Embed Size (px)

Citation preview

ird.govt.nz

B–23

AnnualReport

2015

Crown Copyright © 2015

This work is licensed under the Creative Commons Attribution 3.0 New Zealand licence. In essence, you are free to copy, distribute and adapt the work, as long as you attribute the work to the Crown and abide by the other licence terms. To view a copy of this licence, visit

creativecommons.org

Please note that no departmental or governmental emblem, logo or Coat of Arms may be used in any way that infringes any provision of the Flags, Emblems, and Names Protection Act 1981.

legislation.govt.nz

Attribution to the Crown should be in written form and not by reproduction of any such emblem, logo or Coat of Arms.

ISSN 1176-6654 (Print)

ISSN 2230-4053 (Online)

ird.govt.nz

Presented to the House of Representatives pursuant to the Public Finance Act 1989 and the Tax Administration Act 1994.

ANNUAL REPORT 2015 1

About Inland Revenue 7

Delivering and improving our core business 11

Contributing to the Government’s priorities 23

Business Transformation 31

Organisational health 35

Our performance 43

Measuring our performance 57

Departmental financial statements 93

Non-departmental financial schedules 125

Audit Report 145

Additional information 149

Contents

2 ANNUAL REPORT 2015

From the Commissioner

A year of making tax simpler

As Commissioner I’m enormously proud of how much Inland Revenue has achieved for the people of New Zealand. This year’s Annual Report reflects many of the improvements you’ll notice next time you look for information online, file a return or claim a refund. We’re making the business of tax and entitlements simpler, more open and more certain for customers and businesses across New Zealand.

Easier for customers

Our Business Transformation will completely change how people interact with the revenue system in future. And as we prepare for transformation, we’re making it easier every day for businesses and individuals, through continuous improvement and innovation.

More people are doing a lot more online. During the year we improved our website and myIR online services, and made it easier to register and find information. Since August customers have been able to activate their new myIR account instantly via text. Customers are embracing new digital opportunities – last year 67% of returns and almost 83% of payments were done online. Our mobile app that lets small businesses do GST on the go, developed through crowd-sourcing and research, is hugely popular.

Going digital gives customers increased certainty. But if they need to call us we’re answering more calls and answering them faster: 75% of our 3.24 million calls received last year were answered in less than two minutes. Voice ID, with 1.5 million customers registered, and automatic call-back makes the process even smoother.

These changes and more contribute to Better Public Services, making it simpler and more seamless for New Zealanders to deal with Government. We’re working with many other agencies on a range of projects from sharing information that supports customers to joint service delivery. Businesses are noticing the difference: a recent survey reported a 23% reduction in the effort of dealing with Inland Revenue.

Getting it right

Our new Compliance Model helps us understand customers better and tailor our approaches to respond to different customer behaviours and needs. We want

to help people get it right from the start, make tax simpler and more certain, and help more people avoid debt.

For the first time in five years, Inland Revenue’s overdue debt total has reduced. We’ve done this by contacting businesses and individuals upfront to prevent them getting into debt, following up fast with effective arrangements to manage any debts, and recognising that some debt costs more than it’s worth to collect.

The vast majority of student loan debt is owed by borrowers now living overseas, and much child support debt is owed by liable parents living in Australia. We’ve used innovative campaigns to successfully reach these customers and recover debt. Our student loan campaign was a gold-medal winner in communications awards.

We also reduced overdue tax returns by 21.5% last year, finalising 1.45 million overdue returns and reducing the number outstanding to the lowest level in five years.

We also take further action to ensure everyone pays the tax they should. During the year we tackled the hidden economy, property tax compliance and aggressive tax planning, with an excellent rate of return on each. We also had some outstanding wins in the courts.

Reforming child support

A significant project during the year was changing the child support system to better reflect how families live since child support was introduced in 1992. After earlier public consultation, the first changes took effect on 1 April 2015, with the second stage to come in April 2016.

In preparation we contacted thousands of parents who pay or receive child support to make sure they understood the changes and were well-prepared for their impacts. We used social media and texts as well as more traditional channels. 68,000 visitors used our online calculator to work out how changes could affect them.

ANNUAL REPORT 2015 3

Future Inland Revenue – Business Transformation

Implementing our Business Transformation programme is one of our three strategic priorities for 2014–18. I’m excited to see preparation for changes that will create a modern tax administration by 2023, now coming to fruition.

It’s critical we have the right people helping us develop and implement transformation. After an intensive selection process we appointed Accenture and Fast Enterprises, along with several New Zealand-based supporting companies, to work alongside us. We also completed high-level design for all four transformation stages taking place over the next eight to 10 years and started detailed design of the first stage expected to start next year.

We’re involving stakeholders across all areas, with four advisory panels providing a wide range of advice and opinions. Quality assurance reviews from external organisations who make sure we’re spending taxpayers’ funds wisely, have all been positive.

We asked New Zealanders for their thoughts on the tax system of the future through two significant Government consultations during the year. These received great engagement from the public and tax community, with more than 900 comments online and over 90 written submissions.

Conclusion

It’s a privilege to be Commissioner of Inland Revenue. Alongside great customer service delivered every day this organisation provides advice to Government on tax and social policy; and contributes to solving international tax issues.

This year we helped make New Zealand an even better place to live and work in many ways - including collecting $59.7 billion of tax revenue that helps fund services to benefit all New Zealanders.

I’m proud of our people who are committed to making a difference in people’s lives and adding value every day. As we look forward to next year’s challenges I am confident Inland Revenue has the people, skills and innovation to meet the future.

Naomi FergusonCommissioner of Inland Revenue

4 ANNUAL REPORT 2015

Highlights

KIWISAVER MEMBERSHIP REACHED

2.5MILLION

WE NOW HAVE 1.5 MILLION CUSTOMERS

REGISTERED WITH VOICE ID

MOBILE APPLICATION LAUNCHED FOR APPLE PRODUCTS – SMALL TO MEDIUM ENTERPRISES CAN NOW MANAGE THEIR

GST ON THEIR SMARTPHONES

OVERDUE DEBT CASES HAVE DECREASED BY

16%(67,000)

THIS IS THE FIRST TIME IN

five yearsTHAT WE HAVE BEEN ABLE TO

REDUCE THE TOTAL AMOUNT OF OVERDUE DEBT

WE COLLECTED

$59.7BILLION OF TAX REVENUE FOR

THE GOVERNMENT

WE PAID

$3.4 BILLION IN WORKING FOR

FAMILIES TAX CREDITS, KIWISAVER, PAID PARENTAL LEAVE PAYMENTS AND PAYROLL SUBSIDY

WE TRANSFERRED

$4.8BILLION OF KIWISAVER

CONTRIBUTIONS TO PROVIDERS

BUSINESSES WHOSE MOST RECENT INTERACTION WITH GOVERNMENT WAS WITH INLAND REVENUE REPORTED A

23%REDUCTION IN EFFORT OF DEALING WITH US,

IN THE LATEST BUSINESS REFERENCE GROUP SURVEY

$

ANNUAL REPORT 2015 5

INLAND REVENUE IS THE FIRST AGENCY TO REACH

five stars IN THE ENERGY EFFICIENCY

AND CONSERVATION AUTHORITY (EECA) ONE2FIVE

ENERGY MANAGEMENT RATING

EECA LOOKED AT OUR ENERGY USAGE AND HOW WELL WE DEMONSTRATE CORPORATE

COMMITMENT, TARGETS AND PERFORMANCE INDICATORS, PLANS, AND ACCOUNTABILITY TO ENERGY MANAGEMENT. OUR FIVE STAR

RATING IS AN IMPROVEMENT FROM OUR FOUR STAR RATING IN NOVEMBER 2013.

OUR BUSINESS TRANSFORMATION PROGRAMME ACHIEVED ALL ITS MILESTONES AND

WAS UNDER BUDGET

CHILD SUPPORT REFORMS PHASE ONE COMPLETED AND IMPLEMENTED

SUCCESSFULLY

SIGNIFICANTLY CONTRIBUTED TO THE GOVERNMENT’S RESULT 10 TARGET OF “AN AVERAGE OF 70% OF NEW

ZEALANDERS’ MOST COMMON TRANSACTIONS WITH GOVERNMENT WILL BE COMPLETED IN A DIGITAL

ENVIRONMENT” WITH

88%OF INDIVIDUALS FILING

THEIR TAX RETURNS ELECTRONICALLY AND JUST OVER

81% PAYING INDIVIDUAL TAX ELECTRONICALLY

CONTINUED INCREASE IN CUSTOMERS’ USE OF DIGITAL

SERVICES. WE RECEIVED

67.4%OF RETURNS ELECTRONICALLY,

UP FROM 59.8% LAST YEAR

WE ACHIEVED

91%OF OUR SERVICE PERFORMANCE

TARGETS COMPARED TO 85% LAST YEAR

82.5%OF PAYMENTS ELECTRONICALLY COMPARED TO 74.2% LAST YEAR

$

Tax return

6 ANNUAL REPORT 2015

01About

Inland Revenue

ANNUAL REPORT 2015 7

8 ANNUAL REPORT 2015

About us

Outcomes

Inland Revenue contributes to the economic and social wellbeing of New Zealand by collecting and distributing money. New Zealanders pay tax to and may get money from the Government. We are accountable to the Minister of Revenue.

Inland Revenue’s success is reflected in two outcomes:

• Revenue is available to fund government programmes through people meeting payment obligations of their own accord.

• People receive payments they are entitled to, enabling them to participate in society.

Strategic intentions

Our strategic intentions set out in our Statement of Intent 2014–18 are to:

• Deliver and improve our core business

• Contribute to the Government’s priorities

• Implement our transformation change agenda.

We are working on these three areas to ensure that we deliver for our customers today and transform for tomorrow.

Why paying tax matters

In 2014–15, Inland Revenue collected $59.7 billion in tax revenue, which is around 80% of the money government uses to pay for services that all New Zealanders benefit from, including healthcare, education and policing.

In 2014–15 the Crown expected to spend the following:

Our tax system

An effective tax and social policy system comprises good policy settings plus good administration. A well-functioning tax system supports a more competitive and productive economy and helps the Government achieve its fiscal, economic and social objectives.

