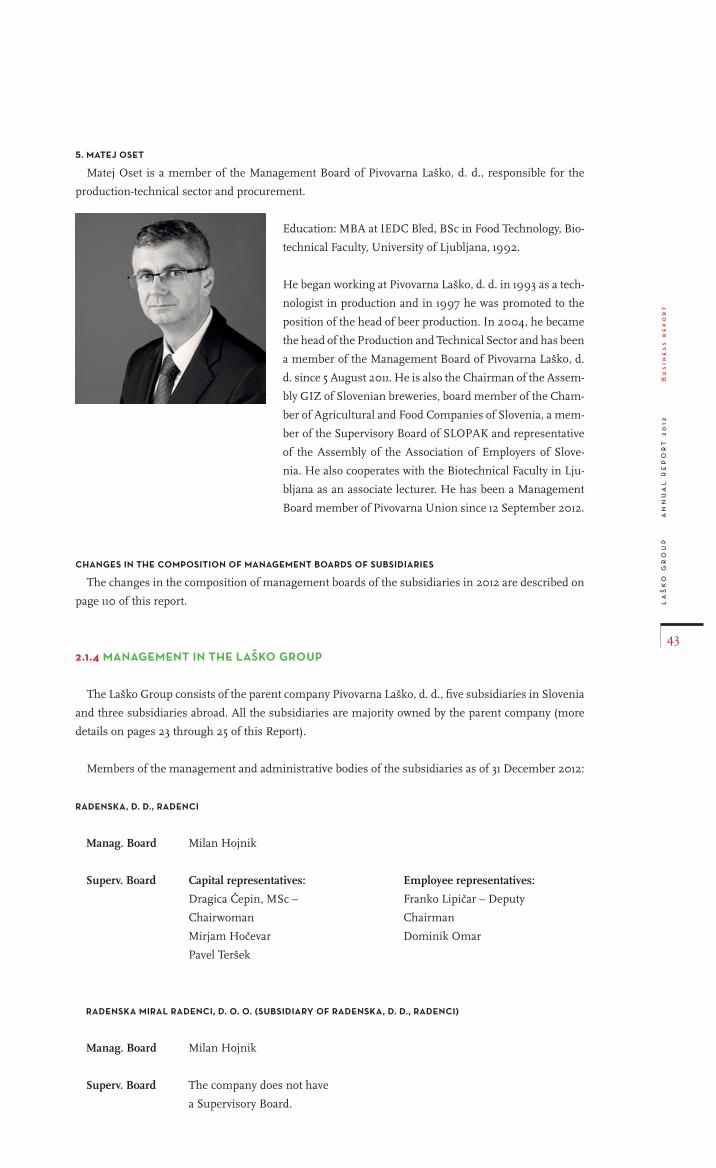

Embed Size (px)

DESCRIPTION

http://www.pivo-lasko.si/uploads/media/Annual_report_2012.pdf

Citation preview

LAŠKO GROUP

ANNUAL REPORT

ANNUAL REPORT OF THE LAŠKO GROUP

AND PIVOVARNA LAŠKO, D. D.

ANNUAL REPORT

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Co

nt

en

ts

2

1. INTRODUCTION 4

1.1 Address by the Chairman of the Management Board 5

1.2 Report of the Supervisory Board on the Annual report verification 7

1.3 Data on the operations of the Laško Group 11

1.4 Data on the operations of the Pivovarna Laško, d. d. 17

1.5 Vision, mission, values and strategic goals 22

1.6 Presentation of the Laško Group 23

1.7 Presentation of the parent company Pivovarna Laško, d. d. 26

2. BUSINESS REPORT 28

2.1 Corporate governance 29

2.2 Statement on corporate governance and the compliance with the Corporate

Governance Code 46

2.3 Report of the Management Board of Pivovarna Laško, d. d. on the extent of

influence according to Article 545 of the Companies ACT (ZGD-1) 50

2.4 Shareholders 53

2.5 Sales and marketing 62

2.6 Supply flows 78

2.7 Quality and standards 81

2.8 Investments 86

2.9 Performance analysis 93

2.10 Risk management 98

2.11 Financing and sale of the investments 103

2.12 Overview of significant events in 2012 106

2.13 Events after the accounting period 112

2.14 Development landmarks 113

Contents

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

3

Co

nt

en

ts

3. SUSTAINABLE DEVELOPMENT 116

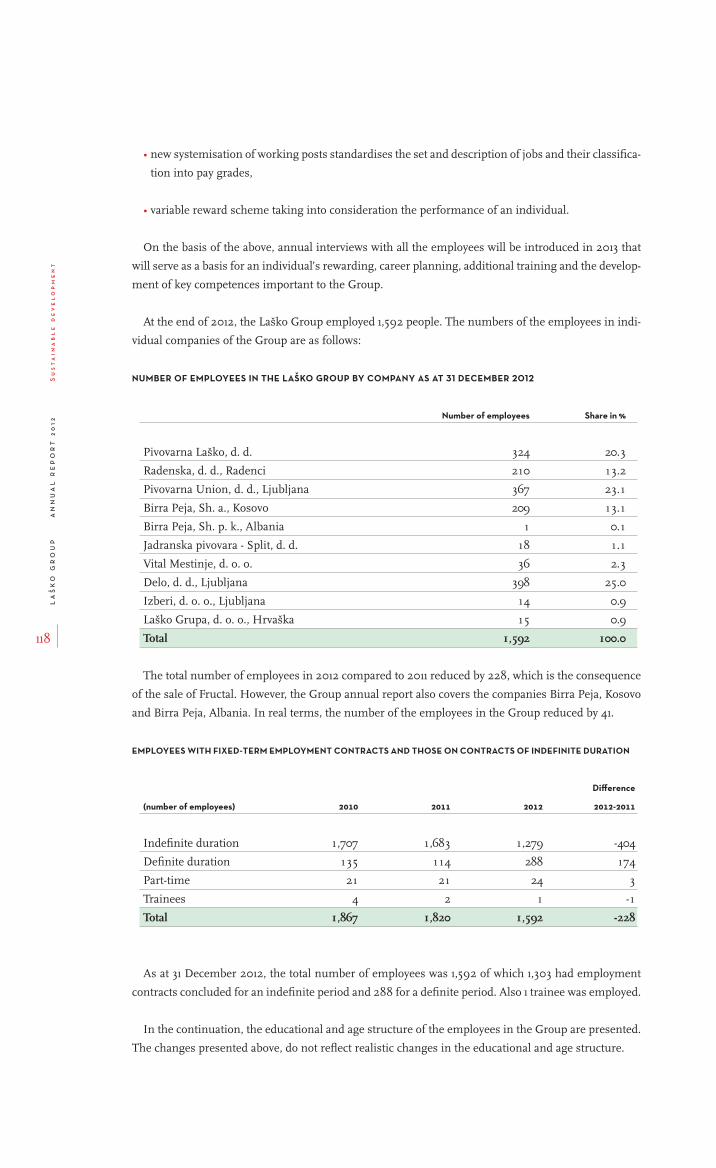

3.1 Human resources management in the Laško Group 117

3.2 Communications 121

3.3 Responsible attitude towards social environment 123

3.4 Environmental protection 124

4. FINANCIAL REPORT OF THE LAŠKO GROUP 132

5. FINANCIAL REPORT OF PIVOVARNA LAŠKO, D. D. 218

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

4

Introduction

12345

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

5

Int

ro

du

ct

ion

GOOD UPDATED RESULTS DESPITE THE ECONOMIC CRISIS

Dear Shareholders, esteemed Business Partners and Colleagues,

2012 was yet another year that can mainly be characterised by the operations in extremely chal-

lenging economic conditions. The economic crisis in Slovenia further intensified and the purchasing

power of the population additionally decreased. The projections of the Management three years ago

when the objectives set in the business strategy were the sales growth on foreign markets and the

maintenance of the leading market shares on the domestic market have been confirmed as correct.

Despite extremely demanding economic environment, the Laško Group managed to achieve good

results. In accordance with the agreement reached with the creditor banks, a part of the principal was

paid back and interest on loans was regularly paid.

In the first half of 2012, we were able to reach an agreement with the creditor banks on rescheduling

the majority of loans; however, some of the creditor banks made it conditional on the cessation of the

activities concerning the establishment of the contractual concern that the shareholders of Pivovarna

Laško had confirmed at the general meeting in January. These requests resulted in the termination of

the controlling contracts between Pivovarna Laško and Pivovarna Union and Radenska.

In 2012, the Laško Group generated EUR 271.5 million of net sales revenues and EUR 22.2 million of

operating profit, which is by 39.5% more than in 2011. Similarly to recent years, high debt of the Group

considerably affected operating results.

In 2012, the Laško Group generated 88.6% of its net sales revenues from sales of products and ser-

vices on the domestic market and 11.4% on foreign markets. The sale of beer represents the greatest

THE OPERATING RESULTS OF THE

LAŠKO GROUP IN 2012 ARE YET

ANOTHER PROOF THAT THIS IS A

GROUP OF HEALTHY COMPANIES

THAT CREATE HIGH ADDED

VALUE AND HAVE OPERATED

WITH PROFITS; HOWEVER IN

THE FUTURE THEY WILL NOT

BE ABLE TO DEAL WITH THE

COMPETITION DUE TO THE

FINANCIAL BURDEN.

1.1

Address by the Chairman of the Management Board

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

6

share in the sales structure with EUR 152.6 million and was followed by other beverages with EUR

59.4 million whereas the revenue resulting from the newspaper and publishing activities amounted

to EUR 50.1 million.

In 2012, the sale of beverages on the domestic market was anticipated to be lower than in the previ-

ous years and the sales on foreign markets increased in accordance with the business strategy. The

markets between Italy in the West and Macedonia in the East were the most important ones.

In 2012, the Group proved that environment that we co-created and with which we interfered was

one of the most important values of all the employees since we believe that such a vision reflects our

business responsibility and sustainability. And our products and the efforts to reduce the use of natu-

ral resources are adapted to this vision. New systematisation was also successfully introduced in the

Group companies.

The performance of the Laško Group in 2012 is further proof that this is a group of healthy com-

panies that creates high added value and generates profit; however, in the future, it will not be able to

contend with the competitors due to high financial burden. This is why the divestment of the assets

that do not represent the core activity remains one of the priorities. More fruitful cooperation with the

creditor banks with regard to long-term solution of the problem of indebtedness can enable our opera-

tions and business results that will be in the interest of the shareholders, creditors and employees.

Dušan Zorko, MSc

Chairman of the Management Board of Pivovarna Laško

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

7

Int

ro

du

ct

ion

THE SUPERVISORY BOARD ASSESSES THAT THE OPERATIONS OF PIVOVARNA LAŠKO AND THE LAŠKO GROUP

AND THE WORK OF THE MANAGEMENT BOARD IN 2012 WERE IN ACCORDANCE WITH EXPECTATIONS IN

THE LIGHT OF THE GENERAL DETERIORATION OF THE ECONOMIC SITUATION AND CHANGED FINANCING

CONDITIONS.

