Embed Size (px)

Citation preview

Annual Report2014JPMorgan Japanese Investment Trust plc

Annual Report & Accounts for the year ended 30th September 2014

Features

Objective

Capital growth from Japanese investments.

Investment Policy

- To maintain a portfolio almost wholly invested in Japan.

- To use gearing to increase potential returns to shareholders. The Company’s gearingpolicy is to operate within a range of 5% net cash to 15% geared in normal marketconditions.

- To invest no more than 15% of its gross assets in any listed company (includinginvestment trusts).

Further details on investment policies and risk management are given in the BusinessReview on page 14.

Benchmark

The Tokyo Stock Exchange 1st Section Index (‘TOPIX’) expressed in sterling terms.

Capital Structure

UK domiciled. Full listing on the London Stock Exchange and the New Zealand StockExchange.

As at 30th September 2014, the Company’s share capital comprised 161,248,078(2013: 161,248,078) ordinary shares of 25p each.

Management Company

The Company employs JPMorgan Funds Limited (‘JPMF’ or the ‘Manager’) as itsAlternative Investment Fund Manager. JPMF delegates the management of theCompany’s portfolio to JPMorgan Asset Management (UK) Limited (‘JPMAM’).

Association of Investment Companies

The Company is a member of the Association of Investment Companies (‘AIC’).

FCA Regulation of ‘Non-Mainstream Pooled Investments’

The Company currently conducts its affairs so that its shares can be recommended byIndependent Financial Advisers to ordinary retail investors in accordance with therules of the Financial Conduct Authority (‘FCA’) in relation to non-mainstreaminvestment products and intends to continue to do so for the foreseeable future.

The shares are excluded from the FCA’s restrictions which apply to non-mainstreaminvestment products because they are shares in an investment trust.

Website

The Company’s website can be found at www.jpmjapanese.co.uk and includes usefulinformation about the Company, such as daily prices, factsheets and current andhistoric half year and annual reports.

Contents

1 Financial Results

Strategic Report

2 Chairman’s Statement5 Investment Manager’s Report8 Performance9 Ten Year Financial Record10 Ten Largest Investments11 Sector Analysis12 List of Investments 14 Business Review

Governance

19 Board of Directors21 Directors’ Report24 Corporate Governance Statement30 Directors’ Remuneration Report33 Statement of Directors’

Responsibilities

34 Independent Auditors’ Report

Financial Statements

38 Income Statement39 Reconciliation of Movements in

Shareholders’ Funds40 Balance Sheet41 Cash Flow Statement42 Notes to the Accounts

Shareholder Information

58 Notice of Annual General Meeting61 Glossary of Terms and Definitions65 Information about the Company

Financial Data 2014 2013 % change

Net asset value, share price and discount at 30th SeptemberShareholders’ funds (£’000) 408,462 431,876 –5.4Net asset value per share 253.3p 267.8p –5.4Share price 218.0p 238.3p –8.5Share price discount to net asset value 13.9% 11.0%Exchange rate £1 = ¥177.8 £1 = ¥158.9 +11.9Shares in issue 161,248,078 161,248,078 —

Revenue for the year ended 30th SeptemberGross revenue attributable to shareholders (£’000) 5,715 6,041 –5.4Net revenue attributable to shareholders (£’000) 3,963 4,480 –11.5Earnings per share 2.46p 2.78p –11.5Dividend per share 2.80p 2.80p —

Gearing5 12.7% 13.7%

Ongoing Charges6 0.78% 0.78%

A glossary of terms and definitions is provided on page 61.

1Total returns (includes dividends reinvested).2S ource: J.P. Morgan.3Source: Morningstar.4Source: Datastream. The Company’s benchmark is The Tokyo Stock Exchange 1st Section Index (TOPIX) expressed in sterling terms.5Gearing represents the excess amount above shareholders’ funds of total assets (including net current assets/(liabilities)) less cash/cash equivalents, expressed as a percentage ofshareholders’ funds. If the amount calculated is negative, this is shown as a ‘net cash’ position.6Management fee and all other operating expenses excluding any finance costs, expressed as a percentage of the average of the daily net assets during the year. Ongoing chargesare calculated in accordance with guidance issued by the Association of Investment Companies in May 2012.

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 1

–7.4%Return to shareholders1,3

(2013: +57.8%)

–5.3%Underperformance of Benchmark4

(2013: +15.6%)

2.80pDividend(2013: 2.80p)

–4.4%Return on net assets1,2

(2013: +45.9%)

+0.9%Benchmark return1,3,4

(2013:+30.3%)

Financial ResultsTotal returns

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 20142

Investment Performance

In the year to 30th September 2014, the Company’s net assets fell by 4.4% in sterlingterms, compared with the Tokyo Stock Exchange First Section (TOPIX) Index (ourbenchmark), which rose by 0.9%. The returns are calculated on a total return basis insterling terms and were impacted by the movement in the yen/sterling rate from yen158.9 at the beginning of the year to yen 177.8 at its conclusion. The share price ofyour Company fell by 7.4% during the year, assuming the reinvestment of thedividend. The results for the year to 30th September 2014 are disappointing though,over the two, three and five years ended 30th September 2014, the portfolio hasoutperformed the benchmark in sterling terms.

Revenue and Dividends

Income received during the year fell with earnings per share for the full year fallingto 2.46p (2013: 2.78p). However, in light of an apparent upward trend in dividendpayments by Japanese companies, the Board proposes, subject to shareholders’approval at the Annual General Meeting, to pay an unchanged final dividend of 2.80pper share (2013: 2.80p) on 23rd December 2014 to shareholders on the register at theclose of business on 28th November 2014 (ex-dividend date 27th November 2014).The objective of the Company is capital growth, any dividend paid being a residual ofthe portfolio structure and, in the event that this revenue increase is not forthcoming,it would be difficult to continue to maintain the dividend at this level. Incomereceived by the Company is subject to certain distribution requirements that must bemet in order to retain the Company’s investment trust status.

Gearing

The Board of Directors sets the overall strategic gearing policy and guidelines,reviewing these at each meeting. The Investment Manager then manages the gearingwithin these agreed levels. On 30th September 2014, the Company had a gearinglevel of 12.7%. This level of gearing at the end of the financial year reflected theconfidence of the Investment Manager in the individual companies held in theportfolio. The management of gearing has also been active during the year with thelevel ranging between geared positions of 11% and 15% (month end figures).

The funds available to be drawn down by the Company are ¥12 billion and the loanfacility provides for additional capacity to increase gearing to ¥15 billion, shouldmarket conditions allow.

Investment Manager

The Company’s objective is to provide shareholders with capital growth from aportfolio of investments in Japanese companies and on a longer term view yourInvestment Manager has achieved this outperformance against our benchmark,equally through stock selection and gearing.

Strategic ReportChairman’s Statement

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 3

Board of Directors

Having been a Director since 1996, I am retiring at the conclusion of the AnnualGeneral Meeting. Over the time I have served on the Board Japan has faced bothglobal and domestic economic difficulties but, despite this, I remain convinced thatthe country will offer continuing investment opportunities for your portfolio.

I am delighted that Andrew Fleming, a Director since 2004, will be appointedChairman in my place.

In selecting a new Director, an outside consultant, Trust Associates, was appointed.Following interviews with all members of the Board, Christopher Samuel is to beappointed as a Director following the close of the Annual General Meeting on19th December 2014. Christopher was previously Chief Executive Officer of Ignis AssetManagement and will bring to the Board considerable experience of the investmentmanagement industry as well as Japan where he was based earlier in his career.

In accordance with the Company’s Articles of Association, Andrew Fleming and KeithPercy, having served on the Board for more than nine years, are retiring and seekingreappointment. Alan Barber will also retire and seek reappointment to comply withthe Company’s Articles of Association which requires a third of the Board to retire byrotation (excluding those with tenure in excess of nine years).

Alan, Andrew and Keith all bring a wealth of experience to the Board and I have nohesitation in recommending their reappointment.

Authority to Repurchase the Company’s Shares

At last year’s Annual General Meeting, shareholders granted the Directors’ authorityto repurchase up to 14.99% of the Company’s shares. No shares have beenrepurchased for cancellation during the year (2013: 70,000). The Directors continueto believe that the power to repurchase shares is of ongoing benefit to shareholdersand therefore propose that the authority be renewed for a further period. Sharerepurchases continue to be a useful tool for decreasing discount volatility and thisapproach will be used when considered to be appropriate by the Board.

Alternative Investment Fund Managers Directive (‘AIFMD’)

As required under AIFMD, with effect from 1st July 2014, the Company appointedJPMorgan Funds Limited as its Alternative Investment Fund Manager under a newinvestment management agreement. Portfolio management is delegated byJPMorgan Funds Limited to JPMorgan Asset Management (UK) Limited, thus retainingprevious portfolio management arrangements. The management fee and noticeperiod arrangements remain unchanged. The Company appointed BNY Mellon Trust& Depositary (UK) Limited to act as the Company’s Depositary, a new requirementunder AIFMD. JPMorgan Chase Bank, NA remains the Company’s Custodian, but as adelegate of the Depositary. JPMorgan Funds Limited was also appointed as CompanySecretary to the Company on 1st July 2014.

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 20144

Independent Auditors

These accounts are the first to be audited by PricewaterhouseCoopers LLP. You willfind their first audit report to shareholders on page 34.

Annual General Meeting

This year’s Annual General Meeting will be held on Friday, 19th December 2014 at2.00 p.m. at 60 Victoria Embankment, London EC4Y 0JP. As in previous years, inaddition to the formal part of the meeting, there will be a presentation from theInvestment Manager who will answer questions on the portfolio and performance.There will also be an opportunity to meet the Board, the Investment Manager andrepresentatives of JPMorgan after the meeting. I look forward to welcoming as manyof you as possible to this meeting.

If you have any detailed or technical questions, it would be helpful if you could raisethese in advance of the meeting with the Company Secretary at 60 VictoriaEmbankment, London EC4Y 0JP. Alternatively, questions may be submitted via theCompany’s website (www.jpmjapanese.co.uk). Shareholders who are unable to attendthe Annual General Meeting are encouraged to use their proxy votes. Proxy votesmay be lodged electronically, whether shares are held through CREST or in certificateform, and full details are set out on the form of proxy.

