Embed Size (px)

Citation preview

Annual Report 2013

Alteo Limited - ANNUAL REPORT 2013

CONTENTSNotice of Annual MeetingCorporate InformationGroup StructureChairman’s StatementExecutives’ ReportCorporate Social Responsibility Corporate GovernanceOther Statutory DisclosuresCompany Secretary’s Certificate

0204

06 - 07 08 - 0910 - 3538 - 4144 - 6566 - 77

79

Independent Auditors’ Report to the MembersStatements of Financial PositionIncome StatementsStatements of Comprehensive IncomeStatements of Changes in EquityStatements of Cash FlowsNotes to the Financial StatementsProxy FormPostal Vote

80 - 81828384

85 - 8687

88 - 149151152

page

1

DEAR SHAREHOLDER,

ThE BOARd Of diRECTORS Of ALTEO LimiTEd iS PLEASEd TO PRESENT iTS ANNUAL REPORT fOR ThE yEAR ENdEd JUNE 30, 2013. ThiS REPORT wAS APPROvEd By ThE BOARd Of diRECTORS AT A mEETiNg hELd ON SEPTEmBER 20, 2013.

ON BEhALf Of ThE BOARd Of diRECTORS Of ALTEO LimiTEd, wE iNviTE yOU TO gO ThROUgh ThE ANNUAL REPORT ANd JOiN US AT ThE ANNUAL mEETiNg Of ThE COmPANy whiCh wiLL BE hELd:

DATE: wEdNESdAy, dECEmBER 18, 2013TIME: 10.00 hOURSPLACE: hENNESSy PARK hOTEL EBONy CONfERENCE ROOm 65 EBÈNE, EBÈNE CyBERCiTy

wE LOOK fORwARd TO SEEiNg yOU.

yOURS SiNCERELy,

ARNAUd LAgESSE CHAIRMAN

Alteo Limited - ANNUAL REPORT 2013

page

3page

2

Alteo Limited - ANNUAL REPORT 2013

NOTICE OF ANNUAL MEETINGTO SHAREHOLDERSNotice is hereby given that the Annual Meeting (“the Meeting”) of Shareholders of Alteo Limited (“the Company”) will be held at Hennessy Park Hotel, Ebony Conference Room, 65 Ebène Cybercity, Ebène on Wednesday, December 18, 2013 at 10.00 hours to transact the following business in the manner required for the passing of ORDINARY RESOLUTIONS:

AGENDA1. To consider the Annual Report 2013 of the Company.

2. To receive the report of BDO & Co, the auditors of the Company.

3. To consider and adopt the Group’s and Company’s audited financial statements for the year ended June 30, 2013.

4. To re-elect, on the recommendation of the Corporate Governance Committee, as Director of the Company to hold office until the next Annual Meeting, in accordance with Section 138(6) of the Companies Act 2001, Mr. G. Christian Dalais1 who offers himself for re-election.

5-13. To re-elect, on the recommendation of the Corporate Governance Committee, as Directors of the Company to hold office until the next Annual Meeting, the following persons1 who offer themselves for re-election (as separate resolutions):

5. Mr. Arnaud Lagesse

6. Mr. Jean-Claude Béga

7. Mr. Jan Boullé

8. Mr. Patrick de L. d’Arifat

9. Mr. P. Arnaud Dalais

10. Mr. Amédée Darga

11. Mr. Jean de Fondaumière

12. Mr. Louis Guimbeau

13. Mr. Thierry Lagesse

14. To re-appoint BDO & Co as auditors for the ensuing year and to authorise the Board of Directors to fix their remuneration.

15. To ratify the remuneration paid to the auditors for the financial year ended June 30, 2013.

By Order of the Board

Nathalie Gallet, ACISFor Navitas Corporate Services LtdCompany Secretary

November 12, 2013

Notes

1. A shareholder of the Company entitled to attend and vote at this meeting may appoint a proxy of his/her own choice to attend and vote on his/her behalf. A proxy need not be a member of the Company.

2. A proxy form and a postal vote are included in this Annual Report and are also available at the registered office of the Company.

3. The instrument appointing a proxy or any general power of attorney shall be deposited at the Share Registry and Transfer Office of the Company, MCB Registry & Securities Ltd, 2nd Floor, MCB Centre, 9-11, Sir William Newton Street, Port-Louis, not less than twenty-four (24) hours before the start of the meeting and in default, the instrument of proxy shall not be treated as valid.

4. Postal votes shall be deposited at the Share Registry and Transfer Office of the Company, MCB Registry & Securities Ltd, 2nd Floor, MCB Centre, 9-11, Sir William Newton Street, Port-Louis, not less than forty-eight (48) hours before the start of the meeting and in default, the postal vote shall not be treated as valid.

5. For the purpose of this Annual Meeting, the Directors have resolved, in compliance with Section 120(3) of the Companies Act 2001, that the shareholders who are entitled to receive notice of the meeting shall be those shareholders whose names are registered in the share register of the Company as at November 20, 2013.

6. The minutes of the Annual Meeting held on December 18, 2012 are available for consultation by the shareholders during office hours at the registered office of the Company, Vivéa Business Park, Saint Pierre.

7. The minutes of the Annual Meeting to be held on December 18, 2013 will be available for consultation and comments during office hours at the registered office of the Company, Vivéa Business Park, Saint Pierre from February 3 to 14, 2014.

Footnote 1: The profiles and categories of the Directors proposed for re-election are set out at pages 50 to 53 of the Annual Report 2013.

Alteo Limited - ANNUAL REPORT 2013

page

5page

4

Alteo Limited - ANNUAL REPORT 2013

MANAGEMENT TEAM

P. Arnaud Dalais – Group Chief Executive

Patrick de L. d’Arifat – Chief Executive Officer

Jérôme De Chasteauneuf – Head of Finance

Robert Baissac – CEO of TPC Ltd

Jean-Luc Harel – COO Sugar Milling & Energy Activities

Sébastien Lavoipierre – Designate COO Sugar Milling & Energy Activities

Christian Marot – COO Agricultural Activities

Jean-Robert Lincoln – Group Agricultural Development Executive

Patrice Legris – CEO of Alteo Properties Ltd

REGISTERED OFFICE

Vivéa Business ParkSaint PierreMauritiusBRN: C06000012Tel: +230 402 9050Fax: +230 432 0729Website: www.alteogroup.com

ALTEO - BEAU CHAMP

Beau ChampGrand River South EastMauritiusTel: +230 417 6000Fax: +230 417 6481

ALTEO - UNION FLACQ

Union FlacqMauritiusTel: +230 402 3300Fax: +230 413 2699

COMPANY SECRETARY

Navitas Corporate Services Ltd 2nd Floor, Navitas Business Centre13, St Clément StreetCurepipeMauritius

SHARE REGISTRY & TRANSFER OFFICE

If you are a shareholder and have inquiries regarding your account, wish to change your name or address, or have questions about lost share certificates, share transfers or dividends, please contact our Share Registry and Transfer Office:

MCB Registry & Securities Limited2nd Floor, MCB Centre9-11, Sir William Newton StreetPort-LouisMauritiusTel: +230 202 5397Fax: +230 208 1167

EXTERNAL AUDITORS

BDO & Co.

INTERNAL AUDITORS

EY

BANKERS

ABC Banking Corporation

AfrAsia Bank Limited

Barclays Bank PLC

Bank of Baroda

Banque des Mascareignes Ltée

Bank One Limited

State Bank of Mauritius Ltd

The Hong Kong and Shanghai Banking Corporation Ltd

The Mauritius Commercial Bank Ltd

CORPORATEINFORMATION

page

7

Alteo Limited - ANNUAL REPORT 2013

World Tropicals Ltd

Sukari Investment Company Limited

Microlab Ltd

TPC Ltd

100%

100%

61%

100%

50%

67.55%

75%

100%

100%

33.33%

Flagstone Property Management Ltd

Anahita World Class Sanctuary Ltd

Trois Ilots Limited

99.89%

100%

100%

Trianon Estates Limited

Société Gonin

Société Ducomet

50.01%Noveprim Limited

93% NoveprimEurope Limited

80% Deep River Beau Champ Milling Company Ltd

80% Contance La Gaiété Milling Company Limited

100% Anahita Centre for Excellence Limited

37.5%Bluefrog Limited

32.5%

39%

50.63%

32.5%

13.13%

Alteo Refinery Ltd (formerly FUEL Refinery Limited)

Alteo Planters Services Ltd(formerly FSMC Planters Services Co Ltd)

Anahita Golf Ltd

Compagnie Usinière de Mon Loisir Ltée

Consolidated Energy Co. Ltd.

