Embed Size (px)

Citation preview

Annual Reportfor the year ended 31 March 2004

ICAP is the world’s largest interdealerbroker with an average daily transactionvolume in excess of $600 billion, morethan 50% of which is electronic. The Groupis active in the wholesale markets for OTCderivatives, fixed income securities, moneymarket products, foreign exchange, energy,credit and equity derivatives.

01 Financial Highlights

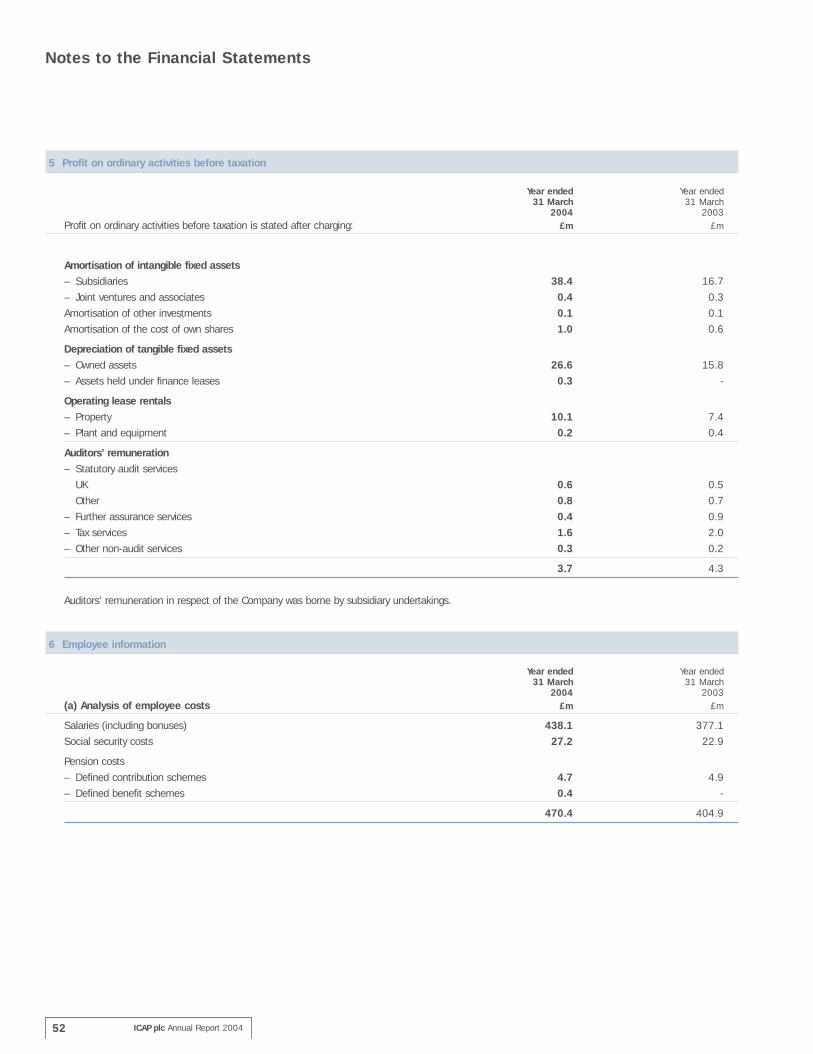

02 Group Profile

05 Developments

06 Chairman’s Statement

08 Group Chief Executive Officer’s Review

10 Operating Review

12 Group Finance Director’s Review

18 Directors and Secretary

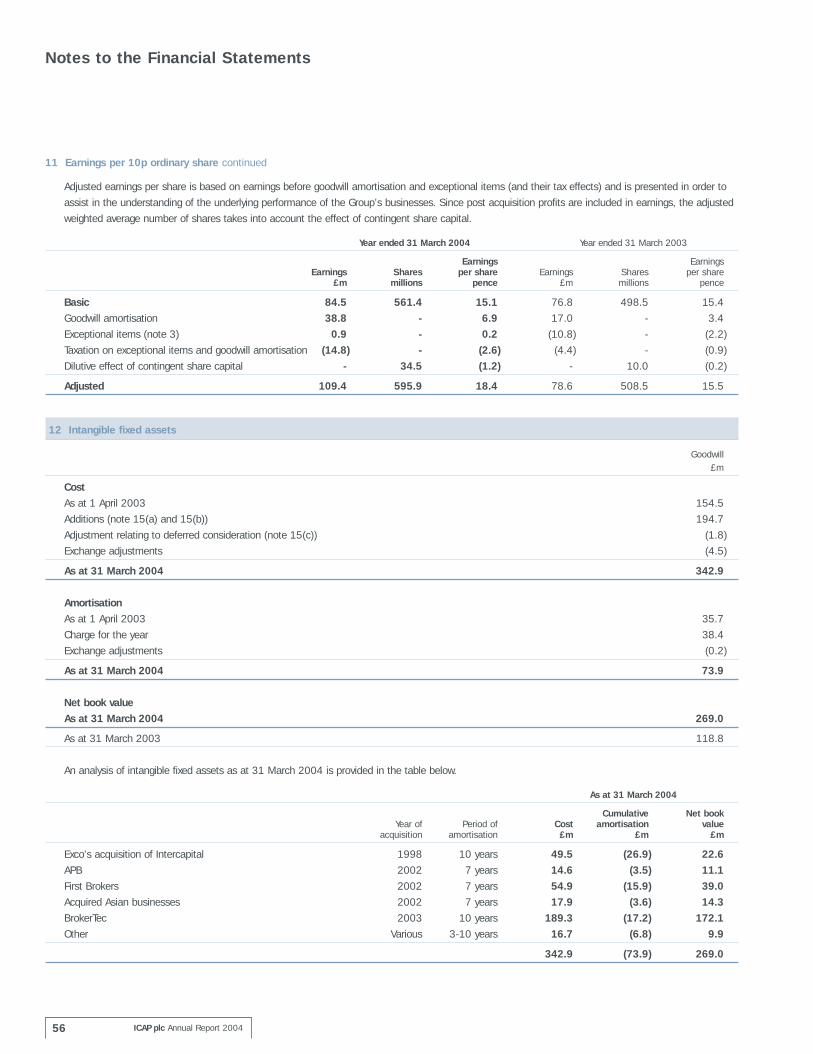

20 Directors’ Report

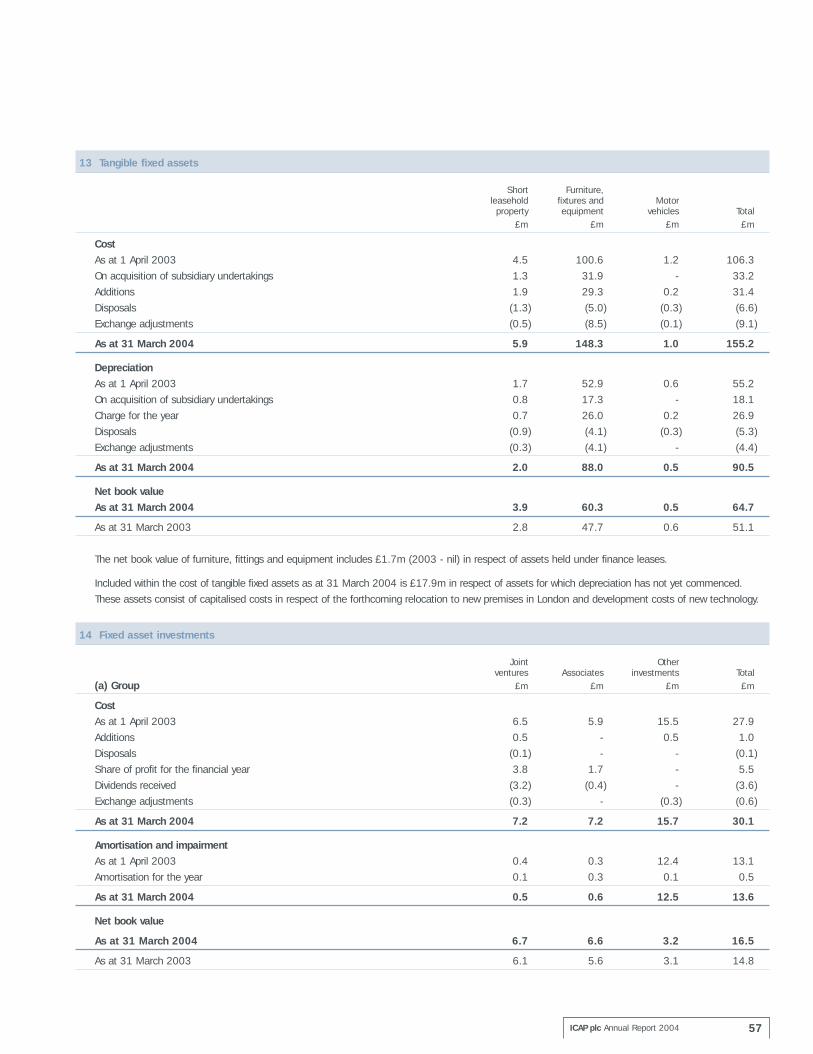

23 Corporate Governance Report

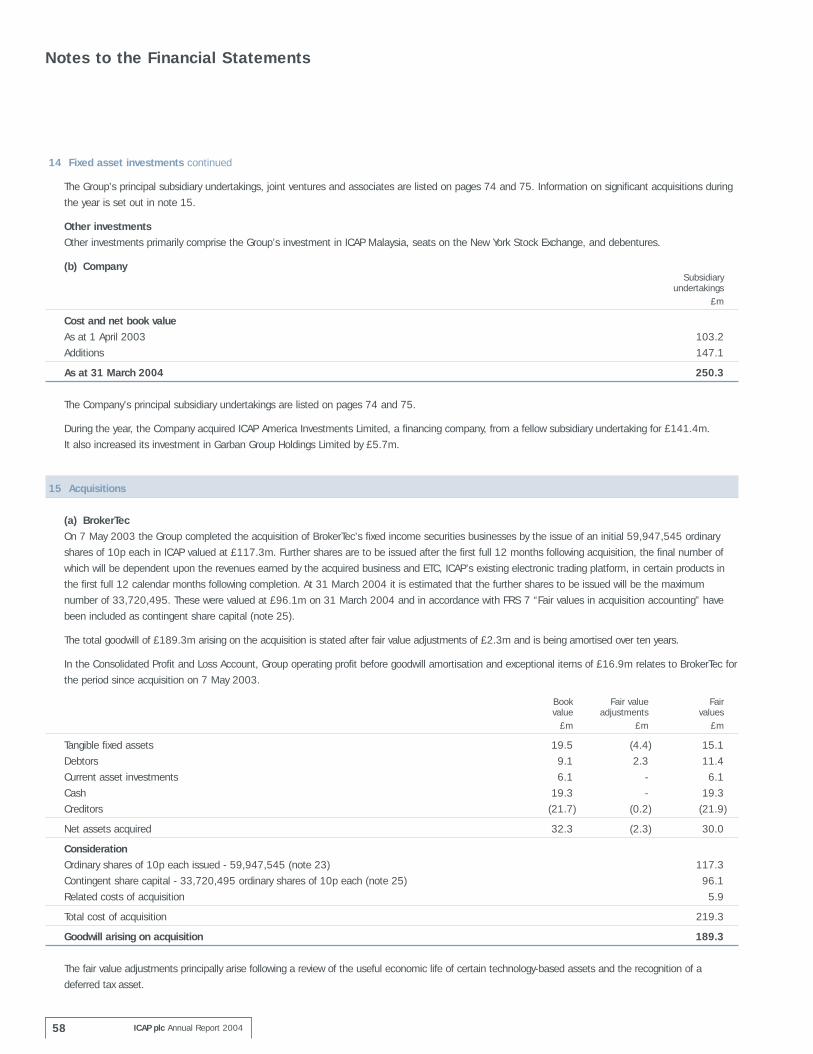

28 Remuneration Committee Report

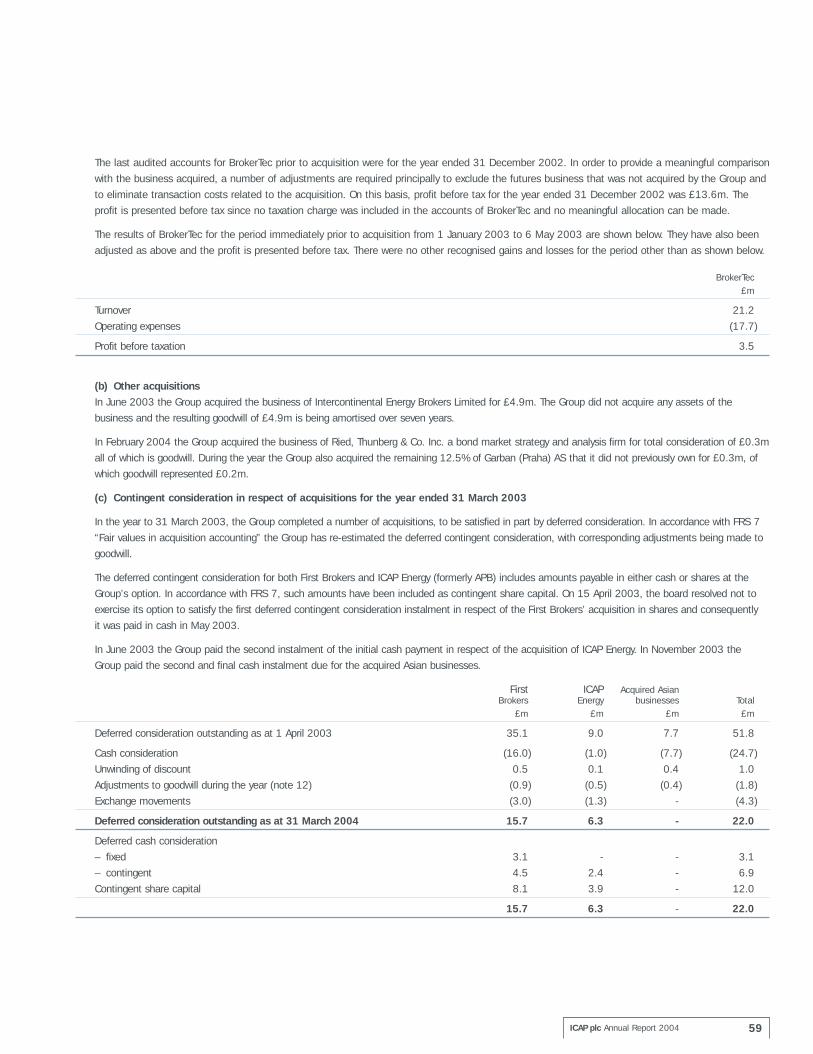

37 Independent Auditors’ Report

38 Consolidated Profit and Loss Account

40 Consolidated Balance Sheet

41 Consolidated Statement of Total Recognised Gains and Losses

41 Reconciliation of Movements in Consolidated Shareholders’ Funds

42 Consolidated Cash Flow Statement

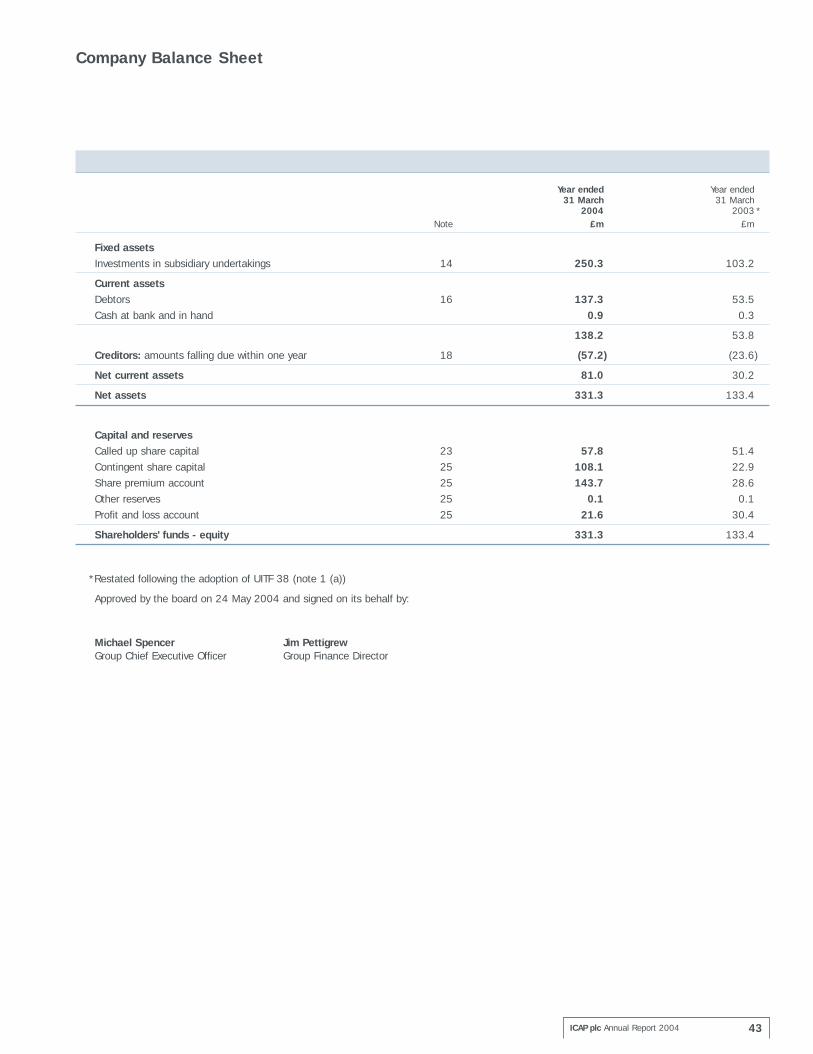

43 Company Balance Sheet

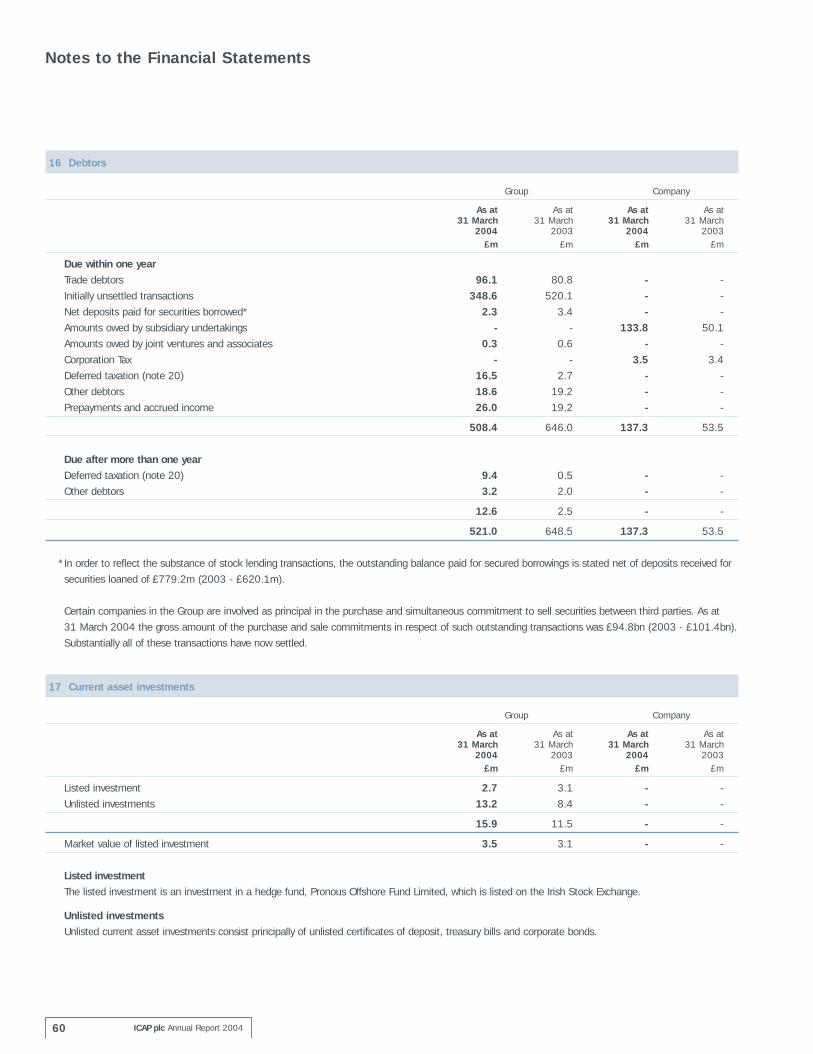

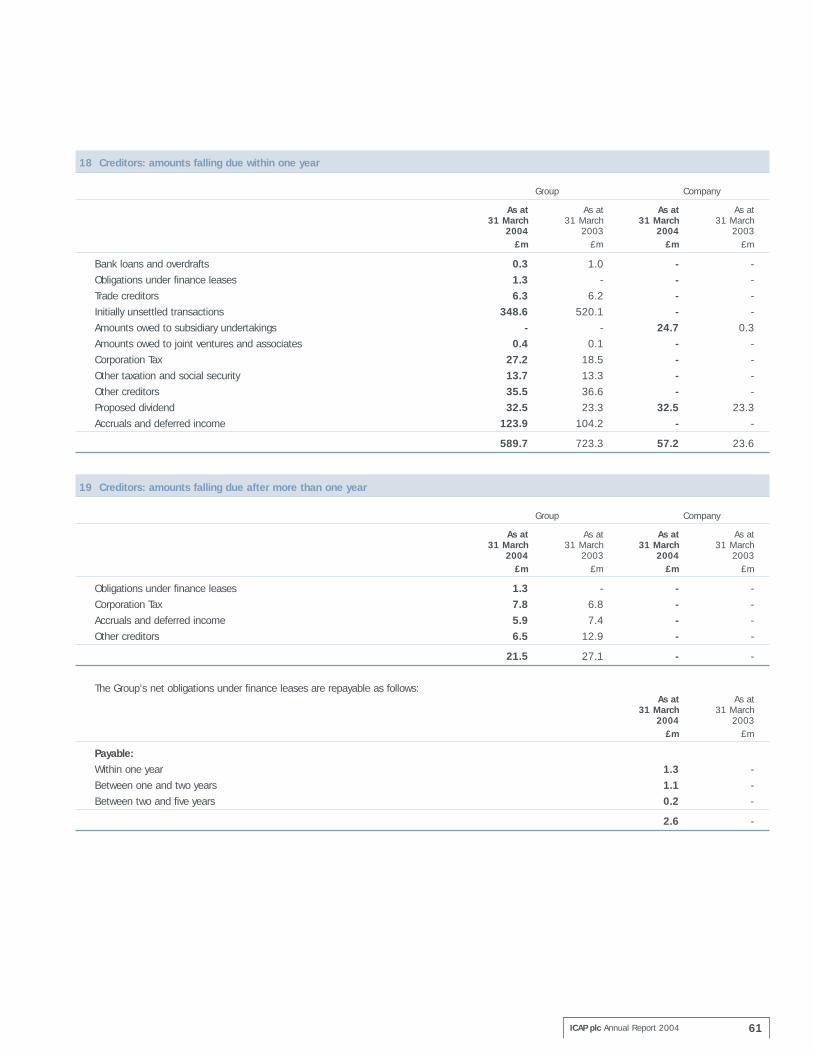

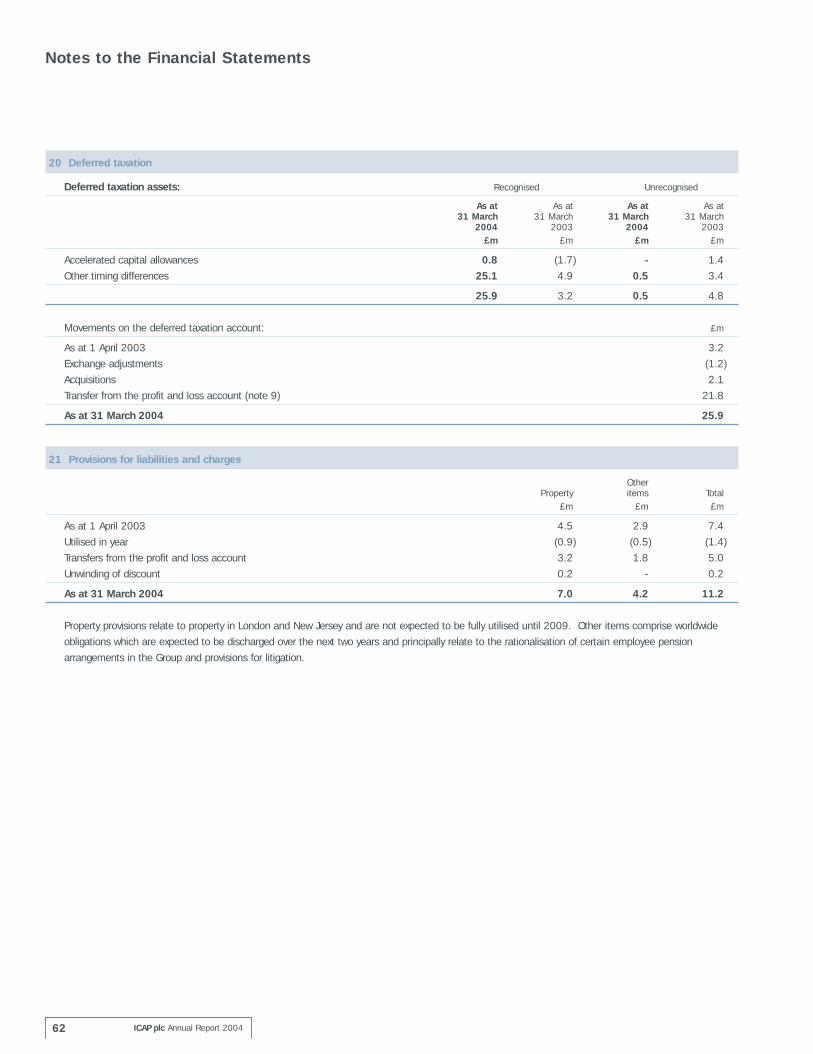

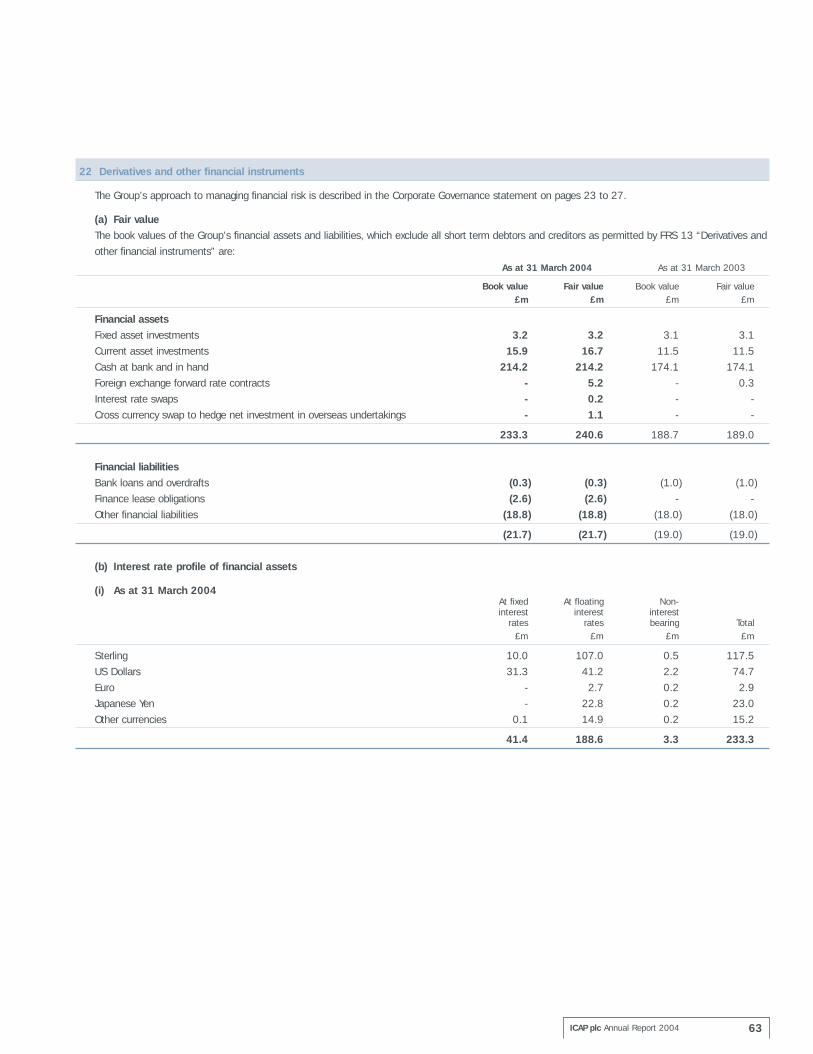

44 Notes to the Financial Statements

74 Principal Subsidiaries, Joint Ventures and Associates

76 Information for Shareholders

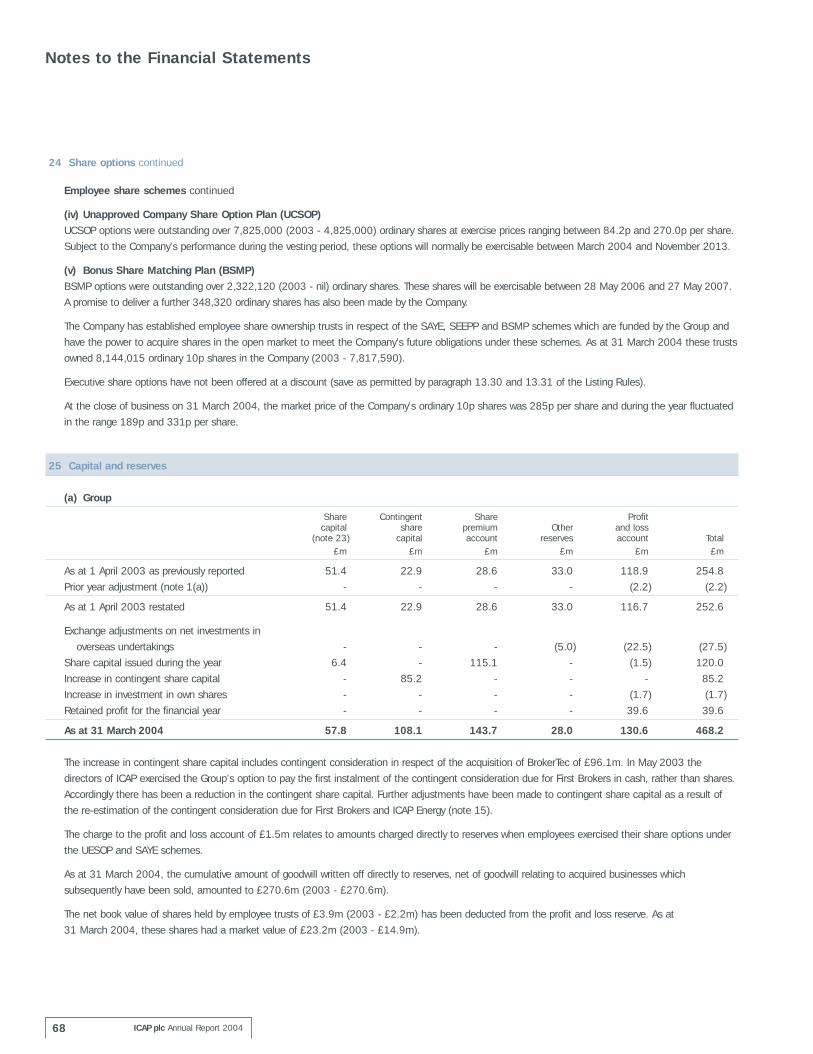

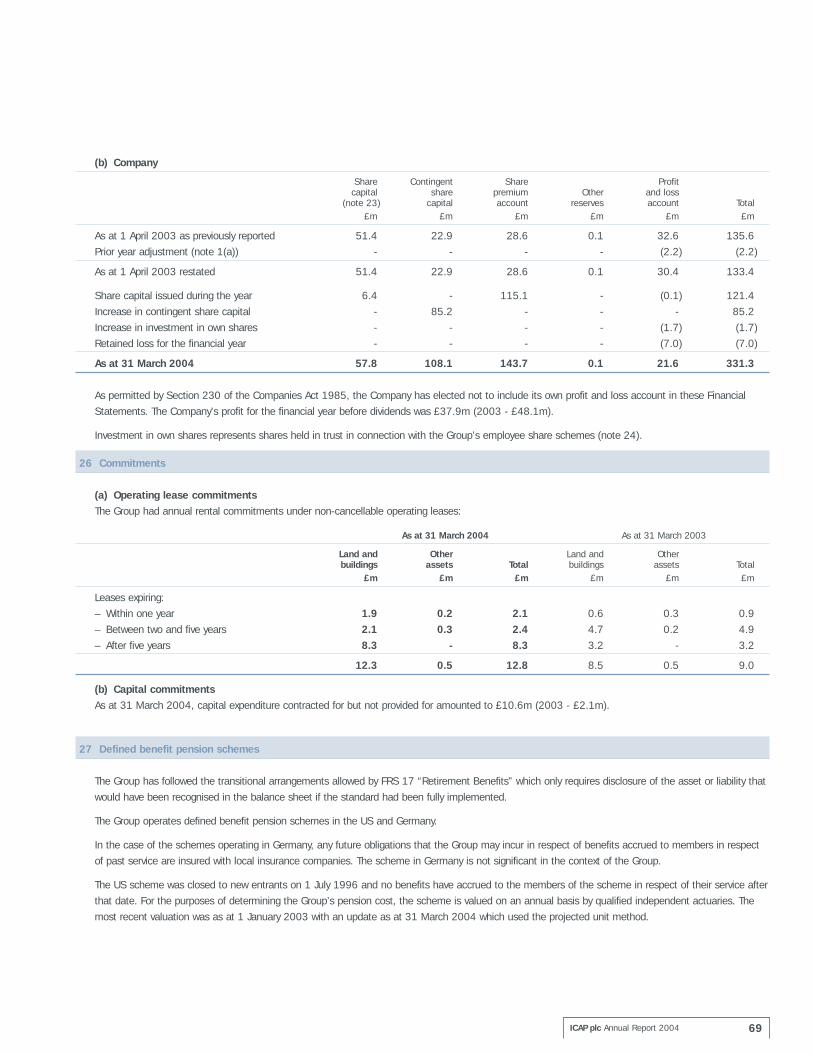

78 Notice of Annual General Meeting

82 Contact Information

84 Definitions

ICAP plc

Registered number: 3611426

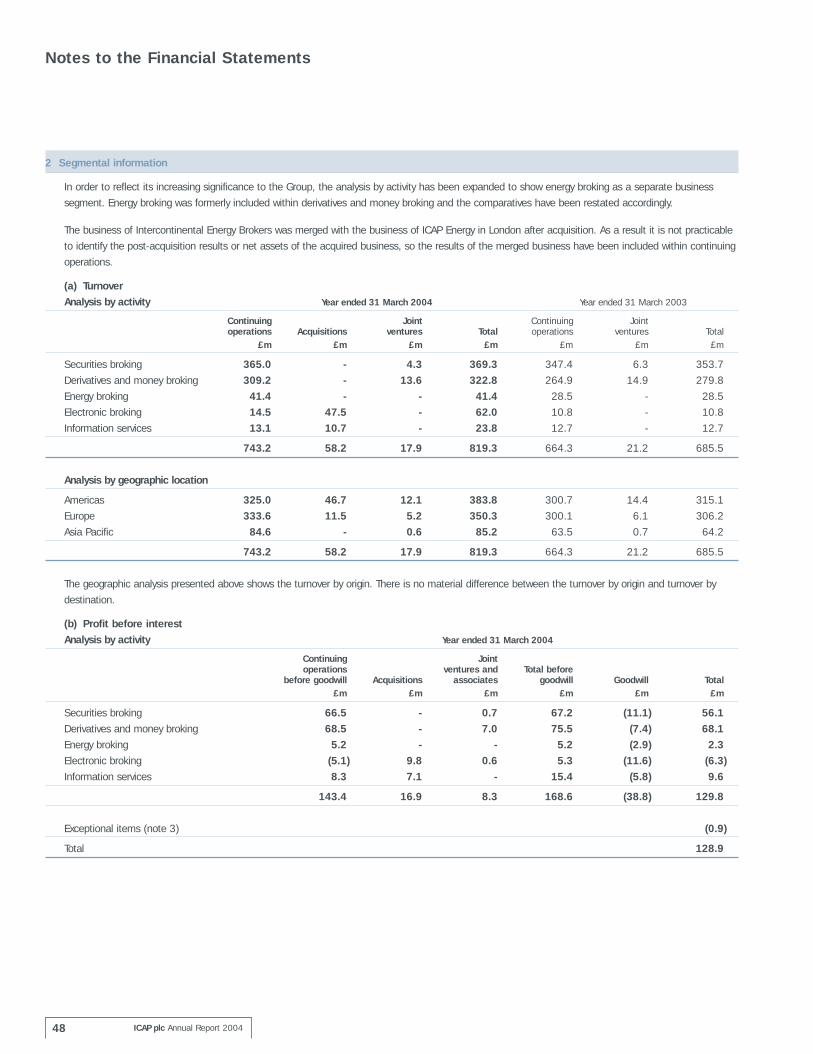

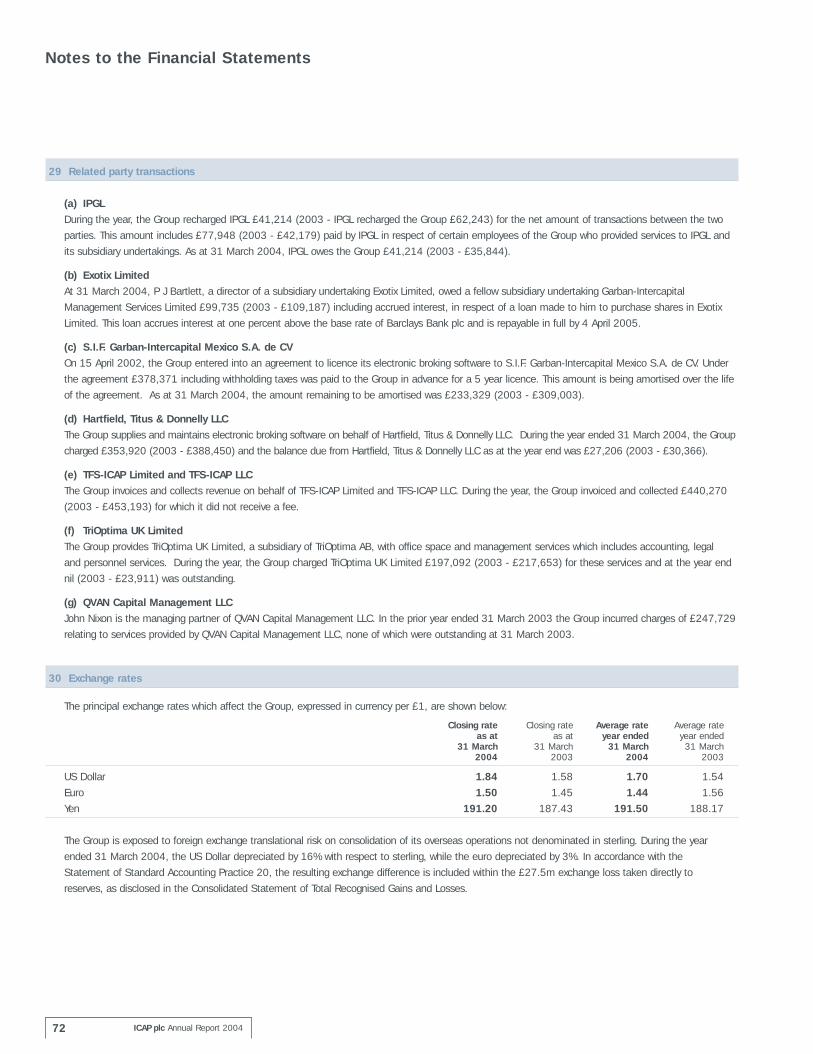

TURNOVER

Financial Highlights

ICAP plc Annual Report 2004 01

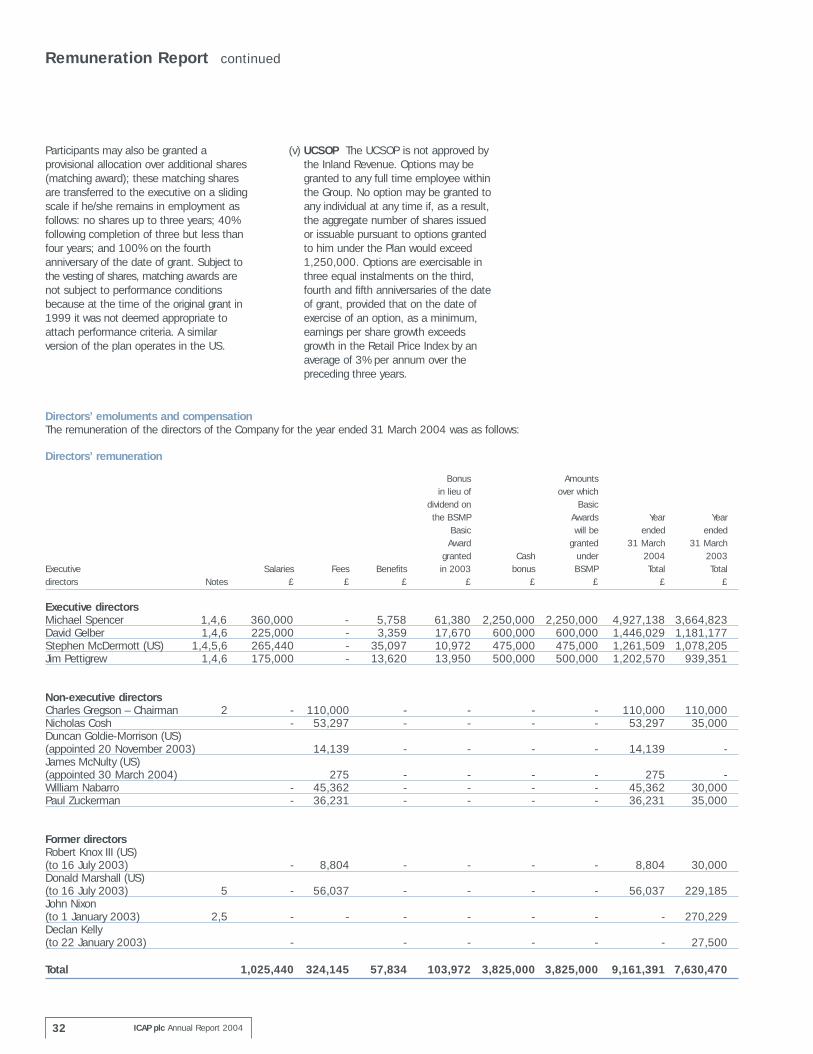

Year ended Year ended31 March 2004 31 March2003

£m US$m(3) £m US$m(3)

Turnover 801.4 1,362.4 664.3 1,023.0Expenses 641.1 1,090.0 550.8 848.2Profit before tax - adjusted (1) 170.2 289.3 123.7 190.5Earnings per share - adjusted (2,4) 18.4p 31.2c 15.5p 23.9cDividends per share (4) 7.4p 12.6c 6.0p 9.2c

Profit before tax - statutory 130.5 221.9 117.5 181.0Earnings per share - basic (4) 15.1p 25.7c 15.4p 23.7c

Notes1 Excludes goodwill amortisation of £38.8 million

(2003 - £17 million) and a net exceptional costof £0.9 million (2003 gain - £10.8 million).

2 Excludes goodwill amortisation and exceptional items but includes 34.5 million contingently issuable shares.

3 Converted at the average exchange rate for theyear of US$1.70 and for the year to March 2003 at US$1.54.

4 Reflects the share split in February 2004 of ordinary shares of 50p each into five ordinaryshares of 10p each.

Profit (before tax, goodwill amortisation and exceptional items)(1)

Statutory profit before tax

Adjusted EPS (before tax, goodwill amortisationand exceptional items)(2)

Basic EPS

2001 2002 2003

472.6 527.9664.3

2004

801.4

£m

DIVIDENDS PER SHARE

2001 2002 2003

4.04.8

6.0

2004

7.4

pence

PROFIT BEFORE TAX

£m

20022001

EARNINGS PER SHARE

pence

9.98.1

11.610.6

2003

15.4

2004

18.415.115.5

20022001

75.667.289.183.8

2003

123.7117.5

2004

170.2

130.5

GLOBAL MARKETS

With more than 2,900 staff, ICAPhas a strong presence in each ofthe three major financial markets;London, New York and Tokyo,together with a local presence in 20 other financial centres.

Group Profile

ICAP plc Annual Report 200402

HOW IT COULD DEVELOP %

HOW THE INDUSTRY IS %

ELECTRONIC

GLOBAL MARKETS

MEXICO CITY LOUISVILLE NEW YORK LONDON AMSTERDAMBERGEN COPENHAGEN

PARISFRANKFURT MADRID

PRAHAWARSAW

THE ROLE OF THE INTERDEALER BROKERICAP provides a specialist intermediarybroking service to commercial banks andinvestment banks in the wholesale financialmarkets. An interdealer broker works in thesemarkets to draw together liquidity and tomatch buyers and sellers so that deals canbe executed by its banking customers. Banks pay a commission when they use abroker to complete a deal.

