Embed Size (px)

Citation preview

APRIL 2 0 0 6

INDEPENDENCE – OBJECTIVITY - EXCELLENCE

Presented by: Emmanuelle Javoy, Director, Planet Rating [email protected]

Pilots of social performance evaluation: Planet rating’s experience

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

2

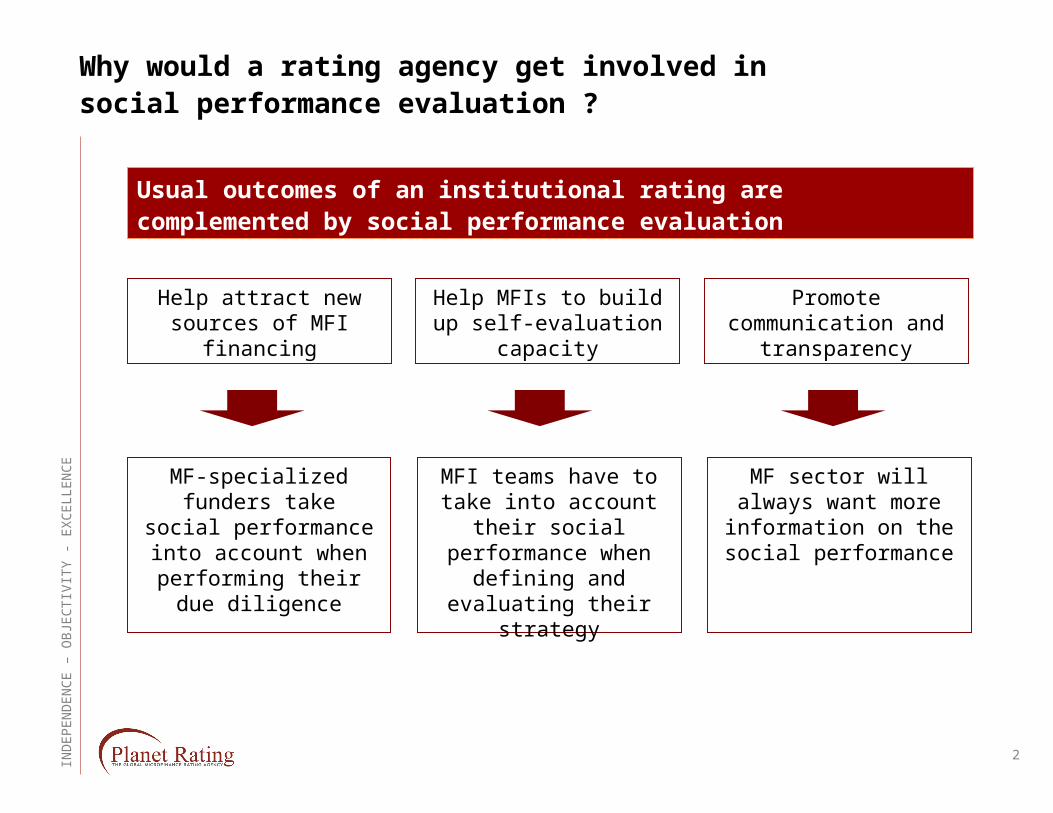

Why would a rating agency get involved in social performance evaluation ?

Help attract new sources of MFI

financing

Help MFIs to build up self-evaluation

capacity

Promote communication and

transparency

MF-specialized funders take social performance into

account when performing their due

diligence

MFI teams have to take into account their

social performance when defining and

evaluating their strategy

MF sector will always want more

information on the social performance

Usual outcomes of an institutional rating are complemented by social performance evaluation

Usual outcomes of an institutional rating are complemented by social performance evaluation

