Embed Size (px)

Citation preview

A N N U A L R E P O R T A N D S U S T A I N A B I L I T Y R E P O R T

2 01 0

LK

AB

A

NN

UA

L

RE

PO

RT

A

ND

S

US

TA

INA

BIL

ITY

R

EP

OR

T

20

10

C O N T E N T S

L KAB , BOx 952 , SE 971 28 LU L Eå , SwEDEN www. l k ab . com

LKAB 2010

Overview of the past year 4

President’s report 6

Group strategies 10

L K A B ’ S A N N U A L R E P O R T 1 2

Market and economic trends 13

International iron ore trade 15

Capacity and logistics 17

Ore reserves and mineral resources 19

Research and development 20

S U S TA I N A B I L I T Y R E P O R T 2 2

Stakeholders and sustainability issues 24

Value creation 25

Urban transformation, Kiruna and Malmberget 27

Environment 31

Significant events during the year 33

Environment per operating location 34

Energy 37

Atmospheric emissions 39

waste 41

water 44

Deformations 45

Seismic events/rock mass displacements 45

Site remediation 46

Co-workers 47

Sustainability Management 110

GRI index 112

Auditors’ statement of assurance,

Sustainability Report 114

C O R P O R AT E G O V E R N A N C E R E P O R T 5 2

Board of Directors and Group Management 56

Auditors’ Report on the Corporate Governance Report 59

F I N A N C E 6 0

Group overview 60

Report of the Directors 62

Financial reports and notes 72

Proposed disposition of unappropriated earnings 108

Auditors’ Report 109

Glossary 115

Addresses 116

Annual General Meeting and financial information 117

A N N U A L R E P O R T A N D S U S T A I N A B I L I T Y R E P O R T

2 01 0

LK

AB

A

NN

UA

L

RE

PO

RT

A

ND

S

US

TA

INA

BIL

ITY

R

EP

OR

T

20

10

C O N T E N T S

L KAB , BOx 952 , SE 971 28 LU L Eå , SwEDEN www. l k ab . com

LKAB 2010

Overview of the past year 4

President’s report 6

Group strategies 10

L K A B ’ S A N N U A L R E P O R T 1 2

Market and economic trends 13

International iron ore trade 15

Capacity and logistics 17

Ore reserves and mineral resources 19

Research and development 20

S U S TA I N A B I L I T Y R E P O R T 2 2

Stakeholders and sustainability issues 24

Value creation 25

Urban transformation, Kiruna and Malmberget 27

Environment 31

Significant events during the year 33

Environment per operating location 34

Energy 37

Atmospheric emissions 39

waste 41

water 44

Deformations 45

Seismic events/rock mass displacements 45

Site remediation 46

Co-workers 47

Sustainability Management 110

GRI index 112

Auditors’ statement of assurance,

Sustainability Report 114

C O R P O R AT E G O V E R N A N C E R E P O R T 5 2

Board of Directors and Group Management 56

Auditors’ Report on the Corporate Governance Report 59

F I N A N C E 6 0

Group overview 60

Report of the Directors 62

Financial reports and notes 72

Proposed disposition of unappropriated earnings 108

Auditors’ Report 109

Glossary 115

Addresses 116

Annual General Meeting and financial information 117

EnvironmEntal gains with “lKaB grEEn PEllEts”Total carbon dioxide emissions from the production of crude steel, about 2,000 kg CO2/tonne, are reduced when LKAB pellets are used as the iron raw material. The manufacture of LKAB pellets generates one seventh of the carbon dioxide emissions as compared to sintering at the steelmill, and one-third as compared to hematite-based pellet manufacture. The reduction is about 215 kg and 95 kg CO2/tonne crude steel, respectively.

Fe3o4 4,100EmPloYEEs

thE high-gradE magnEtitE orE From lKaB’s minEs is somE oF

thE world’s BEstmorE than 200 tradEs and ProFEssions

distriBution oF womEn and mEn in lKaBLKAB’s ambition is to be an attractive employer for all individuals, regardless of gender, disability, cultural background or sexual orientation.

lKaB PEllEt Production 2010 Most of LKAB’s products are iron ore pellets with an iron content of 66%. Carefully tested and measured additives in pellet manufacture increase productivity, reduce energy input, result in lower wear and lead to lower slag volumes in steelmaking.

14% are women

86% are men

66%Iron content

For thE saKE oF thE EnvironmEnt In the ULCOS project (Ultra-Low Carbon dioxide Steelmaking), Europe’s steel and mining industries have joined forces in research collaboration to find solutions for tomorrow’s environmentally friendly, ultra-low carbon dioxide steelmaking.

38kg CO2/tonne

110kg CO2/tonne

250kg CO2/tonne

LKAB PELLETS

HEMATITE-BASED PELLETS SINTER

Other products

13%

PELLETS 87%

SHARE OF PELLETS/ OTHER PRODUCTS IN

LKAB’S PRODUCT RANGE

a rEcord! lKaB Posts an oPErating ProFit For 2010 oF

twElvE thousand two hundrEd and EightY onE million Kronor.

lKaB’s logistics in FigurEsLKAB delivered a total of 26 million tonnes of finished iron ore products during 2010.

Ore harbor in Luleå:

5.8 mt(437 vessels)

Ore harbor in Narvik:

17.2 mt(215 vessels)

Other deliveries to customers and stocks, 3.0 Mt. Payload/train:

6,800 tonnes

68 cars/train, so-called long train.

Payload/car:

100 tonnes

towards thE toPOne aim of LKAB’s sponsorship strategy

is to offer broad sponsorship that contributes to active recreation, and to attract and assist talented young

athletes to reach the elite level. By giving

110%the trio of young wrestlers Johanna

Mattsson, Hanna Johansson and Sofia Mattsson from Gällivare have won

several gold, silver and bronze medals in national, European and world

championships, and their sights are set on winning medals in the 2012 Olympics.17% of LKAB’s managers are women. In 2000 the corresponding figure was 4.6%.

rEducEd atmosPhEric EmissionsAlthough pellet production has more than tripled in the past 30 years, LKAB has managed to halve discharges of particulates and emissions of sulfur dioxide and fluorides.

This dramatic reduction has been achieved thanks to improved efficiency in production, new technologies and improved knowledge of processes. The goal is further reductions.

More information on emissions, including carbon dioxide, is given on pages 39-41.

In the past 30 years LKAB’s production has

increased by more than

300%while emissions of sulfur

dioxide and fluorides and discharges of particulates

have decreased by

50%

EMIS

SIO

NS

PER

TON

NE

PELL

ETS

PRO

DUCE

D, 2

010

189 g/tonne pellets

103 g/tonne pellets

70 g/tonne pellets

31 g/tonne pellets

10 g/tonne pellets

NITROGENOXIDE

SULFUR DIOXIDE PARTICULATES HYDROGEN

CHLORIDEHYDROGENFLUORIDE

50% lowEr co2-Emissions

LKAB Annual Report 2010.Produced by LKAB in collaboration with Vinter.The Sustainability Report has been produced in collaboration with Hallvarsson & Halvarsson.Photo: Fredric Alm, Andreas Lundberg and LKAB.Printed by: Luleå Grafiska.

L KAB 2010

LKAB is one of Sweden’s oldest industrial companies. Founded in 1890, the company has played a vital role in Sweden’s export industry and industrial development for more than a century. And for just as long, the company has been a reliable supplier and partner to the European steel industry. The rich, high-grade iron ore from the North has been complemented with other natural minerals. LKAB is now an international, high-tech

minerals group with large-scale operations on a globally competitive market, and a reliable resource that is constantly developing and aiming for the future.

The largesT sTeel-producing counTries, 2010

r&d supporTs lKaB’s growThA mineral is called ore when it can be mined profitably. R&D activities including process development create ore and contribute to LKAB’s profitability and competitiveness. The growth target is more than 37 million tonnes of iron ore products per year by 2015.

26Million Tonnes

lKaB’s deliveries of iron ore producTs in 2010, of which 21 Million Tonnes was pelleTs.

high qualiTy in producTionDuring 2010 LKAB’s deliveries achieved a quality value of 95.2%. That is the best full-year Q value since quality rating according to this system was adopted in 2000.

The highest quality value,

100%was achieved in December 2010.

