Embed Size (px)

Citation preview

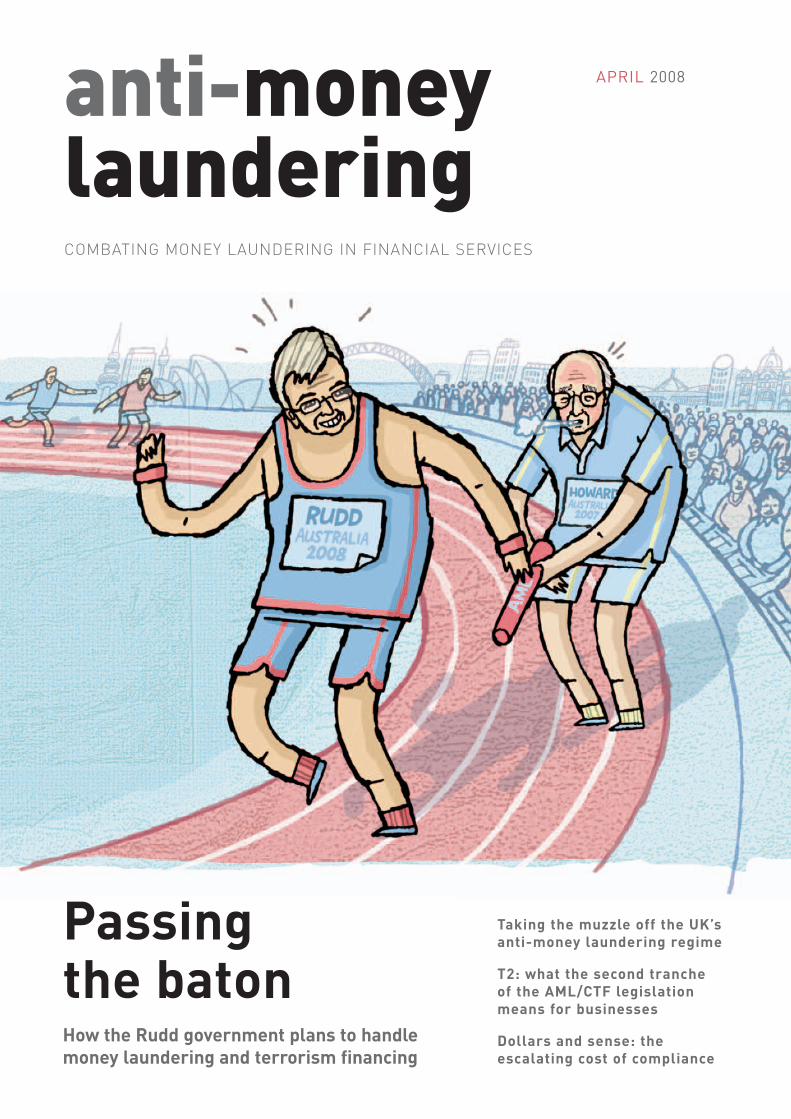

Passing the batonHow the Rudd government plans to handlemoney laundering and terrorism financing

Taking the muzzle off the UK’s anti-money laundering regime

T2: what the second tranche of the AML/CTF legislation means for businesses

Dollars and sense: the escalating cost of compliance

anti-money launderingCOMBATING MONEY LAUNDERING IN FINANCIAL SERVICES

APRIL 2008

CONTENTS

ANTI-MONEY LAUNDERING 1APRIL 2008

REGULARS & CONTRIBUTORS

3 NEWS REVIEWBY ALEXANDRA CAIN

• Deadline looms for Austrac compliance reports

• Possible AML/CTF university course

• 3 minutes with David Bell, Chief Executive of the Australian Bankers Association

• Biometrics could help fight AML/CTF

• FATF issues Iran warning

• Asia/Pacific Group to hold AGM in Bali

5 TRENDSBY MICHELLE HANNAN

The first in a two part series looking at how terrorist organisations raise and channel funds.

6 INSIDE STORY BY KENNETH RIJOCK

What happens when introducers fail to vet prospective customers?

16 PROFILE BY ALEXANDRA CAIN

Alexandra Cain speaks with two leading expertsfrom Anti-Money Laundering Magazine’s 2008Congress – Richard A. Small, Global Head of Anti-Money Laundering, GE Money USA and Steve Hancock, Head of Group Money Laundering,Prudential Plc UK and Chairman, Institute ofMoney Laundering Prevention Officers (IMPLO).

19 Q&A BY ALEXANDRA CAIN

Alexandra Cain interviews Neil Jensen, Austrac’s Chief Executive and leader in Australia’s charge against money laundering.

20 OPINION BY DAVID LEPPAN

When it comes to protecting a reputation, it pays to ask the difficult questions.

7 LABOR WEAVES ITS WEBPaul Ham examines the Rudd government’stough approach to the new AML/CTF laws.

10 IDENTITY VERIFICATION – TURN COMPLIANCE INTO A BUSINESS BENEFITIdentity verification consultancy FCSOnlineexplores why now is a great time to reviewidentity verification compliance.

12 NO MORE MR NICE GUYAdam Courtenay investigates the UK’s strictanti-money laundering regime.

18 TIDAL WAVENick Kochan looks at who will be affected bythe second tranche of the AML/CTF laws.

22 YOU’VE GOT TO BE JOKINGAdam Courtenay researches the escalating cost of compliance of the new AML/CTF laws.

24 SMOOTH RUNNINGJens Meyer profiles the National AustraliaBank’s resident AML guru, Neil Jeans.

25 NEW KIDS ON THE BLOCKAnn-Maree Moodie interviews the latest members of the AML team at Deutsche Bank,Steve Sharp and Scott Williamson.

FEATURES

A REPORTING ENTITY is an individual or business that providesa designated service as defined

in the act. Examples of reporting entitiesinclude banking; non-bank financial services;money transfer, bullion and gambling businesses. Designated services include opening an account, accepting deposits, making a loan, issuing a debit card, issuingtraveller’s cheques, remittance services, funds management, superannuation, life insurance, financial planning and stockbroking.

From 12 December 2007, all businessesproviding one or more designated services are required to have in place an anti-moneylaundering and counter-terrorism financing(AML/CTF) program, as well as customeridentification and verification procedures.Austrac says “submitted compliance reportswill give Austrac an indication of yourprogress in implementing these obligations.The reports should cover the period from 13 December 2006 to 31 December 2007.”

The implementation of an AML/CTF program and the submission of a compliancereport are legislative requirements for reporting entities under the act.

The easiest way to submit a compliancereport is via Austrac Online. To enrol withAustrac Online:

> go to www.Austrac.gov.au

> choose the Austrac Online option

> click on the link to the Austrac Online login page

> select the Sign Up button and follow the instructions

To assist industry in understanding itsobligations, Austrac has developed tools such as the Austrac regulatory guide (the Austrac Typologies and Case StudiesReport 2007) which are available on its website. Sample compliance reports are also available on the site. However, these are only samples.

For further guidance or information about AML/CTF programs or compliancereports, visit the Austrac website(www.Austrac.gov.au), contact the Austrac help desk on 1300 021 037 or email [email protected]. ■

NEWS REVIEW

APRIL 2008 ANTI-MONEY LAUNDERING2

All reporting entities under the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 must submit a compliance report to Austrac by 31 March 2008.

AML/CTF universitycourse on the cards

A USTRAC recently released a requestfor expressions of interest (REOI)document for the development of a

tertiary course in AML/CTF. The REOI saysthe course is required to provide foundationlearning in AML/CTF fundamentals, as well as stimulate discussion and investigation onleading-edge and emerging issues.

Topics that might be considered in thecurriculum include:• the financial sector• AML/CTF and associated legislation• risk models• audit and compliance• criminology• money laundering and the law

enforcement environment• terrorism and counter-terrorism• international factors• money-laundering and terrorism-financ-

ing typologies, transnational crime andemerging trendsThe REOI closed on 31 January 2008 and

responses are currently being considered. ■

Deadline looms for Austrac compliance reports

T HE MANAGING DIRECTOR ofBiometrix, Ted Dunstone, says there is increasing interest from

financial institutions and fraud detection and prevention authorities in using biometrictechnologies to help reduce the incidence of money laundering.

Biometrix has developed technologiesthat link an individual’s biological idiosyn-crasies (such as voice, face or fingerprints) to identity documents.

