Embed Size (px)

Citation preview

A p p lica tion o f R e sp ons ib ility

C e nte r A p p roa ch

(M a na g e m e nt C ontro l Syste m )

for C onve rting D iv is ions in to

“P rofit C e nte rs”

B Y

H EM A N T B . G O D B O LE

S AG /IR AS

R e port su bm itte d in con n ection w ith a cou rse on

Pro ject M a n a g em en t a t C -T A R A

From 1 0th

S e pte m be r to 1 8th

O c tobe r 2 0 1 3

2

A ck now ledg em en t

I am th ank fu l to th e FA& CAO /Sou th Cen tra l

Ra ilw ay , Sm t. U sha A . Kum ar fo r n om ina tin g m e

fo r th is cou rse .

I am a lso th ank fu l to D ire c to r/C -T ARA ,

Sh ri V ijay Kum ar and Ad d l. D ire c to r, Sh r i M u r th y ,

fo r th e ir v a lu ab le h e lp .

I a lso p la ce on re co rd th e h e lp rende red by m y

co lle agues in RS C (n o w ca l le d N A IR ), BR C D iv is ion

o f W R fo r th e ir v a lu ab le h e lp .

H em a n t B . G o d bo le

IRAS /SAG /SC R ,

Se cunde raba d .

3

IN D EX

S l.

N o . D esc rip t ion o f c on ten t

Pa g e

N o .

1 ) Abs tra c t 4

2 ) Background 5

3 )

Th eo re tica l B ack ground o f th e

re le van t con cep ts (M anagem en t

Con tro l S y s tem )

6

4 ) M anagem en t Con tro l th rough

Respon s ib il ity A ccoun tin g 12

5 ) D iscu ss ion re la te d to S ta tu s on

Ra ilw ay s an d Su gges t ion s 17

4

A p plica tion o f R espon s ib ilit y C en ter A p proa ch

(M a n a g em en t C on tro l S ys tem ) fo r C on v ertin g

D iv is ion s in to “ Pro f it C en ters”

Ab stra ct

Zona l R ailw ays (ZR ) in India are headed by General

M anagers (GM s) w ho have to ensu re satisfactory

custom er serv ice by conducting the operations e fficien tly

and e ffectively . W hile w ork ing tow ard s these goa ls, they

have to strive hard to ensu re that they earn the targeted

revenue w ithin budgeted expenses for a tta in ing the

desired operating ratio (OR). T he Indian R ailw ays (IR) can

atta in the budgeted financial targets on ly by atta inm ent of

respective ob jectives by various GM s.

As of today , IR as a w hole; as a lso various ZR s are

attuned to on ly one m ost sign ifican t financia l ob jective,

nam ely the OR. IR s’ l ingo, w h ile re ferr ing to v iab il ity,

nobody ta lks of Profit / N et Profit. Indeed in the last

Budget Speech also it w as em phasized that OR w ou ld

im p rove in 2013-14 from 88 .8% to 87 .8% . Thus, for the

cu rren t d iscussion , it is su ffic ien t to say that O R is a

su rrogate for v iabi lity or p rofitability in IR .

W h ile OR as a ratio of Operating Expenses to

Apportioned Earn ing is calcu la ted and m onitored for IR as

w e ll as for ZR s, such ratio is not com puted for m ost v ita l

un its o f the ZR s, i.e . D iv isions . In stead, a ratio called

Perform ance E ffic iency Index (PE I) i.e. a ratio of Expenses

under Dem ands # 3 to 12 * to O rig inating Earning s is

com puted. Since the denom inator in this ratio does not

indicate Apportioned Earning s of the Div ision , such ratio is

no w ay indicative of p rofitabil ity or v iab ility of the

D iv ision . (* Som e R a ilw ays like SC R LY take Dem and # 3

to 13 w h ile C . R LY , W . RLY take # 3 to 12)

T h is p roject seeks to lay dow n the m echanism for

com puting OR for the Div isions. It also attem p ts to fu rther

re fine the m echanism for even com puting p rofit o f the

5

D iv ision s. T his w ill render the financial targets as m ore

in te llig ible and in teg rated responsibility for facilita ting

M anagem ent C on tro l in consonance with the M anagem ent

C on tro l System (R esponsibility Accoun ting) , in as m uch as

D iv isional geog raphica l structu re lends itse lf to be treated

like that of ZR s as it is a rep lica of the la tte r.

B a ckg rou nd

Ind ian R a ilw ays are a Departm enta l C om m ercial

undertaking o f the Governm ent of Ind ia . T heir budget has

been separated from that of Governm ent of India from

1924 as per the of the Acw orth C om m ittee ’s

recom m endations, w hich had , in ter alia , m en tioned as

fo llow s:

"W e recom m end … … … ..

that the ra ilw ays shou ld have a separate budget of

the ir ow n , (and ) be responsible for

– earn ing and expend ing their ow n in com es and

– for p rov iding such net revenue as is requ ired to m eet

the in terest on the deb t in cu rred or to be in cu rred by

the Governm ent for ra ilw ay pu rpose … … … .”