2010: 67.0

2009: 60.0

+11.7%

#4 RUSSIA Mt

2010: 80.6

2009: 58.2

+38.5%

#3 USA Mt

2010: 66.8

2009: 62.8

+6.4%

#5 INDIA Mt

2010: 58.5

2009: 48.6

+20.3%

#6 SOUTH KOREA Mt

2010: 43.8

2009: 32.7

+34.1%

#7 GERMANY Mt

2010: 33.6

2009: 29.9

+12.4%

#8 UKRAINE Mt

2010: 32.8

2009: 26.5

+23.8%

#9 BRAZIL Mt

2010: 4.8

2009: 2.8

+72.8%

#29 SWEDEN Mt

2010: 626.7

2009: 573.6

+9.3%

#1 CHINA Mt

2010: 109.6

2009: 87.5

+25.2%

#2 JAPAN Mt

lKaB 2010Luossavaara-Kiirunavaara AB (plc). LKAB is wholly owned by the Swedish state.

President and CEO: Lars-Eric Aaro

Chairman of the Board: Björn Sprängare

Corp. ID No.: 556001-5835(Source: worldsteel, January 2011)

perforMance in ironMaKingLKAB is a high-tech minerals group whose success is driven by world-class research, development and production.

#1 Europe’s largest iron ore producer

#2 The world’s second-largest pellet manufacturer

1,25

0 M

eTre

s

1,36

5 M

eTre

s

underground, The MalMBergeT

Mine’s new Main level is Being BuilT

underground, The Kiruna Mine’s new

Main level is Being BuilT

In a research and optimization project during 2010, LKAB’s R&D department increased capacity at the MK3 pelletizing plant in Malmberget by

10%(Source: Sifo, LKAB Framtid, Nov. 2009)

120years of Bel ief in The fuTure

urBan TransforMaTionIn the company’s financial statements for 2010, LKAB allocated 2,997 million kronor towards urban transformation in Kiruna and Malmberget. According to a SIFO survey, 97% of the population of Gällivare and 96% of residents in Kiruna accept the urban transformation in the orefields communities as a consequence of the new main levels.

90%are sympathetic towards the urban transformation, according to SIFO

>

O V E R V I E W O F T H E P A S T Y E A R4

10

J A N F E B M A R C H A P R I L M A Y J U N E

Lars-Eric Aaro is appoint-ed President as of Jan 1. Bolagshotellet in Malm-berget is closed. Derail-ment at Sjöbangården in Kiruna disrupts the de-livery flow. A damaged roof at the old apatite plant in Kiruna causes water and debris to flow down, creating problems loading trains from rock chutes.

LKAB elects to sign an-nual price agreements for its iron ore products, while many major pro-ducers switch to quarter-ly pricing. Construc-tion begins on a stra-tegically important pellet research centre, AggloLab, in Malmber-get. A further SEK 75 million over three years is allocated for the pros-pecting programme to enable exploration of some 50 deposits around the present operating lo-cations. Environmen-tal permits are granted for Gruvberget in Svap-pavaara. Mining begins.

LKAB announces plans for three new open pit mines in the Svappa- vaara area. Ten million tonnes of products have been delivered to Qatar Steel. Skiers Marcus Hell-ner and Charlotte Kalla, then LKAB employ ees, take individual Olym-pic golds in Vancouver. The Malmberget mine re-ports a record month for delivery to the process-ing plants.

The Board votes on a new strategy plan that will include LKAB 37, tar-geting growth of about 35 per cent to 37 mil-lion tonnes of iron ore products per year. Test drilling in Malmberget shows that the Prinzsköld orebody extends at depth. This bodes well for operations in the long term, but will have an im-pact on central Malm-berget. Magne Leinan is appointed president of LKAB Norge AS.

The first modernized, en-vironmentally friendly ter-minal locomotive, T46, is in service. Despite occa-sional problems due to se-vere cold, the interim re-port shows an operating profit of SEK 1,361 mil-lion and a quarterly deliv-ery record of 6.3 million tonnes. LKAB’s athlet-ics and culture grants are awarded to Sofia Matts-son and Agge Theander, respectively.

E V E N T S O F T H E Y E A R I N B R I E F

Four-year summary

SEK MILLIONS 2010 2009 2008 2007 Net sales 28,533 11,558 23,128 16,385Operating profit 12,281 659 10,327 6,148- operating margin, % 43.0 5.7 44.7 37.5 Profit after financial items 12,350 1,192 10,389 6,344- profit margin, % 43.3 10.3 44.9 38.7Tax - 3,267 –473 –2,748 –1,665Net income for the year 9,083 719 7,641 4,679Non-current assets 25,083 23,688 21,414 19,447Current assets 21,546 11,867 14,915 10,233Shareholders’ equity 33,419 25,375 25,218 22,251Cash flow for the year 5,415 –3,140 3,948 –1,159 Return on equity, %* 30.9 2.8 32.2 22.6Equity/assets ratio, % 71.7 71.4 69.4 75Capital expenditures** 3,973 3,543 4,716 5,968Average number of employees 4,030 3,778 4,086 3,885

* After tax ** property, plant and equipment

significanT evenTs 2010:LKAB adopts a new strategy that will include LKAB 37, targeting growth of about 35 per cent to 37 million tonnes of iron ore products per year. Gruv-berget, the first of three planned new open pit mines in Svappavaara, opens in May. A delivery record of 26 million tonnes of iron ore products is set.

L K A B G R O U P

significanT evenTs 2010:A delivery record is set for magnetite products.Production and delivery records are set for huntite products. Investment for manufacturing more refractory and recycled product in England.Robert Boulton, new president, Minelco Group.

SEK MILLIONS 2010 2009

Sales 2,814 2,141Operating profit 433 –95Operating margin, % 15.4 –4.4Operating assets 1,264 1,352Operating liabilities 721 1,029Investments* 10 13Depreciation* 30 47Impairments* 0 317Average number of employees 380 384

* property, plant and equipment

Financial highlights – Minerals

M I N E R A L S D I V I S I O N

Europe is the Group’s biggest market.

Sales per market region (%)

Others 7%

Europe 66%

Middle East/ Asia 27%

Europe is Minelco’s home market. However, most of the growth is taking place on other markets.

Sales per market region (%)

Middle East/ Asia 34%Others 8%

Europe 58%

2005 2006 2007 2008 2009 2010

50

40

30

20

10

0

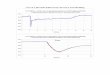

Return on equity (after tax)

Target return on equity (after tax)

The targeted return on equity is 10 per cent over a business cycle.

Return on equity (%)

2005 2006 2007 2008 2009 2010

30,000

25,000

20,000

15,000

10,000

5,000

0

Net sales increased by 147 per cent and amounted to SEK 28,533 million (11,588). Operating profit amounted to SEK 12,281 million (659).

Net sales ( 2010) Operating profit

Net sales and operating profit (SEK MILL IONS)

Test drilling for iron ore begins near Tuollujärvi, Kiruna. One billion tonnes of iron ore products have been shipped via the Nar-vik harbour since opera-tions began. An informa-tion office is opened in Malmberget.

O V E R V I E W O F T H E P A S T Y E A R 5

10

J U L Y A U G S E P T O C T N O V D E C

A new sales office, Villa Schwedenerz, is opened in Essen, Germany. Branding project begins. Operating profit after the second quarter is 6.4 billion kronor.

The president’s debate ar-ticle, Future climate-smart technology is punished by the EU, is published in DN, Sweden’s biggest national daily. Applica-tion is submitted for test mining of 300,000 tonnes at the Mertainen near Svappavaara. Strömsnes Station on the Ore Railway reopens with an extended siding for meeting trains. Operating profit of SEK 11,173 mil-lion is reported after the first three quarters.

Markus Petäjäniemi is appointed Senior Vice President Sales & Marketing, and Robert Boulton becomes President of the Minelco Group. As of 12 Dec., LKAB can only operate the new, 30 per cent more efficient trains on the Ore Railway. LKAB celebrates its 120th anniversary. Total iron ore deliveries for the year amount to 26 Mt, the best result since the mid-1970s.

LKAB sponsors a children’s and youth arena at Kirunafestiva-len. A switchgear fire at the Torneträsk station disrupts traffic on the Ore Railway.

As part of the future recruiting drive, LKAB par-ticipates in Career Days, in Stockholm. International speakers and customers from throughout the world visit the LKAB Dry Bulk Shipping Symposium in Narvik. A new mountain cabin is opened at Ritsem and can be booked by all LKAB employees.

LKAB holds press confer-ences on the search for more iron ore and the new main level in Malm-berget. In collaboration with Norrbottensteatern, LKAB sponsors children’s and youth theatre in the orefields communities for three years. A monthly record for delivery of iron ore products (2.65 Mt) is reached, of which 1.9 Mt is shipped via Narvik, also a monthly record.

significanT evenTs 2010:KGS assumes responsibility for operations and the sorting process at LKAB’s Gruvberget mine, Svappavaara. FAB starts construction on 28 new apart-ments at Bäckåsen in Gällivare, the first of 230 planned new dwellings in the area.

