Embed Size (px)

DESCRIPTION

Anti Evasion Measures In VAT. Presented by- Shri. J.P.Dange Chairman, 4 th State Finance Commission & Former Chief Secretary to the Government of Maharashtra 14/08/2013. Best Practices In Maharashtra. TOPICS FOR DISCUSSION. What is Sales Tax? Revenue Receipts under VAT - PowerPoint PPT Presentation

Citation preview

Anti- Evasion Measures: Best Practices in Maharashtra

ANTI EVASION MEASURES IN VATBest Practices In

Maharashtra

Presented by-

Shri. J.P.DangeChairman, 4th State Finance Commission &

Former Chief Secretary to the Government of Maharashtra

14/08/2013

1

Anti- Evasion Measures: Best Practices in Maharashtra

TOPICS FOR DISCUSSION What is Sales Tax? Revenue Receipts under VAT Functional Branches Types of evasions Evasion Cases Policy options on fraud Anti Evasion Measures

2

Anti- Evasion Measures: Best Practices in Maharashtra

ORGANISATIONAL STRUCTURE Council of Ministers Finance Minister Finance Secretary Commissioner of Sales Tax (1)- Cadre Post IAS Special Commissioner of Sales Tax (1)- Cadre Post IAS Chief Vigilance Officer (Special IGP) (1)- IPS Additional Commissioners of Sales Tax (9) Joint Commissioners of Sales Tax (72)- IAS 3 Deputy Commissioners of Sales Tax (401) Assistant Commissioners of Sales Tax (590) Sales Tax Officers (1191)

3

Anti- Evasion Measures: Best Practices in Maharashtra

SALES TAX In its present form, Sales Tax, a tax on transactions of

sales, came into existence after First World War. The taxable event in case of Sales Tax is the sale of

goods as in case of Customs is bringing of the goods into India and in case of excise, the manufacture of goods.

The powers are derived by State Governments from Entry 54 of State List (List II) of the Seventh Schedule to the Constitution of India and they are subject to Entry 92A of Union List (List I)

4

Anti- Evasion Measures: Best Practices in Maharashtra

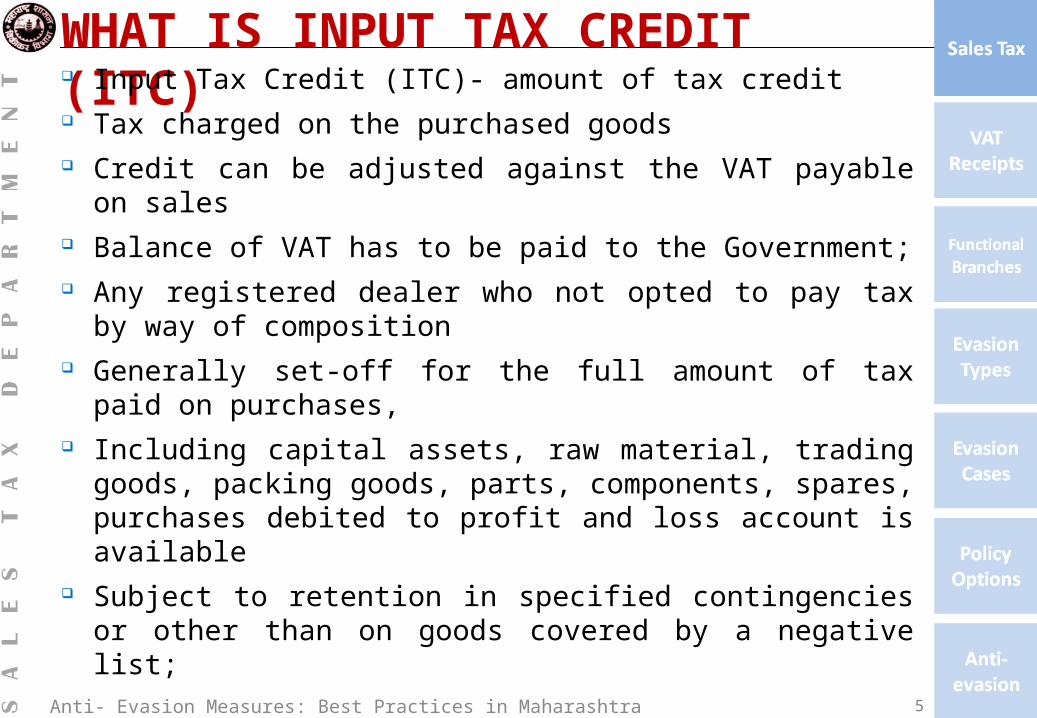

WHAT IS INPUT TAX CREDIT (ITC) Input Tax Credit (ITC)- amount of tax credit Tax charged on the purchased goods Credit can be adjusted against the VAT payable on sales Balance of VAT has to be paid to the Government; Any registered dealer who not opted to pay tax by way of

composition Generally set-off for the full amount of tax paid on purchases, Including capital assets, raw material, trading goods, packing

goods, parts, components, spares, purchases debited to profit and loss account is available

Subject to retention in specified contingencies or other than on goods covered by a negative list;

5

Anti- Evasion Measures: Best Practices in Maharashtra

MAHARASHTRA: FROM ST TO VAT (…CONTD.) Comprehensive Sales Tax Act, viz, Bombay Sales Tax

Act, 1946, from 1st October 1946 and tax on goods dispatched to other States introduced in 1949.

Constitution came into effect from 26th Jan 1950. Powers of State to levy tax came to be controlled by

Entry 54 of State List Bombay Sales Tax Act, 1953 was enforced from Mar

1953 whereas Bombay Sales Tax Act, 1959 came into effect from 1st Jan 1960.

Replaced by Maharashtra Value Added Tax Act, 2002 from 1st April 2005.

6

Anti- Evasion Measures: Best Practices in Maharashtra

MAHARASHTRA: FROM ST TO VAT Generally guided by best international practices with

regard to legal framework Operating procedures and eliminates cascading impact

of double taxation. Self-policing, self-assessment system Improved control mechanism for better compliance Comprehensive legislation covering works contract,

lease transactions etc with Standard VAT rate 12.5%

7

Anti- Evasion Measures: Best Practices in Maharashtra

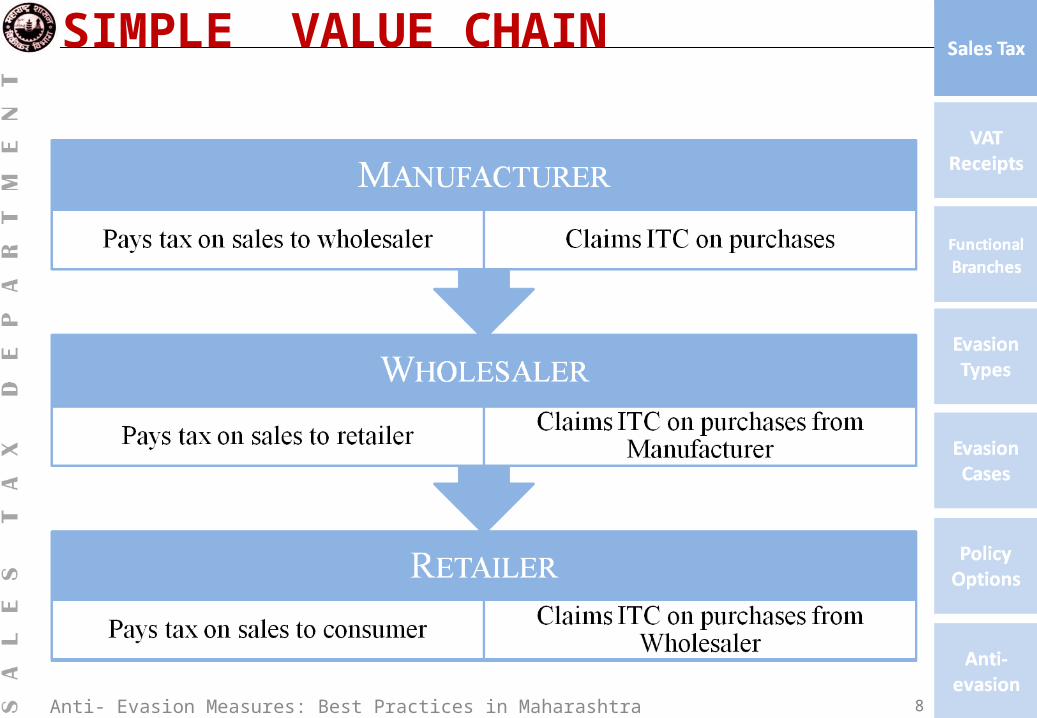

SIMPLE VALUE CHAIN

8

Anti- Evasion Measures: Best Practices in Maharashtra

WHO PAY VAT TO GOVERNMENT Manufacturers Importers Wholesalers Distributors Retailers Works Contractors Lessers

9

Anti- Evasion Measures: Best Practices in Maharashtra

BENEFITS OF VAT OVER SALES TAX(…CONTD.) Lower and stable rates of tax (no frequent changes) Rationalization of tax burden Great reduction in number of rates of 5% and 12.5% Goods taxable @ 5% to be specified and Rest of others liable to tax @ 12.5% Less scope for litigation and full set-off taxes paid at

every stage

10

Anti- Evasion Measures: Best Practices in Maharashtra

BENEFITS OF VAT OVER SALES TAX(…CONTD.) Transparent system, greater reliance on self

assessment and voluntary compliance by dealers; Schedule A (tax free goods), B (gold, silver and

precious stones), C (goods of national importance, industrial raw material, IT products), D (liquor and petroleum products) and E (goods not covered elsewhere) are lists of goods for which rates of tax are @ Nil or 0%, 1%, 5%, 20% or above and 12.5% respectively.

11

Anti- Evasion Measures: Best Practices in Maharashtra

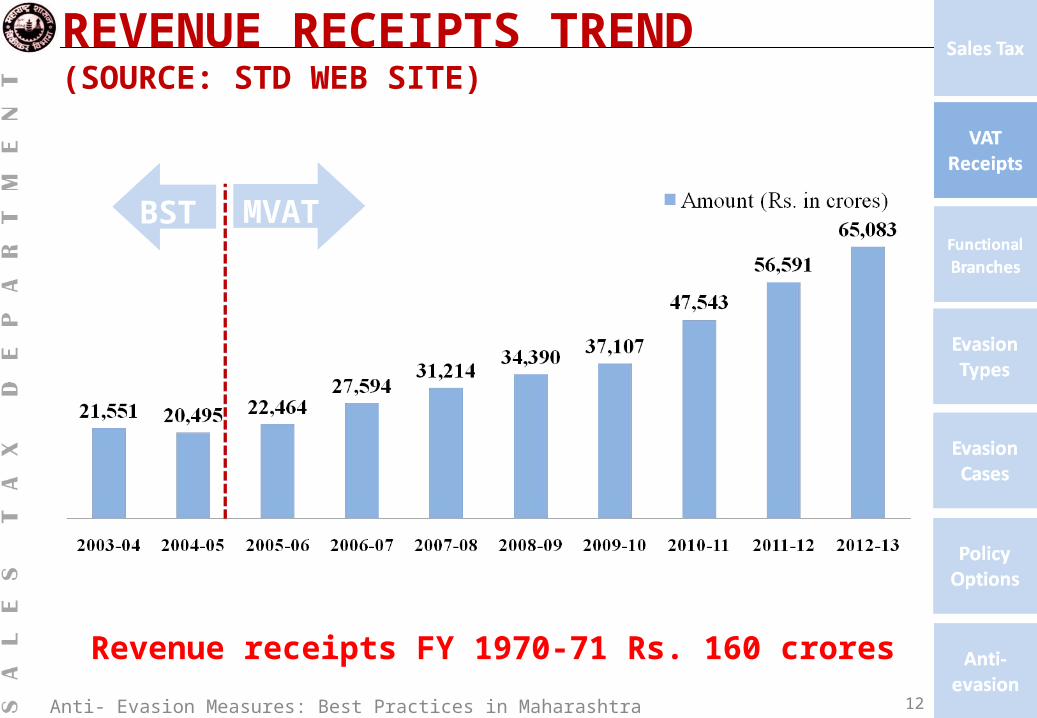

REVENUE RECEIPTS TREND(SOURCE: STD WEB SITE)

