Embed Size (px)

Citation preview

ANNUALREPORT

2014

ANNUALREPORT

2014

www.tpc.com.kh

North

Note: The map is used for TPC’s branch network indication purpose only.

Number of branches : 54

Number of operating provinces : 22

Operating TPC offices

Office opening in 2015

TPC operating areas

Map of Operating Areas

Kep

Koh Kong

Kampong

Chhnang

Pursat

BanteayMeanchey

Preah Vihear

Kampong Cham

Tboung khmum

KratieMondul Kiri

Stung Treng

Prey Veng

Svay Rieng

Siem Reap

Kampong

Speu

Preah Sihanouk

Kampot

ThailandLaos

Vietnam

Otdar Meanchey

Rattanak Kiri

Kampong Thom

Battam Bang

Pailin

Kandal

Annual Report 2014 1

Takeo

Phnom Penh

Vision Statement

Mission Statement

Thaneakea Phum (Cambodia), Ltd.2

Thaneakea Phum (Cambodia), Ltd. (TPC) is a microfinance institution with a social vision and a business orientation that provides entrepreneurs and families at the base of the socio-economic pyramid with the economic opportunities to transform the quality of their lives and their communities through the provision of effective and sustainable client empowering financial services.

Families at the base of the socio-economic

pyramid are empowered to live their lives with

dignity, social and economic security and

justice.

Annual Report 2014 3

Core Values

Client Relationships

Quality

Integrity

Diversity &

NeutralityBalanced Social

& Pro�t

Discipline

Hard Work

Education

CoreValueCore

Value

Client Relationships, our �rst priority is always to ensure thatthe clients are fully satis�ed with our services.

Quality, we will continue to provide e�cient, e�ective and best quality services to our clients.

Integrity, fairness and honesty in all business dealings, trust is the cornerstoneof our business and it will never be compromised.

Education, we believe that it will

provide the foundation for sta� and client lifelong success.

Hard Work, we believe that trust

our future is guaranteed through the maximum

e�ort we give to our responsibilities.

Discipline, we believe in respecting the rules of the company, its stakeholders

and the country.

Diversity & Neutrality, we serve poor people on the basis of need not ethnicity, religion or political a�liation.

Balanced Social & Pro�t, the balance assures the future for

our clients and for ourselves.

Thaneakea Phum (Cambodia), Ltd.4

Lenders and Partners

National Bank of Cambodia

Alterfin

Calvert Foundation

Cyrano-Management

Frankfurt School Financial Services

Foreign Trade Bank of Cambodia

Maruhan Japan Bank

Grameen Credit Agricole

Incofin

Instituto de Credito Oficial

Industrial and Commercial Bank of China Limited

Standard Chartered

Bank Im Bistum Essen E.G

ACLEDA Bank Plc.

Novib Fonds (Trimple Jump)

International Finance Corporation

responsAbility

Proparco

Symbiotics

BlueOrchard

Deutshe Bank

MicroVest

Overseas Private Investment Corporation

Phnom Penh Commercial Bank

Impact Finance

Good Return

Advanced Bank of Asia Limited

Cambodia Microfinance Association

Good Return

Credit Bureau Cambodia

The Smart Campaign

Agence Française de Développement

Banking With The Poor Network

Microcredit summit Campaign

USAID

Wing

MIX Market

Oikocredit

Annual Report 2014 5

Awards, Recognitions and Achievements

Progress out of Powerty Index certification

The S.T.A.R certification from MIX Market

Certificate of “gratitude” from Ministry of Information

Certificate of “gratitude” from Phnom Penh Municipal Department of Education, Youth and Sport

1

1

3

2

4

3

4

2

Thaneakea Phum (Cambodia), Ltd.6

Annual Report 2014 7

Our Clients... Our Services...

Customer service is at the heart of our business model. At every level of our operations, we strive to provide the best quality of customer service by listening attentively to our clients and providing a quick and highly personalized service.

Our staff is polite, courteous and enthusiastic. Employees at every branch frequently attend trainings and re-trainings on how to best present TPC and themselves to our clients. We also offer a customer service help phone number at the head office in case clients have any complaints.

Thaneakea Phum (Cambodia), Ltd.8

Key Performance Highlights

2011 2012 2013 2014Total Assets (USD)

Gross Loan Portfolio (USD)

Equity (USD)

Net Income (USD)

Number of Active Borrowers

Number of Offices (including HO)

Number of Personnel

Operating Expense/ Loan Portfolio

PAR>30 days

Write-offs Ratio

Capital Adequacy Ratio (CAR)

Debt-to-Equity Ratio

Return On Assets

Return On Equity

134,307,474

115,372,296

23,801,643

7,468,659

189,345

54

1,156

10.74%

0.10%

0.09%

17.77%

4.6 x

6.71%

37.14%

45,945,239

33,155,327

8,062,844

1,458,698

96,542

32

545

15.53%

0.13%

1.15%

16.10%

4.7 x

3.87%

21.11%

61,773,992

48,402,754

10,224,431

2,219,658

122,077

39

695

13.61%

0.20%

0.10%

18.20%

4.5 x

4.17%

24.24%

95,025,328

74,946,541

17,088,518

4,284,523

153,952

46

874

12.68%

0.15%

0.09%

16.16%

4.6 x

5.49%

29.83%

Gross Loan Portfolio(USD in million)

Active Borrowers(in thousand)

PAR >30 DaysNet Income(USD in million)

33.16 48.40

74.95

115.37

0

20

40

60

80

100

120

140

2011 2012 2013 Dec-14

CAGR: 51.5%

96.54 122.08

153.95 189.35

020406080

100120140160180200

2011 2012 2013 Dec-14

CAGR: 25.2%

1.46 2.22

4.28

7.47

0

1

2

3

4

5

6

7

8

2011 2012 2013 Dec-14

0.13%

0.20%0.15%

0.10%

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

2011 2012 2013 Dec-14

Annual Report 2014 9

Table of Contents

Map of Operating Areas

Vision / Mission Statement

Core Values

Lenders and Partners

Awards, Recognitions and Achievements

Key Performance Highlights

Table of Contents

Chairperson’s Statement

CEO’s Report

Cambodia at a Glance

Microfinance Sector

Brief Overview of TPC

Brief History of TPC

Responsible Growth

Trend in Product Mix

Business Outlook

Risk Management

How Do We Translate Our Mission?

