Embed Size (px)

Citation preview

Annual Report for the twelve months ended 31 August 2012

Nord Anglia Education (UK) Holdings PLC (the “Issuer”)

7 December 2012

2

Introduction

On 28 March 2012, Nord Anglia Education (UK) Holdings plc (the “Issuer”) issued its 10.25% Senior Secured Notes due 2017 (the “Notes”) pursuant to an indenture dated 28 March 2012 among the Issuer, Citicorp International Limited as Trustee and Security Agent, Citibank N.A. London Branch as Paying Agent and Transfer Agent and Citigroup Global Markets Deutschland AG as Registrar (as amended or supplemented, the “Indenture”). Capitalised terms used herein that are not otherwise defined have the meanings given to such terms in the Indenture. Section 4.03(a)(1) of the Indenture requires, so long as any Notes are outstanding, the Issuer to furnish to the Trustee (who at the Issuer’s expense will furnish by mail to the Holders) and post on the website https://sf.citidirect.com, within 120 days following the end of the fiscal year beginning with the fiscal year ended 31 August 2012, annual reports containing: (i) information that is substantially comparable in all material respects to the sections in the Offering Memorandum entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, “Business” and “Description of Other Material Indebtedness and Certain Financing Arrangements”; (ii) the audited consolidated balance sheet of the Issuer as of the end of the most recent fiscal year and audited consolidated income statements and statements of cash flow of the Issuer for the most recent two fiscal years, including appropriate footnotes to such financial statements, for and as of the end of such fiscal years and the report of the independent auditors on the financial statements and (iii) calculations of Consolidated EBITDA and Consolidated Interest Expense, in each case, for such fiscal year. This Annual Report as of and for the twelve months ended 31 August 2012 and the audited consolidated financial statements of the Issuer for the year ended 31 August 2012 included at Appendix 1 are published to comply with the reporting requirements in the Indenture. In this Annual Report, references to “FY2011”, “FY2012” and “FY2013” refer to the twelve month periods ended 31 August 2011, 31 August 2012 and 31 August 2013, respectively.

Forward-Looking Statements

This Annual Report may include forward-looking statements. All statements other than statements of historical fact contained in the Annual Report, including, without limitation, those regarding the future financial position and results of operations, strategy, plans, objectives, goals and targets, future developments in the markets in which the Issuer and its consolidated subsidiaries (together “Nord Anglia Education”) participate or seek to participate, and any statements preceded by, followed by or that include the words “believe”, “expect”, “aim”, “intend”, “will”, “may”, “anticipate”, “seek”, “should” or similar expressions or the negative thereof, are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, some of which are beyond the control of Nord Anglia Education, which may cause actual results, performance or achievements, or industry results, to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. These forward-looking statements are based on numerous assumptions regarding present and future business strategies and the environment in which Nord Anglia Education will operate in the future. Actual results and the timing of certain events may differ significantly from the results discussed in the forward-looking statements. All forward-looking statements in this document are based on information available to Nord Anglia Education as of the date of the Annual Report and Nord Anglia Education assumes no obligation to update any such forward-looking statements.

Presentation of Financial Information The selected consolidated financial information of the Issuer presented in this Annual Report has been prepared in accordance with International Financial Reporting Standards as adopted by the European Union (“IFRS”) and International Financial Reporting Interpretations Committee interpretations applicable to companies reporting under IFRS. However, please note that this Annual Report does not necessarily include all disclosure required by IFRS. The consolidated financial information included herein does not include all the information and disclosure required in the annual consolidated financial statements, and should therefore be read in conjunction with the Issuer’s annual consolidated financial statements as at 31 August 2012. Detailed information regarding the accounting policies used for preparing the financial information included in this Annual Report is provided in Note 1 to the Issuer’s annual consolidated financial statements for the year ended 31 August 2012.

3

In this Annual Report, reference is made to “EBITDA”, “Adjusted EBITDA” and “Adjusted Revenue”. EBITDA, Adjusted EBITDA and Adjusted Revenue are non-GAAP measures and are not required by or presented in accordance with IFRS. EBITDA is defined as operating profit plus depreciation, amortisation, impairment of assets and exceptional expenses. Adjusted EBITDA is defined as EBITDA adjusted for the impact of acquisitions and dispositions (i.e. assuming that the acquisition or disposition occurred at the beginning of the relevant period) and to exclude certain items that we believe are not related to our normal operations. Adjusted Revenue is defined as Revenue adjusted for the impact of acquisitions and dispositions (i.e. assuming that the acquisition or disposition occurred at the beginning of the relevant period). We use EBITDA, Adjusted EBITDA and Adjusted Revenues as supplemental financial measures of our operating performance. EBITDA, Adjusted EBITDA and Adjusted Revenue should not be considered in isolation or construed as an alternative to cash flows, net income or any other measure of financial performance or as an indicator of our operating performance, liquidity, profitability or cash flows generated by operating, investing or financing activities. EBITDA, Adjusted EBITDA and Adjusted Revenues presented herein may not be comparable to similarly titled measures presented by other companies and Investors should also note that EBITDA and Adjusted EBITDA presented are calculated differently from “Consolidated EBITDA” as defined and used in the Indenture governing the Notes.

Important Note This Annual Report has been prepared exclusively by us for any holder of the Notes or any prospective investor in accordance with Section 4.03 of the Indenture. You are authorised to use this Annual Report solely for the purpose of evaluating your investment in the Notes. Neither the delivery of, nor access to, this Annual Report implies that any information set forth in this Annual Report is correct as of any date after the date of this Annual Report, in whole or in part, and you may not disclose any of the contents of this Annual Report or use any information herein for any purpose other than evaluating your investment in the Notes. You agree to the foregoing by accepting delivery of, or access to, this Annual Report.

4

1. BUSINESS

Overview

We are a leading global operator of premium private schools for K-12 students in Asia,

Switzerland, Central Europe and the Middle East (“Premium Schools”). We operate in markets

characterised by strong wealth creation, significant FDI and economic growth. The two main

drivers of our business are increasing globalisation and a growing emphasis by parents on high

quality education for their children. In addition to our Premium Schools, we provide educational

services to governments in the Middle East, the United Kingdom and Asia (“Learning

Services”).

In FY2012, our Premium Schools accounted for 84.7% and 88.6% of our Adjusted Revenues

and Adjusted EBITDA before central and regional expenses, respectively. Learning Services

accounted for 15.3% and 11.4% of our Adjusted Revenues and Adjusted EBITDA before central

and regional expenses, respectively.

Premium Schools

We own and operate 13 premium schools in 11 locations in Asia, Switzerland and Central

Europe. In addition, we operate the British International School Abu Dhabi (“BISAD”) in the

Middle East, 49% of which is owned by an affiliate of our parent company. On 28 September

2012, we signed a definitive agreement to acquire the 49% interest in the school from the affiliate

of our parent company. Completion of the acquisition, which is subject to the satisfaction of

several conditions precedent, is expected before the end of 2012.1

In FY2012, our schools in China, Switzerland and Central Europe contributed approximately

67.8%, 18.8% and 13.4% of our Premium Schools’ Adjusted EBITDA, respectively.

Our schools in China primarily serve expatriates and our schools in Thailand, Switzerland,

Central Europe and the Middle East serve both expatriates and affluent local families. Our

overall student mix is 78% expatriates and 22% local students. Our Premium Schools are not

directly exposed to government funding risk as all of their revenues are derived from private

sources, of which employers contribute approximately 58%.

As of 18 November 2012, our enrolment was 9,747 students and our capacity was 12,472

places representing a utilisation rate of 78%.

Learning Services

We provide targeted education-related services to governments, government agencies,

regulatory bodies and related educational authorities in the Middle East, the United Kingdom, and

Asia. During FY2012 we did not enter into any new Learning Services contracts and we expect

to continue to see a reduction in the size of our Learning Services operations going forward.

1 In this report, information and statements relating to FY2012 do not include our schools in Chonburi,

Thailand and Abu Dhabi, UAE. Commentary on FY2013, for example current student numbers, capacity and other information on our schools, includes our schools in Chonburi, Thailand and Abu Dhabi, UAE.

