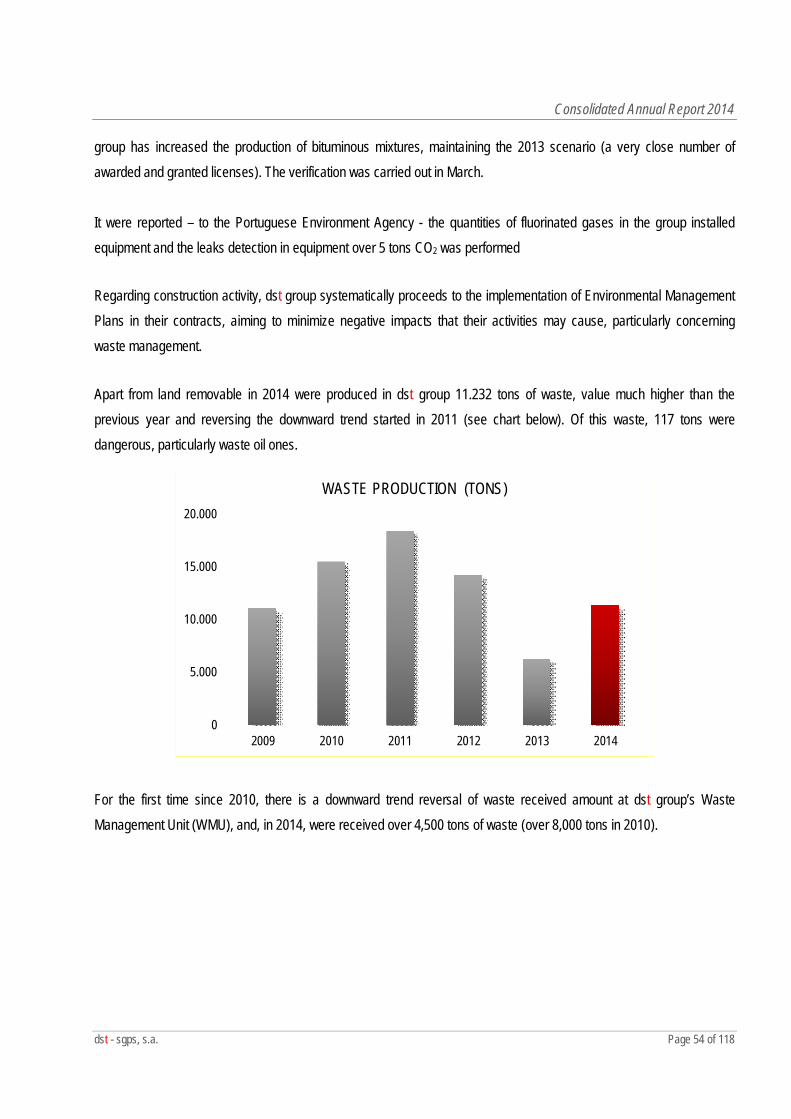

Embed Size (px)

DESCRIPTION

Â

Citation preview

Consolidated Annual Report

dst – sgps, s.a.

December 31, 2014

Index

A) CONSOLIDATED MANAGEMENT REPORT TO THE BOARD OF DIRECTORS 3

1. MACROECONOMICS FRAMEWORK 3 2. BUSINESS ACTIVITY 25 3. MATERIAL EVENTS OCCURRING AFTER THE END OF THE PERIOD 45 4. FINANCIAL RISK MANAGEMENT OBJECTIVES AND POLICIES 45 5. INFORMATION REQUIRED BY LEGISLATION 45 6. AUTHORIZED DISCLOSURE DATE FOR ISSUE THE FINANCIAL STATEMENTS 46 7. FINAL NOTE 46

B) CORPORATE SOCIAL RESPONSIBILITY 47

HUMAN RESOURCES 47 SAFETY, HYGIENE AND HEALTH 50 R&D AND INNOVATION 51 SOCIETY 52 ENVIRONMENT 53 QUALITY AND CERTIFICATIONS 56

C) ANNEX TO THE BOARD OF DIRECTORS CONSOLIDATED REPOR 58

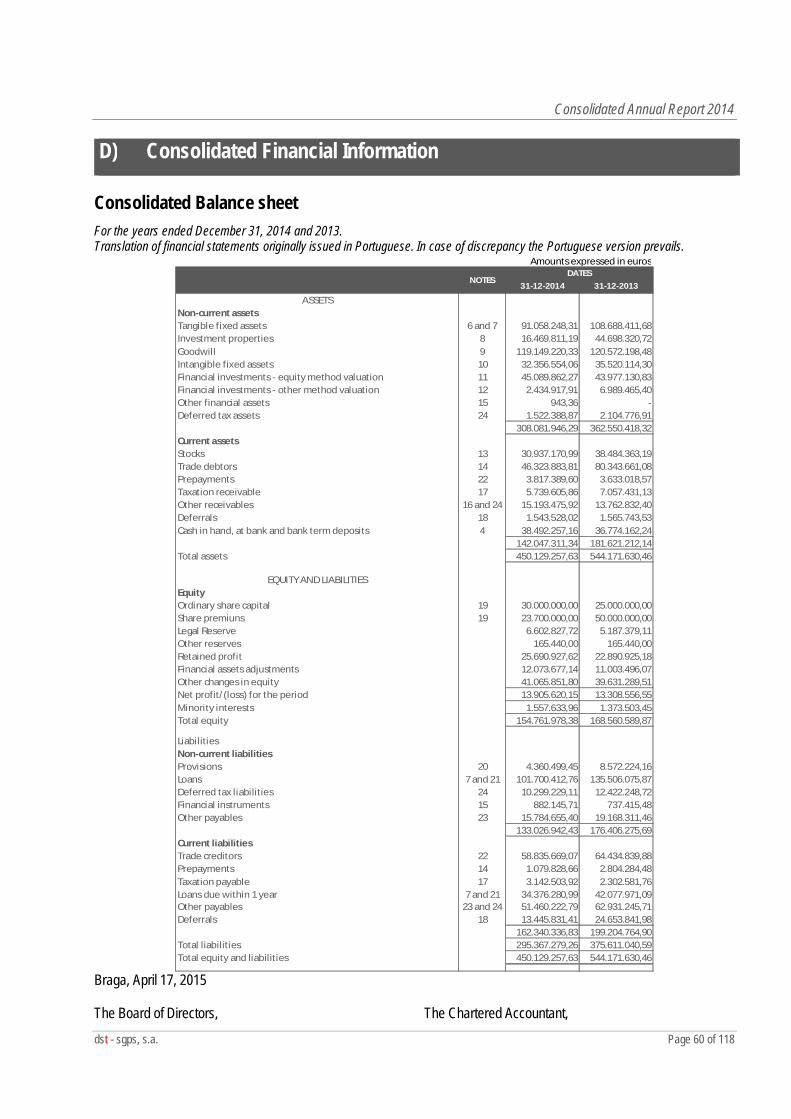

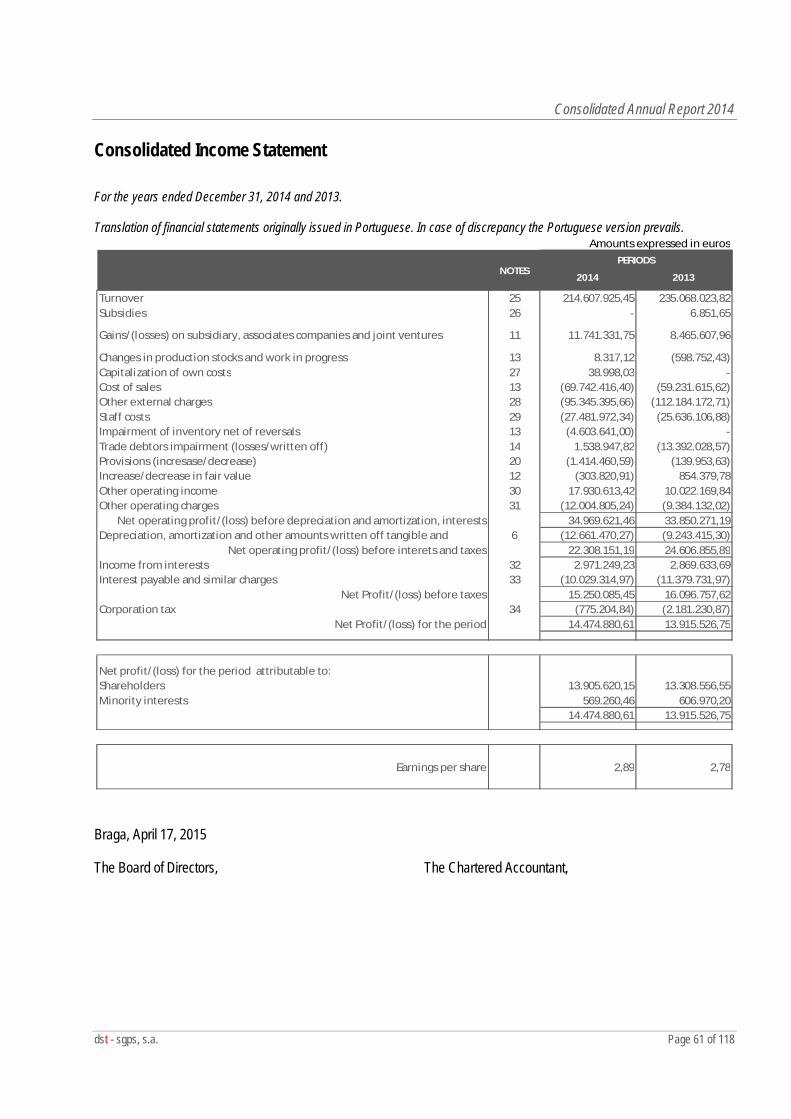

D) CONSOLIDATED FINANCIAL INFORMATION 60

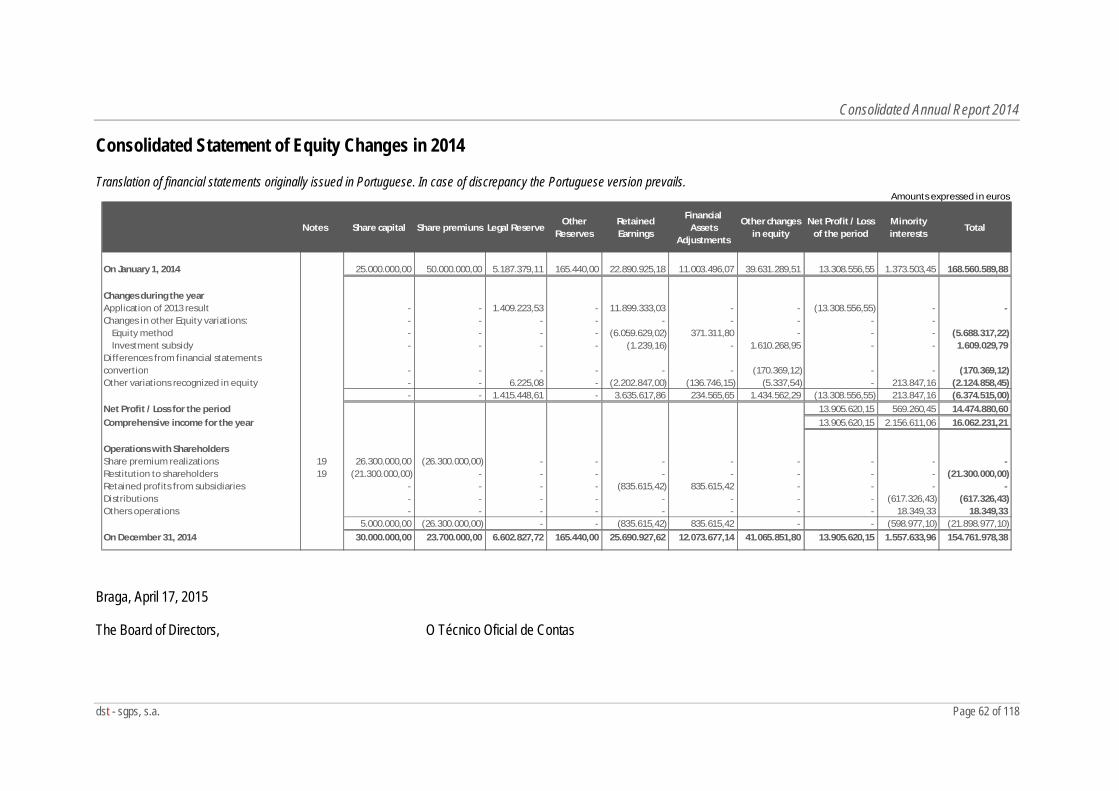

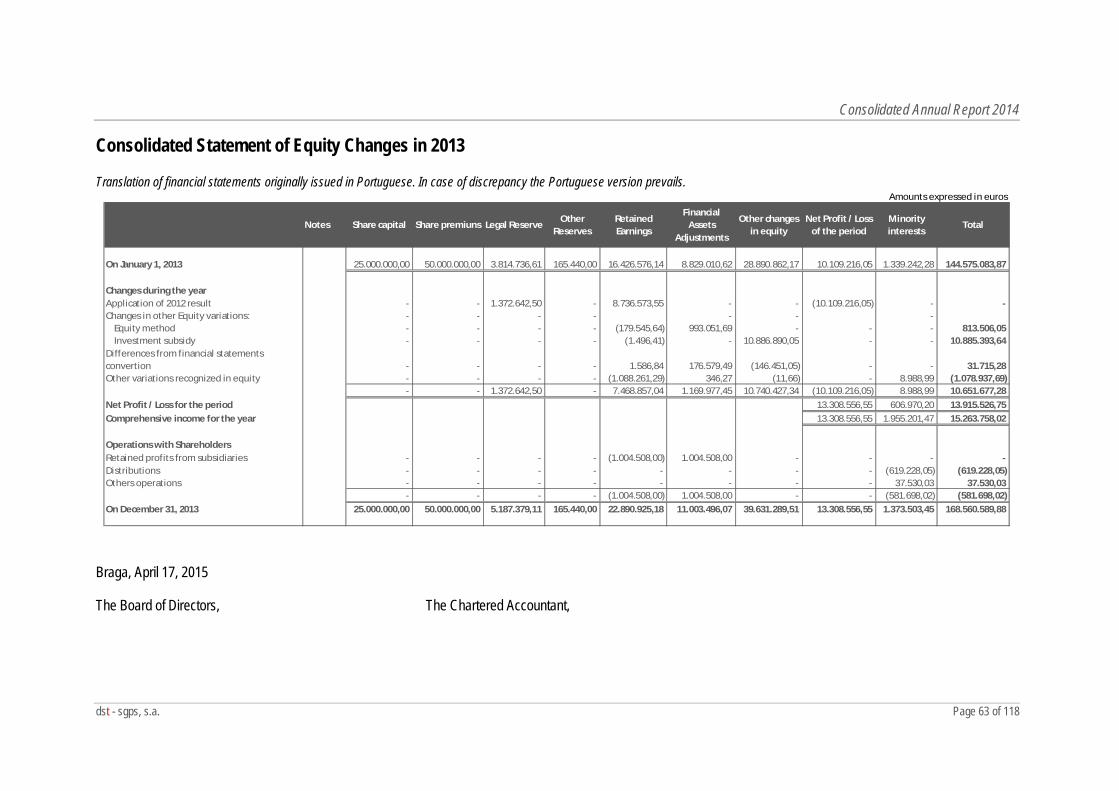

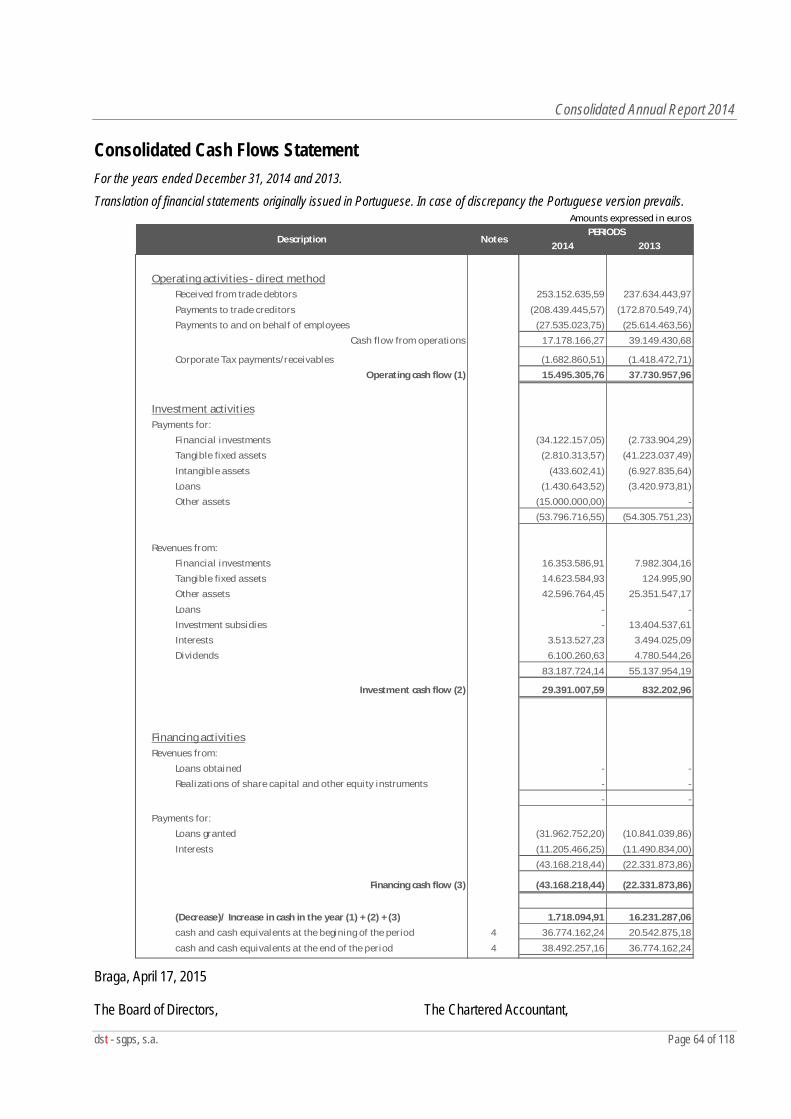

CONSOLIDATED BALANCE SHEET 60 CONSOLIDATED INCOME STATEMENT 61 CONSOLIDATED STATEMENT OF EQUITY CHANGES IN 2014 62 CONSOLIDATED STATEMENT OF EQUITY CHANGES IN 2013 63 CONSOLIDATED CASH FLOWS STATEMENT 64 ANNEX AT DECEMBER 31, 2014 65

E) LEGAL CERTIFICATION OF CONSOLIDATED ACCOUNTS 117

F) REPORT AND OPINION OF THE SOLE FISCAL AUDITOR 118

Consolidated Annual Report 2014

dst - sgps, s.a. Page 3 of 118

A) Consolidated Management Report to the Board of Directors

Dear Shareholders,

In compliance with the legal and statutory regulations, the Board of Directors presents the management report for 2014 fiscal year.

As the environment where we operate is directly related to the positive evolution or downturn of the global economy, before presenting the dst group’s financial information and its business centers we will do a slight approach to the most important national and international macroeconomic data.

1. Macroeconomics framework

1.1 International macroeconomics framework

The uncertainty associated with the global economic outlook remains high. During the last months, the world witnessed the increase in geopolitical tensions in Russia, culminating in the imposition of sanctions by the United States of America (USA) and the European Union (EU). This may affect the recovery of global economic growth and confidence, determining factors for the investment resumption. In addition, geopolitical conflicts installed in the main oil-producing countries (Iraq, Libya, Ukraine and Russia) may also cause disturbances in the oil supply and change prices, to rise, bucking the current downward trend. On the other hand, in the US, the recently decided end by the Federal Reserve of the monetary stimulus has brought some uncertainty in monetary policy. And, any rise in key interest rates could have an impact on the US economy growth rate and increase instability in international financial markets. Still, current projections point to an improvement of the world economy performance, based mainly on boosting growth of the advanced economies, which shows a relatively strong growth in the US, a more moderate one in the European economy, with a very distinct evolution between the members states (stronger in the UK, Sweden and Baltic countries; and weaker for the Eurozone countries). The group of emerging countries has a less strong growth, although still robust in some Asian countries (China and India), reflecting less expansionary economic policies, lower raw materials prices and the heightening of geopolitical tensions surrounding the crisis in Ukraine .

