Embed Size (px)

Citation preview

Appendix 1: Materials used by Ms. Johnson and Mr. Gagnon

June 29-30, 2004 156 of 203

STRICTLY CONFIDENTIAL (FR) CLASS II FOMC

Material for the FOMC presentation on

U.S. External Adjustment

Karen Johnson and Joseph Gagnon Exhibits by James Chavez June 29, 2004

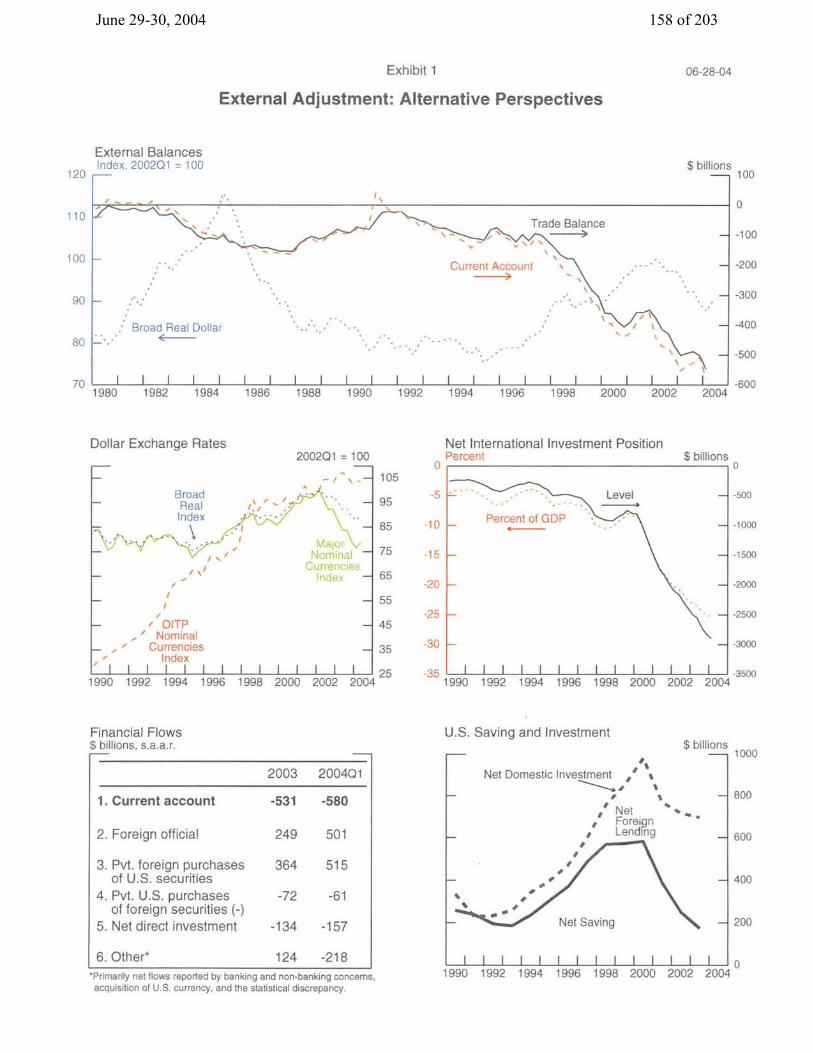

June 29-30, 2004 157 of 203

Exhibit 1

External Adjustment: Alternative Perspectives

External Balances Index, 200201 = 100

120 --

Current Account

, Broad Real Dollar

I I I I I I I I I I I I I I I I I1982 1984 1986 1988 1990 1992 1994

I I I I1996 1998 2000 2002

$ billions 100

0

-100

-200

-300

-400

-500

-600 2004

Dollar Exchange Rates 2002Q1 = 100

- ,. - 105

Broad , Real ,, 95 Index 5't ;.

S '7 - 85

S,/- 75

- 65

-- 55

/ OITP - 45 ,' Nominal

Currencies - 35 Index

I I I I l ll l I I I 25 1990 1992 1994 1996 1998 2000 2002 2004

Financial Flows $ billions, s.a.a.r.

2003 200401

1. Current account -531 -580

2. Foreign official 249 501

3. Pvt. foreign purchases 364 515 of U.S. securities

4. Pvt. U.S. purchases -72 -61 of foreign securities (-)

5. Net direct investment -134 -157

6.Other* 124 -218 *Primarily net flows reported by banking and non-banking concerns,

acquisition of U.S. currency, and the statistical discrepancy.

Net International Investment Position Percent

0

-5 Level Percent of GDP

-15

-20

-25

-30

-35I I I

U.S. Saving and Investment

$ billions

$ billions

Net Domestic Investment / s

, Net , , s Foreign

, Lending

Net Saving

-500

-1000

-1500

-2000

-2500

-3000

-3500

1000

800soo

600

400

200

I I I I I I I I I I I II I I 1990 1992 1994 1996 1998 2000 2002 2004

06-28-04

100

90

80 V

I

,, I

June 29-30, 2004 158 of 203

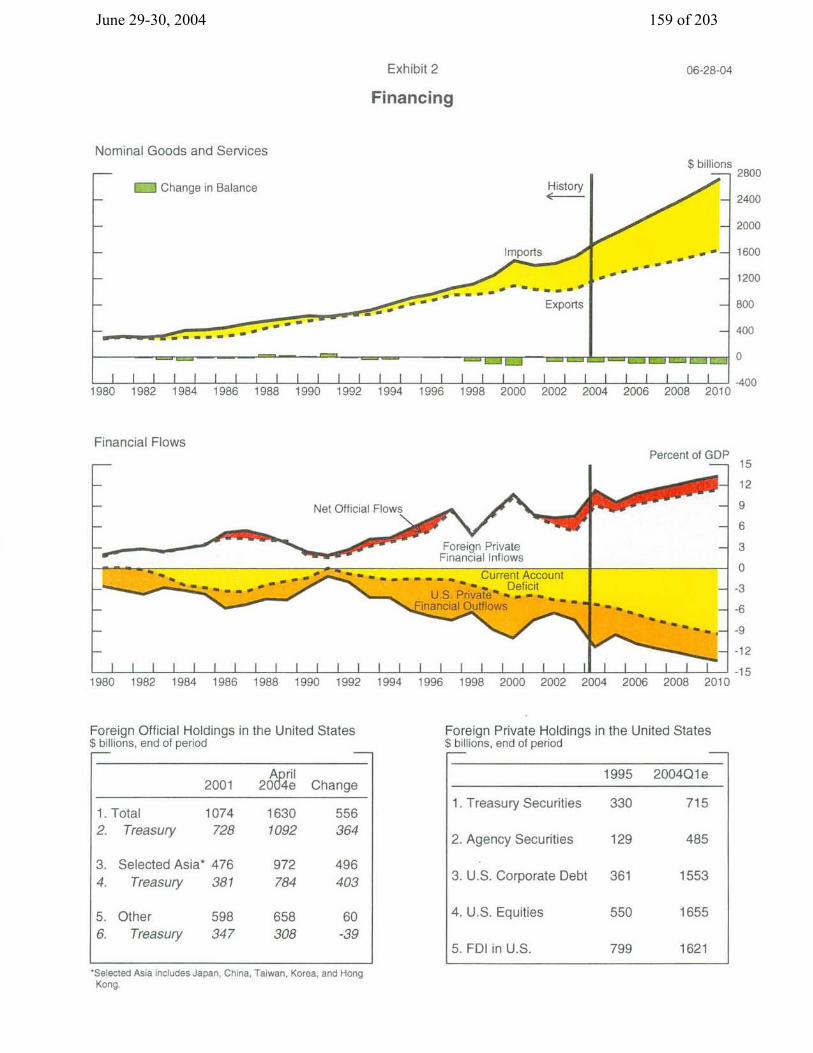

Exhibit 2

Financing

Nominal Goods and Services

K Change in Balance History 4-

Il__[1 111111 11 I11 l II I I Ill980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 20

Financial Flows

$ billions 2800

2400

2000

S, * - 1600

- 1200

800

400

04 ~ 200.8 0

I I I -400 04 2006 2008 2010

Percent of GDP

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Foreign Official Holdings in the United States $ billions, end of period

April 2001 2004e Change

1. Total 1074 1630 556 2. Treasury 728 1092 364

3. Selected Asia* 476 972 496 4. Treasury 381 784 403

5. Other 598 658 60 6. Treasury 347 308 -39

'Selected Asia includes Japan, China, Taiwan, Korea, and Hong Kong.

Foreign Private Holdings in the United States $ billions, end of period

1995 200401e

1. Treasury Securities 330 715

2. Agency Securities 129 485

3. U.S. Corporate Debt 361 1553

4. U.S. Equities 550 1655

5. FDI in U.S. 799 1621

06-28-04

- Imports

. "' _ . - .. Exports

- ;

June 29-30, 2004 159 of 203

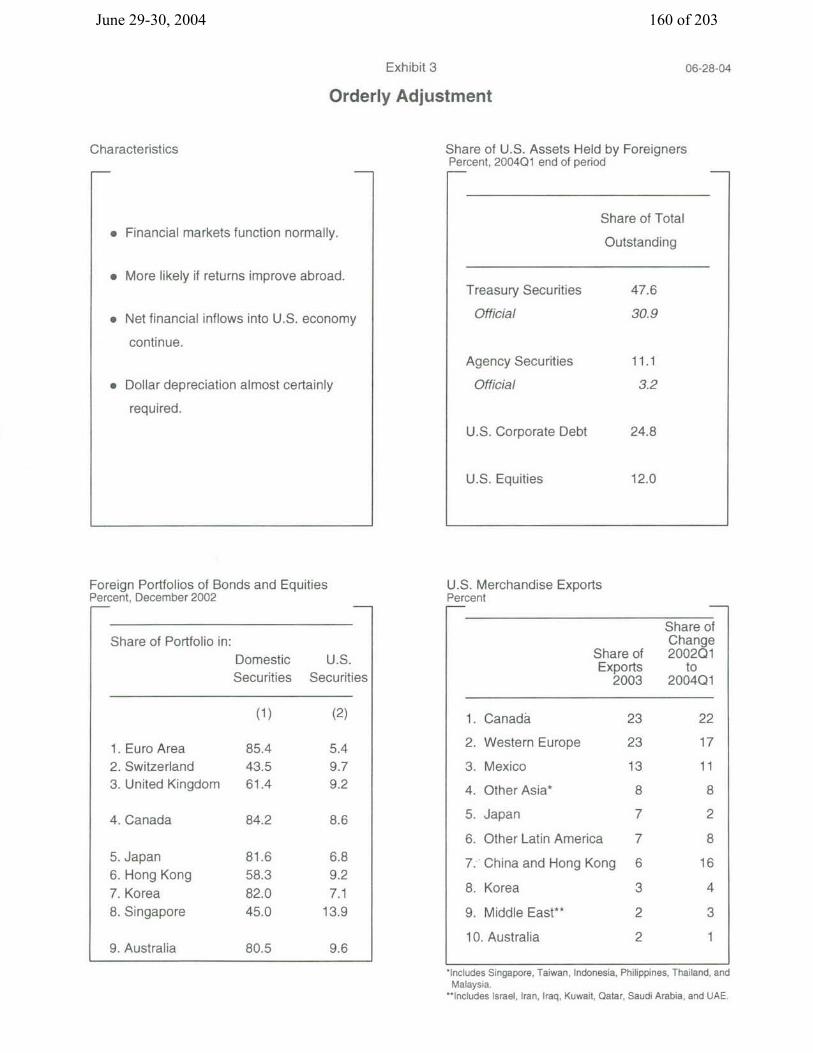

Exhibit 3

Orderly Adjustment

Characteristics

* Financial markets function normally.

* More likely if returns improve abroad.

* Net financial inflows into U.S. economy

continue.

* Dollar depreciation almost certainly

required.

Foreign Portfolios of Bonds and Equities Percent, December 2002

Share of Portfolio in: Domestic U.S. Securities Securities

(1) (2)

1. Euro Area 85.4 5.4 2. Switzerland 43.5 9.7 3. United Kingdom 61.4 9.2

4. Canada 84.2 8.6

5. Japan 81.6 6.8 6. Hong Kong 58.3 9.2 7. Korea 82.0 7.1 8. Singapore 45.0 13.9

9. Australia 80.5 9.6

Share of U.S. Assets Held by Foreigners Percent, 2004Q1 end of period

Share of Total

Outstanding

Treasury Securities 47.6

Official 30.9

Agency Securities 11.1

Official 3.2

U.S. Corporate Debt 24.8

U.S. Equities 12.0

U.S. Merchandise Exports Percent

Share of Change

Share of 200201 Exports to

2003 200401

*Includes Singapore, Taiwan, Indonesia, Philippines, Thailand, and Malaysia.

"Includes Israel, Iran, Iraq, Kuwait, Qatar, Saudi Arabia, and UAE.

06-28-04

1. Canada

2. Western Europe

3. Mexico

4. Other Asia*

5. Japan

6. Other Latin America

7. China and Hong Kong

8. Korea

9. Middle East**

10. Australia

June 29-30, 2004 160 of 203

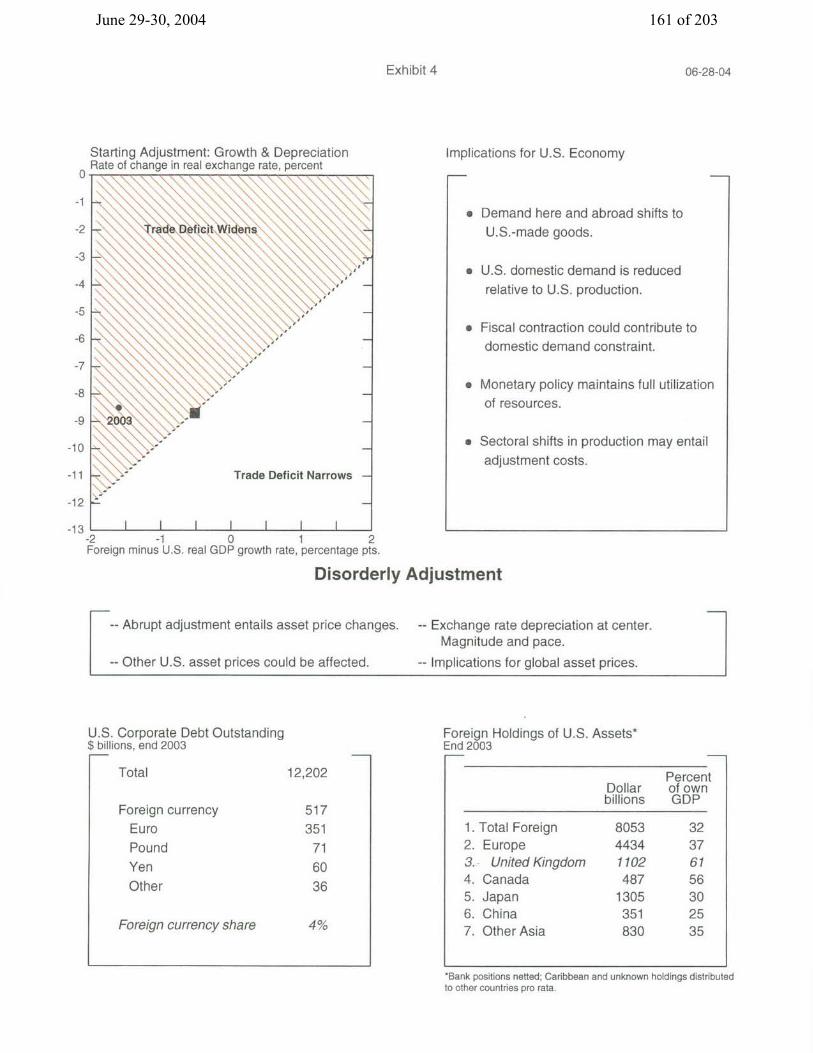

Exhibit 4

Starting Adjustment: Growth & Depreciation Rate of change in real exchange rate, percent

Implications for U.S. Economy

* Demand here and abroad shifts to U.S.-made goods.

* U.S. domestic demand is reduced relative to U.S. production.

* Fiscal contraction could contribute to domestic demand constraint.

* Monetary policy maintains full utilization of resources.

* Sectoral shifts in production may entail adjustment costs.

-2 -1 0 1 2 Foreign minus U.S. real GDP growth rate, percentage pts.

Disorderly Adjustment

-- Abrupt adjustment entails asset price changes.

-- Other U.S. asset prices could be affected.

-- Exchange rate depreciation at center. Magnitude and pace.