5

Our Family of Schools

The following map shows the geographic coverage of our Premium Schools (including

BISAD):

Our Strengths

Diversified Platform with Benefits of Scale

Nord Anglia Education is one of the world’s largest K-12 premium school operators owning and/or operating fourteen schools in twelve locations and eight countries across Asia, Switzerland, Central Europe and the Middle East. No single school in our geographically diverse network accounted for more than 15% of total Adjusted Revenues in FY2012. This platform allows us to leverage expertise and resources across our entire network to enhance the quality of education and create significant operating benefits, including:

• strong brand equity supported by a reputation for quality, which enables us to drive

enrolment growth and set tuition fees at the higher end of the market;

• credibility with our stakeholders, including educational authorities, teachers, parents,

developers, landlords and sellers of premium schools;

• implementation of best practices including cost management and control through

benchmarking;

• creating global citizens of students through initiatives such as the Global Classroom,

which enhances the value proposition of our schools to parents and prospective

students; and

• training and development of principals and teachers through initiatives such as Nord

Anglia University.

Robust and Highly Attractive Business Model

Resilient Performance Across Economic Cycles

Total enrolment in our schools has grown at a CAGR of 23.5% from the end of FY2008 through 18 November 2012. Of this increase in enrolment, 2,700 new student enrolments were

6

through strategic acquisitions and 3,037 were organic.1 We are well positioned to deal with

negative national or regional trends due to our geographically diverse operations across key education markets.

Price Inelasticity

The private-pay nature of our model helps ensure that our schools are not directly exposed to any government funding risk. Approximately 58% of our tuition fees are paid by employers, who are less sensitive to moderate pricing increases as education allowances typically represent only a small percentage of an expatriate’s total compensation. In addition, self-funding expatriates and affluent local families, who contribute approximately 42% of our tuition fees, are also able to afford moderate price increases. We have been able to increase our tuition fees across our markets at an average of 4-6% per annum over the last four years (the weighted average increase from FY2012 to FY2013 was 5.2%), whilst continuing to generate organic enrolment growth.

Strong Business Visibility with Predictable Revenue Streams

We have good visibility on future enrolments through our high persistence rates and average student tenure of 3.6 years. Further, our policy to require a full term’s notice for any potential leavers enhances in-year visibility as we are entitled to receive a full-year of tuition if we are notified of a student’s intention to leave after the start of Term 2 (January).

Our ability to measure student re-enrolment rates among existing students and to estimate new enrolments for subsequent periods provides revenue predictability and enables us to plan student capacity.

Favourable Working Capital Dynamics and a Capital Efficient Approach to Growth

We have historically received approximately 60% of our annual tuition fees in advance of the school year, which starts in late August/early September. We have generally received an additional 20% of our tuition fees prior to the start of Term 2 (January), and the remainder prior to Term 3 (April). In FY2012, approximately half of our students paid the full annual tuition fees in advance of the school year in exchange for a small average discount. As a result, our working capital needs are principally sourced from tuition fees.

Our expansion strategy is based on an “asset-light” model and is focused on securing high quality purpose-built facilities through long-term leases. The capital expenditure for capacity expansion at our existing, new and acquired schools has been primarily funded by the owners of the real estate. Accordingly, we are generally able to expand capacity at our existing schools and secure capacity at new schools without incurring major capital expenditure. Our capital expenditure is generally limited to furniture, equipment and other materials for classroom, sports and extra-curricular activities. In the case of our acquired schools, we have structured the transactions so that we acquire the operating businesses and typically negotiate long-term leases from the sellers who retain ownership of the real estate.

Premium Quality Education and Leading Reputation

Our commitment to quality drives the strong operating performance of our Premium Schools as evidenced by overall enrolment growth and high levels of re-enrolment. We focus on the needs of individual students and offer high quality education across multiple curricula. Our proprietary IT platform supports this by tracking each student’s performance against personalised targets and drawing our attention to the requirements of the individual learner. Through this highly individualised system we are better able to maximise each student’s potential. In addition, the platform allows us to set clear expectations of learning objectives for a classroom, class year or entire school and intervene as required.

Our principals and teaching staff are highly-qualified and experienced, having been through a rigorous recruitment process. We are able to attract highly-qualified staff due to our international scale, long track record and competitive compensation packages. Further, we have an organisation-wide emphasis on the retention of teachers through on-going professional development initiatives and a policy to promote from within wherever suitably capable candidates are identified. Initiatives such as Nord Anglia University, which provides comprehensive professional training programs for teachers and principals, underscore our commitment to professional development.

1 Organic enrolment growth includes the school in Abu Dhabi, which we opened as a greenfield site in

2009.

7

Our students consistently outperform their peers in standardised examinations. In the last five academic years, our students’ average examination results were higher than the average in the United Kingdom for the International General Certificate of Secondary Education (IGCSE), which students take at the age of 16, and globally for the International Baccalaureate Diploma (IBD), which students take at the age of 18. For the 2012 academic year, 86.2% of our students gained 5 A* to C grades compared to 85.6% in the 2011 academic year and the provisional UK average for 2012 of 81.1%. The average IBD score achieved by our students was 33.3 points compared to 32.6 points in the 2011 academic year and a global average score in 2012 of 29.8 points. In addition, 17% of our graduates in 2012 went to the world’s top 30 universities and 75% went to the world’s top 600 universities.

1 Given that our admissions approach is not based upon

academic ability, and the fact that for a large portion of our students English is their second language, we believe our students’ examination results and university destinations demonstrate the quality and effectiveness of our approach to education.

Superior Operational Capabilities

We emphasise operational efficiency and adopt a data-driven approach to managing our business. Our global, regional and school teams track and analyse KPIs on a weekly basis and refine our operating strategy accordingly.

We focus on the following key areas of our operations:

• Student recruitment: We have a systematic approach to student recruitment. Our comprehensive recruitment strategies are adapted to each of our specific markets and executed by each school’s principal, admissions team and marketing manager. We use a relationship management system that enables us to monitor an applicant’s file at every stage, from initial enquiry through enrolment.

• Pricing: We monitor market trends taking into consideration historic and regional economic trends and supply and demand dynamics to set our tuition fee levels.

• Cost management: We use metrics-based management throughout our school operations to enhance efficiencies. We achieve operational efficiencies through various means, including efficient class scheduling and optimising our teaching resources.

• Capacity planning: We have developed expertise in planning and adding capacity to meet demand. This enables us to manage growth by efficiently utilising capacity at existing schools and expanding as necessary. We also work with architectural consultants who specialise in optimising school configurations. Our approach to growing our network of schools is highly analytical and includes the use of demographic and economic models, when identifying opportunities for expansion.

• Cash and financial management: We have a centralised finance team that enables us to monitor and manage our business more effectively. We have a track record of robust cash management and have historically had few instances of bad debt.

Partner of Choice

Our scale and reputation make us a desirable partner for sellers, developers and landlords. We believe that sellers of schools are often focused on the operating track record, financial stability and the reputation of potential buyers. Our acquisitions of schools in Beijing, Switzerland and Thailand resulted from exclusive discussions with sellers who were primarily concerned with these matters. Similarly, developers and landlords seek to attract a recognised operator of schools with a reputation for quality in order to enhance the value of their adjacent residential real estate.

Experienced Management Team

Our senior management team, led by CEO Andrew Fitzmaurice, combines seasoned executives with experience in running publicly-listed companies and strong operational expertise as well as leading academic thinkers. Andrew Fitzmaurice has been with the company for almost ten years and was CEO when Nord Anglia Education was a publicly-listed company in the United Kingdom. Since going private in 2008, we have further invested in building a highly qualified management team, including our CFO and our COO, both of whom have prior public company experience.

1 Top universities as defined by www.topuniversities.com

8

Our Strategies

Continue to increase student enrolments at our existing schools

We have been successful at driving enrolment growth and aim to continue this growth by applying our systematic processes for enquiry generation, converting enquiries to enrolment and retention of existing students. Our school principals lead the recruitment effort with dedicated admissions and marketing teams. We generate enquiries and visits through referrals, web-based strategies and other marketing activities.

Maintain price leadership at our existing schools

We have made significant investments in our schools which enable us to consistently provide high-quality premium education. We intend to leverage our superior quality and reputation to maintain price leadership in each of our markets and realise pricing growth in excess of inflation.