Most of New Zealand’s tax revenue is from three main sources:

• Personal income

• Company income

• GST.

These three main tax types have broad bases, allowing substantial amounts of tax to be collected at modest tax rates.

Scope of operations In the tax year ended March 20141:

Individuals—about 1.08 million individuals filed annual tax returns

Employers—about 196,000 employers filed almost 2.1 million employer monthly schedules with PAYE deductions for employees

Companies—392,000 company tax returns were filed

GST filers—631,000 registered customers filed 3.0 million GST returns.

We also manage or share the administration of:

Working for Families Tax Credits—we distributed, with the Ministry of Social Development, $2.4 billion in entitlements to support working families.

Child support—we collected $463 million from 174,000 liable parents who pay child support and distributed $265 million to parents who are main carers of children. The balance is collected for the Government as an off-set for custodial families supported through the benefit system.

* includes $291 million for forecasted new operating spending and ($875) million top down expense adjustment which are not included in graph

Where taxes go – Total Crown expenses $73,107 million*

Forecast 2015 $million

Social security and welfareHealthEducationCore government servicesFinance costsLaw and order

Transport and communications

Economic and industrial servicesDefenceHeritage, culture and recreationPrimary servicesOtherEnvironmental protectionGSF pension expensesHousing and community development

23,954

15,065

12,827

4,816

3,883

3,486

2,217

2,215

1,984

770

700

543

510

395

326

01

Executive Leadership Team

From left to right:

Greg James, Deputy Commissioner Change

Giles Southwell, Chief Financial Officer

Mary Craig, Deputy Commissioner Corporate Integrity & Assurance

Mike Cunnington, Deputy Commissioner Information, Intelligence & Communications

Naomi Ferguson, Commissioner

Martin Smith, Chief Tax Counsel

Jeanie Truell, Chief People Officer

Arlene White, Deputy Commissioner Service Delivery

Myles Ward, Chief Technology Officer

Struan Little, Deputy Commissioner Policy & Strategy

ANNUAL REPORT 2015 9

Our operating budgetOur operating expenditure for the 2014–15 year was $704.2 million, an increase of $3.7 million over the prior year. Expenditure for 2015–16 is forecast to be $764.9 million, an increase of $60.7 million. Most of the forecast increase relates to expenditure on our Business Transformation programme.

KiwiSaver—we administer the scheme by collecting contributions and transferring them to scheme providers for investment. At 30 June 2015 there were 2.5 million people enrolled in KiwiSaver. We distributed $4.8 billion to scheme providers.

Student loans—we jointly administer this programme with the Ministries of Education and Social Development (StudyLink). We had 728,000 student loan borrowers and collected $1.1 billion in repayments.

Paid parental leave—we make payments, for the Ministry of Business, Innovation and Employment, to parents who take leave from their job or business to care for a baby. We made $180 million in payments to 27,500 parents.

12015 figures not available

10 ANNUAL REPORT 2015

02Delivering and improving our

core business

ANNUAL REPORT 2015 11

12 ANNUAL REPORT 2015

We aim to make it easy for our customers to manage their own tax and social policy obligations and entitlements by providing information, assistance and tools so they can do it themselves.

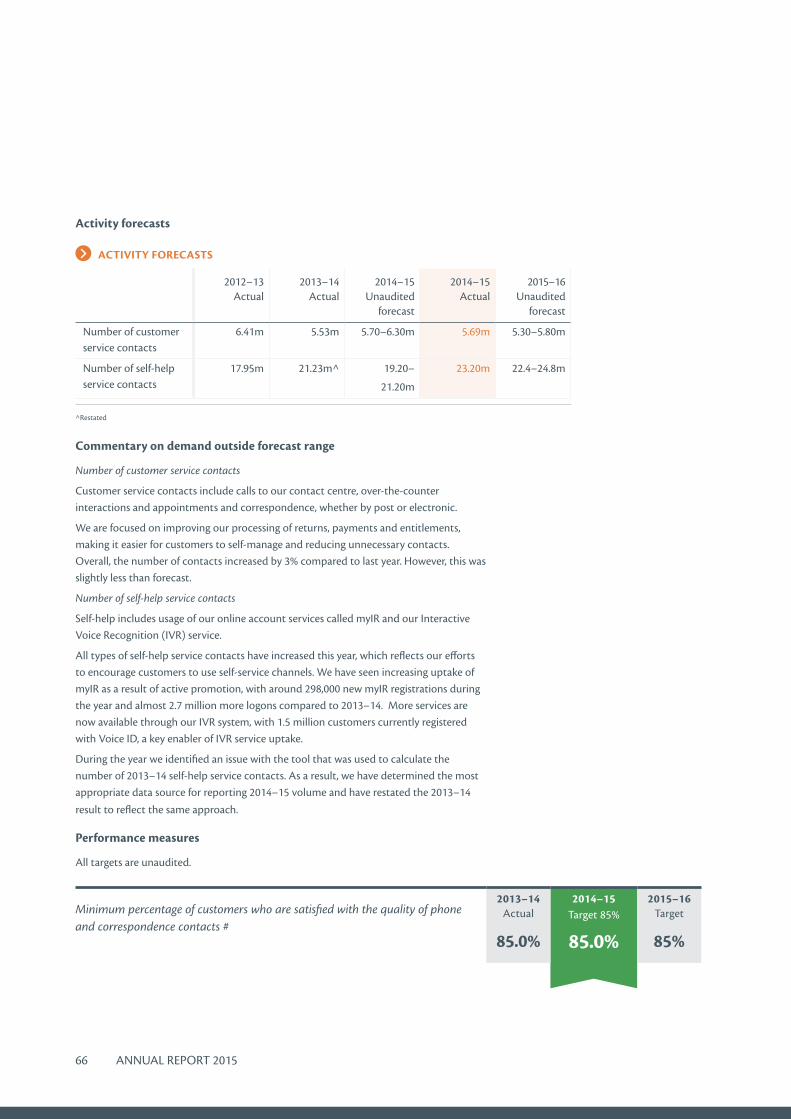

We are enabling our customers to do more online. It is part of our strategy to save our customers and Inland Revenue time and money. Completing their tax and social policy obligations online also helps customers get it right the first time and means we do not have to contact customers to check the information provided is accurate. Over the past year the number of people who have started to file online and use our online tools has increased. The number of returns we received electronically increased by 8.3 percentage points since last year compared to a 4.4 percentage point increase the previous year.

Customers are able to register for a myIR account to manage their own tax and social policy affairs. To make things easier for our customers, we have updated myIR and introduced more online documents to provide access to statements, notices and letters electronically. We made eDocuments available to customers in April 2015. This fits with the objectives of the Government’s Better Public Services Result 9 and 10 goals covered on page 27.

Customers expect to be able to interact with us using all their digital devices.

In January 2015, we launched our new free mobile application myIR on Apple products. This enables small to medium enterprises to manage their GST through their smartphones.

We recognise that our website is the first place most people go when they want to find out information so we work hard to make sure it is the best it can be. We also publish instructional videos on our YouTube channel InlandRevenueNZ. We are continually improving our website and YouTube information to make sure customers are able to find the information they need. One of the improvements we made was to add transcripts of our introductory videos written in Korean and traditional and simplified Chinese to reflect the changing needs of our customers. These are in addition to information in English, Māori and New Zealand Sign Language already available.

Another example of improvements we have made to our website is the employer superannuation contribution tax (ESCT) tool. Customers told us that ESCT was hard to understand so we created an educational tool in July 2014 to help employers. The tool explained what ESCT was and how to calculate, file and pay ESCT. This has been used over 163,000 times.

Our work to make tax easier to understand on our website was recognised again. In December, ird.govt.nz won the ESET NetGuide best Government website award for the eighth time in nine years.

Digital services

02

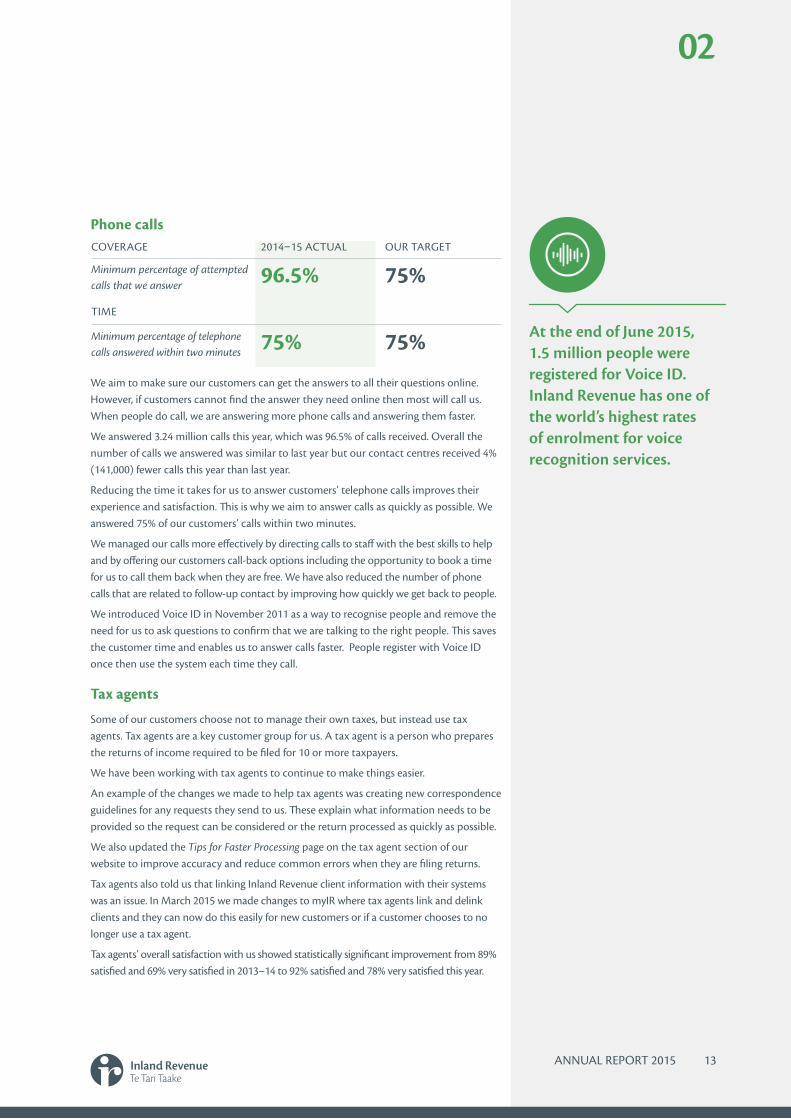

Phone calls

We aim to make sure our customers can get the answers to all their questions online. However, if customers cannot find the answer they need online then most will call us. When people do call, we are answering more phone calls and answering them faster.

