Embed Size (px)

Citation preview

European Global Navigation System Services Programme

“All you need to know to do business with GNSS”

N. Dumesnil , September 2007

WHO MIGHT FIND THIS BOOKLET USEFUL?

Do terms like GNSS, satellite navigation, and geo-positioning sound familiar to you? Have you ever thought of doing business based on satellite navigation services? If so, at first you should have a look at the booklet. The following pages might bring you a clearer overview of the overall landscape of GNSS. This booklet is a guide composed of modules in order to cover each aspect of GNSS, helping you to understand and position yourself in this new challenging environment. Note that the GNSS marketplace is considerably and rapidly evolving, market data can quickly become obsolete. This document will tell what technologies exist, for which applications, in which environment and how to set up successful business in this domain. We wish you a good reading!

TABLE OF CONTENT

CHAPTER 1 INTRODUCTION STRATEGIC BACKGROUND CHAPTER 2 WORLWIDE GNSS TECHNOLOGIES CHAPTER 3 EUROPEAN GNSS TECHNOLOGIES CHAPTER 4 GNSS MARKET PICTURE CHAPTER 5 LOCATION BASED SERVICES CHAPTER 6 ROAD APPLICATIONS CHAPTER 7 OTHER GNSS APPLICATIONS CHAPTER 8 MARKET DRIVERS CHAPTER 9 GNSS INDUSTRY PANORAMA CHAPTER 10 EUROPE POSITIONING IN THE COMPETITIVE

ENVIRONMENT CHAPTER 11 GNSS SMES PROFILES CHAPTER 12 GOLDEN RULES FOR GNSS SMES

All you need to know to do business with GNSS Capital High Tech Page 4 Noémie Dumesnil

CHAPTER 1

INTRODUCTION STRATEGIC BACKGROUND

In this introduction chapter, we will introduce you the strategic interest of global navigation satellite systems (GNSS) and a first insight on Europe motivation for having its own GNSS.

I. The importance of GNSS applications in our day to day life The benefits of global navigation satellite system have already been demonstrated with the availability of the American (USA) Global Positioning System (GPS). Applications are continuously being developed, covering all lifestyle and sectors of the world economy. Satellite navigation is becoming more and more part of the daily life, not only in their cars and portable telephones but also in energy distribution networks or banking systems. Receivers are now found in all kinds of electronic devices for everyday use such as mobile phones, personal digital assistants, cameras, portable PCs or wristwatches. Mobile telephony is a promising market with over 2 billion mobile phone subscribers. Half a billion units are sold every year, with a prospect of 1 billion a year by 2020, allowing for fast market penetration of satellite positioning-based services. Vehicles should increasingly be fitted with navigation equipment. All sectors of modern economies are affected by the development of satellite navigation technologies. Applications span a large range of sectors, not only in transport and communication but also in other markets such as land survey, agriculture, scientific research, tourism and others. Global satellites navigation systems services are penetrating all segments of society and are becoming a common tool in the citizen’s daily life. In combination with even more cheaper and powerful handheld terminals and the demand for ubiquitous services, the role played by satellite global positioning systems is set to grow considerably, and is expected to reveal new sources of business in the years ahead.

II. A political challenge Having control of the satellite constellation technology that is central to the system means having control of the many industrial applications made possible thanks to satellite positioning. The European Union cannot afford not to become involved in what, it is already clear, will be one of the main sectors of industry in the twenty-first century. That would mean becoming dependent on systems and technologies developed outside Europe for applications vital to the running of the society of tomorrow. 1

1 http://ec.europa.eu/dgs/energy_transport/GALILEO/intro/challenge_en.htm

All you need to know to do business with GNSS Capital High Tech Page 5 Noémie Dumesnil

The European Councils at Cologne, Feira, Nice, Stockholm, Laeken and Barcelona all emphasised the strategic importance of Satellite Navigation programme. As a result, the European Union is now building the European global navigation satellite system (GNSS), comprising GALILEO and EGNOS, which will provide a set of positioning, navigation and timing services. GALILEO is a flagship of the European Space Policy. Its objectives are, amongst others, to respond to citizen's needs, to serve other EU policies, to concentrate on space applications and to improve European competitiveness. GALILEO has also to be seen in the wider context for fostering innovation and in the Lisbon strategy to make Europe the most competitive and dynamic knowledge-based economy in the world, capable of sustainable economic growth with more, better jobs, and greater social inclusion.2

III. An economic and social challenge GALILEO will afford considerable advantages in many sectors of the economy. In road and rail transport, for example, it will make it possible to predict and manage journey times, or, thanks to automated vehicle guidance systems, help reduce traffic jams and cut the number of road accidents. However, although transport by road, rail, air and sea is the example most frequently quoted, satellite radio navigation is also increasingly of benefit to fisheries and agriculture, oil prospecting, defence and civil protection activities, building and public works, etc. In the field of telecommunications, allied with other new technologies such as GSM or UMTS, GALILEO will increase the potential to provide positioning information as well as to provide combined services of a very high level. The real impact of satellite global positioning on society and industrial development, as is the case for all major technical innovations, will become clear only gradually, even though many practical applications are already possible. While there is no question but that the future of guidance systems involves satellite radio navigation, there are sectors other than the transport sector which are already dependent on this new technology, even if they are not aware of the fact. This is true of the financial sector when it comes to determining the exact time of bank transactions. With Galileo, Europe will be able to exploit the opportunities provided by satellite navigation fully. GNSS receiver and equipment manufacturers, application providers and service operators will benefit from novel business opportunities Some analysts regard satellite radio navigation as an invention that is as significant in its way as that of the watch: in the same way that no one nowadays can ignore the time of day, in the future no one will be able to do without knowing their precise location.

IV. A technological challenge GALILEO is designed as a non-military application, while nonetheless incorporating all the necessary protective security features. It therefore provides, for some of the services offered, a very high level of continuity required by modern business, in particular with regard to contractual responsibility.

2 http://ec.europa.eu/dgs/energy_transport/galileo/green-paper/doc/com_2006_gp_galileo_en.pdf

All you need to know to do business with GNSS Capital High Tech Page 6 Noémie Dumesnil

It is based on the same technology as GPS and provides a similar - possibly higher - degree of precision, thanks to the structure of the constellation of satellites and the ground-based control and management systems planned. GALILEO is more reliable as it includes a signal "integrity message" informing the user immediately of any errors. In addition, by placing satellites in orbits at a greater inclination to the equatorial plane than GPS, Galileo will achieve better coverage at high latitudes. This will make it particularly suitable for operation over northern Europe, an area not well covered by GPS. It will be possible to receive GALILEO in towns and in regions located in extreme latitudes. It represents a real public service and, as such, guarantees continuity of service provision for specific applications.

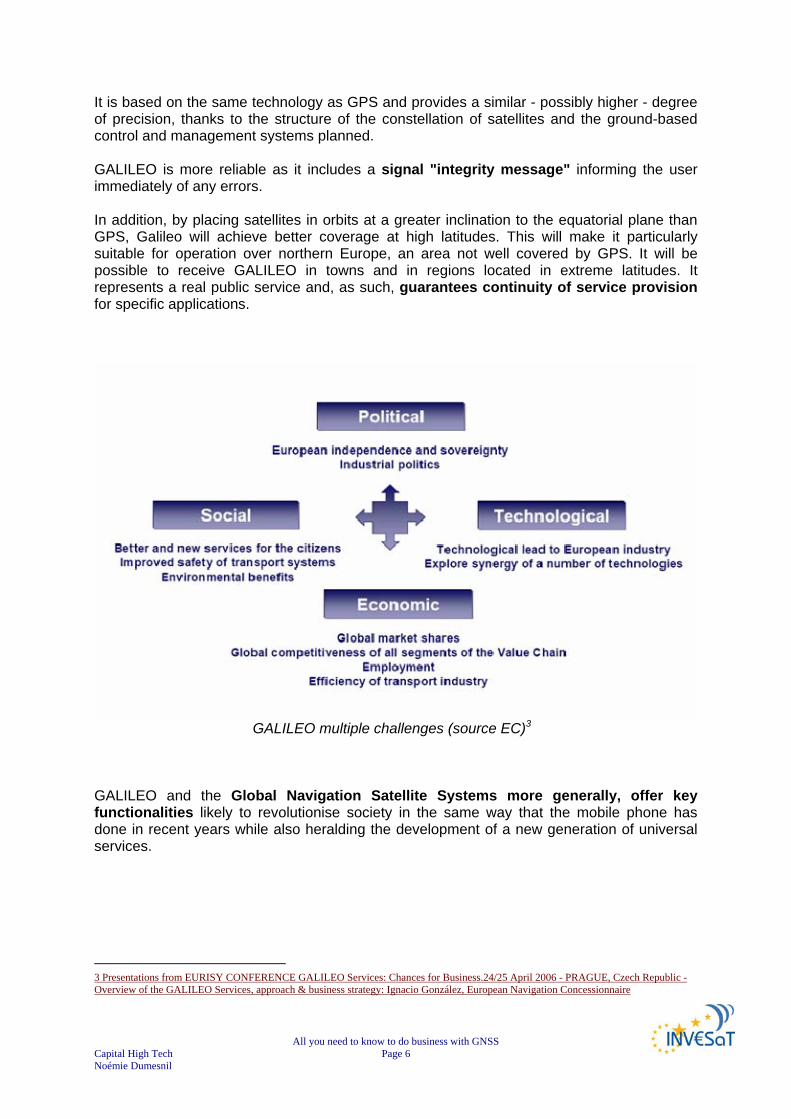

GALILEO multiple challenges (source EC)3

GALILEO and the Global Navigation Satellite Systems more generally, offer key functionalities likely to revolutionise society in the same way that the mobile phone has done in recent years while also heralding the development of a new generation of universal services.

3 Presentations from EURISY CONFERENCE GALILEO Services: Chances for Business.24/25 April 2006 - PRAGUE, Czech Republic - Overview of the GALILEO Services, approach & business strategy: Ignacio González, European Navigation Concessionnaire

All you need to know to do business with GNSS Capital High Tech Page 7 Noémie Dumesnil

CHAPTER 2

GNSS TECHNOLGIES

The 20th century was marked by the definitive takeoff of geopositioning or the advent of radio navigation followed by satellite navigation. We will discuss in this chapter the existing or future technologies, their performances and differences. A full chapter is dedicated to European GNSS (GALILEO & EGNOS): their performances and complementarities/differences with other systems.

I. Introduction Developed in the first half of the 20th century, radio navigation uses radioelectric signals to determine a position. The points obtained do not depend on visibility conditions. In 1957, Sputnik I, the world’s first artificial satellite was launched by Russia. It remained three months in orbit and emitted signals for 21 days. It marked the beginning of research in satellite location. In 1968, the first Global Positioning System (GPS) satellite was launched by the United States. In 1973, the Pentagon designed and financed a GPS system composed of several satellites in orbit around the Earth, which gave the position in real time of any point on the planet. This system was originally designed for military purposes. In 1990, the American government announced that GPS satellites were also open to the civil domain and in 1995; the system was operational with accuracy from 7 to 10 meters. For its part, Europe is working on the EGNOS project, a system designed to inform users about the integrity of positioning signals of the GPS (American) and GLONASS (Russian) systems, as well as correcting errors and improving availability. EGNOS is the first step towards GALILEO, European satellite navigation and positioning system, which will be operational by 2010. GALILEO is a civil system that will provide better accuracy than the current GPS system.4

4 http://www.navigation-satellites-toulouse.com/rubrique.php3?id_rubrique=74

All you need to know to do business with GNSS Capital High Tech Page 8 Noémie Dumesnil

II. Principle of satellite radio navigation

1) Satellite radio navigation, geopositioning & navigation Satellite radio navigation has been developed over the last 30 years or so, essentially for military purposes originally, enables anyone with a receiver capable of picking up signals emitted by a constellation of satellites to instantly determine his position in time and space very accurately. Geopositioning is used to locate the exact position of a mobile element or object on the Earth. Today, it is based on satellite geopositioning systems composed of satellite constellations in orbit around the Earth and receivers. The latter can be on the ground or on board a vehicle or a plane, receives information from satellites, which allows it to calculate its position relative to the Earth. While navigation refers to the science and techniques, which make possible to: Determine the position (coordinates) of a mobile object relative to a reference system or a

determined, fixed point. Calculate or measure the route to be taken to get to another point of known coordinates Calculate any other information relative to the movement of this mobile object (distances

and durations, speed, estimated time of arrival, etc.) All navigation systems are frequently called "GPS", although GPS specifically describes the American system. The systems built so far work according to the same principle. 5

2) Operating principle of GNSS The operating principle is simple: The satellites in the constellation are fitted with an atomic clock measuring time very accurately. The satellites emit personalised signals indicating the precise time the signal leaves the satellite. The ground receiver, incorporated for example into a mobile phone, has in its memory the precise details of the orbits of all the satellites in the constellation. By reading the incoming signal, it can thus recognise the particular satellite, determine the time taken by the signal to arrive and calculate the distance from the satellite. Once the ground receiver receives the signals from at least four satellites simultaneously, it can calculate the exact position. 6

5 http://en.wikipedia.org/wiki/User:Dual_Freq/GNSS 6 http://ec.europa.eu/dgs/energy_transport/GALILEO/index_en.htm

All you need to know to do business with GNSS Capital High Tech Page 9 Noémie Dumesnil

GNSS infrastructure (source EC)