Improve the efficiency and enhance quality and consistency of our teaching resources

Our teaching costs are the largest component of our cost structure and therefore a key driver of margins. We focus on driving teaching efficiencies through class scheduling and effective deployment of our teaching resources. We optimise our teaching resources by minimising the amount of administrative responsibilities allocated to our teachers to ensure that each teacher spends more time focused on teaching.

Incremental capacity addition

Where opportunities arise, we may increase capacity by expanding our current schools, opening new school campuses or acquiring schools. In addition, we may opportunistically enter new markets primarily in Asia, Europe and the Middle East, where we believe there is or could be strong demand and subsequent expansion opportunities for premium schools.

Our Approach to Academic Quality

Our philosophy is to help all our students to be the best that they can be. Our schools are inclusive in that they accept students with a wide range of academic ability. Through our “High Performance” approach we ensure that high academic performance is the goal for all students. The key elements that we focus on to promote a high level of academic quality are:

An academically rigorous educational program

Our curricula meet internationally recognised requirements and are adapted to meet local regulatory requirements, culture and customs. The majority of our schools teach the National Curriculum of England and Wales (the “National Curriculum”).

We utilise a highly customised IT platform designed around each student. It enables us to track performance of students on an individual basis as well as benchmark within and across our schools. We believe that this maximises student learning and performance by giving each student and faculty an accurate gauge on individual progress. In addition, this platform allows us to set clear expectations of learning objectives at a classroom, class year or school level and intervene as required. Further, our IT platform creates accountability among faculty members and drives consistency in instruction by applying comparable metrics across our network.

In addition to our rigorous approach to classroom-based learning, we have a supplementary informal online learning environment which operates across all our schools that we call the Global Classroom. The Global Classroom is an internet-based system which allows our students to learn with other students in our schools throughout the world. This innovative and distinctive learning environment introduces students to a new learning style, which creates independent learners, preparing them well for future university study and turning them into global citizens.

Highly qualified principals, teachers and administrative staff

We demonstrate our commitment to premium quality education by hiring and retaining highly qualified principals, teachers and administrative staff. We require all our teachers to be fully qualified and have significant teaching experience in national or international schools. The minimum credentials we require include formal teacher qualifications, such as a Post Graduate Certification in Education (“PGCE”) or its equivalent and at least two years teaching experience.

Our principals and teachers also benefit from the centralised support and experience of our educational team led by Professor Deborah Eyre. In addition, we have in place various

9

continuing professional development initiatives, including Nord Anglia University which is designed to prepare some of our best teachers for career progression and help continuously improve all of our teaching staff. We regularly and rigorously review the performance of our principals and teaching staff to ensure that their performance meets our high standards.

Class sizes

We restrict classes to a maximum of 22 students, with a few exceptions, in order to provide each student with close teacher interaction and individual attention and support. This benefits students, and provides a rewarding environment for our teachers and promotes staff retention.

High quality school facilities

Our school facilities, such as science laboratories, music and theatre resources, swimming pools and other high quality sports facilities enhance the educational experience of our students. In addition, the majority of classrooms utilise interactive computerised white boards that facilitate students’ participation in learning. We use internationally-recognised architectural consultants specialised in school design to direct the development of new facilities and the expansion or refurbishment of our existing schools in order to promote the efficient use of our facilities by staff and students.

Premium Schools

We own and operate 13 premium co-educational schools in 11 locations across Asia, Switzerland and Central Europe. In addition, we operate the British International School Abu Dhabi (“BISAD”) which is owned 49% by an affiliate of our parent company. On 28 September 2012, we signed a definitive agreement to acquire the 49% interest in BISAD owned by the affiliate of our parent company. Completion of the acquisition, which is subject to the satisfaction of certain conditions precedent (including regulatory approval), is expected before the end of 2012.

The following table sets forth certain information about each of our schools and their educational programs:

School Date Founded

Date Acquired/ Founded Curriculum Qualification

China Sanlitun Beijing, China 2003 2009 National Curriculum

(1)

Shunyi Beijing, China 2009 2009 National Curriculum IGCSE/A levels Pudong Shanghai, China 2002 2002 National Curriculum IGCSE/IBD Puxi Shanghai,China 2005 2005 National Curriculum IGCSE/IBD Asia (non-China)

Chonburi, Thailand 1994 2012 National Curriculum IGCSE/IBD Switzerland Beau Soleil, Villars 1910 2011 French and Swiss Curriculum IBD or French Bac College Champittet, Lausanne 1903 2011 French and Swiss Curriculum French/Swiss Bac/IBD College Champittet, Nyon 2007 2011 French and Swiss Curriculum IBD La Cote, Gland 2008 2011 National Curriculum IBD Central Europe Prague, Czech Republic 1995 1995 National Curriculum IGCSE/IBD Warsaw, Poland 1992 1992 National Curriculum IGCSE/IBD Bratislava, Slovakia 1998 1998 National Curriculum IGCSE/IBD Budapest, Hungary 2002 2002 National Curriculum IGCSE/IBD Middle East Abu Dhabi, UAE 2009 2009 National Curriculum IGCSE (1)

This school educates students from age three to 13, which are pre-qualification years.

Our Four Schools in China

The British International School Shanghai—Pudong, China

We opened this school in 2002, our first school in China, with an initial capacity of 100 places and the school now has a capacity of 1,500 places. The school is located within a large scale residential development in Pudong, approximately five miles from the centre of Shanghai. Its facilities include science laboratories, computer suites, art, music and physical education

10

rooms, libraries, a 1,000 seat state of the art theatre, a new secondary school building, three indoor sports halls and a 25 metre indoor swimming pool. The school experienced good growth in student numbers in FY2012.

As of October 31, 2012, nearly all of the students at this school were expatriates.

The British International School Shanghai—Puxi, China

We opened this school in 2005 with an initial capacity of 500 places. The school is adjacent to several high-end residential developments popular with expatriate families. The school’s facilities include two gymnasiums, two swimming pools of 15 and 25 metres, a dance studio, a fitness suite, outdoor basketball courts, four tennis courts, one astro-turf football field and playing fields. Other facilities include two libraries, a 250 capacity auditorium, a 500 capacity auditorium, a new IB suite, an internet café, science laboratories, music rooms and two cafeterias. We have since expanded capacity to a total of 2,000 places. The expansion to this school was officially opened by His Royal Highness Prince Andrew in 2011. This school had strong student number growth in FY2012.

As of 31 October 2012, nearly all of the students at this school were expatriates.

The British School of Beijing—Shunyi, China

We acquired this school in 2009 with a capacity of 400 places and moved it to new custom built facilities with 1,500 places one mile from its original location. The school is located in a large residential area containing many expatriate developments in suburbs on the outskirts of Beijing. The school’s campus includes outdoor and indoor sport facilities gymnasiums, fitness suites, a football field and tennis and basketball courts, along with an indoor swimming pool and dance studio. In addition, we have two theatres, dedicated music rooms, computer music suites, a recording studio, ICT suites, a Lego robotics lab, science laboratories and art studios. The school was officially opened by His Royal Highness Prince Andrew in 2010. We have recently signed contracts to expand the capacity by up to 300 places. This expansion is expected to be completed in time for September 2013. This school experienced strong student number growth in FY2012.

As of 31 October 2012, nearly all of the students at this school were expatriates.

The British School of Beijing—Sanlitun, China

We acquired this school in 2009 with a capacity of 280 places. The school is located in the heart of the Embassy district of Beijing and educates students from age three to age 13. Its facilities include a football pitch, a full size gym, an assembly hall, tennis and basketball courts and an astroturf play area with climbing frames. The school now has a capacity of 360 places. We have recently signed contracts to expand the capacity of this school by approximately 200 places. The expansion will include additional facilities and a new entrance from the main road in Sanlitun and is expected to be completed in time for September 2013. Student numbers at this school were stable in FY2012.

As of 31 October 2012, nearly all of the students at this school were expatriates.

Our One School in Thailand

The Regent’s School — Chonburi, Thailand

We acquired our school in Chonburi, Thailand on 1 August 2012 with a capacity of 1,200 places. The school is located in the Eastern Seaboard region of the Gulf of Thailand, 120km southeast of Bangkok and 16km north-east of Pattaya. The Eastern Seaboard in general and Chonburi in particular include many of Thailand’s largest industrial developments. The facilities at the school include a 25-metre swimming pool with audience seating, a full sized rugby and football pitch (with two additional, smaller football pitches), a double gymnasium with basketball facilities and tennis courts, a 400 seat theatre and a brand new early-years building for younger children. The boarding houses are home to more than 100 students and are equipped with modern fingerprint security technology.

