Embed Size (px)

Citation preview

*The data for this report is released on a rolling schedule. The presented numbers are current as of publication and are subject to revision.

SYNOPSIS

Retail Sales

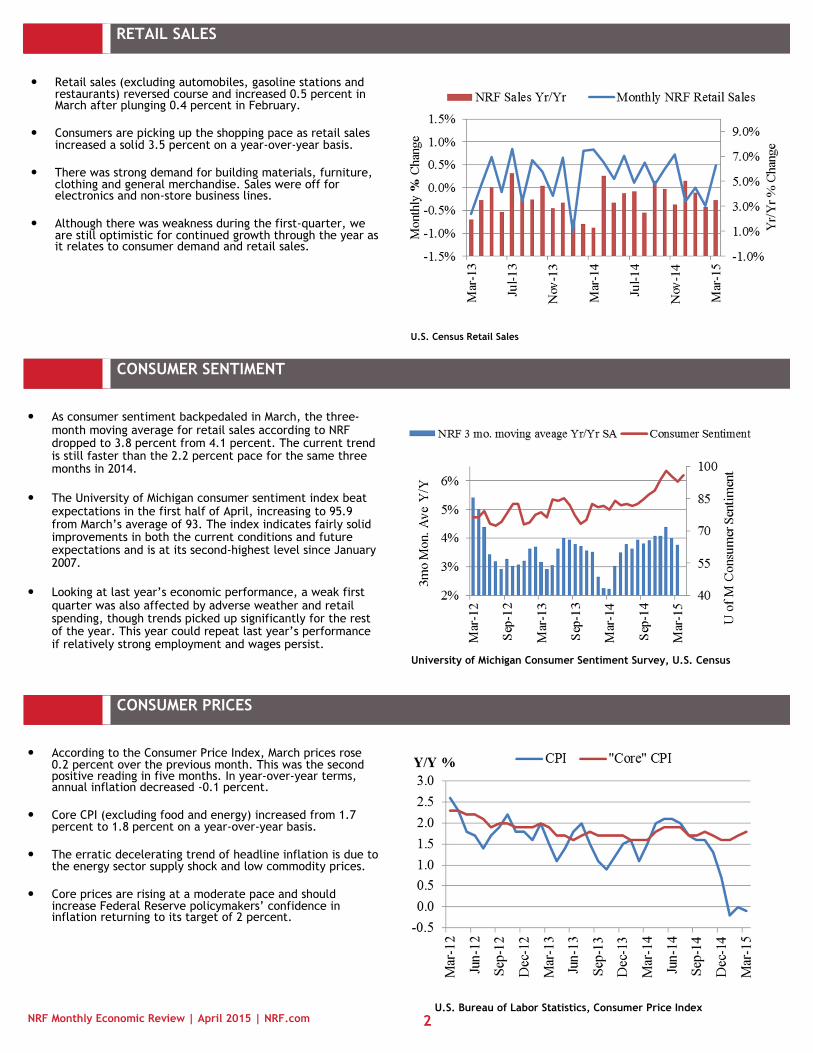

• Retail sales (excluding automobiles, gasoline stations and restaurants) reversed course and increased 0.5 percent in March after dropping 0.4 percent in February.

Consumer Sentiment

• The University of Michigan consumer sentiment index beat expectations in the first half of April, increasing to 95.9 from March’s average of 93.

Consumer Prices

• The March headline Consumer Price Index rose 0.2 percent between March and February. This was the second positive reading in five months.

Gross Domestic Product

• The third estimate of fourth quarter GDP reflected no change to the 2.2 percent rate from the second estimate.

Housing

• Single family starts rebounded by 4.4 percent to 618,000 units in March and homebuilding is off to a good start. Weather appeared to be play a negative role earlier this year not only on starts but on completions.

Employment

• Job growth slowed in March as private payrolls rose an anemic 129,000. Overall employment (public and private sectors combined) increased 126,000 in March.

Retail Jobs and Openings

• Total retail employment across all industry segments increased 25,900 to 15.6 million in March. There were 463,000 job openings in the retail industry on the last business day of February.

