Embed Size (px)

Citation preview

1

ANNUAL REPORT AS OF

31 DECEMBER 2015 OF THE TERNIENERGIA GROUP

2

TerniEnergia S.p.A.

Registered office in Strada dello Stabilimento 1, 05035 Narni (TR)

Authorised, issued and paid-up share capital: Euro 57,007,230

Terni Register of Companies no. 01339010553

Branches and Offices

Narni – Strada dello Stabilimento, 1

Milan – Corso Magenta, 85

Lecce – Via Costadura, 3

Athens – 52, Akadimias Street

Cape Town - Boulevard Office Park, 2nd floor, Block D, Searle. District of Woodstock

Warsaw - Sw. Krolewska 16, 00-103

Bucharest - Str. Popa Petre 5

Board of Directors

Chairman and CEO

Stefano Neri

Directors

Fabrizio Venturi

Sergio Agosta

Giovanni Fabrizi (*)

Francesca Ricci

Monica Federici

Paolo Ottone Migliavacca

Mario Marco Molteni

Domenico De Marinis

(*) Co-opted by the Board on 29 October 2015 as a replacement for Umberto Paparelli whose term of office ended 7 August 2015

Board of Statutory Auditors

Ernesto Santaniello (Chairman)

Vittorio Pellegrini

Simonetta Magni

Independent auditors

PriceWaterhouseCoopers S.p.A.

3

TERNIENERGIA GROUP – 2015 CONSOLIDATED FINANCIAL STATEMENTS

Contents

1 REPORT ON OPERATIONS................................................................................................................................................. 6

1.1 MACROECONOMIC SCENARIO .............................................................................................................................. 6

1.2 TRENDS IN THE MARKET OF REFERENCE ............................................................................................................ 7

1.3 THE GROUP’S BUSINESS AND MISSION ............................................................................................................10

1.4 THE GROUP’S STRUCTURE ...................................................................................................................................12

1.5 MAIN EVENTS DURING THE FINANCIAL YEAR ENDED 31 DECEMBER 2015 ..............................................13

1.5.1 New 2015-2017 Industrial Plan, “Fast on the smart energy road”. ...................................13

1.5.2 Merger by incorporation of the fully owned company Lucos Alternative Energies S.p.A.

into TerniEnergia S.p.A................................................................................................................13

1.5.3 Authorisation of the plant for treatment of liquid waste in Nera Montoro (TR) ...........13

1.5.4 Contracts for the construction of two photovoltaic plants in the Republic of South

Africa for an overall installed power capacity of 148.5 MWp ............................................14

1.5.5 Increased voting rights ................................................................................................................14

1.5.6 Valorisation of photovoltaic assets; 50% of SPV DT Srl sold. ..............................................15

1.5.7 Acquisition of New Gas Trade Srl and the launch of TerniEnergia Gas&Power SpA .....15

1.5.8 Shareholders’ Meeting approves the 2014 financial statements as well as the

distribution of a dividend equal to Euro 0.065 per share ....................................................16

1.5.9 New PFU plant at Borgo Val di Taro .........................................................................................16

1.5.10 Divestment of Free Energia ........................................................................................................17

1.5.11 Valorisation of photovoltaic assets; 50% of JV SAIM Energy 2 Srl sold ............................19

1.5.12 Update of the 2015-2017 Industrial Plan, “Fast on the smart energy road” ...................20

1.5.13 Acquisition of 100% of share capital of Greenled Industry by TerniEnergia ...................21

1.5.14 Multi-year agreement with Avanti Communications to distribute connectivity between

the renewable energy plants in South Africa and Italy ........................................................22

1.5.15 Valorisation of photovoltaic assets continues: 50% of four SPVs sold to Renewable

European Investment Italy 3 ......................................................................................................22

1.6 PERFORMANCE OF OPERATIONS .......................................................................................................................24

1.7 INVESTMENTS ........................................................................................................................................................32

1.8 HUMAN RESOURCES .............................................................................................................................................32

4

1.9 ENVIRONMENTAL POLICY ....................................................................................................................................33

1.10 R&D...........................................................................................................................................................................33

1.11 RISK FACTORS RELATED TO THE REFERENCE SECTOR ....................................................................................34

1.12 RELATIONS WITH RELATED PARTIES .................................................................................................................35

1.13 INFORMATION REQUIRED BY ART. 123 BIS OF THE TUF (CONSOLIDATED F INANCIAL ACT) .................36

1.14 OTHER INFORMATION ..........................................................................................................................................38

1.15 SIGNIFICANT EVENTS AFTER YEAR-END............................................................................................................40

1.16 CORPORATE GOVERNANCE REPORT .................................................................................................................40

1.17 BUSINESS OUTLOOK ..............................................................................................................................................40

2 FINANCIAL STATEMENTS ......................................................................................................................................42

2.1 CONSOLIDATED STATEMENT OF FINANCIAL POSITION ....................................................................42

2.2 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME ..........................................................44

2.3 STATEMENT OF CHANGES IN CONSOLIDATED SHAREHOLDERS’ EQUITY .....................................45

2.4 CONSOLIDATED CASH FLOW STATEMENT ...........................................................................................46

3 EXPLANATORY NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR CLOSED ON 31

DECEMBER 2015 .................................................................................................................................................................47

3.1 GENERAL INFORMATION .........................................................................................................................47

3.2 SEGMENT REPORTING .............................................................................................................................48

3.3 FORM, CONTENT AND APPLIED ACCOUNTING PRINCIPLES .............................................................50

3.4 COMMENTS ON THE MAIN STATEMENT OF FINANCIAL POSITION ITEMS: ..................................72

3.4.1 INTANGIBLE FIXED ASSETS .........................................................................................................72

3.4.2 TANGIBLE FIXED ASSETS ..............................................................................................................74

3.4.3 EQUITY INVESTMENTS .................................................................................................................77

3.4.4 PREPAID TAXES ...............................................................................................................................80

3.4.5 NON-CURRENT FINANCIAL RECEIVABLES .................................................................................83

3.4.6 INVENTORIES .................................................................................................................................84

3.4.7 TRADE RECEIVABLES ....................................................................................................................85

3.4.8 OTHER CURRENT ASSETS ............................................................................................................86

3.4.9 DERIVATIVES ..................................................................................................................................87

3.4.10 FINANCIAL RECEIVABLES.............................................................................................................87

3.4.11 CASH AND CASH EQUIVA LENTS.................................................................................................88

5

3.4.12 ASSETS HELD FOR SALE................................................................................................................88

3.5 COMMENTS ON THE MAIN LIABILITY AND EQUITY ITEMS ..............................................................89

3.5.1 SHAREHOLDERS’ EQUITY ............................................................................................................89

3.5.2 PROVISIONS FOR EMPLOYEE BENEFITS ...................................................................................91

3.5.3 PROVISIONS FOR DEFERRED TAXES..........................................................................................93

3.5.4 NON-CURRENT FINANCIAL PAYABLES......................................................................................94

3.5.5 OTHER NON-CURRENT LIABILITIES ...........................................................................................95

3.5.6 DERIVATIVES ..................................................................................................................................95

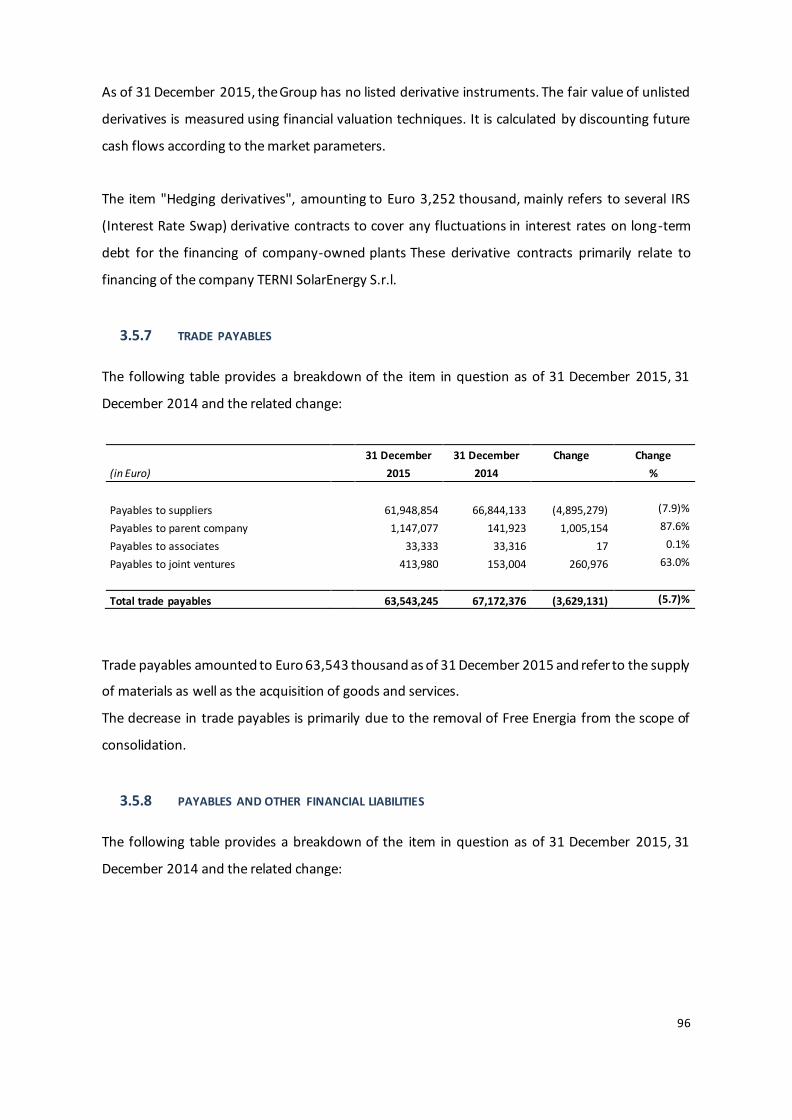

3.5.7 TRADE PAYABLES ..........................................................................................................................96

3.5.8 PAYABLES AND OTHER FINANCIAL LIABILITIES ......................................................................96

3.5.9 INCOME TAX PAYABLES ..............................................................................................................99

3.5.10 OTHER CURRENT LIABILITIES......................................................................................................99

3.5.11 COMMITMENTS AND ISSUED GUARANTEES AS WELL AS POTENTIAL LIABILITIES ..... 100

3.6 COMMENTS ON THE MAIN INCOME STATEMENT ITEMS ............................................................. 106

3.6.1 REVENUES ................................................................................................................................... 106

3.6.2 CHANGE IN INVENTORIES OF SEMI-FINISHED AND FINISHED PRODUCTS .................... 106

3.6.3 COST OF RAW MATERIALS, CONSUMABLES AND GOODS ................................................ 107

3.6.4 COSTS FOR SERVICES ................................................................................................................ 108

3.6.5 PERSONNEL COSTS .................................................................................................................... 108

