and 54% respectively. Even Asian

markets, including Australia, whose volumes are generally less affected by U.S. market closures have

been adversely impacted by the holiday in the past.

It probably doesn’t come as much

of a surprise, but U.S. volumes

surrounding Memorial Day have

been significantly below average

over the past several years. As we

approach this year’s holiday, expect

total U.S. daily volumes to fall

precipitously beginning the Friday

before Memorial Day and to not

recover fully until the following

Friday. On average, over the past

five years U.S. volumes on the

Friday before Memorial Day have

been 25% below their average

levels.

4

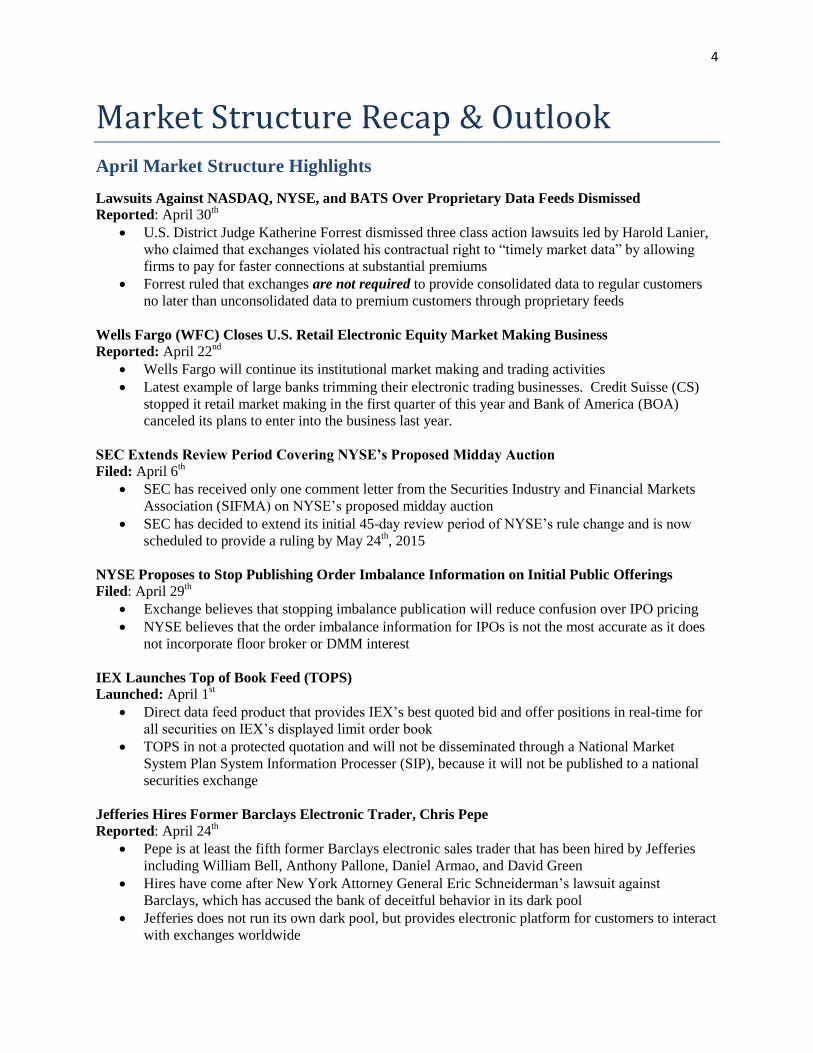

Market Structure Recap & Outlook

April Market Structure Highlights

Lawsuits Against NASDAQ, NYSE, and BATS Over Proprietary Data Feeds Dismissed

Reported: April 30th

U.S. District Judge Katherine Forrest dismissed three class action lawsuits led by Harold Lanier,

who claimed that exchanges violated his contractual right to “timely market data” by allowing

firms to pay for faster connections at substantial premiums

Forrest ruled that exchanges are not required to provide consolidated data to regular customers

no later than unconsolidated data to premium customers through proprietary feeds

Wells Fargo (WFC) Closes U.S. Retail Electronic Equity Market Making Business

Reported: April 22nd

Wells Fargo will continue its institutional market making and trading activities

Latest example of large banks trimming their electronic trading businesses. Credit Suisse (CS)

stopped it retail market making in the first quarter of this year and Bank of America (BOA)

canceled its plans to enter into the business last year.

