Embed Size (px)

Citation preview

Page 1 of 9

Application for review of a

Ministerial decision

Customs Act 1901 s 269ZZE

This is the approved1 form for applications made to the Anti-Dumping Review Panel (ADRP) on or

after 2 March 2016 for a review of a reviewable decision of the Minister (or his or her Parliamentary

Secretary).

Any interested party2 may lodge an application for review to the ADRP of a review of a ministerial

decision.

All sections of the application form must be completed unless otherwise expressly stated in this

form.

Time

Applications must be made within 30 days after public notice of the reviewable decision is first

published.

Conferences

You or your representative may be asked to attend a conference with the Panel Member appointed

to consider your application before the Panel gives public notice of its intention to conduct a review.

Failure to attend this conference without reasonable excuse may lead to your application being

rejected. The Panel may also call a conference after public notice of an intention to conduct a review

is given on the ADRP website. Conferences are held between 10.00am and 4.00pm (AEST) on

Tuesdays or Thursdays. You will be given five (5) business days’ notice of the conference date and

time. See the ADRP website for more information.

1 By the Acting Senior Member of the Anti-Dumping Review Panel under section 269ZY Customs Act 1901. 2 As defined in section 269ZX Customs Act 1901.

Page 2 of 9

Further application information

You or your representative may be asked by the Panel Member to provide further information to the

Panel Member in relation to your answers provided to questions 0, 11 and/or 12 of this application

form (s269ZZG(1)). See the ADRP website for more information.

Withdrawal

You may withdraw your application at any time, by following the withdrawal process set out on the

ADRP website.

If you have any questions about what is required in an application refer to the ADRP website. You

can also call the ADRP Secretariat on (02) 6276 1781 or email [email protected].

Page 3 of 9

PART A: APPLICANT INFORMATION

1. Applicant’s details

Applicant’s name: Scaw South Africa (Pty) Ltd (“Scaw”)

Address: PO Box 61721

Marshalltown

Gauteng

Johannesburg 2107

South Africa

Type of entity (trade union, corporation, government etc.): Proprietary limited company

And

Applicant’s name: Haggie Reid Pty Limited (“Haggie Reid”)

Address: 96 Forrester Road

St Marys

NSW 2760

Australia

Type of entity (trade union, corporation, government etc.): Proprietary limited company

2. Contact person for applicants

Full name: Morgan Pillay Tom Bruce

Position: General Manager Director

Email address: [email protected] [email protected]

Telephone number: +27 11 620 0241 +61 2 9673 8100

Please note that all communications in relation to this application are requested to take place

with and through Scaw and Haggie Reid’s legal representatives. For contact details please refer to

Part E of this application.

3. Set out the basis on which the applicant considers it is an interested party

Pursuant to Section 269ZZC of the Customs Act 1901 (“the Act”) a person who is an interested

party in relation to a reviewable decision may apply for a review of that decision. The reviewable

decision in this case relates to an application made to the Commissioner under Section 269TB

requesting that the Minister publish a dumping duty notice. Under Section 269T of the Act an

“interested party” for the purpose of that kind of a reviewable decision is defined as including,

amongst others, any person who is or is likely to be directly concerned with the importation or

exportation into Australia of the goods the subject of the application; any person who has been or

is likely to be directly concerned with the importation or exportation into Australia of like goods;

Page 4 of 9

and any person who is or is likely to be directly concerned with the production or manufacture of

the goods the subject of the application or of like goods that have been, or are likely to be,

exported to Australia.

Scaw is a manufacturer and exporter, to Australia, of the goods to which the decision relates,

namely steel wire rope. Scaw is thus an “interested party” for the purposes of the Act and this

application.

Haggie Reid is an importer and distributor of the goods exported from Scaw in Australia. Haggie

Reid is thus an “interested party” for the purpose of the Act and this application.

4. Is the applicant represented?

Yes ���� No

If the application is being submitted by someone other than the applicant, please complete the

attached representative’s authority section at the end of this form.

*It is the applicant’s responsibility to notify the ADRP Secretariat if the nominated representative

changes or if the applicant become self-represented during a review.*

Page 5 of 9

PART B: REVIEWABLE DECISION TO WHICH THIS APPLICATION RELATES

5. Indicate the section(s) of the Customs Act 1901 the reviewable decision was made under:

���� Subsection 269TG(1) or (2) –

decision of the Minister to publish a

dumping duty notice

☐Subsection 269TH(1) or (2) – decision

of the Minister to publish a third

country dumping duty notice

☐Subsection 269TJ(1) or (2) – decision

of the Minister to publish a

countervailing duty notice

☐Subsection 269TK(1) or (2) decision

of the Minister to publish a third

country countervailing duty notice

☐Subsection 269TL(1) – decision of the Minister

not to publish duty notice

☐Subsection 269ZDB(1) – decision of the Minister

following a review of anti-dumping measures

☐Subsection 269ZDBH(1) – decision of the

Minister following an anti-circumvention enquiry

☐Subsection 269ZHG(1) – decision of the

Minister in relation to the continuation of anti-

dumping measures

6. Provide a full description of the goods which were the subject of the reviewable decision

The goods the subject of this investigation are stranded wire rope, alloy or non-alloy steel,

whether or not coated or impregnated, having both of the following:

• Not greater than 8 strands;

• Diameter not less than 58mm and not greater than 200mm,

with or without attachments.

Further information regarding the goods is outlined below:

(i) Stranded steel wire rope is rope and strand made of high carbon wire (whether or

not containing alloys);

(ii) The strand or rope can also be sheathed or impregnated and sheathed respectively

in plastic or composites;

(iii) The wires can be layered-up in various configurations in order to give the strand or

rope the desired physical properties;

(iv) Variances can include:

• strand diameter;

• number of wires;

• wire finish (e.g. typically black but may be galvanised);

• wire tensile grade;

• type of lubricant;

• strand or rope length; and

• whether or not an attachment is included (but not limited to ferrules and/or

beckets).

(v) Cores may be made of:

Page 6 of 9

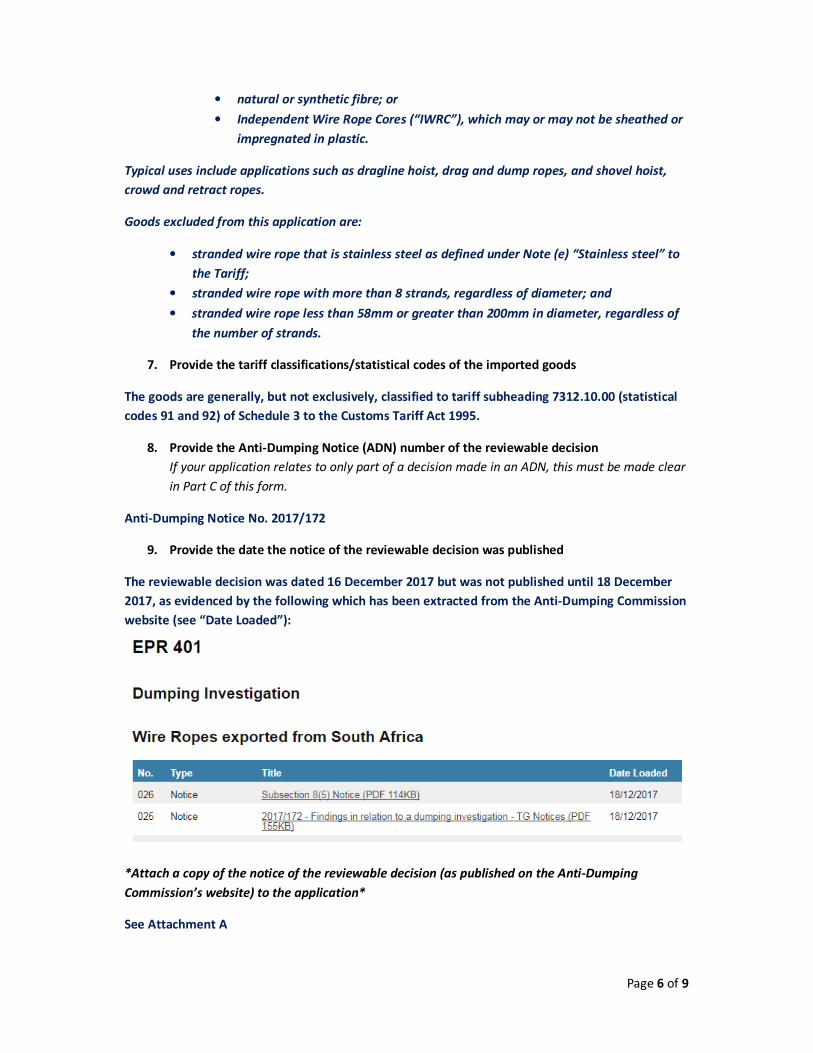

• natural or synthetic fibre; or

• Independent Wire Rope Cores (“IWRC”), which may or may not be sheathed or

impregnated in plastic.

