Embed Size (px)

Citation preview

The following is the text of a report received from the Company’s reporting accountants.SHINEWING (HK) CPA Limited, Certified Public Accountants, Hong Kong, for the purpose ofincorporation in this prospectus, it is prepared and addressed to the Directors and the Sponsor pursuantto the requirement of Auditing Guideline 3.340 ‘‘Prospectuses and the Reporting Accountants’’ issuedby the Hong Kong Institute of Certified Public Accountants.

31 March 2016

The Board of DirectorsA.Plus Group Holdings Limited

Altus Capital Limited

Dear Sirs,

INTRODUCTION

We set out below our report on the financial information (the ‘‘Financial Information’’) regardingA.Plus International Financial Press Limited (‘‘API’’) for each of the two years ended 31 March 2015and the nine months ended 31 December 2015 (the ‘‘Track Record Period’’) for inclusion in theprospectus of A.Plus Group Holdings Limited (the ‘‘Company’’) dated 31 March 2016 (the‘‘Prospectus’’) in connection with the listing of shares of the Company on the Growth EnterpriseMarket of The Stock Exchange of Hong Kong Limited (the ‘‘Stock Exchange’’).

API was incorporated in Hong Kong under the Hong Kong Companies Ordinance with limitedliability on 3 January 2012. Pursuant to a group reorganisation as detailed in the section headed‘‘History, Reorganisation and Group structure’’ to the Prospectus (the ‘‘Reorganisation’’), API becamean indirect wholly-owned subsidiary of the Company on 23 March 2016.

The statutory financial statements of API for the year ended 31 March 2014 were prepared inaccordance with Hong Kong Financial Reporting Standard for Private Entities issued by the Hong KongInstitute of Certified Public Accountants (the ‘‘HKICPA’’) and were audited by W.H. Tang & PartnersCPA Limited. The statutory financial statements of API for the year ended 31 March 2015 wereprepared in accordance with Hong Kong Financial Reporting Standards (‘‘HKFRSs’’) issued by theHKICPA and were audited by W.H. Tang & Partners CPA Limited.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 1

BASIS OF PREPARATION

For the purpose of this report, the directors of API have prepared the financial statements of APIfor the Track Record Period in accordance with HKFRSs issued by the HKICPA (the ‘‘UnderlyingFinancial Statements’’). We have carried out independent audit procedures on the Underlying FinancialStatements in accordance with Hong Kong Standards on Auditing issued by the HKICPA for the TrackRecord Period and carried out such additional procedures as are necessary in accordance with theAuditing Guideline 3.340 ‘‘Prospectuses and the Reporting Accountant’’ issued by the HKICPA.

The Financial Information has been prepared by the directors of API for inclusion in theProspectus based on the Underlying Financial Statements, with no adjustments thereto, and inaccordance with the applicable disclosures required by the Rules Governing the Listing of Securities onthe Growth Enterprise Market of the Stock Exchange (the ‘‘GEM Listing Rules’’) and by the Hong KongCompanies Ordinance.

RESPECTIVE RESPONSIBILITIES OF THE DIRECTORS AND REPORTING ACCOUNTANTS

The directors of API are responsible for the preparation of the Financial Information that gives atrue and fair view in accordance with HKFRSs issued by the HKICPA, the applicable disclosureprovisions of the GEM Listing Rules and the Hong Kong Companies Ordinance, and for such internalcontrol as the directors of API determine is necessary to enable the preparation of the FinancialInformation that is free from material misstatement, whether due to fraud or error.

Our responsibility is to form an independent opinion on the Financial Information based on ourprocedures and to report our opinion thereon to you.

BASIS OF OPINION

As a basis for forming an opinion on the Financial Information, for the purpose of this report, wehave examined the Underlying Financial Statements and have carried out such appropriate procedures aswe considered necessary in accordance with Auditing Guideline 3.340 ‘‘Prospectuses and the ReportingAccountant’’ issued by the HKICPA.

We have not audited any financial statements of API in respect of any period subsequent to 31December 2015.

OPINION

In our opinion, for the purpose of this report, the Financial Information gives a true and fair viewof the financial position of API as at 31 March 2014 and 2015 and 31 December 2015, and of thefinancial performance and cash flows of API for the Track Record Period.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 2

CORRESPONDING FINANCIAL INFORMATION

The comparative statement of profit or loss and other comprehensive income, statement of changesin equity and statement of cash flows of API for the nine months ended 31 December 2014 togetherwith the notes thereon (the ‘‘December 2014 Financial Information’’) have been extracted from API’sunaudited financial statements for the same period, which was prepared by the directors of API solelyfor the purpose of this report. We have reviewed the December 2014 Financial Information inaccordance with Hong Kong Standard on Review Engagements 2410 ‘‘Review of Interim FinancialInformation Performed by the Independent Auditor of the Entity’’ issued by the HKICPA. Ourresponsibility is to express a conclusion on the December 2014 Financial Information based on ourreview.

Our review of the December 2014 Financial Information consists of making enquiries, primarily ofpersons responsible for financial and accounting matters, and applying analytical procedures and otherreview procedures. A review is substantially less in scope than an audit conducted in accordance withHong Kong Standards on Auditing and consequently does not enable us to obtain assurance that wewould become aware of all significant matters that might be identified in an audit. Accordingly, we donot express an audit opinion on the December 2014 Financial Information.

Based on our review, nothing has come to our attention that causes us to believe that theDecember 2014 Financial Information is not prepared, in all material aspects, in accordance with theaccounting policies consistent with those used in the preparation of the Financial Information whichconform with HKFRSs.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 3

A. FINANCIAL INFORMATION

STATEMENTS OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

Notes HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Revenue 7 5,494 9,886 7,645 11,228Cost of services (3,429) (5,283) (4,068) (5,143)

Gross profit 2,065 4,603 3,577 6,085Other income 9 – – – 1Selling and distribution expenses (657) (968) (605) (814)Administrative expenses (945) (1,575) (1,109) (1,556)

Profit before tax 463 2,060 1,863 3,716Income tax expense 10 – (298) (266) (617)

Profit and total comprehensiveincome attributableto the owners of API 11 463 1,762 1,597 3,099