As of 31 October 2012, 75% of the students at this school were expatriates.

11

Our Four Schools in Switzerland

Collège Champittet—Lausanne

An affiliate of our parent company acquired this school in 2009 and it was acquired by Nord Anglia Education in February 2011. The school has a capacity of 944 places and is located near the banks of Lake Geneva in Lausanne. The school includes high quality academic and recreation facilities including, sports fields, playgrounds, library, science laboratories, chapel, dining hall and cafeteria and computer suites. The school also has boarding accommodation for up to 100 students. Founded by Dominican monks in 1903, we believe that Collège Champittet is one of the best known private schools in Switzerland. The school experienced a reduction in student numbers in FY2012, which we believe was due to a combination of reduced expatriate flows into Switzerland and increased competition. We have taken a number of actions to improve the school’s competitive positioning in the market so that it is in a position to capture future expatriate flows.

As of 31 October 2012, 25% of the students at this school were expatriates.

Collège Champittet—Nyon

This school was opened in 2007 and was acquired by an affiliate of our parent company in 2009. It was acquired by Nord Anglia Education in February 2011 in conjunction with the acquisition of Collège Champittet-Lausanne. The school has a capacity of 220 places and is located near the banks of Lake Geneva between Geneva and Lausanne. Its facilities include playgrounds, dining hall and a computer lab. Student numbers at this school were stable in FY2012.

As of 31 October 2012, 13% of the students at this school were expatriates.

Collège Alpin Beau Soleil—Villars-sur-Ollon

We acquired this boarding school in January 2011 with a capacity of 220 places. The school now has a capacity of 240 places and is located in the Alpine region not far from Lake Geneva. The school’s facilities include an astroturf pitch with seating, premium boarding facilities, a recently renovated art centre, a fitness centre, two restaurants, a theatre and a private ski slope. Founded in 1910, Beau-Soleil is one of the oldest Swiss educational establishments. This school experienced good growth in student numbers during FY2012.

As of 31 October 2012, 93% of the students at this school were expatriates.

La Cote International School—La Cote

This school was founded in 2008 and we acquired it in September 2011. The school has a capacity of 220 places and is located near Lake Geneva in Gland. The school experienced a reduction in student numbers in FY2012, primarily due to market conditions and a delay in announcing a potential new campus for this school as current capacity is limited. We intend to move the school to a new purpose built facility with 850 place capacity, expected to complete in September 2014.

As of 31 October 2012, 89% of the students at this school were expatriates.

Our Four Schools in Central Europe

The British International School Bratislava, Slovakia

We opened this school in 1998 with an initial capacity of 100 places. The school is operated out of two locations, with one allocated for the kindergarten and Year 1 students and the other for students in Years 2 to 13. The location for younger students has its own library, information and communication technology room, music area, and a playground. The second building has three well-equipped science labs, three ICT rooms, two specialist music rooms, and a computer-equipped library. The campus also enjoys two gymnasiums, one of which has a climbing wall, a dance studio, basketball courts, a 200 meter athletics track, and a half-size football field. In response to increasing demand, we opened the second building in 2006 bringing the school to its current capacity of 770 places. The new facilities were formally opened by His Royal Highness Prince Andrew. Student numbers at this school were stable in FY2012.

As of 31 October 2012, 71% of the students at this school were expatriates.

12

The British International School Budapest, Hungary

We assumed operations of this school in 2002 with a capacity of 420 places. In 2005, we relocated the school to new custom built facilities in its current location in Budapest’s third district. Its facilities include two science labs, music rooms equipped with computers, a dance and drama studio, an amphitheatre and a library. Its outdoor facilities include an organic wild garden for science lessons as well as an outdoor pavilion classroom. Its sporting facilities include a half-size football pitch, a 220 meter track, outdoor basketball court, and a large indoor gymnasium. The school’s current capacity is 590 places. Student numbers at this school were stable in FY2012.

As of 31 October 2012, 68% of the students at this school were expatriates.

The English International School Prague, Czech Republic

We opened this school in 1995 on a site that we converted for educational use near the centre of the city. In September 2007, we moved the school to a new custom built campus, with a capacity of 550 places. The campus includes modern facilities in two buildings including a sports field, gymnasium, two libraries, art and music rooms and a dance studio. The classrooms are all networked, utilising interactive whiteboard technology and each section of the school is equipped with its own computer suite. The new campus was formally opened by Her Royal Highness Princess Anne. The school experienced a reduction in student numbers in FY2012, which was caused by increased competition in the market. We have taken a number of actions to improve the school’s position in the market and its performance.

As of 31 October 2012, 78% of the students at this school were expatriates.

The British School Warsaw, Poland

Founded by Nord Anglia Education in 1992 in association with a local family, this was our first international school. In 2004, we opened a new building by converting a former electrical engineering college into high quality academic facilities and this building has been further expanded and upgraded on a number of occasions. The school has a capacity of 878 places and its facilities include a sports field, gymnasium, and art and music rooms. The new building was formally opened by His Royal Highness Prince Andrew. The school had good student number growth in FY2012.

As of 31 October 2012, 53% of the students at this school were expatriates.

Our One School in the Middle East

The British International School Abu Dhabi

We opened the British International School Abu Dhabi in September 2009 and in August 2010 sold our 49% equity interest in the school to our parent company and entered into an agreement to manage the school. On 28 September 2012, we entered into a definitive agreement to re-purchase the 49% equity interest held by our parent company in the school. The school has a capacity of 1,500 places. The school’s facilities include dedicated music rooms, a music technology suite, a drama studio with the latest media technology, gardens and outdoor learning areas as well as a wide range of indoor and outdoor sports facilities catering for swimming, rugby, cricket, hockey, netball and athletics. This school experienced strong growth in student numbers in FY2012.

As of 31 October 2012, 71% of the students at this school were expatriates.

Marketing Our Schools

Our marketing strategy is designed to develop brand awareness among prospective parents and students and brand loyalty and advocacy amongst existing parents and students. We seek to build brand awareness in each of our existing and new markets, with respect to our individual schools and the “Nord Anglia Education” name. We believe that this brand building approach also contributes to the recruitment and retention of quality teachers and principals.

We believe that a school’s attractiveness to parents and students is based largely upon its reputation. Accordingly, our marketing strategy is focused on the communication and enhancement of the excellent reputation that our schools enjoy within their respective markets. The effective deployment of our marketing strategy is executed at each school by our principals and the admissions and marketing teams. Our marketing strategy is based upon our online

13

presence, reputation and referrals from existing parents as opposed to costly media campaigns. Accordingly, we achieve our enrolment results in a highly cost effective manner.

We have developed a systematic approach to student recruitment and retention and we ensure that enquiry generation and conversion into new student enrolments is prioritised and well managed.

Student Recruitment

The student recruitment process has three stages:

• Enquiries: parents considering enroling their child at one of our schools register their child’s details and request further information.

• Visits: parents personally visit the school campus often accompanied by the child/children.

• Enrolments: parents register their child with the school, specify a start date and pay a non-refundable application fee. Almost all applicants enrol either within the academic year in which they applied or in the subsequent academic year.

Our marketing strategy has been very successful in generating enquiries, visits and applications. The table below shows an increase in enquiries and visits and the rate at which they have been converted into new enrolments for the past three fiscal years (excluding Abu Dhabi and Chonburi):

FY2010 FY2011 FY2012 Enquiries. 4,305 6,516 7,040 Visits 3,236 4,463 5,284

Enrolments 1,438 2,343 2,579

Percentage Visits to Enrolments 44% 52% 49%

As at 18 November 2012, the number of enquiries and visits year to date (excluding Abu Dhabi and Chonburi) were respectively 17% and 14% less than the enquiries and visits of the same period last year. The largest decrease in enquiries and visits has been experienced by our schools in Beijing. We believe that this is due to a slowing in the growth of the Beijing market compared to the growth experience in 2011 in the lead up to the Communist Party Congress in November 2012 and the change in Communist Party leadership. Excluding the Beijing schools, the number of enquiries and visits as at 18 November were 13% and 8% less respectively than the same period last year. Despite the reduction in the enquiries and visits to 18 November 2012, our in-year starters (excluding Abu Dhabi and Chonburi) as at 18 November 2012 were 25% more than those as at 18 November 2011.

