Embed Size (px)

Citation preview

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITEDRegistered Office: Vidyut Sadan, Vidyut Nagar, Hisar-125005(Haryana)

www.dhbvn.org.in

Annual Report2015-2016

DHBVN

Annual Report2015-2016

CONTENTS

Page Nos.

Board of Directors 2

Notice 3-4

Director's Report 5-24

Managements replies to Comments of C & AG 25-27

Report of Comptroller & Auditor General 28-29

Statutory Auditors Report 30-44

Managements replies to Report of Statutory Auditors 45-74

Balance Sheet 75

Profit and Loss Account 76

Cash Flow Statement 77

Significant Accounting Policies & Notes on Accounts 78-122

CONTENTS

Prepared by:

Sandeep Legha, Sr. AO & Team

2

DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

Board of Directors

Audit Committee Company Secretary

Auditors

Lead Banker Registered Office

1. Sh. Rajan Kumar Gupta, IAS ChairmanAddl. Chief Secretary (Power)

2. Sh. Arun Kumar Verma Managing Director

3. Sh. Vineet Garg, IAS DirectorMD, HVPNL

4. Sh. Nitin Kumar Yadav, IAS DirectorSecy./Power & MD, UHBVNL & HVPNL

5. Sh. Ravi Prakash Gupta Director

6. Sh. Suresh Kumar Bansal Director Projects

7. Sh. Ravinder Kumar Batra Director Operations

8. Sh. M.K.V. Rama Rao DirectorMD, HPGCL

9. Sh. Kalyan Kumar Ghosh Director

10. Sh. R. P. Sasmal Director

11. Ms. Sanghamitra Pyne Director

12. Sh. Anil Gupta Director

Sh. M.K.V. Rama Rao Sh. Harjinder SinghDirector, DHBVNLChairman of the Committee

Sh. Kalyan Kumar GhoshDirector, DHBVNLMember of the Committee

M/s O. Aggarwal & CoMs. Sanghamitra Pyne Chartered AccountantsDirector, DHBVNLMember of the Committee

Oriental Bank of Commerce Vidyut Sadan, Vidyut Nagar,Hisar – 125 005 (Haryana)

3

NOTICE

Endst. No.

Copy of notice is sent to the following with a request to attend the meeting:-

1. Sh. Shatrujeet Singh Kapoor, IPS, Chairman-cum-Managing Director, DHBVNL

2. Sh. Vineet Garg, IAS MD, HVPNL & HPGCL

3. Smt. Ashima Brar, IASSpecial Secretary FinanceGovt. of Haryana, HPUs& Director, DHBVNL

4. Sh. Ravinder Kumar BatraDirector/Operations & Project, DHBVNL

5. Sh. Anil GuptaDirector, DHBVNL

6. Smt. Anjana AgarwalDirector DHBVNL

M/s O. Aggarwal & Co.

Chartered Accountant, Bhiwani

M/s Grish Madan & Associates

Company Secretaries, Panchkula

-Sd/-

(Harjinder Singh)

COMPANY SECRETARY

72/CS/AGM/DH-6 Dated: 17.02.2017

BOARD OF DIRECTORS

STATUTORY AUDITOR

SECRETARIAL AUDITOR

Notice is hereby given that the Adjourned 17th Annual General Meeting of the Shareholders of Dakshin Haryana Bijli Vitran Nigam Ltd. which was scheduled to be held on Thursday, the 16th of February, 2017 at 10:30 AM and was Adjourned due to lack of quorum, will now be held on Thursday, 23rd of February, 2017 at 10.30 AM at the Registered Office of the Company i.e in Conference Hall, Vidyut Sadan, Vidyut Nagar, Hisar, Haryana.

Your are requested to kindly make it convenient to attend the said meeting.

By order of the Boardfor Dakshin Haryana Bijli Vitran Nigam Ltd.

-Sd/-(Harjinder Singh)

Company Secretary

Memo No. Ch-72/CS/AGM/DH-6

Dated: 17.02.2017

1. Hon'ble Governor of Haryana through Sh. Anurag Restogi, IASPrincipal Secretary (Power)Govt. of Haryana.

2. Sh. Anurag Restogi, IASPrincipal Secretary (Power)Govt. of Haryana.

3. Sh. Shatrujeet Singh Kapoor, IPSChairman-cum-Managing Director, DHBVNL.

4. Sh. Nikhil Gajraj, IASD. C. Hissar.

5. Sh. Ravinder Kumar BatraDirector Operation & Projects, DHBVNL.

6. Sh. Sumit Kumar, HCSEstate Officer, HUDA, Hisar.

7. Sh. Arun Kumar Verma

8. M/S Haryana Vidyut Prasaran Nigam Ltd. through Sh. H. C. Gupta, Chief Engineer / TS, HVPNL, Hisar.

Sd/-(Harjinder Singh)

COMPANY SECRETARY

SHAREHOLDERS

4

Subject: Notice for holding Adjourned 17th Annual General Meeting of the Dakshin Haryana Bijli Vitran Nigam Ltd.

SHAREHOLDERS

Please find enclosed herewith the 17th Annual Report of the Company for the Financial Year 2015-16 containing the Notice for holding Adjourned 17th Annual General Meeting scheduled to be held on Thursday, the 16th day of February, 2017 at 10:30 AM at the Registered office of the Company in Conference Hall, Vidyut Sadan, Vidyut Nagar, Hisar, Haryana.

You are requested to kindly make it convenient to attend the meeting.

By order of the BoardFor Dakshin Haryana Bijli Vitran Nigam Ltd

Sd/-(Harjinder Singh)

Memo No.-Ch-71/CS/AGM/DH-6Dated: 13.02.2017

1. Hon'ble Governor of Haryana through Sh. Anurag Restogi, IASPrincipal Secretary (Power)Govt. of Haryana.

2. Sh. Anurag Restogi, IASPrincipal Secretary (Power)Govt. of Haryana.

3. Sh. Shatrujeet Singh Kapoor, IPSChairman-cum-Managing Director, DHBVNL.

4. Sh. Nikhil Gajraj, IASD. C. Hissar.

5. Sh. Ravinder Kumar BatraDirector Operation & Projects, DHBVNL.

6. Sh. Sumit Kumar, HCSEstate Officer, HUDA, Hisar.

7. Sh. Arun Kumar Verma

8. M/S Haryana Vidyut Prasaran Nigam Ltd. through Sh. H. C. Gupta, Chief Engineer / TS, HVPNL, Hisar.

Sd/-(Harjinder Singh)

COMPANY SECRETARYEndst. No.

Copy of notice is sent to the following with a

Company Secretary

71/CS/AGM/DH-6 Dated: 13.02.2017

NOTICE

request to attend the meeting:-

1. Sh. Shatrujeet Singh Kapoor, IPS, Chairman-cum-Managing Director, DHBVNL

2. Sh. Vineet Garg, IAS MD, HVPNL & HPGCL

3. Smt. Ashima Brar, IASSpecial Secretary FinanceGovt. of Haryana, HPUs& Director, DHBVNL

4. Sh. Ravinder Kumar BatraDirector/Operations & Project, DHBVNL

5. Sh. Anil GuptaDirector, DHBVNL

6. Smt. Anjana AgarwalDirector DHBVNL

M/s O. Aggarwal & Co.

Chartered Accountant, Bhiwani

M/s Girish Madan & Associates

Company Secretaries, Panchkula

-Sd/-

(Harjinder Singh)

COMPANY SECRETARY

BOARD OF DIRECTORS

STATUTORY AUDITORS

SECRETARIAL AUDITORS

INCOMESRevenue from the sale of power (including FSA) 12413.67 11170.03Other Income including Revenue Subsidy & Grants 2756.36 2230.83TOTAL INCOME 15170.03 13400.86TOTAL EXPENSES 13670.35 13386.55Gross Loss/Profit before Interest, Depreciation and Taxation 1499.68 14.31Less : Interest 1772.19 950.50Profit/(Loss) before depreciation & Taxation (272.51) (936.19)Less : Depreciation 199.89 180.38Provision for Taxation 0.00 0.01Net Prior Period Charges/Income (0.52) 0.03Profit/Loss after Taxation (472.92) (1116.55)Add: Transfer to Regulatory Assets --------- ---------Less: Amortization of regulatory assets --------- ---------Extraordinary Items 1.34 480.38Profit/(Loss) of Current Year (471.58) (636.17)Profit/(Loss) transferred from UHBVN 0.00 (1356.27)Accumulated losses up to Previous Year (12719.03) (10726.59)Balance carried forward to next year (13190.61) (12719.03)

Financial Results:

Particulars 2015-2016

(Rs. in crore)

ToThe Members,Dakshin Haryana Bijli Vitran Nigam LimitedHissar

Your Directors present the Seventeenth Annual Report and the Audited Accounts of the Company for the financial year ended 31st March, 2016

2014-2015(Rs. in crore)

5

Director's Report

6

Turnover( In Crores) `

Net Profit & Loss( In Crores) `

Capital Expenditure

( In Crores) `

197218

262 265279

2011-12 2012-13 2013-14 2014-15 2015-16

Sub Stations (In Numbers)

33 KV

161177

199749218603

236953 243651

2011-12 2012-13 2013-14 2014-15 2015-16

Distribution T/Fs (in Numbers)

Distribution T/Fs

2470 2721 3088 3237 3261

5202154313

62095

69157

63842

55094 55769

6491562957

70593

2011-12 2012-13 2013-14 2014-15 2015-16

Transmission & Distribution Lines (In KMs)

2848859

3073617

3671255

3985856

4275659

604403

12233511360210

14643841597196

3262733 3190625

35440123710023 3776109

21844112314698

28418243016063

3117068

802723715576

810397910458

1047520

2011-12 2012-13 2013-14 2014-15 2015-16

Connected Load (In KWs)

Domestic

Commercial

Industries

Tube-Wells

Others

-4599.44

-1352.40

-2088.65

-636.16 -471.58

2011-12 2012-13 2013-14 2014-152015-16

24.28

23.29

24.25

26.11

26.89

2011-12 2012-13 2013-14 2014-15 2015-16

AT&C Losses (%)

23.71

22.38

23.66

24.47 24.47

2011-12 2012-13 2013-14 2014-15 2015-16

Distribution Losses (%)

389.61425.15

953.05

704.58587.87

2011-12 2012-13 2013-14 2014-15 2015-16

7067.008407.39

11454.06

13400.8615170.03

2011-12 2012-13 2013-14 2014-15 2015-16

OPERATIONAL PERFORMANCE

INFRASTRUCTURE ADDITIONS

Increase in Revenue

The amount billed to consumers against supply of power increased by 11.14% to Rs. 12414 crore in 2015-16 from Rs. 11170 crore in FY 2014-15.