50%

page

6

Alteo Limited - ANNUAL REPORT 2013

GROUPSTRUCTUREAS AT SEPTEMBER 20, 2013

DEEP RIvER INvESTMENT LTD20.96%

GML INvESTISSEMENT LTéE26.92%

OTHER SHAREHOLDERS 52.12%

ALTEO LIMITED

50%

64.23%

61.72%

65.19%

100%

60%

50%

100%

50%

33.3%

100%

65.10%

65.10%

85.72%

100%

100%

99.99%

57.15%

Anahita Estates Limited

Anahita Hotel Limited

Fondation Nouveau Regard

Commercial and Industrial Enterprises Ltd

100%

50%

6.99%

99.99%

Anahita Residences and villas Limited

Constance La Gaiété Company Limited

Ferney Aquaculture Limited

Société Beaureagrd

Novelife Limited

Alteo Energy Ltd(formerly F.U.E.L. Steam and Power

Generation Company Limited)

Refinest Limited

Alteo Milling Ltd(formerly F.U.E.L. Sugar Milling

Company Limited)

Eastern Energy Company Limited

Compagnie de la vigie Limitée

Usinest Limited

Schoenfeld Co. Ltd

Alteo Properties Ltd (formerly CIEL Properties Ltd)

Island Fresh Ltd

Sucrière des Mascareignes Limited

West East Limited

CIEL et Nature Limitée

Sena Development Ltd

page

9

Alteo Limited - ANNUAL REPORT 2013

page

8

Alteo Limited - ANNUAL REPORT 2013

CHAIRMAN’SSTATEMENT

Associated companies and Joint Ventures contributed Rs 104m (2012: loss Rs 2,4m) mainly resulting from an exceptional revenue by one of the entities.

Following the amalgamation, the Board of Directors decided to align the discount rate applied to third party freehold land valuation throughout the Group. This is largely responsible for the surplus on revaluation of land of Rs 1,368bn stated in the other comprehensive income.

An interim dividend of Rs 0.30 per share based on 318,492,120 ordinary shares (2012: Rs 4.00 based on 9,360,000 ordinary and preference shares) and a final dividend of Rs 0.45 per share (2012: Rs 0.40 based on 186,986,700 ordinary shares) were declared during the financial year under review.

During the year, the Company raised Rs 1bn through the first tranche of a multicurrency note programme at an average cost of funds of 5.40% per year. The proceeds from this issue will be used to refinance existing short term banking facilities and also to fund our obligations in respect of the voluntary retirement scheme.

PROSPECTS

Sugar and Energy

In Mauritius, an average overall sugar crop is expected, which should yield fair results provided export prices to EU are not too adversely affected by the depressed world market. Energy results are likely to remain in line with the previous years on the basis of foreseeable sluggish coal prices.

In the sugar sector, ALTEO is looking forward to start reaping the synergic benefits of the amalgamation in the agricultural activities through a more efficient utilization of resources and in the industrial sector through the closing down of Deep River Beau Champ mill and the concentration of the operations onto Alteo Milling.

In the aftermath of the milling centralization, Alteo Energy will be in an ideal position to maximize its renewable energy potential in the context of any request for proposals from the authorities. In Tanzania, a very good crop is anticipated against more difficult market conditions. The initial investments in the new Business Plan, both at field and factory levels, will be initiated and should have an effect on operational efficiency and production levels.

Property

The sector remains challenging. However, the recent improved trend is expected to gain momentum towards the end of the year with the expected launch of our new product offering, Amalthea, at Anahita. Alteo will also be embarking, with the assistance of external expertise, in a thorough exercise with a view to determining and optimizing the best opportunities for value creation in its significant property portfolio.

Hospitality

The improved trend noted in our activities is expected to consolidate further in the year to come.

Regional Development

ALTEO is looking forward to completing during the year the in-depth studies with regard to the integrated sugar and energy project in Swaziland for which we have recently signed a Memorandum of Understanding. Other projects are also being investigated. ALTEO will, in parallel, further investigate other regional opportunities that have already been identified and that present interesting opportunities for the Company to become a major sugar and energy production in the region.

Social responsibility

ALTEO was very active during this financial year on the social and environmental fronts and contributed to Rs 4.7m to a number of socio-economic development, education, and training, childcare and health projects. Going forward, ALTEO will continue to fulfill the various commitments of ex DRBC as well as those of ex FUEL through, Fondation Nouveau Regard and GML Fondation Joseph Lagesse, respectively, as well as contributing directly to a number of other initiatives.

Appreciation

I would like to express my gratitude to my colleagues of the Board of Directors for their assistance and guidance throughout the year and the management and staff under the leadership of Arnaud Dalais, Group Chief Executive, and of Patrick d’Arifat, Chief Executive Officer, for their valuable contribution during the year.

Arnaud LagesseChairman

September 20, 2013

Dear Shareholder,

July 2012 marked the history of the sugar industry in Mauritius, with the creation of Alteo Ltd (“ALTEO”)further to the amalgamation of FUEL with and into DRBC.

Derived from the Latin word “Altus”, the name Alteo encompasses the vision of the new Group - To reach new heights through its plans of local and international expansion by leveraging on the expertise of employees and combining resources to sustain competitiveness. This vision resulted from the shared objective of its main shareholders, Deep River Investment and GML Investissement, and their dedicated leadership, to ensure the competitiveness of their existing operations in an increasingly liberalized environment, whilst open the way to a number of new exciting avenues.

The setting up of ALTEO and its listing on the Official Market of the Stock Exchange of Mauritius since July 31, 2013 designated the starting points of a new era of tremendous opportunities for the Group which aims to be a regional leader, not only in the cane industry, but across a business mix that spans renewable energy production, sustainable property development and the leisure and hospitality industries.

The present annual report and financial statements for the period ending June 30, 2013, thus constitutes the first such report and statements of the amalgamated entities.

As the amalgamation took place in July 2012, the comparative figures of the Company and Group for the year ended June 2012, as contained in the present financial statements are those of ex-DRBC and its subsidiaries only.

OVERALL REVIEW

The overall financial performance of the Group for its first year of existence has been more than encouraging as more fully described hereunder.

On the organizational side, the main initiatives for the year have been, namely, the setting up of the Company’s Head Office at Vivéa Business Park, St Pierre, where the property development cluster is also based; and, the refurbishment of the Union Flacq offices where the greater part of the agricultural and industrial staff have now been relocated.

On the operational and strategic plan, the year has seen the following main features:

i) The completion of the investment programme at Alteo Milling Ltd and Alteo Energy Ltd to optimize

the capacity and operational efficiencies of these two plants, in view of the forthcoming closure of DRBC Milling factory and the redirection of the canes to Alteo Milling Ltd.

ii) The initial reorganization of the agricultural operations with a view to ensuring that all the potential synergies of the amalgamation materialize over the coming years.

iii) The setting up of a structured financial and technical project appraisal team so as to reinforce the Company’s capacity to identify new investment ventures.

iv) The production of a new 5 year Business Plan for TPC Ltd in Tanzania that identifies the investments required at both agricultural and industrial levels to bring the yearly sugar production to some 110,000 tonnes.

v) On the property front, at Anahita, the finalization of all the preparatory works for the launching, by the end of 2013, of Amalthea, a new phase of 59 units comprising villas, duplexes and golf lodges.

FINANCIAL RESULTS

The Group turnover for the year stood at Rs 6,066m (2012: Rs 3,673m) with an operating profit of Rs 1,908m (2012: Rs 1,401m) and a profit after tax of Rs 1,407m (2012: Rs 700m). This much improved performance is attributable to the following main elements; (i) the amalgamation of FUEL entities; (ii) better operational performances; (iii) profit on disposal of assets and (iv) a gain on fair value of investment property.

Our sugar operations in Tanzania continued to perform very satisfactorily despite a slightly lower production of 87,000 tonnes for the year, (2011-2012: 91,000 tonnes). Mauritian operations also reported an improved performance as a result of a globally average crop and sugar prices at Rs 17,560 per tonne, i.e. 10 % higher than in the previous year. Energy activities in Mauritius also recorded fair results in the face of sustained off take from the national grid (166 GWh) and lower coal costs. The refinery operation also improved its performance with a production of some 163,000 tonnes and higher operational efficiencies.

Our activities in the hospitality industry continued to show improved results despite the still difficult market conditions. The property sector remained tough but encouraging signs were seen at the end of the financial year which leads us to believe that a possible recovery is under way.

Alteo Limited - ANNUAL REPORT 2013

page

11

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’REPORT

page

10

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORT

We are pleased to submit our first executives’report following the merger, in July 2012 of FUEL with and into Deep River Beau Champ Ltd, and which has subsequently been renamed Alteo Limited (“ALTEO”).

Following the merger, the ordinary shares of ALTEO were listed on the Official Market of the Stock Exchange of Mauritius on July 31, 2012.

The year under review has been an exciting one following this successful merger and challenges were numerous. We would like to put on record the excellent performance of the company and the group in their first year of operation. This has been achieved thanks to the good work done by each and every one amongst our management and staff, both locally and abroad. A special tribute to Jean Luc Harel, COO for Industrial activities, and Christian Marot, COO for Growing activities and Logistics, who through their close collaboration, have permitted a very good integration of both teams from ex-FUEL and ex-DRBC into one at the level of ALTEO.

This has also been the case at both head office level and finance and accounts departments where a dedicated team, under the leadership of Jérôme de Chasteauneuf, Head of Finance, have successfully integrated all the systems to allow our operations to run smoothly.

The creation of ALTEO has not only led to significant added impetus to the operations but has also resulted in an excellent financial performance as spelt out hereunder.

The group has recorded a turnover in excess of Rs 6,066m (2012: Rs 3,673m) for the financial year resulting in a profit after tax of Rs 1,407m (2012: Rs 700m). These figures are however not comparable with those of last year which were “pre- merger”.

