Embed Size (px)

Citation preview

Agriculture as an asset class and the finacialisation of the South African farming

sector

Antoine Ducastel & Ward Anseeuw

• Financialisation? The role of South Africa

• Process of financialisation

• Changing the form and conception of SA agricultural sector?

Financialisation -The role of South Africa

Financialisation

Diverse social phenomena related to the expansion of the financial markets’ realm

(proliferation of financial assets, evolution of shareholding structures in companies); this

diversity generates as such vagueness around this concept (Fine, 2012).

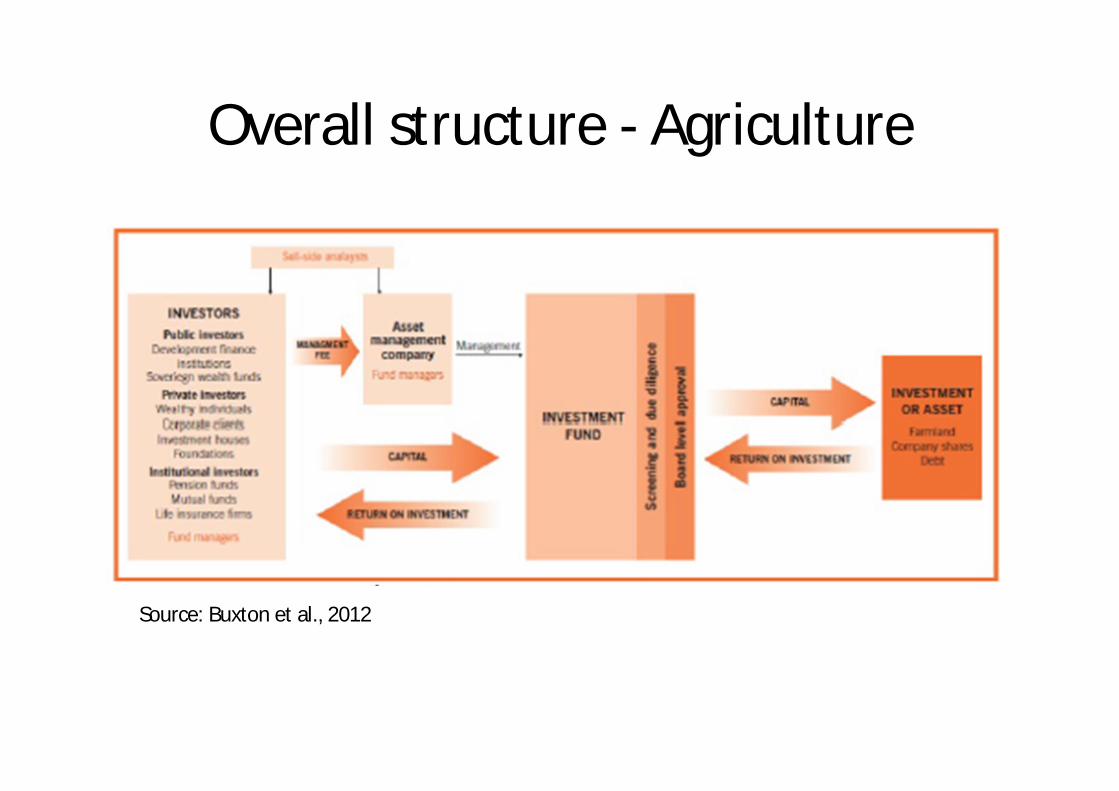

Overall structure - Agriculture

Source: Buxton et al., 2012

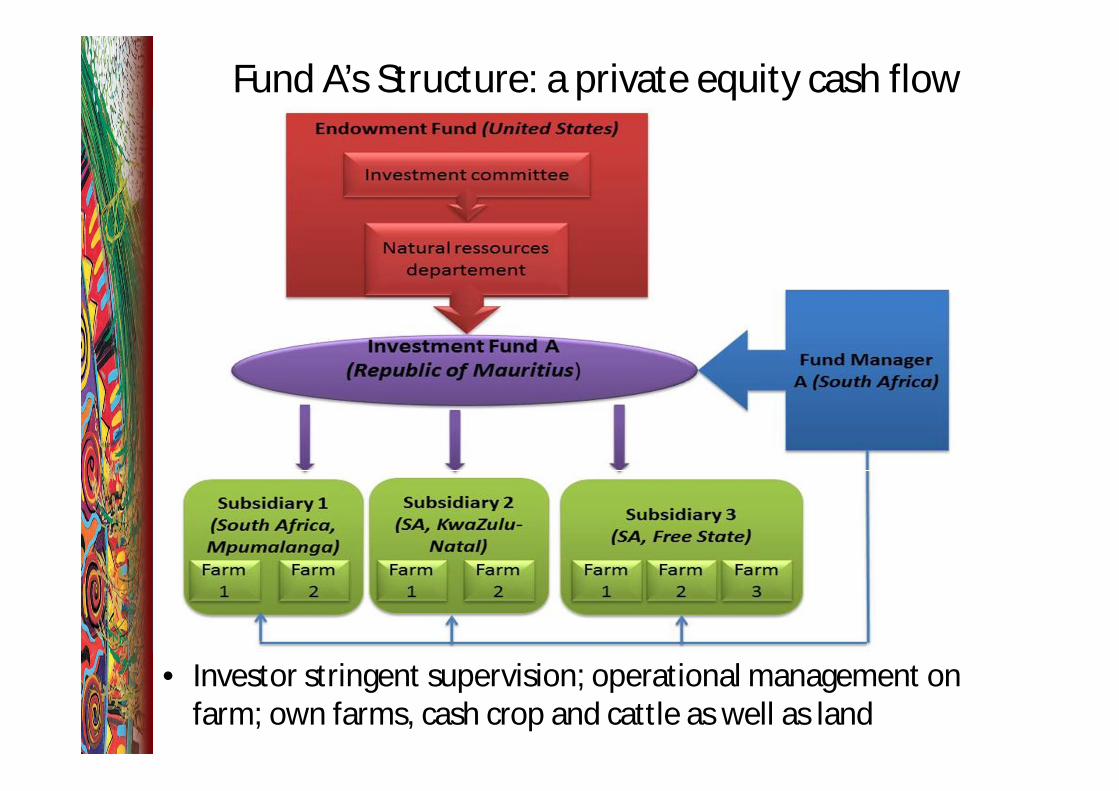

Fund A’s Structure: a private equity cash flow

• Investor stringent supervision; operational management on farm; own farms, cash crop and cattle as well as land