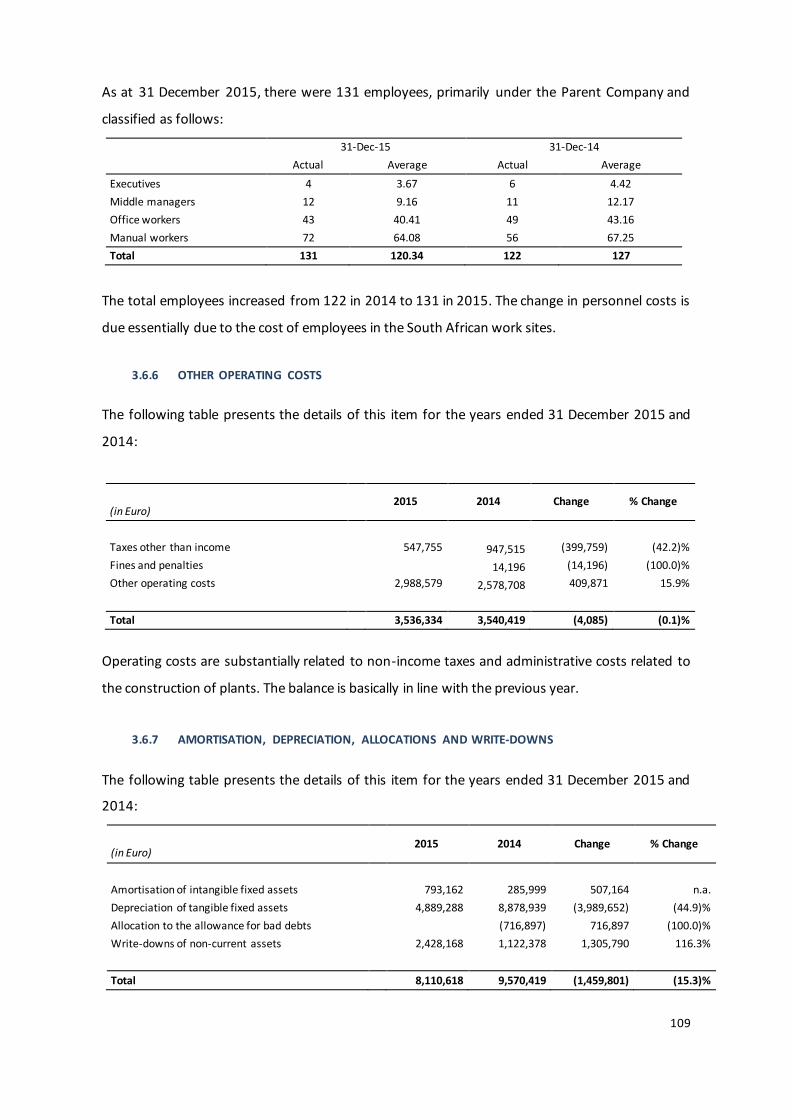

3.6.6 OTHER OPERATING COSTS....................................................................................................... 109

3.6.7 AMORTISATION, DEPRECIATION, ALLOCATIONS AND WRITE-DOWNS ......................... 109

3.6.8 FINANCIAL INCOME AND CHARGES ....................................................................................... 110

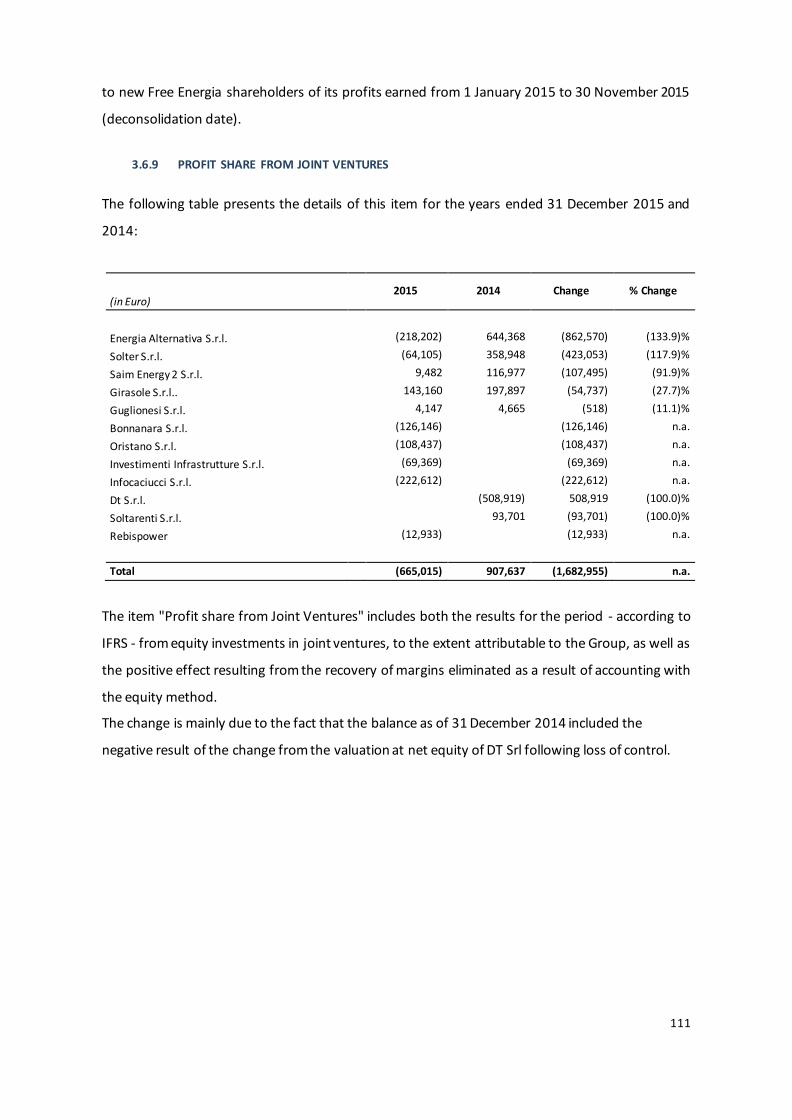

3.6.9 PROFIT SHARE FROM JOINT VENTURES ................................................................................ 111

3.6.10 TAXES ........................................................................................................................................... 112