ICAP offers banks significant economies of scale in price discovery by having anumber of staff covering each product andin constant contact with a range ofcounterparties. Access to a brokertherefore allows a bank to increasemarket coverage in busy times withoutincurring additional overheads. In manymarkets ICAP operates as an agent ormatched principal broker providing bankswith the opportunity to deal anonymouslythrough a neutral party at the mostattractive price available.

ICAP has created a powerful combination:the world’s largest voice and electronicinterdealer broker. There is growingdemand for electronic broking of liquidproducts, which is totally complementaryto voice broking of more bespoke, lessliquid products. The majority of themarkets in which ICAP operates rely on,and will continue to rely on, voice brokingskills. ICAP’s version of electronic brokingnaturally complements voice broking andin most markets combines voice and/orelectronic access to a common pool ofliquidity. This hybrid solution provides

customers with both voice support andelectronic execution.

THE WHOLESALE FINANCIAL MARKETSICAP is an interdealer broker in the overthe counter (OTC) markets for derivatives,fixed income securities, money marketproducts, foreign exchange, energy, creditand equity derivatives. These marketshave grown significantly in recent yearsdriven by:

• demand for significant deficit financingin many of the G7 countries;

• increased issuance in the corporate bondand mortgage backed securities markets;

• volatility in medium term interest rates;

• increased allocation of capital for tradingand position taking by the banks andhedge funds;

• shifts in foreign exchange rates;

• increased use by banks and otherfinancial institutions of the derivativesmarket to unbundle and redistribute arange of financial risks including credit,interest rate and exchange rate risks; and

• changes in the demand for commoditiessuch as oil, coal and gas.

HYBRID VOICE

MANAMA MUMBAI BANGKOKJAKARTA

HONG KONGKUALA LUMPURMANILASINGAPORE

TOKYO

ICAP plc Annual Report 2004 03

The strong growth exhibited in the OTCderivatives markets clearly underscores thebenefits these products provide as financialrisk management tools. Furthermore, thegrowth of both the credit and the interestrate derivatives markets demonstrates thevalue they provide firms seeking to transferthese types of risk.

The credit default swap market, for example,has been effective at redistributing risk awayfrom the banking system to otherinstitutions such as insurance companiesand pension funds, facilitating a transfer ofcredit risk out of the banking system.

There are two types of derivative market:the OTC market and the exchange-tradedfutures market. Significant tradingopportunities exist between these closelyrelated markets. There is ongoing and rapidconvergence between the exchange-tradedand OTC markets due to a greaterpenetration of electronic trading, lowerfinancial barriers to entry, risk mitigationwith greater emphasis on common clearingpools, a demand for more transparentvaluation methodology and commontrading protocols.

MARKET GROWTHICAP estimates that the global interdealerbroker market for OTC derivatives, fixedincome securities, money market products,foreign exchange, energy, credit and equityderivatives increased in 2003 byapproximately 7%, after adjusting for theimpact of exchange rate movements and is worth approximately $4.6 billion. ICAPcontinues to be the global leader with anestimated 27% share of the market, anincrease of approximately 3% from the prioryear as a result of organic growth and theacquisition of BrokerTec in May 2003.

The Bank of International Settlements hasannounced continued strong growth in interestrate derivatives in the first half of 2003,which reached a record $121.8 trillion ofnotional amounts outstanding. Interest rateswaps grew by 20% and interest rate optionsby 23% compared with the second half of 2002.

Overall business in the foreign exchangederivatives markets was especially buoyantwith currency options surging by 42% overthe previous six months. According to a recentsurvey by the International Swaps DealersAssociation, the notional principal outstandingvolume of credit derivatives grew at an evenstronger rate in the second half (33%) thanin the preceding six months (25%); notionalamounts now stand at $3.58 trillion. Thisrepresents a year-on-year growth of 29%.