Sugar and sugar related activities, from both local and regional levels, have generated a turnover of Rs 4,267m, whilst power generation recorded a turnover Rs 1,192m, property development Rs 206m and others Rs 399m for the financial year under review.

Other operating income which includes agricultural diversification, rent & transport recharge, profit on sale of land amongst others stood at Rs 247m.

The operating profit after accounting for the direct expenses and overheads for the Group reached Rs 1,908m compared to Rs 1,401m in the previous year.

The adoption of a uniform discount rate resulted in a fair value gain on investment property for the year of Rs 109m (2012: nil).

Finance cost on interests bearing debts stood at Rs 323m (2012: Rs190m). During the year, as stated in the Chairman’s Statement, Alteo Limited, the Company, raised Rs 1 billion through the issue of multi-currency notes programme. The interest rates on these notes range between 4.10% and 5.75% with repayment terms of 1 to 5 years. The purpose of this fund raising exercise was to refinance existing short term banking facilities and also to fund our obligation regarding the voluntary retirement scheme.

Our share of results of associated companies and Joint ventures stood at Rs 104m (2012: Rs 2m). This is largely as a result of exceptional revenue recorded in one of the companies.

The profit realized at Group level on disposal of land and investment property reached Rs 62m (2012: nil). A gain of Rs 47m (2012: nil) on re-measuring our interest from associate to subsidiary was registered in the year under review.

Alteo Ltd undertook a revaluation of its land assets and investment portfolio and realised a gain on its land of Rs 1,335m, excluding Investment Property, treated separately, and a gain of Rs 537m on its portfolio of investments. In line with prevailing accounting standards, such gains are disclosed in the Statements of Comprehensive Income.

We are pleased to present herewith an extensive review of the different lines of activity where the Group operates, namely:

i) Cane Growing

ii) Sugar Manufacturing

iii) Sugar Refining

iv) Energy

v) Regional Development – TPC Limited (cane growing, milling and energy)

vi) Property & Hospitality

ALTEO AGRI

ALTEO SUGARS

ALTEO ENERGY

ALTEO INTERNATIONAL

ALTEO PROPERTY & HOSPITALITY

CANE GROWING

SUGAR MANUFACTURING

SUGAR REFINING

ENERGY

REGIONAL DEVELOPMENT – TPC LIMITED

(CANE GROWING, MILLING AND ENERGY)

PROPERTY DEVELOPMENT & TOURISM

Alteo Limited - ANNUAL REPORT 2013

page

13

Alteo Limited - ANNUAL REPORT 2013

page

12

The deviations from budgeted cane productivity were an increase of 4.9% for Union Flacq (UF), a drop of 4.0% for Beau Champ (BC) and 9.3% for Mon Loisir (ML). The reduction in the yield at BC and ML, where most of the cane areas are situated in the humid and sub-humid regions, was attributable to low rainfall. A deficit of rainfall of 47% in the North and 21% in the East was registered during the period of October 2011 to February 2012 compared to the Long Term Mean. This shortfall of rainfall in the East was beneficial to the super humid regions of Bel Etang and Sans Souci where a gain in productivity of nearly 9 tonnes cane/ha was recorded representing an increase of 12% over the initial estimate.

CANE GROWING

Review of Operations

ALTEO

2012 Crop

Crop 2012 marked the first harvest of ALTEO. The total area under cane cultivation after the amalgamation of Flacq United Estates Ltd, Deep River–Beau Champ Ltd and the subsequent dissolution of Société de Gérance Mon Loisir Ltd reached an extent of 11,260 ha located in the regions of Olivia, Belle-Rive, Ferney, Queen Victoria, Bel Etang and Mon Loisir. During the 2012 crop, 10,000 ha were harvested for a total cane production of 807,645 tonnes, in line with the estimated figure of 808,240 tonnes.

The precipitations in the North and the East are illustrated by Graphs below.

Rainfall in the North from October 2012 to July 2013 v/s Long Term Mean (source MSIRI)

0

50

100

150

200

250

300

350

400

450

500

cms

Octob

er

Novem

ber

Decem

ber

Janua

ry

Febr

uary

Marc

hApr

ilM

ayJu

ne July

2012

2013

LTM

EXECUTIvES’ REPORTCANE GROWING

Rainfall in the East from October 2012 to July 2013 v/s Long Term Mean (source MSIRI)

0

100

200

300

400

500

600

700

800

cms

Octob

er

Novem

ber

Decem

ber

Janua

ry

Febr

uary

Marc

hApr

ilM

ayJu

ne July

2012

2013

LTM

page

15

Alteo Limited - ANNUAL REPORT 2013

page

14

Alteo Limited - ANNUAL REPORT 2013

Table 1 below gives an overview on the tonnage of cane production for crop 2012 at ALTEO.

RegionsArea (hectares) Cane Production (tonnes) Yield (tonne/hectare)

Estimate Actual Estimate Actual Estimate Actual

Beau Champ

Olivia 1,229 1,220 103,500 100,131 87.2 82.0

Belle Rive 1,413 1,409 109,500 105,115 77.5 74.6

Ferney 837 839 67,000 64,031 80.0 76.3

Union Flacq

Q. Victoria 2,896 2,896 245,000 248,561 84.6 85.8

Bel Etang 1,954 1,936 146,000 161,744 74.7 83.5

Mon Loisir Mon Loisir 1,770 1,778 137,240 128,063 77.5 72.0

TOTAL 10,099 10,077 808,240 807,645 80.0 80.1

In addition, an extent of 1,229 ha was replanted during the year, representing 11% of the total cane area of ALTEO. The total area replanted includes 250 ha under the variety M695/69 which was replaced due the drastic yield drop registered year after year since 2010.

2012/2013 Financial Results

Following the merger of FUEL and DRBC in July 2012 and the subsequent dissolution of Société Gérance de Mon Loisir, the financial statements of ALTEO to June 2013 incorporate for the first time the activities of these three operations.

For the year under review the price of sugar reached Rs17,573, up 9.70% from the previous year. The price of molasses stood at Rs 2,235, which is a 12.8% increase over 2011.

Extraction rate (commercial sugar recovered % cane) was 10.45% on average for ALTEO with the lowest results of 10.22% at BC, followed by 10.48% at UF and the highest result obtained at ML with 10.86%.

On the harvesting side, a total of 447,000 tonnes of canes were harvested mechanically at ALTEO, representing approximately 55% of the total harvest. Some 16,400 tonnes of canes belonging to outgrowers were also harvested by ALTEO’s mechanical harvesters. The total area prepared for mechanical harvest at June 2013 reached 6,990 ha, (including 700 ha at Bel Etang presently harvested manually), which represents 62% of the total cane area and 68% of the total average cane production.

During the year under review, the Company invested in the refurbishing of the irrigation pivot at Trois Ilots and of the drip irrigation system at Grand Port on an extent of 125 ha. In addition, 5 infield tractors of 110 hp were replaced by 5 new tractors of 130 hp for mechanical harvesting and for land preparation during the intercrop.

Table 2 shows the trend in prices in recent years.

The selling price of sugar and molasses (2007-2012) in Rs per tonne.

Crop years 2013 (est.) 2012 2011 2010 2009 2008 2007

Sugar 17,000 17,573 16,020 13,536 14,612 17,427 18,620

Molasses 2,000 2,235 1,982 2,689 3,016 2,181 1,361

EXECUTIvES’ REPORTEXECUTIvES’ REPORT

Taking on the assets of ex-FUEL led to a deferred tax credit of Rs 63m for the year under review.

After allowing for the above, the Company realised a Net Profit of Rs 622m for the year.

Additions to Property, Plant and Equipment amounted to Rs 148m for the year.

2013 Crop

Harvest estimate for crop 2013, undertaken in April 2013, based on prevailing climatic conditions as well as cane growth measurements resulted in a crop forecast of 843,000 tonnes compared to 807,645 tonnes for crop 2012. The deficit rainfall recorded from October 2012 to January 2013, was followed by very favorable rains during the mid-January to end of March period. Unfortunately, as from April to June the whole island experienced another prolonged dry spell, well under the Long Term Mean, which slowed down cane growth. This situation will certainly have an adverse effect on our initial estimate. Extraction rate for the 2013 crop has been estimated to be around 10.50% for the different regions.

As a result of the improved sugar and molasses prices, the turnover of the Company reached Rs 1,238m. Other Operating Income also grew by Rs 44m compared to the previous year due to an increase of Rs 13m in management fees receivable, subsidiaries which did perform better, a Rs 13m rise in rental income and a Rs 15m increase in revenue from agricultural diversification.

After taking into account the positive movement on the valuation of the standing crop as at year end, of Rs 111m, the Company achieved a total income of Rs 1,569m for the year.

Given that the cane production achieved was largely comparable to estimates, the cost of production remained on a similar footing as estimated. The Operating Profit for the Company, as reported, was at Rs 267m.

Investment and Other Income was largely within expectations at Rs 415m. The Company registered a gain on the fair value of its Investment Property to the order of Rs 142m. Net finance costs decreased by Rs 13m on accounts of gains in year-end foreign currency translations and savings on finance charges. The Company also impaired the value of an investment in a subsidiary by Rs 20m, during the year.