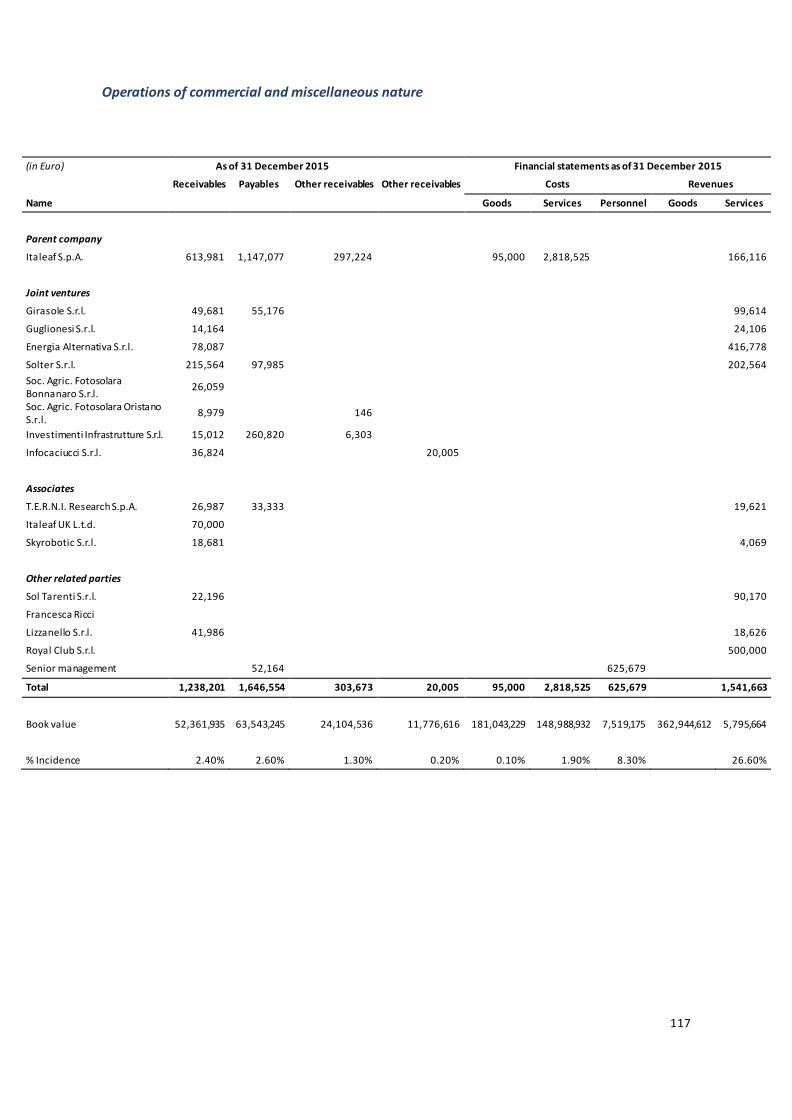

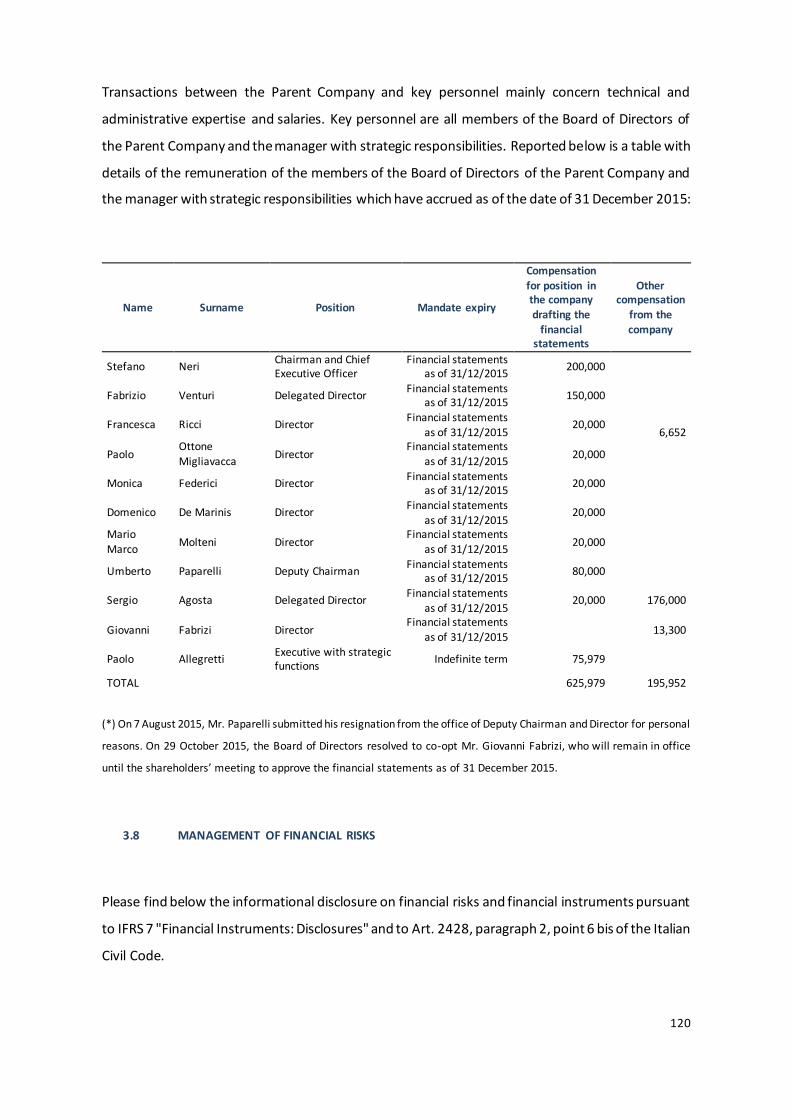

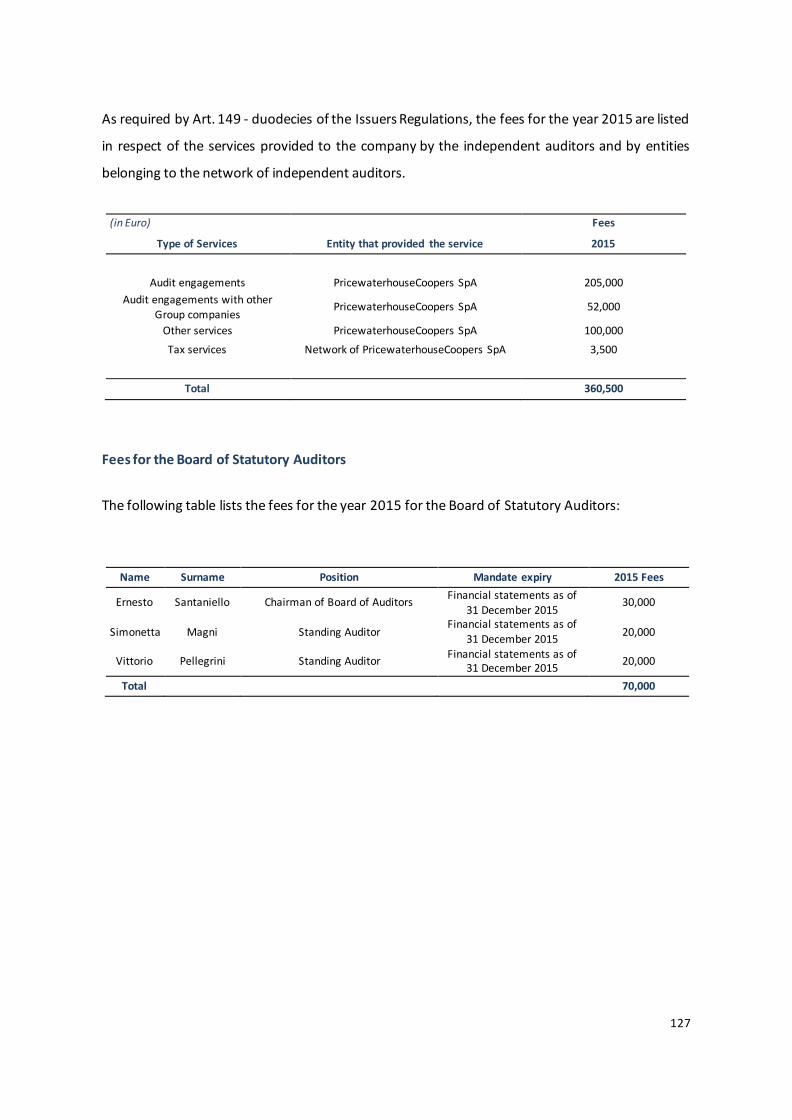

3.7 RELATIONS WITH RELATED PARTIES .................................................................................................. 112

3.8 MANAGEMENT OF FINANCIAL RISKS ................................................................................................. 120

3.9 ATYPICAL AND/OR UNUSUAL TRANSACTIONS ................................................................................ 125

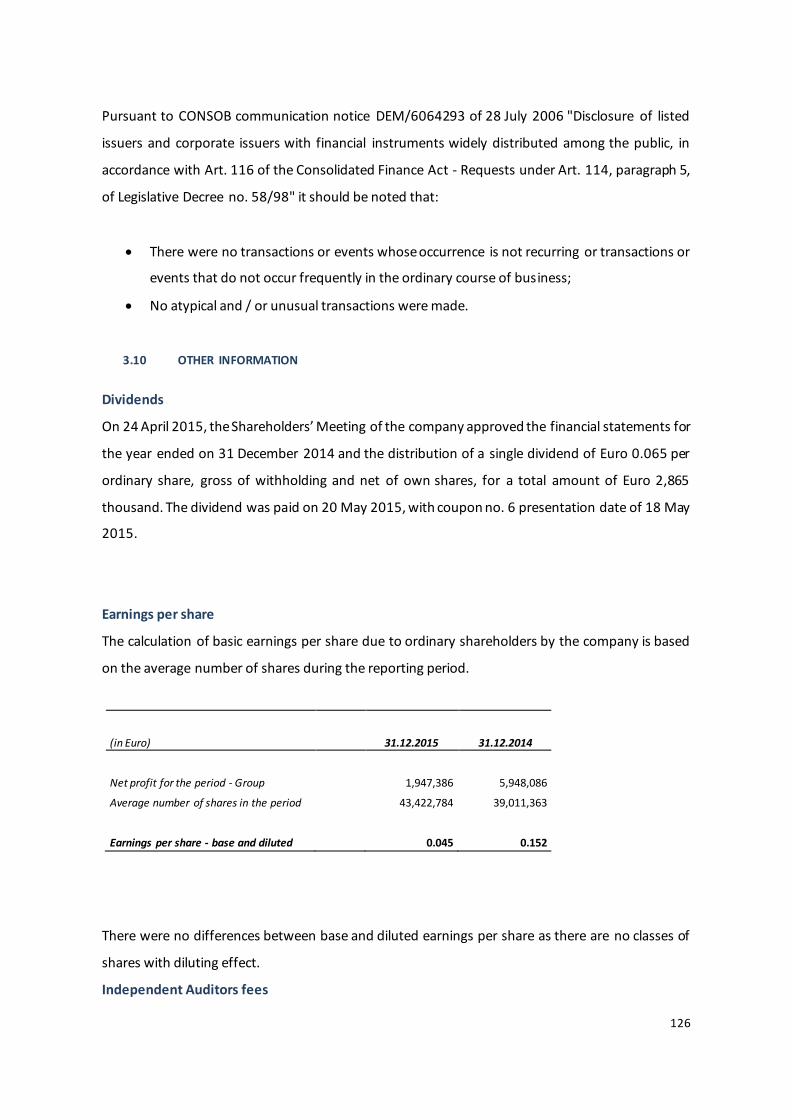

3.10 OTHER INFORMATION .......................................................................................................................... 126

4. CERTIFICATION OF THE CONSOLIDATED FINANCIAL STATEMENTS PURSUANT TO ART. 154-BIS OF

LEGISLATIVE DECREE 58/98 AND ART. 81-TER OF CONSOB REGULATION NO. 11971/99, AND ITS

SUBSEQUENT AMENDMENTS AND SUPPLEMENTS ..................................................................................... 131

6

1 REPORT ON OPERATIONS

1.1 MACROECONOMIC SCENARIO

In 2015, economic growth continued in the principal developed countries, but the slowdown in the

Chinese economy had a negative impact on raw material prices and on the growth rates of emerging

countries. China’s adjustment period from high levels of investment and indebtedness constitutes

an element of weakness for the country and a risk for the global economy.

In the Eurozone, growth is continuing, but remains fragile. The programme to purchase Eurosystem

government bonds has proven to be effective in supporting economic activity as a whole, with the

effects to date in line with the initial forecasts. However, the weakness in external demand and the

drop in petroleum prices gave rise to new risks for lower inflation and growth, which became more

evident in recent months. The ECB’s Governing Council introduced additional expansionary

measures and extended the bond purchase programme in December. The Council is determined to

use all available tools, including the possibility of changing the size, composition and duration of the

purchasing programme for public and private securities, if it becomes necessary in order to combat

downward risks and to ensure inflation returns to values that are consistent with price stability.

In Italy, economic activity began to grow again at the beginning of 2015, with a balance of +0.6% for

the full year. The recovery is continuing gradually in Italy. Spurred by exports, which had sustained

economic activity over the last four years are now reflecting weakness in the markets outside the

EU, and are gradually being replaced by internal demand, in particular in consumer goods and

rebuilding inventories. In addition to the recovery in the manufacturing cycle, there are also signs

of growth in services and, after a prolonged recession, a stabilisation in construction. However,

forecasts for investments reflect uncertainty regarding external demand. During the summer

months, employment figures continued to growth, particularly for young people and in services.

Hiring proceeded with a re-composition that favoured stable contracts. The forecasts of businesses

regarding the employment scenario are cautiously optimistic.

The trend in consumer prices, which reflected the recent drop in petroleum prices, remains very low

(0.2% annual rate in September). However, the slow recovery of core inflation continues, which has

been, until now, supported by the acceleration in prices for services. Households and businesses

expect very limited inflation in the upcoming months, but gradually returning. The portion of

consumers who expect prices to fall has decreased.

Inflation fell in December to 0.1% annually. Forecasts by households and businesses point to a

modest recovery in prices in upcoming months, but they will remain at contained levels. Inflation

7

forecasts reflect the recent decline in energy prices, but also the persistent under-utilisation of

production capacity, which contributes to keeping core prices at minimum values.

Lending to the private sector strengthened in autumn, as loans to businesses grew for the first time

in nearly four years. Supply conditions continued to ease. The cost of new loans to businesses were

at very contained levels from an historic perspective and the differential on the corresponding

average interest rate in the Eurozone was eliminated (it was one percentage point at the end of

2012). However, the dispersion of credit conditions between economic activity sectors and business

size remained high, although lower than the peaks reached during the recession.

Overall, gross domestic product could grow at around 1.5% in 2016 and 2017. Inflation will gradually

increase to 0.3% this year and 1.2% next year. Investments, which have until now been characterised

by modest growth, could benefit from forecasts of more favourable demand and lending conditions

and from the effects of stimulus measures introduced by the Stability Law. Consumer goods may

growth as a result of the recovery in available income, also supported by strength in the labour

market.

Significant risks remain, including, most importantly, those associated with the global context, which

became more evident in recent weeks. In particular, the possibility of a slowdown in emerging

economies, which could become more pronounced and persistent than had been expected until

now, would have serious repercussions on financial and currency markets. At the same time,

monetary policy must decisively combat the risk of downward inflation, which could result from

either growth in demand that is lower than expected, if the unutilised production capacity remains

at current high levels for a long period of time, as well as from additional drops in raw material

prices, if they generate feedback effects on wage dynamics. The scenario described above assumes

that the confidence of households, businesses and financial operators continues in Italy and the

Eurozone, and that decisive cyclical support measures continue.

1.2 TRENDS IN THE MARKET OF REFERENCE

At a global level in 2015, 59 GW of new photovoltaic power was installed, a growth in demand of

34% over 2014. The last quarter of 2015 demonstrated how photovoltaic demand still depends on

the support of public policies, which can be unpredictable, with both positive and negative

consequences.

The reference is to the unexpected extension of the investment tax credit in the United States, which

caused a notable increase in forecasts for that market. With the extension of the ITC, demand in the

U.S. as a percentage of global demand from 2015 to 2020 will grow from an average of 10% to 15%,

8

despite the forecasts for marked growth in the Asia-Pacific region as well. Forecasts for Japan, the

United Kingdom and China remain, however, low.

Emerging markets are increasingly more significant. Beginning this year, India will become a market

in which several GW will be installed annually. Mexico and Brazil should prove to be up to the task

of their commitments. Others, such as the Philippines, Pakistan and Bangladesh in Asia, as well as

Uruguay, Guatemala and Panama in Latin American, will break the 100 MW threshold.

According to analysts, the result of the COP 21 will be important for diversification in PV markets,

driving demand in Latin America, Asia and Africa. In fact, many countries have promised significant

cuts in emissions and photovoltaic power is seen as a quick, effective and scalable solution to obtain

these results.

The collapse in oil prices and declines in other commodity fossil fuels did not stop progress in

renewable sources. In 2015, investments in clean energy reached a new record, with half of the new

global electrical power from wind and photovoltaic sources. In the year just completed, USD 328.9

billion was invested in renewables, a growth of 4% over USD 315.9 billion in 2014, which surpasses

the previous record set in 2011 with USD 318 billion.