In the US fixed income markets in the yearto February 2004, according to the NewYork Federal Reserve Board, volumestransacted by interdealer brokers grew by19% in the US Treasuries market, 23% inthe Mortgage Backed Securities market, but declined by 21% in the US Agenciesmarket. In Europe, according to ISMA, Repomarkets volumes transacted by interdealerbrokers grew by 22%.

NOW

FUTURE

SYDNEY WELLINGTON

USING TECHNOLOGY TO INCREASETRADING EFFICIENCYThe completion of ICAP’s acquisition of BrokerTec in May 2003 was a keystrategic objective, transforming theGroup’s electronic broking capability. ICAP is now the leading global electronicinterdealer broker, as well as the leadingvoice broker. In the first quarter of 2004,ICAP’s electronic broking volumes hadgrown to an average of $305 billion perday. A peak daily electronic brokingvolume of $410 billion was recorded on 4 May 2004.

A technology project to cross-connectBrokerTec’s and ICAP’s electronic platformsin the US Treasury markets was completedin September 2003 and now successfullyprovides voice and/or electronic access to a common pool of liquidity.

ICAP’s electronic broking footprint is muchmore extensive than any other broker andcurrently includes active and off-the-runUS Treasuries, Bills, Notes, Bonds, Strips,TIPS and Basis trading as well as Agenciesand Mortgages; European, UK, Australian,Japanese and South African governmentbonds; US$ and euro repurchase agreementsand Eurobonds.

Outside the fixed income markets, 39 bankshave now been connected and are usingICAP’s iSwap platform (non-interactively)for euro interest rate swaps, 10 more areat various stages of installation. The nextsteps will be to launch iSwap for electronictrading of EONIAS (short term IRS) inSeptember 2004.

A project to provide improved price discoveryand straight through processing in ForwardFX and money market cash products isexpected to go live in late 2004. It willinvolve offices in Europe, the US and Asiasharing access to the liquidity generatedacross the ICAP network.

REGULATIONICAP has a strong balance sheet to meetthe commercial demands of customersand to comply with regulatory capitaladequacy requirements. The ICAP Group isregulated on a consolidated basis by theUK Financial Services Authority (FSA)with the Group’s UK businesses beingauthorised by the FSA to carry onregulated activities in the UK. In the US,the Group’s activities are regulated by theSecurities and Exchange Commission. TheGroup operates in other countries and itsoperations are subject to the relevantlocal regulatory requirements.

Group Profile continued

ICAP plc Annual Report 200404

ELEC

TRONICVO

ICE

Developments

ICAP plc Annual Report 2004 05

2003

APRIL – TriOptima executed the largestderivatives transaction ever, terminatingover €420 billion in interest rate swaps inits launch run. Since April the triReduceservice has become the established methodfor reducing interest rate swap portfoliosfor the world's largest banks with the totalnominal value of mass swap terminationtransactions through TriOptima's servicestanding at $4,454 billion. ICAP owns30% of TriOptima.

MAY – ICAP completed the acquisition ofBrokerTec’s electronic securities brokingbusiness to combine the world’s leadinginterdealer voice broker with one of theworld’s leading electronic brokers of fixedincome securities.

MAY – ICAP entered a partnership withDeutsche Bank and The Goldman SachsGroup to expand the distribution of economicderivatives into the interdealer market.The development of liquid markets in thisproduct will enable the measurement of independent market views on theeconomy and accurate pricing on co-dependent markets.

JUNE – ICAP acquired IntercontinentalEnergy Brokers, a London based energybusiness with strong positions in thenatural gas and some electricity markets.These were combined with ICAP Energy’sexisting market positions in oil, electricity,coal and precious metals.

SEPTEMBER – The technology project tocross-connect BrokerTec’s and ICAP’selectronic broking platforms was completed.This provided both combined voice andelectronic access into a combined liquiditypool, initially in the US Treasury markets.

2004

FEBRUARY – ICAP announced plans tolaunch an independent global futuresbusiness by expanding its small existingfutures activities, focusing particularly onNorth America and Europe. Leveraging offICAP’s strengths in the OTC markets, ICAPaims to become one of the small numberof truly global futures executionbusinesses within two years.