-- Implications for global asset prices.

U.S. Corporate Debt Outstanding $ billions, end 2003

K Total 12,202

Foreign currency Euro Pound

Yen

Other

Foreign currency share

Foreign Holdings of U.S. Assets* End 2003

Percent Dollar of own billions GDP

1. Total Foreign 8053 32 2. Europe 4434 37 3. United Kingdom 1102 61 4. Canada 487 56 5. Japan 1305 30 6. China 351 25 7. Other Asia 830 35

*Bank positions netted; Caribbean and unknown holdings distributed to other countries pro rata.

06-28-04

June 29-30, 2004 161 of 203

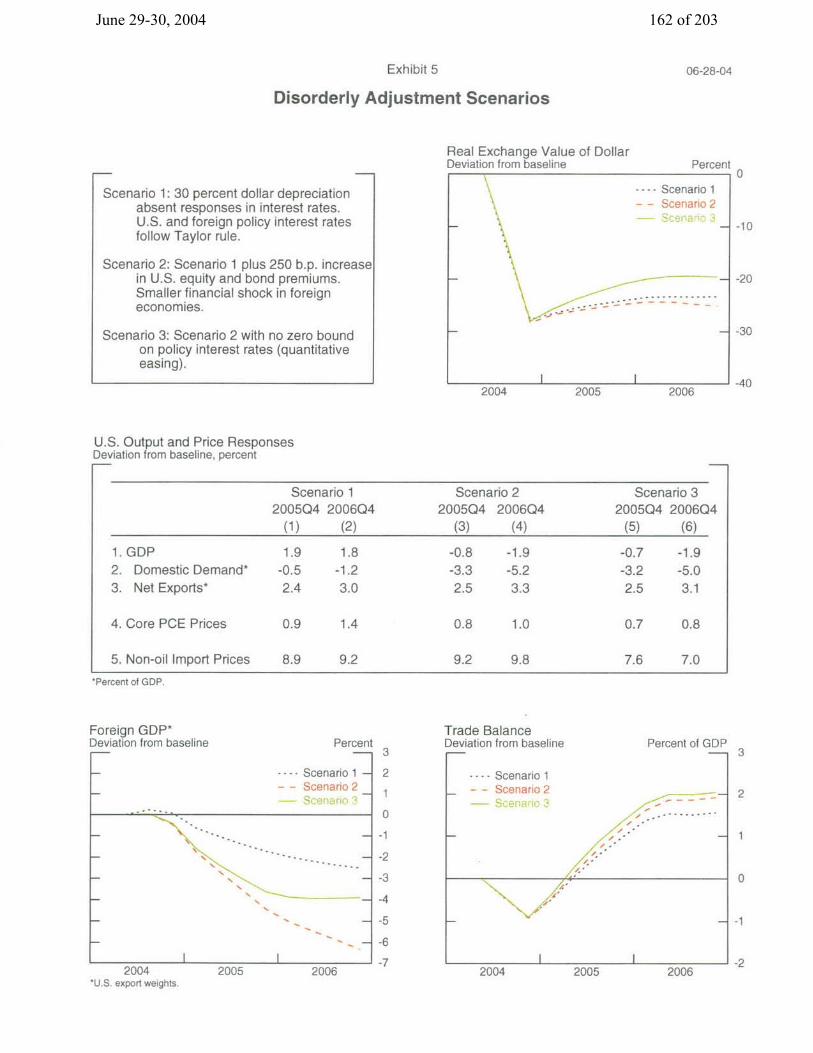

Exhibit 5

Disorderly Adjustment Scenarios

Scenario 1: 30 percent dollar depreciation absent responses in interest rates. U.S. and foreign policy interest rates follow Taylor rule.

Scenario 2: Scenario 1 plus 250 b.p. increase in U.S. equity and bond premiums. Smaller financial shock in foreign economies.

Scenario 3: Scenario 2 with no zero bound on policy interest rates (quantitative easing).

Real Exchange Value of Dollar Deviation from baseline

2004 2005

U.S. Output and Price Responses Deviation from baseline, percent

Scenario 1 200504 2006Q4 (1) (2)

Scenario 2 200504 2006Q4

(3) (4)

Scenario 3 2005Q4 2006Q4

(5) (6)

1. GDP 2. Domestic Demand* 3. Net Exports*

4. Core PCE Prices

5. Non-oil Import Prices

*Percent of GDP.

-1.9

-5.0

3.1

0.8 1.0

9.2 9.8 7.6 7.0

Foreign GDP* Deviation from baseline Percent

.... Scenario 1 - - Scenario 2

-- % --. _ N .

Nz

N . \'

\

Trade Balance Deviation from baseline

---- Scenario 1 - - Scenario 2

Percent of GDP

..

I

II

I 12004

*U.S. export weights.

06-28-04

Percent 0

- -.... Scenario 1 - - Scenario 2

.- -- -

-- -30

2006

2006

i

2005 2006 2004 2005

June 29-30, 2004 162 of 203

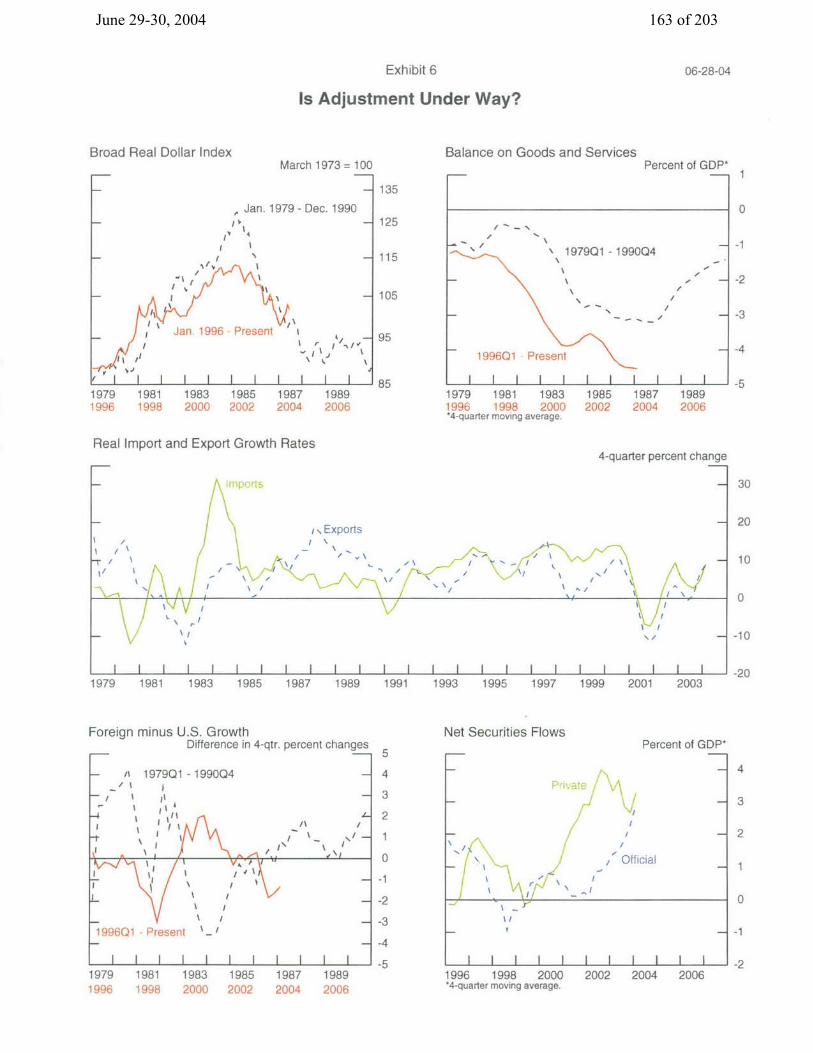

Exhibit 6

Is Adjustment Under Way?

Broad Real Dollar IndexMarch 1973 = 100

Balance on Goods and ServicesPercent of GDP*

-- 1

1979 1981 1983 1985 1987 1989 1996 1998 2000 2002 2004 2006

Real Import and Export Growth Rates

/ I ,

T \ / 1

- l \

//

- \ i

/ Exports

I\

' I _ ..

1979Q1-1990Q4

/ -- 2

199601 Present-4

1 I I t1 I I I -5 1979 1981 1983 1985 1987 1989 1996 1998 2000 2002 2004 2006 *4-quarter moving average.

4-quarter percent change

\I 'I.

N\ N

1

^ I 1

I

IIII I I I I I I I I I I I I

- r 1 1

1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1

1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

Foreign minus U.S. Growth Difference in 4-qtr.

Net Securities FlowsPercent of GDP*

1979 1981 1983 1985 1987 1989 1996 1998 2000 2002 2004 2006

, Official

,.

I ,I

I I I I I I I I I I I 1996 1998 2000 2002 2004 2006 *4-quarter moving average.

06-28-04

2003

June 29-30, 2004 163 of 203

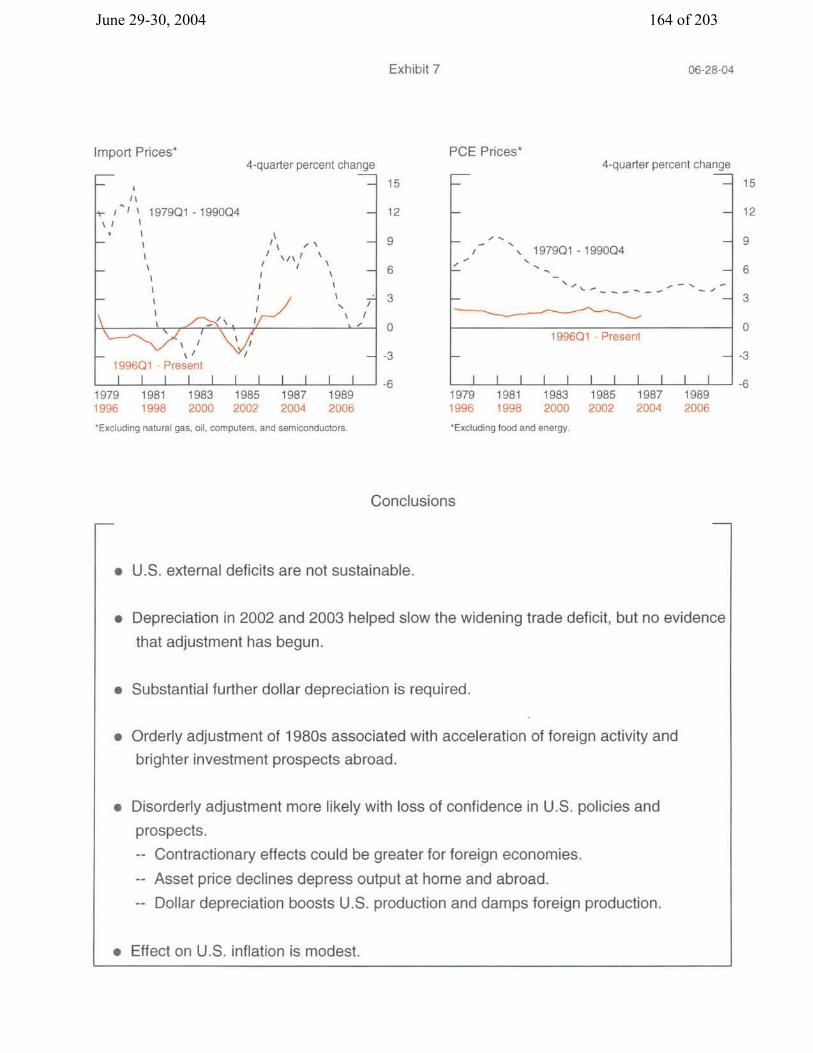

Exhibit 7

Import Prices*

it

I ' 1979(

- I _ \

1996Q1 Pr -1i i

4-quarter percent change

1 -1990Q4

/

t 1

/ /

esent I I I I I I I I

1979 1981 1983 1985 1987 1989 1996 1998 2000 2002 2004 2006

*Excluding natural gas, oil, computers, and semiconductors.

PCE Prices*4-quarter percent change

I/ \ 1979Q1 - 1990Q4

1996Q1 Present

I I I I I I 11979 1981 1983 1996 1998 2000

*Excluding food and energy.

1985 1987 1989 2002 2004 2006

Conclusions

* U.S. external deficits are not sustainable.

* Depreciation in 2002 and 2003 helped slow the widening trade deficit, but no evidence

that adjustment has begun.

* Substantial further dollar depreciation is required.

* Orderly adjustment of 1980s associated with acceleration of foreign activity and

brighter investment prospects abroad.

* Disorderly adjustment more likely with loss of confidence in U.S. policies and

prospects.

-- Contractionary effects could be greater for foreign economies.

-- Asset price declines depress output at home and abroad.

-- Dollar depreciation boosts U.S. production and damps foreign production.

* Effect on U.S. inflation is modest.

06-28-04

June 29-30, 2004 164 of 203

Appendix 2: Materials used by Ms. Goldberg

June 29-30, 2004 165 of 203

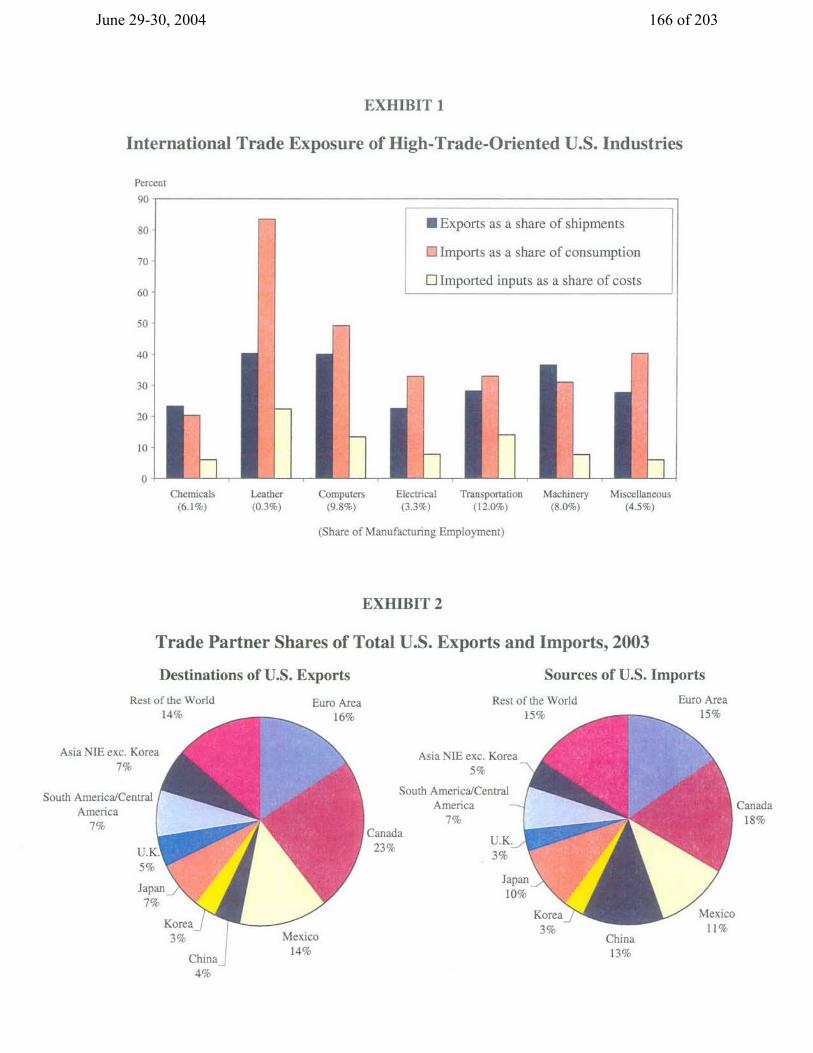

EXHIBIT 1

International Trade Exposure of High-Trade-Oriented U.S. Industries

Percent o0

Exports as a share of shipments

* Imports as a share of consumption

Q Imported inputs as a share of costs

Computers Electrical Transportation

(9.8%) (3.3%) (12.0%)

(Share of Manufacturing Employment)

Machinery (8.0%)

EXHIBIT 2

Trade Partner Shares of Total U.S. Exports and Imports, 2003

Destinations of U.S. Exports Sources of U.S. Imports

Rest of the World Euro Area Rest of the World Euro Area 14% ___ 16% 15% 15%

Asia NIE exc. Korea 7%

South America/Central America 7%

U.K . 5%

Japan 7%

Korea_ 3%

China) 4%

Canada 23%

Asia NIE exc. Korea 5%

South America/Central America

7%

U.K_ 3%

Japan 10%

Mexico 14%

Chemicals (6.1%)