Generation of Enquiries

The majority of our enquiries are generated through the following methods.

Digital Marketing

In our experience, when considering overseas assignments, parents’ first step is often to thoroughly research schools online. We recognise that online marketing is a critical means of communication with prospective parents and students and a key part of our strategy is to prioritise online tools. We ensure that our websites are optimised to deliver important information to prospective parents in a concise and user friendly manner. This enables them to make informed decisions when evaluating our schools.

• Corporate and School Websites: We have designed our corporate website to introduce parents to our company’s commitment to education, network of schools and history. Our corporate website contains direct web links to each individual school and provides details of the innovative educational work undertaken by our educational team. Our school websites inform prospective parents about each individual school’s curriculum, facilities, admissions process and why parents should choose the school for their children. Our websites include publications such as proprietary city guides and educational magazines which are only available to parents who register their interest with the school via the website.

14

• Search Engine Optimisation/Web Advertising: We have tailored each school’s website to maximise effectiveness and ease of use. Our search engine optimisation techniques generate a substantial number of visits to our website. We also identify and advertise on popular websites used by our target families.

Parent Referrals

Parent referrals are important for generating enquiries. We believe that prospective parents seek out parents of current and former students for their opinions on our schools, helping to convert enquiries to visits and applications. We encourage the parents of current and former students to speak positively about our schools and achieve this by providing high quality education, communicating with and involving parents in our schools and seeking to place each of our schools at the centre of its community.

We create parental endorsement by making sure each of our schools is at the centre of their community in three ways:

• Inclusive events for parents: Each school holds regular events, which parents are encouraged to attend and at which they are able to interact with other parents. This is particularly important to the majority of our parents who are expatriates as the school becomes their primary route to social activities and inclusion in a new and often alien environment.

• Community events: Each school runs events such as musical concerts and sports competitions which are open to the parents and students of other schools. We also invite influential individuals such as government officials, relocation agents and diplomatic staff to attend. These events demonstrate educational leadership and showcase our schools to prospective parents and influential leaders in the community.

• Charitable activities: We use initiatives such as our Nordstar community investment programme to involve parents, teachers and students in local charitable activities. These activities demonstrate the school’s role as a leader in the community as well as providing social opportunities for expatriate and local families.

In our most recent parental surveys, over 92% of our parents said that they would be

happy to recommend our school.

Relocation Agents

Relocation agents who settle expatriate families in cities in which our schools are located are an important source of enquiries. We develop close relationships with these relocation agents through a variety of initiatives, such as hosting school visits, providing quality information on our schools and producing user-friendly materials they can share with their clients.

In addition, we invite relocation agents to participate in the community events that the schools run. These events are a useful networking opportunity for relocation agents and also provide us with an excellent opportunity to showcase our schools.

Employers

In each of our markets, we have established relationships with major employers, such as multinational corporations and embassies. From our research, we know that parents consult their employers for school recommendations and information. In addition, we ensure these key personnel participate in the community events the school runs, providing us with an excellent

opportunity to showcase our schools.

Other Marketing Activities

We supplement our marketing strategy with other targeted activities to further enhance our schools’ reputation, promote awareness and generate enquiries, including:

• Promotional materials: We use promotional materials such as school brochures, educational magazines and other publications to enhance the schools’ reputation as high quality and leading academic institutions.

15

• Public Relations: We create and distribute news stories such as our strong academic results and high quality school facilities to promote our schools’ profiles in the media.

• Conferences: We demonstrate leadership in the world of education by speaking at conferences and sponsoring our own events. Nord Anglia Education employees speak at over 100 conferences worldwide annually, while our executives speak at over 50 conferences annually. Most active as public speakers are Andrew Fitzmaurice, our CEO and Professor Deborah Eyre our Education Director who together speak at over 30 events per year.

Converting Enquiries

Parents will typically draw up a shortlist of schools for their child and then physically visit these school campuses. Parents generally visit two or three different schools and usually undertake these visits with an open mind as to which school they will eventually select. Research conducted by an independent education consultancy with respect to our schools in China found that approximately 70% of parents did not have a clear first choice. Management of the school visit is therefore important and we have designed our systems carefully to help maximise the conversion ratio between visit and application.

Each of our schools has a dedicated admissions and marketing team who work closely with our principals during the student recruitment process in order to maximise the conversion of enquiries and visits to enrolments. Our marketing and admissions teams typically have prior education industry experience and are chosen through a highly selective hiring process. In order to ensure that we achieve high conversion rates, our admissions managers participate in proprietary training programs which provide them with the necessary skills to maximise their effectiveness.

Retention

We are focused on retaining our students. Once a student has enroled at one of our schools, the school’s teaching staff and principal are responsible for ensuring that the student receives a premium education and remains enroled.

To this end, we track the number of students who leave for reasons other than those outside of our control such as graduation or family relocation. In FY2012, the percentage of students who left our schools for reasons other than those outside of our control was only 2%, resulting in a persistence rate of 98%. We monitor the number of students leaving on a weekly basis and take immediate corrective action on any weaknesses identified for each school.

16

Teaching and Learning, Administrative, Regional and Central Support Staff

As at 31 October 2012, we had 2,391 full time equivalent employees. Our Premium Schools had 2,026 full time equivalent employees, of whom 1,440 were teaching staff, 563 were school administration and management and 23 were regional support. Our Learning Services business employed 240 education professionals and 83 administrative/regional support staff. In addition, we had 42 Group Central Support staff. The full time equivalent employee numbers as at October 31, 2012 are listed in the table below.

Full time

equivalent

employees

Group Central Support (Globally) . . . . . . . . . . . . .. . . . . . . . . . . . . . .

. . . . . . .

42

Premium Schools

- Teachers and Teaching Assistants . . . . . . . . . . . . . . . . . . . . . . . . . 1,440

- School Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563

- Regional Support . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

23

Learning Services

- Education Professionals . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . .

240

- Learning Services Support . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

- Regional Support . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . .

2,391

Outstanding Teachers for Outstanding Schools

Candidates are attracted to our reputation, commitment to high quality education, established international presence and financial strength. In addition we offer a compensation package that is typically equivalent to the remuneration of similarly qualified personnel in the United Kingdom and is, in most cases, highly competitive.

In our drive to position Nord Anglia Education’s recruitment practices to match our desire to be the leading global premium education company, we launched the Outstanding Teachers for Outstanding Schools project (“OTOS”) across the group in August 2012. The scope of the OTOS project includes: 1. Premium Candidate Attraction, 2. Outstanding Recruitment Process and Administration, 3. Quality Selection, 4. Enhanced Induction. The project will drive improvement and best practice in each of these areas.

Staff Development

Nord Anglia Education is committed to supporting our teachers to be the best that they can be. Through our Nord Anglia University, we provide on-going professional development for our principals and teachers, in the form of online and classroom based training. This programme is vital to ensure that we attract and retain the best possible academic faculty. Nord Anglia Education University offers the following:

• Executive Leadership Programme: an online and classroom based comprehensive

executive leadership programme for all school principals which develops academic and

commercial capabilities. The programme includes individual mentoring and is

independently accredited by the Windsor Leadership Trust, a leading organisation

dedicated to providing opportunities for leaders to develop their own leadership wisdom

and insight.

• Senior Leadership Programme: currently in development and will offer bespoke

development for Vice Principals and Heads of Schools to enable their career progression

and development to more senior posts.

• Management and Leadership Development Programme: an online and classroom based

programme to develop current high potential middle leaders, such as academic department

heads for future senior leadership posts.

17

• Global Staffroom: a proprietary online portal for the development of all our teaching staff.

Both external experts and our own staff, with relevant expertise, are used to enhance high

quality teaching and to share best practice teaching methods throughout the organisation.

Information Technology Systems and Management

We believe that we have a comprehensive and reliable information technology infrastructure that supports our data driven approach to the management of our Premium Schools. This platform enables our executive team, regional management, school principals and teachers to monitor and engage in timely decision-making based on data relating to key operating metrics. We use project management and Information Technology Information Library (“ITIL”) systems to support the high quality and timely delivery of our IT services across the schools and offices of Nord Anglia Education. Our information technology platform is scalable and is able to support the growth of our Premium Schools.