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 4

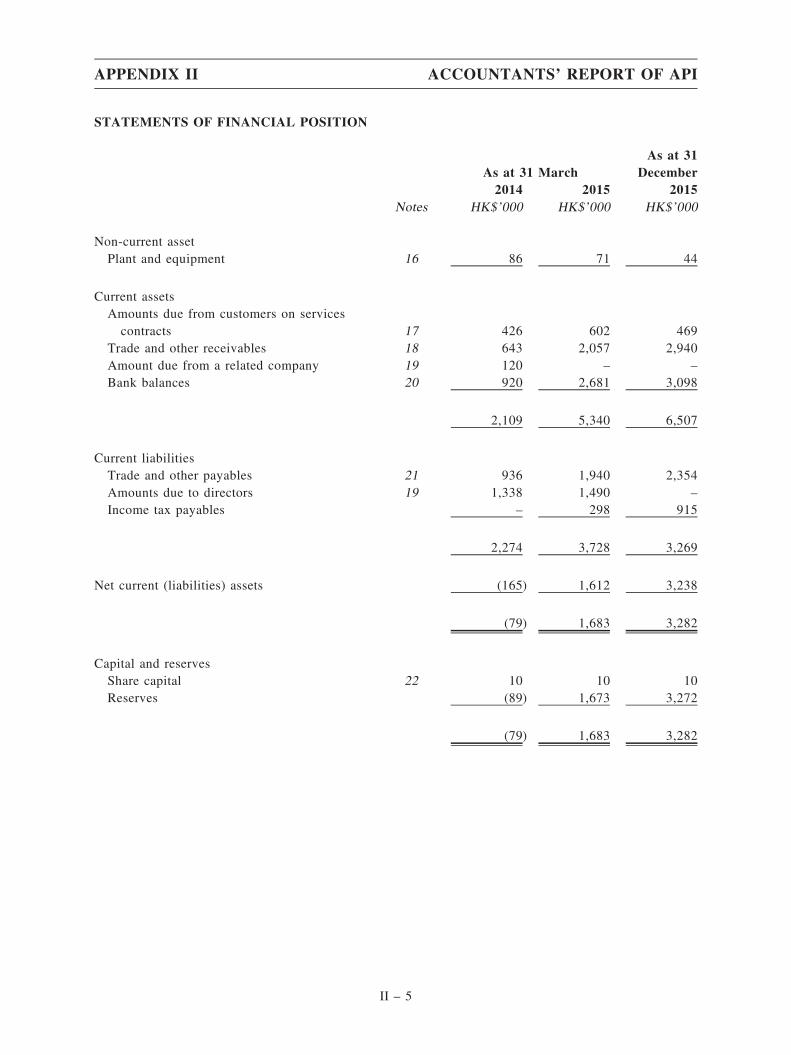

STATEMENTS OF FINANCIAL POSITION

As at 31 MarchAs at 31

December2014 2015 2015

Notes HK$’000 HK$’000 HK$’000

Non-current assetPlant and equipment 16 86 71 44

Current assetsAmounts due from customers on servicescontracts 17 426 602 469

Trade and other receivables 18 643 2,057 2,940Amount due from a related company 19 120 – –

Bank balances 20 920 2,681 3,098

2,109 5,340 6,507

Current liabilitiesTrade and other payables 21 936 1,940 2,354Amounts due to directors 19 1,338 1,490 –

Income tax payables – 298 915

2,274 3,728 3,269

Net current (liabilities) assets (165) 1,612 3,238

(79) 1,683 3,282

Capital and reservesShare capital 22 10 10 10Reserves (89) 1,673 3,272

(79) 1,683 3,282

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 5

STATEMENTS OF CHANGES IN EQUITY

Attributable to owners of API

Share capital

(Accumulatedlosses)

retainedprofits Total

HK$’000 HK$’000 HK$’000

At 1 April 2013 10 (552) (542)Profit and total comprehensive income for the year – 463 463

At 31 March 2014 and 1 April 2014 10 (89) (79)Profit and total comprehensive income for the year – 1,762 1,762

At 31 March 2015 and 1 April 2015 10 1,673 1,683

Profit and total comprehensive incomefor the period – 3,099 3,099

Dividend recognised as distribution (note 14) – (1,500) (1,500)

At 31 December 2015 10 3,272 3,282

At 1 April 2014 (Audited) 10 (89) (79)

Profit and total comprehensive incomefor the period – 1,597 1,597

At 31 December 2014 (Unaudited) 10 1,508 1,518

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 6

STATEMENTS OF CASH FLOWS

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

OPERATING ACTIVITIESProfit before tax 463 2,060 1,863 3,716Adjustments for:

Depreciation of plant and equipment 59 68 52 27Impairment loss of trade receivables – – – 360Bank interest income – – – (1)

Operating cash flows before movements inworking capital 522 2,128 1,915 4,102

(Increase) decrease in amounts due fromcustomers on service contracts (254) (176) (280) 133

Decrease (increase) in trade and otherreceivables 96 (1,414) (1,214) (1,243)

Increase in trade and other payables 395 1,004 1,157 414Increase in amount due to a related

company – – 100 –

NET CASH FROM OPERATINGACTIVITIES 759 1,542 1,678 3,406

INVESTING ACTIVITIESPurchase of plant and equipment (20) (53) (48) –

Bank interest income received – – – 1(Advance to) repayment from related

companies (107) 120 – –

NET CASH (USED IN) FROMINVESTING ACTIVITIES (127) 67 (48) 1

FINANCING ACTIVITIESRepayment to a related company (200) – – –

(Repayment to) advance from directors (395) 152 – (1,490)Dividend paid – – – (1,500)

NET CASH (USED IN) FROMFINANCING ACTIVITIES (595) 152 – (2,990)

NET INCREASE IN CASH AND CASHEQUIVALENTS 37 1,761 1,630 417

CASH AND CASH EQUIVALENTS ATBEGINNING OF THE YEAR/PERIOD 883 920 920 2,681

CASH AND CASH EQUIVALENTS ATEND OF THE YEAR/PERIOD,represented by bank balances 920 2,681 2,550 3,098

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 7

NOTES TO THE FINANCIAL INFORMATION

1. Corporate information

API was incorporated in Hong Kong with limited liability on 3 January 2012. The addresses of theregistered office and the principal place of business of API are stated in the ‘‘Corporate Information’’Section of the Prospectus. During the Track Record Period and before Reorganisation, API was held asto 50% by Brilliant Ray Global Limited (‘‘Brilliant Ray’’) (Incorporated in the British Virgin Islands(the ‘‘BVI’’)) and 50% by Majestic Praise Enterprise Limited (‘‘Majestic Praise’’) (incorporated in theBVI). Its parent is Maplehill Investments Limited (‘‘Maplehill’’) (incorporated in the BVI) and itsultimate parent is Brilliant Ray after Reorganisation.

API is engaged in the business of financial printing services.

The Financial Information is presented in HK$, which is the same as the functional currency ofAPI.

The Financial Information does not constitute API’s statutory annual financial statements for theyears ended 31 March 2014 and 2015. Further information relating to these statutory financialstatements required to be disclosed in accordance with section 436 of the Hong Kong CompaniesOrdinance is as follows:

As API is a private company, it is not required to deliver its financial statements to the Registrarof Companies, and has not done so.

API’s auditor has reported on these financial statements for all two years. The auditor’s report forthe year ended 31 March 2014 was unqualified; included a reference to which the auditor drew attentionby way of emphasis of matters in relation to going concern basis of API without qualifying its report butdid not contain a statement under sections 406(2), 407(2) or (3) of the Hong Kong CompaniesOrdinance. The auditor’s report for the year ended 31 March 2015 was unqualified; did not include areference to any matters to which the auditor drew attention by way of emphasis; and did not contain astatement under either sections 406(2), 407(2) or (3) of the Hong Kong Companies Ordinance.

2. Application of Hong Kong Financial Reporting Standards (‘‘HKFRSs’’)

For the purpose of preparing and presenting the Financial Information of the Track Record Periodand the nine months ended 31 December 2014, API has consistently adopted HKFRSs, the Hong KongAccounting Standards (‘‘HKASs’’), amendments and interpretations (‘‘Ints’’) issued by the HKICPAwhich are effective for API’s financial year beginning on 1 April 2015 throughout the Track RecordPeriod.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 8

At the date of this report, the HKICPA has issued the following new and revised HKFRSs,HKASs, amendments and Ints (hereinafter collectively referred to as ‘‘new and revised HKFRSs’’) whichare not yet effective. API has not early applied the following new and revised HKFRSs that have beenissued but are not yet effective:

HKFRS 9 (2014) Financial Instruments2

HKFRS 15 Revenue from Contracts with Customers2

Amendments to HKFRSs Annual Improvements to HKFRSs 2012 – 2014 Cycle1

Amendments to HKAS 1 Disclosure Initiative1

Amendments to HKAS 16 andHKAS 38

Clarification of Acceptable Methods of Depreciation andAmortisation1

Amendments to HKAS 16 andHKAS 41

Agriculture: Bearer Plants1

Amendments to HKAS 27 Equity Method in Separate Financial Statements1

Amendments to HKFRS 10 andHKAS 28

Sale or Contribution of Assets between an Investor and itsAssociate or Joint Venture3

Amendments to HKFRS 10,HKFRS 12 and HKAS 28

Investment Entities: Applying the Consolidation Exception1

Amendments to HKFRS 11 Accounting for Acquisitions of Interests in Joint Operations1

1 Effective for annual periods beginning on or after 1 January 2016.2 Effective for annual periods beginning on or after 1 January 2018.3 Effective date not yet been determined.

The directors of API anticipate that, except as described below, the application of the new andrevised HKFRSs will have no material impact on the results and the financial position of API.