Social Performance Management

Client Protection Principles

Financial Literacy Education Update

Environmental Assessment Survey

Community Event Highlights

Partnership Update

Client Stories

Overview of Good Governance

Organizational Chart

Ownership Structure

Board of Directors

Management Team

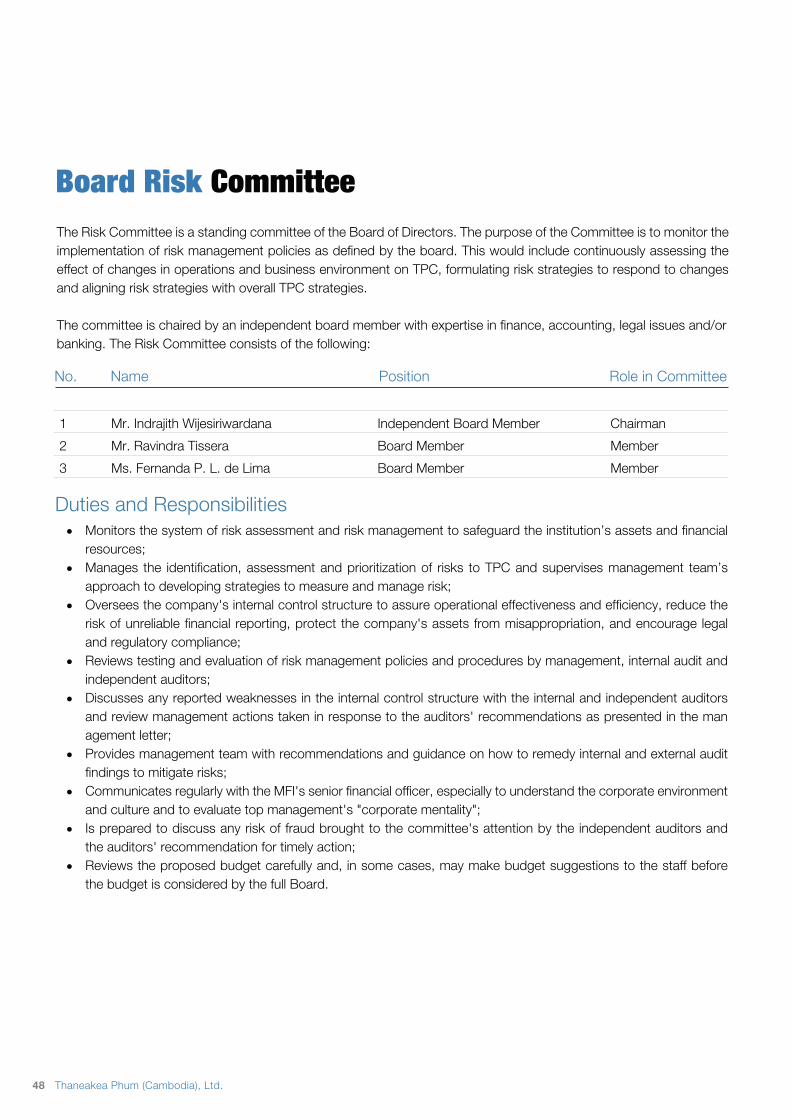

Board Risk Committee

Board Audit Committee

Board Appointments and Remunerations Committee

Directors’ Report

Independent Auditor’s Report

Balance Sheet

Income Statement

Statement of Changes in Equity

Cash Flow Statement

1

2

3

4

5

8

9

10

12

16

17

18

19

22

23

24

26

28

29

30

31

32

34

35

36

38

39

40

42

44

48

49

50

53

55

56

57

58

59

Table of ContentsChairperson’s Statement

and CEO’s Report

About TPC

Business Review

Social andEnvironmental

Performance Review

Corporate Governance

FinancialStatements and

IndependentAudit Reports

Prologue

Thaneakea Phum (Cambodia), Ltd.10

In Retrospect

Chairperson’s Statement

I am pleased to report another outstanding year and share key developments that will positively impact TPC in the years to come. During 2014, DWM made important decisions such as the consolidation of a 100% local senior management, the move to a spacious head office and the sale of a majority stake in the company to LOLC Group from Sri Lanka. We welcome LOLC and especially its board representatives Mr. Ravi Tissera and Mr. Kithsiri Gunawardena, who will take over as Chairman. We expect TPC to strengthen its position in the market with continued innovation in its product offering, technology, geographic expansion and robust support from shareholders.

Global economic growth in 2014 was lower than initially expected, with soft commodity prices, low interest rates but divergent monetary policies across major economies, and weak world trade. The Cambodian economy posted decent growth at 7.0%, only slightly underperforming the 7.3% average of the previous 3 years. Industries and services were the drivers as agriculture lagged. Political tensions and labor unrest in the garment industry in 2013 continued until early 2014, but only temporarily affected investment and disturbed garment manufacturing and tourism - industry as a whole grew by around 10%. The political environment in Cambodia has improved from the turmoil of the last election, as the ruling CPP and the opposition CNRP have worked together on electoral reform.

In 2014, the Cambodian microfinance industry expanded with a Gross Loan Portfolio (GLP) of USD 2,503 million (ACLEDA Bank microfinance portfolio included) and over 2 million borrowers throughout the country. There are currently 39 microfinance licenses (MFI) in Cambodia reaching different parts of the population with a wide range of products from working capital loans and asset financing to consumer finance products and mortgages. The top 5 MFIs and ACLEDA microfinance portfolio account for more than 75% of the total portfolio outstanding.

TPC accomplished outstanding financial and social results during 2014. The company performed above the industry average again, increasing its market share and consolidating its position as the 5th largest MFI in the country in portfolio and number of borrowers. It has exceeded its profitability targets, almost doubling its net income to reach USD 7.5 million in 2014 and serves approximately 190,000 clients in 22 provinces.

Ms. Fernanda Lima

Chairperson

Annual Report 2014 11

Chairperson’s Statement

Outlook

TPC demonstrated strong commitment towards social performance management, with the implementation of the Smart Campaign Client Protection Principles, the use of the Progress out of Poverty Index tool, and the development of policies, that were acknowledged by third party social rating agency Microfinanza and MIX Market. TPC received the S.T.A.R certification from MIX Market for achieving high level of transparency and compliance to social performance standards. These initiatives contribute to the reduction of client-related risks and ensure that TPC treats its clients fairly and with transparency. In partnership with Good Return, an initiative of World Education Australia, TPC provided financial literacy to over 7,000 clients and non-clients as part of its “Learning for a Better Life” program.

Global growth is expected to rise moderately in 2015. Similarly, higher growth is expected in Cambodia based on better prospects for exports and tourism, an easing of domestic political and labor tensions, and lower fuel costs helping private consumption to recover. Prospects are positive for agriculture as well, with increasedinvestments and policy focus. The gross domestic product is projected to increase to approximately 7.3% in 2015. Over the medium term, growth should be stimulated by gradual diversification into light manufacturing and further integration into regional and global supply chains.

In the coming years, TPC intends to develop through innovative products and increased productivity to fulfill its mission of providing effective and sustainable financial services to entrepreneurs and families at the base of socio-economic pyramid. TPC will continue to expand its branch network, leverage technology in the field and take advantage of the agency banking model to take its products and services closer to clients. Board and management are evaluating the investment in a new core banking application that will enable TPC to provide more efficient services and products to customers in real time. In its bid to improve customer service, TPC will continue to train and develop its employees, equipping them with the necessary skills to effectively serve customers. Such training will be geared towards customer care and leadership development aimed at empowering employees.

I look forward to working with TPC towards another outstanding year in 2015. I would also like to sincerely thank the National Bank of Cambodia for their robust regulatory and supervisory role and TPC’s Board of Directors and senior management team for their guidance, dynamism and supervision of TPC’s operation. I would also like to thank TPC staff for their hard work and commitment to our clients’ success and the sustainable growth of the company. Along with the rest of the Board of Directors, I have utmost confidence in TPC’s senior management team to deliver on TPC’s strategic goals going forward. Lastly, I cannot forget to thank all over clients who put their trust in TPC for the prosperity of their families and businesses.

Ms. Fernanda LimaChairperson

Thaneakea Phum (Cambodia), Ltd.12

CEO’s Report

The country’s microfinance sector performed at a high standard in 2014. The 10 largest MFIs posted an average loan portfolio growth of 52%. This growth is partly due to the fact that some of the larger MFIs increased their maximum loans sizes to meet clients’ needs, attracting clients with larger loan sizes mostly in urban and munici-pal town centers. Another reason is that rural-focused MFIs, like TPC, opened more branches, and were able to increase outreach. While maintaining growth, many MFIs, especially the larger ones, have also strengthened their client protection efforts by achieving compliance with all the indicators in the SMART Campaign’s Client Protection Principles. The aim is to ensure the viability and continued growth of the micro-business and SME sectors.

According to Mekong Strategic Partners, the MFI sector in Cambodia is one of the best performing MFI sectors globally in terms of growth and returns. The organization highlights that the Cambodian microfinance sector has achieved this while charging interest rates that are towards the low end of the spectrum for MFIs globally, with a level of transparency and a pro-poor approach that are among the best in the world. These characteristics position the Cambodian microfinance sector for continued growth in the years ahead.

Loan Portfolio Outstanding

As of December 31, 2014, TPC’s gross loan portfolio is

USD 115.4 million, an increase of 54% over 2013.

The portfolio consists of group, individual, and seasonal

loans, which comprise 36%, 47%, and 15% of the

portfolio respectively. On a year-to-year basis, TPC’s

portfolio has been growing an average of 51% annually in

the last four years.

Performance in 2014Loan Portfolio Growth

TPC experienced strong growth in 2014, increasing its loan portfolio by 54% to USD 115.4 million and number of clients by 23% to almost 190,000. Management expanded TPC’s employee base and geographic footprint to meet demand, opening eight new offices while maintaining high productivity standards. The increase in gross loan portfolio and number of borrowers is attributed to TPC’s:

Focus on providing the best customer service in the

industry;

Competitive loan product offerings;

Innovative products;

Strong head office and branch management; and

Strong focus on client protection.