Prospects

While it is disappointing that, to date, Prime Minister Abe has not made as muchprogress with his programme of revitalisation as initially expected, the recentdecision by the Bank of Japan to reinforce the process of monetary easing was asurprise to most observers. It perhaps reflects an opportunity for the Government topush forward their aim of improved economic growth coupled with an element ofinflation.

Your Investment Manager has laid out the areas where he believes opportunities willarise for your portfolio and I continue to think the well-managed and entrepreneurialcompanies in these sectors will provide investment opportunities for the future.

Jeremy Paulson-EllisChairman 12th November 2014

Strategic Report continuedChairman’s Statement continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 5

The benchmark TOPIX index rose by around 1% in sterling terms during the yearended 30th September 2014 with the Company’s NAV falling 4.4%. Over three yearsthe Company has returned 37% versus 25% for the index. Over five years 46% versus29% for the index.

Review

Prime Minister Abe remained popular which is remarkable in a country that hasbecome accustomed to a revolving door of prime ministers. This stability is positive.The global economic recovery, led by the United States, continued. The yenweakened and, perhaps most importantly of all from a stock market perspective,corporate earnings were strong while progress was made with corporate governance.

Economic data was mixed. On the positive side land prices rose, office vacancy ratesfell and the unemployment rate hit a multi-year low of 3.5%. However, although therehas been wage growth this has not kept pace with inflation. The consumption tax hikein April, from 5% to 8%, led to weak GDP numbers in the second quarter and so farthe recovery from this has been tepid. This is one reason why the Bank of Japanadded to its stimulus measures at the end of October 2014. Export data has also beenlacklustre despite the weaker yen. We attribute this softness to the ongoing shift ofproduction overseas by Japanese companies and the loss of competitiveness incertain industries such as consumer electronics.

The yen weakened substantially. The sharp depreciation at the end of the fiscal yearwas driven by the belief that the US Federal Reserve will gradually tighten policy dueto the improving economy while the Bank of Japan will continue its monetary easingprogramme. This view was cemented when the Bank of Japan announced its secondround of quantitative easing in October 2014. Monetary policy in Japan is now moreaggressive than in other developed markets. The weaker yen is a tailwind for most ofcorporate Japan but we have to monitor closely the impact on everyday lives whichhave been affected by rising import prices.

Corporate earnings continue to be the major positive. Earnings have been strong andanalyst projections for 2014 and 2015 have been revised up. This pattern continuedduring the interim results season in November 2014 and shareholder returns areimproving. In the first half of the year almost 250 companies set up share repurchaseprogrammes for a total value of ¥1.85 trillion, the highest tally since the first half of2008. Some companies increased their dividends including a few which hadpreviously eschewed substantial shareholder returns. A total of 160 institutionalinvestors, including J.P. Morgan Asset Management, have signed up to a newstewardship code which aims to boost transparency and improve corporategovernance. One notable point in the October Bank of Japan easing was itsannouncement to buy Exchange Traded Funds (ETFs) including an ETF linked to theJPX 400 index, an index that places emphasis on companies with high and improvingreturns on equity amongst other factors. We hope that progress with corporategovernance is the start of a long-term structural trend.

Portfolio Performance

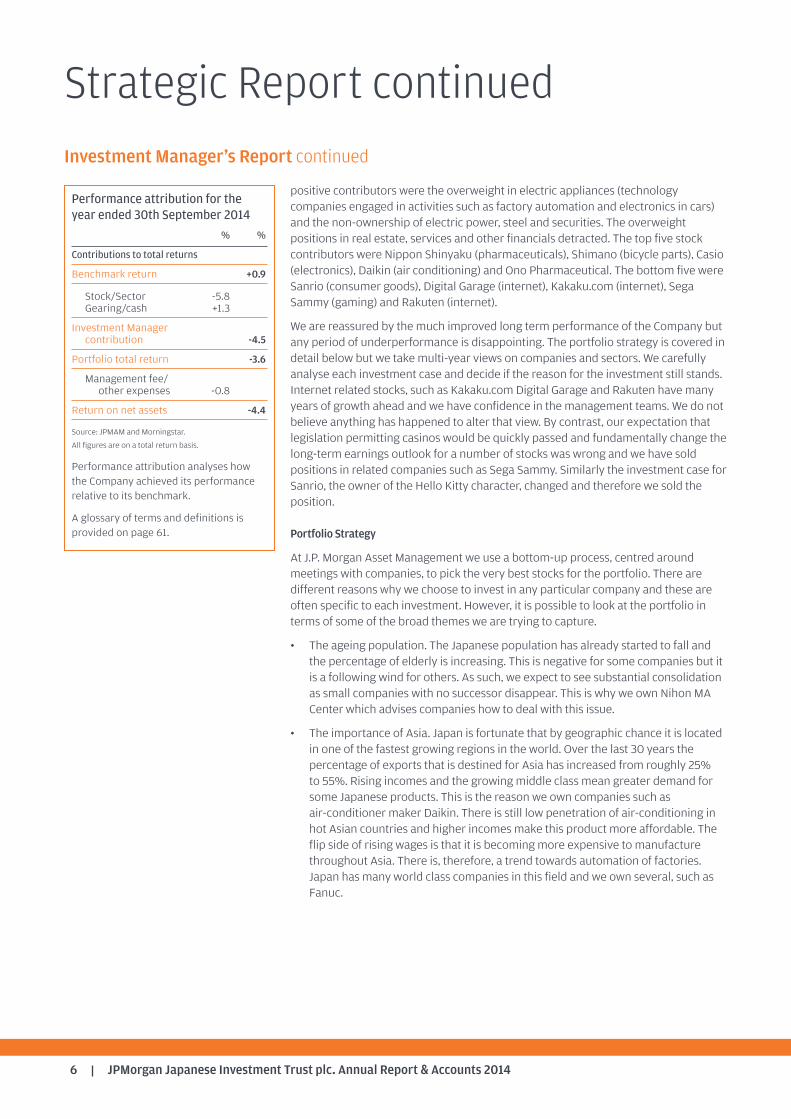

The underperformance versus the benchmark over the year was due to poor stockselection. However, gearing was positive. At the sector allocation level the major

Investment Manager’s Report

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 20146

positive contributors were the overweight in electric appliances (technologycompanies engaged in activities such as factory automation and electronics in cars)and the non-ownership of electric power, steel and securities. The overweightpositions in real estate, services and other financials detracted. The top five stockcontributors were Nippon Shinyaku (pharmaceuticals), Shimano (bicycle parts), Casio(electronics), Daikin (air conditioning) and Ono Pharmaceutical. The bottom five wereSanrio (consumer goods), Digital Garage (internet), Kakaku.com (internet), SegaSammy (gaming) and Rakuten (internet).

We are reassured by the much improved long term performance of the Company butany period of underperformance is disappointing. The portfolio strategy is covered indetail below but we take multi-year views on companies and sectors. We carefullyanalyse each investment case and decide if the reason for the investment still stands.Internet related stocks, such as Kakaku.com Digital Garage and Rakuten have manyyears of growth ahead and we have confidence in the management teams. We do notbelieve anything has happened to alter that view. By contrast, our expectation thatlegislation permitting casinos would be quickly passed and fundamentally change thelong-term earnings outlook for a number of stocks was wrong and we have soldpositions in related companies such as Sega Sammy. Similarly the investment case forSanrio, the owner of the Hello Kitty character, changed and therefore we sold theposition.

Portfolio Strategy

At J.P. Morgan Asset Management we use a bottom-up process, centred aroundmeetings with companies, to pick the very best stocks for the portfolio. There aredifferent reasons why we choose to invest in any particular company and these areoften specific to each investment. However, it is possible to look at the portfolio interms of some of the broad themes we are trying to capture.

• The ageing population. The Japanese population has already started to fall andthe percentage of elderly is increasing. This is negative for some companies but itis a following wind for others. As such, we expect to see substantial consolidationas small companies with no successor disappear. This is why we own Nihon MACenter which advises companies how to deal with this issue.

• The importance of Asia. Japan is fortunate that by geographic chance it is locatedin one of the fastest growing regions in the world. Over the last 30 years thepercentage of exports that is destined for Asia has increased from roughly 25%to 55%. Rising incomes and the growing middle class mean greater demand forsome Japanese products. This is the reason we own companies such asair-conditioner maker Daikin. There is still low penetration of air-conditioning inhot Asian countries and higher incomes make this product more affordable. Theflip side of rising wages is that it is becoming more expensive to manufacturethroughout Asia. There is, therefore, a trend towards automation of factories.Japan has many world class companies in this field and we own several, such asFanuc.

Performance attribution for theyear ended 30th September 2014

% %

Contributions to total returns

Benchmark return +0.9

Stock/Sector -5.8Gearing/cash +1.3

Investment Managercontribution -4.5

Portfolio total return -3.6

Management fee/other expenses -0.8

Return on net assets -4.4

Source: JPMAM and Morningstar.

All figures are on a total return basis.

Performance attribution analyses howthe Company achieved its performancerelative to its benchmark.

A glossary of terms and definitions isprovided on page 61.

Strategic Report continuedInvestment Manager’s Report continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 7

• The increasing use of electronics in cars. Ultimately cars may be able to drivethemselves but even now there is an increasing proliferation of electronics incars. For example, the headlights of some cars already automatically switch fromfull beam to dipped. We own shares in several companies that stand to benefit,including Murata.

• New Japanese brands. Twenty years ago Japanese consumer electronicscompanies were global leaders with very valuable brands. Now, their productshave become commoditised and they have been surpassed by low-costmanufacturers in Taiwan, Korea and China. However, Japan remains very strongin other areas. Shimano is dominant in gears for bicycles, Kikkoman in soy sauce.

• Ecommerce. The percentage of online retail in Japan, at around 4% of total retailsales, is very much lower than other developed countries such as the UnitedKingdom where the equivalent figure is well over 12%. There is no basic reasonwhy this should be the case and growth is strong. This is one reason why wecontinue to hold the number one ecommerce company Rakuten.

