Embed Size (px)

Citation preview

Annual Report 2013

The business year 2013

4

DFS Deutsche Flugsicherung GmbH

In the 2013 business year, the Supervisory Board

performed its functions as prescribed by law and the

Articles of Association. It regularly advised the Board of

Managing Directors and was comprehensively involved in

decisions of fundamental importance to the company.

In its work, the Supervisory Board was supported by its

three committees: an audit, a personnel and a project

committee. The committees intensively discussed deci-

sion papers in advance and prepared recommendations

for the decisions to be taken at the plenary meetings.

With the resolution of the Shareholder Meeting on the

discharging of the Supervisory Board and the Board

of Directors for the business year 2012 on 26 April

2013, the fourth term of office of the Supervisory Board

ended as scheduled. As of the fifth term of office of

the Supervisory Board from 26 April 2013, Dr Martina

Hinricher, Dr Angelika Kreppein, Michael Odenwald and

Ralf Raddatz were again appointed as members of the

Supervisory Board on the Shareholder side. Repre-

sentatives on the Shareholder side for the first time

are Dr Edeltraud Leibrock and Carmen von Bornstaedt-

Radbruch.

The employee representatives were chosen by means of

an election among staff. In the fifth term of office, Peter

Schaaf and Dirk Wendland as well as the new members

Catja Gräber, Volker Möller, Markus Siebers and Andrea

Wächter are the staff representatives on the Supervisory

Board.

In the 83rd and constitutional meeting, the Supervisory

Board elected Michael Odenwald as Chairman of the

Supervisory Board and Markus Siebers as Deputy Chair-

man. In addition, the composition of the three commit-

tees was completely changed.

The Board of Managing Directors reported to the Super-

visory Board in due form by means of comprehensive

quarterly reports in accordance with Article 90 of the Ger-

man Stock Corporation Law (AktG). On the basis of these

reports, the Supervisory Board discussed the situation and

development of the company at four ordinary meetings as

well as at two extraordinary meetings. The Board of Man-

aging Directors provided supplemental ad hoc information

to the Supervisory Board on a case-by-case basis.

In addition to the regular deliberations on the quarterly

reports on the situation of the company, the Supervisory

Board specifically dealt with the following topics:

■ the 2012 annual financial statements, management

report and the audit report on the 2012 annual financial

statements,

■ the economic plan 2014, with the associated investment

and financial plan,

■ the submission of a tender for the apron management

service at Munich Airport and

■ the possible stake in the UK air navigation service

provider NATS.

In addition, the Supervisory Board decided on the replace-

ment investments

■ in the air traffic control system in the Munich Control

Centre as part of the P2 renewal programme

and

■ in the air traffic control system iCAS at the Karlsruhe

Control Centre.

At two extraordinary meetings, the Supervisory Board

passed the economic, investment and finance plans 2013

and dealt with the corporate strategy based on the DFS

five-point programme.

Report of the Supervisory Board

5

After the first year of the term of office of the new Board

of Managing Directors, the Supervisory Board sees itself

confirmed in the progress of the reorientation of DFS. The

Supervisory Board is convinced that DFS is on the right

path to meet demanding challenges in an economically

difficult environment.

The Supervisory Board discussed the 2013 financial

statements and the management report with the assis-

tance of the audit report prepared by the auditors RBS

RoeverBroennerSusat GmbH & Co. KG in accordance with

Article 53 of the German Budgetary Principles Act (HGrG).

The comprehensive risk management system established

in the company was included in the audit. The auditors

participated in the discussions and were available to

answer questions, giving an account of the key results of

their report. The Supervisory Board found no exceptions

to be taken against the audit report and its findings.

The Supervisory Board would like to thank the new Board

of Managing Directors, all members of staff and the mem-

bers of the staff councils for their commitment to DFS

and for their successful work in the business year 2013.

The Supervisory Board

Michael Odenwald

Chairman

Michael Odenwald

6

DFS Deutsche Flugsicherung GmbH

Members of the Supervisory Board

ChairpersonMichael OdenwaldState SecretaryFederal Ministry of Transport and Digital Infrastructure

Deputy ChairmanMarkus SiebersEmployee representativeDFS Deutsche Flugsicherung GmbH

Carmen von Bornstaedt-RadbruchMinisterialrätinFederal Ministry of Defence

Catja GräberEmployee representativeDFS Deutsche Flugsicherung GmbH

Dr Martina HinricherMinisterialdirektorinFederal Ministry of Transport and Digital Infrastructure

Dr Angelika KreppeinRegierungsdirektorinFederal Ministry of Finance

Dr Edeltraud LeibrockMember of the Executive BoardKfW Bankengruppe

Volker MöllerEmployee representativeDFS Deutsche Flugsicherung GmbH

Ralf RaddatzColonel (G.S.)Federal Ministry of Defence

Peter SchaafEmployee representativeDFS Deutsche Flugsicherung GmbH

Andrea WächterEmployee representativeDFS Deutsche Flugsicherung GmbH

Dirk WendlandEmployee representativeDFS Deutsche Flugsicherung GmbH

Correct at March 2014

7

Members of the Advisory Council

Christine AligChairpersonBARIG – Board of Airline Representatives in Germany e.V.

Gerd BechtManagement Board Member for Compliance, Privacy, Legal Affairs and Corporate SecurityDeutsche Bahn AG

Andreas BergerMember of the Board of ManagementAllianz Global Corporate & Specialty AG

Markus BeumerMember of the Board of Managing DirectorsCommerzbank AG

Michael EggenschwilerChief Executive OfficerFlughafen Hamburg GmbH

Dirk FischerMember of ParliamentGerman Bundestag

Prof Dr Elmar GiemullaPresidentAircraft Owners and Pilots Association AOPA Germany

Winfried HermannMinisterMinistry of Transport and Infrastructure Baden-Württemberg

Ulrich LangeMember of ParliamentGerman Bundestag

Kirsten LühmannMember of ParliamentGerman Bundestag

Karl MüllnerLieutenant GeneralChief of Staff, Air ForceFederal Ministry of Defence

Katherina ReicheParliamentary State SecretaryFederal Ministry of Transport and Digital Infrastructure

Paul RiemensChief Executive OfficerLuchtverkeersleiding Nederland (LVNL)

Prof Dr Bernd SannerAGAPLESION BETHESDA KRANKENHAUS WUPPERTAL gGmbHMedical Director

Dr Stefan SchulteChairman of the Executive BoardFraport AG

Carsten SpohrChief Executive Officer of Lufthansa Passenger AirlinesDeutsche Lufthansa AG

Wolfgang StertenbrinkChairman of the Supervisory BoardsALTE LEIPZIGER – HALLESCHE Group

Ralf TeckentrupPresident of the Executive BoardCondor Flugdienst GmbH

Klaus Thiemann

Daniel WederChief Executive Officerskyguide swiss air navigation services ltd

Permanent guest:Michael OdenwaldChairman of DFS Supervisory Board Federal Ministry of Transport and Digital Infrastructure

Correct at March 2014

8

DFS Deutsche Flugsicherung GmbH

Group management report

1. Overview of the DFS Group ...................................................................................................................................9

2. Economic environment .......................................................................................................................................16

3. Personnel ..........................................................................................................................................................33

4. Supplementary report .........................................................................................................................................35

5. Compliance .......................................................................................................................................................36

6. Risk report ........................................................................................................................................................36

7. Outlook .............................................................................................................................................................42

Group financial statements

Annex 1: Group statement of comprehensive income .................................................................................................48

Annex 2: Group balance sheet ..................................................................................................................................49

Annex 3: Group statement of changes in equity .........................................................................................................50

Annex 4: Group cash flow statement .........................................................................................................................51

Annex 5: Notes (group) ............................................................................................................................................52

Notes to the statement of comprehensive income ........................................................................................73

Notes to the balance sheet .........................................................................................................................81

Additional disclosures ..............................................................................................................................111

Acronyms and abbreviations .....................................................................................................................142