Leather (0.3%)

Miscellaneous (4.5%)

Canada 18%

China 13%

June 29-30, 2004 166 of 203

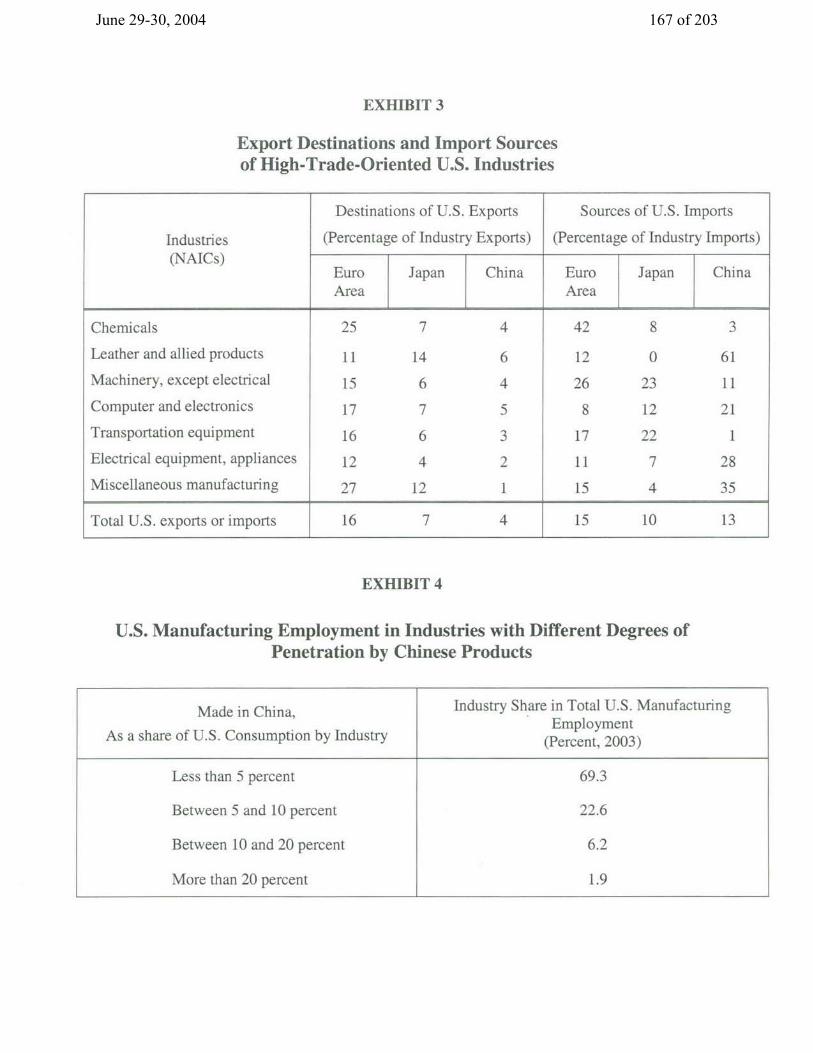

EXHIBIT 3

Export Destinations and Import Sources of High-Trade-Oriented U.S. Industries

Destinations of U.S. Exports Sources of U.S. Imports

Industries (Percentage of Industry Exports) (Percentage of Industry Imports) (NAICs)

Euro Japan China Euro Japan China Area Area

Chemicals 25 7 4 42 8 3

Leather and allied products 11 14 6 12 0 61

Machinery, except electrical 15 6 4 26 23 11

Computer and electronics 17 7 5 8 12 21

Transportation equipment 16 6 3 17 22 1

Electrical equipment, appliances 12 4 2 11 7 28

Miscellaneous manufacturing 27 12 1 15 4 35

Total U.S. exports or imports 16 7 4 15 10 13

EXHIBIT 4

U.S. Manufacturing Employment in Industries with Different Degrees of Penetration by Chinese Products

Made in China,

As a share of U.S. Consumption by Industry

Industry Share in Total U.S. Manufacturing Employment

(Percent, 2003)

Less than 5 percent 69.3

Between 5 and 10 percent 22.6

Between 10 and 20 percent 6.2

More than 20 percent 1.9

June 29-30, 2004 167 of 203

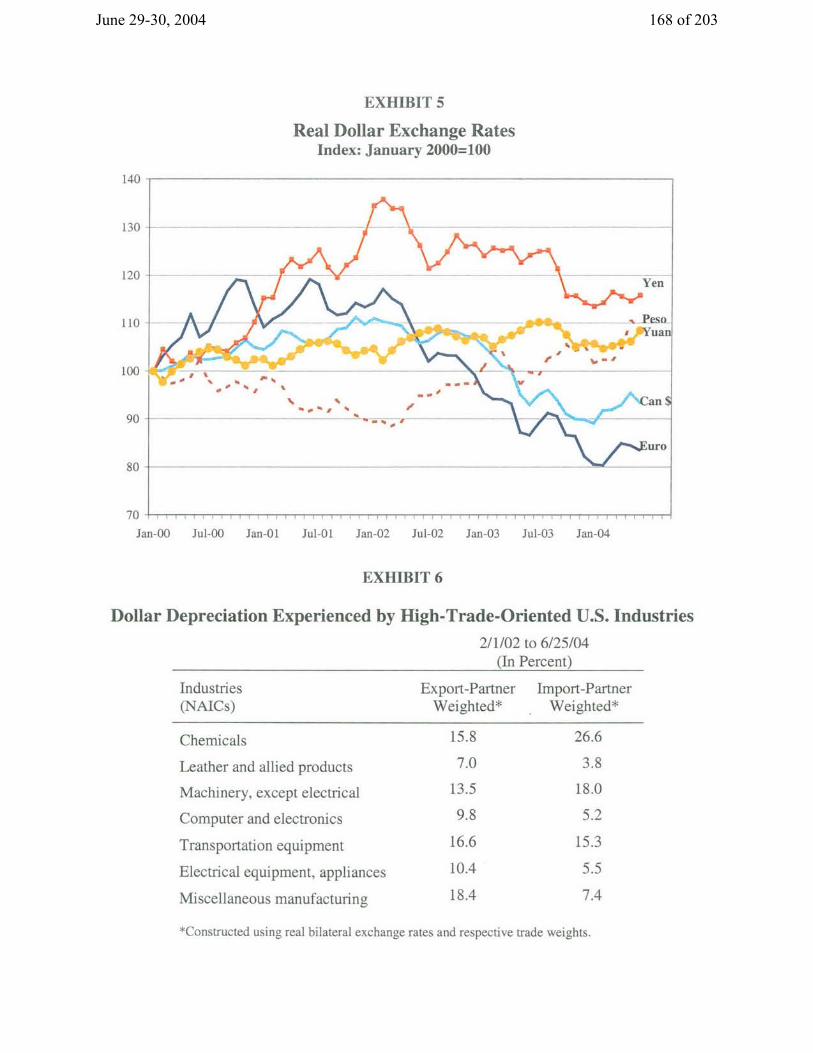

EXHIBIT 5

Real Dollar Exchange Rates Index: January 2000=100

140

130

120

110

100

90 -

80

Yen

_ _ Peso ' Yuan

'I.f

%-- ~-----

- ,_ I) I,

--~--I. i

70

Jan-00 Jul-00 Jan-01 Jul-01 Jan-02 Jul-02 Jan-03 Jul-03 Jan-04

EXHIBIT 6

Dollar Depreciation Experienced by High-Trade-Oriented U.S. Industries

2/1/02 to 6/25/04 (In Percent)

Industries Export-Partner Import-Partner (NAICs) Weighted* Weighted*

Chemicals

Leather and allied products

Machinery, except electrical

Computer and electronics

Transportation equipment

Electrical equipment, appliances

Miscellaneous manufacturing

15.8

7.0

13.5

9.8

16.6

10.4

18.4

26.6

3.8

18.0

5.2

15.3

5.5

7.4

*Constructed using real bilateral exchange rates and respective trade weights.

Can 9,,r

June 29-30, 2004 168 of 203

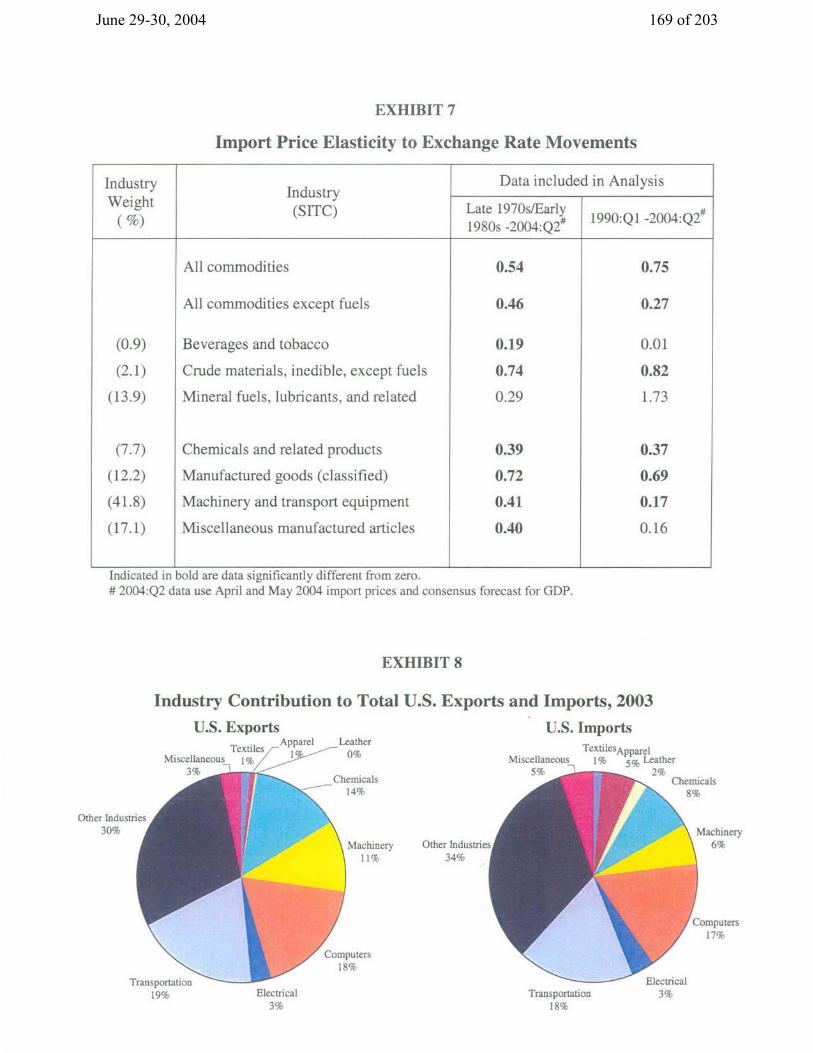

EXHIBIT 7

Import Price Elasticity to Exchange Rate Movements

Industry Data included in Analysis Industry

Weight (SITC) Late 1970s/Early # (%) 1980s -2004:Q2# 1990:Q1 -2004:Q2

All commodities 0.54 0.75

All commodities except fuels 0.46 0.27

(0.9) Beverages and tobacco 0.19 0.01

(2.1) Crude materials, inedible, except fuels 0.74 0.82

(13.9) Mineral fuels, lubricants, and related 0.29 1.73

(7.7) Chemicals and related products 0.39 0.37

(12.2) Manufactured goods (classified) 0.72 0.69

(41.8) Machinery and transport equipment 0.41 0.17

(17.1) Miscellaneous manufactured articles 0.40 0.16

Indicated in bold are data significantly different from zero. # 2004:Q2 data use April and May 2004 import prices and consensus forecast for GDP.

EXHIBIT 8

Industry Contribution to Total U.S. Exports and Imports, 2003

U.S. Exports U.S. Imports Apparel Leather

Textiles App Leather TextilesApparel Miscellaneous 1% Miscellaneous 1% 5% Leather

C m l59 h 2l Chemicals Chemicals 14% 14% 8%

Other Industries 30%

Machinery 11%

Other Industrie: 34%

Machinery 6%

Computers 17%

Computers 18%

Electrical 3%

Transportation 18%

Electrical 3%

June 29-30, 2004 169 of 203

Appendix 3: Materials used by Mr. Kos

June 29-30, 2004 170 of 203

1.00

1.50

2.00

2.50

3.00

3.50

3/15 3/30 4/14 4/29 5/14 5/29 6/13 6/281.00

1.50

2.00

2.50

3.00

3.50

180

190

200

210

220

230

240

3/15 3/30 4/14 4/29 5/14 5/29 6/13 6/28180

190

200

210

220

230

240

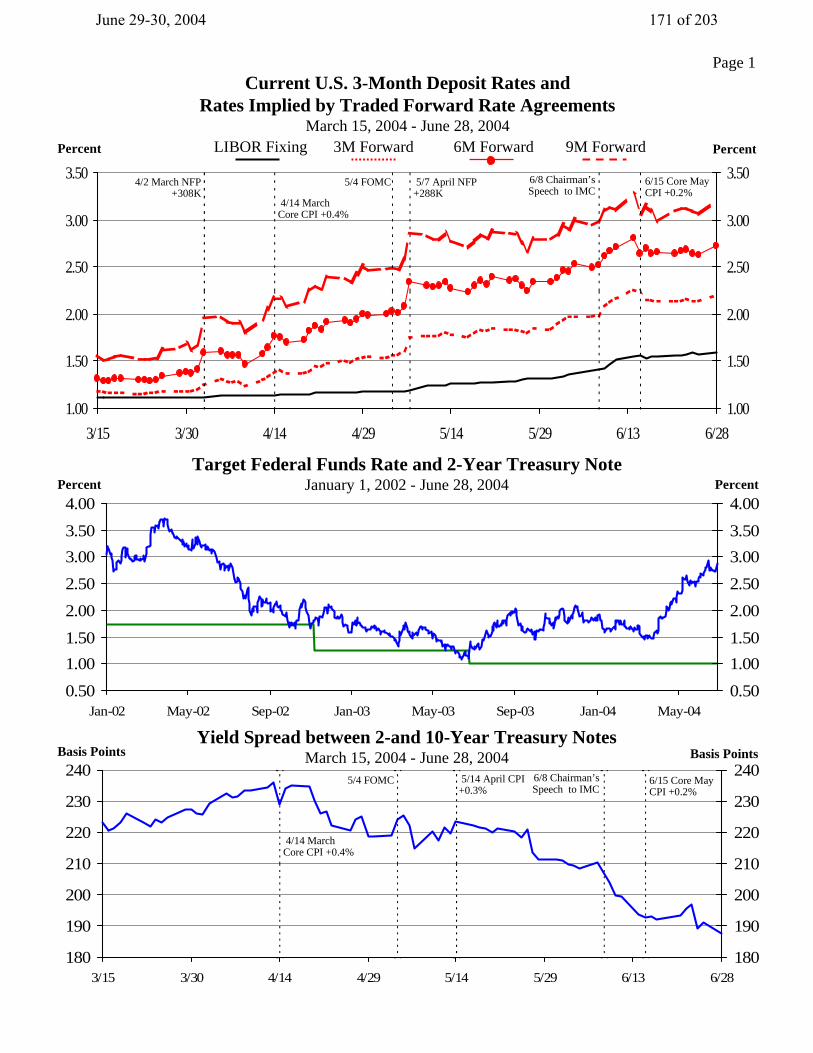

Page 1Current U.S. 3-Month Deposit Rates and

Rates Implied by Traded Forward Rate AgreementsMarch 15, 2004 - June 28, 2004

LIBOR Fixing 3M Forward 6M Forward 9M Forward PercentPercent

0.501.001.502.002.503.003.504.00

Jan-02 May-02 Sep-02 Jan-03 May-03 Sep-03 Jan-04 May-040.501.001.502.002.503.003.504.00

Target Federal Funds Rate and 2-Year Treasury NoteJanuary 1, 2002 - June 28, 2004Percent Percent

Yield Spread between 2-and 10-Year Treasury NotesMarch 15, 2004 - June 28, 2004Basis Points Basis Points