Increase in supply of power:

The power supplied to the consumers of the Company during FY 2015-16 has been 24861 MU in comparison to 24488 MU supplied during FY 2014-15, which is 1.52% higher than the previous year.

Distribution Losses & AT&C Losses:

The Distribution Losses have been same i.e. 24.47% in FY 2015-16 & FY 2014-15 and the AT&C Losses increased from 26.11% in FY 2014-15 to 26.89 in FY 2015-16.

Remittance into Bank (RIB):

The Remittance into Bank during the year under review grew from Rs. 10397.93 crore in 2014-15 to Rs. 11484.17 crore in 2015-16, showing an increase of 10.45% over the previous year.

Detection of theft and recovery thereof:

Theft of energy is the major cause of loss of revenue. During the period, major emphasis was given on checking of theft of energy. Several teams of Operations and Vigilance Staff were deployed for checking the consumer premises to detect theft cases and FIRs were lodged against the guilty besides imposing penalty. A total of 95212 no. connections were checked during FY 2015-16, out of which 24904 theft cases were detected. A sum of Rs. 85.34 crore as penalty was imposed on the consumers in 2015-16 who were found stealing the energy.

HVDS Projects

Under HVDS Scheme, the work of 59 No. feeders amounting to Rs. 195 Cr. approx. for Gurgaon, Faridabad & Dadri Town was allotted. Out of 59 Nos., the work of 11 No. 11 kV feeders has been completed till 31.03.2016 and the work on the remaining feeders is under progress.

Bifurcation of 11 KV Mixed load feeders

Under Bifurcation of 11 KV mixed load feeders, the work of 113 No. feeders amounting to Rs. 73 Cr. approx. for Gurgaon & Faridabad was allotted. Out of 113 Nos., the work of 100 No. 11 kV feeders has been completed till 31.03.2016 and the work on the remaining feeders is under progress.

Creation of 33 KV sub-station along with associated lines and augmentation of 33 KV sub-station.

During the FY 2015-16, 8 No. new 33 KV sub-stations along with the associated lines commissioned and 53 no. sub-stations were augmented with overall cost amounting to Rs. 105.4 Cr. approx.

Restructured Accelerated Power Development and Reforms Program (R-APDRP)

Under the flagship program of RADRP (now subsumed IPDC) Govt. of India, DHBVN has implemented IT part of this program, wherein 18 Towns having population of more than 30,000 as per Census of 2011 has been brought into IT Domain and the entire distribution and retail supply business activities have been made IT enabled. Based on the accomplishment of the above scheme, further penetration of the scheme has also been planned with the financial assistance from Govt. of India so as to cover the other towns having population of more than 5000 as per 2011 census. Under the second phase almost 28 Towns shall be added in the IT domain which will further the operational efficiency of the Nigam, besides focusing towards customer satisfaction. Under the UDAY Scheme further absorption as technology inform of implementation of AMI solutions in a phased manner which will further improve the performance and financial health of the Nigam. For the implementation of AMI/Smart Grid Solutions various approaches i.e. CAPEX & OPEX models are also being discussed with India Smart Grid Cell constituted by Govt. of India under NSGM (National Smart Grid Mission). Under the IT initiatives implementation of SCADA, DMS has also been planned by the Nigam for Faridabad town which has been selected for the Smart City by Ministry of Urban Development, Govt. of India besides plan for developing Smart Grid Infrastructure in the Millennium City of Gurugram which is also priority project for Govt. of Haryana. The CAPEX incurred for the above stated projects during 2015-16 was Rs. 15.23 crores and the budget for the current financial year i.e. 2016-17 is Rs. 60 crores. ..

LOAD AND MARKET RESEARCH DESIGN & DEVELOPMENT OF BASELINE DATA

For design and development of DSM plan a detailed Load Research & Market Analysis had been carried out by Surveying agency M/S Darashaw & Co. (P) Ltd. Hired by EESL. The same has been approved by DHBVN. On the basis of Load Research Report the major findings on saving potential from all category consumers are as under:

DSM PROGRAMME

7

S. No.

Segment

Proposed Activities for saving Saving Potential

1

Commercial

Replacement with LED and EE Fans 140 MU

2

Agriculture

Replacement of inefficient pumps with EE Pumps

219 MU

3

Street Light

Replacement of existing lighting with LED Lights

19 MU

4

Domestic

Replacement with LED and EE Fans 563 MU

5 PWW Replacement of inefficient motor pumps with EE Pumps

21 MU

6 Industry Replacement with Energy Efficient appliances

105 MU

Discom Drawl Info: on the basis of LR Report the Max., Min. and Avg. load requirement is as under:

UJALA Program (Unnat Jyoti Affordable Lamps for All)

UJALA Program was launched by Hon'ble Chief Minister, Haryana Sh. Manohar Lal Khattar on 11th March 2016.in order to reduce the electricity consumption under the program LED Bulbs are to be distributed to the consumers at subsided rates in all the operational circles of DHBVN.

Agriculture Pump Set Program

Under this program old inefficient agriculture pump set will be replaced with 4 or 5 star rates Energy Efficient Agriculture Pump Sets. The detail proposal for agriculture DSM program has been submitted TO DHBVN by EESL which is under the consideration of management.

ØIt was decided vide Sales Circular No. D-16/2015 dated 19.06.2015 to issue Demand notice to the applicants who have applied for tube well connection from 01.01.2012 to 31.12.2012. Further it was decided by the Sales Circular No. D-11/2016 dated 28.04.2016 to issue the demand notice for tubwell connection upto 31.12.2013.

ØFurther Tatkal Facility was floated for releases of tubewell connection vide Sales Circular No. D-30/2015 dated 25.08.2015. The applicant who is desirous of obtaining connection on priority over and above the waiting list can opt for "Tatkal Facility". Under the "Tatkal Facility", the application would be processed expeditiously on payment of Rs. 1 lac over and above the normal charges /cost to be levied on General Category connections.

ØThe Board of Directors in its meeting held on 15/12/2014 had approved laying of electrical infrastructure of 220/33/0.4 KV in Sectors 58-115 of Gurgaon and Sectors 75 to 89 of Faridabad instead of conventional 220/66/11/0.4 KV system.

ØAccordingly, Sales Circular No. D-1/2015 was issued in this regard. The matter was reviewed by the Management and it was decided vide Sales Circular No. D-19/2015 that till such time 220/33/0.4 KV level is created in these sectors of Gurgaon and Faridabad, supply on 11 KV level will be given to the Developers / Builders / Societies etc. wherever possible at their cost, restricting the load upto 5 MVA

IMPORTANT POLICY DECISIONS REGARDING COMMERCIAL ACTIVITIES DURING THE FY 2015-16

through 3 X 300 mm2 11 KV underground XLPE cable. Such release of load on 11 KV will be subject to the condition that the Developers / Builders / Societies will erect the system afresh on 33 KV level from the nearest 220/33 KV sub-station/ switching station at their own cost either by upgrading the 11/0.4 KV distribution transformer to 33/0.4 KV level or by way of installing 33/11 KV Power Transformer. To safeguard the implementation of the above provision, the Developers / Builders / Societies will submit the Bank Guarantee equaling 1.5 times the cost of such changeover from 11 KV level to 33 KV level including 33 KV line at the time of applying for load upto 5 MVA at 11 KV level. Once the 33 KV level is created in these sectors, the Developers / Builders / Societies shall have to mandatorily switchover from 11 KV to 33 KV level within 6 months of issue of notice by DHBVN in this regard failing which the BG shall be encashed and the work shall be got executed by the Nigam at its own level and any extra expenditure incurred in the process shall be suitably recovered from the developer.

ØIn compliance to the Law and legislative Department Notification No. Leg. 07/2014 dated 26th March, 2014 and Administrative Reforms Department Notification No. 07/31/2014-3AR dated 7th May, 2015 vide which Govt. of Haryana has notified the Right to Service Act-2014, the various services to be provided to the citizens within the time frame as notified under Right to Service Act, 2014 were circulated to field offices vide Sales Circular No. D-21/2015 dated 10/7/2015 for strict compliance.