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

3

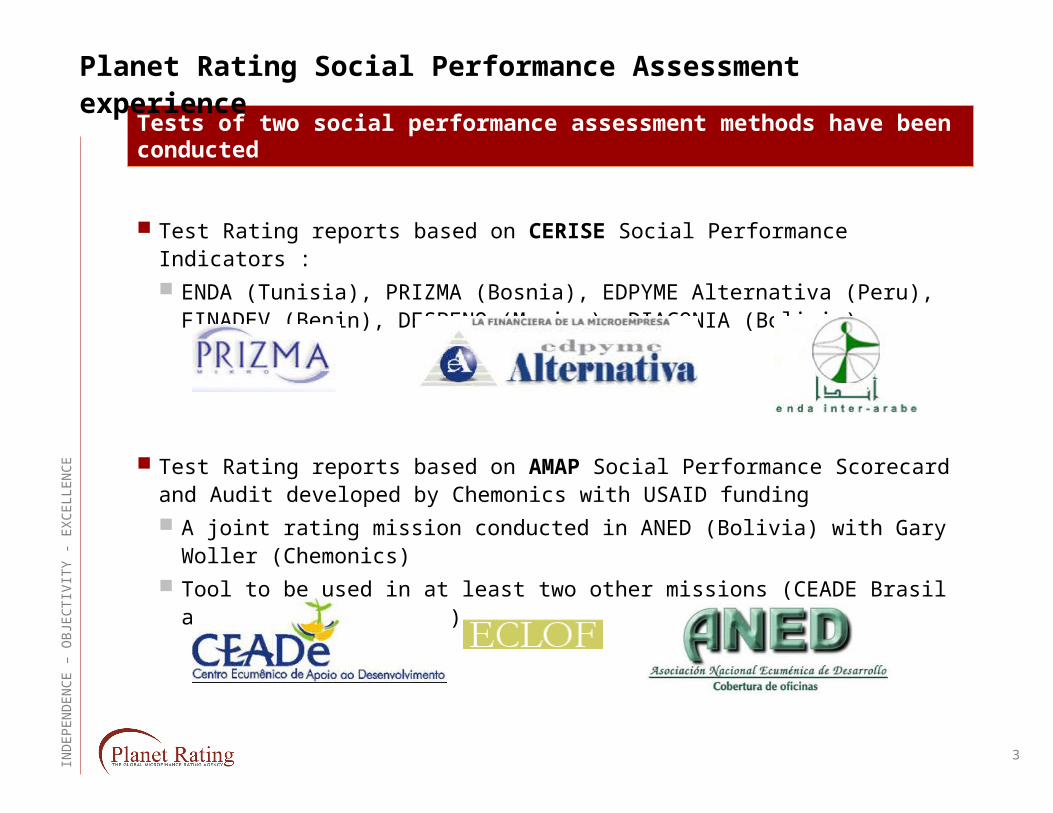

Tests of two social performance assessment methods have been conducted

Tests of two social performance assessment methods have been conducted

Planet Rating Social Performance Assessment experience

Test Rating reports based on CERISE Social Performance Indicators : ENDA (Tunisia), PRIZMA (Bosnia), EDPYME Alternativa (Peru), FINADEV

(Benin), DESPENO (Mexico), DIACONIA (Bolivia)

Test Rating reports based on AMAP Social Performance Scorecard and Audit developed by Chemonics with USAID funding A joint rating mission conducted in ANED (Bolivia) with Gary Woller

(Chemonics) Tool to be used in at least two other missions (CEADE Brasil and ECLOF

Philippines)

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

4

What do “social ratings” rate ?

MFI usually have a social goal which is to create a social impact such as “alleviate poverty” or “participate in the economic development” or contribute to “women empowerment”

Their social mission is to provide microfinance services (efficient and adapted financial services offered to those that are excluded by the traditional financial sector) to a target clientele as a tool to reach that goal

Rating constraints rule out the rating of the social impact dimension (understood as the effects of microfinance on clients’ living conditions) of social performance

But rating can provide an opinion on “the likelihood that the MFI produces significant social impact both now and in the future” (AMAP definition).

Our ratings will not evaluate whether the MFI has reached its social goal, but whether it is likely to do so because it has implemented its social mission in a satisfactory way. Is it offering good microfinance services? It is serving its target clientele ?