1.

2.

3.

4.

5.

Active Borrowers

As of December 31, 2014, TPC served close to 190,000

active borrowers, representing an increase of 23%

compared to the previous year. The vast majority of loans

outstanding are individual and group loans, which reflects

TPC’s mission of serving entrepreneurs and families at

the base of socio-economic pyramid in rural areas.

Mr. SOK Voeun

Chief Executive Officer

Annual Report 2014 13

CEO’s Report

Social Performance

about 8.75% of TPC's new clients were likely to be living

below the national poverty line, and about 29.22% were

likely living below KHR 3,704 a day. Continual tracking of

the PPI tool for all new clients enables TPC to:

In 2014, TPC was awarded the S.T.A.R. certification from

MIX Market for its commitment to being transparent and

responsible towards consumers. In addition, TPC

became the first MFI to receive the new standard PPI

Certification by MicroFinanza for its exemplary use of the

social performance measurement tool. We have

implemented the PPI for selected repeated clients with

the aim of determining improvement in the clients’

socio-economic well-being from one cycle to another

since 2012. Over the last three years from 2012 to 2014,

clients with a poverty likelihood of ‘poor’ dropped from

30% to 19%, while clients with poverty likelihood in the

next category up of ‘low income’ increased from 39% to

48%. This indicates that TPC clients are advancing into

higher socio-economic brackets and moving away from

the lowest categories of ‘very poor’ and ‘poor’.

In compliance with the SMART Campaign’s Client

Protection Principles, policies, management tools,

education tools, forms, procedures, and training have

been integrated into TPC’s business operations using the

detailed framework of standards developed by the

SMART Campaign. This progress has been achieved

with the assistance of TPC’s Australian partner

organization, Good Return, as TPC works towards

obtaining SMART Certification and continues to put

clients first. Additionally, TPC has also collaborated with

Good Return to offer community financial literacy training

to TPC clients, non-clients, and university students in six

branches helping them to understand and better manage

their finances. These achievements demonstrate TPC’s

commitment to delivering responsible financial services to

underserved, low-income portions of the population. Serving and empowering entrepreneurs and low-income

families at the base of the socio-economic pyramid is at

the core of what TPC does. 98% of total borrowers live in

rural areas; 84.58% of them are women and 60% are

engaged in agricultural activities. The Progress out of

Poverty Index (PPI) survey of clients in 2014 showed that

Loan Portfolio Quality

TPC’s growth during 2014 continues to be responsibly

managed to ensure a top quality portfolio. The TPC

Board of Directors and management worked to

continually strengthen TPC’s credit process and made

several enhancements to TPC’s risk management

practices, including:

Return on Assets and Return on Equity

As a result, TPC’s portfolio quality is currently among the

best in the industry, with PAR>30 days of 0.10% as of

December 31, 2014.

TPC’s ROA rose to 6.7% in 2014 from 5.5% in 2013,

while ROE increased to 37.1% in 2014 from 29.8%. Net

income increased by 74% over 2013 to USD 7.5 million.

These improvements were driven by strong portfolio

growth and careful management of operating expenses,

which decreased from 12.7% of GLP in 2013 to 10.7% in 2014.

Strengthening of the credit risk management and

internal controls;

Improving employee incentive structures,

particularly for the Credit Officers;

Integrating the Client Protection Principles as a core

part of risk management;

Effective implementation of the financial literacy

training program with Good Return Australia to

provide clients and other community members the

skills to manage their finances;

Requiring Credit Bureau of Cambodia checks for

100% of borrowers across all branches to

supplement rigorous in-person loan evaluations;

Conducting training to strengthen staff

productivity;

Partnership with USAID/Cambodia HARVEST

Program to provide agricultural training and

technical assistance to TPC credit officers and

branch management.

•

•

•

•

•

•

•

Remain focused on serving marginalized

populations

Improve products to meet the needs of TPC’s clients

Measure the effectiveness of TPC’s services

•

•

•

Thaneakea Phum (Cambodia), Ltd.14

Additional Highlights for 2014

TPC is excited as we prepare for another productive

year! As long as we maintain our passion and

commitment to serving the economically active portions

of the population, we will continue to make headway in

fulfilling our objectives and strengthen our presence in

the market.

Let me again acknowledge all the hard-working and

committed members of TPC’s management and staff.

Your contribution is driving TPC to what it is today—one

of the fastest growing MFIs in the country. I would like to

express my sincere gratitude to our customers, our

shareholders, and development and strategic business

partners for your overwhelming support to TPC. Finally, I

wish to thank our Board of Directors for your oversight

and guidance. May 2015 be another year of growth and

excellence!

We moved to a spacious new head office.

We rolled out more products (such as Life

Improvement Loan, Emergency Loan and

Agriculture Machinery Loan) to meet clients’ needs.

TPC received the standard social rating BB from

Microfinanza in 2014 for TPC’s implementation

of social performance management, client

protection, outreach, and quality of services.

TPC was awarded the MIX S.T.A.R. MFI 2014 from

MIX Market for its commitment to being socially

transparent and responsible.

We received the Progress out of Poverty Index

certification (PPI) at the basic level from

MicroFinanza, a testament to TPC’s exemplary use

of the social performance measurement tool.

TPC received a “Platinum” rating by GIIRS in 2014,

which recognizes business models that are

specifically designed to solve social or

environmental problems through company

products/services.

We further strengthened our efforts on client

protection. We strengthened our client complaint

mechanisms, trained all staff on proper

communications and handling of clients, and

improved our human resource management tools

and materials to encourage all staff to focus on

client protection and continue to reduce

over-indebtedness.

TPC also recruited more staff in 2014 with the aim

to ensure a good succession plan and business

continuity. We also sent more team members to

international training, including exposures by

department heads and branch managers in Sri

Lanka.

We continued to assist the various communities

where we operate. We led numerous community

events; including repainting of public school

classrooms, tree planting activities, road and bridge

reparation, and blood donation, among others.

•

•

•

•

•

•

•

•

•

Providing diversified new products and services;

Applying for Client Protection Principles (CPP)

Certification from a rating agency.

Conducting a feasibility study on Micro-Insurance

subsidiary.

Planning to look for a new, real-time core banking

system to support TPC’s growth and development

of products and services, as well as to improve risk

management.

Planning to explore the potential of technology

oriented delivery channels as a way of improving

customer service and increasing efficiency.

Continuing to intensify our Social Performance

Management (SPM) program; and leverage it to

maintain strong risk management as well as to

increase our market share.

As part of our strategy to broaden our product

offering, we will explore options to reach the

underserved portion of the urban and rural

population through enhanced product offerings that

meet their specific needs.

•

•

•

•

•

•

•

Strategic Priorities for 2015Opening offices in 6 new locations, namely in Kampong Trach, Kampong Tralach, Banan, Angkor Chum, Dambae and Kien Svay. The locations are economically very active, with a stable agriculture base, but are currently underserved by formal financial service providers;

•

Mr. SOK VoeunChief Executive Officer

Annual Report 2014 15

Thaneakea Phum (Cambodia), Ltd.16

Cambodia is one of the “top ten” fastest growing economies in the world, having experienced an average 7% growth rate over the last 10 years. Located in South East Asia with the “New Tiger” economies Thailand and Vietnam as neighbors, Cambodia is quickly emerging and progressively transitioning from a low-income to an emerging-market economy.

The Cambodian population was estimated at 15.18 million people in 2014, with 20.5% of the population aged between 15 and 24 years old, while average population growth is stable at 1.5% (2009-2014). With around 80% of the population living in rural areas, some socio-economic disparities are noticeable between the capital of Phnom Penh, where 2.2 million people live, and the rest of the country. Nevertheless, transport, communication and power infrastructures are improving quickly in Cambodia, creating new opportunities for Cambodians living in rural areas.

Cambodia’s GDP is divided between 34.8% in agriculture, 24.5% in industry and 40.7% in services. While the garment industry remains the main growth driver, the construction sector came second as the tourism and crops sectors are decelerating. Growth prospects are therefore positive for Cambodia’s economy, as its long-lasting growth and renewed political stability are building confidence among international investors and facilitating Foreign Direct Investment (FDI). In 2014 GDP growth remained high at 7%.