In our Premium Schools, we use a proprietary information technology platform to track students’ academic progress, our student recruitment process and to manage billing. We have tailored a platform initially designed by Serco to meet our own specific requirements. This platform is designed to deliver the best outcomes for each individual student by tracking performance at a student and subject specific level. We believe that the key benefits of this platform include the ability to:

• maximise individual student performance;

• implement accountability at a student, teacher, year group, subject group and overall school level;

• encourage parental involvement and ownership of students’ academic objectives; and

• maintain comprehensive benchmarking within and between schools.

In addition, we use a commercial project management software application to support our planning and oversight of the design, development and construction of new schools and expansion of capacity at existing schools.

All of our information technology platforms are managed internally by dedicated IT professionals. We manage the availability of our networks and wireless through the use of well-resourced and modern technology. We monitor our systems on a real-time basis to verify the robustness and availability of our servers, network and data storage. Our server infrastructure uses resilient data storage and backup technology located in data centres, one in the United Kingdom and one in Hong Kong.

Intellectual Property

We are the applicant or registrant of trademarks relating primarily to our logos and the name “Nord Anglia Education” covering as many as 39 regions, including the ones in which we operate. We do not own the rights to the name “British International School”, which may be used by any organisation subject to meeting certain accreditation requirements.

18

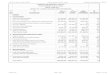

Properties

Our headquarters are located at Worldwide House, Des Voeux Road, Central in Hong Kong where we lease 3,153 square feet. We continue to operate in eight locations in the United Kingdom for our Learning Services business. We believe that these facilities currently meet our needs and that, to the extent necessary, replacement space is or would be available on acceptable terms.

We lease all of our current school facilities under long term leases. For additional information concerning our school facilities, please see “—Premium Schools” above. The table below summarises the main operating leases for each of our schools:

School Termination Date

* Rent Review Guarantee by Nord

Anglia Education Limited/Issuer to the

Landlord Sanlitun Beijing 2023 None None

Shunyi Beijing 2029 None None

Pudong Shanghai 2022 2.5% p.a. None

Puxi Shanghai 2025/2036 None None

Regent’s, Chonburi 2037 Annual CPI None

College Beau Soleil, Villars 2035 Annual CPI Yes

College Champittet, Lausanne & Nyon 2017/2026 Annual CPI None

La Cote International, Gland 2015 Annual CPI None

Prague, Czech Republic 2032 Annual CPI None

Warsaw, Poland 2025 Review 2015 None

Bratislava, Slovakia 2016/2039 None None

Budapest, Hungary 2014/2034 Annual CPI None

Abu Dhabi, UAE 2014/2019 None None

* More than one date indicates the termination date of multiple leases.

The prior owner of the shares of Beau-Soleil has a right for a period of ten years from the date we acquired the shares to purchase, and require us to sell, Beau-Soleil at fair market value, as determined by an independent accounting firm selected by the parties, if (i) we do not pay rent under our lease for the main school building for three months or (ii) the prior owner terminates our lease for the main school building for cause.

Litigation

We may be subject to legal or administrative proceedings or claims arising in the ordinary course of our business. We are not currently subject to any such claims that we believe could reasonably be expected to have a material and adverse effect on our business, results of operations or financial condition.

19

2. SELECTED CONSOLIDATED FINANCIAL DATA

Nord Anglia Education’s fiscal year is based on the twelve month period ending 31 August.

The tables below set out selected consolidated financial information of the Issuer as of and for

the twelve months ended 31 August 2012 (“FY2012") and 31 August 2011 (“FY2011"). All the

information shown is extracted from our audited consolidated financial statements for the twelve

months ended 31 August 2012, included as Appendix 1 to this Annual Report.

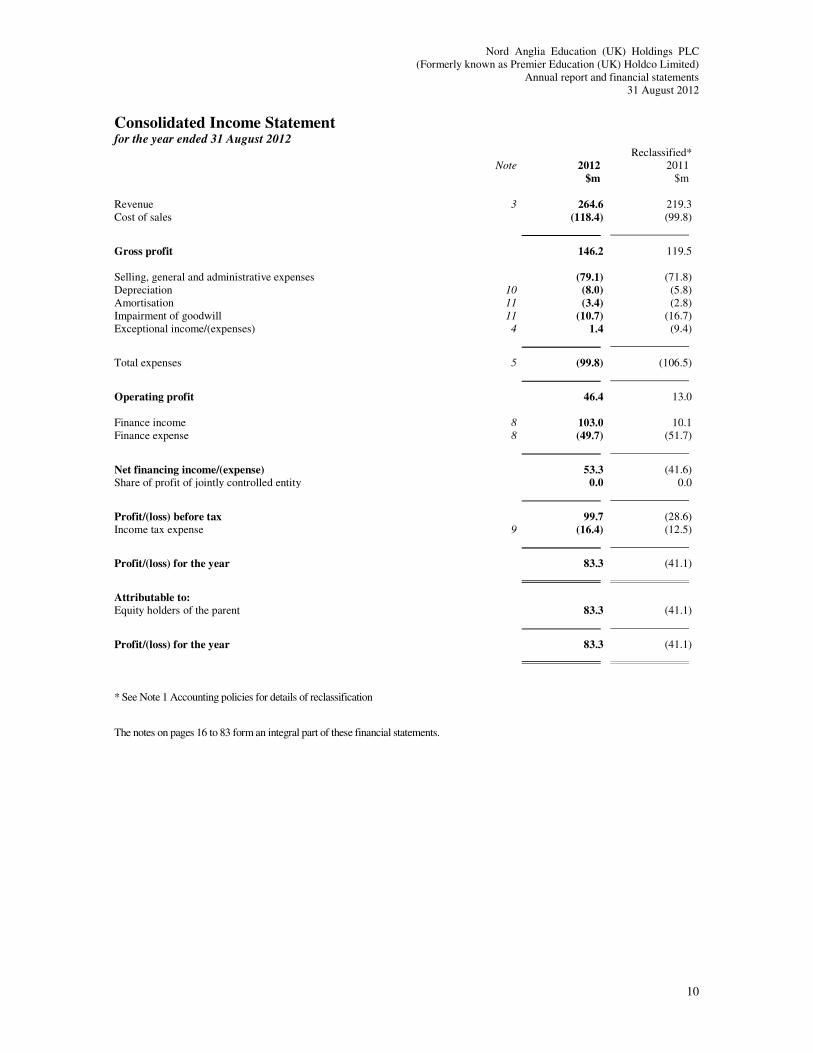

Selected consolidated statement of comprehensive income

Twelve Months Ended

31/08/2012 31/08/2011

$m $m

Revenue 264.6 219.3

Cost of sales (118.4) (99.8)

Gross Profit 146.2 119.5

Selling, general and administrative expenses (79.1) (71.8)

Depreciation (8.0) (5.8)

Amortisation (3.4) (2.8)

Impairment of goodwill (10.7) (16.7)

Exceptional expenses 1.4 (9.4)

Total expenses (99.8) (106.5)

Operating profit 46.4 13.0

Finance income 103.0 10.1

Finance expense

- Shareholder loan notes accrued interest (22.1) (35.5)

- Notes, bank loans and overdrafts (22.9) (13.0)

- Other finance expenses (4.7) (3.2)

Total finance expenses (49.7) (51.7)

Net finance income/(expense) 53.3 (41.6)

Share of profit in joint venture - -

Profit/(loss) before income tax 99.7 (28.6)

Income tax expense (16.4) (12.5)

Profit/(loss) for the period 83.3 (41.1)

Foreign exchange translation differences (20.7) 9.3

Actuarial losses on defined benefit pension plans (16.3) (1.1)

