Embed Size (px)

Citation preview

APEC Fintech E-payment Readiness Index

Ecosystem Assessment and Status Report

supported by PayPal

TableofContents

Preface...................................................................................................................................................1

ExecutiveSummary................................................................................................................................3

1.Introduction.......................................................................................................................................6

2.APECE-paymentIndex.......................................................................................................................9

KeyFindingsbyPillar........................................................................................................................16

Pillar1:RegulatoryandPolicyEnvironment................................................................................16

Pillar2:Infrastructure..................................................................................................................18

Pillar3:Demand...........................................................................................................................20

Pillar4:Innovation.......................................................................................................................22

Conclusion........................................................................................................................................23

3.CaseStudies:In-DepthLookatSelectedEconomies........................................................................25

Australia...........................................................................................................................................25

HongKong........................................................................................................................................27

Indonesia..........................................................................................................................................29

ThePhilippines.................................................................................................................................32

4.ConclusionandRecommendations:LookingAhead........................................................................35

Appendix1.EconometricMethodologyandResults...........................................................................37

Appendix2.APECE-paymentIndex–Methodology............................................................................39

1

Preface

TheAPECFintechE-paymentReadinessIndex:EcosystemAssessmentandStatusReportisajointstudybytheAustralianAPECStudyCentreatRMITUniversityandTRPC,aspecialisttechnologyresearchconsultancy,basedoutofSingapore,withofficesinHongKong,BeijingandSydney.PayPalgenerouslysupportedthedevelopmentofthereportforboththe2015reportandthe2016report.

Thestudyassessesthelevelofreadinessandfuturepotentialofthe21APECeconomiestoengagein,adoptandreapthebroadrangeofeconomicandsocietalbenefitsthate-paymentshold,andtowhichtheroleofFintechisofcriticalimportance.Thereportwasundertakenwithaviewtotestingtheassumptionthatthereisastrongandgrowinglinkbetweene-paymentpenetrationandeconomicgrowth.Andthat,anysuchlinkwasworthidentifyingandbeginningtomeasure,alongwithacanvassingofthebarrierstoe-paymentadoptionacrossthevariousAPECeconomies.

APECeconomiesconstituteanimportantregionaleconomicbloc,representingover40%ofworldtradeand50%ofglobalGDP.Asthestudyattests,theseeconomiesareundergoingaprofoundtransitiontowardscashlesssocieties,drivenbythespreadofmobiledevices,increasingaccesstotheInternet,andtheemergenceofdigitalpayments.Thestudyprovidesatimelysnapshotofe-paymentadoption,andservesasanearlyguideonacceleratingdigitizationofpaymentsinlinewithAPEC’sfoundingobjectivesoftradefacilitation,regionalintegrationandeconomicprosperityforall.Morecrucially,thereportalsohelpspolicymakersassesstowhatextenttheireconomiesaree-paymentsready,andidentifieswhatareasareinneedofimprovement.

Whilee-paymentshavelongbeendiscussedwithinafewspecificforaoftheAPECsystem,theirwide-rangingbenefitsareonlybeginningtobeappreciatedoutsidethetechnologysector.Notsurprisinglytherefore,across-sectoralapproachwithinAPECtosystematicallymeasuretheeconomicimpactofthetransitiontowardse-paymentshasbeenlacking.Atthetimeofwriting,however,theAPECBusinessAdvisoryCouncil(ABAC)AsiaPacificFinancialForum(APFF)hasinitiatedtheprocessofcreatingane-paymentssub-group.Thestudycan,therefore,serveasareferencepointtotracktheregion’sprogressandinvitecollaborationfromvariousmembersintheefforttoimproveone-paymentsreadinessandimpactmeasurement.

Toestimatethemacro-economicimpactofopenaccesstoe-paymentsonAPECeconomies,thereportbeginswithaproof-of-concepteconometricmodellingusingsampledatafromsixAPECeconomies.TheheartofthereportistheAPECE-paymentReadinessIndex,comprising44indicatorsacrossfourpillarsmakingupthee-paymentecosystemthatmeasuretheattractivenessoftheirphysicalandregulatoryenvironments,currentandpotentialdemand,andtheircapacitytoinnovate.Thislatestreportisimprovedbyfine-tuningtheindicatorsusedinordertobetterrepresentexistingandpotentialdemandofe-payments,aswellasincorporatingtheuseofthelatestavailabledata.

Asthefindingsfromtheindexshow,smartphonesande-commercearesettodrivee-paymentadoptioninthefutureandinthiscontext,theroleofgovernmentsindevelopingeconomiesiscriticalife-paymentsaretoforgeahead.Governmentsneedtoensuretheirregulatoryandbusinessenvironmentsareconduciveforinnovationandseamlesstransactionalflowswiththeregion.Thereportalsoarguesthatgovernmentsneedtoshowleadership,especiallyinemergingeconomies,bypromotingashifttodigitalwithinpublicfinances,andtoworkwithstakeholdersfromtheprivatesectorandtheinternationaldevelopmentcommunity.

2

Thisreportillustrateskeyconsiderationsandpotentialpathwaysforexpandinge-paymentadoptionacrossAPECeconomies.TheauthorshopethattheAPECE-paymentReadinessIndex2016willcontributetothedevelopmentofseamlesselectronicpayments,expandingtheoverallmarket,andincreasingthesharedprosperityofallAPECeconomies.

3

ExecutiveSummary

E-paymentsholdabroadrangeofpromisesforindividuals,communitiesandeconomiesatlarge.Adaptationtodigitaltransactionsisalreadyhavingatransformativeimpactonsocietiesthroughaloweringoftransactioncosts,particularlyforSMEs,andtherebyaddingtoproductivity,economicgrowthandsocialbenefits.Constrainingtransactionflows,throughrestrictionsonaccesstoe-payments–whetherintentionalornot–canbeshowntodampeneconomicgrowth,socialequityandequality,andinnovation.However,thisstudyfindsthatAsiaPacificEconomicCooperation(APEC1)economies’levelofadvancementandexperienceinthedevelopmentofane-paymentecosystemvarieswidely.Realisingthefullpotentialofe-paymentswillrequiremoreflexibleregulatoryandbusinessclimatesalongwithcoordinatedandsustainedeffortsfromgovernments,theprivatesectorandtheinternationaldevelopmentcommunitytofosteradoption.

Thisstudysetouttoillustratethelinkagesbetweene-paymentpenetrationandeconomicgrowth,canvassingwherebarriersexistsforeachAPECeconomy.Toestimatethemacro-economicimpactofopenaccesstoelectronicpaymentsonAPECeconomies,aproof-of-conceptexercisewasconductedattheoutsetofthestudy.UsingsampledatafromsixAPECeconomies,thestudyfoundthata1%changeinonlineretailsalesisassociatedwithatleasta0.175%growthinGrossDomesticProduct(GDP)percapitaamongthesesixAPECeconomies.Thisisasubstantivefindingandcallsforafollowupandmoresubstantiveandempiricallybasedsurveyofe-paymentsaccessandopportunitiesacrossAPECeconomies.

Next,anAPECE-paymentIndex,comprisingfourpillarsand44indicators,wasconstructedtogaugethereadinessandcapacityofeachofthe21APECeconomiestoengageine-payment(includingbothe-paymentandm-paymentservices),andtofurtherdeveloptheiroveralle-paymentecosystem.BuildingfromthisIndexthestudyalsousesaseriesofcasestudiesofselectedeconomies–Australia,Indonesia,HongKongChina,andthePhilippines–toillustratekeycontributingfactorstotheprospectsfore-paymentadoptionanddevelopment.

KeytrendsandinsightsthatemergedfromtheIndexandcasestudiesareasfollows:

• Whileeconomiescangenerallybeseentorankinaccordancewiththeirincomebracket(GDPpercapita),thelevelofeconomicgrowthisnotthesoledeterminantofe-paymentreadinessoradoptioninagiveneconomy.Indeed,somemiddle-incomeeconomies,suchasMalaysia,andChina,withafavourablebusinessclimateandsolidinfrastructure,arepunchingabovetheirweight,whilesomehigh-incomeeconomies,suchastheRepublicofKoreaandJapan,fallbelowwheretheywouldotherwisebeexpected,duetoarestrictiveregulatoryenvironmentandalackofcertainconsumerdemand.Thissuggeststhat,byfocusingone-payments,aneconomycanboosteconomicgrowthandeffectively‘leapfrog’initsdevelopmenttrajectory.

• Furtherdevelopingthisissue,theE-paymentIndexshowsthatAPECeconomiesarelargelydividedintothreeclustersaccordingtoreadinessandcapacityfore-paymentusageandadoption.Theclusterscanbesummarisedasfollows:

1The21APECeconomiesare:Australia,BruneiDarussalam,Canada,Chile,China,HongKongChina,Indonesia,Japan,RepublicofKorea,Malaysia,Mexico,NewZealand,PapuaNewGuinea,Peru,Philippines,Russia,Singapore,ChineseTaipei,Thailand,UnitedStatesofAmericaandVietnam.

4

• Cluster1:Economieswithadvancede-paymentecosystems(“Advanced”)–UnitedStatesofAmerica,Singapore,Canada,Australia,NewZealand,RepublicofKorea,HongKongChina,andJapan

• Cluster2:Economieswithtransitioninge-paymentecosystems(“Transitioning”)–ChineseTaipei,Malaysia,BruneiDarussalam,China,RussianFederation,andChile

• Cluster3:Economieswithnascente-paymentecosystems(“Nascent”)–Thailand,Peru,Mexico,Indonesia,Philippines,Vietnam,andPapuaNewGuinea

• Notably,nosingleAPECeconomytrumpsinallpillarsoftheIndex.Ofthefourpillarsthat

comprisetheIndex,SingaporecomesfirstinRegulatory&Policy,KoreatopsthelistinInfrastructure,NewZealandscoreshighestinDemand,whiletheUnitedStatesexcelsinInnovativeProducts&Services.Thismeansthateveryeconomyhasaspectsitcanimproveinordertoreapthebenefitsthate-paymentscanbring.Evenmoresignificantly,nosingleeconomytrumpsinmorethanonepillar.Thisalsoimpliesthatwhilesequencingofstructuralshiftsthattakesplacemaybeimportant,thereisnosinglepathwayoraroadmapforthoseinthelowerclusterstoclimbuptheranking.Everyeconomywillhaveauniquecombinationoffocusareastostrategicallyandsuccessfullyshifttoe-payments.

• Theresultsalsoshowthatwhileaccesstoformalfinancialsystems,suchasbankingincludingcreditanddebitcardusage,isimportanttoday,futuregrowthwillcomedisproportionatelyfromemergingeconomiesusingaffordablesmartphonesandothermobiledevices.EconomiessuchasIndonesiaandthePhilippines,whilestillcashdependent,areshowingnotonlyaremarkablyhighpropensitytogoonline,engageinsocialmediaandshopviasmartphones,butalargeproportionareenteringtheformalfinancialmarketbecauseofthesedevices,andpotentiallybypassingtraditionalplatformssuchascreditcards.Rapidlyexpandinge-commercesectorsintheseeconomieswilloftenleadandfurtherdrivethedevelopmentandusageofe-paymentsincomingyears.

• Nomatterthestageofdevelopmentofthee-paymentecosystem,facilitatinganattractivemarket(includingbusiness)climate,andinvestmentsintoinnovativee-moneysolutionsisimportant.Somedevelopingeconomies,suchasIndonesiaandthePhilippines,areforgingaheadininnovationssuchasFinTechandcryptocurrenciestocapitaliseontheirgrowingmiddleclass’propensitytospendandtransactviamobiledevices.

• Government,asahugeproviderandconsumerofpayments,hasanimportantroletoplayinacceleratingthedigitaltransition,especiallyineconomiesacrossthelowerclusters.Governmenteffortsandinitiativestotransitiontoelectronicpaymentscreatesdemandandnewopportunities,includingnewneedsforpaymentinfrastructureandachangeinconsumers’cashdependence.Asgovernmentsceasetoaccumulate,andproduce,cashandincreasinglymovetoelectronicallydisbursingcitizenfunds–tobankbranches,ATMs,orothercash-outpoints–recipientswillbeincentivizedtoparticipate.

5

IntermsofspecificareasoftheAPECE-paymentIndex,thefindingsareasfollows:

RegulatoryandPolicyEnvironment:Manyeconomiesneedtofocusonfosteringafavourableregulatoryandpolicyenvironmenttoenhancetheconfidenceofbusinessesandconsumers.Therefore,government’svisionandeffortstomakeuseofe-paymentstoimprovetransparency,efficiencyandaccountabilityinitsownfinancescankick-startavirtuouscycleofadoption.

Infrastructure:Thegapordividebetweenhigh-income,upper-middle-incomeandlower-middle-incomeeconomiesismostobviousintheinfrastructurepillarandbridgingthedigitaldividewillbeessentialtofullyleveragingtheopportunitiesine-payments.Thisincludesincreasingsmartphonepenetrationandbroadbandaccessandaffordability.Focusingonavailabilityandaffordabilityofbasicfinancialservicesiskeyindrivinge-payments.

Demand:Demandfore-paymenttodateismoreprominentinadvancedeconomieswherethemajorityofthepopulationarelikelytohavebankaccounts–butthattrendislikelytochangesoon.Rapiduptakeofmobilephones,socialmediaande-commerceindevelopingeconomieswillfacilitatemarketgrowthfore-paymentandm-payment.