Consolidated Annual Report 2014

dst - sgps, s.a. Page 4 of 118

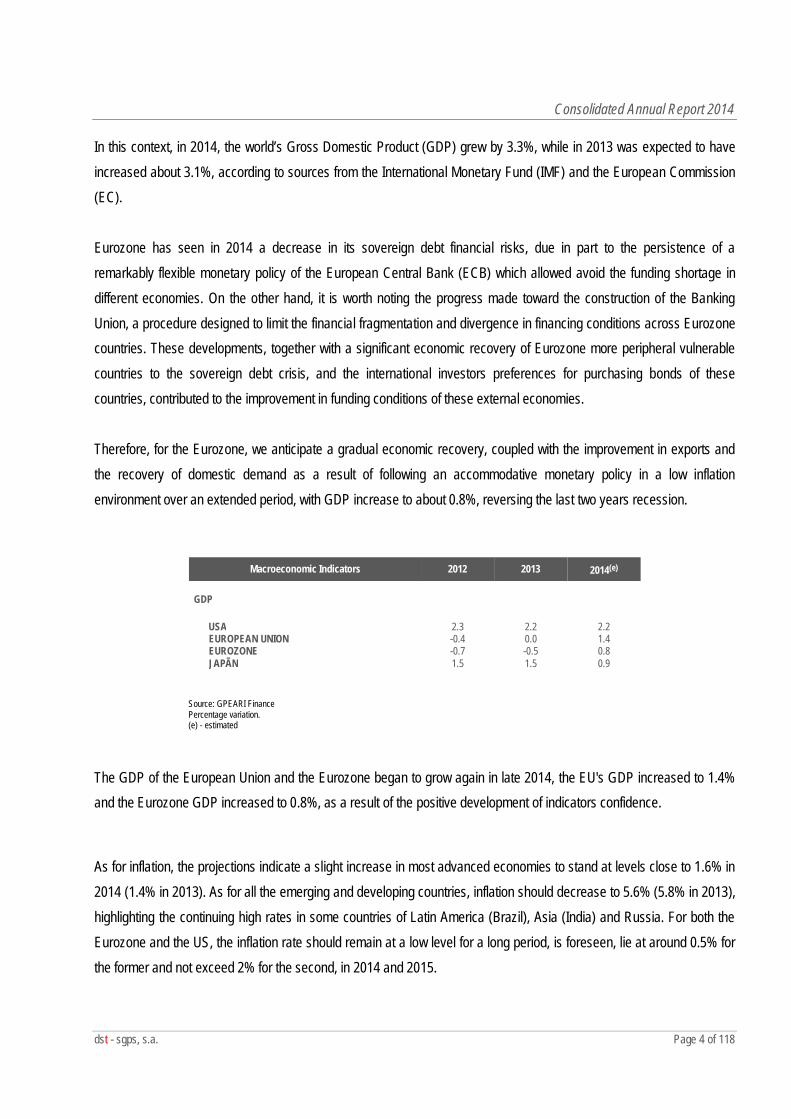

In this context, in 2014, the world’s Gross Domestic Product (GDP) grew by 3.3%, while in 2013 was expected to have increased about 3.1%, according to sources from the International Monetary Fund (IMF) and the European Commission (EC). Eurozone has seen in 2014 a decrease in its sovereign debt financial risks, due in part to the persistence of a remarkably flexible monetary policy of the European Central Bank (ECB) which allowed avoid the funding shortage in different economies. On the other hand, it is worth noting the progress made toward the construction of the Banking Union, a procedure designed to limit the financial fragmentation and divergence in financing conditions across Eurozone countries. These developments, together with a significant economic recovery of Eurozone more peripheral vulnerable countries to the sovereign debt crisis, and the international investors preferences for purchasing bonds of these countries, contributed to the improvement in funding conditions of these external economies. Therefore, for the Eurozone, we anticipate a gradual economic recovery, coupled with the improvement in exports and the recovery of domestic demand as a result of following an accommodative monetary policy in a low inflation environment over an extended period, with GDP increase to about 0.8%, reversing the last two years recession.

Source: GPEARI Finance Percentage variation. (e) - estimated

The GDP of the European Union and the Eurozone began to grow again in late 2014, the EU's GDP increased to 1.4% and the Eurozone GDP increased to 0.8%, as a result of the positive development of indicators confidence.

As for inflation, the projections indicate a slight increase in most advanced economies to stand at levels close to 1.6% in 2014 (1.4% in 2013). As for all the emerging and developing countries, inflation should decrease to 5.6% (5.8% in 2013), highlighting the continuing high rates in some countries of Latin America (Brazil), Asia (India) and Russia. For both the Eurozone and the US, the inflation rate should remain at a low level for a long period, is foreseen, lie at around 0.5% for the former and not exceed 2% for the second, in 2014 and 2015.

Macroeconomic Indicators 2012 2013 2014(e) GDP USA 2.3 2.2 2.2 EUROPEAN UNION -0.4 0.0 1.4 EUROZONE -0.7 -0.5 0.8 JAPÃN 1.5 1.5 0.9

Consolidated Annual Report 2014

dst - sgps, s.a. Page 5 of 118

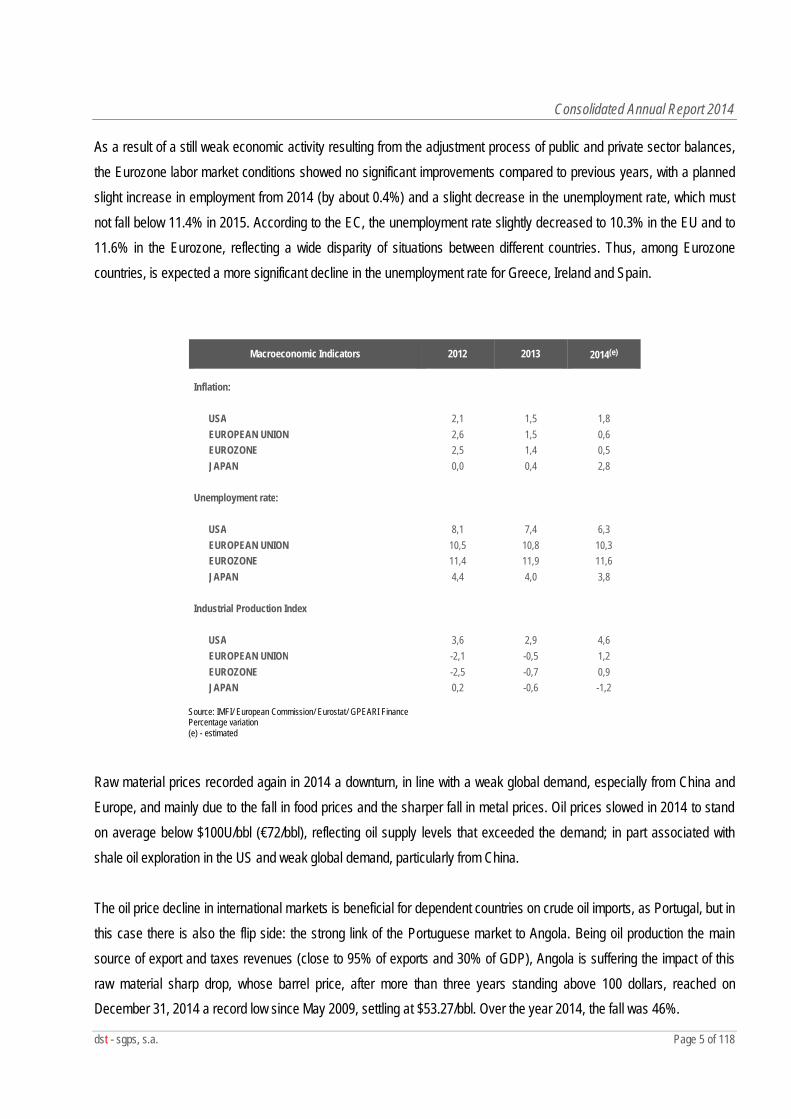

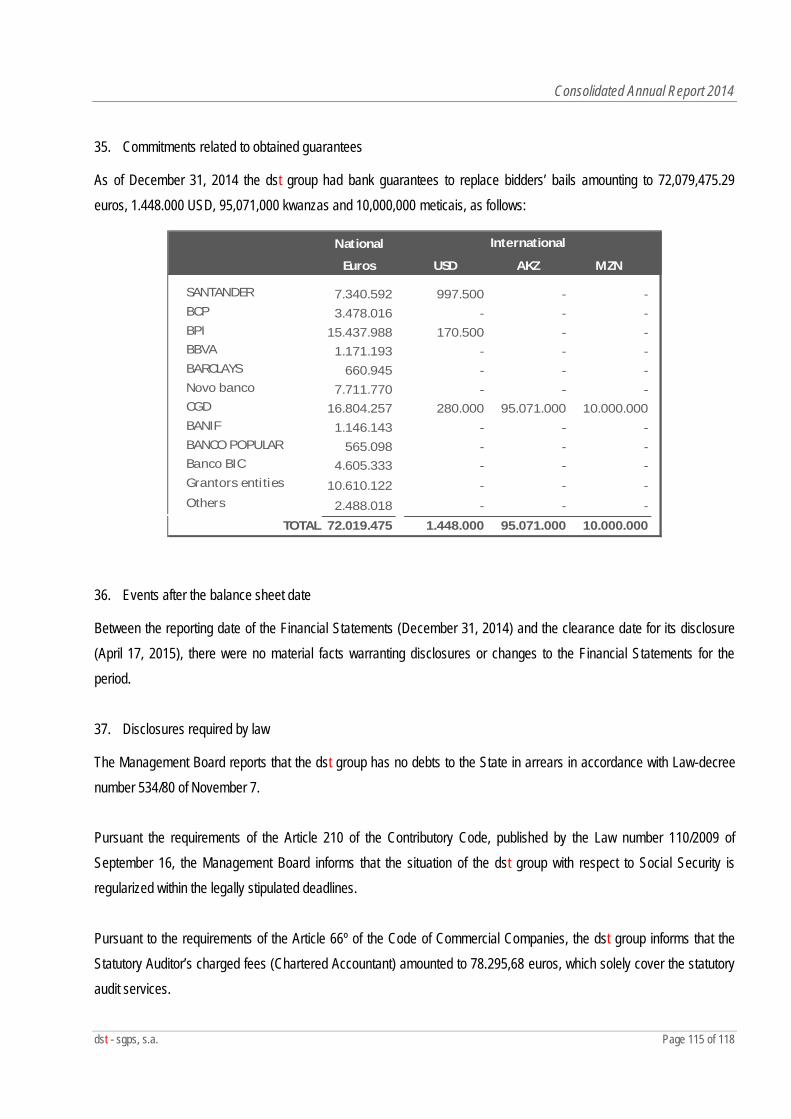

As a result of a still weak economic activity resulting from the adjustment process of public and private sector balances, the Eurozone labor market conditions showed no significant improvements compared to previous years, with a planned slight increase in employment from 2014 (by about 0.4%) and a slight decrease in the unemployment rate, which must not fall below 11.4% in 2015. According to the EC, the unemployment rate slightly decreased to 10.3% in the EU and to 11.6% in the Eurozone, reflecting a wide disparity of situations between different countries. Thus, among Eurozone countries, is expected a more significant decline in the unemployment rate for Greece, Ireland and Spain.

Macroeconomic Indicators 2012 2013 2014(e)

Inflation: USA 2,1 1,5 1,8 EUROPEAN UNION 2,6 1,5 0,6 EUROZONE 2,5 1,4 0,5 JAPAN 0,0 0,4 2,8 Unemployment rate: USA 8,1 7,4 6,3 EUROPEAN UNION 10,5 10,8 10,3 EUROZONE 11,4 11,9 11,6 JAPAN 4,4 4,0 3,8 Industrial Production Index USA 3,6 2,9 4,6 EUROPEAN UNION -2,1 -0,5 1,2 EUROZONE -2,5 -0,7 0,9 JAPAN 0,2

-0,6

-1,2

Source: IMFI/ European Commission/ Eurostat/ GPEARI Finance Percentage variation (e) - estimated

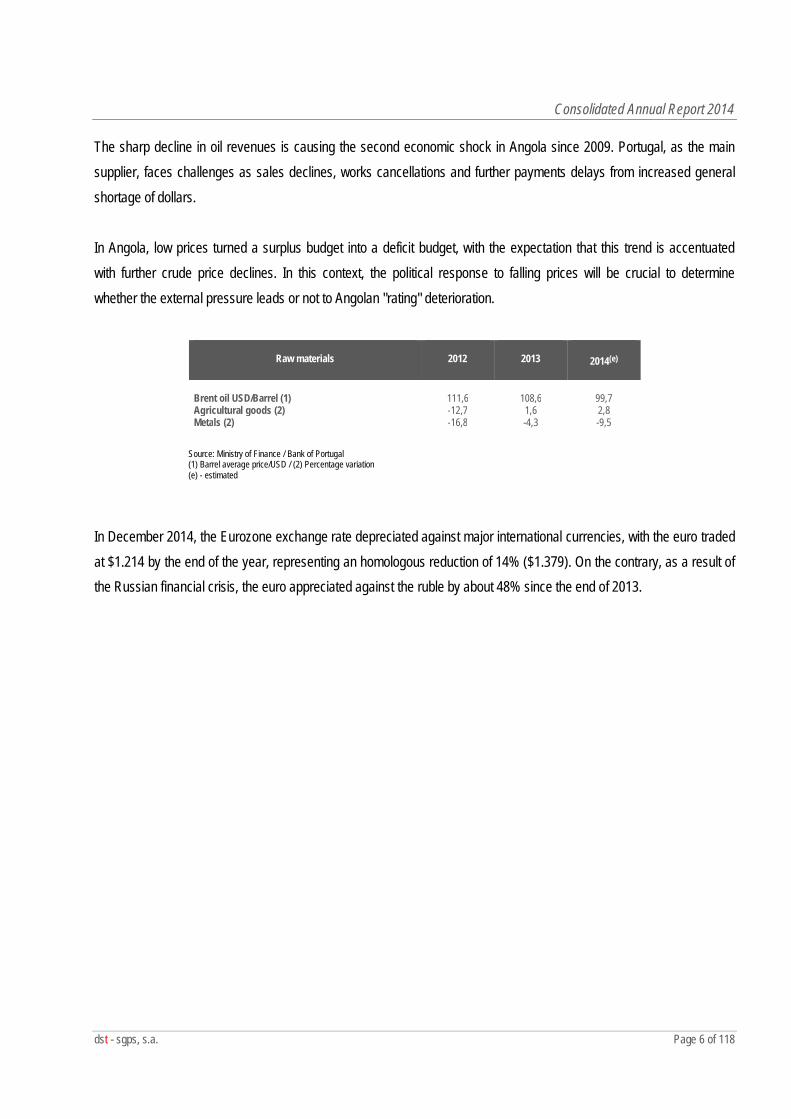

Raw material prices recorded again in 2014 a downturn, in line with a weak global demand, especially from China and Europe, and mainly due to the fall in food prices and the sharper fall in metal prices. Oil prices slowed in 2014 to stand on average below $100U/bbl (€72/bbl), reflecting oil supply levels that exceeded the demand; in part associated with shale oil exploration in the US and weak global demand, particularly from China. The oil price decline in international markets is beneficial for dependent countries on crude oil imports, as Portugal, but in this case there is also the flip side: the strong link of the Portuguese market to Angola. Being oil production the main source of export and taxes revenues (close to 95% of exports and 30% of GDP), Angola is suffering the impact of this raw material sharp drop, whose barrel price, after more than three years standing above 100 dollars, reached on December 31, 2014 a record low since May 2009, settling at $53.27/bbl. Over the year 2014, the fall was 46%.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 6 of 118

The sharp decline in oil revenues is causing the second economic shock in Angola since 2009. Portugal, as the main supplier, faces challenges as sales declines, works cancellations and further payments delays from increased general shortage of dollars. In Angola, low prices turned a surplus budget into a deficit budget, with the expectation that this trend is accentuated with further crude price declines. In this context, the political response to falling prices will be crucial to determine whether the external pressure leads or not to Angolan "rating" deterioration.

Raw materials

2012

2013

2014(e)

Brent oil USD/Barrel (1) 111,6 108,6 99,7 Agricultural goods (2) -12,7 1,6 2,8 Metals (2) -16,8 -4,3 -9,5

Source: Ministry of Finance / Bank of Portugal (1) Barrel average price/USD / (2) Percentage variation (e) - estimated

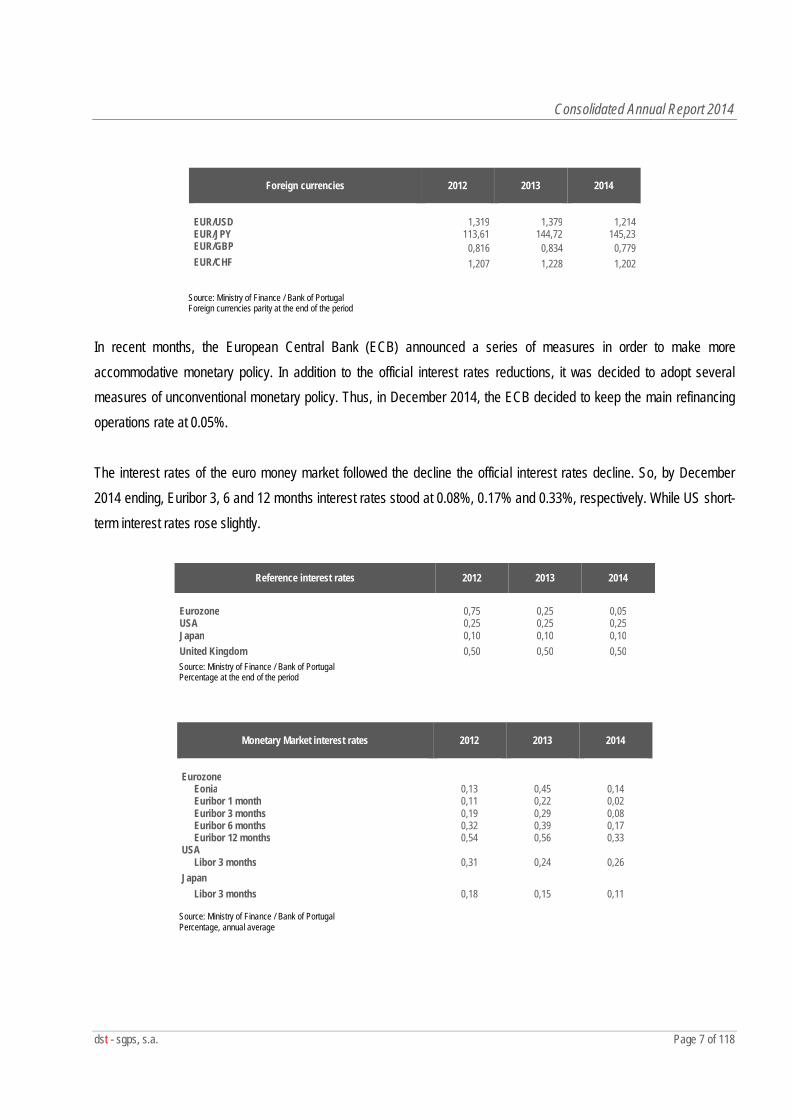

In December 2014, the Eurozone exchange rate depreciated against major international currencies, with the euro traded at $1.214 by the end of the year, representing an homologous reduction of 14% ($1.379). On the contrary, as a result of the Russian financial crisis, the euro appreciated against the ruble by about 48% since the end of 2013.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 7 of 118

Source: Ministry of Finance / Bank of Portugal Foreign currencies parity at the end of the period

In recent months, the European Central Bank (ECB) announced a series of measures in order to make more accommodative monetary policy. In addition to the official interest rates reductions, it was decided to adopt several measures of unconventional monetary policy. Thus, in December 2014, the ECB decided to keep the main refinancing operations rate at 0.05%. The interest rates of the euro money market followed the decline the official interest rates decline. So, by December 2014 ending, Euribor 3, 6 and 12 months interest rates stood at 0.08%, 0.17% and 0.33%, respectively. While US short-term interest rates rose slightly.