ALTEO Union Flacq: Cane Growth 2013

280

260

240

220

200

180

160

140

120

100

80

60

40

Cms

2013

2012

2001

9/1 23/1 6/2 20/2 6/3 20/3 3/4 17/4 1/5 15/5 29/5 12/6 Dates

CANE GROWINGCANE GROWING

page

17

Alteo Limited - ANNUAL REPORT 2013

page

16

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORT CANE GROWINGCANE GROWING

ALTEO Mon Loisir: Cane Growth 2013

260

240

220

200

180

160

140

120

100

80

60

40

20

2013

2012

2001

9/1 23/1 6/2 20/2 6/3 20/3 3/4 17/4 1/5 15/5 29/5 12/6

ALTEO Beau Champ: Cane Growth 2013

280

260

240

220

200

180

160

140

120

100

80

60

40

2013

2012

2001

9/1 23/1 6/2 20/2 6/3 20/3 3/4 17/4 1/5 15/5 29/5 12/6

Health and Safety

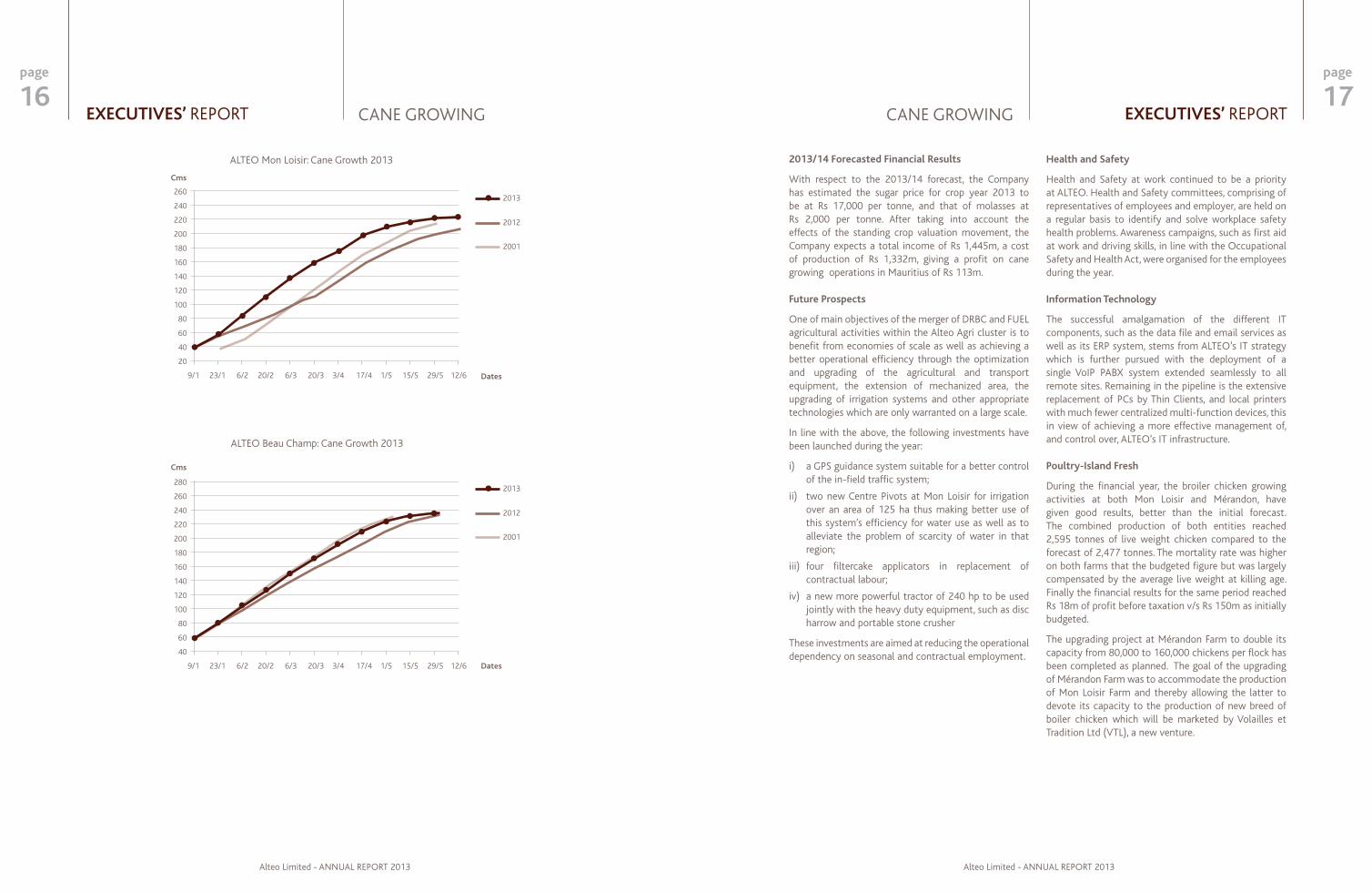

Health and Safety at work continued to be a priority at ALTEO. Health and Safety committees, comprising of representatives of employees and employer, are held on a regular basis to identify and solve workplace safety health problems. Awareness campaigns, such as first aid at work and driving skills, in line with the Occupational Safety and Health Act, were organised for the employees during the year.

Information Technology

The successful amalgamation of the different IT components, such as the data file and email services as well as its ERP system, stems from ALTEO’s IT strategy which is further pursued with the deployment of a single VoIP PABX system extended seamlessly to all remote sites. Remaining in the pipeline is the extensive replacement of PCs by Thin Clients, and local printers with much fewer centralized multi-function devices, this in view of achieving a more effective management of, and control over, ALTEO’s IT infrastructure.

Poultry-Island Fresh

During the financial year, the broiler chicken growing activities at both Mon Loisir and Mérandon, have given good results, better than the initial forecast. The combined production of both entities reached 2,595 tonnes of live weight chicken compared to the forecast of 2,477 tonnes. The mortality rate was higher on both farms that the budgeted figure but was largely compensated by the average live weight at killing age. Finally the financial results for the same period reached Rs 18m of profit before taxation v/s Rs 150m as initially budgeted.

The upgrading project at Mérandon Farm to double its capacity from 80,000 to 160,000 chickens per flock has been completed as planned. The goal of the upgrading of Mérandon Farm was to accommodate the production of Mon Loisir Farm and thereby allowing the latter to devote its capacity to the production of new breed of boiler chicken which will be marketed by Volailles et Tradition Ltd (VTL), a new venture.

2013/14 Forecasted Financial Results

With respect to the 2013/14 forecast, the Company has estimated the sugar price for crop year 2013 to be at Rs 17,000 per tonne, and that of molasses at Rs 2,000 per tonne. After taking into account the effects of the standing crop valuation movement, the Company expects a total income of Rs 1,445m, a cost of production of Rs 1,332m, giving a profit on cane growing operations in Mauritius of Rs 113m.

Future Prospects

One of main objectives of the merger of DRBC and FUEL agricultural activities within the Alteo Agri cluster is to benefit from economies of scale as well as achieving a better operational efficiency through the optimization and upgrading of the agricultural and transport equipment, the extension of mechanized area, the upgrading of irrigation systems and other appropriate technologies which are only warranted on a large scale.

In line with the above, the following investments have been launched during the year:

i) a GPS guidance system suitable for a better control of the in-field traffic system;

ii) two new Centre Pivots at Mon Loisir for irrigation over an area of 125 ha thus making better use of this system’s efficiency for water use as well as to alleviate the problem of scarcity of water in that region;

iii) four filtercake applicators in replacement of contractual labour;

iv) a new more powerful tractor of 240 hp to be used jointly with the heavy duty equipment, such as disc harrow and portable stone crusher

These investments are aimed at reducing the operational dependency on seasonal and contractual employment.

Cms

Cms

Dates

Dates

Alteo Limited - ANNUAL REPORT 2013

page

19

Alteo Limited - ANNUAL REPORT 2013

page

18EXECUTIvES’ REPORTSUGAR MANUFACTURING

SUGAR MANUFACTURING

Review of Operations

DEEP RIvER BEAU CHAMP MILLING LIMITED

2012 Crushing Season

2009 2010 2011 2012

Cane crushed during crop (tonnes) 768,953 720,911 678,453 654,463

TCH 234.5 231.6 224.5 222.4

Canes/day (tonnes) 4,867 4,871 4,744 4,777

Purity mixed juice (%) 85.8 85.7 85.2 85.2

Sugar produced (%) 78.285 76.203 69.493 66.874

Extraction (%) 10.181 10.570 10.243 10.218

OTE (%) 86.5 87.6 88.1 89.5

MTE (%) 93.2 91.7 95.9 95.8

OR (%) 85.97 86.33 86.21 85.55

Muscovado (tonnes) 9,316 9,407 10,139 14,153

Demerara (tonnes) 13,573 12,858 15,815 14,635

Other raws (PWS) 55,367 53,889 43,579 38,040

The main features of the crushing season were:

• An important drop in available cane and resulting sugar production. This is mainly due to adverse climatic conditions and partly to a drop in the acreage harvested by outgrowers.

• Minimal variance otherwise in rates and efficiencies.

