Embed Size (px)

Citation preview

ANNUAL REPORT 2008

AN

NU

AL

REPO

RT 2

008

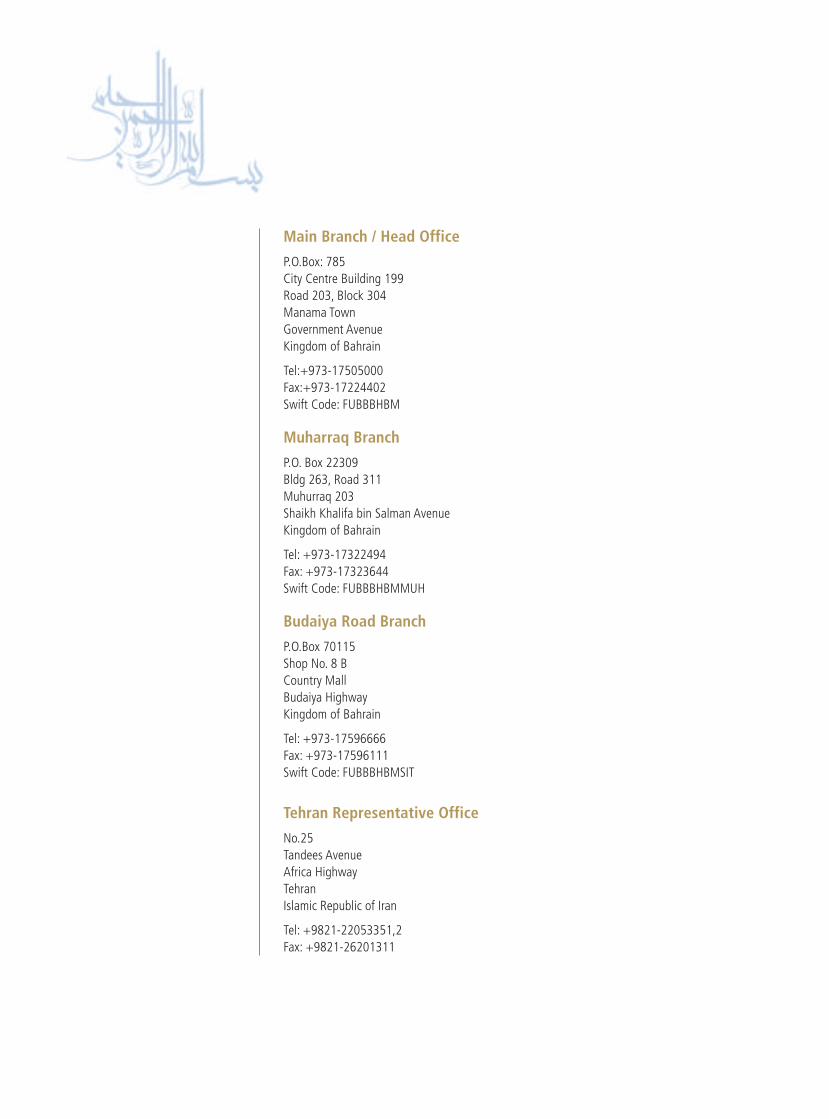

Main Branch / Head Office

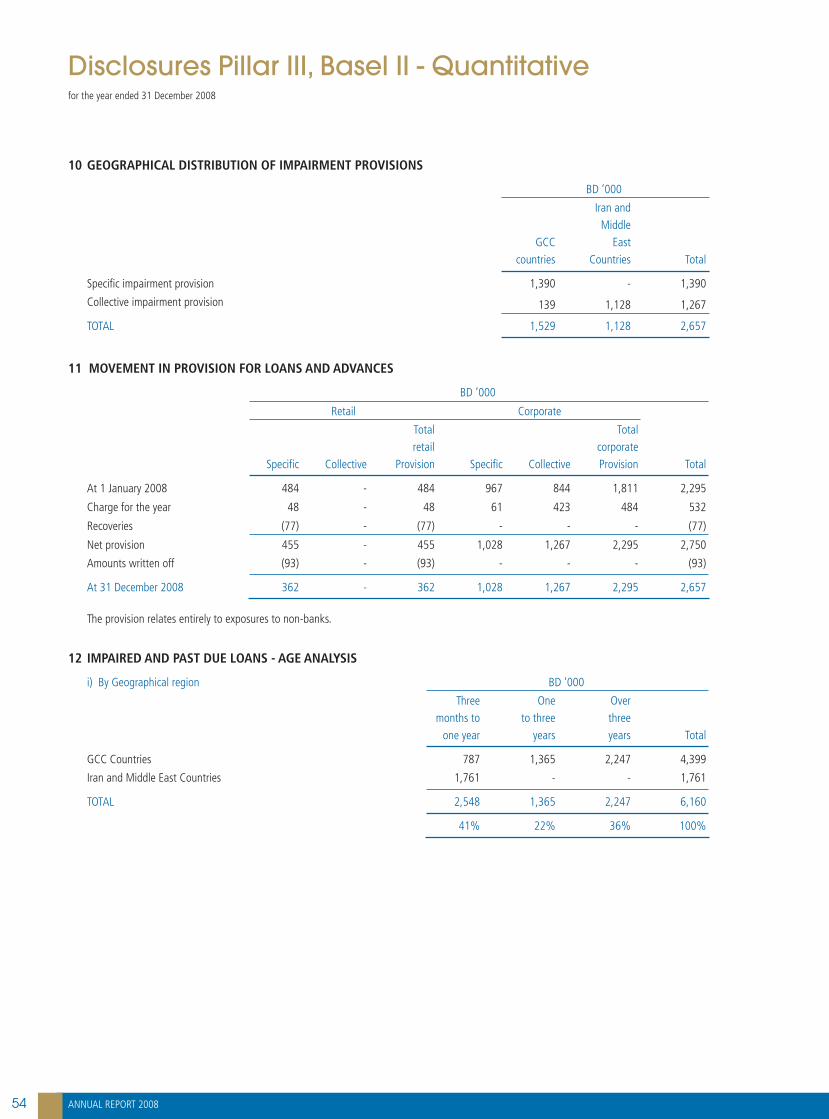

P.O.Box: 785City Centre Building 199Road 203, Block 304Manama TownGovernment AvenueKingdom of Bahrain

Tel:+973-17505000Fax:+973-17224402Swift Code: FUBBBHBM

Muharraq Branch

P.O. Box 22309Bldg 263, Road 311Muhurraq 203Shaikh Khalifa bin Salman AvenueKingdom of Bahrain

Tel: +973-17322494Fax: +973-17323644Swift Code: FUBBBHBMMUH

Budaiya Road Branch

P.O.Box 70115Shop No. 8 BCountry MallBudaiya HighwayKingdom of Bahrain

Tel: +973-17596666Fax: +973-17596111Swift Code: FUBBBHBMSIT

Tehran Representative Office

No.25Tandees AvenueAfrica HighwayTehranIslamic Republic of Iran

Tel: +9821-22053351,2Fax: +9821-26201311

»°ù«FôdG ÖàμŸG / »°ù«FôdG ´ôØdG785 Ü.¢U

199 Îæ°S »à«°S ájÉæH,304 ™ª› ,203 ≥jôW

áeÉæŸGáeƒμ◊G ´QÉ°T

øjôëÑdG áμ∏‡

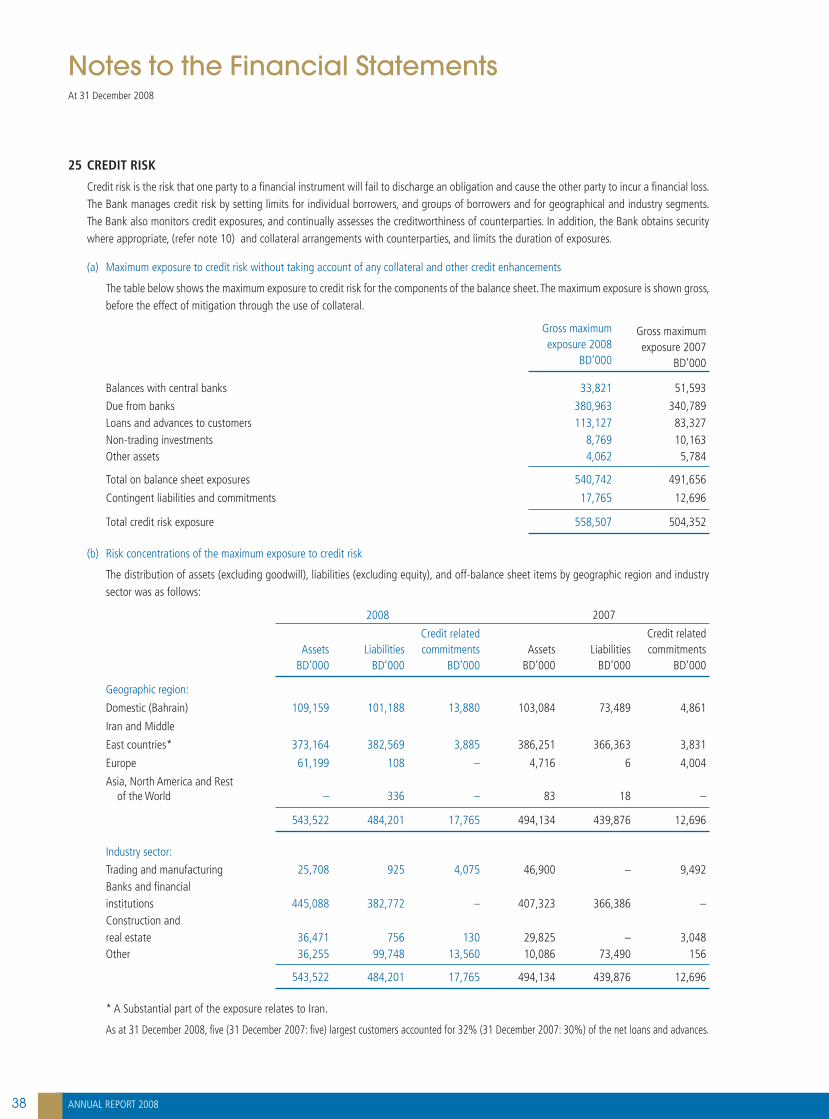

+973 17 505000 :∞JÉg+973 17 224402 :¢ùcÉa

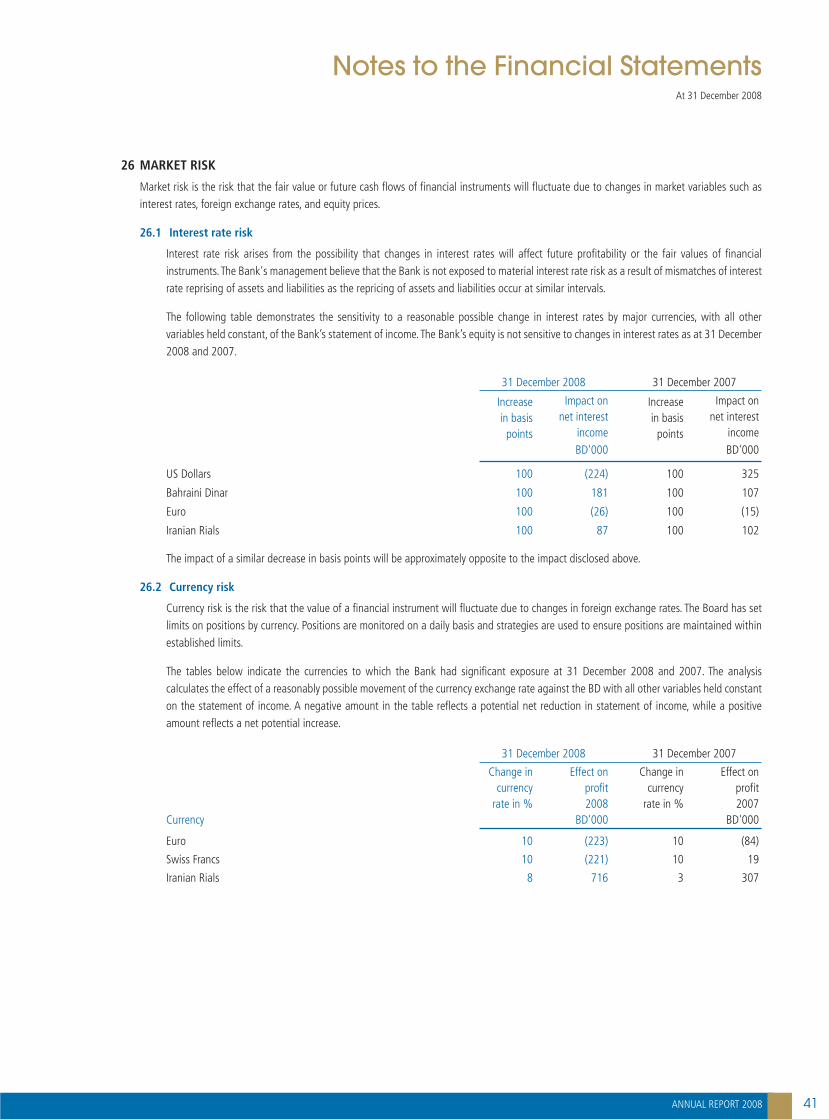

FUBBBHBM :âØjƒ°S

¥ôÙG ´ôa 22309 :Ü.¢U

311 ≥jôW ,263 ájÉæH203 ¥ôÙG

¿Éª∏°S øH áØ«∏N ï«°ûdG ´QÉ°TøjôëÑdG áμ∏‡

+973 17322494 :∞JÉg+973 17 323644 :¢ùcÉaFUBBBHBMMUH :âØjƒ°S

™jóÑdG ´QÉ°T ´ôa70115 Ü.¢U

∫ƒe …Îfƒc Ü 8 ºbQ πfiøjôëÑdG áμ∏‡ - ™jóÑdG ´QÉ°T

+973 17596666 :∞JÉg+973 17596111 :¢ùcÉa

FUBBBHBMSIT :âØjƒ°S

»∏«ãªàdG ¿Gô¡W Öàμe25 ºbQ ¢ùjóæJ ≥jôW

É«≤jôaCG ´QÉ°T¿Gô¡W

á«eÓ°SE’G ¿GôjEG ájQƒ¡ªL

+9821 22053351^2 :∞JÉg+9821 26201311 :¢ùcÉa

Table of Contents:

05 Financial Highlights

06 Chairman's Statement

07 Board of Directors

08 Group Management

09 Board Committee Members and Organization Chart

10 Major Shareholders, Voting Rights & Directors’ Interests

12 CEO's Statement & Management Review

14 Financial Review

16 Ongoing Developments

20 Auditor’s Report

21 Financial Statements - 2008

45 Disclosures

02

03

In this automated and ever changing world, the art of being personal mayseem out of place, but is perhaps the only nurturing and comforting constant.Today more than ever, people need to take time to connect with one another,and increasingly, businessmen all over the world are putting in greater efforttowards understanding their customers better.

This personal culture sets any business apart and makes all the difference indeveloping meaningful and trusting relationships with its customers. For everycustomer is different, every problem is unique and each client deserves personalattention that will cater to his individual needs.

We at Futurebank, have all the convenience of technology…but refuse toabandon our long cherished practice of taking your business personally.

