Embed Size (px)

Citation preview

Natura &Co:A transformational

journey to unlock value

Natura &Co DayApril 20, 2018 São Paulo

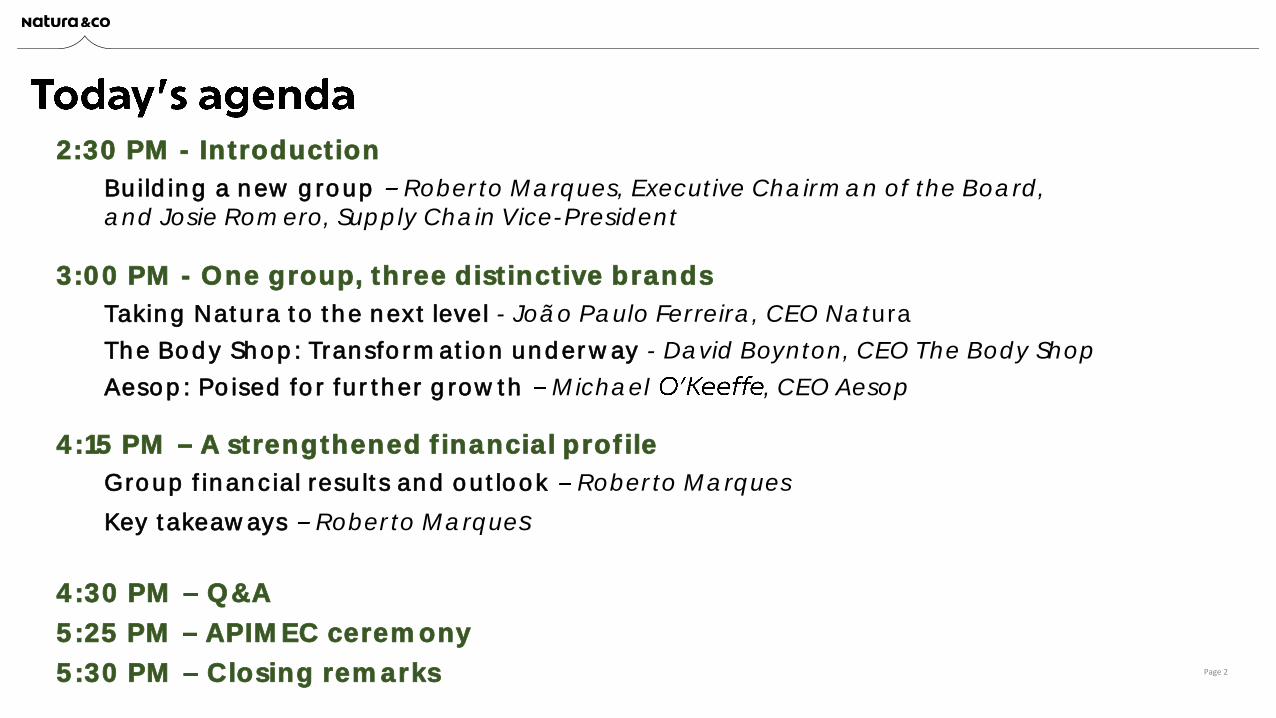

2:30 PM - Introduction

Building a new group Roberto Marques, Executive Chairman of the Board, and Josie Romero, Supply Chain Vice-President

4:15 PM A strengthened financial profile

Group financial results and outlook Roberto Marques

Key takeaways Roberto Marques

4:30 PM Q&A

5:25 PM APIMEC ceremony

5:30 PM Closing remarks

3:00 PM - One group, three distinctive brands

Taking Natura to the next level - João Paulo Ferreira, CEO Natura

The Body Shop: Transformation underway - David Boynton, CEO The Body Shop

Aesop: Poised for further growth Michael , CEO Aesop

Page 2

Building a new group

Roberto MarquesExecutive Chairman of the Board

Aesopacquisition

Leading position in Braziland successful expansion

across Latin America.

First stepsin internationalization

and multichannelexpansion

A global, multibrand, multichannel,

purpose-driven Group

Creation of Natura Passion for cosmetics

and relationships

2013

The Body Shop acquisition

2017

1969

A step-change: From Natura to Natura &Co

Page 4

community

collaboration

co-creation

connection

The power of the co_

economic & social & environment

what & why &how the big & the small

the long & the short

The power of the &

A new corporate identity for a new multibrand group

Page 5

Multibrand model

Leveraging group scale

Three empowered iconic brands

Distinct value proposition per brand

Mantaining strong brand autonomy

Expand internationalfootprint and grow TBS in Latam

Capture synergies

A clear financial strategy focused onprofitable growth, cash generationand deleveraging

Solid corporate governance, focusedon value creation and commitmentto ethical business practices

1

Multichannel growthin multiple geographies

2

3Innovation and sustainability

4

Capitalize on the strengths of each brand• Direct sales• Broad store network (70 countries) • E-commerce• Wholesale

Attract new connected customers

Cruelty free products, sustainably sourced

Fair trade-based, collaborative relationships with supplier communities

Innovation-driven product porftolio

Four key drivers to create value

Page 6

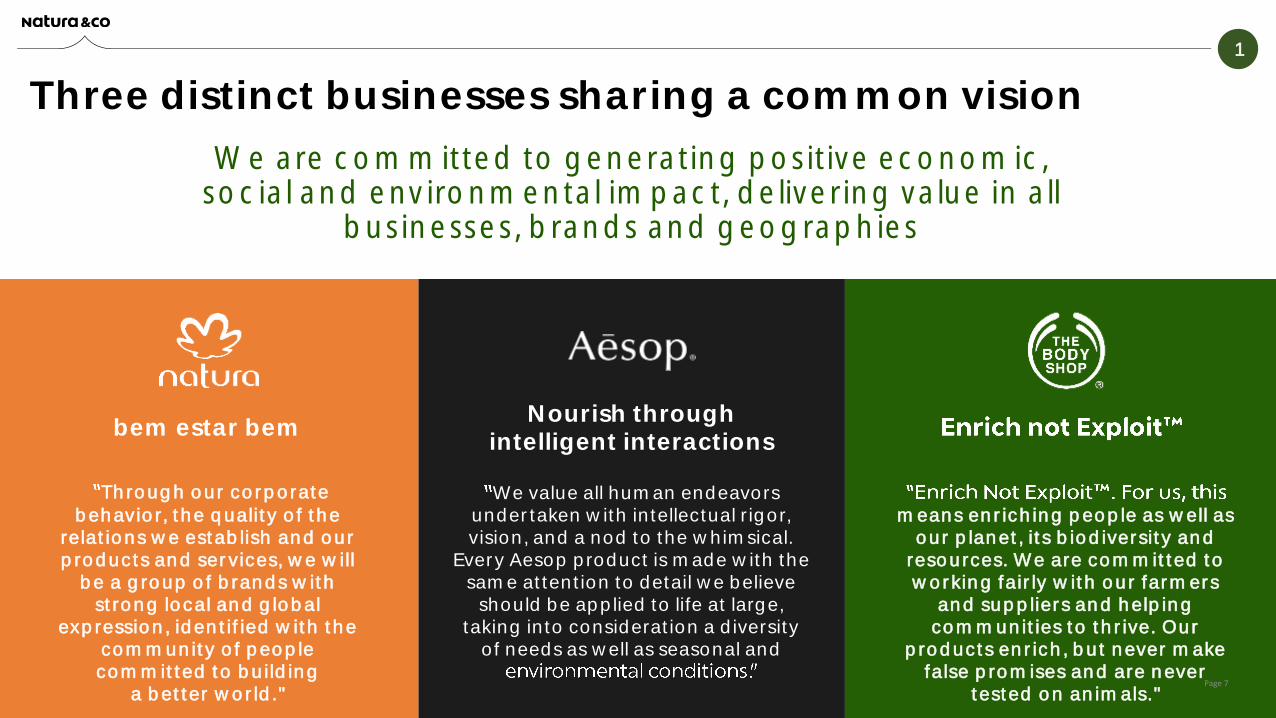

Through our corporatebehavior, the quality of the

relations we establish and our products and services, we will

be a group of brands with strong local and global

expression, identified with the community of people

committed to building a better world."

means enriching people as well as our planet, its biodiversity and

resources. We are committed to working fairly with our farmers

and suppliers and helping communities to thrive. Our

products enrich, but never make false promises and are never

tested on animals."

We value all human endeavors undertaken with intellectual rigor, vision, and a nod to the whimsical.

Every Aesop product is made with the same attention to detail we believe

should be applied to life at large, taking into consideration a diversity

of needs as well as seasonal and

We are committed to generating positive economic, social and environmental impact, delivering value in all

businesses, brands and geographies

1

Three distinct businesses sharing a common vision

bem estar bemNourish through

intelligent interactions

Page 7

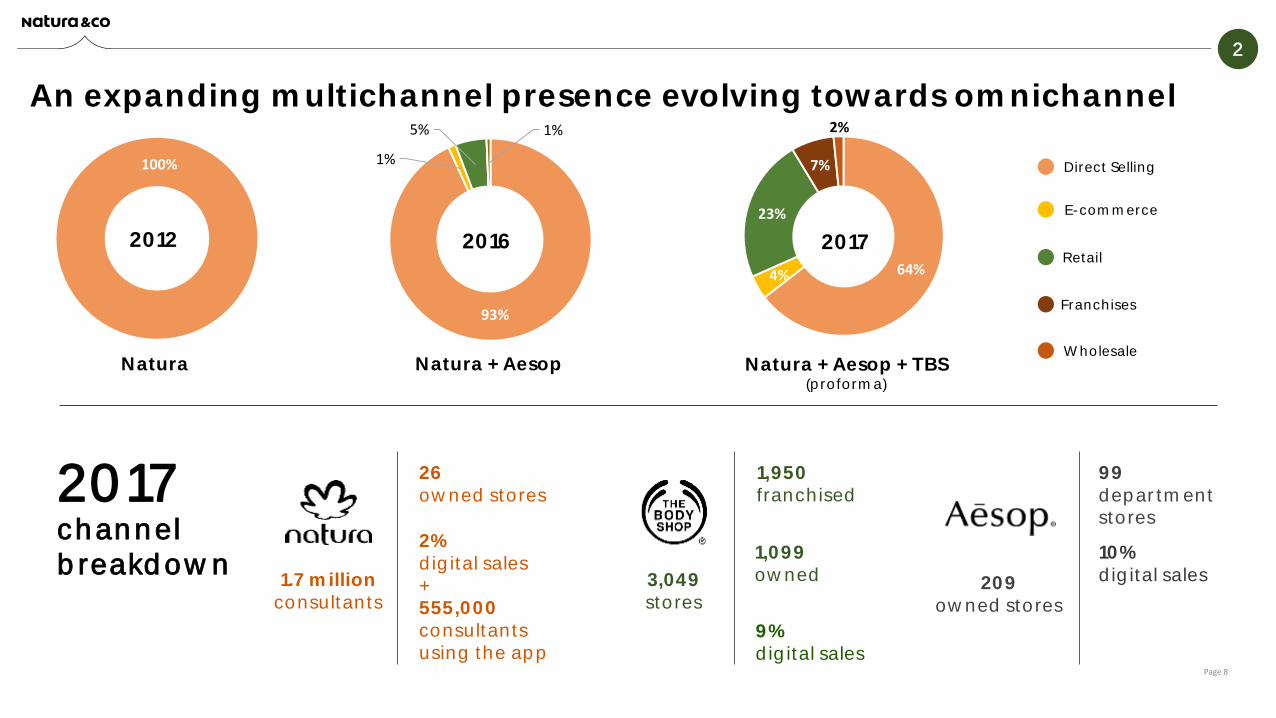

93%

1%

5% 1%

2016

100%

2012

Natura Natura + Aesop Natura + Aesop + TBS (proforma)

64%4%

23%

7%

2%

2017

Direct Selling

E-commerce

Retail

Franchises

Wholesale

1.7 millionconsultants

26owned stores

3,049 stores

1,950 franchised

1,099 owned 209

owned stores

99 departmentstores

channelbreakdown

2%digital sales+555,000consultantsusing the app

9%digital sales

10%digital sales

An expanding multichannel presence evolving towards omnichannel

2

2017

Page 8

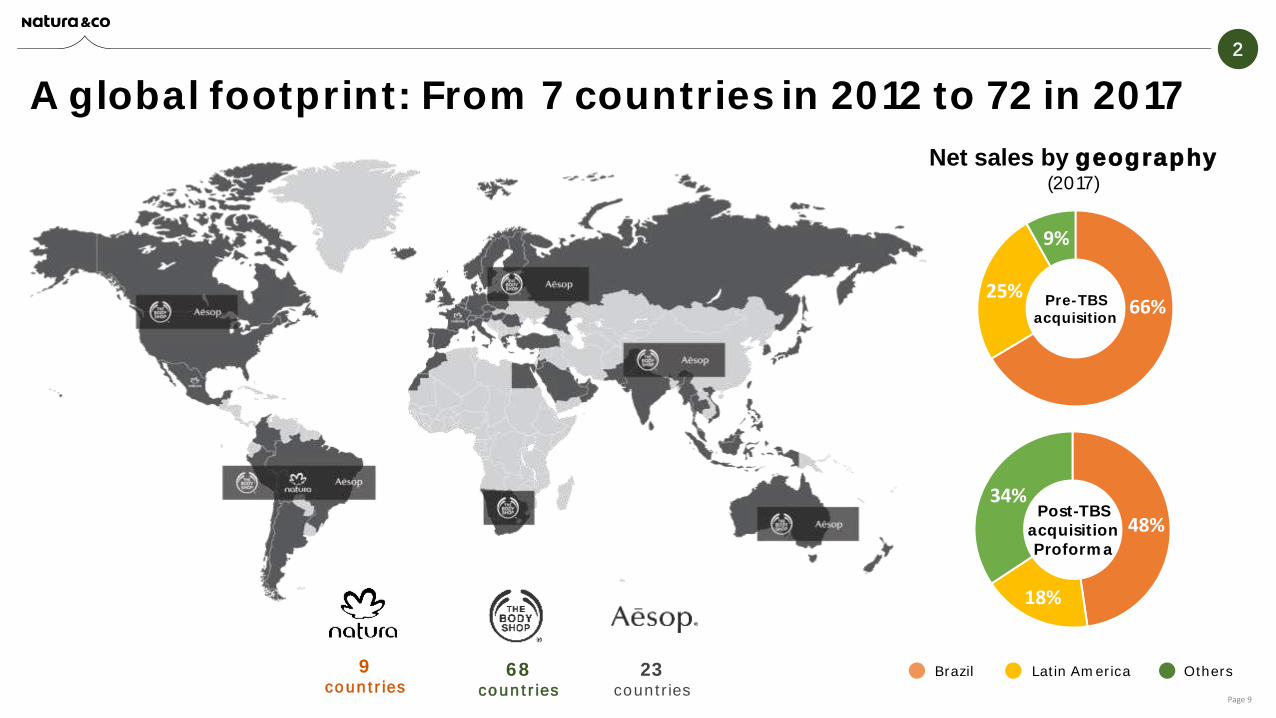

66%25%

9%

Pre-TBS acquisition

Net sales by geography(2017)