We answered 3.24 million calls this year, which was 96.5% of calls received. Overall the number of calls we answered was similar to last year but our contact centres received 4% (141,000) fewer calls this year than last year.

Reducing the time it takes for us to answer customers’ telephone calls improves their experience and satisfaction. This is why we aim to answer calls as quickly as possible. We answered 75% of our customers’ calls within two minutes.

We managed our calls more effectively by directing calls to staff with the best skills to help and by offering our customers call-back options including the opportunity to book a time for us to call them back when they are free. We have also reduced the number of phone calls that are related to follow-up contact by improving how quickly we get back to people.

We introduced Voice ID in November 2011 as a way to recognise people and remove the need for us to ask questions to confirm that we are talking to the right people. This saves the customer time and enables us to answer calls faster. People register with Voice ID once then use the system each time they call.

Tax agents

Some of our customers choose not to manage their own taxes, but instead use tax agents. Tax agents are a key customer group for us. A tax agent is a person who prepares the returns of income required to be filed for 10 or more taxpayers.

We have been working with tax agents to continue to make things easier.

An example of the changes we made to help tax agents was creating new correspondence guidelines for any requests they send to us. These explain what information needs to be provided so the request can be considered or the return processed as quickly as possible.

We also updated the Tips for Faster Processing page on the tax agent section of our website to improve accuracy and reduce common errors when they are filing returns.

Tax agents also told us that linking Inland Revenue client information with their systems was an issue. In March 2015 we made changes to myIR where tax agents link and delink clients and they can now do this easily for new customers or if a customer chooses to no longer use a tax agent.

Tax agents’ overall satisfaction with us showed statistically significant improvement from 89% satisfied and 69% very satisfied in 2013–14 to 92% satisfied and 78% very satisfied this year.

COVERAGE 2014–15 ACTUAL OUR TARGET

Minimum percentage of attempted calls that we answer 96.5% 75%TIME

Minimum percentage of telephone calls answered within two minutes 75% 75% At the end of June 2015,

1.5 million people were registered for Voice ID. Inland Revenue has one of the world’s highest rates of enrolment for voice recognition services.

ANNUAL REPORT 2015 13

14 ANNUAL REPORT 2015

Returns

Returns are the way in which customers give us their tax information for the year. We aim to be more proactive by letting customers know their returns are due before issues arise. This proactive approach is working.

The number of outstanding returns was down 21.5% at the end of June 2015, to reach the lowest number in the last five years. This reflects an ongoing reduction and we had about 234,000 fewer returns outstanding at 30 June 2015 than at 1 July 2014.

We are encouraging as many customers as possible to use our online channels to file their returns.

Making payments

Our proactive approach of letting people know their obligations before their payments are due is also supported by Budget 2012 and 2014 funded projects which improved our predictive modelling capability. These projects looked at how we can identify patterns of compliance and engage with customers before issues arise.

When customers need to make payments, we are making it easier for them to pay electronically. This also makes it easier for us to process payments faster.

To help our customers know all the ways they can pay electronically, we developed a 45-second video on the Make a payment page of our website. We have also made the payment page responsive and easy to use on mobile devices. Around 20% of customers visit our payment page using a mobile device.

We removed the option for cheque payments at Westpac. Now that Westpac only receives cash or EFTPOS payments, we have seen a large reduction in exceptions. Exceptions are payments that cannot be processed or that are missing information like IRD numbers. In December 2014, we had 21 payments which could not be processed. These exceptions were worth $10,000. This compares with 5,400 exceptions worth $56 million in December 2013. During January and February 2015 we had one exception each month and by March we had no exceptions.

For customers who want to pay over the counter at Westpac, we introduced barcodes on payment slips in June 2015. The barcode aims to reduce time and errors for these transactions.

Predictive modelling helps us change customer behaviour before issues arise

Our work on the probability of GST returns being filed shows we can reliably predict customers who are highly unlikely to file GST returns on time. We have changed our processes based on our findings.

This has already resulted in a reduction of more than 98,000 outstanding GST returns during the past year. In the future, we will be able to take a more proactive approach for these customers and contact them before any potential GST filing issues arise.

We had 82.5% of payments made electronically compared to 74.2% in 2013–14 and 70% in 2012–13.

$

2012–13 2013–14 2014–15

INCOME TAX 84.1% 86.9% 88.8%

GST 47.6% 54.9% 64.0%

EMPLOYER MONTHLY SCHEDULES 41.3% 49.6% 60.0%

Electronic returns by tax type

YEAR % GST RETURNS RECEIVED ELECTRONICALLY

% OF GST CUSTOMERS FILING ELECTRONICALLY

30 June 2013 47.6% 44.9%

30 June 2014 54.9% 50.6%

30 June 2015 64.0% 62.5%

GST return

ANNUAL REPORT 2015 15

02

Social policy programmes

We have an important role in administering social policy programmes, often in conjunction with other government agencies. During the year we made changes to our child support, paid parental leave, and KiwiSaver systems to implement Government policy changes.

Child support changes

Inland Revenue collects and distributes child support payments for about 200,000 children whose parents do not live together.

The Government recognised that things have changed for families since child support was first introduced in 1992. After significant public consultation, extensive changes were made to the scheme to better reflect family life today. These changes come into effect in two stages on 1 April 2015 and 1 April 2016.

The first stage went live on 1 April 2015 and changed the way child support was calculated. The calculation moved from focusing on the liable parent’s income to the cost of ongoing care of the child by:

• taking into account the cost of raising children

• taking into account the income of both parents

• recognising lower levels of shared and regular care provided for each child.

To ensure the liable and receiving parents knew how the changes would affect them, we contacted them via either mail, phone, text messaging or email to ensure we had the correct information about their situation and to help them understand the changes.

As part of the changes we developed two new calculators and made them available on our website to help parents work out how the changes would affect them. Since going live in September 2014, the

calculators have had 68,000 visits.

We used social media as a new way to improve engagement with some of our child support customers and also contacted parents through our normal communication channels. We undertook our first question and answer session on Facebook on the privately-run Child Support NZ Facebook page. During the session we had 139 participants in a one-hour discussion, received over 200 questions and had over 680 comments made. We also had over 10,000 views of the Facebook page during the session.

An additional change we made is that parents who received child support payments from more than one liable parent can now see who made the payment.

Changes to paid parental leave

We make paid parental leave payments for the Ministry of Business, Innovation and Employment (MBIE), to parents who take leave from their job or business to care for a baby. We are responsible for ensuring people receive their correct entitlements.

On 1 April 2015 paid parental leave was extended from 14 to 16 weeks. From 1 April 2016 this will be extended to 18 weeks. Also from 1 April 2015, the parental tax credit increased from $150 to $220 a week and the payment period was extended from eight weeks to 10 weeks.

KiwiSaver

Inland Revenue administers members’ KiwiSaver contributions through the PAYE system. We do this by collecting contributions and transferring them to scheme providers for investment.

Through Budget 2015, changes were made to KiwiSaver. The KiwiSaver Budget Measures Act enacted on 27 May 2015 removed the KiwiSaver $1,000 kick-start payment to help contain the cost of the scheme to taxpayers.

Removing the kick-start payment for

One of our outcomes is to ensure people receive payments they are entitled to, enabling them to participate in society.

In the 2014–15 financial year we collected $463 million from 174,000 liable parents and distributed $265 million to receiving caregivers. This is an increase of 3% in payment collection.

16 ANNUAL REPORT 2015

future enrolments will save over $500 million over the next four years.

In March, we got excellent feedback from an Australian research company SuperRatings for the role we play in administering KiwiSaver. Their assessment also recognised our role is critical in maintaining the efficiency of the system and the overall cost-effectiveness of KiwiSaver schemes in comparison to other countries’ retirement systems.

In April 2015, KiwiSaver membership hit a significant milestone of 2.5 million people.

Improving compliance

A key aspect of our core business is helping to maximise voluntary compliance. We assist customers who are willing to meet their compliance obligations but are unaware or uncertain about how to do so. Influencing voluntary compliance, targeting inadvertent non-compliance by providing information, assistance and tools, and detecting and deterring deliberate non-compliance are part of our core activities.

Understanding and influencing customer behaviour

We aim to make it easy for people to understand their obligations and entitlements. In our Statement of Intent 2014–18 we said we would redesign our compliance model so it reflects a more comprehensive range of the factors influencing customer behaviour.

We launched our new compliance model in March 2015. The new model places greater emphasis on understanding our customers, their lifecycles and perspectives. We want to give our customers certainty with the least number of interactions. We also want our customers to be able to get it right first time. We have worked with customers, tax agents, private providers and other government departments to design solutions that fit tax and social policy obligations around customers’ needs, and we will continue to do this. The impacts of changes on customers will also be assessed to ensure we understand how they influence and affect compliance and the customer experience.

Dealing with non-compliance

The majority of our customers file and pay on time, but New Zealanders need to have confidence that we take action when people or businesses do not pay. This encourages compliance and maintains confidence in our tax system. We use a range of tools to identify areas of non-compliance and evaluate the most appropriate response, including investigations of the tax affairs of individuals and businesses. We have focused our efforts on specific areas of non-compliance such as aggressive tax planning, property and the hidden economy and received further funding in Budget 2015 to expand our investigations activity in these areas.