According to Dr Dunstone, “there isincreasing interest in speaker verification for phone banking.”

He says biometric technologies couldbe used to register a person’s voice when

a new customer opens an account with afinancial institution, making it difficult for telephone banking, for example, to be undertaken by someone who is not the account holder.

Another use might be to introduce a system through which credit cards could onlybe activated following the user of the cardtelephoning to activate it.

Dr Dunstone says he is surprised therehas not been more focus on the use of biometric technologies to combat fraud, given “recent issues related to SociétéGénérale traders sharing log-in details intentionally or through theft.”

He says the widespread introduction ofbiometric technologies in financial institutions,for example the linking of speaker verificationto system log-in procedures, would go someway toward reducing fraudulent activity. ■

NEWS REVIEW

NEWS BRIEFSFATF issues Iran warningThe Financial Action Task Force, the global body that sets up international guidelines for AML/CTF, has released a statement condemning Iran for not having a comprehensive AML/CTF regime. FATF says this approach “represents a significant vulnerability within the international financial system.”FATF has urged Iran to immediatelyaddress its AML/CTF shortcomings and is advising financial institutions to“take the risk arising from the deficienciesin Iran’s AML/CTF regime into account for enhanced due diligence”.

Asia/Pacific Group to hold AGM in BaliThe eleventh Asia/Pacific Group on Money Laundering AGM is being held in Bali between 7 and 11 July 2008. The meeting will discuss the APG’s strategic direction, implementation issues facing members and “emerging and evolving money laundering and terrorism financing methods, as well ascounter-terrorism measures.” The APMbrings together national regulatory bodiesand other organisations across the Asia-Pacific region that administer AML laws.

ANTI-MONEY LAUNDERING 3APRIL 2008

How much have banks already spent on AML?

The ABA understands that complying with the reporting requirements of theAML/CTF Act, which will involve systemschanges and staff training, will cost the banking industry more than $100 million.There are also continuing costs.

What are the big-ticket items?The big-ticket items are the changes to banks’ information technology systems

and staff training to make sure employeesunderstand the new rules. Given that ABA member banks employed 131,500domestic employees as at November 2006,this is no mean feat.

Will banks see any return on investment?

Banks and other financial institutions are not predicting any significant commercial benefits. ■

THREE MINUTES WITH ... David Bell, chief executive of theAustralian Bankers Association

Anti-Money Laundering put three tough questionsto the ABA’s chief executive, David Bell, to find out how much compliance with the new AML lawsis really going to cost.

Biometrics could help fight AML/CTF Biometrics could help fight AML/CTF

AFMA / KPMG TRAINING PROGRAM

APRIL 2008 ANTI-MONEY LAUNDERING4

T HE GOVERNMENT’S AML/CTFAct is among the most comprehen-sive and detailed pieces of legislation

ever produced in this country. Passed as legislation, it is now expected that AML practitioners have interpreted it, are designinga program around it and know how to put the tenets of the law into action.

The legislation places implicit demandson practitioners to be fluent in a broad rangeof competencies related to anti-money laun-dering and counter-terrorism financing. The regulator Austrac expects reporting entities to have well-developed complianceprograms in place, as well as the ability toassess and manage the risks to which theirorganisations may now be exposed.

This is why KPMG and AFMA – publisher of Anti-Money Laundering – have co-designed a practical, comprehensiveprogram to help practitioners to understandthe risks, demystify the new legislation and its rules, understand its possible impact ontheir business lines, and consider how toeffectively respond to its challenges.

How is this program structured?The program is in two stages. In the first stageit offers a comprehensive study guide that will inform you of the legislation and rules, and provide many case studies and practicequestions to consider. The second comprises apractical, hands-on one-day workshop that willbring the theory to life. Within this workshopyou will be assessed as proof of your compe-tence in this emerging area. Effective comple-tion of your assessment will earn you threecompetencies from the Diploma of FinancialServices FNS50104, a level 5 qualificationunder the Australian Qualifications Framework,which can be put towards further study.

What will I learn?Completing this program will equip you to:• describe money laundering and terrorist

financing (ML/TF)• explain the responses being developed

at a governmental, regulatory, lawenforcement and industry levels – bothoverseas and in Australia

• detect the ML/TF risk exposure inherentin wholesale financial market products

• investigate the Anti-money Laundering andCounter-terrorist Financing Act and theassociated rules in Australia, and analysethe fundamentals of a risk-based approach

• consider the requirements your organisa-tion will need to adopt for customer duediligence, and any third parties you utilise

• assess the practical implications for establishing an AML/CTF environmentwithin your organisation/business unitand developing an effective resource andaccountability framework

• discuss the requirements for staff aware-ness and training, and pitfalls to avoid

• communicate effectively with stakeholders, both external and internal,regarding the identified ML/TF risk, and the impact of the new regime

• identify the factors to consider whenimplementing internal monitoring, software and reporting procedures.

A six-stage programTopic 1: The foundations of money laundering and terrorist financing This topic examines the fundamentals forunderstanding the process of money laundering and terrorist financing. We’llinvestigate how it’s done, who participates,where they do it and what it costs society.

Topic 2: Money laundering and terrorist financing risk in wholesale financial market products Here we’ll illustrate how money launderersand terrorists, directly or indirectly, use financial market products in the course oftheir operational activities. We will alsoexplain how guidance in this sector remainsan emerging field, and consequently, the importance of applying accepted risk

principles when assessing individual businesslines. Finally, we will provide a detailedbreakdown of the risk factors associated with specific product families.

Topic 3: Understanding your organisational obligations under the AML/CTF Act and RulesIn this topic, we’ll delve into the new legislationand its rules to establish what it may mean foryour organisation. Your AML officers willalready be apprised of this, but this topic takes a practical perspective to explain the differentareas of the legislation with case studies to high-light possible tricky areas or common mistakes.

Topic 4: Practicalities – establishing a ‘risk-based approach’ and customer due diligence In this chapter, we’ll examine the fundamen-tals of taking a risk-based approach to knowyour customer procedures. We’ll discuss theimpact that issues such as politically exposedpersons can have on customer due diligenceprocedures and what enhanced due diligenceyour firm may need to conduct as a result.

Topic 5: Practicalities – managing your AML/CTF Program In this topic, we’ll examine the practical considerations you need to take into accountwhen developing your AML/CTF policy andprocedures and implementing your program –and the options you have available for each.

Topic 6: Practicalities – internal monitoring systems, post-reporting issuesand staff awareness and training In this topic, we’ll examine the role ofAML/CTF software, and key internal andexternal considerations and organisation mustmake during the investigation, purchase andimplementation phase. We’ll also investigatereporting issues, analysing the art of makingsuspicious matter reports, and the best ways to shape staff awareness of the issues.

The cost of the program is $1050 ex GST for a full one-day workshop per person. For further information, contact Diana Zdrilic on (02) 9776 7923 [email protected] ■

Fit for the regulator – getting with the programAFMA and KPMG have co-designed a training program to equip candidatesto translate the demands ofthe new AML/CTF legislationinto a compliance program fit for the regulator.

TRENDS IN TERRORISM FINANCING METHODS

ANTI-MONEY LAUNDERING 5APRIL 2008

T ERRORISM FINANCING, like othercriminal or illegal activities, isresponsive to both the changes in the

operating environment and the respectivelevel of risk represented by different financingmethods and avenues. Over the past 12months, indications of these types of changesin the operating environment for terrorismfinancing have become evident, as the level ofawareness and scrutiny of possible terrorist-related activities has increased throughout themainstream economy.

Terrorism financing continues to operateat two distinct levels – financing for terroristorganisations and financing for cells to undertake terrorist activities. While the political and/or religious motivation for these activities has also continued, what has changed is the preferred methods forfinancing these undertakings.

Financing terrorist organisationsThe operation of terrorist organisationsrequires significant funding and the mainsources of funding continue to be donationsand charities. But as the scrutiny of movementof larger amounts of money to known terroristorganisations through the legitimate financialsystem has become more risky with theincreased level of monitoring by financialinstitutions, other sources of funding areemerging. In particular, these are the increaseduse of aid funds and legitimate businesses.