A GNSS is composed of three segments: Space segment is the satellite constellation Ground segment includes control segment for operation, orbit and time determination,

and the system for integrity monitoring User segment is composed of receivers translating the signals provided by the

satellites into real services for the user

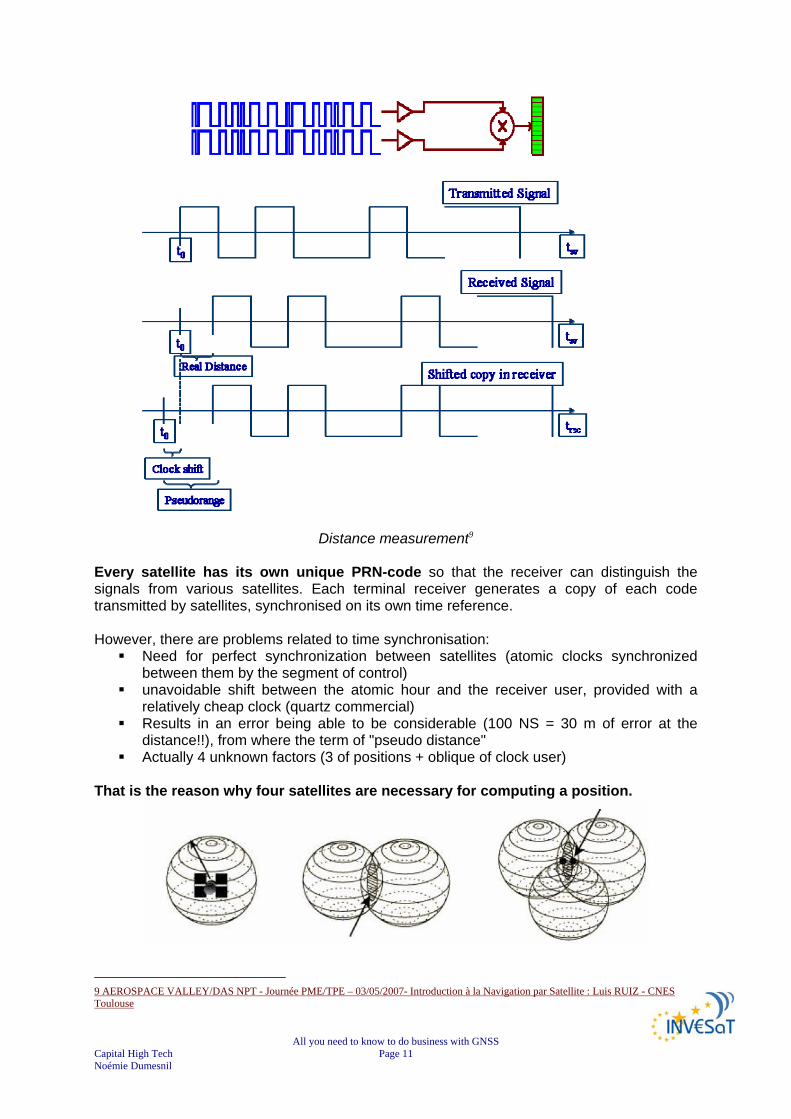

3) To go further into principles: pseudorandom noise codes

Pseudo distance concept7

7 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

Satellite emission time

Propagation time × Speed of light⇒ Distance covered d

Signal reception timeby user terminal

Satellite emission time

Propagation time × Speed of light⇒ Distance covered d

Signal reception timeby user terminal

All you need to know to do business with GNSS Capital High Tech Page 10 Noémie Dumesnil

Each satellite transmits a pseudorandom noise synchronised on GPS time reference. The code consists of a long series of bits (0's and 1's). A sequence of digital 1's and 0's that appear to be randomly distributed like noise but that can be reproduced exactly. Their most important property is a low autocorrelation value for all delays or lags except when they coincide exactly. The codes-patterns used for GPS repeat themselves after the 1023rd bit. These codes can be easily made with very few digital elements. For the 1023-bit pattern, 10 shifting registers and some digital adders are needed.

Source TU Delft

In general, with n shifting registers a series of 2n -1 bits can be generated. For n = 10 this will become 1024 (= 210) - 1 = 1023 bits. The codes are generated with a speed of 1.023 MHz (or 1023000 bits per second). An example with 4 shifting elements is given in below. 8

Source TU Delft

8 http://www.eurofix.tudelft.nl/prncode.htm

All you need to know to do business with GNSS Capital High Tech Page 11 Noémie Dumesnil

Distance measurement9 Every satellite has its own unique PRN-code so that the receiver can distinguish the signals from various satellites. Each terminal receiver generates a copy of each code transmitted by satellites, synchronised on its own time reference. However, there are problems related to time synchronisation:

Need for perfect synchronization between satellites (atomic clocks synchronized between them by the segment of control)

unavoidable shift between the atomic hour and the receiver user, provided with a relatively cheap clock (quartz commercial)

Results in an error being able to be considerable (100 NS = 30 m of error at the distance!!), from where the term of "pseudo distance"

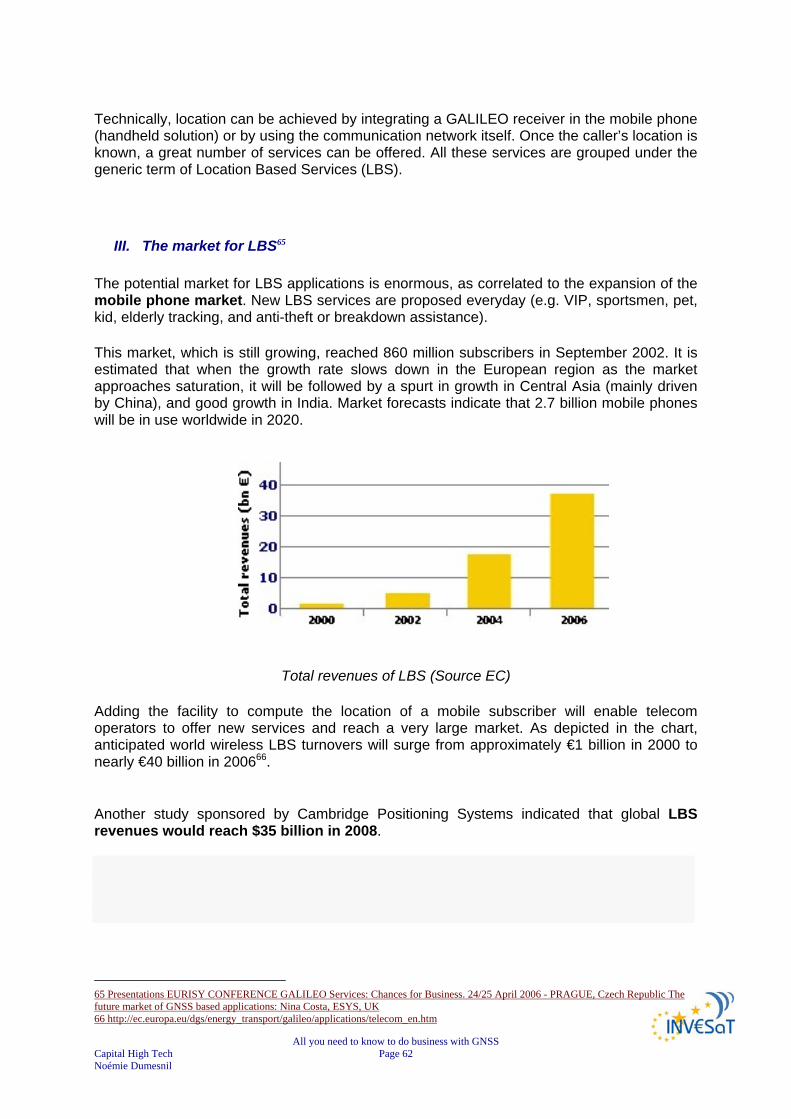

Actually 4 unknown factors (3 of positions + oblique of clock user) That is the reason why four satellites are necessary for computing a position.

9 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 12 Noémie Dumesnil

Based on one satellite, one can define a sphere; with two satellites, one can define a circle. Thanks to a third satellite, one can find the position of a receiver (excluding absurd solution).

III. The navigation satellite systems classification Global Navigation Satellite System (GNSS) is the standard generic term for satellite navigation systems that provide autonomous geo-spatial positioning with global coverage. GNSS that provide enhanced accuracy and integrity monitoring usable for civil navigation are classified as follows:

GNSS-1 is the first generation system and is the combination of existing satellite navigation systems (GPS and GLONASS), with Satellite Based Augmentation Systems (SBAS) or Ground Based Augmentation Systems (GBAS).

GNSS-2 is the second generation of systems that independently provides a full

civilian satellite navigation system, exemplified by the European GALILEO positioning system. These systems will provide the accuracy and integrity monitoring necessary for civil navigation. This system consists of L1 and L2 frequencies for civil use and L5 for system integrity. Development is also in progress to provide GPS with civil use L2 and L5 frequencies, making it a GNSS-2 system.

GNSS steps10

10 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

All you need to know to do business with GNSS Capital High Tech Page 13 Noémie Dumesnil

GNSS may have several layers of infrastructure:

Global Satellite navigation systems: currently GPS (US), GLONASS (Russia), and future GALILEO (Europe) and Beidou 2 (China).

Regional Satellite Navigation Systems: IRNSS (India), and Beidou 1 (China). Regional Satellite Based Augmentation Systems (SBAS): WAAS (US), EGNOS

(EU), MSAS (Japan) and GAGAN (India). Ground Based Augmentation Systems (GBAS) for example Differential GPS

(DGPS) , Local Area Augmentation System (LAAS), local GBAS typified by a single GPS reference station operating Real Time Kinematic (RTK) corrections

GNSS layers by regions

All you need to know to do business with GNSS Capital High Tech Page 14 Noémie Dumesnil

IV. The Global Satellite Navigation Systems

1) GPS

As mentioned previously although the acronym GPS is commonly used for designating GNSS, it only refers to the American GNSS system. The Global Positioning System (GPS) is currently the only fully functional Global Navigation Satellite System (GNSS). Developed by the United States Department of Defence, it is officially named NAVSTAR GPS (NAVigation Satellite Timing And Ranging Global Positioning System). The NAVSTAR GPS Joint Program Office manages the NAVSTAR Global Positioning System.

The Global Positioning System (GPS) satellite network is operated by the U.S. Air Force to provide highly accurate navigation information to military forces around the world. A growing number of commercial products are also using the network. GPS transmits precise radio signals; the system enables a GPS receiver to determine its location, speed and direction. The idea for a global positioning system was first proposed in 1940. There are 4 generations of the GPS satellite: the Block I, Block II/IIA, Block IIR and Block IIF.

Block I satellites were used to test the principles of the system, and lessons learned from those 11 satellites were incorporated into later blocks.

Block II and IIA satellites make up the current constellation. The third generation Block IIR satellites are currently being deployed as the Block

II/IIA satellites reach their end-of-life and are retired. Block IIF satellites will be the fourth generation of satellites and will be used for

operations and maintenance (O&M) replenishment.11

11 http://www.spaceandtech.com/spacedata/constellations/navstar-gps_consum.shtml

All you need to know to do business with GNSS Capital High Tech Page 15 Noémie Dumesnil

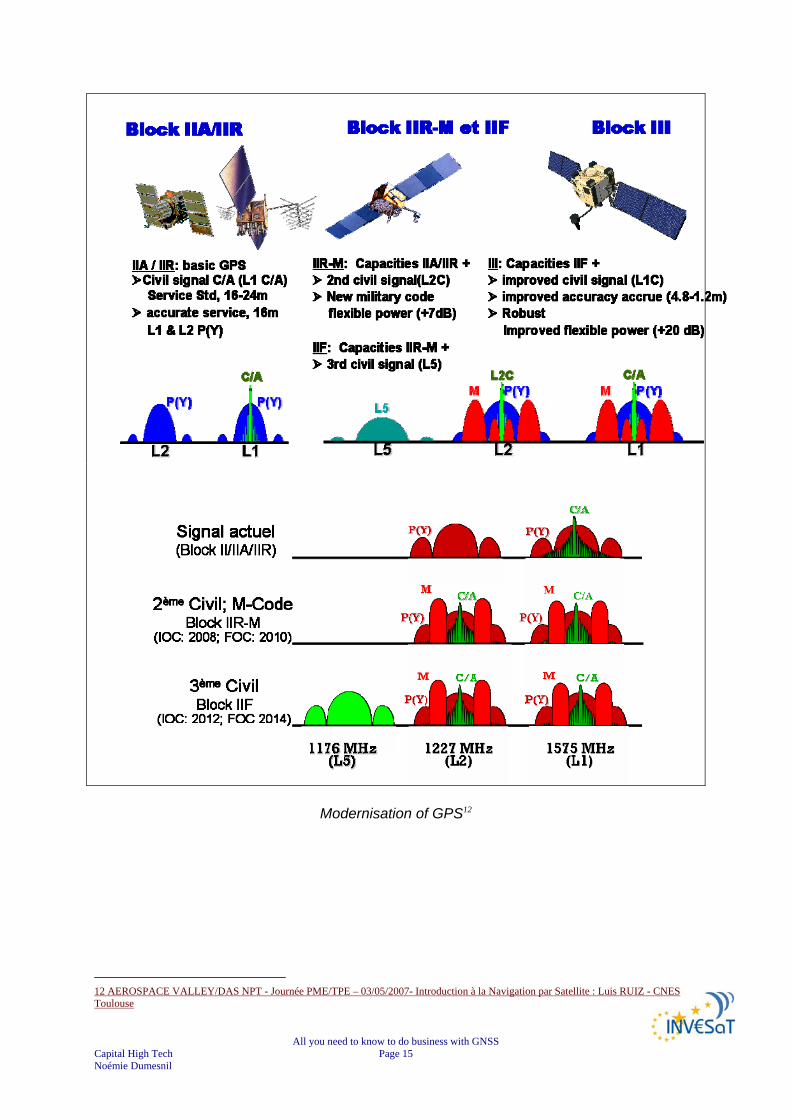

Modernisation of GPS12

12 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 16 Noémie Dumesnil

GPS positioning performance13

The GPS space segment consists of into 6 orbital planes, requiring a minimum of 4 satellites in each, to operate. GPS is based on a constellation of:

24 medium Earth orbit satellites (at least 24 Active and 4 spare) 6 orbital planes Orbital inclination: 55° Altitude: 20200 km

The GPS control segment consists of

5 monitoring stations (Hawaii, Kwajalein, Ascension Island, Diego Garcia, Colorado Springs),

3 ground antennas, (Ascension Island, Diego Garcia, Kwajalein), 1 Master Control station located at Schriever AFB in Colorado.