• The growth in inbound tourism. For the first time ever the number of touristscoming to Japan has outnumbered Japanese going overseas. There are tworeasons for this. First, visa restrictions for some nationalities have been lifted.Second, Japan has become much cheaper following the depreciation of the yen.Retailer Don Quijote, which is a popular shopping destination for tourists, is oneexample of a company we hold that is benefitting from this.

At JPMorgan we have a large team based on the ground in Tokyo trying to identifysignificant changes in sectors and companies. Being based locally is increasinglyunusual and we expect this to be a source of continued competitive advantage.Overall, we are positive on the outlook for the economy, market, active fundmanagement and the performance of the Company.

Nicholas WeindlingInvestment Manager 12th November 2014

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 20148

Performance Relative to BenchmarkFigures have been rebased to 100 at 30th September 2004

Source: Morningstar.

JPMorgan Japanese – share price total return.

JPMorgan Japanese – net asset value total return.

The benchmark index is represented by the grey horizontal line.

Ten Year PerformanceFigures have been rebased to 100 at 30th September 2004

Source: Morningstar/MSCI.

JPMorgan Japanese – share price total return.

JPMorgan Japanese – net asset value total return.

Benchmark.

Strategic Report continuedPerformance

60

80

100

120

140

160

180

20142013201220112010200920082007200620052004

60

70

80

90

100

110

120

20142013201220112010200920082007200620052004

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 9

At 30th September 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total assets less current liabilities (£’m) 393.1 504.3 511.7 431.8 298.1 315.7 306.1 326.6 302.1 494.8 408.4

Net asset value per share (p) 211.6 271.4 275.8 244.3 171.3 185.9 189.6 194.7 187.3 267.8 253.3

Share price (p) 188.5 263.0 254.5 214.5 145.5 157.0 160.0 166.8 154.5 238.3 218.0

Discount (%) 10.9 3.1 7.7 12.2 15.1 15.5 15.6 14.3 17.5 11.0 13.9

Gearing1/(net cash) (%) 6.8 13.8 12.5 12.3 8.0 7.6 (1.8) (0.6) 9.0 13.7 12.7

Yen exchange rate (=£1) 199.4 200.5 220.5 234.3 189.2 143.2 131.6 120.1 125.6 158.9 177.8

Year ended 30th September

Gross revenue attributable to shareholders (£’000) 5,272 6,537 8,450 7,068 7,160 7,596 6,138 7,323 8,121 6,041 5,715

Earnings per share (p) 2.06 2.75 3.60 2.96 2.97 2.96 2.91 3.49 4.10 2.78 2.46

Dividend per share (p) Nil Nil Nil 2.80 2.80 2.80 2.80 3.30 3.65 2.80 2.80

Ongoing charges2 (%) 0.83 0.73 0.78 0.75 0.79 0.77 0.81 0.86 0.77 0.78 0.78

Rebased to 100 at 30th September 2004

Share price total return3 100.0 139.5 135.0 113.8 78.3 86.4 89.8 95.1 89.9 141.9 131.4

Net asset value total return3 100.0 128.3 130.9 114.6 81.0 89.5 92.8 96.3 94.0 137.1 131.1

Benchmark3,4 100.0 128.9 135.0 129.0 109.4 123.3 124.3 127.8 121.0 157.7 159.2

A glossary of terms and definitions is provided on page 61.

1Gearing represents the excess amount above shareholders’ funds of total assets (including net current assets/(liabilities)) less cash/cash equivalents, expressed as a percentage ofshareholders’ funds. If the amount calculated is negative, this is shown as a ‘net cash’ position.2Ongoing charges are calculated in accordance with guidance issued by the AIC in May 2012 as follows. Management fee and all other operating expenses excluding any finance costs,expressed as a percentage of the average of the daily net assets during the year (2009 to 2011: Total Expense Ratio: Management fee and all other operating expenses excluding anyfinance costs, expressed as a percentage of the average of the month end net assets during the year; 2008 and prior years: expressed as the average of the opening and closing netassets).3Source: Morningstar.4Source: Datastream. The Company’s benchmark is The Tokyo Stock Exchange 1st Section Index (TOPIX) expressed in sterling terms.

Ten Year Financial Record

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201410

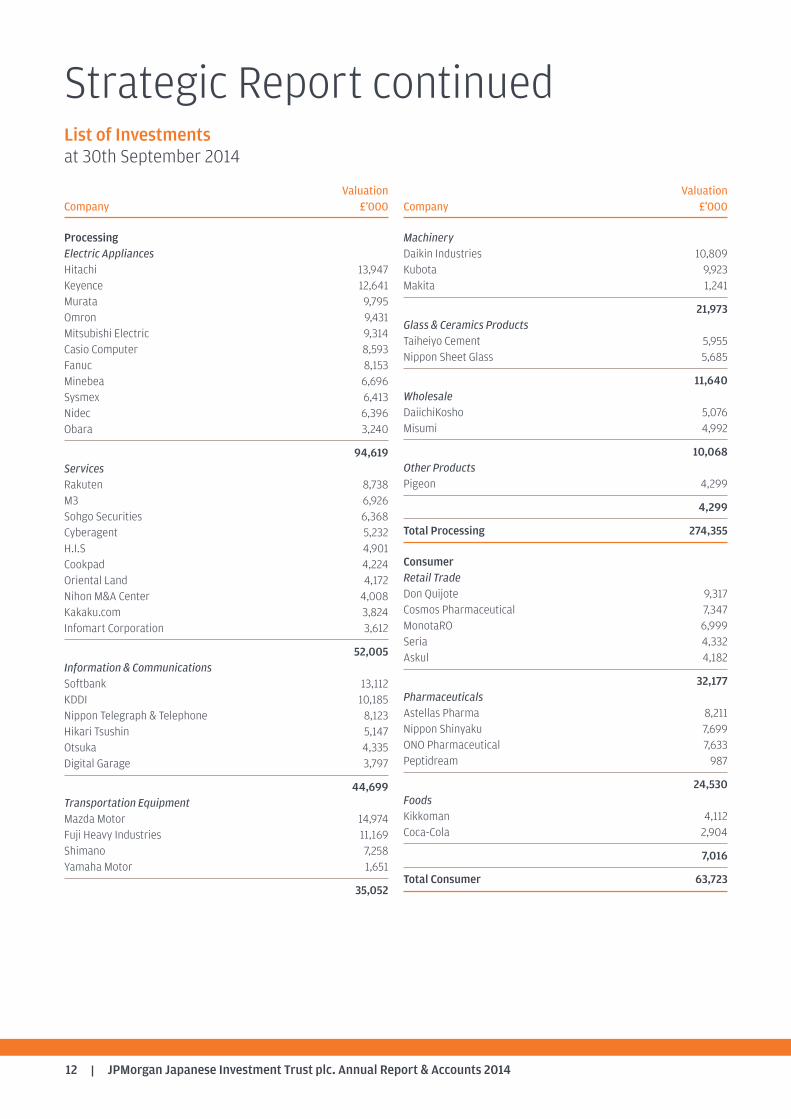

2014 2013Valuation Valuation

Company Sector £’000 %1 £’000 %1

Mazda Motor Transportation Equipment 14,974 3.3 12,226 2.5Mazda Motor manufactures and sells automobiles, trucks and auto parts.The company operates its business worldwide.

Hitachi Electric Appliances 13,947 3.0 12,050 2.5Hitachi manufactures communications and electronic equipment, heavyelectrical and industrial machinery and consumer electronics. Thecompany’s diverse product line ranges from nuclear power systems tokitchen appliances. Hitachi also operates subsidiaries in the wire andcable, metal and chemical industries.

Mitsubishi UFJ Banks 13,767 3.0 18,226 3.7Mitsubishi UFJ is Japan’s largest bank which offers personal banking,corporate banking, investment banking, investment management,mortgage and credit card services worldwide.

Softbank Information & 13,112 2.8 15,778 3.2Softbank provides telecommunication services. The company also Communicationoperates ADSL (Asymmetric Digital Subscriber Line) and fibre optichigh-speed internet connection, ecommerce businesses and internetbased advertising and auction businesses.

Sumitomo Mitsui Financial Banks 12,786 2.8 21,957 4.5Sumitomo Mitsui Financial is Japan’s second largest bank. The companyprovides a wide range of banking services, financial products and servicesworldwide.

Keyence2 Electric Appliances 12,641 2.7 5,502 1.1Keyence develops, manufactures and sells sensors and measuringinstruments used for factory automation and high technology hobbyproducts. The company’s products include fibre optic sensors,photoelectric sensors, programmable logic controllers, laser scanmicrometers, bar code readers and radio-controlled model cars.

Fuji Heavy Industries2 Transportation Equipment 11,169 2.4 9,359 1.9Fuji Heavy Industries manufactures passenger cars, buses, motor vehicleparts and industrial machinery. The company also produces aircraft partsand supplies these to the defence agency and Boeing Co. Fuji HeavyIndustries sells its passenger cars under the Subaru brand.

Orix Other Financing 10,914 2.4 15,779 3.2Orix provides comprehensive financial services throughout the world. BusinessThe company’s business lines include leasing, instalment loans, real estateloans, life insurance, banking, securities brokerage, venture capital andconsumer finance. Orix has also recently purchased an asset managementbusiness in Holland.

Daikin Industries2 Machinery 10,809 2.3 10,442 2.1Daikin manufactures air conditioning equipment for household andcommercial use. The company also produces fluorine chemical productssuch as fluorinated hydrocarbon gas and shells and warheads for thedefence industry.

Sumitomo Electric2 Nonferrous Metals 10,615 2.3 9,457 1.9Sumitomo Electric manufactures electric wires, cables and their relatedequipment. The company’s products include optical fibres, wire harnesses,antennas for broadcasting stations and electric monitoring systems.Sumitomo Electric also produces disc brakes and antilock braking systemsfor automobiles. It also produces printed circuit boards.