SEC Extends Review Period Covering NYSE’s Proposed Midday Auction

Filed: April 6th

SEC has received only one comment letter from the Securities Industry and Financial Markets

Association (SIFMA) on NYSE’s proposed midday auction

SEC has decided to extend its initial 45-day review period of NYSE’s rule change and is now

scheduled to provide a ruling by May 24th, 2015

NYSE Proposes to Stop Publishing Order Imbalance Information on Initial Public Offerings

Filed: April 29th

Exchange believes that stopping imbalance publication will reduce confusion over IPO pricing

NYSE believes that the order imbalance information for IPOs is not the most accurate as it does

not incorporate floor broker or DMM interest

IEX Launches Top of Book Feed (TOPS)

Launched: April 1st

Direct data feed product that provides IEX’s best quoted bid and offer positions in real-time for

all securities on IEX’s displayed limit order book

TOPS in not a protected quotation and will not be disseminated through a National Market

System Plan System Information Processer (SIP), because it will not be published to a national

securities exchange

Jefferies Hires Former Barclays Electronic Trader, Chris Pepe

Reported: April 24th

Pepe is at least the fifth former Barclays electronic sales trader that has been hired by Jefferies

including William Bell, Anthony Pallone, Daniel Armao, and David Green

Hires have come after New York Attorney General Eric Schneiderman’s lawsuit against

Barclays, which has accused the bank of deceitful behavior in its dark pool

Jefferies does not run its own dark pool, but provides electronic platform for customers to interact

with exchanges worldwide

5

Further Delay in FINRA’s Implementation of CARDS Wide Reaching Data Collection System Announced: April 30

th

FINRA Congressional Testimony

Details:

Motivation behind original CARDS proposal was to enhance FINRA’s monitoring capabilities to

identify fraud and abusive sales practices earlier

Financial industry raised serious concerns about availability of data, which if reverse engineered

could identify individual trades

FINRA has decided not to pursue CARDS in its present form and not to pursue revised versions

of a similar program until they have addressed industry concerns

T. Rowe Price (TROW) Experiments with HFT

Reported: May 1st

One of HFT’s biggest critics, T. Rowe, has reportedly launched a high frequency trading trial

through a partnership with Virtu Financial (VIRT)