6/15 Core MayCPI +0.2%

6/8 Chairman’sSpeech to IMC

5/7 April NFP+288K

5/4 FOMC

4/14 MarchCore CPI +0.4%

4/2 March NFP+308K

6/15 Core MayCPI +0.2%

6/8 Chairman’sSpeech to IMC

5/14 April CPI+0.3%

5/4 FOMC

4/14 MarchCore CPI +0.4%

June 29-30, 2004 171 of 203

180

200

220

240

260

280

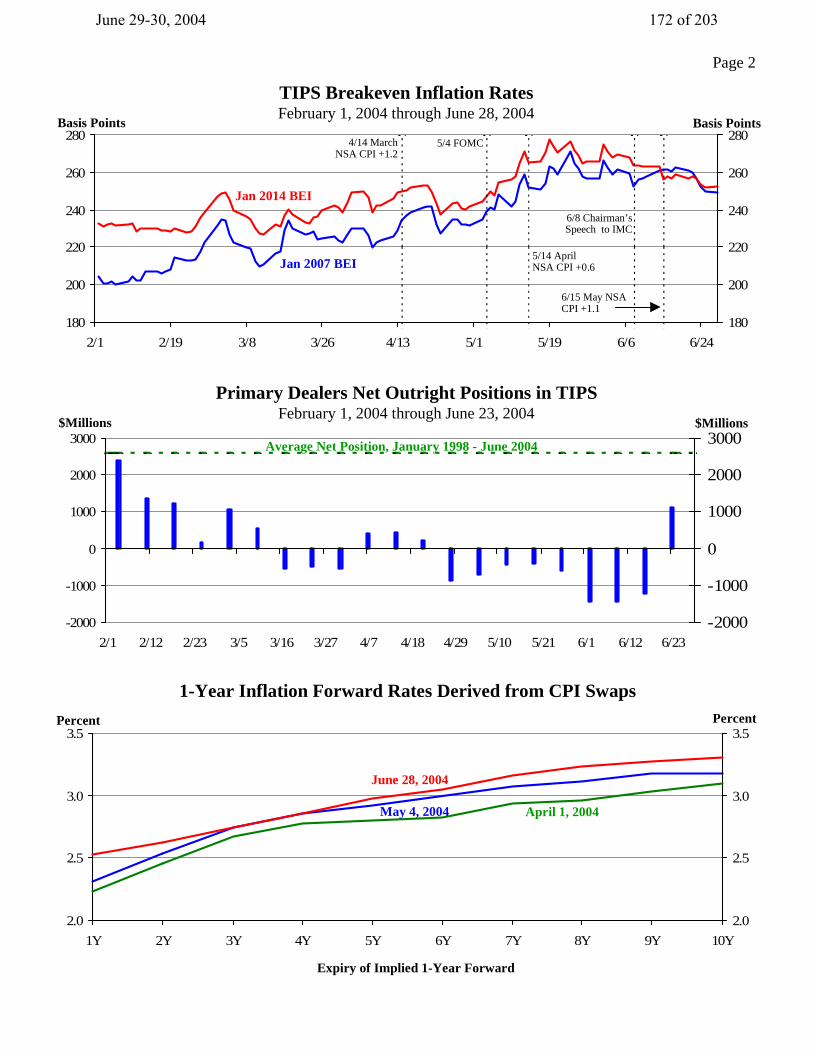

2/1 2/19 3/8 3/26 4/13 5/1 5/19 6/6 6/24180

200

220

240

260

280

TIPS Breakeven Inflation RatesFebruary 1, 2004 through June 28, 2004

-2000

-1000

0

1000

2000

3000

2/1 2/12 2/23 3/5 3/16 3/27 4/7 4/18 4/29 5/10 5/21 6/1 6/12 6/23-2000

-1000

0

1000

2000

3000

Primary Dealers Net Outright Positions in TIPSFebruary 1, 2004 through June 23, 2004

2.0

2.5

3.0

3.5

1Y 2Y 3Y 4Y 5Y 6Y 7Y 8Y 9Y 10Y2.0

2.5

3.0

3.5

1-Year Inflation Forward Rates Derived from CPI Swaps

Basis PointsBasis Points

$Millions$Millions

PercentPercent

Jan 2007 BEI

Jan 2014 BEI

May 4, 2004

June 28, 2004

6/15 May NSACPI +1.1

6/8 Chairman’sSpeech to IMC

5/14 AprilNSA CPI +0.6

5/4 FOMC 4/14 MarchNSA CPI +1.2

Average Net Position, January 1998 - June 2004

April 1, 2004

Page 2

Expiry of Implied 1-Year Forward

June 29-30, 2004 172 of 203

20

40

60

80

100

120

Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-0420

40

60

80

100

120

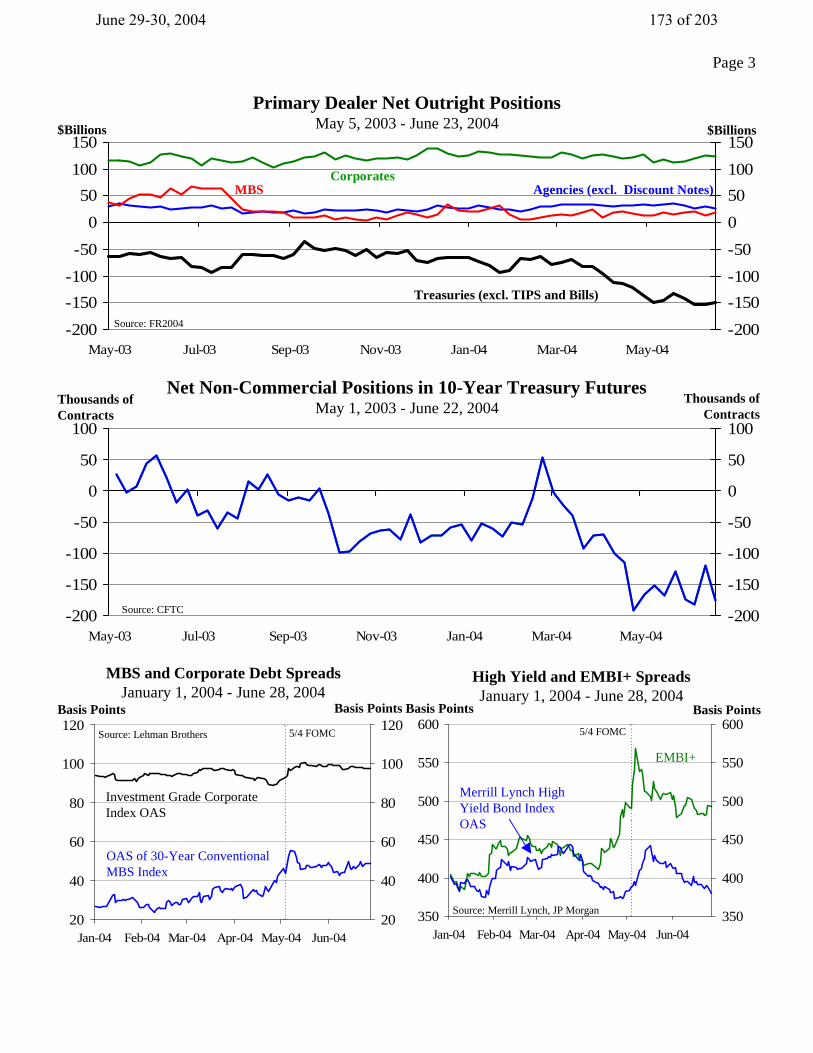

Page 3

350

400

450

500

550

600

Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04350

400

450

500

550

600Basis Points Basis PointsBasis Points

Source: Merrill Lynch, JP Morgan

Merrill Lynch HighYield Bond IndexOAS

EMBI+

High Yield and EMBI+ SpreadsJanuary 1, 2004 - June 28, 2004

MBS and Corporate Debt SpreadsJanuary 1, 2004 - June 28, 2004

Investment Grade CorporateIndex OAS

Basis Points

Source: Lehman Brothers

-200-150-100-50

050

100150

May-03 Jul-03 Sep-03 Nov-03 Jan-04 Mar-04 May-04-200-150-100-50050100150

Primary Dealer Net Outright PositionsMay 5, 2003 - June 23, 2004

-200

-150

-100

-50

0

50

100

May-03 Jul-03 Sep-03 Nov-03 Jan-04 Mar-04 May-04-200

-150

-100

-50

0

50

100

Net Non-Commercial Positions in 10-Year Treasury FuturesMay 1, 2003 - June 22, 2004

Source: FR2004

Treasuries (excl. TIPS and Bills)

CorporatesAgencies (excl. Discount Notes)MBS

$Billions$Billions

Thousands ofContracts

OAS of 30-Year ConventionalMBS Index

Thousands ofContracts

5/4 FOMC 5/4 FOMC

Source: CFTC

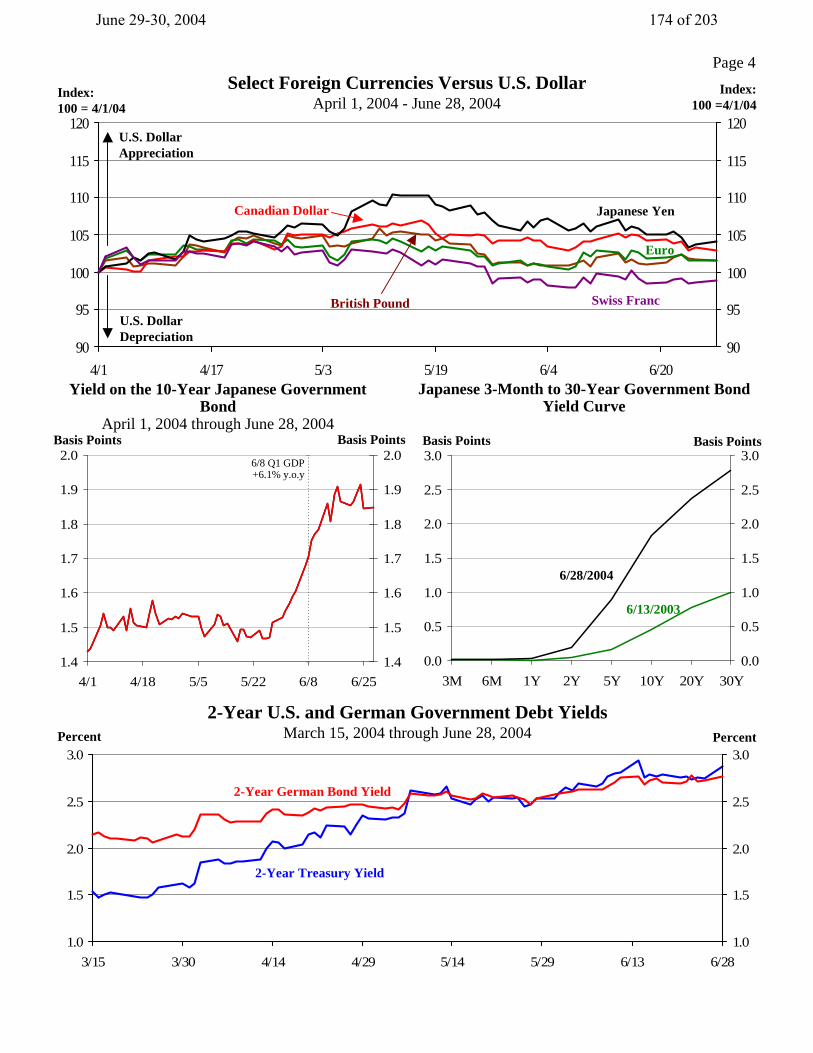

June 29-30, 2004 173 of 203

1.0

1.5

2.0

2.5

3.0

3/15 3/30 4/14 4/29 5/14 5/29 6/13 6/281.0

1.5

2.0

2.5

3.0

Page 4

Yield on the 10-Year Japanese GovernmentBond

April 1, 2004 through June 28, 2004

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3M 6M 1Y 2Y 5Y 10Y 20Y 30Y0.0

0.5

1.0

1.5

2.0

2.5

3.0

1.4

1.5

1.6

1.7

1.8

1.9

2.0

4/1 4/18 5/5 5/22 6/8 6/251.4

1.5

1.6

1.7

1.8

1.9

2.0

6/28/2004

6/13/2003

Basis PointsBasis PointsBasis PointsBasis Points

2-Year U.S. and German Government Debt YieldsMarch 15, 2004 through June 28, 2004

2-Year Treasury Yield

2-Year German Bond Yield

PercentPercent

Japanese 3-Month to 30-Year Government BondYield Curve

6/8 Q1 GDP+6.1% y.o.y

Select Foreign Currencies Versus U.S. DollarApril 1, 2004 - June 28, 2004

90

95

100

105

110

115

120

4/1 4/17 5/3 5/19 6/4 6/2090

95

100

105

110

115

120

Euro

British Pound

U.S. DollarAppreciation

U.S. DollarDepreciation

Canadian Dollar Japanese Yen

Swiss Franc

Index:100 =4/1/04

Index:100 = 4/1/04

June 29-30, 2004 174 of 203

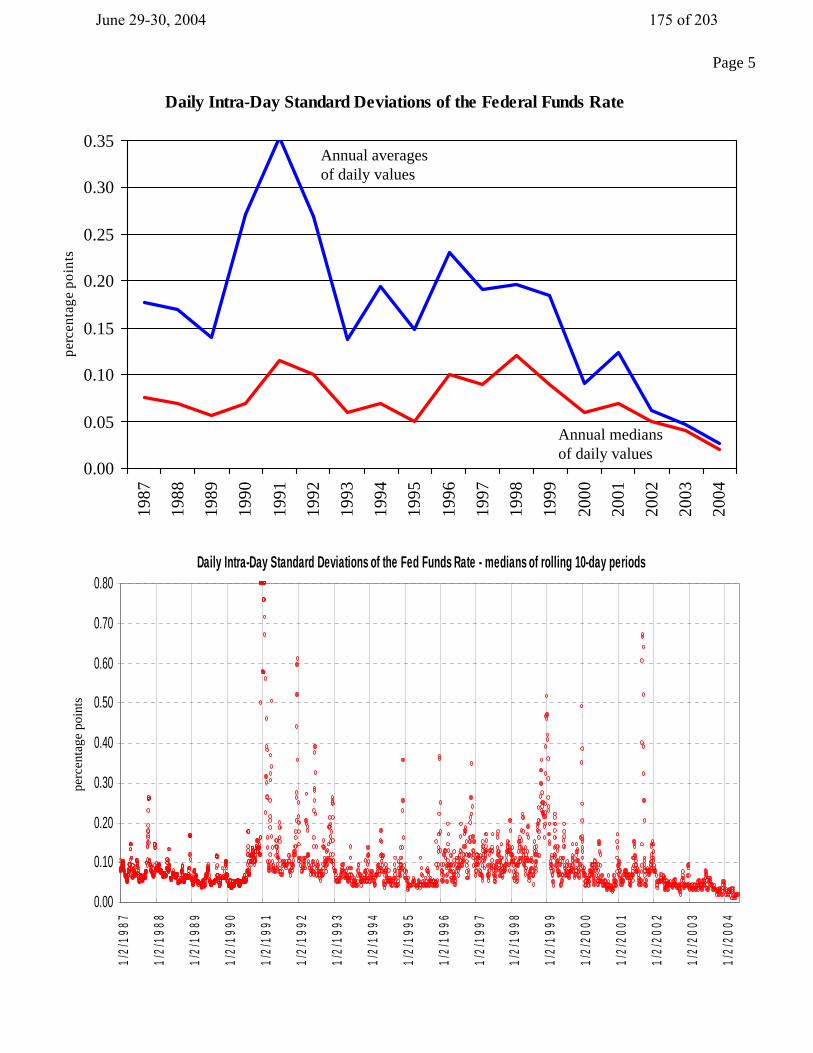

Daily Intra-Day Standard Deviations of the Federal Funds Rate

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.3519

87

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

perc

enta

ge p

oint

s

Annual averagesof daily values

Annual mediansof daily values

Daily Intra-Day Standard Deviations of the Fed Funds Rate - medians of rolling 10-day periods