In 2015, investments in renewable sources were 6 times greater than 2004, and growth continued

despite the 4 factors that acted as a hindrance: the collapse of prices for fossil fuels, reduction in

the cost of photovoltaic power, which reduces investments at an equivalent rate with the installed

power, the recovery in the dollar, and the slowdown of the European economy. This is a clear

response to those who expected investments in the sector to suffer a setback as combustible fossil

fuels became cheaper. In fact, in the 18 months prior to the end of 2015, the price per barrel of

petroleum on the Brent index declined 67%, the price of coal on the north-western European hub

declined 35%, and the price of natural gas on the Henry Hub in the U.S. dropped 48%.

On the other hand, renewables have several strengths: they are increasingly more competitive, they

are now chosen in many developing countries because they can become operational extremely

rapidly, and they reduce the exposure of these countries to price volatility in fossil fuels. It is not

very likely that this trend will reverse, given the climate agreement reached in December in Paris.

The bulk of investments in renewables, USD 199 billion (+4% compared to 2014), was directed at

utility-scale projects such as wind and photovoltaic parks, biomass or waste-to-energy plants, and

small hydropower plants. Note that expenditures on smart grids and utility-scale accumulations

increased by 11% over 2014, reaching USD 20 billion at a global level. Investments in smaller

projects, especially roof photovoltaic systems, grew 12%, to USD 67.4 billion, with Japan in the lead,

followed closely by the United States and China. The largest investment in biomass was for the 330

MW plant in Klabin Ortiguera in Brazil, with USD 921 million, while the largest geo-thermal plant

was the Guris Efeler project in Turkey (170 MW for USD 717 million).

9

Analysing the various markets, China was in the lead in terms of investments, with USD 110 billion

(+17% over 2014), followed by the United States with USD 56 billion (+8%). In contrast, Europe

posted a decline of 18% compared to the previous year, with expenditures of USD 58.5 billion, the

lowest level since 2006. The sole exception to the general decline (Germany -42%, France -53%) was

the British market, where investments rose 24% to USD 23.4 billion. Brazil also saw its investments

decrease by 10%, while expenditures for renewables grew 23% in India. New markets like Mexico

(+116%), Chile, South Africa, and Morocco are becoming increasingly important, which in total

invested tens of billions of dollars.

Africa and the Middle East are the two regions with the largest potential for growth in clean energy.

Together they amounted USD 13.4 billion in 2015, +54% over 2014, due to a combination of strong

demographic growth (and related electricity demand) as well as the abundance of sun and wind.

10

1.3 THE GROUP’S BUSINESS AND MISSION

TerniEnergia aims to establish itself as the first independent Italian “smart energy company”

operating in the sectors of renewable energies, energy efficiency, and waste and energy

management through its individual business model.

The Industrial Plan from February 2015, “Fast on the smart energy road”, was updated and approved

by the TerniEnergia Board of Directors on 29 October 2015. In particular, the plan is based on the

following business assumptions:

- backlog of work orders in the photovoltaic sector, both acquired and those in the process of being

acquired abroad;

- development of significant commercial cross-selling opportunities in the sectors of energy

efficiency (strong growth) and in gas & power management;

- strong diversification of the TerniEnergia business within anti-cyclical sectors and completion of

core activities of the Group along the entire value chain of energy, ranging from the design of plants

to advanced post-sales services.

A new strategic element of the plan approved by the Board of Directors in February 2015 is the

search for potential corporate and business partnerships in the environmental sector, including the

possibility of spinning off the waste management sector in a “newco”, which may represent a

“national leader” industrial platform open to participation of new investors focused on the green &

circular economy sector.

The overall number of photovoltaic plants constructed by TerniEnergia since the start of

operations is equal to 273, with cumulative capacity of circa 284.1 MWp (including 13.2 MWp held

100% by the company and 30 MWp in joint venture, allocated to power generation activities). In

addition, biomass plants for a total of 1.5 Mwe and 2 MWt are connected to the grid.

The overall production of energy in full ownership and joint venture plants for power generation

activities was equal to circa 64 million kWh.

Within the environmental sector, plants for the treatment and recovery of unused tires in Nera

Montoro and Borgo Val di Taro, as well as for biodigestion and GreenAsm composting are

operational, as are the Nera Montoro groundwater purification plants. The Free Energia Group

11

managed 1.3 GWh of energy for heavy consumption customers. The industrial results of Free

Energia S.p.A. are included in the financial statements of the TerniEnergia Group through 30

November 2015, the effective date of the divestment, which will be discussed below.

TerniEnergia Gas&Power, established following the acquisition in 2015, managed 13.2 million of

standard cubic metres of gas, equivalent to 139,800 MWh.

The Group undertook industrial lighting energy efficiency initiatives for 10,200 lighting points, with

expected savings of more than 21.2 million KWh and 3,901 TEP.

Greenled Industry produced 2,000 LED light bulbs for energy eff iciency initiatives and 500 for

direct sales.

12

1.4 THE GROUP’S STRUCTURE

TERNIENERGIA S.P.A.

100%

NEWCOENERGY S.R.L.

REBIS POWER S.R.L.

CAPITAL SOLAR S.R.L.

INVESTIMENTI INFRASTRUTTURE S.R.L.

CAPITAL ENERGY S.R.L.

SOC AGR FOTOSOLARA BONNANARA S.R.L.

ENERGIA NUOVA S.R.L.

SOC AGR FOTOSOLARA ORISTANO S.R.L.

MEET SOLAR S.R.L.

INFOCACIUCCI S.R.L.

RINNOVA S.R.L. 50% ENERGIA ALTERNATIVA S.R.L.

ENERGIA BASILICATA S.R.L.

SOLTER S.R.L.

ENERGIA LUCANA S.R.L.

GIRASOLE S.R.L.

VERDE ENERGIA S.R.L.

GUGLIONESI S.R.L.

FESTINA S.R.L.

GREEN ASM S.R.L.

SOCIETÀ AGRICOLA PADRIA SRL

SOC AGR FOTOSOLARA CHEREMULE S.R.L.

SOC AGR FOTOSOLARA ITTIREDDU S.R.L.

80% TEVASA L.t.d.

TECI S.R.L. TERNIENERGIA PROJECT L.t.d.

MEET GREEN ITALIA S.R.L.

70%

IGREEN PATROL S.R.L.

LYTENERGY S.R.L.

TERNIENERGIA POLSKA Sp.z.o.o.

5%

TERNIENERGIA SOLAR SOUTH AFRICA L.t.d.

SOL TARENTI S.R.L.

TERNIENERGIA S.p.A. HELLAS M.E.P.E.

TERNIENERGIAROMANIA S.R.L.

T.E.R.N.I. SOLARENERGY S.R.L.

ALCHIMIA ENERGY 3 S.R.L.

TERNIENERGIA GAS&POWER S.P.A.

GREENLED INDUSTRY S.P.A.

13

1.5 MAIN EVENTS DURING THE FINANCIAL YEAR ENDED 31 DECEMBER 2015

1.5.1 New 2015-2017 Industrial Plan, “Fast on the smart energy road”.

On 9 February 2015, the Board of Directors of TerniEnergia approved the 2015-2017 Industrial Plan,

“Fast on the smart energy road,” and updated the Group’s 2014 forecast.

1.5.2 Merger by incorporation of the fully owned company Lucos Alternative Energies S.p.A. into

TerniEnergia S.p.A.

On 27 February 2015, the Board of Directors of TerniEnergia and the extraordinary shareholders’

meeting of Lucos Alternative Energies approved the operation for the merger by incorporation of

Lucos (fully owned by TerniEnergia) into TerniEnergia by approval of the relative merger project

drafted in accordance with Articles 2501-ter and 2505 of the Italian Civil Code and previously

rendered public in accordance with the law.

The merger is part of the industrial and strategic policy as well as the 2015-2017 Industrial Plan “Fast

on the smart energy road” presented on 9 February 2015, which aims to develop the energy

efficiency business. In particular, the merger will shorten the control chain which will allow for more

effective financial management of energy efficiency activities, improved industrial coordination of

energy saving activities, the attainment of productive and financial synergies as well as the

attainment of significant savings in fixed operational and managerial costs.

The transaction was concluded on 14 May 2015 with the signature of the merger deed. It was

registered with the Terni Commercial Registry Office on 21 May 2015, the date that the legal effects

of the transaction began.

1.5.3 Authorisation of the plant for treatment of liquid waste in Nera Montoro (TR)

On 3 March 2015, TerniEnergia communicated that, by means of Executive Resolution of the

Province of Terni no. 11458/2015, an “Integrated Environmental Authorisation (IEA)” was issued in

relation to the “Operational plan for restoration of the groundwater of the industrial site of Nera

Montoro (TR) – adjustment to provisions and implementation of current plants with the

introduction of new sections for liquid waste treatment with third parties”.

14

In particular, the attainment of authorisations will allow TerniEnergia to complete the investments

on the biological and chemical/physical plants that are already operational in order to comply with

the provisions for the restoration project of the groundwater of Nera Montoro, as approved by the

Umbria Region in April 2011 (emissions with qualities and characteristics of “deep waters”). Finally,

by means of the IEA, TerniEnergia may expand the treatment capacities of the existing plants by

creating a new purifier for the purposes of starting up the business for treatment of special liquid

wastes (e.g. agricultural, industrial, chemical/organic and inorganic, etc.). The authorisation will

allow for the treatment of 58,000 cubic meters/year of inflowing waste, represented by both liquid

water and pumpable muds. The capex of this additional investment is approximately Euro 3 million

and will allow for the realisation of new plants with elevated quality within the green industrial pole

of Nera Montoro (TR), intercepting flows of liquid waste that are currently send to plants outside

the Umbria region and at the same time meeting the industrial demand of central Italy.

1.5.4 Contracts for the construction of two photovoltaic plants in the Republic of South Africa for

an overall installed power capacity of 148.5 MWp

On 12 March 2015, TerniEnergia – as part of its process of internationalisation of the photovoltaic

EPC (engineering, procurement and construction) business – announced the start-up of construction

of industrial-size photovoltaic plants in South Africa with a total power of 148.5 MWp on behalf of

a primary Italian utility company.

In particular, work began following the definitive EPC and O&M (operation and maintenance)

contracts that provide for the construction by TerniEnergia Project PTY Ltd, a South African

subsidiary of TerniEnergia S.p.A., of two photovoltaic plants with the "EPC Contract" (turnkey)

formula and that include the supply of panels and inverters, respectively, in the locality Paleisheuwel

with a power of 82.5 MWp and in Tom Burke for 66 MWp of installed capacity, for a total

consideration of approximately Euro 120 million, calculated using the 31 December 2015 exchange

rate.

1.5.5 Increased voting rights

On 16 March 2015, the TerniEnergia Extraordinary Shareholders’ Meeting was held with the

attendance of shareholders representing 63.01% of the share capital, passing amendments to the

Articles of Association (Article 6) with a 99.95% favourable vote, which introduce the mechanism of

increased voting rights. The introduction of this mechanism aims to create incentives for medium

15

to long term investment and therefore the stability of the shareholding structure, in compliance

with the right pursuant to Article 127-quinquies of the Consolidated Financial Act – recently

introduced – as well as Article 20 of Law decree 91 of 24 June 2014 (known as the “Competitiveness

Decree”). In particular, the introduced regulations provide, in fact, for the assignment of two votes

to each ordinary share held by the same shareholder for a continuing period of not less than two

years, effective as of the date of registration within a specific list created and maintained by the

Company.

