Embed Size (px)

Citation preview

Apple outlook 2011 Philippe Binard

World Apple and Pear Association ( WAPA )

Freshfel Europe

World Apple and Pear Association ( WAPA)

• WAPA ( 2001 ) = world umbrella organisation for the apple and pear producing countries = global forum of discussion for issues affecting apple and pear production and trading

• Incorporating the 18 leading apple and pear producing countries around the world both in the Northern Hemisphere (Europe + USA) and Southern Hemisphere

• Governance : rotating presidency and secretariat – President: Kevin Moffitt (USA)– Vice-President: Peter Beaven (New Zealand)– Immediate Past President: Alessandro Dalpiaz (Italy)– Brussels based secretariat

WAPA :mission & achievements

• Improve transparency by facilitating exchange of information on production and trade of apple & pear

• Platform for dissemination of sound science relating to apples and pears ( nutrition ,health benefit , organoleptic,... )

• Facilitate internationally the market position of apples and pears by exchanging best practice on promotion/communication

• www.wapa-association.org

APPLE MARKET REVIEW 2010/2011

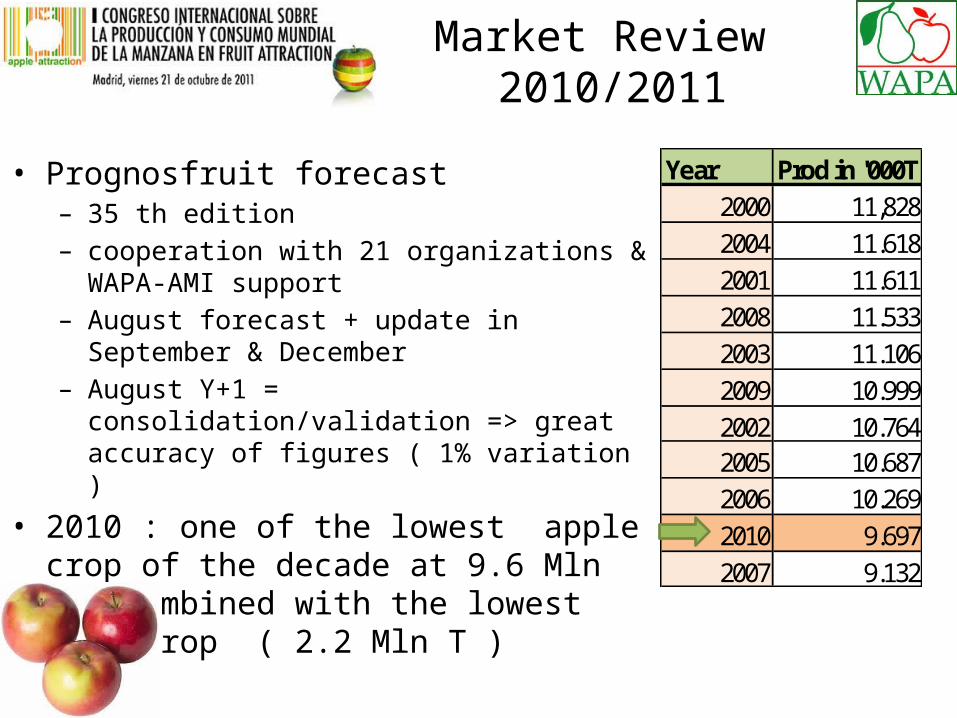

Market Review 2010/2011

• Prognosfruit forecast– 35 th edition – cooperation with 21 organizations & WAPA-AMI

support– August forecast + update in September & December– August Y+1 = consolidation/validation => great

accuracy of figures ( 1% variation )

• 2010 : one of the lowest apple crop of the decade at 9.6 Mln T, combined with the lowest pear crop ( 2.2 Mln T )

Year Prod in '000T2000 11,8282004 11.6182001 11.6112008 11.5332003 11.1062009 10.9992002 10.7642005 10.6872006 10.2692010 9.6972007 9.132

Market Review 2010/2011

• Main parameters of the season ( volume ) : – Late start – No NH stock nor SH overlap – Increasing demand in Eastern Europe ( low crop in Poland ) and strong

demand in Russia ( total import = 1.2 Mln T) – Small imports volume from SH in the EU( ca 570.000 T )– Supply balance => lower fresh consumption at 18.1 kg/capita

1.000 t 2007/08 2008/09 2009/10 2010/11f

Market production 9.117 11.499 10.984 9.697

+ Import EU1) 830 731 585 570

- Export EU1) 746 1.220 1.222 1.180

= Consumption2) 9.201 11.010 10.347 9.087Per capita (kg) 18,4 22,0 20,7 18,1

Source : AMI

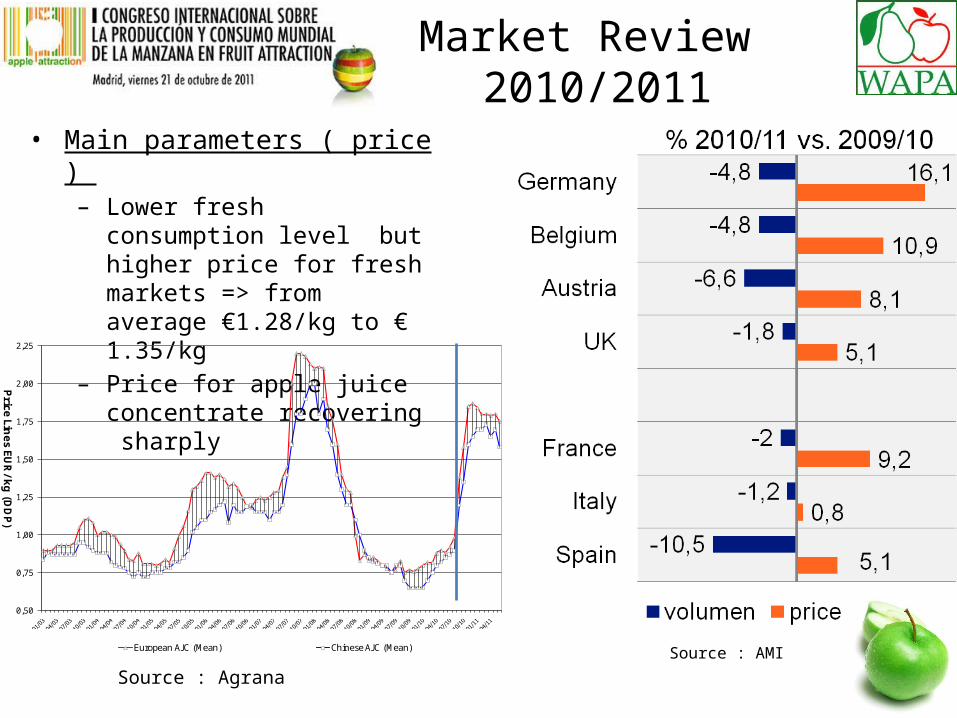

Market Review 2010/2011

• Main parameters ( price ) – Lower fresh consumption level

but higher price for fresh markets => from average €1.28/kg to € 1.35/kg

– Price for apple juice concentrate recovering sharply

Source : AMI

0,50

0,75

1,00

1,25

1,50

1,75

2,00

2,25

Price

Lines E

UR

/kg (D

DP)