Personal Income and Spending

• Personal income rose by 0.4 percent in February while personal consumption inched

up only 0.1 percent.

Chicago Fed National Activity Index

• The economy was growing even slower last month according to the Chicago Fed National Activity Index which recorded activity dropped to –0.42 in March from –0.18 in February.

Jack Kleinhenz, Ph.D. Chief Economist

National Retail Federation

April 2015

RETAIL SALES

• Retail sales (excluding automobiles, gasoline stations and restaurants) reversed course and increased 0.5 percent in March after plunging 0.4 percent in February.

• Consumers are picking up the shopping pace as retail sales increased a solid 3.5 percent on a year-over-year basis.

• There was strong demand for building materials, furniture, clothing and general merchandise. Sales were off for electronics and non-store business lines.

• Although there was weakness during the first-quarter, we are still optimistic for continued growth through the year as it relates to consumer demand and retail sales.

NRF Monthly Economic Review | April 2015 | NRF.com 2

CONSUMER SENTIMENT

• As consumer sentiment backpedaled in March, the three-month moving average for retail sales according to NRF dropped to 3.8 percent from 4.1 percent. The current trend is still faster than the 2.2 percent pace for the same three months in 2014.

• The University of Michigan consumer sentiment index beat expectations in the first half of April, increasing to 95.9 from March’s average of 93. The index indicates fairly solid improvements in both the current conditions and future expectations and is at its second-highest level since January 2007.

• Looking at last year’s economic performance, a weak first quarter was also affected by adverse weather and retail spending, though trends picked up significantly for the rest of the year. This year could repeat last year’s performance if relatively strong employment and wages persist.

CONSUMER PRICES

• According to the Consumer Price Index, March prices rose 0.2 percent over the previous month. This was the second positive reading in five months. In year-over-year terms, annual inflation decreased -0.1 percent.

• Core CPI (excluding food and energy) increased from 1.7 percent to 1.8 percent on a year-over-year basis.

• The erratic decelerating trend of headline inflation is due to the energy sector supply shock and low commodity prices.

• Core prices are rising at a moderate pace and should increase Federal Reserve policymakers’ confidence in inflation returning to its target of 2 percent.