HKFRS 9 (2014) Financial Instruments

HKFRS 9 issued in 2009 introduces new requirements for the classification and measurementof financial assets. HKFRS 9 was amended in 2010 and includes the requirements for theclassification and measurement of financial liabilities and for derecognition. In 2013, HKFRS 9was further amended to bring into effect a substantial overhaul of hedge accounting that will allowentities to better reflect their risk management activities in the financial statements. A finalisedversion of HKFRS 9 was issued in 2014 to incorporate all the requirements of HKFRS 9 that wereissued in previous years with limited amendments to the classification and measurement byintroducing a ‘‘fair value through other comprehensive income’’ (‘‘FVTOCI’’) measurementcategory for certain financial assets. The finalised version of HKFRS 9 also introduces an‘‘expected credit loss’’ model for impairment assessments.

Key requirements of HKFRS 9 (2014) are described below:

• All recognised financial assets that are within the scope of HKAS 39 FinancialInstruments: Recognition and Measurement to be subsequently measured at amortisedcost or fair value. Specifically, debt investments that are held within a business modelwhose objective is to collect the contractual cash flows, and that have contractual cashflows that are solely payments of principal and interest on the principal outstanding aregenerally measured at amortised cost at the end of subsequent accounting periods. Debtinstruments that are held within a business model whose objective is achieved both bycollecting contractual cash flows and selling financial assets, and that have contractual

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 9

terms of the financial asset give rise on specified dates to cash flows that are solelypayments of principal and interest on the principal amount outstanding, are measured atFVTOCI. All other debt investments and equity investments are measured at their fairvalues at the end of subsequent reporting periods. In addition, under HKFRS 9 (2014),entities may make an irrevocable election to present subsequent changes in the fairvalue of an equity investment (that is not held for trading) in other comprehensiveincome, with only dividend income generally recognised in profit or loss.

• With regard to the measurement of financial liabilities designated as at fair valuethrough profit or loss, HKFRS 9 (2014) requires that amount of change in the fair valueof the financial liability that is attributable to changes in the credit risk of that liabilityis presented in other comprehensive income, unless the recognition of the effects ofchanges in the liability’s credit risk in other comprehensive income would create orenlarge an accounting mismatch in profit or loss. Changes in fair value of financialliabilities attributable to changes in the financial liabilities’ credit risk are notsubsequently reclassified to profit or loss. Under HKAS 39, the entire amount of thechange in fair value of the financial liability designated as fair value through profit orloss was presented in profit or loss.

• In the aspect of impairment assessments, the impairment requirements relating to theaccounting for an entity’s expected credit losses on its financial assets and commitmentsto extend credit were added. Those requirements eliminate the threshold that was inHKAS 39 for the recognition of credit losses. Under the impairment approach inHKFRS 9 (2014), it is no longer necessary for a credit event to have occurred beforecredit losses are recognised. Instead, expected credit losses and changes in thoseexpected credit losses should always be accounted for. The amount of expected creditlosses is updated at each reporting date to reflect changes in credit risk since initialrecognition and, consequently, more timely information is provided about expectedcredit losses.

• HKFRS 9 (2014) introduces a new model which is more closely aligns hedgeaccounting with risk management activities undertaken by companies when hedgingtheir financial and non-financial risk exposures. As a principle-based approach, HKFRS9 (2014) looks at whether a risk component can be identified and measured and doesnot distinguish between financial items and non-financial items. The new model alsoenables an entity to use information produced internally for risk management purposesas a basis for hedge accounting. Under HKAS 39, it is necessary to exhibit eligibilityand compliance with the requirements in HKAS 39 using metrics that are designedsolely for accounting purposes. The new model also includes eligibility criteria butthese are based on an economic assessment of the strength of the hedging relationship.This can be determined using risk management data. This should reduce the costs ofimplementation compared with those for HKAS 39 hedge accounting because it reducesthe amount of analysis that is required to be undertaken only for accounting purposes.

HKFRS 9 (2014) will become effective for annual periods beginning on or after 1 January2018 with early application permitted.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 10

The directors of API anticipate that the adoption of HKFRS 9 (2014) in the future may havesignificant impact on the amounts reported in respect of API’s financial assets and financialliabilities. Regarding API’s financial assets and financial liabilities, it is not practicable to providea reasonable estimate of that effect until a detailed review has been completed.

HKFRS 15 Revenue from Contracts with Customers

The core principle of HKFRS 15 is that an entity should recognise revenue to depict thetransfer of promised goods or services to customers in an amount that reflects the consideration towhich the entity expects to be entitled in exchange for those goods or services. Thus, HKFRS 15introduces a model that applies to contracts with customers, featuring a contract-based five-stepanalysis of transactions to determine whether, how much and when revenue is recognised. The fivesteps are as follows:

i) Identify the contract with the customer;

ii) Identify the performance obligations in the contract;

iii) Determine the transaction price;

iv) Allocate the transaction price to the performance obligations; and

v) Recognise revenue when (or as) the entity satisfies a performance obligation.

HKFRS 15 also introduces extensive qualitative and quantitative disclosure requirementswhich aim to enable users of the financial statements to understand the nature, amount, timing anduncertainty of revenue and cash flows arising from contracts with customers.

HKFRS 15 will supersede the current revenue recognition guidance including HKAS 18Revenue, HKAS 11 Construction Contracts and the related Interpretations when it becomeseffective.

HKFRS 15 will become effective for annual periods beginning on or after 1 January 2018with early application permitted. The directors of API anticipate that the application of HKFRS 15in the future may have a material impact on the amounts reported and disclosures made in theAPI’s Financial Information. However, it is not practicable to provide a reasonable estimate of theeffect of HKFRS 15 until API performs a detailed review.

Amendments to HKAS 16 and HKAS 38 Clarification of Acceptable Methods of Depreciationand Amortisation

The amendments to HKAS 16 prohibit the use of revenue-based depreciation methods forproperty, plant and equipment under HKAS 16. The amendments to HKAS 38 introduce arebuttable presumption that the use of revenue-based amortisation methods for intangible assets isinappropriate.

This presumption can be rebutted only in the following limited circumstances:

i) when the intangible asset is expressed as a measure of revenue;

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 11

ii) when a high correlation between revenue and the consumption of the economic benefitsof the intangible assets could be demonstrated.

The amendments to HKAS 16 and HKAS 38 will become effective for financial statementswith annual periods beginning on or after 1 January 2016. Earlier application is permitted. Theamendments should be applied retrospectively.

As API uses straight-line method for depreciation of plant and equipment, the directors ofAPI do not anticipate that the application of the amendments to HKAS 16 and HKAS 38 will havea material impact on API’s Financial Information.

Amendments to HKAS 1 Disclosure Initiative

The amendments clarify that companies should use professional judgement in determiningwhat information as well as where and in what order information is presented in the financialstatements. Specifically, an entity should decide, taking into consideration all relevant facts andcircumstances, how it aggregates information in the financial statements, which include the notes.An entity does not require to provide a specific disclosure required by a HKFRS if the informationresulting from that disclosure is not material. This is the case even if the HKFRS contain a list ofspecific requirements or describe them as minimum requirements.

Besides, the amendments provide some additional requirements for presenting additional lineitems, headings and subtotals when their presentation is relevant to an understanding of the entity’sfinancial position and financial performance respectively. Entities, in which they have investmentsin associates or joint ventures, are required to present the share of other comprehensive income ofassociates and joint ventures accounted for using the equity method, separated into the share ofitems that (i) will not be reclassified subsequently to profit or loss; and (ii) will be reclassifiedsubsequently to profit or loss when specific conditions are met.

Furthermore, the amendments clarify that:

(i) an entity should consider the effect on the understandability and comparability of itsfinancial statements when determining the order of the notes; and

(ii) significant accounting policies are not required to be disclosed in one note, but insteadcan be included with related information in other notes.

The amendments will become effective for financial statements with annual periodsbeginning on or after 1 January 2016. Earlier application is permitted.