SEK MILLIONS 2010 2009

Sales 1,861 1,098Operating profit 244 168Operating margin, % 13.1 15.3Operating assets 1,121 1,063Operating liabilities 449 375Investments* 55 55Depreciation* 56 39Impairments* 0 0Average number of employees 274 236

* property, plant and equipment

Financial highlights – Special Businesses

D I V I S I O N

S P E C I A L B U S I N E S S E S

significanT evenTs 2010:The two newest pelletizing plants in Kiruna and Malmberget set production records. The underground mines in Kiruna and Malmber-get also set production records. The best quality value for deliveries since thequality rating system was adopted in 2000.

SEK MILLIONS 2010 2009Sales 25,908 9,613Operating profit 11,524 537Operating margin, % 44.5 5.6Operating assets 29,331 27,862Operating liabilities 10,031 1,029Investments* 3,908 3,461Depreciation* 1,735 1,741Impairments* 300 0Average number of employees 3,376 3,158– of which Parent Company 2,998 2,800Production, Mt 25.3 17.7Deliveries, Mt 26.0 18.7Stocks, Mt 1.1 1.6

* property, plant and equipment

Financial highlights – Mining

Production per operating location 2010 (Mt)

Iron ore productsPellets Kiruna 12.2Pellets Svappavaara 3.4Pellets Malmberget 6.5Special products Kiruna 0.9Fines Malmberget 2.3Total 25.3

Shipped 2010 Mt

From Narvik, 215 vessels 17.2From Luleå, 437 vessels 5.8

Other deliveries to customers and stocks, 3.0 Total 26.0

Production of iron ore products Mt

2010 2009 2008 2007 2006Pellets 22.1 14.7 19.9 18.8 16.9Fines* 3.2 3.0 3.9 5.9 6.4Total 25.3 17.7 23.8 24.7 23.3

* incl. special products

Deliveries 2010 Mt

Pellets 20.8Fines* 5.2Total 26.0

* incl. special products

1,500

1,200

900

600

300

0

Global iron ore exports and production of crude steel (Mt )

Global iron ore exports (prel. 2010)

World production of crude steel ( 2010)

(Source: CRU, December 2010, worldsteel, January 2011)

1960 1970 1980 1990 2000 2010

S A L E S & M A R K E T I N G D I V I S I O N M I N I N G D I V I S I O N

Europe is the home market for LKAB’s blast furnace products, and direct reduction products are sold to the Middle East and North Africa.

Production, Mt ( 2010)

Productivity, tonne/employee

2005 2006 2007 2008 2009 2010

30

25

20

15

10

5

0

Production and productivity

12 000

10 000

8 000

6 000

4 000

2 000

0

Mt Tonne/employee

Sales per market region (%)

Others 7%

Europe 66%

Middle East/ Asia 27%

P R E S I D E N T ’ S R E P O R T6

10

record year wiTh a focus on growThThe Group posted a profit for 2010 of 12.3 billion kronor, our best financial outcome on record. It is especially pleasing to report that this historic result was achieved during a year when LKAB celebrated its 120th anniversary. This gave us an assurance of LKAB’s success as an enduring, long-term operation in which, despite occasional problems, we have maintained a steadfast belief in our products and continued to develop our business while keeping pace with change and the demands of customers and society. The year’s result would never have been possible without the strategic investments in research and development in recent decades which have laid the foundations for LKAB’s position as the world’s technology-leading manufacturer of iron ore pellets. Expansion of production capacity during the 2000s has equipped the company to meet the strong de-mand which has characterized the market during 2010. Growth continues in the form of further expansion in increased capacity.

econoMic perspecTivesFinancial outcomes have fluctuated dramati-cally in the past three years. This reflects LKAB’s heavy dependency on customers, and sensitivity to world events and economic cycles. When things go well for the compa-ny’s customers, they also go well for LKAB. To mitigate the effects of excessive fluctua-tions and to ensure greater long-term stability in our business, LKAB has elected to sign an-nual contracts with customers. Many other large suppliers have, instead, switched to shorter contracts. The signed contracts imply that LKAB’s iron ore prices for 2010 rose to the same level as in the boom year 2008.

The development of a pricing system for iron ore continues, but is far from complete. Dur-ing the first quarter, LKAB will continue dia-logue with customers concerning price mod-els and will decide on contracts for 2011. The programme of cost-cutting and efficiency improvement that began in 2009 continues. The aim is to reach 2007 cost levels. LKAB has invested 30 billion kronor during the 2000s and now has six pelletizing plants and an efficient logistics system. Production capacity in our processing plants is about 28 million tonnes (Mt) of iron ore products per year and transport capacity exceeds 30 Mt. Without disruptions, the year’s production result, 25.3 Mt of iron ore products, and re-cord deliveries of 26 Mt could have been sur-passed. The bottleneck in the chain of pro-duction is now access to crude ore. In June 2010 the Board established new targets and strategic activities for the years to come. The plan is for LKAB to grow with its customers. Our objective is to continue to be a preferred supplier to each of our custom-ers, so as to maintain high-volume deliveries. This is essential if we are to achieve the earn-ings levels necessary to cover all costs while continuing to invest around SEK 5-6 billion per year. Earnings must also suffice to give our own-er a reasonable return on equity and to fi-nance costs associated with the urban trans-formation of Kiruna and Malmberget, a process that will span several decades. The identified strategic activities focus on areas that are vital for the company’s growth. As LKAB’s customers grow, we grow with them, both to retain market shares and to in-crease them. We estimate that, within five years, we will have reached a production and

delivery capacity of more than 37 Mt of iron ore products, hence the working title LKAB 37. This growth, which is in excess of 35 per cent, requires access to more iron ore that can be upgraded to our high-quality prod-ucts. During the year, LKAB has therefore opened the first of three new open pit mines in what we refer to as the Svappavaara field. Gruvberget was inaugurated in May, and over the next two to three years, LKAB also plans to begin mining in Mertainen and Leveäniemi, provided the necessary environ-mental permits are granted within a reason-able time period. Within a few years, the sup-ply of crude ore from the two underground mines in Kiruna and Malmberget will also increase when the new main levels are in full production.

social perspecTivesOne of the most important strategic tasks for the period 2010–2012 is to reduce the num-ber of accidents leading to absence by at least half. 2010 was a poor start. The frequency of accidents per million work hours increased by 23 per cent, and the worst thing that can happen in our operation also occurred. Two employees of a contractor died while working on the construction of the new main level in Malmberget. Now, work on Safety First will be intensified with a programme entitled Or-der and Upkeep. Safe workplaces are a nec-essary condition for attracting new co-work-ers to LKAB. On a positive note, absence due to illness remains at a relatively low level, at an average of 2.6 per cent. Long-term ab-sence due to illness stands out at a mere 0.4 per cent. We are also pleased to report that our efforts to improve diversity are also show-ing results. The proportion of women em-

P R E S I D E N T ’ S R E P O R T 7

10

record year wiTh a focus on growTh

ployed in the Group rose during the year to 14.3 per cent, and the share of women in managerial positions to 17.8 per cent. Hu-man capital is the key to LKAB’s success; an ongoing programme of competence develop-ment is therefore an important ingredient in LKAB’s recipe for success. The number of training days per employee increased during the year to 4.6. The target is 5 training days per employee and year. The urban transformation that is a conse-quence of mining in Kiruna and Malmberget entails considerable social challenges with respect to LKAB’s present and future opera-tion. For LKAB, these issues are a high prior-ity in our strategic work, and they must be managed responsibly and with a long view in dialogue and mutual understanding with all parties concerned. The respective municipali-ties plan and decide how urban areas will be decommissioned, as well as how new ones are to be designed and how they will func-tion. LKAB takes an active part in this work and funds a large part of the transformation. To date, LKAB has paid out more than SEK 1.9 billion towards urban transformation in the orefields communities and, during 2010, nearly SEK 3 billion was earmarked for the damage we have so far caused. Communica-tion is an important success factor in the day-to-day work with urban transformation. During the year LKAB has distributed ten issues of the magazine LKAB Framtid to all households in the municipalities of Gällivare and Kiruna, and we have opened an informa-tion office in Malmberget. An office will also be opened in Kiruna during the first half of 2011.

LARS-ERIC AARO PRESIDENT AND CEO

P R E S I D E N T ’ S R E P O R T8

10

sources of energy and has invested in five wind turbines with a combined output of 27.4 GWh. This represents only a small por-tion of LKAB’s total energy requirement, but there may be great potential for windpower. Up until 2015, LKAB plans to build 150 wind turbines.