FUTUREBANK…

A personalized culture can set a business

apart.

still personal

05

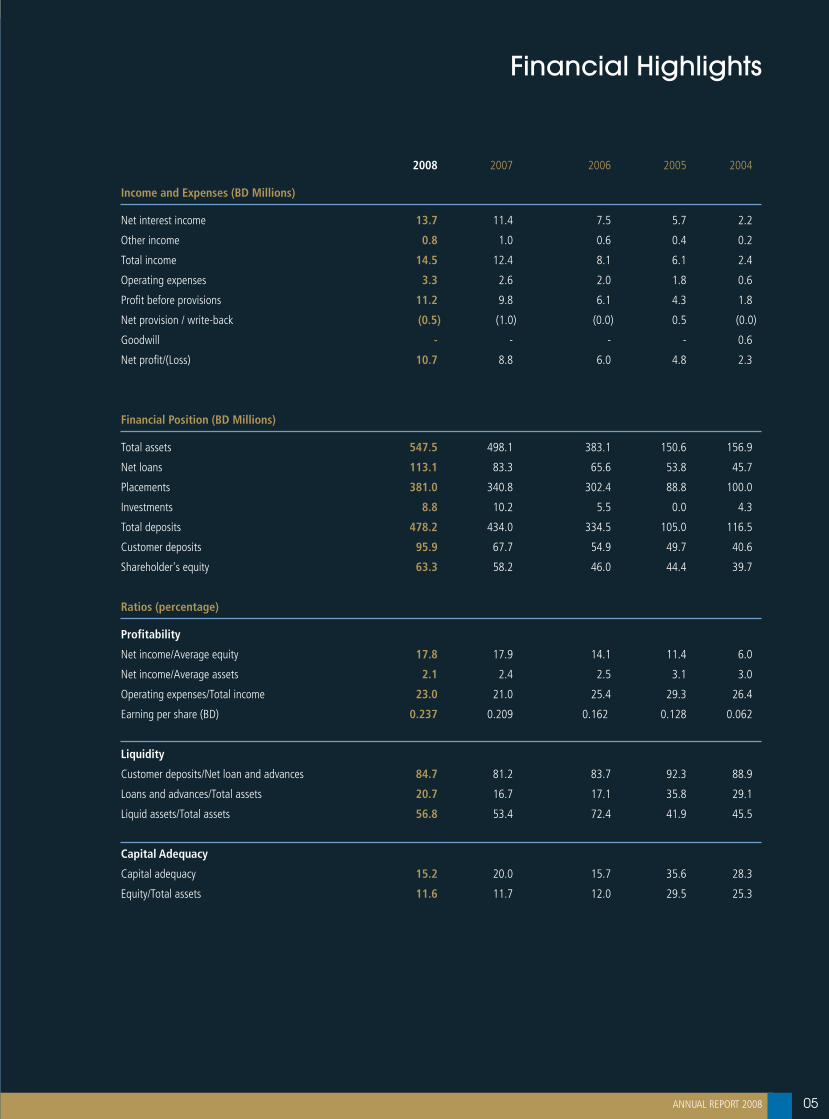

Financial Highlights

2008 2007 2006 2005 2004

Income and Expenses (BD Millions)

Net interest income 13.7 11.4 7.5 5.7 2.2

Other income 0.8 1.0 0.6 0.4 0.2

Total income 14.5 12.4 8.1 6.1 2.4

Operating expenses 3.3 2.6 2.0 1.8 0.6

Profit before provisions 11.2 9.8 6.1 4.3 1.8

Net provision / write-back (0.5) (1.0) (0.0) 0.5 (0.0)

Goodwill - - - - 0.6

Net profit/(Loss) 10.7 8.8 6.0 4.8 2.3

Financial Position (BD Millions)

Total assets 547.5 498.1 383.1 150.6 156.9

Net loans 113.1 83.3 65.6 53.8 45.7

Placements 381.0 340.8 302.4 88.8 100.0

Investments 8.8 10.2 5.5 0.0 4.3

Total deposits 478.2 434.0 334.5 105.0 116.5

Customer deposits 95.9 67.7 54.9 49.7 40.6

Shareholder's equity 63.3 58.2 46.0 44.4 39.7

Ratios (percentage)

Profitability

Net income/Average equity 17.8 17.9 14.1 11.4 6.0

Net income/Average assets 2.1 2.4 2.5 3.1 3.0

Operating expenses/Total income 23.0 21.0 25.4 29.3 26.4

Earning per share (BD) 0.237 0.209 0.162 0.128 0.062

Liquidity

Customer deposits/Net loan and advances 84.7 81.2 83.7 92.3 88.9

Loans and advances/Total assets 20.7 16.7 17.1 35.8 29.1

Liquid assets/Total assets 56.8 53.4 72.4 41.9 45.5

Capital Adequacy

Capital adequacy 15.2 20.0 15.7 35.6 28.3

Equity/Total assets 11.6 11.7 12.0 29.5 25.3

06

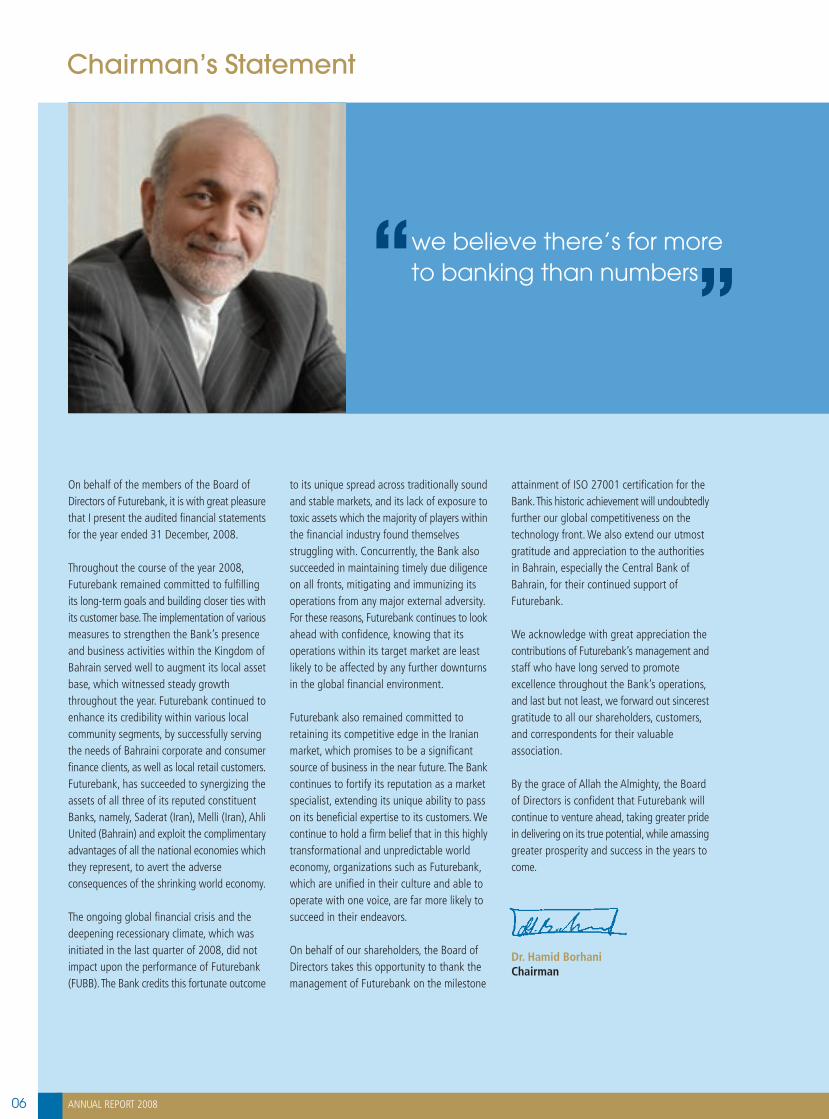

Chairman’s Statement

On behalf of the members of the Board ofDirectors of Futurebank, it is with great pleasurethat I present the audited financial statementsfor the year ended 31 December, 2008.

Throughout the course of the year 2008,Futurebank remained committed to fulfillingits long-term goals and building closer ties withits customer base. The implementation of variousmeasures to strengthen the Bank’s presenceand business activities within the Kingdom ofBahrain served well to augment its local assetbase, which witnessed steady growththroughout the year. Futurebank continued toenhance its credibility within various localcommunity segments, by successfully servingthe needs of Bahraini corporate and consumerfinance clients, as well as local retail customers.Futurebank, has succeeded to synergizing theassets of all three of its reputed constituentBanks, namely, Saderat (Iran), Melli (Iran), AhliUnited (Bahrain) and exploit the complimentaryadvantages of all the national economies whichthey represent, to avert the adverseconsequences of the shrinking world economy.

The ongoing global financial crisis and thedeepening recessionary climate, which wasinitiated in the last quarter of 2008, did notimpact upon the performance of Futurebank(FUBB). The Bank credits this fortunate outcome

to its unique spread across traditionally soundand stable markets, and its lack of exposure totoxic assets which the majority of players withinthe financial industry found themselvesstruggling with. Concurrently, the Bank alsosucceeded in maintaining timely due diligenceon all fronts, mitigating and immunizing itsoperations from any major external adversity.For these reasons, Futurebank continues to lookahead with confidence, knowing that itsoperations within its target market are leastlikely to be affected by any further downturnsin the global financial environment.

Futurebank also remained committed toretaining its competitive edge in the Iranianmarket, which promises to be a significantsource of business in the near future. The Bankcontinues to fortify its reputation as a marketspecialist, extending its unique ability to passon its beneficial expertise to its customers. Wecontinue to hold a firm belief that in this highlytransformational and unpredictable worldeconomy, organizations such as Futurebank,which are unified in their culture and able tooperate with one voice, are far more likely tosucceed in their endeavors.

On behalf of our shareholders, the Board ofDirectors takes this opportunity to thank themanagement of Futurebank on the milestone

attainment of ISO 27001 certification for theBank. This historic achievement will undoubtedlyfurther our global competitiveness on thetechnology front. We also extend our utmostgratitude and appreciation to the authoritiesin Bahrain, especially the Central Bank ofBahrain, for their continued support ofFuturebank.

We acknowledge with great appreciation thecontributions of Futurebank’s management andstaff who have long served to promoteexcellence throughout the Bank’s operations,and last but not least, we forward out sincerestgratitude to all our shareholders, customers,and correspondents for their valuableassociation.

By the grace of Allah the Almighty, the Boardof Directors is confident that Futurebank willcontinue to venture ahead, taking greater pridein delivering on its true potential, while amassinggreater prosperity and success in the years tocome.

Dr. Hamid BorhaniChairman

we believe there’s for moreto banking than numbers

07

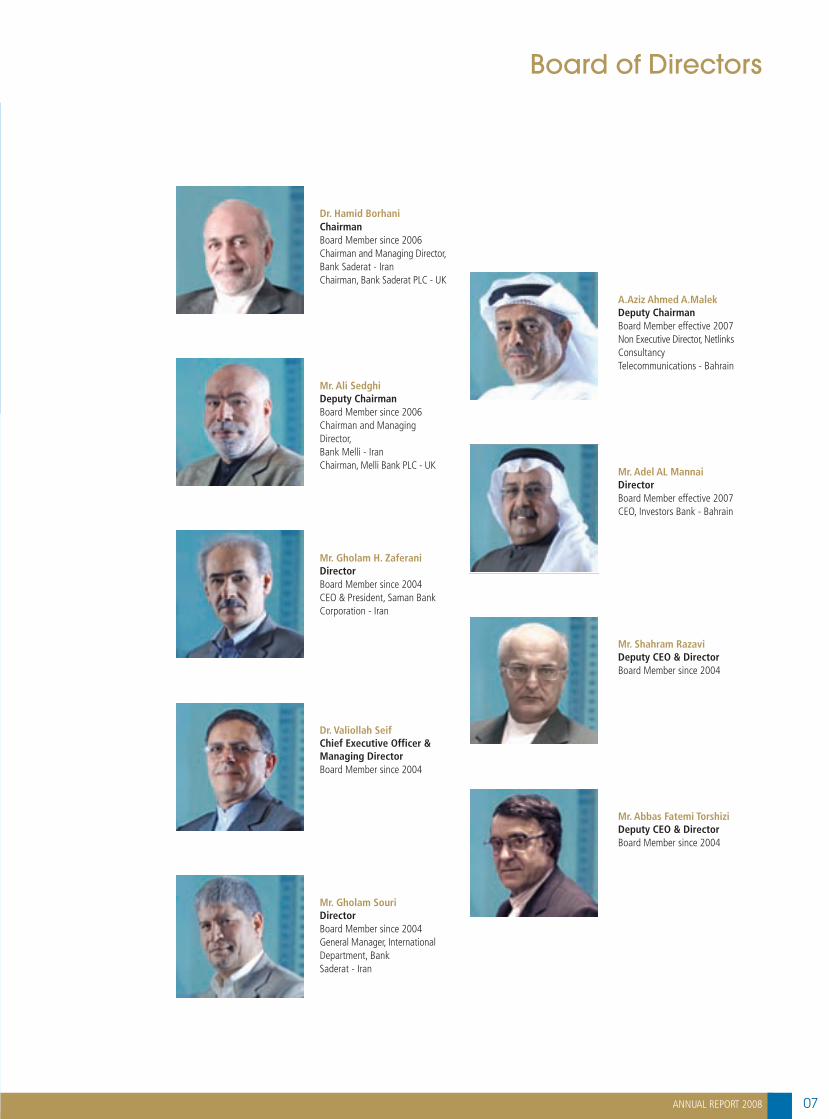

Board of Directors

Mr. Gholam H. ZaferaniDirectorBoard Member since 2004CEO & President, Saman BankCorporation - Iran

Mr. Gholam SouriDirectorBoard Member since 2004General Manager, InternationalDepartment, BankSaderat - Iran

Dr. Valiollah SeifChief Executive Officer &Managing DirectorBoard Member since 2004

Mr. Ali SedghiDeputy ChairmanBoard Member since 2006Chairman and ManagingDirector,Bank Melli - IranChairman, Melli Bank PLC - UK

Mr. Adel AL MannaiDirectorBoard Member effective 2007CEO, Investors Bank - Bahrain

Mr. Abbas Fatemi TorshiziDeputy CEO & DirectorBoard Member since 2004

Mr. Shahram RazaviDeputy CEO & DirectorBoard Member since 2004

A.Aziz Ahmed A.MalekDeputy ChairmanBoard Member effective 2007Non Executive Director, NetlinksConsultancyTelecommunications - Bahrain

Dr. Hamid BorhaniChairmanBoard Member since 2006Chairman and Managing Director,Bank Saderat - IranChairman, Bank Saderat PLC - UK