• An important increase in Muscovado sugars production following additional installed capacity.

Extraction Rate Crop 2010 to 2012

8.00

18/0

6

25/0

6

02/0

7

09/0

7

16/0

7

23/0

7

30/0

7

06/0

8

13/0

8

20/0

8

27/0

8

03/0

9

10/0

9

17/0

9

24/0

9

01/1

0

08/1

0

15/1

0

22/1

0

29/1

0

05/1

1

12/1

1

19/1

1

26/1

1

03/1

2

10/1

2

17/1

2

24/1

2

Week

8.50

9.00

9.50

10.00

10.50

10.1910.25

10.57

Extraction

2012- Extraction (Wkly TD) 2010- Extraction (Wkly TD) 2011- Extraction (Wkly TD)

page

21

Alteo Limited - ANNUAL REPORT 2013

page

20

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORT SUGAR MANUFACTURINGSUGAR MANUFACTURING

In view of the closure of Deep River Beau Champ mill, the investment programme for 2012-2013, had been limited to:

(a) the replacement of the “C” Massecuite Reheater which had reached the end of its useful life and

(b) the upgrade of the Waste Water Treatment plant by the addition of a Highly Charged Aerobic Reactor.

Financial Results 2012-2013

Even with a 6% drop in sugar tonnage accruing for crop 2012, turnover increased to Rs.358m (Rs 328m in 2012).

This is largely attributable to an increase in final raw sugar price at Rs 17,593 per tonnes (Rs 16,020 in 2012) and better premiums for Special Sugars. Special sugar production was on the upside to reach production level of 28,729 tonnes (25,993 tonnes in 2012).

ALTEO MILLING LTD (ex FUEL SUGAR MILLING Co LTD)

2012 Crushing Season

2009 2010 2011 2012

Cane crushed during crop (tonnes) 902,281 888,033 846,018 848,214

TCH 295 289 285 307

Canes/day (tonnes) 5,897 6,001 6,000 6,575

Purity mixed juice (%) 86.8 86.6 85.9 86.7

Sugar Produced (tonnes) 93,397 93,826 86,036 89,382

Extraction (%) 10.35 10.57 10.16 10.54

OTE (%) 83.38 86.46 87.79 89.25

MTE (%) 89.61 90.97 91.33 93.46

OR (%) 87.63 87.66 87.40 87.96

Special Raw Sugar (tonnes) 11,779 11,573 14,999 14,602

After charging for cost of operations including financial charges and taxation for a total amount of Rs 315m (Rs 305m in 2012), the company realised a net profit of Rs 48m (Rs 40m in 2012)

A dividend of Rs 50m (2012: Rs 35m) representing Rs 2.098 per share (2012: Rs 1.468) was declared during the year under review.

Future Prospects

In line with the already agreed sugar sector reform, it is expected that the DRBC Milling operations will cease after the 2013 harvest.

The cane yard and reception will thereafter remain as a transit station for the factory area small planters.

Cane will be reloaded into large carriers to Alteo Milling Ltd of Union Flacq.

The main features of the crushing season were:

• A stable cane availability considering that yields for the upper region was excellent in 2012.

• A higher throughput in TCH and tonnes per day as part of the incremental capacity requirements of the forthcoming centralisation project.

• Minimal variations in extraction and mill efficiencies which remained above island average.

The 2012-2013 investment programme comprised of:

• a juice rotary screen to replace static DSM,

• steam saving from 400 kg/tonne cane to below 300 kg/tonne cane achieved by the installation of additional evaporation and juice heating vessels,

• two new A centrifugals,

• a new C Massecuite crystalliser.

At the time of writing (September 2013), the factory crushing capacity reached a day peak of 390 TCH and 8,900 tonnes of cane for the day.

Centralisation

In 2012/2013, Alteo Milling Ltd continued its factory expansion and consolidation project started in year 2011-2012, in view of the planned closure of Deep River Beau Champ Milling Co. Ltd (DRBC M) in December 2013.

Thus, during the 2012 crop, two important installations were commissioned successfully, namely:

• the heavy duty pressure feeder on mill no. 7, and

• two cooling tower cells in replacement of the cooling pond.

Extraction from crop 2010 to 2012

10.90

10.70

10.50

10.30

10.10

9.90

9.70

9.50

9.30

9.10

8.90

8.70

8.50

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

Extraction

Week

Year 2010

Year 2011

Year 2012

page

23

Alteo Limited - ANNUAL REPORT 2013

page

22

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORT SUGAR REFININGSUGAR MANUFACTURING

Alteo Planters Services Ltd

Alteo Planters Services operates in partnership with sugar cane planters in order to provide them with cost effective and quality services for sustainable sugar cane production. During the period under review, it was mainly involved in the implementation of the FORIP Programme and Harvest Services, as described below. The handing over of planters’ fields replanted in 2012 was completed and the implementation of the following phase was initiated. The table below summarises the extent replanted by the company in the factory area since the inception of FORIP Programme in 2006.

Harvest of planters’ fields spanned from July 2, to December 5, 2012, that is, 131 days. A total of 47,704 tonnes of cane were harvested over an area of around 800 ha belonging to 445 planters. For a measure of comparison, 34,428 tonnes of canes were harvested for 324 planters in 2011, year during which the service was launched.

The department also provided “à La carte services” to 18 planters for an area of around 70 ha. These services included planting, manual weeding, application of fertilisers and herbicides and trash lining.

Financial Results 2012-2013

The results of the milling activity improved on account of the favourable sugar price for the crop year 2012 of Rs 17,573 per tonne (Last Year: Rs 16,020) coupled with a better extraction rate of 10.30% for the year ended 30 June 2013. As a result turnover increased by Rs 52m to Rs 380m.

Costs of operations were maintained to last year level Rs 363m (2012: Rs 367m). Other Income fell by Rs 33m as the 2012 figure accounted for an exceptional reversal of Blue Print provision of Rs 28m alongside with higher interest income. Finance cost rose by Rs 9.6m as a result of the loan financing in relation to the factory expansion.

The company realised of a profit after tax of Rs 28.8m as compared to Rs 18.4m in 2011-2012.

A dividend of Rs 27m (2012: Rs 40m) representing Rs 1.00 per share (2012: Rs1.50) was declared in June 2013.

Future Prospects

In order to complete the factory expansion, the 2013-2014 investment programme will involve mainly the shredding and juice extraction stations and the transfer of the special sugar plant from DRBC M.

The existing effluent treatment plant at DRBC M will be upgraded to a state of the art facility to treat additional waste waters and will be transferred to Alteo Milling Ltd. At the same time, an effluent abatement programme will be launched.

Extent replanted by Alteo for the FORIP Programme and number of planters concerned

Phase Year Area (ha) No. planters concerned

I 2006/07 120 74

II 2008 242 176

III 2009 184 132

IV 2010 198 149

V 2011 201 238

VI 2012 290 243

VII 20131 192 231

TOTAL 1,428 1,243

Prospects

Reduction of sugar production in Mauritius coupled with an increase of special sugar production will result in a decrease of plantation white sugar available for refining. This will be compensated by the import of sugars from the world market for refining for the non EU, regional and domestic markets. The refinery is at task to make this new avenue a technical and commercial success.

SUGAR REFINING

ALTEO REFINERY LTD (ex FUEL REFINERY LTD)

Review of Operations

2010-2011 2011-2012 2012-2013

Originating PWS produced by Alteo Milling Ltd (less recovery) (tonnes)

75,676 70,162 73,880

Originating PWS received from other factories (tonnes) 49,293 80,396 77,217

Non-originating PWS received (tonnes) - 20,650 16,582

White refined sugar exported to EU (tonnes) 125,698 147,208 160,326

White refined sugar for local market (tonnes) 5,316 6,310 2,791

Steam/T sugar (kg) 1.9 1.7 1.1

Electricity/T sugar (kWh) 63 63 62

During the year under review, the refinery reached 96% of its capacity and produced 163,117 tonnes of white sugar for both the export and domestic markets. This represents a 6% increase of production on the previous year. The process has been optimised with a reduction in energy and electricity usage and the target for the coming year will be 170,000 T.

The free flowability of the sugar continued to improve in 2012-2013. The refinery successfully met its Smeta and BRC year audits. The company has successfully been approved in September 2013 as a Coca Cola Supplier for the Africa region.

Financial Results 2012-2013

Turnover for the year rose to EUR 7.6m while operating expenses at EUR 3.2m were lower than the previous year by 19% on account of usage of non-originating sugar available to the refiner and increased efficiency at operational level. Finance Cost amounted to EUR 0.3m (2011-2012: EUR 1m) following repayment of loan instalments and exchange gains recognised during the year.

The Profit after Tax stood at EUR 3.1m for the year ended June 30, 2013 (2011-2012: EUR 1.5m).

1 Provisional figures

Alteo Limited - ANNUAL REPORT 2013

page

25

Alteo Limited - ANNUAL REPORT 2013

page

24EXECUTIvES’ REPORTENERGY

Financial Results 2012-2013

With a drop of 6 GWh production of energy exported to the national grid coupled with lower price per kWh received from the Central Electricity Board (CEB), turnover decreased to Rs 327m (Rs 352m in 2012).