The ouTlooK for The fuTureLKAB’s ambition is to grow with its custom-ers and, by 2015 at the latest, to have the ca-pacity to deliver 37 Mt of iron ore products. The growth strategy requires a haulage ca-pacity on the Ore Railway of at least 40 Mt. In addition, there are indications that other parties wish to traffic the line. Increased use of the railway will necessitate more and lon-ger sidings along the entire line between Luleå and Narvik, and LKAB is depending on Trafikverket (the Swedish Transport Adminis-tration) to include this in its infrastructure planning. LKAB will also have to acquire more of the new, energy-efficient and cli-mate-adapted locomotives and 100-tonne cars of the type we have purchased in recent years. In total, the major strategic investments in future mining and production capacity entail disbursements of about SEK 5–6 billion per year over the coming years. A share of this is attributable to compensation associated with changes at surface level as a result of the new main levels in Malmberget and Kiruna. LKAB’s continued underground mining plac-es high demands on the Group’s capacity to generate strong financial outcomes and cash flows over the coming years. The growth strategy will also entail new and continuous research and development efforts, and a safe, developmental and attrac-tive workplace for those currently employed by LKAB as well as the many new co-workers that will be recruited. Living environment and housing in the operating locations in the orefields are critical factors for recruiting. When new mines are opened, a factor of un-certainty is the burden imposed by the appli-cation process for environmental permits. The Swedish Environmental Protection Agency’s appeal of the permit for the open pit mine at Gruvberget, which opened in May 2010, will entail an even more extensive and time-consuming permit process.Processing of the environmental permit ap-

environMenTal perspecTivesLKAB offers its customers climate-smart products. Our main product is iron ore pel-lets manufactured from magnetite. During pellet manufacture, magnetite oxidizes to he-matite, resulting in the liberation of large amounts of energy that can be utilized in the pelletizing process. Therefore, the process requires significantly less fossil fuel, such as coal and oil, as compared to competing pro-cesses based on, for example, hematite. This means that global carbon dioxide emissions are dramatically reduced if LKAB’s pellets are used in steelmakers’ blast furnaces. Emis-sions are as low as one seventh of the emis-sions resulting from sintering of fines at the steelmills. Even though it is a well-documented fact that LKAB has the world’s most carbon-diox-ide-efficient plants, LKAB’s competitive ad-vantages are jeopardized by the EU’s system of trade in carbon dioxide emissions rights. During 2010, allocation principles for the trading period 2013–2020 were presented by the EU Commission. Owing to the nature of the implementation process, LKAB risks be-ing allocated considerably fewer emissions rights than for the current period. Since the trade system is not global, but applies only to EU member states, LKAB is the only manu-facturer of iron ore pellets to risk being hit by higher costs for emissions rights. This would distort competition to the advantage of pro-ducers of less climate-smart iron ore products. The energy issue is a high priority for LKAB. Planned production increases imply a greater demand for electricity. Within a few years, annual consumption is expected to rise from about 2.2 to 2.8 TWh. Securing delivery of competitively priced power is therefore strategically important. The current long-term energy contracts will expire successively. A third of our portfolio of energy agreements expired a year ago, and the corresponding vol-ume is now open to exposure on the Nordic spot market. There, market prices have risen dramatically since deregulation, and LKAB is working with financial price reductions in an attempt to retain price stability. We rely on stable prices and stable supply 24 hours a day, 365 days a year. As part owner in VindIn AB, LKAB is par-ticipating in a project to harness renewable

plication for Gruvberget took 22 months. The long permitting process is cause for great concern. Being proactive on the market re-quires stable conditions for doing business, and that includes a foreseeable timeframe for environmental permitting. Following a ruling by the Environmental Court of Appeal on March 10, 2011, a new permit application for Gruvberget will be submitted. LKAB will lodge an appeal with the Supreme Court, while at the same time including operations at Gruvberget in the ongoing permitting pro-cess for pellet production in Svappavaara. If the Supreme Court chooses not to grant leave to appeal, operations at Gruvberget will cease until a new environmental permit has been granted. LKAB therefore risks not being able to achieve a planned increase in delivery capacity, and thereby falling behind other global suppliers of iron ore products. This threatens the company’s long-term market position. Despite this situation, LKAB looks to the future with cautious optimism. Demand for iron ore is stronger than ever, even though there are always dark clouds on the horizon, such as political unrest or natural disasters, which can influence the world economy. To-day, the window of opportunity for supplying more iron ore to the world is open. By ex-ploiting the Svappavaara field and ramping up prospecting activities in the vicinity of ex-isting operations in Norrbotten, we plan to secure LKAB’s capacity to grow with custom-ers, in a cost-effective way, even beyond LKAB 37. With our logistics and processing systems in top form, there is a good possibil-ity that we will be able to achieve greater vol-umes and maintain good profitability by opening new mines. LKAB’s record profit in 2010 provides a good foundation for the future-oriented in-vestments that have already been initiated.

March 2011

Lars-Eric Aaro, President and CEO

K O N C E R N S T R A T E G I 9

10

120 yeArs

of Be L i e f in the fu ture

our main markets while at the same time strengthening the company’s long-term com-petitiveness internationally. Together with new mining capacity, the strategic invest-ments in production and infrastructure made during the 2000s give LKAB the means to increase production of upgraded iron ore products by about 35 per cent. To reach the ambitious growth target, annual production of more than 37 million tonnes by 2015, LKAB has identified six strategically impor-tant areas.

G R O U P S T R A T E G Y10

10

QuALity PoLiCy LKAB will exceed customers’ present and future expectations by involving all employees in the process of continuous improvement. We will strive for zero defects in everything we do, and each employee is responsible for the quality of his or her own work.

enVironMent AnD enerGy PoLiCy

through continuous improvement of the work environment, the natural environ-ment and energy use, LKAB’s operations will promote long-term sustainability and profitable development.

ethiCs PoLiCy LKAB will strive to be perceived by its stakeholders as a company that conducts a sound and successful business operation with integrity and rectitude.

PersonneL PoLiCy LKAB’s personnel policy will contribute to making LKAB a company that is an attractive employer and is perceived as such.

inforMAtion PoLiCy LKAB’s employees will always be well informed with respect to the company’s operations, its business environment, goals, strategies and results, and of their own workplace and their role in the company’s operations. LKAB’s external stakeholders will be given, on an ongoing basis, timely and correct information that provides a representative view of the company and its operations.

f inAnCiAL PoLiCies Credit Policy, Currency Policy and Policy for Managing financial Assets and Liabilities; see www.lkab.com.Dividend Policy; see Corporate Governance.

for the complete policies, see www.lkab.com

L K A B ’ s P O L I C I E S I N B R I E F

lKaB aiMs for annual producTion of 37 Million Tonnes of iron ore producTs

LKAB is a high-tech, international minerals group and a technology-leading supplier of iron ore pellets. the company manufactures highly developed products that are the result of research and development on all fronts. LKAB’s principal strategy is to grow with the market and to secure the company’s position as the supplier that creates the greatest added value and business benefit for its customers.

Over 120 years, LKAB has evolved from a raw-materials producer to a world-leading supplier of upgraded iron ore pellets. During the past decade, to meet customers’ demands and expectations on deliveries, product quality and service, LKAB has invest-ed determinedly in human capital, infrastruc-ture and production facilities. LKAB delivers “performance in ironmaking” of absolute world class and is a respected brand among customers, suppliers and competitors. For LKAB, it is critical to be able to keep pace with customers’ growth and thereby maintain the position we have achieved on

G R O U P S T R A T E G Y 11

10

L K A B ’ s M I S S I O N

L K A B ’ s S T R A T E G I C A R E A S

L K A B ’ s V I S I O N

G R O W T H

Grow, together with customers, both through business development and organically via prospecting and opening new iron ore mines to increase access to raw material. Invest in production structure and ef-ficiency improvement. Create added value from mineral resources and human capital, including subsidiaries.

G R E A T E R F L E x I B I L I T Y

Secure the position of iron ore pellets for the steel industry as LKAB’s main product. Always deliver a part of annual production in the form of fines products, and always reserve products for new markets with an aim to keeping pace with trends in the industry.

P E R F O R M A N C E I N I R O N M A K I N G

With the customer in focus, deliver the best “value-in-use” and have a fundamental understanding of customers’ production processes and product features. Develop new pellet products that continue to contrib-ute to carbon-dioxide-reduced and carbon-dioxide-neutral steelmaking. Increase the internal exchange of knowledge, for better understanding of our own production processes.