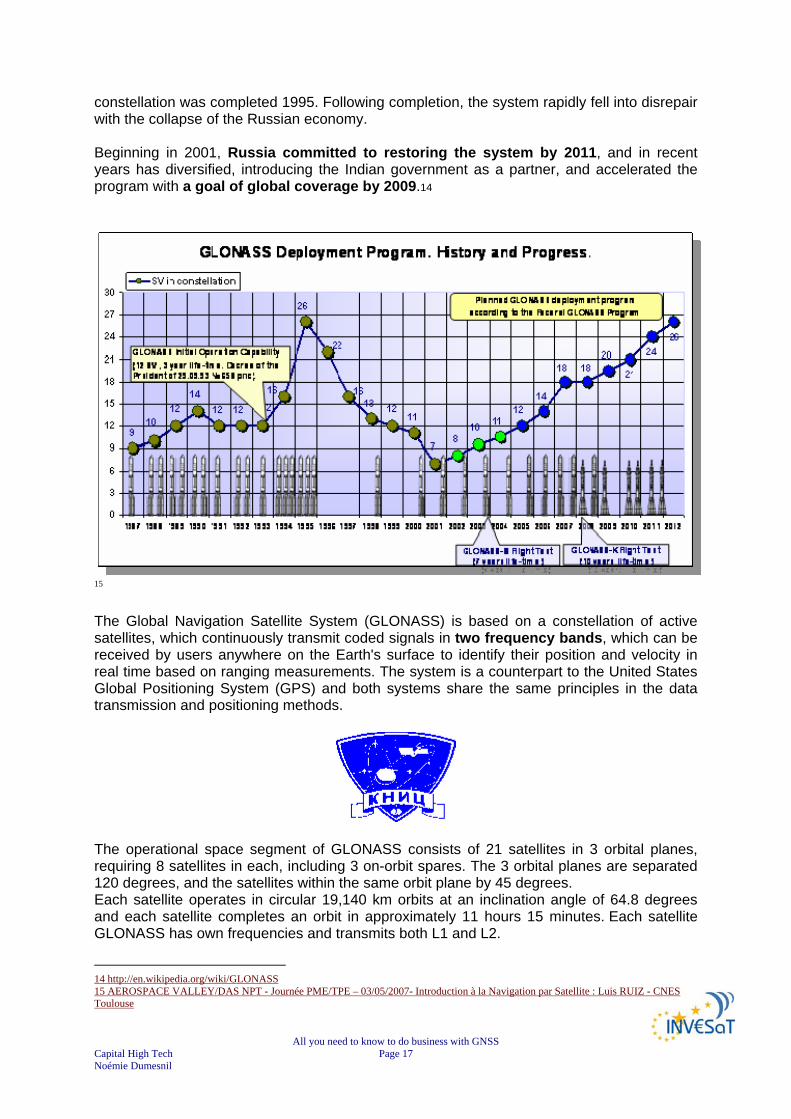

2) GLONASS GLONASS is a radio-based satellite navigation system, developed by the former Soviet Union and now operated for the Russian Federation Government by the Russian Space Forces, and the system is operated by the Coordination Scientific Information Centre (KNITs) of the Ministry of Defence of the Russian Federation. Development on the GLONASS began in 1976, with a goal of global coverage by 1991. Beginning in 1982, numerous satellite launches progressed the system forward until the

13 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 17 Noémie Dumesnil

constellation was completed 1995. Following completion, the system rapidly fell into disrepair with the collapse of the Russian economy. Beginning in 2001, Russia committed to restoring the system by 2011, and in recent years has diversified, introducing the Indian government as a partner, and accelerated the program with a goal of global coverage by 2009.14

15 The Global Navigation Satellite System (GLONASS) is based on a constellation of active satellites, which continuously transmit coded signals in two frequency bands, which can be received by users anywhere on the Earth's surface to identify their position and velocity in real time based on ranging measurements. The system is a counterpart to the United States Global Positioning System (GPS) and both systems share the same principles in the data transmission and positioning methods.

The operational space segment of GLONASS consists of 21 satellites in 3 orbital planes, requiring 8 satellites in each, including 3 on-orbit spares. The 3 orbital planes are separated 120 degrees, and the satellites within the same orbit plane by 45 degrees. Each satellite operates in circular 19,140 km orbits at an inclination angle of 64.8 degrees and each satellite completes an orbit in approximately 11 hours 15 minutes. Each satellite GLONASS has own frequencies and transmits both L1 and L2.

14 http://en.wikipedia.org/wiki/GLONASS 15 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 18 Noémie Dumesnil

GLONASS is based on a constellation of:

24 medium Earth orbit satellites (including 3 on orbit spares) Rotation on 3 orbital planes Orbital of inclination plans 64.8° Altitude is 19.140 Km

The ground control segment of GLONASS is entirely located within former Soviet Union territory.

Ground Control Centre and Time Standards is located in Moscow 4 telemetry and tracking stations are in St. Petersburg, Ternopol, Eniseisk,

Komsomolsk-na-Amure.

Work is underway to modernise the system. The new GLONASS-M satellite will have better signal characteristics as well as a longer design life (7-8 years instead of the current 3 years). In the future, plans are being developed to transition to a low mass third generation GLONASS-K satellites with a guaranteed lifespan of 10 years.

3) GALILEO

The GALILEO positioning system, referred to simply as GALILEO, is the European GNSS programme. It is named after the Italian astronomer GALILEO Galilei. The GALILEO positioning system is referred to as "GALILEO" instead of as the abbreviation "GPS" to distinguish it from the existing United States system. GALILEO is designed to provide a higher precision to all users than is currently available through GPS or GLONASS, to improve availability of positioning services at higher latitudes, and to provide an independent positioning system upon which European nations can rely even in times of war or political disagreement. The GALILEO constellation should become operational by 2012.

GALILEO constellation (source ESA)

FOR MORE INFORMATION SEE CHAPTER “FOCUS ON EUROPEAN GNSS”

All you need to know to do business with GNSS Capital High Tech Page 19 Noémie Dumesnil

4) COMPASS Navigation Satellite System (CNSS)/BeiDou 2

China is planning to build a navigation satellite constellation known as Compass Navigation Satellite System (CNSS), or “BeiDou 2” in its Chinese name. The BeiDou 2 system will be based on its current Compass Satellite Navigation Experimental System (BeiDou-1). BeiDou-1 will be able to provide navigation and positioning services to users in China and its neighbouring countries by 2008. The BeiDou 1 system will gradually be expanded into BeiDou 2 global navigation satellite constellation comprising 5 Geostationary Earth Orbit (GEO) satellites and 30 medium Earth orbit satellites. The BeiDou 2 system is intended to provide navigation and positioning services to global users. The CNSS will provide two types of services:

a free service for civilian users will have positioning accuracy within 10 metres, velocity accuracy within 0.2 metre per second and timing accuracy within 50 nanoseconds;

a licensed service with higher accuracy for authorised and military users only. The system will initially cover China and its neighbouring countries only but will eventually extend into a global navigation satellite network.

The new generation BeiDou 2 will allow ground receiver to calculate its position by measuring the distance between itself and three or more satellites, similar to the method of operation of the GPS and GLONASS systems. An independent satellite navigation network would allow Chinese forces to maintain its satellite navigation capability in time of crisis without relying on foreign satellites. China successfully launched a first medium Earth orbit BeiDou 2 navigation satellite codenamed Compass-M1 on 14 April 2007. The satellite will operate at an altitude of 21,500km orbit. 16

16 http://www.sinodefence.com/strategic/spacecraft/beidou2.asp

All you need to know to do business with GNSS Capital High Tech Page 20 Noémie Dumesnil

V. Regional Satellite Navigation Systems

1) BEIDOU 1

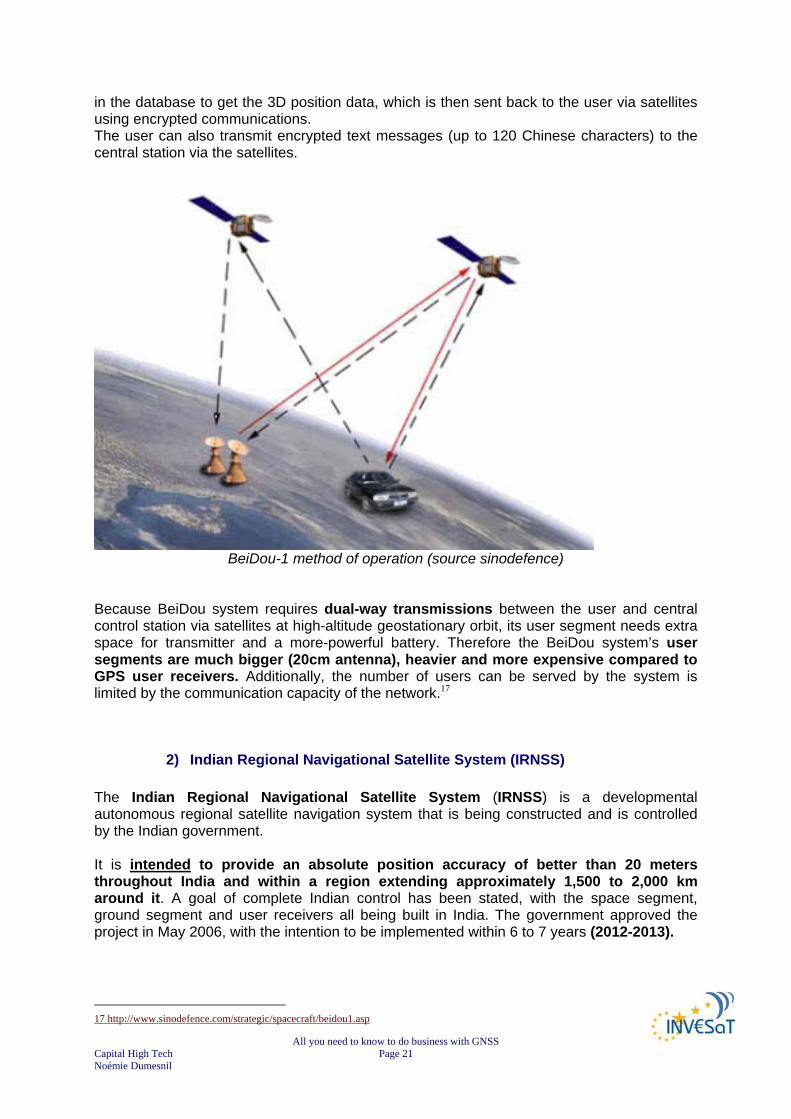

The Compass Navigation Satellite Experimental System, or BeiDou-1 in its Chinese name, is the 3 satellites constellation developed by China Academy of Space Technology (CAST). It is China’s first space-based regional navigation and positioning network. The system provides all weather, two-dimensional positioning data for both military and civilian users. The satellites are capable of communication and horizontal positioning for China’s military within their region. The network covers most areas of East Asia region and has both navigation and communication functions. The system will be able to provide navigation and positioning services to users in China and its neighbouring countries by 2008. The satellite network comprises three BeiDou-1 satellites (2 operational and 1 backup). The first two satellites of the BeiDou-1 navigation experimental system, the BeiDou-1A and BeiDou-1B, were launched on 31 October 2000 and 21 December 2000 respectively. The system began to provide navigation and positioning services in late 2001. The third satellite (backup) BeiDou-1C was launched on 25 May 2003, bringing the system fully operational. The navigation and positioning services became available to civilian users in April 2004. This has made China the third country in world to have deployed an operational space-based navigation and positioning network. Following the three successful launches of the BeiDou-1 satellites, a fourth GEO satellite was launched on 2 February 2007. The satellite suffered from a control system malfunction, which resulted in the solar power panel unable to expand. After some adjustment work from the ground control station, the satellite was said to be fully restored. The satellite was placed into the GEO, presumably to complement the three existing regional Beidou-1 geostationary satellites. At current time, we are not able to say if the satellite is being used. The ground systems include:

central control station, 3 ground tracking stations for orbit determination (at Jamushi, Kashi and

Zhanjiang), ground correction stations, user terminals (receivers/transmitters).