Cambodia has achieved several development-related successes and reached the Millennium Development Goals targets in 2009 by improving maternal health, lowering the child mortality rate, and building the conditions to offer primary education to every child. In 2014, the adult literacy rate reached 74%. Cambodia is among the world’s fastest-growing economies. It has rapidly reduced poverty from nearly 50% of the population in 2007 to just 19% in 2012, although many people have moved only slightly above the poverty line and remain vulnerable.

Cambodia at a Glance

Economic Data for this section is taken from the Asian Development Bank and MEF

Annual Report 2014 17

Source of data is taken from Cambodia Microfinance Association (CMA)

Micro�nance Sector There are 39 microfinance institutions (MFI) in Cambodia, reaching different parts of the population according to their business strategies and target clients. In 2014, the Cambodian microfinance industry operated a Gross Loan Portfolio (GLP) of USD 2,503 million (ACLEDA Bank’s small loans included) and over 2 million borrowers throughout the country. The Cambodian microfinance sector has experienced significant growth since the beginning of the decade from a GLP of USD 572 million and 1 million borrowers in 2011, while experiencing an average of 45% growth during the last five years.

The expansion of the microfinance sector plays an important role in increasing domestic demand and investment in the country, benefiting to the country’s economy. By reaching more and more people in underserved areas, the microfinance sector and the diversification of its product offering are modifying Cambodian attitudes towards savings and consumption as they enjoy greater access to credit, deposits and ATM services.

Finally, the expansion of the Cambodian microfinance sector also comes with better practices, the implementation of risk-averse policies and also further regulations by the National Bank of Cambodia (NBC) and the Credit Bureau of Cambodia (CBC). In the last quarter of 2014 the reported average Portfolio at Risk (PAR > 30 Days) of the microfinance industry (comprised of 39 MFIs, ACLEDA Bank’s small loan and 6 NGOs) was 0.72% and the write-off ratio was only 0.09%. These figures reinforce the image of the Cambodian microfinance sector as one of the most performing and sustainable in the world, with clients strongly benefiting from the services they receive and generally facing a low risk of over-indebtedness. The microfinance sector employed 30,650 people as of December 2014.

Thaneakea Phum (Cambodia), Ltd.18

Brief Overview of TPCto greatly improve its operations and procedures. After four years as TPC’s majority shareholder, Developing World Markets (DWM) sold 55.5% of its equity stake to LOLC Micro Investments, Ltd. (LOMI), a wholly-owned subsidiary of LOLC PLC. With operations in Sri Lanka, Myanmar, and Cambodia and total assets of USD 1.3 billion, LOLC demonstrates both the experience and resources to support TPC’s sustainable and steady development for years to come. LOMI now owns 60% of total shares, while DWM remains a significant minority shareholder with 36.97% of total shares and 3.03% are owned by TPC staff through an Employee Stock Ownership Plan (TPC-ESOP).

With the consolidation of its financial ownership, sound social performance management and twenty years of experience in the microfinance sector celebrated this year, TPC can look at its future with serenity and confidence, pursuing its mission to give the greatest number of clients an access to its financial services.

Thaneakea Phum (Cambodia), Ltd. (TPC) is a rapidly growing regulated microfinance institution with a focus on serving families at the base of the socio-economic pyramid in rural and urban Cambodia. TPC serves close to 190,000 clients through a network of 54 branch offices in 22 provinces, and TPC is the 5th largest MFI in Cambodia (in terms of number of borrowers and gross loan portfolio). TPC stands out among its peers thanks to its commitment to responsibly serving clients, focusing on customer service, providing innovative products, as well as fair and transparent pricing, and thus became a trusted provider of financial services in rural and urban areas.

TPC was established by Catholic Relief Services (CRS) in 1994 to enable rural women to gain access to financial services in order to finance their microenterprises. In January 2010, Developing World Markets (“DWM”), a US-based, socially responsible emerging markets fundmanager acquired a majority equity stake in TPC from CRS. With over 15 years of experience and approximately USD 760 million in assets under management,DWM's oversight and high standards have enabled TPC

Annual Report 2014 19

20-year track record providing socially responsible microfinance services in Cambodia

- Founded by Catholic Relief Services as part of Small Enterprise Development Program

- First regulated by National Bank of Cambodia

- Continued growth through support of USAID and McKnight Foundation

- Incorporated as Thaneakea Phum (Cambodia), Ltd. (Village Bank Cambodia in Khmer)

- Licensed as a Microfinance Institution by National Bank of Cambodia

- Employee Stock Ownership Plan established

- Acquired by Developing World Markets- Gross Loan Portfolio exceeds USD 22 million- Rollout of Seasonal Loan product for agricultural clients

- Develops Microbusiness Expansion Loan product- Develops Collateral Management System and set up Risk Department

- Launches the Home Improvement Loan in partnership with OPIC and Financial Literacy program with Good Return Australia- First MFI to implement credit check through the Credit Bureau of Cambodia

- Established the Environmental and Social Performance Management Committee

- New Head Office established in Phnom Penh- Majority stake in TPC acquired by LOLC Micro Investments Ltd. (LOMI)

Brief History of TPC

1994

1999

2001

2002

2003

2007

2010

2011

2012

2013

2014

Thaneakea Phum (Cambodia), Ltd.20

Annual Report 2014 21

My Farming... My Life...Nearly two thirds of TPC’s clients work in agriculture or farming. Farmers, with seasonal incomes dependent on hard work, use our services to invest in farming equipment and working capital to increase their revenue. Recently, we began offering loans for heavier agricultural machinery, like tractors. Achieving the sustainable economic empowerment of people in rural areas has always been, and will always be, a priority.

Thaneakea Phum (Cambodia), Ltd.22

Responsible Growth2014 was a pivotal year for TPC as the company welcomed a new majority shareholder, LOLC Micro Investments, Ltd. (LOMI), after 4 years and half of a highly successful relationship with Developing World Markets (DWM). Our long-term commitment to empower entrepreneurs and families at the base of the socio-economic pyramid in Cambodia was realized through the development of new products tailored to our clients’ needs, sound internal control policies, and financial literacy programs aimed at enhancing the overall client experience. In 2014, having again experienced impressive growth in our loan portfolio, number of borrowers and operational areas, TPC is continuing on its growth path while exerting due diligence on our operational activities.

TPC’s Gross Loan Portfolio grew by 54% from USD 74.9 million in 2013 to USD 115.4 million in 2014, while the number of clients grew by more than 35,000 from 153,952 in 2013 to 189,345 at the end of 2014. Having consolidated its risk controls and lowered the Portfolio at Risk rate (>30 Days) from 1.96% in 2010 to 0.10% in 2014, TPC built solid grounds for further responsible expansion of its activities in Cambodia. The aforementioned LOMI acquisition of 60% of TPC shares occurs at an appropriate time.

After achieving an average growth of 51% per year, TPC needed a strong stakeholder to support its growth path and further consolidate its risk and internal control policies. TPC maintains a high-quality loan portfolio thanks to strong internal controls, a careful monitoring of its loan products’ disbursement and collection processes, as well as the provision of extensive training and capacity building for its staff. In this regard, LOMI’s leadership will not only allow TPC to expand its operations but will also provide TPC with the expertise of more than 30 years’ experience in financial services in South East Asia. LOMI’s expertise is with microfinance-related challenges and the two organizations have already started working together on IT management issues and client data protection.

TPC’s long-term commitment to prevent over-indebtedness among its clients and to generate fair customer outcomes, illustrated by its strict credit and multiple loan policies, will be backed and pushed forward by its new shareholder. LOMI, the LOLC Group’s microfinance subsidiary was recognized in February 2014 as the first Sri Lankan microfinance institution to receive the Client Protection Certification from the Smart Campaign. TPC also took several steps towards an effective social performance management, such as the implementation of the Smart Campaign Client Protection Principles, the use of the Progress out of Poverty Index tool, and the development of environmental and social performance management, for all of which it has received rewards. In 2014, TPC became the 3rd MFI in Cambodia to receive the S.T.A.R certification from MIX Market for achieving high level of transparency and compliance to social performance standards. These initiatives and their derived processes contribute to the reduction of all client-related risks and ensure that TPC treats its clients fairly.