T he loans taken by R a ilw ays from the Governm ent of

Ind ia for C apita l Exp enditu re are factored in the budget

as budgetary support; cum ulative tota l b eing ca lled as

C apita l a t C harge, w hich bears the rate of D iv idend

( in terest) as recom m ended by R ailw ay C onven tion

C om m ittee of Parliam ent from tim e to tim e.

As stated earlie r, as of now , OR is ca lcula ted only for

IR as w hole and a lso for ZR s, and not for D ivisions. T hus,

the m ost im portan t field level functionaries, called as

D iv isional R a ilw ay M anagers (DR M s), do not have p rofit ,

or its su rrogate , the O R as the financial target. T he only

financial targets they have are: (1 ) expend itu re to be

con tro lled with in Budget G ran ts and (2 ) generating

Budgeted O riginating Earn ing s . T here is no corre la tion

betw een the tw o. In ab sence of Profit (or even operating

6

p rofit in fe rred from O R) as m otivating targets, the DR M s

tend to pay m ore atten tion to other im portan t typica lly

non -financial ob jectives like: Safe ty, S ecu rity , Pub lic

R e lations, Industrial Re lations, Load ing (whether

p rofitable or not), Punctuality, Protoco l for higher up s and

Po litical Dignitaries e tc . W hile all these are im portan t,

accen t on v iab ility and reduction of loss and /or in crease of

p rofit, and (with the ob jective/ m easu rable assessm ent

and not arbitrary or sub jective assessm ent) is a sine qua

non for susta inab ility of the organization is m issing.

A s IR is a C om m ercial Undertaking, there has to be a

re la tionship betw een the M anagem ent C on trol System to

O rganizational Goa ls. H ence there is need for Profitability

or v iability as its perform ance m easu res/m etrics/ targets.

T h eoretica l B a ck grou n d o f th e re leva n t

con ce pts

M an ag em en t Contro l S yste m

B a s ic Con cep ts

F or understanding the m eaning of “M anagem ent C on tro l

System ” it w ould be use fu l to know the m ean ing of these

th ree term s in cluded in th is concep t, in a convenie n t

order.

Con tro l

As you p ress the acce lerator, you r car goes faster , as you

rotate the steering w heel, it changes d irection , and as you

p ress the b rake pedal, it slow s dow n or stop s. W ith these

conso les, you con tro l the speed and direction of the car. I f

any of them is inoperative , the car does not do w hat you

w an t it to do. In other w ord s, it is ou t of con tro l.

7

An organization m ust also be con tro lled; that is, d evices

m ust be in place to ensu re that its strategic in ten tions are

ach ieved . Bu t con tro lling an organ ization is m uch m ore

com p licated than con tro ll ing a car.

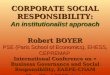

E very c on tro l sys tem h a s a t lea s t fou r

e lem en ts :

1 . A d e te ctor or sen sor – a device that m easu res w hat is

actua lly happen ing in the p rocess be ing con tro lled .

2 . An a ssessor – a dev ice that d eterm ines the

significance of w h at is actua lly happening by com paring

it w ith som e standard or expectation of w hat shou ld

happen .

3 . An e ffe ctor – a dev ice (often called “feedback”) that

a lte rs behavior if the assessor indicates the need to do

so .

4 . Com m un ication s ne tw ork -d e vice s that transm it

in form ation betw een the detector and the assessor and

betw een the assessor and the e ffector.

T hese fou r basic e lem ents of any con tro l system are

show n be low .

Control

device2. Assessor. Comparison

with standard

3. Effector. Behavior

A lteration, if needed

Entity

Being

controlled

1. Detector. Informat ion

about what is happening

By m eans of a speedom eter (detector) d river of

a car notices that the speed is 58 km ph. H e

com pares (assesses) it w ith the m ax im um perm itted

speed say 60 km ph. By suitab le use of conso les,

con tro ls the speed w ithin 60 km ph.

8

M a n a gem en t

An organization consists of a g roup of peo ple w ho

w ork together to achieve certain com m on g oa ls ( in a

b u sin e ss org an ization a m ajor g oa l is to e arn a

sa tis fa ctory p rofit). O rganizations are led by a h ierarchy

of m anagers, with the ch ie f execu tive officer (C EO ) at the

top , and the m anagers of busin ess units, d epartm ents,

sections, and other subunits ranked below h im or her in

the organizationa l chart. T he com plexity of the

organ ization determ ines the num ber of layers in the

h ie rarchy. A ll m anagers other than the C EO are both

superiors and subord inates; they supervise the peop le in

the ir ow n un its, and they are superv ised by the m anagers

to w hom they report.