Innovation:Innovationsespeciallyinmobileandvirtualcurrenciesinovercominginfrastructurechallengesarecontributingtohigheruptakeofe-paymentandm-paymentservices,andareactingasgatewaysintothefinancialsystemforunbanked–orunder-banked–consumersegments.Governmentsneedtoembracecryptocurrency,whilealsoprovidingmuchneededconsumerprotectionandmitigatingillicitactivities,tobeabletobenefitfromthepotentialtoplugconsumerstoglobalpaymentssystems.Asthenumberofnon-bankplayersinthee-paymentsystemincreases,particularlyindevelopingm-paymentsolutions,thereisaneedforcollaborationamongbanksandnon-banksinordertoaccelerateinnovation.Thereisalsoaneedforregulatorycoordinationintheregiontosupportthisendorsement.

6

1.Introduction

Electronicpayments,ore-payments,havebeenmakingever-increasinginroadsintotransactionssincethe1950sbeginningwiththeadventofgeneral-purposepaymentcards.Technologydevelopments,particularlytheincreasingpervasivenessoftheInternetandmobilephones,havepavedthewayforthecurrentproliferationofe-paymentmethods.E-paymentsnowrangefromstandardbanktransfersandcardpayments,toInternet-basedconsumptionandtransactions,tomobilewallets,andontovirtualcurrencyexchangessuchascryptocurrenciesanddistributedledgertechnologies.Commonusecasesofdigitalpaymentshavestretchedbeyondtraditionalretailandpeer-to-peer(P2P)paymentsandnowincludegovernment-to-people(G2P)payments,cross-borderremittances,transportation,andin-apppurchasesonsmartphones.

Withsuchvarietye-paymentsholdabroadrangeofpromisesforindividuals,communities,andespeciallyfordevelopingeconomiesandsmallandmedium-sizedenterprises(SMEs)thathavetypicallybeenleftbehindbythebrick-and-mortarmodeloffinancialservices.Mobilemoney,forexample,canextendfinancialaccesstotheunbanked,enablingthemtotransferfundsconvenientlyandsafely,whileonlineandmobilepaymentsenableSMEstoexpandmarketreachandengageincrossbordertradebyofferingfast,secureandpredictableflowsoffunds.Forgovernments,digitizedpaymentsenablefarmoreeffectivedisbursementsoffundssuchaspensions,salariesandsocialwelfarepayments,increasingreachandtransparency,reducingcorruption,andensuringaccountability.

Despiteitspotential,thepaceofe-paymentsadoptionisstillconstrainedinmanypartsoftheworld.Outofthetwobillionpeoplewithoutaccesstoformalfinancialservices,1.12billionarefromAsiaPacific,wherecashstillremainsthepreferredmediumofpayment.2Moreover,differingregulatoryframeworksacrosstheregionalongwithdifferentdefinitionsofwhatconstitutespayments–orwhatisapaymentsbusiness–constraincross-bordere-payments.

Thispaperispremisedaroundasimplehypothesis:thatbyincreasingopenaccesstopayments(i.e.removingconstraintsonpaymentsaccess)therewillbeacorrespondinggrowthineconomicdevelopment(GDP).

Thepurposeofthisstudythereforeistolookintothetrendsanddifferences,toexaminethestatusofe-paymentpenetrationacrosstheAPECeconomies,andthelevelofadvancementofeacheconomy’se-paymentecosystemforsupportingfuturedevelopmentandadoption.Insodoing,thestudyprovidesaroadmapofpotentialpathwaysandkeyconsiderationsforexpandinge-paymentadoptionacrossAPECeconomies,andthusbeingabletorealisethesocioeconomicbenefitsthatadoptioncanbring.

Thestudyisdividedintotwodistinctcomponents:

1. TheAPECE-paymentIndex,gaugingthereadinessandcapacityofeachofthe21economiesthatcompriseAPECtoengageine-payment,tousebothe-paymentandm-paymentservices,andtofurtherdeveloptheiroveralle-paymentecosystem.The2016APECE-paymentIndexhasfine-tuned19indicatorsoutofthe44usedwithnewerstatisticsormorerelevantindicatorsthathavebecomeavailablesincethepublicationofthe2015APECE-paymentIndex.

2AsiaPacificherereferstoEastAsia,SouthAsiaandthePacificaccordingtotheGSMAclassification.Formoreinformation,seeGSMA(2016)2015TheStateoftheIndustryReport:MobileMoney.

7

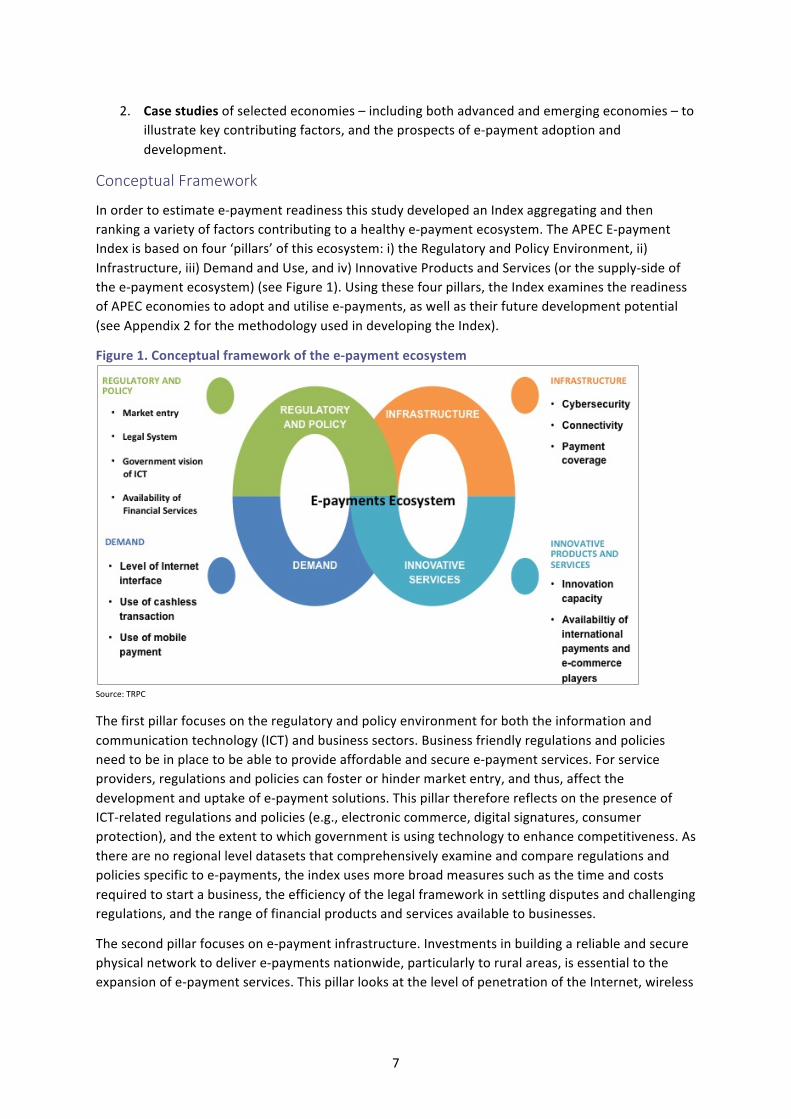

2. Casestudiesofselectedeconomies–includingbothadvancedandemergingeconomies–to

illustratekeycontributingfactors,andtheprospectsofe-paymentadoptionanddevelopment.

ConceptualFramework

Inordertoestimatee-paymentreadinessthisstudydevelopedanIndexaggregatingandthenrankingavarietyoffactorscontributingtoahealthye-paymentecosystem.TheAPECE-paymentIndexisbasedonfour‘pillars’ofthisecosystem:i)theRegulatoryandPolicyEnvironment,ii)Infrastructure,iii)DemandandUse,andiv)InnovativeProductsandServices(orthesupply-sideofthee-paymentecosystem)(seeFigure1).Usingthesefourpillars,theIndexexaminesthereadinessofAPECeconomiestoadoptandutilisee-payments,aswellastheirfuturedevelopmentpotential(seeAppendix2forthemethodologyusedindevelopingtheIndex).

Figure1.Conceptualframeworkofthee-paymentecosystem

Source:TRPC

Thefirstpillarfocusesontheregulatoryandpolicyenvironmentforboththeinformationandcommunicationtechnology(ICT)andbusinesssectors.Businessfriendlyregulationsandpoliciesneedtobeinplacetobeabletoprovideaffordableandsecuree-paymentservices.Forserviceproviders,regulationsandpoliciescanfosterorhindermarketentry,andthus,affectthedevelopmentanduptakeofe-paymentsolutions.ThispillarthereforereflectsonthepresenceofICT-relatedregulationsandpolicies(e.g.,electroniccommerce,digitalsignatures,consumerprotection),andtheextenttowhichgovernmentisusingtechnologytoenhancecompetitiveness.Astherearenoregionalleveldatasetsthatcomprehensivelyexamineandcompareregulationsandpoliciesspecifictoe-payments,theindexusesmorebroadmeasuressuchasthetimeandcostsrequiredtostartabusiness,theefficiencyofthelegalframeworkinsettlingdisputesandchallengingregulations,andtherangeoffinancialproductsandservicesavailabletobusinesses.

Thesecondpillarfocusesone-paymentinfrastructure.Investmentsinbuildingareliableandsecurephysicalnetworktodelivere-paymentsnationwide,particularlytoruralareas,isessentialtotheexpansionofe-paymentservices.ThispillarlooksatthelevelofpenetrationoftheInternet,wireless

8

broadband,mobilephonesandsmartphones,aswellasthenumberofATMsandcommercialbankbranchesineacheconomy.Italsoexaminesnationalcapabilitiesincybersecurity.

Thethirdpillarfocusesontheleveloflatentandactualdemandfore-paymentsfrombusinessesandconsumers,astheiracceptanceandusageofe-paymentservicesarekeytoathrivinge-paymentecosystem.Thepillargaugestheeconomies’useofthevariouschannelsfore-payment,includingcreditanddebitcards,onlineandmobileoptions,andthroughsocialmediasites.

Thefourthpillarfocusesonthesupply-sideofe-paymentandtheeconomies'readinesstodevelopinnovativee-paymentsolutionsandbusinessmodelsbylookingatthelevelofcompetitiveness,venturecapitalavailability,andpresenceofinternationalplayersinbothe-commerceandonlinepaymentssuchasAlibaba,Alipay,Amazon,Bitcoin,eBay,PayPal,TaobaoandTenpay.Intheupdated2016report,thispillarreceivedthemostchanges,with4outofthe9indicatorspreviouslyusedfromtheWorldEconomicForum’sGlobalCompetitivenessReportreplacedwithmorerigorousandrelevantonesfromtheGlobalInnovationIndexpublishedin2015(SeeAppendix2fordetails).

Thecentralpremiseofthisstudyisthatanincreaseinaccesstoandusageofe-paymentswilllead,fairlydirectly,toanincreaseineconomicgrowth.Acorollarypositionisthatthegreaterfinancialdepthcreatedbyatransitiontoe-paymentshasapositiveimpactonsocioeconomicdevelopment.Thereisalreadyampleevidenceestablishingaconcretecorrelationbetweene-paymentsandeconomicgrowthtosupportthisargument.Moody’sAnalytics,forexample,conductedastudylookingatelectroniccardusagein70countries.ThestudyfoundthatelectroniccardusageaddedUSD296billiontorealGDPfrom2011to2015,equivalenttoa0.1cumulativeincreaseinglobalGDPduringthesampletimeperiod.Higherelectroniccardsusagealsoaccountedforanaverageincreaseof2.6millionjobsperyearacrossthecountriessampledduringthesameperiod.3Similarly,ImperialCollegeLondonestimatesthatmoving25%ofpaper-basedtransactionstodigitalinretailpayments,G2P,e-commerce,cross-borderremittancesandSMEs,governments,businessesandconsumerscouldunlockbetweenUSD350to400inannualsavings.4

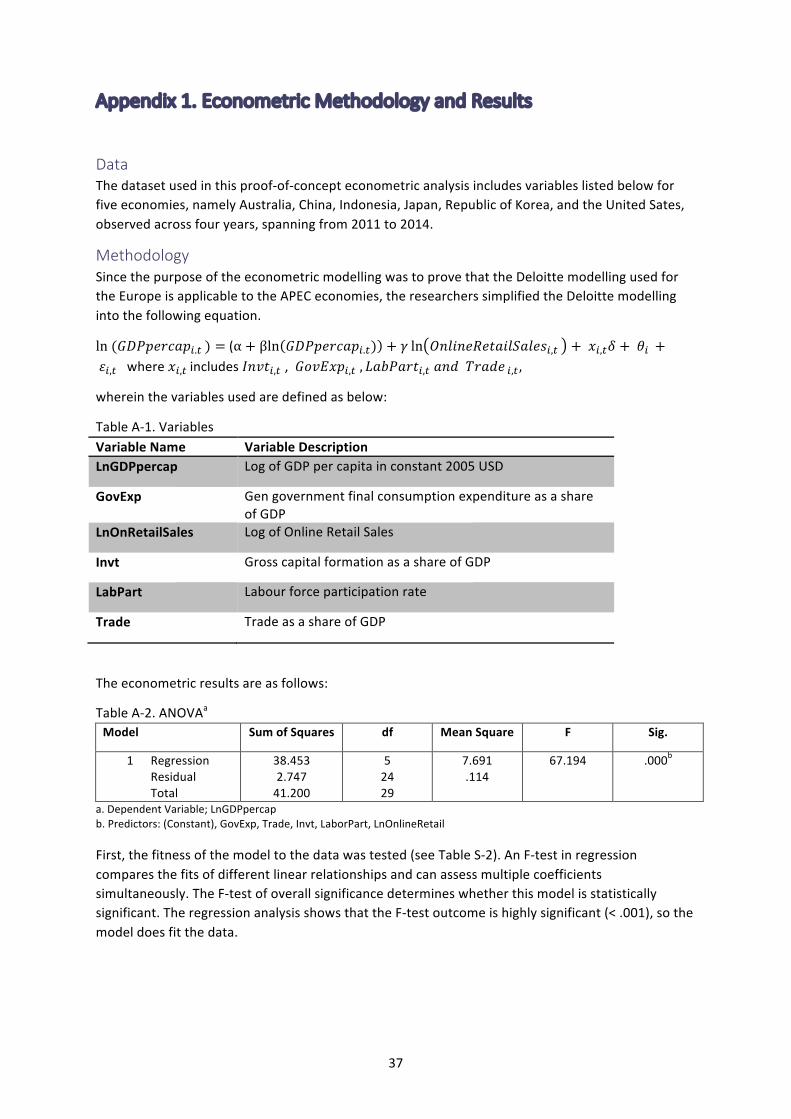

Takingthisastepfurther,Deloitteusedaneconometricmodellingtoquantifytheeffectsofanincreaseinonlineretailasaproxytoe-paymentsoneconomicgrowthacrossEuropeandfoundthatthetotalcontributionofonlineretailenabledbyonlinepayments,between2009and2012,tobeatleast1%ofGDPpercapita.5Asitisbeyondthescopeofthisstudytobuildaseparateeconometricmodeltoquantifytheeconomicimpactofonlinepaymentsacrossall21APECeconomies,aproof-of-conceptexercisewascarriedoutusingDeloitte’sregressionmodeltotestthecorrelation.