TPC also looks at innovative ways to fulfill its mission to empower rural entrepreneurs and families. In 2014, in partnership with Good Return, an initiative of World Education Australia, TPC provided financial literacy courses to 7,000 people in 7 provinces. Additionally, in partnership with Agence Française de Développement (AFD), TPC is seeking to encourage the use of renewable energy in rural and urban Cambodia by developing a new loan product for clients who wish to buy solar energy products.

Finally, our operations and projects have been supported by growing our number of staff from 874 in 2013 to 1,156 in 2014. TPC opened 8 new branches in 2014 – up to a total of 54 branches – and now operates in 22 provinces throughout the country. Our staff members all receive an extensive training on TPC’s internal and credit policies as TPC is dedicated to align our growth path with the quality of our loan portfolio.

Annual Report 2014 23

Trend in Product MixTPC has strengthened and diversified its product offering throughout the years in order to meet its clients’ evolving demands and needs. Our mission to empower people at the base of the socio-economic pyramid is thus shaping our products’ design. Furthermore, we intend to be as flexible as possible in their application and delivery, removing any barriers of access to our services. We have also expanded the size of our individual loans and designed new products aiming at meeting clients’ needs.

TPC’s group loans (Thaneakea Phum Loan and Solidarity Group Loan) are TPC’s most well-established loan products; this is mainly due to their popularity among rural communities and the clients’ knowledge and trust in these products as they are highly representative of the whole microfinance market product offering. The Thaneakea Phum Loan (TPL) and Solidarity Group Loan (SGL) respectively account for 27% and 9% of total Gross Loan Portfolio (GLP) and jointly represent 75% of TPC borrowers. Although these two products are well-functioning and enjoy clients’ satisfaction we are always looking for ways to improve their quality. TPC is currently looking at the possibility of increasing the loan size of the TPL and SGL.

The Individual Loan (IL) accounts for 36% of the GLP and 16% of the clients. With a larger loan size, the IL is intended for entrepreneurs whose growing businesses need working capital. TPC’s Seasonal Loan (SNL) is intended for clients with agricultural activities who need to finance their inputs and repay the loan once the harvest is sold. The SNL allows for balloon or semi-balloon repayment of loan principal. The Micro-Business Expansion (MBE) loan has a maximum loan size of USD 20,000 and provides small and medium-sized business owners ample capital to grow their businesses. While their target client segments are different, the success of these products show a positive market reception for an enhanced product offering.

TPC also offers additional products attached to our core products. This is the case for the Top-Up loan introduced in 2013. This product is offered to IL and MBE clients who wish to borrow additional funds from TPC before repayment of their current loan is completed. As part of TPC’s due diligence and in order to mitigate risks of over-indebtedness, the Top-Up loan can only be granted to clients who have demonstrated strong repayment discipline and a steady repayment capacity.

In 2014, TPC launched a new individual loan product with the name of the Quick Individual Loan (QIL) which is designed for productive purposes for people willing to consolidate their business or create a new one. Its smaller loan size (up to USD 3,000) in comparison with the IL makes it easier and faster to disburse, though the conditions of access are stricter than those of the IL in order to properly manage the risk carried by accelerated procedures.

The Loan for Agricultural Machinery (LAM) is one of the main highlights of year 2014. This individual loan can be accessed for an amount of USD 1,000 up to USD 35,000 constituting the highest loan amount a TPC loan can offer. This is due to the loan purpose, which is primarily the purchasing of agricultural machinery for farmers and service providers (machine rental businesses) in order to raise their productivity, yield, and ultimately generate more profits. The LAM is currently available in the 14 branches where the largest farms are. The LAM is available either in US dollars or in Thai Baht. Furthermore, TPC is planning to expand the LAM’s availability to other provinces.

TPC has also moved forward in the offering of non-productive loans. After rolling out the Home Improvement Loan (HIL) which offers a term loan to allow home owners to improve their homes without the need to extract capital from their businesses, TPC launched a new product in 2014, the Life Improvement Loan (LIL). The LIL provides clients who have stable sources of income with the opportunity to finance further consumption and personal purchases against an affordable interest rate and loan term. As of December 2014, the HIL and LIL respectively represented 4% and 3% of TPC Gross Loan Portfolio (GLP), that is USD 4.6 million and USD 3 million. TPC now provides an Emergency Loan (EL) that is made for existing group loan clients who face an emergency in their life which requires them to engage money to fund an exceptional expense. This loan amount is up to USD 250 and acts as a supportive product.

Thaneakea Phum (Cambodia), Ltd.24

Business Outlook

Strong Risk and ComplianceManagement

In 5 years, TPC has become one of the top 5 MFIs in Cambodia, experiencing a loan portfolio growth of 58.7% from 2010 to December 2014. This success results from strict risk management policies, a top-quality product delivery and customer service, and an enhanced social performance management. Moreover, TPC took the right decisions in order to ensure adequate compliance with the Credit Bureau of Cambodia (CBC) guidance and legislation, therefore making its growth as sustainable and steady as possible.

In 2014, TPC made significant progress towards its goal to operate in every Cambodian province, as it now operates in 22 out of 25 provinces. TPC opened 8 new branches over the course of 2014, up to a total of 54 throughout the country and therefore exceeded its initial goal of 52 fully operational branches by the end of 2014. TPC’s expansion plan continues as the company expects to open 6 more branches in 2015. TPC’s expansion in the country remains an essential component of its ambition to become a leader in the Cambodian microfinance market.

2014 has seen many innovations and new products emerging from TPC’s product development team, as TPC seeks to provide more complex products tailored on its clients’ needs. TPC focused on providing loans corresponding to specific needs and situations, and adapts loan conditions accordingly.

TPC moved forward in providing non-productive loans. TPC sensed that it was the time for aligning its product offering on Cambodia’s economic mutations. As consumption behaviors evolve and more and more standardized goods and services reach underserved areas, people are willing to take part in this economic development. TPC, therefore, launched a new loan, the Life Improvement Loan (LIL) in 2014 to allow people in rural areas to have the resources to buy consumption goods. The LIL comes a year after the Home Improvement Loan was rolled-out, and marks a new step in our product offering diversification. Moreover, the Loan for Agricultural Machinery (LAM) provides solutions for a particular but significant group of TPC’s clients by offering a specific loan to farmers in need of mechanization. TPC will expand its delivery in the course of 2015. Finally, the Quick Individual Loan (QIL) provides more flexible terms to allow entrepreneurs to respond to short-term business needs.

TPC’s individual loan portfolio considerably grew in 2014 as two new loans were introduced: the Loan for Agricultural Machinery (LAM) and the Life Improvement

TPC focuses on building frameworks and exerts due diligence and vigilance over operational risks, financial risks, and regulatory risk as a consequence of increased monitoring and control by the Cambodian regulator, the Credit Bureau of Cambodia. TPC has consequently enlarged its compliance team and added a legal officer in order to support the different departments in all legally-related issues. TPC also made progress in adopting the International Financial Reporting Standards (IFRS), with the objective to achieve full compliance by 2016. In April 2014, it engaged the Cambodian IFRS (CIFRS) conversion service with PricewaterhouseCoo-pers (Cambodia) Ltd (PWC), whose two first phases – Phase 1 “GAAP Difference and Impact Analysis” and Phase 2 “Knowledge transfer”, will be completed in 2015.

Up to now, TPC’s Risk and Compliance management has demonstrated its efficiency and reliability. In this regard, one of the most relevant indicators is the upkeep of a very low Portfolio at Risk (PAR) over 30 days. At the end of 2014, TPC had a PAR>30 Days of 0.10% and had maintained this low rate throughout the year 2014, with very few variations (up to 0.17% in May 2014).

Top Quality Product Delivery andCustomer ServiceHigh-quality product delivery is inherent to TPC’s business strategy and is supported by geographic expansion, broadening of product offerings, and enhanced product delivery channels.

Expansion

Broadening of Product Offering

Annual Report 2014 25

Business Outlook

Enhanced Social Performance Management

TPC maintains its objective to enhance both the quality and speed of its product delivery in the coming years. It will be achieved by pursuing its network expansion, and incorporating more technology and automatic systems in its operations. While developing an upgraded core banking system and field and back-office technology applications, TPC is building a partnership with WING, a telecommunication company, in order to elaborate an automatic repayment system by allowing TPC’s clients to repay their loans through WING Kiosks. These combined new functions will improve TPC’s customer service and serve TPC’s business objectives as an effective customer service stands as a fundamental factor supporting client satisfaction and competitiveness in the Cambodian microfinance market.