Typical uses include applications such as dragline hoist, drag and dump ropes, and shovel hoist,

crowd and retract ropes.

Goods excluded from this application are:

• stranded wire rope that is stainless steel as defined under Note (e) “Stainless steel” to

the Tariff;

• stranded wire rope with more than 8 strands, regardless of diameter; and

• stranded wire rope less than 58mm or greater than 200mm in diameter, regardless of

the number of strands.

7. Provide the tariff classifications/statistical codes of the imported goods

The goods are generally, but not exclusively, classified to tariff subheading 7312.10.00 (statistical

codes 91 and 92) of Schedule 3 to the Customs Tariff Act 1995.

8. Provide the Anti-Dumping Notice (ADN) number of the reviewable decision

If your application relates to only part of a decision made in an ADN, this must be made clear

in Part C of this form.

Anti-Dumping Notice No. 2017/172

9. Provide the date the notice of the reviewable decision was published

The reviewable decision was dated 16 December 2017 but was not published until 18 December

2017, as evidenced by the following which has been extracted from the Anti-Dumping Commission

website (see “Date Loaded”):

*Attach a copy of the notice of the reviewable decision (as published on the Anti-Dumping

Commission’s website) to the application*

See Attachment A

Page 7 of 9

PART C: GROUNDS FOR THE APPLICATION

If this application contains confidential or commercially sensitive information, the applicant must

provide a non-confidential version of the grounds that contains sufficient detail to give other

interested parties a clear and reasonable understanding of the information being put forward.

Confidential or commercially sensitive information must be marked ‘CONFIDENTIAL’ (bold, capitals,

red font) at the top of each page. Non-confidential versions should be marked ‘NON-CONFIDENTIAL’

(bold, capitals, black font) at the top of each page.

For lengthy submissions, responses to this part may be provided in a separate document attached to

the application. Please check this box if you have done so: ☒☒☒☒

See Attachment B, in respect of which confidential and non-confidential versions have been

provided.

10. Set out the grounds on which the applicant believes that the reviewable decision is not the

correct or preferable decision.

11. Identify what, in the applicant’s opinion, the correct or preferable decision (or decisions)

ought to be, resulting from the grounds raised in response to question 0.

12. Set out the reasons why the proposed decision provided in response to question 11 is

materially different from the reviewable decision.

Do not answer question 12 if this application is in relation to a reviewable decision made

under subsection 269TL(1) of the Customs Act 1901.

Page 8 of 9

PART D: DECLARATION

The applicant/the applicant’s authorised representative [delete inapplicable] declares that:

- The applicant understands that the Panel may hold conferences in relation to this

application, either before or during the conduct of a review. The applicant understands that

if the Panel decides to hold a conference before it gives public notice of its intention to

conduct a review, and the applicant (or the applicant’s representative) does not attend the

conference without reasonable excuse, this application may be rejected;

- The information and documents provided in this application are true and correct. The

applicant understands that providing false or misleading information or documents to the

ADRP is an offence under the Customs Act 1901 and Criminal Code Act 1995.

Signature:

Name: Daniel Moulis

Position: Partner Director

Organisation: Moulis Legal

Date: 17 January 2018

Page 9 of 9

PART E: AUTHORISED REPRESENTATIVE

This section must only be completed if you answered yes to question 4.

Provide details of the applicant’s authorised representative

Full name of representative: Daniel Moulis

Organisation: Moulis Legal

Address: 6/2 Brindabella Circuit

Brindabella Business Park

Canberra International Airport

Australian Capital Territory

Australia 2609

Email address: [email protected]

Telephone number: +61 2 6163 1000

Representative’s authority to act

*A separate letter of authority may be attached in lieu of the applicant signing this section*

See Attachment C

The person named above is authorised to act as the applicant’s representative in relation to this

application and any review that may be conducted as a result of this application.

Signature:….………………………………………………………………………..

(Applicant’s authorised officer)

Name:

Position:

Organisation

Date: / /

A T T A C H M E N T A T T A C H M E N T A T T A C H M E N T A T T A C H M E N T BBBB

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

17 January 2018

In the Anti-Dumping Review Panel

Application for review Wire rope exported from South Africa

Scaw South Africa (Pty) Ltd and Haggie Reid Pty Limited

Introduction ........................................................................................................................................... 2

A First ground – the evidence did not establish, and it was unreasonable to conclude, that material injury was caused by exports from South Africa .................................................................. 3

10 Grounds ..................................................................................................................................... 3

(a) Findings as to the economic condition of the Australian industry ...................................... 4

(b) The nature of “injury” that can be “caused” by dumping .................................................... 6

(c) The finding that material injury was caused by dumping is undeveloped and unsafe ....... 8

(d) Evidence on the record – outline and commentary .............................................................. 9

(e) Response to causation analysis set out in the Report ....................................................... 12

11 Correct or preferable decision ................................................................................................ 15

12 Material difference between decisions ................................................................................... 15

B Second ground – the Minister failed to establish corresponding normal values for comparison with the export prices of the goods .................................................................................................... 16

10 Grounds ................................................................................................................................... 16

11 Correct or preferable decision ................................................................................................ 25

12 Material difference between decisions ................................................................................... 25

C Third ground – adjustments were not made to the normal value so as to not affect the comparison, and to ensure a proper comparison, with the export price .......................................... 26

10 Grounds ................................................................................................................................... 26

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 2

(a) Incorrect application of “specification adjustment” for certain goods ............................. 26

(b) Rejection of export rebate based adjustment ..................................................................... 27

(c) Refusal to make domestic bad-debt related adjustment .................................................... 29

(d) Incorrect adjustment concerning reel returns. ................................................................... 30

(e) Failure to make exchange gain based adjustment ............................................................. 32

11 Correct or preferable decision ................................................................................................ 32

12 Material difference between decisions ................................................................................... 33

D Fourth ground – the export price was incorrectly ascertained ................................................. 33

10 Grounds ................................................................................................................................... 33

(a) Lack of consideration of timing difference in working out export price............................ 33

(b) Inappropriate deductions adopted in the work-back export price ..................................... 35

11 Correct or preferable decision ................................................................................................ 37

12 Material difference between decisions ................................................................................... 37

Conclusion and request ...................................................................................................................... 37

Introduction

By way of an application to the Anti-Dumping Commission (“the Commission”) dated 8 March 2017,

Bakaert Wire Ropes Pty Ltd (“BBRG” or “the Australian industry”) applied for a dumping investigation

with respect to certain steel wire rope (“wire rope” or “the goods”) exported from the Republic of South

Africa.1

In response to that application, the Commission initiated the subject anti-dumping investigation in

respect of wire rope exported from South Africa on 26 April 2017.