UsingsampledatafromsixAPECeconomiesoverfouryears,from2011to2014(includingamixofadvancedandemergingeconomies:seeAppendix1),amulti-regressionanalysiswascarriedouttoestimatetheelasticitybetweenonlineretailsaleandeconomicgrowth.Theresultssuggestthata1%changeinonlineretailsalesenabledbye-paymentsisassociatedwith0.175%changeinGDPpercapitaamongtheseeconomies,a57%increasecomparedtothepreviousstudywherea1%changeinonlineretailaccountedfora0.1%changeinGDPpercapitaover2011-2013.

3Moody’sAnalytics(2016)TheImpactofElectronicPaymentsonEconomicGrowth,https://usa.visa.com/dam/VCOM/download/visa-everywhere/global-impact/impact-of-electronic-payments-on-economic-growth.pdf4ImperialCollegeLondon(2016)ReleasingtheFlowofDigitalMoney:HittingtheTippingPointofAdoption,https://www.citibank.com/icg/sa/digital_symposium/digital_money_2016/pdf/releasing_the_flow_of_digital_money.pdf5TheeconomicgrowthliteraturethatDeloitteandthisstudydrewthemethodologicalapproachfromincludesBarro(1992),Mankiw,RomerandWeil(1992)andCaselli,EsquivelandLefort(1998).

9

WhencombinedwiththeconclusionsemergingfromtheE-paymentIndex,webelievethatthisresultmeritsfurtherstudyutilizingpaneldataacrossallAPECeconomiesandoverasustainedperiodoftimetobetterunderstandtheeconomicimpactofe-paymentadoption.

2.APECE-paymentIndex

ThissectiondetailsthedevelopmentoftheAPECE-paymentIndexandsummarisesthekeytrendsandinsightsthatemergefromananalysisoftheIndex.

Table1.TheAPECE-paymentIndex:OverallRanksAPECishighlydiversifiedintermsofreadinessandadvancementofe-paymentecosystems.

Whileintuitive,itisworthrecognizingupfrontthatAPECeconomies’readinesstoadoptandutilisee-paymentsvarieswidely.Overall,theUnitedStatesretaineditsfirstpositionwithintheAPECE-paymentIndexwithascoreof66.9(outofapossible100–seebelowfordetails),whileattheotherendofthetablePapuaNewGuineacameinlastwithascoreof23.9.

Between2015and2016,11ofthe21APECeconomieshadashiftinrankings.Perumarkedthebiggestgainbymovingupthreeplacesto16th.Canadamoveduptwopositionsto3rd,whiletheRepublicofKorea,China,theRussianFederation,andMexicoallmoveduponeplaceto6th,12th,13th,and17threspectively.Chile,IndonesiaandthePhilippinesfelltwoplacesto14th,18th,and19threspectively,whileNewZealandalsofell1placedownto5th.

APEC’soveralle-paymentecosystemisimproving,thankstothetransitioningeconomies

Comparedto2015,theaveragee-paymentreadinessscoreofthe21APECeconomieshasimprovedfrom41.6to44.6.Themedianscoreisalsoupto43.4,from37.2inthepreviousyear.Thissignalsanoverallimprovementinthee-paymentecosystemoftheregionwiththebottomtiergroupmovingupatafasterratethantherestoftheclusters.

Thereadinessandcapacityofaneconomytoengageine-paymentisstronglyinfluencedbyitsstageofdevelopment.

Rank Economy ScoresChangesinRanking

1 UnitedStatesofAmerica 66.9 -

2 Singapore 62.9 -

3 Canada 62.4 (+2)

4 Australia 60.6 -

5 NewZealand 60.4 (-2)

6 Korea,Rep. 59.9 (+1)

7 HongKong,China 59.3 (-1)

8 Japan 55.5 -

9 ChineseTaipei 52.9 -

10 Malaysia 45.5 -

11 BruneiDarussalam 42.4 -

12 China 37.5 (+1)

13 RussianFederation 37.4 (+1)

14 Chile 36.2 (-2)

15 Thailand 33.2 -

16 Peru 29.5 (+3)

17 Mexico 29.1 (+1)

18 Indonesia 28.4 (-2)

19 Philippines 26.0 (-2)

20 Vietnam 25.6 -

21 PapuaNewGuinea 23.9 -

10

Thelevelofeconomicdevelopmentofaneconomyis,ofcourse,onekeyfactordrivingsuchawiderange.Indeed,astrongcorrelationemergeswhentheeconomies’e-paymentindexrankingsareoverlaidagainstGDPpercapita,(Figure2);thehighertheincome,thebettertheeconomytendstodointherankingoftheAPECE-paymentIndex.6Exceptionsdoexistinthiscase;BruneiDarussalam,forinstance,appearstolaginrankingcomparetoitspeersofthesimilarincomerangewhileMalaysiaandChinashowhigherrankingrelativetotheirincomepeers.

Figure2.RelationshipbetweenAPECE-paymentIndexrankingsandincomelevel

Source:WorldDevelopmentIndicators(2014);forChineseTaipei,NominalGDPpercapita,2014obtainedfromNationalStatistics,RepublicofChina(ChineseTaipei)

OncetheAPECe-PaymentIndexscoresareoverlaidagainstincomelevels,thefollowingthreeclustersemerge:advanced,transitioning,and,emerging(Figure3):

• Cluster1:Economieswithadvancede-paymentecosystems(>55points)–UnitedStatesofAmerica,Singapore,Canada,Australia,NewZealand,RepublicofKorea,HongKongChina,andJapan

• Cluster2:Economieswithtransitioninge-paymentecosystems(between35–55points)–ChineseTaipei,Malaysia,BruneiDarussalam,China,RussianFederation,andChile

• Cluster3:Economieswithnascentandemerginge-paymentecosystems(<35points)–Thailand,Peru,Mexico,Indonesia,Philippines,Vietnam,andPapuaNewGuinea

6TheR-squaredvalueofthelogarithmictrendlineis0.7662,whichshowsagoodfitofthedataandthusastrongcorrelationbetweentheAPECe-paymentreadinessrankingsandlevelofeconomicgrowth.

11

Figure3.RelationshipbetweenAPECE-paymentIndexscoresandIncomelevel

Source:WorldDevelopmentIndicators(2014);forChineseTaipei,NominalGDPpercapita,2014obtainedfromNationalStatistics,RepublicofChina(ChineseTaipei)

WhencomparedwiththeWorldBank’sincomeclassification,Clusters1and2arecomprisedmainlyofhigh-incomeeconomies,withtheexceptionofMalaysia,andChina(upper-middleincomeeconomies).ThisdemonstratesthatMalaysia,andChinahaveachievedhighe-paymentreadinessrelativetotheirlevelofeconomicdevelopment.AfurthernotablecomparatorhereisbetweenMalaysiaandMexico,twoeconomieswithroughlysimilarlevelsofGDPpercapitaandyetstarklydifferentlevelsofe-paymentsreadiness.Cluster3comprisesmostlyupper-middleandlower-middleincomeeconomies,againdemonstratingthestrongpositiverelationshipbetweenthelevelofe-paymentreadinessandthelevelofeconomicdevelopment.

Table2.ClustersoftheAPECE-paymentIndexClusters APECE-paymentIndex WorldBankIncome

ClassificationCluster1(>55pts)

1. UnitedStatesofAmerica

2. Singapore3. Canada4. Australia

5. NewZealand6. RepublicofKorea7. HongKong8. Japan

Allhigh-incomeeconomiesexceptMalaysiaandChina

Cluster2(35-55pts)

9. ChineseTaipei10. Malaysia11. BruneiDarussalam

12. China13. RussianFederation14. Chile

Cluster3(<35pts)

15. Thailand16. Peru17. Mexico18. Indonesia

19. Philippines20. Vietnam21. PapuaNewGuinea

Allupper-middleandlower-middleincomeeconomies

High-incomeeconomiesaremorelikelytohaveathrivingecosystemfore-payments.

BasedonthestronglinkagebetweenGDPpercapitaande-paymentreadiness,high-incomeeconomiesarelikelytohavemadesignificantprogressinthefourpillarsthatmakeupthee-paymentecosystem.EconomiesinCluster1,forinstance,havemoreadvancedbankingandpaymentsystems,withwell-establishedregulationsandinfrastructurefore-paymentsinplace.A

12

largerpercentageofitspopulationhasbankaccounts,andisfamiliarwithcreditcardsanddebitcards,andonlineshopping.

Cluster1:Economies

Overall,theUnitedStatesrankshighestbasedonitsstrengthsininnovation(1st),infrastructure(2nd)anddemand(4th).Fromtherankingbypillar(Table3),theUnitedStatestakestheleadintheinnovationpillar.US-foundedcompaniessuchasAmazon,Google,andPayPalaswellasmajorcreditcardcompanieslikeAmericanExpress,MasterCardandVisaareinternationally-recognisedinnovatorsine-payment.TheintensityofcompetitionandtheavailabilityofventurecapitalintheUSareleadingtothedevelopmentofinnovativee-paymentproductsandservices.Forexample,USFinTechcompaniessawa72%risefundingin2015year-on-year,whichtotalledUSD$7.9billion,whichismorethanhalfoftheglobalshare.WhileFinTechactivitiesmayhavetaperedsincethen,fundingrecoveredbyUSFinTechcompaniescontinuetodwarfotherregions(USD$4.5billionforAsiaandUSD$1.5billionforEurope).7Thiscapacitytoinnovateislinkedwithanadvanceddigitalinfrastructureaswellasonlineandsocialtechnologies,whichareinturnsparkingdemandfornewservicesandfunctionalitiesthatincreasetheconvenienceandreliabilityofmakingpayments.

Singapore’srunner-upstatusintheIndexisfuelledbyitstoprankingintheregulatoryandpolicypillar.TheGovernmentofSingaporetakesatop-downapproachindevelopingitsdigitaleconomywithaclear-eyedstrategytobuildaSmartNationandfocusonbusinessstart-ups.Theimportanceoftheanaloguecomponentsofthedigitalpaymentsecosystem,namelyafavourablepolicyandregulatoryenvironmentcannotbestressedenoughandisshownbytheIndexresultstobefundamentalinattractinginvestment,drivinginnovation,andstimulatingthenecessaryemergenceofdemandfore-paymentproductsandservices.

Canada,rankingthirdoverall,moveduptworanksfrom2015,scoreshigh–perhapssurprisinglyforsome–inthedemandpillar(tied2ndwithAustralia)wherethetopthreeeconomiesscorewithin0.1pointfromeachother.Supportingthisresult,aGfKstudycorroboratesCanadian’sstrongpreferencefornon-cashpayments,reportingthatonly1in4transactionsinCanadausedcashin2015.8Thesamestudyalsofoundthatmobilepaymentsweregainingtraction,with63%ofCanadianconsumersreportedmakingatleastonemobiletransactionpermonthinthesameyear,up3%from2014.9Canada’spolicyandregulatoryenvironment(5th)andinfrastructure(4th)fore-paymentsalsoscoredrelativelystrong.ItisworthnotingthatCanadahasasignificantlyhigherpercentageofcreditcardownershipandusage,at77%and73%respectively,thanotherAPECeconomies.(JapanisnextamongAPECeconomieswith66%creditcardownershipand52%creditcarduse–asizeabledifference.ThegapisevengreaterwhencomparedwitheconomiesinClusters2and3.InMalaysia,only20%ofthepopulationownsacreditcard,andinIndonesiaonly2%.)

AccordingtoWorldPay,creditcardsconstitutethegreatestproportionofnon-cashtransactionsconductedgloballyintermsofonlinetransactionpurchasevalue(55%),followedbye-walletaccounts(22%)in2014.10Creditcardande-walletadoptionratesaresignificantlyhigherinhigh-incomeeconomies,whichreinforcesthepointthatpopulationsinhigh-incomeeconomiesaremoreabletoperforme-paymenttransactions.However,asthevarietyofe-paymentoptionsgrowand

7KPMGandCBInsight(2016)PulseofFintech2015Review,https://home.kpmg.com/content/dam/kpmg/pdf/2016/06/pulse-of-fintech-2015-review.pdf8GfK(2016)FutureBuystudy,http://www.gfk.com/en-us/insights/press-release/canadians-preference-for-non-cash-payment-methods-continues-to-grow-gfk-study/9Ibid10WorldPay2015citedinUnitedNationsConferenceonTradeandDevelopment(2016)B2CE-CommerceIndex2016,http://unctad.org/en/PublicationsLibrary/tn_unctad_ict4d07_en.pdf

13

accesstoe-paymentincreasesitispreciselythiscategoryofcredit/debitcardsandbankaccountsweseegivingway,asthetransactionsbasecontinuestotransform.Well-positionedeconomiesinClusters2and3willbeabletomaketheleapbybestenablingtheirpopulationstoadopte-paymentsoutsidetheuseofcredit/debitcardsandbankaccounts.