The use of aid funds for funding criminalactivities and corruption is not new, however.There have been a number of cases where aidfunds have been “redirected” to terroristgroups and their on-the-ground activities, and this appears to be increasing. The use oflegitimate businesses being used is again notnew, but has not previously been a widelyused avenue through which to move money.But as with other criminal organisations with

a need to disguise their activities, the use oflegitimate businesses as fronts or generatorsof legitimate-appearing funds is becomingincreasingly attractive for terrorism financing.So is the use of third parties – or even fourthparties – as conduits to move the moneythrough, as these parties increase the distancebetween the source and the destination of thefunds, and also confuse the money trail withthe aim of minimising the risk of detection.

The regional tendency towards certainfunding sources is likely to continue, althoughthe method of moving the money is likely to alter in line with the general trends in terrorism organisation-funding activities. For instance, funding derived from Africa islikely to continue to be from gun and armssmuggling, diamond smuggling and corrup-tion. Funding sources in Europe and the USare likely to continue to be mainly donations,charities and an increased use of legitimatebusiness operations. In Asia, drugs and corruption continue to be a source of oppor-tunistic funding supplemented by charity, aid and donation funding. In the Middle East,funding from donations and charities areexpected to continue to be the primarysources, with an increase in the use of legitimate business operations not only in the Middle East but also outside the region.

Financing terrorist activitiesCells and local terrorist operations have had tobecome more financially self-sufficient.Although funding from local charities anddonations continues to be a primary source offinancing, there is a strong trend towards theuse of fraud. Again the use of credit card andID fraud by terrorists is not new; however, themove towards these activities becoming thepreferred source of financing rather than asupplement is new. These activities have been further supported by the increased use

of technology to move money or generatefunds through online frauds.

Possible trends in the futureThere are a number of other trends that mayemerge over the next few years in response to heightened anti-terrorism and CTF laws, in particular:• The decreased use of the legitimate

financial system in favour of loose networks to physically move money;

• The increased use of unrelated organisations or individual accountsthrough which to stream funds;

• The increased use of money laundering-type layering activities; and

• A preference for using assets such asshares or bonds to move value to theorganisation, with the organisation then able to sell these assets on openfinancial markets when required.The other key future development that

is already appearing is the increased use oftechnology. It has already become apparentthat the internet is increasingly being used for effective communication between terroristorganisation members and cells. But technolo-gy also provides more effective methods for moving funds globally, with an almostanonymous money trail.

What is reflected in all of these trends, at both the terrorism organisation and the ter-rorist cell level, is the responsiveness of themethods of financing and sourcing activity tochanges in the level of risk detection; and theneed to adapt to a global change in the envi-ronment where possible terrorism activitiesare being looked for not just by governmentsbut also by financial institutions through theirCTF measures. For financial institutions, thekey is in identifying these trends and thenmodifying CTF measures to detect changes in terrorism financing methods. ■

Terrorist financinggets creativeLike their legitimate counterparts, terrorist organisations are constantly looking for more effective ways to raise and channelfunds, writes Michelle Hannan By Michelle Hannan

FINANCIAL CRIME CONSULTANT

REFERENCES: US National Intelligence Council (July 2007), National Intelligence Estimate: The Terrorist Threat to the US Homeland, www.dni.gov.press_releases/2070717_release.pdfTE-SAT (March 2007), EU Terrorism Situation and Trend Report 2007, Europol, The Hague, Netherlands, www.europol.europa.eu

INSIDE STORY

APRIL 2008 ANTI-MONEY LAUNDERING6

L AWYERS SHOULD ENSURE theirtrusted agents and introducers (thosewho refer a prospective customer to

them) ascertain the identity and intentions ofthese parties. This includes, but is not limitedto, effective customer due diligence andsource of funds verification, and adequaterecord keeping. Your law firm must have confidence in the prior inquiries of its introducers, lest subsequent events cause reputation damage upon the lawyers who have relied upon their source of business. In an age of sensational journalism, in whichnegative information about prominent subjectsis often published without adequate verifica-tion, prudent lawyers audit their introducers’ due-diligence programs to reduce the chanceof being engaged by clients who represent an unacceptable level of potential risk.

Agents and introducers of referrals to law firms include the following:• Lawyers and law firms, many of whom

are located in separate countries to the clients;

• Real estate agents;• Accountants and accounting firms;• Bankers; and• Sales representatives.

The introducers must carefully vet theprospective clients they send to a law firm –to do otherwise can be dangerous and consti-tutes negligence. A classic case is the recentBrazilian scandal involving local resellers of the products of Cisco Systems, a leadingsupplier of network equipment and networkmanagement. Here is what happened.

Brazilian authorities conducted severalarrests, charging that the participants defraudedtax authorities out of an estimated $US500 mil-lion in import duties by using a complexscheme that utilised offshore companies.

Negative press in Brazil blamed the lawyersinvolved in company formation for the accuseddefendants, though none were involved in anything more than simple company formation.

The fraudsters engaged the services ofreputable, capable lawyers in Sao Paolo andMiami, who in turn retained the prominentfirst-tier Panama law firm Aleman, Cordero,Galindo and Lee (also known as Alcogal) to form companies in tax haven jurisdictions.The firm relied on existing professional relationships with the referring lawyers, whowere ultimately responsible for identifyingand approving the clients, before sending the business to Alcogal. Unfortunately, theintroducers were negligent in discharging their responsibilities to Alcogal regarding the approval of these clients.

Unknown to the referring lawyers, most likely due to inadequate due diligence,the clients covertly also engaged a Miamiimmigration lawyer with little internationalexperience to form a domestic Florida corpo-ration on their behalf, which would later beused in a complex tax evasion scheme.

Had Alcogal known of the extent of theclients’ operation, it would certainly havetaken precautions to ensure the companies that were being formed would not be used fora criminal purpose, or it could have declinedthe representation altogether.

It is the responsibility of the agents and introducers referring business to law firms to perform adequate due diligence on all prospective clients prior to transmitting the business onward. The failure to discharge this responsibility can constitute professional negligence, ormalpractice, in their respective professions.

Notwithstanding the negative press, no member or employee of Alcogal was

ever subpoenaed, questioned, arrested,charged or convicted of any crime or violationin connection with the Cisco scandal. In fact,the firm voluntarily submitted to the Brazilianauthorities a statement containing all theinformation it had in its files as soon as it discovered that the companies were beinginvestigated by the authorities and resignedforthwith as registered agents for the companies. It did nothing wrong.

The law firm, which had no involvementin the scheme to avoid paying import dutiesto the Brazilian government, suffered badpublicity as the direct result of the arrests ofclients. Alcogal had absolutely no connectionwith the principals involved and were merelyproviders of corporate services – and wereactually victims in this case due to the negative publicity.

It is therefore critical that agents and introducers sending lawyers business do the following:• Create and operate a customer

identification program, includingenhanced due diligence when and as needed;

• Should there be financial aspects to the presentation that source of fundsprovenance be assured;

• Adequate records of these processes be created and maintained;

• An outside periodic audit of the programs be conducted to ensure they are being followed; and

• New business is declined before it isreferred to your law firm should the customer identification program revealthe prospective client is unsatisfactory. ■

Kenneth Rijock is a US-based financial crime consultant for World-Check. Contact: [email protected]

By Kenneth RijockFINANCIAL CRIME CONSULTANT

WORLD-CHECK

What happens when introducers fail to vetprospective customersIf certain important steps are not carried out when a new clientarrives on your doorstep the consequences can be devastating,as shown by what happened to a respectable and completelyinnocent major law firm, writes Kenneth Rijock, financial crimeconsultant for World-Check.

FEATURE: ANTI-MONEY LAUNDERING UNDER LABOR

O NE OF THE FIRST THINGS Labordid after winning office last yearwas to sign into law the first tranche

of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006.

The new laws not only burden banks andfinancial services companies with far moreonerous reporting requirements, they alsoimpose a range of new identity checks on thelives of ordinary investors and allow a degreeof intrusion into corporate and personal privacy that appears to be unprecedented in

the developed world. Its second tranche – yet to become law – will encompass non-bankindustries deemed to be exceptionally vulnerable to money launderers.

Labor’s priorities reflect the Rudd government’s impatience with the coalition’sslow legislative schedule. In opposition, Laborrepeatedly accused the Howard government of delays and criticised the split legislation as “half-baked.”