The test began earlier this year and involves less than 1% of TROW’s orders

6

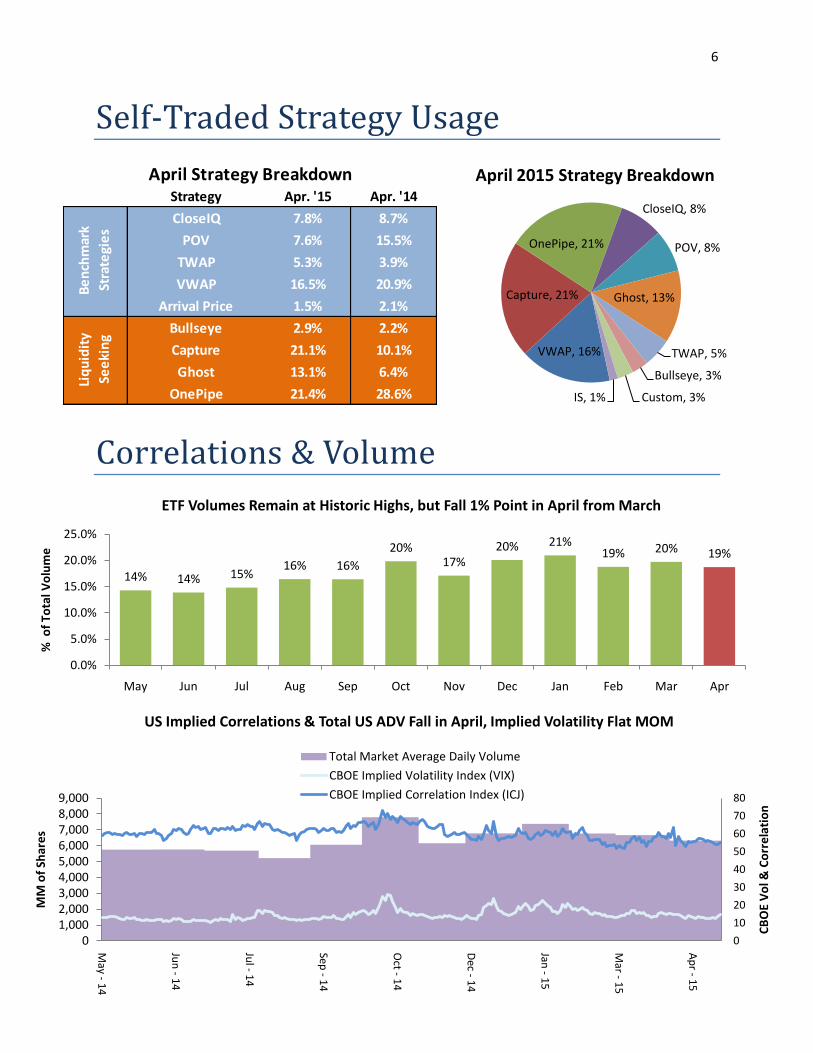

14% 14% 15%16% 16%

20%17%

20% 21%19% 20% 19%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr

% o

f To

tal V

olu

me

ETF Volumes Remain at Historic Highs, but Fall 1% Point in April from March

01,0002,0003,0004,0005,0006,0007,0008,0009,000

May -

14

Jun

-1

4

Jul -

14

Sep -

14

Oct -

14

Dec -

14

Jan -

15

Mar -

15

Ap

r -1

5

0

10

20

30

40

50

60

70

80

MM

of

Shar

es

CB

OE

Vo

l & C

orr

ela

tio

n

US Implied Correlations & Total US ADV Fall in April, Implied Volatility Flat MOM

Total Market Average Daily Volume

CBOE Implied Volatility Index (VIX)

CBOE Implied Correlation Index (ICJ)

VWAP, 16%

Capture, 21%

OnePipe, 21%

CloseIQ, 8%

POV, 8%

Ghost, 13%

TWAP, 5%

Bullseye, 3%

Custom, 3%IS, 1%

April 2015 Strategy BreakdownStrategy Apr. '15 Apr. '14

CloseIQ 7.8% 8.7%

POV 7.6% 15.5%

TWAP 5.3% 3.9%

VWAP 16.5% 20.9%

Arrival Price 1.5% 2.1%

Bullseye 2.9% 2.2%

Capture 21.1% 10.1%

Ghost 13.1% 6.4%

OnePipe 21.4% 28.6%

Be

nch

mar

k

Stra

tegi

es

Liq

uid

ity

See

kin

g

April Strategy Breakdown

Self-Traded Strategy Usage

Correlations & Volume

7

12% 12%

8%7%

7%6% 5% 5%

4% 4% 4% 4% 3% 3% 3%2% 2% 1% 1% 1% 1% 1%

0%

2%

4%

6%

8%

10%

12%

14%

ATS Market Share (Apr. 6 - May 1)IEX Reclaims 50bps of Market Share in April

NYSE12.15%

NASDAQ15.24%

AMEX0.25%

PSX0.99%

Direct Edge9.10%

BATs BYX4.21%

ARCA10.91%

Boston1.76%

BATs BZX7.35%

B/D Internalized & Other ATS

38.06%

Venue April Break Down

2015 Venue Market Share Statistics1

1.8% 1.8%

1.2%1.1% 1.0%

.8% .8% .7% .6% .6% .6% .6% .5% .4% .4%.3% .3% .2% .2% .2% .1% .1%

0.0%

0.5%

1.0%

1.5%

2.0% ATS Market of Total Tier 1 NMS Volumes (Apr. 6 - May 1)