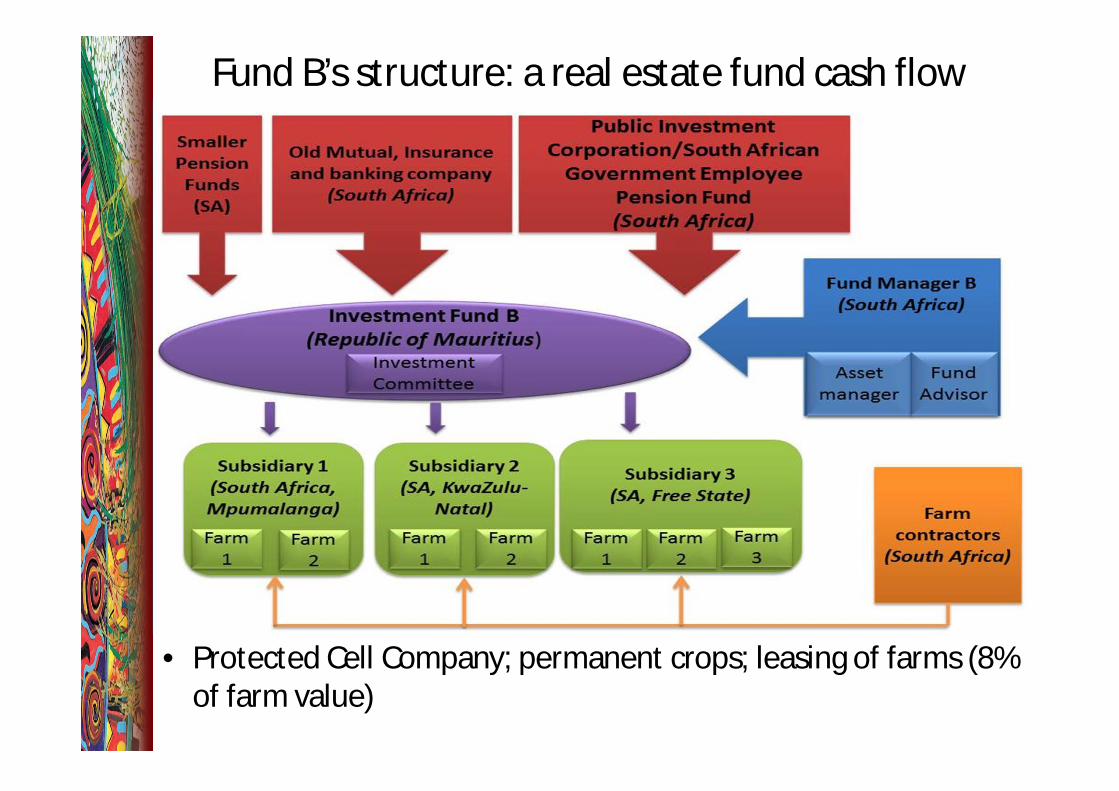

Fund B’s structure: a real estate fund cash flow

• Protected Cell Company; permanent crops; leasing of farms (8% of farm value)

South African actors & intermediaries as farmlandbrokers

• Market intermediaries’ roles (Bessy & Chauvin, 2013):– Mediating the supply and demand– Translating capital and ressources

• Agriculture = asset as a value recognized by financialmarkets:– Financial beliefs (i.e. outperformed the average profit)– Financial devices (i.e. calculation devices) and benchmarks