1.5.6 Valorisation of photovoltaic assets; 50% of SPV DT Srl sold.

On 24 March 2015, as part of its strategy aimed at enhancing the value its photovoltaic assets,

TerniEnergia S.p.A. signed an agreement for the sale to AEGA ENERGY PRIMA AS (a fund governed by

the laws of Norway) of 50% of the share capital of DT Srl, owner of an industrial-sized plant with

total installed capacity of approximately 1 MWp.

The price for 50% of the shares was agreed between the parties at approximately Euro 0.5 million

and AEGA ENERGY PRIMA AS paid in cash.

1.5.7 Acquisition of New Gas Trade Srl and the launch of TerniEnergia Gas&Power SpA

On 23 April 2015, TerniEnergia signed an agreement with La Mercantile Srl of La Spezia for

acquisition of 85% of the share capital of the company New Gas Trade Srl (NGT), an Italian concern

which operates in the upstream and liquefied natural gas sectors, in the integrated management of

energy commodities area. The price for the shares was agreed between the parties at approximately

Euro 150 thousand and TerniEnergia paid in cash.

Subsequently, on 9 July 2015, the Board of Directors of TerniEnergia resolved to acquire the

remaining 15% of the share capital of New Gas Trade Srl (NGT) held by Intermonte Holding SIM, a

MiFID-governed company. The sale price was agreed at Euro 49 thousand, payable in cash.

Through the acquisition of NGT, TerniEnergia is pursuing the objective of competing its energy

management offer through access to the dual fuel market for industrial customers, ensuring real

savings on the "cost component, including due to the Group's energy efficiency activity, thereby

continuing its focus on the objective of promoting growth externally as per the "Fast on the energy

smart road” Industrial Plan.

Finally, on 7 October 2015, the Extraordinary Shareholders’ Meeting of New Gas Trade approved

the transformation of the company from S.r.l. into S.p.A., and the change in company name to

16

TerniEnergia Gas&Power S.p.A., with the resulting amendments to Art. 1 of the Articles of

Association.

The change in the company name is part of the Group’s broader reorganisation plan, aimed at:

- participating in all phases of the energy and gas value chain in Italy, integrating

purchasing, trading and marketing of natural gas and LNG with the activities of generating and

managing electricity;

- optimising growth opportunities in the gas sector which, in Italy as well as globally, posted

positive results in 2015 both in terms of volumes as well as margins, with more compelling growth

forecasts, including in relation to the electricity sector;

- better distinguishing the role of the Company in relationships with institutions, the market, the

financial and business community as well as customers.

Furthermore, the Extraordinary Shareholders’ Meeting resolved a divisible increase in share capital

for cash, from Euro 100 thousand up to a maximum of Euro 1 million. The share capital increase

has already been subscribed for Euro 0.5 million. In order to achieve better industrial coordination

of the business, the company will be merged by incorporation into TerniEnergia in the first half of

2016.

1.5.8 Shareholders’ Meeting approves the 2014 financial statements as well as the distribution of

a dividend equal to Euro 0.065 per share

On 24 April 2015, the Shareholders' Meeting of TerniEnergia examined and unanimously approved

the draft financial statements and the distribution of a dividend of Euro 0.065 per ordinary share,

gross of tax. The dividend was paid on 20 May 2015, with voucher no. 6 paid on 18 May 2015.

1.5.9 New PFU plant at Borgo Val di Taro

On 21 July, the Company inaugurated its second installation for the treatment and recovery of out-

of-use tyres (PFU), located in the Municipality of Borgo Val di Taro (Parma).

The technologically innovative system, installed by TerniEnergia, required an overall investment of

Euro 5.5 million. The plant became operational at the end of 2015 and has a processing capacity of

26,400 tonnes/annum in a restored and converted industrial area of 10,000 square metres, of which

2,000 are covered.

17

Through construction of this plant, TerniEnergia strengthens its national leadership position in the

industrial PFU recovery market, pursuing the objective of sustainability by reducing/cancelling

entirely the dispersion of this waste, implementing the market opportunities provided by the

legislative framework, which provides for full traceability of the tyre at the end of its useful life.

With two plants at Nera Montoro (TR) and Borgo Val di Taro (PR), TerniEnergia is set to reach a

processing capacity of approximately 20% of the domestic requirement.

1.5.10 Divestment of Free Energia

On 2 October 2015, the TerniEnergia Board of Directors resolved to approve a divestment

transaction through the signing of a divestment agreement. The subject of the agreement is the

transfer, for a maximum of all of the shares that TerniEnergia owns in Free Energia S.p.A., equivalent

to 3,674,604 shares, and equivalent to 97.60% of the share capital of the latter, in execution of an

agreement between the Company and the principal former shareholders of Free Energia. The

compensation for the transaction was the repurchase of all of the TerniEnergia shares owned by the

former shareholders of Free Energia, up to a maximum of 6,477,550. Hence, on 7 August 2015, the

TerniEnergia Board of Directors resolved to accept the proposals of the principal former

shareholders of Free Energia, received on 31 July 2015, to suppress the effects of the investment

agreement signed on 1 August 2014, according to which, as part of a share capital increase reserved

to said shareholders, they subscribed 6,477,550 TerniEnergia shares through the transfer of

3,674,604 Free Energia shares, equivalent to 97.60% of its share capital. As a result of this

transaction, Free Energia became part of TerniEnergia Group. In executing said investment

agreement, on 21 October 2014, TerniEnergia informed the market that an authorisation request

was pending with CONSOB for the publication of the prospectus for admission to trading of

TerniEnergia shares resulting from the share capital increase in service of the Free Energia

acquisition. Subsequently, on 31 July 2015, as indicated above, TerniEnergia received from the

principal former shareholders of Free Energia a proposal to suppress the effects of the signed

investment agreement. On 7 August 2015, the Board of Directors resolved to accept this proposal,

also ratifying the withdrawal of the prospectus under review by CONSOB and prepared by the

Chairman of the Board of Directors on 6 August 2015.

Also on 7 August, the Board of Directors accepted the resignation of Umberto Paparelli, one of the

principal former shareholders of Free Energia, from the role of Deputy Chairman and member of

the Board of Directors of TerniEnergia.

The key reasons that the Board of Directors of TerniEnergia S.p.A. decided to accept the proposal of

the principal former shareholders of Free Energia involved certain tax disputes of Free Energia for

18

the years 2009-2013, as well as assessments inherent in the forecasts for energy trading activities

and possible developments in the gas market.

The effectiveness of the divestment agreement as it relates to the transfer of Free Energia shares in

exchange for TerniEnergia shares was subject to the twofold condition of approval by the

Bondholders’ Meeting and the Shareholders’ Meeting.

The compensation for the transfer of the entire investment in Free Energia (with the exception of a

minor amount of shares in the event not all of the former shareholders of Free Energia opted to

participate in the divestment agreement) consisted of TerniEnergia shares subscribed by the

principal former shareholders of Free Energia from the dedicated share capital increase of 21

October 2014. The value of the compensation was confirmed by an opinion issued on 30 September

2015 by an independent expert designated by the parties, who confirmed that the value of the

entire investment in Free Energia was between Euro 15 million and Euro 20 million, indicating that

said value could be considered equivalent to the value assigned to the unlisted TerniEnergia shares,

thereby not necessitating any cash adjustment.

Thus, the Board of Directors decided to proceed with the transfer as per the divestment agreement

at a value that represented the median of the aforementioned range of the appraisal and, therefore,

for a value deemed fair of Euro 17.5 million.

In addition to the reciprocal granting of declarations and guarantees that are typical of this type of

transaction, the divestment agreement also envisaged governance during the interim period

between the subscription date and the closing date, with joint management of certain operating

aspects of Free Energia for specific issues, including treasury and the release of guarantees provided

by TerniEnergia, as co-guarantor, to Free Energia as part of supply relationships.

As a result of analyses performed by TerniEnergia, the transaction was not considered a “transaction

between related parties”.

As regards the effects on the “Fast on the smart energy road” Industrial Plan presented to the

market on 9 February 2015, the Board decided, on 7 August 2015, among other things, to confirm

the strategic and financial objectives envisaged for 2015 and to affirm the business model and

organisational structure based on four business lines (Technical Services, Cleantech, Energy

Management and Energy Saving) that would cover the entire energy value chain.

On 30 November 2015, TerniEnergia S.p.A. concluded the divestment transaction for the transfer of

Free Energia S.p.A. shares, receiving as payment the shares in TerniEnergia owned by shareholders

of Free Energia.

In particular, as communicated to the market on the same date, on 2 October 2015, the Board of

Directors of TerniEnergia resolved to sign the divestment contract for the transfer of the Free

19

Energia shares to the principal formers shareholders of Free Energia, in exchange for unlisted

TerniEnergia shares.

The divestment contract included two precedent conditions: approval expressed (i) by the meeting

of the holders of the “TerniEnergia Euro 25,000,000.00 Notes due 2019” bond, held on 16 November

2015 and (ii) by the Shareholders’ Meeting held on 18 November 2015. Subsequent to the fulfilment

of these conditions, with the reversal of the Free Energia shares and the transfer of the TerniEnergia

shares to the qualified broker, this divestment agreement was completed on 30 November 2015.

Consequently, TerniEnergia sold 3,315,936 shares in Free Energia (equivalent to 88.07% of the entire

share capital of Free Energia) to BA & Partners S.p.A., Sistematica S.p.A., Energetica S.p.A. and Feed

S.p.A., obtaining in exchange 5,845,290 own shares (equivalent to 13.26% of the share capital of

TerniEnergia). Moreover, following the closing of the year, 358,668 shares were sold. Profit

distribution rights for 2015 were retained pro quota by said purchasers. Refer to explanatory note

no. 3.6.8 of the income statement for the effects of this transaction on the financial statements.

Part of the own shares resulting from said divestment transaction were used to purchase shares of

Greenled Industry S.p.A., as will be explained below. The remaining shares can be used for any

transactions that involve third party investors, which have not yet been identified.

1.5.11 Valorisation of photovoltaic assets; 50% of JV SAIM Energy 2 Srl sold

As part of the strategy to enhance the value of the photovoltaic assets, TerniEnergia signed an

agreement to sell 50% of the shares of SAIM Energy 2 Srl, a company that manages a 997.04 kWp

photovoltaic plant located in the city of Torchiarolo in the province of Brindisi, to Fabrizio Venturi.

The total value of the sale was agreed between the parties to be Euro 650 thousand, including 412

thousand pertaining to the value of the shares of the JV SAIM Energy 2 Srl and Euro 238 thousand

pertaining to the value of the dividends resolved but not yet paid for the portion due to

TerniEnergia. The sales deed for the shares in the JV SAIM Energy 2 Srl was subject to a

termination clause in the case of failed approval of the transaction from the leasing company with

which the company had stipulated contracts for the photovoltaic plant, no later than 31 March

2016.

As Fabrizio Venturi is an executive director of TerniEnergia, the transaction is considered an

insignificant transaction with a related party. In applying the procedures for transactions with

related parties as well as CONSOB Regulation no. 17221 of 12 March 2010, the Committee for

Transactions with Related Parties was informed of the terms and conditions of the transaction and

20

expressed its favourable opinion, supported by an appraisal prepared by an independent expert,

on the advantage to and economic interest of TerniEnergia in the transaction.

1.5.12 Update of the 2015-2017 Industrial Plan, “Fast on the smart energy road”

On 29 October 2015, the Board of Directors approved the update to the 2015-2017 Industrial Plan,

which was considered appropriate following the deconsolidation of Free Energia from the Group,

consequent to the divestment contract approved by the Board on 2 October 2015.