Total3 124,734 27.0

1Based on total portfolio investments of £459.6m (2013: £487.9m).2Not included in the ten largest investments at 30th September 2013.3At 30th September 2013, the value of the ten largest investments amounted to £145.2m representing 29.8% of total portfolio investments.

Strategic Report continuedTen Largest Investmentsat 30th September 2014

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 11

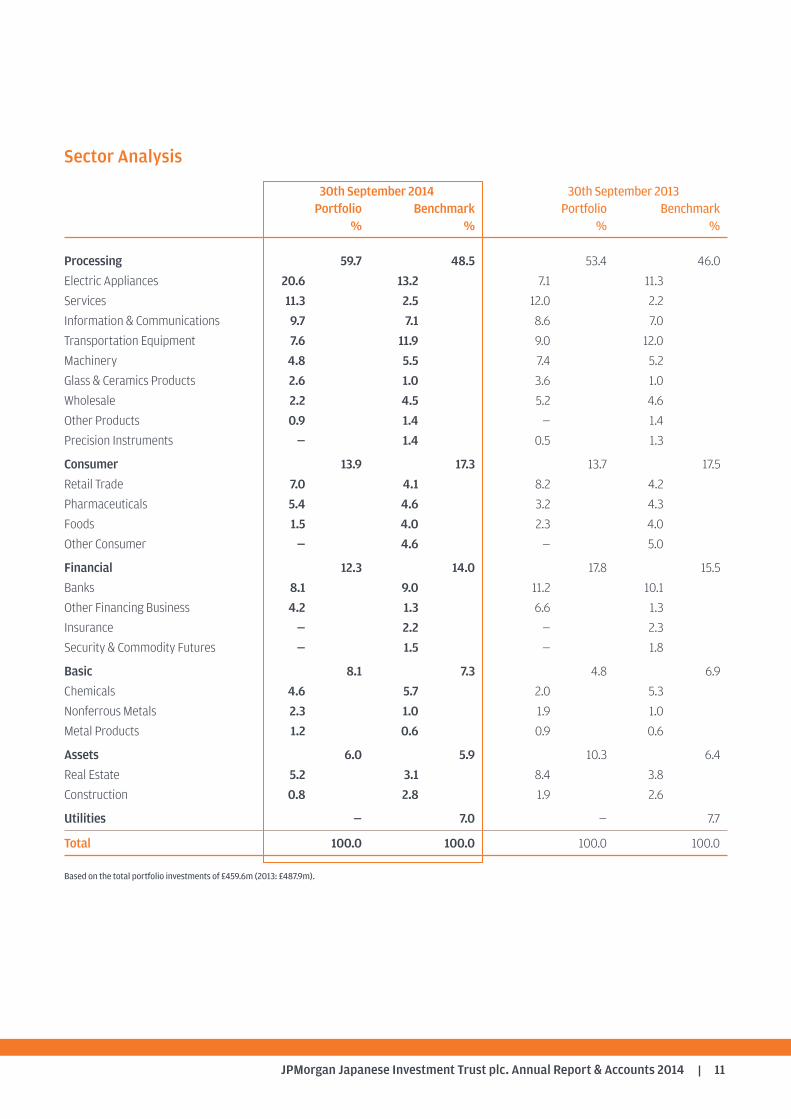

30th September 2014 30th September 2013Portfolio Benchmark Portfolio Benchmark

% % % %

Processing 59.7 48.5 53.4 46.0 Electric Appliances 20.6 13.2 7.1 11.3Services 11.3 2.5 12.0 2.2Information & Communications 9.7 7.1 8.6 7.0Transportation Equipment 7.6 11.9 9.0 12.0Machinery 4.8 5.5 7.4 5.2Glass & Ceramics Products 2.6 1.0 3.6 1.0Wholesale 2.2 4.5 5.2 4.6Other Products 0.9 1.4 — 1.4Precision Instruments — 1.4 0.5 1.3

Consumer 13.9 17.3 13.7 17.5 Retail Trade 7.0 4.1 8.2 4.2Pharmaceuticals 5.4 4.6 3.2 4.3Foods 1.5 4.0 2.3 4.0Other Consumer — 4.6 — 5.0

Financial 12.3 14.0 17.8 15.5 Banks 8.1 9.0 11.2 10.1Other Financing Business 4.2 1.3 6.6 1.3Insurance — 2.2 — 2.3Security & Commodity Futures — 1.5 — 1.8

Basic 8.1 7.3 4.8 6.9 Chemicals 4.6 5.7 2.0 5.3Nonferrous Metals 2.3 1.0 1.9 1.0Metal Products 1.2 0.6 0.9 0.6

Assets 6.0 5.9 10.3 6.4 Real Estate 5.2 3.1 8.4 3.8Construction 0.8 2.8 1.9 2.6

Utilities — 7.0 — 7.7

Total 100.0 100.0 100.0 100.0

Based on the total portfolio investments of £459.6m (2013: £487.9m).

Sector Analysis

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201412

ValuationCompany £’000

ProcessingElectric AppliancesHitachi 13,947Keyence 12,641Murata 9,795Omron 9,431Mitsubishi Electric 9,314Casio Computer 8,593Fanuc 8,153Minebea 6,696Sysmex 6,413Nidec 6,396Obara 3,240

94,619ServicesRakuten 8,738M3 6,926Sohgo Securities 6,368Cyberagent 5,232H.I.S 4,901Cookpad 4,224Oriental Land 4,172Nihon M&A Center 4,008Kakaku.com 3,824Infomart Corporation 3,612

52,005Information & CommunicationsSoftbank 13,112KDDI 10,185Nippon Telegraph & Telephone 8,123Hikari Tsushin 5,147Otsuka 4,335Digital Garage 3,797

44,699Transportation EquipmentMazda Motor 14,974Fuji Heavy Industries 11,169Shimano 7,258Yamaha Motor 1,651

35,052

ValuationCompany £’000

MachineryDaikin Industries 10,809Kubota 9,923Makita 1,241

21,973Glass & Ceramics ProductsTaiheiyo Cement 5,955Nippon Sheet Glass 5,685

11,640WholesaleDaiichiKosho 5,076Misumi 4,992

10,068Other ProductsPigeon 4,299

4,299

Total Processing 274,355

ConsumerRetail TradeDon Quijote 9,317Cosmos Pharmaceutical 7,347MonotaRO 6,999Seria 4,332Askul 4,182

32,177PharmaceuticalsAstellas Pharma 8,211Nippon Shinyaku 7,699ONO Pharmaceutical 7,633Peptidream 987

24,530FoodsKikkoman 4,112Coca-Cola 2,904

7,016

Total Consumer 63,723

Strategic Report continuedList of Investmentsat 30th September 2014

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 13

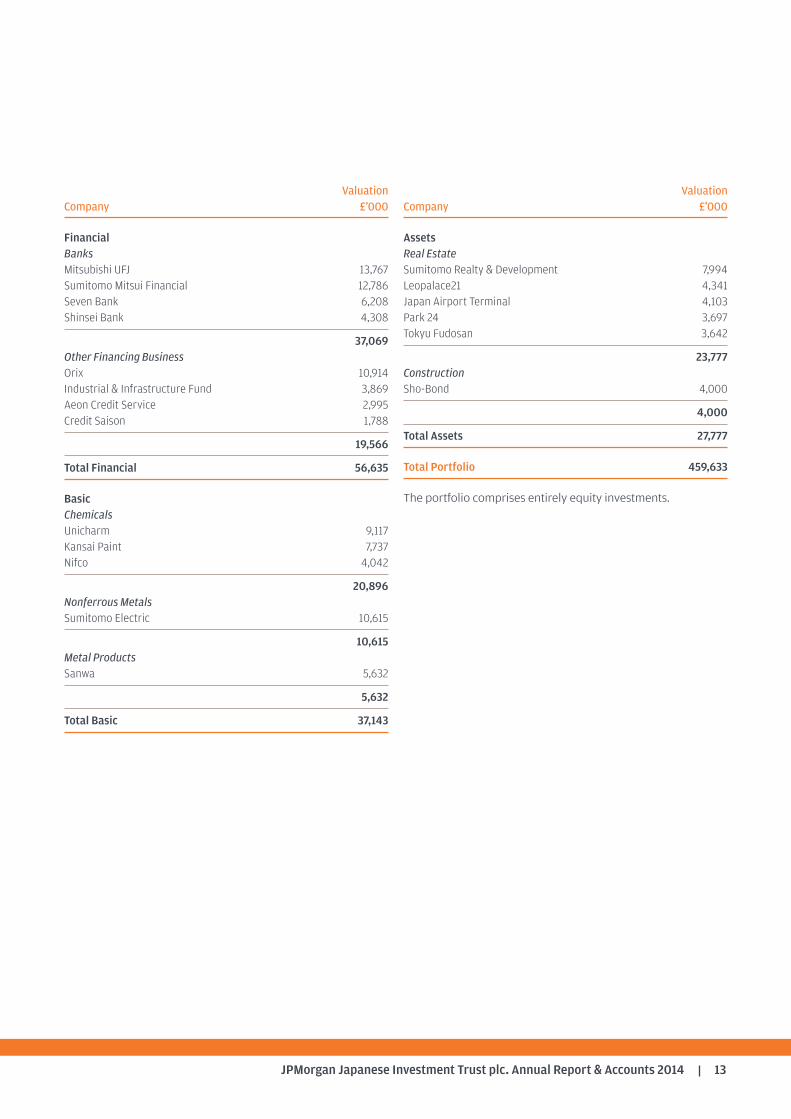

ValuationCompany £’000

FinancialBanksMitsubishi UFJ 13,767Sumitomo Mitsui Financial 12,786Seven Bank 6,208Shinsei Bank 4,308

37,069Other Financing BusinessOrix 10,914Industrial & Infrastructure Fund 3,869Aeon Credit Service 2,995Credit Saison 1,788

19,566

Total Financial 56,635

BasicChemicalsUnicharm 9,117Kansai Paint 7,737Nifco 4,042

20,896Nonferrous MetalsSumitomo Electric 10,615

10,615Metal ProductsSanwa 5,632

5,632

Total Basic 37,143

ValuationCompany £’000

AssetsReal EstateSumitomo Realty & Development 7,994Leopalace21 4,341Japan Airport Terminal 4,103Park 24 3,697Tokyu Fudosan 3,642

23,777ConstructionSho-Bond 4,000

4,000

Total Assets 27,777

Total Portfolio 459,633

The portfolio comprises entirely equity investments.