At the core of our new compliance model are the three factors that form customer behaviour – capability, motivation and opportunity.Capability is how well customers can meet their obligations and access their entitlements. It includes their knowledge of rules that apply to them, their access to tools and assistance, and their ability to understand.

Motivation is about the factors that create the willingness to comply and then actually follow through and do it. Motivation includes both social and personal norms.

Opportunity is about how easy it is for a customer to comply or not to comply with their obligations or access their entitlements.

CAPABILITY M

OTIV

ATIO

N

OPPORTUNITY

CUSTOMER

ANNUAL REPORT 2015 17

02

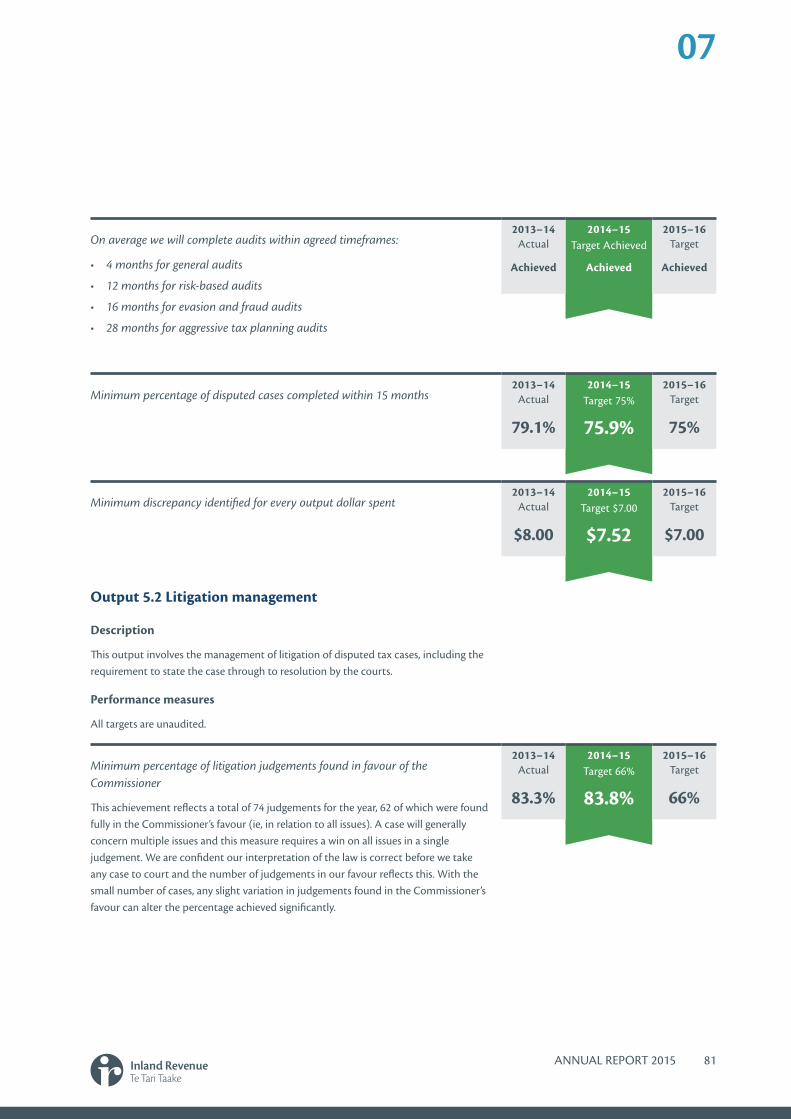

If our investigation detects a discrepancy, a difference between the tax position filed by a taxpayer and the position determined by our investigations, we issue a new assessment and may charge penalties and interest. This year we identified discrepancies of $1.23 billion. The overall return on investment for our investigation activity was $7.52:$1 (target $7.00:$1).

Aggressive tax planning

A small number of people try to avoid paying the tax they should, reduce the amount they should be paying or increase their entitlement to social benefits. They use inappropriate or unlawful tax structures and this is called aggressive tax planning. We match information from different sources to identify potential aggressive tax planning structures and schemes.

Our work to counter aggressive tax planning contributed $336.9 million toward the total discrepancies result. Of this, $191.1 million came from examining complex finance and trust losses. This produced a return on investment of $34.10:$1 (target $11.60:$1). We resolved the last optional convertible notes cases after the settlement with Alesco New Zealand in 2014. This contributed $64.3 million to this year’s discrepancies. This year we have worked on cases

New Zealand has a voluntary compliance approach to tax. This is an environment dependent on an open, honest and transparent tax system where there are high levels of mutual trust and understanding between customers and the revenue agency.

OUR MODEL FOR

facilitatingcompliance

OUR NEW COMPLIANCE MODEL

The movable wheels show we use a range of approaches that change depending on our customers. The more we understand customer needs and behaviours, the better we can tailor our actions so people pay the taxes and get the entitlements they should.

A thinking tool to help us understand customers better so we can work pro-actively and tailor approaches to make compliance easier.>

> Customer centred: Customers are at the centre of our thinking surrounded by context that affects their behaviour.

> Behaviour wheel: we consider the three factors that form customer behaviour so we can tailor our approaches to facilitate compliance.

> Principles wheel: five key principles guide how we work with customers to build compliance. We apply a mix of these in different ways, depending on our role and the customers we work with.

> Activity wheel: whatever our job in IR, we have a role in making sure people pay the taxes and get the entitlements they should. We use different activities to facilitate compliance depending on our customers.

EDUCATE DESIGN LEGISLATE COLLABORATE

ANALYSE

SER

VICE

E

NFO

RCE

Make it easy to comply

and difficult not to

C

APABILITY MO

TIVA

TION

OPPORTUNITY

Understand and involve the customer and stakeholders

CUSTOMER

Build compliance right from the start

Influence norms

Provide certainty

18 ANNUAL REPORT 2015

involving the use of mandatory convertible notes, which led to discrepancies of $91.8 million.

Since we received multi-year funding to work on aggressive tax planning in Budget 2012, we have assessed revenue of $811.1 million. We will use Budget 2015 funding to continue addressing emerging risks such as high-income individuals, in particular high-income new immigrants.

Non-compliance in the property sector

We have continued to focus on identifying property speculation, particularly in Auckland and Christchurch. This focus includes examining residential property sales and new developments to ensure that speculators and developers are paying the correct amount of tax. We have found discrepancies during the year of $67.1 million. The return on investment was $9.97:$1 (target $6.80:$1).

To help clarify the tax position we delivered presentations to different industry groups on this topic. We aim to educate people about how to deal with GST on a property and property investment. We will use funding from Budget 2015 to expand customer education and increase our focus on this sector.

Hidden economy

People operate in the hidden economy by intentionally not declaring or accurately reporting transactions. We focused on higher-risk sectors such as hospitality and construction. We identified discrepancies of $146 million in the hidden economy. Of this, $45 million (target $44 million) came from Budget 2010-funded work, a return on investment of $5.21:$1 (target $5.00:$1). As a last resort we prosecute to recover funds from taxpayers operating in the hidden economy.

In May and June 2015, we ran an advertising campaign to remind tradespeople to declare all of their income. The campaign ran in four suburbs in Auckland and included billboards and posters at construction sites, and advertisements online, on radio, and in trade publications. The reaction was fast, with tax agents reporting a large number of calls from people looking to add cash jobs to the information they had submitted to us.

We list notes of decisions made by the Taxation Review Authority, the High Court, Court of Appeal, Privy Council and the Supreme Court on our website at www.ird.govt.nz/technical-tax/case-notes.

A post-campaign survey with tradies showed strong unprompted awareness (42% aware of the campaign) and 65% awareness after prompting. Of these tradies, 33% discussed the topic with others and the main messages recalled were, “Declare it all” (32%) and “Inland Revenue will catch those doing cash jobs” (25%). We also saw good public interest after the media picked up on our activities.

02

ANNUAL REPORT 2015 19

Clarifying tax law in cases where there are different interpretations

When interpretation of the law is not clear we provide certainty by providing binding rulings on specific transactions, public rulings and statements and disputes reviews. However in some cases we may need to clarify tax law by taking cases to court. The court will decide on the correct interpretation and create a precedent.

In June 2015, our appeal to the Court of Appeal against Trustpower was successful. Trustpower had claimed tax deductions on the costs of getting resource consents for new power generation projects, arguing that these costs were revenue expenses.

We believed these were capital costs and therefore not deductible. In 2013 the High Court agreed with Trustpower and we appealed this judgement. The Court of Appeal found that Trustpower’s spending on resource consents was capital expenditure and that Trustpower was not entitled to the deductions it had claimed.

Trustpower has been granted leave to appeal. Clarifying this question will help us and our customers have certainty over how these expenses should be dealt with.

Litigation against non-compliance

Over a decade of litigation came closer to conclusion in April 2015 when the High Court struck out the remaining 77 Trinity tax challenges. This case, a significant tax avoidance scheme, has been subject to a large number of court proceedings since the Supreme Court found in Inland Revenue’s favour in the 2008 Ben Nevis case.

Prosecutions

We completed 67 prosecutions for tax evasion or knowledge offences. This compares with 74 last year. The decrease was related to the timing of cases before the courts. At 30 June 2015, 79 such cases were pending. There were 89 cases pending at the same time last year.

Tax law is complicated. We need to interpret and apply the law correctly and give our customers certainty on areas of tax law.

So we have teams of legal experts spread across Inland Revenue whose research and consultation provide us and our customers with reliable technical advice.