9

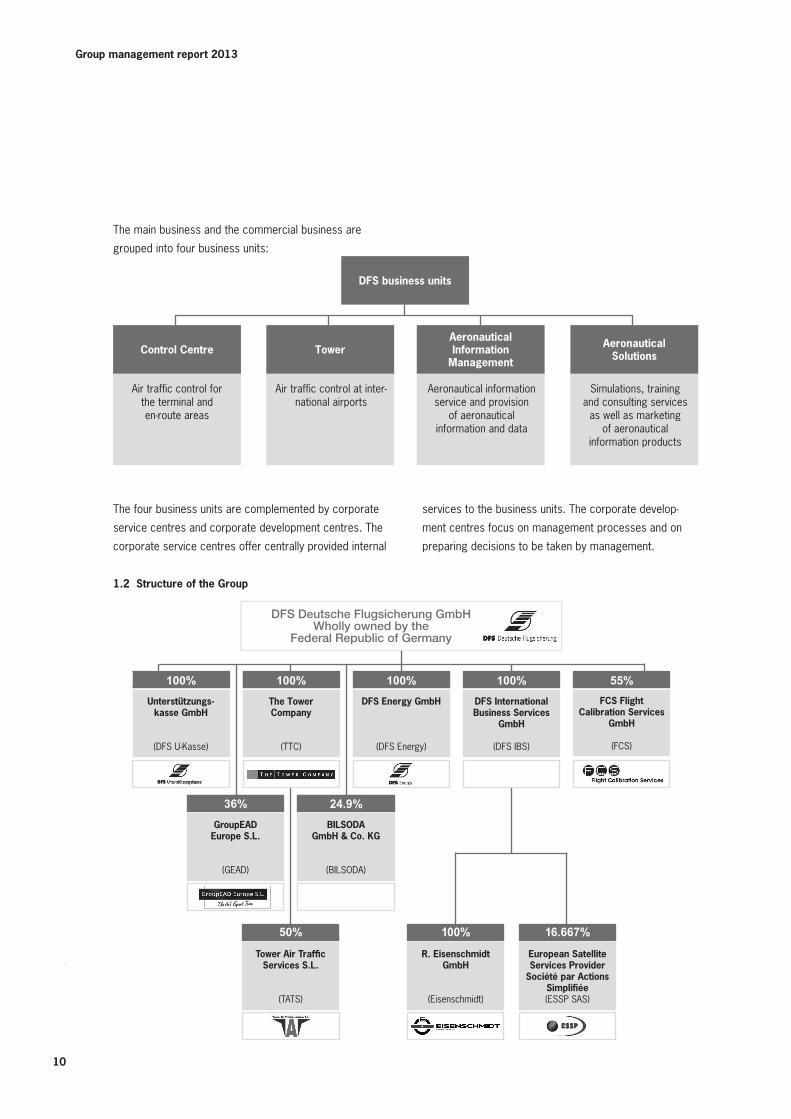

1. Overview of the DFS Group1.1 Business activities

The main business of air navigation services provided

by DFS Deutsche Flugsicherung GmbH is defined by the

tasks set out in Article 27c of the German Aviation Act

(LuftVG). Under this act, DFS is entrusted with providing

air traffic services and air traffic flow management as well

as with managing airspace utilisation (sovereign task). For

this purpose, it develops and operates air traffic service

systems as well as communications, navigation and sur-

veillance systems. DFS operates control centres in Lan-

gen, Bremen, Karlsruhe and Munich as well as 16 control

towers at international airports in Germany. In addition,

DFS is represented at the EUROCONTROL Control Centre

in Maastricht, the Netherlands. Through these activities

and with its 6,000 operational and administrative staff,

DFS ensures that approximately three million flights under

instrument flight rules (IFR) reach their destinations safely

and on time each year.

As payment for its main business, DFS levies air naviga-

tion charges. These charges are set by means of a charg-

ing ordinance issued by the Federal Ministry of Transport

and Digital Infrastructure (BMVI).

DFS also provides commercial services for third parties

on the free market (i.e. services not financed by air navi-

gation charges). These commercial services comprise

project work for national and international air navigation

service providers, consulting services, aeronautical publi-

cations, apron management services as well as the train-

ing services offered by the DFS Academy.

Group management report for the business year 2013

Air navigation services under Article 27c German Aviation Act (LuftVG)■ Air traffic services

■ Air traffic flow management

■ Management of airspace utilisation

■ Aeronautical information services

■ Projects■ Consulting■ Publications■ Apron management

services■ Training

Main business(Control Centre, Tower and AIM)

Commercial business(AS)

Not financed by air navigation charges

Financed by air navigation charges

Overview of business activities

Group management report 2013

10

Group management report 2013

The main business and the commercial business are

grouped into four business units:

1.2 Structure of the Group

Aeronautical information service and provision

of aeronautical information and data

Aeronautical Information

Management

Air traffic control for the terminal and en-route areas

Control Centre

Air traffic control at inter-national airports

Tower

DFS business units

Simulations, training and consulting services

as well as marketing of aeronautical

information products

Aeronautical Solutions

The four business units are complemented by corporate

service centres and corporate development centres. The

corporate service centres offer centrally provided internal

services to the business units. The corporate develop-

ment centres focus on management processes and on

preparing decisions to be taken by management.

100% The Tower Company

(TTC)

BILSODA

GmbH & Co. KG

(BILSODA)

100% DFS Energy GmbH

(DFS Energy)

55% FCS Flight

Calibration Services GmbH

(FCS)

100% Unterstützungs -

kasse GmbH

(DFS U-Kasse)

100% DFS International Business Services

GmbH

(DFS IBS)

GroupEAD Europe S.L.

(GEAD)

36%

Tower Air Traffic Services S.L.

(TATS)

50%

R. EisenschmidtGmbH

(Eisenschmidt)

100%

European Satellite Services Provider

Société par Actions Simplifiée(ESSP SAS)

16.667%

DFS Deutsche Flugsicherung GmbHWholly owned by the

Federal Republic of Germany

24.9%

11

The subsidiaries and investments of the DFS Group sup-

plement the portfolio of services offered by DFS and are

closely related to the aviation industry. Other major activi-

ties of the DFS Group:

Operational

■ Development, provision and conduct of air navigation

services at regional airports as well as the provision of

other services, especially apron management services,

coordination of ground handling and meteorological

observations.

■ Operation of an air transport company for the transport

of persons and the material of third parties for the

flight inspection of navigation aids as well as services,

developments and support of all kinds for the conduct

of flight inspections.

■ Operation of a database of aeronautical information

for the provision of aeronautical data and associated

services.

New since July 2013

■ Production and marketing of aeronautical charts and

publications as well as other aeronautical information,

including in electronic form. This encompasses the

marketing of technical accessories for the preparation,

planning and conduct of flights.

Supporting

■ Generation, provision and sale of energy for the own

use of DFS and for a fixed group of external customers.

■ Construction, rental, operation and administration of a

parking structure for DFS.

As a reaction to the continuing consolidation in the avia-

tion industry and the resulting diversified framework

conditions, DFS has initiated the first measures to adapt

and realign the structure of the Group. In preparation for

its future organisational and financing holding function,

DFS European Satellite Services Provider GmbH (DFS

ESSP) has been renamed and has been trading as DFS

International Business Services GmbH (DFS IBS) since

3 September 2013. The growing national and international

scope of DFS IBS covers primarily the management,

holding, administration and financing of investments in

companies that promote the development, provision and

conduct of services on the air transport market and their

further development. On 3 July 2013, DFS IBS acquired

100 percent of the shares in R. Eisenschmidt GmbH,

Egelsbach, Germany and integrated this long-standing

contracting party into the DFS Group. This step secures

a high level of quality and reliability over the long term for

our customers.

On 14 October 2013, DFS took over the payment of

grants to employees and eligible dependants in the case

of emergencies. These duties had previously been under-

taken by DFS Unterstützungskasse GmbH (DFS U-Kasse).

DFS U-Kasse is being wound up.

The contents of this group management report refer to

DFS only, as the subsidiaries neither individually nor col-

lectively exceed quantitative thresholds or display qualita-

tive characteristics with a material impact on the results

and financial position of DFS.

1.3 Legal framework and management organisation

In 1993, DFS was entrusted with the tasks of the Federal

Administration of Air Navigation Services (BFS). The head-

quarters of DFS is located near Frankfurt, in Langen, Am

DFS-Campus 10. The company is registered under HRB

34977 on the Commercial Register at the local district

court in Offenbach.

The object of the company is the development, provision

and execution of the air navigation services delegated

to the company by the Federal Ministry of Transport and

Digital Infrastructure (BMVI). The company can provide air

navigation services in Europe as well as carry out related

sideline activities in Germany and abroad.

The sole shareholder is the Federal Republic of Germany.

The management organisation is based on the distribution

of responsibilities among the DFS Managing Directors.

12

Group management report 2013

The Board of Managing Directors is supported by a

sixteen-strong Management Committee, whose members

come from the executive management level. The Manage-

ment Committee advises on important issues, shares

information and prepares the decisions of the Board of

Managing Directors.

The Supervisory Board of DFS comprises 12 members,

six appointed by the Shareholder and six elected by

the employees. In 2013, the Supervisory Board was

reformed as scheduled (see Note 42.2 on the composi-

tion of the Supervisory Board).

