Embed Size (px)

Citation preview

Report No. 442a-IVC

Appraisal of .FILE COPYThird Oil Palm ProjectIvory CoastJune 12, 1974

Agriculture Projects DepartmentWestern Africa Regional Office

Not for Public Use

U

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may not be published,quoted or cited without Bank Group authorization. The Bank Group does not accept responsibilityfor the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

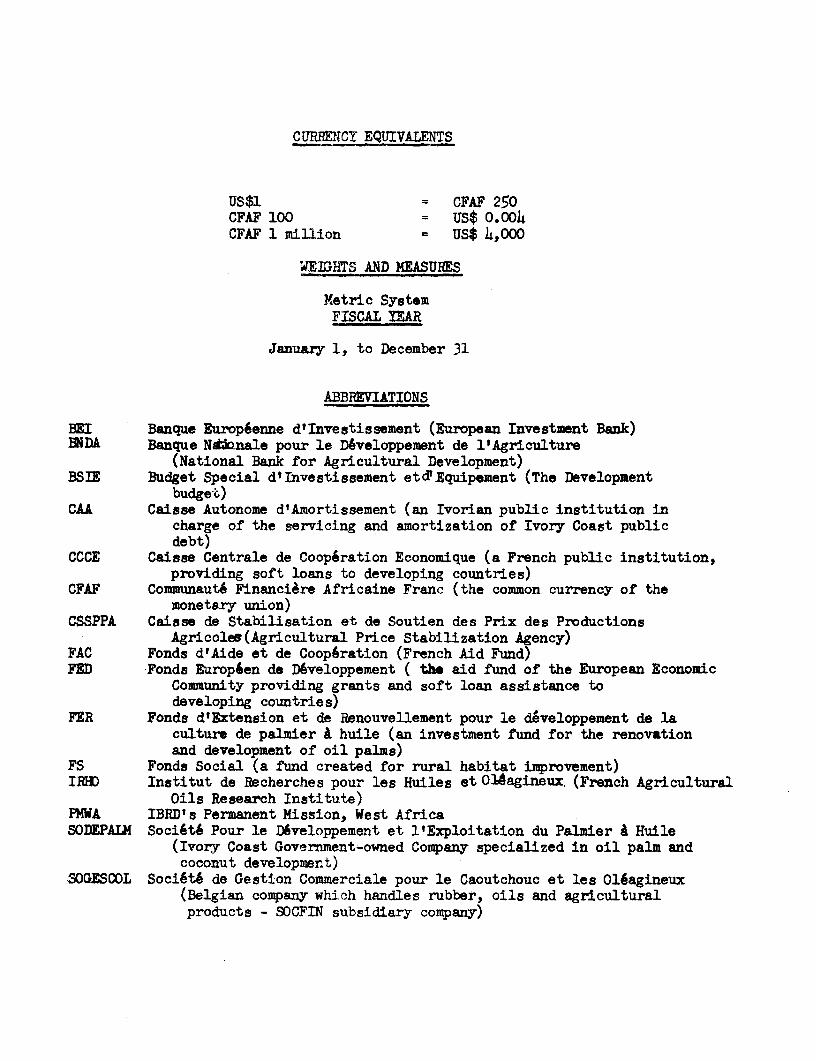

CURENJCY EQUIVALENTS

US$1 = CFAF 250CFAF 100 - US$ 0.004CFAF 1 milion = US$ 4,000

WEI3HTS AND MEASURES

Metric SystemFISCAL YEAR

January 1, to December 31

ABBREVIATIONS

BEI Banque Europ6enne d'Investissement (European Investment Bank)ENDA Banque Nd3anale pour le D6veloppement de l'Agriculture

(National Bank for Agricultural Development)BSIE Budget Special d'Investissement etd'Equipement (The Development

budget)CAA Caisse Autonome d'Amortissement (an Ivorian public institution in

charge of the servicing and amortization of Ivory Coast publicdebt)

CCCE Caisse Centrale de Coopgration Economique (a French public institution,providing soft loans to developing countries)

CFAF Communaut6 Financiere Africaine Franc (the common currency of themonetary union)

CSSPPA Caisse de Stabilisation et de Soutien des Prix des ProductionsAgricoles(Agricultural Price Stabilization Agency)

FAC Fonds d'Aide et de Coop6ration (French Aid Fund)FED Fonds Europ6en de D6veloppement ( the aid fund of the European Economic

Community providing grants and soft loan assistance todeveloping countries)

FER Fonds d'Extension et de Renouvellement pour le developpement de laculture de palmier a huile (an investment fund for the renovationand development of oil palms)

FS Fonds Social (a fund created for rural habitat improvement)IRID Inatitut de Recherches pour les Huiles et Oldagineux. (French Agricultural

Oils Research Institute)PMWA IBRD's Permanent Mission, West AfricaSODEPALN Societ6 Pour le D6veloppement et ltExploitation du Palmier a Huile

(Ivory Coast Government-owned Company specialized in oil palm andcoconut development)

S30GESCOL Soci6t6 de Gestion Commerciale pour le Caoutchouc et les 016agineux(Belgian company which handles rubber, oils and agriculturalproducts - SOCFIN subsidiary company)

IVORY COAST

THIRD OIL PALM PROJECT

Table of Contents

Page No.

SUMMARY AND CONCLUSIONS .................... o.... i - iii

Is INTRODUCTION o.................................* 1

IT* BACKGROUND to....... ................1

A. General ............ .. ................ .... 1

B. Institutional Structure ................... 3C. The Oil Palm and Coconut Sector ........... 5

III. THE PROJECT .......... .... ................ 7

A. General .. ................................. 7B. The Planting Program ...................... 7C. Estate Development ... .... .... ......... .. 8D. Outgrower Field Development .... ........... 9

IV. ORGANIZATION AND MANAGEMENT .................... 9

A. General ............................ ....... 9B. Outgrower Selection, Size of Holdings and

Credit Arrangements ....................... 10C. Processing and Marketing .................. 12

V. OOSTESTIMATES*+AND FINANCING ................... 12

A. Cost Estimates .............. ... 12B. Proposed Financing ....................... 14C. Procurement and Disbursement .............. 15D. Accounts and Audit ........................ 15

VI. YIELDS, OUTPUT, MARKETS AND PRICES ............. 16

A. Yields and Output ......................... 16B. Markets and Prices .......... ........ to 16

This report is based on the findings of an appraisal mission whichvisited Ivory Coast in November-December, 1973, composed of Messrs.G. Losson, J. Tillier and T. Winston.

Table of Contents (Continued)

a _ .

VII. FINANCIAL BENEFITS AND OUTLOOK .................. 17

VIII. ECONOMIC BENEFITS AND JUSTIFICATION .... ......... 19

IX. RECOMMENDATIONS ................................... 20

Annexes

1. Progress of Agricultural Projects Financed by Bank Loans

2. SODEPALM Accounts and Financing

Table 1. SODEPALM/PALMINDUSTRIE/PALMIVOIRE: Audited Balance Sheetson December 31.

Table 2. PALMINDUSTRIE: Audited Balance Sheets on December 31.Table 3. SODEPALM: Oil Palm Estates, Estimated Cash FlowsTable 4. SODEPALM: Oil Palm Outgrowers, Estimated Cash FlowsTable 5. SODEPALM: Coconut Sector, Estimated Cash FlowsTable 6. PALMINDUSTRIE: Estimated Cash FlowsTable 7. Association en Participation: Updated Estimates of Profit

and Loss AccountTable 8. Summarized Overall Cash Position for SODEPALM and PALMINDUSTRIETable 9. FER: Anticipated Cash flows

3. Oil Palm Sector

Table 1. The Planting ProgramTable 2. Oil Mills

4. Technical Features

Table 1. Project's Oil Palm Planting ProgramTable 2. Projected Yields

5. Credit Arrangements

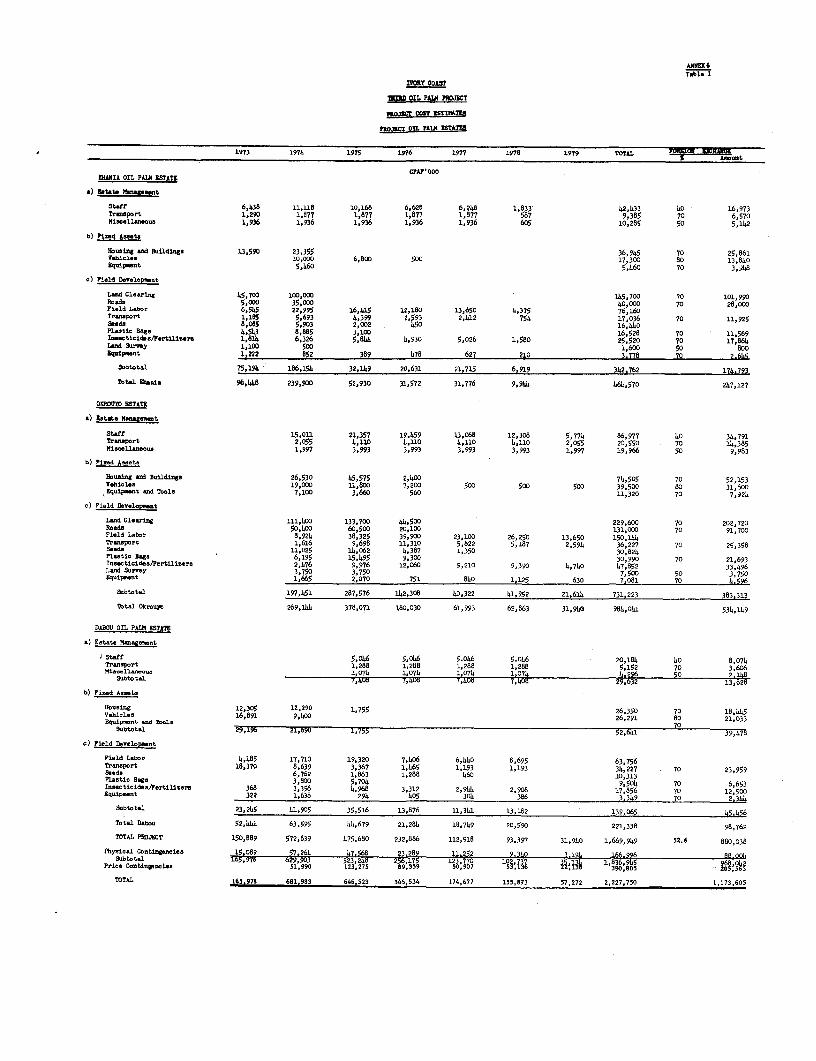

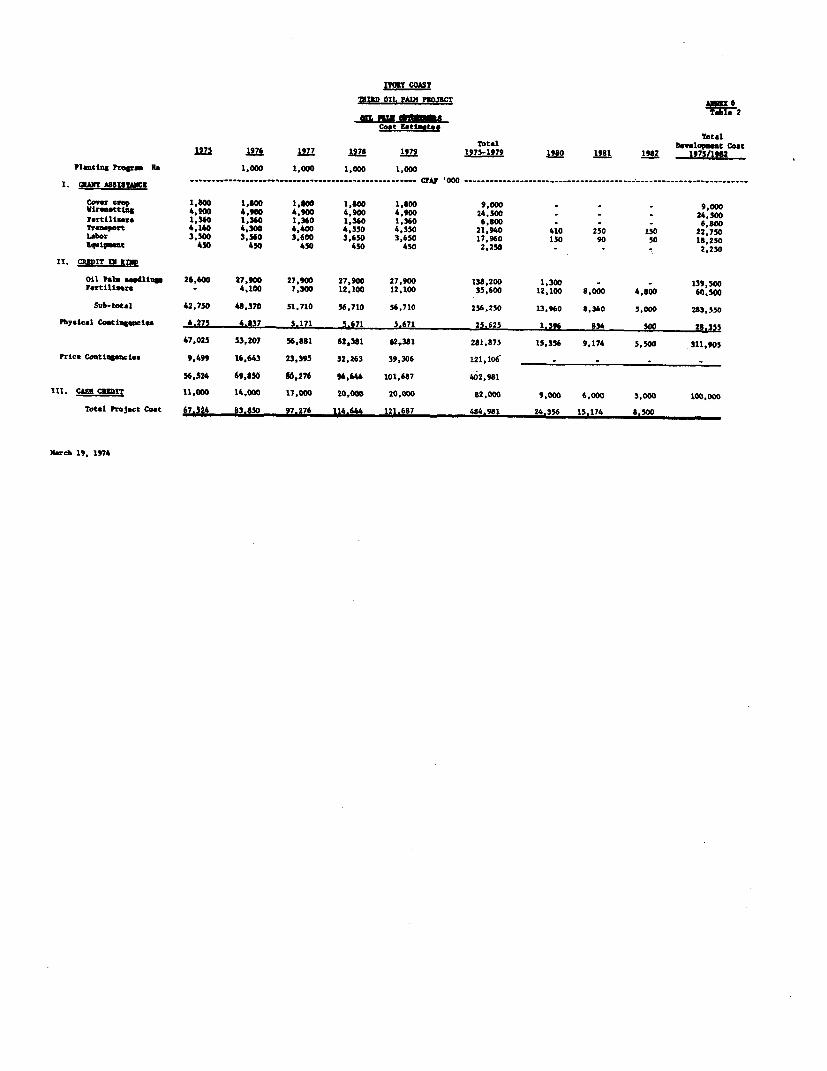

6. Project Costs

Table 1. Project Oil Palm EstatesTable 2. Oil Palm Outgrowers

Table of Contents (Continued)