Reference interest rates 2012 2013 2014

Eurozone 0,75 0,25 0,05 USA 0,25 0,25 0,25 Japan 0,10 0,10 0,10 United Kingdom 0,50 0,50 0,50 Source: Ministry of Finance / Bank of Portugal Percentage at the end of the period

Source: Ministry of Finance / Bank of Portugal Percentage, annual average

Foreign currencies 2012 2013 2014

EUR/USD 1,319 1,379 1,214 EUR/JPY 113,61 144,72 145,23 EUR/GBP 0,816 0,834 0,779 EUR/CHF 1,207 1,228 1,202

Monetary Market interest rates 2012 2013 2014

Eurozone Eonia 0,13 0,45 0,14 Euribor 1 month 0,11 0,22 0,02 Euribor 3 months 0,19 0,29 0,08 Euribor 6 months 0,32 0,39 0,17 Euribor 12 months 0,54 0,56 0,33 USA Libor 3 months 0,31 0,24 0,26 Japan Libor 3 months 0,18 0,15 0,11

Consolidated Annual Report 2014

dst - sgps, s.a. Page 8 of 118

In late 2014, a high volatility of international stock indices continued to be attended. While in the US, the major indexes performed well, in the case of the Eurozone, the stock prices decline was influenced by concerns about the pace of global economic growth, by political instability in some countries (as in Greece) and by the Russian financial crisis expanded with the sharp oil prices decline.

Additionally, given the euro negative trend and the expectation of further falls due to the public debt purchase program that the ECB is to formalize, the Swiss central bank abandoned the Swiss franc indexation to the euro. In 2011, the Swiss central bank had set that country's currency should have a minimum of 1.20 Swiss francs per euro exchange rate, in order to protect the Swiss economy from the turbulence created by the Eurozone sovereign debt crisis. The monetary authority feared that a euro fall, as a result of the debt crisis, threatened the Swiss economy. This measure took the market by surprise and is generating strong reaction of the assets linked to the Swiss economy. On the one hand, the Swiss franc rate against the euro soared; on the other, the fall is being widespread in the Swiss market, but exporting and financial companies, which are the most penalized by the rise of the franc, being the most punished. For the Eurozone, the impact should be limited. The Swiss National Bank has been a major investor in French and German public debt, among others, within the context of the money market intervention to defend the Swiss franc value. However, the public debt demand of these countries is sufficient, anyway, even without the purchases made by the Swiss National Bank.

Stock markets

2012

2013

2014

Dow Jones EURO STOXX -6,5 17,5 13,1 Nikkei 225 -3,5 48,7 48,7 Standard & Poors 500 8,7 19,1 16,9 Source: European Central Bank Percentage variation

Consolidated Annual Report 2014

dst - sgps, s.a. Page 9 of 118

1.2 National macroeconomic framework

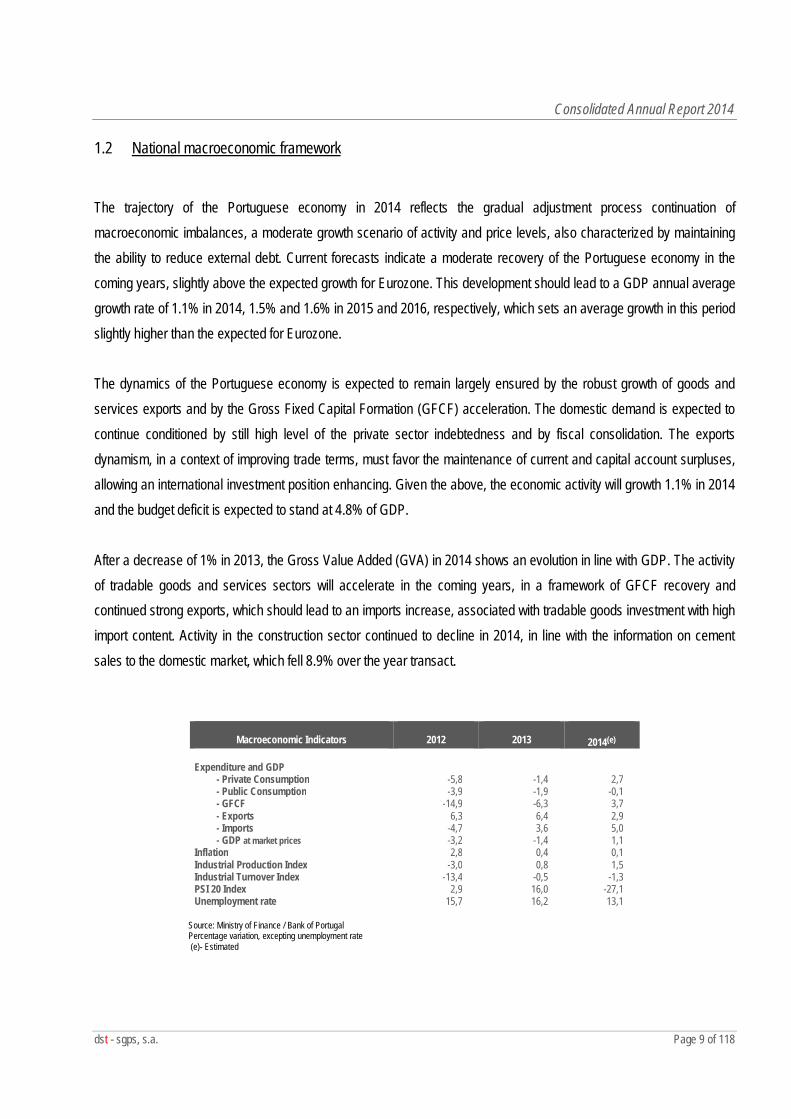

The trajectory of the Portuguese economy in 2014 reflects the gradual adjustment process continuation of macroeconomic imbalances, a moderate growth scenario of activity and price levels, also characterized by maintaining the ability to reduce external debt. Current forecasts indicate a moderate recovery of the Portuguese economy in the coming years, slightly above the expected growth for Eurozone. This development should lead to a GDP annual average growth rate of 1.1% in 2014, 1.5% and 1.6% in 2015 and 2016, respectively, which sets an average growth in this period slightly higher than the expected for Eurozone. The dynamics of the Portuguese economy is expected to remain largely ensured by the robust growth of goods and services exports and by the Gross Fixed Capital Formation (GFCF) acceleration. The domestic demand is expected to continue conditioned by still high level of the private sector indebtedness and by fiscal consolidation. The exports dynamism, in a context of improving trade terms, must favor the maintenance of current and capital account surpluses, allowing an international investment position enhancing. Given the above, the economic activity will growth 1.1% in 2014 and the budget deficit is expected to stand at 4.8% of GDP. After a decrease of 1% in 2013, the Gross Value Added (GVA) in 2014 shows an evolution in line with GDP. The activity of tradable goods and services sectors will accelerate in the coming years, in a framework of GFCF recovery and continued strong exports, which should lead to an imports increase, associated with tradable goods investment with high import content. Activity in the construction sector continued to decline in 2014, in line with the information on cement sales to the domestic market, which fell 8.9% over the year transact.

Macroeconomic Indicators

2012

2013

2014(e) Expenditure and GDP - Private Consumption -5,8 -1,4 2,7 - Public Consumption -3,9 -1,9 -0,1 - GFCF -14,9 -6,3 3,7 - Exports 6,3 6,4 2,9 - Imports -4,7 3,6 5,0 - GDP at market prices -3,2 -1,4 1,1 Inflation 2,8 0,4 0,1 Industrial Production Index -3,0 0,8 1,5 Industrial Turnover Index -13,4 -0,5 -1,3 PSI 20 Index 2,9 16,0 -27,1 Unemployment rate 15,7

16,2

13,1

Source: Ministry of Finance / Bank of Portugal Percentage variation, excepting unemployment rate (e)- Estimated

Consolidated Annual Report 2014

dst - sgps, s.a. Page 10 of 118

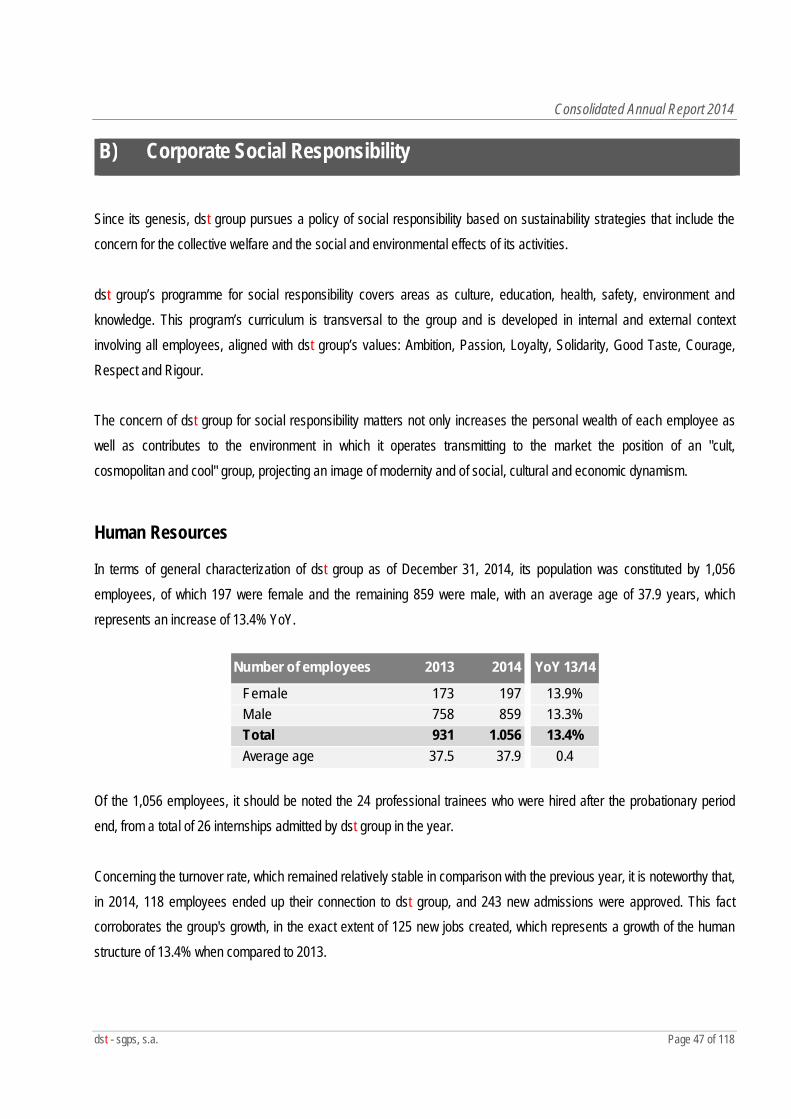

During the year 2014 there has been a recovery in private consumption, 2.7% compared to a fall of 1.4% in 2013, while still conditioned by high levels of debt. GFCF interrupted in mid-2013 its downward trend registered since 2009, projecting an increase of 3.7% in 2014. This development reflects largely the acceleration trajectory in business investment. The GFCF increase in GDP has been more moderate in the current recovery cycle as compared to previous recovery cycle periods. This moderate increase reflects the continued need to reduce the companies’ indebtedness level, which is expected to continue in the upcoming years, inasmuch as, notwithstanding the recent reduction, in the private sector, it remains very high compared to the Eurozone average. Consumer prices have been decelerating since 2012, in a context of cyclical position deterioration of the Portuguese economy. Thus, the Harmonised Index of Consumer Prices (HICP) slowed in 2014 to 0.1% (0.4% in 2013). Inflation is expected to remain at low levels, projecting a progressive increase in the coming years, in a framework of national and global economies moderate recovery. Additionally, there was a recovery in consumer confidence throughout 2014 and remained consistent at higher than the last ten years average values. This improvement was also found in most confidence indicators, leading to an increase in economic sentiment indicator. Also, in the labor market there are some signs of a moderate improvement in employment, reflecting the positive contribution of private employment. The unemployment rate stood at 13.1% at the end of 2014, compared with 16.2% in 2013. Despite the gradual recovery projections of the Portuguese economy, the expected growth potential is relatively limited. In fact, the deleveraging of the private and public sectors, limited levels of per worker productive capital, the low dynamism projected for key trading partners, especially those within Eurozone, will continue to influence the growth potential of the Portuguese economy in the future. In mid-2014 one of the major Portuguese banking groups falls. The crisis in Banco Espírito Santo (BES) naturally had a negative impact on businesses, individuals and the financial sector itself. The tightening of credit conditions for companies increased, while consumer confidence in the Portuguese banking system decreased. Once the BES damage was reported, putting the bank in a clear situation of insolvency, public intervention became necessary. The financial effort of the Portuguese State, through Resolution Fund, reached approximately EUR 4000 million. The impact of BES crisis on of the Portuguese economy growth next year is difficult to predict, but given the strength of the financial system, the economic and financial risk is more mitigated than if the crisis had occurred in previous times, during a more fragile financial system.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 11 of 118

In recent years, the Portuguese economy continued the strong adjustment, which achieved remarkable progress in correcting macroeconomic imbalances. However, the structural rebalancing of the economy is still incomplete and the macroeconomic adjustment still requires further deepening. Simultaneously, the risks of internal and external nature, imposed on the Portuguese economy, should not be ignored. In this context, it is crucial to fulfill the European commitments in terms of fiscal consolidation, which are essential to sustain a debt ratio downward trend. At the same time, the process of structural reforms aimed to create incentives for innovation, factor mobility and investment in physical and human capital must be deepened. All these conditions are essential to promote a better resources allocation and productivity growth, contributing to the sustained increase in economic welfare levels in Portugal.

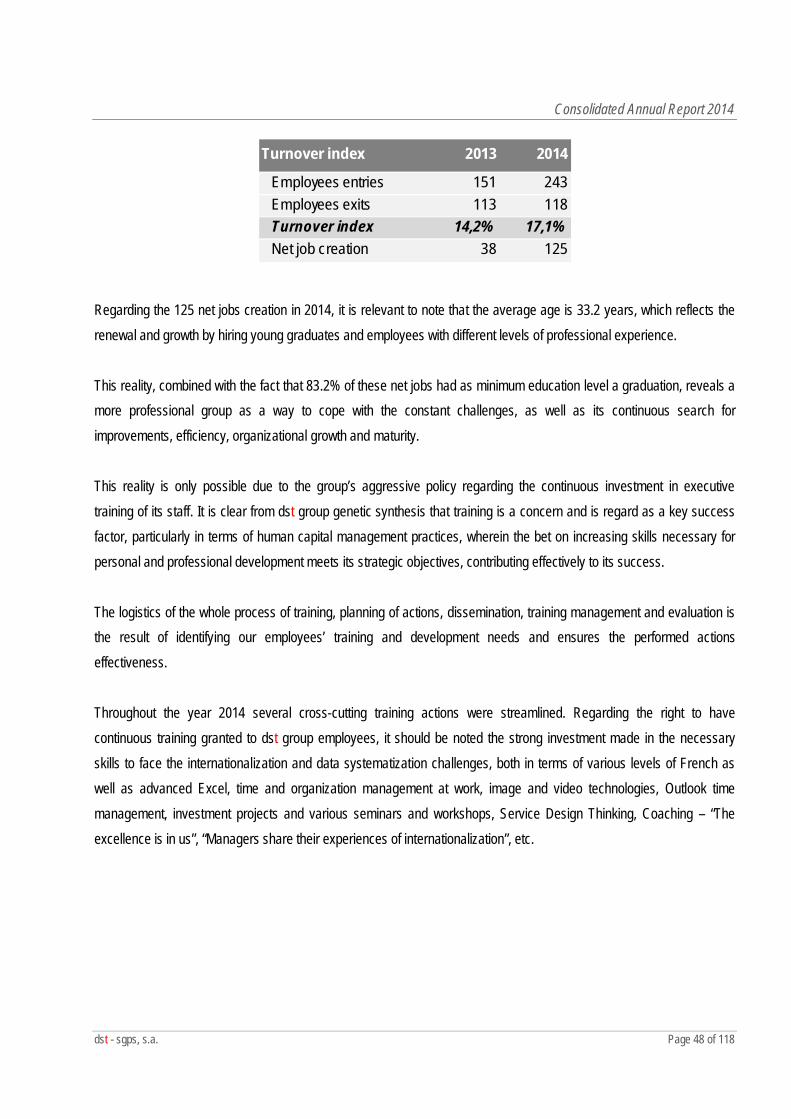

1.2.1 The construction Sector

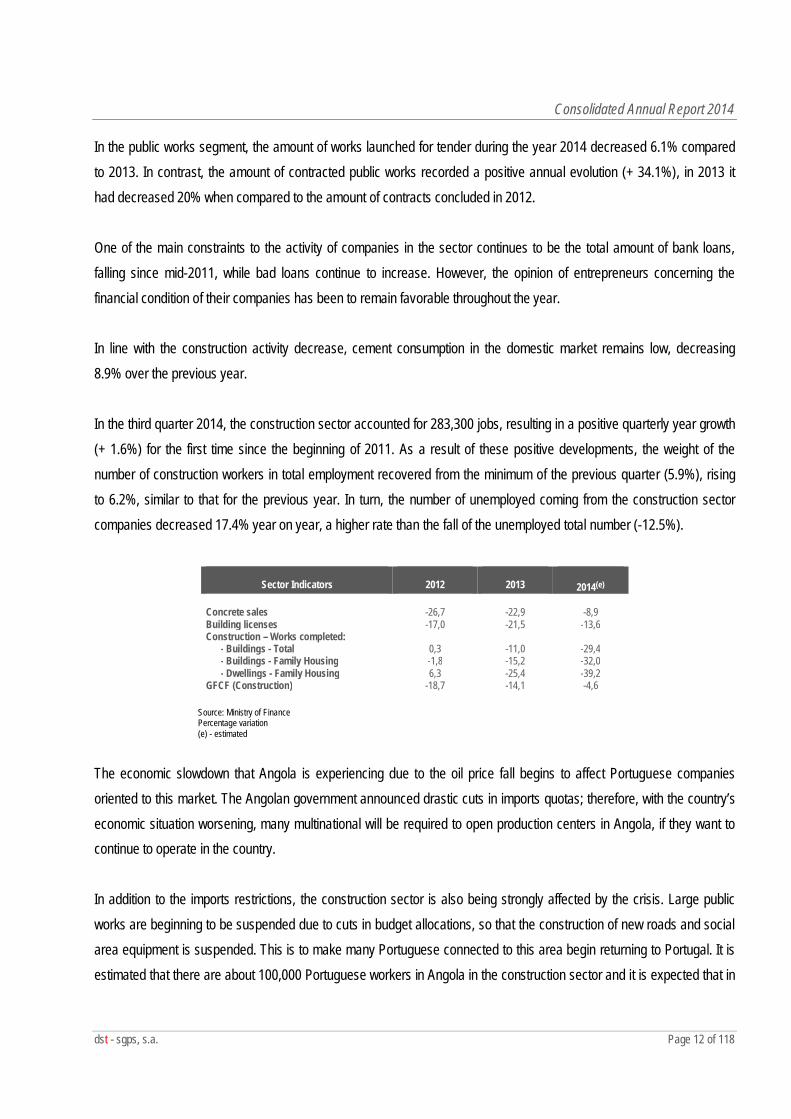

The Portuguese economy during the year 2014 has shown some positive signs, observing a clear slowdown of the construction sector crisis, while developments in this sector remain unfavorable. During the year 2014, the Portuguese entrepreneurs’ confidence indicator of the construction sector maintained a positive change from the assessment recorded a year earlier. This improvement results from the clearly positive entrepreneurs’ evaluations regarding the order book and the future sectorial unemployment level evolution. However, the majority of quantitative indicators have maintained a downward trend in 2014, although more moderate than in 2013. Being a fact that investment in construction fell by 4.6% and the sector GVA decreased by 4.9%, proving that the sector behavior is less unsatisfactory, since the breaks cleared in 2013 were 14.1% for construction GFCF and 13.1% in GVA. The works awarded value increased by 34% compared to 2013, which quickly being translated in works, will have very positive consequences on the companies activity level who work in the public works market. However, the development prospect for the building construction market is not so optimistic, since the housing licensing continues to fall (-13% of licensed dwellings) and the area licensed for non-residential buildings decreased 4% YoY . Thus, regarding building construction, it is worth noting the decrease of 13.6% in the licensing of new dwellings and 13.7% in the licensed area (34% and 30% in 2013, respectively). For non-residential buildings, there was a year on year fall of 3.9% of the licensed area, most notably the licensed area reduction of buildings for tourism, in contrast to the growth of buildings for agriculture and industry.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 12 of 118

In the public works segment, the amount of works launched for tender during the year 2014 decreased 6.1% compared to 2013. In contrast, the amount of contracted public works recorded a positive annual evolution (+ 34.1%), in 2013 it had decreased 20% when compared to the amount of contracts concluded in 2012. One of the main constraints to the activity of companies in the sector continues to be the total amount of bank loans, falling since mid-2011, while bad loans continue to increase. However, the opinion of entrepreneurs concerning the financial condition of their companies has been to remain favorable throughout the year. In line with the construction activity decrease, cement consumption in the domestic market remains low, decreasing 8.9% over the previous year. In the third quarter 2014, the construction sector accounted for 283,300 jobs, resulting in a positive quarterly year growth (+ 1.6%) for the first time since the beginning of 2011. As a result of these positive developments, the weight of the number of construction workers in total employment recovered from the minimum of the previous quarter (5.9%), rising to 6.2%, similar to that for the previous year. In turn, the number of unemployed coming from the construction sector companies decreased 17.4% year on year, a higher rate than the fall of the unemployed total number (-12.5%).