We provide public rulings, interpretation statements and interpretation guidelines, which clarify difficult areas of tax law, give our customers certainty and help them comply. We also research and analyse technical tax issues that come from private or product ruling applications.

www.ird.govt.nz/technical-tax

20 ANNUAL REPORT 2015

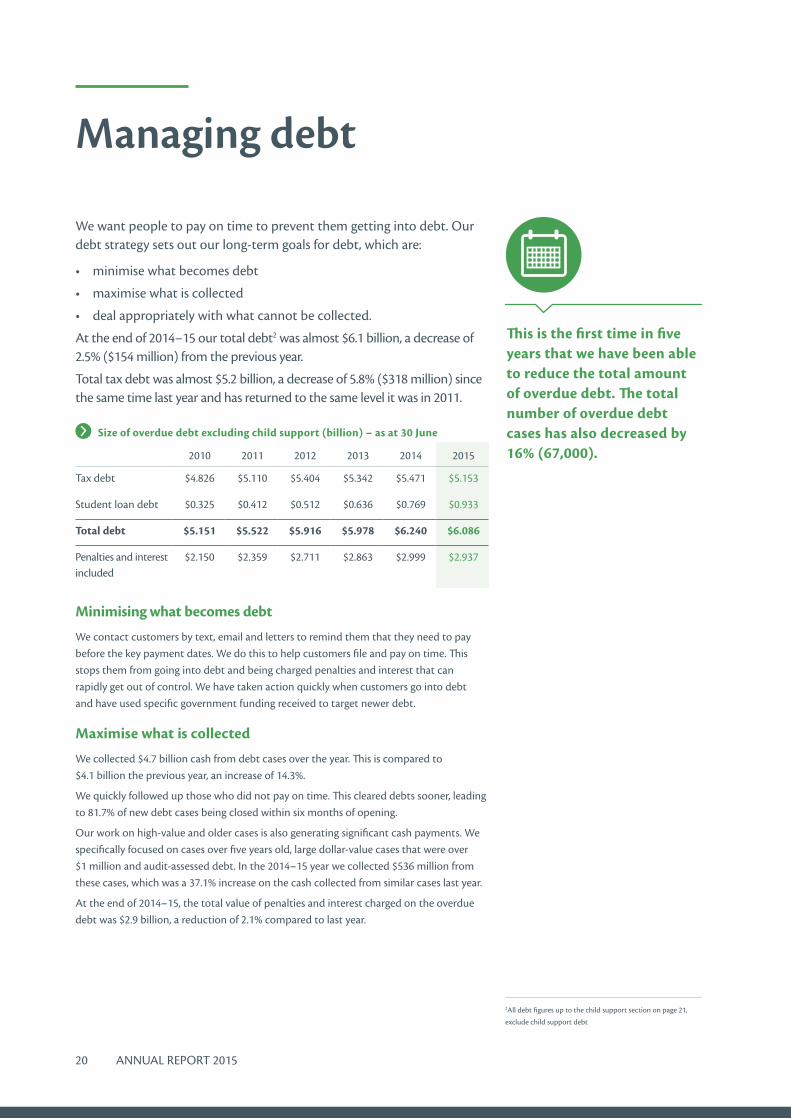

Managing debt

We want people to pay on time to prevent them getting into debt. Our debt strategy sets out our long-term goals for debt, which are:

• minimise what becomes debt

• maximise what is collected

• deal appropriately with what cannot be collected.

At the end of 2014–15 our total debt2 was almost $6.1 billion, a decrease of 2.5% ($154 million) from the previous year.

Total tax debt was almost $5.2 billion, a decrease of 5.8% ($318 million) since the same time last year and has returned to the same level it was in 2011.

This is the first time in five years that we have been able to reduce the total amount of overdue debt. The total number of overdue debt cases has also decreased by 16% (67,000).

Minimising what becomes debt

We contact customers by text, email and letters to remind them that they need to pay before the key payment dates. We do this to help customers file and pay on time. This stops them from going into debt and being charged penalties and interest that can rapidly get out of control. We have taken action quickly when customers go into debt and have used specific government funding received to target newer debt.

Maximise what is collected

We collected $4.7 billion cash from debt cases over the year. This is compared to $4.1 billion the previous year, an increase of 14.3%.

We quickly followed up those who did not pay on time. This cleared debts sooner, leading to 81.7% of new debt cases being closed within six months of opening.

Our work on high-value and older cases is also generating significant cash payments. We specifically focused on cases over five years old, large dollar-value cases that were over $1 million and audit-assessed debt. In the 2014–15 year we collected $536 million from these cases, which was a 37.1% increase on the cash collected from similar cases last year.

At the end of 2014–15, the total value of penalties and interest charged on the overdue debt was $2.9 billion, a reduction of 2.1% compared to last year.

2010 2011 2012 2013 2014 2015

Tax debt $4.826 $5.110 $5.404 $5.342 $5.471 $5.153

Student loan debt $0.325 $0.412 $0.512 $0.636 $0.769 $0.933

Total debt $5.151 $5.522 $5.916 $5.978 $6.240 $6.086

Penalties and interest included

$2.150 $2.359 $2.711 $2.863 $2.999 $2.937

Size of overdue debt excluding child support (billion) – as at 30 June

2All debt figures up to the child support section on page 21,

exclude child support debt

ANNUAL REPORT 2015 21

02

Deal appropriately with what cannot be collected

New Zealanders expect us to take action against those that do not pay their fair share of tax. In the most severe cases we will take legal action against people who refuse to pay their debt. It is rare, but we can ask for people to be arrested if they refuse to pay.

Where necessary we have made decisions over the year to write off debt that would cost more to collect than the cost of the debt.

Child support debt

Child support debt is $3.3 billion, 79% ($2.6 billion) of which is penalties.

Of the total child support debt, around $827 million is owed by liable parents living in Australia, and is mostly in the form of penalties. In accordance with our agreement with the Australian Department of Human Services they collected $50.2 million from these parents on our behalf. A further $778 million is owed by those living in other parts of the world. The remaining $1,671 million debt is owed by liable parents living in New Zealand.

For child support, over the last year there were 56 cases where the lack of action by the liable parent justified Inland Revenue to seek an arrest warrant. We have only been required to execute one arrest warrant. All other cases were able to be resolved by simply having the possibility of a warrant being executed. The total debt relating to the 56 cases amounted to $11.7 million.

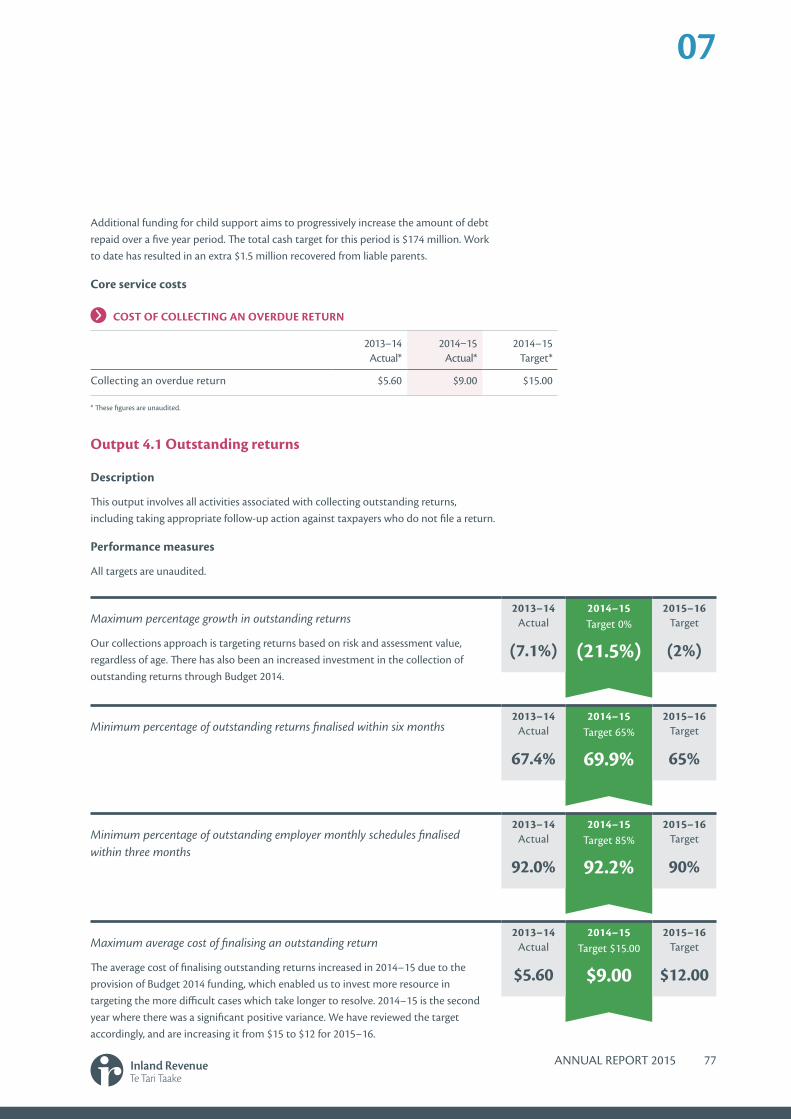

Budget 2014 provided us with additional funding to help improve child support compliance. We are beginning to see positive outcomes from our activities in this area, including more debt cases being closed within 12 months of opening and a reduction in the total number of debtors at the end of the year. Early work has included an education campaign to new child support customers on their obligations, particularly taking into account the child support reform changes, ensuring they understand their obligations to help them get it right from the start. This initiative aims to progressively increase the amount of debt repaid over a five-year period with early work resulting in an extra $1.5 million recovered from liable parents.