7. Estimated Schedule of Disbursements

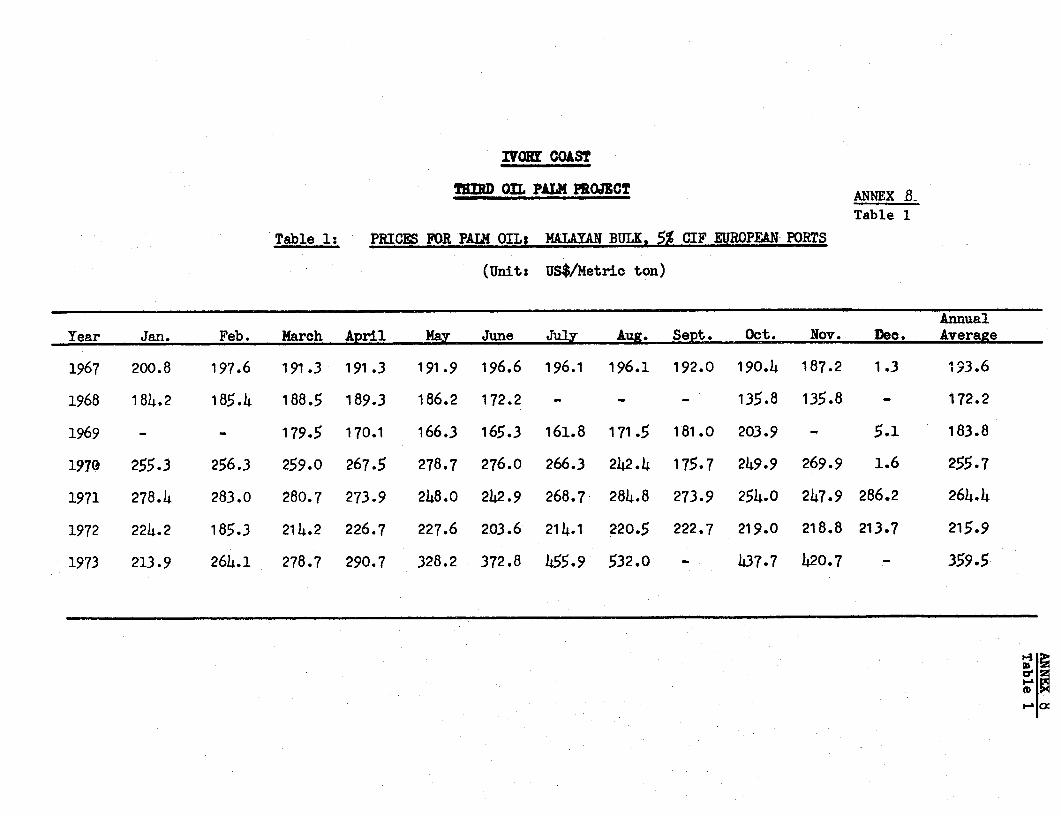

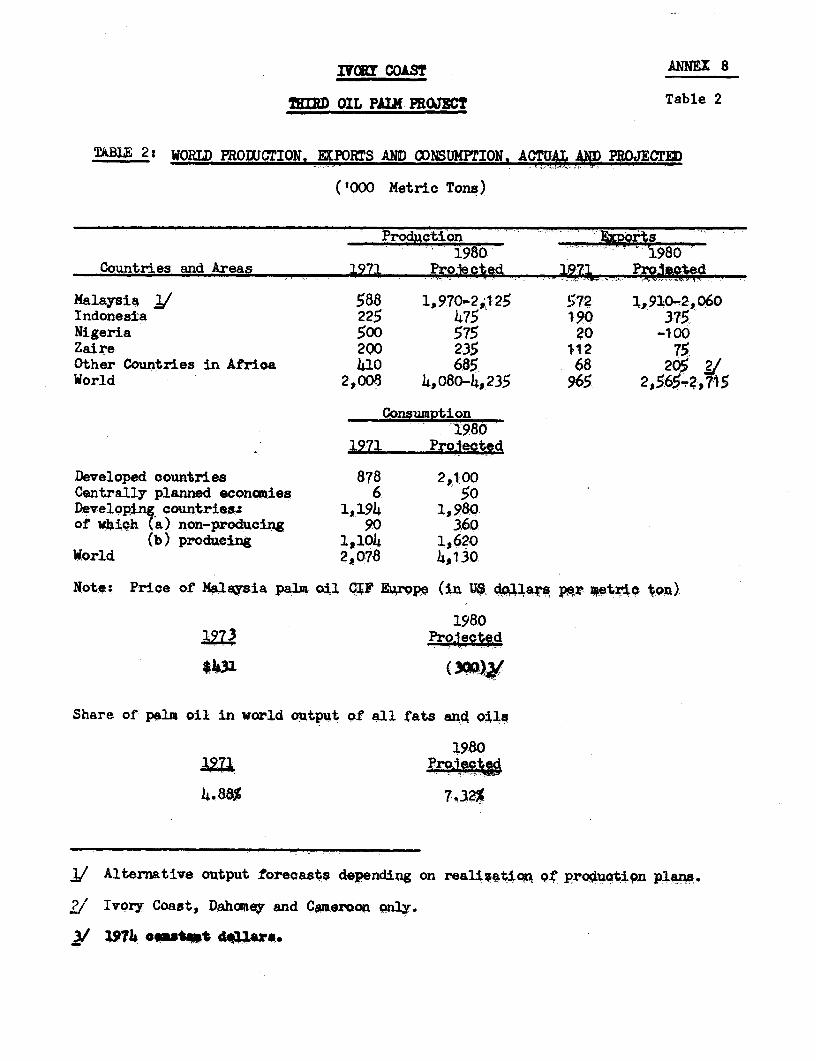

8. Market and Price Outlook fcr Palm Oil

Table 1. Prices for Palm Oil: Malayan bulk, 5% cif European portsTable 2. World Production, exports and consumption actual and

projected

9. Oil Palm Outgrowers: Cost a:,d Return Per Hectare Planted in 1975

10. Project Cash Flows

Table 1. Oil Palm EstatesTable 2. Oil Palm Outgrowers

11. Estimated Government Project Cash Flows

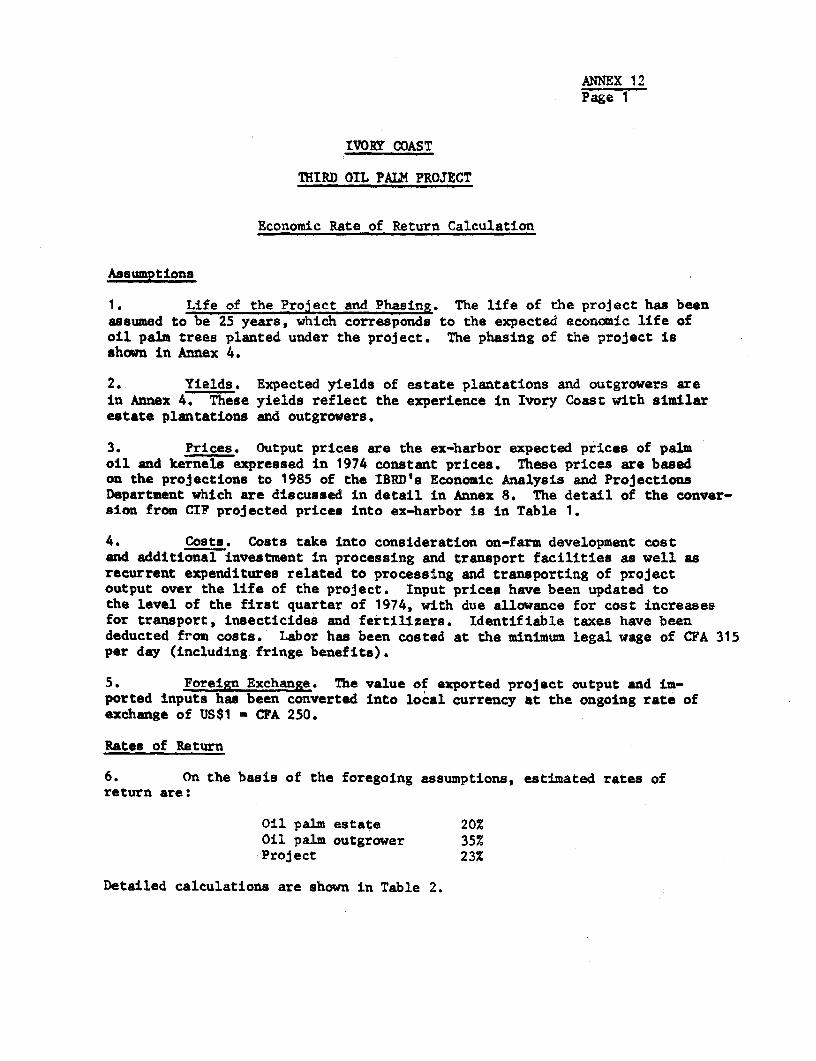

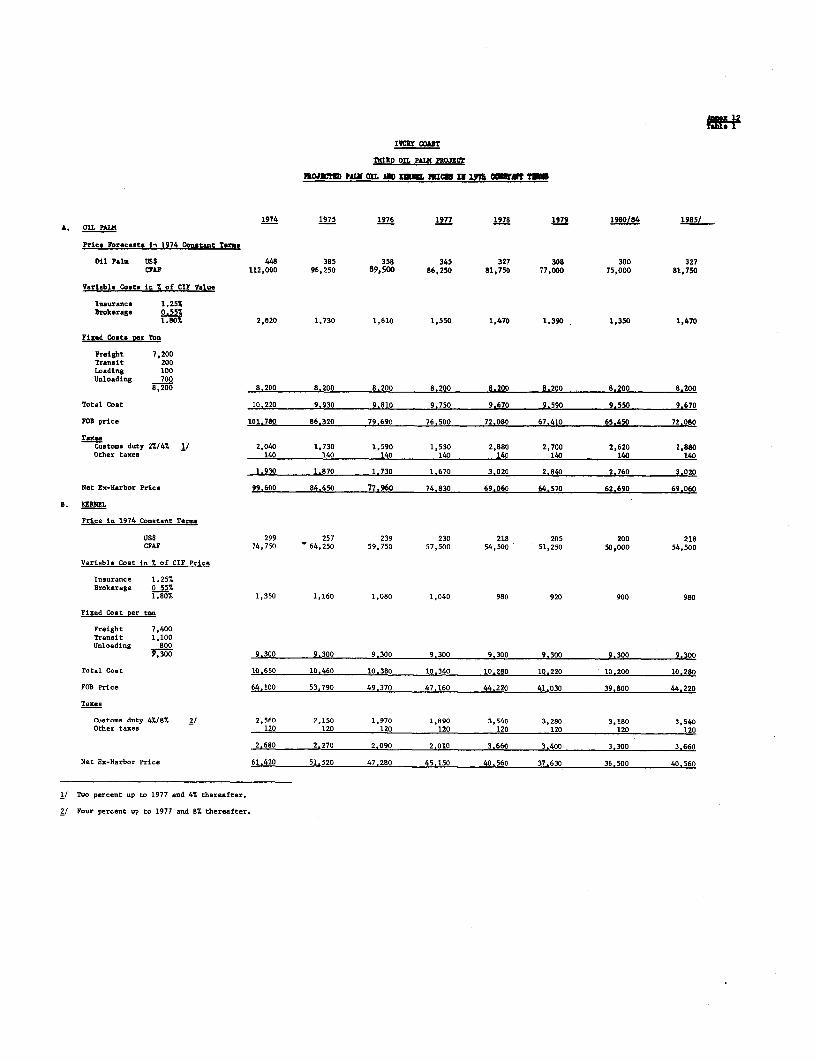

12. Economic Rate of Return Calculation

Table 1. Projected Palm Oil and Kernel Prices in 1974Constant Terms

Table 2. Economic Rate of Return

MAPS

IVORY COAST

THIRD OIL PALM PROJECT

SUMMARY AND CONCLUSIONS

Background

i. The Government of the Ivory Coast has asked the Bank to finance partof the costs of completing its oil palm development program East of theSassandra River. The proposed loan of US$2.6 million would be the Bank'sfinal contribution toward the ongoing program which has been under way sincethe middle 1960's, under the responsibility of an association of companies,SODEPALM, PALMINDUSTRIE and PALMIVOIRE (the Participation). The project wasprepared by the Participation. The appraisal was made by a Bank mission inNovember/December 1973.

Project Description

ii. The project, which aims at further diversifying agricultural produc-tion in forest and fringe savannah areas, and increasing farmers' income andthe country's foreign exchange earnings, would be carried out from 1974 to1979 and would comprise:

(a) planting 5,000 ha with high yield potential oil palm by out-growers, with the help of SODEPALM's technical and supervisedcredit services, to bring the total area of oil palm outgrowingsto 30,000 ha;

(b) planting or replanting 5,520 ha with high yield potential oilpalm, of which 400 ha would be with new hybrid lines onSODEPALM estates.

Project Execution

iii. The principal entity involved in the proposed project is Societepour le Developpement et l'Exploitation du Palmier a Huile (SODEPALM), whichwas founded in 1963 to develop the oil palm and coconut industries. It iswholly owned by Government. It owns oil palm and coconut estates, and isresponsible for providing credit and supervision for the oil palm and coconutoutgrowers. PALMINDUSTRIE, which is 73% owned by Government, owns the palmoil mills and ancillary installations needed to process the production fromestates and outgrowers. PALMIVOIRE, owned 40% by Government and 60% byprivate interests, manages the SODEPALM oil palm estates and PALMINDUSTRIEmills. PALMIVOIRE supplies all staff above the estate manager level. Itsoperating standards and performance are very good. The oil palm outgrowerprogram, as well as coconut estates and outgrowers, is outside the scopeof the Participation, and SODEPALM has its own competent organization forthese. The financial condition of the entities involved in the project issound. Despite production costs that are 20% higher than anticipated, thefinancial results for the Participation and for outgrowers have been betterthan expected due largely to higher than anticipated prices for palm products.

- ii -

iv. On January 1, 1974, in accordance with existing loan covenants,qualified Ivorian citizens were appointed as Director and Deputy DirectorGeneral of SODEPALM/PALMIVOIRE, to replace former expatriate incumbents.SODEPALM/PALMIVOIRE intends to retain the services of seven high level expa-triates to fill key positions for which suitable Ivorian replacements have notyet been found. Consequently, all key managerial positions continue to befilled satisfactorily.