T he C EO (or, in som e organ izations, a team of senior

m anagers) decides on the ove ra ll s tra teg ie s that will

enab le the organ ization to m eet its goa ls. Sub ject to the

app roval o f the C EO , the various business unit m anagers

form u late add itiona l strategies that w ill enable their

respective units to fu rther these goa ls. The m an ag em e nt

con tro l p roce ss is th e p roce ss b y w h ich m a nag e rs at

a ll le ve ls e n su re tha t th e p e op le th e y su pe rvise

im p le m en t th e ir inten ded stra te g ie s .

S ys tem

A system is a p rescrib ed and usually repetitious w ay

of carry ing ou t an activ ity or a se t o f activ ities. System s

are characterized by a m ore or less rhy thm ic, coordinated,

and recu rring series of step s in tended to accom p lish a

specified pu rpose. T he therm ostat, the body tem peratu re

con tro l and con tro l o f a car are the exam ples of system s.

M anagem ent con tro l system s are far m ore com p lex and

judgm enta l.

9

M any m anagem ent actions a re unsystem atic.

M anagers regularly encoun ter situations for w hich the

ru les are not w ell d e fined and thus m ust use their best

judgm ent in deciding w hat actions to take. T he

e ffectiveness of the ir actions is determ ined by their skill in

dea ling w ith peop le, not by a rule specific to the system

(though the system m ay suggest the genera l natu re of the

app rop ria te response). If a ll system s ensu red the correct

action for a ll s ituations, there w ou ld be no need for hum an

m anagers!

M a n a gem en t C on tro l

M anagem ent con tro l is the p rocess by w hich

m anagers in fluence (the behavior of) other m em bers of

the organ ization for im plem enting the organ ization ’s

strateg ies. Several aspects of th is p rocess are am p lified

be low .

M a n a gem en t C on tro l A ctiv ities

M anagem ent con tro l invo lves a varie ty of activities,

in cluding:

P lanning w hat the organization should do.

C oordinating the activities of severa l parts of the

organ ization.

C om m un icating in form ation.

Eva luating in form ation .

Deciding w hat, if any, action shou ld be taken .

In fluencing people to change their behav ior.

C on c e pt o f G oa l C on gru en c e

M anagers have persona l as w ell as organizational

goa ls. The cen tra l con tro l p roblem is to induce them to act

in pu rsuit o f their persona l goa ls in w ays that will he lp

atta in the organ ization ’s g oa ls as w e ll. Goal cong ruence

m eans that, in sofar as is feasib le, the goals of an

10

organ ization ’s ind ividua l m em bers should be consisten t

w ith the goa ls of the organization itse lf. T he m anagem ent

con tro l system shou ld be designed and operated w ith the

p rin ciple of goa l cong ruence in m ind .

S tra te gy fo rm u la tion , M a n a g em en t con t ro l

a n d ta sk con t ro l

There is a b road spectrum of activ ities that an

organ ization undertakes and based on their

characteristics , they are m onitored from the long term ,

m ed ium term or short te rm perspective. T hey are:

S trategy form ulation, M anagem ent con tro l and T ask

con tro l

S tra te g y form u la tion is the p rocess of decid ing on

new strateg ies; wh ile m a na ge m e n t contro l is the

p rocess of im p lem enting those strateg ies. F rom the

standpoin t o f system s design, the m ost im portan t

d istin ction betw een strategy form ulation and m anagem ent

con tro l is that strategy form ulation is essen tially

unsystem atic. T hreats, opportunities, and new ideas do

not occu r at regu lar in terva ls; thus, str ategic decisions

m ay be m ade at any tim e .

Ta sk contro l is the p rocess of assu ring that

specified tasks are carried ou t e ffective ly a nd

e ffic ie n tly. T ask con tro l is transaction -orien ted that is, it

invo lves the perform ance of individual tasks accord ing to

ru les established in the m anagem ent con tro l p rocess.

T ask con tro l o ften consists of see ing that these rules are

fo llow ed, a function that in som e cases does not even

requ ire the p resence of hum an be ing s. CNC m ach ines,

p rocess con tro l com puters, and robots are m echan ical

task con tro l d evices. T heir function involves hum ans only

w hen the la tte r p rove less expensive or m ore reliab le; this

is like ly to happen on ly if unusua l even ts occu r so

frequen tly that prog ram m ing a com puter with rules for

dea ling with the se even ts is not w orthw h ile .