The package of TerniEnergia shares received as compensation for the transfer of the investment in

Free Energia may be used for possible extraordinary transactions in forming business or strategic

alliances that involve third party investors, which have not yet been identified. These transactions

may target:

- Companies in the EPC sector of plants producing energy from renewable sources (not exclusively

photovoltaic), operating at an international level, in order to take advantage of this period of

strong global growth, led by the increase in energy needs of emerging countries, new international

policies on containing global warming, and, above all, the increase in investments in the sector;

- Companies operating in the Gas&Power management sector, also at an international level, in

order to strengthen and accelerate commercial, operational and post-sale services development

for TerniEnergia Gas&Power, a subsidiary of the Group that is active in trading energy, natural gas

and liquefied natural gas;

- Companies operating in “smart technologies” for the demand to reduce energy consumption by

large industrial, commercial and public administration entities, in order to increase the entity’s

energy efficiency margins by implementing proprietary technologies.

The updated plan confirms the organisational structure, which continues to be based on 4

functional business lines: Technical Services, Cleantech, Energy Management and Energy Saving.

TerniEnergia confirms a significant increase in revenues and profitability in 2017 and, at the same

time, a decrease in the NFP and increase in margins.

21

1.5.13 Acquisition of 100% of share capital of Greenled Industry by TerniEnergia

On 30 November 2015, having received the favourable opinion of the Committee for Transactions

with Related Parties, the Board of Directors of TerniEnergia S.p.A. resolved to acquire up to 100%

of the share capital of Greenled Industry S.p.A. (“Greenled”), a company that produces and sells

light bulbs with LED technology.

In particular, on 27 November 2015, the Board of Directors of Italeaf S.p.A., the controlling

shareholder of Greenled, resolved to propose to TerniEnergia the acquisition of Greenled shares

(the “Transaction”) at market value, based on the appraisal of a specially designated independent

expert. The sales price for 100% of the shares representing the share capital of Greenled was

agreed at Euro 3.5 million, as indicated by the assessment performed by the independent expert

appointed by TerniEnergia.

After receiving the proposal from Italeaf, the TerniEnergia Board of Directors decided in favour of

the transaction, resolving to submit it for the approval of the Shareholders’ Meeting called for 28

December 2015.

Greenled produces and sells LED light bulbs, which are considering high performing in terms of

energy efficiency and savings, and with considerable technological capabilities.

For TerniEnergia, the acquisition optimises the supply chain for the Energy Saving business line,

which carries out energy efficiency projects, in which the purchasing of LED light bulbs represents

the most significant cost item. Hence, this transaction is consistent with the objectives of

TerniEnergia and in line with growth in the Energy Saving sector envisaged in the Industrial Plan

presented to the financial community on 30 October 2015.

TerniEnergia’s acquisition of Greenled is considered a transaction between related parties, as it

was carried out with the latter’s parent company, Italeaf S.p.A., which holds an investment

representing 46.78% of the share capital of TerniEnergia, over which it exercises control pursuant

to Art. 2359, paragraph 1, no. 2 of the Italian Civil Code and Art. 93 of the TUF (Consolidated

Financial Act).

In addition, Greenled shareholders are related parties with the company.

22

Therefore, the transaction was approved by the Board of TerniEnergia after receiving the

favourable opinion of the Committee for Transactions with Related Parties, in accordance with

CONSOB Regulation no. 17221/2010 and the procedure adopted by the company.

Consequently, TerniEnergia prepared a disclosure document, in accordance with the instructions

in the governing regulation as well as the Procedure for Transaction with Related Parties,

approved by the Board of Directors of TerniEnergia S.p.A. on 30 November 2010.

On 28 December 2015, the TerniEnergia S.p.A. Shareholders’ Meeting approved this investment

transaction for the purchase of up to 100% of the shares representing the share capital of

Greenled Industry S.p.A. against the transfer, as payment, of up to 2,078,195 own shares,

equivalent to 4.71% of the share capital.

The counter value of Euro 3.5 million, paid through the transfer of 2,078,195 own shares,

corresponds to 4.71% of the share capital of TerniEnergia. Refer to Explanatory Note no. 3.5.1 for

the effects of this transaction on the financial statements.

1.5.14 Multi-year agreement with Avanti Communications to distribute connectivity between the

renewable energy plants in South Africa and Italy

In December 2015, TerniEnergia informed the market that it had signed a multi-year agreement

with Avanti Communications, leading supplier of satellite data communications services in Europe,

the Middle East and Africa. The company will use the Avanti’s Ka-band satellite technology to

provide high speed, broadband connectivity for its giant photovoltaic plants located in

Paleisheuwel and Tom Burke in South Africa, which are under construction by a leading Italian

utility. The satellite service is provided through a VPN (Virtual Private Network) to ensure that the

IP traffic is secure and encrypted between the points of transmission and reception.

1.5.15 Valorisation of photovoltaic assets continues: 50% of four SPVs sold to Renewable

European Investment Italy 3

On 30 December 2015, as part of its strategy to enhance the value of photovoltaic assets,

TerniEnergia signed an agreement to sell 50% of the share capital of the SPVs (Special Purpose

Vehicles) Investimenti Infrastrutture Srl, Società Agricola Fotosolara Oristano Srl, Società Agricola

Fotosolara Bonannaro Srl and Infocaciucci Srl to Renewable European Investment Italy 3 – REI III Srl,

a company belonging to the Radiant Clean Energy Fund. These SPVs own a total of four industrial-

size photovoltaic plants for total installed power of 3.3 MWp.

23

The total sales price was agreed between the parties to be Euro 1.7 million. The cash payment from

Renewable European Investment Italy 3 – REI III Srl was received in January 2016.

The agreements to sell the investments in the SPVs Investimenti Infrastrutture Srl, Società Agricola

Fotosolara Oristano Srl, Società Agricola Fotosolara Bonannaro Srl and Infocaciucci Srl were subject

to precedent conditions, including the negative result of due diligence reviews, failure to receive

approval of the operation by the leasing company with which the company stipulated contracts for

photovoltaic plants by 30 March 2017, and the failure of the seller to issue adequate guarantees on

the restitution of the sales price should the leasing party not give its approval.

24

1.6 PERFORMANCE OF OPERATIONS

Below are summarised the main economic and financial highlights of the TerniEnergia Group as at

31 December 2015 compared to those of the previous year.

2015 2014

Change Change

(in Euro) %

Income Statement

Net revenues from sales and services 368,740,277 95,191,364 273,548,913 n.a.

EBITDA 25,241,031 18,003,466 7,237,565 40%

EBIT 17,130,414 8,433,047 8,697,367 103%

Result for the period 2,557,445 6,203,581 (3,646,136) (59)%

EBITDA margin 6.8% 18.9% (12.1)% (64)%

31 December 31 December Change Change

(in Euro) 2015 2014 %

Financial data

Fixed assets 125,960,176 151,305,332 (25,345,156) (17)%

Net working capital, excluding provisions and other liabilities 17,202,726 28,216,107 (11,013,381) (39)%

Net financial position 87,371,548 108,174,685 (20,803,137) (19)%

Shareholders’ equity 55,791,353 71,346,754 (15,555,401) (22)%

Performance indicators 31 December 31 December

2015 2014

PROFITABILITY RATIOS

ROE 4.8% 9.5%

ROI 10.6% 4.6%

ROS 4.6% 8.9%

FINANCIAL RATIOS

Fixed asset coverage 1.56 1.48

Short-term NFP / Shareholders’ equity 0.15 0.26

NFP / Shareholders’ equity 1.57 1.52

NFP / Net invested capital 0.61 0.60

Shareholders’ equity / Net invested capital 0.39 0.40

NFP / EBITDA 3.46 6.01

NET WORKING CAPITAL ROTATION

Net working capital / Revenues 6.30% 38.10%

25

Consolidated net revenues for the year amount to Euro 368,740 thousand, an increase of Euro

273,549 thousand over the previous year. On one hand, the increase is due to the inclusion of Free

Energia in the scope of consolidation as of 21 October 2014 until 30 November 2015, following the

merger and subsequent divestment transactions described in the previous paragraphs. On the other

hand, it is due to progress in the constructions works for EPC activities related to the two projects

in South Africa. The contribution to 2015 revenues ascribable to Free Energia is equal to Euro

246,414 thousand. EBITDA is Euro 25,241 thousand, a considerable increase (+40%) over 31

December 2014 (Euro 18,003 thousand), due mainly to the inclusion of Free Energia in the scope of

consolidation as well as the status of EPC activities in the construction projects in South Africa.

EBITDA margin is equivalent to 6.8%, down from 2014 (18.9%), due to the modified business model.

Revenues and margins are the highest ever achieved in the Group’s history.

The decline in statement of financial position figures from the previous year is essentially

attributable to the divestment of Free Energia at the end of November 2015, with the resulting

decrease, in particular, of shareholders’ equity, from Euro 71,346 thousand to Euro 55,791

thousand, and the sale of 50% of the share capital of the SPVs Investimenti Infrastrutture Srl, Società

Agricola Fotosolara Oristano Srl, Società Agricola Fotosolara Bonannaro Srl and Infocaciucci Srl to

Renewable European Investment Italy 3 – REI III Srl, which resulted, in particular, in the decrease in

tangible fixed assets and net financial position.

26

ECONOMIC RESULTS

The financial results of the Group are summarised below:

2015 2014 Change

Change

(in Euro) %

Net revenues from sales and services 368,740,277 95,191,364 273,548,913 n.a.

Cost of production (335,980,070) (71,446,441) (264,533,629) n.a.

Added value 32,760,206 23,744,923 9,015,283 37.97%

Personnel costs (7,519,175) (5,741,457) (1,777,718) 30.96%

EBITDA 25,241,031 18,003,466 7,237,565 40.20%

Amortisation, depreciation, allocations and write-downs (8,110,618) (9,570,419) 1,459,801 (15.25)%

Operating result 17,130,414 8,433,047 8,697,367 103.13%

Financial income and expenses (10,351,957) (10,080,568) (271,389) 2.69%

Profit share from joint ventures (665,015) 907,637 (1,572,652) n.a.

Pre-tax result 6,113,442 (739,884) 6,853,326 n.a.

Income taxes (3,555,997) 6,943,465 (10,499,462) n.a.

Net result 2,557,445 6,203,581 (3,646,136) (58.77)%

At 31 December 2015, the Group posted consolidated revenues from sales and services of Euro

368,740 thousand, up from Euro 273,549 thousand in the previous year (Euro 95,191 thousand).

This mainly reflects the inclusion of Free Energia in the scope of consolidation effective from 21

October 2014 to 30 November 2015, following the merger and subsequent divestment transactions

described above, as well as the progress in the constructions projects in South Africa for EPC

activities. The contribution to 2015 revenues ascribable to Free Energia is equal to Euro 246,414

thousand.

Revenues relative to Technical Service activities are Euro 107,831 thousand, broken down as

follows: revenues relative to EPC activities in the photovoltaic sector are Euro 96,476 thousand (Euro

5,210 as of 31 December 2014) and refer to the works for the realisation of photovoltaic plants

during that period in South Africa. Revenues deriving from the management of photovoltaic plants

(Power Generation Fotovoltaico) amounted to Euro 7,083 thousand, a significant decrease with

respect to the previous year (Euro 16,039 thousand) due to the disposal of certain photovoltaic

assets during 2015 as described above.

The Cleantech business line had revenues of Euro 8,678 thousand, up 14.1% compared to the prior

year, mainly due to the full year of operations of the PFU in Nera Montoro as well as the

strengthening of biodigester activities. Revenues from the Energy Saving business line amount to

27

Euro 2,494 thousand, an increase over 2014, due to several important energy efficiency projects

which took place in 2015.