The directors of API anticipate that the application of Amendments to HKAS 1 in the futuremay have a material impact on the disclosures made in the API’s Financial Information.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 12

3. Significant accounting policies

The Financial Information has been prepared in accordance with HKFRSs issued by the HKICPA.In addition, the Financial Information includes applicable disclosures required by the GEM Listing Rulesand by the Hong Kong Companies Ordinance.

The Financial Information has been prepared on the historical cost basis. Historical cost isgenerally based on the fair value of the consideration given in exchange for goods and services.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in anorderly transaction between market participants in the principal (or most advantageous) market at themeasurement date under current market conditions (i.e. an exit price) regardless of whether that price isdirectly observable or estimated using another valuation technique. In estimating the fair value of anasset or a liability, API takes into account the characteristics of the asset or liability if marketparticipants would take those characteristics into account when pricing the asset or liability at themeasurement date. Fair value for measurement and/or disclosure purposes in these financial statements isdetermined on such a basis, except for share-based payment transactions that are within the scope ofHKFRS 2, leasing transactions that are within the scope of HKAS 17, and measurements that have somesimilarities to fair value but are not fair value, such as net realisable value in HKAS 2 or value in use inHKAS 36.

In addition, for financial reporting purposes, fair value measurements are categorised into Level 1,2 or 3 based on the degree to which the inputs to the fair value measurements are observable and thesignificance of the inputs to the fair value measurement in its entirety, which are described as follows:

• Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets orliabilities that the entity can access at the measurement date;

• Level 2 inputs are inputs, other than quoted prices included within Level 1, that areobservable for the asset or liability, either directly or indirectly; and

• Level 3 inputs are unobservable inputs for the asset or liability.

The principal accounting policies are set out below.

Plant and equipment

Plant and equipment are stated in the statements of financial position at cost less subsequentaccumulated depreciation and accumulated impairment losses, if any.

Depreciation is recognised so as to allocate the cost of items of plant and equipment lesstheir residual values over their estimated useful lives, using the straight-line method. The estimateduseful lives, residual values and depreciation method are reviewed at the end of each reportingperiod, with the effect of any changes in estimate accounted for on a prospective basis.

An item of plant and equipment is derecognised upon disposal or when no future economicbenefits are expected to arise from the continued use of the asset. Any gain or loss arising on thedisposal or retirement of an item of plant and equipment is determined as the difference betweenthe sales proceeds and the carrying amount of the asset and is recognised in profit or loss.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 13

Impairment on tangible assets

At the end of the reporting period, API reviews the carrying amounts of its tangible assetswith finite useful lives to determine whether there is any indication that those assets have sufferedan impairment loss. If any such indication exists, the recoverable amount of the asset is estimatedin order to determine the extent of the impairment loss, if any. When it is not possible to estimatethe recoverable amount of an individual asset, API estimates the recoverable amount of the cash-generating unit to which the asset belongs. Where a reasonable and consistent basis of allocationcan be identified, corporate assets are also allocated to individual cash-generating units, orotherwise they are allocated to the smallest group of cash-generating units for which a reasonableand consistent allocation basis can be identified.

Recoverable amount is the higher of fair value less costs of disposal and value in use. Inassessing value in use, the estimated future cash flows are discounted to their present value using apre-tax discount rate that reflects current market assessments of the time value of money and therisks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or a cash-generating unit) is estimated to be less thanits carrying amount, the carrying amount of the asset (or the cash-generating unit) is reduced to itsrecoverable amount. An impairment loss is recognised as expense immediately in profit or loss.

Where an impairment loss subsequently reverses, the carrying amount of the asset (or thecash-generating unit) is increased to the revised estimate of its recoverable amount, but so that theincreased carrying amount does not exceed the carrying amount that would have been determinedhad no impairment loss been recognised for the asset (or the cash-generating unit) in prior years. Areversal of an impairment loss is recognised as income immediately in profit or loss.

Cash and cash equivalents

Bank balances in the statements of financial position comprise cash at banks with a maturityof three months or less. For the purpose of the statements of cash flows, cash and cash equivalentsconsist of bank balances as defined above.

Financial instruments

Financial assets and financial liabilities are recognised in the statements of financial positionwhen the entity becomes a party to the contractual provisions of the instrument.

Financial assets and financial liabilities are initially measured at fair value. Transaction coststhat are directly attributable to the acquisition or issue of financial assets and financial liabilitiesare added to or deducted from the fair value of the financial assets or financial liabilities, asappropriate, on initial recognition.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 14

Financial assets

API’s financial assets are classified as loans and receivables. The classification depends onthe nature and purpose of the financial assets and is determined at the time of initial recognition.All regular way purchases or sales of financial assets are recognised and derecognised on a tradedate basis. Regular way purchases or sales are purchases or sales of financial assets that requiredelivery of assets within the time frame established by regulation or convention in the marketplace.

Effective interest method

The effective interest method is a method of calculating the amortised cost of a debtinstrument and of allocating interest income over the relevant period. The effective interest rate isthe rate that exactly discounts estimated future cash receipts (including all fees and points paid orreceived that form an integral part of the effective interest rate, transaction costs and otherpremiums or discounts) through the expected life of the debt instrument, or, where appropriate, ashorter period to the net carrying amount on initial recognition.

Interest income is recognised on an effective interest basis for debt instruments.

Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable paymentsthat are not quoted in an active market. Subsequent to initial recognition, loans and receivables(including trade and other receivables, amount due from a related company and bank balances) arecarried at amortised cost using the effective interest method, less any identified impairment losses(see accounting policy on impairment of financial assets below).

Impairment of financial assets

Financial assets are assessed for indicators of impairment at the end of each reporting period.Financial assets are considered to be impaired where there is objective evidence that, as a result ofone or more events that occurred after the initial recognition of the financial asset, the estimatedfuture cash flows of the financial assets have been affected.

Objective evidence of impairment could include:

• significant financial difficulty of the issuer or counterparty; or

• breach of contract, such as default or delinquency in interest or principal payments; or

• it becoming probable that the borrower will enter bankruptcy or financial re-organisation; or

• the disappearance of an active market for that financial asset because of financialdifficulties.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 15

For certain categories of financial assets, such as trade and other receivables, assets that areassessed not to be impaired individually are, in addition, assessed for impairment on a collectivebasis. Objective evidence of impairment for a portfolio of receivables could include API’s pastexperience of collecting payments, an increase in the number of delayed payments in the portfoliopast the average credit period of 30 days, observable changes in national or local economicconditions that correlate with default on receivables.

For financial assets carried at amortised cost, the amount of the impairment loss recognised isthe difference between the asset’s carrying amount and the present value of the estimated futurecash flows discounted at the financial asset’s original effective interest rate.

The carrying amount of the financial asset is reduced by the impairment loss directly for allfinancial assets with the exception of trade and other receivables, where the carrying amount isreduced through the use of an allowance account. Changes in the carrying amount of the allowanceaccount are recognised in profit or loss. When a trade or other receivable is considereduncollectible, it is written off against the allowance account. Subsequent recoveries of amountspreviously written off are credited to profit or loss.

For financial assets measured at amortised cost, if, in a subsequent period, the amount of theimpairment loss decreases and the decrease can be related objectively to an event occurring afterthe impairment loss was recognised, the previously recognised impairment loss is reversed throughprofit or loss to the extent that the carrying amount of the asset at the date the impairment isreversed does not exceed what the amortised cost would have been had the impairment not beenrecognised.

Financial liabilities and equity instruments

Debt and equity instruments issued by a group entity are classified as either financialliabilities or as equity in accordance with the substance of the contractual arrangements and thedefinitions of a financial liability and an equity instrument.

Equity instruments

An equity instrument is any contract that evidences a residual interest in the assets of anentity after deducting all of its liabilities. Equity instruments issued by API are recognised at theproceeds received, net of direct issue costs.