On the other hand, coal costs continued its downward trend and reached an average cost of acquisition of Rs 3,420 per tonne (compared to Rs 4,084 in 2012). The rise in operating expenses and financial charges was contained to a 5% increase from Rs 138m to Rs 146m for 2013.

The company thus realised a net profit of Rs 23m, compared to a deficit of Rs 8m for 2012.

CEL declared and paid a dividend of Rs 25m in June 2013.

Future Prospects

The present Power Purchase Agreement (PPA) with the CEB ends in July 2015. Following the closure of Deep River Beau Champ Milling Co. Ltd, the plant will have to operate on coal only but could supply incremental energy normally supplied to the mill during crop season. Amendments to the present PPA are under discussion with the CEB.

ENERGY

CONSOLIDATED ENERGY CO. LIMITED

2012 Crushing Season

2010-2011 2011-2012 2012-2013

Bagasse (tonnes) 228,029 199,916 222,647

Coal (tonnes) 24,812 55,990 46,629

Export Bagasse (GWh) 50.6 42.5 50.9

Export Coal (GWh) 31.8 81.6 67.5

Total Exports (GWh) 82.4 124.1 118.4

kWh/Tonne Bagasse 222 212 229

kWh/Tonne Coal 1,280 1,458 1,447

Mill Electricity Consumption (kWh)/Tonne Cane 28 29 29

Mill Steam Consumption (kg)/Tonne Cane 455 453 421

The main features of the crushing season were:

• A higher fibre % cane, thus more bagasse energy.

• A lower total export due to an unplanned stoppage of 18 days to replace the Turbo Alternator condenser tubes.

• A slight improvement in bagasse energy efficiency due to lower internal consumption of steam at the mill.

• During 2012-13 maintenance stop, the following were undertaken: The GTA 3.8 MW control monitoring system has been replaced.

• The TA maintenance involved the four yearly turbine overhaul.

• The TA condenser tubes have been replaced.

• The boiler front wall top bends were replaced.

• A reduction of 17% of the fly ash has been realised with the optimisation of the grit re-firing reinjection with a gain of 9.6% on losses of unburnt in ash.

page

27

Alteo Limited - ANNUAL REPORT 2013

page

26

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORT ENERGYENERGY

After accounting for other income, financial costs and taxation, the company realised a net profit of Rs 127m (Rs 78m in 2012).

As a result, the company declared in June 2013 the same dividend as the previous year, i.e. Rs 5.50 per share, amounting to a total of Rs 101m.

Future Prospects

A zero effluent disposal is being implemented for Alteo Energy Ltd with the installation of new cooling towers to have the water cooled in a closed circuit.

Alteo Energy Ltd also made representations to the National Energy Commission on a new power project as summarised hereunder.

Two, phased in, 50 MW 110 Bar coal/biomass plants with the following characteristics:

• Incremental use of cane biomass in using trash left in cane fields.

• Use of other biomass such as Arundo Donax and wood chips from locally grown forest.

• A package of incentives to be proposed to planters supporting the use of renewable sources and limiting coal.

ALTEO ENERGY LTD (ex FUEL STEAM AND POWER GENERATION LTD)

2012 Crushing Season

2010-2011 2011-2012 2012-2013

Bagasse (tonnes) 280,099 240,195 250,534

Coal (tonnes) 79,351 83,352 86,313

Export Bagasse (GWh) 55.8 47.7 50.2

Export Coal (GWh) 109.8 110.6 116.6

Total Exports to the grid (GWh) 165.6 158.3 166.8

kWh/Tonne Bagasse 199 198 201

kWh/Tonne Coal 1,383 1,327 1,351

Mill Electricity Consumption (kWh)/Tonne Cane 22.2 21.8 21.4

Mill Steam Consumption (kg)/Tonne Cane 380 380 378

The main features of the crushing season were:

• Higher fibre content in cane with 5% more bagasse energy.

• Higher total export as CEB off-take was higher than the contract minimum.

• Minimal operational efficiency improvements.

During the 2013 maintenance stop, both steam turbines were overhauled by overseas specialists. All machines internals were thoroughly inspected using non destructive testing method to reveal any possible hidden flaws in machine parts. No flaws were detected and both turbines were found fit for operation and the maintenance was in line with the insurer’s recommendations.

2012-2013 Financial Results

The company exported to the grid 6 GWh more than its contractual obligation of 160 GWh towards the Central Electricity Board. Total energy exported to both CEB and Alteo Refinery amounted to 196 GWh (compared to 186 GWh in 2012). This resulted in an increase in turnover from Rs 782m to Rs 827m.

Total cost of sales, operating and administrative expenses amounted to Rs 665m (Rs 694m in 2012). This decrease is largely attributable to the cost of coal which continued its downward trend (Rs 3,646 in 2013 and Rs 4,155 in 2012, per tonne).

PHOTOvOLTAIC PROJECT

In line with its strategy to support the Central Electricity Board’s initiatives and to participate in a greener Mauritius, your Company took part in a tender for Solar Photovoltaic (PV) Farms of Capacity between 1-2 MW.

ALTEO partnered with Astonfield Renewables, a renewable energy group that builds, owns, and operates utility-scale solar power plants in emerging markets with its base of operation in India.

The partnership Astonfield-Ateo was awarded a 2MW Project at Union Flacq on a PV area of 4 hectares.

The Energy Supply and Purchase Agreement (ESPA) is currently being negotiated.

Alteo Limited - ANNUAL REPORT 2013

page

29

Alteo Limited - ANNUAL REPORT 2013

page

28EXECUTIvES’ REPORTINTERNATIONAL

possibility of bringing soil salinity to acceptable levels by conducting reclamation work through overhead irrigation.

Sugar Production

The amount of cane crushed per hour for the 2012-13 season, at 162.6 tonnes, was higher than the previous year (158.5) and slightly higher than budget (160.0) mostly due to the pushing of the crushing rate towards the beginning and end of the season to assess if 170 TCH would be achievable on a sustainable basis.

Higher sucrose than past years’ average made up for the slightly lower mill extraction at 95.8%, and boiling house recovery at 83.7%, thus bringing sugar per cent cane to 10.46% compared to 10.45% for the previous season. Factory time efficiency was higher than the previous season but slightly lower than the budget mainly due to mechanical breakdowns, while overall time efficiency was better than budget and the previous season. Finally, although lower than budget by 5.5%, a near record sugar production of 86,086 tonnes was achieved, just below the previous record of the 2011-12 season by 53 tonnes.

Energy Production

Over and above the production of electricity for irrigation and other internal requirements, power export to the national grid amounted for 13.2 GWh by the end of June 2013. This achieved export is lower than the budget due to the combined effects of a shorter crushing season and a lower fibre content of the cane varieties harvested but also to the decision to produce power for an extended period of time for TPC own irrigation requirements against maximizing exports to the grid.

Industrial Relations

Industrial relations continued to be cordial during the course of the year. The annual wage negotiation between the workers’ union, TASIWU and management was successfully conducted and an agreement was signed on the June 5, 2013 granting a salary increase of 10% to the employees on the back of an equivalent inflation rate, year on year to March 2013.

REGIONAL DEVELOPMENT

TPC Limited (“TPC”)

2012/2013 SEASON

Cane Production

During the 2012-13 season a total of 822,796 tonnes of cane were produced from a harvested area of 7,541 ha. This was again a very good cane production for TPC, at levels comparable to the previous year’s record although lower than original estimate by 3.5%. Excellent cane yields of 109 tonnes per hectare for an average cane age at harvest of 11.25 months were achieved, equivalent to an average productivity of 9.7 tonnes per hectare per month; a 2.9% increase over that of the previous season. Such an increased cane production resulted from the continued replacement of old varieties, which accounted for less than 15% of total cane production, as well as from the improvements in cultural practices. Sucrose content averaged 12.92% which saw a slight increase of 0.12 percentage point compared to the figure recorded during the previous season.

The area re-planted during the 2012-13 season amounted to 1,650 ha, mainly with new varieties from South Africa, Mauritius and Reunion Island. A total of 717,953 tonnes of cane and about 73,912 tonnes of sugar were produced from these newly introduced varieties.

The trial to evaluate the performance of drip irrigation in saline and sodic soils has continued to produce promising results with average yields of 186 tonnes per hectare or 16.6 tonnes per hectare per month for the first ratoon. The control portion under surface irrigation yielded 82.5 tonnes per hectare or 7.5 tonnes per hectare per month. The clogging of the emitters experienced during the previous season seems to have been solved during this season. Extensive canal lining works were carried out during the season, concrete lining was used for the main canals and HDPE for the secondary canals totalling this season an additional 2,000 meters of lining; the objective is to increase the volume of water reaching the fields by reducing seepage in canals.

Further to the detailed soil survey carried out on a portion of about 600 hectare of less productive land in the southern part of Kahe area to evaluate if there is a potential for expanding cane production; a 16 hectare portion has been prepared for evaluating the

page

31

Alteo Limited - ANNUAL REPORT 2013

page

30

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORT INTERNATIONALINTERNATIONAL

2013 Offcrop

The long rains season started in the first week of March. Very good rains were received throughout March, April and early May.

Owing to the good rainy season, major canal lining and pump maintenance works were undertaken without detrimental effect on cane productivity.