SUPERVISORY BOARD COMPOSITION

The Supervisory Board of the Company was active with the following composition in the 2012 fi-

nancial year:

CAPITAL REPRESENTATIVES

Dr Vladimir Malenković, Chairman

Dr Peter Groznik, member

Dr Borut Bratina, member

Mr Borut Jamnik, member

EMPLOYEE REPRESENTATIVES

Mr Bojan Cizej, Deputy Chairman

Dragica Čepin, MSc, member

COMPOSITION OF THE SUPERVISORY BOARD COMMITTEES

The Audit and Human Resources Committees operated within the Supervisory Board in 2012 with

the following compositions:

AUDIT COMMITTEE

Dr Peter Groznik, Chairman

Mr Bojan Cizej, member

Mr Igor Teslić, external member

HUMAN RESOURCES COMMITTEE

Mr Borut Jamnik, Chairman

Dr Borut Bratina, member

Dragica Čepin, MSc, member

1.2

Report of the Supervisory Board on the verification of the annual report

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

8

FUNCTIONING OF THE SUPERVISORY BOARD

The operations of Pivovarna Laško were monitored by the Supervisory Board of the Company in ac-

cordance with the statutory provisions and the Articles of Associations of the Company and it met at

14 regular sessions.

Throughout the year of 2012, the Supervisory Board continuously reviewed the work of the Manage-

ment Board. The Supervisory Board placed special attention to the key indicators of capital adequa-

cy and the solvency of Pivovarna Laško and the companies in the Group, the disposal of the invest-

ments of the Laško Group, activities connected to the rescheduling of financial liabilities of Pivovarna

Laško and the Laško Group companies, cost management, relevant legal issues and verification of the

achievement of business results. Due to the situation in the companies, the Supervisory Board con-

stantly dealt with the abovementioned issues that were regular items on the agenda of the Supervisory

Board meetings.

SIGNIFICANT RESOLUTIONS OF THE SUPERVISORY BOARD

In addition to the above, the Supervisory Board also dealt with other current matters and adopted

the following key resolutions:

• the Supervisory Board approved the business plan of the Laško Group and Pivovarna Laško for the

2012 financial year;

• the Supervisory Board was informed of the content of the contract on the sale of the shares of

Poslovni sistem Mercator and agreed that Pivovarna Laško should sell 317,498 ordinary registered

shares with the MELR ticker symbol issued by Poslovni sistem Mercator representing a 8.43%

stake to the Agrokor Company, namely at EUR 221.00 per share;

• the Supervisory Board was informed of the notification of the financial advisor from ING that the

Agrokor Company decided to withdraw from the sale process of Mercator shares and supported the

Management Board to continue the activities related to the sale of Mercator shares so as to protect

the interests of the Laško Group companies to the fullest extent possible;

• the Supervisory Board took note of the balance of financial liabilities to the banks and their matu-

rity as well as of the proposal of the Management Board and its activities concerning the reschedul-

ing and of the position of the banks with regard to the adopted resolution of the General Meeting.

The Supervisory Board invited the Management Board to protect the interests of Pivovarna Laško

and the Laško Group by reaching an agreement on the rescheduling of the financial liabilities to

the banks and thus reduces the high financial risk;

• the Supervisory Board approved the 2011 audited Annual Report of Pivovarna Laško and the Laško

Group;

• the Supervisory Board was informed of the condition of one of the creditor banks to conduct

the rescheduling of financial commitments of the companies: Pivovarna Laško, Pivovarna Union

and Radenska, namely that these companies terminate the contract-based group. The Supervisory

Board was also acquainted with the view of the Pivovarna Laško Management Board that wanted to

protect the interests of the Laško Group companies by implementing the procedures related to the

termination of the controlling contracts;

• the Supervisory Board got acquainted with the findings and recommendations of the research and

advisory study to support strategic decisions of the Laško Group;

• the Supervisory Board was acquainted with the roadmap of the activities to achieve long-term

rescheduling;

• the Supervisory Board got acquainted with the updated Plan of financial restructuring of Pivovarna

Laško and the Laško Group;

• the Supervisory Board confirmed the Business Plan of the Laško Group and Pivovarna Laško for

the 2013 financial year.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

9

Int

ro

du

ct

ion

FUNCTIONING OF THE AUDIT COMMITTEE

In 2012, the he Audit Committee met seven times. At its sessions, the Committee analysed major

transactions of the Laško Group in 2010 and 2011, individual transactions of the Laško Group as well

as it addressed the findings and recommendations of the external auditor on the basis of the previous

audit of the 2011 financial statements. The Committee adopted the Rules of procedure of the Audit

Committee and got acquainted with the work of a newly established Internal Audit Service. The Audit

Committee regularly reported on its findings to the Supervisory Board.

FUNCTIONING OF THE HUMAN RESOURCES COMMITTEE

In 2012, the Human Resources Committee met four times. At its session the Committee dealt with

the system of risk management related to the management of the Laško Group and it prepared recom-

mendations with regard to the management and the arrangement of remuneration of the manage-

ments in the Group companies and proposed the management employment contracts for the mem-

bers of the Management Board with a dual mandate. The HR Committee regularly reported on its

findings to the Supervisory Board.

ANNUAL REPORT VERIFICATION

The Supervisory Board reviewed the 2012 audited Annual Report of Pivovarna Laško and the Laško

Group at its session on 20 March 2013.

The Annual Report was audited by the audit firm Deloitte Revizija d.o.o., Ljubljana. The audit firm

issued its positive opinion of the Annual Report with notes on 4 March 2013. The Supervisory Board

found no objections to the auditor’s report and approved it.

The Supervisory Board felt that the Annual Report of Pivovarna Laško and the Pivovarna Laško Group

for 2012 required no comment on its part and it unanimously confirmed it at its session on 20 March 2013.

PROPOSAL FOR COVERING NET LOSS

In addition to confirming the 2012 audited Annual Report of Pivovarna Laško and the Laško Group,

the Supervisory Board also confirmed the proposal of the Management Board for covering net loss of

Pivovarna Laško in 2012, namely that net loss amounting to EUR 18,510,265 be covered by profit from

the previous years in the amount of EUR 859,740, by other profit reserves in the amount of EUR

232,097 and by capital reserves in the amount of EUR 17,418,428. Distributable profit of Pivovarna

Laško in the 2012 financial year thus equals EUR 0.0.

The Supervisory Board assesses that the operations of Pivovarna Laško and the Laško Group and the

work of the Management Board in 2012 were in accordance with expectations in the light of the general

deterioration of the economic situation and changed financing conditions.

The Supervisory Board has drawn up this report for the General Meeting of Shareholders of the

Company in accordance with Article 282 of the Companies Act (ZGD-1).

Laško, 20 March 2013

Chairman of the Supervisory Board:

dr. Vladimir Malenković

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

11

Int

ro

du

ct

ion

THE LAŠKO GROUP MANAGED TO REDUCE THE NUMBER OF THE EMPLOYEES, WHICH IS IN ACCORDANCE

WITH THE MULTI-ANNUAL RESTRICTIVE EMPLOYMENT POLICY. IN TERMS OF QUANTITIES, THE SALE ON

THE MARKETS OUTSIDE SLOVENIA INCREASED BY 12.2 PERCENT.

SALES REVENUES AND OPERATING PROFIT INCLUDING AMORTISATION (EBITDA)

0.0

in E

UR

mill

ion

Net sales revenue

EBITDA - normalised

2010 2011 2012

50.347.538.9

271.5323.4306.4

90.0

180.0

270.0

360.0

450.0

In 2012, sales revenues reduced by 16.0% while normalised operating profit including depreciation

(EBITDA) increased by 5.9%.

The Business report provides total net sales revenues unless expressly stated otherwise, while only

revenues from continuing operations are shown in the consolidated income statement.

Normalised EBIT is calculated from operating profit increased or decreased by the impact of one-off

business events such as the revaluation of real estate and investment property and the formation of

more significant revaluation adjustments. Normalised EBITDA is the sum of normalised EBIT and

normalised depreciation.

1.3

Data on the operations of the Laško Group

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

12

In addition to the listed adjustments, normalised EBIT is also adjusted for the impairment of invest-

ments and accrued deferred tax receivables under this heading.

RETURN ON ASSETS (ROA) AND RETURN ON EQUITY (ROE)

0.0

in %

Return on equity (ROE)

Return on assets (ROA)

2010 2011 2012

2.2

0.60.7

11.2

2.92.9

6.0

3.0

9.0

12.0

15.0

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

13

Int

ro

du

ct

ion

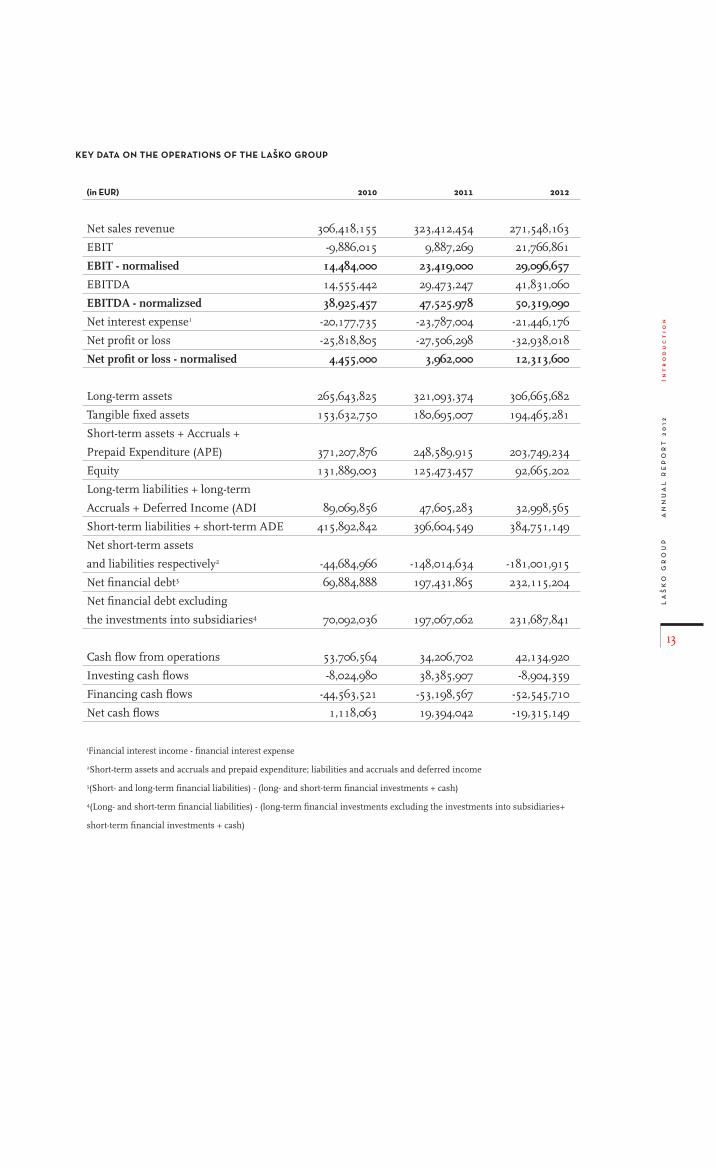

KEY DATA ON THE OPERATIONS OF THE LAŠKO GROUP

(in EUR) 2010 2011 2012

Net sales revenue 306,418,155 323,412,454 271,548,163

EBIT -9,886,015 9,887,269 21,766,861

EBIT - normalised 14,484,000 23,419,000 29,096,657

EBITDA 14,555,442 29,473,247 41,831,060

EBITDA - normalizsed 38,925,457 47,525,978 50,319,090

Net interest expense1 -20,177,735 -23,787,004 -21,446,176

Net profit or loss -25,818,805 -27,506,298 -32,938,018

Net profit or loss - normalised 4,455,000 3,962,000 12,313,600

Long-term assets 265,643,825 321,093,374 306,665,682

Tangible fixed assets 153,632,750 180,695,007 194,465,281

Short-term assets + Accruals +

Prepaid Expenditure (APE) 371,207,876 248,589,915 203,749,234

Equity 131,889,003 125,473,457 92,665,202

Long-term liabilities + long-term

Accruals + Deferred Income (ADI 89,069,856 47,605,283 32,998,565

Short-term liabilities + short-term ADE 415,892,842 396,604,549 384,751,149

Net short-term assets

and liabilities respectively2 -44,684,966 -148,014,634 -181,001,915

Net financial debt3 69,884,888 197,431,865 232,115,204

Net financial debt excluding

the investments into subsidiaries4 70,092,036 197,067,062 231,687,841

Cash flow from operations 53,706,564 34,206,702 42,134,920

Investing cash flows -8,024,980 38,385,907 -8,904,359

Financing cash flows -44,563,521 -53,198,567 -52,545,710

Net cash flows 1,118,063 19,394,042 -19,315,149

1Financial interest income - financial interest expense

2Short-term assets and accruals and prepaid expenditure; liabilities and accruals and deferred income