U.S. Census Retail Sales

University of Michigan Consumer Sentiment Survey, U.S. Census

U.S. Bureau of Labor Statistics, Consumer Price Index

GROSS DOMESTIC PRODUCT

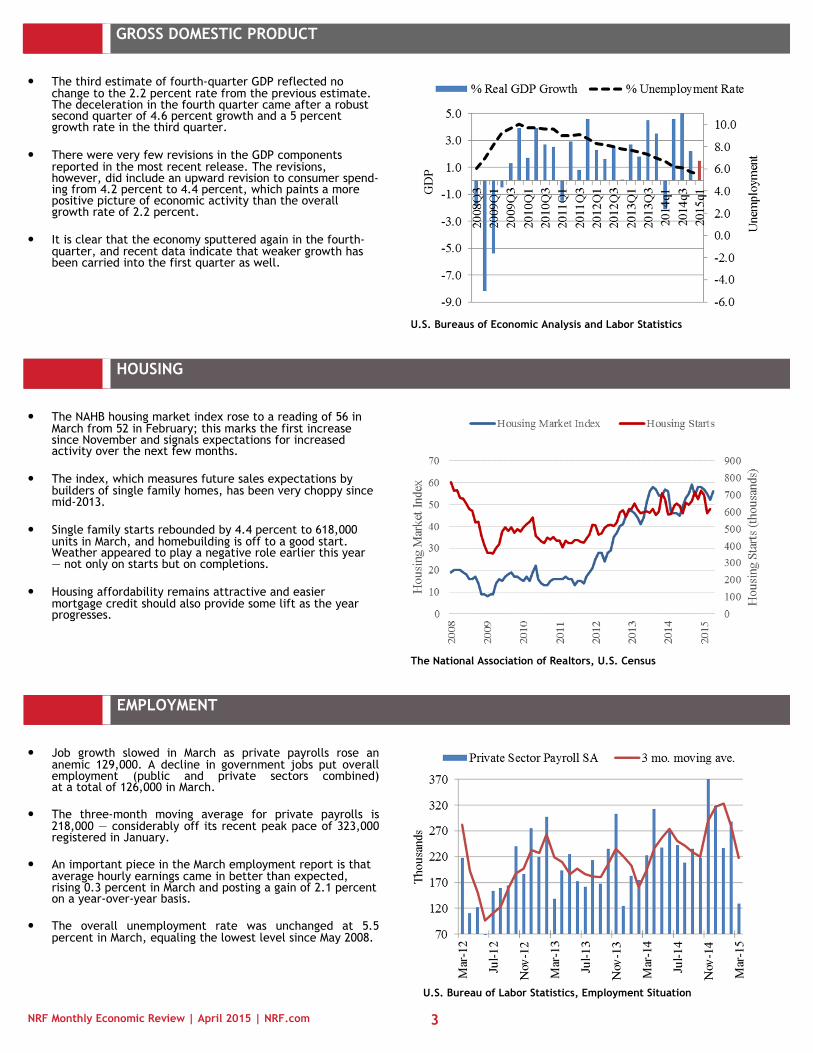

• The third estimate of fourth-quarter GDP reflected no change to the 2.2 percent rate from the previous estimate. The deceleration in the fourth quarter came after a robust second quarter of 4.6 percent growth and a 5 percent growth rate in the third quarter.

• There were very few revisions in the GDP components reported in the most recent release. The revisions, however, did include an upward revision to consumer spend-ing from 4.2 percent to 4.4 percent, which paints a more positive picture of economic activity than the overall growth rate of 2.2 percent.

• It is clear that the economy sputtered again in the fourth-quarter, and recent data indicate that weaker growth has been carried into the first quarter as well.

NRF Monthly Economic Review | April 2015 | NRF.com 3

HOUSING

• The NAHB housing market index rose to a reading of 56 in March from 52 in February; this marks the first increase since November and signals expectations for increased activity over the next few months.

• The index, which measures future sales expectations by builders of single family homes, has been very choppy since mid-2013.

• Single family starts rebounded by 4.4 percent to 618,000 units in March, and homebuilding is off to a good start. Weather appeared to play a negative role earlier this year — not only on starts but on completions.

• Housing affordability remains attractive and easier mortgage credit should also provide some lift as the year progresses.

EMPLOYMENT

• Job growth slowed in March as private payrolls rose an anemic 129,000. A decline in government jobs put overall employment (public and private sectors combined) at a total of 126,000 in March.

• The three-month moving average for private payrolls is 218,000 — considerably off its recent peak pace of 323,000 registered in January.

• An important piece in the March employment report is that average hourly earnings came in better than expected, rising 0.3 percent in March and posting a gain of 2.1 percent on a year-over-year basis.

• The overall unemployment rate was unchanged at 5.5 percent in March, equaling the lowest level since May 2008.