ØIn compliance to Haryana Electricity Regulatory Commission (Rooftop Solar Grid Interactive System based on Net Metering) Regulations (1st Amendment), 2015 dated 09.06.2015, it was notified vide Sales Circular No. D-24/2015 dated 24.07.2015 that "Incentive at the rate of 25 Paise per unit shall be given during the FY 2015-16 on the solar power generated to the extent the same is admissible for off-setting consumer's consumption under Net Metering system".

ØIn compliance to the decision of the Government of Haryana to curb theft of power, improving billing efficiency and quality of service to the consumers of the selected feeder, the 'Mhara Gaon Jag Mag Gaon Scheme' was launched w.e.f. 01.07.2015. Under this scheme one RDS feeder in each of the Haryana Assembly constituencies having least AT&C losses were initially selected for providing increased supply hours from 12 to 15 hours w.e.f. 01.07.2015. The scheme is being carried out in phased manner so that all the RDS feeder are covered in phases.

The salient features of the scheme are as under:-

8

S No. Category Load in MW1 Max. peak demand requirement 3275

2 Min. peak demand requirement 2661

3 Min. Average peak demand 2919

1. The principal amount of the old arrears will be recovered from the consumers of the village in five regular installments along with current bills. After payment of the last bill and arrear installment, entire surcharge amount will be waived off.

2. Reconnection at defaulter premises shall be allowed after payment of first installment without surcharge of outstanding bill. Balance outstanding amount will be paid in four installments along with next current bills.

3. Following activities shall be carried out in the villages to improve the quality of service to consumers:-

i. Replacement of bare conductor with AB cable.

ii. Replacement of defective/electro mechanical meters.

iii. Shifting of meters outside the premises.

iv. Maintenance of DT's.

v. Maintenance of LD system.

vi. As a one time measure, the meter so replaced would not be subject to further checking from the M&T Lab.

4. When the naked LT conductor of the village is fully changed into AB cables as per site requirement and the meters of all the households have been brought out, the power supply to the village will be increased from 15 hours to 18 hours.

Ø5. For measuring the power supplied to the village the meters shall be installed on all the points from which 11 KV lines go into the village. After allowing for the permitted quantum of technical losses i.e. 20%, if the village pays bills to the extent of 90% of power supplied, their electricity supply will be increased from 18 to 21 hours. After the defaulting amount of the feeder becomes less than 10%, 24 Hours supply will be provide

In case a village does not fulfill the obligations cast upon them in terms of helping installation of AB cables, replacement of meters and bringing them outside the houses, eventually leading to reduction of losses, the increased supply hours of power will be withdrawn.

ØVoluntary scheme for declaration of un-authorized load of DS, NDS, LT Industrial & Agriculture Consumers -VDS-2015 was floated vide Sales Circular No. D-27/2015 dated 11/8/2015 whereby consumer can get their unauthorized load regularized from existing system by paying Advance Consumption Security for extended load and Service Connection charges, wherever applicable. This scheme remained applicable upto 30/9/2015.

ØIt was decided vide Sales Circular No. D-29/2015 dated 12.08.2015 to release temporary

connections to the residents of unauthorized /slums colonies with following conditions:-

1. A specific notice by the SDO/OP on prescribed format shall be given to the concerned official/local competent authority e.g. the Commissioner or Executive Officer of Municipal Corporation or Municipal Council or Secretary of the Municipal Committee or E. O HUDA or BDPO/ Gram Panchayat for giving at least four weeks' time for taking suitable action by them regarding the status of premises before the connection is actually released.

2. The connection will be provided purely on temporary basis and the consumer with such an electricity connection would not be entitled to any right over the land or property, if any.

3. The energy meter of the connection will be installed on the pole outside the premises through cable.

4. Only single phase connection will be given to such a consumer.

5. The electricity connection would be charged at the tariff applicable to the concerned category of consumers.

6. The colour of the bill of such a temporary electricity connection shall be different than the usual bills.

7. An affidavit as well as indemnity bond shall be taken from each of such consumer stating clearly that he shall be liable for any legal action regarding his premises by the concerned Local Bodies Department or Town and County Planning Department or Panchayat department or any other legal/competent authority as the case may be.

8. The applicant is required to submit an identity proof (Driving License, PAN No, Adhaar Card, Voter ID Card, Ration Card, Passport, Bank Passbook, etc).

9. All the electricity bills of such consumer will have a detailed disclaimer "clearly stating that release of power connection and collection of bills from the concerned individual does not confer him/her any occupation or ownership rights on the concerned property and that he/she is simply making payment for the electricity actually consumed by him/her and nothing more".

ØThe matter regarding site checking of CT meters has been reviewed keeping in view the fact that it is practically not feasible to check each and every connection by M&P wing, once in a year with the present staff strength due to increased work load and hence, it has been decided vide Sales Instruction No. 11/2015 dated 24/7/2015 to revise the norms for site checking of CT meters by M&P wing as under:-

a) The site checking of all HT CT connections and theft prone industries such as Electroplating Units, Oil

9

Expellers, Plastic Units, Rubber Units, Steel Furnaces, Mobile Towers & Stone Crushers etc. will be carried out by M&P wing, once in a year. The checking report will be prepared by the concerned SDO/M&P in the prescribed format at the time of checking.

b) Seasonal Industries such as Ice Factories, Ice Candies, Cold Storage units, Cotton Ginning Mills and Rice Shellers etc. shall be checked twice during the season i.e. at least once every three months.

c) The connections of all other LT CT consumers will be checked once in every two years.

d) SDO M&P shall invariably check and record a certificate on MT-1 Performa during each such checking that the ratio of CT & PT installed at the consumer's premises as well as that of substation (in case of independent feeder) has been tested and the same is as per record.

Note: However SDO/Op, XEN/Op & XEN/M&P shall monitor the consumption pattern of the consumers and will get the meters checked wherever considered necessary to ensure that the meters are in proper working order.

ØSimplified application form for new connection, reconnection, extension of load, reduction of load and change of name was circulated vide Sales Circular No. D-4/2016 dated 9/2/2016. The applicant is required to submit only 2 nos. documents viz Proof of Ownership / Legal occupation of the premises & Proof of identity along with standard Application and Agreement (A&A) Form.

ØNigam introduced 'Out of Court Settlement Scheme' vide Sales Circular No. D-42/2019 dated 9/12/2015 for Settlement of disputes pertaining to various categories of Electricity consumers which are pending in Courts/Arbitration/ DCDRF/State Commission/National Commission etc, in the Lok Adalats being held regularly under the jurisdiction of DHBVN. This scheme remain applicable upto 31/1/2016. Thereafter the scheme was again extended from 18/3/2016 to 31/7/2016 vide Sales Circular No. D-7/2016 dated 18/3/2016.

SMART GRID PROJECT GURUGRAM:

a. The meeting held on 08.10.2016 under the chairmanship of Hon'ble Chief Minister Haryana and the Hon'ble MoS (IC) Power, Coal and Renewable Energy Departments, GoI, provided the impetus to the development of "Smart Grid Project" leading to smart City Gurugram. The decisions taken in the meeting acted as the way forward guidelines upon which the development of Smart Grid project of Gurugram was to be based. The main objectives in mind to start with are to provide 24x7 uninterrupted electricity to all the consumers, to make Gurugram a Diesel Generator free city

10

within next one year and subsequently scaling up the infrastructure to make it a Smart City.

The Execution was planned in 3 Parts-

¢ Part-l-(sec 1-57 )which was further divided in to 4 phases

i) DLF City S/D

ii) South City & Sohna Road S/D

iii) Maruti & IDC SO

iv) Kadipur, N. Clny & N. Palam Vihar S/D

ØPart-ll(Sector 58 to 115)

ØPart-III(IMT Manesar)

Implementation of Smart Grid will ensure 24 X 7 uninterrupted power supply to the end consumers resulting in reduction in AT&C losses and overhead cost due to integration of various IT tools to make the Grid system more efficient by ensuring consumer participation.

b. The total project cost was estimated of 10000 Cr out of which Rs 7000 Cr was envisaged for Part -1 of the project.

Under the original strategy the NIT was floated for the Part-I, Phase-I of the project with the estimated cost of Rs 504 Cr.

c. After deliberation at various levels the original strategy was changed to implement Smart Grid Project from sector 1 to 57 in Gurugram in different layers as detailed out below

1. Strengthening of infrastructure by laying 11 kV network in ring main along with optical fiber cable to meet with future requirement of communication and by providing SCADA compatible field equipments. Apart from this, strengthening of LT network with additional distribution transformers to meet with the future load growth is also included.

2. In the second layer SCADA with various IT tools will be implemented for entire Gurugram.

3. Advance metering infrastructure (AMI) will be implemented for the entire Gurugram to remove the inefficiency in the system on account of meter reading and improper data analytics.

4. Undergrounding of LT network in such a fashion that the network is in ring main to ensure round the clock supply up to the consumer premises.

SMART CITY PROJECT OF FARIDABAD:

Faridabad town has been shortlisted as one of the fast track cities selected by Ministry of Urban Development, Gol for development as a Smart City. Following area has been selected for development under Faridabad Smart City Project for rolling out the pilot project:

Sector-19, Sector 20, Sector 20A, Sector 21B, Sector 21D, Badhkal Lake, Fatehpur, Village Ajraundi & Village

11

Sant Nagar.