272 275 262

0

50

100

150

200

250

300

350

$B

ln (

USD

)

Average Daily Notional Turnover Falls in April MOM

8

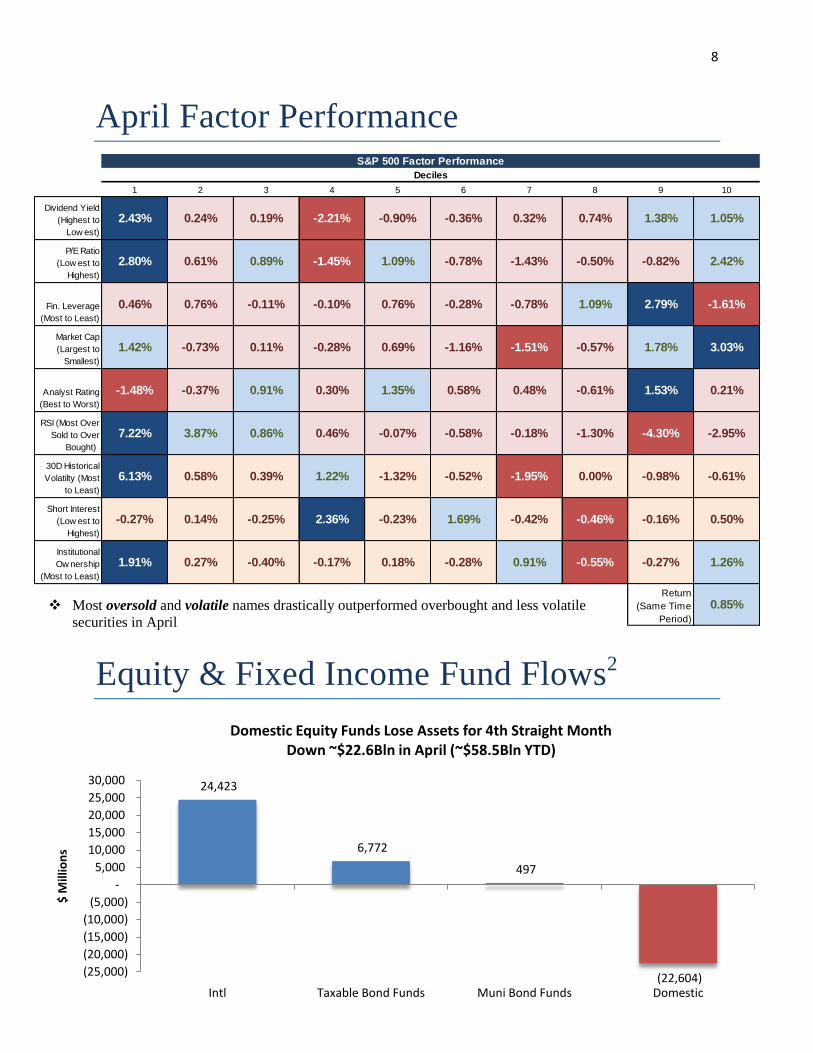

24,423

6,772

497

(22,604)(25,000)

(20,000)

(15,000)

(10,000)

(5,000)

-

5,000

10,000

15,000

20,000

25,000

30,000

Intl Taxable Bond Funds Muni Bond Funds Domestic

$ M

illio

ns

Domestic Equity Funds Lose Assets for 4th Straight Month Down ~$22.6Bln in April (~$58.5Bln YTD)