The system provides positioning data of 100m accuracy. By using ground- and/or space-based (the 3rd and 4th satellites) differential methods, the accuracy can be increased to under 20m. The system capacity is 540,000 users per hour, and serve up to 150 users simultaneously. The method of operation is specific: Beidou 1 Satellite Navigation Experimental System requires dual-way transmissions between the user and the central control station via the satellite. Firstly, the central control station sends inquiry signals to the users via two satellites. When the user terminal received the signal from one satellite, it sends responding signal back to both satellites. The central station receives the responding signals sent by the user from two satellites, and calculates the user’s 2D position based on the time difference between the two signals. This position is then compared with the digital territorial map stored

All you need to know to do business with GNSS Capital High Tech Page 21 Noémie Dumesnil

in the database to get the 3D position data, which is then sent back to the user via satellites using encrypted communications. The user can also transmit encrypted text messages (up to 120 Chinese characters) to the central station via the satellites.

BeiDou-1 method of operation (source sinodefence)

Because BeiDou system requires dual-way transmissions between the user and central control station via satellites at high-altitude geostationary orbit, its user segment needs extra space for transmitter and a more-powerful battery. Therefore the BeiDou system’s user segments are much bigger (20cm antenna), heavier and more expensive compared to GPS user receivers. Additionally, the number of users can be served by the system is limited by the communication capacity of the network.17

2) Indian Regional Navigational Satellite System (IRNSS) The Indian Regional Navigational Satellite System (IRNSS) is a developmental autonomous regional satellite navigation system that is being constructed and is controlled by the Indian government. It is intended to provide an absolute position accuracy of better than 20 meters throughout India and within a region extending approximately 1,500 to 2,000 km around it. A goal of complete Indian control has been stated, with the space segment, ground segment and user receivers all being built in India. The government approved the project in May 2006, with the intention to be implemented within 6 to 7 years (2012-2013).

17 http://www.sinodefence.com/strategic/spacecraft/beidou1.asp

All you need to know to do business with GNSS Capital High Tech Page 22 Noémie Dumesnil

It is unclear if recent dealings with the Russian government to restore their GLONASS system will supersede the IRNSS project or feed additional technical support to enable its completion. The proposed system would consist of a constellation of 7 satellites and a support ground segment.

3 of the satellites in the constellation will be placed in geostationary orbit 4 in geosynchronous inclined orbit of 29° relative to the equatorial plane.

Such an arrangement would mean all 7 satellites would have continuous radio visibility with Indian control stations. The satellite payloads would consist of atomic clocks and electronic equipment to generate the navigation signals. The navigation signals themselves would be transmitted in the S-band frequency (2-4 GHz), and broadcast through a phased array antenna to maintain required coverage and signal strength. The satellites would weigh approximately 1,330 kg and their solar panels generate 1,400 watts of energy. The ground segment of IRNSS constellation would consist of:

a Master Control Centre (MCC), ground stations to track and estimate the satellites' orbits and ensure the integrity of

the network (IRIM), additional ground stations to monitor the health of the satellites with the capability of

issuing radio commands to the satellites (TT&C stations). The MCC would estimate and predict the position of all IRNSS satellites, calculate integrity, makes necessary ionospheric and clock corrections and run the navigation software. In pursuit of a highly independent system, an Indian standard time infrastructure would also be established.18

18 http://fr.wikipedia.org/wiki/Indian_Regional_Navigational_Satellite_System

All you need to know to do business with GNSS Capital High Tech Page 23 Noémie Dumesnil

VI. Augmentation systems Augmentation of a Global Navigation Satellite System is a method of improving the navigation system's attributes, such as accuracy, reliability, and availability, through the integration of external information into the calculation process. There are many such systems in place and they are generally named or described based on how the GNSS sensor receives the external information.

some systems transmit additional information about sources of error (such as clock drift, ephemeris, or ionospheric delay),

others provide direct measurements of how much the signal was off in the past, while a third group provide additional vehicle information to be integrated in the

calculation process.19

VII. The satellite based augmentation systems A Satellite Based Augmentation System (SBAS) is a system that supports wide-area or regional augmentation using additional satellite-broadcast messages.

SBAS worldwide20

Such systems are commonly composed of multiple ground stations, located at accurately surveyed points. The ground stations take measurements of one or more of the GNSS satellites, the satellite signals, or other environmental factors, which may affect the signal received by the users. Using these measurements, information messages are created, and sent to one or more satellites for broadcast to the end users.21 Various SBAS are implemented worldwide. 19 http://en.wikipedia.org/wiki/GNSS_Augmentation 20 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status 21 http://en.wikipedia.org/wiki/GBAS#Satellite_Based_Augmentation_Systems

All you need to know to do business with GNSS Capital High Tech Page 24 Noémie Dumesnil

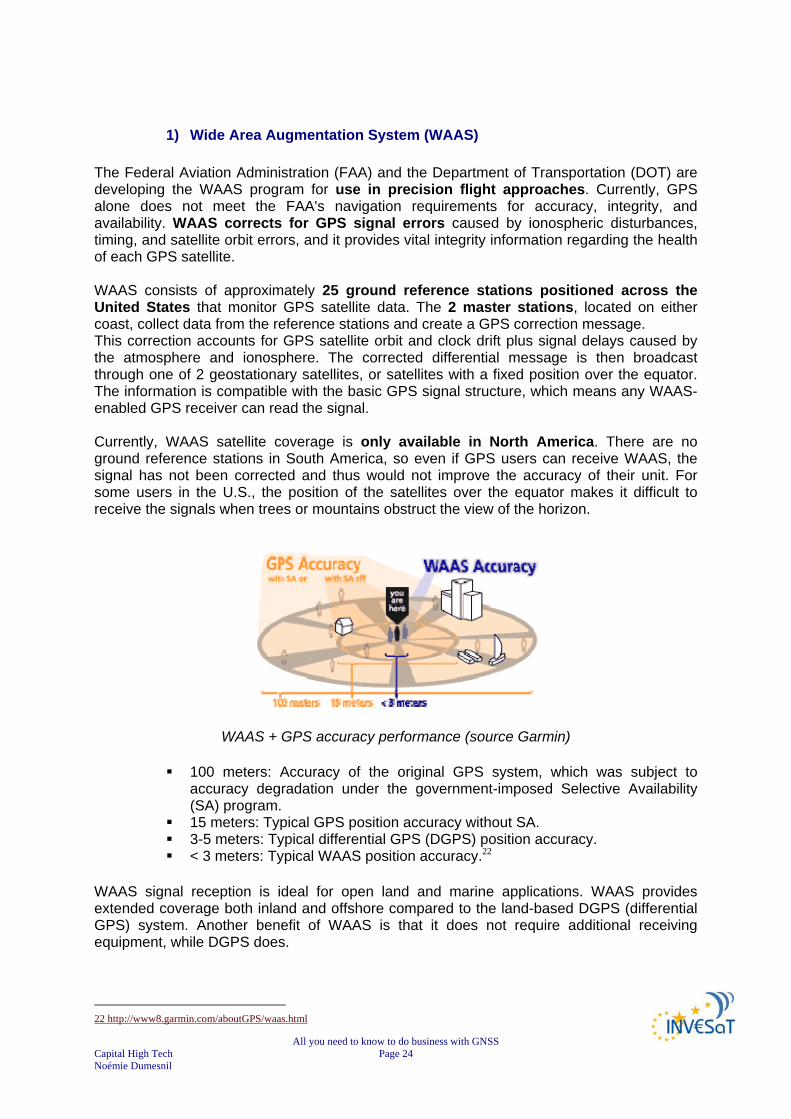

1) Wide Area Augmentation System (WAAS) The Federal Aviation Administration (FAA) and the Department of Transportation (DOT) are developing the WAAS program for use in precision flight approaches. Currently, GPS alone does not meet the FAA's navigation requirements for accuracy, integrity, and availability. WAAS corrects for GPS signal errors caused by ionospheric disturbances, timing, and satellite orbit errors, and it provides vital integrity information regarding the health of each GPS satellite. WAAS consists of approximately 25 ground reference stations positioned across the United States that monitor GPS satellite data. The 2 master stations, located on either coast, collect data from the reference stations and create a GPS correction message. This correction accounts for GPS satellite orbit and clock drift plus signal delays caused by the atmosphere and ionosphere. The corrected differential message is then broadcast through one of 2 geostationary satellites, or satellites with a fixed position over the equator. The information is compatible with the basic GPS signal structure, which means any WAAS-enabled GPS receiver can read the signal. Currently, WAAS satellite coverage is only available in North America. There are no ground reference stations in South America, so even if GPS users can receive WAAS, the signal has not been corrected and thus would not improve the accuracy of their unit. For some users in the U.S., the position of the satellites over the equator makes it difficult to receive the signals when trees or mountains obstruct the view of the horizon.

WAAS + GPS accuracy performance (source Garmin)

100 meters: Accuracy of the original GPS system, which was subject to accuracy degradation under the government-imposed Selective Availability (SA) program.

15 meters: Typical GPS position accuracy without SA. 3-5 meters: Typical differential GPS (DGPS) position accuracy. < 3 meters: Typical WAAS position accuracy.22

WAAS signal reception is ideal for open land and marine applications. WAAS provides extended coverage both inland and offshore compared to the land-based DGPS (differential GPS) system. Another benefit of WAAS is that it does not require additional receiving equipment, while DGPS does.

22 http://www8.garmin.com/aboutGPS/waas.html

All you need to know to do business with GNSS Capital High Tech Page 25 Noémie Dumesnil

2) GPS Aided Geo Augmented Navigation GAGAN Indian Space Research Organization (ISRO), along with Airport Authority of India (AAI) has worked out a joint program to implement the Satellite Based Augmentation System (SBAS) for the Indian region to fill the gap between EGNOS and MSAS. The project called GAGAN (GPS Aided Geo Augmented Navigation) has been taken up with an objective to demonstrate the SBAS technology over the Indian region. There is a plan to have an operational system to provide a seamless navigation facility in the region, which is interoperable with other SBAS. The Airports Authority of India (AAI) plans to use Gagan to meet the civil aviation industry's growing needs in communications, navigation and surveillance and air traffic management. It will result in greater efficiency and safety in over 100 airports in India. Although primarily meant for civil aviation, it is also beneficial for other users. The GAGAN system will have a full complement of the SBAS inclusive of ground and onboard segment. The ground segment consists of

8 reference stations distributed across the country, 1 mission control centre in Bangalore 1 up linking station also in Bangalore.

The onboard segment consists of a navigation payload onboard Indian geostationary satellite GSAT-4. The indigenously designed and developed navigational transponder has the latest features inclusive of L1 and L5 operation, higher EIRP of up to 33 dBw and higher bandwidth of 20 Mhz. The preliminary system acceptance test in 2006 for the Technology Demonstration System (TDS) of the GPS-aided Geo Augmented Navigation (GAGAN), being developed by the Indian Space Research Organisation (ISRO) to improve Air Traffic Control, was successful. The GAGAN -TDS network monitors Global Positioning Satellite (GPS) signals for errors and then generates correction messages to improve accuracy for users. During the test period, average accuracy of GAGAN-TDS was better than 1-metre horizontally and only slightly more than one metre vertically, thus surpassing the 7.6-metre requirement by a significant margin.2324

3) European Geostationary Navigation Overlay Service (EGNOS)

The European Geostationary Navigation Overlay Service (EGNOS) is Europe’s first venture into satellite navigation. It will augment the 2 military satellite navigation systems now operating, the US GPS and Russian GLONASS systems, and make them suitable for safety critical applications such as flying aircraft or navigating ships through narrow channels.

Consisting of 3 geostationary satellites and a network of ground stations, EGNOS will achieve its aim by transmitting a signal containing information on the reliability and accuracy of the positioning signals sent out by the Global Positioning System (GPS) and the Global Orbiting Navigation Satellite System (GLONASS). It will allow users in Europe and beyond to determine their position within 5 m, compared with about 20 m at present.

23 http://www.india-defence.com/reports/2239 24 http://www.aiaa.org/indiaus2004/Sat-navigation.pdf

All you need to know to do business with GNSS Capital High Tech Page 26 Noémie Dumesnil

EGNOS is a joint project of the European Space Agency (ESA), the European Commission (EC) and Eurocontrol, the European Organisation for the Safety of Air Navigation. It is Europe’s contribution to the first stage of the global navigation satellite system (GNSS) and is a precursor to GALILEO, the full global satellite navigation system under development in Europe.

FOR MORE INFORMATION SEE CHAPTER “FOCUS ON EUROPEAN GNSS”

4) Multi-functional Satellite Augmentation System (MSAS)

Throughout Asia, Multi-functional Satellite Augmentation System (MSAS) provides satellite navigation correction and validation, making SBAS-enabled receivers at least 3 times more accurate than standard devices. MSAS relay stations have been set at known positions throughout Asia.