European AJC (Mean) Chinese AJC (Mean)

Source : Agrana

OUTLOOK 2011 : EU-27 AND OTHER EUROPEAN COUNTRIES

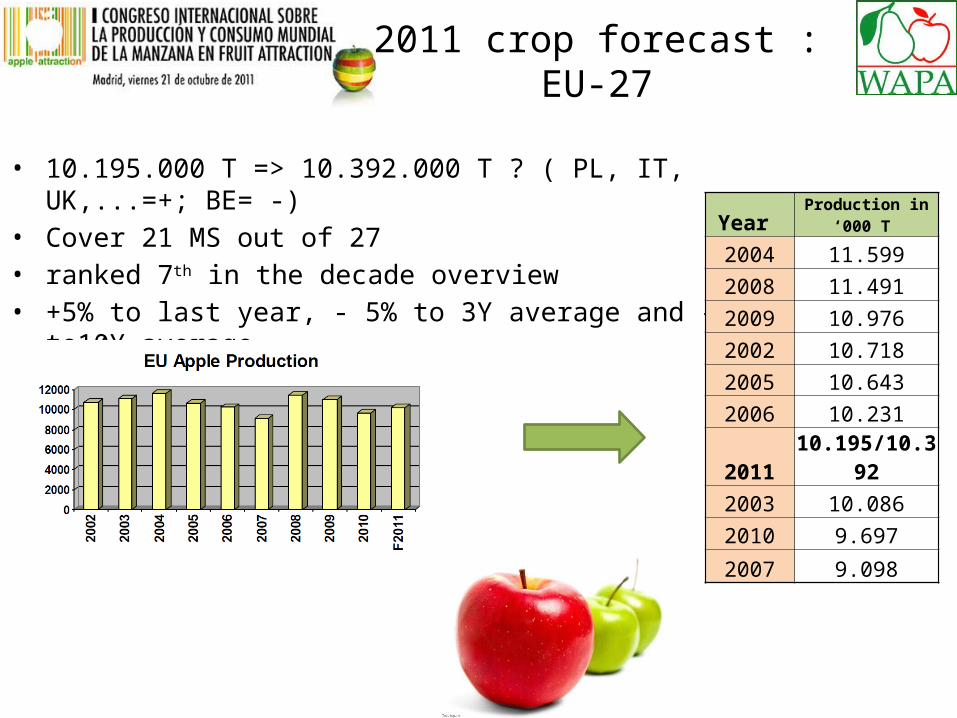

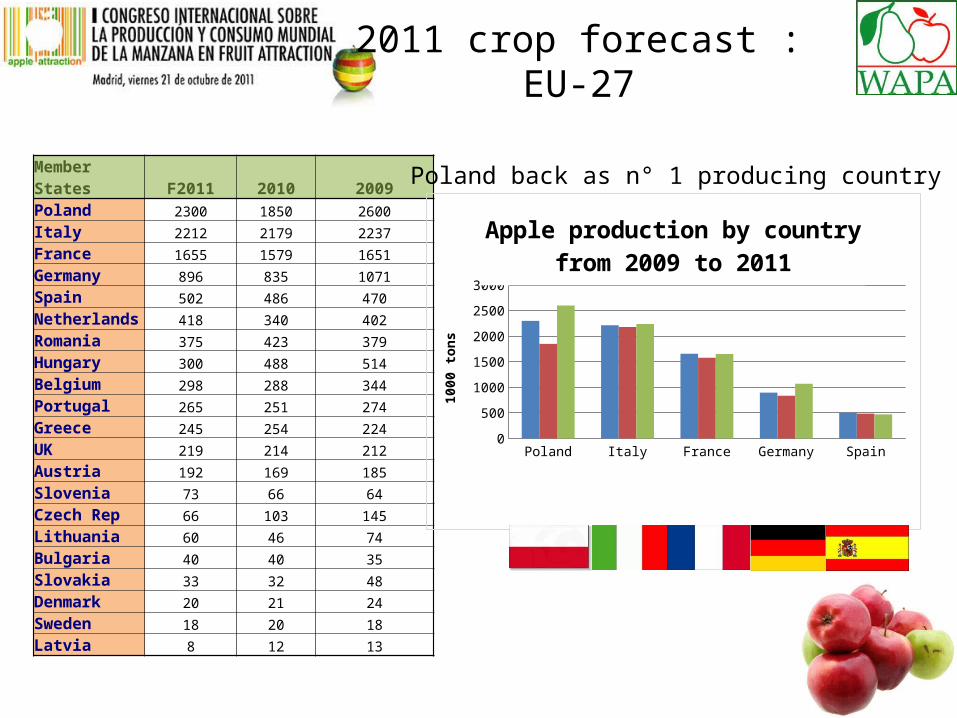

2011 crop forecast :EU-27

• 10.195.000 T => 10.392.000 T ? ( PL, IT, UK,...=+; BE= -)• Cover 21 MS out of 27 • ranked 7th in the decade overview • +5% to last year, - 5% to 3Y average and -4% to10Y average

Year Production in ‘000 T

2004 11.5992008 11.4912009 10.9762002 10.7182005 10.6432006 10.2312011 10.195/10.3922003 10.0862010 9.697

2007 9.098

2011 crop forecast :EU-27

Member States F2011 2010 2009Poland 2300 1850 2600

Italy 2212 2179 2237

France 1655 1579 1651

Germany 896 835 1071

Spain 502 486 470

Netherlands 418 340 402

Romania 375 423 379

Hungary 300 488 514

Belgium 298 288 344

Portugal 265 251 274

Greece 245 254 224

UK 219 214 212

Austria 192 169 185

Slovenia 73 66 64

Czech Rep 66 103 145

Lithuania 60 46 74

Bulgaria 40 40 35

Slovakia 33 32 48

Denmark 20 21 24

Sweden 18 20 18

Latvia 8 12 13

Poland Italy France Germany Spain

F2011 2300 2212 1655 896 502

2010 1850 2179 1579 835 486

2009 2600 2237 1651 1071 470

250

750

1250

1750

2250

2750

Apple production by country from 2009 to 2011

1000

tons

Poland back as n° 1 producing country

EU -27 forecast 2011: comments ( production )