1.4 Strategies and objectives

DFS is committed to delivering an outstanding level of

performance at a first-class, uncompromising safety

level. The company services are provided in a sustain-

able manner and are tailored to the different needs of

our customers. As a certified provider of air navigation

services for complex airspaces and airports, DFS contrib-

utes to enhancing the performance of the air transport

system, while carefully taking noise abatement needs into

account. DFS offers challenging work for aviation enthusi-

asts and innovative people from around the world seeking

the opportunity to shape the future of air transport.

The financial strategy of DFS promotes the financial sta-

bility of the company and is based on the following areas

of focus:

■ A good to very good credit rating: Investors, business

partners and employees should be able to continue

to trust in the financial stability of the company. The

company secures a very good investment grade rating,

both in combination with its Shareholder and from a

stand-alone perspective (see section on Financial man-

agement).

■ Adequate liquidity: The company keeps an operational

reserve of €160 million to be able to react flexibly to

changed conditions in its environment. This ensures the

company's ability to act.

■ Adequate capital structure and equity ratio: The capital

structure and equity ratio are strengthened continu-

ously. The negative impact on the equity as defined

under IFRS stemming from the revised standard on the

recognition of long-term employee benefits (see Note

25.8) from the 2013 business year will be reduced step

by step over the next 15 years, starting from 2015

due to higher air navigation charges. DFS will continue

Distribution of responsibilities among the DFS Managing Directors

Chairman andCEO

■ Strategy, organisation, international affairs■ Institutional and legal affairs, insurances,

risk management, compliance■ Safety and security management systems■ Auditing, quality management■ Corporate communications, public relations,

environment■ Finance incl. taxes and charges■ General administration■ Procurement■ Consulting services and system deliveries

Managing Director Operations

■ Air traffic services■ Airspace management■ Air traffic flow management■ Aeronautical information service■ Communication, navigation

and surveillance services■ Product/system management for

technical systems, logistics■ Research and development■ Military affairs■ Technical and infrastructural facility manage-

ment■ Development of ATM systems

and business and administrative information technology

Managing Director Human Resources – Labour Director –

■ Human resources strategy■ Collective bargaining (strategies

and policies)■ Staff planning, human resources

management■ Human resources development,

initial and continuation training, Academy

■ Payroll accounting■ Compensation and incentive systems■ Occupational pensions■ Social and health management■ Industrial safety, accident prevention■ Labour law, collective bargaining law

13

to maintain the equity ratio shown in 'adjusted equity'

(see Note 35.4) of around 25 percent and to progress

towards a fully funded status for occupational pensions

in a step-by-step manner.

■ Low debt and unencumbered assets: The take-up of

loans is tightly linked to the capital expenditure to be

financed both as regards timing and purpose, and the

loans are paid back over the normal useful life of the

capital expenditure. The infrastructure of the company

is unencumbered and remains the property of the com-

pany. This creates a stable asset base that is for all

intents and purposes freely available.

■ Ability to pay a dividend: The provision of cost-effective

operational air navigation services ensures that the

capital provided by the Shareholder earns an adequate

return.

A modern risk management system supports the planning

and control of financial risks in a consistent manner.

Starting from the DFS vision with its long-term focus,

the Board of Managing Directors has developed strate-

gic guidelines and installed a five-point programme to

realign DFS with the demands of the future. In doing so,

it has defined fundamental strategic objectives. They

focus on cooperation among air navigation service pro-

viders in Europe, the optimisation of air traffic services,

the increase of productivity, the commercial business

and the reorganisation of the human resources function

at DFS.

Air navigation services in Europe

As a strong air navigation service provider, DFS is actively

shaping the European consolidation process. It cooper-

ates with European partners in a reliable and predictable

manner.

It analyses the competition and acquires new business

both in the commercial business and in the business

financed by air navigation charges. The company supports

suitable and appropriate regulations to implement the

SES objectives.

Air traffic services

DFS is reacting to the demands of customers by creat-

ing the conditions for the flexible deployment of staff

and improving both airspace structures and proce-

dures. ATS systems continue to be harmonised across

Europe.

Increase in productivity

By 2019, DFS aims to reduce operating costs by

approximately €100 million per year. The company is in

close dialogue with the employees, staff councils and

trade unions affected to avoid a further increase in head-

count and uses natural staff turnover to reduce staff

numbers. All measures will be introduced in a socially

compatible manner. Mandatory redundancies are not

planned.

The company is critically appraising capital expenditures

and reducing general administrative expenses.

Commercial business

DFS is improving its competitiveness and is systemati-

cally expanding its commercial business.

Human resources

DFS is strengthening its reliable and trust-based working

relationships with its staff, executives and the staff rep-

resentatives. It is improving the ability of staff members

to combine work and family life over the long term and is

reorganising the human resources function.

1.5 Planning and control

Corporate management at DFS is based on the regulation

targets, the strategic guidelines and objectives laid down

by the Board of Managing Directors, the requirements of

the business financed by air navigation charges and the

commercial business as well as the organisational struc-

ture and the five-point programme of DFS. The planning

and control process identifies suitable measures, embeds

14

Group management report 2013

them in the yearly rolling five-year plan and continuously

monitors the results of the Group, the segment financed

by air navigation charges, all other segments and the

group companies.

Performance and cost objectives as well as internal

goals from the five-point programme determine the

requirements placed on the individual organisational units

(business units, corporate service centres and corporate

development centres).

The achievement of these objectives and goals is meas-

ured by means of planned/actual comparisons which

are carried out both on a regular basis and as needed

(monthly, yearly and ad hoc). Achievement is monitored

and reported at a group, corporate, unit and product

level. For this purpose, a system of financial indicators

has been developed. The system is composed of indica-

tors derived primarily from IFRS accounting standards.

The system lays down budgets and cost ceilings. The

goals for operating costs are determined and laid down

using the following framework:

Staff costs

+ Other operating expenses (e.g. material costs)

+ Depreciation and amortisation

= Primary costs

+ Charges from internal cost allocation (ILV)

– Income from internal cost allocation (ILV)

= Operating costs

The commercial business is materially influenced by

the competitive environment in which it operates. Plan-

ning and control is carried out by means of contribution

margins and return on sales metrics, whereby a positive

contribution to earnings should be generated.

Planning and control also uses non-monetary indicators,

such as those from the traffic forecast.

DFS continuously measures safety and air traffic control

capacity. It reviews infringements of separation as well as

punctuality indicators.

1.6 Operating segments

1.6.1 Overview

DFS divides its business activities between the "Segment

financed by air navigation charges" and "All other seg-

ments". The segment financed by air navigation charges

is the focus of the main business in Germany. It is divided

into the material areas en-route services and terminal

services, which fall under the responsibility of the busi-

ness units Control Centre and Tower and their technical

support units

1.6.2 Segment financed by air navigation charges

1.6.2.1 En-route services

Within the scope of adopting of the Single European Sky

(SES) II package, EU Regulation 691/2010 and EU Reg-

ulation 1191/2010 introduced a performance scheme

for air navigation services and network functions from

1 January 2012. EU Regulation 691/2010 lays down

a performance scheme for air navigation services and

network functions (formerly EC Regulation 2096/2005)

and EU Regulation 1191/2010 lays down a common

charging scheme for air navigation services (formerly

EC Regulation 1794/2006). The core elements of these

Regulations are European and national requirements

covering safety, environment, capacity and cost-efficien-

cy. For the first reference period, target values have

been laid down in the performance plan (capacity and

environment) for the Functional Airspace Block Europe

Central (FABEC) and for the German contribution to the

performance plan (cost-efficiency performance area).

The respective national supervisory authority lays down

the charges to be levied for one reference period on the

basis of EU regulations. The first period covers 2012 to

2014. In Germany, the Federal Supervisory Authority for

Air Navigation Services (BAF) is the national supervisory

authority.

15

1.6.2.2 Terminal services

Terminal services will continue to be subject to the

existing system of full cost recovery until the end of

2014. The calculation of charges results in operational

over- and under-recoveries for the business year that

are carried forward as liabilities or receivables into

future periods (business year + 2) and offset when

calculating charges for airspace users. Over-recoveries

reduce the future basis for billing, while under-recover-

ies increase it.

1.6.2.3 All other segments

This segment covers the activities that are not individually

reportable as they are below the quantitative thresholds.

These activities primarily relate to commercial services,

investments and financial transactions that do not impact

air navigation charges. Commercial services are offered

globally. In contrast to the business financed by air navi-

gation charges, the activities under all other segments

are not subject to economic regulation or full cost recov-

ery. Commercial services make up the major component

of all other segments.