SBAS-enabled receivers do not require any additional equipment to use MSAS correction signals and, as with satellite navigation signals, there are no setup or subscription fees. MSAS is scheduled for full operation in 2005 providing accuracy to within 5 meters or less, and will expand safety and air-traffic capacity in the Asia pacific regions.25

25 http://corp.magellangps.com/en/products/aboutgps/augmentation.asp

All you need to know to do business with GNSS Capital High Tech Page 27 Noémie Dumesnil

VIII. Ground Based Augmentation System (GBAS )

The Ground Based Augmentation System (GBAS) is an augmentation to GNSS that focuses its service on the airport area (approximately a 30 km radius). It broadcasts its correction message via a very high frequency (VHF) radio data link from a ground-based transmitter. GBAS will initially provide support for (Category I) Precision Approach operation and ultimately fulfil the extremely high requirements for accuracy, availability, and integrity necessary (for Category I, II, and III) precision approaches. In addition, it will provide the ability for more flexible, curved approach paths, terminal area and regional augmentation in regions, which desire such implementation. The current Instrument Landing System (ILS) suffers from a number of technical limitations such as, VHF interference, multi path effects (for example due to new building works at and around airports), as well as ILS channel limitations. The operational benefits of GBAS include:

One GBAS Ground Station will be able to support multiple runway ends; Flight Inspection and maintenance requirements should be reduced compared to ILS; More stable signal, and less interference with preceding aircraft.

Current GBAS demonstrated accuracy is less than 1 meter in both the horizontal and vertical axis. The Ground-Based Augmentation System (GBAS) supports all phases of approach, landing, departure, and surface operations within its area of coverage. 26

1) The United States' Local Area Augmentation System (LAAS) LAAS, or the Local Area Augmentation System, is the FAA version of the Ground Based Augmentation System, or GBAS, that has been defined by the International Civil Aviation Organization (ICAO). LAAS is based on a single GPS reference station facility located on the property of the airport being serviced. This facility has 3 or more (redundant) reference receivers that independently measure GPS satellite pseudo range and carrier phase (GPS measurements based on the L1 or L2 carrier signal) and generate differential carrier-smoothed-code corrections that are eventually broadcast to user via a 31.5-kbps VHF data broadcast (in the 108 - 118 MHz band) that also includes safety and approach-geometry information. This information allows users within 45 km of the LAAS ground station to perform GPS-based position fixes with 0.5-meter (95%) accuracy and to perform all civil flight operations up to non-precision approach. Aircraft landing at a LAAS-equipped airport will be able to perform precision approach operations up to at least Category I weather minima. The pseudolites shown in the diagram below are optional means of improving user ranging geometries with ground-based GPS-like transmitters but are not likely to be needed in the foreseeable future. 27 26 http://www.ecacnav.com/content.asp?CatID=64 27 http://waas.stanford.edu/research/laas.htm

All you need to know to do business with GNSS Capital High Tech Page 28 Noémie Dumesnil

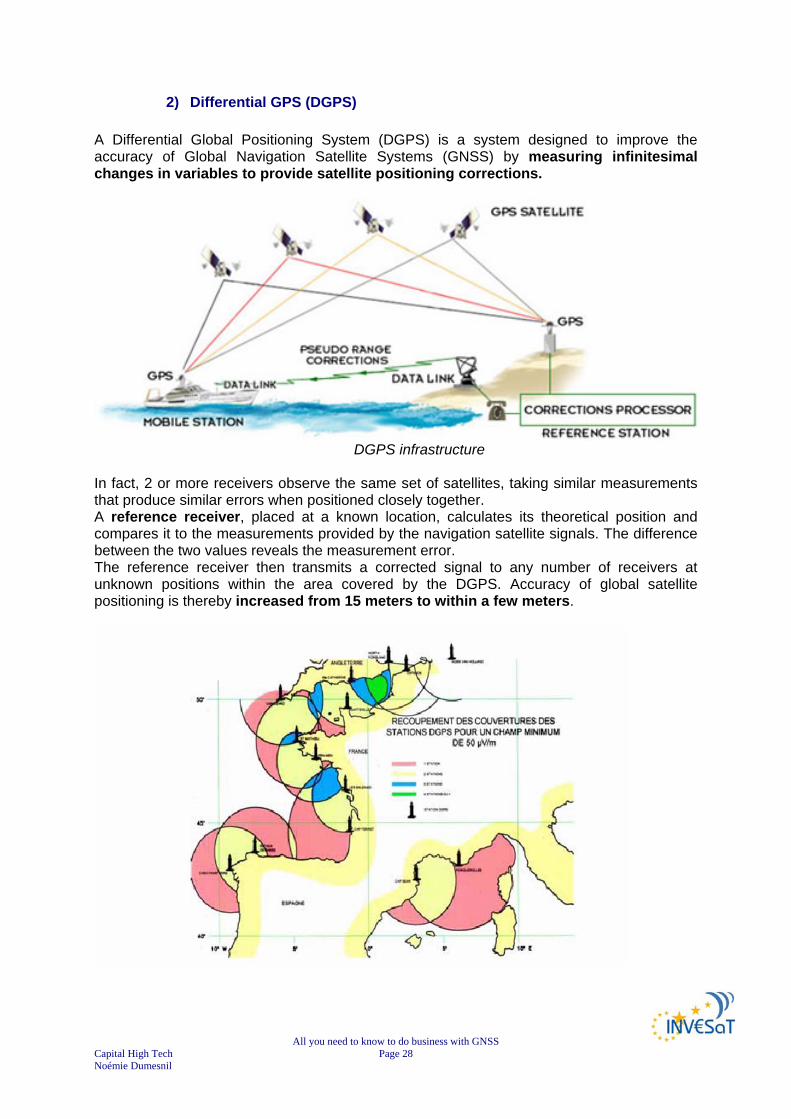

2) Differential GPS (DGPS) A Differential Global Positioning System (DGPS) is a system designed to improve the accuracy of Global Navigation Satellite Systems (GNSS) by measuring infinitesimal changes in variables to provide satellite positioning corrections.

DGPS infrastructure

In fact, 2 or more receivers observe the same set of satellites, taking similar measurements that produce similar errors when positioned closely together. A reference receiver, placed at a known location, calculates its theoretical position and compares it to the measurements provided by the navigation satellite signals. The difference between the two values reveals the measurement error. The reference receiver then transmits a corrected signal to any number of receivers at unknown positions within the area covered by the DGPS. Accuracy of global satellite positioning is thereby increased from 15 meters to within a few meters.

All you need to know to do business with GNSS Capital High Tech Page 29 Noémie Dumesnil

French DGPS network28 This technique compensates for errors in the satellite navigation system itself but may not always correct errors caused by the local environment when satellite navigation signals are reflected off of tall buildings or nearby mountains, creating multi-path signals. The accuracy of DGPS decreases with asynchronous measurement caused by spatial and temporal error decorrelation when the system receivers are set at greater distances apart.

DGPS stations performances29

More sophisticated DGPS techniques can increase positioning accuracy to within a few millimetres. Raw measurements recorded by the reference receiver and one or more roving receivers can be processed using specially designed software that calculates the errors. The corrections may then be transmitted in real time or after the fact (post-processing). By applying the corrections and recalculating the position, accuracy from within several meters to within a few millimetres is achieved, depending on the specific methodology used and the quality of the real-time data link. Satellite navigation receivers calculate position by measuring pseudo distances from the positioning satellites.

Code phase measurement method: most common method, used by all receivers, is to calculate the difference between the time a signal is transmitted from a satellite and the time it is recorded by the receiver, using the code embedded in the satellite's signal. This measurement is called code phase, and produces non-ambiguous meter-level results.

28 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse 29 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 30 Noémie Dumesnil

There are three types of DGPS using code phase measurement methods: o DGPS and LADGPS (Local Area DGPS) typically cover an area up to several

tens of kilometres. o WADGPS greatly increases the coverage area up to several thousand

kilometers by a more sophisticated method known as WADGPS (Wide Area DGPS). WADGPS classifies errors into position-dependent and position-independent components creating a secondary set of measurements that are transmitted to the rover receivers. The rover receivers are then able to reconstruct the pseudo range correction most applicable to their actual position and compute an accurate differential position.

Carrier phase serves to compliment code phase measurement by measuring the

satellite carrier wave. This method provides millimetres-level resolution with measurements that are ambiguous to about 19 centimeters. DGPS using the carrier phase achieves maximum accuracy only when measurement ambiguities are resolved in some way. The static method of ambiguity resolution is related to stationary receivers, with rover receiver point occupation from 30 minutes to several hours or even several days. The rapid static method reduces occupation periods to several minutes, while the kinematic method allows rover receivers to move without constraint.

Measurement Type

Real-time or Post-processing

System Type Accuracy Coverage Area

Code phase Post-processing

Post-processed DGPS, post-processed LADGPS or post-processed WADGPS

from < 1 m to ~10 m

From several x 10 km to several x 1000 km

Code phase Real time DGPS, LADGPS or WADGPS

from < 1 m to ~10 m

From several x 10 km to several x 1000 km

Carrier phase Post-processing

Kinematic, rapid static or static

from < 1 cm to several cm

From several km to several x 1000 km

Carrier phase Real time Real-time kinematic from < 1 cm to several cm

From several km to several x 10 km

3) Real Time Kinematic (RTK) Real Time Kinematic (RTK) satellite navigation is a technique used in land survey based on the use of carrier phase measurements of the GPS, GLONASS and/or GALILEO signals where a single reference station provides the real-time corrections of even to a centimetre level of accuracy. When referring to GPS in particular, the system is also commonly referred to as Carrier-Phase Enhancement, CPGPS. RTK is a process where GPS signal corrections are transmitted in real time from a reference receiver at a known location to one or more remote rover receivers.

All you need to know to do business with GNSS Capital High Tech Page 31 Noémie Dumesnil

The use of an RTK capable GPS system can compensate for atmospheric delay, orbital errors and other variables in GPS geometry, increasing positioning accuracy up to within a centimetre. Used by engineers, topographers, surveyors and other professionals, RTK is a technique employed in applications where precision is paramount. RTK is used, not only as a precision positioning instrument, but also as a core for navigation systems or automatic machine guidance, in applications such as civil engineering and dredging. It provides advantages over other traditional positioning and tracking methods, increasing productivity and accuracy. Using the code phase of GPS signals, as well as the carrier phase, which delivers the most accurate GPS information, RTK provides differential corrections to produce the most precise GPS positioning. The RTK process begins with a preliminary ambiguity resolution. This is a crucial aspect of any kinematic system, particularly in real-time where the velocity of a rover receiver should not degrade either the achievable performance or the system's overall reliability.30

Local augmentation: RTK31

30 http://pro.magellangps.com/en/products/aboutgps/rtk.asp 31 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007- Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 32 Noémie Dumesnil

CHAPTER 3

EUROPEAN GNSS TECHNOLOGIES

This chapter is dedicated to European GNSS, known as GALILEO & EGNOS their performances and complementarities/differences with other systems.

I. European GNSS32 Recognising the strategic importance of satellite navigation and its potential applications, Europe decided to develop its own GNSS capability in following a two-step approach: Step 1: EGNOS to provide civil complement to military GPS and GLONASS initial

services in early 2006. EGNOS is an initiative of the European Commission, Eurocontrol and ESA. EGNOS is a precursor to Galileo

Step 2: GALILEO to achieve European sovereignty through system under civil control. GALILEO is an initiative of the European Commission and ESA.

The European GNSS infrastructure is made of EGNOS and Galileo.

II. EGNOS: the European Geostationary Navigation Overlay Service The European Geostationary Navigation Overlay Service (EGNOS) is:

Europe first development of a satellite navigation ground segment Europe’s first venture into satellite navigation Europe’s contribution to the first stage of the GNSS

EGNOS is being developed under a tripartite agreement between:

the European Commission (EC), the European Organisation for the Safety of Air Navigation (Eurocontrol) the European Space Agency (ESA).

Several air traffic service providers are supporting the development programme with their own investments. EGNOS development phase started in 2000 and initial operations were in 2005. The European Space Agency is currently finalising the qualification of the operator and the deployed infrastructure. The funding of the technical activities is ensured until the Operational Qualification Review in 2008, at which ESA is committed to bring EGNOS to a qualified pre-operational state with a system compliant with the specifications. 32 http://ec.europa.eu/dgs/energy_transport/GALILEO/intro/index_en.htm

All you need to know to do business with GNSS Capital High Tech Page 33 Noémie Dumesnil

In 2007, the Galileo Supervisory Authority and ESA will negotiate and conclude on the EGNOS assets transfer of ownership taking into account the investors. In the same year, the GSA will launch a call for tender for an EGNOS Economic Operator (EEO). The EGNOS Economic Operator will be responsible to obtain certification in the shortest time possible in order to allow service provision to, in particular, the aviation community. The EGNOS Economic Operator will also develop services provision to other user communities. 33

1) EGNOS principles EGNOS will complement the GPS and GLONASS systems over large European area to improve accuracy, and make them suitable for safety critical applications such as flying aircraft or navigating ships through narrow channels.

Consisting of three geostationary satellites and a network of ground stations, EGNOS will send out a ranging signal similar to those transmitted by the GPS and GLONASS satellites. However, the signals will be more than another opportunity for users to fix a position. They will also provide information about the accuracy of position measurements delivered by GPS and GLONASS so that a train driver, for example, will be able to assess whether the position is accurate enough to rely on. EGNOS will disseminate, on the GPS L1 frequency carry out the task of transmitting a signal containing information on the reliability and accuracy of the positioning signals sent out by the GNSS.

This information, or integrity data, will be modulated onto the ranging signal. It will include accurate information on the position of each GPS and GLONASS satellite, the accuracy of the atomic clocks on board the satellites and information on disturbances within the ionosphere that might affect the accuracy of positioning measurements. The EGNOS receiver, which is more sophisticated than a standard satellite navigation receiver, will de-code the signal to give a more accurate position than is possible with GPS or GLONASS alone and an accurate estimate of errors.