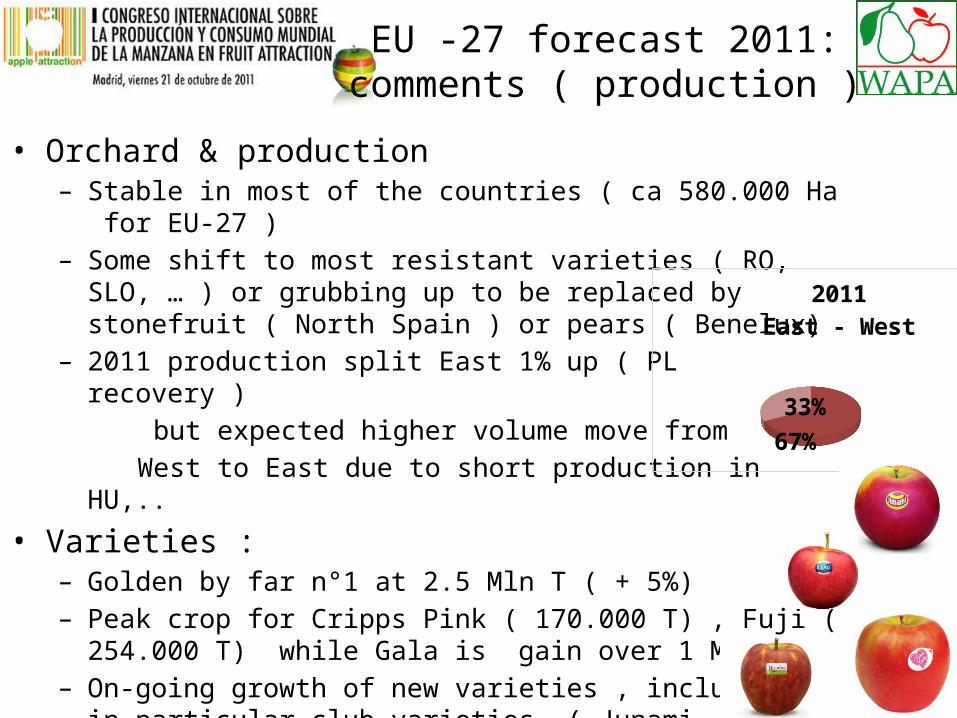

• Orchard & production– Stable in most of the countries ( ca 580.000 Ha for EU-27 )– Some shift to most resistant varieties ( RO, SLO, … ) or grubbing up to

be replaced by stonefruit ( North Spain ) or pears ( Benelux) – 2011 production split East 1% up ( PL recovery ) but expected higher volume move from West to East due to short production in HU,..

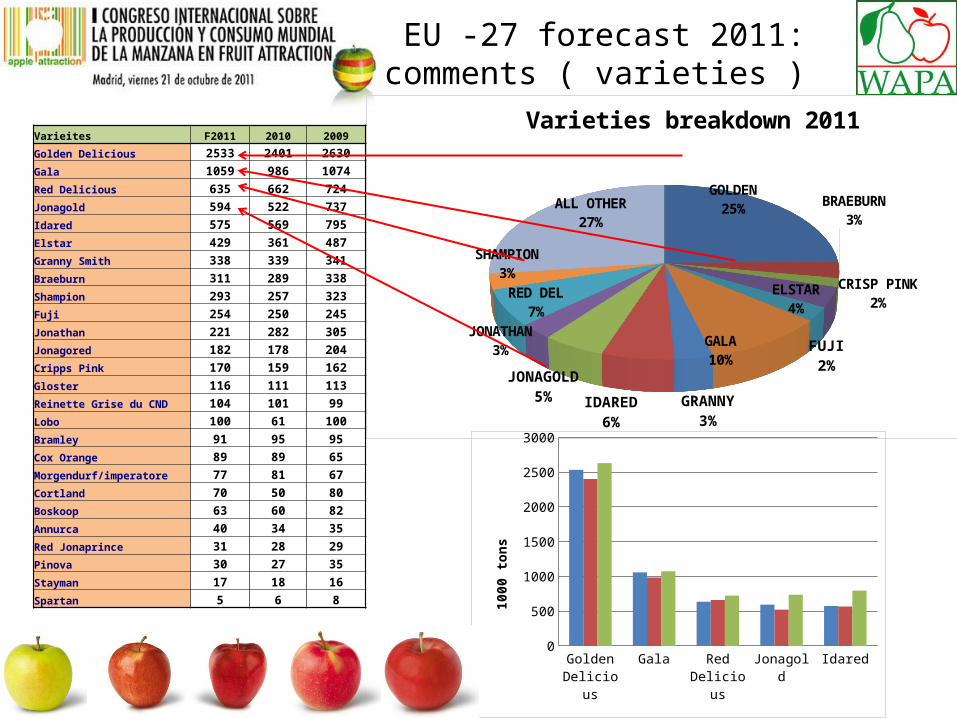

• Varieties :– Golden by far n°1 at 2.5 Mln T ( + 5%) – Peak crop for Cripps Pink ( 170.000 T) , Fuji ( 254.000 T) while Gala is

gain over 1 Mln T – On-going growth of new varieties , including in particular club

varieties ( Junami, Kanzi, Rubens,…)– Decline for Idared, Jonagold , Red Delicious , Morgendurf,..

67%33%

2011 East - West

EU -27 forecast 2011: comments ( varieties )

GOLDEN25%

BRAEBURN3%

CRISP PINK2%ELSTAR

4%

FUJI2%GALA

10%

GRANNY3%

IDARED6%

JONAGOLD5%

JONATHAN3%

RED DEL7%

SHAMPION3%

ALL OTHER27%

Varieties breakdown 2011

Golden Delicious

Gala Red Deli-cious

Jonagold Idared

F2011 2533 1059 635 594 575

2010 2401 986 662 522 569

2009 2630 1074 724 737 795

250

750

1250

1750

2250

2750

1000

tons

Varieites F2011 2010 2009

Golden Delicious 2533 2401 2630

Gala 1059 986 1074

Red Delicious 635 662 724

Jonagold 594 522 737

Idared 575 569 795

Elstar 429 361 487

Granny Smith 338 339 341

Braeburn 311 289 338

Shampion 293 257 323

Fuji 254 250 245

Jonathan 221 282 305

Jonagored 182 178 204

Cripps Pink 170 159 162

Gloster 116 111 113

Reinette Grise du CND 104 101 99

Lobo 100 61 100

Bramley 91 95 95

Cox Orange 89 89 65

Morgendurf/imperatore 77 81 67

Cortland 70 50 80

Boskoop 63 60 82

Annurca 40 34 35

Red Jonaprince 31 28 29

Pinova 30 27 35

Stayman 17 18 16

Spartan 5 6 8

EU -27 forecast 2011: comments ( weather )