Other comprehensive (loss)/income for the

period, net of income tax (37.0) 8.2

46.3 (32.9) Total comprehensive income/(loss)

for the period

20

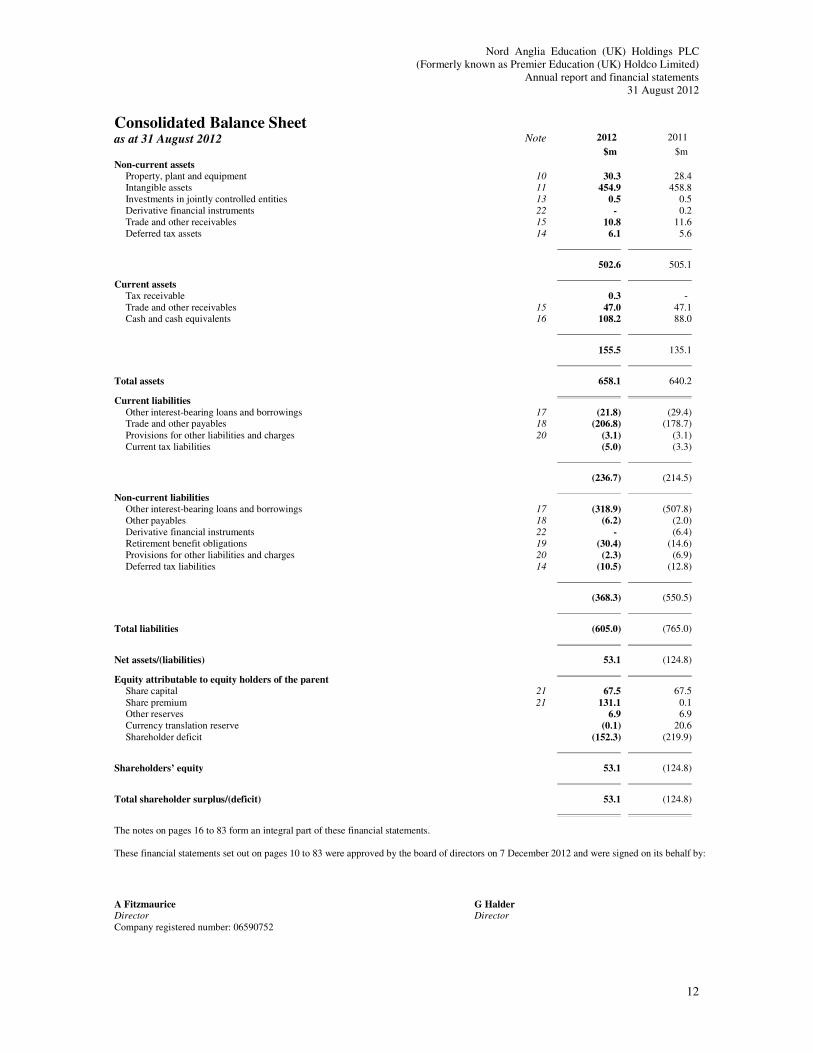

Selected consolidated balance sheet

As at As at

31/08/2012 31/08/2011

$m $m

Property, plant and equipment 30.3 28.4

Intangible assets 454.9 458.8

Deferred income tax assets 6.1 5.6

Derivative financial instruments - 0.2

Trade and other receivables 11.3 12.1

Total non-current assets 502.6 505.1

Tax receivable 0.3 -

Trade and other receivables 47.0 47.1

Cash and cash equivalents 108.2 88.0

Total current assets 155.5 135.1

Total assets 658.1 640.2

Share capital 67.5 67.5

Share premium 131.1 0.1

Other reserves 6.8 27.5

Retained earnings (152.3) (219.9)

Total equity 53.1 (124.8)

Other interest bearing loans and borrowings 21.8 13.0

Shareholder loans - 16.4

Trade and other payables 206.8 178.7

Provisions for other liabilities and charges 3.1 3.1

Current income tax liabilities 5.0 3.3

Total current liabilities 236.7 214.5

Other interest bearing loans and borrowings 318.9 179.1

Shareholder loan notes - 328.7

Other non-current liabilities 49.4 42.7

Total non-current liabilities 368.3 550.5

Total liabilities 605.0 765.0

Total equity and liabilities 658.1 640.2

21

Selected consolidated statement of cash flows

31/08/2012 31/08/2011

$m $m

Cash generated from operations 74.5 56.8

Interest paid (6.8) (10.9)

Tax paid (15.9) (13.9)

Net cash from operating activities 51.8 32.0

Net cash (used in) investing activities (27.1) (11.6)

Net cash from/(used in) financing activities (2.2) (20.4)

Net increase

in cash and cash equivalents 22.5 -

Cash and cash equivalents at beginning of period 88.0 81.8

Exchange (losses)/gains on cash

and cash equivalents (2.3) 6.2

Cash and cash equivalents at end of period 108.2 88.0

Twelve Months Ended

22

3. OPERATING DATA AND NON-GAAP FINANCIAL INFORMATION

The tables below show certain non-GAAP financial information for the twelve months ended

31 August 2012 and 31 August 2011.

Key Performance Indicators

31/08/2012 31/08/2011

Capacity (average for the period)(1)

China 5,360 4,860

Switzerland 1,604 1,374

Central Europe 2,738 2,678

9,702 8,912

Full time equivalent students (average for the period)(2)

China 3,622 3,070

Switzerland 1,437 1,222

Central Europe 2,338 2,190

7,397 6,482

Utilisation (average for the period)(3)

China 68% 63%

Switzerland 90% 89%

Central Europe 85% 82%

76% 73%

Adjusted Revenue per full time equivalent student

(in US$ thousands)(4)

China 30.8 27.9

Switzerland 47.1 47.1

Central Europe 18.6 19.8

Average 30.1 28.8

Twelve Months Ended

(1) We measure average capacity at the measurement date as the total number of FTEs that can be accommodated in a school based on its existing classrooms at each academic calendar month divided by the number of months in such period. (2) We calculate average full time equivalent students (“FTEs”) for a period by dividing the total number of FTEs at each academic calendar month end in such period by the number of academic calendar months in such period. (3) We measure utilisation during a period as a percentage equal to the ratio of average FTEs for the period enroled at that school divided by average capacity. (4) We calculate Adjusted Revenue per student by dividing our total Adjusted Revenue for a relevant period by the average FTEs for such period. See “Calculation of Adjusted Revenue” on page 23.

23

Segment Analysis

31/08/2012 31/08/2011

$m $m

Adjusted Revenue (Segment)

China 111.5 85.6

Switzerland 67.7 57.6

Central Europe 43.5 43.3

Premium Schools 222.7 186.5

Learning Services 40.1 59.9

Other - 0.6

Adjusted Revenue 262.8 247.0

Twelve Months Ended

8/31/2012 8/31/2011

$m $m

Adjusted EBITDA (Segment)

China 53.8 40.8

Switzerland 15.0 13.1

Central Europe 10.6 9.6

Discontinued - (0.4)

Premium Schools 79.4 63.1

Learning Services 10.2 13.7

Regional & Central Costs (15.6) (16.9)

Adjusted EBITDA 74.0 59.9

Twelve Months Ended

Calculation of Adjusted Revenue

31/08/2012 31/08/2011

$m $m

Calculation of Adjusted Revenue

Revenue 264.6 219.3

Full year impact of acquisitions(4) - 29.5

Other (1.8) (1.8)

Adjusted Revenue 262.8 247.0

Twelve Months Ended

24

Calculation of EBITDA and Adjusted EBITDA

31/08/2012 31/08/2011

$m $m

Operating profit 46.4 13.0

Add back:

Exceptional expenses/(income), net(1) (1.4) 9.4

Impairment of goodwill(2) 10.7 16.7

Amortisation 3.4 2.8

Depreciation 8.0 5.8

EBITDA 67.1 47.7

Loss on disposal of property,

plant and equipment and intangible assets 0.3 1.0

Exchange loss/(gain)(3) 4.6 (3.5)