48%

18%

34%Post-TBS

acquisitionProforma

Brazil Latin America Others9countries

68countries

23countries

2

A global footprint: From 7 countries in 2012 to 72 in 2017

Page 9

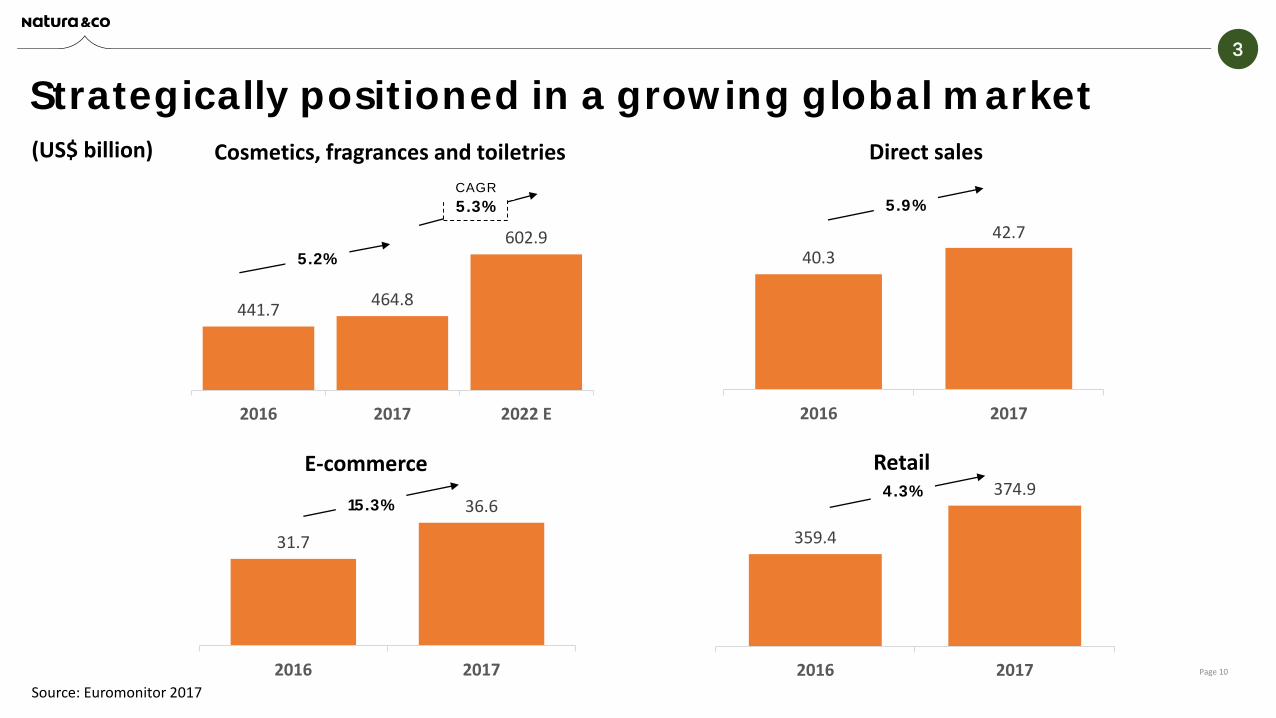

359.4

374.9

2016 2017

31.7

36.6

2016 2017

40.3

42.7

2016 2017

441.7464.8

602.9

2016 2017 2022 E

Direct sales

RetailE-commerce

Cosmetics, fragrances and toiletries

Source: Euromonitor 2017

(US$ billion)

5.3%

5.2%

5.9%

15.3%4.3%

CAGR

3

Strategically positioned in a growing global market

Page 10

• Sourced from a community trade supplier in Ghana, where it helps provide a fair wage to 500 women

• Provides intense moisture and 48 hour hydration

29%

25%18%

8%

9%

7%4%

29%

29%

19%

9%

5%7%

2%

32%

8%

12%9%

29%

5%5%

27%

4%

11%46%

7%5%

Fragrance, body care,gifts and core beauty

Skin andhair care

Body care, skin care and gifts

Body Care Fragrance Gifts Makeup Skin care Hair care Others

• Vegetable waxes to provide a protective layer

• Copper and Zinc PCA are combined with Ginger Root extract to provide soothing and anti-inflammatory properties

• Launch in October 2017 of the first deo parfum in the Kaiakfamily with high quality ingredients

• 100% organic alcohol and 100% recycled glass

Elemental Face Barrier creamShea Body butterK

3

A complementary and innovative product portfolio across categories

Page 11

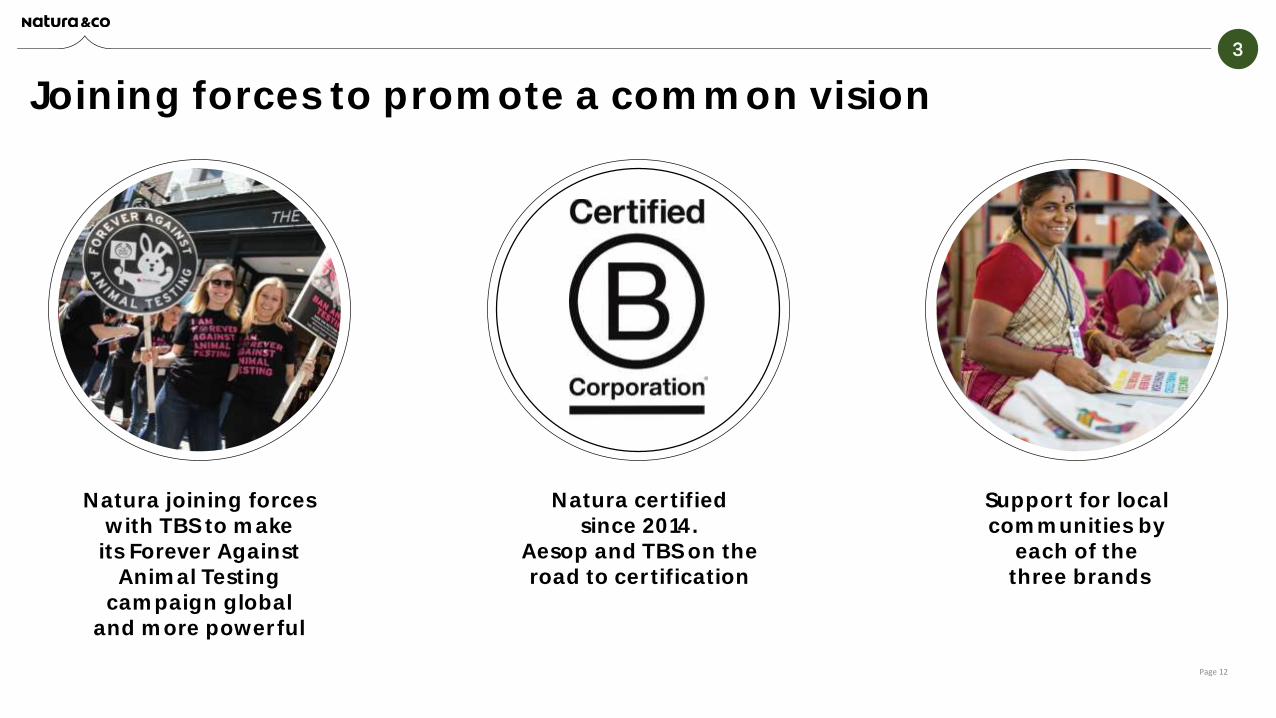

Natura joining forces with TBS to make

its Forever AgainstAnimal Testing

campaign globaland more powerful

Natura certifiedsince 2014.

Aesop and TBS on theroad to certification

Support for local communities by

each of thethree brands

3

Joining forces to promote a common vision

Page 12

Board of Directorsserving the entire group

Group Operating Committee formedto capture synergies, allocate resourcesand carry out consolidation

Natura, TBS and Aesop are runautonomously, each with a CEO and its own Executive Committee

Roberto MarquesExecutive Chairman

Paula FallowfieldHuman Resources

João Paulo FerreiraNatura CEO

David BoyntonTBS CEO

Michael Aesop CEO

Robert ChatwinChief Transformation

Officer

Josie RomeroSupply Chain

Itamar Gaino FilhoLegal and Compliance

Roger SchimidInnovation and Sustainability

José FilippoCFO

Networking organization

Moacir SalzsteinGovernance

4

A governance and management structure combining scale and autonomy

Page 13

Growth synergies

• Natura international growth acceleration, building on

• The Body Shop expansionin Latin America, capitalizing

-how

• Aesop: Entering new geographies

Cost synergies• Efficiency and scale gains

• Global procurement

• Lower group cost of capital

4

Leveraging group scale to unlock synergies

Page 14

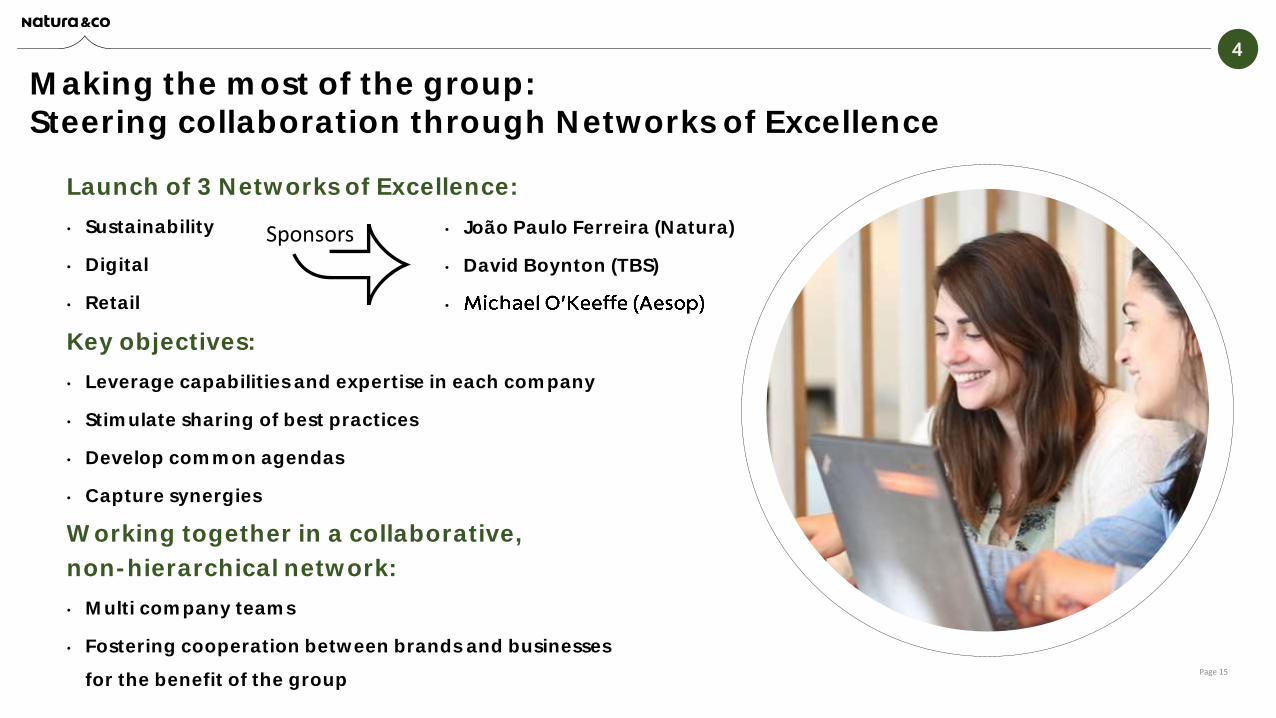

Launch of 3 Networks of Excellence:

• Sustainability

• Digital

• Retail

Key objectives:

• Leverage capabilities and expertise in each company

• Stimulate sharing of best practices

• Develop common agendas

• Capture synergies

Working together in a collaborative,

non-hierarchical network:

• Multi company teams

• Fostering cooperation between brands and businesses

for the benefit of the group

• João Paulo Ferreira (Natura)

• David Boynton (TBS)

•

4

Making the most of the group: Steering collaboration through Networks of Excellence

Sponsors

Page 15

Key objectives:

• Speak to the supplier base with a single Natura &Co voice to optimize costs,

payment terms and inventory management

• Harmonize protocols and policies, reducing compliance and supply risks

• Develop strategic partnerships with key suppliers for co-creation

(faster and bolder innovation)

• Promote purchasing process transparency

Capture of synergies and scale through a Global Procurement Organization, leveraging the expertise available throughout the group