FEBRUARY – ICAP and TradingTechnologies International, Inc. agreed tolaunch an alternative marketplace in USTreasury benchmark issues. Using TradingTechnologies’ system, market professionalsworldwide are able to trade US Treasuryissues with futures-style execution onICAP’s BrokerTec platform.

MARCH – ICAP and MarketAxess Inc.formed a strategic alliance to provideelectronic trading of government bonds,including US Treasury benchmark securities,over the MarketAxess platform. MarketAxessis the leading electronic multi-dealer-to-client trading platform for US and Europeanhigh-grade corporate and emerging marketsbond trading.

DIVIDEND 2003 pence

This was the fourth successive year inwhich ICAP has performed extremely well.Group turnover during that period hasrisen by 73% and profit before tax,goodwill amortisation and exceptionalitems by 225%. ICAP’s total return toshareholders over the past four years hasbeen 507%. This reflects our continuingability to produce very good results in ahighly competitive environment. This yearthere have been strong contributionsfrom almost all products and markets.The markets that have shown outstandinggrowth have been medium term interestrate derivatives, credit derivatives andsegments of the fixed income securitiesmarkets.

The directors recommend a final dividend of5.7p per share to be paid on 27 August2004 to shareholders on the register on30 July 2004 making a total dividend of7.4p per share for the year. The increaseof 23% is consistent with our progressiveapproach to the dividend and our confidencein the cash generative nature of the business.

To improve further the marketability andliquidity in ICAP’s shares, on 9 February2004 we implemented a split of theCompany’s ordinary shares of 50p into five new ordinary shares of 10p each. The daily average volume of sharestraded in the first three months followingthe share split increased from the equivalentof 2.7 million (0.52% of issued sharecapital) in 2003 to 4.7 million (0.82% of issued share capital) in 2004.

Issues of corporate governance commanda significant profile in the management of public companies and we respect thedemand for high standards of governance.We comply fully with the provisions of theCombined Code for the year ended 31 March2004 and believe that we are alreadysubstantially compliant with the newCombined Code that will apply to theGroup for the year ending 31 March 2005.

Chairman’s Statement The Group’s profit before tax, goodwill amortisation and exceptional itemswas £170.2 million for the year to 31 March 2004 compared with £123.7 million for the previous year.Shareholders’ funds at 31 March 2004 were £468.2 million, up £215.6 million. Profit before tax ona statutory basis was £130.5 million, up £13.0 million.

ICAP plc Annual Report 200406

DIVIDEND 2004 pence 7.4

6.0

Two of our non-executive directors, Bob Knoxand Don Marshall, retired from the boardduring the year. I would like to thank themboth for their considerable contributions toICAP during a period when the businesshas grown significantly. Two non-executivedirectors have joined the board, DuncanGoldie-Morrison and Jim McNulty. Theybring broad experience of the globalfinancial markets including management,technology and risk managementtogether with exchange and OTC trading. I am sure that the combination of theirexpertise will be extremely valuable to the Group.

ICAP’s annual Charity Day, held in December,is a very special day for the charities thatbenefit from the proceeds of one day’sbroking revenue. In 2003 an astonishing£4 million was raised. Over the past 11 years,ICAP staff and customers have raisedmore than £17 million. During this timewe have been able to help many peoplearound the world and none of this couldhave been achieved without the generosityand enthusiasm of ICAP’s staff and customers.Once again I would like to thank them all - every deal really counted!

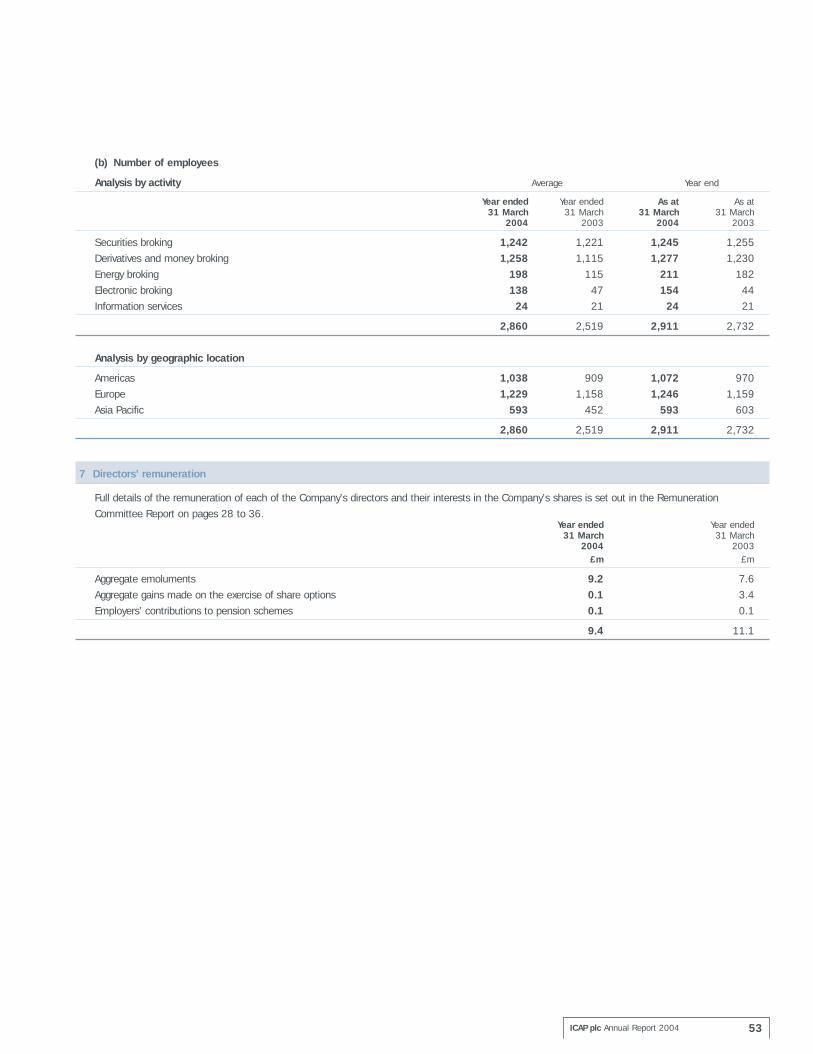

Staff numbers have increased during theyear from 2,700 to 2,900, largely as aresult of the acquisition of the BrokerTecbusiness. Although competition for qualitystaff remains high, we have continued tostrengthen our business through selectiverecruitment. I would like to take theopportunity to thank all our staff for thetremendous effort that they have madethis year.

We have a proven business model that isbased on a successful combination of ourstaff and our technologies. Our strategy isclear and our implementation has beenextremely effective, including theintegration of BrokerTec. As a result weare in a strong position to benefit fromthe continuing development of ourmarkets.

Charles GregsonChairman

ICAP plc Annual Report 2004

CHARLES GREGSON

07

YEAR TO 31 MARCH 2004

YEAR TO 31 MARCH 2003

Without doubt the most significant event for the Group this past year was thecompletion in May 2003 of the purchaseof BrokerTec. This landmark event, afternearly two years of negotiations with theowners, has transformed ICAP overnightfrom a modest operator in electronic brokingof fixed income securities into the clearglobal leader.

Our timing could not have been morepropitious as the pace of electronicbroking has accelerated even further sincethen and we now transact over $300 billionper day (yes, per day) on the BrokerTecplatform. This is some 60% higher thanBrokerTec was transacting only a year agoand the ongoing rapid adoption of electronicbroking in the fixed income universe suggeststo me that these high growth rates aresustainable. BrokerTec has performed aheadof our best expectations.

It is no exaggeration to observe that ICAPis now not only the clear global leader inwholesale voice broking, as we have beenfor many years, but also the leader inelectronic broking. This is a unique criticalcombination as our three largest voicecompetitors have no effective electronicbroking capability and our electroniccompetitors have little or no voice capability.

Our strategy going forward remains thesame as we have espoused for severalyears – with the important exception thatwe now have a powerful electronic armwhich perfectly complements our longestablished market leading voice business.

We intend to expand further our share ofthe electronic and voice markets by acombination of acquisition and organicgrowth. We anticipate that the electronicdivision is likely to grow more rapidly thanthe voice divisions in volume and profitterms as more products are tradedelectronically and we benefit from themajor operating leverage of electronicbroking. We believe that by pursuing thisstrategy it is possible to increase ourglobal market share of industry revenuesfrom a current estimated 27%. Our marginsover time will also improve from theeconomies of scale generated by ourelectronic capabilities.

Industry volumes have been robust duringmost of the financial year with derivativesand fixed income volumes both postingsharp increases. The threat of deflationthat had been of some concern to us ayear ago, threatening to lead to low andstable interest rates, has now completelyreceded. With increasing G7 deficits and

Group Chief Executive Officer’s Review This has been another year of considerable progressat ICAP. We have again outpaced our competitors and significantly increased our share of theinterdealer broking market, our turnover and profit. This has been reflected in the rise of the ICAPshare price during the year by 49% and a cumulative appreciation, since the September 1999creation of ICAP, of 444%.

ICAP plc Annual Report 200408

MARKET SHARE 2003 %

MARKET SHARE 2004 % 27.2

24.2

higher economic growth, I remain optimisticthat we have another year of reasonablevolatility and rising volumes ahead of us.The rapidly expanding hedge fund industryhas also contributed significantly to increasedderivative and fixed income trading. ICAPis very well positioned to capture morethan our previous share of this business.

We are also embarking upon building a global futures broking business. We havesmall existing futures activities in somecentres but we now intend to build aglobal capability, focusing particularly onNorth America and Europe. The overlap interms of clients and products as well asconvergence between OTC products andfutures exchanges drives us inexorably inthis direction. Within a few years I expectthat futures will make a material contributionto our overall profit.

Further strategic and structural changesare in our opinion likely to take place in ourindustry within the next year or so. Ourmanagement team is well prepared andwe will take advantage of the opportunitiesthat will add shareholder value.

I have been fortunate for many years to work with an exceptional and committedmanagement team: broadly the samegroup has led ICAP since the 1999

merger. I am delighted, however, this yearthat our management resources havebeen strengthened by the appointmentof Jay Spencer as Global Chief InformationOfficer, Humphrey Percy as global head offutures and Garry Jones and David Rutteras heads of electronic broking in Europeand North America respectively.

OutlookThere was an upturn in market sentiment inApril regarding the US economic outlookand the prospect for further policy tightening,which has lifted the US yield curve andthe euro curve has followed in its wake.The likelihood of a further global economicupswing is improving and this is expectedto apply continued upward pressure onchanges in interest rate expectations. As aresult we anticipate that industry activitylevels will continue to grow steadily andICAP will continue to benefit from its strongposition in and broad coverage of thewholesale markets in fixed income securitiesand derivatives.

2003/2004 was a good year for ICAP; welook forward to another successful year.

Michael SpencerGroup Chief Executive Officer

ICAP Executive Team

Group Chief Operating OfficerDavid Gelber

Group Finance DirectorJim Pettigrew

Chief Operating Officer – AmericasSteve McDermott

AmericasRon Purpora and Doug Rhoten

Europe & AfricaGeorge MacDonald, David Casterton, Paul McMenemy and Gary Smith

Asia PacificBryan Massey and Mark Webster

Electronic BrokingGarry Jones and David Rutter

FuturesHumphrey Percy

Global Chief Information OfficerJay Spencer

Information ServicesJohn Nixon

ICAP plc Annual Report 2004 09

YEAR TO 31 MARCH 2004

YEAR TO 31 MARCH 2003

MICHAEL SPENCER

ICAP plc Annual Report 200410

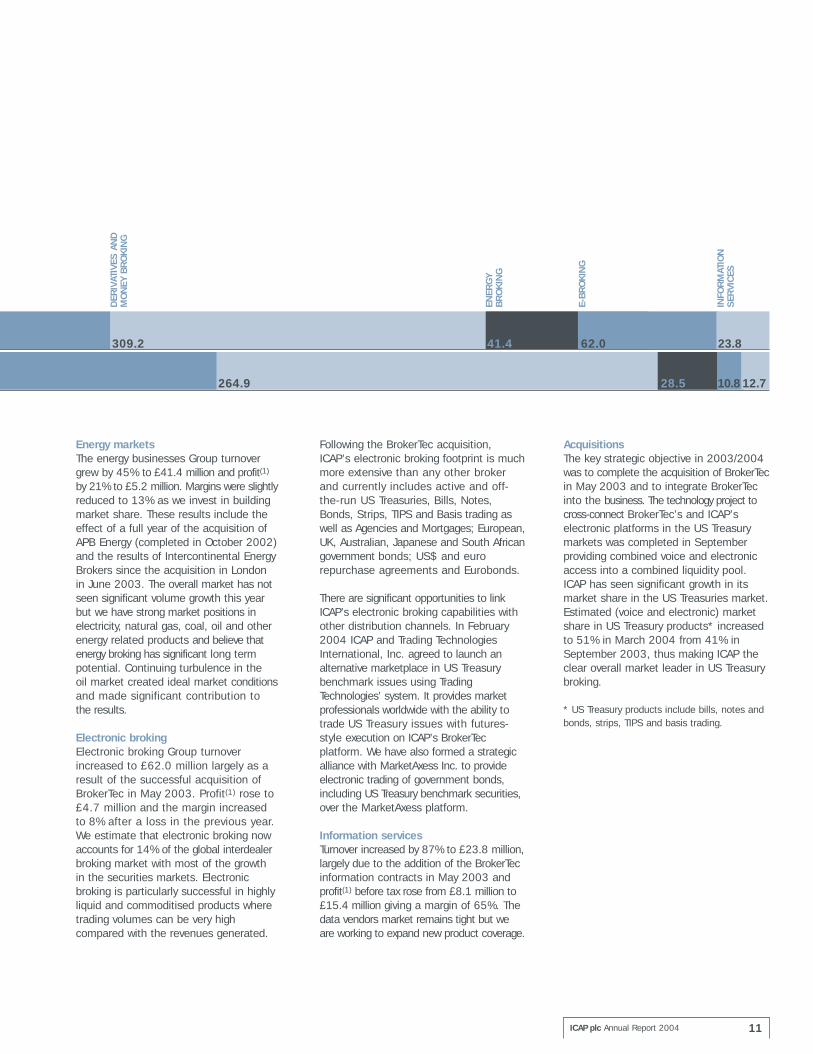

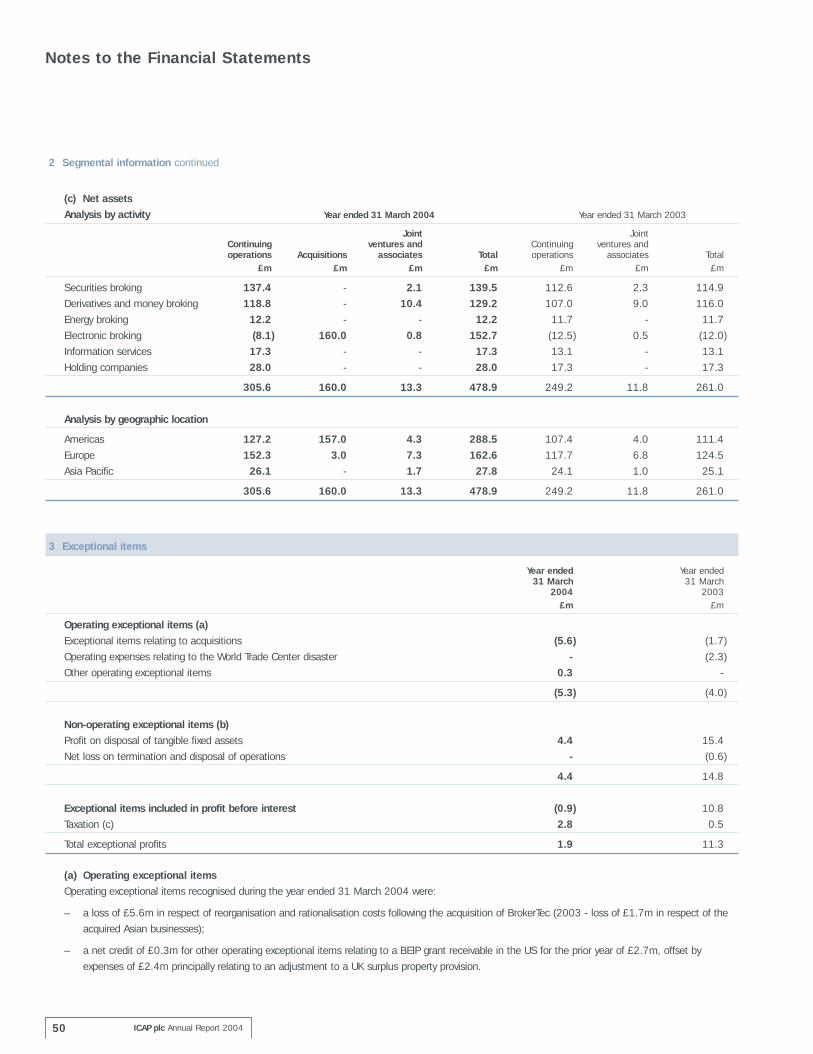

Securities marketsGroup turnover in the securities marketsgrew by 5% to £365.0 million and profit(1)

by 17% to £66.5 million with an improvedmargin of 18%. The securities marketshave had mixed results; US Treasuries andMortgages, UK Gilts, Eurobonds andJapanese Government Bonds have allbeen active as a result of higher levels ofnew issuance for government deficitfinancing or movements in the mediumand longer end of the yield curve. Creditderivatives in London, New York and HongKong have been very busy. In theAmericas and Europe the low interest rateenvironment boosted the volumes ofRepurchase Agreements as customerswere reluctant to undertake longer termtrades. BrokerTec, which operates mainlyin the shorter dated Repurchase Agreementmarkets, benefited with an increase involumes. US agencies saw slower markets.Overall corporate bond markets were slowerthan the very busy markets in the previousyear. However volatility returned to thesemarkets in the second half.