On the factory side, a second mill (No. 4) was electrified and an air pre-heater was installed at the boiler. The civil works for the backup TA/Set were also started.

2013/2014 OUTLOOK

Owing to newer cane varieties and better rains during the offcrop, a higher crop, at 898,395 tonnes – a 9% increase compared to last season, has been estimated for the 2013-14 season and sugar production has been budgeted to the level of 95,050 tonnes. The new season started on time on June 11 and is planned to end on March 9.

For the first few weeks of the season cane yields have been more than 16% above budget with an average of 140 tonnes of cane per hectare achieved. These higher yields may be attributed to the combined effects of good rains received during the previous season as well as increased fertilizer application. These productivity gains may however be partly offset by a lower than budgeted sucrose content as noticed during the same period.

Sugar prices and sales volumes in the first 12 weeks of production have been lower than estimated due to unusually high competition with imports in a distorted market. It is expected that prices will remain under pressure in order to achieve the required sales volumes.

During the course of the year, a new business plan covering years 2013-14 to 2017-18 was prepared; it was subsequently approved by the July 2013 Board of Directors Meeting. The plan projects investments in the fields and the factory to increase cane crushing to over 1 million tonnes and sugar production to about 110,000 tonnes per annum by the last year.

Prospects

Building upon its experience, ALTEO has made it one of its major objectives to pursue the expansion of its sugar operations in the region. In that context, a number of opportunities were identified and investigated on the African continent, during the year under review. In particular, ALTEO has been actively engaged in two of the more promising prospects and has, in this context, signed a Memorandum of Understanding in October 2013 for a project in Swaziland. By signing this MoU, ALTEO and the local promoters have agreed on an exclusivity period of six months during which they will together complete the technical and financial assessment of the project.

Sugar and Molasses Sales

The rate of monthly sugar sales for the year was negatively impacted by high levels of imported sugar, some legal and others illegal. As a result, the company only managed to sell all the production just before the start of the new crop which had not been the case in recent years. The lower demand resulted in selling prices coming under pressure with the average price for the year declining by 1.5%. A total of 85,161 tonnes of sugar was sold for the financial year. Although molasses demand for the year was exceptionally strong the 36,690 tonnes sold was lower than the prior year by 2,006 tonnes on the back of reduced production over the financial year. The stronger demand did however result in better prices being achieved with the result that Molasses turnover increased year on year.

Financial Results

Sales in local currency decreased by 4.3% during the year under review; however due to the devaluation of the Tanzanian shilling to the USD, the decrease in USD came to 5.3% with overall sales at USD 70.5m. Cost of Sales increased by 3.1% (increase of 4.2% in local currency) and Other Expenses by 5.6% (increase of 6.7% in local currency). Finance Costs decreased by USD 1.3m mainly as a result of exchange losses incurred on foreign currency positions held in the prior year and not repeating this year; otherwise due to lower interest costs as the outstanding loan was settled in January. The reduction in turnover and increases in costs coupled with a unfavourable valuation impact on Consumable Biological Assets of USD 6.0m resulted in Net Profit before Tax decreasing to USD 37.5m, a USD 10.3m or 21.5% decrease on prior year. With the resultant decrease in profitability, the tax charge was also reduced by USD 3.1m, leaving Net Profit after Tax for the year at USD 26.2m, a decrease of USD 7.2m or 21.6%. This reduction in profitability for the year and similar cash flow impact from investing and financing activities resulted in the year end cash position declining by USD 4.6m. with a net overdraft position of USD2.2m. Total Assets reflected an increase of USD 4.5m largely as a result of increases in the biological assets valuation and investments in fixed assets. On the liability side the Non-Current portion increased by USD 2.2m due to an increase in the deferred tax liability whilst the Trade and Other Payables decreased by USD 1.7m as a result of lower year end accruals.

Alteo Limited - ANNUAL REPORT 2013

page

33

Alteo Limited - ANNUAL REPORT 2013

page

32EXECUTIvES’ REPORTPROPERTY & HOSPITALITY

Moreover, the launch of Amalthea, a new phase of 59 units comprising Villas, Duplexes and Golf Lodges, should contribute to broaden Anahita’s product offering, having yielded positive feedback from the market to date. Construction works are expected to begin at the end of 2013. Upon completion of this new phase, more than half of Anahita’s planned properties will be built and operational.

Secondary market transaction values on resale properties still enjoy robust growth momentum, particularly for prime ocean front real estate, resulting in net ROI up to 45%.

Anahita Golf Limited (“AGL”)

Four Seasons Golf Club Mauritius at Anahita (“the golf course”) reaffirmed its position as the golf course of choice in Mauritius for the year ending June 30, 2013.

Showing positive year on year growth in all areas of revenue, the twin resort inclusive golf agreement has consistently proven successful with its unlimited golf component.

With the company’s gross operating profit and net operating income attaining a positive figure this year, there are clear signs that an encouraging future is in store.

Although priority continues to be given to its limited number of lifetime members and resort residents, attracting outside players remains a key strategy. Offering favourable rates to local hotels and groups, along with being open and available to the general public, allows a healthy cross section of market segments to supply the golf course with revenue streams.

The golf course once again will play host to the Afrasia Golf Masters tournament in December 2013. This has proven a solid marketing tool towards the European market and attracts a good number of international guests during this pre-end-of-year period.

PROPERTY DEVELOPMENT AND TOURISM

Anahita Hotel Limited (“AHL”)

Four Seasons is a well-established brand with a solid reputation on the international scene and Four Seasons Resort Mauritius at Anahita remains the leading hotel within the range of 5-star hotels in Mauritius.

Four Seasons Resort Mauritius at Anahita (“Four Seasons Resort”) experienced an overall increase in turnover of 10.7% for FY 2013 as compared to FY 2012.

The resort’s average annual occupancy rate showed a 3-point increase to 63% and the realisation of positive EBITDA of MUR 294.9M represented a net improvement of 17.1% for the hotel, compared to the previous year. The company’s RevPar index registered a score of 95% above average, while its occupancy index was of 16.5% above average, ensuring it remains the leader in its competitive set.

The Resort currently holds the position of sixth Best Hotel in the World, according to Trip Advisor.

Four Seasons Resort forecasts growth in EBITDA and Gross Operating Profit year on year and looks forward to continued growth in all areas during FY 2014.

The private residences at Four Seasons, formerly under Anahita IRS Forty, a separate legal entity, were amalgamated within AHL further to the close to 100% sell through of its forty-five properties. Heretofore, they will remain under full management of Four Seasons Resort. At financial year’s end, three villas remained in the inventory. The resale market of such villas continued to be robust with strong net return on investment of 20% on average being achieved.

Anahita Estates Limited (“AEL”)

The year ending June 2013 marked the beginning of Anahita Mauritius’ seventh year of existence.

Anahita maintains its leading position within the local IRS market. Although very difficult international market conditions prevailed, interest in and sales of its real estate and land products continued to grow.

The product diversification strategy of incorporating serviced residential land for sale triggered signs of positive market absorption with the sale of 5 plots of serviced residential land and a bright forecast for the coming year with 9 additional plots of serviced residential land reserved with deposits.

page

35

Alteo Limited - ANNUAL REPORT 2013

page

34

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORT PROPERTY & HOSPITALITY

The marketing focus was to establish an integrated booking engine interfaced with major Online Travel Agencies (OTA) which resulted in increased visibility and higher sales figures (+35%) in this segment.

In an effort to strengthen its positioning, ATR has established an agreement to operate an “Exclusive Beach” at Ile Aux Cerfs. Furthermore, the golf facilities at Ile Aux Cerfs are also included in guests’ packages, thus providing a unique experience on two championship golf courses.

Looking ahead, ATR is showing promising signs of further establishing its position within the east coast local tourism scenery. Reservation levels for the following months until December are indicating that high and peak period occupancy levels should bring in additional revenues.

HORTICULTURE

World Tropicals Ltd

In its endeavor to better focus on its larger sugar operations, following the merger of its operations into ALTEO, the Company decided during the year under review to part from its horticulture operations. At the time of writing, this was being finalized through a management buyout.

Alteo Properties Limited (“APL”) (ex CIEL Properties Ltd)

During the year under review, Alteo Limited consolidated its shareholding in Ciel Properties Ltd from 50% to 100%. Further to that change, the company has now been renamed Alteo Properties Ltd.

In recent years, the company has continued to diversify its revenue stream through a broader client base via its four core strategic activities: asset management, development management, real estate sales and marketing services, and project management.

For the period to June 30, 2013, the promotion and development of Anahita Mauritius remained the main revenue stream of the company which recorded an increase in revenue of 28%, totalling MUR 3.2m, ensuring a strong outlook for Alteo Limited and its subsidiaries.

Anahita Residences and villas Limited (“ARvL”)

Operated by Anahita Residences and Villas Limited (AVRL), Anahita The Resort (ATR) is the administrator of the property rental program at Anahita Mauritius. It manages the resort facilities at La Place Belgath, the lively waterfront village.

With its positioning as a 5-star resort, ATR is well integrated within the Mauritian hotel industry and maintains the esteem and trust of the international travel industry.