Now Labor is cracking down hard. It hasushered in the new regime with great haste

and apparent relish. Fron 12 December 2007,about 40,000 banks, credit unions, brokers,lenders and casinos must verify the identity of customers each time they open an account,obtain a loan, buy traveller’s cheques or makean electronic funds transfer. Labor is expectedto bring forward a planned $13 million publicawareness campaign about the identity checksthat was postponed during the election. Underthe new laws, service providers must also

ANTI-MONEY LAUNDERING 7APRIL 2008

Labor weaves its webPaul Ham examines exactly how the Rudd government will ratchet up its intrusion into the everyday financial transactions of Australians, complete with Orwellian-sounding institutions, and asks whether it can be justified.

�

FEATURE: ANTI-MONEY LAUNDERING UNDER LABOR

report all kinds of “suspicious”‘ activity to the AML regulator, Austrac, which has writtento 19,000 entities that will be affected.

Also in Labor’s sights are potentialdomestic money launderers – real estateagents, jewellers, lawyers and accountants –all of whom will also be required to reportany suspicious transactions under the secondtranche of the laws that is likely to come intoeffect this year. The Attorney-General’sDepartment has consulted with peak bodiesrepresenting these professions and the draftprovisions were circulated in August 2007.

In speeding up the timetable, the govern-ment has sent a strong message to the corpo-rate sector, one that carries a sense of continu-ity and much greater emphasis. Clearly, underLabor, there will be no relaxation or delay in the standards of financial regulation andcompliance in Australia, which are deemed to be among the toughest in the world.

In fact, Labor’s legislative priorities suggest the thin end of a wedge. It appears the very name of the Department of Financeand Deregulation may be an Orwellian euphemism for a solid dose of extra regulation. Notwithstanding his claims that he would resist overburdening the financial sector, Lindsay Tanner, the department’s new minister, decided his first priority was to regulate not deregulate.

It is of a piece with Labor’s understand-ing of power, which, in blunt terms, is towield a lot of it, very quickly and very widely. As Paul Kelly, editor-at-large of The Australian, comments: “Rudd plans vast changes in the system of government.There is, however, one unifying theme:greater prime ministerial power.” Of severalpriority areas, security is shaping up as thenumber one prime-ministerial concern.

“Security” involves not only securingAustralia’s borders and procuring its defenceneeds, of course. It involves protecting thefinancial system, detecting and eradicatingtainted cash flows through the system, andflushing out financial fraudsters, drug dealers,tax evaders and terrorists who hope to escape detection.

To this end, Labor sees financial securityand the fight against money laundering as anational priority and one in which the primeminister himself will be intimately involved.Rudd is expected to enhance the powers of the Office of National Security by appointinga chief adviser answerable directly to theprime minister. Rudd would thus, by default,assume the role of “national security chief”.

In tandem with these moves, Rudd hascommissioned a defence white paper in order

to confront the threat of militant Islam andweapons of mass destruction proliferation inthe region, which would enshrine a sweepingnew approach to defence policy. He alsointends to fulfil Labor’s pledge to create adepartment of homeland security, that would

incorporate, among other functions, those ofASIO, the Australian Federal Police, theAustralian Crime Commission, customs, emer-gency management and anti-money laundering.

Thinly disguised feelings of apprehen-sion, if not outright hostility, from within theexisting security apparatus and the corporateworld have greeted many of these measures –and not only because they will cost a greatdeal of money. As Kelly recently observed,the proposed department of homeland securityhas a disastrous precedent in the US: “Nowthere are three things you need to know [about the proposed department of homelandsecurity]. This is an American concept. It is anAmerican title. It is an American failure. TheUS Department of Homeland Security hasbeen little short of a disaster. Howard wouldnot touch the notion. For Australia, it willconstitute a huge project in governance andthere are many security experts in Canberrawarning Labor to halt this innovation. Theyare in for a shock. Rudd is determined toestablish the homeland security department.”

At ground level, Australian banks andcasinos, and soon, real estate agents, jew-ellers, accountants and lawyers, will shortlybe facing the most rigorous complianceregime anywhere on earth. Companies that donot comply with new client identity checks,for example, face fines of up to $11 million;individuals could be fined up to $2.2 million.

Critical to this awesome regulatoryregime will be the ongoing role of Austrac,the national’s pre-eminent financial intelli-gence agency. Austrac is an extraordinarybeast – a kind of regulatory Sauron, capableof casting its all-seeing eye on virtually anyfinancial transaction. To do this, it has devel-oped proprietary software (called Target) thathas the power to trace every wire transfer intoand out of the country – a gift to ASIO, theOffice of National Assessments and theAustralian Taxation Office in their pursuit offraudsters, tax evaders and traffickers, andanyone, really, who strays under the catch-allphrase of a “risky” customer.

Austrac is the envy of the money laundering regulators of the developed world,thanks to its success in tracing illicit cashflows. The Canadian government recentlypurchased Austrac’s software; and the USadministration, which lacks a system of itsown for monitoring its citizens’ wire transfers,has examined Australia’s achievement.

Anyone wiring more than $10,000 into orout of Australia automatically appears onAustrac’s system. Those details are accessibleto ASIO and the ATO – indeed, 1500 ATOoperatives have instant access to the informa-tion. There is no screening process; so it mat-ters little whether the money has a dubiousprovenance or – as in the vast majority ofcases – is simply a legal transfer.

The know your customer plank of themoney laundering legislation complementsthe role of Austrac, and is seen as even moreinsidious by anyone concerned about the citizen’s right to privacy from an overweeningstate. It obliges complying organisations tomonitor their clients and report any dubious or “risky” customers or transactions. “Peopleneed to understand they are going to be monitored on an ongoing basis,” saysDeacons law firm spokeswoman Alison Deitz.Banks, for example, will be expected to monitor an individual’s pattern of transactionsand report anything suspicious to Austrac.

“If they do, then Austrac can share thatinformation with government agencies,” shesays. “That information cannot be disclosedback to the customer. A lot of informationabout mums and dads may well end up withvarious government agencies and those mumsand dads won’t know that has occurred.”

APRIL 2008 ANTI-MONEY LAUNDERING8

�

�

“RUDD PLANS VAST CHANGES IN THE SYSTEM OF GOVERNMENT. THERE IS,HOWEVER, ONE UNIFYINGTHEME: GREATER PRIME MINISTERIAL POWER.”

PAUL KELLY, EDITOR-AT-LARGE,

THE AUSTRALIAN

FEATURE: ANTI-MONEY LAUNDERING UNDER LABOR

In short, the new laws will extend the government’s tentacles right down to the levelof the ordinary investor, who may even beasked to identify themselves before they makea share trade. As Deitz explains: “As a cus-tomer, you won’t know in advance what identi-fication you are going to be asked for. Peopleare used to providing identifying informationwhen they open a bank account or borrowmoney. But people aren’t used to providing that information when they are trying to buyunits in a managed investment scheme.”

The burden on the financial sector isgoing to be huge: ANZ, for example, reckonsit will have to train 18,000 staff over the next15 months at a cost of up to $66 million.Other banks are similarly obliged. How astruggling real estate agent or jeweller willcope remains to be seen.

So what has justified this massive probeinto the privacy of Australian companies andcitizens? Have money launderers and otherfinancial criminals become so pervasive tojustify such world-beating intrusion? Is Laborright in imposing new layers of security onthe existing system?

On the face of it, the number of investiga-tions of alleged white-collar crime appears to beincreasing, as suggested by recent flashpoints.

Consider Victorian Ombudsman GeorgeBrouwer’s report on the state’s driving licencesystem, which he found riddled with corrup-tion. Brouwer found fake licences had been

used in Medicare and Centrelink fraud, tolaunder money, and organise terrorist acts.

Or take the religious sect, the ExclusiveBrethren: Labor’s allegations against thechurch have been referred to the AustralianFederal Police, the ATO, the AustralianElectoral Commission and Austrac. The coreallegations are that the Brethren failed todeclare the transfer of large sums of moneyacross borders under the Anti-MoneyLaundering and Counter-Terrorist FinancingAct 2006 and the Financial TransactionsReports Act 1987; and have made false decla-rations about domestic financial transactions.

A few spectacular individual cases havealso come to light. In February, for example, aformer senior executive with Woolworths wasarrested and charged with multimillion-dollar

fraud, including multiple counts of cheating ordefrauding, conspiracy to cheat or defraud,receiving a corrupt commission, corruptinducement for advice, and money laundering.