11

Activity Nature of End Product

Strategy

formulation

Management

Control

Task

control

Goals, strategies, and policies

Implementation of strategies

Efficient and effective

Performance of individual tasks

Run indiv idual research

project

Control research

organization

Decide magnitude and

direction of research

Reorder an item Decide inventory levelsDevise inventory

speculation policy

Maintain personnel

records

Implement minority

recruitment program

Adopt affirmative action

policy

Manage cash flowsIssue new debtChange debt/equity ratio

Book TV commercialsDetermine advertising

budget

Add direct mail selling

Schedule productionExpand a plantEnter a new business

Coordinate order entryIntroduce new product or

brand within product line

Acquire an unrelated

business

Task Control Management

Control

Strategy

Formulation

Ex a m p les o f d ec is ion s in p la n n in g a nd con tro l

fu n ction s

12

M a n a gem en t C on tro l th rou gh R esp on s ib i lity

A c cou n t in g

R e sp onsib ility Cen te rs

A responsibility cen ter is an organ ization unit that is

headed by a m anager w ho is responsib le for its activities.

In a sense, an organ ization is a co llection of responsibility

cen ters, each of w h ich is rep resen ted by a box on the

organ izational chart. These responsibility cen te rs form a

h ie rarchy. A t the low est leve l are the cen ters for sections,

w ork sh ifts, and other sm all organ ization units.

Departm ents or business un its com prising severa l o f these

sm aller un its are h igher in the h ie rarchy . F rom the

standpoin t o f sen ior m anag em ent, the en tire organization

is a responsibility cen ter; though the term is usua lly used

even to re fer to sm alle r units w ith in the organ ization .

N a ture of Re sp on sib ility Ce nters

A responsibil ity cen ter exists to accom p lish on e or

m ore p urp ose s , te rm ed its objective s . The organization

as a w hole has goals, and senior m anagem ent decides on

a se t of strateg ies to accom p lish these goa ls. T he

ob jectives of the organ ization ’s various responsibility

cen ters are to he lp im plem ent these strateg ies. Because

every organ ization is the sum of its responsibility cen ters,

if each responsib ility cen ter m eets its ob jectives, the goa ls

of the organ ization w ill have been achieved .

R esponsibility cen ters rece ive inpu ts in the form of

m ateria ls, labor and services. Using w orking capita l (e .g .,

inven tory, receivables), equipm ent, and other assets, the

responsibil ity cen ter p erform s its particular function with

the u ltim ate ob jective of transform ing its inpu ts in to

ou tpu ts, e ither tangible (i.e., goods) or in tang ible ( i.e .,

serv ices). In a p roduction p lan t, the ou tpu ts are goods. In

sta ff un its, such as hum an resou rces, transportation,

eng ineering, accoun ting, and adm in istration, ou tpu ts are

serv ices.

13

T he products (i.e., goods and serv ices) p roduced by

a responsib il ity cen ter m ay be fu rnished e ither to another

responsibil ity cen ter (u s ing de fined tra n sfe r p r ic ing

m e cha n ism ), w here they are inpu ts, or to the ou tside

m arketplace w here they are ou tpu ts of the organ ization as

a w hole . R evenues are the am ounts earned from

p rov id ing these ou tpu ts. R esponsib ility cen ters are

requ ired to function both e fficien tly and e ffectively.

E ffic ien cy an d e ffe ctive n ess

E ffic ien cy is the ratio o f ou tp uts to inp uts, or the

am ount of ou tpu t per un it o f inpu t. R esponsib il ity C en ter A

is m ore e ffic ien t that Responsibility C en ter

if it u ses few er resou rces than R esponsibility

C en ter B bu t p roduces the sam e ou tpu t, or

If it u ses the sam e am ount of resou rces bu t

p roduces a g reater ou tpu t.

In con trast to e ffic iency , w hich is determ ined by the

re la tionship be tw e en a re sp on sib ility ce nter ’s ou tp ut

a n d its objectives . T he m ore th is ou tpu t con tribu tes to

the ob jectives, the m ore e ffective the unit. Since both

ob jectives and ou tpu ts are difficult to quan tify,

e ffectiveness tends to be exp ressed in sub jective, non-

ana ly tical te rm s- for exam ple , “C ollege A is doing a first -

rate job , bu t C ollege B has slipped som ew hat in recen t

years.”

E ffic iency and e ffectiveness are not m utually

exclusive; every responsibility cen ter ough t to be both

e ffic ien t and e ffe ctive in w h ich case , the organization

ough t to be m eeting its goals in an op tim um m anner. A

responsibil ity cen ter, w h ich carries ou t its charge w ith the

low est possible consum p tion of resou rces, m ay be

e ffic ien t, bu t if its ou tpu t fa ils to con tribu te adequ ate ly to

the atta inm ent of the organizations ’ g oa ls, it is not

effective . If a cred it d epartm ent hand les the paperw ork

connected w ith de linquen t accoun ts at a low cost per unit,

14

it is e ffic ien t; bu t if, a t the sam e tim e, it is unsuccessfu l in

m ak ing co llections (or needlessly an tagonizes custom ers

in the p rocess), it is ine ffective.