08

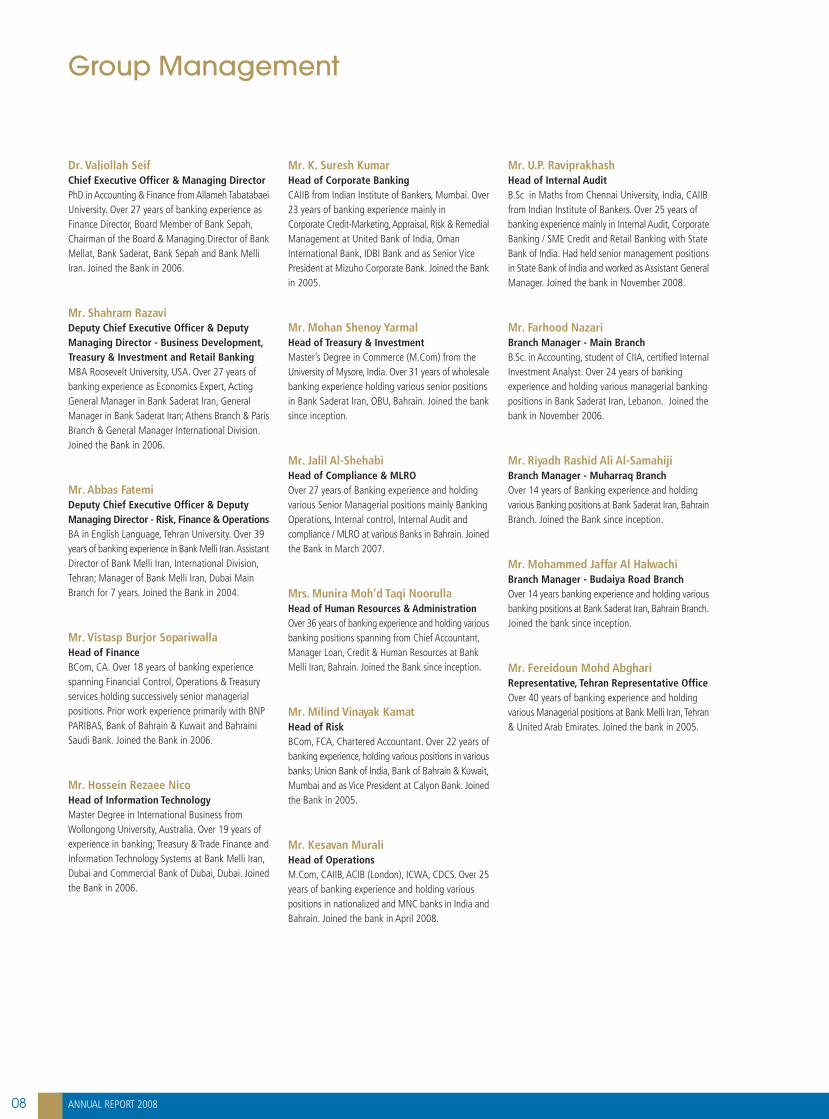

Dr. Valiollah SeifChief Executive Officer & Managing DirectorPhD in Accounting & Finance from Allameh TabatabaeiUniversity. Over 27 years of banking experience asFinance Director, Board Member of Bank Sepah,Chairman of the Board & Managing Director of BankMellat, Bank Saderat, Bank Sepah and Bank MelliIran. Joined the Bank in 2006.

Mr. Shahram RazaviDeputy Chief Executive Officer & DeputyManaging Director - Business Development,Treasury & Investment and Retail BankingMBA Roosevelt University, USA. Over 27 years ofbanking experience as Economics Expert, ActingGeneral Manager in Bank Saderat Iran, GeneralManager in Bank Saderat Iran; Athens Branch & ParisBranch & General Manager International Division.Joined the Bank in 2006.

Mr. Abbas FatemiDeputy Chief Executive Officer & DeputyManaging Director - Risk, Finance & OperationsBA in English Language, Tehran University. Over 39years of banking experience in Bank Melli Iran. AssistantDirector of Bank Melli Iran, International Division,Tehran; Manager of Bank Melli Iran, Dubai MainBranch for 7 years. Joined the Bank in 2004.

Mr. Vistasp Burjor SopariwallaHead of FinanceBCom, CA. Over 18 years of banking experiencespanning Financial Control, Operations & Treasuryservices holding successively senior managerialpositions. Prior work experience primarily with BNPPARIBAS, Bank of Bahrain & Kuwait and BahrainiSaudi Bank. Joined the Bank in 2006.

Mr. Hossein Rezaee NicoHead of Information TechnologyMaster Degree in International Business fromWollongong University, Australia. Over 19 years ofexperience in banking; Treasury & Trade Finance andInformation Technology Systems at Bank Melli Iran,Dubai and Commercial Bank of Dubai, Dubai. Joinedthe Bank in 2006.

Mr. K. Suresh KumarHead of Corporate BankingCAIIB from Indian Institute of Bankers, Mumbai. Over23 years of banking experience mainly inCorporate Credit-Marketing, Appraisal, Risk & RemedialManagement at United Bank of India, OmanInternational Bank, IDBI Bank and as Senior VicePresident at Mizuho Corporate Bank. Joined the Bankin 2005.

Mr. Mohan Shenoy YarmalHead of Treasury & InvestmentMaster’s Degree in Commerce (M.Com) from theUniversity of Mysore, India. Over 31 years of wholesalebanking experience holding various senior positionsin Bank Saderat Iran, OBU, Bahrain. Joined the banksince inception.

Mr. Jalil Al-ShehabiHead of Compliance & MLROOver 27 years of Banking experience and holdingvarious Senior Managerial positions mainly BankingOperations, Internal control, Internal Audit andcompliance / MLRO at various Banks in Bahrain. Joinedthe Bank in March 2007.

Mrs. Munira Moh’d Taqi NoorullaHead of Human Resources & AdministrationOver 36 years of banking experience and holding variousbanking positions spanning from Chief Accountant,Manager Loan, Credit & Human Resources at BankMelli Iran, Bahrain. Joined the Bank since inception.

Mr. Milind Vinayak KamatHead of RiskBCom, FCA, Chartered Accountant. Over 22 years ofbanking experience, holding various positions in variousbanks; Union Bank of India, Bank of Bahrain & Kuwait,Mumbai and as Vice President at Calyon Bank. Joinedthe Bank in 2005.

Mr. Kesavan MuraliHead of OperationsM.Com, CAIIB, ACIB (London), ICWA, CDCS. Over 25years of banking experience and holding variouspositions in nationalized and MNC banks in India andBahrain. Joined the bank in April 2008.

Mr. U.P. RaviprakhashHead of Internal AuditB.Sc in Maths from Chennai University, India, CAIIBfrom Indian Institute of Bankers. Over 25 years ofbanking experience mainly in Internal Audit, CorporateBanking / SME Credit and Retail Banking with StateBank of India. Had held senior management positionsin State Bank of India and worked as Assistant GeneralManager. Joined the bank in November 2008.

Mr. Farhood NazariBranch Manager - Main BranchB.Sc. in Accounting, student of CIIA, certified InternalInvestment Analyst. Over 24 years of bankingexperience and holding various managerial bankingpositions in Bank Saderat Iran, Lebanon. Joined thebank in November 2006.

Mr. Riyadh Rashid Ali Al-SamahijiBranch Manager - Muharraq BranchOver 14 years of Banking experience and holdingvarious Banking positions at Bank Saderat Iran, BahrainBranch. Joined the Bank since inception.

Mr. Mohammed Jaffar Al HalwachiBranch Manager - Budaiya Road BranchOver 14 years banking experience and holding variousbanking positions at Bank Saderat Iran, Bahrain Branch.Joined the bank since inception.

Mr. Fereidoun Mohd AbghariRepresentative, Tehran Representative OfficeOver 40 years of banking experience and holdingvarious Managerial positions at Bank Melli Iran, Tehran& United Arab Emirates. Joined the bank in 2005.

Group Management

09

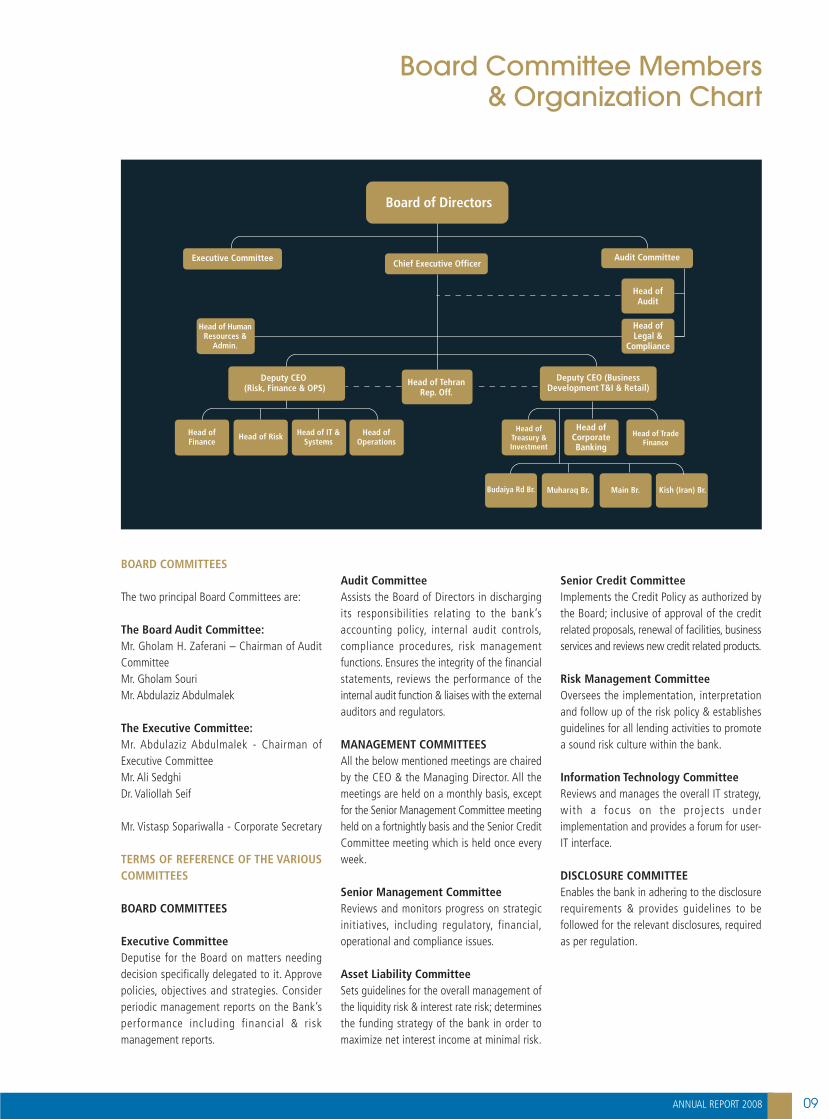

Board Committee Members& Organization Chart

BOARD COMMITTEES

The two principal Board Committees are:

The Board Audit Committee:Mr. Gholam H. Zaferani – Chairman of AuditCommitteeMr. Gholam SouriMr. Abdulaziz Abdulmalek

The Executive Committee:Mr. Abdulaziz Abdulmalek - Chairman ofExecutive CommitteeMr. Ali SedghiDr. Valiollah Seif

Mr. Vistasp Sopariwalla - Corporate Secretary

TERMS OF REFERENCE OF THE VARIOUSCOMMITTEES

BOARD COMMITTEES

Executive CommitteeDeputise for the Board on matters needingdecision specifically delegated to it. Approvepolicies, objectives and strategies. Considerperiodic management reports on the Bank’sperformance including financial & riskmanagement reports.

Audit CommitteeAssists the Board of Directors in dischargingits responsibilities relating to the bank’saccounting policy, internal audit controls,compliance procedures, risk managementfunctions. Ensures the integrity of the financialstatements, reviews the performance of theinternal audit function & liaises with the externalauditors and regulators.

MANAGEMENT COMMITTEESAll the below mentioned meetings are chairedby the CEO & the Managing Director. All themeetings are held on a monthly basis, exceptfor the Senior Management Committee meetingheld on a fortnightly basis and the Senior CreditCommittee meeting which is held once everyweek.

Senior Management CommitteeReviews and monitors progress on strategicinitiatives, including regulatory, financial,operational and compliance issues.

Asset Liability CommitteeSets guidelines for the overall management ofthe liquidity risk & interest rate risk; determinesthe funding strategy of the bank in order tomaximize net interest income at minimal risk.

Senior Credit CommitteeImplements the Credit Policy as authorized bythe Board; inclusive of approval of the creditrelated proposals, renewal of facilities, businessservices and reviews new credit related products.

Risk Management CommitteeOversees the implementation, interpretationand follow up of the risk policy & establishesguidelines for all lending activities to promotea sound risk culture within the bank.

Information Technology CommitteeReviews and manages the overall IT strategy,with a focus on the projects underimplementation and provides a forum for user-IT interface.

DISCLOSURE COMMITTEEEnables the bank in adhering to the disclosurerequirements & provides guidelines to befollowed for the relevant disclosures, requiredas per regulation.

Chief Executive OfficerAudit Committee

Board of Directors

Deputy CEO (Risk, Finance & OPS)

Head ofTreasury &Investment

Head ofCorporateBanking

Head of TradeFinance

Deputy CEO (BusinessDevelopment T&I & Retail)

Executive Committee

Head ofAudit

Head of TehranRep. Off.

Head of HumanResources &

Admin.

Head of Risk Head of IT &Systems

Head ofOperations

Head ofFinance

Budaiya Rd Br. Muharaq Br. Main Br. Kish (Iran) Br.

Head ofLegal &

Compliance

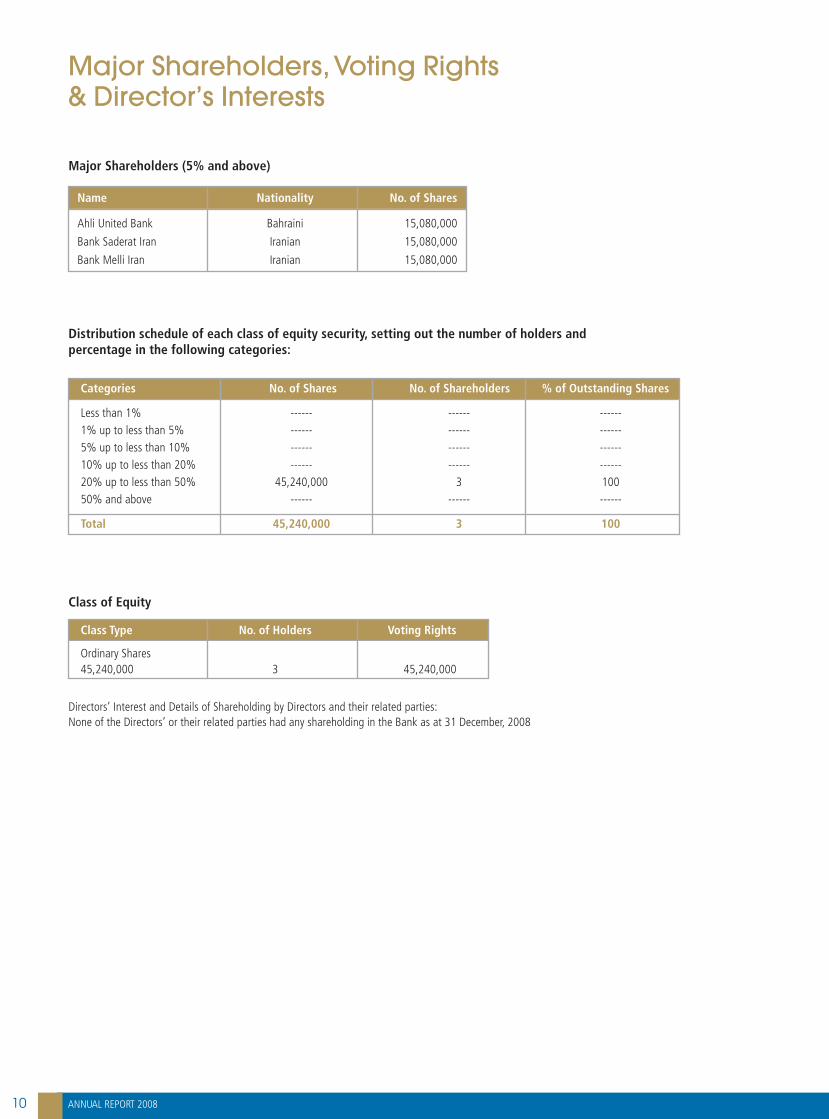

Major Shareholders, Voting Rights& Director’s Interests

10

Major Shareholders (5% and above)

Distribution schedule of each class of equity security, setting out the number of holders andpercentage in the following categories:

Class of Equity

Name Nationality No. of Shares

Ahli United Bank Bahraini 15,080,000

Bank Saderat Iran Iranian 15,080,000

Bank Melli Iran Iranian 15,080,000

Categories No. of Shares No. of Shareholders % of Outstanding Shares

Less than 1% ------ ------ ------1% up to less than 5% ------ ------ ------5% up to less than 10% ------ ------ ------10% up to less than 20% ------ ------ ------20% up to less than 50% 45,240,000 3 10050% and above ------ ------ ------

Total 45,240,000 3 100

Class Type No. of Holders Voting Rights

Ordinary Shares45,240,000 3 45,240,000

Directors’ Interest and Details of Shareholding by Directors and their related parties:None of the Directors’ or their related parties had any shareholding in the Bank as at 31 December, 2008

11

At the heart of our personal working philosophy is the task of turning a financial product or service intoan “experience” thereby defeating commoditization. Essentially it’s about making the right people-productconnect; connecting products to people or connecting solutions to problems. By developing a personalequation with our clients and placing great importance on the quality of this relationship, we ensure highercustomer loyalty and employee productivity. The end result is the ability to create new business opportunitiesthat are mutually beneficial.