3(Short- and long-term financial liabilities) - (long- and short-term financial investments + cash)

4(Long- and short-term financial liabilities) - (long-term financial investments excluding the investments into subsidiaries+

short-term financial investments + cash)

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

14

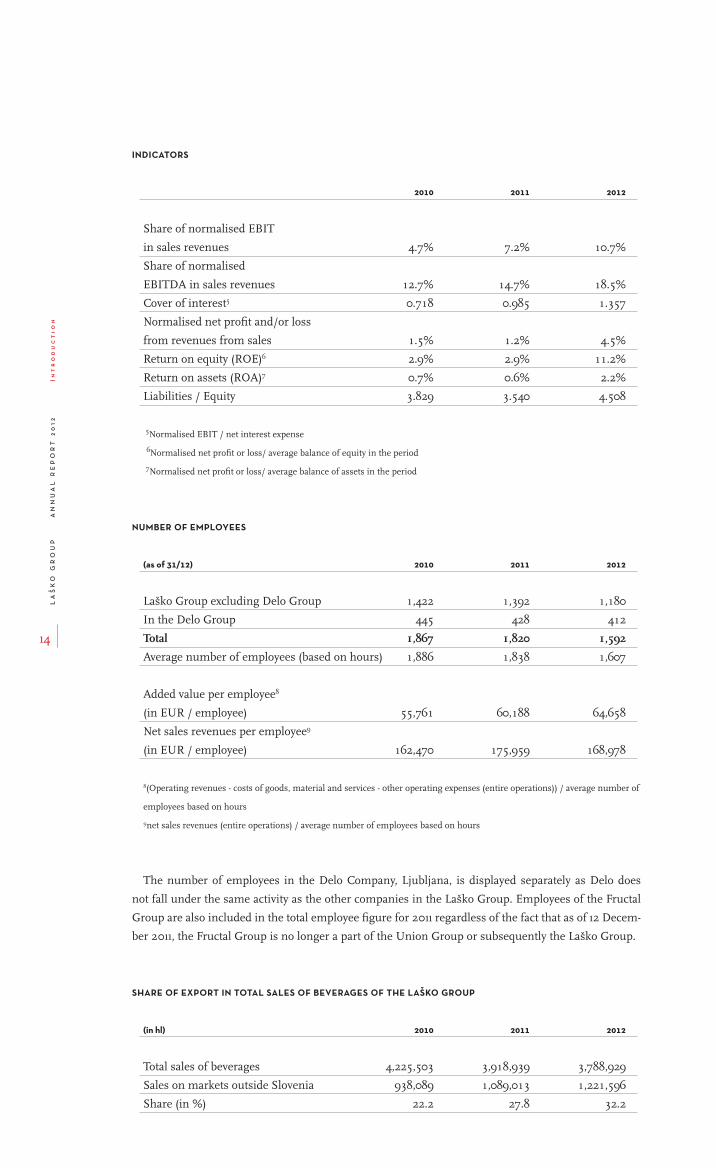

INDICATORS

2010 2011 2012

Share of normalised EBIT

in sales revenues 4.7% 7.2% 10.7%

Share of normalised

EBITDA in sales revenues 12.7% 14.7% 18.5%

Cover of interest5 0.718 0.985 1.357

Normalised net profit and/or loss

from revenues from sales 1.5% 1.2% 4.5%

Return on equity (ROE)6 2.9% 2.9% 11.2%

Return on assets (ROA)7 0.7% 0.6% 2.2%

Liabilities / Equity 3.829 3.540 4.508

5Normalised EBIT / net interest expense

6Normalised net profit or loss/ average balance of equity in the period

7Normalised net profit or loss/ average balance of assets in the period

NUMBER OF EMPLOYEES

(as of 31/12) 2010 2011 2012

Laško Group excluding Delo Group 1,422 1,392 1,180

In the Delo Group 445 428 412

Total 1,867 1,820 1,592

Average number of employees (based on hours) 1,886 1,838 1,607

Added value per employee8

(in EUR / employee) 55,761 60,188 64,658

Net sales revenues per employee9

(in EUR / employee) 162,470 175,959 168,978

8(Operating revenues - costs of goods, material and services - other operating expenses (entire operations)) / average number of

employees based on hours

9net sales revenues (entire operations) / average number of employees based on hours

The number of employees in the Delo Company, Ljubljana, is displayed separately as Delo does

not fall under the same activity as the other companies in the Laško Group. Employees of the Fructal

Group are also included in the total employee figure for 2011 regardless of the fact that as of 12 Decem-

ber 2011, the Fructal Group is no longer a part of the Union Group or subsequently the Laško Group.

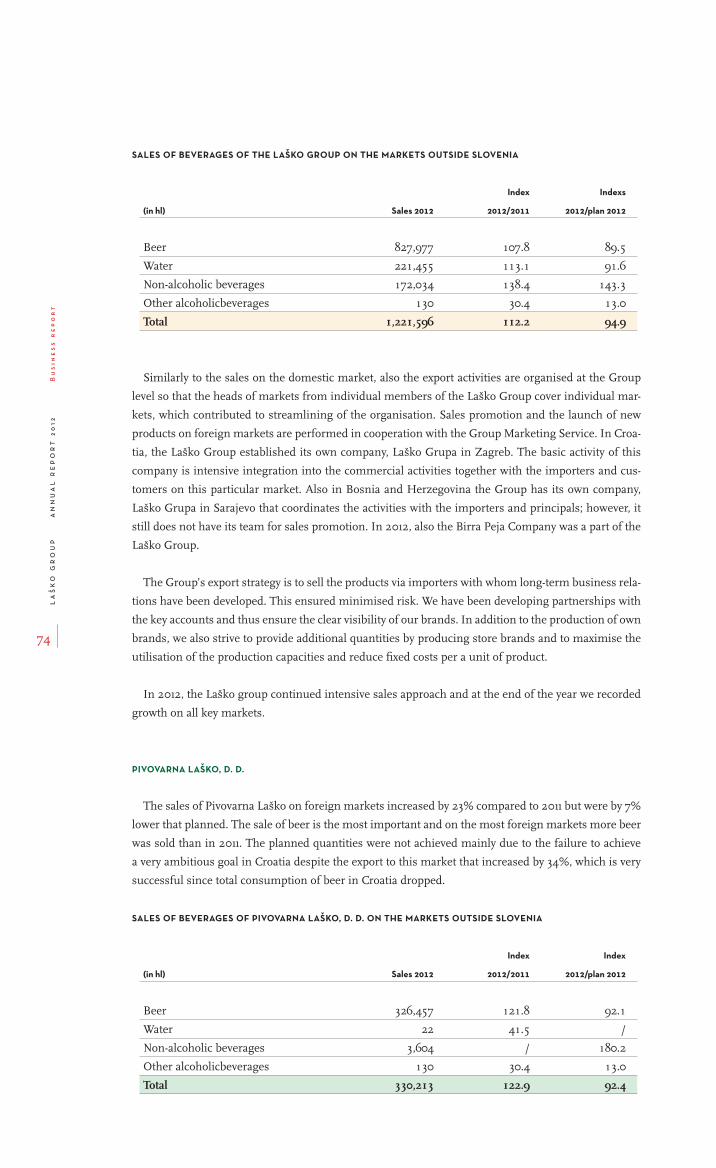

SHARE OF EXPORT IN TOTAL SALES OF BEVERAGES OF THE LAŠKO GROUP

(in hl) 2010 2011 2012

Total sales of beverages 4,225,503 3,918,939 3,788,929

Sales on markets outside Slovenia 938,089 1,089,013 1,221,596

Share (in %) 22.2 27.8 32.2

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

15

Int

ro

du

ct

ion

To ensure comparability of data in 2011, the sales in terms of quantity in 2011 is presented excluding

the Fructal Group; however the volume of sales of Birra Peja from Kosovo is included.

SUMMARY OF THE 2013 BUSINESS PLAN

PLANS CONCERNING THE OPERATIONS OF THE LAŠKO GROUP

(in EUR) 2011 2012 Plans 2013

Net sales revenues from

continuing operations 264,737,273 271,386,948 269,585,102

EBIT 15,923,108 22,216,181 30,453,552

EBITDA 35,509,087 42,280,380 48,892,135

Net profit or loss from

continuing operations -20,801,140 -30,396,363 11,704,846

Sales (in hectolitres) 3,918,939 3,788,929 3,900,035

Added value per employee10

(in EUR / employee) 60,188 64,658 63,156

10(Operating revenues - costs of goods, material and services - other operating expenses (entire operations)) average number of

employees in terms of hours worked

The global and in particular European market has been changing irrepressibly due to the recession.

The continuation of strained economic conditions on the key markets of the Laško Group are reflected

in considerably reduced purchasing power and the redirection of buyers to smaller formats of shops

and the growth of discount store popularity.

The fundamental objective set for the Laško Group in 2013 is to increase the sales of beverages by

2.9%, which should be achieved by the growth on foreign markets and by the maintenance of the lead-

ing position on the domestic market.

EUR 269.6 million of net sales revenue the Group is planning to generate is comprised of EUR 30.5

million of operating profit, EUR 11.7 million of net profit and EUR 48.9 million EBITDA.

In 2013, the Group will, in accordance with the adopted business strategy, invest mainly into produc-

tion, equipment and technology and the achievement of optimum productivity, the balance between

adaptability and efficiency of individual parts of the production process, the achievement of synergy

effects among the Group companies, integration of information technology into the production pro-

cesses, possibilities of the expansion of certain production sets and as high as possible return on

investments.