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

1/2/

1987

1/2/

1988

1/2/

1989

1/2/

1990

1/2/

1991

1/2/

1992

1/2/

1993

1/2/

1994

1/2/

1995

1/2/

1996

1/2/

1997

1/2/

1998

1/2/

1999

1/2/

2000

1/2/

2001

1/2/

2002

1/2/

2003

1/2/

2004

perc

enta

ge p

oint

sPage 5

June 29-30, 2004 175 of 203

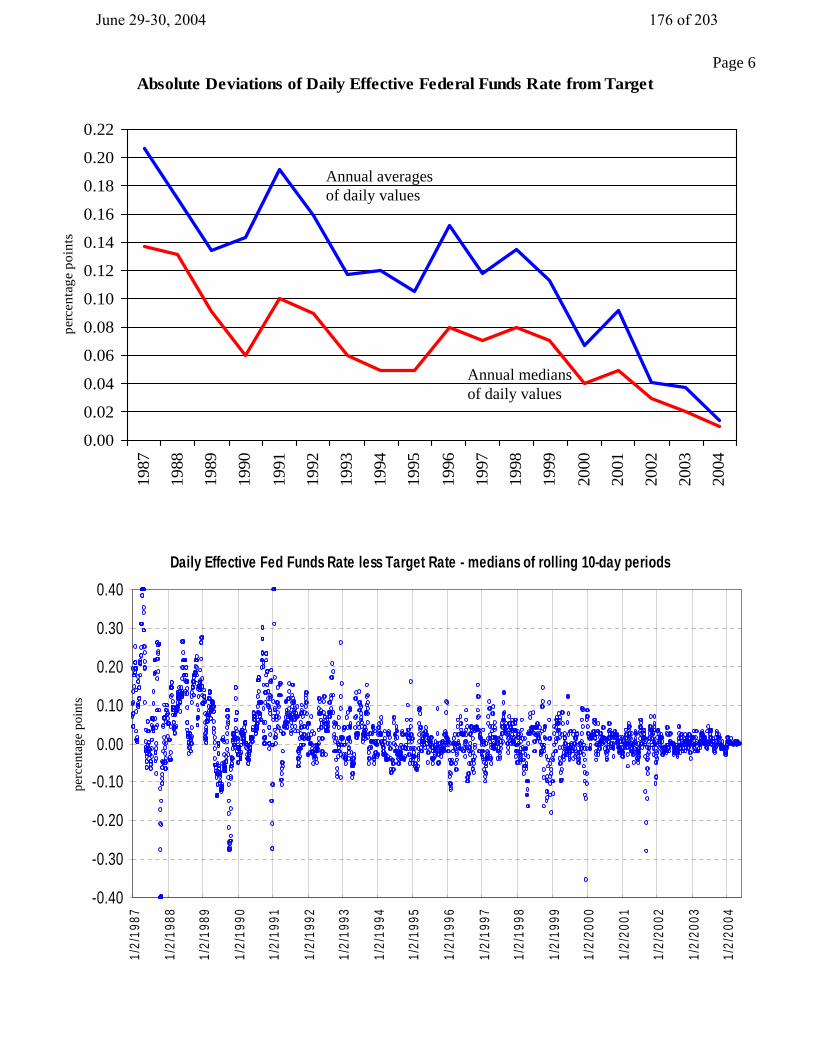

Absolute Deviations of Daily Effective Federal Funds Rate from Target

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

0.18

0.20

0.2219

87

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

perc

enta

ge p

oint

s

Annual mediansof daily values

Daily Effective Fed Funds Rate less Target Rate - medians of rolling 10-day periods

-0.40

-0.30

-0.20

-0.10

0.00

0.10

0.20

0.30

0.40

1/2/

1987

1/2/

1988

1/2/

1989

1/2/

1990

1/2/

1991

1/2/

1992

1/2/

1993

1/2/

1994

1/2/

1995

1/2/

1996

1/2/

1997

1/2/

1998

1/2/

1999

1/2/

2000

1/2/

2001

1/2/

2002

1/2/

2003

1/2/

2004

Annual averagesof daily values

perc

enta

ge p

oint

sPage 6

June 29-30, 2004 176 of 203

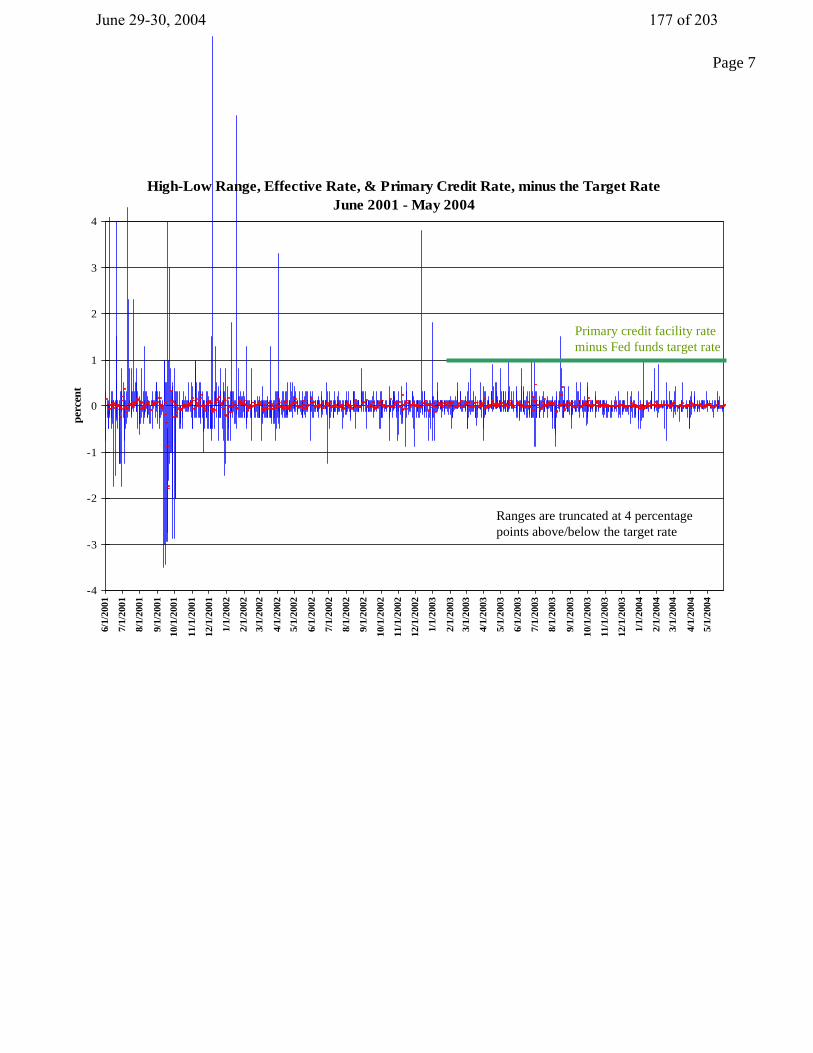

High-Low Range, Effective Rate, & Primary Credit Rate, minus the Target RateJune 2001 - May 2004

-4

-3

-2

-1

0

1

2

3

4

6/1/

2001

7/1/

2001

8/1/

2001

9/1/

2001

10/1

/200

1

11/1

/200

1

12/1

/200

1

1/1/

2002

2/1/

2002

3/1/

2002

4/1/

2002

5/1/

2002

6/1/

2002

7/1/

2002

8/1/

2002

9/1/

2002

10/1

/200

2

11/1

/200

2

12/1

/200

2

1/1/

2003

2/1/

2003

3/1/

2003

4/1/

2003

5/1/

2003

6/1/

2003

7/1/

2003

8/1/

2003

9/1/

2003

10/1

/200

3

11/1

/200

3

12/1

/200

3

1/1/

2004

2/1/

2004

3/1/

2004

4/1/

2004

5/1/

2004

perc

ent

Primary credit facility rateminus Fed funds target rate

Ranges are truncated at 4 percentagepoints above/below the target rate

Page 7

June 29-30, 2004 177 of 203

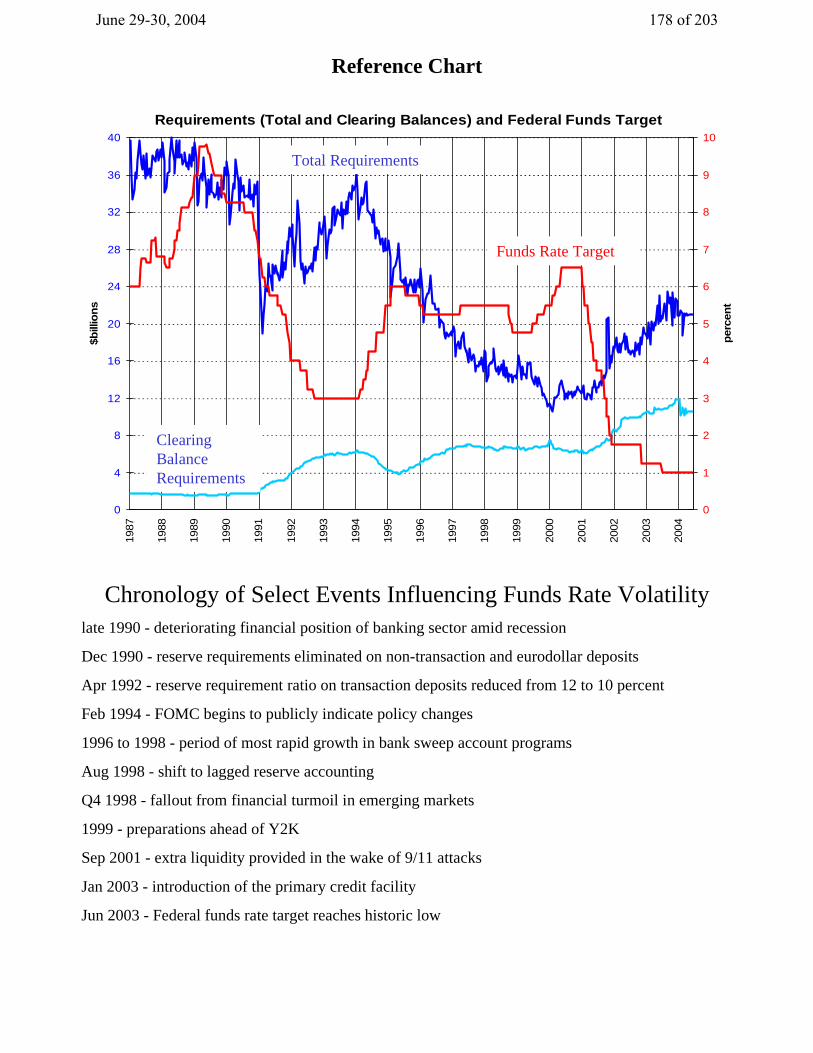

Requirements (Total and Clearing Balances) and Federal Funds Target

0

4

8

12

16

20

24

28

32

36

4019

87

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

$bill

ions

0

1

2

3

4

5

6

7

8

9

10

perc

ent

Total Requirements

ClearingBalanceRequirements

Funds Rate Target

Chronology of Select Events Influencing Funds Rate Volatilitylate 1990 - deteriorating financial position of banking sector amid recession

Dec 1990 - reserve requirements eliminated on non-transaction and eurodollar deposits

Apr 1992 - reserve requirement ratio on transaction deposits reduced from 12 to 10 percent

Feb 1994 - FOMC begins to publicly indicate policy changes

1996 to 1998 - period of most rapid growth in bank sweep account programs

Aug 1998 - shift to lagged reserve accounting

Q4 1998 - fallout from financial turmoil in emerging markets

1999 - preparations ahead of Y2K

Sep 2001 - extra liquidity provided in the wake of 9/11 attacks

Jan 2003 - introduction of the primary credit facility

Jun 2003 - Federal funds rate target reaches historic low

Reference Chart

June 29-30, 2004 178 of 203

Appendix 4: Materials used by Messrs. Oliner, Wilcox, and Sheets

June 29-30, 2004 179 of 203

STRICTLY CONFIDENTIAL (FR) CLASS I-FOMC*

Material for

Staff Presentation on the Economic Outlook

June 30, 2004

*Downgraded to Class II upon release of the July 2004 Monetary Policy Report.