Also intrinsic to this personal approach is the belief that a customer is not just another number, and wetake great pride in the fact that our staff knows each of our clients personally. So just as we offer ourcustomers with a Relationship Manager, or access to a human voice at the end of a phone, what remainsat the core of our working philosophy, is the ability to service their needs face to face.

CEO’s Statement& Management Review

12

I am pleased to report a thriving and prosperousfinancial and corporate performance. In 2008,the Bank’s Balance Sheet size grew by 9.90%,from BD 498.07 million in the previous year toBD 547.46 million in terms of Total Assets. Thissteady growth is attributable mainly to theincrease in the Placements with Bank’s portfolio(by almost 43%) and by a healthy increment inthe Loans & Advances portfolio amounting to36%, as compared with the previous year.

Having successfully achieved the goals andtargets set out by the Board of Directors,Futurebank recorded a net profit of BD 10.7million in 2008, as compared with BD 8.86million in the previous year. This represents anincrease of 20.9% over last year’s performanceand constitutes significant growth inFuturebank’s core operations. This level ofprofitability is also exceptional in the face of thecurrently volatile effects which the global financialmarkets are generally causing across the region.

Operating EnvironmentThe recent turmoil witnessed in global financialmarkets has lead to a recession which seemsto be running much deeper than initiallyanticipated. Vital economic indicators are yet tosignal any signs of recovery, as the worldeconomy continues to spiral downward, despitethe generous capital injections which have beenextended to key international financial marketsby the free economies.

Closer to home, major regional economies inthe GCC region, such as Saudi Arabia and theUAE, struggled to contain the ripple effects ofthe global financial meltdown and experiencedsignificant losses in their asset share values. Inthe face of plunging consumer confidence

indexes, the GCC states pro-actively injectedUS$ 10 billion into their local banks to easeliquidity constraints. The Saudi Central Bank’sstimulus package is estimated to have gone upto US$ 3 billion, in a fierce bid to stabilize theirlocal banks, while the UAE Ministry of Financedelivered AED 25 billion into the banking systemas part of an AED 70 billion overall rescue facility.

While most regional economies witnessed aslow-down, Bahrain’s success as an internationalfinancial centre remained largely unaffectedwith the Central Bank of Bahrain reaffirmingthe security and integrity of Bahraini banks, amove which inspired the financial communityto push on with progressive agendas and plans.Within this environment, Futurebank found itselfin a uniquely advantageous position, at a safedistance from the turmoil in the internationalfinancial markets and speculative practices,focusing on its traditionally sound andfundamentally robust target markets. All of theBank’s assets were gauged to be of the highestquality, with no evident or immediate risks toits target market and customer base.

Operational AchievementsDuring 2008, the Bank focused on strengtheningits operational stance within Bahrain, andenhancing its services to meet the needs of itsgrowing customer base. As a cautionary steptowards meeting its obligations and strategicgoals, the Bank arranged for a new strategicthree-year medium term borrowing facility,effectively securing and stabilizing its depositbase and funds.

Within Bahrain, Futurebank continued to expandon its products, service offerings and branchnetwork, welcoming customers into its newly

relocated Branch in Muharraq, as well as the recentlyinaugurated Budaiya Branch in Country Mall, whichis prominently situated on Budaiya Road.

In addition, an offsite ATM expansion planremained well underway throughout the yearand witnessed the addition of two new ATMunits in strategic locations. This drive will continueinto the upcoming calendar year with an aimto extend coverage across all the main centresof population and commerce..

Advancing state-of-the-art bankingconveniences, the Bank successfully introducedTelephone banking to enable its customer basewith round-the-clock access to the Bank’sproducts and customer services.

Taking stock of its unique identity and position,Futurebank also embarked on an insightful internalculturing program in collaboration with specialists,which allowed for the identification of the Banks’core strengths and essence. This exercise wasdeemed necessary at this juncture in order tosustain organizational cohesion and effectivelyrealize a viable road-map for the future.

The two-stage program culminated with thedevelopment and launch of a promotionaladvertising campaign within Bahrain to createmore awareness and enhance visibility ofFuturebank amongst its target markets and theBahraini community at large.

Corporate BankingFuturebank continued providing high qualitysyndication facilities to Iranian Corporate clientsat competitive rates. The Bank’s expertise insyndicated loans enhanced its capabilities towardsparticipation in other prospective syndications.

13

Futurebank found itself in a uniquely advantageous position, at a safe distance from the turmoil in theinternational financial markets and speculative practices, focusing on its traditionally sound and fundamentallyrobust target markets.

Futurebank’s corporate banking strategy is basedon the provision of comprehensive andcustomized financial solutions to our corporatecustomers, primarily in Bahrain, Iran and theGCC. The Bank extends a wide range of corporatebanking products including Bahraini Dinar andForeign Currency Debt, Working Capital Credit,Structured Financing, along with Syndicationand Transaction banking products and services.

The steady growth achieved during the year inproviding high quality syndication facilities tocorporate enterprises in Iran, at competitive rates,has allowed the Bank to bolster its expertise inSyndicated loans. This in turn has provided anadditional thrust to Futurebank’s attractivenessto other prospective syndication participants.

Information TechnologyFuturebank’s commitment to deploying cuttingedge technology witnessed numerousdevelopments and upgrades in the bank’s ITinvestments.

The steady advances achieved in terms ofeffective technology deployment, such as newsoftware developments implemented for TradeFinance will allow Futurebank to make furtheradvances into the market, as we prepare tolaunch high-potential products into the regionalretail banking sector.

ISO Certificate for Information SecurityFuturebank’s infrastructural credibility remaineda top priority, as information and network securitysystems were enhanced to meet future growthrequirements and expansion plans. In order toachieve and maintain the highest standard ofinformation security, the Bank continues to investa considerable amount of financial and human

resources in information technology and hassucceeded to obtain the prestigious ISO 27001Certificate. I am proud to report that Futurebankis one of the few banks to obtain thisdistinguished credential.

Human ResourcesAt the forefront of Futurebank’s ambitiousgrowth and development plans remains ourongoing commitment to the recruitment andretention of high quality professionals, to guidethe course of the Bank’s core activities.

Progress in this field included furthering theskills of employees, to enable them to adapt tothe ever changing growing requirements of thefinancial industry in general and the bankingindustry in particular.

Staff training and development initiatives wereintensified with the establishment andimplementation of best practice procedurestowards all branch operations.

Future OutlookFuturebank remains confident about itscapabilities, strengths and willingness to faceany challenges which the volatile externalenvironment may present. Looking to the future,

the Bank aligns its aims with the needs of itsgrowing client-base, bringing together the bestof financial opportunities and global prospectswhile providing leading-edge financial productsand banking services.

The planned expansion of our products andservices within our target markets is envisionedto continue well into the upcoming New Yearand beyond. We will remain steadfast on thestrategic path set out by the Board of Directorsof the Bank, and will act to implement growthinducing steps which compliment our customers’needs and aspirations.

Futurebank is committed to servicing theburgeoning economies in Iran and the Kingdomof Bahrain, and is poised to become the preferredchoice of customers who seek to tap into thesemarkets and their potentials. Leading the wayfor regional investors, the Bank has establisheda reputation for acting in the best interest of itscustomers and shareholders.

Dr. Valiollah SeifChief Executive Officer &Managing Director

Futurebank’s corporate banking strategy is based on the provision of comprehensive andcustomized financial solutions to our corporate customers, primarily in Bahrain, Iran and theGCC. The Bank extends a wide range of corporate banking products including Bahraini Dinarand Foreign Currency

Financial Review

14

Income Statement

Futurebank’s robust operating performance hasresulted in a record net profit of BD 10.7 million,registering an increment of 20.9 per cent overlast year’s net profit of BD 8.9 million. Thisexemplary growth is primarily attributed to thestrong revenue growth realized by the Bankacross all of its major business banking activities.This is reflected in its Return on Average Equityratio, which was maintained at 17.8 per cent ona higher capital base for the full year, as comparedto 17.9 per cent in the previous year 2007.

Net Operating Income increased by 22.33 percent from BD 11.5 million to BD 14.1 million.This exceptional financial performance reflectedwell upon the Bank’s continued growth acrossall principal business activities. The significantyear-on-year increase in the Bank’s profitabilitywas attributable to increases in interest earningsas well as an increase in its fees & commissionincome, with containment over the growth ofexpenses during the year.

The Bank saw its Net Interest income rise by BD2.3 million as compared to the previous year. Thisaccounted for an increase of 20.0 per cent whichwas achieved despite the increase in interestexpenses during the year. The increase in interestearnings was principally due to significantly higherloan volumes, with increased focus on the localregional market and a selection of large corporatesin Iran, for financing major Iranian projects.

Considering the markets within which the Bankoperates, increased margins helped Futurebankin maintaining the growth of its earnings, aswell as increasing its profitability to sustainablelevels. Thus, prudent use of liquidity positionsand the deployment of net available funds weremainly responsible for the growth of the netinterest margin, which stood at 2.49 per centas compared to 2.2 per cent in the previous year.

Fees and commission income witnessed asubstantial rise of 42 per cent over the previousyear mainly due to commission income earnedon the Trade Finance portfolio, together withfresh financing deals carried out by the Bank inconjunction with companies based in Iran, andsome note-worthy corporate deals finalized

within Bahrain with major clients. However, dueto the suppressed forex markets and theinternational turmoil currently being witnessed,foreign exchange profits made by the bank inthe previous year, to the extent of BD 0.42million, were not sustainable and reported at anet minor loss of BD 0.01 million. Together withforeign exchange profits, the Bank’s non-interestincome during 2008 represented a contributionof 5.4 per cent (BD 0.8 million) to total income,as compared to 8.3 per cent (BD 1.0 million) inthe previous year.

Although the Bank’s operating expensesincreased from BD 2.6 million to BD 3.3 million,for a comparative 27.2 per cent increase overthe previous year, they were mainly allocatedto the rising costs related to staffing the Bank’soperations. Despite the increase, the Cost toIncome ratio stood at only 23.0 per cent ascompared to 21.0 per cent in 2007 which wasnotably one of the lowest in the industry - atrue testament to the Bank’s operationalefficiency and ability to contain revenueexpenditures.

The Bank follows the International AccountingStandard (IAS) 39 for the provisioningrequirements of its non-performing portfolio.The Bank significantly increased its provisionrequirements during the year and has made acollective impairment provision of BD 1.3 milliontowards a healthier and stronger Balance sheet.Consequently the provision coverage ratio as ofyear-end 2008 stood at 67.8 per cent whencompared to 73.7 per cent as recorded in theprevious year. This is due to the fact that theBank holds significant assets as collateral inregards to many of these facilities.

Balance Sheet

The Bank’s balance sheet has grown from BD498.1 million to BD 547.5 million. This representsa modest but important increase of 10 per centin the Bank’s total assets, which under thecurrent scenario of restrictions and the globalfinancial crisis is credible.This growth in the Balance sheet size isattributable mainly to the significant growthachieved in its Loans & Advances portfolio andthe Placements portfolio with banks.

During the year, the Bank adopted a flexibleapproach to its asset mix which was instrumentalin yielding higher returns. The Bank’s assetallocation model has continued to focus moreon the Loans & Advances portfolio comprisingof 20.7 per cent of its Balance sheet, up from16.7 per cent in the previous year. However, thelucrative Bills discounted under the Banks’Portfolio, which now comprises of 22.8 per centof its Balance sheet at the year-end, as comparedto 32.4 per cent in the previous year.

Net loans and advances to customers rose byBD 29.8 million registering an increase of 35.8per cent during the year, as compared to theprevious year’s increase of only 27 per cent. Thiswas possible mainly due to a surge in corporatelending, along the Bank’s shifting focus onincreasing bilateral loans with Iranian & Bahrainibased companies.

The Inter-bank portfolio now comprises of 46.8per cent of the Bank’s total assets, compared to36 per cent in the previous year. A sum of BD 8.8million comprised specific investments which theBank made in high yielding Iranian Bonds. Theseinvestments are classified under the “Availablefor Sale” (AFS) and the “Held to Maturity” (HTM)category as per IAS 39. The Bank does not seeany risks associated with these securities.

Inter-bank deposits continue to form majorsources of funding for the Bank towards its Inter-bank portfolio. The ratio of Inter-bank depositsto total liabilities and the shareholders fund stoodat 69.8 per cent, as compared to 73.6 per centin the previous year. For the year ended 2008,the loans to customer deposit ratio includingMedium Term loan facilities availed by the Bank,stood at 88.6 per cent, compared to 98.9 percent in the previous year, to reflect betterutilizations.

Equity before appropriation increased to BD 63.3million at the end of 2008, up from BD 58.2million at the end of the previous year. Equity toTotal assets accounted for 11.6 per cent of theTotal assets of the Bank, as compared to 11.7per cent in the previous year.