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

5

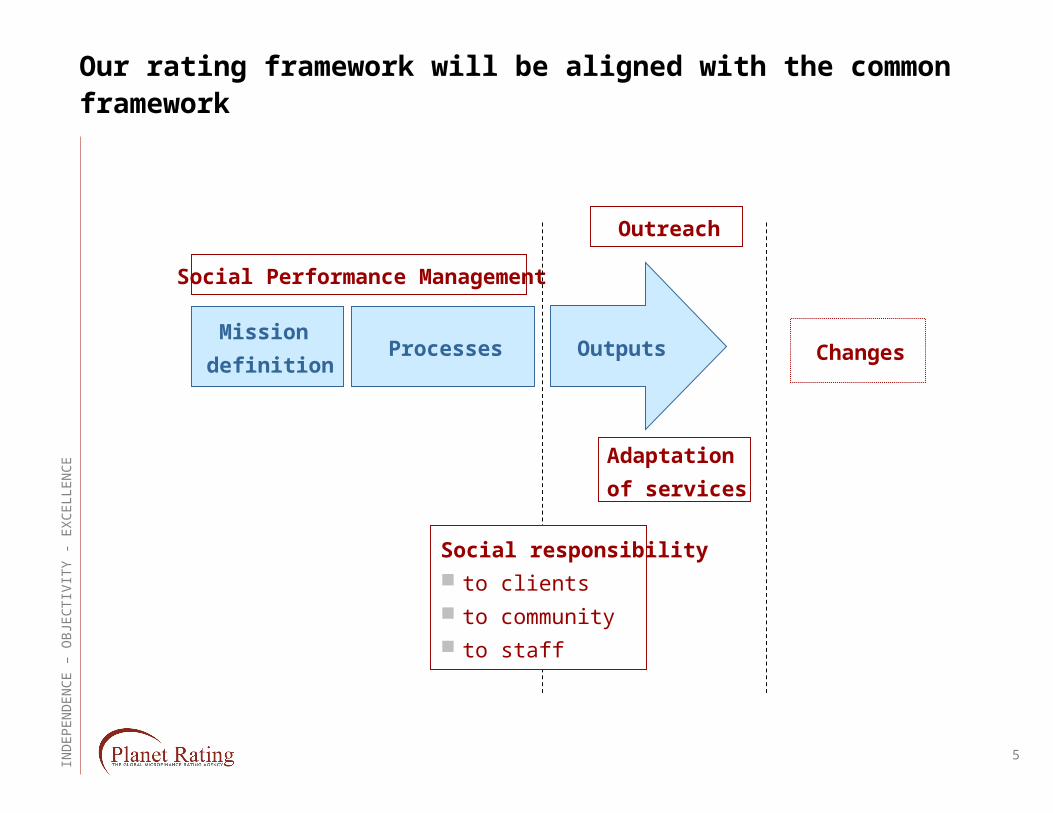

Our rating framework will be aligned with the common framework

Social Performance Management

Mission

definitionProcesses Outputs

Outreach

Adaptation

of services

Changes

Social responsibility to clients to community to staff

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

6

Main differences remaining between social rating frameworks

Outreach : Base our analysis on existing information or create information ? We will stick to information available in the MFI

— Creating information is not the role of raters; who will check the validity of the data we might produce ?

Verify the reliability of the information— One to two additional days of branch visits depending on the volume of “client”

data available

During social rating missions, we will promote / bring the word about tools available to increase MFI knowledge— Any multilingual presentation, leaflet website of existing tools will be very useful

to us

We will try “client surveys”— In order to understand the tools and technical constraints and limitations so that

we can be better assessors of their reliability when we find them in the MFIs

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

7

Main differences remaining between social rating frameworks

Outreach: provide a grade on that dimension ? Does a MFI that targets the poorest have a higher social impact than a

MFI targeting SMEs (both of them being excluded from the classic financial services) ?— Impact studies do not provide strong evidence of that fact— We will remain neutral on that aspect

Provide information on the outreach to usually targeted populations (poor, women, vulnerable, rural, SME ?), but no grade

We will provide a grade on the outreach to the target clientele of the MFI (if it has a specific one) – when the necessary information will be available.

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

8

Institutional and social ratings : What are the relationships ?