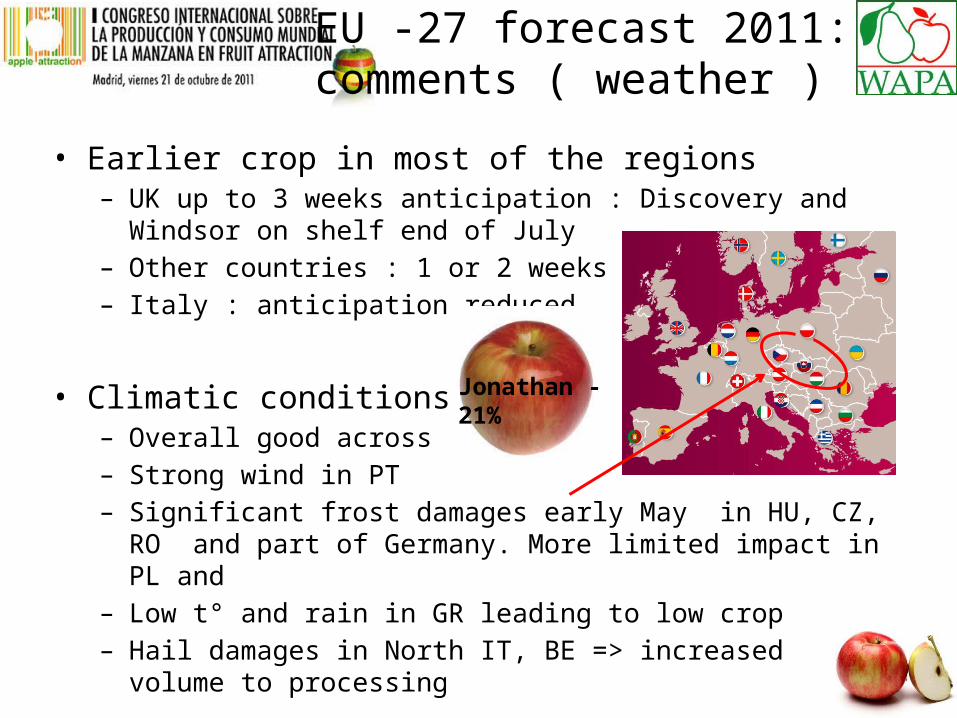

• Earlier crop in most of the regions – UK up to 3 weeks anticipation : Discovery and Windsor on shelf end of

July – Other countries : 1 or 2 weeks– Italy : anticipation reduced

• Climatic conditions– Overall good across Europe – Strong wind in PT– Significant frost damages early May in HU, CZ, RO and part of

Germany. More limited impact in PL and – Low t° and rain in GR leading to low crop– Hail damages in North IT, BE => increased volume to processing

Jonathan -21%

EU -27 forecast 2011: comments ( quality )

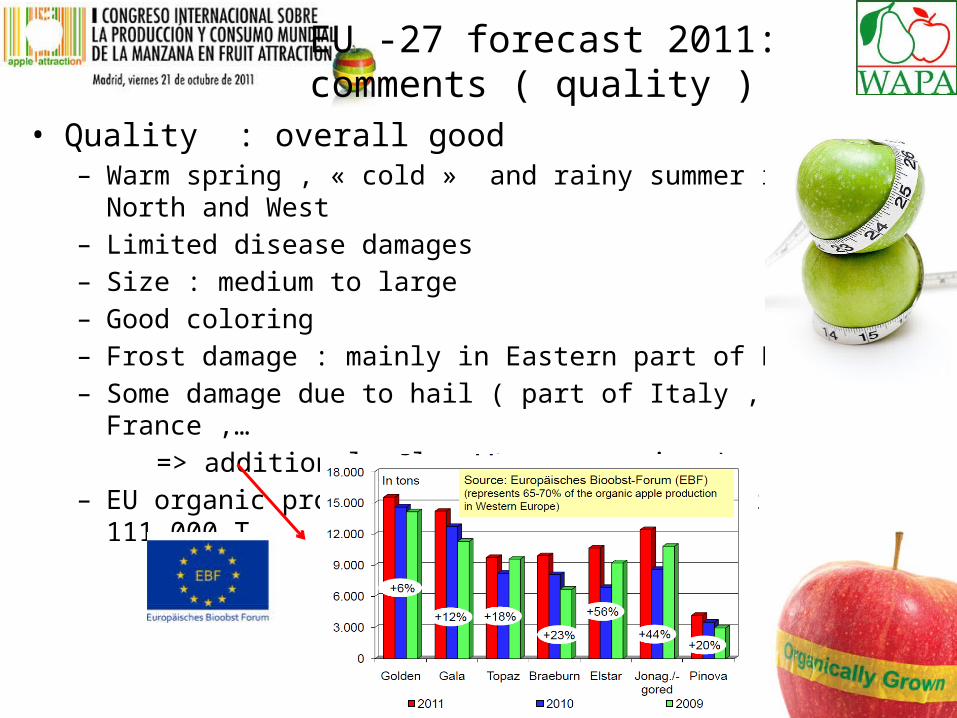

• Quality : overall good – Warm spring , « cold » and rainy summer in North and West– Limited disease damages– Size : medium to large – Good coloring– Frost damage : mainly in Eastern part of Europe– Some damage due to hail ( part of Italy , France ,… => additional volume to processing )– EU organic production up by almost 20% at 111.000 T

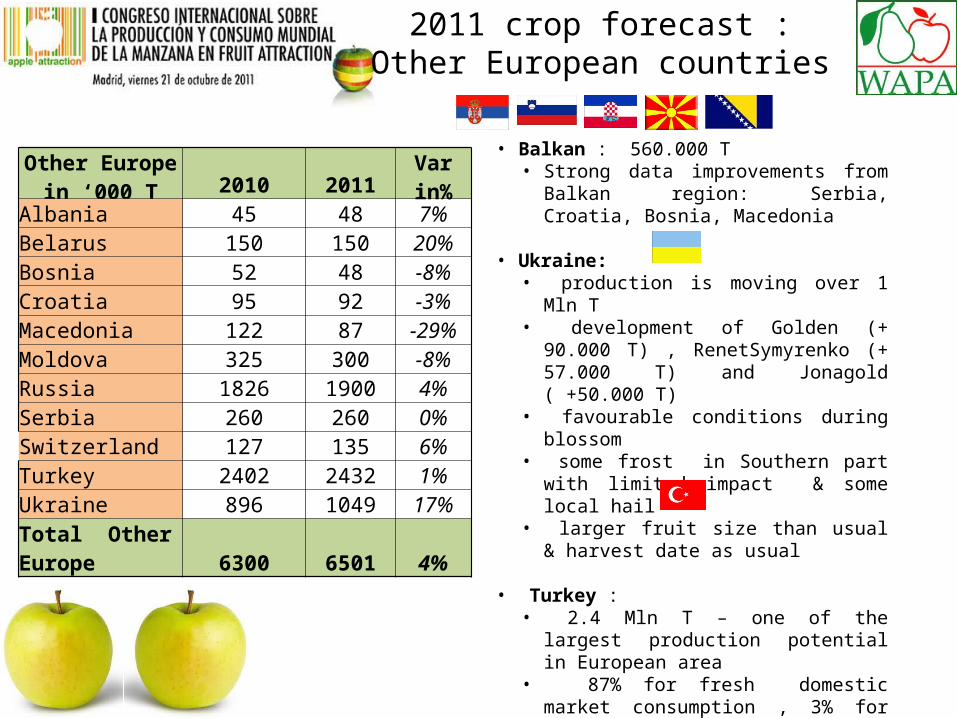

2011 crop forecast :Other European countries

• Balkan : 560.000 T

• Strong data improvements from Balkan region: Serbia, Croatia, Bosnia, Macedonia

• Ukraine: • production is moving over 1 Mln T • development of Golden (+ 90.000 T) ,

RenetSymyrenko (+ 57.000 T) and Jonagold ( +50.000 T)

• favourable conditions during blossom• some frost in Southern part with limited

impact & some local hail • larger fruit size than usual & harvest

date as usual

• Turkey : • 2.4 Mln T – one of the largest production

potential in European area• 87% for fresh domestic market

consumption , 3% for fresh exports and 10 % for juice . Limited import .