33 http://ec.europa.eu/dgs/energy_transport/galileo/doc/staff_doc_galileo_en_final_16052007.pdf

All you need to know to do business with GNSS Capital High Tech Page 34 Noémie Dumesnil

Egnos description34

Consequently, EGNOS will improve the accuracy of positions from about 20 m to 5m, inform users on the health of the constellation, of the errors in position measurements and warn of disruption to a satellite signal within six seconds. EGNOS will have the responsibility to guarantee the integrity of the service, meaning to provide timely warnings to users when the system should not be used for navigation because of errors or failures in the system.

2) EGNOS system components

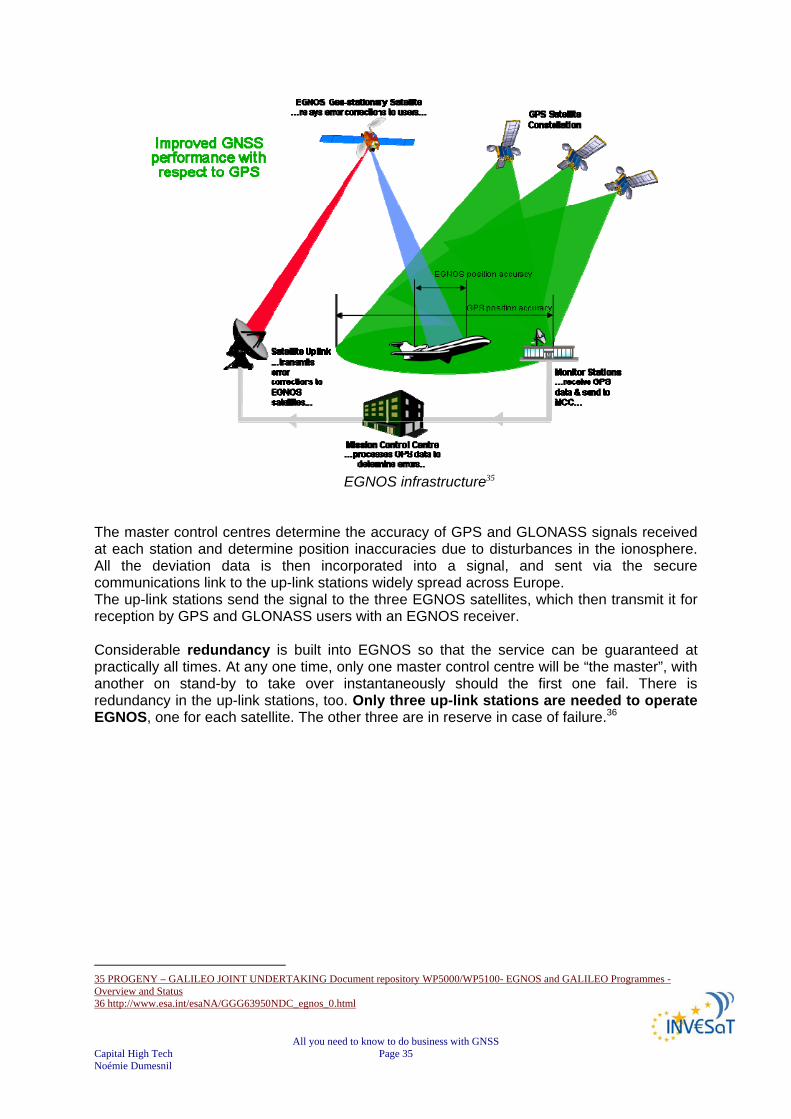

Two Inmarsat-3 satellites, one over the eastern part of the Atlantic, the other over the Indian Ocean, and the ESA Artemis satellite will broadcast the EGNOS signal, which is in Geostationary Earth orbit above Africa. Unlike the GPS and GLONASS satellites, these three will not have signal generators on board. A transponder will transmit signals up-linked to the satellites from the ground, where all the signal processing will take place. The sophisticated ground segment will consist of:

about 30 ranging and integrity monitoring stations (RIMS) 4 master control centres 6 up-link stations

The RIMS measure the positions of each EGNOS satellite and compare accurate measurements of the positions of each GPS and GLONASS satellite with measurements obtained from the satellites’ signals. The RIMS then send this data to the master control centres, via a purpose built communications network.

34 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

All you need to know to do business with GNSS Capital High Tech Page 35 Noémie Dumesnil

EGNOS infrastructure35

The master control centres determine the accuracy of GPS and GLONASS signals received at each station and determine position inaccuracies due to disturbances in the ionosphere. All the deviation data is then incorporated into a signal, and sent via the secure communications link to the up-link stations widely spread across Europe. The up-link stations send the signal to the three EGNOS satellites, which then transmit it for reception by GPS and GLONASS users with an EGNOS receiver. Considerable redundancy is built into EGNOS so that the service can be guaranteed at practically all times. At any one time, only one master control centre will be “the master”, with another on stand-by to take over instantaneously should the first one fail. There is redundancy in the up-link stations, too. Only three up-link stations are needed to operate EGNOS, one for each satellite. The other three are in reserve in case of failure.36

35 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status 36 http://www.esa.int/esaNA/GGG63950NDC_egnos_0.html

All you need to know to do business with GNSS Capital High Tech Page 36 Noémie Dumesnil

EGNOS ground segment37

3) EGNOS coverage

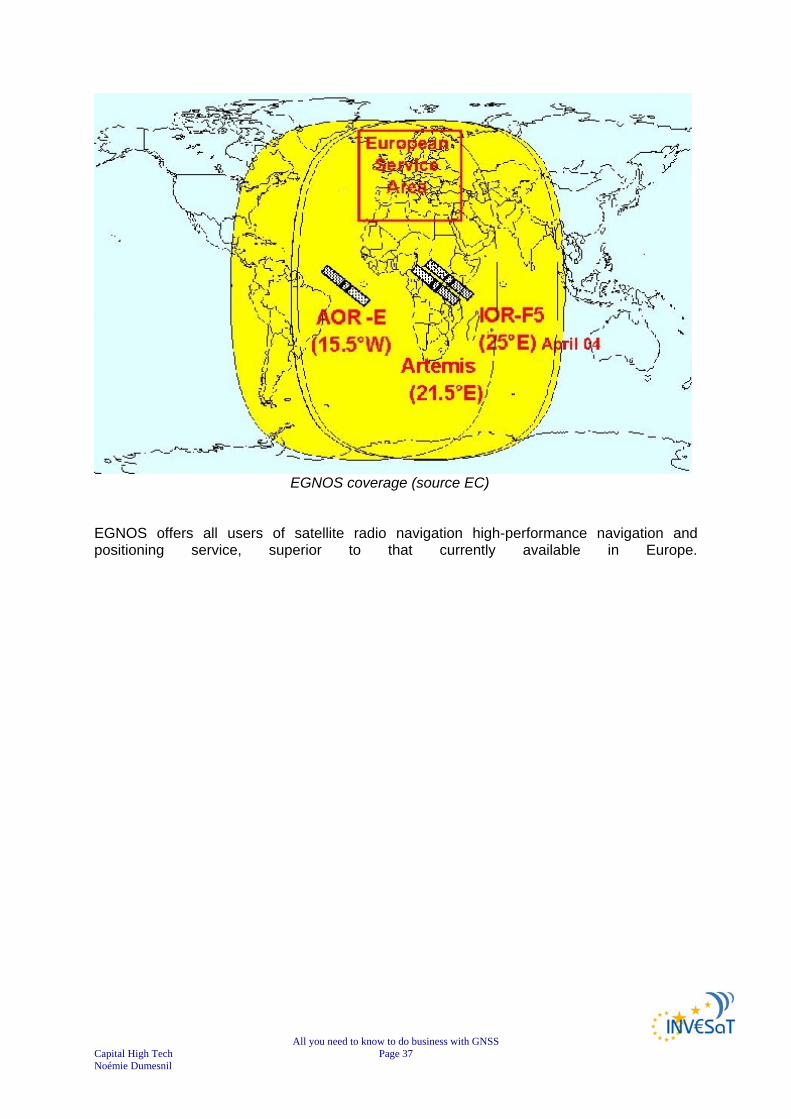

The EGNOS coverage area includes all European states, and could be extended to include other regions, such as South America, Africa, and parts of Asia and Australia, within the coverage of three geostationary satellites being used.

37 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

All you need to know to do business with GNSS Capital High Tech Page 37 Noémie Dumesnil

EGNOS coverage (source EC)

EGNOS offers all users of satellite radio navigation high-performance navigation and positioning service, superior to that currently available in Europe.

All you need to know to do business with GNSS Capital High Tech Page 38 Noémie Dumesnil

4) EGNOS performances

Figure 1: Mean horizontal positioning accuracy (95%) achieved through the GPS

constellation alone (in m) (1)

Figure 2: Mean horizontal positioning accuracy (95%) achieved through the GPS

constellation augmented by EGNOS (in m) (1)

Comparison between GPS constellation alone and GPS Constellation augmented by EGNOS (source EC)

All you need to know to do business with GNSS Capital High Tech Page 39 Noémie Dumesnil

Example of a GPS integrity event38

On 25 December 2005, GPS satellite PRN25 started to malfunction at 21H06. It took ~30 minutes for the GPS operators to take the satellite out of service. During this period, EGNOS managed to correct the satellite error.39

Example of a GPS integrity event40

38 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status 39 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100 - EGNOS_Galileo_overview_270606 40 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

All you need to know to do business with GNSS Capital High Tech Page 40 Noémie Dumesnil

III. GALILEO41 GALILEO is Europe’s initiative for a state-of-the-art global navigation satellite system, providing a highly accurate, guaranteed global positioning service under civilian control. The GALILEO positioning system is referred to as "GALILEO" instead of as the abbreviation "GPS" to distinguish it from the existing United States system.

1) GALILEO background GALILEO is designed to provide a higher precision to all users than is currently available through GPS or GLONASS, to improve availability of positioning services at higher latitudes, and to provide an independent positioning system upon which European nations can rely even in times of war or political disagreement. Galileo will be Europe’s own global navigation satellite system, providing a highly accurate, guaranteed global positioning service under civilian control. It will be inter-operable with GPS and GLONASS. By offering dual frequencies as standard, however, Galileo will deliver real-time positioning accuracy down to the metre range, which is unprecedented for a publicly available system. It will guarantee availability of the service under all but the most extreme circumstances and will inform users within seconds of a failure of any satellite. This will make it suitable for applications where safety is crucial, such as running trains, guiding cars and landing aircraft. GALILEO is to achieve European sovereignty and service guarantees through a dedicated satellite navigation system operated under civil control. Indeed, today, satellite navigation users in Europe have no other alternative than to derive their positions from US GPS or Russian GLONASS satellites. Therefore, not all the operators who make a strong use of navigation data can be guaranteed of an uninterrupted service. This is therefore the major reason why the GALILEO programme was launched: to guarantee European independence. However, other subsidiary reasons also include:

Implementation of European Transport Policy Certifiable for Safety of Life Applications Innovation through new Applications Market share for European Industry Creation of 150,000 new jobs in Europe and much more on a global scale Research & development for present & future generations Contribution to the Lisbon Strategy

