Embed Size (px)

Citation preview

Annual Update on Insurance Law

Professor Rob Merkin QC

BILA

Insurance Law Update

20 November 2015

Professor Rob Merkin QC

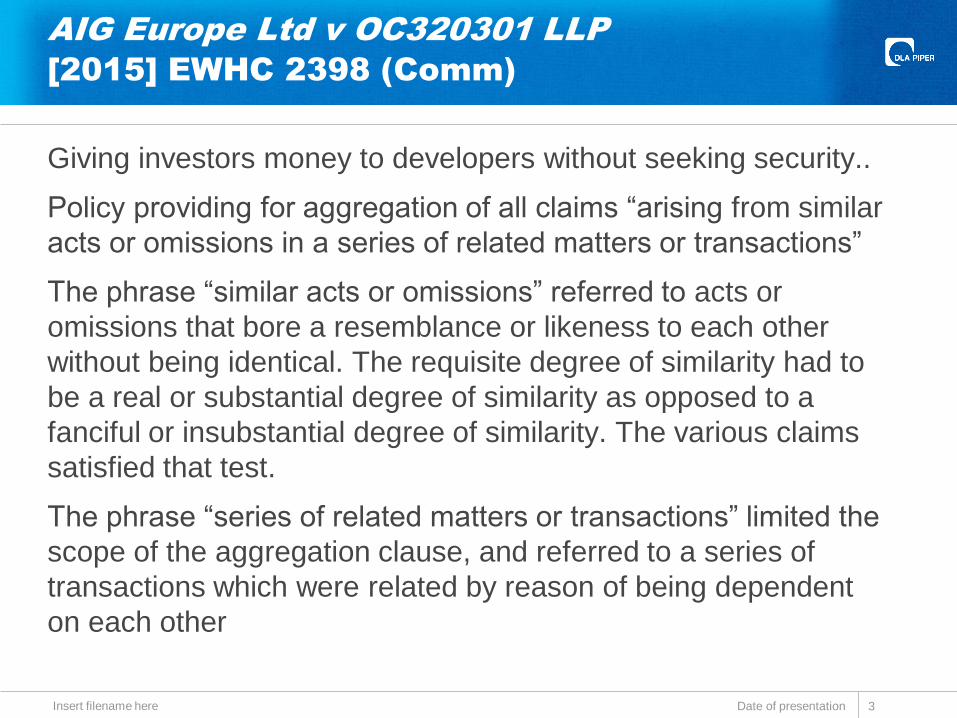

AIG Europe Ltd v OC320301 LLP

[2015] EWHC 2398 (Comm)

Giving investors money to developers without seeking security..

Policy providing for aggregation of all claims “arising from similar

acts or omissions in a series of related matters or transactions”

The phrase “similar acts or omissions” referred to acts or

omissions that bore a resemblance or likeness to each other

without being identical. The requisite degree of similarity had to

be a real or substantial degree of similarity as opposed to a

fanciful or insubstantial degree of similarity. The various claims

satisfied that test.

The phrase “series of related matters or transactions” limited the

scope of the aggregation clause, and referred to a series of

transactions which were related by reason of being dependent

on each other

Date of presentation Insert filename here 3

MacCaferri Ltd v Zurich Insurance Plc

[2015] EWHC 1708 (Comm)

Product liability claim following injury to an employee at work

Policy stating that “The Insured shall give notice in writing to the

Insurer as soon as possible after the occurrence of any event

likely to give rise to a claim”

Accident occurring 22 September 2011, threat of proceedings

made 18 July 2013 and claim was then notified

No breach of the obligation

Date of presentation Insert filename here 4

Zurich v IEG [2015] UKSC 33

Zurich were on risk for 7/27 years of employers’ liabiility cover,

EI were on risk for two years and IEG was uninsured for 19

years. The SC held 4:3:

(1) Zurich was liable 100% under the Fairchild principle.

(2) Zurich was entitled to recover 2/27 from EI.

(3) Zurich was entitled to recoup 19/27 from IEG

(4) Zurich had to bear 100% defence costs

Date of presentation Insert filename here 5

Teal Assurance v Berkley Insurance

Europe [2015] EWHC 1000 (Comm)

Exhaustion of funds under liability insurance

Claims must be met in the order that they are established and

quantified

Date of establishment and quantification where sums are paid

into an escrow account and used to pay invoices for work to

correct defects in work

Date of invoices, not date of payment into escrow account

Date of presentation Insert filename here 6

Lambert Leasing Inc. v QBE Insurance

Ltd (No 2) [2015] NSWSC 1196

Liability policy providing cover “in respect of all sums which the

Insured shall become legally liable to pay, and shall pay, as

compensatory damages (including costs awarded against the

Insured)”

Meaning of “and shall pay”

Not sufficient to oust obligation of insurers to pay on proof of

liability, no postponement to actual payment

Date of presentation Insert filename here 7

Flint v Tittensor [2015] EWHC 466

(QB)