Other Europe in ‘000 T 2010 2011

Varin%

Albania 45 48 7%Belarus 150 150 20%Bosnia 52 48 -8%Croatia 95 92 -3%Macedonia 122 87 -29%Moldova 325 300 -8%Russia 1826 1900 4%Serbia 260 260 0%Switzerland 127 135 6%Turkey 2402 2432 1%Ukraine 896 1049 17%

Total Other Europe 6300 6501 4%

2.2

0.7

1

2.3

0.60.5

2.4

1.911.60.7

0.2

0.2

0.1

European region 201116.7 Mln T

0.2

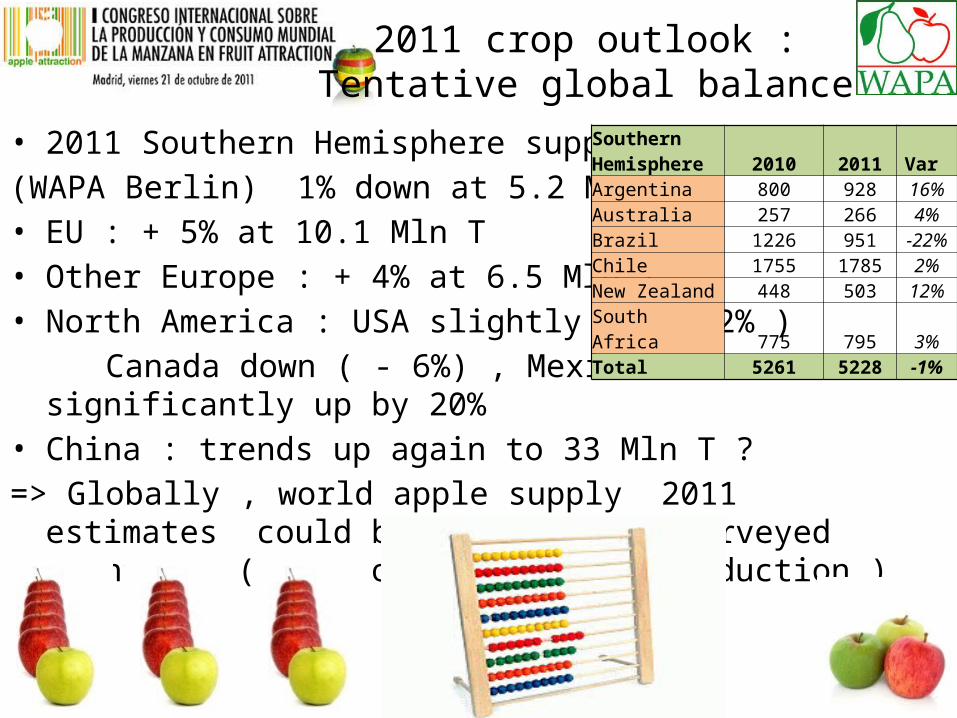

2011 crop outlook :Tentative global balance

• 2011 Southern Hemisphere supply (WAPA Berlin) 1% down at 5.2 Mln T• EU : + 5% at 10.1 Mln T • Other Europe : + 4% at 6.5 Mln T • North America : USA slightly up ( +2% ) Canada down ( - 6%) , Mexico significantly up by 20% • China : trends up again to 33 Mln T ?=> Globally , world apple supply 2011 estimates could be up by 5%

for surveyed countries ( =90% of world apple production )

Southern Hemisphere 2010 2011 Var Argentina 800 928 16%Australia 257 266 4%Brazil 1226 951 -22%Chile 1755 1785 2%New Zealand 448 503 12%South Africa 775 795 3%Total 5261 5228 -1%

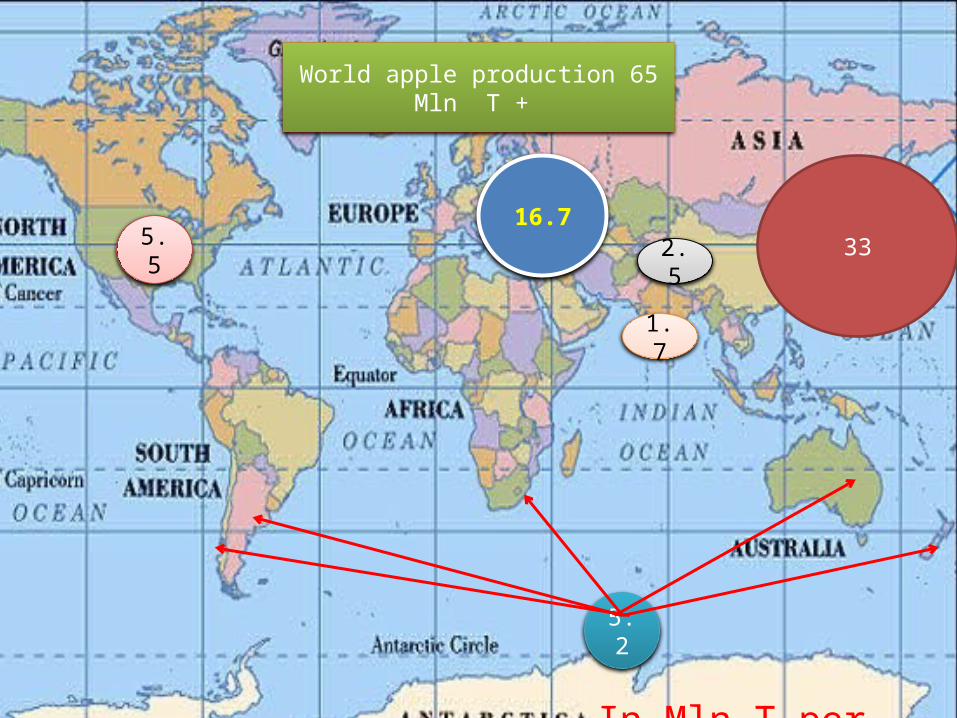

5.516.7

33

5.2

1.7

2.5

In Mln T per region

World apple production 65 Mln T +

MARKET OUTLOOK 2011-2012

?