At the conclusion of the investigation, in a decision published on 18 December 2017 based on the

recommendations contained in Report No. 401 – Alleged Dumping of Wire Rope Exported to Australia

1 See EPR 401 Doc 001.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 3

from the Republic of South Africa2 (“the Report”), the Assistant Minister and Parliamentary Secretary to

the Minister for Industry, Innovation and Science (“the Parliamentary Secretary”) decided to impose

dumping duties on wire ropes exported to Australia from South Africa.3

Specifically, the Parliamentary Secretary decided to publish notices in relation to wire rope exported

from South Africa under Sections 269TG(1) and (2) of the Customs Act 1901 (“the Act”).4 These notices

had the effect of imposing dumping duties on exports from all South African exporters.5

Scaw South Africa (Pty) Ltd (“Scaw”) is a South African manufacturer and exporter of wire rope. Haggie

Reid Pty Limited (“Haggie Reid”) is the importer of wire ropes exported by Scaw from South Africa.6

Scaw and Haggie Reid seek review by the Anti-Dumping Review Panel (“the Review Panel”), under

Sections 269ZZA(1)(a) and 269ZZC, of the decision (or decisions) made by the Parliamentary Secretary

to impose dumping measures against Scaw’s exports of wire ropes to Australia, as outlined in this

application.

We now address the requirements of both the form of application that has been approved by the Senior

Member of the Review Panel under Section 269ZY, and of Section 269ZZE(2), in relation to our clients’

grounds of review, being those requirements not already addressed within the text of the approved form

itself, which hawse have also completed and lodged with the Review Panel.

A First ground – the evidence did not establish, and it was unreasonable to conclude, that material injury was caused by exports from South Africa

10 Grounds

Set out the grounds on which the applicant believes that the reviewable decision is not the correct or preferable decision

2 See EPR 401 Doc 024. 3 Based on the recommendations contained in Report No. 401 – Alleged Dumping of Wire Rope Exported to Australia from the Republic of South Africa, November 2017. 4 A reference in this Application to “the Act”, or to a “Section”, “Subsection” or “Subparagraph” is a reference to a Section, Subsection or Subparagraph of the Act, unless otherwise specified. 5 See EPR 401 Doc 025 and 026. 6 Scaw and Haggie Reid are also referred to as “the Appellants” in this application.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 4

(a) Findings as to the economic condition of the Australian industry

Section 1.4.5 of the Report states the following:

The Commissioner considers that the Australian industry has experienced material injury as a

result of wire rope imported at dumped prices from South Africa.

The Appellants consider that this is not the correct or preferable decision.

The facts as to the economic condition of the Australian industry in the investigation period of 2016, as

recited in the Report, are as follows:

• its sales volumes of wire rope declined;7

• it lost 4.2% of its market share and Haggie Reid gained 4.9%;8

• the gap between its unit sales revenue and unit CTMS narrowed;9

• its sales prices were not depressed, ie did not decrease, after decreasing in 2015;10

• its total profits and unit profitability declined;11

• it was profitable during the investigation period of 2016;12

• its sales revenues decreased;13

• reduced capital investment was not evidenced;14

• its return on investment declined;15

• its capacity utilisation declined;16

7 See Doc 024 – Report 401, Section 6.3.1 at page 36. 8 Ibid, Section 6.3.2 at page 38. 9 Ibid, Section 6.4.2 at page 39. 10 Ibid, Figure 6 on page 39. 11 Ibid, Section 6.5.1 at page 39. 12 Ibid, implied from Figure 6 on page 39 and Section 6.5.2 on page 40. 13 Ibid, Section 6.6.1 on page 41. 14 Ibid, Section 6.6.2 on page 41. 15 Ibid, Section 6.6.3 on page 41. 16 Ibid, Section 6.6.4 on page 42.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 5

• its employment numbers declined;17 and

• its productivity reduced.18

The section of the Report in which these findings are contained is headed “Economic Condition of the

Australian Industry”. Although that section is not meant to deal with the question of causation, the Report

appears to bring forward, into that section of the Report, conclusions on causation that are premature

and unrationalised.

(1) First, it states:

The Commission’s analysis shows that during the investigation period, BBRG Australia

lost 4.2 per cent of market share, whereas Haggie Reid gained 4.9 cent of market share

indicating that BBRG Australia’s lost market share went to Haggie Reid.19 [underlining

supplied]

The word “went” is an active expression, suggesting that an action (in this case, on the part of

Haggie Reid) caused an effect. As we believe is demonstrated in this application, there is

nothing that took place at the point of competition between the Australian and South African wire

rope that constituted an action that could have had that effect.

(2) Secondly, it states:

The Commission accepts that the downturn in the coal-mining industry may have

contributed to BBRG Australia moving from 3 shifts to 2 shifts, however the Commission

considers that dumping and BBRG Australia’s consequent loss of sales volumes to

dumped imports has been a material factor in BBRG Australia operating at 2 shifts rather

than 3 during the investigation period.20 [underlining supplied]

Here we see a statement of causation based on the unrationalised assumption that dumped

imports caused (a “consequent loss”) of sales volume.

17 Ibid, Section 6.6.5 on page 43. 18 Ibid, Section 6.6.6 on page 43. 19 Ibid, Section 6.3.2 at page 38. 20 Ibid, Section 6.6.6 at pages 43 to 44.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 6

(b) The nature of “injury” that can be “caused” by dumping

The factors the Commission identified with respect to the economic condition of the Australian industry

can be broken down into two categories. The first are what might be referred to as operative injury

factors, or primary injury factors. Plainly, these are lower sales volumes, and lower prices.

It is frequently observed that prices might not be able to be increased by a domestic industry, because

of the price of dumped imports, and the Appellants do not deny that. However that does not obviate the

need to work out what it was that caused the injury in the first place, ie what the professed need to

increase prices or to recover lost sales was. In some cases it might be the case that dumping is the only,

single exogenous impact that attracts that need. The instant case does not present in such a way. If

injury has been caused by non-dumping factors but, notwithstanding that, it continues to be alleged by

the domestic industry that dumping has caused material injury, a much more sophisticated analysis is

necessarily called for. The injury that might be alleged to have been caused by dumping “in addition to”,

in the sense of “after”, the impact of a non-dumping factor or factors must be considered with greater

care. An industry that has had a large chunk of its sales withdrawn from its sales volume by reason of

non-dumping factors cannot blame dumped imports for injury simply because the dumped imports were

present in the market. For example, as in this case, the products may be complex, specialised goods

that are not conducive to source-switching, rapid sales disposal and/or resale. In an “exchange” or other

commodity trading environment price signals are immediate and transparent, and the reaction time of

buyers can be almost instantaneous. Where specialised capital goods are involved, and where there are

long term relationships and preferences in place, and where the substitution of one supplier for another

and new price discovery takes place through formalised procedures, price and volume will not be able

to be recovered by one supplier at the expense of the other at “the wave of a wand”, and it would be

improper to assume that dumping was thereafter a further cause of material injury in the period

concerned.

The Report makes just such an assumption. It quotes from the relevant Ministerial Direction as follows:21

The Commission notes that the Australian industry may remain profitable notwithstanding that its

profits have been affected by dumped goods. The Material Injury Direction states that injury may

be found in circumstances where the Australian industry is prospering but less prosperous than

it would be absent dumping.22

21 Ministerial Direction on Material Injury 2012, at http://www.adcommission.gov.au/adsystem/referencematerial/Documents/ACDN2012-24.pdf 22 Report, section 6.5,2 at page 40.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 7

However the Ministerial Direction is prefaced by the statement that it is “[s]ubject always to the law”, as it

must be. Further, the proposition is that injury by dumping may be found in that circumstance. The

coincidence of two facts – dumping, and a “less prosperous” industry – is not enough to establish that

the first fact caused the second. Whether it is at all reasonable to expect that additional injury, being

material injury in the form of price suppression, was caused by dumping after a different factor had

already caused injury is a relevant question, the answer to which must be determined to a proper

standard and not assumed.

Returning now to our categorisation of injury factors, if an industry experiences lower sales and/or lower

prices, it will also experience or may also experience what might be called consequential injury, or

secondary injury. Into that category would fall

• a loss of market share, being a symptom of lower sales;

• a decline in profits or profitability, being a symptom of either or both lower sales and lower

prices;

• decreased sales revenues, being a symptom of either or both lower sales and lower prices;

• declining return on investment, being a symptom of both lower sales and lower prices;

• declined capacity utilisation, being a symptom of lower sales;

• declined employment numbers, being a symptom of either or both lower sales and lower prices;

• reduced productivity, being a symptom of either or both lower sales and lower prices.