June 29-30, 2004 180 of 203

June 29-30, 2004 181 of 203

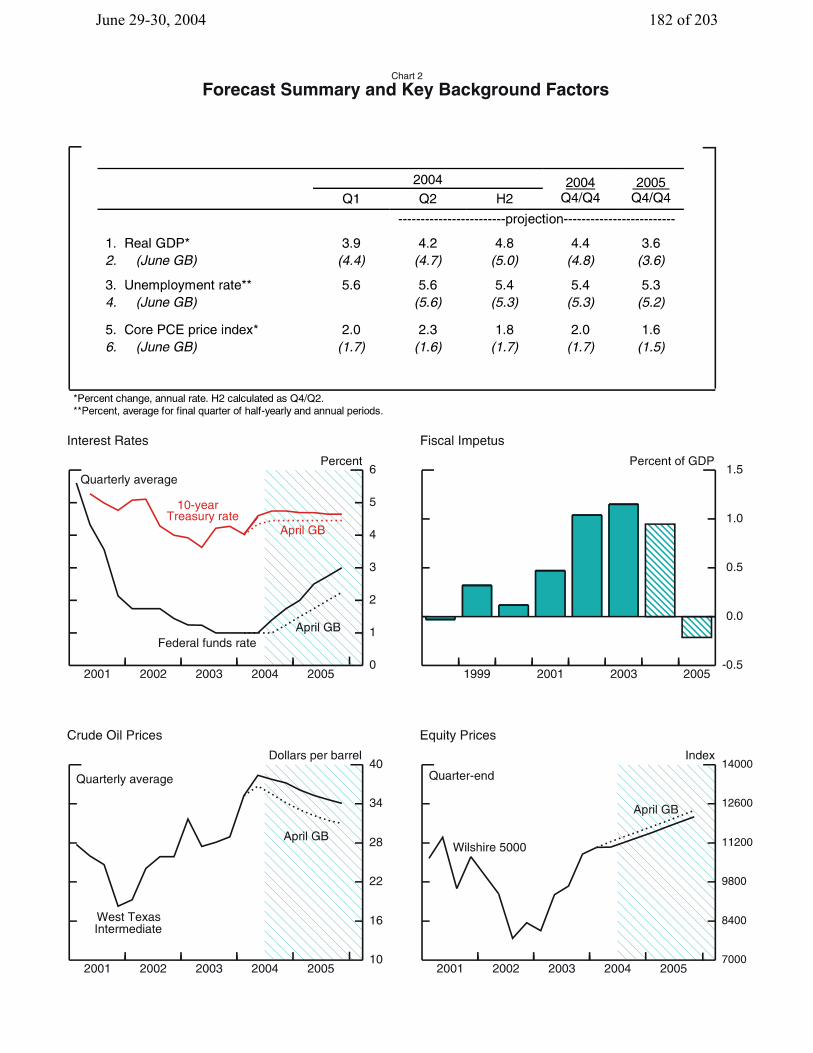

June 29-30, 2004 182 of 203

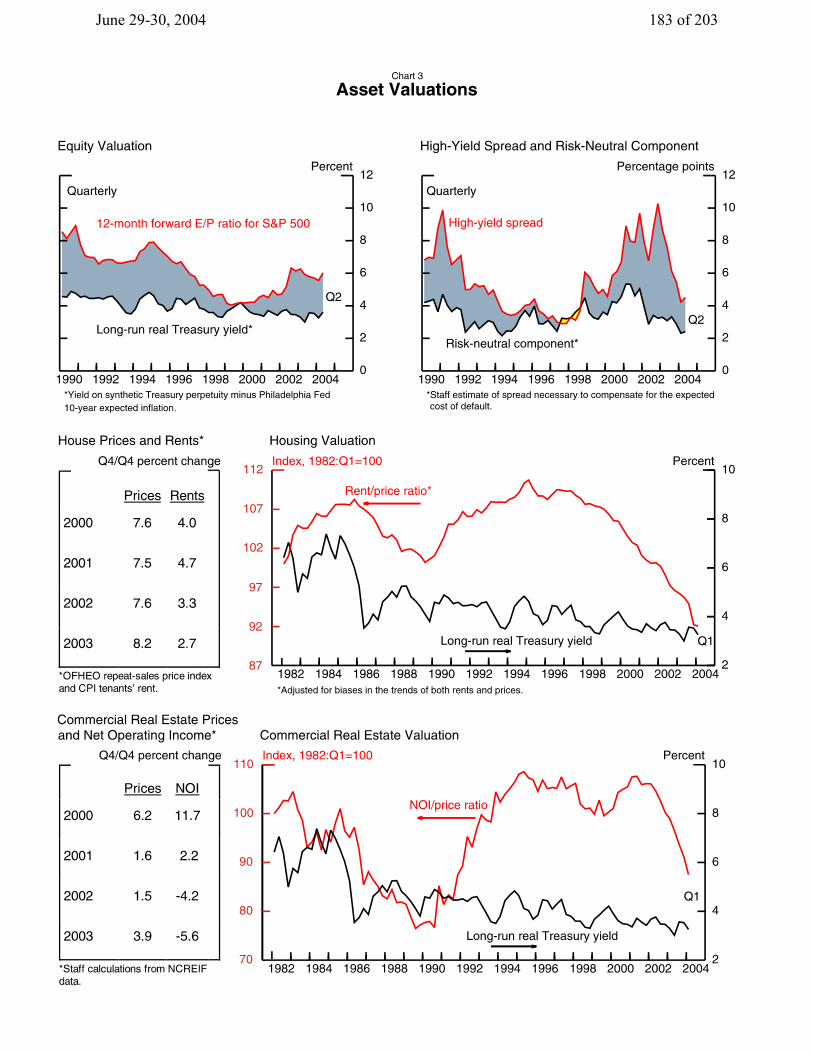

June 29-30, 2004 183 of 203

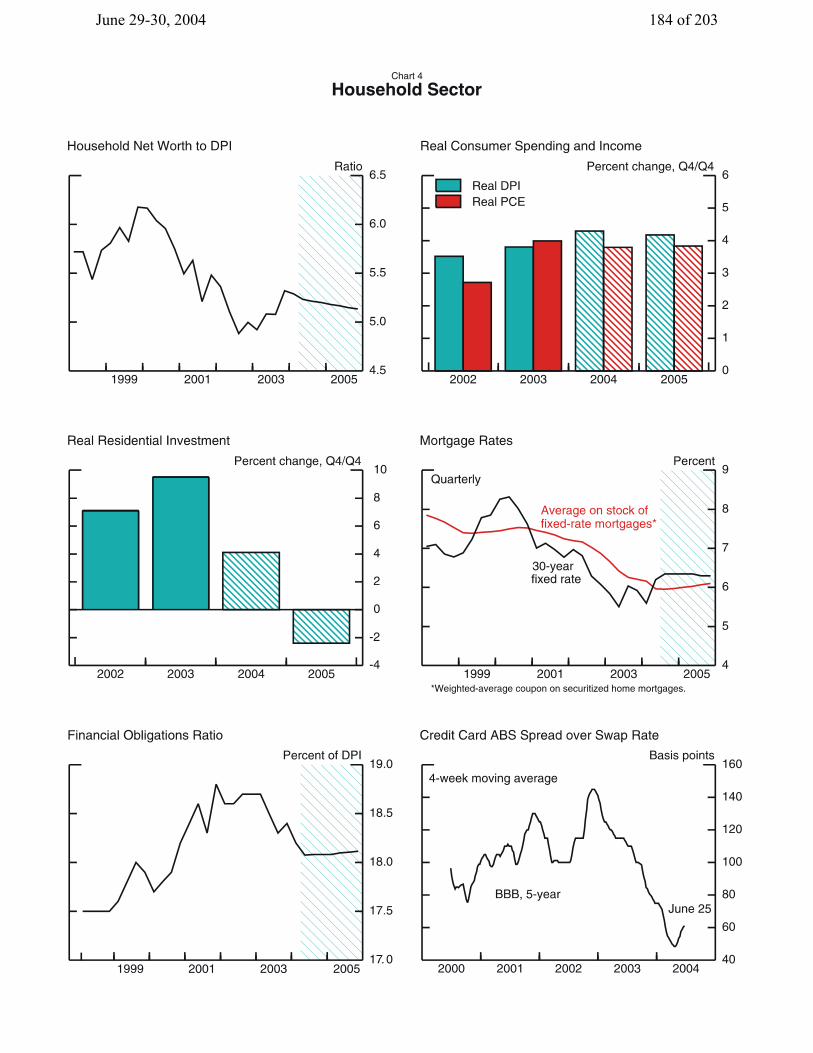

June 29-30, 2004 184 of 203

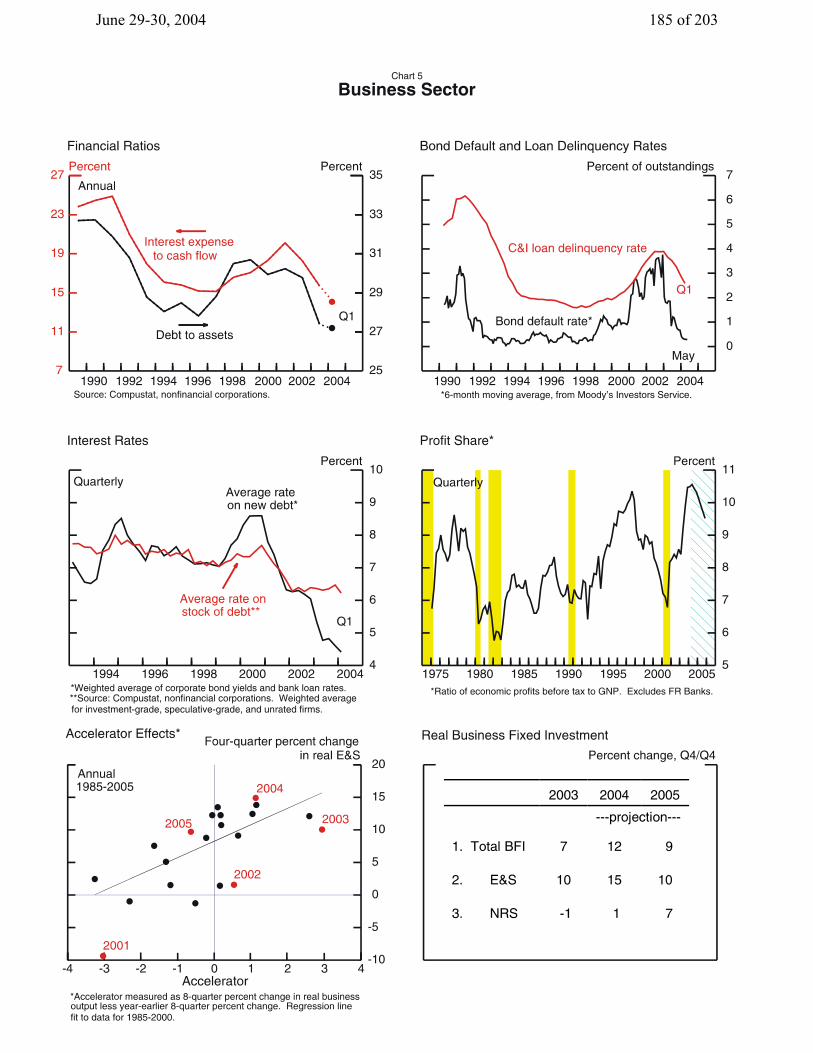

June 29-30, 2004 185 of 203

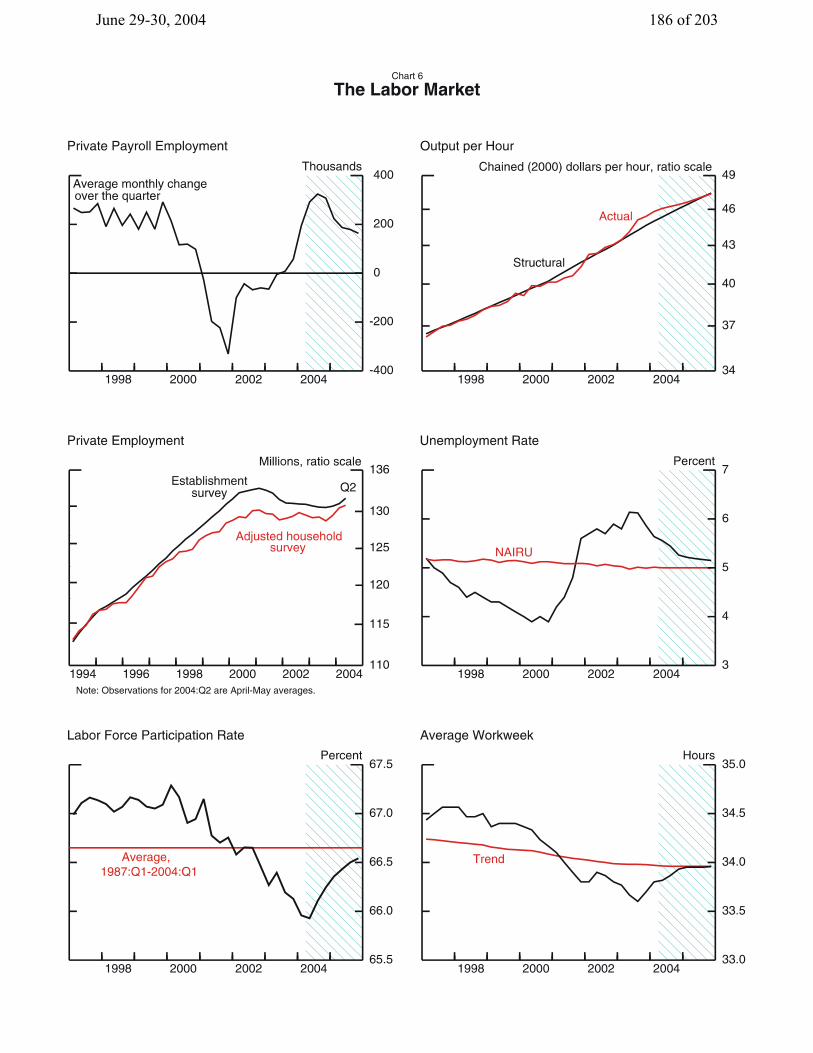

June 29-30, 2004 186 of 203

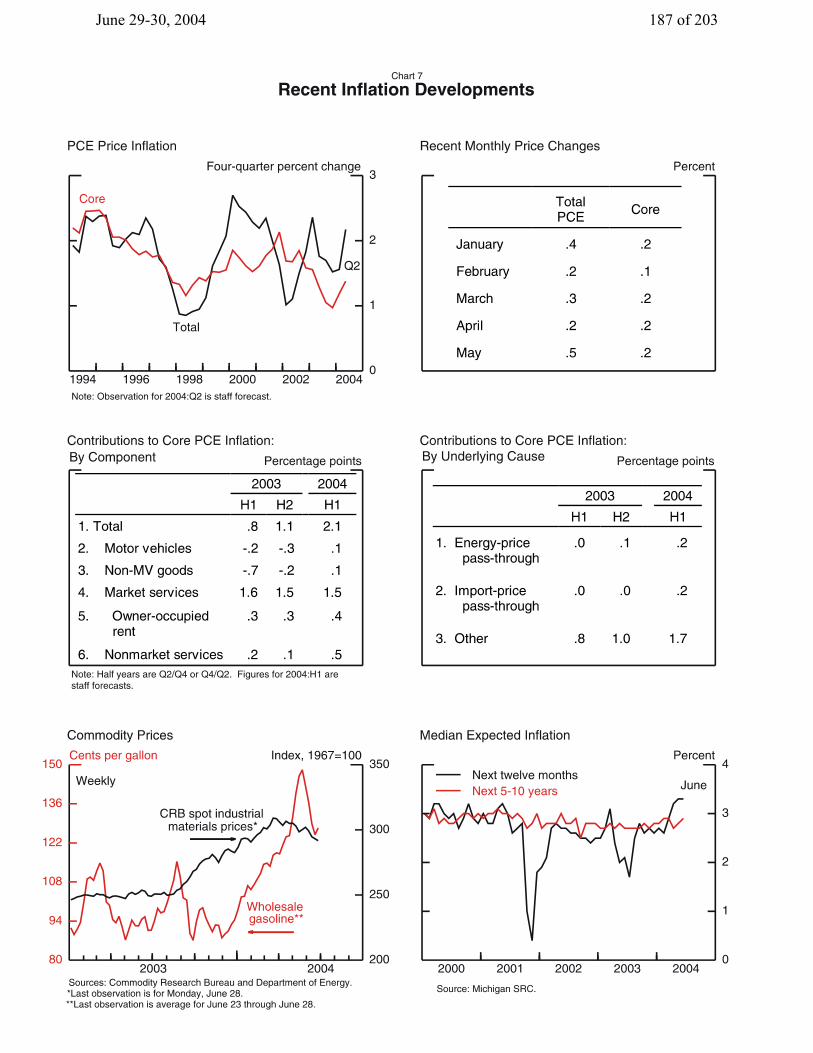

June 29-30, 2004 187 of 203

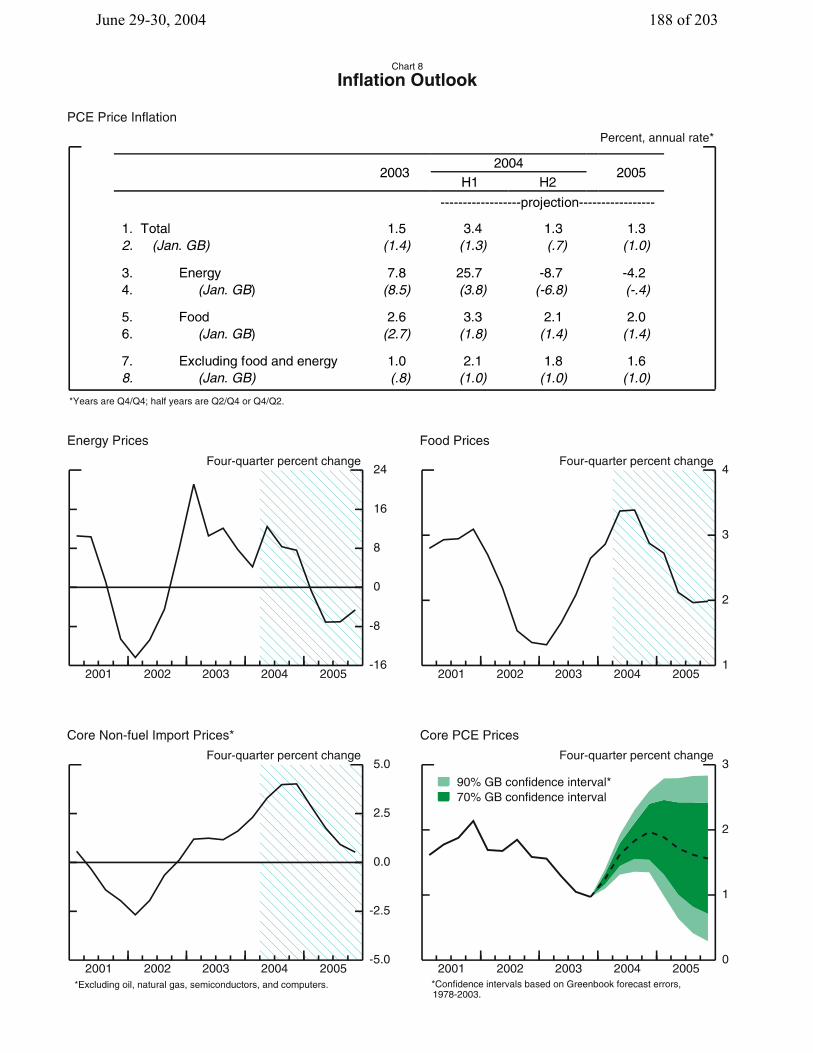

June 29-30, 2004 188 of 203

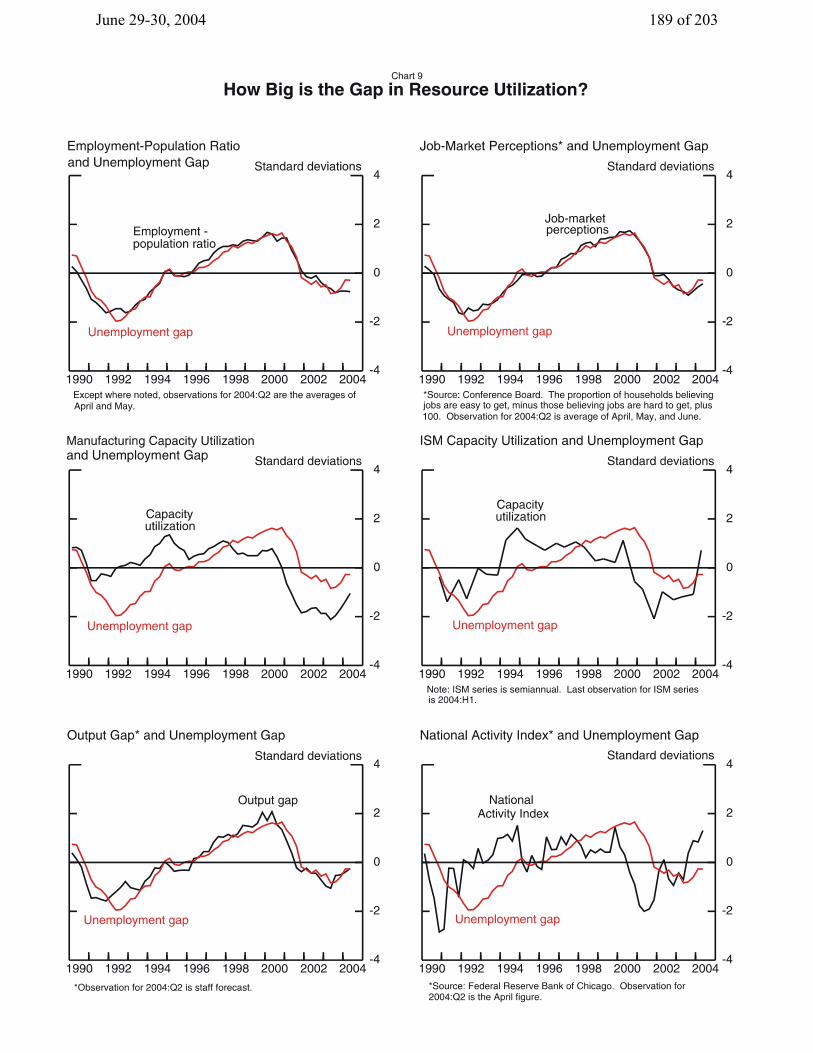

June 29-30, 2004 189 of 203

June 29-30, 2004 190 of 203

June 29-30, 2004 191 of 203

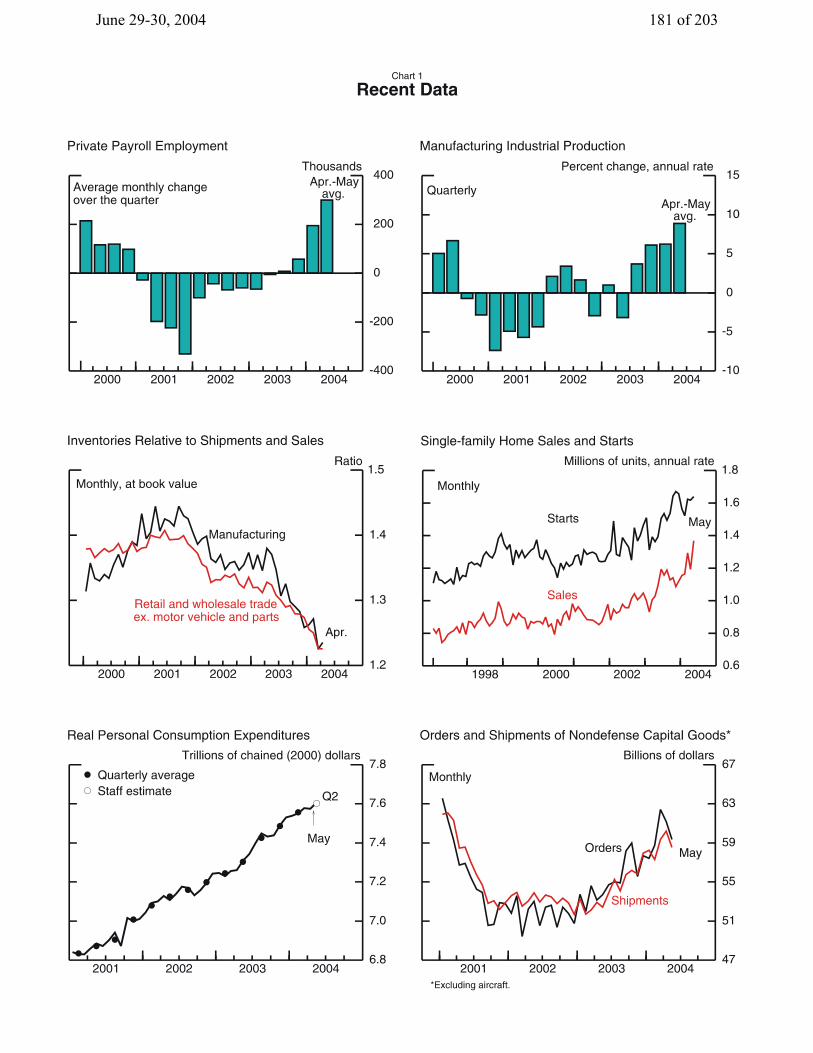

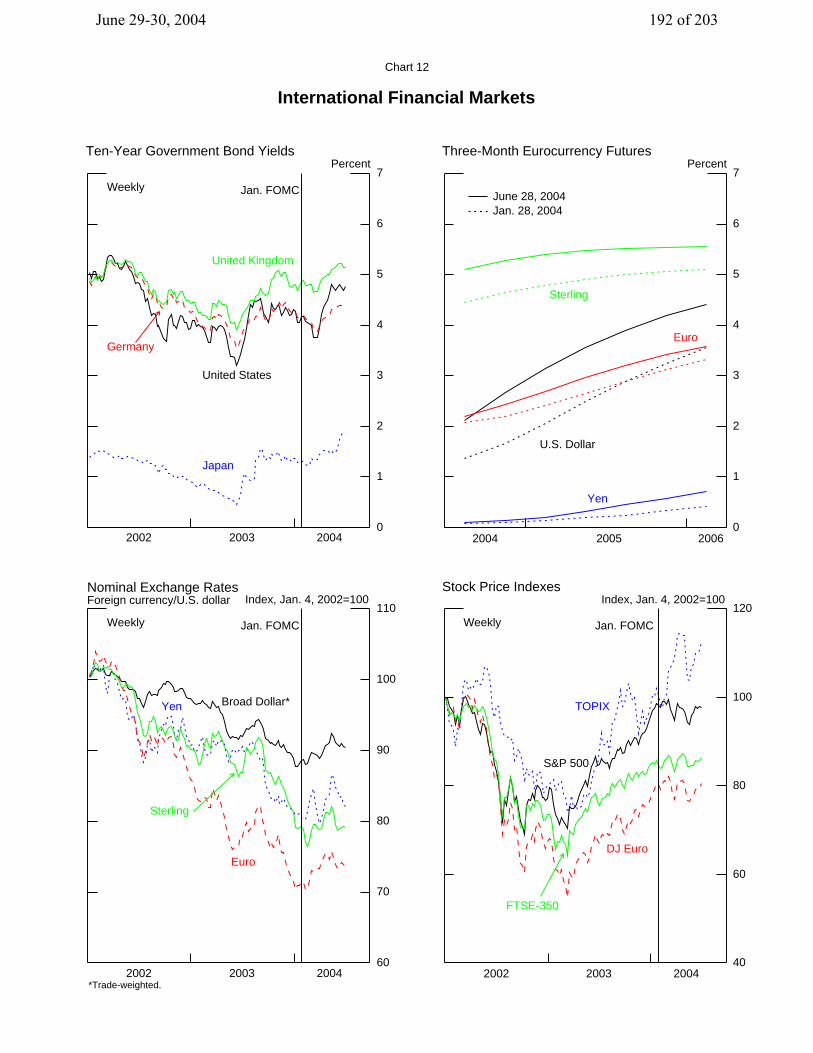

Chart 12

International Financial Markets

0

1

2

3

4

5

6

7

United States

Germany

Japan

United Kingdom

2002 2003 2004

Jan. FOMCWeekly

Ten-Year Government Bond YieldsPercent

0

1

2

3

4

5

6

7

2004 2005 2006

U.S. Dollar

Euro

Sterling

Yen

June 28, 2004Jan. 28, 2004

Three-Month Eurocurrency FuturesPercent

60

70

80

90

100

110

Nominal Exchange RatesForeign currency/U.S. dollar

2002 2003 2004

Broad Dollar*Yen

Euro

Sterling

Jan. FOMC

*Trade-weighted.

Weekly

Index, Jan. 4, 2002=100

40

60

80

100

120

S&P 500

DJ Euro

TOPIX

FTSE-350

2002 2003 2004

Jan. FOMCWeekly

Stock Price IndexesIndex, Jan. 4, 2002=100

June 29-30, 2004 192 of 203

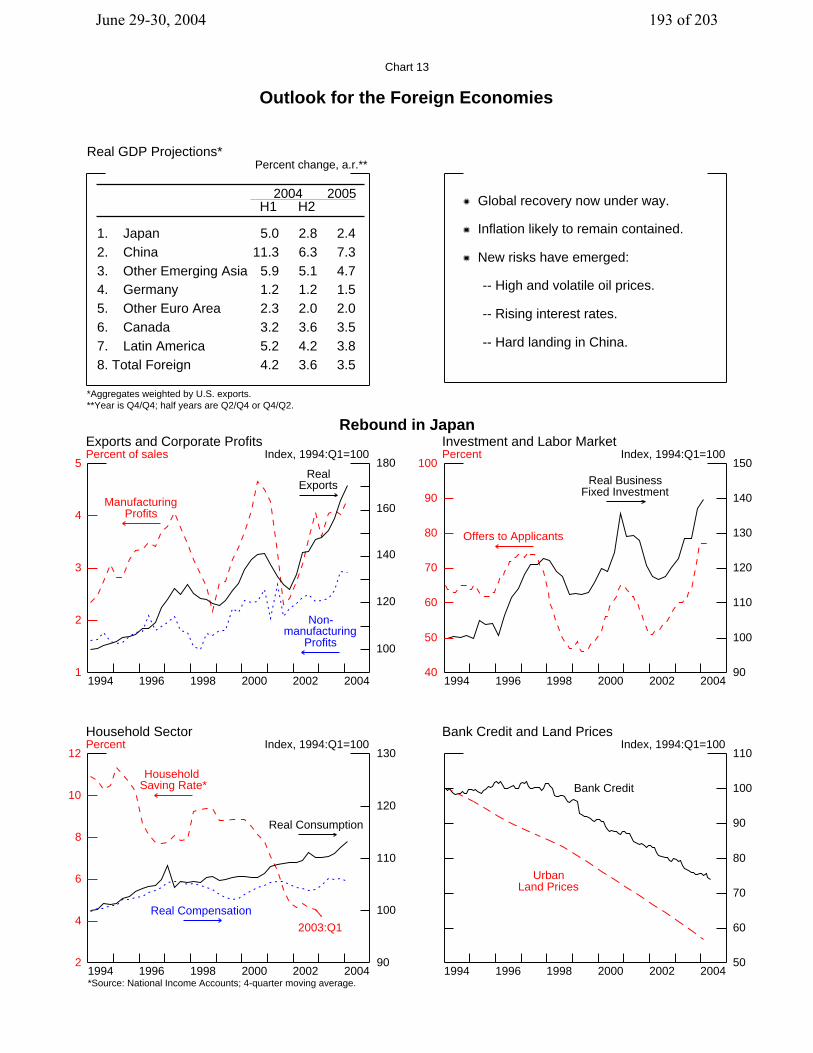

Chart 13

Outlook for the Foreign Economies

Global recovery now under way.

Inflation likely to remain contained.

New risks have emerged:

-- High and volatile oil prices.

-- Rising interest rates.

-- Hard landing in China.

1994 1996 1998 2000 2002 20041

2

3

4

5Real

Exports

ManufacturingProfits

Non-manufacturing

Profits 100

120

140

160

180

Rebound in Japan Exports and Corporate Profits Percent of sales Index, 1994:Q1=100