Items assessed in institutional rating are important components of social performance (Governance, MIS reliability, Internal controls, Financial performance)

Social performance ratings should be done in combination with an institutional rating or incorporate an institutional assessment

Poor institutional performance (for instance a rating of D or E, meaning that the future of the institution is at high risk) is a strong limitation to social performance

Social ratings is likely to be capped by our institutional ratings for bad performers

Social ratings and institutional ratings to be performed during the same mission Synergies between the two processes are important

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

9

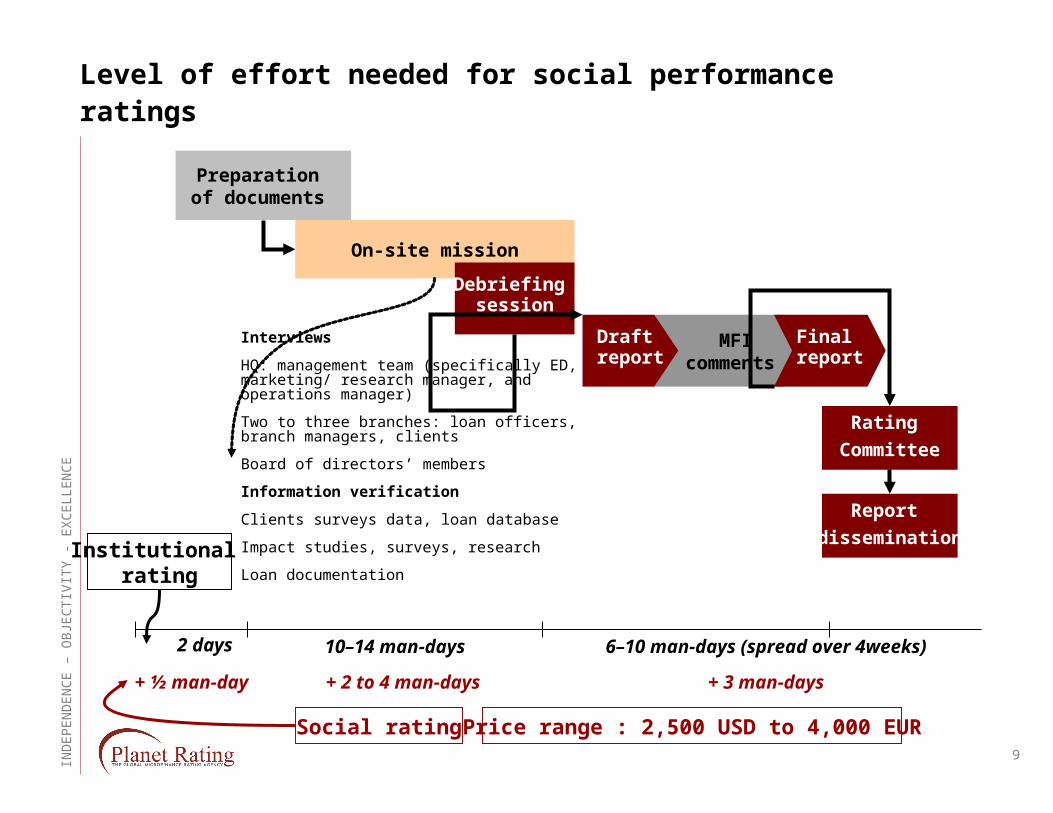

Level of effort needed for social performance ratings

Interviews

HQ: management team (specifically ED, marketing/ research manager, and operations manager)

Two to three branches: loan officers, branch managers, clients

Board of directors’ members

Information verification

Clients surveys data, loan database

Impact studies, surveys, research

Loan documentation

Preparation of documents

On-site mission

Debriefing session

2 days 10–14 man-days 6–10 man-days (spread over 4weeks)