Public policy defence in motor insurance

Defendant run over by assured following alteracation

Court ruling that defendant had a claim in tort and that insurers

were required to indemnify the assured

Date of presentation Insert filename here 8

McCracken v Smith [2015] EWCA Civ

380

Claimant injured while travelling as a passenger on a stolen

motor cycle

Injury sustained as a result of driver speeding and also

negligence of driver of a van colliding with motor cycle

Public policy precluded claim against driver of motor cycle

Public policy did not preclude claim against van driver, no causal

link between illegality and injury

However, 50% deduction from damages for contributory

negligence (as well as 20% deduction for not wearing crash

helmet)

Date of presentation Insert filename here 9

Hammersley v National Transport

Insurance [2015] TASFC 5

Motor policy excluding liability where the vehicle was conveying

any load in excess of: that for which it was constructed; that for

which it was licensed; or that permitted by law. However, these

exclusions did not apply where there was “accidental

overloading”

Further exclusion for vehicle “being used in an unsafe or

unroadworthy condition, unless such condition could not be

readily detected by you.”

Overloading held to be accidental

Overloading did not make vehicle unsafe or unroadworthy

No reckless failure to observe road traffic regulations

Date of presentation Insert filename here 10

Brit v F&B Trenchless Solutions

[2015] EWHC 2237 (Comm)

FBTS’s liability policy in respect of a micro-tunnel was avoided

following a derailment due to settlement above the tunnel. The

following points arose

(1) The information as to the settlement and void was material, a

conclusion which could be reached without expert evidence. Brit

had discharged its burden of showing that, with full disclosure, it

would have excluded the site from cover.

(2) There had been a representation that there would be no work

near active railway lines, and the statement had inducing effect.

(3) Brit had not affirmed the policy. The broker was the agent of

FBTS and not Brit, so that any documents issued by the broker

after the loss did not give rise to waiver. Further, the delay in

avoiding the policy was not significant: Brit had not become

aware until April 2014 that the railway line had been active.

Date of presentation Insert filename here 11

Axa v Arab Insurance Group [2015]

EWHC 1939 (Comm)

Axa sought to avoid an energy risks facultative obligatory first

loss reinsurance treaty made in 1996, and its 1997 renewal, for

non-disclosure of loss statistics for 1989 to 1995, or

misrepresentation to the effect that there were no losses. A

further ground for avoiding the renewal was non-disclosure of

three incidents in the first year. Avoidance was refused.

(1) Loss statistics were generally material facts.

(2) The 1996 Treaty could not be avoided. No statement about

loss statistics had been made. There had been material non-

disclosure but there was no inducement because the risk

would have been written.

(3) There was no waiver of disclosure by failing to ask

questions, as the reinsurers were unaware that the statistics

were available.

Date of presentation Insert filename here 12

Milton Furniture v Brit Insurance

[2015] EWCA Civ 671

Loss by fire. The relevant clause provided that: “The whole of

the protections including any Burglar Alarm provided for the

safety of the premises shall be in use at all times out of business

hours or when the Insured's premises are left unattended and

such protections shall not be withdrawn or varied to the

detriment of the interests of Underwriters without their prior

consent.” The CA held that: (1) the term was to be construed

independently of another narrower clause relating theft loss; (2)

there were two separate restrictions, business hours and left

unattended; (3) the premises had been left unattended; (4) there

was breach because the assured had failed to pay burglar alarm

monitoring charges.

Note that the loss was by fire. Effect of IA 2015 on this decision?

Date of presentation Insert filename here 13

Gard Marine v China National

Chartering [2015] EWCA Civ 16

A (owner) and B charterer agreed that A would insure on behalf

of A and B. The agreement contained a safe port warranty which

was allegedly broken. Insurers paid A and sued B.The CA found

immunity.

(1) Where A and B agree that A shall insure on behalf A and B,

and a loss occurs due to the fault of B, the question whether

the insurers - having paid A - can bring a subrogation action

against B depends entirely on the contract between A and B.

The terms of the insurance are irrelevant.

(2) The Court of Appeal went on to hold that there is a

presumption in the case of co-insurance that A will look to

the insurers and not to B, so that in the absence of words to

the contrary the insurers will not have a subrogation action.

Date of presentation Insert filename here 14

Johnston v Endeavour Energy [2015]

NSWSC 1117

Subrogation and effect of payment by insurers that does not fully

indemnify assured

Insurers, having paid to policy limits, purported to remove

policyholder from a class action

Subrogation rights arise only on full indemnification, so assured

had right to control litigation against third party pending full

indemnification

Insurers had no power to opt-out policyholders

Date of presentation Insert filename here 15

Small Business Consortium v Angas

[2015] NSWSC 1511

Credit policy covering mortgage loans.