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201414

The aim of the Strategic Report is to provide shareholders withthe ability to assess how the Directors have performed theirduty to promote the success of the Company during the yearunder review. To assist shareholders with this assessment, theStrategic Report sets out the structure and objective of theCompany, its investment policies and risk management,investment limits and restrictions, performance and keyperformance indicators, share capital, principal risks and howthe Company seeks to manage those risks, the Company’senvironmental, social and ethical policy and finally its futuredevelopments.

Business Review

Business of the Company JPMorgan Japanese Investment Trust plc is an investment trustcompany that has a premium listing on the London StockExchange and is fully listed on the New Zealand StockExchange. In seeking to achieve its objectives, the Companyemploys JPMorgan Funds Limited (‘JPMF’ or the ‘Manager’)which, in turn, delegates portfolio management to JPMorganAsset Management (UK) Limited, to actively manage theCompany’s assets. The Board has determined investmentpolicies and related guidelines and limits. These objectives,investment policies and related guidelines and limits aredetailed below.

The Company is subject to UK and European legislation andregulations including UK company law, UK Financial ReportingStandards, the UK Listing, Prospectus, Disclosure andTransparency Rules, taxation law and the Company’s ownArticles of Association.

The Company is an investment company within the meaningof Section 833 of the Companies Act 2006 and has beenapproved by HM Revenue & Customs as an investment trust(for the purposes of Sections 1158 and 1159 of the CorporationTax Act 2010). As a result the Company is not liable for taxationon capital gains. The Directors have no reason to believe thatapproval will not continue to be retained. The Company is nota close company for taxation purposes.

Investment ObjectiveThe Company’s objective is to achieve capital growth frominvestments in Japanese companies by long termoutperformance of the Company’s benchmark index, the TokyoStock Exchange 1st Section Index (‘TOPIX’) expressed in sterlingterms.

Investment Policies and Risk ManagementIn order to achieve its stated investment policy and to seek tomanage investment risks, the Company invests in a diversified

portfolio of quoted Japanese companies. The number ofinvestments in the portfolio will normally range between 50and 100. The average number of holdings in the portfolio hasreduced in recent years as the Manager has focused on thosecompanies that have strong balance sheets and are notaffected by macro-economic issues. The Company makes useof both long and short term borrowings to increase returns andfocuses on first hand company research and analysis.

Investment Restrictions and GuidelinesThe Board seeks to manage the Company’s risk by imposingvarious investment limits and restrictions:

• The Company must maintain 97.5% of investments inJapanese securities or securities providing an indirectinvestment in Japan. (30th September 2014: 100%).

• No investment to be more than 5% in excess of benchmarkweighting at time of purchase. (30th September 2014: nil).

• The Company does not normally invest in unquotedinvestments and to do so requires prior Board approval.(30th September 2014: nil).

• The Company’s gearing policy is to operate within a rangeof 5% net cash to 15% geared in normal market conditions.(30th September 2014: 12.7%).

• The Company does not normally enter into derivativetransactions and to do so requires prior Board approval.(30th September 2014: nil).

• The Company will not invest more than 15% of its grossassets in other UK listed investment companies and willnot invest more than 10% of its gross assets in companiesthat themselves may invest more than 15% of gross assetsin UK listed investment companies. (30th September2014: nil).

• The Investment Manager does not hedge the portfolioagainst foreign currency risk.

These limits and restrictions may be varied by the Board at anytime at its discretion.

Monitoring of ComplianceCompliance with the Board’s investment restrictions andguidelines is monitored continuously by the Manager and isreported to the Board on a monthly basis.

PerformanceIn the year ended 30th September 2014, the Companyproduced a total return to shareholders of -7.4% and a totalreturn on net assets of -4.4%. This compares with thereturn on the Company’s benchmark of +0.9%. As at

Strategic Report continuedBusiness Review

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 15

30th September 2014, the value of the Company’s investmentportfolio was £459.6 million. The Investment Manager’sReport on pages 5 to 7 includes a review of developmentsduring the year as well as information on investment activitywithin the Company’s portfolio.

Total Loss, Revenue and Dividends Gross total loss for the year amounted to £14.5 million (2013:return £139.8 million) and the net total loss after deductingthemanagement fee, other administrative expenses, financecosts and taxation, amounted to £18.9 million (2013: return£135.8 million). Distributable income for the year amountedto £4.0million (2013: £4.5 million).

The Directors have declared a dividend of 2.80p (2013: 2.80p)per share. This dividend amounts to £4.5 million (2013:£4.5 million) and the revenue reserve after allowing for thedividend will amount to £1.9 million (2013: £2.4 million).The dividend will be subject to shareholder approval at theforthcoming Annual General Meeting and is detailed furtherbelow.

Key Performance Indicators (‘KPIs’) The Board uses a number of financial KPIs to monitor andassess the performance of the Company. The principal KPIs are:

• Performance against the benchmark indexThis is the most important KPI by which performance isjudged. Information on the Company’s performance isgiven in the Chairman’s Statement and the InvestmentManager’s Report on pages 2 to 4 and 5 to 7 respectively.

Performance Relative to Benchmark IndexFigures have been rebased to 100 at 30th September 2004

Source: Morningstar.

JPMorgan Japanese – share price total return.

JPMorgan Japanese – net asset value total return.

The benchmark index is represented by the grey dotted horizontal line.

Ten Year PerformanceFigures have been rebased to 100 at 30th September 2004

Source: Morningstar/ MSCI.

JPMorgan Japanese – share price total return.

JPMorgan Japanese – net asset value total return.

Benchmark.

• Performance against the Company’s peers Whilst the principal objective is to achieve capital growthrelative to the benchmark, the Board also monitors theperformance relative to a broad range of competitor funds.

• Performance attributionThe purpose of performance attribution analysis is toassess how the Company achieved its performance relativeto its benchmark index, i.e. to understand the impact on theCompany’s relative performance of the variouscomponents such as asset allocation and stock selection.Details of the attribution analysis for the year ended30th September 2014 are given in the InvestmentManager’s Report on page 6.

• Share price discount to net asset value (‘NAV’) per shareThe Board recognises that the possibility of a wideningdiscount can be a key disadvantage of investment truststhat can discourage investors. The Board therefore hasa share repurchase programme which seeks to addressimbalances in supply of and demand for the Company’sshares within the market. Its aim is to minimise the volatilityand absolute level of the discount to NAV per share atwhich the Company’s shares trade in relation to its peers inthe sector. In the year to 30th September 2014, the sharestraded between a discount of 6.3% and 13.9% at an averageof 9.8%.

60

70

80

90

100

110

120

20142013201220112010200920082007200620052004

60

80

100

120

140

160

180

20142013201220112010200920082007200620052004

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201416

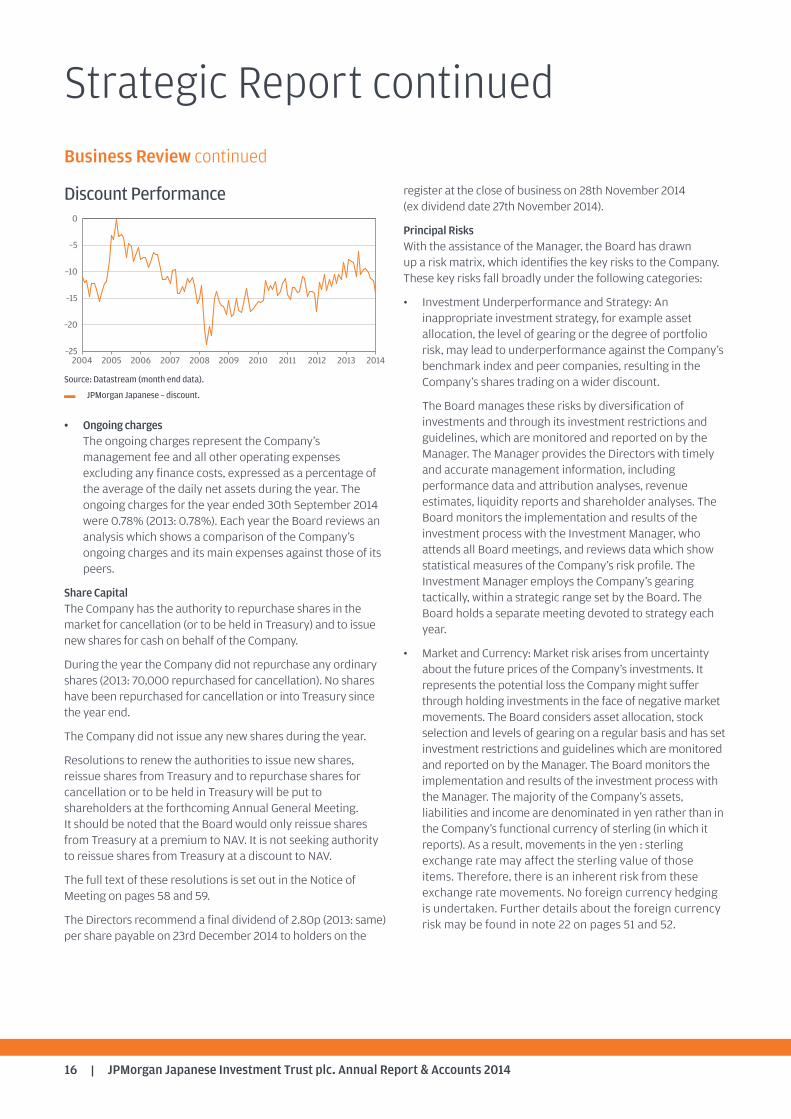

Discount Performance

Source: Datastream (month end data).

JPMorgan Japanese – discount.

• Ongoing chargesThe ongoing charges represent the Company’smanagement fee and all other operating expensesexcluding any finance costs, expressed as a percentage ofthe average of the daily net assets during the year. Theongoing charges for the year ended 30th September 2014were 0.78% (2013: 0.78%). Each year the Board reviews ananalysis which shows a comparison of the Company’songoing charges and its main expenses against those of itspeers.