MFI comments

Draft report

Final report

Rating

Committee

Report

dissemination

+ ½ man-day

+ 2 to 4 man-days + 3 man-days

Social rating

Institutional rating

Price range : 2,500 USD to 4,000 EUR

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

10

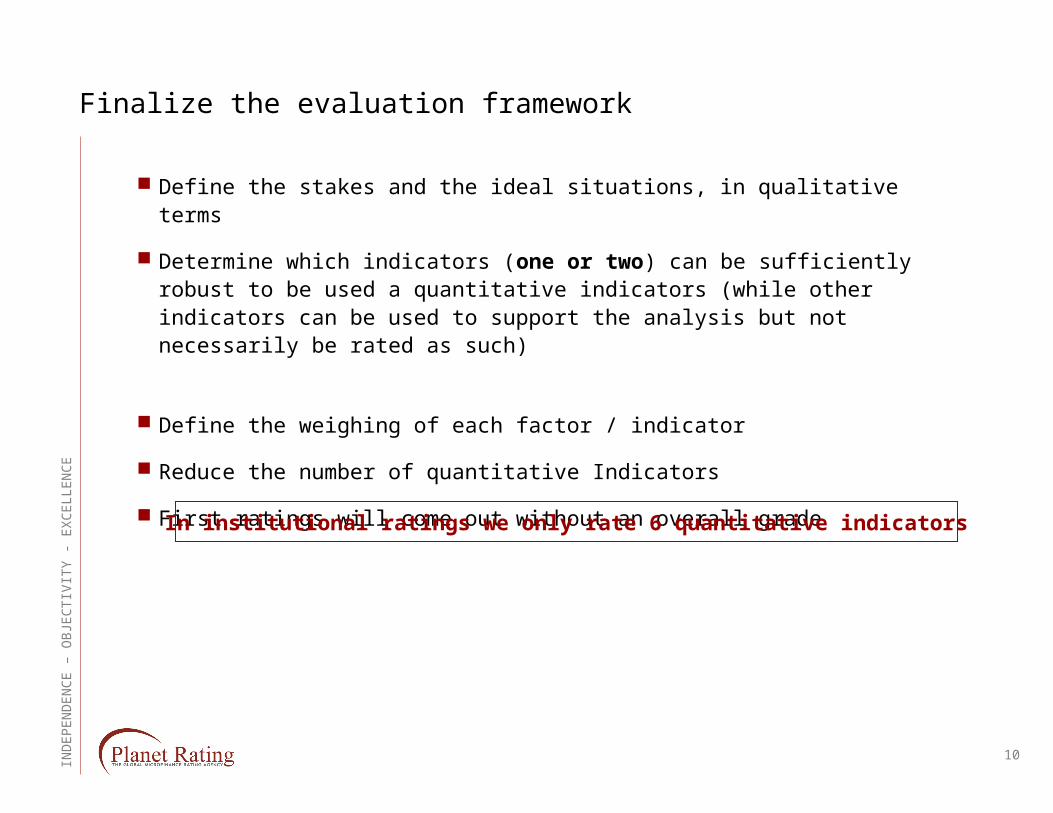

Finalize the evaluation framework

Define the stakes and the ideal situations, in qualitative terms

Determine which indicators (one or two) can be sufficiently robust to be used a quantitative indicators (while other indicators can be used to support the analysis but not necessarily be rated as such)