Under the pilot project in Faridabad the complete electrical infrastructure is being undergrounded in ring main. Apart from this, SCADA and AMI is also being implemented and integrated with the system to bring efficiency in the system by ensuring 24 X 7 quality power supply to the consumers. The system efficiency will also be increased by implementing demand side management (DSM) and with the integration of renewable energy with the Grid.

Online Consumer Grievances Redressal System

As online consumer Grievances Redressal System is already place in DHBVNL. During the year 2015-16 total numbers of 5,411 complaints have been lodged by the consumers through Consumer Grievances Redressal System.

Centralized Call Centre:

DHBVN has established a centralized call center as part of R-APDRP (Part-A) Project, for registering of no current complaints on 24X7 for all consumers falling under its administrative control. The operations of the call centre was started from 26/08/2014. To avoid any charges to the consumer one Toll Free number (i.e. 1800-180-4334) has been provided. A total of 2,32,181 nos. complaints have been received through call centers during 2015-16.

Court Case Monitoring System:

It has been observed that substantial portion of revenue is getting blocked in the court cases for better monitoring of court cases DHBVN has implemented online Court Case Monitoring System (CCMS) wherein the synopsis of all the consumer related court case are being entered by the field offices. Through the system the court cases are being monitored and prompt action against the high stake court cases is being taken up timely.

Online Cash Collection and Reconciliation System:

The source of Company's revenue a vast consumer base and there are many collection centers being operated in the field by Company's staff as well as outsourced staff. For better monitoring of revenue collection in the field and better cash handing process "Online Cash Collection and Reconciliation System" has been implemented in DHBVN wherein all the models of cash collection shall be integrated on a single platform so as to facilitate real time monitoring and further extend the facility of Online Payments to all the consumers of DHBVN. Which was earlier provided to the consumers of Gurgoan, Faridabad & Hisar towns only.

Online application for HT/LT Connections:

Transparent & visible process of submission of online

IT INITIATIVES

application for all industrial (HT/LT) connection and other categories of connections, where the applied load is more than 20 KW has been launched, which facilitates monitoring of pending applications by management and higher offices. The system has been upgraded to cater all categories of consumers, irrespective of load applied.

Capex works:

Various Capex works have been undertaken by the Company such as construction of new sub stations, augmenting existing overloaded sub stations, bifurcation/trifurcation of overloaded 11 KV feeders, shifting of connections to feeder pillar boxes, release of connections etc. An amount of Rs. 587.87 crore was spent as Capex works in 2015-16 as against Rs. 704.58 crore spent in 2014-15.

Your Directors have not recommended any dividend since the Company has incurred losses during the year under review.

As on the date of this report, the Authorized Share capital of the Company is Rs. 5000 crores and the paid up share is Rs. 20051442000/-. The State Govt. is holding 78.20% of the paid up capital of the company and the balance of 21.80% is held by Hayana Vidyut Parasaran Nigam Limited.

During the year under review the Company has not accepted any deposit under Section 73 of the Companies Act, 2013.

The Haryana Electricity Regulatory Commission (HERC) has granted License to the Company for Distribution & Retail Supply of Power in the South of Haryana.

The information on conservation of Energy Technology Absorption as stipulated in section 134 (3)(m) of the Companies Act, 2013 read with Rule 8 of the Companies (Account) Rules 2014 is attached as Annexure-I.

The Board of Directors of the Company comprises of below mentioned Directors and Key Managerial Personals as on 31.03.2016:-

DIVIDEND

SHARE CAPITAL

FIXED DEPOSITS

LICENCE FOR CARRYING OUT BUSINESS

CONSERVATION OF ENERGY, TECHNOLOGY ABSORPTION AND FOREIGN EXCHANGE EARNINGS AND OUTGO

DIRECTORS AND KEY MANAGERIAL PERSONALS

12

The following changes had taken placed in the Board of Directors and Key Managerial Personals of your company since last financial year 2015-16.

(i) Sh. Suresh Kumar Bansal, was appointed to be Director/Projects w.e.f. 08.04.2015.

(ii) Sh. Ravinder Kumar Batra, was appointed as Director/Operation on 09.04.2015.

(iii) Sh. Anil Gupta, Chartered Accountant was appointed as Part Time Director-Independent w.e.f. 28.05.2015.

(iv) Smt. Ashima Brar, IAS was appointed as Nominee Director w.e.f. 03.08.2015.

(v) Sh. Vineet Garg, IAS was appointed as Nominee Director w.e.f. 16.12.2015.

(vi) Sh. Ravi Prakash Gupta, IAS was appointed to be Nominee Director w.e.f. 16.12.2015.

(vii) Sh. Vijay Singh Dahiya, IAS was ceased to be Director w.e.f. 16.12.2015.

(viii) Smt. Ashima Brar, IAS was ceased to be Director w.e.f. 16.12.2015.

The Board places on record its sincere appreciation and gratitude for the valuable contribution & support rendered by the outgoing Directors during their tenure in the Company.

Board of Directors Meeting

DECLARATION BY INDEPENDENT DIRECTORS

COMMITTEES OF THE BOARD OF DIRECTORS

The Board of Directors met Five times during the financial year 2015-16. The meetings of the Board were conducted by the Company Secretary and majority of the Directors had attended each meeting.

All the Independent Directors meet the criteria of independence as provided in Section 149(6) of the Companies Act, 2013, and necessary declarations under section 149(7) of the Companies Act 2013 have been received from them.

1. Audit Committee

The Board of Directors had constituted Audit Committee pursuant to the provisions of section 177 of the Companies Act 2013 read with Rule 6 of the Companies (Meetings of Board & its Powers) Rules 2014 with below mentioned compositions for the financial year 2015-16:-

1. Sh. M. K. V. Rama Rao Chairman

2. Sh. K. K. Ghosh Member

3. Sh. Sanghamitra Pyne Member

During the financial year 2015-16 three meetings of Audit Committee had been conducted. All the recommendations made by the Audit Committee during the year had been accepted by the Board of Directors.

Sr. No.

Name of Directors Designation Category Date of

Appointment

1. Sh. Rajan Gupta ACS/Power & Chairman, DHBVNL

Part Time Director 18.11.2014

2. Sh. Arun Kumar Verma Managing Director Whole Time Director 04.03.2014

3. Sh. Vineet Garg Director Part Time Director Representing Power Utilities

16.12.2015

4. Sh. Nitin Kumar Yadav Director Part Time Director Representing Power Utilities

24.11.2014

5. Sh. Ravi Prakash Gupta Director Part Time Director Representing Power Utilities

16.12.2015

6. Sh. Suresh Kumar Bansal Director/Projects Whole Time Director 08.04.2015

7. Sh. Ravinder Kumar Batra Director/Operation Whole Time Director 09.04.2015

8. Sh. M. K.V. Rama Rao Director Part Time Director Representing Power Utilities

05.11.2013

9. Sh. K. K. Ghosh Director- Independent Part Time Director 17.04.2013

10. Sh. R. P. Sasmal Director- Independent Part Time Director 17.04.2013

11. MS. Sanghamitra Pyne Director- Independent Part Time Director 17.04.2013

12. Sh. Anil Gupta Director- Independent Part Time Director 28.05.2015

13. Sh. Kapil Kumar Marwha Chief Financial Officer /KMP Whole Time 23.07.2014

14. Sh. Harjinader Singh Company Secretary/ KMP Whole Time 24.09.2014

2. Whole Time Directors

To review the functional areas of business and other matters, the Whole Time Directors of the Company hold their meetings from time to time and Twenty such meetings were held during the financial year 2015-16. The Company Secretary acts as Secretary for conducting the meetings.

3. Nomination & Remuneration Committee

The Company is having dully constituted Nomination & Remuneration Committee pursuant to the provisions of section 178 of the Companies Act 2013. The composition of the Nomination & Remuneration Committee for the financial year ending 31.03.2016 is mentioned below:-

1. Sh. M.K.V. Rama Rao Chairman2. Sh. R. P. Sasmal Member3. Ms. Sanghamitra Pyne Member

During the financial year 2015-16 one meetings of Nomination & Remuneration Committee had been conducted.

4. Corporate Social Responsibility

The Company is having dully constituted Corporate Social Responsibility Committee pursuant to the provisions of section 135 of the Companies Act 2013. The composition of the Corporate Social Responsibility Committee for the financial year ending 31.03.2016 is mentioned below:-

1. Sh. Suresh Kumar Bansal, Chairman

2. Sh. R. P. Sasmal Member

3. Sh. Ravinder Kumar Batra Member

The Company has also formulated a Corporate Social Responsibility Policy which inter alia contains guidelines and mechanism for undertaking various projects for developments and welfare of Society at large.

Due to non availability of profits no CSR activities had been carried out by the company during the financial year 2015-16.

During the financial year 2015-16 one meetings of Corporate Social Responsibility Committee had been conducted.

5. Meeting of Independent Directors

During the financial year 2015-16 one meeting of Independent Directors was held. All the independent Directors except Ms. Sanghamitra Pyne had attended the meeting. The meeting was chaired by Sh. K. K. Ghosh.

Pursuant to the provision of section 177 of the Companies Act 2013 the company has formulated and adopted a Vigil Mechanism Policy. The policy provides a channel to Directors and employees to report their genuine concerns about any unethical or improper behavior of an employee of the company or malpractices or events which have taken place or suspected to take place. It also provides adequate

VIGIL MECHANISM

safeguards against the victimization of an employee who has availed the Vigil Mechanism.