S A F E A N D R E S O U R C E - E F F I C I E N T P R O D U C T I O N

Conduct world-class production and provide assured deliveries. Make effective and efficient purchases, invest in our own energy supply and improve energy efficiency. Work for environmental sustainability, based on our own high degree of expertise, and maintain competitive cost levels in production.

U R B A N T R A N S F O R M A T I O N

With responsible solutions, work to create attractive communities and foster good relations with those affected by LKAB’s operations. Work with a long-term perspective, and communicate clearly and openly. Collaborate with the municipalities and other stakehold-ers to create sustainable long-term solutions. Work proactively to ensure that economic impact on LKAB is acceptable.

A T T R A C T I V E L K A B

Focus on healthier co-workers and safe jobs with an aim to reduc-ing accidents by 50 per cent. Be an attractive employer that pro-motes human-resources development and attractive communities, which are an assurance for the supply of human capital. Strengthen LKAB’s brand and position as the climate-smart alternative. Improve the level of knowledge of LKAB among decision-makers.

LKAB’s mission is, based on the Swedish orefields, to manufacture and deliver to the world market upgraded iron ore products and services for ironmaking that create added value for customers. Other closely related products and services that are based on LKAB’s know-how and support the main business can also be included in the company’s operations.

LKAB will be perceived by customers as the supplier that delivers the greatest added value and is thereby the leader in its selected market segments.

L K A B ’ s A N N U A L R E P O R T 12

10

LKAB’s products build Europe’s vehicle industry.

L K A B ’ s A N N U A L R E P O R T 13

10

lKaB and The iron ore MarKeT2010 was a year of strong growth for the global mining and steel industries. LKAB de-livered 26 million tonnes of finished iron ore products during the year, a record volume for the 2000s. World steel consumption reached an all-time high and the great demand for steel pushed iron ore prices to record levels. Rapidly growing economies with major infra-structure projects, such as China, were the main drivers of this market development.

The iron ore market followed the trend from the final quarter of 2009, continuing strong into the first quarter of 2010. There was a reversal during the autumn, when glob-al steel production, which drives demand for iron ore, saw a general lapse. This is ex-plained partly by the fact that economic stim-ulus packages presented during the financial crisis were exhausted. Despite a decline in the third quarter, total world crude steel pro-duction was record-high during 2010, amounting to about 1.4 billion tonnes, an in-crease of 15 per cent over 2009.

Even though the decline in steel produc-tion was felt mainly in Europe, a weaker trend was also evident in China, where iron ore imports were reduced in October and November.

However, the decline is largely explained by domestic energy and environmental regu-lations, which restricted steel production,

and not by lower demand.The statistics show that Chinese imports of iron ore tapered off and that China imported a lower volume of iron ore, just over 618 Mt during 2010, as compared to the 2009 record tonnage of nearly 628 Mt.

Industry analysts are of the opinion, how-ever, that China’s reduced import of iron ore is only temporary and that demand for steel remains high in that country.

Despite the decline in the iron ore market during the third quarter, the price of iron ore did not fall. There are several reasons. India reduced its iron ore exports, since the coun-try has an ever-growing need for iron ore for its own steel production. In China, lower iron content in domestic ores led to a dra-matic increase in production costs. Lower sea-freight rates therefore made it advanta-geous to import iron ore, despite high spot prices.

Sea freight costs, which rose up to four times between 2007 and 2008, were at about the same level in 2010 as they were in 2006. In the coming years, shipping capacity, main-ly to ports in Asia and China, is expected to increase by 50 per cent in terms of dead-weight tonnage. The huge oversupply indi-cates a stable, and perhaps even a further downward trend, in sea freight rates.

Mixed Trends in The sTeel indusTryOutside of Asia, demand for steel is increas-ing, even though recovery after the recession of 2008 is moving slowly, mainly in Europe and the USA. On the weaker markets, eco-nomic development is varied; in Europe, Sweden and Germany have solid finances and are experiencing strong growth while sev-eral countries in southern Europe, as well as Ireland and England, have huge budget defi-cits, which inhibit growth. While the USA has had better success in adapting steel pro-duction according to demand, parts of the steel industry in Europe and the Middle East are struggling to show a profit. Development in the infrastructure and building construc-tion sectors remains weak, and oversupply is pressing the price of steel in relation to the cost of iron ore and finished steel products and consumer goods.

Steelmills in the Middle East, for example, deliver about 70 per cent of their steel to the construction industry and have not yet re-sumed pre-2008 levels.

While some regions are showing weak growth, others are booming. Germany’s rapid economic recovery and growth is strongly tied to that country’s steadily-growing me-chanical engineering and vehicle industries.

Although statistics for new-vehicle regis-tration in Europe as a whole showed a small decline at the close of the 2010, an ever-

LKAB

Others

The diagram shows the flow of iron ore from producer countries to recipient countries.(Source: LKAB, CRU)

(Source: CRU, December 2010

Largest exporting countries

AustraliaBrazilIndiaSouth AfricaCanadaSweden

Global trade in iron ore

Largest importing countries

ChinaJapanEUSouth KoreaMiddle East

L K A B ’ s A N N U A L R E P O R T 14

10

and driving up oil prices. In China, inflation has approached alarmingly high levels and economic recovery is slow in parts of the western world.

In other words, there are some dark clouds on the horizon, even though the market out-look still appears to be good.

LKAB, a smal l i ron ore producerThe world’s three largest iron ore suppliers are Vale, Rio Tinto and BHP Billiton. Together, they accounted for about 31 per cent of the world’s estimated iron ore production in 2010 (approximately 1800 Mt). In the same year, LKAB manufactured 25.3 Mt of iron ore products, which corresponds to about 1.4 per cent of global production. World iron ore exports in 2010 reached an estimated 1000 Mt. Most of LKAB’s deliveries, 21 Mt of 26 Mt in 2010, were exported. That represents a world market share of around two per cent.

LKAB, the world’s second-largest pel let manufacturerWith a capacity of about 45 Mt pellets per year, Vale, in Brazil, is the world’s largest pellet supplier. The sec-ond-largest is LKAB, with a capacity of about 25 Mt, depending on the product mix, i.e. LKAB also produc-es about 3 Mt of fines per year. The third-largest pellet manufacturer is Samarco, in Brazil, with a capacity of about 22 Mt pellets per year. The company is owned by Vale and BHP Billiton.

T R A D E I N I R O N O R E

growing demand for new vehicles in China and Asia has kept the German steel and ve-hicle industries running at high capacity.

For LKAB, the single most important growth factor is a continued recovery and a competitive steel industry in Europe.

Most of LKAB’s steelmill customers are in northern Europe; in Germany, England and Holland.

Turkey has also emerged as a highly inter-esting market with strong growth. Swedish steel production and manufacturing have re-sumed much the same levels as before the recession, though with somewhat weaker de-velopment for strip steel and with lower prof-itability.

Similar conditions prevail on LKAB’s Finn-ish market.

Despite setbacks, the outlook for the Euro-pean steel industry for the coming years is considered good, though the growth rate is expected to remain slow.

difficulT To increase voluMes on The iron ore MarKeTOwing to the tremendous demand for iron ore, most of the world’s iron ore producers are now trying to increase capacity. Some 250 iron ore development projects were un-der way at the start of 2011. If all of these reach fruition, the supply of iron ore may be expected to rise by about 50 per cent in the

During 2010 most of the world’s iron ore producers de-cided not to sign yearly contracts with their customers and switched, instead, to quarterly prices based on an index price for iron ore that is strongly influenced by the spot price for sinter fines in Asia.

Since the spot price of iron ore in Asia is based on the most expensive tonne produced in China, it is cheap-er for Chinese steelmills to import seaborne iron ore.

Advantageous sea-freight rates and strong global de-mand for iron ore helped to push up prices on the Asian iron ore market.

Even though the entire global trade in iron ore was heavily influenced by variable index prices, LKAB nego-tiated and signed annual contracts with its customers for 2010. For LKAB’s iron ore business, stability is impor-tant, both from a customer perspective and a production perspective.

In terms of production, fluctuations in volume in com-bination with a variable price cause imbalance in the

flow from mine to customer. On a spot market, custom-ers try to buy as much as possible when the price is low, which means that LKAB must compensate for fluc-tuations in its own chain of supply. With relatively lim-ited possibilities for intermediate storage in stockpiles and at harbours, LKAB’s most important goal is to ship the largest possible volumes at the most even rate of delivery. Therefore, annual contracts enable maximum utilization of LKAB’s mining, production, logistics and shipping facilities.