Share CapitalThe Company has the authority to repurchase shares in themarket for cancellation (or to be held in Treasury) and to issuenew shares for cash on behalf of the Company.

During the year the Company did not repurchase any ordinaryshares (2013: 70,000 repurchased for cancellation). No shareshave been repurchased for cancellation or into Treasury sincethe year end.

The Company did not issue any new shares during the year.

Resolutions to renew the authorities to issue new shares,reissue shares from Treasury and to repurchase shares forcancellation or to be held in Treasury will be put toshareholders at the forthcoming Annual General Meeting.It should be noted that the Board would only reissue sharesfrom Treasury at a premium to NAV. It is not seeking authorityto reissue shares from Treasury at a discount to NAV.

The full text of these resolutions is set out in the Notice ofMeeting on pages 58 and 59.

The Directors recommend a final dividend of 2.80p (2013: same)per share payable on 23rd December 2014 to holders on the

register at the close of business on 28th November 2014(ex dividend date 27th November 2014).

Principal RisksWith the assistance of the Manager, the Board has drawnup a risk matrix, which identifies the key risks to the Company.These key risks fall broadly under the following categories:

• Investment Underperformance and Strategy: Aninappropriate investment strategy, for example assetallocation, the level of gearing or the degree of portfoliorisk, may lead to underperformance against the Company’sbenchmark index and peer companies, resulting in theCompany’s shares trading on a wider discount.

The Board manages these risks by diversification ofinvestments and through its investment restrictions andguidelines, which are monitored and reported on by theManager. The Manager provides the Directors with timelyand accurate management information, includingperformance data and attribution analyses, revenueestimates, liquidity reports and shareholder analyses. TheBoard monitors the implementation and results of theinvestment process with the Investment Manager, whoattends all Board meetings, and reviews data which showstatistical measures of the Company’s risk profile. TheInvestment Manager employs the Company’s gearingtactically, within a strategic range set by the Board. TheBoard holds a separate meeting devoted to strategy eachyear.

• Market and Currency: Market risk arises from uncertaintyabout the future prices of the Company’s investments. Itrepresents the potential loss the Company might sufferthrough holding investments in the face of negative marketmovements. The Board considers asset allocation, stockselection and levels of gearing on a regular basis and has setinvestment restrictions and guidelines which are monitoredand reported on by the Manager. The Board monitors theimplementation and results of the investment process withthe Manager. The majority of the Company’s assets,liabilities and income are denominated in yen rather than inthe Company’s functional currency of sterling (in which itreports). As a result, movements in the yen : sterlingexchange rate may affect the sterling value of thoseitems. Therefore, there is an inherent risk from theseexchange rate movements. No foreign currency hedgingis undertaken. Further details about the foreign currencyrisk may be found in note 22 on pages 51 and 52.

–25

–20

–15

–10

–5

0

20142013201220112010200920082007200620052004

Strategic Report continuedBusiness Review continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 17

• Political, Economic and Governance: Administrative risks,such as the imposition of restrictions on the free movementof capital. These risks are discussed by the Board on aregular basis.

• Loss of Investment Team or Investment Manager: A suddendeparture of the Investment Manager or several membersof the investment management team could result in a shortterm deterioration in investment performance. TheManager takes steps to reduce the likelihood of such anevent by ensuring appropriate succession planning and theadoption of a team based approach, as well as specialefforts to retain key personnel.

• Discount: A disproportionate widening of the discountrelative to the Company’s peers could result in loss of valuefor shareholders. The Board regularly discusses discountpolicy and has set parameters for the Manager and theCompany’s broker to follow.

• Change of Corporate Control of the Manager: The Boardholds regular meetings with senior representatives of theManager in order to obtain assurance that the Managercontinues to demonstrate a high degree of commitment toits investment trust business through the provision ofsignificant resources.

• Accounting, Legal and Regulatory: In order to qualifyas an investment trust, the Company must complywith Section 1158 of the Corporation Tax Act 2010(‘Section 1158’). Details of the Company’s approval aregiven under ‘Business of the Company’ above. Were theCompany to breach Section 1158, it may lose investmenttrust status and, as a consequence, gains within theCompany’s portfolio would be subject to Capital GainsTax. The Section 1158 qualification criteria are continuallymonitored by the Manager and the results reported to theBoard each month. The Company must also comply withthe provisions of the Companies Act 2006 and, since itsshares are listed on the London Stock Exchange, the UKLAListing Rules, Disclosure and Transparency Rules (‘DTRs’)and, as an investment trust, the Alternative InvestmentFund Managers Directive (‘AIFMD’). A breach of theCompanies Act could result in the Company and/or theDirectors being fined or the subject of criminalproceedings. Breach of the UKLA Listing Rules or DTRscould result in the Company’s shares being suspendedfrom listing which in turn would breach Section 1158. The

Board relies on the services of its Company Secretary, theManager and its professional advisers to ensurecompliance with the Companies Act 2006, the UKLAListing Rules, DTRs and AIFMD.

• Corporate Governance and Shareholder Relations: Detailsof the Company’s compliance with Corporate Governancebest practice, including information on relations withshareholders, are set out in the Corporate GovernanceStatement on pages 24 to 29.

• Operational: Disruption to, or failure of, the Manager’saccounting, dealing or payments systems or the Depositaryor Custodian’s records may prevent accurate reporting andmonitoring of the Company’s financial position. Details ofhow the Board monitors the services provided by JPMF andits associates and the key elements designed to provideeffective risk management and internal control are includedwithin the Risk Management and Internal Controls section ofthe Corporate Governance Statement on pages 28 and 29.

• Going concern: Pursuant to the Sharman Report, Boards arenow advised to consider going concern as a potential risk,whether or not there is an apparent issue arising in relationthereto. Going concern is considered rigorously on anongoing basis and the Board’s statement on going concernis detailed on page 22.

• Financial: The financial risks faced by the Company includemarket price risk, liquidity risk and credit risk. Furtherdetails are disclosed in note 22 on pages 50 to 56.

Board DiversityWhen recruiting a new Director, the Board’s policy is to appointindividuals on merit. Diversity is important in bringing anappropriate range of skills and experience to the Board.

At 30th September 2014, there were five male Directors and nofemale Directors on the Board.

Employees, Social, Community and Human Rights IssuesThe Company is managed by JPMF, has no employees and all ofits Directors are non-executive, the day to day activities beingcarried out by third parties. There are therefore no disclosuresto be made in respect of employees. The Board notes thepolicy statements of JPMorgan Asset Management (UK) Limited(‘JPMAM’) in respect of Social, Community, Environmental andHuman Rights issues, as highlighted in italics.

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201418

Social, Community, Environmental and Human RightsJPMAM believes that companies should act in a socially responsiblemanner. Although our priority at all times is the best economic interestsof our clients, we recognise that, increasingly, non-financial issues suchas social and environmental factors have the potential to impact theshare price, as well as the reputation of companies. Specialists withinJPMAM’s environmental, social and governance (‘ESG’) team are taskedwith assessing how companies deal with and report on social andenvironmental risks and issues specific to their industry.

JPMAM is also a signatory to the United Nations Principles of ResponsibleInvestment, which commits participants to six principles, with the aim ofincorporating ESG criteria into their processes when making stockselection decisions and promoting ESG disclosure. Our detailed approachto how we implement the principles is available on request.

Greenhouse Gas EmissionsThe Company is managed by JPMF with portfolio managementdelegated to JPMAM. It has no employees and all of itsDirectors are non-executive, the day to day activities beingcarried out by third parties. There are therefore no disclosures

to be made in respect of employees. The Company itself has nopremises, consumes no electricity, gas or diesel fuel andconsequently does not have a measurable carbon footprint.JPMAM is a signatory to the Carbon Disclosure Project andJPMorgan Chase is a signatory to the Equator Principles onmanaging social and environmental risk in project finance.

Future Developments The future development of the Company is dependent on thesuccess of the Company’s investment strategy in the lightof economic and equity market developments and thecontinued support of its shareholders. The InvestmentManager discusses the outlook in his report on pages 5 to 7.

By order of the Board Rebecca Burtonwood for and on behalf of JPMorgan Funds Limited Company Secretary

12th November 2014

Strategic Report continuedBusiness Review continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 19

Jeremy Paulson-Ellis (Chairman)

A Director since 1996.

Last reappointed to the Board: 2013.

Until 30th June 2009, he was Chairman of Genesis Investment Management LLP,a specialist institutional investment manager. Prior to that Mr Paulson-Ellis wasChairman of Vickers da Costa Limited where he had responsibility for all their Japanesebusiness.

Connections with Manager: None.

Shared directorships with other Directors: None.

Alan Barber (Chairman of the Audit Committee)

A Director since 2006.

Last reappointed to the Board: 2013.

Currently Non-Executive Chairman of the Management Consulting Group plc anda Director and Audit Committee Chairman of Witan Pacific Investment Trust plc. Formerlya Director of Impax Asian Environmental Markets plc, Mr Barber is a CharteredAccountant and was a partner in KPMG for twenty five years prior to his retirement in2004.

Connections with Manager: None.

Shared directorships with other Directors: None.

Andrew Fleming (Chairman Designate)

A Director since 2004.

Last reappointed to the Board: 2013.

He has over thirty years of international investment management experience, whichincluded six years running an investment company in Tokyo and most recently was ChiefExecutive of Kames Capital. Mr Fleming is a member of the Investment Committee of theNational Trust.

Connections with Manager: None.

Shared directorships with other Directors: None.

GovernanceBoard of Directors

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201420

All Directors, with the exception of Mr Paulson-Ellis, are members of the AuditCommittee. All Directors are members of the Nomination and Remuneration Committee.All Directors are considered independent of the Manager.

Keith Percy

A Director since 2004.

Last reappointed to the Board: 2013.

Currently Chairman of Brunner Investment Trust plc and a Director of Standard LifeEquity Income Trust plc and Henderson Smaller Companies Investment Trust plc,Mr Percy was formerly a Director of F&C Asset Management plc.