2010 2011 2012 2013 2014 2015

Debt value $1.990 $2.335 $2.452 $2.781 $3.047 $3.276

Penalties included $1.430 $1.743 $1.818 $2.109 $2.372 $2.605

Size of overdue child support debt (billion) – as at 30 June

22 ANNUAL REPORT 2015

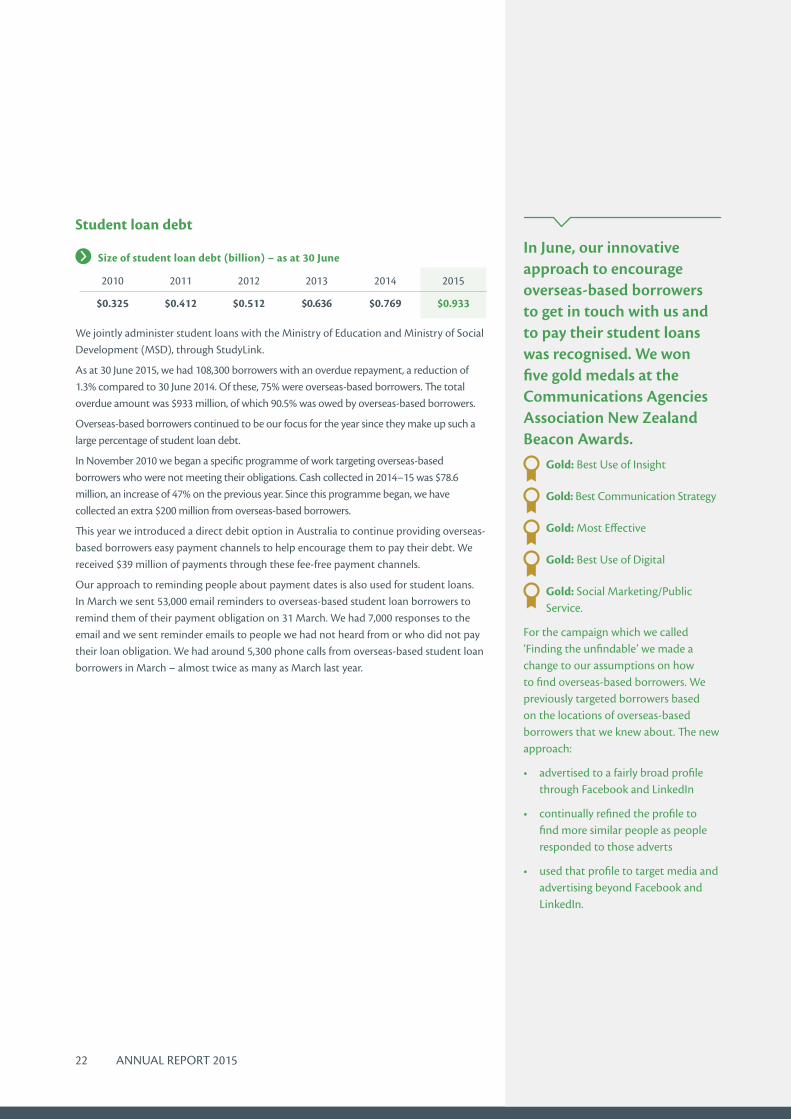

Student loan debt

We jointly administer student loans with the Ministry of Education and Ministry of Social Development (MSD), through StudyLink.

As at 30 June 2015, we had 108,300 borrowers with an overdue repayment, a reduction of 1.3% compared to 30 June 2014. Of these, 75% were overseas-based borrowers. The total overdue amount was $933 million, of which 90.5% was owed by overseas-based borrowers.

Overseas-based borrowers continued to be our focus for the year since they make up such a large percentage of student loan debt.

In November 2010 we began a specific programme of work targeting overseas-based borrowers who were not meeting their obligations. Cash collected in 2014–15 was $78.6 million, an increase of 47% on the previous year. Since this programme began, we have collected an extra $200 million from overseas-based borrowers.

This year we introduced a direct debit option in Australia to continue providing overseas-based borrowers easy payment channels to help encourage them to pay their debt. We received $39 million of payments through these fee-free payment channels.

Our approach to reminding people about payment dates is also used for student loans. In March we sent 53,000 email reminders to overseas-based student loan borrowers to remind them of their payment obligation on 31 March. We had 7,000 responses to the email and we sent reminder emails to people we had not heard from or who did not pay their loan obligation. We had around 5,300 phone calls from overseas-based student loan borrowers in March – almost twice as many as March last year.

In June, our innovative approach to encourage overseas-based borrowers to get in touch with us and to pay their student loans was recognised. We won five gold medals at the Communications Agencies Association New Zealand Beacon Awards.

Gold: Best Use of Insight

Gold: Best Communication Strategy

Gold: Most Effective

Gold: Best Use of Digital

Gold: Social Marketing/Public Service.

For the campaign which we called ‘Finding the unfindable’ we made a change to our assumptions on how to find overseas-based borrowers. We previously targeted borrowers based on the locations of overseas-based borrowers that we knew about. The new approach:

• advertised to a fairly broad profile through Facebook and LinkedIn

• continually refined the profile to find more similar people as people responded to those adverts

• used that profile to target media and advertising beyond Facebook and LinkedIn.

2010 2011 2012 2013 2014 2015

$0.325 $0.412 $0.512 $0.636 $0.769 $0.933

Size of student loan debt (billion) – as at 30 June

03Contributing to

the Government’s priorities

ANNUAL REPORT 2015 23

24 ANNUAL REPORT 2015

Responsibly manage the Government’s finances

Inland Revenue collected $59.7 billion tax revenue and transferred $4.8 billion of KiwiSaver contributions to providers. Total payments for the year ended 30 June 2015 for social policy entitlements were $3.4 billion. Social policy entitlements include Working for Families Tax Credits, KiwiSaver, Paid Parental Leave Payments and Payroll Subsidy. We also managed a departmental budget of $727 million.

Full finance details are covered in parts eight and nine.

We have a responsibility as a government agency to contribute to the Government’s priorities.

These are to:

• responsibly manage the Government’s finances

• build a more competitive and productive economy

• deliver Better Public Services within tight fiscal constraints

• rebuild Canterbury.

We participate in a range of all-of-government activities, collaborate with other agencies to reduce costs, improve efficiency and effectiveness.

Along with the Government’s priorities, we also continued to work on the

Government’s tax policy work programme which was updated and released by the Minister of Revenue on 13 March 2015. This programme focused on three main areas:

• Business Transformation and Better Public Services

• International tax reform and contributing to international efforts to counter base erosion and profit shifting (BEPS)

• Continuing improvement and enhancements to tax and social policy settings to keep the tax system well maintained.

ANNUAL REPORT 2015 25

03

Build a more competitive and productive economy

Inland Revenue contributed to building a more productive economy through legislation changes. These changes are designed to ensure New Zealand is an attractive place to do business. We also want to strengthen tax rules to ensure overseas companies pay their fair share of tax in New Zealand. The Government’s tax policy work programme focuses on improving tax and social policy settings and participating in the global response to the problem of tax base erosion and profit shifting.

Our work to enhance tax and social policy settings

An important part of our approach to the development and review of tax policy is public consultation. This provides transparency of our policy-making process and allows us to listen and respond to New Zealanders, tax professionals and associations.

During the year we asked for public feedback on:

• an officials’ issues paper, Related parties debt remission, released on 24 February 2015. This asked for feedback on proposed changes to make the tax rules on this more certain and fairer.

• a discussion document, Simplifying the tax collection for employee share schemes, released in April 2015. Public feedback helped shape proposals introduced in the Taxation (Transformation: First Phase Simplification and Other Measures) Bill in June 2015, which will allow employers to choose to withhold tax on an employee’s behalf as part of their PAYE return.

• detailed design proposals for the new bright-line test announced in Budget 2015 released on 29 June 2015. The proposal clarifies whether or not gains on the sale of residential property bought and sold within two years are taxable. Feedback helped shape legislation planned for introduction in September 2015.

Legislation

To improve the economic environment for businesses and New Zealanders we provided policy analysis and options to the Government to change legislation. We focused on three main bills during the year.

The Taxation (Annual Rates for 2015–16, Research and Development, and Remedial Matters) Bill introduced on 26 February 2015 contains proposals to reflect the Government’s Business Growth Agenda emphasising the importance of innovation to help grow New Zealand’s economy. The bill removes some distortions relating to Research and Development to encourage businesses to invest in these activities. It also clarified the GST rules for bodies corporate.

The KiwiSaver HomeStart Bill enacted on 31 March 2015 implemented part of the Government’s support package for first home buyers, allowing eligible KiwiSaver members to access more of their KiwiSaver funds to purchase their first home. It also clarified and corrected the tax rules for payments made under the Veterans’ Support Act 2014.

New rules to strengthen the property tax rules were introduced in the Taxation (Land Information and Offshore Persons Information) Bill on 22 June 2015. The proposed rules will require domestic and overseas buyers and sellers of property to provide their IRD number at the time of the property transfer and the equivalent tax identification number for people resident in another country.

26 ANNUAL REPORT 2015

Overseas residents will have to provide a New Zealand bank account number to obtain an IRD number for properties bought on or after 1 October 2015. The IRD number requirement will not apply to New Zealand individuals buying or selling their main home, unless they are selling their third main home in a two-year period.

International tax reforms and base erosion and profit shifting

As outlined in our Statement of Intent 2014–18 we are participating in the Organisation for Economic Co-operation and Development (OECD) led response to the global problem of base erosion and profit shifting, where multinational organisations take advantage of the interaction between the tax rules of different countries to pay little or no tax. We continue to work on projects to strengthen domestic rules on international tax.

We continued to work with the OECD and the G20 forum of countries on implementing an Automatic Exchange of Financial Account Information, a global automatic exchange of information to counter tax evasion.

Over the year we worked on the taxation of cross-border purchasing of services and intangibles, low-value goods and digital downloads. This work aligns with the OECD’s draft guidelines to develop rules to tax consumption fairly.

On 1 January 2015 the Convention on Mutual Administrative Assistance in Tax Matters came into effect for New Zealand. This lets us seek assistance from other tax authorities to discover evasion and pursue tax debt overseas.

An issues paper, NRWT: Related party and branch lending, which explores options to clarify the non-resident withholding rules to help ensure that non-resident investors pay an appropriate amount of tax, was released in May 2015.

Our tax treaty negotiations with other jurisdictions continued, with China completed in July 2014, Korea in April 2015 and Norway in June 2015.

A new tax treaty between New Zealand and Canada came into force in June 2015, replacing the 1980 treaty with a more modern agreement.

Foreign Account Tax Compliance Act

As outlined in our Statement of Intent 2014–18, we need to implement legislative change to help New Zealand’s financial institutions to meet Foreign Account Tax Compliance Act (FATCA) obligations. This legislation requires New Zealand financial institutions to give United States authorities details of accounts held by American citizens, tax residents and others.

In July 2014, New Zealand was granted more favourable terms from the United States Government as part of the FATCA intergovernmental agreement signed between New Zealand and the United States. Implementing Inland Revenue’s obligations set out in the agreement is on track. We started collecting information from New Zealand financial institutions from April 2015. We will start forwarding the information to the United States Government’s Internal Revenue Service in 2015–16.