But do these peculiar cases reflect agroundswell in underlying activity? Austracsays it has identified larger flows of illicitcash. Money laundering in and throughAustralia was estimated at $2.6 billion in1995; now it is almost double that. However,as Neil Jensen, Austrac’s chief executive,makes clear, this is in part due to the fact that“we’re finding a lot more”. By this measure,better and more pervasive detection methodsappear to be working.

On the other hand, according to TheExtent of Money Laundering in and ThroughAustralia in 2004 (a report by Crimes TrendsAnalysis, RMIT University, and Austrac) thecost of money laundering to the economy isvariously quoted as being between $2.8 and$6.3 billion dollars, with a likely figure of$4.5 billion. However, the report also notedthat extent of money laundering in andthrough Australia “was not significantly dif-ferent from that in 1995, when the last reportwas published”. In this light, Australians maybe forgiven for wondering whether the caseagainst money laundering is strong enough tojustify the huge invasion of personal and cor-porate privacy since 1995.

Jensen explains that Austrac’s role isunlikely to change under the new government:“Certainly our major role in partnership withthe private sector and with law enforcement

agencies is primarily to deter money launder-ing and terrorism financing. We’re certainlyidentifying a lot more – and law enforcers are acting upon that.”

In fact, Austrac is likely to get more powerful. It already does a lot more thandeterrence, of course: its cash-tracking soft-ware has helped law enforcement agenciescrack every major case in recent years. “Every international wire transfer is reportedto us as a matter of course,” says Jensen. Heis justly proud of his unit’s role in assistingpre-emptive strikes on criminals. He did arecent study of media releases from police,Customs and the Crime Commission over a12 month period, which alerted the press tomajor successes in thwarting or catching crim-inals. Jensen found that Austrac’s information

was used in almost all cases: “In many cases,it initiated the information. In that 12 monthperiod the law enforcers stopped nearly $1 billion from being laundered.”

Austrac is in fact highly successful. In 2006-07, its information was used in 1529 operational matters. There were morethan 2.3 million searches of Austrac data, and much of that information contributed toATO assessments of more than $87 million.Indeed, tax evaders are under the electronicspotlight as never before, and Labor is certainly expected to enhance the regulators’powers in this regard.

Austrac is snugly plugged into the ATOnetwork: “We report regularly to the ATO,”says Jensen. “1500 tax offices have directaccess to our data,” he says. Over the past five years Austrac has provided informationon tax evasion totalling around half-a-billiondollars. Some involved tax evasion linked to fraud, money laundering, terrorism anddrug trafficking.

Indeed, one little-known element of thenew laws is that entities – companies andindividuals – must now report directly toAustrac. In the past, reporting was industry-based; now it is an individual obligation, towhich end Austrac has recently written to19,000 entities “whom we think would beengaged in designated services” and askedthem to contact the agency, “so we can helpthem build systems required.”

The “entities” – ie any companyembraced by the new laws – will have tolodge a compliance report by 31 March,detailing the levels of compliance in 2007. In this respect Austrac now functions at theheart of Labor’s compliance regime, and is preparing for a deluge of suspicious transaction reports in coming months as the know your client rules take effect.

Nobody can say they weren’t warned. ■

ANTI-MONEY LAUNDERING 9APRIL 2008

�

OVER THE PAST FIVE YEARS AUSTRAC HAS PROVIDEDINFORMATION ON TAX EVASION TOTALLING AROUND HALF-A-BILLION DOLLARS.

APRIL 2008 ANTI-MONEY LAUNDERING10

SPONSORED FEATURE

N OW IS A GREAT TIME to review identity verificationcompliance. This is because 12 December 2007 (the date by which financial institutions were required to

have formal identity verification procedures in place) is welland truly past, and all reporting entities must have their compliance report for the period ending 31 December 2007lodged with Austrac by 31 March 2008.

But how should complying organisations assess the variouselectronic verification providers? Choosing the right provider is of paramount importance. This is not just for compliance reasons, but also to provide:

• A road map for data and product enhancements;• The ability to provide new data sources;• The ability to provide an exception-handling process;• True 24/7 support with guaranteed SLAs; and• Knowledge of legislative and regulatory requirements.

Instead of looking at identity verification as a compliancecost, businesses should view it rather as an opportunity to really get to know their customers. This approach will minimiserisk and increase overall profit margins, and also fulfil compli-ance requirements.

The use of paper-based, unsecured documents to verifyindividuals or companies is unreliable. In contrast, the use of independent, verifiable databases delivered in an online, real-time environment provides a number of benefits. These include:

• The ability to meet regulatory requirements;• The elimination of manual inefficiencies and reduced

referral rates;• Increased workflow;• A decrease in delinquency rates;• The ability to predict potential fraud and therefore

reduce losses; and • The ability to increase and flag CRM attribute anomalies.

When identity verification is performed properly, the benefit to the business is enormous and turns compliance intoa cost benefit.

What is compliance?

According to the anti-money laundering/counter-terrorismfinancing (AML/CTF) rules, compliance is determined by the

level of risk associated with the relationship pertaining to a customer (in this article we deal with medium and low-risk customers). To meet the minimum know your customer require-ments, the following information must be verified:

• The customer’s name and residential address using reliable and independent electronic data from at least two separate data sources; and either

• The customer’s date of birth using reliable and independent electronic data from at least one data source; or

• A transaction history for at least the past three years.

But what is not clearly outlined in the law is the correctdata sources to use; what constitutes a match on name, addressand date of birth information; how to minimise the impact tocustomers; and how to increase identity verification rates.

There are a number of independent government and non-government data sources, but not all providers have access tothese sources. It is therefore important to look for a providerwho uses a number of trusted, independent data sources to ver-ify identity and corroborate the identity particulars provided.Using only one source – or worse, using an internally-createdfile to verify identity – is unacceptable under the AML/CTF laws.

Independently derived data sources

It is important to explore available data sources and look at whyan organisation should ensure these are canvassed as part of anidentity verification solution.

Australian electoral roll

Full name and current residential addresses can be verifiedthrough a number of sources, the most comprehensive andindependent being the Australian electoral roll. This has becomemore reliable due to the recent tightening of the process toupdate or change details. The electoral roll consists of more than13 million individuals covering in excess of 95 per cent of citizenswho are eligible to vote, and is updated quarterly.

Only a select number of organisations have satisfied the rigorous process to gain access to the Australian electoral roll. Information from this roll cannot be purchased by non-authorised companies and can only be used for purposes of verifying an individual to satisfy the AML/CTF legislation, andnot for any other purpose.

Identity verification – turn compliance into a business benefit

�

ANTI-MONEY LAUNDERING 11APRIL 2008

SPONSORED FEATURE

Historical Electoral Roll

In additional to the current Australian electoral roll, it is possible to access historical electoral roll data, affording accessto an in-depth customer history.

This data can be used to confirm or corroborate a customer’s identity, especially relevant to those customers that fall into a Generation X or Y classification. Generations X and Y are well known for regularly changing roles and residential addresses, so verifying their current address detailscan be problematic.

Telephone directories

Sensis White Pages is one of the largest telephone directoryproducers and a great source for identity verification. Otherphone directories, including those from local and regional publishers, are commonly used in combination with the Sensis White Pages for identity verification. Mobile telephonenumbers are more difficult to obtain for identity verification,with only two million or so mobile numbers publicly listed.Working with providers who have close relationships with telephone directory producers can increase the probability ofcorroborating a customer’s identity.

Government watch lists

As well as confirming an individual’s identity, it is important tocheck government watch lists for terrorists or internationallywatched persons. The main lists are:

• OFAC (Office of Foreign Assets Control)• DFAT (Department of Foreign Affairs and Trade)• PEP (politically exposed persons)

Matching

However good a data source, it is useless if paired with poor orobsolete matching technology. Organisations should work witha provider that demonstrates they understand what constitutesa good identity match across various financial products and riskgroups and that caters for their customer demographic – butmost importantly, understands how to use this technology.

An organisation should consider the matching rules andweightings applied to each match type so that it has not onlydocumented its risk process, but has also partnered with a com-pany that provides an auditable and transparent process forverifying customers against the many data sources available.

As this process can be slightly more complex when verifyinga customer’s identity against multiple sources, it is important totake into consideration what happens when there are slightvariances in name or address between different sources.

Questions to consider:• How does the identity verification partner handle

non-exact matches?

• How does it manage and report slight variations in name or address?