RELATED PARTY

All transactions entered with Related Parties for the year were on arm's length basis and in ordinary course of business. The disclosure of related party transactions as required under Section 134 (3) (h) of the Companies Act 2013 in Form AOC-2 has been annexed as Annexure-II.

In accordance with the provisions of the section 134 (3) (a) of the Companies Act 2013 read with Rule 12 of the Companies (Management and Administration) Rules, 2014, the extract of the Annual Return in form MGT-9 has been annexed as Annexure-III.

There are no loans given, guarantee issued or investment made by the Company to which provision of section 186 of the Companies Act, 2013 are applicable.

M/s O. Aggarwal & Co., Chartered Accountants, were appointed as Statutory Auditor to conduct audit of the books of Accounts for the financial year 2015-16 (had appointed the Comptroller and Auditor General of I n d i a , N e w D e l h i v i d e s i t s l e t t e r N o . CA.V/COY/HARYANA, DHBJLI(1)/1176 dated 05.08.2015) The reports of the Statutory Auditor and the Comptroller General of India on the account for the financial year 2015-16 have been received.

As required under Section 134(3) (f) of the Companies Act, 2013, your Directors also offer their fullest information and explanations on the reservations, qualifications and comments of the Statutory Auditors on the accounts of the Company for the year 2015-16 in the addendum to this report.

Further, M/s O. Aggarwal & Co., Chartered Accountants, have also been appointed as Statutory Auditors of the Company for the FY 2016-17 by the C&AG of India vide its letter No. CA.V/COY/ HARYANA,DHBJLI(1)/1259 dated 26.08.2016.

The Comptroller Auditor General of India (CAG) has given comments on the accounts for the financial year ended 31.03.2016 under Section 143(6) of the Companies Act 2013. The comments of the Comptroller Auditor General of India along with replies of Management have been enclosed as addendum to this report.

Pursuant to the provisions of the section 204 of the Companies Act 2013, the Board of Directors had appointed M/s Girish Madan & Associates as Secretarial Auditors of the Company for the financial year 2015-16. M/s Girish Madan & Associates, Panchkula has

RELATED PARTY TRANSACTIONS

ANNUAL RETURN

PERTICULERS OF LOANS, GUARRANTEE AND INVESTMENTS

STATUTORY AUDITORS

Comments of the Comptroller Auditor General of India

SECRETARIAL AUDITORS

13

submitted the Secretarial Audit Report in Form MR-3 for the financial year 2015-16 the copy of the same has been annexed as Annexure-IV. The Report submitted by M/s Girish Madan & Associates does not contain any qualification or adverse remarks for the financial year 2015-16.

In accordance with the provisions of section148 of the Companies Act 2013 read with the Companies (Audit and Auditors) Rule 2014 M/s A.G. Aggarwal & Associates, Cost Accountants, Noida, had been appointed as Cost Auditors by Board of Directors for the financial year 2015-16.

The Cost Audit Report for the financial year 2015-16 had been submitted by M/s A.G. Aggarwal & Associates, Cost Accountants, Noida.

Further, on the recommendations of the Audit Committee the Board of Directors had appointed M/s A.G. Aggarwal & Associates, Noida as Cost Auditors for the financial year 2016-17.

The Company has an internal audit system commensurate with the nature and size of the business of the company. The Chief Auditor, DHBVNL has been appointed as Internal Auditor of the Company under Section 138 of the Companies Act 2013 by the Board of Directors of the Company.

Pursuant to the provisions of Section 134(5) of the Companies Act, 2013, the Board of Directors to the best of their knowledge beliefs, ability and according to the information received confirms that:-

(i) in the preparation of the Annual Accounts for the year ended 31st March, 2016 the applicable accounting standards have been followed and there are no material departures from the same;

(ii) the Directors have selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the Company as at 31st March, 2016 and of the profit of the Company for the year ended on that date;

(iii) the Directors have taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provision of the Act for safeguarding the assets of the Company and for preventing and detecting fraud and other irregularities;

(iv) the Directors have prepared the annual accounts for the financial year 31st March, 2015 on a 'going concern' basis;

(v) the Directors have devised proper systems to ensure compliance with the provisions of all applicable

COST AUDITORS

INTERNAL AUDIT

Directors' Responsibility Statement

laws and that such systems are adequate and operating effectively.

The company has adequate internal financial controls and these internal controls were operating effectively during the year.

As required under Electricity Act 2003 and HERC guidelines, DHBVN had established a Forum for Redressal of grievances of consumer in March, 2006. This Forum prepares monthly schedules to visit all Nine Circles in every month for redressal of consumer grievances in the respective circles as per procedure prescribed under State Electricity Regulation. During the financial year 2015-16, 275 number complaints had been received and decided by the Forum.

As per manpower position of DHBVN as on 31.03.2016, details of technical and Non-technical staff are tabulated below:-

During the year 2015-16, detail of training provided to the employees of DHBVN in man days is as under:

In line with provisions of "Sexual Harassment of Women (Prevention, Prohibition & Redressal) Act, 2013, an "Internal Complaints Committee" has been constituted in the Nigam for Redressal of complaint(s) against sexual harassment of women employees. During the financial year 2015-16, no complaint against the sexual harassment of women employees has been received in the Nigam.

The Ministry of Corporate Affairs vide its notification dated 05.06.2015 has exempted the Govt. Companies from the applicability of section 197 of the Companies Act, 2013. Hence no information is required to be given by the Company under this section.

Ujwal Discom Assurance Yojna (UDAY)

INTERNAL CONTROLS SYSTM AND THEIR ADEQUACY

CONSUMER GRIEVANCE REDRESSAL FORUM

HUMAN RESOURCE ACTIVITIES:

TRAINING IN MAN DAYS

COMPLIANCE WITH THE SEXUAL HARASSMENT OF WOMEN AT WORKPLACE (PREVENTION, PROHIBITION AT REDRESSAL) ACT, 2013

PARTICULARS OF EMPLOYEES

MATERIAL CHANGES AND COMMITMENTS

Sr. No. Category Sanctioned Posts Working Position s

1.

Technical

13527

7186

2. Non-technical 5134 2230

Category Period of training No. of officers/officials attended the training

Man days

Gazetted &

Non-Gazetted

FY 2015-2016 2849 8846

14

The Govt. of India (Ministry of Power) notified Ujwal Discom Assurance Yojna (UDAY) on 20.11.2015 for operational and financial turnaround of State Power Distribution Utilities. The tripartite MoU amongst Govt. of India, Govt. of Haryana and State DISCOMs (UHBVN & DHBVN) was signed at New Delhi on 11.03.2016. The scheme aims at reducing debt burden of DISCOMs, reduces cost of power & reduce AT&C losses to the level of 15% in next 3 years by 2018-19.

Under the scheme, 75% of the loan liabilities of DISCOMs outstanding as on 30th September, 2015, are to be taken over by the State Govt. in two years i.e. 50% in FY 2015-16 and balance 25% in FY 2016-17 by issuing non SLR bonds and treating the same as loan from State Govt. to Power Utilities. The entire loan amount would be converted into equity & grant to Utilities over a period of 5 years starting from 2015-16 to 2019-20 @ 15% every year.

First tranche of UDAY bonds for both the DISCOMs was issued by the State Govt. on 31.03.2016 at coupon rate of 8.21 % for Rs. 17300 crores. The 2nd, 3rd & 4th tranche of UDAY bonds for the balance amount of Rs. 8650 crores were issued from 15.06.2016 to 04.07.2016 through Reserve Bank of India at coupon rate ranging from 8.06% to 8.14%. The weighted average rate of interest for UDAY bonds of Haryana State comes to 8.20% approx.

The DHBVN loan liabilities coered under UDAY are Rs. 11727 crores including 75% of the loans of Rs. 2632.13

crores transferred from UHBVN on account of transfer of Jind distribution circle in FY 2013-14.

The UDAY would result in significant reduction in interest cost for the DISCOMs. The loans in the books of the DHBVN prior to take over by the State Govt. were carried interest at around 11.70% (Base Rate of Lead Bank +2%) to 12.38 % which after issue of bonds reduced to 8.20% resulting into saving of amount Rs. 425 crores approx. in FY 2016-17 as interest cost. The full benefit would, however come after conversion of entire State Govt. loan portion into equity and grant to DISCOMs by the year 2020 @ 15% every year.

During the year under review, the industrial relations with the employees remained cordial and peaceful. The Directors wish to place on the record their sincere appreciation for unstinted support provided to the Company by the employees at all levels.

The Board of Directors acknowledge with gratitude the co-operation and assistance rendered by the Haryana Electricity Regulatory Commission (HERC), Bankers, Financial Institutions and various Departments of the Central and State Governments. The Board also expresses its deep gratitude for the continued co-operat ion and support received from the Shareholders.

.

INDUSTRIAL RELATIONS

ACKNOWLEDGEMENTS

For and on behalf of the Board of Directorsof Dakshin Haryana Bijli Vitran Nigam Ltd.

Shatrujeet Singh Kapoor, IPSChairman-cum-Managing Director,

DHBVNLDate: Place: Panchkula

sd/-

15

PARTICULARS UNDER COMPANIES (ACCOUNTS) RULES 2014 FOR THE YEAR ENDED 31ST MARCH, 2016

a) For conservation of energy a number of steps have been taken by the Company such as replacement of incandescent lamps with CFL, use of solar water heater system, use of energy efficient/ BEG level equipments, use of energy efficient/ star rated transformers, automatic power switching system, automatic power factor correction units, ESCO model for DSM of commercial, industrial and domestic sectors.