Derivatives and money markets Derivatives and money market Groupturnover grew by 17% to £309.2 million andprofit(1) by 31% to £68.5 million, with animproved margin of 22%. There wasreasonable volatility in the medium terminterest rate markets in 2003 and ourinterest rate swaps and options deskshave been very busy. The Americas andEurope are by far the largest markets andthe most significant contributors to profits.Inflation swaps have continued their rapidexpansion in Europe. ICAP’s significantlyincreased market share in US TIPS hasadded the potential to expand the inflationswaps market. Having got off to a slowstart at the beginning of 2004, activity inthe interest rate swaps market picked upsignificantly as a run of economic dataannouncements from the US caused hugeswings in market sentiment regarding theoutlook for the US economy. This, in turn,has exerted a strong influence on mediumand long term interest rates.

Operating Review A particularly buoyant first half of the year was followed by lower levels of activity in quarter three and a generally more active quarter four. ICAP’s Group turnover rose by 21% to £801.4 million for the year to 31 March 2004. Excluding the impact of acquisitions and foreignexchange movements, turnover growth was 12% compared with a 7% growth in the globalinterdealer broker market.

Note1 Profit is defined as pre-tax operating profit before goodwill amortisation, exceptional items, interest and share

of operating profit of joint ventures and associates. We continue to believe that this measure better reflects theGroup’s performance and it is reconciled to statutory profit before interest and tax in the segmental analysis shown in note 2 to the Financial Statements.

GROUP TURNOVER BY ACTIVITY 2003 £m

GROUP TURNOVER BY ACTIVITY 2004 £m 365.0

SEC

UR

ITIE

S

BR

OK

ING

347.4

ICAP plc Annual Report 2004 11

Energy markets The energy businesses Group turnovergrew by 45% to £41.4 million and profit(1)

by 21% to £5.2 million. Margins were slightlyreduced to 13% as we invest in buildingmarket share. These results include theeffect of a full year of the acquisition ofAPB Energy (completed in October 2002)and the results of Intercontinental EnergyBrokers since the acquisition in London in June 2003. The overall market has notseen significant volume growth this yearbut we have strong market positions inelectricity, natural gas, coal, oil and otherenergy related products and believe thatenergy broking has significant long termpotential. Continuing turbulence in the oil market created ideal market conditionsand made significant contribution to the results.

Electronic broking Electronic broking Group turnoverincreased to £62.0 million largely as aresult of the successful acquisition ofBrokerTec in May 2003. Profit(1) rose to£4.7 million and the margin increased to 8% after a loss in the previous year.We estimate that electronic broking nowaccounts for 14% of the global interdealerbroking market with most of the growth in the securities markets. Electronicbroking is particularly successful in highlyliquid and commoditised products wheretrading volumes can be very highcompared with the revenues generated.

Following the BrokerTec acquisition,ICAP’s electronic broking footprint is muchmore extensive than any other brokerand currently includes active and off-the-run US Treasuries, Bills, Notes,Bonds, Strips, TIPS and Basis trading aswell as Agencies and Mortgages; European,UK, Australian, Japanese and South Africangovernment bonds; US$ and eurorepurchase agreements and Eurobonds.

There are significant opportunities to linkICAP’s electronic broking capabilities withother distribution channels. In February2004 ICAP and Trading TechnologiesInternational, Inc. agreed to launch analternative marketplace in US Treasurybenchmark issues using TradingTechnologies’ system. It provides marketprofessionals worldwide with the ability totrade US Treasury issues with futures-style execution on ICAP’s BrokerTecplatform. We have also formed a strategicalliance with MarketAxess Inc. to provideelectronic trading of government bonds,including US Treasury benchmark securities,over the MarketAxess platform.

Information services Turnover increased by 87% to £23.8 million,largely due to the addition of the BrokerTecinformation contracts in May 2003 andprofit(1) before tax rose from £8.1 million to£15.4 million giving a margin of 65%. Thedata vendors market remains tight but weare working to expand new product coverage.

Acquisitions The key strategic objective in 2003/2004was to complete the acquisition of BrokerTecin May 2003 and to integrate BrokerTecinto the business. The technology project tocross-connect BrokerTec’s and ICAP’selectronic platforms in the US Treasurymarkets was completed in Septemberproviding combined voice and electronicaccess into a combined liquidity pool.ICAP has seen significant growth in itsmarket share in the US Treasuries market.Estimated (voice and electronic) marketshare in US Treasury products* increasedto 51% in March 2004 from 41% inSeptember 2003, thus making ICAP theclear overall market leader in US Treasurybroking.

* US Treasury products include bills, notes andbonds, strips, TIPS and basis trading.

ENER

GY

BR

OK

ING

E-B

RO

KIN

G

INFO

RM

ATIO

N

SER

VIC

ES

309.2

DER

IVAT

IVES

AN

D

MO

NEY

BR

OK

ING

264.9 28.5

62.041.4 23.8

10.812.7

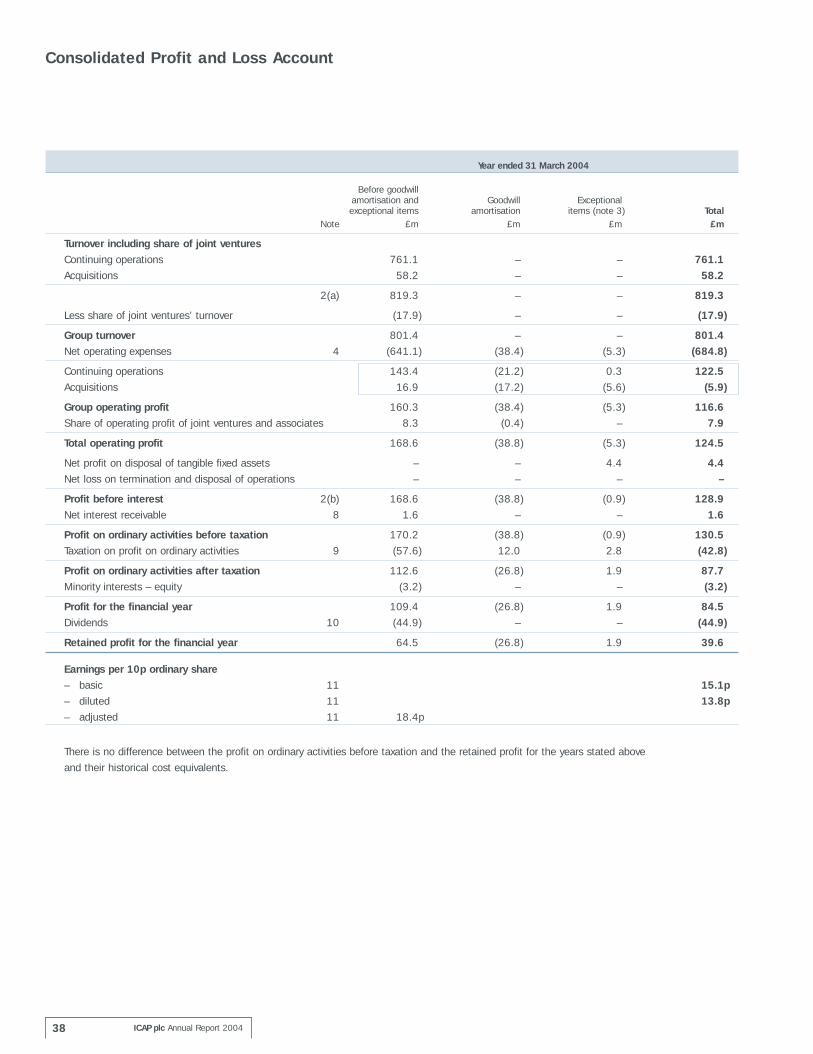

ResultsThe Group reported profit of £170.2 millionbefore taxation, goodwill amortisation andexceptional items; this represents a 38%increase over the prior year. On a statutorybasis profit on ordinary activities beforetaxation was £130.5 million (2003 -£117.5 million). We continue to believethat profit before tax, goodwill amortisationand exceptional items better reflects theGroup’s performance. This measure isreconciled to profit before tax on the face of the profit and loss account.

Group turnover grew by 21%, with anumber of the Group’s broking operationsincreasing their market share and themajority continuing to benefit fromuncertain and volatile financial markets.The acquisition of BrokerTec on 7 May2003 also had a positive effect onturnover. Excluding contributions fromacquisitions and foreign exchangemovements, turnover growth was 12%.

Cost managementCosts continue to be tightly controlled.Although they increased, in headlineterms, over the prior year by £90.3 million(16%), costs before goodwill amortisationand exceptional items increased by only£11.3 million (3%) if the impact ofacquisitions, currency movements andhigher revenue and profit-linked bonusesare excluded.

Broker employment costs, the largestcomponent of the Group’s cost base, were51% of Group turnover in the financial yearto 31 March 2004. This represents areduction from 54% in the previous period

and continues to demonstrate the Group’sdetermination to maintain control over brokerremuneration. The variable component ofbroker remuneration cost, which is linked torevenue and profit growth, has nowincreased to 56% of total broker employmentcosts, and this compares with 54% in theprior year. A further element of the Group’scost base, estimated to be some 10% ofGroup turnover, is also of a variable nature.In total cost terms, under the presentbusiness model, it is estimated that justunder 40% of the Group’s costs are variable.However, the increase in contribution fromelectronic broking is starting to, and willcontinue to, change the Group’s cost baseand profit margin profile. The Group’selectronic business has a lower overall costbase and a higher fixed cost component thanthe traditional voice broking business. Withthe relatively low incremental cost oftransacting business on the Group’selectronic platform, advantage can be takenof operational leverage by increasing volumestraded on the Group’s electronic platform. Ifthis can be achieved, it provides the Groupwith an opportunity to deliver further profitgrowth and margin improvement.

Effective cost management continues to be a major priority.

Operating marginsThe strong revenue performance, combinedwith prudent cost management, has enabledthe Group to increase its operating margin to20% in the financial year ended 31 March2004 (17% in the prior year). This is thefourth year in succession that this marginhas increased.

Group Finance Director’s Review Delivery on strategic objectives has enabled the Group to reportanother strong financial performance in the year ended 31 March 2004. This is the fourth year insuccession that turnover, profit, EPS (on an adjusted basis) and dividend per share have increasedsubstantially. Costs continue to be effectively controlled and margins have risen to 20%. The Group remains highly cash generative.

ICAP plc Annual Report 200412

ICAP plc Annual Report 2004 13

The Group continues to focus on operatingprofit margin enhancement through acombination of growth in market share andthe application of strict cost controls.

This year in our segmental disclosures we have shown profit before and aftergoodwill amortisation. The operating profitmargins summarised in the table below,by business segment and geographiclocation, are based on profit beforeinterest, share of profit of joint venturesand associates, exceptional items andgoodwill amortisation.

Year-on-year margin improvement has beenachieved in most segments. The modestmargin reduction in energy broking reflectsthe difficulties in the energy sector in thepost Enron environment. In addition, theGroup’s conscious decision to grow itsenergy business organically as well as by

acquisition resulted in a number of costsbeing incurred in the current financial yearwhich should place the business in astronger position for the future. There havebeen demonstrable signs of an upturn inbusiness activity levels in the Group’senergy division in recent months.

A particularly encouraging element of thisyear is the electronic broking segment’sperformance following the BrokerTec acquisition.In the post acquisition period (7 May 2003- 31 March 2004) BrokerTec (excluding theGroup’s other electronic broking operationsbut including the related informationservices income) reported an operatingmargin of 29%. The overall electronicbroking margin performance (8%) wasachieved against a background of theintegration of its operations with the Group’sexisting ETC business. In the year to 31 March 2004 we more than exceeded

our cost savings target of £2.2 million.Once this integration process is completedit should deliver further savings to theexisting cost base.

AcquisitionsThe major acquisition in the financial yearwas BrokerTec which has been consolidatedinto the Group’s Financial Statements since7 May 2003. As discussed in the GroupChief Executive Officer’s Review thisacquisition has transformed the Group’selectronic broking capabilities. In last year’sGroup Finance Director’s Review thefinancial profile of the transaction wasdiscussed. More detail is provided in note15 to the Financial Statements, includingthe calculation of the goodwill arising onan acquisition (£189.3 million). Goodwill isbeing amortised over a 10-year period foraccounting purposes.

During the financial year the Group alsocompleted the acquisition of IntercontinentalEnergy Brokers, a London-based energybusiness, for £4.9 million in cash. TheGroup continues to seek to expand itsenergy business organically and throughappropriate acquisition opportunities.

Exceptional itemsNet exceptional costs before tax of £0.9 million were incurred in the financialyear to 31 March 2004.

Year ended Year ended Operating margins 31 March 2004 31 March 2003

ActivitySecurities broking 18% 16%Derivatives and money broking 22% 20%Energy broking 13% 15%Electronic broking 8% (75%)Information services 65% 64%

Geographic locationAmericas 19% 14%Europe 24% 22%Asia Pacific 9% 8%

JIM PETTIGREW

Group Finance Director’s Review continued

ICAP plc Annual Report 200414

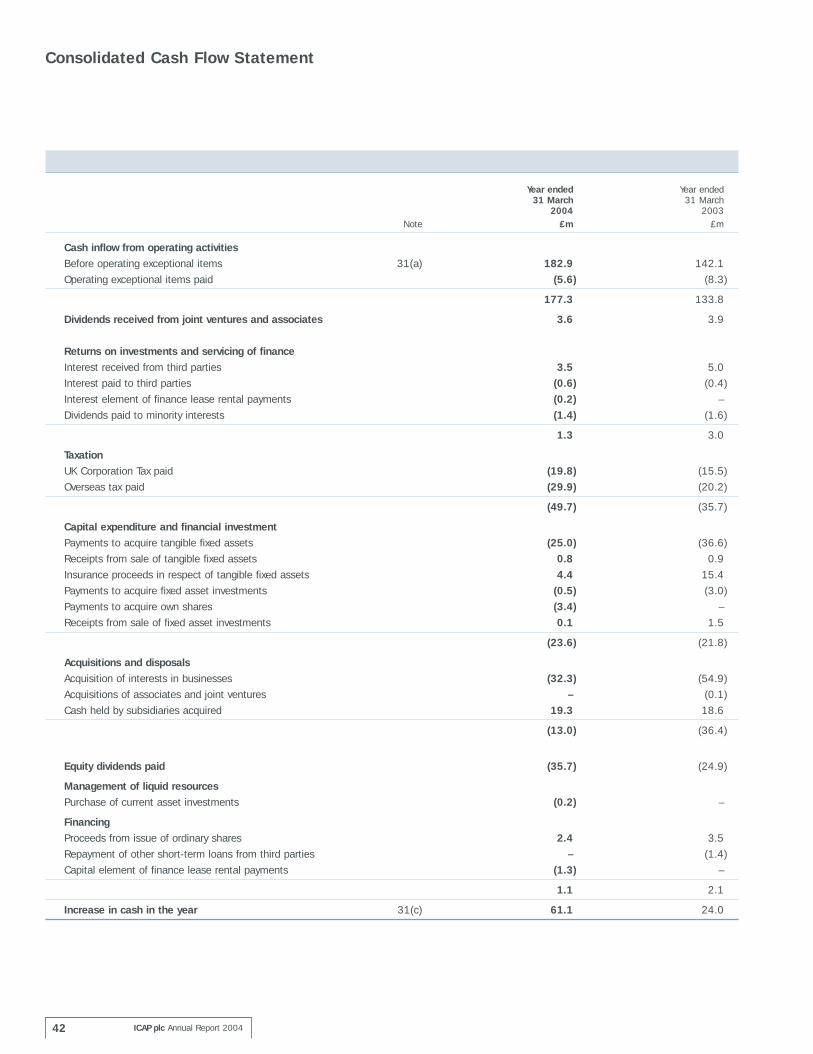

Cash flowThe effective management of cash resourcesremains a key management objective.Regular reviews of cash retained in operatingsubsidiaries are undertaken and whereappropriate surplus cash is repatriated tothe centre. Capital expenditure is rigorouslycontrolled and monitored by the Group’scapital expenditure committee and alsothrough the annual budgeting and quarterlyforecasting cycles. All acquisition opportunitiesare the subject of detailed due diligenceand financial evaluation, including the useof discounted cash flow and return oninvestment criteria.