• How are the results reported against various data sources and how is the overall identity score weighted?

Benefits to business

Implementing a comprehensive electronic identity verificationsolution is a powerful business tool. Businesses want a customer-friendly solution to help improve business perform-ance. The greater the number of independent sources of dataa provider uses, the higher the probability of verifying the customer to a certifiable level, therefore reducing referral ratesand the need for costly manual customer verification. A goodidentity verification provider can help to:

• Turn the AML/CTF legislation into a true business benefit;• Reduce the cost of compliance significantly; • Verify and approve more customers to a certifiable

level in real-time; • Decrease referral rates by increasing identity

verification matches;• Comply with industry legislation, using independently

verifiable government and non-government data sources; and

• Reduce business and fraud risk.

FCS OnLine provides electronic identity verification and has a comprehensive range of independent data sources toensure the highest possible match rates. With some customers,FCS is achieving customer verification rates of up to 80 per cent,depending on product type, risk type and customer demo-graphic on safe-harbour criteria. ■

■ STOP PRESS ■

NEW INFORMATION POWERHOUSE CREATED

FCS OnLine and Dun & Bradstreet have created a strategic alliancebringing together two of Australia’s most powerful identity verification and credit reporting databases.

This partnership provides the largest and most comprehen-sive identity verification service in Australia and positions FCS OnLine as the nation’s leader in turning AML/CTF legislationinto a benefit for organisations.

The partnership provides a powerful framework for growth of the business and brings customers greater access to decision-making data, both business and consumer. Dun &Bradstreet and FCS OnLine have a complementary approach to doing business, while at the same time bringing a uniqueoffering to the partnership. ■

�

For a free demonstration of how FCS OnLine can assist your organisation, please contact (02) 8912 1030 or visit www.fcsonline.com.au

WHAT’S HAPPENING IN UK AML

The UK’s anti-money laundering regime has teeth that can really bite, and now the muzzle is well and truly off, writes Adam Courtenay.

I F AUSTRALIA’S reporting entities want a sneak preview of the future ofanti-money laundering (AML) regulation

and control, they need look no further than the old country.

Australia may no longer take its politicalor economic cues directly from the UK, butour AML regime has been largely borrowedfrom it. The big differences are only in time(that is, the extent to which similar laws havebeen invoked) and, of course, the state ofpreparation of reporting entities.

The UK’s authorised firms (the equivalentof Australian reporting entities) are now, inthe words of one AML practitioner, “right in it”. There are no more periods for industryto absorb, digest and comment on proposedregulations. Nor are there any “assisted com-pliance periods” to help out the less prepared,as is currently the case in Australia.

The UK’s Money Laundering Regulations2007, which bring into effect the EuropeanUnion’s Third Money Laundering Directive,were ushered in on 15 December 2007 and are the final act in European money-laundering legislation – at least for the foreseeable future.

The new regulations provide moredetailed obligations regarding customer duediligence, require firms to vary customer due diligence and monitoring, and to take enhanced due diligence measures in higher risk situations.

They allow firms to rely on certain otherfirms for undertaking customer identification

and they clarify the arrangements for thesupervision of firms.

The new regulations cover most UKfinancial businesses (banks, building societies,money transmitters, bureaux de change,cheque cashers, savings and investment firms)and also bring in legal professionals (whenundertaking certain activities), accountants,tax advisers, auditors, insolvency practition-ers, estate agents, casinos, high-value dealerswhen dealing in goods worth more than€15,000 ($24,000) as well as trust and com-pany service providers.

Rowan Bosworth-Davies, one of theUK’s top AML consultants, says there are no more “comebacks” for any of these regulated entities.

“Whereas before a piece of guidance mayhave said that money laundering reportingofficers should ensure the following is done – it’s now that they must be done,”Bosworth-Davies says.

“They have put in a great deal more serious muscle into the latest legislation. It has teeth.”

Bosworth-Davies says the risk-basedregime may have once prompted AML practitioners to think they were in charge of their programs, as they were able to adaptthem to suit the risk. But the net effect, he says, has been to instil fear.

“In future you’re not going to be judgedon whether you did something that may have permitted money laundering – or even if

APRIL 2008 ANTI-MONEY LAUNDERING12

FROM ADAM COURTENAY IN LONDON

No more Mr Nice Guy

�

WHAT’S HAPPENING IN UK AML

you did something that breached a regulation– in future you’ll be judged on whether you complied with the terms of your ownagreement with your own regulator,”Bosworth-Davies says.

The principal of AML consultancyBridges & Partners, Martyn Bridges, says the new regime is “far more onerous” onreporters. “Before this, nobody really caredabout following the rules unless they gotcaught by the police,” says Bridges.

“But now supervision is the key thing. No one has ever been done before for failingto follow the AML regulations. But now thereare civil penalties and unlimited fines for any failure to comply with them,” he says.

And there’s another rub. The new regula-tions have brought in 27 new supervisory bodies, all of which will be able to regulateand oversee members’ behaviour.

Many of these bodies were once meretrade associations or non-governmental organisations. But since 15 December, theyhave become second-line regulators with powers to inspect and assess the AML proficiency of the firms who once set them up for their own protection and assistance.

Among the new supervisors are theOffice of Fair Trading, the Association ofInternational Accountants, the CharteredInstitute of Management Accountants, theLaw Society, the Law Society of Scotland,

the Faculty of Advocates, the InternationalAssociation of Bookkeepers and the GamblingCommission. And, perhaps most bizarrely, the Faculty Office of the Archbishop ofCanterbury. The archbishop’s office regulatesnotaries public – and for this reason will begiven power to sanction those under its aegis.

There are many who question the abilityof these organisations to supervise their members. The principal of AML consultancyOHL Consulting, Mark Outhwaite, says:“Some of these are trade bodies and somegovernment offices, and I question whethermany of them have set out their own risk-

based regime and whether many of them have set out any guidance.”

Bridges concurs: “The laugh is that halfthe supervisory bodies introduced by the leg-islation don’t have procedures themselves.”

Beyond introducing new supervisory bod-ies, the new regulations have tightened uprules on dealing with the beneficial owners ofcompanies and trusts as well as applyingtougher controls on those doing business withpolitically exposed persons (PEPs).

The regulations now incorporate threecategories of beneficial owner:

• A general definition covering individualswho ultimately control the customer, oron whose behalf a transaction or activityis being conducted;

• A detailed definition of persons who ownor control more than 25 per cent of abody corporate; and

• A detailed definition of the beneficialowner of a legal entity or a legal arrangement (such as a trust).

The new regulations spell out in detail thecustomer due-diligence measures that arerequired – which include greater monitoring.This relates directly to PEPs. Because they areat the top of the risk ladder, their “transaction-al behaviour” must not only be initially veri-fied but regularly checked on.

This is most keenly felt by the bigger UKbanks which tend to have more PEPs on their

books. “You’re now going to have to be farmore responsive to how PEPs and other highrisk entities transact,” says a senior AML headat one of the big four clearing banks.

“You’ll have to know the nature of whothey deal with and how their business growsglobally. Do they get involved with other thirdparties and entities and, if they diversify,where is the beneficial ownership?

“It’s become far more granular – and systems must pick up all those nuances which hitherto haven’t been so clear.”

Another development in the past year hasbeen the UK Financial Services Authority’s

insistence that firms look at financial crimeholistically. Whereas Australian regulatedfirms will soon have to prove that they havethe bones of an effective risk-based AML program, their UK counterparts have to prove that they have much more than this – ie, an effective financial crime policy.

Mark Spiers, the founder of AML consultancy SmithSpiers and a former moneylaundering reporting officer (MLRO) at UBS, says in practice this will mean greaterco-ordination between internal audit, securityand AML departments in big financial services companies.

“While this was announced in 2006, it hasonly been felt organisationally in the past year.It’s quite a difficult management trick to do –and the various different departments are nowencouraged to do joint thinking,” Spiers says.

Money laundering reporting officers are also still smarting from the 2006 case of Stephen Judge, the former MLRO for CFD provider City Index. Judge had made a suspicious activity report about a number of suspicious spread bets but, before theseven-day consent period had expired, he proceeded with the transaction.

The total amount transferred by Judgewas £30,787 ($65,647). There was never a suggestion that Judge had been acting dishonestly. Indeed, he had co-operated withthe authorities throughout and he maintainedthat he proceeded with the transaction only because he was concerned that if hemaintained his refusal the customer would be tipped off.