Cost Estimates and Financial Arrangements

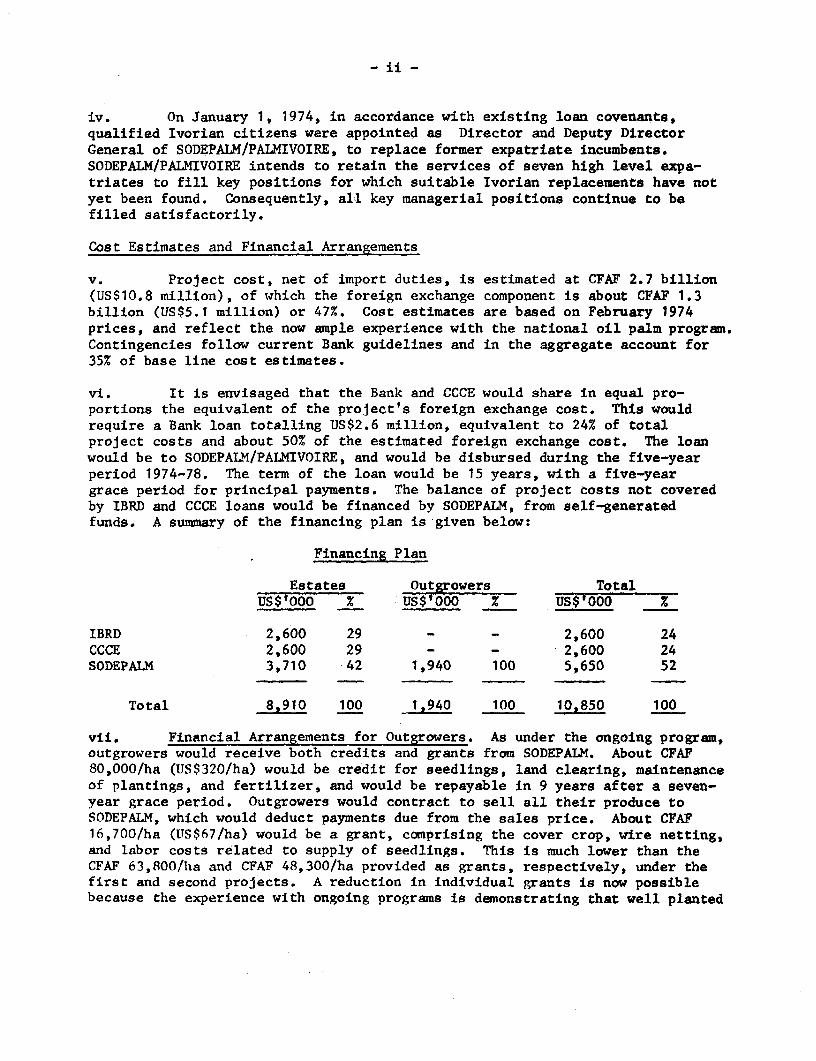

v. Project cost, net of import duties, is estimated at CFAF 2.7 billion(US$10.8 million), of which the foreign exchange component is about CFAF 1.3billion (US$5.1 million) or 47%. Cost estimates are based on February 1974prices, and reflect the now ample experience with the national oil palm program.Contingencies follow current Bank guidelines and in the aggregate account for35% of base line cost estimates.

vi. It is envisaged that the Bank and CCCE would share in equal pro-portions the equivalent of the project's foreign exchange cost. This wouldrequire a Bank loan totalling US$2.6 million, equivalent to 24% of totalproject costs and about 50% of the estimated foreign exchange cost. The loanwould be to SODEPALM/PALMIVOIRE, and would be disbursed during the five-yearperiod 1974-78. The term of the loan would be 15 years, with a five-yeargrace period for principal payments. The balance of project costs not coveredby IBRD and CCCE loans would be financed by SODEPALM, from self-generatedfunds. A summary of the financing plan is given below:

Financing Plan

Estates Outgrowers Totals$_000 x - US$ 000 % US$'000 %

IBRD 2,600 29 - - 2,600 24CCCE 2,600 29 - - 2,600 24SODEPALM 3,710 42 1,940 100 5,650 52

Total 8,910 _ 1,940 100 10,850 100

vii. Financial Arrangements for Outgrowers. As under the ongoing program,outgrowers would receive both credits and grants from SODEPALM. About CFAF80,000/ha (US$320/ha) would be credit for seedlings, land clearing, maintenanceof plantings, and fertilizer, and would be repayable in 9 years after a seven-year grace period. Outgrowers would contract to sell all their produce toSODEPALM, which would deduct payments due from the sales price. About CFAF16,700/ha (US$67/ha) would be a grant, comprising the cover crop, wire netting,and labor costs related to supply of seedlings. This is much lower than theCFAF 63,800/ha and CFAF 48,300/ha provided as grants, respectively, under thefirst and second projects. A reduction in individual grants is now possiblebecause the experience with ongoing programs is demonstrating that well planted

- iii -

and maintained oil palm can compete successfully with other crops in the projectarea and, therefore, prospective participants would be less reluctant to jointhe project than in earlier years.

Procurement and Disbursements

viii. Contracts over US$50,000 would be subject to international compet-itive bidding in accordance with Bank guidelines. ICB would be used to pro-cure goods and services estimated to cost US$1.4 million: fertilizer andinsecticides, US$0.5 million; vehicles and equipment, US$0.9 million. Localmanufacturers would be given preference of 15% against bids quoted in CIFprices. High-yielding palm oil seeds estimated to cost US$0.5 million wouldbe supplied by IRHO, the only supplier of suitable material. Civil worksconsisting of land clearing and earth estate roads, estimated to cost US$2.7million, would be carried out by force account. SODEPALM has the equipment,and has demonstrated that it can conduct it both efficiently and less costlythan contractors. Of the remaining project costs, US$2.6 million would befor staff and labor services, US$0.3 million would be for materials toestablish plant nurseries, US$0.5 million would be for housing, and US$2.8million unallocated. Disbursement of Bank and CCCE loans would occur fromloan signature to the end of the 1978 calendar year. For administrativeconvenience, the Bank and CCCE would finance pari passu, at 35% each, againstthe estates component only. Disbursements would be against contracts, com-pletion certificates and other documents certified by SODEPALM.

ix. Primary benefits from the oil palm outgrower and estate plantingswould be the increased production of palm oil and kernels and resultant netannual incremental foreign exchange earnings amounting to about US$8.8 millionby 1987.

x. Based on expected world prices for these commodities, the returnsto the economy from the project investments are estimated to be about 23%.The rate of return for the estate component alone is estimated at 20%, and therate for the outgrower component at 35%. The project would also have substan-tial secondary benefits through providing employment for some 600 workers onthe oil palm estates, and creating some 265,000 mandays of work per year indeveloping outgrowers holdings. It would further the Government's programof agricultural diversification both directly, through the project output,and indirectly by generating resources with which to pursue other programs.

Recommendations

xi. The assurances and covenants of Loans IVC-611 and IVC-760 would becontinued substantially in the Third Oil Palm Loan. The project is suitablefor a Bank loan to SODEPALM/PALMIVOIRE for US$2.6 million repayable over10 years after five years of grace on principal payments.

IVORY COAST

THIRD OIL PALM PROJECT

I. INTRODUCTION

1.01 The Government of the Ivory Coast has asked the Bank to financepart of the costs of completing its ongoing oil palm and coconut developmentprogram that is being carried out East of the Sassandra River (Map). Theobjectives of the program are to increase output of coconut and oil palmproduce, to further diversify agricultural production in forest and fringesavannah areas, and to increase farmers' inc,xnes and the country's foreignexchange earnings.

1.02 The proposed loan of US$2.6 million would be the Bank's final contri-bution toward the ongoing program, which has been underway since the middle1960's under the responsibility of an association of companies, SODEPALM,PALMINDUSTRIE and PALMIVOIRE, joined together in a Participation (the Partici-pation). The Bank and the prospective cofinancer of the proposed project,France's Caisse Centrale de Cooperation Economique, and the Government believethat the completed program, which involves almost 100,000 ha of oil palm andcoconut and substantial processing and commercial operations, will requirethe undivided attention of the Participation management. For this reason,Government plans to assign responsibility for future development of oil palmsand coconuts (in the Southwest) to a different agency.

1.03 The project was prepared by the Participation. This report is basedon the findings of a Bank mission which visited the Ivory Coast in November/December 1973, composed of Messrs. Losson, Tillier and Winston.

1.04 The Bank has made seven loans for agricultural development in theIvory Coast: three totalling US$17.1 million in 1969 for oil palm and coconutdevelopment; a loan of US$7.5 million in 1970 for smallholder cocoa production;two oil palm and coconut loans of US$7 million in 1971; and a loan of US$8.4million for a rubber project in late 1973. All of the projects financed havebeen completed or are progressing satisfactorily (Annex 1).

II. BACKGROUND

A. General

2.01 The Ivory Coast has a land area of about 324,000 km , broadlydivided into two ecological zones. Tropical rain forest stretches across thecountry in a belt reaching about 200 km inland from the Atlantic Ocean, andfurther North the forest is replaced by savannah which covers the remainderof the country. Shifting cultivation has led to the displacement of forestsby savannah, particularly in the center of the country.

- 2 -

2.02 Population is estimated at about 5.4 million, growing at about 3.3%annually (including 1% growth from immigration). Small scale agricultureprovides about 80% of employment and, according to estimates, jobs for some400,000 foreign workers, mainly from Upper Volta and Mali.

2.03 GDP amounts to about US$1.8 billion and exports to about US$0.5billion (both 1972 figures). Due to the rapid growth of industry and urbanservices, the share of agriculture (including forestry and fishing) in GDPdecreased from 36% in 1965 to only 27% in 1972. However, the agriculturalsector still accounts for 86% of all exports (CFAF 120.7 billion out ofCFAF 139.5 billion in 1972).

2.04 In 1970, 23% of the population lived in towns with more than5,000 inhabitants; by 1985, this figure is expected to reach 43%. There isalso migration within the rural areas, from the savannah to the forest zone.Population in cities is expected to grow at around 6%, that of the forestzone at about 4%, and that of the savannah to decline by about 1% per year.

2.05 Migration is due largely to the wide income disparity between sectorsand regions. In 1970, when overall per capita income was CFAF 81,200 (US$325),money incomes of rural inhabitants varied from CFAF 3,400 (US$14) in the North,to CFAF 17,000 (US$68) in the central rain forest, and CFAF 23,600 (US$94) inthe South around AbidJan.

2.06 The forest zone produces the greatest share of agricultural outputand 86% of agricultural exports, with timber, coffee and cocoa being the mostimportant. Since 1965, the government has undertaken a program of cropdiversification involving pineapples, bananas, coconut, oil palm and rubber(the last three with the assistance of Bank loans). But coffee and cocoaremain the most important crops for small scale agriculture, with almosthalf of all farm families involvel in their production. A second cocoa projectis under consideration by the Bank.

2.07 In contrast, the savannah region is dominated by subsistence crop-ping of maize, rice, cassava, sorghum, beans and peas. Livestock productionis generally limited to poultry and small ruminants, mainly goats; beefproduction is limited by prevalence of tse-tse fly. Until recently, effortsto improve savannah incomes have been limited to rice and cotton developmentprograms. A major program in cotton, rice and other food crops is now inpreparation with Bank assistance.

Development Strategy

2.08 Real growth in the economy has averaged about 7% per year over thepast decade. Government would like to maintain this high growth rate. Thuspolicy emphasis is on commodity output increases, as well as on diversification,and making exports competitive to protect them from adverse trends in worldprices. The economy is very dependent on foreign exchange, and as the countrydoes not possess commercially exploited mineral resources, there is no alter-native to export crops as a source of foreign exchange.

- 3 -

2.09 Until recently, efforts to improve agricultural productivity havetaken the single crop approach ani have generally been successful. Thisapproach was helped by the countr-'s being virtually self-sufficient in foodexcept for livestock products. Urbanization is now changing the situationand the need for increasing food production is pressing. Government is plan-ning to tackle this problem and the related one of rural poverty in the food-producing Savannah zone through regional programs involving a package ofimprovements not only in agriculture but in the physical and social infrastruc-ture. Projects currently under preparation for Bank financing support theseobjectives.

B. Institutional Structure

2.10 Overall development planning is in the hands of the Planning Ministry,while detailed plans and programs for crop production, forestry and fresh waterfisheries are the responsibility of the Ministry of Agriculture. Execution ofthese programs is entrusted to a number of agencies, some of which are Statecompanies, such as Societe d'Assistance Technique pour la Modernisation Agricolede la Cote d'Ivoire (SATMACI) for coffee and cocoa development. Others areforeign companies under contract to the Government, such as Compagnie Francaisede Developpement des Textiles (CFDT) for cotton development.

2.11 The principal entity involved in the proposed project is Societepour le Developpement et 1'Exploitation du Palmier a Huile (SODEPALM), whichwas founded in 1963 to develop the oil palm and coconut industries. It iswholly owned by Government. It owns oil palm and coconut estates and is re-sponsible for providing credit and supervision to oil palm and coconut outgrow-ers. SODEPALM is part of a joint venture (the Participation) which additionallyinvolves PALMINDUSTRIE and PALMIVOIRE. PALMINDUSTRIE is owned 73% by Governmentand 27% by private interests, and owns the palm oil mills and ancillary installa-tions needed to process the production from SODEPALM estates and outgrowers.PALMIVOIRE is owned 40% by Government and 60% by the same private interestswith minority ownership in PALMINDUSTRIE, and manages the SODEPALM oil palmestates and PALMINDUSTRIE mills. PALMIVOIRE supplies all staff above estatemanager level. Its operating standards and performance are very good.PALMIVOIRE does not directly provide services to outgrowers since the out-grower program is outside the scope of the Participation, except in so faras the Participation processes outgrower palm produce on a cost basis; coconutdevelopment, both estates and outgrowers, is also outside the Participation.Consequently, SODEPALM has its own organization for outgrowers and coconutdevelopment. Profits or losses to the Participation are divided proportionatelyamong the three companies on the basis of their investments. PALMIVOIRE, whosefinancial contribution is minimal, is remunerated for its management serviceson a sliding scale based on financial results of the Participation as a whole.The institutional structure is described in detail in the "Appraisal of theSecond Oil Palm and Coconut Project" (PA-89a, June 1, 1971).

- 4 -

2.12 Fonds d'Extension et de Renouvellement (FER). This fund was set upin conjunction with the Participation, at the request of the Fonds Europeen deDeveloppement (FED), initially to finance modern housing for oil palm estateworkers and to assist in financing development of outgrower oil palm produc-tion. Its revenues were to consist of (a) rent paid by SODEPALM on the estatehousing, and (b) transfers from SODEPALM of CFAF 0.80/kg of fresh fruit bunchesproduced on the oil palm estates, as a form of repayment of the CFAF 8.3 bil-lion grant Government received from FED to establish the first 32,000 ha ofSODEPALM estates. Because estate production has been in its initial stages,transfers to FER under the levy on production have been small (CFAF 422 mil-lion). Since FER was short of funds to carry out its housing program,SODEPALM prefinanced its estate housing program, costing CFAF 2 billion. In1973 and early 1974, FER borrowed money from Government sources and repaidSODEPALM. Subsequently, Government decided that SODEPALM should own its ownestate housing outright, and should pay over 15 years the CFAF 2 billionrecently received from FER. As transfers to the FER from the levy on estateproduction will increase rapidly in the years ahead, this fund is expected tobecome a significant source of funds and Government would draw upon it tohelp finance the outgrower development program (para 4.06) and to financeoil palm and coconut development in the Southwest.