In sum m ary , a responsib ility cen ter is e ffic ien t if it

d oe s th ing s r ig ht, an d it is e ffe ctive if it d oe s the

r igh t th ing s.

Th e R o le o f Profit

A m ajor ob jective of any p rofit-orien ted organization

is to earn a satisfactory p rofit. T hus, p rofit is an

im p ortan t m ea sure o f e ffe ctive ne ss . Fu rtherm ore,

sin ce p rofit is the diffe rence betw een revenue (a m easu re

of ou tpu t) and expenses (a m easu re of inpu t), it is a lso a

m e a su re o f e ffic ie ncy . T hus, p rofit m easures both

e ffectiveness and e ffic iency .

Typ e s o f Re sp on sib ility Ce nte rs

T here are fou r types of responsib ility cen ters,

c lassified accord ing to the natu re of the m onetary inpu ts

and /or ou tpu ts that are m easu red for con tro l pu rposes:

re ven ue cen te rs, e xp en se cen ters (a lso ca lled a s

cost cen te rs) , p rofit cen te rs, a nd in ve stm e nt

ce nte rs . T heir characteristics are show n be low.

In re ve n ue ce n te rs , ou tpu t is m easu red in

m onetary term s;

In ex pe n se ce n te rs , inpu ts are so m easu red;

In p rofit ce nters, b oth revenues (ou tpu t) and

expenses (inpu t) are so m easu red; and

In in ve stm e n t cen ters , the rela tionship betw een

p rofit and investm ent is so m easu red .

15

R e ve n ue Ce n te rs

In a revenue cen ter, ou tpu t ( i.e. revenue) is

m easu red in m onetary term s, bu t no form al a ttem p t is

m ade to re la te inpu t (i.e., expense or cost) to ou tpu t.

Ex pe n se Cen te rs

C en ters w hose inpu ts are m easu red in m onetary

term s, bu t ou tpu ts are not. T here are tw o genera l types of

expense cen ters: eng ineered and discre tionary .

En g in ee red Ex pe n se Ce n te rs

Engineered expense cen ters have the fo llow ing

characteristics:

Their inpu t can be m easu red in m onetary term s.

Their ou tpu t can be m easu red in physica l te rm s.

The op tim um m onetary am ount of inpu t requ ired

to p roduce one un it o f ou tpu t can be determ ined.

16

D iscre tion ary Exp en se Ce nters

D iscre tionary expense cen ters in clude adm in istrative

and support un its (e .g ., accoun ting, legal, industrial

re la tions, public re la tions, and hum an resou rces),

research and deve lopm ent operations, and m ost

m arketing activities. T he ou tpu t of these cen ters cannot

be m easu red in m onetary term s.

Profit Ce n te rs

In p rofit cen ters, both revenues and expenses

associa ted w ith g enerating these revenues are

m easu red; giving diffe rence betw een the tw o as p rofit (or

even loss). Actua l p rofit (or loss), com pared to budgeted

p rofit or loss is a m easure of M anager’s perform ance .

17

In ve stm en t Ce nte rs

In these cen ters, both p rofit and the investm ent (i.e.

rep resen ted by assets) dep loyed in carrying ou t such

cen ter’s responsibility are m easu red. The re tu rn o n

investm ent (RO I) is the broadest m easu re of the

M anager’s e ffic iency and e ffectiveness.

D is cu ss ion re la ted to S ta tu s on R a ilw a ys a n d

S u gg es tion s

W h at k in d of Re sp on sib ility ce nters are IR , ZRs,

D iv is ion s e tc. as o f n ow ?

O R is a ratio of O perating Expenses (num erator) as

a percen tage of Operating Incom e (denom inator).

O perating Profit is the Excess of O perating Incom e over

O perating Expenses. Thus OR is a su rrogate of operating

p rofit. S ince OR is com puted every year for IR and ZR s,

they can be treated as “Profit C en ters” in te rm s of

R esponsibility Cen te rs app roach, w here in estim ated or

budgeted OR (from w hich Operating Profit can be

deduced ) can be a M anagem ent C on trol T oo l as per

M anagem ent C on trol System .

It cannot be sa id of the Divis ions as of now that they

can be treated as “Profit C en ters” because, in the ir case ,

apportioned earn ing s are not availab le. As for the

num erator of O R, expenses covered under Dem and

num bers 3 to 12 or 13 as som e R a ilw ays take, (w hich are

18

used for com putation of Perform ance E ffic iency Index or

PE I in case of D ivis ion s) do not com prehensively dep ict

the O perating Expenses as the Dem and num ber 14 w hich

denotes app rop ria tion to Pension Fund and App rop ria tion

to Dep recia tion Reserve Fund (DR F) are not in cluded in

the num erator of PE I. Besides, the denom inator used in

PE I, viz. O rig inating Earning s are not log ically fully

perta inab le to the D iv isions, w h ile apportioned earning s as

used in case of ZR s are . In short, as of today , OR is not

be ing ca lculated for D iv isions and thus they cannot be

treated as “Profit C en ters”.