1994 1996 1998 2000 2002 200440

50

60

70

80

90

100

90

100

110

120

130

140

150

Real BusinessFixed Investment

Offers to Applicants

Investment and Labor Market Percent Index, 1994:Q1=100

1994 1996 1998 2000 2002 20042

4

6

8

10

12

90

100

110

120

130

*Source: National Income Accounts; 4-quarter moving average.

Real Consumption

Real Compensation

Household Saving Rate*

2003:Q1

Household Sector Percent Index, 1994:Q1=100

1994 1996 1998 2000 2002 200450

60

70

80

90

100

110

Bank Credit

UrbanLand Prices

Bank Credit and Land PricesIndex, 1994:Q1=100

Real GDP Projections* Percent change, a.r.**

*Aggregates weighted by U.S. exports.**Year is Q4/Q4; half years are Q2/Q4 or Q4/Q2.

H1 H2

1. Japan 5.0 2.8 2.42. China 11.3 6.3 7.33. Other Emerging Asia 5.9 5.1 4.74. Germany 1.2 1.2 1.55. Other Euro Area 2.3 2.0 2.06. Canada 3.2 3.6 3.57. Latin America 5.2 4.2 3.88. Total Foreign 4.2 3.6 3.5

2004 2005

June 29-30, 2004 193 of 203

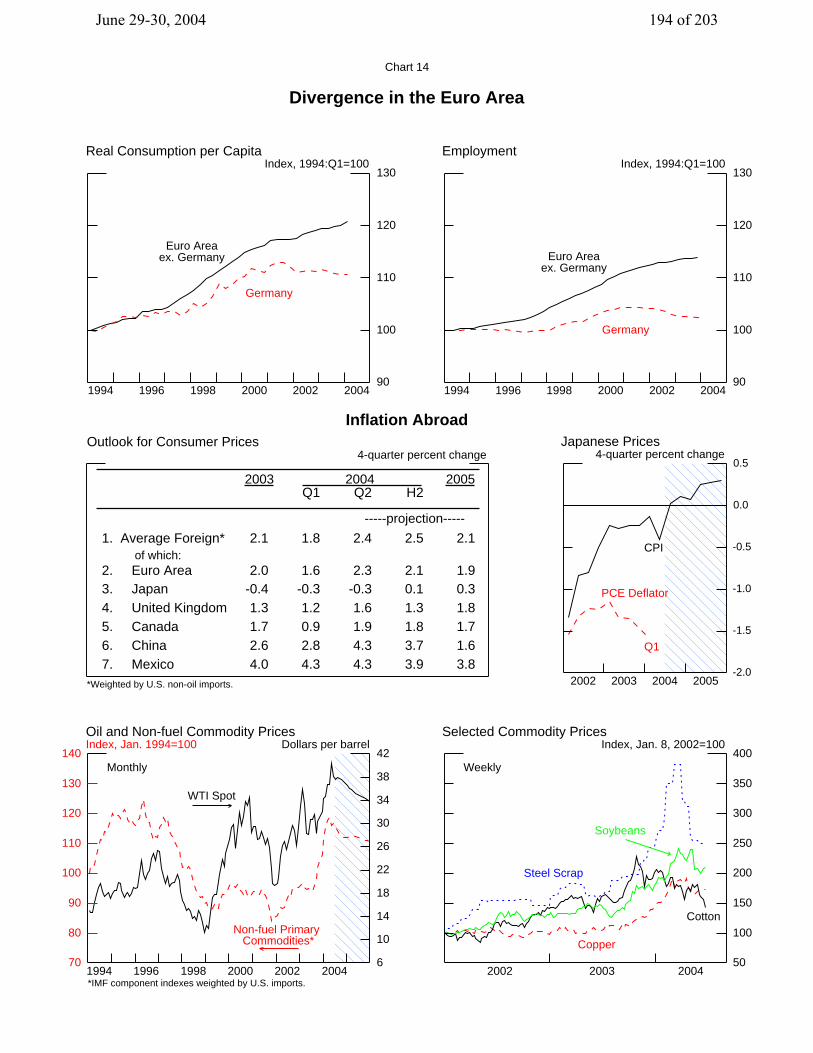

Chart 14

Divergence in the Euro Area

1994 1996 1998 2000 2002 200490

100

110

120

130

Euro Areaex. Germany

Germany

Real Consumption per CapitaIndex, 1994:Q1=100

1994 1996 1998 2000 2002 200490

100

110

120

130

Euro Areaex. Germany

Germany

EmploymentIndex, 1994:Q1=100

2002 2003 2004 2005-2.0

-1.5

-1.0

-0.5

0.0

0.5

CPI

PCE Deflator

Q1

Japanese Prices4-quarter percent change

1994 1996 1998 2000 2002 200470

80

90

100

110

120

130

140

6

10

14

18

22

26

30

34

38

42

*IMF component indexes weighted by U.S. imports.

WTI Spot

Non-fuel Primary Commodities*

Monthly

Oil and Non-fuel Commodity Prices Index, Jan. 1994=100 Dollars per barrel

50

100

150

200

250

300

350

400

Steel Scrap

Soybeans

Copper

Cotton

2002 2003 2004

Weekly

Selected Commodity PricesIndex, Jan. 8, 2002=100

Outlook for Consumer Prices4-quarter percent change

*Weighted by U.S. non-oil imports.