12

Revenue receipts FY 1970-71 Rs. 160 crores

BST MVAT

Anti- Evasion Measures: Best Practices in Maharashtra

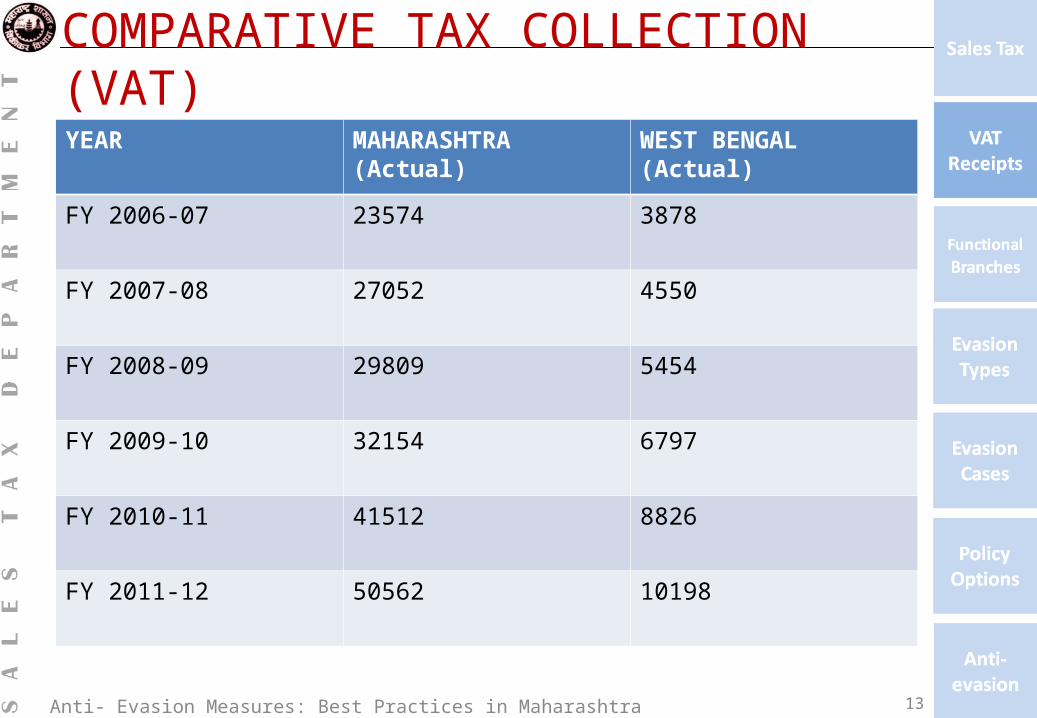

COMPARATIVE TAX COLLECTION (VAT)YEAR MAHARASHTRA (Actual) WEST BENGAL (Actual)

FY 2006-07 23574 3878

FY 2007-08 27052 4550

FY 2008-09 29809 5454

FY 2009-10 32154 6797

FY 2010-11 41512 8826

FY 2011-12 50562 10198

13

Anti- Evasion Measures: Best Practices in Maharashtra

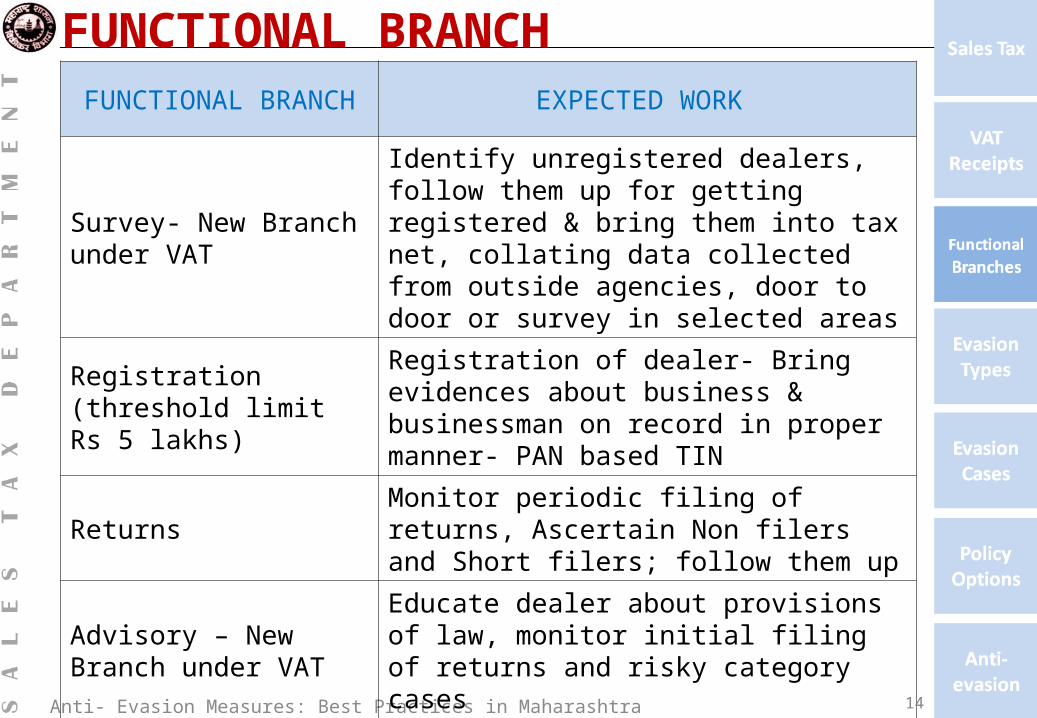

FUNCTIONAL BRANCH FUNCTIONAL BRANCH EXPECTED WORK

Survey- New Branch under VAT

Identify unregistered dealers, follow them up for getting registered & bring them into tax net, collating data collected from outside agencies, door to door or survey in selected areas

Registration (threshold limit Rs 5 lakhs)

Registration of dealer- Bring evidences about business & businessman on record in proper manner- PAN based TIN

Returns Monitor periodic filing of returns, Ascertain Non filers and Short filers; follow them up

Advisory – New Branch under VAT

Educate dealer about provisions of law, monitor initial filing of returns and risky category cases

Central Repository- New Branch

Issuance of declarations under CST Act (Form C, H, F, EI, EII) with proper scrutiny

14

Anti- Evasion Measures: Best Practices in Maharashtra

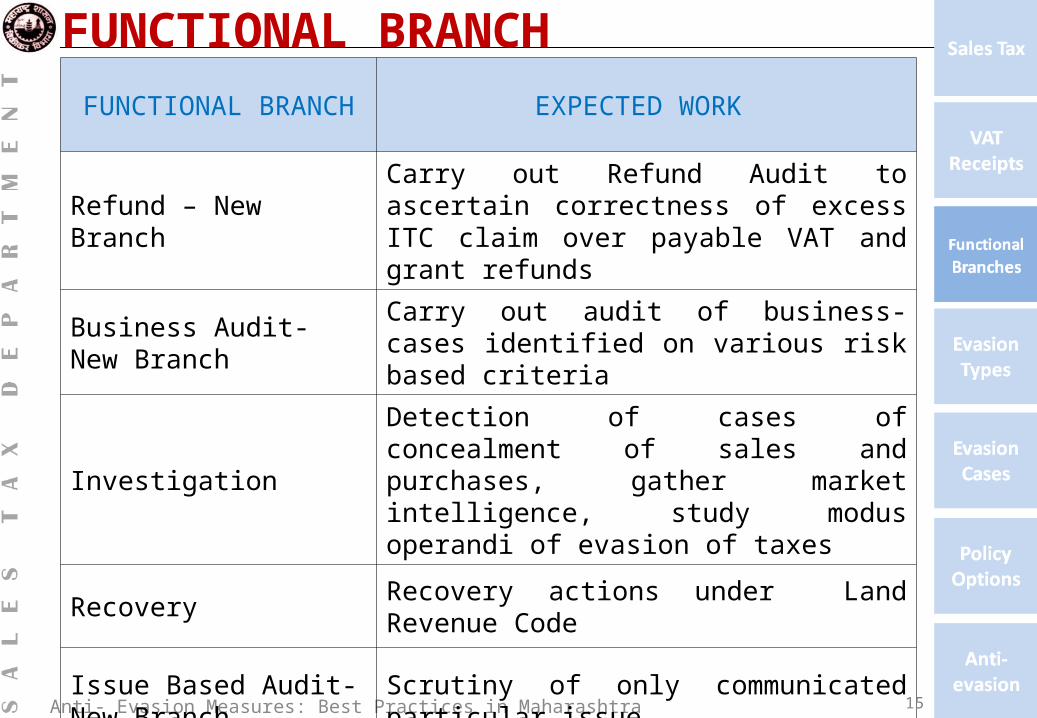

FUNCTIONAL BRANCH FUNCTIONAL BRANCH EXPECTED WORK

Refund – New BranchCarry out Refund Audit to ascertain correctness of excess ITC claim over payable VAT and grant refunds

Business Audit- New Branch

Carry out audit of business- cases identified on various risk based criteria

InvestigationDetection of cases of concealment of sales and purchases, gather market intelligence, study modus operandi of evasion of taxes

Recovery Recovery actions under Land Revenue Code

Issue Based Audit- New Branch

Scrutiny of only communicated particular issue

15

Anti- Evasion Measures: Best Practices in Maharashtra

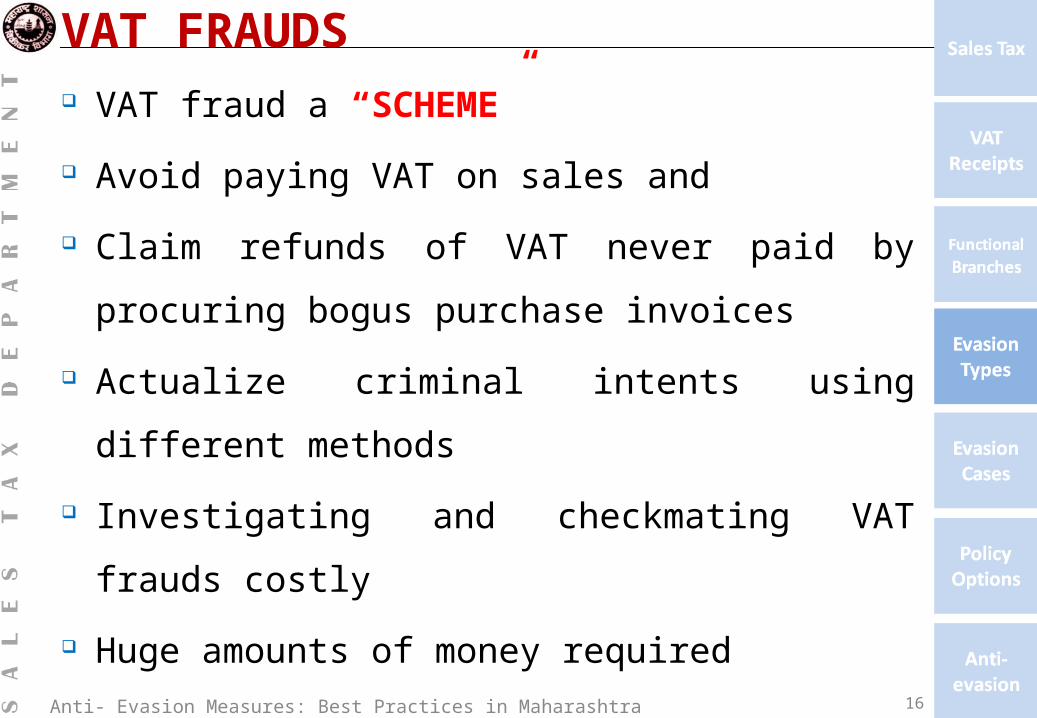

VAT FRAUDS VAT fraud a “SCHEME”