2.13 Agricultural Production Price Stabilization Agency. The "Caisse deStabilisation et de Soutien des Prix des Productions Agricole" (CSSPPA) is re-sponsible for carrying out Government agricultural price support policies. Itsupports producer prices for cotton, cocoa and coffee growers in a conventionalmanner: paying producers a guaranteed minimum price which it fixes annually,selling the commodities on the world market, and absorbing profits or losseson its operations. For oil palm, CSSPPA does not guarantee minimum pricesto outgrowers or to SODEPAIM, nor does it market oil palm products. Ratherits function is limited to moderation of drastic changes in world prices overconsecutive years. SODEPALM/PALMIVOIRE controls its own export sales and re-ports export prices and volume to CSSPPA, which intervenes after the year'sresults are known, but only if the average export prices for palm products varymore than 10% in either direction from the year before. For instance, in theevent of a substantial increase in export price in one year relative to thepreceding year, SODEPALM would be called on to transfer revenue to CSSPPA onthe following basis: (a) none of the marginal revenue from the first 10% ofthe price increase; (b) half of the marginal revenue from the 10-15% tranche;and (c) four-fifths of the marginal revenue from any remaining price increaseabove 15%. A similar formula applies for the transfer of funds from CSSPPAto SODEPALM in the event of a price decrease. CSSPPA does not support coconutprices.

2.14 Agricultural Research. Agricultural research is undertaken by variousFrench organizations under technical assistance agreements with France, andresearch costs are shared by the two Governments. Oil palm and coconut researchis undertaken by the Institut de Recherches pour les Huiles et Oleagineux(IRHO). PALMIVOIRE has a department concerned with collection, processingand end product research. Some of the results of research are described inAnnex 4.

C. The Oil Palm and Coconut Sector

Oil Palm Development

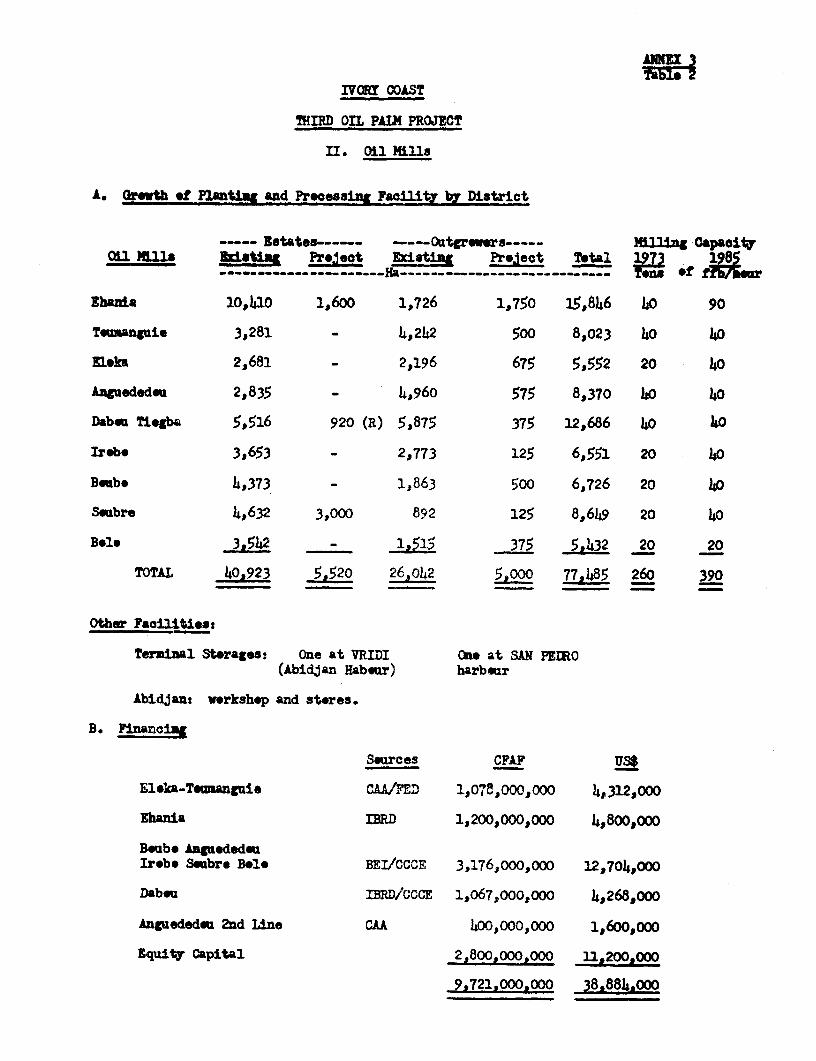

2.15 In the early 1960s Government initiated an oil palm developmentprogram and established SODEPALM to carry it out. Financial help was obtainedfrom Fonds Europeen de Developpement (FED), Banque Europeenne d'Investissement(BEI), Caisse Centrale de Cooperation Economique (CCCE), and IBRD (Annex 1).Some 65,000 ha of oil palms have been planted under the programs, of a nationaltotal of 75,000 ha of improved oil palm; the balance was planted prior to theSODEPALM program by private entrepreneurs. 55,000 ha, of various ages, arenow in production and exports of palm oil are growing rapidly:

Palm Oil Production and Exports

1969 1970 1971 1972 1980 forecast------------------'000 tons-----------------

Production 36 52 69 100 200

Exports 2 13 28 55 110

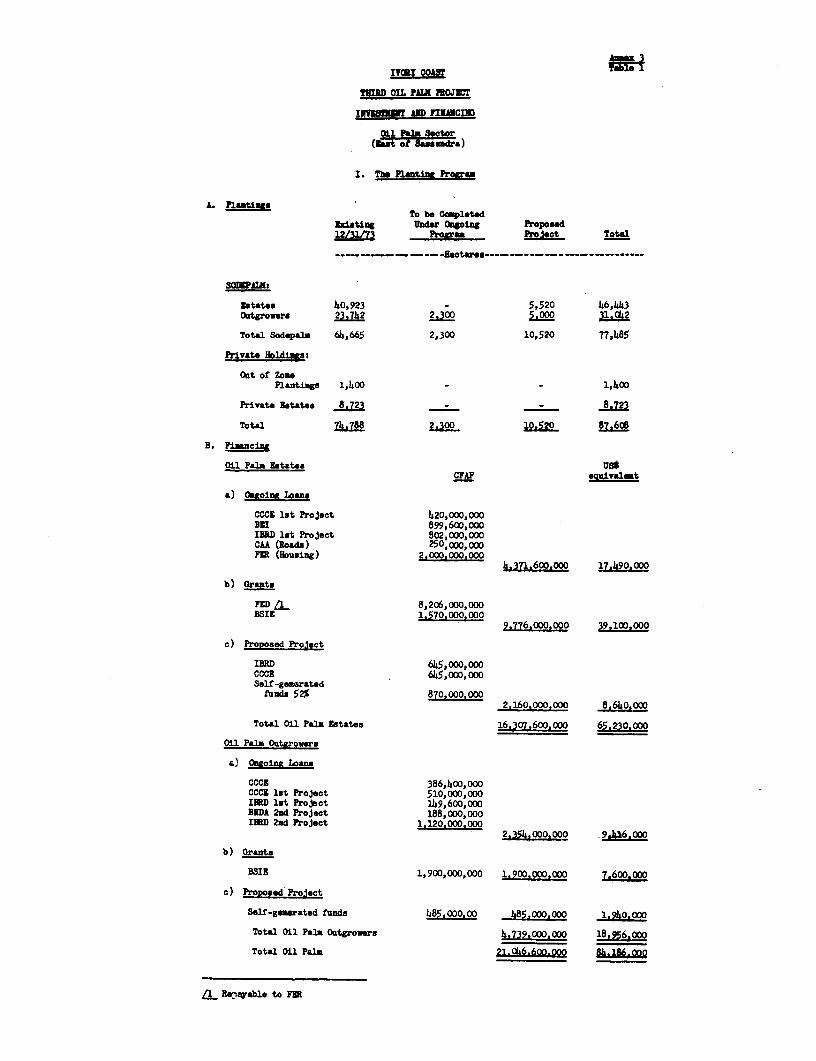

2.16 Both in its oil palm and coconut programs, Government has favored asystem of nucleus industrial estates surrounded by outgrowers, who are smallfarmers plimting, as of now, an average of 4 ha each. Estates are consideredessential go the outgrower program through demonstrating the value of usingmodern cultural practices, providing the potential outgrower with confidencein the future of the crop, and supporting a range of services essential toefficient production and high yields. Under this concept, nine developmentdistricts have been established East of the Sassandra River, each based ona palm oil mill and containing a mixture of estate plantings and outgrowers.The network is complete basically but additional investments to develop thepotential of each district will be required until 1985 (Annex 3). Exceptfor the Bank and CCCE financing under the proposed project, all or most furtherfinance to complete the ongoing program probably would be self-generated bythe Participation.

Coconut Development

2.17 Coconut development has been carried out since 1969 simultaneouslywith the oil palm program, and with financial help from the same sources(para 2.15). SODEPALM is carrying out a 20,000 ha coconut program in linewith the schedule envisaged during the 1969 and 1971 appraisals. Projectplantings will be completed in 1976, and will substantially exhaust thecoconut potential of the zone east of the Sassandra River. In the beginning,difficulties were met in implementing the outgrower program; but these diffi-culties are now being overcome through providing more incentives to farmers.Establishment of the coconut estates is satisfactory. Unit investment costshave generally been in line with appraisal estimates. In the meantime,varietal research is making substantial progress and future yields should be

- 6 -

higher than originally anticipated. Considering the highly favorable marketprospects for coconut, there is every reason to consider the coconut programa success. By 1985, the Ivory Coast will produce only about 60,000 tons ofcopra equivalent, a negligible percentage of world trade in coconut products.

2.18 CKoconut plantings will begin to mature in 1976 but a decision isawaited as to how production will be processed and marketed. As this is im-portant in respect of SODEPALM's financial position and ability to generatefunds, Government has been asked to submit to the Bank, within 12 monthsafter effectiveness of the loan proposed in this report, a plan to processand market coconut production. An assurance on this point has been secured.

Investments and Finance for Oil Palm and Coconut Development (Annex 3)

2.19 The Participation has invested CFAF 30.2 billion (US$120.8 million)in oil palm and coconut development, as of the end of 1972, as follows:

Investments CFAF (billions) US$ (millions)

Oil Palm Estates 15.123 60.5Oil Palm Outgrowers 3.937 15.8Coconut Estates and

Outgrowers 2.360 9.4Oil Palm Processing

Facilities 8.775 35.1

30.195 120.8

The total investment is about CFAF 2.5 billion more than was anticipated bythe Bank at tbr time of appraising the Second Oil Palm and Coconut Project in1971 (Loans ITC 759 and 760) because investments have included expenditureson social infrastructure and housing (CFAF 2 billion) and estate roads (CFAF560 million), which under the original financing arrangements were not intendedto be financed by SODEPALM. Also, SODEPALM purchased land clearing and roadequipment costing 3ome CFAF 1 billion, to enable it to undertake work at lowercost than previous contract arrangements, see para 3.07. Oil palm developmentcosts per hectare, however, are in line with the 1971 appraisal estimates.The cost for oil palm estates is CFAF 260,000/ha. For the outgrower program,the cost is CFAF 140,000/ha. Smallholders have received loans amounting toCFAF 2.1 billion, and grants from Government of CFAF 1.6 billion. SODEPALMnow supervises about 6,500 oil palm outgrowers.

2.20 The sources of funds, as of the end of 1972, are summarized below:

Equity Self-Generated Funds Grants Loan Disbursements Total…_------------------…CFAF million-------------------…----

Oil Palm Estates 300 2,658 10,592 1,640 15,190SODEPALM/PALMIVOIRE 150 774 2,169 3,287 6,380PALMINDUSTRIE 2,800 722 - 4,965 8,487

3,250 4,154 12,761 9,892 30,057

Percentage 10.8 13.8 42.5 32.9 100

Self-generated funds include profits, reserves and depreciation allowances.Grants include a Government contribution of CFAF 3,780 million and FED grantsto Government of CFAF 8,363 million. Disbursements from the five IBRD lo&nsaccount for CFAF 3.2 billion (US$12.8 million), or 10.6% of the total financ-ing of Participation investments.

2.21 Financial results are discussed in Chapter 7. Despite productioncosts that are 20% higher than anticipated, the financial results for theParticipation and for outgrowers have been better than expected due largelyto higher than anticipated prices for palm products.

III. THE PROJECT

A. General

3.01 The project is the final stage of an ongoing investment programaimed at the optimal exploitation of the oil palm growing potential of areasEast of the Sassandra River (Map). The project consists of oil palm plantingcoupled with the necessary support activities to bring the plantings tomaturity.

The project comprises:

(a) plantings of 5,000 ha of hiigh yield potential oil palm byoutgrowers assisted by SODEPALM's technical and supervised creditservices, to bring the total area of outgrower oil palmsto 30,000 ha; and

(b) plantings or replantings of 5,520 ha of high yield potentialoil palm, out of which 400 ha would be new hybrid lines,on SODEPALM estates.

The project would be carried out from 1974 to 1979.

B. The Planting Program

Outgrowers

3.02 The 5,000 ha of outgrower plantings would be divided among allnine of the palm oil mill districts, and phased equally over the five years,1975-1979 (Annex 4, Table 1). In general, the plantings would be as closeas possible to the mill sites. An estimated 1,300 farm families would beinvolved, including 600-800 newcomers to the program.

-8-

Estates

3.03 1,600 ha would be planted on Ehania estate; the planting wouldincrease the area of this estate from 10,410 ha to 12,010 ha. This expansionis based on the availability of an unutilized parcel of land in SODEPALM'sEhania estate holding, which enjoys the best conditions for oil palm in IvoryCoast. The plantings would be in conjunction with an expansion of processingcapacity in Ehania district financed by PALMINDUSTRIE. About 400 ha of IRHO'snew hybrid, E. Melanococca x E. Guineensis, would be planted in 1975 as partof the 1,600 ha planting program. The characteristics of this hybrid aredescribed in Annex 4.

3.04 3,000 ha would be planted on Okrouyo estate, a new estate to thewest of Abidjan. This estate is within the collection perimeter of theexisting Soubre mill-estate complex. The plantings have high priority toprovide a larger throughput for the Soubre oil mill, which would otherwisehave wasted capacity.