Other financial liabilities

Other financial liabilities including trade and other payables and amounts due to directors aresubsequently measured at the amortised cost, using the effective interest method.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 16

Effective interest method

The effective interest method is a method of calculating the amortised cost of a financialliability and of allocating interest expense over the relevant period. The effective interest rate isthe rate that exactly discounts estimated future cash payments (including all fees and points paid orreceived that form an integral part of the effective interest rate, transaction costs and otherpremiums or discounts) through the expected life of the financial liability, or, where appropriate, ashorter period, to the net carrying amount on initial recognition. Interest expense is recognised onan effective interest basis.

Derecognition

API derecognises a financial asset only when the contractual rights to the cash flows from theasset expire, or when it transfers the financial asset and substantially all the risks and rewards ofownership of the asset to another entity.

On derecognition of a financial asset in its entirety, the difference between the asset’scarrying amount and the sum of the consideration received and receivable and the cumulative gainor loss that had been recognised in other comprehensive income and accumulated in equity isrecognised in profit or loss.

API derecognises financial liabilities when, and only when, the API’s obligations aredischarged, cancelled or expired. The difference between the carrying amount of the financialliability derecognised and the consideration paid and payable is recognised in profit or loss.

Revenue recognition

Revenue from provision of financial printing services is recognised when i) the services areprovided and the transactions can be measured reliably, ii) it is probable that the economic benefitsassociated with the transaction will flow to the API and iii) the costs incurred or to be incurred inrespect of the transaction can be measured reliably. Revenue from service contract is recognisedbased on the stage of completion of the contracts as described in the accounting policy for servicecontracts below. The recognition of revenue on this basis provides information on the extent ofservice activities and performance at the end of the reporting period as considerable portion offinancial printing services are spanned for months and sometimes across different reportingperiods.

Interest income from a financial asset is recognised when it is probable that the economicbenefits will flow to API and the amount of income can be measured reliably. Interest income isaccrued on a time basis, by reference to the principal outstanding and at the effective interest rateapplicable, which is the rate that exactly discounts the estimated future cash receipts through theexpected life of the financial asset to that asset’s net carrying amount on initial recognition.

Services contracts

Where the outcome of a service contract can be estimated reliably and it is probable that thecontract will be profitable, service revenue is recognised over the period of the contract byreference to the stage of completion of service contract activity at the end of the reporting period.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 17

When the outcome of a service contract cannot be estimated reliably, service revenue isrecognised only to the extent of service costs incurred that are likely to be recoverable.

API uses the percentage of completion method to determine the appropriate amount ofrevenue and costs to be recognised in a given period. The stage of completion is measured byreference to work performed to date as a percentage of total estimated service cost of the contract.

API presents as an asset the gross amounts due from customers on services contracts for allservice contracts in progress for which service costs incurred plus recognised profits exceedprogress billings. Progress billings not yet paid by customers are included within trade receivables.

Foreign currencies

In preparing the financial statements of an entity, transactions in currencies other than thefunctional currency of that entity (foreign currencies) are recorded in the respective functionalcurrency (i.e. the currency of the primary economic environment in which the entity operates) atthe rates of exchanges prevailing at the dates of the transactions. At the end of the reportingperiod, monetary items denominated in foreign currencies are retranslated at the rates prevailing atthat date.

Exchange differences arising on the settlement of monetary items, and on the retranslation ofmonetary items, are recognised in profit or loss in the period in which they arise. Exchangedifferences arising on the retranslation of non-monetary items carried at fair value are included inprofit or loss for the period.

Retirement benefit costs

Payments to the Mandatory Provident Fund Scheme are recognised as an expense whenemployees have rendered service entitling them to the contributions.

Short-term employee benefits

A liability is recognised for benefits accruing to employees in respect of wages and salariesin the period the related service is rendered at the undiscounted amount of the benefits expected tobe paid in exchange for that service.

Liabilities recognised in respect of short-term employee benefits are measured at theundiscounted amount of the benefits expected to be paid in exchange for the related service.

Taxation

Income tax expense represents the sum of the tax currently payable.

The tax currently payable is based on taxable profit for the year/period. Taxable profit differsfrom ‘‘profit before tax’’ as reported in the statements of profit or loss and other comprehensiveincome because it excludes items of income or expense that are taxable or deductible in otheryears and it further excludes items that are never taxable or deductible. API’s liability for currenttax is calculated using tax rates that have been enacted or substantively enacted by the end of thereporting period.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 18

Current tax is recognised in profit or loss, except when it relate to items that are recognisedin other comprehensive income or directly in equity, in which case, the current tax is alsorecognised in other comprehensive income or directly in equity respectively.

4. Key sources of estimation uncertainty

In the application of API’s accounting policies, which are described in note 3, the directors of APIare required to make judgements, estimates and assumptions about the carrying amounts of assets andliabilities that are not readily apparent from other sources. The estimates and associated assumptions arebased on historical experience and other factors that are considered to be relevant. Actual results maydiffer from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions toaccounting estimates are recognised in the period in which the estimate is revised if the revision affectsonly that period, or in the period of the revision and future periods if the revision affects both currentand future periods.

The followings are the key assumptions concerning the future, and other key sources of estimationuncertainty at the end of the reporting period, that have a significant risk of causing a materialadjustment to the carrying amounts of assets and liabilities within the next financial year.

Revenue recognition

API recognises contract revenue and profit of a service contract in relation to provision offinancial printing services according to the management’s estimation of the total outcome of thecontract as well as the percentage of completion of the service contract. Notwithstanding that themanagement reviews and revises the estimates of both contract revenue and costs for the servicecontract as the contract progresses, the actual outcome of the contract in terms of its total revenueand costs may be higher or lower than the estimates and this will affect the revenue and profitrecognised.

Useful lives of plant and equipment

In applying the accounting policy on plant and equipment with respect to depreciation,management estimates the useful lives of various categories of plant and equipment according tothe industrial experiences over the usage of plant and equipment and also by reference to therelevant industrial norm. If the actual useful lives of plant and equipment is less than the originalestimated useful lives due to changes in commercial and technological environment, suchdifference will impact the depreciation charge for the remaining period. As at 31 March 2014 and2015 and 31 December 2015, the carrying amounts of plant and equipment were approximatelyHK$86,000, HK$71,000 and HK$44,000 respectively.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 19

Impairment of trade receivables

The policy for making impairment loss on trade receivables of API is based on the evaluationof collectability and ageing analysis of accounts and on management’s judgement. A considerableamount of judgement is required in assessing the ultimate realisation of these receivables,including the current creditworthiness and the past collection history of each debtor. If thefinancial conditions of debtors of API were to deteriorate, resulting in an impairment of theirability to make payments, additional impairment loss may be required. As at 31 March 2014 and2015 and 31 December 2015, the carrying amounts of the trade receivables were approximatelyHK$591,000, HK$2,005,000 and HK$2,888,000 respectively, net of accumulated impairment lossof nil, nil and approximately HK$360,000 respectively. API recognised impairment loss ofapproximately HK$360,000 for the nine months ended 31 December 2015.

5. Capital risk management

API manages its capital to ensure that API will be able to continue as a going concern whilemaximising the return to shareholders through the optimisation of the debt and equity balances. API’soverall strategy remains unchanged during the Track Record Period.

The capital structure of API consists of bank balances and equity attributable to owners of API,comprising issued share capital and reserves.

The directors of API regularly review and manage API’s capital structure. As part of this review,the directors of API consider the cost of capital and risks associated with each class of capital. Based onrecommendations of the directors of API, API will balance its overall capital structure through thepayment of dividends and new share issue.

6. Financial instruments

a) Categories of financial instruments

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Financial assetsLoans and receivables (including bankbalances) 1,631 4,686 5,986

Other financial liabilitiesAt amortised cost 2,015 2,728 1,518

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 20

b) Financial risk management objectives and policies

API’s major financial instruments include trade and other receivables, amount due from arelated company, bank balances, trade and other payables and amount(s) due to directors. Detailsof the financial instruments are disclosed in respective notes. The risks associated with thesefinancial instruments include market risk (currency risk and interest rate risk), credit risk andliquidity risk. The policies on how to mitigate these risks are set out below. The managementmanages and monitors these exposures to ensure appropriate measures are implemented on a timelyand effective manner.