• How such intermediaries (re-)shape South African farmsas an investment opportunity for investors, i.e. as anasset class?

Processes

Global farm land attraction from financial industry

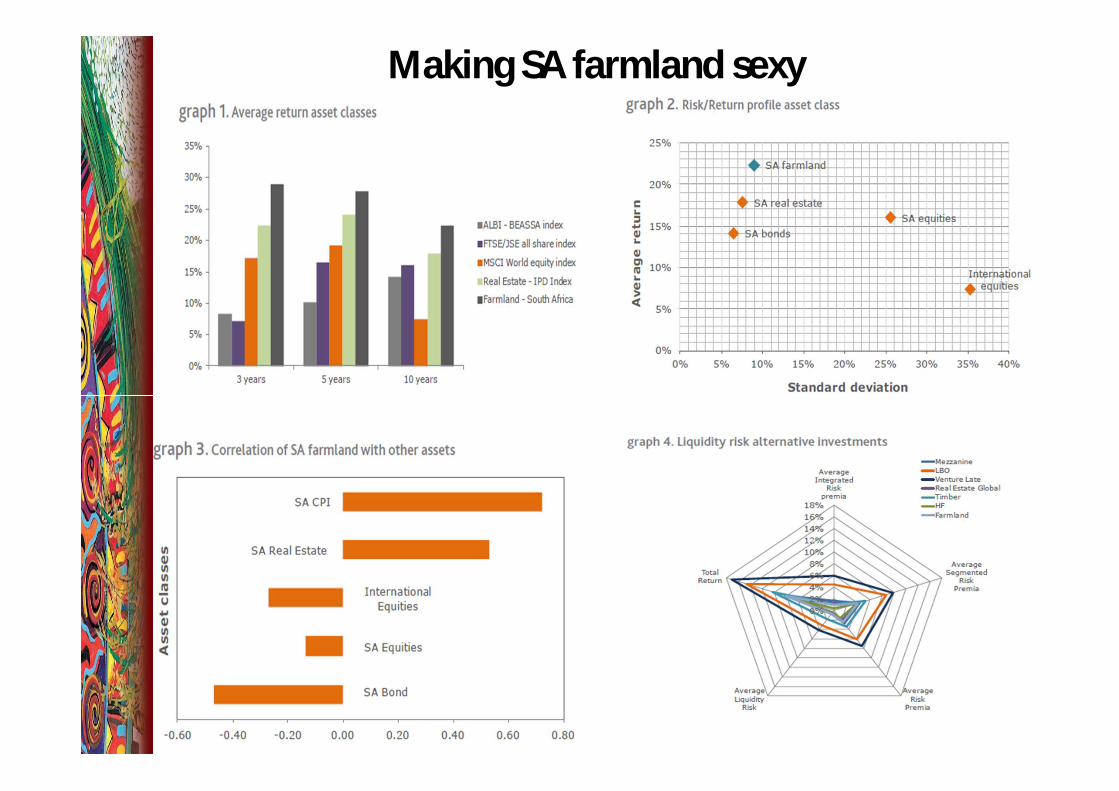

Making SA farmland sexy

Assetisation

SA intermediaries engaged in an “assetisation” process

• 3 steps toward a profitable, tradable, predictable and liquid asset

Diversity of channels toward South African farmlands structured around the relations investor(s)/manager:

o Long term investors and weight of the source of capital (Aglietta & Rigot, 2009)

o Background of the fund manager and forms of its “indigenous capital”