These things are symptoms of the operative or primary causes of injury. It is correct to say that factors

other than dumping could independently cause these heads of injury, for example a fire at the

production facility could cause any or all of them to occur. However the action of exporting dumped

goods to Australia could never cause those things to happen without first causing the Australian industry

to experience lower sales or lower prices.

Thus, the fundamental question in an anti-dumping investigation is whether dumping has caused lower

sales or lower prices. The other effects are flow-on effects that can support the finding that there has

been a materiality to the injury. This requires us to turn to a consideration of whether exports from South

Africa were causative of the operative or primary injury of which the Australian industry complained,

namely reduced sales volumes and reduced prices.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 8

(c) The finding that material injury was caused by dumping is undeveloped and unsafe

The Appellant’s position is that in the investigation period the Australian industry suffered the full force of

a market downturn that almost uniquely affected the mine sites that it serviced with its wire ropes,

causing it to suffer reduced sales volumes, lower throughput, production slowdown, and a resultant

increase in its unit costs of production. In the investigation period the Australian industry’s prices did not

decline, the prices of South African wire ropes did not decline, and South African wire ropes did not

secure any new contracts or customers.

The proposition on which the Australian industry must seek to rely in arguing that dumped exports

caused it material injury is that it should have been able to increase its prices, and take over the sales

and customers of the importer of South African wire ropes. This would need to have been achieved

immediately on the occasion of each machine shutdown, in the face of declining rope usage and

demand, and without trials taking place, and against the settled preference of those customers for the

wire ropes it had been purchasing at all relevant times.

It is submitted by our clients that in these circumstances, the correct or preferable view is that the

material injury that was suffered by the Australian industry was due to the machine shut-downs that

heavily and uniquely affected its market position. To “blame” South African exports is to ignore that

cause, and not to give it the attributive relevance that it must logically have, and to ignore the fact that an

instantaneous or rapid short term recovery that the Australian industry appears to assert that it should

have enjoyed was simply not achievable or available to it in the investigation period. In the absence of

the loss of sales volumes caused by the machine shut-downs that afflicted the Australian industry, it

would not have suffered any injury at all, a finding that is entirely consistent with the Commission’s

finding that it cannot be concluded that injury was caused by dumping in the year prior to the

investigation period:

Therefore, the Commission does not have evidence that 2015 is a time affected by dumping. On

this basis, the Commissioner considers it appropriate to use the Australian industry’s weighted

average selling prices in the 2015 calendar year for the purpose of calculating the USP.23

In this case we submit that the Report adopts an unthinking approach in finding that dumping caused

material injury to the Australian industry. In our submission it is a finding that is simply not justified on the

facts. The Report’s conclusion that:

23 Ibid, Section 9.4 on page 60.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 9

• because there was a dumping margin found; and

• because the Australian industry was less profitable; and

• because the Australian industry would not have been less profitable if it enjoyed higher prices;

then

• it was dumped imports that caused it to be injured,

is a primitive one.

In the circumstances of this case, as supported by the evidence on the record, we submit that this is not

the correct or preferable conclusion, as we will now continue to explain.

(d) Evidence on the record – outline and commentary

Our client made a number of substantial and detailed submissions to the Commission in this matter.

Moreover, our client was open and transparent in its submissions.

We recommend our clients’ submissions on injury matters to the Review Panel, and expressly

incorporate them in this application for review.24 We do not intend to repeat those submissions in their

entirety, but do wish to draw the Review Panel’s attention to salient aspects for the purposes of this

review:

(1) The Appellant’s letter dated 13 June 2017 documented the fact that the Appellants’ sales

volumes decreased in the investigation period, 25 although not to the same degree as those of

the Australian industry.

(2) The Appellants’ letter dated 13 June 2017 documented that the prices of the South African wire

ropes had not changed during the injury review period.26 The Report accepts this to have been

the case.27 Indeed, prices in the Australian market in 2015 were used by the Commission to

establish a non-injurious price. Accordingly, the Report confirms the fact that the non-injurious

price of South African wire ropes remained in place, and was not reduced, in the investigation

24 See Public Record Doc 004, 010 & 019 – Scaw letters to the Commission. 25 See Doc 004 – Scaw letter to the Commission, at page 4. 26 Ibid, at page 6. 27 See Doc 024 – Report 401, Section 5.5.3 at page 25.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 10

period, giving credence to the proposition that some other factor was a cause of the injury

complained of by the Australian industry in that period.

(3) The summary paragraph in that letter presents the consistent view of the Appellants throughout

the investigation, and now in this application for review:

Bekaert has not “lost sales volume to Haggie Reid”. Its Application attempts to exclude

or downplay the effect of the market factors that have truly impacted on it, and that have

“caused” it “injury” (if you can call continued profitability in the presently depressed

conditions “injury”). If there have been any “change agents” in the market in 2016 they

certainly do not include Haggie Reid’s imports which, as we have proven, have declined

in volume and not changed in price. Under the mining industry conditions that are

relevant to this investigation, and on the basis of the evidence you have before you, we

submit that Bekaert’s financial performance in the only period that can be relevant for

that determination, namely, 2016, is clearly and certainly representative of the “normal

ebb and flow of business”. The increased costs it faced are a symptom of reduced

throughput in a downturned mining industry market. That is not a situation that has been

caused by Haggie Reid’s sales in the Australian market. Changes in the market

conditions in 2016 were introduced by factors other than Haggie Reid’s imports.28

(4) The Appellants’ letter dated 19 July 2017 presented a very clear and very detailed breakdown of

the sales positions of the Australian and South African wire rope manufacturers in the

investigation period. Moreover, the Commission requested that our clients agree to provide an

un-redacted version of the table set out at pages 8 to 14 of that letter for the purposes of

allowing the Australian industry to comment thereon. The Appellants complied with that request.

In response to the critical facts set out in those tables, the Australian industry provided a

summary response by way of letter dated 28 July 2017. Our client maintains that this response

obfuscated and misrepresented the true situation. That information is on the Commission’s

record, and the Review Panel can consider it against the detailed information provided by the

Appellants and come to its own conclusions. However a key point that the Review Panel is asked

to take into account is that the Australian industry did not refute the information provided by the

Appellants with respect to the machines that were parked up or the mines that were shut down.

Accordingly, we submit that the Review Panel should accept that the information provided by the

Appellants to the Commission is to be preferred. It was reported to the Commission with great

care as to its accuracy, and was not rebutted by the Australian industry.

28 See Doc 004 – Scaw letter to the Commission, at page 7.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 11

(5) The focus of the Australian industry’s letter dated 28 July 2017 is that the Appellants were busy

undercutting the Australian industry at various mine sites and that this caused material injury to

the Australian industry. This is simply incorrect. Relying only on record evidence, we make the

following observations with respect to the dot points on the penultimate page of that letter:

i. With respect to the first, second, fourth, fifth and sixth dot points – the Australian industry

cannot have lost “xxx tonnes” to South African wire ropes because [CONFIDENTIAL TEXT

DELETED – confidential sales information]. As stated in our clients’ letter dated 19 July

2017, [CONFIDENTIAL TEXT DELETED – confidential sales information] these were not

the goods under investigation.29 [CONFIDENTIAL TEXT DELETED – confidential sales

information]. This can be substantiated in the information provided by Haggie Reid to the

Commission during the importer verification of Haggie Reid. In this scenario sales cannot

have been lost to dumped imports, and that proposition cannot be “supported by email

correspondence”.

ii. With respect to the third dot point – the Australian industry cannot have lost “xxx tonnes” to

South African wire ropes because [CONFIDENTIAL TEXT DELETED – confidential sales

information],30 the Appellants did not change their prices, and in any case

[CONFIDENTIAL TEXT DELETED – confidential sales information] 31

iii. With respect to the seventh dot point – this relates to Rio Tinto/HVO, in respect of which the

only market impact reported in our client’s letter dated 19 July 2017 was [CONFIDENTIAL

TEXT DELETED – confidential sales information] goods that were not under

investigation.32

iv. With respect to the eighth and ninth dot points – this relates to Rio Tinto/MTW. The

Appellants’ explanation of these sales is that [CONFIDENTIAL TEXT DELETED –

confidential sales information] were not purchased for price reasons (and, again, a large

proportion of them were not the goods under investigation).33

29 See Doc 010 – Scaw letter to the Commission, at pages 10 and 11. 30 Ibid, at page 8. 31 Ibid, footnote 10. 32 Ibid, at page 13. 33 Ibid, footnote 13 and page 14.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 12

Thus, the Australian industry’s claim that the loss of “1,121 tonnes of wire rope sales” can be attributed

to pricing competition from the Appellants simply does not withstand careful scrutiny. The mining

industry serviced by the Australian industry and Haggie Reid faced very tough conditions in 2016 and

the market volume declined significantly. Exacerbating this in the case of the Australian industry was its

terribly bad fortune with respect to machine park-ups and mine closures, the evidence of which remains

uncontradicted on the public record.