AustraliaandNewZealandrankfourthandfifth,respectively,scoringrelativelywellinthreeofthefourpillars.InAustralia,thehighInternetandsmartphonepenetration,andhighusageofe-paymentmethodsallowittoscorerelativelywellininfrastructure(3rd)anddemand(tied2ndwithCanada),withfiguressimilartoNewZealand.Forinstance,82%ofAustraliansusedebitcards(comparedwith92%ofNewZealanders),and68%ofAustraliansusetheInternettopaybillsorbuythings(comparedwith72%ofNewZealanders).IntheG20E-tradeReadinessIndex,Australiatoppedtherankings,andoneofthereasonswasduetotheeconomy’shighuseofe-paymentmethods.Anotherreasonwasrelatedtoitsrelativelywell-developeddigitalinfrastructure–althoughthisisoneareawhichtherehasbeendomesticconsternationinrecentyearswithalackofconsensusinpoliticalwill.11

ForNewZealand,itsoverallrankingwentdownby2spotsalthoughitdidmanagetoascendtothetopspotinthedemandpillar,albeitwithaslightlyhigherscorethanAustraliaandCanada,tiedat2ndspot.Italsoscoredrelativelyhighinregulatoryandpolicy(4th),infrastructure(6th)andinnovation(8th).NewZealandhasthemostfavourableregulatoryenvironmentforstartingupabusiness,andtheuseofe-paymentsisalreadyquitehighwithover90%ofitspopulationusingdebitcards,andover70%ofitspopulationusingtheInternettopaybillsormakepurchases.12Forbothoftheseindicators,NewZealandrankshighestamongallAPECeconomies.

NoeconomydominatestheIndexbytoppingmorethanonepillarinthee-paymentecosystem.

FromTable3andfromtheprecedingobservationsonCluster1economies,itcanbeseenthatnoneoftheeconomiestopmorethanoneofthepillarsinthee-paymentecosystem.Moreover,onlyCanadarankedinthetopfiveinallfourpillars,meaningthatmajorityoftheeconomieshavethepotentialtoimproveinoneormoreaspectsoftheire-paymentecosystem.

Forinstance,theUnitedStatesleadsinthedevelopmentofinnovativeproductsandservicesbutranks6thintheprovisionofaregulatoryandpolicyenvironmentfore-payments.Singaporeisthefrontrunnerinofferingafavourableregulatoryandpolicyenvironmentfore-paymentsbutranksonly6thindemandandusage.Oneinterestingindicatorinthisregard:only28%ofSingaporeansusetheInternettopaybillsorbuythings.13Canadaleadsinthedemandpillarbutits5thrankinregulatoryandpolicyenvironmentpullsdownitsoverallranking.TheRepublicofKorea,oneoftheworld’smostdigitallyconnectedsocieties,notsurprisinglyscoreshighestforinfrastructure,butranksonly11thintheregulatoryandpolicyenvironmentpillar.Oneofthereasonsforthisisthat,whilethelawsrelatingtoICTsarewelldevelopedinKorea,lawsrelatingtothebankingandfinancialservicessectorshavenotadjustedquicklytoinnovationsappearinginICT,leavingnewinnovativeareassuchasFinTech,ratherlesscompetitivethanmightotherwisebeexpected.Thereisthusroomforimprovementintheefficiencyofthelegalframeworksforfinancialservices,inparticularwhereitoverlapswithICT.Thisneedforcross-sectoralunderstanding,awarenessandresponsivenessine-paymentsisathemethatcomesthroughtimeandagaininlookingattherankingsacrosstheAPECE-paymentsIndex.

11TheEconomistIntelligenceUnit(2014)TheG20e-TradeReadinessIndex,https://www.eiuperspectives.economist.com/sites/default/files/Laurel%20West%20-%20eBay%20-%20The%20Global%20e-trade%20Readiness%20Index%20Final%20V2_0.pdf12WorldBank(2014)GlobalFindex,http://datatopics.worldbank.org/financialinclusion/13Ibid

14

Table3.TheAPECE-paymentIndexrankingsandscores,bypillar P1.Regulatory

&PolicyEnvironment

P2.Infrastructure

P3.Demand P4.InnovativeProducts&services

Rank Score Rank Score Rank Score Rank Score

1 UnitedStatesofAmerica 6 67.0 2 72.5 4 54.1 1 77.5

2 Singapore 1 96.4 7 59.7 5 48.4 5 55.9

3 Canada 5 68.3 4 66.8 2 56.1 2 59.3

4 Australia 8 62.2 3 70.5 2 56.1 7 51.0

5 NewZealand 4 77.1 6 60.2 1 56.2 8 50.0

6 Korea,Rep. 11 48.8 1 78.9 5 49.3 3 58.3

7 HongKong,China 2 83.8 9 57.7 9 45.8 4 57.4

8 Japan 7 64.7 5 63.2 10 42.7 6 54.0

9 ChineseTaipei 9 58.4 8 58.6 8 46.6 9 48.3

10 Malaysia 3 80.6 11 40.8 11 34.2 13 34.4

11 BruneiDarussalam 12 47.4 12 39.0 7 46.6 12 36.3

12 China 15 42.7 16 37.7 13 28.6 10 45.4

13 RussianFederation 20 24.6 10 50.5 12 32.0 11 38.6

14 Chile 10 52.3 14 38.4 14 28.5 17 28.6

15 Thailand 16 35.6 15 37.9 15 28.2 15 31.2

16 Peru 21 24.1 13 39.3 17 23.1 16 29.8

17 Mexico 19 28.3 17 29.3 16 27.1 14 32.8

18 Indonesia 14 42.8 18 28.9 21 18.9 19 27.7

19 Philippines 17 32.0 19 28.7 18 21.1 20 23.4

20 Vietnam 18 31.1 20 25.4 19 20.4 18 28.0

21 PapuaNewGuinea 13 47.1 21 15.5 20 20.4 21 18.6

Othernotablestrengthsandweaknessesareworthcallingout.TheseincludetheremarkablyrapidpaceofdevelopmentintheChinesemarket,internationallyknownforwidelyadoptede-paymentsolutionssuchasAlipay,TaobaoandTenpay,butstillneedingtoovercomeregulatoryandinfrastructurechallengesinordertofullyleveragetheopportunities.InJapan,itspaymentsinfrastructureismature(ranks5th),whileitsdemandfore-paymentissurprisinglylow(ranked10th).AmongAPECeconomies,theJapanesespendtheleastamountoftimeontheInternetandonsocialmedia,andonly8%ofitspopulationusemobilebanking,despitetheubiquityofmobileusageelsewhereinotheraspectsofJapaneselife.Thelackofprevalentinternationale-paymentsolutionsinJapan,andthelackofsuccessofJapanesee-paymentssolutionsinforeignmarketscouldexplainJapan’slowuptakeofmobilebanking.

Astheresultsshow,thereisnosinglepathwaytopromotinganddevelopinge-payment.Thismeansthatforpolicymakerse-paymentisanareathatneedstobedevelopedholisticallybyconsideringthewaysinwhicheachofthepillarsinthee-paymentecosystemaffecteachother

15

withinthecontextofeachindividualeconomy.Andthismeansthatpolicymakersneedtohaveabroadappreciationofhowthesefactorsworkiftheyaretocreateaneffectiveframework.

Moreover,whilegrowthandinnovationine-paymentcancomefromallincomelevelsandfromallmannerofsocialgroups,thetypesofinnovationfindingtractioninaneconomydifferasdifferentneedsareaddressedanddifferentsocialgroupsserviced.

Cluster1economiesgenerallyhavealongerhistoryofthedevelopmentanduseofe-paymentservices.Theseeconomieshavealargepercentageoftheirpopulationalreadyusingcreditanddebitcards,andarefamiliarwithATMsand,increasingly,withonlinebanking.Heree-paymentinnovationsaimtoincreaseconvenience,flexibilityandsecurityforconsumers;whileforbusinessestheyenhancesalesandreducepaymentprocessingcosts.

ForeconomiesinClusters2and3,theemphasisisoftenonincreasingaccesstobasicfinancialservices,ontheonehand,andempoweringtheSMEe-commerceopportunity,ontheother.Intheseeconomiespeoplearelesslikelytohavebankaccountsandtheownershipofcreditcardsislower,butthosewithsmartphonesareincreasinglyusingthemtomakepaymentsofonesortoranother.ForSMEsthiscanmeanaccesstofundsforsettingupandexpandingtheirbusinesses;itcanmeanaccesstonewmarkets,whetheronthesupplysideordemandside,andunlockingthepotentialfore-commerce;anditcanmeanbeingabletoexecuteonpayrollorfinancewithouthavingtophysicallyvisitabankandcarrylargesumsofcash.Greateraccesstoe-paymentsdrawsmoreenterprisesintotheformalsector,raisingtaxrevenuesandmakingworkerseligibleforbetterprotectionandbenefits.14Forconsumers,accesstopaymentcanmeanaccesstoservicessuchashealthandeducation,andenhancedproductivitybyreducingthetimeittakestopayforservicesandproducts.

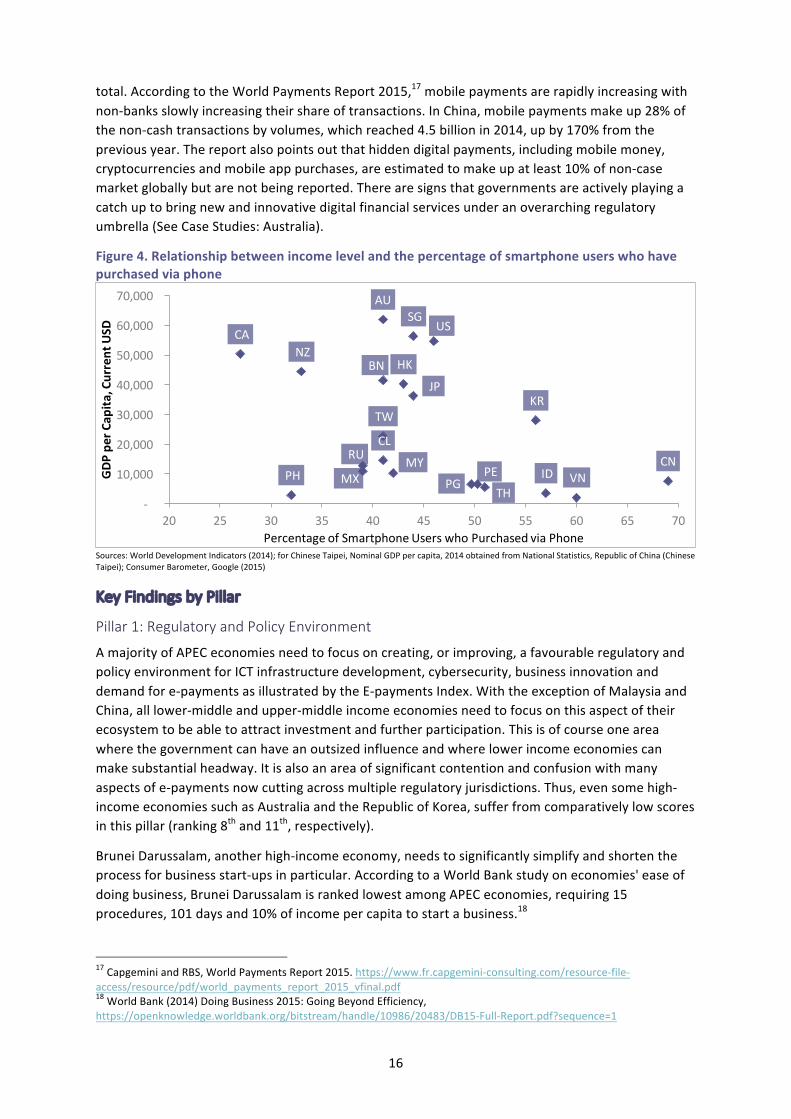

APECisrapidlybecoming‘mobilefirst’andsignificantgrowthwillbedrivenfromeconomieswithhighsmartphoneadoptionandwheretheproportionsofservicesofferedthroughsmartphonesareincreasing.Theseeconomiesarenotnecessarilyhigh-incomeeconomies.Forinstance,theeconomywiththehighestpercentageofsmartphoneuserswhohavemadepurchasesviatheirphoneisChina(69%),withsome930millionpeople–orthreetimesthetotalpopulationoftheUnitedStates–alreadyhavingdoneso.ThisisfollowedbyVietnam(60%),Indonesia(57%),RepublicofKorea(56%)andThailand(51%).However,inCanadaitis27%,NewZealand33%andAustralia41%.15Figure4showstheweakcorrelationbetweenGDPpercapitaandthepercentageofsmartphoneuserswhohavepurchasedviaphone.Thisisanarearequiringsignificantfurtherresearch.

Asmorepeoplebecomeconnected,particularlyinthelower-middleandupper-middleincomeeconomiesofCluster3,throughtherapiduptakeofmobilephonesandsocialmedia,themarketfore-paymentandm-paymentwillgrowexponentially.Furthermore,thevarietyofinnovativeproductsandservicesislikelytoincreasetomeetdemand,includingalternativee-paymentsystemsfortheunbankedconsumersegments.