4

Synergy case study: Creating a common procurement organization

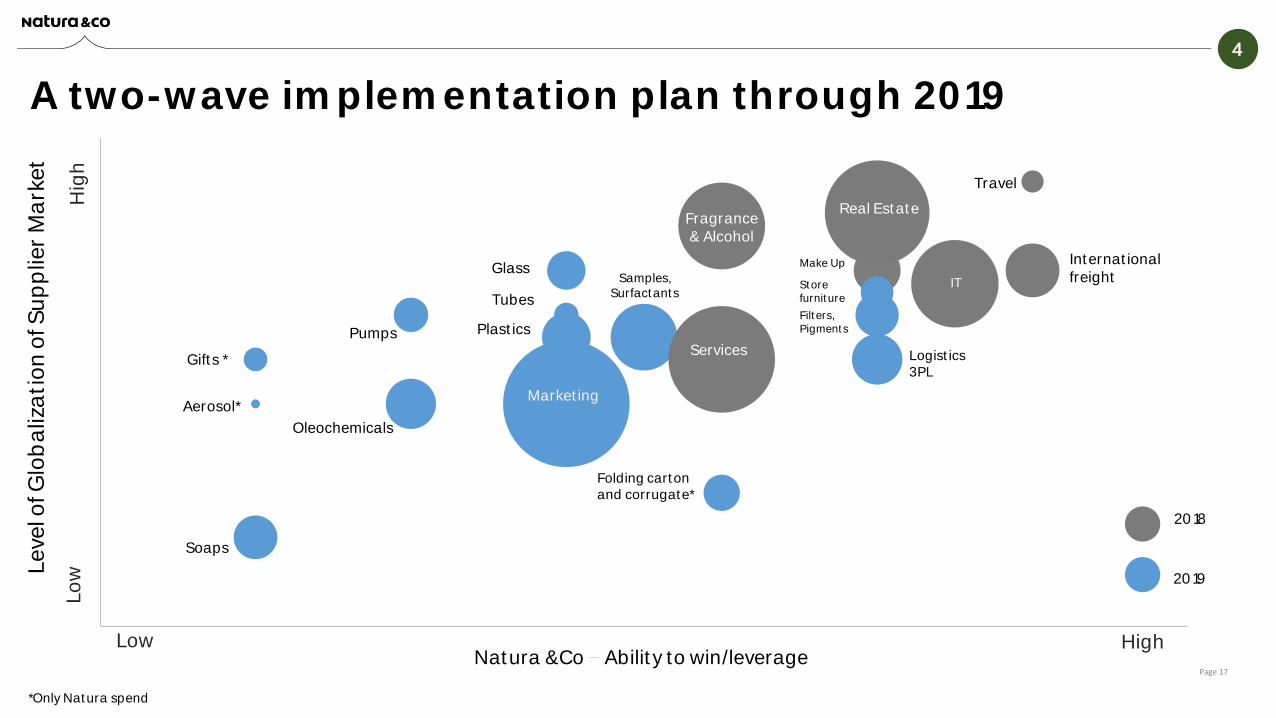

Page 16

Gifts *

Aerosol*

Pumps

Glass

Folding carton and corrugate*

Services

Marketing

Plastics

TubesStore furniture

Real Estate

Travel

Natura &Co Ability to win/leverage

Le

velo

f Glo

ba

liza

tio

no

f Su

pp

lier

Ma

rke

t

Soaps

Oleochemicals

Fragrance& Alcohol

Logistics3PL

IT

Filters, Pigments

Make Up International freightSamples,

Surfactants

Low High

Lo

wH

igh

2018

2019

*Only Natura spend

4

A two-wave implementation plan through 2019

Page 17

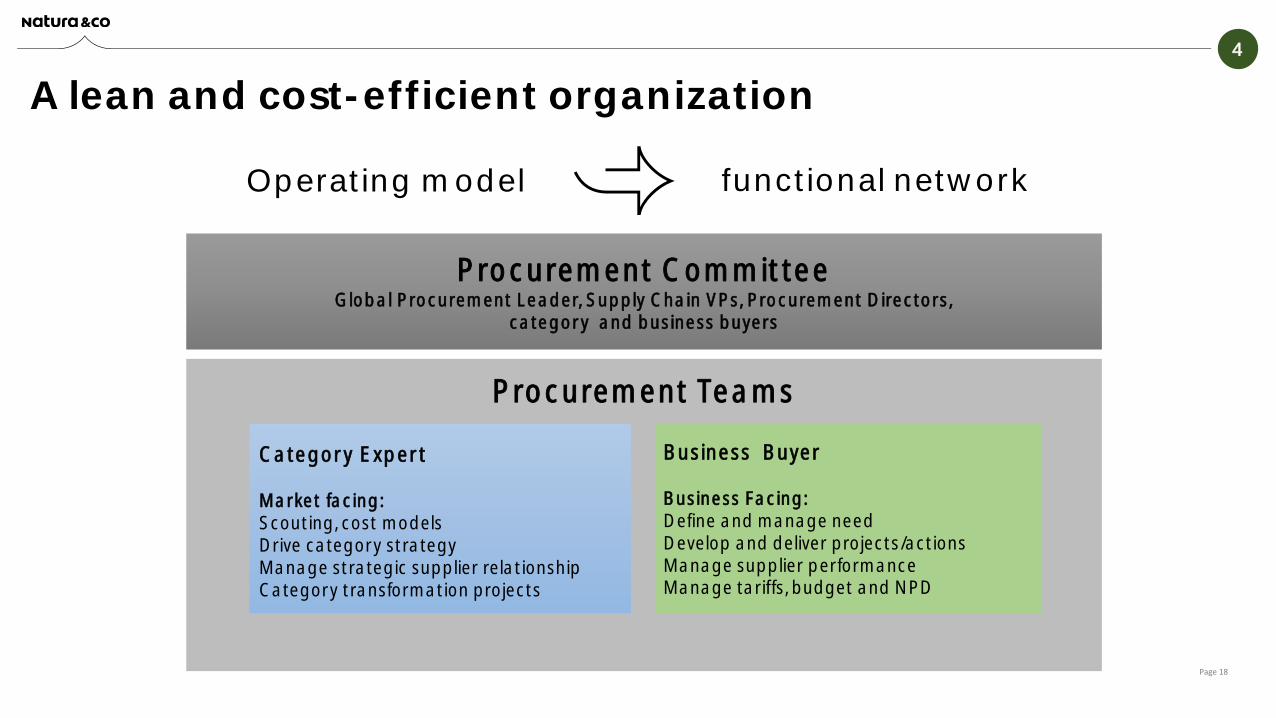

Procurement CommitteeGlobal Procurement Leader, Supply Chain VPs, Procurement Directors,

category and business buyers

Category Expert

Market facing: Scouting, cost modelsDrive category strategyManage strategic supplier relationshipCategory transformation projects

Procurement Teams

Business Buyer

Business Facing:Define and manage needDevelop and deliver projects/actionsManage supplier performanceManage tariffs, budget and NPD

Operating model

4

A lean and cost-efficient organization

functional network

Page 18

4

A R$ 420 million opportunity for the group

R$ 420 million*

Global procurement spend approx.:

5%

R$ 8.5 billion a year

Cumulative cost savings in 3 years:

Page 19

This figure is part of the overall guidance provided further on in this presentation. It is based on a mapping of the scale gainpurchasing volumes in such categories as logistics, third party services, raw materials, packaging, information technology and others. There are other opportunities to capture from access to a larger number of suppliers, currency diversification and centralized negotiations with suppliers. The estimated savings result from a comparative overview of market practices.

*At current exchange rates.

Turn around TBS and accelerate

its growthin Latam

Expand Natura’smultichannel

transformationand international

footprint

Continue Aesop’sgrowth

momentum andexpantion

4

A clear financial strategy focused onprofitable growth,

cash generation anddeleveraging

Establishing governance and culture

Driving value creationGetting the most out of the Group

Capture Natura Group synergies

Strengthengovernance, international capabilities &

processes

Page 20

Taking Natura to the next level

João Paulo FerreiraCEO Natura

Page 21

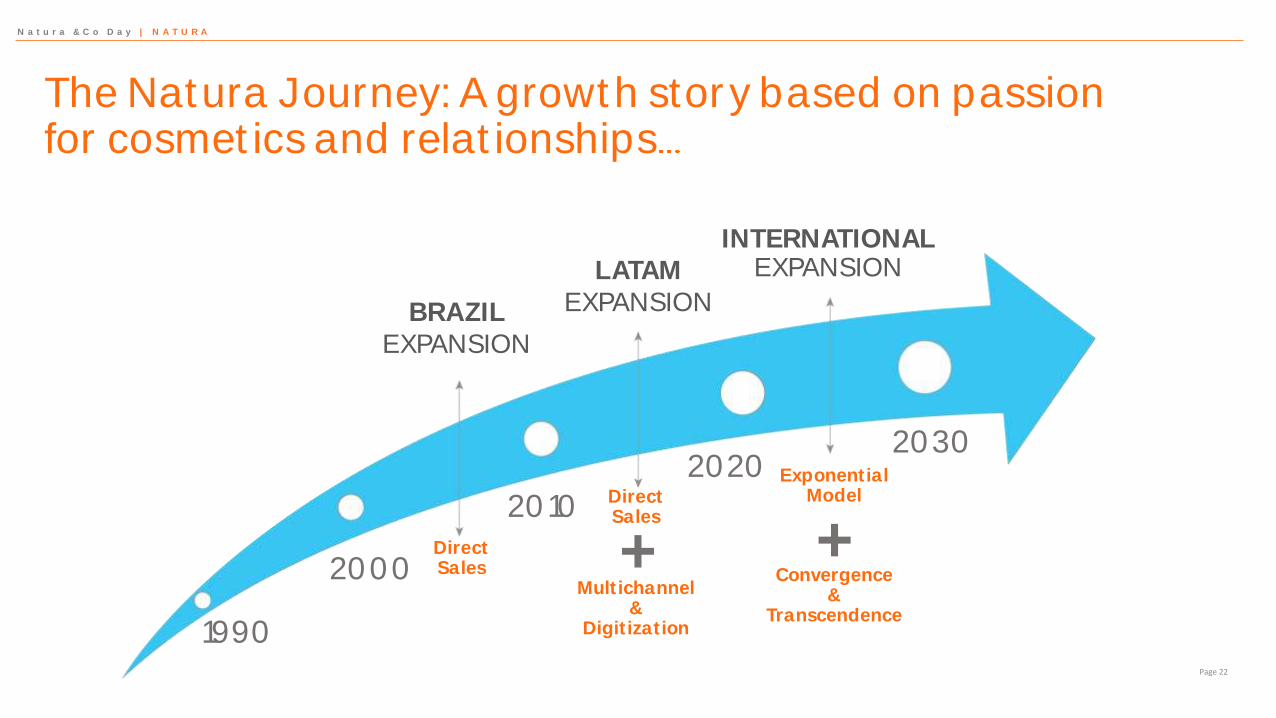

1990

2000

2010

20202030

BRAZILEXPANSION

INTERNATIONALEXPANSION

DirectSales

DirectSales

ExponentialModel

+ +Multichannel

&Digitization

Convergence&

Transcendence

The Natura Journey: A growth story based on passion for cosmetics and relationships

N a t u r a & C o D a y | N A T U R A

LATAMEXPANSION

Page 22

2014 2016:NATURA WAS LOSING MOMENTUM

N a t u r a & C o D a y | N A T U R A

with some short-term bumps on the road

LOSING TOUCH WITH:

Beautyattributes

Higher-income consumers

Young consumers

Lower market share in direct sales

Lower household penetration share-of- wallet

RESULTING IN:

AMID CHANGING STRUCTURAL MARKET TRENDS:

New brands

New competitorsin direct sales

Changing shopping habits and channels

Page 23

4 5 6

REVITALIZATION

OF DIRECT SALES

ONLINE & OFFLINE

CONVERGENCE OF THE

COMMERCIAL MODEL

MULTI-CHANNEL SHOPPING

EXPERIENCE

N a t u r a & C o D a y | N A T U R A

2017: A new roadmap for Natura

A S I X- P I L L A R A C T I O N P L A N TO R E - D Y N A M I Z E O U R B U S I N E S S M O D E L A N D R E S U M E G R O W T H

NATURA BRAND

1

CATEGORIES AND BRANDS

STRATEGY

EXPANSION INTO NEW MARKETS

2 3

1 2

Page 24

Natura brand relaunch

N a t u r a & C o D a y | N A T U R A

WE REPOSITIONED THE NATURA BRAND

Revised brand architecture

Key sub-brands relaunch

1 2

Page 25

Live your living beautyPage 26

We redesigned the brand architecture

• Fragrances• Body care• Gifts

CORE CATEGORIES BRAND STRATEGY

Higher household penetration

• Ekos• Chronos• Tododia• Faces • Aquarela

• Kaiak• Essencial• Humor• Una • Luna

Clear role to reach target consumers

N a t u r a & C o D a y | N A T U R A

2

• Core beauty

Strengthen beauty attributes

Page 27

Ekos ChronosPage 28

Perfumery HousePage 29

Natura HomemPage 30

Tododia (Wear your skin, live your body)Page 31

Faces AquarelaPage 32

N a t u r a & C o D a y | N A T U R A

55.5%

64.6%

Q2-16 Q4-17

+9.1p.p.

Relevant innovation combining cosmetics, technology and biodiversity

Innovation index

1 2

Page 33

jan out nov dez

Fragrance

jan out nov dez jan out nov dez

N a t u r a & C o D a y | N A T U R A

Leadership recovery in key categoriesResuming market share gains in Brazil in 2017

Body care Gifts

Main competitor

Marketshare

%

2017

Page 34

1 2

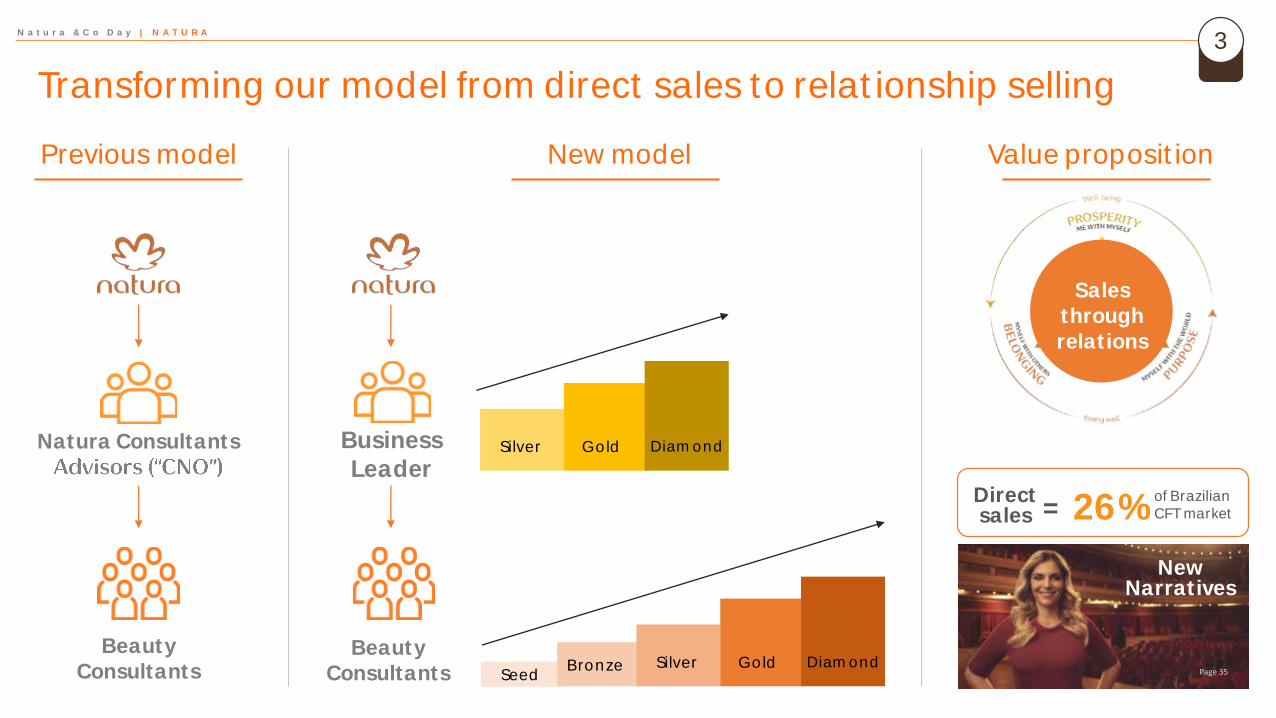

Salesthrough relations

Previous model

Natura Consultants

Beauty Consultants

New model

Business Leader

Silver Gold DiamondSeed

BronzeBeauty

Consultants

Silver Gold Diamond

Value proposition

Transforming our model from direct sales to relationship selling

N a t u r a & C o D a y | N A T U R A

26%Direct sales

of Brazilian CFT market

3

=

New Narratives

Page 35

Relationship SellingPage 36

80

90

100

110

120

130

140

150

More consultants in top 3 tiersand higher overall productivity

Number of consultantsvs. productivity (Brazil)

2017

N a t u r a & C o D a y | N A T U R A

Gross revenue Number of consultantsProductivity

Jul/2017 Feb/2018

Silver, Gold and Diamond

consultants

Totalconsultants

(million)

Productivity per consultant

+5.8%

1.21.0

+18.0%

3

Page 37

N a t u r a & C o D a y | N A T U R A

Digital solutions enhance direct sales shopping experienceProviding our consultants with tools to amplify their potential

v

E-commerce Direct sales

Direct sales revitalization

through digital

Relationship-driven model fostered by digital

Relational e-commerce

4

Page 38

Target:

1 millionconsultants

by 2019

N a t u r a & C o D a y | N A T U R A

Using cutting-

An app designed for consultants

• 10X times more interactions with Natura

• Bots, agumented reality, analytics and CRM

• High customer review rating in app stores

555,000active consultants

21% of total orders

+10% average productivity

gain/consultant

Rapid adoption

4

Outstanding UEx

Growing relevancePage 39

Natura Relationship Selling can deliver an excellent shopping experience:

N a t u r a & C o D a y | N A T U R A

Multiple channels for different shopper profiles and category drivers

• Extensive reach• Assortment with innovation• Endorsement and advocacy marketing• High service level• Advice on products and beauty