Q uestion to be asked is whether they can be treated

as C ost C en ters? In orde r to be treated as such , a ll

revenue expenses perta inable to the period of the year

shou ld be capable of be ing agg regated. As of now ,

expenses like app ropria tion to Pension Fund and

App rop ria tion to DRF are not show n separately for the

D iv isions as a part o f O perating Expenses of the D ivis ion .

S ince these costs perta in ing to D iv isions are not know n to

the D ivis ions, D iv isions can not be log ically ca lled as cost

cen ters e ither.

W h y app ortion ed e a rn ing s are n ot com pu te d for

D iv is ion s sep a ra te ly?

A s of now , earn ing s of the ZR s are apportioned (sp ilt

in to portions or shared ) am ong various ZR s on the basis

o f p roportionate leng th of track of respective ZR s used for

carriage of goods consignm ent over them . Sam e is done

for passenger earn ing s. ZR s on w h ich tra ffic orig inates or

te rm inates are given som e extra share for the ir ex tra

e ffort on hand ling e tc. T his apportionm ent is facil ita ted by

T ra ffic Accoun ts O ffice of the Zona l R ailw ay, w h ich is

cen tra lized for such R ailw ay, w hile the expenditu re

accoun ta l is m ostly decen tralized over the Div isions and is

carried ou t by D ivis ional Accoun ts O ffices headed by S r

DFM s. Thus the DR M s do not know the ir Divis ions’

apportioned earning s.

19

Ca n th e a pp ortione d e arn in g s be com p uted for

D iv is ion s?

Based on the p roportionate d i stance of consignm ent

or passenger travelled over the Zona l R a ilw ay , if the

p roportionate (apportioned ) earn ing s can be calculated for

the Zona l R ailw ays, there is no reason w hy using sim ilar

tab les of distances across the Divis ions, w hy it cannot be

so ca lcu lated for the D ivis ions. W ith he lp of com puters it

w ou ld be im m ense ly possible to do the sam e .

Ca n ope ra tin g e xp en se s, inc lud ing u nde r D e m a nd

n u m b er 13 & 1 4 be ca lcu lated for the D iv is ion s?

It w ou ld be possible to ca lcu late the App ropria tion to

Pension Fund from the D iv ision based on the form ula:

Pe n siona ble e m p loye es

on D iv is ion

------- ----- ----- ------ ----- X Ap propriation to Pe n.

Fu n d on ZR

Pe n siona ble e m p loye es

on the Zon e.

An exam p le of Baroda (BRC ) Divis ion of W estern

R a ilw ay, w here in the sta ff streng th on ro ll h as stead ily

declined over last 6 years, w ould he lp ou r understanding.

as fo llow s.

As on 3 1st

M a rch N u m b er

2008 15427

2009 15081

2010 14760

2011 14278

2012 13857

2013 13257

W hat th is ind icates is that there is a lot o f a ttrition

over the years, due to au tom ation, ou tsou rcing and

20

in creased e ffic iency/ e ffectiveness, the g row th in

expenses is not p roportionate ly h igh. If App rop ria tion to

Pension fund w ere to be com puted for Div ision separate ly,

the sam e w ou ld be in tandem with such reduction in sta ff

on ro ll w hich w ou ld yie ld im p roved OR and p rofit.

D iv ision ’s e fforts to con ta in the sta ff streng th w ou ld

m an ifest in im p roved perform ance figu re on ly if Profit is

com puted.

S im ilarly, App rop ria tion to DR F from the D i v is ion can

be com puted as:

Cap ita l at Charg e

o n the D iv is io n

------------------------ X A p p ro p riatio n to D R F fo r the Z o ne

Cap ita l at Charg e o n

the Z o ne.

W ith such com putation , O perating Expenses for the

D iv ision can be ca lcu lated ana logous to such expenses for

the Zona l R ailw ay .

T h is will help D iv isions to com pute its OR sim ilar to

ZR s.

O ve r a nd ab ove O pe ra ting Profit, ca n Ne t Profit ,

a fter ta k ing into a ccou nt the fina n c in g ch arg e s , be

ca lcu la te d for th e D iv is ion?

Indeed , it can be done by ad ding to the Operating

Expenses, p roportionate D iv idend liab il ity app licable to the

D iv ision based on the p roportionate C apita l a t c harge

invested vis a v is that on the Zona l R a ilw ay .