15

Financial Review

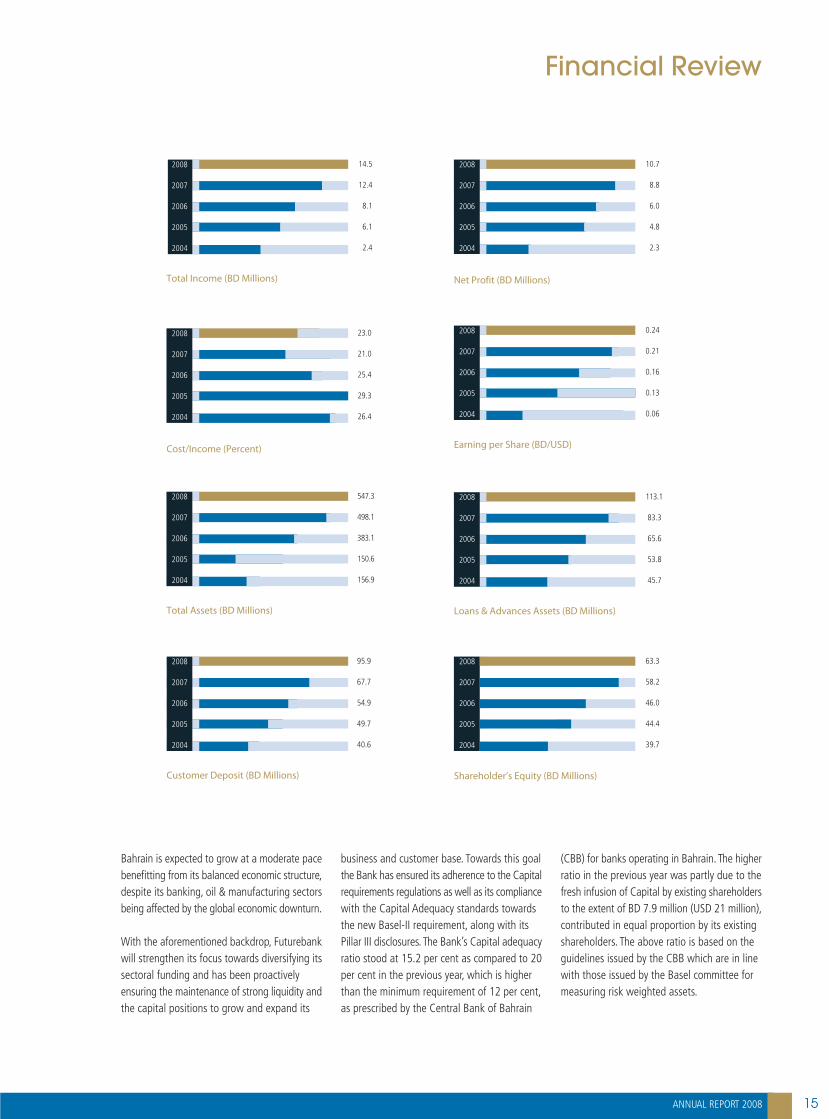

Bahrain is expected to grow at a moderate pacebenefitting from its balanced economic structure,despite its banking, oil & manufacturing sectorsbeing affected by the global economic downturn.

With the aforementioned backdrop, Futurebankwill strengthen its focus towards diversifying itssectoral funding and has been proactivelyensuring the maintenance of strong liquidity andthe capital positions to grow and expand its

business and customer base. Towards this goalthe Bank has ensured its adherence to the Capitalrequirements regulations as well as its compliancewith the Capital Adequacy standards towardsthe new Basel-II requirement, along with itsPillar III disclosures. The Bank’s Capital adequacyratio stood at 15.2 per cent as compared to 20per cent in the previous year, which is higherthan the minimum requirement of 12 per cent,as prescribed by the Central Bank of Bahrain

(CBB) for banks operating in Bahrain. The higherratio in the previous year was partly due to thefresh infusion of Capital by existing shareholdersto the extent of BD 7.9 million (USD 21 million),contributed in equal proportion by its existingshareholders. The above ratio is based on theguidelines issued by the CBB which are in linewith those issued by the Basel committee formeasuring risk weighted assets.

Net Profit (BD Millions)

Cost/Income (Percent) Earning per Share (BD/USD)

Total Assets (BD Millions) Loans & Advances Assets (BD Millions)

Customer Deposit (BD Millions) Shareholder’s Equity (BD Millions)

Total Income (BD Millions)

2008

2007

2006

2005

2004

14.5

12.4

8.1

6.1

2.4

2008

2007

2006

2005

2004

10.7

8.8

6.0

4.8

2.3

2008

2007

2006

2005

2004

23.0

21.0

25.4

29.3

26.4

2008

2007

2006

2005

2004

0.24

0.21

0.16

0.13

0.06

2008

2007

2006

2005

2004

547.3

498.1

383.1

150.6

156.9

2008

2007

2006

2005

2004

113.1

83.3

65.6

53.8

45.7

2008

2007

2006

2005

2004

95.9

67.7

54.9

49.7

40.6

2008

2007

2006

2005

2004

63.3

58.2

46.0

44.4

39.7

Futurebank is taking firm steps towards building its head quarters by starting construction on its new premises in the Seef district. The main idea inthe design approach was to create a branded corporate headquarters that draws from Post-Islamic influence and extends itself into a contemporaryand modern building thereby defining the bank itself as an analogue of future from the past.

Futurebank Tower, with its unique architecture style, infusing contemporary design with Iranian mosaic tiles, arches and minarets, will be an 19 storeybuilding, having a gross floor built-up area of around 15,000 square meters and cost over US$ 15 million (BD 5.9 million). Apart from housing thebank’s new global headquarters, the building will have six podium parking levels, an amenity level, offices and executive floors. The project was inspiredby the Futurebank logo geometry of a series of arches, which have been rearranged to result in a unique façade design.

This significant investment reinforces Futurebank’s contribution towards Bahrain’s long-term vision of becoming the financial centre of the MiddleEast. Since its inception, Futurebank has worked closely with the Central Bank of Bahrain to establish itself as a major player in Bahrain’s commercialbanking sector. By firmly grounding themselves in Bahrain, Futurebank hopes to create an environment conducive to building and furthering strongBahrain-Iran economic ties. To be completed by mid-2010, Futurebank’s new corporate premises will enable it to diversity its client base and expandits business within the MENA region.

Firm Foundations For Future

ANNUAL REPORT 2008 19

Our profitability has increased 20.9% year on

year, which demonstrates Futurebank’s ability

to deliver consistent, positive returns to our

stakeholders. But our priorities are skewed

towards our customers and we believe that

every transaction is a development of their

trust. We want our customers to feel confident

walking into any branch, knowing that his

business needs will be taken care of, face to

face.

In line with our ‘still personal’ philosophy, our

new global headquarters, the Futurebank

Towers, are being built as a reaffirmation of

our commitment to the business and to our

valued customers. We are laying firmer

foundations into the soil of this Kingdom and

the hearts of its people. We feel responsible

for those who deal with us and seek to partner

their dreams and shape their futures. The

Futurebank Tower is just another way of

creating exclusive customer touch-points; a

concrete proof of the fact that like a trusted

and reliable partner, Futurebank is standing

tall and by their side

Dr. Valiollah Seif

CEO & MD

17

18

Business Culture

This year, Futurebank connected with its client base,both current and potential, at an emotional yetprofessional level by employing an advertising strategywhich proposed that the customer is not just anothernumeric data in the system, but someone who isunique with a specific set of needs or problems thatmust be addressed individually. The communicationhighlighted the specific care and focus that is involvedin understanding and meeting a customer’s needs atFuturebank.

The message clearly differentiates Futurebank fromany other bank offering hi-tech banking solutions, bythe fact that while other banks are concentrating onde-humanizing and automating every conceivableaspect of banking, Futurebank continues to retain itstraditional practice of taking time out for its clients,coming face to face and meeting their needspersonally. Needless to say, the bottom line atFuturebank, is a happy and satisfied customer.

Guiding philosophy:

Technology is the means to an end...

and not the end itself.

End is the human touch.

19

ISO Certification

Futurebank receives ISO/IEC 2001:2005certification

Futurebank, has received the prestigious ISO27001 certification. The certification signifiesthat Futurebank’s IT operations conform to theInformation Management System Standard –ISO/IEC 27001:2005.

Futurebank is one of the first few bankinginstitutions in the Kingdom to have complianceto ISO 27001 standard, audited by TÜV SÜDSouth Asia, which is a subsidiary of Germany-based TÜV SÜD Group. The ISO 27001 certificationis the foremost international standard forinformation security management systems.

The certification scope covers Management ofInformation security for providing InfrastructureSetup and Support, Application Support andMaintenance, Backup, Helpdesk, NetworkManagement and System Administration.

Futurebank Chairman Dr. Hamid Borhani andChief Executive Officer Dr. Valiollah Seif receivedthe certificate on behalf of the bank, duringFuturebank’s first Board of Directors meetingof 2009.

Receiving the ISO/IEC 27001:2005 certification,is a milestone achievement for the bank and itunderlines the bank’s commitment to excellenceand to world-class Information Securitystandards.

Futurebank employees realise the paramountimportance of information security in the bankingindustry and this validation from the TÜV SÜDGroup further reinforces the bank’s ability todeliver secure banking services to their valuedcustomer base.

The certification and audit which was performedin a highly efficient and timely manner furtherreflects the efforts of the skilled IT Departmentat Futurebank who played a pivotal role in thisprocess.

Futurebank is dedicated to providing the highestquality of products and services to its customersand the implementation of this world-renownedcertification would further reassure the bank’scustomers about the high calibre of the systemsit has in place to safeguard their informationwith the bank.

About ISO/IEC 27001:2005

ISO/IEC 27001:2005 specifies the requirementsfor establishing, implementing, operating,monitoring, reviewing, maintaining andimproving a documented Information SecurityManagement System within the context of thebank’s overall business risks. The certification isdesigned to ensure the selection of adequateand proportionate security controls that protectinformation assets.

TÜV SÜD conducted the audit in two specificstages. Stage One involved a review of allFuturebank security and risk relateddocumentation including the Statement ofApplicability (SoA) and Risk Treatment Plan(RTP). Stage Two included a detailed audit andtesting of the effectiveness of the informationsecurity controls stated in the SoA and RTP.

About TÜV SÜD Group

TÜV SÜD is a major international service groupengaged in optimizing technology, systems andknow-how, and thus acting as process partners,enhancing the competitive strength of itscustomers throughout the world. Staffed by localexperts and powered by German expertise, TÜV

SÜD in the Asia Pacific region provides the entirerange of TÜV SÜD Group services offering one-stop shopping to secure fast and efficientinternational standard compliance andmanagement system certification.

20 ANNUAL REPORT 2008

Auditors’ Report to the Shareholders of Futurebank B.S.C. (c)

We have audited the accompanying financial statements of Futurebank B.S.C. (c) (“the Bank”), which comprise the balance sheet as at 31 December 2008 and the statements of income, changes in equity and cash flows for the year then ended, and a summary of significant accounting policies and other explanatory notes.

Board of Director’s Responsibility for the Financial Statements

The Board of Directors is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditors’ Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate for the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Board of Directors, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position of the Bank as of 31 December 2008 and its financial performance and its cash flows for the year then ended in accordance with International Financial Reporting Standards.

Other Regulatory Matters

We confirm that, in our opinion, proper accounting records have been kept by the Bank and the financial statements and the content of the chairman’s report relating to these financial statements are in agreement therewith. We further report, to the best of our knowledge and belief, that no violations of the Bahrain Commercial Companies Law, nor of the Central Bank of Bahrain and Financial Institutions Law nor of the memorandum of articles of association of the Bank have occurred during the year ended 31 December 2008 that might have had a material adverse effect on the business of the Bank or on its financial position and that the Bank has complied with the terms of its banking license.

25 January 2009Manama, Kingdom of Bahrain

22 ANNUAL REPORT 2008

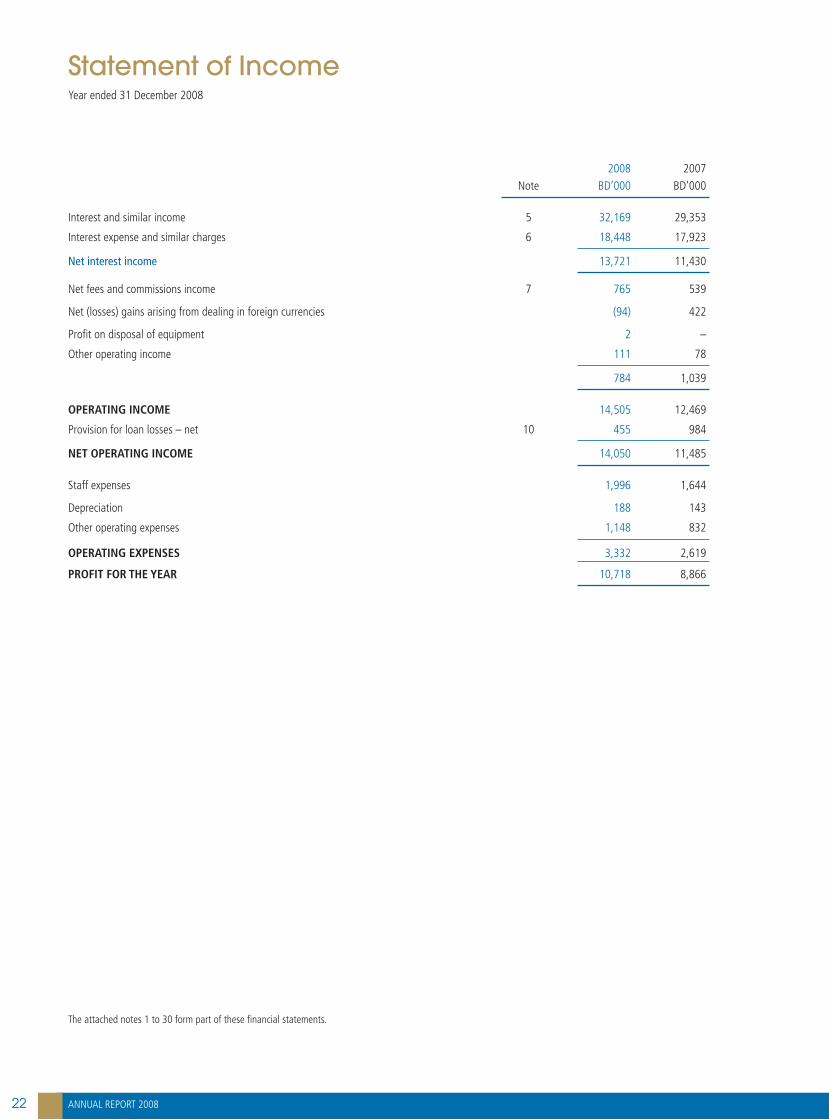

Statement of IncomeYear ended 31 December 2008

Note2008

BD’0002007

BD’000

Interest and similar income 5 32,169 29,353

Interest expense and similar charges 6 18,448 17,923

Net interest income 13,721 11,430

Net fees and commissions income 7 765 539

Net (losses) gains arising from dealing in foreign currencies (94) 422

Profit on disposal of equipment 2 –

Other operating income 111 78

784 1,039

OPERATING INCOME 14,505 12,469

Provision for loan losses – net 10 455 984

NET OPERATING INCOME 14,050 11,485

Staff expenses 1,996 1,644

Depreciation 188 143

Other operating expenses 1,148 832

OPERATING EXPENSES 3,332 2,619

PROFIT FOR THE YEAR 10,718 8,866

The attached notes 1 to 30 form part of these financial statements.