Which can be complemented with other channels

Fragrance/makeup

Face care

Shopperprofile

Personalcare

30% A S S I S TA N C E

36% E X P E R I E N C E

34% C O N V E N I E N C E

5

Page 40

N a t u r a & C o D a y | N A T U R A

Natura is increasingly multichannel to attract younger, more affluent beauty consumers

Natura Beauty Consultants

Natura Beauty Entrepreneurs

Natura Beauty Specialists

Rede Natura

One of the most visited digital sales

channels for beauty products in Brazil

Growing database

of direct consumers

Natura stores

AB1 consumers

26 stores (19 in Brazil)

Makeup and face care

Premium portfolio: Ekos, Chronos, UnaRelationship-

based model

5

Page 41

N a t u r a & C o D a y | N A T U R A | 3 . O N L I N E & O F F L I N E C O N V E R G E N C E O F T H E C O M M E R C I A L M O D E L

We have created a powerful online sales platform: Rede Natura

_Best online store in 2017¹

_Leader in trafficin cosmetics2

_High double-digit growthDouble-digitEBITDA margin

_220,000+digital consultants; 62% of online sales

_3.5 millionconsumers30% aged below 30 (vs. 18% in direct sales)

_50% of sales

through mobile

Source: ¹Ebit popular vote | ²Source: Similarweb. Cosmetics segments (natura.com.br+natura.net),

Rede Natura

5

Page 42

_26 stores (19 in Brazil)

_Average store size: 70m²

_Break-even: Less than 2 years

_Further expansion in 2018

_Premium portfolio

_Focus on core beauty

N a t u r a & C o D a y | N A T U R A

A growing physical store network

5

Page 43

N a t u r a & C o D a y | N A T U R A

Natura resumes no 1 ranking in Brazil

Page 44

1 2 3 4 5

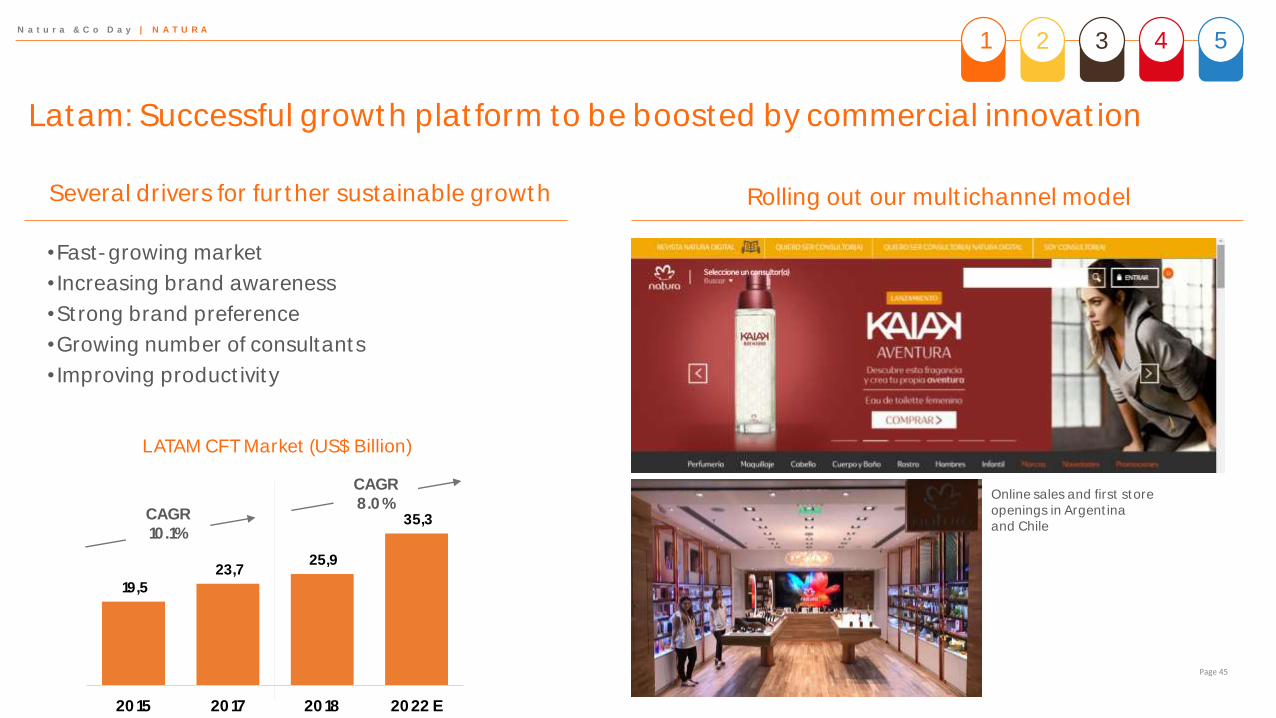

Rolling out our multichannel model

•Fast-growing market

• Increasing brand awareness

•Strong brand preference

•Growing number of consultants

• Improving productivity

LATAM CFT Market (US$ Billion)

Online sales and first storeopenings in Argentina and Chile

Several drivers for further sustainable growth

CAGR 10.1%

CAGR 8.0%

N a t u r a & C o D a y | N A T U R A

Latam: Successful growth platform to be boosted by commercial innovation

19,5 23,7

25,9

35,3

2015 2017 2018 2022 E

1 2 3 4 5

Page 45

302,000

589,000

Q4-12 Q4-13 Q4-14 Q4-15 Q4-16 Q4-17

5.1%Growth 3X above average

of competitors

Market share1

CFT Market1

(USD billion)

Brand awareness2

Market share1

98%

2º

5.4

9.5%

99%

1º

3.3

5.5%

97%

3º

9.4

2.4%

97%

*1º

3.3

4.9%

100%

*1º

2.2

6.5%Number of

consultants

2012 2017

2012 2017

N a t u r a & C o D a y | N A T U R A

Latam: Strong performance across the region

Source: ² Equity Millward Brown, 2017 | *Tied for first place

Source: ¹ Euromonitor International 2017, LATAM Beauty and Personal Care | (Argentina, Chile, Peru, Colombia and Mexico)

2.4%

24

1 2 3 4 5

Brand preference2

Page 46

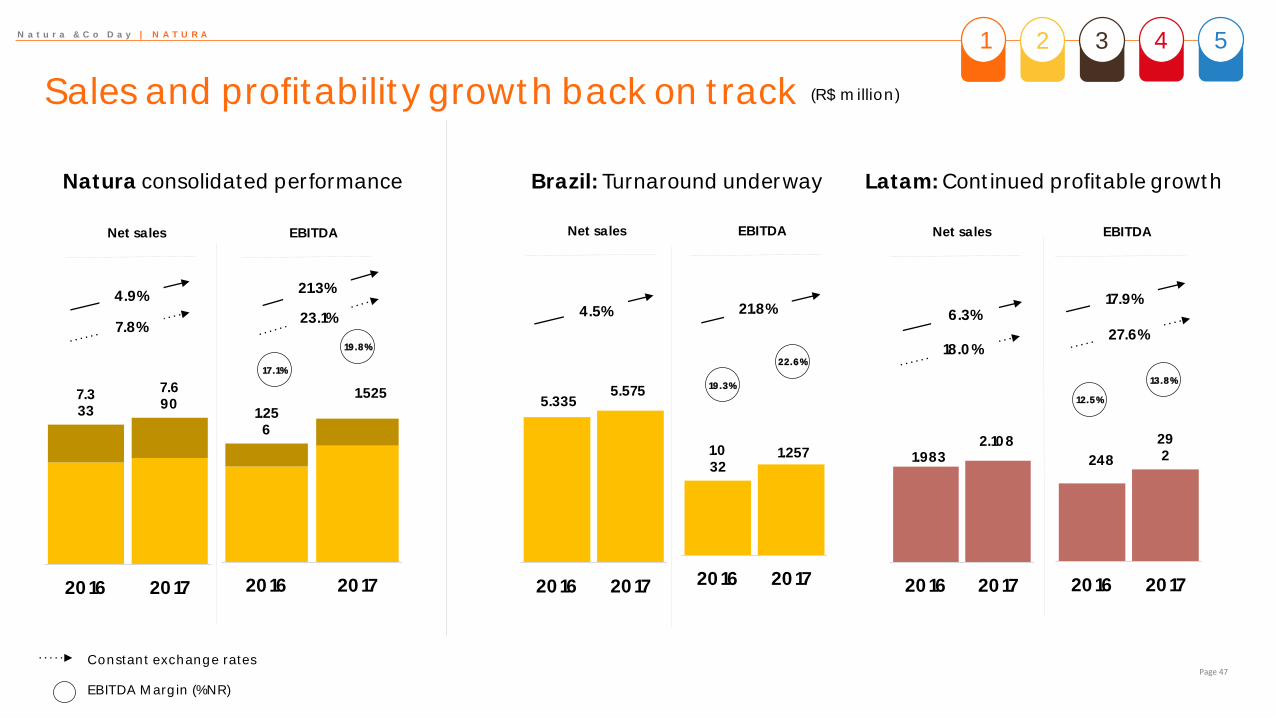

1.256

1.525

2016 2017

7.333

7.690

2016 2017

Natura consolidated performance

EBITDA

Latam: Continued profitable growthBrazil: Turnaround underway

19.3%

EBITDA Margin (%NR)

22.6%

12.5%

13.8%

(R$ million)

Constant exchange rates

23.1%

21.3%

17.1%

19.8%

5.335 5.575

2016 2017

1.032

1.257

2016 2017

21.8%4.5%4.9%

7.8%

1.983 2.108

2016 2017

248

292

2016 2017

17.9%

27.6%

6.3%

18.0%

N a t u r a & C o D a y | N A T U R A

Sales and profitability growth back on track

Net sales EBITDANet sales EBITDANet sales

1 2 3 4 5

Page 47

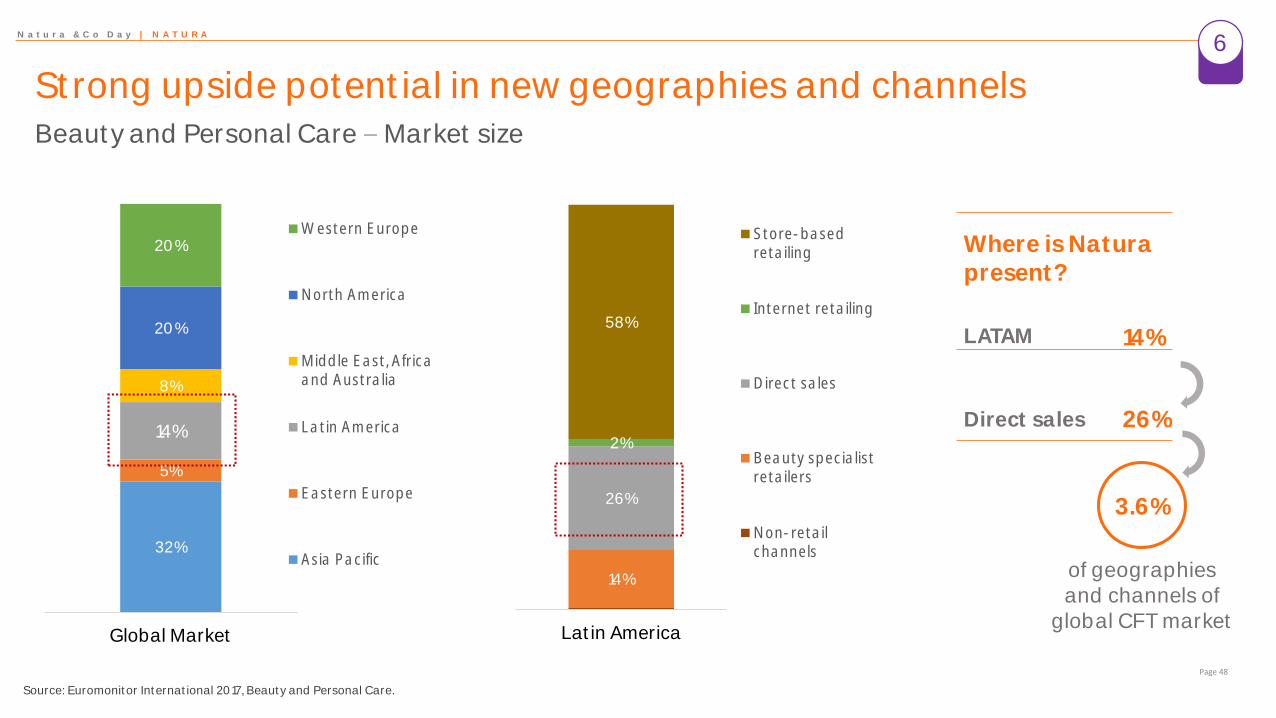

32%

5%

14%

8%

20%

20%

Global Market

Western Europe

North America

Middle East, Africaand Australia

Latin America

Eastern Europe

Asia Pacific

N a t u r a & C o D a y | N A T U R A

Strong upside potential in new geographies and channels

Where is Natura present?

LATAM 14%

Direct sales 26%

3.6%

14%

26%

2%

58%

Latin America

Store-basedretailing

Internet retailing

Direct sales

Beauty specialistretailers

Non-retailchannels

Source: Euromonitor International 2017, Beauty and Personal Care.