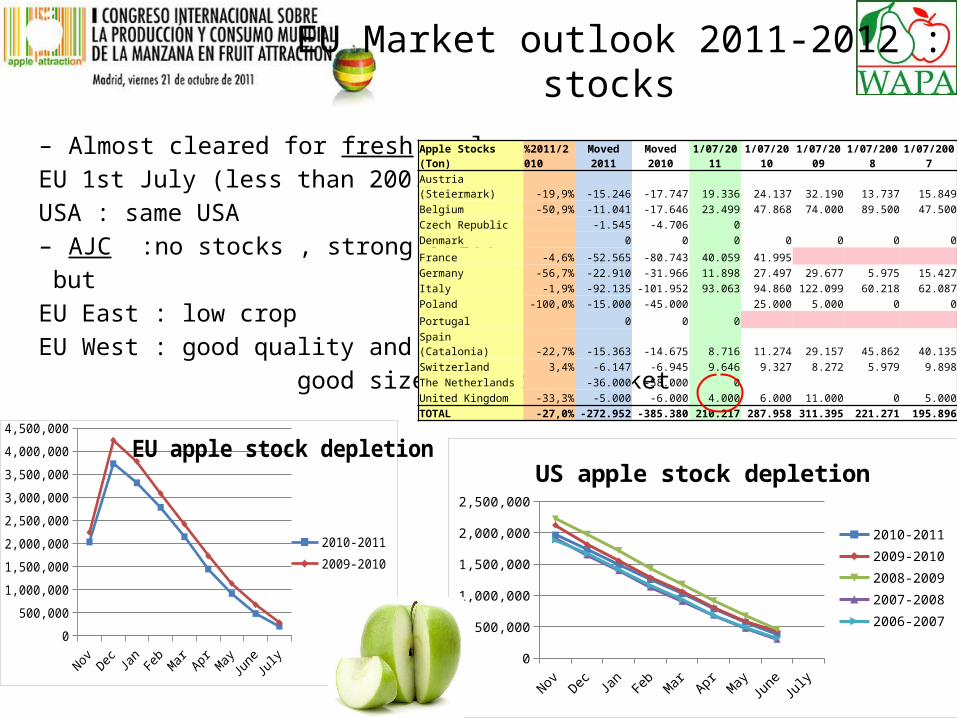

EU Market outlook 2011-2012 :stocks

– Almost cleared for fresh apples EU 1st July (less than 200.000 T) –USA : same USA– AJC :no stocks , strong start but EU East : low cropEU West : good quality and good size for fresh market

Apple Stocks (Ton)%2011/2010

Moved 2011

Moved 2010 1/07/2011 1/07/2010 1/07/2009 1/07/2008 1/07/2007

Austria (Steiermark) -19,9% -15.246 -17.747 19.336 24.137 32.190 13.737 15.849

Belgium -50,9% -11.041 -17.646 23.499 47.868 74.000 89.500 47.500

Czech Republic -1.545 -4.706 0

Denmark 0 0 0 0 0 0 0

France -4,6% -52.565 -80.743 40.059 41.995 Germany -56,7% -22.910 -31.966 11.898 27.497 29.677 5.975 15.427

Italy -1,9% -92.135 -101.952 93.063 94.860 122.099 60.218 62.087

Poland -100,0% -15.000 -45.000 25.000 5.000 0 0

Portugal 0 0 0 Spain (Catalonia) -22,7% -15.363 -14.675 8.716 11.274 29.157 45.862 40.135

Switzerland 3,4% -6.147 -6.945 9.646 9.327 8.272 5.979 9.898

The Netherlands -36.000 -58.000 0

United Kingdom -33,3% -5.000 -6.000 4.000 6.000 11.000 0 5.000

TOTAL -27,0% -272.952 -385.380 210.217 287.958 311.395 221.271 195.896

Nov Dec Jan Feb Mar Apr May June July0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000EU apple stock depletion

2010-20112009-2010

Nov Dec Jan Feb Mar Apr May June July0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

US apple stock depletion

2010-20112009-20102008-20092007-20082006-2007

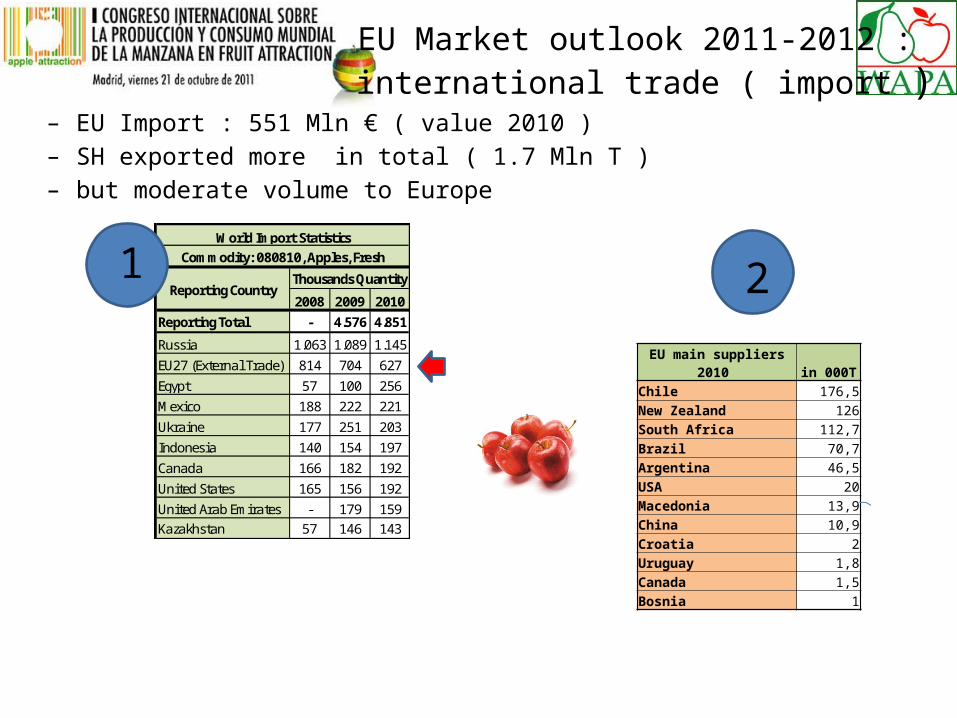

EU Market outlook 2011-2012 : international trade ( import )

– EU Import : 551 Mln € ( value 2010 ) – SH exported more in total ( 1.7 Mln T ) – but moderate volume to Europe

2008 2009 2010

Reporting Total - 4.576 4.851

Russia 1.063 1.089 1.145

EU27 (External Trade) 814 704 627

Egypt 57 100 256

Mexico 188 222 221

Ukraine 177 251 203

Indonesia 140 154 197

Canada 166 182 192

United States 165 156 192

United Arab Emirates - 179 159Kazakhstan 57 146 143

World Import StatisticsCommodity: 080810, Apples, Fresh

Reporting CountryThousands Quantity

EU main suppliers 2010 in 000TChile 176,5New Zealand 126South Africa 112,7Brazil 70,7Argentina 46,5USA 20Macedonia 13,9China 10,9Croatia 2Uruguay 1,8Canada 1,5Bosnia 1