Currency risk

API mainly operated in their local jurisdiction with most of the transactions settled intheir functional currencies of the operations and did not have significant exposure to riskresulting from changes in foreign currency exchange rates. API currently does not have aforeign currency hedging policy. However, the management monitors foreign exchangeexposure and will consider hedging significant foreign currency exposure should the needarise.

The directors of API consider that the currency risk in response to the changes inexchange rate is insignificant, sensitivity analysis on currency risk is not presented.

Interest rate risk

API’s income and operating cash flows are substantially independent of changes inmarket interest rates, as API has no significant interest-bearing assets and liabilities.

Credit risk

As at the end of each reporting period, API’s maximum exposure to credit risk whichwill cause a financial loss to API due to failure to discharge an obligation by thecounterparties is arising from the carrying amount of the respective recognised financialassets as stated in the statements of financial position.

In order to minimise the credit risk, the management of API has delegated a teamresponsible for determination of credit limits, credit approvals and other monitoringprocedures to ensure that follow-up action is taken to recover overdue debts. In addition,API reviews the recoverable amount of each individual trade debt at the end of the reportingperiod to ensure that adequate impairment losses are made for irrecoverable amounts. In thisregard, the directors of API consider that API’s credit risk is significantly reduced.

The credit quality of counterparty in respect of amount due from a related company isassessed by taking into account its financial position and other factors. The directors of APIare of the opinion that the risk of default by the counterparty is low.

The credit risk on liquid funds is limited because the counterparties are banks with highcredit ratings assigned by authorised credit-rating agencies.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 21

As at 31 March 2014 and 2015 and 31 December 2015, API has concentration of creditrisk as 57%, 19% and 40% of the total trade receivables was due from API’s five largestcustomers respectively.

Liquidity risk

In the management of the liquidity risk, API monitors and maintains a level of bankbalances deemed adequate by the management to finance API’s operations and mitigate theeffects of fluctuations in cash flows.

At 31 March 2014 and 2015 and 31 December 2015, API’s remaining maturity for itsfinancial liabilities is mainly within one year from the end of each reporting period. In theopinion of the directors of API, the carrying amounts of the financial liabilities are the sameas undiscounted cash flows based on the earliest date on which API can be required to payand therefore, no further analysis is presented in the Financial Information.

c) Fair value measurements recognised in the statements of financial position

The directors of API consider that the carrying amounts of financial assets and financialliabilities recorded at amortised cost in the Financial Information approximate their fair values dueto their immediate or short-term maturities.

7. Revenue

Revenue represents revenue arising from provision of financial printing services in Hong Kongduring the Track Record Period. An analysis of API’s revenue for the Track Record Period and the ninemonths ended 31 December 2014 is as follows:

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Debt offering circulars and initialpublic offering prospectuses 1,439 4,983 4,203 8,195

Results announcements and financialreports 1,098 1,512 999 1,150

Company announcements andshareholders circulars 518 1,429 1,148 663

Fund documents – – – 132Others 2,439 1,962 1,295 1,088

5,494 9,886 7,645 11,228

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 22

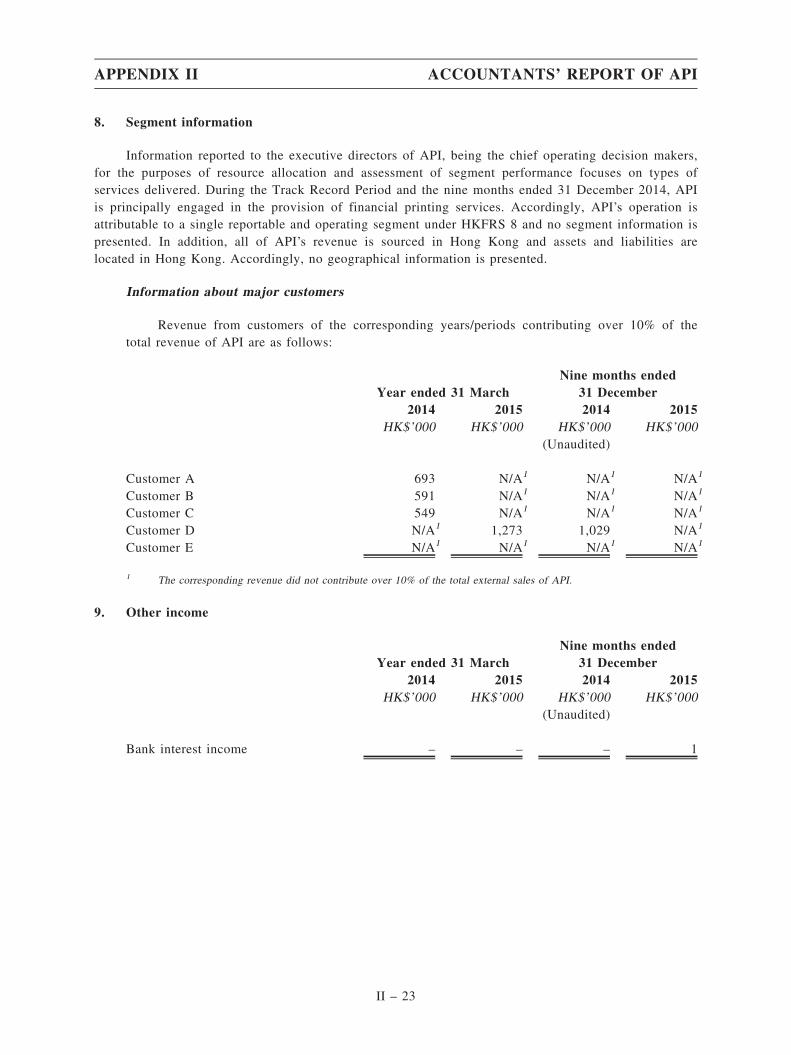

8. Segment information

Information reported to the executive directors of API, being the chief operating decision makers,for the purposes of resource allocation and assessment of segment performance focuses on types ofservices delivered. During the Track Record Period and the nine months ended 31 December 2014, APIis principally engaged in the provision of financial printing services. Accordingly, API’s operation isattributable to a single reportable and operating segment under HKFRS 8 and no segment information ispresented. In addition, all of API’s revenue is sourced in Hong Kong and assets and liabilities arelocated in Hong Kong. Accordingly, no geographical information is presented.

Information about major customers

Revenue from customers of the corresponding years/periods contributing over 10% of thetotal revenue of API are as follows:

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Customer A 693 N/A1 N/A1 N/A1

Customer B 591 N/A1 N/A1 N/A1

Customer C 549 N/A1 N/A1 N/A1

Customer D N/A1 1,273 1,029 N/A1

Customer E N/A1 N/A1 N/A1 N/A1

1 The corresponding revenue did not contribute over 10% of the total external sales of API.

9. Other income

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Bank interest income – – – 1

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 23

10. Income tax expense

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Current tax:Hong Kong Profits Tax – 298 266 617

Hong Kong Profits Tax is calculated at 16.5% on the estimated assessable profits during the TrackRecord Period and the nine months ended 31 December 2014.

No tax is payable on the profit for the year ended 31 March 2014 arising in Hong Kong since theassessable profit is wholly absorbed by tax losses brought forward. Tax losses carried forward for theyears ended 31 March 2014 and 2015 and the nine months ended 31 December 2014 and 2015 amountto approximately HK$275,000, nil, nil and nil respectively.