Connections with Manager: None.

Shared directorships with other Directors: None.

Sir Stephen Gomersall, KCMG

A Director since 2013.

Last reappointed to the Board: 2013.

Deputy Chairman of Hitachi Europe and a director of a number of Hitachi Groupcompanies in the UK. Sir Stephen entered the Foreign & Commonwealth Office in 1970and held a number of appointments overseas including being Ambassador to Japanfrom 1999 to 2004. He has spent more than fourteen years living and working in Japan.

Connections with Manager: None.

Shared directorships with other Directors: None.

Governance continuedBoard of Directors continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 21

The Directors present their report and the audited financialstatements for the year ended 30th September 2014.

A number of disclosures previously incorporated in theDirectors’ Report are now included in the Strategic Report.These include: Business of the Company; Investment Objective;Investment Policies and Risk Management; InvestmentRestrictions and Guidelines; Performance; Total Return.Revenue and Dividends; KPIs; Share Capital; Principal Risks;Employee, Social, Community and Human Rights Issues; andFuture Developments.

Management of the Company

TheManager and Company Secretary to the Company isJPMorgan Funds Limited. The Manager is employed undera contract which can be terminated on six months’ notice,without penalty. If the Company wishes to terminate thecontract on shorter notice, the balance of remuneration ispayable by way of compensation.

The Manager is a wholly-owned subsidiary of JPMorgan ChaseBank which, through other subsidiaries, also providesaccounting, banking, dealing and custodian services to theCompany.

Portfolio management is delegated to JPMorgan AssetManagement (UK) Limited. The current ManagementAgreement was entered into with effect from 1st July 2014following the implementation of a number of changes requiredby the Alternative Investment Fund Managers Directive, asdetailed in the Chairman’s Statement on page 3.

From 1st December 2007, the Board and the Manager agreedthat day-to-day investment management activity would beconducted in Tokyo by JPMorgan Asset Management (Japan)Limited, a fellow investment management subsidiary and partof JPMorgan Chase Bank.

The Board conducts a formal evaluation of the performance of,and contractual relationship with, the Manager on an annualbasis. Part of this evaluation includes a consideration of themanagement fees and whether the service received is value formoney for shareholders. No separate managementengagement committee has been established because allDirectors are considered to be independent of the Managerand, given the nature of the Company’s business, it is felt thatall Directors should take part in the review process.

The Board has thoroughly reviewed the performance of theManager in the course of the year. The review covered theperformance of the Manager, its management processes,investment style, resources and risk controls and the quality ofsupport that the Company receives from the Manager includingthe marketing support provided. As part of this process, theBoard visits Japan each year. The Board is of the opinion thatthe continuing appointment of the Manager is in the bestinterests of shareholders as a whole. Such a review is carriedout on an annual basis.

The Alternative Investment Fund Managers Directive (‘AIFMD’)

JPMF, an affiliate of JPMAM, has been appointed as theCompany’s alternative investment fund manager (‘AIFM’).JPMF has been approved as an AIFM by the Financial ConductAuthority (‘FCA’). For the purposes of the AIFMD the Companyis an alternative investment fund (‘AIF’).

The Company entered into a new investment managementagreement with JPMF on 1st July 2014. JPMF has delegatedresponsibility for the day to day management of the Company’sportfolio to JPMAM. JPMF is required to ensure that a depositaryis appointed to the Company. The Company therefore hasappointed BNY Mellon Trust and Depositary (UK) Limited (‘BNY’)as its depositary. BNY has delegated its safekeeping function tothe custodian, JPMorgan Chase Bank, N.A., however, BNYremains responsible for the oversight of the custody of theCompany’s assets and for monitoring its cash flows.

The AIFMD requires certain information to be made availableto investors in AIFs before they invest and requires thatmaterial changes to this information be disclosed in the annualreport of each AIF. Investor Disclosure Documents, which setout information on the Company’s investment strategy andpolicies, leverage, risk, liquidity, administration, management,fees, conflicts of interest and other shareholder information areavailable on the Company’s website at www.jpmjapanese.co.uk

There have been no material changes (other than thosereflected in these financial statements) to this informationrequiring disclosure. Any information requiring immediatedisclosure pursuant to the AIFMD will be disclosed to theLondon Stock Exchange through a primary informationprovider. As an authorised AIFM, JPMF will make the requisitedisclosures on remuneration levels and polices to the FCA atthe appropriate time.

Directors’ Report

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201422

Management Fee

The fixed basic annual management fee, negotiated in 2005, isa sliding scale based on the Company’s net assets. Themanagement fee is charged monthly in arrears.

Net assets Fee level

First £465 million under management 0.65%£465 million to £930 million under management 0.485%Over £930 million under management 0.40%

The management fee includes a contribution towards theManager’s general marketing and client administration costs.

If the Company invests in funds managed or advised by theManager, or any of its associated companies, those investmentsare excluded from the calculation of the fixed basic annualmanagement fee.

Going Concern

The Directors believe that, having considered the Company’sinvestment objective (see page 14), risk management policies(see page 14), liquidity risk (see note 22 on page 55), capitalmanagement policies and procedures (see note 23 on page 57),the nature of the portfolio and expenditure and cashflowprojections, the Company has adequate resources, anappropriate financial structure and suitable managementarrangements in place to continue in operational existence forthe foreseeable future. For these reasons, they consider thatthere is reasonable evidence to continue to adopt the goingconcern basis in preparing the accounts.

Directors

All Directors served throughout the year and their details areincluded on pages 19 and 20. Details of their beneficialshareholdings may be found in the Directors’ RemunerationReport on page 31.

Andrew Fleming and Keith Percy, having been Directors formore than nine years, will retire and seek reappointment.Jeremy Paulson-Ellis will retire at the conclusion of the AnnualGeneral Meeting and is not seeking reappointment.

In accordance with the Company’s Articles of Associationrequirement that a third of Directors retire by rotation and seekreappointment each year (excluding those required to retireand seek reappointment annually), Alan Barber will retire byrotation and, being eligible, seeks reappointment at theforthcoming Annual General Meeting.

Christopher Samuel will be appointed a Director of theCompany following the Annual General Meeting on19th December 2014.

The Nomination Committee, having considered the Directors’qualifications, performance and contribution to the Board andits Committees, confirms that each Director continues to beeffective and demonstrates commitment to the role and theBoard recommends to shareholders that those standing forreappointment be reappointed.

Director Indemnification and Insurance

As permitted by the Company’s Articles of Association, eachDirector has the benefit of an indemnity which is a qualifyingthird party indemnity, as defined by Section 234 of theCompanies Act 2006. The indemnities were in place duringthe year and as at the date of this report.

An insurance policy is maintained by the Company whichindemnifies the Directors of the Company against certainliabilities arising in the conduct of their duties. There is nocover against fraudulent or dishonest actions.

Disclosure of information to theAuditors

In the case of each of the persons who are Directors of theCompany at the time when this report was approved:

(a) so far as each of the Directors is aware, there is no relevantaudit information (as defined in the Companies Act 2006) ofwhich the Company’s Auditors are unaware, and

(b) each of the Directors has taken all the steps that he ought tohave taken as a Director in order to make himself aware ofany relevant audit information (as defined) and to establishthat the Company’s Auditors are aware of that information.

The above confirmation is given and should be interpreted inaccordance with the provisions of Section 418(2) of theCompanies Act 2006.

Independent Auditors

Further to a review of audit services in 2013, Begbies retired asthe Company’s Auditors at the 2013 Annual General Meeting.PricewaterhouseCoopers LLPwere appointed Auditors of theCompany in their place. PricewaterhouseCoopers LLP haveexpressed their willingness to continue in office as the Auditorsand a resolution to reappoint PricewaterhouseCoopers LLP andauthorise the Directors to determine their remuneration for theensuing year, will be proposed at the Annual General Meeting.

Governance continuedDirectors’ Report continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 23

Section 992 Companies Act 2006

The following disclosures are made in accordance withSection 992 Companies Act 2006.

Capital StructureAs at 30th September 2014, the Company’s issued share capitalcomprised 161,248,078 ordinary shares of 25p each. Therewere no shares held in Treasury.

Voting Rights in the Company’s sharesDetails of the voting rights in the Company’s shares as at thedate of this report are given in note 16 to the Notice of AnnualGeneral Meeting on page 60.

Notifiable Interests in the Company’s Voting RightsAt the year end, the following had declared a notifiable interestin the Company’s voting rights:

Number of Shareholders shares held %

Lazard Asset Management1 29,229,402 18.11607 Capital Partners1 26,353,471 16.3Derbyshire County Council1 6,564,361 4.1Legal & General2 4,928,847 3.1

1Indirect holding.2Direct holding.

No further changes had been notified since the year end to thedate of this report.

The Company is also aware that as at 30th September 2014,approximately 3.5% of the Company’s total voting rights wereheld by individuals through the savings products managed byJ.P. Morgan Asset Management and registered in the name ofChase Nominees Limited as at the year end. If those votingrights are not exercised by the beneficial holders, inaccordance with the terms and conditions of the savingsproducts, under certain circumstances, J.P. Morgan AssetManagement has the right to exercise those voting rights. Thatright is subject to certain limits and restrictions and falls awayat the conclusion of the relevant general meeting.

The rules concerning the appointment, reappointment andreplacement of Directors, amendment of the Company’sArticles of Association and powers to issue or buy back theCompany’s shares are contained in the Articles of Associationof the Company and the Companies Act 2006.

There are no restrictions concerning the transfer of securitiesin the Company; no special rights with regard to control

attached to securities; no agreements between holders ofsecurities regarding their transfer known to the Company; noagreements to which the Company is party that affect itscontrol following a takeover bid; and no agreements betweenthe Company and its Directors concerning compensation forloss of office.

Annual General Meeting

NOTE: THIS SECTION IS IMPORTANT AND REQUIRES YOURIMMEDIATE ATTENTION. If you are in any doubt as to the actionyou should take, you should seek your own personal financialadvice from your stockbroker, bank manager, solicitor or otherfinancial adviser authorised under the Financial Services andMarkets Act 2000.