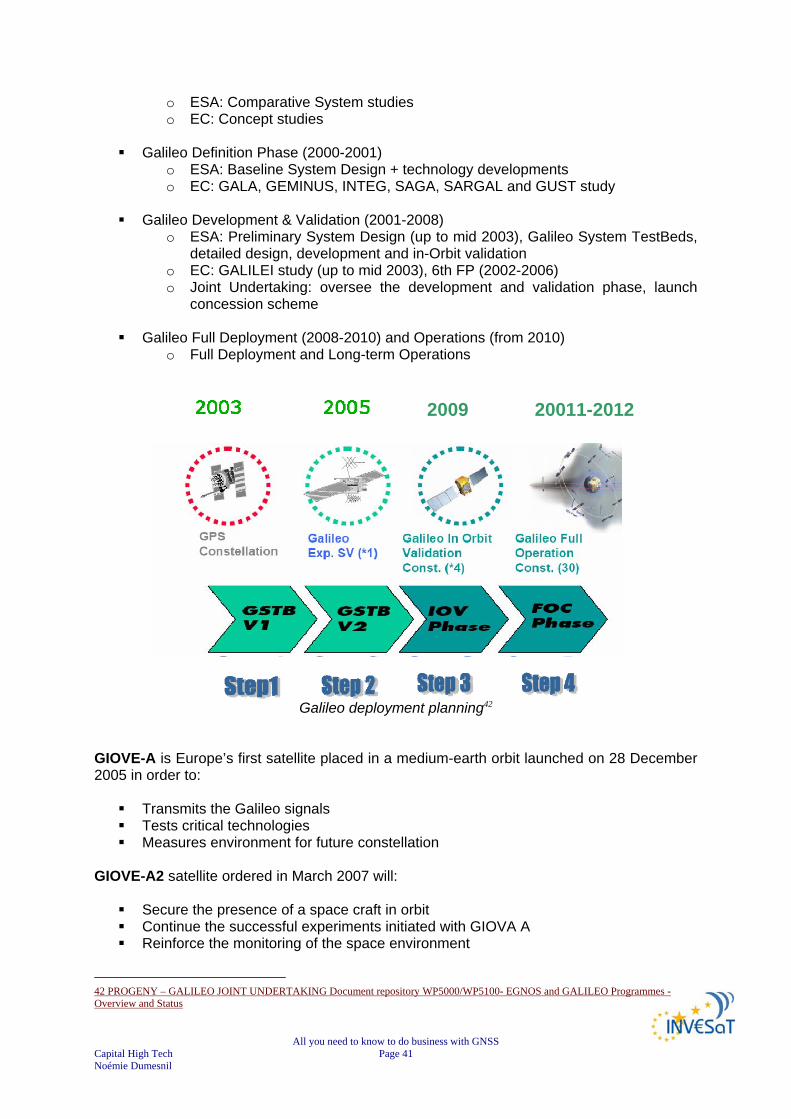

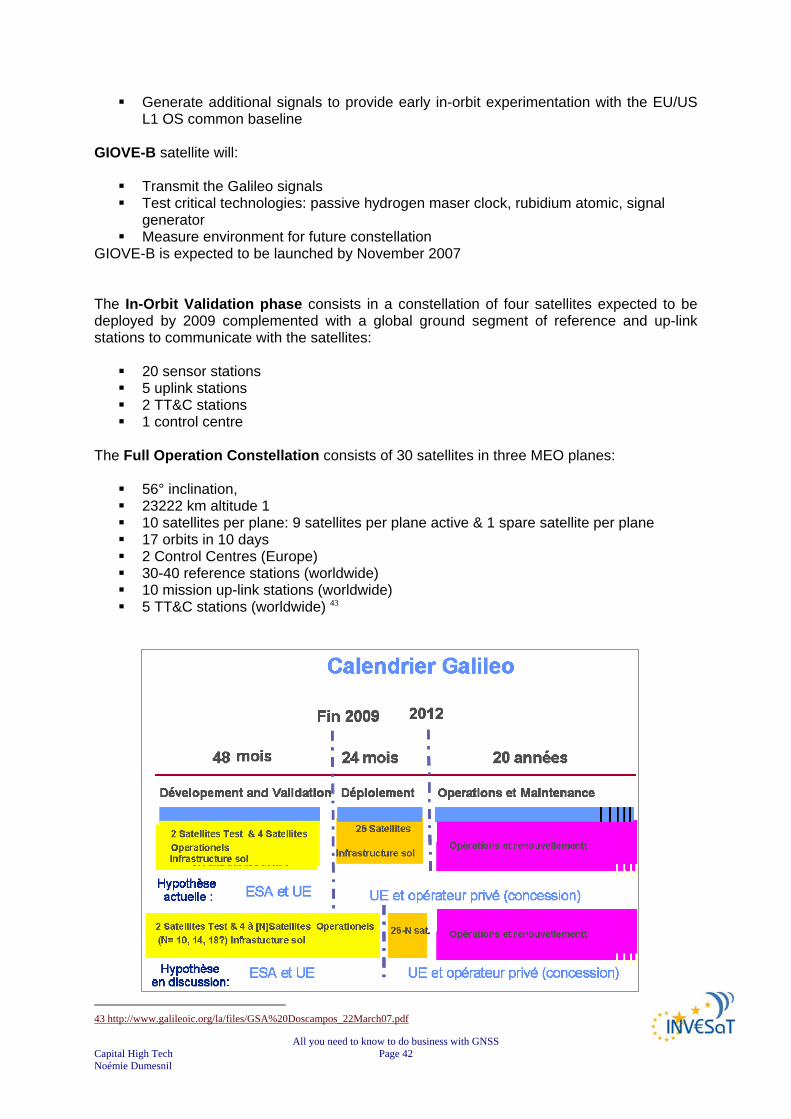

2) GALILEO Planning Originally, the GALILEO programme phase was planned as follows:

Preliminary Studies: (1998-1999)

41 http://www.esa.int/esaNA/GGG28850NDC_galileo_0.html

All you need to know to do business with GNSS Capital High Tech Page 41 Noémie Dumesnil

o ESA: Comparative System studies o EC: Concept studies

Galileo Definition Phase (2000-2001) o ESA: Baseline System Design + technology developments o EC: GALA, GEMINUS, INTEG, SAGA, SARGAL and GUST study

Galileo Development & Validation (2001-2008) o ESA: Preliminary System Design (up to mid 2003), Galileo System TestBeds,

detailed design, development and in-Orbit validation o EC: GALILEI study (up to mid 2003), 6th FP (2002-2006) o Joint Undertaking: oversee the development and validation phase, launch

concession scheme

Galileo Full Deployment (2008-2010) and Operations (from 2010) o Full Deployment and Long-term Operations

Galileo deployment planning42

GIOVE-A is Europe’s first satellite placed in a medium-earth orbit launched on 28 December 2005 in order to:

Transmits the Galileo signals Tests critical technologies Measures environment for future constellation

GIOVE-A2 satellite ordered in March 2007 will:

Secure the presence of a space craft in orbit Continue the successful experiments initiated with GIOVA A Reinforce the monitoring of the space environment

42 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

2009 20011-2012

All you need to know to do business with GNSS Capital High Tech Page 42 Noémie Dumesnil

Generate additional signals to provide early in-orbit experimentation with the EU/US L1 OS common baseline

GIOVE-B satellite will:

Transmit the Galileo signals Test critical technologies: passive hydrogen maser clock, rubidium atomic, signal

generator Measure environment for future constellation

GIOVE-B is expected to be launched by November 2007 The In-Orbit Validation phase consists in a constellation of four satellites expected to be deployed by 2009 complemented with a global ground segment of reference and up-link stations to communicate with the satellites:

20 sensor stations 5 uplink stations 2 TT&C stations 1 control centre

The Full Operation Constellation consists of 30 satellites in three MEO planes:

56° inclination, 23222 km altitude 1 10 satellites per plane: 9 satellites per plane active & 1 spare satellite per plane 17 orbits in 10 days 2 Control Centres (Europe) 30-40 reference stations (worldwide) 10 mission up-link stations (worldwide) 5 TT&C stations (worldwide) 43

43 http://www.galileoic.org/la/files/GSA%20Doscampos_22March07.pdf

All you need to know to do business with GNSS Capital High Tech Page 43 Noémie Dumesnil

GALILEO Calendar (source EC)44

3) GALILEO system description The fully deployed Galileo system consists of 30 satellites (27 operational + 3 active spares), positioned in three circular Medium Earth Orbit (MEO) planes at 23 222 km altitude above the Earth, and at an inclination of the orbital planes of 56 degrees with reference to the equatorial plane. GALILEO constellation is based on:

30 spacecrafts orbital altitude: 23 222 km (MEO) 3 orbital planes, 56° inclination (9 operational satellites and one active spare per orbital plane)

17 orbits in 10 days 2 Control Centres (Europe) 30-40 reference stations (worldwide) 10 mission up-link stations (worldwide) 5 TT&C stations (worldwide)

satellite lifetime: >12 years satellite mass: 675 kg satellite body dimensions: 2.7 m x 1.2 m x 1.1 m

span of solar arrays: 18.7 m power of solar arrays: 1500 W (end of life)

Once this is achieved, the Galileo navigation signals will provide good coverage even at latitudes up to 75 degrees north, which corresponds to the North Cape, and beyond. The large number of satellites together with the optimisation of the constellation, and the availability of the 3 active spare satellites, will ensure that the loss of one satellite has no discernible effect on the user. The two Galileo Control Centres (GCC) will be implemented on European ground to provide for the control of the satellites and to perform the navigation mission management. The data provided by a global network of 20 Galileo Sensor Stations (GSS) will be sent to the Galileo Control Centres through a redundant communications network. The GCC’s will use the data of the Sensor Stations to compute the integrity information and to synchronize the time signal of all satellites and of the ground station clocks. The exchange of the data between the Control Centres and the satellites will be performed through so-called up-link stations. For this purpose, five S-band up-link stations and ten C-band up-link stations will be installed around the globe.

44 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007 - Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse

All you need to know to do business with GNSS Capital High Tech Page 44 Noémie Dumesnil

Galileo constellation45

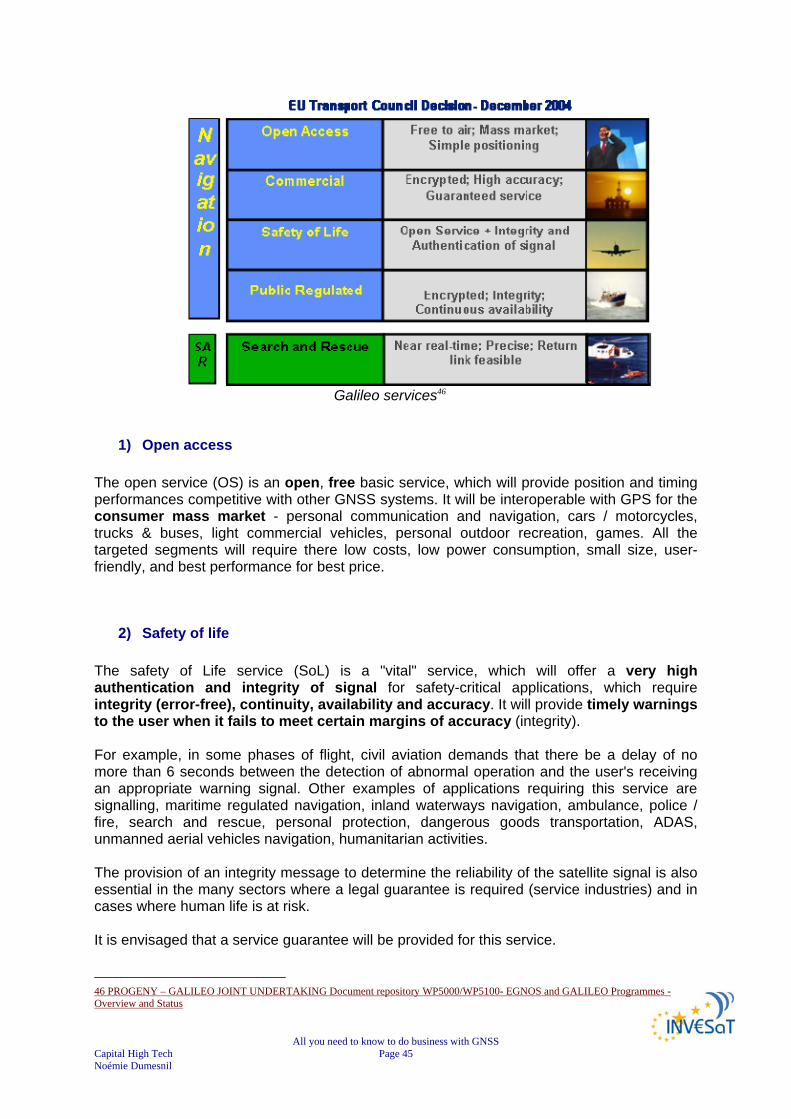

IV. GALILEO services Studies have already been carried out in order to identify future GALILEO users needs and then to define the characteristics of the services. Four navigation services and one service to support Search and Rescue operations have been identified to cover the widest range of users needs, including professional users, scientists, mass-market users, safety of life and public regulated domains.

The range of GALILEO services is designed to meet practical objectives and expectations, from improving the coverage of open-access services in urban environments (to cover 95% of urban districts compared with the 50% currently covered by GPS alone). All services are directly accessible worldwide. However, local bodies may have to make some adaptations to specific environments or user communities (tunnels, airports, ports, etc.). In addition, the satellite infrastructure can be complemented by regional components, particularly for producing the integrity message. It is worth emphasising that the services offered by GALILEO will cover the whole planet, particularly areas at a geographical disadvantage and the outermost regions of the European Union.

45 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

All you need to know to do business with GNSS Capital High Tech Page 45 Noémie Dumesnil

Galileo services46

1) Open access The open service (OS) is an open, free basic service, which will provide position and timing performances competitive with other GNSS systems. It will be interoperable with GPS for the consumer mass market - personal communication and navigation, cars / motorcycles, trucks & buses, light commercial vehicles, personal outdoor recreation, games. All the targeted segments will require there low costs, low power consumption, small size, user-friendly, and best performance for best price.

2) Safety of life The safety of Life service (SoL) is a "vital" service, which will offer a very high authentication and integrity of signal for safety-critical applications, which require integrity (error-free), continuity, availability and accuracy. It will provide timely warnings to the user when it fails to meet certain margins of accuracy (integrity). For example, in some phases of flight, civil aviation demands that there be a delay of no more than 6 seconds between the detection of abnormal operation and the user's receiving an appropriate warning signal. Other examples of applications requiring this service are signalling, maritime regulated navigation, inland waterways navigation, ambulance, police / fire, search and rescue, personal protection, dangerous goods transportation, ADAS, unmanned aerial vehicles navigation, humanitarian activities. The provision of an integrity message to determine the reliability of the satellite signal is also essential in the many sectors where a legal guarantee is required (service industries) and in cases where human life is at risk. It is envisaged that a service guarantee will be provided for this service. 46 PROGENY – GALILEO JOINT UNDERTAKING Document repository WP5000/WP5100- EGNOS and GALILEO Programmes - Overview and Status

All you need to know to do business with GNSS Capital High Tech Page 46 Noémie Dumesnil

3) Commercial service

The Commercial Service (CS) provides access to two additional signals, to allow for a higher data rate throughput and to enable users to benefit from improved accuracy. This service will provide also a limited broadcasting capacity for messages from service centres to users (in the order of 500 bits per second). This commercial service will facilitate the development of professional applications since it will offer enhanced performance compared with the basic service. It is envisaged that a service guarantee will also be provided. This service will offer value added navigation services for users with mission critical positioning requirements, in addition to guarantees regarding the specific basic parameters of the services provided (precision, availability, etc.). All professional and road market applications which require high precision, high accuracy, and high reliability will be able to benefit from this professional service : from the insurance sector (tracking stolen vehicles, premiums adjusted to the actual movements of the vehicles, monitoring movements of goods, etc.), to high-tech sectors such as oil prospecting, precision crop management, freight management, etc. Other examples of applications are oil and gas, mining, timing, environment, fleet management, asset management, geodesy, meteorological forecasting, land survey / GIS, precision survey, precision agriculture, fisheries, vehicle control and robotics, construction and civil engineering.