Besides the above, a number of other steps have also been taken by the Company such as distribution of leaflets and pamphlets on energy conservation on important occasions like India International Trade Fair, Gandhi Jayanti Samaroh, Inaugurat ion/ foundat ion s tone laying programmes of VIPs etc. for mass awakening. Messages were also disseminated through audio cassettes in various programmes.

b) Additional investments and proposals, if any, being implemented for reduction of consumption of energy.

For reduction of consumption of energy new Distribution Transformers are being added wherever required. Rehabilitation and expansion of distribution system has been undertaken and overloaded feeders are being rehabilitated and new feeders are being energized. Rebate is being given in electricity bill of consumers using solar water heater system, Incentive for use of star rated/ energy efficient pump sets is also being given.

c) Impact of measures at (a) and (b) above for reduction in energy consumption and consequent impact on the cost of production of goods.

As a result of the above measures the following benefits have arisen:

?There is a reduction in technical and non-technical line losses and reduction in unauthorized tapping of power supply.

?Supply of quality power to consumers resulting to greater consumer satisfaction.

?Reduction in damage rate of distribution transformers.

A. CONSERVATION OF ENERGY

?Solution to Low Voltage problem and improved voltage to consumer.

?Reduction in overloading of Transformers and reduction in Peak Power Loss.

d) Total energy consumption per unit of production as per Form-A.

DHBVN is not covered in the category of Industries required to furnish the information as contained in the Schedule.

e) Research & Development (R&D): Nil.

(a) Efforts have been made in this regard such as providing high speed internet connections with Computers and Lap Tops to officer's/offices, Installation of advance version of Electronic Energy Meters, Installation of upgraded Distribution Transformers, computerization of energy billing & various other functions of the Nigam.

(b) As a result of the above efforts, the Company has benefited in curbing theft of electricity and reduction in line losses. The above efforts have also lead to supply of quality power and accurate metering resulting to consumer satisfaction, increase in revenue and efficiency & transparency in working.

a) Earning in Foreign Exchange: Nil

b) Foreign Exchange outgo: Nil

For and on behalf of the Board of Directorsof Dakshin Haryana Bijli Vitran Nigam Ltd.

Sd/-

Shatrujeet Singh Kapoor, IPSChairman-cum-Managing Director, DHBVNL

Place: Panchkula

B. TECHNOLOGY ABSORPTION:

C. FOREIGN EXCHANGE EARNING AND OUTGO :

ANNEXURE- I TO DIRECTOR'S REPORT

16

17

Date:

Place: Panchkula

For and on behalf of the Board of Directors

of Dakshin Haryana Bijli Vitran NIgam Ltd.

Shatrujeet Singh Kapoor, IPS

Chairman-cum-Managing Director, DHBVNL

sd/-

18

19

20

21

22

23

Date:

Place: Panchkula

For and on behalf of the Board of Directors

of Dakshin Haryana Bijli Vitran NIgam Ltd.

Shatrujeet Singh Kapoor, IPS

Chairman-cum-Managing Director, DHBVNL

24

sd/-

25

REPLIES OF THE MANAGEMENT ON THE COMMENTS OF THE COMPTROLLER AND AUDITOR GENERAL OF INDIA UNDER

SECTION 143 (6) (B) OF THE COMPANIES ACT 2013 ON THE ACCOUNTS OF DAKSHIN HARYANA BIJLI VITRAN NIGAM LIMITED

HISAR FOR THE YEAR ENDED 31ST MARCH 2016.

MANAGEMENT REPLYCOMMENTSPara No.

ANNEXURE-II TO THE DIRECTOR'S REPORT

The preparation of financial statements of the Dakshin Haryana Bijli Vitran Nigam Limited for the year March 2016 in accordance with financial reporting framework prescribed under the Companies Act, 2013 is the responsibility of the management of the Company. The Statutory Auditors appointed by the Comptroller and Auditor General of India under Section 139 (5) of the Act are responsible for expressing opinion on the financial statements under Section 143 of the Act based on independent audit in accordance with the Standards on auditing prescribed under Section 143(10) of the Act. This is stated to have been done by them vide their Audit Report dated 22 November 2016.

I, on behalf of the Comptroller and Auditor General of India, have conducted a supplementary audit under Section 143(6) (a) of the Act of the stand alone financial statements of Dakshin Haryana Bijli Vitran Nigam Limited for the year ended 31 March 2016. This supplementary audit has been carried out independently without access to the working papers of the statutory auditors and is limited primarily to inquiries of the statutory auditors and company personnel and a selective examination of some of the accounting records. Based on my supplementary audit, I would like to highlight the following significant matters under Section 143 (6)(b) of the Act which have come to my attention and which in my view are necessary for enabling a better understanding of the financial statements and the related Audit Report.

A. Comments on profitability:

I Current Liabilities:

Trade Payables (Note 9): 2193.67 crore

The above does not include

a. Payable of `2.83 crore to Haryana Power Generation Corporation Limited (HPGCL) owing to true up orders of Haryana Electricity Regulatory Commission (HERC) dated 31 March 2016 on the cost of that Company.

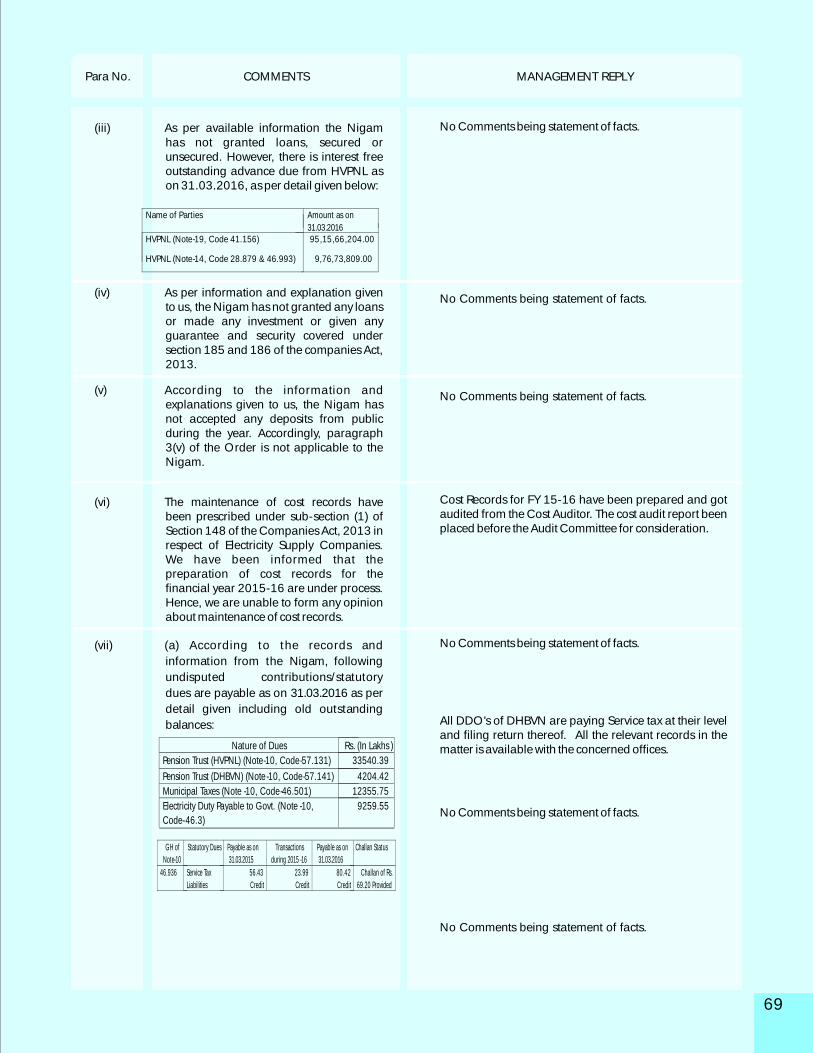

No Comments

No Comments

It is submitted that HPGCL had raised the bill amounting to 69.62 crore as true-up expenses for the FY 2014-15 as per the HERC order dt. 31.03.2016 on 11.04.2016. In response to the HERC order dt. 31.03.2016 and the bill raised by HPGCL for True-up Expenses for FY 2014-15, HPPC had made a reference to HPGCL stating that

b. Payable of `47.17 crore to Lanco Amarkantak Power Limited (LAPL) for power purchased in the years 2011-12 and 2012-13. This has resulted in understatement of Liabilities for purchase of power, Trade payable and Loss by 50.00 crore.

II Current Assets:

Other Current Assets (Note 20): `67.26 crore

The above includes difference of `19.55 crore of written down value of asset and realizable value of assets disposed/retired from active use during 2015-16.This has resulted in overstatement of Current Assets, other current assets and understatement of loss by 19.55 crore.

III Cost of power purchase 12500.40 crore

The power purchase cost includes prior period expenditure of `201.98 crore and prior period income of 217.10 crore which should have been shown separately. This has resulted in understatement of power purchase cost and loss for the year by

as per HERC order dt. 31.03.2016, HPGCL is also directed to reverse the excess amount of fixed cost of `64.45 crore recovered in the FY 2014-15 to the Discoms and requested to revise the bill of 69.62 crores after considering the reversal of fixed cost of `64.45 crores and returned the original copy of the bill for True-up Expenses for FY 2014-15 to HPGCL. But HPGCL vide its letter dated 26.04.2016 had intimated that HPGCL is going to file a review petition against the Hon'ble Commission's order dt. 31.03.2016. HPPC again requested to HPGCL to raise this bill for True-up Expenses for FY 2014-15 dt. 11.04.2016 as a whole only after the outcome of review orders of Hon'ble Commission otherwise stay order by HERC against this order be provided to this office.