Avoid paying VAT on sales and

Claim refunds of VAT never paid by procuring bogus

purchase invoices

Actualize criminal intents using different methods

Investigating and checkmating VAT frauds costly

Huge amounts of money required

16

Anti- Evasion Measures: Best Practices in Maharashtra

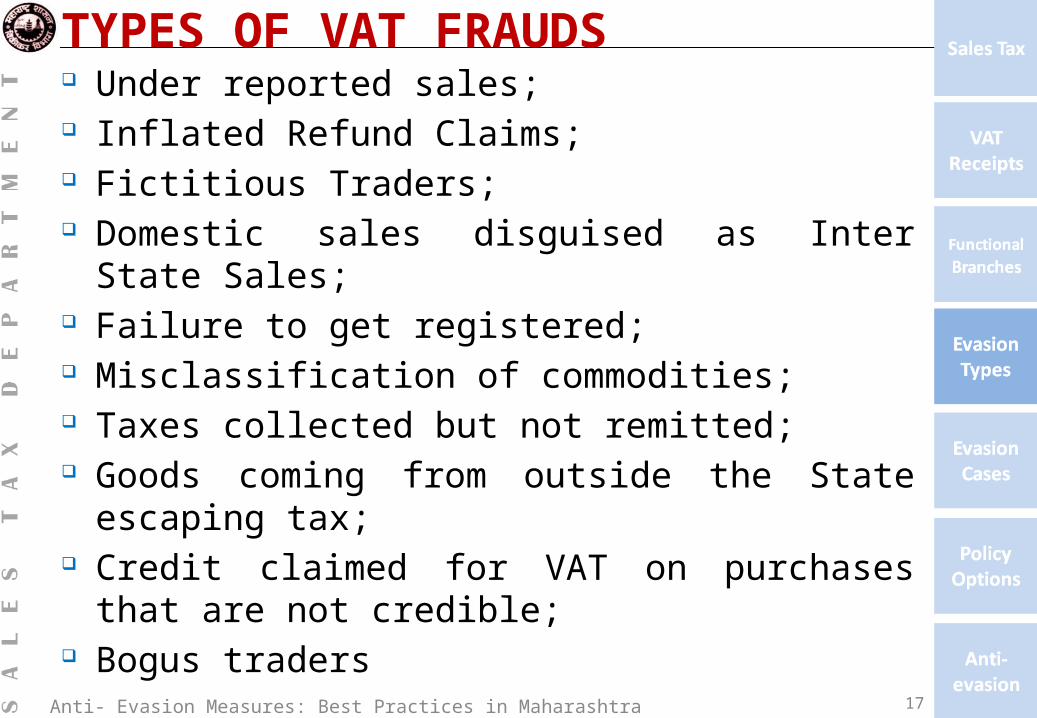

TYPES OF VAT FRAUDS Under reported sales; Inflated Refund Claims; Fictitious Traders; Domestic sales disguised as Inter State Sales; Failure to get registered; Misclassification of commodities; Taxes collected but not remitted; Goods coming from outside the State escaping tax; Credit claimed for VAT on purchases that are not

credible; Bogus traders

17

Anti- Evasion Measures: Best Practices in Maharashtra

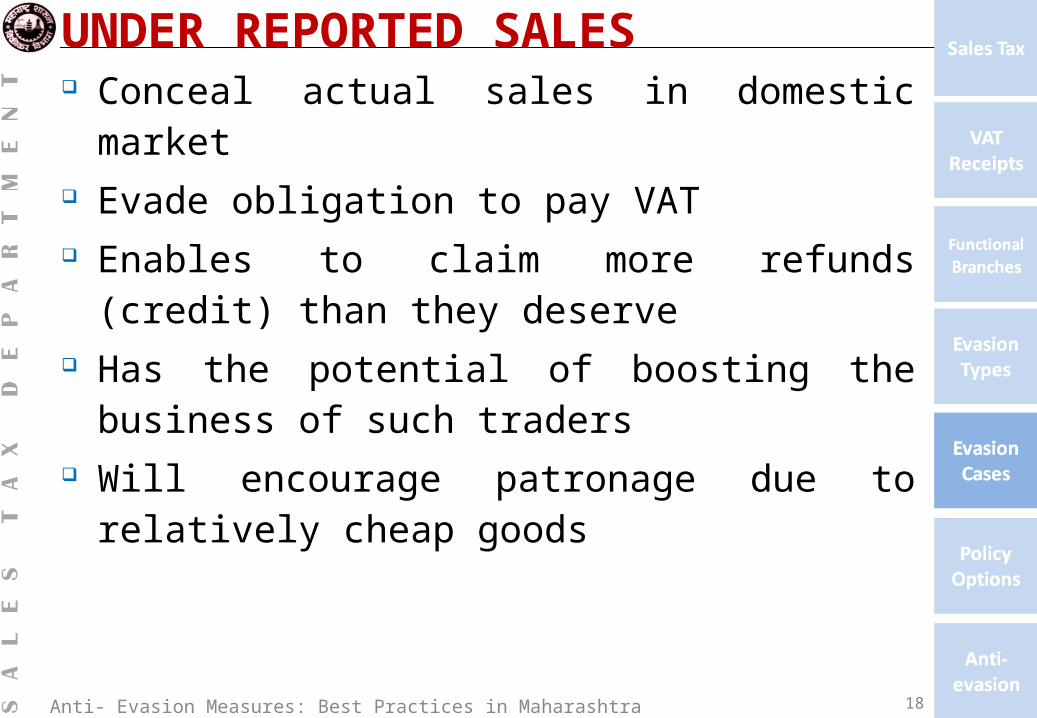

UNDER REPORTED SALES Conceal actual sales in domestic market Evade obligation to pay VAT Enables to claim more refunds (credit) than they

deserve Has the potential of boosting the business of such

traders Will encourage patronage due to relatively cheap

goods

18

Anti- Evasion Measures: Best Practices in Maharashtra

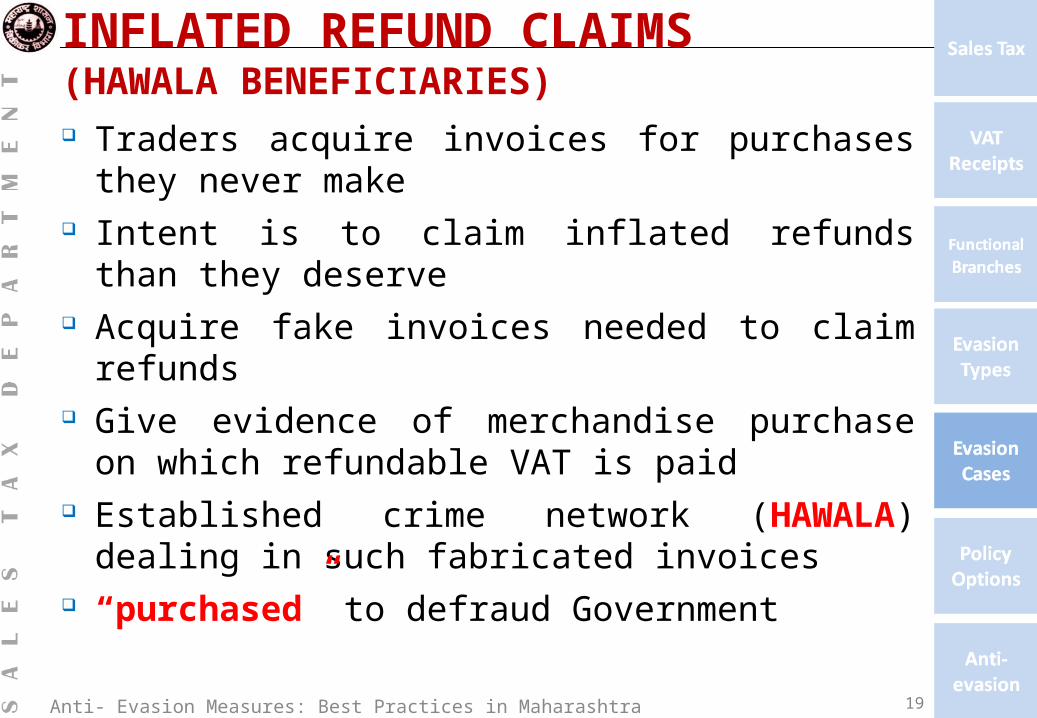

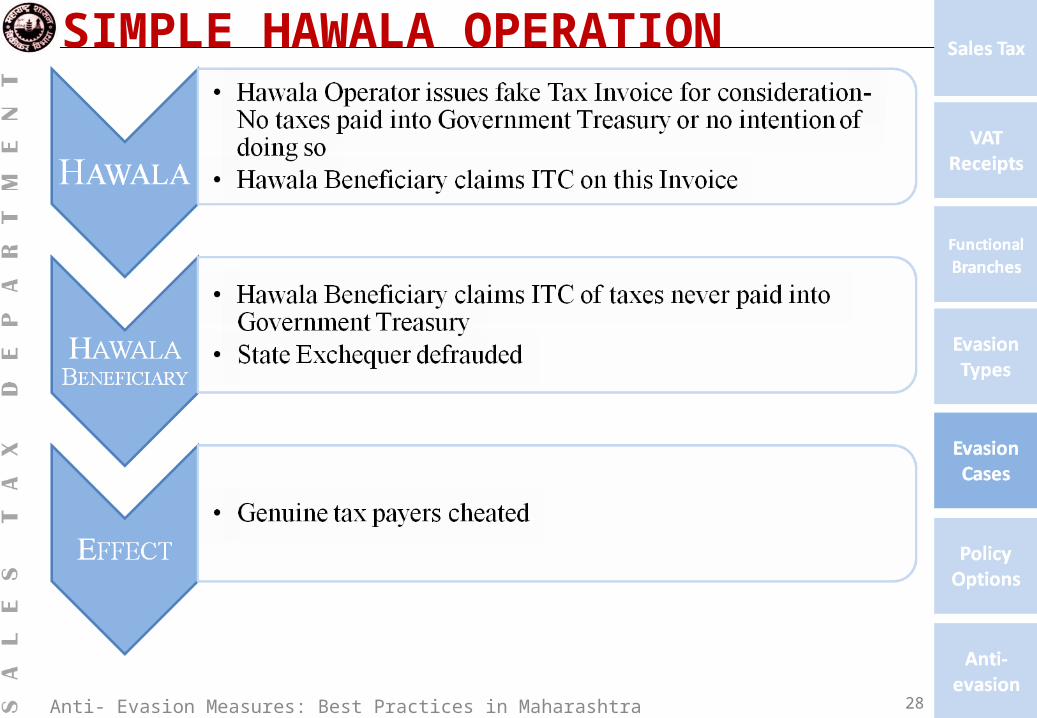

INFLATED REFUND CLAIMS(HAWALA BENEFICIARIES) Traders acquire invoices for purchases they never

make Intent is to claim inflated refunds than they deserve Acquire fake invoices needed to claim refunds Give evidence of merchandise purchase on which

refundable VAT is paid Established crime network (HAWALA) dealing in

such fabricated invoices “purchased” to defraud Government

19

Anti- Evasion Measures: Best Practices in Maharashtra

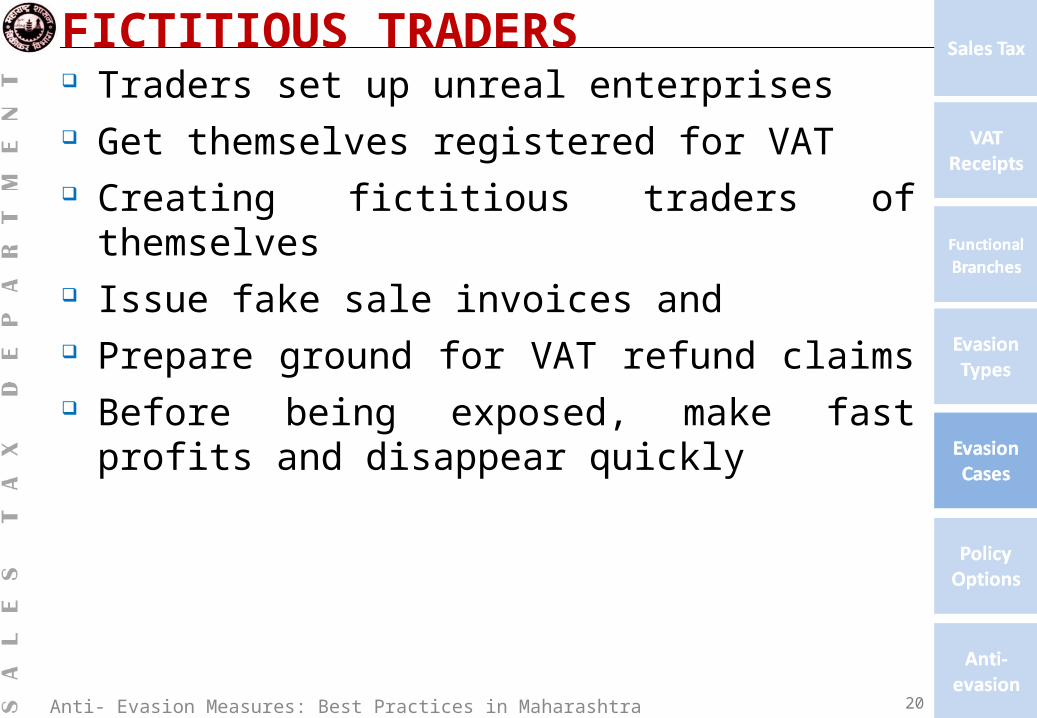

FICTITIOUS TRADERS Traders set up unreal enterprises Get themselves registered for VAT Creating fictitious traders of themselves Issue fake sale invoices and Prepare ground for VAT refund claims Before being exposed, make fast profits and disappear