1 2

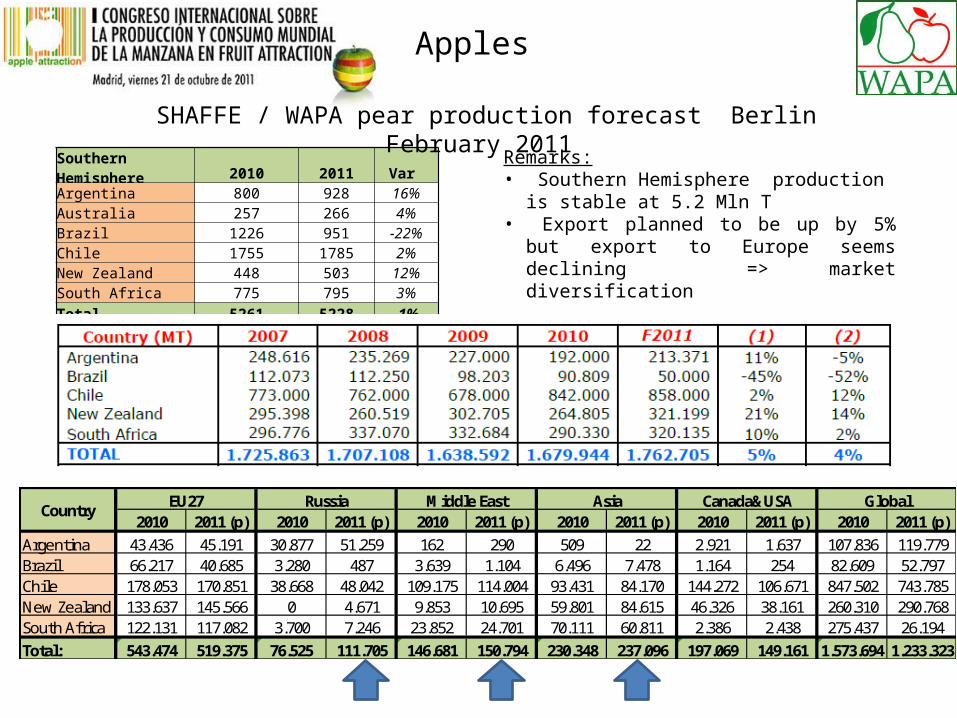

Apples

Remarks:• Southern Hemisphere production is stable

at 5.2 Mln T• Export planned to be up by 5% but export

to Europe seems declining => market diversification

Southern Hemisphere 2010 2011 Var Argentina 800 928 16%Australia 257 266 4%Brazil 1226 951 -22%Chile 1755 1785 2%New Zealand 448 503 12%South Africa 775 795 3%Total 5261 5228 -1%

SHAFFE / WAPA pear production forecast Berlin February 2011

2010 2011 (p) 2010 2011 (p) 2010 2011 (p) 2010 2011 (p) 2010 2011 (p) 2010 2011 (p)Argentina 43.436 45.191 30.877 51.259 162 290 509 22 2.921 1.637 107.836 119.779Brazil 66.217 40.685 3.280 487 3.639 1.104 6.496 7.478 1.164 254 82.609 52.797Chile 178.053 170.851 38.668 48.042 109.175 114.004 93.431 84.170 144.272 106.671 847.502 743.785New Zealand 133.637 145.566 0 4.671 9.853 10.695 59.801 84.615 46.326 38.161 260.310 290.768South Africa 122.131 117.082 3.700 7.246 23.852 24.701 70.111 60.811 2.386 2.438 275.437 26.194Total: 543.474 519.375 76.525 111.705 146.681 150.794 230.348 237.096 197.069 149.161 1.573.694 1.233.323

GlobalEU27 Russia Middle East Asia Canada&USACountry

EU Market outlook 2011-2012 : international trade

– EU Export : 558 Mln € ( value 2010 ) – Uncertainties : SPS , world economy , strenght of the € ….. – Russia : Safety certificates maintained for apples from BE, DE, EL ,FR, HU, IT, NL, PL– Market demand in North Africa : Algeria, Egypt ,…– SPS protocol negotiation

2008 2009 2010

Reporting Total - 5.529 5.785

EU27 (External Trade) 861 1.167 1.241

China 1.153 1.171 1.121

Chile 776 679 843

United States 712 818 791

Iran - 270 360

South Africa 359 339 306

New Zealand 261 303 260

Argentina 236 207 179

Serbia 35 40 107Ukraine 20 59 98

World Export StatisticsCommodity: 080810, Apples, Fresh

Export CountryThousands Quantity

EU Destination in 000TRussia 563Ukraine 195Algeria 89Belarus 43Lybia 42Saudi Arabia 37Norway 34Kazakhstan 31Emirate 25Morocco 13Turkey 13Bosnia 11Switzerland 10Egypt 9Malaysia 9Croatia 8

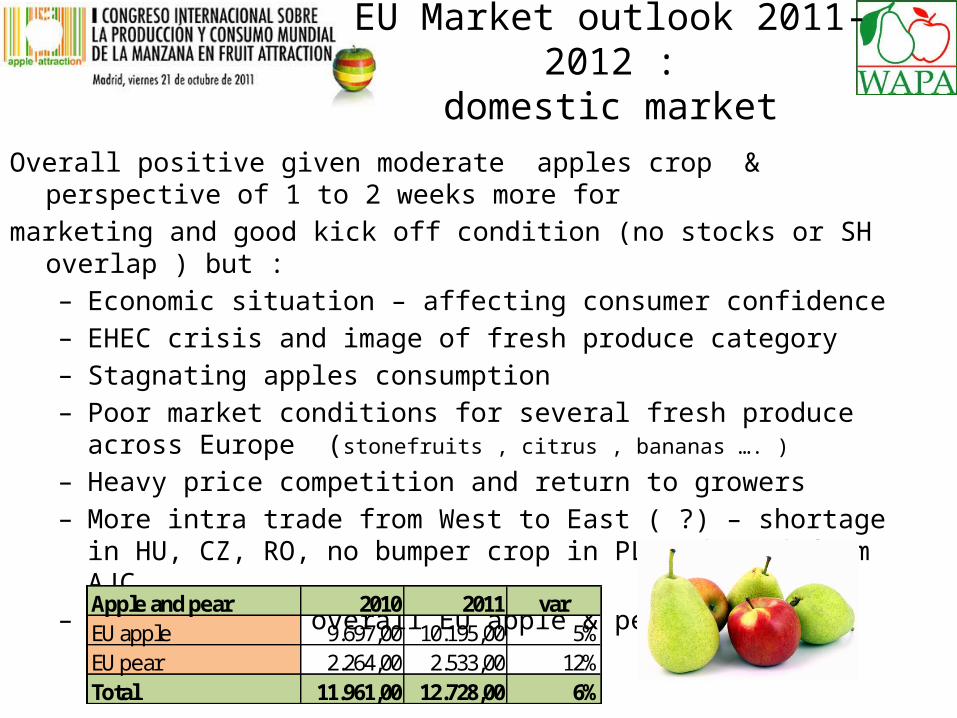

EU Market outlook 2011-2012 : domestic market

Overall positive given moderate apples crop & perspective of 1 to 2 weeks more formarketing and good kick off condition (no stocks or SH overlap ) but :