(e) Response to causation analysis set out in the Report

The causation analysis in the Report does not overcome the reservations that an impartial observer

would have about the conclusion that South African wire ropes had caused material injury to the

Australian industry in the special circumstances of this case.

(1) Price undercutting – the Report states:

The Commission’s price undercutting analysis at the mine level for dragline ropes over

the investigation period is shown in the Figure 12 below. Customer 1 – 4 depict the

mines that are jointly supplied by Haggie Reid and BBRG Australia. The Commission

also calculated the level of price undercutting by Haggie Reid in the sales of dragline

(dump, drag and hoist) ropes for all customers. The Commission calculated that the

overall price undercutting by Haggie Reid in sales of dragline ropes is 16 per cent for

the investigation period.34

The disparity in pricing reported by the Commission was [CONFIDENTIAL TEXT DELETED –

confidential sales information]% for four customers and [CONFIDENTIAL TEXT DELETED –

confidential sales information]% for one other. If that is the true quantum of difference, for the

reported sites, then we would offer the opinion that our clients’ case is strengthened rather than

weakened. It is a matter of record evidence that Haggie Reid did not reduce its prices.

Accordingly, this situation must have existed before the market shocks of 2016 that impacted the

Australian industry in 2016 took place. Its injury, therefore, was because of the effects of those

shocks. It was not due to the price undercutting, because the Australian industry had been

operating without injury with that or those price dynamics with respect to those customers in

place before those shocks took place.

The Australian industry was selling to those customers before the investigation period, when its

prices were unsuppressed, and continued to sell to those customers in the investigation period.

The Appellants did not change their prices, as found by the Commission. Thus, the factor which

34 See Doc 024 – Report 401, Section 7.5 at page 46.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 13

injured the Australian industry was the market downturn and the substantial loss of sales by

reason of machine park ups and mine shutdowns that affected it almost uniquely. The Report

finds that the Australian industry’s selling prices were unsuppressed in 2015, meaning that if

there was no change to Haggie Reid’s pricing in the next year (and there was no change) then it

must have been some other factor that changed to cause the Australian industry to suffer injury.

In this case it is submitted that it was the Australian industry’s loss of sales – which was not

caused by the dumping of South African wire ropes - that caused it to suffer injury. It reduced

the Australian industry’s throughput, and increased its costs.

(2) Price effects – the Appellants strenuously object to the two paragraphs dealing with price effects

in the Report. The Report states:

The Commission understands that when the mining companies received offers that are

below their current purchase prices, they often seek to re-negotiate the prices with the

current supplier benchmarking the price on the newly received offer.

BBRG Australia supplied the Commission with positive evidence by way of email

correspondence with its customers that showed price negotiations expressly referencing

the price of wire rope imported by Haggie Reid from South Africa. It is clear from these

negotiations that BBRG Australia lowered its prices in response to Haggie Reid’s prices

to prevent the risk of losing business. Despite this, Haggie Reid’s prices were below that

of BBRG Australia’s price, placing ongoing price pressure on BBRG Australia’s future

negotiations. 35

We wish to draw the Review Panel’s attention to these matters:

i. What the Commission “understands” falls short of being a finding.

ii. Further, what might happen in price negotiations “in the future” is not a finding with respect

to causation of lower prices or lost sales in the investigation period.

iii. In its application for the investigation the Australian industry was unable to provide case

studies of reduced prices in the investigation period said to be caused by the Appellants.36

35 Ibid, Section 7.6, at pages 48 and 49. 36 See Doc 010 – Scaw letter to the Commission, at page 15.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 14

iv. The Report finds that the Australian industry’s prices were not reduced during the

investigation period. Indeed, on the basis of the unit revenue table presented in the Report,

there appears to have been a subtle price increase.37

v. The facts with respect to Haggie Reid’s few price offers are as Haggie Reid presented them

in its letter dated 19 July 2017, to which we refer the Review Panel.38

(3) Also with respect to “price effects” - the Appellants note that the discussion of price effects in

the Report also includes the following statements:

At a macro level, as shown at Figure 2 of section 4.6, the Australian market for wire rope

declined in 2016 from 2015 levels. The Commission acknowledges that the general

decline in the market has implications for all suppliers of wire rope. However, as

discussed at section 6.3.2, BBRG Australia lost market share to Haggie Reid during the

investigation period.

The Commission has conducted a micro level analysis of BBRG Australia’s lost sales

volumes to Haggie Reid at individual mine sites at section 7.9.2, which showed that

BBRG Australia’s lost sales volume to Haggie Reid exceeded the general decline in the

Australian market.39

These statements maintain the built-in and unreasoned assumption that the Australian industry “lost”

market share to the Appellants, and that market share “went” to the Appellants, by reason of dumping,

without understanding, discussing, or arriving at a conclusion as to whether that had anything to do with

dumping. The Appellants submit that they correctly advised the Commission of the magnitude of sales

“lost” by the Australian industry because of machine park ups and mine shutdowns.40

In conducting its review, the Appellants request the Review Panel to evaluate the information provided

by the Australian industry, as referred to in the following extract from the Report, and to consider whether

it supports what is being said:

In order to support its assessment, BBRG Australia provided comprehensive evidence in

the form of market intelligence, import price offers and email correspondence with its

customers. The Commission considered the evidence provided by BBRG Australia in

quantifying the volume of lost sales to Haggie Reid and observed that provided

evidence supported BBRG Australia’s claims. The Commission further observed within

the evidence provided by BBRG Australia that when the customers selected to switch to

using Haggie Reid’s wire ropes, the price of the imported wire rope was the main

37 See Doc 024 – Report 401, Figure 6 at page 39. 38 See Doc 010 – Scaw letter to the Commission, at pages 15 to17. 39 See Doc 024 – Report 401, Section 7.7 at pages 49 to 50. 40 Ibid, at pages 10-14.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 15

motivation. The Commission then calculated that BBRG Australia’s sales volume was

reduced by some 1,800 metric tonnes between the 2015 and 2016 calendar years. The

Commission also calculated that while the Australian wire rope market contracted by

approximately 650 metric tonnes during the investigation period by means of parked

machinery and mine shut-downs, BBRG Australia lost more than 1,100 metric tonnes

sales volume to Haggie Reid.41

Given that the Appellants and the Australian industry’s assessments of the latter’s sales volume

reduction in the investigation period are said in the Report to be within 1.6% of each other, and given

also that the Appellants only means of estimating that sales volume reduction was to calculate the usage

of wire rope by the shut-down machines, the explanation offered by the Appellants with respect to the

Australian industry’s drop in sales is more likely to be correct, or at least should be preferred over that of

the Australian industry.

11 Correct or preferable decision

Identify what, in the applicant’s opinion, the correct or preferable decision (or decisions) ought to be, resulting from the grounds raised in response to question 10

With regard to this ground, the correct or preferable decision should be that the Australian industry was

not caused material injury by the dumped exports, on the basis that the evidence does not support that

finding. Instead, the correct and preferable decision is that the Australian industry was caused material

injury by the sudden losses of sales volume in the investigation period arising from the market downturn

generally, and more specifically by machine shut-downs, being shocks that had an almost unique and

far more severe effect on the Australian industry in comparison to the effect on the Appellants.