Beauty and Personal Care Market size

6

of geographiesand channels of

global CFT market

Page 48

N a t u r a & C o D a y | N A T U R A

Lower entry costs

Synergies, scale gains

Faster break-even

Intimacy with local markets

68 countries

6

80% of global CFT marketof which 66% is new to Natura

Page 49

A M E R I C A S | N A T U R A

Transcendence: The 2 X 20 X 200 opportunity

Source: PEN 2018 - 2022

2 millionconnected

consultants

20 millionconsumers in Latam, consuming content,

products and cosmetic services

200 millionconsumers connected

to the Natura ecosystem worldwide

6

Page 50

© 2015 The Body Shop International plc

NATURA &CO DAY20 April 2018

David Boynton CEO

ICONIC BRITISH BEAUTY BRAND

• 22,000 PEOPLE

• 68 COUNTRIES

• 3,049 STORES

• 400 GLOBAL

TRAVEL

RETAIL LOCATIONS

Page 52

BUSINESS AS A FORCE FOR

GOOD

Page 53

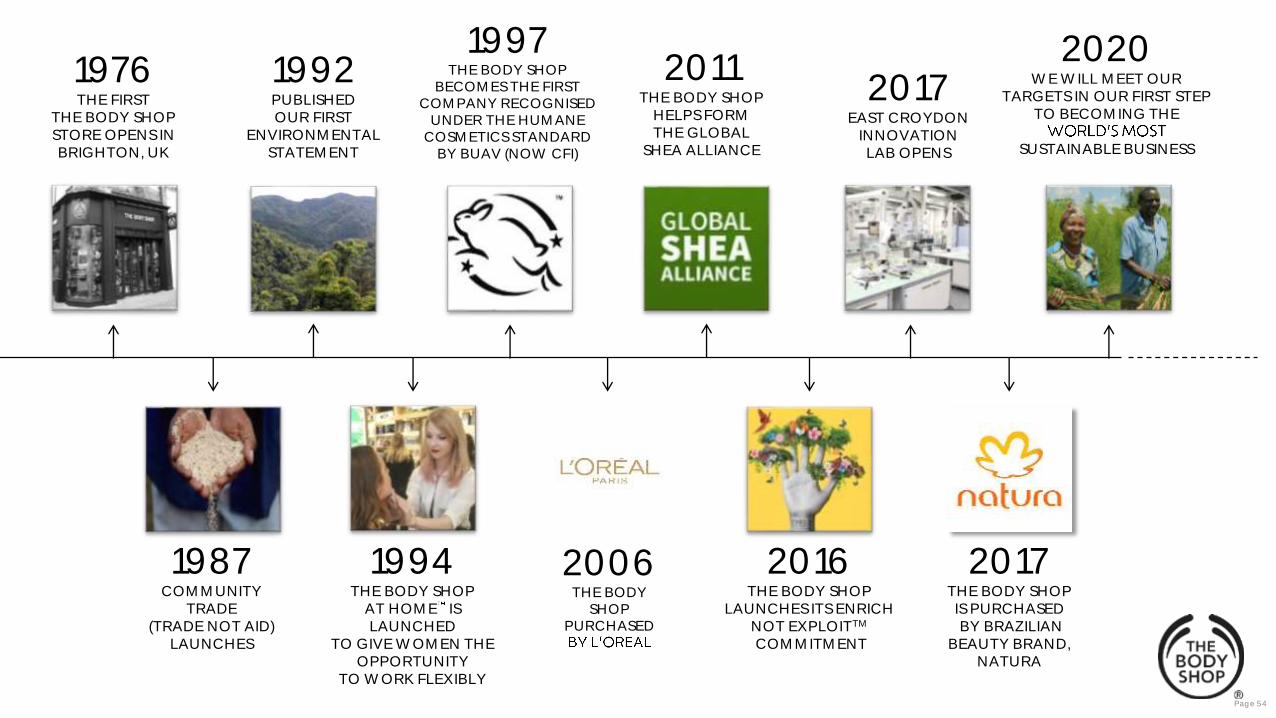

1976THE FIRST

THE BODY SHOP STORE OPENS IN BRIGHTON, UK

1992PUBLISHED OUR FIRST

ENVIRONMENTAL STATEMENT

1987COMMUNITY

TRADE(TRADE NOT AID)

LAUNCHES

1994 THE BODY SHOP

AT HOME IS LAUNCHED

TO GIVE WOMEN THE OPPORTUNITY

TO WORK FLEXIBLY

1997THE BODY SHOP

BECOMES THE FIRST COMPANY RECOGNISED

UNDER THE HUMANE COSMETICS STANDARD

BY BUAV (NOW CFI)

2017 EAST CROYDON

INNOVATION LAB OPENS

2016 THE BODY SHOP

LAUNCHES ITS ENRICH NOT EXPLOITTM

COMMITMENT

2020WE WILL MEET OUR

TARGETS IN OUR FIRST STEP TO BECOMING THE

SUSTAINABLE BUSINESS

2006THE BODY

SHOP PURCHASED

2011THE BODY SHOP

HELPS FORM THE GLOBAL

SHEA ALLIANCE

2017THE BODY SHOP

IS PURCHASEDBY BRAZILIAN

BEAUTY BRAND, NATURA

Page 54

A TRULY GLOBAL BRAND

NORTH AMERICA2 COUNTRIESCOMPANY OWNED257 STORES

EUROPE, MIDDLE EAST

& AFRICA47 COUNTRIES

12 COMPANY-OWNED 35 HEAD FRANCHISE

1,489 STORES

ASIA PACIFIC

16 COUNTRIES3 COMPANY-OWNED

13 HEAD FRANCHISE1,127 STORES

LATIN AMERICA3 COUNTRIESCOMPANY OWNED176 STORES

Page 55

56

MULTI-CHANNEL APPROACH

IN-STORE3,049 STORES GLOBALLY

DIGITAL33 E-COMMERCE SITES

WHOLESALE DIRECT SALESTHE BODY SHOP AT HOME

OUR KEY CATEGORIES

BODYCAREBODY BUTTER, LOTION

HANDS, LIPS, GIFTS

SKINCAREMOISTURISER, SERUMS,

MASKS, CLEANSER, MEN, GIFTS

BODY HYGIENESHOWER GEL SCRUBS,

DEO, MISTS

HAIRCARESHAMPOO, CONDITIONER

MAKEUPFACE, LIP

FRAGRANCEEDT, OILS, BODY LOTION

Page 57

OUR MOST-LOVED PRODUCTS

*AS OF FEBRUARY 2018

GINGER SHAMPOO

400ML

HIMALAYAN CHARCOAL

FACIAL MASK

HEMP HAND PROTECTOR 100ML

DROPS OF YOUTHLIQUID PEEL

DROPS OF YOUTHYOUTH CONCENTRATE

50ML

DROPS OF YOUTHYOUTH

CONCENTRATE 30ML

TEA TREE OIL 20ML

DROPS OF YOUTHDAY CREAM 50ML

SHEA BODY BUTTER 200ML

ALMOND MILK & HONEY BODY BUTTER 200ML

7

TEA TREE OIL 10ML

1 2 3 4 5 6

8 9 10 11 12

TEA TREE SKIN CLEARING FACIAL

WASH 250ML

Page 58

59

MORE INNOVATION IN 2018

• Launch of body yogurt

• Investing in critical body care category

• 100% vegan

• Fast absorbing, 48 hour moisturising

• Initial launch in US and Finland

Specially formulated to apply on damp skin

Contains Community Trade organic almond milk

Available in our six best-selling scents

Page 59

60

IMPROVING PERFORMANCE

Page 60

GROWTH IN REVENUE AND EBITDA IN 2017

Net revenues1

(Constant currency £M)EBITDA 1

(Constant Currency £M)

777.8 794.9

2016 2017

6166

2016 2017

8.6%

1 Pro-forma: includes financial performance prior to the acquisition

• First EBITDA growth since 2013

• Clear opportunities for future growth

2.2%

Page 61

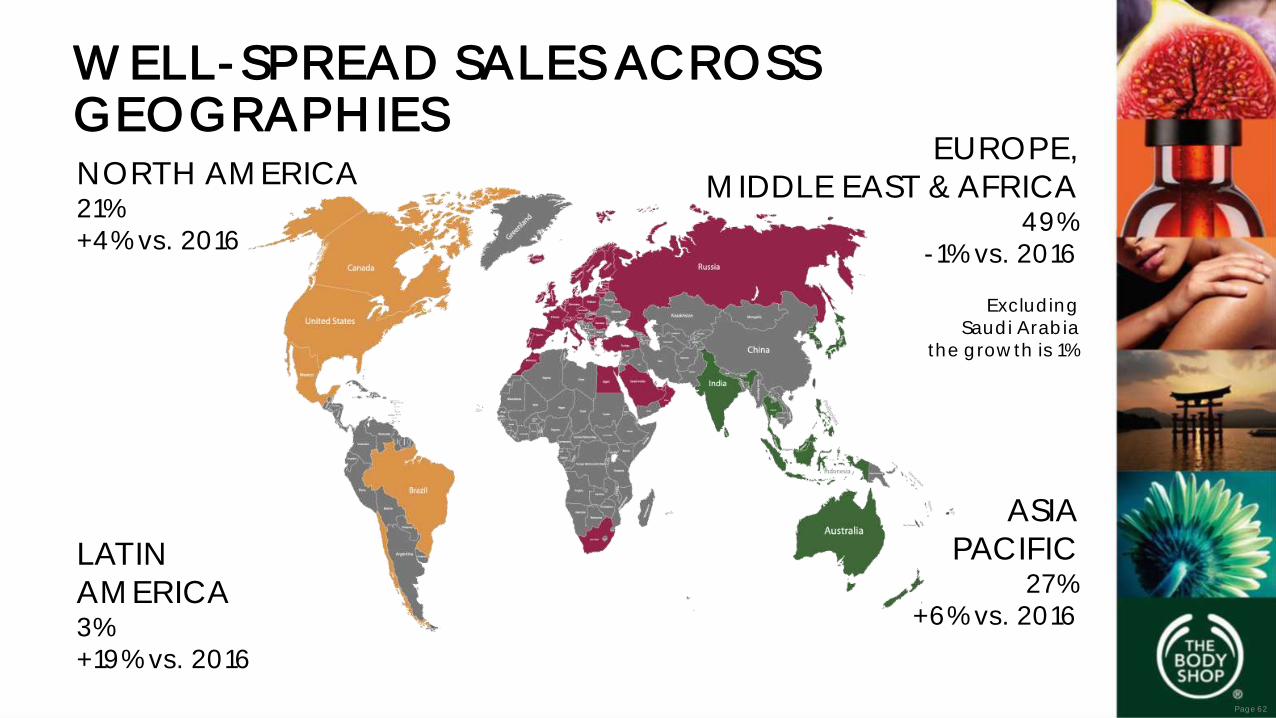

WELL-SPREAD SALES ACROSS GEOGRAPHIES NORTH AMERICA21% +4% vs. 2016

EUROPE, MIDDLE EAST & AFRICA

49%-1% vs. 2016

ASIA PACIFIC

27%+6% vs. 2016

LATIN AMERICA3%+19% vs. 2016

Excluding Saudi Arabia

the growth is 1%

Page 62

WELL-BALANCED SALES BY CHANNEL AND CATEGORY

5823

9

10

By channel

Own Store Franchisee

E-commerce Others

32

29

12

9

85 5

By category

Body Care Skin Care GiftsMake up Fragrance Hair CareOthers

Page 63

2022TRANSFORMATION

UNDERWAY

Page 64

65

A FIVE-PILLAR TRANSFORMATION PLAN

REJUVENATETHE BRAND

1

OPTIMISE RETAIL OPERATIONS

2

RE-DESIGN ORGANISATION

5

ENHANCE OMNI-CHANNEL

3

IMPROVE OPERATIONAL EFFICIENCY

4

• Transformation office with a dedicated team

• Committed and accountable 200-strong transformation team

• 17 workstreams within these five pillars

1REJUVENATE

BRAND

REVITALISE THE BODY SHOP PURPOSE AND BRING IT TO LIFE FOR CUSTOMERS

REDUCE PROMOTIONAL INTENSITY & IMPROVE PRICING ARCHITECTURE

RESET CATEGORY STRATEGIES, EVENT MANAGEMENT AND STOCK MANAGEMENT

SECURE THE SUCCESS OF BODY YOGURT AND CHRISTMAS

3ENHANCE

OMNI-CHANNEL

DRIVE ECOMMERCE IN EXISTING AND NEW MARKETS

DEFINE AND DRIVE THE GLOBAL CHANNEL STRATEGY INCLUDING WHOLESALE

INVEST IN CRM & MARKETING TO INCREASE TRAFFIC

2OPTIMISE

RETAIL OPERATIONS

TURN AROUND THE US

TURN AROUND GERMANY, DENMARK AND SWEDEN

RENEW STORE FOOTPRINT

ENTER NEW HEAD FRANCHISE MARKETS

BOOST LATAM GROWTH

CREATE A WINNING IN-STORE CUSTOMER EXPERIENCE

4IMPROVE

OPERATIONAL EFFICIENCY

REDUCE OPEX THROUGH INDIRECT AND DIRECT SAVINGS

INCREASE CAPEX SPEND EFFICIENCY

5RE-DESIGN

ORGANISATION

STRENGTHEN CULTURE AND TALENT

RE-DESIGN THE OPERATING MODEL TO ENABLE THE STRATEGY

Page 66

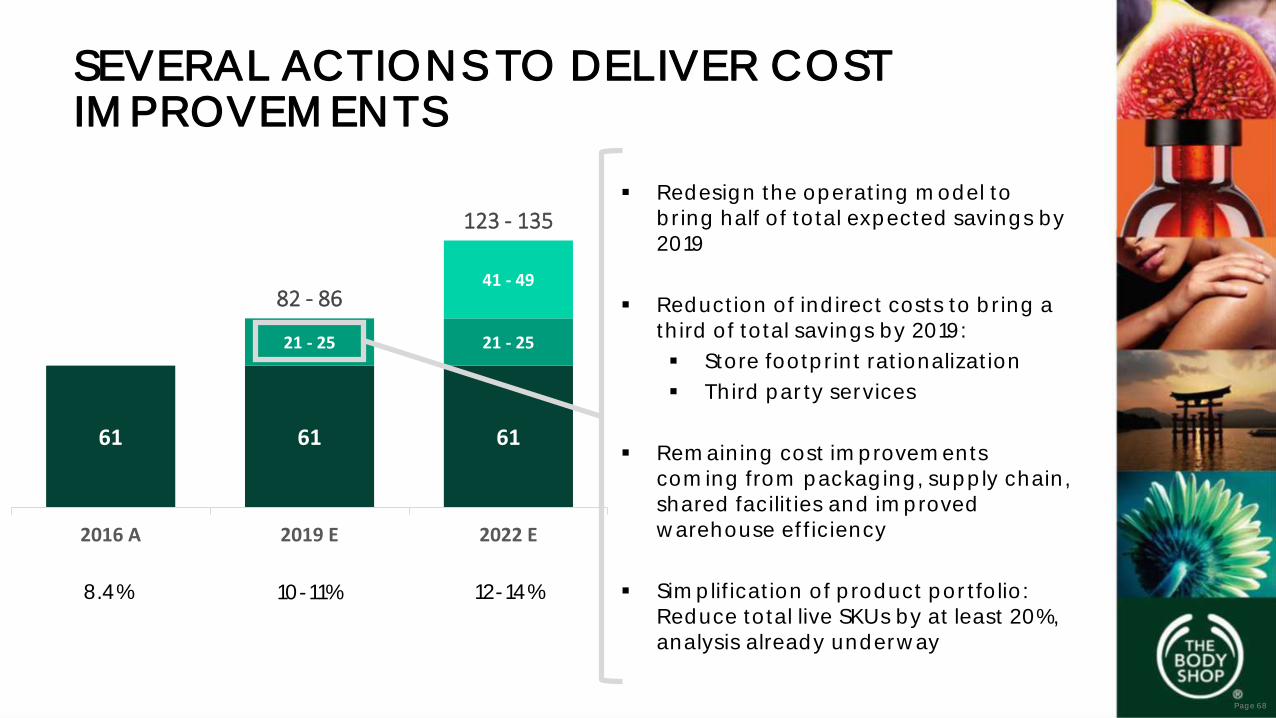

8.4% 10-11% 12-14%

61 61 61

21 - 25 21 - 25

41 - 4982 - 86

123 - 135

2016 A 2019 E 2022 E

WE AIM TO DOUBLE EBITDA TO £123M BY 2022

2016 EBITDAbaseline

Cost improvement

Topline growth

EBITDA margin

Expected EBITDA evolution £M

1 Based on December 2017 rate of 0.75 £ for 1 US$

1

Page 67

8.4% 10-11% 12-14%

61 61 61

21 - 25 21 - 25

41 - 4982 - 86

123 - 135

2016 A 2019 E 2022 E

SEVERAL ACTIONS TO DELIVER COST IMPROVEMENTS

Redesign the operating model to bring half of total expected savings by 2019

Reduction of indirect costs to bring a third of total savings by 2019:

Store footprint rationalization

Third party services

Remaining cost improvements coming from packaging, supply chain, shared facilities and improved warehouse efficiency

Simplification of product portfolio: Reduce total live SKUs by at least 20%, analysis already underway