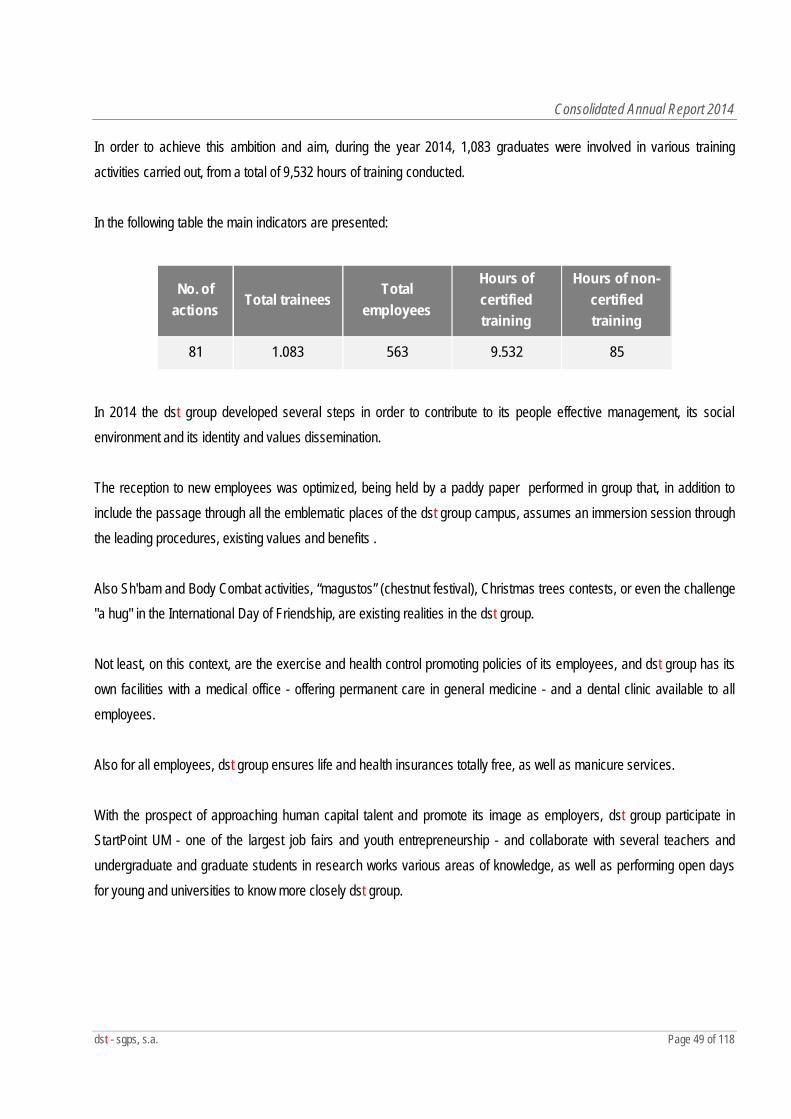

Sector Indicators

2012

2013

2014(e) Concrete sales -26,7 -22,9 -8,9 Building licenses -17,0 -21,5 -13,6 Construction – Works completed: - Buildings - Total 0,3 -11,0 -29,4 - Buildings - Family Housing -1,8 -15,2 -32,0 - Dwellings - Family Housing 6,3 -25,4 -39,2 GFCF (Construction) -18,7 -14,1 -4,6

Source: Ministry of Finance Percentage variation (e) - estimated

The economic slowdown that Angola is experiencing due to the oil price fall begins to affect Portuguese companies oriented to this market. The Angolan government announced drastic cuts in imports quotas; therefore, with the country’s economic situation worsening, many multinational will be required to open production centers in Angola, if they want to continue to operate in the country. In addition to the imports restrictions, the construction sector is also being strongly affected by the crisis. Large public works are beginning to be suspended due to cuts in budget allocations, so that the construction of new roads and social area equipment is suspended. This is to make many Portuguese connected to this area begin returning to Portugal. It is estimated that there are about 100,000 Portuguese workers in Angola in the construction sector and it is expected that in

Consolidated Annual Report 2014

dst - sgps, s.a. Page 13 of 118

the coming months this number will be greatly reduced and that the vast majority of them will return to Portugal without any guarantee of finding new work. On the other hand, construction companies will experience late payments, recurring situation in Angola. The conversion of revenue in kwanza for dollars and its expatriation to Portugal will be a growing problem, due to the lack of foreign currency in the market. Consequently, the Angolan crisis will have a negative impact on the Portuguese companies’ margins, being that Angola is the largest market for Portuguese construction companies, representing 38% of total activity outside Portugal.

1.2.2 The Renewable Energy Sector

Committed to reduce dependency on foreign energy, to increase energy efficiency and to reduce CO2 emissions, the Government has defined strategic lines for the energy sector, approving the National Strategy for Energy (ENE 2020), which estimates that by 2020 dependency on external energy will be reduced in 74%. Thus, renewable energy will have a key role to play, providing up to 2020 an installed capacity of 8,500 MW in wind power, 8,600 MW in hydropower and 1,500 MW in solar energy. In this sense, the renewable energy sector assumes more and more a prominent position in Portugal. At the end of 2014, renewable installed capacity reached 11,603 MW, being the annual production based on renewable sources of 32.461GWh. So, last year, 61% of the electricity consumed in Portugal came from renewable sources, and it should be highlighted the 10.7% increase in hydropower and the 31.7% in the photovoltaic energy. In this context, the Operational Programme of Sustainability and Efficiency in the Use of Resources 2014-2020, will be a structuring tool in the activity development of the energy production from renewable sources, and aims to achieve a sustainable growth path, supported in a competitive development model, in order to mitigate the consumption of natural resources and energy while generating new employment opportunities and economic development. The fundamental transition to a low carbon economy will necessarily be supported by the development of energy efficiency and energy production from renewable sources, themes supported in the Operational Programme mentioned above.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 14 of 118

Wind Energy

In Portugal, the North and Centre regions are the ones that have the higher concentration of national wind farms, due to the greater availability of resources. The installed capacity of wind power in Portugal at the end of 2014 stood at 4.873 GW, spread by 245 wind farms. The production in 2014 was 12,169 GWh, an almost equal value to that obtained in 2013. Most wind turbines currently in operation was installed between 2005 and 2012, and this technology is responsible for the production of more than 10 TWh since 2012. The evolution of this sector will go through over equipping the existing parks or the installation of offshore wind farms. Solar Energy

Due to its energy potential, the photovoltaic solar energy is one of the most promising energy resources. In 2014, the photovoltaic sector continued to consolidate the global position achieved in previous years, as the third most important source of renewable energy.

In Portugal, the installed capacity at the end of the year 2014 reached approximately 414 MW, compared with 229, 244 and 175 MW in the years 2013, 2012 e 2011, respectively.

Last year was marked by the end of micro and minigeneration, and the latest projects within this legal framework were installed, as well as the latest projects still framed in the National Strategic Reference Framework (NSRF) 2007-2013 were finalized, whose deadline for implementation expired on 2014.

The year 2015 will be marked by the entry into force of the self-consumption legal framework, which comes to liberalize the sector, allowing any electrical energy consumer to produce its own energy, exporting the surpluses to the grid utility.

It is expect a revival in the solar photovoltaic industry activity under this new framework, to enable the sector's recovery, affected in recent years by the abrupt reduction of the tariffs applied to the sector.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 15 of 118

The Hydropower

The hydropower is the worldwide leading source of renewable energy, being one of the most attractive for its maturity and predictability, as well as for its ability to compete economically with other non-renewable energy sources. China is by far the world largest producer of hydroelectric power, followed by Canada, USA, Brazil and Russia.

In Portugal, the installed capacity is stabilized with a value of approximately 5,566 MW, which, on an average year, corresponds to slightly more than 30% of the electricity consumed in Portugal is hydropower generated.

In 2007, the hydroelectric sector in Portugal was marked by the launch of the National Programme for High-Potential Hydroelectric Dams, which are currently running. This Programme foresees the Hydroelectric Exploitations implementation of Padroselos, Daivões, Vidago, Gouvães, Foz Tua, Pinhosão, Fridão, Girabolhos, Alvito and Almourol. The completion of these projects will result in an increase of installed capacity of 1.054 MW. By 2020, it is expected to reach 7,000 MW of installed capacity, according to the targets set.

Regarding the Law decree No. 25/2012, of February 6, that suspend the assignment of new injection points into the Public Service Electrical Network, and the Order 3316/2012 from the Ministry of the Economy and the Environment suspended all new hydro-electric licensing and extinguished the ongoing administrative licensing processes, which turns impossible all new hydro-electric licensing and extinguishes the ongoing administrative licensing processes, besides the Dams National Plan, there is no development perspective for this sector.

Despite not having been made any investment in new dams, the year 2014 was a very productive one regarding the water component, with a production of 16 456 GWh, as a result of a year with higher than average rainfall in more than 20%.

The industry has been waiting for some time the publish of new legal framework that will simplify the authorization of existing infrastructure use for the implementation of river SHP (Small Hydro plants) in order to enhance the energy production from renewable sources in rural areas, aiming the sustainable economic development and ensuring the preservation of the ecological ecosystems where these utilities are implemented.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 16 of 118

1.2.3 The Telecommunications Sector

The year 2014, regarding telecommunications market, was essentially marked industry consolidation.

Therefore, it should be pinpointed the following events that took place during this year in the global context:

Comcast, an entity based in Philadelphia, USA, and the biggest American cable operator, bought the Time Warner Cable. This was a transaction valued at about 42.2 billion dollars in shares, equivalent to EUR 33 billion. Thus, the combination of the two biggest American operators results in a total of about 33 million subscribers. Note that Comcast, in addition to the cable TV business, still sells Internet and telephone services, still owns NBC Universal, which olds NBC television station NBC and Universal Studios;

The US telecommunications entity AT & T bought Directv. Known as the second largest mobile phone services provider in the US, AT & T acquired DirectTv by 49 billion dollars. Taken together, the two groups accounts for a total of about 26 million subscribers. One objective of this acquisition, according to AT & T, is to bring broadband to over 15 million homes, especially in the rural areas of the country.

As regards the European context, the following events pinpoints:

At the end of November, Altice, the owner of Portuguese Cabovisão and ONI, bought the French SFR - Société Française de Radiotelephone, a deal valued at 15 billion euros. This purchase will result in the creation of a new operator in France that will unite SFR and Numericable;

In Spain, and in order to strengthen the television and Internet offer in the domestic market, Vodafone bought ONO for a total value of 7.2 billion euros. This deal follows Vodafone's strategic line to expand its activity in Europe through acquisitions. To remember, even in 2013, the same group purchased Kabel Deutschland;

Orange, the French telecommunications group, launched a takeover bid for the Spanish Jazztel. The offer was approximately of EUR 3.4 billion. The French telecommunications group has the intention to finance this transaction through a capital increase over two billion euros;

As fiber optic network management is concerned, the Spanish ADIF was purchased by REE - Red Eléctrica de España, in a deal valued at EUR 525 million;

The neutral fiber optic operator, Gas Natural Fenosa Telecomunicaciones (GNFT) sold its telecommunications subsidiary to Cinven, a venture capital firm, for 510 million euros. Cinven will thus manage GNFT network, which operates in the Spanish market and in Latin America.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 17 of 118

In the national context, the telecommunications sector was marked by the following events:

At May 5, 2014 Portugal Telecom increases its stake in Brazilian Oi from 23.2% to 39.7%;

Vodafone and PT signed a fiber optic sharing agreement. The goal is that each of the operators can access the 450,000 dwellings in geographical locations where the other entity has already invested or intends to invest. Therefore, and from this infrastructure point of view, it is expected to be in dispute for new customers.

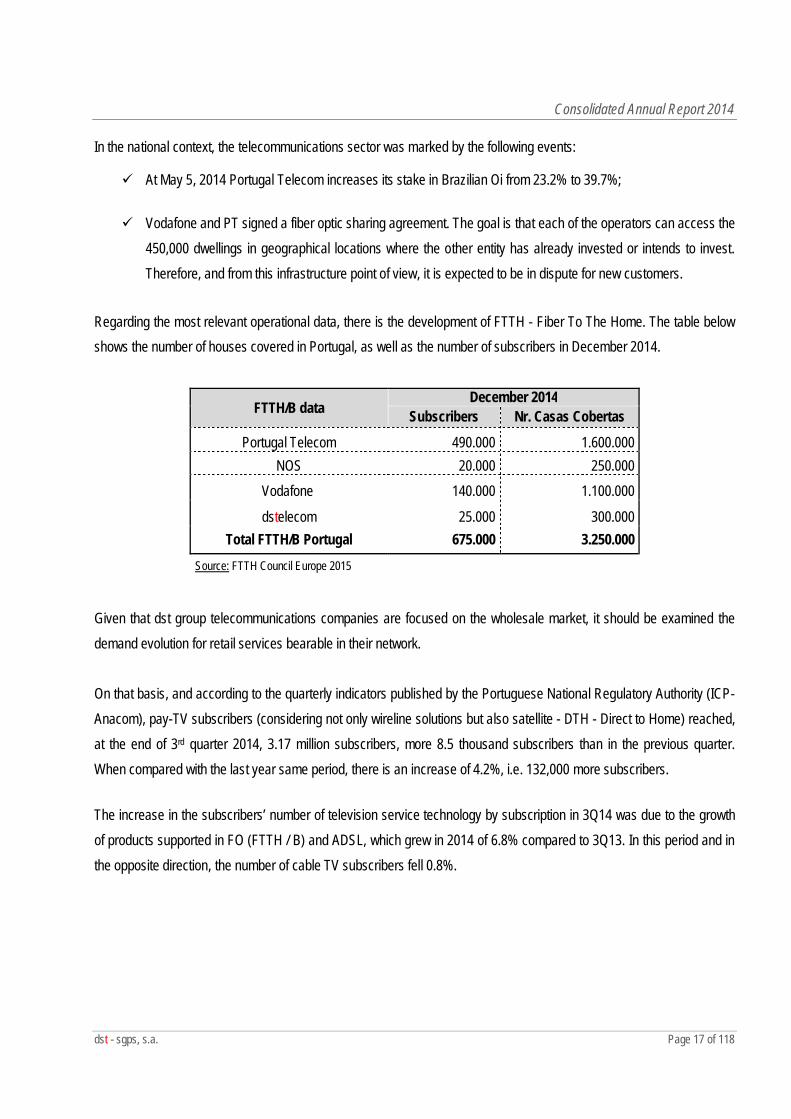

Regarding the most relevant operational data, there is the development of FTTH - Fiber To The Home. The table below shows the number of houses covered in Portugal, as well as the number of subscribers in December 2014.

Given that dst group telecommunications companies are focused on the wholesale market, it should be examined the demand evolution for retail services bearable in their network. On that basis, and according to the quarterly indicators published by the Portuguese National Regulatory Authority (ICP-Anacom), pay-TV subscribers (considering not only wireline solutions but also satellite - DTH - Direct to Home) reached, at the end of 3rd quarter 2014, 3.17 million subscribers, more 8.5 thousand subscribers than in the previous quarter. When compared with the last year same period, there is an increase of 4.2%, i.e. 132,000 more subscribers.

The increase in the subscribers’ number of television service technology by subscription in 3Q14 was due to the growth of products supported in FO (FTTH / B) and ADSL, which grew in 2014 of 6.8% compared to 3Q13. In this period and in the opposite direction, the number of cable TV subscribers fell 0.8%.

FTTH/B data December 2014

Subscribers Nr. Casas Cobertas

Portugal Telecom 490.000 1.600.000 NOS 20.000 250.000

Vodafone 140.000 1.100.000

dstelecom 25.000 300.000 Total FTTH/B Portugal 675.000 3.250.000

Source: FTTH Council Europe 2015

Consolidated Annual Report 2014

dst - sgps, s.a. Page 18 of 118

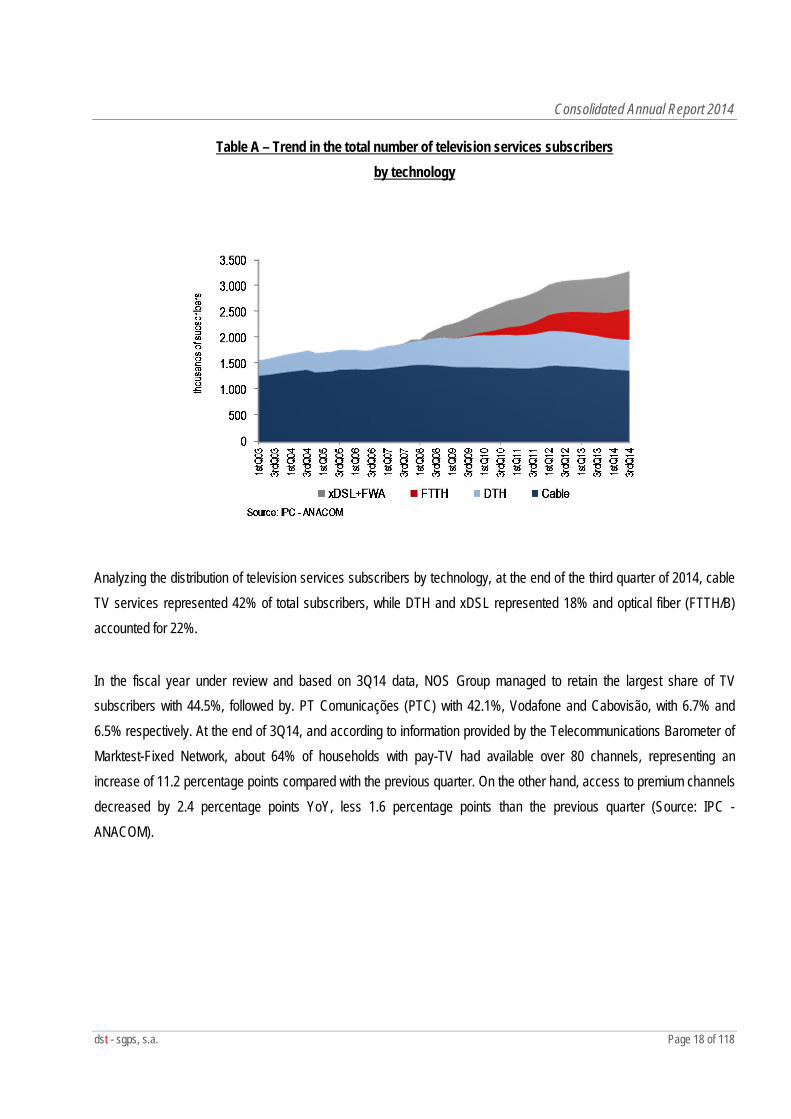

Table A – Trend in the total number of television services subscribers by technology

Analyzing the distribution of television services subscribers by technology, at the end of the third quarter of 2014, cable TV services represented 42% of total subscribers, while DTH and xDSL represented 18% and optical fiber (FTTH/B) accounted for 22%.

In the fiscal year under review and based on 3Q14 data, NOS Group managed to retain the largest share of TV subscribers with 44.5%, followed by. PT Comunicações (PTC) with 42.1%, Vodafone and Cabovisão, with 6.7% and 6.5% respectively. At the end of 3Q14, and according to information provided by the Telecommunications Barometer of Marktest-Fixed Network, about 64% of households with pay-TV had available over 80 channels, representing an increase of 11.2 percentage points compared with the previous quarter. On the other hand, access to premium channels decreased by 2.4 percentage points YoY, less 1.6 percentage points than the previous quarter (Source: IPC - ANACOM).