Most of LKAB’s iron ore production is sold on the Eu-ropean market to customers with whom LKAB has been doing business for decades. LKAB has always striven to maintain long-term, stable business relations based on partnership. Signing yearly contracts for delivery volumes based on a long-term price model is a way of achieving stability and credibility in a business relation-ship with balanced risk-sharing. While the world market price is essentially based on iron content and quality

parameters, the price models have continued to develop since 2008. LKAB’s approach is to discuss price models as a part of the overall business agreement. LKAB’s customers who have thus far preferred the stability implicit in annual contracts appreciate this. The dialogue on the pric-ing system, with an element of flexibility, continues.

L K A B ’ s A N N U A L R E P O R T 15

10

coming decade. However, there are many in-dications that many of these projects will be delayed and that iron content is lower than expected, which means that the volume in-crease will be realized after 2013.

At the same time, the world’s leading iron producers in Brazil and Australia have had difficulty in achieving the expected volumet-ric increases. At the close of 2010, produc-tion volumes at Vale and Rio Tinto were at about the same levels as before the recession in 2008. Despite strong global demand for iron ore, little, if any, extra capacity has been introduced on the market for seaborne trade in iron ore products, which therefore remains narrow and highly priced.

By the time the increased iron ore volumes are finally realized, it is believed that the market will have cooled down and that the iron ore price will have begun to slowly de-cline around 2012–2013. Contrary to this view, it seems that, over the long term, steel consumption will continue to increase in growth economies such as China and India. A falling world-market price will also render many of the ongoing iron ore development projects unfeasible, which will result in re-duced supply and, probably, push the price up.

Current political unrest in the Middle East and North Africa is having a negative effect on demand for steel products in the region

MARKUS PETäJäNIEMI Senior Vice President Sales & Marketing, LKAB

LARGE VOLUMES AT AN EVEN RATE OF DELIVERY, THE KEY TO LKAB’S PROFITABIL ITY

Drilling at LKAB’s Gruvberget open-pit mine in Svappavaara.

High del iver y volumeLKAB delivered 26 million tonnes of upgraded iron ore products in 2010. This is the highest delivery volume in 25 years. Most of it was pellets (20.8 Mt) and the rest fines, incl. special products (5.2 Mt).

High product ionIn total, LKAB produced 25.3 million tonnes of iron ore products, of which 22.1 Mt pellets, 2.3 Mt fines and 0.9 Mt special products. The two newest of LKAB’s six pelletizing plants set production records: KK4 in Kiruna, with 4.7 Mt and MK3 in Malmberget, with 3.3 Mt. Both underground mines set production records. 26.7 Mt of crude ore was produced in Kiruna and 16.1 Mt in Malmberget, totalling 42.8 Mt.

High qual i tyDuring 2010 LKAB’s deliveries achieved a quality rating of 95.2 per cent. That is the best full-year Q value since quality rating according to this system was adopted in 2000. Then, the Q value was 89.3 per cent. The top rating, 100 per cent, was achieved in December 2010.

High avai labi l i tyIn the Svappavaara plant, the oldest of LKAB’s pel-letizing plants, production was very stable during 2010. There, personnel broke the record for the greatest number of days without a production stop.

L K A B I N F I G U R E S 2 0 1 0cent is destined for steel used in the vehicle industry, 25 per cent is made into steel for other consumer, industrial and engineering products, and 50 per cent becomes steel for use in infrastructure, building construction and civil engineering projects.

Iron ore products delivered to customers outside the steel industry are sold by LKAB’s wholly owned subsidiary Minelco. Minelco supports LKAB’s iron ore business and sells about one million tonnes of iron ore annu-ally, mainly for use as ballast in heavy con-crete, for example, in pipe coating for the gas and oil industry, and as a coagulant in water treatment. For many years Minelco has delivered magnetite products for radia-tion shielding applications in, for example, radiation oncology and the nuclear power industry.

In the coming years there will continue to be business opportunities outside the steel industry; these include deliveries to projects in pipe coating, construction and civil engi-neering, and the manufacture of water treat-ment chemicals.

During 2010 Minelco delivered 600,000 tonnes of magnetite as heavy concrete bal-last for the 1,220-km-long Nord Stream gas pipeline, which will carry Russian natural gas across the Baltic Sea to Europe. Minelco has delivery contracts for an additional 410,000 tonnes in 2011 before the conclu-sion of the project.

Digital infrastructure has long played an important role in LKAB’s competitive busi-ness. Since the 1960s, LKAB has striven to

achieve a high degree of automation and process control in the produc-

tion apparatus by means of IT systems. Profitability depends on a high, even flow of delivery, which is why production stops lead quickly to a marked loss of revenue. LKAB’s IT department fulfils an important function in creating and building systems and infrastructure solutions that support LKAB’s strategic goal to produce 37 million tonnes of fin-ished iron ore products per year. Various forms of IT support enable major efficiency improve-ments in day-to-day operations. For example, we can now remotely control production

processes, safely and securely, in the newest pelletizing plant, MK3 in Malmberget. Instead of sending a techni-cian from Luleå to Malmberget to solve a problem, it can be fixed directly via the internet. This saves a lot of money in reduced downtime. Another important parameter for reaching production targets is the ability to make full use of the production structures in the mines. To improve the efficiency of min-ing operations in Kiruna, LKAB is investing about 40 million kronor to improve, among other things, entrance control and the possibilities for communication via one of Europe’s most extensive wireless networks. Today, the communications system in Kiruna consists of several different overlapping systems and standards. With the new wireless network, frequencies and commu-nication underground can be standardized, so the sepa-rate systems do not cause interference. The intention is to use the wireless system for all voice communication and to integrate IP telephony with, for example, radio and other information systems to enable more efficient control and management. The greatest advantage with the Kiruna mine’s new

wireless network is the personnel entrance control and positioning system. Before blasting in the mine, it is nec-essary to know the exact location of all personnel. Pre-cise positioning is therefore of paramount importance, and it can save tens of millions of kronor in improved production efficiency. When fully operational, the Kiruna mine’s wireless network will consist of 1,500 access points, allowing ex-cellent possibilities for accurate positioning. Eventually, it will be possible to tag everything that moves in the mine, such as vehicles, machinery and personnel, with RFID tags. This presents possibilities for interesting future appli-cations whereby, for example, logistics can be planned according to the position of people and equipment in real time, or ventilation systems can be controlled as required, depending on where people are in the mine.

IT MAxIMIZES UTIL IZATION OF THE PRODUCTION STRUCTURE

L K A B ’ s A N N U A L R E P O R T 16

10greaTer flexiBiliTy provides sTaBiliTyMost of LKAB’s annual production is deliv-ered in the form of pellets, mainly to the nearby market in Europe. To respond to rap-id changes in demand, strengthen customer relationships and open new business chan-nels, LKAB is working to broaden its prod-uct portfolio and to deliver to more geo-graphic market regions.

By always producing and delivering a por-tion of annual production in the form of fines products, regardless of the business cycle, LKAB broadens its product offerings. Volumes are secured and sensitivity to fluc-tuations in the business cycle is reduced. A permanent presence in, for example, Chi-na, allows LKAB to follow, at close range, market trends, customer demands and tech-nical developments that have a bearing on LKAB’s own production and research and development.

LKAB also has an interest in the sectors to which our steelmill customers deliver their products, for example, steels for the manufacturing industry, consumer goods and the building construction and infra-structure sectors.

By delivering iron ore products that are used to produce a diversity of steel products, instead of supplying one or a few market segments, we can reduce the impact on LKAB of a possible economic downturn.

Of LKAB’s sales of iron ore products to the European steel industry, about 25 per

DANIEL BERGLUND IT Manager, LKAB

fines, special products

Pelletizing plantssorting and concentrating plants

skip hoisting

shipping

rail transport

Pellets

Crushing

Loading

Drilling/blasting

train/truck haulage in the mine

From underground mine to ship

L K A B ’ s A N N U A L R E P O R T 17

10

cade, LKAB has therefore invested some SEK 30 billion to upgrade processing capac-ity and logistics. The two newest pelletizing plants, MK3 in Malmberget and KK4 and its adjoining con-centrating plant KA3 in Kiruna, have boosted LKAB’s pellet capacity by nine million tonnes per year. Longer trains with new locomotives and cars are now able to haul 60 per cent more on a yearly basis on the Ore Railway. With the completion in 2009 of SILA, the refurbished harbour facility in Narvik, annual shipping capacity at Narvik has increased from 16 to 19 million tonnes.