Page 68

8.4% 10-11% 12-14%

61 61 61

21 - 25 21 - 25

41 - 4982 - 86

123 - 135

2016 A 2019 E 2022 E

FOCUSED ACTIONS TO DELIVER TOP LINE GROWTH

Turn around the US, Germany, Denmark and Sweden through store portfolio and brand rejuvenation

Grow owned ecommerce sales to 15% of total by 2022; roll out new ecommerce sites in all remaining sizeable Head Franchise markets (21 currently live)

Achieve a 25% increase in marketing investments as a percentage of net sales by 2022

Create a clearer and more transparent pricing architecture to reflect the quality of our products

Grow Latam footprint by leveraging Natura's infrastructure and capabilities

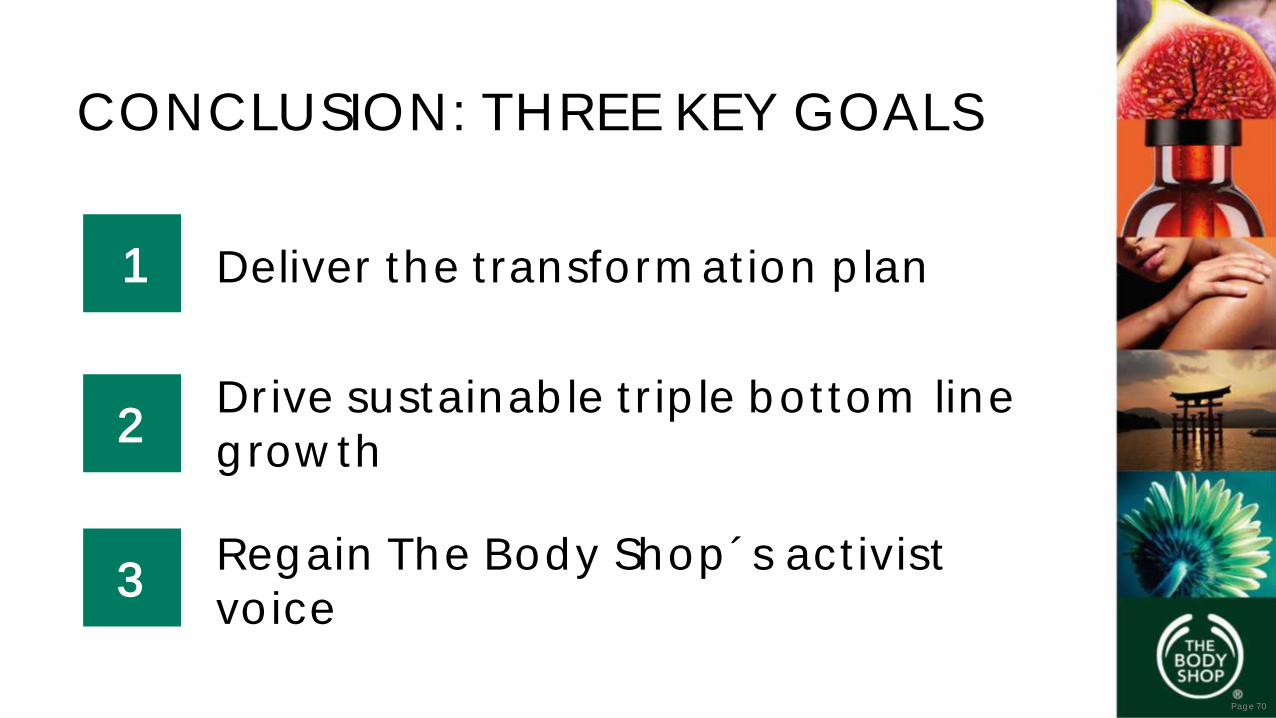

CONCLUSION: THREE KEY GOALS

Deliver the transformation plan1

2

3

Drive sustainable triple bottom line growth

Regain The Body Shop´s activist voice

Page 70

Aesop: Poised for further growthMichael O'Keeffe, CEO

Natura &Co Day. April 20, 2018

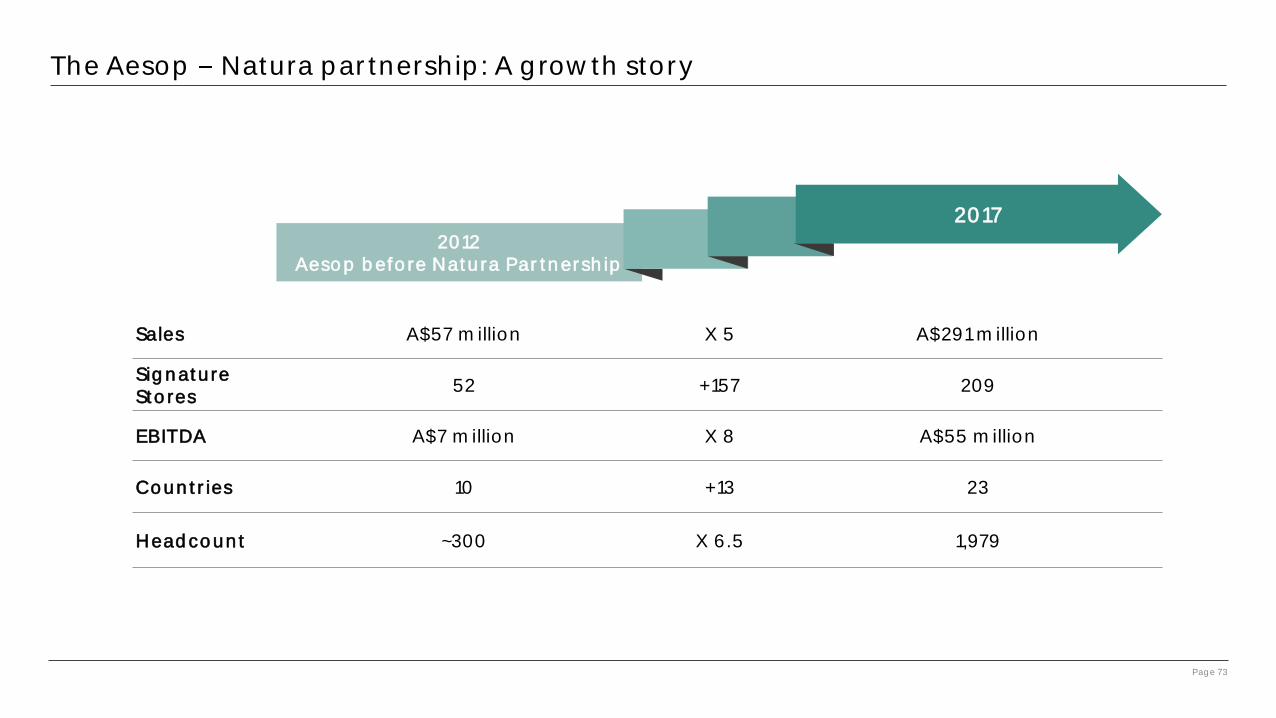

The Aesop Natura partnership: A growth story

2012Aesop before Natura Partnership

2017

Sales A$57 million X 5 A$291 million

Signature Stores

52 +157 209

EBITDA A$7 million X 8 A$55 million

Countries 10 +13 23

Headcount ~300 X 6.5 1,979

Page 73

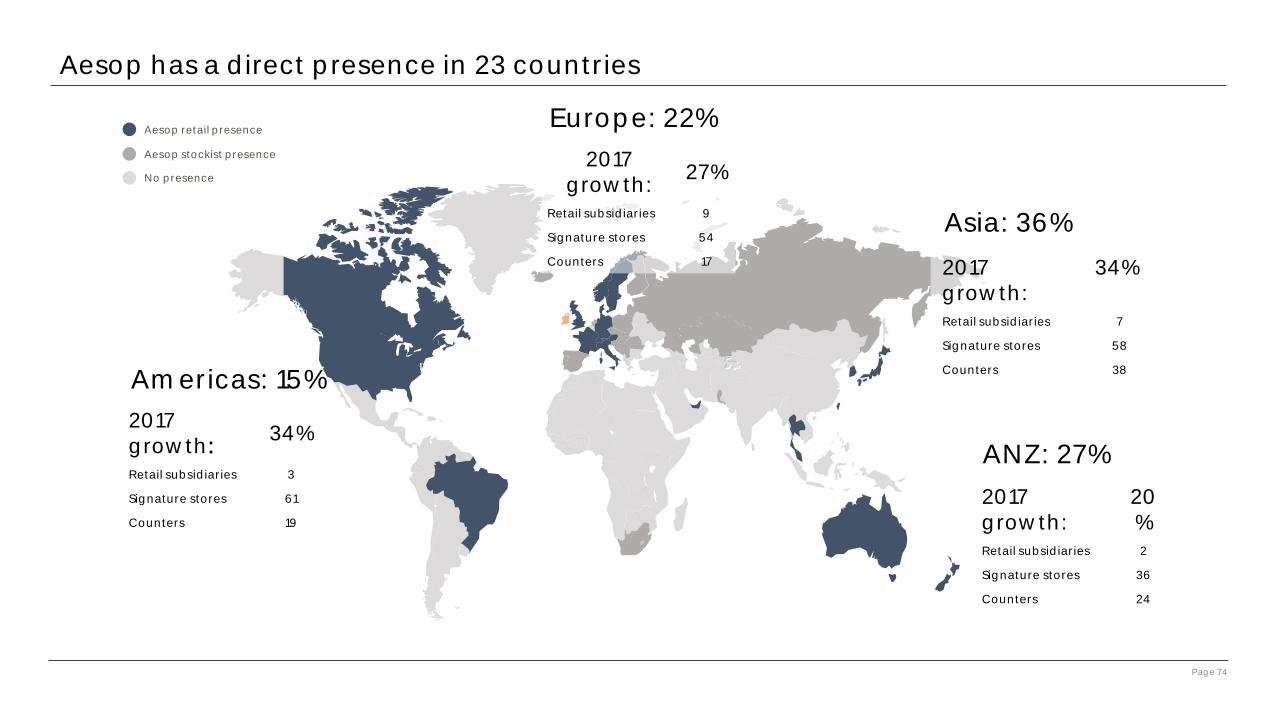

Aesop has a direct presence in 23 countries

Aesop retail presence

Aesop stockist presence

2017 growth:

34%

Retail subsidiaries 3

Signature stores 61

Counters 19

2017 growth:

20%

Retail subsidiaries 2

Signature stores 36

Counters 24

2017growth:

27%

Retail subsidiaries 9

Signature stores 54

Counters 17

No presence

2017 growth:

34%

Retail subsidiaries 7

Signature stores 58

Counters 38Americas: 15%

Europe: 22%

Asia: 36%

ANZ: 27%

Page 74

A customer first approach

Products

Design A non-conformist culture

Page 75

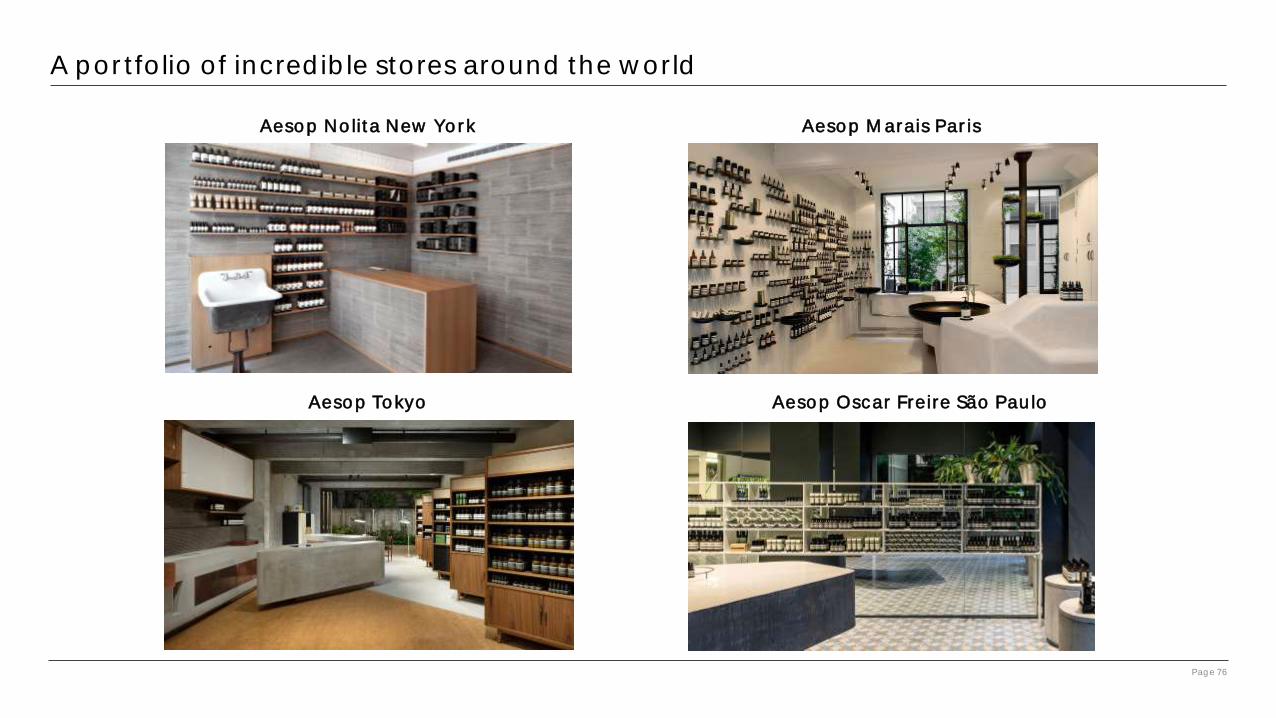

Aesop Nolita New York Aesop Marais Paris

Aesop Tokyo Aesop Oscar Freire São Paulo

A portfolio of incredible stores around the world

Page 76

Aesop | Vision: We are only at the start of an exciting journey

A global integrated network of online and physical stores

that delivers exceptional products and experiences, with

strong connections to core customers in all markets,and good brand recognition among the wider

community.

Growing businesses in all major markets of the worldwith committed leaders and supported staff.