Consolidated Annual Report 2014

dst - sgps, s.a. Page 19 of 118

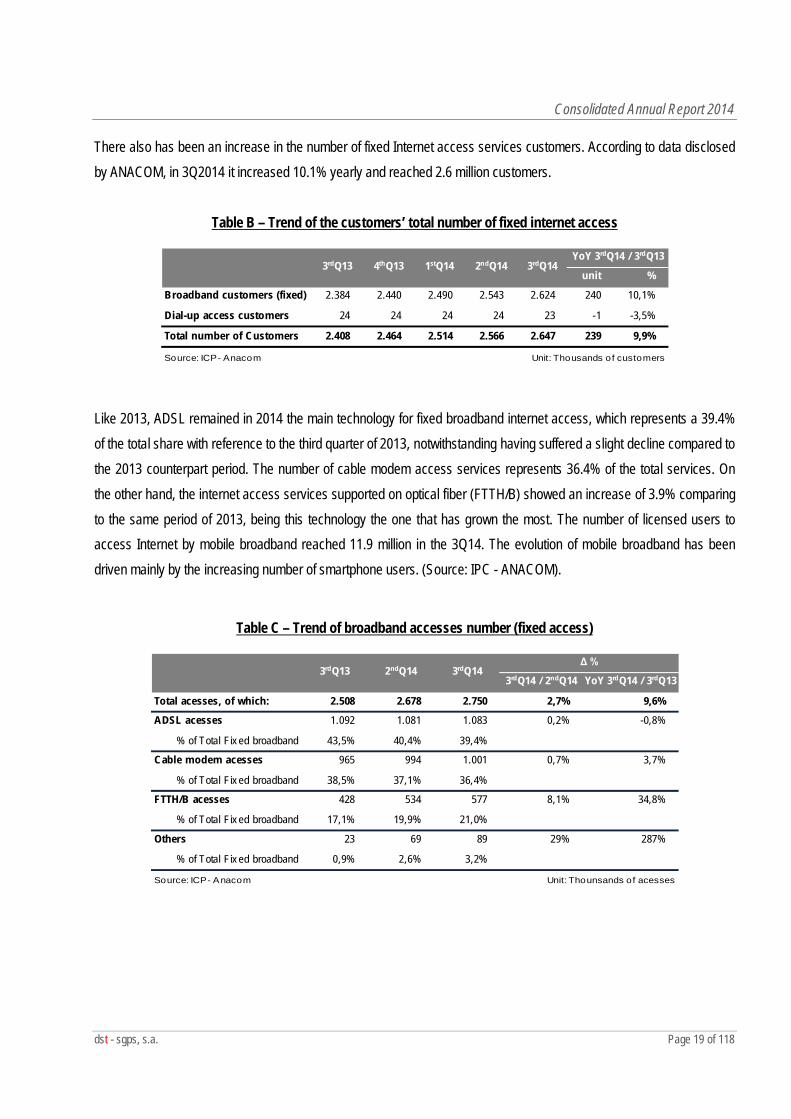

There also has been an increase in the number of fixed Internet access services customers. According to data disclosed by ANACOM, in 3Q2014 it increased 10.1% yearly and reached 2.6 million customers.

Table B – Trend of the customers’ total number of fixed internet access

Like 2013, ADSL remained in 2014 the main technology for fixed broadband internet access, which represents a 39.4% of the total share with reference to the third quarter of 2013, notwithstanding having suffered a slight decline compared to the 2013 counterpart period. The number of cable modem access services represents 36.4% of the total services. On the other hand, the internet access services supported on optical fiber (FTTH/B) showed an increase of 3.9% comparing to the same period of 2013, being this technology the one that has grown the most. The number of licensed users to access Internet by mobile broadband reached 11.9 million in the 3Q14. The evolution of mobile broadband has been driven mainly by the increasing number of smartphone users. (Source: IPC - ANACOM).

Table C – Trend of broadband accesses number (fixed access)

unit %

Broadband customers (fixed) 2.384 2.440 2.490 2.543 2.624 240 10,1%

Dial-up access customers 24 24 24 24 23 -1 -3,5%

Total number of Customers 2.408 2.464 2.514 2.566 2.647 239 9,9%

Source: ICP- Anacom Unit: Thousands of customers

YoY 3rdQ14 / 3rdQ133rdQ13 4thQ13 1stQ14 2ndQ14 3rdQ14

3rdQ14 / 2ndQ14 YoY 3rdQ14 / 3rdQ13

Total acesses, of which: 2.508 2.678 2.750 2,7% 9,6%

ADSL acesses 1.092 1.081 1.083 0,2% -0,8%

% of Total Fix ed broadband 43,5% 40,4% 39,4%

Cable modem acesses 965 994 1.001 0,7% 3,7%

% of Total Fix ed broadband 38,5% 37,1% 36,4%

FTTH/B acesses 428 534 577 8,1% 34,8%

% of Total Fix ed broadband 17,1% 19,9% 21,0%

Others 23 69 89 29% 287%

% of Total Fix ed broadband 0,9% 2,6% 3,2%

Source: ICP- Anacom Unit: Thounsands of acesses

3rdQ13 2ndQ14 3rdQ14Δ %

Consolidated Annual Report 2014

dst - sgps, s.a. Page 20 of 118

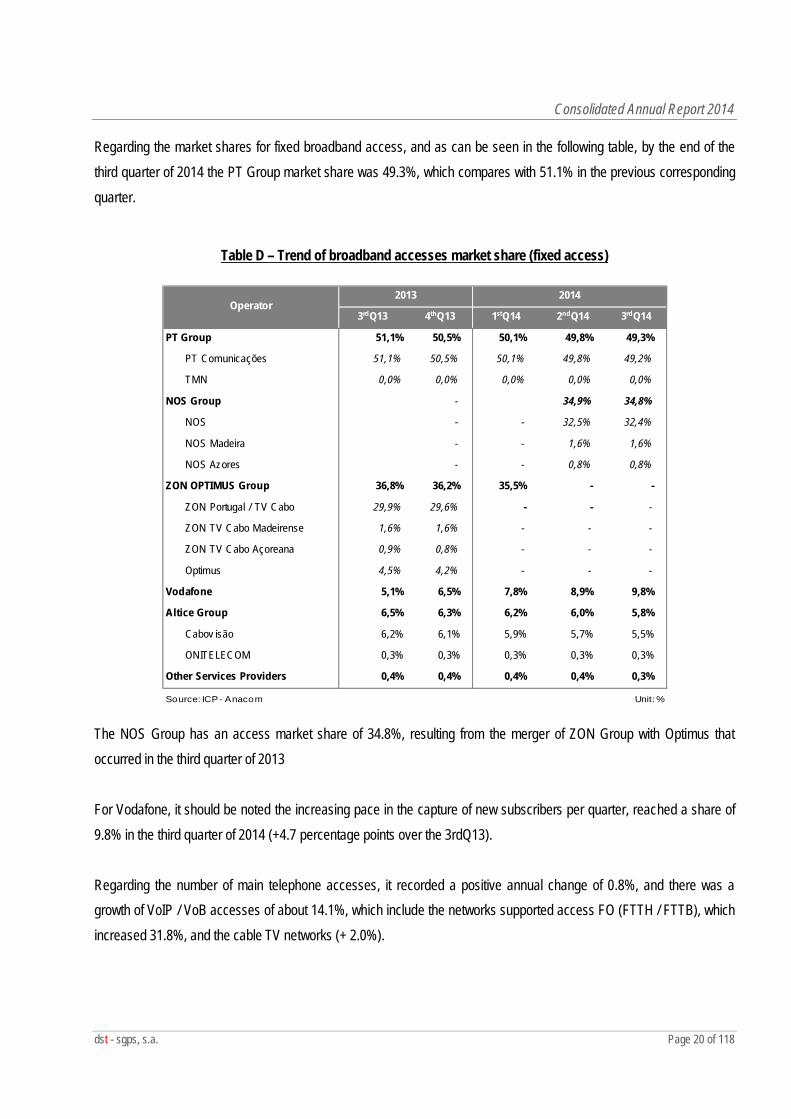

Regarding the market shares for fixed broadband access, and as can be seen in the following table, by the end of the third quarter of 2014 the PT Group market share was 49.3%, which compares with 51.1% in the previous corresponding quarter.

Table D – Trend of broadband accesses market share (fixed access)

The NOS Group has an access market share of 34.8%, resulting from the merger of ZON Group with Optimus that occurred in the third quarter of 2013 For Vodafone, it should be noted the increasing pace in the capture of new subscribers per quarter, reached a share of 9.8% in the third quarter of 2014 (+4.7 percentage points over the 3rdQ13). Regarding the number of main telephone accesses, it recorded a positive annual change of 0.8%, and there was a growth of VoIP / VoB accesses of about 14.1%, which include the networks supported access FO (FTTH / FTTB), which increased 31.8%, and the cable TV networks (+ 2.0%).

3rdQ13 4thQ13 1stQ14 2ndQ14 3rdQ14

PT Group 51,1% 50,5% 50,1% 49,8% 49,3%

PT Comunicações 51,1% 50,5% 50,1% 49,8% 49,2%

TMN 0,0% 0,0% 0,0% 0,0% 0,0%

NOS Group - 34,9% 34,8%

NOS - - 32,5% 32,4%

NOS Madeira - - 1,6% 1,6%

NOS Azores - - 0,8% 0,8%

ZON OPTIMUS Group 36,8% 36,2% 35,5% - -

ZON Portugal / TV Cabo 29,9% 29,6% - - -

ZON TV Cabo Madeirense 1,6% 1,6% - - -

ZON TV Cabo Açoreana 0,9% 0,8% - - -

Optimus 4,5% 4,2% - - -

Vodafone 5,1% 6,5% 7,8% 8,9% 9,8%

Altice Group 6,5% 6,3% 6,2% 6,0% 5,8%

Cabov isão 6,2% 6,1% 5,9% 5,7% 5,5%

ONITELECOM 0,3% 0,3% 0,3% 0,3% 0,3%

Other Services Providers 0,4% 0,4% 0,4% 0,4% 0,3%

Source: ICP- Anacom Unit: %

Operator2013 2014

Consolidated Annual Report 2014

dst - sgps, s.a. Page 21 of 118

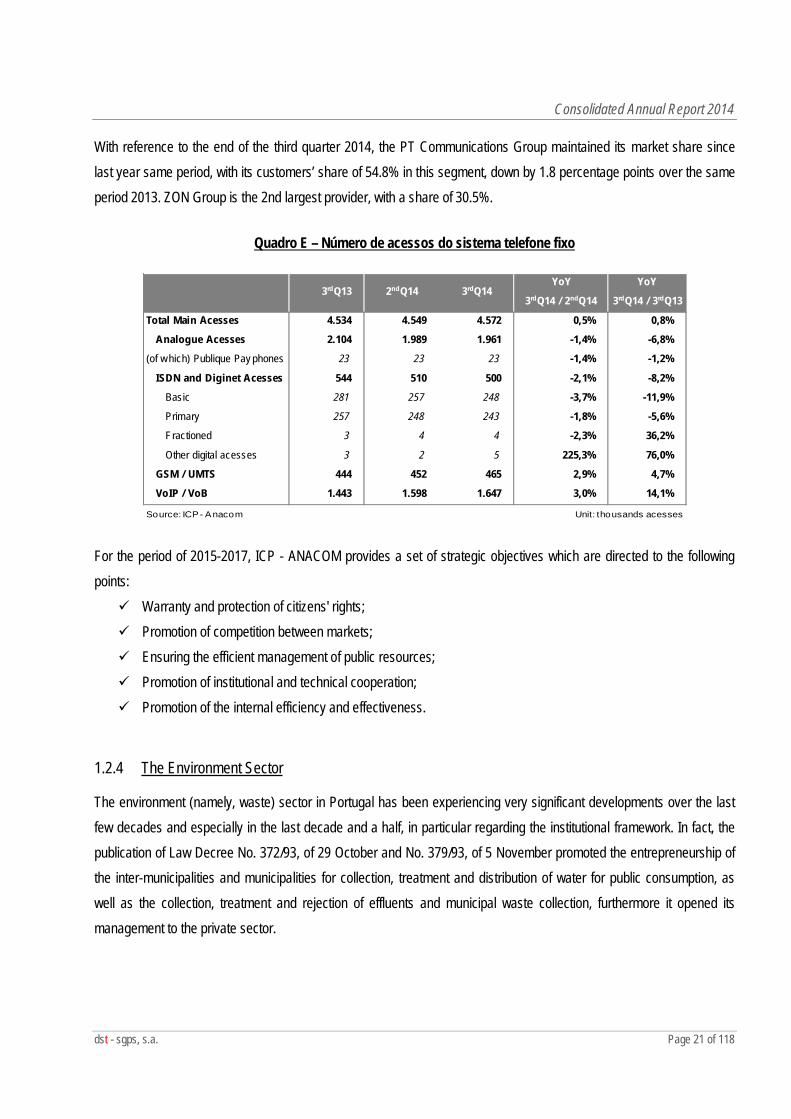

With reference to the end of the third quarter 2014, the PT Communications Group maintained its market share since last year same period, with its customers’ share of 54.8% in this segment, down by 1.8 percentage points over the same period 2013. ZON Group is the 2nd largest provider, with a share of 30.5%.

Quadro E – Número de acessos do sistema telefone fixo

For the period of 2015-2017, ICP - ANACOM provides a set of strategic objectives which are directed to the following points: Warranty and protection of citizens' rights; Promotion of competition between markets; Ensuring the efficient management of public resources; Promotion of institutional and technical cooperation; Promotion of the internal efficiency and effectiveness.

1.2.4 The Environment Sector

The environment (namely, waste) sector in Portugal has been experiencing very significant developments over the last few decades and especially in the last decade and a half, in particular regarding the institutional framework. In fact, the publication of Law Decree No. 372/93, of 29 October and No. 379/93, of 5 November promoted the entrepreneurship of the inter-municipalities and municipalities for collection, treatment and distribution of water for public consumption, as well as the collection, treatment and rejection of effluents and municipal waste collection, furthermore it opened its management to the private sector.

YoY YoY

3rdQ14 / 2ndQ14 3rdQ14 / 3rdQ13

Total Main Acesses 4.534 4.549 4.572 0,5% 0,8%

Analogue Acesses 2.104 1.989 1.961 -1,4% -6,8%

(of which) Publique Pay phones 23 23 23 -1,4% -1,2%

ISDN and Diginet Acesses 544 510 500 -2,1% -8,2%

Basic 281 257 248 -3,7% -11,9%

Primary 257 248 243 -1,8% -5,6%

Fractioned 3 4 4 -2,3% 36,2%

Other digital acesses 3 2 5 225,3% 76,0%

GSM / UMTS 444 452 465 2,9% 4,7%

VoIP / VoB 1.443 1.598 1.647 3,0% 14,1%

Source: ICP- Anacom Unit: thousands acesses

3rdQ13 2ndQ14 3rdQ14

Consolidated Annual Report 2014

dst - sgps, s.a. Page 22 of 118

The strategy outlined in the PEAASAR II defines that management entities along with the necessary implementation of infrastructure for achieving the desired service levels, with the required quality standards, should ensure that the price of services reflects the cost of water and sanitation, thus ensuring the sustainability of services, and promoting the efficient resources use through appropriate environmental practices. Furthermore, it should guarantee the complete compliance with legal obligations, without losing sight of the recommendations for the establishment of socially acceptable fares, in particular those related to the increase of territorial interventions and to the full exploitation of the project funds.

In Portugal, the water supply and wastewater sanitation sector is subdivided in two strands along their value chain: the "high" and "low":

“High” systems of wholesale activity: systems for capture, treatment and supply of water, and also systems for collection, treatment and rejection of waste water.

“Low” systems of retail activity: water distribution systems and domestic waste-water collection.

There are a large number of management entities operating in Portugal and its small size does not allow a desirable – and long-awaited – efficiency, optimization and scale in the water sector. The situation becomes more alarming when adding the dispersion and the small scale of those entities of the water short cycle that they manage.

Currently the imbalances in water sector are an unquestionable fact and recognized by all players in the industry, imposing the need to act urgently to achieve greater rationality, efficiency and optimization.

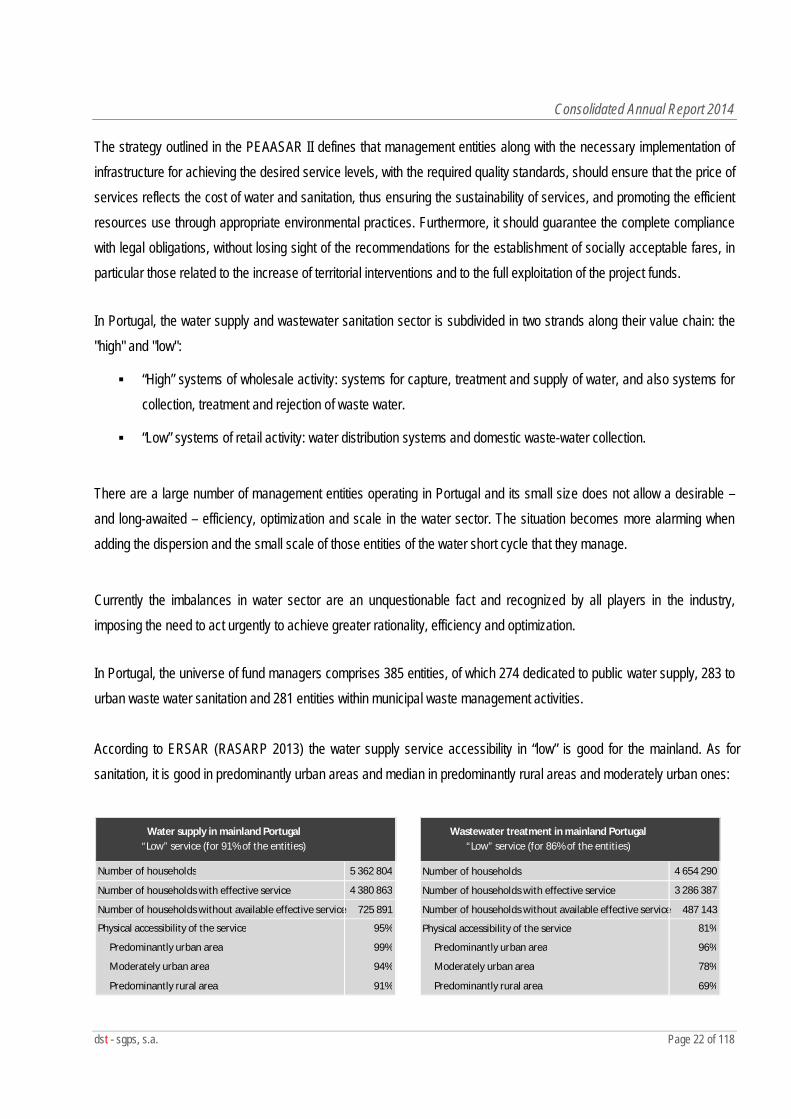

In Portugal, the universe of fund managers comprises 385 entities, of which 274 dedicated to public water supply, 283 to urban waste water sanitation and 281 entities within municipal waste management activities. According to ERSAR (RASARP 2013) the water supply service accessibility in “low” is good for the mainland. As for sanitation, it is good in predominantly urban areas and median in predominantly rural areas and moderately urban ones:

Number of households 5 362 804 Number of households

4 654 290

Number of households with effective service

4 380 863 Number of households with effective service

3 286 387

Number of households without available effective service

725 891 Number of households without available effective service

487 143

Physical accessibility of the service 95% Physical accessibility of the service

81%

Predominantly urban area 99% Predominantly urban area 96%

Moderately urban area 94% Moderately urban area 78%

Predominantly rural area 91% Predominantly rural area 69%

Water supply in mainland Portugal“Low” service (for 91% of the entities)

Wastewater treatment in mainland Portugal “Low” service (for 86% of the entities)

Consolidated Annual Report 2014

dst - sgps, s.a. Page 23 of 118

As for water losses, the mainland average unbilled water was 30.7% (RASARP 2013). A final note regarding consumption, which it has been consistently decreasing since 2007. The trend is widespread throughout the country and is related to several combined factors, namely:

Short-term Factors: - Economic and social crisis; - Emigration; - Unemployment.

Structural Factors: - Demographic reduction; - Population aging; - Environmental awareness; - Climate changes; - Tariffs increasing; - Technological innovations; - Public and building networks efficiency.