Intersegment transactions are conducted at arm's length

conditions and prices (see Note 30).

1.7 Research and development

German airspace demands a particularly well-performing

air navigation services organisation over the long term

as its airspace is considered to be extremely busy and

complex in international comparison. Technological and

operational innovations represent an important means

to manage the growing cost pressure, the increasing

requirements as regards environmental sustainability

and the rise in air traffic predicted in all forecasts for the

medium term. This must all be managed while maintain-

ing an unrestricted safety level. Therefore, DFS has been

involved in international and national research projects for

many years. It concentrates on applied research which

leads to new products, procedures and working methods

and which pursues the path from invention to innovation.

SESAR is the leading project in the international area,

which encompasses all areas of air navigation services.

It is organised within the scope of the SESAR Joint

Undertaking, which DFS joined as an active member in

June 2009, along with other leading organisations (air

navigation service providers, airspace users, airports

and the manufacturing industry). National activities focus

on regional challenges such as the optimisation of flight

routes for overflights and the operation of busy airports

En-route

■ Until the end of 2011: Full cost recovery

■ Since 2012: Economic regulation

Terminal services

■ Until the end of 2014: Full cost recovery

■ From 2015 onwards: Economic regulation

Commercial business

Investments

Financial transactions not impacting air navigation

charges

Segment financed by air navigation charges All other segments

Germany WorldGermany

16

Group management report 2013

such as those in Frankfurt and Munich (including their

approach and departure procedures) by means of real-

time and fast-time simulations. This also covers testing

new key technologies and the subsequent development

of air traffic control software and suitable simulators.

Within the scope of the German aeronautical research

programme with its technology line of funding for effec-

tive, safe and efficient flight guidance and flight control

sponsored by the Federal Ministry for Economic Affairs

and Energy, DFS was able to once again position itself as

a project manager. The goal is to work jointly with German

partners from research and industry to improve the start-

ing basis for later international activities.

DFS advances innovative developments and markets

some of these through the business unit Aeronautical

Solutions (AS) These include:

■ The remote control of airports (see Outlook).

■ Sectorless flying: a revolutionary concept that assigns

aircraft in the entire controlled area to a particular air

traffic controller and which promises more expeditious

traffic handling with less effort.

■ Surveillance systems that use all available sensors,

such as various radar systems, multilateration and the

position determined by the aircraft itself, to be able to

track the aircraft seamlessly from gate to gate, on the

ground as well as in the air.

■ Support systems for air traffic controllers that reduce

the burden on them by means of optimised information

processing, especially as regards conflict avoidance,

and by means of step-by-step automation.

■ The interoperability of European air traffic control

systems that keeps pace with new developments – an

important precondition of the Single European Sky.

A total of approximately 3.5 percent of the costs and

239 staff posts are allocated to research and own devel-

opments. The costs involved are partially offset by grant

funding of approximately €6.7 million awarded from Euro-

pean research framework programmes, including SESAR

and the German aeronautical research programme.

2. Economic environment2.1 Overall economic situation

The global economy stabilised in 2013 on the modest

level of the previous year with a growth rate of 2.4 per-

cent (status: February 2014). Despite the improved condi-

tions on the financial markets, unemployment and excess

capacity continue to have a negative impact on countries

with a high level of national income.

In contrast, the situation in Europe remained unchanged.

Gross domestic product (GDP) in the 28 EU countries

grew by 0.1 percent compared with the previous

year. In particular the expected stagnation in Italy and

France poses a risk for the further economic growth in

Germany.

German GDP rose in contrast to the situation in the EU

countries by an annual average of 0.4 percent in 2013

compared with the previous year. This growth rate was

within the range forecast by the leading economic insti-

tutes (between 0.3 percent and 0.9 percent) and the

Federal Government (0.4 percent).

As in previous years, exports are the foundation of eco-

nomic growth, which is being materially supported by

domestic consumption and the willingness to invest shown

by the corporate sector.

In a robust labour market, employment and income con-

tinued to increase. In 2013, an average of 41.78 million

people were in employment. The rise of 232,000 persons

compared with the previous year led to a record high.

2.2 Development of air traffic

In addition to the overall economic situation, political, legal

and industry-specific factors in particular have a fundamen-

tal influence on the development of air traffic.

Political unrest

Traffic is being negatively impacted by political unrest in

North Africa and the Middle East as well as the continued

stagnation of the European economy.

17

In the first quarter 2013, traffic volume in Europe was

5 percent below the level reached in 2012. After the

change to the summer schedule 2013, traffic volume

rose and reached the level of the previous year. From

August 2013, the trend in traffic volume was upwards,

restricted only by the loss of tourist traffic to/from Egypt

as a consequence of the renewed unrest. Overall, traffic

volume in Europe declined by 1.1 percent compared with

the previous year.

Grassroots movements, night curfew and the new Berlin

Brandenburg Airport

In Germany, citizens are reacting in an increasingly sensi-

tive manner to noise disturbance caused by air traffic. The

night curfew at Frankfurt Airport, the referendum against

the third runway at Munich Airport and the renewed post-

ponement of the opening of the new airport in Berlin are

dampening the growth impulses for the national economy.

Climate action plan and emissions trading system

On 2 February 2009, the EU Directive 2008/101/EC on the

inclusion of international aviation activities in the European

emissions trading scheme came into effect. This Directive

was in force until the end of 2012 and was superseded by

the provisions on the new trading period 2013 until 2020

(EU Directive 2009/29/EC). According to this Directive,

all aircraft taking off or landing at an airport in the EU are

included in the emissions trading system. From the total

number of certificates allocated to aviation, 85 percent

were divided among the air carriers involved. The remaining

15 percent were auctioned off. There was considerable

opposition against the inclusion of airlines from non-EU

States in the European emissions trading system, particu-

larly from the USA, the Russian Federation, China and India.

Following the agreement within the International Civil

Aviation Organisation (ICAO) on a climate action plan

for aviation, the European Commission intends to make

permanent changes to emissions trading in Europe. The

exception that requires airlines to only pay for flights that

take off and land in Europe has been limited to 2016 for

the time being.

Air transport tax

In Germany, the law introducing an air transport tax

(Luftverkehrssteuergesetz – LuftVStG) has been in force

since the beginning of 2011. This law governs the levy-

ing of a tax that has to be paid for every passenger that

departs from a German airport. Proceeds are expected

to come in at around €1 billion for 2013, despite a

slight reduction in the rate of this tax in the previous

year. Overall, this passenger-based air transport tax

increases the costs for the entire air transport industry.

According to the second evaluation report of the German

aviation association BDL (Bundesverband der deutschen Luftverkehrswirtschaft), the growth in air transport in

Germany has remained below the Western European aver-

age because of this and it was noted that passengers are

shifting to neighbouring countries. Overall, the drop in pas-

senger numbers can be quantified at five million per year

at least.

Competition, airlines' pressure to reduce costs and restructure

Low-cost airlines and the fast-growing airlines from the Gulf

region are changing and increasing the competition for

lucrative routes and customers in a fundamental manner.

The large European airlines continue to suffer from con-

siderable pressures as regards costs and the need to

restructure. The lasting high kerosene prices continue to

be a significant cost factor.

The airlines are reacting with far-reaching changes in their

capacity plans and are changing the size and load factors

of the aircraft used. As part of cost-cutting programmes,

Lufthansa German Airlines (DLH) and Air Berlin have

reduced the flights they offer by 7.5 percent and 4.7 per-

cent, respectively.

In addition, Lufthansa has brought together all its Euro-

pean direct connections under the Germanwings brand.

This low-cost airline subsidiary has taken over all routes

that do not involve the large hubs in Frankfurt and Munich.

With over 80 aircraft, the new Germanwings will have

more than doubled in size. Lufthansa expects savings of

hundreds of millions of euro per year from this initiative.

18

Group management report 2013

11.0

11.7

Following Lufthansa's retreat from decentralised Euro-

pean routes, it is becoming apparent that the German

market is attracting more and more low-cost airlines. As

a consequence, the number of flights conducted by low-

cost airlines rose by over 10 percent.