We are making good progress in working with significant enterprises and multinational companies operating in New Zealand and across different countries to identify and address potential risk before non-compliance occurs. Our work with these taxpayers can result in advance pricing agreements (APAs) which represent a more co-operative approach to addressing transfer pricing compliance. We completed 15 APAs this year. This is the best mechanism to achieve certainty for multinationals in their international associated-party dealings as they involve complex issues such as restructuring arrangements and intellectual property transfers.

ANNUAL REPORT 2015 27

03

Deliver Better Public Services within tight fiscal constraints

We play an important role in improving services for New Zealanders and continue to play a key role in:

• the Better Public Services programme

• the delivery of the Government’s ICT Strategy

• all-of-government services

• other cross-agency initiatives.

Our Business Transformation programme, outlined in part four, contributes to the Government’s goal of making it easier for customers to interact with government and delivering a significant reduction in the effort of dealing with government.

We are working closely with other government agencies to deliver the innovative and effective public services that government and our customers expect. We are working to link more of our customer services with those of other government agencies to provide a seamless service. More cross-agency information sharing will be balanced against the need to protect customer privacy and the integrity of the tax system.

In line with Government’s ICT Strategy, we are also using all-of-government services where they are available and where they fit with our Business Transformation programme.

Working with the Ministry of Business, Innovation and Employment (MBIE) and other participating agencies, we have helped to develop the Result 9 roadmap and worked on key initiatives such as the New Zealand Business Number (NZBN). We have also delivered products and services that support Result 9’s intent of improving interaction with government for businesses

including eGST, more digital delivery, a myIR application, online business videos and simplified Tools for business web pages.

We have continued to focus on the digitisation of key processes for individuals and businesses to make it easier to interact with government. We contribute to the Result 10 target of “an average of 70% of New Zealanders’ most common transactions with government will be completed in a digital environment” with over 88% of individuals filing their tax returns electronically and just over 81% paying individual tax electronically.

The Department of Internal Affairs (DIA) digitised the process for applying for an IRD number as part of the birth registration process and this will also contribute to this target.

We are working with the Ministry of Social Development (MSD) to understand if it is possible and practical to share one voice biometric service for customers interacting with multiple agencies. Initial results saw 84% of customers saying they thought sharing one voice identification service across several government agencies would be useful, while 51% of customers surveyed gave consent to their voiceprint and information being shared with MSD.

We have now completed our first year of running a shared financial management information system with DIA. As part of this service we have successfully provided accounts receivable, accounts payable and bank reconciliations for both organisations. We have refined the system during the year and are working with DIA on enhancing the system and processes in the future.

We continue to work with the Property Management Centre of Expertise (PMCoE) and to join with other agencies to lease accommodation, where it makes sense to do so.3

The Better Public Services result areas we contribute to are:

• Result 7: Reduce total crime rate

• Result 9: New Zealand businesses have a one-stop online shop for all government advice and support they need to run and grow their business

• Result 10: New Zealanders can complete their transactions with government easily in a digital environment.

3Hosted by MSD, PMCoE leads and assists agencies in

meeting the goals set by Government for the efficient and

effective management of the property owned or leased by 61

government agencies.

28 ANNUAL REPORT 2015

Information sharing

The Government has increasingly recognised that information is an asset which, under certain circumstances, should be shared across government to support collective outcomes for New Zealand. We continue to work with other government agencies to enable more effective information sharing between government agencies and with third parties by helping to simplify the management and control of agency data.

New Zealanders expect us to responsibly manage their details and only share information between agencies when it is appropriate.

We have Approved Information Sharing Agreements (AISA) in place with DIA and New Zealand Police. Reports of sharing that we have done under these agreements can be found on pages 154 to 156. Full details of the agreements are on our website www.ird.govt.nz/aboutir/agreements.

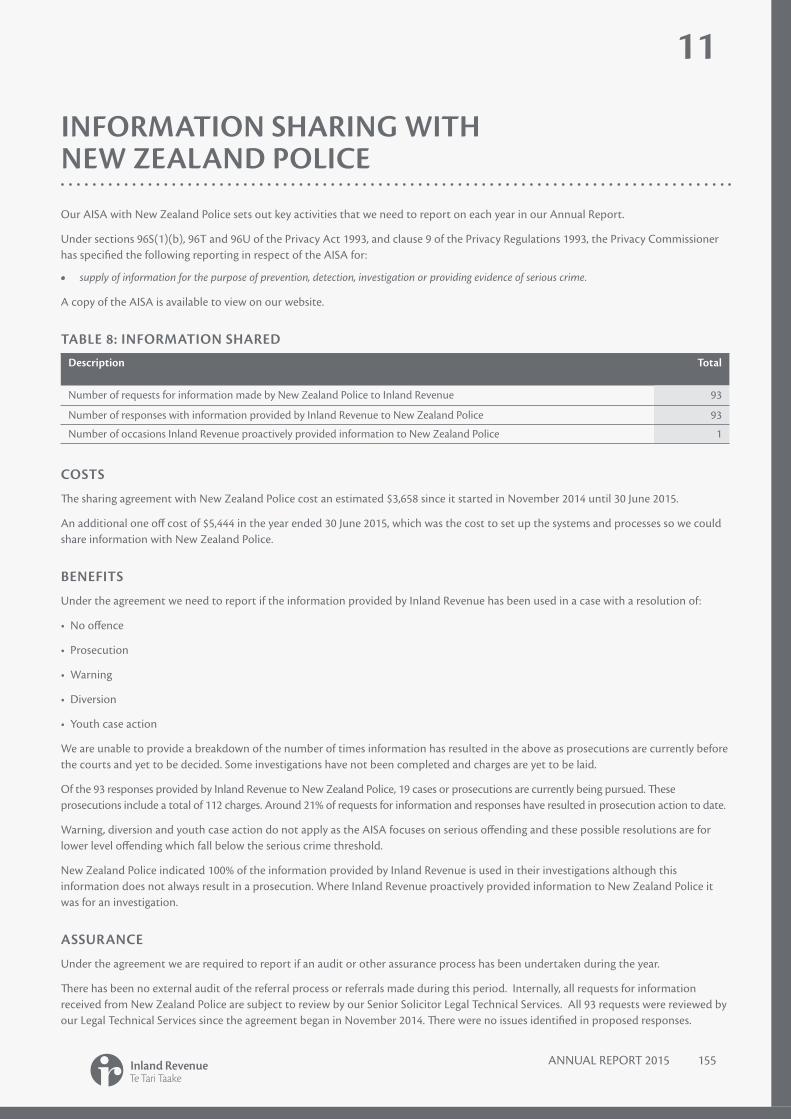

We contribute to Result 7 through an AISA with New Zealand Police. This allows Inland Revenue to share certain personal information with New Zealand Police for the purpose of prevention, detection, investigation or providing evidence of serious crime. We also participate in the Whole-of-Government Gangs Action Plan, a multi-agency approach to reducing the harm caused by gangs, involving intelligence gathering and a range of prevention and enforcement activities.

Over 2014–15, we have continued to enable more effective information sharing between government agencies. This has included:

• working on the development of possible future information sharing initiatives with MSD and the Accident Compensation Corporation (ACC)

• working with MBIE and Worksafe to share information for the enforcement of employment standards as a result of changes to workplace legislation

• participating in cross-agency forums such as the privacy reform group, data futures forums, Government Chief Information Officer information management groups, and Government Chief Privacy Officer leadership forums and working groups.

Our sharing arrangements are supported by our new Information Management Strategy. The strategy enables effective administration of information and helps us to build and manage our intellectual property. This will improve information management capability through collective ownership of information management and simplified guidelines supported by fit for purpose IT capability.

Government Information and Communication Technology Strategy

Inland Revenue’s Information and Communication Technology (ICT) strategy and roadmaps reflect the Government ICT Strategy’s focus on using information and technology to deliver better services to New Zealanders. By 2017, the aim is to enable individuals and businesses to connect with government services through digital channels, joined-up services and technology that will function across agencies.

We already use a number of all-of-government services. One example is Storage as a Service provided through Datacom New Zealand. This approach means that we no longer have to physically manage storage ourselves. By using the all-of-government data storage service we have access to more capacity, flexibility and improved performance at less cost.

Businesses are already noticing the differences we are making. The latest results of the business reference group survey looking at effort of dealing with government and how government agencies compare with the private sector show overall a 16% reduction in effort with dealing with government. For businesses whose most recent interaction with government was with Inland Revenue, the survey showed there was a 23% reduction in effort. The key reasons businesses listed for the improvement were:

• ease of filing returns led by the implementation of online GST filing and increased uptake of other online services

• ease of contacting Inland Revenue, with businesses finding it easy to get through to services and dealing with helpful Inland Revenue staff.

ANNUAL REPORT 2015 29

03

Contributing to other all-of-government services

We are involved in other all-of-government activities. We will continue to work with other agencies to identify where we could adopt new and improved processes and services used elsewhere in the public sector.

Procurement

We are participating in the Government’s new streamlined procurement rules, which have changed the way government does business with suppliers by making agencies’ procurement practices more consistent and business-friendly. The new rules promote a value for money approach to procurement, which means that rather than just getting the lowest price, we consider total cost of ownership and other benefits.

We have a long-term strategy to ‘buy not build’ for our Business Transformation programme. To make it easier for small businesses to engage with Inland Revenue, we developed the Business Transformation Approved Panel in October 2014, which covers a number of the professional services our Business Transformation programme

is likely to need on a recurring basis. This panel is open and allows suppliers to register their interest at any time.

Inland Revenue is committed to using collaborative procurement opportunities such as all-of-government, collaborative and syndicated procurement contracts. We have signed up to a number of these in the past 12 months and are leading the syndicated waste management contract.

All-of-government banking services

The state sector’s banking contract with Westpac has been in place for more than 20 years. During this time the banking requirements of government have changed considerably. We are working with Treasury and MBIE who are leading an all-of-government solution to meet the Government’s current and future banking needs. This solution will provide access to economies of scale, better value for money, process efficiencies and better interaction for financial payments between government, business and taxpayers.