Criminal proceedings were instituted andthe general perception was that, at best, theprosecution was based on a technical breachof the law and that the decision to bring crimi-nal proceedings was misconceived. In theevent, the Crown Prosecution Service droppedthe case, but the fear of prosecution amongMLROs has remained strong ever since.

An MLRO for NIBC Bank in London,Ben Hur, says the case prompted him and oth-ers to set up an MLRO protection committee.

“Quite simply, if an MLRO gets intotrouble, they can come to us. If we feel thecase is justified, we will help them where we can,” Hur says.

“But if we feel they acted unprofessionally,or inappropriately, we will not assist them,” he says.

Australian AML professionals have notyet come to this kind of situation – where theyfeel they need to set up a committee to protectthem from the prosecuting authorities. But ifthe AML scene becomes as tough as it haseffectively become in the UK, and the fear of civil and criminal sanctions as great, then everything may change. ■

ANTI-MONEY LAUNDERING 13APRIL 2008

�

“YOU’RE NOW GOING TO HAVE TO BE FARMORE RESPONSIVE TO HOW PEPS ANDOTHER HIGH RISK ENTITIES TRANSACT.”

APRIL 2008 ANTI-MONEY LAUNDERING14

SPONSORED FEATURE

Anti-money laundering legislation intended toimpede the flow of funds to terrorists andcriminals is just adding another layer ofbureaucracy and potential snares for theunwary. David Rose looks for the real reasonswhy AML legislation has been created

W HO’S IN CHARGE of anti-money laundering andanti-terrorist financing legislation, and is it working? The short answers would appear to be

“no one” and “no”. But let’s not get carried away. Accordingto the US Treasury’s director of public affairs, MollyMillerwise, money laundering and terrorist financing are not one and the same. One of the challenges of detectingterrorist money flows is that funds intended for terrorist useoften enter the financial system clean and move throughlegitimate channels, only to be used for illicit activity on the other end. Money laundering, on the other hand, is aneffort to inject money derived from illicit purposes into thefinancial system and make it appear clean at the other end.

The UN Security Council maintains its own list of entitiesand individuals to be targeted for anti-terrorist financingmeasures, in which governments and the private sector play arole. The US Treasury also maintains its own list of financiersand facilitators of terrorism, thousands of them, which it targets with a view to freezing their assets. However theseactions have no more than a disruptive effect – more to dowith forcing them to shift their focus from planning attacks toconcerns about their financial viability. The authorities believethat they also have a deterrent effect on financiers who wantto keep one foot in the legitimate business world while supporting murder and violence on the side. Is having a bankaccount in Switzerland or the Cayman Islands any protectionagainst intrusion from investigating authorities? The acceptedposition from the banking industry is that it voluntarily goesabove and beyond its legal requirements because it does not want to do business with terrorist supporters, moneylaunderers or proliferators. That’ll be a “no” then.

A key player in the financial war on terrorists is theFinancial Action Task Force, the premier international standard-setting body for anti-money laundering andcounter-terrorist financing (AML/CTF). The FATF has issued40 AML recommendations and, more recently, nine specialrecommendations on CTF. Further, the FATF evaluates the

AML/CTF regimes of its member countries. We took a reallygood look around its website, the tag of which indicatedthat the FATF was part of the OECD, although there’s no indication of that on the website itself. As far as anti-terrorist financing goes, it’s probably true to say that FATF isthe one “in charge” – or at least the one that can best bedescribed as a co-ordinating body.

International cooperation

Valentina Zoghbi is a project lawyer at the International BarAssociation and a member of its AML forum. She says thecomplex nature of money laundering techniques makesinternational harmonisation of legislation and policy difficultto achieve. In Europe, AML directives are “minimum harmonisation”, leaving EU governments free to gold platethem. A report by the British Institute of International andComparative Law claims these efforts “fell some way short ofproducing a uniform AML regime across the EU”. With theimplementation date for the Third EU Money LaunderingDirective on 15 December 2007, Zoghbi believes that it is vital to ensure that efforts are made to maximise the harmonisation of directives, by preventing this gold platingand to facilitate cross border transactions. The directive itself says: “Measures adopted solely at national or even EUlevel, without taking account of international coordinationand cooperation, would have very limited effects.”

Impact of legislation

But the big question for those of us just trying to run a business is what kind of impact does this unco-ordinated legislation have? In a letter to the Financial Times, TheresaVilliers, MEP (Member European Parliament) argued that“[money laundering] rules do almost nothing to catch criminals or terrorists and merely provide inconvenience tolaw-abiding citizens in carrying out innocuous everydayfinancial transactions”. This view is not an uncommon one:many people experience the effects of money launderinglegislation on a day-to-day basis, with increasingly probingbackground checks and security measures. Unfortunately,much of the press coverage and comment on money laundering legislation focuses on the regulatory burden andnot on the actual impact on the legislation on the crime itself.The reason for this is that money laundering, by its verynature, falls off the economic radar, making it impossible togenerate any empirical data on the effects of legislation.

The great anti-money laundering deception

�

ANTI-MONEY LAUNDERING 15APRIL 2008

SPONSORED FEATURE

In 1996, the IMF estimated that money laundering couldaccount for somewhere between two and five per cent of theworld’s gross domestic product. Zoghbi argues that althoughthe regulations may be perceived as onerous to businesses andindividuals, money laundering undermines the integrity andreliability of domestic and international economies and mustbe prevented. Surely then, the argument for international co-ordination and standardisation of legislation becomes evenstronger? In many jurisdictions, failure to comply with anti-money laundering laws and regulations is in itself a criminaloffence with jail sentences up to two years and/or a fine. Firms that are in the regulated sector need to set up variousprocedures such as appointing a money laundering reportingofficer, setting up internal reporting procedures within thefirm, training all staff within the firm so that they are awareof the relevant regulations, and carrying out identificationprocedures and reporting suspicions of money laundering.

It is easy to underestimate the potential for prosecutionunder AML legislation even if you only have a passing suspi-cion about a particular individual or incident. It is a genuineadditional hazard to entrepreneurial life. For example, inEngland and Wales, the numbers of investigations, prosecu-tion and convictions have each been increasing substantiallysince 2003. In the recent UK case of Regina v Saik, the Houseof Lords considered the law of conspiracy with respect to the offence of money laundering, where an individual wassuspected rather than had knowledge of money laundering.

In this case the defendant was sentenced to seven yearsimprisonment. Zoghbi believes one particularly controversialissue surrounding money laundering legislation is the extentto which lawyers should have to comply with disclosure rules,when doing so conflicts with fundamental principles of access to justice through legal proceedings and the ability toobtain confidential legal advice. Legal challenges are beingsubmitted in countries including France, Belgium, Poland,Greece and Japan.

The position relating to those individuals who have conflicting duties and obligations is still unclear. The Third EUMoney Laundering Directive provides that disclosure “shallnot constitute a breach of any restriction on disclosure of information imposed by contract or by any legislative, regulatory or administrative provision, and shall not involvethe institution or person or its directors or employees in liability of any kind”. Some still believe, however, that thethreat these regulations pose to the foundations of client-lawyer trust are not acceptable. All that aside, one gets thefeeling this increasing burden of AML legislation is leavingwealth-creators ever more fearful of committing someobscure AML regulatory offence that could leave businessesand reputations in tatters.

A version of this story appeared in the UK magazine Riskand Reward and was written by the editor, David Rose.

Business benefits THE ARGUMENT RUNS that there are no business benefits to the AML/CTF legislation, and it is just going to cost money … lots of money! But are there any advantages to the necessary expenditure? There are significant benefits if organisations tackle the issue froma value-add perspective and not just a cost of complianceangle. Added value is not anticipated by many, but amore visionary approach is likely to highlight the not soobvious benefits of implementing an AML system.

ML Trac from International Financial Systems canproduce real business benefits and deliver cost-effectivesolutions for the new know your customer (KYC) rules. The software is designed to act as a customer management system, following the complete life cycle of a customer from account opening, with automatedfacilities to update customer records in a timely manner.The system can deliver information to the marketingdepartment that will allow it to drive specific campaignsto meet the customer’s requirements. The potential cost savings to the marketing department by not havingto “carpet bomb” the customer could be enormous. In addition, it reduces customer frustration as they do not receive information on products or services they don’t want.