Social Performance Management is one of TPC’s core commitments as it ensures the company’s operations and practices are aligned with its social mission. TPC has committed itself to numerous international social performance standards, such as the Universal Standards for Social Performance Management (USSPM) and the Client Protection Principles (CPP), and tracks the impact of TPC’s operations on its clients through the Progress out of Poverty Index (PPI). In 2014, TPC received two important certifications: the S.T.A.R Certification from Mix Market, and the new standard PPI certification by Microfinanza rating. These two certifications reward the effectiveness of our Social Performance Management and give TPC’s good prospects for its present and future sustainability. It also makes TPC an important participant in the Social Performance Task Force (SPTF) Annual Conference, to be held in Cambodia for the first time in June 2015.

In the future, TPC will continue to ensure that its social and environmental commitments are fully integrated into its daily operations. In this regard, the Environmental and Social Performance Management committee including top management and the Social Performance Manager will play a key role in maintaining this high level of social responsibility.

Loan (LIL). TPC’s individual loan portfolio reached USD 72.5 million at the end of 2014 (or 63% of total GLP), of which the IL accounted for 36%, the Seasonal Loan for 15%, the Microbusiness Expansion Loan for 4%, the Loan for Agricultural Machinery for 1%, the Home Improvement Loan for 4% and the Life Improvement Loan for 3%. As TPC’s core target clients are low-income (following the Progress out of Poverty Index’s categories), clients’ demand for individual loans which offer larger loan amounts is likely to increase in the coming years. However, it does not mean that TPC is turning its back on group loans as those remain TPC’s core business in terms of number of borrowers and number of loans by products – the Thaneakea Phum Loan (TPL) and Solidarity Group Loan (SGL) accounts for 75% of TPC’s overall loans.

Enhanced Product Delivery

Thaneakea Phum (Cambodia), Ltd.26

TPC applies the following risk management principles in its day to day business transactions:

Promote sustainable long term growth and profitability by embracing prudent risk management and corporate governance practices.Assist the business in producing stable and consistently high returns for its shareholders.Ensure its risk management strategy is based on a clear understanding of the various risks, disciplined assessment, measurement and monitoring processes.

•

•

•

Risk Management Framework

Management Risk Committee

Credit Committee

Board Risk Committee

Assets and Liabilities Committee (ALCO)

Operational Risk and Other Risk Areas Credit Risk Financial Risk

Risk ManagementRisk PhilosophyManaging risk is inherent in any institution’s strategic business plan and Thaneakea Phum (Cambodia), Ltd. (TPC) is no exception. TPC’s risk philosophy is that risk management should help advance our business strategy, assist the decision-making process and enhance management effectiveness.

TPC’s risk framework is aimed at strengthening the company’s ability to identify, measure and manage risk to maximize shareholder value by aligning risk management with corporate strategy, assessing the impact of emerging risks and developing risk tolerance and risk mitigating strategies which ultimately reflect the Company’s corporate governance and control culture.

The Board Risk Committee is established and chaired by an Independent Board member. Its mission is to oversee all types of risks that occur internally and externally in operations, credit and finance to ensure that the practices and procedures are effective for risk identification and management, and comply with internal guidelines and external requirements. In addition, this committee will oversee the company’s risk management and internal control system to safeguard the company’s assets and financial resources. The committee normally meets once per quarter.

The Management Risk Committee is chaired by the Chief Executive Officer and meets once a month. The main responsibility of this committee is to ensure that TPC is operating with a sound, effective, and efficient risk management system and monitor risk assessment and risk management to safeguard the institution’s assets and financial resources. The committee also focuses on monitoring and mitigating operational risk which may arise from inadequate information systems, technology failures, breaches in internal controls, fraud, unforeseen catastrophes, or other operational problems that may result in unexpected losses or reputation risk.

Board Risk Committee Management Risk Committee

Annual Report 2014 27

Risk Management

The objective of the Credit Committee is to minimize credit loss to an acceptable level. The committee is chaired by the Chief Operations Officer. The responsibility of the committee is to ensure that credit policies are in place, up to date, appropriate to the business and consistent with sound lending practice and to monitor portfolio quality, identify any adverse trends and ensure that remedial action is taken. As a result, the overall portfolio quality was very good by the end of 2014 with the portfolio at risk (PAR) over 30 days at 0.10%. The good quality of portfolio comes from internal and external factors. The Credit Committee normally meets once per month.

Management Credit Committee

Financial risks are managed and controlled by the Assets and Liabilities Committee (ALCO) with the primary goal to evaluate, monitor and approve practice relating to liquid-ity, interest rate risk, regulatory risk, currency risk and other financial risks in order to optimize returns while ensuring that appropriate levels of cash are maintained. The ALCO committee is chaired by Chief Financial Officer. The ALCO Committee normally meets once per month.

Management Assets and Liabilities Committee

Thaneakea Phum (Cambodia), Ltd.28

How Do We Translate Our Mission?

An institution with a social vision

and a business orientation that

provides entrepreneurs and families at

the base of the socio-economic pyramid

with the economic opportunities

to transform the quality of their lives and

their communities through the provision

of effective and sustain able client

empowering financial services

Client: Agri = 70%,Production = 1%,

Trade = 12%,Service = 7%,

Salary and Wage = 10%,Other = 0.1%

Track the change of PPI

Adoption of Client Protection Principles

OSS* = 274%,FSS** = 150%

84.58% are women, 29.22% livingbelow KHR 3,704.83 (2012 CPI)

Loan and Non-�nancial products and services

* Operating Self Su�ciency** Financial Self Su�ciency

Annual Report 2014 29

Measuring our Impact through PPI

TPC Poverty Outreach:

Social Performance Management

The Progress out of Poverty index is used to measure TPC outreach to poor clients, determine transformation of the quality of clients’ lives, and ensure that appropriate products are extended to the right target clients. Moreover, using the PPI, TPC can determine its categories of client as below:

For its outstanding use of the PPI tool, TPC is the first recipient of PPI certification certified by Microfinanza in 2014.

As of December 2014, 92,590 new clients are estimated their poverty likelihood through PPI. The result indicates that the majority of TPC’s client is comprised in poor and low-income categories.

Client Poverty Progress:

Since 2012 the poverty likelihood of randomly selected clients has been monitored and surveyed from one year to another. TPC has monitored those clients in 3 consecutive years and clients’ poverty improvements can be estimated, as shown in the graph below.

Very Poor: Those who are living below national poverty linePoor: Those who are living below 150% national poverty lineLow-income: Those who are living below USD 3.57/Day 2005 PPPNon-poor: Those who are living above USD 3.57/Day 2005 PPP

•

•

•

•

20% 12% 8%

30%25%

19%

39%46%

48%

11% 18% 25%

0%

20%

40%

60%

80%

100%

120%

2012 2013 2014

"Non-Poor"

"Low-income"

"Poor"

"Very Poor"

20%12%

8%

50%

37%

27%

89%82%

75%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014

"NPL"

"150% NPL"

"USD 3.75/Day/2005"

Client Poverty Outreach:

Client Poverty Progress by poverty line

Client Poverty Progress by categories

Very Poor,

Moderate poverty/ poor, 20.47%

Low income, 47.64%

Non - Poor,

23.14%

8.75%

Thaneakea Phum (Cambodia), Ltd.30

How Does TPC Integrate Client Protection Principles into Core Business?