30 ANNUAL REPORT 2015

Rebuild Canterbury

Understanding the impact of adverse events and the characteristics of the rebuild workforce

Inland Revenue has sponsored research projects to understand the impact of the earthquakes on SMEs in Canterbury and the characteristics of the Christchurch rebuild workforce. The research has provided insight into SME compliance, debt and employment and the compliance issues associated with the rebuild workforce. The effect of the rebuild on SME GST in different industries and sectors has also been evaluated. These insights are now informing our initiatives in Canterbury.

Providing joined-up government services in Christchurch

We continued to work with the Canterbury Earthquake Recovery Authority (CERA) and other agencies in various forums to support the overall reconstruction effort. This included planning for the Public Sector Precinct and exploring opportunities to co-locate 1,600 public servants from 17 agencies in four new CBD locations from late 2015. We continue to operate and learn from co-location in the New Zealand Government site in Durham Street and work with other agencies to investigate opportunities for cross-government collaboration.

Supporting our people in Canterbury

We provided additional support and wellbeing initiatives for our own Christchurch workforce and other government agencies supporting the Government sector in Christchurch. This included chairing the Public Sector Organisational Resilience Team and contributing to the Greater Christchurch Psychosocial Recovery Committee and work programme.

Improving compliance in Canterbury

We have focused on mitigating and addressing the compliance risks from the $40 billion rebuild. This included working alongside funding distributors, including all major insurance companies and government, to gain assurance in the integrity of their systems and identify any areas of risk. We have continued our compliance focus on identified high-risk sectors, including construction, hospitality and property. We have also provided support to the wider community with educational activities to help customers get it right from the start.

Inland Revenue research has confirmed on-time GST filing and payments have improved in Canterbury since the low point in the 2011 tax year when the earthquakes occurred.

While the proportion of Canterbury small and medium enterprises (SME) in debt spiked at the time of the earthquakes, it has improved since then, with Canterbury SMEs making up a smaller proportion of SMEs in debt nationally than they did in 2011.

04Business

Transformation

ANNUAL REPORT 2015 31

32 ANNUAL REPORT 2015

Business Transformation

Business Transformation is a multi-year, multi-stage change programme that will help us become the modern world-class revenue organisation that is set out in our vision IR for the future. Over the year we got closer to realising this vision.

We are currently managing a range of tax and social policy products on an ageing system and business model. Over the years our role has expanded from solely collecting tax in a paper world, to today where we manage the collection and payments of tax and a range of other services like student loans, child support and KiwiSaver. Adding these social policy products and services to 30 year old technology has resulted in complexity.

Our tax administration needs to catch up and be fit for 21st century needs.

Technology is rapidly advancing, our customers’ lives are busier than ever and businesses want to spend less time on compliance. New Zealand is becoming more diverse and customers want and expect us to interact with them in a digital world.

Modernising our systems and processes will also enable the Government to implement policy more quickly.

The Business Transformation programme consistently met its milestones and spent less than its budget throughout the year.

How we are changing

Our Business Transformation programme is being delivered in four customer-focused stages over eight to 10 years.

High-level design of the four stages has been completed and the detailed design of stage one has begun. We anticipate that the detailed business case will be completed and submitted to the Government for approval by March 2016. Once approved, implementation of stage one will begin. We have delivered some visible, early improvements to our digital services, including improving myIR and making improvements to our website.

This year we focused on designing the foundations for our future revenue system. The design phase began in January 2015, and covers high-level design for stages one to four of the programme, and detailed design for Stage 1: Enabling secure digital services. The design and digital services business case outlining the approach to design and the funding, was approved by Cabinet on 17 November 2014.

We have a regular programme of independent quality assurance reviews to continually check that what we are doing is the best way to do it. Over the year we had a Deloitte review and the Gateway Review in September 2014, KPMG Independent Quality Assurance and Technical Quality Assurance completed in December 2014 and a review from the Office of the Auditor General in April 2015. All were positive and support the way we are transforming and the quality of our processes. Results of the reviews are available on www.ird.govt.nz/transformation.

Cabinet approval and legislative changes

Changes proposed in the Taxation (Transformation: First Phase Simplification and Other Measures) Bill introduced on 30 June 2015 pave the way for modernising and simplifying the tax administration system by removing some current legislative obstacles.

They include:

• proposals to allow earlier tax refunds on personal tax summaries that meet the automatic refund threshold

• reforming the way we are able to communicate with our customers by providing modern rules to support electronic communication in the same way as paper communications

• measures to allow us to share certain information with other agencies when it makes customers’ lives easier.

Choosing design and core software partners

We spent most of the year completing very careful procurement processes to select partners to help us design the next stage of Business Transformation and a software provider to supply the technological core of our future system.

We chose Accenture and two local providers to help us with design. External quality assurance checks found the

ANNUAL REPORT 2015 33

“ The programme has been set up to succeed, and is suitably prepared to begin the design phase, while being aware of the considerable challenge of sustaining the good progress thus far.”

KPMG Independent Quality Assurance and Technical Quality Assurance review, December 2014

04

procurement process that we used was sound and fair.

Accenture joined Inland Revenue in January 2015 and has been helping us with the high-level design of the four stages of the Business Transformation programme. We have developed blueprints outlining our future system.

In June 2015 we announced Fast Enterprises (FAST) as our preferred Commercial Off-the-Shelf (COTS) software vendor. COTS software will form the technological core of our future system. FAST started working with us on the detailed design in August 2015.

To help us prepare for the changes, we have engaged a range of local providers including Optimation, ThinkPlace, Assurity Consulting and Tenzing along with Accenture and FAST.

Stakeholder engagement

A large part of what we are doing is engaging with stakeholders and seeking their input on designing New Zealand’s future tax system.

Discussions continued during the year with GST and payroll software developers on options for how they can better interact with our core systems and reduce compliance costs for businesses. We also met and presented to a wide range of groups including:

• financial services and accounting industry bodies

• software developers

• industry groups including Federated Farmers and Business New Zealand

• social service groups such as Age Concern and Citizens Advice Bureau.

We have set up three key reference groups to help us.

The Taxpayers’ Simplification Panel was created to give New Zealanders a voice in simplifying, modernising and transforming the way we pay tax.

The Transformation Reference Group provides us insights and perspectives from businesses, individuals and the tax community to inform our Business Transformation programme. Members have extensive experience across a broad range of sectors and represent diverse communities.

Our ICT Reference Group provides an independent voice and sounding board on our Business Transformation programme. It is an opportunity for ICT professionals to contribute individual perspectives and experience on the impact of our Business Transformation programme on business and the community.

Public consultation

Improving the customer experience and making it easier and simpler for our customers will require significant policy-related work over the life of the Business Transformation programme.

We ran two significant public consultations asking New Zealanders for their feedback on our Business Transformation and explored options designed to modernise and simplify the tax system. The Minister of Revenue launched both on 31 March 2015.

Making Tax Simpler – A Government Green paper on Tax Administration set out the policy direction for modernising and simplifying the tax administration. This consultation ran until 29 May 2015.

Making Tax Simpler – A Government discussion document on Better Digital Services asked for feedback on approaches to encourage customers to move to better digital services and any barriers that currently prevent them from doing so. This consultation closed on 5 May 2015.

More than 900 online comments and over 90 written submissions were received on the proposals. This was a significantly higher number of responses than we expected. Detailed feedback on these consultations will be published on our website when it is collated.

34 ANNUAL REPORT 2015

Cabinet confirmed a programme roadmap to deliver Business Transformation in a number of steps, enabling the Government to make investment choices throughout the life of the programme:

Enabling secure digital services – to enable the majority of customers to self-manage and reduce businesses’ compliance burden in fulfilling their PAYE obligations.

STAGE 1

Streamline social policy delivery – this will improve the delivery of the social policies that Inland Revenue administers.

STAGE 3

Complete delivery of the future revenue system – this will include transitioning any remaining tax and social policies to a new platform and decommissioning technical platforms that are no longer required.

STAGE 4

Streamline income and business tax processes – this will leverage the foundations delivered in the previous stage and further reduce businesses’ compliance burden to fulfil their tax obligations.

STAGE 2

Organisational health

ANNUAL REPORT 2015 35

05

36 ANNUAL REPORT 2015

Health and Safety

A range of activities have started to ensure Inland Revenue is compliant and has strategies in place that will effectively transition the organisation to the new Health and Safety legislation, which comes into effect 4 April 2016.

We are currently working to bring our health and safety-related policies, processes and systems into line with the requirements of the new legislation. Our activities include exploring a health and safety governance reporting structure that will provide our governance group with regular information on health and safety risks and mitigation and ensuring people including managers and health and safety committees receive education and increased visibility of the legislation.

Organisational health

It is important that we effectively manage our people, our assets and the risks to our business so that we can achieve our strategic intentions.

Governance

To ensure our governance system continues to meet the needs of our transforming organisation, we introduced changes to our governance system in May 2015. The governance system will ensure robust and timely governance of our strategy, investment and performance activities, focusing on transformation, but also ensuring we are meeting the needs of today. Membership across the system is a mix of our Inland Revenue Executive Leadership Team, senior leaders and external members where appropriate.

Preparing our people for change

Changing and streamlining the way we deliver our services, mainly through greater use of digital and online services, will have an impact on our people. As we move towards greater application of technology and streamlined processes, we will make changes to our workforce. To prepare for this, we are designing frameworks and systems to help reshape our organisational capability.

We have updated our workforce strategy to help us identify what we need to do to deliver our strategic intentions. This has supported work on our organisation’s culture and our leadership strategy.

Change leadership and capability

Effective change leadership is essential to lead our people through Business Transformation. We need leaders to be more agile, adaptable and open to new ways of working.

We have revised our leadership framework and are currently redesigning our leadership programmes to reflect this.

Our people leadership strategy includes:

• embedding this leadership framework

• renewing our development programmes for leaders

• encouraging leadership collaboration

• further developing our leadership skill set.