The income tax expense for the Track Record Period and the nine months ended 31 December2014 can be reconciled to the profit before tax per the statements of profit or loss and othercomprehensive income as follows:

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Profit before tax 463 2,060 1,863 3,716

Tax calculated at tax rate of 16.5% 76 340 308 613Tax effect of expenses not deductiblefor tax purpose 6 3 3 4

Utilisation of tax losses previously notrecognised (82) (45) (45) –

Income tax expense – 298 266 617

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 24

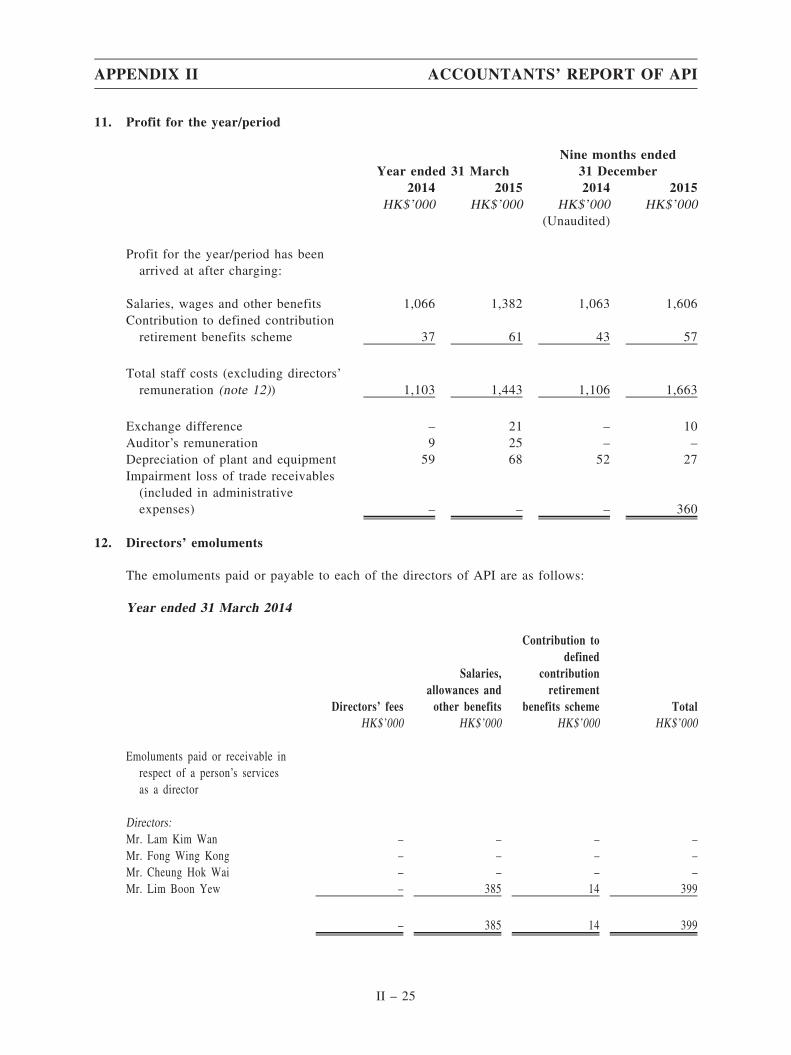

11. Profit for the year/period

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Profit for the year/period has beenarrived at after charging:

Salaries, wages and other benefits 1,066 1,382 1,063 1,606Contribution to defined contributionretirement benefits scheme 37 61 43 57

Total staff costs (excluding directors’remuneration (note 12)) 1,103 1,443 1,106 1,663

Exchange difference – 21 – 10Auditor’s remuneration 9 25 – –

Depreciation of plant and equipment 59 68 52 27Impairment loss of trade receivables(included in administrativeexpenses) – – – 360

12. Directors’ emoluments

The emoluments paid or payable to each of the directors of API are as follows:

Year ended 31 March 2014

Directors’ fees

Salaries,allowances andother benefits

Contribution todefined

contributionretirement

benefits scheme TotalHK$’000 HK$’000 HK$’000 HK$’000

Emoluments paid or receivable inrespect of a person’s servicesas a director

Directors:Mr. Lam Kim Wan – – – –

Mr. Fong Wing Kong – – – –

Mr. Cheung Hok Wai – – – –

Mr. Lim Boon Yew – 385 14 399

– 385 14 399

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 25

Year ended 31 March 2015

Directors’ fees

Salaries,allowances andother benefits

Contribution todefined

contributionretirement

benefits scheme TotalHK$’000 HK$’000 HK$’000 HK$’000

Emoluments paid or receivable inrespect of a person’s servicesas a director

Directors:Mr. Lam Kim Wan – – – –

Mr. Fong Wing Kong – – – –

Mr. Cheung Hok Wai – – – –

Mr. Lim Boon Yew – 921 18 939

– 921 18 939

Nine months ended 31 December 2014 (Unaudited)

Directors’ fees

Salaries,allowances andother benefits

Contribution todefined

contributionretirement

benefits scheme TotalHK$’000 HK$’000 HK$’000 HK$’000

Emoluments paid or receivable inrespect of a person’s servicesas a director

Directors:Mr. Lam Kim Wan – – – –

Mr. Fong Wing Kong – – – –

Mr. Cheung Hok Wai – – – –

Mr. Lim Boon Yew – 663 13 676

– 663 13 676

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 26

Nine months ended 31 December 2015

Directors’ fees

Salaries,allowances andother benefits

Contribution todefined

contributionretirement

benefits scheme TotalHK$’000 HK$’000 HK$’000 HK$’000

Emoluments paid or receivable inrespect of a person’s servicesas a director

Directors:

Mr. Lam Kim Wan – – – –

Mr. Fong Wing Kong – – – –

Mr. Cheung Hok Wai – – – –

Mr. Lim Boon Yew – 774 14 788

– 774 14 788

No chief executive was appointed during the Track Record Period and the nine months ended 31December 2014.

No directors of API waived or agreed to waive any emolument paid by API during the TrackRecord Period and the nine months ended 31 December 2014. No emoluments were paid by API to thedirectors of API as an incentive payment for joining API or as compensation for loss of office duringthe Track Record Period and the nine months ended 31 December 2014.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 27

13. Employees’ emoluments

A director of API was one of the five highest paid individuals for the Track Record Period and thenine months ended 31 December 2014, details of whose remuneration is disclosed in note 12 above. Theemoluments of the remaining individuals for the Track Record Period and the nine months ended 31December 2014 were as follows:

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaduited)

Salaries, allowances, and otherbenefits 685 1,037 726 1,001

Contribution to defined contributionretirement benefits scheme 30 46 33 41

715 1,083 759 1,042

Their emoluments fell within the following bands:

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

Number ofindividuals

Number ofindividuals

Number ofindividuals

Number ofindividuals

(Unaduited)

Nil to HK$1,000,000 4 4 4 4

No emoluments have been paid to the five highest paid individuals as an inducement to join orupon joining API, or as compensation for loss of office during the Track Record Period and the ninemonths ended 31 December 2014.

14. Dividend

No dividend was paid or declared during the two years ended 31 March 2015.

In July 2015, an interim dividend of HK$150 per share amounting to HK$1,500,000 in aggregatewas declared by API to its then shareholders. The amount has been fully paid in August 2015.

15. Earnings per share

Earnings per share information is not presented as its inclusion, for the purpose of the FinancialInformation, is not considered meaningful with regard to the Reorganisation and the presentation of theresults for the Track Record Period and the nine months ended 31 December 2014.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 28

16. Plant and equipment

Leaseholdimprovements

Furniture andfixtures

Officeequipment Total

HK$’000 HK$’000 HK$’000 HK$’000

COSTAt 1 April 2013 68 32 81 181Additions – 1 19 20

At 31 March 2014 and1 April 2014 68 33 100 201

Additions – 27 26 53

At 31 March 2015, 1 April 2015and 31 December 2015 68 60 126 254

ACCUMULATEDDEPRECIATION

At 1 April 2013 24 8 24 56Charge for the year 23 8 28 59

At 31 March 2014 and1 April 2014 47 16 52 115

Charge for the year 21 13 34 68

At 31 March 2015 and 1 April2015 68 29 86 183

Charge for the period – 11 16 27

At 31 December 2015 68 40 102 210

CARRYING VALUESAt 31 March 2014 21 17 48 86

At 31 March 2015 – 31 40 71

At 31 December 2015 – 20 24 44

Depreciation is recognised so as to write off the cost of plant and equipment, using the straight-line method over their estimated useful lives and at the rates per annum as follows:

Leasehold improvements Over the term of the lease or 33.33%, whichever is the shorterFurniture and fixtures 25%Office equipment 33.33%

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 29

17. Amounts due from customers on services contracts

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Contract costs incurred plus attributable profit 426 602 469Progress billings to date – – –

Due from customers on services contracts 426 602 469

18. Trade and other receivables

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Trade receivables 591 2,005 3,248Allowance for impairment of trade receivables – – (360)

591 2,005 2,888Deposits 52 52 52

Trade and other receivables 643 2,057 2,940

API allows an average credit period of 30 days to its trade customers. API does not hold anycollateral over its trade and other receivables. The following is an aged analysis of trade receivables, netof allowance for doubtful debts, presented based on the invoice date, (or date of revenue recognition, ifearlier) at the end of the reporting period.