– Economic situation – affecting consumer confidence– EHEC crisis and image of fresh produce category – Stagnating apples consumption – Poor market conditions for several fresh produce across Europe (stonefruits ,

citrus , bananas …. )

– Heavy price competition and return to growers – More intra trade from West to East ( ?) – shortage in HU, CZ, RO, no bumper

crop in PL -demand from AJC – Pear crop up- overall EU apple & pear +6%

Apple and pear 2010 2011 var EU apple 9.697,00 10.195,00 5%EU pear 2.264,00 2.533,00 12%Total 11.961,00 12.728,00 6%

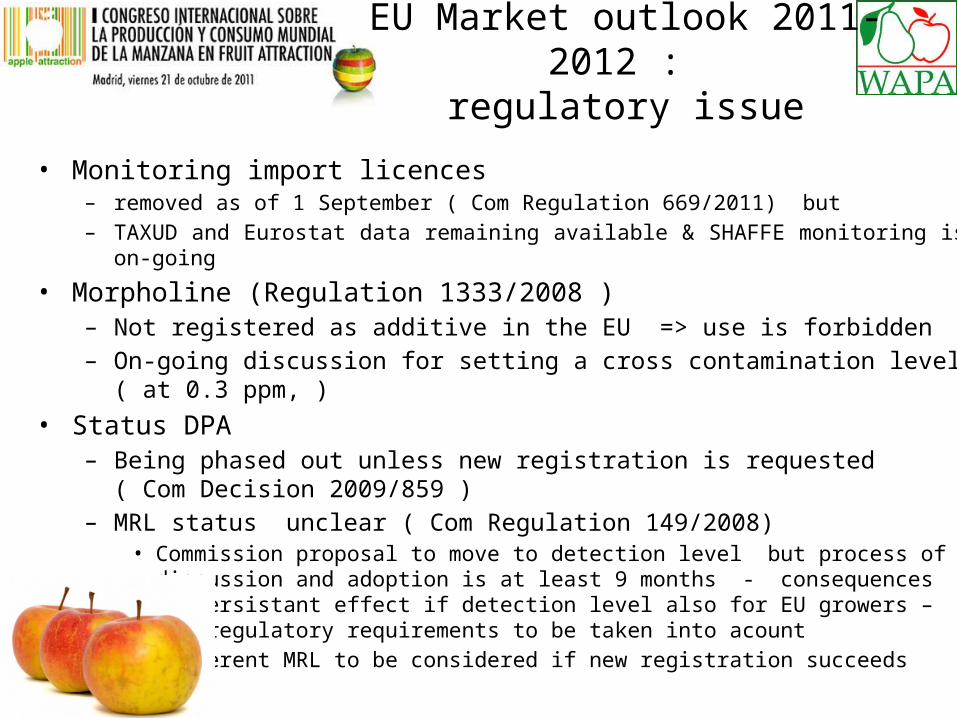

EU Market outlook 2011-2012 : regulatory issue

• Monitoring import licences– removed as of 1 September ( Com Regulation 669/2011) but– TAXUD and Eurostat data remaining available & SHAFFE monitoring is on-going

• Morpholine (Regulation 1333/2008 )– Not registered as additive in the EU => use is forbidden– On-going discussion for setting a cross contamination level ( at 0.3 ppm, )

• Status DPA– Being phased out unless new registration is requested ( Com Decision 2009/859 )– MRL status unclear ( Com Regulation 149/2008)

• Commission proposal to move to detection level but process of discussion and adoption is at least 9 months - consequences of persistant effect if detection level also for EU growers – non regulatory requirements to be taken into acount

• Different MRL to be considered if new registration succeeds

CONCLUSION

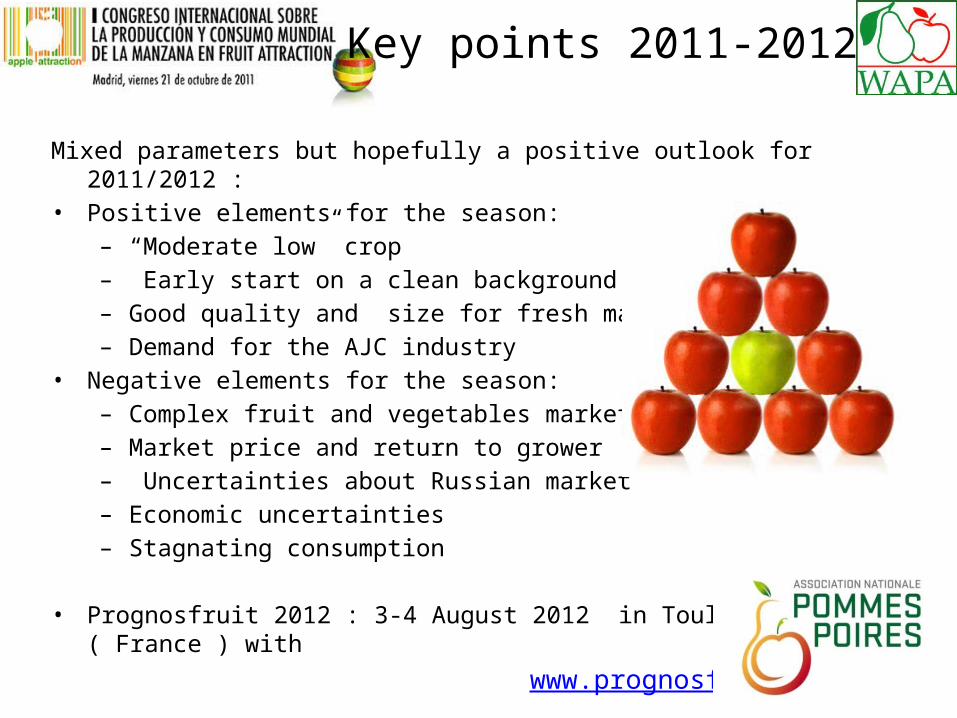

Key points 2011-2012

Mixed parameters but hopefully a positive outlook for 2011/2012 : • Positive elements for the season:

– “Moderate low” crop– Early start on a clean background – Good quality and size for fresh market – Demand for the AJC industry

• Negative elements for the season:– Complex fruit and vegetables markets – Market price and return to grower– Uncertainties about Russian market – Economic uncertainties – Stagnating consumption

• Prognosfruit 2012 : 3-4 August 2012 in Toulouse ( France ) with

www.prognosfruit.eu