1.2.5 The Capital Venture Sector

The Portuguese venture capital industry after experienced a crisis, is currently on a growth phase. This fact mainly stemmed from markets short liquidity, which has led to greater demand for venture capital to strengthen companies’ equity. Consequently, there are new investment funds and different types of market participants. As happened in the '80s, venture capital companies (“VCC”) are currently averse to undertake investments in start-ups, unlike what happens, for example, in the U.S., where they continue to support the expansion of this type of investment

At the end of 2014, as in the previous year, Portugal had 79 venture capital funds ("VCF") and 34 VCC. Data disclosed by Portuguese Securities Market Commission (“CMVM”) indicate that the dynamism of venture capital activity over the last decade mainly results from the increase in VCF and not of VCC, a fact easily explained by the fact that funds hold about 90% of the total amount under management. The revitalization funds had the biggest highlight in transactions in 2014, which is not quite surprising, given that these transactions require greater capital investment, for which has also contributed a considerable increase of foreign private equity investments funds in Portuguese companies. This type of fund operates at a more operational level and they intend to privileged internationalization, cost reduction and consolidation (mergers between companies in the same industry), in order to make profitable companies. With regard to venture capital, more than 60% of this investment type in 2014 was held in internet and technology companies and it is estimated that in 2015 the trend will continue.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 24 of 118

The venture capital investments in Portugal have shown an atypical behavior regarding its industry pattern, since investors rather than taking shareholders risks have instead chosen to make capital contributions through paid provisions, which greatly resembles a bank loan. Thus, the overall risk of operations is substantially reduced, since the return on equity ceases to depend solely on profits from activity or shares sales. The operational program COMPETE, under the Support Financing and Risk Sharing System of Innovation (SAFPRI), had a significant importance to the sector expansion since it continued to support, in 2014, about 22 VCF oriented to SMEs investments, both at the initial phase of its life cycle as in the expansion phase of its activity. On the European scene, like Portugal, funds raised by venture capital have mainly been directed to VCF, with private equity characteristics, specialized in buyout transactions involving the acquisition of an entity’s capital majority, with an eventually use of substantial debt amounts. The year 2014 was also marked by the first steps towards the transposition of Directive No. 2011/61 / EU and Directive No. 2013/14 / EU of the European Parliament and European Council of June 8, 2011 and May 21, 2013 respectively. The result was published by the Law No. 18/2015, of March 4, which substantially changes the regulatory framework for venture capital investment in Portugal, and to highlight the following aspects: (i) introduces regulation on investment in social entrepreneurship and specialized alternative investment; (ii) possibility of fund management regulation to predict funds background division in several independent compartments patrimonial rules; and (iii) a new more demanding regime that now large management companies are subject.

In short, it is still expected a growing influence in this industry, as there is a substantial capacity of funds raised

by operators that has not yet been invested in shares. Moreover, the European Community program Horizon 2020 predicts that about 2 billion euros are available for venture capital investments, primarily for projects in the seed or early stage phases.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 25 of 118

2. Business activity

Global analysis of 2014 period

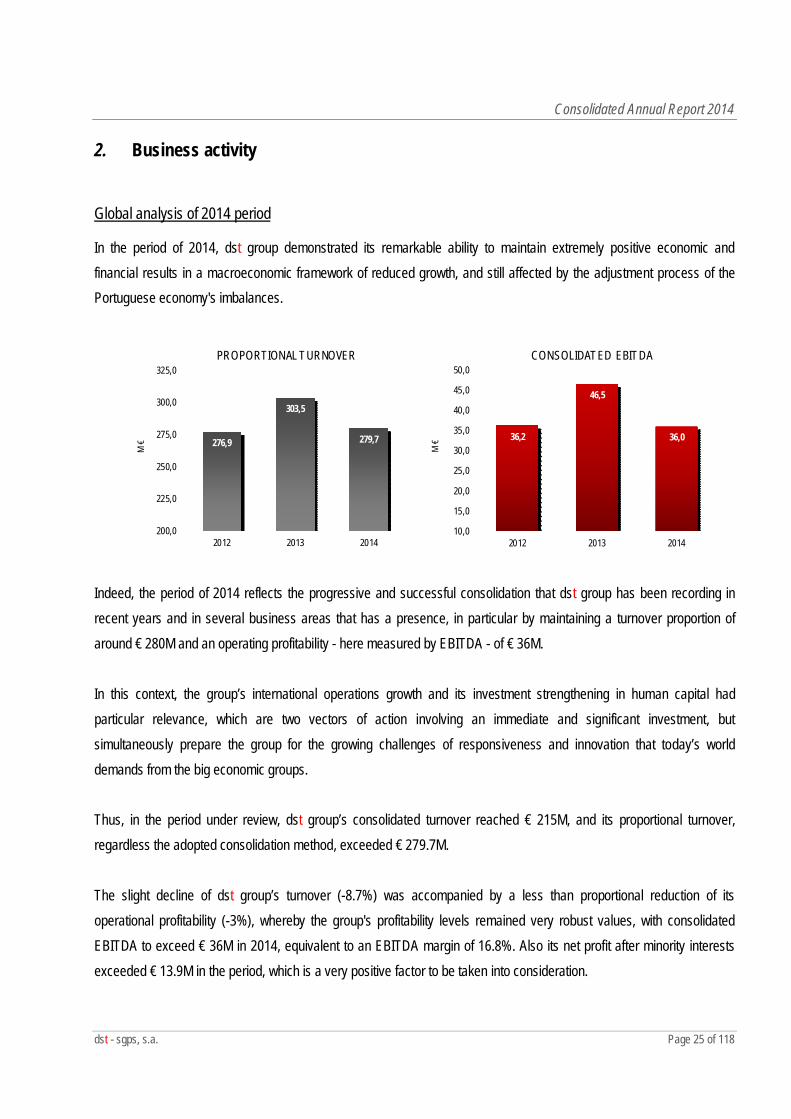

In the period of 2014, dst group demonstrated its remarkable ability to maintain extremely positive economic and financial results in a macroeconomic framework of reduced growth, and still affected by the adjustment process of the Portuguese economy's imbalances.

276,9

303,5

279,7

200,0

225,0

250,0

275,0

300,0

325,0

2012 2013 2014

M €

PROPORTIONAL TURNOVER

36,2

46,5

36,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

45,0

50,0

2012 2013 2014

M €

CONSOLIDATED EBITDA

Indeed, the period of 2014 reflects the progressive and successful consolidation that dst group has been recording in recent years and in several business areas that has a presence, in particular by maintaining a turnover proportion of around € 280M and an operating profitability - here measured by EBITDA - of € 36M. In this context, the group’s international operations growth and its investment strengthening in human capital had particular relevance, which are two vectors of action involving an immediate and significant investment, but simultaneously prepare the group for the growing challenges of responsiveness and innovation that today’s world demands from the big economic groups. Thus, in the period under review, dst group’s consolidated turnover reached € 215M, and its proportional turnover, regardless the adopted consolidation method, exceeded € 279.7M. The slight decline of dst group’s turnover (-8.7%) was accompanied by a less than proportional reduction of its operational profitability (-3%), whereby the group's profitability levels remained very robust values, with consolidated EBITDA to exceed € 36M in 2014, equivalent to an EBITDA margin of 16.8%. Also its net profit after minority interests exceeded € 13.9M in the period, which is a very positive factor to be taken into consideration.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 26 of 118

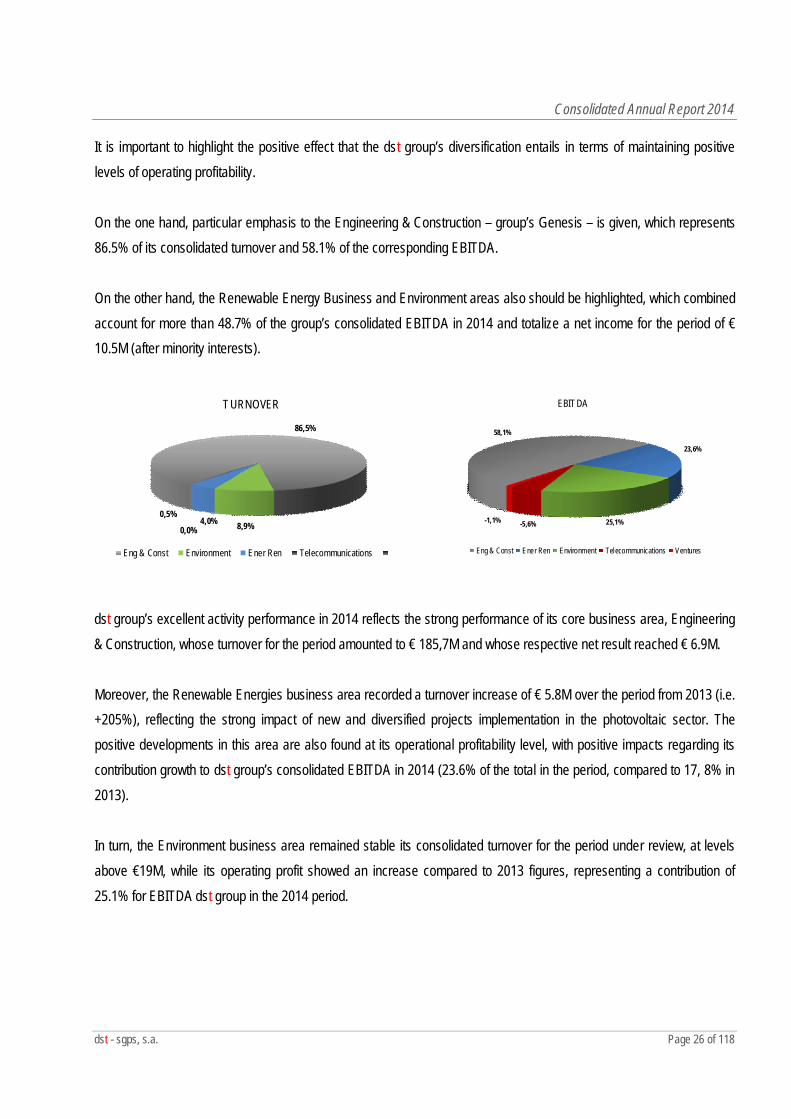

It is important to highlight the positive effect that the dst group’s diversification entails in terms of maintaining positive levels of operating profitability. On the one hand, particular emphasis to the Engineering & Construction – group’s Genesis – is given, which represents 86.5% of its consolidated turnover and 58.1% of the corresponding EBITDA. On the other hand, the Renewable Energy Business and Environment areas also should be highlighted, which combined account for more than 48.7% of the group’s consolidated EBITDA in 2014 and totalize a net income for the period of € 10.5M (after minority interests).

86,5%

8,9%4,0%0,0%

0,5%

TURNOVER

Eng & Const Environment Ener Ren Telecommunications

58,1%

23,6%

25,1%-5,6%-1,1%

EBITDA

Eng & Const Ener Ren Environment Telecommunications Ventures

dst group’s excellent activity performance in 2014 reflects the strong performance of its core business area, Engineering & Construction, whose turnover for the period amounted to € 185,7M and whose respective net result reached € 6.9M. Moreover, the Renewable Energies business area recorded a turnover increase of € 5.8M over the period from 2013 (i.e. +205%), reflecting the strong impact of new and diversified projects implementation in the photovoltaic sector. The positive developments in this area are also found at its operational profitability level, with positive impacts regarding its contribution growth to dst group’s consolidated EBITDA in 2014 (23.6% of the total in the period, compared to 17, 8% in 2013). In turn, the Environment business area remained stable its consolidated turnover for the period under review, at levels above €19M, while its operating profit showed an increase compared to 2013 figures, representing a contribution of 25.1% for EBITDA dst group in the 2014 period.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 27 of 118

The year 2014 continued to be a great investment period in the Telecommunications business area, particularly in trade, so that, although this area does not yet present a relevant turnover on dst group’s global sphere, its turnover growth of 42.8% YoY is remarkable, exceeding in the year, the level of €1M. Nevertheless, the impact of depreciation and amortization from the high investments made by the group in this business implies that its net income for the period is necessarily negative, to the tune of € 2.1M. Moreover, it should be emphasized dst group’s presence in Ventures business area, which bet became intensified in 2014, with the implementation by 2bpartner – sociedade capital de risco, s.a., - the group’s venture capital company – of multiple analysis process and due diligence projects which materialized in the realization of different investments during the period under review, in parallel with the development, by innovationpoint – investigação e desenvolvimento, s.a., of several innovative projects. In this context, naturally, Ventures business area does not yet have a turnover that may be representative of its potential growth, remaining as a big bet vector in the future by dst group.

Economic and financial summary (year 2014)

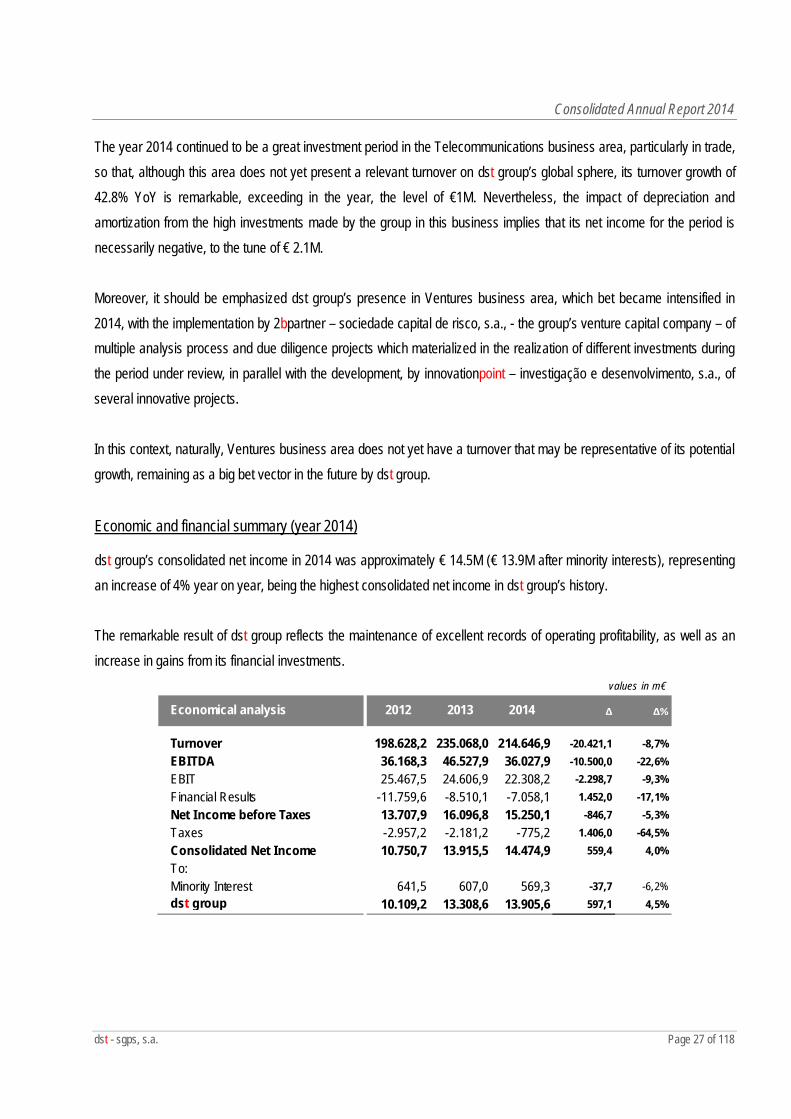

dst group’s consolidated net income in 2014 was approximately € 14.5M (€ 13.9M after minority interests), representing an increase of 4% year on year, being the highest consolidated net income in dst group’s history. The remarkable result of dst group reflects the maintenance of excellent records of operating profitability, as well as an increase in gains from its financial investments.

values in m€

Economical analysis 2012 2013 2014 ∆ ∆%

Turnover 198.628,2 235.068,0 214.646,9 -20.421,1 -8,7%EBITDA 36.168,3 46.527,9 36.027,9 -10.500,0 -22,6%EBIT 25.467,5 24.606,9 22.308,2 -2.298,7 -9,3%Financial Results -11.759,6 -8.510,1 -7.058,1 1.452,0 -17,1%Net Income before Taxes 13.707,9 16.096,8 15.250,1 -846,7 -5,3%Taxes -2.957,2 -2.181,2 -775,2 1.406,0 -64,5%Consolidated Net Income 10.750,7 13.915,5 14.474,9 559,4 4,0%To:Minority Interest 641,5 607,0 569,3 -37,7 -6,2%dst group 10.109,2 13.308,6 13.905,6 597,1 4,5%

Consolidated Annual Report 2014

dst - sgps, s.a. Page 28 of 118

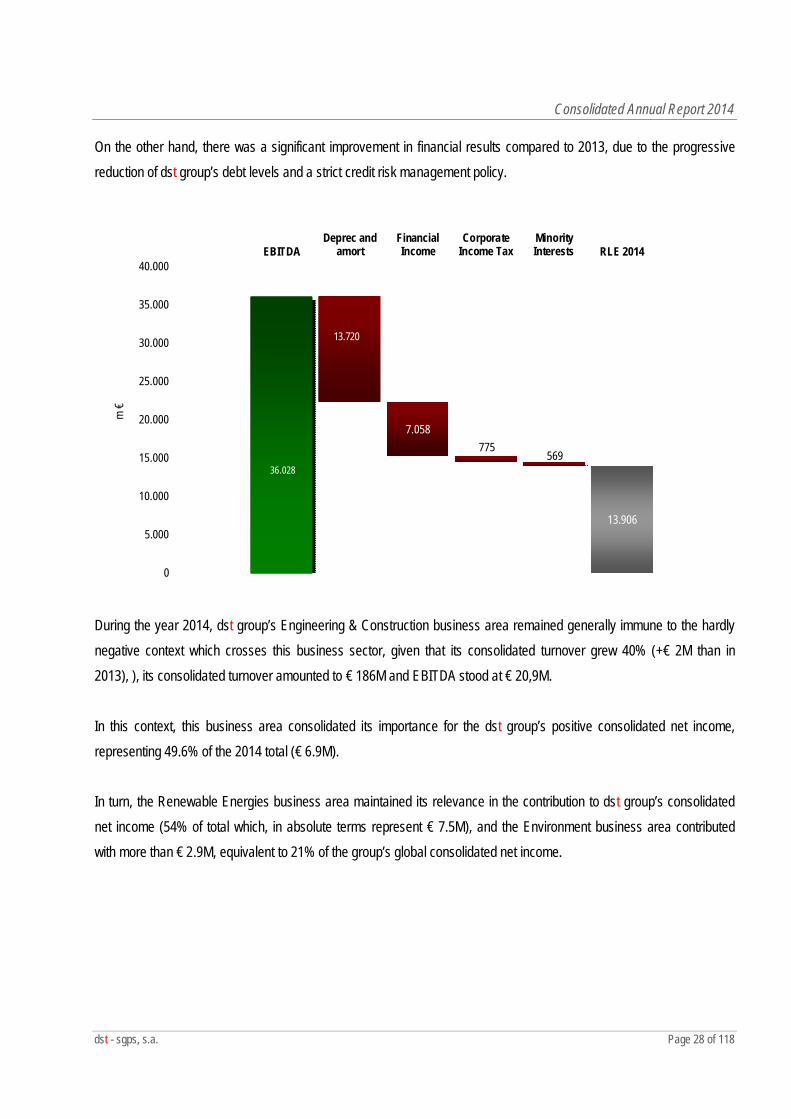

On the other hand, there was a significant improvement in financial results compared to 2013, due to the progressive reduction of dst group’s debt levels and a strict credit risk management policy.