Define the weighing of each factor / indicator

Reduce the number of quantitative Indicators

First ratings will come out without an overall grade

In institutional ratings we only rate 6 quantitative indicators

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

11

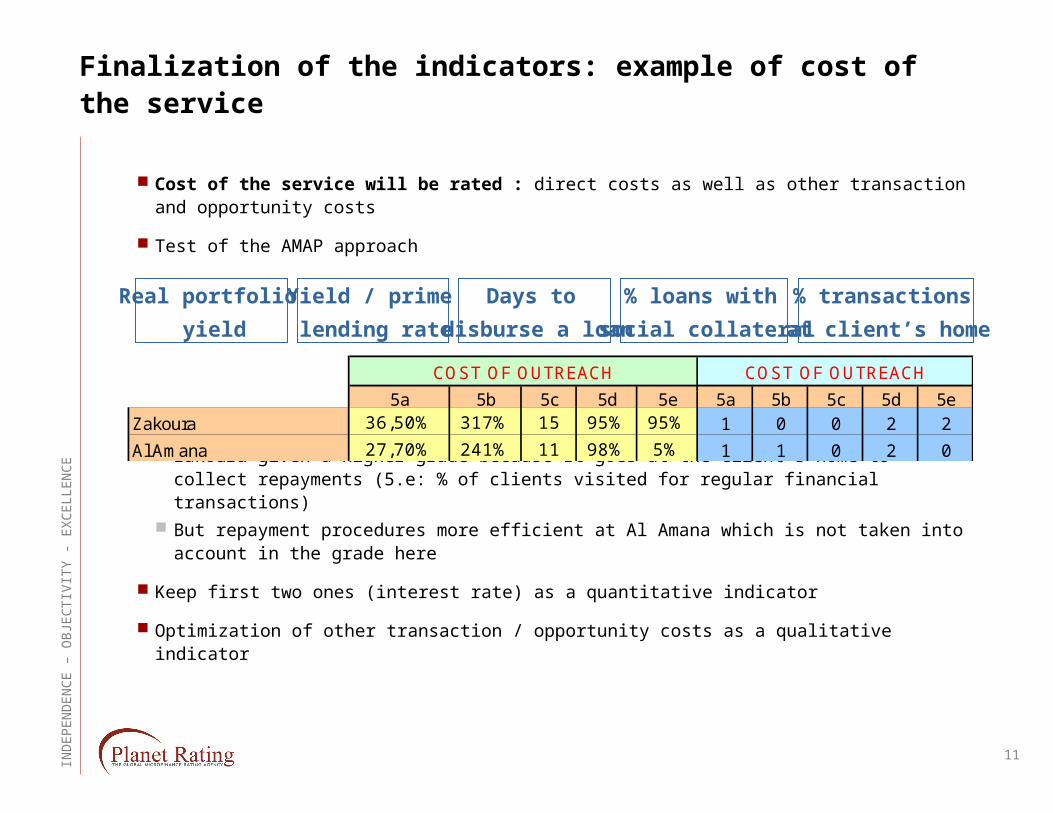

Finalization of the indicators: example of cost of the service

Cost of the service will be rated : direct costs as well as other transaction and opportunity costs

Test of the AMAP approach

Zakoura given a higher grade because It goes at the client’s home to collect repayments (5.e: % of clients visited for regular financial transactions)

But repayment procedures more efficient at Al Amana which is not taken into account in the grade here

Keep first two ones (interest rate) as a quantitative indicator

Optimization of other transaction / opportunity costs as a qualitative indicator

COST OF OUTREACH COST OF OUTREACH WORTH OF OUTREACH

5a 5b 5c 5d 5e 5a 5b 5c 5d 5eZakoura 36,50% 317% 15 95% 95% 1 0 0 2 2

Al Amana 27,70% 241% 11 98% 5% 1 1 0 2 0

Real portfolio

yield

Yield / prime

lending rate

Days to

disburse a loan

% loans with

social collateral

% transactions

at client’s home

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

12

Planned activities

Six social ratings in Mali for medium sized institutions

First update of a social rating (enda-inter arabe, Tunisia)

Inclusion of “client friendliness” section in our Mini-Ratings in Uganda Social responsibility to the client Adaptation of services to client’s needs

IND

EPEN

DEN

CE –

OB

JEC

TIV

ITY -

EX

CELL

EN

CE

13

Created in 1999 and became a private independent rating firm in June 2005

Created in 1999 and became a private independent rating firm in June 2005

Planet Rating SAS: The Global Microfinance Rating Agency

Planet Rating has the most extensive global coverage:

Paris HQ: covering Eastern Europe, Middle East & Asia

Lima Office: covering Latin America

Dakar Office: covering Africa

Most diversified rating team in the industry:

Multicultural: American, Canadian, Colombian, French, Lebanese, Senegalese, Spanish, Vietnamese citizens

Multilingual: Arabic, Italian, English, French, Spanish, Portuguese, Vietnamese, Wolof speakers

Qualified & experienced team:

Planet Rating’s Managing Director is the only head of rating agencies that has operational microfinance experience; he was former General Manager of SPBD – Samoa’s largest MFI

Each senior analyst has conducted at least 12 rating missions on 3 different continents

Analyst backgrounds: investment banking, management consulting, non-profit, microfinance