Most of the ongoing investment in the chain of processing and logistics will be completed during 2011, after which a phase of fine-tun-ing for maximum efficiency, growth and con-solidation will begin. The goal is to realize the full potential of plant and systems, so as to reach maximum capacity and return on capital, even via additional investment. Heavy investment in capacity for process-ing and logistics has shifted the bottleneck to the raw-material supply end of the operation i.e., access to crude ore. Consequently, LKAB’s focus is now on current and planned investments in upgraded mining capacity.

increased processing and haulage capaciTyLKAB’s strategy is to be a principal supplier and a flexible partner that creates maximum benefit for customers. Therefore, LKAB is investing in a major production increase with the aim of growing by 35 per cent and deliv-ering 37 Mt per year by 2015. Increased capacity in raw-material supply, processing, other production structures and logistics is the key to reaching LKAB’s growth target. In the early-2000s LKAB could mine more ore than the company was able to process and deliver. Over the past de-

L K A B ’ s A N N U A L R E P O R T 18

10

Ore reserves

per December 31, 2009 (to dressing plant)

Quantity, Mt Per cent Fe 2010 2009 2010 2009KirunaProven 579 598 48.7 48.6Probable 79 76 46.2 46.4

MalmbergetProven 270 298 42.5 43.8Probable - 52 - 37.8

GruvbergetProven 10 11 53.2 53.2Probable - - - -

Ore reserves include ore within the granted mining concessions. The ore reserve in Kiruna includes ore above 1,365 metres (from levelling point). The ore reserve in Malmberget includes ore above 1,250 meters (from levelling point) in the Eastern Field. For the Western Field, ore above 600 meters is included. Ore reserves for Gruv-berget include magnetite ore above 220 metres. The ratio of mined waste rock to ore in open-pit mines is 1:7. Prices at the turn of the year 2004–2005 have been applied in calculations of ore reserves, which are expected to be valid for duration of the working life of a main level. Iron losses in the upgrading process are about eight per cent.

Mineral resources in addition to ore reserves

per December 31, 2009 (to dressing plant)

Quantity, Mt Per cent Fe 2010 2009 2010 2009Kiruna Measured 95 94 49.0 48.4Indicated 159 153 45.2 44.9Inferred 81 82 46.5 46.8

LeveäniemiMeasured 80 80 47.1 47.1Indicated 30 30 47.0 47.0Inferred - - - -

MalmbergetMeasured 116 51 43.4 42.8Indicated - 2 - 44.1Inferred - 20 - 39.4

Mineral resources in Kiruna down to 1,500 meters (from leveling point) are reported. Mineral resources in Malm-berget are reported for the Eastern Field down to 1,250 metres and between 600 and 800 metres for the Western Field. At deeper levels, there is insufficient data to enable an estimate of grades and quantities. Mineral resources for Gruvberget are not reported in this report. LKAB also has a mining concession for Mertainen.

L K A B ’ s A N N U A L R E P O R T 19

10

In Sweden, anyone wishing to conduct exploration and exploitation of certain mineral deposits on land, regard-less of the ownership of the land, is subject to the pro-visions of the Minerals Act. The Act defines to which mineral substances its provisions apply; these are known as concession minerals. The supervisory authority is the Mining Inspectorate of Sweden (Bergsstaten), the agency responsible for compliance with the Minerals Act. It re-ports to and receives administrative and other support from the Geological Survey of Sweden (SGU).

In Sweden, exploration for ore may be carried out only by the holder of an exploration permit, for which ap-plication must be made. An exploration permit entitles the holder to exclusive right to undertake exploration work, the right of access to the land and preferential right to an exploitation permit (concession). The permit is issued by the Chief Mining Inspector, head of the Mining Inspector-ate of Sweden.

If the mineral deposit is deemed economically viable, the Chief Mining Inspector issues an exploitation conces-sion. An exploitation concession entitles the holder to mine ore in a deposit for 25 years, and to renew the permit. When the Environmental Court has approved the mining operation, the Mining Inspectorate regulates any remuneration to the landowner via a so-called designa-tion of land.

Sweden has a long mining history and is one of the EU’s leading ore and metals producers.

When it comes to iron ore, we are Europe’s largest producer. Sweden’s national interest in minerals exploita-tion derives from the fact that it provides raw materials for domestic industry and creates employment and export incomes.

Permits handled by the Mining Inspectorate relate mainly to iron ore and other base metals such as copper, zinc and gold. During 2010 more than 200 permit appli-cations for projects throughout Sweden were processed. To an increasing degree, applications for exploitation of rare earth elements (used in e.g., the vehicle and elec-tronics industries) are submitted.

LKAB, for example, is investigating the possibility of recovering rare earth metals and apatite from tailings at the company’s production sites.

The economic downturn meant that the total land area for valid exploration permits was significantly less at the close of 2009 than during the previous year. However, for the full year 2010, this area increased by more than 200 square kilometres compared to the previ-ous year, which is indicative of the mining industry’s rapid recovery.

It is both exciting and pleasing to report that the Swedish mining industry is experiencing a strong upward trend. At the same time, it is a highly specialized indus-try with a demand for unique expertise. The industry as a whole therefore faces a great challenge with respect to the recruitment of personnel, both to meet new demands and to offset future attrition due to retirement.

ÅSA PERSSON Chief Mining Inspector, Mining Inspectorate of Sweden

MeeT deMand and secure access To raw MaTerialLKAB has the capacity to process about 28 million tonnes of finished iron ore products per year. After extensive investment in the logistics structure, LKAB can handle 30 mil-lion tonnes or more, if additional investments are made to eliminate bottlenecks in the chain of production and supply. Therefore, LKAB is planning for a major boost in mining capacity, for example, in the Svappavaara area, with open-pit mines at Gruvberget, Mertainen and Leveäniemi.LKAB is also doing extensive prospecting work in the vicinity of the present operating locations. Over a three-year period beginning in 2012, LKAB will spend SEK 75 million on prospecting. On May 27, 2010, the first new mine, Gruv-berget, was officially opened. Mining and sorting at Gruvberget are managed by LKAB’s subsidiary KGS. When fully operational, the mine will deliver two million tonnes of crude ore to the Svappavaara pelletizing plant. Re-sults from test drilling at Mertainen, which is expected to be operational in 2013, are now being analyzed. A production start at the

Leveäniemi open pit is also forecast for 2013. However, production in the Svappavaara field is contingent upon the granting of environ-mental permits within a reasonable time. In-vestments are also being made in the two ex-isting underground mines, where new main levels will augment LKAB’s ore supply and assure access to raw material for decades to come. Overall, the drive to increase mining ca-pacity will lift LKAB’s annual production of finished products from 28 million tonnes by an additional 10 million tonnes within five to ten years. Initially, the additional ore will be used to meet production peaks in the existing six pelletizing plants, but will also ensure a sufficient supply of material for fines products. LKAB also foresees opportunities for creat-ing significant added value and broadening its business by supplying other minerals on markets beyond the steel industry. One ex-ample is the possibility of extracting the min-eral apatite, which is used in the production of artificial fertilizers, and/or recovering rare earth elements from the sand material that is a by-product of iron ore processing.

B I L D S K A

VA R A

Å S A

P E R S S O N

LKAB reports ore reserves in compliance with recommendations adopted by SveMin. Sections of the recommenda-tions correspond to the Ontario Securities Commission’s (OSC) National Instrument 43-101, which stipulates how ore reserves and mineral resources are to be reported. Håkan Selldén, specialist in ore-base development, is recognized as a ‘Qualified Person’ by SveMin. He has more than 30 years of experience in the mining and minerals industry and has compiled LKAB’s figures.

STRONG UPWARD TREND FOR MINING

The refurbished ore harbour in Narvik, with silos built into the bedrock, has boosted shipping capacity and improved the environment.

L K A B ’ s A N N U A L R E P O R T 17

10

LKAB’s direct reduction pellets give the steel industry the market’s best value-in-use.

20

10

PROCESS DEVELOPMENT BUILDS COMPETITIVENESS AND PROFITABIL ITY

A mineral is called ore when it can be mined profitably. Process development

creates ore. With greater efficiency in beneficiation and production processes, LKAB can achieve prof-itability and maintain its competi-tive advantage. LKAB’s R&D de-partment supports the Group’s growth strategy: to maximize yield in the existing production structure towards the target of producing 37 million tonnes of iron ore products per year. During 2010 R&D com-pleted a project of which the aim was to optimize the comminution process at the

concentrating plant in Malm-berget. By replacing the steel

grinding balls that are used to

break down the ore into finer pieces with a somewhat smaller grinding medium, capacity at the concentrator has been increased by 10 per cent. The new grinding balls are somewhat more expensive, but stronger, which means lower consumption and, ultimately, lower costs. Improved efficiency and higher capacity also reduce energy con-sumption by about two per cent per tonne produced. Fine-tuning of the grinding process in Malmberget has resulted in increased production without the need for costly investments in new plant and equipment. Instead, the in-vestments have been made in knowledge, expertise and human capital. The optimized grinding process in Malmberget is one good example of LKAB’s continuous effort to realize the full potential of production processes and maximize the yield on capital employed. Trials are also under way to optimize the grinding process in Kiruna and in KA3, the newest concentrating plant, where another grinding method, au-togenous grinding, is used. It is expected that the results of this project will be presented during 2011.