13.906

7.058775

56936.028

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000EBITDA

Deprec andamort

FinancialIncome

CorporateIncome Tax

MinorityInterests RLE 2014

m €

13.720

During the year 2014, dst group’s Engineering & Construction business area remained generally immune to the hardly negative context which crosses this business sector, given that its consolidated turnover grew 40% (+€ 2M than in 2013), ), its consolidated turnover amounted to € 186M and EBITDA stood at € 20,9M. In this context, this business area consolidated its importance for the dst group’s positive consolidated net income, representing 49.6% of the 2014 total (€ 6.9M). In turn, the Renewable Energies business area maintained its relevance in the contribution to dst group’s consolidated net income (54% of total which, in absolute terms represent € 7.5M), and the Environment business area contributed with more than € 2.9M, equivalent to 21% of the group’s global consolidated net income.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 29 of 118

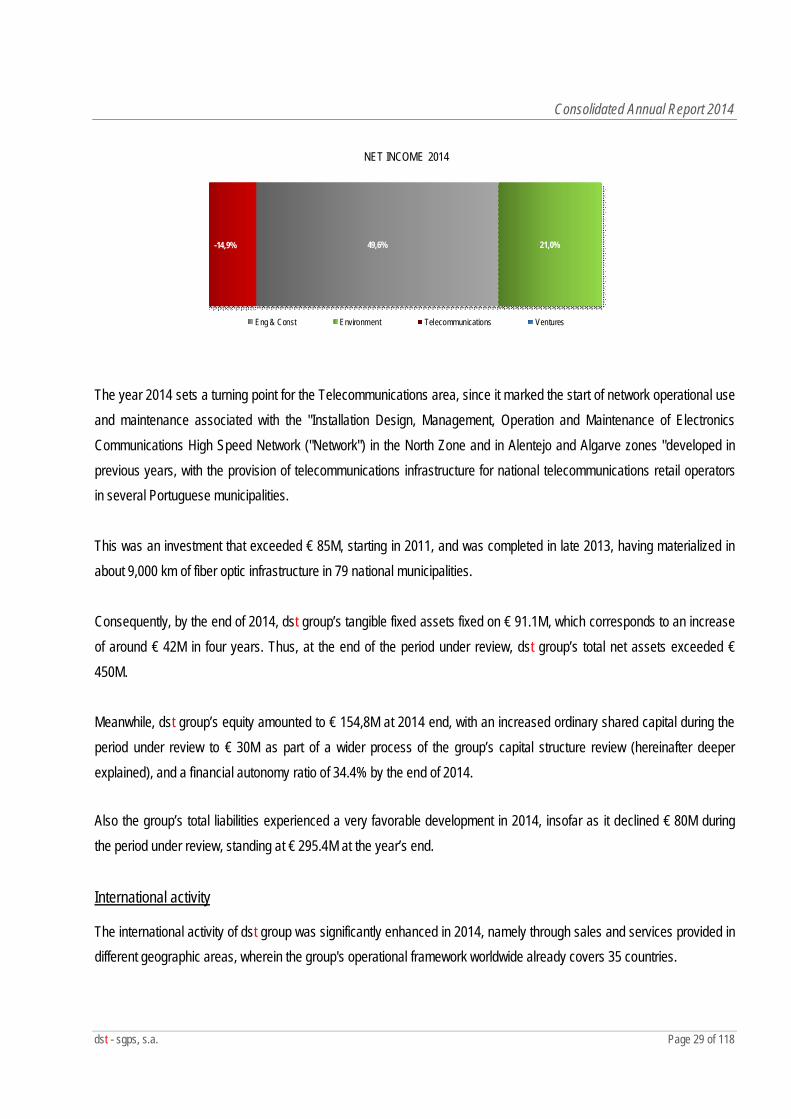

49,6% 21,0%-14,9%

NET INCOME 2014

Eng & Const Environment Telecommunications Ventures

The year 2014 sets a turning point for the Telecommunications area, since it marked the start of network operational use and maintenance associated with the "Installation Design, Management, Operation and Maintenance of Electronics Communications High Speed Network ("Network") in the North Zone and in Alentejo and Algarve zones "developed in previous years, with the provision of telecommunications infrastructure for national telecommunications retail operators in several Portuguese municipalities. This was an investment that exceeded € 85M, starting in 2011, and was completed in late 2013, having materialized in about 9,000 km of fiber optic infrastructure in 79 national municipalities. Consequently, by the end of 2014, dst group’s tangible fixed assets fixed on € 91.1M, which corresponds to an increase of around € 42M in four years. Thus, at the end of the period under review, dst group’s total net assets exceeded € 450M. Meanwhile, dst group’s equity amounted to € 154,8M at 2014 end, with an increased ordinary shared capital during the period under review to € 30M as part of a wider process of the group’s capital structure review (hereinafter deeper explained), and a financial autonomy ratio of 34.4% by the end of 2014.

Also the group’s total liabilities experienced a very favorable development in 2014, insofar as it declined € 80M during the period under review, standing at € 295.4M at the year’s end.

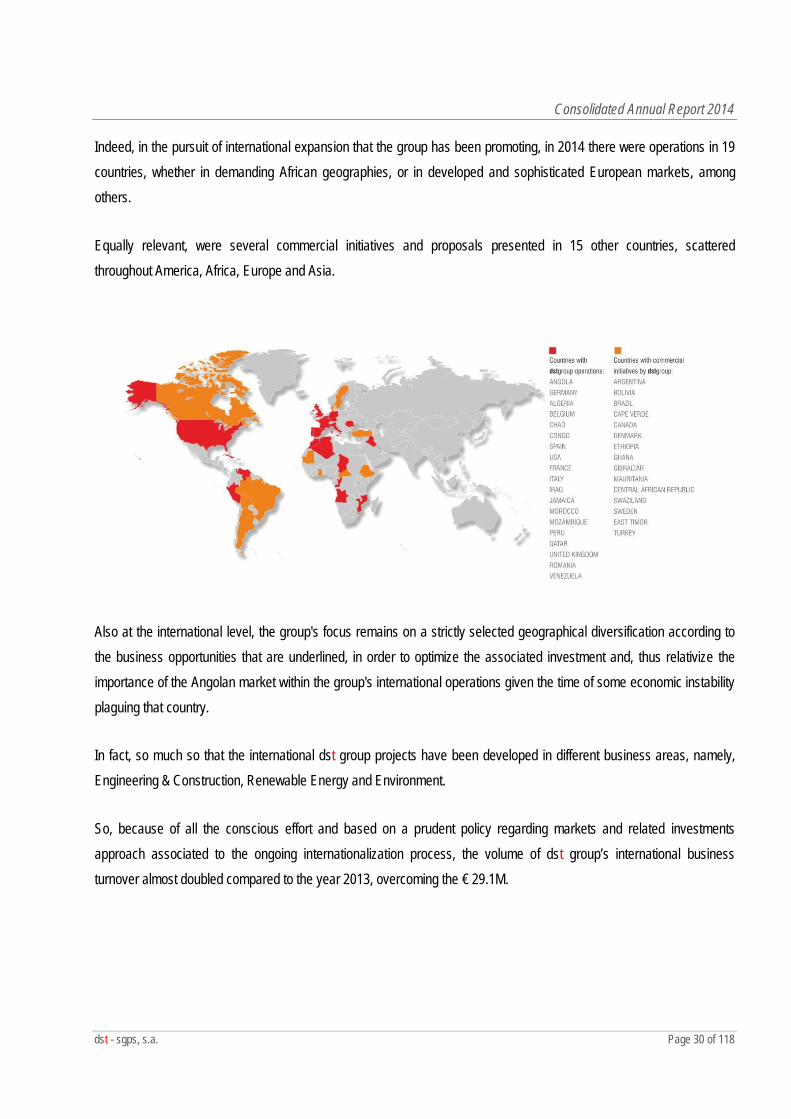

International activity

The international activity of dst group was significantly enhanced in 2014, namely through sales and services provided in different geographic areas, wherein the group's operational framework worldwide already covers 35 countries.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 30 of 118

Indeed, in the pursuit of international expansion that the group has been promoting, in 2014 there were operations in 19 countries, whether in demanding African geographies, or in developed and sophisticated European markets, among others.

Equally relevant, were several commercial initiatives and proposals presented in 15 other countries, scattered throughout America, Africa, Europe and Asia.

Also at the international level, the group's focus remains on a strictly selected geographical diversification according to the business opportunities that are underlined, in order to optimize the associated investment and, thus relativize the importance of the Angolan market within the group's international operations given the time of some economic instability plaguing that country.

In fact, so much so that the international dst group projects have been developed in different business areas, namely, Engineering & Construction, Renewable Energy and Environment.

So, because of all the conscious effort and based on a prudent policy regarding markets and related investments approach associated to the ongoing internationalization process, the volume of dst group’s international business turnover almost doubled compared to the year 2013, overcoming the € 29.1M.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 31 of 118

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014

INTERNATIONAL TURNOVER

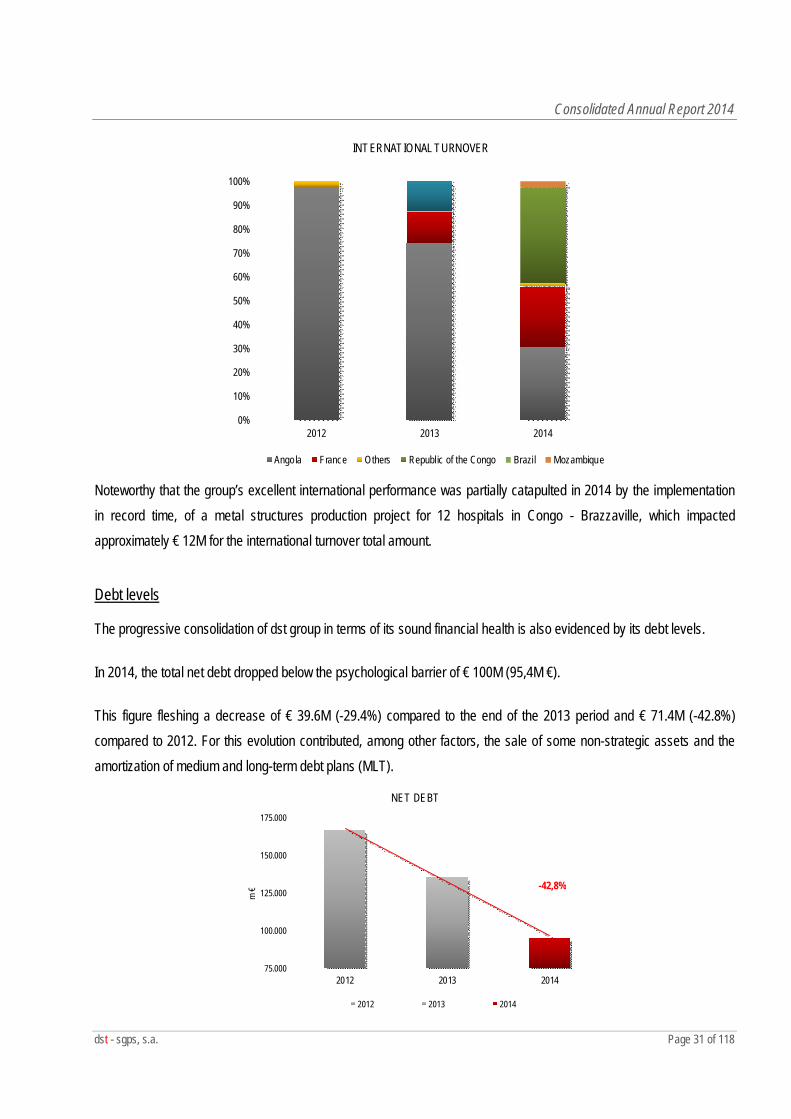

Angola France Others Republic of the Congo Brazil Mozambique Noteworthy that the group’s excellent international performance was partially catapulted in 2014 by the implementation in record time, of a metal structures production project for 12 hospitals in Congo - Brazzaville, which impacted approximately € 12M for the international turnover total amount.

Debt levels

The progressive consolidation of dst group in terms of its sound financial health is also evidenced by its debt levels.

In 2014, the total net debt dropped below the psychological barrier of € 100M (95,4M €).

This figure fleshing a decrease of € 39.6M (-29.4%) compared to the end of the 2013 period and € 71.4M (-42.8%) compared to 2012. For this evolution contributed, among other factors, the sale of some non-strategic assets and the amortization of medium and long-term debt plans (MLT).

75.000

100.000

125.000

150.000

175.000

2012 2013 2014

m €

NET DEBT

2012 2013 2014

-42,8%

Consolidated Annual Report 2014

dst - sgps, s.a. Page 32 of 118

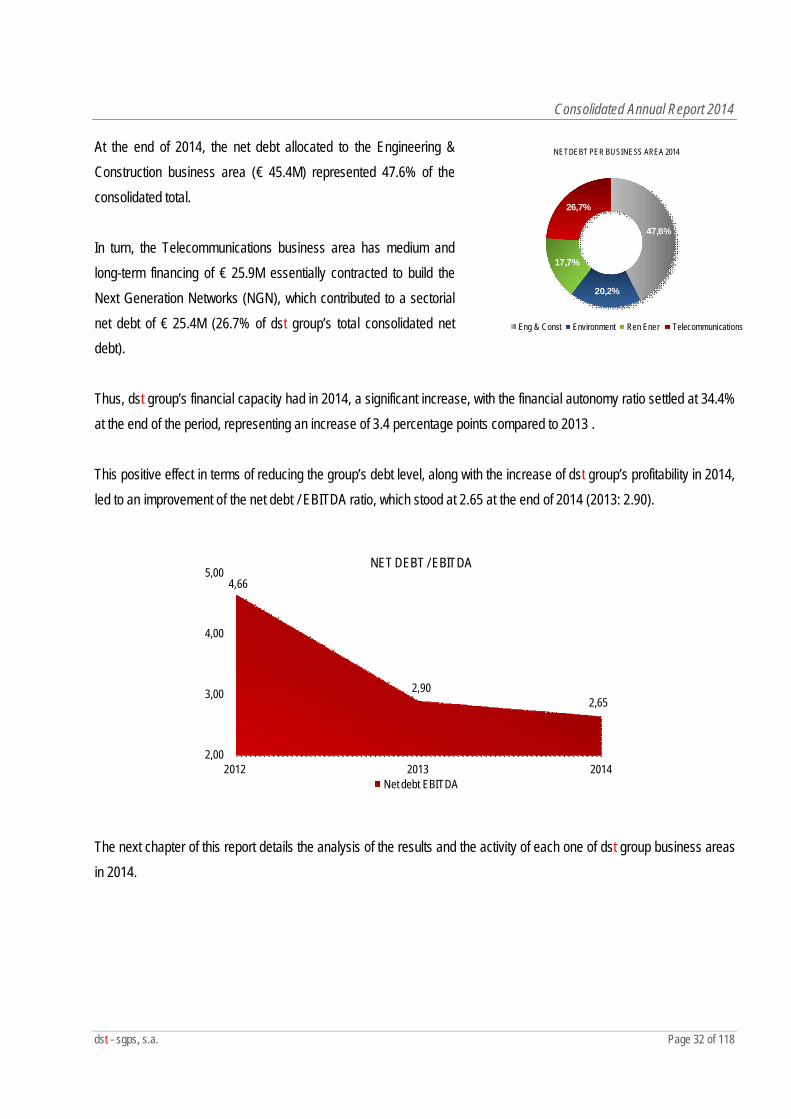

At the end of 2014, the net debt allocated to the Engineering & Construction business area (€ 45.4M) represented 47.6% of the consolidated total. In turn, the Telecommunications business area has medium and long-term financing of € 25.9M essentially contracted to build the Next Generation Networks (NGN), which contributed to a sectorial net debt of € 25.4M (26.7% of dst group’s total consolidated net debt). Thus, dst group’s financial capacity had in 2014, a significant increase, with the financial autonomy ratio settled at 34.4% at the end of the period, representing an increase of 3.4 percentage points compared to 2013 . This positive effect in terms of reducing the group’s debt level, along with the increase of dst group’s profitability in 2014, led to an improvement of the net debt / EBITDA ratio, which stood at 2.65 at the end of 2014 (2013: 2.90).

4,66

2,902,65

2,00

3,00

4,00

5,00

2012 2013 2014

NET DEBT / EBITDA

Net debt EBITDA

The next chapter of this report details the analysis of the results and the activity of each one of dst group business areas in 2014.

47,6%

20,2%

17,7%

26,7%

NET DEBT PER BUSINESS AREA 2014

Eng & Const Environment Ren Ener Telecommunications

Consolidated Annual Report 2014

dst - sgps, s.a. Page 33 of 118

Business Areas

ENGINEERING & CONSTRUCTION

221,3245,2

210,3

100,0

150,0

200,0

250,0

2012 2013 2014

M €

PROPORTIONAL TURNOVER

Turnover

4,3 5,0

6,9

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

2012 2013 2014

M €

NET INCOME

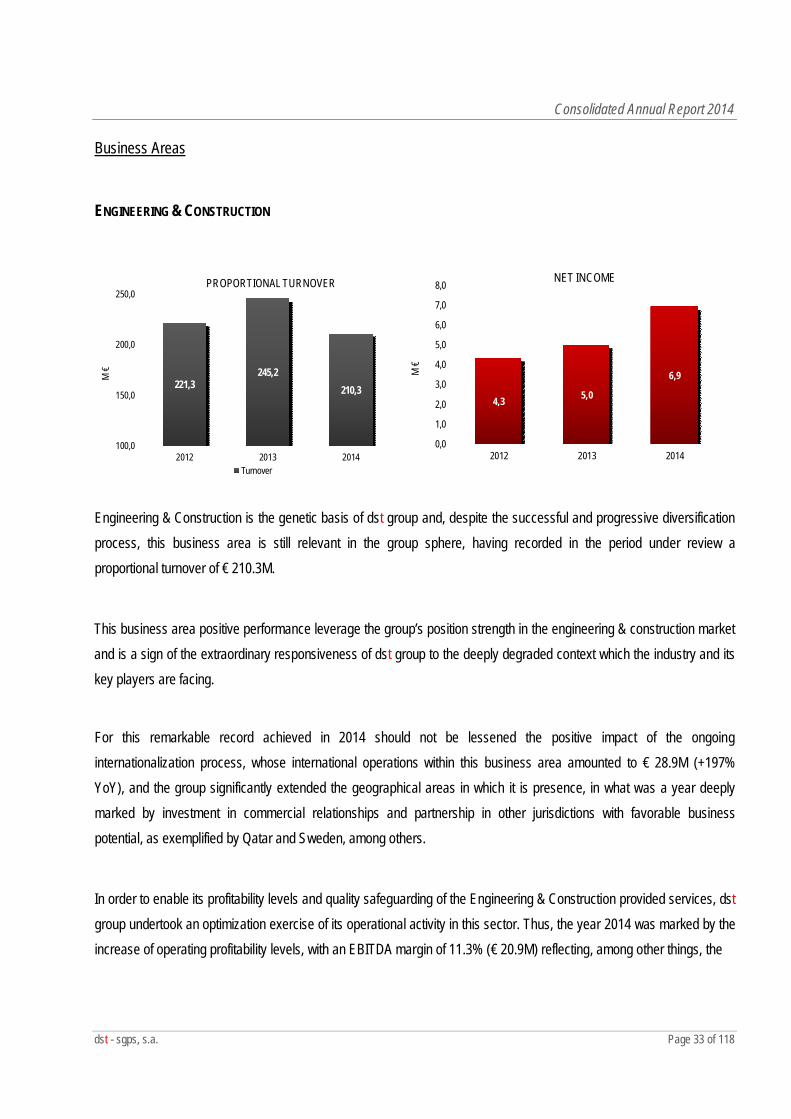

Engineering & Construction is the genetic basis of dst group and, despite the successful and progressive diversification process, this business area is still relevant in the group sphere, having recorded in the period under review a proportional turnover of € 210.3M.

This business area positive performance leverage the group’s position strength in the engineering & construction market and is a sign of the extraordinary responsiveness of dst group to the deeply degraded context which the industry and its key players are facing.

For this remarkable record achieved in 2014 should not be lessened the positive impact of the ongoing internationalization process, whose international operations within this business area amounted to € 28.9M (+197% YoY), and the group significantly extended the geographical areas in which it is presence, in what was a year deeply marked by investment in commercial relationships and partnership in other jurisdictions with favorable business potential, as exemplified by Qatar and Sweden, among others.

In order to enable its profitability levels and quality safeguarding of the Engineering & Construction provided services, dst group undertook an optimization exercise of its operational activity in this sector. Thus, the year 2014 was marked by the increase of operating profitability levels, with an EBITDA margin of 11.3% (€ 20.9M) reflecting, among other things, the

Consolidated Annual Report 2014

dst - sgps, s.a. Page 34 of 118

group's concern on maximizing its operations efficiency, as exemplified by the reduction of about € 17.2M in other external charges (including subcontractors). Moreover, it is noteworthy the continued reduction of this business area debt level, which in the period under review, the net financial expenses were reduced by € 2.1M, to a total of € 3M recorded in 2014. Also, this period registered significant impacts regarding impairment losses, particularly of receivables (with yearly net reversals of € 2.1M) and stocks (reinforcement of € 4.6M) in order to reflect, in a prudent and proper manner, the quality of its balance sheet balances related to trade debtors and with its stocks.

Consequently, the year 2014 was highlighted by the extraordinary contribution that this sector has to dst group’s consolidated net income, whose positive amount of € 6.9M recorded in this business area account for 49.6% of total earnings and show a € 2M growth compared to 2013. dst group has a wide scope of strong technical skills that allow it to be perceived by the market as a landmark of rigour and service quality in Engineering & Construction field. Not only this is taken for granted already for many years at the national market level as, increasingly, it is perceived by key international players with which the group works in its international operations. As such, in 2014, dst group made several works of recognized impact and technical complexity, as is the case, among others, the following contracts:

Block and Hydraulic Circuit Baleizão, in Beja Paper Production Factory of Fortissue, in Viana do CasteloRegional System of Carvoeiro New Headquarters building LIDL , in SintraWarehouse 10:11 Pole 2 Plat. Logistics, in Matosinhos Sanitation subsystem of Torres NovasLandfill Gestal, in Santa Maria da Feira Aeronautics Unit CEIIA, in MatosinhosSanitation networks of Santarém WWTP of PombalModel Continent of Quarteira APDL – Leixões Terminal

It should also be emphasized the unique know-how that dst group has at the level of building up new generation networks broadband, which was consolidated with the implementation of these networks in Rural areas of North and Alentejo and Algarve.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 35 of 118

Moreover, dst group incorporates in its operations the entire value chain of the business sector, particularly in the award of electrical installations, heating, ventilation and air conditioning (HVAC), hydraulic works and telecommunications - through dte – instalações especiais, s.a. (“dte”) - and the construction and assembly of steel structures and roofs and facades coating through bysteel, s.a. (“bysteel”). Therefore, dst group has significant competitive advantages in relation to its main competitors in the Engineering & Construction area.