Environmental protection activities in 2013 are still associated with the implementation of environ-

mental objectives geared towards reducing the environmental burden, quantities of waste water and

waste and towards the rational use of electricity and natural gas. The preservation of the water protec-

tion area, the vital resource of the Group, is the constant objective of the Laško Group.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

17

Int

ro

du

ct

ion

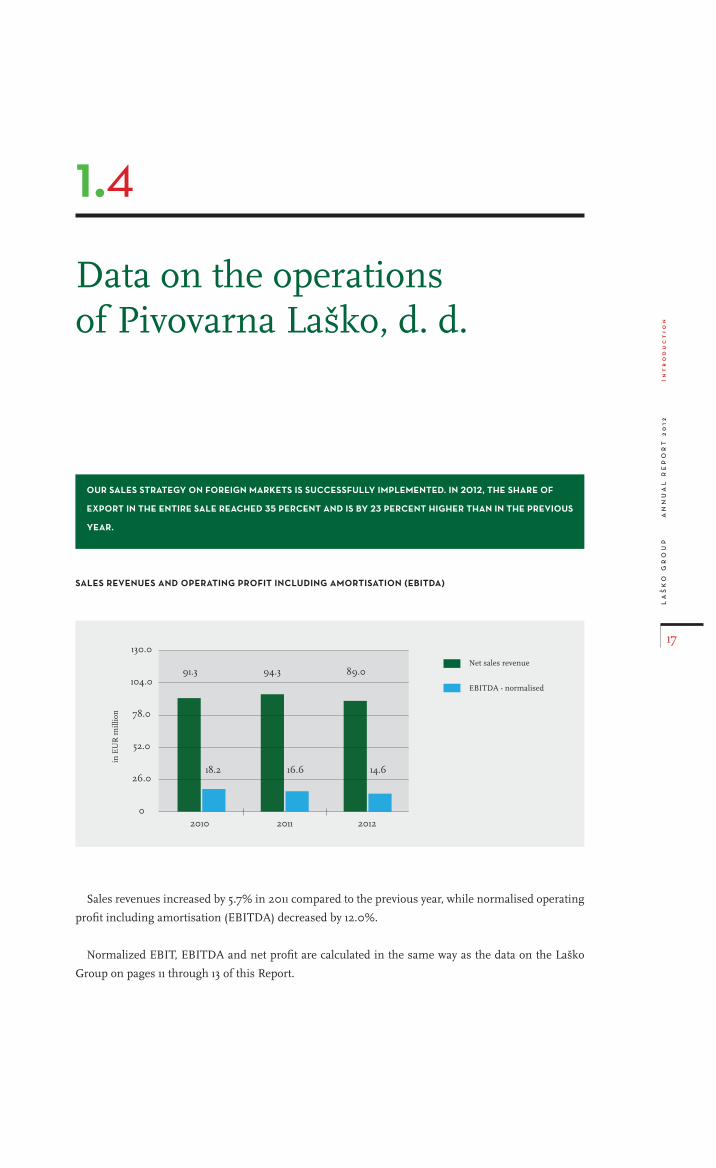

OUR SALES STRATEGY ON FOREIGN MARKETS IS SUCCESSFULLY IMPLEMENTED. IN 2012, THE SHARE OF

EXPORT IN THE ENTIRE SALE REACHED 35 PERCENT AND IS BY 23 PERCENT HIGHER THAN IN THE PREVIOUS

YEAR.

SALES REVENUES AND OPERATING PROFIT INCLUDING AMORTISATION (EBITDA)

0

in E

UR

mill

ion

Net sales revenue

EBITDA - normalised

2010 2011 2012

14.616.618.2

89.094.391.3

26.0

52.0

78.0

104.0

130.0

Sales revenues increased by 5.7% in 2011 compared to the previous year, while normalised operating

profit including amortisation (EBITDA) decreased by 12.0%.

Normalized EBIT, EBITDA and net profit are calculated in the same way as the data on the Laško

Group on pages 11 through 13 of this Report.

1.4

Data on the operations of Pivovarna Laško, d. d.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

18

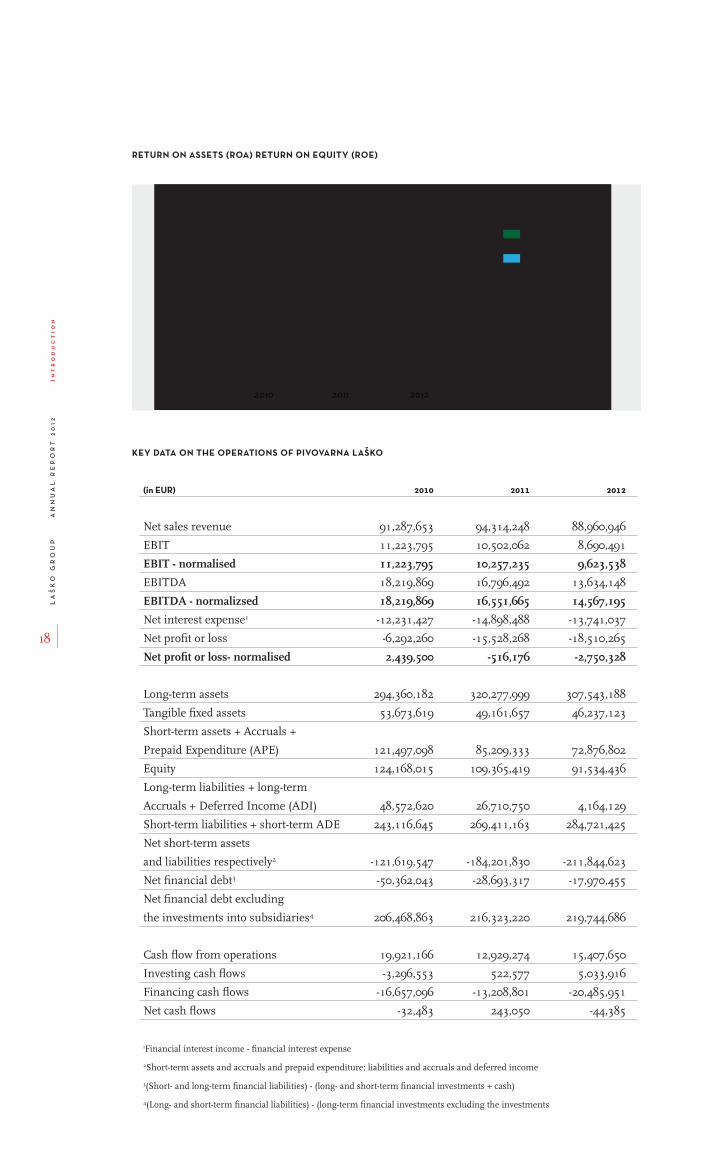

RETURN ON ASSETS (ROA) RETURN ON EQUITY (ROE)

Return on equity (ROE)

Return on assets (ROA)

-3.0

-1.0

-2.0

1.0

0.0

2.0

3.0

in %

2010 2011 2012

-0.7-0.1

0.6

-2.7-0.4

1.9

KEY DATA ON THE OPERATIONS OF PIVOVARNA LAŠKO

(in EUR) 2010 2011 2012

Net sales revenue 91,287,653 94,314,248 88,960,946

EBIT 11,223,795 10,502,062 8,690,491

EBIT - normalised 11,223,795 10,257,235 9,623,538

EBITDA 18,219,869 16,796,492 13,634,148

EBITDA - normalizsed 18,219,869 16,551,665 14,567,195

Net interest expense1 -12,231,427 -14,898,488 -13,741,037

Net profit or loss -6,292,260 -15,528,268 -18,510,265

Net profit or loss- normalised 2,439,500 -516,176 -2,750,328

Long-term assets 294,360,182 320,277,999 307,543,188

Tangible fixed assets 53,673,619 49,161,657 46,237,123

Short-term assets + Accruals +

Prepaid Expenditure (APE) 121,497,098 85,209,333 72,876,802

Equity 124,168,015 109,365,419 91,534,436

Long-term liabilities + long-term

Accruals + Deferred Income (ADI) 48,572,620 26,710,750 4,164,129

Short-term liabilities + short-term ADE 243,116,645 269,411,163 284,721,425

Net short-term assets

and liabilities respectively2 -121,619,547 -184,201,830 -211,844,623

Net financial debt3 -50,362,043 -28,693,317 -17,970,455

Net financial debt excluding

the investments into subsidiaries4 206,468,863 216,323,220 219,744,686

Cash flow from operations 19,921,166 12,929,274 15,407,650

Investing cash flows -3,296,553 522,577 5,033,916

Financing cash flows -16,657,096 -13,208,801 -20,485,951

Net cash flows -32,483 243,050 -44,385

1Financial interest income - financial interest expense

2Short-term assets and accruals and prepaid expenditure; liabilities and accruals and deferred income

3(Short- and long-term financial liabilities) - (long- and short-term financial investments + cash)

4(Long- and short-term financial liabilities) - (long-term financial investments excluding the investments

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

19

Int

ro

du

ct

ion

INDICATORS

2010 2011 2012

Share of normalised EBIT in sales revenues 12.3% 10.9% 10.8%

Share of normalised EBITDA in sales revenues 20.0% 17.5% 16.4%

Cover of interest5 0.918 0.688 0.700

Normalised net profit and/or

loss from revenues from sales 2.7% -0.5% -3.1%

Return on equity (ROE)6 1.9% -0.4% -2.7%

Return on assets (ROA)7 0.6% -0.1% -0.7%

Liabilities / Equity 2.349 2.708 3.156

5Normalised EBIT / net interest expense

6Normalised net profit or loss / average balance of equity in the period

7Normalised net profit or loss / average balance of assets in the period

NUMBER OF EMPLOYEES

2010 2011 2012

Employees as of 31/12 318 329 324

Average number

of employees in terms of hours worked 319 322 330

Added value per employee8

(in EUR / employee) 90,267 91,258 77,511

Net sales revenue per employee9

(in EUR / employee) 286,168 292,901 269,579

8(Operating revenues - costs of goods, material and services - other operating expenses (entire operations)) / average number of

employees in terms of hours worked

9net sales revenues (entire operations) / average number of employees in terms of hours worked

SHARE OF EXPORT IN TOTAL SALES OF BEVERAGES PIVOVARNA LAŠKO, D. D.