On 20.07.2016, HPGCL had raised the bill for True-up Expenses for FY 2014-15 for the net amount of `5.07 crore (`69.52 crore - `64.45 crore) as per HERC order dated 29.06.2016 and `2.83 crore (`5.07 x 55.93%) was booked into the monthly account of the month of July 16 in which the final invoice from HPGCL is received.

It is submitted that HPPC had booked the total amount of monthly invoices of actual energy supplied by Lanco Amarkantak Power Ltd. (LAPL) in the respective months in the FY 2011-12 and FY 2012-13.

As per HERC order dt. 12.07.2016, this payable differential amount of 88.123 crore for the period from 07.05.2011 to 31.03.2013 at the tariff determined by the Commission was paid in three installment starting from the month of August 2016 and same stand accounted far in the books during FY 2016-17.

In this connection it is stated that assets disposed/retired from use during the year, having original value of 47.59 crore mainly includes meters & metering equipments which may be replaced earlier than its useful life ascertained being obsolete or damaged. Under such circumstances, the residual value of the asset cannot be exactly 10% of original value but the value remained after providing depreciation for useful life of assets. Moreover the depreciation is provided at the rates fixed by HERC as per MYT Regulation. The above treatment is in accordance with the provision contained in AS-10. Moreover the amount of loss charged to P&L account on this account is 17.71 Cr.

The issue raised by Audit for the understatement of power purchase cost is a disclosure issue and do not effect the profit or loss of the DHBVN.

DHBVN is recognizing the power purchase cost in the period during which the corresponding liabilities is

26

MANAGEMENT REPLYCOMMENTSPara No.

`15.12 crore (`217.10 - `201.98= `15.12 crore).

B Impact on Profitability:

The impact of above comments is that the losses have been understated by `69.55 crore. If they are taken into account, the losses for the year of `471.58 crore would increase to 541.13 crore.

established and accepted. This process help the DHBVN to correctly ascertain the amount of FSA to be recovered from consumers in future.

The comment of the audit regarding understatement of power purchase cost cannot be accepted in view of position explained above.

This does not impact true & fair view of the financial statement of the Nigam.

As per our replies above.

27

MANAGEMENT REPLYCOMMENTSPara No.

lR;eso t;rs

iathd`r@xksiuh;

dk;kZy; iz/kku egkys[kkdkj ¼ys[kkijh{kk½gfj;k.kk

IykV ua 5] lSDVj 33&ch

nf{k.k ekxZ] p.Mhx<+ 160020

OFFICE OF THE ACCOUNTANT GENERAL (AUDIT)

HARYANA PLOT NO. 5, SECTOR 33-B,

DAKSHIN MARG, CHANDIGARH-160020.

la[;k ES-I/CA III/DHBVNL/BS-2015-2016, 2016-2017/650

fnukad : 25.01.2017

lsok esa]

izcU/k funs'kd]nf{k.k gfj;k.kk fctyh forj.k fuxe fyfeVsM]fo|qr lnu] fo|qr uxjfglkj A

fo"k;%& dEiuh vf/kfu;e 2013 dh /kkjk 143 ¼6½ ¼Ckh½ ds vUrZxr nf{k.k gfj;k.kk fctyh forj.k fuxe fy-] fglkj ds 31 ekpZ 2016 dks lekIr gq, o"kZ ds okf"kZd ys[kksa ij Hkkjr ds fu;a=d ,oa egkys[kkijh{kd dh fVIif.k;kaA

egksn;]

eSa blds lkFk dEiuh vf/fu;e 2013 dh /kkjk 143 ¼6½ ¼ch½ ds vUrZxr nf{k.k gfj;k.kk fctyh forj.k fuxe fyfeVsM] fglkj ds 31 ekpZ 2016 dks lekIr gq, o"kZ ds okf"kZd ys[kksa ij Hkkjr ds fu;a=d ,oa egkys[kkijh{kd dh fVIif.k;ka ,oa izca/ku i= layXu djrk gwaA

fVIif.k;ksa dks daiuh dh okf"kZd egklHkk ¼,- th- ,e-½ esa izLrqr djus dh frfFk rFkk le; dk;kZy; dks lwfpr fd;k tk;sA

Hkonh;]

mi&egkys[kkdkj ¼vkfFkZd {ks= I ½

28

Sd/-

COMMENTS OF THE COMPTROLLER AND AUDITOR GENERAL OF INDIA UNDER SECTION 143(6)(b) OF THE

COMPANIES ACT, 2013, ON THE FINANCIAL STATEMENTS OF THE DAKSHIN HARYANA BIJLI VITRAN

NIGAM LIMITED, HISAR FOR THE YEAR ENDED 31st MARCH 2016

The preparation of financial statements of the Dakshin Haryana Bijli Vitran Nigam Limited for the year March 2016 in

accordance with financial reporting framework prescribed under the Companies Act, 2013 is the responsibility of the

management of the Company. The Statutory Auditors appointed by the Comptroller and Auditor General of India

under Section 139 (5) of the Act are responsible for expressing opinion on the financial statements under Section 143

of the Act based on independent audit in accordance with the Standards on auditing prescribed under Section 143(10)

of the Act. This is stated to have been done by them vide their Audit Report dated 22 November 2016.

I, on behalf of the Comptroller and Auditor General of India, have conducted a supplementary audit under Section

143(6) (a) of the Act of the stand alone financial statements of Dakshin Haryana Bijli Vitran Nigam Limited for the year

ended 31 March 2016. This supplementary audit has been carried out independently without access to the working

papers of the statutory auditors and is limited primarily to inquiries of the statutory auditors and company personnel

and a selective examination of some of the accounting records. Based on my supplementary audit, I would like to

highlight the following significant matters under Section 143 (6)(b) of the Act which have come to my attention and

which in my view are necessary for enabling a better understanding of the financial statements and the related Audit

Report.

A. Comments on Profitability :

I. Current Liabilities:

Trade Payables (Note 9): 2193.67 crore

The above does not include

a. Payable of `2.83 crore to Haryana Power Generation Corporation Limited (HPGCL) owing to true up

orders of Haryana Electricity Regulatory Commission (HERC) dated 31 March 2016 on the cost of that

Company.

b. Payable of 47.17 crore to Lanco Amarkantak Power Limited (LAPL) for power purchased in the years

2011-12 and 2012-13.

This has resulted in understatement of Liabilities for purchase of power, Trade payable and Loss by

`50.00 crore.

II. Current Assets:

Other Current Assets (Note 20): 67.26 crore

The above includes difference of `19.55 crore of written down value of asset and realizable value of assets

disposed/retired from active use during 2015-16.This has resulted in overstatement of Current Assets, other

current assets and understatement of loss by 19.55 crore.

III. Cost of power purchase 12500.40 crore

The power purchase cost includes prior period expenditure of `201.98 crore and prior period income of

`217.10 crore which should have been shown separately. This has resulted in understatement of power

purchase cost and loss for the year by 15.12 crore (`217.10 - 201.98= 15.12 crore).

B. Impact on Profitability:

The impact of above comments is that the losses have been understated by 69.55 crore. If they are taken into

account, the losses for the year of 471.58 crore would increase to 541.13 crore.

1829

For and on the behalf of the

Comptroller & Auditor General of India

Place: Chandigarh

Date: 25.01.2017 Sd/-

(Karan Singh)

A.G. (Audit), Haryana

Chandigarh

The Members,Dakshin Haryana Bijli Vitran Nigam LtdHisar

1. Report on the Standalone financial statements

We have audited the accompanying standalone financial statements of Dakshin Haryana Bijli Vitran Nigam Ltd (“the Company”), which comprise the Balance Sheet as at March 31, 2016 the Statement of Profit and Loss and Cash Flow Statement, and a summary of significant accounting policies and other explanatory information for the year then ended.

2. Management's Responsibility for the Standalone financial statements

The Company's Board of Directors is responsible for the matters stated in Section 134(5) of the Companies Act, 2013 (“the Act”) with respect to the preparation and presentation of these standalone financial statements that give a true and fair view of the financial position, financial performance and cash flows of the Company in accordance with the accounting principles generally accepted in India, including the Accounting Standards specified under Section 133 of the Act, read with Rule 7 of the Companies (Accounts) Rules, 2014. This responsibility also includes maintenance of adequate accounting records in accordance with the provisions of the Act for safeguarding the assets of the Company and for preventing and detecting frauds and other irregularities; selection and application of appropriate accounting policies; making judgments and estimates that are reasonable and prudent; and design, implementation and maintenance of adequate internal financial controls, that were operating effectively for ensuring the accuracy and completeness of the accounting records, relevant to the preparation and presentation of the financial statements that give a true and fair view and are free from material misstatement, whether due to fraud or error.

3. Auditor's Responsibility

Our responsibility is to express an opinion on these standalone financial statements based on our audit. We have taken into account the provisions of the Act, the accounting and auditing standards and matters which are required to be included in the audit report under the provisions of the Act and the Rules made thereunder.