In 2014, the production unit of bysteel turned 7,796 tons of steel, representing an industrial production increase above 100% compared to 2013, while its turnover in the period under review rose to its historical high of € 26.8M (+82.4% compared to 2013).

bysteel keeps its focus on attracting international reference customers (e.g., Angola, France and the UK) as well as on geographies diversification in which is present reflecting the growing international reputation that has been achieving as a result of its rigor, service quality and responsiveness to customer needs.

Thus, 2014 was a positive year for bysteel particularly, to the extent that it’s international business turnover had a very significant growth, mainly with the production and assembly of metallic structures for 12 hospitals in Congo without, thereby, losing focus on the Angolan and French markets.

In this context, it was also awarded several project design, manufacture and execution contracts of steel structures for some European and worldwide reference customers, such as Bouygues and Vinci groups, among others, from which enhance the construction of a new plant for pharma multinational Lilly in Strasbourg, and the rehabilitation of the Hotel

Crillon in La Concorde square in Paris (France).

Notwithstanding the weight of bysteel international operations correspond to 46.4% and 77.9% of its turnover in 2013 and 2014, respectively, this does not neglect any business opportunities in the domestic market, continuing with similar major projects implementation, examples of which are the works of the Port Authority in Oporto and the new Modelo Continente in Quarteira.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 36 of 118

In turn, in 2014, dte activity recorded an overall decrease in its turnover compared to 2013, due exclusively to a single purpose: its activity reduction within the telecommunications business area, resulting from the completion, in 2013, of the North Zone and Alentejo & Algarve NGN contracts.

Nevertheless, dte’s turnover in electricity, HVAC and plumbing areas grew 54% from €14.8M in 2013 to € 22.8M in 2014.

On the other hand, it is worth highlighting dte’s internationalization route that, in the period under review, had significant developments in particular by carrying out electrical works and HVAC in Angola and France.

Finally, it should be noted, that the dst group’s results recorded in this business area not only come from the performed work over the entire value chain of engineering and construction, but also from real estate projects and / or partnership schemes that since long, the group is pursuing.

Indeed, dst group decided to formalize these activities and projects, which nominated as Real Estate and Joint Ventures.

As mentioned, both these activities have been developed by dst group, the former has been the natural consequence of two factors combination that generate undeniable competitive advantages of the group compared to the market: (i) its long experience in urban regeneration work and (ii) its high financial capacity.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 37 of 118

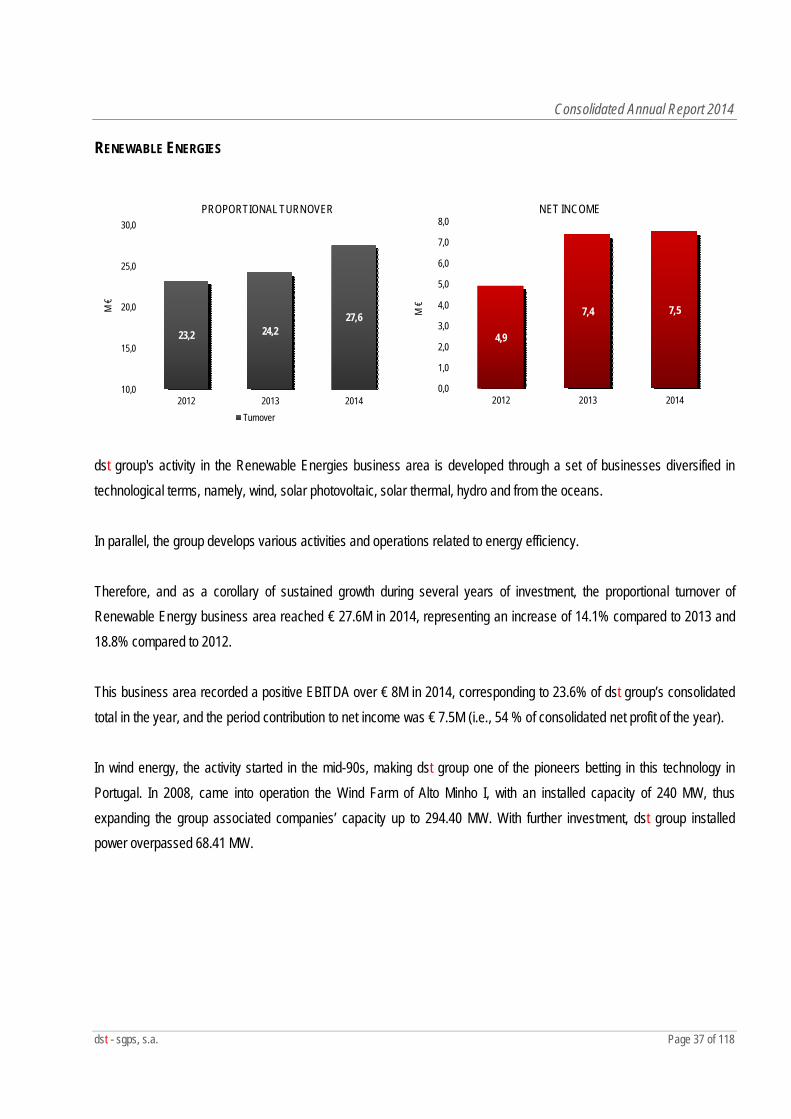

RENEWABLE ENERGIES

23,2 24,227,6

10,0

15,0

20,0

25,0

30,0

2012 2013 2014

M €

PROPORTIONAL TURNOVER

Turnover

4,9

7,4 7,5

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

2012 2013 2014

M €

NET INCOME

dst group's activity in the Renewable Energies business area is developed through a set of businesses diversified in technological terms, namely, wind, solar photovoltaic, solar thermal, hydro and from the oceans. In parallel, the group develops various activities and operations related to energy efficiency. Therefore, and as a corollary of sustained growth during several years of investment, the proportional turnover of Renewable Energy business area reached € 27.6M in 2014, representing an increase of 14.1% compared to 2013 and 18.8% compared to 2012. This business area recorded a positive EBITDA over € 8M in 2014, corresponding to 23.6% of dst group’s consolidated total in the year, and the period contribution to net income was € 7.5M (i.e., 54 % of consolidated net profit of the year). In wind energy, the activity started in the mid-90s, making dst group one of the pioneers betting in this technology in Portugal. In 2008, came into operation the Wind Farm of Alto Minho I, with an installed capacity of 240 MW, thus expanding the group associated companies’ capacity up to 294.40 MW. With further investment, dst group installed power overpassed 68.41 MW.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 38 of 118

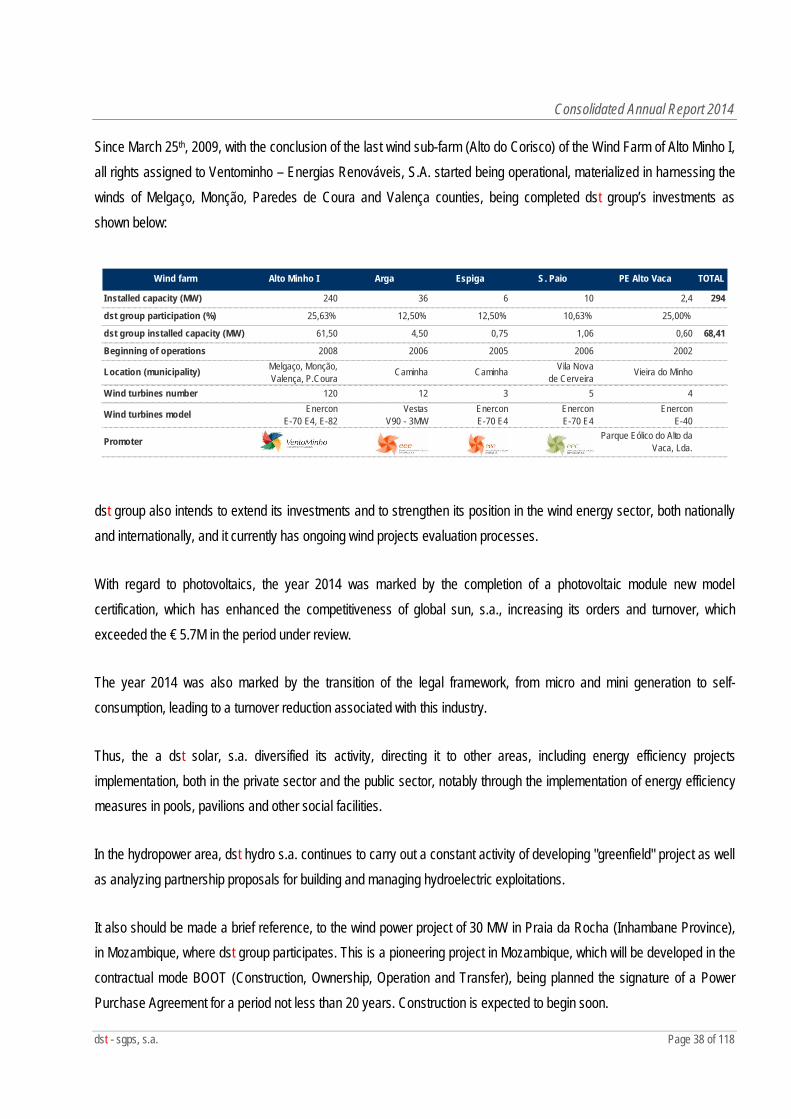

Since March 25th, 2009, with the conclusion of the last wind sub-farm (Alto do Corisco) of the Wind Farm of Alto Minho I, all rights assigned to Ventominho – Energias Renováveis, S.A. started being operational, materialized in harnessing the winds of Melgaço, Monção, Paredes de Coura and Valença counties, being completed dst group’s investments as shown below:

Wind farm Alto Minho I Arga Espiga S. Paio PE Alto Vaca TOTAL

Installed capacity (MW) 240 36 6 10 2,4 294

dst group participation (%) 25,63% 12,50% 12,50% 10,63% 25,00%

dst group installed capacity (MW) 61,50 4,50 0,75 1,06 0,60 68,41

Beginning of operations 2008 2006 2005 2006 2002

Location (municipality) Melgaço, Monção, Valença, P.Coura

Caminha Caminha Vila Novade Cerveira

Vieira do Minho

Wind turbines number 120 12 3 5 4

Wind turbines model EnerconE-70 E4, E-82

VestasV90 - 3MW

EnerconE-70 E4

EnerconE-70 E4

EnerconE-40

Promoter Parque Eólico do Alto da Vaca, Lda.

dst group also intends to extend its investments and to strengthen its position in the wind energy sector, both nationally and internationally, and it currently has ongoing wind projects evaluation processes.

With regard to photovoltaics, the year 2014 was marked by the completion of a photovoltaic module new model certification, which has enhanced the competitiveness of global sun, s.a., increasing its orders and turnover, which exceeded the € 5.7M in the period under review.

The year 2014 was also marked by the transition of the legal framework, from micro and mini generation to self-consumption, leading to a turnover reduction associated with this industry.

Thus, the a dst solar, s.a. diversified its activity, directing it to other areas, including energy efficiency projects implementation, both in the private sector and the public sector, notably through the implementation of energy efficiency measures in pools, pavilions and other social facilities.

In the hydropower area, dst hydro s.a. continues to carry out a constant activity of developing "greenfield" project as well as analyzing partnership proposals for building and managing hydroelectric exploitations.

It also should be made a brief reference, to the wind power project of 30 MW in Praia da Rocha (Inhambane Province), in Mozambique, where dst group participates. This is a pioneering project in Mozambique, which will be developed in the contractual mode BOOT (Construction, Ownership, Operation and Transfer), being planned the signature of a Power Purchase Agreement for a period not less than 20 years. Construction is expected to begin soon.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 39 of 118

In 2014, dst group undertook a reflection about which ones are its projects and strategic assets in the Renewable Energy business area, and therefore divested from some projects, from which stands out the sale of its stake in Sure - Sustainable Renewable Energies, Corp., an US legal entity, with its registered office in the state of New York, in the United States.

ENVIRONMENT

31,5 33,0 33,1

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

2012 2013 2014

M €

PROPORTIONAL TURNOVER

Turnover

2,2 2,32,9

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

2012 2013 2014

M €

NET INCOME

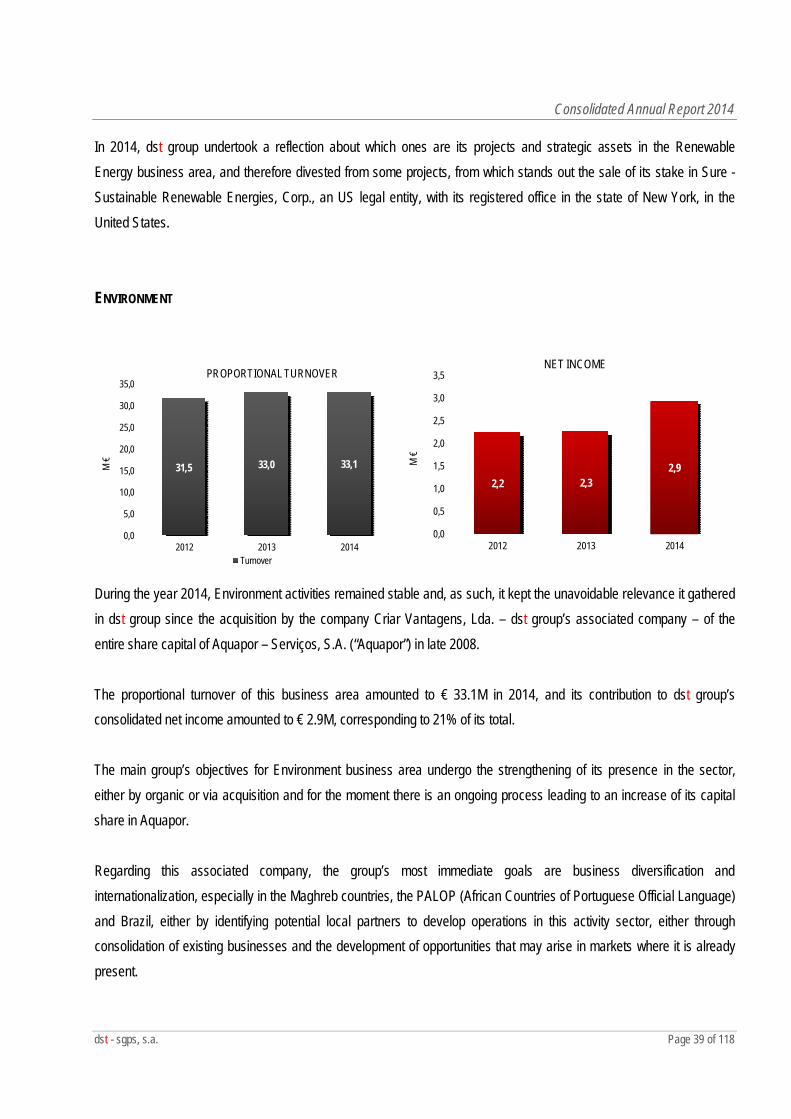

During the year 2014, Environment activities remained stable and, as such, it kept the unavoidable relevance it gathered in dst group since the acquisition by the company Criar Vantagens, Lda. – dst group’s associated company – of the entire share capital of Aquapor – Serviços, S.A. (“Aquapor”) in late 2008. The proportional turnover of this business area amounted to € 33.1M in 2014, and its contribution to dst group’s consolidated net income amounted to € 2.9M, corresponding to 21% of its total. The main group’s objectives for Environment business area undergo the strengthening of its presence in the sector, either by organic or via acquisition and for the moment there is an ongoing process leading to an increase of its capital share in Aquapor. Regarding this associated company, the group’s most immediate goals are business diversification and internationalization, especially in the Maghreb countries, the PALOP (African Countries of Portuguese Official Language) and Brazil, either by identifying potential local partners to develop operations in this activity sector, either through consolidation of existing businesses and the development of opportunities that may arise in markets where it is already present.

Consolidated Annual Report 2014

dst - sgps, s.a. Page 40 of 118

TELECOMMUNICATIONS

0,61,0

8,5

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

8,0

9,0

2012 2013 2014

M €

PROPORTIONAL TURNOVER

-0,7-1,1

-2,1

-2,2-2,0-1,8-1,6-1,4-1,2-1,0-0,8-0,6-0,4-0,20,0

2012 2013 2014

M €

NET INCOME

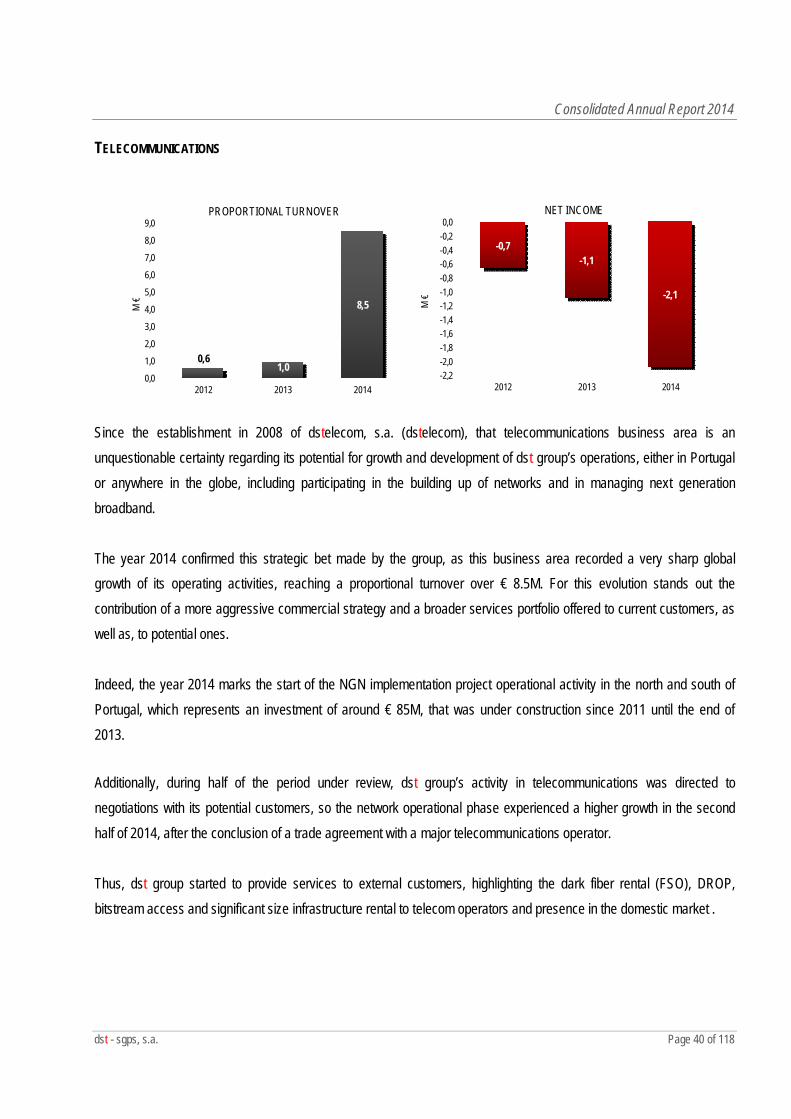

Since the establishment in 2008 of dstelecom, s.a. (dstelecom), that telecommunications business area is an unquestionable certainty regarding its potential for growth and development of dst group’s operations, either in Portugal or anywhere in the globe, including participating in the building up of networks and in managing next generation broadband. The year 2014 confirmed this strategic bet made by the group, as this business area recorded a very sharp global growth of its operating activities, reaching a proportional turnover over € 8.5M. For this evolution stands out the contribution of a more aggressive commercial strategy and a broader services portfolio offered to current customers, as well as, to potential ones. Indeed, the year 2014 marks the start of the NGN implementation project operational activity in the north and south of Portugal, which represents an investment of around € 85M, that was under construction since 2011 until the end of 2013.