1 2 3 4 5 6 7 8 9 10

Dividend Yield

(Highest to

Low est)

2.43% 0.24% 0.19% -2.21% -0.90% -0.36% 0.32% 0.74% 1.38% 1.05%

P/E Ratio

(Low est to

Highest)

2.80% 0.61% 0.89% -1.45% 1.09% -0.78% -1.43% -0.50% -0.82% 2.42%

Fin. Leverage

(Most to Least)

0.46% 0.76% -0.11% -0.10% 0.76% -0.28% -0.78% 1.09% 2.79% -1.61%

Market Cap

(Largest to

Smallest)

1.42% -0.73% 0.11% -0.28% 0.69% -1.16% -1.51% -0.57% 1.78% 3.03%

Analyst Rating

(Best to Worst)

-1.48% -0.37% 0.91% 0.30% 1.35% 0.58% 0.48% -0.61% 1.53% 0.21%

RSI (Most Over

Sold to Over

Bought))

7.22% 3.87% 0.86% 0.46% -0.07% -0.58% -0.18% -1.30% -4.30% -2.95%

30D Historical

Volatilty (Most

to Least)

6.13% 0.58% 0.39% 1.22% -1.32% -0.52% -1.95% 0.00% -0.98% -0.61%

Short Interest

(Low est to

Highest)

-0.27% 0.14% -0.25% 2.36% -0.23% 1.69% -0.42% -0.46% -0.16% 0.50%

Institutional

Ow nership

(Most to Least)

1.91% 0.27% -0.40% -0.17% 0.18% -0.28% 0.91% -0.55% -0.27% 1.26%

S&P 500

Return

(Same Time

Period)

0.85%

Deciles

S&P 500 Factor Performance

April Factor Performance

Equity & Fixed Income Fund Flows2

Most oversold and volatile names drastically outperformed overbought and less volatile