SuchconclusionsaresupportedbyemergingstudiessuchastheUnitedNationsConferenceonTradeandDevelopment’slatestInformationEconomyReport,16whichfindsthatmostretaile-commercepaymentsarestillmadeviacreditcard,butby2017alternatepaymentswillmakeupthemajorityofalle-commercepayments,withe-walletsalonesettorepresentmorethan40%ofthe

14StandardChartered,FinancialInclusion:Reachingtheunbanked,4September2014.15OurMobilePlanet,Google(2014)http://think.withgoogle.com/mobileplanet/en/downloads16UnitedNationsConferenceonTradeandDevelopment(2015)InformationEconomyReport2015:UnlockingthePotentialofE-commerceforDevelopingCountries,http://unctad.org/en/PublicationsLibrary/ier2015_en.pdf

16

total.AccordingtotheWorldPaymentsReport2015,17mobilepaymentsarerapidlyincreasingwithnon-banksslowlyincreasingtheirshareoftransactions.InChina,mobilepaymentsmakeup28%ofthenon-cashtransactionsbyvolumes,whichreached4.5billionin2014,upby170%fromthepreviousyear.Thereportalsopointsoutthathiddendigitalpayments,includingmobilemoney,cryptocurrenciesandmobileapppurchases,areestimatedtomakeupatleast10%ofnon-casemarketgloballybutarenotbeingreported.Therearesignsthatgovernmentsareactivelyplayingacatchuptobringnewandinnovativedigitalfinancialservicesunderanoverarchingregulatoryumbrella(SeeCaseStudies:Australia).

Figure4.Relationshipbetweenincomelevelandthepercentageofsmartphoneuserswhohavepurchasedviaphone

Sources:WorldDevelopmentIndicators(2014);forChineseTaipei,NominalGDPpercapita,2014obtainedfromNationalStatistics,RepublicofChina(ChineseTaipei);ConsumerBarometer,Google(2015)

KeyFindingsbyPillar

Pillar1:RegulatoryandPolicyEnvironment

AmajorityofAPECeconomiesneedtofocusoncreating,orimproving,afavourableregulatoryandpolicyenvironmentforICTinfrastructuredevelopment,cybersecurity,businessinnovationanddemandfore-paymentsasillustratedbytheE-paymentsIndex.WiththeexceptionofMalaysiaandChina,alllower-middleandupper-middleincomeeconomiesneedtofocusonthisaspectoftheirecosystemtobeabletoattractinvestmentandfurtherparticipation.Thisisofcourseoneareawherethegovernmentcanhaveanoutsizedinfluenceandwherelowerincomeeconomiescanmakesubstantialheadway.Itisalsoanareaofsignificantcontentionandconfusionwithmanyaspectsofe-paymentsnowcuttingacrossmultipleregulatoryjurisdictions.Thus,evensomehigh-incomeeconomiessuchasAustraliaandtheRepublicofKorea,sufferfromcomparativelylowscoresinthispillar(ranking8thand11th,respectively).

BruneiDarussalam,anotherhigh-incomeeconomy,needstosignificantlysimplifyandshortentheprocessforbusinessstart-upsinparticular.AccordingtoaWorldBankstudyoneconomies'easeofdoingbusiness,BruneiDarussalamisrankedlowestamongAPECeconomies,requiring15procedures,101daysand10%ofincomepercapitatostartabusiness.18

17CapgeminiandRBS,WorldPaymentsReport2015.https://www.fr.capgemini-consulting.com/resource-file-access/resource/pdf/world_payments_report_2015_vfinal.pdf18WorldBank(2014)DoingBusiness2015:GoingBeyondEfficiency,https://openknowledge.worldbank.org/bitstream/handle/10986/20483/DB15-Full-Report.pdf?sequence=1

USSG

CA

AU

NZ

KR

HK

JP

TW

MY

BN

CNRUCL

THPEMX IDPH VNPG

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

20 25 30 35 40 45 50 55 60 65 70

GDPpe

rCap

ita,CurrentUSD

PercentageofSmartphoneUserswhoPurchasedviaPhone

17

InLatinAmerica,Chileismostadvancedine-payment(ranking14th),whilePeruandMexicorank16thand17th,respectively.Chilehoweverscorescomparativelyhigherintheregulatorypillar(10th)whileMexicoandPeruranklow(19thand21st).Overall,itisrelativelyeasytostartabusinessinthesethreeeconomies—withascoreforthisindicatorofover85outof100,buttheyallneedtoimprovetheefficiencyoftheirlegalframeworksforsettlingdisputesandchallenginggovernmentactionsandregulations.InMexicoandPeru,ICTcontinuestolielowonthegovernment’sagenda,whichisreflectedinthelowdevelopmentofthee-paymentecosystem,evenase-paymentbecomesincreasinglyICT-driven.

Table4.RegulatoryandPolicyEnvironmentTheresultsresonatewiththeG20E-tradeReadinessIndexwhichnotedthat“regulatorsinmanycountriesarestillstrugglingwiththequestionofhowtoregulatethepaymentsindustry.”19Thecreationofnewandinnovativepaymentsystemsonlyaccentuatestheneedforreviewingexistingpaymentsregulations,andreviewingthemonabroadercross-sectoralbasis.

Canada,forexample,hasbecomeoneofthefirstcountriestopassanationallawregulatingvirtualcurrenciessuchasbitcoinandXRP.20InAustralia,theAustralianPaymentsCouncilwasestablishedtobettercoordinatethecountry'spaymentsystemswithaviewtofosteringinnovation,ratherthanmerelyregulatingconservatively.Thisisperhapsthecentralchallengeforalleconomies:successfullyencouraginge-paymentoperatorsrequirescross-sectoralgovernmentcoordination,suchasawhole-of-government

approachoracoordinatinggovernmentagency.ForAPEC,e-paymentsregulatoryalignmentwillacceleratee-paymentsadoptionandusage,andthisinturnwilldrivecross-bordertransactionsandthusregionaleconomicgrowth.

19TheEconomistIntelligenceUnit(2014)TheG20e-TradeReadinessIndex,https://www.eiuperspectives.economist.com/sites/default/files/Laurel%20West%20-%20eBay%20-%20The%20Global%20e-trade%20Readiness%20Index%20Final%20V2_0.pdf20CapgeminiandRBS,WorldPaymentsReport2014,https://www.capgemini.com/thought-leadership/world-payments-report-2014-from-capgemini-and-rbs

Ranking Economy Scores RankingChanges

1 Singapore 96.4 -

2 HongKong,China 83.8 -

3 Malaysia 80.6 -

4 NewZealand 77.1 -

5 Canada 68.3 -

6 UnitedStatesofAmerica 67.0 -

7 Japan 64.7 -

8 Australia 62.2 (+1)

9 ChineseTaipei 58.4 (-1)

10 Chile 52.3 -

11 Korea 48.8 (+2)

12 BruneiDarussalam 47.4 -

13 Indonesia 47.1 (+2)

14 PapuaNewGuinea 42.8 -

15 China 42.7 (-3)

16 Thailand 35.6 -

17 Philippines 32.0 -

18 Vietnam 31.1 -

19 Mexico 28.3 -

20 RussianFederation 24.6 -

21 Peru 24.1 -

18

Pillar2:Infrastructure

Thegapordividebetweenhigh-income,upper-middle-incomeandlower-middle-incomeeconomiesismostobviousintheinfrastructurepillar.

Table5.InfrastructureForexample,thenumberofsecureserversusingencryptiontechnologyinInternettransactionsrangesfromsixperonemillionpeopleinIndonesiato2,178peronemillionpeopleintheRepublicofKorea.Internetpenetrationratesrangefrom9.4%inPapuaNewGuineato90.6%inJapan.Wirelessbroadbandsubscriptionratesrangefrom5.8%inPapuaNewGuineato156.1%inSingapore.Smartphonepenetration,however,showsarelativelysmallervariance,from21.9%inPapuaNewGuineato79.1%inAustralia.

AccordingtotheWorldEconomicForum,“ICTsareneitherasubiquitousnorspreadingasfastasmanybelieve.Some90%ofthepopulationinlow-incomecountries,andover60%globally,arenotonlineyet.”Itgoesontosuggestthat“asdevelopingcountriesleapfrogto4Gtechnology,thusenablingowners

ofsmartphonestoaccesstheInternet,Internetdiffusionmayaccelerateincomingyears.Pricesof4Gsmartphonesremainhigh,but—thankstoinnovationandcompetition—pricesareexpectedtokeepfalling.Alreadyone-sixthofsmartphonessoldin2013costlessthanUS$100.”21

AmongallAPECeconomies,onlyPapuaNewGuineahasachievedlessthan80%mobilepenetration,while15of21APECeconomieshavemobilepenetrationratesover100%,including144%inThailand,147%inVietnam,and128%inIndonesia.Asmorepeoplegetconnected,particularlyinCluster3economies,themarketformobilepaymentswillonlygrow,andgrowstrongly.Bridgingthedigitaldivideisthereforeessentialforfullyleveragingtheopportunitiesine-andm-payment.Thisincludesincreasingsmartphonepenetration,andbroadbandaccessandaffordability.Butthisrequiressignificantup-frontaswellascontinuousinvestmentsintelecommunicationandnetworkinfrastructure.Ensuringalevelplayingfieldandimprovingmarketconditionstoencouragebroad-

21WorldEconomicForum(2015)GlobalInformationTechnologyReport2015,http://www3.weforum.org/docs/WEF_Global_IT_Report_2015.pdf

Ranking Economy Scores RankingChanges

1 Korea 78.9 -

2 UnitedStatesofAmerica 72.5 -

3 Australia 70.5 -

4 Canada 66.8 -

5 Japan 63.2 (+1)

6 NewZealand 60.2 (-1)

7 Singapore 59.7 -

8 ChineseTaipei 58.2 (+1)

9 HongKong 57.7 (-1)

10 RussianFederation 50.5 -

11 Malaysia 40.8 (+2)

12 BruneiDarussalam 39.4 (-1)

13 Peru 39.3 (+3)

14 Chile 38.4 (-2)

15 Thailand 37.9 -

16 China 37.7 (-2)

17 Mexico 29.3 (+1)

18 Indonesia 28.9 (+1)

19 Philippines 28.7 (-2)

20 Vietnam 25.4 -

21 PapuaNewGuinea 15.5 -

19

basedparticipationandcompetitionrequiresregulatorycoordinationacrossregionaleconomiesandwouldhelpattractthenecessaryinvestment.

Innovationsinovercominginfrastructurechallengesarecontributingtohigheruptakeofe-paymentandm-paymentservices,andareactingasgatewaysintothebankingsystemfortheunbanked,orunderbanked,consumersegments.

Forexample,thehighcostoftraditionalbrick-and-mortarbankbrancheshashistoricallyconcentratedfinancialaccesspointsinurbanareaswherehigherpopulationdensitymakesthemprofitable.However,innovationssuchasmobilefinancialservicesandagentbanking,andthemodernisationofpostofficesprovidetheopportunitiesforruralandlow-incomeindividualstoaccessfinancialservices,includinge-payments.

TheWorldPaymentsReport201522notesthattheRussianFederation'snon-cashtransactionsgrewby37.7%during2012-2013,drivenbyanimprovedpaymentinfrastructure.Thenumberofpoint-of-saleterminals,forexample,grew23%annuallysince2011,leadingtoincreasedcardacceptance.TheRussianFederationranks10thininfrastructure–significantlyhigherthanitsrankinginotherpillars.

22CapgeminiandRBS,WorldPaymentsReport2014,https://www.capgemini.com/thought-leadership/world-payments-report-2014-from-capgemini-and-rbs

20

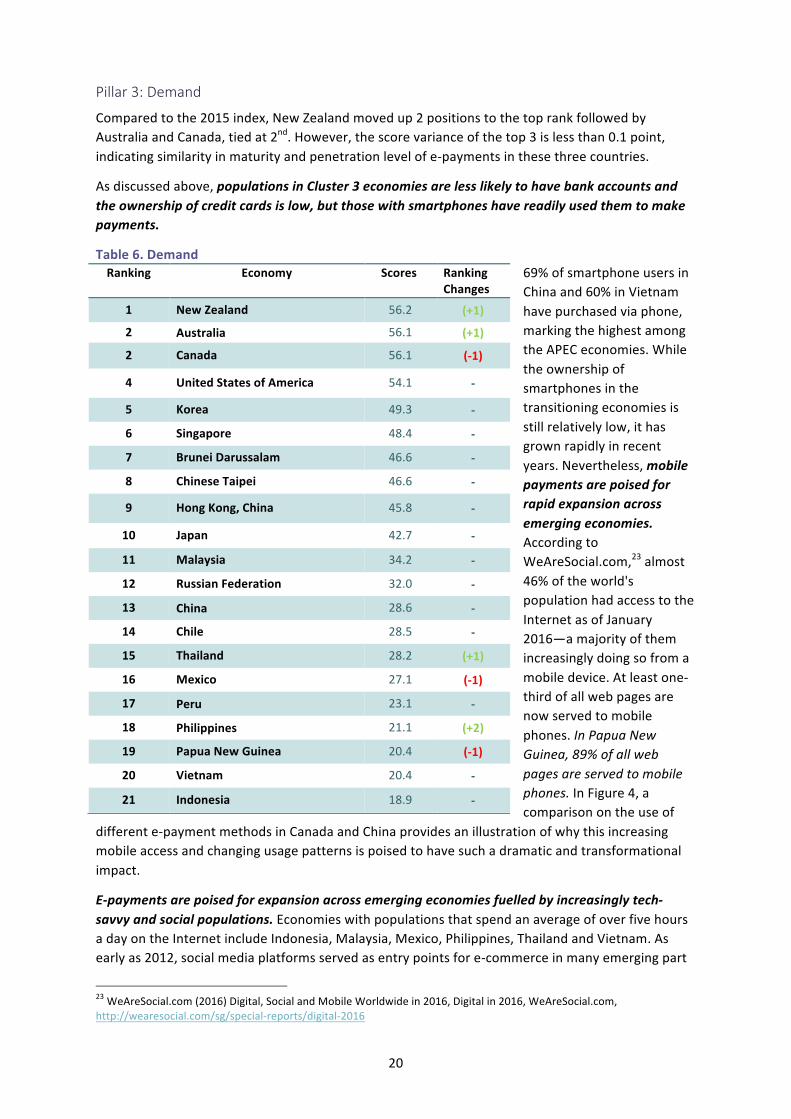

Pillar3:Demand

Comparedtothe2015index,NewZealandmovedup2positionstothetoprankfollowedbyAustraliaandCanada,tiedat2nd.However,thescorevarianceofthetop3islessthan0.1point,indicatingsimilarityinmaturityandpenetrationlevelofe-paymentsinthesethreecountries.