4) Public regulated services The Public Regulated Service (PRS) will provide position and timing capabilities to specific users requiring a high continuity of service with controlled access. Moreover, the public regulated service will be encrypted and resistant to jamming and interference. Two PRS navigation signals with encrypted ranging codes and data will be available. The PRS is aimed at government applications requiring robust navigation services for defence and public safety. In other words, it will be reserved principally for the public authorities responsible for civil protection, national security and law enforcement. It will enable secured applications to be developed in the European Union, and could prove in particular to be an important tool in improving the instruments used by the European Union to combat illegal exports and illegal immigration.

5) Search and rescue As a further feature, Galileo will provide a global Search and Rescue (SAR) function, based on the operational Cospas-Sarsat system.

All you need to know to do business with GNSS Capital High Tech Page 47 Noémie Dumesnil

Cospas-Sarsat is a satellite system designed to provide distress alert and location data to assist search and rescue (SAR) operations, using spacecraft and ground facilities to detect and locate the signals of distress beacons operating on 406 Megahertz (MHz) or 121.5 MHz. The position of the distress and other related information is forwarded to the appropriate Search and Rescue Point of Contact (SPOC) through the Cospas-Sarsat Mission Control Center (MCC) network. The Search and Rescue Service (SAR) will broadcast globally the alert messages received from distress emitting beacons. This service will offer alert and acknowledgement communications for search and rescue activities. It will greatly improve existing relief and rescue services contribute to enhance the performances of the international COSPAS-SARSAT Search and Rescue system.

SAR service infrastructure (source EC) To do so, each satellite will be equipped with a transponder, which is able to transfer the distress signals from the user transmitters to the Rescue Co-ordination Centre, which will then initiate the rescue operation. At the same time, the system will provide a signal to the user, informing him that his situation has been detected and that help is under way. This latter feature is new and is considered a major upgrade compared to the existing system, which does not provide a feedback to the user. The SAR system will support all organizations in the world with responsibility for SAR operations, whether at sea, in the air or on land. SAR benefits:

Reduction of false alarms Better time of detection Better precision of localisation Acknowledgment/receipt of distress message of (ACK) towards the user in

distress

All you need to know to do business with GNSS Capital High Tech Page 48 Noémie Dumesnil

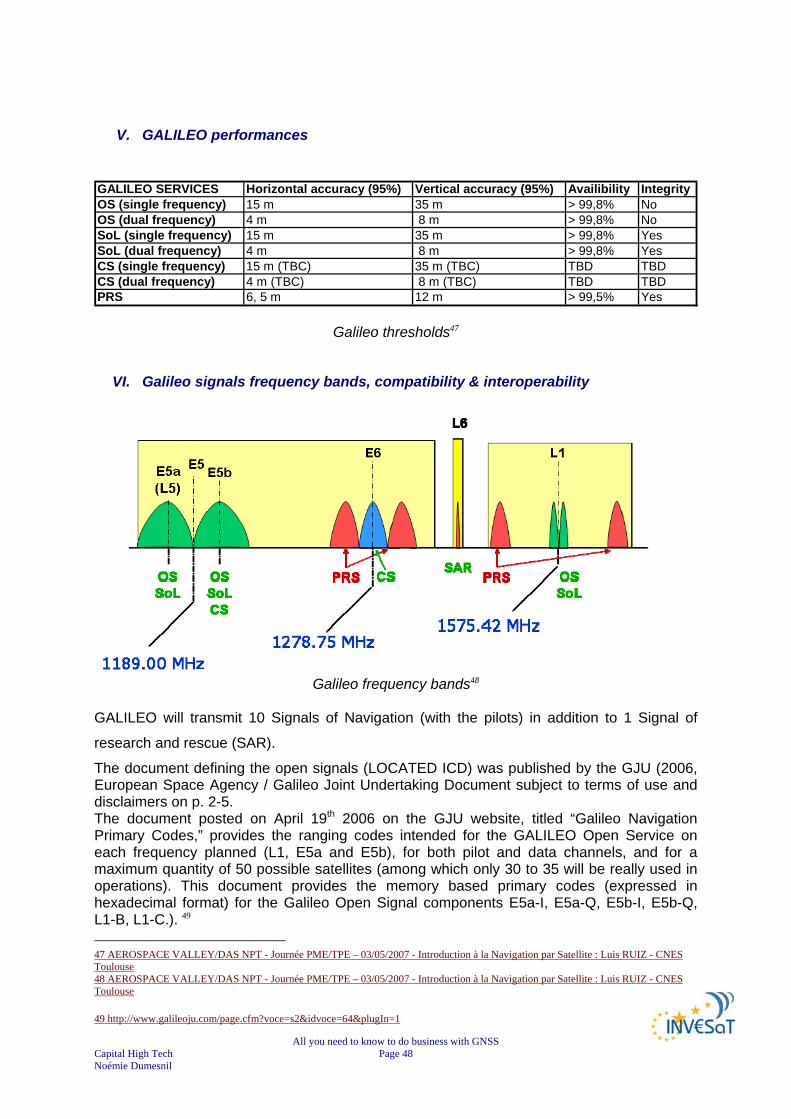

V. GALILEO performances GALILEO SERVICES Horizontal accuracy (95%) Vertical accuracy (95%) Availibility IntegrityOS (single frequency) 15 m 35 m > 99,8% NoOS (dual frequency) 4 m 8 m > 99,8% NoSoL (single frequency) 15 m 35 m > 99,8% YesSoL (dual frequency) 4 m 8 m > 99,8% YesCS (single frequency) 15 m (TBC) 35 m (TBC) TBD TBDCS (dual frequency) 4 m (TBC) 8 m (TBC) TBD TBDPRS 6, 5 m 12 m > 99,5% Yes

Galileo thresholds47

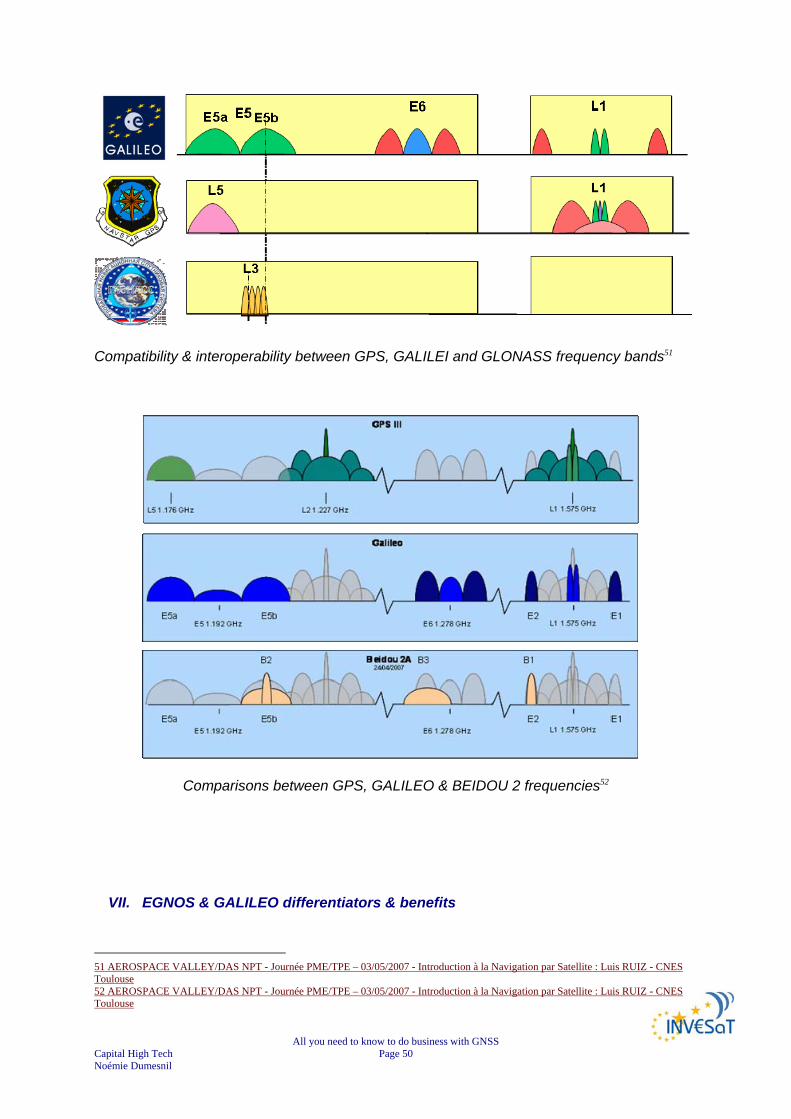

VI. Galileo signals frequency bands, compatibility & interoperability

Galileo frequency bands48

GALILEO will transmit 10 Signals of Navigation (with the pilots) in addition to 1 Signal of

research and rescue (SAR).

The document defining the open signals (LOCATED ICD) was published by the GJU (2006, European Space Agency / Galileo Joint Undertaking Document subject to terms of use and disclaimers on p. 2-5. The document posted on April 19th 2006 on the GJU website, titled “Galileo Navigation Primary Codes,” provides the ranging codes intended for the GALILEO Open Service on each frequency planned (L1, E5a and E5b), for both pilot and data channels, and for a maximum quantity of 50 possible satellites (among which only 30 to 35 will be really used in operations). This document provides the memory based primary codes (expressed in hexadecimal format) for the Galileo Open Signal components E5a-I, E5a-Q, E5b-I, E5b-Q, L1-B, L1-C.). 49 47 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007 - Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse 48 AEROSPACE VALLEY/DAS NPT - Journée PME/TPE – 03/05/2007 - Introduction à la Navigation par Satellite : Luis RUIZ - CNES Toulouse 49 http://www.galileoju.com/page.cfm?voce=s2&idvoce=64&plugIn=1

All you need to know to do business with GNSS Capital High Tech Page 49 Noémie Dumesnil

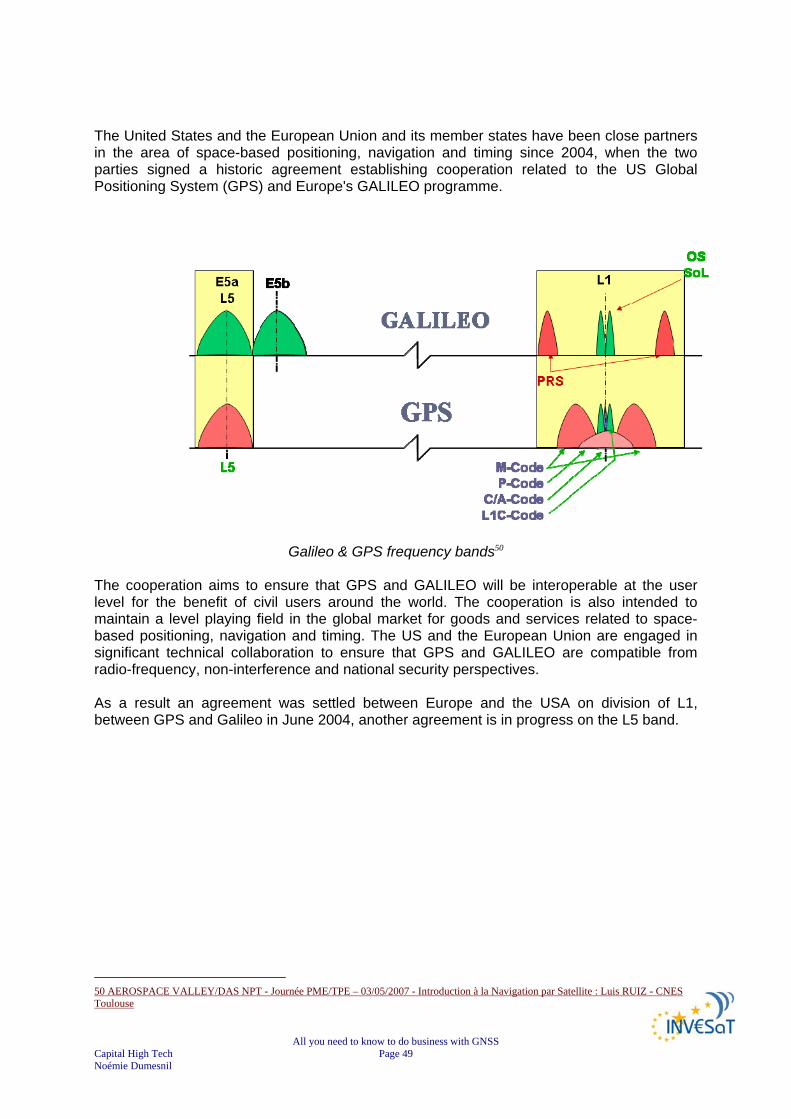

The United States and the European Union and its member states have been close partners in the area of space-based positioning, navigation and timing since 2004, when the two parties signed a historic agreement establishing cooperation related to the US Global Positioning System (GPS) and Europe's GALILEO programme.