(in hl) 2010 2011 2012

Total sales of beverages 968,697 975,838 942,183

Export 250,371 268,631 330,213

Share (in %) 25.8 27.5 35.0

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

20

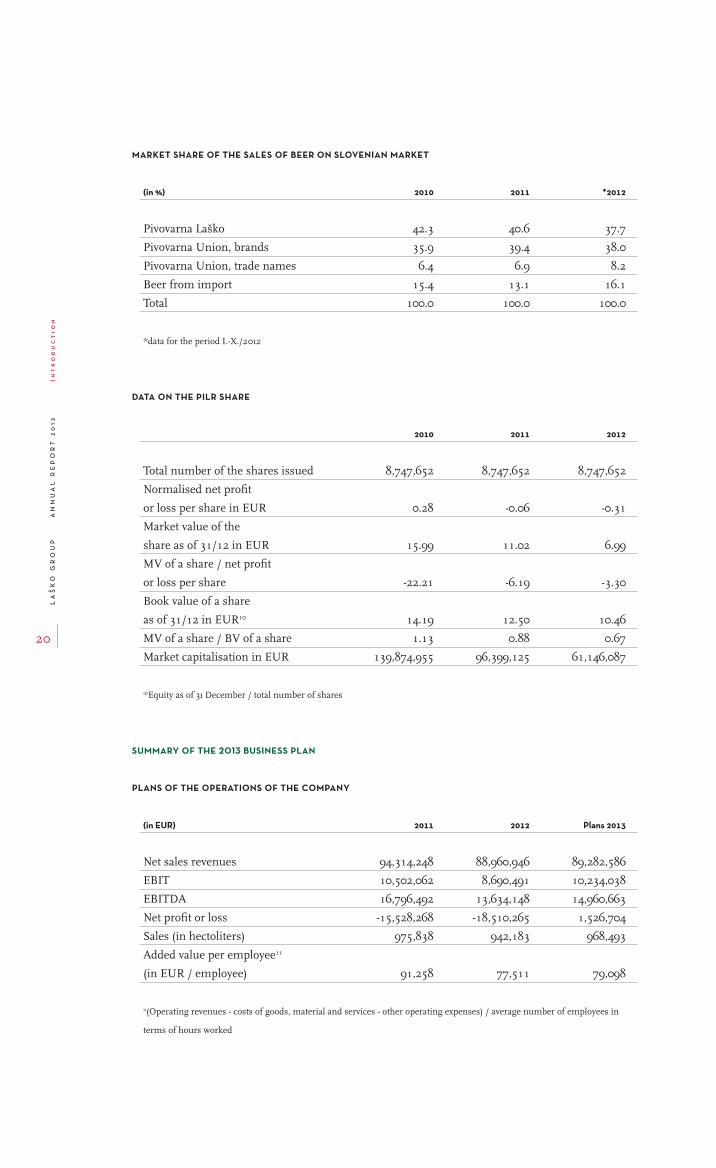

MARKET SHARE OF THE SALES OF BEER ON SLOVENIAN MARKET

(in %) 2010 2011 *2012

Pivovarna Laško 42.3 40.6 37.7

Pivovarna Union, brands 35.9 39.4 38.0

Pivovarna Union, trade names 6.4 6.9 8.2

Beer from import 15.4 13.1 16.1

Total 100.0 100.0 100.0

*data for the period I.-X./2012

DATA ON THE PILR SHARE

2010 2011 2012

Total number of the shares issued 8,747,652 8,747,652 8,747,652

Normalised net profit

or loss per share in EUR 0.28 -0.06 -0.31

Market value of the

share as of 31/12 in EUR 15.99 11.02 6.99

MV of a share / net profit

or loss per share -22.21 -6.19 -3.30

Book value of a share

as of 31/12 in EUR10 14.19 12.50 10.46

MV of a share / BV of a share 1.13 0.88 0.67

Market capitalisation in EUR 139,874,955 96,399,125 61,146,087

10Equity as of 31 December / total number of shares

SUMMARY OF THE 2013 BUSINESS PLAN

PLANS OF THE OPERATIONS OF THE COMPANY

(in EUR) 2011 2012 Plans 2013

Net sales revenues 94,314,248 88,960,946 89,282,586

EBIT 10,502,062 8,690,491 10,234,038

EBITDA 16,796,492 13,634,148 14,960,663

Net profit or loss -15,528,268 -18,510,265 1,526,704

Sales (in hectoliters) 975,838 942,183 968,493

Added value per employee11

(in EUR / employee) 91,258 77,511 79,098

11(Operating revenues - costs of goods, material and services - other operating expenses) / average number of employees in

terms of hours worked

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

21

Int

ro

du

ct

ion

The objectives have been set for 2013 that can be identified as the 2.8% increase in the quantities

of the sales of beer and other beverages. The sales growth is planned for the foreign markets where

the quantities are to increase by more than 13%. At the same time, the shares on the domestic market

should be maintained. 968 thousand hl of all types of beverages are planned to be sold in 2013.

Total of EUR 89.3 million of net sales revenue is expected. 81.8% of all the revenue will be generated

on the domestic market and EUR 16.2 million on foreign markets. The funds amounting to EUR 4.1

million will mainly be invested into the renewal of the technological equipment and into IT as well as

into commercial activities.

Environmental protection activities in 2013 are still linked to the implementation of environmental

objectives geared towards reducing the environmental burden, quantities of waste water and waste and

towards the rational use of electricity and natural gas. The preservation of the water protection area, the

vital resource of the Company, is the constant objective of the Pivovarna Laško, d. d.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

22

TO BECOME THE FIRST CHOICE OF THE BUYERS OF QUALITY BRAND, THE TOP CLASS INVESTMENT FOR

THE SHAREHOLDERS AND AN ATTRACTIVE EMPLOYER. STRENGTHENING THE MARKET POSITION OF THE

COMPANIES IN THE LAŠKO GROUP AND THE PRODUCTION AND SALE OF INNOVATIVE, TRENDY PRODUCTS.

LAŠKO GROUP PIVOVARNA LAŠKO, D. D.

VISION Becoming the first choice of the buyers Becoming the leading one in

of quality brand names in the industry the production and sale of

and on the markets where we operate, beverages, strengthening our

top class investment for our shareholders reputation, recognition and

an attractive employer for the employees market shares of our brand

who strive for excellence, development names on the domestic as

and team work. well as on foreign markets.

MISSION The brands that maintain tradition We create brands with added

and direct the trends generate added value for our buyers and

value for our buyers and shareholders. shareholders.

By stressing social responsibility and Responsible and

motivating the employees we preserve environmentally friendly

the market position of the companies operations enable us to

in the Laško Group on all major achieve top results in

markets. a better world.

STRATEGIC GOALS The production and sale of innovative and trendy products, maintenance of the

market positions of own brand names on the domestic market, and recovery and

expansion of previously achieved positions on foreign markets. Planned cost ef-

fectiveness will be achieved through professionally qualified employees acting as

teams and in accordance with the policies of the Laško Group.

1.5

Vision, mission and strategic goals

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

23

Int

ro

du

ct

ion

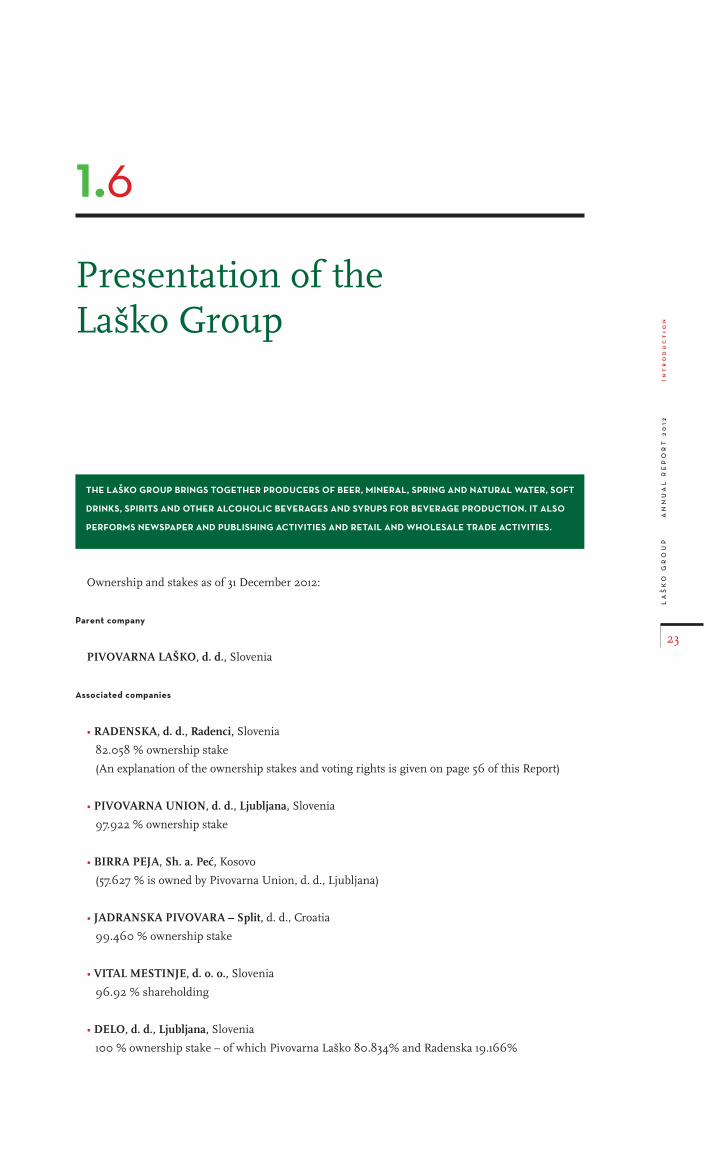

THE LAŠKO GROUP BRINGS TOGETHER PRODUCERS OF BEER, MINERAL, SPRING AND NATURAL WATER, SOFT

DRINKS, SPIRITS AND OTHER ALCOHOLIC BEVERAGES AND SYRUPS FOR BEVERAGE PRODUCTION. IT ALSO

PERFORMS NEWSPAPER AND PUBLISHING ACTIVITIES AND RETAIL AND WHOLESALE TRADE ACTIVITIES.

Ownership and stakes as of 31 December 2012:

Parent company

PIVOVARNA LAŠKO, d. d., Slovenia

Associated companies

• RADENSKA, d. d., Radenci, Slovenia

82.058 % ownership stake

(An explanation of the ownership stakes and voting rights is given on page 56 of this Report)

• PIVOVARNA UNION, d. d., Ljubljana, Slovenia

97.922 % ownership stake

• BIRRA PEJA, Sh. a. Peć, Kosovo

(57.627 % is owned by Pivovarna Union, d. d., Ljubljana)

• JADRANSKA PIVOVARA – Split, d. d., Croatia

99.460 % ownership stake

• VITAL MESTINJE, d. o. o., Slovenia

96.92 % shareholding

• DELO, d. d., Ljubljana, Slovenia

100 % ownership stake – of which Pivovarna Laško 80.834% and Radenska 19.166%

1.6

Presentation of theLaško Group

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

24

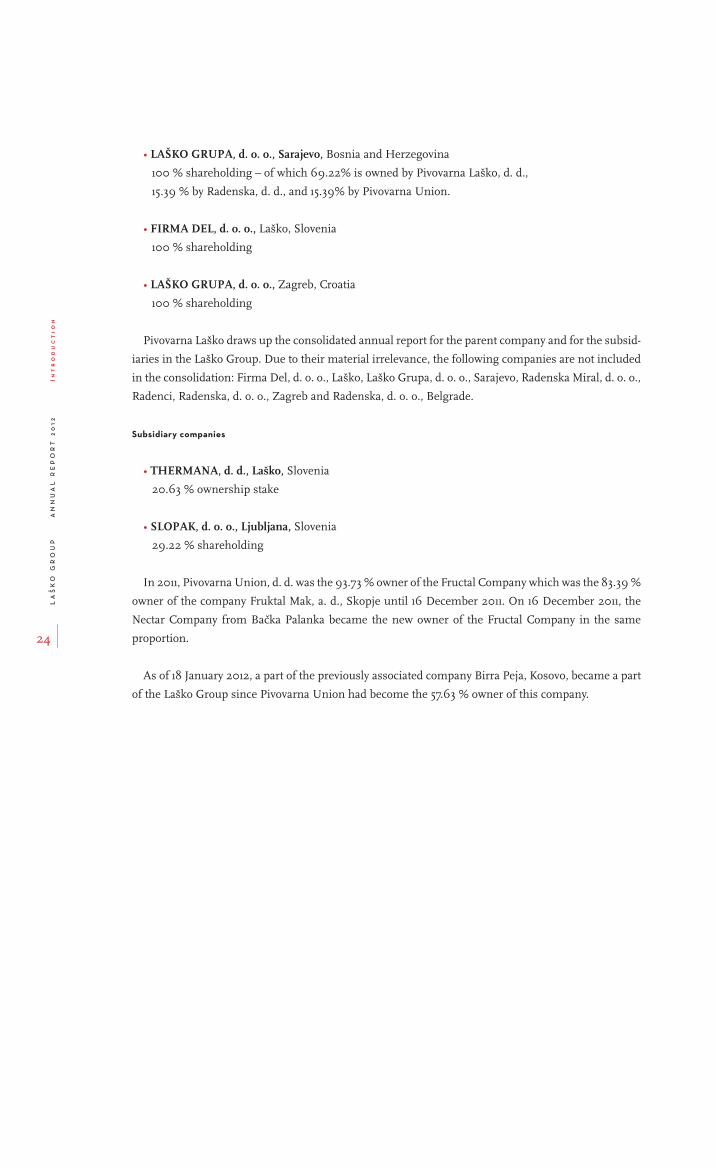

• LAŠKO GRUPA, d. o. o., Sarajevo, Bosnia and Herzegovina

100 % shareholding – of which 69.22% is owned by Pivovarna Laško, d. d.,

15.39 % by Radenska, d. d., and 15.39% by Pivovarna Union.

• FIRMA DEL, d. o. o., Laško, Slovenia

100 % shareholding

• LAŠKO GRUPA, d. o. o., Zagreb, Croatia

100 % shareholding

Pivovarna Laško draws up the consolidated annual report for the parent company and for the subsid-

iaries in the Laško Group. Due to their material irrelevance, the following companies are not included

in the consolidation: Firma Del, d. o. o., Laško, Laško Grupa, d. o. o., Sarajevo, Radenska Miral, d. o. o.,

Radenci, Radenska, d. o. o., Zagreb and Radenska, d. o. o., Belgrade.