quickly

20

Anti- Evasion Measures: Best Practices in Maharashtra

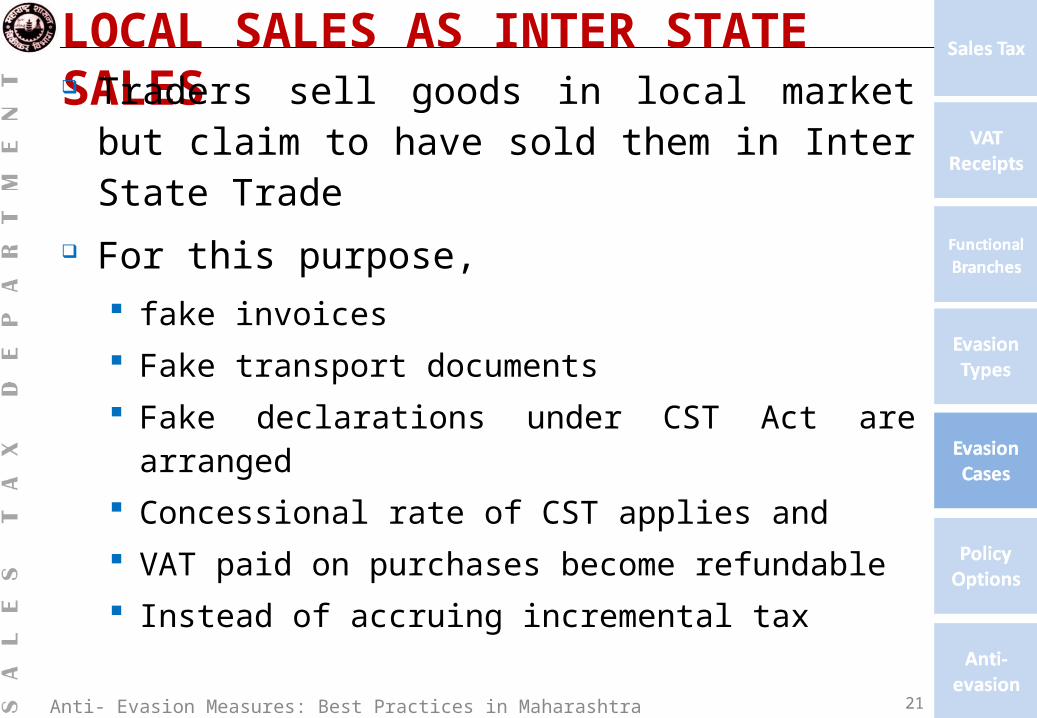

LOCAL SALES AS INTER STATE SALES Traders sell goods in local market but claim to have

sold them in Inter State Trade

For this purpose, fake invoices

Fake transport documents

Fake declarations under CST Act are arranged

Concessional rate of CST applies and

VAT paid on purchases become refundable

Instead of accruing incremental tax

21

Anti- Evasion Measures: Best Practices in Maharashtra

FAILURE TO GET REGISTERED Small businesses operating close to the threshold level

of turnover

At which registration becomes compulsory

Failing to get registered

Saving VAT as well as VAT compliance costs

Mainly retailers predominate this group

22

Anti- Evasion Measures: Best Practices in Maharashtra

MISCLASSIFICATION OF COMMODITIES Sales liable to tax at different rates, or Being goods exempted from VAT May reduce tax liability By exaggerating the proportion of sales in the lower

tax categories

23

Anti- Evasion Measures: Best Practices in Maharashtra

TAX COLLECTED BUT NOT REMITTED By false accounting or By engineering bankruptcy before tax is paid or “missing trader” fraud wherein registered business

disappears

24

Anti- Evasion Measures: Best Practices in Maharashtra

GOODS COMING FROM OUTSIDE THE STATE ESCAPING TAX Levy of tax accounts based

No tax levied at the State border

No record of goods entering into the State

Scope for goods coming from outside the State escaping the tax

No machinery to check that goods meant for Inter State Resale entering State have gone out without being unloaded

25

Anti- Evasion Measures: Best Practices in Maharashtra

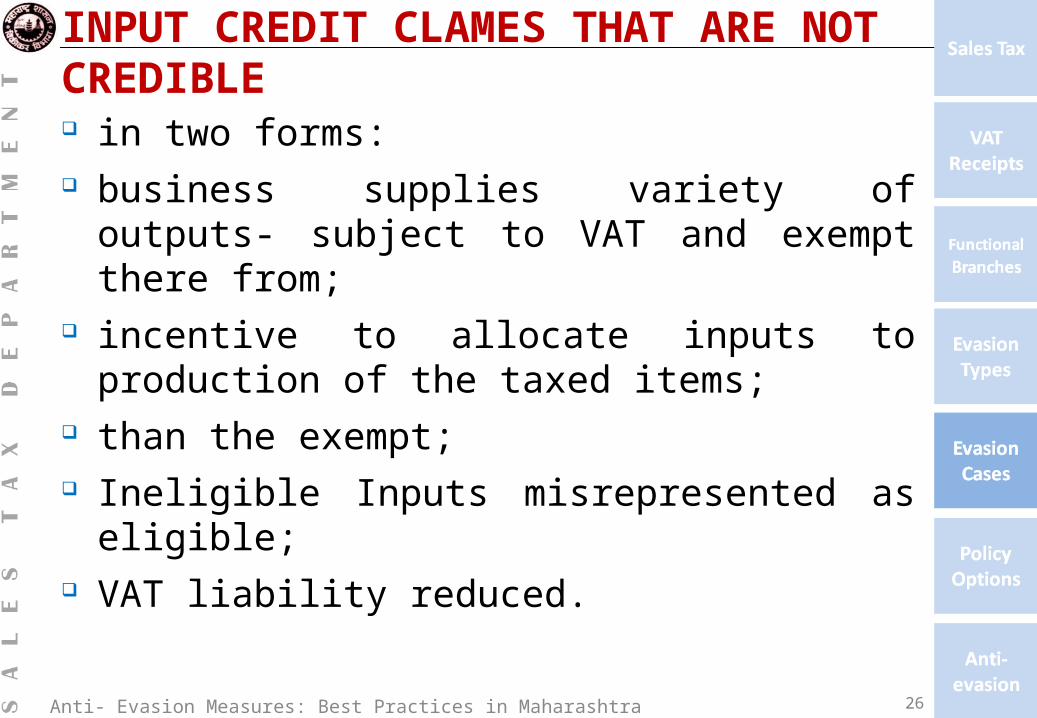

INPUT CREDIT CLAMES THAT ARE NOT CREDIBLE in two forms: business supplies variety of outputs- subject to VAT

and exempt there from; incentive to allocate inputs to production of the taxed

items; than the exempt; Ineligible Inputs misrepresented as eligible; VAT liability reduced.

26

Anti- Evasion Measures: Best Practices in Maharashtra

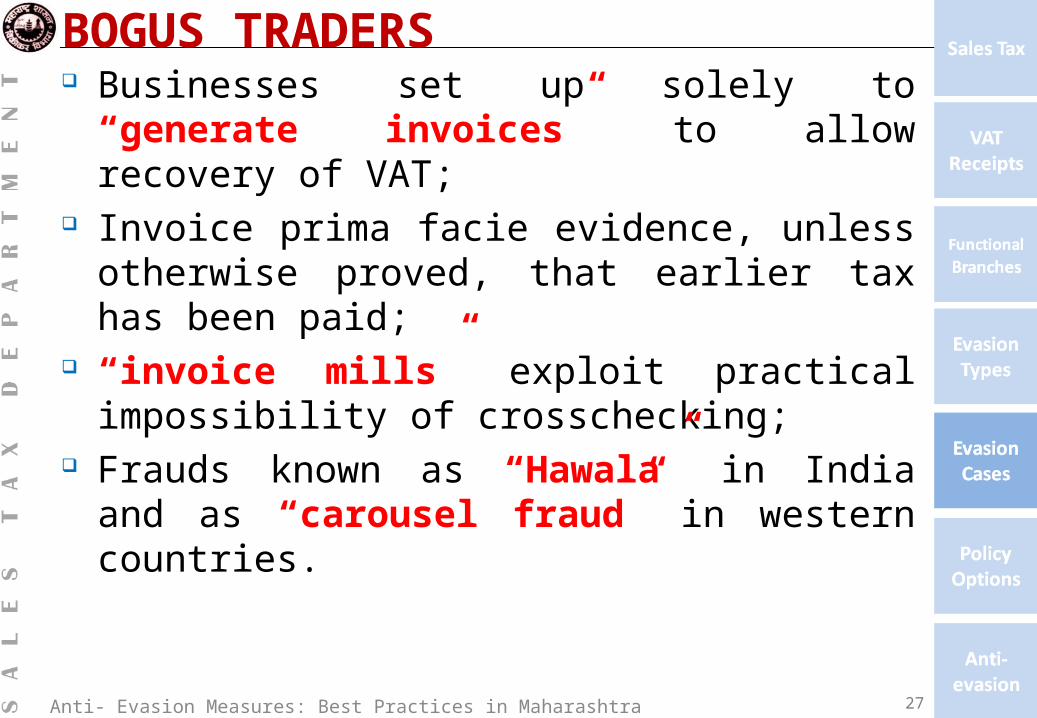

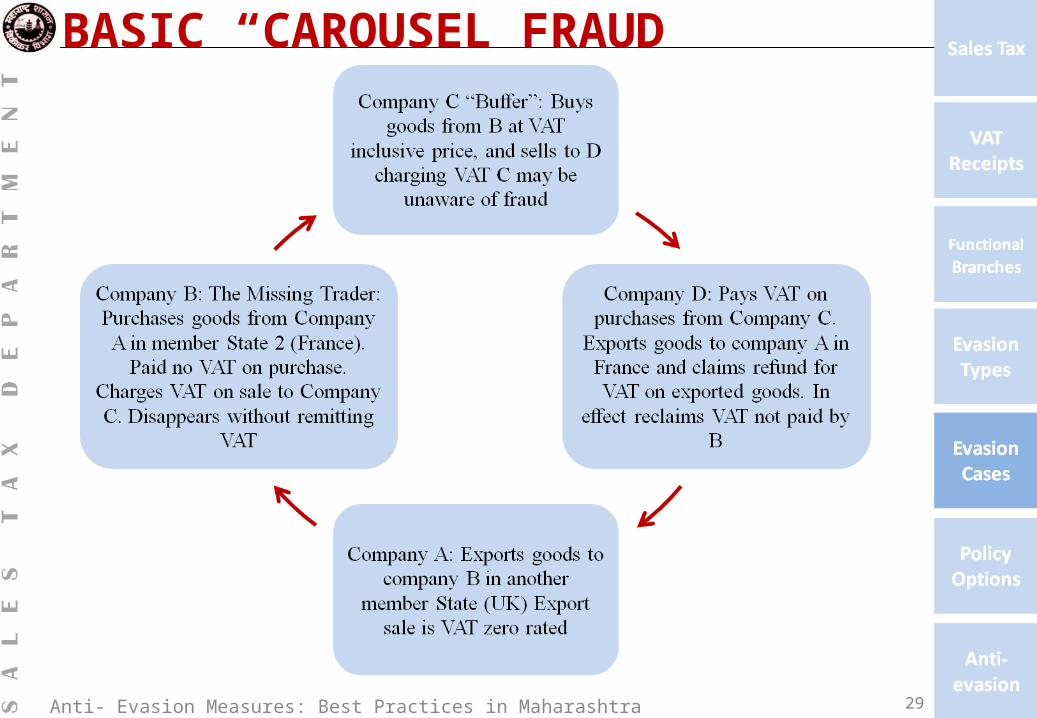

BOGUS TRADERS Businesses set up solely to “generate invoices” to

allow recovery of VAT; Invoice prima facie evidence, unless otherwise

proved, that earlier tax has been paid; “invoice mills” exploit practical impossibility of

crosschecking; Frauds known as “Hawala” in India and as “carousel

fraud” in western countries.