We conducted our audit in accordance with the Standards on Auditing specified under Section 143(10) of the Act. Those Standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and the disclosures in the financial statements. The procedures selected depend on the auditor's judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal financial control relevant to the Company's preparation of the financial statements that give a true and fair view in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on whether the Company has in place an adequate internal financial controls system over financial reporting and the operating effectiveness of such controls. An audit also includes evaluating the appropriateness of the accounting policies used and the reasonableness of the accounting estimates made by the Company's Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our adverse audit opinion on the standalone financial statements.

4. Basis for Adverse Opinion

We draw attention to the matters described in Annexure II, the effects/possible effects of which, individually or in aggregate, are material and/or pervasive to the financial statements and matters where we are unable to obtain appropriate audit evidence. The effects of the matters described in Annexure II, which could be reasonably determined/ quantified, on the basis of accompanying financial statement are tabulated as under:

Profit & Loss A/c (Items) (Rs. In Crore)

INDEPENDENT AUDITOR'S REPORT

O AGGARWAL & CO., Chartered Accountants(A Peer Reviewed Firm)Office: 22420688,22017315, Mob: 9891577403, Email: H-3/11-A, Krishna Nagar, Delhi-110051

30

31

On analysis of above table and keeping in mind the concept of “MATERIALITY” as per AS -1 & SA 320 issued by ICAI , the impact of above are further analysed according to different parameters as under:

Parameters Amount (Rs. in Crore) % of Impact

Net over statement of Loss/ Loss before tax for the FY 2015-16 380.23/471.58 80.63

Net over-statement of Loss / Gross Turnover 380.23/12413.67 3.06

Net over -statement of Loss / Total Assets 380.23/9826.37 3.87

Net over -statement of Loss / Share capital 380.23/1472.36 25.82%

Net over-statement of Loss / Accumulated Losses 380.23/10234.82 3.72%

Sr. No.

Reference P & L Note No.

Head of Account OverstatedLoss

UnderstatedLoss

1. Annexure I, Part – A I -Sr. No. (b)(i)

Note – 22,Code –62.2401- 2481

Delayed Payment Charges from Consumers:

492.71 -

2

Annexure I, Part –

A I-

Sr. No. (b) (ii)

Note – 25,Code – 78.601

Finance Cost:Short

Non booking of income on accrual basis u/s 128 (1) of Companies Act, 2013

making of Interest Provision

on consumer security deposit.

- 75.70

3

Annexure I, Part – A II

Note-25,

Code- 78.553 Finance Cost:

Interest on Loan from UHBVNL has been understated

- 36.85

4

Annexure I, Part –

A

III

Note –

22,

Code –

62.8,

62.9, 62.3

Misc. Receipt:

Short booking of Misc . Receipt

0.07 -

Total 492.78 112.55Net Result is Over- Statement of Losses (Rs. In Crore)

380.23

Balance Sheet (Items) (Rs. In Crore)

Sr. No.

Reference B/s Note No. Head of Account Overstated Understated

1. Annexure I, Part – A, Sr. No. (b) (i)

Note – 17 Code – 23.1701 -81 & 23.5301 -81

Trade Receivables : Understatement of Trade Receivable Balance for Surcharge.

- 492.71

2.

Annexure I, Part –

A I,

Sr. No. (b) (ii)

Note –

10 Code –

46.238

Other Current Liabilities

Understatement of Interest Payable on Consumer Security

-

75.70

3

Annexure I,

Part –

A II,

Note –

3 Code –

55.308

Reserves & Surplus

Understatement of Grant form Govt of

Haryana Under UDAY.

-

115.96

4.

Annexure I,

Part –

A II

Note –

5 Code –

53.553 & 53.554

Long Term Borrowings

Overstatement of Loan from UHBVN

115.96

-

5

Annexure I,

Part – A II

Note –

5

Code – 53.553 &

53.554

Long Term Borrowings

Understatement of loan from UHBVN

-

36.85

Accordingly, the loss for the year is overstated by Rs. 380.23 Crore and Accumulated Loss as at March 31, 2016 by Rs. 380.23 crore. The effects/possible effects of the others qualifications described in Annexure I to the Report on financial statements are not ascertainable.

5. Adverse OpinionIn Our opinion, because of the significance of the matters discussed in Annexure I referred in our Basis for Adverse Opinion paragraph, the financial statements do not give a true and fair view in conformity with the accounting principles generally accepted in India of the state of affairs of the Company as at 31st March ,2016 and its profit/loss and its cash flows for the year ended on that date :

32

(a) In the case of the Balance Sheet, of the state of affairs of the company as at March 31, 2016.

(b) In the case of the Statement of the Profit and Loss, of the loss for the year ended on that date; and

(c) In the case of the Cash Flow Statement, of the cash flows for the year ended on that date.

6. Report on Other Legal and Regulatory Requirements

1. As required by the Companies (Auditor's Report) Order, 2016 ("the Order") issued by the Central Government of India in terms of sub-section (11) of section 143 of the Act, we give in the Annexure 'II' a statement on the matters specified in the paragraph 3 and 4 of the Order, to the extent applicable.

2. As the company is governed by the electricity Act, 2003, the Provisions of the said Act have prevailed wherever they have been inconsistent with the provisions of the Companies Act, 2013.

3. As required by Section 143 (3) of the Act, we report that:

a. We have sought and obtained, except for the possible effects of the matters described in the basis for Adverse Opinion paragraph above, obtained all the information and explanations which to the best of our knowledge and belief were necessary for the purpose of our audit;

b. Except for the possible effects of the matters described in the basis for adverse opinion paragraph above, in our opinion proper books of account as required by law have been kept by the Company so far as it appears from our examination of those books [and proper returns adequate for the purposes of our audit have been received from the branches not visited by us]

c. The Balance sheet, Statement of profit and loss and Cash flow statement dealt with by this report are in agreement with the books of account [ and with the returns received from the branches not visited by us];

d. Except for the effects of matter described in the basis for adverse opinion paragraph above, in our opinion, the aforesaid standalone financial statements comply with the Accounting standards specified under section 133 of the Act, read with Rule 7 of the Companies (Accounts) Rules , 2013 ;

e. The matter described in the basis for Adverse Opinion paragraph above, in our opinion, may have an adverse effect on the functioning of the Company.

f. As per notification No. GSR 463 (E) dated 5th June, 2015 issued by the Ministry of Corporate Affairs, Government of India, Section 164(2) of the Companies Act, 2013 is not applicable to the company.

g. With respect to the adequacy of the internal controls over the financial controls over financial reporting of the company and the operating effectiveness of such controls, refer to our separate Report in Annexure 'III'.

h. The adverse remarks relating to the maintenance of accounts and other matters connected therewith are as stated in the basis for Adverse Opinion paragraph above.

With respect to the other matters to be included in the Auditor's Report in accordance with Rule 11 of the Companies (Audit and Auditors) Rules, 2014, in our opinion and to the best of our information and according to the explanations given to us:

(i) The Company has disclosed the impact of pending litigations on its financial position in its financial statements- Refer Note 1 para 1.21 and para (vii) (b) of annexure-I to the financial statements;

(ii) Except for the possible effects of the matters described in the basis for adverse opinion paragraph above, the company has made provision, as required under the applicable law or accounting standards, for material foreseeable losses, if any, on long term Contracts including derivative contracts.

(iii) As informed to us Rs. 461.00 lying in share application money pending allotment since long time is required to be transferred to the Investor Education and Protection Fund by the Company. However, no such transfer took place so far.

4. As required by section 143 (5) of the Act, we give in Annexure 'IV', a statement on the matters specified by the Comptroller and Auditor General of India for the Company.

For O. Aggarwal & Co.Chartered AccountantsFRN: 005755N

Sd/-CA. ASHOK KUMARPartnerM.No.: 093725

Place : DelhiDate : 22.11.2016

33

(i) Books of Accounts & Accounting Software:

(a) The Nigam has 126 no. of Sub-divisions, 52 no. of divisions and 9 no. of circles with Head Office at Hisar. The system of accounting followed by the Nigam is quite peculiar. To sum up, vouchers for all receipts / income, payments / expenditure are prepared in duplicate on day today at all divisions / sub - divisions indicating suitable a/c code only for debit & credit entries. Subsequently, punching / feeding of these vouchers is also done on daily basis by all sub divisions / divisions on excel sheet thereby respective debit or credit amount of relevant a/c code goes on updated indicating its progressive figure on daily basis. Thus, at the end of the month, a trial balance gets automatically prepared at each sub-division / division a/c code wise. All sub-divisions forward this trial balance to its controlling division along with original set of vouchers for the month as well as supporting documents to vouchers wherever available. The respective division punches / updates the debits / credits a/c code with figures of sub-divisions with their own debits / credits a/c code wise. Thus, a trial balance of a division incorporating the figures or its subordinate sub-division for a particular month is got ready on excel sheet. The respective division forwards this trial balance to Head Office along with original set of vouchers of sub-division and its own for the relevant month. This practice is followed by all sub-divisions & divisions each month for the year.

Thus, Head Office gets 12 no. of Trial balances for a year from each division. The Head Office also prepares its own trial balance a/c code wise each month in the manner explained above. At the end of the year, Head Office merges all trial balances received from Divisions with its own trial balance in Fox Pro and gets one consolidated Trial Balance a/c code wise for the whole organization based on which Profit & Loss a/c & Balance Sheet is prepared at the year end.

From the foregoing it will be evident that this system of accounts is devoid of the following :-

1. Vouchers prepared at different locations do not show as to which Head of A/c is being debited or credited.

2. No date wise posting of debit / credit entry is made under any Head of A/c.