12 Material difference between decisions

Set out the reasons why the proposed decision provided in response to question 11 is materially different from the reviewable decision

The proposed decision would mean that the conditions for the publication of a dumping notice set out in

Section 269TG(1)(b) and Section 269TG(2)(b) of the Act are not made out, and that the dumping notices

should be revoked ab initio.

41 See Doc 024 – Report 401, Section 7.9.2 at page 53.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 16

B Second ground – the Minister failed to establish corresponding normal values for comparison with the export prices of the goods

10 Grounds

Set out the grounds on which the applicant believes that the reviewable decision is not the correct or preferable decision

Pursuant to Section 269TACB(1) of the Act, the Minister must determine whether dumping has occurred

by comparison of export prices of goods the subject of the application established in accordance with

Section 269TAB with corresponding normal values in respect of like goods established in accordance

with Section 269TAC(1). In the investigation that is the subject of this application for review, the

Appellants maintain that the Minister failed to establish corresponding normal values for comparison with

the export prices of the goods.

In a universe of exported goods falling within the scope of an anti-dumping application, there can be

different types. Usually, the exporter will differentiate the types by way of giving them a unique code or

description. In a dumping investigation the investigating authority will “match” the exported types with

the same types sold on the domestic market to work out whether they were dumped. In this way the

obligations to compare corresponding goods under Section 269TACB, and to ensure a fair comparison

between the domestic and the exported goods under Article 2.4 of the WTO Anti-Dumping Agreement,

will be complied with by the investigating authority.

In this case there were some types of wire ropes exported to Australia that were the same (identical) as

types sold on the domestic market of South Africa. In other words, there were direct model matches. For

the other types exported to Australia, there were no direct matches with models sold on the domestic

market.

In these circumstances the Commission had the option of comparing:

• for the directly matched models - the export prices and normal values of those models; and

• for the models which were not directly matched – the export prices of those models with the

domestic price of a closely matched model under Section 269TAC(1) of the Act, adjusted to

remove any distortion to the comparison caused by the difference, or with the normal value for

the exported model calculated under Section 269TAC(2)(c) of the Act.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 17

The Commission did neither of these things. Instead, the Commission created “groups” of exported

models defined by their broad features, and compared each of those groups with a “group” of models

sold on the domestic market having the same broad features.

It is submitted by the Appellants that the manner in which the Commission undertook this exercise

caused significant distortions and a significant exaggeration of the dumping margin with respect to

Scaw’s exports of wire ropes to Australia. The comparison did not achieve the statutory objective of

correspondence, did not ensure a fair comparison, and did not result in the comparison of like goods in

the broader sense. In simple terms, Scaw considers that the Commission’s normal value determination

was based on incorrect model grouping and model matching exercises, resulting in the use of domestic

sales prices of goods that did not correspond to the goods exported to Australia, and without proper

adjustment.

Scaw raised and discussed the normal value calculation issue with the Commission throughout the

investigation. More specifically, Scaw provided a detailed submission on this issue in its comments on

the Statement of Essential Facts published in the investigation dated 6 September 201742 (“the SEF

comment”), part of which stated as follows:

Before and during the exporter verification we submitted Scaw SA’s evidence and suggestions

with respect to the calculation of normal values for the exported models. We clearly stated that

there were some models that were identical on both the domestic and the export markets,

meaning that a TAC(1) normal value43 was available and appropriate with respect to those

exported models. We also informed the Commission that some exported models had closely

similar domestic models, meaning that a TAC(1) normal value with specification adjustments

could be considered for those models. For the other exported models, we advised the

Commission that there were no comparable domestic models, and that a TAC(2)(c) normal

value44 calculation would be appropriate.

This thinking and these manners of calculation of the individual normal values are typically and

regularly adopted by the Commission. We offered the suggestion that if the Commission

intended to proceed differently, it would need to be cautious to ensure that invalid comparisons

were not made.45

We respectfully refer the Review Panel to Scaw’s submission in the SEF comment in this regard.46 In that

submission, we pointed out that the Commission’s model groupings were too broad, distortive,

42 See EPR 401 Doc 019 – the SEF comment. 43 See Section 269TAC(1) of the Act. 44 See Section 269TAC(2)(c) of the Act. 45 See the SEF comment, at pages 1 and 2. 46 See the SEF comment, at pages 1 to 4.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 18

inconsistent, and defied the comparative realities of the goods concerned. We submitted that the

groupings resulted in the treatment, by way of grouping, of a range of goods with substantial physical

and cost differences as essentially the same goods, when they were not the same.

In this application for review, the Appellants maintain the position that the model matching and like

goods identification exercise that was carried out by the Commission resulted in the matching of goods

that did not correspond with each other and could not fairly be compared. They had substantially

different physical characteristics and substantially different costs of production and were not “like

goods” that could be said to properly correspond with each other for model matching and normal value

determination purposes. The Appellants request the Review Panel to consider these matters and to

recommend to the Minister that the original recommendations in the Report led to an incorrect

determination of the overall normal value for the goods exported by Scaw.

We draw the Review Panel’s attention to the following submissions that we made on behalf of the

Appellants in the SEF comments:

As per section 2.3 of the exporter visit report, instead of using the model-to-model matches

advised by Scaw SA, the Commission:

[had] regard to five characteristics:

• end use (i.e. dragline or shovel);

• whether the rope is plasticated;

• whether the rope is compacted;

• diameter range:

o 58 to 74mm;

o 75 to 99mm;

o 100mm to 200mm; and

• number of strands (i.e. six or eight).

The method of grouping wire ropes according to these characteristics (“PCN method”) ignores

our client’s evidence about the importance of design, use and marketing. Wire rope is not a

commodity product. Wire rope exhibits different pricing depending on its specific attributes. We

demonstrated that there was a great variability in the profitability of domestic sales. The profit (or

loss) on different models is not neatly graduated with diameter nor indeed with any other

individual feature. The general superiority of the domestic ropes in terms of their standards and

features as compared to Australian ropes was also advised to the Commission.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 19

The PCN method has created a very pronounced mismatch in the comparison of domestic

models and Australian models. The fact that this amounted to a clear matching of different

products is demonstrated by a “cost to make and sell” (“CTMS”) comparison between the

models, which shows substantial differences between the domestic PCNs and their “matching”

Australian PCNs.

Although the following analysis will not be meaningful to other interested parties, due to the

confidentiality of the information to which the analysis refers, we still wish to have it recorded and

to have it acted upon by the Commission:

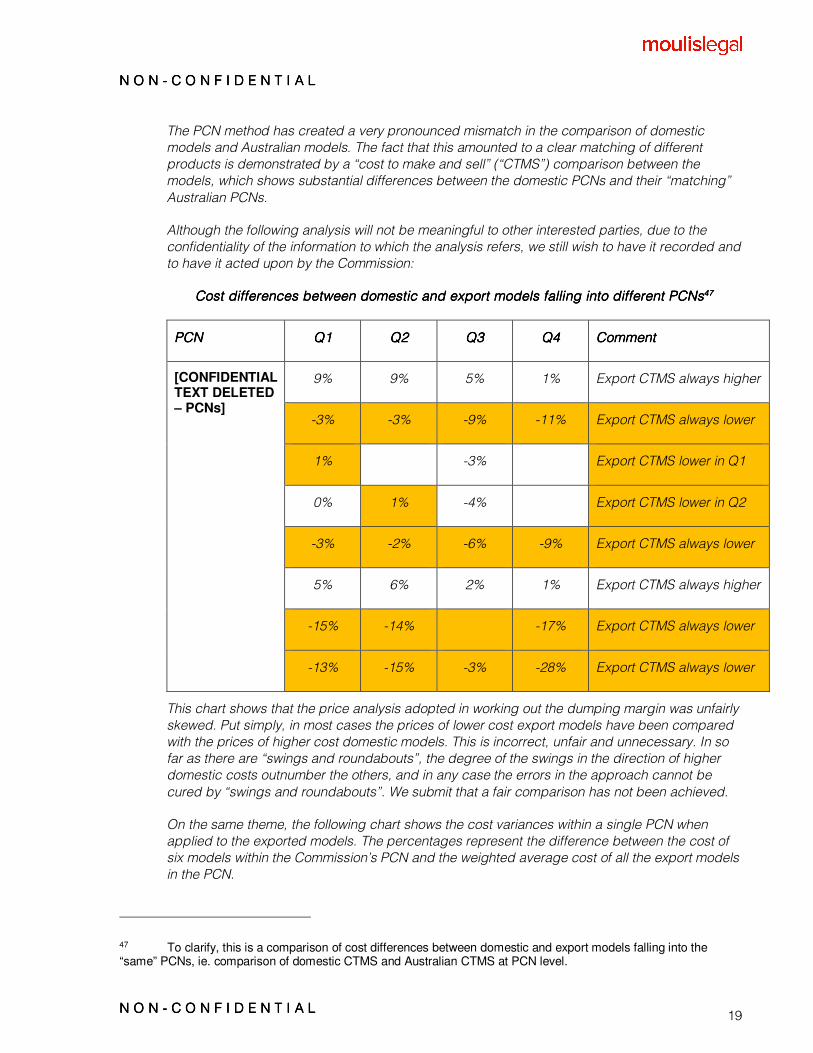

Cost differences between domestic and export models falling into different PCNsCost differences between domestic and export models falling into different PCNsCost differences between domestic and export models falling into different PCNsCost differences between domestic and export models falling into different PCNs47474747

PCNPCNPCNPCN Q1Q1Q1Q1 Q2Q2Q2Q2 Q3Q3Q3Q3 Q4Q4Q4Q4 CommentCommentCommentComment

[CONFIDENTIAL TEXT DELETED – PCNs]

9% 9% 5% 1% Export CTMS always higher

-3% -3% -9% -11% Export CTMS always lower

1% -3% Export CTMS lower in Q1

0% 1% -4% Export CTMS lower in Q2

-3% -2% -6% -9% Export CTMS always lower

5% 6% 2% 1% Export CTMS always higher

-15% -14% -17% Export CTMS always lower

-13% -15% -3% -28% Export CTMS always lower

This chart shows that the price analysis adopted in working out the dumping margin was unfairly

skewed. Put simply, in most cases the prices of lower cost export models have been compared

with the prices of higher cost domestic models. This is incorrect, unfair and unnecessary. In so

far as there are “swings and roundabouts”, the degree of the swings in the direction of higher

domestic costs outnumber the others, and in any case the errors in the approach cannot be

cured by “swings and roundabouts”. We submit that a fair comparison has not been achieved.

On the same theme, the following chart shows the cost variances within a single PCN when

applied to the exported models. The percentages represent the difference between the cost of

six models within the Commission’s PCN and the weighted average cost of all the export models

in the PCN.

47 To clarify, this is a comparison of cost differences between domestic and export models falling into the “same” PCNs, ie. comparison of domestic CTMS and Australian CTMS at PCN level.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 20

Cost differences within the models in export PCNsCost differences within the models in export PCNsCost differences within the models in export PCNsCost differences within the models in export PCNs

PCNPCNPCNPCN Q1Q1Q1Q1 Q2Q2Q2Q2 Q3Q3Q3Q3 Q4Q4Q4Q4

[CONFIDENTIAL TEXT DELETED – PCN]

23.2% 25.6% 24.4% 21.9%

5.3% 7.1% 7.4% 5.3%

3.2% 3.8% 1.9%

1.5% 1.9%

-10.6% -9.4% -7.7% -9.3%

-14.2% -13.1% -11.1% -12.6%

Again, we submit that there is no precision or consistency. This has opened the way for a

dumping margin outcome that is illogical and unfair.48

In the Report the Commission attempted to address Scaw’s submissions as follows:

Interested parties may propose different ways to define models. The Commission takes these

views into consideration but ultimately will determine the models for a particular investigation on

a case by case basis having regard to the circumstances. For certain goods, there may be

many individual characteristics that, to some degree, influence price comparisons. In these

circumstances, the Commission must strike a balance between capturing the key price drivers

(to neutralise or minimise problems relating to comparability) and the practical implications

(including that the number of models increase exponentially with every additional characteristic

considered and that exporters may not keep their CTMS information to such a detailed level).

Where there are too many models identified, it is difficult to identify direct model comparisons.

…

The Commission is of the view that by grouping the domestically sold wire ropes and wire ropes

exported to Australia with respect to the five criteria selected, the Commission is ensuring that

the main physical attributes (e.g. diameter, plastication type, compacting type and number of

strands), methods of production and end-use applications are captured. As a result, the

Commission disagrees with Scaw and Haggie Reid’s claim that the model matching

methodology doesn’t take into account the importance of design, end use or marketing. On the

contrary, the Commission is of the view that its model matching methodology effectively takes

into account all major cost and price drivers pertaining to the goods.

48 See the SEF comment, at pages 2 to 3.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 21

The Commission analysed Scaw’s domestic and export CTMS values during the course of the

investigation. The Commission noted that, for models that are identified to be identical by Scaw

in its exporter questionnaire response, there were significant cost differences between the

domestic CTMS and export CTMS. The Commission found that Scaw incorporated export

rebates it received from its domestic steel rod producer in relation to export sales in the

calculation of its export CTMS. In contrast, no such rebate is given to Scaw in relation to its

domestic sales, therefore Scaw’s domestic CTMS did not include such rebates. As a result, the

cost differential between the domestic CTMS and export CTMS that Scaw highlight in its

submission is explainable in the most part due to these rebates.

Consequently, these cost differences do not detract from the Commission’s approach to model

matching. The cost differences identified are a relevant consideration as to whether or not the

export steel incentive received by Scaw is a basis for an allowable adjustment to normal value.

This issue is discussed in detail in section 5.5.6 of this report.49

These extracts from the Report do not address or remedy the concerns of the Appellants, and we now

provide the following additional comments in respect of those attempted justifications for the Review

Panel’s consideration:

(1) We do not disagree that products can be identified and matched based on their “main physical

attributes” or the main “criteria”. As provided to the Commission during the investigation, the

product code adopted in Scaw’s production and sales system (“the Scaw product code”) is

indeed constructed and based on the key physical characteristics of the goods. The problem is

that the criteria used might not fully capture the key physical characteristics of the product, and

might adopt a range of designs and features that are too broad. This might result in different

products being grouped together as the same or the “one” product, and without proper

adjustment to account for relevant differences. This was a problem that arose in the model

grouping and model matching adopted by the Commission.

(2) Contrary to the example referred to in the Report, where detailed model grouping and matching

is not practical Scaw’s cost system was able to capture the detailed production cost for every

product code. Scaw reported the cost to make and sell (“CTMS”) for each and every Scaw

product code, and those detailed product code-based CTMS were verified, accepted and used

by the Commission in its margin calculation – such as for the purpose of conducting the

“ordinary course of trade” (“OCOT”) analysis on domestic sales of like goods.

(3) TTTThe CTMS analysis in the Report can only partially, at best, address the issue of “Cost

differences between domestic and export models falling into different PCNs” as raised in Scaw’s

49 See the Report, Section 5.4.3 at pages 21 to 22.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 22

SEF comment as cited above. By conducting the analysis only for “models that are identified to

be identical by Scaw in its exporter questionnaire response“, the analysis only dealt with the wire

rope under four Scaw product codes, out of the [CONFIDENTIAL TEXT DELETED –

confidential sales information] models/product codes for the goods exported by Scaw to

Australia, and the [CONFIDENTIAL TEXT DELETED – confidential sales information] models

of goods sold in the domestic market during the investigation period. The volume of the four

models covered by the analysis cited in the Report accounted for only about [CONFIDENTIAL

TEXT DELETED – confidential sales information]% of Scaw’s total Australian sales of the

goods during the investigation period.50 Based on the Commission’s model grouping, the

analysis only covers three models under the Commission’s PCN (ie, “product control number”,

designating a group of models) [CONFIDENTIAL TEXT DELETED – PCN], and one model

under [CONFIDENTIAL TEXT DELETED – PCN]. The cost difference issue as raised for the

other six PCNs remains unaddressed.