ANNUAL REPORT 2008 23

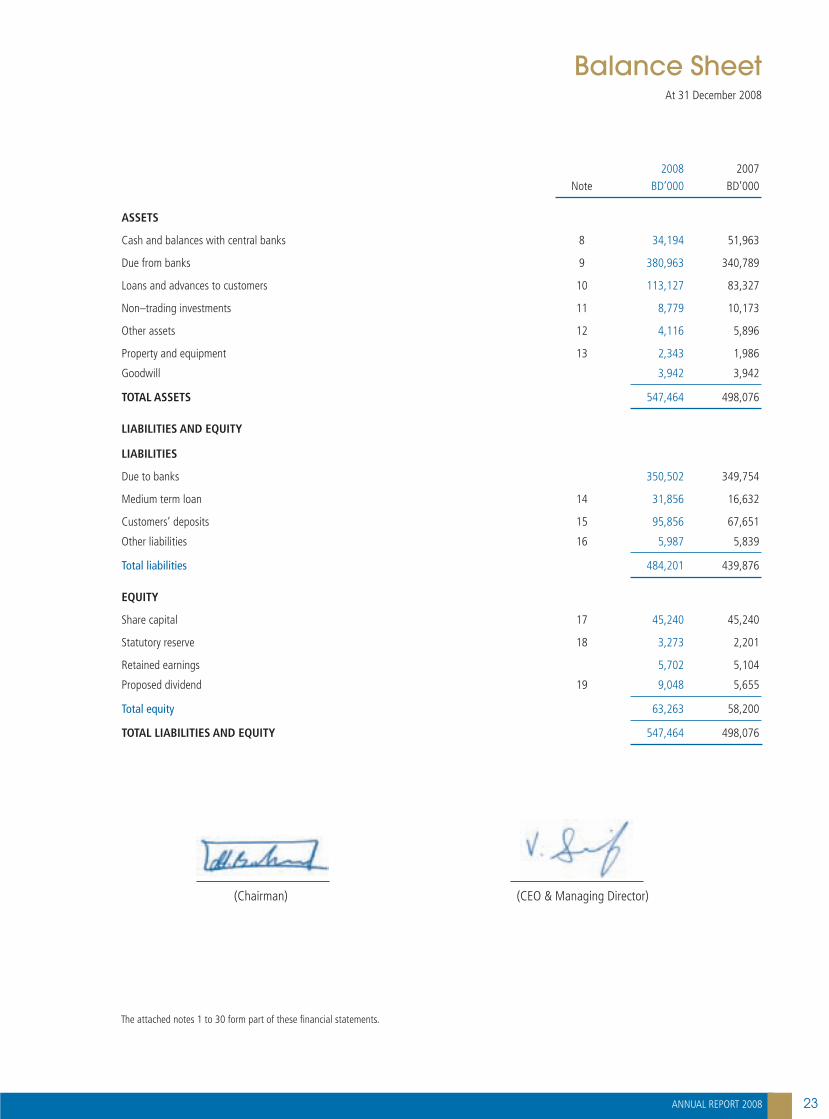

Balance SheetAt 31 December 2008

Note2008

BD’0002007

BD’000

ASSETS

Cash and balances with central banks 8 34,194 51,963

Due from banks 9 380,963 340,789

Loans and advances to customers 10 113,127 83,327

Non–trading investments 11 8,779 10,173

Other assets 12 4,116 5,896

Property and equipment 13 2,343 1,986

Goodwill 3,942 3,942

TOTAL ASSETS 547,464 498,076

LIABILITIES AND EQUITY

LIABILITIES

Due to banks 350,502 349,754

Medium term loan 14 31,856 16,632

Customers’ deposits 15 95,856 67,651

Other liabilities 16 5,987 5,839

Total liabilities 484,201 439,876

EQUITY

Share capital 17 45,240 45,240

Statutory reserve 18 3,273 2,201

Retained earnings 5,702 5,104

Proposed dividend 19 9,048 5,655

Total equity 63,263 58,200

TOTAL LIABILITIES AND EQUITY 547,464 498,076

(Chairman) (CEO & Managing Director)

The attached notes 1 to 30 form part of these financial statements.

24 ANNUAL REPORT 2008

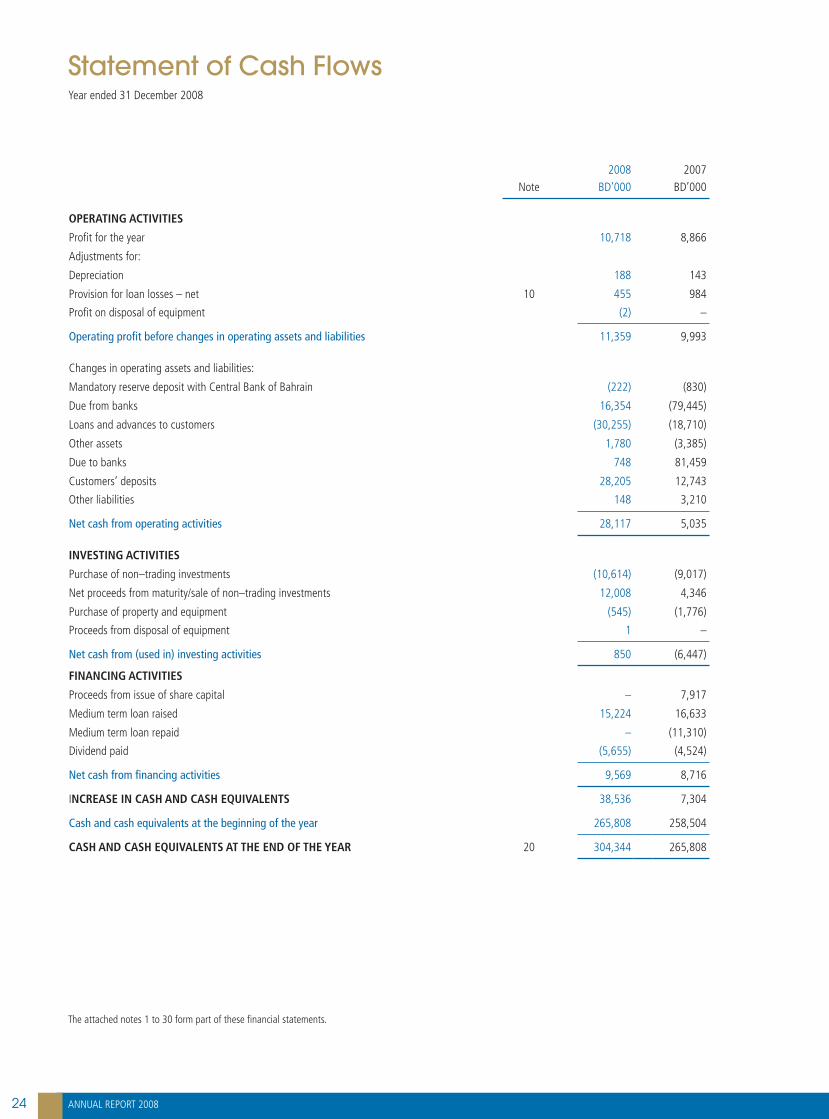

Statement of Cash FlowsYear ended 31 December 2008

Note2008

BD’0002007

BD’000

OPERATING ACTIVITIES

Profit for the year 10,718 8,866

Adjustments for:

Depreciation 188 143

Provision for loan losses – net 10 455 984

Profit on disposal of equipment (2) –

Operating profit before changes in operating assets and liabilities 11,359 9,993

Changes in operating assets and liabilities:

Mandatory reserve deposit with Central Bank of Bahrain (222) (830)

Due from banks 16,354 (79,445)

Loans and advances to customers (30,255) (18,710)

Other assets 1,780 (3,385)

Due to banks 748 81,459

Customers’ deposits 28,205 12,743

Other liabilities 148 3,210

Net cash from operating activities 28,117 5,035

INVESTING ACTIVITIES

Purchase of non–trading investments (10,614) (9,017)

Net proceeds from maturity/sale of non–trading investments 12,008 4,346

Purchase of property and equipment (545) (1,776)

Proceeds from disposal of equipment 1 –

Net cash from (used in) investing activities 850 (6,447)

FINANCING ACTIVITIES

Proceeds from issue of share capital – 7,917

Medium term loan raised 15,224 16,633

Medium term loan repaid – (11,310)

Dividend paid (5,655) (4,524)

Net cash from financing activities 9,569 8,716

INCREASE IN CASH AND CASH EQUIVALENTS 38,536 7,304

Cash and cash equivalents at the beginning of the year 265,808 258,504

CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR 20 304,344 265,808

The attached notes 1 to 30 form part of these financial statements.

ANNUAL REPORT 2008 25

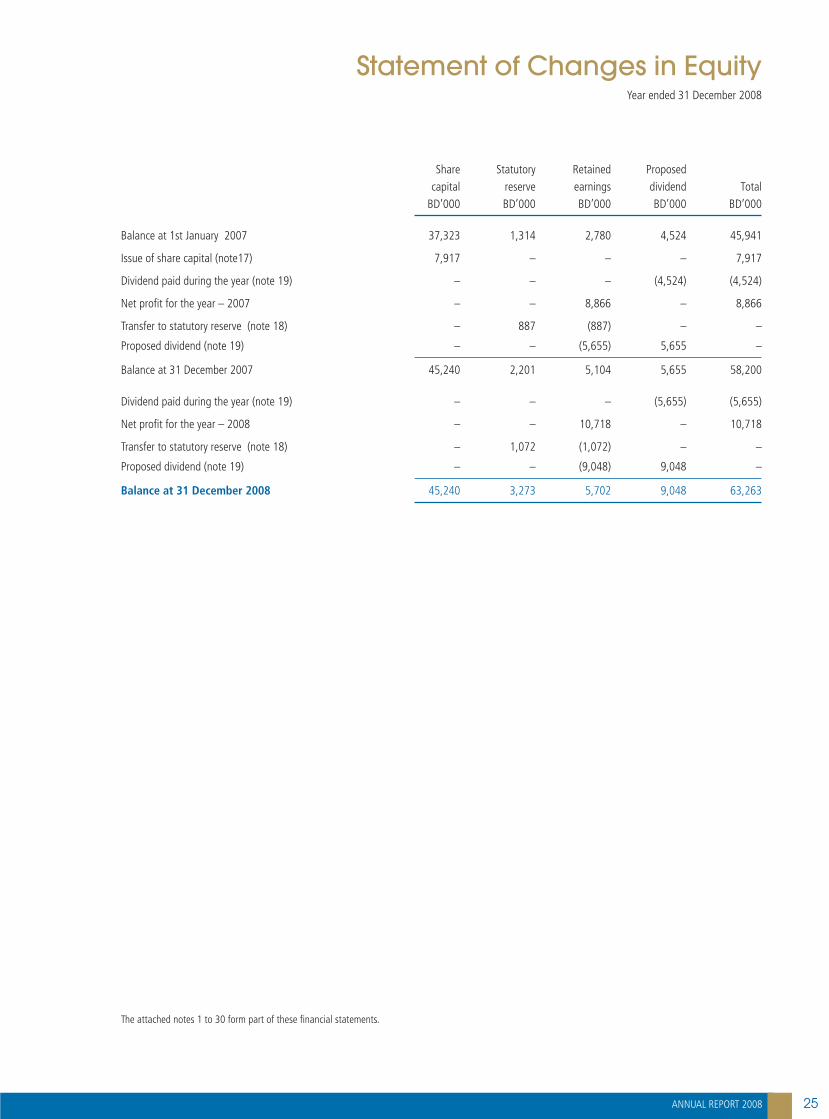

Statement of Changes in EquityYear ended 31 December 2008

The attached notes 1 to 30 form part of these financial statements.

Sharecapital

BD’000

StatutoryreserveBD’000

RetainedearningsBD’000

ProposeddividendBD’000

TotalBD’000

Balance at 1st January 2007 37,323 1,314 2,780 4,524 45,941

Issue of share capital (note17) 7,917 – – – 7,917

Dividend paid during the year (note 19) – – – (4,524) (4,524)

Net profit for the year – 2007 – – 8,866 – 8,866

Transfer to statutory reserve (note 18) – 887 (887) – –

Proposed dividend (note 19) – – (5,655) 5,655 –

Balance at 31 December 2007 45,240 2,201 5,104 5,655 58,200

Dividend paid during the year (note 19) – – – (5,655) (5,655)

Net profit for the year – 2008 – – 10,718 – 10,718

Transfer to statutory reserve (note 18) – 1,072 (1,072) – –

Proposed dividend (note 19) – – (9,048) 9,048 –

Balance at 31 December 2008 45,240 3,273 5,702 9,048 63,263

26 ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

1 ACTIVITIES

Futurebank B.S.C. (c) (“the Bank”) is a closed Bahrain Joint Stock Company incorporated on 1 July 2004 when the Bank acquired the Bahrain commercial branches of Bank Melli Iran (BMI) and Bank Saderat Iran (BSI) and the offshore banking unit of BSI. The Bank operates in the Kingdom of Bahrain under a retail banking license issued by the Central Bank of Bahrain and is engaged in commercial banking activities. The Bank has three branches in Bahrain and has obtained regulatory approval for opening a branch in Kish Island in the Islamic Republic of Iran. The address of the Bank’s registered office is PO Box 785, Manama, Kingdom of Bahrain.

The financial statements for the year ended 31 December 2008 were authorised for issue in accordance with a resolution of the directors on 25 January 2009.

2 BASIS OF PREPARATION

Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) and in conformity with the Bahrain Commercial Companies Law and the Central Bank of Bahrain and Financial Institutions Law.

Accounting convention

The financial statements are prepared under the historical cost convention. The financial statements have been presented in Bahraini Dinars (BD) being the functional currency of the Bank and all values are rounded to the nearest thousand BD except when otherwise indicated.

Change of functional currency

At the Extraordinary General Assembly of Shareholders’ Meeting held on 16 March 2008, the shareholders approved the change in the Bank’s functional currency from US Dollars to Bahraini Dinars. Since the Bank’s transactions are mainly denominated in Bahraini Dinars, the Bank considered it appropriate to change its functional currency to Bahraini Dinars for management, regulatory and external financial reporting.

Standards Issued but not adopted

The Bank has not adopted the revised IAS 1 “Presentation of Financial Statements” which will be effective for the year ending 31 December 2009. The application of this standard will result in amendments to the presentation of the financial statements.

3 SIGNIFICANT ACCOUNTING JUDGMENTS AND ESTIMATES

In the process of applying the Bank’s accounting policies, management has used its judgment and made estimates in determining the amounts recognised in the financial statements. The most significant use of judgments and estimates are as follows:

Impairment losses on loans and advances

The Bank reviews its problem loans and advances at each reporting date to assess whether an allowance for impairment should be recorded in the statement of income. In particular, judgment by management is required in the estimation of the amount and timing of future cash flows when determining the level of allowance required. Such estimates are based on assumptions about a number of factors and actual results may differ, resulting in future changes to such allowance.

Collective impairment provisions on loans and advances

In addition to specific allowances against individually significant loans and advances, the Bank also makes a collective impairment allowance against exposures which, although not specifically identified as requiring a specific allowance, have a greater risk of default than when originally granted. This collective allowance is based on any deterioration in the internal rating of the loan or investment since it was granted or acquired. These internal ratings take into consideration factors such as any deterioration in country risk, industry, and technological obsolescence as well as identified structural weaknesses or deterioration in cash flows.

ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

27

4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The significant accounting policies applied in the preparation of these financial statements are set out below. Policies have been consistently applied to all the years presented, unless otherwise stated.

Foreign currency translation

Transactions in foreign currencies are initially recorded in the functional currency at the rate of exchange ruling at the date of the transaction.

Monetary assets and liabilities denominated in foreign currencies are retranslated at the functional currency rate of exchange ruling at the balance sheet date. All differences are taken to the statement of income.

Financial instruments

The classification of financial instruments at initial recognition depends on the purpose for which the financial instruments were acquired and their characteristics. All financial instruments are initially measured at their fair value plus, any directly attributable incremental costs of acquisition or issue.

(i) Date of recognition Purchases or sales of financial assets that require delivery of assets within the time frame generally established by regulation or convention

in the marketplace are recognised on trade date, i.e. the date that the Bank commits to purchase or sell the asset.