Subsidiary companies

• THERMANA, d. d., Laško, Slovenia

20.63 % ownership stake

• SLOPAK, d. o. o., Ljubljana, Slovenia

29.22 % shareholding

In 2011, Pivovarna Union, d. d. was the 93.73 % owner of the Fructal Company which was the 83.39 %

owner of the company Fruktal Mak, a. d., Skopje until 16 December 2011. On 16 December 2011, the

Nectar Company from Bačka Palanka became the new owner of the Fructal Company in the same

proportion.

As of 18 January 2012, a part of the previously associated company Birra Peja, Kosovo, became a part

of the Laško Group since Pivovarna Union had become the 57.63 % owner of this company.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

25

Int

ro

du

ct

ion

PIVO

VARN

AU

NIO

N, d

. d.,

Ljub

ljana

Ow

ners

hip:

97.9

22%

No

of s

h: 4

41,74

0

JAD

RAN

SKA

PIVO

VARA

- Sp

lit, d

. d.

Ow

ners

hip:

99.

460

%N

o of

sh:

5,3

96,9

32

RAD

ENSK

A, d

. d.,

Rade

nci

Ow

ners

hip

82.0

58%

No

of s

h.: 4

,153,

644

VIT

AL,

d. o

. o.,

Mes

tinje

Buss

. sha

re: 9

6.92

%

DEL

O, d

. d.,

Ljub

ljana

Buss

. sha

re: 1

00

%N

o of

sh:

667

,464

RAD

ENSK

A M

IRA

L,d.

o. o

., Ra

denc

iBu

ss. s

hare

: 10

0%

BIRR

A P

EJA

, Sh.

a.

Peć,

Kos

ovo

No

of s

h: 5

7.627

%N

o of

sh:

1,02

0 BI

RRA

PEJ

A, S

h. p

. k.

Tira

na, A

lban

ija

Buss

. sha

re: 1

00

%

PIV

OVA

RN

A L

AŠK

O, d

. d.

Subs

idia

rySu

bsid

iary

Subs

idia

rySu

bsid

iary

Subs

idia

ry

LA

ŠKO

GR

OU

P

Pare

nt c

ompa

ny Pivo

varn

a La

ško

Ow

ners

hip

in D

elu

80.8

34%

No

of s

h: 5

39,5

36

Rade

nska

Ow

ners

hip

in D

elu

19.16

6%N

o of

sh:

127,9

28

Subs

idia

ry o

f Del

o:IZ

BERI

, d. o

. o.,

Ljub

ljana

Buss

. sha

re: 1

00

%

Subs

idia

rySu

bsid

iary

LAŠK

O G

RUPA

, d.o

.o.,

Sara

jevo

Buss

. sha

re: 1

00

%

FIRM

A D

EL, d

. o. o

.,La

ško

Buss

. sha

re: 1

00

%

Pivo

varn

a La

ško

Buss

. sha

re in

Laš

koG

rupa

Sar

ajev

o69

.22%

Rade

nska

Buss

. sha

re in

Laš

koG

rupa

Sar

ajev

o15

.39%

Pivo

varn

a U

nion

Buss

. sha

re in

Laš

koG

rupa

Sar

ajev

o15

.39%

Subs

idia

ry

LAŠK

O G

RUPA

, d.o

.o.,

Zagr

eb

Buss

. sha

re: 1

00

%

as o

f 31 D

ecem

ber

2012

(Not

es o

n th

e ow

ners

hip

and

votin

g rig

hts

in R

aden

ska

on

page

56

of th

is a

nnua

l re

port

.)

OR

GA

NIS

ATIO

N C

HA

RT

OF

THE

LA

ŠKO

GR

OU

P A

S O

F 31

/12/

2012

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Int

ro

du

ct

ion

26

FROM A HISTORICAL STANDPOINT, THE ORIGINS OF PIVOVARNA LAŠKO LAY IN 1825 WHEN THE MEAD

AND GINGERBREAD MAKER FRANZ GEYER SET UP A BREWERY IN THE FORMER VALVASOR HOSPITAL, THE

BUILDING WHICH STILL EXISTS TODAY AND IS THE LOCATION OF THE SAVINJA HOTEL.

1.7.1 IDENTITY CARD

PIVOVARNA LAŠKO, Trubarjeva 28, 3270 Laško, registered with the District Court in Celje under

the decision No Srg 95/00673 and under the application No 1/00171/00 dating September 1995.

Abbreviated Company’s name: PIVOVARNA LAŠKO, d. d.

Organizational form: Joint-stock company

Share capital: EUR 36,503,305

Number of issued shares: 8,747,652 no par-value shares

Listing of shares: Ljubljana stock Exchange, stock exchange listing of

regular shares

Tycker symbol: PILR

Company registration number: 5049318

Tax ID number: SI90355580

Activity code: 11.050

Type of business and principal activity:

BEER PRODUCTION

1.7

Presentation of the parent company Pivovarna Laško, d. d.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

27

Int

ro

du

ct

ion

Management Board: Dušan Zorko, MSc, Chairman

Marjeta Zevnik

Mirjam Hočevar

Gorazd Lukman

Matej Oset

Supervisory Board: Dr Vladimir Malenković, Chairman

Dr Borut Bratina

Borut Jamnik

Dr Peter Groznik

Bojan Cizej

Dragica Čepin, MSc

TRANSACTION ACCOUNTS:

Nova Ljubljanska banka, d. d., Ljubljana IBAN SI56 0223 2002 0104 463

Hypo Alpe-Adria-bank, d. d. IBAN SI56 3300 0000 2722 975

Nova Kreditna banka Maribor, d. d. IBAN SI56 0451 5000 0909 883

Raiffeisen Krekova banka, d. d. IBAN SI56 2430 0900 0054 863

Unicredit banka Slovenije, d. d. IBAN SI56 2900 0000 1820 159

Banka Celje, d. d., Bančna skupina Celje IBAN SI56 0600 0000 1199 122

Abanka Vipa, d. d. IBAN SI56 0510 0801 2922 332

Banka Sparkasse, d. d. IBAN SI56 3400 0100 1922 773

Probanka, d. d. IBAN SI56 2510 0970 0565 280

Telephone: +386 3 734 80 00

Fax: +386 3 573 18 17

Electronic mail address: [email protected]

Website: http://www.pivo-lasko.si

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

28

Business report

12345

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

29

Bu

sin

es

s r

ep

or

t

IT IS MANAGED ACCORDING TO A TWO-TIER SYSTEM WHEREBY THE COMPANY IS MANAGED BY THE

MANAGEMENT BOARD AND ITS OPERATIONS SUPERVISED BY THE SUPERVISORY BOARD.

The principles of management of Pivovarna Laško arise from valid legal norms in the Republic of

Slovenia, internal acts of the Company and established good work practices. Management is carried

out according to a two-tier system whereby the Company is managed by the Management Board and

its operations monitored by the Supervisory Board.

The bodies of the Company as set out in the Articles of Association of Pivovarna Laško are the Gen-

eral Meeting of Shareholders, Supervisory Board and Management Board of the Company.

2.1.1 GENERAL MEETING OF SHAREHOLDERS

In accordance with the provisions of the Companies Act, the General Meeting of Shareholders is the su-

preme body of the Company. This is where the shareholders’ will is directly realised and they adopt funda-

mental and statutory decisions. One share represents one vote at the General Meeting. Pivovarna Laško, d. d.

has no shares with limited voting rights. Own shares do not enable voting rights at the General Meeting.

The General Meeting of Shareholders is convened by the Management Board on its own initiative, at

the request of the Supervisory Board or at the written request of the shareholders of the Company pos-

sessing at least a 5% equity stake in the Company. The Supervisory Board may also convene a General

Meeting. Shareholders can exercise their rights arising from shares directly at the General Meeting or

through their representatives.

The General Meeting decides by a majority of the votes cast (simple majority) except where other-

wise provided in the Act or Articles of Association. The decisions taken at the General Meeting by a

three-quarters majority mainly concern:

• amendments to the Articles of Association,

• decrease in share capital (including conditional increase),

• approved increase in share capital,

2.1

Corporate governance

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

30

• status changes and winding up of the Company,

• exclusion of the shareholders’ preferential rights when issuing new shares,

• election and early discharge of the Supervisory Board members,

• other matters, if so prescribed by law or the Articles of Association.

The General Meeting takes decisions regarding the granting of discharges to the Management and

Supervisory Boards of the Company, and at the same time, makes decisions regarding the use of

distributable profit. By granting discharges the General Meeting confirms and approves the work of

the Management and Supervisory Boards for the financial year. Discussions regarding the granting

of discharges are carried out in combination with discussions on the use of distributable profit. If the

General Meeting does not grant discharge, it is not considered that the Management Board was given

a vote of no confidence.

Whenever the General Meeting of Shareholders decides that the distributable profit is to be used for

dividends, the dividends belong to the shareholders who as owners have been entered in the central

register of securities at the Central Securities Clearing Corporation on the cut-off date which shall be

decided each time through a decision on the use of distributable profit.

ATTENDANCE AT GENERAL MEETINGS

The right to participate and vote at the General Meeting is held by those shareholders who have been

entered into the share register at the Central Securities Clearing Corporation by the end of the fourth

day prior to the convocation of a General Meeting (cut-off date) and who personally, or through a repre-

sentative or nominee, gave notification of their attendance to the Management Board of the Company

by the end of the fourth day prior to the convocation of the General Meeting.

The Management Board members and the Supervisory Board members may attend the General

Meeting even if they are not shareholders. Media representatives may also attend the General Meeting

if they give notification of their attendance to the Management Board of the Company in writing within

three days at the latest prior to the convocation of the General Meeting.

CONVOCATION AND IMPLEMENTATION OF THE GENERAL MEETING OF SHAREHOLDERS

A General Meeting of Shareholders is convened when it is for the benefit of the Company or when

it is necessary in accordance with law and the Articles of Association.

In 2012, there were two General Meetings of Shareholders. The 19th regular General Meeting of

Shareholders of Pivovarna Laško, d. d. was convened on 29 December 2011 and held on 30 January 2012

and the 20th General Meeting of Shareholders of Pivovarna Laško was convened on 26 July 2012 and

held on 28 August 2012.

RESOLUTIONS OF THE 19TH GENERAL MEETING OF SHAREHOLDERS OF PIVOVARNA LAŠKO

The following important decisions were adopted at the 19th regular General Meeting regarding the

items on the agenda:

ITEM 2: INCREASE IN SHARE CAPITAL BY CASH CONTRIBUTIONS (CAPITAL INJECTION)

Resolution to item 2 provided by the Management Board and Supervisory Board of the Company

was not adopted since only 1,808,249 or 36.01% votes cast supported the resolution. The adoption of

resolutions requires a three-fourths majority or 75% of the votes cast.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

31

Bu

sin

es

s r

ep

or

t

The contrary proposal of a resolution to Item 2 of a shareholder of KS Naložbe was not adopted. The

resolution was not adopted since only 379,028 or 8.85% of the votes cast supported it. The adoption of

resolutions requires a three-fourths majority or 75% of the votes cast.

ITEM 3: APPROVAL OF THE GENERAL MEETING OF THE CONTROLLING CONTRACTS AND THE AMENDMENTS

TO THE ARTICLES OF ASSOCIATION (AUTHORISED CAPITAL)

RESOLUTIONS TO ITEM 3:

3.1. The General Meeting approves the controlling contract concluded on 27 December 2011 between

Pivovarna Laško, the parent company, and Pivovarna Union, the subsidiary.