Q1 Q2 H2

1. Average Foreign* 2.1 1.8 2.4 2.5 2.1

2. Euro Area 2.0 1.6 2.3 2.1 1.93. Japan -0.4 -0.3 -0.3 0.1 0.34. United Kingdom 1.3 1.2 1.6 1.3 1.85. Canada 1.7 0.9 1.9 1.8 1.76. China 2.6 2.8 4.3 3.7 1.67. Mexico 4.0 4.3 4.3 3.9 3.8

Inflation Abroad

2003 2005

of which:

2004

-----projection-----

June 29-30, 2004 194 of 203

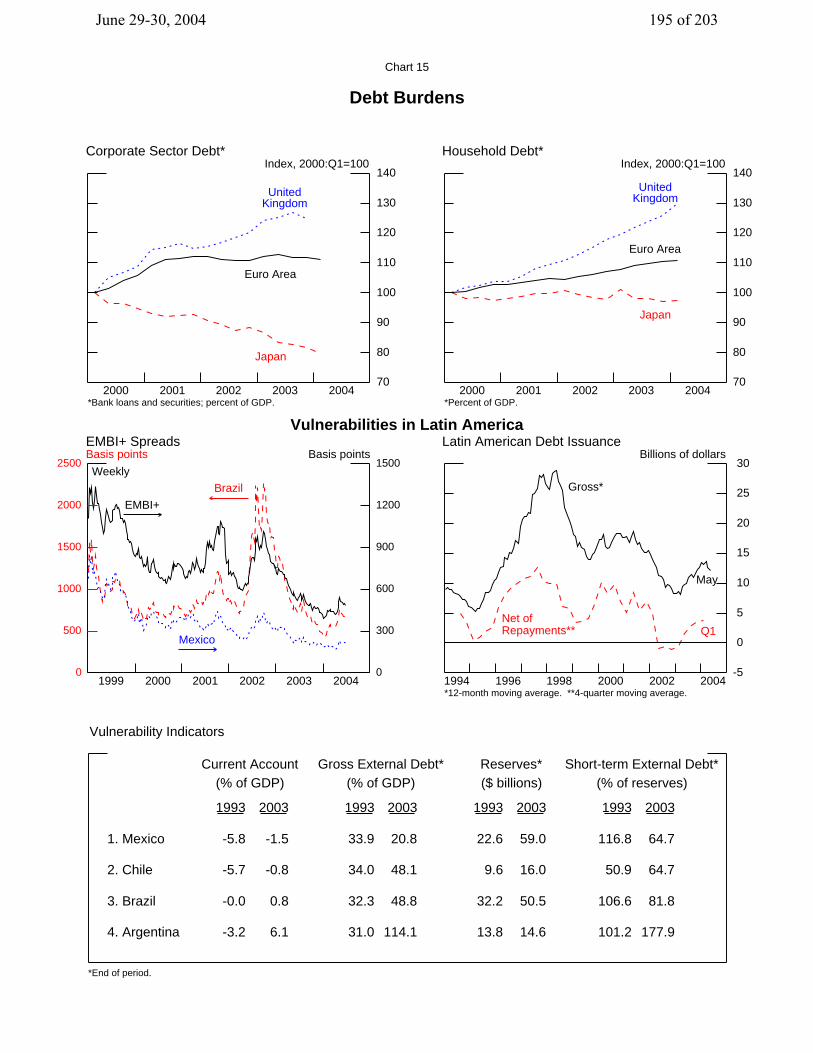

Chart 15

Debt Burdens

2000 2001 2002 2003 200470

80

90

100

110

120

130

140

*Bank loans and securities; percent of GDP.

Euro Area

Japan

UnitedKingdom

Corporate Sector Debt*Index, 2000:Q1=100

2000 2001 2002 2003 200470

80

90

100

110

120

130

140

*Percent of GDP.

UnitedKingdom

Japan

Euro Area

Household Debt*Index, 2000:Q1=100

1999 2000 2001 2002 2003 20040

500

1000

1500

2000

2500

0

300

600

900

1200

1500

Brazil

Mexico

EMBI+

Weekly

Vulnerabilities in Latin America EMBI+ Spreads Basis points Basis points

1994 1996 1998 2000 2002 2004-5

0

5

10

15

20

25

30

*12-month moving average. **4-quarter moving average.

Gross*

Net ofRepayments**

May

Q1

Latin American Debt IssuanceBillions of dollars

*End of period.

Current Account(% of GDP)

Gross External Debt*(% of GDP)

Reserves*($ billions)

Short-term External Debt*(% of reserves)

1993 2003 1993 2003 1993 2003 1993 2003

1. Mexico -5.8 -1.5 33.9 20.8 22.6 59.0 116.8 64.7

2. Chile -5.7 -0.8 34.0 48.1 9.6 16.0 50.9 64.7

3. Brazil -0.0 0.8 32.3 48.8 32.2 50.5 106.6 81.8

4. Argentina -3.2 6.1 31.0 114.1 13.8 14.6 101.2 177.9

Vulnerability Indicators

June 29-30, 2004 195 of 203

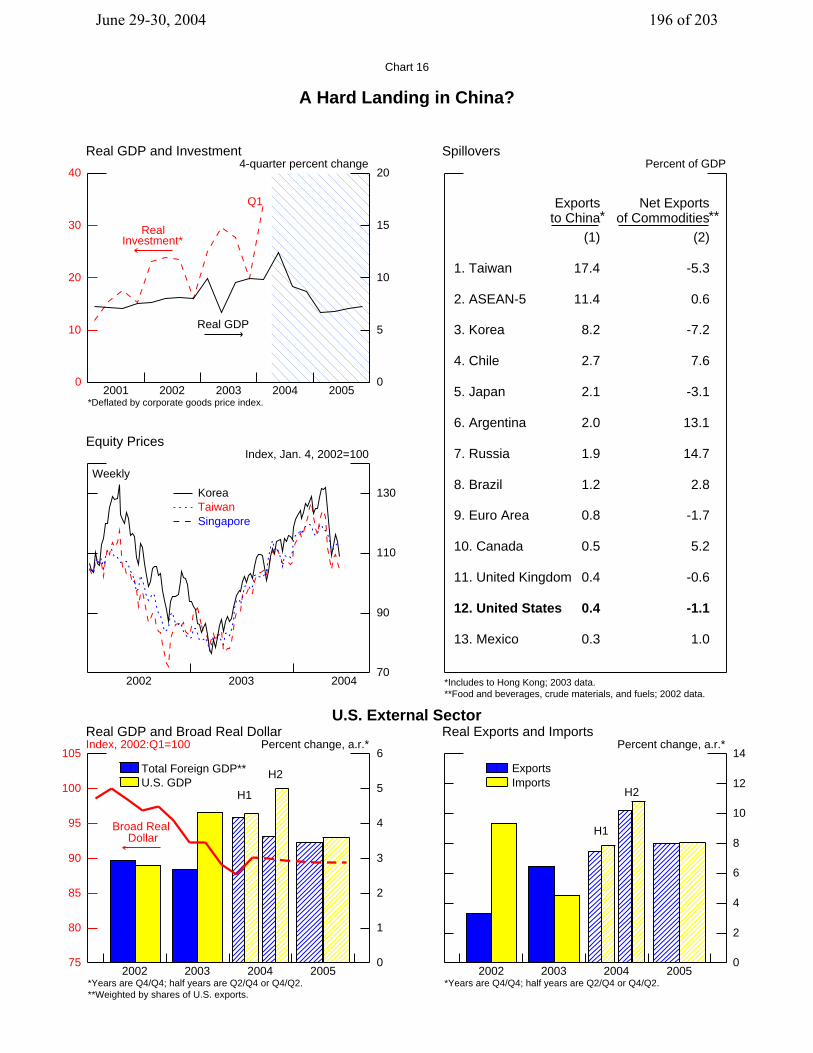

Chart 16

A Hard Landing in China?

2001 2002 2003 2004 20050

10

20

30

40

0

5

10

15

20

*Deflated by corporate goods price index.

RealInvestment*

Real GDP

Q1

Real GDP and Investment4-quarter percent change

*Includes to Hong Kong; 2003 data.**Food and beverages, crude materials, and fuels; 2002 data.

* **Exports Net Exports

to China of Commodities(1) (2)

1. Taiwan 17.4 -5.3

2. ASEAN-5 11.4 0.6

3. Korea 8.2 -7.2

4. Chile 2.7 7.6

5. Japan 2.1 -3.1

6. Argentina 2.0 13.1

7. Russia 1.9 14.7

8. Brazil 1.2 2.8

9. Euro Area 0.8 -1.7

10. Canada 0.5 5.2

11. United Kingdom 0.4 -0.6

12. United States 0.4 -1.1

13. Mexico 0.3 1.0

SpilloversPercent of GDP

2002 2003 200470

90

110

130

Weekly

KoreaTaiwanSingapore

Equity PricesIndex, Jan. 4, 2002=100

2002 2003 2004 200575

80

85

90

95

100

105

0

1

2

3

4

5

6

*Years are Q4/Q4; half years are Q2/Q4 or Q4/Q2.**Weighted by shares of U.S. exports.

Total Foreign GDP**U.S. GDP

H1

H2

Broad Real Dollar

U.S. External Sector Real GDP and Broad Real Dollar Index, 2002:Q1=100 Percent change, a.r.*

2002 2003 2004 20050

2

4

6

8

10

12

14

*Years are Q4/Q4; half years are Q2/Q4 or Q4/Q2.

H1

H2

ExportsImports

Real Exports and ImportsPercent change, a.r.*

June 29-30, 2004 196 of 203

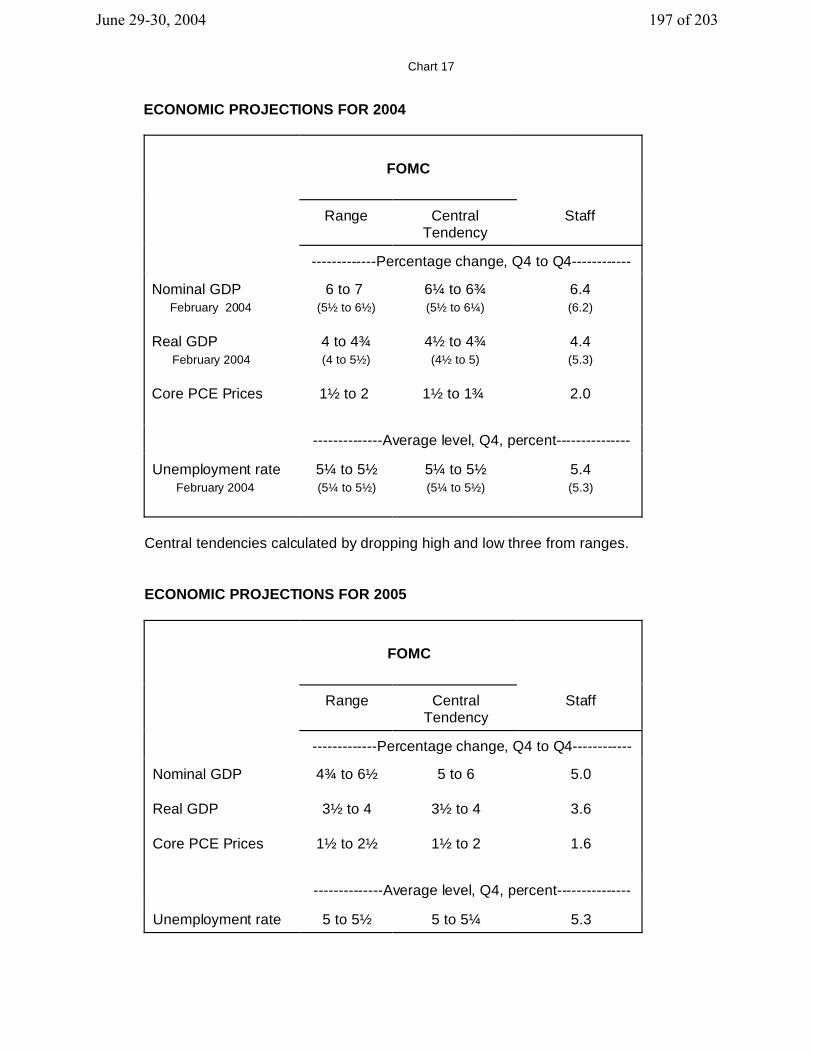

Chart 17

ECONOMIC PROJECTIONS FOR 2004

FOMC

Range CentralTendency

Staff

-------------Percentage change, Q4 to Q4------------

Nominal GDP February 2004

Real GDP February 2004

Core PCE Prices

6 to 7 (5½ to 6½)

4 to 4¾(4 to 5½)

1½ to 2

6¼ to 6¾(5½ to 6¼)

4½ to 4¾(4½ to 5)

1½ to 1¾

6.4(6.2)

4.4(5.3)

2.0

--------------Average level, Q4, percent---------------

Unemployment rate February 2004

5¼ to 5½(5¼ to 5½)

5¼ to 5½(5¼ to 5½)

5.4(5.3)

Central tendencies calculated by dropping high and low three from ranges.

ECONOMIC PROJECTIONS FOR 2005

FOMC

Range CentralTendency

Staff

-------------Percentage change, Q4 to Q4------------

Nominal GDP Real GDP

Core PCE Prices

4¾ to 6½

3½ to 4

1½ to 2½

5 to 6

3½ to 4

1½ to 2

5.0

3.6

1.6

--------------Average level, Q4, percent---------------

Unemployment rate 5 to 5½ 5 to 5¼ 5.3

June 29-30, 2004 197 of 203

Appendix 5: Materials used by Mr. Reinhart

June 29-30, 2004 198 of 203

June 29-30, 2004 199 of 203

June 29-30, 2004 200 of 203

June 29-30, 2004 201 of 203

June 29-30, 2004 202 of 203

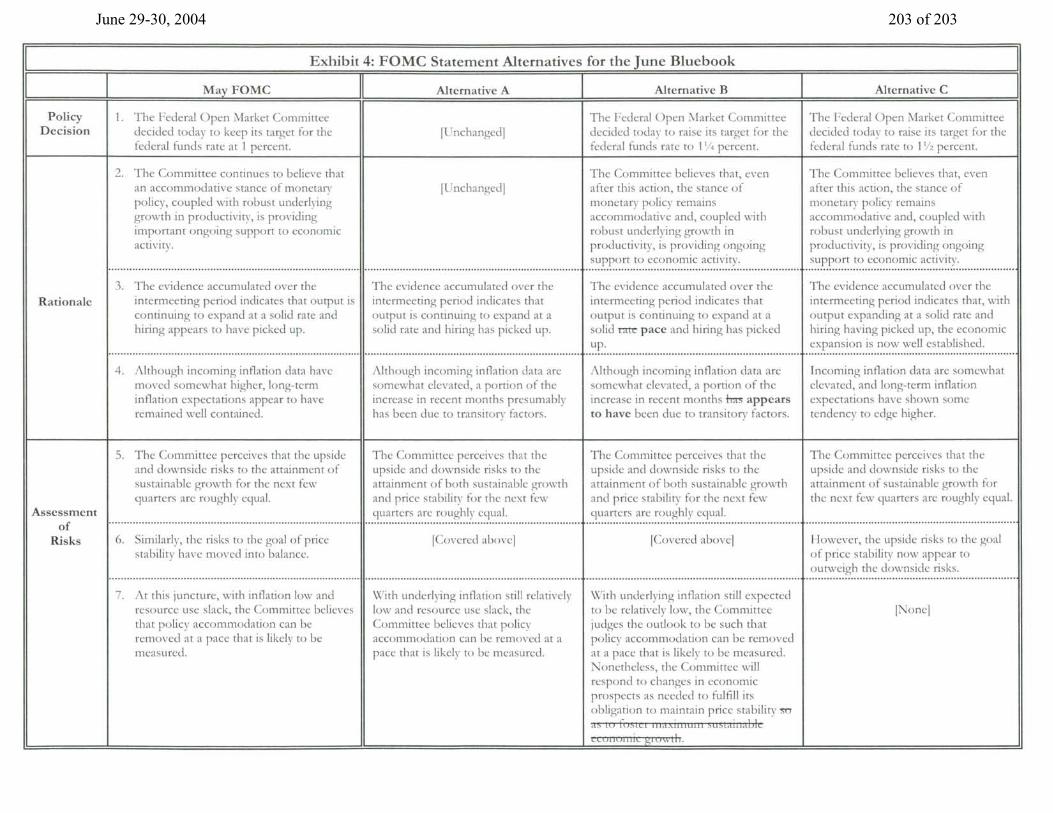

June 29-30, 2004 203 of 203