(ii) Available-for-sale investments Available-for-sale investments are those which are designated as such or do not qualify to be classified as designated at fair value through

profit or loss, held-to-maturity or loans and advances. Available-for-sale investments are initially measured at cost and are subsequently measured at fair value. Unrealised gains and losses are recognised in equity under “cumulative changes in fair value” and foreign exchange gains and losses are recognised in statement of income under “Net gains/(losses) arising from dealing in foreign currencies”.

(iii) Held-to-maturity investments Held-to-maturity investments are those which carry fixed or determinable payments and fixed maturities and which the Bank has the

intention and ability to hold to maturity. After initial measurement, held-to-maturity investments are subsequently measured at amortised cost using the effective interest rate method, less allowance for impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees that are an integral part of the effective interest rate. The amortisation is included in ‘Interest and similar income’ in the statement of income. The losses arising from impairment of such investments are recognised in the statement of income.

(iv) Loans and advances Loans and advances are financial assets with fixed or determinable payments and fixed maturities that are not quoted in an active market.

They are not entered into with the intention of immediate or short-term resale. This accounting policy relates to the balance sheet captions ‘Due from banks’ and ‘Loans and advances to customers’. After initial measurement, the loans and advances are subsequently measured at amortised cost using the effective interest rate method, less allowance for impairment. Amortised cost is calculated by taking into account any discount or premium on acquisition and fees that are an integral part of the effective interest rate. The amortisation is included in ‘Interest and similar income’ in the income statement. The losses arising from impairment of such loans and advances are recognised in the income statement in ‘Provision for loan losses-net’.

(v) Derivatives Derivatives represent forward foreign exchange contracts. Derivatives are recorded at fair value and carried as assets when the fair value is

positive and as liabilities when the fair value is negatives. Changes in fair value of derivatives held for trading are included in the statement of income.

(vi) Medium term loan Medium term loan is stated at amortised cost using the effective interest rate method.

28 ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Derecognition of financial assets and financial liabilities

(i) Financial assetsA financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognised where:

– the rights to receive cash flows from the asset have expired;

– the Bank retains the right to receive cash flows from the asset, but has assumed an obligation to pay them in full without material delay to a third party under a ‘pass–through’ arrangement; or

– the Bank has transferred its rights to receive cash flows from the asset and either (a) has transferred substantially all the risks and rewards of the asset, or (b) has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset.

(ii) Financial liabilitiesA financial liability is derecognised when the obligation under the liability is discharged or cancelled or expired.

Fair value

For investments quoted in an active market, fair value is calculated by reference to quoted bid prices. The fair value of forward exchange contracts is calculated by reference to forward exchange rates with similar maturities.

Impairment of financial assets

The Bank assesses at each balance sheet date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event (or events) has an impact on the estimated future flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the borrower or a group of borrowers is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganisation and where observable data indicates that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults. If such evidence exists, any impairment loss, is recognised in the statement of income.

The carrying amount of the asset is reduced through the use of an allowance account and the amount of the loss is recognised in the statement of income. Interest income continues to be accrued on the reduced carrying amount based on the original effective interest rate of the asset. Loans together with the associated allowance are written off when there is no realistic prospect of future recovery and all collateral has been realised or has been transferred to the Bank. If, in a subsequent year, the amount of the estimated impairment loss increases or decreases because of an event occurring after the impairment was recognised, the previously recognised impairment loss is increased or reduced by adjusting the allowance account and the corresponding amount recognised in the statement of income. If a future write–off is later recovered, the recovery is credited to the ‘Provision for loan losses – net’.

Impairment is determined as follows:

(a) for assets carried at amortised cost, impairment is based on estimated cash flows discounted at the original effective interest rate;

(b) for assets carried at fair value, impairment is the difference between cost and fair value; and

(c) for assets carried at cost, impairment is based on present value of estimated future cash flows discounted at the current market rate of return for a similar financial asset.

In addition, a provision is made to cover impairment for specific groups of assets where there is a measurable decrease in estimated future cash flows.

ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

29

4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Impairment of non–financial assets

The Bank assesses at each reporting date whether there is an indication that an asset may be impaired. If any such indication exists, or when annual impairment testing for an asset is required, the Bank makes an estimate of the asset’s recoverable amount. An asset’s recoverable amount is the higher of an asset’s or cash–generating unit’s fair value less costs to sell and its value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets and then its recoverable amount is assessed as part of the cash–generating unit to which it belongs. Where the carrying amount of an asset (or cash–generating unit) exceeds its recoverable amount, the asset (or cash–generating unit) is considered impaired and is written down to its recoverable amount.

Offsetting financial instruments

Financial assets and financial liabilities are offset and the net amount reported in the balance sheet, if, and only if, there is a currently enforceable legal right to offset the recognised amounts and there is an intention to settle on a net basis, or to realise the asset and settle the liability simultaneously.

Revenue recognition

Revenue is recognised to the extent that it is probable that the economic benefits will flow to the Bank and the revenue can be reliably measured. The following specific recognition criteria must also be met before revenue is recognised.

(i) Interest and similar income For all financial instruments measured at amortised cost, interest–income or expense is recorded at the effective interest rate.

(ii) Fee and commission income Credit origination fees are treated as an integral part of the effective interest rate of financial instruments and are recognised over their lives,

except when the underlying risk is sold to a third party at which time it is recognised immediately. Other fees and commission income are recognised when earned.

(iii) Dividend income Dividend income is recognised when the right to receive payment is established.

Property and equipment

Property and equipment is stated at cost less accumulated depreciation and accumulated impairment in value.

Depreciation is calculated using the straight–line method to write down the cost of equipment to their residual values over their estimated useful life of 5 years. Land is not depreciated.

An item of equipment is derecognised upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the statement of income in the year the asset is derecognised.

Goodwill

Goodwill arising on acquisition is measured at cost, being the excess of the cost of the business combination over the acquirer’s interest in the net fair value of identifiable assets, liabilities and contingent liabilities. Following initial recognition, goodwill is measured at cost less any accumulated impairment losses. Goodwill is not amortised, but reviewed for impairment annually, or more frequently if events or changes in circumstances indicate that the carrying value may be impaired. Impairment is determined by assessing the recoverable amount of the cash generating unit, to which the goodwill relates. Where the recoverable amount of the cash generating unit is less than the carrying amount, an impairment loss is recognised.

Provisions

Provisions are recognised when the Bank has a present obligation (legal or constructive) arising from a past event and the costs to settle the obligation are both probable and able to be reliably measured.

30 ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

4 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Employees’ end of service benefits

The Bank provides end of service benefits to its expatriate employees. The entitlement to these benefits is based upon the employees’ final salary and length of service, subject to the completion of a minimum service period. The expected costs of these benefits are accrued over the period of employment.

With respect to its national employees, the Bank makes contributions to the General Organisation for Social Insurance calculated as a percentage of the employees’ salaries. The Bank’s obligations are limited to these contributions, which are expensed when due.

Cash and cash equivalents

Cash and cash equivalents comprise cash, balances with central banks (excluding mandatory reserve deposits), deposits with banks with original maturities of less than ninety days.

Dividends on ordinary shares

Dividends on ordinary shares are recognised as a liability and deducted from equity when they are approved by the Bank’s shareholders. Interim dividends are deducted from equity when they are paid.

Dividends for the year that are approved after the balance sheet date are dealt with as an event after the balance sheet date.

Financial guarantees

In the ordinary course of business, the Bank gives financial guarantees, consisting of letters of credit, guarantees and acceptances. Financial guarantees are initially recognised in the financial statements at fair value, being the premium received. Subsequent to initial recognition, the Bank’s liability under each guarantee is measured at the higher of the amortised premium and the best estimate of expenditure required to settle any financial obligation arising as a result of the guarantee.

Any increase in the liability relating to financial guarantees is taken to the statement of income in ‘provision for loan losses–net’. The premium received is recognised in the statement of income in ‘Net fees and commissions income’ on a straight line basis over the life of the guarantee.

Renegotiated loans

Where possible, the Bank seeks to restructure loans rather than to take possession of collateral. This may involve extending the payment arrangements and the agreement of the new loan conditions. Once the term have been renegotiated, the loan is no longer considered past due. Management continuously reviews renegotiated loans to ensure that all criteria are met and that future payments are likely to occur. The loans continue to be subject to an individual or collective impairment assessment, calculated using the loan’s original effective interest rate.

ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

31

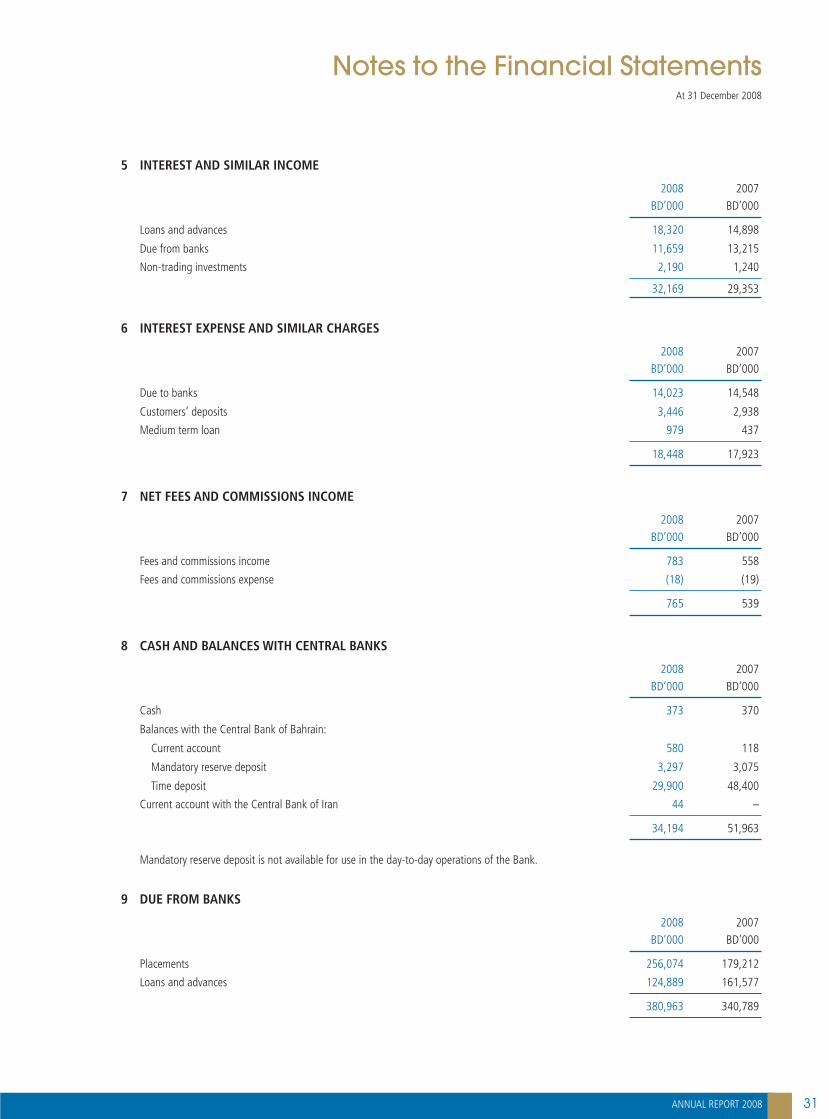

5 INTEREST AND SIMILAR INCOME

2008BD’000

2007BD’000

Loans and advances 18,320 14,898

Due from banks 11,659 13,215

Non-trading investments 2,190 1,240

32,169 29,353

6 INTEREST EXPENSE AND SIMILAR CHARGES

2008BD’000

2007BD’000

Due to banks 14,023 14,548

Customers’ deposits 3,446 2,938

Medium term loan 979 437

18,448 17,923

7 NET FEES AND COMMISSIONS INCOME

2008BD’000

2007BD’000

Fees and commissions income 783 558

Fees and commissions expense (18) (19)

765 539

8 CASH AND BALANCES WITH CENTRAL BANKS

2008BD’000

2007BD’000

Cash 373 370

Balances with the Central Bank of Bahrain:

Current account 580 118

Mandatory reserve deposit 3,297 3,075

Time deposit 29,900 48,400

Current account with the Central Bank of Iran 44 –

34,194 51,963

Mandatory reserve deposit is not available for use in the day-to-day operations of the Bank.

9 DUE FROM BANKS

2008BD’000

2007BD’000

Placements 256,074 179,212

Loans and advances 124,889 161,577

380,963 340,789

32 ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

10 LOANS AND ADVANCES TO CUSTOMERS

2008BD’000

2007BD’000

Retail 7,315 7,770

Corporate 109,990 78,955

117,305 86,725

Less: Provision for loan losses (2,657) (2,295)

Suspended interest (1,521) (1,103)

113,127 83,327

The movements in provision for credit losses were as follows:

2008 2007

RetailBD’000

CorporateBD’000

TotalBD’000

RetailBD’000

CorporateBD’000

TotalBD’000

At 1 January 484 1,811 2,295 492 846 1,338

Charge for the year 48 484 532 36 990 1,026

Recoveries (77) – (77) (25) (17) (42)

Net provision (29) 484 455 11 973 984

Amounts written off (93) – (93) (19) (8) (27)

At 31 December 362 2,295 2,657 484 1,811 2,295

Individual provision 362 1,028 1,390 484 967 1,451

Collective provision – 1,267 1,267 – 844 844

Total provision 362 2,295 2,657 484 1,811 2,295

Gross amount of loans, individually determined to be impaired, before deducting any individually assessed impairment allowance 3,058 3,102 6,160 1,363 3,250 4,613

The fair value of collateral that the Bank holds relating to loans individually determined to be impaired at 31 December 2008 amounts to BD 14.0 million (31 December 2007: BD 7.4 million). The collateral consists of cash, securities, properties and letters of guarantee from banks and corporates.

11 NON–TRADING INVESTMENTS

2008 2007

Available for sale

Held to maturity Total

Available for sale

Held to maturity Total

Unquoted BD’000 BD’000 BD’000 BD’000 BD’000 BD’000

Iranian Government bonds 6,358 2,411 8,769 – 10,163 10,163

Equity 10 – 10 10 – 10

6,368 2,411 8,779 10 10,163 10,173

The Iranian Government bonds are denominated in Iranian Rials. These are stated at cost as on maturity the bonds are redeemable at their face value.

ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

33

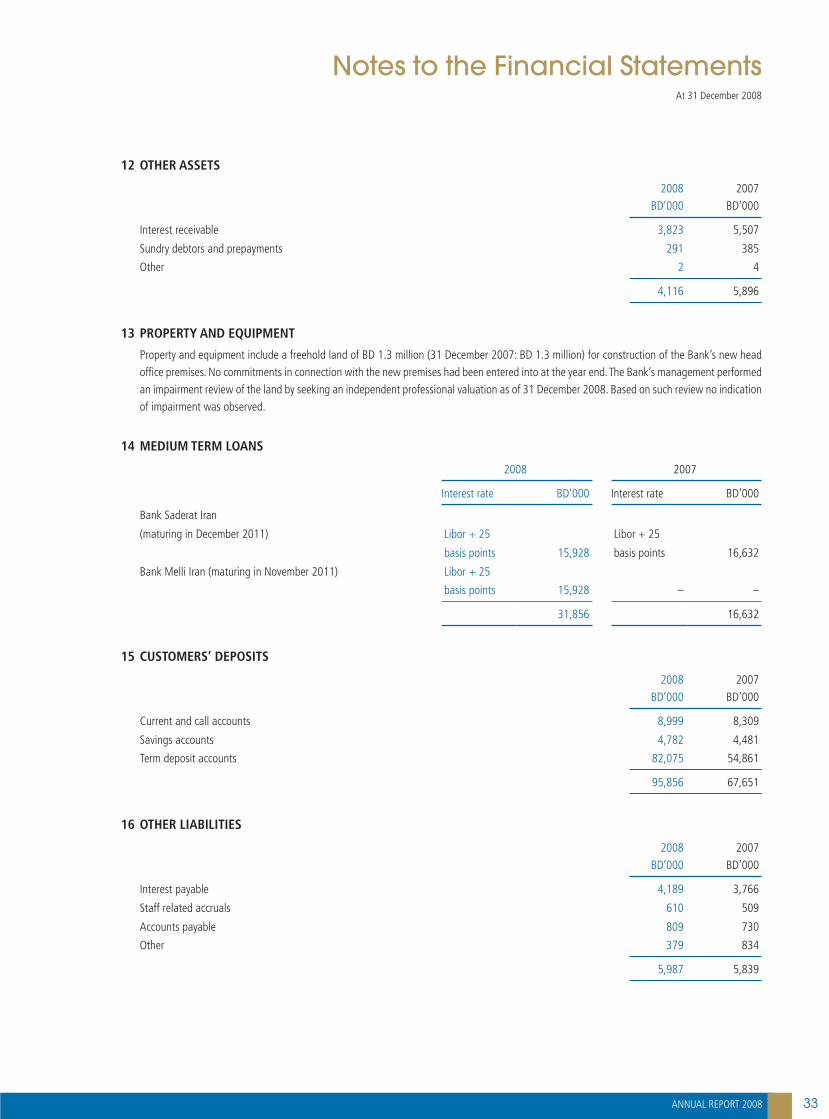

12 OTHER ASSETS

2008BD’000

2007BD’000

Interest receivable 3,823 5,507

Sundry debtors and prepayments 291 385

Other 2 4

4,116 5,896

13 PROPERTY AND EQUIPMENT

Property and equipment include a freehold land of BD 1.3 million (31 December 2007: BD 1.3 million) for construction of the Bank’s new head office premises. No commitments in connection with the new premises had been entered into at the year end. The Bank’s management performed an impairment review of the land by seeking an independent professional valuation as of 31 December 2008. Based on such review no indication of impairment was observed.

14 MEDIUM TERM LOANS

2008 2007

Interest rate BD’000 Interest rate BD’000

Bank Saderat Iran

(maturing in December 2011) Libor + 25 Libor + 25

basis points 15,928 basis points 16,632

Bank Melli Iran (maturing in November 2011) Libor + 25

basis points 15,928 – –

31,856 16,632

15 CUSTOMERS’ DEPOSITS

2008BD’000

2007BD’000

Current and call accounts 8,999 8,309

Savings accounts 4,782 4,481

Term deposit accounts 82,075 54,861

95,856 67,651

16 OTHER LIABILITIES

2008BD’000

2007BD’000

Interest payable 4,189 3,766

Staff related accruals 610 509

Accounts payable 809 730

Other 379 834

5,987 5,839

34 ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

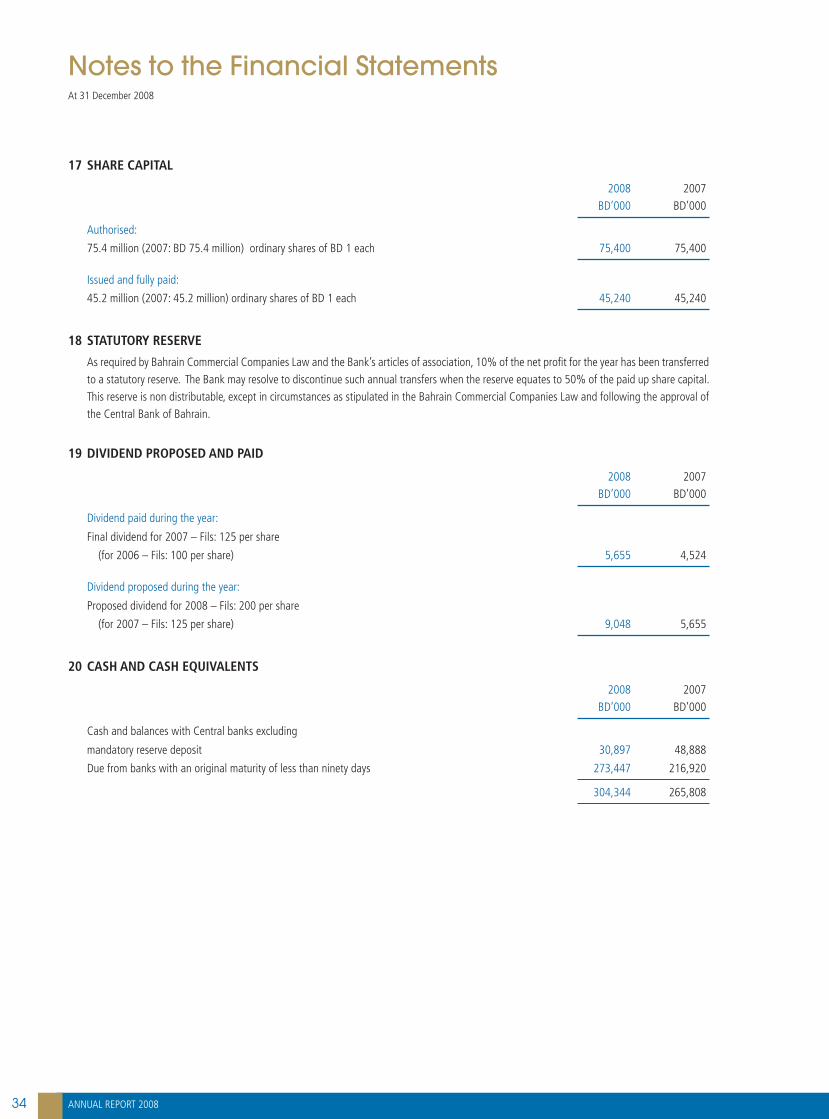

17 SHARE CAPITAL

2008BD’000

2007BD’000

Authorised:

75.4 million (2007: BD 75.4 million) ordinary shares of BD 1 each 75,400 75,400

Issued and fully paid:

45.2 million (2007: 45.2 million) ordinary shares of BD 1 each 45,240 45,240

18 STATUTORY RESERVE

As required by Bahrain Commercial Companies Law and the Bank’s articles of association, 10% of the net profit for the year has been transferred to a statutory reserve. The Bank may resolve to discontinue such annual transfers when the reserve equates to 50% of the paid up share capital. This reserve is non distributable, except in circumstances as stipulated in the Bahrain Commercial Companies Law and following the approval of the Central Bank of Bahrain.

19 DIVIDEND PROPOSED AND PAID

2008BD’000

2007BD’000

Dividend paid during the year:

Final dividend for 2007 – Fils: 125 per share

(for 2006 – Fils: 100 per share) 5,655 4,524

Dividend proposed during the year:

Proposed dividend for 2008 – Fils: 200 per share

(for 2007 – Fils: 125 per share) 9,048 5,655

20 CASH AND CASH EQUIVALENTS

2008BD’000

2007BD’000

Cash and balances with Central banks excluding

mandatory reserve deposit 30,897 48,888

Due from banks with an original maturity of less than ninety days 273,447 216,920

304,344 265,808

ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

35

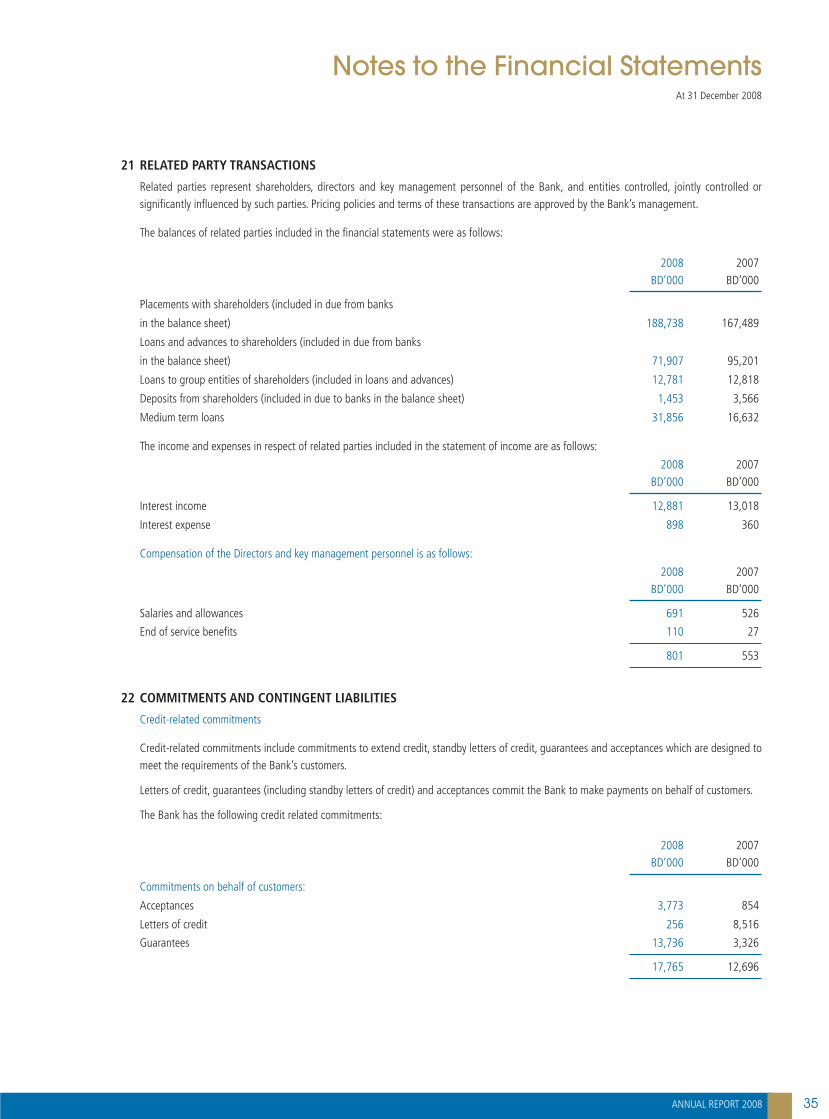

21 RELATED PARTY TRANSACTIONS

Related parties represent shareholders, directors and key management personnel of the Bank, and entities controlled, jointly controlled or significantly influenced by such parties. Pricing policies and terms of these transactions are approved by the Bank’s management.

The balances of related parties included in the financial statements were as follows:

2008BD’000

2007BD’000

Placements with shareholders (included in due from banks

in the balance sheet) 188,738 167,489

Loans and advances to shareholders (included in due from banks

in the balance sheet) 71,907 95,201

Loans to group entities of shareholders (included in loans and advances) 12,781 12,818

Deposits from shareholders (included in due to banks in the balance sheet) 1,453 3,566

Medium term loans 31,856 16,632

The income and expenses in respect of related parties included in the statement of income are as follows:

2008BD’000

2007BD’000

Interest income 12,881 13,018

Interest expense 898 360

Compensation of the Directors and key management personnel is as follows:

2008BD’000

2007BD’000

Salaries and allowances 691 526

End of service benefits 110 27

801 553

22 COMMITMENTS AND CONTINGENT LIABILITIES

Credit-related commitments

Credit-related commitments include commitments to extend credit, standby letters of credit, guarantees and acceptances which are designed to meet the requirements of the Bank’s customers.

Letters of credit, guarantees (including standby letters of credit) and acceptances commit the Bank to make payments on behalf of customers.

The Bank has the following credit related commitments:

2008BD’000

2007BD’000

Commitments on behalf of customers:

Acceptances 3,773 854

Letters of credit 256 8,516

Guarantees 13,736 3,326

17,765 12,696

36 ANNUAL REPORT 2008

Notes to the Financial StatementsAt 31 December 2008

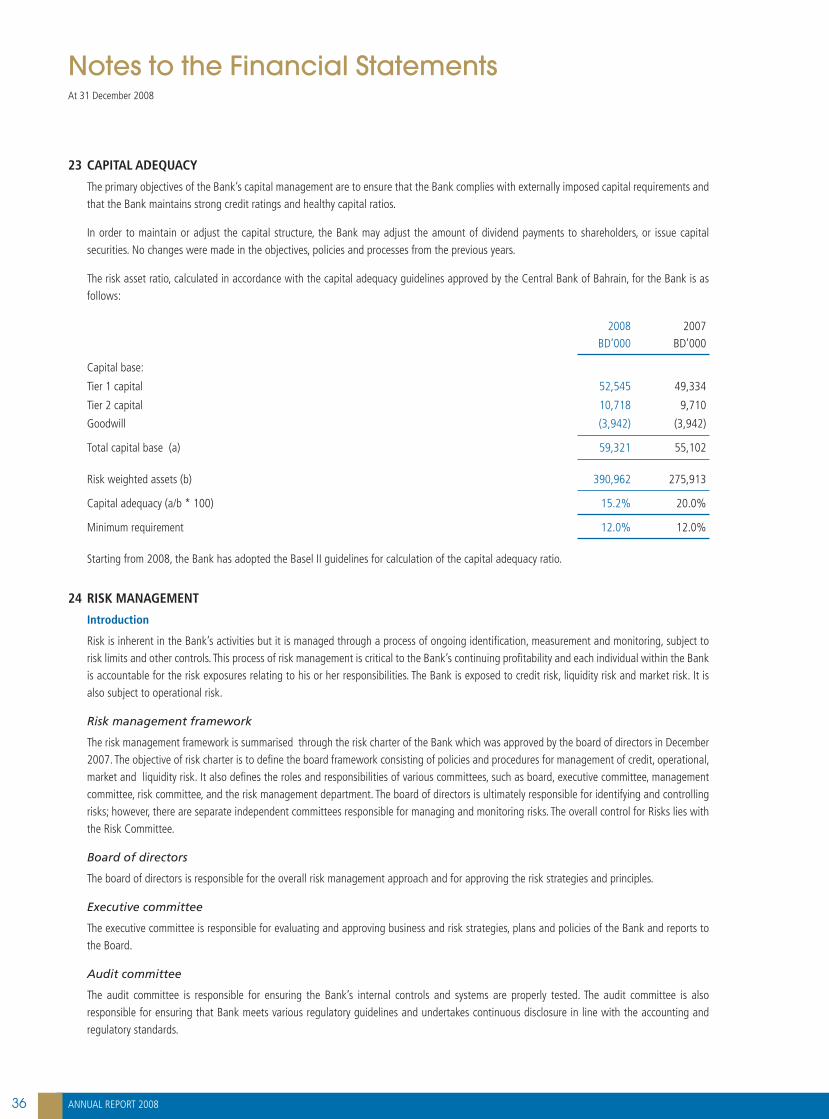

23 CAPITAL ADEQUACY

The primary objectives of the Bank’s capital management are to ensure that the Bank complies with externally imposed capital requirements and that the Bank maintains strong credit ratings and healthy capital ratios.

In order to maintain or adjust the capital structure, the Bank may adjust the amount of dividend payments to shareholders, or issue capital securities. No changes were made in the objectives, policies and processes from the previous years.

The risk asset ratio, calculated in accordance with the capital adequacy guidelines approved by the Central Bank of Bahrain, for the Bank is as follows:

2008BD’000

2007BD’000

Capital base:

Tier 1 capital 52,545 49,334

Tier 2 capital 10,718 9,710

Goodwill (3,942) (3,942)