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Within 30 days 317 936 96631 to 60 days – 591 66061 to 90 days 152 158 716Over 90 days 122 320 546

Total 591 2,005 2,888

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 30

Included in the API’s trade receivables balance are debtors with aggregate carrying amount ofapproximately HK$274,000, HK$1,069,000 and HK$1,922,000 as at 31 March 2014 and 2015 and 31December 2015 respectively which are past due as at the reporting date for which API has not providedfor impairment loss as these balances were either subsequently settled or there has not been a significantchange in credit quality and the amounts are still considered recoverable.

Ageing of trade receivables presented based on due date is as follows:

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Neither past due nor impaired 317 936 966Past due but not impaired:Within 30 days – 591 66031 to 60 days 152 158 716Over 60 days 122 320 546

Total 591 2,005 2,888

The movement in allowance for impairment of trade receivables are as follows:

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

At the beginning of the year/period – – –

Impairment losses recognised – – 360

At the end of the year/period – – 360

Included in the allowance for impairment of trade receivables are individually impaired tradereceivables with an aggregate balance of approximately nil, nil and HK$360,000 as at 31 March 2014and 2015 and 31 December 2015 respectively based on the credit history of its customers, such asfinancial difficulties or default in payments, and current market conditions.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 31

19. Amount(s) due from/to a related company/directors

The amount(s) due from a related company/directors are unsecured, non-interest bearing andrepayable on demand.

Amount due from a related company:

Maximum amount outstanding

Year ended 31 March

Ninemonths

ended 31December As at 31 March

As at 31December

2014 2015 2015 2014 2015 2015HK$’000 HK$’000 HK$’000 HK$’000 HK$’000 HK$’000

Beta Group Limited(‘‘Beta’’) (formerlyknown as A.Plus GroupLimited) 120 120 – 120 – –

During the Track Record Period, Mr. Fong Wing Kong and Mr. Lam Kim Wan were shareholdersof Beta.

Amounts due to directors:

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Mr. Lam Kim Wan 372 372 –

Mr. Fong Wing Kong 373 373 –

Mr. Lim Boon Yew 593 745 –

1,338 1,490 –

20. Bank balances

Bank balances represented short-term deposits with a maturity of three months or less. At 31March 2014 and 2015 and 31 December 2015, bank balances carried at prevailing market rates of 0.01%per annum.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 32

21. Trade and other payables

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Trade payables 498 1,105 1,277Customer deposit 259 702 836Accrued bonus and commission 157 120 225Accruals 22 13 16

Trade and other payables 936 1,940 2,354

The following is an aged analysis of accounts payable presented based on invoice date at the endof the reporting period.

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Within 30 days 157 305 39131 to 60 days 77 123 19661 to 90 days 109 117 197Over 90 days 155 560 493

Trade payables 498 1,105 1,277

The average credit period granted is ranging from 30 to 60 days. API has financial riskmanagement in place to ensure that all payables are settled within the credit timeframe.

22. Share capital

As at 31 MarchAs at 31

December2014 2015 2015

HK$’000 HK$’000 HK$’000

Issued and fully paid:10,000 ordinary shares 10 10 10

Notes:

(i) Under the Hong Kong Companies Ordinance (Cap. 622), which commenced operation on 3 March 2014, the conceptof authorised share capital no longer exists.

(ii) In accordance with section 135 of the Hong Kong Companies Ordinance (Cap. 622), API’s shares no longer have apar or nominal value with effect from 3 March 2014. There is no impact on the number of shares in issue or the

relative entitlement of any of the members as a result of this transition.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 33

23. Retirement benefits plan

API operates a Mandatory Provident Fund Scheme for all qualifying employees in Hong Kong.The assets of the scheme are held separately from those of API, in funds under the control of trustees.API contributes 5% of the relevant payroll costs and up to maximum of HK$1,500 from 1 June 2014onwards (1 April 2013 to 31 May 2014: HK$1,250) for each employee to the scheme, to which the sameamount of contribution is matched by employees.

The only obligation of API with respect to the retirement benefit plans is to make the statutoryspecified contributions. During the two years ended 31 March 2015 and the nine months ended 31December 2014 and 2015, the total retirement benefits scheme contributions charged to the statements ofprofit or loss and other comprehensive income amounted to approximately HK$51,000, HK$79,000,HK$56,000 and HK$71,000 respectively.

24. Related party transactions

(a) Save as disclosed elsewhere in the Financial Information, during the Track Record Period andthe nine months ended 31 December 2014, API entered into transactions with related partiesas follows:

Year ended 31March

Nine months ended31 December

Related party Nature of transaction 2014 2015 2014 2015Notes HK$’000 HK$’000 HK$’000 HK$’000

Beta Management fee expense (i) 360 – – –

APF Management fee expense (ii) – 1,029 772 711

Certain directors of API are the beneficial shareholders and/or directors of the above entities.

Notes:

(i) During the year ended 31 March 2014, amount of approximately HK$360,000 representing the managementfee charged to API in relation to the management services provided by Beta. Such services were no longerprovided by Beta during the year ended 31 March 2015 and the nine months ended 31 December 2014 and2015.

(ii) During the year ended 31 March 2015 and the nine months ended 31 December 2014 and 2015, amount ofapproximately HK$1,029,000, HK$772,000 and HK$711,000 representing the management fee charged to APIin relation to the business operations and administrative services provided by APF respectively. During the

year ended 31 March 2014, the business operations and administrative services were provided at nilconsideration.

(iii) These transactions were carried out at the terms determined and agreed by API and relevant parties.

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 34

(b) Compensation to key management personnel

The remuneration of directors and other members of key management personnel during theTrack Record Period and the nine months ended 31 December 2014 was as follows:

Year ended 31 MarchNine months ended

31 December2014 2015 2014 2015

HK$’000 HK$’000 HK$’000 HK$’000(Unaudited)

Short-term benefits 385 921 663 774Post employment benefits 14 18 13 14

399 939 676 788

B. EVENTS AFTER THE REPORTING PERIOD

As part of the Reorganisation, on 23 March 2016, Brilliant Ray, which was owned as to 50% byMr. Lam Kim Wan and 50% by Mr. Fong Wing Kong, acquired 50% equity interest in API fromMajestic Praise, which was wholly-owned by Mr. Lim Boon Yew. The Company via Maplehillindirectly acquired the entire interest in API on the same day, and API became a wholly-ownedsubsidiary of Maplehill upon the completion of the Reorganisation. These acquisitions form part of theReorganisation and details of which are set out in the section headed ‘‘History, Reorganisation andGroup structure’’ of the Prospectus.

C. SUBSEQUENT FINANCIAL STATEMENTS

No audited financial statements of API have been prepared in respect of any period subsequent to31 December 2015.

Yours faithfully,

SHINEWING (HK) CPA LimitedCertified Public AccountantsTang Kwan LaiPractising Certificate Number: P05299Hong Kong

APPENDIX II ACCOUNTANTS’ REPORT OF API

II – 35