Resolutions relating to the following item of special businesswill be proposed at the forthcoming Annual General Meeting:

The full text of the resolutions is set out in the Notice of AnnualGeneral Meeting on pages 58 and 59.

(i) Authority to allot new shares and to disapply statutorypre-emption rights (resolutions 9 and 10)

The Directors will seek renewal of the authority at the AnnualGeneral Meeting to issue up to 8,062,400 new ordinary sharesfor cash or by way of a sale of Treasury shares up to anaggregate nominal amount of £2,015,600 such amount beingequivalent to 5% of the present issued share capital (excludingTreasury shares) as at the last practicable date before thepublication of this document or, if different, the number ofordinary shares which is equal to approximately 5% of theCompany’s issued share capital (excluding Treasury shares) asat the date of the passing of the resolution.

This authority will expire at the conclusion of the AnnualGeneral Meeting in 2015 unless renewed at a prior generalmeeting.

Resolution 10 will enable the allotment of shares otherwisethan by way of a pro rata issue to existing shareholders. It isadvantageous for the Company to be able to issue new shares(or to sell Treasury shares) to participants purchasing sharesthrough the JPMorgan savings products and also to otherinvestors when the Directors consider that it is in the bestinterests of shareholders to do so. Any such issues would onlybe made at prices greater than the net asset value (‘NAV’),thereby increasing the NAV per share and spreading theCompany’s administrative expenses, other than themanagement fee which is charged on the value of theCompany’s market capitalisation, over a greater number of

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201424

shares. The issue proceeds would be available for investmentin line with the Company’s investment policies. No issue ofshares will be made which would effectively alter the control ofthe Company without the prior approval of shareholders ingeneral meeting.

The Company currently does not hold any shares in the capitalof the Company in Treasury.

(ii) Authority to repurchase the Company’s Shares (resolution 11)The authority to repurchase up to 14.99% of the Company’sissued share capital, granted by shareholders at the 2013Annual General Meeting, will expire on 19th June 2015 unlessrenewed at the forthcoming Annual General Meeting. TheDirectors consider that the renewal of the authority is in theinterests of shareholders as a whole, as the repurchase ofshares at a discount to their underlying NAV enhances the NAVof the remaining shares.

Resolution 11 gives the Company authority to repurchase itsown issued shares in the market as permitted by theCompanies Act 2006. The authority limits the number of sharesthat could be purchased to a maximum of 24,171,000 shares,representing approximately 14.99% of the Company’s issuedshares as at 10th November 2014 (being the latest practicabledate prior to the publication of this document) or, if different,the number of ordinary shares which is equal to 14.99% of theCompany’s issued share capital (excluding Treasury shares) asat the date of the passing of the resolution. The authority alsosets minimum an maximum prices. The authority also setsminimum and maximum prices.

If resolution 11 is passed at the Annual General Meeting, theBoard may repurchase the shares for cancellation or hold themin Treasury pursuant to the authority granted to it for possiblereissue at a premium to NAV.

Any repurchase will be at the discretion of the Board and willbe made in the market only at prices below the prevailing NAVper share, thereby enhancing the NAV of the remaining shares,as and when market conditions are appropriate. The authorityto repurchase shares will expire on 18th June 2016, but it is theBoard’s intention to seek renewal of the authority at the 2015Annual General Meeting.

Recommendation

The Board considers that resolutions 10 to 12 are likely topromote the success of the Company and are in the bestinterests of the Company and its shareholders as a whole.The Directors unanimously recommend that you vote in favourof the resolutions as they intend to do, where voting rights areexercisable, in respect of their own beneficial holdings which

amount in aggregate to 23,349 shares representingapproximately 0.01% of the voting rights of the Company.

Corporate Governance StatementCompliance

The Company is committed to high standards of corporategovernance. This statement, together with the Statement ofDirectors’ Responsibilities on page 33, indicates how theCompany has applied the principles of good governance of theFinancial Reporting Council’s UK Corporate Governance Code(the ‘UK Corporate Governance Code’) and the Association ofInvestment Companies’ (‘AIC’) Code of Corporate Governance(the ‘AIC Code’), which complements the UK CorporateGovernance Code and provides a framework of best practicefor investment trusts.

The Board is responsible for ensuring the appropriate level ofcorporate governance and considers that the Company hascomplied with the best practice provisions of the UK CorporateGovernance Code and of the AIC Code, other than in respect ofthe provision relating to the appointment of a seniorindependent director, and insofar as they are relevant to theCompany’s business, throughout the year under review.

Role of the Board

The Management Agreement between the Company and theManager sets out the matters which have been delegated tothe Manager. This includes management of the Company’sassets and the provision of accounting, company secretarial,administration, and some marketing services. All other mattersare reserved for the approval of the Board. A formal scheduleof matters reserved to the Board for decision has beenapproved. This includes determination and monitoring of theCompany’s investment objective and policy and its futurestrategic direction, gearing policy, management of the capitalstructure, appointment and removal of third party serviceproviders, review of key investment and financial data and theCompany’s corporate governance and risk controlarrangements.

At each Board meeting, Directors’ interests are considered.These are reviewed carefully, taking into account thecircumstances surrounding them, and, if consideredappropriate, are approved. It was resolved that there were noactual or indirect interests of a Director which conflicted withthe interests of the Company, which arose during the year.

Following the introduction of The Bribery Act 2010, the Boardhas adopted appropriate procedures designed to prevent

Governance continuedDirectors’ Report continued

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 2014 25

bribery. It confirms that the procedures have operatedeffectively during the year under review.

The Board meets at least quarterly during the year andadditional meetings are arranged as necessary. Full and timelyinformation is provided to the Board to enable it to functioneffectively and to allow Directors to discharge theirresponsibilities.

There is an agreed procedure for Directors to take independentprofessional advice, if necessary, and at the Company’sexpense. This is in addition to the access that every Directorhas to the advice and services of the Company Secretary, whichis responsible to the Board for ensuring that Board proceduresare followed and for compliance with applicable rules andregulations.

Board Composition

The Board, chaired by Jeremy Paulson-Ellis, consisted of fivenon-executive Directors during the year ended 30th September2014, all of whom are regarded by the Board as independent ofthe Company’s Manager, including the Chairman. JeremyPaulson-Ellis will retire following the Annual General Meetingand Andrew Fleming will be appointed Chairman at that stage.Christopher Samuel will be appointed as a Director of theCompany following the Annual General Meeting. The Directorshave a breadth of investment knowledge, business and financialskills and experience relevant to the Company’s business andbrief biographical details of each Director are set out onpages 19 and 20.

There have been no changes to the Chairman’s othersignificant commitments during the year under review.

A review of Board composition and balance is included as partof the annual performance evaluation of the Board, details ofwhich may be found below. The Board has considered whethera senior independent director should be appointed, and hasconcluded that, due to the Company’s nature of business as aninvestment trust and because the Board is comprised entirelyof non-executive Directors, this is unnecessary at present.However, the Chairman of the Audit Committee leads theevaluation of the performance of the Chairman and is availableto shareholders if they have concerns that cannot be resolvedthrough discussions with the Chairman.

Tenure

Directors are initially appointed until the following AnnualGeneral Meeting when, under the Company’s Articles ofAssociation, it is required that they be reappointed by

shareholders. Thereafter, Directors are required to submitthemselves for reappointment at least every three years.The Chairman will meet with each Director before the Directoris proposed for reappointment, and subject to theperformance evaluation carried out each year, the Board willagree whether it is appropriate for the Director to seek anadditional term. The Board does not believe that length ofservice in itself necessarily disqualifies a Director fromseeking reappointment but, when making a recommendation,the Board will take into account the ongoing requirements ofthe UK Corporate Governance Code, including the needto refresh the Board and its Committees.

Any Directors with more than nine years’ service are requiredto submit themselves annually for reappointment. In this,regard, the Board recommends the reappointment of AndrewFleming and Keith Percy who, having served in excess of nineyears, retire at this year’s AGM. Andrew Fleming and KeithPercy have a wealth of experience in the financial sector andmake a valuable contribution to the workings of the Board. TheBoard considers that Andrew Fleming, who will be appointedChairman with effect from the end of the Annual GeneralMeeting, will demonstrate effective leadership of the Company.As part of the Board’s ongoing refreshment and successionplanning, Jeremy Paulson-Ellis is not seeking reappointmentand will retire immediately following the Annual GeneralMeeting. Christopher Samuel will be appointed as a Director ofthe Company following the Annual General Meeting.

The terms and conditions of Directors’ appointments are setout in formal letters of appointment, copies of which areavailable for inspection on request at the Company’s registeredoffice and at the Annual General Meeting.

Induction and Training

On appointment, the Manager and Company Secretary provideall Directors with induction training. Thereafter, regularbriefings are provided on changes in law and regulatoryrequirements that affect the Company and Directors. Directorsare encouraged to attend industry and other seminars coveringissues and developments relevant to investment trustcompanies. Regular reviews of the Directors’ training needs arecarried out by the Chairman by means of the evaluationprocess described below.

Meetings and Committees

The Board delegates certain responsibilities and functions toCommittees. Details of membership of these Committees areshown with Directors’ profiles on pages 19 and 20.

JPMorgan Japanese Investment Trust plc. Annual Report & Accounts 201426

The table below details the number of formal Board andCommittee meetings attended by each Director. During theyear under review there were five Board meetings, in additionto a meeting devoted to strategy, two Audit Committeemeetings and one meeting of the Nomination andRemuneration Committee. These meetings weresupplemented by additional meetings held to cover proceduralmatters and formal approvals. In addition there is regularcontact between the Directors and the Manager and CompanySecretary throughout the year.

Meetings Attended

Nominationand

Audit RemunerationDirector Board Committee Committee

Alan Barber 5 2 1Andrew Fleming 5 2 1Sir Stephen Gomersall, KCMG 5 2 1

Jeremy Paulson-Ellis1 5 2 1David Pearson2 2 1 1Keith Percy 5 2 1

1Invited to attend the Audit Committee meetings held during the year.2Retired December 2013.

Board Committees