Direct production costs, which are primarily variable in nature, totalled Euro 335,980 thousand, an

increase of Euro 264,534 thousand compared to the previous year (Euro 71,446 thousand), primarily

due to the different types of activities and the entry of the Energy Management business line, in line

with the changes posted in revenues. EBITDA increased from Euro 18,033 thousand in 2014 to Euro

25,241 thousand in 2015. This substantial increase in EBITDA is due to the inclusion of Free Energia

in the scope of consolidation through November 2015 and EPC activities in the two “giant”

construction works in South Africa.

Amortisation, depreciation, allocations and write-downs in the reclassified income statement have

decreased from Euro 9,570 thousand in the previous year to Euro 8,111 thousand. This result is the

combination of lower depreciation for the fewer photovoltaic plants fully owned by the Group,

partially offset by the effect of higher write-downs posted in 2015.

Financial management, which had a negative balance of Euro 10,352 thousand, is essentially in line

with 2014 due to the combined effect of, on one hand, the higher impact of bank commissions,

attributable to sureties guaranteeing the projects in South Africa, net of the reduction in interest

expense deriving from lower average indebtedness over 2015 compared to the prior year, while on

the other, recognition of 2014 dividends disbursed in 2015 by Free Energia, which left the Group at

the end of 2015.

The significant variation in the item “Income taxes” is attributable to the fact that there was a

positive balance in 2014 of Euro 6,943 thousand as a result of the recognition of tax income related

to the “Tremonti Ambientale” (environmental law) for certain Group companies that owned large

photovoltaic parks. However, in 2015 there was a higher tax rate, equivalent to 58%, that is

imputable in particular to the effects of the IRES reduction beginning in 2017, which caused a

recalculation of deferred taxes in 2015.

The net result for the year as at 31 December 2015 has a positive balance of Euro 2,557 thousand,

with a decrease in absolute terms of Euro 3,646 thousand compared to the figure for last year (Euro

6,204 thousand), as a result of the dynamics described above.

With regard to the modalities for representation of results, refer to that reported below in the

paragraph “Alternative performance indicators”.

28

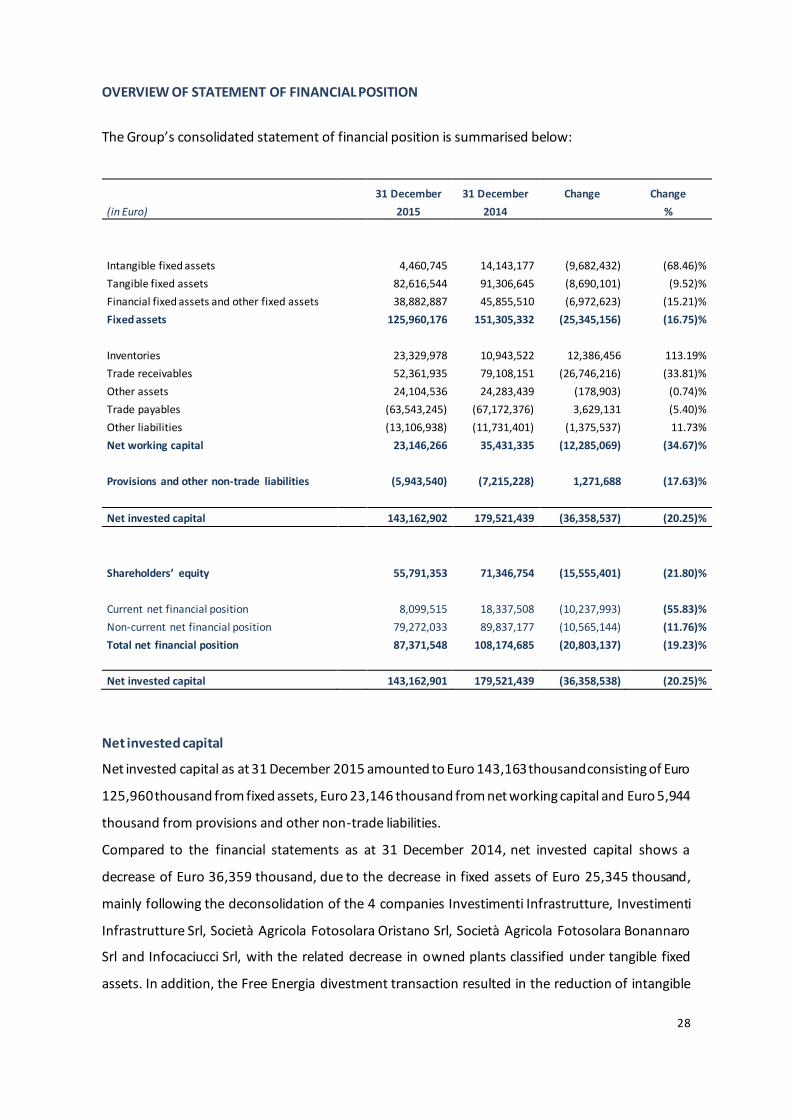

OVERVIEW OF STATEMENT OF FINANCIAL POSITION

The Group’s consolidated statement of financial position is summarised below:

31 December 31 December Change Change

(in Euro) 2015 2014 %

Intangible fixed assets 4,460,745 14,143,177 (9,682,432) (68.46)%

Tangible fixed assets 82,616,544 91,306,645 (8,690,101) (9.52)%

Financial fixed assets and other fixed assets 38,882,887 45,855,510 (6,972,623) (15.21)%

Fixed assets 125,960,176 151,305,332 (25,345,156) (16.75)%

Inventories 23,329,978 10,943,522 12,386,456 113.19%

Trade receivables 52,361,935 79,108,151 (26,746,216) (33.81)%

Other assets 24,104,536 24,283,439 (178,903) (0.74)%

Trade payables (63,543,245) (67,172,376) 3,629,131 (5.40)%

Other liabilities (13,106,938) (11,731,401) (1,375,537) 11.73%

Net working capital 23,146,266 35,431,335 (12,285,069) (34.67)%

Provisions and other non-trade liabilities (5,943,540) (7,215,228) 1,271,688 (17.63)%

Net invested capital 143,162,902 179,521,439 (36,358,537) (20.25)%

Shareholders’ equity 55,791,353 71,346,754 (15,555,401) (21.80)%

Current net financial position 8,099,515 18,337,508 (10,237,993) (55.83)%

Non-current net financial position 79,272,033 89,837,177 (10,565,144) (11.76)%

Total net financial position 87,371,548 108,174,685 (20,803,137) (19.23)%

Net invested capital 143,162,901 179,521,439 (36,358,538) (20.25)%

Net invested capital

Net invested capital as at 31 December 2015 amounted to Euro 143,163 thousand consisting of Euro

125,960 thousand from fixed assets, Euro 23,146 thousand from net working capital and Euro 5,944

thousand from provisions and other non-trade liabilities.

Compared to the financial statements as at 31 December 2014, net invested capital shows a

decrease of Euro 36,359 thousand, due to the decrease in fixed assets of Euro 25,345 thousand,

mainly following the deconsolidation of the 4 companies Investimenti Infrastrutture, Investimenti

Infrastrutture Srl, Società Agricola Fotosolara Oristano Srl, Società Agricola Fotosolara Bonannaro

Srl and Infocaciucci Srl, with the related decrease in owned plants classified under tangible fixed

assets. In addition, the Free Energia divestment transaction resulted in the reduction of intangible

29

fixed assets and financial fixed assets due to, respectively, the goodwill from the consolidation of

the equity investment and the securities used by Free Energia as collateral for guarantees issued on

the supplies of electricity.

The decrease in net working capital is mainly attributable to the combined effect of the increase of

raw material inventories, consisting primarily of panels, used in constructing the two photovoltaic

plants in South Africa, and the reduction in trade receivables after the exclusion of Free Energia

S.p.A. from the scope of consolidation.

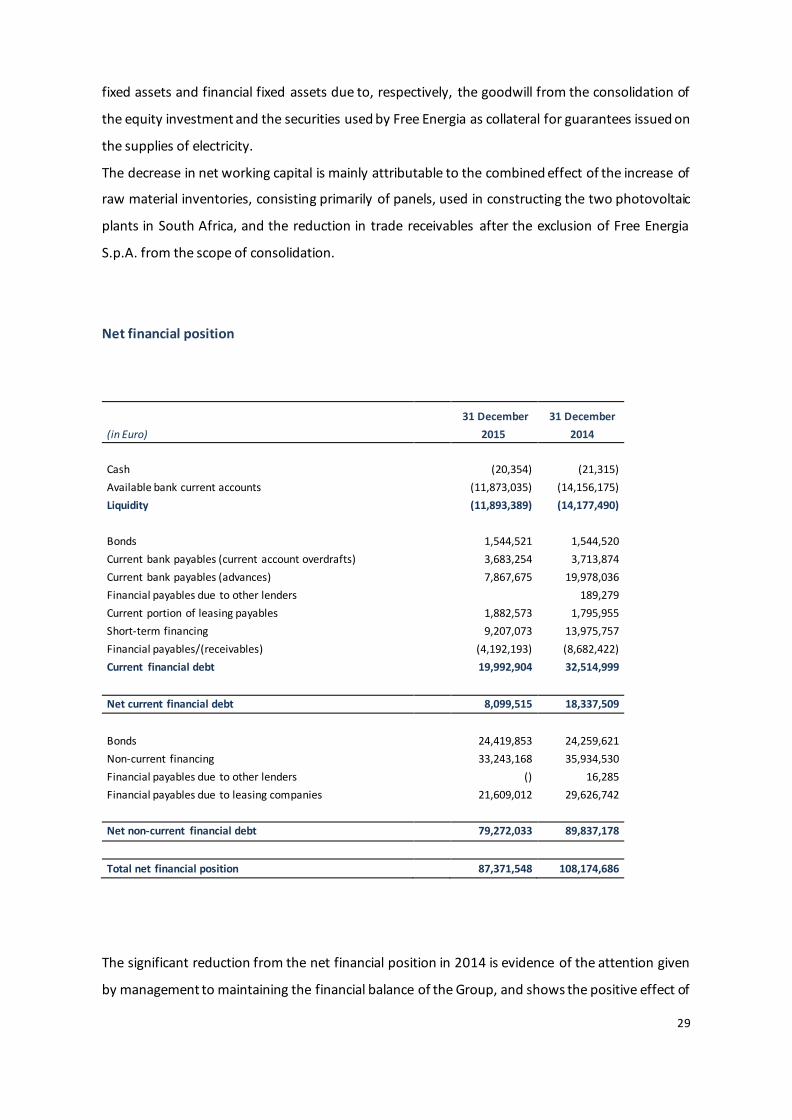

Net financial position

31 December 31 December

(in Euro) 2015 2014

Cash (20,354) (21,315)

Available bank current accounts (11,873,035) (14,156,175)

Liquidity (11,893,389) (14,177,490)

Bonds 1,544,521 1,544,520

Current bank payables (current account overdrafts) 3,683,254 3,713,874

Current bank payables (advances) 7,867,675 19,978,036

Financial payables due to other lenders 189,279

Current portion of leasing payables 1,882,573 1,795,955

Short-term financing 9,207,073 13,975,757

Financial payables/(receivables) (4,192,193) (8,682,422)