3.05 920 ha would be replanted on the Dabou estate, which was originallyplanted in the 1950's with early experimental varieties that are now over-aged and obsolete.

3.06 The schedule of plantings would be as follows:

Planting Program(hectares)

1974 1975 1976 1977 1978 1979 Total

Oil Palm Estates

Ehania 1,100 500 - - - - 1,600Okrouyo - 1,500 1,500 - - - 3,000Dabou - 920 - - - - 920Oil Palm Outgrowers - 1,000 1,000 1,000 1,000 1,000 5,000

Total 1,100 3,920 2,500 1,000 1,000 1,000 10,520

C. Estate Development

3.07 Development and Maintenance. Land for estate plantings would becleared mechanically by SODEPALM, as has been the case in the past. Whilemechanical clearing is more expensive than hand clearing, the Ivory Coast isunable, because of the rapid pace of development in the rural sector, tomobilize in a timely fashion the necessarily large numbers of skilled menneeded to hand-clear the heavy vegetation. Initially clearing was done bycontractors, but since 1970 SODEPALM has cleared land with its own equipmentat about 50% of the contract price.

-9-

3.08 Seedlings are raised by SODEPALM in its own nurseries, from seedsupplied by IRHO. SODEPALM also produces its own cover crop seed.

3.09 SODEPALM would ensure that all project plantings would be maintaineduntil the end of the third year after their planting. The maintenance require-ments are small but important: principal components are maintenance of thecover crop, including circle weeding for each plant; replacement of deadplants; and fertilizer applications and pest control.

3.10 Replanting the Dabou estate - 920 ha - would involve felling theold palms, planting and maintenance, and controlling existing weed infestation.The procedures involved in replanting are described in Annex 4. To meet theplanting schedule, the first phase of land preparation was started in 1973.

3.11 Estate Tenure. Ehania estate is owned by SODEPALM. The land onwhich the Okrouyo estate is located is classified forest land owned by Govern-ment. Dabou estate is Government property, and was put under SODEPALM manage-ment in 1972. Transfer of ownership of both properties to SODEPALM was inprocess at the time of appraisal, and no difficulties are expected. Duringnegotiations, the Bank received assurances that all facilities and title toor rights in respect of land required for the carrying out and operating theproject would be provided to SODEPALM within one year of loan effectiveness.

D. Outgrower lield Development

3.12 There has been no shortage of applicants for participation in theoil palm outgrower scheme, and no shortage of good candidates is expected.All plantings would be on land for which the farmer has the right of usufruct.Lo,cations and choice of planters would be strictly controlled by SODEPALMprocedures (para 4.04-4.05).

3.13 Oil palm holdings would be cleared by their owners. Seedlings,cover crop seed, fertilizer, and cash for hiring labor would be supplied tothe outgrower by SODEPALM. Development and maintenance methods employedby outgrowers and SODEPALM control and supervision procedures have provedsuccessful and no changes are contemplated.

IV. ORGANIZATION AND MANAGEMENT

A. General

4.01 The Bank was involved in the discussions that led to the creationof the Participation and its constituent companies, and approved the corres-ponding legal statutes. The Bank also approved the Participation's managementorganization, with the provisos that a policy of "Ivorization" would be pursued

- 10 -

by SODEPALM/PALIIVOIRE, and that appointments to the key posts of GeneralManager and Assistant General Manager of SODEPALM/PALMIVOIRE and the CreditManager of SODEPALM would be made only following agreement with the Bank. Achange in top management took place on January 1, 1974, when an Ivorian citizenwas appointed as Director General to replace the former expatriate incumbent.He and his new Deputy, also an Ivor:tan, have held senior positions in SODEPALM;both men are qualified to fill their new posts. SODEPALM/PALMIVOIRE intendsto retain the services of seven high level expatriate staff members. Conse-quently all key managerial positions continue to be filled with qualified andexperienced persons.

Estates Management

4.02 SODEPALM estates are managed by PALMIVOIRE from headquarters inAbidjan. Development of plantings at the existing Ehania and Dabou estateswould be supervised by the present estate management, and for Okrouyo super-vision would be provided by the Soubre distrtct staff. These arrangementsare satisfactory.

Management of Outgrower Oil Palm Development

4.03 A Division of SODEPALM is responsible for oil palm outgrowers (para2.11). Within this Division and at field level, area chiefs supervise outgroweractivity in nine principal areas, each covering a zone of about 20 km radiusfrom each mill. Below the area level, group chiefs appointed by SODEPALMsupervise plantings made individually by farmers who are grouped on a villagebasis to facilitate supervision and the supply of technical and marketingservices. For each group, a SODEPALM employee coordinates and records thecollection of fresh fruit bunches to be delivered to the area's mill. Abouthalf of project plantings probably would be made by farmers who have alreadyplanted palms under the SODEPALM program. Because of this factor, and alsobecause more than half of outgrower palms are now in production and thusrequire less supervision, carrying out the outgrower component would requireno increase in headquarters or area field staff. The performance of theSODEPALM outgrower program has been satisfactory and no organizational ormanagement problems are envisaged.

B. Outgrower Selection, Size of Holdings and Credit Arrangements

4.04 Participation in the outgrower scheme would continue to be conditionalon the farmer's agreement to follow, throughout the development period, thetechnical advice provided by SODEPALM. Such an obligation has been containedin the agreements that are signed between SODEPALM and outgrowers and whichhave been approved by the Bank.

4.n5 The local SODEPALM agent inspects each applicant's farm, checkshis standing in the community and ability as a farmer, and makes a recommenda-tion to headquarters. Existing selection arrangements would apply. Under

- 1 1 -

these, outgrower participants are limited to a maximum of 10 ha of oil palm.The farmer's planting site must be within 200 m of a road passable by ffbcollection vehicles; and new outgrower planting sites would be in zones whereadditional plantings could be handled by the existing supervision and ffbcollection services.

4.06 As under the ongoing program, outgrowers would receive both credits,now interest free, and grants from SODEPALM (details in Annex 5). About CFAF80,000/ha (US$320/ha) would be credit: CFAF 60,000 would be for fieldestablishment, specifically seedlings, fertilizer, and cash for land clearingand maintenance of plantings, and CFAF 20,000 for fertilizer supply fromyear 4 to year 7. This credit would be repayable in 9 years after a seven-year grace period. Outgrowers would contract to sell all theit produce toSODEPALM, which would deduct payments due from the sales price. About CFAF16,700/ha (US$67/ha) would be a grant, comprising the cover crop, wirenetting, and labor costs related to supply of seedlings. This is much lowerthan the CFAF 63,800 and CFAF 48,300 per hectare provided as grants, respectively,under the first and second projects. A reduction in individual grant is nowpossible because the experience with ongoing programs is demonstrating thatwell planted and maintained oil palm can compete successfully with other cropsin the project area and therefore prospective participants would be lessreluctant to join the project than in earlier years. FER would continue toreimburse SODEPALM for the grant element.

4.07 rhe system of financing oil palm out3rowers 1/ development in theIvory Coas: through nominally interest-free loans and grants cannot be judgedby the standards of a conventional credit system. The system is not intendedto replace or compete with a conventional system and is simply a financingmethod chosen by Government to attain the dual objectives of: (a) providingadequate incentive to farmers to diversify into oil palm, and (b) assuringGovernment a satisfactory return on its own investment in the outgrowersprogram and which has proved to be very successful. Recent studies show thatin conventional credit programs high interest rates have to be charged, upto 25% and 30% in some cases, if the lending institution is to receive areasonable return on the money lent to farmers after due allowance foradministration and technical service charges and reserves against bad debts.A scheme charging high interest rates would not have been condusive toencouraging farmers to invest in a crop that was essentially new to them,such as oil palm, and consequently of unproved merit. Under the SODEPALMscheme, outgrowers must sell their produce to SODEPALM. The difference betweenthe forecast export price and the price paid to producers accrues to SODEPALM,not to the outgr6wers, and the guiding principle in fixing the producer priceis consistency with a minimum financial return to Government of 7% on its oilpalm outgrower investment. On the basis of the average price paid for out-growers ffb (CFAF 8/kg including bonuses) and the current world market priceforecast, the return to Government from this investment is estimated at 12%;

1/ A conventional credit system has been used for coconut outgrowers sincethe inception of the coconut program.

- 12 -

and even if the producer price to outgrowers were increased by 50%, the re-turn to Government would remain above the target return of 7%. Under themarket conditions prevailing during the early years of outgrowers development(1969-71), it had been felt necessary to charge a 2% interest rate on loans tooutgrowers to secure the desired return to Government. With a greatly im-proved mar;et outlook, SODEPALM suspended the interest charge in 1971, as itwas not neesded to insure a satisfactory return to Government. As the SODEPALMscheme is achieving highly satisfactory results and is not, because of thevery specialized nature of the oil palm program, establishing undesirableprecedents, it is not considered necessary to make any change in the creditarrangements for oil palm outgrowers.

C. Processing and Marketing

4.08 PALMINDUSTRIE would have sufficient capacity to process all ffbproduction with its nine existing oil mill centers and some additionalcapacity scheduled to be constructed at Ehania. PAIMINDUSTRIE would providethe transport services to collect outgrower and estate fresh fruit bunches(ffb).

4.09 Palm oil and kernels produced by the PALMINDUSTRIE mills would bemarketed by PALMIVOIRE, both directly and through contracts concluded withthe Belgian commodity trading company SOGESCOL as broker. These arrangementsare in force and are satisfactory.

V. COST ESTIMATES AND FINANCING

A. Cost Estimates

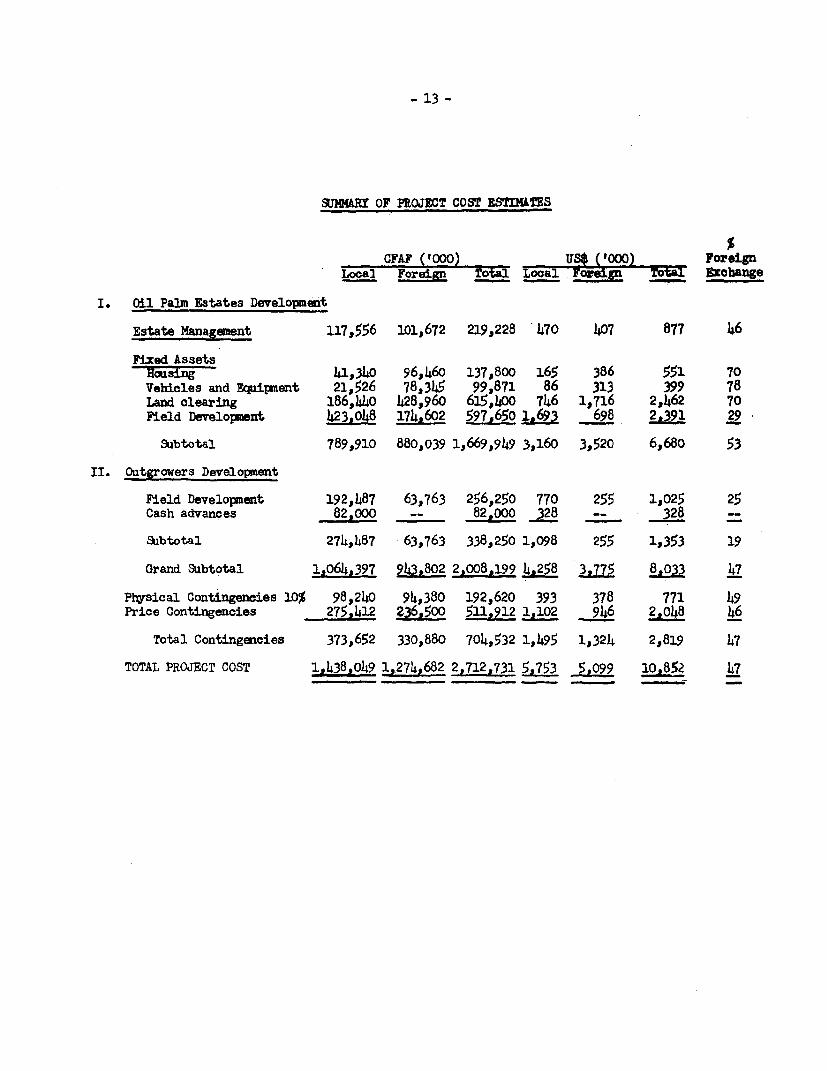

5.01 Project costs during the six-year period 1974 through 1979 areestimated at CFAF 2.7 billion (US$10.8 million), of which the foreign exchangecomponent is about CFAF 1.3 billion (US$5.1 million) or 47%. Detailed costestimates are in Annex 6, and are summarized in the attached table (next page).

5.02 Government has indicated its intention to continue to exempt allimports needed for the project from import duties during the developmentperiod, and confirmation of this has been obtained. Such exemption wouldnegate all preferences enjoyed by foreign companies in the Ivory Coast market.Cost estimates are based on February 1974 prices, and reflect the ample ex-perience gained from the national oil palm program. Cost estimates includeindirect taxes amounting to about US$1 million, and contain the followingcontingencies:

- 13 -

SUMMAY OF PROJECT COST ESTIMATES

CFAE ('000) US$ ('000) ForeignLocal Foreign Total Local Foreign Total Exohange

I. Oil Palm Estates Development

Estate Management 117,556 101,672 219,228 470 407 877 46

Fixed AssetsHousing 41,340 96s460 137s800 165 386 551 70Vehicles and Equipment 21,526 78s345 99,871 86 313 399 78Land clearing 186,440 428,960 615,,400 746 1,716 2,462 70Field Development 423,048 174,602 597,650 2.693 698 2.391 29 -

Subtotal 789s910 88o0,39 1,669s949 3,160 3,520 6,680 53

II. Oatgrawers Develomt

Field Development 192,487 63,763 256,250 770 255 1,025 25Cash advances 82,000 -- 82 000 328 -- 328

Subtotal 274,487 63s763 338,250 1,098 255 1,353 19

Grand Subtotal 1,064,397 943,802 2,008,199 4.258 3.775 8,033 47

Physical Contingencies 10% 98,240 94s380 192,620 393 378 771 49Price Contingencies 275,412 236,500 511,912 1,102 946 2,048 46

Total Contingencies 373,652 330,880 704,532 1,.495 1,324 2,819 47

TOTAL PROJECT COST 1,438,049 IA274s682 2,712,731 5,753 5,099 10,852 47

- 14 -

(a) pnys_a contingencies totalling about 10Z of projectcost are included for oil palm outgrowers and the estates; and

(b) price contingencies compounded as follows: for civil works,construction, and mechanical land clearance, 18Z in 1974,15? in 1975, 12X in 1976 and thereafter; and for all remainingcosts, 14% in 1974, 11Z in 1975, and 7.5? thereafter.