3. Transparency

- Use A4 Metacard (information disclosure) at assessment & disbursement- Client is informed of the ir rights and responsibilities- Interest rate is disclosed when marketing

- Thorough cash flow assessment determine loan size &repayment

capacity- 100% check credit bureau- Refined / develop product

- Incentivize loan quality- Restrict multiple loan

Client Protection Principles

- Range of interest rates is approved by board of directors- Efficiency ratio aligned with peers- Penalty and fee charge are not excessive

4. Responsible Pricing

- Strict implementation on code of conduct- Define appropriate collection practices- Do not endorse/ implement zero tolerance on PAR- Sanction/ penalty on misconduct of code- Inform client of their rights

5. Fair and respectful treatment of clients

- Formalize privacy policy- Inform client about data usage & sharing & ask consent before data collection- Secure IT system and segregation of duties of access- Train staff about confidentiality of information

6. Privacy of Client Data

- Active complaint resolution system- Assigned staff to handle complaint- Client complaint are recorded, reported, audit, and analyzed, used to improve products & services

7. Mechanisms for complaint resolution

2. Prevention of Over-indebtedness,

1. Appropriate Product Design

& Delivery Channel,

- Diversify products,repayment methodology

- Collection and disbursement in community

- Refined/ develop productusing client feedback

- Has proper loan recovery procedure that protect the client

Annual Report 2014 31

Cash Management Savings Debt ManagementSmall Business Management.

••••

Financial Literacy Education UpdateImproving financial literacy in the community is an important social goal for TPC. In partnership with Australian NGO Good Return, TPC developed the “Learning for a Better Life” (LBL) program to train clients and non-clients alike on topics such as:

The program was successfully piloted from July 2013 to June 2014 and began full rollout from June 2014 across six TPC branches. To maximize the program’s usefulness on the ground, priority for the rollout was given to communities with a higher incidence of multiple borrowing. University students were also specifically targeted for raising awareness in the youth age group.

Accumulated from 2013 to 2014, there were 7,324 participants in the LBL program, with 5,590 of these participants being female and 1,934 of participants being university students.

Thaneakea Phum (Cambodia), Ltd.32

TPC randomly samples its clients to assess side effects to the environment through its business operations. The assessment covers all of TPC’s operational regions, having interviewed 316 clients. The research focuses on pollution, health and safety, and labour.

The survey mapping client’s environmental risk along two axes: client risk level and client’s risk management quality. On the horizontal axis is clients’ risk level, which

refers to the potential environmental damage, and ismeasured by the client’s size and type of business (i.e. a large farm poses a higher environmental risk than a small grocery shop). On the vertical axis is clients’ risk management quality, which refers to the ability to identify and mitigate environmental risks, and is measured by their knowledge of environmental risks and their actions to improve/ prevent these.

EnvironmentalAssessment Survey

High(3)

High(3)

Medium(2)

Medium(2)

Clients Risk Level

Clie

nts

Ris

k M

anag

emen

t Qua

lity

High - Mitigate

Medium - Monitor

Low - No action

Low(1)

Low(1)

Environment Affected by sourcesof energy

Emission (kg-CO2)

Electricity (kWh), 16.4

Gasoline (litre), 44.79

Diesel (litre), 83.79

Kerosene (litre), 4.29

LPG (kg), 46.42

Overall, the average TPC client (a household) emitted CO2 195.69 Kg-CO2 per month. The graph below is the distribution of emission energy by categories.

Annual Report 2014 33

Environmental Assessment Survey

9.18% of household’s members have no experience of sickness in the last 12 months, while 90.82% have experience with illness. The most common disease that afflicted household members was general illness

(53.19%) such cough, fever, headache. Other fairly frequent illnesses in the last 12 months were typhoid, malaria, diarrhea, strep throat, dengue fever, pneumonia, and other diseases.

Health and Safety Assessment

Have no experience of sick last year

9.18%

General Illness

53.19%

Diarrhea4.77%

Dengue Fever1.76%

Strep Throat1.76%

Malaria5.77%

Pneumonia1.76%

Typhoid Fever6.77%

15.05%

Have experince of sick last year

90.82%

Other diseases (stomach ache, diabet, excess sugar, hemorrhoid, gallbladder inflammation...)

Work Accident of Client’s Business Activities

Client’s Health Assessment

93.67%

3.71%

1.96%

0.65%6.33%

Have never faced any accident

Have ever faced accident

Dizzy/Tired

Headache

Fever

As an MFI whose activities impact almost 200,000 people and their families, TPC has the opportunity to leverage its outreach to improve the Cambodian people’s living environment. TPC’s Board of Directors and Management Team therefore encourage it all branches and head office to design, develop and organize community events where TPC staff and local communities are invited to work together on socially or environmentally related projects in their communities. These events therefore enhance our service and impact, strengthen our relationships with local communities and directly benefit the people.

In 2014 TPC organized 50 community events throughout the country with almost 10,000 participants. The diversity

of projects conducted by TPC staff and local communities covers material and logistical support such as road improvement, land refilling, school cleaning, garbage collection, hygienic or informational support by raising awareness on hygiene among children, hand washing product distribution, and donation of text books. Community events generally receive a wide and very enthusiastic interest of all community members as they create unique conditions for village leaders, school principals and villagers to contribute to a project that will benefit the whole community. TPC will continue to organize such community events and increase their numbers in the coming years.

Thaneakea Phum (Cambodia), Ltd.34

Community EventHighlights

Annual Report 2014 35

Partnership UpdateIn 2014, TPC established new partnerships and strengthened existing partnerships, in order to offer TPC’s rural client base the opportunities to improve their standards of living.

Since 2013, TPC has partnered with the Australian NGO Good Return to provide financial literacy training to

clients, non-clients, and university students. Good Return and TPC have also collaborated on

strengthening social performance (Universal Standards of Social Performance) and client protection in line

with the SMART Campaign. Good Return supporters continued to fund TPC micro-loan clients through the

Good Return online portal.

USAID – DCA has also been an important partner for TPC, having provided TPC with the means to assist

farmers and other small business owners involved in agriculture value chains to access micro-loans. In 2014,

401 clients with a loan portfolio of USD 552,480 were funded in Battambang, Kampong Thom, Pursat and

Siem Reap provinces. In addition to giving loans, a local project implementer, HARVEST, is also providing

technical agriculture training to TPC field staff and farmers, including TPC clients.

In October 2014, TPC and Agence Française de Développement signed a partnership to commence rollout

of a Solar PV micro-credit product in 2015 to offer rural households not connected to the grid with improved

electrification. Looking forward, this is an exciting development with the prospect of assisting Cambodia’s

under-served rural population to access electricity through environmentally-conscious practices.

To provide more convenient payment options to clients, TPC has partnered with WING to pilot its mobile

repayment procedure. This enables clients with businesses far from home and MFI offices to process

repayment from anywhere. Thus, clients are offered a more secure and cost-effective method of payment,

rather than the traditionally riskier methods of sending repayments to MFI branches via motor-taxi drivers or

other community members. At the end of 2014 WING has more than 660 Cash Xpress vendors throughout

Cambodia that TPC clients can conveniently process their repayments through.

30-year-old Outh Savuth lives with her husband, three young age children and her parents in Prey Nheat village, Kampong Speu province.

In 2010, after the birth of her third child, Outh Savuth and her husband realized that his salary as a construction worker in town was not sufficient to support the family’s expenses. Although they did not have any savings she was told that she could get a loan from TPC, a microfinance institution that her neighbors just got a loan from. She always wanted to buy the farming land located in her house’s backyard but she didn’t have enough capital. Finally, she obtained a loan of USD 2,000, which was disbursed in early 2010. She started growing rice on her new land the same year.

a hand-tractor and a trailer so she could ship more rice to the market. Because she had demonstrated her reliability and that her incomes had significantly increased, TPC approved a bigger individual loan of USD 3,000.

Since then, Outh Savuth’s activities considerably evolved. On the way to the market, Outh Savuth and her husband loaded up to 1 ton of rice and on the way back to their village, they brought fish, meat, vegetables, fruits and all sort of elementary goods such as soaps, coffee bags, biscuits, beers. The main challenge for rice producers is that they can only get revenues during the production period running from July to December. But after this diversification in her activities, she could ensure steady revenues all year through.

Today, Outh Savuth is in her third loan cycle with TPC and she uses the money to buy more products at the market and resell those products in her village, as well as for building a small roof to protect her grocery shop installed right next to her house. Outh Savuth and her husband hope to renovate and expand their house to build a third room for their children.