U.S. Bureaus of Economic Analysis and Labor Statistics

The National Association of Realtors, U.S. Census

U.S. Bureau of Labor Statistics, Employment Situation

RETAIL JOBS AND OPENINGS

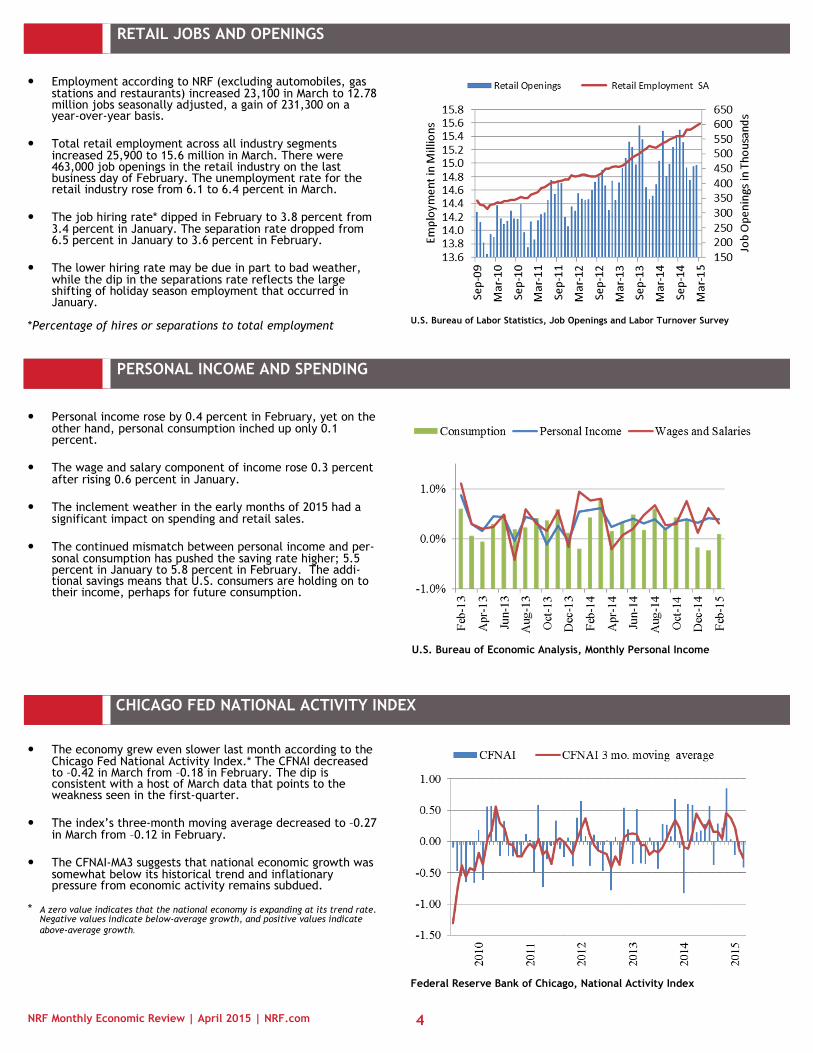

• Employment according to NRF (excluding automobiles, gas stations and restaurants) increased 23,100 in March to 12.78 million jobs seasonally adjusted, a gain of 231,300 on a year-over-year basis.

• Total retail employment across all industry segments increased 25,900 to 15.6 million in March. There were 463,000 job openings in the retail industry on the last business day of February. The unemployment rate for the retail industry rose from 6.1 to 6.4 percent in March.

• The job hiring rate* dipped in February to 3.8 percent from 3.4 percent in January. The separation rate dropped from 6.5 percent in January to 3.6 percent in February.

• The lower hiring rate may be due in part to bad weather, while the dip in the separations rate reflects the large shifting of holiday season employment that occurred in January.

*Percentage of hires or separations to total employment

NRF Monthly Economic Review | April 2015 | NRF.com 4

PERSONAL INCOME AND SPENDING

• Personal income rose by 0.4 percent in February, yet on the other hand, personal consumption inched up only 0.1 percent.

• The wage and salary component of income rose 0.3 percent after rising 0.6 percent in January.

• The inclement weather in the early months of 2015 had a significant impact on spending and retail sales.

• The continued mismatch between personal income and per-sonal consumption has pushed the saving rate higher; 5.5 percent in January to 5.8 percent in February. The addi-tional savings means that U.S. consumers are holding on to their income, perhaps for future consumption.

CHICAGO FED NATIONAL ACTIVITY INDEX

U.S. Bureau of Labor Statistics, Job Openings and Labor Turnover Survey

U.S. Bureau of Economic Analysis, Monthly Personal Income

Federal Reserve Bank of Chicago, National Activity Index

• The economy grew even slower last month according to the Chicago Fed National Activity Index.* The CFNAI decreased to –0.42 in March from –0.18 in February. The dip is consistent with a host of March data that points to the weakness seen in the first-quarter.

• The index’s three-month moving average decreased to –0.27 in March from –0.12 in February.

• The CFNAI-MA3 suggests that national economic growth was somewhat below its historical trend and inflationary pressure from economic activity remains subdued.

* A zero value indicates that the national economy is expanding at its trend rate. Negative values indicate below-average growth, and positive values indicate

above-average growth.