Total contingencies calculated on the foregoing basis amount to 26? of totalproject costs or 35% of base line cost estimates.

B. Proposed Financing

5.03 Government has asked France's Caisse Centrale (CcCE) and the Bankto cofinance part of project costs. It is envisaged that together the Bankand CCCE would-finance roughly the equivalent of the project's foreignexchange costs. This would entail a Bank loan totalling US$2.6 million, equiv-alent to 24% of total project costs and about 50% of estimated foreign exchangecosts.

5.04 The loan would be to SODEPALM/PALMIVOIRE, and would be disbursedduring the five-year period 1974-78. The term of the loan would be 15 years,with a five-year grace period for principal payments. CCCE has agreed in prin-ciple to lend an identical amount to SODEPALM/PALMIVOIRE, to be disbursed overthe same period as the IBRD loan. Tentatively, the CCCE loans would bearinterest at 5.5% and would be for the same term and grace period as on theproposed Bank loan. The balance of project costs not covered by IBRD and CCCEloans would be financed by SODEPALM from self-generated funds.

5.05 The financing plan for the proposed project is summarized below:

Financing Plan

Estates Outgrowers TotalUS$000 X US$ '000 x US$ '000 %

IBRD 2,600 29 - 2,600 24OCCE 2,600 29 - 2,600 24

Government:

SODEPALM 3,710 42 1,940 100 5,650 52

Total 8,910 100 1,940 100 10,850 100

- 15 -

C. Procurement and Disbursement

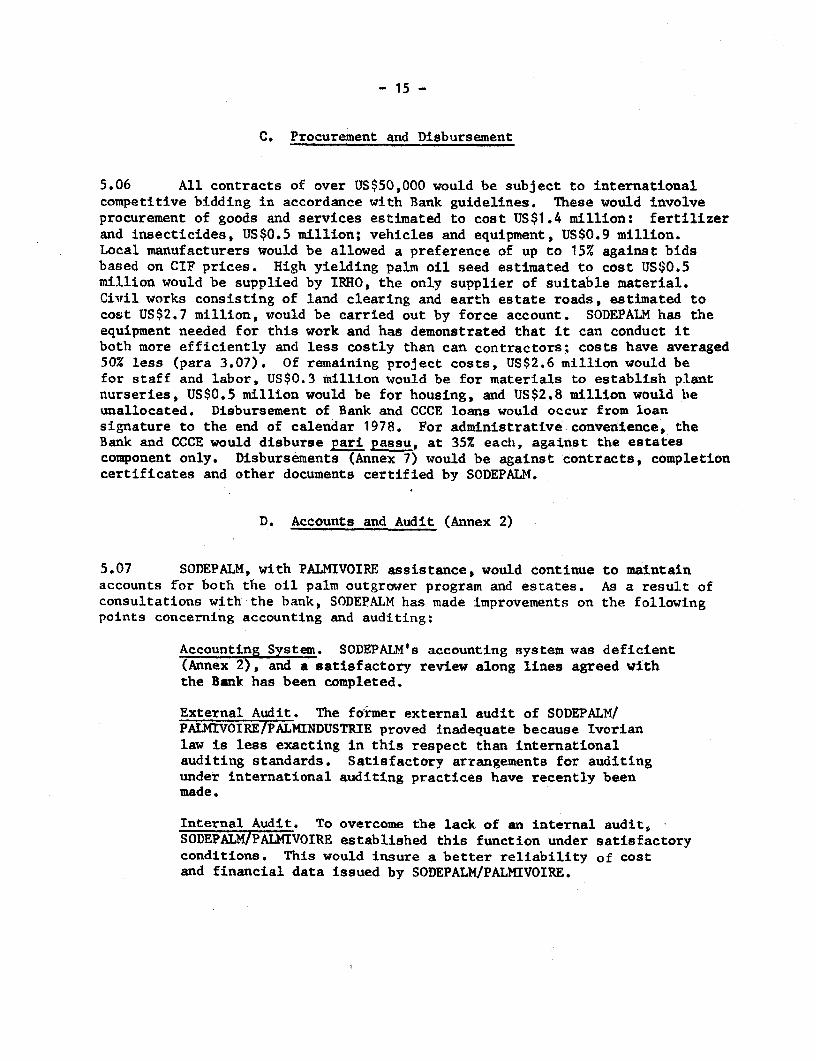

5.06 All contracts of over US$50,000 would be subject to internationalcompetitive bidding in accordance with Bank guidelines. These would involveprocurement of goods and services estimated to cost US$1.4 million: fertilizerand insecticides, US$0.5 million; vehicles and equipment, US$0.9 million.Local manufacturers would be allowed a preference of up to 15% against bidsbased on CIF prices. High yielding palm oil seed estimated to cost US$0.5million would be supplied by IRHO, the only supplier of suitable material.Civil works consisting of land clearing and earth estate roads, estimated tocost US$2.7 million, would be carried out by force account. SODEPALM has theequipment needed for this work and has demonstrated that it can conduct itboth more efficiently and less costly than can contractors; costs have averaged50% less (para 3.07). Of remaining project costs, US$2.6 million would befor staff and labor, US$0.3 million would be for materials to establish plantnurseries, US$0.5 million would be for housing, and US$2.8 million would beunallocated. Disbursement of Bank and CCCE loans would occur from loansignature to the end of calendar 1978. For administrative convenience, theBank and CCCE would disburse pari passu, at 35% each, against the estatescomponent only. Disbursements (Annex 7) would be against contracts, completioncertificates and other documents certified by SODEPALM.

D. Accounts and Audit (Annex 2)

5.07 SODEPALM, with PALMIVOIRE assistance, would continue to maintainaccounts for both the oil palm outgrower program and estates. As a result ofconsultations with the bank, SODEPALM has made improvements on the followingpoints concerning accounting and auditing:

Accounting System. SODEPALM's accounting system was deficient(Annex 2), and a satisfactory review along lines agreed withthe Bank has been completed.

External Audit. The former external audit of SODEPALM/PALMIVOIREfPALMINDUSTRIE proved inadequate because Ivorianlaw is less exacting in this respect than internationalauditing standards. Satisfactory arrangements for auditingunder international auditing practices have recently beenmade.

Internal Audit. To overcome the lack of an internal audit,SODEPALM/PALMIVOIRE established this function under satisfactoryconditions. This would insure a better reliability of costand financial data issued by SODEPALM/PALMIVOIRE.

- 16 -

VI. YIELDS, OUTPUT, MARKETS AND PRICES

A. Yields and Output

6.01 Oil palm outgrowers are estimated to obtain an average yield of 13tons ffb/ha (21% oil and 4.3% kernel contents) when their oil palm plantingsare mature, nine years after planting. Actual results from existing oil palmoutgrowers confirm the validity of this estimate. Estates are expected toobtain a range of yields depending upon their differing potentials (Annex 4),specifically these are: Ehania, 16 tons/ha; Okrouyo, 14 tons/ha; Dabou, 12tons/ha, with oil yields of about 21.5Z and kernel yields of 4.3%.

6.02 Oil palms planted under the project would come into productionafter four years and reach full production in the ninth year. Consequently,project plantings would reach full production in 1984, from which time theirproduction would average 30,800 tons of oil and 6,300 tons of kernels annuallyor less than 1% of the anticipated world trade in these commodities at thattime (Annex 8).

B. Markets and Pricep

6.03 Market prospects are good. About 55X of the palm oil and allkernels produced by project plantings would be exported, and the remaining45% would be absorbed by the growing domestic market. Total world productionof palm oil is estimated to be expanding at about 12% annually, and productionby 1980 is expected to reach about 4.2 million tons and exports 2.7 milliontons. Of the total, the Ivory Coast would export about 110,000 tons or 4.5%.On the basis of the supply and demand outlook, the Bank's commodity analystsexpect palm oil prices to range from US$425/ton, the current price, to US$695/ton cif Europe in 1985. A price equivalent to US$327/ton cif Europe, inconstant 1974 prices, has been assumed for project purposes (Annex 8).

6.04 The principal product of palm kernels is palm kernel oil, whichhas similar chemical characteristics to coconut oil; on the basis of thetrend in coconut prices, palm kernel prices in current terms are expectedto range from US$350/ton, the present level, to US$460/ton cif Europe by1935. A price of US$218/ton, in constant 1974 prices, has been assumedfor project purposes. The price projections for both oil palm productscompare favorably with the outlook under the previous projects.

- 17 -

VII. FINANCIAL BENEFITS AND OUTLOOK

Financial Results

7.01 Whilst production from the first project has been generally in linewith appraisal estimates, the financial results of the Participation havebeen better than expected because of higher than expected palm oil prices,which averaged over US$215/ton in 1972 and US$400/ton in 1973, compared withthe projected figure of US$160/ton, and which have more than offset cost in-creases. The financial results of the smallholder program have been in linewith estimates. The operating results for 1972, before debt service, maybe summarized as follows:

SmallholderSODEPALM Participation Program

CFAF million

Appraisal estimates 4 142 (138)

Effect of increased: - sellingprices 847 761 86

- costs (695) (588) (107)

Actual results 156 315 (159)

7.02 SODEPALM's working capital was severely depleted by the end of 1972,when Bank overdrafts amounted to CPAP 1.6 billion, due to investments outsidethe scope of the original program (para 2.19). By the end of 1973, however,increased revenues and additional long term borrowing from PER had reducedthe overdraft to an estimated CFAF 900 million.

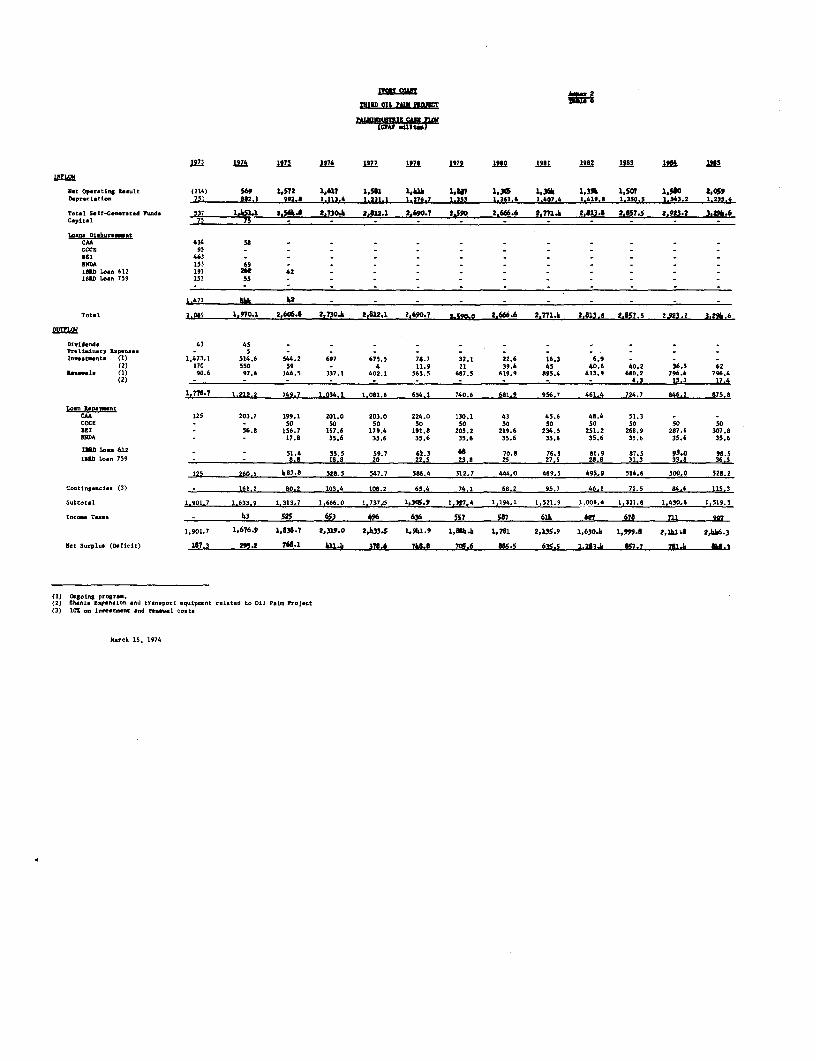

7.03 The estimated cash flows for the period 1973-1988 for SODEPALM andPALMINDUSTRIE are at Annex 2, Table 8; they are based on the latest (April 9)price forecasts for palm oil. For SODEPALM they show the following mainflows of funds up to the end of disbursements, in 1978, under the proposedproject:

- 18 -

Oil PalmOutgrowers

Oil Palm Estates Program -

Ongoing Proposed Ongoing & CoconutTotal Program Project Proposed Program

… -CFAY Billion -------- …

Retained earnings /1 21.6 18.5 - 2.0 1.1Loans /2 8.1 2.9 1.3 0.8 3.1

Inflow 29.7 21.4 1,3 2.8 4.2

Investments 11.0 2,7 2.2 1.3 4.8Debt service /3 8.3 5.4 0.2 0.9 1.8Income tax 6.1 5.2 - 0.9 -

Outflow 25.4 13.3 2.4 3.1 6.6

Surplus (Deficit) 4.3 8.1 (1.1) (0.3) (2.4)

/1 After payments of CFAF 3.5 billion to CSSPPA,72- Including proposed IBRD Loan of CFAP 0.75 billion equivalent.73 Including repayment of CFAF 1.4 billion to FER in respect of estate

housing.

Project Benefits - The Participation

7.04 The main benefits to the Participation would accrue from the outputof the estate plantings (Annex 10), from small reductions in estate and proces-sing overheads and costs due to economies in scale resulting from projectactions. The benefits would be allocated to SODEPALM, PALMINDUSTRIE andPALMIVOIRE in proportion to their investments. Surpluses would begin toaccumulate in 1979 and by 1985, at full development, would amount after debtservice to an estimated CPA? 380 million (US$1.5 million), or 20% of theParticipation's total earnings. At that time, net earnings would be allocated60% to SODEPALM, 39% to PALMINDUSTRIE and 1% to PALMIVOIRE.

7.05 SODEPALM would also benefit directly from the services it providesthe additional smallholders (Annex 5). At full development in 1985, incrementaliurpluses from this source would amount to CFAP 184 million (US$0.7 million),or 45% of the total surpluses accruing to SOEPALM's outgrower servicedivision (Annex 10, Table 2). In other words, due to economies of scale inservicing additional outgrowers with the same staff, the 5,000 ha of projectplantings will produce almost as much surplus as the previous 25,00b ha ofoutgrower plantings.