The General Meeting approves the controlling contract concluded on 27 December 2011 between

Pivovarna Laško, the parent company, and Radenska, Radenci, the subsidiary.

The resolution was passed with 3,983,759 or 81.22% of the votes cast.

3.2. The Articles of association is amended so that article 10.a follows Article 10 and reads as follows:

»Article 10.a

The Management Board of the Company is authorised to issue new, ordinary registered no par value

shares for a consideration other than in cash and thus increases the share capital by issuing new shares

by maximum 5 (five) % of the share capital (authorised capital) existing at the time of adopting amend-

ments to the Articles of Association within 1 (one) year after the entry of the amendment of the Articles

of Association into the Court register. Prior to the issue of new shares, the Management Board needs

to obtain the consent of the Supervisory Board.

On the basis of the previous paragraph the Management Board of the Company is entitled to take a

decision concerning the exclusion of subscriptions rights to purchase new shares when increasing the

share capital provided the Company’s Supervisory Board has given its agreement.

When increasing the share capital based on the first and second paragraph of this Article, the auditor

does not need to verify the issue of shares for a consideration other than in cash.

The Supervisory Board is authorised to adopt the amendments to the Articles of Associations in

order to adjust the text to the implemented increase in the share capital of the Company based on the

provisions on the authorised capital.«

The resolution was passed with 3,965,175 votes cast or with 79.28%.

ITEM 4: AMENDMENT TO THE ARTICLES OF ASSOCIATION OF THE COMPANY (AUTHORISED CAPITAL) –

REQUEST OF KAPITALSKA DRUŽBA OF 20 DECEMBER 2011

RESOLUTION TO ITEM 4:

The Articles of association is amended so that article 11.a follows Article 11 and reads as follows:

»The Management Board of the Company is authorised to increase the share capital of the Company

by 50% of the share capital existing at the time of adopting amendments to the Articles of Association,

which means maximum EUR 18,251,652.48, by issuing new shares for a consideration other than in cash

within 5 (five) years after the entry of the amendment of the Articles of Association into the Court register.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

32

The issue of new shares, the increase in share capital and the content of the rights arising from the

new shares as well as the conditions of the issue of shares are decided by the Management Board pro-

vided the Company’s Supervisory Board has given its agreement.

The Supervisory Board is authorised to adopt the amendments to the Articles of Associations in

order to adjust the text to the implemented increase in the share capital of the Company based on the

provisions on the authorised capital.«

The resolution was not passed since it was supported by only 1,858,354 or 37.01% of the votes cast.

The adoption requires a majority of three-quarters or 75% of the votes cast.

ITEM 5: RESCHEDULING OF FINANCIAL LIABILITIES

RESOLUTION TO ITEM 5:

The General Meeting calls on the creditor banks to agree with Pivovarna Laško and the companies of

the Laško Group on a comprehensive long-term rescheduling of financial liabilities under favourable

market conditions by 30 March 2012. The rescheduling should contain moratorium on the repayment

obligations concerning the principals that should mature with the receipt of the purchase sum after

having sold the investment into Mercator or after the recapitalisation of the parent company but not

later than 30 June 2013. With the debt rescheduling all the Laško Group companies could reach the

sustainable level of debt in 10 years (2–3x EBITDA). The rescheduled dynamics of the payment obliga-

tions should be coordinated with the planned cash flows arising from the core activities of individual

companies in the Group. This rescheduling will result in the reduction of financial risks, which will

enable normal operations, development and long-term existence.

The resolution was passed with 4,192,427 or 93.60% of the votes cast.

ITEM 6: INFORMATION OF THE GENERAL MEETING AND CONSENT GIVEN TO THE SALE/PURCHASE CON-

TRACT WITH REGARD TO THE SHARES OF POSLOVNI SISTEM MERCATOR, D. D.

No resolution was adopted by the General Meeting since the shareholders only got acquainted with

the sale/purchase contract with regard to the shares of Poslovni sistem Mercator.

ITEM 7: APPROVAL OF THE PERFORMANCE OF SUPERVISION IN SUBSIDIARY COMPANIES

RESOLUTION TO ITEM 7:

In accordance with Article 41 of the Companies Act, the General Meeting gives consent to the ap-

pointment of the members of the Supervisory Board of Pivovarna Laško into the supervisory boards of

the subsidiary companies.

The resolution was passed with 3,925,776 or 92.42% of the votes cast.

ITEM 8: AMENDMENTS TO THE ARTICLES OF ASSOCIATION OF THE COMPANY

RESOLUTION TO ITEM 8:

8.1. The Articles of association is amended so that article 14.a follows Article 14 and reads as follows:

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

33

Bu

sin

es

s r

ep

or

t

»Article 14.a

Members of the Management Board of the Company can be appointed members of the manage-

ment boards and supervisory boards in subsidiary companies that are or could be in competitive rela-

tionship with the activity of the Company.«

The Articles of association is amended so that article 16.a follows Article 16 and reads as follows:

»Article 16.a

Members of the Supervisory Board of the Company can be appointed members of the supervisory

boards in subsidiary companies that are or could be in competitive relationship with the activity of the

Company.«

8.2. Article 23 of the Articles of association is amended and reads as follows:

»Article 23

For their work, the members of the Supervisory Board are entitled to the payment for the perfor-

mance of the function, attendance fees and reimbursement of travel cost and other eligible costs due

to the performance of a function.

The level of payment for the performance of the function, attendance fees and reimbursement of

travel cost and other eligible costs from the previous paragraph is defined by the General Meeting.

The payment to external members of the committees of the Supervisory Board is determined by the

Supervisory Board.«

Article 39 of the Articles of association is added a net third paragraph that reads as follows:

»The amendment of article 23 of the Articles of Association adopted at the General Meeting on 30

January 2012 enters into force on 1 January 2012.«

The resolution was passed with 4,690,351 or 93.56% of the votes cast.

ITEM 9: DETERMINATION OF REMUNERATION OF THE MEMBERS OF THE SUPERVISORY BOARD

RESOLUTION TO ITEM 9:

For the attendance at the session, a member of the Supervisory Board is entitled to the attendance

fee that amounts to EUR 275.00 (gross amount). A member of a committee of the Supervisory Board

is entitled to the attendance fee for the attendance at the session of the committee that equals 80% of

the attendance fee of the Supervisory Board member. In the case of a correspondence session the at-

tendance fee equals 80% of the ordinary attendance fee.

A member of the Supervisory Board is entitled to attendance fee irrespective of the number of ses-

sions the Supervisory Board member attends in an individual financial year until the total amount of

the attendance fees paid, for either the Supervisory Board sessions or the sessions of the committees

of the Supervisory Board, in an individual financial year reaches 50% of the remuneration for the per-

formance of the function of a member of the Supervisory Board.

In addition to the attendance fee, a member of the Supervisory Board is also entitled to the basic

remuneration for the performance of the function of a Supervisory Board member equalling EUR

12,000.00 gross annually. The chairman of the Supervisory Board is entitled to the additional payment

equalling 50% of the basic remuneration for the performance of the function of a Supervisory Board

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

34

member whereas the deputy chairman is entitled to the additional payment equalling 10% of the basic

remuneration for the performance of the function of a Supervisory Board member. A member of a

committee of the Supervisory Board is entitled to the additional payment equalling 25% of the basic

remuneration for the performance of the function of a Supervisory Board member whereas the chair-

man of a committee of the Supervisory Board is entitled to the additional payment equalling 50% of the

basic remuneration for the performance of the function of a Supervisory Board member and the dep-

uty chairman of a committee of the Supervisory Board is entitled to the additional payment equalling

10% of the basic remuneration for the performance of the function of a Supervisory Board member.

Regardless of the number of committees the Supervisory Board member is a member of in the

individual financial year, the individual member of the Supervisory Board is entitled to the additional

payment for the performance of the functions of committees until the total amount of these addi-

tional payments in the financial year totals 50% of the basic remuneration for the performance of the

function of a Supervisory Board member. The members of the Supervisory Board receive the basic

remuneration and the additional payment for the performance of functions to which they are entitled

in proportionate monthly payments until they perform the functions. A monthly payment amounts to

one-twelfth of the above listed annual sums.

The members of the Supervisory Board are entitled to the reimbursement of travel cost, daily allow-

ances and accommodation costs resulting from their work in the Supervisory Board or in the Supervi-

sory Board committee up to the level defined in the regulations governing the reimbursement of costs

related to work and other revenues that are not included in the taxable amount. The accommodation

costs can be reimbursed when the place of the work of the Board is at least 100 km distance from the

permanent or temporary residence of the Supervisory Board member and the location of the work of

the Board is at least 100 kilometres and when the member cannot return the same day since according

to the timetable no ride was planned in public transport or for other objective reasons.

This resolution shall apply from 1 January 2012. From the date of entry into force of this resolution,

the resolution adopted by the General Meeting on 31 August 2009 shall expire.

The resolution was passed with 3,958,736 or 80.72% of the votes cast.

PLANNED CHALLENGING ACTION

The KS Naložbe shareholder announced a challenging action regarding the adopted resolutions 3.1.

and 3.2.

The minutes of the General Meeting are available on the external websites of AJPES (Business reg-

ister of Slovenia).

RESOLUTIONS OF THE 20TH GENERAL MEETING OF SHAREHOLDERS OF PIVOVARNA LAŠKO

The 20th General Meeting of the shareholders of Pivovarna Laško adopted the following relevant decisions:

ITEM 2: ACQUAINTANCE OF THE GENERAL MEETING WITH THE REPORT OF THE SUPERVISORY BOARD ON

THE ADOPTION OF THE AUDITED ANNUAL REPORT FOR 2011, ACQUAINTANCE OF THE GENERAL MEETING

WITH THE COVER OF NET LOSS, ACQUAINTANCE OF THE GENERAL MEETING WITH THE REMUNERATION OF

THE MANAGEMENT AND SUPERVISORY BOARD MEMBERS AND THE DECISION CONCERNING THE DISCHARGE

TO BE GIVEN TO THE MANAGEMENT BOARD AND THE SUPERVISORY BOARD

RESOLUTIONS TO ITEM 2:

2.1. The General Meeting is acquainted with the report of the Supervisory Board on the verification

and adoption of the audited Annual Report for financial year 2011.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

35

Bu

sin

es

s r

ep

or

t

2.2. The General Meeting is informed that as of 31 December 2011 the net loss for the financial year

2011 totals EUR 15,528,268 EUR and that the Management in agreement with the Supervisory Board

covered it with other profit reserves in the amount of EUR 391,649 and capital reserves amounting to

EUR 15,136,619.

2.3. The General Meeting is informed of the remuneration of the Management Board and Supervi-

sory Board members in the Company and its subsidiaries in the 2011 financial year.

The resolutions 2.1. to 2.3. are informative and were not put to the vote.

2.4. The General Meeting grants the Management Board the discharge for the 2011 financial year.

The resolution was passed with 7,425,382 or 99.54% of the votes cast. The adoption requires a ma-

jority of the votes cast (simple majority).

2.5. The General Meeting grants the Supervisory Board the discharge for the 2011 financial year.

The resolution was passed with 7,454,151 or 99.93% of the votes cast. The adoption requires a major-

ity of the votes cast (simple majority).

ITEM 3: INCREASE IN SHARE CAPITAL PAID IN CASH (CAPITAL INJECTION)

Resolution to Item 3 proposed by the Management Board and Supervisory Board of the Company

was not passed since it was only supported by 1,853,463 or 25.38% of the votes cast. The adoption of a

resolution requires at least a three-quarter majority vote.