Asdiscussedabove,populationsinCluster3economiesarelesslikelytohavebankaccountsandtheownershipofcreditcardsislow,butthosewithsmartphoneshavereadilyusedthemtomakepayments.

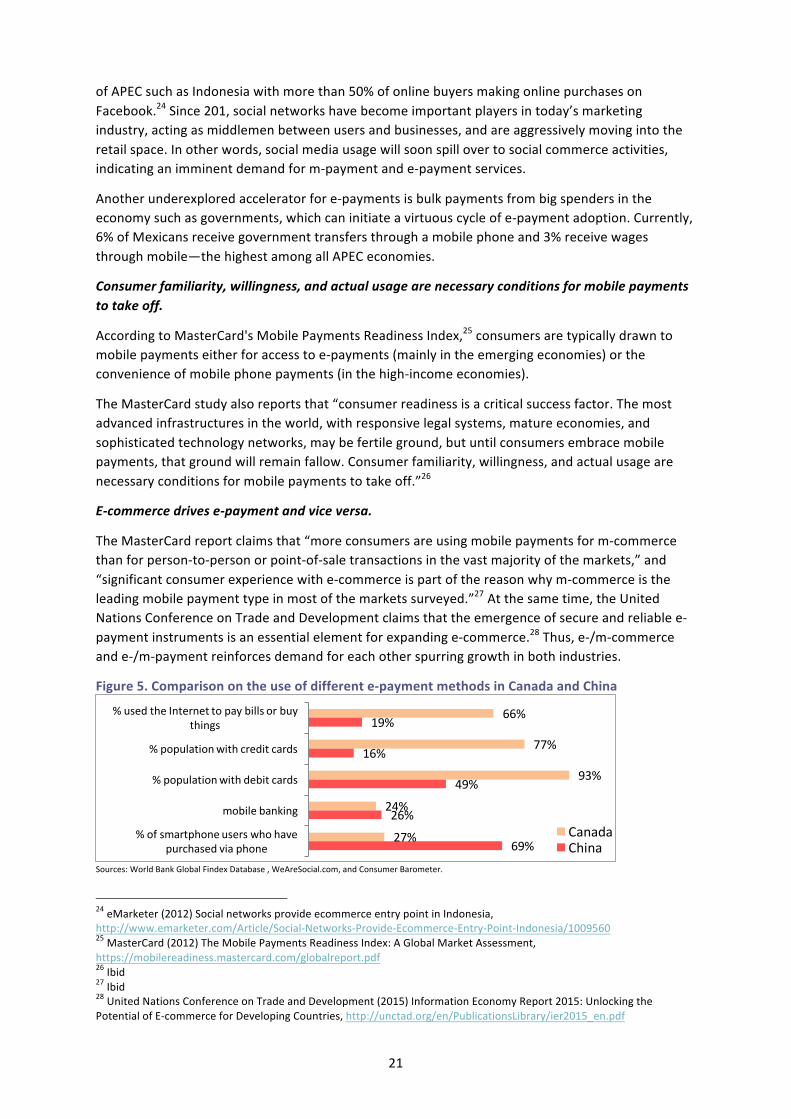

Table6.Demand69%ofsmartphoneusersinChinaand60%inVietnamhavepurchasedviaphone,markingthehighestamongtheAPECeconomies.Whiletheownershipofsmartphonesinthetransitioningeconomiesisstillrelativelylow,ithasgrownrapidlyinrecentyears.Nevertheless,mobilepaymentsarepoisedforrapidexpansionacrossemergingeconomies.AccordingtoWeAreSocial.com,23almost46%oftheworld'spopulationhadaccesstotheInternetasofJanuary2016—amajorityofthemincreasinglydoingsofromamobiledevice.Atleastone-thirdofallwebpagesarenowservedtomobilephones.InPapuaNewGuinea,89%ofallwebpagesareservedtomobilephones.InFigure4,acomparisonontheuseof

differente-paymentmethodsinCanadaandChinaprovidesanillustrationofwhythisincreasingmobileaccessandchangingusagepatternsispoisedtohavesuchadramaticandtransformationalimpact.

E-paymentsarepoisedforexpansionacrossemergingeconomiesfuelledbyincreasinglytech-savvyandsocialpopulations.EconomieswithpopulationsthatspendanaverageofoverfivehoursadayontheInternetincludeIndonesia,Malaysia,Mexico,Philippines,ThailandandVietnam.Asearlyas2012,socialmediaplatformsservedasentrypointsfore-commerceinmanyemergingpart

23WeAreSocial.com(2016)Digital,SocialandMobileWorldwidein2016,Digitalin2016,WeAreSocial.com,http://wearesocial.com/sg/special-reports/digital-2016

Ranking Economy Scores RankingChanges

1 NewZealand 56.2 (+1)

2 Australia 56.1 (+1)

2 Canada 56.1 (-1)

4 UnitedStatesofAmerica 54.1 -

5 Korea 49.3 -

6 Singapore 48.4 -

7 BruneiDarussalam 46.6 -

8 ChineseTaipei 46.6 -

9 HongKong,China 45.8 -

10 Japan 42.7 -

11 Malaysia 34.2 -

12 RussianFederation 32.0 -

13 China 28.6 -

14 Chile 28.5 -

15 Thailand 28.2 (+1)

16 Mexico 27.1 (-1)

17 Peru 23.1 -

18 Philippines 21.1 (+2)

19 PapuaNewGuinea 20.4 (-1)

20 Vietnam 20.4 -

21 Indonesia 18.9 -

21

ofAPECsuchasIndonesiawithmorethan50%ofonlinebuyersmakingonlinepurchasesonFacebook.24Since201,socialnetworkshavebecomeimportantplayersintoday’smarketingindustry,actingasmiddlemenbetweenusersandbusinesses,andareaggressivelymovingintotheretailspace.Inotherwords,socialmediausagewillsoonspillovertosocialcommerceactivities,indicatinganimminentdemandform-paymentande-paymentservices.

Anotherunderexploredacceleratorfore-paymentsisbulkpaymentsfrombigspendersintheeconomysuchasgovernments,whichcaninitiateavirtuouscycleofe-paymentadoption.Currently,6%ofMexicansreceivegovernmenttransfersthroughamobilephoneand3%receivewagesthroughmobile—thehighestamongallAPECeconomies.

Consumerfamiliarity,willingness,andactualusagearenecessaryconditionsformobilepaymentstotakeoff.

AccordingtoMasterCard'sMobilePaymentsReadinessIndex,25consumersaretypicallydrawntomobilepaymentseitherforaccesstoe-payments(mainlyintheemergingeconomies)ortheconvenienceofmobilephonepayments(inthehigh-incomeeconomies).

TheMasterCardstudyalsoreportsthat“consumerreadinessisacriticalsuccessfactor.Themostadvancedinfrastructuresintheworld,withresponsivelegalsystems,matureeconomies,andsophisticatedtechnologynetworks,maybefertileground,butuntilconsumersembracemobilepayments,thatgroundwillremainfallow.Consumerfamiliarity,willingness,andactualusagearenecessaryconditionsformobilepaymentstotakeoff.”26

E-commercedrivese-paymentandviceversa.

TheMasterCardreportclaimsthat“moreconsumersareusingmobilepaymentsform-commercethanforperson-to-personorpoint-of-saletransactionsinthevastmajorityofthemarkets,”and“significantconsumerexperiencewithe-commerceispartofthereasonwhym-commerceistheleadingmobilepaymenttypeinmostofthemarketssurveyed.”27Atthesametime,theUnitedNationsConferenceonTradeandDevelopmentclaimsthattheemergenceofsecureandreliablee-paymentinstrumentsisanessentialelementforexpandinge-commerce.28Thus,e-/m-commerceande-/m-paymentreinforcesdemandforeachotherspurringgrowthinbothindustries.

Figure5.Comparisonontheuseofdifferente-paymentmethodsinCanadaandChina

Sources:WorldBankGlobalFindexDatabase,WeAreSocial.com,andConsumerBarometer.

24eMarketer(2012)SocialnetworksprovideecommerceentrypointinIndonesia,http://www.emarketer.com/Article/Social-Networks-Provide-Ecommerce-Entry-Point-Indonesia/100956025MasterCard(2012)TheMobilePaymentsReadinessIndex:AGlobalMarketAssessment,https://mobilereadiness.mastercard.com/globalreport.pdf26Ibid27Ibid28UnitedNationsConferenceonTradeandDevelopment(2015)InformationEconomyReport2015:UnlockingthePotentialofE-commerceforDevelopingCountries,http://unctad.org/en/PublicationsLibrary/ier2015_en.pdf

66%

77%

93%

24%

27%

19%

16%

49%

26%

69%

%usedtheInternettopaybillsorbuythings

%populationwithcreditcards

%populationwithdebitcards

mobilebanking

%ofsmartphoneuserswhohavepurchasedviaphone

CanadaChina

22

Pillar4:Innovation

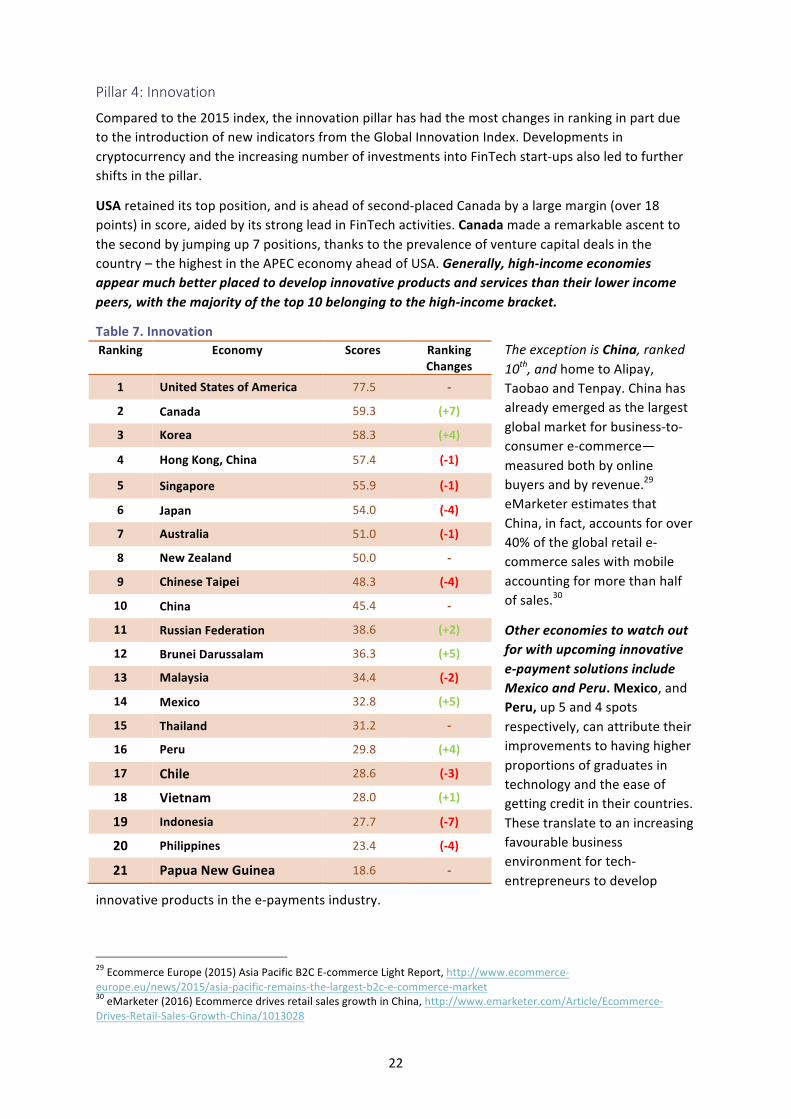

Comparedtothe2015index,theinnovationpillarhashadthemostchangesinrankinginpartduetotheintroductionofnewindicatorsfromtheGlobalInnovationIndex.DevelopmentsincryptocurrencyandtheincreasingnumberofinvestmentsintoFinTechstart-upsalsoledtofurthershiftsinthepillar.

USAretaineditstopposition,andisaheadofsecond-placedCanadabyalargemargin(over18points)inscore,aidedbyitsstrongleadinFinTechactivities.Canadamadearemarkableascenttothesecondbyjumpingup7positions,thankstotheprevalenceofventurecapitaldealsinthecountry–thehighestintheAPECeconomyaheadofUSA.Generally,high-incomeeconomiesappearmuchbetterplacedtodevelopinnovativeproductsandservicesthantheirlowerincomepeers,withthemajorityofthetop10belongingtothehigh-incomebracket.