27

Anti- Evasion Measures: Best Practices in Maharashtra

SIMPLE HAWALA OPERATION

28

Anti- Evasion Measures: Best Practices in Maharashtra

BASIC “CAROUSEL FRAUD”

29

Anti- Evasion Measures: Best Practices in Maharashtra

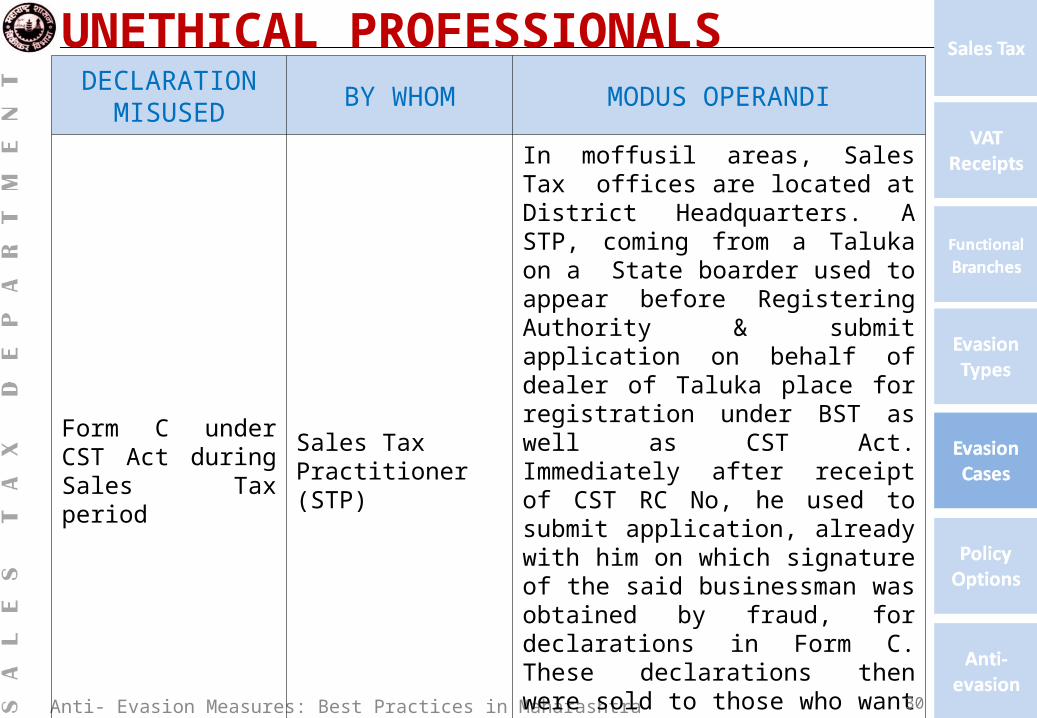

UNETHICAL PROFESSIONALSDECLARATION

MISUSEDBY WHOM MODUS OPERANDI

Form C under CST Act during Sales Tax period

Sales Tax Practitioner (STP)

In moffusil areas, Sales Tax offices are located at District Headquarters. A STP, coming from a Taluka on a State boarder used to appear before Registering Authority & submit application on behalf of dealer of Taluka place for registration under BST as well as CST Act. Immediately after receipt of CST RC No, he used to submit application, already with him on which signature of the said businessman was obtained by fraud, for declarations in Form C. These declarations then were sold to those who want them for a consideration. Later on he was caught and prosecuted.

30

Anti- Evasion Measures: Best Practices in Maharashtra

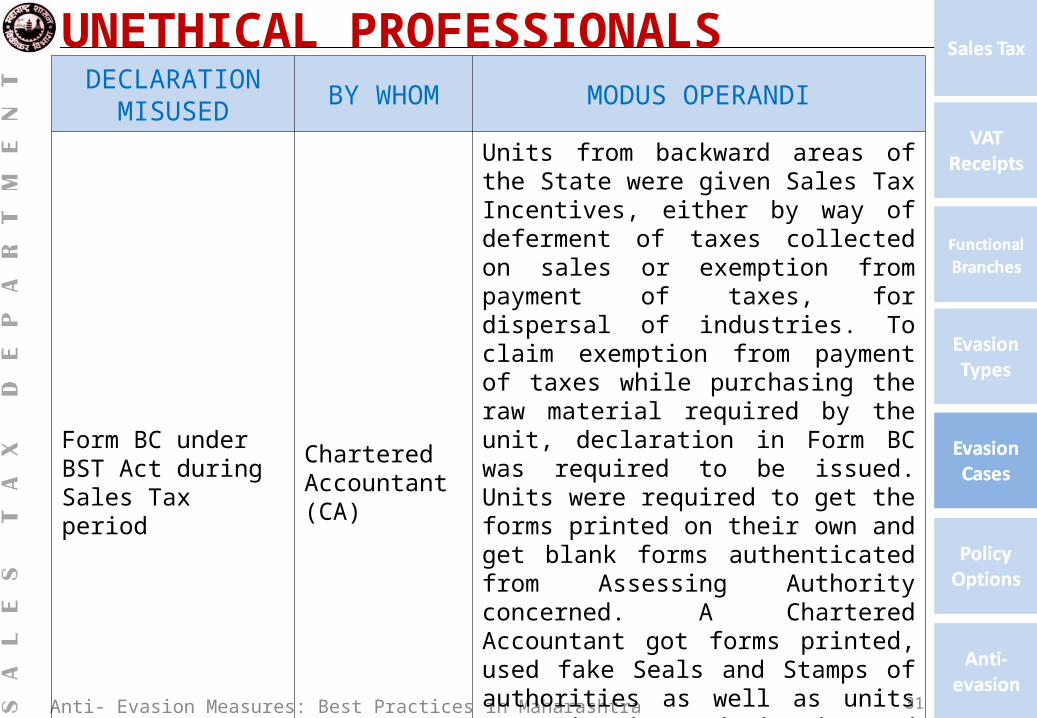

UNETHICAL PROFESSIONALS DECLARATION

MISUSEDBY WHOM MODUS OPERANDI

Form BC under BST Act during Sales Tax period

Chartered Accountant (CA)

Units from backward areas of the State were given Sales Tax Incentives, either by way of deferment of taxes collected on sales or exemption from payment of taxes, for dispersal of industries. To claim exemption from payment of taxes while purchasing the raw material required by the unit, declaration in Form BC was required to be issued. Units were required to get the forms printed on their own and get blank forms authenticated from Assessing Authority concerned. A Chartered Accountant got forms printed, used fake Seals and Stamps of authorities as well as units operating in Beed District and sold forms for consideration. Was caught during cross checks and prosecuted.

31

Anti- Evasion Measures: Best Practices in Maharashtra

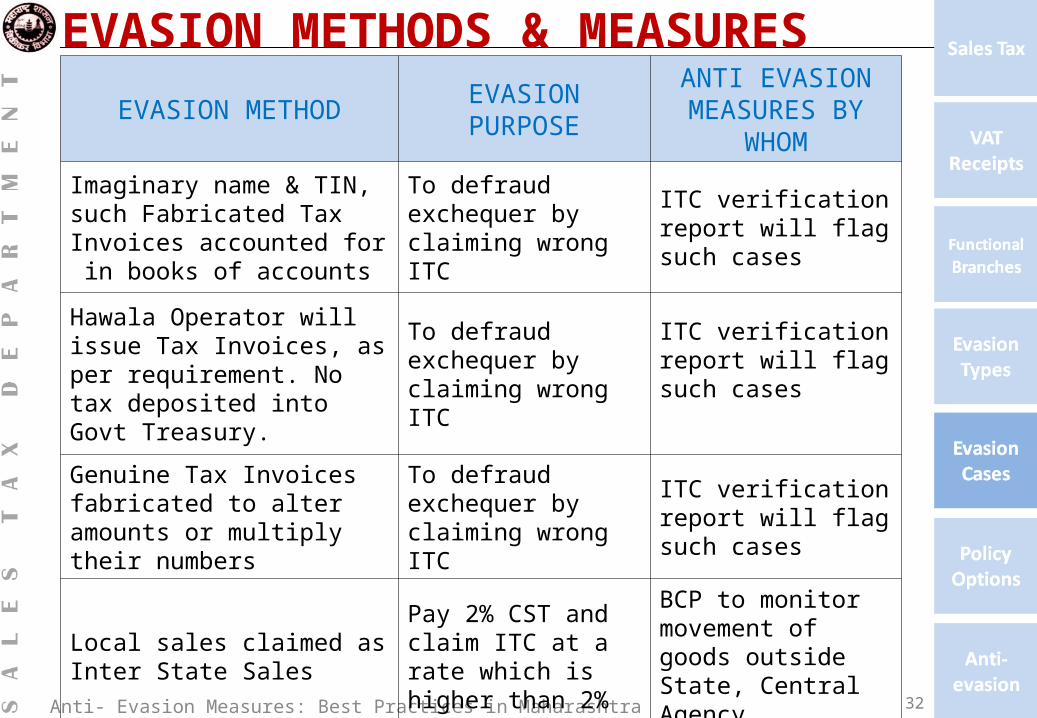

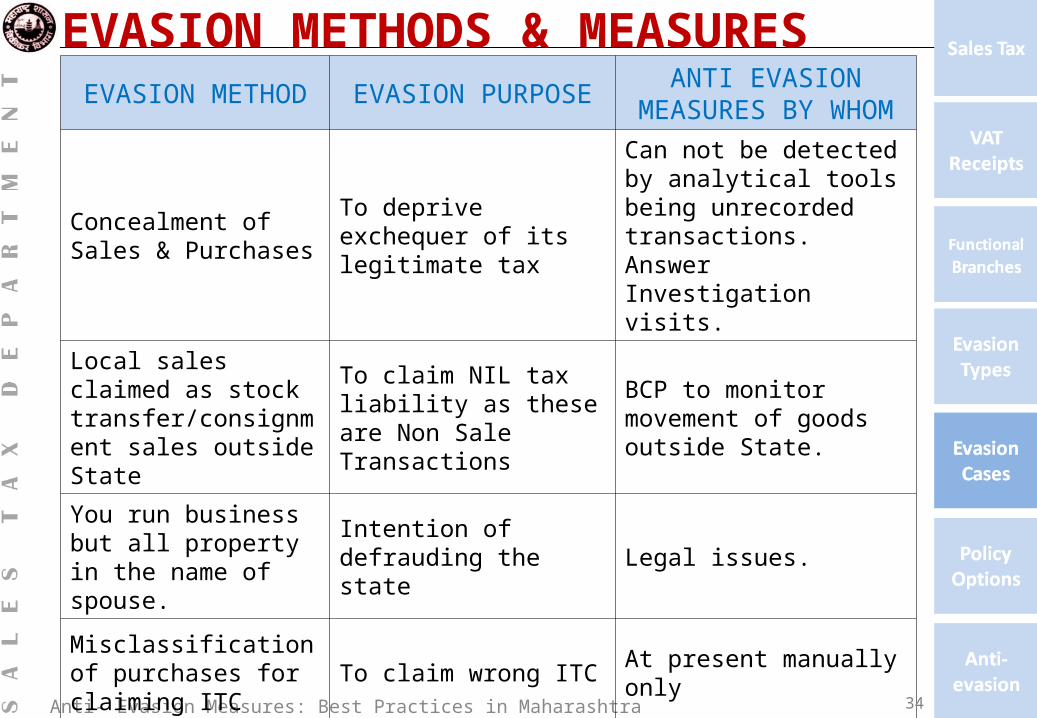

EVASION METHODS & MEASURESEVASION METHOD

EVASION PURPOSE

ANTI EVASION MEASURES BY

WHOM

Imaginary name & TIN, such Fabricated Tax Invoices accounted for in books of accounts

To defraud exchequer by claiming wrong ITC

ITC verification report will flag such cases

Hawala Operator will issue Tax Invoices, as per requirement. No tax deposited into Govt Treasury.

To defraud exchequer by claiming wrong ITC

ITC verification report will flag such cases

Genuine Tax Invoices fabricated to alter amounts or multiply their numbers

To defraud exchequer by claiming wrong ITC

ITC verification report will flag such cases

Local sales claimed as Inter State Sales

Pay 2% CST and claim ITC at a rate which is higher than 2%

BCP to monitor movement of goods outside State, Central Agency

32

Anti- Evasion Measures: Best Practices in Maharashtra

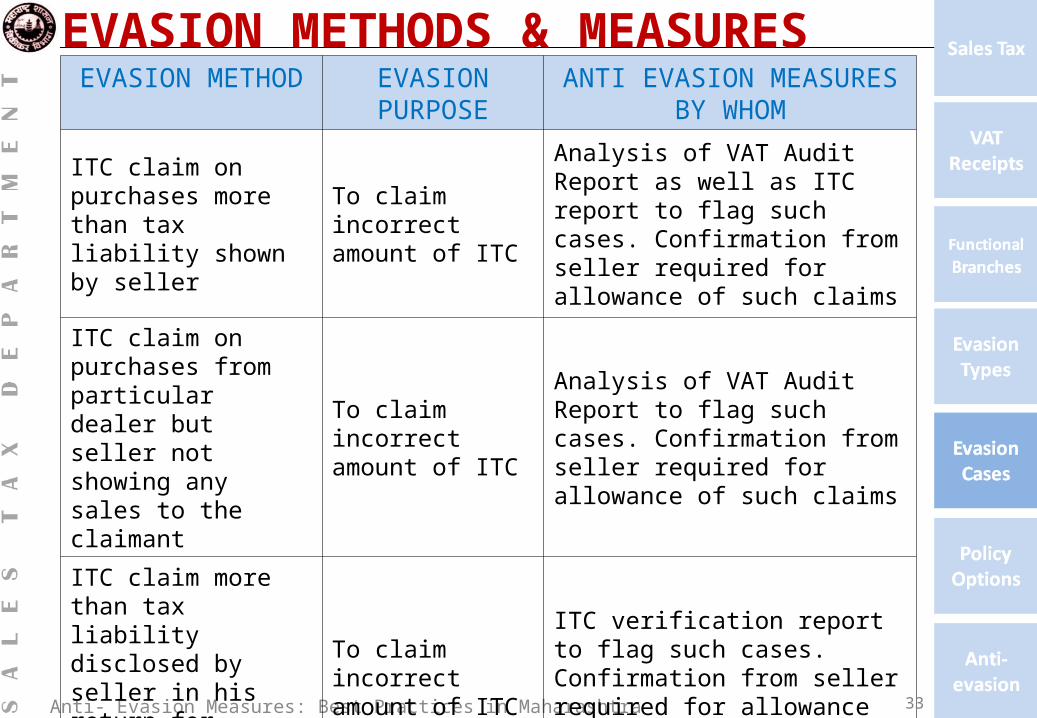

EVASION METHODS & MEASURESEVASION METHOD EVASION

PURPOSEANTI EVASION MEASURES

BY WHOM

ITC claim on purchases more than tax liability shown by seller

To claim incorrect amount of ITC

Analysis of VAT Audit Report as well as ITC report to flag such cases. Confirmation from seller required for allowance of such claims