- 19 -

Project Benefits - Oil Palm Outgrowers

7.06 For outgrowers, average returns from the ongoing projects areabout CFAF 860/manday employed after all costs including debt service, ascompared with estimates made at appraisal of the second project in 1971 ofCFAF 612. Expected benefits for outgrowers ander the project have beenestimated from models prepared from the experience of previous projects.Under current practice SODEPALM pays outgrowers a fixed basic price ofCFAF 4/kg ffb, augmented by a bonus system that enabled growers to attain,in 1973, an average price of CFAF 6/kg ffb. The expected 1974 average priceto outgrowers is CFAF 8/kg ffb; financial projections (para 4.07) show thatthis price is consistent with adequate return to Government. Production onan outgrower's holding would begin in the fourth year after planting, when39 working days would be required to maintain and harvest one hectare of oilpalms and when the return per manday would be CFAF 86 (USd0.34). This wouldincrease and reach a maximum of CFAF 2,000 after debt service by year 9 andCFAF 2,200 (US$8.8) when debt service is completed in year 16. The return tolabor employed is satisfactory compared with the official agricultural wageof CFAF 315/day (including fringe benefits) and with the return from cocoacultivation, another principal crop in the oil palm zone, of about CFAF940 (US$3.75) per manday from traditional plantings and CFAF 1,200 fromimproved plantings. Few outgrowers cultivate only oil palm, as most combineoil palms with coffee and food crops. Indications are that the averageoutgrower holding will be about 4 ha and plantings of this size would generatea t:otal annual income after debt service of approximately CFAF 480,000(US$1,920) as from year 16 after full repayment of debt. The returns areconsidered satisfactory from the viewpoints of inducing farmers to participatein the outgrower program, and of improving their standards of living.

VIII, ECONOMIC BENEFITS AND JUSTIFICATION

8.01 Primary benefits from the oil palm outgrower and estate plantingswould be the increased production of palm oil and kernels and resultant netannual incremental foreign exchange earnings amounting to about US$8.8 millionby 1987.

8.02 Based on expected world prices for these commodities, the returnsto the ecoriomy from the project investments are estimated to be about 23%.In calculating this overall rate, all labor used in the project, for small-holder as well as estate development, has been costed at the average officialrate of CFAF 315/manday including fringe benefits. The rate of return forthe estate component is estimated at 20%, and the rate for the outgrowercomponent at 35%. The difference between the two rates is greater than itwas under the previous project; the reason is that outgrower developmentunder the new project would utilize infrastructure and services already in-stalled during earlier projects. The resultilLg higher rate of return onoutgrower development might suggest that this co"ponent of the project shouldbe expanded. However, the proposed pace of development is based on SODEPALM's

- 20 -

judgment as to how fast additional outgrower plantings could be integratedinto the program. Under Loan IVC-613, it was envisaged that 12,000 ha wouldbe developed by smallholders over a four year period but the developmentperiod subsequently had to be extended by two years. The proposed programis in keeping with that experience. Details of the calculation are givenat Annex 12, which includes an analysis of the sensitivity of the rates ofreturn to changes in costs and benefits. As is often the case with slowlymaturing investments, the rates of return for all project components arerelatively insensitive to changes in the value of output/ha, itself a functionof both yields and prices:

Returns (a)Output/ha 90% 110%

Outgrowers 32% 36%

Estates 17% 23%

8.03 The project would have substantial secondary benefits throughproviding employment for some 600 workers on the oil palm estates, and creat-ing some 265,000 mandays of work per year in developing outgrowers' holdings.The project would further the Government's program of agricultural diversi-fication both directly, through the project output, and indirectly by generat-ing the resources with which to pursue other programs.

IX. RECOMME9NDATIONS

9.01 The assurances and covenants of Loans IVC-611, IVC-613 and IVC-760would be continued, insofar as they are applicable, in the Third Oil PalmLoan. In addition, assurances have been obtained on the following points:

(a) Government would submit to the Bank, within 12 monthsafter loan effectiveness, a plan to process and marketcoconut production (para 2.18); and

(b) facilities and title to or rights in respect of landrequired for the carrying out and operation of theproject would be provided to SODEPALM within one yearof loan effectiveness (para 3.11).

9.02 Subject to the above conditions, the project is suitable for a Bankloan to SODEPALM/PALMIVOIRE for US$2.6 million repayable over 10 years afterfive years of grace on principal payments.

ANNEX 1Page 1

IVORY COAST

THIRD OIL PALM PROJECT

Progress of Agricultural Projects Financed by Bank Loans

A. Loan 611-IVC - Palmivoire US$3.3 Million Equivalent (June 13, 1969)

1. The project consists of establishing and bringing into production4,000 ha of oil palms at Ehania estate and to bring the estate to 10,000 haof oil palms. The loan became effective on December 30, 1969. Planting wascompleted in 1972 and plantation maintenance is satisfactory. Planting costswere slightly lower than estimated at the time of appraisal.

B. Loan 612-IVC - Palmindustrie US$4.8 Million Equivalent (June 13, 1969)

2. The project comprises the construction of a palm oil mill to servicethe 10,000 ha Ehania estate and some outgrowers. The loan became effectiveon December 30, 1969. The mill was constructed with an initial capacity of40 tons/hour ffb, in two processing lines, and these are functioning satis-factorily at full capacity. Costs were within appraisal estimates. Anaddition of a 20-ton/hr processing line was provided for in the project, butPalmindustrie has requested the Bank to approve a change in plans involvingtwo satellite mills of 20 tons/hr each with expanded central mill service,instead of the addition. The proposal is sound and therefore the projectdescription will be changed to delete the third processing line, and theremaining funds ($700,000) will be devoted to help finance the proposedsatellite-central mill complex.

C. Loan 613-IVC - Sodepalm US$9.0 Million Equivalent (June 13, 1969)

3. The project consists of the establishment and bringing into produc-tion of 12,000 ha of outgrower oil palms, the establishment and maintenanceuntil 1974 of 3,500 ha of estate coconuts and 3,000 ha of outgrower coconuts,the provision of credit and supervisory services for oil palm and coconutoutgrowers and the necessary infrastructure associated with the 3,500 ha ofestate coconuts. The loan became effective on December 30, 1969. Projectcoconut estate plantings were due to be completed in 1971. Due to shortageof planting material (because of disease), the Bank agreed to extend theplanting period to 1972. All estate plantings have now been completed. Atthe request of the Borrower, the Bank also agreed to the extension of the oilpalm outgrower program planting period, initially scheduled to be completedin 1970, to 1972 to permit more rigorous selection of outgrowers.

4. The above three loans are the first Bank operations in support ofthe oil palm sector in the Ivory Coast. After a relatively slow start dis-bursements of the Bank have accelereated and are now well within appraisal

ANNEX 1Page 2

estimates. On the other hand, physical progress has been very good. Althoughproduction of the oil palms under the project is just beginning, all indica-tions are that yields in the estates and of outgrowers will be in line withappraisal estimates. The number of outgrowers participating in the projectis also in line with appraisal estimates.

D. Loan 686-IVC - Cocoa Project US$7.5 Million Equivalent (June 5, 1970)

5. The project originally consisted of the planting of 18,800 ha ofcocoa and the rehabilitation of about 38,000 ha of existing cocoa plantationsand became effective in November 1970. The project was amended in July 1973to reduce the rehabilitation ccmponent to 15,500 ha. This revised programhas been completed. Approximately 10,000 ha had been established under thenew planting program by the end of 1973; plantings of 7,800 ha are expectedin 1974 and 1,000 ha in 1975, completing the program one year later thanexpected at appraisal. Disbursements have been delayed by a delay in signingannual operating conventions, between Government and SATMACI, but with theprocessing of outstanding commitments disbursements are expected to reachUS$3 million in early 1974, or about 25% below appraisal estimates. TheBank's share of project costs have been reduced by the reduction of rehabilita-tion and fertilizer programs (evidence has accumulated that, with increasedprices, payoff from fertilizer use on new plantations is not adequate).

E. Loans 759-IVC and 760-IVC - Sodepalm and Palmindustrie US$7.0 MillionEquivalent (June 22, 1971)

6. The project consists of (a) planting 4,500 ha outgrower oil palms,(b) 4,500 ha of outgrower coconut palms, (c) 8,000 ha of coconut palms onGovernment-owned estates, and (d) construction of a palm oil mill. The loansbecame effective on November 15, 1972. The oil mill was commissioned inJuly 1972, and is operating satisfactorily. The planting programs are pro-ceeding satisfactorily and on schedule.

F. Loan 938-IVC-SOCATCI Rubber Estate US$8.4 Million Equivalent(October 23, 1973)

7. This loan was signed in October 1973, but the deadline formeeting conditions of effectiveness was postponed from November 30, 1973,the original date, to April 30, 1974. The purpose of the loan is to finance,pari passu with CCCE and FED, the planting of 13,500 ha of modern rubberestates and the establishment of auxiliary services under the management of".EtablissementsMichelin", a French tire manufacturer.

ANNEX 2Page 1

IVORY COAST

THIRD OIL PALM PROJECT

SODEPALM Accounts and Financing

Accounting

1. Accounting procedures were changed in 1969 to fit with the newlegal structure of the participation, and, in 1972, to meet legal require-ments when Ivory Coast adopted a national accounting chart.

2. These requirements, added to a fast development of the group'sactivities, caused the accounting procedures to be in a state of transitionfor too long a time. As a result, the accounting system has not met therequirements. While SODEPALM has been mostly interested in obtaining reliableproduction costs quickly, it has neglected to produce detailed investmentcosts. This situation is now improving and SODEPALM has reconciled mostof its accounts with physical inventories; this work is expected to be com-pleted in 1974.

3. SODEPALM has reviewed its accounting procedures and is training itsIvorian accounting staff as recommended by the Bank. The Bank has been keptinformed of the progress of this review which is expected to enable SODEPALMto improve and simplify its accounting procedures.

Auditing

4. Two auditors are appointed by the Minister of Economic Affairs andFinance (actually, only one is from the Government Audit Department; theother is from a private firm of auditors, Societe Fiduciaire France-Afrique).Accounts remain provisional until approved by the Minister and submittedto the General Assembly together with an annual report. This must be withinthree months of the end of each fiscal year.

5. This auditing has not been satisfactory under present arrangementsbecause the Ivorian law is less exacting in this respect than internationalauditing standards. The important internal audit function has been lacking.SODEPALM/PALMIVoIRE has made satisfactory arrangements in both of thesematters.

Balance Sheets and Long-Term Forecasts

6. Tables 1 and 2 summarize balance sheets for SODEPALM and PALMINDUSTRIE.

7. Tables 3 to 8 summarize the long-term financing plan. They showthat oil palm activities will generate abundant surpluses on the basis ofcurrent estimates. Nevertheless, from these surpluses SODEPALM will have tofinance about CFAF 3.1 billion of deficits for the coconut sector, insteadof CFAF 1.5 billion as anticipated at appraisal.

IVORY COAST AT lX 2Table I

THIRD OIL PALM PROJnCT

(CPA? Willio-)

A. ASST81967 198 1969 1970 1971 1972

(a) Tiad Assets (Not)

Pteltainawy 5eUsos . - 115.8 453.6 659.7 230.1Vehicles includirm agriultlre.qa84snt 189.0 288.8 345.1 1,895.2 1,264.7 1.446.5

1natalIatione 142.0 200.7 232.8 440.5 577.5 720.9Oil sills 165.0 C08.6 2,095.8 - 1,979.9 5,852.2b.ci1ding and brldgs 457.0 953.0 5G7.3 1,665.4 887.1 3,676.6 2.353.3 5,142.6 2.783.9 7,265.7 3,642.2 11,891.9

Aericulturel De VlOmDnt

Estates: Oil Pdsn 4,098.0 4,763.0 6,312.7 8,815.6 9,405.5 9,390.7Cocenut 56.0 4,154.0 242,1 5,005.1 195.6 6,508.3 949.9 9,765.5 1.211.2 10,616.7 1,752.9 11,143.6

Ou.tposwar 809.0 809.0 - 1,116.1 _ 877.9 1,264.3 1,264.3 - 2,303.1 - 3,778.8Usell"cated - 426.0 - 838.8 _ 732.0 - - . - _

Total Fhed Assgts 6,342.0 8,623.4 11,794.8 16,172.4 20,185.5 - 26,814.3

(b) Current Asets

Av ilable 547.0 - 659.6 - 3,214.9 - 3,330.6 - 4,120.1 - 3,746.0 -Lo:ei curre.t 1ahlilities (518.0) 29.0 (474.5) 185.1 (1,560.2 1,654.7 (1,995.3) 1,335.3 (3,479.5) 640.8 (5,467.1) (1,721.1)

(c) Loes 81.2 - 138.1 _ 138.1 - 232.7 655.1

TOTAL ASSE 6,371.0 - 8,891.7 - 13,587.S _ 17,645.8 _ 21,05930 25,748.3

8. IlIAILlT785

(a) Sharshuldors Pwuda

Share capital 200.0 - 400.0 - 1,712.5 - 2,950.0 - 2,950.0 - 3.250.0Raers.. 278.0 - 2- - 824.6 - 1.074.9 - 772.5

Ttal - 478.0 - 400.0 - 1,712.5 - 3,774.6 _ 4,024,9 - 4,022.5

(b) Grents

SU _ 1,148.0 - 1,253.5 _ 2,027.4 2,390.5 2,390.5 2,900.8 2,900.8 - -3,440.5

IBRD _- - - 499.4 - 1,654.9 - 3,205.0Others - 4,745. _ 7,238.2 - 9,847.7 10,981.3 11,480.7 12.478.4 14,133.3 15.080.2 18.285.2

TOTA.L LTAILITIZS 6 8,371.0 _ 8,891.7 _ 13,587.6 _ 17,645.8 - 21,059.0 - 25,748.2

March 14, 1974

ASiRM 2IVORY COAST Teble 2

THIRD OIL PALM PROJECT

PAUlENDUSTRIE

Audited Balance Sheet; On Deceber 31(CFA Milon)

1969 1970 1971 1972

ASSETS

(a) Fixed Assets

Preliminary expenses 115.8 453.0 649.7 182.0Oil mills and ancillaries 163.8 2,735.0 3,670.6 5,529.4Buildings - - 555.8Vehicles - 64.7 165.1 429.8Other equipment - 26.1 23.9 147.3Infrastructure - 57.4 177.2 272.2Spare ports 1,631.8 _ 2,883.2 _ 4,036.8 203.7 7,138.2