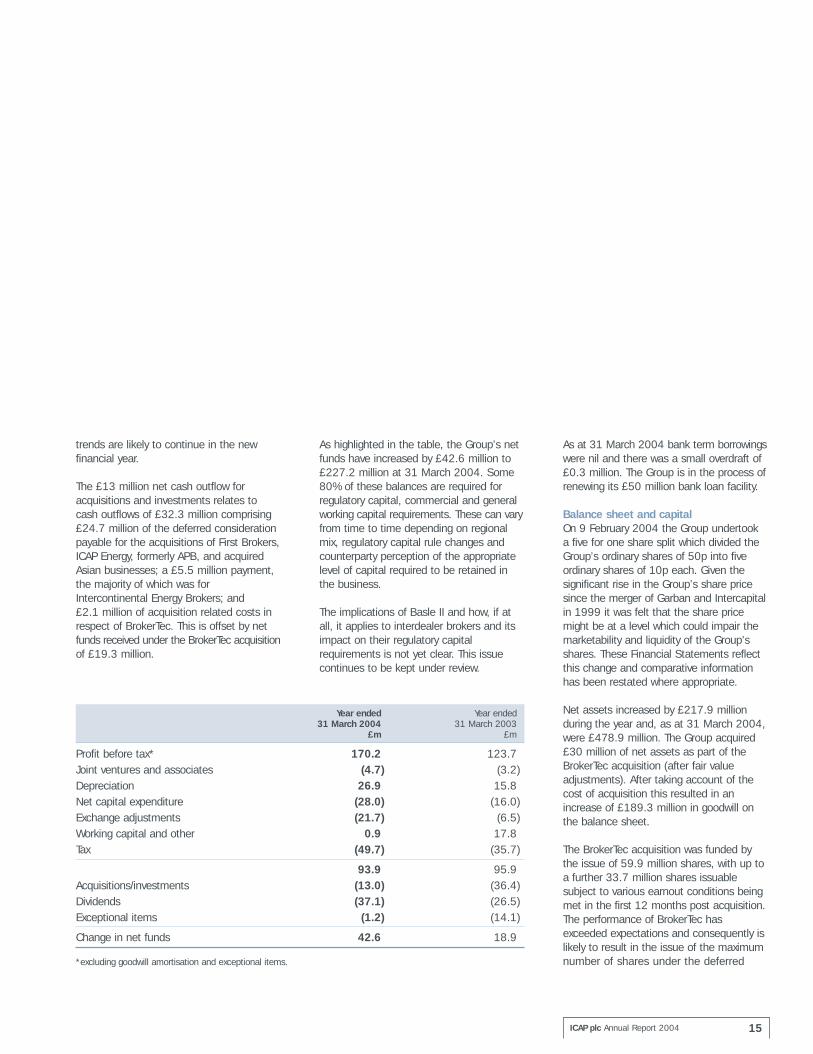

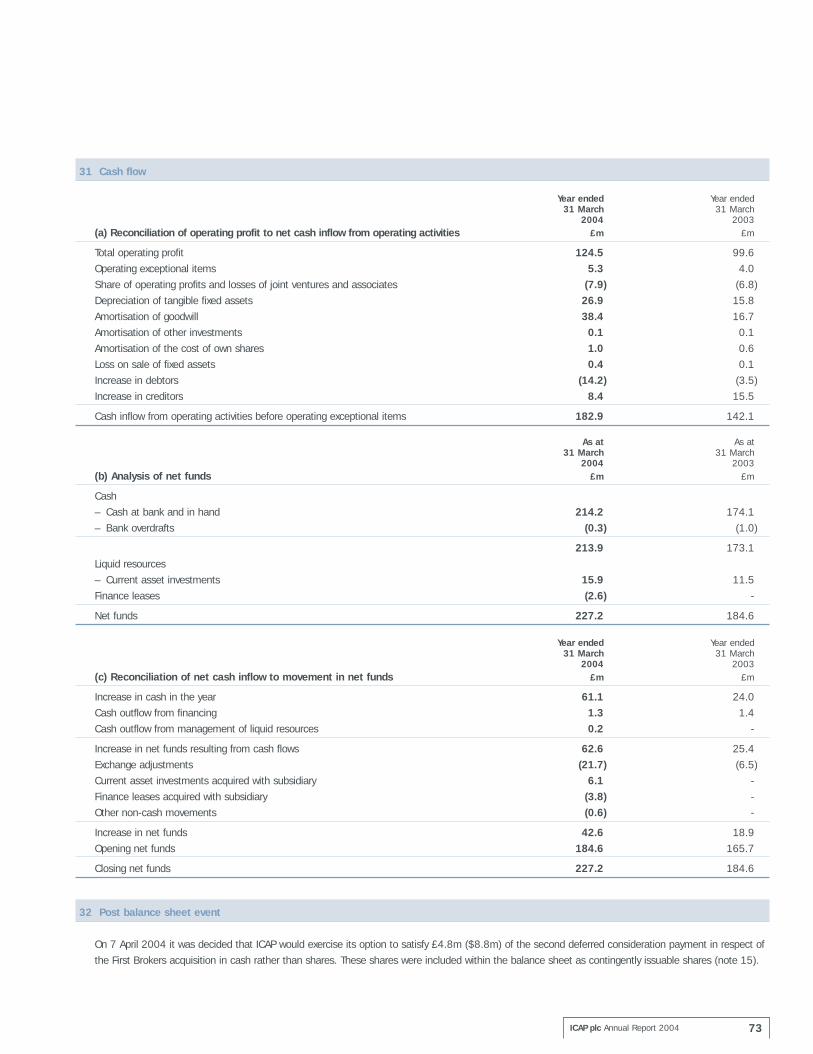

The Group’s FRS1 cash flow is set out onpage 42 of the Financial Statements.Consistent with previous years, cash flow is best understood by reference to themovement in net funds (defined as cash,current asset investments less overdraftsand borrowings).

On this basis, net funds, as defined in note31 (c) to the Financial Statements,increased during the year by £42.6 millionto £227.2 million (2003 - £184.6 million).

The movement in the net funds position issummarised in the table opposite. Thistable demonstrates the continuing cashgenerative nature of the business.

Net capital expenditure was slightly higherthan depreciation reflecting the increase inexpenditure as a result of the move, in theUK, to Broadgate and investment inBrokerTec’s system development. These

The Group received its final insurancereimbursement of £4.4 million in respect of the World Trade Center disaster. A numberof BrokerTec integration costs have beenincurred, mainly provisions for surplusproperty in the US and London, andredundancy costs, amounting to £5.6 million.

In the financial year to 31 March 2005, itis anticipated that the Group will incur some£8 million exceptional costs in respect ofthe relocation of its UK operations to itsnew premises in Broadgate, London. Theremay also be some additional exceptional costsin respect of the BrokerTec integration.

TaxationThe effective tax rate, which excludes goodwillamortisation and exceptional items, hasbeen maintained at 34%. The Group’sbudget for the financial year to 31 March2005 anticipates a 35% effective tax rate.

The Group has recorded a £12 million taxdeduction in respect of goodwill amortisationin the US. This is represented by currenttax of £4 million and deferred tax of £8 million,reflecting the 15 year tax amortisationperiod compared to 10 years foraccounting purposes.

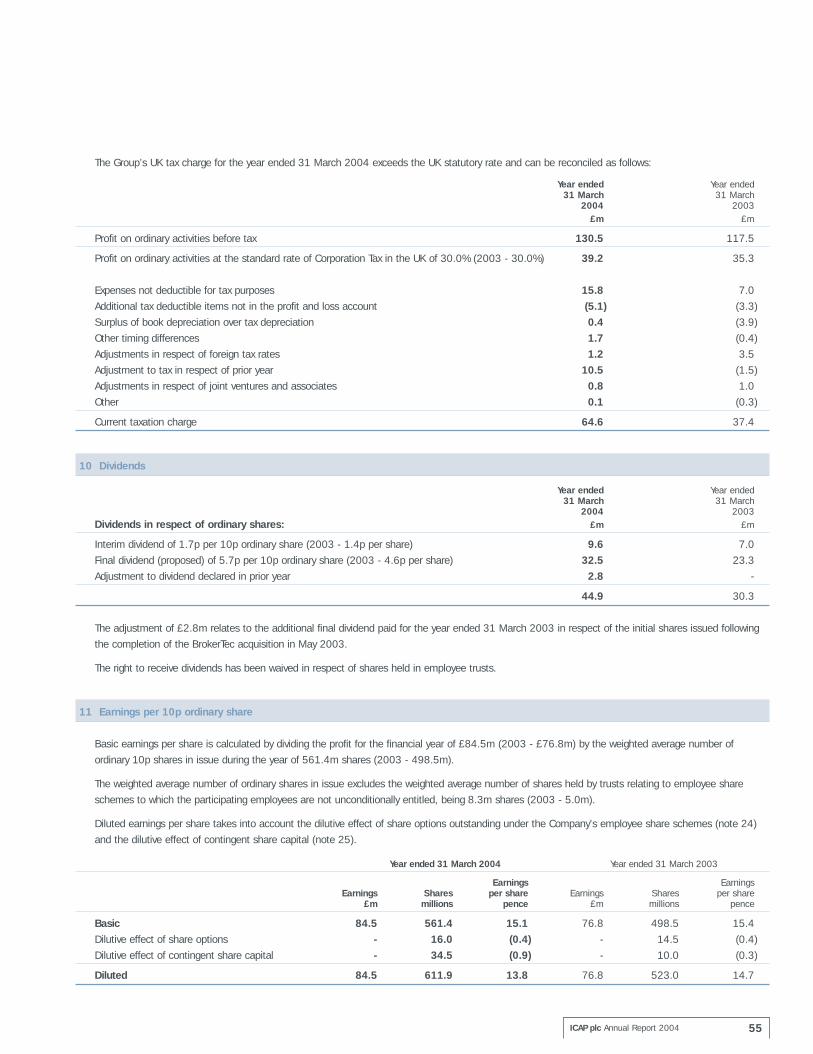

Earnings and earnings per share (EPS)All the Group’s EPS calculations are based onthe number of shares in issue following theGroup’s five for one share split in February 2004.

The 2% reduction in basic EPS reflectsthe net impact of the growth in pre-taxprofit, the increase in goodwillamortisation (mainly arising from theBrokerTec acquisition), and the fact thatthe year ended 31 March 2003 benefitedfrom a net exceptional credit item of£11.3 million.

We continue to believe that the mostappropriate EPS measurement ratio forthe Group is adjusted EPS, which betterreflects the business’s underlying cashearnings. Adjusted EPS excludes goodwillamortisation and exceptional items, butincludes share capital which is contingentlyissuable in respect of the First Brokers,APB and BrokerTec acquisitions.Calculation of EPS is set out in note 11 to the Financial Statements.

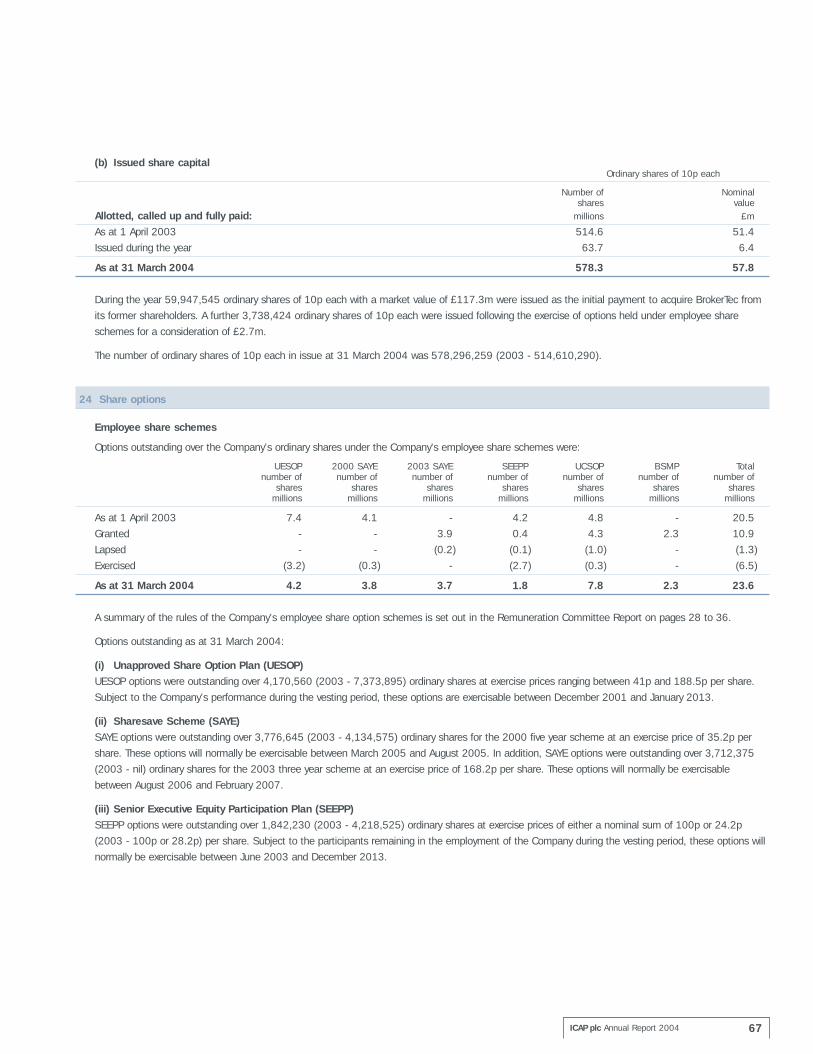

During the year 3.7 million of shares wereissued following the exercise of options heldunder employee share schemes.

Adjusted EPS increased by 19% to 18.4p.

DividendSubject to shareholder approval, a 5.7p finaldividend is proposed. This compares with4.6p in the prior year and would result in afull-year dividend of 7.4p, which representsa 23% increase on the prior year. This is thefourth consecutive year that we have beenable to increase the dividend and reflects thestrong earnings performance. The full-yeardividend remains more than twice coveredby the profit before tax, goodwillamortisation and exceptional items.

ICAP plc Annual Report 2004 15

trends are likely to continue in the newfinancial year.

The £13 million net cash outflow foracquisitions and investments relates tocash outflows of £32.3 million comprising£24.7 million of the deferred considerationpayable for the acquisitions of First Brokers,ICAP Energy, formerly APB, and acquiredAsian businesses; a £5.5 million payment,the majority of which was forIntercontinental Energy Brokers; and £2.1 million of acquisition related costs inrespect of BrokerTec. This is offset by netfunds received under the BrokerTec acquisitionof £19.3 million.

As highlighted in the table, the Group’s netfunds have increased by £42.6 million to£227.2 million at 31 March 2004. Some80% of these balances are required forregulatory capital, commercial and generalworking capital requirements. These can varyfrom time to time depending on regionalmix, regulatory capital rule changes andcounterparty perception of the appropriatelevel of capital required to be retained inthe business.

The implications of Basle II and how, if atall, it applies to interdealer brokers and itsimpact on their regulatory capitalrequirements is not yet clear. This issuecontinues to be kept under review.

Year ended Year ended 31 March 2004 31 March 2003

£m £m

Profit before tax* 170.2 123.7Joint ventures and associates (4.7) (3.2)Depreciation 26.9 15.8Net capital expenditure (28.0) (16.0)Exchange adjustments (21.7) (6.5)Working capital and other 0.9 17.8Tax (49.7) (35.7)

93.9 95.9Acquisitions/investments (13.0) (36.4)Dividends (37.1) (26.5)Exceptional items (1.2) (14.1)

Change in net funds 42.6 18.9

*excluding goodwill amortisation and exceptional items.

As at 31 March 2004 bank term borrowingswere nil and there was a small overdraft of£0.3 million. The Group is in the process ofrenewing its £50 million bank loan facility.

Balance sheet and capitalOn 9 February 2004 the Group undertook a five for one share split which divided theGroup’s ordinary shares of 50p into fiveordinary shares of 10p each. Given thesignificant rise in the Group’s share pricesince the merger of Garban and Intercapitalin 1999 it was felt that the share pricemight be at a level which could impair themarketability and liquidity of the Group’sshares. These Financial Statements reflectthis change and comparative informationhas been restated where appropriate.

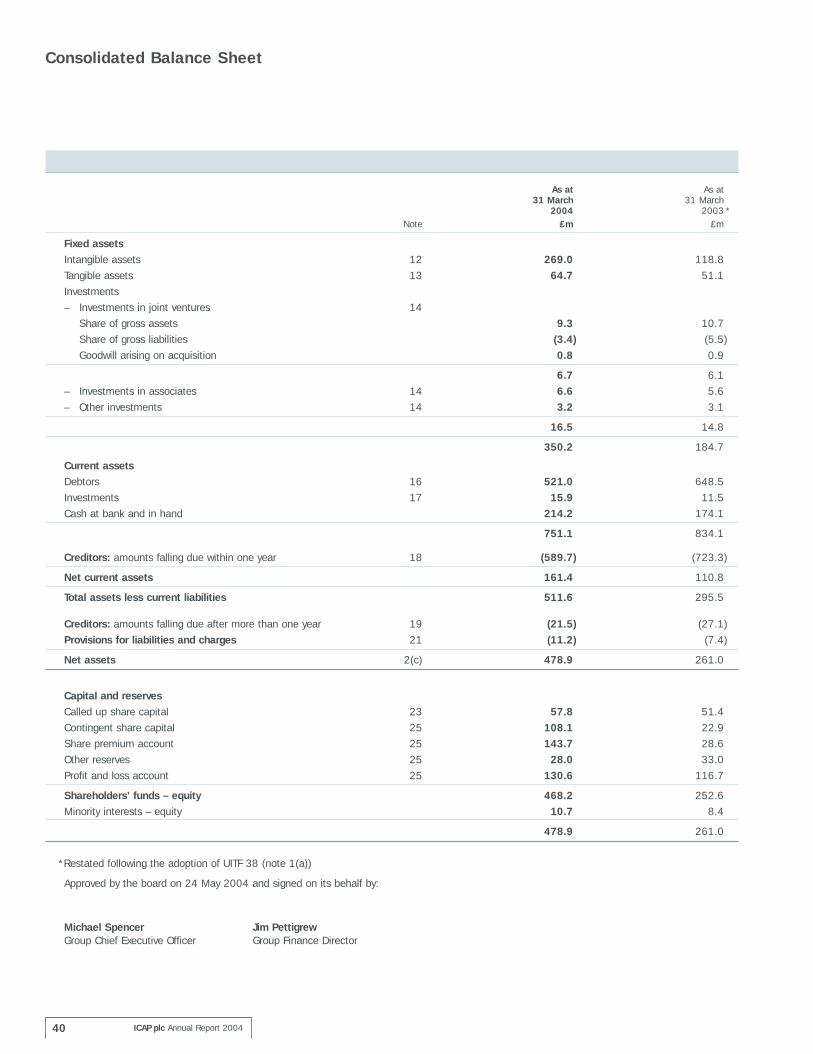

Net assets increased by £217.9 millionduring the year and, as at 31 March 2004,were £478.9 million. The Group acquired£30 million of net assets as part of theBrokerTec acquisition (after fair valueadjustments). After taking account of thecost of acquisition this resulted in anincrease of £189.3 million in goodwill onthe balance sheet.