Table7.InnovationTheexceptionisChina,ranked10th,andhometoAlipay,TaobaoandTenpay.Chinahasalreadyemergedasthelargestglobalmarketforbusiness-to-consumere-commerce—measuredbothbyonlinebuyersandbyrevenue.29eMarketerestimatesthatChina,infact,accountsforover40%oftheglobalretaile-commercesaleswithmobileaccountingformorethanhalfofsales.30

Othereconomiestowatchoutforwithupcominginnovativee-paymentsolutionsincludeMexicoandPeru.Mexico,andPeru,up5and4spotsrespectively,canattributetheirimprovementstohavinghigherproportionsofgraduatesintechnologyandtheeaseofgettingcreditintheircountries.Thesetranslatetoanincreasingfavourablebusinessenvironmentfortech-entrepreneurstodevelop

innovativeproductsinthee-paymentsindustry.

29EcommerceEurope(2015)AsiaPacificB2CE-commerceLightReport,http://www.ecommerce-europe.eu/news/2015/asia-pacific-remains-the-largest-b2c-e-commerce-market30eMarketer(2016)EcommercedrivesretailsalesgrowthinChina,http://www.emarketer.com/Article/Ecommerce-Drives-Retail-Sales-Growth-China/1013028

Ranking Economy Scores RankingChanges

1 UnitedStatesofAmerica 77.5 -

2 Canada 59.3 (+7)

3 Korea 58.3 (+4)

4 HongKong,China 57.4 (-1)

5 Singapore 55.9 (-1)

6 Japan 54.0 (-4)

7 Australia 51.0 (-1)

8 NewZealand 50.0 -

9 ChineseTaipei 48.3 (-4)

10 China 45.4 -

11 RussianFederation 38.6 (+2)

12 BruneiDarussalam 36.3 (+5)

13 Malaysia 34.4 (-2)

14 Mexico 32.8 (+5)

15 Thailand 31.2 -

16 Peru 29.8 (+4)

17 Chile 28.6 (-3)

18 Vietnam 28.0 (+1)

19 Indonesia 27.7 (-7)

20 Philippines 23.4 (-4)

21 PapuaNewGuinea 18.6 -

23

Thepropensitytoadoptdisruptivedigitalpaymenttechnologiesappearstobewidespread,regardlessofincomelevel.Themosthigh-profilevirtualcurrency,Bitcoin,whilepredominantlyusedinNorthAmerica,isgainingtractioninotherpartsoftheworld,forexampleBitnoderecorded182bitcoinnodesintheRussianFederationand118inChina,whichareatcomparablelevelsasJapan(202)andSingapore(200).312016alsowitnessedashiftindiscussiononcryptocurrencywithPWCclaimingthat“itisnolongeroneofwhethercryptocurrencywillsurvivebutratherhowitwillsurvive”.32Whiletheexpandinguseofcryptocurrencyhasthepotentialtoconnectfinanciallyexcludedconsumerstoglobalpaymentssystemsaffordablyandinstantaneously,itsexpansionisfraughtwithchallengessuchaslowuseracceptance,aswellassecurityissues.33

Regulatorysystemsareburgeoning,withmyriadapproachesbeingtakenbyvariousgovernments;ononehand,Australia,Canada,Japan,SingaporeandtheUSAareleadingthewayoflegitimisingcryptocurrencybypromotingconsumerprotectionandissuingguidelinesontaxationwhileontheotherhandtheRussianFederation,China,MexicoandVietnamhavetakenmorerestrictivestances.34Cryptocurrencywillnotreachitstruemarketpotentialunlessregulationsevolvetoembracecryptocurrency,albeitcautiously.

Thereisaneedforcollaborationamongbanksandnon-banksinordertoaccelerateinnovation.Thisincludesmobilemoneyandagentbankingventures,forinstanceencouragingnon-bankplayers—suchasretailers,e-commerceplatforms,andtelecommunicationfirms—tojointhesystemoffinancialservicesdeliveryandaccessprovidersinaninteroperableandopenmanner.Financialregulatorycollaborationinandacrosseconomieswillalsobeessential.

ConclusionThekeytrendsandinsightsthatemergefromthisIndexincludethefollowing:

• Globally,therateofe-paymentadoptioncontinuestorise,andtherangeofe-paymentchannelsisbroadeningsignificantly.

• APECeconomies’levelofadvancementandexperienceinthedevelopmentofane-paymentecosystemvarieswidely.Thegrowthofandinnovationine-paymentcancomefromallincomelevelsbutthetypesofinnovationwillbedifferentastheneedsthattheseinnovationsaretryingtomeetaredifferent.

• Thereadinessandcapacityofaneconomytoengageine-paymentisstronglyinfluencedbyitsstageofdevelopment.High-incomeeconomiesaremorelikelytohaveathrivingecosystemfore-payment.

• Yet,APECisbecomingmobilefirstandmajorgrowthwillcomefromeconomieswheresmartphoneadoptionisgrowingandtheproportionofservicesofferedthroughsmartphonesareincreasing.Theseeconomiesarenotnecessarilyhigh-incomeones.

• NoneoftheeconomiesexceptCanadarankedinthetopfiveofallthepillarsinthee-paymentecosystem.Thus,economiesinallstagesofdevelopmenthaveanopportunitytoimproveononeormoreaspectsofthee-paymentecosystem.

31Bitnode(2016)GlobalBitcoinNodesDistribution,https://bitnodes.21.co/,figuresasofApril2016.32PWC(2015)Moneyisnoobject:Understandingtheevolvingcryptocurrencymarkethttps://www.pwc.com/us/en/financial-services/publications/assets/pwc-cryptocurrency-evolution.pdf33AsrecentlyasinJune2016,DAO,acrowdsourcinginvestingorganization,becameavictimofUSD79millionheistofether,arivalcryptocurrencytoBitcoin.Formore,seehttp://qz.com/710126/a-massive-79-million-heist-just-happened-and-its-threatening-the-future-of-blockchains/34WhartonResearchScholarJournal(2015)AnAnalysisofCryptocurrencyIndustry,http://repository.upenn.edu/cgi/viewcontent.cgi?article=1133&context=wharton_research_scholars

24

• Thereisnosinglepathwaytopromotinganddevelopinge-payments.E-paymentneedstobedevelopedholisticallybyconsideringthewaysinwhicheachofthepillarsinthee-paymentecosystemaffectorreinforcetheotherinthecontextofeachindividualeconomy.

RegulatoryandPolicyEnvironment

• Manyeconomiesneedtoimprovetheireaseofdoingbusinessandfocusonfosteringafavourableregulatoryandpolicyenvironmenttoenhancetheconfidenceofbusinessesandconsumers.

• Government’svisionandeffortstomakeuseoftechnologytoimprovetransparency,efficiencyandaccountabilityinitsownfinancesthroughe-paymentscankick-startavirtuouscycleofadoption.Thisshouldbeachievedthroughpublic-privatepartnershipsinvolvingthefinance,retail,andtelecommunicationssectorsinparticular.

Infrastructure

• Thegapordividebetweenhigh-income,upper-middle-incomeandlower-middle-incomeeconomiesismostobviousintheinfrastructurepillar.

• Bridgingthedigitaldividewillbeessentialtofullyleveragingtheopportunitiesine-payments.Thisincludesincreasingsmartphonepenetration,broadbandaccess,andaffordability.Focusingonavailabilityandaffordabilityofbasicfinancialservicesiskeyindrivinge-payments.

• Atthesametime,innovationsinovercominginfrastructurechallengesarecontributingtohigheruptakeofe-paymentandm-paymentservices,andareactingasgatewaysintothebankingsystemforunbankedconsumersegments.

Demand

• Populationsinupper-middleandlower-middleincomeeconomiesarelesslikelytohavebankaccountsandtheownershipofcreditcardsislow,butthosewithsmartphoneshavereadilyusedittomakepayments.

• Asmorepeoplegetconnectedintheseeconomies,particularlythroughtherapiduptakeofmobilephonesandsocialmedia,themarketfore-paymentandm-paymentislikelytogrowexponentially.

• E-commerceande-paymentarecloselyinterlinked;e-commercecandrivee-paymentgrowthande-paymentwillfacilitatee-commercegrowth.

Innovation

• Generally,high-incomeeconomieshavebetterhumanresourcesandmorefinancialresourcestodevelopinnovativeproductsandservices.

• Butdevelopingeconomiesarecomingupwithinnovativee-paymentsolutionsaswelltomeettheirdevelopmentneeds.Chinahasbeenoneofthekeyinnovatorsine-paymentwithsolutionslikeAlipay,TaobaoandTenpay.

• Othereconomiestowatchoutfortocomeupwithinnovativee-paymentsolutionsareMexicoandPeru.

• Cryptocurrencywillnotreachitstruemarketpotentialunlessregulationsevolvetoembracecryptocurrency,albeitcautiously.

• Asthenumberofnon-bankplayersinthee-paymentsystemincreases,particularlyindevelopingm-paymentsolutions,thereisaneedforcollaborationamongbanksandnon-banksinordertoaccelerateinnovation.ThiswillneedtobeaccompaniedbyregulatorycooperationinandbetweenAPECeconomies.

25

3.CaseStudies:In-DepthLookatSelectedEconomies

TheAPECE-paymentIndexprovidesahigh-levelviewoftheentireAPECeconomyandasystematicanalysisofvariouselementsofthee-paymentecosystem.AsthevastnumberofindicatorsthatwereaggregatedintheIndexshows,however,e-paymentreadinessandadoptiondependonamultitudeoffactors.Eacheconomyalsohasadifferentbaselineandadifferentsetofchallengestosurmount.TocomplementthefindingsfromtheIndex,thissectionprovidesasetofcasestudieswhichassessesamixofadvancedandnascente-paymentecosystems,namelyAustralia,HongKongChina,IndonesiaandthePhilippines.

Australia

Australiamaintaineditspositionin4thplaceinthe2016APECE-paymentReadinessIndex,andremainscloselybehindleaderstheUnitedStates,Singapore,andnowCanadawhichleapfroggedtothirdplace.Withintherespectivepillars,Australiahasshownimprovementintheregulatoryandpolicyenvironmentpillar,whichisreflectedbyitsslightlyhigherscoreandimprovedrankfrom9thto8th.Howeverintheinnovationpillar,Australiahasfallenonepositionto7thplace.Australiacontinuestoremainalucrativeformarketfortheadoptionofe-paymentsandotherinnovativeFinTechservices.

AustraliahasahighGDPpercapitaofoverUSD60,000andisthesixth-largestcountryintheworldintermsofsize,andtheleastdenselypopulated.ThismeansthatAustraliahasaconsiderableamountoflandmasstoprovidecoveragefor,intermsofmobilenetworks,Internetaccess,ATMsandbankbranches.Thegovernmentcontinuestodowellintheseareas,andthelatestiterationoftheNationalBroadbandNetwork(NBN)employsamulti-technologymodelincludingfibre-optic,fixedwirelessandsatelliteinfrastructuretoimproveInternetaccess.AlthoughtheNBNcontinuestorunintoitsfairshareofproblemsandcriticisms,itcontinuestobethegovernment’slong-termnationalinfrastructureprogramtoimproveInternetconnectivitywithfasterandmorereliablebroadbandconnections.35Australiansarefastadoptersoftechnology,andtheincreasedavailabilityandaffordabilityofsmartphonesmeansmanymobilephoneusersareupgrading,orhavealreadyupgradedtotheuseofsmartphones.WiththepromiseofimprovedInternetbroadbandconnectivityoftheNBN,Australianswillfindthemselveswellequippedtonavigatetheopportunitiesofitsdevelopingdigitaleconomy.

Withitsstrongregulatoryenvironmentandemerginginfrastructureprogress,theAustraliangovernmenthasturneditsattentiontosupporttheFinTechindustrytobecomeinternationallycompetitive,andtoattractandretainlocaltalentsinAustralia.Thiswillhelpenabletheuseandspreadofe-paymentsasmoreelectronicservicesbecomeavailableandmoremerchantsreadilyaccepte-payments.

RecentE-paymentDevelopments

TheAustraliangovernmentcontinuestoexpressitscommitmenttosupporttheemerginglocalFinTechindustryandaspiresforAustraliatobecometheFinTechhubofAsia.Tothisextent,theAustraliagovernmenttreasuryannouncedasetofFinTechreformsinMarch2016,outliningitssupporttotheindustry.36

35Tucker,H.(2016)TheNBNisreportedlyfacinghugeproblems,BusinessInsiderAustralia,http://www.businessinsider.com.au/the-nbn-is-reportedly-facing-huge-problems-2016-236Morrison,S.(2016)SupportingAustralia’sFinTechfuture,http://sjm.ministers.treasury.gov.au/media-release/032-2016/

26

TheseincludethecreationofanewFinTechadvisorygroupwhichischairedbyFinTechhub,StoneandChalkchairmanCraigDunn,andincludesrepresentationfrombanks,venturecapitalists,paymentproviders,andotherFinTechstart-ups.37Othernewmeasuresincludeprovidingbetteraccesstoconcessionaltaxtreatmentforventurecapitalinvestmentsinstart-upFinTechfirms,commissioningtheProductivityCommissiontooutlineoptionstoincreasedataavailabilityandaccesstofacilitatenewproductsandbetterconsumeroutcomes,addressingthe‘doubleGST’treatmentofdigitalcurrencies,creatingaregulatorysandboxtotestideaswithminimalregulations,andmanyothers.38

Thegovernmentisalsolookingatamendingthepriorityareasofexistingfinancialregulationtoensuretheyaretechnologyneutral,andthusfutureproofingregulationsonFinTechinnovations.WiththeAttorney-General’sDepartmentalsolookingatmakingobligationsundertheexistinganti-moneylaundering/counterterrorismfinancing(AML/CTF)regimetechneutral,thiswillsignificantlyeasetherestrictionsfore-paymentandFinTechservicesonofferingnewserviceswhichusebiometricidentificationandidentityverification.39

TheNewPaymentsPlatform(NPP)isasystemcreatedbytheAustralianPaymentsClearingAssociationtoallowlow-valuetransactionsamongdifferentfinancialinstitutionstobemadeinrealtimeand24/7.Initiallydesignedin2012,andsetforcompletioninthesecondhalfof2017,theNPPremainsontrackforitsscheduledcompletiondate.BillpaymentsproviderBpayhaswonthetendertoofferapaymentserviceontheNPP,knownasthe"InitialConvenienceService",allowingconsumerstoinstantaneouslytransferfundstoandfromtheirbankaccountsthroughtheirmobilephone,tablet,ortheInternet.40Theservicewillallowusersbettervisibilityoftheirbudgets,astheirtransactionsandaccountsareupdatedinstantly.AstheNPPbeginstonearcompletion,theReserveBankofAustralia(RBA)shouldcontinuetoworkwithfinancialinstitutionsandotherstakeholderstoeducateandbuildawarenessonthebenefitsandservicesavailableontheNPP.