ITC claim on purchases from particular dealer but seller not showing any sales to the claimant

To claim incorrect amount of ITC

Analysis of VAT Audit Report to flag such cases. Confirmation from seller required for allowance of such claims

ITC claim more than tax liability disclosed by seller in his return for corresponding period

To claim incorrect amount of ITC

ITC verification report to flag such cases. Confirmation from seller required for allowance of such claims

33

Anti- Evasion Measures: Best Practices in Maharashtra

EVASION METHODS & MEASURES EVASION METHOD EVASION PURPOSE

ANTI EVASION MEASURES BY WHOM

Concealment of Sales & Purchases

To deprive exchequer of its legitimate tax

Can not be detected by analytical tools being unrecorded transactions. Answer Investigation visits.

Local sales claimed as stock transfer/consignment sales outside State

To claim NIL tax liability as these are Non Sale Transactions

BCP to monitor movement of goods outside State.

You run business but all property in the name of spouse.

Intention of defrauding the state

Legal issues.

Misclassification of purchases for claiming ITC

To claim wrong ITC At present manually only

34

Anti- Evasion Measures: Best Practices in Maharashtra

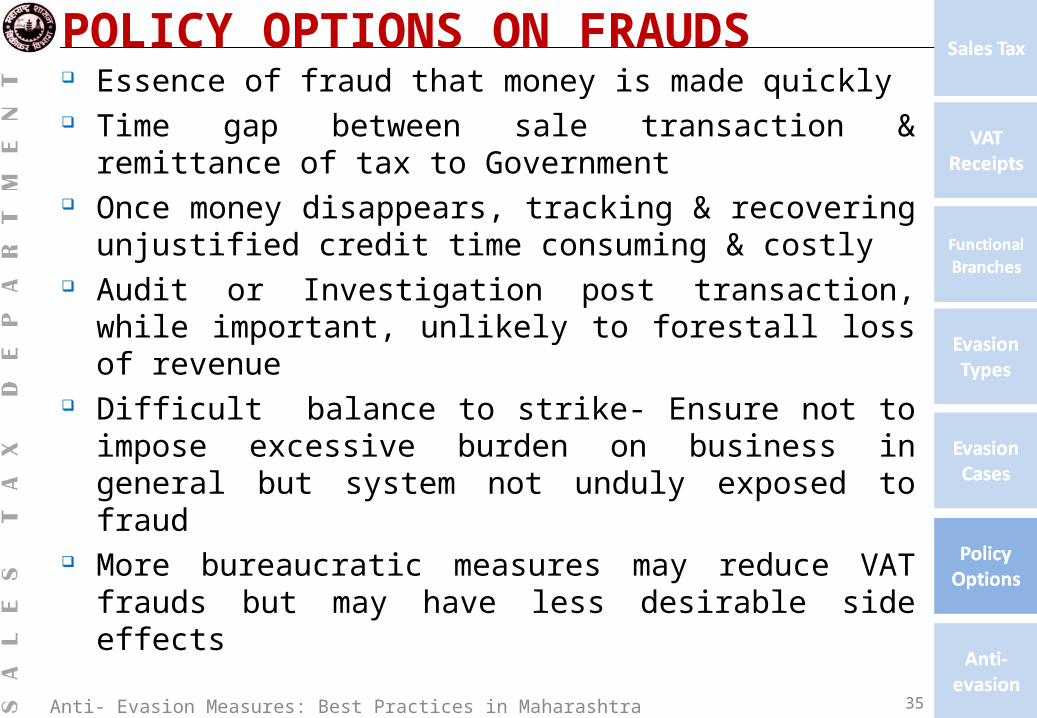

POLICY OPTIONS ON FRAUDS Essence of fraud that money is made quickly Time gap between sale transaction & remittance of tax to

Government Once money disappears, tracking & recovering unjustified

credit time consuming & costly Audit or Investigation post transaction, while important,

unlikely to forestall loss of revenue Difficult balance to strike- Ensure not to impose excessive

burden on business in general but system not unduly exposed to fraud

More bureaucratic measures may reduce VAT frauds but may have less desirable side effects

35

Anti- Evasion Measures: Best Practices in Maharashtra

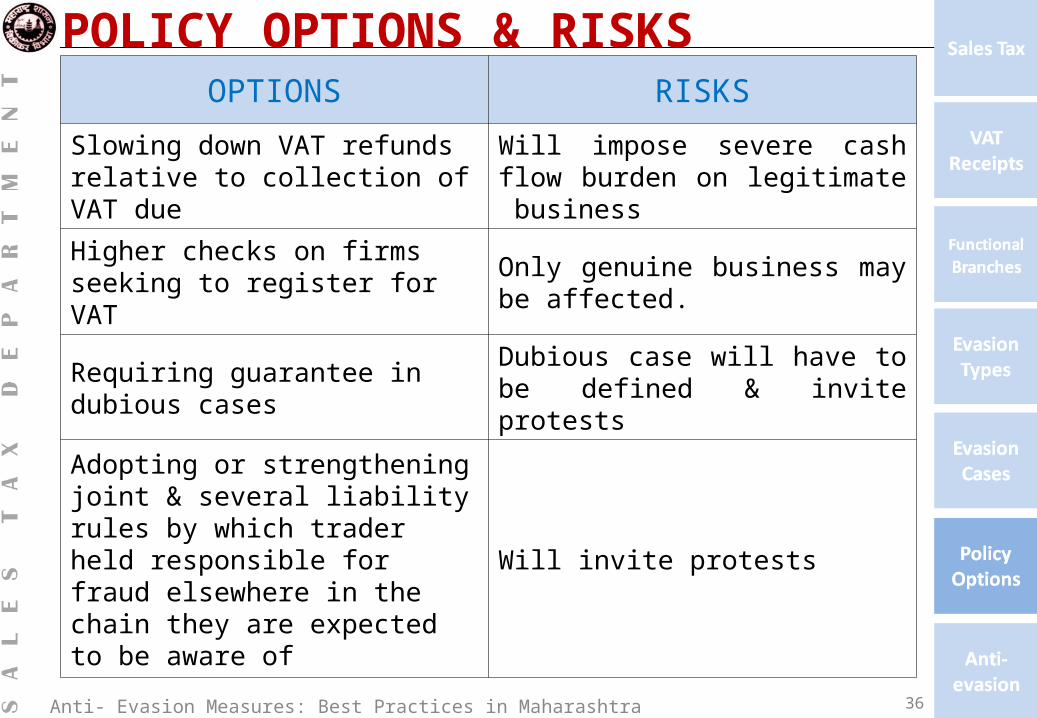

POLICY OPTIONS & RISKSOPTIONS RISKS

Slowing down VAT refunds relative to collection of VAT due

Will impose severe cash flow burden on legitimate business

Higher checks on firms seeking to register for VAT

Only genuine business may be affected.

Requiring guarantee in dubious cases Dubious case will have to be defined & invite protests

Adopting or strengthening joint & several liability rules by which trader held responsible for fraud elsewhere in the chain they are expected to be aware of

Will invite protests

36

Anti- Evasion Measures: Best Practices in Maharashtra

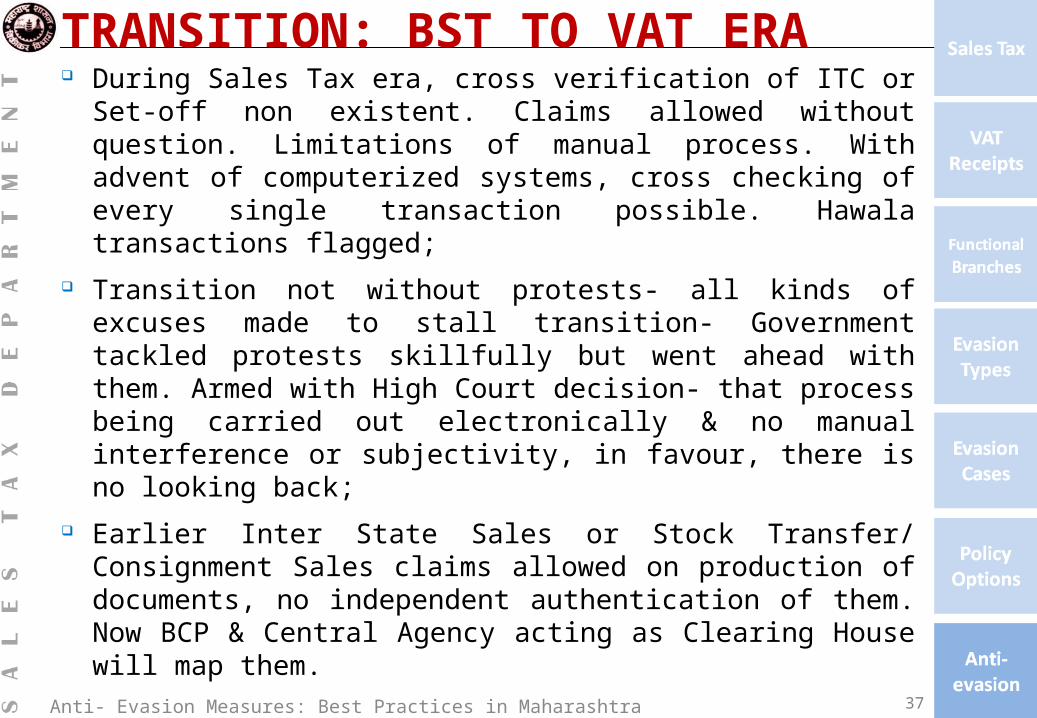

TRANSITION: BST TO VAT ERA During Sales Tax era, cross verification of ITC or Set-off non

existent. Claims allowed without question. Limitations of manual process. With advent of computerized systems, cross checking of every single transaction possible. Hawala transactions flagged;

Transition not without protests- all kinds of excuses made to stall transition- Government tackled protests skillfully but went ahead with them. Armed with High Court decision- that process being carried out electronically & no manual interference or subjectivity, in favour, there is no looking back;

Earlier Inter State Sales or Stock Transfer/ Consignment Sales claims allowed on production of documents, no independent authentication of them. Now BCP & Central Agency acting as Clearing House will map them.