ML Trac can operate as a single-customer repository,which also has many advantages. These include branchaccess, centralised signature verification and automatedreminders to get updated customer information.

So, while AML/CTF can be seen as a burden onresources to meet compliance requirements, it shouldalso be viewed as an ideal opportunity to really get toknow your customers – and deliver the service theyexpect from you.

In other words, correct implementation of AML/CTFcompliance systems should impact your bottom line in a positive manner. To quote an article by AML commentator Adam Courtenay, “ ... it’s more about thezeitgeist of regulation, the curse of every entrepreneur’slife. Best to know that banks and other financial institutions holding your money are under a constantsilent threat from regulators and police authorities bothat home and abroad. Being forewarned is better thanbeing trapped, sequestered and having your namedragged through the mud.”

For further information, contact Martyn Rees, director, International FinancialSystems Australia, 0404 806081.www.i-financial.com.au

PROFILE

G E MONEY’s global anti-moneylaundering leader Richard Small is Mr Anti-Money Laundering.

Having worked in AML for 20 years, including setting up Citigroup’s and GEMoney’s compliance program, Small says the key to a successful AML/counter-terrorismfinancing program is consistency, adviceAustralian banks and reporting entities would do well to heed.

Having travelled to Australia recently for the Anti Money Laundering Magazine2008 conference, Small says the biggest challenge for local banks is “ensuring AMLprocedures don’t change from branch tobranch or location to location.”

“Banks need to have controls in place to mitigate the risk of money laundering –including pinpointing what the identifiablerisks are and what a suspicious activity might look like – and ensuring these identification procedures are same across the business,” Small says.

Consistency is a challenge with which Small is familiar, given that he isimplementing AML/CTF monitoring technology across GE Money’s entire business globally. “Monitoring will be thesame in Australia, India and the US: whereverwe operate, the processes will be the same,”he says, adding “it all comes back to mymantra of consistency”.

When it comes to the domestic approachto AML/CTF, Small says he approves of the risk-based system the AustralianAML/CTF legislation takes, which, he says,helps “financial institutions work out whattheir real threats are. It’s much better than a rules-based approach.”

Small also has a clear picture of the role of banks in the compliance regime and is adamant that “banks should not be police.Banks have a responsibility to identify suspicious things – but they are not responsible for doing criminal investigations.”

According to Small, banks have to conduct appropriate due diligence at the start of a customer relationship, understandwhich products are at a higher risk ofAML/CTF, and put in place due diligence to address this.

In instances where evidence of potential money laundering is found, Small says the obligation is to “Report it to authorities. It’s not our responsibility to investigate it, it’s our responsibility toreport it ... it’s also our responsibility todecide what to do next [if a suspicious transaction is found]. Are we going to continue to do business with the customer, or perhaps to continue to monitor the situation? There needs to be a process to decide what to do after a suspicious transaction report has been filed.”

When it comes to what banks should do after the suspicious activity report has been filed, Small is the expert, having recently written the US law on what banksshould do in those circumstances.

Indeed, Small says Australian banksshould expect a teething period when it comes to filing SARs, though he says that the more refined a system is, the fewer false positives it will throw up. (False positives are potentially suspicioustransactions unrelated to money laundering,for example international transfers of large sums of money for legitimate purposes.)

“But if the process for finding SARsworks, who cares if a few false positives are reported? It will also be hard for banks to know if they are doing the right thing until the regulator has had a chance to review the first compliance reports,” Small says.

His final piece of advice for banks in the process of introducing AML/CTF compliance systems is “to ensure your program both manages risks and also addresses the regulatory regime ... you need to understand your products, your customers,your market and your risks to put a good program in place.

“This is something that needs to bethought out, which is what the regulator willwant to see: there might be disagreementsalong the way, but if banks can show thethinking process behind their compliance program they will go a long way in addressing the regulator’s concerns.” Good advice indeed. ■

APRIL 2008 ANTI-MONEY LAUNDERING16

Consistency’s the key at GE A global perspective has given Richard Small some very clearideas on the best way to implement procedures and practices.By Alexandra Cain.

“... if banks can show the thinking process behind their compliance program they will go a long way inaddressing the regulator’s concerns.”

Richard Small

PROFILE

S TEVE HANCOCK is head of groupmoney laundering prevention at iconic UK financial services company

Prudential and has a big job. As the person in charge of anti-money laundering atPrudential he oversees AML/counter-terrorismfinancing procedures and compliance across 38 businesses in 28 countries and 44 offices.

Unsurprisingly, Hancock says “AlthoughI’m based in London, I spend most of mytime travelling.”

Hancock has been a part of Prudential’sAML compliance team since the global financial services provider started to considerhow to address the problem organisation-wide, which gives him a unique perspectiveon the business and its tackling of AML/CTF.He joined the company’s sales team in 1988before moving across to the compliance division in 1991.

“I was initially asked to take a look at the legislative impact of new AML laws onour UK business; that was the start of it. Now I’m the reporting officer for the entireUK business,” he says.

Hancock’s experience in the sales area of the business stood him in good stead whenhe was setting up Prudential’s complianceregime. “We had 12,000 direct sales agents, so there was lots of time spent working withthe direct sales force.”

Having successfully worked on AMLwith Prudential’s sales people, Hancock thenworked with head office on the company’sAML/CTF compliance program, eventuallytaking on the newly created role of head ofgroup money laundering prevention for theentire Prudential business. “That was the startof our set-up of global procedures,” he says.

Aside from his current role, Hancock

also represents Prudential on a number ofAML/CTF industry groups. And in 2001 he founded the Institute of Money LaunderingPrevention Officers and was its first chairman,resigning only in January this year. He is now its honorary president.

Hancock says the most significant event while working on AML/CTF was the terrorist attacks on New York in 2001.“That really made us tighten our know your customer requirements and ensured terrorism financing became part of the UK legislation,” he says. According toHancock, this has also meant that “there is now no jurisdiction in which legislation has not been thoroughly made-over.”

Aside from this momentous event,Hancock says the shift from a rules-based to arisk-based approach had a significant impacton his work. “Having prescriptive rules wassilly. It was stupid having to go through thesame KYC requirements for an elderly personas you would do with a multimillion-dollartransaction,” he says. The UK regulator intro-duced a risk-based approach in August 2006,having started with a rules-based approachwhen the legislation was put together in 1994.

“This required a rewrite of our rules. The authorities scrapped the old money-laun-dering rules and introduced systems and controls requirements, and the Third EuropeanMoney Laundering Directive has made therisk-based approach compulsory across theEuropean Union,” he says.

Another big change has been the focus onpolitically exposed persons; that is legislationconcerned with high profile and governmentofficials using the proceeds of corruption fortheir own aims. “Monitoring these people isquite a topic of conversation,” he says.

Asked whether he has ever found any evidence of money laundering in Prudential’sbusiness, Hancock says “we have identifiedsuspicious transactions and have identifiedthose to police, but we’re a low-risk business.”

In instances where suspicious activity has been detected, Hancock says Prudentialhas “continued to monitor the situation and be guided by law enforcement. They keeptrack of what’s going on. If you shut down the relationship, then there’s no audit trail for them to work with.”

Hancock’s advice to Australian banks putting in place a compliance program is to “understand the risks involved in yourproducts. If you understand your risks, you understand your vulnerabilities – andthat’s paramount in the prevention of financial crime.” ■

ANTI-MONEY LAUNDERING 17APRIL 2008

Understanding is everything

Prudential’s top AML executive worldwide is a big fan of the risk-based approach, which has played a major role in his career over the years. By Alexandra Cain.

“understand the risks involved in your products. If you understand your risks, you understand your vulnerabilities ... “

Steve Hancock

SMALL GUYS PREPARE ... OR ELSE!

A CCOUNTANTS, real estate dealers,solicitors and jewellers are set to behit by a wide range of anti-money

laundering requirements they won’t welcome.Many of these one and two-man bands will be unfamiliar with the second tranche of the Anti-Money Laundering and Counter-Terrorism Financing Act 2006.

But come the end of this year, or thebeginning of next, these small operators will be required to implement processes like customer due diligence and suspicious report-ing. They form the second part, or tranche, of the AML legislation. This component of thenew anti-money laundering/counter-terrorismfinancing (AML/CTF) law brings in thosefirms that do not handle cash as an integral part of their business.