Page 77

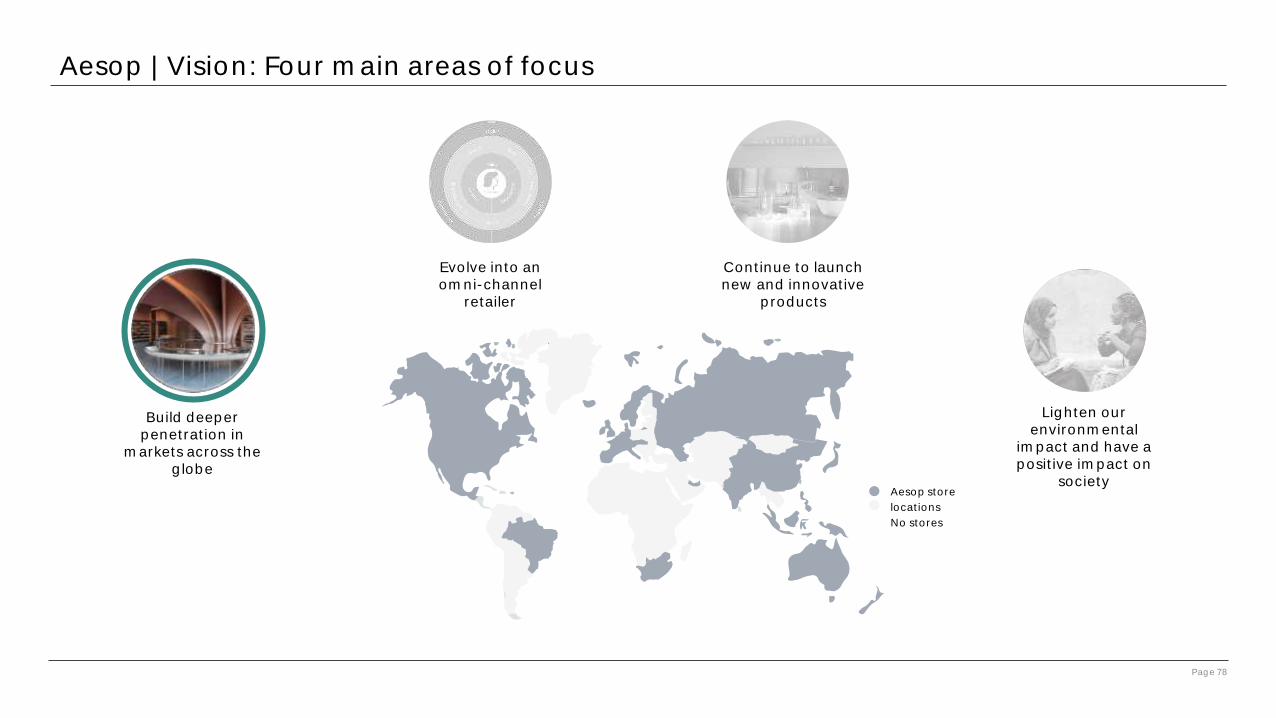

Aesop | Vision: Four main areas of focus

Build deeper penetration in

markets across the globe

Evolve into anomni-channel

retailer

Continue to launch new and innovative

products

Lighten our environmental

impact and have a positive impact on

societyAesop store

locations

No stores

Page 78

2017

2020

Signature Stores 209 Further expansion

Countries 23 29 - 31

Leveraging our regional offices, Aesop will continue to grow its business through both existing and new cities

12 month like-for-like growth rates:• Signature stores 15%• Department stores 15%

Our signature store presence will expand by almost 50% by 2020

In addition to new stores, Aesop will continue to drive its returns from existing stores by increased customer conversion and improved transaction size

Page 79

Build deeper penetration in

markets across the globe

• Through a mix of subsidiaries and distributors, with a focus on leveraging our presence in existing regions.

• In 2017, Aesop entered Austria and UAE (Dubai), with both countries trading strongly.

• A carefully sequenced roll-out plan taking into account market potential and resourcing has been developed.

Asia Pacific• Philippines

• Indonesia

• Vietnam

Europe• Russia (2018)

• Belgium (2018)

• Netherlands

• Spain (2019)

• Portugal

By 2020, our geographical footprint will extend into a further 6-8 countries

Build deeper penetration in

markets across the globe

Page 80

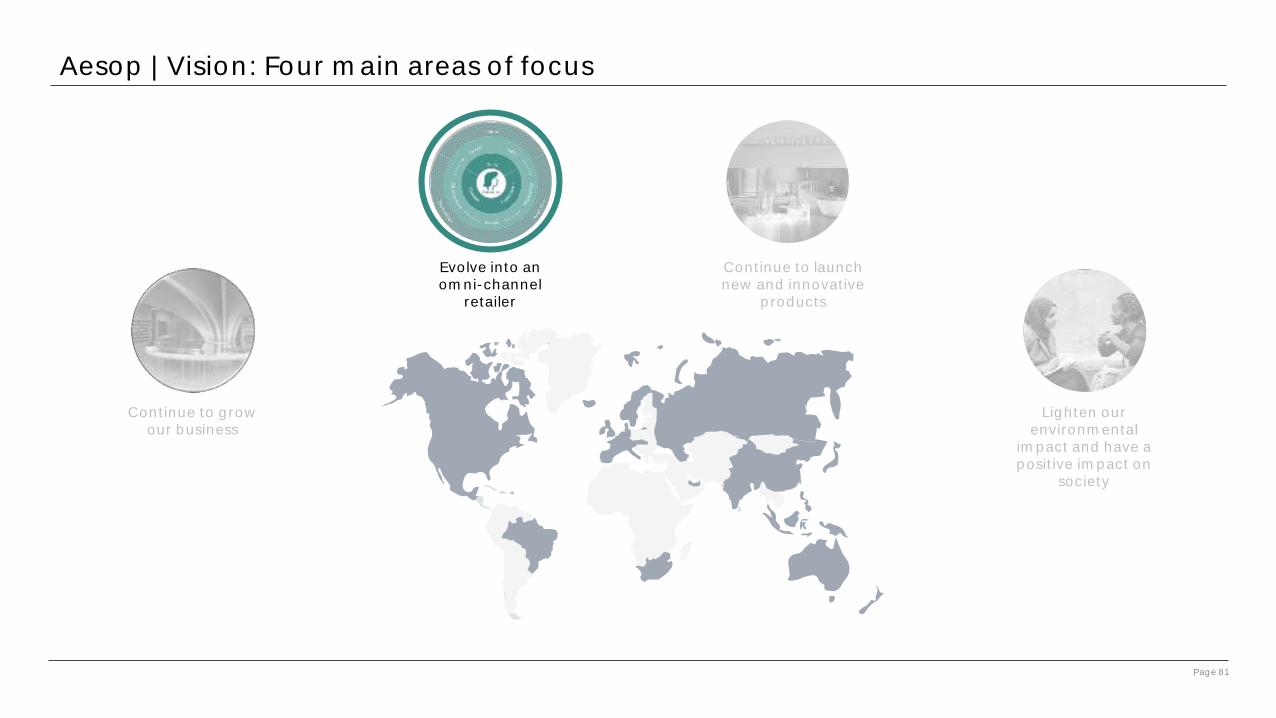

Continue to grow our business

Evolve into anomni-channel

retailer

Continue to launch new and innovative

products

Lighten our environmental

impact and have a positive impact on

society

Aesop | Vision: Four main areas of focus

Page 81

AESOP 2005

AESOP 2025

R&D Brand DistributionR&D Brand Distribution

Retail Customer

PRODUCT-CENTRIC(Aesop 2005)

RETAIL CENTRIC(Aesop 2017)

ONE RETAILSTRATEGY

Customer

D

a

i

Page 82

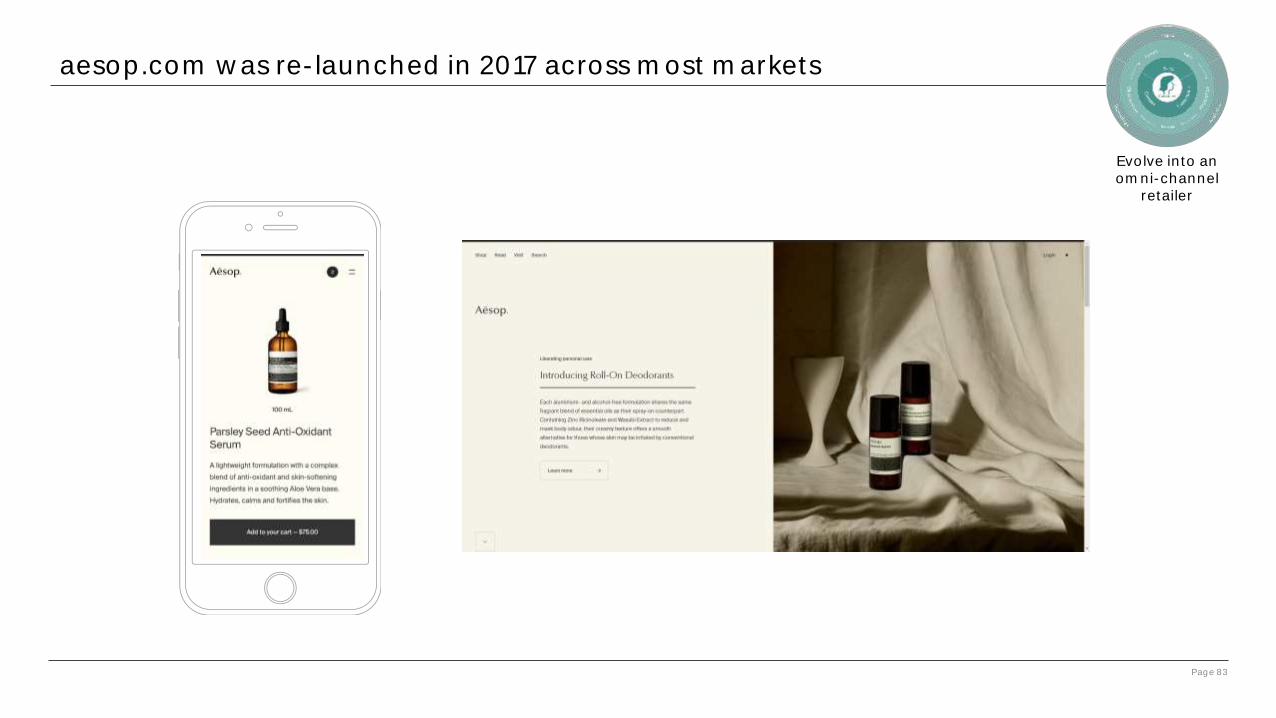

Evolve into anomni-channel

retailer

aesop.com was re-launched in 2017 across most markets

Page 83

Evolve into anomni-channel

retailer

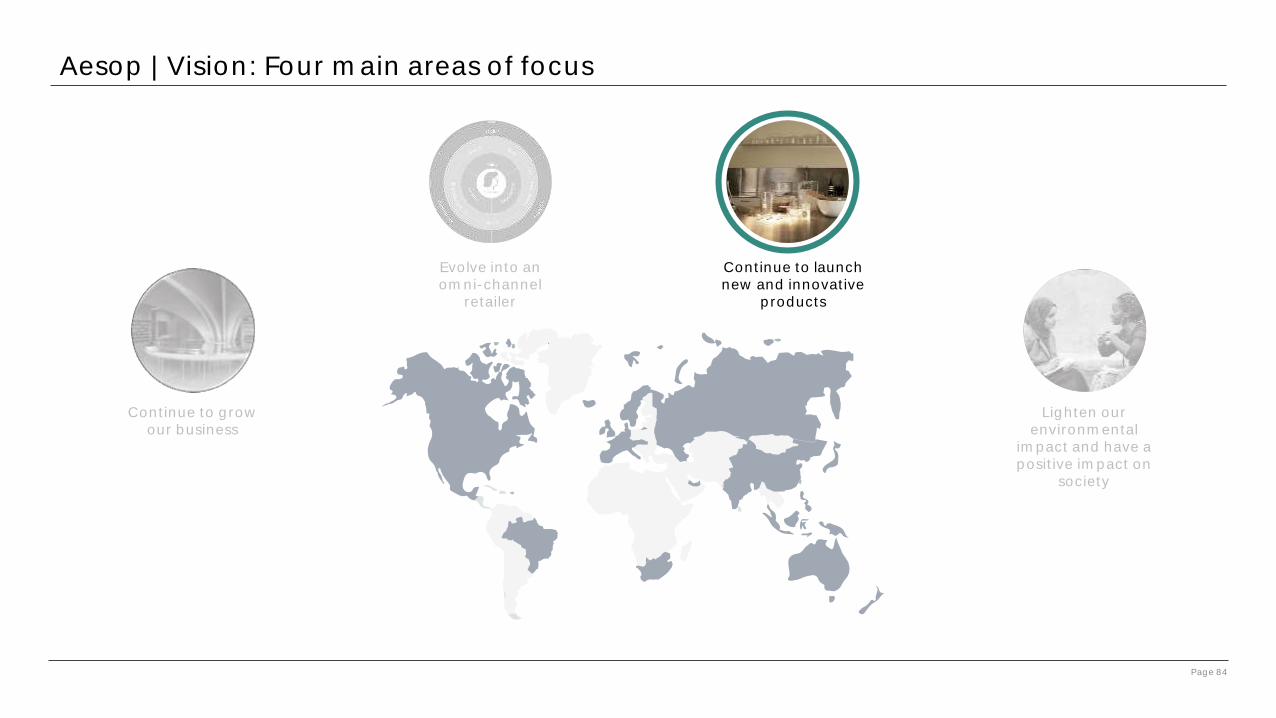

Continue to grow our business

Evolve into anomni-channel

retailer

Continue to launch new and innovative

products

Lighten our environmental

impact and have a positive impact on

society

Aesop | Vision: Four main areas of focus

Page 84

Aesop will continue to release limited, best-in-class products

Continue to launch new and innovative

products

In Two Minds Range

(Cleanser, Toner and Hydrator)

Toothpaste

Deodorants Roll-On

Hwyl Eau de Parfum

Room Sprays

• Skin care is our dominant product category, but Aesop is also strong across body, hair, perfume and home products

Page 85

Continue to grow our business

Evolve into anomni-channel

retailer

Continue to launch new and innovative

products

Lighten our environmental

impact and have a positive impact on

society

Aesop | Vision: Four main areas of focus

Page 86

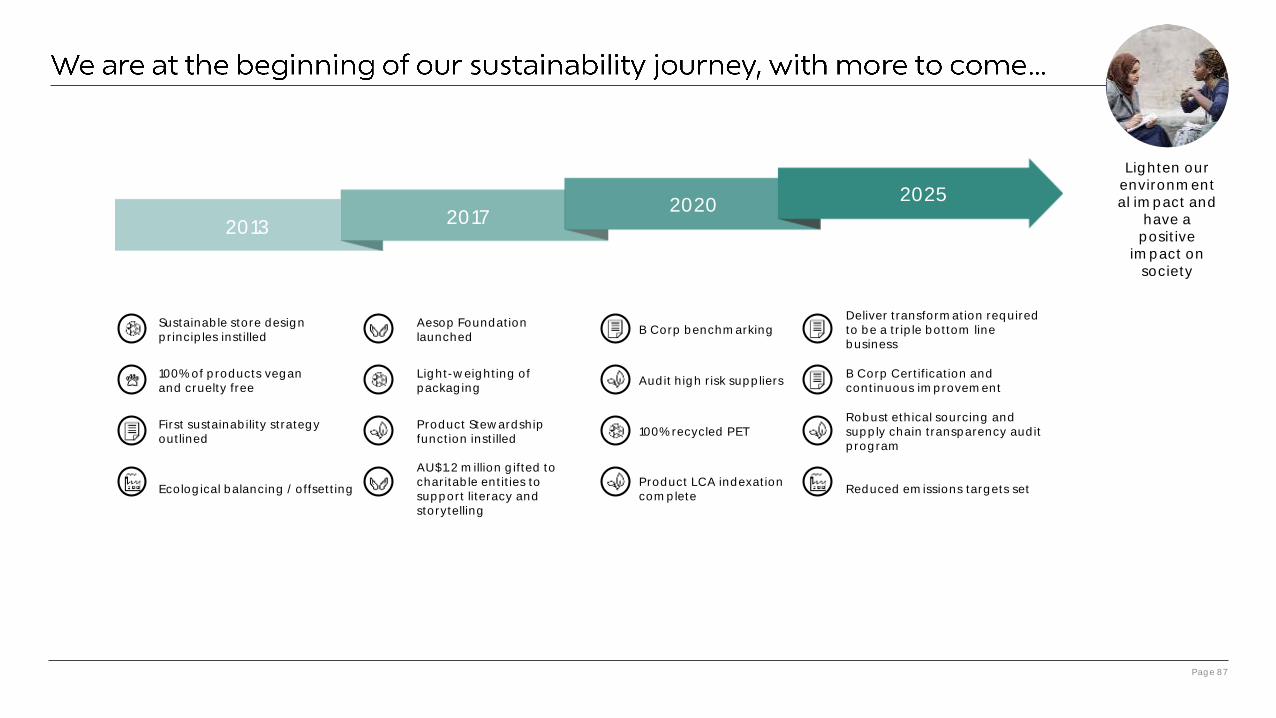

Sustainable store design principles instilled

Aesop Foundation launched

B Corp benchmarkingDeliver transformation required to be a triple bottom line business

100% of products vegan and cruelty free

Light-weighting of packaging

Audit high risk suppliersB Corp Certification and continuous improvement

First sustainability strategy outlined

Product Stewardship function instilled

100% recycled PETRobust ethical sourcing and supply chain transparency audit program

Ecological balancing / offsetting

AU$1.2 million gifted to charitable entities to support literacy and storytelling

Product LCA indexation complete

Reduced emissions targets set

20172020

2025

20132017

20202025

2013

Page 87

Lighten our environmental impact and

have a positive

impact on society

Established the Aesop Foundation

AUD$1.2m

distributed to charities

10 charitable organisations

supported

70+ charities in the pipeline

Development of Global Philanthropy

StrategyStaff engagement

In contribution to our wider community, the Aesop Foundation was established in 2016 to provide individuals with greater opportunities through the development of literacy and storytelling. We partner with organisations to cultivate written and verbal skills, and provide a platform for expression to those who may otherwise struggle to be heard. Through two distinct granting programs, it is our hope that we nurture diversity within the community, and the culture of the arts with resounding effect.