D oe s “Profit cen te r” a lw a ys e arn p ro fit?

A particular responsib il ity C en ter ca lled Profit C en ter

on ly ind icates that both expenses and earning s for that

dom ain can be com puted and thus p rofit or loss can be

21

deduced . It does not m ean that there w ill alw ays be p rofit.

It on ly im p lies that p rofit/ loss is com putab le unlike as pe r

cu rren t d ispensation ob ta ining in the D ivis ions w here it

cannot be so com puted because the earn ing s and

expenses figu res are not ava ilab le for m atch ing them for

assessing p rofit/ loss. C om putability of p rofit/ loss or

operating p rofit/ operating loss or O perating R atio

( favorab le or adverse) in itse lf renders the en tity to be a

Profit C en ter. When it cannot be so com puted, it cannot

be ca lled as a p rofit Cen ter and the responsibility of the

M anager cannot be in te rm s of p rofit to be m ade or /

in creased or loss to be con ta ined or reduced.

H ow w ou ld th e con ce pt he lp the D iv is ion s or

D RM s? .

“W hat cannot be m easured, cannot be m anage d

: Peter D rucker/ D em ing

"If you cannot m easu re it, you can ’t im p rove it"

: Lord Ke lvin

T he logic in above sa id quotes can be benefic ially

ported for m easu rem ent of OR / p rofit for the D ivis ion.

T h is will cast the responsibil ity of earn ing budgeted or

h igher OR /p rofit on DRM s. Y ear-over-year (YO Y)

com parison and in ter Divis ion al com parison w ou ld be

possible , p rom p ting com petition am ong DR M s for

exceed ing targets by h igher m arg ins.

C om putab ility o f O R and operating Profit w ou ld be a

far m ore m otivating target for any Business M anag er

than O riginating Earning and/or Expenses under

Dem and num bers 3 to 12 or 13 . GM s and even the

Board w ou ld be in a better position to com pare and

m on itor the targets of the DR M s in te rm s of Profit /

O R as it w ou ld con tribu te to and be cong ruen t with

the ir ow n financia l targets in te rm s of Profit or O R.

Th is cong ruence of goa ls of DR M s and those of ZR s

and IR are sine qua nan for con tro ll ing in te rm s of

22

R esponsibility C en tre app roach . System s can be

fu rther devised to in cen tiv ize the achievem ent of

such targets so that such achievem ents w ould he lp

IR to im p lem ent the ir strategies. If such a lignm ent is

not forged , there w ould be divergence that will b e

d ifficult to fix .

Such target/s w ill help DR M s to connect the

apportioned earn ing s w ith operating expenses

in stead of targets like O riginating Earn ing and /or

Expenses under Dem and num bers 3 to 12 (or 13

w here in cluded) , w herein there is no good corre la tion

betw een the tw o v is a v is the num erator and

denom inator of the O R.

H av ing O R and O perating Profits as targets w ou ld

he lp DRM s to in crease the Profits over last year or

reduce the losses over last year as m ore in tellig ib le,

tang ib le and in teg rative app roach w ou ld be

facil ita ted . Indeed, a C om m ercia l O rganization,

w ithou t Profit as a target for its Business Un it

M anager does not in fuse any sense of business in

them . Em p loyees can be better sensitiz ed to reduce

the con tro llable expenses for earn ing better p rofit or

O R for the D ivis ions. DR M s can then develop better

m easu res for revenues and costs for various

spending and earn ing au thorities under them . Profit

or O R is a m uch m ore in te llig ible / v isible target for

sharing am ong a ll concerned than otherw ise.

Behav ioral (m otivational) im p lications that push

M anagers (DRM s) to rather vis ib le and d irected

targets are qu ite significan t as behav ioral

consequences of eva luation m echan ism is very

significan t, g iven the hum an natu re .

Profit as a target w ou ld have necessita ted the linkage

betw een expenses and earn ing s, as earn ing s m inus

expenses w ou ld g ive us the p rofit figu re. Because of

such w an t of l inkage, in the Divis ions expenses are

23

m on itored separately from the earning s as these tw o

are separate/ disparate /d iscre te/ targets.

If for exam p le , OR for last fisca l for a D iv is ion w as

78% , target for cu rren t fiscal can be 75% .

A lte rnative ly if OR last year w as 125% , target can be

say 120% now . Exceeding these targets can give far

better satisfaction and recogn ition than som ew hat

am orphous targets like PE I and its com ponen ts.

W ith such perspective, DRM s w ou ld better discern

the tendency of w aste fu l and or fancifu l expenditu re

p roposa ls and thus w ould striv e to cu rtail the

fa t/ flab . T hey w ill tend to in fuse the sp irit o f va lue

eng ineering and Zero Base Budgeting am ong the

B ranch O fficers concerned. There w ill b e better

l ike lihood to see that additional expenses w ould be

m ore than offse t by in crem enta l earning s or by

in crem ental sav ing s due to such expenses.