securities in April

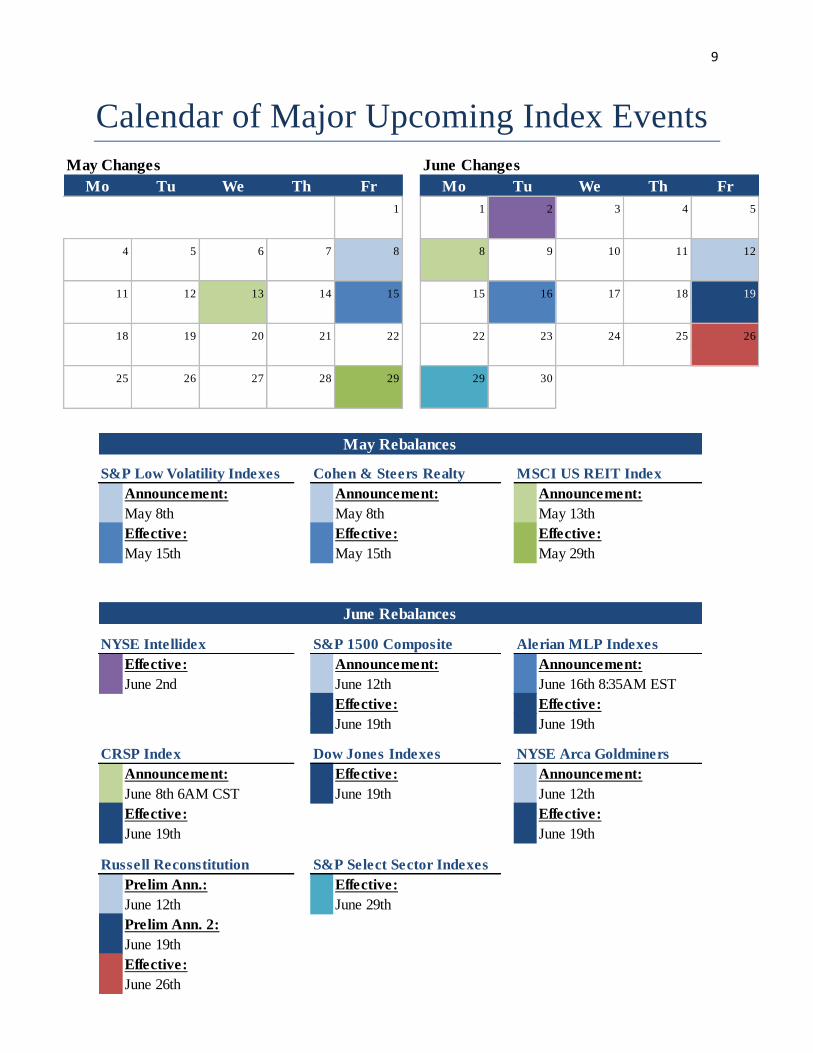

9

Announcement: Announcement: Announcement:

May 8th May 8th May 13th

Effective: Effective: Effective:

May 15th May 15th May 29th

Effective: Announcement: Announcement:

June 2nd June 12th June 16th 8:35AM EST

Effective: Effective:

June 19th June 19th

NYSE Arca Goldminers

Announcement: Effective: Announcement:

June 8th 6AM CST June 19th June 12th

Effective: Effective:

June 19th June 19th

Prelim Ann.: Effective:

June 12th June 29th

Prelim Ann. 2:

June 19th

Effective:

June 26th

June Rebalances

NYSE Intellidex Alerian MLP Indexes

Dow Jones Indexes

S&P 1500 Composite

CRSP Index

Russell Reconstitution

May Rebalances

S&P Low Volatility Indexes Cohen & Steers Realty MSCI US REIT Index

S&P Select Sector Indexes

May Changes June Changes

Mo Tu We Th Fr Mo Tu We Th Fr

1 1 2 3 4 5

4 5 6 7 8 8 9 10 11 12

11 12 13 14 15 15 16 17 18 19

18 19 20 21 22 22 23 24 25 26

25 26 27 28 29 29 30

Calendar of Major Upcoming Index Events

10

How to Read the Factor Analysis

Our factor analysis breaks down the S&P 500 into 100 groups based on the factors listed on the far left of the chart.

Each row takes a factor (e.g. Market Capitalization) and sorts the S&P 500 into 10 groups of 50 based on that factor

(called deciles). For example, the first row listed (Market Cap) is sorted from largest to smallest (as indicated) with

decile one consisting of the 50 largest stocks in the index and decile 10 consisting of the 50 smallest. It’s important

to note that a stock in decile one for Market Cap will likely not be in decile one for any other factor. For example,

GOOG is in decile one for Market Cap, but decile 10 for Dividend Yield, as it does not pay a dividend. Blue shading

means that decile outperformed the S&P, while red shading means the opposite. The growth vs. value decile ranks

the S&P 500 names based on their weights in the growth and value 500 indices as described in the figure.

Contacts

Judd Schwab Quantitative Desk Analyst Weeden Program Trading Group 203.861.9320 [email protected]

1 Venue market share reported by BATs, Direct Edge, BIDs, and Level Daily Trading summary

2All fund flows reported by Thomas Reuters Lipper Funds, formerly AMG

All Market Data is from Bloomberg or NYSE TAQ Disclosure: This publication is prepared by Weeden & Co.'s trading department, and not its research department. This

publication is for information purposes only and is based on information and data from sources considered to be reliable, but it

is not guaranteed as to accuracy and does not purport to be complete and are subject to change without notice. This

publication is neither intended nor should be considered as an offer or the solicitation of an offer to sell or buy any security or

other financial product. Nothing contained herein is intended to be, nor shall it be construed as, investment advice. Information

contained herein provides insufficient information upon which to base an investment decision. Any comments or statements

made herein do not necessarily reflect those of Weeden & Co. LP or its affiliates. 2015 Weeden & Co. LP.