Work in Progress 463.9 4.0 345.5

(b) Inventories - - - - - - -

(c) Current AssetsAvailable 964.5 - 2,230.8 - 1,794.8 - 717.0 -

Legs:Liabilities 347.0 617.5 582.5 1,648.3 343.6 1,451.2 412.9 304.1

(d) Losses - 12.8 - 14.0 - 18.3 - 395.8

2.841.8 5.002.5 6,156.0 8.365.6

LIABILITIES

Shareholder Fund

Share capital 1,291.0 - 2,500.0 - 2,500.0 _ 2,800.0 -Reserves - 1,291.0 - 2,500.0 29.9 2,529.9 8.3 2,808.3

Loans

Long term 367.2 - 830,7 - 2,123.2 - 4,611.9Medium term 219.1 - 318.1 - 225.0 - 228.4 -Draving rights 964.5 1.550.8 1.353.7 2,502.5 1,277.9 3,626.1 717.0 5,557.3

2.841.8 5.002.5 6.156.0 8,365.6

March 14, 1974

9

ITU C00kM

THIRD OCIL PaX 2JS3

80O2MIX on1 ?AIX 39CAM

1972 1973 1k 9W6 1,2L m si 1.51 151 INk

(a) Inn

=S 520h - a~1 7 - - - - - - - - --CL - 205 45 - - - - - -

ca:s 1 000 baEk 42 87ID400 oco mm . 167 148 ;6_

- 152 97 - - - - - - - - -PU~~ ~~~ - 1.1.03 600 - - - - - - - - -

S*b_totzl _ 2, mo 890 44 -

IND - - 91.2 201.3 173.6 91.1 57.9 26.9-OCCc - - 91.2 2C4.3 173.6 91.1 57.9 26.9 - -

Totl 2. 2.mo.0 1.078.4 4L52.6 347.2 182.2 115.8 93.8

(b) *lt _ Pnrd

Do d at1o (a) 720.0 806.o 885.0 886.0 6 o.0 869.0 816.0 856 W.0 840.0 810.0 784.0 775.03b) - - - - - - 19.0 53.0 78.0 79.0 81.0 83.0 86.0

Aflocated p2n fta ft. th.ptn latoo n 313.0 1.686.0 3.080 2.866 2.857 2.$74 2.320 2.3c8 2.422 2,599 2.732 2.76?

Total Self-gert.d food. 1.033 2,490 3.965 3.752 3.763 3.458 3.219 3.231 3.31 3.492 3.599 3.626

Total S _ 3.043 3.568.4 i.1U7.6 h.099.2 3.9S4.2 3.s7.8 3.272.8 3.231 3.3.1 3.90 .I89.0 3.626.0

c_ital memditk

de.e1.~a cost Co tin katet- R NnwaLaL- 1,341.0 520.0 211.0 101.0 121.0 131.0 2c.0 116.0 102.0 82.0 84.0 75.0

-- po.d Pro3.ot 1 72.6 .78.7 232.9 12.9 S3.4 31.9 12.5 12.9 12.5 12.5 12.5

&kb-total 1.491.9 1. 92.6 686.7 333.9 231.5 224.4 236.9 128.5 114.5 94.5 96.5 87.5

DetIEe caiCl C91 _nt

31 _ _ 31.7 64.7 65.9 67.3 68.7 70.0 71.4 72.9 74.3 75.8 77.4CAA- 25.3 26.8 28.4 30.1 31.9 33.8 35.8 38.0 - -CCCZ 1.. OD lb- 28 .0 28 .0 28.0 28.0 28.0 28.0 28.0 28.0 28.0 28.0IDD 4000 Ha -b 34 .6 35 3. 38.3 10.8 413.3 4.5.8 419.6 52.0 55.8 57.6PR _ 39.9 - . - - - - * - - -

.- ned Pfo3eot

I - - D - *- 6.2 39.5 53 1 57 0 61 1 65 6COCZ 5 0.2 93 59.9 58.9 62.2 65.6

Other Cbre

MU %baidy' - 303.0 303.0 -. -. * -- FE Loan Reppmt 43.0 1. 31.6 D 131.0 134.0 3.o 134.. 13.0 134.0 134.0 131.0 131.0FM. ledeo.. CPAI 0.80 per klo - 210.0 . 28.0 331.0 359.0 376.0 383.0 386.0 388.0 388.0 388.0 388.0

kab-total 292.9 685.7 878.6 621.5 655.0 677.6 786.6 801.s 817.3 830.2 804.9 816.2

Pinacinjl Cha..

B1 _ 17.8 17.9 17.1 15.7 14.4 13.1 11.7 10.3 8.8 7.4 5.9 4.4CA _ 6.0 15.0 15.0 13.5 11.9 10.2 8.4 6.5 4.4 2.3 -CCC 124.9 17.2 17.4 16.3 15.1 13.9 12.7 11.7 10.5 9.3 8.1 6.9ioD 37.0 40.8 99.1 52.8 50.4 47.9 43.3 42.4 39.4 36.1 32.7 29.0Jlt-t. In - 65.o 32.5 16.3 16.3 16.3 16.3 16.3 16.3 16.3 16.3 16.3 16.3

Proooa.d Pro tet

IMED - _ 7.8 17.3 29.9 38.4 43.1 46.7 43.4 39.8 35.9 31.8 27.3CCCG _ _ 2.5 10.6 21 28.3 32.4 35.4 32.6 29.7 26.7 23.4 20

PU - 31.0.0 139.0 128.0 19.0 12.0 117 106.0 95.0 85.0 72.0 63.0 93.0 4 2.0N2.aell_ obarsg. - 35.0 29.0 16.0 16.0 10.0 10.0 10.0 10.0 10.0 10.0 10.0 10.0

Skb-tota 289.7 302.7 303.8 309.5 301.8 292.9 279.5 258.2 230.9 207.0 181.2 155.9

W-kl.f Ceoial - 5 590.0 900.0 500.0 - - - - - - - -

o. ?a 4.6 - 10.5 622.5 1,249.1 1,150.4 1,149.8 1,026.5 918.2 922.4 986 1,076.4 1,147.9 1,175Coaxthgeooi.e (3 _ 131.1 52,0 01.1 10.1 11.9 13.1 20.5 11.6 10.2 8.2 8.1. 7.931) _ 15.1 109.2 170.9 112.7 41.2 62.5 25.3 1.3 1.3 1.3 1.3 1.3

ToW klicaut - 2,7864.2 3,364.7 3,810.2 2,538.1 2,421.2 2,297.0 2,267.0 2,123.5 2,160.2 2,217.6 2,240.2 2,243.4

SMw (789.6) 2au8.8 203.7 607.4 1.S61.1 1.S34 1.276.8 1.00A.8 1.107.5 1.180.8 1.272.4 1.138.8 1.382.6

(a) Otgoing prop=

(b) 2rqd 09oj t

IVORY COAST

THIRD OIL PAIX( PROJECT T

SODKPAIL - OILPAIM OUlROWS

BSTTIHUD CASH now

V7 1974 1975 1976 1977 1978 Fil) O 98 1982 1S3 98 1985INFL

146 15 5BNDA 8 111 43 12 6IB.D 14 235 36 34BsIE 28 34 14 11

b) R ep!Vwtsb a) 95 25 6 67 86 103 121 138 148 5 152 359

FU a) 9 25 47 68 87 105 122 139 150 132 106 814b) 3 9 1,5 21

a) Reem %Icales a) 1.354 3,100 3,220 3,518 3,848 3,928 3,933 4,025 4.155 4.207 4,226 4,208 4,634

b) 61 127 245 409 585 748 956DOprociation 36 16 6 39 0 hO 3 3 3

Total OO J,A 1A4 3,705 UZ02 4X0 4,9 4,713 4.956 1, 231 4293

Iovestmenta a) 348 287 160 117 76 38 30 24 18 12 5b) 53.8 62.4 68.7 76.7 76.7 23 14.3 12.8

Renewals 4 15 7 8 10 2 16 16 16 20 17 21 17

Loans R nitsWZFM 38.6 72.6 72.6 72.6 72.6 72.6 72.6 72.6 72.6 72.6 34 34BNDA 6.3 12.5 12.5 12.5 12.5 12.5 12.5 12.5 12.5IBRD 39.6 42.1 48.5 46.6 61.1 66.6 70.2 73.5 80.7 85.9 92.3

* 25.2 37 132 25

Oper itlo Ia) 465 455 195 549 603 643 661 672 673 673 671 676 676b) 3 6 12 19 27 33 38

Proceasing a) 385 454 521 605 682 759 816 849 881 894 874 872 811b) 8 16 30 50 70 85 97

Financial charges 67 80 95 104 110 112 105 97 89 81 73 51 56Stabilization Fund 550

Purchase of Fruits 409 1,453 1,767 1,894 2,153 ,1114 2,080 2,231 2.366 tA,2 2,582 2,657 3,394

Contingencies 121 124 134 14 152 161 161 165 168 166 169 169

Incom Tax 8 108 113 77 58 77 57 85 114 148 185 145

Total 1,703.2 3, 498.6 3,575 3,726.1 4,051.1 4,116.4 4,179.9 4,303.7 415o4.6 4,4.4 4,798.8 41.84.4 5,571.8

(89.2) 50.4 (171) (21.1) (23.1) 23.6 62.1 131.3 208.4 271.6 356.2 424.6 321.2

/ Ongoing Program

P. Project

ANNEX 2

Table 5

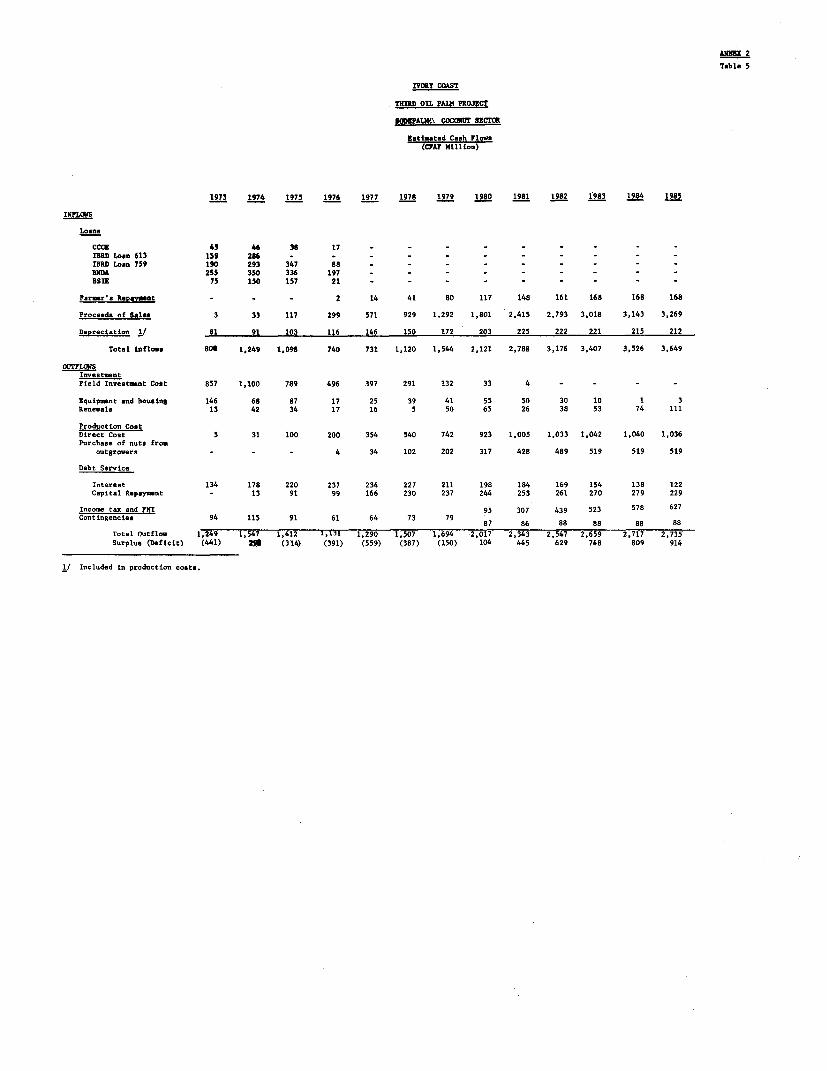

rVORY COAST

THuID 01 PALM PROJECT

SODZPALHU, COCONTE SECTCR

Estimated Cash Flows(ClAP Million)

1973 1974 1975 1976 1977 1978 1979 1980 1981 1982 1983 1984 1985

INPLOWS

Loans

CCCE 45 46 38 17 - - - - - - -rBRD Loan 613 159 286 _ -18RD Loan 759 190 293 347 s8BNDA 255 350 336 197 - - - - - - - -BSIE 75 150 157 21 - - - - - - - - -

Farmr's Reoavmeot - - 2 14 41 80 117 148 161 168 168 168

Proceeds of Sales 3 33 117 299 571 929 1,292 1,801 2,415 2,793 3,018 3,143 3,269

Depreciation 1/ 81 91 103 116 146 150 172 203 225 222 221 215 212

Total inflows 808 1,249 1,098 740 731 1,120 1,544 2,121 2,788 3,176 3,407 3,526 3,649

OUT'FLOWSInvestmentField Investmext Coat 857 1,100 789 496 397 291 132 33 4 - - - -

Equipment and housing 146 68 87 17 25 39 41 55 50 30 10 1 3Renewals 13 42 34 17 16 5 50 65 26 38 53 74 111

Production CostDirect Cost 5 31 100 200 354 540 742 923 1,005 1,033 1,042 1,040 1,036Purchase of nuts from

outgrowers - - - 4 34 102 202 317 428 489 519 519 519

Debt Service

Interest 134 178 220 237 234 227 211 198 184 169 154 138 122Capital Repyment - 13 91 99 166 230 237 244 253 261 270 279 229

Income tax and FNI 95 307 439 523 578 627Contingencies 94 115 91 61 64 73 79 87 86 88 88 88 88

Total Outflow 1,249 1,547 1,412 1,131 1,290 1,507 1,694 2,017 2,343 2,547 2,659 2,717 2,735Surplus (Deficit) (441) 259 (314) (391) (559) (387) (150) 104 445 629 748 809 914

1/ Included in production costs.

T7lkD OIL ?AX NOJICT

1973 1974 U19 1976 19fl 1978 197S 19S0 1981 1982 1983 198M4 19S