The BrokerTec acquisition was funded bythe issue of 59.9 million shares, with up toa further 33.7 million shares issuablesubject to various earnout conditions beingmet in the first 12 months post acquisition.The performance of BrokerTec hasexceeded expectations and consequently islikely to result in the issue of the maximumnumber of shares under the deferred

gains arising from the Group’s transactionalhedging programme which is in place tomanage its UK business’s transactionalexposure to the US dollar. It has alsobeen offset by a £6 million positiveimpact on pre-tax profit as the euro hasappreciated against sterling and this hashad a beneficial impact on the Group’sUK business’s transactional euro exposure.

The Group’s overall pre-tax profit (pre-hedging) sensitivities to movements inexchange rates in respect of itstransactional and translational exposuresare as follows; a 10 cent movement inthe US dollar equates to £7 million; a10 cent movement in the euro equatesto £4 million.

The Group policy, determined by the TreasuryCommittee, is to hedge its transactional foreignexchange exposures by the use of foreignexchange contracts and options. The Group’smajor transactional exposures are to USdollar and euro inflows into the UK. A 10cent movement in the US dollar beforehedging, at current exposure levels andexchange rates, has a £2.5 million impacton pre-tax profit. A 10 cent movement inthe euro before hedging has a £4 millionimpact. As at the date of this report theGroup has 100% of its US dollar exposurefor the year to 31 March 2005 hedged at$1.72 (worse case basis) and for the yearto 31 March 2006, 4% is hedged at$1.74. As at the date of this report theGroup had 61% of its euro exposure forthe year to 31 March 2005 hedged at a

Group Finance Director’s Review continued

ICAP plc Annual Report 200416

consideration provisions of the acquisitionagreement. In accordance with accountingstandards, the 33.7 million of earnoutshares are included as contingent sharecapital in the Group’s balance sheet as at31 March 2004.

The increase in share capital and sharepremium during the year is principallybecause of the shares issued as the initialconsideration under the BrokerTecacquisition.

Deferred consideration is also payable in respect of the First Brokers and APBacquisitions and is dependent on theirfuture performance. At the Company’soption part of this consideration may bepaid by way of issue of shares and this is reflected in the balance sheet ascontingent share capital. The Group haselected, where it has the option to pay ineither shares or cash, to pay the first andsecond instalments of consideration due inconnection with both of these acquisitionsin cash. The cash element of the secondinstalments is included within creditorsunder one year, the first instalment havingbeen paid in cash during the financial yearto 31 March 2004.

Risk managementThe identification, control and monitoringof risks facing the business remain amanagement priority and steps continueto be taken to further improve our riskmanagement procedures. The risks monitoredinclude credit, market, treasury,

operational and reputational risk. Detailsof our approach to risk management areprovided in the Corporate Governancestatement on pages 23 to 27.

Foreign exchange The Group conducts business in manycurrencies. As a result, it is subject toforeign currency exchange risk due to theeffects that exchange rate movementshave on the translation of the results andunderlying net assets of its foreign subsidiaries.The Group also has transactional foreignexchange exposures in its UK businesswhich has underlying US dollar and eurorevenue streams.

Currency movements had a net £4 millionadverse impact on the Group’s pre-taxprofit in the financial year to 31 March 2004when compared with the prior financial year.During the financial year, the US dollardepreciated significantly in value againststerling. With the Group’s substantial USoperations, in terms of both profit and netassets, this has had a number oframifications for the financial year ended31 March 2004. The average USdollar/sterling rate in the financial yearwas $1.70 compared with $1.54 in theprevious financial year and this hasresulted in a £12 million adverse impacton pre-tax profit. (The translation of theGroup’s US dollar profits in sterling had an£8 million impact and the transactionalexposure to the US dollar in the UKbusiness had a £4 million impact.) This hasbeen mitigated by £2 million of hedging

ICAP plc Annual Report 2004 17

blended euro rate of €1.45. There is noeuro cover in place for the financial yearto 31 March 2006.

The Group does not hedge its translationalprofit and loss foreign exchange exposures.The impact of foreign exchange movementson the translation of the Group’s overseassubsidiaries’ profits into sterling is mitigatedby the Group’s policy of translating overseasprofits at average exchange rates. Whereappropriate, structural hedges via inter-company debt are put in place to furthermitigate translational foreign exchangeexposures. The only major translationalforeign exchange exposure is to the US dollar,where a 10 cent movement would have a£4.5 million impact on pre-tax profit.

The Group’s only significant balance sheettranslational foreign exchange exposure is tothe US dollar. This exposure, after structuralhedging, is some $270 millionrepresented by US dollar net assetsexcluding goodwill. The Group has hedged37% of this exposure at $1.80 through toMarch 2005 using a cross currencyswap. The impact of exchange ratemovements on the translation of non-sterlingdenominated net assets into sterling foraccounting purposes is shown as a unrealisedexchange adjustment on net investments inoverseas undertakings in the consolidatedstatement of total recognised gains andlosses shown on page 41 of the FinancialStatements. Mainly as a consequence ofthe decline in the US dollar against sterling

from $1.58 at 31 March 2003 to $1.84at 31 March 2004, there is a £27.5 millionexchange adjustment taken to reserves.

Credit and interest rate riskWe continue to ensure that strict investmentcriteria apply to the management of theGroup’s cash balances. Investments mustbe AA rated or better and for a duration ofno longer than two years. Limits are alsoin place to restrict the amount of fundsthat can be invested in any one institution.Compliance with policy and criteria issubject to regular review by the TreasuryCommittee. The overall Group philosophyis one of capital preservation, liquiditymanagement and then yield enhancement.

The Group has an exposure to interest ratemovements in a number of geographicregions. The main exposures are to USinterest rates where a 1% movement ininterest rates has a £0.6 million sensitivity tothe Group’s pre-tax profit and loss accountand to UK interest rates, where a 1%movement impacts profits by £0.4 million.The Group has hedged the following variableinterest rate exposures: UK 10% is fixed,US 35% is fixed.

International Financial ReportingStandardsUnder the current proposed timetable we willbe required to adopt International FinancialReporting Standards in the preparation ofour Financial Statements for the year ending31 March 2006. The international standard

setter, the International Accounting StandardsBoard (IASB), has undertaken an extensiveexercise to develop new standards andimprove existing ones.

The Group recognises the significantcomplexities which such a conversioninvolves and is working to ensure a timelyand efficient transition. A Group-wide projectwith the objective of ensuring compliancewith International Financial ReportingStandards is well advanced but the impacton the Group cannot be definitivelyquantified at this juncture. We believe,however, that the major areas of impact forthe Group will include goodwill amortisationand share based payments.

The new financial yearThe financial priorities for the new financialyear are to increase profit through acombination of growth in market shareand continuing effective costmanagement. A key factor in achievingthese objectives will be our ability to takeadvantage of operational leverage throughincreased trading volumes on the Group’selectronic trading platforms.

Jim PettigrewGroup Finance Director

Charles Gregson was appointed non-executive Chairman on 1 August 2001having been executive Chairman since 6 August 1998. Between 1978 and 1998,he was responsible for the Garban businessesthat demerged from United and later mergedwith Intercapital. He is also an executivedirector of United. In addition, he is non-executive Deputy Chairman of ProvidentFinancial plc. Aged 56. N

Michael Spencer is Group Chief ExecutiveOfficer. He was the founder of IPGL in 1986and became Chairman and Chief Executiveof Intercapital in October 1998, followingthe Exco/Intercapital merger. He wasappointed non-executive Chairman of NumisCorporation plc in April 2003. Aged 48. N

David Gelber was appointed Group ChiefOperating Officer on 9 September 1999,having been the Chief Operating Officer ofIntercapital, following the Exco/Intercapitalmerger. Prior to joining the Intercapitalcompanies, he held senior trading positionswith Citibank and Chemical Bank and wasChief Operating Officer for HSBC GlobalMarkets. He joined IPGL in 1994 as GroupManaging Director. In addition to his role asGroup Chief Operating Officer, he has managerialresponsibility for the Group’s operations inthe Asia Pacific region. Aged 56. GR, T

Nicholas Cosh, independent non-executivedirector, was appointed on 5 December2000. He is a director of Hornby plc,Bradford & Bingley plc and Computacenterplc. From 1991 to 1997 he was FinanceDirector of JIB Group plc and until 1991Finance Director of MAI plc. He is achartered accountant and is Chairman ofthe Audit Committee. Aged 57. A,N,R,GR

Duncan Goldie-Morrison, independentnon-executive director, was appointed on20 November 2003. He is senior managingdirector of Ritchie Capital Management, amulti-strategy hedge fund based in Geneva,Illinois. Between 1993 and 2003 he was

Managing Director, Head of Global MarketsGroup and Head of Asia at Bank of America.He was also a member of Bank of America’sManagement Operating Committee, theAsset and Liability Committee and theTrading Risk Committee. Aged 48. A,N,R

Stephen McDermott was appointed anexecutive director on 28 October 1998. He is Chief Operating Officer of the Americas.Prior to joining the Company, he managedthe forward foreign exchange business atTullett & Tokyo and joined the foreignexchange business of Garban in 1986. He was appointed a director of the USOperations in December 1995. He is also a board member of Columbia University’sdivision of special programs and services.Aged 47. GR

James McNulty, independent non-executivedirector, was appointed on 30 March 2004.He has 29 years’ experience in the GlobalFinancial Markets, including futures, securities,derivatives and foreign exchange. He wasPresident and Chief Executive Officer ofChicago Mercantile Exchange Holdings Incfrom its formation in August 2001 andChicago Mercantile Exchange Inc (CME)from February 2000 until 1 January 2004.Before joining the CME he was managingdirector and co-head of the CorporateAnalysis and Structuring Team in theCorporate Finance division of the investmentbanking firm now known as UBS Warburg.Aged 53. N,R,GR

William Nabarro, independent non-executivedirector, was appointed on 28 October1998 and is Chairman of the Nominationand Remuneration Committees. He wasVice Chairman of KPMG Corporate Financebetween July 1999 and July 2003. Beforejoining KPMG he was a managing director ofSG Hambros Corporate Finance. He joinedHambros Bank in 1978 and became headof the Corporate Finance Division ofHambros in 1997. He is a non-executivedirector of William Ransom & Son plc and

a member of Council of the University ofLeeds; he also acts as a strategic consultantto Jardine Lloyd Thompson UK Limited. Aged 48. A,N,R

Jim Pettigrew was appointed Group FinanceDirector on 18 March 1999, having becomean executive director on 25 January 1999.In 1988 he joined Sedgwick Group plc asthe Finance Director of its Financial ServicesDivision. Between 1993 and 1996 he wasthe Group Treasurer of Sedgwick Group plcand, from 1996, Deputy Group FinanceDirector. He is a chartered accountant anda member of the Association of CorporateTreasurers. Aged 45. GR,T

Paul Zuckerman, independent non-executive director, was appointed on 28 October 1998. He is Deputy Chairmanand the Senior Independent Director. He isChairman of Zuckerman & Associates LLC,a boutique specialising in start-up companies.He is also a director of a number ofcompanies including Merrill Lynch EuropeanEquity Hedge Fund Ltd and Dabur Oncologyplc. He was a founding member andManaging Director in charge of investmentbanking at Caspian Securities. Prior tojoining Caspian, he was Chairman of SGWarburg Latin America Ltd, Vice Chairmanof SG Warburg International and an executivedirector of SG Warburg & Co Ltd. Aged 58.A,N,R

Helen Broomfield FCIS was appointedGroup Company Secretary on 1 August 2003having previously been Deputy CompanySecretary since 2000. She is also secretaryof all board committees. Aged 38.

Directors and Secretary

ICAP plc Annual Report 200418

Key to membership of committeesA Audit CommitteeN Nomination Committee R Remuneration Committee GR Group Risk Committee T Treasury Committee

ICAP plc Annual Report 2004 19

MICHAEL SPENCER

CHARLES GREGSON

NICHOLASCOSH

DAVIDGELBER

STEPHENMcDERMOTT

DUNCANGOLDIE-MORRISON

WILLIAMNABARRO

JAMESMcNULTY

PAULZUCKERMAN

JIMPETTIGREW

Directors’ Report

ICAP plc Annual Report 200420

The directors present their report and theaudited Financial Statements of the Groupfor the year ended 31 March 2004.

Activities, business review anddevelopmentA review of business activities and futuredevelopments of the Group is given in theGroup Profile, Chairman’s Statement,Group Chief Executive Officer’s Review,Operating Review and Group FinanceDirector’s Review on pages 2 to 17.

Related party transactionsDetails of related party transactions are setout in note 29 to the Financial Statements.

Post balance sheet eventOn 7 April 2004 it was decided that ICAPwould exercise its option to satisfy £4.8million ($8.8 million) of the second deferredconsideration payment in respect of theFirst Brokers acquisition in cash rather thanshares. Further information is given in note32 to the Financial Statements.

Results and dividendsThe results of the Group for the year are set out in the consolidated profit and lossaccount on page 38. Following payment ofthe interim dividend, details of which areset out in note 10 to the FinancialStatements, the directors recommend afinal dividend of 5.7 pence per share for theyear ended 31 March 2004 to be paid on27 August 2004 to shareholders on theRegister on 30 July 2004 (ex-dividend datebeing 28 July 2004). After allowing for thepayment of the proposed dividend, theprofit for the year transferred to reserveswas £39.6 million.

Directors and directors’ interestsBiographical details of the directors whoheld office throughout the year includingDuncan Goldie-Morrison and James McNultywho were appointed on 20 November 2003and 30 March 2004 respectively, aregiven on page 18 and also in the noticeof the Annual General Meeting on pages78 to 81 for those to be re-elected andre-appointed (with the exception of RobertKnox and Donald Marshall who did notstand for re-election at the AnnualGeneral Meeting held on 16 July 2003).Details of the service contracts of thecurrent directors and of the interests of

the directors in the Company’s shares areshown in the Remuneration CommitteeReport on pages 28 to 36.

In accordance with the Company’s articlesof association Duncan Goldie-Morrison andJames McNulty will stand for re-appointmentand Nicholas Cosh will stand for re-electionat the forthcoming Annual General Meeting.

Edward Pank resigned as Company Secretaryon 1 August 2003 and Helen Broomfieldwas appointed Group Company Secretaryon this date.

Corporate Social ResponsibilityEmployee involvement andemployment practicesThe Group is committed to achieving thehighest standards in its workplace. Thepolicies and practices in place within theGroup to deter acts of harassment anddiscrimination are regularly monitored. The Group maintains a zero tolerance policy concerning sexual harassment,discrimination and retaliation againstindividuals who report problems in theGroup’s workplace. These topics arecovered in the training of all US employees.All managers in the UK take part inexternally managed diversity trainingcourses which cover discussion on theexpected and acceptable standards ofconduct and behaviour for employees.

The Group recognises the value ofcommunication with employees at alllevels and incentive schemes and shareownership schemes are run for the benefitof employees. Information on theseschemes is set out in the RemunerationCommittee Report on page 31.

During the year an intranet site wasdeveloped in the UK allowing employeeseasy access to the Company website forinformation on current developments. The intranet brings together informationon employment opportunities, the staffhandbook, including policies and procedures,details of arrangements whereby employeesare able to raise, in confidence, anyconcerns they may have, and complianceprocedures and manuals.

A structured graduate training programmeis offered in the UK. The programme is run over a three-month period and iscomplemented by hands on experience oneach broking desk so that all participants mayobtain a good understanding of the business.

Charity Day and charitable donationsDuring the year the Group donated £4 million(2003 - £3.3 million) to charitableorganisations globally, of which £2.1 million(2003 - £2.0 million) was donated tocharitable organisations in the UK. For thepast 11 years ICAP has held an annualcharity day and our offices around theworld have raised a total of £17 million.Many charities have received significantdonations enabling them to receive enoughmoney to make dreamed of projects areality without spending money fundraising.Further information can be found on ourwebsite, www.icap.com, and in the brochurewhich was sent to all shareholders with the2003 interim report.

Equal opportunitiesThe Group is committed to employmentpolicies that follow best practice and offersopportunities for employment, training andcareer development and promotion basedon individual abilities, regardless of gender,race, national origin, disability, age, sexualorientation, or religious or political beliefs.

Health and safetyThe Company has a health and safetypolicy approved by the board and iscommitted to providing for the health,safety and welfare of all its employeesand to maintaining standards at leastequal to the best practice in the financialservices industry.

EnvironmentRecognising that the Group’s operationsare themselves of minimal environmentalimpact, ICAP’s policy is to operate, as faras practicable, environmentally friendlypolicies and meet the statutory requirementsplaced on the Group.

Creditor payment policyThe Group’s policy with regard to thepayment of its suppliers is to agree theterms of payment at the start of businesswith each supplier, ensure that the suppliersare made aware of the terms of paymentsand pay in accordance with its contractualand legal obligations. The Company doesnot have any trade creditors.

ICAP plc Annual Report 2004 21

Political donationsIn the UK the board approved a donation toBusiness for Sterling of £10,000. (2003 -£50,000 to Business for Sterling).

Share capitalShare split At an Extraordinary GeneralMeeting held on 4 February 2004shareholders approved a five for one sharesubdivision which divided the Group's ordinaryshares of 50p each into five ordinary sharesof 10p each. The subdivision was effectivefrom 9 February 2004. These FinancialStatements (including comparatives) reflectthe change following the share subdivision.