Full year impact of acquisitions (4) - 6.4

Pre-acquisition and business

integration costs (5) 0.6 3.2

Reduction in management charge

to a related party - 1.8

School and contract closure costs (6) - 1.8

Share based payments (7) 0.6 0.3

Others (8) 0.8 1.2

Adjusted EBITDA 74.0 59.9

Capital Expenditures

Capacity Related(9) 4.6 6.7

Non-capacity related(10) 6.1 5.0

Total capital expenditure 10.7 11.7

Adjusted EBITDA after non-capacity

related capital expenditures 67.9 54.9

Twelve Months Ended

(1) In the twelve months ended 31 August 2012, exceptional expenses comprise costs incurred in connection with

the Notes issue and the acquisition of schools. (2) FY2012 comprises the non-cash impairment charge on the remaining balance of the goodwill relating to Learning Services in the Middle East. FY2011 comprises the non-cash impairment charge on the goodwill associated with the UK Learning Services business. (3) Primarily associated with foreign currency translational gains/losses on our inter-company loan balances and bank accounts denominated in foreign currencies as well as actual transactional gains/losses. . (4) Incorporates the full fiscal period historical financial results of the schools we acquired during the relevant fiscal period as if those acquisitions had been completed as of the first day of such period. We acquired College Alpin Beau Soleil SA on 14 January 2011 and College Champittet Lausanne and College Champittet Nyon on 25 February 2011. No adjustment has been made in the twelve months ended 31 August 2012 for the acquisition of our school in Thailand because, even though it was acquired on 1 August 2012, no revenue or costs were recognised during the twelve months ended 31 August 2012. (5) Represents costs associated with legal, tax and accounting advice in relation to the conversion of our US dollar shareholder loans from pound sterling, as well as costs associated with changes to our corporate structure and lending arrangements to enable us to acquire our schools in Switzerland. (6) Represents the costs associated with the closure of our school in Nanxiang, Shanghai in the twelve months ended 31 August 2011. (7) These non-cash charges are associated with the equity investments in the Group by members of our management. (8) Various fees and expenses and redundancy costs relating to the switch in the mix of business from Learning Services to Premium Schools that are one-off in nature and non-recurring. (9) Capacity related capital expenditure means expenditures related to the expansion of student capacity at our existing schools such as fixtures, equipment and related expenses. (10) Non-capacity related capital expenditure means total capital expenditure less capacity related capital expenditure.

25

4. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

You should read the following discussion in conjunction with our audited consolidated

financial statements as of and for the periods ended August 31, 2011 and 2012 and in each

case the related notes. For the purposes of this discussion, references to “FY2011” and

“FY2012” refer to the periods ended 31 August 2011 and 31 August 2012 respectively.

Recent Developments

On 28 March 2012, the Issuer issued the Notes and made available $182.5 million of the proceeds of the Notes to repay the senior and mezzanine facilities outstanding at the time and close out the hedging arrangements in connection with those facilities and $120.0 million of the proceeds to repay outstanding shareholder loans and loan notes held by NAE Inc. NAE Inc. then capitalised all remaining shareholder loans and loan notes owed by the Issuer to it in exchange for additional ordinary shares in the Issuer.

On 21 March 2012, the Issuer entered into a Senior Secured Revolving Credit Facility which provided for borrowings up to an aggregate of $20.0 million and subsequent increases of up to a further $20.0 million. On 23 July 2012, Barclays Bank PLC increased its commitment under the Senior Secured Revolving Credit Facility from $20.0 million to $30.0million.

On 1 August 2012, Nord Anglia Education completed the acquisition of The Regent’s School, a K-12 school in Chonburi Thailand. Nord Anglia Education purchased 49% direct and indirect interests in the share capital of the Thai company formed to hold the acquired school’s business.

On 28 September 2012, Nord Anglia Education entered into a definitive agreement to acquire the 49% interest owned by its parent in the British International School Abu Dhabi. The acquisition is subject to a number of conditions and there is no assurance that these conditions will be satisfied and the transaction will complete. Subject to the foregoing, the acquisition is expected to close before the end of December 2012.

Factors affecting our results of operations and financial condition

Macroeconomic Conditions

Our results of operations are directly affected by our ability to recruit additional students in our

schools, which in turn can be affected by general economic conditions in each of the countries in

which we operate. As a result of the importance of education spend in the markets in which we

operate and the relative resilience shown by expatriate flows during the recent difficult economic

conditions, we believe our revenue and profitability are resilient to fluctuations as a result of macro-

economic conditions.

Acquisitions

In the twelve months ended 31 August 2012, we acquired La Cote International School,

Switzerland and The Regent’s School, Chonburi Thailand. We continue to look for future potential

acquisition opportunities and we may acquire schools in the future which impact our results of

operations.

Currency Translation

We conduct our business on a global basis in several major currencies, most notably the

Chinese renminbi, Swiss franc, Polish zloty, pound sterling, U.A.E dirham, Euro, Thai baht and

Malaysian ringgit, while our reporting currency is the US dollar. During the period under review,

almost all of our revenue was recorded in currencies other than the US dollar. Fluctuations in

exchange rates between the US dollar and our operating currencies affect the translation of our

results and the net assets or liabilities of our overseas entities into US dollars.

In FY2012, most of our operating currencies except the Chinese renminbi weakened against the

US dollar which negatively influenced our results for this period.

Substantially all of our revenues and costs associated with our Premium Schools are

denominated in the local currency of the countries in which we operate and are not denominated in

US dollars. We recognise translational gains and losses primarily upon the conversion of our foreign

currency denominated earnings into US dollars through other comprehensive income.

26

Increased Focus on Premium Schools

Since FY2009, we have shifted our focus toward the operation of our Premium Schools. As a

result, our Premium Schools revenues, as a percentage of our total revenues, have grown

significantly. For FY2009, FY2010, FY2011 and FY2012, revenues from our Premium Schools

represented 49.8%, 62.3%, 75.5% and 84.7% of our total Adjusted Revenues, respectively. Since

FY2009 we have acquired schools in Switzerland, China and Thailand and we have also expanded

capacity in our schools in China post acquisition. We expect in the future to maintain our focus on the

continued expansion of our Premium Schools to continue to see a reduction in our Learning Services

operations.

Key Operating Metrics

In addition to financial performance, we use the following key operating metrics to manage our

Premium Schools: tuition fees; the number of FTEs; capacity; utilisation; and average annual revenue

per student. We monitor these operating metrics on a weekly, monthly, quarterly and annual basis as

we believe that they are the most reliable measures for accurately measuring and predicting the

current and future profitability of our Premium Schools.

Tuition Fees. Approximately 60% of our tuition fees are paid for by expatriate employers who are

less sensitive to moderate pricing increases as education allowances typically represent only a small

percentage of an overall expatriate’s total compensation. Self-funding expatriates and affluent local

families, are also typically less sensitive to moderate price increases. As a result, we have been able

to increase our tuition across our markets at an average of 4-6% p.a. over the last three years

(approximately twice the median rate of inflation in the markets where our schools are located),

without materially impacting enrolment growth.

Full-Time Equivalent Students. We monitor the number of average FTEs at any given time. The

number of FTEs fluctuates throughout the academic year as new students enrol or as current

students depart.

Our average FTEs have grown from 4,292 in FY2009 to an average of 7,397 in FY2012 (not

including our school in Thailand which was acquired on 1 August 2012 or our school in Abu Dhabi).

This increase in FTEs has been primarily due to enrolment growth in our existing schools and

acquisitions of new schools.

Average Capacity. We monitor our average capacity at any given time. We increased our

average capacity from 5,513 places in FY2009 to 9,702 places in FY 2012. This increase in capacity

was primarily due to the acquisition of new schools in Switzerland and capacity expansion at our

schools in China. Between FY2011 and FY2012 we increased our capacity from 8,912 to 9,702.

Utilisation. We measure utilisation at any given time. Our average utilisation increased from

73% in FY2011 to 76% in FY2012. This increase was primarily due to increased enrolment across

our schools in China.

Average Adjusted Revenue per Student. We calculate average Adjusted Revenue per student

as total revenues from our Premium Schools Division for the relevant period divided by the average of

the month-end FTEs throughout the academic year. Our average Adjusted Revenue per student has

steadily increased from FY2009 to FY2012 reflecting tuition fee increases and the impact of the

movement of our foreign operating currencies against the US dollar.

Principal Components of Our Results of Operations

Revenue

Revenue is recognised net of indirect taxes, returns, rebates and discounts. Sales of services

which have been invoiced but not yet recognised as revenue are included on the balance sheet as

deferred income and accounted for within trade and other payables.

School fee income

School fee income comprises tuition fees and income from ancillary sources including

registration fees, examinations, school trips, bus transportation, lunch fees and the tuition fee

insurance scheme. School fee income is generally recognised over the school terms from September

to June and is generally payable in advance on or before the first day of each term and recognised

27

across the months of each term. Where fees are received in advance for more than one term, the

income is recognised over the months in the terms for which payment has been made. Our refund

policy requires a full term’s notice for a refund. Therefore, we are entitled to a full year of tuition fees

if we receive a withdrawal notice after the start of Term 2 in January.

Service contracts

Learning Services contract revenue is recognised proportionally as we provide the services

under each contract. Some degree of judgement is exercised where contracts have an element of