Default amounted to just under A$2.3 million. $1.75 million was

recovered from the sale of property. Insurers paid the difference,

around $600,000 under a Deed of Settlement

The payment was “Subject to and conditional upon the payment

of the Indemnity Sum … Angas Securities agree that repayment

of the indemnity sum to SBC takes priority from any funds

received from any claim against a Third Party for recovery of

damages arising out of the default by the borrower …”

Assured suffered other financial losses. Action brought against

negligent valuers and some $650,000 was recovered. Court held

that in equity the sum belonged to the assured, but under the

policy it belonged to the insurers to the extent of their payment.

Date of presentation Insert filename here 16

Western Trading v Great Lakes [2015]

EWHC 103 (QB)

Buildings managed by WT, claim following fire

WT had insurable interest by virtue of status as manager, tenant

and obligation to insure

No misrepresentation as to occupancy or use of buildings

Obligation to reinstate with reasonable despatch not triggered

until insurers admit liability

Date of presentation Insert filename here 17

Aspen v Adana [2015] EWCA Civ 176

Product and public liability insurance

Product liability excluding liability “arising in connection with the

failure of any Product to fulfil its intended function.”

Public liability covering faulty or inefficient workmanship,

materials or design, but excluding liability for products

Product defined as “any product or goods manufactured,

constructed, installed, altered, repaired, serviced, processed,

treated, sold, leased, supplied or distributed by or on behalf of

the Insured … but only after such item has left the Insured's

care, custody or control.”

Concrete base not a product. Dowels were products but had not

failed to fulfil function

Date of presentation Insert filename here 18

Impact Funding v Barrington [2015]

EWCA Civ 31

Solicitors Indemnity Policy, excluding liability for “breach by any

insured of the terms of any contract or arrangement for the

supply to, or use by, any insured of goods or services in the

course of the Insured Firm's Practice …”

Solicitors becoming liable to litigation funders under a Master

Agreement whereby the solicitors were to recommend suitable

cases for funding.

Loss held to be incurred as part of the assured’s professional

practice and not excluded by the trading exclusion

Date of presentation Insert filename here 19

Kraal v Earthquake Commission

[2015] NZCA 13

Household policy covering “physical loss or damage to the

property”

Property undamaged but ordered to be vacated because of

future threats

No coverage under the policy

Date of presentation Insert filename here 20

Kelly v EQC [2015] NZHC 1690

Insurers had discretion under property policy to pay for

reinstatement or to cash settle.

Delay in exercising option.

Court held that the delay in exercising the election had been

unreasonable, and that it was no longer possible for the insurers

to do so.

Date of presentation Insert filename here 21

Soutern Response v Avonside [2015]

NZSC 110

Assured’s property totally destroyed and incapable of being

rebuilt. Assured entitled to buy or build a new house, indemnity

capped at rebuilding the destroyed house on the original site.

Notional calculation required, and included all notional costs

including: 10% margin for contingencies; and architects’ and

surveyors’ fees

Date of presentation Insert filename here 22

Domenico Trustee v Tower [2015]

NZCA 372

In the event of total loss the insurers had the right to rebuild or to

cash settle. After lengthy negotiations in which cash offers were

made, the assured commenced proceedings.

The CA held that the insurers had not elected to pay cash at any

time but had merely negotiated. Their delay meant that no

election had been made.

In the absence of election, there was no default for cash

payment, and the court would not make the election for the

insurers (contrary to the trial judge’s view). The appropriate

remedy was an application to the court for directions

Date of presentation Insert filename here 23

Matton Developments Pty Ltd v CGU

Insurance Ltd (No 2) [2015] QSC 72

Crane collapsing when overloaded contrary to manufactuter’s

instructions

Policy covering “accidental, sudden and unforeseen” damage

Also coverage for “accidental overloading”

Word “sudden” not necessarily relating to timing and meant only

unexpected and unintended

Words “unforeseen” and “accidental” mean much the same

On the wording, accidental was to be looked at from the

operator’s perspective

Damage sudden and unforeseen, but not accidental

Overloading was not accidental

Date of presentation Insert filename here 24

Involnert v Aprilgrange [2015] EWHC

2225 (Comm)

2011 policy on yacht at an agreed value of €13 million, the sum

paid in 2007. In 2007 the yacht had been valued at €7 million.

Insurers able to set policy aside for non-disclosure of valuation.

Valuation was a material fact: while it was usual to insure yachts

for purchase price, it was different if there was an up to date

valuation

The condition “subject to receipt of satisfactory proposal form”

did not give a defence – the phrase meant satisfactory to

insurers and not free of false statements

Breach of duty to sue within 12 months, but not of duty to

produce documents within 90 months – insurers had not

specified a time and place for production

Sub-broker did not owe duty of care to assured

Date of presentation Insert filename here 25

Hayward v Zurich [2015] EWCA Civ

327

Employers liability insurance

Settlement entered into with injured employee following

proceedings where insurers alleged “lack of candour” and

“exaggeration of difficulties”

Evidence of fraud coming to light two years later

Settlement could not be overturned

Date of presentation Insert filename here 26

BILA would like to thank

Professor Rob Merkin QC