Court cases on the admissibility of wind farms

The disturbance-free operation of the air navigation facili-

ties operated by DFS is being put into question in some

court cases involving the building of numerous wind tur-

bines. Based on the current state of technology, distur-

bance is to be expected when wind turbines are erected

within a radius of 15 kilometres around VOR and DVOR

facilities. (VOR is the short form of VHF omnidirectional

radio range and the acronym VHF itself stands for very

high frequency, while DVOR stands for Doppler VOR.) In

accordance with Article 18a of the German Aviation Act

(LuftVG), such construction projects have to be notified

to the Federal Supervisory Authority for Air Navigation

Services (BAF). On a case-by-case basis, DFS checks

the disturbance potential of any additional wind turbines

to be erected on the operation of a VOR or DVOR facil-

ity. DFS informs the BAF of its assessment in an expert

opinion and the BAF takes its decision on the basis of

this opinion. According to Article 18a of the German

Aviation Act, it is not permitted to erect structures which

might interfere with air navigation services facilities.

In a case before the administrative court of Oldenburg

located in northern Germany, the competent authority of

the German Federal State in question approved five wind

turbines against the decision of the BAF and ordered

the immediate enforcement of the ruling. DFS lodged an

appeal, which has not been finally decided on yet.

DFS views that its right to operate its air navigation

services facilities without disturbance has been infringed

upon. The undisturbed operation of air navigation services

facilities is a precondition for the safe, orderly and expedi-

tious handling of air traffic.

IFR flights 2013

In Germany, the number of civil IFR flights in 2013 fell by

1.4 percent compared with the previous year. The rise

in low-cost airlines could not fully compensate for the

decline in traffic of the traditional air carriers as part of

their cost-cutting programmes, despite the growth in the

economy. There was therefore a significant shortfall in

IFR flights compared with the rise of 0.7 percent planned

for 2013. The volume of civil traffic declined by 1.3 per-

cent over the previous year, while military air traffic saw

7.8 percent fewer flights.

With a share of only 11.0 percent and 51.8 percent

respectively, the number of domestic flights and arrivals

and departures continued to decline, while the share of

overflights at 37.2 percent increased.

IFR flights in Germany

2013 2012

Total 2,952,624 2,993,866

Compared with previous year (%) -1.4 -2.2

2013

2012

51.8

52.2

37.2

36.1

0% 20% 40% 60% 80% 100%

Domestic flights

Flights arriving in or departing from Germany

Overflights

Distribution of IFR flights (%)

19

2.3 Overview of the business development

Impact of the revised IAS 19 standard

DFS offers defined benefit pensions to its staff. The

revised provisions of IAS 19 (Employee Benefits) have had

to be applied since the business year 2013. The amend-

ments to the accounting standard relate to the elimination

of an option for recording actuarial gains and losses.

Since 2013, such gains and losses as well as other

measurement changes have to be immediately recog-

nised in full in equity under other comprehensive income

(OCI). DFS can no longer use the corridor method it had

previously applied. Changes in interest rates that impact

occupational pensions can no longer be smoothed. Gains

and losses from the subsequent measurement of pension

obligations as well as the associated plan assets are fully

recognised in equity without impacting the income state-

ment (see Note 25.8).

The immediate impact of this is increased equity volatil-

ity. This volatility has been dampened when determining

charges by the introduction of an imputed model.

DFS has developed, under the auspices of its regulatory

authority, a model for the calculation of occupational

pensions that conforms to European regulations on the

performance plan and on the determination of charges.

It has been in use since 1 January 2012. Air navigation

charges take the length of service and interest cost into

account in a mutatis mutandis application of IAS 19. The

discount rate used to determine the obligation is orien-

tated in a prospective manner and in the medium term to

the interest rate that can be earned on the plan assets.

The differences between the obligation and plan assets

(plan deficit/plan surplus) are allocated in a rolling fashion

over the average remaining time to work (15 years) of the

staff and also taken into account in the following refer-

ence periods as a component of the charges. Additional

conservative assumptions for interest rate, salary and

inflation trends support the correct matching of the cost

of occupational pensions and avoid random fluctuations in

the cost-base for charges and therefore arbitrary charges

for airspace users.

In a directive dated 12 December 2012, the Federal

Supervisory Authority for Air Navigation Services (BAF)

laid down that the actual financing expense for occupa-

tional pensions should not be subject to the cost-efficien-

cy targets of the performance plan, but is instead to be

considered as a determined cost in the performance plan

and therefore part of the cost-base. The model is adjust-

ed as part of the performance planning when drawing up

the following performance plan. The financing difference

(delta) that is determined in the planning phase for the fol-

lowing reference period is distributed over 15 years (roll-

ing view) and increases revenues and liquidity in the IFRS

group financial statements.

In the first reference period from 2012 to 2014, the

company has used a uniform interest rate of 4.65 per-

cent based on prudent commercial considerations. This

uniform rate is used for the assets underlying the occu-

pational pension scheme as well as for discounting the

corresponding obligations.

A conflict of norms between those governing the levying of

charges and those governing the determination of results

In accordance with European regulations for air navigation

service providers, DFS switched the cost-base for cal-

culating charges from German Commercial Code (HGB)

to the International Financial Reporting Standards (IFRS)

issued by the International Accounting Standards Board

(IASB) as at 1 January 2007.

Since that time, DFS has been exposed to a material con-

flict of norms between the standards used to determine

charges and the standards used to draw up the commer-

cial and tax accounts. This conflict is eating into the sub-

stance of DFS. (See the last paragraph of this section for

the tax solution.) On the one hand, there were European

regulations requiring the application of IFRS for the rec-

ognition and measurement of issues that impact charges

and, on the other hand, there were commercial and tax

regulations that required measurements to be made that

significantly deviated from those required by those same

European regulations.

20

Group management report 2013

There is a divergence between the commercial account-

ing rules and the cost-related basis for determining

revenues from air navigation charges. This divergence

leads to a corresponding divergence in the expense line

items. The regulatory authority has given DFS the right

to spread the effects from the conversion to the new

accounting standards (catch-up effects) that lead to ex-

post financing requirements over a period of 15 years

after first recognising them directly in equity (Article 6 of

EC Regulation 1794/2006). These catch-up effects may

be invoiced to airspace users. They were included in rev-

enues for the first time in 2007.

The catch-up effects relate particularly to the following

balance sheet line items: non-current assets (development

costs, borrowing costs, depreciation and amortisation),

pension obligations and other provisions.

Therefore, the revenues earned in the area financed by

air navigation charges do not match the corresponding

costs in the accounts drawn up under commercial law.

In addition, it must be borne in mind that the day-to-day

accounting treatment of the same underlying issues can

lead to differences between the accounts from a charges

perspective, the accounts under IFRS and the accounts

under German Commercial Code (HGB) when the catch-up

effects are included.

Article 29 of the Law on the Implementation of the Mutual

Assistance Directive as well as on the Change to Tax

Regulations (AmtshilfeRLUmsG) dated 26 June 2013 now

governs the determination of the tax base previously set

out in Article 31b paragraph 3 of the German Aviation

Act (LuftVG). The positive or negative difference between

the profit from air navigation charges as calculated under

income tax law (EStG) and the result from the provision of

air navigation services as calculated under the provisions

governing charges are not considered when determin-

ing income for DFS. Taxation is therefore based on the

charges-related result. At a minimum, this regulation

resolves the existing tension between the charges and tax

perspective for the determination of profit. Nevertheless,

significant differences still remain from the divergence

between the determination of profit under the provisions

governing air navigation charges and those under com-

mercial law.

Unclear legal situation as regards uncontrollable costs

The current debate on the revised Regulations on

performance (EU Regulation 390/2013) and charges

(EU Regulation 391/2013) is still ongoing although

these Regulations have already been adopted. The

European Commission is investigating revising the rules

on uncontrollable costs. This investigation also covers

the approval process as well as amended rules on the

return on equity, on the consideration of the interest

on borrowings and on occupational pensions. The cur-

rent status quo requires the Commission to give the

final approval for each of these cost items. The timing

of this approval (annually/at the end of the reference

period) is currently being negotiated. The new rule

is to apply retroactively to the uncontrollable costs

incurred in the first reference period. Considering the

unclear legal situation, DFS does not yet consider those

costs that DFS itself believes, in its own legal opinion,

should be borne by airspace users when drawing up its

financial statements. On the other hand, provisions for

obligations are being recognised for the uncontrollable

costs that have to be reimbursed.

Five-point programme

The Board of Managing Directors is driving the expan-

sion of the commercial business. With the acquisition

of Eisenschmidt in 2013 (see section 1.2), it expanded

the commercial portfolio to include the production and

sale of aeronautical charts, publications and other aero-

nautical information, also in electronic form, including

the sales of technical devices for the preparation and

conduct of flights. It plans further expansion in those

commercial business areas directly connected to air

navigation services when opportunities arise in the mar-

ket. Our marketing and consulting activities are being

expanded worldwide.