Lighten our environmental

impact and have a positive impact on

society

Page 88

Aesop | Vision: An exciting journey so far. Significantly more growth and development to come

Page 89

Continue to grow our business

Evolve into anomni-channel

retailer

Continue to launch new and innovative

products

Lighten our environmental

impact and have a positive impact on

societyAesop store

locations

No stores

A global integrated network of online and physical stores

that delivers exceptional products and experiences, with

strong connections to core customers in all markets,and good brand recognition among the wider

community.

Growing businesses in all major markets of the worldwith committed leaders and supported staff.

Group financial results and outlook

Roberto MarquesExecutive Chairman

of the Board

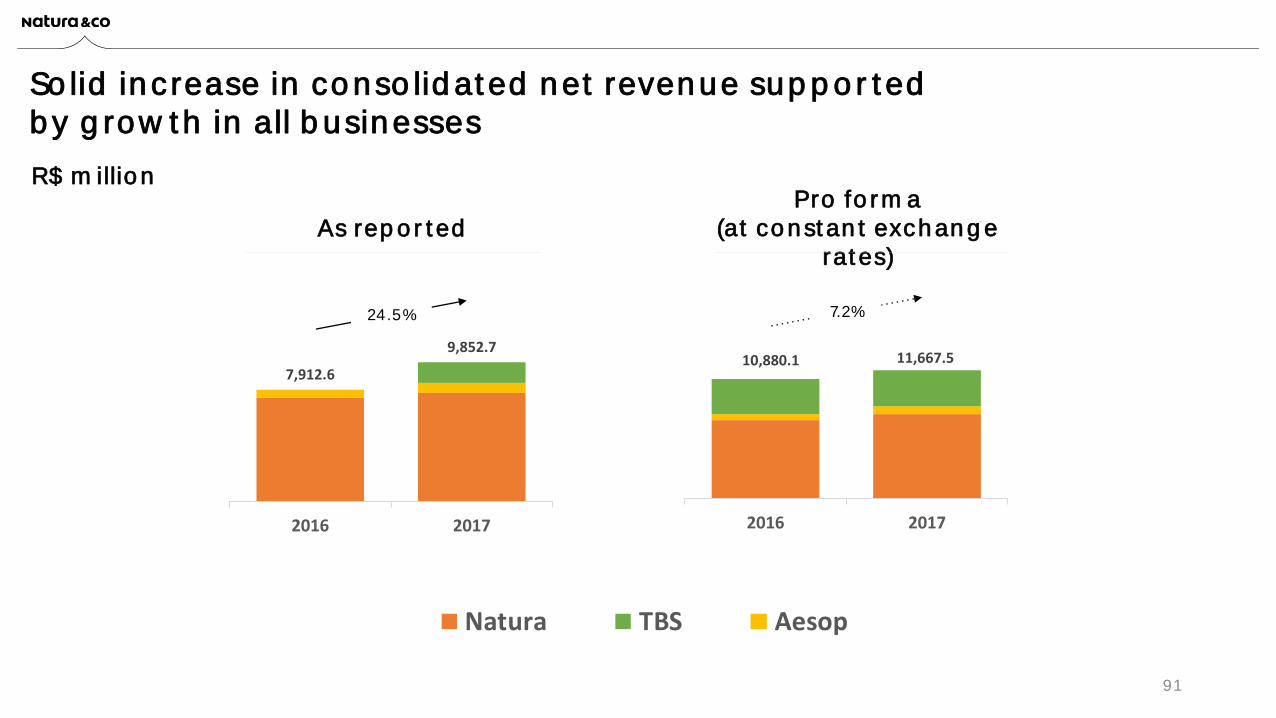

90

7,912.6

9,852.7

2016 2017

24.5% 7.2%

As reportedPro forma

(at constant exchangerates)

91

10,880.1 11,667.5

2016 2017

10.880,1 11.667,5

2016 2017

Natura TBS Aesop

R$ million

Solid increase in consolidated net revenue supported by growth in all businesses

1,565.51,783.2

2016 2017

1,343.6

1,741.9

2016 2017

As reportedPro forma

(at constant exchangerates)

29.6%13.9%

92

10.880,1 11.667,5

2016 2017

Natura TBS Aesop

R$ million

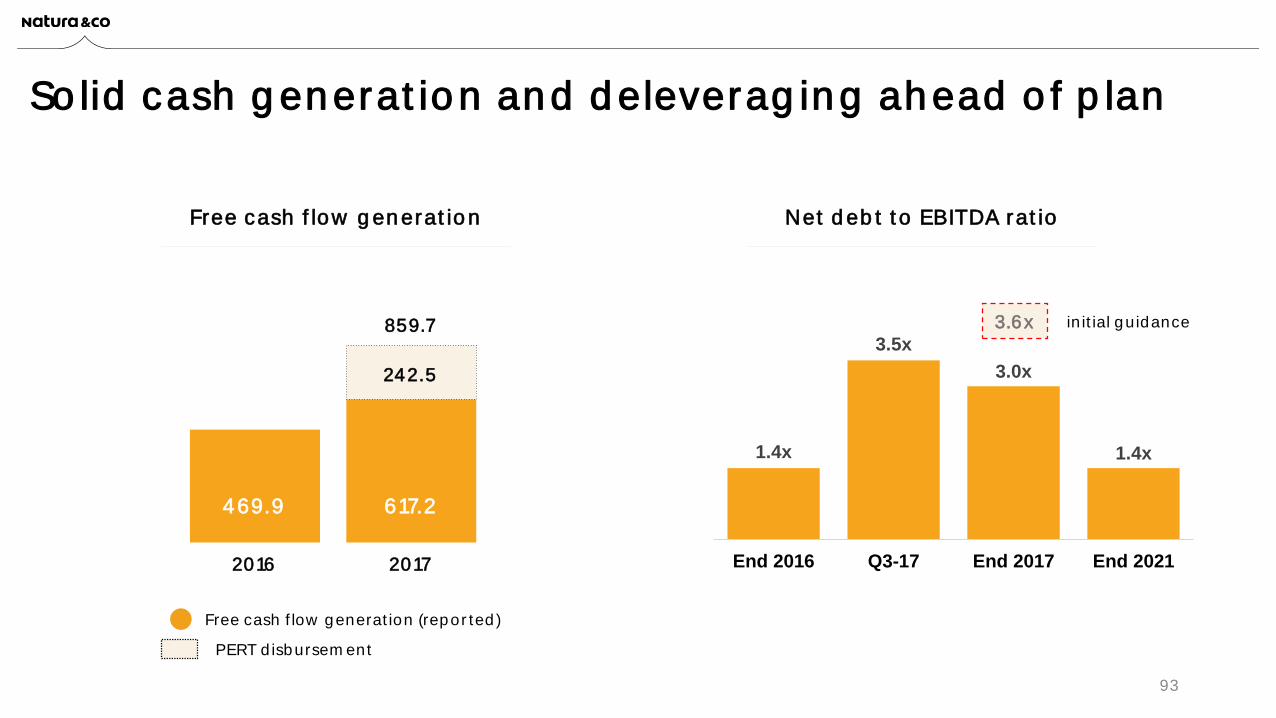

Robust improvement in EBITDA

Free cash flow generation (reported)

617.2

242.5

2017

469.9

2016

859.7

Free cash flow generation

1.4x

3.5x

3.0x

1.4x

End 2016 Q3-17 End 2017 End 2021

Net debt to EBITDA ratio

PERT disbursement

93

3.6x initial guidance

Solid cash generation and deleveraging ahead of plan

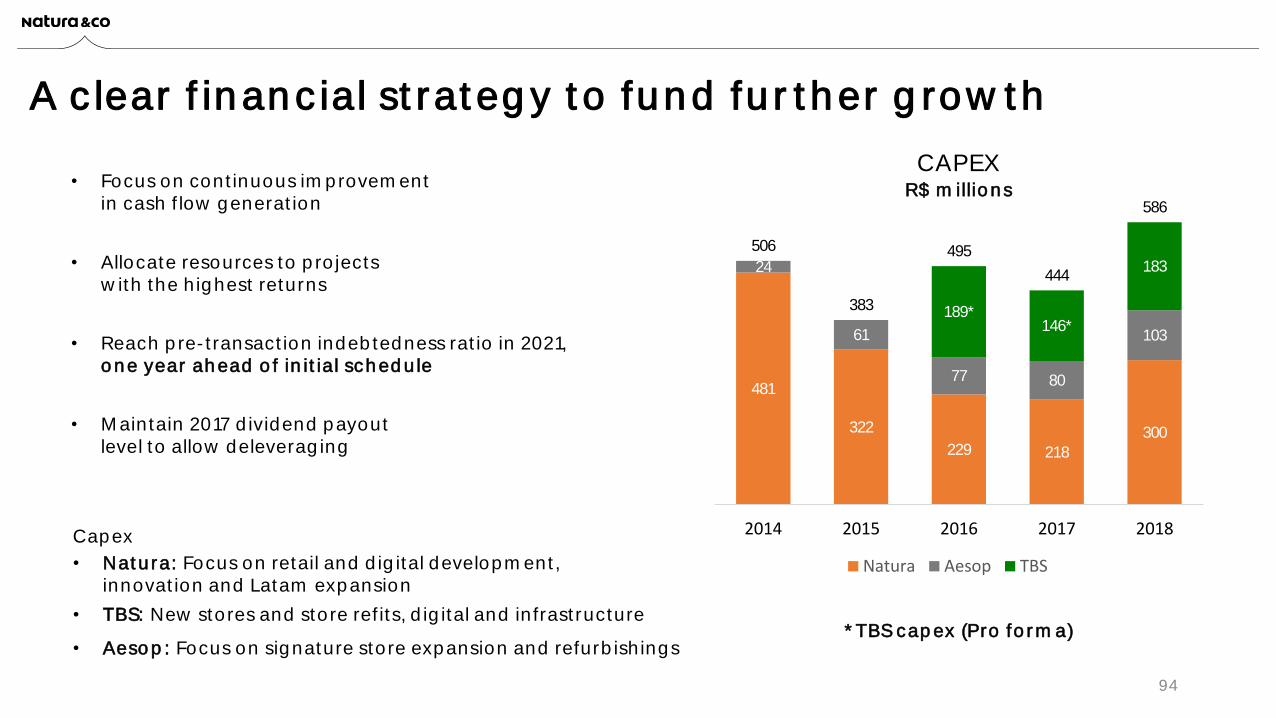

Capex

• Natura: Focus on retail and digital development, innovation and Latam expansion

• TBS: New stores and store refits, digital and infrastructure

• Aesop: Focus on signature store expansion and refurbishings

94

* TBS capex (Pro forma)

*

A clear financial strategy to fund further growth

481

322

229 218300

24

61

77 80

103

189*146*

183

506

383

495

444

586

2014 2015 2016 2017 2018

Natura Aesop TBS

R$ millions• Focus on continuous improvement in cash flow generation

• Allocate resources to projects with the highest returns

• Reach pre-transaction indebtedness ratio in 2021, one year ahead of initial schedule

• Maintain 2017 dividend payout level to allow deleveraging

CAPEX

11,667

17,150

2017 2022

Net sales 1

(in R$ MM)

95

1In BRL, 2017 net sales include full year of The Body Shop pro-forma.2 In BRL, 2017 EBITDA includes full year of The Body Shop pro-forma and was adjusted to exclude non-recurring effects of R$ 127 million, as detailed in appendix I.Under current accounting principles and including estimated foreign exchange rates (see appendix II)

Over the next five years, we target high single-digit growth in net sales1 and low double-digit growth in EBITDA2 on a compound annual growth rate (CAGR) basis,

aiming at a near-doubling of EBITDA by 2022

High single-

digit CAGR

1,656

3,100

2017 2022

EBITDA2

(in R$ MM)

Lowdouble-

digit CAGR

Targeting solid sales and EBITDA growth through 2022

Key takeaways

Roberto Marques Executive Chairman

of the Board

96

A Strengthened consolidated financial performance

• High single digit compound annual growth in net sales through 20221

• Near doubling of EBITDA by 20222

• Return to pre-transaction indebtedness level of 1.4x EBITDA in 202197

Key takeaways: The new group on the moveGovernance in place and first synergies identified, strong potential to

-how to unleash further value creation

Back on a growth path through the transformation of its business

model in Brazil, accelerated expansion in Latin America and a growing international footprint

Revival of an iconic brand underway in

each of the five pillars

turnaround plan

Continue strong growth performance

and increase its relevance within

the group

Clear roadmaps for the three brands:

98

Three empowered, iconic brands with

clear roadmaps

A global, increasinglymultichannel presence

A complementary productportfolio in key categories,

based on innovationand sustainability

Leveraging the Group'sscale and know-how to

share resources andenhance efficiency

A clear financial strategyto fund further growth

Positioned in an attractive, growing industry

1 2 3

4 5 6

Natura &Co: A compelling investment case

Solid sales and EBITDA growth through 2022

Q&A

99

APIMEC

100

APIMEC

101

NATURA COSMÉTICOS S.A.

102

Thank you

103

![IS 6472 (1971): General Requirements for Tinted Ophthalmic ... · IS 6472 (1971): General Requirements for Tinted Ophthalmic Glass [MHD 5: Ophthalmic Instruments and Appliances] Title:](https://img.pdfslide.us/doc/110x75/5f5befe83083e95c2d145594/is-6472-1971-general-requirements-for-tinted-ophthalmic-is-6472-1971-general.jpg)