1. Unlocking and securing financial value: leverageinstruments on SA farms

• Bundling and unbundling strategies/assets:• A farm as a bundle of independent assets: property deeds, water rights, a

“biological asset” and a flow of commodities

• Presence/development of financial instruments (Commodityfuture exchange (SAFEX) in a market economy

• Potfolio approach• Diversification of activities• « Off-shorisation »• Geographic diversification

• Corporate farming andmanagement from a distance

2. Setting up SA farms’ standards and benchmarks

• The corporate finance instruments (i.e.Discounted Cash Flow model)– A set of « calculation devices » (Callon et al., 2007)– A common metric for financial markets: Decision

making support; to compare and evaluate theassets’ profitability and complementarity

• Highlighting the value creation• Framing practices and strategies• A competition challenge

3. Producing a « disembedded » farm

• the « assetisation » process as an extractionfrom its political and social environment– « Occupiers »: “A person residing on land which belongs to another

person, and who has, or on 4 February 1997 or thereafter, had consentor another right in law to do so”, Extension of Security of Tenure Act,1997

• Toward financial enclaves• The « cross-border regulation » attempts

Changing the form and conception of SA agricultural sector?

Changing the form and conception of SA agricultural sector?

• Limits and contraints of the translationprocess• retroaction from resistances and failures• Certainly in other African countries

• From “Land-commodity fiction” (Polanyi,1983) to “land-asset fiction”?

Examples of investment funds specialised in agricultural initiatives in South AfricaInvestment fund(date of establishment)

Fund owner Origin of capital Capitalisation amount

Investment capital Activity area

Emvest(2008)

Emergent Asset Management (UK-based investment fund, specialised in emergent markets) & Russel Stone Group (SA agro-business)

US university endowment funds

-Land acquisition with direct engagement in production, transformation and commercialisation-Several agricultural sub-sectors

Southern Africa

South African agricultural fund & African Agricultural Fund (2010)

Old mutual (SA financial institution)

European and SA life insurance companies and pension funds

R3 billion (Approx 300 million Euros)

Speculative land acquisition (no direct control over agricultural production)

Southern Africa

Zeder(2006)

PSG (SA group dedicated to financial services)

-Minority position (between 20 et 34%) with agri-businesses-No direct implications regarding production but with managerial inference-Downstream and upstream activities

SA now Southern Africa

Agri-Vie(2008)

Sanlam (SA insurance company)

Pension funds, Private foundations (Kellogs), Public institutions (Industrial Development Corporation)

R700 million (70 million Euros)

-Majority position in agri-businesses (cereals, livestock, horticulture…)-Direct control over productionPriority given primary production

Africa

African Agricultural fund(2009)

AFD, AfDB, AGRA, IFAD, West African Dev Bank

US$150 million

-Intégralité de la chaine de production agricole primary (production, transformation, infrastructures…)-Towards commercial agriculture (80% of capital) and family-based agriculture (20%)

Africa

TransFarm Africa(2011)

NEPAD business foundation

Private foundations (Hewlett)

US$20 million

Strategy not developed yet Africa

Fund of the Rand Merchant Bank (RMB – SA commercial bank)

RMB Own funds -Priority to transformation and commercialisation agri-businesses -Shares of minimum 25%-Land acquisition (30 000ha in SA)-Management and direct implications for the company’s activities-Cereal and sugar cane

Africa

Changing the form and conception of SA agricultural sector?

• Development of sub-financial industry:mobilizing dominant instruments, expertise,procedures and staff

• « Desectorisation » of SA agriculture• « Farming without farmers » - Corporate

agriculture, from independant farmer to farmmanager

• New routes of financialisation - Fundingagricultural development through financialindustry?