21

In the core business, the productivity will be boosted,

staff flexibility enhanced and the rise in staff numbers

contained to respond to fluctuating demand. Vacant posi-

tions are not being filled and the natural turnover will be

used to reduce staff numbers. Airspace structures and

procedures are being optimised and capital expenditure

on recoverable, high-performance and harmonised ATM

systems is being stepped up. Project and general costs

are being reduced.

Purchase of a stake in the UK air navigation service

provider NATS

The evaluation process begun in the previous business

year on the possible purchase of a significant stake in the

UK air navigation service provider NATS was completed.

The sellers decided to sell their shares to a financial

investor.

Ryanair

Incomplete information submitted by the low-cost airline

Ryanair in the business years 2010 to 2012 led to a

basis for determining charges that was disadvantageous

for DFS. In 2013, DFS invoiced for the associated short-

fall in terminal services. However, contrary to the position

of DFS on this matter, EUROCONTROL decided not to

invoice for the amounts for en-route services after consul-

tation with the States affected and at its own reasonable

discretion. DFS is currently reviewing if it is possible to

enforce its claims in this matter.

2.4 Results of operations

2.4.1 Service units and unit rates

2.4.1.1 En-route services

For en-route services, a service unit is computed as the

square root of the weight factor multiplied by the distance

factor. The economic value of each flight conducted

is taken into account so that the value of the air traffic

control service performed is considered by the legislator

when establishing the relevant air navigation charges.

Definition of service units:

max. take-off weight in tonnes x

distance in km 50 100

En-route:

The amount to be paid by the airspace user is given by

multiplying the service unit by the unit rate.

The national unit rate for en-route charges comprises

air-traffic-related cost elements of DFS, the German

Meteorological Service (DWD), EUROCONTROL, the

Maastricht Control Centre, and other national bodies that

are involved with air navigation services, such as the Air

Navigation Services Division (LR23) of the German Fed-

eral Ministry of Transport and Digital Infrastructure (BMVI)

and the Federal Supervisory Authority for Air Navigation

Services (BAF). In 2013, the service units rose slightly

compared with 2012 and came in within the forecast of

the economic plan from the year 2012. The development

Development of service units – en-route

2013 2012

Total 12,506,062 12,442,470

Compared with previous year (%) +0.5 -1.7

En-route unit rate (€)

2014 2013 2012 2011 2010 2009

Total 77.32 76.50 74.19 71.84 68.86 67.02

DFS share 62.55 63.22 60.41 58.24 54.39 53.30

Compared with previous year (Total, in %) +1.1 +3.1 +3.3 +4.3 +2.7 +3.6

22

Group management report 2013

of service units remained well below the expectations set

out in the performance plan, as the overall economy has

suffered significantly since the plan was drawn up.

In 2013, the national unit rate for en-route services rose by

around 3.1 percent primarily because of the consideration

of the under-recovery from 2011, which was caused by

the slowdown in traffic. The EU Regulation on the common

charging scheme for air navigation services contains com-

pensation mechanisms within a reference period to partly

offset losses in revenues as a consequence of fluctuations

in traffic volumes as well as an inflation adjustment. The

adjustment to the unit rate from 2014 is primarily attributa-

ble to the two issues from 2012. The DFS share of the en-

route unit rate remains stable at approximately 81 percent.

2.4.1.2 Terminal services

For terminal services, a service unit is the quotient

obtained by dividing by fifty the maximum take-off weight,

expressed as a figure taken to two decimal places, to the

power of 0.7.

Definition of service units:

0.7

max. take-off weight in tonnes50

Terminal services:

The amount to be paid by the airspace user is given by

multiplying the service unit by the unit rate for terminal

services.

The unit rate for terminal services comprises air-traffic-

related cost elements of DFS, the German Meteorologi-

cal Service (DWD), and other national bodies that are

involved with air navigation services, such as the Air

Navigation Services Division (LR23) of the German Fed-

eral Ministry of Transport and Digital Infrastructure (BMVI)

and the Federal Supervisory Authority for Air Navigation

Services (BAF). The service units 2013 remained below

expectations, in particular due to the fact that the Ger-

man airlines conducted fewer flights as a result of their

cost-cutting programmes.

The 2013 unit rate for terminal services rose by 6.2 per-

cent compared with the previous year. Two factors are

primarily responsible for this. Firstly, traffic in 2011 was

below expectations. Secondly, material costs, such as

energy costs, as well as the costs for staff and occupa-

tional pensions rose more strongly than assumed in the

planning process. There are two main factors responsi-

ble for the rise from 2014. DFS was not allowed to fully

offset the under-recovery from 2011 in 2013. Instead,

the under-recovery has to be evenly distributed over

the years 2013, 2014 and 2015 in accordance with a

directive issued by the Federal Supervisory Authority

for Air Navigation Services (BAF). In addition, the carry-

over from the traffic-related under-recovery from 2012

increases the unit rate. The DFS share of costs of the

unit rate for terminal services amounts to approximately

96 percent.

Development of service units – terminal services

2013 2012

Total 1,287,989 1,310,562

Compared with previous year (%) -1.7 -1.3

Terminal unit rate (€)

2014 2013 2012 2011 2010 2009

Total 183.87 181.99 171.29 163.05 162.54 167.78

DFS share 177.20 175.84 165.70 155.76 154.33 160.80

Compared with previous year (Total, in %) +1.0% +6.2 +5.1 +0.3 -3.1 +3.4

23

0.59

-0.55

1.04

1.56

5.17

20.41

71.78

-10 0 10 20 30 40 50 60 70 80

Over-/under-recovery

Government reimbursements:Exempted flights

Other air navigation services

Other revenues

Government reimbursements:Military flights

Terminal services

En-route services

2.4.2 Revenues

In the business year 2013, DFS generated revenues of

€1,109.2 million. Revenues rose slightly compared with

the previous year by 0.7 percent despite the decline in

flight movements.

For DFS, the shift from full cost recovery to a perfor-

mance-oriented charging structure for en-route services

brings with it significant changes in the breakdown of

revenues. Within certain limits, DFS is exposed to oppor-

tunities and risks resulting from the development of air

traffic (see section 2.4.5).

Revenues from air navigation services increased from

€1,080.9 million to €1,091.9 million after netting the

2011 under-recovery (€32.3 million) and taking into

account the 2013 under-recovery (€22.2 million, including

the carry-over from the en-route area).

The increase resulted primarily from adjusted unit rates,

with which DFS can charge retroactively for the under-

recovery from 2011, as well as by a slightly higher num-

ber of service units when compared with the plan.

Revenue breakdown (in %)

(includes result contribution from netting over-/under-recovery)

Revenues from en-route charges (€m)

2013 2012 2011 2010 2009

Total 796.2 753.4 739.1 665.3 629.9

Compared with previous year (%) +5.7 +1.9 +11.1 +5.6 -3.1

24

Group management report 2013

Revenues from government reimbursements (€m)

2013 2012 2011 2010 2009

Military operational air traffic 57.4 57.1 57.7 55.4 60.8

Exempted flights 6.5 6.5 6.5 6.5 6.5

Total 63.9 63.6 64.2 61.9 67.3

Compared with previous year (%) +0.5 -0.9 +3.7 -8.0 +6.5

Revenues from other air navigation services (€m)

2013 2012 2011 2010 2009

Aeronautical publications 7.5 3.3 3.6 2.8 2.9

Flight inspection services 2.5 3.0 3.1 2.9 2.5

Other air navigation services 1.5 1.1 0.9 0.4 0.3

Total 11.5 7.4 7.6 6.2 5.7

Compared with previous year (%) +55.4 -2.6 +22.6 +8.8 +5.6

Other revenues (€m)

2013 2012 2011 2010 2009

Total 17.2 20.4 20.1 18.2 17.2

Compared with previous year (%) -15.7 +2.0 +10.4 +5.8 -23.2

Reimbursements for military flights contain services pro-

vided by the Maastricht unit. The exempted flights relate

to en-route flights under visual flight rules.

DFS generated other revenues primarily from consult-

ing and staff services, apron management services and

training services.

Within other air navigation services and other revenues,

commercial services made up roughly 83.4 percent,

generating revenues of €24.1 million (previous year:

€23.8 million), exceeding the planning forecast due to

increased marketing activities.

Revenues from terminal charges (€m)

2013 2012 2011 2010 2009

Gross 227.3 218.3 207.4 196.8 188.9

Reimbursements paid 1 (0.9) (0.7) (0.6) (0.5) (7.7)

Net 226.4 217.6 206.8 196.3 181.2

Compared with previous year (net, in %) +4.0 +5.2 +5.3 +8.3 -1.8

1 Since 2010, the air-traffic-related cost elements of the German Meteorological Service (DWD) have no longer been considered in the revenues of DFS. The air-traffic-related cost elements of the Federal Supervisory Authority for Air Navigation Services (BAF) remain.