They w ill also try to earn m ore th rough e ffic iency and

e ffectiveness of operations w hich w ill lead to reduced

un it cost and /or in crease in earning s. e .g .

o Increased fue l e fficiency due to better d riving

p ractices w ith the he lp of tra in ing of Loco P ilot

and in cen tivisation for a tta in ing the sam e,

o Speedy clearance of cases like capacitor banks

for better energy e ffic iency ,

o M ore e ffic ien t linkages of crew w ith in H O ER

o M ak ing of expenses/investm ents faced on hard

facts rather than con jectu res

o System ic changes, com puterization e tc. for

reducing costly m istakes w ith in creases

re liab ility

o Expenses giving quicker re tu rns

o Autom ation that will save recu rring costs and

im p rove re liability.

24

O sten tation w ou ld a lso be expected to be reduced as

it m anifests in to avo idable expenses w ith advers e

im pact on OR.

Ex isting targets for earning s are based on orig inating

basis. In fact DR M s have som e con tro l over the sam e

w ith m arketing and facilita ting sm oother load ing and

evacuation . T his leew ay can be re ta ined by

in cen tiv izing such O riginating E arning s by perm itting

D iv isions to re ta in say 5% of such earn ing s be fore

apportionm ent. In any case , som e portion of

originating earn ing s is bound to be apportioned to

that D ivis ion. T here w ou ld be accen t on push ing

th rough the investm ents like au tom ated load ing

m echan ism for quicker tu rnaround of stock and m ore

th roughpu t w ith better asset tu rn (assets like

w agons, track , locoes e tc.) for faster revenue

generation. DR M s w ou ld a lso d o w e ll in facilita ting

p rojects that decongest the rou tes and/or get last

m ile advan tage. Fo llow ing Exam p les from Baroda

(BRC ) Divis ion of W R w ou ld illu strate such benefits.

Last 5 years’ PE Is are as fo llow :

(F ig u res in R s C rores)

YE A R E X PE N DITU R E

D3 -D1 2

O R IG IN A TIN G

E A R N IN G S

PE I %

2008-09 606 .74 980 .04 61 .90

2009-10 744 .00 1035 .40 71 .85

2010-11 747 .00 1231 .94 60 .63

2011-12 785 .14 1251 .65 62 .73

2012-13 864 .56 2 1 47 .7 0 3 9 .9 0

It is seen that there is a sudden upsu rge in

O rig inating Earning s in 2012 -13. Th is w as due to

com m issioning of port connectivity p roject o f

Bharuch -Dahej, lead ing to im ported coa l T ra ffic.

W h ile on one hand , Div ision /DRM had facilita ted the

com p letion and there fore deserve add itiona l share ,

say 5% extra due to hand ling e tc. p lu s apportioned

quan tum that w ould trave l over the D iv ision ’s track ,

25

the revenue due to en tire serv ice of consignm ent

transportation w ould devolve on the basis o f track of

other D ivis ions/ ZR s p roportionate ly used for the

sam e. OR w ou ld dep ict a m ore rea lis tic pictu re.

As of today , bonus is a t com m on rates, not

d istinguishing perform ers with non -perform ers. In

the long run, Bonus in D iv isions c ou ld be based on

im p rovem ent over last year YOY on Profit (or loss

reduction) , Th is w ou ld help em p loyees see the

re la tionship betw een the ir actions/ inactions on the ir

in cen tives w h ich m ay m otivate them to w ork hard

and sm art and a lso cou ld apply peer p ressu re on the

laggard s.

These are on ly illu strative and not exhaustive

exam ples and w ith creativity and ingenuity th at w pol

be unleashed w ith Profit C en ter approach , m any

m ore id eas w ould forth com e.

26

B ib lio g rap hy

“M a n a g em en t C on tro l S ys te m s”

B y R obert N A n th on y , V ijay G ov in dara jan , 1 2th

E d it ion , 1 5th

R epr in t 2 013 , Pu blish ed by M cG raw H ill E du ca t ion (In d ia )

P r iva te L im ite d .

W ebs ites a cc esse d fo r u n de rs ta n d in g

h ttp ://w w w .cob.sjsu.ed u /b uck_c/ im ach 09 .pp t

(M anagem ent C on trol System s and R esponsibility

Accoun ting)

h ttp ://rep ub.e ur.n l/re s/pub /1 08 69 /EPS 20 08 1

2 0 F% 25 26 A9 05 89 2 15 12 N oe ve rm a n.p d f

(M anagem ent C on tro l System s, Eva luative S tyle , and

Behav iou r: Exploring the concep t and behaviou ral

consequences of eva luative sty le. By JA N N O E V E R M A N

-o -