37

Anti- Evasion Measures: Best Practices in Maharashtra

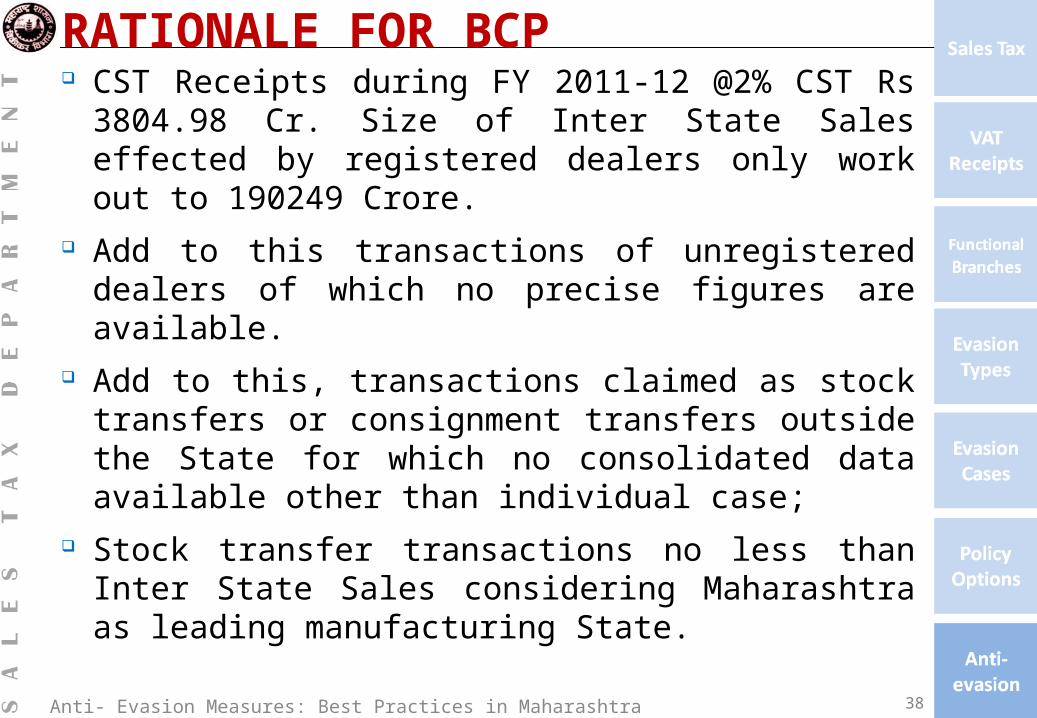

RATIONALE FOR BCP CST Receipts during FY 2011-12 @2% CST Rs

3804.98 Cr. Size of Inter State Sales effected by registered dealers only work out to 190249 Crore.

Add to this transactions of unregistered dealers of which no precise figures are available.

Add to this, transactions claimed as stock transfers or consignment transfers outside the State for which no consolidated data available other than individual case;

Stock transfer transactions no less than Inter State Sales considering Maharashtra as leading manufacturing State.

38

Anti- Evasion Measures: Best Practices in Maharashtra

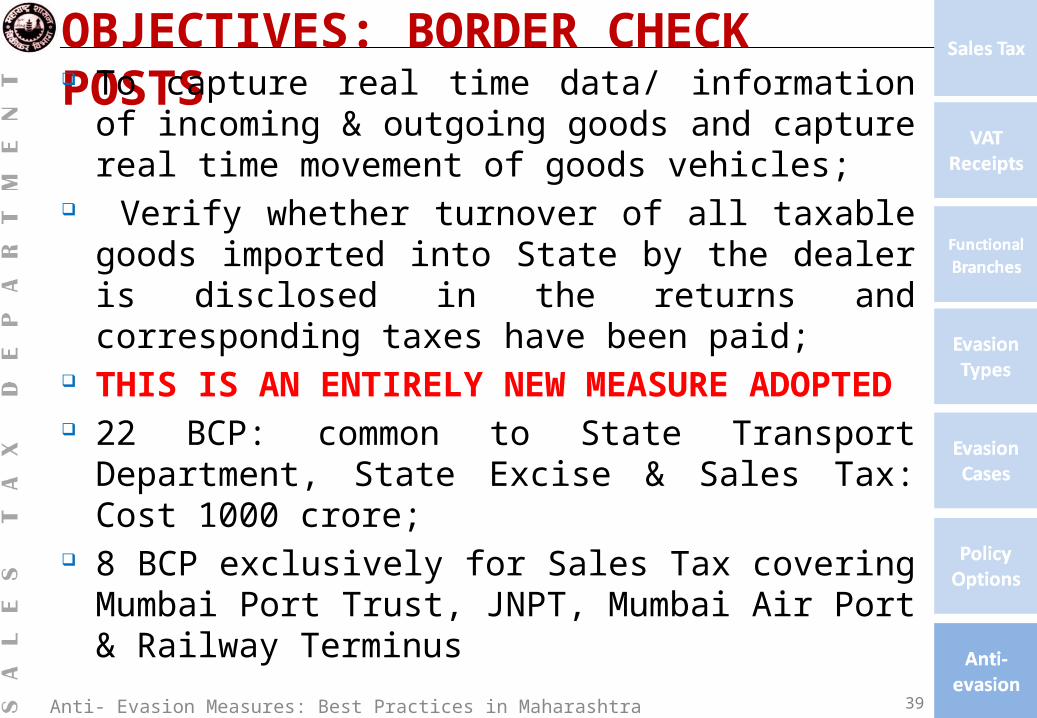

OBJECTIVES: BORDER CHECK POSTS To capture real time data/ information of incoming &

outgoing goods and capture real time movement of goods vehicles;

Verify whether turnover of all taxable goods imported into State by the dealer is disclosed in the returns and corresponding taxes have been paid;

THIS IS AN ENTIRELY NEW MEASURE ADOPTED

22 BCP: common to State Transport Department, State Excise & Sales Tax: Cost 1000 crore;

8 BCP exclusively for Sales Tax covering Mumbai Port Trust, JNPT, Mumbai Air Port & Railway Terminus

39

Anti- Evasion Measures: Best Practices in Maharashtra

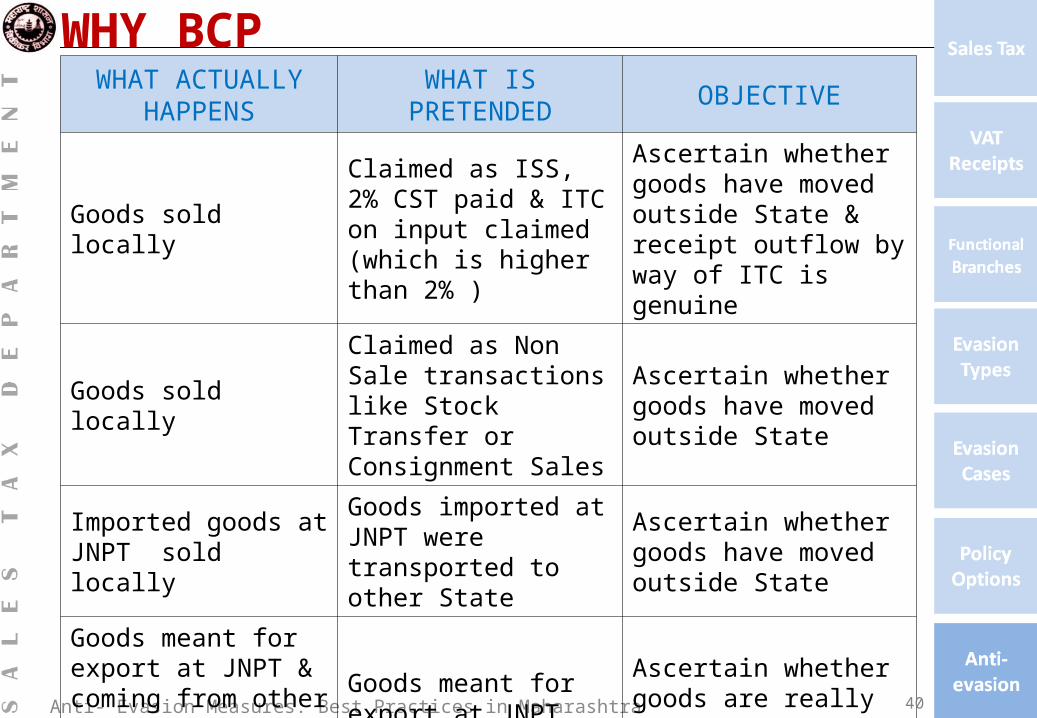

WHY BCPWHAT ACTUALLY

HAPPENSWHAT IS

PRETENDEDOBJECTIVE

Goods sold locally

Claimed as ISS, 2% CST paid & ITC on input claimed (which is higher than 2% )

Ascertain whether goods have moved outside State & receipt outflow by way of ITC is genuine

Goods sold locally

Claimed as Non Sale transactions like Stock Transfer or Consignment Sales

Ascertain whether goods have moved outside State

Imported goods at JNPT sold locally

Goods imported at JNPT were transported to other State

Ascertain whether goods have moved outside State

Goods meant for export at JNPT & coming from other States sold locally

Goods meant for export at JNPT

Ascertain whether goods are really exported

40

Anti- Evasion Measures: Best Practices in Maharashtra

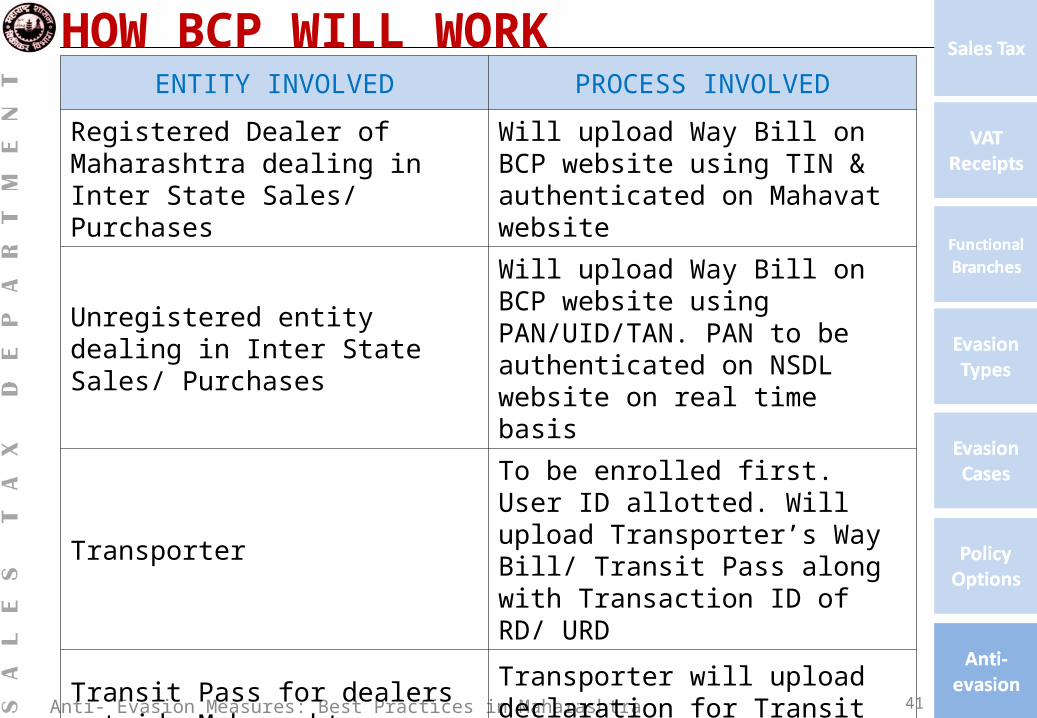

HOW BCP WILL WORKENTITY INVOLVED PROCESS INVOLVED

Registered Dealer of Maharashtra dealing in Inter State Sales/ Purchases

Will upload Way Bill on BCP website using TIN & authenticated on Mahavat website

Unregistered entity dealing in Inter State Sales/ Purchases

Will upload Way Bill on BCP website using PAN/UID/TAN. PAN to be authenticated on NSDL website on real time basis

Transporter

To be enrolled first. User ID allotted. Will upload Transporter’s Way Bill/ Transit Pass along with Transaction ID of RD/ URD

Transit Pass for dealers outside Maharashtra

Transporter will upload declaration for Transit Pass on BCP website

41

Anti- Evasion Measures: Best Practices in Maharashtra

TRANSIT PASS Transit of goods by road through the State require

transit pass u/s 68 to be delivered at last check post or barrier before exit from State;

Failure to comply, to attract penalty equal to twice the amount of tax leviable on the goods transported

42

Anti- Evasion Measures: Best Practices in Maharashtra

ITC VERIFICATION: AUDIT REPORT Matching of VAT Audit Report of Seller and

Purchaser: disclosed tax liability by seller in respect of a dealer

matched with ITC claim by purchaser in respect of that seller.

Claimant purchaser given opportunity to prove claim by obtaining confirmation from seller in case of discrepancies, otherwise claim to be disallowed.

43

Anti- Evasion Measures: Best Practices in Maharashtra

ITC VERIFICATION: RETURN STATUS Seller doing business with number of entities. Tax payable by seller, as per return, must be equal to

greater than ITC claim of claimant for the said corresponding period.

In case of discrepancies, confirmation from seller dealer required for allowing ITC;

If no returns furnished by seller disclosing his tax liability, confirmation required for allowing ITC;

Purchases from identified Hawala and from TIN cancelled cases are flagged in the verification

report.

44

Anti- Evasion Measures: Best Practices in Maharashtra

ITC VERIFICATION: AREAS NOT COVERED BY ANALYTICAL TOOLS There are certain areas which are not covered by analytical

tools and has to be dealt with manually currently; Ineligible Inputs for ITC (NEGATIVE LIST) covered by rule

54; Retention, u/r 53, under contingencies the specified ; Goods purchases of which debited to Profit & Loss Account or

Trading Account-Gifts or other as Sales Promotion expenses; Misclassification of commodity for claiming ITC. Example:

Software, being goods of incorporeal or intangible nature, are eligible for ITC to traders only. Purchasers classify them as Computer Spares to avoid detection and claiming ITC.