(4) We submit that the conclusion attempted to be drawn from the CTMS analysis in the Report, to

the effect that the cost differences highlighted by Scaw are only due to the export rebate that

was taken up in the export CTMS, is unsustainable. As shown in the “Cost differences between

domestic and export models falling into different PCNs” table, cost differences ranged from

[CONFIDENTIAL TEXT DELETED – confidential cost information]% lower (Australian CTMS

lower than the domestic CTMS with the same PCN) to [CONFIDENTIAL TEXT DELETED –

confidential cost information]% higher (Australian CTMS being higher than the domestic

CTMS with same PCN). Such cost variances cannot be explained away as being solely or mainly

caused by the inclusion of the rebated steel cost in the Australian CTMS (which would have the

effect of reducing the Australian CTMS) and the lack of such a rebate in the domestic CTMS.

Further, as shown in the Australian Sales spreadsheet provided by Scaw (which forms the basis

of “Confidential Appendix 5 – dumping margin” to the Report, and the “dumping margin”

worksheet therein), the export rebate only accounted for [CONFIDENTIAL TEXT DELETED –

confidential cost information] of the corresponding Australian CTMS for Scaw’s Australian

sales of the goods during the investigation period. This indicates that the cost variances

between domestic and Australian products falling within the same PCN cannot be attributed

50 This includes one of the four product codes for which all domestic sales were at loss, and therefore not in ordinary course of trade. The volume of Australian sales which have domestic sales of identical models in the ordinary course of trade account for about [CONFIDENTIAL TEXT DELETED – confidential sales information]% of the total Australian sales of the goods.

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 23

solely to the inclusion of the rebated steel cost in the Australian CTMS. For example, for

[CONFIDENTIAL TEXT DELETED – PCN], being a PCN that covers one of the four product

codes subject to the CTMS analysis in the Report, the Australian CTMS was [CONFIDENTIAL

TEXT DELETED – confidential cost information]% lower than the domestic CTMS, whereas

the export rebate accounted for only [CONFIDENTIAL TEXT DELETED – confidential cost

information]% of the Australian CTMS.

(5) Lastly, the Report does not address the issue of “Cost differences within the models in export

PCNs” as was raised by us in the SEF comment, as referred to above. The comparison

demonstrates the cost variances between different product codes within a single PCN, all based

on the Australian CTMS with the steel rebate taken into account. The export rebate would have

had a very limited impact on this comparison, and cannot explain the significant variances. To

further demonstrate this point, we provide another example, showing the cost variances between

each product code which fall within the same [CONFIDENTIAL TEXT DELETED – PCN], based

on domestic CTMS, which is free from the effect of any export rebate. This comparison, which is

the same as the one we presented in the SEF comment, is conducted by comparing the CTMS

for the product codes that fall within the PCN with the weighted average PCN level CTMS for

each corresponding quarter. A negative percentage means the CTMS for the particular product

code is lower than the mean CTMS of the PCN it belongs to, whereas a positive percentage

means the product code CTMS is higher than the mean PCN CTMS. In addition, this table shows

more comparisons (for nine product codes under the PCN) than the one we presented in the

SEF comment for the same PCN, because the PCN covered nine different product codes sold in

the domestic market, whereas the same PCN covered only six product codes for goods

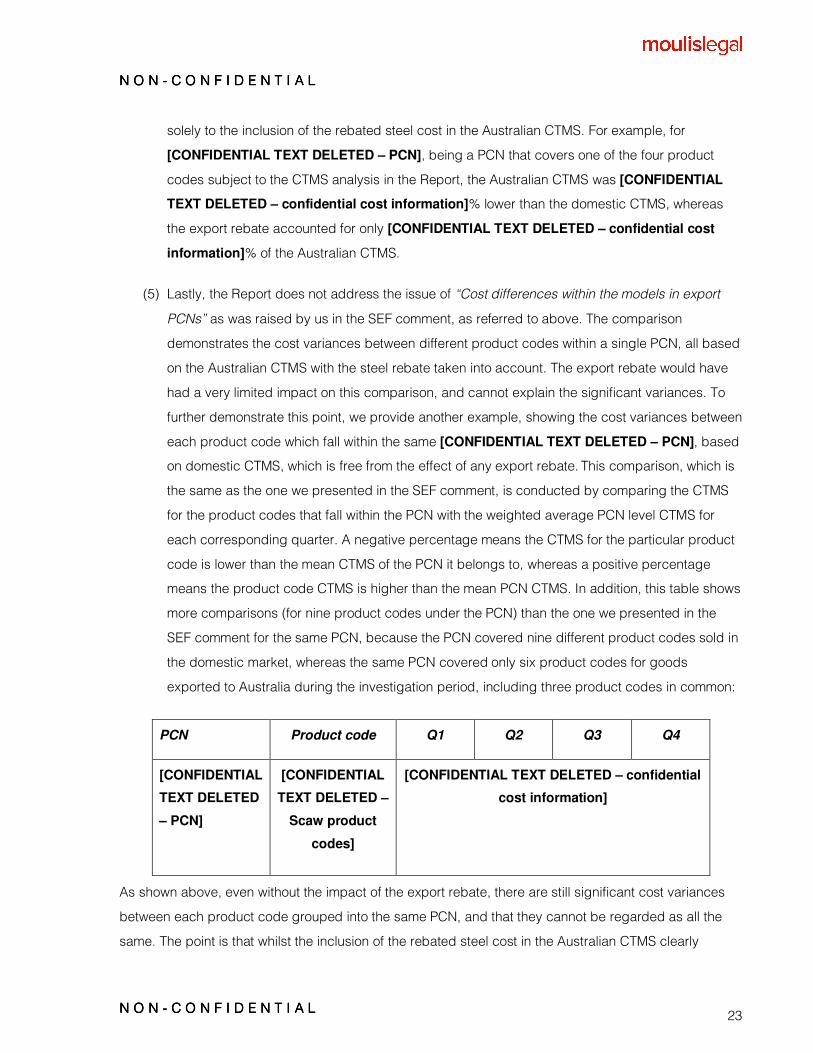

exported to Australia during the investigation period, including three product codes in common:

PCN Product code Q1 Q2 Q3 Q4

[CONFIDENTIAL

TEXT DELETED

– PCN]

[CONFIDENTIAL

TEXT DELETED –

Scaw product

codes]

[CONFIDENTIAL TEXT DELETED – confidential

cost information]

As shown above, even without the impact of the export rebate, there are still significant cost variances

between each product code grouped into the same PCN, and that they cannot be regarded as all the

same. The point is that whilst the inclusion of the rebated steel cost in the Australian CTMS clearly

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L

N O N N O N N O N N O N ---- C O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A LC O N F I D E N T I A L 24

contributed to a situation in which the Australian CTMS was lower than the domestic CTMS for the

identical products, this does not explain or moderate the significant cost variances between domestic

and export products, much less the significant cost variances between products being allocated with

the same PCNs.

Allocating products with a wide range of costs into the one PCN does not provide a safe or fair point of

comparison between the Australian and domestic prices. Indeed, in many circumstances the

Commission’s PCN approach has resulted in products with different product codes – which already

suggest that they are physically different – being compared on the premise that they are the same

goods, because of the same broad and problematic PCN assigned to them. Because the same PCN has

been assigned to a group of different products, the differences between the products sold in the

domestic market and the goods exported to Australia have been ignored. Different products have been

grouped and compared as if they correspond with each other when they do not. We respectfully submit

that this approach is incorrect and does not comply with Section 269TACB(1) and the fair comparison

requirement of the Anti-Dumping Agreement:

2.4 A fair comparison shall be made between the export price and the normal value. This

comparison shall be made at the same level of trade, normally at the ex-factory level, and in

respect of sales made at as nearly as possible the same time. Due allowance shall be made in