Current financial debt 19,992,904 32,514,999

Net current financial debt 8,099,515 18,337,509

Bonds 24,419,853 24,259,621

Non-current financing 33,243,168 35,934,530

Financial payables due to other lenders () 16,285

Financial payables due to leasing companies 21,609,012 29,626,742

Net non-current financial debt 79,272,033 89,837,178

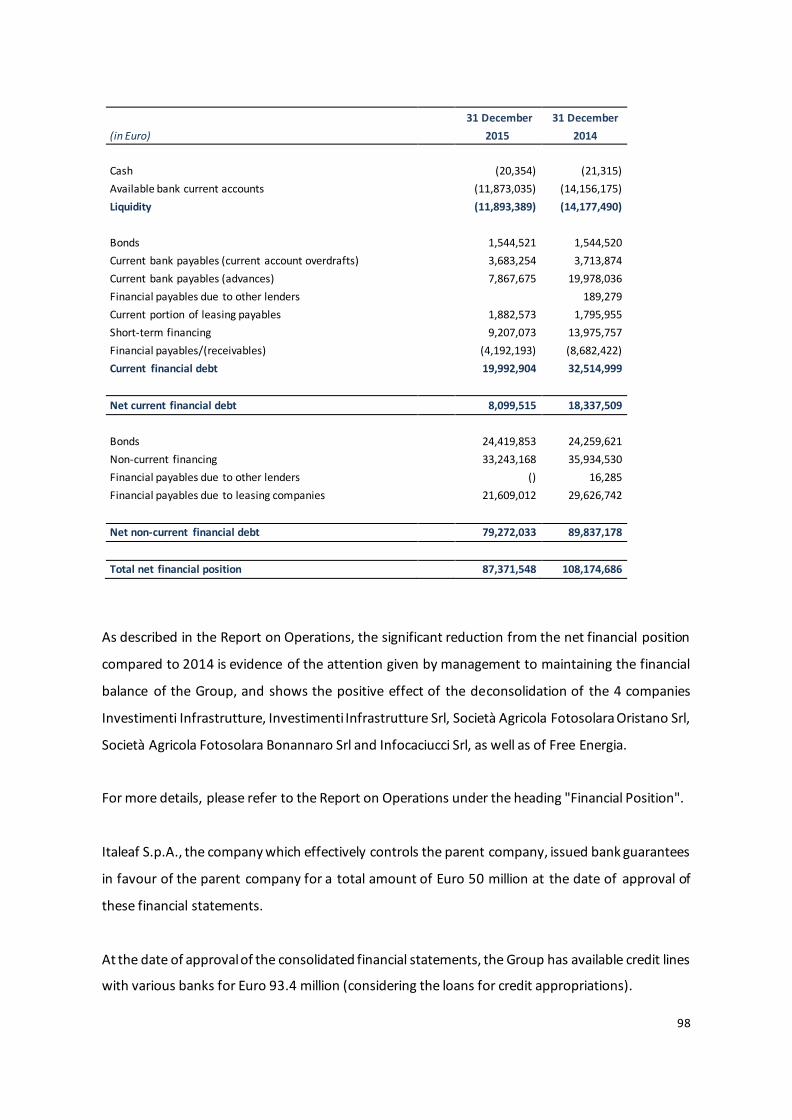

Total net financial position 87,371,548 108,174,686

The significant reduction from the net financial position in 2014 is evidence of the attention given

by management to maintaining the financial balance of the Group, and shows the positive effect of

30

the deconsolidation of the 4 companies Investimenti Infrastrutture, Investimenti Infrastrutture Srl,

Società Agricola Fotosolara Oristano Srl, Società Agricola Fotosolara Bonannaro Srl and Infocaciucci

Srl, as well as of Free Energia.

Net debt at 31 December 2015 amounted to Euro 87,372 thousand, divided into short-term portion

of Euro 8,099 thousand and long-term portion of Euro 79,272 thousand. The long-term portion is

primarily attributable to leases entered into with major financial institutions to cover the financial

requirements necessary for the development of photovoltaic plants that are fully available to the

company and for the investments in the biodigestion plant and the used tire treatment plant in Nera

Montoro. Non-current financial debt also includes the quota due beyond 12 months of the

corporate financing granted to the parent company TerniEnergia at the end of 2013, and mainly

composed of an unsecured loan totalling Euro 10 million with a duration of 60 months and

reimbursement in 20 quarterly instalments, as well as an unsecured loan of Euro 5 million with a

duration of 60 months and lump sum reimbursement at the expiration date, both issued by Veneto

Banca. Finally, the non-current financial debt also includes the bond with a nominal value of Euro

25 million and a duration of 5 years, annual coupon of 6.875%, as well as reimbursement in a lump

sum at the expiration date (month of February 2019). The current quota includes the interest

accrued in 2015, equal to Euro 1,544 thousand, and relative to the coupon paid in the month of

February 2016.

It should also be noted that the current financial payables comprise part of the payments incurred

for investments already made or still under construction and for which on 31 December 2015 the

company had not yet entered into a specific contract financing in the medium/long term. In

particular, they refer to the second treatment plant for used tyres completed at the end of 2015, a

pyrogasification plant and a composting plant under construction in Apulia.

The short-term financial position for an amount of Euro 8,010 thousand is basically made up of

short-term debt to banks for overdrafts (Euro 3,683 thousand) or advances on invoices and/or

contracts (Euro 7,868 thousand), short-term financing to banks for Euro 9,207 thousand, short-term

portion of lease payables for Euro 1,883 thousand, cash for Euro 11,893 thousand, and the short-

term portion of financial receivables and securities for Euro 4,192 thousand.

31

Shareholders' equity

As at 31 December 2015, shareholders' equity, including income for the period, amounted to Euro

55,791 thousand, a decrease from the previous year of Euro 15,555 thousand. For more details,

please refer to the Explanatory Note 3.5.1.

ALTERNATIVE PERFORMANCE INDICATORS

The items shown in the reclassified financial statements are in part extracted from the financial

statements required by law and listed in the remainder of this document and partly aggregated;

with regard to the latter, the following table shows the composition and notes referring to the items

of the statutory financial statements, as required by the CESR Recommendation (CESR/05-17 b).

Revenues: this item is given by the sum of revenues from sales and services.

Cost of production: the item is given by the sum of consumption of raw materials, cost of services

and other operating costs, changes in inventories of raw materials and consumables and finished

products.

Depreciation, amortisation and allocations: this item is given by the sum of amortisation and write-

downs of intangible assets, depreciation and impairment of tangible assets, and provisions for the

write-down of receivables.

EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortisation) is an economic indicator

not defined by the International Accounting Standards. EBITDA is a measure used by management

to monitor and evaluate the operating performance of the Company, considered significant by the

management, as it is not affected by the volatility due to the effects of different criteria for the

determination of tax income, the amount and features of the capital used and

depreciation/amortisation policies. EBITDA is defined as the operating profit before depreciation

and amortisation of tangible and intangible assets, financial income and expenses and income taxes.

EBIT (Earnings Before Interest and Taxes) is the operating profit gross of financial income and

charges as well as income taxes.

The abovementioned values, such as EBITDA and EBIT, are commonly identified without having a

uniform definition in the accounting standards or in the Italian Civil Code and, therefore, might not

be comparable with similarly named values of other entities.

Other assets: this item is given by the sum of the items of other current assets and other financial

assets.

Other liabilities: this item is given by the sum of the items of tax payables and other liabilities.

Fixed assets: this item is given by the sum of intangible and tangible assets as well as financial fixed

32

assets.

Net working capital: this item is given by the sum of closing inventories, trade receivables, other

assets and assets held for sale, excluding trade payables and other liabilities.

Net working capital, excluding provisions and other liabilities: this item is given by the algebraic sum

of net working capital and provisions and other non-current liabilities.

The Net Financial Position (NFP), used as a financial indicator of indebtedness, is represented as the

sum of the following positive and negative components from the statement of financial position, as

required by CONSOB notice no. 6064293 of 28 July 2006.

Positive items: cash and cash equivalents, highly liquid securities under current assets, short-term

financial receivables and derivative instruments. Negative items: payables to banks, payables to

other lenders, leasing and factoring companies.

1.7 INVESTMENTS

(in Euro) Direct

investments Increase from

purchases

Total investments

as of

31/12/2015

31-Dec-2014 Change %

Software 310,810 310,810 809,122 (498,312) (61.6%)

Other intangible assets 1,075,603 1,075,603 1,502,940 (427,337) (28.4%)

Goodwill 145,600 145,600 9,055,368 (8,909,768) (98.4%)

Plant and machinery 2,541,712 2,541,712 1,085,730 1,455,982 134.1%

Industrial equipment 45,599 45,599 39,900 5,699 14.3%

Other goods 17,910 17,910 888,349 (870,439) (98.0%)

Other fixed assets in progress

3,255,318 3,255,318 2,236,011 1,019,307 45.6%

Total 7,246,952 145,600 7,392,552 15,617,420 (8,224,868) (52.66%)

1.8 HUMAN RESOURCES

The Parent Company applied Legislative Decree no. 81/2008, appointing a security manager and

entrusting a qualified and experienced outsourcer with the analysis of risks and the related

evaluation report.

Procedures have been implemented in compliance with currently effective legislation and, in this

regard, medical examinations as well as training and refresher courses on safety at work and within

33

the working environment are regularly carried out for all the employees of the Group.

Incentive plans have been envisaged for managers with strategic responsibilities and executive

directors of the Group in the form of an increase in their remuneration that is directly proportional

to the targets achieved.

As at 31 December 2015, there were 131 employees, primarily under the Parent Company and

classified as follows:

31-Dec-2015 31-Dec-2014

Actual Average Actual Average

Executives 4 3.67 6 4.42

Middle managers 12 9.16 11 12.17

Office workers 43 40.41 49 43.16

Manual workers 72 64.08 56 67.25

Total 131 120.34 122 127

The total employees increased from 122 in 2014 to 131 in 2015.

1.9 ENVIRONMENTAL POLICY

The Group’s mission provides for the respect and protection of the environment. TerniEnergia is

active in the sectors of energy, environment and services, in view of sustainable development, and

its objectives are economic growth, environmentally-friendly efficiency and social progress.

The mission of the TerniEnergia Group reflects the target to try to achieve an increasingly high level

of performance in pursuing a policy of innovation and economic growth, respecting the ecosystem,

through the careful use of natural resources.

More specifically, the construction of energy production plants is subject to authorisation

procedures which may require the implementation of EIA (Environmental Impact Assessment - VIA,

“Valutazione Impatto Ambientale”) procedures.

1.10 R&D

Pursuant to Art. 2428, paragraph 2, number 1, it is hereby acknowledged that in the year ended 31

December 2015, the Group carried out research and development whose costs were fully expensed

in the income statement.

34

1.11 RISK FACTORS RELATED TO THE REFERENCE SECTOR

In order to comply with the provisions pursuant to Italian Legislative Decree no. 58 of 24 February

1998 and, specifically, under Art. 154-ter as to the description of the main risks and uncertainties,

below are reported the risks and/or uncertainties and the related actions taken by the Group to

neutralise their effects on the economic-financial position and performance.

Activities pertaining to the construction and operation of plants for the production of energy from

renewable sources, similarly to new environmental activities, are extremely regulated; TerniEnergia

analyses in detail the regulations of reference in order to be constantly updated and to adopt, if

possible, optimal applicable solutions. During the implementation of its operations, TerniEnergia

therefore is subject to risks deriving respectively from external factors pertaining to the regulatory

and macroeconomic context of reference, including the legislative, financial and credit sectors

where the Group operates or which result from strategic choices adopted during operations and

which expose the Group itself to specific risks as well as internal risks deriving from ordinary

operational management.