Improved performance was realized for FY 2013 through a market diversification strategy during the traditional low-season period and a strong focus on cost monitoring. Efforts were also made to uphold the guest experience with added value services and facilities resulting in the increase of repeat business.

Occupancy was maintained with a positive turnover growth of 6% (MUR 196m). A continued improvement in the bottom line figures with a positive EBITDA of MUR 6m is to be noted.

Alteo Limited - ANNUAL REPORT 2013

page

37

Alteo Limited - ANNUAL REPORT 2013

page

36

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORT

page

39

Alteo Limited - ANNUAL REPORT 2013

page

38

Education

FNR believes in and supports alternative education. Thanks to the ANFEN schools network and to the Zippy programme of ICJM, children with learning difficulties can have access to education. FNR provide its support to other NGOs such as Teen Hope of Groupe Noyau Social de Cité La Cure in Port-Louis, Mahebourg Espoir Education Centre (MEEC), l’association Bâtisseurs de Paix, and scholarships to students from Collège St Patrick.

Disability

FNR is also strongly committed to providing disabled children with access to education: thus, in January 2010 it opened the first secondary school for deaf children in collaboration with the NGO Society for the Welfare of the Deaf. In 2010, the Form 1 pre-vocational programme was launched with 20 pupils, then Form II in 2012 and Form III in 2012. In 2013, FNR has renewed its support to the SWD and is financing 25% of the running cost of its 4 classrooms. Moreover, FNR provides its support to other NGOs such as Eastern Welfare Association for the Disabled (‘EWAD’), Association Dominique Savio and Friends in Hope.

Sport

Sport is a unifying factor for gathering young people in pursuit of sound and positive values. That is why this year ALTEO has supported the Curepipe Starlight Sporting Club and the Faucon Flacq Sporting Club.

FNR has also developed a website- www.ACTogether.mu - where numerous NGOs are represented and able to put all their resources together in the fight against poverty and exclusion in Mauritius. This website enables the NGO’s to better communicate among them and to co-organise events such as the workshop of Chlidren’s rights in partnership with SAFIRE and l’Institut Cardinal Jean Margéot and with the collaboration of Mr Trond Waage, and the Marché de Noel Solidaire which aims at promoting the quality of the craft industry and allowing the crafty persons to gain money.

CORPORATE SOCIAL AND ENVIRONMENTAL RESPONSIBILITY

As at June 30, 2012, i.e. prior to the effective date of the amalgamation of FUEL with and into DRBC, the CSR involvement of FUEL and DRBC was mainly channelled through the Fondation Nouveau Regard (“FNR”) of CIEL Group and the GML Fondation Joseph Lagesse (“GML FJL”) respectively. ALTEO was also directly involved and contributed some Rs 900,000 to a number of regional projects and organisation in order to support the development and well-being of children with disabilities, adults with alcoholic dependency problems, technical education, elders in difficulty and sports.

The Fondation Nouveau Regard (“FNR”) - Presentation and Actions

During the year under review, ALTEO has contributed Rs 1.8 million to the Fondation Nouveau Regard, a Special Purpose Vehicle (“SPV”) accredited by the National CSR Committee (“NCSRC”) for various projects managed by local NGOs in areas as:

• Fight against poverty and social integration

• Education

• Disability

• Sport

Fight against Poverty and Social Integration

In line with government policy, the struggle against poverty has been the spearhead of the FNR’s action this year. Thus, at the end of 2010, FNR launched a large-scale integrated community development project in partnership with Caritas: La Caze Lespwar. This project, situated at Solitude, assists communities living in poverty and facing difficulties in the regions of Solitude, Triolet, Plaine des Papayes, Pointe aux Piments, and now reaching even as far as Arsenal. It provides services adapted to the needs of these population groups: education and training, community gardening, breakfast for pupils, sports, holiday activities for children, activities for women, an emergency service, a solidarity shop and a pre-school centre/creativity centre. FNR provide also its support to other NGOs such as the department of ‘counselling’ of the ICJM, the association Kinouété and la Maison cœur écoute of Barkly.

CORPORATESOCIAL RESPONSIBILITY

CORPORATESOCIAL RESPONSIBILITY

page

41

Alteo Limited - ANNUAL REPORT 2013

page

40

Alteo Limited - ANNUAL REPORT 2013

EXECUTIvES’ REPORTEXECUTIvES’ REPORTCORPORATESOCIAL RESPONSIBILITY

CORPORATESOCIAL RESPONSIBILITY

Community Development

Since its inception GML FJL has established a program of integrated community development in the neighbourhood of Chemin Rail, a small village located in Rivière du Rempart. A whole team of coordinators, social workers, educators and volunteers are working for and are supporting a group of twenty poor families. While aiming to restore their dignity, GML FJL has received the support of ALTEO which has contributed to giving them a better future through the construction of decent houses.

Environment

The focus of GML FJL on education has also an environmental aspect. “GML Think Green” has engaged several projects since last year and some new initiatives are being launched. The specialised ANFEN schools have benefited from the help and expertise of the GML FJL in the implementation of schools garden projects, but also for the conservation of resources and ecosystems. Some other schools have also organised sessions of environmental awareness with Mission Verte supported by GML FJL. For the first time, GML FJL has expanded its activities to Rodrigues through various actions for the protection of native biodiversity of the island, including bats. Moreover, an educational film was realised and produced to accompany the leaders of the Mauritian Wildlife Foundation in their awareness program. The integrated community development program of GML FJL at Chemin Rail has also received an environmental contribution through regular awareness activities, cleaning, and organised trips for educational purposes.

For the Future

ALTEO is committed to continue to fulfil the current undertakings of DRBC and FUEL in CSR activities which are met through FNR and GML FJL. It will thus support the activities of these SPV while defining how it can also more directly, use its financial and human resources against poverty and exclusion.

P. Arnaud Dalais Patrick de L. d’Arifat

Group Chief Executive Chief Executive Officer

September 20, 2013

The GML Fondation Joseph Lagesse (“GML FJL”) – Presentation and Actions

GML FJL has been created in 2005 to provide funds and assistance to social and environmental activities, and has confirmed the commitment that GML has traditionally sustained throughout the years.

The CSR contribution of ALTEO to the GML FJL for the year has amounted to Rs 2 m and has been spent to finance projects in line with the objectives set by the Management Board. These are:

• Education

• Access to medical treatment and health

• Community Development

• Environment

Education

GML FJL’s main objective is education. GML FJL is determined to promote education at all levels and to target the most vulnerable children by starting from early childhood, through its 15 dedicated centres around Mauritius. The education of adolescents is reflected through specialised ANFEN (Adolescent Non Formal Education) schools for students who have experienced failures at CPE. At the tertiary level, GML FJL has sought to broaden its support by also focusing on Rodrigues, and among the 24 students who received scholarships from GML FJL, 13 of them are from Rodrigues and are now studying at the University of Mauritius. In addition to the stipend paid monthly to all students, those Rodrigues’s students also receive a housing allowance and a return ticket to spend Christmas with their parents in Rodrigues. Finally GML FJL supports adult literacy.

Access to Health Treatment

GML FLJ is also resolute in helping poor persons to have a better access to medical treatment and health. Its actions are however somehow limited by some restrictive criteria of CSR “guidelines”.

page

43

Alteo Limited - ANNUAL REPORT 2013

page

42

Alteo Limited - ANNUAL REPORT 2013

page

45CORPORATE GOVERNANCE

Alteo Limited - ANNUAL REPORT 2013

• a Director who has declared his interest shall not vote on any matter relating to the transaction or proposed transaction in which he is interested, and shall not be counted in the quorum present at the meeting;

• in case of equality of votes at either a Board meeting or a Shareholders’ meeting, the Chairperson of the meeting shall not be entitled to a casting vote;

HOLDING STRUCTURE

The holding structure of ALTEO as at reporting date is as follows:

• a Director is not required to hold shares in the Company; and

• the Company may indemnify and/or insure any Director or employee of the Company or a related company.

A copy of ALTEO’s Constitution is available upon request in writing to the Company Secretary at the registered office of the Company, Vivéa Business Park, Saint Pierre.

Deep River Investment Limited

(DRI)

ALTEO LIMITED

GML Investissement Ltée

(GMLI)Others

20.96% 26.92% 52.12%

The Group’s shareholding is found on page 6 of the Annual Report.

COMMON DIRECTORS

The names of the common Directors are as follows:

Directors ALTEO DRI GMLI

Arnaud Lagesse(1) ü** ü*

Jan Boullé ü ü**

G. Christian Dalais ü ü**

P. Arnaud Dalais ü ü

Louis Guimbeau ü ü

Thierry Lagesse(1) ü ü

** Chairman* Alternate Director

(1) Mr. Thierry Lagesse has acted as Chairman of the Board of Directors of the Company up to August 9, 2013, date on which he has decided to step down following an allegation made against him in relation to a case of customs fraud. As a result, on August 13, 2013, the Board has nominated Mr. Arnaud Lagesse as Chairman of the Board of Directors in replacement of Mr. Thierry Lagesse.

page

44

Alteo Limited - ANNUAL REPORT 2013

CORPORATEGOVERNANCEAlteo Limited (formerly known as Deep River-Beau Champ Limited) (“ALTEO” or “the Company”) is a public company incorporated on April 18, 1913.