ITEM 4: ACQUAINTANCE OF THE GENERAL MEETING WITH THE TERMINATION OF THE CONTROLLING CON-

TRACTS AND WITH THE ORGANISATION OF A CONTRACT-BASED GROUP

RESOLUTION TO ITEM 4:

The General Meeting is informed of the termination of the Controlling Contract and of the Organi-

sation of a Contract-based Group concluded on 27 December 2011 between Pivovarna Laško d. d., the

parent company, and Pivovarna Union d. d., the subsidiary company and of the termination of the Con-

trolling Contract and of the Organisation of a Contract-based Group concluded on 27 December 2011 be-

tween Pivovarna Laško d. d., the parent company, and Radenska d. d., Radenci, the subsidiary company.

The resolution is informative and was not put to the vote.

ITEM 5: APPOINTMENT OF THE AUDITOR FOR THE 2012 FINANCIAL YEAR

RESOLUTION TO ITEM 5:

The General Meeting appoints the audit firm Deloitte Revizija, d. o. o., Ljubljana for the purpose of

auditing the 2012 annual accounts.

The resolution was passed with 7,442,153 or 99.77% of the votes cast. The adoption requires a major-

ity of the votes cast (simple majority).

PLANNED CHALLENGING ACTION

No challenging action regarding the adopted resolutions was announced.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

36

2.1.2 SUPERVISORY BOARD

The fundamental function of the Supervisory Board is to supervise the management of the Com-

pany’s business operations. The Supervisory Board appoints and discharges the members and Chair-

man of the Management Board.

The composition of the Supervisory Board is defined in the Articles of Association of the Com-

pany. The Supervisory Board of Pivovarna Laško, d. d. has six members, each of whom has the same

rights and responsibilities unless otherwise stipulated by the Articles of Association. Four members

of the Supervisory Board elected by the General Meeting of Shareholders are capital representatives,

while the other two Supervisory Board members are employee representatives and are elected by the

Worker’s Council.

The Supervisory Board is appointed by the General Meeting of Shareholders by a majority of the

votes of the shareholders cast except for the members of the Supervisory Board who are elected by the

Worker’s Council. The Supervisory Board members are elected for a period of four years and their ap-

pointment is renewable following the expiry of their term of office. The Supervisory Board appoints the

Chairman and Deputy Chairman of the Supervisory Board from amongst their members.

The Chairman convenes and chairs the sessions of the Supervisory Board and is authorised to de-

clare its will and announce decisions adopted by the Supervisory Board. The Chairman of the Supervi-

sory Board represents the Company in disputes with the members of the Management Board and the

Supervisory Board represents the Company in disputes against other bodies of the Company and third

parties, unless otherwise specified in each particular case. The Chairman of the Supervisory Board is

always the representative of the shareholders. Sessions of the Supervisory Board are convened by the

Chairman on his own initiative, on the initiative of any member of the Supervisory Board, or on the

initiative of the Management Board. The Supervisory Board takes decisions at sessions.

Within one month from the submission of the annual report, the Supervisory Board must review the

annual report and proposal for use of the distributable profit and draft a written report for the General

Meeting of Shareholders and deliver it to the Management Board. If the Supervisory Board confirms

the annual report, the annual report is adopted.

SUPERVISORY BOARD COMPOSITION SUPERVISORY BOARD COMPOSITION

AS OF 31 DECEMBER 2011 AS OF 31 DECEMBER 2012

Capital representatives: Capital representatives:

Dr Vladimir Malenković, Chairman Dr Vladimir Malenković, Chairman

Dr Borut Bratina Dr Borut Bratina

Borut Jamnik Borut Jamnik

Dr Peter Groznik Dr Peter Groznik

Employee representatives: Employee representatives:

Bojan Cizej, Deputy Chairman Bojan Cizej, Deputy Chairman

Dragica Čepin, MSc Dragica Čepin, MSc

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

37

Bu

sin

es

s r

ep

or

t

1. DR VLADIMIR MALENKOVIĆ

Vladimir Malenković has been the Supervisory Board member of Pivovarna Laško, d. d. since

31 August 2009 and Chairman of the Supervisory Board of Pivovarna Laško, d. d. since 29 April 2011.

Education: DSc in Strategic Management, the Faculty of Eco-

nomics in Ljubljana in 2005

He has been employed as a member of the Management

Board of Premogovnik Velenje, d. d.

2. DR BORUT BRATINA

Borut Bratina has been a member of the Supervisory Board of Pivovarna Laško, d. d. since June 2011.

Education: DSc in Legal Sciences - Faculty of Law, University

of Maribor, 1997

He has been employed at the Faculty of Economics and Busi-

ness, University of Maribor as Associate Professor of Busi-

ness Law and the Chair of the Business and Corporate law.

3. BORUT JAMNIK

Borut Jamnik has been a member of the Supervisory Board of Pivovarna Laško, d. d. since 24 June 2011.

Education: BSc in mathematics Engineering.

He has been employed as the chairman of the Management

Board of the company Modra zavarovalnica, d. d.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

38

4. DR PETER GROZNIK

Peter Groznik has been a member of the Supervisory Board of Pivovarna Laško, d. d. since 16 July 2010.

Education: DSc in Finance, Kelley School of Business, In-

diana University Bloomington (United States of America),

2003.

He has been employed as a member of the Management

Board of Gorenje, d. d.

5. BOJAN CIZEJ

Bojan Cizej has been a member of the Supervisory Board of Pivovarna Laško, d. d. since 6 April 2011.

Education: BSc in Food Technology, Biotechnical Faculty,

University of Ljubljana, 1993.

He has been employed at Pivovarna Laško, d. d. as the Direc-

tor of the Production-Technical Division.

6. DRAGICA ČEPIN, MSC

Dragica Čepin has been a member of the Supervisory Board of Pivovarna Laško, d. d. since August 2011.

Education: MSc in Economics, Eonomics Business Faculty,

University of Maribor, 2001.

She has been employed by Pivovarna Laško, d. d. since 1981.

CHANGES IN THE COMPOSITION OF THE SUPERVISORY BOARD OF PIVOVARNA LAŠKO, D. D.

In 2012, the composition of the Supervisory Board of Pivovarna Laško, d. d. did not change.

AUDIT COMMITTEE OF THE SUPERVISORY BOARD OF PIVOVARNA LAŠKO, D. D.

The tasks of the Audit Committee are specified in Article 280 of the Companies Act, with the key

ones comprising:

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

39

Bu

sin

es

s r

ep

or

t

• monitoring of the process of financial reporting and statutory audits of the annual and consolidated

financial statements,

• monitoring the independence, impartiality and effectiveness of the auditor for the Company’s an-

nual report,

• submitting a proposal to the Supervisory Board for the appointment of a candidate for the annual

report auditor,

• supervision of the integrity of the financial information provided by the Company,

• assessment of the drawn-up annual report including the formulation of proposal for the Supervi-

sory Board.

AUDIT COMMITTEE COMPOSITION AUDIT COMMITTEE COMPOSITION

AS OF 31 DECEMBER 2011 AS OF 31 DECEMBER 2012

Dr Peter Groznik – Chairman Dr Peter Groznik – Chairman

Bojan Cizej Bojan Cizej

Igor Teslić Igor Teslić

CHANGES IN THE COMPOSITION OF THE AUDIT COMMITTEE OF THE SUPERVISORY BOARD

In 2012, the composition of the Audit committee of the Supervisory Board of Pivovarna Laško, d. d.

did not change.

HUMAN RESOURCES COMMITTEE OF THE SUPERVISORY BOARD OF PIVOVARNA LAŠKO

The Companies Act does not define the tasks of the Human Resources committee. In compliance

with point B.2 Annex B to the Management code for publicly traded companies (Ljubljana, 8 Decem-

ber 2009) the Human Resource committee is mainly responsible for:

• provision of assistance to the Supervisory Boars and preparation of proposals on criteria and candi-

dates for the Management Board members whereby it needs to balance the skills, knowledge and

experience and prepare a description of the qualifications required for each individual post,

• assessment of the size, composition and functioning of the Management Board at regular intervals,

• provision of support in evaluating the work of the Management Board and the preparation of rea-

soned grounds for the recall of individual board members if required

• Provision of the support in the design and implementation of the remuneration system for the

Management Board.

HR COMMITTEE COMPOSITION HR COMMITTEE COMPOSITION

AS OF 31 DECEMBER 2011 AS OF 31 DECEMBER 2012

Borut Jamnik – Chairman Borut Jamnik – Chairman

Dr Borut Bratina Dr Borut Bratina

Dragica Čepin, MSc Dragica Čepin, MSc

CHANGES IN THE COMPOSITION OF THE HUMAN RESOURCES COMMITTEE OF THE SUPERVISORY BOARD

In 2012, the composition of the Human Resources committee of the Supervisory Board of Pivovarna

Laško, d. d. did not change.

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

Bu

sin

es

s r

ep

or

t

40

CHANGES IN THE SUPERVISORY BOARDS IN SUBSIDIARIES

In 2012, the composition of the supervisory boards in subsidiaries of Pivovarna Laško, d. d. did not

change.

2.1.3 MANAGEMENT BOARD

The Management Board runs the Company and adopts business decisions independently and at its

own risk and represents the Company in disputes with third parties, adopts the Company’s develop-

ment strategy, ensures proper risk treatment and management, acts with due care and diligence and

protects the business secrets of the Company.

The Management Board is composed of five members, namely: Dušan Zorko, MSc – Chairman of

the Management Board, Marjeta Zevnik – Management Board member, responsible for legal affairs,

human resources and general affairs, Mirjam Hočevar – Management Board member, responsible

for finance, Gorazd Lukman – Management Board member, responsible for sales and commerce and

Matej Oset – Management Board member, responsible for the production and technical sector.

The Chairman and members of the Management Board are appointed and recalled by the Super-

visory Board, whereby members of the Management Board are appointed at the Chairman of the

Management Board’s recommendation. The term of office of the Chairman and members of the Man-

agement Board is five years. The Chairman of the Management Board and one of the Management

Board members together represent and act on behalf of the Company. The Management Board may

appoint a procurator.

MANAGEMENT BOARD OF PIVOVARNA LAŠKO, D. D.

MANAGEMENT BOARD COMPOSITION MANAGEMENT BOARD COMPOSITION

AS OF 31 DECEMBER 2011 AS OF 31 DECEMBER 2012

Dušan Zorko, MSc – Chairman Dušan Zorko, MSc – Chairman

Marjeta Zevnik Marjeta Zevnik

Mirjam Hočevar Mirjam Hočevar

Gorazd Lukman Gorazd Lukman

Matej Oset Matej Oset

LA

ŠK

O G

RO

UP

A

NN

UA

L R

EP

OR

T 2

012

41

Bu

sin

es

s r

ep

or

t

1. DUŠAN ZORKO, MSC

Chairman of the Management Board of Pivovarna Laško, d. d.

Education: MSc in Economics, VEKŠ, Maribor, 1988.

In 1988, Dušan Zorko began his professional career at Ko-

vinotehna and in 1990 became director of TOZD Zunanja

trgovina. Two years later, he assumed the management of the

company Kovintrade and in 2004 the management of Pivo-

varna Union. On 24 July 2009 he became the Chairman of

the Management Board of Pivovarna Laško, d. d.

2. MARJETA ZEVNIK

Marjeta Zevnik is a member of the Management Board responsible for legal, human resources and

general affairs.

Education: BSc LL, Faculty of Law, University of Ljubljana,

1986, bar exam in 1991.

She began working in 1986 as a legal clerk at Pivovarna Un-