25

2.4.3 Other operating income

Other operating income (€m)

2013 2012 2011 2010 2009

Total 33.7 77.8 38.4* 29.7 33.1

Compared with previous year (%) -56.7 +102.6 +29.3 -10.3 -39.2

* Due to a reclassification, the disclosures are not directly comparable with the previous years.

Other operating income came in within the level reached

in the years 2009 to 2011, after achieving a record high

in the previous year primarily attributed to the special

item from the QTE transaction (€52.2 million). Due to

the end of the principal contracts and the transfer of the

remaining shell structure (see 6.2.2.4), the deferral of the

net present value generated at the start of the transac-

tion was completely reversed in the income statement. In

contrast to the adjusted value of €25.6 million from the

previous year, the figure rose by approximately 31.6 per-

cent in 2013.

Material components:

■ Derecognition of liabilities (€8.6 million)

■ Project-specific funding by the European Commission

(€6.7 million)

■ Reversal of provisions (€5.5 million)

■ Reimbursement of costs of the business year

and of previous years (€4.1 million)

■ Benefits-in-kind (€3.1 million)

■ Income from the QTE transaction,

exchange rate gain (€2.6 million)

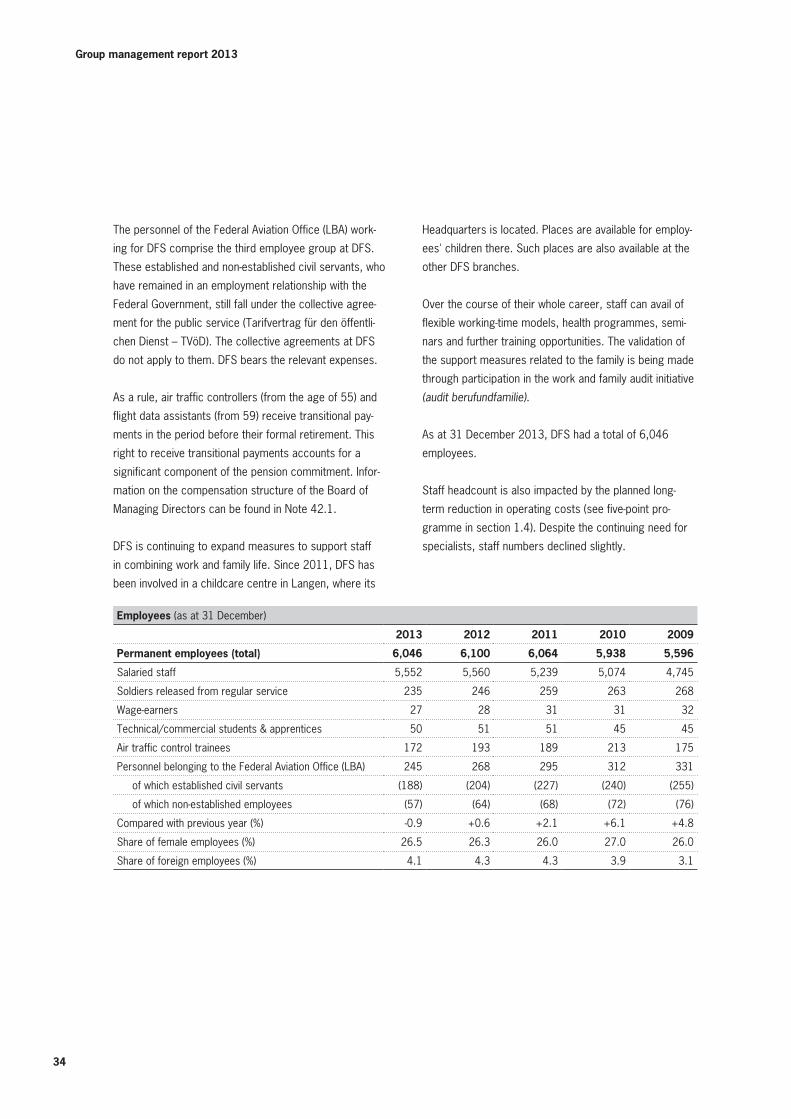

Employee expenses (€m)

2013 2012* 2011 2010 2009

Total 808.5 772.2(789.1) 701.9 625.8 608.1

Thereof wages and salaries 585.7 586.1 550.3 527.6 485.7

Thereof social security costs and expenses for pensions and assistance

197.8 160.2(177.2) 130.2 78.7 96.0

Thereof costs of personnel belonging to the Federal Aviation Office (LBA)**

25.0 25.9 21.3 19.5 26.4

Share of total costs (%) 76.7 75.1(75.5) 72.5 71.4 70.4

Compared with previous year (%) +4.7 +10.0(+12.4) +12.2 +2.9 +3.1

* Prior-year figures adjusted to IAS 19 (revised 2011). Figure in brackets: Originally reported figure.** LBA: Luftfahrt-Bundesamt (Federal Aviation Office)

2.4.4 Principal expense categories

The change compared with the previous year is primarily

attributable to the higher service cost and the changed

recognition of actuarial gains and losses (now only in

equity) due to the revised IAS 19 (revised 2011).

Interest of €98.0 million accruing from provisions for

pensions and early retirement is charged to the financial

result. The return on plan assets (€46.7 million) is cred-

ited to the financial result.

26

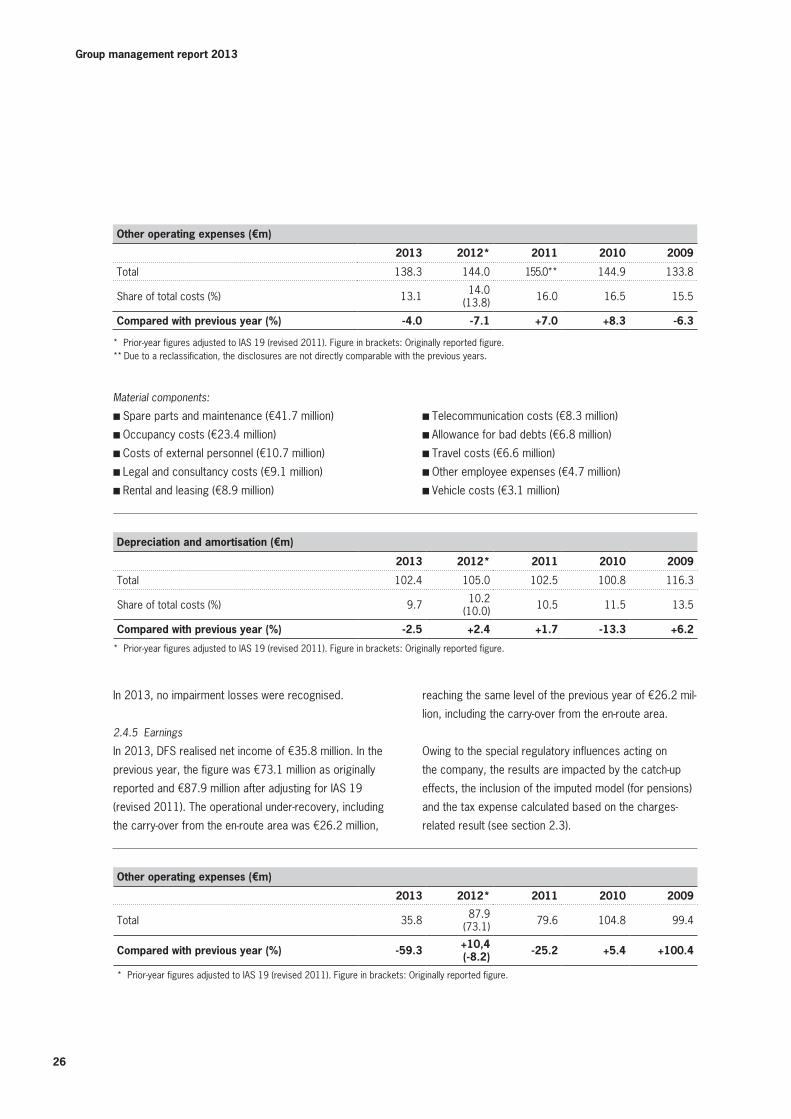

Group management report 2013

Material components:

■ Spare parts and maintenance (€41.7 million)

■ Occupancy costs (€23.4 million)

■ Costs of external personnel (€10.7 million)

■ Legal and consultancy costs (€9.1 million)

■ Rental and leasing (€8.9 million)

■ Telecommunication costs (€8.3 million)

■ Allowance for bad debts (€6.8 million)

■ Travel costs (€6.6 million)

■ Other employee expenses (€4.7 million)

■ Vehicle costs (€3.1 million)

In 2013, no impairment losses were recognised.