Changes in share capital All changes inshare capital are detailed in note 23 to theFinancial Statements. As at 31 March 2004,options existed over 23,648,930 of theCompany’s ordinary shares of 10 pence inrelation to employee share option schemes.Of this figure 7,263,345 are options overexisting shares which are held in Trust andthe remainder are expected to be satisfiedby new issues of shares. Changes in optionsunder the various schemes are detailed in note 24 to the Financial Statements. In accordance with the provisions of theacquisition agreement entered into inconnection with the acquisition of BrokerTec,up to a maximum of 33,720,495 ordinaryshares may be issued to the formershareholders of BrokerTec as deferredconsideration depending on the revenuecreated by the acquired business. In

addition, shares may be issued as deferredconsideration in respect of the acquisitionof First Brokers and APB. More informationis given in the Group Finance Director’sReview.

At the Annual General Meeting held on 16 July 2003, the Company was givenauthority to purchase up to 11,493,644ordinary shares of 50 pence now 57,468,220of 10 pence each. This authority will expireat the conclusion of the Annual GeneralMeeting to be held on 14 July 2004.

Annual General MeetingThe sixth Annual General Meeting of theCompany will be held on Wednesday, 14 July 2004. The Notice of meeting isset out on pages 78 to 81.

In addition to the ordinary business of votingupon receiving the Financial Statements,declaring a dividend, the re-election andre-appointment of directors and theappointment of auditors, the followingspecial business will be considered:

Resolution 7 will be proposed as anOrdinary Resolution to approve theRemuneration Committee Report.

Resolution 8 will be proposed as an OrdinaryResolution. It is to authorise the directorsto allot ordinary shares of the Company toan amount equal to approximately onethird of the existing issued share capital.

Resolution 9 will be proposed as a SpecialResolution. It is to empower the directors to allot ordinary shares, otherwise than on a pro-rata basis to existing shareholders, inconnection with any future rights issue orgrant rights over shares or sell treasuryshares for cash, up to an aggregatenominal amount of £2,891,481 (beingapproximately 5% in value of the existingissued share capital at 31 March 2004 and 4.99% of the issued share capital at29 April 2004).

The authorities in Resolutions 8 and 9 lastfor periods of five and one year respectively,in accordance with institutional guidelines.The directors have no present intention ofexercising these authorities other than tocomply with the Company’s obligationspursuant to the acquisition agreements inconnection with BrokerTec, First Brokersand APB. It is normal for boards of listedcompanies to have these authorities in order to take advantage of marketopportunities as they arise.

Resolution 10 will be proposed as a SpecialResolution. It will empower the Company topurchase its own ordinary shares by marketpurchases not exceeding approximately10% of the Company’s issued share capitalas at 29 April 2004. The maximum andminimum prices are stated in the resolution.Your directors believe that it is advantageousfor the Company to continue to have thisflexibility to make market purchases of itsown shares. In the event that shares arepurchased, they would either be cancelled(and the number of shares in issue wouldbe reduced accordingly) or, subject to theCompanies (Acquisition of Own Shares)(Treasury Shares) Regulations 2003 (theRegulations) which came into force on 1 December 2003, retained as treasuryshares with a view to possible re-sale at afuture date rather than having to cancelthem. The Company would consider holdingrepurchased shares pursuant to the authorityconferred by this resolution as treasuryshares. This would give the Company the

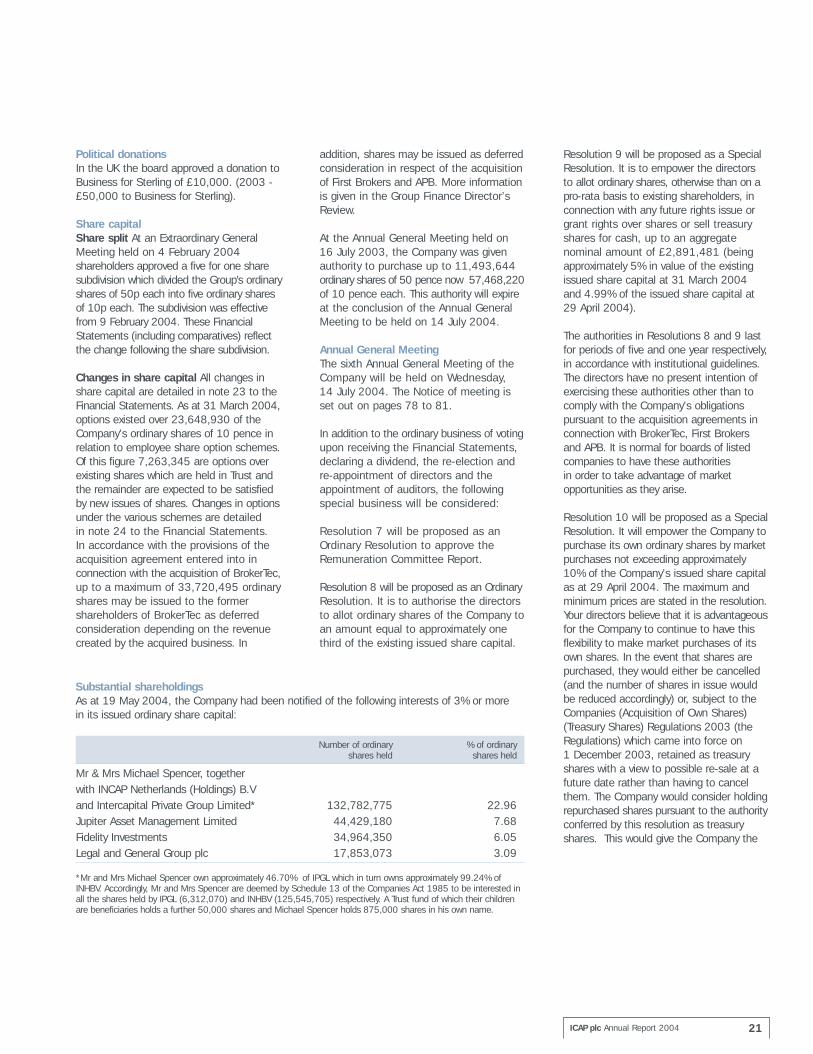

Number of ordinary % of ordinaryshares held shares held

Mr & Mrs Michael Spencer, togetherwith INCAP Netherlands (Holdings) B.Vand Intercapital Private Group Limited* 132,782,775 22.96Jupiter Asset Management Limited 44,429,180 7.68Fidelity Investments 34,964,350 6.05Legal and General Group plc 17,853,073 3.09

*Mr and Mrs Michael Spencer own approximately 46.70% of IPGL which in turn owns approximately 99.24% ofINHBV. Accordingly, Mr and Mrs Spencer are deemed by Schedule 13 of the Companies Act 1985 to be interested inall the shares held by IPGL (6,312,070) and INHBV (125,545,705) respectively. A Trust fund of which their childrenare beneficiaries holds a further 50,000 shares and Michael Spencer holds 875,000 shares in his own name.

Substantial shareholdingsAs at 19 May 2004, the Company had been notified of the following interests of 3% or more in its issued ordinary share capital:

Directors’ Report continued

ICAP plc Annual Report 200422

ability to re-issue treasury shares quicklyand cost effectively and would provide theCompany with additional flexibility in themanagement of its capital base. The directorswould exercise this authority only if theywere satisfied that a purchase would resultin an increase in expected earnings pershare and would be in the interests ofshareholders generally. There is no presentintention of exercising this authority and theauthority given in the resolution will expireat the conclusion of the Annual GeneralMeeting to be held in 2005.

Resolutions 11 and 12 will be proposedas Ordinary Resolutions to approve themaking of political donations and incurringof political expenditure by the Companyand its subsidiary Garban-IntercapitalManagement Services Limited of up to anaggregate amount of £100,000 in theperiod to the Company’s Annual GeneralMeeting to be held in 2005. The PoliticalParties, Elections and Referendums Act2000, contains restrictions on companiesmaking donations to EU political organisationsor incurring EU political expenditurewithout prior shareholder approval.

Details on electronic proxy voting can befound in the Notice of the Annual GeneralMeeting on pages 78 to 81.

AuditorsPricewaterhouseCoopers LLP wereappointed auditors to the Company on 16 July 2003. A resolution to re-appointPricewaterhouseCoopers LLP and toauthorise the directors to set theirremuneration will be proposed. Note 5 tothe Financial Statements sets out detailsof the auditors’ remuneration.

Statement of directors’ responsibilitiesfor the Financial StatementsThe directors are required by the CompaniesAct 1985 to prepare Financial Statementsfor each accounting period that give atrue and fair view of the state of affairs ofthe Company and Group as at the end ofthe financial year and of the profit or lossof the Group for the year. The directorsconfirm that suitable accounting policieshave been used and applied consistentlyand reasonable and prudent judgementsand estimates have been made in thepreparation of the Financial Statementsfor the year ended 31 March 2004. The directors also confirm that applicableUnited Kingdom Accounting Standardshave been followed.

The directors are responsible for keepingproper accounting records, for takingreasonable steps to safeguard the Group’sassets and to prevent and detect fraudand other irregularities.

Going concernThe directors are satisfied that the Companyand the Group have adequate resourcesto continue to operate for the foreseeablefuture and confirm that the Company andthe Group are going concerns. For thisreason they continue to adopt the goingconcern basis in preparing these financialstatements.

By order of the board

Helen BroomfieldGroup Company Secretary

ICAP plc Annual Report 2004 23

Corporate Governance Report

New directors to the board are providedwith appropriate training and briefingswhich take into account their individualqualifications and experience. All directorsreceive, during their term of office, regularbriefings on changes and developments inthe Group’s business and legislative andregulatory changes which are relevant tothe Group.

During the year the board evaluated itsperformance and that of its committeesand individual directors. This was done byway of a questionnaire which was completedby each director to evaluate the board’seffectiveness and accountability. The resultsof this exercise were then summarised tothe board by the Chairman. The Chairman’sperformance was evaluated by the non-executive directors led by the SeniorIndependent Director who then providedthe Chairman with the results of thisevaluation.

The board manages the Group through boardmeetings and a number of committees, eachof which has detailed terms of referenceand meets regularly. The minutes of eachof the Committees are made available toall directors and the board receives a verbalupdate from each committee’s Chairman.

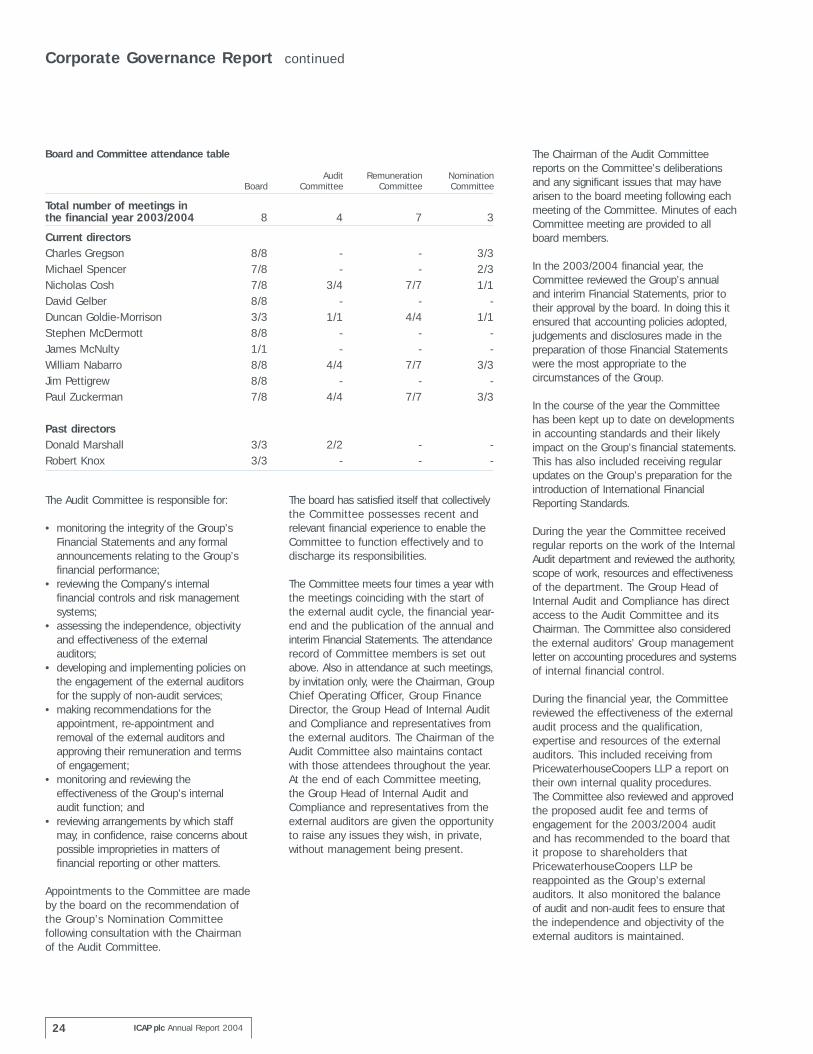

(i) Audit CommitteeThe Committee comprises four independentnon-executive directors. The directors whoserved on the Committee during the yearand at the year end are:

Nicholas Cosh FCA(Chairman)Duncan Goldie-Morrison(appointed 20 November 2003)William NabarroPaul ZuckermanDonald Marshall(did not stand for re-election at 2003 AGM)

The Committee’s full terms of referencewere reviewed, in light of the Smith Reporton Audit Committees, and approved by theboard during the year. They are availableon the Group’s website, www.icap.com, or from the Group Company Secretary.

Corporate Governance StatementThroughout the year ended 31 March 2004and up to the date of this report, the boardconfirms that it fully complied with theprovisions of the Code of Best Practice setout in Section 1 of the Combined Code onCorporate Governance issued in June 1998by the UK Listing Authority. The board hasconsidered the impact of the new revisedCombined Code issued in July 2003 whichwill apply to the Group for the 2004/2005financial year and believes that it is alreadysubstantially compliant with the 2003Combined Code and will make suchadjustments as are necessary to ensure itcan report full compliance with the newcode in its Annual Report and Accounts for2005. This section on corporate governancetogether with the Remuneration CommitteeReport details how the Group has appliedthe Combined Code and includes additionaldisclosures, where appropriate, as a steptowards compliance with the revised code.

DirectorsDirectors and the board The Company is headed by an experienced board ofdirectors consisting of a non-executiveChairman, Group Chief Executive Officer,three further executive directors and fivenon-executive directors. The board meetsat least six times a year, half of thosemeetings being held in the US. During theyear ended 31 March 2004 two additionalboard meetings were held to review andapprove the BrokerTec acquisition.

The board has a schedule of mattersspecifically reserved to it for decision andapproval which include, but are notlimited, to:

• the Group’s long term objectives andcommercial strategy;

• acquisitions, disposals and majorinvestments;

• the Group’s annual and interim financialstatements;

• any significant change in accountingpolicies or practices;

• any interim dividend andrecommendation of the final dividend;

• the annual operating and capitalexpenditure budgets;

• any changes to the company’s capitalstructure or its status as a listedcompany;

• risk management strategy; and• treasury policy.

Information, including monthly managementaccounts, is provided in a timely and regularmanner to directors for all meetings to enablethem to exercise their judgement in thedischarge of their duties. All directors haveaccess to the advice and services of theGroup Company Secretary who is responsiblefor ensuring that board procedures andapplicable rules are observed. Proceduresexist to enable the directors to obtainindependent professional advice in respectof their duties.

There is a clear division of roles andresponsibilities between the Chairman and Group Chief Executive Officer with theChairman being responsible for leadershipof the board and ensuring effectivecommunication with shareholders and theChief Executive Officer being responsiblefor leading and managing the business.There is a balance between non-executiveand executive directors on the board suchthat there is a majority of independentnon-executives who provide a wide rangeof skills and experience to the board. Paul Zuckerman, the Deputy Chairman, is the Senior Independent Director. Withthe exception of the Chairman, who wasexecutive Chairman until 31 July 2001, all the non-executive directors areindependent of management and consideredby the board to be free from any businessor other relationships which could interferewith the exercise of their independence.Biographies of each of the directors anddetails of their membership of boardcommittees is given on page 18.

Board nominations are recommended tothe board by the Nomination Committeeunder its terms of reference. In accordancewith the Combined Code and the Company’sarticles of association all directors aresubject to re-appointment by shareholdersat the first opportunity following theirappointment and, subsequently, must seekre-election at least once every three years.

The Audit Committee is responsible for:

• monitoring the integrity of the Group’sFinancial Statements and any formalannouncements relating to the Group’sfinancial performance;

• reviewing the Company’s internalfinancial controls and risk managementsystems;

• assessing the independence, objectivityand effectiveness of the externalauditors;

• developing and implementing policies onthe engagement of the external auditorsfor the supply of non-audit services;

• making recommendations for theappointment, re-appointment andremoval of the external auditors andapproving their remuneration and termsof engagement;

• monitoring and reviewing theeffectiveness of the Group’s internal audit function; and

• reviewing arrangements by which staffmay, in confidence, raise concerns aboutpossible improprieties in matters offinancial reporting or other matters.

Appointments to the Committee are madeby the board on the recommendation ofthe Group’s Nomination Committeefollowing consultation with the Chairmanof the Audit Committee.

The board has satisfied itself that collectivelythe Committee possesses recent andrelevant financial experience to enable theCommittee to function effectively and todischarge its responsibilities.

The Committee meets four times a year withthe meetings coinciding with the start ofthe external audit cycle, the financial year-end and the publication of the annual andinterim Financial Statements. The attendancerecord of Committee members is set outabove. Also in attendance at such meetings,by invitation only, were the Chairman, GroupChief Operating Officer, Group FinanceDirector, the Group Head of Internal Auditand Compliance and representatives fromthe external auditors. The Chairman of theAudit Committee also maintains contactwith those attendees throughout the year.At the end of each Committee meeting,the Group Head of Internal Audit andCompliance and representatives from theexternal auditors are given the opportunityto raise any issues they wish, in private,without management being present.

The Chairman of the Audit Committeereports on the Committee’s deliberationsand any significant issues that may havearisen to the board meeting following eachmeeting of the Committee. Minutes of eachCommittee meeting are provided to allboard members.