45

Anti- Evasion Measures: Best Practices in Maharashtra

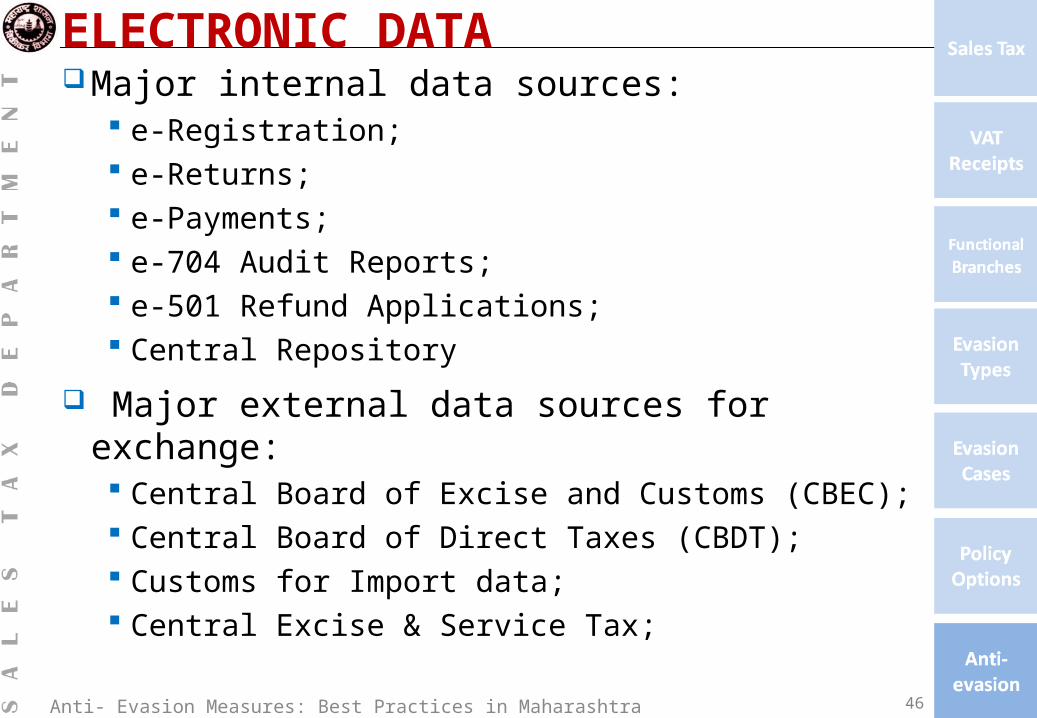

ELECTRONIC DATAMajor internal data sources:

e-Registration; e-Returns; e-Payments; e-704 Audit Reports; e-501 Refund Applications; Central Repository

Major external data sources for exchange: Central Board of Excise and Customs (CBEC); Central Board of Direct Taxes (CBDT); Customs for Import data; Central Excise & Service Tax;

46

Anti- Evasion Measures: Best Practices in Maharashtra

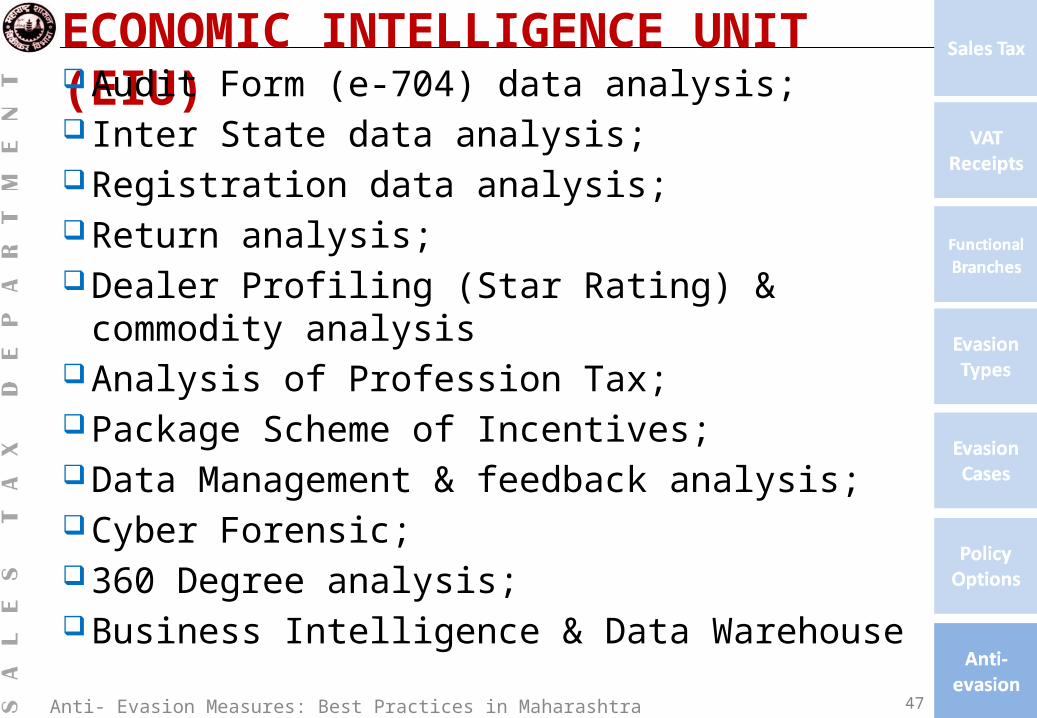

ECONOMIC INTELLIGENCE UNIT (EIU) Audit Form (e-704) data analysis; Inter State data analysis;Registration data analysis;Return analysis;Dealer Profiling (Star Rating) & commodity analysis Analysis of Profession Tax;Package Scheme of Incentives;Data Management & feedback analysis;Cyber Forensic;360 Degree analysis;Business Intelligence & Data Warehouse

47

Anti- Evasion Measures: Best Practices in Maharashtra

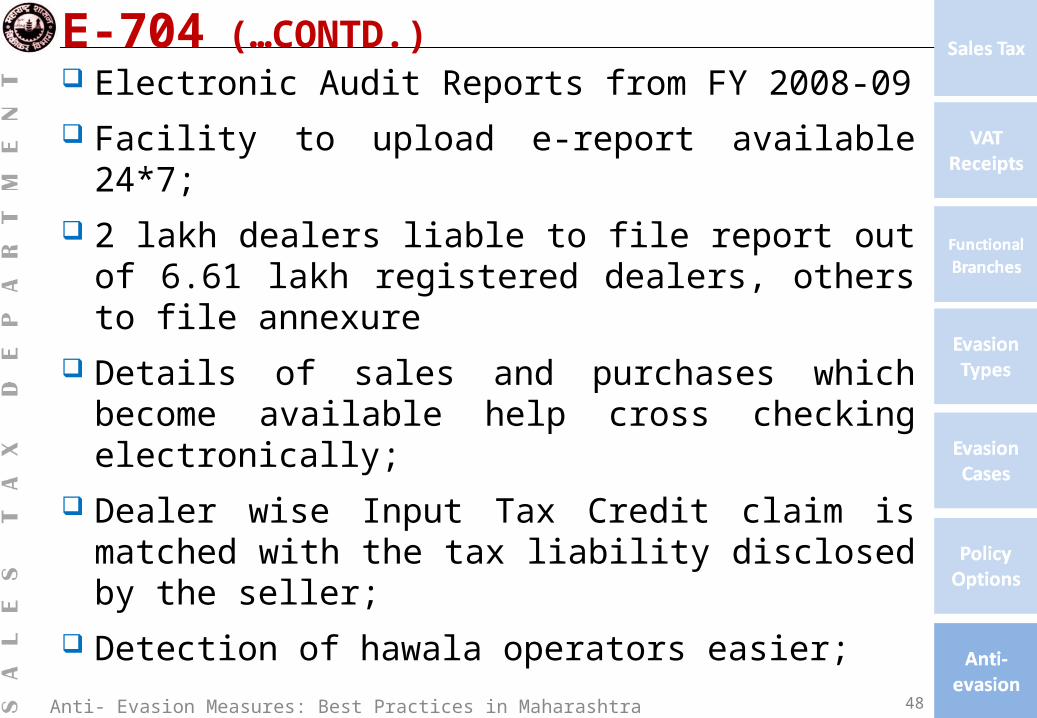

E-704 (…CONTD.) Electronic Audit Reports from FY 2008-09

Facility to upload e-report available 24*7;

2 lakh dealers liable to file report out of 6.61 lakh registered dealers, others to file annexure

Details of sales and purchases which become available help cross checking electronically;

Dealer wise Input Tax Credit claim is matched with the tax liability disclosed by the seller;

Detection of hawala operators easier;

48

Anti- Evasion Measures: Best Practices in Maharashtra

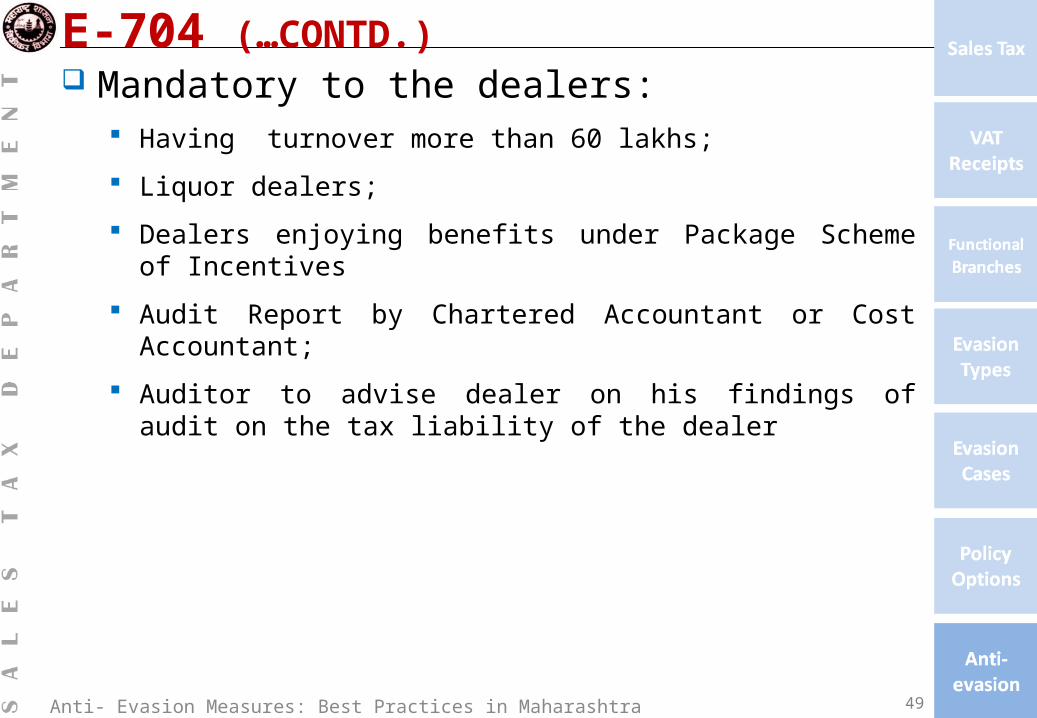

E-704 (…CONTD.) Mandatory to the dealers:

Having turnover more than 60 lakhs;

Liquor dealers;

Dealers enjoying benefits under Package Scheme of Incentives

Audit Report by Chartered Accountant or Cost Accountant;

Auditor to advise dealer on his findings of audit on the tax liability of the dealer

49

Anti- Evasion Measures: Best Practices in Maharashtra

E-ANNEXURE For dealers not filing e-704 VAT Audit report; This way entire data of sales and purchases carried out

by every dealer is captured electronically; Tax Deducted at Source (TDS) Certificates received

and issued by the dealer Declarations under Central Sales Tax Act received and

yet to be received by the dealer Declarations for sale in the course of export (Form H)

received by the dealer Customer wise sales Supplier wise purchases

50

Anti- Evasion Measures: Best Practices in Maharashtra

TINXSYS TINXSYS (Tax Information Exchange System): in

coordination with other States to plug revenue leakages in inter state transactions of sales, purchases or stock / consignment transfers

Exchange of data of declarations issued under CST Act to dealers for claiming reduced rate of CST

51

Anti- Evasion Measures: Best Practices in Maharashtra

VIGILANCE BRANCH Under the direct control of Chief Vigilance

Officer of the rank of Special Inspector General of police (IGP);

Watchdog on complaints against employees; Control over Investigation Proceedings on real

time basis.

52

Anti- Evasion Measures: Best Practices in Maharashtra

THANK YOU !