In the MK3 pelletizing plant in Malmberget, R&D has op-timized pellet manufacture with a system for computer-aided process modelling. MK3 is a successful pilot project where-by mathematical process models can be used to develop new control and regulation principles off-line and to fine-tune processes before they are introduced into production. The stabilized pellet manufacturing process has boosted MK3’s capacity by more than 10 per cent. The efficiency improvement has also resulted in environmental gains, thanks to improved function in the off-gas treatment system. The ambition is to adopt the same approach to improve pellet processes and maximize production in all of LKAB’s pelletizing plants towards the realization of LKAB 37.

coMpeTiTive advanTage Through perforMance in ironMaKingLKAB’s upgrading of iron ore is characterized by focus on the customer and a will to under-stand each and every customer’s processes and needs. World-leading research in combi-nation with customer-driven, practical experi-mentation results in high-quality iron ore products with unique added values. Deliver-ing “performance in ironmaking” and, in all situations, meeting the customer’s expecta-tions on product specifications, quality and full service is one of LKAB’s main competi-tive advantages. LKAB is the world’s second-largest pellet manufacturer, and an international leader in iron ore pellet research and development. LKAB’s pellets for direct reduction improve productivity, reduce energy demand, slag products and wear on equipment, and give the steel industry the market’s best value-in-use. As of 2012, LKAB will also have a model for quantifying value-in-use, even for blast furnace pellets. The fact that LKAB’s pellets have less environmental impact than other pellet products on the market is becoming ever more important. The general consensus among iron ore pro-ducers and in the steel industry is that the share of pellets will increase successively.

The reason is that customers are placing higher demands on efficiency in steelmaking. LKAB’s ambition is to be the global leader in pellet manufacture and to be perceived as such by the customer, a position that will as-sure LKAB’s long-term competitiveness.

world-class researchFor more than 55 years LKAB has worked to achieve a world-leading position in iron ore pellet research and development. Research is conducted in close collaboration with Luleå University of Technology, via two founda-tions: the Hjalmar Lundbohm Research Cen-tre and the LKAB Excellence Centre in Min-ing and Metallurgy. To further widen the company’s technological lead, LKAB has a long-range plan to create a complete “LKAB Research Centre” in northern Sweden. LKAB is the only iron ore producer that is able to carry out tests in its own, world-unique experimental blast furnace. The EBF is located in Luleå. This also gives customers a unique opportunity, in joint projects with LKAB, to develop new products, fine-tune blast furnace processes and perfect new tech-nologies that lead to better profitability. The AggloLab research laboratory, which will be operational in Malmberget during 2011, brings together all of the expertise and

resources that LKAB needs to perfect the pellet process – from mine to finished prod-uct – via interdisciplinary research in areas such as mineral sciences, chemistry, metal-lurgy and control and automation. There are also long-term plans for securing even more knowledge with, for example, an experimental pelletizing plant and a research mine.

At LKAB’s experimental blast furnace in Luleå, iron ore products are optimized

in close collaboration with customers.

KENT TANO R&D Manager, LKAB

L K A B ’ s A N N U A L R E P O R T 21

10

a long-TerM and susTainaBle road Towards growThAs one of sweden’s largest industrial groups, LKAB influences and is influenced by the world around it, both locally and globally. in its dealings with the surrounding world, LKAB’s intention is to be a role model for the industry, to assume responsibility for the impact it causes, and to promote an enduring and sustainable development of the company and its surroundings.

2010 was a successful year for LKAB. LKAB delivered 26 million tonnes of iron ore prod-ucts, the highest volume during the 2000s. Together with record-high iron ore prices, this meant that LKAB posted one its best fi-nancial outcomes ever: a profit of more than SEK 12 billion. LKAB’s expressed strategy is to keep pace with customers’ growth and thereby maintain the position we have achieved on our main markets and strengthen the company’s long-term competitiveness. Increased production also increases LKAB’s impact on people and the environment. The expansion of mining operations has consequences for many resi-dents in Kiruna and Gällivare, and it increas-es environmental and climate impact, which must be minimized both locally and globally. Many co-workers will be affected by LKAB’s efforts in areas including health, safety and work environment. A growing labour demand makes LKAB’s image as an attractive employ-er and the company’s efforts towards greater diversity even more important than ever. During 2010 absence due to illness was at the same level as in 2009. However, the fre-quency of accidents increased, which meant that the targeted 20 per cent reduction over the previous year’s accident rate was not met.

Safety and work environment are high-priori-ty areas in which LKAB works, strategically and with a focus on people, towards the vi-sion of zero accidents. A fatal accident in Malmberget, in which two employees of a contractor died, was a tragic reminder of how important it is to fo-cus even harder on safety training, work-envi-ronment assessments and risk awareness among employees and subcontractors. In-house training and competence devel-opment within LKAB 2010 gained momen-tum during 2010 and reached virtually all set objectives. The proportion of women em-ployed in the group continues to increase, even at managerial level, and the number of women applying to LKAB secondary-school programmes in Malmberget and Kiruna is record high. Despite significantly higher production compared to 2009, per-tonne emissions of particulates were reduced, thanks to system-atic environmental work and an even rate of production. Decommissioning of Minelco’s olivine mine in Greenland has been realized in con-sultation and agreement with local authori-ties and no environmental hazards have been identified.

S U S T A I N A B I L I T Y R E P O R T17

1022

10Gruvberget and the other two planned open-pit mines Leveäniemi and Mertainen are important

for realizing LKAB’s growth plans.

S U S T A I N A B I L I T Y R E P O R T 23

10

sTaKeholders and prioriTized susTainaBiliTy issuesIn light of the considerable impact of LKAB’s operations, the company has identified the most important issues for sustainability man-agement and reporting in order to contribute to long-term sustainable development. These are: the urban transformations, health and safety, environmental and climate impact, and equality and diversity. The re-sults of the company’s sustainability manage-ment are reported here. LKAB has defined a stakeholder as a group with which the company has a reciprocal re-lation by way of LKAB’s operations. Accord-ing to an updated analysis, the most impor-tant stakeholders are the owner, customers, employees, public authorities, suppliers and contractors, people in the local communities and the media. Especially characteristic in the case of LKAB are the close relations with local residents, public authorities, landown-ers and the Sami minority. During 2010 LKAB has communicated

S U S T A I N A B I L I T Y R E P O R T24

10with a large number of stakeholders in all of the defined stakeholder groups. This has tak-en place via direct dialogue and meetings, surveys, joint projects and seminars with the participation of LKAB and individual stake-holders, as well as via digital channels such as the LKAB chat on lkabframtid.com.Digital communications make LKAB more accessible and enable broader, more detailed stakeholder dialogues. More information about these stakeholder dialogues is given under the respective sections.

urBan TransforMaTionLKAB’s mining is the lifeblood of Kiruna and Malmberget, but it also has a great impact on the local communities. LKAB’s continued op-eration means that buildings and infrastruc-ture must be relocated or replaced. LKAB is funding much of the costs associated with the transformations and is conducting an on-going dialogue with affected stakeholders via various forms of consultation. Read more on page 27.

healTh and safeTyDespite prioritization and concerted efforts, LKAB was not fully able to reach all set tar-gets concerning health, safety and work envi-ronment. Short-term absence increased somewhat, but long-term absence due to ill-ness remains at the same level as in 2009. The targeted 20 per cent reduction in acci-dent frequency was not realized. The group-wide effort to change attitudes to safety and to prevent workplace accidents was therefore intensified. Read more on page 47.

environMenTal and cliMaTe iMpacTLKAB is the world leader in the development of iron ore pellets for steelmaking with re-duced environmental and climate impact. With the aid of LKAB’s experimental blast furnace, European steel-industry partners in the ULCOS project have taken a further step towards a 50 per cent reduction in carbon dioxide emissions. “LKAB Green Pellets” are a unique climate-smart offer to customers that strengthens LKAB’s competitive advan-tage globally. Read more on page 35.