LookingAhead

AustralianisalreadyamongthetopfivecountriesintheE-paymentReadinessIndex,andlookssettofurtheradvanceitspositionandimproveitsrankingsinthenear-future.StrongsupportfromthegovernmentonFinTechwillhelpenablethelocalindustrytoflourish,increasingexposuretoe-paymentsforawiderrangeofservices.ThemobilepaymentsmarketisalsobecomingincreasinglycompetitiveasinternationalplatformsincludingApplePay,GoogleWallet,andincomingSamsungPayandAndroidPaycompeteagainstlocalbankpaymentappsinAustralia.

Australiaisinagoodpositiontobecomeagloballeaderine-payments,andthevariouspolicyandregulatoryagencies,includingTreasury,theRBA,ASIC,AustralianPrudentialRegulationAuthority(APRA),andAustralianTransactionReportsandAnalysisCentre(AUSTRAC),havebeenactivelyengagingwiththeFinTechindustrytoremoveunnecessaryregulatoryburdenandredtape,inlinewiththegovernment’sderegulatoryagenda.WhilethiswillhelpFinTechinnovationstotake-off,thepolicyandregulatoryagencieswillstillcontinuetoprovidesomeformofregulatoryoversightovertoensureinvestorandconsumertrustandconfidenceintheseemergingbusinessmodels.

37TheTreasury(2016)WorkingwithAustralia’sFinTechindustry,http://fintech.treasury.gov.au/working-with-australias-fintech-industry/38TheTreasury(2016)Australia’sFinTechpriorities,http://fintech.treasury.gov.au/australias-fintech-priorities/39TheTreasury(2016)AustralianRegulatorsengagementwiththeFinTechindustry,http://fintech.treasury.gov.au/australian-regulators-engagement-with-the-fintech-industry/40Drummond,S.(2015)BPayfirsttoofferinstantpaymentsonbanks'NewPaymentsPlatform,http://www.smh.com.au/business/banking-and-finance/bpay-first-to-offer-instant-payments-on-banks-new-payments-platform-20151029-gkmjkw.html

27

HongKong,China

HongKongfellonespotto7thplaceintheIndex,althoughscoresremainclose,withlessthan4pointsseparatingsecondtoseventhplace.HongKongnowtrailscloselybehindKorea,butcontinuestodemonstratehighscoresfortheregulatoryandpolicyenvironmentpillar(2ndbehindSingapore)andtheinnovationpillar(4thbehindtheUnitedStates,Canada,andKorea).However,HongKongcontinuestobeplaguedbyproblemsinInfrastructureandDemandwithaveragescoresinthosetwopillars.

HongKongisaprominenttradehubandfinancialcentreandissynonymouswithalight-touchregulatedeconomywhichhasattractedmanymultinationalcorporationstosetuptheirregionalofficesandheadquartersthere.Howeverwhileitmaybenon-interventionistinmanyareas,oneareawhereHongKongstillregulatestightlyisthee-paymentsspace.PaymentprovidersofmobileandelectronicpaymentservicesarerequiredtoobtainabankinglicensefromtheHongKongMonetaryAuthority(HKMA).41TheHKMAannouncedanewregulatoryregimeforStoredValueFacilities(SVF)andRetailPaymentSystems(RPS)inNovember2015,withtheHKMAsettoissuenewlicensesinNovember2016.TheHKMAannouncedthemajortoolsitwouldemploytoregulatelicenses,including(a)on-siteexaminations;(b)off-sitereviews;(c)independentassessments;(d)reviewofauditors’reports;and(e)meetingswiththemanagementofthelicensee.42Whilewellintendedtoprotectconsumerdeposits,andmoneylaundering,theregulationsmayinadvertentlyfrightenoffe-paymentsprovidersfromoperatinginHongKong.Todate,ApplePayisalreadyavailableinChina,anddespiteannouncingplanstolaunchinHongKong,Applehaveyettoannounceatimetableforthemobilepaymentservicelaunch.TheHKMArevealedinApril2016,thatofthesome20applicationsithadalreadyreceived,onlyathirdthathadappliedwereseekingtooperateInternetormobilepaymentservices.43

Withthegovernmentannouncinginits2016-17BudgetspeechinFebruarythatitwantstotakeadvantage,andsupportFinTech,theHKMAneedstoconsiderlesseningtheregulatoryburdenfore-paymentproviderstooperateinHongKong.44

RecentE-paymentDevelopments

NineHongKongbankslaunchedane-chequesysteminDecember2015,whichallowsuserstousetheirphonesandInternet-enableddevicestosettlebills,transfermoney,andevengiveoutelectronicredpacketsduringtheLunarNewYear.Thee-chequesystemworkssimilartothatofpapercheque,butaddstheconvenienceofbeingabletobegeneratedelectronicallythroughmobilephones.E-chequeshavetheaddedadvantageovertraditionalelectronicpayment/transferservicesinthattheywouldnotrequirepartiestoregisterwiththepaymentplatform,anddonotrequirethepayeetoprovidehis/heraccountinformationtothepayer.Aspartofitsawarenesscampaigns,theHKMAandtheHongKongAssociationofBanks(HKAB)jointlylaunchedapublicitycampaignincludingaseriesofeducationalmaterialssuchasadvertisementsontelevisionandradio,postersandelectronicbrochures.45

41HongKongMonetaryAuthority(2015)ExplanatoryNoteonLicensingforStoredValueFacilities,http://www.hkma.gov.hk/media/eng/doc/key-functions/finanical-infrastructure/infrastructure/retail-payment-initiatives/Explanatory_note_on_licensing_for_SVF.pdf42HongKongMonetaryAuthority(2015)RegulationofStoredValueFacilities(SVF),http://www.hkma.gov.hk/eng/key-functions/international-financial-centre/regulatory-regime-for-svf-and-rps/regulation-of-svf.shtml43RTHK(2016)HKMAsaysitwon'tsetcapfore-paymentservices,http://news.rthk.hk/rthk/en/component/k2/1252673-20160405.htm44HongKongGovernment(2016)BudgetSpeech,Fintech,http://www.budget.gov.hk/2016/eng/budget11.html45HongKongGovernment(2015)LaunchofElectronicCheque(e-Cheque)publicitycampaign,http://www.info.gov.hk/gia/general/201511/23/P201511230374.htm

28

TheSteeringGrouponFinTechreleaseditsrecommendationstothegovernmenttopromoteFinTechinFebruary2016.ThereporthighlightsthepotentialforHongKongtobecomeapremierFinTechHub,andthatappropriatesupportandmeasuresfromthegovernmentcanhelptodevelopthefledglingsector.ThekeyrecommendationsproposedbytheSteeringGroupinclude:(i)formulatingavisiontounderlineHongKong'scommitmentindevelopingFinTechandpositioningasalaunchpadforcompaniesinthesector;(ii)providingassistancetoFinTechstart-ups;(iii)establishinginandattractingtoHongKongmoreFinTech-themedprogramsandinnovationlaboratories;(iv)encouragingtheapplicationandsettingofstandardsforcutting-edgeFinTechtechnologies;(v)facilitatingcommunicationbetweenfinancialregulatorsandtheFinTechcommunity;(vi)improvingdisseminationofinformationonfundingsourcesandimmigrationpolicy;and(vii)encouragingyoungtalentstoentertheFinTechsector.46

TheHKMAcreatedtheFinTechFacilitationOffice(FFO)inMarch2016tofacilitatethedevelopmentoftheFinTechecosysteminHongKong,andpromoteHongKongasaFinTechhubinAsia,whichwillputitindirectcompetitionagainstSingaporeandAustraliawhosharesimilaraspirations.47TheFFOdescribesitselfamongotherthings,as:(i)aplatformforexchangingideasofinnovativeFinTechinitiativesamongkeystakeholdersandconductingoutreachingactivities;(ii)aninterfacebetweenmarketparticipantsandregulatorswithintheHKMAtohelpimprovetheindustry’sunderstandingaboutthepartsoftheregulatorylandscapewhicharerelevanttothem;and(iii)aninitiatorofindustryresearchinpotentialapplicationandrisksofFinTechsolutions.ThisfollowsasimilarmovebytheSecuritiesandFuturesCommission(SFC),whichalsosetupinMarch2016acontactpointfortheFinTechindustrytoliaiseonregulatoryissues.48

LookingAhead

HongKongremainsontherighttrackfore-paymentsandotherinnovativeFinTechservicestoflourish.TheHongKonggovernmenthasannounceditssupportofthesector,andisalreadytakingstepstoaidthedevelopmentandencouragegreateradoptionofe-payments.However,HongKongstillremainsafewstepsbehinditsclosestregionalcompetitorsSingaporeandAustralia.Tocatch-upswiftly,theHongKonggovernmentshouldlookatrelaxingitsrequirementsfore-payments,forexampleimplementingtransactionlimitsone-payments,ratherthanrequiringbankinglicenses.WhenprovidingfinancialassistancetoFinTechventures,thegovernmentshouldensurethatinformationonhowtoreceiveandapplyforfundingiseasilyavailable,andaccessible.

TheHongKonggovernmentneedstoensureithasaclear,articulatedvisionwiththerelevantsupportingmechanismsonenablinge-paymentsandFinTechlessitgetleftbehind.

46HongKongGovernment(2016)SteeringGrouponFintechreleasesreport,http://www.info.gov.hk/gia/general/201602/26/P201602260497.htm47HongKongMonetaryAuthority(2016)FintechFacilitationOffice(FFO),http://www.hkma.gov.hk/eng/key-functions/international-financial-centre/fintech-facilitation-office-ffo.shtml48SecuritiesandFuturesCommission(2016)SFCFintechContactPoint,http://www.sfc.hk/web/EN/sfc-fintech-contact-point/

29

Indonesia

IndonesiahasbeengainingincreasingattentionasAsia’snextfocalmarketfore-commerceande-payments.Itsgrowingeconomy,emergingmiddleclass,youthfuldemographic,increasingspendingpowerandrapidlygrowingInternetuser-baseareallreasonstobeoptimisticaboutthefutureprospectsofIndonesia’sdigitaleconomy.49

TheimmediatepriorityforIndonesiaappearstobeonimprovingtheICTinfrastructuretoprovidesecureandreliableInternetconnectivity.Whilemobilepenetrationhasreachednearubiquitouslevels,broadbandconnectivityisstilllimited,andnationalcybersecuritycapabilitiesremainquestionable.

Indonesiaalsoneedsastrategyforunlockingthenascentdemandfore-payments,asthisisIndonesia’sweakestpillar(21st).ThelowrankingcanbeexplainedbyIndonesia’sheavycash-dependency.Only36%ofthepopulationwasbankedasof2014,withcreditcardpenetrationataroundonly5%,oneofthelowestamongAPECeconomies.50While1outof4Indonesiansownadebitcard,only1outof10wouldactuallyuseit.51However,Indonesiaisalsotheworld’sfourthlargestcountrybypopulationwithaveryyoungdemographicgroupandthereforethepotentialforgrowthamongstIndonesianconsumersandbusinessesremainspotent,ande-commerceande-payments,particularlywhendeliveredviamobileconnectivityofferwaysaroundmanyoftheexistingmarketconstraints.

IntheregulatoryandpolicypillarIndonesiafaresrelativelybetter(14th),butfellsignificantlyintheprovisioningofe-paymentproductsandservices(19th).Thereis,however,stillalotofroomforIndonesiatoimprovetheeaseofdoingbusiness,theeffectivenessofitslegalsystemandtheinvestmentclimate.BureaucratichurdlesofmarketentryandinvestmentclearlyneedtobeaddressedforIndonesiatofullybenefitfromtheefficienciesandsocialgainspossiblefromdigitalpayments.

RecentE-paymentDevelopments

Morefavourableregulatorychangehasbeguntakingplaceinrecentyearsasthegovernmentrecognisedthepotentialofe-paymentsinfosteringfinancialinclusion.Acaseinpointisbranchlessbanking,whichusesagentsandmobilephonestoprovidebasicsavingsandtransactionservices,thathasrisentoprominenceinIndonesia’snationalagenda.In2013,BankofIndonesia(BI)releasedguidelinesforallowingselectedbanksandmobilenetworkoperatorstopilotagent-modelandmobilewalletinitiativestotesttheviabilityofthebusinessmodel.52Ayearlater,theFinancialServicesAuthority(OJK)formallyopenedthedoorforbankstohireagentstoimprovefinancialinclusionandexpandbasicfinancialservicestoremoteandruralpartsoftheeconomy,53eventually