2.4.5 Earnings

In 2013, DFS realised net income of €35.8 million. In the

previous year, the figure was €73.1 million as originally

reported and €87.9 million after adjusting for IAS 19

(revised 2011). The operational under-recovery, including

the carry-over from the en-route area was €26.2 million,

reaching the same level of the previous year of €26.2 mil-

lion, including the carry-over from the en-route area.

Owing to the special regulatory influences acting on

the company, the results are impacted by the catch-up

effects, the inclusion of the imputed model (for pensions)

and the tax expense calculated based on the charges-

related result (see section 2.3).

Depreciation and amortisation (€m)

2013 2012* 2011 2010 2009

Total 102.4 105.0 102.5 100.8 116.3

Share of total costs (%) 9.7 10.2(10.0) 10.5 11.5 13.5

Compared with previous year (%) -2.5 +2.4 +1.7 -13.3 +6.2

* Prior-year figures adjusted to IAS 19 (revised 2011). Figure in brackets: Originally reported figure.

Other operating expenses (€m)

2013 2012* 2011 2010 2009

Total 35.8 87.9(73.1) 79.6 104.8 99.4

Compared with previous year (%) -59.3 +10,4(-8.2) -25.2 +5.4 +100.4

* Prior-year figures adjusted to IAS 19 (revised 2011). Figure in brackets: Originally reported figure.

Other operating expenses (€m)

2013 2012* 2011 2010 2009

Total 138.3 144.0 155.0** 144.9 133.8

Share of total costs (%) 13.1 14.0 (13.8) 16.0 16.5 15.5

Compared with previous year (%) -4.0 -7.1 +7.0 +8.3 -6.3

* Prior-year figures adjusted to IAS 19 (revised 2011). Figure in brackets: Originally reported figure.** Due to a reclassification, the disclosures are not directly comparable with the previous years.

27

Adjusted earnings before taxes (€m)

Net income 35.8

./. Taxes on income and revenues* 0.1

EBT 35.7

./. Catch-up effects from IFRS conversion 47.7

./. Catch-up effects from occupational pensions 73.9

Adjusted EBT -85.9

* This relates to the correction of a tax relief for 2013 overall.

The result in 2013 contains the costs reimbursed by

airspace users for previous years of €47.7 million

(previous year: €45.8 million) from the conversion of

the basis for calculating charges from the German Com-

mercial Code to IFRS as of 1 January 2007 (catch-up

effects). It also contains an amount of €73.9 million

(previous year: €23.4 million) from the change in the

charges-related parameters for expenses for occupa-

tional pensions (imputed model, see section 2.3) within

the scope of the introduction of regulated charges as of

1 January 2012.

Adjusted for the above factors, the adjusted earnings

before taxes amounts to minus €85.9 million.

The incomplete information provided by the low-cost air-

line Ryanair (see section 2.3) resulted in an allowance for

doubtful accounts of €5.6 million being charged against

receivables in the en-route area for 2010 to 2012.

The changeover from full cost recovery to charges

based on performance in the en-route area has a mate-

rial impact on the cost structures. Savings or additional

expenses are no longer passed on in the following

periods but directly impact the earnings of DFS. Cur-

rently, there are still issues concerning interpretation and

application which could influence the future development

of the company's economic situation. From the point of

view of DFS, there are a small number of measurement,

accounting and charging issues which have not been

unequivocally resolved since the date of the transition

(31 December 2011/1 January 2012). The regulatory

authority and DFS continue to work in a critical dialogue

on drawing up a binding catalogue of qualifying uncontrol-

lable costs. Such costs will have to be borne in full by

airspace users.

For the en-route area, the EU Charging Scheme

1191/2010 has split the chances and risks resulting

from the differences between planned and actual traffic

volume between the airspace users and DFS since 2012.

If defined thresholds are exceeded, DFS is authorised and

obliged to return or demand any over- or under-recoveries

(carry-over). The carry-over for 2013 will be carried

forward and taken into account in the determination of

charges for the second reference period.

Chance/risk transfer from deviation in traffic volume

Deviation in traffic volume (v) DFS share User share

v ≤ 2.0% 100.0% ---

2.0% < v ≤ 10.0% 30.0% 70.0%

v > 10.0% --- 100.0%

28

Group management report 2013

Terminal services will continue to be subject to full cost

recovery until the end of 2014. The principles governing

air navigation charges laid down by ICAO and EUROCON-

TROL continue to stipulate that – after making allowance

for a reasonable return on capital employed – over- or

under-recoveries have to be passed on in subsequent

years. Accordingly, the operational over-recovery from the

business year 2013 for terminal services will be taken into

account when determining charges for the year 2015.

Overall, the positive earnings have been impacted by the

material special items.

2.5 Assets and financial position

2.5.1 Capital expenditure

DFS invests in the preservation and further development

of the necessary infrastructure if the measures are

based on legal obligations or support the development

of earnings in an economically sound manner. Regula-

tions and standards from ICAO, EUROCONTROL and the

EU are adhered to. The safety of air traffic plays a deci-

sive role when it comes to decisions on capital expendi-

ture. Against this background, capital expenditure of

€124.6 million was made in the business year 2013.

As at 31 December 2013, a further €18.5 million of an

inter-Group long-term loan approval of €50 million from

DFS was drawn down.

The following projects are currently underway and repre-

sent the highest share of capital expenditure:

Construction of the Langen technical centre

DFS is constructing a new technical centre to set up ATC

test and reference installations and house the administra-

tive computer centre.

iCAS (interoperability Through European Collaboration Centre

Automation System) software

The future control centre ATS system iCAS will in par-

ticular meet the interoperability requirements of the SES

regulations.

Voice switching system ISIS-XM

(Improved Speech Integrated System) in Langen

DFS is harmonising its voice switching systems and is

replacing the system in Langen within the scope of the

LASER project. In the future, ISIS-XM is to be installed

at all DFS control centres to achieve a homogeneous

system landscape. Using a uniform user interface and

concept will increase training efficiency and create the

necessary conditions to enable the transfer of services

(e.g. consolidating control centres at night) and new con-

cepts to ensure ATC operations in contingencies.

Extension to the Munich Control Centre

Building work was required because of the increase in

space needed for the installation of the P2/ATCAS air

traffic management system. This is the successor system

to P1/ATCAS (P1 air traffic control automation system)

in the control centres for lower airspace. The building

work covers a control room with roughly 100 controller

working positions as well as office and functional rooms

for operations. In addition, two equipment rooms and two

centres each for the provision of air-conditioning, cooling

and electricity were fitted out.

Radio Site Upgrade and Modernisation (RASUM) 8.33

DFS is equipping 95 radio stations for the 8.33 kHz chan-

nel spacing requirements in lower airspace, including the

necessary structural and infrastructural measures. The

project caters for future traffic growth and implements

the Conclusion taken by the ICAO European Air Navigation

Planning Group (EANPG) 48 dated November 2006 and

EU Regulation 1079/2012.

P2 Langen Control Centre

The goal of the project is the installation and commis-

sioning of P2 in the new control room of the Langen

Control Centre. Frankfurt and Düsseldorf have separate

ATS, communication (COM) and air traffic flow manage-

ment (ATFM) systems. These are to be integrated into

one ATS, one COM and one ATFM system. At the same

time, the engineer on duty (EoD) Langen is to start work.

29

When it goes into operation, a centrally developed new

P2 controller working position will be employed that can

be used in various roles and will be used during the tran-

sition to iCAS and during future iCAS operations. After P2

starts up, the old P1/ATCAS systems will be uninstalled

from the old control room and equipment rooms. A new

cooling plant will be commissioned in the Langen Control

Centre for the new P2 components to be installed.

Rehosting ATCAS hardware and software

To ensure the product life cycle, ATCAS is being rehost-

ed. The software is being ported to Linux using Intel-

compatible hardware.

P1/ATCAS software extensions for PSS Langen

PSS is an extension within the area of flight data pro-

cessing and display in the ATS system P1/ATCAS used

in Bremen, Munich and Langen. PSS replaces paper

flight progress strips with electronic flight progress

strips and exchanges data with the FDPS (flight data

processing system) of P1/ATCAS. As PSS is an integral

component of ATCAS, software maintenance and fur-

ther development, especially the different functionality

PSS Langen (different when compared with Bremen and

Munich), will be carried out by the DFS Systems House

as part of the ATCAS maintenance processes. On a