Thaneakea Phum (Cambodia), Ltd.36

With her production quickly growing, Outh Savuth started to sell it at her house’s front door to the people in the village. During the harvesting season, Outh Savuth could harvest around 8 tons of rice per year from her 3 hectares of land. After a few months she increased her revenues to USD 170 per month. Outh Savuth started to sell her production at the market located around 10 kilometers away from Prey Nheat village. Every day she loaded her production on her husband’s motorbike to go to the market. When she paid off her first loan, she had the idea to get a new loan from TPC to buy

Client StoriesOuth Savuth

Annual Report 2014 37

Client Stories

Soem Yun, 56, and her husband Kong Meanleak, 55, live in Koh Krous, about 50 kilometers away from Phnom Penh. Their two children left the house a couple years ago to work in garment factories in the capital city and send their parents money every month. Their support constitutes a safety net that allows them to take care of the house and maintain their standard of living. Back in 2010, the couple established a small bicycle and motorbike repair shop in front of their house, in which Soem Yun was in charge of the retailing of maintenance products and spare parts (lubricant, nuts, tires, electric-related pieces etc.), and Kong Meanleak was in charge of the repairing activity. Although there are many repair shops in the area, Soem Yun and Kong Meanleak have a strong reputation in Koh Krous. “I think that the people around know that we can fix and bring solutions to most of the problems they can meet”, says Kong Meanleak as he points to the air pump he bought thanks to his second TPC loan of USD 250. Although Soem Yun already used two out of her 4 loan cycles to buy spare parts – respectively for USD 125 and USD 325 – she says that their immediate need is to focus on motorbike’s spare parts that are usually more expensive and that people specifically look for.

From a small business in which only Kong Meanleak was repairing bicycles, Soem Yun was able to add more activities and generate more incomes by retailing spare parts for both bicycles and motorbikes. Furthermore, Soem Yun and Kong Meanleak are now able to look at more quality-focused aspects as they recently built a cement slab in order to make it easier for clients to get into the shop with their vehicles and a new wall to close and protect the shop at night.

Their new revenues and recent achievements allow them to apply for a larger TPC loan of USD 500. Soem Yun is very thankful to TPC’s credit officer for supporting her projects throughout the last past years:

“We have a really good relationship with TPC’s credit officer; he really helped us to progressively move to new loans as our incomes were growing”.

When asked about her plans for the future she says she would like to further increase her own household’s revenues so her children would be free to fully enjoy the fruit of their hard work.

Soem Yun

Sound Corporate Governance practices are at the heart of our success at Thaneakea Phum (Cambodia), Ltd. (“TPC”). TPC operates within an integrated Governance framework formulated after taking into consideration the Corporate Governance regulations issued by the National Bank of Cambodia and other Corporate Governance best practices.

The Board of Directors, composed of 5 members and led by the Chairperson, is responsible for the high level governance of TPC and for developing effective Governance Frameworks to meet challenges, both in the short and long term. Three Board Committees, Audit, Risk and Remuneration and Recruitment provide oversight and guidance on the main aspects of TPC. The Board has established an on-going process for identifying, evaluating and managing the significant risks faced by TPC and this process includes enhancing the system of internal controls as and when there are changes to the business environment or regulatory guidelines. Importantly, TPC’s Internal Audit Department is independent of management and reports directly to the Board Audit Committee.

At Management level, the Chief Executive Officer oversees the Finance, Operations, Human Resource, Risk and Compliance, Administration and Procurement,

and IT departments. Four management committees, Credit, Assets and Liabilities, Risk and Executive committees meet monthly and help top management remain focused on accomplishing TPC’s medium and long term strategy.

The TPC Board and Management understand the importance of clear governance guidelines and a free, fair and transparent environment at all levels of the organization, and work hard to become such an organization. We are committed to reviewing and improving our systems to provide transparency and accountability to ensure best practices are maintained and enhanced according to the principles of good Corporate Governance.

TPC’s approach to governance is predicated on the belief that there is a link between high quality governance and the creation of long-term stakeholder value. In pursuing the Corporate Objectives, we have committed to the highest level of governance and strive to foster a culture that values and rewards exemplary ethical standards, personal and corporate integrity and mutual respect.

Thaneakea Phum (Cambodia), Ltd.38

Overview of Good Governance

Annual Report 2014 39

Boa

rd o

f Dire

ctor

s(B

oD)

SH

AR

EH

OLD

ER

S

(LO

MI,

DW

M &

ES

OP

)

App

oint

men

t &R

emun

erat

ion

Com

mitt

ee

Ris

k M

anag

emen

t C

omm

ittee

Aud

it C

omm

ittee

Com

pany

Sec

reta

ry C

hief

Exe

cutiv

e O

ffice

rIn

tern

al A

udit

Dep

artm

ent

Soci

al P

erfo

rman

ce &

En

viro

nmen

tal

Man

agem

ent C

omm

ittee

Exe

cutiv

e C

omm

ittee

Cre

dit

Com

mitt

eeR

isk

Com

mitt

eeA

LCO

Com

mitt

ee

Lega

l & C

ompl

ianc

e

Chi

ef O

pera

tions

Offi

cer

Reg

iona

l Man

ager

s

Bra

nch

Offi

ces

Res

earc

h &

Prod

uct

Dev

elop

men

tB

usin

ess

Dev

elop

men

tD

epar

tmen

tB

rand

& P

rom

otio

nS

avin

g D

epar

tmen

tC

redi

t Dep

artm

ent

Lend

ing

Bra

nch

Sup

port

Dep

artm

ent

Chi

ef F

inan

ce

Offi

cer

Hum

an R

esou

rces

Dep

artm

ent

Fina

nce

Dep

artm

ent

Info

rmat

ion

Tech

nolo

gy D

epar

tmen

tA

dmin

istr

atio

n &

Proc

urem

ent D

epar

tmen

tR

isk

Man

agem

ent

Dep

artm

ent

Not

ice

Cur

rent

pos

ition

In th

e fu

ture

pla

n

Com

mun

icat

ion

line

Dire

ct s

uper

visi

on li

ne

Soci

al P

erfo

rman

ce

Man

agem

ent D

epar

tmen

t

Organizational Chart

Thaneakea Phum (Cambodia), Ltd.40

60.0%

36.97%

3.03%

LOLC Micro Investments Ltd. ("LOMI")

Developing World Markets ("DWM")

TPC Employee Stock Ownership Plan("TPC-ESOP")

Ownership StructureTPC ownership structure has been reshaped by the acquisition of 60% of TPC shares by LOLC Micro Investment Ltd. (“LOMI”) in September 2014. The Sri Lankan socially responsible investment fund is now the majority shareholder, while Developing World Markets (“DWM”) remains a significant minority shareholder with 36.97% of the shares. TPC’s Employee Stock Ownership Plan (“TPC-ESOP”) owns 3.03% of TPC shares.

Shareholding as of December 31, 2014 is as follows:

LOLC Micro Investments Ltd. (”LOMI”), wholly owned by Lanka Orix Leasing Company Plc (LOLC), is a public listed company in Sri Lanka. LOLC was established in 1980 as a pioneering provider of leasing products in Sri Lanka and has since expanded to offer a range of financial and non-financial products and services. As of 31 March 2014, LOLC reported total assets of approximately USD 1.3 billion. Its microfinance subsidiary, LOMC was established in 2009 in partnership with the Dutch development bank, FMO, and was recognized in February 2014 as the first Sri Lankan microfinance institution to receive Client Protection Certification from the Smart Campaign. LOLC also began microfinance operations in Myanmar in 2013 and holds a minority stake in the Cambodian SME lender Prasac.

Developing World Markets is a US-based dedicated emerging markets asset manager with a mission to improve lives at the base of the economic pyramid. As a leading fund manager for microfinance and other impact assets, DWM aims to achieve sustainable development through market-level, financial returns for its investors, and social returns in the developing world. As of December 31, 2013, DWM managed approximately USD 665 million in assets primarily from institutional investors. Over the past 10 years, DWM has structured or advised on over USD 1 billion in microfinance transactions, including work done by DWM’s affiliate, DWM Finance, LLC. DWM has financed over 140 inclusive finance providers in over 40 countries, and currently has a staff of 30+ professionals, speaking over 20 languages.

TPC-ESOP is a vehicle through which eligible employees can acquire an ownership interest in TPC. The ESOP serves as an employee benefit that enables employees to share in the long-term growth and future of TPC.

Shareholders by Percentage

Annual Report 2014 41

Thaneakea Phum (Cambodia), Ltd.42